Washington, D.C. 20549

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non‑acceleratednon-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,company.” and "emerging“emerging growth company"company” in Rule 12b‑212b-2 of the Exchange Act:

sufficient to cover operating expenses and to generate profits. FRE differs from income before taxes computed in accordance with GAAP as it adjusts for the items included in the calculation of ENI andFRE excludes net performance fees, performance fee compensation,income, investment income from our Consolidated Fundsfunds and non-consolidated funds andadjusts for certain other items that we believe are not indicative of our core operating performance;performance. Fee related performance revenues, together with fee related performance compensation, is presented within FRE because it represents incentive fees from perpetual capital vehicles that are measured and eligible to be received on a recurring basis and are not dependent on realization events from the underlying investments;

Amounts and percentages throughout this report may reflect rounding adjustments and consequently totals may not appear to sum.

Ares was built upon the fundamental principle that each of our distinct but complementary investment groups benefits from being part of our broader platform. We believe that our strong performance, consistent growth and high talent retention through economic cycles is due largely to the effective application of this principle across our broad organization of over 1,0002,850 employees. The management of our operating businesses is currently overseen by our Executive Management Committee which meets frequently to discuss strategy and operational matters, and includes as representatives our Holdco Members and other senior leadership from our investment groups and business operations team. We do notalso have a centralizedPartners Committee comprised of senior leadership from across the firm that meets periodically to discuss our business, including investment committee and instead our investment committees are structured with overlapping membership from different investment groups to ensure consistency of approach.operating performance, fundraising, market conditions, strategic initiatives and other firm matters. Each of our investment

groups is led by its own deep leadership team of highly accomplished investment professionals, who average approximately 25 years of investment experience in managing, investments in, advising, underwriting and restructuring companies. While primarily focused on managing strategies within their own investment group, these senior professionals are integrated within our platform through economic, cultural and structural measures. Our senior professionals have the opportunity to participate in the incentive programs of multiple investment groups to reward collaboration across our investment activities. This collaboration takes place on a daily basis butand is formally promoted through sophisticated internal systems and widely attended weekly or monthly meetings.

Each of our investment groups employs a disciplined, credit-oriented investment philosophy and is managed by a seasoned leadership team of senior professionals with extensive experience investing in, advising and underwriting assets held by our funds.

| |

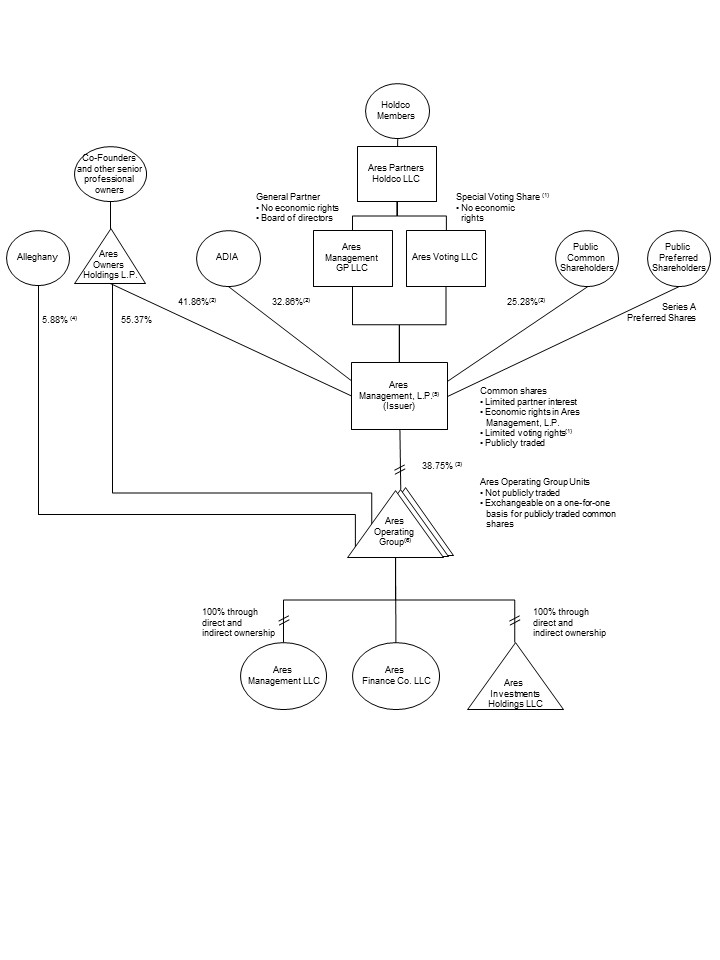

(1) | Ares Management, L.P. common shareholders have limited voting rights and have no right to remove our general partner or, except in the limited circumstances described below, elect the directors of our general partner. On those few matters that may be submitted for a vote of our common shareholders, Ares Voting LLC, an entity owned and controlled by Ares Partners Holdco LLC, which is in turn owned and controlled by the Holdco members, holds a special voting share that provides it with a number of votes, on any matter that may be submitted for a vote of our common shareholders, that is equal to the aggregate number of vested and unvested Ares Operating Group Units held directly or indirectly by the limited partners of the Ares Operating Group that do not directly hold a special voting share. See “Material Provisions of Ares Management, L.P. Partnership Agreement—Withdrawal or Removal of the General Partner,” “—Meetings; Voting” and “—Election of Directors of General Partner.” |

| |

(2) | Assuming the full exchange of Ares Operating Group Units for our common shares, Ares Management, L.P. holds 100% of the Ares Operating Group and Ares Owners Holdings L.P., Alleghany, ADIA and the public hold 71.59%, 5.88%, 12.73% and 9.80%, respectively, of Ares Management, L.P. |

| |

(3) | Each Ares Operating Group entity has both common units and a series of preferred units with economic terms designed to mirror those of the Series A Preferred shares (“GP Mirror units”) outstanding.

|

| |

(4) | Alleghany is expected to exchange all of its Ares Operating Group Units for our common shares in 2018. |

| |

(5) | As of December 31, 2017, Ares Management, L.P. was treated as a partnership for U.S. federal income tax purposes. Effective March 1, 2018, Ares Management, L.P. will be treated as a corporation for U.S. federal income tax purposes. Ares Management, L.P.'s legal structure will remain a Delaware limited partnership. |

| |

(6) | The Ares Operating Group is comprised of Ares Holdings L.P., Ares Offshore Holdings L.P. and Ares Investments L.P. |

Holding Company Structure

The Company has elected to be treated as a corporation for U.S. federal income tax purposes (the “Tax Election”) effective March 1, 2018. In connection with the Tax Election, we have amended and restated our partnership agreement to, among other things, reflect our new tax classification and change the name of our common units and preferred units to common shares and preferred shares, respectively. The terms of such common shares and preferred shares, and the associated rights, otherwise remain unchanged. See "Item 1A. Risk Factors – Our common shareholders do not elect our general partner or, except in limited circumstances, vote on our general partner's directors and have limited ability to influence decisions regarding our businesses."

Accordingly, Ares Management, L.P. and any direct subsidiaries of Ares Management, L.P. that are treated as corporations for U.S. federal income tax purposes and that are the holders of Ares Operating Group Units are (and, in the case of Ares Offshore Holdings, Ltd., may be) subject to U.S. federal, state and local income taxes in respect of their interests in the Ares Operating Group entities. Our legal structure will remain a Delaware limited partnership and the distribution provisions under our limited partnership agreement will remain unchanged. The Ares Operating Group entities are treated as partnerships for U.S. federal income tax purposes. An entity that is treated as a partnership for U.S. federal income tax purposes generally incurs no U.S. federal income tax liability at the entity level. Instead, each partner is required to take into account its allocable share of items of income, gain, loss, deduction and credit of the partnership in computing its U.S. federal, state and local income tax liability each taxable year, whether or not cash distributions are made.

Each of the Ares Operating Group entities has an identical number of partnership units outstanding. Ares Management, L.P. holds, directly or through direct subsidiaries, a number of Ares Operating Group Units equal to the number of common shares that Ares Management, L.P. has issued. The Ares Operating Group Units held by Ares Management, L.P. and its subsidiaries are economically identical in all respects to the Ares Operating Group Units that are not held by Ares Management, L.P. and its subsidiaries. Accordingly, Ares Management, L.P. receives the distributive share of income of the Ares Operating Group from its equity interest in the Ares Operating Group.

The Ares Operating Group Units and our common shares held directly or indirectly by our senior professional owners are generally subject to restrictions on transfer and other provisions. See “Item 11. Executive Compensation.”

Certain Corporate Governance Considerations

Voting Rights. Unlike the holders of common stock in a corporation, our common shareholders have limited voting rights and have no right to remove our general partner or, except in the limited circumstances described below, elect the directors of our general partner. On those few matters that may be submitted for a vote of our common shareholders – certain amendments to our limited partnership agreement, mergers and consolidations and in the limited circumstances described below, election of the directors of our general partner – Ares Voting LLC, an entity wholly owned by Ares Partners Holdco LLC, which is in turn owned and controlled by the Holdco Members, holds a special voting share that provides it with a number of votes, on any matter that may be submitted for a vote of our common shareholders, that is equal to the aggregate number of Ares Operating Group Units held by the limited partners of the Ares Operating Group entities that do not hold a special voting share. We refer to our common shares (other than those held by any person whom our general partner may from time to time, with such person’s consent, designate as a non‑voting common shareholder) and our special voting shares as “voting shares.” Accordingly, on those few matters that may be submitted for a vote of our common shareholders, our public shareholders (other than ADIA) collectively have 9.79% of the voting power of Ares Management, L.P, and the Holdco Members, through Ares Owners Holdings L.P. and the special voting share held by Ares Voting LLC, have approximately 71.59% of the voting power of Ares Management, L.P. Our common shareholders’ voting rights are further restricted by the provision in our partnership agreement stating that any common shares held by a person that beneficially owns 20% or more of any class of our common shares then outstanding (other than our general partner, Ares Owners Holdings L.P., a member of Ares Partners Holdco LLC or their respective affiliates, a direct or subsequently approved transferee of our general partner or its affiliates or a person who acquired such common shares with the prior approval of our general partner) cannot vote on any matter.

Election of Directors. In general, our common shareholders have no right to elect the directors of our general partner. However, when the Holdco Members and other then‑current or former Ares personnel directly or indirectly hold less than 10% of the limited partner voting power, our common shareholders will have the right to vote in the election of the directors of our general partner. This voting power condition will be measured on January 31 of each year, and will be triggered if the total voting power held collectively by (i) holders of the special voting shares in Ares Management, L.P. (including our general partner, members of Ares Partners Holdco LLC and their respective affiliates), (ii) then‑current or former Ares personnel (including indirectly through related entities) and (iii) Ares Owners Holdings L.P. is less than 10% of the voting power of the outstanding voting shares of Ares Management, L.P. For purposes of determining whether the Ares control condition is satisfied, our general partner will treat as

outstanding, and as held by the foregoing persons, all voting shares deliverable to such persons pursuant to equity awards granted to such persons. Unless and until the foregoing voting power condition is satisfied, our general partner’s board of directors will be elected in accordance with its limited liability company agreement, which provides that directors generally may be appointed and removed by the member of our general partner, an entity owned and controlled by the Holdco Members. Unless and until the foregoing voting power condition is satisfied, the board of directors of our general partner has no authority other than that which its member chooses to delegate to it. In the event that the voting power condition is satisfied, the board of directors of our general partner will be responsible for the oversight of our business and operations.

Conflicts of Interest and Duties of Our General Partner. Although our general partner does not engage in any business activities other than the management and operation of our businesses, conflicts of interest may arise in the future between us or our common shareholders, on the one hand, and our general partner or its affiliates or associates, on the other. The resolutions of these conflicts may not always be in our best interests or that of our common shareholders. In addition, we have fiduciary and contractual obligations to the investors in our funds and we expect to regularly take actions with respect to the purchase or sale of investments in our funds, the structuring of investment transactions for those funds or otherwise that are in the best interests of the investors in those funds but that might at the same time adversely affect our near term results of operations or cash flow.

Our partnership agreement limits the liability of, and reduces or eliminates the duties (including fiduciary duties) owed by, our general partner and its affiliates and associates to us and our common shareholders. Our partnership agreement also restricts the remedies available to common shareholders for actions that might otherwise constitute breaches of our general partner’s or its affiliates’ or associates’ duties (including fiduciary duties). Common shareholders are treated as having consented to the provisions set forth in our partnership agreement, including the provisions regarding conflicts of interest situations that, in the absence of such provisions, might be considered a breach of fiduciary or other duties under applicable state law.

Operations Management Group

The OMG consists of five independent, shared resource groups to support our reportableoperating segments by providing infrastructure and administrative support in the areas of accounting/finance, operations/operations, information technology, business development/corporatelegal, compliance, human resources, strategy legal/compliance and human resources.relationship management and distribution. Our clients seek to partner with investment management firms that not only have compelling investment track records across multiple investment products but also possess seasoned infrastructure support functions. As such, significant investments have been made to develop the OMG. The OMG also includes AWMS. We have successfully launched new business lines, integrated acquired businesses into the operations and created scale within the OMG to support a much larger platform in the future.

Organizational Structure

The simplified diagram below (which omits certain intermediate holding companies) depicts our legal organizational structure. Ownership information in the diagram below is presented as of December 31, 2023. Ares Management Corporation (“AMC”) is a holding company and through subsidiaries is the general partner of the Ares Operating Group entity and operates and controls the business and affairs of the Ares Operating Group. AMC consolidates the financial results of the Ares Operating Group, its consolidated subsidiaries and certain consolidated funds.

(1)Assuming the full exchange of AOG Units for shares of our Class A common stock, as of December 31, 2023, Ares Owners Holdings L.P. would hold 42.36%, Sumitomo Mitsui Banking Corporation (“SMBC”) would hold 5.48% and the public would hold 52.16% of AMC. Inclusive of Class A common stock held directly by Ares employees and assuming the full exchange of AOG Units for shares of our Class A common stock, Ares employee ownership would represent 45.90% of all outstanding shares.

Holding Company Structure

Our common stockholders are entitled to vote on all matters on which stockholders of a corporation are generally entitled to vote under the Delaware General Corporation Law (the “DGCL”), including the election of our board of directors. Holders of shares of our Class A common stock are entitled to one vote per share of our Class A common stock. On any date on which the Ares Ownership Condition (as defined in the Certificate of Incorporation) is satisfied, holders of shares of our Class B common stock are, in the aggregate, entitled to a number of votes equal to (x) four times the aggregate number of votes attributable to our Class A common stock minus (y) the aggregate number of votes attributable to our Class C common stock. On any date on which the Ares Ownership Condition is not satisfied, holders of shares of our Class B common stock are not entitled to vote on any matter submitted to a vote of our stockholders. The holder of shares of our Class C common stock is generally entitled to a number of votes equal to the number of AOG Units (as defined in the Certificate of Incorporation) held of record by each Ares Operating Group Limited Partner (as defined in the Certificate of Incorporation) other than the Company and its subsidiaries. Ares Management GP LLC is the sole holder of shares of our Class B common stock and Ares Voting LLC is the sole holder of shares of our Class C common stock. Our Class B common stock and our Class C common stock are non-economic and holders thereof shall not be entitled to: (i) dividends from the Company or (ii) receive any assets of the Company in the event of any dissolution, liquidation or winding up of the Company.Ares Management GP LLC and Ares Voting LLC are both wholly owned by Ares Partners Holdco LLC. As a result, the Company is a “controlled company” within the meaning of the corporate governance standards of the New York Stock Exchange (“NYSE”) and qualifies for exceptions from certain corporate governance rules of the NYSE. The Company also has non-voting common stock solely held by SMBC, which has the same economic rights as the Class A common stock.

Accordingly, AMC and any direct subsidiaries of AMC that are treated as corporations for U.S. federal income tax purposes and that are the holders of AOG Units are subject to U.S. federal, state and local income taxes in respect of their interests in the Ares Operating Group. The Ares Operating Group entity is treated as a partnership for U.S. federal income tax purposes. An entity that is treated as a partnership for U.S. federal income tax purposes generally incurs no U.S. federal income tax liability at the entity level. Instead, each partner is required to take into account its allocable share of items of income, gain, loss, deduction and credit of the partnership in computing its U.S. federal, state and local income tax liability each taxable year, whether or not cash distributions are made.

AMC holds through subsidiaries a number of AOG Units equal to the number of shares of Class A common stock that AMC has issued. The AOG Units held by AMC and its subsidiaries are economically identical in all respects to the AOG Units that are not held by AMC and its subsidiaries. Accordingly, AMC receives the distributive share of income of the Ares Operating Group from its equity interest in the Ares Operating Group.

Structure and Operation of our Funds

We conduct the management of our funds and other similar private vehicles primarily through organizing a limited partnership or other limited liability structure in which entities organized by us accept commitments and/or funds for investment from institutional investors and (to a limited extent) high net worth individuals.other investors. Such commitments are generally drawn down from investors on an as needed basis to fund investments over a specified term. Our Credit Group funds also include hedge funds or structured funds in which the investor’s capital is fully funded into the fund upon or soon after the subscription for interests in the fund. The CLOs that we manage are structured investment vehicles that are generally private companies with limited liability.liability companies. Our drawdown funds and hedge funds are generally organized as limited partnerships or limited liability companies. However, there are non‑U.S.non-U.S. funds that are structured as corporate or non‑partnershipnon-partnership entities under applicable law. We also advise a number of investors through SMA relationships structured as contractual arrangements or single investor vehicles. In the case of our SMAs that are not structured as single investor vehicles, the investor, rather than us, generally controls custody of the investments with respect to which we advise. ThreeWe also manage closed-end interval funds (APMF and CADC) that allow for periodic redemptions of the vehicles that we manage are publicly traded corporations. The publicly tradedvarious share classes, four publicly-traded corporations (AAC II, ACRE, ARCC and ARDC), two non-traded REITs (AIREIT and AREIT) and a non-traded BDC (ASIF). ACRE, ARDC and ARCC do not have redemption provisions or a requirement to return capital to investors upon exiting the investments made with such capital, except as required by applicable law (including distribution requirements that must be met to maintain RICregulated investment company (“RIC”) or REIT status). However, ACRE’s charter includes certain limitations relating to the ownership or purported transfer of its common stock in violation of the REIT ownership requirements. In addition, Class A ordinary shares issued by AAC II are redeemable for cash by the public shareholders in the event that AAC II does not complete a business combination or tender offer associated with stockholder approval provisions.

Our funds are generally advised by Ares Management LLC, which is registered under the Investment Advisers Act of 1940, as amended (the "Investment“Investment Advisers Act"Act”) or, a wholly owned subsidiary thereof.thereof or subsidiary controlled by AMC. Responsibility for the day‑to‑dayday-to-day operations of each investment vehicle is typically delegated to the Ares entity serving as investment adviser pursuant to an investment advisory, (or similar)management or similar agreement. Generally, the material terms of our

investment advisory agreements relate to the scope of services to be rendered by the investment adviser to the applicable vehicle, the calculation of management fees to be borne by investors in our investment vehicles and certain rights of termination with respect to our investment advisory agreements. With the exception of certain of the publicly traded corporations,publicly-traded investment vehicles, the investment vehicles themselves do not generally register as investment companies under the Investment Company Act of 1940, as amended (the “Investment Company Act”), in reliance on applicable exemptions thereunder.

The investment management agreements we enter into with clients in connection with contractual SMAs may generally be terminated by such clients with reasonably short prior written notice. Our investment management agreement with ARCC generally must be approved annually by such company’s board of directors (including a majority of such company’s independent directors). In addition to other termination provisions, each investment advisory and management agreement will automatically terminate in the event of its assignment and may be terminated by either party without penalty upon 60 days’ written notice to the other party.

The governing agreements of many of our funds provide that, subject to certain conditions, third‑partythird-party investors in those funds have the right to terminate the investment period or the fund without cause. The governing agreements of some of our funds provide that, subject to certain conditions, third‑partythird-party investors have the right to remove the general partner. In addition, the governing agreements of certain of our funds provide that upon the occurrence of certain events, including in the event that certain “key persons” in our funds do not meet specified time commitments, the investment period will be suspended or the investors have the right to vote to terminate the investment period in accordance with specified procedures. Such events may include certain “key persons” in our funds that engage in bad acts or depart the firm.

Fee Structure

Management Fees

The investment adviser of each of our funds and certain separately managed accounts generally receives an annual management fee based upon a percentage of the fund’s capital commitments, contributed capital, net assets value or invested capital during the investment period and the fund’s invested capital after the investment period, except for the investment advisers to certain of our hedge funds and separately managed accounts receive an annual management fee that is based upon a percentage of invested capital, contributed capital or net asset value throughout the term of the fund or separately managed account. From time to time we also may receive special fees, including commitment, arrangement, underwriting, agency, portfolio management, monitoring and other similar fees, some of which may be accelerated upon a sale of the underlying portfolio investment. In certain circumstances we are contractually required to offset certain amounts of such special fees against future management fees relating to the applicable fund. In addition, we may receive transaction fees from certain affiliated funds for activities related to fund transactions, such as loan originations. These fees are either recognized as other revenue in the period the transaction related services are rendered or amortized over the life of the investment.

The investment adviser of each of our CLOs typically receives annual management fees based upon a percentage of each CLO's total assets, subject to certain performance measures related to the underlying assets the vehicle owns, and additional management fees which are incentive‑based (that is, subject to meeting certain return criteria). We also classify the ARCC Part I Fees as management fees due to their predictability and frequency of payments without risk of contingent repayment. See “Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations—Components of Consolidated Results of Operations—Revenues.”

The management fees we receive from our drawdown style funds are typically payable on a quarterly basis over the life of the fund and do not depend on the investment performance of the fund (other than to reflect the disposition or decrease in value of assets where the management fees are based on invested capital). The management fees we receive from our hedge funds have similar characteristics, except that such funds often afford investors increased liquidity through annual, semi‑annual or quarterly withdrawal or redemption rights following the expiration of a specified period of time when capital may not be withdrawn and the amount of management fees to which the investment adviser is entitled with respect thereto will proportionately increase as the net asset value of each investor’s capital account grows and will proportionately decrease as the net asset value of each investor’s capital account decreases. The management fees we receive from our SMAs are generally paid on a periodic basis (typically quarterly, subject to the termination rights described above) and may alternatively be based on invested capital or proportionately increase or decrease based on the net asset value of the separately managed account.

We also receive management fees in accordance with the investment advisory and management agreements we have with the publicly traded vehicles we manage. Base management fees we receive from ARCC are paid quarterly and proportionately increase or decrease based on ARCC’s total assets (other than cash and cash equivalents). ARCC Part I Fees are also generally paid quarterly and proportionately increase or decrease based on ARCC’s net investment income (before ARCC Part I Fees and ARCC Part II Fees (as defined in “Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations—Components of Consolidated Results of Operations—Revenues”)), subject to a fixed hurdle rate. Management fees we receive from ARDC are generally paid on a regular basis (typically monthly) and proportionately increase or decrease based on the closed‑end funds’ total assets minus such funds’ liabilities (other than liabilities relating to indebtedness). Management fees we receive from ACRE are generally paid on a quarterly basis and proportionately increase or decrease based on ACRE’s stockholders’ equity (as calculated pursuant to the ACRE management agreement).

Performance Fees

We may also receive performance fees from a majorityOperations” for an overview of our funds, which may be either anfee structure, including management fee, incentive fee or a special allocation of income, which we refer to as aand carried interest in the event that specified investment returns are achieved by the fund. We may, and do in certain cases, award our senior professionals with participation in such performance fees.

Incentive Fees

The general partners or similar entities of certain of our funds receive performance‑based allocation fees ranging from 10% to 20% of the applicable fund’s net capital appreciation per annum, subject to certain net loss carry‑forward provisions (known as a “high‑watermark”). In some cases, the investment adviser of each of our hedge funds and certain SMAs is entitled to an incentive fee generally up to 20% of the applicable fund’s net appreciation per annum, subject to a high‑watermark and in some cases a preferred return. Realized incentive fees are generally higher during the second half of the year due to the nature of certain Credit Group funds that typically realize incentive fees annually. Once realized, the fees earned by our hedge funds generally are not subject to a contingent repayment obligation. Incentive fees are realized at the end of a measurement period, typically quarterly or annually.

Incentive Fees from Publicly TradedVehicles

We also are entitled to receive incentive fees in accordance with the investment advisory and management agreements we have with ARCC and ACRE. We may receive ARCC Part II Fees, which are calculated at the end of each applicable year by subtracting (a) the sum of ARCC’s cumulative aggregate realized capital losses and aggregate unrealized capital depreciation from (b) its cumulative aggregate realized capital gains, in each case calculated from October 8, 2004. Incentive fees we receive from ACRE are based on a percentage of the difference between ACRE’s core earnings (as defined in ACRE’s management agreement) and an amount derived from the weighted average issue price per share of ACRE’s common stock in its public offerings multiplied by the weighted average number of shares of common stock outstanding. We are not entitled to receive incentive fees from ARDC.

Carried Interest

The general partner or an affiliate of certain of our funds may be entitled to receive carried interest from a fund. Carried interest entitles the general partner (or an affiliate) to a special allocation of income and gains from a fund, and is typically structured as a net profits interest in the applicable fund. Carried interest is generally calculated on a “realized gain” basis, and the general partner of a fund is generally entitled to a carried interest between 10% and 20% of the net realized income and gains (generally taking into account unrealized losses) generated by such fund. Net realized income or loss is not netted between or among funds.

For most funds, the carried interest is subject to a preferred return ranging from 5% to 8%, subject in most cases to a catch‑up allocation to the general partner. Generally, if at the termination of a fund (and in some cases at interim points in the life of a fund), the fund has not achieved investment returns that generally exceed the preferred return threshold or the general partner receives net profits over the life of the fund in excess of its allocable share under the applicable partnership agreement, the general partner will be obligated to repay an amount equal to the extent to which performance fees that were previously distributed to it exceeds the amounts to which the general partner is ultimately entitled. These repayment obligations may be related to amounts previously distributed to us and our senior professionals and are generally referred to as contingent repayment obligations.

Although a portion of any distributions by us to our common shareholders may include carried interest received by us, we do not intend to seek fulfillment of any contingent repayment obligation by seeking to have our common shareholders return any portion of such distributions attributable to carried interest associated with any contingent repayment obligation. Contingent repayment obligations operate with respect to a given fund’s own net investment performance only and performance fees of other funds are not netted for determining this contingent obligation. Although a contingent repayment obligation is several to each person who received a distribution, and not a joint obligation, the governing agreements of our funds generally provide that, if a recipient does not fund his or her respective share, we may have to fund such additional amounts beyond the amount of performance fees we retained, although we generally will retain the right to pursue remedies against those performance fee recipients who fail to fund their obligations.

For additional information concerning the contingent repayment obligations we could face, see “Item 1A. Risk Factors—We may need to pay these contingent obligations if and when they are triggered under the governing agreementsarrangements with our investors.”funds.

Capital Invested In and Through Our Funds

To further align our interests with those of investors in our funds, we have invested the firm’s capital and that of our professionals in the funds we sponsor and manage. General partner capital commitments to our funds are determined separately with respect to our funds and, generally, are less than 5% of the total commitments of any particular fund. We determine the general partner capital commitments based on a variety of factors, including regulatory requirements, investor requirements, estimates regarding liquidity over the estimated time period during which commitments will be funded, estimates regarding the amounts of

capital that may be appropriate for other opportunities or other funds we may be in the process of raising or are considering raising, prevailing industry standards with respect to sponsor commitments and our general working capital requirements. We may from time to time offer to our senior professionals a part of the general partner commitments to our funds. Our general partner capital commitments are typically funded with cash and not with carried interest or deferral of management fees. We generally offer a portion of the general partner commitments to our eligible professionals in accordance with the Investment Company Act. Ares employees had capital commitments of $2.4 billion in Ares-managed funds as of December 31, 2023. For more information, see “Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations—Liquidity and Capital Resources—Sources and Uses of Liquidity.”

Regulatory and Compliance Matters

Our businesses, as well as the financial services industry, generally are subject to extensive regulation, including periodic examinations, by governmental agencies and self‑regulatoryself-regulatory organizations or exchanges in the U.S. and foreign jurisdictions in which we operate relating to, among other things, antitrust laws, anti‑moneyanti-money laundering laws, anti‑briberyanti-bribery laws relating to foreign officials, tax laws and data privacy laws with respect to client and other information, and some of our funds invest in businesses that operate in highly regulated industries. Each of the regulatory bodies with jurisdiction over us has regulatory powers dealing with many aspects of financial services, including the authority to grant, and in specific circumstances to cancel, permissions to carry on particular activities. Any failure to comply with these rules and regulations could expose us to liability and/or reputational damage. In addition, additionalAdditional legislation, increasing global regulatory oversight of fundraising activities, changes in rules promulgated by self‑regulatoryself-regulatory organizations or exchanges or changes in the laws or rules, or interpretation or enforcement of existing laws and rules, either in the United StatesU.S. or elsewhere, may directly affect our mode of operation and profitability. See “Item 1A. Risk Factors-RisksFactors—Risks Related to Our Businesses-Extensive regulation in the United States affects our activities and creates the potential for significant liabilities and penalties that could adversely affect our businesses and results of operations,” “-Failure to comply with “pay to play” regulations implemented by the SEC, FINRA and certain states, and changes to the “pay to play” regulatory regimes, could adversely affect our businesses,” “-Regulatory changes and other developments in the United States and regulatory compliance failures could adversely affect our reputation, businesses and operations” and “-Regulatory changes in jurisdictions outside the United States could adversely affect our businesses.Regulation.”

Rigorous legal and compliance analysis of our businesses and investments is important to our culture. We strive to maintain a culture of compliance through the use of policies and procedures such as oversight compliance, codes of ethics, compliance systems, communication of compliance guidance and employee education and training. All employees must annually certify their understanding of, compliance with and adherence to key global Ares policies, procedures and code of ethics. We havemaintain a compliance group, supervised by our Chief Compliance Officer, that monitorsis responsible for monitoring our compliance with the regulatory and legal requirements to which we are subject and managesmanaging our compliance policies and procedures. Our Chief Compliance Officer, together with our Chief Legal Officer, supervises our compliance group, which is responsible for monitoring all regulatory and compliance matters that affect our activities. Our compliance policies and procedures seek to address a variety of regulatory and compliance risks such as the handling of material non‑publicnon-public information, position reporting, personal securities trading, valuation of investments on a fund‑specificfund-specific basis, document retention, potential conflicts of interest and the allocation of investment opportunities.

Many jurisdictions in which we operate have laws and regulations relating to data privacy, cybersecurity and protection of personal information, including the General Data Protection Regulation (“GDPR”), a European Union (“EU”) regulation designed to protect privacy rights of individuals residing in the European Economic Area (the “EEA”), the GDPR as it forms part of the laws of England and Wales, Scotland and Northern Ireland by virtue of Section 3 of the European Union Withdrawal Act 2018 (as amended) and the Data Protection Act 2018 (collectively, “U.K. GDPR”) with respect to individuals residing in the United StatesKingdom (the “U.K.”), and various state and federal privacy laws applicable to individuals residing in the U.S., including the California Consumer Privacy Act (the “CCPA”), as amended by the California Privacy Rights Act. Other comprehensive privacy laws have been enacted or passed in numerous U.S. states, including Colorado, Connecticut, Delaware, Indiana, Iowa, Montana, New Jersey, Oregon, Tennessee, Texas, Utah and Virginia. Various global privacy laws also apply to our business, including those in Australia, the Cayman Islands, Hong Kong, India, Korea, Japan, Dubai and Singapore. These privacy laws are quickly evolving and may conflict with one another. Any failure to comply with such laws or regulations could result in substantial fines, penalties and/or sanctions, litigation, as well as reputational harm. Moreover, to the extent that these laws and regulations or the enforcement of the same become more stringent, or if new laws or regulations or enacted, our financial performance or plans for growth may be adversely impacted.

U.S.

The SEC oversees the activities of our subsidiaries that are registered investment advisers under the Investment Advisers Act. The Financial Industry Regulatory Authority (“FINRA”) overseesand the SEC oversee the activities of our subsidiarywholly owned subsidiaries, AWMS and Ares Management Capital Markets LLC (formerly known as Ares Investor Services LLC ("AIS"LLC) (“AMCM”), as a registered broker‑dealer. In connection with certain investments made by funds in our Private Equity Group, certain of our subsidiaries and funds are subject to audits by the Defense Security Service to determine whether we are under foreign ownership, control or influence.broker-dealers. In addition, we regularly rely on exemptions from various requirements of the Securities Act, of 1933, as amended (the “Securities Act”), the Securities Exchange Act, of 1934, as amended (the “Exchange Act”), the Investment Company Act, the Commodity Exchange Act and ERISA.the U.S. Employee Retirement Income Security Act of 1974, as amended (“ERISA”). These exemptions are sometimes highly complex and may in certain circumstances depend on compliance by third parties who we do not control.

Additionally, the SEC and various self-regulatory organizations have in recent years increased their regulatory activities in respect of investment management firms. See “Item 1A. Risk Factors—Risks Related to Regulation—Extensive regulation affects our activities, increases the cost of doing business and creates the potential for significant liabilities and penalties that could adversely affect our businesses and results of operations.” Since September 2019, the SEC has required broker-dealers, or natural persons who are associated persons of broker-dealers, to act in the best interest of a retail customer when making a recommendation of any securities transaction or investment strategy involving securities, without placing the financial or other interest of the broker, dealer or natural person who is an associated person of a broker-dealer making the recommendation ahead of the interest of the retail customer (“Regulation Best Interest”). Regulation Best Interest requires broker-dealers to evaluate available alternatives, including those that may have lower expenses and/or lower investment risk than our investment funds. The term “retail customer” is defined as a natural person who uses such a recommendation primarily for personal, family or household purposes, without reference to investor sophistication or net worth. The “best interest” standard is satisfied through compliance with certain disclosure, duty of care, conflict of interest mitigation and compliance obligations. Under Regulation Best Interest, high cost, high risk and complex products may be subject to greater scrutiny by broker-dealers and their salespersons. The full impact of Regulation Best Interest and state fiduciary standards on broker-dealers cannot be determined at this time. However, it may negatively impact whether broker-dealers and their associated persons are willing to recommend investment products, including our funds, to retail customers, which may adversely impact our ability to distribute our products to certain investors. As such, Regulation Best Interest may reduce the ability of our funds to raise capital, which would adversely affect our business and results of operations. In addition, the U.S. Department of Labor as well as several states have proposed regulations or taken other actions pertaining to conduct standards for investment advisers and broker-dealers that may result in additional regulatory requirements related to our business.

Funds and Portfolio Companies of our Funds

All of our funds are advised by SEC registered investment advisers that are registered with the SEC (or wholly owned subsidiaries thereof). Registered investment advisers are subject to more stringent requirements and regulations under the Investment Advisers Act than unregistered investment advisers. Such requirements relate to, among other things, fiduciary duties to clients, maintaining an effective compliance program, managing conflicts of interest and general anti‑fraudanti-fraud prohibitions. In addition, the SEC requires investment advisers registered or required to register with the SEC under the Investment Advisers Act that advise one or more private funds and have at least $150 million in private fund assets under management to periodically file reports on Form PF. We have filed, and will continue to file, quarterly reports on Form PF.PF, which has resulted in increased administrative costs and a significant amount of attention and time to be spent by our personnel. The SEC adopted changes to Form PF in 2023, which, among other requirements, requires current reporting upon the occurrence of certain fund-level events. In 2024, the SEC and the Commodity Futures Trading Commission (the “CFTC”) adopted joint amendments to Form PF that will require additional basic information about advisers and the private funds they advise, including identifying information, assets under management,

withdrawal and redemption rights, gross asset value and net asset value, inflows and outflows, base currency, borrowings and types of creditors, fair value hierarchy, beneficial ownership and fund performance, as well as additional specific information regarding funds that must report as hedge funds on the form. These amendments will likely increase related administrative costs and burdens.

ARCC is aand ASIF are registered investment companycompanies that hashave each elected to be treated as a business development company under the Investment Company Act. APMF, ARDC and certain other fundsCADC are registered investment companies under the Investment Company Act. Each of the registered investment companies has elected, for U.S. federal tax purposes, to be treated as a regulated investment companyRIC under Subchapter M of the U.S. Internal Revenue Code of 1986, as amended (the “Code”). As such, each registered investment company is requiredTo maintain its RIC status under the Code, a RIC must timely distribute an amount equal to distribute at least 90% of its ordinaryinvestment company taxable income and realized,(as defined by the Code, which generally includes net short‑term capital gains in excess of realized net long‑term capital losses, if any, to its shareholders. In addition, to avoid excise tax, each registered investment

company is required to distribute at least 98% of its income (such income to include both ordinary income and net capital gains), which would take into account short‑term and long‑short term capital gains and losses. Each registered investment company, at each ofgains) to its discretions, may carry forward taxable income in excess of calendar year distributions andstockholders. In addition, a RIC generally will be required to pay an excise tax equal to 4% on this income.certain undistributed taxable income unless it distributes in a timely manner an amount at least equal to the sum of: (i) 98% of its ordinary income recognized during a calendar year; (ii) 98.2% of its capital gain net income, as defined by the Code, recognized during the one-year period ending on October 31 of the calendar year; and (iii) any income recognized, but not distributed, in preceding years. The taxable income on which a RIC pays excise tax is generally distributed to its stockholders in the next tax year. Depending on the level of taxable income earned in a tax year, a RIC may choose to carry forward such taxable income for distribution in the following year, and pay any applicable excise tax. In addition, as a business development company,companies, ARCC and ASIF must not acquire any assets other than “qualifying assets” specified in the Investment Company Act unless, at the time the acquisition is made, at least 70% of ARCC’sARCC and ASIF’s respective total assets are qualifying assets (with certain limited exceptions). Qualifying assets include investments in “eligible portfolio companies.” ARCC and ASIF are also generally prohibited from issuing and selling its common stock at a price below net asset value per share and from incurring indebtedness (including for this purpose, preferred stock), if ARCC and ASIF’s respective asset coverage, as calculated pursuant to the Investment Company Act, equals less than 150% after such incurrence.

ACRE, hasAREIT and AIREIT have each elected and qualified to be taxed as a real estate investment trust, or REIT, under the Code. To maintain its qualification as a REIT, ACREeach must distribute at least 90% of its taxable income to its shareholdersstockholders and meet, on a continuing basis, certain other complex requirements under the Code.

AIS,AWMS and AMCM, our wholly owned subsidiary, issubsidiaries, are registered as a broker‑dealerbroker-dealers with the SEC, maintain licenses in many states, and is a memberare members of FINRA. As a broker‑dealer, thisbroker-dealer, each subsidiary is subject to regulation and oversight by the SEC and state securities regulators. In addition, FINRA a self‑regulatory organization that is subject to oversight by the SEC, promulgates and enforces rules governing the conduct of, and examines the activities of, its member firms. Due to the limited authority granted to each of our subsidiarysubsidiaries in its capacity as a broker‑dealer, it isbroker-dealers, they are not required to comply with certain regulations covering trade practices among broker‑dealersbroker-dealers and the use and safekeeping of customers’ funds and securities. As a registered broker‑dealerbroker-dealers and membermembers of a self‑regulatoryself-regulatory organization, AIS is,AWMS and AMCM are, however, subject to the SEC’s uniform net capital rule. Rule 15c3‑115c3-1 of the Exchange Act, which specifies the minimum level of net capital a broker‑dealerbroker-dealer must maintain and also requires that a significant part of a broker‑dealer’sbroker-dealer’s assets be kept in relatively liquid form.

The SEC See “Item 1A. Risk Factors—Risks Related to Our Businesses—Political and various self‑regulatory organizations haveconditions, including the effects of negative publicity surrounding the financial industry in recent years increased their regulatory activities in respect of investment management firms. In July 2010, the Dodd‑Frank Wall Street Reformgeneral and Consumer Protection Act (the “Dodd‑Frank Act”) was signed into law and has imposed significant regulations on nearly every aspect of the U.S. financial services industry.

In October 2011, the Federal Reserve and other federal regulatory agencies issued a proposed rule implementing a section of the Dodd‑Frank Act that has become known as the “Volcker Rule.” The Volcker Rule generally prohibits insured banks or thrifts, any bank holding company or savings and loan holding company, any non‑U.S. bank with a U.S. branch, agency or commercial lending company and any subsidiaries and affiliates of such entities, regardless of geographic location, from investing in or sponsoring “covered funds,” which include private equity funds or hedge funds. The final Volcker Rule became effective on April 1, 2014, and , except with respect to certain foreign banking entities, the conformance period ended on July 21, 2017. It contains exemptions for certain “permitted activities” that would enable certain institutions subject to the Volcker Rule to continue investing in covered funds under certain conditions.

In 2013, the Office of the Comptroller of the Currency, the Department of the Treasury, the Board of Governors of the Federal Reserve System and the Federal Deposit Insurance Corporation published revised guidance regarding expectations for banks’ leveraged lending activities. This guidance, in addition to the Dodd‑Frank Act risk retention rules approved in October 2014,legislation, could further restrict credit availability, as well as potentially restrict the activities of certain funds who invest in broadly syndicated loans in our Credit Group, which supports many of its portfolio investments from banks’ lending activities.

Pursuant to the Dodd-Frank Act, regulation of the derivatives market is bifurcated between the U.S. Commodities Futures Trading Commission (the “CFTC”) and the SEC. Under the Dodd‑Frank Act, the CFTC has jurisdiction over swaps and the SEC has jurisdiction over security‑based swaps. As part of its Dodd-Frank Act related rule‑making process, the CFTC made changes to its rules with respect to the registration and oversight of commodity pool operators (“CPOs”). Such rules require that an entity that is a CPO must register with the CFTC unless an exemption from registration is available. Previously, the CPO registration rules had applied to the operator of a fund invested in “commodity interests,” meaning that the fund entered into futures or options with respect to commodities. As a result of the CFTC’s revisions to these rules, all swaps (other than security‑based swaps) are now included in the definition of commodity interests. As a result, funds that utilize swaps (whether or not related to a commodity) as part of their business model may fall within the statutory definition of a commodity pool. If a fund qualifies as a commodity pool, then, absent an available exemption, the operator of such a fund is required to register with the CFTC as a CPO. Registration with the CFTC renders such CPO subject to regulation, including with respect to disclosure, reporting, recordkeeping and business conduct.

Certain of our funds may from time to time, directly or indirectly, invest in instruments that meet the definition of a “swap” under the Commodity Exchange Act and the CFTC’s rules promulgated thereunder. As a result, such funds may qualify as commodity pools, and the operators of such funds may need to register as CPOs unless an exemption applies such as the so-called “de minimis” exemption, codified in CFTC rule 4.13(a)(3). If any of our funds cease to qualify for this (or another applicable) exemption, certain Ares entities associated with and/or affiliated with those funds will be required to register with the CFTC as commodity pool operators.

The Dodd‑Frank Act requires the CFTC, the SEC and other regulatory authorities to promulgate certain rules relating to the regulation of the derivatives market. Such rules require or will require the registration of certain market participants, the clearing of certain derivatives contracts through central counterparties, the execution of certain derivatives contracts on electronic platforms, as well as reporting and recordkeeping. The Dodd-Frank Act also provides expanded enforcement authority to the CFTC and SEC. While certain rules have been promulgated and are already in effect, the rulemaking and implementation process is still ongoing. In particular, the CFTC has finalized most of its rules under the Dodd‑Frank Act, and the SEC has proposed a number of rules regarding security‑based swaps but has only finalized some of these rules. We cannot therefore yet predict the ultimate effect of the rules and regulations on our business.

Under CFTC and SEC rules, an entity may be required to register as a major swap participant (“MSP”) or major security-based swap participant (“MSBSP”) if it has substantial swaps or security-based swaps positions or has substantial counterparty exposure from its swaps or security-based swaps positions. If any of our funds were required to register as an MSP or MSBSP, it could make compliance more expensive, affect the manner in which we conduct our businesses and adversely affect our profitability. Additionally, if any of our funds qualify as “special entities” under CFTC rules, it could make it more difficult for them to enter into derivatives transactions or make such transactions more expensive.businesses.”

The CFTC has issued final rules imposing reporting and recordkeeping requirements on swaps market participants. Such rules are currently effective and could significantly increase operating costs. These additional recordkeeping and reporting requirements may require additional compliance resources and may also have a negative effect on market liquidity, which could negatively impact commodity prices and our ability to hedge our price risks.

Pursuant to rules finalized by the CFTC in December 2012 and September 2016, certain classes of interest rate swaps and certain classes of credit default swaps are subject to mandatory clearing, unless an exemption applies. Many of these swaps are also subject to mandatory trading on designated contract markets or swap execution facilities. At this time, the CFTC has not proposed any rules designating other classes of swaps for mandatory clearing, but it may do so in the future. Mandatory clearing and trade execution requirements may change the cost and availability of the swaps that we use, and exposes us to the credit risk of the clearing house through which any cleared swap is cleared. In addition, federal bank regulatory authorities and the CFTC have adopted initial and variation margin requirements for swap dealers, security-based swap dealers, MSPs and MSBSPs (“swap entities”), including permissible forms of margin, custodial arrangements and documentation requirements, for uncleared swaps and security-based swaps. As a result, swap entities will be required to collect margin for transactions and positions in uncleared swaps and security-based swaps by financial end users. The new rules became effective for end users on March 1, 2017. The CFTC’s Division of Swap Dealer and Intermediary Oversight subsequently extended, until September 1, 2017, the time to comply with the variation margin requirements for swaps that are subject to a March 1, 2017 compliance date. The effect of the regulations on us is not fully known at this time. However, these rules may increase the cost of our activity in uncleared swaps and security-based swaps to the extent we are determined to be a financial end user.

In December 2016, the CFTC reproposed rules that would set federal position limits for certain core physical commodity futures, options and swap contracts (“referenced contracts”), and issued final rules on aggregation among entities under common ownership or control, unless an exemption applies, for position limits on certain futures and options contracts that would apply to the proposed position limits on referenced contracts. It is possible that the CFTC could propose to expand such requirements to other types of contracts in the future. The proposal could affect our ability and the ability for our funds to enter into derivatives transactions if and when the CFTC’s position limits rules become effective.

The CFTC has finalized regulations requiring collateral used to margin cleared swaps to be segregated in a manner different from that applicable to the futures market and has finalized other rules allowing parties to an uncleared swap to require that any collateral posted as initial margin be segregated with a third party custodian. Collateral segregation may impose greater costs on us when entering into swaps.

Finally, the Dodd‑Frank Act gave the CFTC expanded anti‑fraud and anti‑manipulation authority, including authority over disruptive trading practices and insider trading. Several investigations have commenced in the United States related to manipulation of the foreign exchange, LIBOR and indices markets. It is possible that new standards will emerge from these proceedings that could impact the way that we trade.

The Dodd‑Frank Act authorizes federal regulatory agencies to review and, in certain cases, prohibit compensation arrangements at financial institutions that give employees incentives to engage in conduct deemed to encourage inappropriate risk‑taking by covered financial institutions. In 2016, federal bank regulatory authorities and the SEC revised and re-proposed a rule that generally (1) prohibits incentive-based payment arrangements that they determine encourage inappropriate risks by certain financial institutions by providing excessive compensation or that could lead to material financial loss and (2) requires those financial institutions to disclose information concerning incentive-based compensation arrangements to the appropriate federal regulator.

The Dodd‑Frank Act also directs the SEC to adopt a rule that requires public companies to adopt and disclose policies requiring, in the event the company is required to issue an accounting restatement, the contingent repayment obligations of related incentive compensation from current and former executive officers. The SEC has proposed but not yet adopted such rule. To the extent the aforementioned rules are adopted, our ability to recruit and retain investment professionals and senior management executives could be limited.

The Dodd‑Frank Act amends the Exchange Act to compensate and protect whistleblowers who voluntarily provide original information to the SEC and establishes a fund to be used to pay whistleblowers who will be entitled to receive a payment equal to between 10% and 30% of certain monetary sanctions imposed in a successful government action resulting from the information provided by the whistleblower.

Many of these provisions are subject to further rulemaking and to the discretion of regulatory bodies, such as the Council and the Federal Reserve. Many of these provisions are subject to further rulemaking and to the discretion of regulatory bodies, such as the Council and the Federal Reserve. On February 3, 2017, President Trump signed Executive Order 13772 (the “Executive Order”) announcing the new administration’s policy to regulate the U.S. financial system in a manner consistent with certain “Core Principles,” including regulation that is efficient, effective and appropriately tailored. The Executive Order directed the Secretary of the Treasury, in consultation with the heads of the member agencies of the Financial Stability Oversight Council, to report to the President on the extent to which existing laws, regulations and other government policies promote the Core Principles and to identify any laws, regulations or other government policies that inhibit federal regulation of the U.S. financial system.

On June 12, 2017, the U.S. Department of the Treasury (“Treasury”) published the first of several reports in response to the Executive Order on the depository system covering banks and other savings institutions. On October 6, 2017, the Treasury released a second report outlining ways to streamline and reform the U.S. regulatory system for capital markets, followed by a third report, on October 26, 2017, examining the current regulatory framework for the asset management and insurance industries. Subsequent reports are expected to address: retail and institutional investment products and vehicles, as well as non‑bank financial institutions, financial technology and financial innovation.

On June 8, 2017, the U.S. House of Representatives passed the Financial Choice Act, which includes legislation intended to repeal or replace substantial portions of the Dodd‑Frank Act. Among other things, the proposed law would repeal the Volcker Rule limiting certain proprietary investment and trading activities by banks, eliminate the authority of regulators to designate asset managers and other large non‑bank institutions as “systemically important financial institutions” or “SIFIs,” and repeal the Department of Labor (“DOL”) “fiduciary rule” governing standards for dealing with retirement plans until the SEC issues standards for similar dealings by broker‑dealers and limiting the substance of any subsequent DOL rule to the SEC standards. The bill was referred to the Senate, where it is unlikely to pass as proposed. On November 16, 2017, a bipartisan group of U.S. Senators, led by Senate Banking Committee Chairman, introduced the Economic Growth, Regulatory Relief, and Consumer Protection Act (the “Senate Regulatory Relief Bill”). The Senate Regulatory Relief Bill would revise various post-crisis regulatory requirements and provide targeted regulatory relief to certain financial institutions. Among the most significant of its proposed amendments to the Dodd-Frank Act are a substantial increase in the $50 billion asset threshold for automatic regulation of bank holding companies as SIFIs, an exemption from the Volcker Rule for insured depository institutions with less than $10 billion in consolidated assets and lower levels of trading assets and liabilities, as well as amendments to the liquidity leverage ratio and supplementary leverage ratio requirements. On December 5, 2017, the Senate Banking Committee approved the Senate Regulatory Relief Bill. If the legislation is adopted in the Senate, it remains unclear whether and how it would be reconciled with its House-passed counterpart, the Financial Choice Act, which is substantially different in scope and substance, and ultimately approved by both chambers of Congress. The ultimate impact of this order and its implementation on existing and proposed regulations under the Dodd-Frank Act and other rules and regulations applicable to the U.S. financial system are uncertain; however, such impact could be material to our industry, business and operations.

Other Jurisdictions

Certain of our subsidiaries operate outside the United States.U.S. In Luxembourg, Ares Management Luxembourg (“AM Lux”) is subject to authorization and regulation by the Commission de Surveillance du Secteur Financier (“CSSF”). In the United Kingdom,U.K., Ares Management Limited (“AML”) and Ares Management UKU.K. Limited (“AMUKL”) are subject to regulation and authorization by the U.K. Financial Conduct Authority (“FCA”(the “FCA”). Ares European Loan Management LLP (“AELM”), which is not a subsidiary, but in which we are indirectly invested and which procures certain services from Ares Management Limited,AML, is also subject to regulation by the FCA. In some circumstances, Ares Management Limited, Ares Management UK Limited, Ares European Loan Management LLPAML, AMUKL, AELM (the “U.K. Regulated Entities”) and other Ares entities are or may become subject to UKU.K. or EU laws, for instance in relation to marketing our funds to investors in the European Economic Area (“EEA”).EEA.

The UK is scheduled to leaveU.K. exited the EU in March 2019. Some formon January 31, 2020. The withdrawal agreement which provided for a transitional period to allow for the terms of transitional agreement by which UK based financial services firms can continuethe U.K.’s future relationship with the EU to operatebe negotiated, ended on a cross-border basis seems likely. However,December 31, 2020. EEA passporting rights are no longer available to the durationrelevant U.K. entities following the end of the transitional agreementperiod. Various EU laws were “on-shored” into domestic U.K. legislation and certain transitional regimes and deficiency-correction powers exist to ease the transition. The Trade and Cooperation Agreement (the “TCA”) between the U.K. and the end-state relationshipEU formally came into force on May 1, 2021 and since its effectiveness, the TCA has governed certain matters between the UKU.K. and EUthe EU. In addition, the Temporary Marketing Permission Regime (the “TMPR”) allows our alternative investment fund managers (“AIFMs”) to continue to market those funds in the U.K. that were in existence on December 31, 2020, on broadly the same terms as previously applied. Unless extended, the TMPR lasts until December 31, 2025. Any marketing of a new fund coming into

existence after December 31, 2020 must comply with the U.K.’s national private placement regime. Notwithstanding the TCA and the TMPR, there remains unclear. There is a risk that following Brexit the UK may be denied accessconsiderable uncertainty as to the single market. Thisnature of the U.K.’s future relationship with the EU, creating continuing uncertainty as to the full extent to which the businesses of the U.K. Regulated Entities and our businesses generally could be highly disruptiveadversely affected by Brexit. See “Item 1A. Risk Factors—Risks Related to Regulation—The U.K.’s exit from the EU (“Brexit”) could adversely affect our business and may result in us having to increase our presence in other EEA member states which would result in additional costs.

operations.” Despite the U.K.’s departure from the EU, new and existing EU legislation couldis expected to continue to impact our business in the United KingdomU.K. (whether because its effect is preserved in the U.K. as a matter of domestic policy or because compliance with such legislation (whether in whole or part) is a necessary condition for market access into the EEA) and other EEA member states where we have operations. The U.K.’s departure has the potential to change the U.K. legislative and regulatory frameworks within which the U.K. Regulated Entities operate, which could adversely affect our businesses or cause a material increase in our tax liability.

AM Lux operates under the EU legislative frameworks. Notwithstanding the U.K.’s withdrawal from the EU, the U.K. Regulated Entities generally continue to be regulated under these frameworks to the extent they were preserved in U.K. law. In some circumstances other Ares entities are or may become subject to EU laws or the law of EEA member states, including with respect to marketing our funds to investors in the EEA.

AM Lux and AMUKL are both AIFMs. Their operations are primarily governed by Directive 2011/61/EU on Alternative Investment Fund Managers and other associated legislation, rules and guidance (“AIFMD”). The U.K. implemented AIFMD while it was still a member of the EU and similar requirements therefore continue to apply in the U.K. notwithstanding Brexit. The AIFMD imposes significant regulatory requirements on AIFMs established in the EEA. AIFMD regulates fund managers by, amongst other things, prescribing authorization conditions for an AIFM, restricting the activities that can be undertaken by an AIFM and prescribing the organizational requirements, operating conditions, and regulatory standards relating to such things as initial capital, remuneration, conflicts, risk management, leverage, liquidity management, delegation of duties, transparency and reporting requirements.

In the EU (but not the U.K.), AIFMD is expected to be amended in 2024. On November 10, 2023, the European Commission published a near-final amending directive, commonly referred to as “AIFMD II”. Assuming AIFMD II is adopted promptly and published in the Official Journal without delay in 2024, most of the changes will become effective in 2026, subject to the grandfathering period for certain of the loan origination provisions and certain Annex IV disclosure requirements which will become effective a year later. It is not yet clear to what extent (if any) the U.K. will seek to reflect AIFMD II in its domestic rules implementing AIFMD.

AML and AELM are both investment firms within the meaning of Directive 2014/65/EU on Markets in Financial Instruments (“MiFID II”). Notwithstanding Brexit, the U.K.’s rules implementing MiFID II continue to have effect and the accompanying Markets in Financial Instruments Regulation 600/2014/EU (“MiFIR”) has been on-shored into U.K. law in connection with this withdrawal. The operations of AML and AELM are primarily governed by U.K. laws and regulatory rules implementing MiFID II, MiFIR and other associated legislation, rules and guidance. AMUKL is subject to certain provisions of U.K.-retained MiFID II because it has top-up permissions to provide certain U.K.-retained MiFID investment services. AM Lux is subject to certain provisions of EU MiFID II because it has top-up permissions to provide certain MIFID investment services. The main business of AM Lux and the U.K. Regulated Entities is to provide asset management services to clients in Europe.

MiFID II and MiFIR extended the Markets and Financial Instruments Directive (“MiFID”) requirements in a number of areas with more prescriptive and onerous obligations with respect to costs and charges disclosure, product design and governance, the receipt and payment of inducements, the receipt of and payment for investment research, suitability and appropriateness assessments, conflicts of interest, record-keeping, best execution, transaction and trade reporting, remuneration, training and competence and corporate governance. Certain aspects of MIFID II and MiFIR are subject to review and change in both the EU and the U.K.

Effective January 1, 2022, the U.K. introduced a prudential regulatory framework for U.K. investment firms (the “Investment Firm Prudential Regime” or “IFPR”). IFPR applies to AML and AELM as U.K. MiFID investment firms as well as to AMUKL, as a U.K. AIFM with MiFID “top-up” permissions. Under IFPR, among other requirements, AML, AMUKL and AELM are required to maintain more onerous policies regarding remuneration of staff, to set an appropriate ratio between the variable and fixed components of total remuneration and to meet requirements on the structure of variable remuneration. AML and AMUKL are considered to be part of the same “prudential consolidation group”, and many of the requirements of IFPR (including but not limited to capital, liquidity and remuneration) apply at the consolidated group level. Under IFPR, each of AML, AMUKL and AELM have made public disclosures on their websites in relation to their: (i) own funds, own funds requirements and governance structures; (ii) risk management; and (iii) remuneration. The new public disclosure requirements mandate more detail, including quantitative information on remuneration paid to staff, split in between classes of employees, and confirmation of the highest severance payment awarded to an individual material risk taker. The requirements of this

regime may lead to additional operational and compliance complexity in the short to medium term and possibly higher regulatory capital requirements for the affected firms.

The U.K. has introduced an important and substantial regime, the Consumer Duty, designed to improve outcomes for retail investors, aspects of which became effective on July 31, 2023. Although Ares entities do not generally deal with consumers in the ordinary sense, the regime will apply to certain of our funds.

Our operations and our investment activities worldwide are subject to a variety of regulatory regimes that vary by country. These include operating subsidiaries of Ares Management Asia (Holdings) Limited, which are subject to regulation by various regulatory authorities, including the Securities and Futures Commission of Hong Kong and Monetary Authority of Singapore. In addition, as the ultimate parent of the controlling entity of Aspida Re, a Bermuda Class E insurance company, we are considered its “shareholder controller” (as defined in the Bermuda Insurance Act) by the Bermuda Monetary Authority (the “BMA”).

Competition

The investment management industry is intensely competitive, and we expect it to remain so. We compete globally and on a regional, industry and asset basis.

We face competition both in the pursuit of fund investors and investment opportunities. Generally, our competition varies across business lines, geographies and financial markets. We compete for outside investors based on a variety of factors, including investment performance, investor perception of investment managers’ drive, focus and alignment of interest, quality of service provided to and duration of relationship with investors, breadth of our product offering, business reputation and the level of fees and expenses charged for services. We compete for investment opportunities both at our funds and for strategic acquisitions by us based on a variety of factors, including breadth of market coverage and relationships, access to capital, transaction execution skills, the range of products and services offered, innovation and price.

We face competition in our direct lending, trading, acquisitions and other investment activities primarily from traditional asset managers, business development companies, specialized funds, investment managers and other financial institutions, and we expect that competition will continue to increase. Many of these competitors in some of our businesses are substantially larger and have considerably greater financial, technical and marketing resources than are available to us. Many of these competitors have similar investment objectives to us, which may create additional competition for investment opportunities. Some of these competitors may also have a lower cost of capital and access to funding sources that are not available to us, which may create competitive disadvantages for us with respect to investment opportunities. In addition, some of these competitors may have higher risk tolerances, different risk assessments or lower return thresholds, which could allow them to consider a wider variety of investments and to bid more aggressively than us for investments that we want to make. Corporate buyers may be able to achieve synergistic cost savings with regard to an investment that may provide them with a competitive advantage in bidding for an investment. Lastly, institutional and individual investors are allocating increasing amounts of capital to alternative investment strategies. Several large institutional investors have announced a desire to consolidate their investments in a more limited number of managers. We expect that this will cause competition in our industry to intensify and could lead to a reduction in the size and duration of pricing inefficiencies that many of our funds seek to exploit.

Competition is also intense for the attraction and retention of qualified employees. Our ability to continue to compete effectively in our businesses will depend upon our ability to attract new employees and retain and motivate our existing employees.

For additional information concerning the competitive risks that we face, see “Item 1A. Risk Factors—Risks Related to Our Businesses—The investment management business is intensely competitive.”

Available Information