D t

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

☒ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15 (d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 20162017

OR

☐ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15 (d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission file number: 000-54685

CNL Healthcare Properties, Inc.

(Exact name of registrant as specified in its charter)

Maryland |

| 27-2876363 |

(State or other jurisdiction of incorporation or organization) |

| (I.R.S. Employer Identification No.) |

CNL Center at City Commons

|

|

|

(Address of principal executive offices) |

| (Zip Code) |

Registrant’s telephone number, including area code (407) 650-1000

Securities registered pursuant to Section 12(b) of the Act:

Title of each class |

| Name of each exchange on which registered |

|

|

Securities registered pursuant to Section 12(g) of the Act: Common Stock, $0.01 par value per share

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐ No ☒

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ☒ No ☐

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ☒

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company or emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer”filer,” “smaller reporting company” and “smaller reporting“emerging growth company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer | ☐ | Accelerated filer | ☐ | |

Non-accelerated filer | ☒ (Do not check if a smaller reporting company) | Smaller reporting company | ☐ | |

Emerging growth company | ☐ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No☒

There is currently no established public market for the registrant’s shares of common stock. Based on the Company’s $9.75$10.04 net asset value per share as of June 30, 20162017 (the last business day of the registrant’s most recently completed second fiscal quarter), the aggregate market value of the stock held by non-affiliates of the registrant on such date was $1.7$1.8 billion.

The number of shares of common stock of the registrant outstanding as of March 3, 20175, 2018 was 175,069,562.174,634,263.

DOCUMENTS INCORPORATED BY REFERENCE

Registrant incorporates by reference portions of the CNL Healthcare Properties, Inc.

Definitive Proxy Statement for the 2017 Annual Meeting of Stockholders

(Items 10, 11, 12, 13 and 14 of Part III) to be filed no later than

April 30, 2017.

None

|

|

|

| Page | |

|

|

|

| ||

|

|

| 3 | ||

| Item 1. |

| 4 | ||

| Item 1A. |

|

| ||

| Item 1B. |

|

| ||

| Item 2. |

|

| ||

| Item 3. |

|

| ||

| Item 4. |

|

| ||

|

|

|

|

| |

|

|

|

| ||

| Item 5. |

|

| ||

| Item 6. |

|

| ||

| Item 7. | Management’s Discussion and Analysis of Financial Condition and Results of Operations |

|

| |

| Item 7A. |

|

| ||

| Item 8. |

|

| ||

| Item 9. | Changes in and Disagreements With Accountants on Accounting and Financial Disclosure |

|

| |

| Item 9A. |

|

| ||

| Item 9B. |

|

| ||

|

|

|

|

| |

|

|

|

| ||

| Item 10. |

|

| ||

| Item 11. |

|

| ||

| Item 12. | Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters |

|

| |

| Item 13. | Certain Relationships and Related Transactions, and Director Independence |

|

| |

| Item 14. |

|

| ||

|

|

|

|

| |

|

|

|

| ||

| Item 15. |

|

| ||

| Item 16. |

|

| ||

|

|

|

|

| |

|

| ||||

STATEMENT REGARDING FORWARD LOOKING INFORMATION

Statements contained under “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and elsewhere in this Annual Report on Form 10-K for the fiscal year ended December 31, 20162017 (“Annual Report”) that are not statements of historical or current fact may constitute “forward-looking statements” within the meaning of the Federal Private Securities Litigation Reform Act of 1995. The Company intends that such forward-looking statements be subject to the safe harbor created by Section 21E of the Securities Exchange Act of 1934, as amended (“Exchange Act”). Forward-looking statements are statements that do not relate strictly to historical or current facts, but reflect management’s current understandings, intentions, beliefs, plans, expectations, assumptions and/or predictions regarding the future of the Company’s business and its performance, the economy, and other future conditions and forecasts of future events and circumstances. Forward-looking statements are typically identified by words such as “believes,” “expects,” “anticipates,” “intends,” “estimates,” “plans,” “continues,” “pro forma,” “may,” “will,” “seeks,” “should,” “could” and words and terms of similar substance in connection with discussions of future operating or financial performance, business strategy and portfolios, projected growth prospects, cash flows, costs and financing needs, legal proceedings, amount and timing of anticipated future distributions, estimates of per share net asset value of the Company’s common stock, and/or other matters. The Company’s forward-looking statements are not guarantees of future performance. While the Company’s management believes its forward-looking statements are reasonable, such statements are inherently susceptible to uncertainty and changes in circumstances. As with any projection or forecast, forward-looking statements are necessarily dependent on assumptions, data and/or methods that may be incorrect or imprecise, and may not be realized. The Company’s forward-looking statements are based on management’s current expectations and a variety of risks, uncertainties and other factors, many of which are beyond the Company’s ability to control or accurately predict. Although the Company believes that the expectations reflected in such forward-looking statements are based upon reasonable assumptions, the Company’s actual results could differ materially from those set forth in the forward-looking statements due to a variety of risks, uncertainties and other factors. Given these uncertainties, the Company cautions you not to place undue reliance on such statements.

For further information regarding risks and uncertainties associated with the Company’s business, and important factors that could cause the Company’s actual results to vary materially from those expressed or implied in its forward-looking statements, please refer to the factors listed and described under “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and the “Risk Factors” sections of the Company’s documents filed from time to time with the U.S. Securities and Exchange Commission (“SEC” or “the Commission”), including, but not limited to, this Annual Report and the Company’s quarterly reports on Form 10-Q, copies of which may be obtained from the Company’s website at www.cnlhealthcareproperties.com.

All written and oral forward-looking statements attributable to the Company or persons acting on its behalf are qualified in their entirety by this cautionary note. Forward-looking statements speak only as of the date on which they are made, and the Company undertakes no obligation to, and expressly disclaims any obligation to, publicly release the results of any revisions to its forward-looking statements to reflect new information, changed assumptions, the occurrence of unanticipated subsequent events or circumstances, or changes to future operating results over time, except as otherwise required by law.

General

CNL Healthcare Properties, Inc. (“Company”) is a Maryland corporation incorporated on June 8, 2010 that elected to be taxed as a real estate investment trust (“REIT”) beginning with the year ended December 31, 2012 for United States (“U.S.”) federal income tax purposes. The terms “us,” “we,” “our,” “Company” and “CNL Healthcare Properties” include CNL Healthcare Properties, Inc. and each of its subsidiaries.

We are externally managed and advised by CNL Healthcare Corp. (“Advisor”), which serves as our advisor and is responsible for managing our day-to-day affairs and for identifying and making acquisitions and investments on our behalf. We have also retained CNL Healthcare Manager Corp. (“Property Manager”) to manage our properties.

We contributed the net proceeds from our public offerings (“Offerings”) to CHP Partners, LP (“Operating Partnership”) in exchange for partnership interests. Substantially all of our assets are held by, and all operations are conducted, either directly or indirectly, through: (1) the Operating Partnership in which we are the sole limited partner and our wholly owned subsidiary, CHP GP, LLC, is the sole general partner; (2) a wholly owned taxable REIT subsidiary (“TRS”), CHP TRS Holding, Inc.; (3) property owner subsidiaries and lender subsidiaries, which are single purpose entities; and (4) investments in joint ventures.

Our offices are located at 450 South Orange Avenue within the CNL Center at City Commons in Orlando, Florida, 32801, and our telephone number is (407) 650-1000.

Investment Objectives and Strategy

Our primary investment objectives have been to invest in a diversified portfolio of assets that will allow us to:

provide stockholders with attractive and stable cash distributions;

preserve, protect and grow stockholders’ invested capital; and

explore liquidity opportunities in the future, such as the sale of either the Company or our assets, potential merger, or the listing of our common shares on a national securities exchange.

There can be no assurance that we will be able to achieve our investment objectives. In 2017, we began evaluating strategic alternatives to provide liquidity to the Company’s stockholders. The Company continues to evaluate strategic alternatives for an outcome in the best interests of its stockholders and will announce publicly the Company’s formation of a special committee and/or engagement of any investment banker when either occurs. Until such time, we continue to strategically manage and position our portfolio to drive performance and value during what is now our maturation phase of the Company’s lifecycle.

With the completion of our Offerings, our Advisor is focused on actively managing our diversified portfolio of healthcare real estate and real estate-related assets within the seniors housing, medical office, post-acute care and acute care asset classes. The types of seniors housing properties that we have acquired include independent and assisted living facilities, continuing care retirement communities and Alzheimer’s / memory care facilities. The types of medical office facilities that we have acquired include medical office buildings, specialty medical and diagnostic service facilities, surgery centers, outpatient rehabilitation facilities, and other facilities designed for clinical services. The types of post-acute care facilities that we have acquired include skilled nursing facilities and inpatient rehabilitative facilities. The types of acute care facilities that we have acquired include specialty surgical hospitals. We view, manage and evaluate our portfolio homogeneously as one collection of healthcare assets with a common goal of maximizing revenues and property income regardless of the asset class or asset type.

We have primarily leased our seniors housing properties to wholly owned TRS entities and engaged independent third-party managers under management agreements to operate the properties as permitted under the REIT Investment Diversification and Empowerment Act of 2007 (“RIDEA”). We have also leased certain of our seniors housing properties to third-party tenants under triple-net or similar lease structures, where the tenant bears all or substantially all of the costs (including cost increases, for real estate taxes, utilities, insurance and ordinary repairs). Medical office, post-acute care and acute care properties have been leased on a triple-net, net or modified gross basis to third-party tenants. In addition, most of our investments are wholly owned, although, we have invested through partnerships with other entities where we believe it is appropriate and beneficial. We have and continue to invest in existing property developments or properties that have not reached full stabilization.

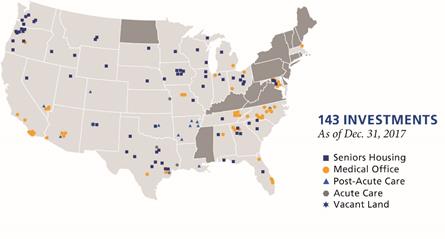

We believe recent demographic trends and compelling supply and demand indicators present a strong case for an investment focus on healthcare real estate and real estate-related assets. We believe that the healthcare sector will continue to provide attractive opportunities as compared to other asset sectors over the long-term. Our healthcare investment portfolio is geographically diversified with properties in 34 states. The map below shows our current property allocations across geographic regions as of December 31, 2016:2017:

As of December 31, 2016,2017, our healthcare investment portfolio consisted of interests in 143 properties, including 72 seniors housing communities,properties, 54 medical office buildings (“MOB”), 12 post-acute care facilities and five acute care hospitals. Of our properties held at December 31, 2016,2017, five of our 72 seniors housing communities currently have real estate under development or current expansion projects and fiveproperties were owned through an unconsolidated joint venture. Oneventure and one was comprised of our 12 post-acute care facilities currently has real estate under development.unimproved land. The following table summarizes our healthcare portfolio by asset class and investment structure as of December 31, 2016:2017:

|

|

|

|

|

| Amount of |

|

| Percentage |

| |||||||||||||

Type of Investment |

| Number of Investments |

|

| Amount of Investments (in millions) |

|

| Percentage of Total Investments |

|

| Number of Investments |

|

| Investments (in millions) |

|

| of Total Investments |

| |||||

Consolidated investments: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

Seniors housing leased (1) |

| 16 |

|

| $ | 360.9 |

|

| 12.0 | % |

|

| 15 |

|

| $ | 311.0 |

|

|

| 10.2 | % | |

Seniors housing managed (2) |

| 48 |

|

|

| 1,260.6 |

|

| 41.9 | % |

|

| 51 |

|

|

| 1,427.5 |

|

|

| 46.9 | % | |

Seniors housing developments (3) (6) |

| 3 |

|

|

| 80.5 |

|

| 2.7 | % | |||||||||||||

Seniors housing expansion projects (3) |

| ― | (4) |

|

| 3.8 |

|

| 0.1 | % | |||||||||||||

Seniors housing unimproved land |

|

| 1 |

|

|

| 1.1 |

|

|

| 0.0 | % | |||||||||||

Medical office leased (1) |

| 54 |

|

|

| 931.4 |

|

| 30.9 | % |

|

| 54 |

|

|

| 931.4 |

|

|

| 30.6 | % | |

Post-acute care leased (1) |

| 11 |

|

|

| 176.6 |

|

| 5.9 | % |

|

| 12 |

|

|

| 190.8 |

|

|

| 6.3 | % | |

Post-acute care development (3) |

| 1 |

|

|

| 12.9 |

|

| 0.4 | % | |||||||||||||

Acute care leased (1) |

| 5 |

|

|

| 153.9 |

|

| 5.1 | % |

|

| 5 |

|

|

| 153.9 |

|

|

| 5.0 | % | |

Unconsolidated investments: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

Seniors housing managed (5) |

| 5 |

|

|

| 31.1 |

|

| 1.0 | % | |||||||||||||

Seniors housing managed (3) |

|

| 5 |

|

|

| 31.1 |

|

|

| 1 | % | |||||||||||

|

| 143 |

|

| $ | 3,011.7 |

|

| 100.0 | % |

|

| 143 |

|

| $ | 3,046.8 |

|

|

| 100 | % | |

_____________

FOOTNOTES:

(1) | Properties that are leased to third-party tenants for which we report rental income |

(2) | Properties that are leased to TRS entities and managed pursuant to third-party management contracts (i.e. RIDEA structure) where we report resident fees and services, and the corresponding property operating expenses. |

(3) |

|

|

|

|

|

We monitor the performance of our tenants and third-party operators to stay abreast of any material changes in the operations of the underlying properties by (1) reviewing the current, historical and prospective operating margins (measured by a tenant’s earnings before interest, taxes, depreciation, amortization and facility rent), (2) monitoring trends in the source of our tenants’ revenue, including the relative mix of public payors (including Medicare, Medicaid, etc.) and private payors (including commercial insurance and private pay patients), (3) evaluating the effect of evolving healthcare legislation and other regulations on our tenants’ profitability and liquidity, and (4) reviewing the competition and demographics of the local and surrounding areas in which the tenants operate.

In addition to operating statistics of the underlying properties, whenWhen evaluating the performance of our healthcare portfolio within the seniors housing and post-acute care asset classes, management reviews occupancy levels and monthly revenue per occupied unit, (“RevPOU”), which we define as total revenue divided by average number of occupied units or beds during a month and is considered an established keya performance metric within these asset classes. Similarly, within the medical office and acute care asset classes, management reviews operating statistics of the underlying properties, including occupancy levels and monthly rent per square foot. Lastly, when evaluating the performance of our third-party operators or developers, management reviews monthly financial statements, property-levelproperty level operating performance versus budgeted expectations, conducts periodic operational review calls with operators and conducts periodic property inspections or site visits. AllWe do not consider this information to be a non-GAAP measure that can be reconciled to our GAAP financial statements because it includes the performance of properties that are leased to third-party tenants. However, all of the aforementioned operating and statistical metrics assist us in determining the ability of our properties or operators to achieve market rental rates, to assess the overall performance of our diversified healthcare portfolio, and to review compliance with leases, debt, licensure, real estate taxes, and other collateral.

Furthermore, in our evaluation of the properties, we consider the operating stage of the investments within the following stages: development, value-add or stabilizing and stabilized. DevelopmentWhile we do not currently have any real estate under development, development properties are those in which we or our joint venture have purchased land for the development of new operating properties. We typically hold rights as the owner or managing member of the development properties while a third-party or our joint venture partner manages the development, construction and certain day-to-day operations of the property subject to our oversight. Stabilizing properties are either developed properties that have been fully constructed and in lease-up phase (typically 18 months post-construction) or existing (“value-add”) properties in which we expect to make capital investments to upgrade or expand. A property is considered stabilized upon the earlier of (i) when the property reaches 85% occupancy for a trailing three month period, or (ii) a two year period from acquisition or completion of development. For those assets that are above an 85% occupancy level and subsequently drop below 85%, they are reclassified to stabilizing until the assets attain the trailing three month 85% occupancy metric.

During the year ended December 31, 2016,2017, we continued to invest in existing ground-up development and value-add or stabilizing properties. During the construction and lease-up phase, these types of investments are expected to generate limited cash flows from operations and may result in near term downward pressure on our results of operations and net asset valuation. However, we believe that investing a portion of our capital into these types of properties is beneficial because they are expected to provide a higher yield on cost and higher net asset valuations in the long-term as compared to stabilized acquisitions. Additionally, these types of assets will result in our portfolio having a lower average age, which we believe will enhance our overall market value over the long-term.

Based on revenues as of December 31, 2016, the Company’s portfolio is comprised of 93.6% stabilized properties, of which 1.2% are completed developments, and 6.4% value-add or stabilizing properties, of which 0.6% are recently completed developments that are currently in the lease-up phase.

The following table lists our occupancy, RevPOU and rent per square feet by asset class within our healthcare portfolio as of December 31, 2016:

Operating Stage |

| Occupancy % |

|

| RevPOU |

| Rent per Square Feet | |||

Value-add or Stabilizing: |

|

|

|

|

|

|

|

|

| |

| Seniors Housing |

| 65.4% |

|

| $ | 4,216 |

| $ | ― |

| Medical Office |

| 80.1% |

|

| $ | ― |

| $ | 2.70 |

Stabilized: |

|

|

|

|

|

|

|

|

| |

| Seniors Housing |

| 88.6% |

|

| $ | 4,256 |

| $ | ― |

| Medical Office |

| 94.8% |

|

| $ | ― |

| $ | 2.65 |

| Acute Care |

| 100.0% |

|

| $ | ― |

| $ | 3.08 |

| Post-Acute Care (1) |

| 100.0% |

|

| $ | 7,115 |

| $ | 3.04 |

_____________

FOOTNOTE:

|

|

Real Estate Under Development

As of December 31, 2016, we had interests in four properties under development and two properties with expansion projects that will provide us with 524 additional units upon completion as follows:

Property Name (and Location) |

| Developer |

| Number of Units Upon Completion |

| Development Costs Incurred (in millions) (1) |

| Remaining Development Budget (in millions) (2) |

| Construction Loan Capacity (in millions) |

| Estimated Completion Date | |||

Developments |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Welbrook Senior Living Grand Junction (Grand Junction, CO) |

| Embree Asset Group, Inc. |

| 50 units |

| $ | 12.9 |

| $ | 1.9 |

| $ | ― |

| February 2017 |

Waterstone on Augusta (Greenville, SC) |

| T&D Greenville, LLC |

| 114 units |

|

| 24.2 |

|

| 5.0 |

|

| 6.2 |

| February 2017 |

Wellmore of Lexington (Lexington, SC) |

| Maxwell Group, Inc. |

| 200 units |

|

| 39.0 |

|

| 20.1 |

|

| 22.1 |

| 2nd quarter 2017 |

Dogwood Forest of Grayson (Grayson, GA) |

| Solomon Development Services, LLC |

| 99 units |

|

| 17.3 |

|

| 12.9 |

|

| 13.0 |

| 3rd quarter 2017 |

Expansion Projects |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Tranquillity at Fredericktowne (Frederick, MD) |

| Capital Health Partners |

| 32 units |

|

| 1.4 |

|

| 4.5 |

|

| ― |

| 2nd quarter 2017 |

Brookridge Heights Assisted Living & Memory Care (Marquette, MI) |

| Capital Health Partners |

| 29 units |

|

| 2.4 |

|

| 2.6 |

|

| ― |

| 2nd quarter 2017 |

|

| Total |

| 524 units |

| $ | 97.2 |

| $ | 47.0 |

| $ | 41.3 |

|

|

_____________

FOOTNOTES:

|

|

|

|

The development budgets include the cost of the land, construction costs, development fees, financing costs, start-up costs and initial operating deficits of the respective properties. Generally, we have delegated to an affiliate of the developer of the respective community the management and administration of the development and construction. Each developer is generally responsible for any cost overruns beyond the approved development budget for the applicable project.

Significant Tenants and Operators

Our real estate portfolio is operated by a mix of national or regional operators and the following represent the significant tenants and operators that lease or manage 5% or more of our rentable space as of December 31, 2016:2017:

Tenants |

| Number of Properties |

| Rentable Square Feet (in thousands) |

| Percentage of Rentable Square Feet |

| Lease Expiration Year |

| Number of Properties |

|

| Rentable Square Feet (in thousands) |

|

| Percentage of Rentable Square Feet |

|

| Lease Expiration Year | |||

TSMM Management, LLC |

| 13 |

| 1,261 |

| 21.6% |

| 2022-2025 |

|

| 13 |

|

|

| 1,261 |

|

|

| 22.7 | % |

| 2022-2025 |

Parc Communities, LLC (1) |

| 2 |

| 385 |

| 6.6% |

| 2017 | ||||||||||||||

Wellmore, LLC |

|

| 2 |

|

|

| 366 |

|

|

| 6.6 | % |

| 2026-2027 | ||||||||

Novant Medical Group, Inc. |

| 5 |

| 320 |

| 5.5% |

| 2017-2025 |

|

| 5 |

|

|

| 305 |

|

|

| 5.5 | % |

| 2018-2025 |

Other tenants and vacancies (2) |

| 66 |

| 3,881 |

| 66.3% |

| 2017-2038 | ||||||||||||||

Other (1) |

|

| 66 |

|

|

| 3,617 |

|

|

| 65.2 | % |

| 2018-2038 | ||||||||

|

| 86 |

| 5,847 |

| 100.0% |

|

|

|

| 86 |

|

|

| 5,549 |

|

|

| 100.0 | % |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Operators |

| Number of Properties |

| Rentable Square Feet (in thousands) |

| Percentage of Rentable Square Feet |

| Operator Expiration Year |

| Number of Properties |

|

| Rentable Square Feet (in thousands) |

|

| Percentage of Rentable Square Feet |

|

| Operator Expiration Year | |||

Integrated Senior Living, LLC |

| 6 |

| 1,803 |

| 31.7% |

| 2019-2021 |

|

| 7 |

|

|

| 2,039 |

|

|

| 32.2 | % |

| 2019-2021 |

Prestige Senior Living, LLC |

| 13 |

| 895 |

| 15.8% |

| 2019 |

|

| 13 |

|

|

| 895 |

|

|

| 14.1 | % |

| 2019 |

MorningStar Senior Management, LLC |

| 4 |

| 834 |

| 14.7% |

| 2018-2019 | ||||||||||||||

Morningstar Senior Management, LLC |

|

| 4 |

|

|

| 834 |

|

|

| 13.2 | % |

| 2018-2019 | ||||||||

SLH Austin Manager, LLC |

| 3 |

| 432 |

| 7.6% |

| 2020-2025 |

|

| 3 |

|

|

| 431 |

|

|

| 6.8 | % |

| 2020-2025 |

HarborChase Retirement, LLC |

| 4 |

| 380 |

| 6.7% |

| 2018-2024 | ||||||||||||||

Other operators (2) |

| 18 |

| 1,336 |

| 23.5% |

| 2017-2025 | ||||||||||||||

Parc Communities, LLC |

|

| 2 |

|

|

| 385 |

|

|

| 6.1 | % |

| 2022 | ||||||||

Harborchase Retirement, LLC |

|

| 4 |

|

|

| 380 |

|

|

| 6.0 | % |

| 2018-2024 | ||||||||

Other (1) |

|

| 18 |

|

|

| 1,363 |

|

|

| 21.6 | % |

| 2018-2025 | ||||||||

|

| 48 |

| 5,680 |

| 100.0% |

|

|

|

| 51 |

|

|

| 6,327 |

|

|

| 100.0 | % |

|

|

___________________

FOOTNOTES:FOOTNOTE:

(1) |

|

| Comprised of various tenants or operators each of which comprise less than 5% of our consolidated rentable square footage. |

While we are not directly impacted by the performance of the underlying properties leased to third-party tenants, we believe that the financial and operational performance of our tenants provides an indication about the stability of our tenants and their ability to pay rent. To the extent that our tenants, managers or joint venture partners experience operating difficulties and become unable to generate sufficient cash to make rent payments to us, there could be a material adverse impact on our consolidated results of operations, liquidity and/or financial condition. Our tenants and managers are generally contractually required to provide this information to us in accordance with their respective lease, management and/or joint venture agreements. Therefore, in order to mitigate the aforementioned risk, we monitor our investments through a variety of methods determined by the type of property.

We monitor the credit of our tenants to stay abreast of any material changes in quality. We monitor tenant credit quality by (1) reviewing financial statements that are publicly available or that are required to be delivered to us under the applicable lease, (2) direct interaction with onsite property managers, (3) monitoring news and rating agency reports regarding our tenants (or their parent companies) and their underlying businesses, (4) monitoring the timeliness of rent collections and (5) monitoring lease coverage.

Tenant Lease Expirations

As of December 31, 2016,2017, we owned 86 properties that were leased to tenants on a triple-net, net or modified gross basis, and accounted for as operating leases. During the year ended December 31, 2016,2017, our rental revenues from operating leasesincome represented approximately 33.1%32.5% of our total revenues. As of December 31, 2016,2017, approximately 67.2%57.0% of our rental revenues from operating leases wereincome was scheduled to expire in 20212023 or later. We do not expect lease turnover to have a significant impact on our cash flows from operations in the near term as approximately 55.9% of our 2017 expiring leased square feet relates to the Parc Communities (discussed above).term.

Our asset management team collaborates with existing tenants to understand their current and anticipated space needs in advance of their lease term renewal date. As of December 31, 2016,2017, approximately 32.8%43.0% of our rental revenues from operating leases wereincome was scheduled to expire through 2020.2022. We work with and begin lease-related negotiations well in advance of the lease expirations or renewal period options in order for us to maintain a balanced lease rollover schedule and

high occupancy levels, as well as to enhance the value of our properties through extended lease terms. Lease extensions are likely to create an obligation to pay lease commissions, lease incentives and/or tenant improvements and may also provide our tenants with some periods of reduced and/or “free rent.”Certain amendments or modifications to the terms of existing leases could require lender approval.

Under the terms of our triple-net lease agreements, each tenant is responsible for the payment of property taxes, general liability insurance, utilities, repairs and maintenance, including structural and roof expenses (“Triple-net Lease”). Each tenant is expected to pay real estate taxes directly to taxing authorities. However, if the tenant does not pay, we will be liable.

Under the terms of our net, modified gross or similar lease agreements for multi-tenant properties with third-party property managers, each tenant is responsible for the payment of their proportionate share of property taxes, general liability insurance, utilities, repairs and common area maintenance (“Modified Lease”). These amounts are billed monthly and recorded as tenant reimbursement income in the accompanying consolidated statements of operations.

The following table lists, on an aggregate basis, scheduled expirations for the next 10 years ending December 31st and thereafter on our consolidated healthcare investment portfolio (excluding real estate under development), assuming that none of the tenants exercise any of their renewal options (in thousands, except for number of tenants and percentages) as of December 31, 2016:2017:

Year of Expiration (1) |

| Number of Tenants |

| Expiring Leased Square Feet |

|

| Expiring Annualized Base Rents (2) |

| Percentage of Expiring Annual Base Rents |

| Number of Tenants |

|

| Expiring Leased Square Feet |

|

| Expiring Annualized Base Rents (2) |

|

| Percentage of Expiring Annual Base Rents |

| ||||

2017 |

| 87 |

| 689 |

|

| 11,320 |

| 10.1% | ||||||||||||||||

2018 |

| 99 |

| 396 |

| 8,139 |

| 7.3% |

|

| 83 |

|

|

| 372 |

|

|

| 9,614 |

|

|

| 8.0 | % | |

2019 |

| 77 |

| 328 |

| 6,496 |

| 5.8% |

|

| 74 |

|

|

| 337 |

|

|

| 7,958 |

|

|

| 6.6 | % | |

2020 |

| 57 |

| 324 |

| 6,146 |

| 5.5% |

|

| 67 |

|

|

| 400 |

|

|

| 9,185 |

|

|

| 7.6 | % | |

2021 |

| 46 |

| 246 |

| 4,863 |

| 4.4% |

|

| 57 |

|

|

| 295 |

|

|

| 7,331 |

|

|

| 6.1 | % | |

2022 |

| 26 |

| 1,027 |

| 15,210 |

| 13.6% |

|

| 42 |

|

|

| 1,088 |

|

|

| 17,571 |

|

|

| 14.7 | % | |

2023 |

| 83 |

| 768 |

| 18,345 |

| 16.4% |

|

| 74 |

|

|

| 815 |

|

|

| 19,392 |

|

|

| 16.1 | % | |

2024 |

| 8 |

| 239 |

| 5,712 |

| 5.1% |

|

| 14 |

|

|

| 272 |

|

|

| 6,742 |

|

|

| 5.6 | % | |

2025 |

| 32 |

| 604 |

| 11,660 |

| 10.4% |

|

| 33 |

|

|

| 555 |

|

|

| 10,789 |

|

|

| 9.0 | % | |

2026 |

| 4 |

| 154 |

| 1,538 |

| 1.4% |

|

| 6 |

|

|

| 160 |

|

|

| 3,509 |

|

|

| 2.9 | % | |

2027 |

|

| 14 |

|

|

| 496 |

|

|

| 6,367 |

|

|

| 5.3 | % | |||||||||

Thereafter |

| 38 |

| 798 |

| 22,322 |

| 20.0% |

|

| 23 |

|

|

| 759 |

|

|

| 21,665 |

|

|

| 18.1 | % | |

Total |

| 557 |

| 5,573 |

| $ | 111,751 |

| 100.0% |

|

| 487 |

|

|

| 5,549 |

|

| $ | 120,123 |

|

|

| 100.0 | % |

Weighted Average Remaining Lease Term (in years): (3)6.8 |

|

|

_________________

FOOTNOTES:

(1) | Represents current lease expiration and does not take into consideration lease renewals available under existing leases at the option of the tenants. |

(2) | Represents the current base rent, excluding tenant reimbursements and the impact of future rent bumps included in leases, multiplied by 12 and included in the year of expiration. |

(3) | Weighted average remaining lease term is the average remaining term weighted by annualized current base rents. |

Share Price Valuation

We have adopted a valuation policy designed to follow recommendations of the Investment Program Association (“IPA”), in the IPA Practice Guideline 2013-01, Valuations of Publicly Registered Non-Listed REITs, which was adopted by the IPA effective May 1, 2013 (“IPA Valuation Guideline”). The purpose of our valuation policy is to establish guidelines to be followed in determining the net asset value per share of our common stock for regulatory and investor reporting and on-going evaluation of investment performance. Net asset value (“NAV”) means the fair value of real estate, real estate-related investments and all other assets less the fair value of total liabilities. Our NAV will be determined based on the fair value of our assets less liabilities under market conditions existing as of the time of valuation and assuming the allocation of the resulting net value among our stockholders after any adjustments for incentive, preferred or special interests, if applicable.

In accordance with our valuation policy and as recommended by the IPA Valuation Guideline, we expect to produce an estimated NAV per share at least annually as of December 31 and disclose such amount as soon as possible after year-end. The audit committee of our board of directors, comprised of our independent directors (“Valuation Committee”), oversees our valuation process and engages one or more third-party valuation advisors to assist in the process of determining the estimated NAV per share of our common stock.

To assist our board of directors in its determination of the estimated NAV per share of our common stock, our board of directors engaged an independent valuation firm, CBRE Capital Advisors, Inc. (“CBRE Cap”), to provide property-level and aggregate valuation analyses of the Company and a range for the NAV per share of our common stock and to consider other information provided by our Advisor.

Upon the recommendation of our Valuation Committee, our board of directors approved our estimateestimated NAV per share to be $10.04$10.32 as of December 31, 2016. In accordance with our valuation policy and as recommended by the IPA Valuation Guideline, we expect to produce an2017, which includes deductions for estimated NAV per share at least annually as of December 31 and disclose such amount as soon as possible after year-end.

transaction costs.

For a detailed discussion of the determination of the estimated NAV per share of our common stock, including our valuation process and methodology, see Item 5. “Market For Registrant’s Common Equity, Related Stockholder Matters And Issuer Purchases Of Equity Securities – Stock Valuation.”

Distribution Policy

In order to qualify as a REIT, we are required to make distributions, other than capital gain distributions, to our stockholders each year in the amount of at least 90% of our taxable income. We may make distributions in the form of cash or other property, including distributions of our own securities. While we generally expect to pay distributions from cash flows provided by operating activities, we have and may continue to cover periodic shortfalls between distributions paid and cash flows provided by operating activities from other sources; such as from cash flows provided by financing activities (“Other Sources”), a component of which could include borrowings, whether collateralized by our assets or unsecured, or proceeds from our distribution reinvestment plan (“Reinvestment Plan”). Refer to Item 5. “Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities – Distributions” for additional information regarding our distributions.

Borrowings

We have borrowed funds to acquire properties, make loans and other permitted investments and to pay certain related fees. We may borrow money to pay distributions to stockholders, for working capital and for other corporate purposes. We also intend to encumber assets in connection with such borrowings and are subject to certain customary covenants and limitations in connection with our borrowings. The aggregate amount of long-term financing is not expected to exceed 60% of the carrying value of our total assets on an annual basis.

There is no limitation on the amount we may invest in any single property or other asset or on the amount we can borrow for the purchase of any individual property or other investment. Our board of directors has adopted a policy to generally limit our aggregate borrowings to approximately 75% of the aggregate value of our assets, unless substantial justification exists that borrowing a greater amount is in our best interests. Our intent is to target our aggregate borrowings ranging from 40% to 60% of the aggregate value of our assets now that we own a seasoned and stable asset portfolio. As of December 31, 20162017 and 2015,2016, we had an aggregate debt leverage ratio of approximately 55.8%59.5% and 52.6%55.8%, respectively, of the aggregate carrying value of our assets.

Competition

The current market for healthcare real estate is highly competitive as is the leasing market for such properties. We compete for investments and financing with many other entities engaged in real estate investment activities, including individuals, corporations, bank and insurance company investment accounts, REITs, real estate limited partnerships, many of which will have greater resources and lower costs of capital than we do. The level of competition impacts both our ability to manage our investments and locate suitable tenants. We may also compete with affiliates to acquire properties and other investments if we determine to make additional investments.

Our tenants and operators compete with other properties that provide comparable services in their local markets. Tenants and operators compete for patients, tenants and residents based on a variety of factors including, but not limited to: quality of care, reputation, location, services offered, physician groups, staff and price. We also face competition from other properties for tenants or residents, such as physicians and other health care providers that provide comparable facilities and services.

Employees

We are externally managed and as such we do not have any employees.

Financial Information about Industry Segments

We have determined that we operate in one business segment, real estate ownership, which consists of owning, managing, leasing, acquiring, developing, investing in, and as conditions warrant, disposing of real estate assets. We internally evaluate all of our real estate assets as one operating segment and, accordingly, we do not report segment information.

The following summary of the taxation of the Company and the material federal income tax consequences to the holders of our equity securities is for general information only and is not tax advice. This summary does not address all aspects of taxation that may be relevant to certain types of holders of securities (including, but not limited to, insurance companies, tax-exempt entities, financial institutions or broker-dealers, persons holding our securities as part of a hedging, integrated conversion, or constructive sale transaction or a straddle, traders in securities that use a mark-to-market method of accounting for their securities, investors in pass-through entities and foreign corporations and persons who are not citizens or residents of the United States)U.S.).

This summary does not discuss all of the aspects of U.S. federal income taxation that may be relevant in light of a particular investment or other circumstances. In addition, this summary does not discuss any state or local income taxation or foreign income taxation or other tax consequences. This summary is based on current U.S. federal income tax law. Subsequent developments in U.S. federal income tax law, including changes in law or differing interpretations, which may be applied retroactively, could have a material effect on the U.S. federal income tax consequences of purchasing, owning and disposing of our securities as set forth in this summary.

On December 22, 2017, the U.S. President signed into law H.R. 1, the “Tax Cuts and Jobs Act,” (the “Tax Act”) which generally took effect for taxable years beginning on or after January 1, 2018 and, in certain instances, is scheduled to expire for taxable years beginning on or after January 1, 2026.

The Tax Act makes many changes to the U.S. federal income tax laws that significantly impact the taxation of individuals, corporations (both regular subchapter C corporations as well as corporations that have elected to be taxed as REITs), and the taxation of taxpayers with overseas assets and operations. Among its changes, the Tax Act (1) temporarily reduces the top individual income tax rate to 37% (from 39.6%), (2) permanently replaces the progressive corporate tax rate structure with a flat corporate tax rate of 21%, (3) repeals the corporate alternative minimum tax, (4) generally limits net operating loss (“NOLs”) deductions to 80% of the taxable income in the carryforward year and eliminates the ability to carryback NOLs that arise in taxable years ending after December 31, 2017, and (5) generally limits the deduction for net business interest expense to 30% of “adjusted taxable income” with certain exceptions for electing real property trades or businesses.

To date, the U.S. Internal Revenue Service (“IRS”) has issued only limited guidance with respect to certain provisions of the Tax Act. There are numerous interpretive issues and ambiguities that will require guidance and that are not clearly addressed in the conference report that accompanied the Tax Act. Technical corrections legislation will likely be needed to clarify certain of the new provisions and give proper effect to congressional intent. There can be no assurance, however, that technical corrections or other legislative changes that may be needed to prevent unintended or unforeseen tax consequences will be enacted by Congress anytime soon. Although this summary addresses material provisions enacted by the Tax Act, which may affect REITs and their stockholders, given the complexity of this new law, and the limited administrative guidance issued as of the date of this Annual Report, prospective stockholders should consult their own tax advisors regarding its potential impact on the U.S. federal income tax consequence to them in light of their particular circumstances.

General. We elected to be taxed as a real estate investment trustREIT under the U.S. Internal Revenue Code of 1986, as amended (the “Code”) beginning with our taxable year ended December 31, 2012. We believe that, commencing with such taxable year, we have been organized and have operated in a manner so as to qualify as a REIT for U.S. federal income tax purposes.

Qualification and taxation as a REIT has depended upon, and will continue to depend upon, our ability to meet on a continuing basis, through actual operating results, distribution levels, diversity of share ownership and various qualification requirements imposed upon REITs by the Code. Our ability to qualify as a REIT also requires that we satisfy certain asset tests (discussed below), some of which depend upon the fair market values of assets directly or indirectly owned by us. Such values may not be susceptible to a precise determination. While we intend to continue to operate in a manner that will allow us to qualify as a REIT, no assurance can be given that the actual results of our operations for any taxable year will satisfy such requirements for qualification and taxation as a REIT.

As a REIT, we generally will not be subject to federal corporate income taxes on that portion of our ordinary income or capital gain we distribute currently to our stockholders, because the REIT provisions of the Code generally allow a REIT to deduct distributions, which are taxable dividends, paid to its stockholders. This substantially eliminates the federal double taxation on earnings (taxation at both the corporate level and stockholder level) that usually results from an investment in a corporation. With limited exceptions, dividends from us or from other entities that are taxed as REITs are generally not eligible for the capital gain rate and will continue to be taxed at rates applicable to ordinary income. Commencing with taxable years beginning on or after January 1, 2018 and continuing through 2025, the Tax Act temporarily reduces the effective tax rate on ordinary REIT dividends (i.e., dividends other than capital gain dividends and dividends attributable to certain qualified dividend income received by us) for U.S. stockholders (as hereinafter defined) of our common stock that are individuals, estates or trusts by permitting such stockholders to claim a deduction in determining their taxable income equal to 20% of any such dividends they receive. Taking into account the Tax Act’s reduction in the maximum individual federal income tax rate from 39.6% to 37%, this results in a maximum effective rate of regular income tax on ordinary REIT dividends of 29.6% through 2025 (as compared to the 20% maximum federal income tax rate applicable to qualified dividend income received from a non-REIT corporation).

Any net operating losses,NOLs, foreign tax credits and other tax attributes generally do not pass through to our stockholders, subject to special rules for certain items such as the capital gains that we recognize.

As a result of the enactment of the Tax Act, effective for taxable years beginning on or after January 1, 2018 our domestic taxable REIT subsidiaries (“TRSs”) are subject to U.S. federal income tax on their taxable income at a rate of 21% (as well as applicable state and local income tax), but NOL carryforwards of TRS losses arising in taxable years beginning after December 31, 2017 may be deducted only to the extent of 80% of TRS taxable income in the carryforward year (computed without regard to the NOL deduction). In contrast to prior law, which permitted unused NOL carryforwards to be carried back two years and forward 20 years, the Tax Act provides that losses arising in taxable years ending after December 31, 2017 can no longer be carried back but can be carried forward indefinitely.

Commencing in taxable years beginning after December 31, 2017, Section 163(j) of the Code, as amended by the Tax Act, limits the deductibility of net interest expense paid or accrued on debt properly allocable to a trade or business to 30% of “adjusted taxable income,” subject to certain exceptions. Any deduction in excess of the limitation is carried forward and may be used in a subsequent year, subject to the 30% limitation. “Adjusted taxable income” is determined without regard to certain deductions, including those for net interest expense, NOL carryforwards and, for taxable years beginning before January 1, 2022, depreciation, amortization and depletion. Provided the taxpayer makes a timely election (which is irrevocable), the 30% limitation does not apply to a trade or business involving real property development, redevelopment, construction, reconstruction, rental, operation, acquisition, conversion, disposition, management, leasing or brokerage, within the meaning of Section 469(c)(7)(C) of the Code. If this election is made, depreciable real property (including certain improvements) held by the relevant trade or business must be depreciated under the alternative depreciation system under the Code, which is generally less favorable than the generally applicable system of depreciation under the Code. In general, while there is no authority under such provision or in the legislative history of the Tax Act that specifically addresses healthcare properties or other facilities, including senior housing facilities and MOB, we believe that our leasing, management and operation of such facilities and buildings should constitute a real property trade or business, and we, or our TRSs, may elect not to have the interest deduction limitation apply to that trade or business. If we, or our TRSs, do

not make the election or if the election is determined not to be available with respect to all or certain of our, or our TRSs, business activities, the new interest deduction limitation could result in us having more REIT taxable income and thus increase the amount of distributions we must make to comply with the REIT requirements and avoid incurring corporate level tax. Similarly, the limitation could cause our TRSs to have greater taxable income and thus potentially greater corporate tax liability.

Even if we qualify for taxation as a REIT, however, we will be subject to federal income taxation as follows:

We will be taxed at the regular corporate ratesrate on our undistributed taxable income, including undistributed net capital gains.

Under some circumstances, we may be subject to an “alternative minimum tax.”

If we have net gain for tax purposes from prohibited transactions (which are, in general, sales or other dispositions of property, other than foreclosure property, held primarily for sale to customers in the ordinary course of business), such gain will be subject to a 100% tax.

If we elect to treat property that we acquire in connection with a foreclosure of a mortgage loan or certain leasehold terminations as “foreclosure property,” we may avoid the 100% tax on gain from a sale of that property (if the sale would otherwise constitute a prohibited transaction), but the income from the sale or operation of the property may be subject to corporate income tax at the highest applicable rate.

If we should fail to satisfy the asset test other than certain de minimis violations or other requirements applicable to REITs, as described below, yet nonetheless maintain our qualification as a REIT because there is reasonable cause for the failure and other applicable requirements are met, we may be subject to an excise tax. In that case, the amount of the tax will be at least $50,000 per failure, and, in the case of certain asset test failures, will be determined as the amount of net income generated by the assets in question multiplied by the highest corporate tax rate if that amount exceeds $50,000 per failure.

If we fail to satisfy either of the 75% or 95% income tests (discussed below) but have nonetheless maintained our qualification as a REIT because certain conditions have been met, we will be subject to a 100% tax on an amount based on the magnitude of the failure, as adjusted to reflect the profit margin associated with our gross income.

If we fail to distribute during each year at least the sum of (i) 85% of our REIT ordinary income for the year, (ii) 95% of our REIT capital gain net income for such year, and (iii) any undistributed taxable income from prior periods, then we will be subject to a 4% excise tax on the excess of the required distribution over the sum of (A) the amounts actually distributed, plus (B) retained amounts on which corporate level tax is paid by us.

We may elect to retain and pay tax on our net long-term capital gains. In that case, a U.S. stockholder would be taxed on its proportionate share of our undistributed long-term capital gains and would receive a credit or refund for its proportionate share of the tax we paid.

If we acquire appreciated assets from a C corporation that is not a REIT (i.e., a corporation generally subject to corporate level tax) in a transaction in which the C corporation would not normally be required to recognize any gain or loss on disposition of the asset and we subsequently recognize gain on the disposition of the asset during the five-year period beginning on the date on which we acquired the asset, then a portion of the gain may be subject to tax at the highest regular corporate rate, unless the C corporation made an election to treat the asset as if it were sold for its fair market value at the time of our acquisition. We will also be required to distribute prior non-REIT earnings and profits.

We may be required to pay monetary penalties to the Internal Revenue Service (“IRS”)IRS in certain circumstances, including if we fail to meet record keeping requirements intended to monitor our compliance with rules relating to the composition of a REIT’s stockholders.

The earnings of our taxable REIT subsidiariesTRSs are subject to federal corporate income tax. In addition, a 100% excise tax will be imposed on the REIT and a corporate level tax on the TRS for transactions between a TRS and the REIT that are deemed not to be conducted on an arm’s length basis.

In addition, we and our subsidiaries may be subject to a variety of taxes, including payroll taxes and state, local, foreign, property and other taxes, on our assets and operations. We could also be subject to tax in situations and on transactions not presently contemplated.

Requirements for Qualification as a REIT. Our qualification as a REIT has depended upon and will continue to depend upon our meeting and continuing to meet the requirements discussed below relating to our organization, sources of income, nature of assets and distributions of income to our stockholders.

Organizational Requirements. In order to qualify for taxation as a REIT under the Code we must meet tests regarding our income and assets described below and we must (i) be a corporation, trust or association that would be taxable as a domestic corporation but for the REIT provisions of the Code; (ii) be managed by one or more trustees or directors; (iii) have our beneficial ownership evidenced by transferable shares; (iv) not be a financial institution or an insurance company subject to special provisions of the federal income tax laws; (v) use a calendar year for federal income tax purposes; (vi) have at least 100 stockholders for at least 335 days of each taxable year of 12 months or during a proportionate part of a taxable year of less than 12 months; and (vii) not be closely held, as defined for purposes of the REIT provisions of the Code.

We would be treated as closely held if, during the last half of any taxable year, more than 50% in value of our outstanding capital shares is owned, directly or indirectly through the application of certain attribution rules, by five or fewer individuals, as defined in the Code to include certain entities. Items (vi) and (vii) above do not apply until after the first taxable year for which we elect to be taxed as a REIT. If we comply with U.S. Department of Treasury Regulationsregulations (“Treasury Regulations”) that provide procedures for ascertaining the actual ownership of our common stock for each taxable year and we did not know, and with the exercise of reasonable diligence could not have known, that we failed to meet item (vii) above for a taxable year, we will be treated as having met item (vii) for that year.

We have elected to be taxed as a REIT commencing with our taxable year ended December 31, 2012, and we intend to satisfy the other requirements described in items (i) through (v) above at all times during each of our taxable years. In addition, our charter contains restrictions regarding ownership and transfer of shares of our common stock that are intended to assist us in continuing to satisfy the share ownership requirements in items (vi) and (vii) above.

For purposes of the requirements described herein, any corporation that is a qualified REIT subsidiary of ours will not be treated as a corporation separate from us and all assets, liabilities and items of income, deduction and credit of our qualified REIT subsidiaries will be treated as our assets, liabilities and items of income, deduction and credit. A qualified REIT subsidiary is a corporation, other than a TRS (described below under “— Operational Requirements — Asset Tests”), of which all of its capital shares are owned by a REIT.

In the case of a REIT that is a partner in an entity treated as a partnership for federal tax purposes, the REIT is treated as owning its proportionate share, based on its capital interest, of the assets of the partnership and as earning its allocable share of the gross income of the partnership for purposes of the requirements described herein. In addition, the character of the assets and gross income of the partnership will retain the same character in the hands of the REIT for purposes of the REIT requirements, including the asset and income tests described below. As a result, our proportionate share, based on our capital interest, of the assets, liabilities and items of income of our operating partnership and of any other partnership, joint venture, limited liability company or other entity treated as a partnership for federal tax purposes in which we or the operating partnership have an interest, will be treated as our assets, liabilities and items of income.

The Code provides relief from violations of the REIT gross income requirements, as described below under “— Operational Requirements — Gross Income Tests,” in cases where a violation is due to reasonable cause and not willful neglect, and other requirements are met, including the payment of a penalty tax that is based upon the magnitude of the violation. In addition, the Code includes provisions that extend similar relief in the case of certain violations of the REIT asset requirements (see “— Operational Requirements — Asset Tests” below) and other REIT requirements, again provided that the violation is due to reasonable cause and not willful neglect, and other conditions are met, including the payment of a penalty tax. If we fail to satisfy any of the various REIT requirements, there can be no assurance that these relief provisions would be available to enable us to maintain our qualification as a REIT. If relief provisions are available, the amount of any resultant penalty tax could be substantial.

Operational Requirements — Gross Income Tests. To maintain our qualification as a REIT, we must satisfy annually two gross income requirements:

At least 75% of our gross income, excluding gross income from prohibited transactions, for each taxable year must be derived directly or indirectly from investments relating to real property or mortgages on real property and from other specified sources, including qualified temporary investment income, as described below. Gross income includes “rents from real property” (as defined in the Code) and, in some circumstances, interest, but excludes gross income from dispositions of property held primarily for sale to customers in the ordinary course of a trade or business. These dispositions are referred to as “prohibited transactions.” This is the “75% Income Test.”

At least 95% of our gross income, excluding gross income from prohibited transactions, for each taxable year must be derived from the real property investments described above and generally from dividends and interest and gains from the sale or disposition of shares of common stock or securities or from any combination of the foregoing. This is the “95% Income Test.”

The rents we will receive or be deemed to receive will qualify as “rents from real property” for purposes of satisfying the gross income requirements for a REIT only if the following conditions are met:

The amount of rent received from a tenant must not be based in whole or in part on the income or profits of any Person; however, an amount received or accrued generally will not be excluded from the term “rents from real property” solely by reason of being based on a fixed percentage or percentages of gross receipts or sales.

In general, neither we nor an owner of 10% or more shares of our common stock may directly or constructively own 10% or more of a tenant, which we refer to as a “Related Party Tenant,” or a subtenant of the tenant (in which case only rent attributable to the subtenant is disqualified).

Rent attributable to personal property leased in connection with a lease of real property cannot be greater than 15% of the total rent received under the lease, as determined based on the average of the fair market values as of the beginning and end of the taxable year.

We normally must not operate or manage the property or furnish or render services to tenants, other than through an “independent contractor” (as defined in the Code) who is adequately compensated and from whom we do not derive any income or through a TRS (discussed below). However, a REIT may provide services with respect to its properties, and the income derived therefrom will qualify as “rents from real property” if the services are “usually or customarily rendered” (as defined in the Code) in connection with the rental of space only and are not otherwise considered “rendered to the occupant” (as defined in the Code). Even if the services provided by us with respect to a property are impermissible customer services, the income derived therefrom will qualify as “rents from real property” if such income does not exceed 1% of all amounts received or accrued with respect to that property.

Interest income constitutes qualifying mortgage interest for purposes of the 75% Income Test to the extent that the obligation upon which such interest is paid is secured by a mortgage on real property. If we receive interest income with respect to a mortgage loan that is secured by both real property and other property, and the highest principal amount of the loan outstanding during a taxable year exceeds the fair market value of the real property on the date that we acquired or originated the mortgage loan, the interest income will be apportioned between the real property and the other collateral, and our income from the arrangement will qualify for purposes of the 75% income test only to the extent that the interest is allocable to the real property. Even if a loan is not secured by real property, or is under-secured, the income that it generates may nonetheless qualify for purposes of the 95% Income Test.

To the extent the terms of a loan provide for contingent interest that is based on the cash proceeds realized upon the sale of the property securing the loan (a “Shared Appreciation Provision”), income attributable to the participation feature will be treated as gain from sale of the underlying property, which generally will be qualifying income for purposes of both the 75% Income Test and 95% Income Test, provided that the real property is not held as inventory or dealer property or primarily for sale to customers in the ordinary course of business. Similar to the treatment of contingent rents from real property (discussed above), to the extent that we derive interest income from a mortgage loan where all or a portion of the amount of interest or rental income payable is contingent, such income generally will qualify for purposes of the 75% Income Test and 95% Income Test only if it is based upon the gross receipts or sales and not on the net income or profits of the borrower.

We may invest in mezzanine loans, which are loans secured by equity interests in an entity that directly or indirectly owns real property, rather than by a direct mortgage of the real property. The IRS has issued Revenue Procedure 2003-65, which provides a safe harbor applicable to mezzanine loans. Under the Revenue Procedure, if a mezzanine loan meets each of the requirements contained in the Revenue Procedure, (i) the mezzanine loan will be treated by the IRS as a real estate asset for purposes of the Asset Tests described below, and (ii) interest derived from the mezzanine loan will be treated as qualifying mortgage interest for purposes of the 75% Income Test. Although the Revenue Procedure provides a safe harbor on which taxpayers may rely, it does not prescribe rules of substantive tax law. We intend to structure any investments in mezzanine loans or similar products in a manner that generally complies with the various requirements applicable to our qualification as a REIT. Certain of our mezzanine loans may qualify under the safe harbor set forth in the Revenue Procedure. However, we may make or acquire some mezzanine loans that do not qualify for the safe harbor. To the extent that any of our mezzanine loans do not meet all of the requirements for reliance on the safe harbor set forth in the Revenue Procedure, there can be no assurance that the IRS will not challenge the tax treatment of these loans.

We may, from time to time, enter into hedging transactions with respect to interest rate exposure or currency fluctuation on one or more of our assets or liabilities. Any such hedging transactions could take a variety of forms, including the use of derivative instruments such as interest rate swap contracts, interest rate cap or floor contracts, futures or forward contracts, and options. To the extent that we or a pass-through subsidiary enters into a hedging transaction (i) to reduce interest rate risk on indebtedness incurred to acquire or carry real estate assets, (ii) to manage risk of currency fluctuations with respect to any item of income that would qualify under the 75% Income Test or the 95% Income Test, or (iii) for taxable years beginning after December 31, 2015, new hedging transactions entered into to hedge the income or loss from prior hedging transactions, where the property or indebtedness which was the subject of the prior hedging transaction was extinguished or disposed of, and the instrument is properly identified as a hedge along with the risk it hedges within prescribed time periods, any periodic income from the instrument, or gain from the disposition of such instrument, would be excluded altogether from the 95% Income Test or the 75% Income Test.

To the extent that we hedge in certain other situations, the resultant income will be treated as income that does not qualify under the 75% Income Test or the 95% Income Test, provided that certain requirements are met. We intend to structure any hedging transactions in a manner that does not jeopardize our status as a REIT. We may conduct some or all of our hedging activities through a TRS or other corporate entity, the income from which may be subject to federal, state, and/or international income tax, rather than by participating in the arrangements directly or through pass-through subsidiaries. No assurance can be given, however, that our hedging activities will not give rise to income that does not qualify for purposes of either or both of the REIT income tests, or that our hedging activities will not adversely affect our ability to satisfy the REIT qualification requirements.

Prior to the making of investments in real properties, we may invest the Net Offering Proceeds in liquid assets such as government securities or certificates of deposit. For purposes of the 75% Income Test, income attributable to a stock or debt instrument purchased with the proceeds received by a REIT in exchange for stock in the REIT (other than amounts received pursuant to a distribution reinvestment plan)Reinvestment Plan) constitutes qualified temporary investment income if such income is received or accrued during the one-year period beginning on the date the REIT receives such new capital. To the extent we hold any proceeds of the offering for longer than one year, we may invest those amounts in less liquid investments such as mortgage-backed securities, maturing mortgage loans purchased from mortgage lenders or shares of common stock in other REITs in order to satisfy the 75% Income Test and the 95% Income Test and the Asset Tests described below. We expect the bulk of the remainder of our income to qualify under the 75% Income and 95% Income Tests as rents from real property, gains from the sale of real property interests and interest on mortgages on real property in accordance with the requirements described above.

With regard to rental income, we anticipate most of our leases will be for fixed rentals with annual CPI or similar adjustments and that none of the rentals under our leases will be based on the income or profits of any Person. Rental leases may provide for payments based on gross receipts, which are generally permissible under the REIT income tests. In addition, none of our tenants are expected to be “Related Party Tenants” and the portion of the rent attributable to personal property is not expected to exceed 15% of the total rent to be received under any lease. We anticipate that all or most of the services to be performed with respect to our real properties will be performed by our property manager, and such services are expected to be those usually or customarily rendered in connection with the rental of real property and not rendered to the occupant of such real property. Finally, we anticipate any non-customarynon-

customary services will be provided by a TRS or, alternatively, by an independent contractor that is adequately compensated and from whom we derive no income. However, we can give no assurance that the actual sources of our gross income will allow us to satisfy the 75% Income Test and the 95% Income Test described above.

Further, we and our subsidiaries may hold investments in, and pay taxes to, foreign countries. Taxes that we pay in foreign jurisdictions may not be passed through to, or used by, our stockholders or us as a foreign tax credit or otherwise. Our foreign investments might also generate foreign currency gains and losses. Foreign currency gains that we derive from certain of our investments will be excluded for purposes of computing the REIT income tests if such foreign currency gain is “real estate foreign exchange gain” (as defined in the Code), that is, if such gains are attributable to any item of income that itself qualifies for purposes of the 75% Income Test or other specified sources. Other foreign currency gains, however, if such foreign currency gain is “passive foreign exchange gain” (as defined in the Code), will be excluded for purposes of computing the 95% Income Test but will be treated as income that does not qualify under the 75% Income Test. Generally, “passive foreign exchange gain” includes foreign exchange gain attributable to any item of income that itself qualifies for purposes of the 95% Income Test or other specified sources.

The Tax Act made fundamental changes to the U.S. international tax system that could affect the amount, timing or character of income we recognize with respect to any foreign subsidiary and, thus, may impact our decision to make investments in foreign jurisdictions. For example, if we were to form a foreign subsidiary, we would be subject to new rules enacted under the Tax Act which could subject us to current U.S. federal income tax on a portion of our income attributable to such foreign subsidiary.

Notwithstanding our failure to satisfy one or both of the 75% Income and the 95% Income Tests for any taxable year, we may still qualify as a REIT for that year if we are eligible for relief under specific provisions of the Code. These relief provisions generally will be available if:

our failure to meet these tests was due to reasonable cause and not due to willful neglect; and

following our identification of the failure, we file a schedule with a description of each item of gross income that caused the failure in accordance with Treasury Regulations.

It is not possible, however, to state whether, in all circumstances, we would be entitled to the benefit of these relief provisions. In addition, as discussed above, even if these relief provisions apply, a tax would be imposed with respect to the excess net income.