UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

|

|

☒ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31 2018, 2023

OR

|

|

☐TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 FOR THE TRANSITION PERIOD FROM TO

Commission File Number 001-38467

Ceridian HCM Holding

Dayforce, Inc.

(Exact name of Registrant as specified in its Charter)

Delaware | 46-3231686 |

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer |

3311 East Old Shakopee Road

Minneapolis, Minnesota55425

(952) (952) 853-8100

(Address, Including Zip Code, and Telephone Number, Including Area Code, of Registrant’s Principal Executive Offices)

Securities registered pursuant to Section 12(b) of the Act:

|

| |||

|

| Trading Symbol(s) | Name of each exchange on which registered | |

Common Stock, $.01 par value | DAY | New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act: None

None

(Title of class)

Indicate by check mark if the Registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. YES Yes☒No☐ NO ☒

Indicate by check mark if the Registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act. YES Yes☐ NO No☒

Indicate by check mark whether the Registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. YES Yes☒ NO No☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). YES Yes☒ NO No☐

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405) is not contained herein, and will not be contained, to the best of Registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ☒

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer |

| Accelerated filer | ☐ | |||

Non-accelerated filer |

| Small reporting company | ☐ | |||

Emerging growth company |

|

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☒

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☒

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☒

Indicate by check mark whether the Registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). YES Yes☐ NO No☒

The aggregate market value of the voting and non-voting common equity held by non-affiliates of the Registrant, based on the $33.19$66.97 closing price of the shares of common stock on the New York Stock Exchange on June 30, 2018,2023, was $938.7 million.$10.2 billion.

The number of shares of Registrant’s Common Stock outstanding as of February 25, 201923, 2024 was 140,514,889.156.6 million.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the Registrant’s Definitive Proxy Statement relating to the 20192024 Annual Meeting of Stockholders scheduled to be held on May 1, 2019, are incorporated by reference into Part III of this Annual Report on Form 10-K. Such Definitive Proxy Statement will be filed with the Securities and Exchange Commission within 120 days of the Registrant’s fiscal year ended December 31, 2023.

1 |  2023 Form 10-K

2023 Form 10-K

Table of Contents

Page | ||

PART I | ||

Item 1. |

| |

Item 1A. |

| |

Item 1B. |

| |

Item |

| |

Item |

| |

Item |

| |

Item 4. | 27 | |

| ||

PART II | ||

Item 5. |

| |

Item 6. |

| |

Item 7. | Management’s Discussion and Analysis of Financial Condition and Results of Operations |

|

Item 7A. |

| |

Item 8. |

| |

Item 9. | Changes in and Disagreements With Accountants on Accounting and Financial Disclosure |

|

Item 9A. |

| |

Item 9B. |

| |

Item 9C. | Disclosure Regarding Foreign Jurisdictions that Prevent Inspections | 96 |

| ||

PART III | ||

Item 10. |

| |

Item 11. |

| |

Item 12. | Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters |

|

Item 13. | Certain Relationships and Related Transactions, and Director Independence |

|

Item 14. |

| |

PART IV | ||

Item 15. |

|

2 | 2023 Form 10-K

i

Unless the context requires otherwise, references in this Annual Report on Form 10-K for the fiscal year ended December 31, 2018 of Ceridian HCM Holding Inc. and subsidiaries (“Form 10-K”) to “our company,” the “Company,” “we,” “us,” “our,” and “Ceridian”“our” refer to Ceridian HCM HoldingDayforce, Inc. and its direct and indirect subsidiaries on a consolidated basis. References to Dayforce reflect the Dayforce people platform. Effective January 31, 2024, Ceridian HCM Holding Inc. changed its corporate name to Dayforce, Inc. We ceased trading under the ticker symbol "CDAY" and began trading under our new ticker symbol, "DAY," on the New York Stock Exchange ("NYSE"), and Toronto Stock Exchange ("TSX") effective on February 1, 2024.

We and our subsidiaries own or have the rights to various trademarks, trade names and service marks, including the following: CeridianDayforce®, DayforceCeridian®, Makes Work Life Better™, Powerpay® and various logos used in association with these terms. Solely for convenience, the trademarks, trade names and service marks and copyrights referred to herein are listed without the ©, ®, and ™, symbols, but such references are not intended to indicate, in any way, that Ceridian,Dayforce, Inc., or the applicable owner, will not assert, to the fullest extent under applicable law, Ceridian’sour or their, as applicable, rights to these trademarks, trade names, and service marks. Other trademarks, service marks, or trade names appearing in this Form 10-K are the property of their respective owners.

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

This Form 10-K contains, or incorporates by reference, not only historical information, but also forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended (“Securities Act”), and Section 21E of the Securities Exchange Act of 1934, as amended (“Exchange Act”) and that are subject to the safe harbor created by those sections. All statements other than statements of historical fact or relating to present facts or current conditions included in this Form 10-K are forward-looking statements. Forward-looking statements including, without limitation, statements concerning the conditions of the human capital management solutions industrygive our current expectations and our operations, performance, and financial condition, including, in particular, statementsprojections relating to our business, growth strategies, product development efforts,financial condition, results of operations, plans, objectives, future performance and future expenses. Forward-lookingbusiness. You can identify forward-looking statements can be identified by the fact that they do not relate strictly to historical or current facts. These statements may include words such as “anticipates,“anticipate,” “intends,“estimate,” “plans,“expect,” “seeks,"assume", “project,” “believes,“seek,” “estimates,“plan,” “expects,“intend,” “assumes,“believe,” “projects,“will,” “may,” “could,” “may,“continue,” “will,“likely,” “should,” and other words and terms of similar references tomeaning in connection with any discussion of the timing or nature of future periods,operating or by the inclusion of forecastsfinancial performance or projections.other events but not all forward-looking statements contain these identifying words.

Forward-looking statements are based on our current expectations and assumptions regarding our business, the economy, and other future conditions. Because forward-looking statements relate to the future, by their nature, they are subject to inherent uncertainties, risks, and changes in circumstances that are difficult to predict. As a result, our actual results may differ materially from those contemplated by the forward-looking statements. Important factors that could cause actual results to differ materially from those in the forward-looking statements include regional, national, or global political, economic, business, competitive, market, and regulatory conditions and those risks described in Part I, Item IA, “Risk Factors” of this Form 10-K. Although we have attempted to identify important risk factors, there may be other risk factors not presently known to us or that we presently believe are not material that could cause actual results and developments to differ materially from those made in or suggested by the forward-looking statements contained in this Form 10-K. If any of these risks materialize, or if any of the above assumptions underlying forward-looking statements prove incorrect, actual results and developments may differ materially from those made in or suggested by the forward-looking statements contained in this Form 10-K. For the reasons described above, we caution you against relying on any forward-looking statements. Any forward-looking statement made by us in this Form 10-K speaks only as of the date on which we make it. Factors or events that could cause our actual results to differ may emerge from time to time, and it is not possible for us to predict all of them. We undertake no obligation to publicly update or to revise any forward-looking statement, whether as a result of new information, future developments, or otherwise, except as may be required by law. Comparisons of results for current and any prior periods are not intended to express any future trends or indications of future performance, unless specifically expressed as such, and should be viewed as historical data.

3 | 2023 Form 10-K

Overview

Dayforce, Inc., formerly known as Ceridian HCM Holding Inc. was incorporated in Delaware on July 3, 2013. On April 30, 2018, we completed our initial public offering (“IPO”), in which we issued and sold 24,150,000 shares of common stock at a public offering price of $22.00 per share. Concurrently with our IPO, we issued an additional 4,545,455 shares of our common stock in a private placement at $22.00 per share. Contemporaneously with our IPO, we distributed our controlling financial interest in LifeWorks Corporation Ltd (“LifeWorks”) to our stockholders of record prior to the IPO on a pro rata basis in accordance with their pro rata interests in us.

Following our IPO, we remain a controlled company by our financial sponsors: affiliates and co-investors of Thomas H. Lee Partners, L.P. (“THL”) and Cannae Holdings, Inc. (“Cannae”). Collectively, THL and Cannae are referred to as our “Sponsors.”

Overview

Ceridian is a global human capital management (“HCM”) software company. Dayforce, our flagship cloudCloud HCM platform, provides a full suite of HCM functionality, including global human resources (“HR”), payroll benefits,and tax, workforce management, benefits, and talent managementintelligence functionality. In addition to Dayforce, we sell Powerpay, a cloudCloud HR and payroll solution for the Canadian small business market, through both direct sales and established partner channels. We also continue to support customers using our Bureaulegacy North America solutions which we generally stopped actively selling to newand customers using our acquired solutions in 2012, following the acquisition of Dayforce.Asia Pacific Japan ("APJ") region. We invest in maintenance and necessary updates with the legacy technology to support our Bureau customers and continue to migrate them to Dayforce. Revenue from our recurring solutions includes investment income generated from holding customer funds, also referred to as float revenue or float.

The following five strategic growth levers drive our long-term perspectives, near-term decision making, and stockholder alignment:

Products and ServicesSolutions

Dayforce

Dayforce our principle cloud HCM platform, is a single application that provides continuous real-time calculations across all modules to enable, for example, payroll administrators access to data through the entire pay period, and managers access to real-time data to optimize work schedules. Dayforce offers a comprehensive range of functionality, including global HR, payroll, benefits, workforce management, and talent management on web and native iOS and Android platforms. Our Dayforce mobile app enables employees not only to request and to trade schedules, but also to see the real-time impact of schedule changes on their pay. Our Dayforce platform is used by organizations, regardless of industry or size, to optimize management of the entire employee lifecycle, including attracting, hiring, engaging, paying, deploying, and developing their people. Key functionality ofIn 2023, we received several accolades for our Dayforce platform includessolution, including being named as a Leader in the 2023 Gartner® Magic Quadrant™ for Cloud HCM Suites for 1,000+ Employee Enterprises for the fourth consecutive year; Leader in compliance, payroll administration, and overall product satisfaction in the Gartner Critical Capabilities for Cloud HCM suites for 1000+ Employee Enterprises; Top 5 solution in the 2023 Constellation Shortlist™ for both Global HCM Suites and Workforce Management Suites; Leader in the Sapient Insights Group HR payrollSystems Survey for Time Management Systems and tax, benefits, workforce management,in the Sapient Insights HR Survey - HRMS Voice of the Customer User Experience and talent management.Vendor Satisfaction.

Human Resources

Dayforce Human Resources functionality provides customers withHR professionals, managers, and employees a single, complete record for all employees.of their HR information. Our HR functionality is centered on a comprehensive, flexible workflow engine that streamlines and automates administrative tasks. The component maintains a record of critical forms for the employee, such as signed workplace policy agreements, Occupational Safety and Health Administration regulations, and direct deposit information.

In addition to its primary record-keeping functionality, Dayforce HR comes with an organizational management system that allows managers to view the profiles of their team members, which includes contact and time off details, as well as pay, benefits, and performance data. It is also accessible to employees, who can view the organizational chart, appropriate information about other employees in the organization, and their own pay and time details. There are several self-service options available in the product as well, such as change of address or adding a dependent, making it easy for employees to keep their profiles up to date.

4 | 2023 Form 10-K

Payroll and Tax

Our payroll capabilities provide customers with the tools neededDayforce empowers employers to accurately and compliantly manage their global payroll processes.needs within a single system. Through our Dayforce platform, users in the United States, Canada, and the United Kingdompayroll administrators with localized payroll functionality are able to make updates to time and pay in real-time. InDayforce supports payroll in over 200 countries where we do not currently offer localizedand territories around the world, whilst providing employers with a centralized global view of their payroll Dayforce ConnectedPay providesdata. This global payroll aggregation featuresmodel is powered by a combination of company-owned and partner unified payroll engines with an automated data exchange that allow an organizationaffords employees and administrators to have a centralized viewconsistent, intuitive single user experience. Native payroll is available in certain countries across North America, APJ, and Europe, the Middle East, and Africa ("EMEA"), where Dayforce’s continuous calculation engine offers flexibility, accuracy, and efficiency in the payroll process. In these native markets, we also manage the movement and remittance of their global payroll. ConnectedPay automatestaxes to tax authorities on behalf of our customers. With a flexible rules-based configuration and regional partnerships, Dayforce helps organizations with regulation and compliance concerns regardless of where employees work or live. We are continuing to innovate and expand payroll functionality into new markets to enhance the data exchange with in-country payroll providers and provides a consistent self-servicecustomer experience for employeeslarge enterprises operating globally.

In addition to view earnings statements and associatedcustomers who use our payroll documentation.services, certain customers use our tax filing services on a stand-alone basis. We recently modernized the technology platforms used to provide stand-alone tax services. Beginning in 2023, with the technology migration complete, we classified recurring revenues from stand-alone tax customers as Dayforce calculates, withholds, and files payroll related taxes in the United States and Canada as part of our localized payroll offering.

Dayforce Benefits assists users from benefits enrollment to ongoing benefits administration, including eligibility, open enrollment and Affordable Care Act (“ACA”) management.

Workforce Management

Dayforce Workforce Management provides functionality to helphelps organizations equitably manage their workforces, improve operational efficiency, and enhance compliance by configuring the system to meet complex laboremployment and employmentworking time rules and policies. Through Dayforce usersWorkforce Management, customers are offered absence management, time and attendance, schedule,absence management, scheduling, task management, and labor planning. A variety of options are available for organizations to capture time and attendance data such as physical clocks and the mobile application.

Dayforce Wallet

Dayforce Wallet is a digital payment solution that gives employeesinstant access to their net earnings through on-demand pay requests. With Dayforce Wallet, employees’ funds are loaded onto a paycard, which generates interchange fee revenue when used. As of December 31, 2023, we had more than 1,860 customers signed onto Dayforce Wallet with over 1,150 customers live on the product and the average registration rate was above 60% of all eligible employees.

Benefits

Dayforce Benefits assists benefits administrators from enrollment to ongoing benefits administration, including eligibility, open enrollment and Affordable Care Act ("ACA") management. Our proprietary Benefits Decision Support scoring system guides employees through a self-service experience, giving information about each of the available benefit plans and the impact of plan options, to help them choose the best option for their specific needs.

The system integrates with hundreds of benefits carriers, contains a library of qualifiers to help define eligibility rules, and leverages real-time connections to payroll and HR to inform eligibility and calculate employee deductions. In addition, we offer Benefits Intelligence, which leverages enrollment data to get visibility into elections at the plan and option levels to help administrators analyze their program.

Talent ManagementIntelligence

Dayforce Talent Management enablesIntelligence, a suite of next generation talent acquisition and talent management solutions powered by Artificial Intelligence (“AI”) and driven by data, helps organizations to attract, to engage, torecruit, hire, retain, and develop and to motivate their workforce. UsersDayforce Talent Intelligence transforms talent management and recruitment strategies by using AI in conjunction with talent data from across the employee lifecycle to provide organizations insights that enable them to make more efficient, accurate, and fair talent decisions. Talent Intelligence can also objectively measure workforce demographics while identifying inequity in everything from payroll to promotion opportunities to help employers create actionable policy changes. Customers can leverage Talent Intelligence tools for recruiting, onboarding, engagement, performance management, succession planning, compensation management, and employee learning. career planning and skills development.

Powerpay5 | 2023 Form 10-K

Powerpay

Powerpay is a Cloud platform that provides scalable and straightforward payroll and HR solutions. We offer Powerpay for Canadian organizations with fewer than 100 employees. Powerpay is a cloud platform that provides scalable and straightforward payroll and HR solutions. Specifically designed for small businesses, Powerpay enables clients to pay their employees accurately and on-time. As of December 31, 2018, Powerpay had over 38,000 customer accounts.

BureauOther

Our Bureau solutionsWe also offer payroll and payroll-related services using legacy technology.technology and on-premise technology from our acquired businesses in APJ, which we formerly referred to as Bureau. We invest in maintenance and necessary updates to support our Bureau customers. WeHowever, we generally stopped selling our Bureaulegacy North America payroll solutions to new customers in the United States in 2012("U.S.") and in Canada, in 2015, and we intend to stop actively selling our acquired on-premise payroll solutions to new customers on a stand-alone basis. In addition to customers who use our legacy payroll services, prior to modernizing the technology platforms utilized for stand-alone tax services, certain customers used our legacy tax filing services on a stand-alone basis through 2022.

Services and Support

We offer a broad portfolio of services to enable customer success. We believe it is important to work closely with our customers to understand their needs and deliver technology solutions and support that address them. We continue to convert Bureau customers toincrease our Dayforce platform.

Revenue by Productglobal reach in supporting and Service

For a quantitative discussionserving our customers. As part of our revenueinternational strategy, we work with partners to perform services in certain geographies where we do not currently have international operations or the particular service required by our customers.

Implementation and Professional Services

Our internal implementation team leverages proprietary onboarding technology for new customer activation and professional services work. Our internal team is supplemented by third party services partners and system integration partners (“SI”). Our implementation services include solution please referconfiguration and activation for new customers. Professional services include add-on implementation services for existing customers, ongoing product configuration changes when the customer does not have the resources to Part II, Item do it themselves, product usage consulting and a variety of additional services, such as report writing, usage audits, and process improvement.

Customer Support

Our global customer support organization provides 24/7 “Management’s Discussionapplication support from locations across North America, APJ, and AnalysisEMEA. Our support function is organized into teams of Financial Conditionrepresentatives with deep product and Resultsdomain expertise across our platform. These teams are aligned to groups of Operations”customers based on geography and product type to provide a combination of this Form 10-K. deep product and industry knowledge, consistent relationships, and high availability.

Customers

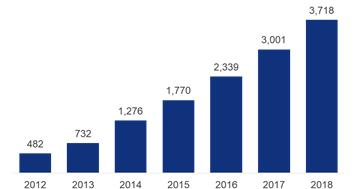

Dayforce is designed to serve organizations with 100 to over 100,000 employees. The Dayforce customer base has increased from 482 as of December 31, 2012 to 3,718 customers live6,393 customers* on the platform as of December 31, 2018. In addition, we had over 450 net new Dayforce customers contracted, but not yet live on Dayforce as of December 31, 2018. We expect the majority of these Dayforce customers to be taken live in 2019. For 2018, our 3,718 live Dayforce customers represented over 3.12023 representing approximately 6.84 million active users.global employees*. We define a customer as a single organization, such as a company, a non-profit association, an educational institution, or government entity. We also have overapproximately 38,000 Powerpay customer accounts. No single customer accounted for more than 1%2% of our revenues during the year ended December 31, 2018.2023.

SalesSelling and Marketing

We sell our Cloud solutions through a direct sales force and a variety of third partythird-party channels, organized by customer size and geography. We market Dayforce to organizations with more than 100 employees. We market Powerpay to organizations with fewer than 100 employees in Canada. The majority of our revenue growth comes from new customers, but we also have a small, dedicated account management team focused on servingCloud customers.

* Excluding the needs2021 acquisitions of our Bureau customersAscender HCM Pty Limited ("Ascender") and helping them to migrate to ourATI ROW, LLC and Dayforce platform.Mexico S. de R.L. de C.V. (formerly known as ADAM HCM MEXICO, S. de R.L. de C.V.) (collectively, "ADAM HCM")

6 | 2023 Form 10-K

Implementation and Professional Services

Our internal implementation team leverages proprietary onboarding technology for new customer activation and professional services work. Our internal team is supplemented by a small number of third party services partners. Our implementation services include solution configuration and activation for new customers. Professional services include add-on implementation services for existing customer, ongoing product configuration changes when the customer does not have the resources to do it themselves, product usage consulting and a variety of additional services, such as report writing, usage audits, and process improvement.

Customer Support

Our global customer support organization provides 24/7 application support from offices across North America and in the United Kingdom, Mauritius, and Australia. Our support function is organized into specialized pods of approximately 18 representatives with deep domain expertise across our platform. These pods are grouped by customer and product type to provide a combination of deep product knowledge, consistent relationships, and high availability.

Technology, Hosting, and Research and Development (“R&D”)

Technology and innovation are at the core of Ceridian.Dayforce, Inc. Our innovation and development process is customer-driven. We work directly with customers to understand their needs and to deliver solutions that address their challenges, through the lens oftaking into consideration the entire user experience, without being constrained by individual modules or applications. We are committed to protecting the information of our customers, our employees, and our contractors, along with other business data.

Our R&D team is responsible for the design, development, and testing of our applications. We believe that our modern cloudCloud technology stack, agile design and development methodology, and efficient software deployment process enable us to innovate quickly in response to industry trends. We host Dayforce and PowerpayCloud-based applications and serve allthe majority of our customers from data centers operated by third party providers, primarily NaviSite, in Boston, Massachusetts; Redhill, England; Santa Clara, California; Toronto, Canada; Vancouver, Canada; and Woking, England. We also host Dayforce Australia in Microsoft Azure, in Melbourne, AustraliaAWS, VMWare Cloud on AWS, and Sydney, Australia.Navisite. While we control and have access to our servers and all of the components of our network that are located in our external data centers, we do not control the operation of these facilities. Additionally, we host our internal systems through data centers that we operate and lease or own in Atlanta, Georgia; Fountain Valley, California; Louisville, Kentucky; St. Petersburg, Florida; and Winnipeg, Canada.

Competition

The market for HCM technology solutions is rapidly changing, with legacy service bureau and on-premise software providers facing increased competition from emerging cloud players. We currently compete with firms that provide both integrated and point solutions for HCM. Legacy payroll service providers, such as Automatic Data Processing (“ADP”), provide HCM solutions primarily through service bureau models. These vendors often have more in-house resources, greater name recognition, and longer operating histories than Dayforce and may seek to expand their cloud offerings through acquisition or organic product development. We also compete with cloud-enabled client-server HCM providers, such as The Ultimate Software Group, Inc. (“Ultimate Software”). These companies, whose products were developed over 20 years ago as on-premise solutions, have modified and redeployed their platforms as hybrid software as a service (“SaaS”) offerings. This has allowed them to transition their business model to offer hosted and cloud solutions, resulting in significantly larger customer bases. More recently, we face competition from modern HCM providers, such as Workday, Inc. (“Workday”), whose solutions have been specifically built as single application platforms in the cloud. In addition, we also face competition from large, long-established enterprise application software vendors, suchU.S. and APJ.

Dayforce National Trust Bank

The Office of Comptroller of the Currency (the "OCC") authorized the Ceridian National Trust Bank (the "CNTB") to open on January 3, 2023. Effective on this date, the CNTB commenced banking operations, acting as Oracle Corporation (“Oracle”) and SAP SE (“SAP”). These companies are seeking to expand their cloud offerings through both acquisition and internal development efforts. We also compete with point solutions, such as Kronos Incorporated (“Kronos”)trustee for workforce management and Cornerstone OnDemand Inc. (“Cornerstone OnDemand”) for talent management.

We believe the principal competitive factors in our market include the following:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Employees and Culture

As of December 31, 2018, we had 4,444 active employees, including 3,759 in North America, Europe, and Australia, and 685 in Mauritius. We also engage temporary employees and consultants when needed to enhance our workforce. NoneU.S. payroll trust. Historically, certain aspects of our U.S. client money movement activity were subject to regulation at both the federal and individual state levels with resulting inherent complexity across multiple jurisdictions. With the establishment of the CNTB, U.S. regulatory oversight will now be under the OCC, a single federal government agency. Our payroll trust structure will continue to benefit our customers by providing bankruptcy-remoteness protection for client funds pending remittance to employees are represented by a labor union,of our clients, tax authorities, and we have never experienced any work stoppages.other payees. On January 31, 2024, the CNTB became the Dayforce National Trust Bank (the "DNTB").

Ceridian believes in diversity and equality for all people and fosters a culture that engages and celebrates our employees. In 2018, we were recognized with over 20 awards related to our company culture and workplace experiences, including Glassdoor Employees’ Choice Awards for 2018 Best Places to Work (Canada and United States), Best Workplaces certification (Canada and United States), Brandon Hall’s Excellence in Talent Management Award for Best Advance in High Potential Development, and 2018 Working Mother 100 Best Companies.

Intellectual Property

Our success depends, in part, on our ability to protect our proprietary technology and intellectual property. We rely on a combination of patents, copyrights, trade secrets, trade names, and trademarks, as well as confidentiality and nondisclosure agreements and other contractual protections, to establish and to safeguard our intellectual property rights.

BacklogCompetition

The market for HCM technology solutions is highly competitive and Seasonalitysubject to changing technology and shifting client needs. We compete with firms that provide both integrated and point solutions for HCM, as well as with local providers in each jurisdiction that we operate. Globally, we compete with legacy payroll service providers, as well as Cloud-enabled client-server HCM providers. We also face competition from modern HCM providers, whose solutions have been specifically built as single application platforms in the Cloud. In addition, we face competition from large, long-established enterprise application software vendors.

For a discussionCompetition in the global HCM market is primarily based on product and service quality, including ease of backloguse and accessibility of technology, breadth of offerings, reputation, and price. We believe that we are competitive in each of these areas and that our single application always-on technology and product innovations, combined with our commitment to service and our geographic reach, distinguishes us from our competitors.

Seasonality

We have in the past and expect in the future to experience seasonal fluctuations in our revenues and new customer contracts with the fourth quarter historically being our strongest quarter for new customer contracts, renewals, and customer go-lives. Although the growth of our Cloud solutions and the ratable nature of our fees makes this seasonality please referless apparent in our overall results of operations, we expect our revenue to Part II, Item 7. “Management’s Discussionfluctuate quarterly and Analysisto be higher in the fourth and first quarters of Financial Conditioneach year. Fourth quarter revenue is driven by year-end processing fees and ResultsDayforce customer go-lives; and first quarter revenue is driven by revenue earned for printing of Operations” of this Form 10-K. year-end tax packages.

Available InformationEnvironmental, Social, and Governance ("ESG") and Human Capital

We believe that transparency and accountability are essential to any company’s success. Our annual reports onapproach to ESG and Human Capital is guided by five pillars: Governance and Trust; Our People; Tech for Good; Our Communities; and the Environment.

7 | 2023 Form 10-K quarterly reports

Governance and Trust

We safeguard the trust given to us by our partners, our customers, and their employees. This means upholding high standards of corporate governance and ethics, ensuring customer data is protected, and developing products that are reliable and effective.

Our People

As of December 31, 2023, we had 9,084 employees, including 4,563 employees in North America, 2,906 in APJ, and 1,615 in EMEA. We provide a wide range of compensation and benefits to our employees that enhance the workplace experience. In addition to salaries, these benefits (which vary by country and region) include annual bonuses, equity awards, a global employee stock purchase program, retirement savings plans, healthcare and insurance benefits, fertility and family building benefits, health savings and flexible savings spending accounts, unlimited time away from work, parental leave, flexible and remote work options, employee assistance programs, and tuition reimbursement.

Promoting diversity, equity, and inclusion within our workforce is also a priority for us. We have a company-wide employee Global Diversity Advisory Council, and our nine employee resource groups foster inclusion, connection, and career development opportunities for their members. Our Achieving Corporate Equity program helps to empower high-potential diverse talent and improve the internal mobility of employees from underrepresented and underserved communities.

As of December 31, 2023, women represented approximately 50% of our global workforce, including approximately 44% of employees in manager-level roles and above, and approximately 36% in vice president-level roles and above. In the U.S., approximately 12% of our workforce was Asian, 11% was Black or African American, 6% was Hispanic or Latino, 3% was multiracial, less than 1% was Native Hawaiian or Pacific Islander, American Indian or Alaska Native, and approximately 65% was White. In the U.S., people of color represented approximately 24% of employees in manager-level roles and above, and approximately 27% of employees in vice president-level roles and above.

The health, safety, and wellbeing of our employees is of high importance to us. We host an annual global Mental Health Summit, and we offer two paid wellness days to all employees. In addition, our global emergency threat monitoring and mass communications system helps to ensure connectivity and support for our employees both during and after natural disasters and other dangerous events.

We are committed to providing meaningful professional development opportunities to our workforce. We maintain a culture of continuous learning and empowerment through programs that include professional skills training, leadership development, and job shadowing and job rotation opportunities.

Our ability to attract and retain top talent remains critical to our continued success as a business, and our employee Net Promoter Score in 2023 was 50.

Tech for Good

We believe that Tech for Good and responsible innovation can have a positive impact on Form 10-Q, current reports on Form 8-K, proxy and information statements, and amendmentsall stakeholders. Our Dayforce Wallet product provides individuals with on-demand access to reports andtheir earned pay, which enables them to better cover both everyday expenses as well as any registration statements filedurgent or furnished pursuant to Sections 13(a), 14 and 15(d)unplanned costs. Our AI Governance Framework closely evaluates the potential use of AI from idea through all key stages of the Exchange Actproduct development lifecycle. Our Dayforce Engagement product helps our customers build a culture of inclusion and respect within their workforce, and it gives them the ability to measure employee sentiment on equity and belonging. Our Career Explorer product provides our customers’ employees access to data-driven career pathing, gives them information about open internal roles that match their interests and abilities, and provides actionable steps to help them reach their career goals.

Our Communities

We are electronically filedcommitted to giving back to the communities in which we live and work. Through our employee-led charity Dayforce Cares, formerly Ceridian Cares, we provide financial support to individuals and families struggling with basic needs and quality of life across the SecuritiesU.S. and Exchange Commission (“SEC”). The SEC maintainsCanada. Since its inception, the foundation has given over $6.5 million in grants to over 4,500 people in need. In addition, 50% of our employees globally participated in our giving and volunteering program in 2023.

8 | 2023 Form 10-K

Environment

We are committed to doing our part to help address the climate crisis. This includes actively working to decrease our carbon footprint by pursuing two near-term reduction targets that cover Scope 1, 2, and 3 emissions. Our decarbonization strategy includes consolidating our physical footprint globally, expanding our cloud strategy to sustainably deliver our data and technology solutions, and significantly reducing our in-house print operations. Each year, we source 100% renewable electricity across our global operations through the purchase of high-quality Energy Attribute Certificates. In 2023, we launched a website that contains reports, proxynew Responsible Sourcing Initiative to enhance the sustainability of our supply chain. We also developed a company-wide Environmental Sustainability Policy and added new provisions to our Vendor Code of Conduct to further embed sustainable practices into our direct operations and procurement processes.

We encourage you to review our ESG Report for more detailed information statements, and other information regarding issuers that file electronically with the SEC. These materials maywhich can be obtained electronically by accessing the SEC’s website at http://www.sec.gov.

We make available, free of chargefound on our website at http:https://investors.ceridian.com, our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, proxy and information statements, Section 16 reports, amendments to those reports, and other documents filed or furnished pursuant to Section 13(a) or 15(d) of the Exchange Act as soon as reasonably practicable after we electronically file such material with, or furnish it to, the SEC.www.dayforce.com/who-we-are/corporate-responsibility. In addition, the following governance materials are availablepast ESG reports, our Task Force on our website at https://investors.ceridian.com/corporate-governance/governance-documents: (i) our current charterClimate-related Financial Disclosures Index, SASB Index, consolidated EEO-1 report, and bylaws; (ii) charters of our Audit, Corporate GovernanceESG-related policies and Nominating Committees of our Board of Directors (our “Board”); (iii) our Corporate Governance Guidelines; and (iv) our Code of Conduct, as well as any waivers from and amendments to our Code of Conduct. Our corporate website address is http://www.ceridian.com.principles can be found here. Our website and the information contained on, or that can be accessed through, the website is not deemed to be incorporated by reference into, and shouldis not be considered part of, this Form 10-K.

Available Information

Our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, proxy and information statements, Section 16 reports, and amendments to reports and any registration statements filed or furnished pursuant to Sections 13(a), 14 and 15(d) of the Exchange Act are available, free of charge at http://investors.dayforce.com as soon as reasonably practicable after we file such material with, or furnish it to, the Securities and Exchange Commission (“SEC”), and are also available on the SEC’s website at http://www.sec.gov.

Our restated certificate of incorporation, our fourth amended and restated bylaws, charters of our Acquisition and Finance, Audit, Compensation, and Corporate Governance and Nominating Committees of our Board of Directors (the “Board”), our Corporate Governance Guidelines, and our Code of Conduct, as well as any waivers from and amendments to our Code of Conduct are available on our website at https://investors.dayforce.com/corporate-governance/governance-documents. Our website and the information contained on, or that can be accessed through, the website is not deemed to be incorporated by reference into, and is not considered part of, this Form 10-K.

Information about Our Executive Officers

The following table sets forth the names and ages,Our executive officers as of February 15, 2019, and titles of the individuals who serve28, 2024 are as our executive officers. Certain biographical information with respect to those executive officers follows the table.follows:

Name | Age | Position | ||

David D. Ossip |

|

| ||

|

| Executive Vice President and Chief Revenue Officer | ||

|

| Executive Vice President and Chief Operating Officer | ||

|

| President, Customer and Revenue Operations | ||

Jeffrey S. Jacobs | 48 | Head of Accounting and Financial Reporting | ||

Jeremy R. Johnson | 40 | Executive Vice President and Chief Financial Officer | ||

|

| Executive Vice President, Chief Product and | ||

|

| Executive Vice President, General Counsel and | ||

|

|

| ||

|

|

|

David D. Ossip

Mr. Ossip is our ChairmanChair of the Board and Chief Executive Officer, positions heOfficer. Mr. Ossip has held the position of Chair since August 2015 and sole Chief Executive Officer since November 2023. Previously, Mr. Ossip served as our Co-Chief Executive Officer from February 2022 until November 2023, and our Chief Executive Officer from July 2013 respectively.until February 2022. Mr. Ossip joined the Company following the Company’s acquisition of Dayforce Corporation in 2012, where he held the position of chief executive officer.Chief Executive Officer. Mr. Ossip is currentlypreviously served as a director for Ossip Consulting Inc.Dragoneer Growth Opportunities Corp., a NYSE listed company, Dragoneer Growth Opportunities Corp. II, a Nasdaq listed company, and OSDACDragoneer Growth Opportunities Corp. III, a Nasdaq listed company.

Leagh E. Turner9 | 2023 Form 10-K

Ms. Turner

Samer Alkharrat

Mr. Alkharrat is our Executive Vice President and Chief Revenue Officer, positions he has served as our Presidentheld since August 2018.June 2023. Prior to joining the Company, Ms. TurnerMr. Alkharrat served as Chief Partner Officer at Workday, Inc., a provider of enterprise cloud applications, from March 2022 to February 2023. Previously, he held the position of global chief operating officer, strategic customer programPresident and Chief Revenue Officer at C3 AI, an artificial intelligence software provider, from June 2021 to February 2022. Prior to that, he served as the Senior Vice President of SAPWorldwide Sales at VMware LLC, a cloud service provider, from October 2016November 2019 to 2021. From August 2018. In addition, Ms. Turner2010 to November 2019, Mr. Alkharrat held the positionsposition of acting chief operating officer ofChief Operating Officer at SAP Europe, Middle East, and Africa region from March 2017 to August 2017, acting president of SAP Canada Inc. from August 2015 to January 2016, chief operating officer of SAP Canada Inc. from February 2014 to October 2016, and vice president, sales central region of SAP Canada Inc. from July 2010 to February 2014.SE, an enterprise application software provider.

Paul D. ElliottChristopher R. Armstrong

Mr. ElliottArmstrong is our Executive Vice President, Chief Operating Officer, a position he has held since April 2016. Additionally,February 2022. Mr. Elliott served as ourArmstrong joined the Company in 2004, and since then has held several commercial and operational leadership roles, including Executive Vice President, Chief Customer Officer from February 2020 until February 2022, Executive Vice President, Chief Operating Officer from May 2019 until February 2020, Executive Vice President, Operations from March 2018 until May 2019, and Executive Vice President, Customer Support from April 2016 until AugustMarch 2018.

Stephen H. Holdridge

Mr. Holdridge is our President, Customer and Revenue Operations, a position he has held since February 2023. Mr. Holdridge joined the Company in January 2020, serving as Global Head of Services until February 2022 and Executive Vice President, Chief Customer Officer from February 2022 until February 2023. Prior to that,joining the Company, Mr. ElliottHoldridge held the position of chief operatingSenior Executive Vice President, Worldwide Services at MicroStrategy, Inc., an analytics and business intelligence company, from November 2017 until July 2019.

Jeffrey S. Jacobs

Mr. Jacobs is our Head of Accounting and Financial Reporting and serves as the principal accounting officer, at two ofpositions he has held since May 2020. Mr. Jacobs served as our affiliate companies, first at Ceridian Canada whereVice President, Finance from December 2016 until May 2020. Mr. Elliott held the position from August 2009 to February 2013, and then at Ceridian HCM, Inc., where Jacobs is a certified public accountant (inactive).

Jeremy R. Johnson

Mr. Elliott held the position from March 2013 to March 2016.

Arthur Gitajn

Mr. GitajnJohnson is our Executive Vice President, and Chief Financial Officer, positionsa position he has held since October 2016.January 2024. Prior to joining us,the Company, Mr. GitajnJohnson held the position of chief financial officerChief Financial Officer at SmartRecruiters, Inc., a talent acquisition software platform, from September 2021 until December 2023. In addition to his role as Chief Financial Officer, for SAP Canadathe period August 2022 to April 2023, Mr. Johnson also served as interim Chief Executive Officer for SmartRecruiters, Inc. from July 2007Prior to January 2012 and from January 2015 to September 2016, andthat, Mr. Johnson held the position of chief financial officerSenior Vice President, Financial Planning and Analysis and Investor Relations at the Company from December 2020 to August 2021, and a variety of SAP’s Europe, Middle East, and Africa regionother roles within Finance at the Company from FebruaryJanuary 2012 to December 2014.

Ozzie J. Goldschmied2020. Mr. Johnson is a certified public accountant.

Joseph B. Korngiebel

Mr. GoldschmiedKorngiebel is our Executive Vice President, Chief Product and Chief Technology Officer, positions he has held since October 2014. Mr. Goldschmied previously served as our senior vice president of research and development from February 2012July 2020. Prior to September 2014. Mr. Goldschmied joinedjoining the Company, following the Company’s acquisitionMr. Korngiebel held various positions at Workday, Inc., a provider of Dayforce Corporation in 2012, where he held the position of senior vice president of engineering.enterprise cloud applications, since March 2006, including Chief Technology Officer from May 2017 until July 2020.

Scott A. KitchingWilliam E. McDonald

Mr. KitchingMcDonald is our Executive Vice President and General Counsel, positions he has held since July 2021, and Corporate Secretary, a position he has held since February 2016, and2016. Mr. McDonald served as Senior Vice President, Deputy General Counsel and Assistant Secretary, positions he has held since December 2013. Prior to that time, Mr. Kitching heldof the position of executive vice president and general counsel at our affiliate subsidiary Ceridian Canada from May 2003 to December 2013.

Lisa M. Sterling

Ms. Sterling is our Executive Vice President and Chief People and Culture Officer, positions she has held since March 2016. Ms. Sterling previously served as our vice president of product strategy from June 2015 to March 2016. Prior to joining us, Ms. Sterling was a partner and talent technology solutions leader at Mercer LLC from March 2013 to May 2015. Prior to that, Ms. Sterling served as the head of people engagement for Ultimate SoftwareCompany from February 2010 to March 2013.2016 until July 2021.

Erik J. Zimmer10 | 2023 Form 10-K

Mr. Zimmer is our Executive Vice President and Chief Strategy Officer, positions he has held since August 2018. Mr. Zimmer previously served as a managing director of Thomas H. Lee Partners, L.P. from February 2011 to August 2018.

Our business ordinarily encounters and addresses risks, some of which can cause our future results to be different than we currently anticipate. The risk factors described below represent our current view of some of the most important risks facing our business and are important to its understanding. The following information includes a number of forward-looking statements and should be read in conjunction with information contained in this Annual Report on Form 10-K, including the Management’s Discussion and Analysis of Financial Condition and Results of Operations, the Quantitative and Qualitative Disclosures About Market Risk and the consolidated financial statements and related notes.

Risks Related to Our Business and Industry

We have a history of losses and negative cash flows from operating activities, and we may not be able to attain or to maintain profitability or positive cash flows from operating activities in the future.

We have incurred net losses and negative cash flows from operating activities over the last few years as we made substantial investments in developing, launching, and selling our Cloud solutions. In addition, our highly leveraged capital structure has had a negative effect on our profitability. As a result, we have incurred net losses of $92.9 million in the year ended December 31, 2016, $9.2 million in the year ended December 31, 2017, and $63.4 million in the year ended December 31, 2018. As of December 31, 2018, we had an accumulated deficit of $419.3 million. We incurred negative cash flows from operating activities of $75.5 million in the year ended December 31, 2016, $39.8 million in the year ended December 31, 2017 and positive cash flows from operating activities of $9.5 million in the year ended December 31, 2018. To the extent we are successful in increasing our Cloud customer base, we may also incur increased net losses and negative cash flows from operating activities because costs associated with acquiring and implementing new Cloud customers are generally incurred up front, while subscription revenues are generally recognized ratably over the terms of the agreements. Our recent growth in revenues may not be indicative of our future performance.

We also expect our expenses to increase in the future due to anticipated increases in sales, general, and administrative expenses, including expenses associated with being a public company, and product development and management expenses, which could impact our ability to achieve or to sustain profitability or positive cash flows from operating activities in the future. Additionally, while the majority of our revenue comes from fees charged for use of the software, we are developing new products and services, which may initially have a lower profit margin than our existing Cloud solutions, which could have a material adverse effect on our business, financial condition, and results of operations. Although we believe we will be able to reach profitability and attain positive cash flows from operating activities in the next few years, we cannot provide any assurance that we will able to do so in the future.

The markets in which we participate are highly competitive, and if we do not compete effectively, it could have a material adverse effect on our business, financial condition, and results of operations.

The markets in which we participate are highly competitive, and competition could intensify in the future. We believe the principal competitive factors in our market include breadth and depth of product functionality, scalability and reliability of applications, robust workforce management, comprehensive tax services, modern and innovative cloud technology platforms combined with an intuitive user experience, multi-country and jurisdiction domain expertise in payroll and HCM, quality of implementation and customer service, integration with a wide variety of third party applications and systems, total cost of ownership and ROI, brand awareness, and reputation, pricing and distribution. We face a variety of competitors, some of which are long-established providers of HCM solutions. Many of our current and potential competitors are larger, have greater name recognition, longer operating histories, larger marketing budgets, and significantly greater resources than we do, and are able to devote greater resources to the development, promotion, and sale of their products and services. Some of our competitors could offer HCM solutions bundled as part of a larger product offering. Furthermore, our current or potential competitors may be acquired by third parties with greater available resources and the ability to initiate or to withstand substantial price competition. In addition, many of our competitors have established marketing relationships, access to larger customer bases, and major distribution agreements with consultants, system integrators, and resellers. Our competitors may also establish cooperative relationships among themselves or with third parties that may further enhance their product offerings or resources.

In order to capitalize on customer demand for cloud applications, legacy vendors are modernizing and expanding their applications through cloud acquisitions and organic development. Legacy vendors may also seek to partner with other leading cloud HCM providers. We also face competition from vendors selling custom software and point solutions, some of which offer cloud solutions. Our competitors include, without limitation: ADP, Ultimate Software, and Workday for HCM; Kronos for workforce management; and Cornerstone OnDemand for talent management. In addition, other companies, such as NetSuite and Microsoft, that provide cloud applications in different target markets, may develop applications or acquire companies that operate in our target markets, and some potential customers may elect to develop their own internal applications. Some large businesses may be hesitant to adopt cloud applications such as ours and prefer to upgrade the more familiar applications offered by these vendors that are deployed on-premise, such as Oracle and SAP. Our competitors could offer HCM solutions on a standalone basis at a low price or bundled as part of a larger product sale. With the introduction of new technologies and market entrants, competition could intensify in the future.

If our competitors’ products, services, or technologies become more accepted than our applications, if they are successful in bringing their products or services to market earlier than ours, or if their products or services are more technologically capable than ours, it could have a material adverse effect on our business, financial condition, and results of operations. In addition, some of our competitors may offer their products and services at a lower price. If we are unable to achieve our target pricing levels or if we experience significant pricing pressures, it could have a material adverse effect on our business, financial condition, and results of operations.

Our growth strategy has focused on developing our Cloud solutions, which have experienced rapid revenue growth in recent periods that has been offset by revenue declines in our Bureau solutions. If we fail to manage our growth effectively or if our strategy is not successful, we may be unable to execute our business plan, to maintain high levels of service, or to adequately address competitive challenges.

We have recently experienced a period of rapid growth in our operations related to our Cloud solutions. In particular, our recurring services revenue for our Cloud solutions has continued to increase while our recurring services revenue for our Bureau solutions has continued to decline. As we implement our growth strategy for our Cloud solutions, we will continue to migrate employees and resources from our Bureau solutions to our Cloud solutions. Additionally, we are continuing to invest in the infrastructure shared by our Bureau and Cloud solutions, although we are no longer marketing our Bureau solutions to new customers. The growth of our Cloud solutions has placed, and future growth will place, a significant strain on our management, administrative, operational, and financial infrastructure. In order to manage this growth effectively, we will need to continue to improve our operational, financial, and management controls, and our reporting systems and procedures. Failure to effectively manage growth and failure to achieve our growth strategy could result in difficulty or delays in implementing customers, declines in quality or customer satisfaction, increases in costs, difficulties in introducing new features, or other operational difficulties; and any of these difficulties could have a material adverse effect on our business, financial condition, and results of operations.

Our Bureau solutions, which comprise a significant portion of our revenue, may decline at a rate faster than we anticipate, and we may not be able to successfully migrate our Bureau customers to our Cloud solutions or to offset the decline in Bureau revenue with Cloud revenue.

Our growth strategy is focused on the growth and expansion of our Cloud solutions; however, a portion of our revenue continues to be derived from our Bureau customers. We generally ceased marketing our Bureau solutions to new customers in the United States in 2012, and since that time have maintained the Bureau applications for existing customers while migrating customers to our Cloud solutions. Maintenance of our Bureau business requires investment, specifically with respect to compliance updates and security controls. If our investments are not sufficient to adequately update our Bureau solutions, such solutions may lose market acceptance and we may face security vulnerabilities.

In addition, we have marketed our Cloud solutions to our Bureau customers, and some of our Bureau customers have migrated to our Cloud solutions, but there is no guarantee that our remaining Bureau customers will migrate to our Cloud solutions. If such Bureau customers do not migrate, we may lose them in the future or we may be required to make ongoing investments to serve a smaller pool of customers. If our revenue from our Bureau solutions declines at a rate faster than anticipated, we are required to make significant investments in infrastructure shared by our Bureau and Cloud solutions that are not offset by increased revenue, we are not able to successfully convert the remaining Bureau customers to our Cloud solutions, or our Cloud solutions revenue does not grow fast enough to offset the decline in our Bureau solutions revenue, it could have a material adverse effect on our business, financial condition, and results of operations.

If the market for enterprise cloud computing develops slower than we expect or declines, it could have a material adverse effect on our business, financial condition, and results of operations.

The enterprise cloud computing market is not as mature as the market for on-premise enterprise software, and it is uncertain whether cloud computing will achieve and sustain high levels of customer demand and market acceptance. Our success will depend to a substantial extent on the widespread adoption of cloud computing in general, and of HCM solutions in particular. Many enterprises have invested substantial personnel and financial resources to integrate traditional enterprise software into their businesses and therefore may be reluctant or unwilling to migrate to cloud computing. It is difficult to predict customer adoption rates and demand for our applications, the future growth rate and size of the cloud computing market, or the entry of competitive applications. The expansion of the cloud computing market depends on a number of factors, including the cost, performance, and perceived value associated with cloud computing, as well as the ability of cloud computing companies to address security and privacy concerns. If we or other cloud computing providers experience security incidents, loss of customer data, disruptions in delivery, or other problems, the market for cloud computing applications as a whole, including our applications, may be negatively affected. If cloud computing does not achieve widespread adoption or there is a reduction in demand for cloud computing caused by a lack of customer acceptance, technological challenges, weakening economic conditions, security or privacy concerns, competing technologies and products, reductions in corporate spending, or otherwise, it could have a material adverse effect on our business, financial condition, and results of operations.

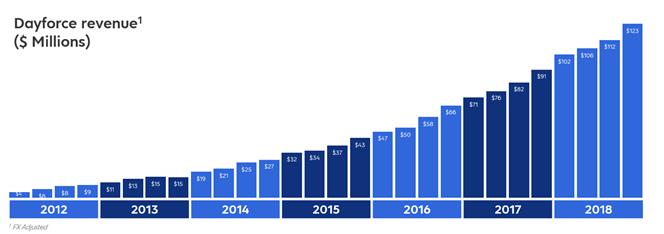

Our revenuesRevenues from our Cloud solutions have grown substantially over the last few years.years, and we believe a significant portion of our market capitalization is based upon maintaining our high Cloud solutions growth rate. Our efforts to increasecontinue increasing use of our Cloud solutions and our other applications may not succeed and may reduce our revenue growth rate.

Our ability to continue to grow the revenues from our Cloud solutions have grown substantially overthrough execution against our growth levers depends on the last few years. Our total Cloud revenues grew from $297.8 million in 2016quality of our platform and solutions, and our ability to $404.3 million in 2017 and $534.3 million in 2018, a growth rate of 35.8% and 32.2%, respectively. Any factor adversely affecting sales ofdesign our Cloud solutions including application release cycles, delays, or failures in new product functionality, market acceptance, product competition, performanceto meet consumer demand; and reliability, reputation, price competition, and economic and market conditions, could have a material adverse effectour ability to increase sales from existing customers depends on our business, financial condition,customers’ satisfaction with our product and results of operations.need for additional solutions. Our participation in new markets for native payroll, sales to our existing base of customers, and application expansion in succession management, learning management,various modules and compensation management,features, including the Dayforce Wallet, is relatively new, and it is uncertain whether these areas will ever result in significant revenues for us. Further, the entry into new markets, sales to our existing base of customers, or the introduction of new features, functionality, or applications beyond our current markets and functionality may not be successful.

Our quarterly results of operations may fluctuate significantly and may not fully reflect the underlying performanceThe success of our business.

Our quarterly results of operations, including the levels of our revenues, gross margin, profitability, cash flow, and deferred revenue, may vary significantly in the future, and period-to-period comparisons of our results of operations may not be meaningful. Accordingly, the results of any one quarter should not be relied upon as an indication of future performance. Our quarterly financial results may fluctuate as a result of a variety of factors, many of which are outside of our control, and as a result, may not fully reflect the underlying performance of our business. Fluctuation in quarterly results may negatively impact the value of our common stock. Factors that may cause fluctuations in our quarterly financial results include, without limitation:

our ability to attract new Cloud customers;

our ability to replace declining Bureau revenue with Cloud revenue;

the addition or loss of large Cloud customers, including through acquisitions or consolidations;

the addition or loss of employees by our Cloud customers;

the timing and number of paydays in a period;

the timing of recognition of revenues;

the tenure of our Cloud customers during that period;

the amount and timing of operating expenses related to the maintenance and expansion of our business, operations, and infrastructure;

network outages or security breaches;

general economic, industry, and market conditions;

customer renewal rates;

increases or decreases in the number of elements of our services or pricing changes upon any renewals of customer agreements;

changes in our pricing policies or those of our competitors;

seasonal variations in sales of our applications, which has historically been highest in the fourth quarter of a calendar year;

fluctuation in market interest rates, which impacts debt interest expense as well as float revenue;

the timing and success of new application and service introductions by us or our competitors or any other change in the competitive dynamics of our industry, including consolidation among competitors, customers, or strategic partners; and

the impact of new accounting rules.

If we are not able to provide new or enhanced functionality and features or keep pace with rapid technological changes and evolving industry standards, we will not be able to remain competitive and the demand for our services will likely decline, which could have a material adverse effect on our business, financial condition, and results of operations.

The markets in which we operate are characterized by changes due to rapid technological advances, additional qualification requirements related to technological challenges, and evolving industry standards and changes in the regulatory and legislative environment. Our future successgrowth strategies will depend upon our ability to anticipate and to adapt to changes in technology and industry standards, and to effectively develop, to introduce, to market, and to gain broad acceptance of new product and service offerings and enhancements incorporating the latest technological advancements. Our success is also subject to the risk of future disruptive technologies, such as large language models, AI, and machine learning. The failure to develop enhancements to our applications for, or that incorporate, technologies such as AI, machine learning, and large language models may impact our ability to increase the efficiency of and reduce costs associated with our customers’ operations. We may not be able to successfully provide new or enhanced functionality and features for our existing solutions, including those that may involve AI or machine learning or be created using AI or machine learning, that achieve market acceptance or that keep pace with rapid technological developments. For example,

We believe a significant portion of our market capitalization is based upon our high Cloud revenue growth rate, and if we are focusedunable to sell our Cloud solutions, including the Dayforce Wallet, into new markets or to further penetrate existing markets, or to increase sales from existing customers, or we have failures in new product functionalities, our revenue may not grow as expected, which could have a material adverse effect on enhancingour market capitalization, and our business, financial condition, and results of operations.

If the features and functionalitymovement of funds to initiate payroll-related transactions on behalf of our HCM solutions to enhance their utility for larger customers with complex, dynamic, and global operations. The success of new or enhanced functionality and features depends on several factors, including their overall effectiveness and the timely completion, introduction, and market acceptance of the enhancements, new features, or applications. Failure in this regardis disrupted, we may significantly impair our revenue growth. In addition, because our solutions are designed to operate on a variety of systems, we will need to continuously modify and enhance our solutions to keep pace with changes in internet-related hardware, iOS, and other software, and communication, browser, and database technologies. We may not be successful in developing these new or enhanced functionality and features, or in bringing them to market in a timely fashion. If we do not continue to innovate and to deliver high-quality, technologically advanced products and services, we will not remain competitive,suffer significant losses which could have a material adverse effect on our business, financial condition, and results of operations. Furthermore, uncertainties about

Our payroll and tax processing services involve the timingmovement of significant funds from the account of a customer to its employees and nature of new functionality, or new functionality to existing platforms or technologies, could increase our research and development expenses. Any failurerelevant taxing authorities. Typically, we rely upon third party vendors to initiate payments on behalf of our applicationscustomers. These payments are made in a large number of jurisdictions, in great volume and in short time windows, all of which raise the possibility of an error that disrupts the movement of funds. Further, these types of transactions are subject to operate effectivelyan increasingly complex series of regulations and laws that we, and/or our third-party vendors must comply with. Failure to comply with future network platformsthese regulations and technologieslaws could reduce the demand for our applications, result in consequences up to and including a regulator enjoining us and/or our third-party vendors from engaging in the movement of funds. In addition, as described elsewhere, the systems on which these payroll-related transactions are based are in some cases antiquated or manual or may be subject to processing and/or technological errors in communicating with third-party technology systems. Any disruption or delay to data flow in these critical time periods could lead to the disruption of fund movement. Any disruption of fund movement could have significant consequences, including defaults under our customer dissatisfaction,agreements and exposure to monetary damages, in addition to reputational harm, that could have a material adverse effect on our business, financial condition and results of operations.

Our aging software infrastructure, technology, and sophistication of these systems, and our migration to new platforms, has and will continue to lead to increased costs, vulnerability to cyber-attack, or disruptions in operations that could have a material adverse effect on our business, market brand, financial condition, and results of operations.

11 | 2023 Form 10-K

Our business continues to demand the use of sophisticated systems and technology, including technology infrastructure assets. These systems and technologies must be refined, updated and/or replaced with more advanced systems on a regular basis in order for us to meet both our customers’ and employees’ demands and expectations. Some of the crucial platforms on which we host our back office and legacy systems are aged and need to be replaced or are in the process of being replaced. Some of our customer instances have, and in the future will be, migrated to public Cloud environments. These technological changes are expensive and have and will continue to impact our profitability and demand attention from our senior leadership. If we are unable to replace our aged, crucial platforms, if some or all these platforms fail to operate due to a software error or infrastructure failure, if we fail to continue to refine and update our systems and technologies on a timely basis or within reasonable cost parameters, if we do not appropriately and timely train our employees to operate any of these new systems, if we fail to migrate to new systems in a manner free from disruption, if the new systems fail to perform as desired, or if we are unable to appropriately protect any of these systems, we could suffer the loss of data, vulnerabilities to cyber-attack, system outages or other performance problems, which could have a material adverse effect on our business, financial condition, and results of operations.

An information security breach of our systems or the loss of, or unauthorized access to, customer information or sensitive company information; the failure to comply with the U.S. Federal Trade Commission’s (“FTC”) ongoing consent order regarding data protection,protection; or a system disruption could have a material adverse effect on our business, market brand, financial condition, and results of operations.