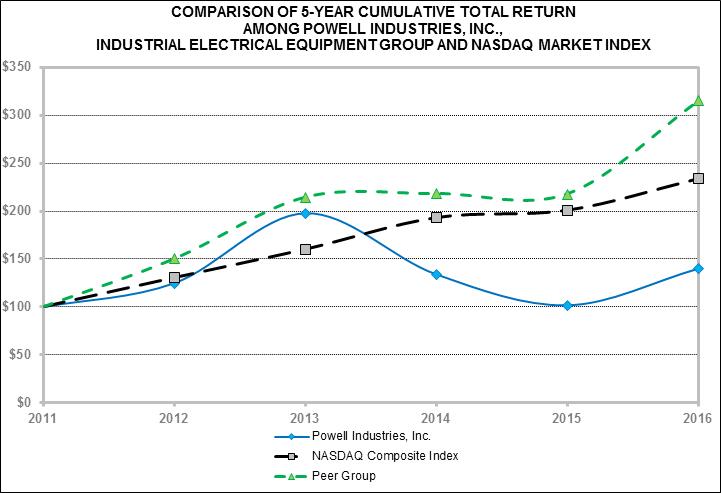

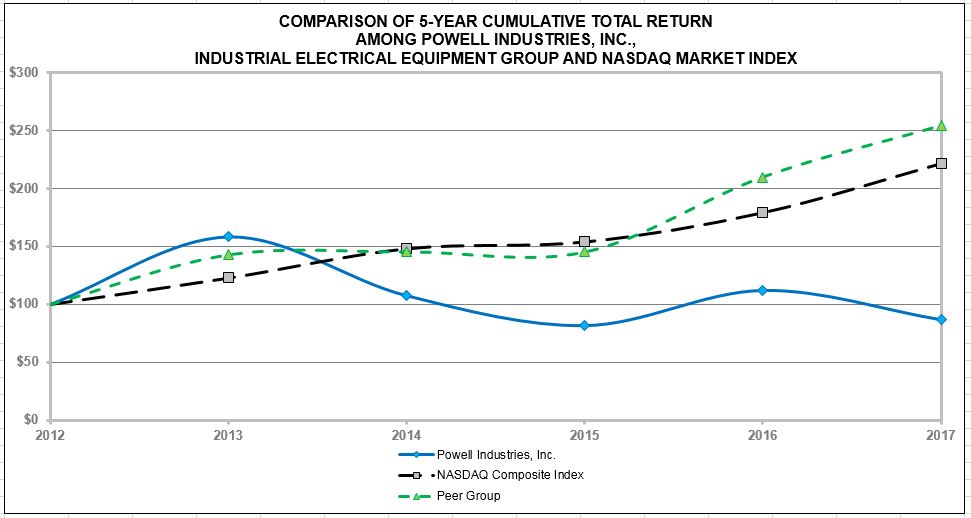

nonrecurring. Thus, multiple and/or continuous projects of similar magnitude with the same customer may vary. As such, the timing of large project awards may cause material fluctuations in revenues and gross profits. 2015. adjustments, with material-cost predictive estimating and by actively pursuing internal cost reduction efforts. We did not enter into any derivative contracts to hedge our exposure to commodity price changes in Fiscal 2017, 2016 2015. future operating results. Our backlog is subject to unexpected adjustments and cancellations and, therefore, may not be a reliable indicator of our future earnings. of operations. of operations. failure to compete effectively could adversely affect future regulations. " net income or loss and cash flow. The departure of key personnel could disrupt our business. Losses arising from such events may or may not be fully covered by our various insurance policies or may be subject to deductibles or exceed coverage limits. policy limits operations. operations. Location Description Acres Approximate Square Footage Houston, TX Corporate office and manufacturing facility 21.4 428,515 Houston, TX Office and manufacturing facility 53.4 290,554 Houston, TX Office, fabrication facility and yard 63.3 82,320 North Canton, OH Office and manufacturing facility 8.0 115,200 Northlake, IL Office and manufacturing facility 10.0 103,500 Bradford, U.K. Office and manufacturing facility 7.9 129,200 Acheson, Alberta, Canada Office and manufacturing facility 20.1 330,168 High Low Fiscal 2015: First Quarter $ 51.33 $ 38.12 Second Quarter 49.93 31.54 Third Quarter 39.45 32.54 Fourth Quarter 35.44 25.60 Fiscal 2016: First Quarter $ 35.89 $ 25.99 Second Quarter 30.41 23.00 Third Quarter 39.47 26.22 Fourth Quarter 41.10 34.40 Years ended September 30, 2016 2015 2014 2013 2012 Statement of Operations: (In thousands, except per share data) Revenues $ 565,243 $ 661,858 $ 647,814 $ 640,867 $ 690,741 Cost of goods sold 459,038 553,597 522,340 502,375 557,938 Gross profit 106,205 108,261 125,474 138,492 132,803 Selling, general and administrative expenses 74,924 76,801 87,756 79,707 76,961 Research and development expenses 6,731 6,980 7,608 7,615 6,286 Amortization of intangible assets 352 435 779 1,659 2,599 Restructuring and separation expenses 8,441 3,397 — 3,927 — Operating income 15,757 20,648 29,331 45,584 46,957 Gain on settlement — — — (1,709 ) — Other income (2,029 ) (2,402 ) (1,522 ) — — Interest expense (net) (7 ) 59 165 167 158 Income from continuing operations before income taxes 17,793 22,991 30,688 47,126 46,799 Income tax provision (1) 2,283 13,552 11,068 7,387 18,056 Income from continuing operations 15,510 9,439 19,620 39,739 28,743 Income from discontinued operations, net of tax — — 9,604 2,337 914 Net income $ 15,510 $ 9,439 $ 29,224 $ 42,076 $ 29,657 Earnings per share: Continuing operations $ 1.36 $ 0.80 $ 1.63 $ 3.32 $ 2.43 Discontinued operations — — 0.80 0.20 0.07 Basic earnings per share $ 1.36 $ 0.80 $ 2.43 $ 3.52 $ 2.50 Continuing operations $ 1.36 $ 0.79 $ 1.62 $ 3.32 $ 2.41 Discontinued operations — — 0.80 0.19 0.08 Diluted earnings per share $ 1.36 $ 0.79 $ 2.42 $ 3.51 $ 2.49 (1) For an explanation of the effective tax rate for the last three fiscal years, see Note H of the Notes to Consolidated Financial Statements included elsewhere in this Annual Report. Years ended September 30, 2016 2015 2014 2013 2012 Balance Sheet Data: (In thousands) Cash and cash equivalents $ 97,720 $ 43,569 $ 103,118 $ 107,411 $ 89,669 Property, plant and equipment, net 144,977 154,594 156,896 144,495 78,489 Total assets 462,516 468,824 541,443 530,903 448,312 Long-term debt, including current maturities 2,400 2,800 3,200 3,616 4,355 Total stockholders' equity 335,317 333,262 371,097 355,226 310,103 Total liabilities and stockholders' equity 462,516 468,824 541,443 530,903 448,312 Dividends paid on common stock 11,845 12,358 11,998 — — petrochemical markets. Fiscal 2016, compared to Fiscal 2015. These decreases Statements. We have a $75.0 million revolving credit facility in the Statements. short-term investments and reclassified $24.9 million as restricted cash for pledged collateral as stipulated by our amended credit agreement. As of September 30, 2016, Payments Due by Period: Long-Term Debt Obligations Operating Lease Obligations Total Less than 1 year $ 420 $ 2,495 $ 2,915 1 to 3 years 829 2,657 3,486 3 to 5 years 812 2,840 3,652 More than 5 years 400 2,485 2,885 Total long-term contractual obligations $ 2,461 $ 10,477 $ 12,938 2017. As of September 30, 2016, Payments Due by Period: Letters of Less than 1 year $ 11,417 1 to 3 years 18,362 More than 3 years 986 Total long-term commercial obligations $ 30,765 Off-Balance Sheet Arrangements cycle. necessary. Under the percentage-of-completion method of accounting, revenues are recognized as work is performed. The revenue earned to date is calculated by multiplying the total contract price by the percentage of performance to date, which is based on total costs or total labor dollars incurred to date compared to the total estimated costs or total labor dollars estimated at completion. The method used to determine the percentage of completion is typically the cost method, unless the labor method is a more accurate method of measuring the progress of the project. Application of the percentage-of-completion method of accounting requires the use of estimates of costs to be incurred for the performance of the contract. Contract costs include all direct material costs, direct labor costs and those indirect costs related to contract performance, such as indirect labor, supplies, tools, repairs and all costs associated with operation of equipment. The cost estimation process is based upon the professional knowledge and experience of our engineers, project managers and financial professionals. Factors that are considered in estimating the work to be completed and ultimate contract recovery include the availability and productivity of labor, the nature and complexity of the work to be performed, the effect of change orders, the availability of materials, the effect of any delays on our project performance and the recoverability of any claims. Changes in job performance, job conditions, estimated profitability and final contract settlements, including our estimate of liquidated damages, if any, may result in revisions to costs and income, with their effects being recognized in the period in which the revisions are determined. Whenever revisions of estimated contract costs and contract values indicate contract. This statements, we believe accounting for variable consideration and the number of performance obligations contained in each contract will have the greatest significance. The materiality of this guidance on our financial statements will be determined in large part by the contracts that are in progress as of the adoption date. decreased. Page Financial Statements: and Stockholders of Powell Industries, Inc. September 30, 2016 2015 ASSETS Current Assets: Cash and cash equivalents $ 97,720 $ 43,569 Accounts receivable, less allowance for doubtful accounts of $811 and $746 101,048 101,784 Costs and estimated earnings in excess of billings on uncompleted contracts 66,106 104,793 Inventories 26,521 32,891 Income taxes receivable 1,713 1,232 Deferred income taxes 4,006 3,910 Prepaid expenses 4,569 5,004 Other current assets 2,457 3,916 Total Current Assets 304,140 297,099 Property, plant and equipment, net 144,977 154,594 Goodwill and intangible assets, net 2,059 2,393 Other assets 11,340 10,117 Deferred income taxes — 2,288 Long-term receivable (Note E) — 2,333 Total Assets $ 462,516 $ 468,824 LIABILITIES AND STOCKHOLDERS' EQUITY Current Liabilities: Current maturities of long-term debt $ 400 $ 400 Income taxes payable 1,459 784 Accounts payable 34,985 48,008 Accrued salaries, bonuses and commissions 22,550 19,223 Billings in excess of costs and estimated earnings on uncompleted contracts 43,974 42,057 Accrued product warranty 4,639 4,930 Other accrued expenses 8,212 7,521 Deferred credit ─ short term (Note E) 2,029 2,029 Total Current Liabilities 118,248 124,952 Long-term debt, net of current maturities 2,000 2,400 Deferred compensation 4,840 4,950 Deferred income taxes 138 — Other long-term liabilities 1,466 723 Deferred credit ─ long term (Note E) 507 2,537 Total Liabilities 127,199 135,562 Commitments and Contingencies (Note G) Stockholders' Equity: Preferred stock, par value $.01; 5,000,000 shares authorized; none issued — — Common stock, par value $.01; 30,000,000 shares authorized; 12,199,511 and 12,031,243 shares issued, respectively 122 121 Additional paid-in capital 52,003 48,507 Retained earnings 331,959 328,294 Treasury stock, 806,018 and 670,181 shares at cost (24,999 ) (21,259 ) Accumulated other comprehensive loss (23,768 ) (22,401 ) Total Stockholders' Equity 335,317 333,262 Total Liabilities and Stockholders' Equity $ 462,516 $ 468,824 Year Ended September 30, 2016 2015 2014 Revenues $ 565,243 $ 661,858 $ 647,814 Cost of goods sold 459,038 553,597 522,340 Gross profit 106,205 108,261 125,474 Selling, general and administrative expenses 74,924 76,801 87,756 Research and development expenses 6,731 6,980 7,608 Amortization of intangible assets 352 435 779 Restructuring and separation expenses 8,441 3,397 — Operating income 15,757 20,648 29,331 Other income (See Note E) (2,029 ) (2,402 ) (1,522 ) Interest expense 149 145 178 Interest income (156 ) (86 ) (13 ) Income from continuing operations before income taxes 17,793 22,991 30,688 Income tax provision 2,283 13,552 11,068 Income from continuing operations 15,510 9,439 19,620 Income from discontinued operations, net of tax (Note N) — — 9,604 Net income $ 15,510 $ 9,439 $ 29,224 Earnings per share: Continuing operations $ 1.36 $ 0.80 $ 1.63 Discontinued operations — — 0.80 Basic earnings per share $ 1.36 $ 0.80 $ 2.43 Continuing operations $ 1.36 $ 0.79 $ 1.62 Discontinued operations — — 0.80 Diluted earnings per share $ 1.36 $ 0.79 $ 2.42 Weighted average shares: Basic 11,400 11,869 12,003 Diluted 11,431 11,908 12,058 Dividends per share $ 1.04 $ 1.04 $ 1.00 Year Ended September 30, 2016 2015 2014 Net income $ 15,510 $ 9,439 $ 29,224 Foreign currency translation adjustments (928 ) (16,104 ) (4,447 ) Postretirement benefit adjustment, net of tax (439 ) 206 17 Comprehensive income (loss) $ 14,143 $ (6,459 ) $ 24,794 Accumulated Additional Other Common Stock Paid-in Retained Treasury Stock Comprehensive Shares Amount Capital Earnings Shares Amount Income/(Loss) Total Balance, September 30, 2013 11,971 $ 119 $ 43,193 $ 313,987 — $ — $ (2,073 ) $ 355,226 Net income — — — 29,224 — — — 29,224 Foreign currency translation adjustments — — — — — — (4,447 ) (4,447 ) Stock-based compensation 44 — 3,385 — — — — 3,385 Excess tax benefit from share-based compensation — — 407 — — — — 407 Shares withheld in lieu of employee tax withholding — — (718 ) — — — — (718 ) Issuance of restricted stock 16 1 — — — — — 1 Retirement of stock — — — (11,998 ) — — — (11,998 ) Postretirement benefit adjustment, net of tax of $9 — — — — — — 17 17 Balance, September 30, 2014 12,031 $ 120 $ 46,267 $ 331,213 — $ — $ (6,503 ) $ 371,097 Net income — — — 9,439 — — — 9,439 Foreign currency translation adjustments — — — — — — (16,104 ) (16,104 ) Stock-based compensation 53 — 3,171 — — — — 3,171 Excess tax benefit from share-based compensation — — (191 ) — — — — (191 ) Shares withheld in lieu of employee tax withholding — — (740 ) — — — — (740 ) Issuance of restricted stock 16 1 — — — — — 1 Purchase of treasury shares — — — — (670 ) (21,259 ) — (21,259 ) Dividends paid — — — (12,358 ) — — — (12,358 ) Postretirement benefit adjustment, net of tax of $123 — — — — — — 206 206 Balance, September 30, 2015 12,100 $ 121 $ 48,507 $ 328,294 (670 ) $ (21,259 ) $ (22,401 ) $ 333,262 Net income — — — 15,510 — — — 15,510 Foreign currency translation adjustments — — — — — — (928 ) (928 ) Stock-based compensation 81 — 4,883 — — — — 4,883 Excess tax benefit from share-based compensation — — (387 ) — — — — (387 ) Shares withheld in lieu of employee tax withholding — — (1,000 ) — — — — (1,000 ) Issuance of restricted stock 18 1 — — — — — 1 Purchase of treasury shares — — — — (136 ) (3,740 ) — (3,740 ) Dividends paid — — — (11,845 ) — — — (11,845 ) Postretirement benefit adjustment, net of tax of $(237) — — — — — — (439 ) (439 ) Balance, September 30, 2016 12,199 $ 122 $ 52,003 $ 331,959 (806 ) $ (24,999 ) $ (23,768 ) $ 335,317 Year Ended September 30, 2016 2015 2014 Operating Activities: Net income $ 15,510 $ 9,439 $ 29,224 Adjustments to reconcile net income to net cash provided by operating activities: Depreciation 12,979 13,120 11,386 Amortization 352 435 779 Gain on sale of discontinued operations, net of tax — — (8,563 ) Stock-based compensation 4,883 3,171 3,385 Excess tax benefit from stock-based compensation 387 191 (407 ) Bad debt expense/(recovery) 187 (29 ) 1,074 Deferred income tax expense (benefit) 2,330 10,521 (3,212 ) Gain on amended supply agreement (2,029 ) (2,029 ) (1,522 ) Cash received from amended supply agreement 2,333 2,333 10,000 Changes in operating assets and liabilities: Accounts receivable, net 369 391 1,959 Costs and billings in excess of estimates on uncompleted contracts 39,612 (17,430 ) (17,089 ) Inventories 6,159 (572 ) (3,959 ) Prepaid expenses and other current assets 1,342 2,656 (1,101 ) Accounts payable and income taxes payable (12,334 ) (5,073 ) 1,002 Accrued liabilities 3,927 (3,373 ) (4,997 ) Other, net (1,101 ) (833 ) 1,524 Net assets held for sale — — (10,355 ) Net cash provided by operating activities 74,906 12,918 9,128 Investing Activities: Proceeds from sale of property, plant and equipment 187 112 118 Proceeds from sale of Transdyn — — 14,819 Purchases of property, plant and equipment (3,044 ) (34,719 ) (16,495 ) Net cash used in investing activities (2,857 ) (34,607 ) (1,558 ) Financing Activities: Payments on industrial development revenue bonds (400 ) (400 ) (400 ) Excess tax benefit from stock-based compensation (387 ) (191 ) 407 Shares withheld in lieu of employee tax withholding (1,000 ) (740 ) (499 ) Purchase of treasury shares (3,740 ) (21,259 ) — Dividends paid (11,845 ) (12,358 ) (11,998 ) Payments on short-term and other financing — — (16 ) Net cash used in financing activities (17,372 ) (34,948 ) (12,506 ) Net increase (decrease) in cash and cash equivalents 54,677 (56,637 ) (4,936 ) Effect of exchange rate changes on cash and cash equivalents (526 ) (2,912 ) 643 Cash and cash equivalents, beginning of period 43,569 103,118 107,411 Cash and cash equivalents, end of period $ 97,720 $ 43,569 $ 103,118 Year Ended September 30, 2016 2015 2014 Cash paid (received) during the period for: Interest, net of interest income $ 4 $ 70 $ 149 Income taxes, net of refunds (352) 2,298 18,889 Non-cash capital expenditures 221 147 13,527 property, plant and equipment, the cost and related accumulated depreciation are removed from the accounts, and any resulting gain or loss is recognized in the Consolidated Statements of Operations. statements, we believe accounting for variable consideration and the number of performance obligations contained in each contract will have the greatest significance. The materiality of this guidance on our financial statements will be determined in large part by the contracts that are in progress as of the adoption date. The following table reconciles basic and diluted weighted average shares used in the computation of earnings per share for the years ended September 30, 2017, 2016 Year Ended September 30, 2016 2015 2014 Numerator: Income from continuing operations $ 15,510 $ 9,439 $ 19,620 Income from discontinued operations — — 9,604 Net income $ 15,510 $ 9,439 $ 29,224 Denominator: Weighted average basic shares 11,400 11,869 12,003 Dilutive effect of restricted stock units 31 39 55 Weighted average diluted shares with assumed conversions 11,431 11,908 12,058 Net earnings per share: Continuing operations $ 1.36 $ 0.80 $ 1.63 Discontinued operations — — 0.80 Basic earnings per share $ 1.36 $ 0.80 $ 2.43 Continuing operations $ 1.36 $ 0.79 $ 1.62 Discontinued operations — — 0.80 Diluted earnings per share $ 1.36 $ 0.79 $ 2.42 September 30, 2016 2015 Balance at beginning of period $ 746 $ 1,577 Bad debt expense (recovery) 187 (29 ) Uncollectible accounts written off, net of recoveries (120 ) (749 ) Change due to foreign currency translation (2 ) (53 ) Balance at end of period $ 811 $ 746 September 30, 2016 2015 Raw materials, parts and subassemblies $ 29,639 $ 36,575 Work-in-progress 996 1,084 Provision for excess and obsolete inventory (4,114 ) (4,768 ) Total inventories $ 26,521 $ 32,891 September 30, 2016 2015 Costs incurred on uncompleted contracts $ 1,088,921 $ 912,237 Estimated earnings 350,125 271,640 1,439,046 1,183,877 Less: Billings to date (1,416,914 ) (1,121,141 ) Net underbilled position $ 22,132 $ 62,736 Included in the accompanying balance sheets under the following captions: Costs and estimated earnings in excess of billings on uncompleted contracts – underbilled $ 66,106 $ 104,793 Billings in excess of costs and estimated earnings on uncompleted contracts – overbilled (43,974 ) (42,057 ) Net underbilled position $ 22,132 $ 62,736 September 30, Range of 2016 2015 Asset Lives Land $ 22,107 $ 22,380 — Buildings and improvements 119,512 120,983 3 - 39 Years Machinery and equipment 103,268 100,306 3 - 15 Years Furniture and fixtures 3,806 3,564 3 - 10 Years Construction in process 1,009 1,013 — $ 249,702 $ 248,246 Less: Accumulated depreciation (104,725 ) (93,652 ) Total property, plant and equipment, net $ 144,977 $ 154,594 September 30, 2016 2015 Balance at beginning of period $ 4,930 $ 4,557 Increase to warranty expense 4,249 3,364 Deduction for warranty charges (4,464 ) (2,738 ) Change due to foreign currency translation (76 ) (253 ) Balance at end of period $ 4,639 $ 4,930 September 30, 2016 September 30, 2015 Gross Net Gross Net Carrying Accumulated Carrying Carrying Accumulated Carrying Value Amortization Value Value Amortization Value Purchased technology $ 11,749 $ (10,693 ) $ 1,056 $ 11,749 $ (10,359 ) $ 1,390 million. Years Ending September 30, Total 2017 $ 352 2018 352 2019 352 2020 ― 2021 ― As of September 30, 2017, there is approximately $0.5 million remaining in the deferred credit balance. September 30, 2016 2015 Industrial development revenue bonds $ 2,400 $ 2,800 Less: current portion (400 ) (400 ) Total long-term debt $ 2,000 $ 2,400 Year Ending September 30, Long‑Term 2017 $ 400 2018 400 2019 400 2020 400 2021 400 Thereafter 400 Total long-term debt maturities $ 2,400 In June 2017, we entered into the Third Amendment to the Credit Agreement (the Third Amendment). The Third Amendment, among other things, (i) extended the Maturity Date from December 2018 to June 2022; (ii) amended the definition of Applicable Rate by (a) providing that Pricing Level I shall apply when a Cash Collateral Period (described below) is in effect and that Pricing Level II shall apply when no Cash Collateral Period is in effect, (b) decreasing the Letter of Credit Fee percentage for Pricing Level I from 1.00% to 0.875% and (c) increasing the Commitment Fee percentage for both Pricing Level I and Pricing Level II from 0.1875% to 0.20%; (iii) added a new requirement that during a Cash Collateral Period we maintain a cash balance in a pledged cash collateral account equal to at least 102% of the Outstanding Amount of Revolving Loans and Letter of Credit Obligations and (iv) modified the Financial Covenants by requiring that, during any Cash Collateral Period, the Consolidated Current Ratio be no less than 1.10 to 1.0. Price Level 3 in the prior agreement was removed and our ability to pay dividends remains subject to financial covenant restrictions. 2017. There were no borrowings outstanding under the U.S. Revolver as of September 30, June 27, 2022. weekly by the Bonds’ remarketing agent, which was the underwriter for the Bonds and is an affiliate of the bank. This interest rate was 2017. We also sublease certain facilities that we are no longer occupying. Our sublease terms do not fully cover the existing rental commitments on certain facilities. Years Ending September 30, Operating 2017 $ 2,495 2018 1,491 2019 1,167 2020 1,470 2021 1,370 Thereafter 2,485 Total lease commitments $ 10,478 as follows (in thousands): 2017. Liquidated Damages Year Ended September 30, 2016 2015 2014 Current: Federal $ (1,395 ) $ 2,638 $ 12,184 State 449 699 2,226 Foreign 899 (306 ) (130 ) (47 ) 3,031 14,280 Deferred: Federal 1,923 3,296 (1,798 ) State 47 420 (311 ) Foreign 360 6,805 (1,103 ) 2,330 10,521 (3,212 ) Total income tax provision $ 2,283 $ 13,552 $ 11,068 Year Ended September 30, 2016 2015 2014 U.S. $ 5,087 $ 33,549 $ 35,131 Other than U.S. 12,706 (10,558 ) (4,443 ) Income before income taxes $ 17,793 $ 22,991 $ 30,688 Year Ended September 30, 2016 2015 2014 Statutory rate 35 % 35 % 35 % State income taxes, net of federal benefit 2 3 3 Research and development credit (8 ) (21 ) — Foreign rate differential (8 ) 4 1 Domestic production activities deduction — (3 ) (3 ) Foreign valuation allowance (11 ) 43 — Other 3 (2 ) — Effective rate 13 % 59 % 36 % January 1, 2015 to September 30, 2015. 2016. September 30, 2016 2015 Current deferred income taxes: Gross assets $ 4,384 $ 3,910 Gross liabilities (378 ) — Net current deferred income tax asset 4,006 3,910 Noncurrent deferred income taxes: Gross assets 16,170 5,005 Gross liabilities (16,308 ) (2,717 ) Net noncurrent deferred income tax asset (liability) (138 ) 2,288 Net deferred income tax asset $ 3,868 $ 6,198 September 30, 2016 2015 Deferred Tax Assets: Net operating loss $ 10,453 $ 9,877 Uniform capitalization and inventory 1,596 1,895 Deferred compensation 1,853 1,848 Stock-based compensation 760 993 Reserve for accrued employee benefits 1,679 1,482 Warranty accrual 1,388 915 Goodwill 345 398 Postretirement benefits liability 503 — Allowance for doubtful accounts 220 166 Accrued legal 294 60 Credit carryforwards 1,292 1,329 Other 171 8 Deferred tax assets 20,554 18,971 Deferred Tax Liabilities: Depreciation and amortization (8,247 ) (2,705 ) Other — (12 ) Deferred tax liabilities (8,247 ) (2,717 ) Less: valuation allowance (8,439 ) (10,056 ) Net deferred tax asset $ 3,868 $ 6,198 At September 30, 2017, the valuation allowance of $8.8 million was primarily related to these Canadian net deferred tax assets. Balance at September 30, 2013 $ 135 Charged to cost and expenses 80 Charged to other accounts 688 Balance at September 30, 2014 $ 903 Charged to cost and expenses 10,048 Charged to other accounts (895 ) Balance at September 30, 2015 $ 10,056 Charged to cost and expenses (1,934 ) Charged to other accounts 317 Balance at September 30, 2016 $ 8,439 Year Ended September 30, 2016 2015 2014 Balance at beginning of period $ 784 $ 4,026 $ 3,845 Increases related to tax positions taken during the current period 293 954 225 Increases related to tax positions taken during a prior period ― 2 14 Decreases related to expiration of statute of limitations (31 ) (49 ) (58 ) Decreases related to settlement with taxing authorities ― (4,149 ) — Balance at end of period $ 1,046 $ 784 $ 4,026 2017. Of the $6.4 million of total assets held by the trustee, $5.6 million is invested in company-owned life insurance policies and the remainder in mutual funds. 2017. Total RSU activity (number of shares) for the past Number of Weighted Restricted Average Stock Fair Value Units Per Share Outstanding at September 30, 2013 81,555 $ 38.66 Granted 57,200 66.15 Vested (29,832 ) 44.88 Forfeited (2,078 ) 56.34 Outstanding at September 30, 2014 106,845 $ 51.30 Granted 89,500 41.75 Vested (55,431 ) 45.23 Forfeited (7,408 ) 43.82 Outstanding at September 30, 2015 133,506 $ 47.83 Granted 168,800 31.64 Vested(1) (116,568 ) 33.10 Forfeited (25,750 ) 50.28 Outstanding at September 30, 2016 159,988 $ 43.12 available. 2017. measurement date. As such, fair value is a market-based measurement that should be determined based on assumptions that market participants would use in valuing an asset or liability. The accounting guidance requires the use of valuation techniques to measure fair value that maximize the use of observable inputs and minimize the use of unobservable inputs. As a basis for considering such assumptions and inputs, a fair value hierarchy has been established that identifies and prioritizes three levels of inputs to be used in measuring fair value. Fair Value Measurements at September 30, 2016 Quoted Prices in Significant Other Significant Active Markets for Observable Unobservable Fair Value at Identical Assets Inputs Inputs September 30, (Level 1) (Level 2) (Level 3) 2016 Assets: Cash equivalents $ 435 $ — $ — $ 435 Deferred compensation 1,643 4,130 — 5,773 Liabilities: Deferred compensation — 4,449 — 4,449 Fair Value Measurements at September 30, 2015 Quoted Prices in Significant Other Significant Active Markets for Observable Unobservable Fair Value at Identical Assets Inputs Inputs September 30, (Level 1) (Level 2) (Level 3) 2015 Assets: Cash equivalents $ 434 $ — $ — $ 434 Deferred compensation 1,879 2,904 — 4,783 Liabilities: Deferred compensation — 4,487 — 4,487 an interest-bearing savings account. See Note F for further discussion on restricted cash. Year Ended September 30, 2016 2015 2014 United States $ 405,298 $ 474,038 $ 365,085 Canada 77,252 101,191 137,684 Middle East and Africa 40,294 40,557 84,330 Europe 26,200 23,567 34,920 Far East 7,895 12,026 15,127 Mexico, Central and South America 8,304 10,479 10,668 Total revenues $ 565,243 $ 661,858 $ 647,814 September 30, 2016 2015 Long-lived assets: United States $ 88,304 $ 95,694 Canada 52,292 53,879 United Kingdom 4,381 5,021 Total $ 144,977 $ 154,594 Expenses in Fiscal 2017. Year Ended September 30, 2016 2015 2014 Revenues $ — $ — $ 13,923 Income from discontinued operations, net of tax of $633 $ — $ — $ 1,041 Gain on sale of discontinued operations, net of tax of $5,218 — — 8,563 Net income from discontinued operations, net of tax $ — $ — $ 9,604 Earnings per share information: Basic $ — $ — $ 0.80 Diluted $ — $ — $ 0.80 2015 Quarters First Second Third Fourth 2015 Revenues $ 152,601 $ 170,199 $ 176,733 $ 162,325 $ 661,858 Gross profit 21,069 24,301 32,944 29,947 108,261 Net income (loss) (239 ) (3,683 ) 7,049 6,312 9,439 Earnings (loss) per share: Basic $ (0.02 ) $ (0.31 ) $ 0.60 $ 0.54 $ 0.80 Diluted $ (0.02 ) $ (0.31 ) $ 0.60 $ 0.54 $ 0.79 2017. 3.1 3.2 10.1 Description of Supplemental Executive Benefit Plan (filed as Exhibit 10 to our Form 10-K for the fiscal year ended October 31, 1984, and incorporated herein by reference). Powell Industries, Inc. Directors’ Fees Program (filed as Exhibit 10.7 to our Form 10-K for the fiscal year ended October 31, 1992, and incorporated herein by reference). Powell Industries, Inc. Deferred Compensation Plan (filed as Exhibit 10.9 to our Form 10-K for the fiscal year ended October 31, 2002, and incorporated herein by reference). Banking facilities between HSBC Bank plc and Switchgear & Instrumentation Limited and Switchgear & Instrumentation Properties Limited dated September 12, 2005 (filed as Exhibit 10.16 to our Form 10-K for the fiscal year ended October 31, 2005, and incorporated herein by reference). Lease Agreement between the Company and C&L Partnership, Ltd. dated April 19, 2006 (filed as Exhibit 10.2 to our Form 8-K filed August 9, 2006, and incorporated herein by reference). Employment Agreement dated as of May 8, 2012 between the Company and Don R. Madison (filed as Exhibit 10.1 to our Form 10-Q for the quarter ended March 31, 2012, and incorporated herein by reference). Amended and Restated Credit Agreement dated as of April 26, 2012, between Powell PowerComm Inc., as Borrower, Powell Industries, Inc., Nextron Limited, PPC Technical Services Inc., as Guarantors, and HSBC Bank Canada, as Lender (filed as Exhibit 10.4 to our Form 10-Q for the quarter ended March 31, 2012, and incorporated herein by reference). Stock Purchase Agreement dated as of January 15, 2014, between the Company and Kapsch TrafficCom IVHS, Inc. (filed as Exhibit 10.1 to our Form 8-K filed January 17, 2014, and incorporated herein by reference). ** Description of Exhibits Severance Agreement and Release effective as of December 24, 2015, between the Company and Michael A. Lucas (filed as Exhibit 10.1 to our Form 10-Q filed February 3, 2016 and incorporated herein by reference). 10.27 * *31.1 *31.2 *32.1 Number — Certification of Chief Financial Officer Pursuant to Section 18 U.S.C. Section 1350, as Adopted Pursuant to Section 906 of the Sarbanes-Oxley Act of 2002. 101.INS — XBRL Instance Document 101.SCH — XBRL Taxonomy Extension Schema Document 101.CAL — XBRL Taxonomy Extension Calculation Linkbase Document 101.DEF — XBRL Taxonomy Extension Definition Linkbase Document 101.LAB — XBRL Taxonomy Extension Label Linkbase Document 101.PRE — XBRL Taxonomy Extension Presentation Linkbase Document Portions of this exhibit have been omitted based on a request for confidential treatment pursuant to Rule 24b-2 of the Securities Exchange Act of 1934. Such omitted portions have been filed separately with the Commission. By: Chairman of the Board Thomas W. Powell /s/Brett A. Cope Brett A. Cope /s/Don R. Madison Don R. Madison /s/Milburn Honeycutt Milburn Honeycutt /s/ Eugene L. Butler Director Eugene L. Butler /s/ Christopher E. Cragg Director Christopher E. Cragg /s/ Bonnie V. Hancock Director Bonnie V. Hancock /s/ Scott E. Rozzell Director Scott E. Rozzell /s/ Stephen W. Seale, Jr. Director Stephen W. Seale, Jr. /s/ John D. White Director John D. White /s/Richard E. Williams Richard E. Williams 3.1 3.2 10.1 Description of Supplemental Executive Benefit Plan (filed as Exhibit 10 to our Form 10-K for the fiscal year ended October 31, 1984, and incorporated herein by reference). Powell Industries, Inc. Directors’ Fees Program (filed as Exhibit 10.7 to our Form 10-K for the fiscal year ended October 31, 1992, and incorporated herein by reference). Banking facilities between HSBC Bank plc and Switchgear & Instrumentation Limited and Switchgear & Instrumentation Properties Limited dated September 12, 2005 (filed as Exhibit 10.16 to our Form 10-K for the fiscal year ended October 31, 2005, and incorporated herein by reference). ** Description of Exhibits * *31.1 *31.2 *32.1 *32.2 101.INS 101.SCH 101.CAL 101.LAB — XBRL Taxonomy Extension Label Linkbase Document 101.PRE — XBRL Taxonomy Extension Presentation Linkbase Document Portions of this exhibit have been omitted based on a request for confidential treatment pursuant to Rule 24b-2 of the Securities Exchange Act of 1934. Such omitted portions have been filed separately with the Commission.corporationcompany was the successor to a company founded by William E. Powell in 1947, which merged into the Company in 1977. We are headquartered in Houston, Texas, and our major subsidiaries, all of which are wholly owned, include: Powell Electrical Systems, Inc.; Powell (UK) Limited; Powell Canada Inc. and Powell Industries International, B.V.ourthis Annual ReportsReport on Form 10-K Quarterly Reports on Form 10-Q, Current Reports on Form 8-Kand other reports, and amendments to those reports, filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934 as soon as is reasonably practicable after we electronically file such material with, or furnish it to, the Securities and Exchange Commission (SEC). Additionally, all of our reports filed with the SEC are available via their website at http://www.sec.gov, or may be read and copied at the SEC Public Reference Room at 100 F Street, NE, Washington, DC 20549.equipmentproducts and systems for the distribution, control and monitoring of electrical energy designed towhich (1) distribute, control and monitor the flow of electrical energy and (2) provide protection to motors, transformers and other electrically powered equipment. Our principal products include integrated power control room substations (PCRs®), custom-engineered modules, electrical houses (E-Houses), traditional and arc-resistant distribution switchgear and control gear, medium-voltage circuit breakers, monitoring and control communications systems, motor control centers and bus duct systems. These products are designed for application voltages ranging from 480 volts to 38,000 volts and are used in oil and gas refining, onshore and offshore oil and gas production, petrochemical, pipeline, terminal, mining and metals, light rail traction power, electric utility, pulp and paper and other heavy industrial markets. Our product scope includes designs tested to meet both U.S. standards (ANSI) and international standards (IEC). We assist customers by providing value-added services such as spare parts, field service inspection, installation, commissioning, modification and repair, retrofit and retrofill components for existing systems and replacement circuit breakers for switchgear that is obsolete or that is no longer produced by the original manufacturer. We seek to establish long-term relationships with the end users of our systems as well as the designengineering, procurement and construction engineering(EPC) firms contracted by those end users. and Fiscal 2014 used throughout this Annual Report relate to our fiscal years ended September 30, 2017, 2016 and 2015, and 2014, respectively.72%71%, 72% and 56%72% of our consolidated revenues for Fiscal 2017, 2016 2015 and 2014,2015, respectively. Revenues from customers located in Canada accounted for approximately 14%12%, 15%14% and 21%15% of consolidated revenues for Fiscal 2017, 2016 2015 and 2014,2015, respectively. Approximately 61%60% of our long-lived assets were located in the U.S. at September 30, 2016,2017, with 36%37% of long-lived assets located in Canada and 3% of long-lived assets located in the United Kingdom (U.K.). Detailed geographic information is included in Note L of the Notes to Consolidated Financial Statements included elsewhere in this Annual Report.In January 2014, we sold our wholly owned subsidiary Transdyn Inc. (Transdyn). We have presented the results of these operations as income from discontinued operations, net of tax, in the accompanying consolidated statements of operations. Additionally, all current and historical financial information presented in this Annual Report excludes the financial information for Transdyn or presents it as discontinued operations where applicable. For more information about this disposition, see Note N of the Notes to Consolidated Financial Statements included elsewhere in this Annual Report.engineering, procurement and construction (EPC)EPC firm on behalf of the end user. Each project is specifically engineered and manufactured to meet the exact specifications and requirements of the individual customer. Powell’s expertise is in the design and engineering, manufacturing, project management and integration of the various systems into a single custom-engineered deliverable. We market and sell our products and services, which are typically awarded in competitive bid situations, to a wide variety of customers, governmental agencies, markets and geographic regions. Contracts often represent large-scale and complex projects with an individual customer. By their nature, these projects are typicallymargins.2016,2017, Fiscal 20152016 or Fiscal 2014. and withas well as smaller, regional competitors that typically have limited capabilities and scope of supply. Our principal competitors include ABB, Eaton, General Electric Company, Schneider and Siemens. The competitive factors used during bid evaluation by our customers vary from project to project and may include technical support and application expertise, engineering and manufacturing capabilities, equipment rating, delivered value, scheduling and price. While projects are typically non-recurring, a significant portion of our business is from repeat customers and many times involves third-party EPC firms hired by the end user and with which we also have long and established relationships. Ultimately, our competitive position is dependent upon our ability to provide quality custom-engineered products, services and systems on a timely basis at a competitive price.20162017 totaled $291.4$250.1 million compared to $441.4$291.4 million at September 30, 2015.2016. Backlog declined primarily due to lower demand in our core oil, gas and petrochemical markets. We anticipate that approximately $228$235.3 million of Fiscal 20162017 ending backlog will be fulfilled during our fiscal year ending September 30, 2017.2018. Backlog may not be indicative of future operating results as orders in our backlog may be cancelled or modified by our customers.and 46% of revenues in both Fiscal 2017 and Fiscal 2016 and 46% in Fiscal 2015, respectively.2015. Unanticipated changes in material requirements, disruptions in supplies or price increases could impact production costs and affect our consolidated results of operations.2015 or 2014.2016,2017, we had 2,3231,841 full-time employees located primarily in the United States,U.S., Canada and the U.K. Our employees are not represented by unions, and we believe that our relationship with our employees is good.most significant risks and uncertainties described below. If any of the following risks actually occur, our business, financial condition, cash flows, liquidity and results of operations could be negatively impacted and we may not be able to achieve our quarterly, annual or long-range plans. Additional risks and uncertainties not known to us or not described below may also impairnegatively impact our business operations. If any of the following risks actually occur, our business, financial condition, cash flows and results of operations could be harmed and we may not be able to achieve our goals.operations. This Annual Report also includes statements reflecting assumptions, expectations, projections, intentions or beliefs about future events that are intended as “forward-looking statements” under the Private Securities Litigation Reform Act of 1995 and should be read in conjunction with the discussion under “Forward-Looking Statements,” above.Due to the cyclical nature ofindustry, our business may bemarkets and we are adversely impacted by extended periods of low oil or gas prices, or unsuccessful exploration efforts which may decrease our customers’ spending, the demand for our products and thereforeservices and the prices we are able to charge. This has had, and may continue to have, an adverse effect on our results in the future.have declinedwhile improving somewhat in 2017, are still down from 2014 levels and are expected to remain unpredictable.volatile. This decline in oil and gas prices since 2014 has had a negative effect on our markets and led to the reduction of projects available and thus reduced our revenue and our backlog of projects. These unfavorableUnfavorable commodity prices have caused oil and gas companies to change their strategies, reduce project spending and delay and/or cancel projects. The price for oil and gas can be influenced by many factors, including global economic growth, inventory levels and supply and demand for these commodities. These factors could cause oil and gas prices to remain depressed or decrease further, which could result in a continued decrease in customer projects that could adversely impact our operations. Continued periods of reduced oil and gas prices couldwill negatively impact our consolidatedbusiness and results of operations cash flows and financial position and would likely result in operating losses and could result in impairment losses on our long-lived assets. Additionally, the loss of significant volume from one particular customer at one of our facilities could materially impact that facility. Furthermore, our ability to maintain or expand our business would be limited in the future if we are unable to maintain or increase our bonding capacity or our credit facility on favorable terms or at all. These disruptions could lead to reduced demand for our products and services and could materiallyadversely impact our business financial condition, cash flows and results of operations and could potentially impact the trading price of our common stock.Our stock price could decline or fluctuate significantly due to unforeseen circumstances. These fluctuations may cause our stockholders to incur losses.Our stock price could fluctuate or decline from quarter to quarter due to a variety of factors including, but not limited to, the timing and cancellation of projects, changes in our estimated costs to complete projects, or failure of our operating results to meet the expectations of securities analysts or investors which could reduce investor confidence. Additionally, we are required to assess and report on our internal controls each year. Findings of inadequate or failed internal controls could reduce investor confidence in the reliability of our financial information. These factors could adversely affect our operating results and the trading price of our common stock could decline significantly.that appeared to have a high certainty of going forward at the time the order was recorded. In the event of a project cancellation, or modification,modified and while we may be reimbursed for certain costs, butwe may not have a contractual right to the total revenue reflected in our backlog. In addition to our being unable to recover certain direct costs, cancelled projects may also result in additional unrecoverable costs due to the underutilization of our assets. Accordingly, the amounts recorded in backlog may not be a reliable indicator of our future earnings.a significantan adverse impact on our operating results for any fiscal quarter or year.them, could subject us to penalty provisions, liquidated damages or claims against the company or our outstanding letters of credit or performance bonds. In addition, some customer contracts stipulate protection against our gross negligence or willful misconduct. Each individual contract defines the conditions under which the customer may make a claim against us. It is possible that adjustments arising from such claims, or our failure to manage our contract risk, may not be covered by insurance and could have a significantan adverse impact on our operating results for any fiscal quarter or year.materiallyadversely impact our ability to meet commitments to our customers.2016.2017. Unanticipated increases in raw material requirements or prices, as well as changes in supplier availability or price increasessupplier consolidation, could increase production costs and adversely affect profitability as fixed-price contracts may prohibit our ability to charge the customer for the increase in raw material prices. We purchase a wide variety of materials and component parts from various suppliers to manufacture our products, including steel, aluminum, copper and various components. Our supply base for certain key components and raw materials is limited and may come from a single supplier. If we are unable to obtain key components and raw materials from these suppliers, the key components and raw materials may not be readily available from other suppliers or available with acceptable terms. Our success depends on our ability to meet customer commitments and could be negatively impacted if a supplier experiences a disruption or discontinuance in their operations. The time and effort associated with the selection and qualification of a new supplier and changes in our design and testing to accommodate similar components from other suppliers could be significant. Additionally, we rely on certain competitors for key materials used in our products. This could put us at risknegatively impact our ability to manufacture our products if the relationships change or become adversarial. around the world such as engineering, manufacturing and marketing resources. Competition in the industry depends on a number of factors, including the number of projects available, technical ability, production capacity, location and price. Certain of our competitors may have lower cost structures and may, therefore, be able to provide their products or services at lower prices than we are able to provide. Similarly, we cannot be certain that we will be able to maintain or enhance our competitive position within our industry, maintain our customer base at current levels, increase our customer base or continue to provide technologically superior products at a competitive price. New companies may enter the markets in which we compete, or industry consolidation may occur, further increasing competition in our markets. Oursalesrevenues and have a materialan adverse impact on our business model, financial position and our consolidated results of operations.regulations, including regulations related to conflict minerals. We may incur significant costs associated with the compliance with SEC reporting and due diligence requirements. In our industry, conflict minerals are most commonly found in metals. As there may be only a limited number of suppliers offering "conflict free" metals, we cannot be sure that we will be able to obtain necessary metals in sufficient quantities or at competitive prices. Also, we may face challenges with our customers and suppliers if we are unable to sufficiently verify that the metals used in our products are "conflict free.”United StatesU.S. and numerous foreign jurisdictions. A change in tax laws, deductions or credits, treaties or regulations, or their interpretation, in the countries in which we operate could result in a higher tax rate on our pre-tax income, which could have a material impact on our net income and cash flows from operations.income. We are regularly under audit by tax authorities, and our tax estimates and tax positions could be materially affected by many factors including the final outcome of tax audits and related litigation, the introduction of new tax accounting standards, legislation, regulations and related interpretations, our global mix of earnings, the extent to which deferred tax assets are realized and changes in uncertain tax positions. A significant increase in our tax rate could have a material effectimpact on our profitability.28%29% of our consolidated revenues in Fiscal 2016.2017. While our manufacturing facilities are located in developed countries with historically stable operating and fiscal environments, our consolidatedbusiness and results of operations cash flows and financial condition could be adversely affected by a number of factors, including: political and economic instability; social unrest, acts of terrorism, force majeure, war or other armed conflict; inflation; changes in tax laws; the pending exitapplication of the U.K. from the European union; inflation;foreign labor regulations; currency fluctuations, devaluations and conversion restrictions;restrictions and/or governmental activities that limit or disrupt markets, restrict payments or limit the movement of funds and trade restrictions or economic embargoes imposed by the U.S. or other countries. Additionally, the compliance with foreign and domestic import and export regulations and anti-corruption laws, such as the U.S. Foreign Corrupt Practices Act, or similar laws of other jurisdictions outside the United States,U.S., could adversely impact our ability to compete for contracts in such jurisdictions. Moreover, the violation of such laws or regulations, by us or our representatives, could result in severe penalties including monetary fines, criminal proceedings and suspension of export privileges.Our operating results may vary significantly from quarter to quarter.Our quarterly results may be materially and adversely affected by a number of factors, including: changes in estimates relating to revenues, costs, project scheduling; the timing and volume of work under new agreements; changes in existing customer schedules; general economic conditions; the spending patterns of customers; variations in the margins of projects performed during any particular quarter; losses experienced in our operations not otherwise covered by insurance; a change in the demand or production of our products and our services caused by severe weather conditions; a change in the mix of our customers, contracts and business; increases in design and manufacturing costs; the ability of customers to pay their invoices owed to us and disagreements with customers related to project performance on delivery. Accordingly, our operating results in any particular quarter may vary significantly and may not be indicative of future results.and profitabilityat competitive levels may be limited by our ability to employ, train and retain personnel necessary to meet our requirements. We face significant competition for qualified personnel in our industry. We may experience shortages of qualified personnel such as engineers, project managers and select skilled trades. We cannot be certain that we will be able to maintain an adequate skilled labor force or key technical personnel necessary to operate efficiently and to support our growth strategy and operations. We cannot be certain that our labor expensescosts will not increase as a result of a shortage in the supply of skilled and technical personnel. Labor shortages or increased labor costs could impair our ability to maintain our business, meet customer commitments or grow our revenues, and may adversely impact our business and results of operations.consolidatedbusiness and results of operations cash flows and financial condition could be adversely affected. In addition, claims, lawsuits and proceedings may harm our reputation or divert management resources away from operating our business.or telecommunications failures, cyber security attacks or other similar events, our business or results of operations could be adversely affected. In addition, despite implementation of security measures, our business systems may be vulnerable to computer viruses, cyber-attacks and other unauthorized access; and theseaccess.These security breaches could result in a disruption to our operations or in legal claims or proceedings. A material network breach of our business systems could involve the theft of intellectual property, financial data, employee data, or customer data, which may be used by competitors. We rely on third-party systems which could also suffer operational system failure or cyber-attacks. Any of these occurrences could disrupt our business, result in potential liability or reputational damage or otherwise have an adverse effect on our business or results of operations.andwhich could adversely impact our consolidatedbusiness and results of operations, cash flows and financial position. In addition, we may not be able to continue to obtain insurance at commercially reasonable rates or may be faced with liabilities not covered by insurance such as, but not limited to, environmental contamination or terrorist attacks.SuchWe may declare the existence of a force majeure event under our contracts in certain situations; however, a customer may dispute our force majeure claim, which may result in additional liabilities. Losses arising from such events may or may not be fully covered by our various insurance policies or may be subject to deductibles or exceed coverage limits. In addition, such events could result in temporary or long-term delays and/or cancellations of orders for raw materials from our suppliers which could impact our project execution. These situations or other disruptions are outside of our control and could have a significant adversemay adversely impact on our consolidatedbusiness and results of operations, cash flows and financial position.operationsbusiness and may adversely impact our profitability.Acquisitions involveresults of operations.pose risks tomay impact our strategy.operating results. Due diligence may not be adequate or reveal all risks and challenges associated with our acquisitions. Companies that we acquire may not achieve revenues, profitability or cash flows that we expected, or that ultimately justify the investment. It is possible that impairment charges resulting from the overpayment for an acquisition may negatively impact our results of operations. Financing for acquisitions may require us to obtain additional equity or debt financing which may not be available on attractive terms, if at all.all or which may be restricted under the terms of our credit facilities or other financing arrangements. Any failure to successfully complete or successfully integrate acquisitions could have a material adverse effect on our business consolidatedand results of operations.condition.reporting, however, any system of controls has limitations, including the possibility of human error, the circumvention or overriding of controls and/or fraud. Our failure to maintain effective internal controls over financial reporting could adversely affect our ability to report our financial results on a timely and accurate basis, which could result in a loss of investor confidence in our financial reports or have an adverse impact on our business and results of operations.United States,U.S., Canada and the U.K. Our facilities are generally located in areas that are readily accessible to materials and labor pools and are maintained in good condition. These facilities are expected to meet our needs for the foreseeable future.2016,2017, are as follows:Location Description Acres Houston, TX Corporate office and manufacturing facility 21.4 428,515 Houston, TX Office and manufacturing facility 53.4 290,554 Houston, TX Office, fabrication facility and yard 63.3 82,320 North Canton, OH Office and manufacturing facility 8.0 115,200 Northlake, IL Office and manufacturing facility 10.0 103,500 Bradford, U.K. Office and manufacturing facility 7.9 129,200 Acheson, Alberta, Canada Office and manufacturing facility 20.1 330,168 High Low Fiscal 2016: First Quarter $ 35.89 $ 25.99 Second Quarter 30.41 23.00 Third Quarter 39.47 26.22 Fourth Quarter 41.10 34.40 Fiscal 2017: First Quarter $ 46.68 $ 34.81 Second Quarter 40.00 30.86 Third Quarter 35.58 31.12 Fourth Quarter 33.47 27.28 2, 2016,1, 2017, the closing price of our common stock on the NASDAQ was $43.38$28.53 per share. As of December 2, 2016,1, 2017, there were 405308 stockholders of record of our common stock. All common stock held in street names are recorded in the Company’s stock register as being held by one stockholder.$11.8$11.9 million and $12.4$11.8 million in dividends in Fiscal 20162017 and Fiscal 2015,2016, respectively. The Board anticipates declaring cash dividends in future quarters; however, there is no assurance as to future dividends or their amounts because they depend on future earnings, capital requirements, financial condition and financial condition. debt covenants. Securities and Exchange Commission,SEC, nor shall such information be incorporated by reference into any future filing under the Securities Act of 1933 or Securities Act of 1934, each as amended, except to the extent that we specifically incorporate it by reference into such filing.20112012 to September 30, 2016,2017, the cumulative stockholder return on our common stock with the cumulative total return on the NASDAQ Market Index and the Industrial Electrical Equipment Group (a select group of peer companies – Altra Industrial Motion Corp.; Ameresco, Inc.; AZZ Inc.; Belden Inc.; Daktronics Inc.; Electro Scientific Industries, Inc.; EnerSys; Franklin Electric Co, Inc.; GrafTech International Ltd; Littelfuse Inc.; LSI Industries Inc.; Preformed Line Products; A O Smith Corporation and Woodward, Inc.). The comparison assumes that $100 was invested on October 1, 2011,2012, in our common stock, the NASDAQ Market Index and the Industrial Electrical Equipment Group, and that all dividends were re-invested. The stock price performance reflected on the following graph is not necessarily indicative of future stock price performance.

Years ended September 30, 2017 2016 2015 2014 2013 Statement of Operations: (In thousands, except per share data) Revenues $ 395,911 $ 565,243 $ 661,858 $ 647,814 $ 640,867 Cost of goods sold 345,142 459,038 553,597 522,340 502,375 Gross profit 50,769 106,205 108,261 125,474 138,492 Selling, general and administrative expenses 61,524 74,924 76,801 87,756 79,707 Research and development expenses 6,906 6,731 6,980 7,608 7,615 Amortization of intangible assets 355 352 435 779 1,659 Restructuring and separation expenses 1,322 8,441 3,397 — 3,927 Operating income (19,338 ) 15,757 20,648 29,331 45,584 Gain on settlement — — — — (1,709 ) Other income (2,029 ) (2,029 ) (2,402 ) (1,522 ) — Interest expense (net) (390 ) (7 ) 59 165 167 Income (loss) from continuing operations before income taxes (16,919 ) 17,793 22,991 30,688 47,126 Income tax provision (benefit) (1) (7,433 ) 2,283 13,552 11,068 7,387 Income (loss) from continuing operations (9,486 ) 15,510 9,439 19,620 39,739 Income from discontinued operations, net of tax (2) — — — 9,604 2,337 Net income (loss) $ (9,486 ) $ 15,510 $ 9,439 $ 29,224 $ 42,076 Earnings (Loss) per share: Continuing operations $ (0.83 ) $ 1.36 $ 0.80 $ 1.63 $ 3.32 Discontinued operations — — — 0.80 0.20 Basic earnings (loss) per share $ (0.83 ) $ 1.36 $ 0.80 $ 2.43 $ 3.52 Continuing operations $ (0.83 ) $ 1.36 $ 0.79 $ 1.62 $ 3.32 Discontinued operations — — — 0.80 0.19 Diluted earnings (loss) per share $ (0.83 ) $ 1.36 $ 0.79 $ 2.42 $ 3.51 Years ended September 30, 2017 2016 2015 2014 2013 Balance Sheet Data: (In thousands) Cash, cash equivalents and short-term investments (3) $ 95,188 $ 97,720 $ 43,569 $ 103,118 $ 107,411 Property, plant and equipment, net 139,420 144,977 154,594 156,896 144,495 Total assets 414,986 462,516 468,824 541,443 530,903 Long-term debt, including current maturities 2,000 2,400 2,800 3,200 3,616 Total stockholders' equity 321,296 335,317 333,262 371,097 355,226 Total liabilities and stockholders' equity 414,986 462,516 468,824 541,443 530,903 Dividends paid on common stock 11,875 11,845 12,358 11,998 — Our strategy in Canada has been to replicateAs a result, our project-based integration model which allows for the design, fabrication, integration and testing of our products at a single location. This strategic initiative has presented challenges for our Canadian operations in prior years, resulting in inefficiencies that led to higher operating costs, gross margin deterioration and operating losses. We took various actions in Canada and have seen improvements in our operational efficiencies during Fiscal 2016. However, the depressed oil and gas market conditions will likely have a negative impact on our Canadian operations for the foreseeable future.During Fiscal 2015, our consolidated operating results were negatively impacted by operational inefficiencies resulting from increased volumerevenues and project scheduling delays. Our inabilitybacklog have declined, and may continue to meet contractual commitments on existing projects, as well as delays in customer construction schedules,decline, which may further negatively impacted the timing and costs related to project execution. Our operating results were negatively impacted by the timing and resolution of change orders, project close-out and resolution of potential liquidated damage claims, all of which impacted gross margins during the period in which these items are resolved withimpact our customers. During Fiscal 2016, continued weakness in the oil and gas markets caused further declines in the number and size of projects leading to a decrease in revenues and backlog of projects.operations. In response to our reduced project backlog and the challenging market outlook in our core oil, gas and petrochemical markets, we took steps in Fiscal 2016, and have taken stepsadditional actions in Fiscal 2017, to reduce our overall cost structure restructureand better align our costs with current and future production requirements.alignworkforce reductions as a result of our salariedadverse market outlook and hourly workforcereduction in project backlog.future production requirements.On January 15, 2014,a valuation allowance. Additionally, the effective tax rates for both Fiscal 2017 and 2016 were favorably impacted by discrete items recognized, primarily related to the Research and Development Tax Credit (R&D Tax Credit), in the amounts of $0.9 million and $0.8 million, respectively. See Note H of the Notes to Consolidated Financial Statements. sold our wholly-owned subsidiary Transdynrecorded a net loss of $9.5 million, or $0.83 per diluted share, a decrease from net income of $15.5 million, or $1.36 per diluted share that we recorded in Fiscal 2016. The reduction in net income compared to the prior year was primarily due to a global providerdecline in our project backlog due to depressed market conditions and competitive pricing pressures, primarily in our core oil, gas and petrochemical markets.electronic toll collection systems, headquarteredwhich are petrochemical, oil and gas construction and transportation infrastructure projects which take a number of months to produce. The order backlog at September 30, 2017 was $250.1 million, compared to $291.4 million at September 30, 2016. New orders placed in Vienna, Austria. The purchase priceFiscal 2017 totaled $355.1 million, compared to $417.5 million in Fiscal 2016. This decrease in orders was primarily due to lower demand from the sale of this subsidiary totaled $16.0 million, subject to working capital adjustments. We received cash of $14.4 millionour customers in our core oil, gas and the remaining $1.6 million was placed into an escrow account and released to us in July 2015. We have presented the results of these operations as income from discontinued operations, net of tax, in the consolidated statements of operations for all periods presented. Accordingly, we have removed Transdyn from the Results of Operations discussions below.Results of Operationscontinuecontinued to see lower demand from our customers in the oil and gas markets. Domestic revenues decreased 15%, or $69.4 million, to $405.3 million and international revenues decreased 15%, or $27.2 million, to $159.9 million inarewere due to the overall reduction in revenues year over year primarily driven by the decline in backlog resulting from lower demand from our customers in the oil and gas markets. Revenues from commercial and industrial customers decreased 20%, or $105.4 million, to $419.1 million in Fiscal 2016, compared to Fiscal 2015, primarily from lower demand from our customers in the oil and gas markets. Revenues from public and private utilities increased 20%, or $16.8 million, to $101.9 million in Fiscal 2016, compared to Fiscal 2015. Revenues from municipal and transit projects decreased 15%, or $8.0 million, to $44.2 million in Fiscal 2016, compared to Fiscal 2015.have also overcomeovercame the operational challenges and cost overruns that occurred in previous years from their expansion and relocation into our new Canadian facility. Additionally, gross profit at our United Kingdom (U.K.)U.K. operations improved due to project execution. The increase in gross profit from our international operations was partially offset by a decline in gross profit from our domestic operations as margins were negatively impacted primarily by our reduced volume as a result of weak oil and gas market conditions and cost overruns related to a large U.S.-based transit project.Research and DevelopmentR&D Tax Credit (R&D Tax Credit) for the previously expired period from January 1, 2015 to September 30, 2015. The effective tax rate in Fiscal 2015 was above the combined U.S. federal and state statutory rate as no tax benefit was recorded against Canadian pre-tax losses due to the $9.0 million valuation allowance recorded in Fiscal 2015, partially offset by the resolution of an IRS audit and the retroactive reinstatement of the R&D Tax Credit for the second through fourth quarters of Fiscal 2014 (see2014. See Note H of the Notes to Consolidated Financial Statements included elsewhere in this Annual Report).

BacklogTwelve Months Ended2015 Compared2017, current assets exceeded current liabilities by 2.9 times and our debt to Twelve Months Endedtotal capitalization was 0.62%.2014Revenue and Gross ProfitRevenues increased 2%, or $14.02017, compared to $97.7 million to $661.9at September 30, 2016. In addition, at September 30, 2017, we had restricted cash of $24.9 million held in Fiscal 2015, primarily due to the increase in domestic revenues. Domestic revenues increased 30%, or $109.6 million, to $474.7 million in Fiscal 2015 primarily duea pledged collateral account related to our production efforts on various large petrochemical projects awarded in Fiscal 2014. International revenues decreased 34%, or $95.6 million, to $187.2 million in Fiscal 2015 primarily due to the substantial completionamended credit agreement. As of several large projects for both the Canadian market and the U.S. export projects. Revenues from commercial and industrial customers increased $50.0 million to $524.5 million in Fiscal 2015. Revenues from public and private utilities decreased $41.9 million to $85.1 million in Fiscal 2015. Revenues from municipal and transit projects increased $5.9 million to $52.2 million in Fiscal 2015. Gross profit decreased 14%, or $17.2 million, to $108.3 million in Fiscal 2015. Gross profitSeptember 30, 2016, we did not have any cash balances classified as a percentage of revenues decreased to 16% in Fiscal 2015 compared to 19% in Fiscal 2014. Our gross profit and gross profit as a percentage of revenues decreased in Fiscal 2015 compared to Fiscal 2014, primarily due to inefficiencies resulting fromrestricted. For further information regarding our production efforts and incremental costs required to maintain our customer’s schedules, as well as the overall mix of project types.Selling, General and Administrative ExpensesSelling, general and administrative expenses decreased by $11.0 million to $76.8 million in Fiscal 2015 compared to Fiscal 2014. Selling, general and administrative expenses, as a percentage of revenues, decreased to 12% in Fiscal 2015 compared to 14% in Fiscal 2014. These decreases were primarily due to a decrease in performance-based compensation, sales commissions, personnel and administrative costs resulting from reductions in force, reduced bad debt expense and overall cost reduction efforts.Restructuring and Separation ExpensesIn Fiscal 2015, we incurred $3.4 million in restructuring and separation costs. Of this, $2.6 million was from separation and severance costs and the remaining $0.8 million resulted from the exit of a Canadian facility lease and the write-off of associated leasehold improvements. Other IncomeWe recorded other income of $2.4 million in Fiscal 2015, of which $2.0 million related to the amortization of the deferred gain from the amended supplycredit agreement, discussed insee Note EF of the Notes to Consolidated Financial Statements, and $0.4 million was from a death benefit received from our company-owned life insurance policy. We recorded other income of $1.5 million in Fiscal 2014, which was solely from the amortization of the deferred gain.Income Tax ProvisionOur provision for income taxes was $13.6 million in Fiscal 2015, compared to $11.1 million in Fiscal 2014. The effective tax rate in Fiscal 2015 was 59% compared to an effective tax rate of 36% for Fiscal 2014. This increase in effective tax rate in Fiscal 2015 was primarily due to the establishment of a valuation allowance against the Canadian net deferred tax assets, partially offset by the resolution of an IRS audit and the retroactive reinstatement of the Federal Research and Development Tax Credit for the second through fourth quarters of Fiscal 2014 (see Note H of the Notes to Consolidated Financial Statements included elsewhere in this Annual Report). The effective tax rate for Fiscal 2014 approximated the combined U.S. federal and state statutory rate as the majority of our income was attributable to the U.S.Income from Continuing OperationsIn Fiscal 2015, we recorded income from continuing operations of $9.4 million, or $0.79 per diluted share, compared to $19.6 million, or $1.62 per diluted share in Fiscal 2014. This reduction to net income was primarily due to a valuation allowance recorded against our Canadian deferred tax assets (as discussed above) and higher domestic productions costs caused by inefficiencies resulting from our production efforts and incremental costs to maintain our customers’ scheduling requirements. These reductions to net income were partially offset by lower selling, general and administrative costs.Income from Discontinued OperationsIn Fiscal 2014, we recorded $9.6 million, or $0.80 per diluted share, of income from discontinued operations which included the gain on the sale. For additional information about this disposition, see Note N of the Notes to Consolidated Financial Statements.BacklogOur backlog includes various projects, some of which are petrochemical, oil and gas construction and transportation infrastructure projects which take a number of months to produce. The order backlog at September 30, 2015 was $441.4 million, compared to $507.1 million at September 30, 2014. New orders placed in Fiscal 2015 totaled $606.8 million, compared to $725.8 million in Fiscal 2014. This decrease in orders was due to reduced capital investments by our customers primarily in oil and gas and petrochemical industries.Liquidity and Capital ResourcesCash and cash equivalents increased to $97.7 million at September 30, 2016, compared to $43.6 million at September 30, 2015. As of September 30, 2016, current assets exceeded current liabilities by 2.6 times and our total debt-to-capitalization ratio was 0.71%.U.S., which expires in December 2018. AsU.S, and as of September 30, 2016,2017, there were no amounts borrowed under this line of credit. We also have a $7.6Total letters of credit outstanding under our U.S. credit facility, which reduce our availability, were $24.1 million at September 30, 2017 and $26.8 million at September 30, 2016. The amount available under the U.S. revolving credit facility in Canada. Atat September 30, 2016, there2017 was no balance outstanding under the Canadian revolving credit facility.$50.9 million. Total long-term debt, obligations, including current maturities, totaled $2.0 million at September 30, 2017, compared to $2.4 million at September 30, 2016, compared to $2.8 million at September 30, 2015. Total letters of credit outstanding were $26.8 million and $21.1 million at September 30, 2016 and 2015, respectively, which reduce our availability under our U.S. credit facility. Amounts available at September 30, 2016 under the U.S. and Canadian revolving credit facilities were $48.3 million and $7.6 million, respectively.2016. For further information regarding our debt, see Notes F and G of the Notes to Consolidated Financial Statements included elsewhere in this Annual Report.$30$36 million of our cash and short-term investments at September 30, 20162017 was held outside of the United StatesU.S. for international operations. It is our intention to indefinitely reinvest all current and future foreign earnings internationally in order to ensure sufficient working capital to support and expand theseour international operations. In the event that we elect to repatriate some or all of the foreign earnings that were previously deemed to be indefinitely reinvested outside the U.S., under current tax laws we would incur additional tax expense upon such repatriation.facilitiesfacility should be sufficient to finance future operating activities, capital improvements and debt repayments for the foreseeable future. We continue to monitor the factors that drive our markets and will continue to strive to maintain our leadership and competitive advantage in the markets we serve while aligning our cost structures with market conditions.million. Duringmillion and in Fiscal 2015, net cash provided by operating activities was $12.9 million and in Fiscal 2014, net cash provided by operating activities was $9.1 million. Cash flow from operations is primarily influenced by the timing of milestone payments from our customers and the payment terms with our suppliers, and is favorably impacted during a down cycle as project milestones are billed and collected as projects are completed. Cash flow from operations declined during Fiscal 2017 compared to Fiscal 2016 primarily as a result of our decrease in operating income and the payments of prior year accrued bonuses and commissions. Cash flow from operations in Fiscal 2017 was favorably impacted by the collection of accounts receivable and the reduction in inventories during our down cycle in project activity. During Fiscal 2016, our cash provided by operations increased over Fiscal 2015 primarily due to our ability to reduce working capital as projects were completed and payments on contracts were received. In Fiscal 2014, we received the $10.0 million payment related to the amended supply agreement discussed in Note E of the Notes to Consolidated Financial Statements included elsewhere in this Annual Report. 20162017 totaled $3.0$3.6 million compared to $34.7$3.0 million and $16.5$34.7 million in Fiscal 2016 and 2015, and 2014, respectively. This decreaseThe reduction in capital spending in Fiscal 2017 and 2016 was in response to our challenging market conditions. The $34.7 million spent in Fiscal 2015 was primarily due to the completion of the expansion of our Canadian facilitiesfacilities. During Fiscal 2017, we invested a net $26.8 million in Fiscal 2015.$17.4$12.7 million in Fiscal 2017, $17.4 million in Fiscal 2016 and $34.9 in Fiscal 2015 and $12.5includes approximately $12 million of dividends paid in each of the three years. The reduction in financing activities from Fiscal 2014. This reduction2015 was primarily due to the completion of our share repurchase program in December 2015, which is discussed below.Repurchase Programrepurchase of shares was funded from cash on hand and cash provided by operating activities. The Repurchase Programshare repurchase program expired on December 31, 2015. As of December 31, 2015, we had purchased 806,018 shares at an aggregate cost of $25 million under the Repurchase Program.this program. The average purchase price per share from inception of the program until its expiration was $31.02.2016,2017, our long-term contractual obligations were limited to debt and leases. The table below details our commitments by type of obligation, including interest if applicable, and the period that the payment will become due (in thousands). Long-Term Debt Obligations Net Operating Lease Obligations Total Less than 1 year $ 419 $ 1,890 $ 2,309 1 to 3 years 1,229 3,580 4,809 3 to 5 years 400 3,510 3,910 More than 5 years — 1,172 1,172 Total long-term contractual obligations $ 2,048 $ 10,152 $ 12,200 2016,2017, the total unrecognized tax benefit related to uncertain tax positions was $1.0$1.2 million. We estimate that none of this will be paid within the next 12 months. However, we believe that it is reasonably possible that within the next 12 months, the total unrecognized tax benefits will decrease by approximately 65%11% due to the expiration of certain statutes of limitations or resolution of tax audits. We are unable to make reasonably reliable estimates regarding the timing of future cash outflows, if any, associated with the remaining unrecognized tax benefits.$30.8$28.5 million as of September 30, 2016, of which $26.8 million reduces our borrowing capacity.