UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

☒ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 20202021

OR

☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from [ ] to [ ]

Commission file number 001-38025

U.S. WELL SERVICES, INC.

(Exact name of registrant as specified in its charter)

Delaware | 81-1847117 | |

(State or other jurisdiction of | (I.R.S. Employer incorporation or | |

organization) | Identification No.) |

1360 Post Oak Boulevard, Suite 1800, Houston, TX | 77056 | |

(Address of principal executive offices) | (Zip Code) |

Registrant’s telephone number, including area code (832) (832) 562-3730

Securities registered pursuant to Section 12(b) of the Act:

Title of each class | Trading Symbol(s) | Name of each exchange on which registered |

CLASS A COMMON SHARES $0.0001, par value WARRANTS | USWS USWSW | NASDAQ Capital Market NASDAQ Capital Market |

Securities registered pursuant to section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. ☐ Yes ☑ No

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. ☐ Yes ☑ No

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. ☑Yes☐ No

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). ☑Yes☐ ☐ No

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and "emerging growth company" in Rule 12b-2 of the Exchange Act.

Large accelerated filer | ☐ | Accelerated filer | ☐ | |

Non-accelerated filer | ☑ | Smaller reporting company | ☑ | |

Emerging growth company | ☑ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). ☐Yes ☐Yes ☑No

The aggregate market value of the voting and non-voting common stock held by non-affiliates of the registrant computed as of June 30, 20202021 (the last business day of the registrant’s most recent completed second fiscal quarter) based on the closing price of the Class A common stock on the Nasdaq Capital Market was $21,639,925.$37,768,341.

As of March 2, 2021,15, 2022, the registrant had 83,600,44577,093,277 shares of Class A Common Stockcommon stock and 2,296,5250 shares of Class B Common Stockcommon stock outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Certain information required to be disclosed in Part III of this report is incorporated by reference from the registrant’s definitive proxy statement or an amendment to this report, which will be filed with the SEC not later than 120 days after the end of the fiscal year covered by this report.

TABLE OF CONTENTS

Cautionary Note Regarding Forward Looking Statements

This Annual Report on Form 10-K (“Annual Report”) contains “forward-looking statements” as defined in Section 27A of the United States Securities Act of 1933, as amended (the “Securities Act”), and Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”). Forward-looking statements usually relate to future events, conditions and anticipated revenues, earnings, cash flows or other aspects of our operations or operating results. All statements, other than statements of historical information, should be deemed to be forward-looking statements. Forward-looking statements are often identified by the words such as “believes,” “expects,” “intends,” “estimates,” “projects,” “anticipates,” “will,” “plans,” “may,” “should,” “would,” “foresee,” or the negative thereof. The absence of these words, however, does not mean that these statements are not forward-looking. These statements are based on our current expectations, beliefs and assumptions concerning future developments and business conditions and their potential effect on us. While management believes that these forward-looking statements are reasonable as and when made, there can be no assurance that future developments affecting us will be those that we anticipate.

All our forward-looking statements involve risks and uncertainties (some of which are significant or beyond our control) and assumptions that could cause actual results to differ materially from our historical experience and our present expectations or projections. Known material factors that could cause actual results to differ materially from those contemplated in the forward-looking statements include those set forth in “Item 1A. Risk Factors” and elsewhere in this Annual Report. We caution you not to place undue reliance on any forward-looking statements, which speak only as of the date hereof. We undertake no obligation to publicly update or revise any of our forward-looking statements after the date they are made, whether because of new information, future events, or otherwise, except to the extent required by law.law.

3

PART I

ItemITEM 1. Business.

BUSINESS

Overview

We are one of the pioneer companies in developing the electric hydraulic fracturingpressure pumping industry. We are based in Houston, Texas and provide our services to oil and natural gas exploration and production (“E&P”) companies in the United States. We are one of the first companies to develop and commercially deploy electric-powered hydraulic fracturingpressure pumping technology (“Clean Fleet®”), which we believe is an industry-changing technology. Our Clean Fleet® technology has a demonstrated track record for successful commercial operation, with over 18,75029,900 electric fracpressure pumping stages completed since the first Clean Fleet® was deployed in July 2014. Our Clean Fleet® technology is supported by a robustan intellectual property portfolio, consisting of 3862 granted patents and an additional 189201 pending patents. We believe that the following characteristics of the Clean Fleet® technology provide the Company with a distinct competitive advantage:

In May 2021, we announced the next generation of our Clean Fleet® technology withthe unveiling of our newly designed Nyx Clean Fleet®. Nyx Clean Fleet® will use our patented PowerCube, driving two independently controlled electric motors and frac pumps to provide 6,000 hydraulic horsepower on a single trailer. We anticipate the first Nyx Clean Fleet® to be delivered in the second quarter of 2022.

Since our announcement in May 2021 of our commitment to becoming an all-electric pressure pumping services provider, we have sold most of our legacy, diesel-powered pressure pumping equipment. We have retained some of our legacy, diesel-powered pressure pumping equipment for use during our transition to support our electric fleets and bridge the time gap between our customers' current service needs and the deployment of our newbuild Nyx Clean Fleets®. Upon delivery, our Nyx Clean Fleets® are intended to replace any conventional fleet in operation.

We currently have five electric fleets representing 258,350 electric hydraulic horsepower and legacy, diesel-powered equipment representing 90,250 hydraulic horsepower. |

|

|

|

|

|

|

|

|

|

|

Currently, we provide our services in the Appalachian, Basin, the Eagle Ford,Permian and the Permian Basin.Uinta Basins. We have demonstrated the capability to expeditiously deploy our fleets to new oil and gas basins when requested by customers. Our customers include ApacheEQT Corporation, Marathon Oil, Range Resources, Shell, BP,Olympus Energy and other leading E&P companies.

Company Formation

On February 21, 2012, U.S. Well Services, LLC (“USWS LLC”) was formed as a Delaware limited liability company and subsequently grew organically from one diesel powered hydraulic fracturing fleet (“Conventional Fleets”) in April 2012 to 14 available fleets representing 684,545 hydraulic horsepower (“HHP”); five of which utilize our patented electric-powered hydraulic fracturing technology (the “Clean Fleet®”).

company. As part of a corporate restructuring in February 2017, all of the outstanding equity interest of USWS LLC was acquired by a newly formed entity, USWS Holdings, LLC (“USWS Holdings”), a Delaware limited liability company that was formed for the purposes of effecting the corporate restructuring and that had no operations of its own. USWS Holdings was acquired by U.S. Well Services, Inc. (f/k/a Matlin & Partners Acquisition Corporation, or “MPAC”) on November 9, 2018, as discussed further under Business Combination herein.

Business Combination

On March 10, 2016, MPAC was incorporated in Delaware as a special purpose acquisition company for the purpose of effecting a merger, capital stock exchange, asset acquisition, stock purchase, reorganization, or other similar business combination with one or more target businesses. On March 15, 2017, MPAC consummated its initial public offering (the “IPO”), following which its shares began trading on the Nasdaq Capital Market (“Nasdaq”).

On November 9, 2018, MPAC acquired USWS Holdings (the “Transaction”) pursuant to a Merger and Contribution Agreement, dated as of July 13, 2018 (as amended, the “Merger and Contribution Agreement”). The Transaction was accounted for as a reverse recapitalization. Under this method of accounting, USWS Holdings iswas treated as the acquirer and MPAC iswas treated as the acquired party.

In connection with the closing of the Transaction, MPAC changed its name to U.S. Well Services, Inc. (“USWS Inc.”) and its trading symbols on Nasdaq from “MPAC,” and “MPACW,” to “USWS” and “USWSW”.

4

Pursuant to the Merger and Contribution Agreement, on November 9, 2018, USWS Inc. issued Class A common stock to certain members of USWS Holdings in exchange for their interests in USWS Holdings and Class B common stock to certain

members of USWS Holdings who retained their interests in USWS Holdings.

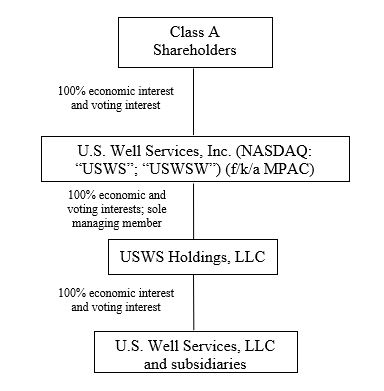

Following the completion of the Transaction, the Company was organized as an “Up-C” structure, meaning that substantially all the Company’s assets and operations are held and conducted by USWS LLC. The Company’s only assets are equity interests representing 97% ownership of USWS Holdings as of December 31, 2020. The Transaction did not include a tax receivable agreement.

During the year ended December 31, 2021, the remaining outstanding shares of Class B common stock were converted into shares of Class A common stock. As of December 31, 2021, there were no shares of Class B common stock issued and outstanding.

During the first quarter of 2021, the remaining noncontrolling interest holders of USWS Holdings exchanged all of their respective shares for the Company’s Class A common stock. Accordingly, USWS Holdings became the Company’s wholly owned subsidiary as of December 31, 2021.

Organizational Structure

The following diagram illustrates the ownership structure of the Company as of December 31, 2020:2021:

Each share of Class B common stock has no economic rights in USWS Inc. but entitles its holder to one vote on all matters to be voted on by shareholders generally. Holders of Class A common stock and Class B common stock vote together as a single class on all matters presented to our shareholders for their vote or approval, except as otherwise required by applicable law. We do not intend to list the Class B common stock on any exchange.

Under the Amended and Restated Limited Liability Company Agreement of USWS Holdings, each share of Class B common stock of USWS Inc., together with one unit of USWS Holdings and subject to certain limitations, is exchangeable (the "Exchange Right") for one share of Class A common stock of USWS Inc. or, at the Company's election, the cash equivalent to the market value of one share of Class A common stock of USWS Inc. The exchange is subject to conversion rate adjustments for stock splits, stock dividends, reclassifications, and other similar transactions. In addition, upon a change in control of USWS Inc., USWS Inc. has the right to require each holder of USWS Holdings units (other than USWS Inc.) to exercise its Exchange Right with respect to some or all of such holder's USWS Holdings units. An exchange of Class B common stock of USWS Inc., together with the corresponding one unit of USWS Holdings, will result in both being cancelled.

Operations

Our operations are organized into a single business segment, which consists of hydraulic fracturingpressure pumping services, and we have one reportable geographical business segment, the United States.

Services

Services

We provide hydraulic fracturingpressure pumping services to E&P companies. Hydraulic fracturingPressure pumping services are performed to enhance the production of oil and natural gas from formations with low permeability and restricted flow of hydrocarbons. Our customers benefit from our expertise in fracturing ofproviding pressure pumping services on horizontal and vertical oil and natural gas-producing wells in shale and other unconventional geological formations.

The process of hydraulic fracturingpressure pumping involves pumping a pressurized stream of fracturing fluid — typically a mixture of water, chemicals, and proppant — into a well casing or tubing to cause the underground mineral formation to fracture or crack. Fractures release trapped hydrocarbon particles and provide a conductive channel for the oil or natural gas to flow freely to the wellbore for collection. The propping agent, or proppant, becomes lodged in the cracks created by the hydraulic fracturingpressure pumping process, “propping” them open to facilitate the flow of hydrocarbons from the reservoir to the well.

5

Our fleets consist mostly of all-electric, mobile hydraulic fracturing unitspressure pumping equipment and other auxiliary heavy equipment to perform fracturingpressure pumping services. We have two designs for our hydraulic fracturing units: (1) Our legacy conventional fleets, which are powered by diesel fuel and utilize traditional internal combustion engines, transmissions, and radiators and (2) our next-generation Clean Fleet®technology, which replaceselectric fleets replace the traditional engines, transmissions, and radiators used in conventional diesel fleets with electric motors powered by electricity createdgenerated by natural gas-fueled turbine generators. Both designsWe utilize high-pressure hydraulic fracturing pumps mounted on trailers. Wetrailers and refer to the group of pump trailers and other equipment necessary to perform a typical fracturing job as a “fleet,”“fleet” and the personnel assigned to each fleet as a “crew.”“crew”.

Since our announcement in May 2021 of our commitment to becoming an all-electric pressure pumping services provider, we have sold most of our legacy, diesel-powered pressure pumping equipment. We have retained some of our legacy, diesel-powered pressure pumping equipment for use during our transition to support our electric fleets and bridge the time gap between our customers' current service needs and the deployment of our newbuild Nyx Clean Fleets®. Upon delivery, our Nyx Clean Fleets® are intended to replace any conventional fleet in operation.

Clean Fleet® Technology

Our Clean Fleet® equipment also allows us to pursue business opportunities outside of the upstream oil and gas sector. We offer power generation services, leasing turbine generators and ancillary power generation equipment under short or long-term arrangements, along with skilled personnel, to provide peaking power and other power generation needs to customers in a variety of industries and markets. Although this has not been a material source of revenue for us historically, we believe that power generation services represent an attractive avenue for future growth.

Clean Fleet® Technology

Our Clean Fleet® combines natural gas turbine generators with uses electric motors and other existing industry equipment to provide fracturingpressure pumping services with numerous advantages over conventional diesel fleets. Our Clean Fleet® technology is a proven technology that has been in commercial operations since July 2014, making us a leading provider of electric-powered hydraulic fracturingpressure pumping services. Our Clean Fleet®technology is supported by a robustan intellectual property portfolio. We have been granted, or have received notice of allowance, for 3862 patents and have an additional 189201 patents pending.

We believe Clean Fleet®technology provides the Company with a distinct competitive advantage over our competitors because of the following characteristics:

| • Industry Leading Environmental Profile – Clean Fleet® technology offers superior emissions performance as compared to traditional diesel-powered pressure pumping equipment. • Reduced Fuel Costs – Clean Fleet® technology uses electric motors to drive its frac pumps instead of internal combustion engines and transmissions used on traditional, diesel-powered pressure pumping equipment. Clean Fleet®’s electric motors are powered by mobile turbine generators or other power sources that can use natural gas produced and conditioned in the field (“Field Gas”), compressed natural gas (“CNG”), liquefied natural gas (“LNG”) or diesel as a fuel source. Our customers typically provide Field Gas or CNG to fuel Clean Fleet®’s turbine generators, which offers a significant cost savings relative to purchasing diesel fuel to power traditional pressure pumping equipment in the current market environment. • Enhanced Wellsite and Community Safety Profile – Clean Fleet® offers superior safety benefits relative to conventional diesel fleets for both workers at the wellsite and inhabitants of nearby communities. • Lower Cost of Ownership – We believe Clean Fleet® offers the best cost of ownership of any commercially available pressure pumping technology. Also, Clean Fleet® uses long-lived components such as electric motors, switchgears, and turbine generators that we estimate will be capable of operating for more than 15 years, while conventional diesel fleets can be expected to operate for less than five years before requiring major component replacements. • Superior Operational Efficiency Profile – Clean Fleet® technology allows us to garner operational efficiencies that are difficult to achieve with traditional diesel-powered pressure pumping technology. By eliminating moving parts associated with internal combustion engines and transmissions, as well as eliminating the need for preventative maintenance activities such as oil filter changes, we are able to reduce maintenance-related downtime. Additionally, the ability of our Clean Fleet® technology to automatically capture and transmit vast amounts of operational, logistical, and environmental data provide us with insights that offer opportunities for continuous improvements in our operational efficiencies.

|

|

|

|

|

|

|

|

|

|

|

Competitive Strengths

We believe that the following strengths will position us to provide high-quality service to our customers and create value for our stockholders:

| • Proprietary Clean Fleet® technology. We are a market leader in electric pressure pumping technology, with five all-electric fleets. Our fleets utilizing Clean Fleet® technology provide substantial cost savings by replacing diesel fuel with natural gas and offer considerable operational, safety and environmental advantages. Clean Fleet® technology offers superior operational efficiency resulting from reduced non-productive time due to repairs, maintenance and failures associated with diesel-powered engines and transmissions. Additionally, Clean Fleet® technology can substantially reduce emissions of air pollutants and noise from the wellsite. With an increasing focus on ESG and increasing returns by our customers, we believe that adoption of this technology in the near term will materially increase and allow us to continue to significantly expand our market share over the next several years. 6 • Strong, employee-centered culture. Our employees are critical to our success and are a key source of our competitive advantage. We continuously invest in training and development for our employees, and as a result, we can provide consistent, high-quality service and safe working conditions for both employees and customers. • Track record for safety. Safety is a critical element of our operations. We focus on providing customers with the highest quality of service by employing a trained and motivated workforce that is rigorously focused on safety. We continuously review safety data and work to develop and implement policies and procedures that ensure the safety and wellbeing of our employees, customers, and the communities in which we operate. Our field operators are empowered to stop work and question the safety of a situation or task performed. We use specialized technology to improve safety for our truck drivers and employ measures to mitigate the risk of respirable silica dust exposure on the wellsite. We believe our record of safe operations makes us an attractive partner for both our customers and our employees. Additionally, we continue to take proactive measures to safeguard the physical health of our employees in response to the novel coronavirus 2019 ("COVID-19") pandemic. Employees capable of working from home were allowed to do so and all individuals entering a Company facility or work location are required to undergo a screening process. • Strong customer relationships supported by contracts and dedications. We have cultivated strong relationships with a diverse group of customers because of the quality of our service, safety performance and ability to work with customers to establish mutually beneficial service agreements. Our contracts and dedications provide customers with certainty of service pricing, allowing them to efficiently budget and plan the development of their wells. Additionally, our contracts and dedications allow us to maintain higher utilization of our fleet and generate revenue and cash flow through industry cycles. We believe our relationships and the structure of our contracts and dedications position us to continue to build long-term partnerships with customers and support stable financial performance. • Modern, high-quality equipment and rigorous maintenance program. Our fleets consist of modern, well-maintained equipment. We invest in high-quality equipment from leading original equipment manufacturers. Moreover, we take proactive measures to maintain the quality of our equipment, using specialized equipment to monitor frac pump integrity and our proprietary FRAC MD® data analytics platform to support preventative maintenance efforts. We believe the quality of our equipment is critical to our ability to provide high quality service to our customers. • Proven, cycle-tested management team. Our management team has a proven track record for building and operating oilfield service companies. Our operating and commercial teams have significant industry experience and longstanding relationships with our clients. We believe our management team’s experience and relationships position us to generate business and create value for stockholders. Additionally, our management team’s rapid response to the COVID-19 pandemic enabled us to maintain adequate liquidity and develop operational procedures allowing for business continuity during a turbulent market environment.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Customer Concentration

Our customers include a broad range of leading E&P companies. For the year ended December 31, 2020, Apache Corporation, Shell, Marathon, Range, and EQT2021, three customers each comprised greater than 10% of our consolidated revenues and collectively represented 50.4% of our consolidated revenues. For the year ended December 31, 2020, five customers each comprised greater than 10% of our consolidated revenues and collectively represented 80.7% of our consolidated revenues.

Suppliers

Suppliers

We purchase a wide variety of raw materials, parts and components that are manufactured and supplied for our operations. We currently rely on a limited number of suppliers from which we procure major equipment components used to maintain, build, or upgrade our custom Clean Fleet® hydraulic fracturing pressure pumping equipment. In addition, some of these components have few suppliers and long lead times to acquire. Historically, we have generally been able to obtain the equipment, parts and supplies necessary to support our operations on a timely basis. While we believe that we will be able to make satisfactory alternative arrangements in the event of any interruption in the supply of these materials and/or equipment by one of our suppliers, we may not always be able to do so. In addition, certainCertain materials for which we do not currently have long-term supply agreements could experience shortages and significant price increases in the future. As a result, we may be unable to mitigate any future supply shortages and our results of operations, prospects and financial condition could be adversely affected.

It is also possible that supply chain constraints or disruptions will result in significant delivery delays with respect to the equipment that we need to build our new Nyx Clean Fleets®. If we are unable to build out our new Nyx Clean Fleets® as a result of any equipment delivery delays, we may not be in position to enter into contracts with customers, which would negatively impact our results of operations.

CompetitionFor the year ended December 31, 2021, purchases from our three largest suppliers represented approximately 27.3% of our overall purchases.

7

Competition

The markets in which we operate are very competitive. We provide services in various geographic regions across the United States, and our competitors include many large and small oilfield service providers, including some of the largest integrated service companies.providers. Our hydraulic fracturingpressure pumping services compete with large, integrated companies such as Halliburton Company, and Schlumberger Limited as well as other companies including Evolution Well Services, Calfrac Well Services Ltd., FTS International Inc., Liberty Oilfield Services Inc., NexTier Oilfield Solutions Inc., Patterson-UTI Energy Inc., ProFrac Services, LLC and ProPetro Services Inc., and RPC Inc. In addition, our industry is highly fragmented, and we compete regionally with a significant number of smaller service providers. Although several of our larger competitors have announced their intention to develop or adopt new electric hydraulic fracturingwell service technologies, we believe that only U.S. Well Services, Inc.the Company and one privately owned competitor are currently offeringsignificant providers of all-electric hydraulic fracturingpressure pumping services.

We believe that the principal competitive factors in the markets we serve are technical expertise, equipment capacity, workforce competency, efficiency, safety record, reputation, experience, and price. Additionally, projects are often awarded on a bid basis, which tends to create a highly competitive environment.

Cyclical Nature of Industry

We operate in a cyclical industry. The key factor driving demand for our services is the level of well completions by E&P companies, which in turn depends largely on the current and anticipated economics of new well completions. Global supply and demand for oil and the domestic supply and demand for natural gas are critical in assessing industry outlook. Demand for oil and natural gas is cyclical and subject to large, rapid fluctuations. E&P companies tend to increase capital expenditures in response to increases in oil and natural gas prices, which generally results in greater revenues and profits for oilfield service companies like us. Increased E&P capital expenditures ultimately lead to greater production, which historically has resulted in increased supplies and reduced prices which in turn tend to reduce demand for oilfield services. For these reasons, the results of our operations may fluctuate from quarter to quarter and from year to year, and these fluctuations may distort comparisons

of results across periods.

Insurance

Insurance

Although we maintain insurance coverage of types and amounts that we believe to be customary in the industry, we are not fully insured against all risks, either because insurance is not available or because of the high premium costs relative to perceived risk. Further, insurance rates have in the past been subject to wide fluctuation and changes in coverage could result in less coverage, increases in cost or higher deductibles and retentions. Liabilities for which we are not insured, or which exceed the policy limits of their applicable insurance, could have a material adverse effect on our business and financial condition.

Environmental and Occupational Health and Safety Regulations

Our operations are subject to stringent laws and regulations governing the discharge of materials into the environment or otherwise relating to environmental protection, and occupational health and safety. Numerous federal, state, and local governmental agencies issue regulations that often require difficult and costly compliance measures that could carry substantial administrative, civil and criminal penalties and may result in permit revocations or modifications, operational disruptions, or injunctive obligations for noncompliance. These laws and regulations may, for example, restrict the types, quantities and concentrations of various substances that can be released into the environment, limit or prohibit construction or drilling activities on certain lands lying within wilderness, wetlands, ecologically or seismically-sensitive areas and other protected areas, or require action to prevent or remediate pollution from current or former operations. Moreover, it is not uncommon for neighboring landowners and other third parties to file claims for personal injury and property damage allegedly caused by the release of hazardous substances, hydrocarbons, or other waste products into the environment. Changes in environmental, health and safety laws and regulations occur frequently, and any changes in the laws or regulations or the interpretation thereof that result in more stringent and costly requirements could materially adversely affect our operations and financial position. We have not experienced any material adverse effect from compliance with these requirements. This trend, however, may not continue in the future.

Below is an overview of some of the more significant environmental, health and safety requirements with which we must comply. Our customers’ operations are subject to similar laws and regulations. Any material adverse effect of these laws and regulations on our customers’ operations and financial position may also have an indirect material adverse effect on our operations and financial position.

Waste Handling. We engage third parties to handle, transport, store and dispose of wastes that are subject to the Resource Conservation and Recovery Act (“RCRA”) and comparable state laws and regulations, which impose requirements regarding the generation, transportation, treatment, storage, disposal and cleanup of hazardous and nonhazardous wastes. With federal approval, the individual states administer some or all the provisions of RCRA, sometimes in conjunction with our own, more stringent requirements. Although certain petroleum production wastes are exempt from regulation as hazardous wastes under RCRA, such wastes may be regulated under state law or constitute “solid wastes” that are subject to the less stringent requirements of nonhazardous waste provisions.

8

Administrative, civil, and criminal penalties can be imposed for failure to comply with waste handling requirements. Moreover, the Environmental Protection Agency (“EPA”) or state or local governments may adopt more stringent requirements for the handling of nonhazardous wastes or re-categorize some nonhazardous wastes as hazardous for future regulation. Indeed, legislation has been proposed from time to time in Congress to re-categorize certain oil and natural gas exploration, development, and production wastes as hazardous wastes. Several environmental organizations have also petitioned the EPA to modify existing regulations to re-categorize certain oil and natural gas exploration, development, and production wastes as hazardous. Any such changes in these laws and regulations could have a material adverse effect on our capital expenditures and operating expenses. Although we do not believe the current costs of managing our wastes, as presently classified, to be significant, any legislative or regulatory reclassification of oil and natural gas exploration and production wastes could increase our costs to manage and dispose of such wastes.

Remediation of Hazardous Substances. The Comprehensive Environmental Response, Compensation and Liability Act (“CERCLA” or “Superfund”) and analogous state laws generally impose liability without regard to fault or legality of the original conduct, on classes of persons who are considered to be responsible for the release of a hazardous substance into the environment or, under some state CERCLA-analogous laws, the release of solid waste. These persons include the current owner or operator of a contaminated facility, a former owner or operator of the facility at the time of contamination, those persons that disposed or arranged for the disposal of the substance at the facility, and transporters who selected the disposal site.

Liability for the costs of removing or remediating previously disposed wastes or contamination, damages to natural resources, and the costs of conducting certain health studies, amongst other things, is strict and joint and several. In addition, it is not uncommon for neighboring landowners and other third parties to file claims for personal injury and property damage allegedly caused by the hazardous substances released into the environment. During our operations, we use materials that, if released, would be subject to CERCLA and comparable state laws. Therefore, governmental agencies or third parties may seek to hold us responsible under CERCLA and comparable state statutes for all or part of the costs to clean up sites at which such substances have been released.

NORM. During our operations, some of our equipment may be exposed to naturally occurring radioactive materials (“NORM”) associated with oil and gas deposits and accordingly may result in the generation of wastes and other materials containing NORM. NORM exhibiting levels of naturally occurring radiation in excess of established state standards are subject to special handling and disposal requirements, and any storage vessels, piping and work area affected by NORM may be subject to remediation or restoration requirements.

Water Discharges. The Clean Water Act, Safe Drinking Water Act, Oil Pollution Act and analogous state laws and regulations impose restrictions and strict controls regarding the unauthorized discharge of pollutants, including produced waters and other gas and oil wastes, into regulated waters. The discharge of pollutants into regulated waters is prohibited, except in accordance with the terms of a permit issued by the EPA, the U.S. Army Corps of Engineers (the “Corps”), or the applicable state. The Clean Water Act has been interpreted by these agencies to apply broadly. The EPA and the Corps releasedAttempting to clarify what constitutes a rule to revise the definition of “watersregulated “water of the United States,”States”, or WOTUS, for all Clean Water Act programs, which went into effect in August 2015. Litigation and political maneuverings surrounding the revised WOTUS definition have been ongoing since that time. On October 22, 2019, the EPA and the Corps issued a final rule to repealpromulgated the 2015 Clean Water Rule in 2015. Following legal challenges and re-codifypolitical maneuverings, the regulatory text that existed prior to 2015 (the “Step One Rule”). The Step OneClean Water Rule became effective on December 23, 2019. On January 23, 2020, the EPAwas repealed and the Corps announcedreplaced with the final Navigable Waters Protection Rule (the “NWPR”), which in 2020. The NWPR revised and narrowed the WOTUS definition. The NWPR replacedwas vacated by an Arizona district court in August 2021, and the Step One Rule and became effective on June 22, 2020. The Biden administration will conduct a reviewagencies announced they would halt implementation of the NWPR and werevert to pre-2015 WOTUS interpretation, which is broader than the NWPR. On December 21, 2021, the EPA and the Corps published a proposed rule in the Federal Register that, once finalized, will formally re-establish the pre-2015 WOTUS definition, with some updates to reflect consideration of Supreme Court decisions. In the proposed rulemaking, the agencies indicated they anticipate a second, future rulemaking that would build upon the foundation of the proposed rule. We expect political maneuverings and litigation regarding the WOTUS definition to continue, creating uncertainty as to what constitutes a protected “water of the United States.” In addition, spill prevention, control and countermeasure plan requirements require appropriate containment berms and similar structures to help prevent the contamination of regulated waters.

Air Emissions. The Clean Air Act (“CAA”) and comparable state laws and regulations regulate emissions of various air pollutants through the issuance of permits and the imposition of other emissions control requirements. The EPA has developed, and continues to develop, stringent regulations governing emissions of air pollutants from specified sources. New facilities may be required to obtain permits before work can begin, and existing facilities may be required to obtain additional permits and incur capital costs to remain in compliance. These and other laws and regulations may increase the costs of compliance for some facilities where we operate, and significant administrative, civil, and criminal penalties can be imposed for failure to comply with air regulations. Obtaining or renewing permits also has the potential to delay the development of oil and natural gas projects.

9

Climate Change. The EPA has determined that greenhouse gases (“GHGs”) present an endangerment to public health and the environment because such gases contribute to warming of the Earth’s atmosphere and other climatic changes. Based on these findings, the EPA has adopted and implemented, and continues to adopt and implement, regulations that restrict emissions of GHGs under existing provisions of the CAA. The EPA also requires the annual reporting of GHG emissions from certain large sources of GHG emissions in the United States, including certain oil and gas production facilities. The U.S. Congress has from time to time considered adopting legislation to reduce emissions of GHGs and almost one-half of the states have already taken legal measures to reduce emissions of GHGs primarily through the development of GHG emission inventories and/or regional GHG cap and trade programs and through the establishment of emissions reduction targets. In December 2015, the United States joined the international community at the 21st Conference of the Parties of the United Nations Framework Convention on Climate Change in Paris, France. The resulting Paris Agreement calls for the parties to undertake “ambitious efforts” to limit the average global temperature, and to conserve and enhance sinks and reservoirs of GHGs. The Paris Agreement entered into force in November 2016. The United States exited the Paris Agreement in November 2020, but rejoined it effective on February 19, 2021. Additional federal and/or state regulations targeting climate change could significantly affect our operations or compliance costs.

Moreover, climate change may cause more extreme weather conditions and increased volatility in seasonal temperatures. Extreme weather conditions can interfere with our operations and increase our costs, and damage resulting from extreme

weather may not be fully insured.

Endangered and Threatened Species. Environmental laws such as the Endangered Species Act (“ESA”) and analogous state laws may impact exploration, development, and production activities in areas where we operate. The ESA provides broad protection for species of fish, wildlife and plants that are listed as threatened or endangered. Similar protections are offered to migratory birds under the Migratory Bird Treaty Act and various state analogs. The U.S. Fish and Wildlife Service may identify previously unidentified endangered or threatened species or may designate critical habitat and suitable habitat areas that it believes are necessary for survival of a threatened or endangered species, or a state may impose new rules limiting oil and gas operations to protect wildlife or habitat, which could cause us or our customers to incur additional costs or become subject to operating restrictions or operating bans in the affected areas.

Regulation of Hydraulic Fracturing and Related Activities. Hydraulic fracturing is an important and common practice that is used to stimulate production of hydrocarbons, particularly natural gas, from tight formations, including shales. The process, which involves the injection of water, sand, and chemicals under pressure into formations to fracture the surrounding rock and stimulate production, is typically regulated by state oil and natural gas commissions. However, federal agencies have asserted regulatory authority over certain aspects of the process. For example, on January 20, 2021, the Biden administration issued an order implementing a 60-day suspension on new oil and gas leases and drilling permits for federal lands and water. On January 27, 2021, the Biden administration issued an executive order that indefinitely pauses new oil and gas leases on federal lands while the administration undertakes a comprehensive review on climate change impacts. In June 2021, a federal judge issued a preliminary injunction to block the leasing pause. The Biden administration resumed approving oil and gas drilling permits on federal lands but is appealing the ruling. Additionally, beginning in August 2012, the EPA issued a series of rules under the CAA that establish new emission control requirements for certain oil and natural gas production and natural gas processing operations and associated equipment. Various political maneuverings resulted in September 2020 amendments to New Source Performance Standards issued in 2016. These amendments rescinded certainwere reversed in June 2021, following a joint resolution passed by Congress and signed by President Biden pursuant to the Congressional Review Act. On November 15, 2021, the EPA published in the Federal Register a proposed rule that would for the first time regulate emissions of methane control requirements(a GHG) and removed the transmission and storage segmentvolatile organic compounds (“VOCs”) from theexisting oil and natural gas source categoryfacilities. The proposed rule would also update, strengthen and were promptly challengedexpand existing rules applicable to new, reconstructed and modified oil and gas facilities. The agency did not provide proposed regulatory text in court, resultingthe proposed rule, but instead sought public comments for a supplemental proposal the agency expects to issue in a temporary stay issued by2022 that may expand on or modify the D.C. Circuit. The amendments are currently under review by the Biden Administration, which could further revise or rescind them.2021 proposed rule, including potentially regulating additional sources of methane and VOC emissions, such as abandoned and unplugged wells The U.S. Department of Interior’s Bureau of Land Management (“BLM”) finalized similar rules in November 2016 that limitwould have limited methane emissions from new and existing oil and natural gas operations on federal lands through limitations on the venting and flaring of gas, as well as enhanced leak detection and repair requirements. The BLM adopted final rules in January 2017. Operators generally had one year from the January 2017 effective date to come into compliance with the rule’s requirements. In December 2017, the BLM temporarily suspended or delayed certain of these requirements set forth in its VentingThis rule and Flaring Rule until January 2019, and ina September 2018 the BLM published a final rule whichamendment to it that scaled back the waste-prevention requirements of the 2016 rule. Both the 2016 rule and the September 2018 revision of that rule were both vacated in 2020 court decisions. LitigationIn a November 2021 multi-agency Emissions Reduction Action Plan, the Biden administration indicated BLM’s intent to promulgate a rule to disincentivize excessive venting or flaring of gas by requiring oil and administrative review of these rules remain ongoing.gas operators to pay royalties to the federal government for vented or flared gas, and to strengthen financial assurance requirements for oil and gas operators. Moreover, in March 2015, the BLM issued a final rule that imposessought to impose requirements on hydraulic fracturing activities on federal and Indian lands, including new requirements relating to public disclosure, wellbore integrity and handling of flowback water. However, the BLM rescinded this rule in December 2017. In January 2018, California and a coalition of environmental groups filed suit in the Northern District of California to challenge the BLM’s rescission of the 2015 rule. In March 2020, the California district court upheld the BLM’s rescission of the hydraulic fracturing rule, and the plaintiff groups appealed. This litigation and administrative review of federal hydraulic fracturing regulations is ongoing. Many states also have hydraulic fracturing regulations in place that may be duplicative of the rescinded

10

federal regulations, and the BLM requires operators to comply with the law of the state where the federal or Indian land is located.

Further, legislation to amend the Safe Drinking Water Act to repeal the exemption for hydraulic fracturing (except when diesel fuels are used) from the definition of “underground injection” and require federal permitting and regulatory control of hydraulic fracturing have been proposed in recent sessions of Congress. Several states and local jurisdictions in which we or our customers operate also have adopted or are considering adopting regulations that could require disclosure of the chemical constituents of the fluids used in the fracturing process, restrict, or prohibit hydraulic fracturing in certain circumstances, impose more stringent operating standards and/or require the disclosure of the composition of hydraulic fracturing fluids.

Federal and state governments have also begun investigating whether the disposal of produced water into underground injection wells has caused increased seismic activity in certain areas. For example, in December 2016, the EPA released its final report regarding the potential impacts of hydraulic fracturing on drinking water resources, concluding that “water cycle” activities associated with hydraulic fracturing may impact drinking water resources under certain circumstances such as water withdrawals for fracturing in times or areas of low water availability, surface spills during the management of fracturing fluids, chemicals or produced water, injection of fracturing fluids into wells with inadequate mechanical integrity, injection of fracturing fluids directly into groundwater resources, discharge of inadequately treated fracturing wastewater to surface waters, and disposal or storage of fracturing wastewater in unlined pits. The results of these studies could lead the federal government

and has led some state governments to develop and implement additional regulations, including stricter regulatory requirements relating to the location and operation of underground injection wells or requirements regarding the permitting of produced water disposal wells or otherwise.

Increased regulation of hydraulic fracturing and related activities (whether as a result of the EPA study results or resulting from other factors) could restrict or prohibit our ability to operate in certain areas or subject us and our customers to additional permitting and financial assurance requirements, more stringent construction specifications, increased monitoring, reporting and recordkeeping obligations, and plugging and abandonment requirements. New requirements could result in increased operational costs for us and our customers and reduce the demand for our services.

OSHA Matters. The Occupational Safety and Health Act (“OSHA”) and comparable state statutes regulate the protection of the health and safety of workers. In addition, the OSHA hazard communication standard requires that information be maintained about hazardous materials used or produced in operations and that this information be provided to employees, state and local government authorities, and the public.

Employees

As of December 31, 2020,2021, we had 638414 full-time employees and no part-time employees. We are not a party to any collective bargaining agreements and have not experienced any strikes or work stoppages. We believe our relationships with our employees are excellent. From time to time, we will utilize the services of independent contractors to perform various field and/or other services.

Intellectual Property

We have been granted or have received notice of allowance for 3862 patents, which begin to expire in late 2033, and have an additional 189201 patents pending. OurWe have filed patents in an effort to protect our Clean Fleet® technology from being duplicated by competitors. These patents should help provide unique competitive advantages in operating areas where noise and emissions are key concerns. We also use proprietary FRAC MD® technology to support our preventative maintenance program and prolong equipment useful life. This technology utilizes specialized equipment to capture and analyze vibrations to identify component stress so maintenance can be performed prior to catastrophic failures. Our fleets continuously transmit data captured in the field to our IoT platform. This data is analyzed by our team of data scientists in order improve our operations by garnering insights that inform real-time decision making in the field and drive our machine learning capabilities to increase efficiency and extend equipment useful life.

Availability of Information

Our website address is www.uswellservices.com. Information contained on our website is not part of this Annual Report on Form 10-K. Our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, and any other materials filed with, or furnished to, the U.S. Securities and Exchange Commission (“SEC”) by us are available on our website (under “Investor Relations”) free of charge, as soon as reasonably practicable after such reports are filed with, or furnished to, the SEC. Alternatively, you may access these reports at the SEC’s website at www.sec.gov.

ItemITEM 1A. Risk Factors.RISK FACTORS

The following risk factors apply to our business and operations and the industry in which we operate. These risk factors are not exhaustive, and investors are encouraged to perform their own investigation with respect to our business, financial condition, and prospects. You should carefully consider the following risk factors in addition to the other information included in this Annual Report, including matters addressed in the section entitled “Cautionary Note Regarding Forward-Looking Statements.” We may face additional risks and uncertainties that are not presently known to us, or that we currently deem immaterial, which may also impair our business, financial condition, or prospects. The following discussion should be read in conjunction with our consolidated financial statements and notes to the consolidated financial statements included in this Annual Report.Report on Form 10-K.

Risk Factors Summary

The following is a summary of the risk factors that apply to our business and operations.operations and the industry in which we operate. The list below is not exhaustive, and investors should read this “Risk Factors” section in full. Some of the risks we face include:

Risks related to our business and industry

12

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Risks related to our securities

13

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Risks related to general and other factors

| • We are subject to risks related to pandemics or epidemics, including the ongoing COVID-19 global pandemic. • Competition may adversely affect our ability to market our services. • We may be subject to interruptions or failures in our information technology systems. • We are subject to cyber security risks. A cyber incident could occur and result in information theft, data corruption, operational disruption and/or financial loss. • We are exposed to risks related to our ability to employ and retain key employees, technical personnel and other skilled or qualified workers. • Anti-indemnity provisions enacted by many states may restrict or prohibit a party’s indemnification of us. • A terrorist attack or armed conflict could harm our business. • We are exposed to the credit risk of our customers, and any material nonpayment or nonperformance by our customers could adversely affect our financial results. • Delays or restrictions in obtaining permits by us for our operations or by our customers for their operations could impair our business. • We may be negatively impacted by inflation. • Rising interest rates may adversely impact our business. • Unanticipated changes in effective tax rates or adverse outcomes resulting from examination of our income or other tax returns could adversely affect our financial condition and results of operations. • Failure to maintain an effective system of internal controls could adversely impact our ability to report our results of operations and financial condition accurately and in a timely manner.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Risks Related to Our Business and Industry

Our transition from the diesel pressure pumping market has negatively impacted and may continue to negatively impact our liquidity and our ability to generate revenues and service our outstanding indebtedness for a period of time.

Since our announcement in May 2021 of our commitment to becoming an all-electric pressure pumping services provider, we have sold most of our legacy, diesel-powered pressure pumping equipment, which has resulted in a reduction in the number of fleets we have available to provide pressure pumping services. Until we can complete the build out of additional all-electric pressure pumping equipment, we expect to generate less revenue, which has adversely impacted and may continue to adversely impact our ability to service our outstanding indebtedness. Additionally, the decrease in revenue has resulted in and may continue to result in a reduction in the borrowing base available under our ABL Credit Facility, which may adversely impact our liquidity. Furthermore, we have also expanded our operations into new geographical areas as our fleet availability has been reduced, which has resulted in a reduction in our economies of scale which has and may continue to have an adverse impact on the profitability of our operations.

Our business depends on the level of capital spending and exploration and production activity by the onshore oil and natural gas industry in the United States, and the level of such activity is affected by industry conditions that are beyond our control.

Our business is directly affected by the willingness of our customers to make expenditures to explore for, develop and produce oil and natural gas from onshore resources in the United States. The willingness of our customers to undertake these activities depends largely upon prevailing industry conditions that are influenced by numerous factors over which we have no control, including:

| • prices, and expectations about future prices, for oil and natural gas; • domestic and foreign supply of, and demand for, oil and natural gas and related products; • the level of global and domestic oil and natural gas inventories; • the supply of and demand for hydraulic fracturing and other oilfield services and equipment in the United States; 14 • the cost of exploring for, developing, producing and delivering oil and natural gas; • available pipeline, storage and other transportation capacity; • lead times associated with acquiring equipment and products and availability of qualified personnel; • the discovery rates of new oil and natural gas reserves; • federal, state and local regulation of hydraulic fracturing and other oilfield service activities, as well as exploration and production activities, including public pressure on governmental bodies and regulatory agencies to regulate our industry; • the availability of water resources, suitable proppant and chemicals in sufficient quantities for use in hydraulic fracturing fluids; • geopolitical developments and political instability in oil and natural gas producing countries; • actions of the Organization of the Petroleum Exporting Countries (“OPEC”), its members and other state-controlled oil companies relating to oil price and production controls; • advances in exploration, development and production technologies or in technologies affecting energy consumption; • the price and availability of alternative fuels and energy sources; • weather conditions, natural disasters and other catastrophic events such as an epidemic or pandemic disease outbreak; • uncertainty in capital and commodities markets and the ability of oil and natural gas producers to raise equity capital and debt financing; • U.S. federal, state and local and non-U.S. governmental regulations and taxes; and • epidemics, pandemics, or other major public health issues, such as the COVID–19 pandemic.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

The oil and natural gas industry is volatile. For example, the price of oil has fallen significantly since the beginning of 2020, due in part to concerns about the COVID–19 coronavirus pandemic and its impact on the worldwide economy and global demand for oil. We expect continued volatility in oil and natural gas prices, as well as in the level of exploration and development activities by our customers. A prolonged economic slowdown or recession in the United States, adverse events relating to the energy industry or regional, national, and global economic conditions and factors could negatively impact exploration and production activity and the level of drilling and completion activity by some of our customers. This volatility may result in a decline in the demand for, or adversely affect the price of, our services. In addition, material declines in oil and natural gas prices, the development of oil and natural gas reserves in our market areas or drilling or completion activity in the U.S. oil and natural gas shale regions, could have a material adverse effect on our business, financial condition, prospects, results of operations and cash flows.

The volatility of oil and natural gas prices may adversely affect the demand for our services and negatively impact our results of operations.

The demand for our services is substantially influenced by current and anticipated crude oil and natural gas commodity prices and the related levels of capital spending and drilling activity in the areas in which we have operations. Volatility or weakness in crude oil and natural gas commodity prices (or the perception that crude oil and natural gas commodity prices will decrease) affects the spending patterns of our customers, and the products and services we provide are, to a substantial extent, deferrable in the event oil and natural gas companies reduce capital expenditures. As a result, we may experience lower utilization of, and may be forced to lower our rates for, our equipment and services.

Historical prices for crude oil and natural gas have been extremely volatile and are expected to continue to be volatile. The market prices for crude oil and natural gas depend on factors beyond our control, including worldwide and domestic supplies of crude oil and natural gas and actions taken by foreign oil and gas producing nations. For example, the price of oil has fallen significantly since the beginning of 2020, due to the COVID–19 coronavirus pandemic and its impact on the worldwide economy and global demand for oil. Weaker economic activity and lower demand for crude oil, driven by the onset of the COVID-19 coronavirus pandemic, has adversely impacted our business resulting in a sharp decrease in both our active fleet count and the utilization of our active fleets. As such, we are experiencing considerable uncertainty in our near-term business prospects and ability to forecast future performance. We expect that our financial performance will be highly uncertain until global economic activity recovers. Beyond the current significant reduction in crude oil prices resulting from the COVID-19 coronavirus pandemic, we expect continued volatility in oil and natural gas prices, as well as in the level of exploration and development activities by our customers.

As a result of declines and volatility in commodity prices, E&P companies moved to significantly cut costs, both by decreasing drilling and completion activity and by demanding price concessions from their service providers, including providers of hydraulic fracturing services. In turn, service providers, including hydraulic fracturing service providers, were forced to lower their operating costs and capital expenditures, while continuing to operate their businesses in an extremely competitive environment. Prolonged periods of price instability in the oil and natural gas industry will adversely affect the demand for our products and services, our financial condition, prospects and results of operations and our ability to service our debt or fund capital expenditures.

For example, the price of oil fell significantly in 2020, due to the COVID–19 pandemic and its impact on the worldwide economy and global demand for oil. As a result, E&P companies moved to significantly cut costs, both by decreasing drilling and completion activity and by demanding price concessions from their service providers, including providers of pressure pumping services. In turn, service providers, including pressure pumping service providers, were forced to lower their operating costs and capital expenditures, while continuing to operate their businesses in an extremely competitive environment.

Oil and natural gas prices continued to fluctuate in fiscal year 2021, with the ongoing COVID-19 pandemic contributing to volatility and uncertainty. Towards the end of the year, prices increased significantly and with the increase in commodity prices demand for our services improved. However, persistent commodity price volatility, supply chain disruptions and deteriorating economic conditions could impact our near-term business prospects and ability to forecast future performance. We expect our customers to react to commodity price volatility by adjusting their level of capital spending accordingly.

15

Additionally, fuel conservation measures, alternative fuel requirements and increasing consumer demand for alternatives to oil and natural gas could reduce the demand for oil and natural gas products, creating downward pressure on commodity prices and the prices we are able to charge for our services.

Our level of current and future indebtedness could adversely affect our financial condition.

As of December 31, 2020,March 15, 2022, we had $23.7$6.4 million of borrowings outstanding, with available capacity of $8.7$9.5 million, under our ABL credit facility, $246.3Credit Facility. Our ABL Credit Facility is scheduled to mature on April 1, 2025. As of March 15, 2022, we had $116.7 million of borrowings outstanding under our senior secured term loan, $10.0Term A Loan and Term B Loan (collectively the "Senior Secured Term Loan") and an additional $21.5 million outstanding under our Paycheck Protection ProgramTerm C Loan (“PPP Loan”),pursuant to our Senior Secured Term Loan Agreement. Our Senior Secured Term Loan and $22.0Term C Loan are scheduled to mature on December 5, 2025. On our Senior Secured Term Loan, we are required to make quarterly principal payments of $1.25 million until March 31, 2023 and $5.0 million from June 30, 2023 through September 30, 2025, with final payment due at maturity. Our Term C Loan has a PIK interest rate of 14.0% and contains provisions with up to a 100% premium payable upon any repayment, prepayment or acceleration. Our obligations under our ABL Credit Facility, Senior Secured Term Loan and Term C Loan are secured by substantially all our assets.

As of March 15, 2022, we had $25.0 million outstanding under our Business Loan Agreement (“USDA Loan”) pursuant to the U.S. Department of Agriculture, Business & Industry Coronavirus Aid, Relief, and Economic Security Act Guaranteed Loan Program. Our PPP Loan is scheduled to mature in five years from July 2020.Loan. Our USDA Loan is scheduled to mature on November 12, 2030, subject to equal monthly principal payments beginning on December 12, 2023. We are required to make quarterly principal payments of 2.0% per annum of the initial principal balanceOur USDA Loan is secured by certain of our seniorpressure pumping equipment.

As of March 15, 2022, the aggregate outstanding balance under our equipment financing notes was $7.7 million, of which $3.1 million is due within one year. Our equipment financing notes are secured term loan,by certain of our pressure pumping equipment.

Certain of our debt instruments include provisions, such as PIK interest, repayment and other premiums, and fees which commenced on January 15, 2020,will result in additionthe amount of outstanding debt to certain principal payments as required by the Fourth Amendment to the senior secured term loan which we entered into on November 12, 2020, with final payment due at maturity on December 25, 2025. Our ABL credit facility is scheduled to mature on February 6, 2024.increase significantly over time. Upon maturity of our indebtedness, we will be required to repay, extend or refinance our indebtedness. We may not be able to extend, replace or refinance any one or all of our existing debt financing agreements on terms reasonably acceptable to us, or at all. Our obligations under both our ABL credit facility and senior secured term loan are secured by substantially all our assets. Our PPP Loan is unsecured, and our USDA Loan is secured by certain of our fracturing equipment. In addition, we have entered into several security agreements with financial institutions for the purchase of certain fracturing equipment. As of December 31, 2020, the aggregate outstanding balance under our equipment financing arrangements was $12.9 million, of which $3.5 million is due within one year. Our equipment financing arrangements are secured by certain of our fracturing equipment. If we are unable to meet our debt service obligations, our lenders under our ABL credit facility, senior secured term loan,Credit Facility, Senior Secured Term Loan, Term C Loan, USDA Loan, or equipment financing arrangementsnotes can seek to foreclose on our assets. For more information about our debt financing agreements and equipment financing arrangements,notes, please see “Item 8. Financial Statements and Supplementary Data – Note 911 - Debt.Debt and Note 20 - Subsequent Events.”

As of March 15, 2022, we had $126.9 million of principal, including PIK interest, outstanding of the Convertible Senior Notes, which are convertible into shares of the Company’s Class A common stock at the option of the holders. The Convertible Senior Notes, subject to earlier conversion, are due and payable on June 5, 2026 in shares of Class A common stock equal to the entire outstanding and unpaid principal balance, plus any PIK interest, subject to certain limitations on the number of shares of Class A common stock that may be issued and which would require the Company to settle the conversion in payment partially in cash.

Our ability to meet our debt service obligations will be dependent upon future performance, which in turn will be subject to general economic conditions, industry cycles and financial, business, and other factors affecting our operations, many of which are beyond our control. Our business may not continue to generate sufficient cash flow from operations to pay our debt service obligations when due. Moreover, we may incur additional indebtedness, which would increase the amount of cash flow we need to service debt obligations. If we are unable to generate sufficient cash flow from operations, we may be required to sell assets, to restructure or refinance all or a portion of such indebtedness or to obtain additional financing. We cannot assure you, however, that we would be able to sell assets, restructure, or refinance all or a portion of our indebtedness or obtain additional financing on commercially reasonable terms or at all. Moreover, any failure to make scheduled payments of interest and principal on our outstanding indebtedness would likely result in a reduction of our credit rating,profile, which could harm our ability

to incur additional indebtedness on acceptable terms. To the extent inadequate liquidity or other considerations require us to seek to restructure or refinance our indebtedness, our ability to do so will depend on numerous factors, including many beyond our control, such as the condition of the capital markets and our financial condition at such time. Any new or refinancing or restructuring of our indebtedness could be at higher interest rates or other unfavorable terms and may require us to comply with more onerous covenants, which could further restrict our business operations. Furthermore, our current and future indebtedness may discourage acquisition bids or merger proposals, which may adversely affect the market price of our Class A common stock.

16

Our debt financing agreements subject us to financial and other restrictive covenants. These restrictions may limit our operational or financial flexibility and could subject us to potential defaults under our credit facilities.

Our debt financing agreements subject us to restrictive covenants, including, among other things, limitations (each of which is subject to certain exceptions) on our ability to incur debt, grant liens, enter into transactions resulting in fundamental changes (such as mergers or sales of all or substantially all of our assets) and asset sales or other types of dispositions, restrict subsidiary dividends or other subsidiary distributions, enter into transactions with affiliates and swap counterparties, make investments and restricted payments, permit subsidiaries to provide guarantees to other material debt, and enter into leases and sale and lease back arrangements.

Additionally, our ABL credit facilityCredit Facility is subject to a springing fixed charge coverage covenant. For a description of the covenants under our ABL credit facility,Credit Facility, please see “Item 8. Financial Statements and Supplementary Data – Note 911 - Debt.” If we are unable to remain in compliance with the covenants of our ABL credit facility,Credit Facility, then amounts outstanding thereunder may be accelerated and become due immediately. We might not have, or be able to obtain, sufficient funds to make these accelerated payments, and any such acceleration could have a material adverse effect on our financial condition and results of operations.

Moreover, subject to the limits contained in our debt financing agreements, we may incur substantial additional debt from time to time. Any borrowings we may incur in the future would have several important consequences for our future operations, including that:

The phase-out of the London Interbank Offered Rate, or LIBOR, may adversely affect a portion of our outstanding debt.

|

|

|

|

|

|

|

|

In July 2017, the United Kingdom’s Financial Conduct Authority, which regulates LIBOR, announced that it intends to phase out LIBOR by the end of 2021. The ICE Benchmark Administration, the administrator of LIBOR, has ceased to publish USD LIBOR for the one week and two month USD LIBOR tenors. Further, on March 5, 2021, the ICE Benchmark Administration announced its intention to cease the publication of the remaining USD LIBOR tenors after June 30, 2023. While this announcement extends the transition period to June 2023, the United States Federal Reserve concurrently issued a statement advising banks to stop new USD LIBOR issuances by the end of 2021. In light of these recent announcements, the future of LIBOR at this time is uncertain and any changes in the methods by which LIBOR is determined or regulatory activity related to LIBOR’s phase-out could cause LIBOR to perform differently than in the past or cease to exist. Changes in the method of determining LIBOR, or the replacement of LIBOR with an alternative referencefloating borrowing rate, may adversely affect our ability to refinance our indebtedness.

Financial regulators are working to transition away from the London Interbank Offered Rate (“LIBOR”) as a reference rate for financial contracts. On July 27, 2017, the Financial Conduct Authority announced that it would phase out LIBOR as a benchmark by the end of 2021. It is unclear whether new methods of calculating LIBOR will be established such that it continues to exist after 2021.borrowing costs. While our ABL credit facilityCredit Facility and senior secured term loanSenior Secured Term Loan are scheduled to mature in February 2024April 2025 and May 2024,December 2025, respectively, potential changes, or uncertainty related to such potential changes in interest rate benchmarks may adversely affect our ability to refinance our indebtedness. ThereWe cannot predict the effect of the potential changes to LIBOR or the establishment and use of alternative floating borrowing rates on the portion of our outstanding debt that is no guarantee thatLIBOR based. Challenges in changing to a transition from LIBOR to an alternative will notdifferent borrowing interest rate may result in financial market disruptions, significant increases in benchmark rates, or borrowing costs to borrowers, anyless favorable pricing on certain of whichour debt instruments and could have an adverse effect on our business, financial condition,results and results of operations.

We may not be entitled to forgiveness of our recently received PPP Loan, and our application for the PPP Loan could in the future be determined to have been impermissible or could result in damage to our reputation.

On July 28, 2020, we received proceeds of $10.0 million from a loan under the Paycheck Protection Program (the “PPP”), of the Coronavirus Aid, Relief and Economic Security Act (as amended, the “CARES Act”), which we used to retain current employees, maintain payroll, and make lease and utility payments. A portion of the PPP Loan may be forgiven by the Small Business Administration (the “SBA”) upon our application in accordance with the SBA requirements and in compliance with the CARES Act. Under the CARES Act, loan forgiveness is available for the sum of documented payroll costs, covered lease payments, covered mortgage interest and covered utilities during the twenty-four-week period beginning on the date the loan