UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-K

|

| | |

| x | | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the Fiscal Year ended December 31, 2015.2016. |

| | | |

| o | | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the Transition period from to . |

Commission File Number: 001-36002

NRG Yield, Inc.

(Exact name of registrant as specified in its charter)

|

| | |

Delaware (State or other jurisdiction of incorporation or organization) | | 46-1777204 (I.R.S. Employer Identification No.) |

| | | |

211804 Carnegie Center, Princeton, New Jersey

(Address of principal executive offices) | | 08540 (Zip Code) |

(609) 524-4500

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

|

| | |

| Title of Each Class | | Name of Exchange on Which Registered |

| Common Stock, Class A, par value $0.01 | | New York Stock Exchange |

| Common Stock, Class C, par value $0.01 | | New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act:

None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes x No o

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Exchange Act. Yes o No x

Indicate by check mark whether the registrant (1) has filed all reports to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405 of this chapter) is not contained herein, and will not be contained, to the best of the registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of "large accelerated filer," "accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act.

|

| | | | | | |

Large accelerated filer x | | Accelerated filer o | | Non-accelerated filer o | | Smaller reporting company o |

| | | | | (Do not check if a smaller reporting company) | | |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes o No x

As of the last business day of the most recently completed second fiscal quarter, the aggregate market value of the common stock of the registrant held by non-affiliates was approximately $1,944,615,167$1,502,686,604 based on the closing sale prices of such shares as reported on the New York Stock Exchange.

Indicate the number of shares outstanding of each of the registrant's classes of common stock as of the latest practicable date.

|

| | |

| Class | | Outstanding at January 31, 20162017 |

| Common Stock, Class A, par value $0.01 per share | | 34,586,250 |

| Common Stock, Class B, par value $0.01 per share | | 42,738,750 |

| Common Stock, Class C, par value $0.01 per share | | 62,784,25062,789,804 |

| Common Stock, Class D, par value $0.01 per share | | 42,738,750 |

Documents Incorporated by Reference:

Portions of the Registrant's Definitive Proxy Statement relating to its 20162017 Annual Meeting of Stockholders

are incorporated by reference into Part III of this Annual Report on Form 10-K

TABLE OF CONTENTS

Index

|

| |

| GLOSSARY OF TERMS | |

| PART I | |

| Item 1 — Business | |

| Item 1A — Risk Factors | |

| Item 1B — Unresolved Staff Comments | |

| Item 2 — Properties | |

| Item 3 — Legal Proceedings | |

| Item 4 — Mine Safety Disclosures | |

| PART II | |

| Item 5 — Market for Registrant's Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities | |

| Item 6 — Selected Financial Data | |

| Item 7 — Management's Discussion and Analysis of Financial Condition and Results of Operations | |

| Item 7A — Quantitative and Qualitative Disclosures About Market Risk | |

| Item 8 — Financial Statements and Supplementary Data | |

| Item 9 — Changes in Disagreements With Accountants on Accounting and Financial Disclosure | |

| Item 9A — Controls and Procedures | |

| Item 9B — Other Information | |

| PART III | |

| Item 10 — Directors, Executive Officers and Corporate Governance | |

| Item 11 — Executive Compensation | |

| Item 12 — Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters | |

| Item 13 — Certain Relationships and Related Transactions, and Director Independence | |

| Item 14 — Principal Accounting Fees and Services | |

| PART IV | |

| Item 15 — Exhibits, Financial Statement Schedules | |

| EXHIBIT INDEX | |

| Item 16 — Form 10-K Summary | |

GLOSSARY OF TERMS

When the following terms and abbreviations appear in the text of this report, they have the meanings indicated below:

|

| | |

| 2017 Drop Down Assets | | (i) a 16% interest (approximately 31% of NRG's 51% interest) in the Agua Caliente solar farm and (ii) NRG's 50% interests in seven utility-scale solar farms located in Utah. Both are subject of the definitive purchase agreements that the Company entered into with NRG on February 24, 2017 |

| 2019 Convertible Notes | | $345 million aggregate principal amount of 3.50% Convertible Notes due 2019 |

| 2020 Convertible Notes | | $287.5 million aggregate principal amount of 3.25% Convertible Notes due 2020 |

Alta Sellers2024 Senior Notes | | Terra-Gen Finance Company,$500 million aggregate principal amount of 5.375% unsecured senior notes due 2024, issued by NRG Yield Operating LLC and certain |

| 2026 Senior Notes | | $350 million aggregate principal amount of its affiliates5.00% unsecured senior notes due 2026, issued by NRG Yield Operating LLC |

| 2037 Notes | | $200 million aggregate principal amount of 4.68% senior secured notes due 2037, issued by CVSR Holdco |

| Alta TE Holdco | | Alta Wind X-XI TE Holdco LLC |

| Alta Wind Portfolio | | Seven wind facilities that total 947 MW located in Tehachapi, California and a portfolio of associated land leases |

| AOCL | | Accumulated Other Comprehensive Loss |

| ARO | | Asset Retirement Obligation |

| ARRA | | American Recovery and Reinvestment Act of 2009 |

| ASC | | The FASB Accounting Standards Codification, which the FASB established as the source of authoritative U.S. GAAP |

| ASU | | Accounting Standards Updates – updates to the ASC |

| ATM Program | | At-The-Market Equity Offering Program |

| Buffalo Bear | | Buffalo Bear, LLC, the operating subsidiary of Tapestry Wind LLC, which owns the Buffalo Bear project |

| CAA | | Clean Air Act |

| CAFD | | Cash Available For Distribution, which the Company defines as net income before interest expense, income taxes, depreciation and amortization, plus cash distributions from unconsolidated affiliates, cash receipts from notes receivable, less cash distributions to noncontrolling interests, maintenance capital expenditures, pro-rata EBITDA from unconsolidated affiliates, cash interest paid, income taxes paid, principal amortization of indebtedness and changes in other assets.prepaid and accrued capacity payments |

| CfD | | Contract for Differences |

| CFTC | | U.S. Commodity Future Trading Commission |

CO2

| | Carbon Dioxide |

| COD | | Commercial Operations Date |

| Code | | Internal Revenue Code of 1986, as amended |

| Company | | NRG Yield, Inc. together with its consolidated subsidiaries |

| CVSR | | California Valley Solar Ranch |

| CVSR Drop Down | | The Company's acquisition from NRG of the remaining 51.05% interest of CVSR Holdco |

| CVSR Holdco | | CVSR Holdco LLC, the indirect owner of CVSR |

| DGCL | | Delaware General Corporation Law |

| DGPV Holdco 1 | | NRG DGPV Holdco 1 LLC |

| DGPV Holdco 2 | | NRG DGPV Holdco 2 LLC |

| Distributed Solar | | Solar power projects, typically less than 20 MW in size, that primarily sell power produced to customers for usage on site, or are interconnected to sell power into the local distribution grid |

Dodd-Frank Act | | The Dodd-Frank Wall Street Reform and Consumer Protection Act of 2012 |

| Drop Down Assets | | Collectively, the June 2014 Drop Down Assets, the January 2015 Drop Down Assets, and the November 2015 Drop Down Assets, and CVSR Drop Down |

Economic gross marginGross Margin | | Energy and capacity revenue, less cost of fuels |

| EDA | | Equity Distribution Agreement |

| EGU | | Electric Utility Generating Unit |

|

| | |

| El Segundo | | NRG West Holdings LLC, the subsidiary of Natural Gas Repowering LLC, which owns the El Segundo Energy Center project |

| EME | | Edison Mission Energy |

| EME Assets | | The January 2015 Drop Down Assets and the November 2015 Drop Down Assets (other than Elbow Creek), originally acquired by NRG from EME on April 1, 2014 |

| EPC | | Engineering, Procurement and Construction |

| ERCOT | | Electric Reliability Council of Texas, the ISO and the regional reliability coordinator of the various electricity systems within Texas |

|

| | |

| EWG | | Exempt Wholesale Generator |

| Exchange Act | | The Securities Exchange Act of 1934, as amended |

| FASB | | Financial Accounting Standards Board |

FCM | | Forward Capacity Market |

| FERC | | Federal Energy Regulatory Commission |

FFB | | Federal Financing Bank |

| FPA | | Federal Power Act |

| GAAP | | Accounting principles generally accepted in the U.S. |

| GenConn | | GenConn Energy LLC |

| GHG | | Greenhouse gasesgas |

| GW | | Gigawatt |

| HLBV | | Hypothetical Liquidation at Book Value |

| IASB | | International Accounting Standards Board |

IPO | | Initial Public Offering |

| IRS | | Internal Revenue Service |

| ISO | | Independent System Operator, also referred to as Regional Transmission Organization, or RTO |

ISO-NE | | ISO New England Inc. |

| ITC | | Investment Tax Credit |

| January 2015 Drop Down Assets | | The Laredo Ridge, Tapestry and Walnut Creek projects, which were acquired by Yield Operating LLC from NRG on January 2, 2015 |

| June 2014 Drop Down Assets | | The TA High Desert, Kansas South and El Segundo projects, which were acquired by Yield Operating LLC from NRG on June 30, 2014 |

| Kansas South | | NRG Solar Kansas South LLC, the operating subsidiary of NRG Solar Kansas South Holdings LLC, which owns the Kansas South project |

| KPPH | | 1,000 Pounds Per Hour |

| Laredo Ridge | | Laredo Ridge Wind, LLC, the operating subsidiary of Mission Wind Laredo, LLC, which owns the Laredo Ridge project |

| LIBOR | | London Inter-Bank Offered Rate |

| Marsh Landing | | NRG Marsh Landing LLC, formerly GenOn Marsh Landing LLC |

| MMBtu | | Million British Thermal Units |

| MW | | Megawatt |

| MWh | | Saleable megawatt hours, net of internal/parasitic load megawatt-hours |

| MWt | | Megawatts Thermal Equivalent |

| NECP | | NRG Energy Center Pittsburgh LLC |

| NERC | | North American Electric Reliability Corporation |

| Net Exposure | | Counterparty credit exposure to NRG Yield, Inc. net of collateral |

| NOLs | | Net Operating Losses |

| November 2015 Drop Down Assets | | 75% of the Class B interests of NRG Wind TE Holdco, which owns a portfolio of 12 wind facilities totaling 814 net MW, which was acquired by Yield Operating LLC from NRG on November 3, 2015 |

NOx | | Nitrogen OxideOxides |

| NPNS | | Normal Purchases and Normal Sales |

| NRG | | NRG Energy, Inc. |

| NRG Wind TE Holdco | | NRG Wind TE Holdco LLC |

| NRG Yield, Inc. | | NRG Yield, Inc., together with its consolidated subsidiaries, or the Company |

|

| | |

| NRG Yield LLC | | The holding company through which the projects are owned by NRG, the holder of Class B and Class D units, and NRG Yield, Inc., the holder of the Class A and Class C units |

| NRG Yield Operating LLC | | The holder of the project assets that belong to NRG Yield LLC |

NSPS | | New Source Performance Standards |

| OCI/OCL | | Other comprehensive income/loss |

| OSHA | | Occupational Safety and Health Administration |

| PG&E | | Pacific Gas & Electric Company |

|

| | |

| Pinnacle | | Pinnacle Wind, LLC, the operating subsidiary of Tapestry Wind LLC, which owns the Pinnacle project |

| PJM | | PJM Interconnection, LLC |

| PPA | | Power Purchase Agreement |

| PTC | | Production Tax Credit |

| PUCT | | Public Utility Commission of Texas |

| PUHCA | | Public Utility Holding Company Act of 2005 |

| PURPA | | Public Utility Regulatory Policies Act of 1978 |

| QF | | Qualifying Facility under PURPA |

| REC | | Renewable Energy Certificate |

| Recapitalization | | The adoption of the Company's Second Amended and Restated Certificate of Incorporation which authorized two new classes of common stock, Class C common stock and Class D common stock, and distributed shares of such new classes of common stock to holders of the Company’s outstanding Class A common stock and Class B common stock, respectively, through a stock split on May 14, 2015 |

| ROFO Agreement | | Amended and Restated Right of First Offer Agreement between the Company and NRG |

| RPM | | Reliability Pricing Model |

| RPS | | Renewable Portfolio Standards |

| RPV Holdco | | NRG RPV Holdco 1 LLC |

| RTO | | Regional Transmission Organization |

| SCE | | Southern California Edison |

| SEC | | U.S. Securities and Exchange Commission |

| Senior Notes | | NRG Yield Operating LLC's $500 million of 5.375% unsecured senior notes dueCollectively, the 2024 Senior Notes and the 2026 Senior Notes |

SO2 | | Sulfur Dioxide |

| TA High Desert | | TA-High Desert LLC, the operating subsidiary of NRG Solar Mayfair LLC, which owns the TA High Desert project |

| Taloga | | Taloga Wind, LLC, the operating subsidiary of Tapestry Wind LLC, which owns the Taloga project |

| Tapestry | | Collection of the Pinnacle, Buffalo Bear and Taloga projects |

Terra-Gen | | Terra-Gen Operating Company, LLC |

| Thermal Business | | The Company's thermal business, which consists of thermal infrastructure assets that provide steam, hot water and/or chilled water, and in some instances electricity, to commercial businesses, universities, hospitals and governmental units |

| UPMC | | University of Pittsburgh Medical Center |

| U.S. | | United States of America |

| U.S. DOE | | U.S. Department of Energy |

U.S. GAAP | | Accounting principles generally accepted in the United States |

| Utility Scale Solar | | Solar power projects, typically 20 MW or greater in size (on an alternating current, or AC, basis), that are interconnected into the transmission or distribution grid to sell power at a wholesale level |

| VaR | | Value at Risk |

| VIE | | Variable Interest Entity |

| Walnut Creek | | NRG Walnut Creek, LLC, the operating subsidiary of WCEP Holdings, LLC, which owns the Walnut Creek project |

PART I

Item 1 — Business

General

NRG Yield, Inc., together with its consolidated subsidiaries, or the Company, is a dividend growth-oriented company formed to serve as the primary vehicle through which NRG owns, operates and acquires contracted renewable and conventional generation and thermal infrastructure assets. The Company believes it is well positioned to be a premier company for investors seeking stable and growing dividend income from a diversified portfolio of lower-risk, high-quality assets.

The Company owns a diversified portfolio of contracted renewable and conventional generation and thermal infrastructure assets in the U.S. The Company’s contracted renewable and conventional generation portfolio collectively represents 4,563 net MW as of December 31, 2015 collectively represents2016 4,435 net MW.. Each of these assets sells substantially all of its output pursuant to long-term offtake agreements with creditworthy counterparties. The weighted average remaining contract duration of these offtake agreements was approximately 1716 years as of December 31, 20152016, based on CAFD. The Company also owns thermal infrastructure assets with an aggregate steam and chilled water capacity of 1,3151,319 net MWt and electric generation capacity of 124123 net MW. These thermal infrastructure assets provide steam, hot water and/or chilled water, and, in some instances, electricity to commercial businesses, universities, hospitals and governmental units in multiple locations, principally through long-term contracts or pursuant to rates regulated by state utility commissions.

A complete listing of the Company's interests in facilities, operations and/or projects owned or leased as of December 31, 20152016 can be found in Item 2 — Properties.

History

The Company was formed by NRG Energy, Inc., or NRG, as a Delaware corporation on December 20, 2012. On July 22, 2013, the Company2012 and closed theits initial public offering of 22,511,250 shares of its Class A common stock at an offering price of $22.00 per share.on July 22, 2013. In connection with theits initial public offering, the Company’sCompany's shares of Class A common stock began trading on the New York Stock Exchange under the symbol “NYLD”. The net proceeds to the Company from the offering, after deducting underwriting discounts, were approximately $468 million, of which the Company used $395 million to purchase 19,011,250 NRG Yield LLC Class A units from NRG and $73 million to purchase 3,500,000 NRG Yield LLC Class A units directly from NRG Yield LLC. At the time of the offering, NRG owned 42,738,750 NRG Yield LLC Class B units.

On July 29, 2014, the Company issued 12,075,000 shares of Class A common stock for net proceeds, after underwriting discount and expenses, of $630 million. The Company utilized the proceeds of the offering to acquire 12,075,000 additional Class A units of NRG Yield LLC.“NYLD.”

Effective May 14, 2015, the Company completed a stock split in connection with whichwhereby each outstanding share of Class A common stock was split into one share of Class A common stock and one share of Class C common stock, and each outstanding share of Class B common stock was split into one share of Class B common stock and one share of Class D common stock. The stock split is referred to as the Recapitalization and all references to share or per share amounts in the accompanying consolidated financial statements and applicable disclosures have been retrospectively adjusted to reflect the Recapitalization. Following the Recapitalization, the Company's Class A common stock continued trading on the New York Stock Exchange under the new ticker symbol "NYLD.A" and the Class C common stock began trading under the ticker symbol "NYLD". In addition, on June 29, 2015, the Company completed the issuance of 28,198,000 shares of Class C common stock for net proceeds of $599 million and utilized the proceeds of the offering to acquire 28,198,000 Class C units of NRG Yield LLC."NYLD."

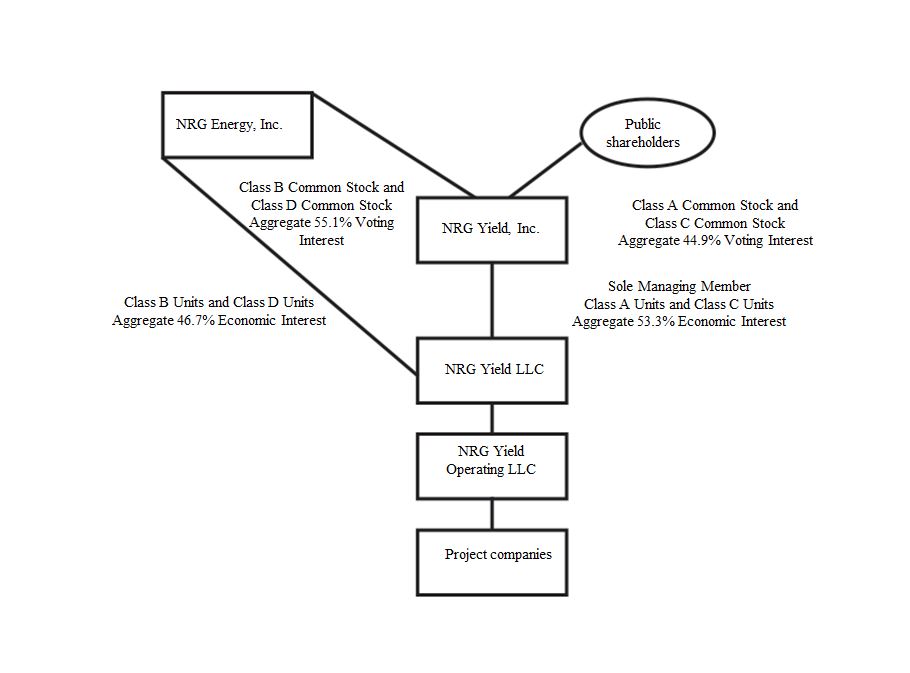

NRG, through its holdings of Class B common stock and Class D common stock, has a 55.1% voting interest in the Company and receives distributions from NRG Yield LLC through its ownership of Class B units and Class D units. The holders of the Company's issued and outstanding shares of Class A common stock and Class C common stock are entitled to dividends as declared and have 44.9% of the voting power in the Company.

As of December 31, 2015, NRG owned 42,738,750 NRG Yield LLC Class B units and 42,738,750 NRG Yield LLC Class D units and the Company owned 34,586,250 NRG Yield LLC Class A units and 62,784,250 NRG Yield LLC Class C units. As of December 31, 2015, the Company and NRG have 53.3% and 46.7% economic interests in NRG Yield LLC, respectively. The Company is the sole managing member of NRG Yield LLC and operates and controls all of its business and affairs and consolidates the financial results of NRG Yield LLC and its subsidiaries. NRG Yield LLC is a holding company for the companies that directly and indirectly own and operate the Company's business. As of December 31, 2016, the Company and NRG have 53.3% and 46.7% economic interests in NRG Yield LLC, respectively. As a result of the current ownership of the Class B common stock and Class D common stock, NRG continues at the present time to control the Company, and the Company in turn, as the sole managing member of NRG Yield LLC, controls NRG Yield LLC and its subsidiaries.

The diagram below depicts the Company’s organizational structure as of December 31, 2015:2016:

Business Strategy

The Company's primary business strategy is to focus on the acquisition and ownership of assets with predictable, long-term cash flows in order that it may be able to increase the cash dividends paid to holders of the Company's Class A and Class C common stock over time without compromising the ongoing stability of the business. The Company's plan for executing this strategy includes the following key components:

Focus on contracted renewable energy and conventional generation and thermal infrastructure assets. The Company owns and operates utility scale and distributed renewable energy and natural gas-fired generation, thermal and other infrastructure assets with proven technologies, low operating risks and stable cash flows. The Company believes by focusing on this core asset class and leveraging its industry knowledge, it will maximize its strategic opportunities, be a leader in operational efficiency and maximize its overall financial performance.

Growing the business through acquisitions of contracted operating assets.The Company believes that its base of operations and relationship with NRG provide a platform in the conventional and renewable power generation and thermal sectors for strategic growth through cash accretive and tax advantaged acquisitions complementary to its existing portfolio. In connectionaddition to acquiring renewable generation, conventional generation and thermal infrastructure assets from third parties where the Company believes its knowledge of the market and operating expertise provides it with its initial public offering,a competitive advantage, the Company entered into a Right of First Offer Agreement with NRG, which was amended and restated in connection withor the Recapitalization, or asROFO Agreement. On February 24, 2017, the Company amended and restated the ROFO Agreement.Agreement, expanding the NRG ROFO pipeline with the addition of 234 net MW of utility-scale solar projects, consisting of Buckthorn, a 154 net MW solar facility in Texas, and Hawaii solar projects, which have a combined capacity of 80 net MW. Under the ROFO Agreement, NRG has granted the Company and its affiliates a right of first offer on any proposed sale, transfer or other disposition of certain assets of NRG for a period of seven years from the completion of the Recapitalization.until February 24, 2022. In addition to the assets described in the table below which reflects the remaining assets subject to sale, the ROFO Agreement also provides the Company with a right of first offer with respect to up to $250 million of equity in one or more residential or distributed solar generation portfolios developed by affiliates of NRG, together with the assets listed in the table below, the NRG ROFO Assets.

| | | Asset | | Fuel Type | | Rated Capacity (MW)(a) | | COD | | Fuel Type | | Rated Capacity (MW)(a) | | COD |

CVSR(b) | | Solar | | 128 | | 2013 | |

Ivanpah(c) | | Solar | | 193 | | 2013 | |

Agua Caliente(d) | | Solar | | 148 | | 2014 | |

Ivanpah(b) | | | Solar | | 193 | | 2013 |

Agua Caliente(c) | | | Solar | | 148 | | 2014 |

| Buckthorn | | | Solar | | 154 | | 2018 |

| Hawaii | | | Solar | | 80 | | 2019 |

| Carlsbad | | Conventional | | 527 | | 2018 | | Conventional | | 527 | | 2018 |

| Puente/Mandalay | | Conventional | | 262 | | 2020 | | Conventional | | 262 | | 2020 |

TE Wind Holdco(e): | | |

Wind TE Holdco(d): | | |

| Elkhorn Ridge | | Wind | | 13 | | 2009 | | Wind | | 13 | | 2009 |

| San Juan Mesa | | Wind | | 22 | | 2005 | | Wind | | 22 | | 2005 |

| Wildorado | | Wind | | 40 | | 2007 | | Wind | | 40 | | 2007 |

| Crosswinds | | Wind | | 5 | | 2007 | | Wind | | 5 | | 2007 |

| Forward | | Wind | | 7 | | 2008 | | Wind | | 7 | | 2008 |

| Hardin | | Wind | | 4 | | 2007 | | Wind | | 4 | | 2007 |

| Odin | | Wind | | 5 | | 2007 | | Wind | | 5 | | 2007 |

| Sleeping Bear | | Wind | | 24 | | 2007 | | Wind | | 24 | | 2007 |

| Spanish Fork | | Wind | | 5 | | 2008 | | Wind | | 5 | | 2008 |

| Goat Wind | | Wind | | 37 | | 2008/2009 | | Wind | | 37 | | 2008/2009 |

| Lookout | | Wind | | 9 | | 2008 | | Wind | | 9 | | 2008 |

| Elbow Creek | | Wind | | 30 | | 2008 | | Wind | | 30 | | 2008 |

| Community | | Wind | | 30 | | 2011 | | Wind | | 30 | | 2011 |

| Jeffers | | Wind | | 50 | | 2008 | | Wind | | 50 | | 2008 |

Minnesota Portfolio(f) | | Wind | | 40 | | 2003/2006 | |

Minnesota Portfolio(e) | | | Wind | | 40 | | 2003/2006 |

(a) Represents the maximum, or rated, electricity generating capacity of the facility in MW multiplied by NRG's percentage ownership interest in the facility as of December 31, 2015.2016.

(b)Represents NRG’s remaining 51.05% ownership interest in CVSR.

(c) Represents 49.95% of NRG's 50.01% ownership interest in Ivanpah. Following a sale of this 49.95% interest, the remaining 50.05% of Ivanpah would be owned by NRG, Google Inc. and BrightSource Energy Inc.

(d)(c) Represents NRG’s 51% ownership interest in Agua Caliente. The remaining 49% of Agua Caliente is owned by MidAmerican EnergyBHE AC Holdings, Inc.LLC. As further described below, the Company has entered into an agreement with NRG to acquire 16% of Agua Caliente.

(e)(d) Represents NRG's remaining 25% of the Class B interests of NRG Wind TE Holdco. NRG Yield, Inc. acquired 75% of the Class B interests in November 2015. A tax equity investor owns the Class A interests in NRG Wind TE Holdco.

(f)(e) Includes Bingham Lake, Eastridge, and Westridge projects.

NRG is not obligated to sell the remaining NRG ROFO Assets to the Company and, if offered by NRG, the Company cannot be sure whether these assets will be offered on acceptable terms, or that the Company will choose to consummate such acquisitions. In addition, NRG may offer additional assets to the Company, as described in Item 7 — Management's Discussion and Analysis of Financial Condition and Results of Operations.

In December 2016, NRG offered the Company the opportunity to purchase the following assets: (i) the Minnesota Portfolio, a 40 MW portfolio of wind projects; (ii) the 30 MW Community wind project; (iii) the 50 MW Jeffers wind projects; and (iv) a 16% interest in the 290 MW Agua Caliente solar project, pursuant to the ROFO Agreement. In addition to these ROFO Assets, NRG also offered the Company the opportunity to purchase NRG's 50% interests in seven utility-scale solar projects located in Utah, representing 265 net MW of capacity, based on cash to be distributed, that were part of NRG's recent acquisition of projects from SunEdison.

On February 24, 2017, the Company and NRG entered into a definitive agreement regarding the acquisition of the following facilities: (i) a 16% interest (approximately 31% of NRG's 51% interest) in the Agua Caliente solar farm, one of the NRG ROFO assets, representing ownership of approximately 46 net MW of capacity. Agua Caliente is located in Yuma County, AZ and sells power subject to a 25-year PPA with Pacific Gas and Electric, with 22 years remaining on that contract; and (ii) NRG's 50% interests in seven utility-scale solar farms located in Utah representing 265 net MW of capacity, based on cash to be distributed, that were part of NRG's recent acquisition of projects from SunEdison. The Utah assets achieved commercial operations in 2016, sell power subject to 20-year PPAs with PacifiCorp, a subsidiary of Berkshire Hathaway and are part of a tax equity structure with Dominion Solar Projects III, Inc., or Dominion, from which NRG currently receives 50% of cash to be distributed. The Company may also have opportunitiesexpects to acquire other generationpay total cash consideration of $130 million for the transaction, excluding adjustments for working capital and thermal infrastructure assets from third parties whereassume non-recourse project debt of approximately $328 million, which will be consolidated, as well as its pro-rata share of non-recourse project level debt of $136 million. The Company elected not to pursue the Company believes its knowledgeacquisition of the marketMinnesota Portfolio, Community and operating expertise provides itJeffers wind projects at this time, but may continue its evaluation of the projects. The Company has retained the right with NRG, pursuant to the ROFO Agreement, to participate in any third party process to the extent NRG elected to pursue a competitive advantage.third party sale of these assets.

Primary Focusfocus on North America. The Company intends to primarily focus its investments in North America (including the unincorporated territories of the U.S.). The Company believes that industry fundamentals in North America present it with significant opportunity to acquire renewable, natural gas-fired generation and thermal infrastructure assets, without creating significant exposure to currency and sovereign risk. By primarily focusing its efforts on North America, the Company believes it will best leverage its regional knowledge of power markets, industry relationships and skill sets to maximize the performance of the Company.

Maintain sound financial practices to grow the dividend. The Company intends to maintain a commitment to disciplined financial analysis and a balanced capital structure to enable it to increase its quarterly dividend over time and serve the long-term interests of its stockholders. The Company's financial practices include a risk and credit policy focused on transacting with credit-worthy counterparties; a financing policy, which focuses on seeking an optimal capital structure through various capital formation alternatives to minimize interest rate and refinancing risks, ensure stable long-term dividends and maximize value; and a dividend policy that is based on distributing a significant portion of CAFD each quarter that the Company receives from NRG Yield LLC, subject to available capital, market conditions, and compliance with associated laws, regulations and other contractual obligations. The Company intends to evaluate various alternatives for financing future acquisitions and refinancing of existing project-level debt, in each case, to reduce the cost of debt, extend maturities and maximize CAFD. The Company believes it has additional flexibility to seek alternative financing arrangements, including, but not limited to, debt financings at a holding company level.and equity-like instruments.

Competition

Power generation is a capital-intensive business with numerous and diverse industry participants. The Company competes on the basis of the location of its plants and on the basis of contract price and terms of individual project.projects. Within the power industry, there is a wide variation in terms of the capabilities, resources, nature and identity of the companies with whom the Company competes with depending on the market. Competitors for energy supply are utilities, independent power producers and other providers of distributed generation. The Company also competes to acquire new projects with solarrenewable developers who retain solarrenewable power plant ownership, independent power producers, financial investors and other dividend, growth-oriented companies. Competitive conditions may be substantially affected by capital market conditions and by various forms of energy legislation and regulation considered by federal, state and local legislatures and administrative agencies.agencies, including tax policy. Such laws and regulations may substantially increase the costs of acquiring, constructing and operating projects, and it could be difficult for the Company to adapt to and operate under such laws and regulations.

The Company's thermal business has certain cost efficiencies that may form barriers to entry. Generally, there is only one district energy system in a given territory, for which the only competition comes from on-site systems. While the district energy system can usually make an effective case for the efficiency of its services, some building owners nonetheless may opt for on-site systems, either due to corporate policies regarding allocation of capital, unique situations where an on-site system might in fact prove more efficient, or because of previously committed capital in systems that are already on-site. Growth in existing district energy systems generally comes from new building construction or existing building conversions within the service territory of the district energy provider.

Competitive Strengths

Stable, high quality cash flows. The Company's facilities have a highly stable, predictable cash flow profile consisting of predominantly long-life electric generation assets that sell electricity under long-term fixed priced contracts or pursuant to regulated rates with investment grade and certain other credit-worthy counterparties. Additionally, the Company's facilities have minimal fuel risk. For the Company's five conventional assets, fuel is provided by the toll counterparty or the cost thereof is a pass-through cost under the CfD. Renewable facilities have no fuel costs, and most of the Company's thermal infrastructure assets have contractual or regulatory tariff mechanisms for fuel cost recovery. The offtake agreements for the Company's conventional and renewable generation facilities have a weighted-average remaining duration of approximately 1716 years as of December 31, 2015,2016, based on CAFD, providing long-term cash flow stability. The Company's generation offtake agreements with counterparties for whom credit ratings are available have a weighted-average Moody’s rating of A3 based on rated capacity under contract. All of the Company's assets are in the U.S. and accordingly have no currency or repatriation risks.

High quality, long-lived assets with low operating and capital requirements. The Company benefits from a portfolio of relatively newly-constructed assets, other than thermal infrastructure assets. The Company's assets are comprised of proven and reliable technologies, provided by leading original solar and wind equipment manufacturers such as General Electric, Siemens AG, SunPower Corporation, or SunPower, First Solar Inc., or First Solar, Vestas, Suzlon and Mitsubishi. Given the modern nature of the portfolio, which includes a substantial number of relatively low operating and maintenance cost solar and wind generation assets, the Company expects to achieve high fleet availability and expend modest maintenance-related capital expenditures. The Company estimates each of its solar and wind portfolios have weighted average remaining expected lives based on CAFD of approximately 20 years. Additionally, with the support of services provided by NRG, the Company expects to continue to implement the same rigorous preventative operating and management practices that NRG uses across its fleet of assets. In 2015, NRG achieved a 0.71 OSHA recordable rate, which is within the top quartile plant operating performance for its entire fleet, based on applicable OSHA standards.

Significant scale and diversity. The Company owns and operates a large and diverse portfolio of contracted electric generation and thermal infrastructure assets. As of December 31, 2015,2016, the Company's 4,4354,563 net MW contracted generation portfolio benefits from significant diversification in terms of technology, fuel type, counterparty and geography. The Company's thermal business consists of twelve operations, seven of which are district energy centers that provide steam and chilled water to approximately 695705 customers, and five of which provide generation. The Company believes its scale and access to best practices across the fleet improves its business development opportunities through enhanced industry relationships, reputation and understanding of regional power market dynamics. Furthermore, the Company's diversification reduces its operating risk profile and reliance on any single market.

Relationship with NRG. The Company believes its relationship with NRG, including NRG’s expressed intention to maintain a controlling interest in the Company, provides significant benefits including management and operational expertise, and future growth opportunities. The Company's executive officers have considerable experience in owning and operating, as well as developing, acquiring and integrating, generation and thermal infrastructure assets:to the Company, including:

• NRG Management and Operational Expertise. The Company has access to the significant resources of NRG, the largest competitive power generator in the U.S., to support theits operational, finance,financial, legal, regulatory and environmental aspects, and growth strategy of its business. As such, the Company believes it avails itself of best-in-class resources, including management and operational expertise.functions.

• NRG Asset Development and Acquisition Track Record. NRG's development and strategic teams are focused on the development and acquisition of renewable and conventional generation assets. They have successfully helped grow NRG's powerassets, which may provide future growth opportunities for the Company in addition to the assets set forth in the ROFO Agreement. The Company believes NRG’s ownership position in the Company incentivizes NRG to support the Company's growth strategy, including through the development of renewable and conventional generation portfolio from 24,365 netprojects. During 2016, NRG acquired 1,639 MWs at the end of 2009 to 49,324 netutility scale solar and wind projects and 107 MWs as of December 31, 2015.distributed generation and community solar projects that are currently under development or in operation.

• NRG Financing Experience.Expertise. The Company, believeswith the support of NRG, has demonstratedbeen able to achieve a successful track record of sourcing attractive low-cost, long duration capital to fund project development and acquisitions. The Company expects to continue to realize significant benefits from NRG’s financing and structuring expertise as well as its relationships with financial institutions and other lenders.

Environmentally well-positioned portfolio of assets. On a net capacity basis, theThe Company's portfolio of electric generation assets consists of 2,4902,618 net MW of renewable generation capacity that are non-emitting sources of power generation. The Company's conventional assets consist of the dual fuel-fired GenConn assets as well as the Marsh Landing and Walnut Creek simple cycle natural gas-fired peaking generation facilities and the El Segundo combined cycle natural gas-fired peaking facility. The Company does not anticipate having to expend any significant capital expenditures in the foreseeable future to comply with current environmental regulations applicable to its generation assets. Taken as a whole, the Company believes its strategy will be a net beneficiary of current and potential environmental legislation and regulatory requirements that may serve as a catalyst for capacity retirements and improve market opportunities for environmentally well-positioned assets like the Company's assets once its current offtake agreements expire.

Thermal infrastructure business has high entry costs. Significant capital has been invested to construct the Company's thermal infrastructure assets, serving as a barrier to entry in the markets in which such assets operate. As of December 31, 2015,2016, the Company's thermal gross property, plant, and equipment was approximately $452$467 million. The Company's thermal district energy centers are located in urban city areas, with the chilled water and steam delivery systems located underground. Constructing underground delivery systems in urban areas requires long lead times for permitting, rights of way and inspections and is costly. By contrast, the incremental cost to add new customers in existing markets is relatively low. Once thermal infrastructure is established, the Company believes it has the ability to retain customers over long periods of time and to compete effectively for additional business against stand-alone on-site heating and cooling generation facilities. Installation of stand-alone equipment can require significant modification to a building as well as significant space for equipment and funding for capital expenditures. The Company's system technologies often provide economies of scale in terms of fuel procurement, ability to switch between multiple types of fuel to generate thermal energy, and fuel conversion efficiency. The Company's top ten thermal customers, which make up approximately 7% of the Company's consolidated revenues for the year ended December 31, 2015, have had a relationship with the Company for an average of over 20 years.

Segment Review

The following table summarizestables summarize the Company's operating revenues, net income (loss) and assets by segment for the years ended December 31, 2016, 2015 2014, and 2013,2014, as discussed in Item 15 — Note 12,13, Segment Reporting, to the Consolidated Financial Statements. Refer to that footnote for additional information about the Company's segments. In addition, refer to Item 2 — Properties, for information about the facilities in each of the Company's segments. All amounts have been recast to include the effect of the acquisitions of the Drop Down Assets, which were accounted for as transfers of entities under common control. The accounting guidance requires retrospective combination of the entities for all periods presented as if the combination has been in effect since the inception of common control. Accordingly, the Company prepared its consolidated financial statements to reflect the transfers as if they had taken place from the beginning of the financial statements period or from the date the entities were under common control (if later than the beginning of the financial statements period).

|

| | | | | | | | | | | | | | | | | | | |

| Year ended December 31, 2015 |

| (In millions) | Conventional Generation |

| Renewables |

| Thermal |

| Corporate |

| Total |

| Operating revenues | $ | 336 |

| | $ | 359 |

| | $ | 174 |

| | $ | — |

| | $ | 869 |

|

| Net income (loss) | 156 |

| | (35 | ) | | 22 |

| | (88 | ) | | 55 |

|

| Total assets | 2,102 |

| | 5,056 |

| | 428 |

| | 189 |

| | 7,775 |

|

| | | | Year ended December 31, 2014 | Year ended December 31, 2016 |

| (In millions) | Conventional Generation | | Renewables | | Thermal | | Corporate | | Total | Conventional Generation |

| Renewables |

| Thermal |

| Corporate |

| Total |

| Operating revenues | $ | 317 |

| | $ | 234 |

| | $ | 195 |

| | $ | — |

| | $ | 746 |

| $ | 333 |

| | $ | 518 |

| | $ | 170 |

| | $ | — |

| | $ | 1,021 |

|

| Net income (loss) | 141 |

| | (28 | ) | | 31 |

| | (45 | ) | | 99 |

| 153 |

| | (103 | ) | | 29 |

| | (94 | ) | | (15 | ) |

| Total assets | 2,169 |

| | 4,790 |

| | 436 |

| | 465 |

| | 7,860 |

| 1,993 |

| | 5,535 |

| | 426 |

| | 429 |

| | 8,383 |

|

| | | | Year ended December 31, 2013 | Year ended December 31, 2015 |

| (In millions) | Conventional Generation | | Renewables | | Thermal | | Corporate | | Total | Conventional Generation | | Renewables | | Thermal | | Corporate | | Total |

| Operating revenues | $ | 138 |

| | $ | 97 |

| | $ | 152 |

| | $ | — |

| | $ | 387 |

| $ | 336 |

| | $ | 443 |

| | $ | 174 |

| | $ | — |

| | $ | 953 |

|

| Net income (loss) | 87 |

| | 31 |

| | 20 |

| | (15 | ) | | 123 |

| 156 |

| | (25 | ) | | 22 |

| | (88 | ) | | 65 |

|

| Total assets | | 2,102 |

| | 5,970 |

| | 428 |

| | 189 |

| | 8,689 |

|

|

| | | | | | | | | | | | | | | | | | | |

| | Year ended December 31, 2014 |

| (In millions) | Conventional Generation | | Renewables | | Thermal | | Corporate | | Total |

| Operating revenues | $ | 317 |

| | $ | 316 |

| | $ | 195 |

| | $ | — |

| | $ | 828 |

|

| Net income (loss) | 141 |

| | (19 | ) | | 31 |

| | (45 | ) | | 108 |

|

Government Incentives

Government incentives, including PTCs and ITCs, can enhance the economics of the Company's generating assets and investments by providing, for example, loan guarantees, cash grants, favorable tax treatment, favorable depreciation rules or other incentives. Certain recentThe Company cannot predict the effects that the new U.S. presidential administration will have on government approvals have enhanced federal incentives for renewable generation — including through the extension of the wind power Production Tax Credit and the extension of the solar Investment Tax Credit as further described in Regulatory Developments and could incentivize the development of additional renewable energy projects that would fit within the Company’s asset portfolio. In addition, direct cash incentives may encourage additional renewable energy development by entities that cannot presently benefit from tax credits.

incentives.

Regulatory Matters

As owners of power plants and participants in wholesale and thermal energy markets, certain of the Company's subsidiaries are subject to regulation by various federal and state government agencies. These agencies include FERC and the PUCT, as well as other public utility commissions in certain states where the Company's assets are located. Each of the Company's U.S. generating facilities qualifies as an EWG or QF. In addition, the Company is subject to the market rules, procedures and protocols of the various ISO and RTO markets in which it participates. Likewise, the Company must also comply with the mandatory reliability requirements imposed by NERC and the regional reliability entities in the regions where the Company operates. The Company's operations within the ERCOT footprint are not subject to rate regulation by FERC, as they are deemed to operate solely within the ERCOT market and not in interstate commerce. These operations are subject to regulation by PUCT.

CFTC

The CFTC, among other things, has regulatory oversight authority overregulates the trading of swaps, futures and many commodities under the Commodity Exchange Act, or CEA. Since 2010, there have been a number of reforms to the regulation of the derivatives markets, both in the U.S. and internationally.markets. These regulations, and any further changes thereto, or adoption of additional regulations, including any regulations relating to position limits on futures and other derivatives or margin for derivatives, could negatively impact the Company’s ability to hedge its portfolio in an efficient, cost-effective manner by, among other things, potentially decreasing liquidity in the forward commodity and derivatives markets or limiting the Company’s ability to utilize non-cash collateral for derivatives transactions.

FERC

FERC, among other things, regulates the transmission and the wholesale sale of electricity in interstate commerce under the authority of the FPA. The transmission of electric energy occurring wholly within ERCOT is not subject to FERC’s jurisdiction under Sections 203 or 205 of the FPA. Under existing regulations, FERC determines whether an entity owning a generation facility is an EWG, as defined in the PUHCA. FERC also determines whether a generation facility meets the ownership and technical criteria of a QF under the PURPA. Each of the Company’s non-ERCOT U.S. generating facilities qualifies as an EWG.

The FPA gives FERC exclusive rate-making jurisdiction over the wholesale sale of electricity and transmission of electricity in interstate commerce of public utilities (as defined by the FPA). Under the FPA, FERC, with certain exceptions, regulates the owners of facilities used for the wholesale sale of electricity or transmission in interstate commerce as public utilities, and establishes market rules that are just and reasonable.

Public utilities are required to obtain FERC’s acceptance, pursuant to Section 205 of the FPA, of their rate schedules for the wholesale sale of electricity. All of the Company’s non-QF generating entities located outside of ERCOT make sales of electricity pursuant to market-based rates, as opposed to traditional cost-of-service regulated rates. Every three years FERC will conduct a review of the Company’s market based rates and potential market power on a regional basis.

In accordance with the Energy Policy Act of 2005, FERC has approved the NERC as the national Energy Reliability Organization, or ERO. As the ERO, NERC is responsible for the development and enforcement of mandatory reliability standards for the wholesale electric power system. In addition to complying with NERC requirements, each NRG entity must comply with the requirements of the regional reliability entity for the region in which it is located.

The PURPA was passed in 1978 in large part to promote increased energy efficiency and development of independent power producers. The PURPA created QFs to further both goals, and FERC is primarily charged with administering the PURPA as it applies to QFs. Certain QFs are exempt from regulation, either in whole or in part, under the FPA as public utilities.

The PUHCA provides FERC with certain authority over and access to books and records of public utility holding companies not otherwise exempt by virtue of their ownership of EWGs, QFs, and Foreign Utility Companies. The Company is exempt from many of the accounting, record retention, and reporting requirements of the PUHCA.

Regulatory Developments

U.S. Supreme Court Agrees to Consider the Constitutionality of Maryland's Generator Contracting Programs — On October 19, 2015, the U.S. Supreme Court agreed to hear challenges to one of two cases involving the rights of states to enter into long-term contracts for power generation facilities. The case involves the right of the Maryland Public Service Commission to award long-term power purchase contracts to a generation developer to encourage the construction of new generation capacity in Maryland. The constitutionality of the long-term contracts was challenged in the U.S. District Court for the District of Maryland, which, in an October 24, 2013, decision, found that the contract violated the Supremacy Clause of the U.S. Constitution and was invalid. On June 30, 2014, the U.S. Court of Appeals for the Fourth Circuit affirmed the Maryland District Court's decision. A companion case alleging similar facts in New Jersey will be decided in accordance with the Supreme Court’s decision in the Maryland case. NRG filed a friend-of-the-court brief urging the Supreme Court to uphold the right of states to enter into long-term contracts, which play an important role in financing new generation resources. The Supreme Court heard oral argument on February 24, 2016, and the outcome of this litigation could have broad impacts on how states contract with new generation resources, as well as how such contracted resources interact with the wholesale markets.

Solar ITC and Wind PTC Extensions — In December 2015, the U.S. Congress enacted an extension of the 30% solar ITC so that projects that begin construction in 2016 through 2019 will continue to qualify for the 30% ITC. Projects beginning construction in 2020 and 2021 will be eligible for the ITC at the rates of 26% and 22%, respectively. The same legislation also extended the 10-year wind PTC for wind projects that begin construction in years 2016 through 2019. Wind projects that begin construction in the years 2017, 2018 and 2019 are eligible for PTC at 80%, 60% and 40% of the statutory rate per kWh, respectively. The extension of the ITC and PTC could promote additional development of solar and wind energy resources.

Environmental Matters

The Company is subject to a wide range of environmental laws in the development, construction, ownership and operation of projects. These laws generally require that governmental permits and approvals be obtained before construction and during operation of facilities. The Company is also subject to laws regarding the protection of wildlife, including migratory birds, eagles, and threatened and endangered species. EnvironmentalFederal and state environmental laws have become increasinglymore stringent and the Company expectsover time, although this trend could change in the near term with respect to continue.federal laws under the new U.S. presidential administration.

In October 2015, the EPA promulgated a GHG emissions rule for existing fossil-fuel-fired electric generating units. The rule is calledfinalized the Clean Power Plan, or CPP.CPP, addressing GHG emissions from existing EGUs. On February 9, 2016, the U.S. Supreme Court stayed the CPP. The CPP faces numerousU.S. Court of Appeals for the D.C. Circuit, sitting en banc, heard oral argument on the legal challenges that likely will take several years to resolve. Ifthe CPP in September 2016. Due to the ongoing litigation and the potential impact of the new U.S. presidential administration, the Company believes the CPP is eventually upheld, it may take several more years for the impacts of this rulenot likely to be clear as states would be required to develop and put in place plans to implement the rule to achieve state-specific goals.survive.

Customers

The Company sells its electricity and environmental attributes, including RECs, primarily to local utilities under long-term, fixed-price PPAs. During the year ended December 31, 2015,2016, the Company derived approximately 43%42% of its consolidated revenue from Southern California Edison, or SCE, and approximately 17%23% of its consolidated revenue from Pacific Gas and Electric, or PG&E.

Employees

The Company employs Christopher Sotos as its President and Chief Executive Officer and Chad Plotkin as its Senior Vice President and Chief Financial Officer. Other than Messrs. Sotos and Plotkin, the Company does not employ any of the individuals who manage operations.other employees. The personnel that carry out these activitiesmanage operations of the Company are employees of NRG or third parties managed by NRG, and their services are provided for the Company's benefit under the Management Services Agreement and project operations and maintenance agreements with NRG as described in Item 15 — Note 1415, Related Party Transactions, to the Consolidated Financial Statements.

Available Information

The Company's annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, and amendments to those reports filed or furnished pursuant to section 13(a) or 15(d) of the Exchange Act are available free of charge through the Company's website, www.nrgyield.com, as soon as reasonably practicable after they are electronically filed with, or furnished to, the SEC. The Company also routinely posts press releases, presentations, webcasts, and other information regarding the Company on its website.

Item 1A — Risk Factors

Risks Related to the Company's Business

Certain facilities are newly constructed and may not perform as expected.

Certain of the Company's conventional and renewable assets are newly constructed. The ability of these facilities to meet the Company's performance expectations is subject to the risks inherent in newly constructed power generation facilities and the construction of such facilities, including, but not limited to, degradation of equipment in excess of the Company's expectations, system failures, and outages. The failure of these facilities to perform as the Company expects could have a material adverse effect on the Company's business, financial condition, results of operations, and cash flows and its ability to pay dividends to holders of the Company's common stock.

Pursuant to the Company's cash dividend policy, the Company intends to distribute all or substantially all of the CAFD through regular quarterly distributions and dividends, and the Company's ability to grow and make acquisitions through cash on hand could be limited.

The Company expects to distribute all or substantially all of the CAFD each quarter and to rely primarily upon external financing sources, including the issuance of debt and equity securities and, if applicable, borrowings under the Company's amended and restated revolving credit facility to fund acquisitions and growth capital expenditures. The Company may be precluded from pursuing otherwise attractive acquisitions if the projected short-term cash flow from the acquisition or investment is not adequate to service the capital raised to fund the acquisition or investment, after giving effect to the Company's available cash reserves. The Company's growth may not be as fast as that of businesses that reinvest their available cash to expand ongoing operations. To the extent the Company issues additional equity securities in connection with any acquisitions or growth capital expenditures, the payment of dividends on these additional equity securities may increase the risk that the Company will be unable to maintain or increase its per share dividend. The incurrence of bank borrowings or other debt by NRG Yield Operating LLC or by the Company's project-level subsidiaries to finance the Company’s growth strategy will result in increased interest expense and the imposition of additional or more restrictive covenants, which, in turn, may impact the cash distributions the Company receives to distribute to holders of the Company’s common stock.

The Company may not be able to effectively identify or consummate any future acquisitions on favorable terms, or at all.

The Company's business strategy includes growth through the acquisitions of additional generation assets (including through corporate acquisitions). This strategy depends on the Company’s ability to successfully identify and evaluate acquisition opportunities and consummate acquisitions on favorable terms. However, the number of acquisition opportunities is limited. In addition, the Company will compete with other companies for these limited acquisition opportunities, which may increase the Company’s cost of making acquisitions or cause the Company to refrain from making acquisitions at all. Some of the Company’s competitors for acquisitions are much larger than the Company with substantially greater resources. These companies may be able to pay more for acquisitions and may be able to identify, evaluate, bid for and purchase a greater number of assets than the Company’s financial or human resources permit. If the Company is unable to identify and consummate future acquisitions, it will impede the Company’s ability to execute its growth strategy and limit the Company’s ability to increase the amount of dividends paid to holders of the Company’s common stock.

Furthermore, the Company’s ability to acquire future renewable facilities may depend on the viability of renewable assets generally. These assets currently are largely contingent on public policy mechanisms including ITCs, cash grants, loan guarantees, accelerated depreciation, RPS and carbon trading plans. These mechanisms have been implemented at the state and federal levels to support the development of renewable generation, demand-side and smart grid and other clean infrastructure technologies. The availability and continuation of public policy support mechanisms will drive a significant part of the economics and viability of the Company’s growth strategy and expansion into clean energy investments.

The Company’s ability to effectively consummate future acquisitions will also depend on the Company’s ability to arrange the required or desired financing for acquisitions.

The Company may not have sufficient availability under the Company’s credit facilities or have access to project-level financing on commercially reasonable terms when acquisition opportunities arise. An inability to obtain the required or desired financing could significantly limit the Company’s ability to consummate future acquisitions and effectuate the Company’s growth strategy. If financing is available, utilization of the Company’s credit facilities or project-level financing for all or a portion of the purchase price of an acquisition could significantly increase the Company’s interest expense, impose additional or more restrictive

covenants and reduce CAFD. Similarly, the issuance of additional equity securities as consideration for acquisitions could cause significant stockholder dilution and reduce the Company’s per share CAFDdividends if the acquisitions are not sufficiently accretive. The Company’s ability to consummate future acquisitions may also depend on the Company’s ability to obtain any required regulatory approvals for such acquisitions, including, but not limited to, approval by FERC under Section 203 of the FPA.

Finally, the acquisition of companies and assets are subject to substantial risks, including the failure to identify material problems during due diligence (for which the Company may not be indemnified post-closing), the risk of over-paying for assets (or not making acquisitions on an accretive basis) and the ability to retain customers. Further, the integration and consolidation of acquisitions requires substantial human, financial and other resources and, ultimately, the Company's acquisitions may divert management’s attention from the Company's existing business concerns, disrupt the Company's ongoing business or not be successfully integrated. There can be no assurances that any future acquisitions will perform as expected or that the returns from such acquisitions will support the financing utilized to acquire them or maintain them. As a result, the consummation of acquisitions may have a material adverse effect on the Company's business, financial condition, results of operations, and cash flows and ability to pay dividends to holders of the Company’s common stock.

Even if the Company consummates acquisitions that it believes will be accretive to CAFD per share of Class A common stock and Class C common stock, those acquisitions may decrease the CAFD per share of Class A common stock and Class C common stock as a result of incorrect assumptions in the Company’s evaluation of such acquisitions, unforeseen consequences or other external events beyond the Company’s control.

The acquisition of existing generation assets involves the risk of overpaying for such projects (or not making acquisitions on an accretive basis) and failing to retain the customers of such projects. While the Company will perform due diligence on prospective acquisitions, the Company may not discover all potential risks, operational issues or other issues in such generation assets. Further, the integration and consolidation of acquisitions require substantial human, financial and other resources and, ultimately, the Company’s acquisitions may divert the Company’s management’s attention from its existing business concerns, disrupt its ongoing business or not be successfully integrated. Future acquisitions might not perform as expected or the returns from such acquisitions might not support the financing utilized to acquire them or maintain them. A failure to achieve the financial returns the Company expects when it acquires generation assets could have a material adverse effect on the Company’s ability to grow its business and make cash distributions to its Class A and Class C stockholders. Any failure of the Company’s acquired generation assets to be accretive or difficulty in integrating such acquisition into the Company’s business could have a material adverse effect on the Company’s ability to grow its business and make cash distributions to its Class A and Class C stockholders.

The Company’s indebtedness could adversely affect its ability to raise additional capital to fund the Company’s operations or pay dividends. It could also expose the Company to the risk of increased interest rates and limit the Company’s ability to react to changes in the economy or the Company’s industry as well as impact the Company’s CAFD.results of operations, financial condition and cash flows.

As of December 31, 2015,2016, the Company had approximately $4,863$5,770 million of total consolidated indebtedness, $3,461$4,314 million of which was incurred by the Company's non-guarantor subsidiaries. In addition, the Company’s share of its unconsolidated affiliates’ total indebtedness and letters of credit outstanding as of December 31, 2015,2016, totaled approximately $842$453 million and $83$86 million, respectively (calculated as the Company’s unconsolidated affiliates’ total indebtedness as of such date multiplied by the Company’s percentage membership interest in such assets).

The Company’s substantial debt could have important negative consequences on the Company’s financial condition, including:

increasing the Company’s vulnerability to general economic and industry conditions;

requiring a substantial portion of the Company’s cash flow from operations to be dedicated to the payment of principal and interest on the Company’s indebtedness, therefore reducing the Company’s ability to pay dividends to holders of the Company’s capital stock (including the Class A and Class C common stock) or to use the Company’s cash flow to fund its operations, capital expenditures and future business opportunities;

limiting the Company’s ability to enter into long-term power sales or fuel purchases which require credit support;

limiting the Company’s ability to fund operations or future acquisitions;

restricting the Company’s ability to make certain distributions with respect to the Company’s capital stock (including the Class A and Class C common stock) and the ability of the Company’s subsidiaries to make certain distributions to it, in light of restricted payment and other financial covenants in the Company’s credit facilities and other financing agreements;

exposing the Company to the risk of increased interest rates because certain of the Company’s borrowings, which may include borrowings under the Company’s amended and restated revolving credit facility, are at variable rates of interest;

limiting the Company’s ability to obtain additional financing for working capital including collateral postings, capital expenditures, debt service requirements, acquisitions and general corporate or other purposes; and

limiting the Company’s ability to adjust to changing market conditions and placing it at a competitive disadvantage compared to the Company’s competitors who have less debt.

The Company's amended and restated revolving credit facility contains financial and other restrictive covenants that limit the Company’s ability to return capital to stockholders or otherwise engage in activities that may be in the Company’s long-term best interests. The Company’s inability to satisfy certain financial covenants could prevent the Company from paying cash dividends, and the Company’s failure to comply with those and other covenants could result in an event of default which, if not cured or waived, may entitle the related lenders to demand repayment or enforce their security interests, which could have a material adverse effect on the Company’s business, financial condition, results of operations and cash flows. In addition, failure to comply with such covenants may entitle the related lenders to demand repayment and accelerate all such indebtedness.

The agreements governing the Company’s project-level financing contain financial and other restrictive covenants that limit the Company’s project subsidiaries’ ability to make distributions to the Company or otherwise engage in activities that may be in the Company’s long-term best interests. The project-level financing agreements generally prohibit distributions from the project entities to the Company unless certain specific conditions are met, including the satisfaction of certain financial ratios. The Company’s inability to satisfy certain financial covenants may prevent cash distributions by the particular project(s) to it and, the Company’s failure to comply with those and other covenants could result in an event of default which, if not cured or waived may entitle the related lenders to demand repayment or enforce their security interests, which could have a material adverse effect on the Company’s business, results of operations and financial condition. In addition, failure to comply with such covenants may entitle the related lenders to demand repayment and accelerate all such indebtedness. If the Company is unable to make distributions from the Company’s project-level subsidiaries, it would likely have a material adverse effect on the Company’s ability to pay dividends to holders of the Company’s common stock.

Letter of credit facilities to support project-level contractual obligations generally need to be renewed after five to seven years, at which time the Company will need to satisfy applicable financial ratios and covenants. If the Company is unable to renew the Company’s letters of credit as expected or replace them with letters of credit under different facilities on favorable terms or at all, the Company may experience a material adverse effect on its business, financial condition, or results of operations and cash flows. Furthermore, such inability may constitute a default under certain project-level financing arrangements, restrict the ability of the project-level subsidiary to make distributions to it and/or reduce the amount of cash available at such subsidiary to make distributions to the Company.

In addition, the Company’s ability to arrange financing, either at the corporate level or at a non-recourse project-level subsidiary, and the costs of such capital, are dependent on numerous factors, including:

general economic and capital market conditions;

credit availability from banks and other financial institutions;

investor confidence in the Company, its partners, NRG, as the Company’s principal stockholder (on a combined voting basis) and manager under the Management Services Agreement, and the regional wholesale power markets;

the Company’s financial performance and the financial performance of the Company subsidiaries;

the Company’s level of indebtedness and compliance with covenants in debt agreements;

maintenance of acceptable project credit ratings or credit quality;

cash flow; and

provisions of tax and securities laws that may impact raising capital.

The Company may not be successful in obtaining additional capital for these or other reasons. Furthermore, the Company may be unable to refinance or replace project-level financing arrangements or other credit facilities on favorable terms or at all upon the expiration or termination thereof. The Company's failure, or the failure of any of the Company’s projects, to obtain additional capital or enter into new or replacement financing arrangements when due may constitute a default under such existing indebtedness and may have a material adverse effect on the Company's business, financial condition, results of operations and cash flows.

Certain of the Company's long-term bilateral contracts result from state-mandated procurements and could be declared invalid by a court of competent jurisdiction.

A significant portion of the Company's revenues are derived from long-term bilateral contracts with utilities that are regulated by their respective states, and have been entered into pursuant to certain state programs. Certain long-term contracts that other companies have with state-regulated utilities have been challenged in federal court and have been declared unconstitutional on the grounds that the rate for energy and capacity established by the contracts impermissibly conflicts with the rate for energy and capacity established by FERC pursuant to the FPA. To date, federal district courts in New Jersey and Maryland have struck down contracts on similar grounds, and the U.S. Courts of Appeals for the Third and Fourth Circuits, respectively, have affirmed the lower court decisions. On October 19, 2015, the U.S. Supreme Court granted certiorari in the Fourth Circuit case, and the Court heard oral argument on February 24, 2016. The outcome of this litigation could affect future capacity prices

in PJM, as well as the legal status of the Company's bilateral contracts with state-regulated utilities. If certain of the Company's state-mandated agreements with utilities are ever held to be invalid, the Company may be unable to replace such contracts, which could have a material adverse effect on the Company's business, financial condition, results of operations and cash flows.

The generation of electric energy from solar and wind energy sources depends heavily on suitable meteorological conditions.

If solar or wind conditions are unfavorable, the Company's electricity generation and revenue from renewable generation facilities may be substantially below the Company's expectations. The electricity produced and revenues generated by a solar electric or wind energy generation facility is highly dependent on suitable solar or wind conditions, as applicable, and associated weather conditions, which are beyond the Company's control. Furthermore, components of the Company's systems, such as solar panels and inverters, could be damaged by severe weather, such as hailstorms or tornadoes. In addition, replacement and spare parts for key components may be difficult or costly to acquire or may be unavailable. Unfavorable weather and atmospheric conditions could impair the effectiveness of the Company's assets or reduce their output beneath their rated capacity or require shutdown of key equipment, impeding operation of the Company's renewable assets. In addition, climate change may have the long-term effect of changing wind patterns at our projects. Changing wind patterns could cause changes in expected electricity generation. These events could also degrade equipment or components and the interconnection and transmission facilities’ lives or maintenance costs.

Although the Company bases its investment decisions with respect to each renewable generation facility on the findings of related wind and solar studies conducted on-site prior to construction or based on historical conditions at existing facilities, actual climatic conditions at a facility site, particularly wind conditions, may not conform to the findings of these studies and may be affected by variations in weather patterns, including any potential impact of climate change. Therefore, the Company's solar and wind energy facilities may not meet anticipated production levels or the rated capacity of the Company's generation assets, which could adversely affect the business, financial condition, and results of operations and cash flows.

Operation of electric generation facilities involves significant risks and hazards customary to the power industry that could have a material adverse effect on the Company's business, financial condition, results of operations and cash flows.