Page | ||||

3 | ||||

Item 1. | 4 | |||

Item 1A. |

| |||

Item 1B. |

| |||

Item | 23 | |||

Item 2. |

| |||

Item 3. |

| |||

Item 4. |

| |||

Item 5. |

| |||

Item 6. |

| |||

Item 7. | Management’s Discussion and Analysis of Financial Condition and Results of Operations |

| ||

Item 7A. |

| |||

Item 8. |

| |||

Item 9. | Changes in and Disagreements with Accountants on Accounting and Financial Disclosure |

| ||

Item 9A. |

| |||

Item 9B. |

| |||

Item 10. |

| |||

Item 11. |

| |||

Item 12. | Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters |

| ||

Item 13. | Certain Relationships and Related Transactions, and Director Independence |

| ||

Item 14. |

| |||

Item 15. |

| |||

| ||||

2

SPECIAL NOTE REGARDING FORWARD-LOOKING STATEMENTS

This Annual Report contains “forward-looking statements.” Such statements can be identified by the use of forward-looking terminology such as “objectives,” “goals,” “preliminary,” “range,” “believes,” “expects,” “may,” “estimates,” “will,” “should,” “plans” or “anticipates” or the negative thereof or other variations thereon or comparable terminology, or by discussions of strategy. Readers are cautioned that any such forward-looking statements are not guarantees of future performance and may involve significant risks and uncertainties, and that actual results may vary materially from those anticipated or implied in the forward-looking statements as a result of various factors. Among the factors that significantly impact the metals distribution industry and our business are:

| • highly cyclical fluctuations resulting from, among others, seasonality, market uncertainty, and costs of goods sold; • remaining competitive and maintaining market share in the highly competitive and fragmented metals distribution industry; • managing the costs of purchased metals relative to the price at which we sell our products during periods of rapid price escalation or deflation; • the management of inventory and other costs and expenses; • customer, supplier, and competitor consolidation, bankruptcy, or insolvency; • the impairment of goodwill that could result from, among other things, volatility in the markets in which we operate; • the impact of geopolitical events; • future funding for postretirement employee benefits may require substantial payments from current cash flow; • the failure to effectively integrate newly acquired operations; • the regulatory and other operational risks associated with our operations located outside of the United States (“U.S.”); • the ability of management to focus on North American and foreign operations; • currency fluctuations in the U.S. dollar versus the Canadian dollar, the Chinese renminbi, the Mexican peso, and the Hong Kong dollar; • the adequacy of our efforts to mitigate cyber security risks and threats; • reduced production schedules, layoffs or work stoppages by our own, our suppliers’, or customers’ personnel; • certain employee retirement benefit plans are underfunded and the actual costs could exceed current estimates; • prolonged disruption of our processing centers; • the ability to retain and attract management and key personnel; • our risk management strategies may result in losses; • the incurrence of substantial costs or liabilities to comply with, or as a result of violations of, environmental laws; • the impact of new or pending litigation against us; • the risk of product liability claims; • our indebtedness and the covenants in instruments governing such indebtedness; • the ability to comply with the terms of our asset-based credit facility; and • the influence of a single investor group over our policies and procedures.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

These risks and uncertainties could cause actual results to differ materially from those suggested by the forward-looking statements. Forward-looking statements should, therefore, be considered in light of various factors, including those set forth in this Annual Report under “Risk Factors” and the caption “Industry and Operating Trends” included in “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and elsewhere in this Annual Report. Moreover, we caution you not to place undue reliance on these forward-looking statements, which speak only as of the date they were made. We do not undertake any obligation to revise or publicly release any revisions to these forward-looking statements to reflect events or circumstances after the date of this Annual Report or to reflect the occurrence of unanticipated events.

3

PART I

ITEM 1. BUSINESS.

|

|

Ryerson Holding Corporation (“Ryerson Holding”), a Delaware corporation, is the parent company of Joseph T. Ryerson & Son, Inc. (“JT Ryerson”), a Delaware corporation. Affiliates of Platinum Equity, LLC (“Platinum”) own approximately 21,037,5003,924,478 shares of our common stock, which is approximately 55%11.5% of our issued and outstanding common stock.

We are a leading metals service center, value-added processor and distributor of industrial metals with operations in the United States ("U.S.") through JT Ryerson and other U.S. subsidiaries, in Canada through our indirect wholly-owned subsidiary Ryerson Canada, Inc., a Canadian corporation (“Ryerson Canada”), and in Mexico through our indirect wholly-owned subsidiary Ryerson Metals de Mexico, S. de R.L. de C.V., a Mexican corporation (“Ryerson Mexico”). In addition to our North American operations, we conduct metal processing and distribution operations in China through an indirect wholly-owned subsidiary, Ryerson China Limited, a Chinese limited liability company (“Ryerson China”). Unless the context indicates otherwise, Ryerson Holding, JT Ryerson, Ryerson Canada, Ryerson Mexico, and Ryerson China together with their subsidiaries, are collectively referred to herein as “Ryerson,” “we,” “us,” “our,” or the “Company.”

Our Company

We are one of the largest value-add processors and distributors of industrial metals in North America measured in terms of sales. We have approximately 4,0004,600 employees across 91110 facilities in North America and four facilities in China. Through this network we serve approximately 40,000 customers across a wide range of manufacturing end-markets. Our customers range from local, independently owned fabricators and machine shops to large, international original equipment manufacturers. We carry a full line of nearlyapproximately 75,000 products in stainless steel, aluminum, carbon steel, and alloy steels and a limited line of nickel and red metals in various shapes and forms. In addition to our metals products, we offer numerous value-added processing and fabrication services, and nearly 80% of the products we sell are processed to meet customer requirements.

Our business strategy includes providing a superior level of customer service and responsiveness, technical services, and inventory management solutions while maintaining low operating costs in order to maximize financial results. Our growth strategy is based on increasing our operating results through organic growth activities and strategic acquisitions.

To that end, we continue to focus on our interconnected network, systems, and to enhanceenhancing our value-added services and online presence to provide increased access, functionality, and flexibility to our customers. We are using advanced analytics to improve pricing and inventory utilization. Our service centers are strategically located near our customers, which permits us to quickly process and deliver our products and services, often the day after receiving an order. We own, lease, or contract a fleet of tractors and trailers, allowing us to efficiently meet our customers’ delivery demands. Our range of products together with our breadth of services allows us to service a diverse customer base and to create long-term partnerships with our customers and enhances our profitability.

We focus on strategic acquisitions that complement and enhance our product, customer, and geographic diversification. Ryerson’s M&A strategy includes both transformative turnaround acquisitions and value-add, bolt-on acquisitions. Recently, Ryerson has focused on bolt-on acquisitions. In 2023, Ryerson's acquisitions such as its September 1, 2021 acquisitionincluded BLP Holdings, LLC, Norlen Incorporated, TSA Processing, and Hudson Tool Steel Corporation. Please refer to the Section titled “Acquisitions” of Specialty Metals Processing, Inc. (“SMP”). SMP is a toll processorItem 7, “Management’s Discussion and Analysis of stainless steel, aluminum, titanium,Financial Conditions and nickel alloy products that expanded the Company’s value-add servicesResults of Operations,” and Note 2 — “Acquisitions” of Part II, Item 8 "Financial Statements and Supplementary Data" for further information regarding all acquisitions made in a variety of industries including aerospace. SMP was purchased for $14.0 million, net of cash acquired.2023.

Industry Overview

Metals service centers serve as key intermediaries between metal producers and end users of metal products. They purchase in scale and sell in smaller quantities. End-users often look for “one-stop” suppliers that offer lower order volumes, shorter lead times, more reliable delivery, and processing services. Metal producers mainly sell metals in the form of standard-sized coils, sheets, plates, structurals, bars, and tubes in large quantities, with longer lead times, and limited inventory. Metal service centers serve as key intermediaries closing the gap between metal producers’ supply and end-users’ demand.

By aggregating end-users’ demand and purchasing metal in bulk to take advantage of economies of scale, metals service centers may purchase, process, and deliver metal to end‑users in a more efficient and cost‑effective manner than the end‑user may achieve by dealing directly with the primary producer. Further, specialized metals processing equipment is costly and requires high‑volume production to be cost effective. In addition,effective, and many customers are not able or willing to invest in the necessary technology, equipment, and warehousing of inventory to efficiently and effectively perform metal processing for their own operations. Due to this, many customers have reduced their in-house processing capabilities, opting to source processed metal from service centers like us. This

4

saves our customers time, labor, and expense, reducing their overall manufacturing costs, while permitting us to increasingly focus on value-added

services and increasingexpanding our mix of fabrication mix.products, which typically sell at higher margins. This supports our capital expenditures on processing equipment to grow annual gross profit margin.

Our industry is highly fragmented with the largest companies accounting for only a small percentage of total market share. The majority of metals services companies have limited product lines and inventories, with customers located in a specific geographic area. In general, competition is based on quality, service, price, and geographic proximity. We primarily compete with other metals service centers and to a lesser extent with metal producers.

The metals service center industry typically experiences cash flow trends that are counter-cyclical to the revenue and volume growth of the industry. During an industry downturn, companies generally reduce working capital assets and generate cash as inventory and accounts receivable balances decline. Asdecline, and as a result, operating cash flow and liquidity tend to increase during a downturn, which typically facilitates industry participants’ ability to cover fixed costs and repay outstanding debt.downturn.

Competitive Strengths

Leading Market Position in North America.

Based on sales, we believe we are one of the largest service center companies for carbon, stainless steel, and aluminum in the North American market where we have a broad geographic presence with 91110 facilities.

Our service centers are located near our customer locations, enabling us to provide timely deliverydeliver to customers across numerous geographic markets. Additionally, our widespread network of locations in the United States,U.S., Canada, and Mexico helps us to utilize our expertise to more efficiently serve customers with complex supply chain requirements across multiple manufacturing locations. We believe this is a key differentiator for customers who need a supplier that can reliably and consistently support them. Our ability to transfer inventory among our facilities better enables us to more timely and profitably source and process specialized items at regional locations throughout our network than if we were required to maintain inventory of all products and specialized equipment at each location.

Broad Geographic Reach Across Attractive End Markets.

Our operations serve a diverse range of industries including commercial ground transportation, metal fabrication and machine shops, industrial machinery and equipment manufacturing, consumer durable equipment, HVAC manufacturing, construction equipment manufacturing, food processing and agricultural equipment manufacturing, and oil and gas. We believe this broad range of industries in which we sell our products and services reduces our risk related to a downturn in a specific industry. We believe that our ability to quickly adjust our offeringofferings based on regional and industry specific trends creates stability while also providing the opportunity to access specific growth markets. We are focused on expanding our presence within growing, secular markets, including electric vehicles and renewable energy.

Established Platform for Organic and Acquisition Growth.

Our growth strategy is based on increasing our operating results through organic growth activities and strategic acquisitions that enhance our service, product, customer, and geographic diversification. Our strategies include investing in value-added processing capabilities, analytically targeting attractive customers and end markets with our supply chain optimization service model, industry consolidation through targeted M&A, and providing customers faster and easier solutions to their metal needs, which we believe will provide us with growth opportunities.

Given the highly fragmented nature of the metals service center industry, we believe there are numerous additional opportunities to acquire businesses and incorporate them into our existing infrastructure. In addition, due to our large scale and geographic reach, we believe we can improve operating performance through efficiencies byWhen integrating acquired businesses into our operational model, thus providingwe may draw on our large scale and geographic reach to improve operational and financial performance through greater purchasing power, improvingimproved expense and working capital management, increased access to additional end markets, and broadening product mix.

Lean Operating Structure Providing Operating Leverage.

Ryerson has demonstrated the ability to effectively manage expenses through tactical productivity and spending improvements. In a stronger metals service center environment characterized by increases in demand and/or pricing, we believe that most additional expenses to service higher revenue and margins would come from variable expenses while further leveraging economies of scale on our existing fixed expenses. In 2021, although impacted by supply chain tightness, industry volumes improved compared to 2020. In response to increased volumes, our warehousing, selling, general, and administrative expenses increased by $156.9 million compared to 2020, but decreased as a percentage of sales by 350 basis points, illustrating our ability to manage cost pressures and realize expense leverage.

Throughout 2021, we continued to focus on and execute strong inventory management and had average inventory days excluding LIFO of 73 days in 2021, within our target inventory range.

Extensive Breadth of Products and Services for Diverse Customer Base.

We believe our broad product mix and marketing approach provides customers with a “one-stop shop” solution few other metals service center companies are able to offer. We provide a broad range of processing and fabrication services to meet the needs of our approximately 40,000 customers and typically fulfill more than 1,100,000approximately 1,000,000 orders per year. We provide supply chain solutions, including just-in-time delivery and value-added processing, to many original equipment manufacturing customers.

5

For the year ended December 31, 2021,2023, no single customer, including their subcontractors, accounted for more than 5%8% of our sales, and our top 10 customers, including their subcontractors accounted for less than 13%16% of our sales.

Strong Relationships with Suppliers.

We are among the largest purchasers of metals in North America and have long-term relationships with many of our North American suppliers. We believe we are frequently one of the largest customers of our suppliers and that concentrating our orders among a core group of suppliers is effective for obtaining favorable pricing and service. We believe we have the opportunity to further leverage this strength through continued focus on price and volume using an analytics-driven approach to procurement. In addition, we view our strategic suppliers as supply chain partners. We focus on logistics, lead times, rolling schedules, and scrap return programs to drive value-based buying that is advantageous for us. Metals producers worldwide are consolidating, and large, geographically diversified customers, such as Ryerson, are desirable partners for these larger suppliers. Our relationships with suppliers often provide us with access to metals when supply is constrained. Through our knowledge of the global metals marketplace and capabilities of specific mills, we believe we have developed an advantageous global purchasing strategy.

Experienced Management Team with Deep Industry Knowledge.

Our senior management team has extensive industry and operational experience and has been instrumental in optimizing and implementing our strategy. Our senior management has an average of more than 30 years of experience in the metals or service center industries. Our Chief Executive Officer (“CEO”) and President, Mr. Edward Lehner, who joined the Company in August 2012 as Chief Financial Officer (“CFO”) and became CEO in June 2015, has 3032 years of experience, predominantly in the metals industry. Mr. Mike Burbach, our Chief Operating Officer, has over 3840 years of experience with the Company and previously served as the President of the North-West Region of the Company. Mr. Jim Claussen, Executive Vice President & CFO, has 2729 years of industry experience.

Industry Outlook

The Institute for Supply Management’s Purchasing Managers’ Index (“PMI”) reported growthcontracting factory activity throughout 20212023 with readings above 50%, indicating expansionconsistently below the growth threshold of 50. The contractionary trend indicated by PMI began with readings dropping below 50 starting in factory activity. This growth trend continued intoNovember 2022 and continuing through December of 2023, marking 14 consecutive months, with athe most recent reading of 57.647.4 for January. While PMI reported contraction in March, April, and May of 2020 due to the onset of the COVID-19 pandemic in the U.S., PMI has overall reported general economic expansion for the last three years as readings have exceeded 50% for 28 of the last 36 months.December 2023. The PMI measures the economic health of the manufacturing sector and is a composite index based on five indicators: new orders, inventory levels, production, supplier deliveries, and the employment environment. PMI readings can be a good indicator of industrial activity and general economic growth.

Additionally, theThe Department of Commerce announced that real GDP increased 5.72.5 percent in 20212023 and the Federal Reserve Bank of Philadelphia projected that the median growth rate in real GDP would be 4.0%, 2.2%,1.7 percent, 1.8 percent, and 2.0%2.1 percent for 2022, 2023,2024, 2025, and 2024,2026, respectively.

Steel demand in North America is largely dependent on growth of the automotive, industrial equipment, consumer appliance, and construction end markets. Our end markets are supported byreflect the strengthperformance of the manufacturing economy, and according to the latest Livingston Survey, published by the Federal Reserve Bank of Philadelphia, U.S. industrial production is expected to have expanded by 5.5%0.3 percent in 20212023 and is further expected to grow by 4.2%0.5 percent in 20222024 and 2.8%1.4 percent in 2023.2025.

Products and Services

We carry a full line of carbon steel, stainless steel, alloy steels, and aluminum, and a limited line of nickel and red metals. These materials are stocked in a number of shapes, including coils, sheets, rounds, hexagons, square and flat bars, plates, structurals, and tubing.

We also provide a wide variety of processing services to meet our customers’ needs. Most of the products that we carry require expensive specialized equipment for material handling and processing. We believe few of our customers have the capability to process the metal into the desired sizes, forms, or finishes or they are unwilling to incur the significant capital expenditures to acquire the necessary equipment. We are growing and diversifying our product mix mainly as a result of our targeted growth strategy to provide increased levels of value-added processing services. We believe our enhanced processing capabilities will increase our ability to sell higher-margin metals processing services to a larger group of customers. We expect this, together and with our focus on maintaining pricing discipline related to our processing services, will increase our gross profit margin.

We had capital expenditures of $194.6$358.1 million in the five-year period ended December 31, 2021.2023. We are increasing our investments in processing equipment due to offer more value-added processing to our customers requesting higher levels of value-added processing. We expect thisin an effort to increase our margins and profitability. We currently perform processing services on nearly 80% of the materials sold by us.

6

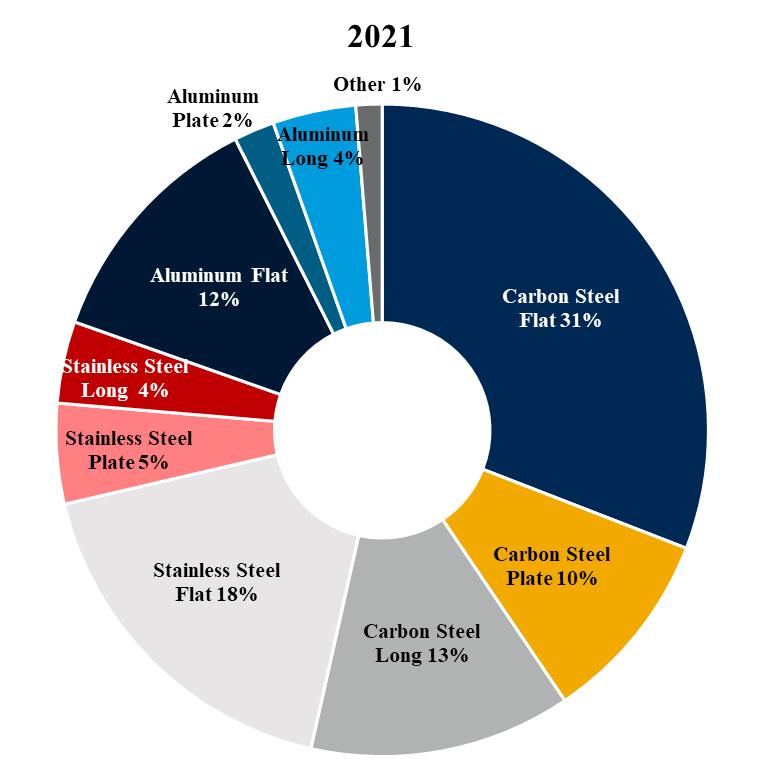

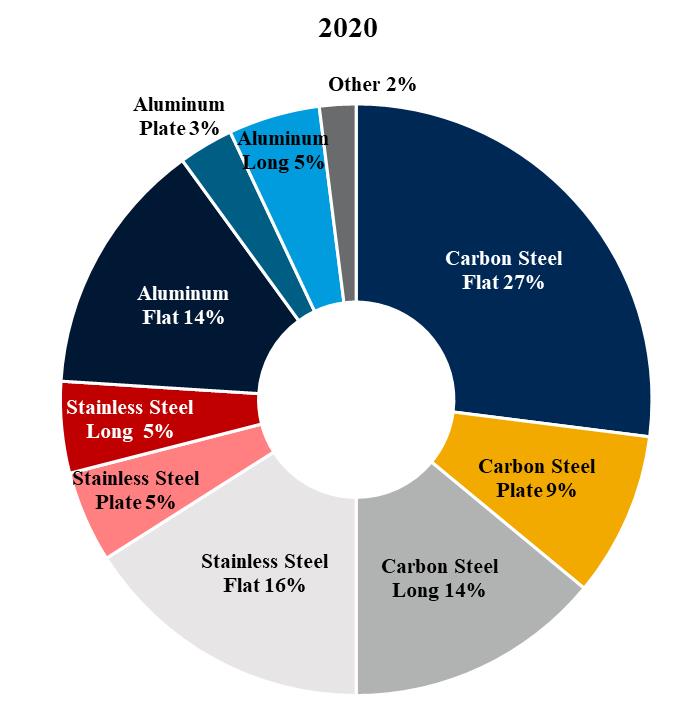

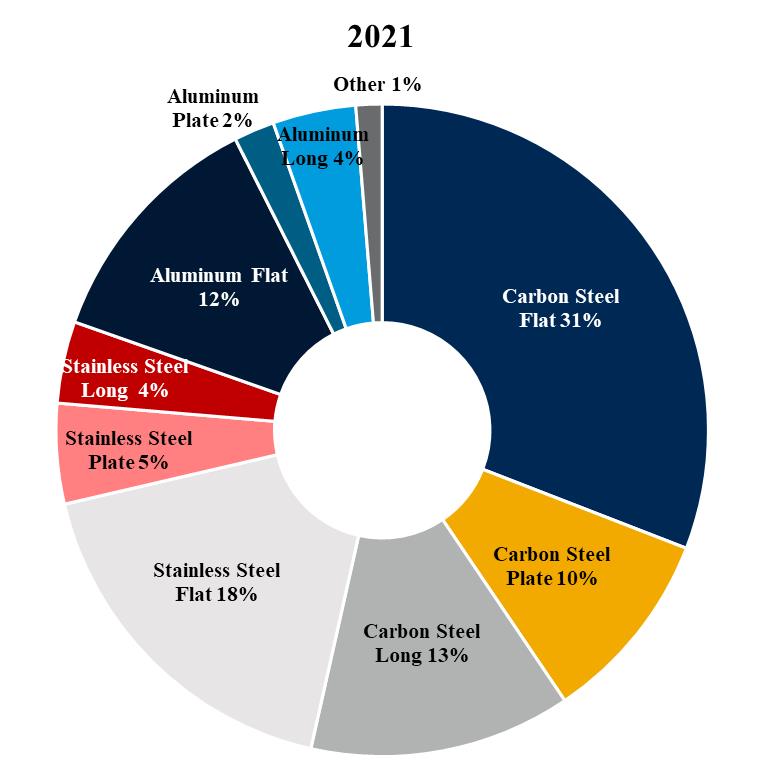

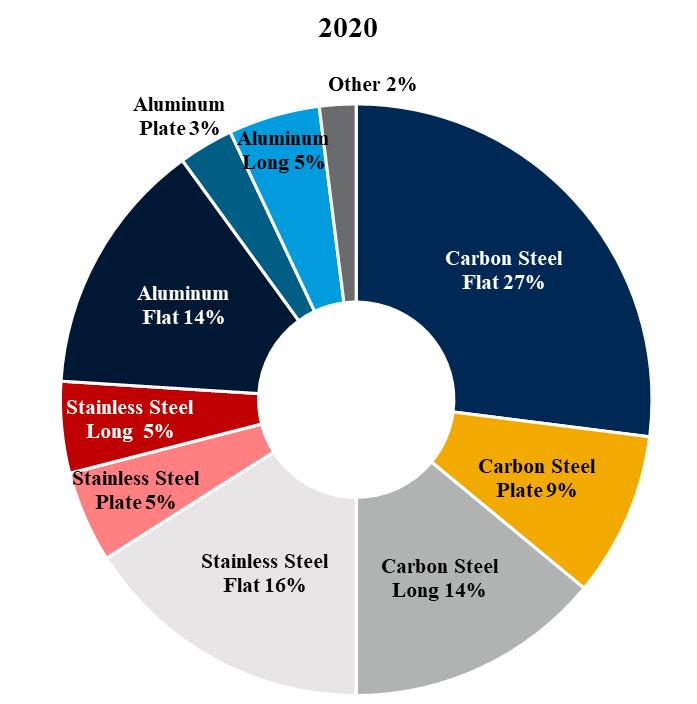

The following pie charts show our percentage of sales by major product lines for 20212023 and 2020:

We are not dependent on any particular customer group or industry because we process and distribute a variety of metals. This diversity of product type and material reduces our exposure to fluctuations or other weaknesses in the financial or economic stability of particular customers or industries. We are also less dependent on any particular suppliers as a result of our product diversification. See pie charts showing our sales by metal consuming industry within “Customers and Markets” discussion below.

Customers and Markets

Our customer base is diverse, numbering approximately 40,000 in a variety of industries, including metal fabrication and machine shops, industrial machinery and equipment, commercial ground transportation, consumer durable, food processing and agricultural equipment, construction equipment, HVAC, and HVAC.oil & gas. Although we sell directly to many large original equipment manufacturers, the majority of our sales are to smaller customers, including small machine shops and fabricators, in small quantities with frequent deliveries, helping them manage their working capital and credit needs more efficiently.

For the year ended December 31, 2021,2023, no single customer, including their subcontractors, accounted for more than 5%8% of our sales, and ourtop 10 customers, including their subcontractors, accounted for approximately 13%less than 16% of our sales. Substantially all of our sales are attributable to our U.S. operations and substantially all of our long-lived assets are located in the United States.U.S.

7

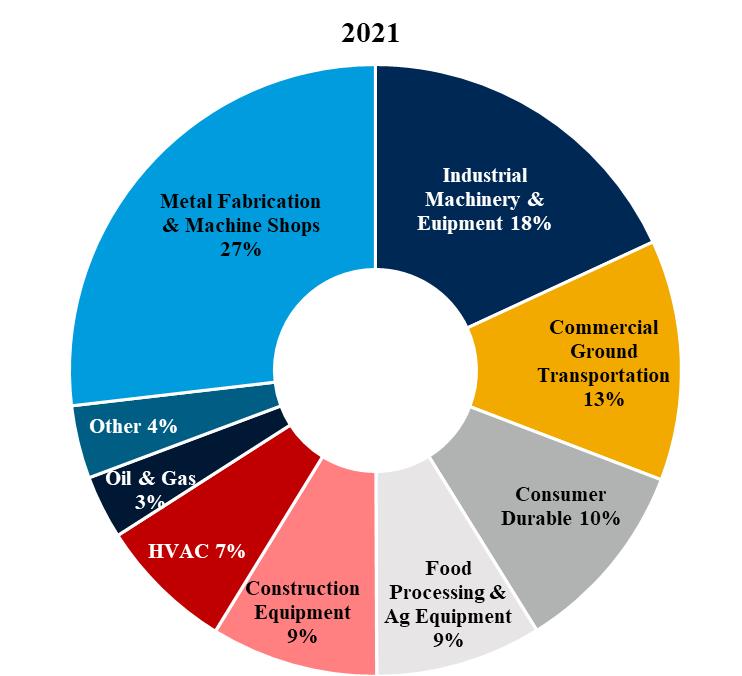

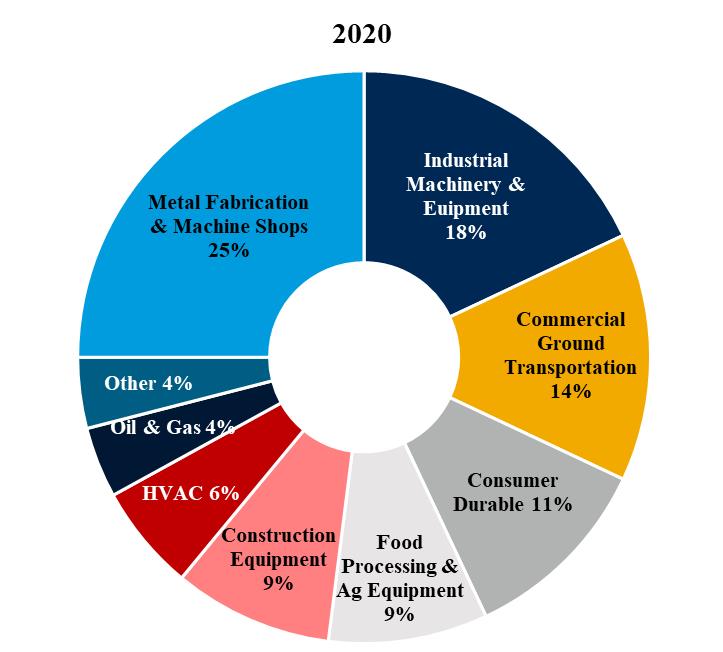

The following pie charts show the Company’s percentage of sales by metal consuming industry for 20212023 and 2020:2022:

Our customers are primarily located throughout the United States,U.S., but we also have international customers. Most customers areOur decentralized operating structure and facilities located near oneor close to most of our facilities, thus enablingcustomers enable an efficient delivery system capable of handling a high frequency of short lead time orders. We transport our products directly to customers via our in-house and dedicated truck fleet, which further supports the just-in-time delivery requirements of our customers, and via third-party trucking firms.

We process our metals to specific customer orders as well as for stocking programs. Many of our larger customers commit to purchase on a regular basis at agreed upon or indexed prices for periods ranging from three to twelve months. To help mitigate price volatility risks, these price commitments are generally matched with corresponding supply arrangements, or to a lesser degree by commodity hedges. Customers notify us of specific release dates for processed products. Customers typically notify us of release dates anywhere from on a just-in-time basis to one month before the release date. Consequently, we are required to carry sufficient inventory to meet the short lead time and just-in-time delivery requirements of our customers.

We also have international facilities located in Canada, Mexico, and China. Net sales of our international locations (based on where the shipments originated) accounted for 9.7%9.1% of our consolidated 20212023 net sales, or $551.6$466.4 million. See Note 1413 — “Segment information” of Part II, Item 8 “Financial Statements and Supplementary Data” for further information on U.S. and foreign revenues and assets.

Customer demand may change from time to time based on, among other things, general economic conditions and industry capacity. Many of the industries in which our customers compete are cyclical in nature. We believe that our various and diverse offerings, ways-to-markets,ways-to-market, and end markets reduce the volatility of our business in the aggregate, thus somewhat reducing earnings volatility. A portion of our customers experience seasonal slowdowns. Our sales, as measured in tonnage sold, in the months of July, November, and December traditionally have been lower than in other months because of a reduced number of shipping days and holiday or vacation closures for some customers. Consequently, our sales in the first two quarters of the year are usually higher than in the third and fourth quarters.

Suppliers

We purchase the majority of our inventories from key domestic metals suppliers. Because of our total volume of purchases and our long‑term relationships with our suppliers, we believe that we are generally able to purchase inventory at the best prices offered by our suppliers.

For the year ended December 31, 2021,2023, our top 25 suppliers, including their subcontractors, accounted for approximately 77%78% of our purchase dollars. We are generally able to meet our materials requirements because we use many suppliers, there is a substantial overlap of product offerings from these suppliers, and there are several other suppliers able to provide identical or similar

8

products. While the metals producing supply base has experienced significant consolidation and supply interruptions duringin the past,

year, we believe both our size and our long-term relationships with our suppliers has enabled us to meet our material requirements and will continue to allow us to do so in the future.

Sales and Marketing

We maintain our own professional sales force. In addition to our office sales staff, we market and sell our products through the use of our field sales force that we believe has extensive product and customer knowledge and offers a comprehensive catalog of our products. Our office and field sales staff, which together consist of approximately 800850 employees, include technical personnel. Additionally, we offer our customers the ability to purchase our products through our e-commerce website.

Because much of our business is relationship-based, we operate under many different trade names. Businesses we acquire often have strong customer relationships and solid reputations, and we will often continue to use the acquired business name to maintain existing customer relationships.

Capital Expenditures

In 2021,2023, we continued to focus on organic growth by expanding and modernizing existing facilities, adding new state-of -the-art facilities, and adding processing equipment.equipment to support value-added business. Investments by us in property, plant, and equipment, together with asset retirements for the five years ended December 31, 2021,2023, excluding the initial purchase price of acquisitions are set forth below. The net capital change during such period aggregated to an increase of $38.0$223.2 million.

|

| Additions |

|

| Retirements |

|

| Net |

| |||

|

| (In millions) |

| |||||||||

2023 |

| $ | 121.9 |

|

| $ | 0.4 |

|

| $ | 121.5 |

|

2022 |

|

| 105.1 |

|

|

| 8.3 |

|

|

| 96.8 |

|

2021 |

|

| 59.3 |

|

|

| 68.5 |

|

|

| (9.2 | ) |

2020 |

|

| 26.0 |

|

|

| 0.2 |

|

|

| 25.8 |

|

2019 |

|

| 45.8 |

|

|

| 57.5 |

|

|

| (11.7 | ) |

|

| Additions |

|

| Retirements or Sales |

|

| Net |

| |||

|

| (In millions) |

| |||||||||

2021 |

| $ | 59.3 |

|

| $ | 68.5 |

|

|

| (9.2 | ) |

2020 |

|

| 26.0 |

|

|

| 0.2 |

|

|

| 25.8 |

|

2019 |

|

| 45.8 |

|

|

| 57.5 |

|

|

| (11.7 | ) |

2018 |

|

| 38.4 |

|

|

| 5.5 |

|

|

| 32.9 |

|

2017 |

|

| 25.1 |

|

|

| 24.9 |

|

|

| 0.2 |

|

The net reductions in 2019 and 2021 are related to sale lease-back transactions. See Part II, Item 8, Note 5: Property, Plant, and Equipment for additional information on the 2021 sale-leaseback transactions. The lower amount of additions in 2020 was caused by maintenance capital expenditures deferred to 2021 and 2022 as spending was reduced due to uncertainties surrounding the COVID-19 pandemic. We currently anticipate capital expenditures, excluding acquisitions, of up to approximately $100$110 million for 2022,2024, much of which is related to organic activities comprised of maintenance and purchases geared towards highly accretive strategic initiatives, IT infrastructure investment, and growth, along with maintenance projects. We expect nearly halfall of the 20222024 capital expenditures to be funded using proceeds from the 2021 sale-leasebacks of two properties with the remainder funded from cash generated by operations and available borrowings.operations. We will continue to evaluate and execute each growth project in light of the economic conditions and outlook at the time of investment and may significantly reduce our capital expenditures if economic conditions warrant a more conservative approach to capital allocation. For the long term, we expect capital expenditures to normalize to a rate that approximates depreciation.

Environmental, Health, and Safety Matters

Our facilities and operations are subject to many foreign, federal, state, local, and localforeign laws and regulations relating to the protection of the environment and to health and safety. In particular, our operations are subject to extensive requirements relating to waste disposal, recycling, air and water emissions, the handling of regulated materials, remediation, underground storage tanks, asbestos-containing building materials, workplace exposure, and other matters. We believe that our operations are currently in substantial compliance with all such laws and do not presently anticipate substantial expenditures in the foreseeable future in order to meet environmental, workplace health or safety requirements, or to pay for any investigations, corrective action, or claims. However, claims, enforcement actions, or investigations regarding personal injury, property damage, or violation of environmental laws could result in substantial costs to us, divert our management’s attention, and result in significant liabilities, fines, or the suspension or interruption of our facilities.

We continue to analyze and implement safeguards to mitigate any environmental, health, and safety risks we may face. As a result, additional costs and liabilities may be incurred to comply with future requirements, including California and the proposed SEC climate disclosure requirements, or to address newly discovered conditions, and these costs and liabilities could have a material adverse effect on the results of operations, financial condition, or cash flows. For example, there is increasing likelihood that additional regulation of greenhouse gas emissions will occur at the foreign, federal, state, and local level, which could affect us, our suppliers, and our customers. While the costs of compliance could be significant, given the uncertain outcome and timing of future action by the U.S. federal government and states on this issue, we cannot accurately predict the

full financial impact of current and future greenhouse gas regulations on our operations or our customers at this time. We do not currently anticipate any new programs disproportionately impacting us compared to our competitors.

9

Some of the properties currently or previously owned or leased by us are located in industrial areas or have a long history of heavy industrial use. We may incur environmental liabilities with respect to these properties in the future including costs of investigations, corrective action, claims for natural resource damages, claims by third parties relating to property damages, or claims relating to contamination at sites where we have sent waste for treatment or disposal. Based on currently available information we do not expect any investigation, remediation matters, or claims related to properties presently or formerly owned, operated, or to which we have sent waste for treatment or disposal would have a material adverse effect on our financial condition, results of operations, or cash flows.

In October 2011, the United States Environmental Protection Agency (the “EPA”) named JT Ryerson as one of more than 100 businesses that may be a potentially responsible party (“PRP”) for the Portland Harbor Superfund Site (the “PHS Site”). On January 6, 2017, the EPA issued an initial Record of Decision (“ROD”) regarding the site. The ROD includes a combination of dredging, capping,Site. See Note 12: Commitments and enhanced natural recovery that would take approximately thirteen years to construct plus additional time for monitored natural recovery, at an estimated present value cost of $1.05 billion. At a December 4, 2018 meeting with the Portland Harbor Participation and Common Interest Group (“PCI Group”), of which JT Ryerson is a member, the EPA indicated that it expected PRPs to submit a plan during 2019 to start remediation of the river and harbor per the ROD within the next two to three years. The EPA also indicated that it expected allocation of amounts among the parties to be determinedContingencies in the same two to three-year time frame.

The EPA met with various PRPs throughout 2019 and 2020 regarding remedial design. The EPA did not include JT Ryerson in those meetings. It did include Schnitzer Steel, which is developing a remedial design plan for the river area which includes the area where the former JT Ryerson facilities were located. Schnitzer Steel’s 2020 disclosures filed with the EPA acknowledged that Schnitzer Steel is the legal successornotes to the prior operators (including JT Ryerson)consolidated financial statements included in the designated area. On February 12, 2021, the EPA announced that one hundred percent (100%)Part II, Item 8 of the PHS Site is now in the active remedial design phase.

In June 2021, the EPA issued a Fact Sheet setting forth the status of the entire site. The primary area of relevance for JT Ryerson is River Mile 3.5 East, with Swan Island Basin being of secondary interest. For River Mile 3.5, remedial design work is ongoing; the Sufficiency Assessment and the Pre-Design Investigation work plans are finalized, and design investigation sampling is underway. Schnitzer Steel and MMGL Corp. are the working parties for River Mile 3.5. For Swan Island, remedial design is just beginning, with Daimler Trucks, Shipyard Commerce, and various government entities as the working parties. JT Ryerson has not been asked to participate in the remedial design phase.

The PCI Group has engaged a third party to prepare cost estimates for each of the Sediment Management Areas at the site. That work is still in progress and is expected to be completed in early 2022. Once the cost estimates are completed, the voting parties of the PCI Group (which does not include JT Ryerson) will likely begin the “advocacy process,” during which the voting parties submit written arguments to the Allocation Team regarding how costs should be allocated among the various PRPs. This process is anticipated to be completed sometime in 2022. Once the advocacy process is completed, the Allocation Team will prepare a proposed allocation of costs among the PRPs. All PRPs, including JT Ryerson, will then participate in the “mediation process,” during which the PRPs will attempt to agreethis Report on a final cost allocation. The mediation process is currently anticipated to occur sometime in 2022 or 2023.

The EPA has stated that it is willing to consider de minimis settlements, which JT Ryerson is trying to pursue; however, the EPA has not begun meeting with any of the smaller parties who have requested de minimis or de micromis status, stating that it does not have sufficient information to determine whether any parties meet such criteria and does not intend to begin those considerations until after the remedial design work is completed. It has met with selected parties that we believe to be larger targets. JT Ryerson has not been invited to meet with the EPA. As a result of the ongoing negotiations and filings over the ROD and the EPA’s decision not to meet with smaller parties, we cannot determine how allocations will be made and whether a de minimus settlement can be reached with the EPA.

Form 10-K. As the EPA has not yet allocated responsibility for the contamination among the potentially responsible parties, including JT Ryerson, we do not currently have sufficient information available to us to determine whether the RODRecord of Decision will be executed as currently stated, whether and to what extent JT Ryerson may be held responsible for any of the identified contamination, and how much (if any) of the final plan’s costs might ultimately be allocated to JT Ryerson. Therefore, management cannot predict the ultimate outcome of this matter or estimate a range of potential loss at this time.

There are various other claims and pending actions against the Company. The amount of liability, if any, for those claims and actions as of December 31, 20212023 is not determinable but, in the opinion of management, such liability, if any, will not have a material

adverse effect on the Company’s financial position, results of operations, or cash flows. We maintain liability insurance coverage to assist in protecting our assets from losses arising from or related to activities associated with business operations.

Our United StatesU.S. operations are also subject to the Department of Transportation Federal Motor Carrier Safety Regulations. We operate a private trucking motor fleet for making deliveries to some of our customers. Our drivers do not carry any material quantities of hazardous materials. Our foreign operations are subject to similar regulations. Future regulations could increase maintenance, replacement, and fuel costs for our fleet. These costs could have a material adverse effect on our results of operations, financial condition, or cash flows.

Intellectual Property

We own several U.S. and foreign trademarks, service marks, and copyrights. Certain of the trademarks are registered with the U.S. Patent and Trademark Office and, in certain circumstances, with the trademark offices of various foreign countries. We consider certain other information owned by us to be trade secrets. We protect our trade secrets by, among other things, entering into confidentiality agreements with our employees regarding such matters and implementing measures to restrict access to sensitive data and computer software source code on a need-to-know basis. We believe that these safeguards adequately protect our proprietary rights and we vigorously defend these rights. While we consider all our intellectual property rights as a whole to be important, we do not consider any single right to be essential to our operations as a whole.

Environmental, SocialSustainability

In December 2023, Ryerson released its second Sustainability Report. The report builds on the Company’s inaugural 2022 report and Governance

Ryerson is committed to operating with a high level of integrity. We are driven by our dedication to support our employees andprovides an update on ongoing sustainability efforts, the communities we serve, deliver products that meet our stringent quality and compliance standards, and maintain high environmental, health, and safety standards to protect ourinvestments being made in its people and service center network, and how it is serving its communities. Similar to the places where we operate. Weinaugural report, the 2023 edition illustrates the Company’s focus on energy and emissions reductions, sustainable products, data security, diversity, equity, and inclusion ("DEI"), and talent and future workforce while also providing updates on Ryerson’s advancement in these categories. A few achievements include Ryerson’s recognition by Forbes as one of America’s best mid-sized companies to work to continually improve eachfor, its launch of these areas to makethe award-winning Ryerson an even better company for tomorrow.

Below are some highlights of our corporate responsibility programs.Illuminator app, and its continued role in the circular metals economy.

Additionally, the Sustainability

As part of our efforts to operate with a high level of integrity, Report includes important content on governance practices, including how we continuously monitor and analyze ourselves and our supply-chain relationships.relationships in order to operate with a high level of integrity and how we protect Company and stakeholder information through strong cybersecurity practices. We strive, and expect our suppliers, to comply with all applicable laws and regulations andas well as Ryerson's Human Rights Policy, Conflict Minerals Policy,and Code of Ethics and Business Conduct.

We are committed to mitigating the impact our operations and products have on the environment. As an operator of metals service centers, our day-to-day business consists of the sale, distribution, and processing of a broad variety of metal products sourced from numerous primary metal producers. Our operations, by their nature, do not emit significant amounts of carbon dioxide or other greenhouse gases. Further, according to the Steel Recycling Institute, we believe steel, one of our most significant products,is the most recycled material on the planet—more than plastic, paper, and glass combined each year—which provides a strong foundation for our sustainability efforts. The Steel Recycling Institute notes that two out of every three tons of new steel are produced from old steel. As part of our commitment to environmental sustainability, we:

|

|

|

|

|

|

|

|

|

|

We alsouse propane fuel to operate forklifts, have installed energy efficient lighting in many of our facilities, and utilize energy efficient diesel tractors that consume less fuel and reduce emissions for the majority of our trucking fleet to further mitigate our impact on the environment.

Community & Social Vitality

Being a responsible neighbor and helping build better communities in the areas we operate is a central part of our company culture. We understand that supporting our communities through giving back is an important and increasing interest of our current and future employees.Human Capital

Employees are provided the opportunity to volunteer their time in the communities they call home through the Ryerson Gives Back program. Established in 2017, Ryerson Gives Back encourages teams across the Company to volunteer in their community, allotting four paid volunteer hours annually to each employee. From food banks to local construction projects, we have watched employees step up to support underserved groups and areas on behalf of Ryerson.

In addition to giving back, we encourage employees to exercise their civic responsibilities. Employees were granted an additional four hours of paid time off to vote in the 2020 presidential election. We also support various charitable organizations, including those that promote social justice and equality, good health, children's causes, educational advancement, and community programs.

Human Capital

In order to provide best in class customer experiences, it is crucial that we continue to work to attract and retain top talent. To facilitate talent attraction and retention, we strive to create a diverse, inclusive, and safe workplace, with opportunities for our

10

employees to grow and develop in their careers, supported by strong compensation, benefits, and wellness programs, and by programs that build connections between our employees and their communities.

Employees.Talent and Future Workforce. AsOur recruitment and talent management teams lead our mission to attract, retain and develop diverse talent. These teams are organized under our Talent Management Office ("TMO"), which includes our Chief Human Resources Officer, our Director of December 31, 2021, we employed approximately 3,700 persons in North AmericaTalent Management, and 300 persons in China. Our North American workforce was comprised of approximately 1,600 office employeesother senior leaders. The TMO is responsible for our recruiting efforts, attracting the best talent, increasing diversity and approximately 2,100 plant employees. Seventeen percent of our plant employees were members of various unions, including the United Steel Workershiring efficiencies, facilitating onboarding, and The International Brotherhood of Teamsters.

Five renewal contracts covering 100 employees were successfully negotiated in 2021. Four contracts covering 104 employees are currently scheduled to expire in 2022.

Employee Development & Engagement. Ryerson believes in promoting from within and provides the resources for long-term career development. Our summer internship program and Ryerson Academy provide meaningful training to entry-level employees. Ryerson Academy is a unique, 12-week immersive training program that runs three sessions per year for entry-level inside sales associates. The program provides intensive training and experience in sales and customer service with up to 15 participants in each session. Ryerson Academy also teaches critical communication, negotiation, and presentation skills, and participants regularly interact with Ryerson’s senior leadership and subject matter experts.

For decades, we have supported the continuing education of our employees’ families through a college scholarship program. In 2021,opportunities to engage employees as they join Ryerson and build their careers with us.

As part of this program, we awarded almost $32,000 in academic scholarships to students graduating from high school that are children or dependents ofretaining and developing talent, Ryerson employees. We also support the continuing education of ouroffers employees competitive compensation, expanded benefits including a parental leave policy, career growth through its learning platform, mentorship and tuition reimbursement programs.

We have a robust training platform, Ryerson EDvantage, available to all employees which offers Ryerson product training along with general skills courses that are customized for our employees’ development. We focus on succession planning and ensure that proper cross-training and knowledge transfer is in place.

Our commitment to listening to and working with our employees led to the launch of our company-wide engagement survey in 2018. Using Quantum Workplace, a leading engagement survey software, our employees anonymously provided their perspectives on a variety of topics. Ryerson achieved overall favorability of 67% with a participation rate of nearly 80%, which exceeded industry benchmarks. We distributed the results to our department heads and managers to hold team meetings to discuss the outcomes and gain additional insights. We identified key improvement opportunities and established advisory teams to address them. In early 2020, we conducted a follow-up “pulse” survey with a subset of the organization and, encouragingly, found that favorability scores increased in locations where leaders had worked to affect change. From this collective effort came company-wide initiatives including new health and wellness programs, and improved sick, vacation, and parental leave policies for U.S. employees.engagement through all-employee surveys conducted periodically.

Diversity and Inclusion.Ryerson is dedicated to building a diverse workplaceembracing diversity and inclusion via our Diversity, Equity, and Inclusion council ("DEI Council") that focuses on employee engagement, DEI training, and community outreach efforts with the mission of associates from a variety of cultures, educational backgrounds, and life experiences. A well-rounded community of talent helps cultivate new ideas and perspectives that help the Company expand its thinking and refine its practices and processes to continue growing in a smart way. Ryerson is aggressively working to engage diverse and under-represented individuals through its recruiting efforts in diverse and underserved communities. We have a Diversity & Inclusion Council whose mission is to fosterfostering an environment across the organization that values

diversity of experiences and perspectives and encourages inclusivity in all aspects of the business. Only

In 2023, Ryerson’s DEI Council announced the establishment of three employee resource groups ("ERGs") to be available to employees in 2024: Women in Search of Excellence (WISE), Next Generation of Leaders (NextGen), and Leveraging All Diversity (LEAD). These ERGs are voluntary, employee-led groups that work to foster a more inclusive workplace by respecting eachuniting people with common interests, identities, or backgrounds. Each of the three ERGs established is purposefully aligned with Ryerson’s DEI mission and strategic goals.

Further, Ryerson is invested in DEI training by providing employees with training on being inclusive, avoiding bias, and workplace intervention. Training is available at any time on the Company’s learning platform, where employees can select from a growing catalog of DEI courses.

Employee Health, Wellness, and Safety. Health, safety, and wellness are fundamental expectations of our unique perspectives, experiences,Board, executives, employees, and needs can we unlock the full potential of our workforce and attract the best talent. The council seeks to achieve this through:

|

|

|

|

|

|

|

|

We promote the advancement of women in our organization through our Women’s Sponsorship Program which provides sponsorship of women in various levels and positions throughout the organization. Ryerson’s employees also participate in Association of Women in the Metals Industry membership and events. Additionally, effective January 1, 2022, we adopted a new parental leave policy which provides all U.S. non-union, full-time employees with four weeks of fully paid parental leave plus eight weeks of fully paid maternity leave.

From a governance perspective, Ryerson has adopted a Code of Ethics & Business Conduct, a Board Corporate Governance Guidelines and Nominating Corporate Governance Committee Charter, an Equal Employment Opportunity Policy, and Anti-harassment Policy to support our diversity, equity, and inclusion values. Our Board of Directors and Compensation Committee provide oversight of our policies, programs, and initiatives focusing on workforce diversity and inclusion.

Employee Safety. Upholding a safe workplace is one of our core values and a part of the company's culture.customers. Our safety standards, which go beyond industry standards and the minimum legal requirements, required by applicable law, have helped protect the well-being of our people and prevent workplace injuries that can impact business productivity. We continuously work to maintaininjuries. Our commitment towards a safety performance rating that consistently outperforms the industry averagezero-injury workplace is constant and have implementeddriven by an Environmental, Health, and Safety policy that reinforces the goal of a zero-injury workplace.goal. Our low recordable injury rate compared to our peers in the metal services industry, based on U.S. Occupational Safety and Health Administration (“OSHA”) criteria, reflects our effectiveness in protecting our employees. Our 20212023 performance at our facilities, measured as the number of OSHA recordable injuries per 200,000 labor hours, was 2.08,2.26, which was better than the industry average as reported by the Bureau of Labor Statistics.

Health and Wellness. The success of our business is fundamentally connected to the well-being of our people. Accordingly, we are committed to the health and wellness of our employees. We provide our employees and their families with access to a variety of innovative, flexible, and convenient health and wellness programs, including benefits that provide protection and security so they can have peace of mind concerning events that may require time away from work or that impact their financial well-being; that support their physical and mental health by providing tools and resources to help them improve or maintain their health status, and encourage engagement in healthy behaviors; and that offer choice where possible so they can customize their benefits to meet their needs and the needs of their families.In response to the COVID-19 pandemic, we implemented significant changes that we determined were in the best interests of our employees and the communities in which we operate, and which comply with government regulations, such as having office employees work from home and implementing additional safety measures for employees continuing critical on-site work.

Compensation and Benefits. We provide robust compensation and benefits programs to help meet the financial needs of our employees. In addition to salaries, we provide annual and quarterly sales incentive plans, healthcare and insurance benefits, health savings and flexible spending accounts, retirement savings contribution matching, paid time off, parental and maternity leave, employee assistance programs, and tuition assistance. Additionally, we have targeted equity-based grant programs with vesting conditions to facilitate retention of personnel, particularly those with critical skills and experience.

Employee Headcount and Unions. See Item 1A, Risks Related to Operating our Business, sub-section "Any significant work stoppages can harm our business", as well as Note 12: Commitments and Contingencies within Part II, Item 8 "Financial Statements and Supplementary Data" for further information.

Available Information

All periodic and current reports and other filings that we are required to file with the Securities and Exchange Commission (“SEC”), including our annual report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, and amendments to those reports filed or furnished pursuant Section 15(d) of the Securities Exchange Act of 1934, as amended, are available free of charge from the SEC’s website (www.sec.gov) or through our Investor Relations website at http://ir.ryerson.com. Such documents are available as soon as reasonably practicable after electronic filing of the material with the SEC. Copies of these reports (excluding

11

exhibits) may also be obtained free of charge, upon written request to: Investor Relations, Ryerson Holding Corporation, 227 W. Monroe St., 27th Floor, Chicago, Illinois 60606.

The Company also posts its Code of Ethics on its website. See Part III, Item 10 for more information regarding our Code of Ethics.

Our website address is included in this report for informational purposes only. Our website and the information contained therein or connected thereto are not incorporated into this annual report on Form 10-K.

ITEM 1A. RISK FACTORS.

|

|

Our business faces many risks. You should carefully consider the risks and uncertainties described below, together with the other information in this report, including the consolidated financial statements and notes to consolidated financial statements. We cannot assure you that any of the events discussed in the risk factors below will not occur. These risks could have a material and adverse impact on our business, results of operations, financial condition, and cash flows.

RISKS RELATED TO OUR INDUSTRY

Weakness in the economy, market trends, and other conditions affecting the profitability and financial stability of our customers could negatively impact our sales growth and results of operations.

Economic and industry trends affect our business environments. We serve several metals-consuming industries in which the demand for our products and services is sensitive to the production activity, capital spending, and demand for products and services of our customers. Many of these customers operate in markets that are subject to highly cyclical fluctuations resulting from seasonality, market uncertainty, costs of goods sold, currency exchange rates, foreign competition, offshoring of production, oil and natural gas prices, geopolitical developments, and a variety of other factors beyond our control. Any of these factors could cause customers to idle or close facilities, delay purchases, reduce production levels, or experience reductions in the demand for their own products or services.

Any of these events could impair the ability of our customers to make full and timely payments or reduce the volume of products and services these customers purchase from us and could cause increased pressure on our selling prices and terms of sale.

We do not expect the cyclical nature of our industry to change and any downturn in our customers’ industries could reduce our revenues and profitability or a significant or prolonged slowdown in activity in the U.S., Canada, or any other major world economy, or a segment of any such economy, could negatively impact our sales growth and results of operations.

The metals services business is very competitive and increased competition could reduce our revenues and gross margins.

We face competition in all markets we serve, from metals producers that sell directly to certain customers or segments of the market, to other metal services companies. The metals services industry itself is highly fragmented and competitive. There are a few large competitors, but most of the market is served by small local and regional competitors. Competition is based principally on price, service, quality, production capabilities, inventory availability, and timely delivery.

We are experiencing increased pressure from online businesses that compete with price transparency. We expect technological advancements and the increased use of e-commerce solutions within the industry to continue to evolve at a rapid pace. As a result, our ability to effectively compete requires us to respond and adapt to new industry trends and developments, and implement new technology and innovations that may result in unexpected costs or may take longer than expected.

To remain competitive, we must be willing and able to respond to market pressures.pressures timely. These pressures, and the implementation, timing, and results of our strategic pricing and other responses, could have a material effect on our sales and profitability. If we are unable to grow sales or reduce costs, among other actions, to wholly or partially offset the effect on profitability of our pricing actions, our results of operations and financial condition may be adversely affected.

Changing metals prices may have a significant impact on our liquidity, net sales, gross margins, operating income, and net income.

The metals services industry as a whole is cyclical and, at times, pricing and availability of metal can be volatile due to numerous factors beyond our control, including, but not limited to, general domestic and international economic conditions, labor costs, sales levels, competition, levels of inventory held by other metals service centers, consolidation of metals producers, higher raw material costs for the producers of metals, import duties and tariffs, and currency exchange rates. This volatility can significantly

12

affect the availability and cost of materials for us. Our ability to pass on increases in costs in a timely manner depends on market conditions and may result in lower gross margins. In addition, higher prices could impact demand for theseour products, resulting in lower sales volumes. Moreover, we maintain substantial inventories of metal to accommodate the short lead times and just-in-time delivery requirements of our customers. Accordingly, we purchase metals in an effort to maintain inventory at levels that we believe to be appropriate to satisfy

the anticipated needs of our customers based upon historic buying practices, contracts with customers, and market conditions. Commitments for metal purchases are generally at prevailing market prices in effect at the time orders are placed or at the time of shipment. During periods of rising metal prices, we may be negatively impacted by delays between the time of increases in the cost of metals to us and increases in the prices that we charge for our products if we are unable to pass these increased costs on to our customers. In addition, when metal prices decline, this could result in lower selling prices for our products and, as we use existing inventory that we purchased at higher metal prices, lower gross profit margins. Declines in prices or further reductions in sales volumes could adversely impact our ability to maintain our liquidity and to remain in compliance with certain financial covenants under our $1.0$1.3 billion revolving credit facility (“the Ryerson Credit Facility”), as well as result in us incurring inventory or goodwill impairment charges. Consequently, changing metals prices could significantly impact our liquidity, net sales, gross margins, operating income, and net income.

Unexpected product shortages could negatively impact customer relationships, resulting in an adverse impact on results of operations.

Disruptions could occur due to factors beyond our control, including economic downturns, political unrest, port slowdowns, trade issues, including increased export or import duties or trade restrictions, health crises, climate related disruptions, and other factors, anyfactors. Recent unrest in the Red Sea has increased both shipping times and costs presenting new challenges to the metals industry. Any of whichthe aforementioned items could adversely affect a supplier’s ability to manufacture or deliver products to us. Public health problems may result in quarantines, business closures, transportation restrictions, import and export complications, and otherwise cause shortages in the supply of materials, higher costs for available supplies, or cause other disruptions within our operations and supply chain. Public health problems may cause increased costs of certain supplies and disruptions and delays within our supply chain, and may expose us to unanticipated liability or require us to change our business practices.

Any disruption resulting from these events could cause significant delays in shipments of products or difficulties in obtaining products, any of which may expose us to unanticipated liability or require us to change our business practices in a manner materially adverse to our business, results of operations, and financial condition. For our sources of lower cost products from Asia and other areas of the world, the effect of disruptions is typically increased due to the additional lead time required and distances involved. Further, the risk of disruption is increased due to the current political climate seeking trade reform. In addition, we have strategic relationships with a number of vendors. In the event we are unable to maintain those relations, there might be a loss of competitive pricing advantages which could, in turn, adversely affect results of operations.

Changes in customer or product mix could cause our gross margin percentage to decline.

From time to time, we experience changes in customer and product mix that affect gross margin. Changes in customer and product mix result primarily from business acquisitions, changes in customer demand, customer acquisitions, selling and marketing activities, and competition. If rapid growth with lower margin customers occurs, we will face pressure to maintain current gross margins, as these customers receive more discounted pricing due to their higher sales volume. There can be no assurance that we will be able to maintain historical gross margins in the future.

We may not be able to retain or expand our customer base if the North American manufacturing industry erodes through acquisition and merger or consolidation activity in our customers’ industries.

Our customer base primarily includes manufacturing and industrial firms. Some of our customers operate in industries that are undergoing consolidation through acquisition and merger activity and some customers have closed as they were unable to compete successfully with overseas competitors. Our facilities are predominately located in the United StatesU.S. and Canada. To the extent that our customers cease U.S. operations or relocate to regions in which we do not have a presence, we could lose their business. Acquirers of manufacturing and industrial firms may have suppliers of choice that do not include us, which could impact our customer base and market share.

Global metal overcapacity and imports of metal products into the United States have adversely affected, and may again adversely affect, United States metal prices, which could impact our sales and results of operations.

At times, global metal production capacity may exceed global consumption of metal products. Such excess capacity sometimes results in metal manufacturers in certain countries exporting steel at prices that are lower than prevailing domestic prices and sometimes at or below their cost of production. Excessive imports of metal into the United States, such as in recent years,U.S. have exerted and may exert in the future, downward pressure on United StatesU.S. steel prices which may negatively affect our results of operations.

13

Lead time and the cost of our products could increase if we were to lose one of our primary suppliers.

If, for any reason, our primary suppliers of aluminum, carbon steel, stainless steel, or other metals should curtail or discontinue their delivery of such metals in the quantities needed and at prices that are competitive, our business could suffer. The number of available suppliers could be reduced by factors such as industry consolidation and bankruptcies affecting steel and metal producers. For the year ended December 31, 2021,2023, our top 25 suppliers represented approximately 77%78% of our purchases. We could be significantly and adversely affected if delivery were disrupted from a major supplier. If, in the future, we were unable to obtain sufficient amounts of the necessary metals at competitive prices and on a timely basis from our traditional suppliers, we may not be able to obtain such metals from alternative sources at competitive prices to meet our delivery schedules, which could have a material adverse effect on our sales and profitability.

RISKS RELATED TO MARKET AND ECONOMIC VOLATILITY

Changes in inflation may adversely affect financial performance.

Fluctuations in inflation could result in, and recent inflationary pressures have resulted in, lower revenues, higher costs, and decreased margins, profits, and earnings. Rapid or significant inflation could continue to increase the costs we incur to procure, process, package, and deliver our metal to customers and we may not be able to increase selling prices to customers at the same rate, resulting in decreased margins and operating profits. Prolonged periods of deflation could adversely affect the degree to which we are able to maintain or increase selling prices resulting in decreased revenues, margins, and operating profits. Additionally, prolonged deflation could impact our availability on the Ryerson Credit Facility as the value of our accounts receivable and inventory decreases.

In addition, we rely on arrangements with third-party shipping and freight companies for the delivery of our products. Freight and shipping costs may increase due to inflation, and any such increases could adversely affect our margins unless we are able to increase selling prices at the same rate.

We monitor the risk that the principal markets in which we operate could continue to experience increased inflationary conditions. The onset, duration, and severity of an inflationary period cannot be estimated with precision.

The volatility of the market could result in a material impairment of goodwill.

We evaluate goodwill annually on October 1 and whenever events or changes in circumstances indicate potential impairment. Events or changes in circumstances that could trigger an impairment review include significant underperformance relative to our historical or projected future operating results, significant changes in the manner or the use of our assets or the strategy for our overall business, and significant negative industry or economic trends. We test for impairment of goodwill by assessing various qualitative factors with respect to developmentdevelopments in our business and the overall economy and calculating the fair value of a reporting unit using a combination of an income approach based on discounted future cash flows and a market approach at the date of valuation, as necessary. Under the discounted cash flow method, the fair value of each reporting unit is estimated based on expected future economic benefits discounted to a present value at a rate of return commensurate with the risk associated with the investment. Projected cash flows are discounted to present value using an estimated weighted average cost of capital, which considers both returns to equity and debt investors. Please refer to the Section titled “Critical Accounting Estimates - Goodwill,” of Item 7, “Management’s Discussion and Analysis of Financial Conditions and Results of Operations,” and Note 1 — “Summary of Accounting and Financial Policies” of Part II, Item 8 "Financial Statements and Supplementary Data" for further information.

Poor investment performance or other factors could require us to make significant unplanned contributions to our pension plan and future funding for postretirement employee benefits other than pensions also may require substantial payments from current cash flow.

We provide defined benefit pension plans for certain eligible employees and retirees. The performance of the debt and equity markets affect the value of plan assets. A decline in the market value may increase the funding requirements for these plans. The cost of providing pension benefits is also affected by other factors, including interest rates used to measure the required minimum funding levels, the rate of return on plan assets, discount rates used in determining future benefit obligations, future government regulation, and prior contributions to the plans. Significant unanticipated changes in any of these factors may have an adverse effect on our financial condition, results of operations, liquidity, and cash flows.

14

RISKS RELATED TO EXPANSION AND INTERNATIONAL OPERATIONS

We may not be able to successfully consummate and complete the integration of future acquisitions, and if we are unable to do so, it could disrupt operations and cause unanticipated increases in costs and/or decreases in revenues and results of operations.

We have grown through a combination of internal expansion, acquisitions, and joint ventures. We intend to continue to grow through selective acquisitions, but we may not be able to identify appropriate acquisition candidates, obtain financing on satisfactory terms, consummate acquisitions, or integrate acquired businesses effectively and profitably into our existing operations. Restrictions contained in the agreements governing our notes, the Ryerson Credit Facility, or our other existing or future debt may also inhibit our ability to make certain investments, including acquisitions, and participations in joint ventures.

Acquisitions, partnerships, joint ventures, and other business combination transactions, both foreign and domestic, involve various inherent risks, such as uncertainties in assessing value, strengths, weaknesses, liabilities, and potential profitability. There is also risk relating to our ability to achieve identified operating and financial synergies anticipated to result from the transactions. Additionally, problems could arise from the integration of acquired businesses, including unanticipated changes in the business or industry or general economic conditions that affect the assumptions underlying the acquisition. Our future success will depend on our ability to complete the integration of these future acquisitions successfully into our operations. Specifically, after any acquisition, customers may choose to diversify their supply chains to reduce reliance on a single supplier for a portion of their metals needs. We may not be able to retain all of our and an acquisition’s customers, which may adversely affect our business and sales. Integrating acquisitions, particularly large acquisitions, requires us to enhance our operational and financial systems and employ additional qualified personnel, management, and financial resources, and may adversely affect our business by diverting management away from day-to-day operations. Further, failure to successfully integrate acquisitions may adversely affect our profitability by creating significant operating inefficiencies that could increase our operating expenses as a percentage of sales and reduce our operating income. In addition, we may not realize expected cost savings from acquisitions. Any one or more of these factors could cause us to not realize the benefits anticipated or have a negative impact on the fair value of the reporting units. Accordingly, goodwill and intangible assets recorded as a result of acquisitions could become impaired.

Certain of our operations are located outside of the United States, which subjects us to risks associated with international activities.

Certain of ourWe have certain operations which are located outside of the United States, primarilyU.S., in Canada, China, and Mexico. We are subject to the Foreign Corrupt Practices Act (“FCPA”), which generally prohibits U.S. companies and their intermediaries from making corrupt payments or otherwise corruptly giving anything of value to foreign officials for the purpose of obtaining or keeping business or otherwise obtaining favorable treatment, and requires companies to maintain adequate record-keeping and internal accounting practices. The FCPA applies to covered companies, individual directors, officers, employees, and agents. Under the FCPA, U.S. companies may be held liable for some actions taken by strategic or local partners or representatives. If we or our intermediaries fail to comply with the requirements of the FCPA, governmental authorities in the United StatesU.S. could seek to impose civil and/or criminal penalties.

Our international operations and potential joint ventures may cause us to incur costs and risks that may distract management from effectively operating our North American business, and such operations or joint ventures may not be profitable.