UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

| (Mark One) | |||||

| ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the fiscal year ended: December 31, 2019

2021

| OR | |||||

| TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

| For the transition period from _______ to ________ | |||||

Commission file number: 001-36062

(Exact name of registrant as specified in its charter)

(State or other jurisdiction of Incorporation or Organization) | 46-2613366 (I.R.S. Employer Identification No.) | ||||

Five Concourse Parkway

Suite 2500

Atlanta, Georgia 30328

(Address of Principal Executive Offices) (Zip Code)

Registrant’s telephone number, including area code: (770) 375-2300

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||||||

| Common units representing limited partnership interests | New York Stock Exchange | |||||||

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No þ☒

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No þ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes þ☒ No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (Section 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes þ☒ No ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer”, “accelerated filer”, “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer | Accelerated filer ☒ | Non-accelerated filer ☐ | Smaller reporting company | ||||||||||

Emerging growth company | |||||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ¨

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report.☒

Indicate by check mark whether the registrant is a shell company (as defined in Exchange Act Rule 12b-2). Yes ¨☐ No þ

The aggregate market value, as of June 30, 2019,2021, of the common units held by non-affiliates of the registrant, based on the reported closing price of such units on the New York Stock Exchange on such date ($19.3914.50 per common unit), was approximately $98.3$75.3 million.

The registrant had 19,757,26019,788,208 common units and 399,000 general partner units outstanding at February 28, 2020,March 10, 2022, the most recent practicable date.

Documents Incorporated by Reference: None

1

ANNUAL REPORT ON FORM 10-K

TABLE OF CONTENTS

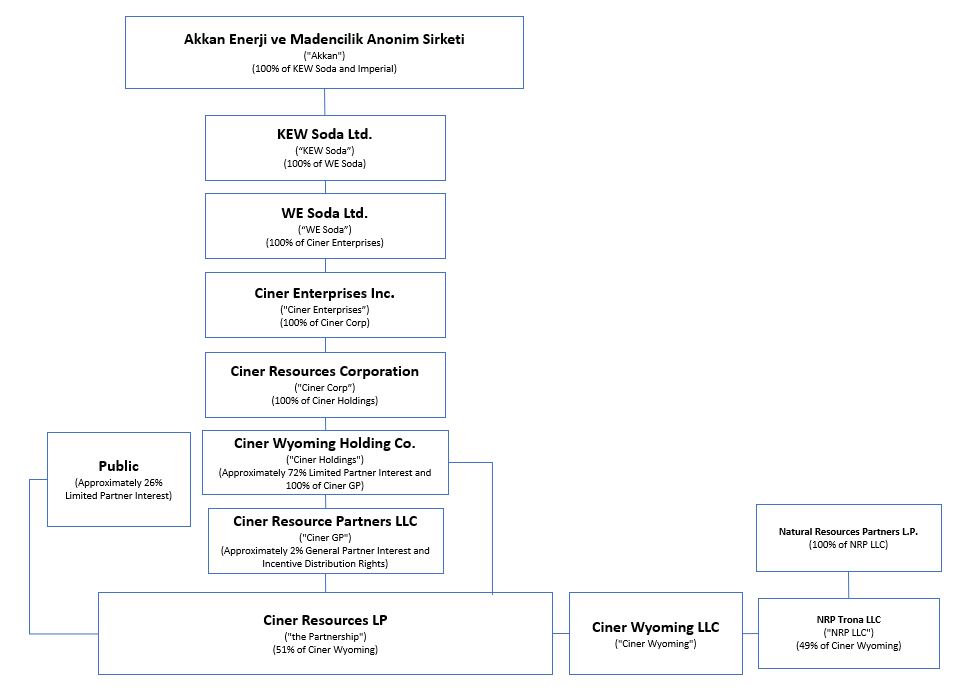

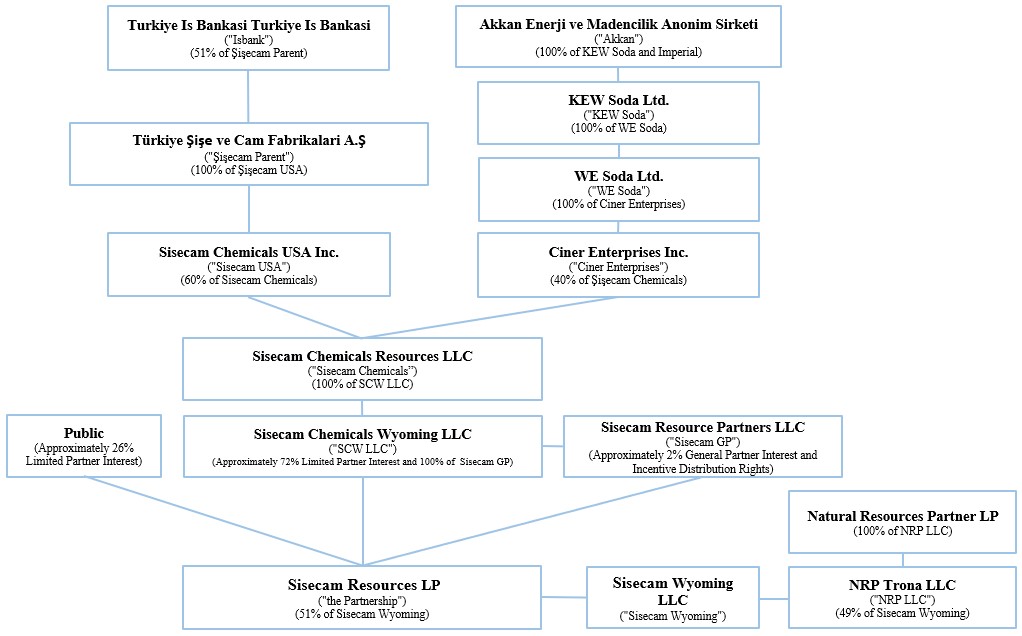

References in this Annual Report on Form 10-K (“Report”) to the “Partnership,” “CINR,” “Ciner Resources,“SIRE,” “we,” “our,” “us,” or like terms refer to Sisecam Resources LP (formerly known as Ciner Resources LPLP) and its subsidiary, Sisecam Wyoming LLC (formerly known as Ciner Wyoming LLC,LLC), which is the consolidated subsidiary of the Partnership and referred to herein as “Ciner Wyoming”.“Sisecam Wyoming.” Sisecam Chemicals Resources LLC ("Sisecam Chemicals" formerly known as Ciner Resources Corporation) is 60% owned by Sisecam Chemicals USA Inc. ("Sisecam USA") and 40% owned by Ciner Enterprises Inc. References to “our general partner” or “Ciner“Sisecam GP” refer to Sisecam Resource Partners LLC (formerly known as Ciner Resource Partners LLC,LLC), the general partner of CinerSisecam Resources LP and a direct wholly-owned subsidiary of Sisecam Chemicals Wyoming LLC ("SCW LLC" formerly known as Ciner Wyoming Holding Co. (“Ciner Holdings”), which is a direct wholly-owned subsidiary of Ciner Resources Corporation (“Ciner Corp”). Ciner CorpSisecam Chemicals. Sisecam Chemicals is a 60%-owned subsidiary of Sisecam USA, which is a direct wholly-owned subsidiary of Türkiye Şişe ve Cam Fabrikalari A.Ş, a Turkish corporation ("Şişecam Parent") which is an approximately 51%-owned subsidiary of Turkiye Is Bankasi Turkiye Is Bankasi ("Isbank"). Şişecam Parent is a global company operating in soda ash, chromium chemicals, flat glass, auto glass, glassware glass packaging and glass fiber sectors. Şişecam Parent was founded 86 years ago, is based in Turkey and is one of the largest industrial publicly-listed companies on the Istanbul exchange. With production facilities in four continents and in 14 countries, Sisecam is one of the largest glass and chemicals producers in the world. Ciner Enterprises Inc. (“Ciner Enterprises”), which is a direct wholly-owned subsidiary of WE Soda Ltd., a U.K. corporationCorporation (“WE Soda”). WE Soda is a direct wholly-owned subsidiary of KEW Soda Ltd., a U.K. corporation (“KEW Soda”), which is a direct wholly-owned subsidiary of Akkan Enerji ve Madencilik Anonim Şirketi (“Akkan”). Akkan is directly and wholly owned by Turgay Ciner, the Chairman of the Ciner Group (“Ciner Group”), a Turkish conglomerate of companies engaged in energy and mining (including soda ash mining), media and shipping markets. All of our soda ash processed is sold to various domestic and international customers including American Natural Soda Ash Corporation (“ANSAC”), which is currently an affiliate for export sales.customers.

We include cross references to captions elsewhere in this Report where you can find related additional information. The following table of contents tells you where to find these captions.

2

| Page Number | |||||||||

| Item 1. | |||||||||

| Item | |||||||||

| Item | |||||||||

| Item 2. | |||||||||

| Item 3. | |||||||||

| Item 4. | |||||||||

| Item 5. | |||||||||

| Item 6. | Reserved | ||||||||

| Item 7. | |||||||||

| Item 7A. | |||||||||

| Item 8. | |||||||||

| Item 9. | |||||||||

| Item 9A. | |||||||||

| Item 9B. | |||||||||

| Item 9C. | |||||||||

| Item 10. | |||||||||

| Item 11. | |||||||||

| Item 12. | |||||||||

| Item 13. | |||||||||

| Item 14. | |||||||||

| Item 15. | |||||||||

| Item 16. | |||||||||

3

CAUTIONARY STATEMENT CONCERNING FORWARD-LOOKING STATEMENTS

This Report contains, and our other public filings and oral and written statements by us and our management may include, statements that constitute “forward-looking statements” within the meaning of the United States securities laws. Forward-looking statements include the information concerning our possible or assumed future results of operations, reserve estimates, business strategies, financing plans, competitive position, potential growth opportunities, potential operating performance, the effects of competition and the effects of future legislation or regulations. Forward-looking statements include all statements that are not historical facts and in some cases may be identified by the use of forward-looking terminology such as the words “believe,” “expect,” “plan,” “intend,” “seek,” “anticipate,” “estimate,” “predict,” “forecast,” “project,” “potential,” “continue,” “may,” “will,” “could,” “should” or the negative of these terms or similar expressions. Examples of forward-looking statements include, but are not limited to, statements concerning cash available for distribution and future distributions, if any, and such distributions are subject to the approval of the board of directors of our general partner and will be based upon circumstances then existing. We have based our forward-looking statements on management’s beliefs and assumptions and on information currently available to us.

Forward-looking statements involve risks, uncertainties and assumptions. You should not put undue reliance on any forward-looking statements. After the date of this Report, we do not have any intention or obligation to update any forward-looking statement, whether as a result of new information or future events, and expressly disclaim any obligation to do so except as required by applicable law.

The risk factors discussed in Item 1A. “Risk Factors” and the factors discussed in Item 7. “Management’s Discussion and Analysis of Financial Condition and Results of Operations” could cause our actual results to differ materially from those expressed in forward-looking statements. These factors should not be construed as exhaustive and there may also be other risks that we are unable to predict at this time. All forward-looking statements included in this Report are expressly accompanied and qualified in their entirety by these cautionary statements.

4

PART I

Item 1. BusinessBusiness

Overview

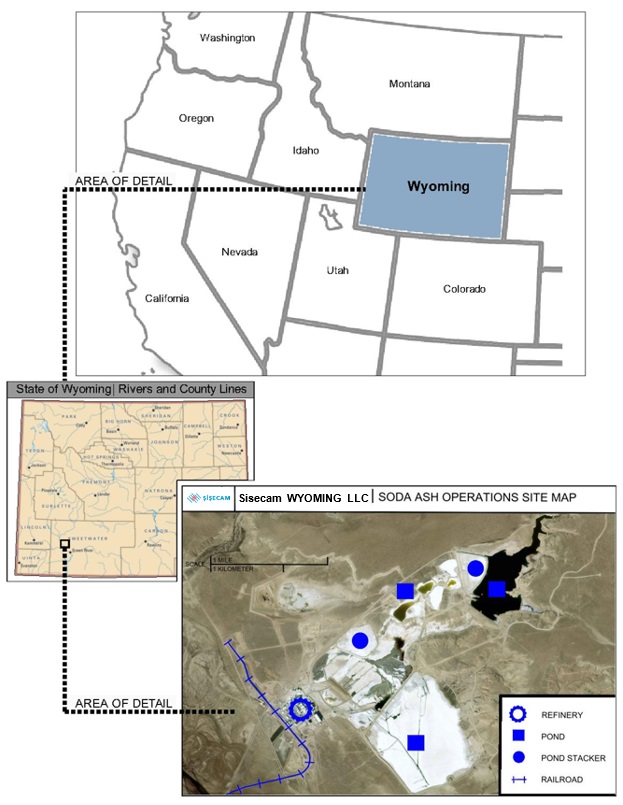

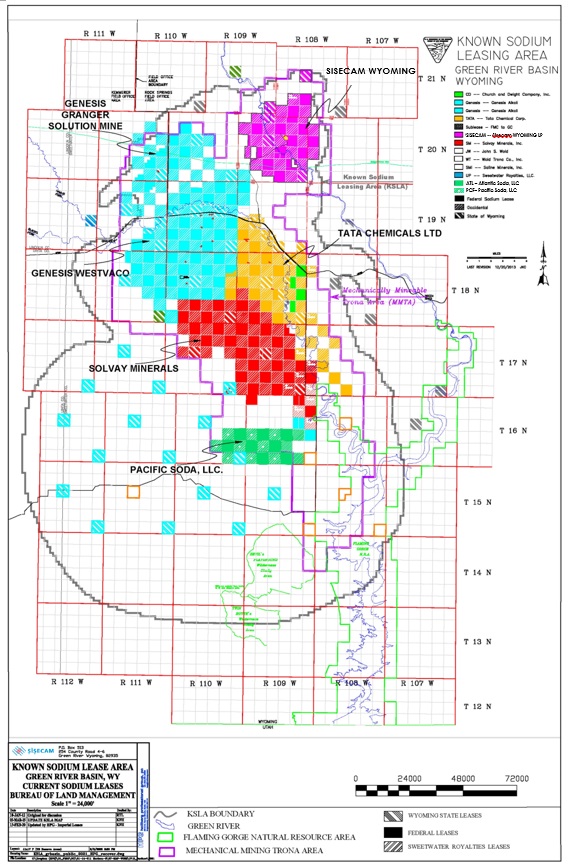

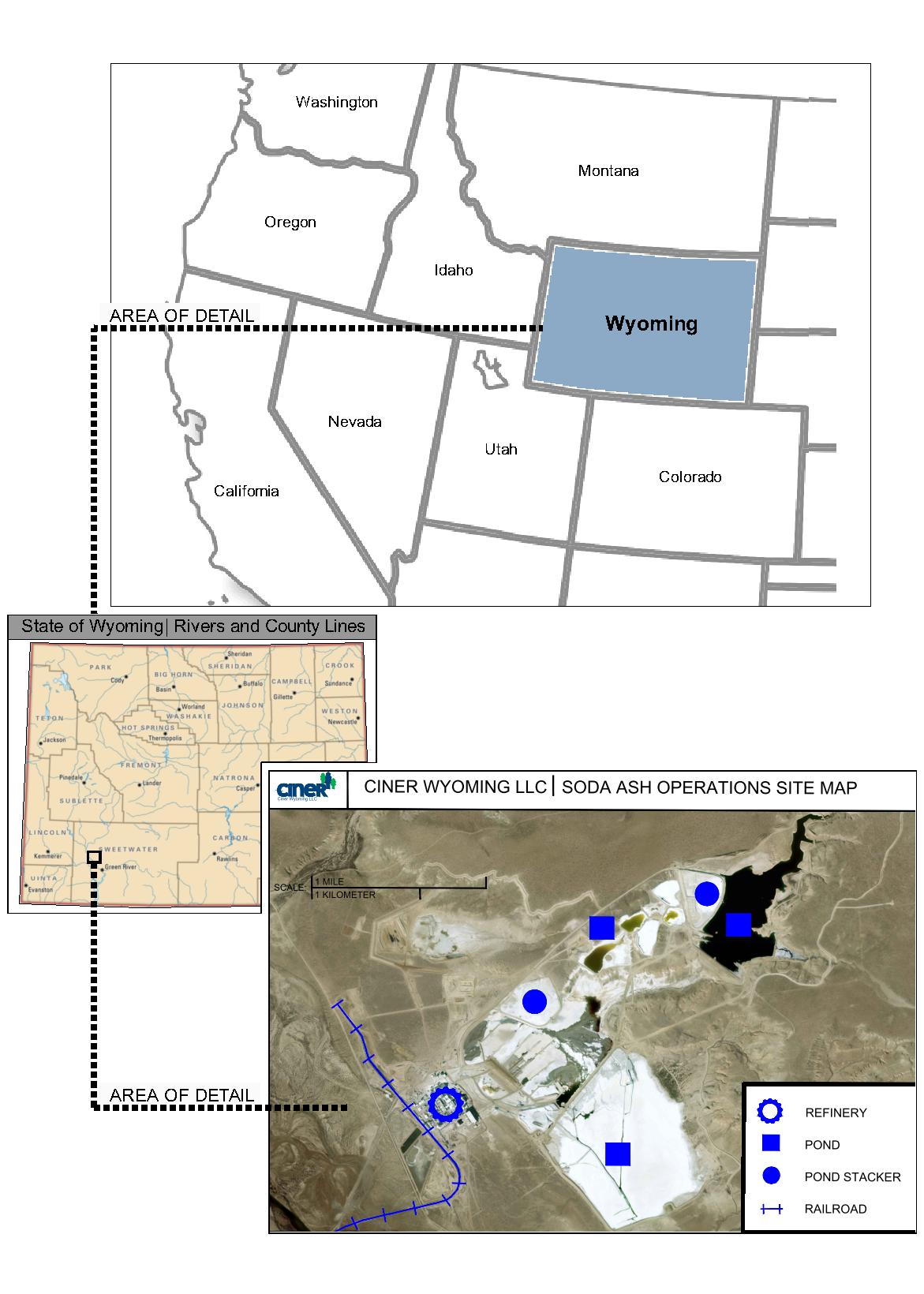

The Partnership was formed in April 2013 by Ciner Holdings.SCW LLC. The Partnership owns a controlling interest comprised of 51.0% membership interest in CinerSisecam Wyoming, which is one of the largest and lowest cost producers of natural soda ash in the world, serving a global market from our facility in the Green River Basin of Wyoming. Our facility has been in operation for more than 50 years.

The following table sets forth certain operating data regarding our business:

expect will eventually lower our cost position and improve our ability to optimize our market share both domestically and internationally. Further, being able to work with the global Ciner Group will provide us the opportunity to attract and efficiently serve larger global customers.

On November 9, 2018, Ciner Corp delivered a notice to terminate its membership in ANSAC, a cooperative that serves as the primary international distribution channel for us as well as two other U.S. manufacturers of trona-based soda ash. The effective termination date of Ciner Corp’s membership in ANSAC is December 31, 2021 (the “ANSAC termination date”). Between now and the ANSAC termination date, Ciner Corp continues to have full ANSAC membership benefits and services. We believe that by combining our volumes with Ciner Group’s soda ash exports from Turkey, Ciner Corp’s withdrawal from ANSAC will allow us to leverage the larger, global Ciner Group’s soda ash operations which we expect will eventually lower our cost position and improve our ability to optimize our market share both domestically and internationally. After the ANSAC termination date, the Partnership will need access to an international logistics infrastructure that includes, among other things, a domestic port for export capabilities. These export capabilities are currently being developed by Ciner Enterprises and options being evaluated range from continued outsourcing in the near term to developing its own port capabilities in the longer term. The development costs of export capabilities are currently being paid by Ciner Enterprises, who is evaluating how these costs might be allocated to the Partnership, which could include ownership by us and repayment for the development costs and related assets or a service agreement model for logistics services which includes reimbursements for development costs. Since a decision to allocate costs to the Partnership has not been made yet and the Partnership is not currently using any Ciner Enterprises export services, none of these development costs have been recorded by the Partnership through December 31, 2019.While Ciner Corp has deliveredHistorically, by design and prior to Sisecam Chemicals’ exit from ANSAC, ANSAC managed most of our international sales, marketing and logistics, and as a notice to terminate its membership in ANSAC effective onresult, was our largest customer for the ANSAC termination date, we anticipate that the impactyears ended December 31, 2020 and 2019, accounting for 45.4% and 60.4%, respectively, of such termination on our net sales, net income and liquidity will be limited. We made this determination primarily based upon the belief that we will continue to be one of the lowest cost producers ofsales. ANSAC takes soda ash orders directly from its overseas customers and then purchases soda ash for resale from its member companies pro rata based on each member’s allocated volumes. ANSAC is the exclusive distributor for its members to the markets it serves. The ANSAC exit allowed Sisecam Chemicals to improve access to customers and gain control over placement of its sales in the international marketplace in 2021. This enhanced view of the global market that has historically seen allows Sisecam Chemicals to better understand supply/demand fundamentals thus allowing better decision making for soda ash exceed supply of soda ash. After the ANSAC termination date, we expect Ciner Corp will begin marketing soda ash directly on our behalf into international markets which are currently being served by ANSAC and intendsits business. Sisecam Chemicals continues to utilize theoptimize its distribution network that has already been established by the global Ciner Group. We believe that by combiningleveraging strengths of existing distribution partners while expanding as our volumes with Ciner Group’s soda ash exports from Turkey, Ciner Corp’s withdrawal from ANSAC will allow us to leverage the

larger, global Ciner Group’s soda ash operations which we expect will eventually lower our cost position and improve our ability to optimize our market share both domestically and internationally. Further, being able to work with the global Ciner Group will provide us the opportunity to attract and efficiently serve larger global customers.Please read “Risk Factors-Risks Inherent in our Business and Industry-A significant portion of our historical international sales of soda ash have been to ANSAC, and therefore, Ciner Corp’s decision to terminate its membership in ANSAC could adversely affect our ability to competebusiness requires in certain international markets, materially adversely impact our business, results of operations and financial condition and limit our ability to make distributions to our unitholders.”target areas.

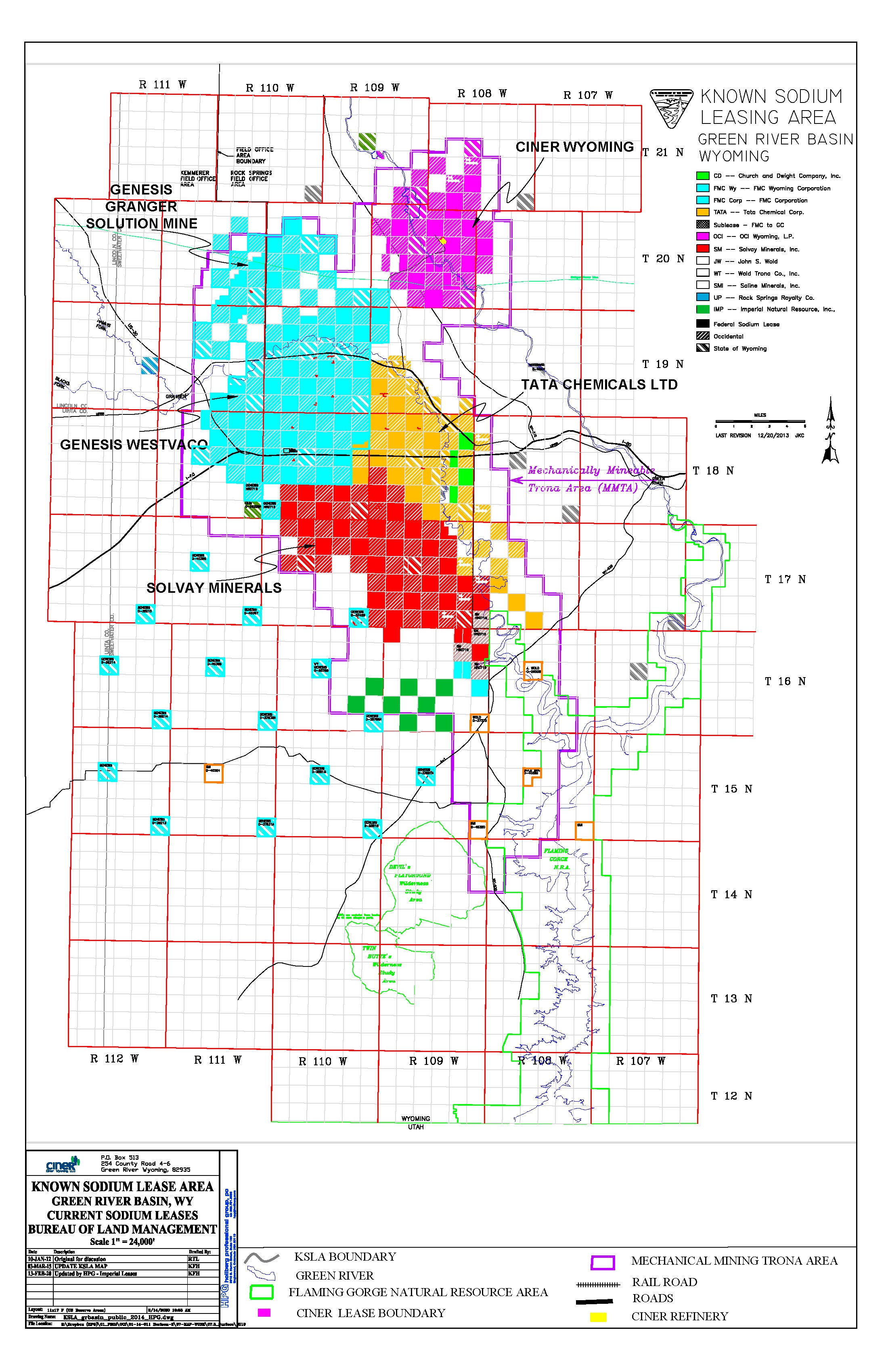

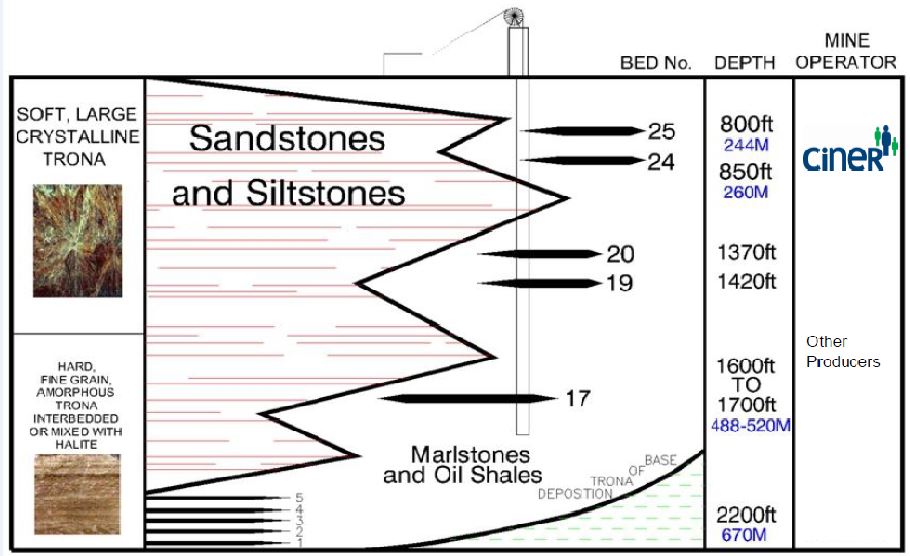

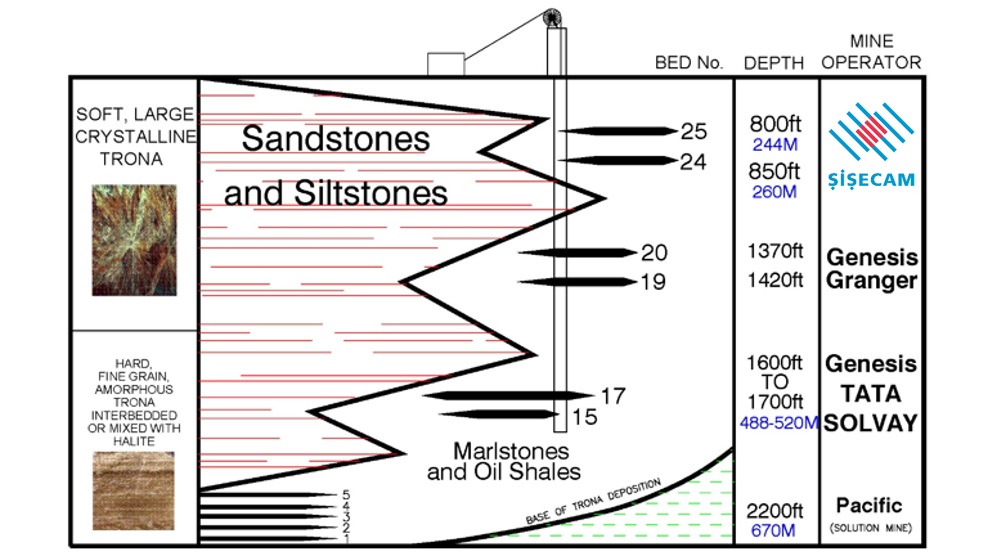

AsInformation concerning our mining property and estimated mineral resources and mineral reserves in this Annual Report on Form 10-K has been prepared in accordance with the requirements of subpart 1300 of Regulation S-K, which first became applicable to us for the fiscal year ended December 31, 2021. These requirements differ significantly from the previously applicable disclosure requirements of SEC Industry Guide 7. Among other differences, subpart 1300 of Regulation S-K requires us to disclose our mineral resources, in addition to our mineral reserves, at our mining property as of the end of our most recently completed fiscal year.The information that follows is derived, for the most part, from, and in some instances is an extract from the technical report summary prepared by Hollberg Professional Group (HPG) in compliance with Item 601(b)(96) and subpart 1300 of Regulation S-K.Portions of the following information are based on assumptions, qualifications and procedures, that are not fully described herein. Reference should be made to the full text of the technical report summary prepared by HPG attached as Exhibit 96.1 and incorporated herein by reference and made a part of this Report on Form 10-K. We have used the term “trona” as in “trona resources” and “trona reserves” interchangeably with “mineral.”

HPG calculated aThe mineral reserve estimate on our tronais the economically mineable part of a measured or indicated mineral assets,resource, which are contained in beds 24includes diluting materials and 25 ofallowances for losses that may occur when the Green River Basin, at depths of 800 and 1,100 feet below the surface, respectively. HPG estimates are based on geological data generated from historical exploration drill holes, borings within the mine space, and mine observations and measurements, including core samples. In addition, HPG reviewed and analyzed our reserve base maps and current mining plans, and developed a life of mine plan with respect to the predicted life of our reserves using a non-subsidence design.Our trona reserve estimates include reserves that can be economically and legally extracted and processed into soda ash at the time of their determination.material is mined or extracted. Our trona reserves are categorized as “proven (measured)“Proven mineral reserves” and “probable (indicated)“Probable mineral reserves,” which are defined as follows:Probable (Indicated) Reserves—Reserves for which quantity and grade and/or quality are computed from information similar to that used for proven (measured) reserves, but the sites for inspection, sampling, and measurement are farther apart or are otherwise less adequately spaced. The degree of assurance, although lower than that for proven (measured) reserves, is high enough to assume continuity between points of observation.For purposes of categorizing our proven reserves, HPG estimates applied exploration and mine measurements and drill hole data within a one-quarter mile radius, and required at least 8-feet of trona thickness and a trona ore grade of at least 85% (with 15% of clays, shales and other impurities). To assess the economic viability of our reserves, HPG reviewed our cost of products sold and average sales price of soda ash for the three years ended December 31, 2019.resource.

our•the cost of products sold excluding depreciation, depletion and amortization expense per short ton will remain consistent with ourSisecam Wyoming’s cost of products sold for the threefive years ended December 31, 2019, which was approximately $80 per short ton of soda ash;2021;we•Sisecam Wyoming’s mining costs will remain consistent with 2021 levels with two-seam mining costs 30% higher for the two-seam production (the Partnership estimates that this increase would not impact its overall production cost by more than 1% and thus would not have a material overall impact to the Partnership’s production costs);we•Sisecam Wyoming will process soda ash with a 90% rate of recovery, rate without accounting for ourthe deca rehydration process;our•The run-of-mine ore estimate contains dilution from the mining process;we will, in approximately 10 years, make necessary equipment modifications to operate at a seam height of 7-feet, although our current mining limit is 9.5 to 10 feet;we will, within the next one to six years, conduct “two-seam mining,” which means to perform continuous mining simultaneously on beds 24 and 25 in close proximity;our mining costs will remain consistent with 2019 levels until we begin two-seam mining, at which time mining costs for the two-seam mining tonnage could increase by as much as 50%;our processing costs will remain consistent with 2019 levels;we•Sisecam Wyoming will continue to conduct only conventional mining using the room and pillar method and a non-subsidence mine design;we•Sisecam Wyoming will, in approximately 10 years, make necessary modifications to the processing facilities to allow localized mining of 75% ore grade in areas where the floor seam or insoluble disruptions have moved up into the mining horizon causing mining to be halted early due to processing facility limitations;we have•Sisecam Wyoming has and will continue to have the necessary permits to conduct mining operations with respect to the reserves; andwe•Sisecam Wyoming will maintain the necessary tailings storage capacity to maintain tailings disposal between the mine and surface placement for the life-of-mine.

The following table presents our estimated proven and probable tronamineral reserves at December 31, 2019:

Our reserve estimates will change from time to time as a result of mining activities, analysis of new engineering and geologic data, modification of mining plans or mining methods and other factors. For additional information, see Item 1A, Risk Factors, “Risks Inherent in our Business and Industry” for more information regarding risks surrounding our reserves.

The We believe our commitment to safety and reliability is an integral component to our fulfillment of our corporate responsibility and long term success. Through rigorous training, sharing of expertise within the Partnership, continuous monitoring and promoting a culture of excellence in operations, we continuously strive to keep our workforce, the communities in which we operate and the environment safe.

favorable.

We maystatus as a partnership for U.S. federal income tax purposes, as well as our not have sufficient available cash each quarterbeing subject to pay the quarterly distribution at the current distribution level of $0.340 per unit, or $1.360 per unit on an annualized basis, or at all. In order to pay the quarterly distribution at the current distribution level, we will require available cash of approximately $6.9 million per quarter, or $27.4 million per year, based on the number of common and general partner units currently outstanding.Thea material amount of cash we can distributeentity-level taxation by individual states; the tax treatment of publicly traded partnerships or an investment in our common units could be subject to potential legislative, judicial or administrative changes and differing interpretations, possibly on our units principally depends upon the amount of cash we generate from our operations, which will fluctuate from quarter to quarter based on several factors, some of which are beyond our control, including, among other things:a retroactive basis.•the volume of natural and synthetic soda ash produced worldwide, including potential additional soda ash from affiliates of the Ciner Group;domestic and international demand for soda ash in the flat glass, container glass, detergent, chemical and paper industries in which our customers operate or serve;•the freight costs we pay to transport our soda ash to customers or various delivery points;•the cost of electricity and natural gas used to power our operations;the amount of royalty payments weUnitholders are required to pay to our lessors and licensor and the durationtaxes on their respective shares of our leases and license;income even if they do not receive any cash distributions.political disruptions in•Tax gain or loss on the markets we or our customers serve, including any changes in trade barriers;our relationships with our customers, including changes to such relationships as a result of Ciner Corp’s expected termination as a member of ANSAC as of the ANSAC termination date, and our or our sales agent’s ability to renew contracts on favorable terms to us;•the creditworthinessdisposition of our customers;•a cybersecurity event;•a pandemiccommon units could be more or epidemic;regulatory action affecting the supply of, or demand for, soda ash; our ability to mine trona ore; our transportation logistics; our operating costs or our operating flexibility;•new or modified statutes, regulations, governmental policies and taxes or their interpretations; and•prevailing U.S. and international economic conditions and foreign exchange rates.In addition, the actual amount of cash we will have available for distribution will depend on other factors, some of which are beyond our control, including, among other things:the level and timing of capital expenditures we make, including the amount and timing of increased capital expenditures with respect to the new Green River Expansion Project at our facility to increase its soda ash production levels;the level of our operating, maintenance and general and administrative expenses, including reimbursements to our general partner for services provided to us;•the cost of acquisitions, if any;less than expected.

•our debt service requirements and other liabilities;•fluctuationsRisks Inherent in our working capital needs;•our ability to borrow fundsBusiness and access capital markets;restrictions on distributions contained in debt agreements to which we, Ciner Wyoming or our affiliates are a party;•the amount of cash reserves established by our general partner; and•other business risks affecting our cash levels.IndustryMostA significant amount of soda ash is sold inclusive of transportation costs, which make up a substantial portion of the total delivered cost to the customer. We transport our soda ash by rail and/or truck and, for exports, ocean vessel. As a result, our business and financial results are sensitive to increases in rail freight, trucking and ocean vessel rates. Increases in transportation costs, including increases resulting from emission control requirements, port taxes and fluctuations in the price of fuel, could make soda ash a less competitive product for glass manufacturers when compared to glass substitutes or recycled glass, or could make our soda ash less competitive than soda ash produced by competitors that have other means of transportation or are located closer to their customers. Our rail freight rates may increase year-over-year. Also, we may be unable to pass on our freight and other transportation costs in full because market prices for soda ash are generally determined by supply and demand forces.A significant portion of our international sales of soda ash has been to ANSAC, a U.S. export cooperative, and therefore adverse developments at ANSAC or its customers, or in any of the markets in which we make direct international sales, could adversely affect our ability to compete in certain international markets.We, along with two other U.S. trona-based soda ash producers, currently utilize ANSAC as our exclusive export vehicle for sales to customers in all countries excluding Canada, South Africa and members of the European Community and European Free Trade Area. Because ANSAC makes sales to its end customers directly and then allocates a portion of such sales to each member,

we do not have direct access to ANSAC’s customers and we have no direct control over the credit or other terms ANSAC extends to its customers. As a result, we are indirectly vulnerable to ANSAC’s customer relationships and the credit and other terms ANSAC extends to its customers, and if, prior to Ciner Corp’s expected termination from ANSAC as of the ANSAC termination date, ANSAC ceased to exist, we could face costs and risks of securing customers in those markets and related logistics arrangements on favorable terms. Any adverse change in ANSAC’s customer relationships, while Ciner Corp remains a member in ANSAC, could have a direct impact on ANSAC’s ability to make sales and our ability to make sales to ANSAC. In addition, to the extent ANSAC extends credit or other favorable terms to its end customers and those customers subsequently default under sales contracts or otherwise fail to perform, we would have no direct recourse against them.For more information about ANSAC, see Item 1, “Business—Customers” and “Risk Factors-Risks Inherent in our Business and Industry- “A significant portion of our historical international sales of soda ash have been to ANSAC, and therefore, Ciner Corp’s decision to terminate its membership in ANSAC could adversely affect our ability to compete in certain international markets, materially adversely impact our business, results of operations and financial condition and limit our ability to make distributions to our unitholders.”A significant portion of our historical international sales of soda ash have been to ANSAC, and therefore, Ciner Corp’s decision to terminate its membership in ANSAC could adversely affect our ability to compete in certain international markets, materially adversely impact our business, results of operations and financial condition and limit our ability to make distributions to our unitholders.On November 9, 2018, Ciner Corp delivered a notice to terminate its membership in ANSAC with an effective termination of December 31, 2021. ANSAC has historically been our largest customer for the years ended December 31, 2019, 2018 and 2017, accounting for 60.4%, 52.0% and 44.7%, respectively, of our net sales. As a result, we cannot be assured that we will be able to retain existing foreign customers or secure new foreign customers or the related logistics arrangements on favorable terms after the ANSAC termination date, which could materially adversely impact our business, results of operations and financial condition and limit our ability to make distributions to our unitholders.

Ciner Corp,Sisecam Chemicals, on our behalf, typically enters into contracts and arrangements with our customers that have terms of one to three years, and our customers are not obligated to purchase any specific amount of soda ash from us.

Provisions in the Facilities Agreement could limit our ability to grow the business and restrict our operational and financial flexibility.

On August 1, 2018, Ciner Enterprises, the entity that indirectly owns and controls our general partner, refinanced its existing credit agreement and entered into a new facilities agreement, to which WE Soda and Ciner Enterprises (as borrowers), and KEW Soda, WE Soda, certain related parties and Ciner Enterprises, Ciner Holdings and Ciner Corp (as original guarantors and together with the borrowers, the “Ciner obligors”), are parties (as amended and restated or otherwise modified, the “Facilities Agreement”), and certain related finance documents. The Facilities Agreement expires on August 1, 2025.

Even though neither we nor Ciner Wyoming is a party or a guarantor under the Facilities Agreement, while any amounts are outstanding under the Facilities Agreement, we will be indirectly affected by certain affirmative and restrictive covenants that apply to WE Soda and its subsidiaries (which include us). Besides the customary covenants and restrictions, the Facilities Agreement includes provisions that, without a waiver or amendment approved by lenders whose commitments are more than 66-2/3% of the total commitments under the Facilities Agreement to undertake such action, would (i) prevent transactions with our affiliates that could reasonably be expected to materially and adversely affect the interests of certain finance parties, (ii) restrict the ability to amend our limited partnership agreement or our general partner’s limited liability company agreement or our other constituency documents if such amendment could reasonably be expected to materially and adversely affect the interests of the lenders to the Facilities Agreement; and (iii) prevent actions that enables certain restrictions or prohibitions on our ability to upstream cash (including via distributions) to the borrowers under the Facilities Agreement.

Any debt instruments that Ciner Enterprises or any of its affiliates enter into in the future, including any amendments to the Facilities Agreement or the related finance documents, may include additional or more restrictive limitations that may impact our ability to conduct our business. These additional restrictions could adversely affect our ability to finance our future operations or capital needs or engage in, expand or pursue our business activities.

Each of Ciner Holdings and Ciner Corp, the sole member of Ciner Holdings, which is in turn the sole member of our general partner, is a guarantor under, and its respective equity interests in us and Ciner Holdings are pledged as collateral under, the Facilities Agreement; if any of the Ciner obligors is unable to meet its obligations under the Facilities Agreement, or is declared bankrupt, the lenders under the Facilities Agreement may gain control of the sole member of our general partner or, in the case of bankruptcy, our partnership may be dissolved.

Ciner Holdings, the sole member of our general partner, is a guarantor under the Facilities Agreement, and Ciner Corp, the sole member of Ciner Holdings, is also a guarantor thereunder. Ciner Corp’s membership interests in Ciner Holdings and Ciner Holdings’ limited partnership interests in us are subject to a lien under the Facilities Agreement. If any of the Ciner obligors is unable to satisfy its obligations under the Facilities Agreement and the lenders foreclose on the applicable collateral, the lenders would own the sole member of our general partner, and effectively all of its assets, which include 100% of the membership interest in the general partner. In such event, the lenders would own and control our general partner, the entity that controls our management and operation. In addition, such a change of control could result in our indebtedness becoming due. Please read the risks factors in this Report, including the discussion under the following risk factors: “Restrictions in the Ciner Resources Credit Facility could adversely affect our business, financial condition, results of operations and ability to make quarterly cash distributions to our unitholders” and “Restrictions in the agreements governing Ciner Wyoming’s indebtedness, including the Ciner Wyoming Credit Facility, could limit its operations and adversely affect our business, financial condition, results of operations and ability to make quarterly cash distributions to our unitholders.”

Restrictions in the agreements governing Ciner Wyoming’s indebtedness, including the Ciner Wyoming Credit Facility, could limit its operations and adversely affect our business, financial condition, results of operations and ability to make quarterly cash distributions to our unitholders.On August 1, 2017, Ciner Wyoming entered into a $225.0 million senior unsecured revolving credit facility (the “Ciner Wyoming Credit Facility”). The Ciner Wyoming Credit Facility contains various covenants and restrictive provisions that limit (subject to certain exceptions) Ciner Wyoming’s ability to:make distributions on or redeem or repurchase its units;incur or guarantee additional debt;make certain investments and acquisitions;incur certain liens or permit them to exist;enter into certain types of transactions with affiliates of Ciner Wyoming;merge or consolidate with another company; andtransfer, sell or otherwise dispose of assets.The Ciner Wyoming Credit Facility also contains covenants requiring Ciner Wyoming to maintain certain financial ratios. Ciner Wyoming is subject to a consolidated interest coverage ratio (as defined in the Ciner Wyoming Credit Facility) of not less than 3.00 to 1.00 and a consolidated leverage ratio (as defined in the Ciner Wyoming Credit Facility) of not greater than 3.00 to 1.00. Ciner Wyoming’s ability to meet those financial ratios and tests can be affected by events beyond our control, and we cannot assure you that Ciner Wyoming will meet those ratios and tests.In addition, the Ciner Wyoming Credit Facility contains events of default customary for transactions of this nature, including (1) failure to make payments required under the Ciner Wyoming Credit Facility, (2) events of default resulting from Ciner Wyoming’s failure to comply with covenants and financial ratios in the Ciner Wyoming Credit Facility, (3) the institution of insolvency or similar proceedings against Ciner Wyoming, (4) the occurrence of a default under any other material indebtedness Ciner Wyoming may have, and (5) the occurrence of a change of control.Under the Ciner Wyoming Credit Facility, a change of control is triggered if Ciner Corp and its wholly-owned subsidiaries, in the aggregate, directly or indirectly, cease to own all of the equity interests, or cease to have the ability to elect a majority of the board of directors (or equivalent governing body) of Ciner GP (or any entity that performs the functions of our general partner). In addition, a change of control would be triggered if we cease to own at least 50.1% of the economic interests in Ciner Wyoming or cease to have the ability to elect a majority of the members of Ciner Wyoming’s board of managers.On February 28, 2020, the Ciner Wyoming Credit Agreement was amended to, among other things, enable greater flexibility for debt financing to be incurred by Ciner Wyoming in connection with its new natural gas-fired turbine co-generation facility, including, among other things (i) increasing the basket for purchase money indebtedness permitted under the Ciner Wyoming Credit Agreement from $5.0 million to $30.0 million; (ii) adding procedures under the Ciner Wyoming Credit Agreement for transition to a benchmark other than the Eurodollar Rate to determine the applicable interest rate (including reference to the secured overnight financing rate, or SOFR, published by the Federal Reserve Bank of New York), with provisions applying to that alternate benchmark; and (iii) adding customary new provisions to the Ciner Wyoming Credit Agreement relating to qualified financial contracts, sanctions and anti-money laundering rules and laws.The provisions of the Ciner Wyoming Credit Facility may affect Ciner Wyoming’s ability to obtain future financing and pursue attractive business opportunities and its flexibility in planning for, and reacting to, changes in business conditions. In addition, Ciner Wyoming’s failure to comply with the provisions of the Ciner Wyoming Credit Facility could result in an event of default, which could enable its lenders, subject to the terms and conditions of the Ciner Wyoming Credit Facility, to terminate all outstanding commitments and declare any outstanding principal of that debt, together with accrued and unpaid interest, to be immediately due and payable. If the payment of Ciner Wyoming’s debt is accelerated, its assets may be insufficient to repay such debt in full. As a result, our results of operations and, therefore, our ability to distribute cash to unitholders, could be materially and adversely affected, and our unitholders could experience a partial or total loss of their investment. Please read Part II, Item 7, “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Liquidity and Capital Resources—Debt—Ciner Wyoming Credit Facility” for more information.

Restrictions in the Ciner Resources Credit Facility could adversely affect our business, financial condition, results of operations and ability to make quarterly cash distributions to our unitholders.On August 1, 2017, the Partnership entered into a $10.0 million senior secured revolving credit facility (the “Ciner Resources Credit Facility”). The Ciner Resources Credit Facility contains various covenants and restrictive provisions that limit (subject to certain exceptions) our ability (and the ability of our subsidiaries, including Ciner Wyoming) to:make distributions on or redeem or repurchase units;incur or guarantee additional debt;make certain investments and acquisitions;incur certain liens or permit them to exist;enter into certain types of transactions with our affiliates;merge or consolidate with another company; andtransfer, sell or otherwise dispose of assets.The Ciner Resources Credit Facility also contains a covenant requiring us to maintain a consolidated leverage ratio (as defined in the Ciner Resources Credit Facility) of not greater than 3.00 to 1.00 and a consolidated interest coverage ratio of not less than 3.00 to 1.00. Our ability to meet that financial ratio and test can be affected by events beyond our control, and we cannot assure you that we will meet that ratio and test.In addition, the Ciner Resources Credit Facility contains events of default customary for transactions of this nature, including (1) failure to make payments required under the Ciner Resources Credit Facility, (2) events of default resulting from our failure to comply with covenants and financial ratios in the Ciner Resources Credit Facility, (3) the institution of insolvency or similar proceedings against us, (4) the occurrence of a default under any other material indebtedness we (or any of our subsidiaries) may have, including the Ciner Wyoming Credit Facility, and (5) the occurrence of a change of control. In addition, our obligations under the Ciner Resources Credit Facility are secured by a pledge of substantially all of our assets (subject to certain exceptions), including the membership interests in Ciner Wyoming held by us.

Under the Ciner Resources Credit Facility, a change of control is triggered if Ciner Corp and its wholly-owned subsidiaries, in the aggregate, directly or indirectly, cease to own all of the equity interests, or cease to have the ability to elect a majority of the board of directors (or equivalent governing body) of, Ciner Holdings or Ciner GP (or any entity that performs the functions of our general partner). In addition, a change of control would be triggered if we cease to own at least 50.1% of the economic interests in Ciner Wyoming or cease to have the ability to elect a majority of the members of Ciner Wyoming’s board of managers.On February 28, 2020, the Ciner Resources Credit Agreement was amended to, among other things, enable greater flexibility for debt financing to be incurred by Ciner Wyoming in connection with its new natural gas-fired turbine co-generation facility, including, among other things (i) increasing the basket for purchase money indebtedness permitted under the Ciner Resources Credit Agreement from $5.0 million to $30.0 million; (ii) adding procedures under the Ciner Resources Credit Agreement for transition to a benchmark other than the Eurodollar Rate to determine the applicable interest rate (including reference to SOFR published by the Federal Reserve Bank of New York), with provisions applying to that alternate benchmark; and (iii) adding customary new provisions to the Ciner Resources Credit Agreement relating to qualified financial contracts, sanctions and anti-money laundering rules and laws.The provisions of the Ciner Resources Credit Facility may affect our ability to obtain future financing and pursue attractive business opportunities and our flexibility in planning for, and reacting to, changes in business conditions. In addition, a failure to comply with the provisions of the Ciner Resources Credit Facility could result in an event of default, which could enable our lenders to, subject to the terms and conditions of the Ciner Resources Credit Facility, terminate all outstanding commitments and declare any outstanding principal of that debt, together with accrued and unpaid interest, to be immediately due and payable. If the payment of our debt is accelerated, our assets may be insufficient to repay such debt in full, the lenders could foreclose on our assets, including without limitation our ownership interests in Ciner Wyoming, and our unitholders could experience a partial or total loss of their investment. Please read Part II, Item 8, Financial Statements and Supplementary Data - Note 9, “Debt-Ciner Resources Credit Facility.”Our level of indebtedness may increase, reducing our financial flexibility.In the future, we may incur significant indebtedness in order to make future acquisitions or to develop or expand our facilities and mining capabilities. Our level of indebtedness could affect our operations in several ways, including:a significant portion of our cash flows could be used to service our indebtedness;a high level of debt would increase our vulnerability to general adverse economic and industry conditions;the covenants contained in the agreements governing our outstanding indebtedness will limit our ability to borrow additional funds, dispose of assets, pay distributions and make certain investments;a high level of debt may place us at a competitive disadvantage compared to our competitors that are less leveraged, and therefore may be able to take advantage of opportunities that our indebtedness would prevent us from pursuing;our debt covenants may also affect our flexibility in planning for, and reacting to, changes in the economy and our industry; anda high level of debt may impair our ability to obtain additional financing in the future for working capital, capital expenditures, acquisitions, distributions or for general corporate or other purposes.A high level of indebtedness increases the risk that we may default on our debt obligations. Our ability to meet our debt obligations and to reduce our level of indebtedness depends on our future performance. General economic conditions and financial, business and other factors affect our operations and our future performance. Many of these factors are beyond our control. We may not be able to generate sufficient cash flows to pay the interest on our debt, and future working capital, borrowings or equity financing may not be available to pay or refinance such debt. Factors that will affect our ability to raise cash through an offering of our units or a refinancing of our debt include financial market conditions, the value of our assets and our performance at the time we need capital.

The amount of cash we have available for distribution to holders of our units depends primarily on our cash flow and not solely on profitability, which may prevent us from making cash distributions during periods when we record net income.The amount of cash we have available for distribution depends primarily upon our cash flow, including cash flow from reserves and working capital or other borrowings, and not solely on profitability, which will be affected by non-cash items. As a result, we may pay cash distributions during periods when we record net losses for financial accounting purposes and may not pay cash distributions during periods when we record net income.

our largest customer is ANSAC, of which our affiliate, Ciner Corp, is one of three current members,•dispute may arise under any commercial agreements between us and certain officers of our general partner currently and periodically serve as board members of ANSAC;

between Imperial Natural Resources Trona Mining Inc. and a third partyboth Sisecam USA and Ciner Corp, our sales agent for soda ash, acts as sales agent for soda ash imports by Ciner Group to the U.S.Enterprises ;

Ciner Holdings, an entity indirectly controlled byPursuant to the global Ciner Group, has the ability to, among other things, (i) appoint all directors toSisecam Chemicals Operating Agreement, the board of directors of our general partner (ii) set the numbershall consist of six designees from Sisecam USA, two designees from Ciner Enterprises and three independent directors on the board of directors offor as long as our general partner subjectis legally required to the limitations set forth in our general partner’s governing documents, and (iii) fill any newly created directorships or vacancies on the board of directors of our general partner.appoint such independent directors. As a publicly traded limited partnership, the NYSE rules do not require, and the board of directors of our general partner does not currently have, a majority of independent directors or a compensation committee or a nominating and corporate governance committee comprised of independent directors-.directors. In addition, while our partnership agreement permits our general partner to seek review by the conflicts committee comprised of independent directors of matters involving conflicts of interest between our general partner or any of its affiliates, on the one hand, and us, our partners and any of our subsidiaries, on the other hand, our general partner is not required or obligated to seek conflicts committee approval for any such matter. As a result, the lack of control of the independent directors on the board of directors of our general partner may create the potential for conflicts of interest and deprive us of the benefits of having entirely independent director approval of various decisions. Accordingly, unitholders do not have the same protections afforded to equity holders of entities that have a board of directors comprised of a majority of independent directors or are otherwise subject to all of the NYSE corporate governance requirements.

ended September 30, 2020, December 31, 2020, March 31, 2021, and June 30, 2021.

other Ciner Group affiliates.Enterprises. Any such person or entity that becomes aware of a potential transaction, agreement, arrangement or other matter that may be an opportunity for us will not have any duty to communicate or offer such opportunity to us. Any such person or entity will not be liable to us or to any limited partner for breach of any fiduciary duty or other duty by reason of the fact that such person or entity pursues or acquires such opportunity for itself, directs such opportunity to another person or entity or does not communicate such opportunity or information to us. This may create actual and potential conflicts of interest between us and affiliates of our general partner and result in less than favorable treatment of us and our common unitholders.

The Tax Cuts and Jobs Act of 2017 also imposes a federal income tax withholding obligation of 10% ofMoreover, the amount realized upon a non-U.S. person’s sale or exchangetransferee of an interest in a partnership that is engaged in a U.S.United States trade or business. However, applicationbusiness is generally required to withhold 10% of this withholding rule to dispositionsthe “amount realized” by the transferor unless the transferor certifies that it is not a non-U.S. person. While the determination of a partner’s “amount realized” generally includes any decrease of a partner’s share of the partnership’s liabilities, Treasury Regulations provide that the “amount realized” on a transfer of an interest in a publicly traded partnership, interests has been suspended bysuch as our common units, will generally be the amount of gross proceeds paid to the broker effecting the applicable transfer on behalf of the transferor, and thus will be determined without regard to any decrease in that partner’s share of a publicly traded partnership’s liabilities. The Treasury Regulations and recent guidance from the IRS until regulations or other guidance have been issued. Itfurther provide that withholding on a transfer of an interest in a publicly traded partnership will not be imposed on a transfer that occurs prior to January 1, 2023, and after that date, if effected through a broker, the obligation to withhold is not clear when or if such regulations or guidance will be issued.imposed on the transferor’s broker. Non-U.S. persons should consult a tax advisor before investing in our common units.

Ciner Corp Sisecam Chemicals leases 21,68812,234 square feet of office space for its headquarters in Atlanta, Georgia.Georgia which it utilizes to provide management and other shared services to the Partnership, pursuant to the various shared services agreements.

March 10, 2022.

units);

On JanuaryOur general partner has considerable discretion in determining the amount of available cash, the amount of distributions and the decision to make any distribution. Although our partnership agreement requires that we distribute all of our available cash quarterly, there is no guarantee that we will make quarterly cash distributions to our unitholders or at any other rate, and we have no legal obligation to do so.

The following table provides selected historical financial data of the Partnership for the periods and as of the dates indicated. The financial data provided should be read in conjunction with management’s discussion and analysis of financial condition and results of operations and our audited consolidated financial statements and related notes included elsewhere in this Annual Report on Form 10-K.

Notice to Terminate MembershipChange in ANSAC

Control of Sisecam Chemicals

ANSAC was our largest customereligible for the years ended December 31, 2019, 2018 and 2017, accounting for 60.4%, 52.0% and 44.7%, respectively, of our net sales. Although ANSAC has been our largest customer forvaccine in the years ended December 31, 2019, 2018, and 2017, we anticipate thatU.S.

repayment for the development costs and related assets or a service agreement model for logistics services which includes reimbursements for development costs. Since a decision to allocate costs to the Partnership has not been made yet and the Partnership is not currently using any Ciner Enterprises export services, none of these development costs have been recorded by the Partnership through December 31, 2019.

Quarterly DistributionFor each of the four quarters in 2019,On October 29, 2021, the Partnership declared aits third quarter 2021 quarterly cash distribution of $0.340 per unit. unit to both the limited partners and general partners. The quarterly cash distribution was paid on November 19, 2021 to unitholders of record on November 9, 2021.We continueIn connection with the CoC Transaction, we believe we have further opportunities to develop plansdebottleneck our facility and executeare incorporating several of these in our holistic approach as we further explore whether to proceed with the early phases for a potential new Green River Expansion Project that, should we decide to proceed, we believe willcould increase production levels up to approximately 3.5 million short tons of soda ash per year or up to approximately 134% of the last five-year average of soda ash produced per year. We have recently conducted the initial basic design and secured certain related permits and are currently evaluating and pursuing the related permits and detailed cost and market analysis pursuant to the basic design. ThisIf we proceed with this project, it will require capital expenditures materially higher than have been recently incurred by CinerSisecam Wyoming.To maintain a disciplined financial policy and what we believe is a conservative The timing of the new Green River Expansion Project as well as any other expansion capital structure, we intend to pay for the investment in part through cash generatedexpenditures may also be impacted by the business and in part through debt. When consideringPartnership’s financial results including further negative volatility caused by the significant investment required by this expansion and the infrastructure improvements designed to increase our overall efficiency, we lowered our quarterly cash distributions beginning in May 2019 by approximately 40% from previously announced cash distributions which we believe will continue until satisfying approximately 50%ongoing COVID-19 pandemic, including resurgences or subsequent variants of the funding for the project.virus.We have a self-bond agreement withOur operations are subject to oversight by the WDEQ under which we currently commit to pay directly for reclamation costs. The amount of the bond was $36.2 million and $32.9 million as of December 31, 2019 and December 31, 2018. In May 2019, the StateLand Quality Division of Wyoming enacted legislation that limits our and otherDepartment of Environmental Quality (“WDEQ”). Our principal mine operators’ ability to self-bond, which will require us to seek other acceptable financial instrumentspermit issued by the Land Quality Division, requires the Partnership to provide additionalfinancial assurances for our reclamation obligations. We expectobligations for the estimated future cost to providereclaim the area of our processing facility, surface pond complex and on-site sanitary landfill. The Partnership provides such assurances by securingthrough a third-party surety bond no later than November 2020. While we expect(the “Surety Bond”). According to obtain such surety guarantee by that time, we cannot guarantee the availability, costsannual recalculation and terms of such surety bond. As ofsubmittal, the date of this Report, we anticipate that any such impact on our net incomeSurety Bond amount was $41.8 million and liquidity will be limited.$36.2 million at December 31, 2021 and 2020, respectively. The amount of such surety guaranteeassurances that we are required to provide is subject to change upon periodic re-evaluationannual recalculation according to Department of Environmental Quality’s Guideline 12, annual site inspection and subsequent evaluation/approval by the WDEQ’s Land Quality Division.

DemandHistorically, long-term demand for soda ash in the United States ishas been driven in large part by general economic growth and activity levels in the end-markets that the glass-making industry serves, such as the automotive and construction industries. Because the United States is a well-developed market, we expect that domestic demand levels will remain stable for the near future. Because future U.S. capacity growth is expected to come from the four major producers in the Green River Basin, we also expect that U.S. supply levels will remain relatively stable in the near term.SodaLong-term soda ash demand in international markets has continued to growgrown in conjunction with GDP.Gross Domestic Product. We expect that over the long-term, future global economic growth will positively influence global demand, which will likely result in increased exports, primarily from the United States, Turkey and to a limited extent, from China, the largest suppliers of soda ash to international markets. Currently, and in the near and mid-term we expect customers across all segments to continue managing and mitigating the impact of COVID-19 to their operations. Soda ash demand in the U.S. as well as the global market have recovered to pre-pandemic levels in 2021. There are select markets which continue to bear the impacts, however in most cases we see recovery taking place even where the demand was impacted to a great extent for a prolonged period.On November 9, 2018, Ciner Corp delivered a notice to terminateAs previously disclosed, Sisecam Chemicals, an affiliate of the Partnership, terminated its membership in ANSAC a cooperative that serves as the primary international distribution channel for us as well as two other U.S. manufacturers of trona-based soda ash. The effective

termination date of Ciner Corp’s membership in ANSAC is December 31, 2020. As of January 1, 2021, (the “ANSAC termination date”). Between nowSisecam Chemicals began managing the Partnership’s sales and marketing efforts for exports with the ANSAC termination date, Ciner Corpexit being complete. In connection with the settlement agreement with ANSAC, Sisecam Chemicals continued to sell, at substantially lower volumes, product to ANSAC for export sales purposes, with a fixed rate per ton selling, general and administrative expense, and also fulfilled its obligation to purchase a limited amount of export logistics services in 2021. In connection with the settlement agreement with ANSAC, there remains sales commitments to ANSAC in 2022 where Sisecam Chemicals will continue to sell, at substantially lower volumes than 2021, product to ANSAC for export sales purposes, with a fixed rate per ton selling, general and administrative expense. Further, in 2022 there are no required export logistics services with ANSAC. The ANSAC exit allowed Sisecam Chemicals to improve access to customers and gain control over placement of its sales in the international marketplace in 2021. This enhanced view of the global market allows Sisecam Chemicals to better understand supply/demand fundamentals thus allowing better decision making for its business. Sisecam Chemicals continues to have fulloptimize its distribution network leveraging strengths of existing distribution partners while expanding as our business requires in certain target areas.

Union Pacific Railroad Company (“Union Pacific”) is our largest providerSisecam Chemicals enters into contracts with one railroad company for the majority of the domestic rail freight services.services that the Partnership receives and the related freight and logistics costs are allocated to the Partnership. For the year ended December 31, 2019, we2021 and 2020, the Partnership shipped approximately 96.9%over 90% of our soda ash to our customers initially via a single rail line owned and controlled by Union Pacific. Ourthe railroad company. The Partnership’s plant receives rail service exclusively from Union Pacificthe railroad company and shipments by rail accounted for 86.4%over 60% and 78.6%over 80% of our total freight costs for the yearsyear ended December 31, 20192021 and 2018,2020, respectively. The increasedecrease in the percentage of freight that is related to Union Pacificthe railroad company is due primarily to ourthe increased usageocean freight in the year ended December 31, 2021 of Union Pacific to accommodate changes indirect international sales mix between domestic and international and their respective delivery locations. Our agreement with Union Pacific expires on

December 31, 2021 and there can be no assurance that it will be renewed on terms favorable to us or at all. If we doSisecam Chemicals does not ship at least a significant portion of our soda ash production on the Union Pacificrailroad company’s rail line during a twelve-month period, weit must pay Union Pacificthe railroad company a shortfall payment under the terms of our transportation agreement. For the year ended December 31, 2019, we assistedThe Partnership assists the majority of ourits domestic customers in arranging their freight services. During 2019, wethe year ended December 31, 2021 and 2020, Sisecam Chemicals had no shortfall payments and dodoes not expect to make any such payments in the future. Sisecam Chemicals renewed its agreement with the railroad company in October 2021, which now expires on December 31, 2025.SalesUntil the end of 2020, sales prices for sales through ANSAC include the cost of freight to the ports of embarkation for overseas export or to Laredo, Texas for sales to Mexico. Sales prices for other international sales may include the cost of rail freight to the port of embarkation and the cost of ocean freight to the port of disembarkation for import by the customer and the cost of inland freight required for delivery to the customer.

for a given period attributable to the soda ash sold by us to ANSAC. On October 23, 2015, theThe Partnership has a Services Agreement (the “Services Agreement”), with our general partner and Ciner Corp.Sisecam Chemicals. Pursuant to the Services Agreement, Ciner CorpSisecam Chemicals has agreed to provide the Partnership with certain corporate, selling, marketing, and general and administrative services, in return for which the Partnership has agreed to pay Ciner CorpSisecam Chemicals an annual management fee, subject to quarterly adjustments, and reimburse Ciner CorpSisecam Chemicals for certain third-party costs incurred in connection with providing such services. In addition, under the joint venture agreement governing CinerSisecam Wyoming, CinerSisecam Wyoming reimburses us for employees who operate our assets and for support provided to CinerSisecam Wyoming.Ciner Group also owns and operates port facilities in Turkey, and since 2017 one of its other North American subsidiaries has an arrangement to exclusively import soda ash into a port on the east coastEffective as of the U.S. Ciner Corp, which isend of day on December 31, 2020, Sisecam Chemicals exited ANSAC. As of January 1, 2021, Sisecam Chemicals began managing the exclusivePartnership’s sales agentand marketing efforts for exports with the Partnership, serves as the exclusive sales agent of that material and receives a commission on those sales. We believe by having access to that material, Ciner Corp isANSAC exit being complete. Sisecam Chemicals was able to offerestablish business relationships with distributors by leveraging the Ciner Group’s distributor network and offering its customers an improved level of service and greater certainty of supply to the Partnership’s end customers,customers. In connection with the settlement agreement with ANSAC, the Partnership met its 2021 sales commitments to ANSAC which were at substantially lower volumes than prior years. These 2021 sales to ANSAC were for export sales purposes, and over time lower our overall costsrequired a fixed rate per ton selling, general and administrative expense. There remains a commitment to servesell additional tons to ANSAC in 2022, which are subsequently chargedat substantially lower volumes than 2021. Additionally, in connection with the settlement agreement, the Partnership met its obligation to purchase a limited amount of export logistics services in 2021. There is not an obligation to purchase logistic services from ANSAC beyond 2021. Through in part the Partnership.Partnership’s affiliates, the Partnership has amongst other things: (i) obtained its own international customer sales arrangements, (ii) obtained third-party export port services, and (iii) chartered and executed its own international product delivery.

Cash provided by operating activities during the twelve monthsyear ended December 31, 2019 was offset by cash used2021 compared to 2020 resulted in investing activities of $65.4 million for capital expenditures andslightly more cash used in financing activities during the twelve monthsyear ended December 31, 2019 of $33.7 million. The decrease in cash used in financing activities during the twelve months ended December 31, 2019 was due to distributions paid of $63.7 million and net borrowings of long-term debt of $30.5 million during the twelve months ended December 31, 2019 compared to distributions paid of $92.1 million and $50.4 million in net repayments of long-term debt during the twelve months ended December 31, 2018. The increase in net borrowings during the twelve months ended December 31, 2019 was primarily related to funding of capital expenditures.2021

Contractual ObligationsMaterial Cash Requirements

Although theThe impact of inflation has slowedbecome significant in recent years, it is still a factormonths and in the U.S. economy and may increase our cost to acquire or replace properties, plant and equipment. Inflation may also increase our costs of labor and supplies. To the extent permitted by competition, regulation and existing agreements, we pass along increased costs to our customers in the form of higher selling prices, and we expect to continue this practice.See Part II, Item 8, Financial Statements and Supplementary Data - Note 14, Commitments and Contingencies - “Off-Balance-Sheet Arrangements”, for more information regarding our off-balance-sheet arrangements.

our operating performance as compared to other publicly traded partnerships in our industry, without regard to historical cost basis or, in the case of Adjusted EBITDA, financing methods;•the viability of capital expenditure projects and the returns on investment of various investment opportunities.expenditures.

The Partnership receivesAgreements and transactions with affiliates have a significant amountimpact on the Partnership’s financial statements because the Partnership is a subsidiary and investee within two different global group structures. Agreements directly between the Partnership and other affiliates, or indirectly between affiliates that the Partnership does not control, can have a significant impact on recorded amounts or disclosures in the Partnership's financial statements, including any commitments and contingencies between the Partnership and affiliates, or potentially, third parties.

Ciner Enterprises, an affiliate that indirectly owns and controls our general partner, is a borrower under the Facilities Agreement which allows for the lenders under the Facilities Agreement to take control of the Partnership’s general partner if Ciner Enterprises or the guarantors are unable to satisfy the obligations under the Facilities Agreement. In addition thereThere may be certain items that Ciner Enterprises isaffiliates are in the process of evaluating how the Partnership may benefit or participate in the development, including participating in the related expenditures. For more information related to Ciner EnterprisesIn addition, the general partner may contract and/or develop certain transactions or assets on its own or through affiliates. Further upstream affiliates of the Partnership, including affiliates of Şişecam Parent may enter into agreements that limit or otherwise adversely impact the Partnership.

disclosure of affiliate relationships, transactions, and commitments and contingencies.

Supplementary Selected Quarterly Financial DataThe following is selected unaudited condensed consolidated data for Ciner Resources LP for the quarters indicated:

ofat December 31, 20192021 and three individual $12.5 million swaps with an aggregate notional value of $37.5 million at December 31, 2020. The swaps have various maturities through 2023.2024. The fair value liability of these interest rate swaps were $0.9was $0.4 million as of December 31, 2019.2021. The Partnership’s variable rate debt had a weighted average interest rate, inclusive of designated interest rate swap contracts, of 2.69% as of December 31, 2021 (as of December 31, 2020: 2.88%). Based on the variable rate debt in our debt instruments as of December 31, 2021 including the impact of the interest rate swap contract discussed below, a change in interest rates of 1% would result in an increase or a decrease of our annual interest expense of approximately $0.3 million.

The

CinerSisecam Resources LP

Critical Audit Matter

The critical audit matter communicated below is a matter arising from the current-period audit of the financial statements that was communicated or required to be communicated to the audit committee and that (1) relates to accounts or disclosures that are material to the financial statements and (2) involved our especially challenging, subjective, or complex judgments. The communication of critical audit matters does not alter in any way our opinion on the financial statements, taken as a whole, and we are not, by communicating the critical audit matter below, providing a separate opinion on the critical audit matter or on the accounts or disclosures to which it relates.

SISECAM RESOURCES LP

| Year Ended December 31, | ||||||||||||||

| 2019 | 2018 | 2017 | 2016 | 2015 | ||||||||||

| Operating and Other Data: | (thousands of short tons, except for ratio data) | |||||||||||||

| Trona ore consumed | 4,157.0 | 4,018.3 | 4,001.3 | 4,050.4 | 4,040.3 | |||||||||

Ore to ash ratio(1) | 1.51: 1.0 | 1.54: 1.0 | 1.50: 1.0 | 1.50: 1.0 | 1.52: 1.0 | |||||||||

Ore grade(2) | 86.6 | % | 85.8 | % | 88.4 | % | 87.5 | % | 85.8 | % | ||||

| Soda ash volume produced | 2,752.0 | 2,613.4 | 2,666.9 | 2,695.3 | 2,662.9 | |||||||||

| Soda ash volume sold | 2,759.1 | 2,613.2 | 2,705.4 | 2,735.7 | 2,655.4 | |||||||||

| Year Ended December 31, | |||||||||||||||||||||||||||||

| 2021 | 2020 | 2019 | 2018 | 2017 | |||||||||||||||||||||||||

| Operating and Other Data: | (thousands of short tons, except for ratio data) | ||||||||||||||||||||||||||||

| Trona ore consumed | 4,251.2 | 3,653.8 | 4,157.0 | 4,018.3 | 4,001.3 | ||||||||||||||||||||||||

Ore to ash ratio(1) | 1.56: 1.0 | 1.60: 1.0 | 1.51: 1.0 | 1.54: 1.0 | 1.50: 1.0 | ||||||||||||||||||||||||

Ore grade(2) | 86.3 | % | 86.6 | % | 86.6 | % | 85.8 | % | 88.4 | % | |||||||||||||||||||

| Soda ash volume produced | 2,720.5 | 2,279.3 | 2,752.0 | 2,613.4 | 2,666.9 | ||||||||||||||||||||||||

| Soda ash volume sold | 2,813.5 | 2,221.9 | 2,759.1 | 2,613.2 | 2,705.4 | ||||||||||||||||||||||||

(1)Ore to ash ratio expresses the number of short tons of trona ore used to produce one short ton of soda ash and liquor and includes our deca rehydration recovery process. In general, a lower ore to ash ratio results in lower costs and improved efficiency.

(2)Ore grade is the percentage of raw trona ore that is recoverable as soda ash free of impurities. A higher ore grade will produce more soda ash than a lower ore grade.

Trona, a naturally occurring soft mineral, is also known as sodium sesquicarbonate and consists primarily of sodium carbonate, or soda ash, sodium bicarbonate and water. We process trona ore into soda ash, which is an essential raw material in flat glass, container glass, detergents, chemicals, paper and other consumer and industrial products. The vast majority of the world’s accessible trona reserves are located in the Green River Basin. According to historical production statistics, approximately 30% of global soda ash is produced by processing trona, with the remainder being produced synthetically through chemical processes. The processing of soda ash from trona is the cheapest manner in which to produce soda ash. The costs associated with procuring the materials needed for synthetic production are greater than the costs associated with mining trona for trona-based production. In addition, trona-based production consumes less energy and produces fewer undesirable by-products than synthetic production.

Our principal executive offices are located at Five Concourse Parkway, Suite 2500, Atlanta, Georgia 30328, and our telephone number is (770) 375-2300. We make available, free of charge on our website at www.ciner.us.com our annual report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934, as amended, or the Exchange Act, as soon as reasonably practicable after we electronically file such material with, or furnish such material to, the U.S. Securities and Exchange Commission (“SEC”). A hard copy of this annual report on Form 10-K may also be requested free of charge by emailing investorrelations@ciner.us.com.

Our website also includes certain governance documents and policies such as our Code of Conduct, our Supplier Code of Conduct, our Corporate Governance Guidelines, our Internal Reporting and Whistleblower Protection Policy, our Insider Trading Policy and the charters of our Audit Committee and Conflicts Committee. The information on our website, or information about us on any other website, is not incorporated by reference into this Report. The SEC maintains an internet site at www.sec.gov that contains reports, proxy and information statements, and other information regarding issuers that file electronically with the SEC.

Change in Control of Sisecam Chemicals

On December 21, 2021, Ciner Enterprises (which was the indirect owner of approximately 74% of the common units in the Partnership and 100% of the general partner), completed the following transactions pursuant to the definitive agreement which Ciner Enterprises entered into with Sisecam USA, a direct subsidiary of Şişecam Parent on November 20, 2021 (“Purchase Agreement”):

•Ciner Enterprises converted Ciner Resources Corporation into Sisecam Chemicals Resources LLC, a Delaware limited liability company ("Sisecam Chemicals"), and Ciner Wyoming Holding Co., a direct wholly-owned subsidiary of Sisecam Chemicals, into Sisecam Chemicals Wyoming LLC (“SCW LLC”), with SCW LLC in turn then directly owning approximately 74% of the common units in the Partnership and 100% of the general partner (collectively, the “Reorganization Transactions”);

5

•subsequent to the Reorganization Transactions, Ciner Enterprises sold to Sisecam USA, and Sisecam USA purchased, 60% of the outstanding units of Sisecam Chemicals owned by Ciner Enterprises for a purchase price of $300 million (the “Sisecam Chemicals Sale”); and

•at the closing of the Sisecam Chemicals Sale, Sisecam Chemicals, Ciner Enterprises, and Sisecam USA entered into a unitholders and operating agreement (the “Sisecam Chemicals Operating Agreement”) (collectively such transactions, the “CoC Transaction”).

Pursuant to the terms of the Sisecam Chemicals Operating Agreement, Sisecam USA and Ciner Enterprises have a right to designate six directors and four directors, respectively, to the board of directors of Sisecam Chemicals. In addition, the Sisecam Chemicals Operating Agreement provides that (i) the board of directors of the general partner (the “MLP Board”) shall consist of six designees from Sisecam USA, two designees from Ciner Enterprises and three independent directors for as long as the general partner is legally required to appoint such independent directors and (ii) the Partnership’s right to appoint four managers to the board of managers of Sisecam Wyoming (the “Wyoming Board”) shall be comprised of three designees from Sisecam USA and one designee from Ciner Enterprises. Each of Sisecam USA and Ciner Enterprises shall vote all units over which such unitholder has voting control in Sisecam Chemicals to elect to the board of directors any individual designated by Sisecam USA and Ciner Enterprises. The Sisecam Chemicals Operating Agreement also requires the board of directors of Sisecam Chemicals to unanimously approve certain actions and commitments, including without limitation taking any action that would have an adverse effect on the master limited partnership status of the Partnership or any of its subsidiaries. As a result of Sisecam USA’s and Ciner Enterprise’s respective interests in Sisecam Chemicals and their respective rights under the Sisecam Chemicals Operating Agreement, each of Ciner Enterprises and Sisecam USA and their respective beneficial owners may be deemed to share beneficial ownership of the approximate 2% general partner interest in the Partnership and approximately 74% of the common units in the Partnership owned directly by SCW LLC and indirectly by Sisecam Chemicals as parent entity of SCW LLC.

Our Competitive Strengths

We believe that the following competitive strengths better enable us to execute our business strategies and to achieve our objective of generating and growing cash available for distribution to our unitholders: