UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

ý☒ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 20172019

or

o☐TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from ____ to ____

Commission File Number: 001-36316

AgroFresh Solutions, Inc.

(Exact Name of Registrant as Specified in Its Charter)

|

| | | | | | | |

Delaware

| | 46-4007249

|

| (State or other jurisdiction of incorporation) | | 46-4007249

(IRS Employer Identification Number) |

One Washington Square

510-530 Walnut Street, Suite 1350

Philadelphia, PA 19106

(Address of principal executive offices)

(267) 317-9139

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

|

| | | | | | | | | | | | | |

| Title of each class | | Trading Symbol(s) | | Name of each exchange on which registered |

| Common Stock, par value $0.0001 per share | | AGFS | | The NASDAQ Global Market |

| Warrants to purchase shares of Common Stock | | AGFSW | | The NASDAQ Global Market |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. o☐ Yes ý☒ No

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Exchange Act o☐ Yes ý☒ No

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. ý☒ Yes o☐ No

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (Section 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). ý☒ Yes o☐ No

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S—K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10—K or any amendment to this Form 10—K. o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company, or an emerging growth company. See the definitions of large accelerated filer,” “accelerated filer” andfiler,” “smaller reporting company”

and "emerging growth company" in Rule 12b-2 of the Exchange Act. (Check one): |

| | | | | | | | | | | | | |

Large accelerated filer o☐ | Accelerated filer x☐ | Non-accelerated filer o☒ (Do not check if a

smaller reporting company)

| Smaller reporting company o ☒ | Emerging growth company o ☐ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. o☐

Indicate by check mark whether the registrant is a shell company (as defined by Rule 12b-2 of the Act). o☐ Yes ý☒ No

As of June 30, 2017,2019, the aggregate market value of the common stock held by nonaffiliates of the registrant, based on the $7.81$1.51 closing price of the registrant’s common stock as reported on the NASDAQ Stock Market on that date, was approximately $170$33 million. For purposes of this computation, all officers, directors and 10% beneficial owners of the registrant are deemed to be affiliates. Such determination should not be deemed to be an admission that such officers, directors or 10% beneficial owners are, in fact, affiliates of the registrant.

The number of shares of the registrant’s common stock outstanding as of March 9, 2018February 25, 2020 was 50,903,047.51,195,101.

DOCUMENTS INCORPORATED BY REFERENCE

The information required by Part III of this annual report on Form 10-K, to the extent not set forth in this Form 10-K, is incorporated herein by reference from the registrant’s definitive proxy statement relating to the annual meeting of stockholders to be held in 2018,2020, to be filed with the Securities and Exchange Commission within 120 days after the end of the registrant’s fiscal year ended December 31, 2017.2019.

TABLE OF CONTENTS

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

Certain of the statements contained in this annual report on Form 10-K constitute “forward-looking statements” for purposes of federal securities laws. Our forward-looking statements include, but are not limited to, statements regarding our or our management’s expectations, hopes, beliefs, intentions or strategies regarding the future. In addition, any statements that refer to projections, forecasts or other characterizations of future events or circumstances, including any underlying assumptions, are forward-looking statements. The words “anticipate,” “believe,” “continue,” “could,” “estimate,” “expect,” “intend,” “may,” “might,” “plan,” “possible,” “potential,” “predict,” “project,” “should,” “would,” “will” and similar expressions may identify forward-looking statements, but the absence of these words does not mean that a statement is not forward-looking. Forward-looking statements in this report may include, for example, statements relating to:

•our future financial performance;

•growth plans and opportunities, including planned product and service offerings;

•changes in the markets in which we compete;

•our ability to increase brand loyalty and awareness;

•our ability to enter into alliances and complete acquisitions of other businesses;

•protection of our intellectual property rights; and

•the outcome of any known and unknown litigation.

The forward-looking statements contained in this report are based on our current expectations and beliefs concerning future developments and their potential effects on us. Future developments affecting us may not be those that we have anticipated. These forward-looking statements involve a number of risks, uncertainties (some of which are beyond our control) or other assumptions that may cause actual results or performance to be materially different from those expressed or implied by these forward-looking statements. These risks and uncertainties include, but are not limited to, those factors described under the heading “Risk Factors” elsewhere in this report. Should one or more of these risks or uncertainties materialize, or should any of our assumptions prove incorrect, actual results may vary in material respects from those projected in these forward-looking statements. We undertake no obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise, except as may be required under applicable securities laws.

PART I

ITEM 1. BUSINESS

Overview

AgroFresh Solutions, Inc. (the “Company”, “AgroFresh”, “we”, “us” or “our)“our”) is a global leader in delivering innovative food preservation and waste reduction solutions forthat extend the shelf life of fresh produce. The Company is empowering the food industry with Smarter FreshnessTM, a range of integrated solutions designed to help growers, packers and retailers improve produce freshness and quality while preventing shrinkage and reducing waste.

AgroFresh’s solutions range from pre-harvest with HarvistaTMmarket leadership is underpinned by our global footprint, extensive applied scientific expertise, customer intimacy, and LandSpringTM to its marqueeSmartFreshTM Quality System, which includes SmartFreshTM, AdvanStoreTMa growing portfolio of value-added products and ActiMistTM, working together to maintain the quality of stored produce. AgroFresh has a controlling interest in Tecnidex Fruit Protection, S.A.U. (“Tecnidex”), a leading provider of post-harvest fungicides, waxes and biocides for the citrus market. Additionally, the company’s initial retail solution, RipeLockTM, optimizes banana ripening for the benefit of retailers and consumers. AgroFresh hasmission-critical advisory services. Our key products registeredare approved for sale in over 4550 countries, supports approximately 3,700 directand support customers and serviceswith over 25,000 storage rooms globally.

In addition, we provide in-depth plant physiology expertise and offer a comprehensive list of solutions spanning from near-harvest to post-harvest, from storage through retail. More importantly, AgroFresh uses proprietary technologyhas been able to regulate the ripening effectsgain a high level of ethylene, the naturally occurring plant hormonetrust from our customers, which is built on nearly 20 years of interaction and support. Our direct market approach, high touch service and science-based model best position us to address our customers’ needs. We believe that triggers ripening in certain fruits and vegetables. Our portfolio of products, that span the supply chain of fresh produce, from orchard to retail shelves, differentiates usthis is a key differentiator compared to other companies that have more narrow product offerings. offer limited service levels.

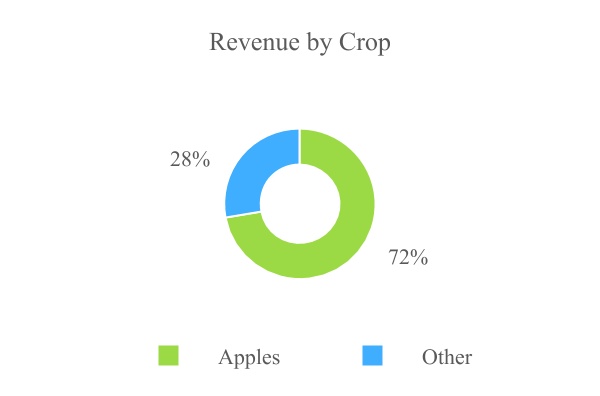

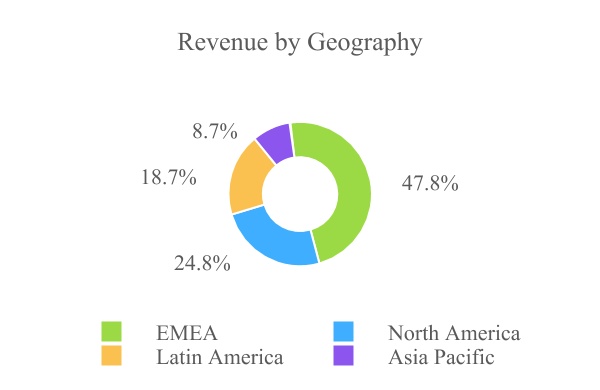

The active ingredient of severalfollowing tables present a breakdown of our products, 1-Methylcyclopropene ("1-MCP")revenue based on solutions, crop and geography for the year ended December 31, 2019.

Note: “EMEA” comprises Europe, the Middle East, and Africa. “Other” include revenue from pears, citrus, kiwifruit, avocados, bananas, and other crops.

AgroFresh’s core business provides solutions to extend the shelf life of fresh produce for both growers and packers. SmartFreshTM, blocks the effects of ethylene. All of AgroFresh’s 1-MCP products are naturally biodegradable and leaves no detectable residue, which has significant consumer appeal.

We believe that SmartFresh our current principal productflagship solution, preserves the texture, firmness, taste and appearance of produce during storage, transportation and retail display. SmartFreshIt allows growers and packers to deliver “just harvested” freshness on a year-round basis and enables retailers to increase customer satisfaction with fresh, high quality produce. An integral part of the SmartFresh sales processvalue proposition is a direct service model providing customers with on-site applications of SmartFresh at their storage facilities together with mission-critical and value-added advisory services. Overall, the SmartFreshTM Quality System offers growers and packers an integrated freshness management solution that is highly effective and easy to deploy.

AgroFresh has two solutions for the pre-harvest market. Our Harvista™ technology is used in pre-harvest management of pome fruit, such as apples and pears. Just as we believe SmartFresh revolutionizedextended its post-harvest apple storage, we believe Harvista can have a similar impact in the orchard. Harvista slows ripening (starch conversion), reduces fruit drop, and holds fruit on the tree longer to promote better color and fruit size, thereby bringing new benefits to the grower and the retailer. It also extends the harvest window to allow growers maximum flexibility in harvest timing while providing peace of mind. LandSpring is a plant-growth regulator ("PGR") for pre-transplant use on seedlings to help them withstand transplanting and other stresses encountered in the field. 2017 was the first year of sales for LandSpring and it received positive reaction from key launch customers.

Our range of solutions for packers and distributors includes innovative storage monitoring systems, StorEdge and AdvanStore, as well as a new delivery system for fungicides, ActiMist. StorEdge and AdvanStore provide customers insights into their storage rooms to help them better manage their storage inventory. Through its novel thermofogging application, ActiMist introduces a better and more efficient way to apply fungicides to stored apples that saves customers money and reduces the complexity of their fungicide protocols. Tecnidex broadens our portfolio of products to post-harvest fungicides, waxes, and biocides, primarily for the citrus market.

RipeLock, a solution designed to improve the quality and consumer appeal of bananas, combines proprietary modified atmosphere packaging and 1-MCP. RipeLock is sold to retailers and enables them to offer consumers bananas that are in better condition and hold the consumer-preferred color longer, reducing shrink and increasing sales. AgroFresh also has a commercial agreementleadership with Food Freshness Technology Holdings Limited ("FFT") that permits us to offer retailers their It’s Fresh!TM ethylene absorbing filters, another novel technology to preserve the freshness of produce at retail.

History

We are a former blank check company that completed our initial public offering on February 19, 2014. On July 31, 2015 (the “Closing Date”), we consummated a business combination (the “Business Combination”) pursuant to a Stock Purchase Agreement, dated April 30, 2015 (the “Purchase Agreement”), with The Dow Chemical Company (“Dow”), providing for the acquisition by us of the AgroFresh business from Dow, resulting in AgroFresh Inc. becoming our wholly-owned, indirect subsidiary. On the Closing Date, we changed our name from Boulevard Acquisition Corp. to AgroFresh Solutions, Inc. Prior to

the closing of the Business Combination, the business that now comprises our business was operated through a combination of wholly-owned subsidiaries and operations of Dow, including through AgroFresh Inc. in the United States.

In December 2017 AgroFresh acquiredof a controlling interest in Tecnidex Fruit Protection, S.A. (“Tecnidex”) which is based in Valencia, Spain, one of the largest citrus producing regions in the world. Tecnidex, a leading provider of post-harvest fungicides, sanitizers, waxes and biocides forcoatings, is primarily focused on the citrus market. Through its portfolio of post-harvest products, technology, consulting, and after-sale services, Tecnidex improves the quality and value of its clients’ fruit and vegetables while respecting the environment.

Tecnidex brought a broad catalog of solutions that enhanced our existing offering, including fungicides that can be added to our innovative ActiMistTM delivery system of foggable fungicides. The expanded offerings further diversified our revenue by expanding our ability to provide more solutions and service the citrus industry. With this acquisition, AgroFresh expanded its industry-leading post-harvest presence into additional crops and increased its penetration of the produce market in southern Europe, Latin America and Africa. We continually seek opportunities to leverage this range of products across new geographies for both existing and new customers.

For over 35 years, Tecnidex has been helping

Complementing our post-harvest solutions, AgroFresh’s HarvistaTM technology is used for near-harvest management of pome fruit (apples and vegetable producers offer clean, safepears), blueberries and high-quality productscherries. Just as SmartFresh revolutionized post-harvest apple storage, we believe Harvista is starting to customershave a similar impact in 18 countries. Through its portfoliothe orchard. In apples, Harvista slows ripening, reduces fruit drop, and holds fruit on the tree longer to promote better color and fruit size. With maximum flexibility in application timing, it extends the harvest window by allowing growers to factor in ever-changing weather conditions and labor availability. We have found that the combination of post-harvest products,Harvista in the orchard and SmartFresh in the storage room results in improved apple quality compared to use of either product individually. When applied to cherries, Harvista offers an increase to yield of a minimum of 10%.

AgroFreshprovides freshness solutions across the supply chain, including retail where much of the ripening process and shrinkage occurs for certain crops. This includes bananas, the largest retail fruit category, and avocados, the fastest growing fruit category. According to data from the Journal of Consumer Affairs and Food and Agriculture Organization of United Nations, it is estimated that 12-16% of banana loss occurs after the fruit reaches the grocery store. SmartFresh technology consulting,can also address this problem and after-sale services, Tecnidex improvesimprove the quality and consumer appeal of bananas. SmartFresh application enables retailers to extend the consumer-preferred yellow life of bananas an additional 2-4 days, reducing shrinkage at the store level. As part of the same diversification efforts, we are also developing and promoting applications of SmartFresh adapted to diverse customer requirements for avocados, broccoli, melons, prunes, tomatoes and mangos.

Our FreshCloud™ platform is an example of how we continue to evolve and increase the value we provide to our customers. The FreshCloudTM platform consists of its clients’produce monitoring and screening solutions with real time information delivered in the “cloud” to customers. FreshCloud capitalizes on our decades-long history of innovation and scientific know-how in the physiology of fruits and vegetables. FreshCloud consists of both enhancements to our existing service offering and customer base and new solutions to reach more crops and steps in the distribution chain. FreshCloud Storage Insights combines proprietary sensor technology and data analytics in the storage room to offer customers real-time access to unique insights into the condition of their stored fruit. FreshCloud Predictive Screening predicts the risk of disorder development during storage by analyzing gene expression at commercial harvest, resulting in more informed storage management decisions. FreshCloud Transit Insights combines sensor technology and proprietary algorithms to provide insights into the condition and quality of fruit during transit. We continue to expand the scope of our FreshCloud offerings, and vegetables while respectingwe are in the environment. Tecnidex is based in Valencia, Spain.process of launching FreshCloud Quality Insights, which aims to integrate quality control and machine learning to drive better decisions through integrated data, as well as digitalization of current solutions such as Harvista.

In December of 2017, AgroFresh invested approximately $10$10.0 million for an approximate 15% ownership stake in and entered into a commercial agreement with FFT, provider of the award-winning It’s Fresh! ethylene removal filters in North America, Europe, the Middle East and Africa (“EMEA”) and Latin America. The proprietary active ingredient of It’s Fresh! has been found to be 100 times more powerful than any other ethylene-absorbing substances, providing a powerful tool to preserve food freshness. We expect It’s Fresh! to complement the RipeLockTM Quality System, our retail solution for extending the freshness of bananas. Through our commercial agreement with FFT, AgroFresh will market It’s Fresh! for high value crops such as berries, stone fruit, avocadoes, tomatoes and cherries, and open up new opportunities to address food waste in retail. FFT’s filters create a protective "Freshasphere"TM around fruit and vegetables to significantly improve their quality, reduce waste and increase sales. Although both companies will continue to operate independently, a key goal of the mutual collaboration is to increase penetration of each company’s respective technology at leading retailers. Where FFT has developed strong retailer relationships, it will serve asrecently shifted its strategic focus away from retailers to growers and packers and is devoting commercial efforts to the launch of a sales agentnew film technology. Due to lower projections while FFT ramps up for AgroFresh’s RipeLock program anda new product launch, AgroFresh will perform the same role for FFT’s It’s Fresh!TM filters with AgroFresh’s retail partners.recognized an impairment charge on its investment in FFT during 2019.

We are subject to extensive national, state and local government regulations. We have completed more than 400 comprehensive international health and environmental tests that have shown the AgroFresh family of products, including SmartFresh and Harvista, to be safe for consumers, workers and the environment. 1-MCP,1-Methylcyclopropene ("1-MCP"), the active ingredient in the AgroFresh products, is metabolized by the natural processes in fruits and leaves no residue. The AgroFresh products have been approved by over 50 authorities including the U.S. Environmental Protection Agency and the European Commission.

Competitive Strengths

We believe that the following strengths differentiate us from our competitors and serve as the foundation for our planned continued growth:

GlobalLeading Agricultural Innovator and Solutions Provider with Proprietary Technical Know-HowKnow-How. AgroFresh has been at the forefront of fresh produce preservation solutions since our inception. Our research and Solutions. We are an agricultural innovatordevelopment team include over 40 scientists, about half with operations in over 45 countries. Our scientists and research staffadvanced degrees, who are leaders in the fieldfields of post-harvestplant physiology. SinceBeginning with our creation of the launchcommercial market for 1-MCP applications for use in the preservation of SmartFresh in 2002,apples, we have developedproduced an extensive and exclusive database onof produce physiology and preferences ofconsumer preferences. Building on our approximately 3,700 customers. Using this extensive proprietary technical expertise, AgroFresh providesknowledge, we have developed an intellectual property portfolio, including over 500 granted and pending patents, that has enabled us to provide comprehensive and innovative solutions to a range of integrated solutions.global customer base. SmartFresh delivers a step-changesubstantial improvement in storage solutions for apples, pears, and pears,other crops, allowing for significantly less waste and greater productivity, as well as a constant supply of high qualityhigh-quality fruit throughout the year. We believeIn the U.S., we estimate that 90% of stored apples are treated with 1-MCP, and our SmartFresh technology continues to enjoy a strong leadership position in this treatment protocol. Extending our record of innovation in the post-harvest market, we entered the near-harvest market with the introduction of Harvista, haswhich extends the potentialideal harvest window for apples and pears, and increases production yields for cherries and blueberries to significantly impact the pre-harvest stage, allowing appleimprove harvest management and pear growers to better manage their harvest, reduce waste and improveenhance fruit quality. Building on this success, we entered the fungicide market with ActiMist and

subsequently enhanced our fungicide portfolio with the acquisition of Tecnidex in 2017. Our recent launch of FreshCloud is the latest milestone in our new product innovation. With StorEdge and AdvanStore,the FreshCloud platform, we expect to be able to provide packers unparalleled informationcustomers real time insights about the condition of their fruit while in cold storage using novel monitoring technologies. The introduction of ActiMist,

Diversified Global Presence Across All Major Growing Regions. We have established a fungicide platform delivered via thermofogging offers a more efficient and quicker application of fungicidesglobal footprint with key products approved in over 50 countries that supports customers with over 25,000 storage rooms simplifying operationsglobally. Our top ten customers represent less than 15% of the Company's total revenue, a sign of the strength and reducing complexity.resilience of our business. The combinationCompany's global commercial platform is unique in the post-harvest industry, positioned across six continents, bringing a full suite of Harvista, SmartFresh, ActiMist, StorEdgeAgroFresh solutions and AdvanStore offers apple and pear growers a unique solutionhigh-touch advisory services to improve the results they are ablecustomers in every key produce-growing region. Our ability to deliver to their customers. LandSpringin-depth technical services and products across every major continent is an additional pre-harvest technology that benefits seedling growers by making the seedlings less sensitive to stresses such as heat, cold and flooding. RipeLock is an innovative fruit quality management system for bananas, offering flexibility and consistency to growers, ripeners and retailers to deliver bananas at a ripeness preferred by consumers.fundamental competitive advantage in our pursuit of capturing growth opportunities. We believe that our storage solutionsglobal footprint provides not only a platform for growth but also greater diversification. Our participation in a wide range of markets protects the business from crop size fluctuations in any particular market. For the year ended December 31, 2019, EMEA, North America, Latin America and portfolioAsia Pacific (including China and India) represented 47.8%, 24.8%, 18.7% and 8.7% of pre- and post-harvest services are well positioned to help address customer needs.sales, respectively. The acquisition of a controlling interest in Tecnidex and the investment in FFT reflectmeaningfully contributed to our ability to expand beyond 1-MCP solutions and develop additional sources of revenue through a variety of crops.global diversification.

Compelling Benefits for Value Chain. Consumer surveys have found that freshness is the most important driver of satisfaction with produce purchased at retail. The ability to store produce longer while preserving just-harvested quality allows growers and packers to extend their marketing window and capitalize on seasonal pricing trends. We believe that SmartFresh revolutionized the apple industry by allowing growers and packers to meet year-round consumer demand for just-harvested quality. This

extension of post-harvest life substantially increases the value of produce that is harvested on a seasonal basis but is sold to consumers throughout the year, particularly during the summer months when apple prices have historically peaked. The cost of SmartFresh translates into less than one cent per pound of apples, and can provide up to a 20-fold increase in value to the grower or packer over the cost of the service. Due to its high effectiveness and low cost relative to the value of the crop treated, we believe that SmartFresh provides compelling benefits across the value chain, from grower to retailer.

UniqueService-Oriented Business Model withCreates Sustainable Competitive StrengthsAdvantages. AgroFresh’s direct service model provides better margins than the industry average, and comprises not only product applications but also “mission critical”mission-critical technical advisory services. We have established a global footprintOur sales and technical support personnel maintain direct interaction with operationsour customers in over 45 countries, allowing us to make over 38,000 monitored applicationsareas of SmartFresh in 2017. Wecontract negotiations and overall customer service. Furthermore, we currently have approximatelyover 40 employees indedicated research and development scientists, about half with advanced degrees, working inacross seven global AgroFresh locations, around the world and at numerous research institutes, and customer sites. This infrastructure investment has allowed us over the past decade, to amass a proprietary database of technical data regardingof plant physiology collected across our 20+ year history. In 2019, we made approximately 36,000 monitored applications of SmartFresh. Our proprietary database gives us unique insights into the causes of produce spoilage for various crops varieties in different regions as well as best practices for the effective use of SmartFreshSmartFresh. As a result, our local sales and technical service teams are best positioned to provide custom advice and solutions, giving our customers “peace of mind” between and during harvest season.

We believe FreshCloud can further bolster our integrated offerings with a wide rangethe addition of apple varieties in variable conditions. Our advisory services utilize this informationdata-backed solutions for the monitoring of produce quality across the supply chain. FreshCloud is designed to assistdeliver timely, predictive insights that will ultimately help our customers in maximizing the profitability of their operations. improve efficiency and enhance produce freshness.

We believe that our direct service model, extensive technical know-how, and brand loyalty will continue todifferentiate us from competitors and sustain our competitive strengths. The credibility

Strong Momentum and trust thisGrowth Opportunities across the Produce Supply Chain. We believe there are significant growth opportunities to expand and diversify our business, model has created positions AgroFresh wellsupported by our track record of new product introductions, market penetration, and mergers and acquisition (“M&A”) execution.

One key initiative is to provideincrease penetration of existing technologies into current and new customers with other solutions such as storage monitoringgeographic markets. While many apple growers and fungicides.

Multiple Drivers of Future Growth.packers in the U.S. have adopted SmartFresh, there is potential for further growth. The market penetration of apples treated with SmartFresh outside the U.S. has been growing internationally but has not yet reachedremains below the levels achieved in the U.S. We have also concentrated on accelerating penetration of SmartFresh into pears outside of the U.S., as well as plums, kiwifruit and persimmons. Based on successful trials with customers, we are increasingalso expanding our salescommercial activities for SmartFresh to increase its use on avocados, bananas, melons, tomatoes, broccoli and marketing efforts in non-U.S. regionsmangos, where we believe SmartFresh can optimize the consumer experience for ripeness, color, taste, and texture. Related to seek to capture these penetration opportunitiesthis effort, we are repositioning RipeLock as our brand for packaging- based freshness technology solutions for fruits and vegetables.

Harvista is another key product where we are actively working to increaseexpand geographic adoption. As of December 31, 2019, Harvista is registered in eight countries and we are currently working to obtain registrations in more than ten additional countries including the European Union (the "EU"). In the past few years, we received regulatory approval to apply Harvista to cherry crops in the U.S., blueberries in Chile, and apples in Australia and our team is working to achieve similar registrations in other markets. Additionally, in 2020 we received approval for use of SmartFreshHarvista on other crops, including pears, kiwifruit, plums,apples in Brazil. The main limitation to accelerated growth of Harvista is the long regulatory approval cycle in important markets like the EU.

We have further augmented our crop solutions portfolio through our acquisition of Tecnidex. The addition of Tecnidex fungicides, sanitizers, waxes and bananas. Harvista extendscoatings has diversified our crop exposure, reduced revenue seasonality, and provided new growth opportunities via cross-pollination of Tecnidex technologies into AgroFresh core fruit categories. As a result of all these initiatives, we have successfully diversified our proportion of sales attributable to apples from nearly 90% in July 2015 down to approximately 72% as of December 31, 2019.

Building on these growth initiatives, we continuously seek opportunities to leverage our research and development (“R&D”) capabilities to commercialize new products for currently unserved markets. At the same time, we are looking at M&A opportunities as another key strategy to enhance our value proposition and drive growth.

Long-Standing Relationships with Highly Diverse Customer Base. We believe our direct service model coupled with our proprietary technology into pre-harvest managementsolutions have helped us develop deep, trusted and long-tenured relationships with a diverse array of applesglobal customers including packers, growers, and pears. Harvista is undergoing an expandedretailers. For more than a decade, we have operated a large team of commercial launchand technical experts located in key geographies around the U.S. We also currently sell Harvista in Turkey, Argentinaworld to provide on-site custom advisory services. This infrastructure helps us maintain intimate and Israel, and plan further launches in South Africa and Chile soon. In addition, we are investing in and launching new solutions that we anticipate will drive continued business growth. LandSpring is another pre-harvest application approved for use on tomato and pepper seedlings and 14 other crops. It is applied to seedlings prior to transplant from the plant house to the field because transplanting is a stress event that causes the plant to produce ethylene. LandSpring blocks the negative effects of ethylene and allows for increased plant vigor including better root establishment, development of greater leaf surface, and less susceptibility to disease which all can lead to better yields. StorEdge and AdvanStore offer atmospheric monitoring that storage operators are not capable of achieving with existing controlled atmosphere (“CA”) technology. This advanced monitoring system is being developedconsistent interaction with our extensive understanding of fruit physiology, fruit respiration, current CA technology, and new proprietary diagnostic tools for measuring fruit volatiles and is designed to provide solutions to customers to help them protect the value of their crops. ActiMist is a platform for delivering fungicides in the storage rooms via thermofogging which enable packhouses to get their storage rooms to desired conditions faster and with less complexity. RipeLock combines 1-MCP with modified atmosphere packaging designed specifically for preserving the quality of bananas during transportation and extending their yellow shelf life for retailers and consumers.

High Customer Touch and Retention. Our personnel interact with our customers face to face throughout the year to addressunderstand all aspects of post-harvestharvest operations, andaddress a variety of customer specificcustomer-specific issues, toand ultimately improve the economics for growers, packers, and retailers across the supply chain. As a result of growersour unique service model and packers.comprehensive solutions, we have cultivated direct customer relationships in more than 50 countries. We believe that this, in turn, has producedhave also started some strategic customer relationships as a high levelway to penetrate new geographies and markets.

High Profit Margins, Strong, and Consistent Cash Flow Generation. Our technical expertise, long-standing customer relationships, and asset-light business model drive attractive, sustainable profit margins. For the year ended December 31, 2019, we generated gross margins and EBITDA margins of customer retention74% and trust in23%, respectively1. In addition, we employ an “asset-light”, outsourced production model. We use a single third-party manufacturer for our key active ingredient, 1-MCP, under a long-term contract with strict confidentiality obligations, to manufacture, and several other suppliers to formulate products and provide packaging services. For the manufacturing of waxes, sanitizers, and equipment servicing the citrus market, we have a combination of a manufacturing plant and several suppliers to formulate products and assemble equipment. As a result, our manufacturing footprint requires minimal capital investment and manufacturing personnel. For the year ended December 31, 2019, capital expenditures were $3.6 million, or 2.1% of net sales. Our attractive margin profile coupled with our asset-light solutions result in free cash flow generation, which will be used to reinvest in the business and repay debt.

ProvenStrong Management Team with Deep Industry Experience. Our management team has extensive food, agricultural and relatedchemical industry experience long-standing customer relationships, and a longproven track record of success in bringing valuable services andinnovative, value-added solutions to market. Commercialcustomers and technical experts are locatedmarkets around the world. The Company’s management team boasts over 125 years of combined relevant industry experience and is led by Jordi Ferre, our chief executive officer, who has over 25 years of experience in key geographies worldwide to provide on-site advisory services, which help customers optimize crop potential. We encourage an independentglobal food operations and entrepreneurial spirit amongmanufacturing.

During the past several years, our management team has effectively launched new products, established new partnerships across the supply chain and employees.completed a successful acquisition of the majority control of Tecnidex. Supported by a deep bench of professionals and a track record of execution, we believe our management team has the vision, expertise, and experience to position us for continued success and to implement our business and growth strategies.

1 EBITDA margin is a non-GAAP measure. See “Management’s Discussion and Analysis of Financial Condition and Results of Operations” in Item 7 of this Annual Report on Form 10-K for more information, and for a reconciliation of EBITDA to net (loss) income.

Industry Overview

Food Preservation and Freshness

According to the FAO,Food and Agriculture Organization of the United Nations, over 1.3 billion metric tons of food, or approximately one third of the total food produced worldwide, is lost to spoilage or waste each year, includingyear. Euromonitor reports that retailers are often judged on their fresh food valued at an estimated $48.3 billion in the U.S. alone. An October 2013 TESCO Consumer Study found that nearly 45% of all fresh fruits and vegetables, including 40% of apples and 20% of bananas, are lost to spoilage. Loss or waste along the food supply chain has a variety of causes, including degradation of fresh produce during storage and transportation.

Food waste is a major economic cost for retailers.selection. A large percentage of food waste at the retail level is based on qualitative factors related to consumer perception of freshness. A consumer survey conductedIn the U.S., the Environmental Protection Agency announced in 2015 the first-ever domestic goal to reduce food loss and waste by Oliver Wyman50 percent by 2030.

Loss or shrinkage along the food supply chain has a variety of causes, including degradation of fresh produce during storage and Ipsos Interactivetransportation.

AgroFresh strives to be the guardian of the world’s fresh produce and stands ready to lead the fresh produce industry into a more sustainable future. In 2019, we completed a detailed sustainability study about the influence of SmartFresh on the apple industry. From 2002 to 2018, we estimate that 259,500 metric tons of apple waste were diverted in the U.S., France and Italy alone. This reduced apple spoilage equates to more than 2.5 million metric tons of water. Improving the apple supply chain in those three countries during the same period took more than 10 million metric tons of carbon dioxide out of the air. This is equivalent to taking approximately two million cars off the road for one year or eliminating one billion smartphone charges. In other countries throughout the world, we estimate that SmartFresh reduced CO2 emissions by approximately 342,000 metric tons during that same period.

the U.S. in 2007 indicated that freshness is the most important driver of customer satisfaction with a store’s produce department.

Pre-HarvestNear-Harvest Treatments

Pre-harvestNear-harvest treatments commonly used to increase the value of crops and reduce pre-harvestharvest losses include the use of

“plant “plant growth regulators” (“PGRs”). during the last stages of crop growth. PGRs influence the rate of growth or development of crops or affect their reaction to stress events such as harsh weather. PGRs interact with the biochemical make-up of the plant and work by mimicking or blocking the production of naturally occurring plant hormones, like ethylene. Blocking the production of ethylene allows a grower to slow down the maturation of fruit to achieve better control over the timing of harvest. PGRs have a range of effectiveness depending on factors such as environmental conditions and the timing of applicationapplication. We consider applications in the orchard as “near-harvest” since they are applied right before the fruit is harvested and have synergistic effect with our post-harvest solutions.

Post-Harvest Treatments

Post-harvest treatments to maximize quality and reduce loss include treatments to manage the effects of ethylene and to prevent microbial contamination. Naturally occurring ethylene triggers the acceleration of ripening in certain crops which results in a reduction of post-harvest life.

One class of post-harvest treatments enhances quality and reduces losses by controlling the environment in which produce is stored. CAControlled Atmosphere ("CA") and Dynamic Controlled Atmosphere (“DCA”) systems are used to keep stored crops within their optimal ranges of temperature and levels of oxygen and carbon dioxide. Specific oxygen and carbon dioxide levels can lower respiration in fresh produce and delay ripening. CA systems have been used for many decades with fruits and vegetables to preserve freshness. DCA, a more recent innovation, seeks to adjust levels of oxygen and carbon dioxide dynamically as the produce in storage breathes and matures. CA and DCA are only effective at preserving freshness while the fruit is kept in cold storage. However, 1-MCP treatments have been found to be complementary to these technologies by helping to better maintain the quality of apples and pears during cold storage and maintaining freshness for up to 90 days after the applesthey are removed from cold storage.

Our Business

We are an agricultural innovator in proprietary advanced technologies that enhance the freshness, quality, and value of fresh produce. We currently offer SmartFresh applications at customer sites predominately through a direct service model utilizing third-party contractors. We also provide advisory services based on our extensive knowledge on the use of 1-MCP collected through tens of thousands of monitored applications done as a part of the service model. Our pricing to customers is based on the service provided, not on the product sold. We operate in over 4550 countries and derive the majority of our revenue working with customers to protect the value of apples, pears and other produce during storage. We also offer Harvista pre-harvest technology in the U.S,U.S., Canada, Argentina, Chile, Turkey, Israel, ChileAustralia and South Africa.Africa, and are expanding into Brazil starting in 2020. LandSpring an additional pre-harvest technology for seedlings, is being marketed primarily in the U.S. RipeLock, an innovative quality management system isand SmartFresh diversification efforts are being marketed mainly in the U.S., EuropeMexico and Australia.Peru. ActiMist a platform of foggable fungicides was launched in the U.S. and is being expanded into other countries subject to regulatory approval. Line extensions and new services are planned for introduction to seek to strengthen our global position in post-harvest storage and to capitalize on adjacent growth opportunities in pre-harvestnear-harvest markets.

Tecnidex’s business,AgroFresh has extended its post-harvest leadership with the acquisition of Tecnidex, a leading provider of fungicides, sanitizers, waxes, and coatings primarily focused on the citrus is mainly concentratedmarket. For over 35 years, Tecnidex has been helping fruit and vegetable producers offer clean, safe and high-quality products to customers in southern Europe18 countries with particular strength in the Mediterranean region. Tecnidex brought a broad catalogue of solutions that enhanced our fungicide offering, ActiMist, an innovative delivery system of foggable fungicides. Our fungicide offerings further diversify our revenue by expanding our ability to provide solutions and North Africa and expands our product offering into other types of fungicides, as well as waxes and coatings.service to the citrus industry.

1-MCP, the active ingredient in SmartFresh, LandSpring Harvista and RipeLock,Harvista, is an ethylene action inhibitor with a proven ability to maintain freshness and extend the shelf life of certain fresh produce. The 1-MCP molecule is structurally similar to ethylene, a naturally occurring plant hormone that occurs in certain fruits and vegetables. Ethylene helps produce grow and ripen, but eventually causes over-ripening and spoilage. 1-MCP works by blocking the ethylene receptors in plant cells, which temporarily delays the ripening process, enabling the produce to better maintain the qualities associated with freshness.

Today, two types of SmartFresh formulations are used to deliver 1-MCP into store rooms, powder and tablets. In a typical SmartFresh powder application, an AgroFresh service provider mixes a pouch of water-soluble powder with water in a SmartFresh generator and activates the generator to release the gaseous form of 1-MCP in the sealed storeroom. When using tablets, a service provider adds the tablets into a prepackaged formulated solution, the tablets dissolve in the solution and the gaseous form of 1-MCP is released in the storeroom. The gas released by either process interacts with the stored fruit, and firmly binds to the fruit’s ethylene receptor sites.

Fruits and vegetables are classified as climacteric or non-climacteric, a term referring to the process of fruit maturation. The climacteric event is a stage of fruit ripening associated with higher ethylene production and changes in the fruit including pigment changes and sugar release. The climacteric event marks the peak of edible ripeness, with fruits having the best taste and texture for consumption. The role of SmartFresh is to delay the onset of the climacteric stage until the product is ready for consumption. Apples, pears, kiwifruit, plums, persimmon, bananas, melons, peaches and tomatoes are examples of climacteric fruit. Our managementThe Company continues to evaluate the commercial value of 1-MCP with a range of other climacteric fruit.

SmartFresh Value Proposition

SmartFresh, our flagship solution, preserves the texture, firmness, taste and appearance of produce during storage, transportation and retail display. It allows growers and packers to deliver “just harvested” freshness on a year-round basis and enables retailers to increase customer satisfaction with fresh, high quality produce. An integral part of the SmartFresh value proposition is a direct service model providing customers with on-site applications of SmartFresh at their storage facilities together with mission-critical and value-added advisory services.

The value of SmartFresh with any crop is determined by both the biological efficacy with that crop and the utility value the application delivers to the customer. The biological efficacy with apples is high; apples are sensitive to ethylene and SmartFresh is effective at delaying ripening. In addition, SmartFresh brings high utility value by helping to keep apples fresh year-round despite their limited harvest window. This has resulted in the widespread adoption of SmartFresh by apple growers and packers throughout the world. The cost of SmartFresh translates into less than one cent per pound of apples, which is small relative to both the value of the crop and the importance of maintaining the quality of that crop during storage. Retail prices of apples in the U.S. typically range from $1.30-$4.50 per pound depending on the variety. The use of SmartFresh gives growers and packers the ability to store apples from one season to the next without losing their just picked quality characteristics.

Beneficial effects of SmartFresh have been proven across numerous apple varieties throughout the world. SmartFresh is also effective with other crops that are highly sensitive to ethylene, including pears, kiwifruit, plums, persimmons, avocados, melons, tomatoes and broccoli, each of which requires a different application method and supply chain logistics beyond storage rooms. We also offer a corresponding solution for flowers, the latter marketed under the EthylBloc brand name through two strategic partners that have a strong position in the global flower market.

AgroFresh’s business historically has been highly seasonal, driven by the timing of apple harvests in the northern and various private label brands.southern hemispheres. The first half of the year is when the southern hemisphere harvest occurs, and the second half of the year is when the northern hemisphere harvest occurs. Since the northern hemisphere harvest of our two core crops of apples and pears is typically larger, a significant portion of our sales and profits are historically generated in the second half of the year. In addition to this seasonality, factors such as weather patterns may impact the timing of the harvest within the two halves of the year. Crop diversification is an important way to achieve balanced revenues across the year, and the ability to service the citrus segment provides an opportunity for the Company to increase revenue in the fourth and first quarters, which are the two strongest quarters for citrus crops. Our acquisition of a controlling interest in Tecnidex and an increased presence in the citrus category has moderately reduced the historic concentration of sales in the second half of the year.

SmartFresh Service Model

We believe that we have developed deep, trusted relationships with our customers by combining our effective SmartFresh product with application expertise and trusted advisory services. Over the past decade we have amassed a valuable proprietary database of technical information on the best practices for the effective use of SmartFresh on a wide range of apple and pear varieties.varieties, since each fruit and fruit variety requires a different treatment protocol. The advisory services component utilizes this information to help maximize the profitability of our customers’ operations.

Seasonality

Our business is highly seasonal, driven by the timing of harvests in the northern and southern hemispheres. The first half of the year is when the southern hemisphere harvest occurs and the second half of the year is when the northern hemisphere harvest occurs. Since the northern hemisphere harvest is typically larger, a significant portion of our sales are historically generated in the second half of the year. In addition to this seasonality, factors such as weather patterns may impact the timing of the harvest within the two halves of the year.

Our Other Products

Harvista

Complementing our post-harvest solutions, Harvista is a pre-harvestused for near-harvest management product that brings ethylene management into orchardsof apples, pears, cherries and fields.blueberries. Our Harvista product line includes several proprietary 1-MCP formulations that are specifically designed to keepslow ripening, reduce fruit drop, and hold fruit on the tree longer which allows moreto promote better color and fruit size, developmentthereby bringing new benefits to the grower. With maximum flexibility in application timing, it extends the harvest window by allowing growers to factor in ever-changing weather conditions and reduceslabor availability, providing peace of mind. We have found that the combination of Harvista in the orchard and SmartFresh in the storage room results in improved fruit stress.

Harvista provides flexibility for fruit harvesters when it is needed the most - within a few days before harvest or when bad weather strikes. Additionally, application prior to, or following, a stress event such as bad weather helps to reduce the incidence of fruit drop or other adverse reactions triggered by these events, which can lower crop yields and cause significant economic loss. We believe the flexibility to apply treatment close to harvest provides growers using Harvista with valuable harvest management benefitsquality metrics compared to competing solutions using older technology that require applications well in advanceuse of harvest.either product individually.

Harvista extends the “ideal harvest window,” the period during which fruit quality is at its peak, by keeping the fruit on the tree longer. For pome fruits, Harvista can extend the length of the harvest windowwindow” for up to an additional 14 days. This added flexibility creates significant benefits both in terms of harvest logistics and crop profitability. Widening the harvest window allows for better scheduling and the optimization of limited resources, such as harvest crews and equipment. The extended harvest window can result in increased average size and weight of fruit. Overall, the value of the crop is enhanced by bigger average sizes,fruit size, better color, and fewer defects.

We offer Harvista for apples, pears, cherries and pearsblueberries through a pre-scheduled application service including aerial and/or ground applications.applications depending on the crop and growing region. Typically, our technical staff designs the protocol in consultation with the customer, and either a third-party service providers makeprovider or the applications. We have also implemented a program to allow customers to make their own applications through AgroFresh-owned sprayers or using kits to modifycustomer makes the customers' own sprayers. This gives orchard operators flexibility to manage the application timing to meet orchard conditions.application.

Harvista is currently available in the U.S., Canada, Turkey, Argentina, Brazil, Israel, Chile, Australia and South Africa, and the Company is currently compiling data for registrations in more than ten more countries, which are expected to be granted on a country by country basis over the next five years. In 2017, we received regulatory approval to apply Harvista to cherries.cherries in the U.S. and blueberries in Chile. Additional registrations and label expansions are expected to be pursued as new formulations and/or crop concepts are validated.

StorEdge & AdvanStoreFreshCloud

Our StorEdgeTo continue to evolve and AdvanStore platforms are usefulincrease the value we provide to our customers, we recently launched our FreshCloud suite of produce monitoring and screening solutions. FreshCloud Storage Insights combines proprietary sensor technology and data analytics in monitoringthe storage room to offer customers real-time access to unique insights into the condition of producetheir stored fruit. FreshCloud Predictive Screening predicts the risk of disorder development during storage. StorEdge provides confirmation, within days that a SmartFresh application was completed successfullystorage by analyzing gene expression at commercial harvest, resulting in more informed storage management decisions. FreshCloud Transit Insights combines sensor technology and provides additional data about storage room conditions the customers can useproprietary algorithms to identify issues. The AdvanStore offering includes on-going monitoring, analytics and feedbackprovide insights as to enable the customer to more optimally manage the condition of the stored commodity and receive early notice of conditions present in the room that may be detrimental to the quality of the produce. Through internal innovation, use of sophisticated analysis and external alliances, the AdvanStore platform reflects our strategy to provide proprietary complete storage solutions to customers by leveraging our extensive knowledge of fruit physiology.during transit.

RipeLock

RipeLock is an innovative fruit quality management system specifically designed for the banana industry. The patented RipeLock system combines a specially-engineered, micro-perforated form of Modified Atmosphere Packaging (“MAP”) and our proprietary 1-MCP formulation. The combination of MAP with 1-MCP provides greater control over the ripening progression of bananas during shipping, distribution, and display. We believe that bananas handled with RipeLock technology retain their bright-yellow color, firm texture, fresh taste, and appealing look for significantly longer than untreated bananas. As a result, RipeLock maximizes the marketable “yellow life” of the fruit, providing economic benefits to brand owners and retailers. Commercial launch of RipeLock began in 2015, and it is now generating revenue among ripeners, food service companies and retailers in the U.S., Europe and Central/Latin America.

LandSpring

LandSpring technology is a PGR for use on seedlings to help them withstand transplanting and other stresses encountered in the field. LandSpring’s active ingredient, 1-MCP, preventsLandSpring suppresses the ethylene signals that would prompt a stress event in the seedling and reduce growth. Among the number of protective benefits, this technology makes seedlings less sensitive to stresses such as heat, cold, UV radiation, drought, flooding and salinity that often occur after planting. When applied before transplanting, LandSpring results in greater plant vigor and a healthier crop that is better able to withstand adverse environmental conditions and give growers the opportunity to increase yield.

Growth Strategy

Our mission is to provide technology, service and support targeted at preserving the quality, freshness and value of produce, through the value chain, worldwide. We have a high touch, asset light, technology driven solutions philosophy. We intend to pursue profitable growth by building on our current capabilities and competencies, expanding into adjacent markets and pursuing related, accretive acquisitions.

Our focus is to:

Strengthen our brand awareness and loyalty through customer relationship programs, intellectual property protection and year-round customer engagement. AgroFresh believes this focus, building on its philosophy of customer intimacy and its sustainable competitive advantages, will allow it to secure and grow its current business.

Further penetrate short term cold storage opportunities in all regions. AgroFresh currently provides its offering to over 80% of U.S. apples stored beyond 30 days. This percentage is much lower in Latin America, Asia Pacific and Europe.

Penetration is typically driven by the pace of registrations, which were earliest in the U.S., and AgroFresh sees these other geographies presenting further opportunities for growth moving forward, as well as shorter term apple storage opportunities in all regions with existing customers.

Extend to other produce, including bananas, pears, and other crops that have the ethylene physiology which responds positively to 1-MCP. One example is RipeLock for bananas. AgroFresh believes it will be able to provide a measurable extension of “yellow life” as well as prevent disorders like split-peel, both of which are highly desired value drivers throughout the supply chain, especially at retail and consumer levels where consistent quality is expected to increase sales.

Expand into other segments such as pre-harvest fruit quality management, fungal and microbial control solutions, diagnostics and storage management solutions. Solutions developed in-house include Harvista, LandSpring, ActiMist and AdvanStore.

Diversify and grow via alliances and accretive acquisitions, building on our numerous core competencies. AgroFresh anticipates proactively pursuing these opportunities. Our acquisition of a controlling interest in Tecnidex is one such example facilitating our expansion into fungicides, biocides, waxes and coatings. In addition, we expect our agreement with FFT to complement RipeLock by bringing a new type of freshness solution to the same retailers we are engaging.

Operations

We operate in more than 45 countries around the world. Currently, we use a single third-party manufacturer (and have a second supplier qualified), under a long-term contract that includes strong confidentiality obligations, to manufacture our key active ingredient, 1-MCP, and several other third parties, primarily to manufacture formulated products and provide product packaging services. We have no owned manufacturing facilities or manufacturing personnel.

We use a high-touch service model for our commercially available products including SmartFresh and Harvista. Sales and sales support personnel maintain direct relationships with customers year-round, which our technical sales and support personnel work directly with customers to provide value-added advisory services regarding the application of SmartFresh and Harvista. The actual application of SmartFresh and Harvista is performed by service providers that are typically third-party contractors. In addition to providing Harvista full service at customer orchards in 2017, we provide retrofit kits to customers to allow them to use their own sprayers to make applications themselves.

We have a dedicated customer service organization responsible for fulfilling customer-related requirements as well as coordinating all services being delivered by our service providers. During the harvest season, temporary third-party resources are added to the customer service organization to support the high volume of transactions and activities.

Marketing and Sales

Our success depends on our ability to attract and develop the talent to effectively implement our strategy. AgroFresh changed its organizational structure and leadership team to support its strategic growth and diversification objectives. The goal of the organizational change is to consolidatehas consolidated the Company’s core business units under a global general managerfour seasoned commercial directors while adding leadership and focus to accelerate new business development activities. Over the past year,In 2018, we have been strengthening and deepening our management organization. We have hired a vice president and global general manager to lead our post-harvest offerings and a director of global retail solutionscrop diversification to lead the RipeLockdiversification of commercial opportunities.opportunities as well as expansion into crops other than pome fruit and citrus. In 2019, we added a business leader to target citrus expansion in California, Peru and Mexico.

The Company’sCompany's core post-harvest business includes SmartFresh, ActiMist, StorEdge and AdvanStore, allsolutions designed to strengthenimprove the company’s leadership inyields of growers and packers. These solutions include SmartFresh, Harvista, ActiMist, FreshCloud Storage Insights, FreshCloud Predictive Screening and a large range of fungicides, waxes and coatings, marketed under the post-harvest space. There is one global general manager with separate regional leads for North America, EMEA, Latin Americabrands Textar and APAC.Teycer, respectively.

The 2017 acquisitionIntegration of Tecnidex continued to progress well in 2019, with all functional departments now aligned with AgroFresh’s global structure, including consolidation of all sales teams. In addition, SAP was managed as a separate business unit and integration is well under wayimplemented across the Tecnidex organization in 2018.April 2019.

The technical sales support group housed within the Research and Development organization, supports the sales team. Technical sales supportteam and runs customer-specific trials for local crop varieties or specialized storage and distribution conditions and conducts follow-up with customers. These individuals workThis team works closely with customers to provide advice on appropriate protocols for SmartFresh, Harvista and Harvistaother product applications depending on crop, variety, region, and climatic conditions. The technical sales support group draws on our extensive knowledge base of 1-MCP applications across all regions and conditions.

Marketing and communications functions areThe marketing function is organized on a global and regional basis. The regionalThis includes global brand management and corporate brand/image stewardship and regionally developed marketing strategies and tactics to drive growth and customer penetration. Marketing personnel are embedded within the Company’s operating regions to provide maximum ability to collaborate with local sales teams manage the core post-harvest business'sand capitalize on business opportunities. Regional marketing needs, while the Global marketing department is responsible for corporate brand stewardship

and communications, as well as serving as a center of excellence to support all product launches, advertising and trade shows. The teams reach out tointeract with customers to keep them up to date on the latest research and news about AgroFresh products. Market research, including product penetration, collecting competitive intelligence and tracking other relevant market and industry information, is managed globally in conjunction with the regional teams.

No single customer accounted for more than 10% of net sales in 2017, 2016,2019, 2018 or 2015.2017.

Competition

TheWe estimate the size of the core post-harvest market forto be approximately $500 million on a global basis. The post-harvest solutions is fragmented with various regional suppliers or products.offered include 1-MCP-based solutions, fungicides and coatings, representing approximately 36%, 20% and 24% of the total market, respectively. The market for the use of 1-MCP is evolving and we expect to continue to facehave faced growing competition as oursince the expiration of the 1-MCP use patent in 2014. We estimate that citrus applications represent approximately 60% of the total core

post-harvest market, which is why we are focused on seeking to grow in this important crop segment. The market for post-harvest solutions is fragmented with various regional suppliers. Including AgroFresh, there are three leading providers with global reach that account for about two thirds of global post-harvest sales. Other regional players, mainly in citrus, account for approximately another 20% of post-harvest sales. Additional key patent expires. We compete with other pre- andplayers in the post-harvest crop preservation providers that have similar product claims and offer potential functional substitutes for our products. Current competitors include: dynamic controlled atmosphere storage companies, including Harvest Watch; Janssen Pharmaceutical and Pace International; and 1-MCP generic sellersindustry include fungicide suppliers such as AgroBest, FitomagSyngenta and several Chinese companies.Janssen PMP who hold post-harvest registrations of fungicides previously approved for pre-harvest applications. In the near-harvest segment, ReTainTM is used pre-harvest for extending the harvest season acrossa competitive technology to Harvista that is offered by Valent in all regions withexcept for the exception of the European Union.EU. We believe that the principal factors of competition in our industry include reputation, product quality, customer service and customer intimacy, product innovation, technical service and value creation. We believe that we compete favorably with competitors on the basis of these and other factors. See the subsection titled “Competitive Strengths” above.

Research and Development

Research and development plays an important role at AgroFresh in supporting customers as well as developing line extensions and new products. ApproximatelyResearch and development is a truly global function with less than half of our research and developmentR&D resources are located in facilities in North America, withand the remainder across theour other regions. Approximately 30% of our research and development resources are third-party contractors. During fruit harvest times (August to November in the Northern Hemisphere and late January to early May in the Southern Hemisphere), we hire additional third-party contract scientists to assist AgroFresh in the execution of experiments involving Harvista, SmartFresh, and AdvanStoreFreshCloud technologies. Most of the regional research and development facilities focus on business aligned research and development initiatives to develop line extensions and create new products. Research and development makes use of core competencies in a number of technical areas including post-harvest physiology, analytical chemistry, regulatory sciences, regulatory affairs, formulation science, formulation process development, organic chemistry and delivery systems. Initiatives focused on next generation solutions utilize expertise in material science, molecular biology, postharvestpost-harvest pathology, diagnostics and sensor technology.

Intellectual Property

We are a technology-based solutions provider and, as such, rely on a combination of important intellectual property strengths, including licenses, patents, trademarks, copyrights and trade secret protection laws to protect our proprietary technology and our intellectual property. We seek to control access to and distribution of our proprietary information. We enter into confidentiality agreements with our employees, consultants, customers, service providers and vendors that generally provide that any confidential or proprietary information developed by us or on our behalf be kept confidential including, but not limited to, information related to our proprietary manufacturing process and SmartFresh service model. In the normal course of business, we provide our intellectual property and/or our products protected by our intellectual property to third parties through licensing or restricted use agreements.

We obtainedToday a majority of our SmartFresh applications use ProTabsTM, an exclusive license from North Carolina State University under the Sisler patent (U.S. 5,518,988) for the use of 1-MCPapplication method patented through 2022, and we continue to delay ripening of fruit and flowers. This patent has expiredinvest in the United States and Europe and continues only in Japan until May of 2020. We also acquired the Daly patent (U.S. 6,017,849) for the encapsulation complex of 1-MCP and alpha-cyclodextrin, usedapplication technologies as the foundational component in SmartFresh and Harvista. Depending on the country, SmartFresh is currently protected by a patent for the encapsulation complex through 2018 or 2019.means to continue to facilitate an even better service to our customers. We have also generated an impressive portfolio of intellectual property with over 30 patents granted in at least one country (pending in other countries) covering 1-MCP and next generation technologies, most of which do not expire until 2025 or beyond. RipeLock and Harvista formulations are patent protected through at least 2027.

Regulation and Compliance

We are subject to extensive national, state and local government regulation, and we have an internalthe Company has a regulatory team that we believe is best in class, which leverages a global network of highly-experienced regulatory consultants. Through this network, we have successfully obtained registrations for SmartFresh, Harvista, RipeLock, and LandSpring in every country where the review process has been completed, and the registration process for Harvista continues in many additional countries. We have completed more than 400

comprehensive international health and environmental tests that have shown the AgroFresh family of products, including SmartFresh and Harvista are safe for consumers, workers, and the environment. 1-MCP, the active ingredient in the AgroFresh products, is metabolized by the natural processes in apples and other fruits and leaves no residue. The products have been approved by over 50 authorities including the U.S. Environmental Protection Agency and the European Commission. We do not anticipate any significant problems in obtaining future required licenses, permits or approvals that are necessary to expand our business. We leverage our regulatory capabilities as we expand the fungicide product lines into new countries.

For a discussion of the various risks we may face from regulation and compliance matters, see “Risk Factors” in Item 1A of this report.

Employees

As of December 31, 2017,2019, we had approximately 284292 full-time employees. None of our employees in North America are members of a union or subject to the terms of a collective bargaining agreement. In certain other countries where we operate (including

(including Brazil, France, Germany, Italy, Netherlands and Spain), employees are members of unions or are represented by works councils. In addition, certain of our activities have been performed historically by seasonal and part-time third-party contingent staff.

Geographic Information

Please see Note 1619 to the audited consolidated and combined financial statements for geographic sales information.

Available Information

Our website is at http://www.agrofresh.com. We make available free of charge, on or through our website, our annual report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and amendments to those reports, if any, or other filings filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934, as amended (the "Exchange Act"), as soon as reasonably practicable after electronically filing or furnishing these reports to the Securities and Exchange Commission ("SEC"). Information contained on our website is not a part of this Annual Report on Form 10-K. We have adopted a code of business conduct applicable to our employees including our principal executive, financial and accounting officers, and it is available free of charge, on our website’s investor relations page.

The SEC maintains an Internet site at http://www.sec.gov that contains our annual report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and amendments to those reports, if any, or other filings filed or furnished pursuant to Section 13(a) or 15(d) of the Exchange Act, and our proxy and information statements. All reports that we file with the SEC may be read and copied at the SEC’s Public Reference Room at 100 F Street, N.E., Washington, DC, 20549. Information about the operation of the Public Reference Room can be obtained by calling the SEC at 1-800-SEC-0330.

ITEM 1A. RISK FACTORS

Ownership of our securities involves a high degree of risk. Holders of our securities should carefully consider the following risk factors and the other information contained in this report, including our historical financial statements and related notes included herein. Additional risks and uncertainties not presently known to us, which we currently deem immaterial or which are similar to those faced by other companies in our industry or businesses in general, may also impair our business or operations. If any of the following risks or uncertainties actually occur, our business, financial condition and operating results could be adversely affected in a material way. This could cause the trading prices of our securities to decline, perhaps significantly, and you may lose part or all of your investment.

Risks Related to Our Business and Industry

Increased competition in our industry can lead to pricing pressure, reduced margins or the inability of our products and services to achieve market acceptance.

We serve established and knowledgeable customers in the business of growing, storing and handling fresh produce and flowers. Key SmartFresh patents have expired or will expire over the next two years.

Actions by new or existing competitors, including introduction of competing products or services, promotions, combinations with other products or services, or price-cutting may lower our sales or require actions to retain and attract customers which could adversely affect our profitability. Increased competition from existing or new competitors could result in price reductions, increased competition for materials, reduced margins or loss of market share, any of which could materially and adversely affect our business and our operating results and financial condition. For example, during 2017 and 2018, we decreased our pricespricing in the U.S. to defend market share against increased competition, andcompetition. We believe the situation stabilized during the 2019 season. We may be requiredelect to take similar actionsaction in other regions such as Europe in the future.future, depending on competitive pressures.

In addition, if the prices at which our customers sell their products increase or decrease, the demand for our products or services may change. If the demand for our products or services decreases, there could be a significant impact on our business in the applicable location or region resulting inand a material adverse effect on our revenues and results of operations.

Our relationship with our employees could deteriorate, and certain key employees could leave, which could adversely affect our business, financial condition and results of operations.