UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

(Mark One)

ý ☒ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the Fiscal Year Ended: December 31, 20172019

¨ ☐TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

Commission File Number: 001-11590

|

| | |

| | | |

CHESAPEAKEUTILITIESCORPORATION |

| (Exact name of registrant as specified in its charter) |

| | | |

|

| | |

| State of Delaware | | 51-0064146 |

| (State or other jurisdiction of | | (I.R.S. Employer |

| incorporation or organization) | | Identification No.) |

909 Silver Lake Boulevard, Dover, Delaware19904

(Address of principal executive offices, including zip code)

302-734-6799302-734-6799

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

|

| | |

| Title of each class | Trading Symbol | Name of each exchange on which registered |

| Common Stock—par value per share $0.4867 | CPK | New York Stock Exchange, Inc. |

Securities registered pursuant to Section 12(g) of the Act:

None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yesý☒ No ¨☐

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨☐Noý☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15 (d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yesý☒ No ¨☐

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yesý☒ No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendments to this Form 10-K. ý☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “accelerated“large accelerated filer,” “large accelerated“accelerated filer,” “smaller reporting company,” and "emerging growth company" in Rule 12b-2 of the Exchange Act.

|

| | | | | | |

| Large accelerated filer | | ý☒ | | Accelerated filer | | ¨

☐ |

| | | | |

| Non-accelerated filer | | ¨☐ | (Do not check if a smaller reporting company" | Smaller reporting company | | ¨☐ |

| | | | | Emerging growth company | | ¨

☐ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ¨☐

Indicate by a check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ¨☐ No ý

☒

The aggregate market value of the common shares held by non-affiliates of Chesapeake Utilities Corporation as of June 30, 2017,2019, the last business day of its most recently completed second fiscal quarter, based on the last tradesale price on that date, as reported by the New York Stock Exchange, was approximately $1.2$1.5 billion.

The number of shares of Chesapeake Utilities Corporation's common stock outstanding as of February 20, 20182020 was 16,344,442.16,407,017

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the Proxy Statement for the 20182020 Annual Meeting of Stockholders are incorporated by reference in Part II and Part III, which Proxy Statement shall be filed with the Securities and Exchange Commission within 120 days after the end of registrant's fiscal year ended December 31, 2017.2019.

CHESAPEAKE UTILITIES CORPORATION

CHESAPEAKE UTILITIES CORPORATION

FORM 10-K

YEAR ENDED DECEMBER 31, 20172019

TABLE OF CONTENTS

GLOSSARY OF DEFINITIONS

AFUDC: Allowance for funds used during construction

Amendment: The Second Amendment to the Rights Agreement, which was executed on February 27, 2018, and which has the effect of terminating the Rights Agreement at 5:00 P.M., New York City time on that date.

ARM: ARM Energy Management, LLC, a natural gas supply and supply management company servicing commercial and industrial customers in Western Pennsylvania, which sold certain assets to PESCO in August 2017

ASC: Accounting Standards Codification

ASU: Accounting Standards Update

Aspire Energy: Aspire Energy of Ohio, LLC, a wholly-owned subsidiary of Chesapeake Utilities, into which Gatherco merged on April 1, 2015Boulden: Boulden, Inc., an entity from whom we acquired certain propane operating assets

AutoGas: Alliance AutoGas, a national consortium of companies providing an industry-leading complete program for fleets interested in shifting from gasoline to clean-burning propane, of which Sharp is a memberCDD: Cooling Degree-Day

CDD: Cooling degree-day, which is the measure of the variation in weather based on the extent to which the daily average temperature (from 10:00 am to 10:00 am) is above 65 degrees Fahrenheit

Central Gas: Central Gas Company of Okeechobee, Incorporated, a propane distribution provider in Southeast Florida, which sold certain assets to Flo-gas in December 2017

CGC: Consumer Gas Cooperative, an Ohio natural gas cooperative

Chesapeake or Chesapeake Utilities: Chesapeake Utilities Corporation, its divisions and subsidiaries, as appropriate in the context of the disclosure

Chesapeake Pension Plan: A defined benefit pension plan sponsored by Chesapeake UtilitiesCHP: Combined Heat and Power Plant

Chesapeake Postretirement Plan: An unfunded postretirement health care and life insurance plan sponsored by Chesapeake Utilities

Chesapeake SERP: An unfunded supplemental executive retirement pension plan sponsored by Chesapeake Utilities

Chesapeake Service Company:Chesapeake Service Company, a wholly-owned subsidiary of Chesapeake Utilities and the parent company of Skipjack, CIC and ESRE

Chipola: Chipola Propane Gas Company, Inc., a propane distribution service provider in Northwest Florida, which sold certain assets to Flo-gas in August 2017

CHP: Combined heat and power plant

CIAC: Contributions from customers that are used to construct facilities

CIC: Chesapeake Investment Company, a wholly-owned subsidiary of Chesapeake Service Company, which is an investment company incorporated in Delaware

Columbia Gas: Columbia Gas Transmission, LLC, an unaffiliated interstate pipeline interconnected with Eastern Shore's pipeline

Columbia Gas of Ohio: An unaffiliated local distribution company based in Ohio

Company: Chesapeake Utilities Corporation, its divisions and subsidiaries, as appropriate in the context of the disclosure

CP: Certificate of Public Convenience and Necessity

Credit Agreement: The Credit Agreement dated October 8, 2015, among Chesapeake Utilities and the Lenders related to the Revolver

Degree-day: A degree-day is the measure of the variation in the weather based on the extent to which the average daily temperature (from 10:00 am to 10:00 am) falls above or below 65 degrees Fahrenheit

Delaware Division: Chesapeake Utilities' natural gas distribution operation serving customers in Delaware

Delmarva Peninsula: A peninsula on the east coast of the United States of AmericaU. S. occupied by Delaware and portions of Maryland and Virginia

Delmarva Peninsula natural gas distribution: Chesapeake Utilities' natural gas distribution operations, which includes the Delaware Division, Chesapeake Utilities' Maryland division, and SandpiperDFS: Dominion Field Services, Inc., a subsidiary of Dominion Energy, Inc.

Dodd-Frank Act: The Dodd-Frank Wall Street Reform and Consumer Protection Act

DNREC: Delaware Department of Natural Resources and Environmental Control

Dt(s): Dekatherm(s), which is a natural gas unit of measurement that includes a standard measure for heating value

Dts/d: Dekatherms per day

Eastern Shore: Eastern Shore Natural Gas Company, a wholly-owned interstate natural gas transmission subsidiary of Chesapeake Utilities

EGWIC: Eastern Gas & Water Investment Company, LLC, an affiliate of Eastern Shore Gas Company

Eight Flags: Eight Flags Energy, LLC, a subsidiary of ChesapeakeChesapeake's OnSight Services, LLC which owns and operates a CHP plant on Amelia Island,

FASB: Financial Accounting Standards Board

FERC: Federal Energy Regulatory Commission

FGT: Florida that supplies electricity to FPU and industrial steam to RayonierGas Transmission Company

EPA: United States Environmental Protection Agency

ESG: Eastern Shore Gas Company and its affiliates

ESRE: Eastern Shore Real Estate, Inc.,Flo-gas: Flo-gas Corporation, a wholly-owned subsidiary of Chesapeake Utilities that owns and leases office buildings in Delaware and Maryland to divisions and subsidiaries of Chesapeake Utilities

FASB: Financial Accounting Standards Board

FERC: Federal Energy Regulatory Commission, an independent agency of the United States government that regulates the interstate transmission of electricity, natural gas, and oil

FDEP: Florida Department of Environmental Protection

FDOT: Florida Department of Transportation

FGT: Florida Gas Transmission Company

Flo-gas: Flo-gas Corporation, a wholly-owned subsidiary of FPU

Florida Division: Chesapeake Utilities' natural gas distribution operation serving customers in Florida

Fort Meade: Fort Meade natural gas division of FPU

FPL: Florida Power & Light Company, an unaffiliated electric company that supplies electricity to FPU

FPU: Florida Public Utilities Company, a wholly-owned subsidiary of Chesapeake Utilities

FPU Medical Plan: A separate unfunded postretirement medical plan for FPU sponsored by Chesapeake UtilitiesGAAP: Generally Accepted Accounting Principles

FPU Pension Plan: A separate defined benefit pension plan for FPU sponsored by Chesapeake UtilitiesGas South: Gas South LLC

GAAP: Accounting principles generally accepted in the United States of America

Gatherco: Gatherco, Inc., a corporation that merged with and into Aspire Energy on April 1, 2015

GRIP: The Gas Reliability Infrastructure Program

Gross Margin: a non-GAAP measure defined as operating revenues less the cost of sales. The Company's cost of sales includes purchased fuel cost for natural gas, pipeline replacement program in Florida, pursuant to which we collect a surcharge from certainelectricity and propane and the cost of our customers to recover capitallabor spent on direct revenue-producing activities and other program-related costs associated with the replacement of qualifying distribution mainsexcludes depreciation, amortization and servicesaccretion

GSR: Gas Service Rates

Gulf Power: Gulf Power Company, an unaffiliated electric company which supplies electricity to FPU

Gulfstream: Gulfstream Natural Gas System, LLC, an unaffiliated pipeline network that supplies natural gas to FPU

HDD: Heating degree-day, which is a measure of the variation in weather based on the extent to which the daily average temperature (from 10:00 am to 10:00 am) is below 65 degrees FahrenheitDegree Day

ICE: Intercontinental Exchange is an electronic trading platform

IGC: Indiantown Gas Company, a division of FPU

IRS: Internal Revenue Service

JEAMetLife: The unaffiliated community-owned utility located in Jacksonville, Florida, formerly known as Jacksonville Electric Authority

Lenders: PNC, Bank of America, N.A., Citizens Bank N.A., Royal Bank of Canada, and Wells Fargo Bank, National Association, which are collectively the lenders that entered into the Credit Agreement with Chesapeake Utilities

MDE: Maryland Department of Environment

MetLife: MetLife Investment Advisors, an institutional debt investment management firm, with which weChesapeake Utilities has entered into the MetLifea Shelf Agreement

MetLife Shelf Agreement: An agreement entered into by Chesapeake Utilities and MetLife pursuant to which Chesapeake Utilities may request that MetLife purchase, through March 2, 2020, up to $150.0 million of unsecured senior debt at a fixed interest rate and with a maturity date not to exceed 20 years from the date of issuance

MetLife Shelf Notes: Unsecured senior promissory notes issuable under the MetLife Shelf Agreement

MGP: Manufactured gas plant, which is a site where coal was previously used to manufacture gaseous fuel for industrial, commercial and residential use

MTM: Fair Mark-to-Market (fair value (mark-to-market) accounting required for derivatives in accordance with ASC 815accounting)

MW: Megawatts, Megawatt, which is a unit of measurement for electric base load power or capacity

Non-Qualified Deferred Compensation Plan: A non-qualified, deferred compensation plan under which certainNJRES: New Jersey Resource Energy Services Company a subsidiary of our executives and members of the Board of Directors are able to defer payment of all or a part of certain specified types of compensation, including executive salaries, cash bonuses, executive performance shares and directors’ retainersNew Jersey Resources Inc.

NYL: New York LifeNYL: NYL Investors LLC, an institutional debt investment management firm, with which weChesapeake Utilities has entered into the NYLa Shelf Agreement and issued Shelf Notes

NYL Shelf Agreement: An agreement entered into by Chesapeake Utilities and NYL pursuant to which Chesapeake Utilities may request that NYL purchase, through March 2, 2020, up to $100.0 million of unsecured senior debt at a fixed interest rate and with a maturity date not to exceed 20 years from the date of issuance

NYL Shelf Notes: Unsecured senior promissory notes issuable under the NYL Shelf Agreement

NYSE: New York Stock Exchange

OPT Service: Off Peak ≤ 30 or ≤ 90 Firm Transportation Service, a tariff associated with Eastern Shore's firm transportation service that allows Eastern Shore to not schedule service for up to 30 or 90 days during the peak months of November through April each year

OTC: Over-the-counter

Peninsula Pipeline: Peninsula Pipeline Company, Inc., a wholly-owned subsidiary of Chesapeake Utilities' wholly-owned Florida intrastate pipeline subsidiaryUtilities

Peoples Gas: The Peoples Gas System division of Tampa Electric Company an unaffiliated utility in Florida that has a joint pipeline with Peninsula Pipeline

PESCO: Peninsula Energy Services Company, Inc., a wholly-owned subsidiary of Chesapeake Utilities' wholly-owned natural gas marketing subsidiaryUtilities

PNC: PNC Bank, National Association, the administrative agent and primary lender for our Revolver

Proxy Statement: Chesapeake Utilities’ definitive Proxy Statement to be filed no later than March 31, 2018, in connection with our Annual Meeting to be held on or about May 9, 2018

Prudential:Prudential: Prudential Investment Management Inc., an institutional investment management firm, with which we haveChesapeake Utilities has entered into the Prudentiala Shelf Agreement

Prudential Shelf Agreement: An agreement entered into by Chesapeake Utilities and Prudential pursuant to which Chesapeake Utilities may request that Prudential purchase, through October 7, 2018, up to $150.0 million of Prudentialissued Shelf Notes at a fixed interest rate and with a maturity date not to exceed 20 years from the date of issuance

Prudential Shelf Notes: Unsecured senior promissory notes issuable under the Prudential Shelf Agreement

PSC: Public Service Commission, which is the state agency that regulates theutility rates and/or services provided by Chesapeake Utilities' natural gas and electric distribution operations in Delaware, Maryland and Florida and Peninsula Pipeline in Floridacertain of our jurisdictions

RAP: Remedial Action Plan, which is a plan that outlines the procedures taken or being considered in removing contaminants from a MGP formerly owned by Chesapeake Utilities or FPU

Rayonier: Rayonier Performance Fibers, LLC, the company that owns the property on which Eight Flags' CHP plant is located and a customer of the steam generated by the CHP plant

Retirement Savings Plan: Chesapeake Utilities' qualified 401(k) retirement savings plan

Revolver: Our unsecured revolving credit facility with the Lenderscertain lenders

Rights Agreement: The Rights Agreement by and between the Company and BankBoston, N.A., dated August 20, 1999, as amended by that certain First Amendment to Rights Agreement by and between the Company and Computershare Trust Company N.A., as successor rights agent, dated September 12, 2008

Sandpiper: Sandpiper Energy: Sandpiper Energy, Inc., Chesapeake Utilities'a wholly-owned subsidiary which provides a tariff-based distribution service to customers in Worcester County, Marylandof Chesapeake Utilities

Sanford Group: FPU and other responsible parties involved with the Sanford MGP site

SCO: Standard Choice Offer, a program offered by Columbia Gas of Ohio in which PESCO was selected as a natural gas supplier pursuant to a competitive auction to serve a pool of customers within Columbia Gas of Ohio's service territory from April 2016 through March 2017

SEC: Securities and Exchange Commission

Senior Notes: Our unsecured long-term debt issued primarily to insurance companies on various dates

Sharp: Sharp Energy, Inc., Chesapeake Utilities' wholly-owned propane distribution subsidiary

Sharpgas: Sharpgas, Inc., a subsidiary of Sharp

SICP: 2013 Stock and Incentive Compensation Plan

SIR: A system improvement rate adder designed to fund system expansion costs within the city limits of Ocean City, Maryland

Skipjack: Skipjack, Inc., a wholly-owned subsidiary of Chesapeake Service CompanyUtilities

Shelf Agreement: An agreement entered into by Chesapeake Utilities and a counterparty pursuant to which Chesapeake Utilities may request that ownsthe counterparty purchase our unsecured senior debt with a fixed interest rate and leases office buildings in Delawarea maturity date not to exceed 20 years from the date of issuance

Shelf Notes: Unsecured senior promissory notes issuable under the Shelf Agreement executed with various counterparties

SICP: 2013 Stock and Maryland to affiliates of Chesapeake UtilitiesIncentive Compensation Plan

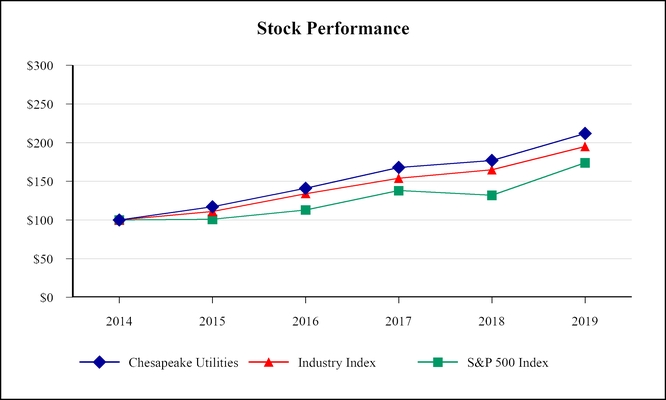

S&P 500 Index: Standard & Poor’s 500 Index, a stock market index based on the market capitalization of 500 leading companies, which is intended to represent the overall composition of the economy

TCJA: Tax Cuts and Jobs Act of 2017, legislation passed by Congress and signed into law by the Presidentenacted on December 22, 2017 which among other things reduced the corporate income tax rate from 35 percent to 21 percent, effective January 1, 2018

TETLP: Texas Eastern Transmission, LP an interstate pipeline interconnected with Eastern Shore's pipeline

Third Participation Agreement: An agreement signed by FPU and the Sanford Group, which provides for the fundingUET: United Energy Trading, LLC

U.S.: The United States of the final remedy approved by the EPA for the property owned by FPU in Sanford, FloridaAmerica

Transco: Transcontinental Gas Pipe Line Company, LLC, an interstate pipeline interconnected with Eastern Shore's pipeline

Xeron: Xeron, Inc., an inactive subsidiary of Chesapeake Utilities which previously engaged in propane and crude oil trading

PART I

References in this document to “Chesapeake,” “Chesapeake Utilities,” the “Company,” “we,” “us” and “our” mean Chesapeake Utilities Corporation, its divisions and/or its wholly-owned subsidiaries, as appropriate in the context of the disclosure.

Safe Harbor for Forward-Looking Statements

We make statements in this Annual Report on Form 10-K that do not directly or exclusively relate to historical facts. Such statements are “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933, as amended, Section 21E of the Securities Exchange Act of 1934, as amended, and the Private Securities Litigation Reform Act of 1995. One can typically identify forward-looking statements by the use of forward-looking words, such as “project,” “believe,” “expect,” “anticipate,” “intend,” “plan,” “estimate,” “continue,” “potential,” “forecast” or other similar words, or future or conditional verbs such as “may,” “will,” “should,” “would” or “could.” These statements represent our intentions, plans, expectations, assumptions and beliefs about future financial performance, business strategy, projected plans and objectives of the Company. Forward-looking statements speak only as of the date they are made or as of the date indicated and we do not undertake any obligation to update forward-looking statements as a result of new information, future events or otherwise. These statements are subject to many risks and uncertainties. In addition to the risk factors described under Item 1A,Risk Factors, the following important factors, among others, could cause actual future results to differ materially from those expressed in the forward-looking statements:

state and federal legislative and regulatory initiatives (including deregulation) that affect cost and investment recovery, have an impact on rate structures, and affect the speed and the degree to which competition enters the electric and natural gas industries;

the outcomes of regulatory, tax, environmental and legal matters, including whether pending matters are resolved within current estimates and whether the related costs associated with such matters are adequately covered by insurance or recoverable in rates;

the impact of climate change, including the impact of greenhouse gas emissions or other legislation or regulations intended to address climate change;

the impact of significant changes to current tax regulations and rates;

the timing of certification authorizations associated with new capital projects;

projects and the ability to construct facilities at or below estimated costs;

changes in environmental and other laws and regulations to which we are subject and environmental conditions of property that we now, or may in the future, own or operate;

possible increased federal, state and local regulation of the safety of our operations;

generalthe inherent hazards and risks involved in transporting and distributing natural gas and electricity;

the economy in our service territories or markets, the nation, and worldwide, including the impact of economic conditions including any potential effects arising from terrorist attacks and any hostilities(which we do not control ) on demand for electricity, natural gas, propane or other external factors over which we have no control;fuels;

long-term global climate change, whichrisks related to cyber-attacks or cyber-terrorism that could adversely affectdisrupt our business operations or result in failure of information technology systems or result in the loss or exposure of confidential or sensitive customer, demandemployee or cause extremeCompany information;

adverse weather conditions, that disrupt the Company's operations;

the weather and other natural phenomena, including the economic, operational and other effects of hurricanes, ice storms and other damaging weather events;

customers' preferred energy sources;

industrial, commercial and residential growth or contraction in our markets or service territories;

the effect of competition on our businesses;businesses from other energy suppliers and alternative forms of energy;

the timing and extent of changes in commodity prices and interest rates;

the ability to establish new, and maintain key, supply sources;

the effect of spot, forward and future market prices on our various energy businesses;

the extent of our success in connecting natural gas and electric supplies to transmission systems, establishing and inmaintaining key supply sources; and expanding natural gas and electric markets;

the creditworthiness of counterparties with which we are engaged in transactions;

the capital-intensive nature of our regulated energy businesses;

our ability to access the results of financing efforts,credit and capital markets to execute our business strategy, including our ability to obtain financing on favorable terms, which can be affected by various factors, including credit ratings and general economic conditions;

the ability to successfully execute, manage and integrate a merger, acquisition or divestiture plans;of assets or businesses and the related regulatory or other limitations imposed as a result of a merger; acquisition or divestiture, andconditions associated with the success of the business following a merger, acquisition or divestiture;

the impact on our costs and funding obligations, under our pension and other post-retirement benefit plans, of potential downturns in the financial markets, lower discount rates, and costs associated with the Patient Protectionhealth care legislation and Affordable Care Act;regulation;

the ability to continue to hire, train and retain appropriately qualified personnel; and

the effect of accounting pronouncements issued periodically by accounting standard-setting bodies;bodies.

the timing and success of technological improvements; and

risks related to cyber-attacks or cyber-terrorism that could disrupt our business operations or result in failure of information technology systems.

ITEM 1. BUSINESS.Business.

CORPORATE OVERVIEWCorporate Overview and Strategy

Chesapeake Utilities Corporation is a Delaware corporation formed in 1947.1947 with operations primarily in the Mid-Atlantic region, Florida and Ohio. We are a diversifiedan energy delivery company engaged through our operating divisionsin the distribution of natural gas, propane and subsidiaries, in various energyelectricity; the transmission of natural gas; the generation of electricity and other businesses. We operate primarily on the Delmarva Peninsulasteam, and in Florida, Pennsylvania and Ohio and provide natural gas distribution, transmission, supply, gathering, processing and marketing; electric distribution and generation; propane distribution; steam generation; and other energy-related services.providing related services to our customers.

|

|

Our strategy is to consistently produce industry leading total shareholder return by profitably investing capital into opportunities that leverage our skills and expertise in energy distribution and transmission to achieve high levels of service and growth. The key elements of our strategy include: • capital investment in growth opportunities that generate our target returns;• expanding our energy distribution and transmission operations within our existing service areas as well as into new geographic areas;• providing new services in our current service areas;• expanding our footprint in potential growth markets through strategic acquisitions that complement our businesses;• entering new energy markets and businesses that complement our existing operations and growth strategy; and• operating as a customer-centric full-service energy supplier/partner/provider, while providing safe and reliable service.Our employees strive to build meaningful connections that generate opportunities to grow our businesses, develop new markets, and enrich the communities in which we live, work and serve. |

Operating Segments

We operate within two reportable segments: Regulated Energy and Unregulated Energy. The remainder of our operations is presented as “Other businesses and eliminations." These segments are described below in detail.

The following chart shows our principal business structure by segment

Regulated Energy

Our regulated energy businesses are comprised of natural gas and other businesses:

electric distribution as well as natural gas transmission services. The following table shows operatingpresents net income for the year ended December 31, 2017,2019 and total assets as of December 31, 2017,2019, for our operating segmentsRegulated Energy segment by operation and other businesses and eliminations:area served:

|

| | | | | | | |

| (dollars in thousands) | Operating Income | | Total Assets |

| Regulated Energy | $ | 73,160 |

| | $ | 1,121,673 |

|

| Unregulated Energy | 12,477 |

| | 261,541 |

|

| Other businesses and eliminations | 206 |

| | 34,220 |

|

| Total | $ | 85,843 |

| | $ | 1,417,434 |

|

|

| | | | | | | | | | |

| | | | | | | |

| Operations | | Areas Served | | Net Income | | Total Assets |

| (in thousands) | | | | | | |

| Natural Gas Distribution | | | | | | |

| Delmarva Natural Gas (Delaware division, Maryland division and Sandpiper Energy) | | Delaware/Maryland | | $ | 9,873 |

| | $ | 280,002 |

|

| Central Florida Gas and FPU | | Florida | | 13,721 |

| | 420,483 |

|

| Natural Gas Transmission | | | | | | |

| Eastern Shore | | Delaware/Maryland/ Pennsylvania | | 17,965 |

| | 447,041 |

|

| Peninsula Pipeline | | Florida | | 5,571 |

| | 115,685 |

|

| | | | | | | |

| Electric Distribution | | | | | | |

| FPU | | Florida | | 640 |

| | 170,855 |

|

| Total Regulated Energy | | | | $ | 47,770 |

| | $ | 1,434,066 |

|

Additional financial information by business segment is set forth in Item 7, Management’s Discussion and Analysis of Financial Condition and Results of Operation, and Item 8, Financial Statements and Supplementary Data (see Note 5, Segment Information, in the consolidated financial statements).

The following charts present operating income by type of energy delivered and areas served for the year ended December 31, 2017 and average investment by type of energy delivered and areas served as of December 31, 2017.

REGULATED ENERGY

Regulated Energy is our largest segment and consists of: (i) our natural gas distribution operations in Delaware, Maryland and Florida; (ii) our electric distribution operations in Florida; and (iii) our natural gas transmission operations on the Delmarva Peninsula and in Florida. All operationsRevenues in this operating segment are regulated, as to theirbased on rates and service,regulated by the PSC having jurisdiction in each statethe states in which we operate or, by the FERC in the case of Eastern Shore. Our natural gas and electric distribution operations are local distribution utilities and generate revenues based on tariff rates approvedShore, which is an interstate business, by the PSC of each state in which we operate.FERC. The PSCs have also authorized our utilities to negotiate rates, based on approved methodologies, with customers that have competitive alternatives. Some of our customers in Maryland are, and will continue to be, served with propane through our underground propane distribution system under PSC-approved tariff rates until we complete the conversion of the system and these customers to natural gas. These customers are included in the Delmarva Peninsula natural gas distribution operation's results and customer statistics.

Eastern Shore generates revenues based upon the FERC-approved tariff rates. Eastern Shore is also authorized by the FERC to negotiate rates with its customers above or below the FERC-approved tariff rates. Peninsula Pipeline, our Florida intrastate pipeline subsidiary, is subject to regulation by the Florida PSC and has negotiated contracts with customers, including certain affiliates. Our rates are designed to provide the opportunity to generate revenues to recover all prudently incurredprudent operating and financing costs and provide a return on our rate base that is sufficient to pay interest on debt and a reasonable return for our stockholders. Each of our utilitiesdistribution and transmission operations has a rate base, which generally consists of the original cost of the utility'soperation's plant, less related accumulated depreciation, working capital and certain other assets. In certain jurisdictions, theFor Delmarva Natural Gas and Eastern Shore, rate base may also includeincludes deferred income tax liabilities and other additions or deductions. Our Regulated Energy operations in Florida do not include deferred income tax liabilities in their rate base.

The

Our natural gas commodity marketand electric distribution operations bill customers at standard rates approved by their respective state PSC. Each state PSC allows us to negotiate rates, based on approved methodologies, for Chesapeake Utilities' Florida Divisionlarge customers that can switch to other fuels. Some of our customers in Maryland receive propane through our underground distribution system in Worcester County, which we are in the process of converting to natural gas. We bill these customers under PSC-approved rates and FPU’s Indiantown division is deregulated. Accordingly, marketers, rather than a traditional utility, sellinclude them in the natural gas distribution results and customer statistics.

Our natural gas and electric distribution operations earn profits on the delivery of natural gas or electricity to end-use customers in those jurisdictions. For all of our other local distribution utilities, we have fuel cost recovery mechanisms authorized by the PSCs that allow us to periodically adjust fuel rates to reflect changes in the wholesalecustomers. The cost of natural gas andor electricity andthat we deliver is passed through to ensure wecustomers under PSC-approved fuel cost recovery mechanisms. The mechanisms allow us to adjust our rates on an ongoing basis without filing a rate case to recover allchanges in the cost of the costs prudently incurred in purchasing natural gas and electricity that we purchase for customers. Therefore, while our distribution operating revenues fluctuate with the cost of natural gas or electricity we purchase, our distribution margin (which we define as operating revenues less purchased gas or electric cost) is generally not impacted by fluctuations in the cost of natural gas or electricity.

Our natural gas transmission operations bill customers under rate schedules approved by the FERC or at rates negotiated with customers.

Operational Highlights

The following table presents operating revenues, volumes and the average number of customers by customer class for our natural gas and electric distribution operations for the year ended December 31, 2017:2019:

| | | | | | | | | |

| | | Delmarva Natural Gas Distribution | | Florida Natural Gas Distribution (2) | | FPU Electric Distribution | | Delmarva Natural Gas Distribution | | Florida Natural Gas Distribution (2) | | FPU Electric Distribution |

Operating Revenues (in thousands) | | | | | | | | | | | | | | | | | | |

| Residential | | $ | 57,365 |

| 57 | % | | $ | 38,703 |

| 38 | % | | $ | 44,082 |

| 53 | % | | $ | 62,708 |

| 60 | % | | $ | 38,248 |

| 34 | % | | $ | 45,738 |

| 59 | % |

| Commercial | | 31,585 |

| 32 | % | | 36,039 |

| 36 | % | | 41,141 |

| 50 | % | | 33,070 |

| 32 | % | | 33,126 |

| 30 | % | | 38,254 |

| 49 | % |

| Industrial | | 7,619 |

| 8 | % | | 28,182 |

| 28 | % | | 3,561 |

| 4 | % | | 8,314 |

| 8 | % | | 37,202 |

| 34 | % | | 2,128 |

| 3 | % |

Other (1) | | 3,504 |

| 3 | % | | (1,495 | ) | (2 | )% | | (5,918 | ) | (7 | )% | | 152 |

| <1% |

| | 2,327 |

| 2 | % | | (8,704 | ) | (11 | )% |

| Total Operating revenues | | $ | 100,073 |

| 100 | % | | $ | 101,429 |

| 100 | % | | $ | 82,866 |

| 100 | % | |

| Total Operating Revenues | | | $ | 104,244 |

| 100 | % | | 110,903 |

| 100 | % | | $ | 77,416 |

| 100 | % |

| | | | | | | | | | | | | | | | | | | |

Volumes (in Dts for natural gas/MWHs for electric) | | | | | | | | | | |

Volumes (in Dts for natural gas/KW Hours for electric) | | | | | | | | | | |

| Residential | | 3,368,603 |

| 28 | % | | 1,690,983 |

| 6 | % | | 291,510 |

| 46 | % | | 3,871,032 |

| 29 | % | | 1,744,486 |

| 4 | % | | 306,445 |

| 47 | % |

| Commercial | | 3,274,975 |

| 28 | % | | 7,019,970 |

| 26 | % | | 304,235 |

| 48 | % | | 3,776,388 |

| 29 | % | | 6,190,350 |

| 14 | % | | 310,856 |

| 49 | % |

| Industrial | | 5,125,633 |

| 43 | % | | 16,105,084 |

| 60 | % | | 27,380 |

| 4 | % | | 5,358,474 |

| 40 | % | | 32,736,870 |

| 76 | % | | 27,929 |

| 4 | % |

| Other | | 95,415 |

| 1 | % | | 1,875,761 |

| 8 | % | | 7,511 |

| 2 | % | | 220,541 |

| 2 | % | | 2,574,925 |

| 6 | % | | — |

| — | % |

| Total Volumes | | 11,864,626 |

| 100 | % | | 26,691,798 |

| 100 | % | | 630,636 |

| 100 | % | | 13,226,435 |

| 100 | % | | 43,246,631 |

| 100 | % | | 645,230 |

| 100 | % |

| | | | | | | | | | | | | | | | | | | |

Average Number of Customers (4)(3) | | | | | | | | | | | | | | | | | | |

| Residential | | 68,699 |

| 91 | % | | 70,206 |

| 90 | % | | 24,574 |

| 77 | % | | 73,995 |

| 91 | % | | 74,915 |

| 90 | % | | 24,573 |

| 77 | % |

| Commercial | | 6,845 |

| 9 | % | | 5,475 |

| 7 | % | | 7,450 |

| 23 | % | | 7,097 |

| 9 | % | | 5,478 |

| 7 | % | | 7,243 |

| 23 | % |

| Industrial | | 147 |

| — | % | | 2,157 |

| 3 | % | | 2 |

| — | % | | 169 |

| <1% |

| | 2,453 |

| 3 | % | | 2 |

| <1% |

|

| Other | | 5 |

| — | % | | 3 |

| — | % | | — |

| — | % | | 15 |

| <1% |

| | 12 |

| <1% |

| | — |

| — | % |

| Total Average Customers | | 75,696 |

| 100 | % | | 77,841 |

| 100 | % | | 32,026 |

| 100 | % | |

| Total Average Number of Customers | | | 81,276 |

| 100 | % | | 82,858 |

| 100 | % | | 31,818 |

| 100 | % |

(1)Operating Revenues from "Other" sources include revenue, unbilled revenue, under (over) recoveries of fuel cost, conservation revenue, other miscellaneous charges, fees for billing services provided to third parties, and adjustments for pass-through taxes.

(2) Florida natural gas distribution includes Chesapeake Utilities' Central Florida Division,Gas division, FPU and FPU's Indiantown and Fort Meade divisions.

(3) Average number of customers is based on the twelve-month average for the year ended December 31, 2017.2019.

The following table presents operating revenues, and design day capacityby customer type, for Eastern Shore and Peninsula Pipeline for the year ended December 31, 2017 and2019, as well as contracted firm transportation capacity by customer type, and design day capacity at December 31, 2017:

2019:

| | | | Eastern Shore | Eastern Shore | | Peninsula Pipeline |

Operating Revenues (in thousands) | | | | | | | |

Local distribution companies - affiliated (1) | $ | 18,350 |

| 32 | % | $ | 24,709 |

| 33 | % | | $ | 14,003 |

| 85 | % |

| Local distribution companies - non-affiliated | 22,782 |

| 39 | % | 25,171 |

| 35 | % | | 840 |

| 5 | % |

| Commercial and industrial | 20,485 |

| 35 | % | |

| Commercial and industrial - affiliated | | — |

| — | % | | 1,120 |

| 7 | % |

| Commercial and industrial - non-affiliated | | 22,527 |

| 31 | % | | 490 |

| 3 | % |

Other (2) | (3,847 | ) | (6 | )% | 516 |

| 1 | % | | — |

| — | % |

| Total Operating Revenues | $ | 57,770 |

| 100 | % | $ | 72,923 |

| 100 | % | | $ | 16,453 |

| 100 | % |

| | | | | | | | |

Contracted firm transportation capacity (in Dts/d) | | | | | | | |

| Local distribution companies - affiliated | 100,652 |

| 43 | % | 125,152 |

| 42 | % | | 243,500 |

| 95 | % |

| Local distribution companies - non-affiliated | 66,182 |

| 28 | % | 76,619 |

| 26 | % | | 4,825 |

| 2 | % |

| Commercial and industrial | 67,923 |

| 29 | % | |

| Total | 234,757 |

| 100 | % | |

| Commercial and industrial - affiliated | | — |

| — | % | | 1,500 |

| 1 | % |

| Commercial and industrial - non-affiliated | | 96,348 |

| 32 | % | | 5,100 |

| 2 | % |

| Total Contracted firm transportation capacity | | 298,119 |

| 100 | % | | 254,925 |

| 100 | % |

| | | | | | | | |

Design day capacity (in Dts/d) | 234,757 |

| 100 | % | 298,119 |

| 100 | % | | 254,925 |

| 100 | % |

(1) Eastern Shore's and Peninsula Pipeline's service to our local distribution affiliates is based on FERC-approvedthe respective regulator's approved rates and is an integral component of the cost associated with providing natural gas supplies for those affiliates. We eliminate operating revenues of Eastern Shorethese entities against the cost of sales of those affiliates in our consolidated financial information; however, our local distribution affiliates include this amount in their purchased fuel cost and recover it through fuel cost recovery mechanisms.

(2) Operating revenues from "Other" sources are from the rental of gas properties and reserve for rate case refund.

Peninsula Pipeline contracts with both affiliated and non-affiliated customers to provide firm transportation service. For the year ended December 31, 2017, operating revenues of Peninsula Pipeline were $7.2 million, of which $4.5 million was related to service to our affiliates, FPU and Eight Flags, under contracts which were previously approved by the Florida PSC. Peninsula Pipeline's operating revenues from FPU and Eight Flags are eliminated against the cost of sales in our consolidated financial information; FPU, however, includes this amount in its purchased fuel cost and recovers it through the fuel cost recovery mechanism.

As of December 31, 2017, our investments in our regulated operations were as follows: $136.5 million for Delmarva Peninsula natural gas distribution; $316.0 million for Florida natural gas and electric distribution; and $250.1 million for natural gas transmission.

Weather

Revenues from our residential and commercial sales are affected by seasonal variations in weather conditions, which directly influence the volume of natural gas and electricity sold and delivered. Specifically, customer demand substantially increases during the winter months, when natural gas and electricity are used for heating. For electricity, customer demand also increases during the summer months, when electricity is used for cooling. We measure the relative impact of weather by using a degree-day methodology accepted by the utility industry. Degree-day data is used to estimate amounts of energy required to maintain comfortable indoor temperature levels based on each day’s average temperature. Normal heating and cooling degree-days are based on the most recent 10-year average.

Our Maryland division and Sandpiper's rates include a weather normalization adjustment for residential heating and smaller commercial heating customers. A weather normalization adjustment is a billing adjustment mechanism (or "decoupled" rate mechanism) that is designed to eliminate the effect of deviations from average seasonal temperatures on utility net revenues. Sandpiper received approval from the Maryland PSC to include in its rates a revenue normalization mechanism for residential heating and smaller commercial heating customers in 2016.

We do not currently have any weather or revenue normalization or “decoupled” rate mechanisms for our other local distribution utilities.

Regulatory MattersOverview

The following table identifies thehighlights key regulatory agencies and highlights the most recent base rate proceeding information for each of our major utilities:principal Regulated Energy operations. Peninsula Pipeline is not regulated with regard to cost of service by either the Florida PSC or FERC and is therefore excluded from the table. The table reflects rate increases and rates of return approved prior to the enactment of the TCJA on December 22, 2017. See Item 8, Financial Statements and Supplementary Data (Note 19, Rates and Other Regulatory Activities and Note 12, Income Taxes in the consolidated financial statements) for further discussion on the impact of this legislation on our regulated businesses.

|

| | | | | | | |

| | Chesapeake Utilities - Delaware Division | Chesapeake Utilities - Florida Division | FPU Natural Gas | FPU Electric | Chesapeake Utilities - Maryland Division | Eastern Shore | Sandpiper |

| Regulatory Agency: | Delaware PSC | Florida PSC | Florida PSC | Florida PSC | Maryland PSC | FERC | Maryland PSC |

| Commission Structure: | 5 commissioners | 5 commissioners | 5 commissioners | 5 commissioners | 5 commissioners | 5 commissioners | 5 commissioners |

| | Part-Time | Full-Time | Full-Time | Full-Time | Full-Time | Full-Time | Full-Time |

| | Gubernatorial Appointment | Gubernatorial Appointment | Gubernatorial Appointment | Gubernatorial Appointment | Gubernatorial Appointment | Presidential Appointment | Gubernatorial Appointment |

| Base Rate Proceeding: |

|

|

|

|

|

|

|

| Delay in collection of rates subsequent to filing application | 60 days | 90 days | 90 days | 90 days | 180 days | Up to 180 days | 180 days |

| Application date associated with the most recent permanent rates | 12/21/2015 | 07/14/2009 | 12/17/2008 | 07/03/2017 | 05/01/2006 | 1/27/2017 | 12/02/2015 |

| Effective date of permanent rates | 01/01/2017 | 01/14/2010 | 01/14/2010(1) | 01/03/2018 | 12/01/2007 | 08/01/2017(2) | 12/01/2017 |

Annual rate increase approved(6) | $2,250,000 | $2,536,300 | $7,969,000 | $1,558,050 | $648,000 | $9,800,000(2) | N/A(7) |

Rate of return approved(6) | 9.75% (3) | 10.80%(3) | 10.85%(3) | 10.25%(3), (4) | 10.75%(3) | Not Stated(2) | Not Stated (5) |

|

| | | | | | | |

| | Natural Gas Distribution | | |

| | Delmarva | Florida | Electric Distribution | Natural Gas Transmission |

| Operation/Division | Delaware | Maryland | Sandpiper | Chesapeake's Florida natural gas division | FPU | FPU | Eastern Shore |

| Regulatory Agency | Delaware PSC | Maryland PSC | Maryland PSC | Florida PSC | Florida PSC | Florida PSC | FERC |

| Effective date - Last Rate Order | 01/01/2017 | 12/1/2007 | 12/01/2019 | 01/14/2010 | 01/14/2010(1) | 01/03/2018 | 08/01/2017 |

| Rate Base (in Rates) | Not stated | Not stated | Not stated | $46,680,000 | $68,940,000 | $11,850,000 | Not stated |

| Annual Rate Increase Approved | $2,250,000 | $648,000 | N/A(2) | $2,540,000 | $7,970,000 | $1,560,000 | $9,800,000 |

Capital Structure (in rates)(3)* | Not stated | LTD: 42.00% STD: 5.00% Equity: 53.00% | Not stated | LTD: 30.63% STD: 6.26% Equity: 43.49% Other: 19.62% | LTD: 30.75% Equity: 46.67% Other: 22.58% | LTD: 21.91% STD: 23.50% Equity: 54.59% | Not stated |

| Allowed Return on Equity | 9.75% (4) | 10.75%(4) | Not Stated (5) | 10.80%(4) | 10.85%(4) | 10.25%(4), (6) | Not Stated |

| TJCA Refund Status associated with customer rates | Refunded | Refunded | Refunded | Retained | Retained | Refunded | Refunded |

(1) The effective date of the order approving the settlement agreement, which adjusted the rates originally approved on June 4, 2009.

(2) Eastern Shore filed an uncontested settlement agreement with the FERCThe Maryland PSC approved a declining return on equity that will result in December 2017. FERC approved the settlement agreement by letter order on February 28, 2018. The order will be deemed final upon the expiration of the right to rehearing on March 30, 2018.a decline in our rates.

(3) Other components of capital structure include customer deposits, deferred income taxes and tax credits.

(4) Allowed after-tax return on equity.

(4)(5) The terms of the agreement include revenue neutral rates for the first year (December 1, 2016 through November 30, 2017), followed by a schedule of rate reductions in subsequent years based upon the projected rate of propane to natural gas conversions.

(6) The terms of the settlement agreement for the FPU electric division limited proceeding with the Florida PSC prescribed an authorized return on equity range of 9.25 to 11.25 percent, with a mid-point of 10.25 percent. The FPU electric division cannotcould not file for a base rate increase prior to December 2019, unless its allowed return on equity iswas below the authorized range and it experiencesexperienced an unanticipated and unforeseen event that impactsimpacted the annual revenue requirement in excess of $800,000 within any contiguous four-month period.

(5)* LTD-Long-term debt; STD-Short-term debt.

In October 2018, Hurricane Michael passed through FPU’s electric distribution service territory in Northwest Florida. The termshurricane caused widespread and severe damage to FPU’s infrastructure resulting in 100 percent of its customers in the service territory losing electrical service. FPU expended more than $65.0 million to restore service, which has been recorded as new plant and equipment, charged against FPU’s accumulated depreciation or charged against FPU’s storm reserve. While there is a short-term negative impact, the storm is not expected to have a significant impact on our financial results going forward, assuming permanent recovery is granted through the regulatory process.

In August 2019, FPU filed a limited proceeding requesting recovery of storm-related costs associated with Hurricane Michael (capital and expenses) through a change in base rates. FPU also requested treatment and recovery of certain storm-related costs as a regulatory asset for items currently not allowed to be recovered through the storm reserve as well as the recovery of capital replaced as a result of the agreement include revenue neutral rates forstorm. Recovery of these costs includes a component of an overall return on capital additions and regulatory assets. In the first year, followedfourth quarter of 2019, FPU along with the Office of Public Counsel in Florida, filed a joint motion with the Florida PSC to approve an interim rate increase, subject to refund, pending the final ruling on the recovery of the restoration costs incurred. The petition was approved by a schedule of rate reductions in subsequent years based upon the projected rate of propane to natural gas conversions.

(6) The table reflectsFlorida PSC on November 5, 2019 and interim rate increases became effective January 2, 2020. FPU continues to work with the Florida PSC and ratesexpects to reach a final ruling in the second half of return approved prior to the enactment of the TCJA on December 22, 2017.2020. SeeItem 8, Financial Statements and Supplementary Data (Note 18, 19, Rates and Other Regulatory Activities and Note 11, Income Taxes in the consolidated financial statements) for further discussion on the impact of this legislation on our regulated businesses.information.

(7)The Maryland PSC approved a declining return on equityfollowing table presents surcharge and other mechanisms that will result in a decline in our rates.

In addition to the base rateshave been approved by the PSCs, certain ofrespective PSC for our localregulated energy distribution utilities have additional surcharge mechanisms that were separately approved by their respective PSC. The most notable surcharge mechanismsbusinesses. These include Delaware’s surcharge to increaseexpand natural gas service in eastern Sussex County; Maryland's surcharge to fund natural gas conversions and system improvement in Worcester County; Florida’s GRIP surcharge which provides accelerated recovery of the costs of replacing older portions of the natural gas distribution system to improve safety and reliability and the Florida electric distribution operation's limited proceeding.

availability |

| | | | | | |

| Operation(s)/Division(s) | | Jurisdiction | | Infrastructure mechanism | | Revenue normalization |

| Delaware division | | Delaware | | Yes | | No |

| Maryland division | | Maryland | | No | | Yes |

| Sandpiper Energy | | Maryland | | Yes | | Yes |

| FPU and Central Florida Gas natural gas divisions | | Florida | | Yes | | No |

| FPU electric division | | Florida | | Yes | | No |

Weather

Weather variations directly influence the volume of natural gas and electricity sold and delivered to residential and commercial customers for heating and cooling and changes in portions of eastern Sussex County, Delaware; Maryland's surcharge designed to recovervolumes delivered impact the costs associated with conversions torevenue generated from these customers. Natural gas volumes are highest during the winter months, when residential and commercial customers use more natural gas and to improve infrastructure in Worcester County, Maryland; and Florida’s GRIP surcharge designed to recover capital and other costs, inclusivefor heating. Demand for electricity is highest during the summer months, when more electricity is used for cooling. We measure the relative impact of an appropriate return on investment, associated with acceleratingweather using degree-days. A degree-day is the replacementmeasure of qualifying distribution mains.

TCJA

At the end of December 2017, the United States Congress passed and the President signed into law, the TCJA, which is effective beginning with the 2018 tax year. Among other things, the TCJA substantially reduces the corporate income tax rate to 21 percent, effective January 1, 2018. Each state PSC, with jurisdiction over the areas that we serve, has issued, or isvariation in the processweather based on the extent to which the average daily temperature falls above or below 65 degrees Fahrenheit. Each degree of issuing, requests for information or orders directing utilities to make filings estimatingtemperature below 65 degrees Fahrenheit is counted as one heating degree-day, and each degree of temperature above 65 degrees Fahrenheit is counted as one cooling degree-day. Normal heating and cooling degree-days are based on the impacts of the TCJA on their respective costs to serve and to propose how the tax law changes are to be reflected in rates. We will comply with these orders and will make any necessary changes, as directed by the applicable PSC. The FERC has not yet issued any procedural orders on this matter; however, the settlement agreement that we filed with the FERC in December 2017 outlined the procedures and proposed customer rates in the event of tax reform. We believe that the ultimate resolution of these matters will not have a material impact on our financial position, operating results or cash flows.

See Item 8, Financial Statements and Supplementary Data (Note 11, Income Taxes, and Note 18, Rates and Other Regulatory Activities, in the consolidated financial statements), for more information.most recent 10-year average.

Competition

Our natural gas and electric distribution operations andNatural Gas Distribution

While our natural gas transmissiondistribution operations do not compete directly with other distributors of natural gas for residential and commercial customers in our service areas, we do compete with other formsnatural gas suppliers and alternative fuel providers for sales to industrial customers. Large customers could bypass our natural gas distribution systems and connect directly to interstate transmission pipelines, and we compete in all aspects of our natural gas business with alternative energy sources, including electricity, oil, propane and renewables. The principal competitive factorsmost effective means to compete against alternative fuels are lower prices, superior reliability and flexibility of service. Natural gas historically has maintained a price advantage in the residential, commercial

and industrial markets, and reliability of natural gas supply and service has been excellent. In addition, we provide flexible pricing to a lesser extent, accessibility. our large customers to minimize fuel switching and protect these volumes and their contributions to the profitability of our natural gas distribution operations.

Natural Gas Transmission

Our natural gas transmission business competes with other pipeline companies to provide service to large industrial, generation and distribution customers, primarily in the northern portion of Delmarva Peninsula and in Florida.

Electric Distribution

While our electric distribution operations have severaldo not compete directly with other distributors of electricity for residential and commercial customers in our service areas, we do compete with other electricity suppliers and alternative fuel providers for sales to industrial customers. Some of our large industrial customers that are able to use fuel oil or propane as an alternative to natural gas. When oil or propane prices decline, these interruptible customers may convert to an alternative fuel source to satisfy their fuel requirements, and our sales volumes may decline. To address the uncertainty of alternative fuel prices, we use flexible pricing arrangements on both the supply and sales sides of our business to compete with alternative fuel price fluctuations.

Large industrial natural gas customers may be able to bypass our distribution and transmission systems and make direct connections with “upstream” interstate transmission pipelines when such connections are economically feasible. Certain large industrial electric customers may be capable of generating electricity for their own consumption. Although the risk of bypassing our systems is not considered significant,electricity, and we may adjust servicesstructure rates, flexibility and rates forservice offerings to retain these customers in order to retain their business in certain situations.and contributions to the profitability of our electric distribution operations.

Supplies, Transmission and Storage

Natural Gas Distribution

Our natural gas distribution operations purchase natural gas from marketers and producers and maintain contracts for transportation and storage with several interstate pipeline companies to meet projected customer demand requirements. We believe that the availability ofour supply and transmission ofcapacity strategy will adequately meet our customers’ needs over the next several years.

The Delmarva natural gas is adequate under existing arrangementsdistribution systems are directly connected to meet the needs of our customers.

Our Delaware, Maryland and Sandpiper divisions use their firm transportation resources to meet a significant percentage of their projected demand requirements. They purchase firm natural gas supplies to meet those projected requirements with purchases of base load, daily spot supplies and storage service. They have both firm and interruptible transportation service contracts with four interstate “open access” pipeline companies (Eastern Shore, Transco, Columbia Gas and TETLP) in order to meet customer demand. Their distribution system is directly interconnected with Eastern Shore’s pipeline, which is directly interconnectedhas connections to the other pipelines that provide us with the upstream pipelines of Transco, Columbia Gastransportation and TETLP. The following table summarizes the firm transportation agreements for Delaware and Maryland divisions:

|

| | | | | | |

| | | | | Maximum Daily Firm Transportation Capacity (Dts) | | Contract Expiration Date |

| Division | | Counterparty | | |

| Delaware | | Eastern Shore | | 72,029 | | 2018 - 2028 |

| | | Columbia Gas | | 10,960 | | 2019 - 2020 |

| | | Transco | | 21,423 | | 2018 - 2028 |

| | | TETLP | | 34,100 | | 2027 |

| | | | | | | |

| Maryland | | Eastern Shore | | 26,673 | | 2018 - 2027 |

| | | Columbia Gas | | 4,200 | | 2018 - 2019 |

| | | Transco | | 6,128 | | 2018 |

| | | TETLP | | 15,900 | | 2027 |

The Delaware and Maryland divisionsstorage. These operations can also have the capability to use propane-air and liquefied natural gas peak-shaving equipment to supplement or displaceserve customers. Our Delmarva Peninsula natural gas purchases.

Our Delaware and Maryland divisions contract with our natural gas marketing subsidiary, PESCO, through andistribution operations had asset management agreement,agreements with PESCO to optimizemanage their natural gas transportation and storage capacitycapacity. The agreements were effective as of April 1, 2017, and secure an adequate supplyeach has a three-year term, expiring on March 31, 2020. As a result of natural gas. Pursuant to the three-year asset management agreement,sale of PESCO's assets and contracts, effective October 1, 2019, these agreements are now managed by NJRES. Our Delmarva operations receive a fee, which we share with our customers, from the asset manager, payswho optimizes the transportation, storage and natural gas supply for these operations.

Our Florida natural gas distribution operation uses Peninsula Pipeline and the Peoples Gas System division of Tampa Electric Company ("Peoples Gas") to transport natural gas where there is no direct connection with FGT. In May 2019, FPU natural gas distribution and Eight Flags entered into separate asset management agreements with Emera Energy Services, Inc. to manage their natural gas transportation capacity. Short-term agreements were entered for a one year term beginning July 2019 through July 2020 with the expectation that long-term agreements will then be executed for a 10-year term commencing on or about July 2020.

A summary of our divisions a fee, which our divisions share with their customers.

Sandpiper is a party to apipeline capacity supply and operating agreement with EGWIC to purchase propane, with a contract ending in May 2019. Sandpiper's current annual commitment is estimated at approximately 2.7 million gallons. Sandpiper has the option to enter into either a fixed per-gallon price for some or all of the propane purchases or a market-based price utilizing one of two local propane pricing indices. Sandpiper also has 1,950 Dts of maximum daily firm transportation capacity available from Eastern Shore through contracts expiring on various dates between 2018 and 2027.

The following table summarizes the firm transportation agreements for our Florida Division and FPU:follows:

|

| | | | | | |

| | | | | Maximum Daily Firm Transportation Capacity (Dts) | | Contract Expiration Date |

| Division | | Counterparty | | |

| Florida Division | | Gulfstream (1) | | 10,000 | | 2022 |

| | | | | | | |

| FPU | | FGT | | 41,909 - 73,317 | | 2020 - 2041 |

| | | Peninsula Pipeline | | 25,000 - 32,000 | | 2033 - 2038 |

| | | Peoples Gas System | | 2,660 | | 2024 - 2035 |

| | | Florida City Gas | | 300 | | 2032 |

|

| | | | | | |

| | | | | Maximum Daily Firm Transportation Capacity (Dts) | | Contract Expiration Date |

| Division | | Pipeline | | |

| Delmarva Natural Gas Distribution | | Eastern Shore | | 125,152 | | 2020-2028 |

| | | Columbia Gas(1) | | 15,160 | | 2020-2024 |

| | | Transco(1) | | 27,732 | | 2019-2028 |

| | | TETLP(1) | | 50,000 | | 2027 |

| | | | | | | |

| Florida Natural Gas Distribution | | Gulfstream(2) | | 10,000 | | 2022 |

| | | FGT | | 53,409 - 84,817 | | 2020-2041 |

| | | Peninsula Pipeline | | 237,500 | | 2033-2048 |

| | | Peoples Gas | | 2,660 | | 2024-2035 |

| | | Florida Southeast Connection | | 5,000 | | 2045 |

| | | Southern Natural Gas Company | | 5,000 | | 2020 |

(1) Transcontinental Gas Pipe Line Company, LLC ("Transco"), Columbia Gas Transmission, LLC ("Columbia Gas") and Texas Eastern Transmission, LP ("TETLP") are interstate pipelines interconnected with Eastern Shore's pipeline

(2) Pursuant to a capacity release program approved by the Florida PSC, all of the capacity under this agreement has been released to various third parties, including PESCO.parties. Under the terms of these capacity release agreements, Chesapeake Utilities is contingently liable to Gulfstream should any party, that acquired the capacity through release, fail to pay the capacity charge.

FPU uses gas marketers and producers to procure all of its gas supplies to meet projected requirements. FPU also uses Peoples Gas to provide wholesale gas sales service in areas far from FPU's interconnections with FGT.

Eastern Shore has three agreements with Transco for a total of 7,292 Dts/d of firm daily storage injection and withdrawal entitlements and total storage capacity of 288,003 Dts. These agreements expire on various dates between 2018 andin March 2023. Eastern Shore retains these firm storage services in order to provide swing transportation service and firm storage service to customers requesting such services.

During 2017, FPU purchasedElectric Distribution

Our Florida electric distribution operation purchases wholesale electricity primarily from three main suppliers: JEA, Gulf Powerunder the power supply contracts summarized below:

|

| | | |

| Counterparty | Area Served by Contract | Contracted Amount (MW) | Contract Expiration Date |

| Gulf Power Company | Northwest Florida | Full Requirement* | 2026 |

| FPL | Northeast Florida | Full Requirement* | 2026 |

| Eight Flags | Northeast Florida | 21 | 2036 |

| Rayonier | Northeast Florida | 1.7 to 3.0 | 2036 |

| WestRock Company | Northwest Florida | As-available | N/A |

*The counter party is obligated to provide us with the electricity to meet our customers’ demand, which may vary.

Unregulated Energy

In the third and Eight Flags.fourth quarter of 2019, we reached agreements with four entities to sell PESCO's assets and contracts. These transactions closed during the fourth quarter of 2019. As a result of January 2018, FPU purchases its wholesale electricity primarily from Gulf Power, FPLthe sale, we have fully exited the natural gas marketing business, which provided natural gas management and Eight Flags.supply services to commercial and industrial customers in Florida, Delaware, Maryland, Pennsylvania, Ohio and other states. Accordingly, PESCO’s historical financial results are reflected in our consolidated financial statements as discontinued operations, which required retrospective application to financial information for all periods presented. See Item 8, Financial Statements and Supplementary Data (Note 4, Acquisitions and Divestitures in the consolidated financial statements) for further information. The following table summarizespresents net income for the supply contractsyear ended December 31, 2019 and total assets as of December 31, 2019, for FPU:our Unregulated Energy segment by operation and area served:

|

| | |

| Counterparty | Contracted Amount (MW) | Contract Expiration Date |

| Gulf Power | Full Requirement | 2019 |

| FPL | Full Requirement | 2024 |

| Eight Flags | 21 | 2036 |

| Rayonier | 1.7 to 3.0 | 2036 |

| WestRock Company | As-available | N/A |

The Gulf Power contract provides generation and transmission service to the Northwest Florida service territory. The FPL contract provides generation and transmission service to the Northeast Florida service territory. The electricity purchased from Eight Flags, Rayonier and WestRock Company serves a portion of FPU's electric distribution customers' base load in Northeast Florida.

UNREGULATED ENERGY

Our Unregulated Energy segment provides: (i) propane distribution; (ii) natural gas marketing; (iii) unregulated natural gas supply, gathering and processing; (iv) electricity and steam generation; and (v) other unregulated energy-related services to customers. Revenues generated from this segment are not subject to any federal, state or local pricing regulations. Our businesses in this segment typically complement our regulated energy businesses based on the products and services they sell.

|

| | | | | | | | | | |

| Operations | | Area Served | | Net Income | | Total Assets |

| (in thousands) | | | | | | |

| Propane Operations (Sharp, FPU and Flo-gas) | | Delaware, Maryland, Virginia, Pennsylvania, Florida | | $ | 6,297 |

| | $ | 134,791 |

|

| Energy Transmission (Aspire Energy) | | Ohio | | 3,822 |

| | 94,124 |

|

| Energy Generation (Eight Flags) | | Florida | | 1,908 |

| | 38,569 |

|

| Marlin Gas Services | | The Eastern U.S. | | 986 |

| | 27,269 |

|

| Other | | Other | | 382 |

| | 171 |

|

| Total | | | | $ | 13,395 |

| | $ | 294,924 |

|

Propane DistributionOperations

Our propane distribution operations sell propane to residential, commercial/industrial, and wholesale customers, includingand AutoGas customers, in Delmarva and southeastern Pennsylvania,the Mid-Atlantic region, through Sharp Energy, Inc. and Sharpgas, Inc., and in Florida through FPU and Flo-gas. Many ofWe deliver to and bill our propane distribution customers are “bulk delivery” customers. We make deliveries of propane to thebased on two primary customer types: bulk delivery customers as needed, based on the level of propane remaining in the tank locatedand metered customers. Bulk delivery customers receive deliveries into tanks at the customer’s premises.their location. We invoice and record revenues for our bulk delivery servicethese customers at the time of delivery, rather than upon customers’ actual usage, since thedelivery. Metered customers typically own the propane gas in the tanks on their premises. We also haveare either part of an underground propane distribution systems serving various neighborhoodssystem or have a meter installed on the tank at their location. We invoice and communities. Suchrecognize revenue for these customers are billed monthly based on actualtheir consumption which is measuredas dictated by meters installed on their premises. In Florida, we also offer metered propane distribution service to residential and commercial customers. We read the meters on such customers' tanks and bill customers monthly.scheduled meter reads. As a member of AutoGas Sharp and AutoGasAlliance, we install and support propane vehicle conversion systems for vehicle fleets. Sharp continues to convert fleets to bi-fuel propane-powered engines and provides onsiteprovide on-site fueling infrastructure.

Propane DistributionOperations - Operational Highlights

For the year ended December 31, 2017,2019, operating revenues, volumes sold and average number of customers by customer class for our Delmarva Peninsula and PennsylvaniaMid-Atlantic and Florida propane distribution operations were as follows:

| | | | | Delmarva Peninsula and Pennsylvania | | Florida | | Operating Revenues (in thousands) | | Volumes (in thousands of gallons) | | Average Number of Customers (1) |

Operating Revenues (in thousands) | | | | | |

| | | | Mid-Atlantic | | Florida | | Mid-Atlantic | | Florida | | Mid-Atlantic (2) | | Florida |

| | | | | | | | | | | | | | | | | | | | | | |

| Residential bulk | | $ | 21,051 |

| | 28 | % | | $ | 6,123 |

| | 28 | % | | $ | 26,190 |

| | 30 | % | | $ | 6,639 |

| | 34 | % | | 10,491 |

| | 18 | % | | 1,489 |

| | 23 | % | | 27,729 |

| | 67 | % | | 10,416 |

| | 60 | % |

| Residential metered | | 7,904 |

| | 11 | % | | 4,735 |

| | 22 | % | | 9,407 |

| | 11 | % | | 4,852 |

| | 25 | % | | 4,146 |

| | 7 | % | | 818 |

| | 13 | % | | 9,863 |

| | 23 | % | | 5,922 |

| | 34 | % |

| Commercial bulk | | 13,655 |

| | 18 | % | | 5,104 |

| | 23 | % | | 20,079 |

| | 23 | % | | 4,506 |

| | 23 | % | | 13,979 |

| | 24 | % | | 2,372 |

| | 36 | % | | 4,418 |

| | 10 | % | | 934 |

| | 5 | % |

| Commercial metered | | — |

| | — | % | | 2,119 |

| | 10 | % | | — |

| | — | % | | 1,971 |

| | 10 | % | | — |

| | — | % | | 814 |

| | 13 | % | | — |

| | — | % | | 271 |

| | 1 | % |

| Wholesale | | 24,667 |

| | 33 | % | | 920 |

| | 4 | % | | 21,154 |

| | 24 | % | | 862 |

| | 4 | % | | 25,629 |

| | 44 | % | | 983 |

| | 15 | % | | 26 |

| | <1% |

| | 6 |

| | <1% |

|

| AutoGas | | 2,318 |

| | 3 | % | | — |

| | — | % | | 4,806 |

| | 6 | % | | — |

| | — | % | | 3,895 |

| | 7 | % | | — |

| | — | % | | 86 |

| | <1% |

| | — |

| | — | % |

Other (1) | | 5,033 |

| | 7 | % | | 2,946 |

| | 13 | % | |

| Total Operating Revenues | | $ | 74,628 |

| | 100 | % | | $ | 21,947 |

| | 100 | % | |

Other (3) | | | 6,822 |

| | 6 | % | | 676 |

| | 4 | % | | — |

| | — | % | | — |

| | — | % | | — |

| | — | % | | — |

| | — | % |

| Total | | | $ | 88,458 |

| | 100 | % | | $ | 19,506 |

| | 100 | % | | 58,140 |

| | 100 | % | | 6,476 |

| | 100 | % | | 42,122 |

| | 100 | % | | 17,549 |

| | 100 | % |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Volumes (in thousands of gallons) | | | | | | | | | |

| Residential bulk | | 8,718 |

| | 17 | % | | 1,433 |

| | 23 | % | |

| Residential metered | | 3,352 |

| | 6 | % | | 893 |

| | 14 | % | |

| Commercial bulk | | 9,032 |

| | 18 | % | | 2,371 |

| | 37 | % | |

| Commercial metered | | — |

| | — | % | | 827 |

| | 13 | % | |

| Wholesale | | 24,463 |

| | 48 | % | | 812 |

| | 13 | % | |

| AutoGas | | 2,159 |

| | 4 | % | | — |

| | — | % | |

| Other | | 3,500 |

| | 7 | % | | — |

| | — | % | |

| Total Volumes | | 51,224 |

| | 100 | % | | 6,336 |

| | 100 | % | |

| | | | | | | | | | |

Average Number of Customers (2) | | | | | | | | | |

| Residential bulk | | 25,452 |

| | 66 | % | | 9,059 |

| | 55 | % | |

| Residential metered | | 8,669 |

| | 23 | % | | 6,089 |

| | 37 | % | |

| Commercial bulk | | 4,166 |

| | 11 | % | | 930 |

| | 6 | % | |

| Commercial metered | | — |

| | — | % | | 278 |

| | 2 | % | |

| Wholesale | | 35 |

| | — | % | | 8 |

| | — | % | |

| AutoGas | | 74 |

| | — | % | | — |

| | — | % | |

| Total Average Customers | | 38,396 |

| | 100 | % | | 16,364 |

| | 100 | % | |

(1)Average number of customers is based on a twelve-month average for the year ended December 31, 2019.

(2) Average numbers of customers for the Mid-Atlantic propane operations includes approximately 5,200 customers added in December 2019 in the acquisition of certain propane operating assets of Boulden. See Item 8, Financial Statements and Supplementary Data (Note 4, Acquisitions and Divestitures in the consolidated financial statements) for further information.

(3) Operating revenues from "Other" sources include revenues from energy-related merchandise; customer loyalty programs; delivery, service and appliance fees; and unbilled revenues.

(2)Average number of customer is based on twelve-month average for the year ended December 31, 2017.

Propane Distribution - Competition

WeOur propane operations compete with several other propane distributors in our geographic markets,national and local independent companies primarily on the basis of price and service. Our competitorsPropane is generally include local outlets of national distributors and local independent distributors, whose proximity to customers entails lower costs to provide service. As an energy source, propane competes witha cheaper fuel for home heating than oil and electricity which are typicallybut more expensive (based on equivalent unit of heat value). Sincethan natural gas has historically been less expensive thangas. Our propane propane is generallyoperations are largely concentrated in areas that are not utilized for home heating in geographic areascurrently served by natural gas pipelines or distribution systems.

Propane Distribution - Supplies, Transportation and Storage

We purchase propane for our propane distribution operations primarily from suppliers, including major oil companies and independent producers of natural gas liquids. Although suppliesliquids producers. Propane is transported by truck and rail to our bulk storage facilities in Delaware, Maryland, Florida, Pennsylvania and Virginia, which have a total storage capacity of propane7.4 million gallons. Deliveries are made from these and other sources are generally readily available for purchase, extreme market conditions, such asfacilities by truck to tanks located on customers’ premises or to central storage tanks that feed our underground propane distribution systems. While propane supply has traditionally been adequate, significant fluctuations in weather, closing of refineries and disruption in supply chains, could result in a reductioncause temporary reductions in available supplies.