UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-K

| | | | | | | | | | | | | | |

| (Mark One) | | | | |

| ☑ | | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES

EXCHANGE ACT OF 1934 |

| | For the fiscal year ended | January 29, 2021February 3, 2023 | |

| or |

| ☐ | | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES

EXCHANGE ACT OF 1934 |

For the transition period from to |

Commission File Number: 001-37867

Dell Technologies Inc.

(Exact name of registrant as specified in its charter)

| | | | | | | | |

| Delaware | | 80-0890963 |

| (State or other jurisdiction of incorporation or organization) | | (I.R.S. Employer Identification No.) |

One Dell Way, Round Rock, Texas 78682

(Address of principal executive offices) (Zip Code)

1-800-289-3355

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

| | | | | | | | |

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered |

| Class C Common Stock, par value of $0.01 per share | DELL | New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes þ No ¨

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No þ

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes þ No ¨

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes þ No ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| | | | | | | | | | | | | | | | | |

| Large accelerated filer | ☑ | | | Accelerated filer | ☐ |

| Non-accelerated filer | ☐ | | | Smaller reporting company | ☐ |

| | | | Emerging growth company | ☐ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☑

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ☐ No þ

As of July 31, 2020,29, 2022, the last business day of the registrant’s most recently completed second fiscal quarter, the aggregate market value of the shares of the registrant’s common stock held by non-affiliates was approximately $15.1$11.4 billion (based on the closing price of $59.83$45.06 per share of Class C Common Stock reported on the New York Stock Exchange on that date).

As of March 23, 2021,27, 2023, there were 762,667,390731,204,853 shares of the registrant’s common stock outstanding, consisting of 276,565,287257,374,103 outstanding shares of Class C Common Stock, 384,416,886378,480,523 outstanding shares of Class A Common Stock, and 101,685,21795,350,227 outstanding shares of Class B Common Stock.

DOCUMENTS INCORPORATED BY REFERENCE

The information required by Part III of this report, to the extent not set forth herein, is incorporated by reference from the registrant’s proxy statement relating to its annual meeting of stockholders to be held in 2021.2023. The proxy statement will be filed with the Securities and Exchange Commission within 120 days after the end of the fiscal year to which this report relates.

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

This report contains “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934. The words “may,” “will,” “anticipate,” “estimate,” “expect,” “intend,” “plan,” “aim,” “seek,” and similar expressions as they relate to us or our management are intended to identify these forward-looking statements. All statements by us regarding our expected financial position, revenues, cash flows and other operating results, business strategy, legal proceedings future responses to and effects of the coronavirus disease 2019 (“COVID-19”), and similar matters are forward-looking statements. Our expectations expressed or implied in these forward-looking statements may not turn out to be correct. Our results could be materially different from our expectations because of various risks, including the risks discussed in “Part I — Item 1A — Risk Factors” and in our other periodic and current reports filed with the Securities and Exchange Commission (“SEC”). Any forward-looking statement speaks only as of the date as of which such statement is made, and, except as required by law, we undertake no obligation to update any forward-looking statement after the date as of which such statement was made, whether to reflect changes in circumstances or our expectations, the occurrence of unanticipated events, or otherwise.

DELL TECHNOLOGIES INC.

TABLE OF CONTENTS

Unless the context indicates otherwise, references in this report to “we,” “us,” “our,” the “Company,” and “Dell Technologies” mean Dell Technologies Inc. and its consolidated subsidiaries, references to “Dell” mean Dell Inc. and Dell Inc.’s consolidated subsidiaries, and references to “EMC” mean EMC Corporation and EMC Corporation’s consolidated subsidiaries.

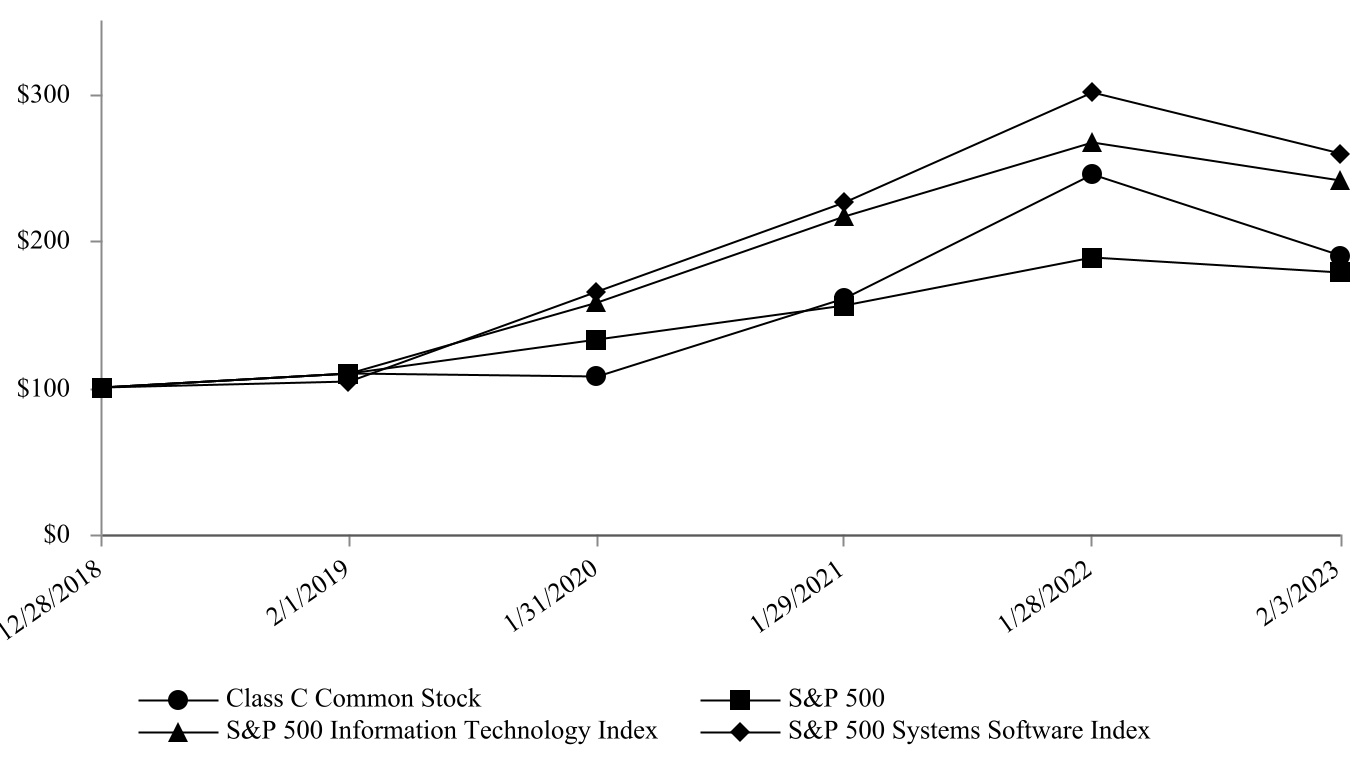

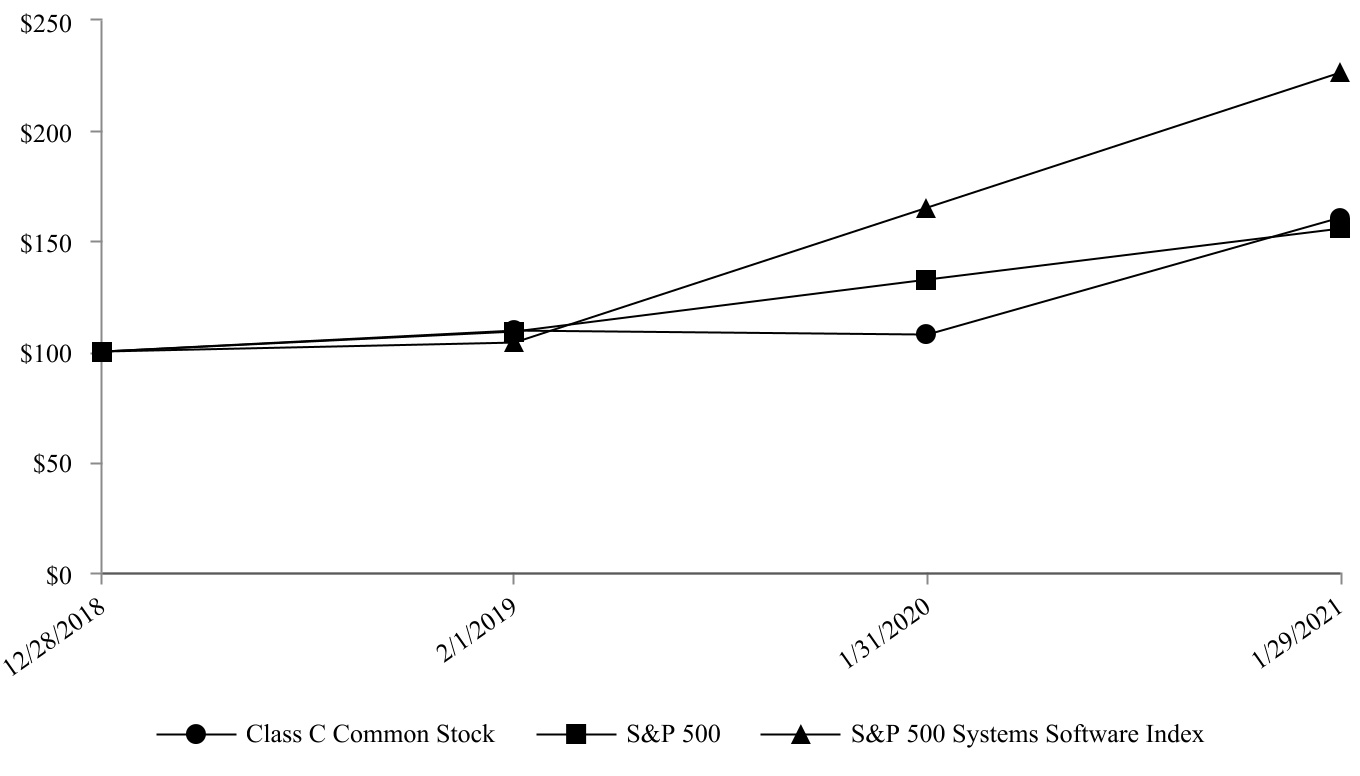

Our fiscal year is the 52- or 53-week period ending on the Friday nearest January 31. We refer to our fiscal years ended February 3, 2023, January 28, 2022, and January 29, 2021 January 31, 2020,as “Fiscal 2023,” “Fiscal 2022,” and February 1, 2019 as “Fiscal 2021,” “Fiscal 2020,” and “Fiscal 2019,” respectively. Fiscal 2021,2023 included 53 weeks, while Fiscal 2020,2022 and Fiscal 20192021 each included 52 weeks.

PART I

ITEM 1 — BUSINESS

BusinessCompany Overview

Dell Technologies helps organizations and individuals build their digital futurefutures and individuals transform how they work, live, and play. We provide customers with one of the industry’s broadest and most innovative technology and servicessolutions portfolio for the data era, spanning bothincluding traditional infrastructure and extending to multi-cloud technologies. We continue to seamlessly deliverenvironments. Our differentiated and holistic information technology (“IT”)IT solutions benefit our results and enable us to our customers, which has driven significantcapture revenue growth and share gains.as customer spending priorities evolve.

Dell Technologies’ integrated solutions help customers modernize their IT infrastructure, manage and operate in a multi-cloudmulticloud world, address workforce transformation, and provide critical solutions that keep people and organizations connected, which has proven even more important in this current time of disruption caused by the coronavirus pandemic.connected. We are helping customers accelerate their digital transformations to improve and strengthen business and workforce productivity. With our extensive portfolio and our commitment to innovation, we offer secure, integrated solutions that extend from the edge to the core to the cloud, and we are at the forefront of the software-defined and cloud native infrastructure era. As further evidence of our commitment to innovation, in Fiscal 2021 we announced our plan to evolve and expand our IT as-a-Service and cloud offerings through Apex. Apex will provide our customers with greater flexibility to scale IT to meet their evolving business needs and budgets.solutions.

Dell Technologies’ end-to-end portfolio isTechnologies operates globally in approximately 180 countries, supported by a world-class organization with unmatched size and scale. We operate globally in 180 countries across key functional areas, including technology and product development, marketing, sales, financial services, and global services. We have a number of durable competitive advantages that provide a critical foundation for our success. Our go-to-market engine includes a 39,000-person31,000-person direct sales force and a global network of over 200,000approximately 240,000 channel partners. We employ approximately 35,000 full-time service and support professionals and maintain approximately 2,200 vendor-managed service centers. We also manage a world-class supply chain at significant scale with approximately $77 billion in annual procurement expenditures and over 725 parts distribution centers.

We further strengthen customer relationships through our financing offerings provided by Dell Financial Services and its affiliates (“DFS”) offer customer paymentand our flexible consumption models, including utility, subscription, and as-a-Service models, which we continue to expand under Dell APEX. These offerings enable our customers to pay over time and provide them with financial flexibility and enables synergies across the business. DFS funded $9 billion of originations in Fiscal 2021 and maintains a $10 billion global portfolio of high-quality financing receivables. We employ 34,000 full-time service and support professionals and maintain more than 2,400 vendor-managed service centers. We manage a world-class supply chain that drives long-term growth and operating efficiencies, with approximately $70 billion in annual procurement expenditures and over 750 parts distribution centers. Together, these elements provide a critical foundation for our success.to meet their changing technological requirements.

Class V TransactionVision and Strategy

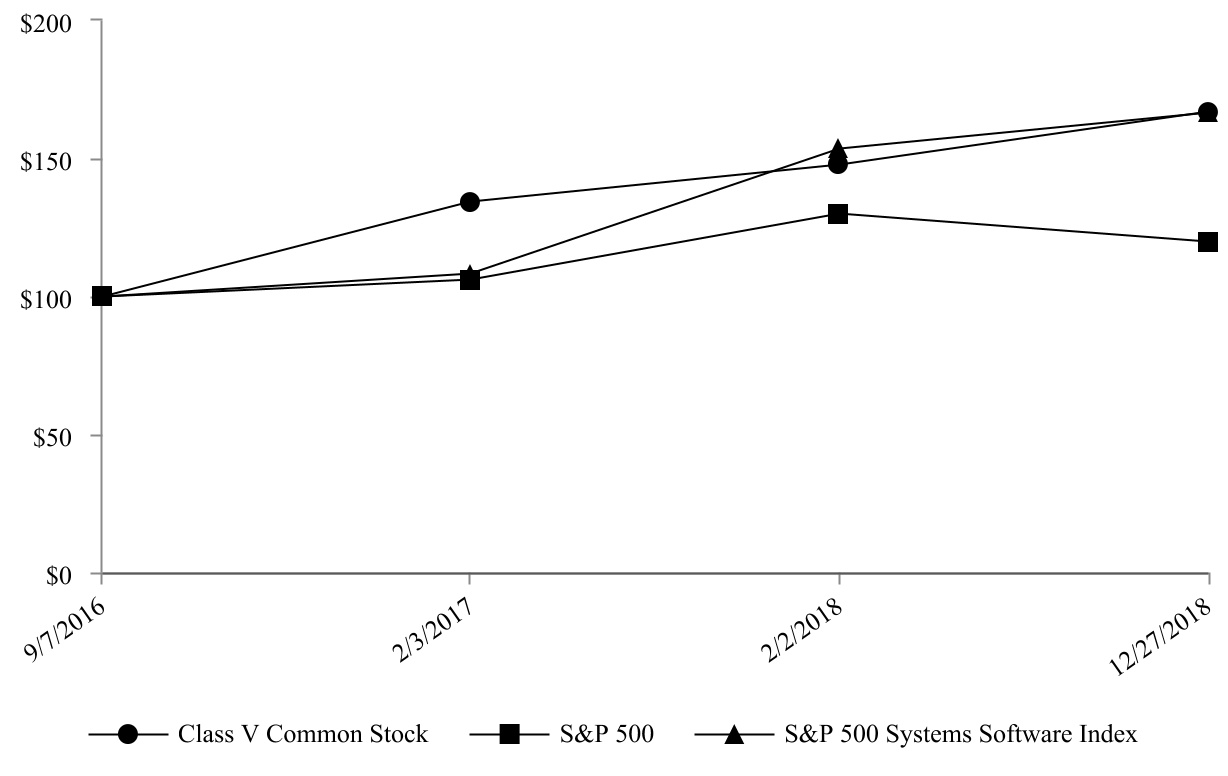

On December 28, 2018, we completed a transaction (“Class V transaction”)Our vision is to become the most essential technology company for the data era. We help customers address their evolving IT needs and their broader digital transformation objectives as they embrace today’s multicloud world. We intend to execute our vision by focusing on two strategic priorities:

•Grow and modernize our core offerings in the markets in which we paid $14.0 billion in cash and issued 149,387,617 shares of our Class C Common Stock to holders of our Class V Common Stock in exchange for all outstanding shares of Class V Common Stock. The non-cash consideration portion of the Class V transaction totaled $6.9 billion. As a result of the Class V transaction, the tracking stock feature of Dell Technologies’ capital structure was terminated. The Class C Common Stock is traded on the New York Stock Exchange.predominantly compete

VMware, Inc. Ownership•Pursue attractive new growth opportunities such as Edge, Telecom, data management, and as-a-Service consumption models

On July 15, 2020, we announced thatWe believe we are exploring potential alternatives with respectuniquely positioned in the data and multicloud era and that our results will continue to benefit from our ownership in VMware, Inc., including a potential spin-offdurable competitive advantages. We intend to continue to execute our business model and position our company for long-term success while balancing liquidity, profitability, and growth and keeping our purpose at the forefront of our decision-making: to create technologies that ownership interest to Dell Technologies’ stockholders. Although this process is currently only at an exploratory stage, we believe a spin-off could benefit both Dell Technologies’ and VMware, Inc.’s stockholders by simplifying capital structures and enhancing strategic flexibility, while still maintaining a mutually beneficial strategic and commercial partnership. Any potential spin-off would not occur prior to September 2021. Other strategic options include maintaining the status quo with respect to our ownership interest in VMware, Inc.drive human progress.

The IT industry is rapidly evolving with demand for simpler, more agile solutions as companies leverage multiple clouds across their increasingly complex IT environments. To meet our customer needs, we continue to invest in research and development, sales, and other key areas of our business to deliver superior products and solutions capabilities and to drive long-term sustainable growth.

Business Model Transformation

Our customers are seeking new and innovative models that address how they consume our solutions. In part, customers are looking to remove unnecessary cost and complexity, align solution offerings to their business needs, and provide consistent operations throughout their IT enterprise.

We offer options including as-a-Service, subscription, utility, leases, loans, and immediate pay models designed to match customers' consumption and financing preferences. We believe these options are particularly advantageous for our customers during times of economic uncertainty as they provide financial flexibility to further enable them to procure our solutions.

These offerings typically result in multiyear agreements which generate recurring revenue streams over the term of the arrangement. We expect that these offerings will further strengthen our customer relationships and provide a foundation for growth in recurring revenue. We define recurring revenue as revenue recognized that is primarily related to hardware and software maintenance as well as subscription, as-a-Service, usage-based offerings, and operating leases.

As we pursue our strategy of modernizing our core business solutions, we continue to evolve and build momentum across our family of as-a-Service offerings under Dell APEX.

Products and Services

We design, develop, manufacture, market, sell, and support a wide range of comprehensive and integratedIT solutions, products, and services. We are organized into the followingtwo business units which are also our reportable segments:segments, referred to as Infrastructure Solutions Group;Group and Client Solutions Group; and VMware.Group.

•Infrastructure Solutions Group (“ISG”) — ISG enables theour customers’ digital transformation of ourwith solutions that address the fundamental shift to multicloud environments, machine learning, artificial intelligence, and data analytics. ISG enables customers through our trusted multi-cloudto simplify, streamline, and big data solutions, which are built upon a modern data center infrastructure. ISG works with customers in the area of hybrid cloud deployment with the goal of simplifying, streamlining, and automatingautomate their cloud operations. ISG solutions are built for multi-cloudmulticloud environments and are optimized to run cloud native workloads in both public and private clouds, as well as traditional on-premise workloads.

Our comprehensive portfolio of advanced storage solutionsportfolio includes traditional storage solutions as well as next-generation storage solutions, (such asincluding all-flash arrays, scale-out file, object platforms, hyper-converged infrastructure, and software-defined solutions).storage. We have simplified our storage portfolio to ensure that we deliver the technology needed for our customers’ digital transformation. Weand continue to make enhancements to our storage solutions offerings andthat we expect that these offerings, including our new PowerStore storage array released in May 2020, will drive long-term improvements in the business.

Our server portfolio includes high-performance rack, blade, and tower and hyperscaleservers. Our servers optimized forare designed with the capability to run high value workloads across customers’ IT environments, including artificial intelligence, and machine learning, and edge workloads. Our networking portfolio helps our business customers transform and modernize their infrastructure, mobilize and enrich end-user experiences, and accelerate business applications and processes.

Our strengths in server, storage, and virtualization software solutions enableallow us to offer leading converged and hyper-converged solutions, allowingenabling our customers to accelerate their IT transformation by acquiringwith scalable integrated IT solutions instead of building and assembling their own IT platforms. ISG also offers attached software, peripherals, and services, including configuration, support and deployment, configuration, and extended warranty services.warranties.

Approximately half of ISG revenue is generated by sales to customers in the Americas, with the remaining portion derived from sales to customers in the Europe, Middle East, and Africa region (“EMEA”) and the Asia-Pacific and Japan region (“APJ”).

•Client Solutions Group (“CSG”) — CSG includes branded hardware (such asPCs including notebooks, desktops, workstations, and notebooks)workstations and branded peripherals (such asincluding displays and projectors),docking stations, as well as third-party software and peripherals. CSG also includes services offerings, including support and deployment, configuration, and extended warranties. Our computing devicesCSG offerings are designed with our commercial and consumer customers’ needs in mind and we seek to optimize performance, reliability, manageability, design, and security. In addition to our traditional hardware business, we have a

Our commercial portfolio of thin client offerings that we believe will allow us to benefit from the growth trends in cloud computing. Forprovides our customers that are seekingwith solutions centered around flexibility to simplify client lifecycle management, Dell PCaddress their complex needs such as a Service offering combines hardware, software, lifecycle services,IT modernization, hybrid work transformation, and financing into one all-encompassing solution that provides predictable pricing per seat per month. CSG also offers attached software, peripherals,other critical needs. Within our high-end consumer offerings, we provide our customers’ with powerful performance, processing, and services, including support and deployment, configuration, and extended warranty services.end-user experiences.

Approximately half of CSG revenue is generated by sales to customers in the Americas, with the remaining portion derived from sales to customers in EMEA and APJ.

•VMware— The VMware reportable segment (“VMware”) reflects the operationsOur “other businesses,” described below, primarily consists of our resale of standalone offerings of VMware, Inc. (NYSE: VMW) within(individually and together with its subsidiaries, “VMware”), referred to as “VMware Resale,” and offerings of SecureWorks Corp. (“Secureworks”). These businesses are not classified as reportable segments, either individually or collectively.

•VMware Resale consists of our sale of standalone VMware offerings. Under our Commercial Framework Agreement with VMware discussed in this report, Dell Technologies. Technologies continues to act as a key channel partner for VMware, reselling VMware’s offerings to our customers. This partnership is intended to facilitate mutually beneficial growth for both Dell Technologies and VMware.

VMware works with customers in the areas of hybrid and multi-cloud,multicloud, modern applications, networking, security, and digital workspaces, helping customers manage their IT resources across private clouds and complex multi-cloud,multicloud, multi-device environments. VMware’s portfolio supports and addresses the key IT priorities of customers: accelerating their cloud journey, migrating and modernizing their applications, empowering digital workspaces, transforming networking, and embracing intrinsic security. VMware enables its customers to digitally transform their operations as they ready their applications, infrastructure, and employees for constantly evolving business needs.

During the third quarter of Fiscal 2020, VMware, Inc. completed the acquisition of Carbon Black, Inc. (“Carbon Black”), a developer of cloud-native endpoint protection.

On December 30, 2019, VMware, Inc. completed its acquisition of Pivotal Software, Inc. (“Pivotal”). Before the transaction, Pivotal was a majority-owned subsidiary of Dell Technologies through EMC and VMware, Inc. Pivotal provides a leading cloud-native platform that makes software development and IT operations a strategic advantage for

customers. Pivotal’s cloud-native platform, Pivotal Cloud Foundry, accelerates and streamlines software development by reducing the complexity of building, deploying, and operating new cloud-native applications, and modernizing legacy applications. With the acquisition, which aligns key software assets, VMware, Inc. builds on a comprehensive development platform with Kubernetes.

The purchase of the controlling interest in Pivotal from Dell Technologies was accounted for as a transaction between entities under common control. This transaction required retrospective combination of the VMware, Inc. and Pivotal entities for all periods presented, as if the combination had been in effect since the inception of common control on the date of the EMC merger transaction in September 2016. Dell Technologies now reports Pivotal results within the VMware reportable segment, and the historical segment results were recast to reflect this change. Pivotal results were previously reported within Other businesses. See Note 19 of the Notes to the Consolidated Financial Statements included in this report for the recast of segment results.

Approximately half of VMware revenue is generated by sales to customers in the United States.

Our other businesses, described below, consist of product and service offerings of SecureWorks Corp. (“Secureworks”), Virtustream, and Boomi, each of which is majority-owned by Dell Technologies. These businesses are not classified as reportable segments, either individually or collectively, as the results of the businesses are not material to our overall results and the businesses do not meet the criteria for reportable segments.

•Secureworks (NASDAQ: SCWX) is a leading global cybersecurity provider of intelligence-driven informationtechnology-driven security solutions singularly focused on protecting its clients from cyberattacks.customers by outpacing and outmaneuvering the adversary. The solutions offered by Secureworks enable organizations of varying size and complexity to fortify their cyber defenses to prevent security breaches, detect malicious activity, in near real time, prioritize and respond rapidly towhen a security incidents,breach occurs, and predictidentify emerging threats.

•Virtustream offers cloud software and infrastructure-as-a-service solutions that enable customersOur offerings are continually evolving in response to migrate, run, and manage mission-critical applications in cloud-based IT environments.

•Boomi specializes in cloud-based integration, connecting information between existing on-premise and cloud-based applications to ensure business processes are optimized, data is accurate and workflow is reliable.

On February 18, 2020, Dell Technologies announced its entry intocustomer needs. As a definitive agreement with a consortiumresult, reclassifications of investors to sell RSA Security, which provides cybersecurity solutions. On September 1, 2020, the parties closed the transaction. At the completion of the sale, we received total cash consideration of approximately $2.082 billion, resulting in a pre-tax gain on sale of $338 million. The Company ultimately recorded a $21 million loss net of taxes. The transaction is intended to further simplify our product portfolio and corporate structure. Prior to the divestiture, RSA Security’s operating results were included within Other businesses.

We believe the collaboration, innovation, and coordination of the operations and strategies across all segments of our business, as well as our differentiated go-to-market model, will continue to drive revenue synergies. Through our coordinated research and development activities, we are able to jointly engineer leading innovative solutions that incorporate the distinct set of hardware, software,certain products and services across all segments of our business.

See Note 19 of the Notes to the Consolidated Financial Statements includedsolutions in this report for more information aboutmajor product categories may be required. For further discussion regarding our reportable segments.

Seesegments, see “Part II — Item 7 — Management’s Discussion and Analysis of Financial Condition and Results of Operations — Results—Results of Operations — Business Unit Results” for a discussionand Note 19 of our reportable segment operating results.the Notes to the Consolidated Financial Statements included in this report.

Dell Financial Services

DFS supports our businesses by offering and arranging various financing options and services for our customers primarily in North America, Europe, Australia, and New Zealand.globally. DFS originates, collects, and services customer receivables primarily related to the purchase or use of our product, software, and services solutions. We also arrange financing for some of our customers in various countries where DFS does not currently operate as a captive. DFScaptive entity. We further strengthens ourstrengthen customer relationships through its flexible consumption models, including utility, subscription, and as-a-Service models, which enable us to offer our customers the option to pay over time and, in certain cases, based on utilization,to provide them with financial flexibility to meet their changing technological requirements. The

originations in Fiscal 2023 and maintains an $11 billion global portfolio of high-quality financing receivables. The results of these operations are allocated to our segments based on the underlying product or service financed.financed and may be impacted by, among other items, changes in the interest rate environment and the translation of those changes to pricing. For additional information about our financing arrangements, see Note 46 of the Notes to the Consolidated Financial Statements included in this report.

Research and Development

We focus on developing scalable technology solutions that incorporate desirable features and capabilities at competitive prices. We employ a collaborative approach to product design and development in which our engineers, with direct customer input, design innovative solutions and work with a global network of technology companies to architect new system designs, influence the direction of future development, and integrate new technologies into our products. products and solutions. Through our collaborative, customer-focused approach to innovation, we strive to deliver new and relevant products to the market quickly and efficiently.

Our team of software engineers isare focused on developing the next generation of solutions for newinnovative solutions. Our software simplifies the complex through automation, increasingly leveraging artificial intelligence and innovative technologies.machine-learning technology. Most of our research and development (“R&D”) expenditures represent costs to develop the software that powers ourthese solutions. This software simplifies the complex through automation, increasingly leveraging artificial intelligence and machine learning technology.

We manage our R&D spending by targeting those innovations and solutions that we believe are most valuable to our customers and by relying on the capabilities of our strategic relationships. Our customer base includesWe have a growing numberglobal R&D presence, with total R&D expenses of service providers, such as cloud service providers, software-as-a-service companies, consumer webtech providers,$2.8 billion, $2.6 billion, and telecommunications companies.$2.5 billionfor Fiscal 2023, Fiscal 2022, and Fiscal 2021, respectively. These service providers turninvestments reflect our commitment to Dell Technologies forR&D activities that ultimately support our advanced solutions that enable efficient service delivery at cloud scale. Throughgoal to help our collaborative, customer-focused approachcustomers build their digital future and to innovation, we strive to deliver new and relevant products to the market quickly and efficiently.transform IT.

Additionally, we invest in early-stage, privately-held companies that develop software, hardware, and other technologies or provide services supporting our technologies. We manage our investments through our venture capital investment arm, Dell Technologies Capital.

VMware represents a significant portion of our R&D activities and has assembled an experienced group of developers with expertise in software-defined data centers, hybrid and multiple public clouds, the modernization, migration and management of applications, networking, security, and digital workspaces. VMware also has strong ties to leading academic institutions around the world and invests in joint research with those institutions. Product development efforts are prioritized through a combination of engineering-driven innovation and customer- and market-driven feedback.

Dell Technologies has a global R&D presence, with total R&D expenses of $5.3 billion, $5.0 billion, and $4.6 billion, for Fiscal 2021, Fiscal 2020, and Fiscal 2019, respectively. These investments reflect our commitment to R&D activities that ultimately support our mission to help our customers build their digital future and to transform IT.

Manufacturing and Materials

We own manufacturing facilities located in the United States, Malaysia, China, Brazil, India, Poland, and Ireland. See “Item 2 — Properties” for information about our manufacturing and distribution facilities.

We also utilize contract manufacturers throughout the world to manufacture or assemble our products under the Dell Technologies brand as part of our strategy to enhance our variable cost structure and to achieve our goals of generating cost efficiencies, delivering products faster, better serving our customers, and enhancing our world-class supply chain.

When using contract manufacturers, we purchase components from suppliers and subsequently sell those components to the manufacturer. Our manufacturing process consists of assembly, software installation, functional testing, and quality control. We conduct operations utilizing a formal, documented quality management system to ensure that our products and services satisfy customer needs and expectations. Testing and quality control are also applied to components, parts, sub-assemblies, and systems obtained from third-party suppliers.

Our quality management system is maintained through the testing of components, sub-assemblies, software, and systems at various stages in the manufacturing process. Quality control procedures also include a burn-in period for completed units after assembly, ongoing production reliability audits, failure tracking for early identification of production and component problems, and processing of information from customers obtained through services and support programs. This system is certified to the ISO 9001 International Standard that includes most of our global sites and organizations that design, manufacture, and service our products.

Our order fulfillment, manufacturing, and test facilities in Massachusetts, North Carolina, and Ireland are also certified to the ISO 9001 International Standard for quality management systems, the ISO 14001 International Standard for environmental management systems, the ISO 45001 International Standard for health and also have achieved OHSAS 18001 certification, an international standardsafety management systems, and the ISO 50001 International Standard for facilities with world-class safety and healthenergy management systems. These internationally-recognized endorsements of ongoing quality, environmental, health and environmentalsafety, and energy management are among the highest levels of certifications

available. We also have implemented Lean Six Sigmaprograms and 7S (Customer, Safety, Quality, Delivery, Cost, Team, and Green) methodologies to ensure that the quality of our designs, manufacturing, test processes, and supplier relationships isare continually improved.

We maintain a robust Supplier Code of Conduct, actively manage recycling processes for our returned products, and are certified by the Environmental Protection Agency as a Smartway Transport Partner.

We purchase materials, supplies, product components, and products from a large number of qualified suppliers. In some cases, where multiple sources of supply are not available, we rely on a single source or a limited number of sources of supply if we believe it is advantageous to do so because of performance, quality, support, delivery, capacity, or price considerations. We believe that any disruption that may occur because of our dependence on single- or limited-source vendors would not disproportionately disadvantage us relative to our competitors. See “Item 1A — Risk Factors — Risks Relating to Our Business and Our Industry — Reliance on vendors for products and components, many of which are single-source or limited-source suppliers, could harm our business by adversely affecting product availability, delivery, reliability, and cost” for information about the risks associated with Dell Technologies’ use of single- or limited-source suppliers.

Geographic Operations

Our global corporate headquarters is located in Round Rock, Texas. We have operations and conduct business in many countries located in the Americas, Europe, the Middle East, Asia, and other geographic regions. To increase our global presence,reach, we continue to focus on emerging markets outside of the United States, Western Europe, Canada, and Japan. We continue to view these geographical markets, which include the vast majority of the world’s population, as a long-term growth opportunity. Accordingly, we pursue the development of technology solutions that meet the needs of these markets. Our expansion in emerging markets creates additional complexity in coordinating the design, development, procurement, manufacturing, distribution, and support of our product and services offerings. For information about the amount of net revenue we generated from our operations outside of the United States during the last three fiscal years, see Note 19 of the Notes to the Consolidated Financial Statements included in this report.

Seasonality

Our sales arecan be affected by seasonal trends. Among the trends with the most significant effect onWithin ISG, our operating results,storage sales to government customers (particularly the U.S. government) generally are typically stronger in our thirdfourth fiscal quarter,quarter. Our sales within the Americas are typically stronger in the second and fourth fiscal quarters, with sales in Europe,EMEA typically stronger during the Middle East and Africa are often weaker in our third fiscal quarter, and sales to consumers are typically strongest during our fourth fiscal quarter. Historical seasonal patterns may not continue in the future and have been impacted by, and may continue to be impacted by, the COVID-19 pandemic, the changing macroeconomic environment, and our mix of business.

Competition

We operate in an industry in which there are rapid technological advances in hardware, software, and services offerings. We face ongoing product and price competition in all areas of our business, including from both branded and generic competitors. We compete based on our ability to offer customers competitive, scalable, and integrated solutions that provide the most current and desired product and services features at a competitive price. We closely monitor market pricing, and solutions trends, including the effect of foreign exchange rate movements, in an effort to provide the best value for our customers. We believe that our strong relationships with our customers and channel partners allow us to respond quickly to changing customer needs and other macroeconomic factors.

We also face competition from non-traditional IT companies, such as cloud serviceincluding large Infrastructure-as-a-Service providers, also known as hyperscalers, that often buy their infrastructure directly from original design manufacturers. Competitive pressures could increase if customers choose to move applicationexisting workloads to cloud service providers away from traditional or private data centers.these Infrastructure-as-a-Service providers.

The markets in which we compete are comprised of largespan countries around the world with customers that range from the world’s largest corporations to small and small companies across all areas of our business.medium-sized businesses to consumers and also includes government and not-for-profit organizations. We believe that new businesses will continue to enter these markets and develop technologies that, if successfully commercialized, may compete with our products and services. Moreover, current competitors may enter into new strategic relationships with new or existing competitors, which may further increase the competitive pressures. See “Item 1A — Risk Factors — Risks Relating to Our Business and Our Industry” for information about our competitive risks.

Sales and Marketing

Our sales and marketing efforts are organized around the evolving needs of our customers, and our marketing initiatives reflect this focus.customers. Our unified global sales and marketing team createshas created a salesgo-to-market organization that is customer-focused, collaborative, and innovative. OWe generally organize our go-to-market operations with a focus on geographic and customer segments which encompass large gur customers include large globallobal and national enterprises, public institutions that include government,governmental agencies, educational institutions, healthcare organizations, and law enforcement agencies, small and medium-sized businesses, and consumers.

Go-to-market strategy — We sell products and services directly to customers and through other sales channels, which include value-added resellers, system integrators, distributors, and retailers. We continuemanage our many channels to pursueoffer a unified customer experience.

We believe our direct business strategy, whichmodel is a significant competitive advantage and emphasizes direct communication with customers, thereby allowing us to refine our products and marketing programs for specific customer groups. and enabling us to successfully navigate environments with constrained supply chains.

In addition to our direct business model, we rely onuse our network of channel partners to sell our products and services, enabling us to efficiently serve a greater number of customers. The Dell Technologies partner program contributes to the development of

channel sales by providing appropriate incentives for revenueto encourage sales generation. We also provide our channel partnersfacilitate access to third-party financing to help our channel partners manage their working capital. We believe that building long-term relationships with our channel partners enhances our ability to deliver an excellenta high-quality customer experience. During Fiscal 2021,2023, our other sales channels contributed overgenerated approximately 50% of our net revenue.

Large enterprises and public institutions — For large enterprises and public institutions, we maintain a field sales force throughout the world. Dedicated account teams, which include technical sales specialists, form long-term relationships to provide our largest customers with a single source of assistance, develop tailored solutions for these customers, position the capabilities of Dell Technologies, and provide us with customer feedback. For these customers, we offer several programs designed to provide single points of contact and accountability with dedicated account managers, special pricing, and consistent service and support programs. We also maintain specific sales and marketing programs targeting federal, state, and local governmental agencies, as well as healthcare and educational customers.

Small and medium-sized business and consumers — We market our products and services to small and medium-sized businesses and consumers through various advertising media. To react quickly to our customers’ needs, we track our Net Promoter Score, a customer loyalty metric that is widely used across various industries. Net Promoter Score is a trademark of Satmetrix Systems, Inc., Bain & Company, Inc., and Fred Reichheld. We also engage with customers through our social media communities on our website and in external social media channels.

Product Backlog

Product backlog represents the value of unfulfilled manufacturing orders.orders and is included as a component of remaining performance obligations to the extent we determine that the manufacturing orders are non-cancelable. Our business model generally gives us the ability to optimize product backlog at any point in time, for example,by such actions as expediting shipping or prioritizing customer orders towardfor products that have shorter lead times. Because productWe ended Fiscal 2022 with elevated backlog at any point in time may notlevels as a result of industry-wide constraints in the generationsupply of any predictable amount of net revenue in any subsequent period,limited-source components. During Fiscal 2023, we do not believe productlowered our backlog to be a meaningful indicator of future net revenue. Product backlog is includedlevels across both CSG and ISG as a component of remaining performance obligation to the extent we determine that the manufacturing orders are non-cancelable.supply positions improved and demand declined.

Patents, Trademarks, and Licenses

As of January 29, 2021,February 3, 2023, we held a worldwide portfolio of 21,87620,693 granted patents and 10,108 pending patent applications. Of those, VMware, Inc. held 5,230 granted patents and 3,1548,045 pending patent applications. We continue to obtain new patents through our ongoing research and development activities. The inventions claimed in our patents and patent applications cover aspects of our current and possible future offerings, computer system andsystems, software products, manufacturing processes, and related technologies. We also hold licenses to use numerous third-party patents. Although we use our patented inventions and license some of them to others, we are not substantially dependent on any single patent or group of related patents. Our product and process patents may establish barriers to entry, and we anticipate that our worldwide patent portfolio will continue to be of value in negotiating intellectual property rights with others in the industry.

We have used, registered, or applied to register certain trademarks and copyrights in the United States and in other countries. We believe that Dell Technologies, DELL, Dell EMC, VMware, Alienware, Secureworks, Pivotal, and VirtustreamSecureworks word marks and logo marks in the United States are material to our operations.

We have entered into software licensing agreements with other companies. We also license certain technology and intellectual property from third parties for use in our offerings and processes, and license some of our technologies and intellectual property to third parties.

Government Regulation

Our business is subject to regulation by various U.S. federal and state governmental agencies and other governmental agencies. Such regulation includes the activities of the U.S. Federal Communications Commission; the anti-trust regulatory activities of the U.S. Federal Trade Commission, the U.S. Department of Justice, and the European Union; the consumer protection laws and financial services regulation of the U.S. Federal Trade Commission and various stateU.S. governmental agencies; the export regulatory activities of the U.S. Department of Commerce and the U.S. Department of the Treasury; the import regulatory activities of the U.S. Customs and Border Protection; the product safety regulatory activities of the U.S. Consumer Product Safety Commission and the U.S. Department of Transportation; the health information privacy and security requirements of the U.S. Department of Health and Human Services; and the environmental, employment and labor, and other regulatory activities of a variety of governmental authorities in each of the countries in which we conduct business.

Our operations are subject to a variety of environmental, performance, and safety regulations in all areas in which we conduct business. Product design and procurement operations must comply with new and future requirements relating to climate change laws and regulations, materials composition, sourcing, radiated emissions, energy efficiency and collection, recycling, treatment, transportation, and disposal of electronics products, including restrictions on mercury, lead, cadmium, lithium metal, lithium ion, and other substances. Operations may also become subject to new or emergent standards relating to climate change laws and regulations. The costsamount and timing of costs under environmental and safety laws are difficult to predict. We were not assessed any material environmental fines, nor did we have any material environmental remediation or other environmental costs, during Fiscal 2021.2023.

We and our subsidiaries are subject to various anti-corruption laws that prohibit improper payments or offers of payments to foreign governments and their officials for the purpose of obtaining or retaining business, and are also subject to export controls, customs regulations, economic sanctions laws, including those currently imposed on Russia, and embargoes imposed by the U.S. government. Violations of the U.S. Foreign Corrupt Practices Act or other anti-corruption laws or export control, customs, or economic sanctions laws and regulations may result in severe criminal or civil sanctions and penalties.

We are subject to provisions of the Dodd-Frank Wall Street Reform and Consumer Protection Act intended to improve transparency and accountability concerning the supply of minerals originating from the conflict zones of the Democratic Republic of the Congo or adjoining countries. We incur costs to comply with the disclosure requirements of this law and other costs relating to the sourcing and availability of minerals used in our products.

Environmental, Social, Impact and SustainabilityGovernance

Dell Technologies is committed to driving human progress by putting our technology and expertise to work where it can do the most good for both people and the planet. AllWe recognize that all of our stakeholders — shareholders, customers, suppliers, employees, and communities — as well as the environment and society, — are essential to our business.

Dell Technologies launched its Social Impact Planis committed to progressing towards the goals set forth in our plan for 2030 (theand beyond (our “2030 Plan”Goals”) in November 2019.. Our goals under the 2030 PlanGoals represent an extension of our purpose as a company — to create technologies that drive human progress. We are using these goals to build our social impact strategies over the next decade. TheOur 2030 Plan hasGoals have four critical areas of focus:

•Advancing Sustainability — We believe we have a responsibility to protect and enrich our planet together with our customers, suppliers, and communities. Dell Technologies willWe continue workingto prioritize sustainability across our business ecosystem, valuing natural resources and minimizingseeking to minimize our impact. With the power of our global supply chain, Dell Technologies has the scale and responsibility to drivepursues the highest standards of sustainability and ethical practices.

•Cultivating Inclusion — We view diversity and inclusion as a business imperative that will enable us to build and empower our future workforce.workforce and we strive to cultivate inclusion for our team members, customers, and communities. It is essential that our workforce be fully representative of the diversity in our global customer base. DiversityFurther, we believe that diversity of leadership increases innovation and ensures that company decisions reflect a wide variety of perspectives.

•Transforming Lives — We believe our scale, support, and the innovative application of our portfolio can play an important role in advancing fundamental human rights and addressing complex societal challenges, including improving health, education, and economic opportunities for the underserved. We endeavor to harness the power of technology to create a future that is capable of fully realizing human potential.

•Upholding Ethics and Data Privacy — Ethics and privacy play a critical role in establishing a strong foundation for positive social impact. We are committed to ensuring that new talent and existing team members align with our ethical culture. We will continue to invest in our advanced privacy governance and risk-management technology. And we willtechnology and continue seeking to select, evaluate, and do business with third parties who share our level of dedication to ethics and privacy.

Dell Technologies is measuring itsmeasures progress against each of theour 2030 social impact goalsGoals in our annually released social impact reports. The Dell Technologies Social Impact Plan for 2030 and annual social impact reports are available on the social impact reporting page of our website.

Climate Change

At Dell Technologies, we believe that by addressing climate change, we are demonstrating our commitment to protect our planet and the community. We have a responsibility to manage the greenhouse gas emissions associated with our direct and indirect footprint, and technology plays an important role in this undertaking. We aim to achieve net zero greenhouse gas emissions across Scopes 1, 2, and 3 by 2050.

Human Capital Management

Powered byWe are a diverse workforce, we create solutions that harnessteam with unique perspectives, united in our purpose, our strategy, and amplify technology in the most meaningful ways.our culture. Our goal is to ensure that Dell Technologies is a compelling destination where team membersemployees of different backgrounds feel valued, engaged, and inspired to do their best work. Through our ongoing diversity and inclusion efforts, flexible workplace transformation programs,working environments, training and development offerings, and health and wellness resources for our team members,employees, we are striving toward this goal — to attract, develop, and retain an empowered workforce for maximum impact internallyworkforce. We believe the success of our commitment is demonstrated through our employee tenure and externally for our customersrecognition by Newsweek as America’s Most Loved Workplace of 2022 and communities.by Forbes in its ranking of the 2022 World’s Best Employers.

As of January 29, 2021,February 3, 2023, we had approximately 158,000 total full-time133,000 employees, approximately 34,00032% of whom were employees of VMware, Inc. In comparison, as of January 31, 2020, we had approximately 165,000 total full-time employees, approximately 31,000 of whom were employees of VMware, Inc. As of January 29, 2021, approximately 36% of our full-time employees were located in the United StatesStates. As a result of rapidly evolving macroeconomic conditions during Fiscal 2023, we took certain measures to reduce cost, including limiting external hiring. Further, subsequent to the close of Fiscal 2023, we announced to our employees reorganizations and other actions to align our investments more closely with our previously discussed strategic and customer priorities. These actions will reduce our employee population by approximately 5%. We are committed to supporting those impacted as they transition to their next opportunities. Despite these difficult decisions, we continue to make investments and focused efforts to develop and empower our employees and attract and retain talent.

Diversity and InclusionWe seek to support our culture in four key focus areas:

Diversity and Inclusion — At Dell Technologies, we believe diversity is power. Within our 2030 Plan, described above, one critical area of focus — cultivating inclusion — highlights how our human capital resources are vital to our social impact and long-term success. We are making stridesCultivating inclusion is a core component of our culture, and we believe that closing the diversity gap is critical to increase gendermeeting future talent needs and ethnic diversity throughout Dell Technologies.ensuring that new perspectives reflect our global customer base. We still have work to do, and are committed to providing transparency into our progress via annual Dell Technologies Diversity & Inclusion Reports. Weequal employment opportunity for all and upholding ethics and integrity in all we do and will continue to champion forpursue inclusive policies that support women, members of the LGBTQ+ community, people with different abilities, and other underrepresented groups. Our goal is to build a workforce that champions racial equity, values different backgrounds and celebrates unique perspectives by:full-spectrum diversity.

•building and attractingAs of February 3, 2023, excluding employees of Secureworks, the future workforce to createoverall representation of employees who self-identify as women was approximately 35%. Of our global people leaders, 29% self-identified as women. We define people leaders as employees in a workplace that is accessible, equitable and attractive to a diverse talent pipeline;management level or executive position.

•developingAs of the same date, our U.S. employee base was composed of employees who self-identified with the following races and retaining an empowered workforce to foster an internal community that is engaged, productiveethnicities: 63% as White or Caucasian; 15% as Asian; 10% as Hispanic or Latino; 6% as Black or African American; 2% with two or more races; and innovative;1% with additional groups (including American Indian, Alaska Native, Native Hawaiian or Other Pacific Islander). Approximately 3% of our U.S. employee base did not self-report or specify race and ethnicity status. Of our U.S. people leaders, 12% self-identified as Hispanic or Latino or as Black or African American.

•scaling for maximum impact to develop stronger customer alliances and an external community that recognizes, respects and embraces our shared value.

To serve tomorrow’s customers well, we need more students of all genders and backgrounds studying STEM (science, technology, engineering, and math) today. We cannot fill our talent pipeline without closing the diversity gap. As the composition of the workforce evolves, we recognize that companies embracing diversity and inclusion are experiencing

greater innovation, productivity, engagement, and employee satisfaction — along with better business performancesatisfaction. We are committed to increasing gender and ethnic diversity throughout Dell Technologies and, as part of our 2030 Plan, have goals focused on this objective. We seek to achieve the following diversity goals within our workforce (excluding employees of Secureworks):

•.By 2030, 50% of our global workforce and 40% of our global people leaders will be those who self-identify as women.

Dell Technologies Diversity & Inclusion Reports are available on the social impact reporting page•By 2030, 25% of our website.U.S. workforce and 15% of our U.S. people leaders will be those who self-identify as Black or African American or as Hispanic or Latino.

Our Culture and Benefits

We seek to meet these goals by:

•building and attracting the future workforce by investing in innovative recruiting and hiring programs intended to attract the best talent possible and address the global technology talent gap; and

•developing and retaining our current team members through a supportive corporate culture focused on equity of access to career advancement and upskilling programs.

Achievement Through Learning, Development, and Total Rewards — We offer a competitive and comprehensive benefits package and strive to provide the best choice and value at the best cost. Our culturecomprehensive rewards programs are designed to attract, reward, and retain high-quality talent and to inspire employees to be their best and do their best work for our customers and the growth of our business. We recognize and reward performance through awards aligned with business strategy and individual objectives while supporting team members’ mental, physical, and financial health, and promoting workplace flexibility and connection. Further, Dell Technologies’ focus on cultivating inclusion is definedan important component of our total rewards philosophy: We believe that equal pay is a business imperative and we are committed to it.

We provide a multitude of programs to support employees’ career growth and development through a centralized experience called “Build Your Career.” Through this program, we offer formal training options, individualized development programs and sponsorship, tools for 360-degree feedback, mentoring, networking, stretch assignments, and growth opportunities. Our tools and resources are designed to empower and inspire employees to direct their own career paths and build a portfolio of transferable skills for success in the technology industry. Our internal Career Hub supports employee growth by our values.providing personalized development suggestions, such as mentors and job opportunities, that align with their skills and development goals. We workare committed to building a diverse leadership pipeline with a broad spectrum of skills, including the ability to lead with integrity and lead by acknowledging the importance of relationships, drive, judgment, vision, optimism, humility,inspire others.

Balance and selflessness Wellness — itWork flexibility is part of our Culture Code. Itculture and remains a significant priority for us. We have built tools and a culture that provide choice and flexibility to employees, the majority of whom work in a hybrid environment. Dell’s global Connected Workplace program allows eligible employees to choose from a variety of flexible work arrangement options that best meet their needs. This program provides technologies to support employees to excel and progress regardless of their physical location.

We support our employees’ wellness through a comprehensive approach focused on mental, physical, and financial health, flexibility, and connection. We provide wellness resources to help employees and their families develop and sustain healthy habits. We further support employee wellness via regular communications, virtual live and on-demand educational sessions, counseling and support services, fitness and wellness challenges, voluntary progress tracking, and other incentives.

Connection and Engagement — We believe that employee feedback is who we are. Ouran important part of our culture matters in how we run the business, how we go to market, and how we treatdrive our strategy. Through our annual Tell Dell survey, employees can confidentially voice their perceptions of the Company and our leadership, culture, and inclusiveness so that we can continue to improve the employee experience. We drive further employee engagement and connection through a variety of initiatives including, but not limited to, our team members.member listening strategy and our Employee Resource Groups (“ERGs”). We have a total of 13 unique ERGs that cultivate inclusion and bring many collective voices together for a greater business impact. Our ERGs also provide personal and professional development through networking opportunities, mentoring, volunteerism, and community involvement.

Human Rights

At Dell Technologies, upholding and advancing respect for the fundamental human rights of all people is core to our business strategy, purpose, and commitment to drive human progress and create a positive and lasting social impact. We believe everyone deserves to be treated equally with dignity and respect, and we are committed to responsible, ethical, inclusive, and sustainable business practices. We believe in winning with integrity, and we leverageuse training and technology and deploy state-of-the-art tools to assist our team members in applying the principles of integrity and compliance as part of everyday business transactions, activities, and decisions.

We seek to create a professional environment where everyone can grow and thrive, and provide a multitude of programs to enhance team members’ career growth and development. We offer formal training options, individualized development programs and sponsorship, tools for 360-degree feedback, mentoring, networking, stretch assignments, and growth opportunities. Our programs are designed to empower and inspire team members to direct their own career paths and build a portfolio of valuable skills for success in the technology industry. We are committed to building a diverse leadership pipeline with a broad spectrum of skills, including the ability to lead with integrity and inspire others. We believe our ability to innovate and cultivate breakthrough thinking is an engine for growth, success, and progress.

We also recognize that the workplace is changing, how people work is changing, and the impact of COVID-19 has only accelerated the “do anything from anywhere” workforce. Dell Technologies offers various flexible work solutions, including our Connected Workplace program, which allows eligible team members to choose from a wide variety of flexible work arrangement options that best meet their needs. Work flexibility is part of our culture, and a recent employee survey indicated that team members strongly believe flexible work arrangements contribute positively to our performance as a company. Our Connected Workplace program is now available in 83 countries across the globe.

During the challenges of the past year, the health and wellness of our team members across the globe has never been more important. We offer a highly competitive and comprehensive benefits package, and strive to provide the best choice and value at the best cost. Additionally, wellness resources are available online through the Dell Wellness Hub to help employees and their families develop and sustain healthy habits. Dell Wellness Hub provides a relevant, personalized, and fun experience that is tailored to each individual’s interests in one easy and convenient place, including physical, mental, and financial wellbeing. We further encourage a focus on wellness via regular communications, virtual live and on-demand educational sessions, voluntary progress tracking, wellness challenges, and other incentives.

Supply Chain Resources

We manage our responsible business practices in one of the world’s largest supply chains. Our supply chain has always demonstrated high standards of responsibility and integrity, and we continue our efforts to drive responsible manufacturing our stakeholders can trust. Our supply chainchains, which involves hundreds of thousands of people around the world. We continue our efforts to drive responsible manufacturing through robust assurance practices, including human rights due diligence and environmental stewardship. We recognize that looking after the wellbeing of people in our supply chain is important and have set goals for our work in this area, including:

•providing healthy work environments where people can thrive;environments;

•delivering future-ready skills development for employees in our supply chain; and

•continuing our engagement with the people who make our products.

We support supplier employees at all levels with training on key topics, including forced labor and health and safety, and we continue to work with suppliers to deliver training directly to employees via their mobile phones. Through this program,initiative, Dell Technologies covers the cost of developing training modules and shares training costs with suppliers who deliver them.

Dell Technologies continuesworks to make significant progress to help ensure that we and our suppliers manufacture our products responsibly. Dell Technologies has one of the largestresponsibly, in part through our social and environmental responsibility assurance programs in the technology sector, both in terms of number ofprogram. Through risk assessments and audits and the program’s reach across the supply chain. Through these audits,conducted under this program, we are ableseek to monitor a supplier factory’sfactories’ adherence to the Responsible Business Alliance (“RBA”) Code of Conduct. Audits are conducted by third-party auditors that have been trained and certified by the RBA. AuditsThe audits cover topics across five areas: labor, including risks of forced labor and weekly working hours; employee health and safety; environment; ethics; and management systems. Through our audit program, we aim to identify and solve concerns in our supply chain, and seek continuouscontinual improvements to address issues and enable suppliers to build their own in-house capabilities. We supplement our audits with targeted assessments of suppliers when we identify opportunities to drive further improvements.

Dell Technologies Supply Chain Sustainability Progress Reports areOur supply chain sustainability progress is available through annual reporting on the social impact reporting page of our website.

Corporate Information

We are a holding company that conducts our operations through subsidiaries.

We were incorporated in the state of Delaware on January 31, 2013 under the name Denali Holding Inc. in connection with Dell’s going-private transaction, which was completed in October 2013. We changed our name to Dell Technologies Inc. on August 25, 2016. The mailing address of our principal executive offices is One Dell Way, Round Rock, Texas 78682. Our telephone number is 1-800-289-3355.

Our website address is www.delltechnologies.com. We make available free of charge through our website our annual report on Form 10-K, quarterly reports on Form 10-Q, and current reports on Form 8-K, and all amendments to those reports, as soon as reasonably practicable after we electronically file such material with, or furnish it to, the SEC. The contents ofinformation on, or accessible through, our website referred to above and the contents ofor any other website we refer to herein arein this report is not a part of, and is not incorporated by reference into, this annual report on Form 10-K.report.

Information about our Executive Officers

The following table sets forth, as of March 5, 2021,4, 2023, information about our executive officers, who are appointed by our boardBoard of directors.Directors.

| | | | | | | | | | | | | | |

| Name | | Age | | Position |

| Michael S. Dell | | 5658 | | Chief Executive Officer and Chairman |

| Jeffrey W. Clarke | | 5860 | | ChiefCo-Chief Operating Officer and Vice Chairman |

| Allison Dew | | 5153 | | Chief Marketing Officer |

| Howard D. Elias | | 6365 | | Chief Customer Officer and President, Services and Digital |

| Richard J. Rothberg | | 59 | | General Counsel |

| Jennifer D. Saavedra, Ph.D. | | 5153 | | Chief Human Resources Officer |

Richard J. Rothberg | | 57 | | General Counsel |

| William F. Scannell | | 5860 | | President, Global Sales and Customer Operations |

| Thomas W. Sweet | | 6163 | | Chief Financial Officer |

| Anthony Charles Whitten | | 46 | | Co-Chief Operating Officer |

Michael S. Dell — Mr. Dell serves as Chairman of the Board and Chief Executive Officer of Dell Technologies. Mr. Dell served as Chief Executive Officer of Dell Inc., a wholly-owned subsidiary of Dell Technologies, from 1984 until July 2004 and resumed that role in January 2007. In 1998, Mr. Dell formed MSD Capital, L.P., a private investment firm, for the purpose of managing his and his family’s investments, and, in 1999, he and his wife established the Michael & Susan Dell Foundation to provide philanthropic support to a variety of global causes. HeMr. Dell is an honorary member of the Foundation Board of the World Economic Forum and is an executive committee member of the International Business Council. He serves as a member of the Technology CEO Council and is a member of the Business Roundtable. He also serves on the advisory board of Tsinghua University’s School of Economics and Management in Beijing, China, on the governing board of the Indian School of Business in Hyderabad, India, and as a board member of Catalyst, Inc., a non-profit organization that promotes inclusive workplaces for women. In June 2014, Mr. Dell was named the United Nations Foundation’s first Global Advocate for Entrepreneurship. Mr. Dell is also Chairman of the Board of Directors of VMware, Inc., a cloud infrastructure and digital workspace technology company that was formerly a public majority-owned subsidiary of Dell Technologies, and Non-Executive Chairman of SecureWorks Corp., a public majority-owned subsidiary of Dell Technologies. Mr. Dell was a board member of Pivotal Software, Inc., formerly a public majority-owned subsidiary of Dell Technologies that provides a leading cloud-native platform, from September 2016 until it was merged with VMware, Inc. in December 2019.

Jeffrey W. Clarke — Mr. Clarke serves as ChiefCo-Chief Operating Officer and Vice Chairman of Dell Technologies, responsible for running day-to-day business operations, shaping the Company’s strategic agenda, and aligningsetting priorities across the Dell Technologies executive leadership team. In partnership with Mr. Whitten, Mr. Clarke overseesdirects the Company’s operations,Infrastructure Solutions Group and the Client Solutions Group and manages Global Operations, including its global manufacturing, procurement, and supply chain activities. Additionally, Mr. Clarke oversees the engineering, design, development,chain. He is also responsible for setting long-term strategy and sales of the Infrastructure Solutions Group across servers, storage, data protection,leads planning for emerging technology areas such as Cloud, Edge, Telecom, and networking products. He also oversees the engineering, design, development, and sales of the Client Solutions Group, including computer desktops, notebooks, workstations, cloud client computing, and end-user computing software solutions.as-a-Service. Mr. Clarke has served as Co-Chief Operating Officer since August 2021, Chief Operating Officer sincefrom December 2019 to August 2021 and Vice Chairman, Products and Operations since September 2017, before which he served as Vice Chairman and President, Operations and Client Solutions with Dell Technologies and, previously, Dell, since January 2009. From January 2003 until January 2009, Mr. Clarke served as Senior Vice President, Business Product Group. From November 2001 to January 2003, Mr. Clarke served as Vice President and General Manager, Relationship Product Group. In 1995, Mr. Clarke became the director of desktop development. Mr. Clarke joined Dell in 1987 as a quality engineer and has

and has served in a variety of other engineering and management roles. Prior toBefore joining Dell Technologies, Mr. Clarke served as a reliability and product engineer at Motorola, Inc.Inc, a global technology company.

Allison Dew — Ms. Dew serves as the Chief Marketing Officer of Dell Technologies. In this role, in which she has served since March 2018, Ms. Dew is directly responsible for the global marketing organization, strategy, and all aspects of Dell Technologies’ marketing efforts, including brand and creative, product marketing, communications, digital, and field and channel marketing. Since joining Dell Technologies in 2008, Ms. Dew has been instrumental in Dell Technologies’ marketing transformation, leading an emphasis on data-driven marketing, customer understanding, and integrated planning. Most recently, prior to her current position, Ms. Dew led marketing for the Dell Technologies Client Solutions Group from December 2013 to March 2018. Before joining Dell Technologies, Ms. Dew served in various marketing leadership roles at Microsoft Corporation, a global technology company. Ms. Dew also worked in both a regional advertising agencyfirm in Tokyo, Japan and and an independent multicultural agency in New York.

Howard D. Elias — Mr. Elias serves as Chief Customer Officer and President, Services and Digital at Dell Technologies. He leads a global organization devoted to customer advocacy and oversees global support, deployment, consulting, education, managed services, services sales, the IT organization, and Virtustream.strategic partnerships. He is executive sponsor for more than a dozen of Dell Technologies’ largest enterprise accounts and is responsible for setting and driving strategy to enable and accelerate the mission-critical business transformations of customers and Dell’s own global operations. Mr. Elias previously served as President and Chief Operating Officer, EMC Global Enterprise Services from January 2013 until EMC’s acquisition by Dell Technologies in September 2016, and was President and Chief Operating Officer, EMC Information Infrastructure and Cloud Services from September 2009 to January 2013. In these roles, Mr. Elias was responsible for setting the strategy, driving the execution, and creating the best practices for services that enabled the digital transformation and data center modernization of EMC’s customers. Mr. Elias also had responsibility at EMC for leading the integration of the Dell and EMC businesses, including overseeing the cross-functional teams that drove all facets of integration planning. Previously, Mr. Elias was EMC’s Executive Vice President, Global Marketing and Corporate Development, responsible for all marketing, sales enablement, technology alliances, corporate development, and new ventures. Mr. Elias was also a co-founder and served on the board of managers for the Virtual Computing Environment Company, now part of Dell Technologies’ converged platform division. Before joining EMC, Mr. Elias served in various capacities at Hewlett-Packard Company, a provider of information technology products, services, and solutions for enterprise customers, most recently as Senior Vice President of Business Management and Operations for the Enterprise Systems Group. Mr. Elias currently serves as chairman of TEGNA Inc., a media and digital business company, and is a member of the Massachusetts Business Roundtable.

Jennifer D. Saavedra, Ph.D. — Dr. Saavedra is Dell Technologies' Chief Human Resources Officer. In this role, Dr. Saavedra leads Dell’s Global Human Resources and Facilities function and accelerates the performance and growth of the company through its culture and its people. Dr. Saavedra previously served as Dell’s Senior Vice President, Human Resources – Sales from December 2019 to March 2021 and as Dell’s Senior Vice President, Human Resources – Talent and Culture from November 2017 to December 2019. Dr. Saavedra joined Dell in 2005 and has served in many key leadership roles throughout the Human Resources organization, including talent development and culture, business partner, strategy, and learning and development. Before joining Dell in 2005, Dr. Saavedra served as a Human Resources consultant to private and public companies. Dr. Saavedra also serves on the executive board for the Black Networking Alliance at Dell Technologies.

Richard J. Rothberg — Mr. Rothberg serves as General Counsel and Secretary for Dell Technologies. In this role, in which he has served since November 2013, Mr. Rothberg oversees the global legal department and manages government affairs, compliance, and ethics. He is also responsible for global security. Mr. Rothberg joined Dell in 1999 and has served in critical leadership roles throughout the legal department. He served as Vice President of Legal, supporting Dell’s businesses in the Europe, Middle East, and Africa region before moving to Singapore in 2008 as Vice President of Legal for the Asia-Pacific and Japan region. Mr. Rothberg returned to the United States in 2010 to serve as Vice President of Legal for the North America and Latin America regions. In this role, he was lead counsel for sales and operations in the Americas and for the enterprise solutions, software, and end-user computing business units. He also led the government affairs organization worldwide. Before joining Dell, Mr. Rothberg served nearly eight years at Caterpillar Inc., an equipment manufacturing company, in senior legal roles in Nashville, Tennessee and Geneva, Switzerland. Mr. Rothberg was also an attorney for IBM Credit Corporation and at Rogers & Wells, a law firm.