0001601669us-gaap:CommonStockMember2020-12-31

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

☒ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the Fiscal Year Ending December 31, 20192020 Commission file number: 001-38788

Watford Holdings Ltd.

(Exact Name of Registrant as Specified in its Charter)

| | | | | | | | |

| Bermuda | | 98-1155442 |

(State or other jurisdiction

of incorporation or organization) | | (I.R.S. Employer Identification Number) |

|

| | | | | | | | | | | | | | | | | | | |

Bermuda

(State or other jurisdiction

of incorporation or organization)

| 98-1155442

(I.R.S. Employer Identification Number)

|

Waterloo House, 1st Floor | | | | (441) | 278-3455 |

| 100 Pitts Bay Road, | Pembroke | HM 08, Bermuda(Address of principal executive offices)

|

(441) 278-3455

Bermuda | | (Registrant’s telephone number, including area code) |

| (Address of principal executive offices) | |

Securities registered pursuant to Section 12(b) of the Act:

|

| | | | | | | | | | | | | |

| Title of each class | | Trading Symbol(s) | | Name of each exchange on which registered |

| Common Shares | | WTRE | | Nasdaq Global Select Market |

| 8½% Cumulative Redeemable Preference Shares | | WTREP | | Nasdaq Global Select Market |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐ No ☒

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

|

| | | | | | | | | | | | | | | | | | | | | | | | | |

| Large accelerated filer ☐ | Accelerated filer ☐ | ☒ | Non-accelerated filer ☒ | ☐ | Smaller reporting company | ☐ | Emerging growth company | ☒ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☒

Indicate by check mark whether the registrant has filed a report on and attestation to its management's assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

The aggregate market value of the voting and non-voting equity held by non-affiliates, computed by reference to the closing price as reported by the Nasdaq Global Select Market as of the last business day of the registrant’s most recently completed second fiscal quarter, was approximately $548.9$282.9 million.

As of February 28, 2020,26, 2021, there were 19,902,89519,886,979 of the registrant’s common shares outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant’s definitive proxy statement for its 2021 annual meeting of shareholders are incorporated by reference into Part III of this Annual Report on Form 10-K, provided that if such proxy statement is not filed with the U.S. Securities and Exchange Commission within 120 days after the end of the fiscal year covered by this Annual Report on Form 10-K, an amendment to this Annual Report on Form 10-K will be filed no later than the end of such 120-day period.

| | | | | | | | |

| Watford Holdings Ltd. |

| Index to Form 10-K | |

| | Page |

| | |

| | |

| | |

| | |

| Item 1. | | |

| Item 1A. | | |

| Item 1B. | | |

| Item 2. | | |

| Item 3. | | |

| Item 4. | | |

| | |

| Watford Holdings Ltd. |

| Index to Form 10-K | |

| | Page |

| | |

| | |

| | |

Item 1. | | |

Item 1A. | | |

Item 1B. | | |

Item 2. | | |

Item 3. | | |

Item 4. | | |

| | |

| | |

| Item 5. | | |

| Item 6. | | |

| Item 7. | | |

| Item 7A. | | |

| Item 8. | | |

| Item 9. | | |

| Item 9A. | | |

| Item 9B. | | |

| | |

| | |

| Item 10. | | |

| Item 11. | | |

| Item 12. | | |

| Item 13. | | |

| Item 14. | | |

| | |

| | |

| Item 15. | | |

| Item 16. | | |

Explanatory note - Certain defined terms

Unless the context suggests otherwise, any reference in this report to:

•“ACGL” refers to Arch Capital Group Ltd. and its controlled subsidiaries;

•“Arch” refers to any one or more of the following direct or indirect subsidiaries of ACGL, as applicable in the context in which such term appears:

•Arch Investment Management Ltd., or AIM, which manages the majority of our investment grade portfolio;

•Arch Reinsurance Company, or ARC, which is a party to certain quota share agreements with one or more of our operating subsidiaries and a services agreement with Watford Holdings (U.S.) Inc.;

•Arch Reinsurance Ltd., or ARL, which is a party to certain quota share agreements with one or more of our operating subsidiaries and owned approximately 12.5%12.6% of our outstanding common shares as of December 31, 2019;

2020;•Arch Underwriters Inc., or AUI, which manages the underwriting business of our U.S. operating subsidiaries;

•Arch Underwriters Ltd., or AUL, which manages the underwriting business of our non-U.S. operating subsidiaries, including Watford Re;

•“HPS” refers to HPS Investment Partners, LLC (formerly known as Highbridge Principal Strategies, LLC), which manages our non-investment grade portfolio, as well as accounts in our investment grade portfolio;

•our “Investment Managers” refers to AIM, HPS or any other investment managers that manage our investment grade portfolio or our non-investment grade portfolio from time to time;

•“Watford,” “we,” “us” and “our” refers to Watford Holdings Ltd. and its subsidiaries;

•“Watford Holdings” refers to our company, Watford Holdings Ltd., a Bermuda exempted company;

•“Watford Re” refers to Watford Re Ltd., a Bermuda domiciled insurance company and a wholly-owned subsidiary of our company;

•“Watford Trust” refers to Watford Asset Trust I, a statutory trust organized under the laws of the State of Delaware;

•“WIC” refers to Watford Insurance Company, a New Jersey domiciled insurance company and a wholly-owned subsidiary of our company;

•“WICE” refers to Watford Insurance Company Europe Limited, a Gibraltar domiciled insurance company and a wholly-owned subsidiary of our company; and

•“WSIC” refers to Watford Specialty Insurance Company, a New Jersey domiciled insurance company and a wholly-owned subsidiary of our company.

In addition, unless the context suggests otherwise, any reference in this report to:

•“HoldCo” refers to Greysbridge Holdings Ltd., a newly formed entity of which ACGL will own approximately 40%, and funds managed by Warburg Pincus LLC and Kelso & Company will each own approximately 30%;

•“Merger” refers to the merger of Merger Sub with and into Watford Holdings pursuant to the Merger Agreement, with Watford Holdings surviving as a wholly-owned subsidiary of HoldCo;

•“Merger Agreement” refers to the Agreement and Plan of Merger, dated as of October 9, 2020, among Watford Holdings, ACGL and Merger Sub, as amended by Amendment No. 1 to Agreement and Plan of Merger, dated as of November 2, 2020, among Watford Holdings, ACGL and Merger Sub; and

•“Merger Sub” refers to Greysbridge Ltd., a newly formed entity that is a wholly-owned subsidiary of HoldCo.

Explanatory note - Proposed merger

On October 9, 2020, we announced that we had entered into an Agreement and Plan of Merger with ACGL and Merger Sub pursuant to which, among other things, Merger Sub will merge with and into Watford Holdings, with Watford Holdings surviving as a wholly-owned subsidiary of ACGL. On November 2, 2020, we announced that we had entered into an amendment to the merger agreement with ACGL and Merger Sub to amend certain terms of the agreement. Further, on November 2, 2020, ACGL assigned its interests and obligations in connection with this acquisition to HoldCo, a newly formed entity of which ACGL will own approximately 40%, and funds managed by Warburg Pincus LLC and Kelso & Company will each own approximately 30%. Unless stated otherwise, all forward-looking information contained in this Annual Report on Form 10-K does not take into account or give any effect to the impact of the Merger (as defined herein). For additional details regarding the Merger, see Part I Item 1 “Business”, Part I Item 1A “Risk factors”, Part I Item 3 “Legal proceedings” and Part II Item 7 “Management’s discussion and analysis of financial condition and results of operations” of this Annual Report on Form 10-K.

Cautionary note regarding forward-looking statements

The Private Securities Litigation Reform Act of 1995 (or the PSLRA) provides a “safe harbor” for forward-looking statements. This report contains forward-looking statements that are intended to enhance the reader’s ability to assess our future financial and business performance. These statements are based on the beliefs and assumptions of our management, and are subject to risks and uncertainties. Generally, statements that are not about historical facts, including statements concerning our possible or assumed future actions or results of operations are forward-looking statements. Forward-looking statements include, but are not limited to, statements that represent our beliefs, expectations or estimates concerning future operations, strategies, financial results or performance, financings, investments, acquisitions, expenditures or other developments and anticipated trends and competition in the markets in which we operate. Forward-looking statements, for purposes of the PSLRA or otherwise, can also be identified by the use of forward-looking terminology such as “may,” “believes,” “intends,” “anticipates,” “plans,” “estimates,” “expects,” “should” or similar expressions.

Forward-looking statements involve our current assessment of risks and uncertainties. Actual events and results may differ materially from those expressed or implied in these statements. Important factors that could cause actual events or results to differ materially from those indicated in such statements are discussed below and elsewhere in this report and in our other reports and other documents filed with the Securities and Exchange Commission, or the SEC, and include:

◦adverse general, societal, economic and market conditions, including those caused by pandemics, including the current global pandemic related to the novel coronavirus, or COVID-19, and government actions in response thereto;

◦our limited operating history;

◦fluctuations in the results of our operations;

◦our ability to compete successfully with more established competitors;

◦our losses exceeding our reserves;

◦downgrades, potential downgrades or other negative actions by rating agencies;agencies, including the announcements by A.M. Best Company, or A.M. Best, that it has placed under review with negative implications status for our financial strength and credit ratings and Kroll Bond Rating Agency, or KBRA, that it has revised the outlook of our financial strength and credit ratings to negative;

◦our dependence on key executives and inability to attract qualified personnel, or the potential loss of Bermudiansuitably qualified personnel as a result of Bermuda employment and immigration restrictions;

◦our dependence on letter of credit facilities and borrowing facilities that may not be available on commercially acceptable terms;

◦our potential inability to pay dividends or distributions;

◦our potential need for additional capital in the future and the potential unavailability of such capital to us on favorable terms or at all;

◦our dependence on clients’ evaluations of risks associated with such clients’ insurance underwriting;

◦the suspension or revocation of our subsidiaries’ insurance licenses;

◦Watford Holdings potentially being deemed an investment company under U.S. federal securities law;

◦the potential characterization of us and/or any of our subsidiaries as a passive foreign investment company, or PFIC;

◦our dependence on Arch for services critical to our underwriting operations;

◦changes to our strategic relationship with Arch or the termination by Arch of any of our services agreements or quota share agreements;

◦our dependence on HPS and AIM to implement our investment strategy;

◦the termination by HPS or AIM of any of our investment management agreements;

◦risks associated with our investment strategy being greater than those faced by competitors;

◦changes in the regulatory environment;

◦our potentially becoming subject to U.S. federal income taxation;

◦our potentially becoming subject to U.S. withholding and information reporting requirements under the U.S. Foreign Account Tax Compliance Act, or FATCA, provisions;

◦our ability to complete acquisitions and integrate businesses successfully;

◦one or more closing conditions to the Merger, including certain regulatory approvals, may not be satisfied or waived, on a timely basis or otherwise, including that a governmental entity may prohibit, delay or refuse to grant approval for the consummation of the Merger, or that the required approval of the Merger Agreement by our shareholders may not be obtained;

◦uncertainties regarding the proposed acquisition of Watford Holdings by HoldCo;

◦our business may suffer as a result of uncertainty surrounding the proposed transaction with HoldCo, and there may be challenges with employee retention as a result of the proposed transaction with HoldCo;

◦the proposed transaction with HoldCo may involve unexpected costs, liabilities or delays;

◦legal proceedings that have been, and additional proceedings that may be initiated against us or our directors related to the proposed transactions with HoldCo;

◦an event, change or other circumstance may occur that could give rise to the termination of the Merger Agreement (including circumstances requiring us to pay HoldCo a termination fee pursuant to the Merger Agreement); and

◦the other risks identified in this report, including, without limitation, thosematters set forth under the sections titled Part I Item 1A “Risk factors” and Part II Item 7 “Management’s discussion and analysis of financial condition and results of operations.”operations” as well as the other factors set forth in the Company’s other documents on file with the SEC and management’s response to any of the aforementioned factors.

Consequently, such forward-looking statements should be regarded solely as our current plans, estimates or belief as of the date of this report. All subsequent forward-looking statements attributable to us or persons acting on our behalf are expressly qualified in their entirety by these cautionary statements. The foregoing review of important factors should not be construed as exhaustive and should be read in conjunction with other cautionary statements that are included herein or elsewhere. We do not intend, and do not undertake, any obligation to update any forward-looking statements to reflect future events or circumstances after the date of this report.

Risk factors summary

The following is a summary of the principal risks that could adversely affect our business, operations and financial results. This summary does not address all of the risks and uncertainties that we face. Additional discussion of the risks and uncertainties summarized below, as well as other risks and uncertainties that we face, can be found under “Risk Factors” in Part I, Item 1A of this Annual Report on Form 10-K. The summary below is qualified in its entirety by that more complete discussion of such risks and uncertainties. You should carefully consider the risks and uncertainties described under “Risk Factors” in Part I, Item 1A of this Annual Report on Form 10-K as part of your evaluation of an investment in our securities.

Risks related to the COVID-19 global pandemic

•The impact of the COVID-19 global pandemic and related risks could materially affect our results of operations, financial position and/or liquidity.

Risks related to our insurance and reinsurance business

•We operate in a highly competitive environment and we may not be able to compete successfully in our industry.

•The insurance and reinsurance industry is from time to time subject to regulatory, legislative, judicial or other unforeseen developments, which could adversely affect our business.

Risks related to our company

•We began operations in March 2014 and, therefore, limited historical information is available for investors to evaluate our performance or a potential investment in our shares.

•The failure of any of the loss limitation methods we employ could have a material adverse effect on our financial condition or results of operations.

•We depend heavily on the performance of Arch, HPS and other third-party service providers under their respective agreements. In particular, we rely on Arch for services critical to our underwriting operations and we depend upon HPS to manage the investments of the funds in our non-investment grade portfolio.

•Our business is dependent upon insurance and reinsurance brokers, intermediaries and program administrators and the loss of these important relationships could materially adversely affect our ability to market our products and services.

•We may not be able to write as much premium as expected on business with the desired level of targeted profitability.

•A downgrade or withdrawal of our financial strength ratings by insurance rating agencies could adversely affect the volume and quality of business presented to us and could negatively impact our relationships with clients and the sales of our products.

•If we are unsuccessful in managing our underwriting operations and investments in relation to each other, our ability to conduct our business could be significantly and negatively affected.

•A single or series of insurable events could result in simultaneous, correlated and substantial losses from underwriting operations and investment losses, which would adversely affect our financial condition and results of operations.

•The failure to maintain our credit facilities and letter of credit facilities or to have adequate available collateral in connection with reinsurance contracts may negatively affect our ability to successfully implement our business strategy.

•Our liquidity position is affected by our underwriting, investment and internal operations, and adverse developments in any of these inputs could have a significantly negative impact on our business and liquidity.

Risks related to Arch

•Arch may take actions in the future that cause its and our interests to be less aligned.

Risks related to our investments

•The performance of our investments is highly dependent upon conditions in the global economy or financial markets that are outside of our Investment Managers’ control and can be difficult to predict.

Risks related to HPS and the HPS-managed non-investment grade portfolio

•HPS utilizes investment strategies and employs trading techniques that involve inherent exposures, which could result in substantial losses to our non-investment grade portfolio and, as a result, to us.

•Our investments differ from those of many insurers and reinsurers because our non-investment grade portfolio is predominantly invested in corporate credit investments, which can be speculative and volatile and which could increase the riskiness and volatility of our results. In addition, the use of financial leverage could increase the riskiness of our non-investment grade portfolio’s investment strategy and volatility of our net income.

•We do not control the decisions of HPS, and HPS may invest the assets in our non-investment grade portfolio in its discretion within the framework of the applicable non-investment grade investment guidelines. The performance of our non-investment grade portfolio depends on the ability of HPS to select and manage appropriate investments.

Risks related to regulation of us and our operating subsidiaries

•Any suspension or revocation of Watford Re’s license as a Bermuda Class 4 insurer would materially impact our ability to do business and implement our business strategy.

•Our non-Bermuda operating insurance subsidiaries are subject to regulation in various jurisdictions, and violations of existing regulations or material changes in the regulation of their operations could adversely affect us.

Risks related to taxation

•U.S. Holders may be subject to certain adverse tax consequences based on the application of rules regarding passive foreign investment companies, or PFICs.

•Changes in U.S. federal tax laws, which may be retroactive, including the finalization of proposed Treasury Regulations, could subject Watford Holdings, Watford Re or U.S. Holders to U.S. federal income taxation on the earnings of Watford Holdings, Watford Re or our subsidiaries or could otherwise adversely impact Watford Holdings and its subsidiaries or shareholders.

Risks related to our common shares

•The share voting limitations that are contained in our bye-laws may result in our shareholders having fewer voting rights than a shareholder would otherwise have been entitled to based upon such shareholder’s economic interest in our company.

Risks related to the proposed Merger

•The Merger is subject to closing conditions, including governmental, regulatory and shareholder approvals, as well as other uncertainties and there can be no assurances as to whether and when it may be completed. Failure to complete the Merger could negatively impact our share price, future business and financial results.

•The pendency of the Merger may cause disruptions in our business, which could have an adverse effect on our business, financial condition or results of operations.

Part I.

Item 1. Business

Our company

We are a global property and casualty, or P&C, insurance and reinsurance company with approximately $1.1$1.2 billion in capital as of December 31, 20192020 and with operations in Bermuda, the United States and Europe. Our strategy combines a diversified, casualty-focused underwriting portfolio, accessed through our multi-year, renewable strategic underwriting management relationship with Arch, with a disciplined investment strategy comprising primarily non-investment grade corporate credit assets, managed by HPS Investment Partners, LLC, or HPS. We have designed our investment strategy to complement the characteristics of our target underwriting portfolio in order to generate attractive risk-adjusted returns for our shareholders. Our strategy involves a greater degree of investment risk balanced with a less volatile underwriting portfolio, especially in relation to the amount of catastrophe exposure we assume, as compared with traditional insurers and reinsurers.

We were formed in Bermuda in the second quarter of 2013. In March 2014, we raised $1.1 billion in our initial funding and began underwriting reinsurance in the first half of 2014. Our operating subsidiaries all carry a financial strength rating of “A-” (Excellent) with a stable outlook from A.M. Best Company, or A.M. Best, which is the fourth highest of 1516 ratings that A.M. Best confers. As of December 31, 2020, A.M. Best has maintained its “under review with negative implications” status for the “A-” financial strength rating of our operating subsidiaries. Each of our operating subsidiaries also carries a financial strength rating of “A” with a stable outlook from Kroll Bond Rating Agency, or KBRA, which is the sixth highest of 22 ratings that KBRA confers. On June 17, 2020, KBRA revised the outlook for all of our ratings to negative. These ratings are each intended to provide an independent opinion of an insurer’s ability to meet its obligations to policyholders and are not ratings of our common shares.

We manage our insurance and reinsurance underwriting through our relationship with Arch, which, through Arch Reinsurance Ltd., or ARL, is one of our founding equity investors. ARL, which is a subsidiary of Arch Capital Group Ltd., or ACGL, a leading global insurance and reinsurance company whose shares are listed on the Nasdaq Global Select Market under the symbol “ACGL,” invested $100 million in our common shares. ACGL had approximately $13.2$15.8 billion in capital and a market capitalization of approximately $17.4$14.7 billion as of December 31, 20192020 and provides a full range of property, casualty and mortgage insurance and reinsurance lines, with a particular focus on writing specialty lines on a worldwide basis through operations in Bermuda, the United States, Canada, Europe Australia and South Africa.Australia.

Our strategic relationship with Arch provides us with unique underwriting expertise and market access based upon our ability to leverage Arch’s global underwriting infrastructure and distribution platform and has enabled us to build a diversified global portfolio of insurance and reinsurance risks. Our operating subsidiaries have written an aggregate of approximately $3.4$4.1 billion in gross premiums written from inception to December 31, 2019.2020.

Our main operating subsidiary is Watford Re Ltd., or Watford Re, a Bermuda-based company that began writing business in early 2014 and is registered as a Class 4 insurer with the Bermuda Monetary Authority, or the BMA. Bermuda is one of the largest insurance and reinsurance centers in the world, particularly for P&C markets, providing insurance and reinsurance capacity for risks on a global basis. In addition to traditional P&C lines, Watford Re also writes mortgage insurance and reinsurance on a worldwide basis. Our Bermuda presence gives us direct and efficient access to reinsure these risks. In mid-2015, we formed and capitalized Watford Insurance Company Europe Limited, or WICE, in Gibraltar to conduct business in Europe. In December 2015, WICE began writing business with access to markets across the European Union, targeting both personal lines and commercial lines of P&C insurance, which it distributes through coinsurance relationships and

specialized insurance agents (also known as program managers). Following the United Kingdom and Gibraltar’s exit from the European Union, WICE now focuses solely on United Kingdom business with all relevant regulatory approvals obtained to run off its remaining European Union exposures. In addition, in December 2019, we entered into an agreement to acquire Axeria IARD, a P&C insurance company based in France. The

completion of this acquisition is subject to regulatory approval and other customary closing conditions, and is expected to close in the secondfirst quarter of 2020.2021.

In late 2015, we formed and capitalized Watford Specialty Insurance Company, or WSIC, a U.S.-based excess & surplus, or E&S, lines insurer. In April 2016, WSIC began writing insurance business in the U.S. E&S market, concentrating its efforts on commercial lines of property and casualty coverage, which it distributes through program managers. We further expanded our U.S. capabilities in August 2016 through the acquisition and capitalization of Watford Insurance Company, or WIC, which has enabled us to access the larger admitted (or licensed) U.S. insurance market, also through program managers. Between WSIC and WIC, we are able to access the entire U.S. P&C insurance market, offering either admitted insurance products or E&S insurance products to service market demand.

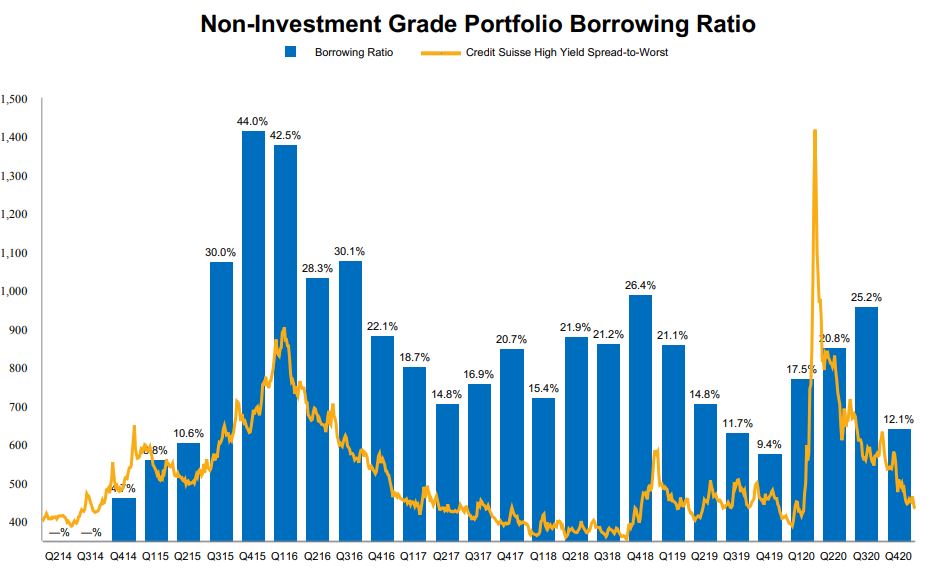

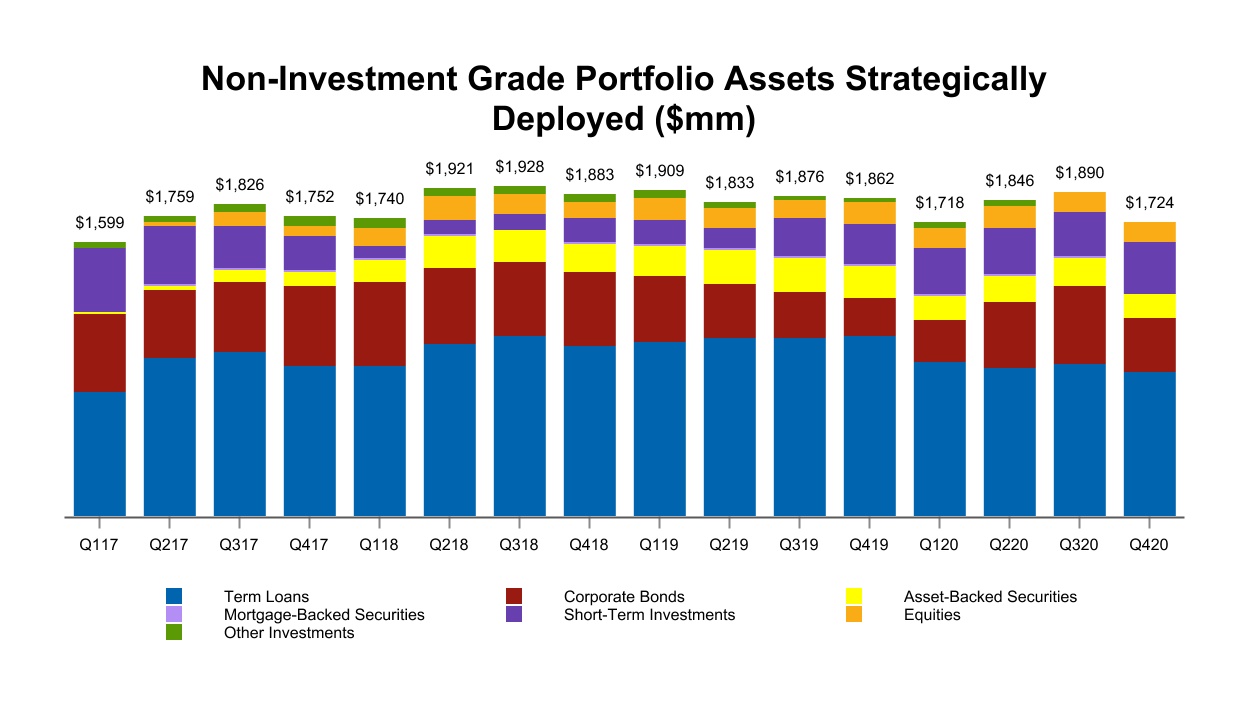

The majority of our investments are allocated to non-investment grade corporate credit assets managed by HPS, which we refer to as our non-investment grade portfolio.

HPS is a global investment platform with a focus on non-investment grade credit. HPS had approximately $61$68 billion of assets under management as of December 31, 2019.2020. HPS manages our non-investment grade portfolio pursuant to investment guidelines formulated to complement our underwriting portfolio. The primary objective of our non-investment grade investment strategy is to generate attractive risk-adjusted returns comprising current interest income, trading gains and capital appreciation, with an emphasis on capital preservation. As of December 31, 2019,2020, non-investment grade corporate credit assets comprised approximately 69% of our overall investment portfolio.

We refer to the remainder of our invested assets as our investment grade portfolio, which is primarily managed by Arch Investment Management Ltd., or AIM, a subsidiary of Arch that manages the investments of Arch’s own funds. We also have several investment grade accounts managed by other Investment Managers, including HPS.

Since formation, we have meaningfully grown our business, generating sizable underwriting revenue and significant interest income. We believe that we are well-positioned to continue delivering prudent growth by balancing our complementary underwriting and investment strategies. From inception through December 31, 2019,2020, our net premiums written and net interest income were as follows:

| | | | Year Ended December 31, | | ITD | | Year Ended December 31, | | ITD |

| | 2019 | | 2018 | | 2017 | | | 2020 | | 2019 | | 2018 | |

| | ($ in thousands) | | ($ in thousands) |

| Net premiums written | $ | 532,862 |

| | $ | 604,175 |

| | $ | 553,117 |

| | $ | 2,944,357 |

| Net premiums written | $ | 537,589 | | | $ | 532,862 | | | $ | 604,175 | | | $ | 3,481,946 | |

| Net interest income | 116,211 |

| | 107,533 |

| | 86,523 |

| | 491,192 |

| Net interest income | 106,390 | | | 116,211 | | | 107,533 | | | 597,582 | |

On March 28, 2019, we completed a direct listing of our common shares on the Nasdaq Global Select Market. On June 28, 2019, we also completed a direct listing of our 8½% Cumulative Redeemable Preference Shares, or our preference shares, on the Nasdaq Global Select Market.

Further, in 2019,In the first quarter of 2020, our board of directors authorized a share repurchase program, which allowed us to make repurchases of up to $75$50 million of our common shares from time to time in open market or privately negotiated transactions. From the inception of the share repurchase program in September 2019 through December 31, 2019,2020, we repurchased 2.82.9 million common shares for a purchase price of $75$77.9 million, excluding transaction costs, fully utilizing the program. costs.

In the firstthird quarter of 2020, our boardwe entered into the Merger Agreement, pursuant to which, among other things, Merger Sub will merge with and into Watford Holdings, which we refer to as the Merger, with Watford Holdings surviving as a wholly owned subsidiary of directors authorized an additionalHoldCo.

We do not anticipate making any further repurchases under the current share repurchase program underas a result of our entry into the Merger Agreement, which generally prohibits us from repurchasing our shares as well as certain other securities prior to the consummation of the Merger or the earlier termination of the Merger Agreement. Accordingly, at the present time, we maydo not expect to repurchase upcommon shares, declare or pay dividends on our common shares or otherwise return capital to $50 millionour common shareholders for the foreseeable future.

Pursuant to the Merger Agreement, subject to certain conditions set forth therein, at the effective time of ourthe Merger, (a) each issued and outstanding common share of Watford Holdings (other than (i) shares to be canceled pursuant to the Merger Agreement and (ii) restricted share units to be canceled and exchanged pursuant to the Merger Agreement (as described below)), will be converted into the right to receive $35.00 in cash, without interest, and (b) each issued and outstanding preference share will remain outstanding as a preference share of the surviving company and will be entitled to the same dividend and other relative rights, preferences, limitations and restrictions as are now provided to the preference shares.

Consummation of the Merger is subject to customary conditions, including without limitation, (i) approval of the Merger Agreement and the transactions contemplated thereby by the affirmative votes of not less than 50% of the holders of the outstanding common shares and the preference shares, voting as a single class, at a meeting of our shareholders, (ii) the receipt of certain remaining regulatory approvals without the imposition of a Burdensome Condition (as defined in the Merger Agreement), (iii) the absence of any law, judgment or other legal restraint that prevents, makes illegal or prohibits the consummation of the Merger and the other transactions contemplated by the Merger Agreement, (iv) the accuracy of each party’s representations and warranties (subject to certain qualifications), (v) each party’s performance in all material respects of its obligations contained in the Merger Agreement and (vi) the absence of a Company Material Adverse Effect (as defined in the Merger Agreement). In addition, HoldCo’s obligation to consummate the Merger is conditioned on our non-investment grade portfolio not suffering a loss of more than $208 million from timeSeptember 30, 2020, through the date that is two business days prior to timethe closing of the Merger.

The Merger Agreement includes customary representations, warranties and covenants of Watford Holdings, HoldCo, and Merger Sub. Among other things, Watford Holdings has agreed to customary covenants regarding the operation of the business of Watford prior to the closing.

The Merger Agreement contains specified termination rights for each of the parties. Upon termination of the Merger Agreement under specified circumstances, including with respect to our entry into an agreement with respect to a qualifying Superior Proposal (as defined in open market or privately negotiated transactions.the Merger Agreement), we will be required to pay HoldCo a termination fee of $28.1 million.

The Merger is expected to close in the first half of 2021, subject to the closing conditions described above and contained in the Merger Agreement.

Strategy

Execute a dynamic business model focused on total returns

We are a total return-driven insurance and reinsurance company. We strive to deliver attractive long-term returns to our shareholders by writing a diversified underwriting portfolio through a proven, disciplined approach, augmented by an investment strategy comprising primarily non-investment grade fixed income corporate credit assets and designed to complement our target underwriting business mix. We feel that this combination enhances our opportunity to thoughtfully

deploy our capital in the most effective manner and to produce attractive risk-adjusted returns across both sides of the balance sheet, thereby maximizing the total return for our shareholders.

Build an insurance platform that supplements our reinsurance business

In 2015, we expanded our platform to include P&C insurance business in the United States and European markets. The business we access at the insurance level generally has lower acquisition costs than similar business accessed at the reinsurance level, and provides other operating efficiencies. In addition, we expect that our insurance business will produce further diversification benefits resulting in lower volatility of our underwriting results.

The table below shows the net insurance premiums written generated by our insurance business for the years ended December 31, 2020, 2019 2018 and 2017.2018. We intend to continue to grow our insurance business opportunistically by leveraging our strategic relationship with Arch.

|

| | | | | | | | | | | |

| | Year Ended December 31, |

| | 2019 | | 2018 | | 2017 |

| | ($ in thousands) |

| Insurance programs and coinsurance - net premiums written | $ | 176,711 |

| | $ | 139,838 |

| | $ | 103,213 |

|

| | | | | | | | | | | | | | | | | |

| Year Ended December 31, |

| 2020 | | 2019 | | 2018 |

| ($ in thousands) |

| Insurance programs and coinsurance - net premiums written | $ | 213,459 | | | $ | 176,711 | | | $ | 139,838 | |

Capitalize on the expertise and infrastructure of Arch, our exclusive underwriting manager

We have partnered with Arch to source and manage our underwriting portfolio in accordance with our underwriting guidelines. We believe this relationship will enable us to execute our chosen, casualty-focused underwriting strategy based on Arch’s expertise in our target lines of business. This arrangement provides us with access to Arch’s global underwriting infrastructure and distribution platform, and has allowed us to quickly build a global portfolio of diversified insurance and reinsurance risks.

Pursue an investment approach that complements our underwriting strategy

Our investment strategy seeks to generate attractive risk-adjusted returns comprising interest income, trading gains and capital appreciation with an emphasis on capital preservation. This investment strategy complements our underwriting portfolio, which predominantly targets medium- to long-tail casualty business. Our non-investment grade portfolio, which is managed by HPS, consists of high yielding corporate credit assets. Our goal in pursuing this strategy is to generate superior investment returns, as compared with investment returns achieved by our peers, through disciplined and prudent credit risk analysis and proper pricing for the risk assumed. We seek to achieve risk-adjusted returns that exceed those of typical reinsurer investment portfolios while also producing stable cash flows from scheduled interest payments. Our lower volatility, casualty-focused underwriting portfolio should have predictability in terms of the timing of payments to insurance claimants, thereby mitigating the risk of having to sell assets during times of temporary investment market stresses.

Maintain a robust risk management program

We have a strong risk management function, overseen by our Chief Risk Officer. We benefit from our ability to leverage the risk management infrastructures in place within each of Arch and HPS. We regularly receive relevant exposure and modeling information from Arch and HPS. On that data we overlay our proprietary analytics, tailored risk appetites and controls for an integrated approach to monitoring and reviewing our exposures. We maintain active oversight of our underwriting and investment management service providers at both the management and board level.

Conservative approach to underwriting risk

We have designed our underwriting and investment strategies toward the goal of maintaining our balance sheet strength on a long-term basis through varying phases of market cycles. We target a

medium-to long-term, lower volatility underwriting portfolio with tightly managed natural catastrophe exposure. We seek to limit our modeled net probable maximum loss, or PML, for property catastrophe exposures for each peak peril and peak zone from a 1-in-250 year occurrence to no more than 10% of the value of our total shareholders’ equity plus our senior notes and our preference shares, or our total capital, which is less than most of our principal reinsurance competitors. As of January 1, 2020,2021, this modeled net PML was 4.2%4.4% of our total capital. Our conscious effort to limit our catastrophe exposure lowers the volatility of our overall underwriting portfolio and provides greater certainty as to future claims-related payout patterns and timing. Our casualty-focused underwriting portfolio’s payout pattern is slower than that of most of our competitors due to the longer tail lines of business we write, and that slower payout pattern provides us with the potential for greater investment income on those premiums, thereby providing us an underwriting modeling advantage when competing for those target lines of business.

We have a robust process for setting loss reserves, leveraging the established processes and procedures employed by Arch, making our own analyses and judgments, and through periodic reviews by external actuarial firms. We also regularly monitor our investment portfolios, including performance of the underlying credits, overall liquidity and how well that liquidity matches with the projected claims payments related to our underwriting portfolio. Being prudent stewards of our balance sheet allows us to maintain the confidence of all of our constituents and thereby to position ourselves to better achieve our goals.

Our operations

Underwriting operations: insurance and reinsurance

Through our underwriting operations we are able to offer a variety of P&C insurance and reinsurance products on a global basis. We target an underwriting portfolio that is diversified by line of business and geography, with a focus on medium- to long-tail casualty business. Given the inception of our insurance operations, our underwriting portfolio to-date has been predominantly reinsurance, although we expect our insurance writings to continue to increase going forward. We have built a diversified, low volatility portfolio by purposely limiting our modeled natural catastrophe exposure to a level lower than many other insurers and reinsurers. Our strategy is to operate in lines of business in which underwriting skill and specialized knowledge can make a meaningful difference in operating results.

We have been well-received in the market and successful in writing what we believe to be attractive underwriting opportunities. We benefit from Arch’s broad underwriting expertise and worldwide distribution network. Arch’s global, multi-line market presence facilitates the ability for Arch to strategically adapt our mix of business by geography, product line or type, as we or Arch perceive potential opportunities. In addition, as a result of our operating subsidiaries’ “A-” (Excellent) rating from A.M. Best and “A” rating from KBRA, as well as our strong balance sheet, we are well-positioned to increase our premium volume in favorable market cycles, creating additional attractive underwriting opportunities.

Similar to other reinsurers and to other insurers writing business through program managers, we do not separately evaluate each individual risk assumed and are, therefore, largely dependent upon the original underwriting decisions made by the ceding companies and program managers in accordance with agreed underwriting guidelines. However, we believe Arch’s experience in portfolio risk selection and detailed monitoring of cedants and program managers provides us with a competitive advantage.

Our Bermuda-based operating subsidiary, Watford Re, writes a broad range of P&C coverages. In addition to traditional P&C lines, Watford Re also writes mortgage insurance and reinsurance on a worldwide basis. Our reinsurance business leverages Arch’s global underwriting platform to distribute a wide variety of products covering lines of business around the world. We write business for third-party cedants and also assume a meaningful portion of our business as a reinsurance or

retrocession of business that Arch has underwritten for its own portfolio and that also meets our underwriting guidelines and return metrics. The table below provides the percentage of our total gross premiums written assumed from Arch for years ended December 31, 2020, 2019 2018 and 2017.2018.

|

| | | | | | | | |

| | Year Ended December 31, |

| | 2019 | | 2018 | | 2017 |

| Gross premiums written - assumed from Arch | 26.6 | % | | 34.4 | % | | 48.2 | % |

| | | | | | | | | | | | | | | | | |

| Year Ended December 31, |

| 2020 | | 2019 | | 2018 |

| Gross premiums written - assumed from Arch | 27.7 | % | | 26.6 | % | | 34.4 | % |

Arch competes with us and will continue to underwrite business for its own distinct portfolios in accordance with its own policies, strategies and business plans. In sourcing insurance and reinsurance opportunities through its worldwide platform, Arch evaluates the perceived risk exposure pursuant to its proprietary underwriting methodology, and then models the required pricing based on both its and our underwriting criteria. In furtherance of our underwriting philosophy to pursue lines of business in which underwriting knowledge and expertise can drive attractive returns, our underwriting guidelines are based largely on Arch’s own, leveraging the experience of Arch’s underwriting professionals. Our underwriting guidelines differ from Arch’s in several aspects, most notably in that our guidelines purposely limit catastrophe risk and our portfolio focus is on mid- to long-tail casualty and other lines of business with similar tenor, whereas Arch’s target business mix includes more catastrophe exposure and a higher percentage of shorter-tail lines.

In underwriting business on our behalf, Arch fundamentally employs the same qualitative and quantitative evaluation and selection criteria for our underwriting portfolio as it does for its own account and each potential contract is evaluated qualitatively and quantitatively for both Arch’s portfolio and ours. For each opportunity that passes Arch’s qualitative and quantitative screening, when performing the pricing evaluation of a contract on our behalf, Arch applies our investment return assumptions to determine our expected return on the allocated capital for each such business opportunity. The determination by Arch as to whether to offer only Arch capacity, only our capacity, or both as side-by-side capacity, depends on the result of the pricing analysis using differing investment assumptions for us and Arch, reflecting our differentiated investment strategies. The mid- to long-tail business on which we focus can benefit from a higher return on the premium float and thus, certain opportunities that meet our metrics may not meet those of insurers and reinsurers like Arch with a more traditional investment strategy. In underwriting operations, “float” arises when premiums are received before losses and other expenses are paid and is an interval that sometimes extends over many years. During that time, the insurer invests the premiums, earns interest income and may generate capital gains and losses. In order to provide solutions to its reinsurance brokers and potential insurance clients, Arch has a strategic incentive to place that business with us rather than simply declining to provide capacity to the broker or potential client in such circumstances.

Other than renewals of business previously written by our underwriting subsidiaries, Arch is not required to allocate any particular business opportunities to us. However, we believe that Arch has

strong incentives to allocate attractive business to us, based on Arch’s investments in us, our contractual arrangements through which Arch earns premium-based fees and a profit commission for business written on our behalf, and Arch’s ability to offer potential clients additional solutions, thus gaining a strategic benefit in the competitive, syndicated reinsurance market in which it is often necessary to be on an expiring contract to have the opportunity to bid to provide capacity at the next annual renewal.

Through our relationship with Arch, we have built a diversified portfolio of medium- to long-tail commercial lines casualty, other specialty and property risks. Our underwriting segment captures

the results of our underwriting lines of business, which are comprised of specialty products on a worldwide basis. Our four major lines of business are described as follows:

•Casualty reinsurance: coverage provided to ceding company clients on third-party liability and workers’ compensation exposures, primarily on a treaty basis. Business written includes coverages such as: executive assurance, medical malpractice liability, other professional liability, workers’ compensation, excess and umbrella liability and excess auto liability.

•Other specialty reinsurance: coverage provided to ceding company clients for personal and commercial auto (other than excess auto liability), mortgage, surety, accident and health, workers’ compensation catastrophe, agriculture and marine and aviation.

•Property catastrophe reinsurance: protects ceding company clients for most catastrophic losses that are covered in the underlying policies. Perils covered may include hurricane, earthquake, flood, tornado, hail and fire, and coverage for other perils on a case-by-case basis. Property catastrophe reinsurance provides coverage on an excess of loss basis when aggregate losses and loss adjustment expense from a single occurrence of a covered peril exceed the retention specified in the contract.

•Insurance programs and coinsurance: targeting program managers and/or coinsurers with unique expertise and niche products offering primary and excess general liability, umbrella liability, professional liability, workers’ compensation, personal and commercial automobile, inland marine and property business with minimal catastrophe exposure.

Our insurance operations are conducted in the United States and Europe. We established our insurance platform as a complement to our reinsurance strategy to expand our distribution channels. Our insurance strategy is focused on pursuing attractive underwriting opportunities in the U.S. and European insurance markets and we view our insurance platform as having the potential to provide meaningful premium growth.

In the United States, we are authorized to write commercial P&C lines of business in both the admitted market and the E&S market through our WIC and WSIC subsidiaries, respectively, with distribution through coinsurance relationships or through select program managers that develop and distribute specialized insurance products for these subsidiaries. In Europe,the U.K., we write direct insurance and coinsurance business, primarily in personal P&C lines, through lead insurers and program managers that develop and distribute specialized insurance products for our WICE subsidiary.

The acquisition of Axeria will extend our insurance platform across the European Union.

We operate and monitor our lines of business through our underwriting operations. The table below provides a breakdown of our gross premiums written for the years ended December 31, 2020, 2019 2018 and 2017:2018:

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Year Ended December 31, |

| 2020 | | 2019 | | 2018 |

| Amount | | % | | Amount | | % | | Amount | | % |

| ($ in thousands) |

| Casualty reinsurance | $ | 188,042 | | | 25.8 | % | | $ | 279,967 | | | 37.1 | % | | $ | 274,661 | | | 37.4 | % |

| Other specialty reinsurance | 117,177 | | | 16.1 | % | | 119,518 | | | 15.8 | % | | 196,170 | | | 26.7 | % |

| Property catastrophe reinsurance | 27,334 | | | 3.8 | % | | 16,226 | | | 2.1 | % | | 10,424 | | | 1.4 | % |

| Insurance programs and coinsurance | 395,993 | | | 54.3 | % | | 339,170 | | | 45.0 | % | | 253,760 | | | 34.5 | % |

| Total | $ | 728,546 | | | 100.0 | % | | $ | 754,881 | | | 100.0 | % | | $ | 735,015 | | | 100.0 | % |

|

| | | | | | | | | | | | | | | | | | | | |

| | Year Ended December 31, |

| | 2019 | | 2018 | | 2017 |

| | Amount | | % | | Amount | | % | | Amount | | % |

| | ($ in thousands) |

| Casualty reinsurance | $ | 279,967 |

| | 37.1 | % | | $ | 274,661 |

| | 37.4 | % | | $ | 284,481 |

| | 47.4 | % |

| Other specialty reinsurance | 119,518 |

| | 15.8 | % | | 196,170 |

| | 26.7 | % | | 169,100 |

| | 28.2 | % |

| Property catastrophe reinsurance | 16,226 |

| | 2.1 | % | | 10,424 |

| | 1.4 | % | | 12,740 |

| | 2.1 | % |

| Insurance programs and coinsurance | 339,170 |

| | 45.0 | % | | 253,760 |

| | 34.5 | % | | 133,983 |

| | 22.3 | % |

| Total | $ | 754,881 |

| | 100.0 | % | | $ | 735,015 |

| | 100.0 | % | | $ | 600,304 |

| | 100.0 | % |

Reinsurance operations

Watford Re is a licensed, Class 4 Bermuda-based reinsurer operating under the supervision of the BMA. Arch serves as our exclusive reinsurance portfolio manager and provides reinsurance-related services including exposure modeling, loss reserve recommendations, claims handling and other related services as part of our long-term services agreements with them. All reinsurance contracts are bound on our behalf by designated employees made available to us by Arch, or, in certain circumstances, by Watford Re management.

We assume reinsurance from third-party cedants or from Arch entities on a reinsurance or retrocessional basis. The retrocessions from Arch are from its reinsurance operations in the United States, Bermuda, Europe, and Australia, levering Arch’s distribution and local expertise in its markets. We also have provided, and may continue to provide, reinsurance to Arch’s insurance operations in the United States, the United Kingdom and elsewhere.

Insurance operations

In 2015 and 2016, we established insurance operations in Europe and the United States. These insurance operations provide additional points of access to our target lines of business, with the potential added benefit for lower acquisition costs and other distribution efficiencies. All of our insurance subsidiaries carry ouran A.M. Best “A-” (Excellent) rating and oura KBRA “A” rating and through them we pursue insurance product lines similar to those we target through our reinsurance operations.

In the United States, our principal insurance subsidiaries are WSIC and its wholly-owned subsidiary, WIC, both of which are domiciled in New Jersey. WSIC is an eligible E&S lines insurer in all 50 states and the District of Columbia. WIC is an admitted insurer in all 50 states and the District of Columbia. Following our acquisition of WIC in 2016, we have expanded our certificates of authority to cover a broad range of lines of business in 4649 states and the District of Columbia, and we are in the process of similarly expanding our authority in theone remaining seven states.state. Both WSIC and WIC are located in New Jersey. Through WSIC and WIC we have the flexibility to access both the E&S and admitted sectors of the U.S. P&C market. Our U.S. insurance subsidiaries concentrate primarily on commercial casualty lines of insurance and have initiated writing business through select program managers.

Our insurance operations in Europe are conducted through WICE, which has its principal office in the British Overseas Territory of Gibraltar. WICE was initially formed to provide access to insurance risks across the European Union. Following Brexit, WICE concentrates on U.K. and Western European risks, predominantly in personal lines of insurance but will also entertain commercial casualty lines.

The acquisition of Axeria will provide access to insurance risks across the European Union.

Our goal within our insurance operations is to be a valued, long-term capacity partner with a select group of well-established, proven program managers, with our integrated total return strategy providing them with competitive solutions for their clients. We have a strong market position with approximately $1.1$1.2 billion in capital and an “A-” rating from A.M. Best for each of our operating subsidiaries. Many of the insurers providing capacity to program managers are neither as substantially capitalized nor as highly rated as we are; having a strong insurance partner gives program managers an edge when promoting products to clients.

We believe that our ability to enter insurance markets on a largely variable cost basis, unburdened by the fixed costs that would otherwise be required to create a standalone insurance operation, provides us with another significant and fundamental advantage. We benefit from AUI’s and AUL’s industry contacts and market acumen to identify, attract and retain those program managers that satisfy our guidelines in terms of reputation, technical track record and quality of administration. While we benefit from AUI’s and AUL’s infrastructure, our acquisition and administrative costs are largely based on premiums actually produced.

Subject to our overall underwriting guidelines, on our behalf, AUL, for WICE, or AUI, for WSIC and WIC, thoroughly conducts due diligence on each prospective program manager and approves underwriting guidelines for each specific line and class of business before delegation of the underwriting and/or claims-handling authority to any such program manager. We believe that by stringently vetting potential program managers we can advantageously and efficiently access a broad customer base while maintaining underwriting control and discipline. Fundamentally, AUL and AUI employ the same evaluation and selection criteria in scrutinizing our prospective program managers as they do for Arch’s own account. The determination by AUL and AUI as to whether to offer our policies, Arch’s policies, or both, depends on the result of the pricing analysis using the differing return assumptions of each company. On an ongoing basis, we and AUL or AUI, as applicable, monitor the business produced and financial condition of each program manager through periodic audits of underwriting, claims and operations.

Sourcing and underwriting

We have a strategic relationship pursuant to which Arch assists us in our pursuit of a highly disciplined underwriting approach, targeting lines of business that we believe will allow us to generate attractive risk-adjusted returns throughout industry market cycles. On our behalf, Arch continuously monitors the broad insurance and reinsurance market for opportunities. Specifically, Arch monitors opportunities that are anticipated to provide attractive risk-adjusted returns with a particular focus on product lines, which may have previously experienced adverse results and are therefore beginning to benefit from an increase in premium rates, and thus provide a potentially beneficial time to enter, or increase activity in, those markets. Similarly, on our behalf, Arch analyzes the market for softening product lines for which the applicable rates may provide less attractive risk-adjusted returns and potentially reduces our exposure to such lines accordingly at renewal.

Our strategy is to operate in lines of business in which underwriting expertise can make a meaningful difference in operating results. We are opportunistic in our pursuit of underwriting risks and binding business where we believe we have a competitive advantage in risk evaluation, distribution, investment strategy, or a combination of these factors. Our recentThe establishment of our U.S. and European insurance operations enables us to directly access similar types of underlying risk premium as we underwrite as reinsurance, with what we believe to be better risk-adjusted pricing. Accessing premium through our insurance operations should also provide the benefit of lower acquisitions costs.

Our underwriting philosophy is based on prudent risk selection, risk diversification and comprehensive pricing analysis. We believe that the key to our approach is adherence to underwriting rigor across all types of business we underwrite. We employ a disciplined, analytical approach to underwriting. As part of the underwriting process, a variety of factors are typically assessed, including: (i) adequacy of underlying rates combined with the expected return on equity

for a given insurance or reinsurance program; (ii) the industry reputation, track record, perceived financial strength and stability of the proposed client, or program manager in the case of our insurance business; (iii) the likelihood of establishing a long-term relationship with the client or program manager; (iv) the specialized knowledge and access to business that they possess; (v) the geographic area in which the client or program manager does business, together with our aggregate exposures in that area; (vi) historical loss data for the client or program manager; and (vii) projections of future loss frequency and severity.

Pursuant to our underwriting guidelines, we target an underwriting portfolio with tightly managed natural catastrophe exposure. We currently seek to limit our modeled PML for property catastrophe exposures for each peak peril and peak zone from a 1-in-250 year occurrence to no more than 10% of our total capital, which is less than most of our principal reinsurance competitors. Our conscious effort to limit our catastrophe exposure lowers the volatility of our overall underwriting portfolio and provides greater certainty as to future claims-related payout patterns and timing, dovetailing

well with our non-investment grade investment strategy by minimizing the possibility of needing to sell investments at inopportune times in the investment market cycles.

We believe that our experienced senior management, combined with Arch’s underwriting expertise and broad market access, allows us to identify business with attractive risk-reward characteristics. As new underwriting opportunities are identified, we explore the suitability of underwriting the new business in order to take advantage of perceived market trends, particularly in lines of business for which Arch already possesses deep underwriting expertise.

Policy service and claims management

Arch provides underwriting services, portfolio management, exposure modeling, loss reserve recommendations, claims-handling, legal oversight, regulatory compliance, policy issuance and development, underwriting systems review, program manager audits, accounting support and administrative support, in each case, subject to the terms and conditions of our services agreements with Arch, including our underwriting and operational guidelines, as well as the oversight of our management and board of directors.

We believe that handling claims is an important component of customer service through which we can differentiate ourselves from our competitors. The ability to handle claims in accordance with industry best practices and standards fosters credibility in the market both with customers and with program managers. Through this arrangement with Arch, we gain access on a very cost-effective basis to highly experienced underwriting, claims and support function professionals and benefit from the exemplary customer service reputation Arch has earned over its 16-year19-year history.

In administering claims on our behalf, Arch may engage third-party claims-handling firms to monitor, adjust and pay claims up to designated approval levels. Arch provides close supervision over any such third-party managers. Claims-handling firms are monitored and audited on an ongoing basis by Arch. When considering any proposed claims-handling delegation, Arch evaluates the candidate’s expertise, track record, staffing adequacy, reputation and licensing as required.

Reinsurance relationships

We have entered into outward quota share reinsurance agreements with Arch for each of our operating subsidiaries, which we believe provides a strong alignment of interest through Arch’s assuming a direct and meaningful sharing of the risk it underwrites for us. Subject to limited exceptions, Arch participates in a minimum 15% interest in all risks written by us, either by its own original participation, writing a companion line with us, or by accepting a minimum 15% quota share participation on all other contracts.

From time to time, we purchase third-party reinsurance when deemed advantageous from a portfolio management standpoint. We only use reinsurers carrying an “A-” or higher rating from

A.M. Best or Standard & Poor’s or, alternatively, reinsurers that provide sufficient collateral to mitigate credit risk exposure.

Investment operations

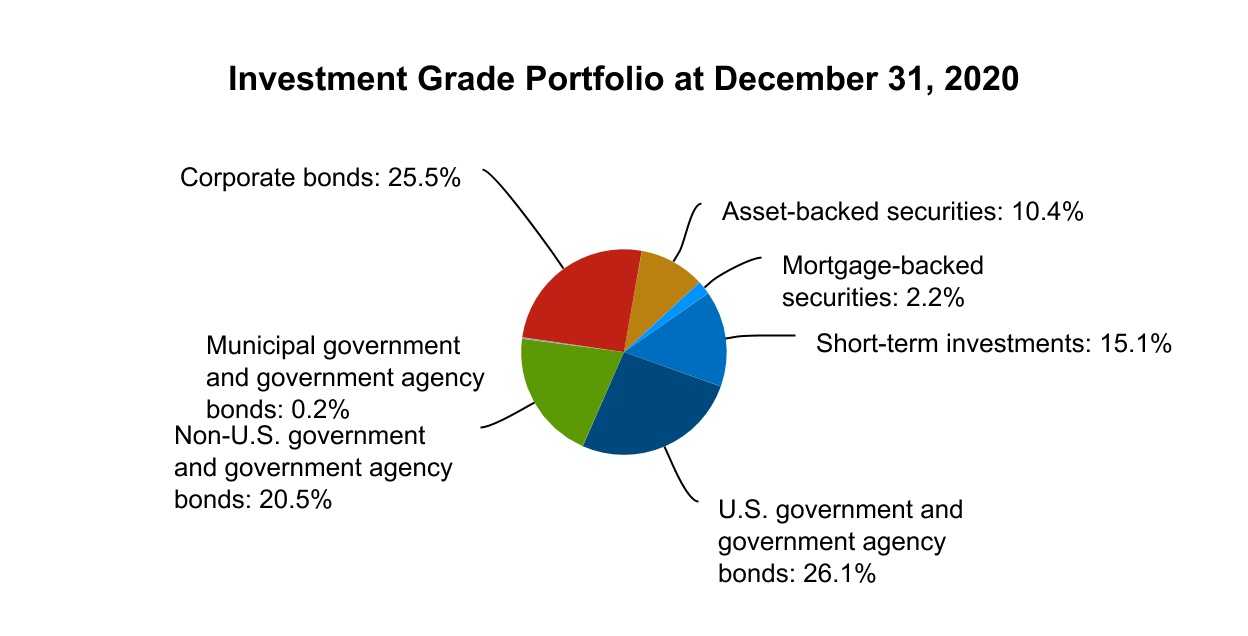

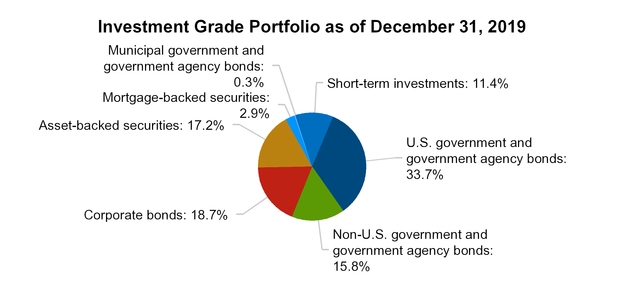

Overview

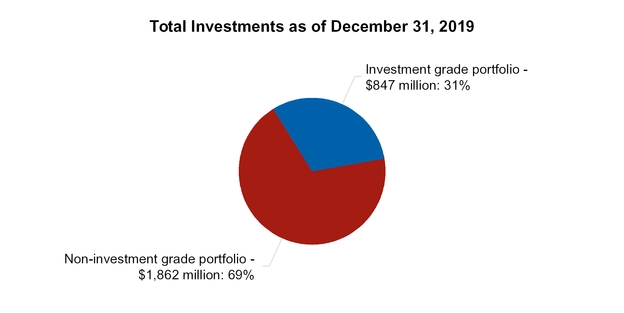

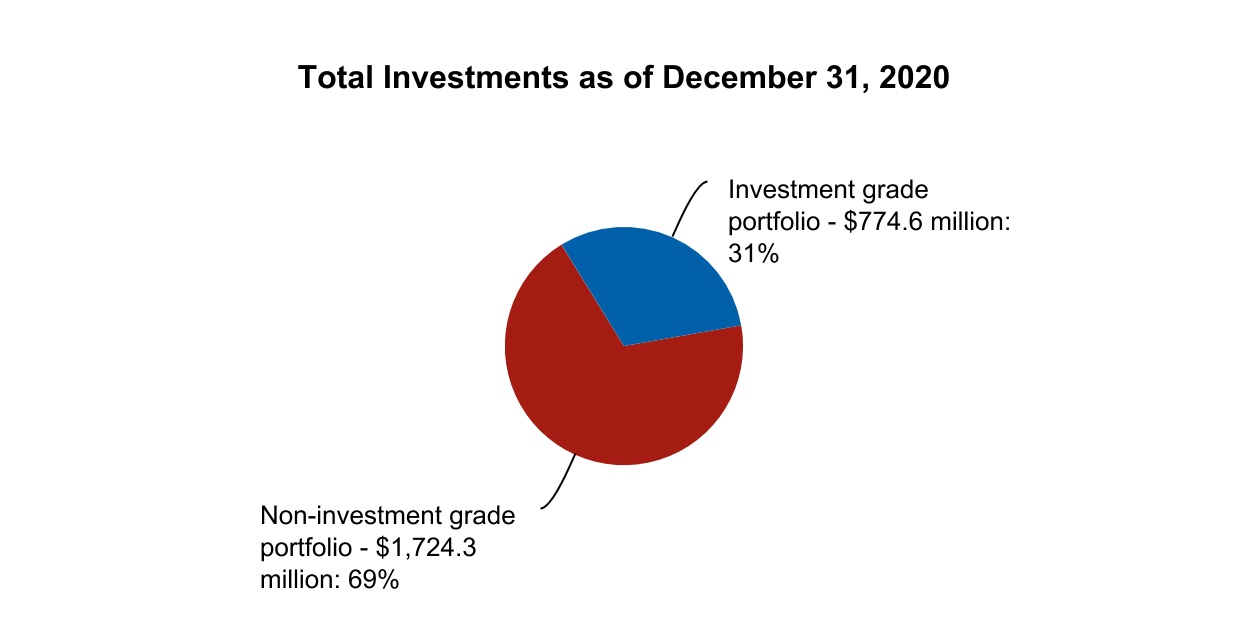

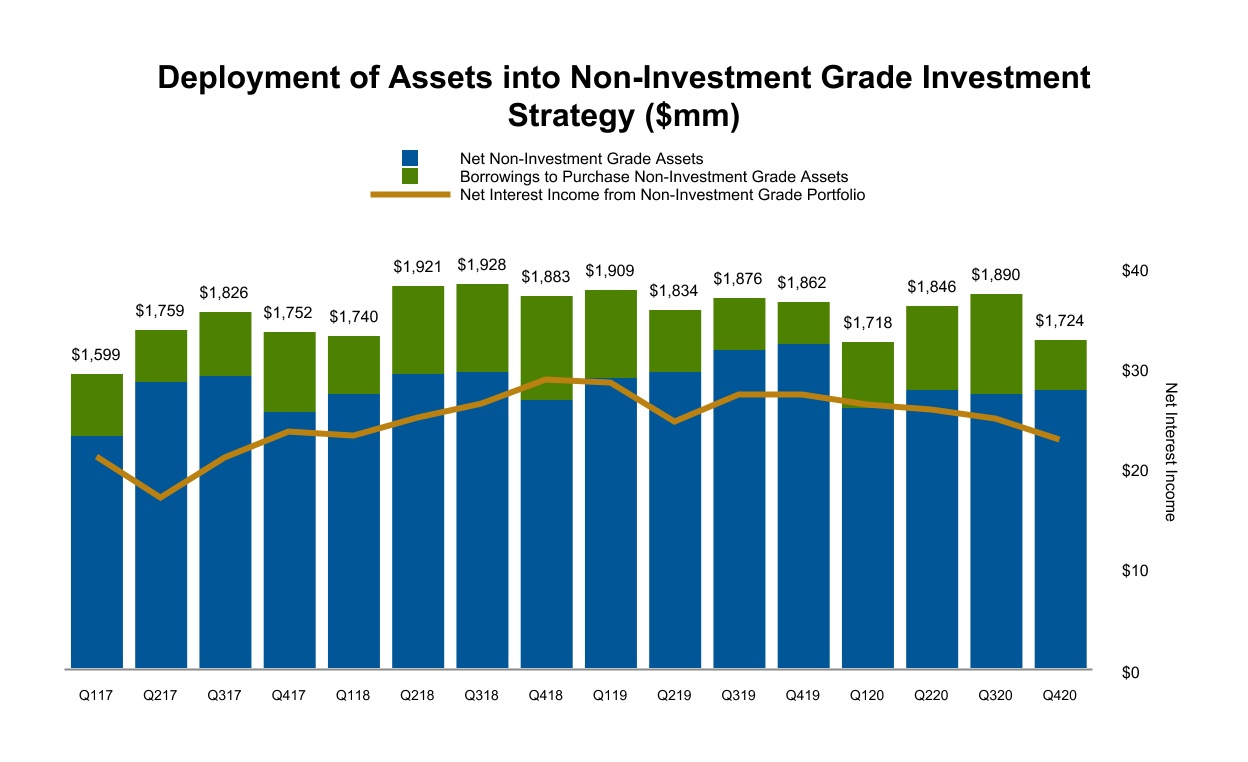

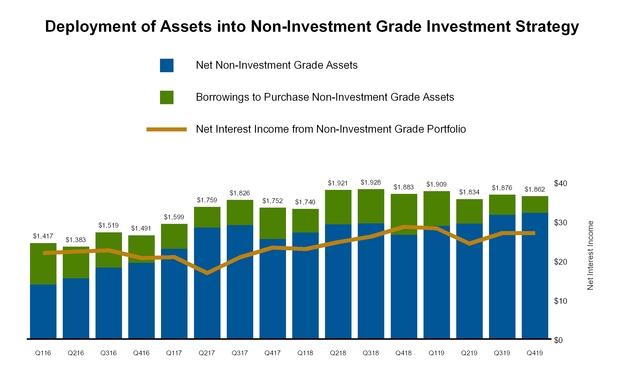

Our invested assets are funded with our capital, accumulated net underwriting float, reinvested net interest income, net capital gains and borrowings to purchase investments. These invested assets are allocated between our non-investment grade portfolio and our investment grade portfolio. As of December 31, 2019,2020, our non-investment grade portfolio represented approximately 69% of our invested assets and our investment grade portfolio represented approximately 31% of our invested assets. Our investment operations are monitored by our PresidentChief Executive Officer, and our Chief Risk Officer and the investment committee of our board of directors.

Our non-investment grade portfolio is comprised principally of corporate credit assets managed by HPS pursuant to separate investment management agreements with Watford Re, Watford Asset Trust I, or Watford Trust, and each of our insurance subsidiaries. Each such investment management agreement with HPS includes investment guidelines. Subject to these guidelines, HPS makes all investment decisions with respect to our non-investment grade portfolio on our behalf. Our non-investment grade investment strategy and guidelines are formulated to complement our target underwriting portfolio, and are designed to meet the projected payout characteristics of the medium- to long-tail, lower-volatility underwriting portfolio we underwrite.

The remainder of our investment portfolio is invested in investment grade assets, the largest portion of which is managed by AIM. We also have several investment grade accounts managed by other Investment Managers, including HPS.

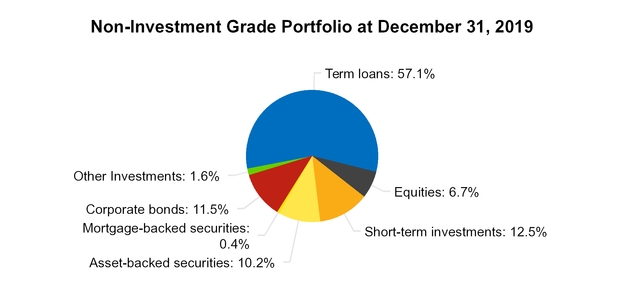

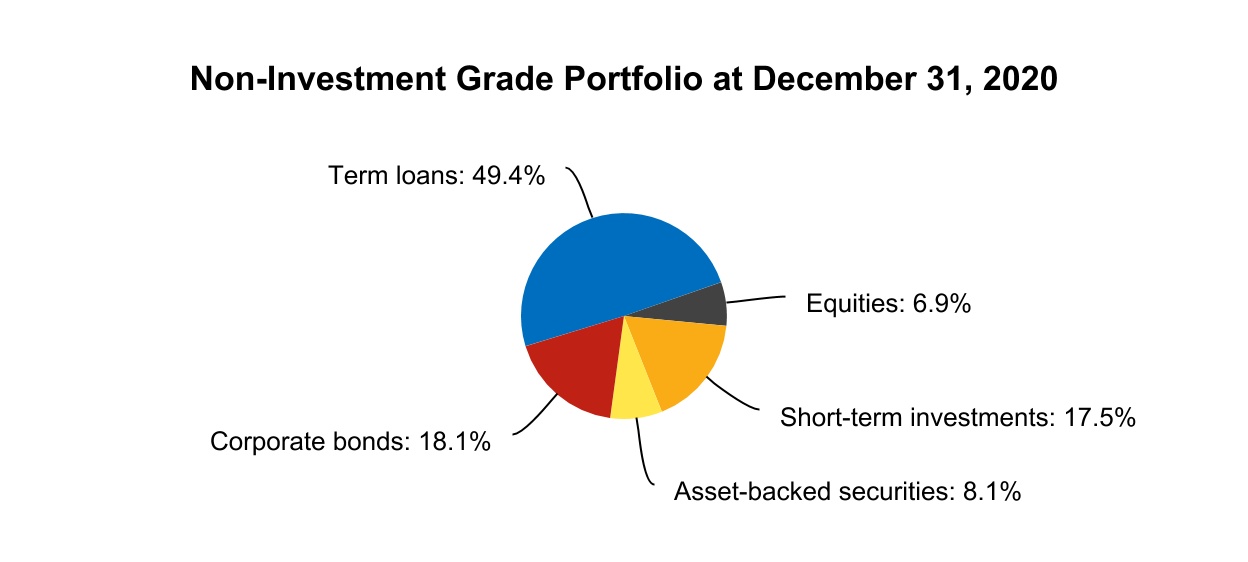

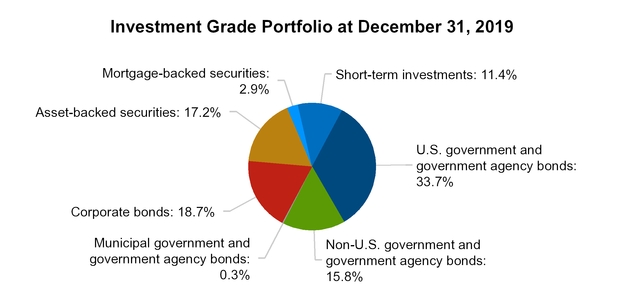

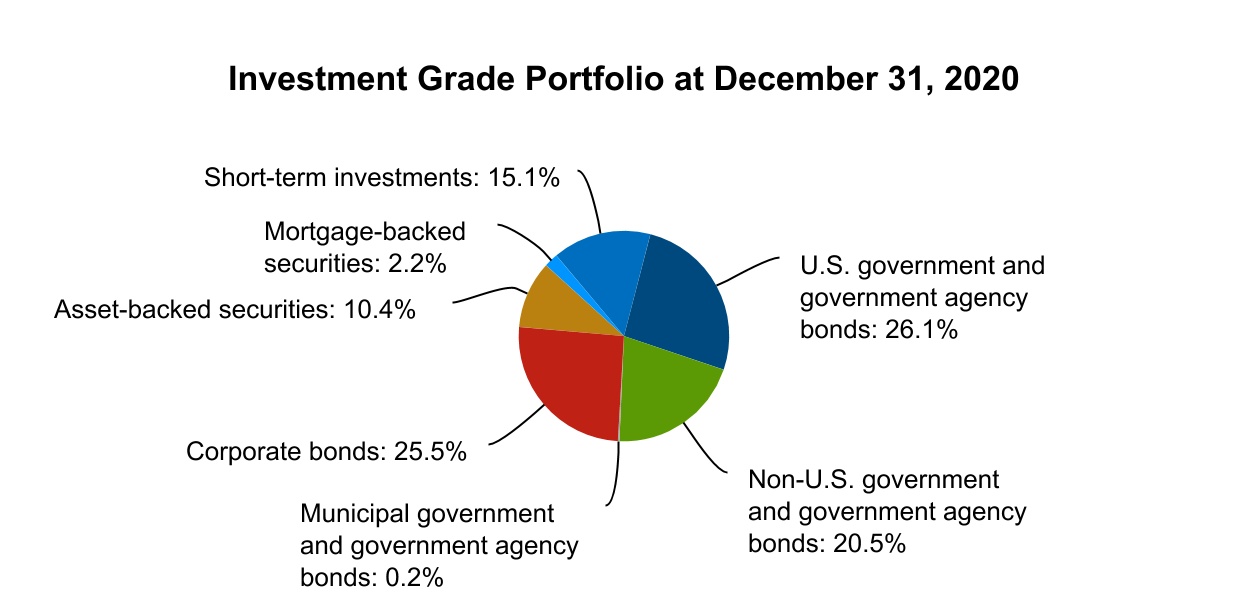

The following chart shows the breakdown of our total investments among our non-investment grade portfolio and our investment grade portfolio as of December 31, 2019:2020:

Total: $2,709.1 million$2.5 billion

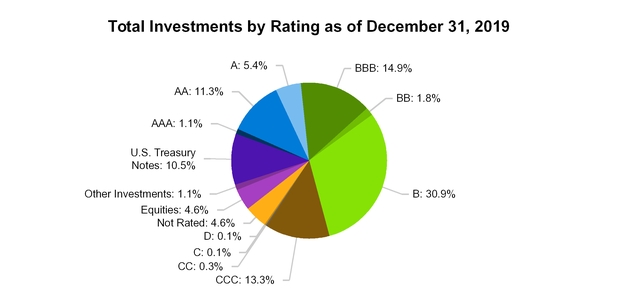

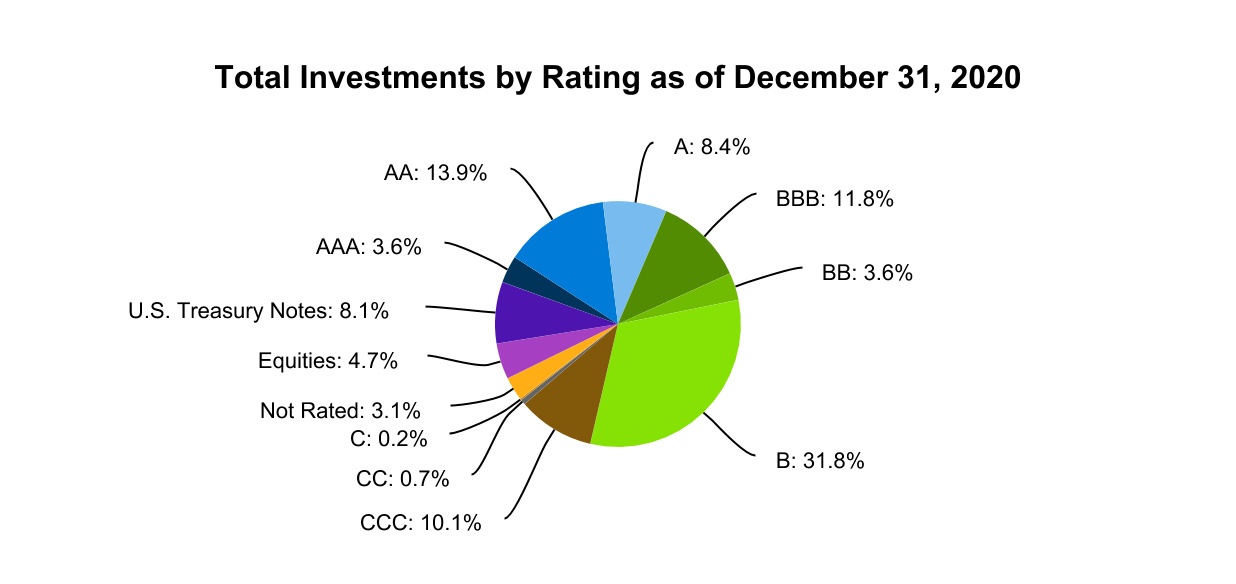

The following chart shows the breakdown of our investments by rating within our total investment portfolio as of December 31, 2019:2020:

Total: $2,709.1 million$2.5 billion

Investment grade ratings, such as “BBB” and above, indicate the applicable rating agency’s view that the investment has a low risk of credit default and that the obligor has at least adequate capacity to meet its financial commitments on the obligation.

Ratings below investment grade, such as “BB”, “B” and “CCC,” indicate the applicable rating agency’s view that the investment is speculative, that the obligor is more vulnerable than investment grade-rated obligors, and that, in the event of adverse business, financial, or economic conditions, the obligor is less likely to have the capacity to meet its financial commitments on the obligation. Based on published criteria, a “BB” rating reflects the applicable rating agency’s view that, while the obligation is less vulnerable to non-payment than other speculative issues, it faces major ongoing uncertainties or exposure to adverse business, financial, or economic conditions, which could lead to the obligor’s inadequate capacity to meet its financial commitment on the obligation. A rating of “B” reflects the applicable rating agency’s view that the obligor currently has the capacity to meet its financial commitment on the obligation, but adverse business, financial, or economic conditions will likely impair the obligor’s capacity or willingness to meet its financial commitment on the obligation. A rating of “CCC” indicates the applicable rating agency’s view that the obligation is currently vulnerable to non-payment and is dependent upon favorable business, financial, and economic conditions for the obligor to meet its financial commitment on the obligation. A rating below “CCC” indicates the applicable rating agency’s view that the obligation is currently highly vulnerable to non-payment.

The following is a representative list of the industries in which we may invest: Consumer Products, Food and Beverage, Healthcare,Health Care, Pharmaceuticals, Tobacco, Technology, Automotive, Consumer Cyclical Services, Home Construction, Restaurants, Retailers, Insurance (Health, Life and Property and Casualty), Communications (Cable and Satellite, Media and Entertainment, Wireless and Wirelines), Banking and Other Financial Services, Capital Goods (Aerospace and Defense, Building Materials, Construction Machinery, Diversified Manufacturing), Energy, Other Industrial, and Transportation. However, we may invest in other industries if presented with attractive opportunities.

As of December 31, 2019,2020, the composition of our portfolio by industry, excluding asset-backed securities and mortgage-backed securities, was as follows: 12.2%15.3% of our portfolio was invested in

Consumer Products, 8.3% Financial Services, 10.3% in Technology, 6.2%9.7% in Health Care, 8.4% in Consumer Cyclical Services and 5.7% 7.5%

in Insurance,Industrials with the remainder invested in other industries (with no other industry comprising greater than 5%). As of December 31, 2019,2020, the geographic composition of our portfolio, excluding asset-backed securities and mortgage-backed securities, was as follows: 78.6%81.6% in the United States, 10.9%10.3% in the United Kingdom, 2.4%3.6% in the Cayman Islands, and the remainder in other regions (with no other geographic region comprising greater than 2%).

A portion of our investment portfolio consists of assets that do not have a rating from one of the major rating agencies. Just as is done in connection with a potential investment in a rated debt obligation, when offered the opportunity to invest our assets into an unrated obligation, HPS thoroughly evaluates the obligor and the potential investment and makes a determination as to the inherent risks and whether the terms provide an attractive risk-adjusted return. A debt issuer may choose to forgo obtaining a rating for a number of reasons, particularly if the debt issuer is conducting a small privately placed transaction for which the ratings fees would be a burdensome expense or if the desired transaction date does not allow sufficient time for the completion of the rating process. It is also possible that a prospective issuer or the terms of the proposed obligation would not meet the rating agency requirements for the level of rating desired by the obligor company.

The following table shows the components of our net investment income (loss) on investments for the periods indicated:

| | | | Year Ended December 31, | | Year Ended December 31, |

| | 2019 | | 2018 | | 2017 | | 2020 | | 2019 | | 2018 |

| | ($ in thousands) | | ($ in thousands) |

| Interest income | $ | 163,888 |

| | $ | 152,916 |

| | $ | 125,463 |

| Interest income | $ | 140,390 | | | $ | 163,888 | | | $ | 152,916 | |

| Investment management fees - related parties | (18,392 | ) | | (17,006 | ) | | (21,451 | ) | Investment management fees - related parties | (17,193) | | | (18,392) | | | (17,006) | |

| Borrowing and miscellaneous other investment expenses | (29,285 | ) | | (28,377 | ) | | (17,489 | ) | Borrowing and miscellaneous other investment expenses | (16,807) | | | (29,285) | | | (28,377) | |

| Net interest income | 116,211 |

| | 107,533 |

| | 86,523 |

| Net interest income | 106,390 | | | 116,211 | | | 107,533 | |

| Realized and unrealized gain (loss) on investments | 24,243 |

| | (113,834 | ) | | 1,120 |

| Realized and unrealized gain (loss) on investments | 19,629 | | | 24,243 | | | (113,834) | |

| Investment performance fees - related parties | (12,191 | ) | | (48 | ) | | (14,905 | ) | Investment performance fees - related parties | (12,037) | | | (12,191) | | | (48) | |

| Net investment income (loss) | $ | 128,263 |

| | $ | (6,349 | ) | | $ | 72,738 |

| Net investment income (loss) | $ | 113,982 | | | $ | 128,263 | | | $ | (6,349) | |

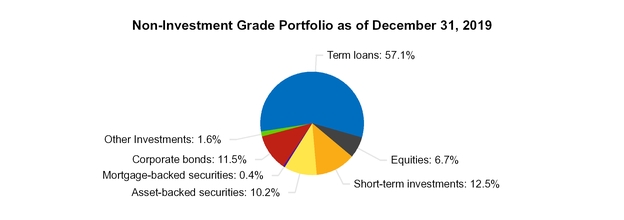

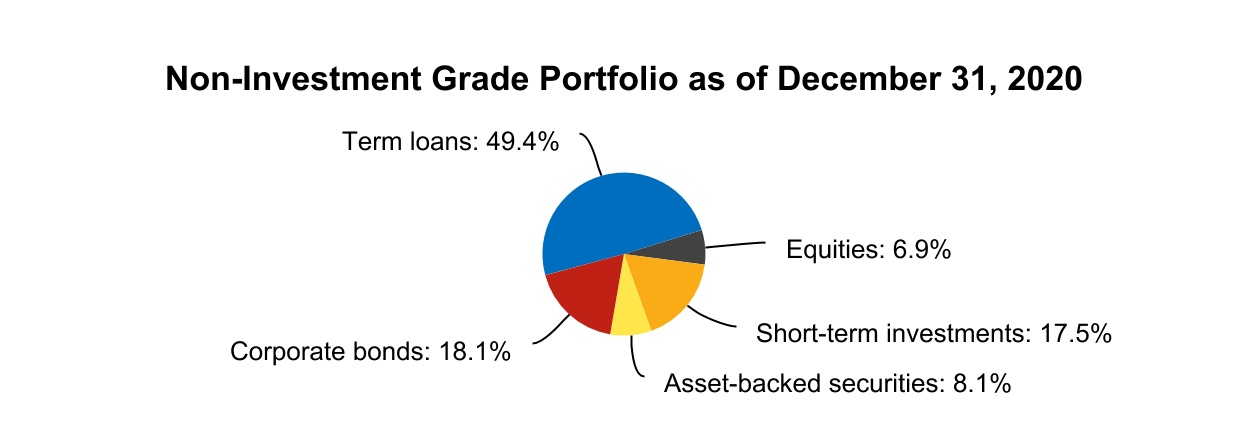

Non-investment grade portfolio

Background on HPS. HPS is a global investment firm with a focus on non-investment grade credit. Established in 2007, HPS has over 100150 investment professionals and over 350380 total employees. HPS manages capital for sophisticated investors, including financial institutions, public and corporate pension funds, sovereign wealth funds, funds of funds, endowments, foundations and family offices, as well as individuals. HPS is headquartered in New York with teneleven additional offices globally. HPS has approximately $61$68 billion of assets under management as of December 31, 2019.2020.

HPS was originally formed as a unit of Highbridge, a subsidiary of JPMorgan Asset Management Holdings Inc. In March 2016, the principals of HPS acquired the firm from JPMorgan Asset Management Holdings Inc., which retained Highbridge’s hedge fund strategies.

Investment strategy.

Our non-investment grade portfolio seeks to generate attractive risk-adjusted returns comprising current interest income, trading gains and capital appreciation, with an emphasis on capital preservation. To execute the non-investment grade component of our investment strategy, we mandated HPS with a strategy that (i) is designed to meet the projected payout characteristics of the medium- to long-term, lower-volatility underwriting portfolio we underwrite and (ii) seeks to achieve risk-adjusted returns that exceed those of typical reinsurer investment portfolios by focusing on non-investment grade assets, with the flexibility to invest a limited portion of this portfolio in less liquid assets. Specifically, we seek to achieve investment

returns that exceed those returns achieved by our competitors from their fixed-income portfolios. We believe this strategy provides us with risk-adjusted returns that are both attractive and appropriate given our underwriting portfolio.

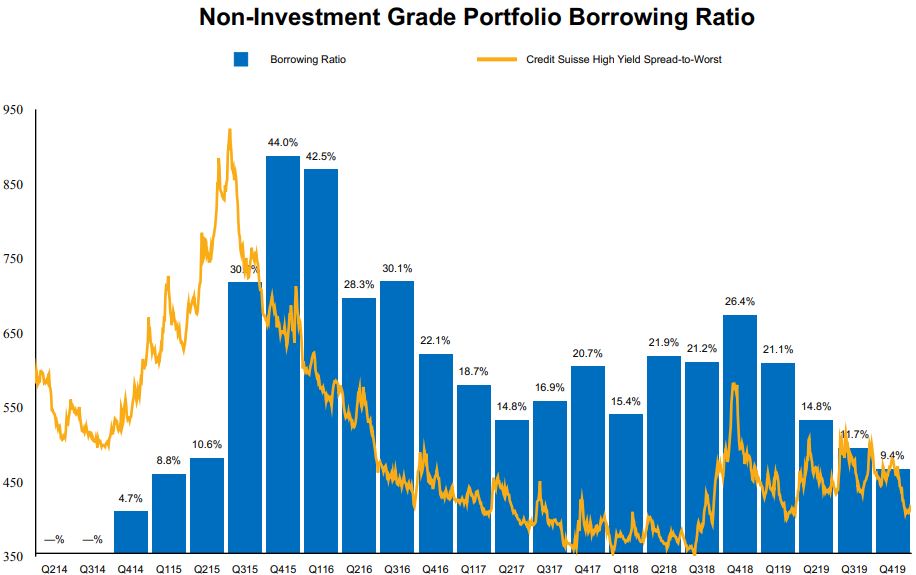

HPS manages our non-investment grade corporate credit assets, including bank loans and high yield bonds, and may also invest in other instruments such as mezzanine debt, equities, credit default swaps, structured credit instruments and other derivative products. Our non-investment grade portfolio seeks to generate attractive risk-adjusted returns comprising current interest income, trading gains and capital appreciation, with an emphasis on capital preservation. Pursuant to these investment guidelines, HPS is permitted to hedge the assets in our non-investment grade portfolio to reduce volatility and protect against systemic risks, as well as to enter into opportunistic short positions. Other than cash and cash equivalents, investment positions with a single issuer will comprise no more than 7.5% of the aggregate Long Market Value (defined as the value of the long investments of the portfolio of Watford Re or Watford Trust, valued using the methodologies set forth in Watford Re’s or Watford Trust’s investment management agreement with HPS, as applicable) of our non-investment grade portfolio. Positions established primarily for hedging purposes (including, without limitation, index positions) are not subject to this limit, and capital structure arbitrage positions in an issuer are deemed separate investments for the purposes of these limitations.

Through this strategy, we seek to achieve risk-adjusted returns that exceed those of typical reinsurer investment portfolios by focusing on non-investment grade assets, with the flexibility to invest a limited portion of this portfolio in less liquid assets. Limited positions in equity securities are also permitted, subject to our non-investment grade investment guidelines, which are an integral component of each applicable investment management agreement. Generally, any equity investments are not expected, in the aggregate, to represent more than 10% of the Long Market Value of our non-investment grade portfolio, and are expected to be focused on either a value-oriented approach or a catalyst to a realization event, which include restructurings, lawsuits and regulatory changes, among other examples. Equity investments resulting in ownership exceeding 18.5% of the outstanding equity securities of an issuer, measured at the time of investment, will require our prior approval. HPS may also utilize other investment instruments for our non-investment grade portfolio, subject to our non-investment grade investment guidelines.

The non-investment grade investment guidelines under Watford Trust’s and our insurance subsidiaries’ respective investment management agreements with HPS also contain certain limitations relating to, among other things, the concentration of investments and utilization of leverage. As of December 31, 2019,2020, HPS was in compliance with all non-investment grade investment guidelines.