00015776702020FYFALSEus-gaap:AccountingStandardsUpdate201613MemberP4Yus-gaap:AccountingStandardsUpdate201613MemberP3Y1,7751,7751,7751,7751,7751,775us-gaap:OtherLiabilities0001577670srt:MaximumMemberus-gaap:FairValueInputsLevel3Memberus-gaap:CommercialMortgageBackedSecuritiesMemberus-gaap:MeasurementInputDiscountRateMember2020-12-31

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-K

(Mark One)

☒ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 20202023

Or

☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from to

Commission file number:

001-36299

Ladder Capital Corp

(Exact name of registrant as specified in its charter)

| | | | | | | | | | | | | | |

| Delaware | | 80-0925494 |

(State or other jurisdiction of

incorporation or organization) | | (IRS Employer

Identification No.) |

| | | | |

345320 Park Avenue, | New York, | NY | | 1015410022 |

| (Address of principal executive offices) | | (Zip Code) |

(212) 715-3170

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

| | | | | | | | |

| Title of Each Class | Trading Symbol(s) | Name of Each Exchange on Which Registered |

| Class A common stock, $0.001 par value | LADR | New York Stock Exchange |

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☒ No ☐

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act:

| | | | | | | | | | | |

| Large accelerated filer | ☒ | Accelerated filer | ☐ |

| | | |

| Non-accelerated filer | ☐ | Smaller reporting company | ☐ |

| | | |

| | Emerging growth company | ☐ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☒

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act):

Yes ☐ No ☒

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

The aggregate market value of the Class A common stock held by non-affiliates of the registrant was $855,736,869$1,222,489,920 as of June 30, 2020,2023, based on the closing price of the registrant’s Class A common stock reported on the New York Stock Exchange on such date of $8.10$10.85 per share. The registrant has no non-voting common stock.

Indicate the number of shares outstanding of each of the registrant’s classes of common stock, as of the latest practicable date.

| | | | | | | | |

| Class | | Outstanding at February 19, 20212, 2024 |

| Class A common stock, $0.001 par value | | 126,825,760126,617,221 |

| Class B common stock, $0.001 par value | | 0— |

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the definitive proxy statement for the Company’s 20212023 Annual Meeting of ShareholdersStockholders have been incorporated by reference into Part III of this Report.

LADDER CAPITAL CORP

FORM 10-K

December 31, 20202023

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K (this “Annual Report”) includes forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended (the “Securities Act”), and Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”). All statements other than statements of historical fact contained in this Annual Report, including statements regarding our future results of operations and financial position, strategy and plans, and our expectations for future operations, are forward-looking statements. The words “anticipate,” “estimate,” “expect,” “project,” “plan,” “intend,” “believe,” “may,” “might,” “will,” “should,” “can have,” “likely,” “continue,” “design,” and other words and terms of similar expressions are intended to identify forward-looking statements.

We have based these forward-looking statements largely on our current expectations and projections about future events and trends that we believe may affect our financial condition, results of operations, strategy, short-term and long-term business operations and objectives and financial needs. Although we believe that the expectations reflected in our forward-looking statements are reasonable, actual results could differ from those expressed in our forward-looking statements. Our future financial position and results of operations, as well as any forward-looking statements are subject to change and inherent risks and uncertainties. You should consider our forward-looking statements in light of a number of factors that may cause actual results to vary from our forward-looking statements including, but not limited to:

•risks discussed under the heading “Risk Factors” in this Annual Report,herein, as well as our consolidated financial statements, related notes, and the other financial information appearing elsewhere in this Annual Report and our other filings with the United States Securities and Exchange Commission (“SEC”(the “SEC”);

•labor shortages, supply chain imbalances, inflation, and the ongoing impact of the COVID-19 pandemic and of responsive measures implemented by various governmental authorities, businesses and other third parties;potential for a global economic recession;

•increasing geopolitical uncertainty, including the impactbroader impacts of the newUkraine-Russia and Hamas-Israel conflicts and escalating tension between the U.S. presidential administration and congressional majority on the regulatory landscape, capital markets, and the response to, and management of, the COVID-19 pandemic;China;

•changes in general economic conditions in our industry and in the commercial finance and the real estate markets;

•changes to our business and investment strategy;

•our ability to obtain and maintain financing arrangements;

•the financing and advance rates for our assets, including the potential effects of LIBOR replacement rates;assets;

•our actual and expected leverage and liquidity;

•the adequacy of collateral securing our loan portfolio and a decline in the fair value of our assets;

•interest rate mismatches between our assets and our borrowings used to fund such investments;

•changes in interest rates andaffecting the market value of our assets;assets and the related impacts on our borrowers, including any unforeseen impacts of the transition to Term Secured Overnight Financing Rate (“SOFR”);

•changes in prepayment rates on our mortgages and the loans underlying our commercial mortgage-backed and other asset-backed securities;

•the effects of hedging instruments and the degree to which our hedging strategies may or may not protect us from interest rate and credit risk volatility;

•the increased rate of default or decreased recovery rates on our assets;

•the adequacy of our policies, procedures and systems for managing risk effectively;

•a potential downgrade in the credit ratings assigned to subsidiaries of Ladder Capital Corp (“Ladder,” “Ladder Capital,” and the “Company”) or our investments;investments or corporate debt;

•our compliance with, and the impact of, and changes in laws, governmental regulations, tax laws and rates, accounting guidance and similar matters;

•our ability to maintain our qualification as a real estate investment trust (“REIT”) for U.S. federal income tax purposes and our ability and the ability of our subsidiaries to operate in compliance with REIT requirements;

•our ability and the ability of our subsidiaries to maintain our and their exemptions from registration under the Investment Company Act of 1940, as amended (the “Investment Company Act”);

•the effects of climate change or the potential liability relating to environmental matters that impact the value of properties we may acquire or the properties underlying our investments;

•the inability of insurance covering real estate underlying our loans and investments to cover all losses;

•the availability of investment opportunities in mortgage-related and real estate-related instruments and other securities;

•fraud by potential borrowers;

•the availability ofour ability to attract and retain qualified personnel;employees;

•the impact of any tax legislation or IRS guidance;

•volatility in the equity capital markets and the impact on our Class A common stock;

•the degree and nature of our competition; and

•the market trends in our industry, interest rates, real estate values and the debt securities markets.

You should not rely upon forward-looking statements as predictions of future events. In addition, neither we nor any other person assumes responsibility for the accuracy and completeness of any of these forward-looking statements. The forward-looking statements contained in this Annual Report are made as of the date hereof, and the Company assumes no obligation to update or supplement any forward-looking statements.

REFERENCES TO LADDER CAPITAL CORP

Ladder Capital Corp is a holding company, and its primary assets are a controlling equity interest in Ladder Capital Finance Holdings LLLP (“LCFH” or the “Operating Partnership”) and in each series thereof, directly or indirectly. Unless the context suggests otherwise, references in this report to “Ladder,” “Ladder Capital,” the “Company,” “we,” “us” and “our” refer (1) prior to the February 2014 initial public offering (“IPO”) of the Class A common stock of Ladder Capital Corp and related transactions, to LCFH (“Predecessor”) and its consolidated subsidiaries and (2) after our IPO and related transactions, to Ladder Capital Corp and its consolidated subsidiaries.

Part I

Item 1. Business

Overview

We areLadder is an internally-managed real estate investment trust (“REIT”) that is a leader in commercial real estate finance. We originate and invest in a diverse portfolio of commercial real estate and real estate-related assets, focusing on senior secured assets. Our investment activities include: (i) our primary business of originating senior first mortgage fixed and floating rate loans collateralized by commercial real estate with flexible loan structures; (ii) owning and operating commercial real estate, including net leased commercial properties; and (iii) investing in investment grade securities secured by first mortgage loans on commercial real estate; and (iii) owning and operating commercial real estate, including net leased commercial properties.estate. We believe that our in-house origination platform, ability to flexibly allocate capital among complementary product lines, credit-centric underwriting approach, access to diversified financing sources, and experienced management team position us well to deliver attractive returns on equity to our shareholders through economic and credit cycles.

Our businesses, including balance sheet lending, conduit lending, securities investments, and real estate investments, provide for a stable base of net interest and rental income. We have originated $25.8$29.7 billion of commercial real estate loans from our inception in October 2008 through December 31, 2020.2023. During this timeframe, we also acquired $12.7$13.2 billion of predominantly investment grade-rated securities secured by first mortgage loans on commercial real estate and $1.8$2.0 billion of selected net leased and other real estate assets.

As part of our commercial mortgage lending operations, we originate conduit loans, which are first mortgage loans on stabilized, income producing commercial real estate properties that we intend to make available for sale in commercial mortgage-backed securities (“CMBS”) securitizations. From our inception in October 2008 through December 31, 2020,2023, we originated $16.6$16.9 billion of conduit loans, of which $16.8 billion were sold into 6971 CMBS securitizations, making us, by volume, the second largest non-bank contributor of loans to CMBS securitizations in the United States in such period. Our sales of loans into securitizations are generally accounted for as true sales, not financings, and we generally retain no ongoing interest in loans which we securitize unless we are required to do so as issuer pursuant to the risk retention requirements of the Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010, as amended, (the “Dodd-Frank Act”). The securitization of conduit loans enables us to reinvest our equity capital into new loan originations or allocate it to other investments.

As of December 31, 2020, we had $5.9 billion in total assets and $1.5 billion of total equity. Our assets primarily consist of $2.3 billion of loans, $1.1 billion of securities, $1.0 billion of real estate, and $1.3 billion of unrestricted cash.

We maintain a diversified and flexible financing strategy supporting our investment strategy and overall business operations, including the use of unsecured corporate bonds, non-recourse, non-mark-to-market Collateralized Loan Obligations (“CLO”) debt issuances and significant committed term financing from leading financial institutions. Refer to “Our Financing Strategies” and “Liquidity and Capital Resources” for further information.

Ladder was founded in October 2008 and we completed our IPO in February 2014. We are led by a disciplined and highly aligned management team. As of December 31, 2020,2023, our management team and directors held interests in our Company comprising 10.8%over 11% of our total equity. On average, our management team members have 2728 years of experience in the industry. Our management team includes Brian Harris, Chief Executive Officer; Pamela McCormack, President; Marc Fox,Paul J. Miceli, Chief Financial Officer; Robert Perelman, Head of Asset Management; and Kelly Porcella, Chief Administrative Officer & General Counsel. Kevin Moclair,Anthony V. Esposito, Chief Accounting Officer, is an additional officer of Ladder. Additionally, effective March 1, 2021, Paul J. Miceli, the Company’s Director of Finance, will succeed Marc Fox as Chief Financial Officer (refer to “Management’s Discussion and Analysis of Financial Condition and Results of Operations - Business Developments - Recent Developments”). As of December 31, 2020, we employed 58 full-time industry professionals.

COVID-19 Impact on the Organization

On March 11, 2020, the World Health Organization declared the novel strain of coronavirus (“COVID-19”) a global pandemic and recommended containment and mitigation measures worldwide. As of the date of this filing, the majority of our employees continue to work remotely in compliance with state guidelines. We continue to actively manage the liquidity and operations of the Company in light of the market conditions, including the current interest rate environment, and overall financial impact caused by the COVID-19 pandemic across most industries in the United States.potential recessionary conditions. The Company has disclosed the impact of the COVID-19 global pandemiccurrent market conditions on our business throughout this Annual Report. However, given the ongoing uncertainty related to the severity and duration

Our Businesses

We invest primarily in loans, securities and other interests in U.S. commercial real estate, with a focus on senior secured assets. Our complementary business segments are designed to provide us with the flexibility to opportunistically allocate capital in order to generate attractive risk-adjusted returns under varying market conditions. The following tablechart summarizes the carrying value of our investment portfolio as reported in our consolidated financial statements as of the dates indicated belowDecember 31, 2023 ($ in thousands):

| | | | | | | | | | | | | | | | | | | | | | | |

| | December 31, 2020 | | December 31, 2019 |

| Loans | | | | | | | |

| Balance sheet loans: | | | | | | | |

| Balance sheet first mortgage loans | $ | 2,232,749 | | | 37.9 | % | | $ | 3,127,173 | | | 46.9 | % |

| Other commercial real estate-related loans | 121,310 | | | 2.1 | % | | 129,863 | | | 1.9 | % |

| | | | | | | |

| Allowance for credit losses | (41,507) | | | (0.7) | % | | (20,500) | | | (0.3) | % |

| Total balance sheet loans | 2,312,552 | | | 39.3 | % | | 3,236,536 | | | 48.5 | % |

| Conduit first mortgage loans | 30,518 | | | 0.5 | % | | 122,325 | | | 1.8 | % |

| Total loans | 2,343,070 | | | 39.8 | % | | 3,358,861 | | | 50.3 | % |

| Securities | | | | | | | |

| CMBS investments | 1,025,514 | | | 17.4 | % | | 1,673,468 | | | 25.3 | % |

| U.S. Agency Securities investments | 32,804 | | | 0.6 | % | | 34,857 | | | 0.5 | % |

| | | | | | | |

| Equity securities | — | | | — | % | | 12,980 | | | 0.2 | % |

| Allowance for current expected credit losses | (20) | | | — | % | | — | | | — | % |

| Total securities | 1,058,298 | | | 18.0 | % | | 1,721,305 | | | 26.0 | % |

| Real Estate | | | | | | | |

| Real estate and related lease intangibles, net | 985,304 | | | 16.8 | % | | 1,048,081 | | | 15.7 | % |

| | | | | | | |

| Total real estate | 985,304 | | | 16.8 | % | | 1,048,081 | | | 15.7 | % |

| Other Investments | | | | | | | |

| Investments in and advances to unconsolidated joint ventures | 46,253 | | | 0.8 | % | | 48,433 | | | 0.7 | % |

| Federal Home Loan Bank (“FHLB”) stock | 31,000 | | | 0.5 | % | | 61,619 | | | 0.9 | % |

| Total other investments | 77,253 | | | 1.3 | % | | 110,052 | | | 1.6 | % |

| Total investments | 4,463,925 | | | 75.9 | % | | 6,238,299 | | | 93.6 | % |

| Cash, cash equivalents and restricted cash | 1,284,284 | | | 21.8 | % | | 355,746 | | | 5.3 | % |

| Other assets | 133,020 | | | 2.3 | % | | 75,107 | | | 1.1 | % |

| Total assets | $ | 5,881,229 | | | 100.0 | % | | $ | 6,669,152 | | | 100.0 | % |

The unique nature

(1)CRE equity asset amounts represent undepreciated asset values.

There are a number of COVID-19 has had a broad impactfactors that influence our operating results. Some of these factors include: (1) our competition; (2) market and economic conditions, including inflation; (3) loan origination and repayment volume; (4) profitability of securitizations; (5) avoidance of credit losses; (6) availability of debt and equity funding and the costs of that funding; (7) the net interest margin on commercialour investments; (8) effectiveness of our hedging and other risk management practices; (9) real estate specificallytransaction volumes; (10) occupancy rates; and (11) expense management. Refer to Part II, Item 7 “Management’s Discussion and Analysis of Financial Condition and Results of Operations” under the hotel and retail sectors. Loans on hotel and retail properties comprised approximately 12.5% and 11.3%, respectively,heading “Results of our loan portfolio at December 31, 2020. Hotel and retail properties comprised approximately 6.0% and 47.0%, respectively, of our real estate portfolio at December 31, 2020; however, the majority of our retail properties are necessity-based businesses and have remained open and stable during the COVID-19 pandemic. We are in regular communication with our borrowers and tenants and are closely monitoring property performance.

Loans

Balance Sheet First Mortgage Loans. We originate and invest in balance sheet first mortgage loans secured by commercial real estate properties that are typically undergoing transition, including lease-up, sell-out, and renovation or repositioning. These mortgage loans are structured to fit the needs and business plans of the property owners, and generally have LIBOR basedTerm SOFR-based floating rates and terms (including extension options) ranging from one to five years. Our loans are directly originated by an internal team that has longstanding and strong relationships with borrowers and mortgage brokers throughout the United States. We follow a rigorous investment process, which begins with an initial due diligence review; continues through a comprehensive legal and underwriting process incorporating multiple internal and external checks and balances; and culminates in approval or disapproval of each prospective investment by our Investment Committee. Balance sheet first mortgage loans in excess of $50.0 million also require the approval of our board of directors’ Risk and Underwriting Committee.

We generally seek to hold our balance sheet first mortgage loans for investment although we also maintain the flexibility to contribute such loans into a collateralized loan obligation (“CLO”)CLO or similar structure, sell participation interests or “b-notes” in our mortgage loans or sell such mortgage loans as whole loans. Our balance sheet first mortgage loans have been typically repaid at or prior to maturity (including by beingmay be refinanced by us into a new conduit first

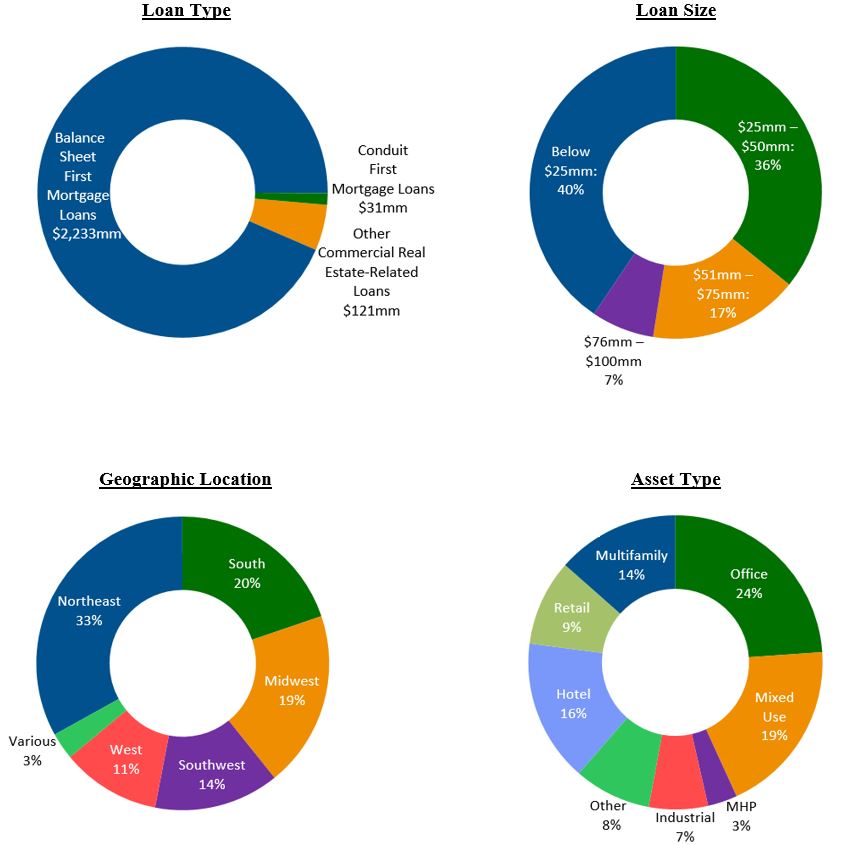

mortgage loan upon property stabilization).stabilization. As of December 31, 2020,2023, we held a portfolio of 99107 balance sheet first mortgage loans with an aggregate book value of $2.2$3.1 billion. Based on the loan balances and the “as-is” third-party Financial Institutions Reform, Recovery and Enforcement Act of 1989 (“FIRREA”) appraised values at origination, the weighted average loan-to-value ratio of this portfolio was 67.4%65.5% at December 31, 2020.

We continue to actively manage and monitor the credit and liquidity risk associated with the balance sheet first mortgage loan portfolio. Due to the nationwide limitations placed on many businesses in response to the COVID-19 pandemic, significant cash flow disruptions have occurred across the economy, which have impacted and likely will continue to impact certain of our borrowers. We have used, and continue to use, a variety of legal and structural options to manage that risk effectively, including forbearance and default provisions, as is generally being utilized throughout the credit lending industries.2023.

Other Commercial Real Estate-Related Loans. We selectively invest in note purchase financings, subordinated debt, mezzanine debt and other structured finance products related to commercial real estate that are generally held for investment. As of December 31, 2020,2023, we held a portfolio of 23 other commercial real estate-related9 mezzanine loans with an aggregate book value of $121.3$32.4 million. Based on the loan balance and the “as-is” third-party FIRREA appraised values at origination, the weighted average loan-to-value ratio of the portfolio was 66.6%82.0% at December 31, 2020.2023.

Conduit First Mortgage Loans. We also originate conduit loans, which are first mortgage loans that are secured by cash-flowing commercial real estate and are available for sale to securitizations. These first mortgage loans are typically structured with fixed interest rates and generally have five- to ten-year terms. Conduit first mortgage loans are originated, underwritten, approved and funded using the same comprehensive legal and underwriting approach, process and personnel used to originate our balance sheet first mortgage loans. Conduit first mortgage loans in excess of $50.0 million also require approval of our board of directors’ Risk and Underwriting Committee. We held one conduit loan with an aggregate carrying value of $26.9 million at December 31, 2023.

Although our primary intent is to sell our conduit first mortgage loans to CMBS trusts, we generally seek to maintain the flexibility to keep them on our balance sheet, sell participation interests or “b-notes” in such loans or sell the loans as whole loans. As of December 31, 2020, we held four first mortgage loans that were available for contribution into a securitization with an aggregate book value of $30.5 million. Based on the loan balances and the “as-is” third-party FIRREA appraised values at origination, the weighted average loan- to-value ratio of this portfolio was 66.7% at December 31, 2020. The Company holds these conduit loans in its taxable REIT subsidiary (“TRS”). upon origination. As of December 31, 2023, we held one conduit first mortgage loan that was available for contribution into securitizations. Based on the loan balance and the “as-is” third-party FIRREA appraised values at origination, loan-to-value ratio of this loan was 59.4% at December 31, 2023.

The following charts set forth our total outstanding balance sheet first mortgage loans, other commercial real estate-related loans, and conduit first mortgage loans as of December 31, 20202023, and a breakdown of our loan portfolio by loan size and geographic location and asset type of the underlying real estate.estate by loan balance.

Securities

CMBS Investments. We invest in CMBS, including CRE CLOs, secured by first mortgage loans on commercial real estate and own predominantly AAA-rated securities. These investments provide a stable and attractive base of net interest income and help us manage our liquidity. We have significant in-house expertise in the evaluation and trading of these securities, due in part to our experience in originating and underwriting mortgage loans that comprise assets within CMBS trusts, as well as our experience in structuring CMBS transactions. AAA-rated CMBS or U.S. Agency securities investments in excess of $76.0 million and all other investment grade CMBS or U.S. Agency securities investments in excess of $51.0 million, each in any single class of any single issuance, require the approval of our board of directors’ Risk and Underwriting Committee. The Risk and Underwriting Committee also must approve any investments in non-rated or sub-investment grade CMBS or U.S. Agency Securities in any single class of any single issuance in excess of the lesser of (x) $21.0 million and (y) 10% of the total net asset value of the respective Ladder investment company.

The Company invests in primarily AAA-rated real estate securities, typically front pay securities, with relatively short duration and significant subordination. The hyperamortization features included in many of the securities positions we own help mitigate potential credit losses even in the current market conditions. At the onset of the COVID-19 pandemic in March 2020, there was a significant decrease in liquidity and trading activity for the real estate securities we own. During the three months ended December 31, 2020, liquidity and trading activity continued to return to the market and the value of our securities portfolio as of December 31, 2020 had an unrealized mark-to-market gain of $18.1 million.

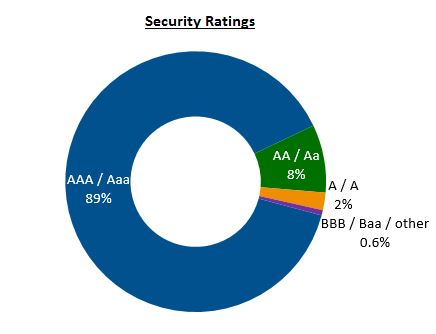

As of December 31, 2020, the estimated fair value of our portfolio of CMBS investments totaled $1.0 billion in 105 CUSIPs ($9.8 million average investment per CUSIP). As of December 31, 2020, included in the $1.0 billion of CMBS securities are $11.7 million of CMBS securities designated as risk retention securities under the Dodd-Frank Act which are subject to transfer restrictions over the term of the securitization trust. The following chart summarizes our securities investments, 94.4% of which were rated investment grade by Standard & Poor’s Ratings Group, Moody’s Investors Service, Inc. or Fitch Ratings Inc. as of December 31, 2020:

In the future, we may invest in CMBS securities or other securities that are unrated. As of December 31, 2020, our CMBS investments had a weighted average duration of 2.0 years. The commercial real estate collateral underlying our CMBS investment portfolio is located throughout the United States. As of December 31, 2020, by property count and market value, respectively, 53.2% and 74.2% of the collateral underlying our CMBS investment portfolio was distributed throughout the top 25 metropolitan statistical areas (“MSAs”) in the United States, with 7.9% and 37.6%, by property count and market value, respectively, of the collateral located in the New York-Newark-Edison MSA, and the concentrations in each of the remaining top 24 MSAs ranging from 0.2% to 4.5% by property count and 0.1% to 10.6% by market value.

Real Estate

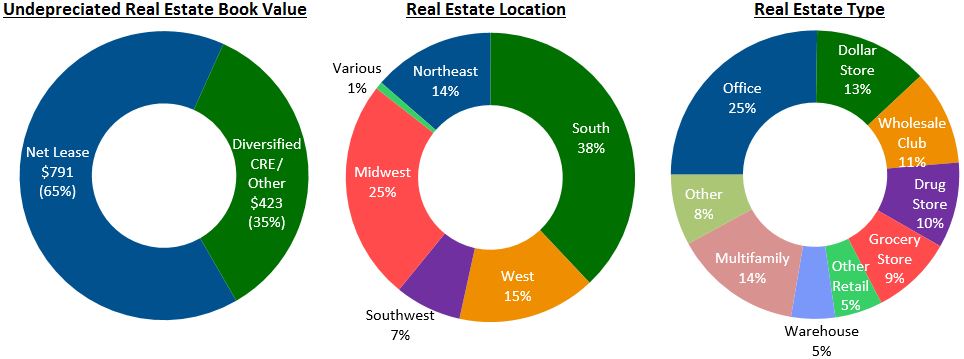

Net Leased Commercial Real Estate Properties. As of December 31, 2020,2023, we owned 164156 single tenant net leased properties with an aggregateundepreciated book value of $639.6$653.5 million. These properties are fully leased on a net basis where the tenant is generally responsible for payment of real estate taxes, property, building and general liability insurance and property and building maintenance expenses. As of December 31, 2020,2023, our net leased properties comprised a total of 5.33.8 million square feet, 100% leased with an average age since construction of 15.718.6 years and a weighted average remaining lease term of 11.48.5 years. Commercial real estate investments in excess of $20.0 million require the approval of our board of directors’ Risk and Underwriting Committee. The majority of the tenants in our net leased properties in our real estate portfolio are necessity-based businesses and have remained open and stable during the COVID-19 pandemic.businesses. During the three monthsyear ended December 31, 2020,2023, we collected 100% of rent on these properties.

Diversified Commercial Real Estate Properties. As of December 31, 2020,2023, we owned 6253 diversified commercial real estate properties throughout the U.S.U.S with an undepreciated book value of $293.7 million. During the three monthsyear ended December 31, 2020,2023, we collected approximately 96.4%99% of rent on these properties.

The following charts summarize the composition of our real estate investments as atof December 31, 2020:2023 ($ in millions):

Residential Real Estate.Securities

The Company from time to time, has made investmentsinvests in residentialprimarily AAA-rated real estate securities, typically front pay securities, with relatively short duration and significant subordination. We invest primarily in CMBS, including condominium developments. DuringCLOs, secured by first mortgage loans on commercial real estate. These investments provide a stable and attractive base of net interest income and help us manage our liquidity and hyper-amortization features included in many of these securities positions help mitigate potential credit losses in the year ended December 31, 2020,event of adverse market conditions. We have significant in-house expertise in the Company sold its remaining investmentevaluation and trading of these securities, due in such investments for immaterial gains.part to our experience in originating and underwriting mortgage loans that comprise assets within CMBS trusts, as well as our experience in structuring CMBS transactions.

As of December 31, 2023, the estimated fair value of our portfolio of CMBS investments totaled $431.5 million in 73 CUSIPs ($5.9 million average investment per CUSIP). Included in the $431.5 million of CMBS securities are $9.3 million of CMBS securities designated as risk retention securities under the Dodd-Frank Act, which are subject to transfer restrictions over the term of the securitization trust. The following chart summarizes our securities investments by market conditions due tovalue, 98.9% of which were rated investment grade by Standard & Poor’s Ratings Group, Moody’s Investors Service, Inc. or Fitch Ratings Inc. as of December 31, 2023:

In the COVID-19 pandemic and the resulting economic disruption have broadly impacted thefuture, we may invest in CMBS securities or other securities that are unrated. As of December 31, 2023, our CMBS investments had a weighted average duration of 2.0 years. The commercial real estate sector.collateral underlying our CMBS investment portfolio is located throughout the United States. As expected,of December 31, 2023, by property count and market value, respectively, 65.2% and 66.3% of the net leased commercial real estate properties, which comprisecollateral underlying our CMBS investment portfolio was distributed throughout the majoritytop 25 metropolitan statistical areas (“MSAs”) in the United States, with 7.9% and 20.2%, by property count and market value, respectively, of the collateral located in the New York-Newark-Jersey City MSA, and the concentrations in each of the remaining top 24 MSAs ranging from 0.1% to 7.6% by property count and 0.1% to 8.5% by market value.

AAA-rated CMBS or U.S. Agency securities investments in excess of $76.0 million and all other investment grade CMBS or U.S. Agency securities investments in excess of $51.0 million, each in any single class of any single issuance, require the approval of our portfolio, have remained minimally impacted as the majorityboard of directors’ Risk and Underwriting Committee. The Risk and Underwriting Committee also must approve any investments in non-rated or sub-investment grade CMBS or U.S. Agency securities in any single class of any single issuance in excess of the lesser of (x) $21.0 million and (y) 10% of the total net leased properties in our real estate portfolio are necessity-based businesses and have remained open and stable duringasset value of the COVID-19 pandemic. We continuerespective Ladder subsidiary or other entity for which Ladder has authority to actively monitor our diversified commercial real estate properties as well to determine the immediate and long term impacts on the buildings, tenants, business plans and the ability to execute those business plans.make investment decisions.

Other Investments

Unconsolidated Joint Venture. In connection with the origination of a loanFrom time to time we invest in April 2012, we received a 25% equity interest with the right to convert upon a capital event. On March 22, 2013, we refinanced the loan, and we converted our equity interest into a 19% limited liability company membership interest in Grace Lake JV, LLC (“Grace Lake LLC”).real estate related ventures. As of December 31, 2020, Grace Lake LLC owned an office building campus with a2023, the carrying value of $50.9 million, which is net of accumulated depreciation of $36.5 million, that is financed by $61.6 million of long-term debt. Debt of Grace Lake LLC is non-recourse to the limited liability company members, except for customary non-recourse carve-outs for certain actions and environmental liability. As of December 31, 2020, the book value of our investment in Grace Lake LLCunconsolidated ventures was $4.0 million.

Unconsolidated Joint Venture. On August 7, 2015, the Company entered into a joint venture, 24 Second Avenue Holdings LLC (“24 Second Avenue”), with an operating partner (the “Operating Partner”) to invest in a ground-up residential/retail condominium development and construction project located at 24 Second Avenue, New York, NY. 24 Second Avenue consists of residential condominium units and one commercial condominium unit. As of December 31, 2020, 24 Second Avenue had sold 20 residential condominium units for $53.0 million in sales proceeds. As of December 31, 2020, the Company had no remaining additional capital commitment to 24 Second Avenue and the book value of the Company’s investment in 24 Second Avenue was $42.2$6.9 million.

FHLB Stock.United States Treasury Securities. Tuebor Captive Insurance Company LLC (“Tuebor”) is a member of the FHLB. Each member of the FHLB must purchaseWe invest in short-term and hold FHLB stocklong-term U.S. Treasury securities. Short-term U.S. Treasury securities are classified as a condition of initialcash and continuing membership, in proportion to their borrowings from the FHLB and levels of certain assets. The Company earns dividend incomecash equivalents on FHLB stock and it is redeemable by Tuebor upon five years’ prior written notice, subject to certain restrictions and limitations. Under certain conditions, the FHLB may also, at its sole discretion, repurchase FHLB stock from its members.our consolidated balance sheet. As of December 31, 2020, the book value2023, we held $1.0 billion of U.S. Treasury securities classified as cash and cash equivalents and held $53.7 million of U.S. Treasury securities classified as securities on our investment in FHLB Stock was $31.0 million.consolidated balance sheet.

Investment Process

Origination

Our team of originators is responsible for sourcing and directly originating new commercial first mortgage loans from the brokerage community and directly from real estate owners, operators, developers and investors. The extensive industry experience of our management team and origination team has enabled us to build a strong network of mortgage brokers and direct borrowers throughout the commercial real estate community in the United States.

Credit and Underwriting

Our underwriting and credit process commences upon receipt of a potential borrower’s executed loan application and non-refundable deposit.

Our underwriters conduct a thorough due diligence process for each prospective investment. The team coordinates in-house and third-party due diligence for each prospective loan as part of a checklist-based process that is designed to ensure that each loan receives a systematic evaluation. Elements of the underwriting process generally include:

Cash Flow Analysis. We create an estimated cash flow analysis and underwriting model for each prospective investment. Creation of the cash flow analysis generally draws on an assessment of current and historical data related to the property’s rent roll, operating expenses, net operating income, leasing cost, and capital expenditures. Underwriting evaluates and factors in assumptions regarding current market rents, vacancy rates, operating expenses, tenant improvements, leasing commissions, replacement reserves, renewal probabilities and concession packages based on observable conditions in the subject property’s sub-market at the time of underwriting. The cash flow analysis may also rely upon third-party environmental and engineering reports to estimate the cost to repair or remediate any identified environmental and/or property-level deficiencies. The final underwritten cash flow analysis is used to estimate the property’s overall value and its ability to produce cash flow to service the proposed loan.

Borrower Analysis. Careful attention is also paid to the proposed borrower, including an analysis based on available information of its credit history, financial standing, existing portfolio and sponsor exposure to leverage and contingent liabilities, capacity and capability to manage and lease the collateral, depth of organization, knowledge of the local market, and understanding of the proposed product type. We also generally commission and review a third-party background check of our prospective borrower and sponsor.

Site Inspection. A Ladder underwriter typically conducts a physical site inspection of each property. The site inspection gives the underwriter insights into the local market and the property’s positioning within it, confirms that tenants are in-place, and generally helps to ensure that the property has the characteristics, qualities, and potential value represented by the borrower.

Legal Due Diligence. Our in-house transaction management team includes experienced attorneys that manage, negotiate, structure and close all transactions and complete legal due diligence on each property, borrower, and sponsor, including evaluating documents such as leases, title, title insurance, opinion letters, tenant estoppels, organizational documents, and other agreements and documents related to the property or the loan.

Third-party Appraisal. We generally commission an appraisal from a member of the Appraisal Institute to provide an independent opinion of value as well as additional supporting property and market data. Appraisals generally include detailed data on recent property sales, local rents, vacancy rates, supply, absorption, demographics and employment, as well as a detailed projected cash flow and valuation analysis. We typically use the independent appraiser’s valuation to calculate ratios such as loan-to-value and loan-to-stabilized-value ratio, as well as to serve as an independent source to which the in-house cash flow and valuation model can be compared.

Third-party Engineering Report. We generally engage an approved licensed engineer to complete property condition/engineering reports and a seismic report for applicable properties. The engineering report is intended to identify any issues with respect to the safety and soundness of a property that may warrant further investigation, and provide estimates of ongoing replacement reserves, overall replacement cost, and the cost to bring a property into good repair.

Third-party Environmental Report. We also generally engage an approved environmental consulting firm to complete a Phase I Environmental Assessment to identify and evaluate potential environmental issues at the property and may also order and review Phase II Environmental Assessments and/or Operations & Maintenance plans, if applicable. Environmental reports and supporting documentation are typically reviewed in-house as well as by our dedicated outside environmental counsel who prepares a summary report on each property.

Third-party Insurance Review. A third-party insurance specialist reviews each prospective borrower’s existing insurance program to analyze the specific risk exposure of each property and to ensure that coverage is in compliance with our standard insurance requirements. Our transaction management team oversees this third-party review and makes the conclusions of their analysis available to the underwriting team.

A credit memorandum is prepared to summarize the results of the underwriting and due diligence process for the consideration of the Investment Committee. We thoroughly document the due diligence process up to, and including, the credit memorandum and maintain an organized digital archive of our work.

Transaction Management

The transaction management team is generally responsible for coordinating and managing outside counsel, working directly with originators, underwriters and borrowers to manage, structure, negotiate and close all transactions, including the securitization of our loans. The transaction management team plays an integral role in the legal underwriting of each property, consults with outside counsel on significant business, credit and/or legal issues, and facilitates the funding and closing of all investments and dispositions. The transaction management team also supports asset management and investment realization activities, including coordination of post-closing issues and assistance with loan sales, financings, refinancing and repayments.

Investment Committee Approval

All loan and real estate investments require approval from our Investment Committee, comprised of Brian Harris, CEO; Pamela McCormack, President; and Michael Scarola, Chief Credit Officer.Officer; and Craig Robertson, Head of Underwriting. The Investment Committee generally requires each investment to be fully described in a comprehensive Investment Committee memorandum that identifies the investment, the due diligence conducted and the findings, as well as all identified related risks and mitigants. The Investment Committee meets regularly to ensure that all investments are fully vetted prior to issuance of Investment Committee approval.

In addition to Investment Committee approval, the Risk and Underwriting Committee of our board of directors approves all loan and real estate investments above certain thresholds, which are currently set at $50.0 million for loans and $20.0 million for real estate investments. Additional investment opportunities, which include but are not limited to land, residential, or non-U.S. loans are also approved.

Financing

Prior to securitization or other disposition, or in the case of balance sheet loans, maturity, we evaluate most of the loans we originate for secured financing usingvia the CLO market or our multiple committed term facilities from leading financial institutions. Our finance team endeavors to match the characteristics and expected holding periods of the assets being financed with the characteristics of the financing options available and our short and long term cash needs in determining the appropriate financing approaches to be applied. The approaches we apply to financing our assets are a key component of our asset/liability risk management strategy with respect to managing liquidity risk. These approaches, supplemented by the use of hedging

primarily via the use of standard derivative instruments, facilitate the prudent management of our interest rate and credit spread exposures. Refer to “Our Financing Strategies” for further information.

Asset Management

Our in-house asset management team pro-actively manages the Company’s loan and real estate portfolios, demonstrating our Company-wide focus and emphasis on principal preservation and maximizing asset performance. The asset management team, together with our underwriting and transaction management teams, monitors the credit performance of our investment portfolio in concert with our third-party servicers and property managers, working closely with borrowers and/or joint-venture partners to manage all of our positions and monitor financial performance of our collateral assets, including execution of business plans and daily activities within our real estate portfolio. We focus on asset-specific issues and market surveillance, active enforcement of loan and security rights, and regular review of potential disposition strategies. Ladder performs detailed asset reviews, endeavors to perform periodic site inspections on every investment and provides comprehensive internal asset-level performance reporting. As applicable, we evaluateour asset management team evaluates loan modifications, debt and/or equity recapitalizations and other changes or variations to a borrower’s or joint venture partner’s business plan or budget and recommend a course of action to the Investment Committee.

Disposition and Distribution

Our securitization team works with our transaction management and underwriting teams to realize our disposition strategy of selling certain first mortgage loans into CMBS securitization trusts. We typically partner with other leading financial institutions to contribute loans to multi-asset securitizations. We have also led single asset securitizations on single loans we have originated.

In addition to contributing first mortgage loans into CMBS securitization trusts, we also maintain the flexibility to keep such loans on our balance sheet, contribute loans into a CLO or similar structure, sell participation interests or “b-notes” in our first mortgage loans or sell first mortgage loans as whole loans. Balance sheet loans that are refinanced by us into a new conduit first mortgage loan upon property stabilization and intended for securitization are re-underwritten and structured by our origination, underwriting and transaction management teams and approved by our Investment Committee.

Our asset management team also manages sales of our real property.

Factors Impacting Operating Results

There are a number of factors that influence our operating results in a meaningful way. The most significant factors include: (1) our competition; (2) market and economic conditions, including the continuing impact from COVID-19 on the economy; (3) loan origination and repayment volume; (4) profitability of securitizations; (5) avoidance of credit losses; (6) availability of debt and equity funding and the costs of that funding; (7) the net interest margin on our investments; (8) effectiveness of our hedging and other risk management practices; (9) real estate transaction volumes; (10) occupancy rates; and (11) expense management.

Our Financing Strategies

Our financing strategies are critical to the success and growth of our business. We manage our financing to complement our asset composition and to diversify our exposure across multiple capital markets and counterparties. In addition to cash flow from operations, we fund our operations and investment strategy through a diverse array of funding sources, including:

•Unsecured corporate bonds

•CLO transactions

•Secured loan and securities repurchase facilities

•Loan sales and securitizations

•Secured financing facility

•CLO transactions

•Non-recourse mortgage debt

•FHLB financingRevolving credit facility

•Revolving credit facilityLoan sales and securitizations

•Unencumbered assets available for financing

•Equity

From time to time, we may add financing counterparties that we believe will complement our business, although the agreements governing our indebtedness may limit our ability and the ability of our present and future subsidiaries to incur additional indebtedness. Our amended and restated charter and by-laws do not impose any threshold limits on our ability to use leverage. Refer to our discussion below and Part II, Item 7 “Management’s Discussion and Analysis of Financial Condition and Results of Operations—LiquidityOperations” under the heading “Liquidity and

Capital Resources” and Note 76, Debt Obligations, Net, into our consolidated financial statements included elsewhere in this Annual Report, for moreadditional information about our financing arrangements.

Unsecured Corporate Bonds

As of December 31, 2020,2023, we had $1.6 billion of unsecured corporate bonds outstanding. These unsecured financings were comprised of $146.7 million in aggregate principal amount of 5.875% senior notes due 2021 (the “2021 Notes”), $465.9 million in aggregate principal amount of 5.25% senior notes due 2022 (the “2022 Notes”), $348.0$327.8 million in aggregate principal amount of 5.25% senior notes due 2025 (the “2025 Notes”) and $651.8, $611.9 million in aggregate principal amount of 4.25% senior notes due 2027 (the “2027 Notes”) and $635.9 million in aggregate principal amount of 4.75% senior notes due 2029 (the “2029 Notes,” and collectively with the 2021 Notes, the 20222025 Notes and the 20252027 Notes, the “Notes”). During the year ended December 31, 2020, we repurchased an aggregate principal of the Notes of $303.9 million, recognizing an aggregate gain on extinguishment of debt of $20.1 million. Refer to Note 7 to the Consolidated Financial Statements for further detail.

Due in large part to devoting such a large portion of the Company’s capital structure to equity and unsecured corporate bond debt, Ladder maintains a $2.8$3.0 billion pool of unencumbered assets, comprised primarily of first mortgage loans and unrestricted cash as of December 31, 2020.2023.

CLO Debt

As of December 31, 2023, the Company had $1.1 billion of matched term, non-mark-to-market and non-recourse CLO debt included in debt obligations on its consolidated balance sheets.

On July 13, 2021, a consolidated subsidiary of the Company completed a privately-marketed CLO transaction, which generated $498.2 million of gross proceeds to Ladder, financing $607.5 million of loans (“Contributed July 2021 Loans”) at an 82% advance rate on a matched term, non-mark-to-market and non-recourse basis. A consolidated subsidiary of the Company retained an 18% subordinate and controlling interest in the CLO. The Company retained control over major decisions made with respect to the administration of the Contributed July 2021 Loans, including broad discretion in managing these loans, and has the ability to appoint the special servicer under the CLO.

On December 2, 2021, a consolidated subsidiary of the Company completed a privately-marketed CLO transaction, which generated $566.2 million of gross proceeds to Ladder, financing $729.4 million of loans (“Contributed December 2021 Loans”) at a 77.6% advance rate on a matched term, non-mark-to-market and non-recourse basis. A consolidated subsidiary of the Company retained an 15.6% subordinate and controlling interest in the CLO. The Company also held two additional tranches as investments totaling 6.8% interest in the CLO. The Company retained control over major decisions made with respect to the administration of the Contributed December 2021 Loans, including broad discretion in managing these loans, and has the ability to appoint the special servicer under the CLO.

Committed Loan Financing Facilities

We are parties to multiple committed loan repurchase agreement facilities, totaling $1.6$1.2 billion of credit capacity. As of December 31, 2020,2023, the Company had $255.4$605.0 million of borrowings outstanding, with an additional $1.3 billion$637.0 million of committed financing available. Assets pledged as collateral under these facilities are generally limited to first mortgage whole mortgage loans, mezzanine loans and certain interests in such first mortgage and mezzanine loans. Our repurchase facilities include covenants covering net worth requirements, minimum liquidity levels, and maximum debt/equity ratios.

We have the option to extend some of our existing facilities subject to a number of customary conditions. The lenders have sole discretion to include collateral in these facilities and to determine the market value of the collateral on a daily basis, and, if the estimated market value of the included collateral declines, the lenders have the right to require additional collateral or a full and/or partial repayment of the facilities (margin call) sufficient to rebalance the facilities. Typically, the lender establishes a maximum percentage of the collateral asset’s market value that can be borrowed. We often borrow at a lower percentage of the collateral asset’s value than the maximum, leaving us with excess borrowing capacity that can be drawn upon at a later date and/or applied against future margin calls so that they can be satisfied on a cashless basis.

Securities Repurchase Facilities

We are a party to a committed term master repurchase agreement with a major U.S. banking institution for CMBS, totaling $400.0$100.0 million of credit capacity, or more depending on our utilization of a loan repurchase facility with the same lender.capacity. As we do in the case of borrowings under committed loan facilities, we often borrow at a lower percentage of the collateral asset’s value than the maximum, leaving us with excess borrowing capacity that can be drawn upon at a later date and/or applied against future margin calls so that they can be satisfied on a cashless basis. As of December 31, 2020,2023, the Company had $149.6 millionno borrowings outstanding, with an additional $638.4$100.0 million of committed financing available.

Additionally, we are a party to multiple uncommitted master repurchase agreements with several counterparties to finance our investments in CMBS and U.S. Agency Securities.securities. The securities that servedserve as collateral for these borrowings are typically

AAA-rated CMBS with relatively short duration and significant subordination. The lenders have sole discretion to determine the market value of the collateral on a daily basis, and, if the estimated market value of the collateral declines, the lenders have the right to require additional cash collateral. If the estimated market value of the collateral subsequently increases, we have the right to call back excess cash collateral.

Mortgage Loan Financing

We generally finance our real estate using long-term non-recourse mortgage financing. During the year ended December 31, 2023, we did not execute any long term debt agreement to finance real estate. Our mortgage loan financings have primarily fixed rates ranging from 4.39% to 9.03%, mature between 2024 - 2031 and total $437.8 million as of December 31, 2023. These long-term non-recourse mortgages include net unamortized premiums of $1.8 million at December 31, 2023, representing proceeds received upon financing greater than the contractual amounts due under the agreements. The premiums are being amortized over the remaining life of the respective debt instruments using the effective interest method. We recorded $0.6 million of premium amortization, which decreased interest expense, for the year ended December 31, 2023. The loans are collateralized by real estate and related lease intangibles, net, of $474.7 million as of December 31, 2023.

Revolving Credit Facility

The Company’s revolving credit facility (the “Revolving Credit Facility”) provides for an aggregate maximum borrowing amount of $266.4$323.9 million, including a $25.0 million sublimit for the issuance of letters of credit. The Revolving Credit Facility is available on a revolving basis to finance the Company’s working capital needs and for general corporate purposes. TheBorrowings under the Revolving Credit Facility hasincur interest at a fixed margin of 2.50% over the index rate, with reductions in the fixed margin upon the achievement of investment grade credit ratings. On January 25, 2024, the Company amended its Revolving Credit Facility to extend the final maturity date assuming all extensions options are exercised,to January 25, 2029. As of February 2025. The amendment also provided for a reduction inDecember 31, 2023, the interest rateCompany had no outstanding borrowings on the Revolving Credit Facility, but still maintains the ability to one-month LIBOR plus 3.00% on Eurodollar advances upon the upgrade of the Company’s credit ratings, which occurred in January 2020.draw $323.9 million.

The obligations under the Revolving Credit Facility are guaranteed by the Company and certain of its subsidiaries. The Revolving Credit Facility is secured by a pledge of the shares of (or other ownership or equity interests in) certain subsidiaries to the extent the pledge is not restricted under existing regulations, law or contractual obligations.

LCFH is subject to customary affirmative covenants and negative covenants, including limitations on the incurrence of additional debt, liens, restricted payments, sales of assets and affiliate transactions under the Revolving Credit Facility. In addition, under the Revolving Credit Facility, LCFH is required to comply with financial covenants relating to minimum net worth, maximum leverage, minimum liquidity, and minimum fixed charge coverage, consistent with our other credit facilities.

FHLB Financing

We have maintained membership in the FHLB since 2012 through our subsidiary, Tuebor Captive Insurance Company LLC (“Tuebor”). As of December 31, 2020, Tuebor had $288.0 million of borrowings outstanding from the FHLB (with an additional $1.2 billion of committed term financing available), with terms of overnight to 3.75 years, interest rates of 0.41% to 2.74%, and advance rates of 45.0% to 95.7% on eligible collateral, including cash collateral. As of December 31, 2020, collateral for the borrowings was comprised of $280.1 million of CMBS and U.S. Agency Securities, and $108.3 million of first mortgage commercial real estate loans. The weighted-average borrowings outstanding were $578.6 million for the year ended December 31, 2020. FHLB advances amounted to 6.8% of the Company’s outstanding debt obligations as of December 31, 2020.

Mortgage Loan Financing

We generally finance our real estate using long-term non-recourse mortgage financing. During the year ended December 31, 2020, we executed ten term debt agreements to finance real estate. All of our mortgage loan financings have fixed rates ranging from 3.75% to 6.16%, mature between 2021- 2030 and total $766.1 million at December 31, 2020. These long-term non-recourse mortgages include net unamortized premiums of $4.6 million at December 31, 2020, representing proceeds received upon financing greater than the contractual amounts due under the agreements. The premiums are being amortized over the remaining life of the respective debt instruments using the effective interest method. We recorded $1.2 million of premium amortization, which decreased interest expense, for the year ended December 31, 2020. The loans are collateralized by real estate and related lease intangibles, net, of $909.4 million as of December 31, 2020.

Secured Financing Facility

On April 30, 2020, the Company entered into a strategic financing arrangement (the “Agreement”) with an American multinational corporation (the “Lender”), under which the Lender provided the Company with approximately $206.4 million in senior secured financing (the “Secured Financing Facility”) to fund transitional and land loans. The Secured Financing Facility is secured on a first lien basis on a portfolio of certain of the Company’s loans and will mature on May 6, 2023, and borrowings thereunder bear interest at LIBOR (or a minimum of 0.75% if greater) plus 10.0%, with a minimum interest premium of approximately $39.2 million minus the aggregate sum of all interest payments made under the Secured Financing Facility prior to the date of payment of the minimum interest premium, which is payable upon the earlier of maturity or repayment in full of the loan. The Senior Financing Facility is non-recourse, subject to limited exceptions, and does not contain mark-to-market provisions. Additionally, the Senior Financing Facility provides the Company optionality to modify or restructure loans or forbear in exercising remedies, which maximizes the Company’s financial flexibility.

As part of the strategic financing, the Lender also had the ability to make an equity investment in the Company of up to 4.0 million Class A common shares at $8.00 per share, subject to certain adjustments (the “Purchase Right”). The Purchase Right was exercised in full at $8.00 per share on December 27, 2020.

The Lender has agreed not to sell, transfer, assign, pledge, hypothecate, mortgage, dispose of or in any way encumber the shares acquired as a result of exercising the Purchase Right for a period of time following the exercise date. In connection with the issuance of the Purchase Right, the Company and the Lender entered into a registration rights agreement, pursuant to which the Company has agreed to provide customary demand and piggyback registration rights to the Lender.

As of December 31, 2020, the Company had $192.6 million of borrowings outstanding under the Secured Financing Facility included in debt obligations on its consolidated balance sheets. Unamortized debt issuance costs of $7.2 million were included in secured financing facility as of December 31, 2020.

Collateralized Loan Obligation (“CLO”) Debt

On April 27, 2020, a consolidated subsidiary of the Company completed a private CLO transaction with a major U.S. bank which generated $310.2 million of gross proceeds to Ladder, financing $481.3 million of loans (“Contributed Loans”) at a 64.5% advance rate on a matched term, non-mark-to-market and non-recourse basis. A consolidated subsidiary of the Company will retained a 35.5% subordinate and controlling interest in the CLO. The Company retained control over major decisions made with respect to the administration of the Contributed Loans, including broad discretion in managing these loans in light of the COVID-19 pandemic, and has the ability to appoint the special servicer under the CLO. The CLO is a Variable Interest Entity (“VIE”) and the Company was the primary beneficiary and, therefore, consolidated the VIE - See Note 10, Consolidated Variable Interest Entities. Proceeds from the transaction were used to pay off other secured debt including bank and FHLB financing that was subject to mark-to-market provisions.

As of December 31, 2020, the Company had $276.5 million of matched term, non-mark-to-market and non-recourse basis CLO debt included in debt obligations on its consolidated balance sheets. Unamortized debt issuance costs of $2.6 million were included in CLO debt as of December 31, 2020.

Hedging Strategies

We may enter into interest rate and credit spread derivative contracts to mitigate our exposure to changes in interest rates and credit spreads. We generally seek to hedge the interest rate risk on the financing of assets that have a duration longer than five years, including newly-originated conduit first mortgage loans, securities in our CMBS portfolio if long enough in duration, and most of our U.S. Agency Securitiessecurities portfolio. We monitor our asset profile and our hedge positions to manage our interest rate and credit spread exposures, and we seek to match fund our assets according to the liquidity characteristics and expected holding periods of our assets.

Financing Strategy in Current Market Conditions

In March 2020, as the COVID-19 health crisis rapidly transformed into a financial crisis, management took swift action to increase liquidity resources and actively manage its financing arrangements with its bank partners. In an abundance of caution, the Company first drew down on its $266.4 million unsecured revolving credit facility, which continues to be fully-drawn, and the proceeds continue to be held as unrestricted cash on the Company’s balance sheet as of February 19, 2021.

Securities Repurchase Facilities: The Company invests in AAA-rated CRE CLO securities, typically front pay securities, with relatively short duration and significant subordination. These securities have historically been financed with short-term maturity, repurchase agreements with various bank counterparties. The Company has been able to continue to access securities repurchase funding and the pricing of such borrowings has improved during the three months ended December 31, 2020 as liquidity continued to return to the market and pricing for the securities that serve as collateral improved. Furthermore, during the year ended December 31, 2020, the Company paid down $548.2 million of securities repurchase financing, primarily through sales of securities.

FHLB Financing: In 2016, the FHFA adopted a final rule that limited our captive insurance subsidiary’s membership in the FHLB, requiring us to significantly reduce the amounts of FHLB borrowings outstanding by February of 2021. The Company has complied with such targeted paydowns. Refer to “Management’s Discussion and Analysis of Financial Condition and Results of Operations - Liquidity and Capital Resources - FHLB financing” for further information.

Total paydowns on FHLB financing for the year ended December 31, 2020 were $785.5 million. As a part of paydowns in the second quarter, the Company incurred $6.5 million in prepayment penalties. The remaining FHLB debt maturities are staggered out through 2024. Funding for future advance paydowns is expected be obtained from the natural amortization of securities over time and/or sales of securities collateral.

Loan Repurchase Financing: The Company has maintained a consistent dialogue with its loan financing counterparties since the COVID-19 crisis began to unfold in late March 2020. In addition to using proceeds from the Company’s 2027 Notes offering in January to reduce secured debt, for the year ended December 31, 2020, the Company paid down over $446.9 million on such loan repurchase financing through loan collateral pay offs and loans securitized through a CLO financing transaction. (refer to below). Loan repurchase debt outstanding as of December 31, 2020 was $255.4 million. The Company continues to maintain an active dialogue with its bank counterparties as it expects loan collateral on each of their lines to experience some measure of forbearance.

Secured Financing Facility: On April 30, 2020, the Company entered into a strategic financing arrangement with an American multinational corporation, under which the lender will provide the Company with approximately $206.4 million in senior secured financing to fund transitional and land loans. (refer to above).

Completion of Private CLO: On April 27, 2020, the Company completed a private CLO financing transaction with a major U.S. bank which generated $310.2 million of gross proceeds, financing $481.3 million of loans at a 64.5% advance rate on a matched term, non-mark-to-market and non-recourse basis.

Based on the financing actions described above, the Company has significantly decreased its exposure to mark-to-market financing in 2020. As of February 19, 2021, the Company is holding over $1.3 billion of unrestricted cash.

Financial Covenants

We generally seek to maintain a debt-to-equity ratio of approximately 3.0:1.0 or below. We expect this ratio to fluctuate during the course of a fiscal year due to the normal course of business inbusiness. This ratio may also fluctuate as a result of our conduit lending operations, in which we generally securitize our inventory of conduit loans at intervals, and also because of changes in our asset mix, due in part to such securitizations. We generally seek to match fund our assets according to their liquidity characteristics and expected hold period. We believe that the defensive positioning of our predominantly senior secured assets and our financing strategy has allowed us to maintain financial flexibility to capitalize on an attractive range of market opportunities as they have arisen.

We and our subsidiaries may incur substantial additional debt in the future. However, we are subject to certain restrictions on our ability to incur additional debt in the indentures governing the Notes (the “Indentures”) and our other debt agreements. Under the Indentures, we may not incur certain types of indebtedness unless our consolidated non-funding debt to equity ratio (as defined in the Indentures) is less than or equal to 1.75 to 1.75:1.00 or if the unencumbered assets of the Company and its

subsidiaries is less than 120% of their unsecured indebtedness, although our subsidiaries are permitted to incur indebtedness where recourse is limited to the assets and/or the general credit of such subsidiary.

Our borrowings under certain financing agreements and our committed repurchase facilities are subject to maximum consolidated leverage ratio limits (either a fixed ratio ranging from 3.503.5:1.0 to 1.00 to 4.00 to 1.00,4.0:1.0, or a maximum ratio based on our asset composition at the time of determination), minimum net worth requirements (ranging from $400.0 million to $871.4 million), maximum reductions in net worth over stated time periods, minimum liquidity levels (typically $30.0 million of cash or a higher standard that often allows for the inclusion of different percentages of liquid securities in the determination of compliance with the requirement), and a fixed charge coverage ratio of 1.25x, and, in the instance of one lender, an interest coverage ratio of 1.50x, in each case, if certain liquidity thresholds are not satisfied. Leverage ratio limits exclude CLO financing for purposes of this covenant calculation. These restrictions, which would permit us to incur substantial additional debt, are subject to significant qualifications and exceptions.

Further, certain of our financing arrangements and loans on our real property are secured by the assets of the Company, including pledges of the equity of certain subsidiaries or the assets of certain subsidiaries. From time to time, certain of these financing arrangements and loans may prohibit certain of our subsidiaries from paying dividends to the Company, from making distributions on such subsidiary’s capital stock, from repaying to the Company any loans or advances to such subsidiary from the Company or from transferring any of such subsidiary’s property or other assets to the Company or other subsidiaries of the Company.

We are in compliance with all covenants as described elsewhere in this Annual Report as of December 31, 2020.2023.

Net of the $1.3 billion of unrestricted cash held as of December 31, 2020, our adjusted leverage ratio would be significantly below 3.0x. In late March 2020, as the COVID-19 crisis evolved, management began executing on a plan to mitigate uncertainty in financial markets by increasing liquidity and obtaining additional non-recourse and non-mark-to-market financing. Partly as a result of maintaining conservative cash levels as of March 31, 2020, the Company was not in compliance with its 3.5x maximum leverage covenant with certain of its lenders but had the benefit of a contractually provided 30-day cure period during which the Company cured such non-compliance by paying down debt (as defined in the relevant borrowing agreements). Refer to “Financing Strategy in Current Market Conditions” for further disclosures surrounding deleveraging actions completed during 2020.

Competition

The commercial real estate finance markets are highly competitive. We face competition for lending and investment opportunities from a variety of institutional lenders and investors and many other market participants, including specialty finance companies, other REITs, commercial banks and thrift institutions, investment banks, insurance companies, hedge funds and other financial institutions. These competitors may enjoy competitive advantages over us, including greater name recognition, established lending relationships with certain borrowers and brokers, financial resources, and access to capital, including through a corporate parent.

We compete on the basis of relationships, product offering, loan structure, terms, pricing and customer service. Our success depends on our ability to maintain and capitalize on relationships with borrowers and brokers, offer attractive loan products, remain competitive in pricing and terms, and provide superior service.

Taxation

We have elected to be subject to tax as a REIT under Sections 856 through 860 of the Internal Revenue Code (the “Code”), commencing with the taxable year ending December 31, 2015. Additionally, onecertain of our subsidiary entities hashave also elected to be subject to tax as a REIT commencing with taxable year ending December 31, 2016.REITs. To qualify as a REIT, we must make qualifying distributions to shareholders and satisfy, on a continuing basis, through actual investment and operating results, certain asset, income, organizational, distribution, stock ownership and other REIT requirements. If we fail to qualify as a REIT, and do not qualify for certain statutory relief provisions, we will be subject to U.S. federal, state and local income taxes and may be precluded from qualifying as a REIT for the subsequent four taxable years following the year in which we lost our REIT qualification. The failure to qualify as a REIT could have a material adverse impact on our results of operations and amounts available for distribution to shareholders.

We utilize TRSs to reduce the impact of the prohibited transaction tax and to avoid penalty for the holding of assets not qualifying as real estate assets for purposes of the REIT asset tests. Any income associated with a TRS is fully taxable because a TRS is subject to federal and state income taxes as a domestic C corporation based upon its net income. Refer to “Risk factors—Risks related to our taxation as a REIT.”

Regulation

Our operations are subject, in certain instances, to supervision and regulation by U.S. federal and state governmental authorities and may be subject to various laws and judicial and administrative decisions imposing various requirements and restrictions. In addition, certain of our subsidiaries’ businesses may rely on exemptions from various requirements of the Securities Act, the Exchange Act, the Investment Company Act, and the U.S. Employee Retirement Income Security Act of 1974, as amended (“ERISA”). These exemptions are sometimes highly complex and may in certain circumstances depend on compliance by third-parties who we do not control.

Regulation of Commercial Real Estate Lending Activities

Although most states do not regulate commercial finance, certain states impose limitations on interest rates and other charges and on certain collection practices and creditor remedies, and require licensing of lenders and financiers and adequate disclosure of certain contract terms. We also are required to comply with certain provisions of, among other statutes and regulations, certain provisions of the Equal Credit Opportunity Act that are applicable to commercial loans, the USA PATRIOT Act, regulations promulgated by the Office of Foreign Asset Control and U.S. federal and state securities laws and regulations.

Regulation as a Captive Insurance Companyan Investment Adviser