Contents

| Investment Team and Strategy | AUM as of December 31, 2017 | Composite Inception Date | Value-Added Since Inception Date (1) as of December 31, 2017 | Fund Rating(2) as of December 31, 2017 | |

| (in millions) | |||||

| Growth Team | |||||

| Global Opportunities | 15,469 | February 1, 2007 | 579 | ««««« | |

| Global Discovery | 16 | September 1, 2017 | (178) | Not yet rated | |

| U.S. Mid-Cap Growth | 12,798 | April 1, 1997 | 453 | ««« | |

| U.S. Small-Cap Growth | 2,345 | April 1, 1995 | 99 | ««« | |

Global Equity Team(3) | |||||

| Global Equity | 1,439 | April 1, 2010 | 406 | ««« | |

| Non-U.S. Growth | 27,101 | January 1, 1996 | 542 | «« | |

| Non-U.S. Small-Cap Growth | 695 | January 1, 2002 | 302 | «« | |

| U.S. Value Team | |||||

| Value Equity | 2,269 | July 1, 2005 | (5) | ««« | |

| U.S. Mid-Cap Value | 6,496 | April 1, 1999 | 388 | ««« | |

| Global Value Team | |||||

| Global Value | 19,930 | July 1, 2007 | 482 | «««« | |

| Non-U.S. Value | 21,757 | July 1, 2002 | 628 | ««««« | |

| Emerging Markets Team | |||||

| Emerging Markets | 282 | July 1, 2006 | 54 | ««« | |

| Credit Team | |||||

| High Income | 2,517 | April 1, 2014 | 296 | ««««« | |

| Privately offered strategy | 37 | July 1, 2017 | Not disclosed | Not applicable | |

| Developing World Team | |||||

| Developing World | 2,253 | July 1, 2015 | 353 | Not yet rated | |

| Thematic Team | |||||

| Thematic | 32 | May 1, 2017 | 1,612 | Not yet rated | |

| Privately offered strategy | 58 | November 1, 2017 | Not disclosed | Not applicable | |

| Total AUM as of December 31, 2017 | 115,494 | ||||

(1) Value-added since inception date is the amount in basis points by which the average annual gross composite return of each of our strategies has outperformed or underperformed the broad-based market index most commonly used by our clients to compare the performance of the relevant strategy since its inception date. Value-added for periods less than one year are not annualized. The broad-based market indices used to compute the value added since inception date for each of our strategies are as follows: Non-U.S. Growth Strategy / Non-U.S. Value Strategy-MSCI EAFE Index; Global Equity Strategy / Global Opportunities Strategy / Global Value Strategy / Global Discovery Strategy-MSCI ACWI Index; Non-U.S. Small-Cap Growth Strategy-MSCI EAFE Small Cap Index; U.S. Mid-Cap Growth Strategy / U.S. Mid-Cap Value Strategy-Russell Midcap® Index; U.S. Small-Cap Growth Strategy-Russell 2000® Index; Value Equity Strategy-Russell 1000® Index; Developing World Strategy / Emerging Markets Strategy-MSCI Emerging Markets Index; High Income Strategy-ICE BofAML US High Yield Master II Total Return Index; Thematic Strategy-S&P® 500 Index. Unlike the ICE BofAML US High Yield Master II Total Return Index, the Artisan High Income strategy may hold loans and other security types. At times, this causes material differences in relative performance. | |||||

(2) The Overall Morningstar RatingTM for a fund is derived from a weighted average of the performance figures associated with its three-year, five-year, and ten-year (if applicable) Morningstar Ratings metrics. The ratings which form the basis for the information reflected in this report, and the fund categories in which they are rated, relating to each Fund’s Investor Share Class are: Artisan Emerging Markets Fund—Diversified Emerging Markets; Artisan Global Equity Fund—World Stock; Artisan Global Opportunities Fund—World Stock; Artisan Global Value Fund—World Stock; Artisan High Income Fund—High Yield Bond; Artisan International Fund—Foreign Large Blend; Artisan International Small Cap Fund—Foreign Small/Mid Growth; Artisan International Value Fund—Foreign Large Blend; Artisan Mid Cap Fund—Mid-Cap Growth; Artisan Mid Cap Value Fund—Mid-Cap Value; Artisan Small Cap Fund—Small Growth; Artisan Value Fund—Large Value. Morningstar ratings are initially given on a fund’s three year track record and change monthly. | |||||

(3) On January 20, 2017, we ceased managing assets in the Global Small-Cap Growth Strategy. | |||||

Growth Team

Our Growth team, which was formed in 1997 and is based in Milwaukee, Wisconsin, manages four investment strategies: Global Opportunities, Global Discovery, U.S. Mid-Cap Growth and U.S. Small-Cap Growth. James D. Hamel, Matthew H. Kamm, Craigh A. Cepukenas, and Jason L. White and Jay C. Warner are the portfolio co-managersmanagers of all four strategies. Mr. Hamel is the lead portfolio manager of the Global Opportunities strategy; Mr. White is the lead portfolio manager of the Global Discovery strategy; Mr. Kamm is the lead portfolio manager of the U.S. Mid-Cap Growth strategy; and Mr. Cepukenas is the lead portfolio manager of the U.S. Small-Cap Growth strategy. The U.S. Mid-Cap Growth and U.S. Small-Cap Growth strategies are currently closed to most new investors and client relationships. The Global Opportunities strategy is open across pooled vehicles, but closed to most new separate account clients.

| As of December 31, 2021 | |||||||||||||||||||||||||||||

| Investment Strategy (Composite Inception Date) | 1 Year | 3 Years | 5 Years | 10 Years | Inception | ||||||||||||||||||||||||

| Global Opportunities (February 1, 2007) | |||||||||||||||||||||||||||||

| Average Annual Gross Returns | 15.17 | % | 30.66 | % | 22.22 | % | 18.32 | % | 13.27 | % | |||||||||||||||||||

MSCI ACWI® Index | 18.54 | % | 20.36 | % | 14.39 | % | 11.84 | % | 7.02 | % | |||||||||||||||||||

| Global Discovery (September 1, 2017) | |||||||||||||||||||||||||||||

| Average Annual Gross Returns | 14.01 | % | 34.48 | % | — | % | — | % | 23.86 | % | |||||||||||||||||||

MSCI ACWI® Index | 18.54 | % | 20.36 | % | — | % | — | % | 13.06 | % | |||||||||||||||||||

| U.S. Mid-Cap Growth (April 1, 1997) | |||||||||||||||||||||||||||||

| Average Annual Gross Returns | 11.68 | % | 35.59 | % | 24.22 | % | 18.62 | % | 16.58 | % | |||||||||||||||||||

Russell Midcap® Index | 22.58 | % | 23.26 | % | 15.09 | % | 14.89 | % | 11.13 | % | |||||||||||||||||||

Russell Midcap® Growth Index | 12.73 | % | 27.43 | % | 19.82 | % | 16.61 | % | 10.72 | % | |||||||||||||||||||

| U.S. Small-Cap Growth (April 1, 1995) | |||||||||||||||||||||||||||||

| Average Annual Gross Returns | (7.77) | % | 28.69 | % | 23.16 | % | 18.21 | % | 12.18 | % | |||||||||||||||||||

Russell 2000® Index | 14.82 | % | 20.00 | % | 12.01 | % | 13.22 | % | 9.83 | % | |||||||||||||||||||

Russell 2000® Growth Index | 2.83 | % | 21.14 | % | 14.52 | % | 14.12 | % | 8.67 | % | |||||||||||||||||||

| As of December 31, 2017 | ||||||||||||||

| Investment Strategy (Inception Date) | 1 Year | 3 Years | 5 Years | 10 Years | Inception | |||||||||

| Global Opportunities (February 1, 2007) | ||||||||||||||

| Average Annual Gross Returns | 32.73 | % | 15.18 | % | 14.87 | % | 10.46 | % | 11.00 | % | ||||

MSCI ACWI® Index | 23.97 | % | 9.29 | % | 10.79 | % | 4.65 | % | 5.21 | % | ||||

| Global Discovery (September 1, 2017) | ||||||||||||||

| Average Annual Gross Returns | — | — | — | — | 5.99 | % | ||||||||

MSCI ACWI® Index | — | — | — | — | 7.77 | % | ||||||||

| U.S. Mid-Cap Growth (April 1, 1997) | ||||||||||||||

| Average Annual Gross Returns | 21.96 | % | 8.14 | % | 13.46 | % | 9.95 | % | 15.06 | % | ||||

Russell Midcap® Index | 18.52 | % | 9.57 | % | 14.95 | % | 9.10 | % | 10.54 | % | ||||

Russell® Midcap Growth Index | 25.27 | % | 10.29 | % | 15.30 | % | 9.09 | % | 9.28 | % | ||||

| U.S. Small-Cap Growth (April 1, 1995) | ||||||||||||||

| Average Annual Gross Returns | 28.38 | % | 11.71 | % | 15.15 | % | 10.30 | % | 10.56 | % | ||||

Russell 2000® Index | 14.65 | % | 9.95 | % | 14.11 | % | 8.70 | % | 9.56 | % | ||||

Russell 2000® Growth Index | 22.17 | % | 10.27 | % | 15.20 | % | 9.18 | % | 7.98 | % | ||||

Global Equity Team

Our Global Equity team was formed in 1996 and is primarily based in San Francisco and New York. The Global Equity team currently manages threefour investment strategies: Global Equity, Non-U.S. Growth, Non-U.S. Small-Mid Growth and Non-U.S. Small-Cap Growth. China Post-Venture.

Mark L. Yockey is the founder of our Global Equity team and has beenserves as portfolio manager of each of the team’s strategies since their inception.Global Equity and Non-U.S. Growth strategies. Charles-Henri Hamker and Andrew J. Euretig are also portfolio managers of the Global Equity strategy and associate portfolio managers of the Non-U.S. Growth strategy andstrategy. Rezo Kanovich serves as the sole portfolio co-managers (with Mr. Yockey)manager of the Global EquityNon-U.S. Small-Mid Growth strategy. Mr. Hamker alsoTiffany Hsiao serves as portfolio co-managermanager and Yuanyuan Ji serves as associate portfolio manager of the Non-U.S. Small-Cap Growth strategy with Mr. Yockey. The Non-U.S. Growth and Non-U.S. Small-Cap Growth strategiesChina Post-Venture strategy.

3

| As of December 31, 2021 | |||||||||||||||||||||||||||||

| Investment Strategy (Composite Inception Date) | 1 Year | 3 Years | 5 Years | 10 Years | Inception | ||||||||||||||||||||||||

| Global Equity (April 1, 2010) | |||||||||||||||||||||||||||||

| Average Annual Gross Returns | 6.56 | % | 22.55 | % | 19.20 | % | 15.89 | % | 14.07 | % | |||||||||||||||||||

MSCI ACWI® Index | 18.54 | % | 20.36 | % | 14.39 | % | 11.84 | % | 10.10 | % | |||||||||||||||||||

| Non-U.S. Growth (January 1, 1996) | |||||||||||||||||||||||||||||

| Average Annual Gross Returns | 10.07 | % | 16.03 | % | 13.31 | % | 10.37 | % | 10.29 | % | |||||||||||||||||||

MSCI EAFE® Index | 11.26 | % | 13.53 | % | 9.54 | % | 8.02 | % | 5.25 | % | |||||||||||||||||||

| Non-U.S. Small-Mid Growth (January 1, 2019) | |||||||||||||||||||||||||||||

| Average Annual Gross Returns | 5.17 | % | 25.33 | % | — | % | — | % | 25.33 | % | |||||||||||||||||||

| MSCI All Country World Index Ex USA Small Mid Cap (Net) | 10.16 | % | 14.71 | % | — | % | — | % | 14.71 | % | |||||||||||||||||||

China Post-Venture (April 1, 2021) 1 | |||||||||||||||||||||||||||||

| Average Annual Gross Returns | — | % | — | % | — | % | — | % | (9.06) | % | |||||||||||||||||||

| MSCI China SMID Cap Index | — | % | — | % | — | % | — | % | (14.45) | % | |||||||||||||||||||

1 Periods less than one year are currently closed to most new investors and client relationships. On January 20, 2017, the Global Equity team ceased managing assets in a fourth strategy, the Artisan Global Small-Cap Growth strategy.not annualized.

| As of December 31, 2017 | ||||||||||||||

| Investment Strategy (Inception Date) | 1 Year | 3 Years | 5 Years | 10 Years | Inception | |||||||||

| Global Equity (April 1, 2010) | ||||||||||||||

| Average Annual Gross Returns | 33.31 | % | 10.66 | % | 13.20 | % | — | 13.14 | % | |||||

MSCI ACWI® Index | 23.97 | % | 9.29 | % | 10.79 | % | — | 9.08 | % | |||||

| Non-U.S. Growth (January 1, 1996) | ||||||||||||||

| Average Annual Gross Returns | 32.55 | % | 5.48 | % | 8.57 | % | 3.87 | % | 10.54 | % | ||||

MSCI EAFE® Index | 25.03 | % | 7.79 | % | 7.89 | % | 1.94 | % | 5.12 | % | ||||

| Non-U.S. Small-Cap Growth (January 1, 2002) | ||||||||||||||

| Average Annual Gross Returns | 35.54 | % | 10.39 | % | 9.67 | % | 5.51 | % | 13.87 | % | ||||

MSCI EAFE® Small Cap Index | 33.01 | % | 14.19 | % | 12.85 | % | 5.77 | % | 10.86 | % | ||||

U.S. Value Team

Our U.S. Value team, which was formed in 1997 and is based in Atlanta and Chicago, manages two investment strategies: Value Equity and U.S. Mid-Cap Value. James C. Kieffer, Thomas A. Reynolds, and Daniel L. Kane, and Craig Inman are the portfolio co-managersmanagers for both strategies. George O. Sertl, Jr., previously a portfolio co-managerDuring the first quarter of 2022, the team’s two strategies, stepped down from portfolio management in October 2017 and provided notice of his intent to retire. On May 23, 2016, the U.S. Value team ceasedwill begin managing assets in a third strategy, the Value Income strategy. James C. Kieffer, who relinquished portfolio management responsibilities of the Value Equity and U.S. Mid-Cap Value strategies effective February 1, 2021, remains a managing director of Artisan U.S. Small-Cap Value strategy.

| As of December 31, 2021 | |||||||||||||||||||||||||||||

| Investment Strategy (Composite Inception Date) | 1 Year | 3 Years | 5 Years | 10 Years | Inception | ||||||||||||||||||||||||

| Value Equity (July 1, 2005) | |||||||||||||||||||||||||||||

| Average Annual Gross Returns | 24.43 | % | 21.90 | % | 12.83 | % | 12.88 | % | 9.67 | % | |||||||||||||||||||

Russell 1000® Index | 26.45 | % | 26.18 | % | 18.41 | % | 16.53 | % | 11.07 | % | |||||||||||||||||||

Russell 1000® Value Index | 25.16 | % | 17.62 | % | 11.16 | % | 12.96 | % | 8.43 | % | |||||||||||||||||||

| U.S. Mid-Cap Value (April 1, 1999) | |||||||||||||||||||||||||||||

| Average Annual Gross Returns | 27.76 | % | 19.43 | % | 11.12 | % | 11.78 | % | 12.98 | % | |||||||||||||||||||

Russell Midcap® Index | 22.58 | % | 23.26 | % | 15.09 | % | 14.89 | % | 10.43 | % | |||||||||||||||||||

Russell Midcap® Value Index | 28.34 | % | 19.60 | % | 11.21 | % | 13.43 | % | 10.28 | % | |||||||||||||||||||

4

| As of December 31, 2017 | ||||||||||||||

| Investment Strategy (Inception Date) | 1 Year | 3 Years | 5 Years | 10 Years | Inception | |||||||||

| Value Equity (July 1, 2005) | ||||||||||||||

| Average Annual Gross Returns | 16.99 | % | 11.78 | % | 13.41 | % | 8.44 | % | 9.00 | % | ||||

Russell 1000® Index | 21.69 | % | 11.22 | % | 15.70 | % | 8.59 | % | 9.05 | % | ||||

Russell® 1000 Value Index | 13.66 | % | 8.64 | % | 14.03 | % | 7.10 | % | 7.77 | % | ||||

| U.S. Mid-Cap Value (April 1, 1999) | ||||||||||||||

| Average Annual Gross Returns | 13.69 | % | 8.70 | % | 12.64 | % | 10.17 | % | 13.51 | % | ||||

Russell Midcap® Index | 18.52 | % | 9.57 | % | 14.95 | % | 9.10 | % | 9.63 | % | ||||

Russell® Midcap Value Index | 13.34 | % | 8.99 | % | 14.67 | % | 9.09 | % | 10.20 | % | ||||

Our GlobalInternational Value team, was formed in 2002 andled by N. David Samra, is based in San Francisco and Chicago. The team manages two investment strategies: GlobalInternational Value and Non-U.S.International Small Cap Value. N. David Samra and Daniel J. O’Keefe are the portfolio co-managers of both strategies. Mr. Samra is theserves as lead portfolio manager of the Non-U.S.International Value strategy and managing director of the International Small Cap Value strategy. Ian P. McGonigle and Joseph Vari serve as co-portfolio managers of the International Value strategy. Beini Zhou and Anand Vasagiri serve as co-portfolio managers of the International Small Cap Value strategy.

| As of December 31, 2021 | |||||||||||||||||||||||||||||

| Investment Strategy (Composite Inception Date) | 1 Year | 3 Years | 5 Years | 10 Years | Inception | ||||||||||||||||||||||||

| International Value (July 1, 2002) | |||||||||||||||||||||||||||||

| Average Annual Gross Returns | 18.10 | % | 17.64 | % | 11.73 | % | 11.79 | % | 12.10 | % | |||||||||||||||||||

MSCI EAFE® Index | 11.26 | % | 13.53 | % | 9.54 | % | 8.02 | % | 6.59 | % | |||||||||||||||||||

| International Small Cap Value (October 1, 2020) | |||||||||||||||||||||||||||||

| Average Annual Gross Returns | 20.65 | % | — | % | — | % | — | % | 40.85 | % | |||||||||||||||||||

| MSCI All Country World Index Ex USA Small Cap (Net) | 12.93 | % | — | % | — | % | — | % | 31.41 | % | |||||||||||||||||||

Global Value Team

Our Global Value team, led by Daniel J. O’Keefe, is primarily based in Chicago. Mr. O’Keefe is theserves as lead portfolio manager and Michael J. McKinnon serves as portfolio manager of the team’s Global Value strategy. The Non-U.S. Value strategy is closed to most new investors and client relationships. The Global Value strategy is open to new relationships through pooled investment vehicles, but generally closed to most new separate account relationships.Select Equity strategies.

| As of December 31, 2021 | |||||||||||||||||||||||||||||

| Investment Strategy (Composite Inception Date) | 1 Year | 3 Years | 5 Years | 10 Years | Inception | ||||||||||||||||||||||||

| Global Value (July 1, 2007) | |||||||||||||||||||||||||||||

| Average Annual Gross Returns | 16.94 | % | 16.46 | % | 11.40 | % | 12.37 | % | 9.17 | % | |||||||||||||||||||

MSCI ACWI® Index | 18.54 | % | 20.36 | % | 14.39 | % | 11.84 | % | 6.60 | % | |||||||||||||||||||

| Select Equity (March 1, 2020) | |||||||||||||||||||||||||||||

| Average Annual Gross Returns | 16.87 | % | — | % | — | % | — | % | 21.61 | % | |||||||||||||||||||

| S&P 500 Index | 28.71 | % | — | % | — | % | — | % | 31.80 | % | |||||||||||||||||||

| As of December 31, 2017 | ||||||||||||||

| Investment Strategy (Inception Date) | 1 Year | 3 Years | 5 Years | 10 Years | Inception | |||||||||

| Global Value (July 1, 2007) | ||||||||||||||

| Average Annual Gross Returns | 23.47 | % | 10.49 | % | 13.88 | % | 10.45 | % | 9.40 | % | ||||

MSCI ACWI® Index | 23.97 | % | 9.29 | % | 10.79 | % | 4.65 | % | 4.58 | % | ||||

| Non-U.S. Value (July 1, 2002) | ||||||||||||||

| Average Annual Gross Returns | 25.34 | % | 9.84 | % | 12.14 | % | 9.04 | % | 13.03 | % | ||||

MSCI EAFE® Index | 25.03 | % | 7.79 | % | 7.89 | % | 1.94 | % | 6.74 | % | ||||

Sustainable Emerging Markets Team

Our Sustainable Emerging Markets team, which was formed in 2006 and is based in New York, manages a single investment strategy. Maria Negrete-Gruson is the portfolio manager for the Sustainable Emerging Markets strategy.

| As of December 31, 2021 | |||||||||||||||||||||||||||||

| Investment Strategy (Composite Inception Date) | 1 Year | 3 Years | 5 Years | 10 Years | Inception | ||||||||||||||||||||||||

| Sustainable Emerging Markets (July 1, 2006) | |||||||||||||||||||||||||||||

| Average Annual Gross Returns | (0.27) | % | 14.40 | % | 12.64 | % | 7.72 | % | 6.78 | % | |||||||||||||||||||

| MSCI Emerging Markets Index | (2.54) | % | 10.93 | % | 9.87 | % | 5.48 | % | 5.72 | % | |||||||||||||||||||

5

Table of company-specific and macroeconomic risks into its valuation analysis to develop a risk adjusted target price. The risk-rating assessment includes a review of country-appropriate macroeconomic risk factors to which a company is exposed. Finally, the team believes that investment opportunities develop when businesses with sustainable earnings are undervalued relative to peers and historical industry, country and regional valuations. The team values a business and develops a price target for a company based on its assessment of the business’s sustainable earnings and risk analysis.

| As of December 31, 2017 | ||||||||||||||

| Investment Strategy (Inception Date) | 1 Year | 3 Years | 5 Years | 10 Years | Inception | |||||||||

| Emerging Markets (July 1, 2006) | ||||||||||||||

| Average Annual Gross Returns | 41.19 | % | 13.72 | % | 6.83 | % | 2.28 | % | 6.89 | % | ||||

MSCI Emerging Markets IndexSM | 37.28 | % | 9.09 | % | 4.35 | % | 1.68 | % | 6.35 | % | ||||

Credit Team

Our Credit team, which was formed in 2014 and is currently based in Mission Woods, Kansas,Denver, manages twothree investment strategies: High Income, Credit Opportunities and a privately offered credit long-short strategy.Floating Rate. Bryan L. Krug is theserves as portfolio manager for both strategies. The following description applies toof the High Income strategy. Information for the privately offered strategy has been intentionally omitted.

| As of December 31, 2021 | |||||||||||||||||||||||||||||

| Investment Strategy (Composite Inception Date) | 1 Year | 3 Years | 5 Years | 10 Years | Inception | ||||||||||||||||||||||||

| High Income (April 1, 2014) | |||||||||||||||||||||||||||||

| Average Annual Gross Returns | 7.16 | % | 11.03 | % | 8.35 | % | — | % | 7.93 | % | |||||||||||||||||||

| ICE BofA U.S. High Yield Master II Total Return Index | 5.36 | % | 8.56 | % | 6.09 | % | — | % | 5.36 | % | |||||||||||||||||||

| Credit Opportunities (July 1, 2017) | |||||||||||||||||||||||||||||

| Average Annual Gross Returns | 18.44 | % | 18.84 | % | — | % | — | % | 14.44 | % | |||||||||||||||||||

| ICE BofA U.S. High Yield Master II Total Return Index | 0.17 | % | 1.28 | % | — | % | — | % | 1.45 | % | |||||||||||||||||||

Floating Rate (January 1, 2022) 1 | |||||||||||||||||||||||||||||

| Average Annual Gross Returns | — | % | — | % | — | % | — | % | — | % | |||||||||||||||||||

| Credit Suisse Leveraged Loan Total Return Index | — | % | — | % | — | % | — | % | — | % | |||||||||||||||||||

1 The Floating Rate strategy composite performance began on January 1, 2022. As a result, there is not a performance track record as of industry participants, and the decision-making history of the issuer’s management. The team believes that analyzing the history and trend of free cash flow generation is critical to understanding an issuer’s financial health. The team also considers an issuer’s capital structure, refinancing options, financial covenants, amortization schedules and overall financial transparency. The team seeks to manage the risk of loss on an investment with what it believes to be conservative financial projections that account for industry position, competitive dynamics and positioning within the capital structure. To determine the value of an investment opportunity the team uses multiple metrics. The team looks for credit improvement potential, relative value within an issuer’s capital structure, catalysts for business improvement and potential value stemming from market or industry dislocations.December 31, 2021.

| As of December 31, 2017 | ||||||||||||

| Investment Strategy (Inception Date) | 1 Year | 3 Years | 5 Years | 10 Years | Inception | |||||||

| High Income (April 1, 2014) | ||||||||||||

| Average Annual Gross Returns | 9.90 | % | 9.07 | % | — | — | 7.90 | % | ||||

| ICE BofA Merrill Lynch U.S. High Yield Master II Total Return Index (Net) | 7.48 | % | 6.38 | % | — | — | 4.94 | % | ||||

Developing World Team

Our Developing World team, which was formed in 2015 and is based in San Francisco, manages a singleone investment strategy. Lewis S. Kaufman is the portfolio manager for the Developing World strategy.

| As of December 31, 2021 | |||||||||||||||||||||||||||||

| Investment Strategy (Composite Inception Date) | 1 Year | 3 Years | 5 Years | 10 Years | Inception | ||||||||||||||||||||||||

| Developing World (July 1, 2015) | |||||||||||||||||||||||||||||

| Average Annual Gross Returns | (8.71) | % | 33.88 | % | 22.94 | % | — | % | 17.16 | % | |||||||||||||||||||

| MSCI Emerging Markets Index | (2.54) | % | 10.93 | % | 9.87 | % | — | % | 6.11 | % | |||||||||||||||||||

| As of December 31, 2017 | |||||||||||

| Investment Strategy (Inception Date) | 1 Year | 3 Years | 5 Years | 10 Years | Inception | ||||||

| Developing World (July 1, 2015) | |||||||||||

| Average Annual Gross Returns | 36.87 | % | — | — | — | 13.24 | % | ||||

| MSCI Emerging Markets Index | 37.28 | % | — | — | — | 9.71 | % | ||||

| As of December 31, 2021 | |||||||||||||||||||||||||||||

| Investment Strategy (Composite Inception Date) | 1 Year | 3 Years | 5 Years | 10 Years | Inception | ||||||||||||||||||||||||

| Antero Peak (May 1, 2017) | |||||||||||||||||||||||||||||

| Average Annual Gross Returns | 25.17 | % | 29.95 | % | — | % | — | % | 28.08 | % | |||||||||||||||||||

| S&P 500 Index | 28.71 | % | 26.04 | % | — | % | — | % | 18.12 | % | |||||||||||||||||||

| Antero Peak Hedge (November 1, 2017) | |||||||||||||||||||||||||||||

| Average Annual Gross Returns | 19.56 | % | 21.97 | % | — | % | — | % | 20.18 | % | |||||||||||||||||||

| S&P 500 Index | 28.71 | % | 26.04 | % | — | % | — | % | 18.04 | % | |||||||||||||||||||

Emerging Markets Debt Team

The following description appliesEmerging Markets Debt team was formed in 2021 and is based in Boston. We are working with the team to develop active, differentiated strategies with broad exposure to the Thematic strategy. Information foremerging markets debt asset class and expect the privately offered strategy has been intentionally omitted.team’s first strategies will launch during the first half of 2022.

6

Table of a top-down thematic framework and bottom-up analysis will position a portfolio to deliver attractive risk-adjusted returns over the long term.

Contents

Distribution, Investment Products and Client Relationships

The goal of our marketing, distribution and client service efforts is to establishgrow and maintain a client base that is diversified by investment strategy, investment vehicle (for example, across mutual funds and separate accounts),client type, distribution channel (for example, institutional, intermediary and retail) and geographic region. We focus our distribution and marketing efforts on sophisticated investors and asset allocators, including institutions and on intermediaries that operate with institutional-like, centralized decision-making processes and longer-term investment horizons. We have designed our distribution strategies and structured our distribution teams to use knowledgeable, seasoned marketing and client service professionals in a way intended to limit the time our investment professionals are required to spend inon marketing and client service activities. We believe that minimizing other demands allows our portfolio managers and other investment professionals to focus their energies and attention on the investment decision-making process, which we believe enhances the opportunity to achieve superior investment returns. Our distribution efforts are centrally managed by our Head of Global Distribution, who oversees and coordinates the efforts of our marketing and client service professionals.

Institutional Channel

Our institutional distribution channel includes institutional clients, such as U.S.-registered mutual funds, non-U.S. funds and collective investment trusts we sub-advise; state and local governments; employee benefit plans including Taft-Hartley plans; foundations; and endowments. Our institutional distribution channel also includes assets under management sourced from defined contribution/401(k)contribution plans. We offer our investment products to institutional clients directly and by marketing our services to the investment consultants and advisors that advise them. As of December 31, 2017,2021, approximately 45%36% of our assets under management were attributed to clients represented by investment consultants.

As of December 31, 2017, 66%2021, 64% of our assets under management were sourced through our institutional channel.

Intermediary Channel

We maintain relationships with a number of major brokerage firms and larger private banks and trust companies at which the process for identifying which funds to offer has been centralized to a relatively limited number of key decision-makers that exhibit institutionalinstitutional-like decision-making behavior. We also maintain relationships with a number of financial advisory firms and broker-dealer advisors that offer our investment products to their clients. These advisors range from relatively small firms to large organizations.

As of December 31, 2017,2021, approximately 30%32% of our assets under management were sourced through our intermediary channel.

Retail Channel

We primarily access retail investors indirectly through mutual fund supermarkets through which investors have the ability to purchase and redeem fund shares. InvestorsU.S. investors can also invest directly in the series of Artisan Funds. Our subsidiary, Artisan Partners Distributors LLC, a registered broker-dealer, distributes shares of Artisan Funds. Publicity and ratings and rankings from Morningstar, Lipper and others are important inessential to building the Artisan Partners brand, which is important infor attracting retail investors. As a result, we publicize the ratings and rankings received by the series of Artisan Funds and work to ensure that potential retail investors have appropriate information to evaluate a potential investment in Artisan Funds. We do not generally use direct marketing campaigns as we believe that their cost outweighs their potential benefits.

As of December 31, 2017,2021, approximately 4% of our assets under management were sourced from investors we categorize as retail investors.

Access Through a Range of Investment Vehicles

Our clients access our investment strategies through a range of investment vehicles, including separate accounts and mutual funds.pooled vehicles. As of December 31, 2017, approximately 50% of our assets under management were in separate accounts, and2021, Artisan Funds and Artisan Global Funds accounted for approximately 50%48% of our total assets under management.management, and approximately 52% of our assets under management were managed in separate accounts and other pooled vehicles.

Separate Accounts and Other

We manage traditional separate account assetsaccounts within most of our investment strategies. As of December 31, 2017,2021, we managed 215235 traditional separate accounts spanning 141138 client relationships and our largest separate account relationship represented approximately 9%8% of our assets under management. OurThese separate account clients include both institutional and intermediary channel relationships.relationships, such as pension and profit sharing plans, corporations, trusts, endowments, foundations, charitable organizations, high net worth individuals, governmental entities, insurance companies, commingled investment vehicles, investment advisers and other financial institutions, trustees of collective investment trusts and investment companies and similar pooled investment vehicles. We generally require a minimum relationship of $20 million to $100 million, depending on the strategy, to manage a separate account. We also offer access to a number of our strategies through Artisan-branded collective investment trusts and through funds (both public and private) that we sub-advise. The fees we charge ouron separate accounts vary by client, investment strategy and the size of the account. Fees are accrued monthly, but generally are paid quarterly in arrears.

7

A number of our investment strategies are accessible to certain types of employee benefit plans through Artisan-branded collective investment trusts, or CITs. We act as investment adviser to the CITs and earn a management fee for providing this service. As of December 31, 2021, Artisan-branded collective investment trusts represented approximately 5% of our own privatelyassets under management.

Certain of our investment strategies are primarily offered funds. through Artisan-sponsored unregistered pooled investment vehicles, referred to as Artisan Private Funds. For serving as investment adviser to Artisan Private Funds, we earn a management fee and, for certain funds, are entitled to receive either an allocation of profits or a performance-based fee. As of December 31, 2021, Artisan Private Funds comprised approximately 1% of our assets under management.

In our reporting materials, unless otherwise stated, our separate account“separate accounts and other” AUM includes assets we manage in traditional separate accounts, Artisan-branded collective investment trusts and Artisan Private Funds, as well as assets under advisement related to clients for whom we manage in Artisan-branded collectiveprovide investment trusts, in funds (both public and private) that we sub-advise, and in our own privately offered funds.models but do not have discretionary investment authority.

Artisan Funds and Artisan Global Funds

U.S. investors that do not meet our minimum account size for a separate account, or who otherwise prefer to invest through a mutual fund, can invest in our strategies through Artisan Funds. We serve as the investment adviser to each series of Artisan Funds, SEC-registered mutual funds that offer no-load, no 12b-1 share classes designed to meet the needs of a range of investors. Each series of Artisan Funds corresponds to an investment strategy we offer to clients. In contrast to some mutual funds, investors in Artisan Funds pay no 12b-1 fees, which are fees charged to investors in addition to management fees to pay for marketing, advertising and distribution services associated with the mutual funds. Rebates and expenses for marketing, advertising and distribution services related to Artisan Funds, including distribution payments to broker-dealers and other intermediaries with respect to the Investor and Advisor Shares, are paid out of the investment management fees we earn. The Institutional Shares do not include any payments to intermediaries. We earn investment management fees, which are based on the average daily net assets of each Artisan Fund and are paid monthly, for serving as investment adviser to these funds. As of December 31, 2021, Artisan Funds represented approximately 45% of our assets under management.

We also serve as investment manager of Artisan Global Funds, a family of Ireland-based UCITS funds. Artisan Global Funds which began operations in 2011, provides non-U.S. investors with access to a number of our investment strategies. Expenses for marketing, advertising and distribution services related to Artisan Global Funds, including payments to broker-dealers and other intermediaries, are paid out of thestrategies in a pooled vehicle structure. We earn investment management fees, we earn, which are based on the average daily net assets of each sub-fund and are generally paid monthly.monthly, for serving as investment adviser to these funds. As of December 31, 2021, Artisan Global Funds represented approximately 3% of our assets under management.

Regulatory Environment and Compliance

Our business is subject to extensive regulation in the United States at the federal level and, to a lesser extent, the state level, as well as by self-regulatory organizations and regulators located outside the United States. Under these laws and regulations, agencies that regulate investment advisers, investment funds and other related entities have broad administrative powers, including the power to limit, restrict or prohibit an investment adviserthe regulated entity from carrying on itsconducting business in the event that it fails to comply with such laws and regulations. PossibleBreaches of these laws and regulations could also result in regulatory enforcement, civil liability, criminal liability and/or the imposition of other sanctions, that may be imposed includeincluding monetary damages, fines, censures, the suspension of individual employees, limitations on engaging in certain lines of business for specified periods of time, and the revocation of investment adviser and other registrations, censures and fines. Aregistrations. In addition, a regulatory proceeding, regardless of whether it results in a sanction, can require substantial expenditures and can have an adverse effect on our reputation or business.

U.S. Regulation

As a publicly traded company, we are subject to U.S. federal securities laws, state securities and corporate laws, and the rules and regulations of U.S. regulatory and self-regulatory organizations. In particular, we are subject to the Securities Act of 1933, the Securities Exchange Act of 1934, the Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010 (“Dodd-Frank”), the Sarbanes-Oxley Act of 2002 and, because we are listed on the New York Stock Exchange, the NYSE listed company rules.

Artisan Partners Limited Partnership and Artisan Partners UK LLP are registered with the SEC as investment advisers under the Investment Advisers Act of 1940, or Advisers Act, and Artisan Funds and several of the investment companies we sub-advise are registered under the Investment Company Act of 1940, or 1940 Act. The Advisers Act and the 1940 Act, together with other applicable securities laws and the SEC’s regulations and interpretations thereunder, impose substantive and material restrictions and requirements on the operations of investment advisers and mutual funds. The Securities Act and the Exchange Act, along with the regulations and interpretations thereunder, impose additional restrictions and requirements on mutual funds. The SEC is authorized to institute proceedings and impose sanctions for violations, of those Acts, ranging from fines and censures to, in the case of investment advisers, the termination of an adviser’s registration.

8

Table of investment opportunities among clients; use of soft dollars; execution of transactions; and recommendations to clients. We manage accounts for our clients on a discretionary basis, with authority to buy and sell securities for each portfolio, select broker-dealers to execute trades and negotiate brokerage commission rates. In connection with certain of these transactions, we receive soft dollar credits from broker-dealers that have the effect of reducing certain of our expenses.Contents

Artisan Partners Distributors LLC, our SEC-registered limited purpose broker-dealer subsidiary, is subject to the Securities Exchange Act of 1934, the SEC’s rules promulgated thereunder and the rules and regulations of the Financial Industry Regulatory Authority, which generally relate to sales practices, registration of personnel, compliance and supervision, and compensation and disclosure. FINRA has the authority to conduct periodic examinations of member broker-dealers, and may initiate administrative proceedings. Artisan Partners Distributors LLC is also subject to the SEC’s Uniform Net Capital Rule and the National Securities Clearing Corporation’s excess net capital requirement, which require that at least a minimum part of a registered broker-dealer’s assets be kept in relatively liquid form.

Artisan Partners Limited Partnership is a fiduciary under ERISAthe Employee Retirement Income Security Act of 1974, as amended, with respect to assets that we manage for benefit plan clients subject to ERISA. ERISA regulations promulgated thereunder and applicable provisions of the Internal Revenue Code impose certainimposes duties on persons who are ERISA fiduciaries, under ERISA, prohibitand prohibits certain transactions involvingbetween related parties to a retirement plan. The U.S. Department of Labor administers ERISA and regulates plan clientsfiduciaries, including investment advisers who service retirement plan clients.

Artisan Partners Limited Partnership is registered with the Commodity Futures Trading Commission (CFTC) as a commodity pool operator, and provide monetary penalties for violationsexpects to become a member of the National Futures Association (NFA), with respect to its management of the Artisan Emerging Markets Debt Opportunities Fund and Artisan Global Unconstrained Fund, each of which we expect to launch in the first half of 2022. The CFTC and NFA each administer a comparable regulatory system covering futures, swaps and other derivative instruments. As the commodity pool operator of these prohibitions.Funds, Artisan Partners expects to claim relief under the Commodity Exchange Act from certain reporting and recordkeeping requirements.

The legislative and regulatory environment in the U.S. is subject to continual change. Political and electoral changes and developments have in the past introduced, and may in the future introduce, additional uncertainty. New legal or regulatory requirements often add further complexity to our business and operations, and addressing such new requirements may require substantial expenditures of time and capital. Certain regulatory reforms in the U.S. that have, or may in the future, impact our business include the following items:

•The SEC has recently proposed and/or adopted several new rules impacting registered investment advisers (e.g. private fund advisor rules, cybersecurity risk management rules, beneficial ownership rules, T+1 settlement cycle, amendments to Form PF and amended advertising rule) and registered investment companies (e.g. new or amended rules on mutual fund use of derivatives, liquidity risk management, reporting modernization, valuation). In addition, the SEC’s current regulatory agenda indicates that the SEC will be proposing a number of rules impacting public companies (e.g. new disclosure requirements on topics such as climate change, human capital management, cybersecurity risk governance, and pay versus performance). These rules impact us and the mutual funds we manage to varying degrees.

•In recent years there has been an increased focus on the protection of customer privacy and data, and the need to secure sensitive information. We are subject to the California Consumer Privacy Act, which took effect in January 2020, and provides for enhanced consumer protections for California residents. Since then, several additional states have proposed and/or adopted data privacy laws with which we may be required to comply.

Non-U.S. Regulation

In addition to the extensive regulation we are subject to in the United States, onea number of our subsidiaries and certain of our non-U.S. operations are subject to regulation in non-U.S. jurisdictions. Some laws in non-U.S. jurisdictions are also extra-territorial and may apply to our business.

Artisan Partners UK LLP is authorized and regulated by the U.K. Financial Conduct Authority, which is responsible for the conduct of business and supervision of financial firms in the United Kingdom. The FCA imposes a comprehensive system of regulation that is primarily principles-based (compared to the primarily rules-based U.S. regulatory system).

Artisan Partners Europe is authorized and regulated by the Central Bank of Ireland, imposes requirements on UCITS fundswhich regulates our Irish business activities. Artisan Partners Europe has a branch office in Sweden, which is also regulated by the Central Bank of Ireland and is further subject to the regulation by it, including of the Swedish financial supervisory authority.

Artisan Global Funds, as doa family of Ireland-domiciled UCITS funds, are regulated by the regulators in certain other markets in which sharesCentral Bank of Ireland. Artisan Global Funds are offeredregistered for sale in many countries around the world, both in the EU and with which we are required to comply. Webeyond, and thus are also subject to regulation internationallythe laws of, and supervision by, the governmental authorities of those countries.

Artisan Partners Hong Kong Limited, our Hong Kong subsidiary, is licensed and regulated by the Hong Kong Securities and Futures Commission (the “SFC”). Artisan Partners Hong Kong Limited and its employees conducting regulated activities under the Securities and Futures Ordinance are subject to the rules, codes and guidelines issued by the SFC from time to time.

Artisan Partners Australia Pty Ltd has historically operated in Australia on the basis of a “sufficient equivalence relief” exemption from local licensing with the Australian Securities and Investments Commission, where we operate pursuantCommission. This relief is expiring for foreign financial service providers like us and, as a result, Artisan Partners Australia Pty Ltd or one of its affiliates may need to ordersapply for and obtain a securities license or a new exemption by April 1, 2023.

9

Certain Artisan Private Funds are regulated as mutual funds under the Mutual Funds Law (as amended) of the Cayman Islands, and by various Canadian regulatory authorities in the Canadian provinces where we operate pursuantCayman Islands Monetary Authority has supervisory and enforcement powers to exemptions from registration. ensure the funds’ compliance with the Mutual Funds Law.

Our business is also subject to the rules and regulations of the countries in which we marketconduct distribution or investment management activities. We have relationships with clients located outside of the United States, which relationships may be subject to laws and regulations of the jurisdictions in which the client is domiciled. In addition, 45% of our fundsassets under management were invested in securities denominated in currencies other than the U.S. dollar as of December 31, 2021. Our investments in these non-U.S. securities may subject us to certain laws and regulations of the jurisdictions in which the issuer resides or servicesis traded. We may also be subject to U.S. laws and conductregulations with respect to our distribution or investment management activities in non-U.S. markets, including the countriesin jurisdictions that may be considered higher risk.

Further expansion of our business into new international jurisdictions and regulatory reforms in jurisdictions in which we currently operate or invest, further complicate our compliance efforts. Addressing these legal and regulatory matters may require substantial time and expense. Certain non-U.S. regulatory reforms or guidance regarding such regulations that have, or may in the future, impact our business include the following items:

•In October 2020, the Central Bank of Ireland issued further guidance regarding the fund company management effectiveness framework (“CP86”). As a result of the guidance, fund management companies, including Artisan Global Funds, were required to assess their operational resources and governance arrangements and increase their level of resources to meet the new minimum requirements. During 2021, Artisan Global Funds retained a third-party management company to meet the requirements of CP86 in Ireland.

•The EU’s Markets in Financial Instruments Directive II regulates the use of soft dollars to pay for research and other soft dollar services. MiFID II’s soft dollar rules do not directly apply to our business because we currently conduct our investment strategies make investments. management activities in the United States. However, in response to MiFID II and the industry-wide changes prompted by it, we have experienced requests from clients to bear research expenses that are currently paid for using soft dollars. In response to such requests or as a result of changes in our operations, we may eventually bear a significant portion or all of the costs of research that are currently paid for using soft dollars, which would increase our operating expenses materially.

We may become subject to additional regulatory demands in the future to the extent we expand our business in existing and new jurisdictions. See “Risk Factors—Risks Related to our Industry—We are subject to extensive, regulation”complex and sometimes overlapping rules, regulations and legal interpretations.” and “Risk Factors—Risks Related to our Industry—The regulatory environment in which we operate is subject to continual change, and regulatory developments designed to increase oversight may adversely affect our business.”

Competition

The investment management industry is highly competitive. In order to be successful and grow our business, we must be able to compete effectively for assets under management. Historically, we have competedWe compete to attract assets to our managementclients and investors principally on the basis of:

•the performance of our investment strategies;strategies

•the continuity of our investment professionals;and distribution professionals

•the quality of the service we provide to our clients;clients

•the range of investment strategies and vehicles we offer

•our brand recognition and reputation within the institutional investing community.community

•the fees we charge for the investment management services we provide

Human Capital Resources

As of December 31, 2017,2021, we employed approximately 400 full-time and part-time employees. None498 associates. Approximately 30% of our employeesassociates work within our investment teams, 17% within our distribution teams and 53% within our business management and operations teams. Approximately 94% of our associates operate from our U.S. offices and 6% operate from our offices outside of the U.S. As of December 31, 2021, 40% of our U.S. associates were female and 20% of our U.S. associates self-identified as ethnically diverse.

10

We commit significant energy to the recruitment of our associates as they are critical to ensuring the long-term success of our firm. We strive to recruit and hire outstanding associates who thrive in broad roles and want the freedom to grow their talents and careers. We are also committed to seeking professionals from different backgrounds, experiences and locations to foster creative thinking and differentiated perspectives that remain a pillar of the firm’s culture. We have built relationships with a variety of recruitment partners and community organizations to broaden our candidate pools and increase our access to diverse talent.

We actively support associate development, both formally and informally, and encourage advancement from within the firm. Our tuition reimbursement program is subjectavailable to collective bargaining agreements.associates who are pursuing applicable undergraduate and graduate degrees or certifications or licenses relevant to the business. Our diversity and inclusion committee champions our diversity and inclusion initiatives by bringing together a group of individuals with broad representation across the firm, as well as diverse social, regional and cultural identities. We consideralso actively support a number of associate-led groups including the Pride Alliance, Multicultural Exchange, diffAbilities and the Women’s Networking Initiative. These groups create supportive and collaborative networks, encourage engagement and a sense of belonging, and enhance professional and personal growth. Our support of these and other associate-led programs are part of our relationshipongoing commitment to providing an environment that allows our talented associates to thrive.

We believe in order to attract and retain talent, it is critical that we continue to foster an engaging environment and provide attractive compensation and benefits programs. We regularly review compensation paid to associates to ensure it is competitive and fair for the role, experience, location and individual contribution. We provide equity or equity-linked incentives to all of our associates in order to align their economic interests with those of our employeesclients and stockholders. We encourage our associates to be goodsave for retirement. In the U.S., we match 100% of associate 401(k) contributions dollar for dollar (fully vested), up to the IRS limit. We also maintain competitive retirement programs or benefits for all non-U.S. associates. In addition, we offer a comprehensive benefits program that is available to all associates regardless of title, role, or responsibility.

Sustainability

Artisan Partners' purpose is to generate and have not experienced interruptionscompound wealth over the long-term for our clients. The wealth we generate improves retirement outcomes, pays for education, funds charitable purposes and in general improves people's lives. We are proud of operations dueour track record for the people we serve and are dedicated to labor disagreements.continuing to improve it.

To achieve our purpose, we must continue to thoughtfully grow our business over the long term while preserving a consistent environment in which our talented investment professionals and associates can thrive. Maintaining our talent-driven business model and investment-focused culture is critical to providing a stable environment for our associates, generating sustainable, long-term investment outcomes for clients, and creating long-term successful financial outcomes for shareholders.

To us, sustainability means the following:

•Long-term relationships with the right clients, on the right terms and with the right time horizons. We foster client relationships by prioritizing investment returns. Prioritizing clients’ investment returns may, at times, require us to limit client cash flows and overall assets managed in a strategy—a practice we refer to as capacity management.

•A deliberate process to bring on new investment talent, launch new strategies and build sustainable franchises. We are patient in developing our talent, teams and strategies. We are comfortable with evolving—and sometimes even disrupting—our firm to increase the probability of long-term successful investment outcomes through market cycles.

•Compelling work in a tailored environment, with long-term opportunities for associates across our firm. Our culture promotes associates’ success—ideally over their entire careers—with economic alignment in the form of variable compensation and long-duration incentive awards.

•Growing our business value while maintaining financial discipline and continuing to generate and distribute significant cash to our shareholders. By taking care of our people and fulfilling our fiduciary duty to our clients we create a waterfall effect that generates sustainable financial outcomes for our shareholders over the long term.

Our Structure and Reorganization

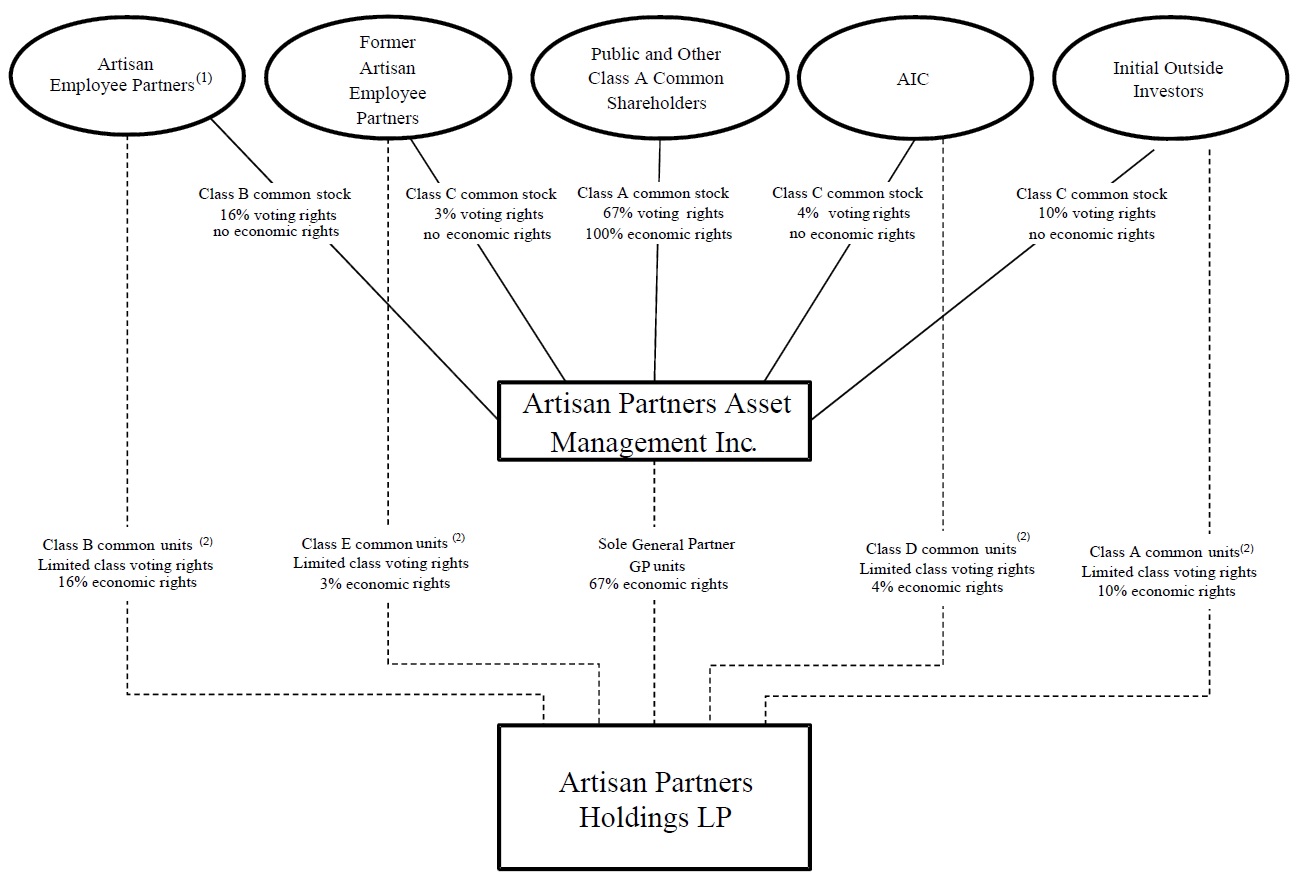

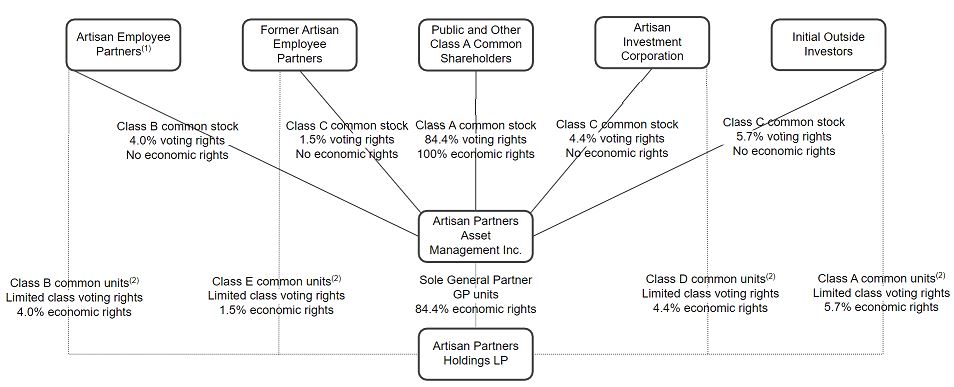

Holding Company Structure

We are a holding company and our assets principally consist of our ownership of partnership units of Artisan Partners Holdings, deferred tax assets and cash. As the sole general partner of Artisan Partners Holdings, we operate and control all of its business and affairs, subject to certain voting rights of its limited partners. We conduct all of our business activities through operating subsidiaries of Artisan Partners Holdings. Net profits and net losses are allocated based on the ownership of partnership units of Artisan Partners Holdings. As of December 31, 2017,2021, we owned approximately 67%84% of Artisan Partners Holdings, and the other 33%16% was owned by the limited partners of Artisan Partners Holdings.

11

IPO Reorganization

In March 2013, we completed our IPO. In connection with the IPO, we and Artisan Partners Holdings completed a series of reorganization transactions, which we refer to as the IPO Reorganization, in order to reorganize our capital structures in preparation for the IPO. The IPO Reorganization was designed to create a capital structure that preserves our ability to conduct our business through Artisan Partners Holdings, while permitting us to raise additional capital and provide access to liquidity through a public company. Multiple classes of securities at the public company level were necessary to achieve those objectives and maintain a corporate governance structure consistent with that of Artisan Partners Holdings prior to the IPO Reorganization. The IPO Reorganization included, among other changes, the following:

•Our appointment as the sole general partner of Artisan Partners Holdings.

•The modification of our capital structure into three classes of common stock and a series of convertible preferred stock. We issued shares of our Class B common stock and Class C common stock and convertible preferred stock to pre-IPO partners of Artisan Partners Holdings. Each share of Class B common stock corresponds to a Class B common unit of Artisan Partners Holdings. Each share of Class C common stock corresponds to either a Class A, Class D or Class E common unit of Artisan Partners Holdings. Subject to certain restrictions, each common unit of Artisan Partners Holdings (together with the corresponding share of Class B or Class C common stock) is exchangeable for a share of our Class A common stock.

•A corporation (“H&F Corp”) merged with and into Artisan Partners Asset Management, which we refer to in this document as the H&F Corp Merger. As consideration forIn connection with the merger, the shareholder of H&F Corp received shares of our convertible preferred stock contingent value rights, or CVRs, issued by Artisan Partners Asset Management and the right to receive an amount of cash. In November 2013, the CVRs issued by Artisan Partners Asset Management were terminated with no amounts paid or payable thereunder.certain other considerations. In June 2014, the shareholder of H&F Corp converted all of its then-remaining shares of convertible preferred stock into shares of Class A common stock and sold those shares. We no longer have any outstanding shares of convertible preferred stock, and Artisan Partners Holdings no longer has any outstanding preferred units.

•The voting and certain other rights of each class of limited partnership units of Artisan Partners Holdings were modified. In addition, Artisan Partners Holdings separately issued CVRs to the holders of the preferred units. In November 2013, the CVRs issued by Artisan Partners Holdings were terminated with no amounts paid or payable thereunder.

•We entered into two tax receivable agreements (“TRAs”), one with a private equity fund (the “Pre-H&F Corp Merger Shareholder”) and the other with each limited partner of Artisan Partners Holdings. Pursuant to the first TRA, APAM will paypays to the assignees of the Pre-H&F Corp Merger Shareholder a portion of certain tax benefits APAM realizes as a result of the H&F Corp Merger. Pursuant to the second TRA, APAM will paypays to current or former limited partners of Artisan Partners Holdings (or their assignees) a portion of certain tax benefits APAM realizes as a result of the purchase or exchange of their limited partnership units of Artisan Partners Holdings.

The diagram below depicts our organizational structure as of February 9, 2018:December 31, 2021:

| (1) | Our employees to whom we have granted equity have entered into a stockholders agreement with respect to all shares of our common stock they have acquired from us and any shares they may acquire from us in the future, pursuant to which they granted an irrevocable voting proxy to a stockholders committee currently consisting of Eric R. Colson | ||||

| (2) | Each class of common units generally entitles its holders to the same economic and voting rights in Artisan Partners Holdings as each other class of common units, except that the Class E common units have no voting rights except as required by law. | ||||

12

Available Information

Our principal executive offices are located at 875 E. Wisconsin Avenue, Suite 800, Milwaukee, Wisconsin 53202. Our telephone number at this address is (414) 390-6100 and our website address is www.artisanpartners.com. We make available free of charge through our website all of the materials we file with or furnish withto the SEC as soon as reasonably practicable after we electronically file such material with, or furnish such materials withit to, the SEC. Information contained on our website is not part of, nor is it incorporated by reference into, this Form 10-K. The company was incorporated in Wisconsin on March 21, 2011 and converted to a Delaware corporation on October 29, 2012.

13

Table of the materials we file with the SEC at the SEC’s Public Reference Room at 100 F Street, NE, Washington, DC 20549. Information on the operation of the Public Reference Room may be obtained by calling the SEC at 1-800-SEC-0330. The SEC also maintains an Internet site that contains reports, proxies and information statements, and other information regarding issuers that file electronically with the SEC at www.sec.gov.Contents

Item 1A. Risk Factors

Risks Related to our Business

The loss of key investment professionals or senior members of our seniordistribution and management teamteams could have a material adverse effect on our business. In addition, a substantial portion of our total assets under management is in six of our strategies, several of which are closed to most new investors and client relationships.

The loss of any of these key professionals could limit our ability to successfully execute our business strategy and may prevent us from sustaining the historically strong investment performance we have achieved or adversely affect our ability to retain existing and attract new client assets and related revenues.

Any of our investment or managementkey professionals may resign at any time, join our competitors or form a competing company. Although many of our portfolio managers and each of our named executive officers are subject to post-employment non-compete obligations, these non-competition provisions may not be enforceable or may not be enforceable to their full extent. In addition, we may agree to waive non-competition provisions or other restrictive covenants applicable to former investment or managementkey professionals in light of the circumstances surrounding their relationship with us. We do not carry “key man” insurance that would provide us with proceeds in the event of the death or disability of any of the key members of our investment or management teams.

Changes to our management structure, corporate culture and corporate governance arrangements could also negatively impact our ability to retain key personnel.

Attracting, developing and retaining talented investment professionals is an essential component of our business strategy. To do so, it is critical that we continue to foster an environment and provide compensation that is attractive for our existing investment professionals and for prospective investment professionals. If we are unsuccessful in maintaining such an environment (for instance, because of changes in management structure, corporate culture, corporate governance arrangements, or applicable laws and regulations) or compensation levels or structures for any reason, our existing investment professionals may leave our firm or fail to produce their best work on a consistent, long-term basis and/or we may be unsuccessful in attracting talented new investment professionals, any of which could negatively impact the performance of our investment strategies, our financial results and our ability to grow.

Over our firm’s history we have sought to successfully design and implement compensation structures that align our investment professionals’ economic interests with those of our clients, investors partners, and shareholders.stockholders. We believe our historical structures have been important to our long-term growth and that objective, predictable, and transparent structures work best to incentivize investment professionals to perform over the long-term.

With respect to cash compensation,asset-based revenues, we use a single revenue share arrangement across all of our investment teams. Under the revenue share, each team shares a bonus pool consisting of 25% of the asset-based revenues earned by the strategies managed by the respective team. The revenue share directly links the majority of the investment teams’ cash compensation to long-term growth in revenues, which, over the long-term, we believe is primarily linked to investment performance. The asset-based revenue share is objective, predictable, transparent, and the same for all teams.

In addition, each team is generally entitled to a share of performance-based revenues earned by the strategies managed by the team. In the future, we expect that performance fees will represent a higher proportion of our total revenues, as some of our new products will use performance fees, while only a few of our separate accounts use performance fees today. We expect to design and implement new or modified compensation arrangements with respect to performance fee revenues. We do not expect that these new or modified compensation arrangements will have a significant impact on any of our existing arrangements, including the revenue share described above. However, the design and implementation of these new arrangements could cause instability within our existing investment teams and/or impact our ability to attract and retain new investment talent. These arrangements could also negatively impact the amount of profits that we recognize with respect to performance fee revenues, as compared to the asset-based revenues we earn today.

Over our firm’s history we have used a variety of equity incentives to align the long-term interests of our investment professionals and other senior personnel with the interests of our clients, investors, partners and shareholders. Untilstockholders. Prior to our IPO in 2013, firm equity awards were in the formconsisted of partnership profits interests, which entitled recipients to a percentage of future profits and future appreciation in the value of the firm.interests. Award recipients had the right to cash out their profits interests only after the end of their careers, and 50% of the awards were subject to forfeiture if the recipient left Artisan without proper notice or was terminated. Prior to the IPO Reorganization, the profits interests were converted into partnership units and, as part of the IPO Reorganization, the 50% forfeiture feature was eliminated and employee-partners were given the right to liquidate a portion of their partnership units during each year that they remained employed withby Artisan. At the time of

Since our IPO, the partnership units held by employee-partners represented 53% of the ownership interests inequity we’ve awarded to our firm. At the time of this report, the partnership units held by employee-partners represented approximately 16% of the ownership interests in our firm.

14

In 2014,2021 we made our first award of franchise capital awards to investment professionals. We designed franchise capital awards as we continuedan added feature to evolve our equity incentives, we introduced Career Shares, whichlong-term incentive award program to enhance the alignment between our investment professionals and clients, and to provide investment professionals with greater control over their long-term economic outcome. Franchise capital awards are restricted stockcash awards that in general, remainare subject to the same long-term vesting and forfeiture untilprovisions as the recipient’s qualifying retirement from Artisan. In general, since 2014, excluding sign-onrestricted share-based awards described above. Prior to vesting, though, the franchise capital awards will generally be invested in one or walk away awards, approximately 50%more of the awards we have made to our senior employees have been Career Shares, and the other 50% Standard Restricted Shares. Unlike our pre-IPO profits interests, the APAM restricted stock awards are “full value” awards (as opposed to “option-style” awards) and the Standard Restricted Shares provide recipients with liquidity prior to the end of their careers. The percentage ownership in our firm representedinvestment strategies managed by the newly granted restricted stock each year is less than the percentage ownership represented by the partnership units that employee-partners may exchange and sell each year. Therefore, the amount of our firm owned by employees, including our portfolio managers, is expected to continue to decline.award recipient’s investment team.

As we have since our founding, we continue to assess the effectiveness of our compensation arrangements and equity structures in aligning the long-term interests of our investment professionals with those of our clients, investors partners, and shareholdersstockholders and whether different, types of, or modified, awards or structures would enhance incentives for long-term growth and succession planning. The design and implementation of new or modified compensation arrangements and equity structures is complicated. We will only pursue changes that we believe will improve the alignment between our most important investment talent and our clients, investors, partners, and shareholders.

The performance of our investment strategies is critical in retaining existing client assets as well asand in attracting new client assets. If our investment strategies perform poorly for any reason, our earnings could decline because:

Our investment strategies can perform poorly for a number of reasons, including general market conditions; investor sentiment about market and economic conditions; investment styles and philosophies; investment decisions; the performance of the companies in which our investment strategies invest and the currencies in which those investmentinvestments are made; the liquidity of securities or instruments in which our investment strategies invest; and our inability to identify sufficient appropriate investment opportunities for existing and new client assets on a timely basis. In addition, while we seek to deliver long-term value to our clients, volatility may lead to under-performanceunder performance in the near term, which could adversely affect our results of operations.

In contrast, when our strategies experience strong results relative to the market, clients’ allocations to our strategies typically increase relative to their other investments and we sometimes experience withdrawals as our clients rebalance their investments to fit their asset allocation preferences despite our strong results.

While clients do not have legal recourse against us solely on the basis of poor investment results, if our investment strategies perform poorly, we are more likely to become subject to litigation brought by dissatisfied clients. In addition, to the extent clients are successful in claiming that their losses resulted from fraud, negligence, willful misconduct, breach of contract or other similar misconduct, these clients may have remedies against us, the mutual funds and other funds we advise and/or our investment professionals under various U.S. and non-U.S. laws.

Difficult market conditions can adversely affect our business in many ways, including by reducing the value of our assets under management and causing clients to withdraw funds, each of which could materially reduce our revenues and adversely affectimpact our financial condition.

Difficult market conditions may cause investors in the mutual funds we advise to redeem their investments in those funds which they can do at any time and without prior notice. Our separate accounts clients may also reduce the aggregate amount of assets under management with us with minimal or no notice for any reason, including due to declining financial market conditions. In addition, the prices of the securities held in the portfolios we manage may decline for any number of reasons beyond our control, including, among others, a declining market, general economic downturn, political uncertainty, natural disasters, acts of terrorism, or other unpredictable events such as a global pandemic.

In connection with the severe market dislocations of 2008 and 2009, for example, the value of our assets under management declined substantially due primarily to the sizable decline in stock prices worldwide. In the period from June 30, 2008 through March 31, 2009, our assets under management decreased by approximately 43%, primarily as a result of general market conditions. More recently, during the first quarter of 2020, AUM levels fell from $125.4 billion on February 19, 2020 to $95.2 billion on March 31, 2020, as a result of sharp global equity market declines related to the COVID-19 pandemic.

The fees we earn under our investment management agreements are typically based on the market value of our assets under management, and to a much lesser extent based directly on investment performance. Investors in the mutual funds we advise can redeem their investments in those funds at any time without prior notice and our clients may reduce the aggregate amount of assets under management with us with minimal or no notice for any reason, including financialIf difficult market conditions, and the absolute or relative investment performance we achieve for our clients. In addition, the prices of the securities held in the portfolios we manage may decline duehowever caused, lead to any number of factors beyond our control, including, among others, a declining market, general economic downturn, political uncertainty or acts of terrorism. In connection with the severe market dislocations of 2008 and 2009, for example, the value of our assets under management declined substantially due primarily to the sizeable decline in stock prices worldwide. In the period from June 30, 2008 through March 31, 2009, our assets under management decreased by approximately 43%, primarily as a result of general market conditions.

15

Table of December 31, 2007 to $115.5 billion as of December 31, 2017. The absolute measure of our assets under management represents a significant rate of growth that has been and may continue to be difficult to sustain. For instance, between June 30, 2014, and December 31, 2016, our assets under management declined from $112.0 billion to $96.8 billion. The continued long-term growth of our business will depend on, among other things, retaining key investment professionals, attracting and recruiting new investment professionals, maintaining existing investment strategies and selectively developing new, value-added investment strategies. Our business growth will also depend on our success in achieving superior investment performance from our investment strategies, as well as our ability to maintain and extend our distribution capabilities, to deal with changing market conditions, to maintain adequate financial and business controls and to comply with new legal and regulatory requirements arising in response to both the increased sophistication of the investment management industry and the significant market and economic events of the last decade. We may not be able to manage our growing business effectively or be able to sustain the level of long-term growth we have achieved historically.Contents

Our efforts to establish and develop new teams and strategies may face challenges or ultimately be unsuccessful, which would likely negativelycould impact our results of operations, and could negatively impact our reputation and culture.

We seek to addrecruit new investment teams that invest in a way that is consistent with our philosophy of offeringmanage high value-added investment strategies and would allow us to grow strategically. We also look to offerdevelop new, differentiated strategies managed by our existing teams. We expect the costs associated with establishing a new team and/or strategy to initially to exceed the revenues generated, which will likely negatively impact our results of operations. New strategies, whether managed by a new team or by an existing team may invest in instruments (such as certain types of derivatives)make investments or present operational, (including legal, and regulatory)regulatory, or distribution-related issues and risks with which we have little or no experience.not yet encountered. Our lack of experience could strain our resources and increase the likelihood of an error or failure. The establishment of new teams and/or strategies (in particular, alternative investment teams or strategies) may also cause us to depart from our traditional compensation and economic model, which could reduce our profitability and harm our firm’s culture.

We generally support the development of new strategies by making one or more seed investments using capital that would otherwise be available for our general corporate purposes. Making such seed investments exposes us to capital losses.

Failure to properly address conflicts of interest could harm our reputation or cause clients to withdraw funds, each of which could adversely affect our business and results of operations.

The SEC and other regulators have increased their scrutiny ofcontinued to focus on potential conflicts of interest and weour fiduciary duties as an adviser. We have implemented procedures and controls that we believe are reasonably designed to address these issues. However, appropriately dealing with conflicts of interest is complex and if we fail, or appear to fail, to deal appropriately with conflicts of interest, we could face reputational damage, litigation or regulatory proceedings or penalties, any of which may adversely affect our results of operations.

revenue and impact our financial condition.

Several of our investment strategies invest principally in the securities of non-U.S. companies, which involve foreign currency exchange, tax, political, social and economic uncertainties and risks.

As of December 31, 2017,2021, approximately 54%51% of our assets under management were invested in strategies that primarily invest in securities of non-U.S. companies. In addition, someSome of our other strategies also invest on a more limited basis in securities of non-U.S. companies. Approximately 47%45% of our assets under management were invested in securities denominated in currencies other than the U.S. dollar. Fluctuations in foreign currency exchange rates could negatively affect the returns of our clients who are invested in these strategies. In addition, an increase in the value of the U.S. dollar relative to non-U.S. currencies is likely to result in a decrease in the U.S. dollar value of our assets under management, which, in turn, would likely result in lower revenue and profits. See “Qualitative and Quantitative Disclosures Regarding Market Risk-Exchange Rate Risk” in Item 7A of this report for more information about exchange rate risk.

Investments in non-U.S. issuers may also be affected by tax positions taken in countries or regions in which we are invested as well as political, social and economic uncertainty. Declining tax revenues may cause governments to assert their ability to tax the local gains and/or income of foreign investors, (including our clients), which could adversely affect clients’ interests in investing outside their home markets. Many financial markets are not as developed, or as efficient, as the U.S. financial markets and, as a result, those markets may have limited liquidity and higher price volatility, and may lack established regulations.