SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

|

| |

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 20162017

OR

|

| |

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission file number: 001-36710

Shell Midstream Partners, L.P.

(Exact name of registrant as specified in its charter)

|

| | |

| Delaware | | 46-5223743 |

(State or other jurisdiction of incorporation or organization) | | (I.R.S. Employer Identification No.) |

One Shell Plaza, 910 Louisiana Street,150 N. Dairy Ashford, Houston, Texas 7700277079

(Address of principal executive offices) (Zip Code)

Registrant’s telephone number, including area code: (888) 737-2377(832) 337-2034

Securities registered pursuant to Section 12(b) of the Act: |

| | |

| Title of each class | | Name of each exchange on which registered |

Common Units, Representing Limited PartnershipPartner Interests | | New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. x Yes ¨ No

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. ¨ Yes x No

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. x Yes ¨ No

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). x Yes ¨ No

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of the registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer”filer,” “smaller reporting company” and “smaller reporting“emerging growth company” in Rule 12b-2 of the Exchange Act.

|

| | | | |

| Large accelerated filer | x | | Accelerated filer | ¨ |

| Non-accelerated filer | ¨ | | Smaller reporting company | ¨ |

| Emerging growth company | o | | | |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. o

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). ¨ Yes x No

The aggregate market value of the registrant’s common units held by non-affiliates of the registrant as of June 30, 2016,2017, was $2,983$2,677 million, based on the closing price of such units of $33.79$30.30 as reported on the New York Stock Exchange on such date. The registrant had 177,317,444223,811,781 common units and no subordinated units outstanding as of February 23, 2017.27, 2018.

Documents incorporated by reference:

None

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING STATEMENTS

This report includes forward-looking statements. You can identify our forward-looking statements by the words “anticipate,” “estimate,” “believe,” “budget,” “continue,” “could,” “intend,” “may,” “plan,” “potential,” “predict,” “seek,” “should,” “would,” “expect,” “objective,” “projection,” “forecast,” “goal,” “guidance,” “outlook,” “effort,” “target” and similar expressions.

We based the forward-looking statements on our current expectations, estimates and projections about us and the industries in which we operate in general. We caution you these statements are not guarantees of future performance as they involve assumptions that, while made in good faith, may prove to be incorrect, and involve risks and uncertainties we cannot predict. In addition, we based many of these forward-looking statements on assumptions about future events that may prove to be inaccurate. Accordingly, our actual outcomes and results may differ materially from what we have expressed or forecast in the forward-looking statements. Any differences could result from a variety of factors, including the following:

The continued ability of Royal Dutch Shell plc and our non-affiliate customers to satisfy their obligations under our commercial and other agreements and the impact of lower market prices for crude oil, refined petroleum products and refined products.refinery gas.

The volume of crude oil, and refined petroleum products and refinery gas we transport or store and the prices that we can charge our customers.

The tariff rates with respect to volumes that we transport through our regulated assets, which rates are subject to review and possible adjustment imposed by federal and state regulators.

Changes in revenue we realize under the loss allowance provisions of our fees and tariffs resulting from changes in underlying commodity prices.

Fluctuations in the prices for crude oil, and refined petroleum products.products and refinery gas.

The level of production of refinery gas by refineries and demand by chemical sites.

The level of onshore and offshore (including deepwater) production and demand for crude oil by U.S. refiners.

Changes in global economic conditions and the effects of a global economic downturn on the business of Shell and the business of its suppliers, customers, business partners and credit lenders.

Liabilities associated with the risks and operational hazards inherent in transporting andand/or storing crude oil, and refined petroleum products.products and refinery gas.

Curtailment of operations or expansion projects due to unexpected leaks, spills, or spills, severe weather disruption; riots, strikes, lockouts or other industrial disturbances; or failure of information technology systems due to various causes, including unauthorized access or attack.

Costs or liabilities associated with federal, state and local laws and regulations relating to environmental protection and safety, including spills, releases and pipeline integrity.

Costs associated with compliance with evolving environmental laws and regulations on climate change.

Costs associated with compliance with safety regulations and system maintenance programs, including pipeline integrity management program testing and related repairs.

Changes in tax status.

Changes in the cost or availability of third-party vessels, pipelines, rail cars and other means of delivering and transporting crude oil, and refined petroleum products.products and refinery gas.

Direct or indirect effects on our business resulting from actual or threatened terrorist incidents or acts of war.

Availability of acquisitions and financing for acquisitions on our expected timing and acceptable terms.

Changes in, and availability to us, of the equity and debt capital markets.

The factors generally described in Part I, Item 1A. Risk Factors of this report.

GLOSSARY OF TERMS

Barrel: One stock tank barrel, or 42 U.S. gallons liquid volume, used in reference to crude oil or other liquid hydrocarbons.

BOEM: Bureau of Ocean Energy Management.

BSEE: Bureau of Safety and Environmental Enforcement.

Capacity: Nameplate capacity.

Common carrier pipeline: A pipeline engaged in the transportation of crude oil, refined products or natural gas liquids as a common carrier for hire.

Crude oil: A mixture of raw hydrocarbons that exists in liquid phase in underground reservoirs.

DOT: Department of Transportation.

EPAct: Energy Policy Act of 1992.

Expansion capital expenditures: Expansion capital expenditures is a defined term under our partnership agreement. Expansion capital expenditures are cash expenditures (including transaction expenses) for capital improvements. Expansion capital expenditures do not include maintenance capital expenditures or investment capital expenditures. Expansion capital expenditures do include interest payments (including periodic net payments under related interest rate swap agreements) and related fees paid during the construction period on construction debt. Where cash expenditures are made in part for expansion capital expenditures and in part for other purposes, the general partner determines the allocation between the amounts paid for each.

FERC: Federal Energy Regulatory Commission.

GAAP: United States generally accepted accounting principles.

HCAs: High Consequence Areas.

ICA: Interstate Commerce Act.

kbpd: Thousand barrels per day.

kbls: Thousand barrels.

Life-of-lease transportation agreement: A contract in which the producer dedicates shipments of all current and future reserves pertaining to a specific lease or area to a specific carrier.

LNG: Liquefied natural gas.

LTIP: Shell Midstream Partners, L.P. 2014 Incentive Compensation Plan.

Maintenance capital expenditures: Maintenance capital expenditures is a defined term under our partnership agreement. Maintenance capital expenditures are cash expenditures (including expenditures for (a) the acquisition (through an asset acquisition, merger, stock acquisition, equity acquisition or other form of investment) by the Partnership or any of its subsidiaries of existing assets or assets under construction, (b) the construction or development of new capital assets by the Partnership or any of its subsidiaries, (c) the replacement, improvement or expansion of existing capital assets by the Partnership or any of its subsidiaries or (d) a capital contribution by the Partnership or any of its subsidiaries to a person that is not a subsidiary in which the Partnership or any of its subsidiaries has, or after such capital contribution will have, directly or indirectly, an equity interest, to fund the Partnership or such subsidiary’s share of the cost of the acquisition, construction or development of new, or the replacement, improvement or expansion of existing, capital assets by such person), in each case if and to the extent such acquisition, construction, development, replacement, improvement or expansion is made to maintain, over the long-term, the operating capacity or operating income of the Partnership and its subsidiaries, in the case of clauses (a), (b) and (c), or such person, in the case of clause (d), as the operating capacity or operating income of the Partnership and its subsidiaries or such person, as the case may be, existed immediately prior to such acquisition, construction, development, replacement, improvement, expansion or capital contribution. For purposes of this definition, “long-term” generally refers to a period of not less than twelve months.

mbls: Million barrels.

mscf/d: Million standard cubic feet per day.

Partnership Agreement: First Amended and Restated Agreement of Limited Partnership of Shell Midstream Partners, L.P., dated as of November 3, 2014.

PHMSA: Pipeline and Hazardous Materials Safety Administration.

Product loss allowance or PLA: An allowance for volume losses due to measurement difference set forth in crude oil product transportation agreements, including long-term transportation agreements and tariffs for crude oil shipments.

Refined products: Hydrocarbon compounds, such as gasoline, diesel fuel, jet fuel and residual fuel that are produced by a refinery.

Refinery gas: Non-condensable gas obtained during distillation of crude oil or treatment of oil products in refineries.

Ship-or-pay contract: A contract requiring payment for the transportation of crude oil or refined products even if the crude oil or refined products are not transported.

Tension-leg platform: A vertically moored floating structure normally used for the offshore production of oil or gas, and particularly suited for water depths greater than 300 meters. The platform is permanently moored by means of tethers or tendons grouped at each of the structure’s corners. A group of tethers is called a tension leg. A feature of the design of the tethers is that they have relatively high axial stiffness (low elasticity), such that vertical motion of the platform is significantly reduced. Tension-leg platforms equipped with a drilling rig have direct vertical access for drilling and completing wells, as well as intervention operations.

Throughput: The volume of crude oil, refined products or natural gas transported or passing through a refinery, pipeline, terminal or other facility during a particular period.

SHELL MIDSTREAM PARTNERS, L.P.

TABLE OF CONTENTS

PART I

Unless the context otherwise requires, references in this report to “Shell Midstream Partners,” “the Partnership,” “us,” “our,” “we,” or similar expressions for the time period from and after November 3, 2014, the closing date of our Initial Public Offering (“IPO”), refer to Shell Midstream Partners, L.P. and its subsidiaries. References to “our general partner” refer to Shell Midstream Partners GP LLC, a wholly owned subsidiary of Shell Pipeline Company LP (“SPLC”). References to “Shell” or “Parent” refer collectively to Royal Dutch Shell plc and its controlled affiliates, other than us, our subsidiaries and our general partner.

The following businesses were acquired from our Parent and accounted for as acquisitions between entities under common control. As such, our consolidated financial statements include the financial results of these businesses, which were derived from the financial statements and accounting records of SPLC and Shell for the periods prior to acquisition. Specifically, such businesses are reflected for the following periods prior to the effective date of such acquisition:

Houston-to-Houma crude oil pipeline system (“Ho-Ho”) for periods prior to July 1, 2014;

Zydeco Pipeline CompanyPecten Midstream LLC (“Zydeco”) for the period from July 1, 2014 through November 2, 2014; and

Shell Auger and Lockport Operations as defined below for periods prior to October 1, 2015.2015;

Shell Delta, Na Kika and Refinery Gas Pipeline Operations (as defined below) for periods prior to May 10, 2017; and

December 2017 Acquisition (as defined below) for periods prior to December 1, 2017, including the effect of fully consolidating Odyssey Pipeline L.L.C.

Our consolidated statements of income exclude the results of these businesses from net income attributable to the Partnership for the periods indicated above by allocating these results to our Parent.

Items 1 and 2. BUSINESS AND PROPERTIES

Overview

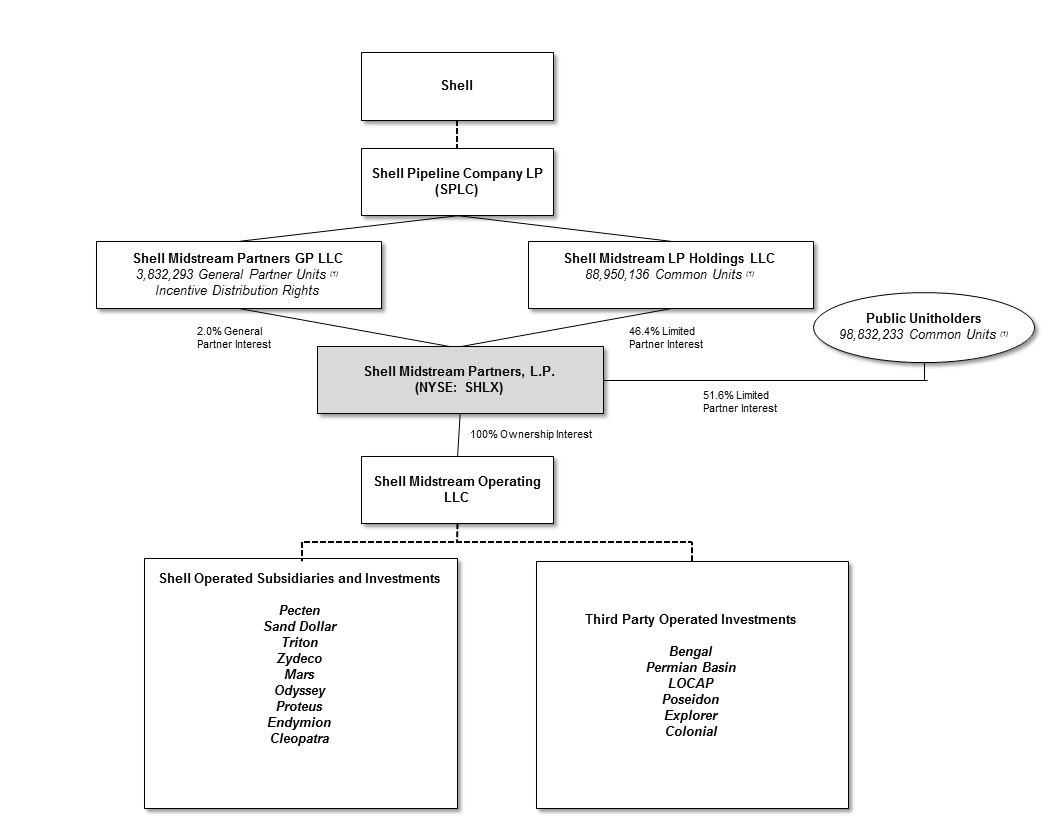

Shell Midstream Partners, L.P. is a Delaware limited partnership formed by Shell on March 19, 2014 to own and operate develop and acquire pipelinespipeline and other midstream assets. On November 3, 2014, we completedassets, including certain assets acquired from SPLC and its affiliates. We conduct our IPO.operations through our wholly owned subsidiary Shell Midstream Operating, LLC (“Operating Company”). Our general partner is Shell Midstream Partners GP LLC (“general partner”). Our common units are tradedtrade on the New York Stock Exchange (“NYSE”) under the symbol “SHLX.” As of December 31, 2016, SPLC, through Shell Midstream LP Holdings LLC, owned 21,475,068 common units and 67,475,068 subordinated units, representing a 49.2% limited partner interest in us. Our subordinated units converted to common units on February 15, 2017. SPLC also owned a 100% interest in Shell Midstream Partners GP LLC, our general partner, which in turn owned 3,618,723 general partner units, representing a 2% general partner interest in us.

We are a fee-based, growth-oriented master limited partnership.partnership that owns, operates, develops and acquires pipelines and other midstream assets. Our assets consist ofinclude interests in entities that own crude oil and refined products and natural gas pipelines and a crude tank storage and terminal system. Our pipelines and crude tank storage and terminal systemterminals that serve as key infrastructure to (i) transport and store onshore and offshore crude oil production to Gulf Coast and Midwest refining markets to deliver Gulf Coast natural gas production to market hubs, and to(ii) deliver refined products from Gulf Coastthose markets to major demand centers. Our assets also include interests in entities that own natural gas and refinery gas pipelines that transport offshore natural gas to market hubs and deliver refinery gas from refineries and plants to chemical sites along the Gulf Coast. We generate the majoritya substantial portion of our revenue under long-term agreements by charging fees for the transportation orand storage of crude oil and refined products through our pipelines the transportation of natural gas throughand storage tanks, and from income from our pipeline,equity and crude tank storage and terminal services. We do not engage in the marketing and trading of any commodities.cost method investments. Our operations compriseconsist of one reportable segment containing our portfolio of pipelines and other midstream assets.segment. See Note 1—Description of the Business and Basis of Presentation in the Notes to Consolidated Financial Statements included in Part II, Item 8 of this report.

We

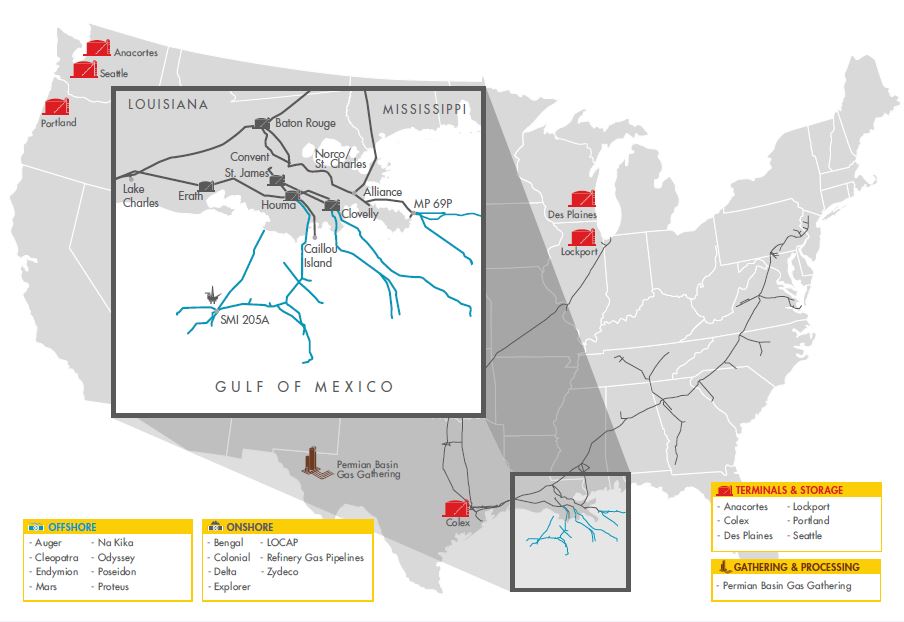

As of December 31, 2017, we own interests in seven crude oil, products and gas gathering and pipeline systems, three refined products systems, one natural gas pipeline system andas well as in a crude tanknumber of storage and terminal system. The crude oil pipeline systems, which are the Auger Pipeline System (“Auger”), held by Pecten Midstream LLC (“Pecten”), Zydeco, Odyssey Pipeline LLC (“Odyssey”), Mars Oil Pipeline Company (“Mars”), Poseidon Oil Pipeline Company LLC (“Poseidon”), Proteus Oil Pipeline Company, LLC (“Proteus”), and Endymion Oil Pipeline Company, LLC (“Endymion”), are strategically located along the Texas and Louisiana Gulf Coast and in the Gulf of Mexico. These systems link major onshore and offshore production areas with key refining markets. The refined products pipeline systems held by Bengal Pipeline Company LLC (“Bengal”) and Colonial Pipeline Company (“Colonial”) connect Gulf Coast and southeastern U.S. refineries to major demand centers from Alabama to New York, while the system held by Explorer Pipeline Company (“Explorer”) serves more than 70 major cities in 16 states from the Gulf Coast to the Midwest. The natural gas pipeline system, Cleopatra Gas Gathering Company, LLC (“Cleopatra”), brings Gulf of Mexico gas production to the market hub at Ship Shoal 332. The crude storage terminal, Lockport Terminal (“Lockport”), is located southwest of Chicago and serves Midwest refineries.

facilities. The following table reflects our ownership, and Shell’s retained ownership as of December 31, 2016.2017.

|

| | | | | |

| | SHLX Ownership | | Shell's Retained Ownership |

| | | | |

| Pecten Midstream LLC | 100 | % | | — | % |

| Zydeco | 92.5 | % | | 7.5 | % |

| Bengal Pipeline Company LLC | 50.0 | % | | — | % |

| Odyssey Pipeline LLC | 49.0 | % | | 22.0 | % |

| Mars Oil Pipeline Company | 48.6 | % | | 22.9 | % |

| Poseidon Oil Pipeline Company LLC | 36.0 | % | | — | % |

| Proteus Oil Pipeline Company, LLC | 10.0 | % | | — | % |

| Endymion Oil Pipeline Company, LLC | 10.0 | % | | — | % |

| Colonial Pipeline Company | 6.0 | % | | 10.12 | % |

| Explorer Pipeline Company | 2.62 | % | | 35.97 | % |

| Cleopatra Gas Gathering Company, LLC | 1.0 | % | | — | % |

|

| | | | | |

| | SHLX Ownership | | Shell's Retained Ownership |

| | | | |

| Pecten Midstream LLC (“Pecten”) | 100.0 | % | | — | % |

| Sand Dollar Pipeline LLC (“Sand Dollar”) | 100.0 | % | | — | % |

| Triton West LLC (“Triton”) | 100.0 | % | | — | % |

| Zydeco Pipeline Company LLC (“Zydeco”) | 92.5 | % | | 7.5 | % |

| Mars Oil Pipeline Company LLC (“Mars”) | 71.5 | % | | — | % |

| Odyssey Pipeline L.L.C. (“Odyssey”) | 71.0 | % | | — | % |

| Bengal Pipeline Company LLC (“Bengal”) | 50.0 | % | | — | % |

| Crestwood Permian Basin LLC (“Permian Basin”) | 50.0 | % | | — | % |

| LOCAP LLC (“LOCAP”) | 41.48 | % | | — | % |

Poseidon Oil Pipeline Company LLC (“Poseidon”)

| 36.0 | % | | — | % |

| Explorer Pipeline Company (“Explorer”) | 12.62 | % | | 25.97 | % |

| Proteus Oil Pipeline Company, LLC (“Proteus”) | 10.0 | % | | — | % |

| Endymion Oil Pipeline Company, LLC (“Endymion”) | 10.0 | % | | — | % |

| Colonial Pipeline Company (“Colonial”) | 6.0 | % | | 10.12 | % |

| Cleopatra Gas Gathering Company, LLC (“Cleopatra”) | 1.0 | % | | — | % |

Acquisitions

In 2017, we completed two acquisitions from Shell and one acquisition from a third party, with an aggregate purchase price of $1,504.9 million. These acquisitions are as follows:

On December 1, 2017, we acquired a 100% interest in 2016Triton, a 41.48% interest in LOCAP, an additional 22.9% interest in Mars, an additional 22.0% interest in Odyssey, and 2015an additional 10.0% interest in Explorer from SPLC and Equilon Enterprises LLC d/b/a Shell Oil Products US (“SOPUS”) for $825.0 million in cash (the “December 2017 Acquisition”).

On October 17, 2017, we acquired a 50.0% interest in Permian Basin from a third party for $49.9 million in cash and initial capital contribution.

On May 10, 2017, we acquired (i) approximately 130 miles of pipeline aggregating volumes from five offshore pipelines (“Delta”), (ii) approximately 80 miles of pipeline serving as host to eight different subsea fields and connecting to Delta at Main Pass 69 (“Na Kika”) and (iii) approximately 100 miles of refinery gas pipeline connecting multiple refineries and plants operated along the Gulf Coast to Shell Chemical LP sites and Norco and Deer Park refineries (the “Refinery Gas Pipeline” and, together with Delta and Na Kika, the “Shell Delta, Na Kika and Refinery Gas Pipeline Operations”), from SPLC and Shell GOM Pipeline Company LP for $630.0 million in cash.

In 2016, we completed three acquisitions from Shell and one acquisition from a third parties,party, with an aggregate purchase price of $1,118.2 million. These acquisitions are as follows:

On December 27, 2016, we acquired a 10.0% interest in Proteus, a 10.0% interest in Endymion and a 1.0% interest in Cleopatra from subsidiaries of BP Pipelines (North America) Inc. (collectively, “BP Pipelines”) for $42.0 million in cash.

On October 3, 2016, we acquired a 49.0% interest in Odyssey from Equilon Enterprises LLC, d/b/a Shell Oil Products US (“SOPUS”)SOPUS and an additional 20.0% interest in Mars from SPLC for $350.0 million in cash.

On August 9, 2016, we acquired a 2.62% equity interest in Explorer from SPLC for $26.2 million in cash.

On May 23, 2016, we acquired an additional 30.0% interest in Zydeco, an additional 1.0% interest in Bengal and an additional 3.0% interest in Colonial from SPLC for $700.0 million in cash.

In 2015, we completed three acquisitions from Shell with an aggregate purchase price of $1,188.0 million. These acquisitions are as follows:

On November 17,15, 2015, we acquired a 100% interest in Pecten which owns Auger and Lockport (collectively, the “Shell Auger and Lockport Operations”), from SPLC for $390.0 million in cash.

On July 1, 2015, we acquired a 36.0% interest in Poseidon from SOPUS for $350.0 million in cash.

On May 18, 2015, we acquired an additional 19.5% interest in Zydeco and an additional 1.388% interest in Colonial from SPLC for $448.0 million in cash.

See Note 3 – Acquisitions and Divestiture in the Notes to Consolidated Financial Statements in Part II, Item 8 of this report for additional information.

Organizational Structure

The following simplified diagram depicts our organizational structure as of December 31, 2016.2017.

*SPLC intends to assume operatorship(1) The sale of these systems bycommon units on February 6, 2018 is not reflected in the end of 2017.

units outstanding.

Our Assets and Operations

Our assets consist of the following systems:

Crude Oil Pipelines

Onshore Crude Pipeline

Delta. Delta is wholly owned by Pecten, and we own a 100% interest in Pecten. SPLC is the operator of Delta.

Delta is an approximately 130-mile onshore pipeline aggregating volumes from five offshore pipelines including the Odyssey and Na Kika Pipelines. Delta connects offshore oil production in the eastern corridor of the Gulf of Mexico to key onshore markets. Delta receives the majority of its revenue from volumes transported on posted transportation rates, some of which are indexed annually. The system originates at Main Pass 69P and Main Pass 69A for the transportation of Heavy Louisiana Sweet (“HLS”) crude oil from the Main Pass, Viosca Knoll, and northeast section of Mississippi Canyon areas in the Gulf of Mexico to onshore demand centers at Empire Terminal, Houma Terminal, and the Norco and Alliance refineries.

Zydeco. We own a 92.5% interest in Zydeco, which owns the Zydeco pipeline system. SPLC owns the remaining 7.5% interest in, and is the operator of Zydeco.

Zydeco is a FERC-regulated pipeline system. It spans over 350 miles and currently has a mainline capacity of approximately 375 kbpd. Zydeco consists of four main segments: (i) the Houston, Texas to Port Neches, Texas segment, which has a capacity of 250 kbpd, (ii) the Port Neches, Texas to Houma, Louisiana segment which has a capacity of 375 kbpd, (iii) the Houma, Louisiana to Clovelly, Louisiana segment, which has a capacity of 500 kbpd, and (iv) the Houma, Louisiana to St. James, Louisiana segment, which has a capacity of 260 kbpd. Zydeco also includes tankage in Port Neches, Texas and Erath and Houma, Louisiana, a dock in Houma, Louisiana and a 16-inch pipeline that indirectly connects to the offshore Boxer pipeline system. We added new tankage at Port Neches and a new third-party connection in late 2016. In August 2016, a joint tariff with LOCAP was filed that allowed for movement of Poseidon crude oil from Houma to St. James beginning in

September 2016. Moving Poseidon crude oil via LOCAP opened up an additional 100 to 140 kbpd of capacity for Zydeco's shippers on the Houma to St. James 18-inch pipeline, while enabling the Poseidon shippers to ship under the joint tariff at the same rate structure as the existing 18-inch pipeline. Also, a new connection into Zydeco at Channelview Houston with Transcanada’s Market Link pipeline became available in August 2016. This connection provides access to additional volumes from Cushing, OK.Oklahoma.

Zydeco’s customers include traders, marketers, refiners, producers and affiliates of Shell. For 2017, 2016 and 2015, four third-party customers accounted for 76.1% and 75.0%, respectively,approximately 70.0% of total Zydeco revenue.

Offshore Crude Pipelines

Auger. Auger is wholly owned by Pecten, and we own a 100% interest in Pecten. SPLC is the operator of Auger.

Auger is a 174-milean approximately 175-mile offshore Gulf of Mexico corridor pipeline that transports medium sour crude from producers in eastern Garden Bank and Keathley Canyon blocks. Auger offers producers two crude market options: (i) the 20-inch pipeline delivers to Ship Shoal pipeline at Ship Shoal 28 for delivery to the St. James market hub (Bonito Sour crude), and (ii) the 12-inch pipeline delivers to Eugene Island pipeline for delivery to the Houma market hub (Eugene Island crude). The 14/16 inch pipeline brings crude from the Auger platform to the 20-inch and 12-inch segments at Garden Banks 128. Auger shares a complementary strategic connection to the Poseidon pipeline system through South Marsh Island 205, which provides the producers connected to Southeast Keathley Canyon Pipeline Company L.L.C. (“SEKCo”) the option to access either Poseidon or Auger delivery markets.

Auger provides transportation for major oil producers and from more than 13 different production fields in the Gulf of Mexico. Auger has several direct connected producers, including the Shell operated Garden Banks 426 (Auger) and Garden Banks 128 (Enchilada) platforms, and the ConocoPhillips operated Garden Banks 783 platform, connected via the Magnolia lateral pipeline. Auger also receives production from producers connected to Poseidon and SEKCo, including the Anadarko operated Keathley Canyon 875 platform (Lucius), via the South Marsh Island 205 Poseidon pipeline connection. The Auger pipeline system provides transportation for a number of customers from offshore to St. James via Ship Shoal and Houma via Eugene Island.

Auger receives the majority of its revenues from volumes transported on posted transportation rates, some of which are indexed annually. For direct connected producers, including Garden Banks 426 and Garden Banks 128 platforms, Auger captures transportation revenue for 100% of those volumes. Auger also receives transportation revenue from receipts at the South Marsh Island 205 connection, as producers seek to deliver into the typically advantaged Bonito Sour market at St. James.

Na Kika. Na Kika is wholly owned by Pecten and we own a 100% interest in Pecten. SPLC is the operator of Na Kika.

Na Kika is an approximately 75-mile offshore pipeline anchored by the Na Kika platform which serves as a host to eight different subsea fields and connects to Delta at Main Pass 69. Na Kika receives the majority of its revenue from volumes transported on posted transportation rates some of which are indexed annually. The system originates at the Na Kika platform for the transportation of HLS crude oil delivered to the Delta pipeline system for further delivery to onshore demand centers at Empire Terminal, Houma Terminal, and the Norco and Alliance refineries.

Mars. We own a 71.5% interest in Mars, which owns the Mars pipeline system. BP Midstream Partners LP owns the remaining 28.5% interest in Mars. SPLC is the operator of Mars.

The Mars pipeline system is approximately 160 miles in length and has 16-, 18- and 24-inch diameter pipelines with mainline capacity of up to 600 kbpd. Transportation on certain segments of the Mars pipeline system are subject to the jurisdiction of FERC and the Louisiana Public Service Commission. Mars delivers production received from the Mississippi Canyon area, including the Olympus and Mars A platform and the Medusa and Ursa pipelines, and from the Green Canyon and Walker Ridge areas via the Amberjack pipeline connection, to shore, terminating in salt dome caverns in Clovelly, Louisiana, which is a major trading hub. Mars leases its main storage cavern at Clovelly from LOOP LLC. For 2017 and 2016, a substantial portion of volumes transported on Mars were moved either under life-of-lease transportation agreements or posted tariffs from production areas where there was established and consistent production activity and where there was limited take-away capacity beyond what our pipelines offered. Mars tariffs are subject to annual adjustment based on the FERC index. Such tariff adjustments allow for annual cash flow increases without commensurate incremental capital expenditures. In addition, Mars entered into life-of-lease transportation agreements with certain producers that include a guaranteed return for Mars for an initial period of time and thereafter will continue for the life of the lease. Mars also receives significant volume from

Amberjack at Fourchon, Louisiana, the terminus of the Amberjack pipeline system. This connection is governed by a FERC tariff.

Odyssey. We own a 49.0%71.0% interest in Odyssey, which owns the Odyssey pipeline system. SOPUS and GEL Offshore PipelineOdyssey, LLC (“GEL”) ownowns a 22.0% interest and 29.0% interest respectively, in Odyssey. SPLC is the operator of Odyssey.

The Odyssey pipeline system is an approximately 106-mile105-mile pipeline system for the transportation of crude oil in the offshore eastern Gulf of Mexico to markets in Louisiana. Odyssey provides transportation for major oil producers and from more than 20 different production fields in the eastern Gulf of Mexico. Major production platforms connected to Odyssey include: Delta House operated by LLOG Exploration Company, L.L.C., Ram Powell operated by Shell, Petronius operated by Chevron Corporation, and Horn Mountain operated by Freeport-McMoRan Inc.Anadarko Petroleum Corporation. Crude oil transported via Odyssey is delivered to the Delta pipeline system for further delivery to onshore demand centers at Empire Terminal, Houma Terminal, and Norco and Alliance refineries.

Odyssey provides for the transportation of crude oil through the use of buy-sellbuy/sell arrangements where crude is purchased at the receipt location into the pipeline and sold back to the counterparty at the destination at that price plus a transportation differential.

Mars. We own a 48.6% interest in Mars, which owns the Mars pipeline system. SPLC owns a 22.9% ownership interest in, and is the operator of, Mars. An affiliate of BP Pipelines owns the remaining 28.5% interest in Mars.

The Mars pipeline system is approximately 163 miles in length and has 16-, 18- and 24-inch diameter pipelines with mainline capacity of up to 600 kbpd. Mars delivers production received from the Mississippi Canyon area, including the Olympus and Mars A platform and the Medusa and Ursa pipelines, and from the Green Canyon and Walker Ridge areas via the Amberjack pipeline connection, to shore, terminating in salt dome caverns in Clovelly, Louisiana, which is a major trading hub. Mars leases its main storage cavern at Clovelly from LOOP LLC, an affiliate of Shell. Mars has maintained a set of well-established customers, including an affiliate of Shell. For 2016 and 2015, 56.0% and 57.0%, respectively, of volumes transported on Mars were moved either under life-of-lease agreements or posted tariffs from production areas where there was established and consistent production activity and where there was limited take-away capacity beyond what our pipelines offered. Mars tariffs are subject to annual adjustment based on the FERC index. Such tariff adjustments allow for annual cash flow increases without commensurate incremental capital expenditures. In addition, in connection with the expansion described below, Mars entered into life-of-lease transportation agreements with certain producers that include a guaranteed return for Mars for an initial period of time and thereafter will continue for the life of the lease. Mars also receives significant volume from Amberjack at Fourchon, Louisiana, the terminus of the Amberjack pipeline system. This connection is governed by a FERC tariff.

Poseidon. We own a 36.0% interest in Poseidon, which owns the Poseidon pipeline system. Genesis Energy, L.P.GEL Poseidon, LLC (“Genesis”) owns the remaining 64.0% interest in, and is the operator of Poseidon.

The Poseidon pipeline system is a 367-milean approximately 365-mile Gulf of Mexico offshore crude oil pipeline with a 350 kbpd capacity transporting to key markets in Texas and Louisiana. A key corridor pipeline, Poseidon connects to approximately 50 Gulf of Mexico fields and delivers to three locations. It provides access to major crude trading hubs via connecting carriers (i.e., Gibson/Houma to St James and Clovelly, Louisiana and via Cameron Highway Oil Pipeline System to Texas hubs in Texas City and Port Arthur). Poseidon delivers crude oil (i) into Zydeco’s tankage at Houma, Louisiana via Poseidon’s 24-inch line from Ship Shoal 332A,332A; (ii) into connecting carriers at St. James, Louisiana via Zydeco’s 18-inch line from Houma, Louisiana,Louisiana; (iii) into Raceland Pipeline subject to a new connection projected to be effective March 15, 2017;Pipeline; and (iv) for barrels on the west side of the Poseidon system and for certain barrels at Ship Shoal 332A, Poseidon can deliver oil into Auger via South Marsh Island 205A in addition to receiving oil from Auger, if needed. Poseidon owns the strategic platform South Marsh Island 205A.

Poseidon’s largest customers are major oil producers who ship from a variety of production fields in the Gulf of Mexico. Each accounts for material throughput on the system, and together these shippers account for 90.0% of the throughput. Poseidon earns income through buy/sell arrangements, pursuant to which it purchases crude oil from its customer at the time the crude oil enters its pipeline system, and then resells the crude oil to the customer at the time the crude oil reaches its destination. At the resell point, Poseidon receives the original purchase price plus an agreed differential (referred to as the buy/sell differential). Many of Poseidon’s customers have dedicated production to the pipeline. Some of Poseidon’s customers have agreed to pay for the transportation of minimum periodic volumes whether or not they actually deliver those volumes for transportation.

Proteus. We own a 10.0% interest in Proteus, which owns the Proteus pipeline system. Mardi Gras Transportation System IncInc. (“Mardi Gras”) and ExxonMobil Pipeline Company ("ExxonMobil"(“ExxonMobil”) own a 65.0% interest and 25.0% interest, respectively, in Proteus. BP Pipelines, an affiliate of Mardi Gras, is currently the operatorSPLC assumed operatorship of Proteus and SPLC intends to assume operatorship of this system by the end ofeffective July 1, 2017.

The Proteus pipeline system is a 71-milean approximately 70-mile crude oil pipeline with a 425 kbpd capacity and provides transportation for multiple oil producers in the eastern Gulf of Mexico. The pipeline provides access to the Mississippi Canyon area of the Gulf of Mexico from the Thunder Horse and Thunder Hawk platforms to the Proteus SP 89E Platform. Noble Energy Inc.’s Big Bend and Dantzler fields are tied back to Thunder Hawk platform. SPLC is currently building the Mattox pipeline which will connect to Proteus and transport all of the volumes from the recently-sanctioned Appomattox platform. Volumes transported on Proteus move via private oil transportation agreements, which are a mix of term and life-of-lease transportation agreements, rather than posted tariffs.

Endymion. We own a 10.0% interest in Endymion, which owns the Endymion pipeline system. Mardi Gras Endymion Oil Pipeline Company, LLC (“Mardi Gras Endymion”) and ExxonMobil own a 65.0% interest and 25.0% interest, respectively, in Endymion. BP Pipelines, an affiliate of Mardi Gras Endymion, is currently the operatorSPLC assumed operatorship of Endymion and SPLC intends to assume operatorship of this system by the end ofeffective July 1, 2017.

The Endymion pipeline system, which originates downstream of the Proteus SP 89E Platform, is an 89-mileapproximately 90-mile crude oil pipeline with a 425 kbpd capacity and provides transportation for multiple oil producers in the eastern Gulf of Mexico. Endymion provides access to the Mississippi Canyon area of the Gulf of Mexico and is connected to the LOOP Clovelly storage terminal with access to multiple markets. Endymion leases a cavern from LOOP LLC. Volumes transported on

Endymion move via private oil transportation agreements, which are a mix of term and life-of-lease transportation agreements, rather than posted tariffs. Such agreements also allow for storage at the LOOP Clovelly storage terminal.

Refined Products Pipelines

Bengal. We own a 50.0% interest in Bengal and Colonial owns athe remaining 50.0% interest in Bengal.interest. Colonial is the system operator for regulatory reporting purposes and operates Bengal’s tankage. SPLC operates Bengal’s pipelines.

The Bengal pipeline system is a 159-milean approximately 160-mile refined products pipeline system connecting four refineries in southern Louisiana to long-haul transportation pipelines. The pipeline system consists of two primary pipelines. The 24-inch diameter pipeline has a capacity of 305 kbpd and connects the MotivaShell and Valero refineries in Norco, Louisiana and the Marathon Petroleum Corporation refinery in Garyville, Louisiana to Bengal’s Baton Rouge, Louisiana tankage and the Plantation pipeline. The 16-inch diameter pipeline has a capacity of 210 kbpd and runs from Motiva’sShell's Convent, Louisiana refinery to the Plantation pipeline and Bengal’s Baton Rouge, Louisiana tankage.

The Bengal pipeline system provides transportation for a number of customers from connected refineries and terminals to the Plantation and Colonial pipelines, and from refineries to the Baton Rouge tankage. Bengal’s revenue is primarily dependent on ship-or-pay contracts. As of December 31, 2016, approximately 67.0% of Bengal’s capacity was subject to minimum volume commitments under ship-or-pay contracts with an average remaining term of 5 years. These contracts are renewable at the election of the shipper. Rates for Bengal’s transportation services are governed by Bengal’s FERC-approved tariffs. These

tariffs are subject to annual adjustment based on the FERC index. Rates under the index ceiling do not require adjustment downward.

Bengal also has a joint tariff division agreement with Colonial covering transportation of refined products from refineries connected to the Bengal pipeline system to destinations in the southeast and eastern United States via the Colonial pipeline system. Under this joint tariff, Colonial bills and collects the tariff from the product shippers and remits to Bengal its share of the joint tariff.

Explorer. We own a 12.62% interest in Explorer, which owns the Explorer pipeline system. SPLC owns a 25.97% interest in Explorer, and MPL Investment LLC, Phillips 66 Partners Holdings LLC and Sunoco Pipeline L.P. collectively own the remaining 61.41% interest. The pipeline system is operated by Explorer.

The Explorer pipeline system is a FERC-regulated 1,830-mile common carrier petroleum products pipeline system, which extends from the Gulf Coast to the Midwest serving more than 70 major cities in 16 states. In 2016, Explorer placed into service a new 24-inch diluent pipeline extension from its existing Peotone, Illinois Station to Manhattan, Illinois allowing shippers to transport diluent volumes into Western Canada via this new Manhattan, Illinois origin. Explorer transports refined products with more than 70 different specifications for more than 60 different shippers.

Explorer has rates that are subject to annual adjustment based on the FERC index. In addition, Explorer has an auction program for certain excess capacity when the pipeline is fully subscribed. Explorer also has ship-or-pay contracts for condensate delivered to the Southern Lights system.

Colonial. We own a 6.0% interest in Colonial, which owns the Colonial pipeline system. SPLC owns a 10.12% interest in Colonial, and CDPQ Colonial Partners, LP; Koch Capital Investments Company, LLC; KKR-Keats Pipeline Investors LP and IFM (US) Colonial Pipeline 2, LLC collectively own the remaining 83.88% interest, in Colonial.interest. The pipeline system is operated by Colonial.

The Colonial pipeline system is the largest refined products pipeline in the United States based on barrel-miles transported. Colonial includes more than 5,500 miles of pipeline connecting refineries along the Gulf Coast to approximately 265 marketing terminals between Houston, Texas and Linden, New Jersey. Colonial transports more than 100 million gallons a day of gasoline, jet fuel, kerosene, home heating oil, diesel fuel and national defense fuels to shipper terminals in 13 states and the District of Columbia.

Since its inception in 1963, Colonial has served a diverse set of customers, including refiners, marketers, airports and airlines. In 2016,2017, more than 100 shippers transported product through Colonial’s system, including an affiliate of Shell. Colonial is subject to FERC regulation and has both market-based rates and rates that are subject to annual adjustment based on the FERC index.

Terminals and Storage

ExplorerTriton.. We own a 2.62%100% interest in Explorer,Triton which wholly owns the Explorer pipeline system.Anacortes (Washington), Colex (Texas), Des Plaines (Illinois), Portland (Oregon) and Seattle (Washington) refined products terminals. Our general partner is the operator of these

five terminals. The necessary personnel are employed by SPLC owns a 35.97% interest, and MPL Investment LLC, Phillips 66 Partners Holdings LLC and Sunoco Pipeline L.P. collectively own the remaining 61.41% interest, in Explorer. The pipeline system is operated by Explorer.

The Explorer pipeline system is a FERC-regulated 1,830-mile common carrier petroleum products pipeline system, which extends from the Gulf Coastare assigned to our general partner pursuant to the Midwest serving more than 70 major citiesoperating agreement among SPLC, our general partner and our subsidiary. These terminals receive products from pipelines and, in 16 states. In 2016, Explorer placed into servicecertain cases, barges, ships or railroads, and distribute them to third parties, who in turn deliver them to end-users and retail outlets. These terminals play a new 24-inch diluent pipeline extension from its existing Peotone, Illinois Station to Manhattan, Illinois allowing shippers to transport diluent volumes into Western Canada via this new Manhattan, Illinois origin. Explorer transports refinedkey role in moving products with more than 72 different specifications for more than 60 different shippers. For the year ended December 31, 2016, the Explorer Owner Companies accounted for 12.72% of the total volume moved on the line as well as 9.31% of Explorer’s total revenue.

Explorer has rates that are subject to annual adjustment based on the FERC index. In addition, Explorer has an auction program for certain excess capacity when the pipeline is fully subscribed. Explorer also has take-or-pay contracts for condensate delivered to the Southern Lights system.

Other Midstream Assetsend-user market by providing efficient product receipt, storage and distribution capabilities, inventory management, ethanol and biodiesel blending, and other ancillary services that include the injection of various additives. Typically, terminaling facilities consist of multiple storage tanks and are equipped with automated truck loading equipment that is available 24 hours a day.

Lockport. Lockport is wholly owned by Pecten, and we own a 100% interest in Pecten. SPLC is the operator of Lockport.

Lockport is a crude terminal facility located southwest of Chicago with two2.0 million barrels of storage capacity that feeds regional refineries, while also offering strategic trading opportunities. Lockport receives Canadian crude from the Enbridge pipeline and serves as a distribution point for movements originating on the Mustang and Westshore pipeline systems. Lockport provides storage services for a number of customers, receives primarily Canadian and Midwest crude and supplies Midwest refineries, such as Citgo LamontLemont Refinery and via connection to Patoka, a regional distribution hub. Lockport receives its revenues from contracted storage capacity.

Other Midstream Assets

Refinery Gas Pipeline. Refinery Gas Pipeline is wholly owned by Sand Dollar, and we own a 100% interest in Sand Dollar.

Refinery Gas Pipeline is a network of approximately 105 miles of gas pipeline connecting multiple refineries and plants operated along the Gulf Coast to Shell Chemical sites, including Shell’s Norco refinery and Deer Park refinery. The pipelines transport refinery gas which is a mix of methane, natural gas liquids and olefins.

Permian Basin. We own a 50% interest in Permian Basin. Permian Basin owns and operates the Nautilus gas gathering system in the Permian Basin. CPB Member LLC (a jointly owned subsidiary of Crestwood Equity Partners LP and First Reserve) owns the remaining 50% interest.

The Nautilus gas gathering system includes 20 receipt point meters, approximately 95 miles of pipeline, a 24-mile high pressure header system, 10,800 horsepower of compression and a high-pressure delivery point. Nautilus is designed to serve a dedication area of about 100,000 acres in West Texas across Loving, Reeves and Ward counties.The Nautilus system gathers the majority of Shell’s operated Delaware Basin gas under a 20-year tiered, fixed-fee contract. We generate revenue on this system under a long-term agreement with SWEPI LP, a subsidiary of Shell.

LOCAP. We own a 41.48% interest in LOCAP. MPLX Operations LLC, an indirect subsidiary of MPLX LP, owns the remaining 58.52% interest. LOOP LLC is the operator of LOCAP.

The LOCAP pipeline connects the LOOP Clovelly Salt Dome storage facility to the active trading hub of St. James, Louisiana, approximately 55 miles to the north. Crude oil arriving at the St. James terminal can be dispatched to any one of four local refineries serving Louisiana and can also be dispatched to other pipeline systems transmitting more than 30% of the nation’s refining capacity to refineries throughout the Midwest. The LOCAP St. James terminal facility has 8 breakout tanks with over 2.6 million barrels of storage capacity situated on 140 acres of land. The 48-inch diameter LOCAP pipeline has a throughput capacity of 1.7 million barrels per day and can expand to 2.4 million barrels per day. The LOCAP pipeline is FERC-regulated and charges rates subject to FERC's indexing rate methodology.

Cleopatra. We own a 1.0% interest in Cleopatra, which owns the Cleopatra pipeline system. Mardi Gras, BHP Billiton Petroleum (Deepwater) Inc., Enbridge Offshore (Gas Transmission) LLC, and Chevron Midstream Investments LLC collectively own the remaining 99.0% interest in Cleopatra. BP Pipelines, an affiliate of Mardi Gras, is currently the operatorSPLC assumed operatorship of Cleopatra and SPLC intends to assume operatorship of this system by the end ofeffective July 1, 2017.

The Cleopatra pipeline system is aan approximately 115-mile gas gathering pipeline and provides gathering and transportation for multiple gas producers and third party gas shippers in Southern Green Canyon, with access to Atwater Valley, Walker Ridge, and Lund areas of the Gulf of Mexico. Cleopatra is currently connected to the Holstein, Atlantis and Mad Dog platforms. The system will transport new volumes from the Mad Dog 2 field once it comes online. Additionally, Neptune and Shenzi platforms have access through third party pipelines into Cleopatra.shippers. Volumes transported on Cleopatra move via private gas gathering agreements, which are life-of-lease transportation agreements, rather than posted tariffs. Such agreements are not subject to annual escalation.

Pipeline Systems and Terminal Systems

The following table sets forth certain information regarding our pipeline and terminal systems:systems as of December 31, 2017:

| | | Pipeline System/Terminal System | | Diameter (inches) | | Length (miles) | | Approximate Capacity

(kbpd) | | Diameter (inches) | | Approximate Length (miles) | | Approximate Capacity

(kbpd) (2) | | Approximate Tank Storage Capacity

(kbls) |

| Zydeco crude oil system - Mainlines | | | | | | | | | | | | | | |

| Houston to Port Neches | | 20 | | 87 | | 250 | | 20 | | 85 | | 250 | | - |

| Port Neches to Houma | | 22 | | 213 | | 375 | | 22 | | 215 | | 375 | | - |

| Houma to Clovelly | | 24 | | 34 | | 500 | | 24 | | 35 | | 500 | | - |

| Houma to St James | | 18 | | 48 | | 260 | | 18 | | 50 | | 260 | | - |

| Auger crude oil system - Mainlines | | |

| Auger crude oil system | | |

| Enchilada Platform to EI315 | | 12 | | 34 | | 35 | | 12 | | 35 | | 35 | | - |

| Enchilada Platform to SS28P | | 20 | | 100 | | 200 | | 20 | | 100 | | 200 | | - |

| Mars crude oil system | | |

| 14/16" Auger export line | | | 14/16 | | 40 | | 150 | | - |

| Delta crude oil system | | | 16/20 | | 130 | | 420 | | - |

| Na Kika crude oil system | | | 18 | | 75 | | 160 | | - |

Mars crude oil system (1) | | |

| Mars TLP to WD 143 | | 18 | | 41 | | 100 | | 18 | | 40 | | 100 | | - |

| Olympus TLP to WD 143 | | 16/18 | | 41 | | 100 | | 16/18 | | 40 | | 100 | | - |

| WD 143 to Fourchon | | 24 | | 55 | | 400 | | 24 | | 55 | | 400 | | - |

| Fourchon to Clovelly | | 24 | | 27 | | 600 | | 24 | | 25 | | 600 | | - |

| Bengal product system | | |

| Norco to Baton Rouge tank farm | | 24 | | 94 | | 305 | | 24 | | 95 | | 305 | | - |

| Convent to Baton Rouge tank farm | | 16 | | 64 | | 210 | | 16 | | 65 | | 210 | | - |

| Poseidon crude oil system | | | Various | | 365 | | 350 | | - |

| Poseidon crude oil system | | Various | | 367 | | 350 | |

| Odyssey crude oil system | | |

| Odyssey crude oil system | | Various | | 106 | | 220 | | Various | | 105 | | 220 | |

| Proteus crude oil system | | |

| Thunder Horse TLP to SP 89E | | 24/28 | | 71 | | 425 | | 24/28 | | 70 | | 425 | | - |

| Endymion crude oil system | | |

| SP 89E to Clovelly | | 30 | | 89 | | 425 | | 30 | | 90 | | 425 | | - |

Cleopatra gas gathering system (1) | | |

Cleopatra gas gathering system (2) | | |

| Atlantis TLP to SS 332A | | 16/20 | | 115 | | 500 | | 16/20 | | 115 | | 500 | | - |

| Colonial product system | | Various | | 5,500 | | 2,500 | | Various | | 5,500 | | 2,500 | | - |

| Explorer product system | | Various | | 1,830 | | 660 | | Various | | 1,830 | | 660 | | - |

Lockport terminal system (2) | | - | | - | | - | |

Permian Basin gas gathering system (2) | | | Various | | 95 | | 250 | | - |

| LOCAP pipeline system and storage facility | | | 48 | | 55 | | 1,700 | | 2,600 |

| Lockport terminal system | | | n/a | | n/a | | - | | 2,000 |

Refinery Gas Pipelines (2) | | |

| Houston Ship Channel | | | 8 | | 10 | | 3,960 | | - |

| Texas City | | | 12 | | 35 | | 5,280 | | - |

| Garyville - Norco | | | 12 | | 20 | | 3,720 | | - |

| Convent to Garyville | | | 12 | | 20 | | 3,840 | | - |

| Norco - Paraffinic | | | 8/12 | | 20 | | 3,720 | | - |

| Triton refined products terminals | | |

Anacortes (3) | | | n/a | | n/a | | - | | - |

| Colex | | | n/a | | n/a | | - | | 2,585 |

|

| | | | | | | | |

| Des Plaines | | n/a | | n/a | | - | | 1,060 |

| Portland | | n/a | | n/a | | - | | 405 |

Seattle (3) | | n/a | | n/a | | - | | 490 |

(1) In addition to the pipeline capacity above, Mars also has storage capacity under its lease of a storage cavern with a related party.

(1)(2) The approximate capacity information presented is in kbpd with the exception of the approximate capacity related to Cleopatra gas

gathering system and Permian Basin which are presented in mscf/d, and Refinery Gas Pipelines which is presented in mscf/klbs/d.

(2)(3) The Anacortes and Seattle refined products terminals have truck racks which are not included in the above table. The Anacortes refined products terminal does not have tank storage capacity on the Lockport terminal system is 2 mbls.storage.

Our Relationship with Shell

Shell is one of the world’s largest independent energy companies in terms of market capitalization and operating cash flow, and Shell and its joint ventures are a leading producer and transporter of onshore and offshore hydrocarbons as well as a major refiner in the United States. As one of the largest producers in the Gulf of Mexico, Shell is currently developing several deepwater prospects and associated infrastructure. In addition to its offshore production, Shell has significant onshore exploration and production interests and produces crude oil and natural gas throughout North America. Shell’s downstream portfolio includes interests in refineries throughout the United States. Shell’s portfolio of midstream assets provides key infrastructure required to transport and store crude oil and refined products for Shell and third parties. Shell’s ownership

interests in transportation and midstream assets include crude oil and refined products pipelines, crude oil and refined products terminals, chemicals pipelines, natural gas pipelines and processing plants, and LNG infrastructure assets. Shell or its affiliates are customers of most of our businesses.

SPLC is Shell’s principal midstream subsidiary in the United States. As of December 31, 2017, SPLC owns our general partner, a 49.2%46.4% limited partner interest in us and all of our incentive distribution rights.

Customers

See Note 12—Transactions with Major Customers and Concentration of Credit Risk in the Notes to Consolidated Financial Statements included in Part II, Item 8 of this report.

Competition

Our pipeline systems compete primarily with other interstate and intrastate pipelines and with marine and rail transportation. Some of our competitors may expand or construct transportation systems that would create additional competition for the services we provide to our customers. In addition, future pipeline transportation capacity could be constructed in excess of actual demand, which could reduce the demand for our services, in the market areas we serve, and could lead to the reduction of the rates that we receive for our services. While we do see some variation from quarter-to-quarter resulting from changes in our customers’ demand for transportation, this risk is mitigated by the long-term, fixed rate basis upon which we have contracted a substantial portion of our capacity.

Competition among onshore common carrier crude oil pipelines is based primarily on posted tariffs, quality of customer service and connectivity to sources of supply and demand. We believe that our position along the Gulf Coast provides a unique level of service to our customers. Additionally, Zydeco is supported by FERC-approved transportation services agreements for the majority of the capacity available on the mainline Houston to Houma segment of the pipeline. Our pipelines and terminals face competition from a variety of alternative transportation methods including rail, water borne movements including barging, shipping and imports and other pipelines that service the same origins or destinations as our pipelines.

Our offshore crude oil pipelines are partially supported by life-of-lease transportation agreements or direct connected production. However, our offshore pipelines will compete for new production on the basis of geographic proximity to the production, cost of connection, available capacity, transportation rates and access to onshore markets. The principal competition for our offshore pipelines include other crude oil pipeline systems as well as producers who may elect to build or utilize their own production handling facilities. In addition, the ability of our offshore pipelines to access future oil and gas reserves will be subject to our ability, or the producers’ ability, to fund the capital expenditures required to connect to the new production. In general, our offshore pipelines are not subject to regulatory rate-making authority, and the rates our offshore pipeline charges for services are dependent on market conditions.

Competition for refined product transportation in any particular area is affected significantly by the end market demand for the volume of products produced by refineries in that area, the availability of products in that area and the cost of transportation to that area from distant refineries. As a result of our contractual relationships, the markets they serve, and the size and scale of

our refined products pipelines, we believe that our refined product pipelines will not face significant new competition in the near-term.

Our refined products terminals generally compete with other terminals that serve the same markets. These terminals may be owned by major integrated oil and gas companies or by independent terminaling companies. While fees for terminal storage and throughput services are not regulated, they are subject to competition from other terminals serving the same markets. However, our contracts provide for stable, long-term revenue, which is not impacted by market competitive forces during the term of the contracts.

At Lockport, our storage tanks continue to be utilized at 100%80% capacity via three service and throughput contracts. TwoOne of thesethe contracts expireexpired in 2017; they areearly 2017, was extended for one year under revised terms, and is currently under re-negotiation.re-negotiation, and another expired on December 31, 2017 and has been extended one year under revised terms effective January 1, 2018. The third contract expires December 31, 2019. In addition to these three contracts, we are actively developing new business for the facility. Additionally, some contracts also guarantee payments for minimum monthly throughput volumes. A competing pipeline from Flannigan to Patoka, Illinois, owned by Enbridge Inc.Our storage terminal competes with surrounding providers of storage tank services. Some of our competitors have expanded terminals and Marathon Petroleum Company, was completed in the fourth quarter of 2015 primarily to transport Bakken crude oil, which was being previously shipped via railcars. Thisbuilt new pipeline had noconnections, and third parties may construct pipelines that bypass our location, which could have a material adverse material impact on our Lockport operations due to our contracts in place. The use of pipelines to transport Bakken crude oiloperations. However, other developments may eventually increase demand for storage and throughput at Lockport.Lockport as pipelines are used to transport crude types previously shipped in other ways.

FERC and State Common Carrier Regulations

Our interstate common carrier and intrastate pipeline systems are subject to economic regulation by various federal, state and local agencies.

FERC regulates interstate transportation on our common carrier pipeline systems under the Interstate Commerce Act of 1887 as modified by the Elkins Act (“ICA”), the Energy Policy Act of 1992 (“EPAct”)EPAct and the rules and regulations promulgated under those laws. FERC regulations require that rates and terms and conditions of service for interstate service pipelines that transport crude oil and refined products (collectively referred to as “petroleum pipelines”) and certain other liquids, be just and reasonable and must not be unduly discriminatory or confer any undue preference upon any shipper. FERC’s regulations also require interstate common carrier petroleum pipelines to file with FERC and publicly post tariffs stating their interstate transportation rates and terms and conditions of service.

Under the ICA, FERC or interested persons may challenge existing or proposed new or changed rates, services, or terms and conditions of service. FERC is authorized to investigate such charges and may suspend the effectiveness of a new rate for up to seven months. Under certain circumstances, FERC could limit a common carrier pipeline’s ability to charge rates until completion of an investigation during which FERC could find that the new or changed rate is unlawful. In contrast, FERC has clarified that initial rates and terms of service agreed upon with committed shippers in a transportation services agreement are not subject to protest or a cost-of-service analysis where the pipeline held an open season offering all potential shippers service on the same terms.

A successful rate challenge could result in a common carrier pipeline paying refunds of revenue collected in excess of the just and reasonable rate, together with interest for the period the rate was in effect, if any. FERC may also order a pipeline to reduce its rates prospectively, and may require a common carrier pipeline to pay shippers reparations retroactively for rate overages for a period of up to two years prior to the filing of a complaint. FERC also has the authority to change terms and conditions of service if it determines that they are unjust or unreasonable or unduly discriminatory or preferential.

We may at any time also be required to respond to governmental requests for information, including compliance audits and rate case reviews conducted by FERC, such as the audit of Explorer and rate complaints filed against Colonial. FERC’sFERC's Office of Enforcement concluded an audit of ColonialExplorer in Docket No. FA14-4-000FA16-5000 for the period January 1, 20112013 to December 31, 2014,2016, and issued a letter order on June 17, 2015January 12, 2018 adopting the audit’s findings and recommendations and requiring ColonialExplorer to submit a compliance plan and quarterly compliance reports. ColonialExplorer accepted the audit’s findings and recommendations, which had nodid not have a financial impact to us. FERC's OfficeOn November 22, 2017, Epsilon Trading LLC, Chevron Products Company, and Valero Marketing and Supply Company filed a complaint with FERC against Colonial challenging its rates for the transportation of Enforcement is currently conducting an auditpetroleum products, including whether it should be permitted to continue charging market-based rates for certain movements originating at the Gulf Coast. Additionally, on February 2, 2018, BP Products North America Inc., Trafigura Trading LLC and TCPU Inc. also filed a complaint with FERC against Colonial regarding rates. These pending complaints have been docketed as Docket Nos. OR18-7-000 and OR18-12-000, respectively, and in both cases, the FERC has not taken any action on the complaints as of Explorer in Docket No. FA16-5-000.this time.

Additionally, EPAct deemed certain interstate petroleum pipeline rates then in effect to be just and reasonable under the ICA. These rates are commonly referred to as “grandfathered rates.” For example, Colonial’s rates in effect at the time of the passage of EPAct for interstate transportation service were deemed just and reasonable and therefore are grandfathered. New rates have since been established after EPAct for certain grandfathered pipeline systems such as Zydeco. FERC may change grandfathered rates upon complaint only after it is shown that:

a substantial change has occurred since enactment in either the economic circumstances or the nature of the services that were a basis for the rate;

the complainant was contractually barred from challenging the rate prior to enactment of EPAct and filed the complaint within 30 days of the expiration of the contractual bar; or

a provision of the tariff is unduly discriminatory or preferential.

EPAct required FERC to establish a simplified and generally applicable methodology to adjust tariff rates for inflation for interstate petroleum pipelines. As a result, FERC adopted an indexing rate methodology which, as currently in effect, allows common carriers to change their rates within prescribed ceiling levels that are tied to changes in the U.S. Producer Price Index for Finished Goods (“PPI-FG”). The indexing methodology is applicable to existing rates, including grandfathered rates, with the exclusion of market-based rates. FERC’s indexing methodology is subject to review every five years. FERC recently completed its five-year review, revised its indexing methodology and determined that during the five-year period commencing July 1, 2016 and ending June 30, 2021, common carriers charging indexed rates are permitted to adjust their indexed ceilings annually by PPI-FG plus 1.23%. The FERC ruling was appealed and the appeal was denied by the D.C. Circuit Court on November 28, 2017. No further appeal is still subject to appeal.expected at this time. We cannot predict whether or to what extent the index factor may change in the future. A pipeline is not required to raise its rates up to the index ceiling, but it is permitted to do so; however a pipeline must reduce its indexed rates to the extent they exceed the index ceiling when a negative index applies. The index adjustment effective July 1, 2016 was a negative 2.0135%. Some indexed rates on our systems were reduced in 2016 in response to the lower index ceiling, such as certain spot rates on Zydeco. The majority of our systems’ rates subject to the index, however, were below the index ceiling and were unchanged. Rate increases made under the index methodology are presumed to be just and reasonable and require a protesting party to demonstrate that the portion of the rate increase resulting from application of the index is substantially in excess of the pipeline’s increase in costs. Despite these procedural limits on challenging the indexing of rates, the overall rates are not entitled to any specific protection against rate challenges. Under the indexing rate methodology, in any year in which the index is negative, pipelines must file to lower their rates if those rates would otherwise be above the rate ceiling.

While common carrier pipelines often use the indexing methodology to change their rates, common carrier pipelines may elect to support proposed rates by using other methodologies such as cost-of-service ratemaking,rate making, market-based rates, and settlement rates. A common carrier pipeline can propose a cost-of-service approach when seeking to increase its rates above the rate ceiling (or when seeking to avoid lowering rates to the reduced rate ceiling), but must establish that a substantial divergence exists between the actual costs experienced by the pipeline and the rates resulting from application of the indexing methodology. A common carrier can charge market based rates if it establishes that it lacks significant market power in the

affected markets. A common carrier can establish rates under settlement if agreed upon by all current shippers. Rates for a new service on a common carrier pipeline can be established through a negotiated rate with an unaffiliated shipper.

The rates shown in our FERC tariffs have been established using the indexing methodology, by settlement or by negotiation. If we used cost-of-service rate making to establish or support our rates on our different pipeline systems, the issue of the proper allowance for federal and state income taxes could arise. In 2005, FERC issued a policy statement stating that it would permit common carrier pipelines, among others, to include an income tax allowance in cost-of-service rates to reflect actual or potential tax liability attributable to a regulated entity’s operating income, regardless of the form of ownership. Under FERC’s policy, a tax pass-through entity seeking such an income tax allowance must establish that its partners or members have an actual or potential income tax liability on the regulated entity’s income. Whether a pipeline’s owners have such actual or potential income tax liability is subject to review by FERC on a case-by-case basis. Although this policy is generally favorable for common carrier pipelines that are organized as pass-through entities, it still entails rate risk due to FERC’s case-by-case review approach. The application of this policy, as well as any decision by FERC regarding our cost of service, is also subject to review in the courts.

Under its current policy, FERC permits regulated interstate oil and gas pipelines, including those owned by master limited partnerships, to include an income tax allowance in their cost of service used to calculate cost-based transportation rates. The allowance is intended to reflect the actual or potential tax liability attributable to the regulated entity’s operating income, regardless of the form of ownership. On July 1, 2016, in United Airlines, Inc. v FERC, the United States Court of Appeals for the D.C. Circuit vacated a pair of FERC orders to the extent they permitted an interstate refined petroleum products pipeline owned by a master limited partnership to include an income tax allowance in its cost-of-service-basedcost-of-service rates. The D.C. Circuit held that FERC had failed to demonstrate that the inclusion of an income tax allowance in the pipeline’s rates would not lead to an over-recoveryover-

recovery of costs attributable to regulated service. The D.C. Circuit instructed FERC on remand to fashion a remedy to ensure that the pipeline’s rates do not allow it to over-recover its costs. Following the D.C. Circuit’s decision, FERC issued a Notice of Inquiry on December 15, 2016 in Docket No. PL17-1-000 requesting comments regarding how to address any double recovery from FERC’s current income tax allowance and rate of return policies. Initial comments are duewere filed on March 8, 2017, and reply comments are duewere filed on April 7, 2017.2017, and certain parties subsequently filed additional comments. The outcome of this proceeding could affect FERC’s income tax allowance policy for cost-based rates charged by regulated pipelines going forward. To the extent that we charge cost-of-service based rates, those rates could be affected by any changes in FERC’s income tax allowance policy to the extent our rates are subject to complaint or challenge by FERC acting on its own initiative, or to the extent that we propose new cost-of-service rates or changes to our existing rates.

On October 20, 2016, the Federal Energy Regulatory CommissionFERC issued an Advance Notice of Proposed Rulemaking (“ANOPR”) in Docket No. RM17-1-000 regarding changes to the oil pipeline rate index methodology and data reporting on the Page 700 of the FERC Form No. 6. In an effort to improve the Commission’s ability to ensure that oil pipeline rates are just and reasonable under the Interstate Commerce Act (“ICA”),ICA, the Commission is considering making the following changes to their current indexing methodologies for oil pipelines:

| |

| 1) | Deny index increases for any pipeline whose Form No. 6, Page 700 revenues exceed costs by 15% for both of the prior two years; |

| |

| 2) | Deny index increases that exceed by 5% the cost changes reported on Page 700; and |

| |

| 3) | Apply the new criteria to costs more closely associated with the pipeline’s proposed rates than with total company-wide costs and revenues now reported on Page 700. |

Initial comments were filed on January 19, 2017, and reply comments will be duewere filed on March 17, 2017. We will continue to monitor developments in this area.

Intrastate services provided by certain of our pipeline systems are subject to regulation by state regulatory authorities, such as the Texas Railroad Commission, which currently regulates Zydeco and Colonial pipeline rates; and the Louisiana Public Service Commission, which currently regulates the Zydeco, Mars, Delta and Colonial pipeline rates. State agencies typically require intrastate petroleum pipelines to file their rates with the agencies and permit shippers to challenge existing rates and proposed rate increases. State agencies may also investigate rates, services, and terms and conditions of service on their own initiative. State regulatory commissions could limit our ability to increase our rates or to set rates based on our costs, or could order us to reduce our rates and require the payment of refunds to shippers.

Further, rate investigations by FERC or a state commission could result in an investigation of our costs, including the:

overall cost of service, including operating costs and overhead;

allocation of overhead and other administrative and general expenses to the regulated entity;

appropriate capital structure to be utilized in calculating rates;

appropriate rate of return on equity and interest rates on debt;

rate base, including the proper starting rate base;

throughput underlying the rate; and

proper allowance for federal and state income taxes.

Shippers can always file a complaint with FERC or a state agency challenging rates or conditions of services. If they were successful, FERC or a state agency could order reparations or service charge.

Certain of our pipelines, including Auger, Na Kika, Odyssey, Poseidon, Proteus, Endymion, Cleopatra and parts of Mars, are located offshore in the Outer Continental Shelf. As such, they are not subject to FERC or state rate regulation, but are subject to the Outer Continental Lands Act (“OCSLA”). Under the OCSLA, we must provide open and nondiscriminatory access to both pipeline owner and non-owner shippers, and comply with other requirements.

Pipeline and Terminal Safety

Our assets are subject to increasingly strict safety laws and regulations. Our transportation and storage of crude oil, and refined products, involveand dry gas involves a risk that hazardous liquids or gas may be released into the environment, potentially causing harm to the public or the environment. In turn, such incidents may result in substantial expenditures for response actions, significant government penalties, liability to government agencies for natural resources damages, liability and/or reparations to land owners and significant business interruption. The Pipeline and Hazardous Materials Safety Administration (“PHMSA”)PHMSA of the Department of Transportation (“DOT”)DOT has adopted safety regulations with respect to the design,