TABLE OF CONTENTS | |||

Page | |||

1 | |||

3 | |||

3 | |||

28 | |||

76 | |||

76 | |||

78 | |||

78 | |||

78 | |||

79 | |||

79 | |||

79 | |||

80 | |||

88 | |||

89 | |||

110 | |||

110 | |||

110 | |||

111 | |||

112 | |||

112 | |||

112 | |||

113 | |||

113 | |||

113 | |||

114 | |||

114 | |||

116 | |||

SPECIAL NOTE REGARDING FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K and the information incorporated by reference in this Annual Report contain(this "Annual Report"), contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, or Securities Act, and Section 21E of the Securities Exchange Act of 1934, or Exchange Act,as amended, (the "Exchange Act"), that involve substantial risks and uncertainties. AllThe forward-looking statements are contained principally in Part I, Item 1. “Business,” Part I, Item 1A. “Risk Factors,” and Part II, Item 7. “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” but are also contained elsewhere in this Annual Report. In some cases, you can identify forward-looking statements by the words “may,” “might,” “will,” “could,” “would,” “should,” “expect,” “intend,” “plan,” “objective,” “anticipate,” “believe,” “estimate,” “predict,” “project,” “potential,” “continue” and “ongoing,” or the negative of these terms, or other thancomparable terminology intended to identify statements relatedabout the future. These statements involve known and unknown risks, uncertainties and other factors that may cause our actual results, performance or achievements to present facts, current conditionsbe materially different from the information expressed or historical facts,implied by these forward-looking statements. Although we believe that we have a reasonable basis for each forward-looking statement contained in this Annual Report, we caution you that these statements are based on Form 10-K, including but not limiteda combination of facts and factors currently known by us and our expectations of the future, about which we cannot be certain. Forward-looking statements include statements about:

1

You should refer to Item 1A. “Risk Factors” in this Annual Report for a discussion of important risks and uncertaintiesfactors that couldmay cause our actual results to differ materially from the results discussed in thethose expressed or implied by our forward-looking statements. Factors that could cause actual results to differ materially from those in the forward-looking statements, include, but are not limited to, the possibility that we may not succeed in developing EggPC cell derived eggs that can be fertilized; the risks implicit in the development process of preparing bovine and human EggPC derived eggs for fertilization; regulatory risks associated with obtaining authorization to fertilize human EggPCSM cells for research; the possibility that international in vitro fertilization (“IVF”) clinics that we work with may determine not to provide or continue providing the OvaPrime or AUGMENT treatments, or to delay providing such treatments, or to limit the population of patients receiving the treatments based on clinical efficacy, safety or commercial, logistic, economic, available data, regulatory or other reasons; challenges associated with enrolling and completing clinical trials, and the possibility that the results may not be favorable; the science underlying our treatments (including OvaPrime treatment, OvaTure treatment and AUGMENT treatment), which is unproven; scientific and regulatory challenges associated with characterizing and fertilizing an EggPC cell-derived egg; our ability to obtain regulatory approval or licenses where necessary for our treatments; risks associated with reliance on third parties, in particular our partner IVF clinics and the contract research organizations and academic partners that we plan to work with in our OvaTure development efforts; our ability to develop our treatments on the timelines we expect, if at all; our ability to commercialize our treatments on the timelines we expect, if at all, as well as other risks described under "Risk Factors" and elsewhere in this Annual Report on Form 10-K and other filings with the Securities and Exchange Commission, or SEC. As a result of these and other factors, we may not actually achievecannot assure you that the plans, intentions or expectations disclosedforward-looking statements in this Annual Report will prove to be accurate. Furthermore, if our forward-looking statements andprove to be inaccurate, the inaccuracy may be material. In light of the significant uncertainties in these forward-looking statements, you should not place undue reliance onregard these statements as a representation or warranty by us or any other person that we will achieve our forward-looking statements. Ourobjectives and plans in any specified time frame, or at all. The forward-looking statements do not reflectin this Annual Report represent our views as of the potential impactdate of any future acquisitions, mergers, dispositions, joint ventures or investmentsthis Annual Report. We anticipate that subsequent events and developments may cause our views to change. However, while we may make. We do not assume anyelect to update these forward-looking statements at some point in the future, we undertake no obligation to publicly update any forward-looking statements, whether as a result of new information, future events or otherwise, except as required by law. You should, therefore, not rely on these forward-looking statements as representing our views as of any date subsequent to the date of this Annual Report.

As used herein, the words “Tempest,” “we,” “us,” “our,” and "company" refer to Tempest Therapeutics, Inc. and its direct and indirect subsidiaries, as applicable.

2

PART I

ITEM 1. BUSINESS

Overview

We are a clinical-stage biotechnology company moving into late-stage development with a diverse portfolio of novel targeted and immune-mediated product candidates with the potential to be first-in-class treatments for a wide range of cancers. The company’s programs range from early research to the lead program, TPST-1120, that is poised to begin a pivotal study in first-line liver cancer. Our philosophy is to build a company based upon not only good ideas and creative science, but also upon the efficient translation of those ideas into therapies that will improve patients’ lives. Each of our programs are designed to provide different and independent approaches to fighting cancer, providing a portfolio of truly diversified assets.

Our two clinical-stage therapeutic product candidates are TPST-1120 and TPST-1495, which we believe are the first clinical-stage molecules designed to inhibit their respective targets.

TPST-1120 is a company focused onselective antagonist of peroxisome proliferator-activated receptor alpha (“PPARα”). On October 11, 2023, we announced new and updated positive results from the discoveryplanned data analysis of the ongoing global randomized Phase 1b/2 trial of TPST-1120 combined with the standard-of-care first-line regimen of atezolizumab and development of new treatment options for women and families strugglingbevacizumab in patients with infertility. OvaScience is leveraging the breakthrough discovery of egg precursor,advanced or EggPC

In addition to the overall data, the new biomarker subpopulation findings are poor, however,consistent with the mechanism of action of TPST-1120: patients with b-catenin activating mutations (21% in this study or n=7) showed a confirmed ORR of 43% and a disease control rate (“DCR”) of 100% in the TPST-1120 arm; and distinct from the control arm, the TPST-1120 arm was consistently active across PD-L1 negative tumors with a confirmed ORR of 27% in the TPST-1120 arm, compared to a reduced ORR of 7% for the control arm.

These randomized data build upon clinical data from Phase 1 trials that were reported at a podium presentation at the American Society of Clinical Oncology (“ASCO”) annual meeting in June 2022. RECIST responses were also observed in this study at the two highest TPST-1120 doses, administered in combination with nivolumab, for an average live birth rate per cycleORR of 28 percentthose cohorts of 30% (3 of 10 patients), including in patients who previously progressed on anti-PD-1 (-L1) therapy. We believe the next step in TPST-1120 development is a pivotal Phase 3 trial in first-line HCC and are planning to meet with the FDA in 2024 in order to advance that goal. In addition, given the totality of the data, we are considering pursuing development of TPST-1120 for use in kidney cancer (“RCC”) and potentially other indications.

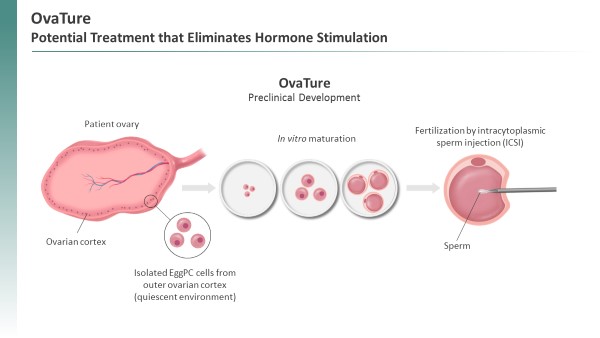

Our second clinical program, TPST-1495, a dual antagonist of the EP2 and EP4 receptors of prostaglandin E2, is in an ongoing Phase 1 combination trial in patients with endometrial cancer. Data from the TPST-1495 Phase 1 trial was presented at the ASCO annual meeting in June 2023. Additionally, we are planning to advance TPST-1495 in a new indication, Familial Adenomatous Polyposis (“FAP”), for which there are no approved therapies. Given that prostaglandin signaling is implicated in FAP and based on positive preclinical data in a CDC report. For womenrelevant mouse model, we believe there is strong mechanistic support for this approach. We are working with Diminished Ovarian Reserve, including those with Primary Ovarian Insufficiency (POI) or Poor Ovarian Reserve (POR), IVF is largely ineffective. In these women, the average live birth rate per cycle is only six percent. Market research suggests that many patients with POI or POR resort to a donor egg or adoption, with some giving up on having a child altogether (Fulcrum Research Group). Other women are unable or unwilling to undergo hormone stimulation, which is a required component of standard IVF treatment. The EggPC cell technology has the potential to offer new treatment options to these women.

3

Beyond these clinical programs, we plan to continue to leverage our drug development and matured in vitro into healthy, fertilizable eggs. This potential treatment may be an option for all women undergoing IVF, which represents approximately 1.9 million women per year globally.

Our Pipeline

Our product development pipeline consists of the ovary usingfollowing orally-available therapies, which if approved by the U.S. Food and Drug Administration (the "FDA"), we believe will be first in class:

1. Timing is an antibody that binds specificallyestimate based on current projections and status of programs

2. Estimated for either year-end 2024 or the first quarter of 2025, subject to discussions with FDA.

3. Received initial approval from NCI; study start subject to final approval.

Strategy

Our team has come together to build an integrated company to deliver meaningful therapies to cancer patients by leveraging our collective capabilities and experience. We expect to build value for our stockholders with the following over-arching strategy:

4

Clinical Programs

TPST-1120: PPARαTranscription Factor Antagonist

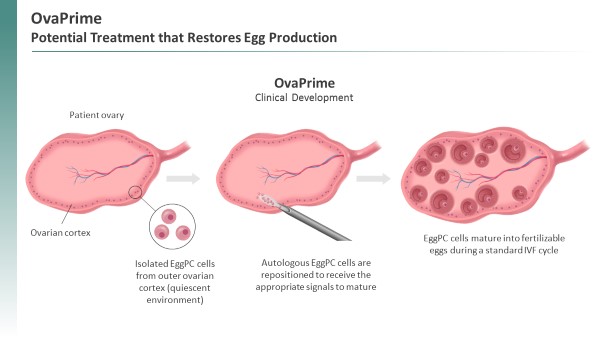

TPST-1120, a restorepotentially first-in-class oral small molecule antagonist of PPARα, has completed a woman’s egg production,Phase 1a/b trial, and is currently being studied in clinical development. With OvaPrime,an ongoing randomized Phase 1b/2 trial. The Phase 1a/b trial was a woman’s own EggPC cells are isolated frommulticenter, open-label, dose-escalation, that evaluated TPST-1120 as both a niche within her ovary where they are

Tumors evolve to promote their own survival by alternating energy sources, promoting angiogenesis and evading immune recognition. PPARα is a transcription factor that is activated through binding of long-chain fatty acid ligands, which in turn regulates the expression of genes that control glucose and lipid homeostasis, inflammation, proliferation, differentiation and cell death. Included among these regulated genes are those that enable fatty acid oxidation, or FAO, and β-oxidation metabolic pathways in cellular peroxisomes and in mitochondria. An FAO metabolic profile is associated with tumor proliferation, induction of angiogenesis and immune suppression. Published studies and internal Tempest analyses of over 9,000 primary ovarian insufficiency (POI)or metastatic tumor samples in the Human Cancer Genome public database reveal a metabolic gene expression profile characterized by increased PPARα, FAO genes and secondarily, assess changeslipogenesis associated with increased metastatic potential and reduced survival enrichment among multiple cancers, including HCC, CCA, breast carcinoma, colorectal adenocarcinoma, RCC, lung adenocarcinoma and prostate adenocarcinoma. TPST-1120 is designed to block the pathways that support tumor cell proliferation, angiogenesis and immune suppression, resulting in women’s hormone levels, follicular developmentreduced disease and occurrencepatient benefit.

5

Summary of pregnancy.

We have conducted pre-clinical pharmacology studies along with pharmacokinetics, or PK, and toxicology studies with TPST-1120 to the EggPC cells, while the other ovary is exposed to the EggPC vehicle as a means to have each subject serve as her own control. Results betweensupport its ongoing evaluation for the treatment and control ovary are examined for relevant endpoints such as antral follicle counts.

Immune checkpoint blockade enhances anti-tumor immunity by restoring the activity of cytotoxic T (Teff) cells. Emerging experimental results suggest that inhibiting FAO with a PPARα antagonist may target resistance mechanisms to both anti-PD-L1/PD-1 and anti-VEGF therapies, supporting the combination of TPST-1120 with either or both therapies. We have conducted preclinical studies showing that while both TPST-1120 or anti-PD-1 monotherapy inhibited outgrowth of established flank MC38 tumors, the combination of these two agents resulted in synergistic anti-tumor activity. In addition, MC38 tumor-bearing mice cured by the combination therapy, unlike age-matched naïve control mice, were completely resistant to tumor growth when rechallenged with autologous MC38 tumor cells, demonstrating that TPST-1120 in combination with anti-PD-1 induced lasting tumor-specific immune memory. In addition, activating mutations in the Wnt/B-catenin pathway represent the most frequently dysregulated pathway in HCC. Such mutations render a tumor cell reintroduction, OvaPrime was generally safedependent upon FAO for its energy source, and well-tolerated. Amongin preclinical studies, Tempest has shown reduction and long-term durable cures in mice bearing Wnt/B-catenin activated HCC tumors treated with TPST-1120 and an immune checkpoint inhibitor. The promise of these pre-clinical results have been observed in the first 20 patients evaluable for safety six-months post-EggPC cell reintroduction, there were no treatment related serious adverse events (SAEs) and no adverse events (AEs) related to the EggPC cells. There were seven mild AEs, four of which were deemed unrelated to OvaPrime and three of which were related to the standard laparoscopic procedure used to reintroduce EggPC cells into the ovary. No patients discontinued treatment because of an AE. The mean duration of follow-up among these 20 patients was nine months.

Efficacy in Syngeneic β-Catenin-driven Hepatocellular Carcinoma Model

Tumor resistance to anti-angiogenic drugs is also associated with elevated lipogenesis and FAO, primarily through the vascular regression and hypoxic environment that this class of therapies engenders. In response, tumor cells can switch to FAO as a readoutmechanism of secondary endpoints byresistance against anti-angiogenic therapy. In a preclinical study, we confirmed that combination of TPST-1120 with tyrosine kinase inhibitor-, or TKI-, based anti-angiogenesis therapy confers potent anti-tumor activity.

The preclinical data for TPST-120 are consistent with the end of the third quarter of 2019. However, based on preliminary blinded data we do not expect this Phase 1 clinical trial to produce strong signals on any of our secondary endpoints. We believe this may be due to the delivery of a sub-optimal EggPC cell dose.

6

the potential evaluation of developmental competence.

Overview of TPST-1120 Clinical Trials

We completed a Phase 1a/b study of TPST-1120 and a randomized Phase 1b/2 clinical study is ongoing. We have released positive data from both studies and expect updated data from the OvaTure Collaboration rather than underPhase 1b/2 clinical study in 2024. The Phase 1a/b trial evaluated both monotherapy and combination therapy with the OvaXon joint venture. We areanti-PD-1 agent nivolumab in discussionspatients with Intrexon regardingadvanced solid tumors that our PPARα-dependent transcriptome analysis of diverse human cancers revealed favor the futureusage of FAO. Results from both the monotherapy and the combination arms were presented in an oral presentation at the ASCO conference in 2022.

TPST-1120 demonstrated monotherapy clinical benefit in patients with late-line, treatment-refractory cancers where objective responses (RECIST v1.1) would not be expected, including pancreatic, CCA, and colorectal cancers ("CRC"). Results showed that 53% (10/19) of patients experienced clinical benefit in the form of disease control, including tumor shrinkage in 21% of the OvaXon joint venture.

In the combination therapy portion of the OvaTure Collaboration, effective 90 days following notice.trial, 15 evaluable patients with heavily pretreated RCC, HCC and CCA were treated with oral twice-daily TPST-1120 and the anti-PD-1 therapy, nivolumab. All the HCC and RCC patients had received an approved anti-PD-1 therapy in at least one prior line of therapy and discontinued that treatment due to disease progression. We believe thatobserved objective responses (RECIST v1.1) in two patients with late-line RCC who had previously progressed on anti-PD-1 therapy without having achieved an objective response (ORR 50%, n=2/4, in evaluable RCC patients), and we can best continueobserved mixed response in a third RCC IO-refractory patient with significant reduction (>30%) in the target lesion, but the appearance of new disease precluded designation as a RECIST PR. A third RECIST response was observed in a patient with late-line, heavily pre-treated CCA, a tumor type generally not responsive to anti-PD-1 therapy alone. All the RECIST responses were observed at the two highest doses.

Notably, one RCC patient who achieved a response after treatment with TPST-1120 and nivolumab had previously been treated with nivolumab in combination with ipilimumab without experiencing an objective response and progressed on treatment, followed by further progression of cancer on both cabozantinib and everolimus. The initial RECIST PR was seen at the first on-study assessment at eight weeks and included a response in all target lesions as well as complete radiographic resolution of multiple sites of metastatic disease (see CT scan below) and has been confirmed at subsequent assessments beyond 12 months.

7

Partial Response in Late-Line RCC Patient Treated with TPST-1120

and Nivolumab Combination Therapy

Randomized Data in HCC

On October 11, 2023, we announced updated positive results from the planned data analysis from the ongoing global randomized Phase 1b/2 trial of TPST-1120, combined with the standard-of-care first-line regimen of atezolizumab and bevacizumab, in patients with advanced or metastatic HCC. The study is comparing the TPST-1120 arm to standard of care alone, and enrolled 40 patients randomized to the TPST-1120 arm and 30 patients randomized to the control arm. With a median follow-up of 9.2 and 9.9 months for the TPST-1120 arm and standard-of-care arm, respectively, the data showed a 30% confirmed ORR achieved in the TPST-1120 arm compared to 13.3% for atezolizumab and bevacizumab in the control arm, a substantial increase specific to the TPST-1120 arm as compared to the previously released interim data cut of 17.5% in the TPST-1120 arm versus 10.3% in the control arm. The results also showed a favorable progression free survival and OS hazard ratio for the TPST-1120 arm as compared to the standard-of-care control arm. In the TPST-1120 arm 40% of patients remained on treatment versus 16.7% in the control arm, while 72.5% of the TPST-1120 arm patients remained on study versus 46.7% in the control arm.

1. Data not provided by Roche

New biomarker subpopulation findings are consistent with the mechanism of action of TPST-1120. Patients with b-catenin activating mutations (21% in this study (n=7)) showed an increased confirmed ORR of 43% and a disease control rate (“DCR”) of 100% in the TPST-1120 arm. In addition, and distinct from the control arm, the TPST-1120 arm was consistently active across

8

PD-L1 negative tumors with a confirmed ORR of 27% in the TPST-1120 arm, compared to a reduced ORR of 7% for the control arm. We expect updated data to be available in 2024.

Early in the development of OvaTureTPST-1120, given the expression profile and attributes of PPARα, we selected HCC, RCC and CAA as cancers of interest and checkpoint inhibitors and anti-angiogenic therapeutics as potential companion therapies with the goal

9

to maximize the opportunity to bring meaningful benefit to patients with these cancers. Based on the pre-clinical and clinical data released to date, we believe that the emerging clinical benefit profile of TPST-1120 for patients shows alignment with these predictions, and we look forward to the potential benefit TPST-1120 could bring to patients with these cancers.

We own worldwide rights to TPST-1120, and have filed and been issued patents, including composition of matter, pharmaceutical compositions, and related methods of use, which are expected to expire between December 2033 and November 2043, without giving effect to any patent term extensions.

TPST-1495: Dual EP2/EP4 Prostaglandin Receptor Antagonist

Our second clinical molecule is TPST-1495, a potentially first-in-class, oral, small molecule dual antagonist of the prostaglandin E2, or PGE2, receptors, EP2 and EP4. TPST-1495 is engineered to inhibit only these receptors while sparing the homologous - but differentially active - EP1 and EP3 receptors.

There is extensive literature demonstrating that PGE2 both enhances tumor proliferation and inhibits anti-cancer immune function; it is known from the scientific literature that many tumors express elevated levels of the cyclooxygenase enzymes that produce PGE2. Elevated expression of COX-2 and overproduction of PGE2 is correlated with progression of diverse malignancies by building out our internal capabilitiesstimulating tumor cell proliferation, survival, evasion and expertise undermetastasis as well as host angiogenesis. In addition, PGE2 suppresses anti-tumor immunity by inhibiting the leadershipfunction of Dr. James Lillie, our Chief Scientific Officer,critical anti-tumor immune effector cell populations such as dendritic cells, natural killer ("NK cells"), T cells, and engagingM1 macrophages, while promoting the activity of suppressive immune cell populations including myeloid-derived suppressor cells ("MDSCs"), M2 macrophages, and regulatory T cells. Recent studies have also shown that increased expression of COX-2 and production of PGE2 can play a role in the effectiveness of immune checkpoint inhibitor therapy and in the development of adaptive resistance to therapy. This body of literature provides the scientific rationale for developing therapeutics that maximally inhibit the prostaglandin pathway, as well as for combining TPST-1495 with immune checkpoint inhibitor monoclonal antibodies.

We conducted preclinical studies to evaluate TPST-1495, including its ability to reverse PGE2-mediated suppression of primary human monocyte to dendritic cell differentiation and activation in vitro, as well as comparisons to other agents designed to operate in the same pathway such as a single EP4 antagonist and, as described, COX2.

We have also conducted preclinical studies to evaluate TPST-1495 in a spontaneous APCMin/+ mouse model of FAP that demonstrated a significant survival advantage in comparison to other inhibitors in the prostaglandin pathway.

Source: Francica et al., Cancer Res Commun; 3(8) August 2023 https://doi.org/10.1158/2767-9764.CRC-23-0249

10

Overview of Ongoing TPST-1495 Clinical Trials

TPST-1495 was evaluated in a first-in-human, Phase 1, multicenter, open-label, schedule and dose optimization trial in subjects with late-stage solid tumor cancers that are deemed incurable. Study objectives include evaluation of safety, tolerability, PK, PD, and preliminary anti-tumor activity of TPST-1495 as monotherapy and in combination with the checkpoint inhibitor, pembrolizumab. TPST-1495 has been evaluated on a once daily (“QD”) or twice daily (“BID”) schedule and with continuous or intermittent administration as monotherapy and in combination with pembrolizumab. Results from the Phase 1 study were presented at ASCO 2023. The data showed that in a diverse and treatment-refractory patient population, treatment with TPST-1495 as a monotherapy and in combination with pembrolizumab resulted in tumor shrinkage and prolonged stable disease in certain patients, as well as a durable confirmed partial response (“PR”) in a combination therapy patient with microsatellite stable colorectal cancer (“MSS CRC”), an indication not normally responsive to immunotherapy. The safety profile for TPST-1495 monotherapy on the recommended once-daily schedule was tolerable, with predominantly Grade 1-2 treatment related adverse events (“TRAEs”), including abdominal pain (17.9% All Grade and 0% Grade 3+), nausea (20.5% All Grade and 0% Grade 3+), and diarrhea (15.4% All Grade and 2.6% Grade 3+). For the combination with pembrolizumab, the most common TRAEs were nausea (29.2% All Grade and 0% Grade 3+), fatigue (20.8% All Grade and 4.2% Grade 3+) and diarrhea (20.8% All Grade, 0% Grade 3+). No TRAEs of Grade ≥4 were reported. On the recommended once-daily schedule, the DCR by RECIST v1.1 was 44% for patients on monotherapy TPST-1495 and 40.9% for patients on TPST-1495 with pembrolizumab (including a confirmed PR in a patient with MSS CRC and a stable disease rate of 36.4%). An ongoing combination arm in patients with endometrial cancer is expected to complete and data will be reported in 2024.

Our preclinical results in the APCMin/+ lead us to consider the application of TPST-1495 in familial adenomatous polyposis syndrome (“FAP”). FAP is a hereditary condition characterized by the development of numerous polyps in the colon and rectum. These polyps have the potential to become cancerous if left untreated. FAP is caused by mutations in the APC gene, which normally helps regulate cell growth and division in the intestinal lining. Individuals with FAP have a significantly increased risk of developing colorectal cancer at a young age, often before the age of 40. Additionally, FAP can lead to the development of polyps in other parts of the gastrointestinal tract, as well as other non-gastrointestinal tumors. Management of FAP typically involves regular surveillance with colonoscopies and surgical intervention to remove the polyps and reduce the risk of cancer. Currently, there are no systemic therapies approved to treat FAP. We are working with the Cancer Prevention Clinical Trials Network on a National Cancer Institute (“NCI”)-funded Phase 2 study, and subject to final approval of NCI, plan to start the study in 2024.

We own worldwide rights to TPST-1495, and have filed and been issued patents, including composition of matter and pharmaceutical compositions, which are expected to expire between April 2038 and October 2042, without giving effect to any patent term extensions.

Discovery Research

Our Discovery Research team is dedicated to identifying and validating novel therapeutic targets in oncology. We are not bound to a single technology platform, which allows us the scientific freedom to pursue targets and modalities that we believe have the highest probability to benefit patients. Rigorous medicinal chemistry and a broad set of preclinical validation studies are conducted to further evaluate lead compounds and inform decision-making for advancement into clinical development. Collaboration with academic institutions, contract research organizations that have specific, complementary capabilities(“CROs”), and strategic partners provides opportunity to enrich our own,pipeline, as well, asenhancing our academic collaborators.

License Agreements

In February 2018,2021, we provided Intrexon with written notice of termination of the OvaTure Collaboration, effective 90 days following notice. The OvaTure Collaboration provided for Intrexon to deliver laboratory and animal data to support OvaTure development, and provided that upon the delivery of laboratory and animal data, we would incur an obligation to pay Intrexon a mid-single digit royalty on net sales of any OvaTure fertility treatment in the future, and the exact royalty will depend upon the timing of the completion of the milestone. The royalty will apply if Intrexon intellectual property is utilized in the continued development of OvaTure.

11

trial, and we retain global development and commercialization rights to TPST-1120. Pursuant to the agreement, Roche provides us with notice of the amount of TPST-1120 required and the delivery timeline, and we supply the TPST-1120. All rights to invention and discoveries relating solely to TPST-1120 or biomarkers solely related to TPST-1120 made during any study will be our technologyexclusive property. All data generated in the field utilizing Intrexon's synthetic biology platform.

The agreement applies on a study-by-study basis until the futurelast treatment of the OvaXon joint venture.

Sales and Marketing

We recordedintend to retain significant development and commercial rights to our initial investment in OvaXon as an equity method investment in December 2013. As of December 31, 2017product candidates and, 2016,if marketing approval is obtained, to commercialize our equity investment in OvaXon was $0.1 million and included within other current assetsproduct candidates on our consolidated balance sheets. We and Intrexon both made additional contributions of $1.1 million and $1.8 million for the years ending December 31, 2017 and 2016, respectively.

Manufacturing

We do not own or operate, and currently have no plans to establish, any manufacturing facilities. We rely and expect to continue to rely, on third parties for the manufacture of our product candidates for preclinical and clinical testing, as well as for commercial manufacture if any of our product candidates obtain marketing approval. We also rely, and expect to continue to rely, on third parties to package, label, store and distribute our investigational product candidates, as well as for our commercial products if marketing approval is obtained. We have internal personnel and utilize consultants with extensive technical, manufacturing, analytical and quality experience to oversee contract manufacturing and testing activities. We will continue to workexpand and strengthen our network of third-party providers but may also consider investing in internal manufacturing capabilities in the future if there is a technical need, or a strategic or financial benefit.

Manufacturing is subject to extensive regulations that impose procedural and documentation requirements. At a minimum these regulations govern record keeping, manufacturing processes and controls, personnel, quality control and quality assurance. Our systems, procedures and contractors are required to comply with these regulations and are assessed through regular monitoring and formal audits.

Competition

The biopharmaceutical and immuno-oncology industries are characterized by intense competition and rapid innovation. Any product candidates that we successfully develop and commercialize will have to compete with existing and future new therapies. While we believe that our technology, development experience and scientific knowledge provide us with competitive advantages, we face potential competition from many different sources, including large and specialty pharmaceutical and biotechnology companies, academic research institutions, government agencies and public and private research institutions that conduct research, seek patent protection, and establish collaborative arrangements for research, development, manufacturing and commercialization.

12

If our TPST-1120, TPST-1495, or any future product candidates are approved for the FDA under its available procedurestreatment of tumors, they may compete with other products used to determinetreat such diseases. There are a variety of treatments used for cancerous tumors that include chemotherapy drugs, small molecules, monoclonal antibodies, antibody-drug conjugates, bi-specific antibodies, cell therapies, oncolytic viruses and vaccines, as well as other approaches. In addition, there are several competitors in clinical development for the most appropriate regulatory pathway for potential entry intotreatment of HCC, RCC, cholangiocarcinoma, and other indications that we may be targeting with TPST-1120 and TPST-1495, including companies such as Ono, Adlai Nortye, Merck, Roche, Exelixis, and AstraZeneca.

TPST-1120, our small molecule designed to be a selective antagonist of PPARα, is the U.S. market.

Many of our competitors, either alone or (ii)with strategic partners, have substantially greater financial, technical and human resources than we do. Accordingly, our competitors may be more successful than us in research and development, manufacturing, preclinical testing, conducting clinical trials, obtaining approval for treatments and achieving widespread market acceptance, rendering our treatments obsolete or non-competitive. Merger and acquisition activity in the eventbiotechnology and biopharmaceutical industries may result in even more resources being concentrated among a smaller number of a material breach that is not cured within 30 days. During the Initial Term, IVF Japan Group will payour competitors. These companies also compete with us a fixed amount of $1,000 per AUGMENT cyclein recruiting and will reimburse usretaining qualified scientific and management personnel, establishing clinical trial sites and patient registration for all lab operationsclinical trials and personnel costs, which we anticipateacquiring technologies complementary to, or necessary for, our programs. Smaller or early-stage companies may also prove to be approximately $0.2 million forsignificant competitors, particularly through collaborative arrangements with large and established companies.

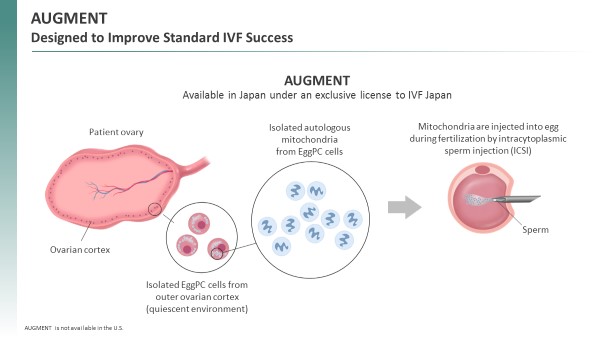

Our commercial opportunity could be substantially limited if our competitors develop and commercialize products that are more effective, safer, less toxic, more convenient or less expensive than our comparable products. In geographies that are critical to our commercial success, competitors may also obtain regulatory approvals before us, resulting in our competitors building a strong market position in advance of the Initial Term,entry of our products. The key competitive factors affecting the success of all our programs are likely to be their efficacy, safety, convenience and are payableavailability of reimbursement. In addition, our ability to compete may be affected in nonrefundable quarterly installments on the first day of each quarter. The IVF Japan Group is also responsible to reimburse us for the cost of materials for AUGMENT for all cycles in excess of 100 which are estimated at $2,000 per cycle. We will retain the worldwide commercialization rights for AUGMENT outside of Japan.

Intellectual Property

We strive to use AUGMENTprotect and enhance the proprietary technology, inventions and improvements that are commercially important to our business, including obtaining, maintaining, and defending our patent rights. Our policy is to seek to protect our proprietary position by, among other methods, filing patent applications and obtaining issued patents in Japan was made by the Japan Society of Obstetrics and Gynecology (JSOG). In some other countries, there

As of February 20, 2018, we own or have exclusively licensed 65December 31, 2023, our patent portfolio consisted of issued patents in 44 countries and jurisdictions and have more than 170 applications pending in more than 130 countries (including applications directly filed in countries and applications filed in regional patent offices); communications indicating allowance have been received for three of these applications.

With respect to TPST-1120, as of December 31, 2023, we own issued patents and pending patent applications pending with patent officesin the United States, Europe, China, Japan, and other markets outside of the U.S. whichUnited States as well as one pending PCT application. The issued

13

United States patents covering TPST-1120 as composition of matter, pharmaceutical compositions, and related methods of use are owned by MGH, twoexpected to expire in December 2033, absent any patent term extensions for regulatory delay. Any additional patents that may issue from these pending patent applications are expected to expire between December 2033 and November 2043, absent any patent term adjustments or patent term extensions for regulatory delay.

With respect to TPST-1495, as of December 31, 2023, we own issued patents including one U.S.and pending patent co-owned by MGHapplications in the United States, Europe, China, Japan, and The President and Fellows of Harvard College, or Harvard, one pending U.S. non-provisional application co-owned by MGH and Harvard, and seventeen applications pending in patent officesother markets outside of the U.S. whichUnited States as well as one pending PCT application. The issued United State patents covering TPST-1495 as composition of matter, pharmaceutical composition, and related methods of use are co-ownedexpected to expire between April 2038 and April 2039, absent any patent term extensions for regulatory delay. Any additional patents that may issue from these pending patent applications are expected to expire between April 2038 and November 2043, absent any patent term adjustments or patent term extensions for regulatory delay.

As of December 31, 2023, our patent portfolio also included pending patent applications in the United States and Europe that are exclusively licensed to us by MGHthe University of California at Berkeley. The licensed patent applications do not cover any of our current product candidates.

We also possess substantial know-how and Harvard.

With respect to our product candidates and processes that we have licensed from MGH is directedintend to female germline stem cells, includingdevelop and commercialize in the normal course of business, we intend to pursue patent protection covering, when possible, compositions, methods of isolating such female germline stem cellsuse, dosing, and various usesformulations. We may also pursue patent protection with respect to manufacturing and drug development processes and technologies.

Issued patents can provide protection for such female germline stem cells, including methods for IVF, methods for egg production, methods to treat infertilityvarying periods of time, depending upon the date of filing of the patent application, the date of patent issuance and methods to restore ovarian function. This family includes issuedthe legal term of patents in the U.S., Canada and 30 European countries allin which they are obtained. In general, patents issued for patent applications filed in the United States can provide exclusionary rights for 20 years from the earliest effective filing date. The term of which will expireUnited States patents may be extended by delays encountered during prosecution that are caused by the USPTO, also known as patent term adjustment. In addition, in May 2025. We believecertain instances, the term of an issued United States patent that somecovers or claims an FDA approved product can be extended to recapture a portion of the term effectively lost as a result of the FDA regulatory review period, which is called patent term extension. The restoration period cannot be longer than five years and the total patent term, including the restoration period, must not exceed 14 years following FDA approval. The term of patents outside of this family providethe United States varies in accordance with the laws of the foreign jurisdiction, but typically is also 20 years from the earliest effective filing date. However, the actual protection for therapeutic compositions comprising EggPC cells, whichafforded by a patent varies on a product-by-product basis, from country-to-country and depends upon many factors, including the type of patent, the scope of its coverage, the availability of regulatory-related extensions, the availability of legal remedies in a particular country and the validity and enforceability of the patent.

The patent positions of companies like ours are referred togenerally uncertain and involve complex legal and factual questions. No consistent policy regarding the scope of claims allowable in patents in the patents as female germline stem cells,field of oncology has emerged in the United States. The relevant patent laws and that sometheir interpretation outside of the United States are also uncertain. Changes in either the patent laws or their interpretation in the United States and other countries may diminish our ability to protect our technology or product candidates and could affect the value of such intellectual property. In particular, our ability to stop third parties from making, using, selling, offering to sell, or importing products that infringe our intellectual property will depend in part on our success in obtaining and enforcing patent claims that cover our technology, inventions, and improvements. We cannot guarantee that patents will be granted with respect to any of this family provide protection for elements of the manufacturing process for obtaining such therapeutic compositions.

Moreover, even its issued patents and any additional patents claiming prioritymay not guarantee us the right to practice our technology in relation to the underlying provisional applications, will expire in April 2032 unless patent term extension is granted. We believe that these patents,commercialization of its products. Patent and any patents issuing from this family, provide protection for AUGMENT and several important aspects thereof.

14

commercializing our product candidates and know-how. Trade secrets and know-how can be difficult to protect. We seek to protectpracticing our proprietary technology, and processes, in part, by confidentiality agreements with our employees, consultants, scientific advisors and contractors. We also seek to preserve the integrity and confidentiality of our data and trade secrets by maintaining physical security of our premises and physical and electronic security of our information technology systems. While we have confidence in these individuals, organizations and systems, agreements or security measuresissued patents may be breached andchallenged, invalidated, or circumvented, which could limit our ability to stop competitors from marketing related products or could limit the term of patent protection that otherwise may exist for its product candidates. In addition, the scope of the rights granted under any issued patents may not provide us with protection or competitive advantages against competitors with similar technology. Furthermore, our competitors may independently develop similar technologies that are outside the scope of the rights granted under any issued patents. For these reasons, we may not have adequate remedies for any breach. In addition, our trade secrets and know-how may otherwise become known or may be independently discovered by competitors. To the extent that our consultants, contractors or collaborators use intellectual property owned by others in their work for us, disputes may arise as to the rights in related or resulting know-how and inventions.

Government Regulation

Government authorities in the need for hormonal hyperstimulation for egg retrieval. We anticipate that price also will be an important competitive factor for all our fertility treatment options. At this time, we cannot evaluate how our

FDA Approval Process

In the United States, pharmaceutical products are subject to extensive regulation by the FDA, the Federal Food, Drug, and Cosmetic Act (“FFDCA”), and other federal and state statutes and regulations govern, among other things, the research, development, testing, manufacture, storage, recordkeeping, approval, labeling, promotion and marketing, distribution, post-approval monitoring and reporting, sampling and import and export of drugs, biologicspharmaceutical products. Failure to comply with applicable U.S. requirements may subject a company to a variety of administrative or judicial sanctions, such as clinical hold, FDA refusal to approve pending a New Drug Applications ("NDA") warning or untitled letters, product recalls, product seizures, total or partial suspension of production or distribution, injunctions, fines, civil penalties and medical devices, as well as other types of medical productscriminal prosecution.

Our investigational medicines and procedures. Most countries also have rules relatingany future investigational medicines must be approved by the FDA pursuant to procurement and use of human tissues or cells, and rules relating to assisted human reproduction. Although the specific rules vary country by country, in general different levels of regulation are applicable depending on the nature of the treatment, the level of risk involved, and/or its intended uses. Some classes of products (e.g., treatments regulated as drugs or biologicsan NDA before they may be legally marketed in the United States, or treatments regulated as medicinal products inStates. The process generally involves the EU) requirefollowing:

15

The preclinical and clinical testing and approval requirements. In these jurisdictions,process requires substantial time, effort and financial resources, and we cannot be certain that any approvals for our product candidates will be granted on a timely basis, or at all.

Preclinical Studies

Before testing any drug product candidates in humans, the developmentproduct candidate must undergo rigorous preclinical testing. Preclinical tests include laboratory evaluation of product chemistry, formulation and marketing of such therapies generally do not requiretoxicity, as well as in vitro and animal studies to assess the potential for adverse events and in some cases to establish a rationale for therapeutic use. The conduct of the preclinical tests must comply with federal regulations and requirements, including GLP. An IND sponsor must submit the results of the preclinical tests, together with manufacturing information, analytical data, any available clinical trialsdata or pre-reviewliterature and approval of a marketing application by the relevant regulatory authority. In addition, although many such therapies are still subject to post-marketing requirements, these requirements typically are substantially reduced as comparedplans for clinical studies, among other things, to the requirementsFDA as part of an IND. An IND is a request for drugs, biologics, medicinal products or medical devices.

Clinical Trials

Clinical trials involve the administration of the United States. We metinvestigational new drug to healthy volunteers or patients under the supervision of a qualified investigator, generally a physician not employed by or under the trial sponsor’s control. Clinical trials must be conducted: (i) in compliance with federal regulations; (ii) in compliance with GCP, an international standard meant to protect the FDArights and health of patients and to define the roles of clinical trial sponsors, administrators and monitors; as well as (iii) under protocols detailing, among other things, the objectives of the trial, the parameters to be used in monitoring safety and the effectiveness criteria to be evaluated in the second quarter of 2017 regarding AUGMENT,trial. Each protocol involving testing on U.S. patients and will continue to work with the FDA under its available procedures to determine the most appropriate regulatory pathway for potential entry into the U.S. market. We cannot provide any assurance, however, that the FDA will ultimately change the position taken in the "untitled" letter. In March 2018, Health Canada informed us that performing AUGMENT violates Canada's Assisted Human Reproduction Act, and requested that we cease offering AUGMENT in Canada. Accordingly, we are no longer making AUGMENT available in Canada while we consider next steps.

Furthermore, each EU member state inclinical trial must be reviewed and approved by an IRB for each institution at which the clinical trial will be conducted. Underconducted to ensure that the new Regulation on Clinical Trials, which is expectedrisks to take effectindividuals participating in the clinical trials are minimized and are reasonable in relation to anticipated benefits. The IRB also approves the informed consent form that must be provided to each clinical trial subject or after October 2018, there will be a centralized application procedure where one

There also are requirements governing the reporting of ongoing clinical trials and completed clinical trial results to public registries. Information about certain clinical trials, including clinical trial results, must be notifiedsubmitted within specific timeframes for publication on the www.clinicaltrials.gov website. Information related to the product, patient population, phase of investigation, clinical trial sites and investigators and other aspects of the clinical trial is then made public as part of the registration. Disclosure of the results of these clinical trials can be delayed in certain circumstances for up to two years after the date of completion of the trial.

16

A sponsor who wishes to conduct a clinical trial outside of the United States may, but need not, obtain FDA authorization to conduct the clinical trial under an IND. If a foreign clinical trial is not conducted under an IND, the sponsor may submit data from the clinical trial to the FDA in support of an NDA. The FDA will accept a well-designed and well-conducted foreign clinical trial not conducted under an IND if the clinical trial was conducted in accordance with GCP requirements, and the FDA is able to validate the data through an onsite inspection if deemed necessary.

Clinical trials are generally conducted in three sequential phases, known as Phase 1, Phase 2 and Phase 3:

These Phases may overlap or be combined. For example, a Phase 1/2 clinical trial may contain both a dose-escalation stage and a dose expansion stage, the latter of which may confirm tolerability at the recommended dose for expansion in future clinical trials (as in traditional Phase 1 clinical trials) and provide insight into the anti-tumor effects of the investigational therapy in selected subpopulation(s).

Typically, during the development of oncology therapies, all subjects enrolled in Phase 1 clinical trials are disease-affected patients and, as a medicinal product EMA,result, considerably more information on clinical activity may be collected during such trials than during Phase 1 clinical trials for non-oncology therapies. A single Phase 3 or Phase 2 trial with other confirmatory evidence may be sufficient in rare instances to provide substantial evidence of effectiveness (generally subject to the requirement of additional post-approval studies). The manufacturer of an investigational drug in a phase 2 or 3 clinical trial for a serious or life-threatening disease is required to make available, such as by posting on its website, its policy on evaluating and national medicines regulatorsresponding to requests for expanded access.

Phase 1, Phase 2, Phase 3 and other types of clinical trials may not be completed successfully within any specified period, if at all. The FDA, the EU provideIRB, or the opportunity for dialogue and guidancesponsor may suspend or terminate a clinical trial at any time on various grounds, including non-compliance with regulatory requirements or a finding that the development program. Atpatients are being exposed to an unacceptable health risk. Similarly, an IRB can suspend or terminate approval of a clinical trial at its institution if the EMA level, thisclinical trial is usually donenot being conducted in accordance with the formIRB’s requirements or if the drug has been associated with unexpected serious harm to patients. Additionally, some clinical trials are overseen by an independent group of scientific advice, which is givenqualified experts organized by the Scientific Advice Working Partyclinical trial sponsor, known as a data safety monitoring board or committee. This group provides authorization for whether a trial may move forward at designated checkpoints based on access to certain data from the trial.

Concurrent with clinical trials, companies usually complete additional animal studies and must develop additional information about the chemistry and physical characteristics of the Committeedrug as well as finalize a process for Medicinal Products for Human Use, or CHMP. A fee is incurredmanufacturing the product in commercial quantities in accordance with each scientific advice procedure. Advice from the EMA is typically provided based on questions concerning, for example,cGMP requirements. The manufacturing process must be capable of consistently producing quality (chemistry, manufacturing and controls testing), nonclinical testing and clinical studies, and pharmacovigilance plans and risk-management programs. Advice is not legally binding with regard to any future marketing authorization applicationbatches of the product concerned. To date, we haveand, among other things, companies must develop methods for testing the identity, strength, quality, potency and purity of the final product. Additionally, appropriate packaging must be selected and tested, and

17

stability studies must be conducted to demonstrate that the investigational medicines do not initiated any scientific advice procedures or other discussions with the EMA or any national regulatory authorities in the EU.

FDA Review Process

After completion of the required clinical testing, we must obtain aan NDA is prepared and submitted to the FDA. FDA approval of an NDA is required before marketing authorization before weof the product may place a medicinal product on the marketbegin in the EU. ThereU.S. An NDA must include the results of all preclinical, clinical and other testing and a compilation of data relating to the product’s pharmacology, chemistry, manufacture and controls. To support marketing approval, the data submitted must be sufficient in quality and quantity to establish the safety and efficacy of the investigational product to the satisfaction of the FDA. FDA approval of an NDA must be obtained before a drug may be marketed in the United States. The cost of preparing and submitting an NDA is substantial. Under the Prescription Drug User Fee Act (“PDUFA”), each NDA must be accompanied by a substantial user fee. The FDA adjusts the PDUFA user fees on an annual basis. Fee waivers or reductions are variousavailable in certain circumstances, including a waiver of the application procedures available,fee for the first application filed by a small business. Additionally, no user fees are assessed on NDAs for products designated as orphan drugs, unless the product also includes a non-orphan indication. The applicant under an approved NDA is also subject to an annual program fee.

The FDA reviews each submitted NDA before it determines whether to file it and may request additional information. The FDA must make a decision on whether to file an NDA within 60 days of receipt, and such decision could include a refusal to file by the FDA. Once the submission is filed, the FDA begins an in-depth review of an NDA. The FDA has agreed to certain performance goals in the review of an NDA. Most applications for standard review drug products are reviewed within ten to twelve months; most applications for priority review drugs are reviewed in six to eight months. Priority review can be applied to drugs that the FDA determines may offer significant improvement in safety or effectiveness compared to marketed products or where no adequate therapy exists. The review process for both standard and priority review may be extended by the FDA for three additional months to consider certain late-submitted information, or information intended to clarify information already provided in the submission. The FDA does not always meet its goal dates for standard and priority timeframes for an NDA, and the review process can be extended by FDA requests for additional information or clarification.

The FDA may also refer applications for novel drug products, or drug products that present difficult questions of safety or efficacy, to an outside advisory committee—typically a panel that includes clinicians and other experts—for review, evaluation and a recommendation as to whether the application should be approved and under what conditions, if any. The FDA is not bound by the recommendation of an advisory committee, but it generally follows such recommendations.

Before approving an NDA, the FDA will conduct a pre-approval inspection of the manufacturing facilities for the new product to determine whether they comply with cGMP requirements. The FDA will not approve the product unless it determines that the manufacturing processes and facilities are in compliance with cGMP requirements and adequate to assure consistent production of the product within required specifications. The FDA also typically inspects clinical trial sites to ensure compliance with GCP requirements and the integrity of the data supporting safety and efficacy.

After the FDA evaluates an NDA and the manufacturing facilities, it issues either an approval letter or a complete response letter. A complete response letter ("CRL"), generally outlines the deficiencies in the submission and may require substantial additional testing, or information, in order for the FDA to reconsider the application, such as additional clinical data, additional pivotal clinical trial(s), and/or other significant and time-consuming requirements related to clinical trials, preclinical studies or manufacturing. If a CRL is issued, the applicant may resubmit an NDA addressing all of the deficiencies identified in the letter, withdraw the application, engage in formal dispute resolution or request an opportunity for a hearing. The FDA has committed to reviewing resubmissions in two or six months depending on the type of information included. Even if such data and information are submitted, the FDA may decide that an NDA does not satisfy the criteria for approval.

As a potential condition of an NDA approval, the FDA may require a REMS to help ensure that the benefits of the drug outweigh the potential risks to patients. A REMS can include medication guides, communication plans for healthcare professionals and elements to assure a product’s safe use ("ETASU"). An ETASU can include, but is not limited to, special training or certification

18

for prescribing or dispensing the product, involved. Alldispensing the product only under certain circumstances, special monitoring and the use of patient-specific registries. The requirement for a REMS can materially affect the potential market and profitability of the product. Moreover, the FDA may require substantial post-approval testing and surveillance to monitor the product’s safety or efficacy.

Changes to some of the conditions established in an approved application, proceduresincluding changes in indications, labeling, or manufacturing processes or facilities, require submission and FDA approval of an applicationNDA supplement or, in some case, a new NDA, before the change can be implemented. An NDA supplement for a new indication typically requires clinical data similar to that in the common technical document,original application, and the FDA uses the same procedures and actions in reviewing NDA supplements as it does in reviewing NDAs.

Orphan Drug Designation

Under the Orphan Drug Act, the FDA may grant orphan drug designation to drugs intended to treat a rare disease or CTD, format,condition, which includes the submission of detailed information about the manufacturing and quality of the product, and non-clinical and clinical trial information. There is an increasing trendgenerally a disease or condition that affects fewer than 200,000 individuals in the EU towards greater transparency and, while the manufacturing or quality information is currently generally protected as confidential information, the EMA and national regulatory authorities are now liable to disclose much of the non-clinical and clinical information in marketing authorization dossiers, including the full clinical trial reports, in response to freedom of information requests after the marketing authorization has been granted. Clinical trial reports will also be posted on the EMA's website following the grant, denial or withdrawal of a marketing authorization application, subject to procedures for limited redactions and protection against unfair commercial use.

Orphan drug designation must be requested before submitting an NDA. After the FDA grants orphan drug designation, the identity of the drug and its potential orphan use are disclosed publicly by the FDA. Orphan drug designation does not convey any advantage in, or shorten the duration of, the regulatory review and approval process.

If a product that has orphan designation subsequently receivedreceives the first FDA approval for the disease or condition for which it has such designation, the product is entitled to a seven-year exclusive marketing period in the U.S. for that product, for that indication. During the seven-year exclusivity period, the FDA may not approve any other applications to market the same drug for the same disease, except in limited circumstances, such as a showing of clinical superiority to the product with orphan drug exclusivity by means of greater effectiveness, greater safety, or providing a major contribution to patient care, or in instances of drug supply issues. Orphan drug exclusivity does not prevent the FDA from approving a different drug for the same disease or condition, or the same drug for a different disease or condition. Other benefits of orphan drug designation include tax credits for certain research and an exemption from the NDA user fee.

Expedited Development and Review Programs

The FDA is authorized to designate certain products for expedited review if they are intended to address an "untitled" letter questioningunmet medical need in the statustreatment of AUGMENTa serious or life-threatening disease or condition.

Fast Track Designation

Fast track designation may be granted for products that are intended to treat a serious or life-threatening disease or condition for which there is no effective treatment and preclinical or clinical data demonstrate the potential to address unmet medical needs for the condition. Fast track designation applies to both the product and the specific indication for which it is being studied. The sponsor of an investigational drug product may request that the FDA designate the drug candidate for a specific indication as a section 361 HCT/P,fast track drug concurrent with, or after, the submission of the IND for the drug candidate. The FDA must determine if the drug candidate qualifies for fast track designation within 60 days of receipt of the sponsor’s request. For fast track products, sponsors may have greater interactions with the FDA and advising usthe FDA may initiate review of sections of a fast track product’s NDA before the application is complete. This rolling review is available if the FDA determines, after preliminary evaluation of clinical data submitted by the sponsor, that a fast track product may be effective. The sponsor must also provide, and the FDA must approve, a schedule for the submission of the remaining information and the sponsor must pay applicable user fees. At the time of an NDA filing, the FDA will determine whether to filegrant priority review designation. Additionally, fast track designation may be withdrawn if the FDA believes that the designation is no longer supported by data emerging in the clinical trial process.

Breakthrough Therapy Designation

19

Breakthrough therapy designation may be granted for products that are intended, alone or in combination with one or more other products, to treat a serious or life-threatening condition and preliminary clinical evidence indicates that the product may demonstrate substantial improvement over currently approved therapies on one or more clinically significant endpoints. Under the breakthrough therapy program, the sponsor of a new drug candidate may request that the FDA designate the candidate for a specific indication as a breakthrough therapy concurrent with, or after, the submission of an IND for the potential fertility treatment, following which we suspended our commercialization effortsdrug candidate. The FDA must determine if the drug product qualifies for breakthrough therapy designation within 60 days of receipt of the sponsor’s request. The FDA may take certain actions with respect to breakthrough therapies, including holding meetings with the sponsor throughout the development process, providing timely advice to the product sponsor regarding development and approval, involving more senior staff in the United States. We believereview process, assigning a cross-disciplinary project lead for the review team and taking other steps to design the clinical studies in an efficient manner.

Priority Review

Priority review may be granted for products that AUGMENTare intended to treat a serious or life-threatening condition and, if approved, would provide a significant improvement in safety and effectiveness compared to available therapies. The FDA will attempt to direct additional resources to the evaluation of an application designated for priority review in an effort to facilitate the review.

Accelerated Approval

Accelerated approval may be granted for products that are intended to treat a serious or life-threatening condition and that generally provide a meaningful therapeutic advantage to patients over existing treatments. A product eligible for accelerated approval may be approved on the basis of either a surrogate endpoint that is reasonably likely to predict clinical benefit, or on a clinical endpoint that can be measured earlier than irreversible morbidity or mortality, that is reasonably likely to predict an effect on irreversible morbidity or mortality or other clinical benefit, taking into account the severity, rarity or prevalence of the condition and the availability or lack of alternative treatments. In clinical trials, a surrogate endpoint is a measurement of laboratory or clinical signs of a disease or condition that substitutes for a direct measurement of how a patient feels, functions or survives. The accelerated approval pathway is most often used in settings in which the course of a disease is long, and an extended period of time is required to measure the intended clinical benefit of a product, even if the effect on the surrogate or intermediate clinical endpoint occurs rapidly. Thus, accelerated approval has been used extensively in the development and approval of products for treatment of a variety of cancers in which the goal of therapy is generally to improve survival or decrease morbidity and the duration of the typical disease course requires lengthy and sometimes large studies to demonstrate a clinical or survival benefit. The accelerated approval pathway is contingent on a sponsor’s agreement to conduct additional post-approval confirmatory studies to verify and describe the product’s clinical benefit. These confirmatory trials must be completed with due diligence and, in some cases, the FDA may require that the trial be designed, initiated and/or fully enrolled prior to approval. Failure to conduct required post-approval studies, or to confirm a clinical benefit during post-marketing studies, would allow the FDA to withdraw the product from the market on an expedited basis. All promotional materials for product candidates approved under accelerated regulations are subject to prior review by the FDA.

Even if a product qualifies for one or more of these programs, the FDA may later decide that the product no longer meets the conditions for qualification or the time period for FDA review or approval may not be shortened. Furthermore, fast track designation, breakthrough therapy designation, priority review and accelerated approval do not change the standards for approval, but may expedite the development or approval process.

Pediatric Information

Under the Pediatric Research Equity Act ("PREA"), an NDA or supplements to an NDA must contain data to assess the safety and effectiveness of the drug for the claimed indications in all relevant pediatric subpopulations and to support dosing and administration for each pediatric subpopulation for which the drug is safe and effective. The FDA may grant full or partial waivers, or deferrals, for submission of data. Unless otherwise required by regulation, PREA does not apply to any drug for an indication for which orphan designation has been granted, with certain exceptions.

20

The Best Pharmaceuticals for Children Act ("BPCA"), provides NDA holders a six-month extension of any exclusivity—patent or nonpatent—for a drug if certain conditions are met. Conditions for exclusivity include the FDA’s determination that information relating to the use of a new drug in the pediatric population may produce health benefits in that population, the FDA making a written request for pediatric studies, and the applicant agreeing to perform, and reporting on, the requested studies within the statutory timeframe. Applications under the BPCA are treated as priority applications, with all of the benefits that designation confers.

Post-Approval Requirements

Once an NDA is approved, a product will be subject to certain post-approval requirements. For instance, the FDA closely regulates the post-approval marketing and promotion of drugs, including standards and regulations for direct-to-consumer advertising, off-label promotion, industry-sponsored scientific and educational activities and promotional activities involving the internet. Drugs may be marketed only for the approved indications and in a manner consistent with the approved labeling.

Adverse event reporting and submission of periodic reports are required following FDA approval of an NDA. The FDA also may require post-marketing testing, known as phase 4 testing, REMS, and surveillance to monitor the effects of an approved product, or the FDA may place conditions on an approval that could meetrestrict the criteriadistribution or use of the product. In addition, quality control, drug manufacture, packaging and labeling procedures must continue to conform to cGMP after approval. Drug manufacturers and certain of their subcontractors are required to register their establishments with the FDA and certain state agencies. Registration with the FDA subjects entities to periodic unannounced inspections by the FDA, during which the Agency inspects manufacturing facilities to assess compliance with cGMP. Accordingly, manufacturers must continue to expend time, money and effort in the areas of production and quality-control to maintain compliance with cGMP. Regulatory authorities may withdraw product approvals or request product recalls if a company fails to comply with regulatory standards, if it encounters problems following initial marketing, or if previously unrecognized problems are subsequently discovered.

Once an approval is granted, the FDA may withdraw the approval if compliance with regulatory requirements and standards is not maintained or if problems occur after the product reaches the market. Later discovery of previously unknown problems with a product, including adverse events of unanticipated severity or frequency, or with manufacturing processes or failure to comply with regulatory requirements, may result in revisions to the approved labeling to add new safety information, imposition of post-market studies or clinical studies to assess new safety risks or imposition of distribution or other restrictions under a REMS program. Other potential consequences include, among other things:

The Hatch-Waxman Act Orange Book Listing

Under the Drug Price Competition and Patent Term Restoration Act of 1984, commonly referred to as the Hatch Waxman Amendments, NDA applicants are required to identify to the FDA each patent whose claims cover the applicant’s drug or approved method of using the drug. Upon approval of a drug, the applicant must update its listing of patents to the NDA in timely fashion and each of the patents listed in the application for regulationthe drug is then published in the FDA’s Approved Drug Products with Therapeutic Equivalence Evaluations, commonly known as the Orange Book.

21

Drugs listed in the Orange Book can, in turn, be cited by potential generic competitors in support of approval of an abbreviated new drug application ("ANDA"). An ANDA provides for marketing of a drug product that has the same active ingredient(s), strength, route of administration, and dosage form as the listed drug and has been shown through bioequivalence testing to be therapeutically equivalent to the listed drug. An approved ANDA product is considered to be therapeutically equivalent to the listed drug. Other than the requirement for bioequivalence testing, ANDA applicants are not required to conduct, or submit results of, pre-clinical or clinical tests to prove the safety or effectiveness of their drug product. Drugs approved under the ANDA pathway are commonly referred to as “generic equivalents” to the listed drug and can often be substituted by pharmacists under prescriptions written for the original listed drug pursuant to each state’s laws on drug substitution.

The ANDA applicant is required to certify to the FDA concerning any patents identified for the reference listed drug in the Orange Book. Specifically, the applicant must certify to each patent in one of the following ways: (i) the required patent information has not been filed; (ii) the listed patent has expired; (iii) the listed patent has not expired but will expire on a particular date and approval is sought after patent expiration; or (iv) the listed patent is invalid or will not be infringed by the new product. A certification that the new product will not infringe the already approved product’s listed patents, or that such patents are invalid, is called a Paragraph IV certification. For patents listed that claim an approved method of use, under certain circumstances the ANDA applicant may also elect to submit a section 361 HCT/P, butviii statement certifying that its proposed ANDA label does not contain (or carves out) any language regarding the patented method-of-use rather than certify to a listed method-of-use patent. If the applicant does not challenge the listed patents through a Paragraph IV certification, the ANDA application will not be approved until all the listed patents claiming the referenced product have expired. If the ANDA applicant has provided a Paragraph IV certification to the FDA, the applicant must also send notice of the Paragraph IV certification to the NDA-holder and patentee(s) once the ANDA has been accepted for filing by the FDA (referred to as the “notice letter”). The NDA and patent holders may then initiate a patent infringement lawsuit in response to the notice letter. The filing of a patent infringement lawsuit within 45 days of the receipt of a Paragraph IV certification automatically prevents the FDA from approving the ANDA until the earlier of 30 months from the date the notice letter is received, expiration of the patent, the date of a settlement order or consent decree signed and entered by the court stating that the patent that is the subject of the certification is invalid or not infringed, or a decision in the patent case that is favorable to the ANDA applicant.

The ANDA application also will not be approved until any applicable non-patent exclusivity listed in the Orange Book for the referenced product has expired. In some instances, an ANDA applicant may receive approval prior to expiration of certain non-patent exclusivity if the applicant seeks, and the FDA permits, the omission of such exclusivity-protected information from the ANDA prescribing information.

Exclusivity

Upon an NDA approval of a new chemical entity ("NCE"), which is a drug that contains no active moiety that has been approved by the FDA in any other NDA, that drug receives five years of marketing exclusivity during which the FDA cannot receive any ANDA seeking approval of a generic version of that drug unless the application contains a Paragraph IV certification, in which case the application may be submitted one year prior to expiration of the NCE exclusivity. If there is no guaranteelisted patent in the Orange Book, there may not be a Paragraph IV certification, and, thus, no ANDA for a generic version of the drug may be filed before the expiration of the exclusivity period.

Certain changes to an approved drug, such as the approval of a new indication, the approval of a new strength, and the approval of a new condition of use, are associated with a three-year period of exclusivity from the date of approval during which the FDA cannot approve an ANDA for a generic drug that includes the change. In some instances, an ANDA applicant may receive approval prior to expiration of the three-year exclusivity if the applicant seeks, and the FDA would agreepermits, the omission of such exclusivity-protected information from the ANDA package insert.

Patent Term Extension

The Hatch Waxman Amendments permit a patent term extension as compensation for patent term lost during the FDA regulatory review process. Patent term extension, however, cannot extend the remaining term of a patent beyond a total of 14 years from the

22