| ||||||||

UNIVERSAL INSURANCE HOLDINGS, INC. | ||||||||

| (Exact name of registrant as specified in its charter) | ||||||||

| ☒ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | ||||

2023

| ☐ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | ||||

UNIVERSAL INSURANCE HOLDINGS, INC.

(Exact name of registrant as specified in its charter)

| ||||||||

UNIVERSAL INSURANCE HOLDINGS, INC. | ||||||||

| (Exact name of registrant as specified in its charter) | ||||||||

| Delaware | 65-0231984 | ||||

| (State or other jurisdiction of

| (I.R.S. Employer

| ||||

(Zip Code)

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||||||

Common Stock, | UVE | New York Stock Exchange | ||||||

Securities registered pursuant to Section 12(g) of the Act:

None.

| Securities registered pursuant to Section 12(g) of the Act: None. | ||||||||

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ☐

| Large accelerated filer |

| Accelerated filer |

| ||||||||||

| Non-accelerated filer | ☐ | Smaller reporting company | ☐ | ||||||||||

| Emerging growth company | ☐ |

|

| ||||||||||

State the aggregate

2023, the last trading day of the registrant’s most recently completed second fiscal quarter: $405,608,782

this Annual Report on Form 10-K, to the extent not set forth herein, is incorporated herein by reference to the registrant’s definitive proxy statement relating to the Annual Meeting of Shareholders to be held in 2024, which definitive proxy statement shall be filed with the Securities and Exchange Commission within 120 days after the end of the fiscal year to which this Annual Report on Form 10-K relates.

Page No. | ||||||||||||||||

| Item 1. | ||||||||||||||||

|

| |||||||||||||||

Item 1A. |

| |||||||||||||||

Item 1B. |

| |||||||||||||||

| Item 1C. | ||||||||||||||||

Item 2. |

| |||||||||||||||

Item 3. |

| |||||||||||||||

Item 4. |

| |||||||||||||||

Item 5. |

| |||||||||||||||

| Item 6. | ||||||||||||||||

|

| |||||||||||||||

Item 7. |

| |||||||||||||||

Item 7A. |

| |||||||||||||||

Item 8. |

| |||||||||||||||

Item 9. |

| |||||||||||||||

Item 9A. |

| |||||||||||||||

Item 9B. |

| |||||||||||||||

| Item 9C. | ||||||||||||||||

Item 10. |

| |||||||||||||||

Item 11. |

| |||||||||||||||

Item 12. |

| |||||||||||||||

Item 13. |

| |||||||||||||||

Item 14. |

| |||||||||||||||

Item 15. |

| |||||||||||||||

Item 16. |

| |||||||||||||||

|

| |||||||||||||||

|

| |||||||||||||||

2

DOCUMENTS INCORPORATED BY REFERENCE

Information called for in PART III of this Form 10-K is incorporated by reference to the registrant’s definitive Proxy Statement to be filed within 120 days of the close of the registrant’s fiscal year in connection with the registrant’s annual meeting of shareholders.

INTRODUCTION

We generate revenues primarily from the collection of premiums. Other sources of revenue include: commissions paid by our reinsurers to our reinsurance intermediary subsidiary on reinsurance it places for the Insurance Entities; policy fees collected from policyholders by our managing general agent subsidiary; service revenue frombenefits, solicited claims handling on ceded claims; and financing fees charged to policyholders who choose to defer premium payments. We also generate income by investing our assets.

Over the past several years, we have grown our business both within Floridaother first-party litigation), technological advancements in distribution, underwriting, claims management and elsewhere in the United States through our distribution network of approximately 8,800 licensed independent agents. In writing business, we adhere to a disciplined underwriting approach – writing risks that are priced adequately and meet our underwriting standards – designed to achieve profitable growth as opposed to merely increasing the total number of policies written. We believe we are better positioned than many of our competitors to expand profitably and service our policyholders due to our established internal capabilities; protection afforded us by our reinsurance program; our experienced management team that successfully navigated prior active hurricane seasons, including 2017, 2016, 2005 and 2004; our strong surplus and capital base; our success in growing organically in Florida without relying on the

3

assumption of policies from Citizens Property Insurance Corporation (“Citizens”), the Florida state-sponsored insurer of last resort; and our growing geographic diversification. We also believe that our reinsurance program is structured such that, in the event of an active hurricane season, we are able to pay policyholder claims, maintain sufficient surplus to grow profitably and take advantage of the resulting market dislocation that could potentially follow.

Below is an organization chart that summarizes our corporate structure:

The Insurance Entities are our insurance operating subsidiaries. Most of our policies are written by UPCIC. Universal Risk Advisors (“URA”) is our managing general agent and manages our distribution network and negotiates our reinsurance. Universal Inspection Corporation (“UIC”) conducts inspections as part of our underwriting process, and Universal Adjusting Corporation (“UAC”) manages our claims processing and adjustment functions. Blue Atlantic Reinsurance Corporation (“BARC”) is our reinsurance intermediary. These service companies are vertically aligned with our Insurance Entities to maintain quality throughout the policy origination and claim settlement process. In addition, our servicing subsidiaries help reduce the costs typically associated with outsourced business functions, enhance our ability to expand geographically due to economies of scale in our operations and allow us to expand our business incrementally and more effectively.

OUR STRATEGY

Pursue Profitable Growth with a Focus on Organic Development

We continue to pursue profitable growth both within Florida and through expansion into other states, while continuing to expand Universal DirectSM and adding new products when prudent (such as the Fire, Commercial Multi-Peril, and Other Liability (collectively, “Commercial Residential”) lines of business in Florida that we introduced in late in 2016). Each of these areas is discussed further below.

4

|

Other States – We intend to continue our geographical expansion outside of Florida primarily to take advantage of opportunities to write profitable business as well as to diversify our revenue and risk. We target states with underserved homeowners insurance markets where we believe there is price adequacy for our products and where policyholders would benefit from our market knowledge and integrated service model. In new markets, we seek to replicate the successful growth strategy we implemented in Florida, including the careful appointment of new agents that we believe will generate profitable business for our Company. We intend to leverage our existing agent network to generate new relationships and business. We will continue in our commitment to careful, profitable business growth through such independent agents, with the intent to grow quickly when the opportunity arises, including following any market dislocation. Our strategy involves taking the time to learn about each new market and its unique risks in order to carefully develop our own policy forms, rates and informed underwriting standards. We also believe further geographic diversification will decrease our relative reinsurance costs as our risk profile changes to include more risks not tied to the Florida hurricane exposure. We believe that such diversification will produce more earnings stability as we expand to states with different market cycles than Florida and where the risks insured could offset Florida losses during an active hurricane season such as 2017 which included the impact of Hurricane Irma. Apart from Florida, we currently write homeowners insurance policies in Alabama, Delaware, Georgia, Hawaii, Indiana, Maryland, Massachusetts, Michigan, Minnesota, New Jersey, New York, North Carolina, Pennsylvania, South Carolina, and Virginia, and are also licensed to issue policies in Illinois, Iowa, New Hampshire, and West Virginia. As of December 31, 2017, policies outside of Florida accounted for 26% of our total insured value, or $51.8 billion, as compared to 21% as of December 31, 2016.

|

|

New Products – We evaluate potential new product offerings, such as the Commercial Residential business we launched in Florida late in 2016, and look to add new products to our portfolio when prudent after careful consideration and substantial planning and development. On August 3, 2016 we announced that APPCIC received authorization from the FLOIR to amend its Certificate of Authority to add Commercial Residential lines of business in Florida. During the fourth quarter of 2016, our rates were approved and we wrote our first Commercial Residential policy.Expansion into the Commercial Residential business is a step forward for the Company, and will allow us to tap into a large complementary market that will advance our organic growth strategy. We believe there is an opportunity in the Commercial Residential marketplace in Florida and expect to leverage our robust independent agent distribution network to grow this new product. While we view the Commercial Residential market as an untapped opportunity, we intend to approach this expansion cautiously in order to establish a solid framework onto which we can build our Commercial Residential portfolio in order to ensure proper risk selection and that adequate pricing is achieved.

5

Optimize our Reinsurance Program as our Risk Profile Changes

We will continue to obtain what we believe to be appropriate reinsurance limits, coverage and terms so that our policyholders and shareholders are adequately protected in the event of an active hurricane season. Significant additional new capital entering portions of the reinsurance marketplace has afforded us the opportunity to obtain favorable pricing and contract terms in recent years. Our dedicated reinsurance team at BARC includes seasoned industry professionals whom we hired from Willis Re almost 12 years ago, as well as additional key personnel more recently from leading global reinsurance intermediaries. BARC differentiates us from our competitors by enabling us to act as our own reinsurance intermediary, developing a bespoke reinsurance program tailored to our needs in both soft and hard reinsurance markets. This team has developed and enhanced existing strong long-term relationships with world leading reinsurance companies, providing better efficiency in the manner in which we buy reinsurance. We had in excess of 60 reinsurance partners for the 2017-2018 reinsurance year from companies in the United States, Bermuda, London, Continental Europe and Asia. BARC works in conjunction with URA in providing these services. We also receive reinsurance intermediary services from Guy Carpenter and thereby benefit from its depth of experience and knowledge of market standards. Guy Carpenter works closely with our teams at BARC and URA in designing our reinsurance program and allowing us to obtain favorable pricing. Our internal team and Guy Carpenter continually evaluate prevailing costsoverall operational efficiencies, and the levelrisk appetite of coverage that we determine is necessary in order to proactively capitalize on favorable market conditions.

Effective June 1, 2015, we eliminated our quota share reinsurance arrangements; purchased additional excess of loss catastrophe cover; and converted from a two-tower reinsurance program to a single tower reinsurance program covering our nationwide business based on our improving financial condition, our evaluation of market conditions and our changing coverage needs. We also supplemented this nationwide reinsurance program with a stand-alone supplemental non-Florida catastrophe reinsurance program for the 2017-2018 period, which provides coverage for catastrophic events affecting states outside of Florida in which we write policies. We believe that restructuring our reinsurance program in this manner and continuously re-evaluating that structure has allowed us to take advantage of attractive reinsurance pricing and terms and to retain profitable business by eliminating our quota share program, while still maintaining reinsurance coverage that we believe is sufficient to protect our policyholders and shareholders. As an example, our reinsurance program generally performed as designed following Hurricane Irma in 2017, limiting the net loss and loss adjustment expenses (“LAE”) to our net retention levels. Further, fees generated from our service subsidiary companies produced income after Hurricane Irma, and this, combined with other benefits derived from our reinsurance program, helped to offset losses and reduce the overall effect that Hurricane Irma had on our consolidated financial statements. See Item 7 – Management’s Discussion and Analysis of Financial Condition and Results of Operations - “Overview” for further discussion about Hurricane Irma.

Continue to Build and Enhance Our Claims Operations

Over the last decade, we have developed a proprietary claims administration system that allows us to efficiently process nearly all aspects of claims resolution for our policyholders. Our technology system has shortened claims handling and processing times, reduced associated claims resolution costs and has generated positive feedback from our policyholders and independent insurance agents. In addition, we launched our Fast Track (“Fast Track”) initiative in 2015, which expedites the claims settlement process to close certain types of claims in as little as 24 hours. The initiative sends select field adjusters to make on-site evaluations, with authorization to make payments to policyholders for certain types of claims. Our internal claims operation allows us to identify any trends or problems that may become apparent as claims are processed such that we can revise and bolster our underwriting guidelines as necessary in order to continue adequately pricing risks. Further, we continue to retain select third-party Florida claims administrators and adjusters as well as one national administrator to perform field services for and adjust a portion of our claims in order to maintain our relationships with them so that they can assist us during periods of high claims volume in providing high quality and timely service to our policyholders. We recognize the importance of claims processing and will continue to invest in this functionality.

Maintain an Emphasis on Underwriting Discipline

We seek to generate a consistent underwriting profit on the business we write in hard and soft markets through carefully developed underwriting guidelines informed by our experience in evaluating risks and in handling and processing claims. By focusing on identifying and assessing key risks and exposures in the market, we believe we are able to accurately price eligible risks and generate consistent profits. We assumed only one small group of policies from Citizens’ predecessor in 1998 when we first began our operations. Since then, we have grown our business by leveraging our network of approximately 4,300 independent agents in Florida, and by expanding to other geographic areas that present market opportunities. We periodically review the renewal rates and quality of business generated by our independent agents to ensure underwriting profitability and work with agents where we believe improvement is warranted. As a result of this organic expansion and our vertically integrated structure, all of our operating units possess extensive knowledge of the personal residential homeowners insurance market.

6

Provide High Quality Service to our Policyholders

We strive to provide excellent customer service to each of our policyholders throughout every aspect of our business. We believe our vertically integrated business model provides a superior level of customer service for our policyholders, enhancing our reputation and increasing the likelihood that our policyholders will renew their policies with us. We believe that when policyholders have high levels of customer satisfaction with our Company, we are able to strengthen our reputation and relationships with our independent insurance agent network. We are committed to managing our losses, loss adjustment expenses and claims administration procedures through prudent underwriting and the use of internal claims adjustment services. We believe our personnel growth and commitment to an in-house claims handling process has improved the policyholder experience and, therefore, our relationship with the policyholders agents, which we believe increases retention of policies in-force. Our monthly weighted average renewal retention rate for the year ended December 31, 2017 was 88.1%.

OUR COMPETITIVE STRENGTHS

We believe that our success, historical growth and ability to capitalize on our future growth prospects are a result of the following competitive strengths of our business and management team.

Experienced Leadership Team

We have a deep and experienced leadership team with extensive experience in the Florida personal residential homeowners insurance market. Our Chief Executive Officer, Sean P. Downes, has more than 25 years of experience in the insurance industry. Prior to Mr. Downes’ arrival, all of our claims processing was outsourced to third parties. When Mr. Downes joined our company in 1999, he oversaw our claims operations and later oversaw the development of our vertically integrated structure. Mr. Downes has worked in the Florida insurance industry during all of its most recent active hurricane seasons. In particular, Mr. Downes led the claims team of a multi-line insurance claims adjusting corporation following Hurricane Andrew and served as Chief Operating Officer of UPCIC during the 2005 and 2004 active hurricane seasons. Jon W. Springer, our President and Chief Risk Officer, has over 25 years of experience in the insurance industry, including nine years leading a team of reinsurance specialists for Willis Re before joining us to implement and oversee our reinsurance program. Prior to becoming our President and Chief Risk Officer, Mr. Springer was Chief Operating Officer and an Executive Vice President of URA and BARC.

We believe this leadership team has led us in a strategic direction that has realized many benefits for our shareholders and policyholders, evidenced in part by the 155.0% increase in our stockholders’ equity and the 136.1% increase in policyholders’ surplus that we have realized since their tenure began. Further, they are supported by a group of highly qualified individuals with industry expertise and extensive operational experience, which enables us to capitalize on our experience of having emerged from the 2004, 2005, and 2017 active hurricane seasons in sound financial condition, whereas many of our competitors are new to the market and have not experienced the challenges of an active Florida hurricane season.

Vertically Integrated Structure

We are vertically integrated with substantially all aspects of insurance underwriting, policy issuance, general administration and claims processing and settlement performed internally. Our ability to provide these services ourselves allows us to compress the cycle time of claim resolution in order to promptly pay valid claims and to control claims handling costs. In particular, by performing our own claims adjustment processes, we can better expedite meritorious claims as well as devote attention to potentially suspicious or inflated claims. As a result, we are generally able to begin the adjustment and mitigation process much earlier than if we relied more heavily on third parties, thereby reducing LAE and ultimate loss payouts. Our statutory net loss and LAE ratio for the nine months ended September 30, 2017 was 53.0%, lower than most of our peer companies. We are also able to retain a significant portion of the management and service fees that we and, indirectly, our reinsurers would otherwise pay to third parties for rendering such services. We do, however, intend to continue having a small portion of claims handled by select third parties, as we believe that maintaining relationships with third-party service providers will benefit us in the event we need their assistance in handling claims due to a catastrophic event.

In the future, we will continue to capitalize on our vertically integrated structure by retaining certain fees that we pay to our subsidiary service providers for, managing general agent, reinsurance brokerage, adjusting and other services. We currently administer 100% of all claims and outsource 35% of on-site field adjustment assignments, and thereby retain a corresponding portion of fees that would have otherwise been paid to external adjusters. These cost efficiencies will help us better withstand the financial impact of potential catastrophic storms. We also continue to retain select third-party claims adjusters to perform field services and adjust the remaining portion of our claims in order to maintain our relationships with them, so they can assist us during periods of high claims volume in providing high quality and timely service to our policyholders. Accordingly, we believe we are able to reduce expenses during non-catastrophe years while providing a high level of customer service during all years.

7

Robust Independent Agent Distribution Network

We have developed long-term relationships with a network of approximately 8,800 licensed independent insurance agents – with approximately 4,300 in Florida and approximately 4,500 outside of Florida. Of our 4,300 independent Florida agents, approximately 1,600 have written business with us for over a decade. Our relationships with our Florida independent agents are critical to our success in growing our business in the future and are key differentiators when compared with competitors that have relied upon assumptions of policies from Citizens for their growth and, as a result, may not have developed the same degree of loyalty with as large a group of independent agents in Florida. We believe we have been able to build this network due to our reputation, commitment to the Florida market, experience, and integrity in the underwriting process, as well as our consistency in offering our products through hard and soft markets. Further, the responsiveness of our operating units due to our vertically integrated structure enhances our relationships with our independent agents. By developing and controlling our proprietary technology system, we can rapidly respond to enhancement requests from our independent agents regarding our policy processing system.

Strong Balance Sheet, with a Proven Capital Return Strategy

We have a strong balance sheet, including a stable investment portfolio, a conservative reserve position, a strong and growing capital base, and a proven capital return strategy. Our investment portfolio is largely fixed maturities with a modest allocation of equities and real estate. Our fixed maturities portfolio is ~99% investment grade securities with a AA- average credit rating. We have a strong and growing capital position that contains minimal goodwill, no intangible assets, and minimal debt. We take a conservative approach to loss reserving, and have made substantial efforts in recent years to improve our claims operation, including the addition of our Fast Track team (which has reduced claim resolution time) and an intensified effort to collect subrogation. Since the Company was formed in 1997, we have posted substantial growth in stockholders’ equity and book value per share. We have demonstrated an ability and willingness to return capital to our shareholders, paying both a regular dividend and, over each of the past six years a special dividend, as well as repurchasing shares of our common stock in the open market and in private transactions.

MARKET

Florida

According to the U.S. Census Bureau, at June 30, 2017, Florida was the third largest state in terms of population, with approximately 21 million people. The University of Florida Bureau of Economic and Business Research estimates that Florida is expected to reach a population of approximately 26 million people by 2040, an increase of 41% from 2010. Property ownership and development represent key drivers of the Florida economy. Because of its location, Florida is exposed to an increased risk of hurricanes during the entire six months of the Atlantic hurricane season, which spans from June 1 through November 30. Eight hurricanes in 2004 and 2005, including Hurricanes Charley, Katrina, Rita and Wilma, caused combined estimated nationwide property damage of over $127 billion, a significant portion of which occurred in Florida. In September 2017, Hurricane Irma caused an estimated $17.2 billion in property damage, the majority of which occurred in Florida. Given the potential for significant personal property damage, the availability of personal residential insurance and claims servicing are vitally important to Florida residents.

The Florida residential insurance market is highly fragmented and dominated by in-state insurance companies, and the state’s residual insurance market, Citizens. Significant dislocation in the Florida property insurance market began following Hurricane Andrew in 1992 and accelerated following the 2004 and 2005 hurricane seasons. National and regional insurers significantly reduced their share of the market in Florida between 1999 and 2012. As national and regional insurance companies reduced their exposure in Florida, Citizens, which was at the time and remains today, by law, an insurer of last resort, increased efforts to provide affordable residential insurance to those residents unable to obtain coverage in the private market. As a result, Citizens’ policy count grew from roughly 800,000 policies in 2005 to a peak level of approximately 1.5 million policies in late 2011. To reduce Citizens’ risk exposure, beginning in 2010, Florida’s elected officials encouraged Citizens to focus on reducing the size of its portfolio by returning policies to the private market. Depopulation efforts have been successful, as Citizens’ policy count at September 30, 2017 was approximately 452,000. To be eligible for a Citizens policy, an applicant must either be denied comparable coverage offers from the private insurance market or have received coverage offerings from the private insurance market requiring premium payments that are more than 15% higher than a comparable Citizens policy.

According to data compiled by the FLOIR, Citizens was the second largest residential insurer in Florida as of September 30, 2017, with a market share of approximately 8.1% based on total direct premiums written in-force for personal residential insurance (excluding mobile homeowners and farmowners). As of December 31, 2017, less than 1,000 of our 618,280 Florida in-force policies, or 0.1%, were assumed from Citizens’ predecessor, as compared to some of our competitors that collectively have assumed more than 785,000 policies from Citizens since January 1, 2014. We believe we have the opportunity to significantly expand the size of our personal residential homeowners insurance business both inside and outside of Florida by pursuing organic growth, and have demonstrated this ability within Florida since 1998 and outside of Florida since 2008.

8

All residential insurance companies that write business in Florida, including the Insurance Entities, are required to obtain a form of reinsurance through the Florida Hurricane Catastrophe Fund (the “FHCF”), a state-sponsored entity that provides a layer of reinsurance protection at a price that is typically lower than what would otherwise be available in the general market. The purpose of the FHCF is to protect and advance the state’s interest in maintaining insurance capacity in Florida by providing reimbursements to insurers for a portion of their catastrophe hurricane losses. Currently, the FHCF provides $17 billion of aggregate capacity annually to its participating insurers, which may be adjusted by statute from time to time.

Other States

While we are concentrated in Florida, part of our strategy is to continue our geographic expansion outside of Florida primarily, to take advantage of opportunities to write profitable business as well as to diversify our revenue and risk. We are targeting states with underserved homeowners insurance markets where we believe there is price adequacy for our products and where policyholders would benefit from our market knowledge and integrated service model. We currently write homeowners insurance policies in Alabama, Delaware, Georgia, Hawaii, Indiana, Maryland, Massachusetts, Michigan, Minnesota, New Jersey, New York, North Carolina, Pennsylvania, South Carolina, and Virginia, and are also licensed to issue policies in Illinois, Iowa, New Hampshire, and West Virginia. We look to expand to markets that have opportunities for reasoned, profitable growth and that allow us to position ourselves to take advantage of market dislocation opportunities similar to what we capitalized on in Florida (e.g. following the 2017, 2005 and 2004 hurricane seasons).

COMPETITION

The market for personal residential homeowners insurance is highly competitive. In our primary market, Florida, there are approximately 127 licensed insurance companies that write residential homeowners insurance policies. See “Item 1A—Risk Factors—Risks Relating to Our Business—Our future results are dependent in part on our ability to successfully operate in a highly competitive insurance industry.”

The table below shows policy count, direct written premium in-force and total insured value by market share (excluding mobile homeowners and farmowners) for the top 20 personal residential homeowners insurance companies by direct written premium in Florida as of September 30, 2017, which is the most recent date that the information is publicly available. We compete to varying degrees with all of these companies and others, including large national carriers.

9

| Florida Homeowners Insurance Market - Personal Residential - |

| ||||||||||||||||||||||

|

| Ranked by Direct Written Premium In-Force* |

| |||||||||||||||||||||

|

|

|

|

|

|

|

|

|

| Direct |

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

|

|

|

|

|

|

|

|

| Written |

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

| Policies |

|

| Percentage |

|

| Premium |

|

| Percentage |

|

| Total Insured |

|

| Percentage |

| ||||||

Company Name |

| in-Force |

|

| Distribution |

|

| in-Force |

|

| Distribution |

|

| Value** |

|

| Distribution |

| ||||||

Universal Insurance Holdings, Inc. |

|

| 612,670 |

|

|

| 10.5 | % |

| $ | 927,593 |

|

|

| 10.1 | % |

| $ | 140,293,797 |

|

|

| 7.5 | % |

Citizens Property Insurance Corporation |

|

| 389,990 |

|

|

| 6.7 | % |

|

| 745,951 |

|

|

| 8.1 | % |

|

| 93,360,665 |

|

|

| 5.0 | % |

Tower Hill |

|

| 353,530 |

|

|

| 6.0 | % |

|

| 635,426 |

|

|

| 6.9 | % |

|

| 152,405,375 |

|

|

| 8.1 | % |

Federated National Insurance Company |

|

| 277,379 |

|

|

| 4.7 | % |

|

| 487,640 |

|

|

| 5.3 | % |

|

| 98,376,805 |

|

|

| 5.2 | % |

Heritage Insurance Holdings, Inc. |

|

| 232,854 |

|

|

| 4.0 | % |

|

| 439,461 |

|

|

| 4.8 | % |

|

| 75,153,790 |

|

|

| 4.0 | % |

USAA |

|

| 219,057 |

|

|

| 3.7 | % |

|

| 403,752 |

|

|

| 4.4 | % |

|

| 66,863,296 |

|

|

| 3.6 | % |

Progressive |

|

| 341,891 |

|

|

| 5.8 | % |

|

| 398,679 |

|

|

| 4.3 | % |

|

| 112,792,465 |

|

|

| 6.0 | % |

Security First Insurance Company |

|

| 342,192 |

|

|

| 5.8 | % |

|

| 378,932 |

|

|

| 4.1 | % |

|

| 94,267,005 |

|

|

| 5.0 | % |

HCI Group, Inc. |

|

| 135,154 |

|

|

| 2.3 | % |

|

| 345,804 |

|

|

| 3.8 | % |

|

| 42,596,761 |

|

|

| 2.3 | % |

United Insurance Holdings Corp. |

|

| 177,340 |

|

|

| 3.0 | % |

|

| 301,781 |

|

|

| 3.3 | % |

|

| 71,438,025 |

|

|

| 3.8 | % |

First Protective Insurance Company |

|

| 117,170 |

|

|

| 2.0 | % |

|

| 295,098 |

|

|

| 3.2 | % |

|

| 66,800,316 |

|

|

| 3.6 | % |

St. Johns Insurance Company, Inc. |

|

| 169,181 |

|

|

| 2.9 | % |

|

| 257,153 |

|

|

| 2.8 | % |

|

| 72,357,431 |

|

|

| 3.9 | % |

American Integrity Insurance Company of Florida |

|

| 237,913 |

|

|

| 4.1 | % |

|

| 256,563 |

|

|

| 2.8 | % |

|

| 82,883,738 |

|

|

| 4.4 | % |

People’s Trust Insurance Company |

|

| 129,626 |

|

|

| 2.2 | % |

|

| 248,733 |

|

|

| 2.7 | % |

|

| 38,458,616 |

|

|

| 2.1 | % |

Florida Peninsula Holdings, LLC |

|

| 114,201 |

|

|

| 1.9 | % |

|

| 244,551 |

|

|

| 2.7 | % |

|

| 41,938,043 |

|

|

| 2.2 | % |

Federal Insurance Company |

|

| 33,479 |

|

|

| 0.6 | % |

|

| 200,750 |

|

|

| 2.2 | % |

|

| 62,136,743 |

|

|

| 3.3 | % |

Southern Fidelity |

|

| 131,073 |

|

|

| 2.2 | % |

|

| 179,617 |

|

|

| 2.0 | % |

|

| 33,363,734 |

|

|

| 1.8 | % |

American International Group, Inc. |

|

| 14,894 |

|

|

| 0.3 | % |

|

| 172,063 |

|

|

| 1.9 | % |

|

| 45,122,732 |

|

|

| 2.4 | % |

Allstate Corp. (Castle Key) |

|

| 168,793 |

|

|

| 2.9 | % |

|

| 169,003 |

|

|

| 1.8 | % |

|

| 31,979,446 |

|

|

| 1.7 | % |

Safepoint Insurance Company |

|

| 71,904 |

|

|

| 1.2 | % |

|

| 140,932 |

|

|

| 1.5 | % |

|

| 16,695,872 |

|

|

| 0.9 | % |

Total - Top 20 Insurers |

|

| 4,270,291 |

|

|

| 72.8 | % |

| $ | 7,229,482 |

|

|

| 78.7 | % |

| $ | 1,439,284,655 |

|

|

| 76.8 | % |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total - All Insurers |

|

| 5,858,776 |

|

|

| 100.0 | % |

| $ | 9,167,584 |

|

|

| 100.0 | % |

| $ | 1,875,697,224 |

|

|

| 100.0 | % |

|

|

|

|

We compete primarily on the basis of the strength of our distribution networks, high-quality service to our independent agents and policyholders, our reputation and commitment to the Florida market, claims handling ability, product features tailored to our markets and price, among other factors. Our successful track record in writing residential homeowners insurance in catastrophe-exposed areas has enabled us to develop sophisticated risk selection and pricing techniques that endeavorstrive to identify desirable risks and accurately reflectprice the risk of loss while allowing us to be competitive in our target markets. This risk selection and pricing approach allows us to profitably offer competitive products in areas that have a high demand for property insurance yet are underserved by the national carriers. Each of the Insurance Entities is currently rated “A” (“Exceptional”) by Demotech, Inc. (“Demotech”), a rating agency specializing in evaluating the financial stability of insurers.

PRODUCTS AND DISTRIBUTION

Products

Our focus and our primary product is personal residential homeowner insurance, which accounts for the vast majority of business that we write. Our homeowners insurance products provide policyholders with the ability to receive homeowners, renters, condominium, dwelling, fire, other structures, personal property, personal liability and personal articles coverages. For the year ended December 31, 2017, we wrote an average of 19,829 new policies per month, an increase of 18.3% as compared to the prior year, and residential

10

homeowners policies produced direct written premium of $982.4 million. Homeowners insurance policies accounted for 93.0% of our total direct written premium, with the remaining 7.0% comprised of Commercial Residential and fire and allied lines coverage.

The nature of our business, with respect to both claims and sales, tends to be seasonal over the course of a year, reflecting consumer behaviors in connection with the Florida residential real estate market and the need to be insured before the start of the hurricane season. The amount of written premium tends to increase just prior to the second quarter of our fiscal year and to decrease approaching the fourth quarter. We also face cyclicality resulting from hard and soft market cycles. See “Item 1A—Risk Factors—Risks Relating to Our Business—Our financial condition and operating results and the financial condition and operating results of our Insurance Entities may be adversely affected by the cyclical nature of the property and casualty insurance business.”

The geographical distribution of our policies in-force, in-force premium and total insured value for Florida by county were as follows as of December 31, 2017 (dollars in thousands, rounded to the nearest thousand):

|

| As of December 31, 2017 |

| |||||||||||||||||||||

|

|

|

|

|

|

|

|

|

| In-Force |

|

|

|

|

|

| Total Insured |

|

|

|

|

| ||

County |

| Count |

|

| % |

|

| Premium |

|

| % |

|

| Value |

|

| % |

| ||||||

South Florida |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Broward |

|

| 92,991 |

|

|

| 15.1 | % |

| $ | 184,217 |

|

|

| 19.9 | % |

| $ | 24,626,640 |

|

|

| 16.8 | % |

Palm Beach |

|

| 79,122 |

|

|

| 12.8 | % |

|

| 144,032 |

|

|

| 15.6 | % |

|

| 21,790,700 |

|

|

| 14.9 | % |

Miami-Dade |

|

| 82,352 |

|

|

| 13.3 | % |

|

| 165,001 |

|

|

| 17.8 | % |

|

| 18,516,985 |

|

|

| 12.6 | % |

South Florida exposure |

|

| 254,465 |

|

|

| 41.2 | % |

|

| 493,250 |

|

|

| 53.3 | % |

|

| 64,934,325 |

|

|

| 44.3 | % |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Other significant* Florida counties |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Pinellas |

|

| 39,366 |

|

|

| 6.4 | % |

|

| 45,955 |

|

|

| 5.0 | % |

|

| 6,893,810 |

|

|

| 4.7 | % |

Hillsborough |

|

| 26,248 |

|

|

| 4.2 | % |

|

| 33,540 |

|

|

| 3.6 | % |

|

| 6,188,844 |

|

|

| 4.2 | % |

Escambia |

|

| 19,173 |

|

|

| 3.1 | % |

|

| 29,943 |

|

|

| 3.2 | % |

|

| 5,489,568 |

|

|

| 3.8 | % |

Collier |

|

| 21,039 |

|

|

| 3.4 | % |

|

| 27,011 |

|

|

| 2.9 | % |

|

| 3,572,248 |

|

|

| 2.4 | % |

Lee |

|

| 26,534 |

|

|

| 4.3 | % |

|

| 26,254 |

|

|

| 2.8 | % |

|

| 4,158,638 |

|

|

| 2.8 | % |

Polk |

|

| 18,309 |

|

|

| 3.0 | % |

|

| 25,030 |

|

|

| 2.7 | % |

|

| 5,529,038 |

|

|

| 3.8 | % |

Pasco |

|

| 23,575 |

|

|

| 3.8 | % |

|

| 24,170 |

|

|

| 2.6 | % |

|

| 7,615,170 |

|

|

| 5.2 | % |

Brevard |

|

| 19,354 |

|

|

| 3.1 | % |

|

| 24,078 |

|

|

| 2.6 | % |

|

| 3,944,004 |

|

|

| 2.7 | % |

Total other significant* counties |

|

| 193,598 |

|

|

| 31.3 | % |

|

| 235,981 |

|

|

| 25.4 | % |

|

| 43,391,320 |

|

|

| 29.6 | % |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| In-Force |

|

|

|

|

|

| Total Insured |

|

|

|

|

| ||

Summary for all of Florida |

| Count |

|

| % |

|

| Premium |

|

| % |

|

| Value |

|

| % |

| ||||||

South Florida exposure |

|

| 254,465 |

|

|

| 41.2 | % |

|

| 493,250 |

|

|

| 53.3 | % |

|

| 64,934,325 |

|

|

| 44.3 | % |

Total other significant* counties |

|

| 193,598 |

|

|

| 31.3 | % |

|

| 235,981 |

|

|

| 25.4 | % |

|

| 43,391,320 |

|

|

| 29.6 | % |

Other Florida counties |

|

| 170,217 |

|

|

| 27.5 | % |

|

| 196,856 |

|

|

| 21.3 | % |

|

| 38,298,825 |

|

|

| 26.1 | % |

Total Florida |

|

| 618,280 |

|

|

| 100.0 | % |

| $ | 926,087 |

|

|

| 100.0 | % |

| $ | 146,624,470 |

|

|

| 100.0 | % |

|

|

11

The geographical distribution of our policies in-force, in-force premium and total insured value across all states were as follows, as of December 31, 2017, 2016 and 2015 (dollars in thousands, rounded to the nearest thousand):

|

| As of December 31, 2017 |

| |||||||||||||||||||||

|

|

|

|

|

|

|

|

|

| In-Force |

|

|

|

|

|

| Total Insured |

|

|

|

|

| ||

State |

| Count |

|

| % |

|

| Premium |

|

| % |

|

| Value |

|

| % |

| ||||||

Florida |

|

| 618,280 |

|

|

| 80.9 | % |

| $ | 926,087 |

|

|

| 87.6 | % |

| $ | 146,624,470 |

|

|

| 73.9 | % |

North Carolina |

|

| 48,866 |

|

|

| 6.4 | % |

|

| 36,993 |

|

|

| 3.5 | % |

|

| 14,275,508 |

|

|

| 7.2 | % |

Georgia |

|

| 31,305 |

|

|

| 4.1 | % |

|

| 32,343 |

|

|

| 3.1 | % |

|

| 11,380,109 |

|

|

| 5.7 | % |

South Carolina |

|

| 13,769 |

|

|

| 1.8 | % |

|

| 13,372 |

|

|

| 1.3 | % |

|

| 4,120,728 |

|

|

| 2.1 | % |

Massachusetts |

|

| 10,132 |

|

|

| 1.3 | % |

|

| 13,162 |

|

|

| 1.2 | % |

|

| 5,857,450 |

|

|

| 3.0 | % |

Indiana |

|

| 11,622 |

|

|

| 1.5 | % |

|

| 9,236 |

|

|

| 0.9 | % |

|

| 3,768,044 |

|

|

| 1.9 | % |

Pennsylvania |

|

| 10,554 |

|

|

| 1.4 | % |

|

| 7,292 |

|

|

| 0.7 | % |

|

| 4,047,997 |

|

|

| 2.1 | % |

Minnesota |

|

| 4,769 |

|

|

| 0.6 | % |

|

| 5,198 |

|

|

| 0.5 | % |

|

| 2,103,731 |

|

|

| 1.1 | % |

Virginia |

|

| 4,908 |

|

|

| 0.6 | % |

|

| 3,867 |

|

|

| 0.4 | % |

|

| 2,263,923 |

|

|

| 1.1 | % |

Alabama |

|

| 2,861 |

|

|

| 0.4 | % |

|

| 2,934 |

|

|

| 0.3 | % |

|

| 895,380 |

|

|

| 0.5 | % |

Maryland |

|

| 2,354 |

|

|

| 0.3 | % |

|

| 1,901 |

|

|

| 0.2 | % |

|

| 869,685 |

|

|

| 0.4 | % |

Hawaii |

|

| 2,009 |

|

|

| 0.3 | % |

|

| 1,830 |

|

|

| 0.2 | % |

|

| 842,740 |

|

|

| 0.4 | % |

Michigan |

|

| 1,330 |

|

|

| 0.2 | % |

|

| 1,574 |

|

|

| 0.1 | % |

|

| 491,906 |

|

|

| 0.2 | % |

Delaware |

|

| 828 |

|

|

| 0.1 | % |

|

| 903 |

|

|

| 0.0 | % |

|

| 400,076 |

|

|

| 0.2 | % |

New Jersey |

|

| 877 |

|

|

| 0.1 | % |

|

| 858 |

|

|

| 0.0 | % |

|

| 428,072 |

|

|

| 0.2 | % |

New York |

|

| 54 |

|

|

| 0.0 | % |

|

| 52 |

|

|

| 0.0 | % |

|

| 27,191 |

|

|

| 0.0 | % |

Total |

|

| 764,518 |

|

|

| 100.0 | % |

|

| 1,057,602 |

|

|

| 100.0 | % |

|

| 198,397,010 |

|

|

| 100.0 | % |

|

| As of December 31, 2016 |

| |||||||||||||||||||||

|

|

|

|

|

|

|

|

|

| In-Force |

|

|

|

|

|

| Total Insured |

|

|

|

|

| ||

State |

| Count |

|

| % |

|

| Premium |

|

| % |

|

| Value |

|

| % |

| ||||||

Florida |

|

| 577,783 |

|

|

| 84.6 | % |

| $ | 862,332 |

|

|

| 90.2 | % |

| $ | 134,493,470 |

|

|

| 79.1 | % |

North Carolina |

|

| 41,393 |

|

|

| 6.1 | % |

|

| 30,858 |

|

|

| 3.2 | % |

|

| 11,972,066 |

|

|

| 7.0 | % |

Georgia |

|

| 24,257 |

|

|

| 3.6 | % |

|

| 23,849 |

|

|

| 2.5 | % |

|

| 8,450,315 |

|

|

| 5.0 | % |

South Carolina |

|

| 12,230 |

|

|

| 1.8 | % |

|

| 12,393 |

|

|

| 1.3 | % |

|

| 3,592,203 |

|

|

| 2.1 | % |

Massachusetts |

|

| 7,451 |

|

|

| 1.1 | % |

|

| 9,964 |

|

|

| 1.0 | % |

|

| 4,352,990 |

|

|

| 2.6 | % |

Indiana |

|

| 6,835 |

|

|

| 1.0 | % |

|

| 5,381 |

|

|

| 0.6 | % |

|

| 2,162,967 |

|

|

| 1.3 | % |

Pennsylvania |

|

| 5,303 |

|

|

| 0.8 | % |

|

| 3,677 |

|

|

| 0.4 | % |

|

| 1,925,226 |

|

|

| 1.1 | % |

Minnesota |

|

| 2,089 |

|

|

| 0.3 | % |

|

| 2,251 |

|

|

| 0.2 | % |

|

| 896,969 |

|

|

| 0.5 | % |

Virginia |

|

| 269 |

|

|

| 0.0 | % |

|

| 224 |

|

|

| 0.0 | % |

|

| 130,556 |

|

|

| 0.1 | % |

Alabama |

|

| 624 |

|

|

| 0.1 | % |

|

| 624 |

|

|

| 0.1 | % |

|

| 182,456 |

|

|

| 0.1 | % |

Maryland |

|

| 1,756 |

|

|

| 0.2 | % |

|

| 1,413 |

|

|

| 0.1 | % |

|

| 640,919 |

|

|

| 0.4 | % |

Hawaii |

|

| 1,767 |

|

|

| 0.2 | % |

|

| 1,689 |

|

|

| 0.2 | % |

|

| 756,428 |

|

|

| 0.4 | % |

Michigan |

|

| 538 |

|

|

| 0.1 | % |

|

| 651 |

|

|

| 0.1 | % |

|

| 190,360 |

|

|

| 0.1 | % |

Delaware |

|

| 621 |

|

|

| 0.1 | % |

|

| 663 |

|

|

| 0.1 | % |

|

| 289,941 |

|

|

| 0.2 | % |

New Jersey |

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

New York |

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

Total |

|

| 682,916 |

|

|

| 100.0 | % |

|

| 955,969 |

|

|

| 100.0 | % |

|

| 170,036,866 |

|

|

| 100.0 | % |

12

| As of December 31, 2015 |

| ||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

| In-Force |

|

|

|

|

|

| Total Insured |

|

|

|

|

| ||

State |

| Count |

|

| % |

|

| Premium |

|

| % |

|

| Value |

|

| % |

| ||||||

Florida |

|

| 550,800 |

|

|

| 88.2 | % |

| $ | 821,631 |

|

|

| 92.6 | % |

| $ | 127,705,731 |

|

|

| 84.0 | % |

North Carolina |

|

| 34,084 |

|

|

| 5.4 | % |

|

| 25,411 |

|

|

| 2.9 | % |

|

| 9,981,069 |

|

|

| 6.6 | % |

Georgia |

|

| 17,425 |

|

|

| 2.8 | % |

|

| 16,013 |

|

|

| 1.8 | % |

|

| 5,716,851 |

|

|

| 3.8 | % |

South Carolina |

|

| 10,479 |

|

|

| 1.7 | % |

|

| 11,744 |

|

|

| 1.3 | % |

|

| 3,135,568 |

|

|

| 2.1 | % |

Massachusetts |

|

| 4,720 |

|

|

| 0.8 | % |

|

| 6,455 |

|

|

| 0.7 | % |

|

| 2,790,054 |

|

|

| 1.8 | % |

Indiana |

|

| 2,694 |

|

|

| 0.4 | % |

|

| 2,146 |

|

|

| 0.3 | % |

|

| 851,536 |

|

|

| 0.6 | % |

Pennsylvania |

|

| 1,017 |

|

|

| 0.2 | % |

|

| 738 |

|

|

| 0.1 | % |

|

| 360,991 |

|

|

| 0.2 | % |

Minnesota |

|

| 251 |

|

|

| 0.0 | % |

|

| 277 |

|

|

| 0.0 | % |

|

| 108,337 |

|

|

| 0.1 | % |

Virginia |

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

Alabama |

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

Maryland |

|

| 1,278 |

|

|

| 0.2 | % |

|

| 1,026 |

|

|

| 0.1 | % |

|

| 464,081 |

|

|

| 0.3 | % |

Hawaii |

|

| 1,523 |

|

|

| 0.2 | % |

|

| 1,547 |

|

|

| 0.2 | % |

|

| 680,701 |

|

|

| 0.4 | % |

Michigan |

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

Delaware |

|

| 396 |

|

|

| 0.1 | % |

|

| 407 |

|

|

| 0.0 | % |

|

| 181,857 |

|

|

| 0.1 | % |

New Jersey |

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

New York |

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

|

| — |

|

Total |

|

| 624,667 |

|

|

| 100.0 | % |

|

| 887,395 |

|

|

| 100.0 | % |

|

| 151,976,776 |

|

|

| 100.0 | % |

Also see “Item 7—Management’s Discussion and Analysis of Financial Condition and Results of Operations” and “Item 1A—Risk Factors—Risks Relating to Our Business—Because we conduct the substantial majority of our business in Florida, our financial results depend on the regulatory, economic and weather conditions in Florida” for discussion on geographical diversification.

Product Pricing

The premiums we charge are based on rates specific to individual risks and locations and are generally subject to regulatory review and approval before they are implemented.review. We periodically submit our rate revisions to regulators as required by law or as we deem necessary or appropriate for our business. The premiums we charge to policyholders are affected by legislative enactments and administrative rules, including state-mandated programs in Florida requiring residential property insurance companies like us to provide premium discounts when policyholders verify that insured properties have certain construction features, orsuch as windstorm loss reduction features.

13

The following table shows UPCIC’s most recently approved rate changes. All percentage increasesthe customer experience include reliability and decreases are expressed as statewide averages.

|

| 2017 Rate Changes |

|

| 2016 Rate Changes |

|

| 2015 Rate Changes |

| |||||||||||||||

|

|

|

|

|

| Percentage Increase |

|

|

|

|

|

| Percentage Increase |

|

|

|

|

|

| Percentage Increase |

| |||

|

| Effective Dates |

| State |

| (Decrease) |

|

| Effective Dates |

| State |

| (Decrease) |

|

| Effective Dates |

| State |

| (Decrease) |

| |||

Homeowners |

| December 7, 2017 for new business; January 26, 2018 for renewal business |

| FL |

| 3.40% |

|

| None |

| FL |

| None |

|

| April 15, 2015 for new business; May 25, 2015 for renewal business |

| FL |

|

| 2.20% |

| ||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| None |

| NC |

| None |

|

| None |

| NC |

| None |

|

| June 1, 2015 for new business and renewal business |

| NC |

|

| 0.60% |

| ||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| None |

| SC |

| None |

|

| None |

| SC |

| None |

|

| November 20, 2015 for new business; January 6, 2016 for renewal business |

| SC |

|

| 2.46% |

| ||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| None |

| GA |

|

| None |

|

| June 1, 2016 for new business and renewal business |

| GA |

|

| 7.50% |

|

| None |

| GA |

| None |

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Fire |

| February 3, 2018 for new business; March 25, 2018 for renewal business |

| FL |

|

| 6.00% |

|

| August 31, 2016 for new business; October 19, 2016 for renewal business |

| FL |

|

| 3.70% |

|

| April 20, 2015 for new business; June 5, 2015 for renewal business |

| FL |

|

| 4.90% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| None |

| NC |

| None |

|

| None |

| NC |

| None |

|

| April 1, 2015 for new business and renewal business |

| NC |

|

| 1.22% |

| ||

Distribution

value, financial strength, and ease-of-use. We marketstrive to provide excellent reliability and sellvalue through the strength of our products primarily throughdistribution networks, high-quality service to our network of approximately 8,800 licensedpolicyholders and independent agents, which we continueour claims handling ability and product features tailored to build bothour markets.

A key part of our distribution strategy is to utilize an attractive commission-based compensation plan as an incentiveinsurer. Excess-of-loss reinsurance indemnifies the primary insurer for independent agents to place business with us. We also attempt to provide excellent service to our independent agents and brokers, maintaining a

14

long-standing partnership with our independent agents and a consistent presence in our target markets through hard and soft market cycles. Our internal staff and specialists provide support to our independent agents, including use of various technologies to assist with the delivery of service to our policyholders. Our independent agents have access to all policy and payment information through our online, proprietary system. This system allows our independent agents to provide quotes within minutes, and because we control our technology, we are able to quickly respond to agents who need troubleshooting assistance or who offer recommendations for improvement. This system has evolved into a highly valued tool that enables agents to quickly understand the status of a policy and assist their clients with any policy-related questions. We regularly monitor and enhance the system to provide the best point of sale tools possible. Agents are provided dedicated internal contacts should they need assistance, and agencies are proactively contacted on a quarterly basis to solicit feedback.

As a result of the superior service and compensation we provide, we have relatively little turnover among many of our key independent agents. Approximately 1,600, or 18%, of our independent agents have relationships with us that span a decade or more.

In addition to distributing our products through our independent agent network, we also utilize our unique direct-to-consumer platform, Universal DirectSM, to sell products directly to consumers. In April 2016, the Company launched a direct-to-consumer online platform called Universal DirectSM, which enables homeowners to directly purchase, pay for and bind homeowners policies online without the need to directly interface with any intermediaries. Universal DirectSM was offered in all 16 states in which the Company offers policies as of December 31, 2017. During the year ended December 31, 2017, 7,361 policies were written representing $8.6 million in direct written premium, as compared to 1,320 policies written representing $1.4 million in direct written premium during the year ended December 31, 2016.

Services

We are vertically integrated with substantially all aspects of insurance underwriting, policy issuance, general administration and claims processing and settlement performed internally, which allows us to retain a majority of the economics associated with the issuance and administration of our insurance policies in-force. Vertical integration also maintains quality service throughout the policy life cycle. Below is a summary of the services we provide.

Underwriting

All underwriting is performed internally utilizing our state-approved underwriting manuals as the basis of our rate-making and risk assessment. Our manuals have been developed and enhanced over a number of years based on our deep knowledge of the homeowners insurance industry, and based on an ongoing analysis of our own loss experience. Initially, all new business must be submitted to us through our proprietary policy processing system and risk criteria, which allows our independent agent partners to generate quotes and bind policies subject to compliance with our binding authority guidelines and risk criteria. Policies that are bound by either independent agents or through Universal DirectSM are further reviewed by our underwriting staff for accuracy of data, including reports of on-site inspections. Our underwriting process is constantly evolving as new and different type of risks and claim types become prevalent. However, see “Item 1A—Risk Factors—Risks Relating to Our Business—The failure of the risk mitigation strategies we utilize could have a material adverse effect on our financial condition or results of operations.”

Policy Administration

We have developed a proprietary suite of applications that provide underwriting, policy and claim administration services, including billing, policy maintenance, inspections, refunds, commissions and data analysis. Our proprietary rating engine aligns with various state requirements to support our geographic expansion. This sophisticated policy processing system is solely managed by our employees, and enhancements are implemented while adhering to strict internal control requirements to ensure business continuity.

Claims Administration

We closely manage all aspects of the claims process, from processing the initial filing to claim conclusion. When a policyholder contacts us to report a claim, members of our claims department create a claim file and aggregate the appropriate supporting documentation. Claims are then reviewed by our managers and staff adjusters, who assess the extent of the loss, complete on-site investigations when required, and determine the resources needed to adjust each claim. We perform or supervise the adjusting services rendered for our policyholders at all stages of the claims process, which we believe allows us to reduce cost and provide a high level of customer service. We assign a small percentage of field inspections to third-party adjusters in order to maintain relationships that will allow us to continue to provide high quality and timely service following a catastrophe or any other period of unusually high claim volume, such as the increase in claims that occurred after Hurricane Irma in September 2017.

15

We manage our reinsurance program through our internal reinsurance intermediary, BARC, in conjunction with URA. Approximately 10 years ago, we hired a dedicated team of reinsurance specialists from Willis Re, including our President and Chief Risk Officer, Jon W. Springer, to design a customized reinsurance strategy for us and to develop our in-house analytical capabilities. Our reinsurance team has an average of 25 years of knowledge and expertise of the reinsurance industry. We have two experienced actuaries and analytics modeling personnel on staff at BARC to assist in evaluating and designing our reinsurance program. Not only do we receive a portion of the fees that otherwise would be paidloss in commissions to a third-party reinsurance intermediary, we also develop and maintain long-term relationships with our reinsurers. We also utilize Guy Carpenter as a third-party reinsurance intermediary as needed, enabling us to capitalize on its market experience and knowledge as well as our internal capabilities. Guy Carpenter works closely with our teams at BARC and URA in designing our reinsurance program to obtain favorable pricing, as well as continually evaluating prevailing costs and the levelexcess of coverage we feel we need in order to capitalize on favorable market conditions.

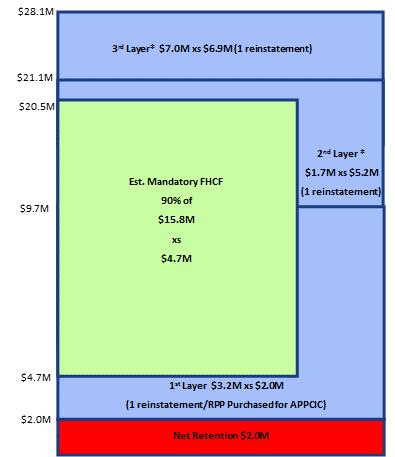

REINSURANCE

an agreed upon amount or retention.

May 31, 2024.

UPCIC’s 2017-2018 Reinsurance Program

Third-Party Reinsurance

Our annual reinsurance program, which is segmented into layersimpact. Furthermore, as part of coverage, as is industry practice, protects us against excess propertyour operational excellence initiatives, we continually look to enable new technology to refine our data intelligence on catastrophe losses. Our 2017-2018 reinsurance program includes the mandatory coverage required by lawrisk modeling.

16

The total cost of UPCIC’s private catastrophe reinsurance program for all states as described below, effective June 1, 2017 through May 31, 2018, is $155.5 million. In addition, UPCIC has purchased reinstatement premium protection as described below, the cost of which is $25.7 million. The largest private participants in UPCIC’s reinsurance program include leading reinsurance companies and providers such as Nephila Capital, Everest Re, RenaissanceRe, Chubb Tempest Re and Lloyd’s of London syndicates.

hurricane season. We have usedhistorically experienced higher direct premiums written in the model results noted above to stress test the completeness of the program by simulating a recurrence of the 2004 calendar year, in which four large catastrophic hurricanes made landfall in Florida. This season is considered to be the worst catastrophic year in Florida’s recorded history. Assuming the reoccurrence of the 2004 calendar year events, including the same geographic path of each such hurricane, the modeled estimated net loss to us in 2017 with the reinsurance coverage described herein would be approximately $84 million (after tax, net of all reinsurance recoveries), the same as it would have been in 2016. We estimate that, based on our portfolio of insured risks as of December 31, 2017second and 2016, a repeat of the four 2004 calendar year events would have exhausted approximately 27.0% and 25.0%, respectively,third quarters of our property catastrophe reinsurance coverage.

UPCIC’s Retention

UPCIC has a net retention of $35 million per catastrophe event for losses incurred, in all states, up to a first event loss of $2.778 billion. UPCIC also purchases a separate underlying catastrophe program to further reduce its retention for all losses occurring in any state other than Florida (the “Other States Reinsurance Program”). UPCIC retains only $5 million under its Other States Reinsurance Programfiscal year and lower direct premiums written in the first event and only $1 million under its Other States Reinsurance Program for the second through fourth events. These retention amounts are grossquarters of any potential tax benefit we would receive in paying such losses.

First Layer

Immediately above UPCIC’s net retention,our fiscal year. Correspondingly, we have $55 millionhistorically experienced a higher volume of reinsurance coverage from third-party reinsurers for up to four separate catastrophic events, for all states. Specifically, we have purchased reinsurance coverage forclaims submitted in the first and third catastrophic events, and each such coverage allows for one reinstatement upon the payment of reinstatement premiums, which would cover the second and fourth catastrophic events. This coverage has been obtained from three contracts as follows:

68.33%quarters of $55 millionour fiscal year during and immediately subsequent to the peak of hurricane season, and a lower volume of claims submitted in excess of $35 million provides coverage on a multi-year basis through May 31, 2019;

31.67% of $55 million in excess of $35 million provides coverage for the 2017-2018 period; and

100% of $55 million in excess of $35 million and in excess of $110 million otherwise recoverable (from the first and second events) provides the third and fourth event coverage for the 2017-2018 period.

For the first two contracts above, to the extent that allquarters of our coverage or a portion thereof is exhausted in a catastrophic event, we have purchased reinstatement premium protection to pay the required premium necessary for the reinstatement of these coverages.

Second Layer

Above the first layer, for losses exceeding $90 million, we have purchased a second layer of coverage for losses up to $445 million – in other words, for the next $355 million of losses. This coverage has been obtained from two contracts as follows:

58% of $355 million in excess of $90 million provides coverage through May 31, 2020; and

42% of $355 million in excess of $90 million provides coverage for the 2017-2018 period

In this layer, to the extent that all of our coverage or a portion thereof is exhausted in a catastrophic event, we have purchased reinstatement premium protection insurance to pay the required premium necessary for the reinstatement of these coverages. Both of these contracts extend coverage to all states.

Third Layer

Above the first and second layers, we have purchased a third layer of coverage for losses up to $540 million – in other words, for the next $95 million of losses. This coverage was obtained from two contracts as follows:

68.33% of $95 million in excess of $445 million provides coverage on a multi-year basis through May 31, 2019; and

31.67% of $95 million in excess of $445 million provides coverage for the 2017-2018 period.

In this layer, to the extent that all of our coverage or a portion thereof is exhausted in a catastrophic event, we have purchased reinstatement premium protection insurance to pay the required premium necessary for the reinstatement of these coverages. Both of these contracts extend coverage to all states.

17

Fourth, Fifth and Sixth Layers

In the fourth, fifth and sixth layers, we have purchased reinsurance for $55 million of coverage in excess of $540 million in losses incurred by us (net of the FHCF layer), $193 million of coverage in excess of $595 million in losses incurred by us (net of the FHCF layer), and $125 million of coverage in excess of $788 million, respectively, for a total of $878 million of coverage (net of the FHCF layer) by third-party reinsurers. With respect to the fourth layer, to the extent that all of our coverage or a portion thereof is exhausted in a catastrophic event, we have purchased reinstatement premium protection to pay the required premium necessary for the reinstatement of this coverage. All three layers’ coverage extends to all states.

UPCIC structures its reinsurance coverage into layers and utilizes a cascading feature such that the second, third, fourth, fifth and sixth reinsurance layers all attach at $90 million. Any layers above the $90 million attachment point are excess of loss over the immediately preceding layer. If the aggregate limit of the preceding layer is exhausted, the next layer cascades down in its place for future events. This means that, unless losses exhaust the top layer of our coverage, we are exposed to only $35 million in losses, pre-tax, per catastrophe for each of the first four events. In addition to tax benefits that could reduce our ultimate loss, we anticipate that certain fees paid to our subsidiary service providers by our Insurance Entities and, indirectly, our reinsurers, would also increase during an active hurricane season, which could also offset claim-related losses we would have to pay on our insurance policies. The subsidiary companies, and UPCIC in particular, experienced a significant volume of claims from Hurricane Irma which surpassed the Company’s per occurrence retention of $35 million and triggered its reinsurance program. The program responded according exactly to plan and the weighted average of funds received from third party reinsurance partners was less than 4 business days. Fees paid to our subsidiary service providers increased due to both the volume of claims administered as well as additional premiums paid to reinstate reinsurance coverage.

Other States Reinsurance Program

The total cost of UPCIC’s private catastrophe reinsurance program for other states as described below, effective June 1, 2017 through May 31, 2018, is $8.9 million. In addition, UPCIC has purchased reinstatement premium protection as described below, the cost of which is $1.85 million.

Effective June 1, 2017 through June 1, 2018, under an excess catastrophe contract specifically covering risks located outside the state of Florida and intended to further reduce UPCIC’s $35 million net retention, as noted above, UPCIC has obtained catastrophe coverage of $30 million in excess of $5 million covering certain loss occurrences, including hurricanes, in states outside of Florida. This catastrophe coverage has a second full limit available with additional premium calculated pro rata as to amount and 100% as to time, as applicable. All catastrophe layers are placed with a cascading feature so that all capacity could be made available in excess of $5 million under certain loss scenarios. Further, UPCIC purchased subsequent catastrophe event excess of loss reinsurance specifically covering risks outside of Florida to cover certain levels of loss through four catastrophe events including hurricanes. Specifically, UPCIC obtained catastrophe coverage that covers 100% of $4,000,000 excess of $1,000,000 in excess of $4,000,000 otherwise recoverable. This coverage has two free reinstatements and a total of $12,000,000 of coverage available to UPCIC.