AUTOLIV TECHNICAL CENTERS AND CRASH TEST TRACKS Country / Company

| | Location

| | | Product(s) Supported

| | | | | | | Country/Company | | Location | | Product(s) supported | China | | | | | | Autoliv (Shanghai) Vehicle Safety System Technical Center Co., Ltd. | | Shanghai | | | Airbags and seatbelts customer applications and platform development with full-scale test laboratory

| France

| | | | | | Autoliv France SNC

| | Gournay-en-Bray

| | | Airbags and seatbelts customer applications and platform development with full-scale test laboratory

| Livbag SAS

| | Pont-de-Buis

| | | Inflator and pyrotechnic development

| | | | | | | Germany

| | | | | | Autoliv B.V. & Co. KG

| | Dachau

| | | Customer applications and platform development, airbags with full-scale test laboratory

| | | Elmshorn

| | | Seatbelts with full-scale test laboratory

| | | | | | | India

| | | | | | Autoliv India Private Ltd.

| | Bangalore

| | | Airbags and seatbelts with sled testing

| Japan

| | | | | | Autoliv Japan Ltd.

| | Tsukuba

| | | Airbags and seatbelts customer applications and platform development with sled test laboratory

| | | | | | | Poland

| | | | | | Autoliv Poland Sp.z.o.o.

| | Olawa

| | | Airbags and seatbelts customer applications and platform development with full-scale test laboratory | | | | | | France | | | | | Autoliv France SNC | | Gournay-en-Bray | | Airbags and seatbelts customer applications and platform development with full-scale test laboratory | Livbag SAS | | Pont-de-Buis | | Inflator and pyrotechnic development | | | | | | Germany | | | | | Autoliv B.V. & Co. KG | | Dachau | | Customer applications and platform development, airbags with full-scale test laboratory | | | Elmshorn | | Seatbelts with full-scale test laboratory | | | | | | India | | | | | Autoliv India Private Ltd. | | Bangalore | | Airbags and seatbelts with sled testing | | | | | | Japan | | | | | Autoliv Japan Ltd. | | Tsukuba | | Airbags and seatbelts customer applications and platform development with sled test laboratory | | | | | | Poland | | | | | Autoliv Poland Sp. zo.o. | | Olawa | | Airbags applications and platform development | | | | | | Romania | | | | | Autoliv Romania S.R.L. | | Brasov | | Seatbelts with sled test laboratory | | | | | | South Korea | | | | | Autoliv Corporation | | Seoul | | Airbags and seatbelts customer applications and platform development with sled test laboratory | | | | | | Sweden | | | | | Autoliv Development AB | | Vårgårda | | Research center | Autoliv Sverige AB | | Vårgårda | | Airbags customer applications and platform development with full-scale test laboratory and Inflator development | | | | | | USA | | | | | Autoliv ASP, Inc. | | Auburn Hills | | Airbags, steering wheels, and seatbelts customer applications and platform development with full-scale test laboratory | | | Ogden | | Airbags, inflators and pyrotechnics customer applications and platform development | | | | | | | Romania

| | | | | | Autoliv Romania S.R.L.

| | Brasov

| | | Seatbelts with sled test laboratory

| | | | | | | South Korea

| | | | | | Autoliv Corporation

| | Seoul

| | | Airbags and seatbelts customer applications and platform development with sled test laboratory

| Sweden

| | | | | | Autoliv Development AB

| | Vårgårda

| | | Research center

| Autoliv Sverige AB

| | Vårgårda

| | | Airbags customer applications and platform development with full-scale test laboratory

| USA

| | | | | | Autoliv ASP Inc.

| | Auburn Hills

| | | Airbags, steering wheels, and seatbelts customer applications and platform development with full-scale test laboratory

| | | Ogden

| | | Airbags, inflators and pyrotechnics customer applications and platform development

|

Item 3. Legal Proceedings

In the ordinary course of our business, we are subject to legal proceedings brought by or against us and our subsidiaries.

See Note 18 to the Consolidated Financial Statements in this Annual Report for a summary of certain ongoing legal proceedings. Such information is incorporated into this Part I, Item 3 – “Legal Proceedings” by reference.

Item 4. Mine Safety Disclosures

Not applicable.

Item 3. Legal Proceedings In the ordinary course of our business, we are subject to legal proceedings brought by or against us and our subsidiaries. See Note 18 to the Consolidated Financial Statements in this Annual Report for a summary of certain ongoing legal proceedings. Such information is incorporated into this Part I, Item 3 – “Legal Proceedings” by reference. Item 4. Mine Safety Disclosures Not applicable.

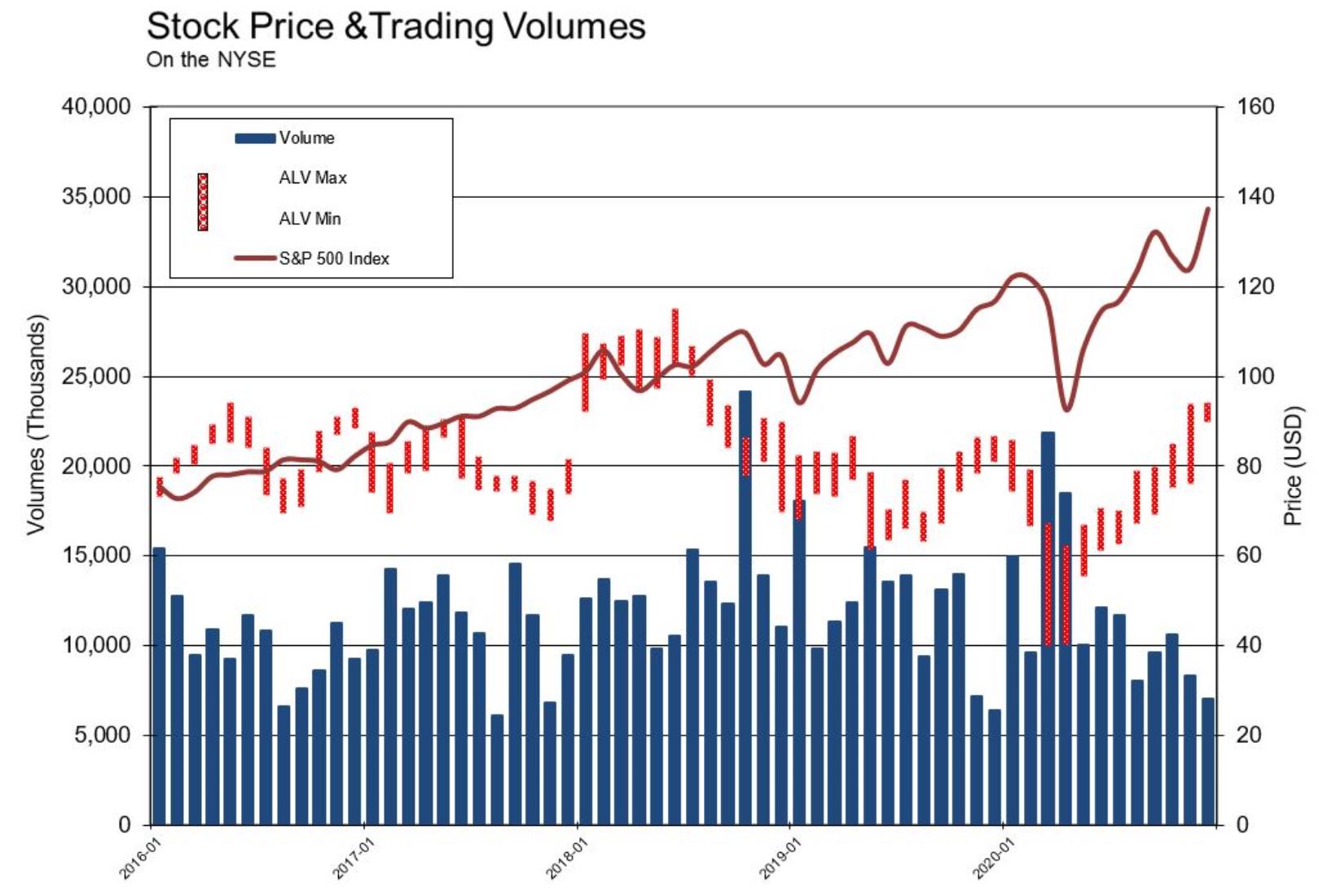

PARTII Item5.MarketforRegistrant’sCommonEquity,RelatedStockholderMattersandIssuerPurchasesofEquitySecurities Shareholder information The primary exchange market for Autoliv’s securities is the New York Stock Exchange (NYSE) where Autoliv’s common stock trades under the symbol “ALV”. Autoliv’s Swedish Depositary Receipts (SDRs) are traded on NASDAQ Stockholm’s list for large market cap companies under the symbol “ALIV SDB”. Options in SDRs trade on Nasdaq Stockholm under the name “Autoliv SDB”. Options in Autoliv shares are traded on NASDAQ OMX PHLX and on NYSE Amex Options under the symbol “ALV”. Share price information*

PARTII

Item 5. Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities

Shareholder Information

The primary exchange market for Autoliv’s securities is the New York Stock Exchange (NYSE) where Autoliv’s common stock trades under the symbol “ALV”. Autoliv’s Swedish Depositary Receipts (SDRs) are traded on NASDAQ Stockholm’s list for large market cap companies under the symbol “ALIV SDB”. Options in SDRs trade on Nasdaq Stockholm under the name “Autoliv SDB”. Options in Autoliv shares are traded on NASDAQ OMX PHLX and on NYSE Amex Options under the symbol “ALV”.

Share price performance*

* For all periods before the distribution date of Veoneer on June 29, 2018, the Autoliv share prices are adjusted by a factor of 72.04%. Number of shares During 2020, the weighted average number of shares outstanding (excluding dilution and treasury shares) increased to 87.3 million from 87.2 million in 2019. The weighted average number of shares outstanding for the full year 2020, assuming dilution, increased to 87.5 from 87.4 million in 2019. Stock options (if exercised) and granted Restricted Stock Units (RSUs) and Performance Shares (PSs) could increase the number of shares outstanding by 0.5 million shares in the aggregate. Combined, this would add 0.6% to the number of shares outstanding. On December 31, 2020, 3.0 million shares were available for repurchase pursuant to the stock repurchase program authorized by the Board of Directors in 2014. On December 31, 2020, the Company had 15.4 million treasury shares. Shareholders As of the end of 2020 around 20% of Autoliv’s securities were held by U.S.-based shareholders and close to 57% by Sweden-based shareholders. Most of the remaining Autoliv securities were held in the U.K., Switzerland, Norway, France and Denmark. Dividends If declared by the Board of Directors, quarterly dividends are usually paid on the first Thursday in the last month of each quarter. Declared dividends are announced in press releases and published on Autoliv’s corporate website. Autoliv has a history of paying quarterly cash dividends; however, on April 2, 2020, our Board of Directors suspended our quarterly dividend after determining that a suspension was necessary in light of the evolving global COVID-19 pandemic, decline in global LVP, the uncertainty surrounding the recession at that time and the inherent risk of customer defaults. The Board revisits dividends on a quarterly basis. There can be no assurance that our Board of Directors will declare dividends in the future. See Autoliv’s corporate website for additional details regarding historical dividends. Stock incentive plan Autoliv employees participate in the Autoliv, Inc. 1997 Stock Incentive Plan, as amended (the “Stock Incentive Plan”) and receive Autoliv stock-based awards from time to time. In connection with the spin-off, each outstanding Autoliv stock-based award as of June 29, 2018 was converted to stock awards that have underlying shares of both Autoliv and Veoneer common stock (see Note 17 to the Consolidated Financial Statements in this Annual Report). Additional information regarding the securities authorized for issuance under the Stock Incentive Plan is included in Item 12 of this Annual Report. Autoliv has adopted a Stock Ownership Policy for Executives requiring the Company’s Chief Executive Officer (CEO) to accumulate and hold the number of Autoliv shares having a value of twice his annual base salary. For other executives, the minimum requirement is, over time, a holding equal to each executive’s annual base salary. Stockrepurchaseprogram Autoliv initiated its repurchase program in 2000 with 10 million shares and has subsequently increased the total authorization four times between 2000 and 2014 to 47.5 million shares.Such purchases may be made from time to time on the open market or otherwise at the discretion of management. There is no expiration date for the share repurchase authorization to provide management flexibility in the Company’s repurchases. In total, Autoliv repurchased 44.5 million shares between May 2000 and December 31, 2017 for cash of $2,498 million, including commissions. No repurchases were made during 2019 or 2020. Autoliv has made no share repurchases since June 30, 2017. The maximum number of shares that may still be purchased under the stock repurchase program amounted to 2,986,288 shares at December 31, 2020. Of the total number of repurchased shares, 23.6 million shares were utilized for the equity units offering during 2009-2012. In addition, approximately 5.5 million shares have been utilized by the Stock Incentive Plan. At December 31, 2020, 15.4 million of the repurchased shares remain in treasury stock.

Item 6. Selected Financial Data Selected financial data for the last five fiscal years ended December 31 for the Continuing Operations, unless noted, is summarized in the table below. (DOLLARS IN MILLIONS, EXCEPT PER SHARE DATA) | | 2020 | | | 2019 | | | 2018 | | | 2017 | | | 2016 | | Sales and Income | | | | | | | | | | | | | | | | | | | | | Net sales | | $ | 7,447 | | | $ | 8,548 | | | $ | 8,678 | | | $ | 8,137 | | | $ | 7,922 | | Operating income4) | | | 382 | | | | 726 | | | | 686 | | | | 860 | | | | 831 | | Income before income taxes4) | | | 291 | | | | 648 | | | | 612 | | | | 792 | | | | 784 | | Net income attributable to controlling interest4) | | | 187 | | | | 462 | | | | 376 | | | | 586 | | | | 558 | | Financial Position | | | | | | | | | | | | | | | | | | | | | Current assets excluding cash | | | 3,091 | | | | 2,557 | | | | 2,670 | | | | 2,598 | | | | 2,269 | | Property, plant and equipment, net | | | 1,869 | | | | 1,816 | | | | 1,690 | | | | 1,609 | | | | 1,329 | | Intangible assets (primarily goodwill) | | | 1,412 | | | | 1,410 | | | | 1,423 | | | | 1,440 | | | | 1,430 | | Non-interest bearing liabilities | | | 3,182 | | | | 2,397 | | | | 2,595 | | | | 2,418 | | | | 2,154 | | Capital employed5) | | | 3,637 | | | | 3,772 | | | | 3,516 | | | | 4,538 | | | | 4,225 | | Net debt6, 8) | | | 1,214 | | | | 1,650 | | | | 1,619 | | | | 368 | | | | 299 | | Total equity5) | | | 2,423 | | | | 2,122 | | | | 1,897 | | | | 4,169 | | | | 3,926 | | Total assets | | | 8,157 | | | | 6,771 | | | | 6,722 | | | | 6,947 | | | | 6,565 | | Long-term debt6) | | | 2,110 | | | | 1,726 | | | | 1,609 | | | | 1,311 | | | | 1,313 | | Share data | | | | | | | | | | | | | | | | | | | | | Earnings per share (US$) – basic4) | | | 2.14 | | | | 5.29 | | | | 4.32 | | | | 6.70 | | | | 6.33 | | Earnings per share (US$) – assuming dilution4) | | | 2.14 | | | | 5.29 | | | | 4.31 | | | | 6.68 | | | | 6.32 | | Total parent shareholders’ equity per share (US$)5) | | | 27.56 | | | | 24.19 | | | | 21.63 | | | | 46.38 | | | | 41.69 | | Cash dividends paid per share (US$) | | | 0.62 | | | | 2.48 | | | | 2.46 | | | | 2.38 | | | | 2.30 | | Cash dividends declared per share (US$) | | | — | | | | 2.48 | | | | 2.48 | | | | 2.40 | | | | 2.32 | | Share repurchases | | | — | | | | — | | | | — | | | | 157 | | | | — | | Number of shares outstanding (million)2) | | | 87.4 | | | | 87.2 | | | | 87.1 | | | | 87.0 | | | | 88.2 | | Ratios | | | | | | | | | | | | | | | | | | | | | Gross margin (%) | | | 16.7 | | | | 18.5 | | | | 19.7 | | | | 20.6 | | | | 20.6 | | Operating margin (%)4) | | | 5.1 | | | | 8.5 | | | | 7.9 | | | | 10.6 | | | | 10.5 | | Pretax margin (%)4) | | | 3.9 | | | | 7.6 | | | | 7.1 | | | | 9.7 | | | | 9.9 | | Return on capital employed (%)7) | | | 10 | | | | 20 | | | | 17 | | | n/a | | | n/a | | Return on total equity (%)4, 7) | | | 9 | | | | 23 | | | | 13 | | | n/a | | | n/a | | Total equity ratio (%)5) | | | 30 | | | | 31 | | | | 28 | | | | 49 | | | | 48 | | Days receivables outstanding | | | 86 | | | | 70 | | | | 71 | | | | 76 | | | | 70 | | Days inventory outstanding | | | 42 | | | | 35 | | | | 35 | | | | 35 | | | | 32 | | Other data | | | | | | | | | | | | | | | | | | | | | Airbag sales3) | | | 4,824 | | | | 5,676 | | | | 5,699 | | | | 5,342 | | | | 5,256 | | Seatbelt sales | | | 2,623 | | | | 2,872 | | | | 2,980 | | | | 2,794 | | | | 2,665 | | Capital expenditures, net | | | 340 | | | | 476 | | | | 486 | | | | 464 | | | | 398 | | Net cash provided by operating activities1) | | | 849 | | | | 641 | | | | 591 | | | | 936 | | | | 868 | | Net cash used in investing activities1) | | | (340 | ) | | | (476 | ) | | | (628 | ) | | | (697 | ) | | | (726 | ) | Net cash (used in) provided by financing activities1) | | | 160 | | | | (338 | ) | | | (245 | ) | | | (566 | ) | | | (200 | ) | Number of employees, December 31 | | | 61,000 | | | | 58,900 | | | | 57,700 | | | | 56,700 | | | | 55,800 | |

1) | Including Discontinued Operations for comparable years 2016-2018. |

2) | At year end, excluding dilution and net of treasury shares. |

3) | Including steering wheels, inflators and initiators. |

4) | Including antitrust provision expense of $210 million in 2018. |

5) | Impacted by the distribution of Veoneer on June 29, 2018 the Autoliv share prices are adjustedof approximately $2 billion recorded as a reduction of equity. |

6) | The increase in debt in 2018 is primarily driven by a factorour capitalization of 72.04%.

NumberVeoneer of shares

During 2018, the number of shares outstanding increased by 0.1 million to 87.1 million (excluding dilution and treasury shares). The weighted average number of shares outstanding for the full year 2018, assuming dilution, was reduced to 87.3 from 87.7 million in 2017.

Stock options (if exercised) and granted Restricted Stock Units (RSUs) could increase the number of shares outstanding by 0.4 million shares in total. Combined, this would add 0.5%approximately $1 billion prior to the Autoliv shares outstanding. On December 31, 2018, 3.0 million shares were available for repurchase underdistribution to the current Board authorization from 2014. On December 31, 2018,shareholders.

|

7) | The Company has decided not to recalculate prior periods since the Companydistribution of Veoneer had 15.7 million treasury shares. Number of shareholders

Autoliv estimates that there were approximately 70,000 beneficial Autoliv owners as of December 31, 2018. Close to 21% of Autoliv’s securities were held by U.S.-based shareholdersa significant impact on total equity and around 60% by Sweden-based shareholders. Most ofcapital employed making the remaining Autoliv securities were held in the U.K., other Nordic countries, Central Europe, Japan and Canada.comparison less meaningful.

|

8) | Dividends

If declared by the Board of Directors, quarterly dividends are usually paid on the first Thursday in the last month of each quarter. Declared dividends are announced in press releases and published on Autoliv’s corporate website. Autoliv has a history of paying quarterly cash dividends and intends to pay similar dividends in the future but may not because of certain factors as set forth in Risk Factors – “You should not anticipate or expect the payment of cash dividends on our common stock”See section Non-U.S. GAAP Performance Measures in Item 1A of this Annual Report.7.

See Autoliv’s corporate website for additional details regarding historical dividends.

Stock incentive plan

Autoliv employees participate in the Autoliv, Inc. 1997 Stock Incentive Plan (the “Stock Incentive Plan”) and receive Autoliv stock-based awards from time to time. In connection with the spin-off, each outstanding Autoliv stock-based award as of June 29, 2018 was converted to stock awards that have underlying shares of both Autoliv and Veoneer common shares (see Note 17 to the Consolidated Financial Statements in this Annual Report). Additional information regarding the securities authorized for issuance under the Stock Incentive Plan is included in Item 12 of this Annual Report.

Autoliv has adopted a Stock Ownership Policy for Executives requiring the Company’s CEO to accumulate and hold the number of Autoliv shares having a value of twice his annual base salary. For other executives, the minimum requirement is, over time, a holding equal to each executive’s annual base salary.

Stock repurchase program

Autoliv initiated its repurchase program in 2000 with 10 million shares and has subsequently increased the total authorization four times between 2000 and 2014 to 47.5 million shares.

Such purchases may be made from time to time on the open market or otherwise at the discretion of management. There is no expiration date for the share repurchase authorization to provide management flexibility in the Company’s repurchases.

In total, Autoliv repurchased 44.5 million shares between May 2000 and December 31, 2017 for cash of $2,498 million, including commissions. No repurchases were made during 2018. Autoliv has made no share repurchases since June 30, 2017. The maximum number of shares that may yet be purchased under the stock repurchase program amounted to 2,986,288 shares at December 31, 2018.

Of the total number of repurchased shares, 23.6 million shares were utilized for the equity units offering during 2009-2012. In addition, approximately 5.3 million shares have been utilized by the Stock Incentive Plan. At December 31, 2018, 15.7 million of the repurchased shares remain in treasury stock.

Item 6. Selected Financial Data

Selected financial data for the last five fiscal years ended December 31 for the Continuing Operations, unless noted, is summarized in the table below.

(DOLLARS IN MILLIONS, EXCEPT PER SHARE DATA) | | 2018 | | | 2017 | | | 2016 | | | 2015 | | | 20141) | | | Sales and Income | | | | | | | | | | | | | | | | | | | | | | Net sales | | $ | 8,678 | | | $ | 8,137 | | | $ | 7,922 | | | $ | 7,636 | | | $ | 9,240 | | | Operating income4) | | | 686 | | | | 860 | | | | 831 | | | | 708 | | | | 723 | | | Income before income taxes4) | | | 612 | | | | 792 | | | | 784 | | | | 655 | | | | 667 | | | Net income attributable to controlling interest4) | | | 376 | | | | 586 | | | | 558 | | | | 443 | | | | 468 | | | Financial Position | | | | | | | | | | | | | | | | | | | | | | Current assets excluding cash | | | 2,670 | | | | 2,598 | | | | 2,269 | | | | 2,259 | | | | 2,607 | | | Property, plant and equipment, net | | | 1,690 | | | | 1,609 | | | | 1,329 | | | | 1,265 | | | | 1,390 | | | Intangible assets (primarily goodwill) | | | 1,423 | | | | 1,440 | | | | 1,430 | | | | 1,445 | | | | 1,661 | | | Non-interest bearing liabilities | | | 2,595 | | | | 2,418 | | | | 2,154 | | | | 2,049 | | | | 2,400 | | | Capital employed5) | | | 3,516 | | | | 4,538 | | | | 4,225 | | | | 3,670 | | | | 3,504 | | | Net debt6, 8) | | | 1,619 | | | | 368 | | | | 299 | | | | 202 | | | | 62 | | | Total equity5) | | | 1,897 | | | | 4,169 | | | | 3,926 | | | | 3,468 | | | | 3,442 | | | Total assets | | | 6,722 | | | | 6,947 | | | | 6,565 | | | | 6,518 | | | | 7,443 | | | Long-term debt6) | | | 1,609 | | | | 1,311 | | | | 1,313 | | | | 1,499 | | | | 1,521 | | | Share data | | | | | | | | | | | | | | | | | | | | | | Earnings per share (US$) – basic4) | | | 4.32 | | | | 6.70 | | | | 6.33 | | | | 5.03 | | | | 5.08 | | | Earnings per share (US$) – assuming dilution4) | | | 4.31 | | | | 6.68 | | | | 6.32 | | | | 5.02 | | | | 5.06 | | | Total parent shareholders’ equity per share (US$)5) | | | 21.63 | | | | 46.38 | | | | 41.69 | | | | 39.22 | | | | 38.64 | | | Cash dividends paid per share (US$) | | | 2.46 | | | | 2.38 | | | | 2.30 | | | | 2.22 | | | | 2.12 | | | Cash dividends declared per share (US$) | | | 2.48 | | | | 2.40 | | | | 2.32 | | | | 2.24 | | | | 2.14 | | | Share repurchases | | | — | | | | 157 | | | | — | | | | 104 | | | | 616 | | | Number of shares outstanding (million)2) | | | 87.1 | | | | 87.0 | | | | 88.2 | | | | 88.1 | | | | 88.7 | | | Ratios | | | | | | | | | | | | | | | | | | | | | | Gross margin (%) | | | 19.7 | | | | 20.6 | | | | 20.6 | | | | 20.5 | | | | 19.5 | | | Operating margin (%)4) | | | 7.9 | | | | 10.6 | | | | 10.5 | | | | 9.3 | | | | 7.8 | | | Pretax margin (%)4) | | | 7.1 | | | | 9.7 | | | | 9.9 | | | | 8.6 | | | | 7.2 | | | Return on capital employed (%)7) | | | 17 | | | n/a | | | n/a | | | n/a | | | | 21 | | | Return on total equity (%)4, 7) | | | 13 | | | n/a | | | n/a | | | n/a | | | | 12 | | | Total equity ratio (%)5) | | | 28 | | | | 49 | | | | 48 | | | | 46 | | | | 46 | | | Net debt to capitalization (%)5, 6) | | | 46 | | | | 8 | | | | 7 | | | | 6 | | | | 2 | | | Days receivables outstanding | | | 71 | | | | 76 | | | | 70 | | | | 71 | | | | 71 | | | Days inventory outstanding | | | 35 | | | | 35 | | | | 32 | | | | 31 | | | | 32 | | | Other data | | | | | | | | | | | | | | | | | | | | | | Airbag sales3) | | | 5,699 | | | | 5,342 | | | | 5,256 | | | | 5,036 | | | | 5,019 | | | Seatbelt sales | | | 2,980 | | | | 2,794 | | | | 2,665 | | | | 2,599 | | | | 2,800 | | | Capital expenditures, net | | | 486 | | | | 464 | | | | 398 | | | | 397 | | | | 453 | | | Net cash provided by operating activities1) | | | 591 | | | | 936 | | | | 868 | | | | 751 | | | | 713 | | | Net cash used in investing activities1) | | | (628 | ) | | | (697 | ) | | | (726 | ) | | | (591 | ) | | | (453 | ) | | Net cash (used in) provided by financing activities1) | | | (245 | ) | | | (566 | ) | | | (200 | ) | | | (319 | ) | | | 226 | | | Number of employees, December 31 | | | 57,700 | | | | 56,700 | | | | 55,800 | | | | 51,300 | | | | 50,800 | | |

|

1)

Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations | Including Discontinued Operations. This period has not been restated to reflect just continuing operations because it was not practicable to do so.

|

2)

| At year end, excluding dilution and net of treasury shares.

|

3)

| Including steering wheels, inflators and initiators.

|

4)

| Including antitrust provision expense of $210 million.

|

5)

| Impacted by the distribution of Veoneer on June 29, 2018 of approximately $2 billion recorded as a reduction of equity.

|

6)

| The increase in debt is primarily driven by our capitalization of Veoneer of approximately $1 billion prior to the distribution to the shareholders.

|

7)

| The Company has decided not to recalculate prior periods since the distribution of Veoneer had a significant impact on total equity and capital employed making the comparison less meaningful.

|

8)

| See section Non-U.S. GAAP Performance Measures in item 7.

|

Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations

Important Trends The discussions and analysis in this section isare focused on our continuing operations. For more information on our discontinuedthe Company’s results of operations see Note 3for the year ended December 31, 2020 compared to the Consolidatedyear ended December 31, 2019. Discussions of our results of operations for the year ended December 31, 2019 compared to the year ended December 31, 2018 can be found in Part II, Item 7. Management's Discussion and Analysis of Financial StatementsCondition and Results of Operations in this Annual Report.our Form 10-K for the year ended December 31, 2019, which was filed with the United States Securities and Exchange Commission on February 21, 2020. Autoliv, Inc. (the “Company”) provides automotive safety systems to the automotive industry with a broad range of product offerings, primarily passive safety systems. In the three-yeartwo-year period ended December 31, 2018,2020, a number of factors have influenced the Company’s results of operations. The most notable factors have been: Growth in light vehicle production and safety content per vehicle

| • | Substantial decline in global light vehicle production |

Continued strong order intake

| • | Growth of safety content per vehicle |

Continued focus on operational excellence and quality

| • | High order intake share maintained |

Changes in competitive environment

| • | Continued focus on operational excellence and quality |

| 20181) | | | 20171) | | | | 20161) | | 20201) | | | 20191) | | | YEARS ENDED DEC. 31 (DOLLARS IN MILLIONS, EXCEPT EPS) | Reported | | | change | | | Reported | | | change | | | | Reported | | | change | | Reported | | | change | | | Reported | | | change | | | Global light vehicle production (in thousands) | | 91,344 | | | | (1 | ) | % | | 92,128 | | | | 2 | | % | | | 90,056 | | | 5 | % | | 71,573 | | | | (17 | ) | % | | 85,862 | | | | (6 | ) | % | Consolidated net sales | $ | 8,678 | | | | 7 | | % | $ | 8,137 | | | | 3 | | % | | $ | 7,922 | | | 4 | % | $ | 7,447 | | | | (13 | ) | % | $ | 8,548 | | | | (1 | ) | % | Operating income3) | | 686 | | | | (20 | ) | % | | 860 | | | | 3 | | % | | | 831 | | | 17 | % | | 382 | | | | (47 | ) | % | | 726 | | | | 6 | | % | Operating margin, %3) | | 7.9 | | | | (2.7 | ) | pp | | 10.6 | | | | 0.1 | | pp | | | 10.5 | | | 1.2 | pp | | 5.1 | | | | (3.4 | ) | pp | | 8.5 | | | | 0.6 | | pp | Net income attributable to controlling interest from Continuing Operations3) | | 376 | | | | (36 | ) | % | | 586 | | | | 5 | | % | | | 558 | | | 26 | % | | Earnings per share Continuing Operations2, 3) | | 4.31 | | | | (35 | ) | % | | 6.68 | | | | 6 | | % | | | 6.32 | | | 26 | % | | Net cash provided by operating activities4) | | 591 | | | | (37 | ) | % | | 936 | | | | 8 | | % | | | 868 | | | 16 | % | | Return on capital employed, %5) | | 16.8 | | | n/a | | pp | n/a | | | n/a | | pp | | n/a | | | n/a | pp | | Net income attributable to controlling interest3) | | | 187 | | | | (60 | ) | % | | 462 | | | | 23 | | % | Earnings per share2) | | | 2.14 | | | | (60 | ) | % | | 5.29 | | | | 23 | | % | Net cash provided by operating activities3) | | | 849 | | | | 32 | | % | | 641 | | | | 8 | | % | Return on capital employed, % | | | 10.4 | | | | (9.3 | ) | pp | | 19.7 | | | | 2.9 | | pp |

1) | Reported figures impacted by costs for capacity alignments, and antitrust related matters in 2016-2018, and for 2019 by separation costs in 2018.costs. See section Items affecting comparability and Notes 3, 12 and 18 to the Consolidated Financial Statements included herein. |

2) | Assuming dilution and net of treasury shares. |

3) | Including EC antitrust provision expensepayment of $210 million. |

4)

| Including Discontinued Operations

|

5)

| The Company has decided not to recalculate prior periods since the distribution of Veoneer had a significant impact on capital employed making the comparison less meaningful.$203 million in 2019.

|

COVID-19 PANDEMIC The COVID-19 pandemic had a substantial impact on our operations in the first half year of 2020. In the first quarter the impact was focused on China, where most of our customers’ plants were closed for several weeks in February and operated at low levels in March. In Europe and North America, sales declined substantially in the second half of March as the pandemic led to customer plant closures. A large number of customer plants were closed in April and parts of May, followed by a ramp-up in June. The decline in global LVP and the slow and volatile restart and ramp-up had a significant impact on our sales and profitability in the first six months of 2020. In the second half of the year, we managed to achieve improvements in sales, profitability and cash flow as our cost reduction initiatives and positive sales development more than offset the 0.4% global LVP year over year decline in the second half of the year. According to IHS Markit, global light vehicle production declined by 17% in 2020 vs. 2019. There were a number of liquidity and management actions undertaken to manage this challenging period. During the first six months of 2020, Autoliv undertook a number of actions to support employee health and safety, corporate liquidity, cash flow, and profitability. Actions included introducing a Smart Start Playbook for safe re-start and ramp-up, investing in employee safety equipment, and re-designing production lines and work places as necessary. Other initiatives included drawing on our Revolving Credit Facility (which is now fully repaid), withdrawing full year guidance (now provided again), extensive use of furloughing, reducing headcount, sharply reducing capital expenditures, close monitoring of working capital, reducing or suspending discretionary spending, and accelerating cost savings initiatives, cancelling the dividend and suspending future dividends, although the Board of Directors will review such suspension on a quarterly basis. Direct COVID-19 related costs, such as personal protective equipment, temporary supplier support, and premium freight was around $10 million in the second quarter, around $5 million in the third quarter and around $5 million in the fourth quarter. Support from governments in connection with furloughing, short-term work weeks, and other similar activities was around $25 million in the second quarter, around $10 million in the third quarter, and around $2 million in the fourth quarter. In all regions, the automotive industry, including Autoliv, is in different stages of ramp-up of operations. Visibility and predictability of customer demand has improved but is still limited, particularly regarding the sustainability of current demand levels, including the effects on LVP of inventory build-ups, government vehicle subsidies, and the risks of another wave of COVID-19 infections in one or more of the regions where we operate or have customers or suppliers. Although we are not directly affected by current semiconductor supply issues highlighted in December 2020 and January and early February 2021 by several OEMs, it could potentially have a negative impact on LVP in the first half of 2021. We believe some of the production that might be lost in the first half of the year could be recovered in the second

half of the year. While we continue to focus on health and safety and cost optimization, we are adjusting our production in coordination with our customers and suppliers. GROWTH INIMPACTED BY LIGHT VEHICLE PRODUCTION, AND SAFETY CONTENT PER VEHICLE AND HIGH ORDER INTAKE The most important driver for Autoliv’s sales is the light vehicle production (LVP). During 2018the past ten years LVP has shown year-over-year growth with the exception of the past three years. During 2020 we experienced deterioration of market conditions as a consequence of the COVID-19 pandemic, resulting in declines of LVP in all regions. The most significant changesdecline in LVP, especiallycame in Americas and Europe impacted by the new emission testing WLTP and in China due to lower consumer demand for vehicles. As a result, full-year 2018declining more than 20% with Asia declining more than 10%. Full-year 2020 global LVP declined by 1%around 17%. This came after eight straight years of LVP growth. In 2017, the LVP grew by 2% anda 6% decline in 2016, the year-over-year growth in LVP was 5%.2019. Light Vehicle Production | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | 2018 | | | 2017 | | | 2016 | | | Change '18 vs ´16 | | | | (000´) units | | | % global | | | (000´) units | | | % global | | | (000´) units | | | % global | | | (000´) units | | | % | | Americas | | | 19,124 | | | | 21 | % | | | 19,185 | | | | 21 | % | | | 19,421 | | | | 22 | % | | | (296 | ) | | | (2 | )% | | North America | | 15,751 | | | | 17 | % | | | 15,920 | | | | 17 | % | | | 16,678 | | | | 19 | % | | | (927 | ) | | | (6 | )% | | South America | | 3,373 | | | | 4 | % | | | 3,265 | | | | 4 | % | | | 2,743 | | | | 3 | % | | | 630 | | | | 23 | % | Europe | | | 21,887 | | | | 24 | % | | | 22,180 | | | | 24 | % | | | 21,458 | | | | 24 | % | | | 429 | | | | 2 | % | Asia | | | 47,811 | | | | 52 | % | | | 48,233 | | | | 52 | % | | | 46,890 | | | | 52 | % | | | 921 | | | | 2 | % | | China | | 25,696 | | | | 28 | % | | | 26,575 | | | | 29 | % | | | 25,952 | | | | 29 | % | | | (256 | ) | | | (1 | )% | | Japan | | 9,052 | | | | 10 | % | | | 9,021 | | | | 10 | % | | | 8,517 | | | | 9 | % | | | 535 | | | | 6 | % | | South Korea | | 3,951 | | | | 4 | % | | | 4,023 | | | | 4 | % | | | 4,143 | | | | 5 | % | | | (192 | ) | | | (5 | )% | | India | | 4,712 | | | | 5 | % | | | 4,420 | | | | 5 | % | | | 4,136 | | | | 5 | % | | | 577 | | | | 14 | % | | Other Asia | | 4,400 | | | | 5 | % | | | 4,194 | | | | 5 | % | | | 4,142 | | | | 5 | % | | | 258 | | | | 6 | % | Other | | | 2,522 | | | | 3 | % | | | 2,530 | | | | 3 | % | | | 2,287 | | | | 3 | % | | | 235 | | | | 10 | % | Global Total | | | 91,344 | | | | 100 | % | | | 92,128 | | | | 100 | % | | | 90,056 | | | | 100 | % | | | 1,288 | | | | 1 | % | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Light Vehicle Production1) | | | | | | | | | | | | | | | | | | | | | | | | 2020 | | | 2019 | | | Change '20 vs ´19 | | | | (000´) units | | | % global | | | (000´) units | | | % global | | | (000´) units | | | % | | Americas | | | 14,184 | | | | 20 | % | | | 18,343 | | | | 21 | % | | | (4,159 | ) | | | (23 | )% | | North America | | 11,955 | | | | 17 | % | | | 15,085 | | | | 18 | % | | | (3,130 | ) | | | (21 | )% | | South America | | 2,229 | | | | 3 | % | | | 3,258 | | | | 4 | % | | | (1,029 | ) | | | (32 | )% | Europe | | | 16,461 | | | | 23 | % | | | 20,994 | | | | 24 | % | | | (4,533 | ) | | | (22 | )% | Asia | | | 39,257 | | | | 55 | % | | | 44,550 | | | | 52 | % | | | (5,293 | ) | | | (12 | )% | | China | | 22,130 | | | | 31 | % | | | 23,292 | | | | 27 | % | | | (1,162 | ) | | | (5 | )% | | Japan | | 7,593 | | | | 11 | % | | | 9,024 | | | | 11 | % | | | (1,431 | ) | | | (16 | )% | | South Korea | | 3,476 | | | | 5 | % | | | 3,879 | | | | 5 | % | | | (403 | ) | | | (10 | )% | | India | | 3,199 | | | | 4 | % | | | 4,168 | | | | 5 | % | | | (969 | ) | | | (23 | )% | | Other Asia | | 2,859 | | | | 4 | % | | | 4,187 | | | | 5 | % | | | (1,328 | ) | | | (32 | )% | Other | | | 1,671 | | | | 2 | % | | | 1,975 | | | | 2 | % | | | (304 | ) | | | (15 | )% | Global Total | | 71,573 | | | | | | | | 85,862 | | | | | | | | (14,289 | ) | | | (17 | )% | 1) Source: IHS Markit | |

The main markets contributing to the global LVP growth during 2016 to 2018 were South America and India. Affected by political factors and microeconomics in the second half of 2018, Chinese LVP, the world’s largest automotive market, declined by 1%1.2 million units or by 5% from 20162019 to 2018.2020. In Europe, which is an important market for automotive safety systems, LVP increaseddecreased by 2%22% or by approximately 0.44.5 million light vehicles during the same three-year period. In North America, LVP declined by 6%21% or 0.93.1 million light vehicles. Thanks to strong domestic demand and growing export to other countries, LVP in India increased by 14% during the three-year period to 4.7 million light vehicles in 2018.

Europe’s share of global LVP has remaineddeclined to 23% from 24% and Americas share declined to 20% from 21%, while China’s share increased from 27% to 31%. Japan’s share was unchanged at 24%, while North America has declined from 19% to 17% and China from 29% to 28% during the same three-year period.11%. Thanks

Due to more stringent crash ratings, by institutes such as EuroNCAP;Euro NCAP; and increasing consumer demand for more safety in emerging markets, we see vehicle manufacturers installing more airbags and more advanced seatbelt systems in their vehicles. This generally happenstakes place when new models are introduced. The safety standards of vehicles are increasing in China, India and other growth markets such as Brazil, partially due to new regulations and crash test rating programs. For example, the Indian government has decided on a new traffic regulation that mandates more rigid crash test standards offor light vehicles. This should eventually lead to a higher installation rate of airbags and more advanced seatbelts. Thanks to these positive worldwide trends, as well as currency translationseatbelts, impacting CPV positively, partly offset by negative effects the average global safety content (airbags, seatbelts and steering wheels) per light vehicle (CPV) has increased from around $220 to around $225 during the period 2017-2018. This increase comes despite the fact that growth in global LVP is mostly in markets with lower average safety CPV such as South America and India, where the CPV is only approximately $170 and $80, respectively. In addition, there is a negative effect from continued pricing pressure from vehicle manufacturers. The trend of increasing CPV was negatively impacted in 2020 by the unfavorable regional CPV mix development, as the decline in LVP was more pronounced in markets with high average safety content per vehicle (CPV) such as North America and Western Europe, where the CPV is approximately $350 and $270, respectively. In 2020, currency translation effects impacted global CPV positively. The average global safety CPV (airbags, pedestrian safety, seatbelts and steering wheels) amounted to $245 in 2020. These trends

The more stringent crash ratings and consumer demand for more safety should enable the global automotive safety market to grow faster than the global LVP during the next three years. The past five years’ high order intake share have resulted in our sales development outperforming the underlying light vehicle production significantly in the past three years. In 2020, our organic sales development outpaced global LVP by around 5 percentage points, due to increased safety content per vehicle and as an effect of recent years high order intake share. WELL BALANCED GLOBAL FOOTPRINT Autoliv’s regional sales mix continues to be balanced with 32%28% of sales in Europe, 31% in the Americas and 37%41% in Asia in 2018,2020, compared to 32%29%, 32%34% and 36%37%, respectively, in 2017.2019. In Asia, our sales in the important Chinese market represents 18%increased to 21% of total sales in 2018, despite2020, partly a reflection of the first drop in LVP in the country in decades. Regardless of the short-term weakness in the Chinese market we remain well positioned in this market, which isbeing less effected by the world’s largest automotive producing market.pandemic. The balanced regional sales mix has been achieved through timely investments and strengthening of technical and support capabilities in growth markets and early introduction and execution of our restructuring and capacity alignment activities. To further improve our competitiveness, we have also made substantial investments to increase manufacturing capacity for vertical integration in China and Thailand.markets. For Asia as a whole, the effect of the higher sales in China, Japan and India was partly offset by declining sales in South Korea.

A fast-growing customer from 2016 to 2018 has been Honda. Their share ofWe estimate that our sales has increased from close to 7% to 8% during the three-year period. The largest customer based in Asia is Hyundai/Kia, accounting for 8% of Autoliv sales. The local Chinese OEMs as a groupElectric Vehicles (EV) and Plug-in Hybrid Electric Vehicles (PHEV) accounted for around 4% of our sales in 2018, with Great Wall representing 2%.

Our sales to premium brand OEMs accounted for around 18% of total sales, while their share of global LVP is approximately 11%. Our strong position with premium OEMs reflects the higher safety content in their vehicles along with our position as a technology leader in the automotive safety market. Of the European OEMs, Daimler stands out, accounting for 6% of Autoliv’s total sales, representing more than two times their global LVP market share. This is a result of our strong position within advanced safety solutions in their vehicles.

The Detroit Three automobile manufacturers, Ford, Fiat Chrysler and GM, account for 8%, 8% and 4%10% of our total sales respectively. Because Autoliv was on a new business hold with GM during 2011-2012 and PSA’s acquisition of GM’s European brand Opel, GM’s share of Autoliv total sales declined from 8% in 2016 to 4% in 2018. This has affected most regions not only Europe and North America.2020.

CONTINUED STRONG ORDER INTAKE SHARE Building on a strong base, including supplying our delivering products to approximately 1,300around 1,200 vehicle models and around 100 car brands, Autoliv recorded its highesta high order intake evershare during the past six-year period, 2016-2018, winning around 50%45% or more of available orders. Our share of order intake in the past threeprior years is significantly above our sales market share in 2020 of around 40% in 2018. Part of the high order intake is the consequence of major recalls by another airbag manufacturer. The most substantial increase in order intake was in 2015, where it increased by 80% compared to 2014, to $11.9 billion. Since 2016, order intake has continued to increase and reached in 2018 $15.5 billion in estimated life-time sales, an increase of 26% compared to 2016. Due to the lead time from order to start of production, 2017 was the first year the increased level of order intake began to impact our sales. The sales growth has substantially accelerated during 2018, outgrowing LVP with close to 10% in the fourth quarter. During 2018, growth was positively affected through recent launches of several new models, including e.g. Dodge Ram 1500, Tesla Model 3 and Honda Accord.42%. The lead time from order intake to start of production is typically 18-36 months. During this period the products are engineered into the vehicle to provide the expected protection for occupants in case of a crash and to meet legal and regulatory requirements, as well as other requirements from the vehicle manufacturer. This investment in new products is the main reason for the increase inhigh level of RD&E expenses, net, between 2016 and 2018.net. Additionally, we have to build up production capacity, in the form of new lines, and buildings, to meet future product launches.

Our order intake share for 2020 continued on a high level. We estimate that we booked around 45% of available order value in 2020, making 2020 the sixth consecutive year of order intake share which is higher than our sales market share. The estimated life-time sales for all orders booked in 2020 is around $10 billion, compared to $11 billion in 2019. New order intake is defined as the sales value of awards for future business, received within that year. The life time value is calculated using detailed assumptions of price and volumes over the years of production and the exchange rates prevailing at the time of receiving the order. Due to the lead time from order to start of production, 2017 was the first year that the increased level of order intake began to impact our sales. Over the last two years, sales have substantially outperformed the change in global LVP. In 2020 and 2019 the outperformance was around 5 pp and 7 pp, respectively. During 2020, growth was positively affected through recent launches of several new models, including Honda Fit, Toyota Yaris, Buick Encore and Chevrolet Trailblazer, Peugeot 208 and 2008, Genesis G80 and Opel Corsa. OPERATIONALSTRATEGIC INITIATIVES

OverAs market weakness has continued in 2020, we stepped up the years we have seen an uneven capacity utilization in severalcost improvement actions and launched a second Structural Efficiency Program, including targeting a reduction of our plants, mainlyindirect workforce by approximately 850 more workers. The cost for Structural Efficiency Program 1 and 2 are estimated to be approximately $52 million and $65 million respectively. The first program was fully implemented in Europe. 2020 and the second program is expected to be fully implemented by early 2021. Annualized savings is estimated to be around $65 million each for the two programs.

In addition to the Structural Efficiency Programs, we made a provision of around $35 million in 2020 for footprint optimization in Europe, involving planned plant closures in Germany and Sweden. The costs for restructuring activities in 20182020 amounted to $9$99 million compared to $23$54 million in 2017 and to $21 million in 20162019. The current restructuring activitiesStructural Efficiency Programs are expected to have a payback period of around 3 years, or more,1 year, after cash-out. The cash payments in 2018 were $14 million compared to $23 million in 2017 and $71 million in 2016. As of December 31, 2018,2020, we have $33$126 million reserved in our balance sheet related to restructuring (see Note 12 to the Consolidated Financial Statements included herein). Capital expenditures, netWith more than 200 improvement projects being evaluated, we have set a high pace in the planning and implementation of $486 million in 2018, was $22 millionstrategic initiatives and $88 million higher than in 2017structural improvements. These initiatives are key drivers to our medium-term target and 2016, respectively. In relationbuilding the foundation to sales Capital expenditures, net was 5.6% in 2018 and 5.7% in 2017 and 5.0% in 2016. The level of Capital expenditures, net, supports our growth strategy and reflects the high order intake for the period 2016continue to 2018.

create shareholder value. IMPROVED EFFICIENCIES THROUGH OPERATIONAL EXCELLENCE Pricing pressure is an inherent part of the automotive supplier business. Price reductions are generally higher on newer products with strong volume growth compared to older products, where both the possibilities to re-design the product to reduce costs and market growth are less. Price reductions can also depend on the business cycle. For the period 2016-2018,2019-2020, we estimate the average reduction of our market prices to have been in the range of 2-4% annually. As described below, to meet these price reductions, we have implemented several programs and taken actions to address every item in our cost structure. Additionally, during the period 2016-2018, we have experienced raw material commodity costs increase of around $30 million. Our productivity improvement target is to achieve at least 5% savings per year. To meet this target, Autoliv has developed a set of strategies to reduce costs in manufacturing: Autoliv production system (APS) is based on lean manufacturing methodology which aims to continuously increase output with less resources. APS provides the target conditions and tools to achieve the delivery of goods and services at the right time, in the right amount, at the required quality and at the lowest cost possible to all our customers.

| • | Autoliv production system (APS) is based on lean manufacturing methodology which aims to continuously increase output with less resources. APS provides the target conditions and tools to achieve the delivery of goods and services at the right time, in the right amount, at the required quality and at the lowest cost possible to all our customers. |

| • | Our One Product One Process (1P1P) strategy focuses on product and process standardization and reducing cost and complexity. The 1P1P strategy, combined with initiatives to reduce costs for components from external suppliers, ensures that we continuously optimize our supply base footprint, consolidate purchase volumes to fewer suppliers, improve productivity in our supply chain, standardize components and redesign our products. |

| • | Strategic Initiatives including Automation, Digitalization, Supply Chain Management Effectiveness and RD&E Effectiveness. |

Our One Product One Process (1P1P) strategy focuses on product and process standardization and reducing cost and complexity. The 1P1P strategy, combined with initiatives to reduce costs for components from external suppliers, ensures that we continuously optimize our supply base footprint, consolidate purchase volumes to fewer suppliers, improve productivity in our supply chain, standardize components and redesign our products. Thesecontinuous improvement strategies have enabled productivity improvementsimprovement at or above our target of 5% over the last years, except 2018 and 2020. 2018 due to a sharp increase in Autoliv’s manufacturinglaunch activities. Excluding impact from Force Majeure situation in our plant in Mexico, we came back to around historical performance during 2019. This was achieved despite the increased launch activities also impacted us during 2019. In 2020, the sharp deterioration of over 5% for four out oflight vehicle production in the five past years. It was onlyfirst half year and the sharp recovery in 2018 that the target was not achieved because of elevated launch related costs.

To reduce labor costs while offsetting the price erosion on our products, we continuously implementsecond half year limited productivity improvement programs, expand production in Best Cost Countries (BCCs) and institute restructuring and capacity alignment activities. The number of employees in the BCCs in relation to total headcount has increased slightly from 78% in 2016 to over 80% in 2018.

These initiatives, in combination with our restructuring activities, investment in vertical integration and several other actions, are in place to offset the market price erosion.opportunities.

We foresee opportunities for further productivity on gains from increasing use of automation in our assembly for lean manufacturing processes. Additionally, automated cells typically perform the manufacturing process with reduced variability. This results in greater control and consistency of product quality.

Reducing labor costs to offset the price erosion on our products is achieved through continuously implementing productivity improvement programs, optimizing our production footprint and instituting restructuring and capacity alignment activities. These initiatives, in combination with our restructuring activities, investment in vertical integration and several other actions, are in place to offset the market price erosion. FOCUS ON QUALITY INCREASING The number of vehicle recalls in the automotive industry has risen sharply over the last fewin recent years. InStarting in 2015, and 2016, Takata’s airbag inflators recall generated a record number of recalls in the automotive industry. We expect overall recall numbers to remain high for years to come and, although we strive for the highest quality in our processes, it cannot be ruled out that we may also be adversely impacted by a future recall. Quality has been and always will be our number one priority, and we continue to sharpen our focus in this area. We now commandhold a market share of 40%around 42% in passive safety. At the same time,while we have been involved in less than 2% of passive safety recalls in the industry in the past ten years;since 2010; an important indicator that we are delivering on our quality strategy. For more information see product warranty and recalls in Note 13 to the Consolidated Financial Statements in this Annual Report. CHANGES IN COMPETITIVE LANDSCAPE During the period 2016 to 2018,past six years, we experienced significant changes in our competitive landscape. In 2015, TRW, a key competitor in passive safety, was acquired by German group ZF Friedrichshafen. Combined, the new company is the third-largestsecond largest passive safety supplier globally. In 2016, Key Safety Systems (“KSS”) was acquired by Ningbo Joyson Electronic Corp. Beginning in 2014, Takata, our largest competitor at the time, experienced severe issues and recalls related to malfunctioning airbag inflators, leading the company to file for bankruptcy protection in the U.S. and Japan. In 2018, Joyson substantially acquired all of Takata's global assets and operations and combined it with KSS, forming the new company JSS.

Combined, the new company is the third largest passive safety supplier globally. European Commission AntitruSt Investigation

Since 2011, Autoliv has been subject to an investigation of anti-competitive behavior among suppliers of occupant safety systems by the European Commission (EC). We now have reason to believe that the EC will seek to impose a fine of approximately 185 million Euros in connection with the remaining portion of the EC investigation. Therefore, the Company accrued $210 million in the fourth quarter of 2018. The Company believes that a fine could be issued during the first half of 2019, although this may be delayed.

CAPITAL STRUCTURE The Company’s net debt wasstood at $1,619$1,214 million on December 31, 2018.2020. This was an increase by $1,250a decrease of $436 million compared to December 31, 2017. The increase was mainly driven by the $972 million capitalization of Veoneer prior to the spin-off.2019. Total interest bearing debt at December 31, 20182020 amounted to $2,230$2,411 million, an increase by $899of $317 million compared to December 31, 2017.2019. Cash flow from operations including discontinued operations, was $591$849 million in 20182020 and $936$641 million in 2017.2019. Capital expenditures, net amounted to $555$340 million in 20182020 and $570$476 million in 2017.2019. During the two-year period 2017-20182019-2020, the Company paid dividends of $423$271 million. In 2020, the Company paid dividends of $54 million in the first quarter and repurchased shares for $157 million. Afterthen suspended the latest declared dividend of 62 cents per share,dividends due to the annualized run rate is $216 million, based on number of shares outstanding at December 31, 2018.COVID-19 pandemic It is the Company’s policy to maintain a financial leverage commensurate with a “strong investment grade credit rating” and our. The long-term target is to have a leverage ratio (see section Non-U.S. GAAP Performance Measures) of around 1.0 times and to be within the range of 0.5 times to 1.5 times. We monitor our1.5. At December 31, 2020, the current leverage ratio is 1.8. The Company monitors its capital structure and the financial markets closely and intendintends to maintain a high level of financial flexibility while being shareholder friendly. As part of the adjustment of the capital structure, the Company historically has repurchased shares of its common stock. During 2018,2020 and 2019, the Company did not repurchase any shares, during 2017, the Company repurchased 1.4 million shares for approximately $157 million, including commissions.shares. At December 31, 2018,2020, the remaining number of shares authorized by the board of directors for repurchase is approximately 3.0 million shares. CURRENCY IMPACTS The Company is exposed to around 50 currency pairs, with exposures in excess of $1 million each. We are monitoring our currency exposure but do not hedge currency flows. Rather we strive to have sales and costs in the same currency to reduce the transaction exposure risk. The total net transaction exposure in 20182020 was approximately $2.4$2.2 billion or 28%25% of sales. The 5 largest exposures in 2020 were USD/MXN (sell USD), USD/CAD (sell USD), EUR/RON (sell EUR), USD/KRW (buy USD) and EUR/CNY (buy EUR) which combined amounted to a net transaction exposure of around $1.2 billion. Approximately three quarters of our sales are denominated in currencies other currencies than U.S. dollars, which is leading to currency translation effects.

Outlook for 20192021 MainlyOur outlook indications for 2021 reflect continuing uncertainty in the automotive markets and are mainly based on our customer call-offs and a light vehicle production outlook that is slightly below theLVP according to IHS estimate, the indication for organic sales growth for the full year 2019 is around 5%. Currency translations are expected to have a combined negative effect of around 1%, resulting in a consolidated sales increase of around 4%. The indication for adjusted operating margin for the full year 2019 is around 10.5%.Markit.

The projected tax rate, excluding unusual items, for the full year 2019, is expected to be around 28%, and is subject to change due to nonrecurring events that may occur.

Financial measure | | Full year indication | Net sales growth | | Around 25% | Organic sales growth | | Around 20% | Adjusted operating margin 1) | | Around 10% | R,D&E, net % of sales | | Around 4.5 | Tax rate 2) | | Around 30% | Operating cash flow3) | | Similar level as 2020 | Capital expenditures, net % of sales | | Below 6% | Leverage ratio at year end | | Within target range |

The projected operating cash flow for the full year 2019, excluding any unusual items, is expected to be higher than for Continuing Operations full year 2018 of around $810 million. The projected capital expenditures as percent of sales, net, for the full year 2019 is expected to be lower than for Continuing Operations full year 2018 of around 5.6%.

The projected R,D&E, net, as percent of sales, for the full year 2019 is expected to be lower than for Continuing Operations full year 2018 of around 4.8%. The projected leverage ratio is expected to be well within our target range of 0.5x to 1.5x at the end of 2019.

1) | Excluding costs for capacity alignments and anti-trust related matters. |

2) | Excluding unusual tax items. |

3) | Excluding unusual items. |

The forward-looking non-U.S. GAAP financial measures above are provided on a non-U.S. GAAP basis. Autoliv has not provided a U.S. GAAP reconciliation of these measures because items that impact these measures, such as costs related to capacity alignments and antitrust matters cannot be reasonably predicted or determined. As a result, such reconciliation is not available without unreasonable efforts and Autoliv is unable to determine the probable significance of the unavailable information. Significant Legal Matters The Company is subject to ongoing antitrust investigations by governmental authorities in several jurisdictions as well as related civil litigation. For further discussion of these antitrust matters and other legal proceedings seeSee Item 3. Legal Proceedings and Note 18 Contingent Liabilities to the Consolidated Financial Statements in this Annual Report.

Year Ended December 31, 20182020 Versus 20172019 Sales by Product | | | | | | | | | | | | | | Components Of Change In Net Sales | | | | | | | | | | | | | | | Components of Change in Net Sales | | | | 2018 Sales (MUSD) | | | 2017 Sales (MUSD) | | | Reported change | | | Currency effects1) | | | Organic | | | 2020 (MUSD) | | | 2019 (MUSD) | | | Reported change | | | Currency effects1) | | | Organic | | Airbags products and Other2) | | $ | 5,698 | | | $ | 5,343 | | | | 6.7 | % | | | 1.8 | % | | | 4.9 | % | | $ | 4,824 | | | $ | 5,676 | | | | (15.0 | )% | | | (0.8 | )% | | | (14.2 | )% | Seatbelt products2) | | | 2,980 | | | | 2,794 | | | | 6.7 | % | | | 2.2 | % | | | 4.5 | % | | | 2,623 | | | | 2,872 | | | | (8.6 | )% | | | (0.9 | )% | | | (7.7 | )% | Total | | $ | 8,678 | | | $ | 8,137 | | | | 6.7 | % | | | 1.9 | % | | | 4.8 | % | | $ | 7,447 | | | $ | 8,548 | | | | (12.9 | )% | | | (0.9 | )% | | | (12.0 | )% |

1) | Effects from currency translations. |

2) | Including Corporate and Other sales. |

Consolidated net sales increaseddecreased by 6.7%12.9% compared to full year 2017 with an2019. Excluding negative currency translation effects of 0.9%, the organic growthsales decrease (see section Non-U.S. GAAP Performance Measures) was 12.0%. Sales of 4.8% and positive currency translation effects of 1.9%. Airbag sales grewall our airbag products except textiles declined organically (see section Non-U.S. GAAP Performance Measures) by 4.9%between 11% and 53% (depending on the region) for the full year, reflecting the 16.8% decline in LVP. Textiles increased by 66%, mainly drivenreflecting new sales of textiles for manufacturing of personal protection equipment. Sales of replacement inflators decreased by steering wheels in North America, Europe and China and from inflatable curtains in North America, partly offset by organic sales decline of inflatable curtains in Europe.around $85 million to $57 million.

Seatbelt sales grewdeclined organically (see section Non-U.S. GAAP Performance Measures) by 4.5%, mainly driven by7.7%. Japan showed a slight organic seatbelt sales growth, while all other regions showed organic sales declines between 1% and 21%. Sales of more advanced and higher value-added seatbelts declined significantly less than total seatbelts sales did and grew strongly in North America, IndiaChina and China, partly offset by declines in Europe.Japan. Sales by Region | | | | | | | | | | | | | | Components Of Change In Net Sales | | | | | | | | | | | | | | | Components of Change in Net Sales | | | | 2018 Sales (MUSD) | | | 2017 Sales (MUSD) | | | Reported change | | | Currency effects1) | | | Organic | | | 2020 (MUSD) | | | 2019 (MUSD) | | | Reported change | | | Currency effects1) | | | Organic | | Asia | | $ | 3,195 | | | $ | 2,998 | | | | 6.6 | % | | | 1.9 | % | | | 4.7 | % | | $ | 3,043 | | | $ | 3,177 | | | | (4.2 | )% | | | (0.0 | )% | | | (4.2 | )% | Whereof: China | | | 1,522 | | | | 1,421 | | | | 7.1 | % | | | 2.2 | % | | | 4.9 | % | | | 1,541 | | | | 1,525 | | | | 1.0 | % | | | 0.0 | % | | | 1.0 | % | Japan | | | 828 | | | | 787 | | | | 5.2 | % | | | 1.6 | % | | | 3.6 | % | | | 733 | | | | 811 | | | | (9.6 | )% | | | 1.9 | % | | | (11.5 | )% | Rest of Asia | | | 845 | | | | 790 | | | | 6.9 | % | | | 1.3 | % | | | 5.6 | % | | | 769 | | | | 841 | | | | (8.5 | )% | | | (2.0 | )% | | | (6.5 | )% | Americas | | | 2,735 | | | | 2,435 | | | | 12.3 | % | | | (1.0 | )% | | | 13.3 | % | | | 2,337 | | | | 2,907 | | | | (19.6 | )% | | | (3.3 | )% | | | (16.3 | )% | Europe | | | 2,748 | | | | 2,704 | | | | 1.7 | % | | | 4.5 | % | | | (2.8 | )% | | | 2,067 | | | | 2,464 | | | | (16.1 | )% | | | 0.9 | % | | | (17.0 | )% | Global | | $ | 8,678 | | | $ | 8,137 | | | | 6.7 | % | | | 1.9 | % | | | 4.8 | % | | $ | 7,447 | | | $ | 8,548 | | | | (12.9 | )% | | | (0.9 | )% | | | (12.0 | )% |

1) | Effects from currency translations. |

For the full year 2018,2020, Autoliv’s sales grewdecreased organically (see section Non-U.S. GAAP Performance Measures) by 4.8%12.0% compared to full year 2017, almost 6pp more2019, around 5pp better than LVP growth according(according to IHS. The largest contributors to theIHS Markit). Sales declined organically in all regions except China. Our organic growth were North America,sales development outperformed LVP in all regions - by around 7pp in Americas, 6pp in China, and India, partly offset by Europe and South Korea. The organic sales increase (see section Non-U.S. GAAP Performance Measures) from Autoliv’s companies5pp in China of 4.9% was driven by both domestic and global OEMs. Sales growth to domestic OEMs was mainly with Geely, including Lynk & Co, and Great Wall while growth with the global OEMs was mainly with VW, Honda and Nissan.

Organic sales growth (see section Non-U.S. GAAP Performance Measures) of 3.6% from Autoliv’s companies in Japan was mainly derived from sales to Subaru and Mitsubishi as well as inflator replacement sales.

Organic sales growth (see section Non-U.S. GAAP Performance Measures) from Autoliv’s companies in the Rest of Asia of 5.6% was driven by strong sales development in India, which grew organically by 26%, mainly from sales to Suzuki, Honda, Tata and Hyundai/Kia. Sales in South Korea decreased, driven mainly by lower sales to Hyundai/Kia.

The organic growth (see section Non-U.S. GAAP Performance Measures) from Autoliv’s companies in Americas was 13.3%. North America grew organically by 13.1% mainly due to new model launches with FCA, Honda, Nissan, Tesla and VW, partly offset by lower sales to Daimler, GM and Ford. Overall growth was driven by all main product groups. Sales in South America grew organically by 18.2%, mainly due to increased sales to FCA and VW.

The 2.8% organic sales decline (see section Non-U.S. GAAP Performance Measures) from Autoliv’s companies in Europe was mainly driven by Renault, FCA, BMW, JLR, PSA and Ford, partly offset by strong performance with premium brands such as Daimler and Volvo. Europe.

| Years ended December 31 | | | | | | (Dollars in millions, except per share data) | 2018 | | | 2017 | | | Change | | Net Sales | $ | 8,678 | | | $ | 8,137 | | | | 6.7 | % | Gross profit | | 1,711 | | | | 1,680 | | | | 1.9 | % | % of sales | | 19.7 | % | | | 20.6 | % | | | (0.9 | )pp | S,G&A | | (390 | ) | | | (407 | ) | | | (4.0 | )% | % of sales | | (4.5 | )% | | | (5.0 | )% | | | (0.5 | )pp | R,D&E net | | (413 | ) | | | (371 | ) | | | 11.3 | % | % of sales | | (4.8 | )% | | | (4.6 | )% | | | 0.2 | pp | Other income (expense), net | | (211 | ) | | | (32 | ) | | | 565.9 | % | % of sales | | (2.4 | )% | | | (0.4 | )% | | | 2.0 | pp | Operating income | | 686 | | | | 860 | | | | (20.2 | )% | % of sales | | 7.9 | % | | | 10.6 | % | | | (2.7 | )pp | Interest expense, net | | (59 | ) | | | (54 | ) | | | 9.3 | % | Income before taxes | | 612 | | | | 792 | | | | (22.7 | )% | Tax rate | | 38.4 | % | | | 25.8 | % | | | 12.6 | pp | Income attributable to controlling interest from Continuing Operations | | 376 | | | | 586 | | | | (35.9 | )% | Earnings per share Continuing Operations, diluted1, 2) | | 4.31 | | | | 6.68 | | | | (35.5 | )% |

2020 Organic growth1) | | Americas | | | Europe | | | China | | | Japan | | | Rest of Asia | | | Global | | Autoliv | | | (16.3 | )% | | | (17.0 | )% | | | 1.0 | % | | | (11.5 | )% | | | (6.5 | )% | | | (12.0 | )% | Main growth drivers | | Tesla, Mazda | | | Toyota, PSA | | | GM, Ford, Toyota | | | Honda, Suzuki, Toyota | | | GM, Renault, Nissan | | | Tesla, GM, Suzuki | | Main decline drivers | | FCA, Honda, Nissan | | | Daimler, Renault, VW | | | Nissan, Geely, Daimler | | | Mitsubishi, Nissan, Mazda | | | Mitsubishi, Toyota, Suzuki | | | Nissan, FCA, Daimler | | 1) Non-U.S. GAAP Measure | | | | | | | | | | | | | | | | | | | | | | | | |

| Years ended December 31 | | | | | | (Dollars in millions, except per share data) | 2020 | | | 2019 | | | Change | | Net Sales | $ | 7,447.4 | | | $ | 8,547.6 | | | | (12.9 | )% | Gross profit | | 1,246.9 | | | | 1,584.4 | | | | (21.3 | )% | % of sales | | 16.7 | % | | | 18.5 | % | | | (1.8 | )pp | S,G&A | | (389.2 | ) | | | (398.9 | ) | | | (2.4 | )% | % of sales | | (5.2 | )% | | | (4.7 | )% | | | 0.5 | pp | R,D&E net | | (375.5 | ) | | | (405.5 | ) | | | (7.4 | )% | % of sales | | (5.0 | )% | | | (4.7 | )% | | | 0.3 | pp | Other income (expense), net | | (90.1 | ) | | | (42.7 | ) | | | 111.0 | % | Operating income | | 382.1 | | | 725.8 | | | | (47.4 | )% | % of sales | | 5.1 | % | | | 8.5 | % | | | (3.4 | )pp | Adjusted operating income | | 481.6 | | | 774.4 | | | | (37.8 | )% | % of sales | | 6.5 | % | | | 9.1 | % | | | (2.6 | )pp | Financial and non-operating items, net | | (90.9 | ) | | | (77.4 | ) | | | 17.4 | % | Income before taxes | | 291.2 | | | | 648.4 | | | | (55.1 | )% | Tax rate | | 35.3 | % | | | 28.6 | % | | | 6.7 | pp | Net income | | 188.3 | | | | 462.8 | | | | (59.3 | )% | Earnings per share, diluted1, 2) | 2.14 | | | 5.29 | | | | (59.5 | )% | Adjusted earnings per share, diluted1, 2) | 3.15 | | | 5.72 | | | | (44.9 | )% |

1) | Assuming dilution and net of treasury shares. |

2) | Participating share awards with right to receive dividend equivalents are (under the two classtwo-class method) excluded from the EPS calculation. |

GROSS PROFIT The grossGross profit fordeclined by $338 million and the full year 2018 increased by $32 million, compared to the prior year, as a result of higher sales partly offset by a lower gross margin. The gross margin decreaseddeclined by 0.9pp1.8pp compared to full year 2017, mainly due to adverse impact2019. The gross margin decline was primarily driven by lower sales and lower utilization of our assets from launch relatedthe decline in LVP. The sharp sales decline followed by a volatile restart and ramp-up with limited visibility and predictability had a significant effect on our gross margin, despite significant reductions in costs rawfor material costs and currency changes which more than offset the operating leverage on the increased sales.labor.

OPERATING INCOME Operating income decreased by $174$344 million, to $686 million. The reported operating margin was 7.9%mainly as a consequence of sales, compared to 10.6% of salesthe declines in the prior year. The decrease of 2.7pp of sales was mainly due togross profit and higher costs for antitrust related matters, compared to, reported as Otherin other income (expense), net, partially offset by lower gross margincosts for S,G&A and higher R,D&E, net costs. net. Selling, General and Administrative (S,G&A) expenses decreased by $16$10 million, or 0.5pp of sales driven by transition service agreement income,2.4%, mainly due to lower bonus accruals and lower legalpersonnel costs. Research, Development & Engineering (R,D&E) expenses, net as percent of sales was 4.8% compareddeclined by $30 million, or by 7.4%, mainly due to 4.6% in the same period the priorpositive year mainly as a result of the significant increase in product launches during the first half of 2018 and continued strong order intake. INTEREST EXPENSE, NET

Interestover year effects from lower personnel costs partially offset by lower engineering income. Other income (expense), net expense net in full year 2018 was $59 million. The increase of $5increased by $47 million compared to $54 million in fullthe previous year, 2017 is related to interest expenses after issuing the 500 million Eurobond in June 2018 partly offset by less USPP debt. Interest income was close to $7 million in full year 2018, $0.5 million lower compared to full year 2017mainly due to lower cash balances.higher costs for capacity alignments.

FINANCIAL AND NON-OPERATING ITEMS, NET Financial and non-operating items, net, costs were $14 million higher than the previous year, mainly due to unfavorable effects of exchange rate changes and higher pension related expenses. INCOME TAXES The effective tax

Tax rate in 2018 was 38.4%35.3%, compared to 25.8%28.6% in 2017. The tax rate for 2018 excluding discrete tax items was 29.1% compared to 24.8% in 2017. The tax rate for 2018 was2019, impacted by several items, including additionalunfavorable country mix and losses without tax cost recorded related to the U.S. transition tax and the impact of the antitrust accrual, which is not deductible for tax purposes. The tax rate for 2017 was impacted by the reversal of the valuation allowance for certain deferred tax assets and the estimate of the negative impact of the U.S. tax reform (specifically the deemed repatriation of non-U.S. earnings and the revaluation of U.S. deferred tax assets to the new lower U.S. tax rate). See Note 6 to the Consolidated Financial Statements included herein.benefit.

NET INCOME AND EARNINGS PER SHARE Net income attributabledecreased by $275 million compared to controlling interest from Continuing Operations decreased year on year2019 primarily driven by the antitrust accruallower gross profit and operating income as noted above. Earnings per share, (EPS) from Continuing Operations assuming dilutiondiluted, decreased by 35.5% to $4.31 compared to $6.68$3.15 where the main drivers were $2.36 from lower adjusted operating income, $0.58 from mainly higher accruals for the same period one year ago. The mainrestructuring activities, $0.11 from financial items affecting EPS negatively were 208 centsand $0.10 from higher costs primarily relating to antitrust related matters and 42 cents from higher underlying tax rate. The main offsetting effects were 15 cents from discrete tax items.taxes.(see section Non-U.S. GAAP Performance Measures). The weighted average number of shares outstanding assuming dilution in 2020 was 87.387.5 million compared to 87.7 million for full year of 2017.

Year Ended December 31, 2017 Versus 2016

Sales by Product

| | | | | | | | | | | | | | Components Of Change In Net Sales | | | | 2017 (Sales MUSD) | | | 2016 (Sales MUSD) | | | Reported change | | | Currency effects1) | | | Organic | | Airbags products and Other2) | | $ | 5,343 | | | $ | 5,257 | | | | 1.6 | % | | | 0.3 | % | | | 1.3 | % | Seatbelt products2) | | | 2,794 | | | | 2,665 | | | | 4.8 | % | | | 0.8 | % | | | 4.0 | % | Total | | $ | 8,137 | | | $ | 7,922 | | | | 2.7 | % | | | 0.5 | % | | | 2.2 | % |

1)

| Effects from currency translations.

|

2)

| Including Corporate and Other sales.

|

Consolidated sales increased by 2.7% to $8,137 million. Excluding positive currency translation effects, the organic sales growth (see section Non-U.S. GAAP Performance Measures) was 2.2%, in line with global light vehicle production despite negative impact from lower inflator sales.

Airbag sales had solid organic growth (see section Non-U.S. GAAP Performance Measures) for the full year in Asia, especially in India, Japan and China. South America grew strongly while Europe and South Korea showed more modest organic growth. North American sales declined organically.

Seatbelt sales grew organically (see section Non-U.S. GAAP Performance Measures) for the full year in all regions except in North America and South Korea, with Europe and Japan as the largest growth drivers.

Inflator replacement sales affected the segment’s organic sales growth (see section Non-U.S. GAAP Performance Measures) for the full year negatively by around 0.4pp.

Sales by Region

| | | | | | | | | | | | | | Components Of Change In Net Sales | | | | 2017 Sales (MUSD) | | | 2016 Sales (MUSD) | | | Reported change | | | Currency effects1) | | | Organic | | Asia | | $ | 2,998 | | | $ | 2,831 | | | | 5.9 | % | | | (0.9 | )% | | | 6.8 | % | Whereof: China | | | 1,421 | | | | 1,385 | | | | 2.6 | % | | | (1.6 | )% | | | 4.2 | % | Japan | | | 787 | | | | 719 | | | | 9.5 | % | | | (3.3 | )% | | | 12.8 | % | Rest of Asia | | | 790 | | | | 727 | | | | 8.8 | % | | | 3.0 | % | | | 5.8 | % | Americas | | | 2,435 | | | | 2,547 | | | | (4.4 | )% | | | 0.1 | % | | | (4.5 | )% | Europe | | | 2,704 | | | | 2,544 | | | | 6.3 | % | | | 2.5 | % | | | 3.8 | % | Global | | $ | 8,137 | | | $ | 7,922 | | | | 2.7 | % | | | 0.5 | % | | | 2.2 | % |

1)

| Effects from currency translations.

|

For the full year 2017, Autoliv’ sales grew organically (see section Non-U.S. GAAP Performance Measures) by 2.2% compared to full year 2016, in line with global LVP growth according to IHS. The largest contributors to the organic growth were Europe, Japan, and China, partly offset by North America and South Korea.

The organic sales increase (see section Non-U.S. GAAP Performance Measures) from Autoliv’s companies in China was mainly driven by the global OEMs, primarily Renault/Nissan and Daimler, partly offset by Hyundai/Kia. Organic sales to the domestic OEMs also increased, with increases to models from Geely and Great Wall, partly offset by decreases to models from Haima. Inflator replacement sales contributed positively to organic sales growth.

Organic sales growth (see section Non-U.S. GAAP Performance Measures) from Autoliv’s companies in Japan was driven by Toyota, Renault/Nissan and Mitsubishi. Offsetting effects are mainly from decreasing inflator replacement sales.

Organic sales growth (see section Non-U.S. GAAP Performance Measures) from Autoliv’s companies in the Rest of Asia was driven by strong sales development in India, mainly to Suzuki and Hyundai/Kia. Sales in South Korea decreased, driven by Ssangyong and GM.

Sales from Autoliv’s companies in Americas declined organically (see section Non-U.S. GAAP Performance Measures) by 4.5%. North America declined by 6.0% organically, driven primarily by GM due to unfavorable platform shifts and declining LVP. Inflator replacement sales had a 0.7pp negative impact on organic growth in North America. South America grew organically by about 45%.

The 3.8% organic sales growth (see section Non-U.S. GAAP Performance Measures) from Autoliv’s companies in Europe was mainly driven by Volvo, Toyota and VW. Offsetting effects were mainly from Opel.

| Years ended December 31 | | | | | | (Dollars in millions, except per share data) | 2017 | | | 2016 | | | Change | | Net Sales | $ | 8,137 | | | $ | 7,922 | | | | 2.7 | % | Gross profit | | 1,680 | | | | 1,628 | | | | 3.2 | % | % of sales | | 20.6 | % | | | 20.6 | % | | | 0.0 | pp | S,G&A | | (407 | ) | | | (394 | ) | | | 3.3 | % | % of sales | | (5.0 | )% | | | (5.0 | )% | | | 0.0 | pp | R,D&E net | | (371 | ) | | | (357 | ) | | | 3.9 | % | % of sales | | (4.6 | )% | | | (4.5 | )% | | | 0.1 | pp | Other income (expense), net | | (32 | ) | | | (35 | ) | | | (8.6 | )% | % of sales | | (0.4 | )% | | | (0.4 | )% | | | (0.0 | )pp | Operating income | | 860 | | | | 831 | | | | 3.5 | % | % of sales | | 10.6 | % | | | 10.5 | % | | | 0.1 | % | Interest expense, net | | (54 | ) | | | (58 | ) | | | (6.9 | )% | Income before taxes | | 792 | | | | 784 | | | | 1.0 | % | Tax rate | | 25.8 | % | | | 28.6 | % | | | (2.8 | )pp | Net income attributable to controlling interest from Continuing Operations | | 586 | | | | 558 | | | | 5.0 | % | Earnings per share Continuing Operations, diluted1, 2) | | 6.68 | | | | 6.32 | | | | 5.7 | % |

1)

| Assuming dilution and net of treasury shares.

|

2)

| Participating share awards with right to receive dividend equivalents are (under the two class method) excluded from the EPS calculation.

|

GROSS PROFIT

The gross profit for the full year 2017 increased by $52 million, compared to the prior year, as a result of higher sales. The gross margin was basically unchanged compared to 2016, as improved operational performance and higher organic sales (see section Non-U.S. GAAP Performance Measures), were offset by costs related to investments for capacity and growth, as well as negative impact from raw material prices.

OPERATING INCOME