UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

ý ☒ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 20172019

OR

o ☐TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from _______ to _______

Commission file number: 000-55039

BioTelemetry, Inc.

(Exact name of registrant as specified in its charter)

|

| | |

DELAWARE

Delaware | | 46-2568498 |

| (State or other jurisdiction of incorporation or organization) | | 46-2568498

(I.R.S.IRS Employer Identification No.) |

|

| | | |

| 1000 Cedar Hollow Road | | |

1000 Cedar Hollow Road #102

Malvern, | Pennsylvania | | 19355 |

| (Address of principal executive offices) | | 19355

(Zip Code) |

(610)729-7000

(Registrant’s telephone number, including area code)

(Former name, former address and former fiscal year, if changed since last report)

Securities registered pursuant to Section 12(b) of the Act:

|

| | |

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered |

Common Stock, $0.001 par value $0.001 per share | BEAT | NASDAQ Global Select Market |

Securities registered pursuant to Section 12(g) of the Act:None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yesý No o

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Exchange Act. Yes oNoý

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yesý No o

Indicate by check mark whether the registrant has submitted electronically, and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yesý No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ý

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company, or an emerginggrowth company. See the definitions of “large accelerated filer,” “accelerated filer,” and “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act. (Check one):

|

| | | | | | | | |

Large accelerated filerý | ☒ | Accelerated filer | ☐ | Emerging growth company | ☐ |

| Non-accelerated filer | ☐ | Smaller reporting company | ☐ | | Accelerated filer o

| | Non-accelerated filer o

(Do not check if a

smaller reporting company)

| | Smaller reporting company o

| | Emerging growth company o

|

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes o No ý

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. o

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ý

The aggregate market value of the registrant’s common stock held by non-affiliates of the registrant was $931.4 million$1.6 billion based on the closing sale price of the registrant’s common stock as reported by the NASDAQ Global Select Market on June 30, 2017, the last business day of the registrant’s most recently completed second fiscal quarter.

quarter ended June 30, 2019. As of February 15, 2018, 32,531,36517, 2020, 34,023,053 shares of the registrant’s common stock were outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant’s definitive proxy statement for its 20182020 annual meeting of stockholders, which proxy statement will be filed no later than 120 days after the close of the registrant’s fiscal year ended December 31, 2017,2019, are incorporated by reference into Part III of this Annual Report on Form 10-K to the extent stated herein.

BioTelemetry, Inc.

Annual Report on Form 10-K

For The Fiscal Year Ended December 31, 20172019

|

| | |

| | | Page |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | | |

| | |

| | |

| | |

| | |

| | |

| | |

| | | |

| | |

| | |

| Item 16. | Form 10-K Summary | |

| |

| |

Unless the context otherwise indicates or requires, the terms “we,“we,” “our,“our,” “us,“us,” “BioTelemetry”“BioTelemetry” and the “Company,“Company,” as used in this Annual Report on Form 10-K, refer to BioTelemetry, Inc. and its directly and indirectly owned subsidiaries as a combined entity, except where otherwise stated or where it is clear that the terms mean only BioTelemetry, Inc. exclusive of its subsidiaries. We do not use the ® or ™ symbol in each instance in which one of our registered or common law trademarks appears in this Annual Report on Form 10-K, but this should not be construed as any indication that we will not assert our rights thereto to the fullest extent permissible under applicable law.

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

This document includes certain forward-looking statements within the meaning of the “Safe Harbor”“Safe Harbor” provisions of the Private Securities Litigation Reform Act of 1995 regarding, among other things, our growth prospects, the prospects for our products and our confidence in our future. These statements may be identified by words such as “expect,“expect,” “anticipate,“anticipate,” “estimate,“estimate,” “intend,“intend,” “plan,“plan,” “believe,“believe,” “promises”“promises” and other words and terms of similar meaning. Examples of forward-looking statements include statements we make regarding our ability to increase demand for our products and services, to leverage our Mobile Cardiac Outpatient Telemetry platform, to expand into new markets, to grow our market share, our expectations regarding revenue trends in our segments and the achievement of cost efficiencies through process improvement and gross margin improvements.improvement. Such forward-looking statements are based on current expectations and involve inherent risks and uncertainties, including important factors that could delay, divert or change any of these expectations, and could cause actual outcomes and results to differ materially from current expectations. These factors include, among other things:

our ability to identify acquisition candidates, acquire them on attractive terms and integrate their operations into our business, including our recent acquisition of LifeWatch AG (“LifeWatch”);business;

our ability to educate physicians and continue to obtain prescriptions for our products and services;

changes to insurance coverage and reimbursement levels by Medicare and commercial payors for our products and services;

our ability to attract and retain talented executive management and sales personnel;

the commercialization of new competitive products;

| |

| • | acceptance of our new products and services, such as our mobile cardiac telemetry (“MCT”) patch; |

the impact of the October 2019 information technology incident;

our ability to obtain and maintain required regulatory approvals for our products, services and manufacturing facilities;

changes in governmental regulations and legislation;

adverse regulatory action;

our ability to obtain and maintain adequate protection of our intellectual property;

acceptance of our new products and services;

adverse regulatory action;

interruptions or delays in the telecommunications systems and/or information technology systems that we use;

our ability to successfully resolve outstanding legal proceedings; and

the other factors that are described in “Part I; Item 1A. Risk Factors” of this Annual Report on Form 10-K.

| |

| • | the other factors that are described in “Part I; Item 1A. Risk Factors” of this Annual Report on Form 10-K. |

We undertake no obligation to publicly update any forward-looking statement, whether as a result of new information, future events, or otherwise, except as may be required by law.

PART I

Item 1. Business

Overview

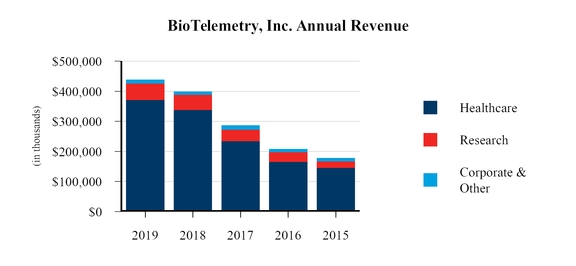

BioTelemetry, Inc. providesis the leading remote medical technology company focused on delivery of health information to improve quality of life and reduce cost of care. We provide remote cardiac monitoring, services and digital population health management for healthcare providers, medical device manufacturing and centralized core laboratory services for clinical research.trials, remote blood glucose monitoring, and original equipment manufacturing that serves both healthcare and clinical research customers.

With over 30,000 unique referring physicians per month, we provide cardiac monitoring and reporting for over one million patients per year, processing over four billion heart beats per day. More information can be found at www.gobio.com. Information on our website or linked to our website is not incorporated by reference into this Annual Report on Form 10-K.

BioTelemetry operates under two reportable segments: Healthcare and Research. Our smaller brands are aggregated in the Corporate and Other category.

The Healthcare segment, which generated 85% of our revenue in 2019, is focused on remote cardiac monitoring to identify cardiac arrhythmias or heart rhythm disorders and to monitor the functionality of implantable cardiac devices. Since we became focusedfocusing on cardiac monitoring in 1999, we have developed a proprietary integrated patient management platform that incorporates a wireless data transmission, network, U.S. Food and Drug Administration (“FDA”FDA”) cleared algorithms, medical devices and 24-hour monitoring service centers.

In July 2017, we acquired LifeWatch, a supplier of mobile cardiac monitoring solutions, headquartered in Zug, Switzerland with U.S. operations based in Rosemont, IL. We believe the integration of LifeWatch will create one of the most comprehensive connected healthcare platforms in the world, by continuing to develop innovative remote cardiac monitoring solutions and delivering those solutions to meet today’s healthcare challenges. See “Part II; Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations; Recent Developments” and “Part II; Item 8. Financial Statements and Supplementary Data; Notes to Consolidated Financial Statements; Note 3. Acquisitions” below for further discussions related to this transaction.

BioTelemetry operates under three reportable segments: (1) Healthcare, (2) Research and (3) Technology. The Healthcare segment, which generated 81% of our revenue in 2017, is focused on the diagnosis and monitoring of cardiac arrhythmias or heart rhythm disorders. We offer cardiologists, and electrophysiologists, neurologists and primary care physicians a full spectrum of solutions, which provides them with a single source of remote cardiac monitoring services. These services range from the differentiated mobile cardiac telemetry service (“MCT”)

include MCT, to event, traditional Holter, extended-wearextended Holter, Pacemaker, and International Normalized Ratio (“INR”INR”), implantable loop recorder (“ILR”) and other implantable cardiac device monitoring. The majority of our Healthcare revenue is derived from the monitoring of devices that BioTelemetry has developed, manufactured and marketed. The Research segment, which generated 14%12% of our revenue in 2017,2019, is engaged in centralcentralized core laboratory services providing cardiac monitoring, imaging services, scientific consulting and data management services for drug and medical device trials. The Technology segment, which generated 5%

During the first quarter of 2018, as part of the LifeWatch AG (“LifeWatch”) integration, our forward-looking integration and rebranding plans, as well as re-evaluating the significance and materiality of our revenuesegments, we aggregated our Technology operating segment into the Corporate and Other category. Included in 2017, focuses on the development,Corporate and Other category is the manufacturing, testing and marketing of cardiovascularcardiac and blood glucose monitoring devices to medical companies, clinics and hospitals.hospitals and corporate overhead and other items not allocated to any of our reportable segments. See “Part II; Item 8. Financial Statements and Supplementary Data; Notes to Consolidated Financial Statements; Note 17.18. Segment Information” below of this Annual Report on Form 10-K for further discussions related to our segments.

As of July 31, 2013, we reorganized to create a holding company structure. CardioNet, Inc., which was previously the public company, became a wholly owned subsidiary of a newly formed entity, BioTelemetry, Inc., a Delaware corporation, and all the outstanding shares of CardioNet, Inc. were exchanged, on a one-for-one basis, for shares of BioTelemetry, Inc. Our new holding company began trading on August 1, 2013common stock is traded on the NASDAQ Global Select Market under our same symbolsymbol: “BEAT.”

Business Strategy

Our goals are to solidify our position as the leading provider of outpatient cardiac monitoring services, expand our presence in the research market and leverage our monitoring platform in new markets. The key elements of the business strategy by which we intend to achieve these goals include:

| |

| • | Increase Overall Demand for Our Cardiac Monitoring Services. We believe that we can increase demand for our comprehensive portfolio of cardiac monitoring solutions by educating cardiologists, electrophysiologists, neurologists and primary care physicians on the benefits of using our services, including MCT, to meet their arrhythmia monitoring needs, stressing the increased diagnostic yield and their ability to use the clinically significant data to make timely interventions and guide more effective treatments. We also believe we can become further incorporated into the medical practices’ workflow by remotely monitoring patients with implanted devices, such as pacemakers, defibrillators and loop recorders, and by offering solutions such as the bi-directional integration of our data into Electronic Medical Record systems. |

| |

| • | Expand Our Presence in the Clinical Research Market. We continue to focus our efforts on increasing our presence in the clinical research market, diversifying our service offerings and expanding our preferred global provider relationships with clinical trial sponsors. We have experienced an increase in dual-service studies that require both cardiac and imaging service, which we see as a key element of our strategic growth plan. We have had success incorporating our proprietary ePatch™ extended-wear monitor as an element of our new cardiac studies creating cross-segment, top-line synergies. |

| |

| • | Leverage Our Core Competencies to New Market Opportunities. We believe our core competencies can be leveraged for applications in multiple markets. While our initial focus has been on remote cardiac monitoring to identify cardiac arrhythmias or heart rhythm disorders and to monitor the functionality of implantable cardiac devices, we intend to expand into new market areas that require outpatient or ambulatory monitoring and management. During the second quarter of 2018, we announced the commercial introduction of our latest generation |

Increase Demand for Our Comprehensive Cardiac Monitoring Solutions. We believe that we can increase demand for our comprehensive portfolio of outpatient cardiac monitoring solutions by educating cardiologists, electrophysiologists and neurologists on the benefits of using mobile cardiac telemetry to meet their arrhythmia monitoring needs, stressing the increased diagnostic yield and their ability to use the clinically significant data to make timely interventions and guide more effective treatments.

Expand Our Presence in the Research Market. In December 2010, we entered the core lab services business through our acquisition of Agility Centralized Research. We later were able to expand our presence in clinical research with our acquisition of Cardiocore Lab, LLC (“Cardiocore”) in August 2012 and our purchase of the assets of RadCore Lab, LLC (“RadCore”) in June 2014. In 2016, we further expanded our core lab capabilities with the acquisition of VirtualScopics, Inc. (“VirtualScopics”), a leading provider of clinical trial imaging solutions. We continue to focus our efforts on increasing our presence in the research market and on becoming a preferred global provider as it provides us with the ability to diversify our service offerings.

Leverage Our Core Competencies to New Market Opportunities. We believe our core competencies can be leveraged for applications in multiple markets. While our initial focus has been on arrhythmia diagnosis and monitoring, we intend to expand into new market areas that require outpatient or ambulatory monitoring and management. In line with this goal, we acquired Telcare, the first company to receive FDA clearance for a cellular-enabledwireless Blood Glucose Monitoring (“BGM”BGM”) system, increasing our presence in the large and rapidly growing digital population health management market. This wireless BGM system transmits real-time results to a cloud-based analytical engine, which synthesizes the data, monitors trends and provides caregivers with critical information about a patient’s health status and the potential need to intervene. We have been leveraging our wireless platform and proprietary technology to develop new opportunities for growth in the digital population health management business through key partnerships and internal investments. We continue to evaluate numerous connected health technologies and solutions to better understand where we can best leverage our capabilities.

The Healthcare segment, or BioTel Heart, operating under the legal entities of CardioNet, LLC (“CardioNet”), LifeWatch and Heartcare Corporation of America, Inc. (“Heartcare”)Heart®, is focused on the diagnosis andremote cardiac monitoring ofto identify cardiac arrhythmias or heart rhythm disorders.disorders and to monitor the functionality of implantable cardiac devices. We provideoffer cardiologists, electrophysiologists, neurologists and primary care physicians who prefer to use a single source of cardiac monitoring services with a full spectrum of solutions, ranging from our differentiated MCTwhich provides them with a single source of remote cardiac monitoring services. These services toinclude MCT, event, to extended wear and Holter monitoring and traditional Holter, extended Holter, Pacemaker, INR, ILR and other implantable cardiac device monitoring. We also provide PacemakerThe majority of our Healthcare revenue is derived from the monitoring of devices that BioTelemetry has developed, manufactured and INR monitoring.marketed.

MCT

Our MCT services incorporate a lightweight patient-worn sensor attached to electrodes that capture two-channel electrocardiogram (“ECG”ECG”) data, measuring electrical activity of the heart, on a compact wireless handheld monitor. The monitor analyzes incoming heartbeat-by-heartbeat information from the sensor on a real-time basis by applying proprietary algorithms designed to detect arrhythmias. The monitor can detect an arrhythmic event even in the absence of symptoms noticed by the patient. When the monitor detects an arrhythmic event, it automatically transmits the ECG to our monitoring centers. At our 24/7 monitoring centers, which operate 24/7, experienced certifiedtrained cardiac monitoring specialiststechnicians analyze the sent data, respond to urgent events and report results in the manner prescribed by the physician. The MCT devices employ two-way wireless communications, enabling continuous transmission of patient data to the

monitoring centers and permitting physicians to remotely adjust monitoring parameters and request previous ECG data from the memory stored in the monitor. The MCT devices have the capability of storing 30 days of continuous ECG data, in contrast to a maximum of 10 minutes for a typical event monitor and a maximum of 24 hours for a typical Holter monitor.

|

| | |

In 2016, we obtained FDA approval of our next generation MCT in a patch form factor. The MCT patch is a four-lead, two-channel system which provides the same best in class technology as the current MCT device, in a patch form factor. The MCT patch is a four-lead, two-channel system that provides the same best-in-class technology as our traditional MCT devices, in a more convenient form factor. The MCT patch was commercially launched in limited accounts during 2017, with a full launch expected in the first quarter of 2018. | | |

Event

Our event monitoring services provide physicians with the flexibility to prescribe wireless event monitors, digital loop event monitors, memory loop event monitors and non-loop event monitors. Event data is transmitted, either through automatic transmission of event data with wireless event monitors or through telephonic transmission of stored event data with our traditional event monitors, to one of our 24/7 monitoring centers where our trained cardiac technicians analyze the data.

Traditional Holter and extended-wear Holter monitors store an image of the electrical impulses of every heartbeat or irregularity in digital format on a compact memory card. The memory card is mailed or the data is sent electronically through a secure web transfer to one of our Holter labs, where our trained cardiac technicians analyze the data. Our next generation Holter monitor, the CardioKey™ and ePatch™ are small, lightweight cardiac monitors, which can continuously store up to 7-14 days of cardiac images.

|

| | |

| Traditional Holter and extended Holter monitors locally store, on a compact memory card, ECG data of every heartbeat or irregularity. At the end of service, the device is returned. Our trained cardiac technicians then analyze the data. Our next generation Holter monitors, the CardioKey® and ePatch™ are small, lightweight cardiac monitors, which can continuously store up to 14 days of ECG data. | | |

Geneva

|

| | |

| Our Geneva platform is a cloud-based solution for point of care and remote monitoring data that consolidates and manages information from ILRs and other implantable cardiac devices of several manufacturers into a single workflow. When combined with Geneva’s cardiac monitoring services, our trained cardiac technicians analyze and report the data. | | |

We market our services generally throughout the United States and receive reimbursement for the monitoring provided to patients from Medicaregovernment and other third-party commercial payors.

The Research segment, or BioTel Research, operating under the legal entities of Cardiocore and VirtualScopics,Research™, is engaged in centralcentralized core laboratory services that provideproviding cardiac monitoring, imaging services, scientific consulting and data management services for drug and medical treatment and device trials. We entered the research field through the acquisition of Agility Centralized Research in December 2010, and later expanded our presence with the asset acquisition of Cardiocore in August 2012 and RadCore in June 2014. The centralized services include ECG, Holter monitoring, ambulatory blood pressure monitoring, echocardiography, multigated acquisition scan (“MUGA”MUGA”), a full range of imaging services, protocol development, expert reporting and statistical analysis. Our imaging servicesservice offerings were bolstered by our 2016 acquisition of VirtualScopics, Inc. (“VirtualScopics”), a leading provider of clinical trial imaging solutions and services in the cardiovascular,cardiac, oncology, metabolic, musculoskeletal and neurologic therapeutic areas. Through these acquisitions, we gained global experience in central core laboratory services, which includes experience in Phase I-IV and Thorough QT Trials. We also provide a full range of support services in Phase I-IV trials and Thorough QT Trials, that include project coordination, setup and management, equipment rental, data transfer, processing, analysis and 24/7 customer support and site training. Our data management systems enable

complete customization for sponsors’ preferred data specifications, and our web service, CardioPortal™, provides access to rich data from any web browser, without client-side plug-ins.browser. Our primary customers in this segment are pharmaceutical companies and contract research organizations. We operate locations domestically,organizations (“CROs”).

In late 2017, we collaborated with Apple, Stanford Medicine and American Well in the Apple Heart Study, to improve the technology used to identify irregular heart rhythms and advance heart science. The study enrolled over 400,000 participants and was expected to discover undiagnosed irregular heart rhythms, such as AFib, using the Apple Watch and dedicated “Apple Heart Study” App. As part of the study, participants who experienced an irregular pulse received BioTelemetry’s ePatch™ for additional monitoring. In November 2019, Stanford Medicine published its findings, “Large-Scale Assessment of a Smartwatch to Identify Atrial Fibrillation” in the New England Journal of Medicine, which support both domestic and international operations.confirmed that wearable technology can safely identify heart rate irregularities that subsequent clinical evaluations confirmed to be AFib. This is an example of a customer outside the traditional CRO or pharmaceutical company utilizing our services.

The Technology segment,Corporate and Other category contains our other operating under the legal entities of Braemar Manufacturing, LLC (“Braemar”)business brands: BioTel Alliance™, Telcare (“Telcare”) and to a lesser extent, LifeWatch,which focuses on manufacturing, testing and marketing of cardiac devices to medical companies, clinics and hospitals, and BioTel Care®, which manufactures blood glucose monitoring devices and is actively working to expand our position in the manufacturing, engineering and development of non-invasive cardiac monitors for leading healthcare companies worldwide.digital population health management space. We have been able to build successful customer relationships by providing reliable, quality products and engineering services. We offer contract manufacturing services, developing and producing devices to the specific requirements set by customers.

Braemar manufacturesWe manufacture various devices, including but not limited to, cardiacMCT, event monitors, digitaland Holter monitors and MCT monitors utilized by our Healthcare segment. and Research segments. Our facilities located in San Diego, CA, and Eagan, MNConcord, MA, are responsible for research and product development under FDA guidelines. Manufacturing of devices is performed in part in our Eagan, MN, facility. We believe that our manufacturing facilitiescapacity will be sufficient to meet our manufacturing needs for the foreseeable future.

In addition, in December 2016, we acquired Telcare, the first company to receive FDA clearance for a cellular-enabled BGM system. This wireless BGM system transmits real-time results to a cloud-based analytical engine, which synthesizes the data, monitors trends and provides caregivers with critical information about the patients’ health status and the potential need to intervene.

We believe our manufacturing operations are in compliance with regulations mandated by the applicable regulatory governing bodies. We are subject to unannounced inspections by the FDA, and we successfully completed routine inspections by the FDA in October 2017 (Eagan, MN), May 2016 (Rosemont, IL) and February 2016 (Concord, MA),recent years with no significant findings noted or warnings issued. Our Eagan, MN, San Diego, CA, and Concord, MA, facilities are ISO 13485 certified13485-certified and registered with the FDA.FDA. ISO 13485 is aan international quality system standard used by medical companies providing design, development,device manufacturing installation and servicing,companies and is the basis for acquiring European Conformity Marking (“CE Marking”Marking”) for medical device product distribution in the European Union. ManyIn addition to FDA clearance, many of our devices also carry a CE Marking.Marking, which is a certification mark that indicates conformity with health, safety and environmental protection standards for products used and sold within the European Economic Area (“EEA”).

There are a number of critical components and sub-assemblies in the devices. The vendors for these materials are qualified through stringent evaluation and testing of their performance. We implement a strict no-change policy with our contract manufacturers to ensure that no components are changed without our approval.

Research and Development

For the years ended December 31, 2017, 2016 and 2015, we spent $11.1 million, $8.4 million and $7.1 million, respectively, onWe make significant investments in research and development activities focused on developing new products and enhancements to our existing products. We intend to continue to develop proof of superiority of our technology through clinical data. Our aim is to create products that are smaller, faster, more efficient and that provide more useful and relevant information to physicians on a more timely basis. We employ a dedicated internal core research and development team, primarily based in San Diego. We have been consolidating parts of the process across the organization to bring cross-company synergies and benefits. Our San Diego location also houses our rapid prototype lab, which has 3-D printing capability. In addition, we consult with external consultants and partners on certain projects or prototype work.

The three primary sources of clinical data that we have used to date to illustrate the clinical value of MCT include: (i) a randomized 300-patient clinical study; (ii) our cumulative actual monitoring experience from our databases; and (iii) numerous other published studies.

We sponsored and completed a 17-center, 300-patient randomized clinical trial in March 2007.2007 - Steven A. Rothman M.D. etal. “The Diagnosis of Cardiac Arrhythmias: A Prospective Multi-Center Randomized Study Comparing Mobile Cardiac Outpatient Telemetry Versus Standard Loop Event Monitoring,” Journal of Cardiovascular Electrophysiology. We believe this study at that time, represented the largest randomized study comparing two non-invasive arrhythmia monitoring methods. The study was designed to evaluate patients who were suspected to have an arrhythmic cause underlying their symptoms but who were a diagnostic challenge given that they had already had a non-diagnostic 24-hour Holter monitoring session or four hours of telemetry monitoring within 45 days prior to enrollment. Patients were randomized to either MCT or to a loop event monitor

for up to 30 days. Of the 300 patients who were randomized, 266 patients who completed a minimum of 25 days of monitoring were analyzed (134 patients using MCT and 132 patients using loop event monitors).

The study specifically compared the success of MCT against loop event monitors in detecting patients with clinically significant arrhythmias and demonstrated the superiority of MCT for confirming the diagnosis of these types of arrhythmias. The study also demonstrated the advantage of using MCT compared to the loop event monitor in the detection of asymptomatic atrial fibrillation (“AFib”) or flutter. Diagnosis and treatment of atrial fibrillationAFib is important because it can lead to many other medical problems, including stroke. The study concluded that MCT provided a significantly higher diagnostic yield, in detecting an arrhythmic event in patients with symptoms of cardiac arrhythmia, compared to traditional loop event monitoring, including such monitoring designed to automatically detect certain arrhythmias.

In addition to the aforementioned 300-patient randomized clinical trial, MCT has been cited and referenced in over 40 publications and abstracts, which lends support to its clinical efficacy.

In 2016, we obtained FDA approval of our next generation MCT device, in a patch form factor. The MCT patch is a four-lead, two-channel system that provides the same best-in-class technology as our traditional MCT devices, in a more convenient form factor. We continue to explore unique designs to improve patient experience while maintaining clinical efficacy.

We also continue to research study setup automation and workflow management for use in our Research segment. Our continued efforts to integrate machine learning and artificial intelligence to improve our automated patient management tracking in our Research segment services will drive efficiencies, and we believe it will help us acquire more dual-service studies from our partners.

Additionally, we continue to build out our coaching platform for our wireless BGM, through patient and third-party feedback. We are analyzing data to determine where machine learning can provide additional technological leverage and efficiencies to the physician and the patient.

Sales and Marketing

We market our cardiac monitoring solutions in our Healthcare segment through aour direct sales force primarily to cardiologists, electrophysiologists, neurologists and neurologists who are the physician specialistsprimary care physicians who most commonly diagnose and managetreat patients with arrhythmias. We sponsor peer-to-peer educational eventsdifferentiate ourselves through our clinical efficacy and participatethe seamless integration of our data in targeted public relations opportunities. the practice’s electronic medical records.

We are athe leading member of the Remote Cardiac Service Provider Group. Group (“RCSPG”), with our Senior Vice President of Medical Affairs being the current President of the RCSPG. The RCSPG collaborates with physician specialty societies as well as the American Telemedicine Association to advocate to the Centers for Medicare and Medicaid Services (“CMS”) and Congress for appropriate valuation of remote diagnostic services that the RCSPG members provide.

We market our researchResearch segment services to pharmaceutical companies, medical device companies, contract research organizationsCROs and academic research organizations. Cardiocore isWe are a founding member and the first cardiac core lablaboratory to join the Cardiac Safety Research Consortium (“CSRC”CSRC”). Through the CSRC, we are able to network with representativeskey thought leaders and decision makers of major pharmaceutical companies, as well as discuss key cardiac safety issues during the drug development process. Through the 2016 acquisitionour integration of VirtualScopics, we have broadenedexperienced an increase in acquiring studies that include both cardiac and imaging requirements. Expanding our research service offerings is a key element of our strategic growth plan, allowing us to more favorably compete for research studies requiring a wider range of research services. We marketOur team has also had success incorporating our proprietary ePatch™ monitor as a critical element of new cardiac studies creating cross-segment, top-line synergies.

Our BioTel Alliance™ brand, currently included in the Corporate and Other category, markets our manufactured products to physicians, hospitals and other cardiac monitoring providers. BioTel Care® is actively working to expand our position in the digital population health space, and continues to evaluate numerous connected health technologies and solutions to better understand where we can best leverage our capabilities. Specifically, we are engaged in increasing awareness and utilization of our wireless BGM and our diabetes management platform. Our commercial team is primarily focused on securing contracted relationships for our diabetes management services with:

commercial managed care plans;

accountable care organizations;

integrated delivery networks;

physicians groups;

durable medical equipment distributors; and

employer groups.

We attend trade shows and medical conferences to promote our various product and service offerings. The trade shows and conferences we attend are related to organizations such as: the Heart Rhythm Society,

American College of Cardiology, American Telemedicine Association, Society of Thoracic Surgeons, European Society of Cardiology, American Heart Association and the American Telemedicine Association.European Society of Cardiology. We also attend the Medica, DIADrug Information Association and Partnerships in Clinical Trials trade shows, as well as the annual Boston Atrial Fibrillation Conference.Symposium. We have had limited product and service-based advertising in certain national newspapers and medical journals.

Healthcare Reimbursement

Seasonality

Our Healthcare segment experiences some seasonality during the third quarter as well as during the year-end holiday season. We believe that this is the result of patients electing to delay our monitoring services during the summer months or holidays.

Healthcare Reimbursement

In the Healthcare segment, services are billed to government and commercial payors using specific codes describing the services. Those codes are part of the CommercialCurrent Procedural Terminology (“CPT”CPT”) coding system, which was established by the American Medical Association (“AMA”) to describe services provided by physicians and other suppliers. Physicians select the code that best describes the medical services being prescribed. Approximately 34%35% of our total revenue is subject to reimbursement directly from the Medicare program, a federal government health insurance program administered by the Centers for Medicare and Medicaid Services (“CMS”)CMS, at rates that are set nationally and adjusted for certain regional indices.

In addition to receiving reimbursement from Medicare,government payors, we enter into contracts with commercial payors to receive reimbursement at specified rates for our technical services. Such contracts typically provide for an initial term of between one and three years and provide for automatic renewal thereafter.

Either party can typically terminate these contracts by providing between 6030 and 120180 days’ prior notice to the other party at any time following the end of the initial term of the agreement. The contracts provide for an agreed upon reimbursement rate, which in some instances is tied to the rate of reimbursement we receive from Medicare.

In addition to receiving reimbursement from government and commercial payors, we have direct arrangements with physicians who may purchase our monitoring services and then submit claims for these services directly to commercialgovernment and governmentcommercial payors. In some cases, patients pay for their service out-of-pocket.

Competition

Although we believe that we have a leading market shareposition in the mobile cardiac monitoring industry,in the marketU.S., the industry in which our Healthcare segment operates is fragmented and characterized by a large number of smaller regional service providers. Additionally, several larger healthcare companies

Our Research segment competes directly with other core labs as well as CROs that offer certaincentralized core laboratory services. We believe that we compete favorably based on our comprehensive cardiac monitoring solutions, primarily Holter monitors. and imaging service offerings, the scale of our operation and our ability to support the entire life cycle of new drug development.

We also compete directly with other original diagnostic equipment manufacturers.

We believe that the principal competitive factors that impact the success of our cardiac monitoring solutionsbusinesses include some or all of the following:

quality of our algorithms used to detect symptoms;arrhythmias;

quality and accuracy of clinical data;

turnaround times;

ease of use and reliability of cardiac monitoring solutions for patients and physicians;

technology performance, innovation, flexibility and range of application;application generating the highest yields;

timeliness and clinical relevance of new product introductions;

quality and availability of superior customer support services;

size, experience, knowledge and training of sales and marketing staff;

reputation;

relationships with referring physicians, hospitals, managed care organizations and other third-party payors;

reporting capabilities;

| |

| • | providing a full spectrum of remote cardiac monitoring solutions, including MCT, event, traditional Holter, extended Holter, Pacemaker, INR, ILR and other implantable cardiac device monitoring; |

spectruma widening range of solutions, ranging from our differentiated MCTclinical cardiac and imaging services to event and Holter monitoring, making us a single source for cardiac monitoring services; andbest-in-class solutions;

perceived value.value; and

extensive industry expertise.

We believe that we compete favorably based on the factors described above. However, our industry is evolving rapidly and is becoming increasingly competitive, and the basis on which we compete may change over time. In addition, if companies with substantially greater resources than ours enter our market, we will face increased competition.

Our Research segment competes directly with other core labs

Charitable Giving

In recent years, we have supported the American Heart Association through sponsorship and employee fund-raising at local Heart Walk events in the Philadelphia area as well as contract research organizations that offer core lab services. We believe that we compete favorably based on our comprehensive cardiac and imaging service offerings,at various other locations across the scaleU.S. as a way to share a portion of our operation andsuccess. In 2019, we began our ability“Heart for Hope” initiative, whereby we committed to supportfund life-saving heart procedures for children in need. To date, we have funded 200 surgeries for children from parts of Southeast Asia whose families do not have the entire life cycle of new drug development.resources to do so. That funding also includes the follow-up care after the surgery is completed. More information about “Heart for Hope” can be found at www.gobio.com/heartforhope.

Our Technology segment competes directly with other original equipment manufacturers. We believe that we compete favorably based on our suite of quality products and innovative solutions, our superior customer service and our extensive industry experience.

Intellectual Property

We rely on a combination of intellectual property laws, non-disclosure agreements and other measures to protect our proprietary rights. We attempt to protect our intellectual property rights by filing patent applications for new features and products we develop. In addition, we also seek to maintain certain intellectual property and proprietary know-how as trade secrets, and generally require our partners to execute non-disclosure agreements prior to any substantive discussions or disclosures of our technology or business plans. Our business and competitive positions are dependent in part upon our ability to protect our proprietary technology and our ability to avoid infringing the patents or proprietary rights of others.

We hold patents in the United States as well as many international jurisdictions on our products, processes and related technologies. In furtherance of our overall global intellectual property strategy, we also have patent applications currently on file in the United States and internationally. While we have several patents expiring between 2018 andthrough 2032, including patents that relate, in part, to our key products, we do not believe such expirations will have a material impact on our ability to compete in the short term since our technology is typically covered by several patents, creating a system of protected technology.

Our trademarks, certain of which are material to our business, are registered or otherwise legally protected in the United States and in certain foreign countriesinternational jurisdictions and include, among others, the registered trademarks CardioNet®BioTelemetry®, BioTelemetry®BioTel Heart®, Geneva Healthcare®, BioTel Care®, and LifeWatch®BioTel Europe® and the unregistered trademarks Mobile Cardiac Outpatient Telemetry™, MCOT™, CardioPortal™ePatch™, BioTel Heart™, BioTel Care™CardioPortal™, BioTel Research™ and BioTel Technology™Alliance™. We also have a significant amount of copyright-protected materials.

Government Regulation

The health carehealthcare industry is highly regulated, with no guarantee that the regulatory environment in which we operate will not change significantly and adversely in the future. We believe that health carehealthcare legislation, rules, regulations and interpretations will change, and we expect we will have to modify our agreements and operations in response to these changes.

U.S. Food and Drug Administration. Administration

The medical devices that we use to provide patient monitoring services are regulated by the FDA under the Federal Food, Drug, and Cosmetic Act. The basic regulatory requirements that manufacturers ofAct (“FDCA”). Unless exempt, medical devices distributed in the United SatesStates must comply with arereceive marketing authorization by the FDA through either a full Premarket Approval (“PMA”) or the Premarket Notification 510(k), unless exempt, process. Based on the classification and characteristics of a medical device, it may receive marketing authorization through a PMA pathway, which requires the demonstration of safety and effectiveness through adequate and well-controlled clinical studies, or Premarket Approval,receive clearance under the 510(k) pathway after demonstrating substantial equivalence to a predicate device. In addition to marketing authorization requirements, device manufacturers must also comply generally with establishment registration, medical device listing, quality system regulation, labeling requirements and medical device reporting.reporting requirements, and any special controls specific to a particular device and used to support reclassification.

The algorithms we use in the MCT service maintain FDA 510(k) clearance as a Class II device (“510(k) Clearance”).device. On October 28, 2003, the FDA issued a guidance document entitled: “Class“Class II Special Controls Guidance Document: Arrhythmia Detector and Alarm.” In addition to conforming to the general requirements of the Federal Food, Drug, and Cosmetic Act,FDCA, including the Premarket Notification requirements described above, all of our cardiac related

510(k) submissions address the specific issues covered in this special controls guidance document. The algorithms we use in the BGM service also maintain FDA 510(k) Clearanceclearance as a Class II device.

Failure to comply with applicable regulatory requirements can result in enforcement action by the FDA which may include, including certain sanctions, such as fines, injunctions and civil penalties;penalties or injunctions; recall or seizure of our devices and intellectual property; operating restrictions; partial suspension or total shutdown of

production; withdrawal of 510(k) Clearanceclearance of new components or algorithms; withdrawal of 510(k) Clearanceclearance already granted to one or more of our existing components or algorithms; and criminal prosecution.

CE Marking. Marking

Medical devices distributed within the EEA require the CE Marking, which is a certification mark that indicates conformity with health, safety, and environmental protection standards for products sold within the EEA. The CE Marking is also found on products sold outside the EEA that are manufactured in, or designed to be sold in, the EEA. Although ISO 13485 certification is not a direct requirement for CE Marking medical devices under the European Economic Area requireMedical Device Directives, it is recognized as a CE Marking.harmonized standard by the European Commission. ISO 13485 is a quality system standard used by medical companies providing design, development, manufacturing, installation and servicing, and isaligned with the basis for acquiring CE Marking forthree European medical device product distributiondirectives that are applicable to different types of medical devices in the European Union. Europe.Failure to maintain appropriate CE Marking could have an adverse effect on our ability to use or sell our devices within the European Union.

Health CareHealthcare, Fraud, Waste and Abuse. Abuse

In the United States, there are state and federal laws and regulations restrict healthcare providers from billing and collecting for products or services connected with fraudulent, wasteful or abusive conduct. These state and federal laws include civil and criminal false claims provisions, health fraud and false statements provisions, anti-kickback provisions, physician self-referral provisions, and more, violation of which may subject us to criminal penalties as well as potential exclusion from federal healthcare programs and civil monetary penalties.

Federal and state anti-kickback laws that generally prohibit the payment or receipt of kickbacks, bribesanything of value to induce prescription or other remuneration in exchange for the referral of patientsreimbursed products or other health care-related business. In addition, federalservices. Stark law (e.g., the “Stark” law) and some state laws prohibit the existence oflimits certain financial relationships between referring physicians and health care providers and suppliers unless those relationships meet the requirements of specific exceptions to the law.certain designated healthcare services. Anti-kickback laws constrain our sales, marketing and promotional activities by limiting the kinds ofrestrict financial arrangements we may have with physicians, medical centers and otherscertain healthcare professionals in a position to purchase, recommend or refer patients for our cardiac monitoring services or other products or services we may develop and commercialize. Due to the breadth of some of these laws, it is possible that some of our current or future practices might be challenged under one or more of these laws.

Furthermore, federalFederal and state false claims laws prohibit anyone from presenting, or causing to be presented, claims for payment to third-party payors that are false or fraudulent. Violations may result in substantial civil penalties including treble damages, andas well as criminal penalties, including imprisonment, fines and exclusion from participation in federal health care programs. The Federal False Claims Act (“FCA”) also contains “whistleblower” or “qui tam” provisions that allow private individuals to bring actions on behalf of the government alleging that the defendant has defrauded the government.false claims and potentially other violations of fraud and abuse laws. Various states have enacted laws modeled after the Federal False Claims Act,FCA, including “qui tam” provisions, and some of these laws apply to claims filed with commercial insurers. Any violationsViolation of anti-kickbackfederal and false claimsstate fraud and abuse laws could have a material adverse effect on our business, financial condition and results of operations.

The Patient Protection and Affordable Care Act. Act

On March 23, 2010, the Patient Protection and Affordable Care Act was signed into law, and on March 30, 2010, the Health Care and Education Reconciliation Act of 2010 was signed into law. Together, the two measures, collectively known as the Affordable Care Act make the most sweeping and(“ACA”), made fundamental changes to the United States health care system since the creation of Medicare and Medicaid.healthcare system. The Affordable Care ActACA expanded Medicaid eligibility, required most individuals to have health insurance or pay a penalty, imposed new requirements for health plans and insurance policy standards, established health insurance exchanges, changed Medicare payment systems to encourage more cost-effective care and newnewly expanded tools to address fraud and abuse and required manufacturers of medical devices and other products reimbursed by Medicare to report annually to the government certain payments to physicians and teaching hospitals.

As a result In 2018, certain provisions of the passage ofACA were modified and repealed effective 2019 and beyond, and in December 2019, the Affordable Care Act, manufacturers of certain medical devices are subject to andevice excise tax applicable to sales of taxable medical devices beginning January 1, 2013. Several devices that are manufactured by our Technology segment are subject to these taxes. The tax equals 2.3% of the sale price of the applicable medical device. As a manufacturer, we are responsible for remitting these taxes to the federal government. The Consolidated Appropriations Act of 2016, enacted on December 18, 2015, included a moratorium on the medical devices tax commencing on January 1, 2016 and ending onwas permanently repealed.

December 31, 2017. Budget legislation signed in January 2018 extended that moratorium through December 31, 2019.

Health Insurance Portability and Accountability Act of 1996. 1996

The Health Insurance Portability and Accountability Act (“HIPAA”) was enacted in 1996, amended by the United States CongressHealth Information Technology for Economic and Clinical Health (“HITECH”) Act in 1996. Numerous state2009, and federalimplemented through regulation (collectively, “HIPAA”). HIPAA, together with other data privacy and security laws governsuch as the General Data Protection Regulations (“GDPR”) in Europe, dictate privacy and security standards governing the collection, storage, maintenance, dissemination, use and confidentiality of individually identifiable patient health information and other personal information. HIPAA applies directly to “covered entities,” which include health plans, healthcare clearinghouses and many healthcare providers, who electronically transmit health information includingand thereby engage in HIPAA “covered transactions.” HIPAA also applies to “business associates,” individuals who perform certain functions or activities for or on behalf of covered entities that require the administrative simplificationindividuals to create, receive, maintain, or transmit protected health information (“PHI”). HIPAA is concerned primarily with the privacy of PHI when it is used and/or disclosed; the confidentiality, integrity and availability of electronic PHI; notifying federal regulators and impacted patients in the event of a breach of unsecured PHI; and the content and format of certain identified electronic healthcare transactions. The laws governing healthcare information privacy provisionsand security impose civil and criminal penalties for their violation. Compliance with these laws requires substantial expenditures of HIPAA.financial and other resources for information technology system compliance, maintenance, monitoring, validation and evaluation. Historically, state law has governed confidentiality issues, and HIPAA preserves these laws to the extent they are more protective of a patient’s privacy or provide the patient with greater access to his or her health information. As a result of the implementation of the HIPAA regulations, manyMany states are consideringcontinue to consider revisions to their existing laws and regulations that may or may not be more stringent or burdensome than the federal HIPAA provisions. HIPAA applies directly to covered entities, which include health plans, health care clearinghouses and many health care providers. The HIPAA statute, as amended by the Health Information Technology for Economic and Clinical Health (“HITECH”) Act in 2009, and its implementation rules are concerned primarily with the privacy of protected health information when it is used and/or disclosed; the confidentiality, integrity and availability of electronic health information; notifying federal regulators and impacted patients in the event of a breach of unsecured protected health information; and the content and format of certain identified electronic health care transactions. The laws governing health care information privacy and security impose civil and criminal penalties for their violation and can require substantial expenditures of financial and other resources for information technology system modifications and for ongoing operational compliance.

Medicare. Medicare

Medicare is a federal program administered by CMS and its Medicare administrative contractors.Administrative Contractors (“MAC”). The Medicare program provides qualified persons with health carehealthcare benefits that cover the major costs of medical care within prescribed limits, subject to certain deductibles and co-payments. The Medicare program has established guidelines for local and national coverage determinations and reimbursement of certain equipment, supplies and services, which are subject to change. The methodology for determining coverage status and the basis and amount of Medicare reimbursement varies based upon, among other factors, the settinglocation in which a Medicare beneficiary receives health carehealthcare items and services.services, the type of items and services provided, and the benefits available to individual beneficiaries.

The Medicare program is subject to statutory and regulatory changes, retroactive and prospective rate adjustments, administrative rulings, interpretations of policy, Medicare administrativebilling guidelines, MAC contractor local coverage determinations and government funding restrictions. All of these policies may materially increase or decrease the rate of program payments to health carehealthcare facilities and other health carehealthcare suppliers and practitioners, including those paid for our cardiac monitoring or other services. Other regulations such as facility standards, billing requirements, rules of participation and other regulations affecting the provision of and reimbursement for products and services also affect the ability to provide, bill and receive reimbursement for services or products provided under the program. Any changes in federal legislation, regulations or other policies affecting Medicare coverage, reimbursement or reimbursementeligibility relative to our cardiac monitoring or other services could have an adverse effect on our performance.

Certain of our facilities are enrolled in Medicare as Independent Diagnostic Testing Facilities (“IDTFs”IDTFs”). An IDTF is defined by CMS as an entity independent of a hospital or physician’s office in which diagnostic tests are performed, often by licensed or certified non-physician personnel, and under appropriate physician supervision. Medicare has set veryprescribes detailed performancecertification standards that every IDTF must meet in order to obtain or maintain its billing privileges, including requirements to, among other things, operate in compliance with all applicable federal and state licensure and regulatory requirements for the health and safety of patients; maintain a physical facility on an appropriate site meeting specific criteria; have a comprehensive liability insurance policy of at least $0.3 million per location; disclose certain ownership information; have its testing equipment calibrated and maintained in accordance with specific standards; have technical staff on duty with the appropriate credentials to perform tests; and permit on-site inspections.

These requirements are subject to change. WeOur IDTF facilities are periodically inspected by CMS to confirm our compliance with the IDTF standards, and we believe that our facilities are in compliance with the IDTFthese standards.

Environmental Regulation. Regulation

We use materials and products regulated under environmental laws, primarily in the manufacturing and sterilization processes. While it is difficult to quantify, we believe the ongoing cost of compliance with environmental protection laws and regulations will not have a material impact on our business, financial position or results of operations.

Supply Chain Diligence and Transparency

Section 1502 of the Dodd Frank Wall Street Reform and Consumer Protection Act was adopted to further the humanitarian goal of ending the violent conflict and human rights abuses in the Democratic Republic of the Congo and adjoining countries (“DRC”). This conflict has been partially financed by the exploitation and trade of tantalum, tin, tungsten and gold (so called “conflict minerals”) that originate from mines or smelters in the region. United States Securities and Exchange Commission (“SEC”) rules adopted in August 2012 under Section 1502 require reporting companies to disclose annually on Form SD whether any such minerals that are necessary to the functionality or production of products they manufactured, or for which they contracted the manufacture, during the prior calendar year did, in fact, originate in the DRC and, if so, if the related revenue was used to support the conflict and/or abuses.Some of the products we manufacture may contain tantalum, tin, tungsten and/or gold. Consequently, in compliance with SEC rules, we have adopted a policy on conflict minerals, which can be found on our website, and have implemented a supply chain due diligence and risk mitigation process with reference to the Organization for Economic Cooperation and Development (“OECD”) guidance approved by the SEC to assess and report annually whether our products are “conflict free.”

We support efforts to end the violence and human rights abuses in the mining of certain minerals in the DRC. We expect our suppliers to comply with the OECD guidance and industry standards and to ensure that their supply chain conforms to our policy and the OECD guidance. We will mitigate identified risks by working directly with our suppliers; however, we may need to alter our sources of supply or modify our product design if circumstances require. We may incur certain costs in order to comply with these disclosure requirements, including for due diligence to determine the source of the subject minerals used in our products and other potential changes to products, processes or sources of supply as a consequence of such verification activities. In addition, these rules could adversely affect the sourcing, supply and pricing of materials used in our products throughout the supply chain beyond our control, whether or not the subject minerals are “conflict free.”

Product Liability and Insurance

The design, manufacture and marketing of medical devices and services of the types we produce entail an inherent risk of product liability claims. In addition, we provide information to health carehealthcare providers and payors upon which determinations affecting medical care are made, and claims may be made against us resulting from adverse medical consequences to patients allegedly resulting from the information we provide. To protect ourselves from product liability claims, we maintain professional liability and general liability insurance on a “claims made” basis. Insurance coverage under such policies is contingent upon a policy being in effect when a claim is made, regardless of when the events whichevent(s) that caused the claim occurred. While, as of the date of this Annual Report on Form 10-K, a material product liability claim has never been made against us and we believe our insurance policies are adequate in amount and coverage for our current operations, there can be no assurance that the coverage maintained by us is sufficient to cover all future

claims. In addition, there can be no assurance that we will be able to obtain such insurance on commercially reasonable terms in the future.

Employees

As of December 31, 2017,2019, we employedhad approximately 1,6001,700 employees. None of our employees are represented by a collective bargaining agreement. We consider our relationship with our employees to be good.

Available Information

We file electronically with the SEC our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934 (“Exchange Act”Act”). We make these reports available on our website at www.gobio.com, free of charge. Copies of these reports are made available as soon as reasonably practicable after we electronically file such material with, or furnish it to, the SEC. Further copies of these reports are located at the SEC’s Public Reference Room at 100 F Street, NE, Washington, D.C. 20549. Information on the operation of the Public Reference Room can be obtained by calling the SEC at 1-800-SEC-0330.. The SEC maintains a website that contains reports, proxy and information statements, and other information regarding our filings, at www.sec.gov. We do not utilize social media platforms as our primary means of distributing material company information.

Item 1A. Risk Factors

The risk factors discussed below are cautionary statements that identify important factors and risks that could cause actual results to differ materially from those anticipated by the forward-looking statements described under “Cautionary Note Regarding Forward-Looking Statements” contained in this Annual Report on Form 10-K. For more information regarding the forward-looking statements contained in this report, see the Table of Contents of this Annual Report on Form 10-K. You should carefully consider the risks and uncertainties described below, together with all of the other information included in this Annual Report on Form 10-K, in considering our business and prospects.prospects as the occurrence of any of the following risks could affect our business, liquidity, results of operations, financial condition or cash flows. The risks and uncertainties described below are not the only ones facing BioTelemetry. Additional risks and uncertainties not presently known to us may also impair our business operations. The occurrence of any of the following risks could affect our business, liquidity, results of operations, financial condition or cash flows.

Our businesses and those of many of our clients have been and continue to be subject to increased legislation and regulatory scrutiny, and we face the risk of changes to this regulatory environment and business in the future.

U.S. income tax reform efforts could have a material impact on our business. On December 22, 2017, the Tax Cuts and Jobs Act (“TCJA”) was signed into law. The TCJA enacts broad changes to the existing U.S. federal income tax code, including reducing the federal corporate income tax rate from 35% to 21% beginning in 2018, amongst many other complex provisions. The ultimate impact of such tax reforms may differ from our current estimates due to changes in interpretations and assumptions made by us as well as the issuance of any further regulations or guidance that may alter the operation of the U.S. federal income tax code. Various uncertainties also exist in terms of how U.S. states and any foreign countries within which we operate will react to these U.S. federal income tax reforms, which could have additional impacts on our business.

Reimbursement by Medicare is highly regulated, and subject to change and our failure to comply with applicable regulations could decrease our revenue, subject us to penalties or adversely affect our results of operations.

The Medicare program is administered by CMS, which imposes extensive and detailed requirements on medical product and services providers, including, but not limited to, rules that govern how we structure our relationships with physicians, how and when we submit reimbursement claims, how we operate our monitoring centers and how and where we provide our arrhythmia monitoring solutions. Our failure to comply with applicable Medicare rules could result in the discontinuation of our reimbursement under the Medicare payment program, a requirement to return funds already paid to us, civil monetary penalties, criminal penalties and/or exclusion from the Medicare program.

Changes in the reimbursement rate that commercial payors and Medicare will pay for our products and services could adversely affect our revenue.operating performance.

We receiveReductions in reimbursement for our products and servicesrates from consolidation of, or contract negotiations with, commercial payors and from Medicare administrative contractors with jurisdiction in the state where the services are performed. In addition,could adversely affect our prescribing physicians receive reimbursement for professional interpretation of the information provided by our products and services from commercial payors or Medicare. Average commercial reimbursement rates have declined over a three and five year period.operating performance. When commercial payors combine their operations, the combined company may electdecide to reimburse for our products and services at the lowest rate paid by any of the participants in the consolidation. If one of the payors participating in the consolidation

does not reimburse for one of our products or services, the combined company may electdecide not to reimburse for such product or service.

Additionally, our agreements with commercial payors can typically allow either party to the contract to terminate these contractsthe contract by providing between 6030 and 120180 days’ prior written notice to the other party at any time following the end of the initial term of the agreement. contract. Our commercial payors may elect to terminate or not to renew their contracts with us for any reason. A commercial payor who terminates or does not renew their contract with us may, or may not, alter their coverage for the type of services we provide. In the event any of our key commercial payors terminate their agreements with us, elect not to renew or enter into new agreements with us upon expiration of their current agreements, or do not renew or establish new agreements on terms as favorable as are currently contracted, our business, operating results and prospects would be adversely affected.

In addition, CMS may reduce the reimbursement rate for our services, as it has in the past. CMS updates the reimbursement rate via the Medicare physician fee schedule annually. Furthermore, CMS has adopted a complex new system for reimbursing Medicare physician services as required by the Medicare Access and CHIP Reauthorization Act of 2015. Under the new program, which began January 1, 2017, physicians will either report under the Merit-based Incentive Payment System or an Advanced Alternative Payment Model, and their 2017past performance will impact 2019future rates. CMS published a final rule on November 16, 2017, modifying program requirements for performance year 2018. The rule designates use of certain patient-generated health data with an active feedback loop as a “high” weighted activity for purposes of the Advancing Care Information bonus. We cannot predict the impact of this new framework or potential future revisions to physician payment policy on reimbursement for our services. A decrease in Medicare or commercial reimbursement rates or termination of commercial payor contracts would adversely affect our financial results.

The operationFinally, patients may continue to move to Medicare Advantage plans from traditional Medicare plans, which may change the nature of our monitoring centers is subject to rules and regulations governing IDTFs and state licensure requirements; failure to comply with these rules could preventthe reimbursements received by us from receivingtraditional Medicare programs and may negatively affect our revenue.

Our revenues could be affected by third-party reimbursement from Medicarepolicies and some commercial payors.potential cost constraints.

We have several monitoring centers throughoutIn the United States, that analyze the data obtained from cardiac monitors and report the results to physicians. In order for us towe receive reimbursement from Medicarefor our products and someservices from commercial payors our monitoring centers must be certified as IDTFs. Certification as an IDTF requires that we follow strict regulations governing how our monitoring centers operate, such as requirements regardingand from the experience and certifications of the technicians who review data transmitted from our monitors. These rules and regulations vary from location to location and are subject to change. If they change, we may have to change the operating procedures at our monitoring centers, which could increase our costs significantly. If we fail to obtain and maintain IDTF certification, our services may no

longer be reimbursed by Medicare and some commercial payors, which could have a material adverse impact on our business.

Our failure to maintain accreditation could impact our DMEPOS operations.

Accreditation is required by most of our managed care payors and became a mandatory requirement for all Medicare durable medical equipment, prosthetics, orthotics and supplies (“DMEPOS”) providers effective October 1, 2009. In 2016, we acquired Telcare, a diabetes care management company. In 2017, Telcare completed a nationwide accreditation renewal process conducted by the Healthcare Quality Association on Accreditation, which renewed our accreditation for another three years. The Company will undergo the next survey cycle in 2020. If we lose accreditation, our failure to maintain accreditation could have an adverse effect on our business, financial condition, results of operations, cash flow, capital resources and liquidity.

Failure to appropriately track and report certain payments to physicians and teaching hospitals may violate certain federal reporting laws and subject us to fines and penalties.

Section 6002 of the Affordable Care Act requires certain medical device manufacturers that produce devices covered by the Medicare and Medicaid programs to report annually to the government certain payments to physicians and teaching hospitals. If we fail to appropriately track and report such payments to the government, we could be subject to civil fines and penalties, which could adversely affect the results of our operations.

Audits or denials of our claims by government agencies and private payors could reduce our revenue and have an adverse effect on our results of operations.

As part of our business operations, we submit claims on behalf of patients directly to, and receive payments from, Medicare, Medicaid and other third-party payors. We are subject to extensive government regulation, including requirements for submitting reimbursement claims under appropriate codes and maintaining certain documentation to support our claims. Medicare contractors and Medicaid agencies periodically conduct pre-and post-payment reviews and other audits of claims and are under increasing pressure to more closely scrutinize health care claims and supporting documentation. We have previously been subject to pre-and post-payment reviews as well as audits of claims under CMS’ Recovery Audit Program and may experience such reviews and audits of claimsMAC with jurisdiction in the future. Such reviews and similar audits of our claims could result in material delays in payment, as well as material recoupments or denials, which would reduce our net sales and profitability, or result in our exclusion from participation instate where the Medicare or Medicaid programs. Weservices are also subject to similar review and audits from private payors, which may result in material delays in payment and material recoupments and denials.performed. In addition, state agencies may conduct investigationsour prescribing physicians or submit requests for information relating to claims data submitted to private payors.

We have a concentrated number of payors and losing one of them would reduce our sales and adversely affect our business and operating results.

Medicare, our largest payor, represents a significant percentage of our revenue. For the year ended December 31, 2017, Medicare accounted for approximately 34% of our total revenue. No other payor accounted for more than 4% of total revenue. Our agreements with commercial payors typically allow either party to the contract to terminate the contract by providing between 60 and 120 days’ prior written notice to the other party at any time following the end of the initial term of the contract. Our commercial payors may elect to terminate or not to renew their contracts with us for any reason and, in some instances,

can unilaterally change the reimbursement rates they pay. A commercial payor who terminates or does not renew their contract with us may, or may not, alter their coverage of our services. In the event any of our key commercial payors terminate their agreements with us, elect not to renew or enter into new agreements with us upon expiration of their current agreements, or do not renew or establish new agreements on terms as favorable as are currently contracted, our business, operating results and prospects would be adversely affected.

Violation of federal and state laws regarding privacy and security of patient information may adversely affect our business, financial condition or operations.