Washington, D.C. 20549

FORM

10-K/A

Amendment No. 1

| ☒ | |

ANNUAL REPORT PURSUANT TO SECTION 13 or 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended September 29, 2017October 2, 2020

OR

| ☐ | |

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period fromto

Commission File Number:

1-7598

VARIAN MEDICAL SYSTEMS, INC.

(Exact name of Registrant as specified in its charter)

Delaware | 94-2359345 | |

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification Number) | |

3100 Hansen Way Palo Alto California | 94304-1038 | |

(Address of principal executive offices) | (Zip Code) | |

(650)

493-4000

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

Title of each class | Trading Symbol | Name of each exchange on which registered | ||

Common Stock, $1 par value | VAR | New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the Registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ý☒ No ¨☐

Indicate by check mark if the Registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨☐ No ý☒

Indicate by check mark whether the Registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ý☒ No ¨☐

Indicate by check mark whether the Registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulationand post such files). Yes ý☒ No ¨

S-T

during the preceding 12 months (or for such shorter period that the registrant was required to submit Indicate by check mark whether the Registrant is a large accelerated filer, an accelerated filer, a"emerging“emerging growth company"company” in Rule

non-accelerated

filer, smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and 12b-2

of the Exchange Act. (Check one):Large accelerated filer | ☒ | Accelerated filer | ☐ | |||||

Non-accelerated filer | ☐ | Smaller reporting company | ☐ | |||||

| Emerging growth company | ☐ | |||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ¨☐

Indicate by check mark whether the Registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report.

¨☒

Indicate by check mark whether the Registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

Yes As of March 31, 2017,April 3, 2020, the last business day of Registrant’s most recently completed second fiscal quarter, the aggregate market value of shares of Registrant’s common stock held byMarch 31, 2017)April 3, 2020) was $8,340,019,028. Shares of Registrant’s common stock held by the Registrant’s executive officers and directors and by each entity that owned 10% or more of Registrant’s outstanding common stock have been excluded in that such persons may be deemed to be affiliates. This determination of affiliate status is not necessarily a conclusive determination for other purposes.

non-affiliates

of Registrant (based upon the closing sale price of such shares on the New York Stock Exchange on $6,905,810,423. At November 21, 2017,13, 2020, the number of shares of the Registrant’s common stock outstanding was 91,616,924.91,355,469

.

DOCUMENTS INCORPORATED BY REFERENCE

None.

EXPLANATORY NOTE | ||

10-K/A

(this “Amendment”) to file certain This Amendment amends the Company’s Annual Report on Form(“SEC”(the “SEC”) on November 25, 2020 (the “Original Filing”). ForThe Company is filing this purpose, statements concerning: industry or market segment outlook; market acceptanceAmendment to amend Part III of or transitionthe Original Filing to new products or technology such as fixed field intensity-modulated radiation therapy, image-guided radiation therapy, stereotactic radiosurgery, volumetric modulated arc therapy, brachytherapy, software, treatment techniques, proton therapy; growth drivers; future orders, revenues, backlog, earnings or other financial results;include the information required by and any statements usingnot included in Part III of the terms “believe,” “expect,” “anticipate,” “can,” “should,” “would,” “could,” “estimate,” “may,” “intended,” “potential,” and “possible” or similar statements are forward-looking statements that involve risks and uncertainties that could cause our actual results andOriginal Filing because the outcome and timingCompany no longer intends to file its definitive proxy statement within 120 days of certain events to differ materially from those projected or management’s current expectations. By making forward-looking statements, we have not assumed any obligation to, and you should not expect us to, update or revise those statements becausethe end of new information, future events or otherwise.

10-K

for the fiscal year ended October 2, 2020, originally filed with the Securities and Exchange Commission 13a-14(a)

promulgated by the S-K,

paragraphs 3, 4 and 5 of the certifications have been omitted.Except as Varex Imaging Corporation (“Varex”), and isdescribed above, no longer part of continuing operations. See “Distribution” below.other changes have been made to the Original Filing. The operating segments were determined based on how our Chief Executive Officer, who is our Chief Operating Decision Maker (“CODM”), views and evaluates our operations. The CODM allocates resourcesOriginal Filing continues to and evaluates the financial performance of each operating segment primarily based on operating earnings.

2

PART III

Item 10. | Directors, Executive Officers and Corporate Governance |

Executive Officers

The information required by this item with respect to our executive officers is set forth in Part I of the Original Filing.

Directors

Below is information, including biographical information, about our current directors as well as a discussion of the specific experiences, qualifications, attributes and skills considered by our Board of Directors (the "Record Date"“Board”) received 0.4 of a share of Varex common stock for every one sharein concluding that such individuals should serve as directors.

Anat Ashkenazi Age: 48 Director Since: 2018 Independent Occupation: Public Company Executive | Principal occupation, business experience and directorships • Positions at Eli Lilly and Company, a global pharmaceutical company: • Senior Vice President, Controller and Chief Financial Officer, Lilly Research Labs (September 2016—present) • Vice President, Finance and Chief Financial Officer, Lilly Diabetes and Lilly Global Manufacturing and Quality (April 2015—September 2016) • Chief Financial Officer, Lilly Oncology (October 2013—April 2015) • Other Current Public Company Board Memberships: None • Prior Public Company Board Memberships in Past Five Years: None Experience, qualifications, attributes or skills supporting directorship • Over 20 years of in-depth financial management and planning experience including corporate finance and financial services• Extensive experience in the pharmaceutical industry having worked for Eli Lilly and Company across different therapeutic areas and disciplines • Experience in global and regional strategic planning, organizational redesign, and Six Sigma implementation | |

Jeffrey R. Balser Age: 59 Director Since: 2018 Independent Occupation: CEO of an Academic Medical Center | Principal occupation, business experience and directorships • President and Chief Executive Officer of Vanderbilt University Medical Center (May 2016—present) • Dean, Vanderbilt University School of Medicine (October 2008—present) • Vice Chancellor for Health Affairs, Vanderbilt University Medical Center (June 2009—April 2016) • Associate Vice Chancellor for Research, Vanderbilt University Medical Center (January 2004—October 2008) • Other Current Public Company Board Memberships: None • Prior Public Company Board Memberships in Past Five Years: None Experience, qualifications, attributes or skills supporting directorship • In-depth knowledge of the healthcare industry, hospital operations and managed care industry• Experience in management and strategic planning of hospital and physician practice, medical education, clinical and basic research through service as Chief Executive Officer and Dean, and previously as chief research officer, of a leading academic medical institution • Licensed Medical Doctor, Board certified in Anesthesiology and Critical Care Medicine | |

3

Judy Bruner Age: 62 Director Since: 2016 Independent Occupation: Former Public Company Executive | Principal occupation, business experience and directorships • Positions at SanDisk Corporation, a global leader in flash memory storage solutions: • Executive Vice President, Administration and Chief Financial Officer (June 2004—May 2016) • Member of Board of Directors (June 2002—July 2004) • Senior Vice President and Chief Financial Officer, Palm, Inc., a manufacturer of personal digital assistants (September 1999—June 2004) • Vice President, Finance & Corporate Controller, 3Com Corporation, a digital electronics manufacturer (May 1998—September 1999) • Other Current Public Company Board Memberships: Applied Materials, Inc., a provider of engineering solutions; Rapid7, a security data and analytics solutions provider; Seagate Technology PLC, a data storage company • Prior Public Company Board Memberships in Past Five Years: Brocade Communications Systems, Inc., a technology company specializing in data and storage networking products Experience, qualifications, attributes or skills supporting directorship • Over 35 years of financial management experience in the high technology industry • Deep experience with compliance and enterprise risk management • Audit committee chair experience • Significant mergers and acquisitions experience • Membership on boards of other public companies | |

Jean-Luc ButelAge: 64 Director Since: 2017 Independent Occupation: Former Public Company Executive | Principal occupation, business experience and directorships • Positions at Baxter International, a health care company providing a portfolio of renal and hospital products: • President, International (January 2015—June 2015) • Corporate Officer, Operating Committee Member, Corporate Vice President and President, International (February 2012—December 2014) • Positions at Medtronic, Inc., a global leader in medical technology: • Corporate Officer, Executive Committee Member, Executive Vice President; Group President International (January 2011—January 2012) • Corporate Officer, Executive Committee Member, Senior Vice President and President, Medtronic International (May 2008—December 2010) • Corporate Officer, Executive Committee Member, Senior Vice President, Medtronic and President, Medtronic Asia Pacific (August 2003—April 2008) • Other Senior Management Experience: President, Johnson & Johnson Independence Technology; President, Worldwide Consumer Healthcare, Becton Dickinson • Other Current Public Company Board Memberships: Takeda Pharmaceutical Company Limited, a global pharmaceuticals company focused on metabolic disorders, gastroenterology, neurology, inflammation and oncology • Prior Public Company Board Memberships in Past Five Years: Biosensors International Group, Ltd., a medical device company specializing in interventional cardiology procedures and critical care technologies Experience, qualifications, attributes or skills supporting directorship • Extensive experience in sales, operations and general management of healthcare companies through his service as an executive of several large U.S. healthcare companies • Extensive experience leading international business operations of large U.S. healthcare companies, including in Europe, Asia and North and South America | |

4

Regina E. Dugan Age: 57 Director Since: 2013 Independent Occupation: CEO | Principal occupation, business experience and directorships • President and Chief Executive Officer, Wellcome Leap, Inc., a nonprofit focused on accelerating innovations in global human health challenges (March 2020—present) • Vice President of Engineering, Facebook, Inc., leading Building 8, a team charged with developing and delivering next generation consumer hardware to market (May 2016—January 2018) • Vice President of Engineering, Google, Inc., leading the Advanced Technology and Products group, a group charged with breakthrough innovations in mobile computing and accelerating the development of promising technologies to market (February 2014—April 2016) • Senior Vice President, Google owned Motorola Mobility LLC, a mobile technology company Google acquired in May 2012 (March 2012— February 2014) • Director, Defense Advanced Research Projects Agency (DARPA), a breakthrough product development organization of the U.S. Department of Defense (July 2009—March 2012) • Co-Founder, President and Chief Executive Officer, RedXDefense LLC, a security solutions company (2005—July 2009)• Co-Founder, President and Chief Executive Officer, Dugan Ventures, an investment firm (currently anon-voting partner) (2001—July 2009)• Other Current Public Company Board Memberships: Zynga Inc., a social game developer • Prior Public Company Board Memberships in Past Five Years: None Experience, qualifications, attributes or skills supporting directorship • Experience leading DARPA, the principal agency within the U.S. Department of Defense responsible for product development, research, demonstration and fielding of high-risk, high-payoff capabilities • Familiarity with defense, security and commercial industries • Expertise with a wide range of advanced technologies and demonstrated track record in moving to use new technologies, from sensor systems to big data products • Years of experience serving in senior executive positions with responsibilities including fostering innovation and developing strategic business relationships across diverse industries and commercial entities large and small • Experience serving on the board of another public company |

5

R. Andrew Eckert Age: 59 Director Since: 2004 Chairman Since: 2014 Independent Occupation: CEO | Principal occupation, business experience and directorships • Chief Executive Officer, Zelis, Inc., a financial technology company specializing in healthcare claims and payment solutions (August 2020—Present) • Chief Executive Officer, Acelity L.P., Inc., a global advanced wound care company (April 2017—October 2019) • Chief Executive Officer, Valence Health, a healthcare solutions company (August 2015—October 2016) • Chief Executive Officer, TriZetto Corporation, a healthcare IT solutions firm (March 2014—November 2014) • Chief Executive Officer, CRC Health Corporation, a provider of substance abuse treatment and adolescent youth services (January 2011—March 2014) • Managing Director, Symphony Technology Group, a private equity firm (October 2009—January 2011) • President and Chief Executive Officer, Eclipsys Corporation, a former publicly traded healthcare information management software provider (October 2005—May 2009) • Chief Executive Officer, SumTotal Systems, Inc., an enterprise software provider (2004—2005) • Chief Executive Officer, Docent Inc., an enterprise software provider that was acquired by SumTotal Systems (2002—2004) • Chairman and Chief Executive Officer, ADAC Laboratories, a former publicly traded medical imaging company (1997—2001) • Other Current Public Company Board Memberships: Becton, Dickinson and Company, a global medical technology company • Prior Public Company Board Memberships in Past Five Years: None Experience, qualifications, attributes or skills supporting directorship • Extensive experience obtained over 15 years serving as an executive officer of several public companies, including a medical imaging company and healthcare information management company • Deep knowledge of operational, financial, strategic planning, product development and marketing matters • Experience serving on the board of directors of several public companies in the healthcare industry | |

Phillip G. Febbo Age: 54 Director Since: 2019 Independent Occupation: Public Company Executive | Principal occupation, business experience and directorships • Chief Medical Officer, Illumina, Inc. (March 2018—present) • Chief Medical Officer, Genomic Health, Inc. (2013—March 2018) • Professor of Medicine and Urology at the University of California, San Francisco (UCSF) (2010—2013) • Service on the board of directors of the American College of Medical Genetics and Genomics Foundation (2018—2019) • Other Current Public Company Board Memberships: None • Prior Public Company Board Memberships in Past Five Years: None Experience, qualifications, attributes or skills supporting directorship • Broad experience in medical strategy and managing resources strategically on a global scale across areas like product development, evidence generation, product marketing, and sales, gained from service as the Chief Medical Officer of two genomic health companies • Deep knowledge in cancer research, clinical and academic research programs, including through service as the principal investigator of clinical trials funded by National Institute Institutes of Health, Department of Defense, and various industry and non-profit foundation grants• Critical insights in evaluating data of various cancer treatments and leveraging multidisciplinary care to optimize patient outcomes | |

6

David J. Illingworth Age: 67 Director Since: 2011 Independent Occupation: Former Public Company CEO | Principal occupation, business experience and directorships • Smith & Nephew plc, a medical devices company • Chief Executive Officer (July 2007—April 2011) • Chief Operating Officer and Division President (2002—July 2007) • Other Senior Management Experience: President, XL Vision, Inc.; Chairman and Chief Executive Officer, VidaMed, Inc.; President, Nellcor Puritan Bennett LLC; and Managing Director, Asia/Pacific, GE Medical Systems • Other Current Public Company Board Memberships: Domtar, Inc., a manufacturer of fiber-based products • Prior Public Company Board Memberships in Past Five Years: None. Experience, qualifications, attributes or skills supporting directorship • In-depth knowledge of the medical technology industry• Extensive experience in sales, operations and general management in the United States, United Kingdom and Asia through his service as an executive of various medical technology companies • Service on the board of directors and as a member of the audit committee and the environmental, health, safety and sustainability committee, of another public medical device company | |

Michelle M. Le Beau Age: 66 Director Since: 2019 Independent Occupation: Professor and Director of an Academic Cancer Center | Principal occupation, business experience and directorships • Positions at the University of Chicago: • Arthur and Marian Edelstein Professor of Medicine, Section of Hematology/Oncology (1986—present) • Director, University of Chicago Medicine Comprehensive Cancer Center (2004—present) • Board Member of the University of Chicago Medicine Cancer Council (2012—present) • Director, Cancer Cytogenetics Laboratory (1986—present) • Other Current Public Company Board Memberships: None • Prior Public Company Board Memberships in Past Five Years: None Experience, qualifications, attributes or skills supporting directorship • Extensive experience with cancer research, clinical and research program development, and structure and operation of academic cancer centers • Deep knowledge of academic and government cancer research priorities, and opportunities across the cancer research and care continuum • Service on (i) numerous scientific advisory boards for academic cancer centers, including advisory boards and working groups for the National Cancer Institute of the U.S. National Institutes of Health, (ii) the board of directors of professional organizations in oncology and cancer research (e.g. the American Association for Cancer Research and the American Society of Hematology), and (iii) multiple non-profit organizations in cancer research, advocacy, outreach and education (e.g. the American Cancer Society)• Doctoral degree in Genetics, and board-certified in clinical cytogenetics by the American Board of Medical Genetics and Genomics • In-depth knowledge of the biology and development of human cancers | |

7

Dow R. Wilson Age: 62 Director Since: 2012 Occupation: President and CEO of Varian | Principal occupation, business experience and directorships • Positions at the Company: • President and Chief Executive Officer (September 2012—present) • Corporate Executive Vice President and Chief Operating Officer (October 2011—September 2012) • Corporate Executive Vice President and President, Oncology Systems (August 2005—September 2011) • Corporate Vice President and President, Oncology Systems (January 2005—August 2005) • Prior to joining the Company in January 2005, held various senior management positions in and outside of the United States with General Electric Company, a diversified industrial company • Other Current Public Company Board Memberships: Agilent Technologies, a research, development and manufacturing company for life science • Public Company Board Memberships in Past Five Years: Saba Software, an e-learning software provider; Varex Imaging Corporation, a leading independent supplier of medicalX-ray tubes and image processing solutions• U.S. Government Appointments: • Presidential appointment to U.S. President’s Advisory Council on Doing Business in Africa (November 2014—January 2019) • Appointed to U.S. Department of Commerce’s US-Brazil CEO Forum in April 2019• Board member of the US-India Strategic Partnership Forum, anon-profit focused on driving economic growth, job creation, innovation, inclusion, and entrepreneurship in the U.S. and India (2018—present)Experience, qualifications, attributes or skills supporting directorship • Deep knowledge of our business, strategy and technology gained through serving as President of our Oncology Systems business and Chief Operating Officer before becoming our President and Chief Executive Officer • Significant knowledge of domestic and international medical and healthcare industries gained from serving in management positions at General Electric • Critical insight into operational requirements of a company with worldwide reach, knowledge of corporate and business unit strategies, and operational expertise, each gained from executive management experience at two large, global organizations • Experience serving on the board of directors and as lead director of another public company |

Delinquent Section 16(a) Reports

Under U.S. securities laws, directors, certain officers and persons holding more than 10% of our common stock as of the Record Date. Varex is now an independent publicly traded company and is listed on The NASDAQ Global Select Market under the ticker symbol "VREX." Varian continues to trade on the New York Stock Exchange under the ticker symbol "VAR." see Note 2, "Discontinued Operations" of the Notes to the Consolidated Financial Statements.

10b5-1

plan.Code of products in foreign countries are also subject to regulation of matters such as product standards, packaging requirements, labeling requirements, import restrictions, environmental and product recycling requirements, tariff regulations, duties and tax requirements. In some countries, we rely on our foreign distributors and agents to assist us in complying with foreign regulatory requirements.Conduct

1. From our main web page, first click “Investors.”

2. Next click on “Governance.”

3. Finally, click on “Code of Conduct” in the Audit Committee, Compensation and Management Development Committee, Ethics and Compliance Committee, Nominating and Corporate Governance Committee and Executive Committee are also available on the Investors page of our website. Investors and others should note that we announce material financial and operational information to our investors using our investor relations website (http://investors.varian.com/), press releases, SEC filings and public conference calls and webcasts. drop-down navigation bar.

8

Please note that information on, or that can be accessed through, our website is not deemed “filed” with the SEC and is not to be incorporated by reference into any of our filings under the Securities Act of 1933, as amended, (the “Securities Act”), or the Securities Exchange Act of 1934, as amended (the “Exchange Act”).

| High | Low | |||||||

| Fiscal Year 2017 | ||||||||

| First Quarter | $ | 94.48 | $ | 75.94 | ||||

| Second Quarter | $ | 92.57 | $ | 76.29 | ||||

| Third Quarter | $ | 105.30 | $ | 87.49 | ||||

| Fourth Quarter | $ | 107.87 | $ | 95.23 | ||||

| Fiscal Year 2016 | ||||||||

| First Quarter | $ | 72.76 | $ | 65.04 | ||||

| Second Quarter | $ | 72.01 | $ | 64.80 | ||||

| Third Quarter | $ | 76.37 | $ | 68.75 | ||||

| Fourth Quarter | $ | 88.62 | $ | 71.49 | ||||

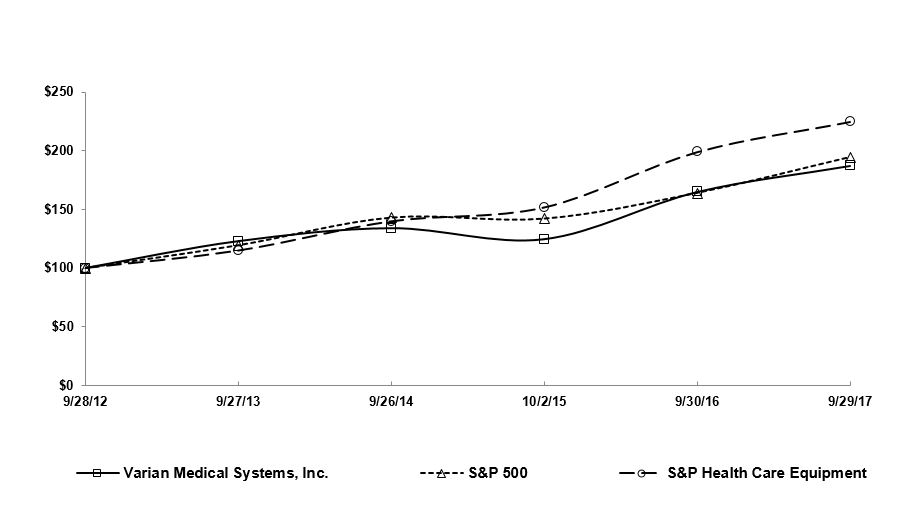

| 9/28/2012 | 9/27/2013 | 9/26/2014 | 10/2/2015 | 9/30/2016 | 9/29/2017 | |||||||

| Varian Medical Systems, Inc. | 100.00 | 122.98 | 134.12 | 124.65 | 165.00 | 187.32 | ||||||

| S&P 500 | 100.00 | 119.34 | 142.89 | 142.02 | 163.93 | 194.44 | ||||||

| S&P Health Care Equipment | 100.00 | 114.92 | 139.91 | 151.75 | 199.02 | 224.92 | ||||||

| Period | Total Number of Shares Purchased | Average Price Paid Per Share | Total Number of Shares Purchased as Part of Publicly Announced Plans or Programs | Maximum Number of Shares that May Yet Be Purchased Under the Plans or Programs (1) | ||||||||

| July 1, 2017 – July 28, 2017 | — | $ | — | — | 5.5 | |||||||

| July 29, 2017 – August 25, 2017 | 0.1 | $ | 97.00 | 0.1 | 5.4 | |||||||

| August 26, 2017 – September 29, 2017 | 0.2 | $ | 105.30 | 0.2 | 5.2 | |||||||

| Total | 0.3 | $ | 101.98 | 0.3 | 5.2 | |||||||

| Summary of Operations: | Fiscal Years (1) | |||||||||||||||||||

| (In millions, except per share amounts) | 2017 | 2016 | 2015 | 2014 | 2013 | |||||||||||||||

| Revenues | $ | 2,668.2 | $ | 2,621.1 | $ | 2,490.7 | $ | 2,392.7 | $ | 2,304.0 | ||||||||||

Earnings from continuing operations before taxes (2) | 344.8 | 440.6 | 401.3 | 374.2 | 417.8 | |||||||||||||||

| Taxes on earnings | 87.7 | 115.3 | 89.9 | 100.2 | 107.1 | |||||||||||||||

| Net earnings from continuing operations | 257.1 | 325.3 | 311.4 | 274.0 | 310.7 | |||||||||||||||

| Net earnings (loss) from discontinued operations | (6.8 | ) | 77.4 | 100.6 | 129.7 | 127.5 | ||||||||||||||

| Net earnings | 250.3 | 402.7 | 412.0 | 403.7 | 438.2 | |||||||||||||||

| Less: Net earnings attributable to noncontrolling interests | 0.7 | 0.4 | 0.5 | — | — | |||||||||||||||

| Net earnings attributable to Varian | $ | 249.6 | $ | 402.3 | $ | 411.5 | $ | 403.7 | $ | 438.2 | ||||||||||

| Net earnings (loss) per share - basic | ||||||||||||||||||||

| Continuing operations | $ | 2.78 | $ | 3.41 | $ | 3.13 | $ | 2.63 | $ | 2.87 | ||||||||||

Discontinued operations | (0.08 | ) | 0.81 | 1.00 | 1.25 | 1.17 | ||||||||||||||

| Net earnings per share - basic | $ | 2.70 | $ | 4.22 | $ | 4.13 | $ | 3.88 | $ | 4.04 | ||||||||||

| Net earnings (loss) per share – diluted | ||||||||||||||||||||

| Continuing operations | $ | 2.75 | $ | 3.39 | $ | 3.10 | $ | 2.60 | $ | 2.82 | ||||||||||

| Discontinued operations | (0.07 | ) | 0.80 | 0.99 | 1.23 | 1.16 | ||||||||||||||

| Net earnings per share - diluted | $ | 2.68 | $ | 4.19 | $ | 4.09 | $ | 3.83 | $ | 3.98 | ||||||||||

| Financial Position at Fiscal Year End: | ||||||||||||||||||||

Working capital (3) | $ | 640.2 | $ | 1,002.0 | $ | 1,016.4 | $ | 1,177.3 | $ | 1,429.5 | ||||||||||

Total assets (3) (4) | 3,179.4 | 3,814.8 | 3,576.9 | 3,336.3 | 3,455.2 | |||||||||||||||

| Short-term borrowings | 350.0 | 329.6 | 108.4 | — | — | |||||||||||||||

Long-term debt (including current maturities) (4) | — | 336.3 | 385.7 | 435.1 | 503.3 | |||||||||||||||

Total equity (3) | $ | 1,499.3 | $ | 1,744.2 | $ | 1,726.3 | $ | 1,616.4 | $ | 1,713.8 | ||||||||||

| Revenues by sales classification | Fiscal Years | ||||||||||||||||

| (Dollars in millions) | 2017 | Percent Change | 2016 | Percent Change | 2015 | ||||||||||||

| Product | $ | 1,555.5 | (2 | )% | $ | 1,583.9 | 6 | % | $ | 1,497.1 | |||||||

| Service | 1,112.7 | 7 | % | 1,037.2 | 4 | % | 993.6 | ||||||||||

| Total Revenues | $ | 2,668.2 | 2 | % | $ | 2,621.1 | 5 | % | $ | 2,490.7 | |||||||

| Product as a percentage of total revenues | 58 | % | 60 | % | 60 | % | |||||||||||

| Service as a percentage of total revenues | 42 | % | 40 | % | 40 | % | |||||||||||

| Revenues by region | Fiscal Years | ||||||||||||||||||||||

| (Dollars in millions) | 2017 | Percent Change | Constant Currency (1) | 2016 | Percent Change | Constant Currency | 2015 | ||||||||||||||||

| Americas | $ | 1,363.8 | 6 | % | 6 | % | $ | 1,285.4 | (3 | )% | (3 | )% | $ | 1,329.4 | |||||||||

| EMEA | 771.6 | (6 | )% | (5 | )% | 824.7 | 13 | % | 18 | % | 730.5 | ||||||||||||

| APAC | 532.8 | 4 | % | 3 | % | 511.0 | 19 | % | 17 | % | 430.8 | ||||||||||||

| Total Revenues | $ | 2,668.2 | 2 | % | 2 | % | $ | 2,621.1 | 5 | % | 7 | % | $ | 2,490.7 | |||||||||

| North America | $ | 1,283.0 | 7 | % | 7 | % | $ | 1,201.2 | (4 | )% | (4 | )% | $ | 1,248.3 | |||||||||

International (2) | 1,385.2 | (2 | )% | (2 | )% | 1,419.9 | 14 | % | 17 | % | 1,242.4 | ||||||||||||

| Total Revenues | $ | 2,668.2 | 2 | % | 2 | % | $ | 2,621.1 | 5 | % | 7 | % | $ | 2,490.7 | |||||||||

| North America as a percentage of total revenues | 48 | % | 47 | % | 51 | % | |||||||||||||||||

| International as a percentage of total revenues | 52 | % | 53 | % | 49 | % | |||||||||||||||||

| Revenues by sales classification | Fiscal Years | ||||||||||||||||||||||

| (Dollars in millions) | 2017 | Percent Change | Constant Currency | 2016 | Percent Change | Constant Currency | 2015 | ||||||||||||||||

| Product | $ | 1,383.0 | (3 | )% | (3 | )% | $ | 1,430.3 | 5 | % | 6 | % | $ | 1,359.2 | |||||||||

| Service | 1,102.7 | 7 | % | 7 | % | 1,027.7 | 4 | % | 5 | % | 987.6 | ||||||||||||

| Total Oncology Systems Revenues | $ | 2,485.7 | 1 | % | 1 | % | $ | 2,458.0 | 5 | % | 6 | % | $ | 2,346.8 | |||||||||

| Product as a percentage of Oncology Systems revenues | 56 | % | 58 | % | 58 | % | |||||||||||||||||

| Service as a percentage of Oncology Systems revenues | 44 | % | 42 | % | 42 | % | |||||||||||||||||

| Oncology Systems revenues as a percentage of total revenues | 93 | % | 94 | % | 94 | % | |||||||||||||||||

| Revenues by region | Fiscal Years | ||||||||||||||||||||||

| (Dollars in millions) | 2017 | Percent Change | Constant Currency | 2016 | Percent Change | Constant Currency | 2015 | ||||||||||||||||

| Americas | $ | 1,276.0 | 4 | % | 4 | % | $ | 1,229.8 | 1 | % | 2 | % | $ | 1,212.1 | |||||||||

| EMEA | 703.5 | (5 | )% | (3 | )% | 739.3 | 5 | % | 9 | % | 703.9 | ||||||||||||

| APAC | 506.2 | 4 | % | 3 | % | 488.9 | 13 | % | 12 | % | 430.8 | ||||||||||||

| Total Oncology System Revenues | $ | 2,485.7 | 1 | % | 1 | % | $ | 2,458.0 | 5 | % | 6 | % | $ | 2,346.8 | |||||||||

| North America | $ | 1,195.2 | 4 | % | 4 | % | $ | 1,145.6 | 1 | % | 1 | % | $ | 1,131.0 | |||||||||

| International | 1,290.5 | (2 | )% | (1 | )% | 1,312.4 | 8 | % | 10 | % | 1,215.8 | ||||||||||||

| Total Oncology System Revenues | $ | 2,485.7 | 1 | % | 1 | % | $ | 2,458.0 | 5 | % | 6 | % | $ | 2,346.8 | |||||||||

| North America as a percentage of total Oncology Systems revenues | 49 | % | 47 | % | 49 | % | |||||||||||||||||

| International as a percentage of total Oncology Systems revenues | 51 | % | 53 | % | 51 | % | |||||||||||||||||

| Revenues by sales classification | Fiscal Years | ||||||||||||||||

| (Dollars in millions) | 2017 | Percent Change | 2016 | Percent Change | 2015 | ||||||||||||

| Product | $ | 172.5 | 13 | % | $ | 153.1 | 11 | % | $ | 137.9 | |||||||

| Service | 10.0 | 4 | % | 9.5 | 70 | % | 5.6 | ||||||||||

| Total VPT revenues | $ | 182.5 | 12 | % | $ | 162.6 | 13 | % | $ | 143.5 | |||||||

| VPT revenues as a percentage of total revenues | 7 | % | 6 | % | 6 | % | |||||||||||

| Fiscal Years | |||||||||||||||||

| Dollars by segment | 2017 | Percent Change | 2016 | Percent Change | 2015 | ||||||||||||

| (Dollars in millions) | |||||||||||||||||

| Oncology Systems | $ | 1,139.6 | 5 | % | $ | 1,087.7 | 9 | % | $ | 998.9 | |||||||

| Varian Particle Therapy | 16.0 | (36 | )% | 25.2 | (24 | )% | 33.2 | ||||||||||

| Gross margin | $ | 1,155.6 | 4 | % | $ | 1,112.9 | 8 | % | $ | 1,032.1 | |||||||

| Percentage by segment | |||||||||||||||||

| Oncology Systems | 45.8 | % | 44.3 | % | 42.6 | % | |||||||||||

| Varian Particle Therapy | 8.8 | % | 15.4 | % | 23.1 | % | |||||||||||

| Total Company | 43.3 | % | 42.5 | % | 41.4 | % | |||||||||||

| Fiscal Years | |||||||||||||||||

| (Dollars in millions) | 2017 | Percent Change | 2016 | Percent Change | 2015 | ||||||||||||

| Research and development | $ | 210.0 | 5 | % | $ | 200.4 | 3 | % | $ | 195.4 | |||||||

| As a percentage of total revenues | 8 | % | 8 | % | 8 | % | |||||||||||

| Fiscal Years | |||||||||||||||||

| (Dollars in millions) | 2017 | Percent Change | 2016 | Percent Change | 2015 | ||||||||||||

| Selling, general and administrative | $ | 552.3 | 16 | % | $ | 475.3 | 8 | % | $ | 441.0 | |||||||

| Impairment charges | $ | 51.4 | n/m | $ | 2.2 | n/m | $ | — | |||||||||

| Selling, general and administrative as a percentage of total revenues | 21 | % | 18 | % | 18 | % | |||||||||||

| Impairment charges as a percentage of total revenues | 2 | % | — | % | — | % | |||||||||||

| Fiscal Years | |||||||||||||||||

| (Dollars in millions) | 2017 | Percent Change | 2016 | Percent Change | 2015 | ||||||||||||

| Interest income, net | $ | 2.9 | (49 | )% | $ | 5.6 | — | % | $ | 5.6 | |||||||

| Fiscal Years | ||||||||||||||

| 2017 | Percent Change | 2016 | Percent Change | 2015 | ||||||||||

| Effective tax rate | 25.4 | % | (0.8 | )% | 26.2 | % | 3.8 | % | 22.4 | % | ||||

| Fiscal Years | |||||||||||

| (in millions) | 2017(1) | 2016 | 2015 | ||||||||

| Revenues | $ | 194.0 | $ | 596.7 | $ | 608.4 | |||||

| Cost of revenues | 117.3 | 348.3 | 357.9 | ||||||||

| Gross margin | 76.7 | 248.4 | 250.5 | ||||||||

Operating expenses (2) | 76.1 | 132.6 | 97.2 | ||||||||

| Operating earnings | 0.6 | 115.8 | 153.3 | ||||||||

| Taxes on earnings | 7.4 | 38.4 | 52.7 | ||||||||

| Net earnings (loss) from discontinued operations | (6.8 | ) | 77.4 | 100.6 | |||||||

| Less: Net earnings from discontinued operations attributable to noncontrolling interests | 0.1 | 0.5 | 0.7 | ||||||||

| Net earnings (loss) from discontinued operations attributable to Varian | $ | (6.9 | ) | $ | 76.9 | $ | 99.9 | ||||

| Fiscal Years | |||||||||||||||||

| 2017 | Percent Change | 2016 | Percent Change | 2015 | |||||||||||||

| Net earnings per diluted share - continuing operations | $ | 2.75 | (19 | )% | $ | 3.39 | 9 | % | $ | 3.10 | |||||||

| Net earnings per diluted share - discontinued operations | (0.07 | ) | (109 | )% | 0.80 | (19 | )% | 0.99 | |||||||||

| Total net earnings per diluted share | $ | 2.68 | (36 | )% | $ | 4.19 | 2 | % | $ | 4.09 | |||||||

| Total Gross Orders (by segment) | Fiscal Years | ||||||||||||||||

| (Dollars in millions) | 2017 | Percent Change | 2016 | Percent Change | 2015 | ||||||||||||

| Oncology Systems | $ | 2,905.8 | 7 | % | $ | 2,724.5 | 1 | % | $ | 2,699.7 | |||||||

| Varian Particle Therapy | 229.2 | 120 | % | 104.3 | (67 | )% | 316.9 | ||||||||||

| Other | — | (100 | )% | 0.4 | 7 | % | 0.3 | ||||||||||

| Total Gross Orders | $ | 3,135.0 | 11 | % | $ | 2,829.2 | (6 | )% | $ | 3,016.9 | |||||||

| Gross Orders by region | Fiscal Years | ||||||||||||||||||||||

| (Dollars in millions) | 2017 | Percent Change | Constant Currency | 2016 | Percent Change | Constant Currency | 2015 | ||||||||||||||||

| Americas | $ | 1,479.0 | 3 | % | 3 | % | $ | 1,438.4 | 4 | % | 4 | % | $ | 1,384.1 | |||||||||

| EMEA | 878.2 | 14 | % | 14 | % | 772.9 | (6 | )% | (4 | )% | 826.0 | ||||||||||||

| APAC | 548.6 | 7 | % | 7 | % | 513.2 | 5 | % | 3 | % | 489.6 | ||||||||||||

| Total Oncology Systems Gross Orders | $ | 2,905.8 | 7 | % | 7 | % | $ | 2,724.5 | 1 | % | 1 | % | $ | 2,699.7 | |||||||||

| North America | $ | 1,386.2 | 6 | % | 5 | % | $ | 1,313.8 | 4 | % | 4 | % | $ | 1,258.2 | |||||||||

| International | 1,519.6 | 8 | % | 8 | % | 1,410.7 | (2 | )% | (1 | )% | 1,441.5 | ||||||||||||

| Total Oncology Systems Gross Orders | $ | 2,905.8 | 7 | % | 7 | % | $ | 2,724.5 | 1 | % | 1 | % | $ | 2,699.7 | |||||||||

| Trailing 12 months ended | |||||||

| September 29, 2017 | June 30, 2017 | March 31, 2017 | December 30, 2016 | ||||

| Americas | 3% | 4% | 5% | 4% | |||

| EMEA | 14% | (3)% | (4)% | (2)% | |||

| APAC | 7% | 13% | 15% | 13% | |||

| North America | 6% | 2% | 5% | 6% | |||

| International | 8% | 5% | 3% | 3% | |||

| Total Oncology Systems Gross Orders | 7% | 3% | 4% | 4% | |||

| September 29, | September 30, | ||||||||||

| (In millions) | 2017 | 2016 | Increase (Decrease) | ||||||||

| Cash and cash equivalents in continuing operations | $ | 716.2 | $ | 811.4 | $ | (95.2 | ) | ||||

| Cash and cash equivalents in discontinued operations | — | 32.1 | (32.1 | ) | |||||||

| Total cash and cash equivalents. | $ | 716.2 | $ | 843.5 | $ | (127.3 | ) | ||||

| Fiscal Years | ||||||||||||

| (In millions) | 2017 | 2016 | 2015 | |||||||||

| Net cash flow provided by (used in): | ||||||||||||

| Operating activities | $ | 399.1 | $ | 356.3 | $ | 469.6 | ||||||

| Investing activities | (130.1 | ) | (109.2 | ) | (210.9 | ) | ||||||

| Financing activities | (392.4 | ) | (245.8 | ) | (276.7 | ) | ||||||

| Effects of exchange rate changes on cash and cash equivalents | (3.9 | ) | (3.3 | ) | 14.2 | |||||||

| Net decrease in cash and cash equivalents | $ | (127.3 | ) | $ | (2.0 | ) | $ | (3.8 | ) | |||

| September 29, 2017 | September 30, 2016 | ||||||||||||

| (In millions, except for percentages) | Amount | Weighted-Average Interest Rate | Amount | Weighted-Average Interest Rate | |||||||||

| 2017 Revolving Credit Facility | $ | 350.0 | 2.36 | % | $ | — | — | % | |||||

| Current portion of 2013 Term Loan Facility | — | — | % | 50.0 | 1.65 | % | |||||||

| 2013 Revolving Credit Facility | — | — | % | 300.0 | 1.91 | % | |||||||

| Sumitomo Credit Facility | — | — | % | 29.6 | 0.53 | % | |||||||

| Debt issuance costs | — | (0.6 | ) | ||||||||||

| Total short-term debt | $ | 350.0 | $ | 379.0 | |||||||||

| 2013 Term Loan Facility | $ | — | — | % | $ | 287.5 | 1.65 | % | |||||

| Debt issuance costs | — | (0.6 | ) | ||||||||||

| Total long-term debt | $ | — | $ | 286.9 | |||||||||

| Fourth Quarter of Fiscal Year 2017 | Fiscal Years | ||||||||||||||

| (In millions except for percentages) | 2017 | 2016 | 2015 | ||||||||||||

| Amount outstanding (at end of period) | $ | 350.0 | $ | 350.0 | $ | 329.6 | $ | 108.4 | |||||||

| Weighted average interest rate (at end of period) | 2.36 | % | 2.36 | % | 1.78 | % | 1.41 | % | |||||||

| Average amount outstanding (during period) | $ | 146.0 | $ | 192.6 | $ | 320.8 | $ | 104.5 | |||||||

| Weighted average interest rate (during period) | 2.30 | % | 1.90 | % | 1.68 | % | 1.48 | % | |||||||

| Maximum month-end amount outstanding during period | $ | 350.0 | $ | 350.0 | $ | 431.6 | $ | 140.0 | |||||||

| Fiscal Years | |||||||||||

| (In millions, except per share amounts) | 2017 | 2016 | 2015 | ||||||||

| Number of shares | 3.3 | 5.7 | 4.8 | ||||||||

| Average repurchase price per share | $ | 90.63 | $ | 81.61 | $ | 87.47 | |||||

| Total cost | $ | 294.5 | $ | 461.3 | $ | 422.0 | |||||

| Payments Due By Period | |||||||||||||||||||

| Fiscal Year | Fiscal Years | Fiscal Years | |||||||||||||||||

| (In millions) | 2018 | 2019-2020 | 2021-2022 | Beyond | Total | ||||||||||||||

Operating leases (1) | $ | 24.9 | $ | 37.3 | $ | 25.6 | $ | 19.1 | $ | 106.9 | |||||||||

Purchase obligations (2) | 31.0 | 39.7 | 3.6 | — | 74.3 | ||||||||||||||

Defined benefit pension plans (3) | 8.7 | — | — | — | 8.7 | ||||||||||||||

Total (4) | $ | 64.6 | $ | 77.0 | $ | 29.2 | $ | 19.1 | $ | 189.9 | |||||||||

| (Dollars in millions) | Notional Value Sold | Notional Value Purchased | Weighted Average Contract Rate (Foreign Currency Units per USD) | ||||||||

| Australian Dollar | $ | 29.1 | $ | — | 1.28 | ||||||

| Brazilian Real | 5.2 | — | 3.18 | ||||||||

| British Pound | 14.8 | 0.1 | 0.75 | ||||||||

| Canadian Dollar | 8.2 | — | 1.25 | ||||||||

| Danish Krone | — | 0.3 | 6.29 | ||||||||

| Euro | 247.2 | 6.1 | 0.85 | ||||||||

| Hungarian Forint | 3.1 | — | 262.83 | ||||||||

| Indian Rupee | 12.7 | — | 65.65 | ||||||||

| Japanese Yen | 47.1 | — | 112.45 | ||||||||

| Polish Zloty | 4.6 | — | 3.65 | ||||||||

| Swedish Krona | 0.6 | — | 8.16 | ||||||||

| Swiss Franc | — | 59.8 | 0.97 | ||||||||

| Thai Baht | 4.8 | — | 33.31 | ||||||||

| Totals | $ | 377.4 | $ | 66.3 | |||||||

| Fiscal Years | ||||||||||||

| (In millions, except per share amounts) | 2017 | 2016 | 2015 | |||||||||

| Revenues: | ||||||||||||

| Product | $ | 1,555.5 | $ | 1,583.9 | $ | 1,497.1 | ||||||

| Service | 1,112.7 | 1,037.2 | 993.6 | |||||||||

| Total revenues | 2,668.2 | 2,621.1 | 2,490.7 | |||||||||

| Cost of revenues: | ||||||||||||

| Product | 1,025.3 | 1,071.3 | 1,035.3 | |||||||||

| Service | 487.3 | 436.9 | 423.3 | |||||||||

| Total cost of revenues | 1,512.6 | 1,508.2 | 1,458.6 | |||||||||

| Gross margin | 1,155.6 | 1,112.9 | 1,032.1 | |||||||||

| Operating expenses: | ||||||||||||

| Research and development | 210.0 | 200.4 | 195.4 | |||||||||

| Selling, general and administrative | 552.3 | 475.3 | 441.0 | |||||||||

| Impairment charges | 51.4 | 2.2 | — | |||||||||

| Total operating expenses | 813.7 | 677.9 | 636.4 | |||||||||

| Operating earnings | 341.9 | 435.0 | 395.7 | |||||||||

| Interest income | 13.6 | 17.2 | 13.5 | |||||||||

| Interest expense | (10.7 | ) | (11.6 | ) | (7.9 | ) | ||||||

| Earnings from continuing operations before taxes | 344.8 | 440.6 | 401.3 | |||||||||

| Taxes on earnings | 87.7 | 115.3 | 89.9 | |||||||||

| Net earnings from continuing operations | 257.1 | 325.3 | 311.4 | |||||||||

| Net earnings (loss) from discontinued operations | (6.8 | ) | 77.4 | 100.6 | ||||||||

| Net earnings | 250.3 | 402.7 | 412.0 | |||||||||

| Less: Net earnings attributable to noncontrolling interests | 0.7 | 0.4 | 0.5 | |||||||||

| Net earnings attributable to Varian | $ | 249.6 | $ | 402.3 | $ | 411.5 | ||||||

| Net earnings (loss) per share - basic | ||||||||||||

| Continuing operations | $ | 2.78 | $ | 3.41 | $ | 3.13 | ||||||

| Discontinued operations | (0.08 | ) | 0.81 | 1.00 | ||||||||

| Net earnings per share - basic | $ | 2.70 | $ | 4.22 | $ | 4.13 | ||||||

| Net earnings (loss) per share - diluted | ||||||||||||

| Continuing operations | $ | 2.75 | $ | 3.39 | $ | 3.10 | ||||||

| Discontinued operations | (0.07 | ) | 0.80 | 0.99 | ||||||||

| Net earnings per share - diluted | $ | 2.68 | $ | 4.19 | $ | 4.09 | ||||||

| Shares used in the calculation of net earnings per share: | ||||||||||||

| Weighted average shares outstanding - basic | 92.5 | 95.4 | 99.7 | |||||||||

| Weighted average shares outstanding - diluted | 93.2 | 96.0 | 100.6 | |||||||||

| Fiscal Years | ||||||||||||

| (In millions) | 2017 | 2016 | 2015 | |||||||||

| Net earnings | $ | 250.3 | $ | 402.7 | $ | 412.0 | ||||||

| Other comprehensive earnings (loss), net of tax: | ||||||||||||

| Defined benefit pension and post-retirement benefit plans: | ||||||||||||

| Net gain (loss) arising during the year, net of tax (expense) benefit of ($2.5), $4.3 and $0.9 | 10.0 | (21.4 | ) | (4.7 | ) | |||||||

| Prior service credit arising during the year, net of tax expense of ($0.7), ($0.2) and $0.0 | 4.3 | 1.1 | — | |||||||||

| Amortization of prior service cost included in net periodic benefit cost, net of tax benefit of $0.2, $0.2 and $0.1 | (0.8 | ) | (0.4 | ) | (0.2 | ) | ||||||

| Amortization, settlement and curtailment of net actuarial loss included in net periodic benefit cost, net of tax expense of ($1.0), ($0.5) and ($0.6) | 5.7 | 3.5 | 2.9 | |||||||||

| 19.2 | (17.2 | ) | (2.0 | ) | ||||||||

| Derivative instruments: | ||||||||||||

| Change in unrealized gain (loss), net of tax (expense) benefit of $0.0, $0.4 and ($0.8) | — | (0.6 | ) | 1.4 | ||||||||

| Reclassification adjustments, net of tax (expense) benefit of $0.0, ($0.4) and $1.4 | — | 0.6 | (2.4 | ) | ||||||||

| — | — | (1.0 | ) | |||||||||

| Available-for-sale securities: | ||||||||||||

| Change in unrealized loss, net of tax benefit of $0.0, $0.1 and $0.1 | — | (0.3 | ) | (0.1 | ) | |||||||

| Reclassification adjustments, net of tax expense of $0.0, ($0.2) and $0.0 | — | 0.4 | — | |||||||||

| — | 0.1 | (0.1 | ) | |||||||||

| Currency translation adjustment | 12.8 | 2.8 | (24.8 | ) | ||||||||

| Other comprehensive earnings (loss) | 32.0 | (14.3 | ) | (27.9 | ) | |||||||

| Comprehensive earnings | 282.3 | 388.4 | 384.1 | |||||||||

| Less: Comprehensive earnings attributable to noncontrolling interests | 0.7 | 0.4 | 0.5 | |||||||||

| Comprehensive earnings attributable to Varian | $ | 281.6 | $ | 388.0 | $ | 383.6 | ||||||

| September 29, | September 30, | ||||||

| (In millions, except par values) | 2017 | 2016 | |||||

| Assets | |||||||

| Current assets: | |||||||

| Cash and cash equivalents | $ | 716.2 | $ | 811.4 | |||

| Short-term investments | — | 95.3 | |||||

| Accounts receivable, net of allowance for doubtful accounts of $45.9 at September 29, 2017 and $24.2 at September 30, 2016 | 823.5 | 769.6 | |||||

| Inventories | 439.7 | 442.4 | |||||

| Prepaid expenses and other current assets | 199.8 | 141.1 | |||||

| Current assets of discontinued operations | 11.1 | 355.6 | |||||

| Total current assets | 2,190.3 | 2,615.4 | |||||

| Property, plant and equipment, net | 255.3 | 258.6 | |||||

| Goodwill | 222.6 | 220.0 | |||||

| Intangible assets | 71.6 | 84.1 | |||||

| Deferred tax assets | 138.8 | 136.8 | |||||

| Other assets | 300.8 | 227.0 | |||||

| Non-current assets of discontinued operations | — | 272.9 | |||||

| Total assets | $ | 3,179.4 | $ | 3,814.8 | |||

| Liabilities, Redeemable Noncontrolling Interests and Equity | |||||||

| Current liabilities: | |||||||

| Accounts payable | $ | 162.3 | $ | 159.2 | |||

| Accrued liabilities | 394.7 | 383.6 | |||||

| Deferred revenues | 640.6 | 608.6 | |||||

| Short-term borrowings | 350.0 | 329.6 | |||||

| Current maturities of long-term debt | — | 49.4 | |||||

| Current liabilities of discontinued operations | 2.5 | 83.0 | |||||

| Total current liabilities | 1,550.1 | 1,613.4 | |||||

| Long-term debt | — | 286.9 | |||||

| Other long-term liabilities | 130.0 | 155.8 | |||||

| Non-current liabilities of discontinued operations | — | 4.2 | |||||

| Total liabilities | 1,680.1 | 2,060.3 | |||||

| Commitments and contingencies (Note 9) | |||||||

| Redeemable noncontrolling interests of discontinued operations | — | 10.3 | |||||

| Equity: | |||||||

| Varian stockholders' equity: | |||||||

| Preferred stock of $1 par value: 1.0 shares authorized; none issued and outstanding | — | — | |||||

| Common stock of $1 par value: 189.0 shares authorized; 91.7 and 93.7 shares issued and outstanding at September 29, 2017 and at September 30, 2016, respectively | 91.7 | 93.7 | |||||

| Capital in excess of par value | 716.1 | 678.6 | |||||

| Retained earnings | 756.0 | 1,069.0 | |||||

| Accumulated other comprehensive loss | (68.8 | ) | (100.8 | ) | |||

| Total Varian stockholders' equity | 1,495.0 | 1,740.5 | |||||

| Noncontrolling interests | 4.3 | 3.7 | |||||

| Total equity | 1,499.3 | 1,744.2 | |||||

| Total liabilities, redeemable noncontrolling interests and equity | $ | 3,179.4 | $ | 3,814.8 | |||

| Fiscal Years | |||||||||||

| (In millions) | 2017 | 2016 | 2015 | ||||||||

| Cash flows from operating activities: | |||||||||||

| Net earnings | $ | 250.3 | $ | 402.7 | $ | 412.0 | |||||

| Adjustments to reconcile net earnings to net cash provided by operating activities: | |||||||||||

| Share-based compensation expense | 41.2 | 48.3 | 46.3 | ||||||||

| Tax benefits from exercises of share-based payment awards | 0.7 | 3.0 | 12.6 | ||||||||

| Excess tax benefits from share-based compensation | (1.0 | ) | (3.9 | ) | (12.6 | ) | |||||

| Depreciation | 58.5 | 64.2 | 60.1 | ||||||||

| Amortization of intangible assets | 18.4 | 15.6 | 8.4 | ||||||||

| Deferred taxes | (14.9 | ) | (23.9 | ) | 5.4 | ||||||

| Provision for doubtful accounts receivable | 43.7 | 3.5 | 1.1 | ||||||||

| Impairment charges | 51.4 | 2.2 | — | ||||||||

| Other, net | 3.0 | 2.1 | 1.4 | ||||||||

| Changes in assets and liabilities, net of effects of acquisitions: | |||||||||||

| Accounts receivable | (52.6 | ) | (168.3 | ) | (79.4 | ) | |||||

| Inventories | (0.1 | ) | (27.7 | ) | (41.6 | ) | |||||

| Prepaid expenses and other assets | (46.7 | ) | 8.0 | (8.2 | ) | ||||||

| Accounts payable | 5.5 | 9.7 | 6.5 | ||||||||

| Accrued liabilities and other long-term liabilities | 11.7 | 61.0 | (14.0 | ) | |||||||

| Deferred revenues | 30.0 | (40.2 | ) | 71.6 | |||||||

| Net cash provided by operating activities | 399.1 | 356.3 | 469.6 | ||||||||

| Cash flows from investing activities: | |||||||||||

| Purchases of property, plant and equipment | (59.1 | ) | (80.4 | ) | (91.4 | ) | |||||

| Issuance of notes receivable | (18.2 | ) | (21.7 | ) | (23.7 | ) | |||||

| Purchase of senior secured debt | (24.5 | ) | — | — | |||||||

| Investment in available-for-sale securities | (13.4 | ) | (3.3 | ) | (1.8 | ) | |||||

| Sale of available-for-sale securities | — | 8.6 | 0.6 | ||||||||

| Sale of notes receivable | — | 8.3 | — | ||||||||

| Investment in privately-held companies | (8.4 | ) | (0.6 | ) | — | ||||||

| Acquisitions, net of cash acquired | (3.0 | ) | (21.1 | ) | (95.3 | ) | |||||

| Net amounts received from (paid to) deferred compensation plan trust account | (4.4 | ) | 0.3 | 1.8 | |||||||

| Other | 0.9 | 0.7 | (1.1 | ) | |||||||

| Net cash used in investing activities | (130.1 | ) | (109.2 | ) | (210.9 | ) | |||||

| Cash flows from financing activities: | |||||||||||

| Repurchases of common stock | (294.5 | ) | (461.3 | ) | (422.0 | ) | |||||

| Proceeds from issuance of common stock to employees | 72.1 | 60.6 | 91.0 | ||||||||

| Excess tax benefits from share-based compensation | 1.0 | 3.9 | 12.6 | ||||||||

| Employees' taxes withheld and paid for restricted stock and restricted stock units | (10.7 | ) | (11.0 | ) | (16.3 | ) | |||||

| Cash received from Varex term facility | 200.0 | — | — | ||||||||

| Cash and cash equivalents contributed to Varex Imaging Corporation | (42.6 | ) | — | — | |||||||

| Borrowings under credit facility agreement | 231.0 | 83.0 | 145.0 | ||||||||

| Repayments under credit facility agreement | (223.5 | ) | (133.0 | ) | (195.0 | ) | |||||

| Net (repayments) borrowings under the credit facility agreements with maturities less than 90 days | (322.0 | ) | 217.1 | 108.6 | |||||||

| Contingent consideration and hold back | (1.4 | ) | (5.6 | ) | (3.4 | ) | |||||

| Other | (1.8 | ) | 0.5 | 2.8 | |||||||

| Net cash used in financing activities | (392.4 | ) | (245.8 | ) | (276.7 | ) | |||||

| Effects of exchange rate changes on cash and cash equivalents | (3.9 | ) | (3.3 | ) | 14.2 | ||||||

| Net decrease in cash and cash equivalents | (127.3 | ) | (2.0 | ) | (3.8 | ) | |||||

Cash and cash equivalents at beginning of period* | 843.5 | 845.5 | 849.3 | ||||||||

Cash and cash equivalents at end of period* | $ | 716.2 | $ | 843.5 | $ | 845.5 | |||||

| Common Stock | |||||||||||||||||||||||||||||||

| (In millions) | Shares | Amount | Capital in Excess of Par Value | Retained Earnings | Accumulated Other Comprehensive Loss | Total Varian Stockholders' Equity | Noncontrolling Interests | Total Equity | |||||||||||||||||||||||

| Balances at September 26, 2014 | 101.0 | $ | 101.0 | $ | 642.8 | $ | 931.2 | $ | (58.6 | ) | $ | 1,616.4 | $ | — | $ | 1,616.4 | |||||||||||||||

| Net earnings | — | — | — | 411.5 | — | 411.5 | 0.5 | 412.0 | |||||||||||||||||||||||

| Other comprehensive loss | — | — | — | — | (27.9 | ) | (27.9 | ) | — | (27.9 | ) | ||||||||||||||||||||

| Issuance of common stock | 2.1 | 2.1 | 88.9 | — | — | 91.0 | — | 91.0 | |||||||||||||||||||||||

| Tax benefits from exercises of share-based payment awards | — | — | 12.6 | — | — | 12.6 | — | 12.6 | |||||||||||||||||||||||

| Shares repurchased for tax withholdings on vesting of restricted stock and restricted stock units | (0.2 | ) | (0.2 | ) | (16.1 | ) | — | — | (16.3 | ) | — | (16.3 | ) | ||||||||||||||||||

| Share-based compensation expense | — | — | 46.3 | — | — | 46.3 | — | 46.3 | |||||||||||||||||||||||

| Repurchases of common stock | (4.8 | ) | (4.8 | ) | (92.3 | ) | (324.9 | ) | — | (422.0 | ) | — | (422.0 | ) | |||||||||||||||||

| Acquisition of MeVis Medical Solutions AG | — | — | — | — | — | — | 10.2 | 10.2 | |||||||||||||||||||||||

| Capital contributions by Noncontrolling interests | — | — | — | — | — | — | 4.0 | 4.0 | |||||||||||||||||||||||

| Balances at October 2, 2015 | 98.1 | 98.1 | 682.2 | 1,017.8 | (86.5 | ) | 1,711.6 | 14.7 | 1,726.3 | ||||||||||||||||||||||

| Net earnings | — | — | — | 402.3 | — | 402.3 | (0.1 | ) | 402.2 | ||||||||||||||||||||||

| Other comprehensive loss | — | — | — | — | (14.3 | ) | (14.3 | ) | — | (14.3 | ) | ||||||||||||||||||||

| Issuance of common stock | 1.4 | 1.4 | 60.5 | — | — | 61.9 | — | 61.9 | |||||||||||||||||||||||

| Tax benefits from exercises of share-based payment awards | — | — | 3.0 | — | — | 3.0 | — | 3.0 | |||||||||||||||||||||||

| Shares repurchased for tax withholdings on vesting of restricted stock and restricted stock units | (0.1 | ) | (0.1 | ) | (10.9 | ) | — | — | (11.0 | ) | — | (11.0 | ) | ||||||||||||||||||

| Share-based compensation expense | — | — | 48.3 | — | — | 48.3 | — | 48.3 | |||||||||||||||||||||||

| Repurchases of common stock | (5.7 | ) | (5.7 | ) | (104.5 | ) | (351.1 | ) | — | (461.3 | ) | — | (461.3 | ) | |||||||||||||||||

| Reclassification of noncontrolling interest in MeVis to redeemable noncontrolling interest | — | — | — | — | — | — | (10.4 | ) | (10.4 | ) | |||||||||||||||||||||

| Other | — | — | — | — | — | — | (0.5 | ) | (0.5 | ) | |||||||||||||||||||||

| Balances at September 30, 2016 | 93.7 | 93.7 | 678.6 | 1,069.0 | (100.8 | ) | 1,740.5 | 3.7 | 1,744.2 | ||||||||||||||||||||||

| Net earnings | — | — | — | 249.6 | — | 249.6 | 0.6 | 250.2 | |||||||||||||||||||||||

| Other comprehensive earnings | — | — | — | — | 32.0 | 32.0 | — | 32.0 | |||||||||||||||||||||||

| Issuance of common stock | 1.4 | 1.4 | 69.3 | — | — | 70.7 | — | 70.7 | |||||||||||||||||||||||

| Tax benefits from exercises of share-based payment awards | — | — | 0.7 | — | — | 0.7 | — | 0.7 | |||||||||||||||||||||||

| Shares repurchased for tax withholdings on vesting of restricted stock and restricted stock units | (0.1 | ) | (0.1 | ) | (10.6 | ) | — | — | (10.7 | ) | — | (10.7 | ) | ||||||||||||||||||

| Share-based compensation expense | — | — | 40.8 | — | — | 40.8 | — | 40.8 | |||||||||||||||||||||||

| Repurchases of common stock | (3.3 | ) | (3.3 | ) | (62.7 | ) | (228.5 | ) | — | (294.5 | ) | — | (294.5 | ) | |||||||||||||||||

| Distribution of Varex | — | — | — | (334.1 | ) | — | (334.1 | ) | — | (334.1 | ) | ||||||||||||||||||||

| Balances at September 29, 2017 | 91.7 | $ | 91.7 | $ | 716.1 | $ | 756.0 | $ | (68.8 | ) | $ | 1,495.0 | $ | 4.3 | $ | 1,499.3 | |||||||||||||||

| Fiscal Years | |||||||||||

| (In millions) | 2017(1) | 2016 | 2015 | ||||||||

| Revenues | $ | 194.0 | $ | 596.7 | $ | 608.4 | |||||

| Cost of revenues | 117.3 | 348.3 | 357.9 | ||||||||

| Gross margin | 76.7 | 248.4 | 250.5 | ||||||||

Operating expenses (2) | 76.1 | 132.6 | 97.2 | ||||||||

| Operating earnings | 0.6 | 115.8 | 153.3 | ||||||||

| Taxes on earnings | 7.4 | 38.4 | 52.7 | ||||||||

| Net earnings (loss) from discontinued operations | (6.8 | ) | 77.4 | 100.6 | |||||||

| Less: Net earnings from discontinued operations attributable to noncontrolling interests | 0.1 | 0.5 | 0.7 | ||||||||

| Net earnings (loss) from discontinued operations attributable to Varian | $ | (6.9 | ) | $ | 76.9 | $ | 99.9 | ||||

| (In millions) | September 29, 2017 | September 30, 2016 | |||||

| Assets: | |||||||

| Cash | $ | — | $ | 32.1 | |||

| Accounts receivable, net | 8.1 | 122.2 | |||||

| Inventories | 2.9 | 197.3 | |||||

| Prepaid expenses and other current assets | 0.1 | 4.0 | |||||

| Current assets of discontinued operations | 11.1 | 355.6 | |||||

| Property, plant and equipment, net | — | 120.6 | |||||

| Goodwill | — | 74.7 | |||||

| Intangible assets | — | 20.6 | |||||

| Deferred tax assets | — | 2.1 | |||||

| Other assets | — | 54.9 | |||||

| Total assets of discontinued operations | $ | 11.1 | $ | 628.5 | |||

| Liabilities: | |||||||

| Accounts payable | $ | 2.0 | $ | 41.9 | |||

| Accrued liabilities | 0.5 | 29.1 | |||||

| Deferred revenues | — | 12.0 | |||||

| Current liabilities of discontinued operations | 2.5 | 83.0 | |||||

| Other long-term liabilities | — | 4.2 | |||||

| Total liabilities of discontinued operations | $ | 2.5 | $ | 87.2 | |||

| Redeemable noncontrolling interests of discontinued operations | $ | — | $ | 10.3 | |||

| Fiscal Years | |||||||||||

| (In millions) | 2017 | 2016 | 2015 | ||||||||

| Operating activities: | |||||||||||

| Share-based compensation expense | $ | 2.0 | $ | 6.1 | $ | 6.4 | |||||

| Depreciation expense | 4.8 | 10.5 | 10.5 | ||||||||

| Amortization expense | 1.8 | 5.5 | 2.7 | ||||||||

| Investing activities: | |||||||||||

| Purchases of property, plant & equipment | (6.4 | ) | (28.9 | ) | (34.3 | ) | |||||

Acquisition of business, net of cash acquired (1) | — | (1.2 | ) | (67.9 | ) | ||||||

| Sale of available-for-sale securities | $ | — | $ | 8.6 | $ | — | |||||

| September 29, 2017 | |||||||||||||||

| (In millions) | Amortized Cost | Gross Unrealized Gains | Gross Unrealized Losses | Fair Value | |||||||||||

| Original CPTC Loans | $ | 47.4 | $ | — | $ | — | $ | 47.4 | |||||||

| DRTC Securities | 8.0 | — | — | 8.0 | |||||||||||

| GPTC securities | 4.4 | — | — | 4.4 | |||||||||||

| Total available-for-sale securities | $ | 59.8 | $ | — | $ | — | $ | 59.8 | |||||||

| September 30, 2016 | |||||||||||||||

| (In millions) | Amortized Cost | Gross Unrealized Gains | Gross Unrealized Losses | Fair Value | |||||||||||

| Original CPTC Loans | $ | 95.3 | $ | — | $ | — | $ | 95.3 | |||||||

| Total available-for-sale securities | $ | 95.3 | $ | — | $ | — | $ | 95.3 | |||||||

| September 29, | September 30, | |||||||

| (In millions) | 2017 | 2016 | ||||||

| Raw materials and parts | $ | 296.5 | $ | 257.9 | ||||

| Work-in-process | 47.7 | 69.6 | ||||||

| Finished goods | 95.5 | 114.9 | ||||||

| Total inventories | $ | 439.7 | $ | 442.4 | ||||

| September 29, | September 30, | |||||||

| (In millions) | 2017 | 2016 | ||||||

| Prepaid income taxes | $ | 69.4 | $ | 41.3 | ||||

RPTC senior secured debt (1) | 25.4 | — | ||||||

| Prepaid compensation | 11.6 | 9.9 | ||||||

| Advance payments to suppliers | 11.1 | 16.9 | ||||||

| Other current receivables | 32.5 | 29.2 | ||||||

| Other prepaid expenses | 49.8 | 43.8 | ||||||

| Total prepaid expenses and other current assets | $ | 199.8 | $ | 141.1 | ||||

| September 29, | September 30, | |||||||

| (In millions) | 2017 | 2016 | ||||||

| Land and land improvements | $ | 44.2 | $ | 44.2 | ||||

| Buildings and leasehold improvements | 220.4 | 211.7 | ||||||

| Machinery and equipment | 375.9 | 358.3 | ||||||

| Construction in progress | 14.6 | 15.9 | ||||||

| 655.1 | 630.1 | |||||||

| Accumulated depreciation and amortization | (399.8 | ) | (371.5 | ) | ||||

| Total property, plant and equipment, net | $ | 255.3 | $ | 258.6 | ||||

| September 29, | September 30, | |||||||

| (In millions) | 2017 | 2016 | ||||||

| Long-term receivables, net | $ | 101.3 | $ | 113.8 | ||||

| Deferred Compensation Plan ("DCP") assets | 72.7 | 61.1 | ||||||

| Long-term available-for-sale securities | 59.8 | — | ||||||

| Investments in privately-held companies | 27.1 | 18.7 | ||||||

| Other | 39.9 | 33.4 | ||||||

| Total other assets | $ | 300.8 | $ | 227.0 | ||||

| September 29, | September 30, | |||||||

| (In millions) | 2017 | 2016 | ||||||

| Accrued compensation and benefits | $ | 109.7 | $ | 105.1 | ||||

| DCP liabilities | 70.7 | 61.5 | ||||||

| Product warranty | 42.9 | 44.2 | ||||||

| Income taxes payable | 38.8 | 54.4 | ||||||

| Other | 132.6 | 118.4 | ||||||

| Total accrued liabilities | $ | 394.7 | $ | 383.6 | ||||

| September 29, | September 30, | |||||||

| (In millions) | 2017 | 2016 | ||||||

| Long-term income taxes payable | $ | 48.6 | $ | 46.2 | ||||

| Deferred income taxes | 19.8 | 24.5 | ||||||

| Other | 61.6 | 85.1 | ||||||

| Total other long-term liabilities | $ | 130.0 | $ | 155.8 | ||||

| Fair Value Measurement Using | ||||||||||||||||

| Type of Instruments | Quoted Prices in Active Markets for Identical Instruments (Level 1) | Significant Other Observable Inputs (Level 2) | Significant Unobservable Inputs (Level 3) | Total Balance | ||||||||||||

| (In millions) | ||||||||||||||||

| Assets at September 29, 2017: | ||||||||||||||||

| Available-for-sale securities: | ||||||||||||||||

| Original CPTC Loans | $ | — | $ | — | $ | 47.4 | $ | 47.4 | ||||||||

| DRTC securities | — | 8.0 | — | 8.0 | ||||||||||||

| GPTC securities | — | 4.4 | — | 4.4 | ||||||||||||

| Total assets measured at fair value | $ | — | $ | 12.4 | $ | 47.4 | $ | 59.8 | ||||||||

| Assets at September 30, 2016: | ||||||||||||||||

| Available-for-sale securities: | ||||||||||||||||

| Original CPTC Loans | $ | — | $ | — | $ | 95.3 | $ | 95.3 | ||||||||

| Total assets measured at fair value | $ | — | $ | — | $ | 95.3 | $ | 95.3 | ||||||||

| Liabilities at September 30, 2016: | ||||||||||||||||

| Contingent consideration | $ | — | $ | — | $ | (1.3 | ) | $ | (1.3 | ) | ||||||

| Total liabilities measured at fair value | $ | — | $ | — | $ | (1.3 | ) | $ | (1.3 | ) | ||||||

| (In millions) | Available-for-sale Securities | Contingent Consideration | ||||||

| Balance at October 2, 2015 | $ | 83.9 | $ | (4.1 | ) | |||

Additions (1) | 11.4 | — | ||||||

Settlements (2) | — | 3.5 | ||||||

| Change in fair value recognized in earnings | — | (0.7 | ) | |||||

| Balance at September 30, 2016 | 95.3 | (1.3 | ) | |||||

Additions (1) | 3.3 | — | ||||||

Settlements (2) | — | 1.6 | ||||||

| Change in fair value recognized in earnings | (51.2 | ) | (0.3 | ) | ||||

| Balance at September 29, 2017 | $ | 47.4 | $ | — | ||||

| September 29, | September 30, | ||||||

| (In millions) | 2017 | 2016 | |||||

| Accounts receivable, gross | $ | 901.2 | $ | 848.4 | |||

| Allowance for doubtful accounts | (63.1 | ) | (24.2 | ) | |||

| Accounts receivable, net | $ | 838.1 | $ | 824.2 | |||

Short-term | $ | 823.5 | $ | 769.6 | |||

Long-term (1) | $ | 14.6 | $ | 54.6 | |||

| Notes receivable | $ | 91.7 | $ | 65.0 | |||

Short-term (2) | $ | 5.0 | $ | 5.8 | |||

Long-term (1) | $ | 86.7 | $ | 59.2 | |||

| (In millions) | Oncology Systems | Varian Particle Therapy | Total | |||||||||

| Balance at October 2, 2015 | $ | 158.8 | $ | 50.0 | $ | 208.8 | ||||||

| Business combinations | 11.4 | — | 11.4 | |||||||||

| Foreign currency translation adjustments | — | (0.2 | ) | (0.2 | ) | |||||||

| Balance at September 30, 2016 | 170.2 | 49.8 | 220.0 | |||||||||

| Foreign currency translation adjustments | — | 2.6 | 2.6 | |||||||||

| Balance at September 29, 2017 | $ | 170.2 | $ | 52.4 | $ | 222.6 | ||||||

| September 29, 2017 | September 30, 2016 | |||||||||||||||||||||||

| (In millions) | Gross Carrying Amount | Accumulated Amortization | Net Carrying Amount | Gross Carrying Amount | Accumulated Amortization | Net Carrying Amount | ||||||||||||||||||

| Technologies and patents | $ | 102.0 | $ | (60.9 | ) | $ | 41.1 | $ | 99.6 | $ | (50.2 | ) | $ | 49.4 | ||||||||||

| Customer contracts and supplier relationship | 33.9 | (14.3 | ) | 19.6 | 32.3 | (10.8 | ) | 21.5 | ||||||||||||||||

| Other | 5.5 | (3.4 | ) | 2.1 | 5.6 | (1.2 | ) | 4.4 | ||||||||||||||||

| Total intangible with finite lives | 141.4 | (78.6 | ) | 62.8 | 137.5 | (62.2 | ) | 75.3 | ||||||||||||||||

| In-process research and development with indefinite lives | 8.8 | — | 8.8 | 8.8 | — | 8.8 | ||||||||||||||||||

| Total intangible assets | $ | 150.2 | $ | (78.6 | ) | $ | 71.6 | $ | 146.3 | $ | (62.2 | ) | $ | 84.1 | ||||||||||

| Fiscal Years | Total | |||

| 2018 | $ | 17.4 | ||

| 2019 | 13.0 | |||

| 2020 | 9.3 | |||

| 2021 | 7.2 | |||

| 2022 | 6.0 | |||

| Thereafter | 9.9 | |||

| Total remaining amortization | $ | 62.8 | ||

| September 29, 2017 | September 30, 2016 | ||||||||||||

| (In millions, except for percentages) | Amount | Weighted-Average Interest Rate | Amount | Weighted-Average Interest Rate | |||||||||

| Short-term debt: | |||||||||||||

| 2017 Revolving Credit Facility | $ | 350.0 | 2.36 | % | $ | — | — | % | |||||

| Current portion of 2013 Term Loan Facility | — | — | % | 50.0 | 1.65 | % | |||||||

| 2013 Revolving Credit Facility | — | — | % | 300.0 | 1.91 | % | |||||||

| Sumitomo Credit Facility | — | — | % | 29.6 | 0.53 | % | |||||||

| Debt issuance costs | — | (0.6 | ) | ||||||||||

| Total short-term debt | $ | 350.0 | $ | 379.0 | |||||||||

| Long-term debt: | |||||||||||||

| 2013 Term Loan Facility | $ | — | — | % | $ | 287.5 | 1.65 | % | |||||

| Debt issuance costs | — | (0.6 | ) | ||||||||||

| Total long-term debt | $ | — | $ | 286.9 | |||||||||

| Gain (Loss) Recognized in Other Comprehensive Income (Effective Portion) | Location of Gain (Loss) Reclassified from Accumulated Other Comprehensive Income into Net Earnings (Effective Portion) | Gain (Loss) Reclassified from Accumulated Other Comprehensive Income into Net Earnings (Effective Portion) | ||||||||||||||||||||||||

| Fiscal Years | Fiscal Years | |||||||||||||||||||||||||

| (In millions) | 2017 | 2016 | 2015 | 2017 | 2016 | 2015 | ||||||||||||||||||||

| Foreign currency forward contracts | $ | — | $ | (1.0 | ) | $ | 2.2 | Revenues | $ | — | $ | (1.0 | ) | $ | 3.8 | |||||||||||

| September 29, 2017 | ||||||||

| (In millions) | Notional Value Sold | Notional Value Purchased | ||||||

| Australian Dollar | $ | 29.1 | $ | — | ||||

| Brazilian Real | 5.2 | — | ||||||

| British Pound | 14.8 | 0.1 | ||||||

| Canadian Dollar | 8.2 | — | ||||||

| Danish Krone | — | 0.3 | ||||||

| Euro | 247.2 | 6.1 | ||||||

| Hungarian Forint | 3.1 | — | ||||||

| Indian Rupee | 12.7 | — | ||||||

| Japanese Yen | 47.1 | — | ||||||

| Polish Zloty | 4.6 | — | ||||||

| Swedish Krona | 0.6 | — | ||||||

| Swiss Franc | — | 59.8 | ||||||

| Thai Baht | 4.8 | — | ||||||

| Totals | $ | 377.4 | $ | 66.3 | ||||

| Location of Gain (Loss) Recognized in Income on Derivative | Amount of Gain (Loss) Recognized in Net Earnings on Derivative | |||||||||||

| Fiscal Years | ||||||||||||

| (In millions) | 2017 | 2016 | 2015 | |||||||||

| Selling, general and administrative expenses | $ | (10.9 | ) | $ | (5.3 | ) | $ | 27.6 | ||||

| Fiscal Years | ||||||||

| (In millions) | 2017 | 2016 | ||||||

| Accrued product warranty, at beginning of period | $ | 48.0 | $ | 39.8 | ||||

| Charged to cost of revenues | 46.9 | 46.4 | ||||||

| Actual product warranty expenditures | (47.7 | ) | (38.2 | ) | ||||

| Accrued product warranty, at end of period | $ | 47.2 | $ | 48.0 | ||||

| (In millions) | Recurring Costs | Non-Recurring Costs | Total Anticipated Future Costs | |||||||||

| Fiscal Years: | ||||||||||||

| 2018 | $ | 0.4 | $ | 0.7 | $ | 1.1 | ||||||

| 2019 | 0.4 | 0.5 | 0.9 | |||||||||

| 2020 | 0.4 | 0.4 | 0.8 | |||||||||

| 2021 | 0.4 | 0.2 | 0.6 | |||||||||

| 2022 | 0.4 | 0.4 | 0.8 | |||||||||

| Thereafter | 1.7 | 0.9 | 2.6 | |||||||||

| Total costs | $ | 3.7 | $ | 3.1 | $ | 6.8 | ||||||

| Less imputed interest | 0.8 | |||||||||||

| Reserve amount | $ | 6.0 | ||||||||||

| (in millions) | September 30, 2016 | Restructuring Charges (Reversals) | Cash Payments | September 29, 2017 | |||||||||||

| 2017 Restructuring Plan | $ | — | $ | 13.2 | $ | (9.3 | ) | $ | 3.9 | ||||||

| 2016 Restructuring Plan and prior plans | 1.6 | (0.6 | ) | (1.0 | ) | — | |||||||||

| $ | 1.6 | $ | 12.6 | $ | (10.3 | ) | $ | 3.9 | |||||||

| (In millions) | September 29, 2017 | September 30, 2016 | |||||

| Change in benefit obligation: | |||||||

| Benefit obligation - beginning of fiscal year | $ | 238.3 | $ | 206.9 | |||

| Service cost | 7.1 | 5.9 | |||||

| Interest cost | 2.4 | 4.0 | |||||

| Plan participants’ contributions | 8.7 | 8.6 | |||||

| Plan amendments | (5.0 | ) | (1.2 | ) | |||

| Plan settlements | (6.9 | ) | (4.0 | ) | |||

| Net transfer in | 0.5 | — | |||||

| Actuarial (gain) loss | (11.3 | ) | 31.6 | ||||

| Foreign currency changes | 1.6 | (8.8 | ) | ||||

| Benefit and expense payments | (4.7 | ) | (4.7 | ) | |||

| Benefit obligation - end of fiscal year | $ | 230.7 | $ | 238.3 | |||

| Change in plan assets: | |||||||

| Plan assets - beginning of fiscal year | $ | 199.3 | $ | 186.9 | |||

| Employer contributions | 8.2 | 8.0 | |||||

| Actual return on plan assets | 8.0 | 12.9 | |||||

| Plan participants’ contributions | 8.7 | 8.6 | |||||

| Plan settlements | (6.9 | ) | (4.0 | ) | |||

| Foreign currency changes | 2.0 | (8.6 | ) | ||||

| Acquisitions / divestitures | 0.5 | — | |||||

| Benefit and expense payments | (4.7 | ) | (4.5 | ) | |||

| Plan assets - end of fiscal year | $ | 215.1 | $ | 199.3 | |||

| Funded status | $ | (15.6 | ) | $ | (39.0 | ) | |

| Amounts recognized within the consolidated balance sheet: | |||||||

| Other assets | $ | 3.6 | $ | — | |||

| Other long-term liabilities | (19.2 | ) | (39.0 | ) | |||

| Net amount recognized | $ | (15.6 | ) | $ | (39.0 | ) | |

| (In millions) | September 29, 2017 | September 30, 2016 | |||||

| Prior service credit | $ | 6.3 | $ | 1.8 | |||

| Net loss | (61.5 | ) | (79.5 | ) | |||

| Accumulated other comprehensive loss | $ | (55.2 | ) | $ | (77.7 | ) | |

| (In millions) | September 29, 2017 | September 30, 2016 | |||||

| Projected benefit obligation | $ | 16.6 | $ | 17.2 | |||

| Accumulated benefit obligation | $ | 15.4 | $ | 16.3 | |||

| Fair value of plan assets | $ | 13.4 | $ | 12.8 | |||

| Fiscal Years | ||||||||||||

| (In millions) | 2017 | 2016 | 2015 | |||||||||

| Net Periodic Benefit Costs: | ||||||||||||

| Service cost | $ | 7.1 | $ | 5.9 | $ | 5.6 | ||||||

| Interest cost | 2.4 | 4.0 | 4.4 | |||||||||

| Loss due to settlement | 1.4 | 1.0 | 1.1 | |||||||||

| Expected return on assets | (7.1 | ) | (6.7 | ) | (7.1 | ) | ||||||

| Amortization of prior service cost | (0.5 | ) | — | 0.1 | ||||||||

| Recognized actuarial loss | 4.3 | 2.9 | 2.4 | |||||||||

| Net periodic benefit cost | 7.6 | 7.1 | 6.5 | |||||||||

| Other Amounts Recognized in Other Comprehensive (Income) Loss: | ||||||||||||

| New prior service credit | (5.0 | ) | (1.2 | ) | (1.1 | ) | ||||||

| Net (gain) loss arising during the year | (12.2 | ) | 25.3 | 6.7 | ||||||||

| Amortization of prior service credit (cost) | 0.5 | — | (0.1 | ) | ||||||||

| Amortization or settlement of net actuarial loss | (5.7 | ) | (3.9 | ) | (3.5 | ) | ||||||

| Total recognized in other comprehensive (income) loss | (22.4 | ) | 20.2 | 2.0 | ||||||||

| Total recognized in net periodic benefit cost and other comprehensive (income) loss | $ | (14.8 | ) | $ | 27.3 | $ | 8.5 | |||||

| (In millions) | Total | |||

| Prior service credit | $ | 0.6 | ||

| Net loss | (2.9 | ) | ||

| Total | $ | (2.3 | ) | |

| Fiscal Years | |||||||||

| Net Periodic Benefit Cost | 2017 | 2016 | 2015 | ||||||

| Discount rate | 1.03 | % | 2.05 | % | 2.59 | % | |||

| Rate of compensation increase | 2.33 | % | 2.42 | % | 2.46 | % | |||

| Expected long-term return on assets | 3.56 | % | 3.57 | % | 3.76 | % | |||

| Benefit Obligation | September 29, 2017 | September 30, 2016 | ||||

| Discount rate | 1.40 | % | 1.03 | % | ||

| Rate of compensation increase | 2.40 | % | 2.33 | % | ||

| (In millions) | Quoted Prices in Active Markets for Identical Assets (Level 1) | Significant Observable Inputs (Level 2) | Significant Unobservable Inputs (Level 3) | Total | ||||||||||||

| As of September 29, 2017: | ||||||||||||||||

| Investment funds: | ||||||||||||||||

| Mutual funds - equities | $ | — | $ | 62.6 | $ | — | $ | 62.6 | ||||||||

| Mutual funds - debt | — | 36.3 | — | 36.3 | ||||||||||||

| Mutual funds - real estate | — | 4.9 | — | 4.9 | ||||||||||||

| Other | — | 3.2 | — | 3.2 | ||||||||||||

| Assets held by insurance company: | ||||||||||||||||

| Insurance contracts | — | 107.6 | — | 107.6 | ||||||||||||

| Cash and cash equivalents | 0.5 | — | — | 0.5 | ||||||||||||

| Total | $ | 0.5 | $ | 214.6 | $ | — | $ | 215.1 | ||||||||

| As of September 30, 2016: | ||||||||||||||||

| Investment funds: | ||||||||||||||||

| Mutual funds - equities | $ | — | $ | 51.7 | $ | — | $ | 51.7 | ||||||||

| Mutual funds - debt | — | 27.1 | — | 27.1 | ||||||||||||

| Mutual funds - real estate | — | 4.6 | — | 4.6 | ||||||||||||

| Other | — | 2.9 | — | 2.9 | ||||||||||||

| Assets held by insurance company: | ||||||||||||||||

| Insurance contracts | — | 112.7 | — | 112.7 | ||||||||||||

| Cash and cash equivalents | 0.3 | — | — | 0.3 | ||||||||||||

| Total | $ | 0.3 | $ | 199.0 | $ | — | $ | 199.3 | ||||||||

| (In millions) | Total | |||

| Fiscal Years: | ||||

| 2018 | $ | 6.6 | ||

| 2019 | 6.9 | |||

| 2020 | 6.2 | |||

| 2021 | 7.6 | |||

| 2022 | 7.9 | |||

| Thereafter | 41.4 | |||

| Total | $ | 76.6 | ||

| Fiscal Years | |||||||||||

| (In millions, except per share amounts) | 2017 | 2016 | 2015 | ||||||||

| Number of shares | 3.3 | 5.7 | 4.8 | ||||||||

| Average repurchase price per share | $ | 90.63 | $ | 81.61 | $ | 87.47 | |||||

| Total cost | $ | 294.5 | $ | 461.3 | $ | 422.0 | |||||

Fiscal Years(1) | |||||||

| (In millions, except per share amounts) | 2016 | 2015 | |||||

| Number of shares | 1.0 | 2.3 | |||||

| Average repurchase price per share | $ | 83.98 | $ | 90.00 | |||

| Total cost | $ | 85.8 | $ | 203.9 | |||

| (In millions) | Net Unrealized Gains (Losses) Defined Benefit Pension and Post-Retirement Benefit Plans | Net Unrealized Gains (Losses) Cash Flow Hedging Instruments | Net Unrealized Gains (Losses) Available-for- Sale Securities | Cumulative Translation Adjustment | Accumulated Other Comprehensive Earnings (Loss) | |||||||||||||||

| Balance at September 26, 2014 | $ | (44.1 | ) | $ | 1.0 | $ | — | $ | (15.5 | ) | $ | (58.6 | ) | |||||||

| Other comprehensive earnings (loss) before reclassifications | (4.5 | ) | 2.2 | (0.2 | ) | (24.8 | ) | (27.3 | ) | |||||||||||