UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

| | | | | |

| ☒ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 20212023

OR

| | | | | |

| ☐ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period to

Commission File No. 001-36629

CAESARS ENTERTAINMENT, INC.

(Exact name of registrant as specified in its charter)

Delaware

(State or other jurisdiction of

incorporation or organization)

46-365678146-3657681

(I.R.S. Employer

Identification No.)

100 West Liberty Street, 12th Floor

Reno, Nevada 89501

(Address of principal executive offices)

Telephone: (775) 328-0100

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

| | | | | | | | | | | | | | |

| Title of each class | | Trading symbol | | Name of each exchange on which registered |

Common Stock, $.00001,$0.00001, par value | | CZR | | NASDAQ Stock Market |

Securities registered pursuant to section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☒ No ☐

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No ☒

Indicate by check mark whether the registrant (1) has filed reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| | | | | | | | | | | | | | | | | |

| Large accelerated filer | ☒ | Accelerated filer | ☐ | Non-accelerated filer | ☐ |

| Smaller reporting company | ☐ | Emerging growth company | ☐ | | |

If an emerging growth company, indicate by checkmark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☒

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that require a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to Section §240.10D-1(b). ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

The aggregate market value of the common stock held by non-affiliates of the Registrant was $21.1$10.5 billion at June 30, 20212023 based upon the closing price for the shares of CZR’s common stock as reported by The Nasdaq Stock Market.

As of February 17, 2022,15, 2024, there were 214,123,451216,299,768 outstanding shares of the Registrant’s Common Stock, net of treasury shares.

Documents Incorporated by Reference

Portions of the Registrant’s definitive proxy statement to be filed with the Commission pursuant to Regulation 14A in connection with the Registrant’s Annual Meeting of Stockholders (the “Proxy Statement”) are incorporated by reference into Part III of this report. Such Proxy Statement will be filed with the Commission not later than 120 days after the conclusion of the Registrant’s fiscal year ended December 31, 2021.2023.

CAESARS ENTERTAINMENT, INC.

ANNUAL REPORT FOR THE YEAR ENDED DECEMBER 31, 20212023

TABLE OF CONTENTS

PART I

In this filing, Caesars Entertainment, Inc., a Delaware corporation, isand its subsidiaries may be referred to as the “Company,” “CEI,” “Caesars,” or the “Registrant,” and together with its subsidiaries may also be referred to as “we,” “us” or “our.“our” or the “Registrant.”

We also refer to (i) our Consolidated Financial Statements as our “Financial Statements,” (ii) our Consolidated Statements of Operations and Consolidated Statements of Comprehensive Income (Loss) as our “Statements of Operations,” (iii) our Consolidated Balance Sheets as our “Balance Sheets,” and (iv) our Consolidated Statements of Cash Flows as our “Statements of Cash Flows.Flows,” which are prepared in accordance with accounting principles generally accepted in the United States (“GAAP”). References to numbered “Notes” refer to Notes to our Consolidated Financial Statements included in Item 8.

Item 1. Business

Overview

We are a geographically diversified gaming and hospitality company that was founded in 1973 by the Carano family with the opening of the Eldorado Hotel Casino in Reno, Nevada. Beginning in 2005, we grew through a series of acquisitions, including the acquisition of MTR Gaming Group, Inc. in 2014, Isle of Capri Casinos, Inc. (“Isle” or “Isle of Capri”) in 2017, and Tropicana Entertainment, Inc. in 2018. On July 20, 2020, we completed the merger with2018, Caesars Entertainment Corporation (“Former Caesars”in 2020, and William Hill PLC (the “William Hill Acquisition”) pursuant to which Former Caesars became our wholly-owned subsidiary (the “Merger”) and we changed the Company’son April 22, 2021. Our ticker symbol on the NASDAQ Stock Market from “ERI” to “CZR”. On April 22, 2021, we completed the acquisition of William Hill PLC (the “William Hill Acquisition”).is “CZR.”

Our primary source of revenue is generated by our casino properties’ gaming operations, which includes our retail and online sports betting as well asand online gaming, and we utilize our hotels, restaurants, bars, entertainment, racing, retail shops and other services to attract customers to our properties.

As of December 31, 2023, we own, lease or manage an aggregate of 52 domestic properties in 18 states. We also operate and conduct sports wagering across 31 jurisdictions in North America, 25 of which offer online sports betting, and operate iGaming in five jurisdictions in North America. We continue to expand into additional markets as jurisdictions legalize forms of retail and online gaming and sports betting. In addition, we have other properties in North America that are authorized to use the brands and marks of Caesars Entertainment, Inc., as well as other non-gaming properties. We lease certain real property assets from third parties, including GLP Capital, L.P., the operating partnership of Gaming and Leisure Properties, Inc. (“GLPI”) and VICI Properties L.P., a Delaware limited partnership (“VICI”).

As of December 31, 2021, we own, lease or manage an aggregate of 52 domestic properties in 16 states with approximately 55,700 slot machines, video lottery terminals and e-tables, approximately 2,900 table games and approximately 47,700 hotel rooms. We also operate and conduct sports wagering across 21 states and domestic jurisdictions, 14 of which are mobile for sports betting, and operate regulated online real money gaming in five states. We continue to expand into additional markets as jurisdictions legalize forms of retail and online sports betting. In addition, we have other domestic and international properties that are authorized to use the brands and marks of Caesars Entertainment, Inc., as well as other non-gaming properties. See

Item 2, “Properties,” for more information about our properties.Significant Transactions in 2021

On September 30, 2020, the Company announced that it had reached an agreement with William Hill PLC on the terms of a recommended cash acquisition pursuant to which the Company would acquire the entire issued and to be issued share capital (other than shares owned by the Company or held in treasury) of William Hill PLC, in an all-cash transaction. On April 22, 2021, the Company completed the acquisition of William Hill PLC for £2.9 billion, or approximately $3.9 billion.

In connection with the William Hill Acquisition, on April 22, 2021, a newly formed subsidiary of the Company (the “Bridge Facility Borrower”) entered into a Credit Agreement (the “Bridge Credit Agreement”) with certain lenders party thereto and Deutsche Bank AG, London Branch, as administrative agent and collateral agent, pursuant to which the lenders party thereto provided the Debt Financing (as defined below). The Bridge Credit Agreement provides for (a) a 540-day £1.0 billion asset sale bridge facility, (b) a 60-day £503 million cash confirmation bridge facility and (c) a 540-day £116 million revolving credit facility (collectively, the “Debt Financing”). The proceeds of the bridge loan facilities provided under the Bridge Credit Agreement were used (i) to pay a portion of the cash consideration for the acquisition and (ii) to pay fees and expenses related to the acquisition and related transactions. The proceeds of the revolving credit facility under the Bridge Credit Agreement may be used for working capital and general corporate purposes. The £1.5 billion Interim Facilities Agreement (the “Interim Facilities Agreement”) entered into on October 6, 2020 with Deutsche Bank AG, London Branch and JPMorgan Chase Bank, N.A., and amended on December 11, 2020, was terminated upon the execution of the Bridge Credit Agreement. On May 12, 2021, we repaid the £503 million cash confirmation bridge facility. On June 14, 2021, the Company drew down the full £116 million from the revolving credit facility and the proceeds, in addition to excess Company cash, were used to make a partial repayment of the asset sale bridge facility in the amount of £700 million. Outstanding borrowings under the Bridge Credit Agreement are expected to be repaid upon the sale of William Hill’s non-U.S. operations including the UK and international online divisions and the retail betting shops (collectively, “William Hill International”), all of which are held for

sale as of the date of the closing of the William Hill Acquisition and reflected within discontinued operations. Certain investments acquired have been excluded from the held for sale asset group.

On September 8, 2021, the Company entered into an agreement to sell William Hill International to 888 Holdings Plc for approximately £2.2 billion. After repayment of the outstanding debt under the Bridge Credit Agreement, described above, the Company expects to receive approximately £835 million, or $1.2 billion, subject to any permitted leakage, which is customary for sale transactions in the UK. In order to manage the risk of changes in the GBP denominated sales price and expected proceeds, the Company has entered into foreign exchange forward contracts. The sale is subject to satisfaction of customary conditions, including receipt of the approval of shareholders of 888 Holdings Plc and regulatory approvals, and is expected to close in the second quarter of 2022.

On April 6, 2021, the Company consummated the sale of the equity interests of MontBleu Casino Resort & Spa (“MontBleu”) to Bally’s Corporation for $15 million, subject to a customary working capital adjustment, resulting in a gain of less than $1 million. The purchase price for MontBleu is due no later than the first anniversary of the consummation of the transaction. MontBleu was within the Regional segment.

On June 3, 2021, the Company consummated the sale of the real property and equity interests of Tropicana Evansville (“Evansville”) to GLPI and Bally’s Corporation (formerly “Twin River” or Twin River Worldwide Holdings, Inc.), respectively, for $480 million, resulting in a gain of $12 million. Evansville was within the Regional segment.

On September 3, 2021, the Company consummated the sale of Caesars Southern Indiana to the Eastern Band of Cherokee Indians (“EBCI”) for $250 million, subject to a customary working capital adjustment, resulting in a gain of $12 million. In connection with the transaction, the Company’s annual base rent payments to VICI Properties under the Regional Master Lease (as defined below) were reduced by $33 million. Additionally, the Company and EBCI extended their existing relationship by entering into a 10-year brand license agreement, with cancellation rights in exchange for a termination fee at the buyer’s discretion following the fifth anniversary of the agreement, for the continued use of the Caesars brand and Caesars Rewards loyalty program at Caesars Southern Indiana. Caesars Southern Indiana was previously reported within the Regional segment and subsequent to the sale, as a result of the license agreement relating to the continued use of the Caesars brand and Caesars Rewards loyalty program at Caesars Southern Indiana, is reported within the Managed and Branded segment.

On November 1, 2021, the Company and VICI consummated the sale of Harrah’s Louisiana Downs Casino, Racing & Entertainment (“Harrah’s Louisiana Downs”) to Rubico Acquisition Corp. for $22 million, subject to a customary working capital adjustment. The proceeds from the sale were split between the Company and VICI. The annual base rent payments under the Regional Lease between Caesars and VICI remain unchanged.

On August 26, 2021, the Company increased its ownership interest in CBAC Borrower, LLC (“Horseshoe Baltimore”), a property which it also manages, to approximately 75.8%. Caesars was subsequently determined to have a controlling financial interest in Horseshoe Baltimore and we began to consolidate the results of operations of the property following our change in ownership. Our previously held investment was remeasured as of the date of our change in ownership and the Company recognized a gain of $40 million during the year ended December 31, 2021. Management fees received prior to the consolidation event have been presented within our Managed and Branded segment. Following the increase in ownership, the operations of Horseshoe Baltimore are presented within the Regional segment.

On December 1, 2020, the Company entered into an agreement to sell the operations of Belle of Baton Rouge Casino & Hotel (“Baton Rouge”) to CQ Holding Company, Inc. The transaction has received regulatory approvals and is expected to close in the first quarter of 2022, subject to other customary closing conditions.

Developments related to COVID-19

In January 2020, an outbreak of a new strain of coronavirus (“COVID-19”) was identified and spread throughout much of the world, including the U.S. All of the Company’s casino properties were temporarily closed for the period from mid-March 2020 through mid-May 2020 due to orders issued by various government agencies and tribal bodies as part of certain precautionary measures intended to help slow the spread of COVID-19. During the year ended December 31, 2021, most of our properties experienced positive trends as restrictions on maximum capacities and amenities available were eased.

Following temporary furloughs and salary reductions during 2020, the Company has emphasized a focus on labor efficiencies as operations resumed. As properties began to reopen during the year ended December 31, 2020, certain capacity restrictions, mask mandates, sanitation guidelines, and the federal COVID-19 vaccine and testing emergency temporary standard were adhered to as required by governmental or tribal orders, directives, and guidelines.

The Company experienced positive operating trends in 2021, with a continued focus on operational efficiencies. Although we have experienced a decline in net income, Adjusted EBITDA and Adjusted EBITDA margins for the year ended December 31, 2021 exceeded pre-pandemic levels experienced in 2019 within our Las Vegas and Regional segments. However, certain revenue streams, such as convention and entertainment revenues, continued to be negatively impacted due to capacity restrictions in the first half of 2021. Future effects of COVID-19 from further outbreaks, including new variants, mask mandates or other restrictions are uncertain and could result in additional closures such as the temporary closure of Caesars Windsor from January 5, 2022 through January 31, 2022. Extensive closure periods impacting many of our properties would have a material adverse effect on future results of operations.

Business Operations

Our consolidated business is composed of five complementary businesses that reinforce, cross-promote, and build upon each other: casino, which includes our retail and online sports betting and iGaming, food and beverage, hotel, casino management services, entertainment, retail and entertainment and other business operations.

Casino Operations

Our casino operations generate revenues from approximately 55,70051,300 slot machines, and 2,9002,700 table games, including poker, as well assports betting from our retail and online sportsbooks, iGaming and other games such as keno, and race and online sportsbooks, all of which comprised approximately 61%55% of our total net revenues in 2021.2023. Slot revenues generate the majority of our casino revenues.

Retail and Online Sports Betting and iGaming

We previously entered into a 25-year agreement with William Hill PLC’s U.S. subsidiary, William Hill U.S. Holdco, Inc. (“William Hill US” and together with William Hill PLC, “William Hill”), which became effective January 29, 2019, and granted to William Hill the right to conduct betting activities, including operating sportsbooks, in retail channels and under certain skins for online channels with respect to our current and future properties and conduct certain real money online gaming activities. On April 22, 2021, we consummated our previously announced acquisition of William Hill PLC in an all-cash transaction. Prior to the transaction, we accounted for our investment in William Hill PLC as an investment in equity securities we accounted for our investment in William Hill US as an equity method investment.

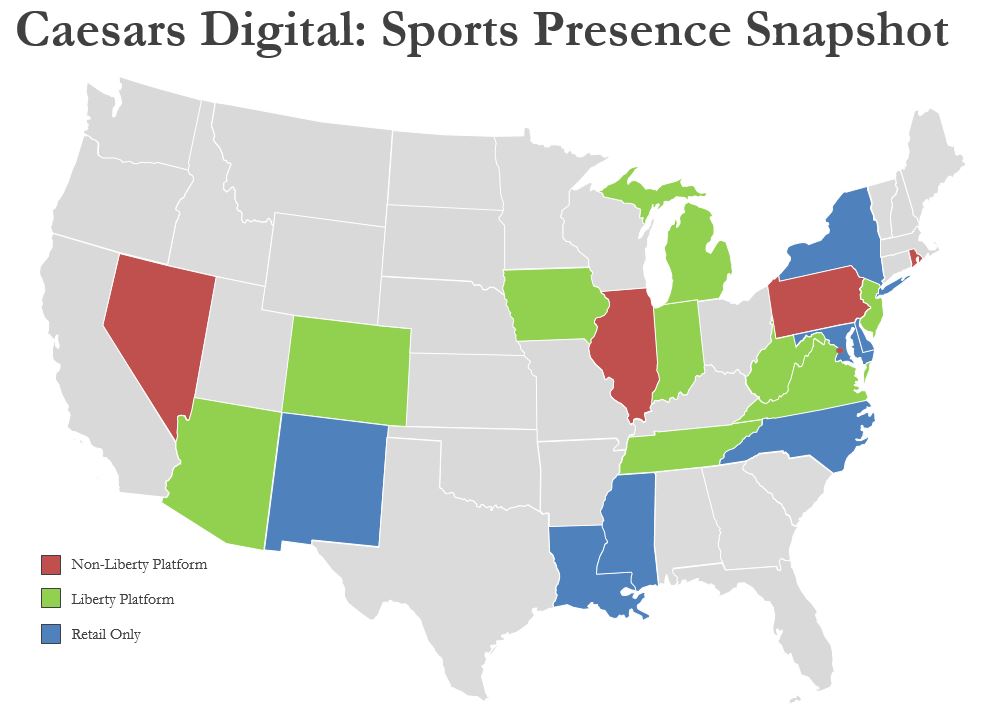

Prior to the acquisition, William Hill operated 37 sportsbooks at our properties in eight states. Subsequent to the William Hill Acquisition, we operate and conduct retail and online sports wagering across 21 U.S. states and domestic31 jurisdictions in North America as of December 31, 2021. Additionally,2023. In addition to our online poker operations, we operate regulated online real money gaming businessesiGaming in five statesjurisdictions in North America and continue to leverage the World Series of Poker (“WSOP”) brand and license the WSOP trademarks for a variety of products and services. Players in markets such as New Jersey can playWe offer hundreds of online casino games including slots, table games, live dealer and video poker and we expect to similarly increase our product offerings in Pennsylvania, Michigan and additional states as iGaming is legalized.

Extensive usage of digital platforms, continued legalizationlegalized in additional states, and growing bettor demand are driving the market for online sports betting platforms in the United States and the William Hill Acquisition positioned us to address this growing market.states.

We launched our Caesars Sportsbook app on our owned and integrated technology platform we have labeled Liberty (“Liberty”). We have launched a significant marketing campaign with distinguished actors, athletes and media personalities promoting the launch of the Caesars Sportsbook app. in 2021. The app offers extensive pre-match and live markets, extensive odds and flexible limits, player props, and same-game parlays. In addition to the Caesars Sportsbook app, the Company and NYRABets LLC, the official online wagering platform of the New York Racing Association, Inc., launched the Caesars Racebook app in 2022. The Caesars Racebook app operates in 20 states and provides access for pari-mutuel wagering at over 300 racetracks around the world as well as livestreaming of races. Additionally, we launched our new Caesars Palace Online Casino application in states and territories where we operate iGaming in 2023. Wagers placed can earn credits towards the Caesars Rewards loyalty program or points which can be redeemed for free wagering credits. No customers under 21 years old are allowed to wager on any of our Caesars Sportsbook, Caesars Racebook and iGaming mobile apps. Growth in the Caesars Digital segment continues to be realized with the strategic expansion into new states as jurisdictions legalize retail and online sports betting and online horse race wagering.

Sports Brand Partnerships — Caesars Sportsbook has partnerships with the NFL, NBA, NHL, MLB, and several individual teams, while being the exclusive odds provider for ESPN and CBS Sports.teams. We continuehave continued to create new partnerships among collegiate and professional sports teams including theand, in 2021, entered into a 20-year exclusive naming-rights partnership that rebrandedbranding the Caesars Superdome. GrowthSuperdome in the Caesars Digital segment continues to be realized with the expansion into new states as jurisdictions legalize retail and online sports betting.

Sports Brand Partnerships — New Orleans. Our strategy includes developing local and national partnerships that align our sportsbooks, casinos, resorts and brands with sports fans. In 2019, we announcedWe have high-profile exclusive sports entertainment partnerships with the NFL, making Caesars the first-ever “Official Casino Sponsor” in the history of the league. This historic partnership combines the NFL’s legendary events with our properties to bring unique experiences to Caesarsour patrons. This includes exclusive rights to use NFL trademarks to promote our properties alsoand enabling Caesars to host exclusive special events and experiences. Caesars willWe expect to continue to host brand activations at prominent, high-profile NFL events, including the NFL Draft, NFL playoffs, and the Super Bowl during this multi-year partnership.

Food and Beverage Operations

Our food and beverage operations generate revenues from our dining venues, bars, nightclubs, and lounges located throughout our casinos and represented approximately 12%15% of our total net revenues in 2021.2023. Many of our properties include several dining options, ranging from upscale dining experiences to moderately-priced restaurants, some of which offer pickup or in-room delivery options.

Hotel Operations

Hotel operations generate revenues from hotel stays at our properties in our approximately 47,70044,700 guest rooms and suites worldwide and represented approximately 16%18% of our total net revenues in 2021.2023. Our properties operate at various price and service points, allowing us to host a variety of casino guests, who are visiting our properties for gaming and other casino entertainment options, and non-casino guests who are visiting our properties for other purposes, such as vacation travel or conventions.

Management and Branding Arrangements

We earn revenue from fees paid for the management of four domestic casinos.other hotels and casinos in North America. Managed properties represent Caesars-branded properties where we provide certain staffing and management services under management agreements. In addition, we authorize the use of certain brands and marks of Caesars Entertainment, Inc. Wefrom which we earn revenue from brand license fees received based on the arrangements.

Entertainment and Other Non-Gaming Operations

We provide a variety of retail and entertainment offerings at our properties. We operate various entertainment venues across the United States, including the Colosseum at Caesars Palace Las Vegas and ZapposBakkt Theater at Planet Hollywood.Hollywood Resort & Casino. These award-winning entertainment venues host or have announced plans to host, prominent headliners such as Adele, John Legend, Sting, Donny OsmondGarth Brooks, The Killers, Kelly Clarkson, Jerry Seinfeld, Shania Twain and Keith Urban.Miranda Lambert.

The LINQ Promenade is an open-air dining, entertainment, and retail development located between The LINQ Hotel & Casino and Flamingo Las Vegas, which features The High Roller, a 550-foot observation wheel, and Fly LINQ, the first and only zipline on the Las Vegas Strip. The retail stores offer guests a wide range of options from high-end brands and accessories to souvenirs and decorative items.

CAESARS FORUM is a 550,000 square-foot state-of-the-art conference center located at the center of the Las Vegas Strip. CAESARS FORUM can accommodate more than 10,000 participants and features more than 300,000 square feet of flexible meeting space, the two largest pillarless ballrooms in the world, a LEED silver-rating, andsilver-rated FORUM Plaza, and the first 100,000 square-foot outdoor meeting and event space in Las Vegas. Though currently available for use with no restrictions, COVID-19 related restrictions limited our ability to utilize the convention center and meeting space at full capacity during the first half

Market Activities

Trends

COVID-19 and Related ImpactsEconomic Factors Impacting Discretionary Spending — Gaming and other leisure activities we offer represent discretionary expenditures which may be sensitive to economic downturns. The extentresurgence of the ongoingOmicron variant of COVID-19 continued to impact the beginning of 2022, however, many of our properties experienced positive trends during much of the year ended December 31, 2022 including higher hotel occupancy and futurerates, particularly in Las Vegas, and increased gaming and food and beverage volumes coupled with improved product mix.

We continue to monitor the effects of COVID-19 on our businessrecent inflation and the casino resort industry and economy generallypossible implications on certain customers most affected by lower discretionary income. Although we have seen periods of reduced visitation from those customers, visitation from customers who are not as affected by inflation remains uncertain. While we experienced positive operating trends in 2021, we continuedsteady or has slightly improved. In addition, our leases with VICI are impacted by inflation as they are subject to see a prolonged impact of COVID-19annual escalators based on the economy,Consumer Price Index (“CPI”).

We are also continuing to monitor rising interest rates which have a direct impact on certain of our debt instruments, in addition to an effect on consumer spending. We evaluate projected changes in interest rates when entering into borrowing arrangements and manage our mix of fixed versus variable debt.

We continue to manage the economic challenges affecting our industry and our Company with increased challenges arising fromthat arise including labor shortages, higher labor costs, supply chain challenges, increasingdisruptions, increased costs of goods and services, inflation and rising interest rates, among other impacts. The continuing impact of COVID-19 and such related challenges on our business will depend on future developments, including but not limited to, the duration and severityFurther discussion of the outbreak or new variants, restrictions on operations imposed by governmental authorities, the potential for authorities reimposing stay at home orders, internationaleffects of these trends are described throughout this Form 10-K. The extent and domestic travel restrictions or additional restrictions in response to continued developments with COVID-19, the Company’s ability to adapt to evolving operating procedures and maintain adequate staffing in response to increased consumer demand and discretionary spending, the efficacy and acceptance of vaccines in response to any potential new variants, and the Company’s ability to adjust its cost structures for the duration of the outbreak’s effect on our operations. We also expect that our businessthese trends is uncertain and the casino resort industry and economy generally will continue to be impacted by shortages of labor, supply chain challenges, increasing costs of goods and services, inflation and rising interest rates and that such impacts may intensify.

Online Betting and Gaming — Online betting and gaming is a rapidly developing sector of the e-commerce industry and we believe the digital segment of the global betting and gaming industry will continue to grow in popularity and consumer confidence. The market for online betting platforms is being driven by the increased use of digital processes and global, growing bettor demand. We anticipate that the United States market will begincontinue to have a strong and steady uptake in active wagers as

state-by-state legislation in the United States continues to evolve in response to recent legislation resulting in new opportunities in the United States sports betting market. The extent and future effects of online betting and gaming on our casino properties is uncertain but we expect that our online betting and gaming offeringofferings will be complementary to our brick-and-mortar casino business.

Competition

The casino entertainment business is highly competitive. The industry is comprised of a diverse group of competitors that vary considerably in size and geographic diversity, quality of facilities and amenities available, marketing and growth strategies, and financial condition. In most regions, we compete directly with other casino facilities operating in the immediate and surrounding areas. There has been increased competition from openings of newly developed casinos and plans of development in certain regions, as well as increased competition from recent legalization of casino gambling and sports betting in states such as Nebraska. In Las Vegas, our largest jurisdiction, competition is expected to increase in the coming years. In response to changing trends, Las Vegas operators have been focused on expanding their non-gaming offerings, including upgrades to hotel rooms, new food and beverage offerings, and new entertainment offerings. There have also been openings and proposals for other large scale gaming and non-gaming development projects in Las Vegas by various other developers. Our Las Vegas Strip hotels and casinos also compete, in part, with each other.

In recent years, many casino operators, including us, have been reinvesting in existing facilities, developing or rebranding new casinos or complementary facilities, and acquiring established facilities. These reinvestment and expansion efforts combined with aggressive marketing strategies by us and many of our competitors have resulted in increased competition in many regions. As companies have completed new expansion projects, supply has grown at a faster pace than demand in some areas. The expansion of properties and entertainment venues into new jurisdictions also presents competitive issues.

Our properties also compete with legalized gaming from casinos located on Native American tribal lands. While the competitive impact on operations in Las Vegas from the continued growth of Native American gaming establishments in California remains uncertain, the proliferation of gaming in California and other areas located in the same regions as our properties could have an adverse effect on our results of operations. In some instances, particularly in the case of Native American casinos, our competitors pay lower taxes or no taxes. In addition, certain states have legalized, and others may legalize, casino gaming in specific areas, including metropolitan areas from which we traditionally attract customers. These factors create additional challenges for us in competing for customers and accessing cash flow or financing to fund improvements for our casino and entertainment products that enable us to remain competitive.

We also compete with other non-gaming resorts and vacation areas, various other entertainment businesses, and other forms of gaming, such as state lotteries, on-track and off-track wagering, video lottery terminals, and card parlors. Our non-gaming offerings also compete with other retail facilities, amusement attractions, food and beverage offerings, and entertainment venues. Internet gaming and sports betting also create additional competition for our brick-and-mortar operations.

We face significant competition in our online sports betting, online horse racing wagering and iGaming businesses in jurisdictions where we currently operate.operate and those jurisdictions in which we wish to expand. Although we have experienced recent success in obtaining approval for sports betting and iGaming licenses in new jurisdictions, new state launches may require significant upfront investment. Our investment into new markets is executed through promotional incentives, marketing and advertising spend to establish ourselves as an industry leader.may not be successful.

Resources Material to Business

Rewards Programs

We believe Caesars Rewards, with a networkone of more than 60 million people,the largest loyalty programs, enables us to compete more effectively and capture a larger share of our customers’ entertainment spending when they travel among regions or engage in online wagering and gaming versus that of a standalone property, and engage in online wagering and gaming, which is core to our cross-market strategy.

Members who have joined Caesars Rewards canmembers earn Reward Credits for qualifying gaming activity,activities, including sports betting, online gaming and iGaming apps and wagering in the Caesars Sportsbook and Caesars Racebook apps. Members also earn Reward Credits for qualifying hotel, dining and retail spending at all Caesars-affiliated propertiesCaesars Entertainment destinations in the United States Canada and Dubai. Members can also earn additionalCanada. Additionally, Reward Credits are earned when theymembers use their Caesars Rewards VISA credit card or make a purchase through a Caesars Rewards partner. Members can redeem their earned Reward Credits with Caesars for hotel amenities, retail and online casino free play and other items such as merchandise, gift cards, and travel.those same experiences.

Caesars Rewards is structured in tiersby member tier level (designated as Gold, Platinum, Diamond, Diamond Plus, Diamond Elite or Seven Stars), each and member value. This structure allows a member to progressively access the full range of benefits available across our portfolio of destinations as they progress through tier levels. Caesars Rewards is designed to cultivate a gratifying and frictionless relationship with increasingour customers, motivating members to enhance both their frequency of visits and expenditures. Additionally, member benefits and privileges. Members are provided promotional offers based on their Tier Level, their engagementdata is utilized in conjunction with Caesars-affiliated properties, aspects of their retail and online casino gaming play, and their preferred spending choices outside of gaming. Member information is also used in connection with variousdiverse marketing promotions, includingpromotions. This includes campaigns involvingspanning direct mail, email, our websites, mobile devices, social media, and interactive slot machines.

Intellectual Property and Resources

We use a variety of trade names, service marks, trademarks, patents and copyrights in our operations and believe that we have all the licensesrights necessary to conduct our continuing operations. The development of intellectual property is part of our overall business strategy. We regard our intellectual property to be an important element of our success. We have registered several service marks,file applications for and obtain patents, trademarks patents and copyrights within the United States Patent and Trademark Office or otherwise acquired the licenses to use those which are material to conduct our business. We also own patents relating to unique casino games.foreign countries where we believe filing for such protection is appropriate. While our business as a whole is not substantially dependent on any one patent, trademark, or copyright, we seek to establish and maintain our proprietary rights in our business operations and technology through the use of patents, trademarks, copyrights, and trade secret laws. We file applications for and obtain patents, trademarks, and copyrights in the United States and foreign countries where we believe filing for such protection is appropriate, including United States and foreign patent applications covering certain proprietary technology of Caesars Enterprise Services, LLC (“CES”). We also seek to maintain our trade secrets and confidential information by nondisclosure policies and through the use of appropriate confidentiality agreements. CES’Our United States patents have varying expiration dates.

We have not applied for the registration of all of our trademarks, copyrights, proprietary technology, or other intellectual property rights, as the case may be, and may not be successful in obtaining all intellectual property rights for which we have applied. Despite our efforts to protect our proprietary rights, parties may infringe upon our intellectual property and use information that we regard as proprietary, and our rights may be invalidated or unenforceable. The laws of some foreign countries do not protect proprietary rights or intellectual property to as great of an extent as do the laws of the United States. In addition, others may independently develop substantially equivalent intellectual property.

We own or have the right to use proprietary rights to a number of trademarks that we consider, along with the associated name recognition, to be valuable to our business, including Eldorado, Silver Legacy, Isle, Lady Luck, Tropicana, Circus Circus, Caesars, Flamingo, Harrah’s, Horseshoe, Paris, Planet Hollywood, Caesars Rewards, Caesars Sportsbook, William Hill WSOP, and a license for the Planet Hollywood trademark used in connection with the Planet Hollywood in Las Vegas.WSOP.

As of December 31, 2023, our Caesars Sportsbook and iGaming app is powered by our Liberty platform. We currently operate the Liberty platform in 14 mobile sports betting states. The Liberty platform resulted in a significant upgrade to our user interface and significant product upgrades including numerous pre-match and live markets, extensive odds and flexible limits, player props, and same-game parlays. Our Liberty platform also integrates customers with the Caesars Rewards loyalty program. In addition, we and NYRABets LLC, the official online wagering platform of the New York Racing Association, Inc., have launched the Caesars Racebook app in more than 20 jurisdictions. The Caesars Racebook app provides access for pari-mutuel wagering at over 300 racetracks around the world. Wagers placed can earn credits towards the Caesars Rewards loyalty program.

Industry Overview

Seasonality

We believe that business at our regional properties outside of Las Vegas is subject to seasonality, including seasonality based on the weather in the marketsregion in which they operate and the travel habits of visitors. Business in our properties can also fluctuate due to specific holidays or other significant events, such as Easter (particularlyparticularly when thea holiday falls in a different quarter than the prior year),year, the timing of the WSOP tournament (with respect to our Las Vegas properties), city-wide conventions, a large sporting eventevents or a concert,concerts, or visits by our premium players. We also believe that any seasonality, holiday, or other significant event may affect our various properties or regions differently. We may also experience seasonality with retail and online sports betting which coincides with certain sporting events, as well as seasons of professional and collegiate basketball and football.sports teams.

Gaming Licenses and Governmental Regulations

The gaming and racing industries are highly regulated, and we must maintain our licenses and pay gaming taxes to continue our operations. We are subject to extensive regulation under laws, rules and supervisory procedures. These laws, rules and regulations generally concern the responsibility, financial stability and characters of the owners, managers, and persons with financial interests in the gaming operations. If additional gaming regulations are adopted in a jurisdiction in which we operate, such regulations could impose restrictions or costs that could have a significant adverse effect on us. From time to time, various proposals have been introduced in legislatures of jurisdictions in which we have operations that, if enacted, could adversely affect the tax, regulatory, operational or other aspects of the gaming industry and us. We do not know whether or when such legislation will be enacted. Gaming companies are currently subject to significant state and local taxes and fees in addition to normal federal and state corporate income taxes, and such taxes and fees are subject to increase at any time. Any material increase in these taxes or fees could adversely affect us.

Some jurisdictions, including those in which we are licensed, empower their regulators to investigate participation by licensees in gaming outside their jurisdiction and require access to periodic reports respecting those gaming activities. Violations of laws in one jurisdiction could result in disciplinary action in other jurisdictions.

Under provisions of gaming laws in jurisdictions in which we have operations, and under our organizational documents, certain of our securities are subject to restriction on ownership which may be imposed by specified governmental authorities. The restrictions may require a holder of our securities to dispose of the securities or, if the holder refuses, or is unable to dispose of the securities, we may be required to repurchase the securities.

A more detailed description of the regulations to which we are subject is contained in Exhibit 99.1 to this Annual Report on Form 10-K, which is incorporated herein by reference.

Internal Revenue Service Regulations

The Internal Revenue Service requires operators of casinos and online sports betting apps located in the United States to file information returns for U.S. citizens, including names and addresses of winners for certain table games, keno, bingo, slot machine and retail and online sports betting winnings in excess of stipulated amounts. The Internal Revenue Service also requires operators to withhold taxes on some table games, keno, bingo, slot machine and retail and online sports betting winnings of nonresident aliens. We are unable to predict the extent to which these requirements, if extended, might impede or otherwise adversely affect operations of, and/or income from, other games.

Regulations adopted by the Financial Crimes Enforcement Network of the Treasury Department (“FINCEN”) requires the reporting of currency transactions in excess of $10,000 occurring within a gaming day, including identification of the patron by name and social security number. This reporting obligation began in May 1985 and may have resulted in the loss of gaming revenues to jurisdictions outside the United States which are exempt from the ambit of these regulations. In addition to currency transaction reporting requirements, suspicious financial activity is also required to be reported to FINCEN.

Other Laws and Regulations

Our businesses are subject to various federal, state and local laws and regulations in addition to gaming regulations. These laws and regulations include, but are not limited to, restrictions and conditions concerning alcoholic beverages, food service, smoking, environmental matters, employees and employment practices, currency transactions, taxation, zoning and building codes, and marketing and advertising. Such laws and regulations could change or could be interpreted differently in the future, or new laws and regulations could be enacted. Material changes, new laws or regulations, or material differences in interpretations by courts or governmental authorities could adversely affect our operating results.

The sale of alcoholic beverages is subject to licensing, control and regulation by applicable local regulatory agencies. All licenses are revocable and are not transferable. The agencies involved have full power to limit, condition, suspend or revoke any license, and any disciplinary action could, and revocation would, have a material adverse effect upon our operations.

We also deal with significant amounts of cash in our operations and are subject to various reporting and anti-money laundering regulations. Such laws and regulations could change or could be interpreted differently in the future, or new laws and regulations could be enacted. Material changes, new laws or regulations, or material differences in interpretations by courts or governmental authorities could adversely affect our operating results. See Item 1A, “Risk Factors,” for additional discussion.

Taxation

Gaming companies are typically subject to significant taxes and fees in addition to normal federal, state and local income taxes, and such taxes and fees are subject to increase at any time. We pay substantial taxes and fees with respect to our operations. From time to time, federal, state, local and provincial legislators and officials have proposed changes in tax laws, or in the administration of such laws, affecting the gaming industry. It is not possible to determine with certainty the likelihood of changes in tax laws or in the administration of such laws.

Environmental Matters

We are subject to various federal, state and local environmental, health and safety laws and regulations, including but not limited to air quality, indoor air quality, water quality, bulk storage of regulated materials, and disposal of waste, including hazardous waste. Such laws and regulations can impose liability on potentially responsible parties (owner/operators of real property) to clean up, or contribute to the cost of cleaning up, sites at which regulated materials were disposed of or released. In addition to investigation and remediation liabilities that could arise under such laws and regulations, we could face personal injury, property damage, fines or other claims by third parties concerning environmental compliance, contamination or exposure to hazardous conditions. Environmental regulatory violations also include monetary penalties assessed by the

jurisdictional regulatory agency and civil or criminal penalties for intentional negligence. Occasionally and under certain circumstances, we have investigated and remediated (or contributed to remediation costs) contamination located at or near our facilities. Examples included contamination related to underground storage tanks and groundwater contamination arising from prior uses of land on which certain facilities are located. In addition, we have and continue to contain, manage, and dispose of manure and wastewater generated by concentrated animal feeding operations due to our racetrack operations; manage, abate, or remove indoor air quality concerns such as mold, lead, or asbestos-containing materials; and manage operations within applicable environmental permitting requirements. Although we have incurred and expect to incur costs related to various environmental matters such as investigations, remediation, and management of hazardous materials or conditions known or discovered to exist at our properties, those costs have not had, and are not expected to have, a material adverse effect on our financial condition, results of operations or cash flow. However, such matters in the future could have a material adverse effect on our business.

Climate Change

There has been an increasing focus of international, national, state, regional and local regulatory bodies on greenhouse gas (“GHG”), including carbon dioxide and methane, emissions, and climate change issues. The United States is a member of the Paris Agreement, a climate accord reached at the Conference of the Parties (“COP 21”) in Paris, that set many new goals, and many related policies are still emerging. The Paris Agreement requires set GHG emission reduction goals every five years beginning in 2020. Stronger GHG emission targets were set at COP 26 in Glasgow in November 2021.

Future regulation could impose stringent standards to substantially reduce GHG emissions. Legislation to regulate GHG emissions has periodically been introduced in the U.S. Congress. The current Administration has taken steps to further regulate GHG emissions. Those reductions could be costly and difficult to implement or estimate.

Beyond financial and regulatory effects, the projected severe effects of climate change – such as property damage or supply chain issues stemming from extreme weather events – has already and may continue to directly affect our facilities and operations. Caesars recognizes the impacts of climate change and is engaged in long-term initiatives to identify, assess, and manage the risks and opportunities associated with climate change (see “Environmental Stewardship” below).

Reporting and Record-Keeping Requirements

We are required periodically to submit detailed financial and operating reports and furnish any other information about us and our subsidiaries that gaming authorities may require. We are required to maintain a current stock ledger that may be examined by gaming authorities at any time. If any securities are held in trust by an agent or by a nominee, the record holder may be required to disclose the identity of the beneficial owner to gaming authorities. A failure to make such disclosure may be grounds for finding the record holder unsuitable. Gaming authorities may, and in certain jurisdictions do, require certificates for our securities to bear a legend indicating that the securities are subject to specified gaming laws.

Human Capital Management

We aim to provide a workplace that is engaging, empowering, inclusive and respectful for all employees (our “Team Members”), embracing a culture of openness, passion for service and recognition. Our ongoing investment in professional training and development, safety, health and wellbeing, and Team Member recognition linked to guest satisfaction are all important drivers of our success in delivering strong financial results and creating value for our communities. We have approximately 49,000 employees at our domestic properties51,000 Team Members throughout our organization.organization, excluding the Team Members of certain of our tribal partners.

Labor Relations

Approximately 23,00024,000, or 47% of our employeesTeam Members, are covered by collective bargaining agreements with certain of our subsidiaries. The majority of these employees in various job positions are covered by the following agreements:

| | | | | | | | | | | | | | | | | | | | |

| Employee Group | | Approximate Number of Active Employees Represented | | Union | | Date on which Collective Bargaining Agreement Becomes Amendable |

| Las Vegas Culinary Employees | | 11,50011,000 | | Culinary Workers Union, Local 226 | | May 31, 2023September 30, 2028 |

| Atlantic City Food & Beverage and Hotel Employees | | 2,0005,400 | | UNITE HERE, Local 54 | | May 31, 20222026 |

| Las Vegas Dealers | | 2,000 | | United Auto Workers | | September 30, 2023* |

| Las Vegas Teamsters | | 1,100 | | Teamsters, Local 986 | | March 31, 2024 |

| Las Vegas Bartenders | | 1,300 | | Bartenders Union, Local 165 | | May 31, 2023 |

Las Vegas Dealers | | 2,100 | | United Auto Workers | | September 30, 20232028 |

We aim to support Team Member Engagement, Compensation, Benefits, Development, SafetyMembers throughout their career with Caesars. We are committed to providing opportunities to help Team Members achieve their professional goals. We maintain a wide range of channels for diverse recruiting, including outreach to academic institutions and Wellbeingnonprofits that help us source diverse candidates. Our leadership receives training on our inclusive and equitable talent management recruitment and retention processes. Additionally, to support hiring initiatives across the enterprise, we maintain a recruiting website that includes information describing our culture, benefits and diversity initiatives. The website highlights our commitment to corporate social responsibility (“CSR”) diversity, equity and inclusion (“DEI”), and we welcome candidates from all backgrounds.

We strive to inspire our Team Members through our mission, vision and values, and our Code of Commitment (described below). To evaluate our Team Member experience and our retention efforts, we monitor a number of employeeTeam Member measures, such as turnover rates and Team Member satisfaction. In 2021, we implemented newWe send out Team Member experience surveys to help us further understand the drivers of engagement and areas where we can improve. These surveys will beare completed on a regular basis alongside additional surveys targeted at specific events within a Team Member cycle includingsuch as new hires, anniversary milestoneshire onboarding and exit inquiries.

Our compensation and benefits programs are designed to attract, retain and motivate our Team Members. In addition to competitive salaries and wages, we provide a variety of short-term, long-term and incentive-based compensation programs to reward performance relative to key metrics relevant to our business. We offer comprehensive benefit options including, but not limited to, retirement savings plans, health insurance coverage (including medical, mental health, dental, vision and pharmacy), parental leave, educational assistance, training opportunities, and company-paid life insurance.insurance and a Team Member assistance program.

We place utmost importance on creating a safe workplace for our Team Members, embedding procedures so that all our Team Members have the awareness, knowledge and tools to make safe working a habit.

We also have maintainedmaintain a wellness program to help our Team Members improve their health and wellbeing. This program has demonstrated improved health metrics for participating employeesTeam Members and their covered family members helping reduce the cost of healthcare for Team Members and for the Company. Effective in 2022, we consolidated our group health plans and made significantWe continue to make enhancements to our offerings and wellness program includingprograms with a wide range of affordable options, mental health initiatives and expanded onsite and virtualprimary care clinics across the US.

Diversity, Equity and Inclusion

We embrace diversity and aim to create an inclusive working environment that celebrates all our Team Members as individuals. Our diversity, equity and inclusion (“DEI”) framework identifies five pillars of activity: advocacy, Team Members, suppliers, communities and guests for a holistic approach to embedding DEI in everything we do. We publish our DEI data in our annual Corporate Social Responsibility (“CSR”)CSR report (described below). Currently, 45%

We set goals to increase the representation of leadership roles in the Company are held by women and 43% are held by people of color excluding the recent acquisition of William Hill. In addition, we set our newin leadership roles (supervisory and above). Our 2025 goals around gender and racial diversity with a target ofoutlined 50% of leadershipmanagement roles to be held by women in both the mid-level and senior leadership populations, and 50% of leadership roles to be held by people of color by 2025.color. We also commitcommitted to increase the representation of people of color in senior leadership roles by 50%. Furthermore, in 2021 we became the first gaming company named as a “Best Place to Work for Disability Inclusion”As of December 31, 2023, 45% of mid-level roles and 29% of senior leadership roles in the 2021 Disability Equality Index.Company were held by women. Additionally, 44% of leadership roles were held by people of color and the representation of people of color in senior leadership positions has increased by 116% since October 2020.

Corporate Social Responsibility

Caesars’ Board of Directors (the “Board”) and senior executives view CSR as an integral element in the way we do business, inwith the belief that being a good corporate citizen helps protect the companyCompany against risk, contributes to improved performance and helps foster positive relationships with all those with whom we connect. The Board and our executive management are committed to being an industry leader in CSR (which includes diversity, equity and inclusion, social impact, and environmental sustainability). In 2021,2023, the Board and our leadership continued to engage with our CEO-level external CSR Advisory Board comprised of experts representing DEI, sustainability, business strategy, academia and investors, and used their guidance to confirm our CSR priorities. These priorities are reflected in our 12th14th annual CSR report, published in 20212023 in accordance with Global Reporting Initiative Standards.

CSR Committee of the Board

Following the Merger in July 2020, Caesars’ Board formedhas a CSR committee that defines the duties and responsibilities of the Board in supporting delivery of our corporate purpose and CSR strategy as well as CSR-related aspects of corporate governance such as Board diversity.

Code of Commitment

Caesars is committed to being a responsible corporate citizen and environmental steward through our CSR strategy, PEOPLE PLANET PLAY. This is reflected in our Code of Commitment which is our public pledge to our guests, Team Members, communities, business partners and all those we reach that we will honor the trust they have placed in us through ethical conduct and integrity. We commit to:

•PEOPLE: Supporting the wellbeing of our Team Members, guests and local communities.

•PLANET: Taking care of the world we all call home.

•PLAY: Creating memorable experiences for our guests and leading responsible gaming practices in the industry.

PEOPLE PLANET PLAY Strategy

Our PEOPLE PLANET PLAY strategy defines how we meet the obligations of our Code of Commitment and is aligned with global priorities articulated by the United Nations as the Sustainable Development Goals. PEOPLE PLANET PLAY establishes multi-year targets in key areas of impact, including science-based greenhouse gas emissions-reduction formally approved by the Science Based Targets Initiative (“SBTi”),goals aligning with global best practices on climate change action. We planIn 2022, we conducted a comprehensive CSR assessment to complete a stakeholder analysisevaluate our

assumptions. With the help of an external specialist, our assessment gathered input from internal and comprehensive doubleexternal stakeholders, reviewed multiple industry and environmental, social and governance (“ESG”) disclosures, standards and frameworks and yielded 21 material topics. Our materiality assessment in 2022, reflectingis available on our website at www.investor.caesars.com within the latest sustainability and social trends, transparency demands andESG resource hub on our business strategy that will also align with the investor community’s Environment,Corporate Social and Governance requirements. Following our stakeholder analysis and materiality assessment, we plan to revise our strategic goals under the PEOPLE PLANET PLAY framework, with the expectation that we will commit to additional multi-year targets beyond those we continue to advance.Responsibility page.

Responsible Gaming

For more than thirty years, Caesars has maintained its Responsible Gaming (“RG”) program. We train tens of thousands of Team Members each year and a cadrecohort of RG Ambassadors throughout our properties to identify guests in need of assistance and provide support. In recent years, Caesars has contributed to the National Center for Responsible Gaming, the National Council on Problem Gaming and other state programs to help advance responsible practices in the gaming industry. Caesars Digital also maintains responsible gaming programs tailored to each state in which it operates, participates in Caesars’ overarching Responsible Gaming program, and offers users in-application RG tools such as time on device restrictions and wagering limits. No customers under 21 years old are allowed to wager on any of our Caesars Sportsbook, Caesars Racebook and iGaming mobile apps.

Caesars maintains a comprehensive risk-based Bank Secrecy Act (“BSA”) and Anti-Money Laundering (“AML”) program. It includes strong governance and effective internal controls and procedures to comply with applicable BSA requirements, regulatory guidance, and any related laws, and to take measures to prevent its affiliated casinos from being used for money laundering or other criminal activity. Execution of the program is governed with reference to FINCEN’s guidance on the Culture of Compliance. CaesarsCaesars’ internal AML Policy, Know Your Customer Policy and BSA Identification Policy outline the Caesars AML Program and set the minimum standards for the related procedures and internal controls of the Caesars casino affiliates. EmployeesCertain employees are required to complete annual trainings related company policies, including AML.

Caesars also maintains a Code of Ethics and Business Conduct (the “Code”) that includes standards designed to deter wrongdoing and to promote, amongst other standards, honest and ethical conduct and full, fair, accurate, timely and understandable disclosure in reports and documents that the Company files with the Securities and Exchange Commission. Caesars’ Chief Legal Officer serves as the compliance officer of the Code and Caesars provides periodic training regarding the contents and importance of the Code.

Caesars also maintains an Amended and restatedRestated Gaming Compliance Plan (the “Plan”), which is approved by various gaming regulators. The Plan is designed to overseeimplement procedures to enhance the likelihood that no activities of the Company or any Affiliateaffiliate of the Company will impugn the reputation and integrity of Caesars. The Plan and also establishes a Compliance Committee that assists the Company in implementing its strict policy that its business be conducted with honesty and integrity, and in accordance with high moral, legal and ethical standards. Caesars’ Senior Vice President & Assistant General Counsel & SVP – Regulatory & Compliance serves as the Compliance Officer as defined by the Plan.

Environmental Stewardship

We take a proactive approach to environmental sustainability through our CodeGreen strategy established by Former Caesars in 2007, consistently improvingstriving to improve our performance across energy and GHG emissions efficiencies, reduction of water consumption and increasing diversion of waste diversion from landfills. Caesars recognizes the impact climate change can play both on our business and the guests we serve. Identifying, assessing, and managing the risks and opportunities therefore plays a vital role in our long-term strategic thinking on climate and water, and how we approach our CSR goals. Former Caesars adopted Science Based Targets (“SBTs”)Our goals are based in science as part of itsour strategy to reduce our environmental impact. TheseIn 2023, we began the process to establish new goals to align with a 1.5-degree Celsius limit to global warming, measured against a 2019 base-year and we expect to announce our new goals in 2024.

Our existing GHG targets, approvedestablished in 2018 to be in line with wellSBTi’s guidance to achieve a level of decarbonization required to keep global temperature increase below 2

degrees Celsius, per SBTi are (i) reducing absolute Scope 1 and 2 GHG emissions by 35% by 2025, and 100% by 2050, from a 2011 base-year and (ii) having 60% of suppliers by spend institute science-based GHG reduction targets for their operations by 2023. In 2022, we expect to establish a new baseline to reaffirm GHG emission reduction goals as a combined company. For 2020, following the Merger, we modeled our GHG emissions data to create an estimate for 2018 and prior years back to 2011. This enabled us to compare our progress against our SBTs using actual data from 2019 and 2020 against a modeled 2011 base year. Between 2011 and 2020,2022, Caesars estimated a reduction in absolute Scopes 1 and 2 GHG emissions of 36.1%.41.8%, thereby achieving our interim Scope 1 and 2 reduction target ahead of schedule. We recognizefell short of our supplier engagement goal; however, in 2023 we revisited our Scope 3 emissions and intend to set an absolute reduction target in 2024 as part of our new GHG goals that 2020 was an atypical yearbetter align with property closures and business interruptions resulting from COVID-19 that had a material impact on1.5-degree Celsius pathway.

To achieve our results. Caesars isgoals, we have taken initiatives such as pursuing renewable energy sources and low-carbon options, including on site solar developments. For example, we have contracts to purchase energy from solar covered parking canopies recently completed at two Atlantic City properties and we installed solar covered parking at Harrah’s Pompano Beach. Our long-term goals include a continued focus on energy efficiency and conservation as well as evaluating renewable energy supply opportunities for each of our properties in pursuitproperties.

We voluntarily participate in the CDP (formerly the Carbon Disclosure Project), an international nonprofit that runs a global disclosure system for investors, companies, and regions to manage their environmental impacts. In 2021,2023, Caesars scored an A forA-for water security and a B for climate change for our 2020 performance and earned a spot on the Supplier Engagement Leaderboard from CDP. Justchange. Approximately 2% of companies assessed by CDP makein 2023 made the A List and only 8% make the Supplier Engagement Leaderboard.for either climate change or water security.

We are engaged in extensive waste reduction efforts across our facilities, including recycling, food donation, and manure composting. In 2020,2022, we diverted 45%59% of our total waste from landfills.

Community Investment

Caesars contributes extensively to our local communities to help them develop and prosper, through funding community projects, employeeTeam Member volunteering and cash donations from the Caesars Foundation, a private foundation funded from our operating income. In 2021,2023, the Caesars Foundation contributed $1.8$3.7 million to communities across the United States. The Caesars Foundation also continued to support significant national relationships that support diversity, equity and inclusion. In addition, we donated $3.1 million generated from parking fees at Las Vegas properties to nine local nonprofit organizations. During 2020,2023, our Team Members volunteered over 91,00082,000 hours through the HERO program.

ManyWe focus on multi-faceted support of our community partners are long-term collaborations.non-profit partners. For example, in 2023 we have many years of partnership with Meals on Wheels Americademonstrated our commitment to combat the issues of senior hunger and isolation. We also partner with Clean the World to reduce waste from soap bars and plastics from our hotel operations, and Boys and Girls Club of America to support the mission of enabling young peopleBoys & Girls Clubs of America through regional giving to reach their full potential as productive, caring, responsible citizens.local Clubs, HERO volunteering, hosting fundraising events, collecting customer donations through Caesars Makes Change, in addition to providing several Caesars Foundation grants at the national and local levels, all totaling nearly $1 million in value to the organization and the communities where we operate.

We host national Economic Equity Tours through live webinars and on-line resources for thousandsseek to encourage DEI dialogue in our communities as part of women of color owned small businesses, and diverse non-profits. Expert-led webinars provided resources in the areas of financial empowerment, nonprofit organization development, and entrepreneurship.our advocacy approach to raise awareness. In Spring of 2022,2023, we will host ahosted our DEI Summit in alignment with our nonprofit andwhich bring together corporate partners, nonprofit partners, advocacy groups and suppliers in supporting and promoting efforts to support the advancement of inclusionadvance DEI initiatives. The Summit included several educational sessions and advocacypanel discussions led by notable DEI leaders and promotion and support of DEI.practitioners.

Available Information

We are required to file annual, quarterly and other current reports and information with the Securities and Exchange Commission (“SEC”). Because we submit filings to the SEC electronically, access to this information is available at the SEC’s website (www.sec.gov). This site contains reports and other information regarding issuers that file electronically with the SEC.

We make our Annual Reports on Form 10-K, our Quarterly Reports on Form 10-Q, our Current Reports on Form 8-K, and all amendments to these reports, available free of charge on our corporate website (www.caesars.com/corporate) as soon as reasonably practicable after such reports are filed with, or furnished to, the SEC. In addition, our Code of Ethics and Business Conduct and charters of the Audit Committee, Compensation Committee, Corporate Social Responsibility Committee, and the Nominating and Corporate Governance Committee are available on our website. We will provide reasonable quantities of electronic or paper copies of filings free of charge upon request. In addition, we will provide a copy of the above referenced charters to stockholders upon request.

References in this document to our website address do not incorporate by reference the information contained on the website into this Annual Report on Form 10-K.

Cautionary Statement Regarding Forward-Looking Information

This Annual Report on Form 10-K includes “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. Forward-looking statements include statements regarding our strategies, objectives and plans for future development or acquisitions of properties or operations, as well as expectations, future operating results, trends and other information that is not historical information. When used in this report, the terms or phrases such as “anticipates,” “believes,” “projects,” “plans,” “intends,” “expects,” “might,” “may,” “estimates,” “could,” “should,” “would,” “will likely continue,” and variations of such words or similar expressions and their negative forms are intended to identify forward-looking statements. Specifically, forward-lookingThese statements may include, among others, statements concerning:are made on the basis of management’s current views and assumptions regarding future events.

•the impact of COVID-19 on our business and financial condition;

•projections of future results of operations or financial condition;

•expectations regarding our business and results of operations of our existing casino properties and prospects for future development;

•expectations regarding trends that will affect our markets and the gaming industry generally, including expansion of internet betting and gaming, and the impact of those trends on our business and results of operations;

•our ability to comply with the covenants in the agreements governing our outstanding indebtedness and leases;

•our ability to meet our projected debt service obligations, operating expenses, and maintenance capital expenditures;

•expectations regarding availability of capital resources;

•our ability to consummate the announced dispositions of William Hill International and Belle of Baton Rouge;

•our intention to pursue development opportunities and additional acquisitions and divestitures; and

•the impact of regulation on our business and our ability to receive and maintain necessary approvals for our existing properties and future projects and operation of online sportsbook, poker and gaming.

Any forward-lookingForward-looking statements are based upon certain underlying assumptions, including any assumptions mentioned with the specific statements, as of the date such statements were made. Such assumptions are in turn based upon internal estimates and analyses of market conditions and trends, management plans and strategies, economic conditions and other factors. Such forward-looking statements are only predictions and involve known and unknown risks and uncertainties, many of which are beyond our control, and are subject to change. By their nature, forward-looking statements involve risks and uncertainties because they relate to events and depend upon future circumstances that may not occur. Actual results and trends may differ materially from any future results, trends, performance or achievements expressed or implied by such statements. Forward-looking statements speak only as of the date they are made, and we assume no duty to update forward-looking statements. Forward-looking statements should not be regarded as a representation by us or any other person that the forward-looking statements will be achieved. Undue reliance should not be placed on any forward-looking statements. Some of the contingencies and uncertainties to which any forward-looking statement contained herein are subject include, but are not limited to, the following:

•our sensitivity to reductions in discretionary consumer spending as a result of downturns in the extenteconomy and durationother factors outside our control;

•projections of future results of operations or financial condition;

•expectations regarding our business and results of operations of our existing casino properties and prospects for future development;

•the impact of COVID-19,economic trends, inflation supply chain challenges and labor shortagespublic health emergencies on our business and financial condition;

•expectations regarding trends that will affect our market and the Company’sgaming industry generally, including expansion of internet betting and gaming, and the impact of those trends on our business and results of operations;

•our ability to comply with the covenants in the agreements governing our outstanding indebtedness and leases;

•our ability to meet our projected debt service obligations, operating expenses, and maintenance capital expenditures;

•expectations regarding availability of capital resources;

•our intention to pursue development opportunities and additional acquisitions and divestitures;

•the impact of regulation on our business and our ability to receive and maintain necessary approvals for our existing properties and future projects and operation of online sportsbook, poker and gaming.

•the impact of the Data Incident (as defined below) and any other future cybersecurity breaches on our business, financial conditions and results of operations;

•factors impacting our ability to successfully operate our digital betting and liquidity;iGaming platform and expand its user base;

•our ability to adapt to the very competitive environments in which we operate, including the online market;

•the impact of economic downturns and other factors that impact consumer spending;

•the impact of win rates and liability management risks on our results of operations;

•our reliance on third parties for strategic relationships and essential services;

•costs associated with investments in our online offerings and technological and strategic initiatives;

•risk relating to fraud, theft and cheating;

•our ability to collect gaming receivables from our credit customers;

•the impact of our substantial indebtedness and significant financial commitments, including our obligations under our lease arrangements;

•restrictions and limitations in agreements governing our debt and leased properties could significantly affect our ability to operate our business and our liquidity;

•financial, operational, regulatory or other potential challenges that may arise as a result of leasing of a number of our properties;

•the effect of disruptions or corruption to our information technology and other systems and infrastructure;

•the ability to identify suitable acquisition opportunities and realize growth and cost synergies from any future acquisitions;

•the impact of governmental regulation on our business and the cost of complying or the impact of failing to comply with such regulations;

•changes in gaming taxes and fees in jurisdictions in which we operate;

•risks relating to pending claims or future claims that may be brought against us;

•changes in interest rates and capital and credit markets;

•the effect of seasonal fluctuations;

•our particular sensitivity to energy and water prices;

•deterioration in our reputation or the reputation of our brands;

•potential compromises of our information systems or unauthorized access to confidential information and customer data;

•our reliance on information technology, particularly for our digital business;

•our ability to protect our intellectual property rights;

•our reliance on licenses to use the intellectual property of third parties and our ability to renew or extend our existing licenses;