Our net product sales from Wal-Mart Stores, Inc. aggregated approximately 22.7%, 23.5%, and 24.2% of net product sales during the years ended December 31, 2021, 2020 and 2019, respectively. Our net sales from Dollar Tree, Inc. (which includes net sales from Family Dollar which is owned by Dollar Tree) aggregated approximately 12.1%, 11.7%, and 11.3% of net product sales during the years ended December 31, 2021, 2020 and 2019, respectively. Some of the aforementioned sales to Wal-Mart and Dollar Tree were sold to McLane Company, a large national grocery wholesaler, which services and delivers certain of the Company’s products to Wal-Mart, Dollar Tree and other retailers in the U.S.A. Net product sales revenues from McLane, which includes these Wal-Mart and Dollar Tree sales as well as sales and deliveries to other Company customers, were 21.0% in 2021 and 22.1% in 2020 and 17.7% in 2019. At December 31, 2021 and 2020, the Company’s three largest customers discussed above accounted for approximately 36% and 21% of total accounts receivable, respectively. Although no customer, other than McLane Company, Inc., Wal-Mart Stores, Inc. and Dollar Tree, accounted for more than 10% of net product sales, the loss of one or more significant customers could have a material adverse effect on the Company’s business. The Company historically offers extended credit terms for sales made under seasonal sales programs, including Halloween. Each year, after accounts receivables related to third quarter sales have been collected, the Company invests such funds in various marketable securities.

Sales revenues from Wal-Mart Stores, Inc. aggregated approximately 24.0%, 23.3%, and 23.7% of net product sales during the years ended December 31, 2017, 2016 and 2015, respectively. Some of the aforementioned sales to Wal-Mart are sold to McLane Company, a large national grocery wholesaler, which services and delivers certain of the Company’s products to Wal-Mart and other retailers in the U.S.A. Net product sales revenues from McLane, which includes these Wal-Mart sales as well as sales and deliveries to other Company customers, were 16.9% in 2017 and 16.3% in 2016 and 16.7% in 2015. Although no customer other than McLane Company, Inc. and Wal-Mart Stores, Inc. accounted for more than 10% of net product sales, the loss of one or more significant customers could have a material adverse effect on the Company’s business.

For a summary of sales and long-lived assets of the Company by geographic area see Note 9 of the “NotesNotes to Consolidated Financial Statements”Statements which is incorporated herein by reference.

4

Information regarding the Company’s Form 10-K, Form 10-Q, current reports on Form 8-K, and any amendments to these reports, will be made available, free of charge, upon written request to Tootsie Roll Industries, Inc., 7401 South Cicero Avenue, Chicago, Illinois 60629, Attention: Barry Bowen, Treasurer and Assistant Secretary. The Company does not make all such reports available on its website at www.tootsie.com because it believes that they are readily available from the Securities Exchange Commission at www.sec.gov, and because the Company provides them free of charge upon request. The information on our website is not incorporated into this Annual Report on Form 10-K. Interested parties, including shareholders, may communicate to the Board of Directors or any individual director in writing, by regular mail, addressed to the Board of Directors or an individual director, in care of Tootsie Roll Industries, Inc., 7401 South Cicero Avenue, Chicago, Illinois 60629, Attention: Ellen R. Gordon, Chairman and Chief Executive Officer. If an interested party wishes to communicate directly with the Company’s non-employee directors, it should be noted on the cover of the communication.

Significant factors that could impact the Company’s financial condition or results of operations include, without limitation, the following:

Risk factors which we believe affect all competitors in our industry

|

|

a. Significant reductions in demand for one or more of our products - Changes in demand may be caused by, among other things, the temporary inability of consumers to purchase our products due to illness, quarantine, travel restrictions, financial hardship, “shelter in place” directives, or overall fear to return to past behaviors.

5

Shifts in demand for one or more of our products, changes in trade and distribution patterns, or changes in consumer buying habits, if prolonged, could negatively impact our results.

b. The inability to meet our customers’ needs and achieve efficient production of finished products - Disruptions in our manufacturing operations or supply chain delivery disruptions caused by the loss or disruption of essential manufacturing ingredients, materials, supplies and services, transportation resources, workforce availability, or other manufacturing and distribution capability could have significant adverse effects on our business and financial results.

c. Significant adverse changes in the political conditions and government mandates or directives - In markets in which we manufacture, sell or distribute our products, governmental or regulatory actions, closures or other restrictions such as quarantine or travel restrictions, that limit or close our manufacturing, distribution or office facilities, or otherwise prevent our third-party suppliers, sales brokers, or customers from achieving the level of operations necessary for the production, distribution, sale, and support of our products, could negatively impact our results.

d. Risk related to Halloween and other seasonal sales - The Company’s net product sales are highest during the Halloween season which have historically comprised approximately 50% of third quarter domestic net product sales. Changes in consumer behavior, traditions, behaviors, and interest in Halloween activities and events, or changes mandated or recommended by government or health officials, as well as negative media coverage, could significantly affect the Company’s seasonal sales.

e. Risks relating to potential employer liability – The effects of Covid-19 relating to employer liability remains uncertain, and if it is determined that employers are to have liability for employee or other matters related to Covid-19, this could have significant adverse effects on our financial results.

| Risk of changes in the price and availability of ingredients and raw materials - The principal ingredients used by the Company are subject to price volatility. Although the Company engages in commodity hedging transactions and annual supply agreements as well as leveraging the high volume of its annual purchases, the Company may experience price increases in |

| Risk of changes in product performance and competition - The Company competes with other well-established manufacturers of confectionery products. A failure of new or existing products to be favorably received, a failure to retain preferred shelf space at retail or a failure to sufficiently counter aggressive promotional and price competition could have an adverse impact on the Company’s results of operations and financial condition. |

| Risk of discounting and other competitive actions - Discounting and pricing pressure by the Company’s retail customers and other competitive actions could make it more difficult for the Company to maintain its operating margins. Actions taken by major customers and competitors may make shelf space less available for |

| Risk of pricing actions |

| Risk related to seasonality of sales - The Company’s sales are highest during the Halloween |

6

| Halloween, such as, widespread adverse weather or other widespread events that affect consumer behavior and related media coverage at that time of year or general changes in consumer interest in Halloween, could significantly affect the Company’s sales. |

|

|

5

|

| Risk of changes in consumer preferences and tastes - Failure to adequately anticipate and react to changing demographics, consumer trends, consumer health concerns and product preferences, including product ingredients and packaging materials, could have an adverse impact on the Company’s results of operations and financial condition. |

| Risk of economic conditions on consumer purchases - The Company’s sales are impacted by consumer spending levels and impulse purchases which are affected by general macroeconomic conditions, consumer confidence, employment levels, disposable income, inflation, availability of consumer credit and interest rates on that credit, consumer debt levels, energy costs and other factors. Volatility in food and energy costs, rising unemployment and/or underemployment, declines in personal spending, |

| Risks related to environmental matters - The Company’s operations are not particularly impactful on the environment, but increased government environmental regulation or legislation, including various “green” initiatives could adversely impact the Company’s profitability. |

| ● | Risk of new governmental laws and regulations - Governmental laws and regulations, including those that affect food advertising and marketing to children, use of certain ingredients in products, new labeling requirements, income and other taxes and tariffs, including the effects of changes to international trade agreements, new taxes targeted toward confectionery products and the environment, both in and outside the U.S.A., are subject to change over time, which could adversely impact the Company’s results of operations and ability to compete in domestic or foreign marketplaces. |

| ● | Risk of labor stoppages - To the extent the Company experiences any significant labor stoppages, strikes or possible labor shortages, could negatively affect overall operations including production or shipments of finished product to customers. The Company’s union labor agreement at its Chicago plant was executed in 2018 and will continue through September 2022. |

| ● | Risk of the cost of energy increasing - Higher energy costs would likely result in higher plant overhead, distribution, freight and delivery, and other operating costs. The Company may not be able to offset these cost increases or pass such cost increases onto customers in the form of price increases, which could have an adverse impact on the Company’s results of operations and financial condition. In addition, higher energy costs also adversely affect the cost of many resins which are used as a foundation material for many of our packaging materials. |

| ● | Risk of a product recall - Issues related to the quality and safety of the Company’s products could result in a voluntary or involuntary large-scale product recall. Costs associated with a product recall and related litigation or fines, and marketing costs relating to the re-launch of such products or brands, could negatively affect operating results. In addition, negative publicity associated with this type of event, including a product recall relating to product contamination or product tampering, whether valid or not, could negatively impact future demand for the Company’s products. |

| ● | Risk of operational interruptions relating to computer software or hardware failures, including cyber-attacks - The Company is reliant on computer systems to operate its business and supply chain. Software failure or corruption, including cyber-based attacks or network security breaches, or catastrophic hardware or software failures or other disasters could disrupt communications, supply chain planning and activities relating to sales demand forecasts, materials procurement, production and inventory planning, customer orders, shipments, and collections, and financial and accounting, all of which could negatively impact sales and profits. |

7

| Risk of releasing sensitive information - Although the Company does not believe that it maintains a large amount of sensitive data, a system breach, whether inadvertent or perpetrated by hackers, could result in identity theft, ransomware and/or a disruption in operations which could expose the Company to financial costs and adversely affect profitability. |

| ● | Disruption to the Company’s supply chain could impair the Company’s ability to produce or deliver its finished products, resulting in a negative impact on operating results - Disruption to the manufacturing operations or supply chain, some of which are discussed above, could result from, but are not limited to adverse tariffs which could effectively limit supply or make supply more costly, natural disasters, pandemics, weather, fire or explosion, earthquakes, terrorism or other acts of violence, unavailability of ingredients or packaging materials which could result if our suppliers are unable to obtain certain raw materials or make timely deliveries, labor strikes or other labor activities, labor shortages including over-the-road truck drivers, logistical delays including materials from foreign locations, operational and/or financial instability of key suppliers, and other vendors or service providers. Although precautions are taken to mitigate the impact of possible disruptions, if the Company is unable, or if it is not financially feasible to effectively mitigate the likelihood or potential impact of such disruptive events, the Company’s results of operations and financial condition could be negatively impacted. |

Risk factors which we believe are principally specific to our Company (although some may apply to varying degrees to competitors in our industry)

| ● | Risks relating to participation in the multi-employer pension plan for certain Company union employees - As outlined in the Note 7 of the Company’s Notes to |

|

|

|

|

| Risk of impairment of goodwill or indefinite-lived intangible assets - In accordance with authoritative guidance, goodwill and indefinite-lived intangible assets are not amortized but are subject to an impairment evaluation annually or more frequently upon the occurrence of a triggering event. Other long-lived assets are likewise tested for impairment upon the occurrence of a triggering event. Such evaluations are based on assumptions and variables including sales growth, profit margins and discount rates. Adverse changes in any of these variables could affect the carrying value of these intangible assets and the Company’s reported profitability. |

|

|

6

|

|

|

|

|

|

|

| Risk of production interruptions - The majority of the Company’s products are manufactured in a single production facility on specialized equipment. In the event of a disaster, such as a fire or earthquake, at a specific plant location, or other disruption, it would be difficult to transfer production to other facilities or a new location in a timely manner, which could result in loss of market share for the affected products. In addition, from time to time, the Company upgrades or replaces this specialized equipment. In many cases these are integrated and complex installations. A failure or delay in implementing such an installation could impact the availability of one or more of the Company’s products which would have an adverse impact on sales and profits. |

| ● | Risk related to investments in marketable securities - The Company invests its surplus cash in a diversified portfolio of highly rated marketable securities, including corporate bonds, with maturities of generally up to three years, and variable rate demand notes with weekly resets of interest rates and “puts’ to redeem the investment each week. Nonetheless, such investments could become impaired in the event of certain adverse economic and/or geopolitical events which, if severe, would adversely affect the Company’s financial condition. |

8

| Risk of further losses in Spain - The Company has restructured its Spanish subsidiary and is exploring a variety of programs to increase sales and profitability. These efforts thus far are resulting in reductions in operating losses, and our efforts are continuing. Nonetheless, if our efforts are not successful, additional losses and impairments may be reported in the future. See also Management’s Discussion and Analysis. |

| ● | Risk of dependence on large customers - The Company’s largest customers, McLane Company, Wal-Mart and Dollar Tree, accounted for approximately 36% of net product sales in 2021, and other large national chains are also material to the Company’s sales. The loss of any of these customers, or one or more other large customers, or a material decrease in purchases by one or more large customers, could result in decreased sales and adversely impact the Company’s results of operations and financial condition. |

| ● | Risk related to acquisitions - From time to time, the Company has purchased other confectionery companies or brands. These acquisitions generally come at a high multiple of earnings and are justified based on various assumptions related to sales growth, and operating margins. Were the Company to make another acquisition and be unable to achieve the assumed sales and operating margins, it could have an adverse impact on future sales and profits. In addition, it could become necessary to record an impairment which would have a further adverse impact on reported profits. |

| ● | Risk of “slack fill” litigation - The Company, as well as other confectionery and food companies, have experienced a number of plaintiff claims that certain products are sold in boxes that are not completely full, and therefore such “slack filled” products are misleading, and even deceptive, to the consumer. Although the Company believes that these claims are without merit and has generally been successful in litigation and court decrees, the Company could be exposed to significant legal fees to defend its position, and in the event that it is not successful, could be subject to fines and costs of settlement, including class action settlements. |

| ● | Risk related to international operations - To the extent there |

|

|

|

|

|

|

7

|

|

|

|

|

| The Company is a controlled company due to the common stock holdings of the Gordon family - The Gordon family’s share ownership represents a majority of the combined voting power of all classes of the Company’s common stock as of December 31, |

The factors identified above are believed to be significant factors, but not necessarily all of the significant factors, that could impact the Company’s business. Unpredictable or unknown factors could also have material effects on the Company.

Additional significant factors that may affect the Company’s operations, performance and business results include the risks and uncertainties listed from time to time in filings with the Securities and Exchange Commission and the risk factors or uncertainties listed herein or listed in any document incorporated by reference herein.

ITEM 1B. Unresolved Staff Comments.

None.

89

The Company owns its principal manufacturing, warehousing and distribution, and offices facilities which are locatedfacilities. The Company’s largest operating facility in Chicago, Illinois also serves as the Corporate headquarters. The Company also owns domestic manufacturing, warehousing and distribution facilities in a building consisting of approximately 2,354,000 square feet.Tennessee (Covington), Massachusetts (Cambridge), and Wisconsin (Delavan) and international manufacturing facilities in Mexico (Mexico City), Spain (Barcelona) and two in Canada (Concord, Ontario). In addition, the Company leases manufacturing and warehousing facilities at a second location in Chicago which comprises 137,000 square feet.Chicago. The lease is renewable by the Company every five years through June 2041; the Company expects to renew this lease prior to termination. The Company also periodically leases additional warehousing space at this second location as needed on a month-to-month basis.2041.

The Company’s other principal manufacturing, warehousing and distribution facilities, all of which are owned, are:

|

| ||

|

| ||

|

| ||

|

| ||

|

|

| |

|

|

| |

|

| ||

|

|

|

|

|

|

|

|

|

|

|

The Company owns substantially all of the production machinery and equipment located in its plants.plants, warehouses and distribution centers. The Company also holds four commercial real estate properties for investment which were acquired with the proceeds from a sale of surplus real estate in 2005.2005 as well as two warehouse facilities (in Concord, Ontario, Canada, and Hazelton, Pennsylvania, USA) that are currently leased to third parties.

There are no material pendingIn the ordinary course of business, the Company is, from time to time, subject to a variety of active or threatened legal proceedings knownand claims. While it is not possible to predict the Companyoutcome of such matters with certainty, in the Company’s opinion, both individually and in the aggregate, they are not expected to which the Company or any of its subsidiaries ishave a party or of which any of their property is the subject, and no penalties have been imposed by the Internal Revenue Servicematerial effect on the Company.Company’s financial condition, results of operations or cash flows.

ADDITIONAL ITEM. Executive Officers of the Registrant.

See the information on Executive Officers set forth in the table in Part III, Item 10.

ITEM 4. Mine Safety Disclosures.

None.

910

PART II

ITEM 5. Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities.

The Company’s common stock is traded on the New York Stock Exchange. The Company’s Class B common stock is subject to restrictions on transferability. The Class B common stock is convertible at the option of the holder into shares of common stock on a share-for-share basis. As of March 1, 2018,February 21, 2022 there were approximately 2,6002,300 and 1,000900 registered holders of record of common and Class B common stock, respectively. In addition, the Company estimates that as of March 1, 2018February 21, 2022 there were 12,50021,000 and 4,3001,000 beneficial holders of common and Class B common stock, respectively.

The following table sets forth information about the shares of its common stock the Company purchased on the open market during the fiscal quarter ended December 31, 2017:

Issuer Purchases of Equity Securities

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Total Number of |

| Maximum Number (or |

|

|

| Total |

| Average |

| Shares Purchased |

| Approximate Dollar Value) |

| |

|

| Number |

| Price |

| as Part of Publicly |

| of Shares that May Yet |

| |

|

| of Shares |

| Paid per |

| Announced Plans |

| be Purchased Under the |

| |

Period |

| Purchased |

| Share |

| or Programs |

| Plans or Programs |

| |

|

|

|

|

|

|

|

|

|

|

|

Oct 1 to Oct 31 |

| — |

| $ | — |

| Not Applicable |

| Not Applicable |

|

Nov 1 to Nov 30 |

| 54,631 |

|

| 36.36 |

| Not Applicable |

| Not Applicable |

|

Dec 1 to Dec 31 |

| 58,028 |

|

| 36.45 |

| Not Applicable |

| Not Applicable |

|

Total |

| 112,659 |

| $ | 36.40 |

|

|

|

|

|

While the Company does not have a formal or publicly announceddividend policy, but has historically issued quarterly dividends and in 2021 issued a quarterly dividend of $0.09 per share. The Company commonhas also historically distributed an annual 3% stock purchase program,dividend. While the Company repurchases its common stock on the open market from timeplans to time as authorized by the Board of Directors.

Quarterly Stock Prices and Dividends

The high and lowcontinue to issue quarterly prices for the Company’s common stock, as reported on the New York Stock Exchange and quarterly dividends in 2017 and 2016 were:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| 2017 |

| 2016 | ||||||||||||||||||||

|

| 4th |

| 3rd |

| 2nd |

| 1st |

| 4th |

| 3rd |

| 2nd |

| 1st | ||||||||

|

|

| Quarter |

|

| Quarter |

|

| Quarter |

|

| Quarter |

|

| Quarter |

|

| Quarter |

|

| Quarter |

|

| Quarter |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

High |

| $ | 38.45 |

| $ | 38.00 |

| $ | 38.90 |

| $ | 40.55 |

| $ | 41.55 |

| $ | 38.44 |

| $ | 39.54 |

| $ | 34.98 |

Low |

|

| 34.75 |

|

| 34.95 |

|

| 34.45 |

|

| 37.00 |

|

| 34.35 |

|

| 36.48 |

|

| 34.08 |

|

| 30.41 |

Dividends per share |

|

| 0.09 |

|

| 0.09 |

|

| 0.09 |

|

| 0.09 |

|

| 0.09 |

|

| 0.09 |

|

| 0.09 |

|

| 0.09 |

NOTE: In addition to the above cash dividends a 3%and the annual stock dividend was issued on April 17, 2017 and April 8, 2016. there can be no assurance that it will continue to do so in the future.

10

Performance Graph

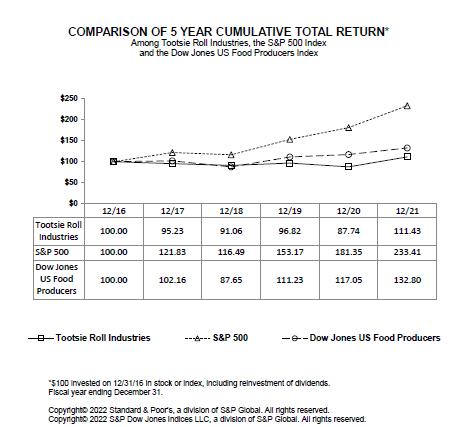

The following performance graph compares the cumulative total shareholder return on the Company’s common stock for a five-year period (December 31, 20122016 to December 31, 2017)2021) with the cumulative total return of Standard & Poor’s 500 Stock Index (“S&P 500”) and the Dow Jones Industry Food Index (“Peer Group,” which includes the Company), assuming (i) $100 invested on December 31 of the first year of the chart in each of the Company’s common stock, S&P 500 and the Dow Jones Industry Food Index and (ii) the reinvestment of cash and stock dividends.

![]()

11

ITEM 6. Selected Financial Data.

Five Year Summary of Earnings and Financial Highlights

(Thousands of dollars except per share, percentage and ratio figures)

| | | | | | | | | | | | | | | | |

|

| 2021 |

| 2020 |

| 2019 |

| 2018 |

| 2017 |

| |||||

Sales and Earnings Data | | | | | | | | | | | | | | | | |

Net product sales | | $ | 566,043 | | $ | 467,427 | | $ | 523,616 | | $ | 515,251 | | $ | 515,674 | |

Product gross margin | |

| 195,938 | |

| 167,717 | |

| 194,514 | |

| 185,371 | |

| 189,263 | |

Interest expense | |

| 46 | |

| 164 | |

| 220 | |

| 181 | |

| 144 | |

Provision for income taxes | |

| 20,421 | |

| 17,288 | |

| 20,565 | |

| 16,401 | |

| 3,907 | |

Net earnings attributable to Tootsie Roll Industries, Inc. | |

| 65,326 | |

| 58,995 | |

| 64,920 | |

| 56,893 | |

| 80,864 | (2) |

% of net product sales | |

| 11.5 | % |

| 12.6 | % |

| 12.4 | % |

| 11.0 | % |

| 15.7 | % |

% of shareholders’ equity | |

| 8.5 | % |

| 7.7 | % |

| 8.5 | % |

| 7.6 | % |

| 11.0 | % |

Per Common Share Data (1) | | | | | | | | | | | | | | | | |

Net earnings attributable to Tootsie Roll Industries, Inc. | | $ | 0.97 | | $ | 0.86 | | $ | 0.94 | | $ | 0.81 | | $ | 1.14 | (2) |

Cash dividends declared | |

| 0.36 | |

| 0.36 | |

| 0.36 | |

| 0.36 | |

| 0.36 | |

Stock dividends | |

| 3 | % |

| 3 | % |

| 3 | % |

| 3 | % |

| 3 | %�� |

Additional Financial Data (1) | | | | | | | | | | | | | | | | |

Working capital | | $ | 188,333 | | $ | 250,851 | | $ | 273,786 | | $ | 242,655 | | $ | 207,132 | |

Net cash provided by operating activities | |

| 85,298 | |

| 74,710 | |

| 100,221 | |

| 100,929 | |

| 42,973 | |

Net cash provided by (used in) investing activities | |

| (91,899) | |

| 9,501 | |

| (15,009) | |

| (44,510) | |

| (9,320) | |

Net cash used in financing activities | |

| (54,146) | |

| (55,846) | |

| (57,187) | |

| (42,353) | |

| (56,881) | |

Property, plant & equipment additions | |

| 31,426 | |

| 17,970 | |

| 20,258 | |

| 27,612 | |

| 16,673 | |

Net property, plant & equipment | |

| 208,906 | |

| 187,328 | |

| 188,455 | |

| 186,101 | |

| 178,972 | |

Total assets | |

| 1,018,618 | |

| 984,558 | |

| 977,864 | |

| 947,361 | |

| 930,946 | |

Long-term debt | |

| 7,500 | |

| 7,500 | |

| 7,500 | |

| 7,500 | |

| 7,500 | |

Total Tootsie Roll Industries, Inc. shareholders’ equity | |

| 769,042 | |

| 763,327 | |

| 759,854 | |

| 750,622 | |

| 733,840 | |

Average shares outstanding | |

| 67,431 | |

| 68,482 | |

| 69,386 | |

| 70,042 | |

| 70,874 | |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| 2017 |

| 2016 |

| 2015 |

| 2014 |

| 2013 |

| |||||

Sales and Earnings Data |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Net product sales |

| $ | 515,674 |

| $ | 517,373 |

| $ | 536,692 |

| $ | 539,895 |

| $ | 539,627 |

|

Product gross margin |

|

| 189,750 |

|

| 197,083 |

|

| 196,602 |

|

| 198,962 |

|

| 188,667 |

|

Interest expense |

|

| 144 |

|

| 105 |

|

| 76 |

|

| 99 |

|

| 92 |

|

Provision for income taxes |

|

| 3,907 |

|

| 30,593 |

|

| 26,451 |

|

| 28,434 |

|

| 23,634 |

|

Net earnings attributable to Tootsie Roll Industries, Inc. |

|

| 80,864 |

|

| 67,510 |

|

| 66,089 |

|

| 63,298 |

|

| 60,849 |

|

% of net product sales |

|

| 15.7 | % |

| 13.0 | % |

| 12.3 | % |

| 11.7 | % |

| 11.3 | % |

% of shareholders’ equity |

|

| 11.0 | % |

| 9.5 | % |

| 9.5 | % |

| 9.2 | % |

| 8.9 | % |

Per Common Share Data (1) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Net earnings attributable to Tootsie Roll Industries, Inc. |

| $ | 1.28 |

| $ | 1.05 |

| $ | 1.02 |

| $ | 0.96 |

| $ | 0.91 |

|

Cash dividends declared |

|

| 0.36 |

|

| 0.36 |

|

| 0.35 |

|

| 0.32 |

|

| 0.32 |

|

Stock dividends |

|

| 3 | % |

| 3 | % |

| 3 | % |

| 3 | % |

| 3 | % |

Additional Financial Data (1) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Working capital |

| $ | 207,132 |

| $ | 235,739 |

| $ | 221,744 |

| $ | 200,162 |

| $ | 179,990 |

|

Net cash provided by operating activities |

|

| 42,973 |

|

| 98,550 |

|

| 91,073 |

|

| 88,769 |

|

| 109,823 |

|

Net cash provided by (used in) investing activities |

|

| (9,343) |

|

| (51,884) |

|

| (8,523) |

|

| (30,459) |

|

| (47,963) |

|

Net cash used in financing activities |

|

| (56,881) |

|

| (51,387) |

|

| (53,912) |

|

| (44,664) |

|

| (37,425) |

|

Property, plant & equipment additions |

|

| 16,673 |

|

| 16,090 |

|

| 15,534 |

|

| 10,704 |

|

| 15,752 |

|

Net property, plant & equipment |

|

| 178,972 |

|

| 180,905 |

|

| 184,586 |

|

| 190,081 |

|

| 196,916 |

|

Total assets |

|

| 930,946 |

|

| 920,101 |

|

| 908,983 |

|

| 910,386 |

|

| 888,409 |

|

Long-term debt |

|

| 7,500 |

|

| 7,500 |

|

| 7,500 |

|

| 7,500 |

|

| 7,500 |

|

Total Tootsie Roll Industries, Inc. shareholders’ equity |

|

| 733,840 |

|

| 711,364 |

|

| 698,183 |

|

| 690,809 |

|

| 680,305 |

|

Average shares outstanding |

|

| 63,179 |

|

| 64,086 |

|

| 65,103 |

|

| 66,020 |

|

| 66,857 |

|

| (1) |

| Per common share data and average shares outstanding adjusted for annual 3% stock dividends. |

| (2) | The 2017 net earnings and earnings per share includes $20,318 or $0.29 per share relating to a favorable accounting adjustment to revalue the Company’s deferred income tax liabilities resulting from the enactment of the U.S. Tax Cuts and Jobs Act in December 2017. |

12

ITEM 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations.

(Thousands(Thousands of dollars except per share, percentage and ratio figures)

The following discussion should be read in conjunction with the other sections of this report, including the consolidated financial statements and related notes contained in Item 8 of this Form 10-K.

FINANCIAL REVIEW

This financial review discusses the Company’s financial condition, results of operations, liquidity and capital resources, significant accounting policies and estimates, new accounting pronouncements, market risks and other matters. It should be read in conjunction with the Consolidated Financial Statements and related Notes that follow this discussion.

FINANCIAL CONDITION

The Company’s overall financial position remains strong as a result of net earnings increasing from $67,318 in 2016 to 80,654 in 2017, andgiven that aggregate cash, cash equivalents and investments including long-term investments, of $328,430is $436,983 at December 31, 2017.2021, including $89,736 in trading securities discussed below. Cash flows from 20172021 operating activities totaled $42,973$85,298 compared to $74,710 in 2020, and are discussed in the section entitled Liquidity and Capital Resources. During 2017,2021, the Company paid cash dividends of $22,621,$24,136, purchased and retired $34,133$30,184 of its outstanding shares, and made capital expenditures of $16,673.$31,426.

The Company’s net working capital was $207,132$188,333 at December 31, 20172021 compared to $235,739$250,851 at December 31, 2016 which generally2020. This change principally reflects lower aggregate cash, cash equivalents and short-term investments.the effects of a $71,155 increases in long-term investments because more of our investments have maturities greater than one year at December 31, 2021 compared to December 31, 2020. As of December 31, 2017,2021, the Company’s total cash, cash equivalents and investments, including all long-term investments, in marketable securities, was $328,430$436,983 compared to $351,323$428,951 at December 31, 2016, a decrease2020, an increase of $22,893, which generally reflects increases in prepaid expenses and current income taxes receivable as well as payments of deferred compensation in 2017.$8,032. See Liquidity And Capital Resources section below. The aforementioned includes $60,520$89,736 and $67,995$73,828 of investments in trading securities as of December 31, 20172021 and 2016,2020, respectively. The Company invests in trading securities to provide an economic hedge for its deferred compensation liabilities, as further discussed herein and in Note 7 of the Company’s Notes to Consolidated Financial Statements.

Shareholders’ equity increased from $711,364$763,327 at December 31, 20162020 to $733,840$769,041 as of December 31, 2017,2021, which principally reflecting 2017reflects 2021 net earnings of $80,864,$65,326, less cash dividends of $22,621,$24,136 and share repurchases of $34,133, and an increase in accumulated other comprehensive loss, primarily foreign translation, of $1,545 during 2017.$30,184.

The Company has a relatively straight-forward financial structure and has historically maintained a conservative financial position. Except for an immaterial amount of operating leases, theThe Company has no special financing arrangements or “off-balance sheet” special purpose entities. Cash flows from operations plus maturities of short-term investments are expected to be adequate to meet the Company’s overall financing needs, including capital expenditures, in 2018.2021. Periodically, the Company considers possible acquisitions, and if the Company were to pursue and complete such an acquisition, that could result in bank borrowings or other financing.

RESULTS OF OPERATIONS

20172021 vs. 20162020

Twelve months 20172021 consolidated net product sales were $515,674$566,043 compared to $517,373$467,427 in twelve months 2016, a decrease2020, an increase of $1,699$98,616 or 0.3%21.1%. Twelve months 2017 consolidatedFourth quarter 2021 net product sales were adversely affected by currency translation of $2,047 due to a stronger U.S. dollar in 2017$166,598 compared to 2016, principally relating to the Company’s Mexican subsidiary. Fourth quarter 2017 net sales were $125,179 compared to $124,279$127,866 in fourth quarter 2016,2020, an increase of $900$38,732, or 0.7%30%. Unfavorable foreign exchange, primarily Mexico, also contributed to lower salesThe growth in fourth quarter 2017 comparedand twelve months 2021 sales reflect effective sales and marketing programs as well as the favorable effects of the continuing economic recovery from the adverse effects of the Covid-19 pandemic. The Company had continuing improvement in customer orders and sales throughout 2021 as consumers returned to more activities which included planned purchases of the Company’s products for “sharing” and “give-a-way” occasions. Many of the Company’s products are consumed at group events, outings, and other gatherings which had been significantly curtailed or in some cases eliminated in response to the Covid-19 virus. Fourth quarter 2021 sales also exceeded fourth quarter 2019 sales by 24% which provides a quarterly sales comparison to a period prior year corresponding period. The Company’s unit selling prices and price realization in 2017 was consistent with 2016. Theto the

13

Company’spandemic, and twelve months 2021 sales results inwere 8% ahead of twelve months 2019 sales. Fourth quarter 2021 sales also benefited from the United States continuetiming of some sales that were rescheduled from third to reflect the challenges of many of the Company’s retail customers including their profit margin pressures and other competitive factors.fourth quarter due to supply chain disruptions.

Product cost of goods sold were $325,924$370,105 in 20172021 compared to $320,290$299,710 in 2016,2020, an increase of $5,634$70,395 or 1.8%23.5%. Product cost of goods sold includes $1,953$687 and $1,137$610 in certain deferred compensation expenses in 20172021 and 2016,2020, respectively. These deferred compensation expenses principally result from changes in the market value of investments and investment income from trading securities relating to compensation deferred in previous years and are not reflective of current operating results. Adjusting for the aforementioned, product cost of goods sold increased from $319,153$299,100 in 20162020 to $323,971$369,418 in 2017,2021, an increase of $4,818$70,318 or 1.5%23.5%. As a percent of net product sales, these adjusted costs increased from 61.7%64.0% in 20162020 to 62.8%65.3% in 2017, an2021, a 1.3 unfavorable increase of 1.1% as a percent of net product sales. Higherpercentage point change. Fourth quarter and twelve months 2021 gross profit margins were adversely affected by increasing costs for ingredients, packaging materials, and certain manufacturing plant overhead, including increases in wages, salariessupplies and benefits, contributed to higherservices. Fourth quarter and twelve months product cost of goods sold compared to the corresponding prior year periods, were also adversely impacted by inefficiencies caused by higher than expected sales demand, supply chain challenges and adversely affecteddisruptions, longer supplier lead times, and some labor shortages. These factors resulted in additional costs related to our efforts to meet this higher demand. Certain cost and expense reductions, including Company initiatives to reduce costs did provide some benefit to 2021 gross profit margins in 2017 compared to 2016. Continuing improvements in manufacturing plant efficiencies driven by capital investments and ongoing cost containment programs mitigated some of these higher costs and expenses. The Company is continuing its focus on capital expenditures that will result in operational efficiencies and cost reductions, as well as product improvements.margins.

Selling, marketing and administrative expenses were $120,977$132,108 in 20172021 compared to $107,377$112,117 in 2016,2020, an increase of $13,600$19,991 or 12.7%17.8%. Selling, marketing and administrative expenses include $8,024$13,521 and $3,138$11,909 in certain deferred compensation expenses in 20172021 and 2016,2020, respectively. These deferred compensation expenses principally result from changesincreases in the market value of investments and investment income from trading securities relating to compensation deferred in previous years and are not reflective of current operating results. Adjusting for the aforementioned, theseselling, marketing and administrative expenses increased from $104,239$100,208 in 20162020 to $112,953$118,587 in 2017,2021, an increase of $8,714$18,379 or 8.4%18.3%. AsThis increase was principally driven by the increase in certain variable expenses, primarily freight and delivery and direct selling expenses, relating to the increase in sales as discussed above. However, as a percent of net product sales, these adjusted expenses increaseddecreased from 20.1%21.4% of net product sales in 20162020 to 21.9%21.0% of net product sales in 2017,2021, a 1.7% unfavorable increase as a0.4 favorable percentage of sales.point change.

Selling, marketing and administrative expenses include freight, delivery and warehousing expenses. These expenses increased from $40,629$42,593 in 20162020 to $43,973$55,289 in 2017,2021, an increase of $3,344$12,696 or 8.2%29.8%. As a percent of net product sales, these adjusted expenses increased from 7.9%9.1% in 20162020 to 8.5%9.8% in 2017, an2021, a 0.7 unfavorable increasepercentage point change. Increasing energy costs and related effects on fuel surcharges, and the adverse effects of 0.6% as a percentthe continuing shortage of net product sales. Increasingover-the-road drivers and high demand for over-the-road truckcarriers, were the principal drivers of these higher freight and delivery expenses in 2021 compared to 2020.

In response to the higher input costs discussed above, the confectionary industry, as well as many companies in the broader consumer products industry, announced increases in selling prices. We have followed with price increases as well, with the objective of improving sales price realization and an imbalance in supply and demand for freight carriers, has resulted in higher prices for these services, particularlyrestoring margin declines. Price increases, which principally became effective during fourth quarter 2021, contributed to the improved results in fourth quarter 2017. There is a shortage of over-the-road trucks and truck drivers, and2021 as well as the Company expects these related cost pressurestwelve months 2021. Price increases for certain products that were not increased in 2021 have also been announced for first half 2022 in our continuing efforts to continue in 2018. Increases in marketing and sales expenses relatingrestore margins.

Our input costs continued to new product development and packaging changes to comply with product labeling requirements also contributed to higher selling, marketing and administrative expenses in 2017 compared to 2016, and these expenses also were much higherremain elevated in fourth quarter 2017.2021 and we expect even higher costs in 2022 as our 2021 supply contracts and hedging programs come to closure and new contracts and hedging at higher 2022 costs begin to take effect. Higher commodity markets are driving up our costs for key ingredients, packaging materials and energy, including the adverse effects of higher energy costs on freight and delivery fuel surcharges and plant manufacturing utilities. We expect these higher input costs and the overall increase in inflation, some of which is driven by supply chain problems, to continue through most of, and possibly all of, 2022. The Company uses the Last-In-First-Out (LIFO) method of accounting for inventory and costs of goods sold which results in lower current income taxes during such periods of increasing costs, but this method does charge the most current costs to cost of goods sold and thereby accelerates the realization of these higher costs. Although the Company continues to monitor these higher input costs and price increases in the industry, we are mindful of the effects and limits of passing on all of the above discussed higher input costs to consumers of our products. As a result, we believe that margins for part or all of 2022 will not fully recover to historical norms.

14

The Company has foreign operating businesses in Mexico, Canada and Spain, and exports products to many foreign markets. Such foreign sales were $43,452 and comprised 8%The Company’s Spanish subsidiary (97% owned by the Company) incurred an operating loss of the Company’s consolidated net product sales$598 in 2017. In fourth quarter 2017, the Company recorded a pre-tax impairment charge of $2,371 relating2021 which was an improvement compared to its Spanish subsidiaries. The Company currently has a 97% ownership of two Spanish companies (93% ownership at December 31, 2016). During 2017 and 2016, these Spanish subsidiaries incurred operating losses of $3,212 and $1,689, respectively, and the Company provided approximately $2,734 and $886, respectively, of additional cash to finance these losses.$691 loss in 2020. Company management expects the competitive and business challenges in Spain to continue and expectsbut believes that there will be continued reductions in operating losses in 20182022 compared to 2021. Nonetheless, management believes that operating losses will likely continue beyond 2022 and likely beyond; andthat these future losses, as well as some capital expenditures, will likely require some additional cash financing.

The Company believes that the carrying values of its goodwill and trademarks have indefinite lives as they are expected to generate cash flows indefinitely. In accordance with current accounting guidance, these indefinite-lived intangible assets are assessed at least annually for impairment as of December 31 or whenever events or circumstances indicate that the carrying values may not be recoverable from future cash flows. No impairments were recorded in 2017, 20162021, 2020 or 2015.2019. Current accounting guidance provides entities an option of performing a qualitative assessment (a "step-zero" test) before performing a quantitative analysis. If the entity determines, on the basis of certain qualitative factors, that it is more-likely-than-not that the intangibles (goodwill and certain trademarks) are not impaired, the entity would not need to proceed to the two step impairment testing process (quantitative analysis) as prescribed in the guidance. During fourth quarter 2017,2021 (and fourth quarters 2020 and 2019), the Company performed a “step zero” test of its goodwill and certain trademarks, and concluded that there was no impairment based on this guidance. For the fair value assessment of certain trademarks where the “step-zero” analysis was not considered appropriate, impairment testing was performed in fourth quarter 20172021 (and fourth quarters 2020 and 2019) using discounted cash flows and

14

estimated royalty rates. For these trademarks, holding all other assumptions constant at the test date, a 100 basis point increase in the discount rate or a 100 basis point decrease in the royalty rate would reduce the fair value of suchthese trademarks by approximately 16% and 10%, respectively. Individually, a 100 basis point increase in the discount rate or a 100 basis point decrease in the royalty rate would not result in a potential impairment of these trademarks as of December 31, 2017.2021.

Earnings from operations were $71,416$67,133 in 20172021 compared to $92,414$58,244 in 2016, a decrease2020, an increase of $20,998.$8,889. Earnings from operations include $9,977$14,208 and $4,275$12,519 in certain deferred compensation expense in 20172021 and 2016,2020, respectively, which are discussed above. Adjusting for these deferred compensation expenses, adjusted earnings from operations decreasedincreased from $96,689$70,763 in 20162020 to $81,393$81,341 in 2017, a decrease2021, an increase of $15,296$10,578 or 15.8%14.9%. Twelve months results were adversely affected by lower gross profit margins, includingThe above discussed increase in net product sales was the effectsprincipal driver of higher operating earnings in 2021 compared to 2020. Although higher 2021 sales contributed to improved operating earnings compared to the corresponding prior year periods, higher input costs and expenses for ingredients, packaging materials, and manufacturing plant overhead as discussed above. In addition, earnings from operations were also adversely affected by higher selling, marketing and administrative expenses, primarily freight and delivery, marketing and sales expenses relating to new product development and packaging changes to comply with product labeling requirements, and declines in foreign results and an impairmentmitigated much of foreign subsidiaries, allthe benefits of which are discussed above. Many of these increased costs and expenses accelerated in fourth quarter 2017. sales.

Management believes the comparisons presented in the preceding paragraphs, after adjusting for changes in deferred compensation, are more reflective of the underlying operations of the Company.

Other income, net was $13,145$18,596 in 20172021 compared to $5,498$18,018 in 2016,2020, an increase of $7,647.$578. Other income, net principally reflects $9,977$14,208 and $4,275$12,519 of aggregate net gains and investment income on trading securities in 20172021 and 2016,2020, respectively. These trading securities provide an economic hedge of the Company’s deferred compensation liabilities; and the related net gains and investment income were offset by a like amount of expense in aggregate product cost of goods sold and selling, marketing, and administrative expenses in the respective years as discussed above. Other income, net includes investment income on available for sale securities including variable rate demand notes, of $2,851$2,740 and $2,130$4,005 in 20172021 and 2016,2020, respectively. Other income, net also includes foreign exchange gains/(losses)gains of $259$667 and $(955)$534 in 20172021 and 2016,2020, respectively.

In connection with enactment of the U.S. Tax Cuts and Jobs Act (Tax Reform Act) in December 2017, the Company recorded a favorable accounting adjustment of $20,318, or $0.32 per share, during the fourth quarter of 2017. This reflects the estimated benefit from the revaluation of net deferred income tax liabilities based on the new lower U.S. corporateThe Company’s effective income tax rate effective January 1, 2018. U.S. tax reform also includes a one-time toll charge resulting fromwas 23.8% and 22.7% in 2021 and 2020, respectively. The increase in the mandatory deemed repatriation of undistributed foreign earnings and profits. The Company determined that there were no net undistributed foreign earnings and profits subject to this toll charge. Based on SEC guidance in Staff Accounting Bulletin No. 118, the Company considers its accounting for the effects of U.S. tax reform to be provisional as of December 31, 2017. The ultimate impact may differ from these provisional amounts, possibly materially, due to, among other things, additional regulatory guidance that may be issued by the Internal Revenue Service and state authorities.

The consolidated effective tax rate was 4.6% and 31.2%rates in 2017 and 2016, respectively. The principal drivers of the lower 2017 effective2021 generally reflects higher rates for state income tax rate are the effects of U.S. tax reform and a worthless stock deduction relating to the Company’s Spanish subsidiaries, which favorably reduced the Company’s effective 2017 tax rate by 24.2% and 3.8%, respectively.provisions. A reconciliation of the differences between the U.S. statutory rate and these effective tax rates is provided in Note 4 of the Company’s Notes to Consolidated Financial Statements. At December 31, 2017 and 2016, the Company’s deferred tax assets include $3,740 and $6,346 of income tax benefits relating to its Canadian subsidiary tax loss carry-forwards which the Company expects to realize before their expiration dates (2029 through 2031). The Company utilized $2,606 and $1,776 of these tax carry-forward benefits in 2017 and 2016, respectively. The Company has concluded that it is more-likely-than-not that it would realize these deferred tax assets relating to its Canadian tax loss carry-forwards because it is expected that sufficient levels of taxable income will be generated during the carry-forward periods.

The Company has provided a full valuation allowance on its Spanish subsidiaries’ tax loss carry-forward benefits of $3,038$4,376 and $2,106$4,508 as of December 31, 20172021 and 2016,2020, respectively, because the Company has concluded that it is not more-likely-than-not that these losses will be utilized before their expiration dates. The Spanish subsidiaries havesubsidiary has a history of net operating losses and it is not known when and if they will generate taxable income in the future.

15

U.S. tax reform changes(US Tax Cuts and Jobs Act enacted in December 2017) changed the United States approach to the taxation of foreign earnings to a territorial system by providing a one hundred percent dividends received deduction for certain qualified dividends received from foreign subsidiaries. These provisions of the U.S. tax reform significantly impact the accounting for the undistributed earnings of foreign subsidiaries, and as a result the Company intends to distribute approximately $10,000 of the earnings held in excess cash by its foreign subsidiaries in 2018.subsidiaries. The tax costs associated with a future distribution, including foreign withholding taxes, are not material to the Company’s financial statements. After carefully considering these facts, the Company has determined that it willwould not be asserting permanent reinvestment of all of its foreign subsidiaries earnings as of December 31, 2017.2017, and the Company continued to take this position as of December 31, 2021.

Net earnings attributable to Tootsie Roll Industries, Inc. were $80,864$65,326 in 20172021 compared to $67,510$58,995 in 2016,2020, and net earnings per share were $1.28$0.97 and $1.05$0.86 in 20172021 and 2016,2020, respectively, an increase of $0.23$0.11 per share or 21.9%13%. The increase in earningsEarnings per share in 2017 principally resulted from U.S. tax reform ($20,318 or $.32 per share), however, many of the above discussed increases in input costs and operating expenses and the impairment of the Company’s Spanish subsidiaries adversely affected 2017 net earnings when compared to 2016. In addition, 2017 earning per share2021 benefited from the reduction in average shares outstanding resulting from purchases of the Company’s common stock in the open market by the Company. Average shares outstanding decreased from 64,08668,482 in 20162020 to 63,17967,431 in 2017.2021 which reflects share repurchases of $30,184 during 2021.

Fourth quarter 20172021 and 2020 net earnings attributable to Tootsie Roll Industries, Inc. were $31,985 compared to $17,841 in fourth quarter 2016,$20,032 and $14,952, respectively, and net earnings per share were $0.51$0.30 and $0.28 in fourth quarter 2017 and 2016,$0.22, respectively, an increase of $0.23$0.08 per share or 82.1%36%. This increase wasThe Company’s fourth quarter 2021 results were principally driven by the favorable accounting adjustment relating to U.S. tax reform of $20,318, or $0.32 per share. Higher input costs and expenses as discussed above also adversely affected fourth quarter results, and many of the input cost increases, primarily freight and delivery, acceleratedits 30% increase in fourth quarter 2017 compared tosales and price increases that became effective in fourth quarter 2016.2021 as discussed above.

Beginning in 2012, the Company received periodic notices from the Bakery and Confectionery Tobacco WorkersUnion and Grain MillersIndustry International Union Pension PlanFund (Plan), a multi-employer defined benefit pension plan for certain Company union employees, that the Plan’s actuary certified the Plan to be in “critical status”, the “Red Zone”, as defined by the Pension Protection Act (PPA) and the Pension Benefit Guaranty Corporation (PBGC); and that a plan of rehabilitation was adopted by the trustees of the Plan in fourth quarter 2012. During 2015, the Company received notices that theThe Plan’s status was changed to “critical and declining status”, as defined by the PPA and PBGC, for the plan year beginning January 1, 2015, and that the Plan was projected to have an accumulated funding deficiency for the 2017 through 2024 plan years. A designation of “critical and declining status” implies that the Plan is expected to become insolvent in the next 20 years. In second quarter 2016, theThe Company received newhas continued to receive annual notices each year (2016 to 2021) that the Plan’s trustees adopted an updated Rehabilitation Plan effective January 1, 2016, and that thethis Plan remains in “critical and declining status” and is projected to become insolvent within the year 2030.next 20 years. These new notices have also adviseadvised that the Plan trustees were considering the reduction or elimination of certain retirement benefits and may seek assistance from the PBGC. Plans in “critical and declining status” may elect to suspend (temporarily or permanently) some benefits payable to all categories of participants, including retired participants, except retirees that are disabled or over the age of 80. Suspensions must be equally distributed and cannot drop below 110% of what would otherwise be guaranteed by the PBGC.

Based on these updated notices, the Plan’s funded percentage (plan investment assets as a percentage of plan liabilities), as defined, were 57.0%48.3%, 62.8%50.4%, and 65.1%51.6% as of the most recent valuation dates available, January 1, 2016, 2015,2020, 2019, and 2014,2018, respectively (these valuation dates are as of the beginning of each Plan year). These funded percentages are based on actuarial values, as defined, and do not reflect the actual market value of Plan investments as of these dates. If the market value of investments had been used as of January 1, 20162020 the funded percentage would be 53.0%51.6% (not 57.0%48.3%). The Plan’s market value of its investments declined by 3.7% and its unfunded vested benefits increased by 6.4% during 2016. As of the January 1, 20162020 valuation date (most recent valuation available), only 20%16% of Plan participants were current active employees, 51%53% were retired or separated from service and receiving benefits, and 29%31% were retired or separated from service and entitled to future benefits. The number of current active employee Plan participants as of January 1, 20162020 fell 2%4% from the previous year and 4%17% over the past two years. When compared to the Plan valuation date of January 1, 2011 (five years earlier)(just prior to the Plan being certified to be in “critical status”), current active employeesemployee participants have declined 31%49%, whereas participants who were retired or separated from service and receiving benefits increased 6%4% and participants who were retired or separated from service and entitled to future benefits increased 8%12%. The bankruptcy of a major participating employer in the Plan contributed to the above discussed Plan results. The Company understands that the Plan is currently exploring additional restructuring measures which include incentives to participating employers in exchange for providing additional future cash contributions as well as suspension of certain retirement benefits.

16

The Company has been advised that its withdrawal liability would have been $82,200, $72,700,$104,300, $99,300 and $61,000$99,800 if it had withdrawn from the Plan during 2017, 20162021, 2020 and 2015,2019, respectively. The increase from 2016 to 2017 principally reflects a decrease in the PBGC interest rates, a decrease in the assets and increase in the Plan’s unfunded vested benefits during 2016 and the Company comprising a largerCompany’s relative share of the Plan’s contribution base.base, driven by employer withdrawals, has increased for the last several years, and management believes that this trend could continue indefinitely which will continue to add upward pressure on the Company’s withdrawal liability. Based on the above, including the Plan’s projected insolvency in the year 2030,next 20 years, management believes that the Company’s withdrawal liability will likelycould increase further in future years.

16

Based on the Company’s updated actuarial study and certain provisions in ERISA and the law relating to withdrawal liability payments, management believes that the Company’s liability would likely be limited to twenty annual payments of $3,059$2,793 which have a present value in the range of $35,900$32,800 to $46,900$46,600 depending on the interest rate used to discount these payments. While the Company’s actuarial consultant does not believe that the Plan will suffer a future mass withdrawal (as defined) of participating employers, in the event of a mass withdrawal, the Company’s annual withdrawal payments would theoretically be payable in perpetuity. Based on the Company’s updated actuarial study, the present value of such perpetuities is in the range of $45,764 to $142,447 and would apply in the unlikely event that substantially all employers withdraw from the Plan. The aforementioned is based on a range of valuationvaluations and interest rates which management understandsthe Company’s actuary has advised is provided under the statute. Should the Company actually withdraw from the Plan at a future date, a withdrawal liability, which could be higher than the above discussed amounts, could be payable to the Plan.

The Company and the union are currently inconcluded a new labor contract negotiations and are continuing to operate under extensions of the recently expired contractin 2018 which requires the Company’s continued participation in this Plan.Plan through September 2022 (the expiration of this union contract). The amended rehabilitation plan, which also continues, requires that employer contributions include 5% compounded annual surcharge increases each year for an unspecified period of time beginning in 2012 as well as certain plan benefit reductions. The Company’s pension expense for this Plan for 2017, 20162021, 2020 and 20152019 was $2,617, $2,541$3,156, $2,866 and $2,574,$2,961, respectively. The aforementioned expense includes surcharges of $656, $542$1,112, $1,010 and $447$948 in 2017, 20162021, 2020 and 2015,2019, respectively, as required under the planamended rehabilitation plan.

In fourth quarter 2020, the Plan Trustees advised the Company that the surcharges would no longer increase annually and therefore be “frozen” at the rates and amounts in effect as of rehabilitationDecember 31, 2020 provided that the local bargaining union and the Company executed a formal consent agreement by March 31, 2021. The Trustees advised that they have concluded that continuing increases in surcharges would likely have a long-term adverse effect on the solvency of the Plan. The Trustees concluded that further increases would result in increasing financial hardships and withdrawals of participating employers, and that this change will not have a material effect on the Plan’s insolvency date. In first quarter 2021, the local bargaining union and the Company executed this agreement which resulted in the “freezing” of such surcharges as amended.of December 31, 2020.

The Plan recently advised the Company that it will be applying for benefits available to financial troubled plans under the American Rescue Plan Act of 2021. Company management understands that this legislation would provide financial assistance from the PBGC to shore up financially distressed multi-employer plans to ensure that they can remain solvent and continue to pay benefits to retirees through 2051 without any reduction in retiree benefits. Nonetheless, the Company’s actuary believes that given the Plan’s projected insolvency date of 2031 as well as other factors, that it still remains unclear if the Plan can remain solvent through the targeted date of 2051. The Company’s actuary also advised that the regulations under the aforementioned PBGC financial assistance could result in a higher withdrawal liability even with PBGC financial assistance. The Company is currently unable to determine the ultimate outcome of the above discussed multi-employer union pension matter and therefore is unable to determine the effects on its consolidated financial statements, but the ultimate outcome or the effects of any modifications to the current rehabilitation plan could be material to its consolidated results of operations or cash flows in one or more future periods. See also Note 7 inof the Company’s Note to Consolidated Financial Statements on Form 10-K for the year ended December 31, 2017.2021.

17

2020 vs. 2019

2016 vs. 2015

Twelve months 20162020 consolidated net product sales were $517,373$467,427 compared to $536,692$523,616 in twelve months 2015,2019, a decrease of $19,319$56,189 or 3.6%10.7%. Twelve months 2016 consolidatedNet product sales were adversely impacted by the effects of the Covid-19 pandemic, which curtailed and limited access to certain channels of trade where the Company has historically sold its products. Response to this pandemic has resulted in the disruption and changes in lifestyles, shopping habits, daily work routines, and consumer behaviors, all of which have adversely affected planned consumer purchases of the Company’s products for “sharing” and “give away” occasions. Many of the Company’s products are consumed at group events, outings, and other gatherings which have been significantly curtailed or in some cases eliminated due to concern of possible infection or spreading of the Covid-19 virus. Impulse purchases of Company products at retail outlets have also been adversely affected by currency translation of $3,473 due to a stronger U.S. dollarthese changes in 2016 compared to 2015, principally relating to Mexico and Canada. The timing of sales between fourth quarter 2016 and first quarter 2017consumer behavior. Unfavorable foreign exchange also had some adverse effectimpact on twelve months 20162020 net product sales compared to 2019.

Fourth quarter 2020 net product sales were $127,866 compared to $134,663 in fourth quarter 2019, a decrease of $6,797 or 5.0%. After a 2% sales increase in first quarter 2020, sales declined 25% in second quarter 2020 at the height of the pandemic and economic downturn. In third quarter 2020 sales declined 14%, while in fourth quarter 2020 the sales decline was narrowed to 5% when compared to the twelve monthscorresponding quarterly periods in the prior year. The Company had higher sales price realization in 2016 compared to 2015 in order to recover increased costs for ingredients and certain other inputs. Fourth quarter 2016 net sales were $124,279 compared to $139,881 in fourth quarter 2015, a decrease of $15,602 or 11.2%. Fourth quarter 2016 net sales were adversely affected by the timing of certain customer sales at both the beginning and end of the quarter when compared to the prior year fourth quarter in 2015. Unfavorable foreign exchange also contributed to lower sales in fourth quarter 2016 compared to the prior year corresponding period.2019.

Product cost of goods sold were $320,290$299,710 in 20162020 compared to $340,090$329,102 in 2015,2019, a decrease of $19,800$29,392 or 5.8%8.9%. Product cost of goods sold includes $1,137$610 and $497$408 in certain deferred compensation expenses in 20162020 and 2015,2019, respectively. These deferred compensation expenses principally result from changes in the market value of investments and investment income from trading securities relating to compensation deferred in previous years and are not reflective of current operating results. Adjusting for the aforementioned, product cost of goods sold decreased from $339,593$328,694 in 20152019 to $319,153$299,100 in 2016,2020, a decrease of $20,440$29,594 or 6.0%9.0%. As a percent of net product sales, these adjusted costs decreasedincreased from 63.3%62.8% in 20152019 to 61.7%64.0% in 2016,2020, a favorable1.2 unfavorable percentage point change. Lower sales and production volumes had an unfavorable impact on plant manufacturing overhead costs included in the aforementioned adjusted product cost of goods sold. These plant overhead costs are primarily fixed and recurring each year, and only partially decline with lower volumes.

Product gross margin was $167,717 in 2020 compared to $194,514 in 2019, a decrease of 1.6% as a percent of net product sales. Higher price realization on$26,797 or 13.8%. The above discussed sales continuing improvements in manufacturing plant efficiencies driven by capital investments, and ongoing cost containment programs contributed to this improvement in lower costs of goods sold anddecline was the resulting improvement inprincipal driver that adversely impacted gross profit margins in twelve months 2016 compared2020. Certain cost and expense reductions, including Company initiatives to 2015. Higherreduce costs for ingredients and additional manufacturing costs relatingdid provide some benefit to changes in and uncertainties relating to product labeling requirements adversely affected2020 gross profit margins in 2016. These higher manufacturing costs in 2016 include the effects of lower production volumes runs for many products

17

in order to reduce and minimize finished goods inventory levels and additional costs to meet new product labeling requirements. This inventory reduction was in response to uncertainties surrounding changes in state and national labeling regulations and requirements during 2016.margins. The Company is continuing its focus on cost reductions and savings, including savings resulting from capital investments in orderits plant manufacturing operations to meet new consumer and customer demands, achieve manufacturing efficienciesquality improvements, provide genuine value to consumers, and productivity improvements. The Company has made progress on restoring margins to their historical levels before the increases in commodity and other input costs in past years.increase operational efficiencies.

Selling, marketing and administrative expenses were $107,377$112,117 in 20162020 compared to $108,051$127,802 in 2015,2019, a decrease of $674$15,685 or 0.6%12.3%. Selling, marketing and administrative expenses include $3,138$11,909 and $953$10,884 in certain deferred compensation expenses in 20162020 and 2015,2019, respectively. These deferred compensation expenses principally result from changes in the market value of investments and investment income from trading securities relating to compensation deferred in previous years and are not reflective of current operating results. Adjusting for the aforementioned, theseselling, marketing and administrative expenses decreased from $107,098$116,918 in 20152019 to $104,239$100,208 in 2016,2020, a decrease of $2,859$16,710 or 2.7%14.3%. As a percent of net product sales, these adjusted expenses increased slightlydecreased from 20.0%22.3% of net product sales in 20152019 to 20.1%21.4% of net product sales in 2016,2020, a 0.1% unfavorable increase0.9 favorable percentage point change. Reductions in travel and trade show expense resulting from changes in Company policies in response to the Covid-19 pandemic, and more favorable freight and delivery unit costs were the principal drivers in this expense reduction as a percentage of sales. sales in 2020.

Selling, marketing and administrative expenses include $40,629 and $42,619 of freight, delivery and warehousing expenses. These expenses decreased from $49,288 in 2016 and 2015, respectively, were 7.9%2019 to $42,593 in 2020, a decrease of $6,695 or 13.6%. As a percent of net product sales, these adjusted expenses decreased from 9.4% in both 20162019 to 9.1% in 2020, a 0.3 favorable percentage point change. More favorable freight and 2015. Internal expensedelivery rates from third-party over-the-road truck carriers, and certain operational and cost reduction initiatives, mitigated some of the higher costs of freight, delivery and warehousing in 2016 comparedcontributed to 2015.this favorable change.

The Company has foreign operating businesses in Mexico, Canada and Spain, and exports products to many foreign markets. The strength of the U.S. dollar and related devaluations of most these related foreign currencies, primarily Mexico and Canada, have adversely affected these foreign and export operations in 2016 compared to 2015. The operating income of these foreign and export operations decreased by $3,269 in 2016 compared to 2015. The Company currently has a 93% ownership of two Spanish companies (93% and 83% ownership at December 31, 2016 and 2015, respectively) which had operating losses for each of the years 2008 through 2016. Company management has restructured the Spanish operations and made other changes to its business plan but these companies continue to have operating losses.

Earnings from operations were $92,414$58,244 in 20162020 compared to $91,082$69,214 in 2015, an increase2019, a decrease of $1,332.$10,970. Earnings from operations include $4,275$12,519 and $1,450$11,292 in certain deferred compensation expense in 20162020 and 2015,2019, respectively, which are discussed above. Adjusting for these deferred compensation expenses, adjusted earnings from operations increased decreased

18

from $92,532$80,506 in 20152019 to $96,689$70,763 in 2016, an increase2019, a decrease of $4,157$9,743 or 4.5%12.1%. Although ingredient costs and results from foreign operations adversely affected adjusted 2016The above discussed decline in net product sales was the principal driver of lower operating income in 2020 compared to 2019, however, 2020 earnings from operations higher price realization on sales and thedid benefit from some cost and expense reductions as discussed above, allowed the Company to achieve these higher adjusted operating earnings in 2016 despite the decline in 2016 net sales compared to 2015.above.

Management believes the comparisons presented in the preceding paragraphs, after adjusting for changes in deferred compensation, are more reflective of the underlying operations of the Company.

Other income, net was $5,498$18,018 in 20162020 compared to $1,496$16,190 in 2015,2019, an increase of $4,002.$1,828. Other income, net principally reflects $4,275$12,519 and $1,450$11,292 of aggregate net gains and investment income on trading securities in 20162020 and 2015,2019, respectively. These trading securities provide an economic hedge of the Company’s deferred compensation liabilities; and the related net gains and investment income were offset by a like amount of expense in aggregate product cost of goods sold and selling, marketing, and administrative expenses in the respective years as discussed above. Other income, net includes investment income on available for sale securities including variable rate demand notes, of $2,130$4,005 and $1,421$4,423 in 20162020 and 2015,2019, respectively. Other income, net also includes foreign exchange lossesgains (losses) of $955$534 and $1,427$(533) in 20162020 and 2015,2019, respectively.

The consolidatedCompany’s effective income tax rate was 22.7% and 24.1% in 2020 and 2019, respectively. The decrease in the effective tax rate was 31.2% and 28.6% in 2016 and 2015, respectively. The lower effective2020 reflects more favorable foreign tax rate for 2015 principally reflects benefits from favorable prior yearrates, income tax settlements, including a $1,066 release of ancredits and adjustments for reserves for uncertain income tax liability resulting from a decision by a foreign court in second quarter 2015. positions.

The Company utilized $1,776$617 and $2,758$1,227 of its Canadian subsidiary’s tax carry-forward benefits in 20162020 and 2015,2019, respectively. At December 31, 2019, the Company’s deferred tax assets included $617 of income tax benefits relating to its Canadian subsidiary tax loss carry-forwards. The Company hasfully utilized this deferred tax asset in 2020 as expected. The Company provided a full valuation allowance on its Spanish subsidiaries’ tax loss carry-forward benefits of $2,106$4,508 and $1,834$4,584 as of December 31, 20162020 and 2015,2019, respectively, because the Company has concluded that it is not more-likely-than-not that these losses will be utilized before their expiration dates.