UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

☒ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 20172023

or

☐ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from ____________ to ____________

Commission file number: 001-11015

Viad Corp

(Exact name of registrant as specified in its charter)

Delaware | 36-1169950 | |

(State or other jurisdiction of incorporation or | (I.R.S. Employer Identification No.) | |

|

| |

(Address of principal executive offices) | (Zip Code) |

(602) (602) 207-1000

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||

Common Stock, $1.50 | VVI | New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined by Rule 405 of the Securities Act. Yes☒ No ☐

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act. Yes ☐No☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes☒ No ☐

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files.) Yes☒ No ☐

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ☒

Indicate by check mark whether registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act. (Check One):

Large accelerated filer |

| Accelerated filer |

| |||

Non-accelerated filer | ☐ | Smaller reporting company | ☐ | |||

Emerging growth company | ☐ |

If an emerging growth company, indicatedindicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☒

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ☐ No ☒

The aggregate market value of the Common Stock (based on its closing price per share on such date) held by non-affiliates on the last business day of the registrant’s most recently completed second fiscal quarter (June 30, 2017)2023) was approximately $948$541.2 million.

Registrant had 20,422,76221,041,920 shares of Common Stock ($1.50 par value) outstanding as of January 31, 2018.February 26, 2024.

Documents Incorporated by Reference

A portionPortions of the Proxy Statement for the Viad Corp Annual Meeting of Shareholders of Viad Corp, which is scheduled to be held onfor May 17, 2018,15, 2024, is incorporated by reference into Part III of this Annual Report.

Auditor Firm Id: 34 | Auditor Name: Deloitte & Touche LLP | Auditor Location: Tempe, AZ USA |

INDEX

Page | ||

Item 1. |

| |

Item 1A. |

| |

Item 1B. |

| |

Item |

| |

Item |

| |

Item |

| |

|

| |

Other. | 16 | |

Item 5. |

| |

Item 6. |

| |

Item 7. | Management’s Discussion and Analysis of Financial Condition and Results of Operations |

|

Item 7A. |

| |

Item 8. |

| |

Item 9. | Changes in and Disagreements With Accountants on Accounting and Financial Disclosure |

|

Item 9A. |

| |

Item 9B. |

| |

Item 9C. | Disclosure Regarding Foreign Jurisdictions that Prevent Inspections | 81 |

Item 10. |

| |

Item 11. |

| |

Item 12. | Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters |

|

Item 13. | Certain Relationships and Related Transactions, and Director Independence |

|

Item 14. |

| |

Item 15. |

82 | |

Item 16. |

|

In this report, for periods presented, “we,” “us,” “our,” “the Company,” and “Viad Corp” refer to Viad Corp and its subsidiaries and affiliates.subsidiaries.

Forward-Looking Statements

This Annual Report on Form 10-K (“2023 Form 10-K”) contains a number of forward-looking statements.statements within the meaning of the Private Securities Litigation Reform Act of 1995. Forward-looking statements may appear throughout this 2023 Form 10-K, including the following sections: “Business” (Part I, Item 1), “Risk Factors” (Part I, Item 1A), “Management’s Discussion and Analysis of Financial Condition and Results of Operations” (Part II, Item 7), and “Quantitative and Qualitative Disclosures About Market Risk” (Part II, Item 7A). Words, and variations of words, such as “will,“aim,” “anticipate,” “believe,” “could,” “deliver,” “estimate,” “expect,” “intend,” “may,” “expect,” “would,” “could,” “might,” “intend,“outlook,” “plan,” “believe,” “estimate,” “anticipate,” “deliver,“potential,” “seek,” “aim,” “potential,” “target,” “outlook,“will,” and similar expressions are intended to identify our forward-looking statements. Similarly, statements that describe our business strategy, outlook, objectives, plans, initiatives, intentions, or goals also are forward-looking statements. These forward-looking statements are not historical facts but reflect our current estimates, projections, expectations, or trends concerning future growth, operating cash flows, availability of short-term borrowings, consumer demand, new or renewal business, investment policies, productivity improvements, ongoing cost reduction efforts, efficiency, competitiveness, strategic actions, acquisitions, the timing of new and damaged attractions openings, the sufficiency of our legal services, projections of 2018 revenue, show rotation, same-show rotation, segment operating income, attraction start-up costs, the realization of deferred tax assets, contributionsare subject to pension and postretirement benefit plans, legal expenses, tax rates and other tax matters, and foreign exchange rates. Actual results could differ materially from those discussed in the forward-looking statements. Viad’s businesses can be affected by a host of risks and uncertainties, many of which are beyond our control. control, which could cause actual results to differ materially from those in the forward-looking statements.

Important factors that could cause actual results to differ materially from those described in our forward lookingforward-looking statements include, but are not limited to, the following:

For a more complete discussion of the risks discussed inand uncertainties that may affect our business or financial results, refer to “Risk Factors” (Part I, Item 1A “Risk Factors,” includedof this 2023 Form 10-K). The forward-looking statements in this Annual Report on2023 Form 10-K forare made as of the year ended December 31, 2017 (“2017 Form 10-K”).date hereof. We disclaim and do not undertake any obligation to update or revise any forward-looking statement in this 20172023 Form 10-K except as required by applicable law or regulation.

1

We are an internationala leading provider of extraordinary experiences, including hospitality and leisure activities, experiential services company with operations principally in the United States, Canada, the United Kingdom, continental Europe,marketing, and the United Arab Emirates. We are committedlive events. Our mission is to providing unforgettabledrive significant and sustainable growth by delivering extraordinary experiences tofor our teams, clients, and guests.

We operate through two mainthree reportable business groups:

segments: Pursuit, Spiro, and GES is a world-classExhibitions. Spiro and GES Exhibitions are both live event service providerbusinesses and are referred to some of the most visible and influential events and global brands.collectively as “GES.”

Pursuit is a collection of iconic naturalinspiring and cultural destinationunforgettable travel experiences that enjoy perennial demand.

|

|

GESExhibitions

GES’ clients include event organizers and corporate brand marketers. Event organizers schedule and run the event from start to finish. Corporate brand marketers include exhibitors and domestic and international corporations that want to promote their brands, services and innovations, feature new products, and build business relationships. GES serves corporate brand marketers when they exhibit at shows and when GES is engaged to manage their global exhibit program or produce their proprietary corporate events.

GES operates through two reportable business segments based on geography:

GES U.S. has a leading position in the U.S. with full-service operations in every major exhibition market, including Las Vegas, Nevada; Chicago, Illinois; Orlando, Florida; New York, New York; and Los Angeles, California.

GES International has operating facilities at many of the most active and popular international event destinations and venues, including seven cities in Canada, seven cities in the United Kingdom, two cities in Germany, two cities in the United Arab Emirates, two cities in the Netherlands, one city in Hong Kong, Switzerland, and Romania, and through these facilities offers full-service event operations across the United Kingdom, Europe, and the Middle East.

Markets Served

GES provides a full suite of services for event organizers and corporate brand marketers across four live event markets: Exhibitions, Conferences, Corporate Events, and Consumer Events (collectively, “Live Events”).

|

| |||||

|

|

| ||||

|

|

| ||||

|

|

| ||||

|

|

| ||||

GES offers a comprehensive range of services and innovative technology, including Core Services, Event Technology, and Audio-Visual, to event organizers and corporate brand marketers.

|

|

In general, GES provides the following exclusive and discretionary services and products to Live Event organizers and corporate brand marketers:

|

| |||

|

|

| ||

|

|

| ||

|

|

| ||

|

|

| ||

|

|

| ||

|

|

| ||

|

|

| ||

|

| |||

|

| |||

|

| |||

|

| |||

|

| |||

| ||||

|

| |||

|

| |||

|

| |||

|

| |||

| ||||

Under various agreements with Live Events organizers, GES is the official services contractor with the exclusive right to provide certain services to exhibitors participating in a Live Event. This gives exhibitors a single point of contact to facilitate a timely, safe, and efficient move-in/out of a Live Event and to facilitate an organized, professional, during-show experience. GES also competes with other service providers to sell discretionary services to exhibitors. Discretionary services include complete event program management, such as creative design, strategy, and planning to corporate brand marketers across all Live Events in which they participate.

|

|

|

|

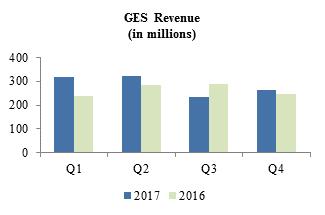

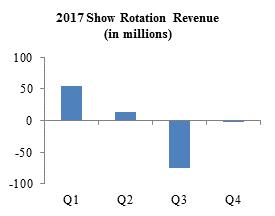

GES’ exhibition and event activity can vary significantly from quarter to quarter and year to year depending on the frequency and timing of shows: some shows are not held annually, and some shift between quarters. During 2017, GES U.S. reported its highest revenue during the first and second quarters. During 2016, GES U.S. reported its highest revenue during the second and third quarters. GES International generally reports its highest revenue during the second and fourth quarters. The following show rotation revenue metric refers to the net change in revenue from 2016 to 2017 due to show movement between quarters and years. Show rotation refers to shows that occur less frequently than annually, as well as annual shows that shift quarters from one year to the next.

Competition

In the Live Events industry, GES generally competes across all classes of services and all markets on the basis of discernible differences, value, quality, price, convenience, and service. GES has a competitive advantage through its worldwide network of resources, history of serving as an extension of clients’ teams, experienced and knowledgeable personnel, client-focus, creativity, reliable execution, proprietary technology platforms, and financial strength. All known U.S. competitors and most international competitors are privately held companies that provide limited public information regarding their operations. GES’ primary competitor within its Core Services is The Freeman Company (a privately-held, U.S.-headquartered company); however, there is substantial competition from a large number of service providers in GES’ other service offerings.

Growth Strategy

GES is committed to become the preferred global, full-service provider for Live Events. GES holds a leading market position in Exhibitions and is pursuing a focused and disciplined growth strategy with the goal of expanding its market share in the currently under-penetrated Conferences, Corporate Events, and Consumer Events markets. GES has uniquely combined the art of high-impact creativity, service, and expertise with the science of easy-to-use technology, strategy, and worldwide logistics to help clients gain a greater return from their events and enhance the exhibitor experience.

Global Reach. Leverage global capabilities and large customer base to drive continued growth in new services and other Live Events.

Full-Service Provider. Growth of adjacent services to create a unique and integrated offering to deepen client relationships, expand client base, and increase share of total event spend.

Live Events. Penetration into other live events to extend industry leadership and leverage capabilities.

With our recent acquisitions, GES made significant progress toward creating the most comprehensive suite of services for the Live Events industry, which enhanced overall competitiveness, facilitated growth in under-penetrated areas, and formed a basis for a data platform. We continue to pursue opportunities to acquire businesses with proven products and services that complement, enhance, or expand current businesses or offer growth opportunities.

Poken Acquisition. In March 2017, we completed the acquisition of the Poken event engagement technology,a leading cloud-based visitor engagement and measurement platform. The Poken platform offers a seamless ecosystem of tools that enable digital document collection (through its patented “Touch and Glow” technology), visitor-to-visitor engagement, gamification, and metrics reporting.

Cross-selling opportunities. GES is effectively positioned to cross-sell an increasingly comprehensive suite of service offerings with a convenient approach to service delivery that differentiates GES from its competition.

Registration and data analytic services entrance in the Asia markets. In early 2017, GES officially launched registration and data analytic services in the Asia market with a Hong Kong office.

Pursuit is a global attractions and hospitality company that owns and operates a collection of iconic naturalinspiring and cultural destinationunforgettable travel experiences in North America that showcase the best of Banff, Jasper, Waterton Lakes, Glacier, Denali,iconic destinations. Pursuit’s mission is to connect guests and Kenai Fjords National Parks, and Vancouver, Canada. Through Pursuit’s collection of unique hotels and lodges, world-class recreational attractions, and ground transportation services, it connects guestsstaff to iconic places through unforgettable inspiring experiences. From world-class attractions, distinctive hotels, and engaging tours in stunning national parks and renowned global travel locations, Pursuit’s elevated attraction and hospitality experiences enable visitors to discover and connect with these iconic destinations. With a strategic direction to build an expanding portfolio of extraordinary experiences, Pursuit remains focused on refreshing, improving, and growing its collection in outstanding places around the globe. Pursuit draws its guests from major markets, including Canada, the United States, Canada, China, the United Kingdom, Australia/New Zealand, Asia Pacific, and Europe. Pursuit markets directly to consumers, as well as through distribution channels that include tour operators, tour wholesalers, destination management companies, and retail travel agencies and organizations.agencies. Pursuit comprises the following collections:following:

Banff Jasper Collection |

portfolio. |

Alaska Collection | The Alaska Collection services. |

Glacier Park Collection |

guided river rafting attraction, lodging, culinary and retail experiences, all designed to enable guests to experience both Montana and Southern Alberta’s stunning outdoors. |

FlyOver Attractions | Pursuit’s FlyOver

|

Sky Lagoon | Pursuit’s Sky Lagoon is cold pool and sauna experiences. It also features an in-lagoon bar, dining experiences and retail offerings. |

2

Pursuit comprises fourPursuit’s collection of experiences focuses on three distinct lines of business: Hospitality, includingAttractions (including food and beverage services and retail operations; Attractions, includingoperations); Hospitality (including food and beverage services and retail operations; Transportation;operations); and Travel Planning. These four linesTransportation.

Attractions |

BANFF JASPER COLLECTION

Banff Gondola transports visitors to an elevation of business work together, driving economiesover 7,000 feet above sea level to the top of scopeSulphur Mountain in Banff, Alberta, Canada offering an unobstructed view of the Canadian Rockies and meaningful scaleoverlooking the town of Banff and the Bow Valley. The Banff Gondola and the Sky Bistro restaurant, which is located at the top of the Banff Gondola, were 2023 Trip Advisor Travelers Choice award winners.

Lake Minnewanka Cruise provides guests a unique sightseeing experience through interpretive boat cruises on Lake Minnewanka in the Canadian Rockies. The Lake Minnewanka Cruise operations are located adjacent to the town of Banff and aroundinclude boat tours, small boat rentals, and charter fishing expeditions. The Lake Minnewanka Cruise was a 2023 Trip Advisor Travelers Choice award winner.

Glacier Adventure is a tour of the Athabasca Glacier on the Columbia Icefield, which provides guests a view of one of the largest accumulations of ice and snow south of the Arctic Circle. Guests ride in a giant “Ice Explorer,” a unique vehicle specially designed for glacier travel. The Glacier Adventure was a 2023 Trip Advisor Travelers Choice award winner.

Columbia Icefield Skywalk is a 1,312-foot guided interpretive walkway with a 98-foot glass-floored observation area overlooking the Sunwapta Valley, near our Glacier Adventure attraction in Jasper National Park, Alberta, Canada.

Maligne Lake Cruise provides interpretive boat tours at Maligne Lake, the largest lake in Jasper National Park, Alberta, Canada. In addition to boat tours, Maligne Lake has a marina and day lodge that offers food and beverage and retail services, an historic chalet complex and boat house that offers canoes, kayaks, and rowboats for rental. The Maligne Lake Cruise was a 2023 Trip Advisor Travelers Choice award winner.

Golden Skybridge is in the mountain town of Golden, British Columbia, which is 90 minutes from Banff. It consists of two suspension bridges that are connected through forested trails. The upper skybridge is 426 feet above the canyon floor while the lower skybridge is 262 feet above the canyon floor. The attraction also includes a zip line, a canyon challenge course, and a mountain coaster. The Golden Skybridge was a 2023 Trip Advisor Travelers Choice award winner.

Open Top Touring is a guided sightseeing tour of Banff with a historic twist. Guests ride in a custom-made, open-topped automobile inspired by local tours from the 1930s. Open Top Touring was a 2023 Trip Advisor Travelers Choice award winner.

ALASKA COLLECTION

Kenai Fjords Tours is a wildlife, whale watching, and glacier cruise, offering guests unforgettable sights of towering glaciers, humpback and grey whales, orcas, arctic birdlife, sea lions, seals, and porpoises in Kenai Fjords National Park. Tours range from a few hours to full days, with some tours including a culinary experience and visit to Fox Island. Kenai Fjords Tours was a 2023 Trip Advisor Travelers Choice award winner.

SKY LAGOON

Sky Lagoon is a 230-foot premium oceanfront geothermal lagoon that is located in Kársnes Harbour, Kópavogur, just minutes from Reykjavik. Sky Lagoon showcases expansive ocean vistas punctuated by awe-inspiring sunsets, Northern Lights, and dark sky views. Sky Lagoon was a 2023 Trip Advisor Travelers Choice award winner.

3

FLYOVER ATTRACTIONS

FlyOver flight ride attractions provide guests with an exhilarating flying experience over iconic destinationsnatural wonders, hard to reach locations, and picturesque scenery. Utilizing state-of-the-art ride and audio-visual technology, each FlyOver experience features moving ride vehicles with six degrees of motion and multi-sensory special effects before a spherical screen.

GLACIER PARK COLLECTION

Glacier Raft Company provides guided river rafting trips in West Glacier, Montana.

Hospitality |

BANFF JASPER COLLECTION | GLACIER PARK COLLECTION | ALASKA COLLECTION | |||||

Elk + Avenue Hotel | 164 rooms | Glacier Park Lodge | 162 rooms | Seward Windsong Lodge | 216 rooms | ||

Forest Park Woodland | 152 rooms | Grouse Mountain Lodge | 145 rooms | Talkeetna Alaskan Lodge | 212 rooms | ||

Lobstick Lodge | 139 rooms | St. Mary Lodge | 116 rooms | Denali Cabins | 46 rooms | ||

Mount Royal Hotel | 133 rooms | Prince of Wales Hotel | 86 rooms | Denali Backcountry Lodge | 42 rooms | ||

Chateau Jasper Hotel | 119 rooms | Apgar Village Lodge & Cabins | 48 rooms | Kenai Fjords Wilderness Lodge | 8 rooms | ||

The Crimson Hotel | 99 rooms | West Glacier Village | 18 rooms | 524 rooms | |||

Forest Park Alpine | 88 rooms | Glacier Basecamp Lodge | 29 rooms | ||||

Marmot Lodge | 81 rooms | Belton Chalet | 27 rooms | ||||

Pyramid Lake Resort | 68 rooms | Motel Lake McDonald | 27 rooms | ||||

Miette Mountain Cabins | 56 rooms | Glacier Raft Co. Lodging | 23 rooms | ||||

Glacier View Lodge | 32 rooms | West Glacier RV Park & Cabins | 25 rooms | ||||

1,131 rooms | 706 rooms | ||||||

Transportation |

BANFF JASPER COLLECTION

Transportation operations include sightseeing tours, airport shuttle services, and seasonal charter motorcoach services. The sightseeing services include seasonal half- and full-day tours from Calgary, Banff, Lake Louise, and Jasper, Canada and bring guests to the most scenic areas of Banff, Jasper, and Waterton LakesYoho National ParksParks. The charter business operates a fleet of luxury motorcoaches, available for groups of any size, for travel throughout the Canadian provinces of Alberta and Vancouver in Canada, and Glacier,British Columbia during the winter months.

ALASKA COLLECTION

Transportation includes a Denali and Kenai FjordsBackcountry Adventure, which is a unique photo safari tour 92 miles deep into Denali National Parks in the United States.Park.

4 |

|

|

|

| ||||

|

|

|

|

| ||||

|

|

|

|

| ||||

|

| |||||||

|

|

|

|

|

|

|

|

|

|

| Pursuit

|

|

| |

|

| |

|

| |

|

|

|

|

Seasonality

Pursuit experiencesPursuit’s peak activity occurs during the summer months. During 2017, 87%2023, 79% of Pursuit’s revenue was earned in the second and third quarters.

Competition

Pursuit generally competes based on the basis of location, uniqueness of facilities, service, quality, and price. Competition exists both locally and regionally across all fourthree lines of business. The hospitality businessindustry has a large number of competitors and competes for leisure travelers (both individual and tour groups) across the United States and Canada. Pursuit’s competitive advantage isadvantages are its distinctive attractions, iconic destinations, and iconic destinations.strong culture of hospitality and guest services.

Pursuit remains focused on delivering inspiring and unforgettable experiences in iconic locations while growing and enhancing its unique portfolio of integrated tourism assetsPursuit’s growth strategy is to become a leading attractions hospitality company through its Refresh-Build-Buy growth initiatives.Refresh, Build, Buy initiatives:

Refresh. RefreshRefreshing our existing assets and processes to optimize the guest and team member experience, market position, and maximize returns.

Build. BuildBuilding new assets thatto create new guest experiences and additional revenue streams with economies of scale and scope.

Buy. BuyBuying strategic assets that drive guest experience, economies of scale and scope, with strong returns.

We continue to search for opportunities to acquire or to build high return tourism assets in iconic natural and cultural destinations that enjoy perennial demand, bring meaningful scale and market share, and offer cross-selling advantages with a combination of attractions and hotels.

Recent Pursuit DevelopmentsDevelopment

Mount Royal Hotel. On December 29, 2016,FlyOver Chicago, located near the Mount Royal Hotel was damaged by fire and closed. In July 2017, we resolved our property and business interruption insurance claims related to the fire for $36.3 million. We allocated $2.2 million to an insurance receivable, $29.3 million was recorded as an impairment recovery (partially offset by impairment chargesfront entrance of $0.2 million) related to construction costs to re-open the hotel, $2.5 million was recorded as a business interruption gain for the recovery of lost profits, $1.3 million was recorded as contra-expense to offset non-capitalizable costs incurred, and the remaining $1.0 million was recorded as deferred revenue that will be recognized over the periods the business interruption losses are actually incurred. Restorations and improvements will provide an elevated guest experience to room finishes and furnishings, lobby and lounge areas, exterior appearance, heating/cooling, sound insulation, and building systems. We anticipate re-opening the hotel in mid-year 2018.

Expansion of FlyOver Concept. On November 3, 2017, we acquired the controlling interest (54.5% of the common stock) in Esja Attractions ehf. (“Esja”). Esja, a private Iceland corporationChicago’s Navy Pier, is developing and will operate Pursuit’s new FlyOver Iceland attraction. This attraction expands our virtual flight ride theater concept into Iceland’s capital city of Reykjavik. Modeled after our highly successful FlyOver Canada attraction, FlyOver Iceland will provide guests an exhilarating virtual flight experience over some of Iceland’s most spectacular scenery and natural wonders. The new attraction is expectedscheduled to open in 2019.March 2024.

5

Tiny Home Village. On July 15, 2017, we added ten tiny homes

GES is a global, full-service live events company offering a comprehensive range of services to the St. Mary Lodge property as partworld’s leading brands and event organizers from the design and production of compelling, immersive live and digital experiences that engage audiences and build brand awareness, through to logistics, including material handling, rigging, electrical, and other on-site event services. GES’ mission is to create the most meaningful and memorable experiences for marketers, organizers, and attendees.

GES has a leading position in the United States, serving every major exhibition market, including Las Vegas, Chicago, and Orlando. Additionally, GES produces events at many of the Glacier Park Collection. The tiny home’smost active and popular international event destinations and venues in the United Kingdom, Canada, the Middle East, the Netherlands, and Germany.

SPIRO

Spiro is an experiential marketing agency that partners with leading brands around the world to manage and elevate their global experiential marketing activities. Spiro builds immersive experiences with its clients starting with the strategic plan, creating the content and design, embracesand finishing with the delivery and execution. Spiro delivers a broad range of unique and impactful experiences for its clients, including meetings and events, exhibition and program management, environments and permanent installations, brand and product activations, and marketing and measurement.

Spiro Competition

Within brand experiences, Spiro generally competes on the basis of creative design, value, quality, and service offerings. Spiro maintains competitive advantages through its breadth of service offerings, worldwide network of resources, state-of-the-art creative solutions, advanced technology platforms, longstanding reputation for customer service and execution, and financial strength. Most known competitors are privately-held companies that provide limited public information regarding their operations. There is substantial competition from a large number of eco-forward elements, suchservice providers, however Spiro’s primary competitors are experiential marketing agencies and trade show design-and-build companies.

GES EXHIBITIONS

GES Exhibitions is a global exhibition services company with a legacy spanning over 90 years and teams throughout North America, Europe, and the Middle East. GES Exhibitions partners with leading exhibition and conference organizers as a fresh water/gray water systemfull-service provider of strategic and pint-sized, energy-efficient appliances. Elementslogistics solutions to manage the complexity of luxurytheir shows, including strategy, creative & design, registration & engagement, accommodations, logistics & management, material handling, overhead sign hanging, graphics and other rental and labor services. GES Exhibitions also serves as an in-house or preferred provider of electrical and other event services within event venues, including convention centers and conference hotels.

GES Exhibitions Competition

In the live events industry, GES Exhibitions generally competes across all classes of services and all markets on the basis of discernible differences, value, quality, price, convenience, and service. GES Exhibitions has a competitive advantage through its worldwide network of resources, history of serving as an extension of clients’ teams, experienced and knowledgeable personnel, client focus, creativity, reliable execution, proprietary technology platforms, and financial strength. All known United States competitors and most international

6

competitors are woven intoprivately held companies that provide limited public information regarding their operations. GES Exhibition’s primary competitor is a privately-held, United States-headquartered company; however, there is substantial competition from a large number of service providers in GES Exhibition’s other service offerings.

GES Seasonality and Show Rotation

GES’ live event activity can vary significantly from quarter to quarter and year to year depending on the design. Homes can accommodate upfrequency and timing of shows. Some shows are not held annually and some shift between quarters. Show rotation refers to four guests, withshows that occur less frequently than annually, as well as annual shows that shift quarters from one year to the next.

GES Strategic Transformation

Over the past few years, we accelerated our transformation and streamlining efforts at GES to significantly reduce costs and create a sliding barn-style door separating a compact sleeping area from the cozy living area.

RV and Cabin Park Development. In 2017, we began developing approximately 100 acres of undeveloped land adjacent to Glacier National Park that we acquired in connection with our 2014 purchase of the West Glacier properties. The new development will include a new RV and cabin park with 102 RV slips, 20 guest cabins, five employee housing cabins, guest registration, and a laundromat. Our site is ideally located at the Glacier Park entrance. We expect half of the new RV and Cabin Park to open during the 2019 season with the remainder opening for the 2020 season.

Financial information for our reportable segments and geographic areas is included in Note 22 – Segment Information of the Notes to Financial Statements (Part II, Item 8 of this 2017 Form 10-K).lower cost structure focused on servicing GES’ more profitable market segments.

Intellectual Property

Our intellectual property rights (including trademarks, patents, copyrights, registered designs, technology, and know-how) are material to our business.

We own or have the right to use numerous trademarks and patents in many countries. Depending on the country, trademarks remain valid for as long as we use them, or as long as we maintain their registration status. Trademark registrations are generally for renewable, fixed terms. We also have patents for current and potential products. Our patents cover inventions ranging from a modular structure having a load-bearing surface that we use in our event and exhibition services, to a surface-covering installation tool and method that reduces our labor costs and improves worker safety. Our U.S.United States issued utility patents extend for 20 years from the patent application filing date;date, and our U.S.United States issued design patents are currently granted for 14 years from the grant date. We also have an extensive design library. Many of the designs have copyright protection and we

have also registered many of the copyrights. In the U.S.,United States, copyright protection is for 95 years from the date of publication or 120 years from creation, whichever is shorter. While we believe that certain of our patents, trademarks, and copyrights have substantial value, we do not believe the loss of any one of them would not have a material adverse effect on our financial condition or results of operations.

Our Trademarks

Our U.S.United States registered trademarks and trademarks pending registration include Global Experience Specialists & design®, Spiro, GES®, Viad ®, GES Servicenter®, GES National Servicenter®, GES MarketWorks®Connect®, The Art and Science of Engagement®GES Exhibit Ready®, GES Measurement & Insight®, GES Project Central,Trade Show Rigging TSR®, TSE Trade Show Electrical & design®, Earth Explorers®, Compass Direct®, ethnoMetrics®, eXPRESSO®, FIT®, ON Services, ON Site Audio VisualFLYOVER® & design, FLYOVER®FLYOVER Canada & design®, eco-sense®FLYOVER Iceland & design®, FLYOVER LAS VEGAS®, ONPEAK®, Above Banff®, Alaska Denali Travel®, Alaska Denali Escapes®, Alaska Heritage Tours®, Kenai Fjords Tours & design®, Kenai Fjords Wilderness Lodge®, Seward Windsong Lodge & design®, Talkeetna Alaskan Lodge®,design, Explore Rockies®, Denali Backcountry Adventure®, Denali Backcountry Lodge®, and Denali Cabins®. Cabins & design®

We also own or have the right to use many registered trademarks and trademarks pending registration outside of the United States, including GES®, Spiro®, ShowTech®, Poken®Visit®, Visit Blitz,by GES®, Brewster Inc. & design®, Brewster Attractions Explore & design®, Brewster Hospitality Refresh & design®, Glacier Skywalk®, Above Banff®, Banff Gondola®, Explore Rockies®, FLYOVER®FLYOVER & design®, FLYOVER ICELAND & design, FLYOVER Canada & design, Forest Park Hotel®, Mount Royal, GES Event Intelligence AG®, Pursuit®, by Pursuit®, Kaffi Grandi, Ský Lagoon®, Soaring Over Canada®, Elk + Avenue Hotel®, Brewster Epic Summer Pass®, and escape.connect.refresh.explore®.

Government Regulation and Compliance

Compliance with legal requirements and government regulations represents a normal cost of doing business. The principal rules and regulations affecting our day-to-day business relate to transportation (such as regulations promulgated by the U.S. Department of Transportation and its state counterparts),our employees (such as regulations implemented by the Occupational Safety and Health Administration, equal employment opportunity laws, guidelines implemented pursuant to the Americans with Disabilities Act, and general federal and state employment laws), unionized labor (such as guidelines imposed by the National Labor Relations Act), and U.S.United States and Canadian regulations relating to national parks (such as regulations established by Parks Canada, the U.S.United States Department of the Interior, and the U.S.United States National Park Service)., United States and Canadian regulations relating to boating (such as regulations implemented by the United States Coast Guard and Canadian Coast Guard and state boating laws), transportation (such as regulations promulgated by the United States Department of Transportation and its state counterparts), and consumer and employee privacy regulations implemented by agencies in the jurisdictions where we operate.

Some of ourOur current and former businesses are subject to U.S. federal and state environmental regulations, including laws enacted under the Comprehensive Environmental Response, Compensation and Liability Act, or our state law counterparts.regulations. Compliance with federal, statethese provisions, and local environmental health and safetystewardship generally, is key to our ongoing operations. To date, these provisions including, but not limited to, those regulating the discharge of materials into the environment and other actions relating to the environment, have not had, and arewe do not expectedexpect them to have, a material effect on our capital expenditures, competitive position, financial condition or results of current and discontinued operations.

Employees

7

On July 18, 2020, an off-road Ice Explorer operated by our Pursuit business was involved in an accident while enroute to the Athabasca Glacier, resulting in three fatalities and multiple other serious injuries. We immediately reported the accident to our relevant insurance carriers, who have supported our investigation and subsequent claims relating to the accident. In May 2023, we resolved charges from the Canadian office of Occupational Health and Safety in relation to this accident, resulting in fines and related payments in an aggregate amount of $0.5 million Canadian dollars (approximately $0.3 million U.S. dollars). We continue to manage our legal defense of various claims from the victims and their families. In addition, we believe that our reserves and, subject to customary deductibles, our insurance coverage is sufficient to cover potential claims related to this accident.

Human Capital

Our people drive our success. We foster a culture that is equitable and inclusive, celebrates our talent, and prioritizes the safety and wellness of our teams, clients, and guests. We are committed to cultivating an environment where people of all different backgrounds feel a sense of belonging and contribute to our continued success.

We had the following number of employees as of December 31, 2017:2023:

Number of | ||||

GES | 2,765 | |||

Pursuit | 1,237 | |||

Viad Corporate | 33 | |||

Total | 4,035 | |||

|

| Number of Employees |

|

| Regular Full-Time Employees Covered by Collective Bargaining Agreements |

| ||

GES |

|

| 3,092 |

|

|

| 1,142 |

|

Pursuit |

|

| 365 |

|

|

| 41 |

|

Viad Corporate |

|

| 64 |

|

|

| — |

|

Total |

|

| 3,521 |

|

|

| 1,183 |

|

(1)

GES hires temporary employees on a show-by-show basis. The number of temporary employees fluctuates depending on the size and location of the exhibition or event. Pursuit hires approximately 2,000 seasonal employees during the peak summer months to help operate its attractions and hospitality properties.

We are governed by a Board of Directors comprised of sevencomprising eight non-employee directors and one employee director, and we have an executive management team consistingwith seven executive officers.

Diversity, equity, and inclusion

We take pride in our diverse community. We believe diversity and gender equality are critical to building a thriving workplace. We strive to create an environment where people of four executive officers.all different backgrounds feel a sense of belonging and contribute to our continued success. To make our workplace as inclusive and safe as possible, we have diversity and inclusion training integrated into our Always Honest Compliance and Ethics Program.

Financial Information about SegmentsWe do not discriminate against employees or applicants based on race, color, age, disability, ethnicity, citizenship, religion, sex, national origin, sexual orientation, genetics or genetic information, or any other categories protected by applicable law. We are committed to equal opportunity in all of our employment activities, including, but not limited to, recruitment, hiring, compensation, determination of benefits, training, promotion, and Geographic Areasdiscipline. We also provide reasonable accommodations to disabled persons, so all employees can achieve success in the workplace.

ReferAs a devoted steward to Note 22 – Segment Informationour communities, we are committed to increasing the diversity of our workforce to better reflect the communities in which we operate. We have undertaken initiatives, which go beyond legal compliance, to recruit from diverse audiences, such as minorities, women, and veterans. These efforts include leveraging inclusive job-posting sites and sharing job postings with community partners.

As part of our commitment to developing our employees and furthering their professional growth, we have programs in place including GES’ Business Development Mentor Program and newly launched training platforms for people leaders, including “Spiro.You” at Spiro, “Sales Leadership Program” at GES Exhibitions, and “Leaders’ Journey” at Pursuit. These programs connect employees with leaders within our organization and are designed to accelerate their career trajectory.

Our emphasis on a positive employee experience permeates throughout the organization and helps drive our success. For example, we conduct periodic employee engagement surveys to help us understand, recognize, and respect the diversity within our team. These

8

surveys help shape our training and development plans to ensure we are maintaining an inclusive culture by engaging, developing, and retaining our talented team members across the globe.

We believe that diversity, equity, and inclusion (“DEI”) is an ongoing journey, and we are proud of our DEI achievements so far, yet also cognizant of the Noteswork we still have ahead.

We take pride in the diverse and talented group of people that make up our Board of Directors, executive management, and employees. We understand the value that a diverse workforce of varying genders, ethnicity, background, and experience brings to Consolidated Financial Statements (Part II, Item 8the Company and we are focused on improving diversity at all levels.

An important part of our work and how we will ensure continual progress is by monitoring our diversity metrics. Out of a total of eight non-employee Board members, two are minorities of which one is a female for a total of three females on the Board. In 2023, almost 50% of our overall global workforce was female.

Workplace safety

The safety and well-being of team members, clients, and guests is a leading core value. We believe that maintaining strong standards of health and safety improves employee productivity and operational efficiency and enhances employee well-being.

We have a responsibility to maintain a safe and healthy work environment. We take prompt action to correct unsafe or hazardous conditions; we promptly report work-related accidents and injuries in accordance with established procedures and applicable laws; we strive to follow all established work rules related to safety; and we educate our workers to ensure they understand the risks, know how to handle hazardous products safely, and are familiar with available information for all hazardous materials used.

Both Pursuit and GES have implemented business-specific programs that support our commitment to the safety and well-being of our team members, clients, and guests.

Pursuit’s Safety Promise is our commitment to the safety and well-being of our guests and staff. Through this 2017 Form 10-K) program, we ensure that everyone feels safe when visiting or working at our experiences and that these places can continue to make a positive impact.

GES’ Always On Health and Safety Program was designed by our safety team to protect our employees, customers, partners, and event attendees. GES employees are committed to adhering to all local government and facility requirements and those established in conjunction with our partners and clients. Safe, reliable delivery of events is one of our most significant responsibilities.

In 2023, Viad had a global reportable incident rate of 1.2, which is below the U.S. industry standard average rateof 2.7. Global reportable incident rate is defined as employee incidents reportable in the operating jurisdiction. It is calculated as reportable incidents divided by payroll hours, multiplied by 200,000 to normalize the results. The overall industry average of incidence rates of non-fatal occupational injuries and illnesses for segment financial information.all industries including private, state, and local government, provided by U.S. Bureau of Labor Statistics 2022. Published data lags one calendar year. We continue to strive toward our goal of zero reportable incidents.

Always honest compliance and ethics program

We believe that maintaining a culture of high ethical standards gives us a distinct advantage in recruiting and retaining top talent, delivering the best experience for our customers, and attracting shareholders. Our Always Honest Compliance and Ethics Program, with the full support of our Board of Directors, has guided us since 1994 to translate integrity into our everyday behavior and actions. The Always Honest Compliance and Ethics Program guides our employees to act honestly, ethically, and always in compliance with the law.

Community involvement

Giving back to the community is very important to us. We are committed to making a positive impact within the communities we serve through educational programs such as GES’ Exhibition Sponsorships, volunteer services, and environmental/economic sustainable efforts in the community. Many of our locations pull together to volunteer and support local and national organizations. The Banff Jasper Collection was awarded the 2022 Corporate Citizen of the Year in Jasper, Alberta in recognition of its community building efforts. Pursuit also supported an exchange of learning and renewed its dedication to reconciliation with local Indigenous communities through a variety of initiatives and programs.

Rewards and performance management

Beyond a competitive salary, we offer a range of healthcare benefits to full-time employees, their spouses, and dependents. We encourage our employees to grow professionally with ongoing training and internal career opportunities. We utilize a performance review process, which aligns our core competencies to our core values, and a performance management cycle, which provides a framework designed to maximize performance and cultivate talent. Short- and long-term incentive compensation for senior managers and executives is based on the Company’s performance and/or stock performance.

9

We were incorporated in Delaware in 1991. Our common stock trades on the New York Stock Exchange under the symbol “VVI.”

Our website address is www.viad.com. All of our SECSecurities and Exchange Commission (“SEC”) filings, including our Annual Reportsannual report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, and amendments to those reports, are available free of charge on our website as soon as reasonably practicable after we electronically file that material with, or furnishedfurnish it to, the SEC. The information contained on our website is neither a part of, nor incorporated by reference into, this 20172023 Form 10-K.

Our investor relations website is www.viad.com/investors/investor-center/default.aspx and includes key information about our corporate governance initiatives, including our Corporate Governance Guidelines, our Board of Directors committee charters, our Code of Ethics, and information concerning our Board members and how to communicate with them.

Our operations and financial results are subject to known and unknown risks. As a result, past financial performance and historical trends may not be reliable indicators of our future performance.

Macroeconomic Risks

We are vulnerable to deterioration in general economic conditions. Our business is particularly sensitive to fluctuations in general economic conditions in the United States and other global markets in which we operate. A decline in global or regional economic conditions, or consumers’ fears that economic conditions will decline, whether due to inflation, elevated interest rates, or other economic, pandemic or geopolitical uncertainties could cause declining consumer or corporate spending, travel disruptions, unemployment, fluctuations in stock markets and interest rates, contraction of credit availability, or other dynamic factors generally affecting economic conditions. For example, high inflation and the resulting rise in interest rates have increased our interest expense on our variable rate debt. The additional impacts of these macroeconomic developments on our operations cannot be predicted with certainty. The success of our GES business largely depends on the number of exhibitions or other live events held, exhibitor presence and attendee volume at those events, the size of marketing expenditures at those events, and on the strength of particular industries that support those events. The number and size of live events and related marketing expenditures generally decrease when the economy weakens. We also could suffer from reduced spending for our services because many live event marketing budgets are partly discretionary and are frequently among the first expenditures reduced when economic conditions deteriorate. In addition, revenue from our Pursuit operations depends largely on the amount of disposable income that consumers have available for travel and vacations, which decreases during periods of weak general economic conditions. As a result, any deterioration in general economic conditions could materially and adversely affect our business, financial condition, and results of operations.

Travel industry disruptions, particularly those affecting the hotel and airline industries, could adversely affect our business. Our business depends largely on the ability and willingness of people, whether exhibitors, event attendees, tourists, or others, to travel. Factors adversely affecting the travel industry, and particularly the airline and hotel industries, generally also adversely affect our business and results of operations. Factors that could adversely affect the travel industry include high or rising fuel prices, levels of consumer discretionary or corporate marketing spendings, international political instability and hostilities, acts of terrorism, weather conditions, health epidemics, pandemics and endemics, and airline accidents. For example, our business, operations and financial results were negatively impacted by dramatically reduced travel, demand for travel-related services, and live event experiences resulting from lockdowns and other restrictions related to the COVID-19 pandemic. A decline in travel-related consumer discretionary or corporate marketing spend, or the occurrence of other pandemic or geopolitical events or hostilities that affect the availability and pricing of air travel and accommodations, could materially and adversely affect our business and results of operations.

Our overall level of indebtedness, as well as our financial covenants under our revolving credit facility, could limit our operational and financial flexibility and make us more vulnerable to adverse economic conditions.As of December 31, 2023, our debt totaled $462.1 million, including $378 million outstanding on our $500 million credit facility (the “2021 Credit Facility”), financing lease obligations of $63.9 million, and $20.2 million in other debt. The 2021 Credit Facility includes a term loan (“Term Loan B”) with an outstanding balance of $321 million as of December 31, 2023 and a $170 million revolving credit facility (“Revolving Credit Facility”). As of December 31, 2023, capacity remaining under the Revolving Credit Facility was $108.0 million. As a result of our indebtedness, we are required to make interest and principal payments on our borrowings, which are significant. These payments reduce our cash available, which could limit our ability to respond to market conditions or take advantage of potential acquisitions and strategic investments. To manage our exposure to interest rate movements, we entered into an interest rate cap agreement that provides an interest rate hedge on $300 million of borrowings for a two-year period, which commenced on January 31, 2023. We also we entered into an amendment to the 2021 Credit Facility on October 6, 2023, which among other things, increased the principal amount of the revolving credit facility by $70 million, bringing the total amount of revolving capacity to $170 million. In connection with the amendment, we prepaid $70 million of the outstanding balance on our existing Term Loan B.

In addition, our ability to draw on our revolving credit facility depends on our ability to meet certain financial covenants. This exposes us to various risks, uncertainties, and events beyond our control, including but not limited to the impact of adverse economic conditions (including inflation, rising interest rates, or a recession), public health crises, and other factors described herein. If we are unable to maintain compliance with these covenants, our lenders may exercise remedies against us, including the acceleration of any outstanding

10

indebtedness on our revolving credit facility. Under this circumstance, we might not have sufficient funds or other resources to satisfy all of our obligations, which could materially and adversely affect our business and results of operations.

Transportation disruptions and increases in transportation costs could adversely affect our business and results of operations. GES relies on independent transportation carriers to send materials and exhibits to and from exhibitions, warehouses, and customer facilities. If our customers and suppliers are unable to secure the services of those independent transportation carriers at favorable rates, it could materially and adversely affect our business and results of operations. In addition, disruption of transportation services, including import/export services due to weather-related problems; labor strikes; lockouts; or other events could adversely affect our ability to supply services to customers and could cause the cancellation or curtailment of exhibitions, which could materially and adversely affect our business and results of operations.

Natural disasters, weather conditions, accidents, and other catastrophic events could negatively affect our business. The occurrence of catastrophic events ranging from natural disasters (such as hurricanes, fires, floods, volcanoes, and earthquakes), acts of war or terrorism, accidents involving our travel offerings or experiences, the effects of climate change, including any impact of global warming, or the prospect of these events could disrupt our business. Changes in climates may increase the frequency and intensity of adverse weather patterns and make certain destinations less desirable.

Such catastrophic events have had, and could in the future have, an adverse impact on Pursuit, which is heavily dependent on the ability and willingness of its guests to travel and/or visit our attractions. Pursuit guests tend to delay or postpone vacations if natural conditions differ from those that typically prevail at competing lodges, resorts, and attractions, and catastrophic events and heightened travel security measures instituted in response to such events could impede the guests’ ability to travel, and interrupt our business operations, including damaging our properties. For example, the accident on July 18, 2020, at Pursuit’s Glacier Adventure attraction, which involved one of our off-road Ice Explorers and resulted in three fatalities and other serious injuries, may have a negative impact on our reputation and traveler willingness to visit that attraction in the future.

Such catastrophic events could also have a negative impact on GES, causing a cancellation or relocation of exhibitions and other events held in public venues or disrupt the services we provide to our customers at convention centers, exhibition halls, hotels, and other public venues. Such events could also have a negative impact on GES’ production facilities, preventing us from timely completing exhibit fabrication and other projects for customers. In addition, unfavorable media attention, or negative publicity, in the wake of any catastrophic event or accident could damage our reputation or reduce the demand for our services. If the conditions arising from such events persist or worsen, they could materially and adversely affect our results of operations and financial condition.

Strategic, Business, and Operational Risks

The seasonality of our business makes us particularly sensitive to adverse events during peak periods. The peak activity for our Pursuit business is during the summer months, as the vast majority of Pursuit’s revenue is earned in the second and third quarters. Our GES exhibition and event activity varies significantly because it is based on the frequency and timing of shows, many of which are not held each year, and which may shift between quarters. If adverse events or conditions occur during these peak periods, for example natural disasters such as hurricanes, volcanoes, forest fires and/or smoke resulting from those events or a similar event, our results of operations could be materially and adversely affected.

New capital projects may not be commercially successful. From time to time, we pursue capital projects in order to enhance and expand our business, such as FlyOver, which includes FlyOver Canada in Vancouver, FlyOver Iceland, FlyOver Las Vegas, and the current development of FlyOver Chicago and FlyOver Canada Toronto, as well as other efforts to upgrade and update some of our Pursuit offerings. Capital projects are subject to a number of risks, including the failure to achieve established financial and strategic goals. For example, our FlyOver attractions are all considered one reporting unit and goodwill is assigned to, and tested at, the reporting unit level. Significant reductions in FlyOver’s expected future revenue, operating income, or cash flow forecasts and projections, or changes in macroeconomic facts and circumstances, particularly high inflation and the resulting rise in interest rates, may result in impairment charges in the future. Capital projects are also subject to unanticipated delays and cost overruns as well as additional project-specific risks. For example, we had to postpone FlyOver Canada Toronto due to permitting and other related delays. A prolonged delay in a capital project, or our failure to accurately predict the revenue or profit that will be generated from a project, could prevent it from performing in accordance with our commercial expectations and could materially and adversely affect our business and results of operations.

We operate in a highly competitive and dynamic industry. Competition in the live events markets is driven by price and service quality, among other factors. To the extent competitors seek to gain or retain market presence through aggressive underpricing strategies, we may be required to lower our prices and rates to avoid the loss of related business. Moreover, customer consolidations and other actions within the industry have caused downward pricing pressure for our products and services and could affect our ability to negotiate favorable terms with our customers. If we are unable to anticipate and respond as effectively as our competitors to changing business conditions, including new technologies and business models, we could lose market share. Our inability to meet the challenges presented by the competitive and dynamic environment of our industry could materially and adversely affect our results of operations.

11

We depend on our large exhibition event clients to renew their service contracts and on our exclusive right to provide those services. GES has a number of large exhibition event organizers and large customer accounts. If any of these large clients do not renew their service contracts, our results of operations could be materially and adversely affected.

Moreover, when event organizers hire GES as the official services contractor, they usually also grant GES an exclusive right to perform material handling, electrical, rigging, and other services at the exhibition facility. However, some exhibition facilities have taken certain steps to in-source certain event services (either by performing the services themselves or by hiring a separate service provider) as a result of conditions generally affecting their industry, such as an increased supply of or reduced demand for exhibition space. If exhibition facilities choose to in-source certain event services, GES will lose the ability to provide certain event services, and our results of operations could be materially and adversely affected.

Show rotation affects our profitability and makes comparisons between periods difficult. GES results are largely dependent upon the frequency, timing, and location of exhibitions and events. Some large exhibitions are not held annually (they may be held once every two, three, or four years) or may be held at different times of the year from when they were previously held. In addition, the same exhibition may change locations from year to year resulting in lower margins if the exhibition shifts to a higher-cost location. Any of these factors could cause our results of operations to fluctuate significantly from quarter to quarter or from year to year, making periodic comparisons difficult.

Completed acquisitions may not perform as anticipated or be integrated as planned. We regularly evaluate and pursue opportunities to acquire businesses that complement, enhance, or expand our current business, or offer growth opportunities. Our acquired businesses might not meet our financial and non-financial expectations or yield anticipated benefits. Our success depends, in part, on our ability to conform controls, policies and procedures, and business cultures; consolidate and streamline operations and infrastructures; identify and eliminate redundant and underperforming operations and assets; manage inefficiencies associated with the integration of operations; and retain the acquired business’business’s key personnel and customers. Moreover, our acquisition activity potentially increases our debt, subjectsmay subject us to new regulatory requirements, distractsdistract our senior management and employees, and exposesexpose us to unknown liabilities or contingencies that we may fail to, or are unable to identify prior to closing. If our acquisitions cause uswe are forced to make changes to our business strategy or if external conditions adversely affect our business operations, such as unfavorable macroeconomic conditions (particularly high inflation and the resulting rise in interest rates), it may be difficult for us to accurately forecast revenue, operating income, or cash flow, and we may also be required to record an impairment chargecharges in the future. Additionally, we may borrow funds to goodwill or intangible assets.finance strategic acquisitions. Debt leverage resulting from future acquisitions would reduce our debt capacity, increase our interest expense, and limit our ability to capitalize on future business opportunities. Such borrowings may also be subject to fluctuations in interest rates. Any of these risks could materially and adversely affect our business, product and service sales, financial condition, and results of operations.

We depend on our large exhibition event clients to renew their service contracts and on our exclusive right to provide those services. During 2017, no single client accounted for more than 6% of our consolidated revenue. However, GES has a number of large exhibition event organizers and large customer accounts. If any of these large clients do not renew their service contracts, our results of operations could be materially adversely affected.

Moreover, when event organizers hire GES as the official services contractor, they also grant GES an exclusive right to perform electrical, plumbing services, and other services (the “Event Services”) at the exhibition facility. However, exhibition facilities are under increasing financial pressure to in-source Event Services (either by performing the services themselves or by hiring a separate service provider) as a result of conditions generally affecting their industry, such as an increased supply of exhibition space. If a large number of exhibition facilities choose to in-source Event Services, GES will lose the ability to provide Event Services despite being hired as the official services contractor, and our results of operations could be materially and adversely affected.

Our business is relationship driven. Our GES business is heavily focused on client relationships, and, specifically, on having close collaboration and interaction with our clients. To be successful, our account team must be able to understand a client’s desires and expectations in order to provide top-quality service. If we lose a key member of our account team, we could also lose customers and our results of operations could be materially and adversely affected.

We operate in highly competitive industries. We are engaged in a number of highly competitive industries. Competition in the Live Events industry and the exhibits and experiential environments industries is driven by price and service quality, among other factors. To the extent competitors seek to gain or retain their market presence through aggressive underpricing strategies, we may be required to lower our prices and rates to avoid the loss of related business, thereby adversely affecting our results of operations. In addition, if we are unable to anticipate and respond as effectively as competitors to changing business conditions, including new technologies and business models, we could lose market share to our competitors. Our inability to meet the challenges presented by the competitive environment could materially and adversely affect our results of operations.

Travel industry disruptions, particularly those affecting the hotel and airline industries, could adversely affect our business. Our business depends largely on the ability and willingness of people, whether exhibitors, exhibition attendees, or others, to travel. Factors adversely affecting the travel industry, and particularly the airline and hotel industries, generally also adversely affect our business and results of operations. Factors that could adversely affect the travel industry include high or rising fuel prices, increased security and passport requirements, weather conditions, airline accidents, and international political instability and hostilities. Any of these factors, or other unexpected events that affect the availability and pricing of air travel and accommodations, could materially and adversely affect our business and results of operations.

Transportation disruptions and increases in transportation costs could adversely affect our business and results of operations. GES relies on independent transportation carriers to send materials and exhibits to and from exhibition, warehouse, and customer facilities. If our customers and suppliers are unable to secure the services of those independent transportation carriers at favorable rates, it could materially and adversely affect our business and results of operations. In addition, disruption of transportation services due to weather-related problems, labor strikes, lockouts, or other events could adversely affect our ability to supply services to customers and could cause the cancellation of exhibitions, which could materially and adversely affect our business and results of operations.

The seasonality of our business makes us particularly sensitive to adverse events during peak periods. Our GES exhibition and event activity varies significantly because it is based on the frequency and timing of shows, many of which are not held each year and which may shift between quarters. The peak activity for our Pursuit business is during the summer months. Consequently, during 2017, 87% of Pursuit’s revenue was earned in the second and third quarters. If adverse events or conditions occur during these peak periods our results of operations could be materially and adversely affected.

Terrorist attacks, natural disasters, or other catastrophic events could negatively affect our business. The occurrence of catastrophic events ranging from natural disasters (such as hurricanes, fires, and floods), health epidemics or pandemics, acts of war or terrorism, accidents involving our travel offerings or experiences, or the prospect of these events could disrupt our business. Such catastrophic events could have a negative impact on GES’ production facilities, preventing us from timely completing exhibit fabrication and other projects for customers. They could also cause a cancellation of exhibitions and other events held in public venues or disrupt the services we provide to our customers at convention centers, exhibition halls, hotels, and other public venues. Such catastrophic events could also have an adverse impact on Pursuit, which is heavily dependent on the ability and willingness of its guests to travel. Pursuit guests tend to delay or postpone vacations if natural conditions differ from those that typically prevail at competing lodges, resorts and attractions, and catastrophic events could impede the guests’ ability to travel, interrupt our business operations, and/or cause damage to our properties. In addition, unfavorable media attention, or negative publicity, in the wake of a catastrophic event could damage our reputation or reduce the demand for our services. If the conditions arising from such events persist or worsen, they could materially and adversely affect our results of operations and financial condition.

We are vulnerable to deterioration in general economic conditions. Our business is sensitive to fluctuations in general economic conditions that affect the cost of materials and operating supplies. The success of our GES business largely depends on the number of exhibitions held, the size of exhibitors’ marketing expenditures, and on the strength of particular industries in which exhibitors operate. The number and size of exhibitions generally decrease when the economy weakens. We also suffer from reduced spending for our services because many exhibitors’ marketing budgets are partly discretionary, and are frequently among the first expenditures reduced when economic conditions deteriorate. Consequently, marketing expenditures often are not increased until economic conditions improve. Revenue from our Pursuit operation depends largely on the amount of disposable income that consumers have available for travel and vacations. This amount decreases during periods of weak general economic conditions. Any of these risks could materially and adversely affect our business, product sales, financial condition, and results of operations.

Recent U.S. tax legislation may materially and adversely affect our financial condition, results of operations, and cash flows. The Tax Cuts and Jobs Act (the “Tax Act”), enacted in late 2017, makes significant changes to U.S. tax laws and includes numerous provisions that could affect our business. For instance, as a result of lower corporate tax rates, the Tax Act tends to reduce both the value of deferred tax assets and the amount of deferred tax liabilities. It also limits interest rate deductions and the amount of net operating losses that can be used each year and alters the expensing of capital expenditures. Other provisions have tax consequences for our international operations. The Tax Act is unclear in certain respects and will require interpretations and implementing regulations by the Internal Revenue Service, as well as state tax authorities. The Tax Act could also be subject to amendments and technical corrections, any of which could lessen or increase the adverse impacts on our business operations. The accounting treatment of these tax law changes is complex, and some of the changes may affect both current and future periods. Others will primarily affect future periods. As we have discussed elsewhere in this Report on Form 10-K, we believe our analysis and computations of the tax effects of the Tax Act on financial results is substantially, but not entirely, complete. Consistent with guidance from the SEC, our financial statements reflect our estimates of the tax effects of the Tax Act on our business. Although we believe these estimates are reasonable, they are

provisional and may be adjusted prior to the end of 2018. Any such adjustments could affect our current or future financial statements, or both.We continue to examine the impact of this tax reform legislation, and as its overall impact is uncertain, we note that the Tax Act could adversely affect our business and financial condition.

We are subject to currency exchange rate fluctuations.We have operations outside of the U.S.United States primarily in Canada, the United Kingdom, Iceland, the Netherlands, Germany,the Middle East, and to a lesser extent, in certain other countries.Germany. During 2017, GES International and Pursuit’s2023, our international operations accounted for approximately 30%44% of our consolidated revenue and 58%89% of our segment operating income. Consequently, a significant portion of our business is exposed to currency exchange rate fluctuations. We do not currently hedge equity risk arising from the translation of non-United States denominated assets and liabilities. Our financial results and capital ratios are sensitive to movements in currency exchange rates because a large portion of our assets, liabilities, revenue, and expenses must be translated into U.S. dollars for reporting purposes. The unrealized gains or losses resulting from the currency translation are included as a component of accumulated other comprehensive income (loss) in our consolidated balance sheets.Consolidated Balance Sheets. We also have certain loans and leases in currencies other than the entity’s functional currency, which results in gains or losses as exchange rates fluctuate. As a result, significant fluctuations in currency exchange rates could result in material changes to our results of operations and the net equity position we report in our consolidated balance sheets. Consolidated Financial Statements.