0001043219srt:RetailSiteMembersrt:MinimumMemberstpr:COnly:RealEstateDebtInvestmentsMember2020-01-012020-12-31

| | |

UNITED STATES SECURITIES AND EXCHANGE COMMISSION WASHINGTON, D.C. 20549

|

FORM 10-K

☒ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

FOR THE FISCAL YEAR ENDED: December 31, 20202023

OR

☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

FOR THE TRANSITION PERIOD FROM _______________ TO _________________

COMMISSION FILE NUMBER: 1-13447

ANNALY CAPITAL MANAGEMENT INC

(Exact Name of Registrant as Specified in its Charter)

| | | | | | | | |

| Maryland | 22-3479661 |

| (State or other jurisdiction of incorporation or organization) | (IRS Employer Identification No.) |

| | | |

| 1211 Avenue of the Americas | |

| New York, | New York | 10036 |

| (Address of principal executive offices) | (Zip Code) |

(212) 696-0100

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

| | | | | | | | |

| Title of Each Class | Trading Symbol(s) | Name of Each Exchange on Which Registered |

| | | |

| Common Stock, par value $0.01 per share | NLY | New York Stock Exchange |

| | |

| | |

| | |

| | |

| 6.95% Series F Fixed-to-Floating Rate Cumulative Redeemable Preferred Stock | NLY.F | New York Stock Exchange |

| 6.50% Series G Fixed-to-Floating Rate Cumulative Redeemable Preferred Stock | NLY.G | New York Stock Exchange |

| 6.75% Series I Fixed-to-Floating Rate Cumulative Redeemable Preferred Stock | NLY.I | New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark whether the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes ☑ No ☐

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

Yes ☐ No ☑

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☑ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☑ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Large accelerated filer | ☑ | | Accelerated filer | ☐ | | Non-accelerated filer | ☐ | | Smaller reporting company | ☐ | | Emerging growth company | ☐ |

| | | | | | | | | | | | | |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☑

If an emerging growth company,securities are registered pursuant to Section 12(b) of the Act, indicate by check mark ifwhether the financial statements of the registrant has elected notincluded in the filing reflect the correction of an error to usepreviously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the extended transitionregistrant’s executive officers during the relevant recovery period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act.§240.10D-1(b). ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ☐ No ☑

At June 30, 2020,2023, the aggregate market value of the voting common stock held by non-affiliates of the registrant was approximately $9.2$9.8 billion, based on the closing sales price of the registrant’s common stock on such date as reported on the New York Stock Exchange.

The number of shares of the registrant’s Common Stockcommon stock outstanding on February 2, 2021January 31, 2024 was 1,398,502,906.500,080,287.

DOCUMENTS INCORPORATED BY REFERENCE

The registrant intends to file a definitive proxy statement pursuant to Regulation 14A within 120 days of the end of the fiscal year ended December 31, 2020.2023. Portions of such proxy statement are incorporated by reference into Part III of this Form 10-K.

| | | | | | | | |

| ANNALY CAPITAL MANAGEMENT, INC.

2020 2023 FORM 10-K ANNUAL REPORT

TABLE OF CONTENTS | |

| | Page |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| |

| | |

Special Note Regarding Forward-Looking Statements

This presentation, other written or oral communications, and our public documents to which we refer contain or incorporate by reference certain forward-looking statements which are based on various assumptions (some of which are beyond our control) and may be identified by reference to a future period or periods or by the use of forward-looking terminology, such as “may,” “will,” “believe,” “expect,” “anticipate,” “continue,” or similar terms or variations on those terms or the negative of those terms. Such statements include those relating to the Company’s future performance, macro outlook, the interest rate and credit environments, tax reform and future opportunities. Actual results could differ materially from those set forth in forward-looking statements due to a variety of factors, including, but not limited to, changes in interest rates; changes in the yield curve; changes in prepayment rates; the availability of mortgage-backed securities (“MBS”) and other securities for purchase; the availability of financing and, if available, the terms of any financing; changes in the market value of the Company’s assets; changes in business conditions and the general economy; the Company’s ability to grow its residential credit business; the Company's ability to grow its mortgage servicing rights business; credit risks related to the Company’s investments in credit risk transfer securities and residential mortgage-backed securities and related residential mortgage credit assets; risks related to investments in mortgage servicing rights; the Company’s ability to consummate any contemplated investment opportunities; changes in government regulations or policy affecting the Company’s business; the Company’s ability to maintain its qualification as a REIT for U.S. federal income tax purposes; the Company’s ability to maintain its exemption from registration under the Investment Company Act of 1940; and operational risks or risk management failures by us or critical third parties, including cybersecurity incidents. For a discussion of the risks and uncertainties which could cause actual results to differ from those contained in the forward-looking statements, see “Risk Factors” in our most recent Annual Report on Form 10-K and any subsequent Quarterly Reports on Form 10-Q. The Company does not undertake, and specifically disclaims any obligation, to publicly release the result of any revisions which may be made to any forward-looking statements to reflect the occurrence of anticipated or unanticipated events or circumstances after the date of such statements, except as required by law.

Website and Social Media Disclosure

We use our website (www.annaly.com) and LinkedIn account (www.linkedin.com/company/annaly-capital-management) as channels of distribution of company information. The information we post through these channels may be deemed material. Accordingly, investors should monitor these channels, in addition to following our press releases, SEC filings and public conference calls and webcasts. In addition, you may automatically receive email alerts and other information about Annaly when you enroll your email address by visiting the “Investors” section of our website, then clicking on “Investor Resources” and selecting “Email Alerts” to complete the email notification form. Our website, any alerts and social media channels are not incorporated into this annual report on Form 10-K.

ANNALY CAPITAL MANAGEMENT, INC. AND SUBSIDIARIES

ITEM 1. BUSINESS

PART I

“Annaly,” “we,” “us,” or “our” refers to Annaly Capital Management, Inc. and our wholly-owned subsidiaries, except where it is made clear that the term means only the parent company.

Refer to the section titled “Glossary of Terms” located at the end of Part II, Item 7. “Management’s Discussion and Analysis of Financial Condition and Results of Operations.” for definitions of certain of the commonly used terms in this annual report on Form 10-K.

The following description of our business should be read in conjunction with the Consolidated Financial Statements and the related Notes thereto, and the information set forth under the heading “Special Note Regarding Forward-Looking Statements” in Item 7. “Management’s Discussion and Analysis of Financial Condition and Results of Operations.”

INDEX TO ITEM 1. BUSINESS

| | | | | |

| | Page |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

Closing of the Internalization and Termination of the Management Agreement | |

| Information about our Executive Officers | |

| |

| |

| |

| |

| |

| |

ANNALY CAPITAL MANAGEMENT, INC. AND SUBSIDIARIES

ITEM 1. BUSINESS

Business Overview

Introduction

We are a leading diversified capital manager that invests in and finances residential and commercial assets.with investment strategies across mortgage finance. Our principal business objective is to generate net income for distribution to our stockholders and optimize our returns through prudent management of our diversified investment strategies. We are an internally-managed Maryland corporation founded in 1997 that has elected to be taxed as a real estate investment trust (“REIT”). Prior to the closing of the Internalization (as defined below under “Closing of the Internalization and Termination of the Management Agreement”) on June 30, 2020, we were externally managed by Annaly Management Company LLC (our “Former Manager”). Our common stock is listed on the New York Stock Exchange under the symbol “NLY.”

We use our capital coupled with borrowed funds to invest primarily in real estate related investments, earning the spread between the yield on our assets and the cost of our borrowings and hedging activities.

We believe that our business objectives are supported by our size and conservative financial posture relative to the industry, the extensive experience of our employees, the diversity of our investment strategy, a comprehensive risk management approach, the availability and diversification of financing sources and our operational efficiencies.

Investment Groups

Our fourthree investment groups are primarily comprised of the following:

| | | | | |

| Investment Groups | Description |

| Annaly Agency Group | Invests in Agency mortgage-backed securities (“MBS”) collateralized by residential mortgages which are guaranteed by Fannie Mae, Freddie Mac or Ginnie Mae.Mae and complementary investments within the Agency market, including Agency commercial MBS. |

| Annaly Residential Credit Group | Invests primarily in non-Agency residential mortgage assetswhole loans and securitized products within securitized productthe residential and whole loancommercial markets. |

Annaly Commercial Real EstateMortgage Servicing Rights Group | Originates and investsInvests in commercialmortgage servicing rights ("MSR"), which provide the right to service residential mortgage loans securities, and other commercial real estate debt and equity investments.in exchange for a portion of the interest payments made on the loans. |

| Annaly Middle Market Lending Group | Provides financing to private equity-backed middle market businesses, focusing primarily on senior debt within select industries.

In April 2022, we entered into a definitive agreement to sell substantially all of the assets that comprise our Middle Market Lending (“MML”) portfolio, including assets held on balance sheet as well as assets managed for third parties. During the year ended December 31, 2022, the assets comprising the MML portfolio were legally transferred. For additional information about this transaction, see the Note titled “Sale of Middle Market Lending Portfolio” in the Notes to the Consolidated Financial Statements included in Item 15. “Exhibits, Financial Statement Schedules.”

In March 2021, we entered into a definitive agreement to sell and exit our Commercial Real Estate (“CRE”) business with the platform and the significant majority of the assets transferred during the year ended December 31, 2021. During the year ended December 31, 2022, the remaining CRE assets and associated liabilities were transferred. For additional information about this transaction, see the Note titled “Sale of Commercial Real Estate Business” in the Notes to the Consolidated Financial Statements included in Item 15. “Exhibits, Financial Statement Schedules.”

Operating Platform

Our operating platform reflects our investments in systems, infrastructure and personnel. Our technology investments have led to the development of proprietary portfolio analytics, financial and capital allocation modeling, portfolio cash and accounting sub-ledger systems, and other risk and reporting tools, which, coupled with cutting-edge digital transformation applications, support the diversification and operating efficiency of our business.business and our ability to implement new investment strategies. Our operating platform supports our investments in Agency assets as well as residential credit assets, commercial real estate assets, residential mortgage loans, and mortgage servicing rights and corporate loans.rights. We believe that the diversity of our investment alternatives provides us the flexibility to adapt to changes in market conditions and to take advantage of potential opportunities.

Business and Investment Strategy

Shared Capital Model

Our company is comprised of fourthree investment groups, each of which has multiple investment options to capitalize on attractive relative returns and market opportunities. In aggregate, we maintain numerous investment options across our investment groups. Our shared capital model drives our capital allocation strategy allowing us to rotate our investments based on relative value while also managing risk.

Strategic Relationships

A key element of our strategy is to establish and grow strategic relationships with industry leading partners in order to develop and broaden access to quality originations flow as well as to leverage third party operations to efficiently manage operating

ANNALY CAPITAL MANAGEMENT, INC. AND SUBSIDIARIES

ITEM 1. BUSINESS

costs, all in an effort to generate attractive risk adjustedrisk-adjusted returns for our shareholders. Additionally, we have attracted capital partners to our business, augmenting our public capital markets efforts, which has resulted in increased scale without sacrificing balance sheet liquidity. Certain of our strategic relationships also afford us the opportunity to support communities through socially responsible investing.

We have created multiple strategic and capital partnerships across our investment groups including the following:

ANNALY CAPITAL MANAGEMENT, INC. AND SUBSIDIARIES

ITEM 1. BUSINESS

–Annaly Residential Credit Group has established relationships with key mortgage loan originators and aggregators including well-known money center banks, allowing us to efficiently source proprietary originations suited to our risk parameters.

–Annaly Commercial Real Estate Group maintains a partnership with Pearlmark Real Estate Partners, a leading real estate private equity sponsor, providing access to co-investment opportunities through their seasoned commercial real estate investment team.

–We have partnered with Pingora Loan Servicing, a premier mortgage servicer for MSR assets and a wholly-owned subsidiary of Bayview Asset Management, through our joint venture with GIC Private Limited (“GIC”), a leading Sovereign Wealth Fund.

–We have also partnered with GICsovereign wealth fund, through the creation of a joint venture with the purpose of investing in residential credit assets, including newly-originated residential loans and securities issued by our subsidiaries.

–We have partnered with Capital Impact Partners, a national community development financial institution, to create a social impact joint venture supporting projects in underserved communities across the country.

–We have partnered with Fifth Wall Ventures, the largest venture capital firm focused on technology for the real estate industry, through a commitment to invest in their funds that target investments in North American early- and late-stage real estate software and marketplace companies. The partnership aims to identify innovative platforms and services that provide efficiencies across our core investment strategies.

Our Portfolio and Capital Allocation Policy

Under our capital allocation policy and subject to oversight by our Board of Directors (“Board”), we may allocate our investments within our target asset classes as we determine to be appropriate from time to time.

Our Board may adopt changes to our capital allocation policy and targeted assets at its discretion.

The nature of our assets and our operations are intended to meet our REIT qualification requirements and our exemption from registration as an investment company under the Investment Company Act of 1940, as amended (“Investment Company Act”).

Our portfolio composition and capital allocation at December 31, 20202023 and 20192022 were as follows:

| | | | | | | | | | | | | | | | | | | | | | | |

| | December 31, 2020 | | December 31, 2019 |

| Investment Group | Percentage of Portfolio | | Capital Allocation (1) | | Percentage of Portfolio | | Capital Allocation (1) |

| Residential | | | | | | | |

Annaly Agency Group (2)(3) | 93% | | 78% | | 93% | | 74% |

Annaly Residential Credit Group (3) | 3% | | 7% | | 3% | | 10% |

| Commercial | | | | | | | |

Annaly Commercial Real Estate Group (3) | 2% | | 5% | | 2% | | 7% |

| Annaly Middle Market Lending Group | 2% | | 10% | | 2% | | 9% |

(1)Capital allocation represents the percentage of equity allocated to each category.

(2)Includes MSRs and TBA purchase contracts.

(3)Includes assets transferred or pledged to securitization vehicles net of debt issued by securitization vehicles.

| | | | | | | | | | | | | | | | | | | | | | | |

| | December 31, 2023 | | December 31, 2022 |

| Asset Classes | Percentage of Portfolio | | Capital Allocation (2) | | Percentage of Portfolio | | Capital Allocation (2) |

| | | | | | | |

Agency (1)(2) | 88% | | 61% | | 90% | | 66% |

Residential Credit (2) | 8% | | 20% | | 7% | | 19% |

MSR (2) | 3% | | 18% | | 2% | | 14% |

| | | | | | | |

| Commercial Real Estate | 1% | | 1% | | 1% | | 1% |

| | | | | | | |

(1) Includes to-be-announced forward contracts (“TBAs”). (2) Assets exclude assets transferred or pledged to securitization vehicles, include TBA purchase contracts (market value), unsettled MSR commitments, CMBX derivatives (market value), and retained securities that are eliminated in consolidation and are shown net of participations issued. |

Risk Appetite

We maintain a firm-wide risk appetite statement which defines the types and levels of risk we are willing to take in order to achieve our business objectives, and reflects our risk management philosophy. We engage in risk activities based on our core expertise that aim to enhance value for our stockholders. Our activities focus on income generation and capital preservation through proactive portfolio management, supported by a conservative liquidity and leverage posture.

The risk appetite statement asserts the following key risk parameters to guide our investment management activities:

ANNALY CAPITAL MANAGEMENT, INC. AND SUBSIDIARIES

ITEM 1. BUSINESS

| | | | | |

| Risk Parameter | Description |

Portfolio compositionComposition | We will maintain a portfolio comprised of target assets approved by our Board and in accordance with our capital allocation policy. |

| Leverage | We generally expect to maintain an economic leverage ratio no greater than 10:1.1 considerate of our overall capital allocation framework. |

Liquidity riskRisk | We will seek to maintain an unencumbered asset portfolio sufficient to meet our liquidity needs even under adverse market conditions. |

Interest rate riskRate Risk | We will seek to manage interest rate risk to protect the portfolio from adverse rate movements utilizing derivative instruments targeting both income generation and capital preservation. |

Credit riskRisk | We will seek to manage credit risk by making investments which conform withinto our specific investment policy parameters and optimize risk-adjusted returns. |

Capital preservationPreservation | We will seek to protect our capital base through disciplined risk management practices. |

ComplianceOperational Risk | We will seek to limit impacts to our business through disciplined operational risk management practices addressing areas including but not limited to, management of key third party relationships (i.e. originators, sub-servicers), human capital management, cybersecurity and technology related matters, business continuity and financial reporting risk. |

| Compliance, Regulatory and Legal | We will seek to comply with regulatory requirements needed to maintain our REIT status and our exemption from registration under the Investment Company Act and the licenses and registrationsapprovals of our regulated and licensed subsidiaries. |

ANNALY CAPITAL MANAGEMENT, INC. AND SUBSIDIARIES

ITEM 1. BUSINESS

Our Board has reviewed and approved the investment and operating policies and strategies that support our risk appetite statement set forth in this Form 10-K. Our Board has the power to modify or waive these policies and strategies to the extent that our Board, in its discretion, determines that the modification or waiver is in theour best interests of our stockholders.interests. Among other factors, market developments whichthat affect our policies and strategies or whichthat change our assessment of the market may cause our Board to revise our policies and strategies.

We may seek to expand our capital base in order to further increase our ability to acquire new and different types of assets when the potential returns from new investments appear attractive relative to the targeted risk-adjusted returns. We may in the future acquire assets or companies by offering our debt or equity securities in exchange for such opportunities.

Target Assets

Within the confines of the risk appetite statement, we seek to generate the highest risk-adjusted returns on capital invested, after consideration of the following:

•The amount, nature and variability of anticipated cash flows from the asset across a variety of interest rate, yield, spread, financing cost, credit loss and prepayment scenarios;

•The liquidity of the asset;

•The ability to pledge the asset to secure collateralized borrowings;

•When applicable, the credit of the underlying borrower;

•The costs of financing, hedging and managing the asset;

•The impact of the asset to our REIT compliance and our exemption from registration under the Investment Company Act; and

•The capital and operational requirements associated with the purchase and financing of the asset.

We target the purchase and sale of the following assets listed below as part of our investment strategy. Our targeted assets and asset acquisition strategy may change over time as market conditions change and as our business evolves.

ANNALY CAPITAL MANAGEMENT, INC. AND SUBSIDIARIES

ITEM 1. BUSINESS

| | | | | | | | |

| Investment Group | Targeted Asset Class | Description |

| Annaly Agency Group | Agency mortgage-backed securitiesMBS | Agency pass-through certificates issued or guaranteed by Freddie Mac, Fannie Mae or Ginnie Mae.Agencies. Other Agency MBS include collateralized mortgage obligations (“CMOs”), interest-only securities and inverse floaters |

| To-be-announced forward contracts (“TBAs”) | Forward contracts for Agency pass-through certificates |

Agency commercial mortgage-backed securitiesCMBS | Pass-through certificates collateralized by commercial mortgages guaranteed by Freddie Mac, Fannie Mae or Ginnie Mae |

Mortgage Servicing Rights (“MSRs”) | Rights to service a pool of residential loans in exchange for a portion of the interest payments made on the loansAgencies |

| Annaly Residential Credit Group | Residential mortgage loans | Residential mortgage loans that are not guaranteed by Freddie Mac, Fannie Mae or Ginnie Maethe Agencies |

Residential mortgage-backed securitiesMBS | Securities collateralized by pools of residential loans that are not guaranteed by one of the Agencies |

| Agency or private label credit risk transfer securities (“CRT”) | Risk sharing transactions issued by Freddie Mac and Fannie Mae and similarly structured transactions arranged by third party market participants, designed to synthetically transfer mortgage credit risk to private investors |

Annaly Commercial Real EstateMortgage Servicing Rights Group | CommercialMortgage Servicing Rights (“MSR”) | Rights to service a pool of residential mortgage loans | Loans collateralized by commercial real estate properties |

Commercial mortgage-backed securities | Securities collateralized by pools in exchange for a portion of commercial mortgagethe interest payments made on the loans |

| Mezzanine loans | Loans collateralized by commercial real estate properties subordinate to first mortgage loans |

| Real property | Commercial real estate properties that generate current cash flow

| Annaly Middle Market Lending Group | First lien middle market loansSenior secured loans made to middle market companies that are the first to be repaid in the event of a borrower default |

| Second lien middle market loans | Senior secured loans to middle market companies that have a junior claim on collateral to those of first lien loans

| | |

| | |

We believe that future interest rates and mortgage prepayment rates are very difficult to predict. Therefore, we seek to acquire assets which we believe will provide attractive returns over a broad range of interest rate and prepayment scenarios.

ANNALY CAPITAL MANAGEMENT, INC. AND SUBSIDIARIES

ITEM 1. BUSINESS

Capital Structure and Financing

Our capital structure is designed to offer an efficient complement of funding sources to generate positive risk-adjusted returns for our stockholders while maintaining appropriate liquidity to support our business and meet our financial obligations under periods of market stress. To maintain our desired capital profile, we utilize a mix of debt and equity funding. Debt funding may include the use of repurchase agreements, loans, securitizations, participations issued, lines of credit, asset backed lending facilities, corporate bond issuance, convertible bonds, mortgages payable or other liabilities. Equity capital primarily consists of common and preferred stock.

We finance our Agency mortgage-backed securities and residential credit investments primarily with repurchase agreements. We also finance certain commercial real estate investments with repurchase agreements. We seek to diversify our exposure and limit concentrations by entering into repurchase agreements with multiple counterparties. We enter into repurchase agreements with broker-dealers, commercial banks and other lenders that typically offer this type of financing. We enter into collateralized borrowings with financial institutions meeting internal credit standards and we monitor the financial condition of these institutions on a regular basis. At December 31, 2020,2023, we had $64.8$62.2 billion of repurchase agreements outstanding.

Additionally, our wholly-owned subsidiary, Arcola Securities, Inc. (“Arcola”), provides direct access to third party funding as a FINRA member broker-dealer.broker-dealer of the Financial Industry Regulatory Authority (“FINRA”). As an eligible institution, Arcola also raises funds through the General Collateral Finance Repo service offered by the Fixed Income Clearing Corporation (“FICC”), with FICC acting as the central counterparty. Arcola provides us greater depth and diversity of repurchase agreement funding while also limiting our counterparty exposure.

To reduce our liquidity riskrisk. we maintain a laddered approach to our repurchase agreements. At December 31, 2020,2023, the weighted average days to maturity was 6444 days.

We utilize diverse funding sources toalso finance our commercial investments, including bilateral borrowing facilities, securitization funding and, in the case of equity investments in commercial real estate,residential mortgage financing.loans through the issuance of securitization transactions sponsored by our wholly-owned subsidiary Onslow Bay Financial LLC (“Onslow Bay”) under the Onslow Bay private-label securitization program (“OBX”). We are a programmatic securitization sponsor of new origination, residential whole loans with 51 deals as of December 31, 2023 comprising $20.0 billion of issuance since the beginning of 2018. During the year ended December 31, 2023, we issued 13 OBX securitizations backed by $4.9 billion of residential whole loans.

We utilize leverage to enhance the risk-adjusted returns generated for our stockholders. We generally expect to maintain an economic leverage ratio of no greater than 10:1.1 considerate of our overall capital allocation framework. This ratio varies from time to time based upon various factors, including our management’s opinion of the level of risk of our assets and liabilities, our mix of assets, our liquidity position, our level of unused borrowing capacity, the availability of credit, over-collateralization levels required by lenders when we pledge assets to secure borrowings and, lastly, our assessment of domestic and international market conditions. Since the financial crisis beginning in 2007, we have maintained an economic leverage ratio below 8:1 which is generally lower than what ourand since the Coronavirus Disease 2019 (“COVID-19”) pandemic began, an economic leverage ratio had been priorcloser to 2007.or below 7:1. For

ANNALY CAPITAL MANAGEMENT, INC. AND SUBSIDIARIES

ITEM 1. BUSINESS

purposes of calculating this ratio, our economic leverage ratio is equal to the sum of Recourse Debt, cost basis of TBA and CMBX derivatives outstanding, and net forward purchases (sales) of investments divided by total equity.

Our target economic leverage ratio is determined under our capital management policy. Should our actual economic leverage ratio increase above the target level, we will consider appropriate measures. Our actions may include asset sales, changes in asset mix, reductions in asset purchases or originations, issuance of capital or other capital enhancing or risk reduction strategies.

The following table presents our leverage economic leverage and capital ratios as of the periods presented.

| | | | | | | | | | | |

| | December 31, 2020 | | December 31, 2019 |

| Leverage ratio | 5.1:1 | | 7.1:1 |

| Economic leverage ratio | 6.2:1 | | 7.2:1 |

| Capital ratio | 13.6% | | 12.0% |

| | | | | | | | | | | |

| | December 31, 2023 | | December 31, 2022 |

| GAAP leverage ratio | 6.8:1 | | 6.0:1 |

Economic leverage ratio * | 5.7:1 | | 6.3:1 |

| GAAP capital ratio | 12.2% | | 13.9% |

Economic capital ratio * | 14.0% | | 13.4% |

| * Represents a non-GAAP financial measure. Refer to the “Non-GAAP Financial Measures” section for additional information. |

Operating Platform

We maintain a flexible and scalable operating platform to support the management and maintenance of our diverse asset portfolio. We have invested in our infrastructure to enhance resiliency, efficiency, cybersecurity and scalability while also ensuring coverage of our target assets. Our information technology applications span the portfolio life-cycle including pre-trade analysis, trade execution and capture, trade settlement and financing, monitoring, management and financial accounting and reporting.

Technology applications also support our control functions including risk, compliance, and middle- and back-office functions.back-offices. We have added breadth to our operating platform to accommodate diverse asset classes and drive automation-based efficiencies.

ANNALY CAPITAL MANAGEMENT, INC. AND SUBSIDIARIES

ITEM 1. BUSINESS

Our business operations include a centralized collateral management function that permits in-house settlement and self-clearing, thereby creating greater control and management of our collateral. Through technology, we have also incorporated exception basedexception-based processing, critical data assurance and paperless workflows. Our infrastructure investment has driven operating efficiencies while expanding the platform. Routine disaster recovery and penetration testing enhances our systems resiliency, security and recovery of critical systems throughout the computing estate, and positioned us for a smooth transition to the remote work environment in which we currently operate due to Coronavirus Disease 2019 (“COVID-19”).estate.

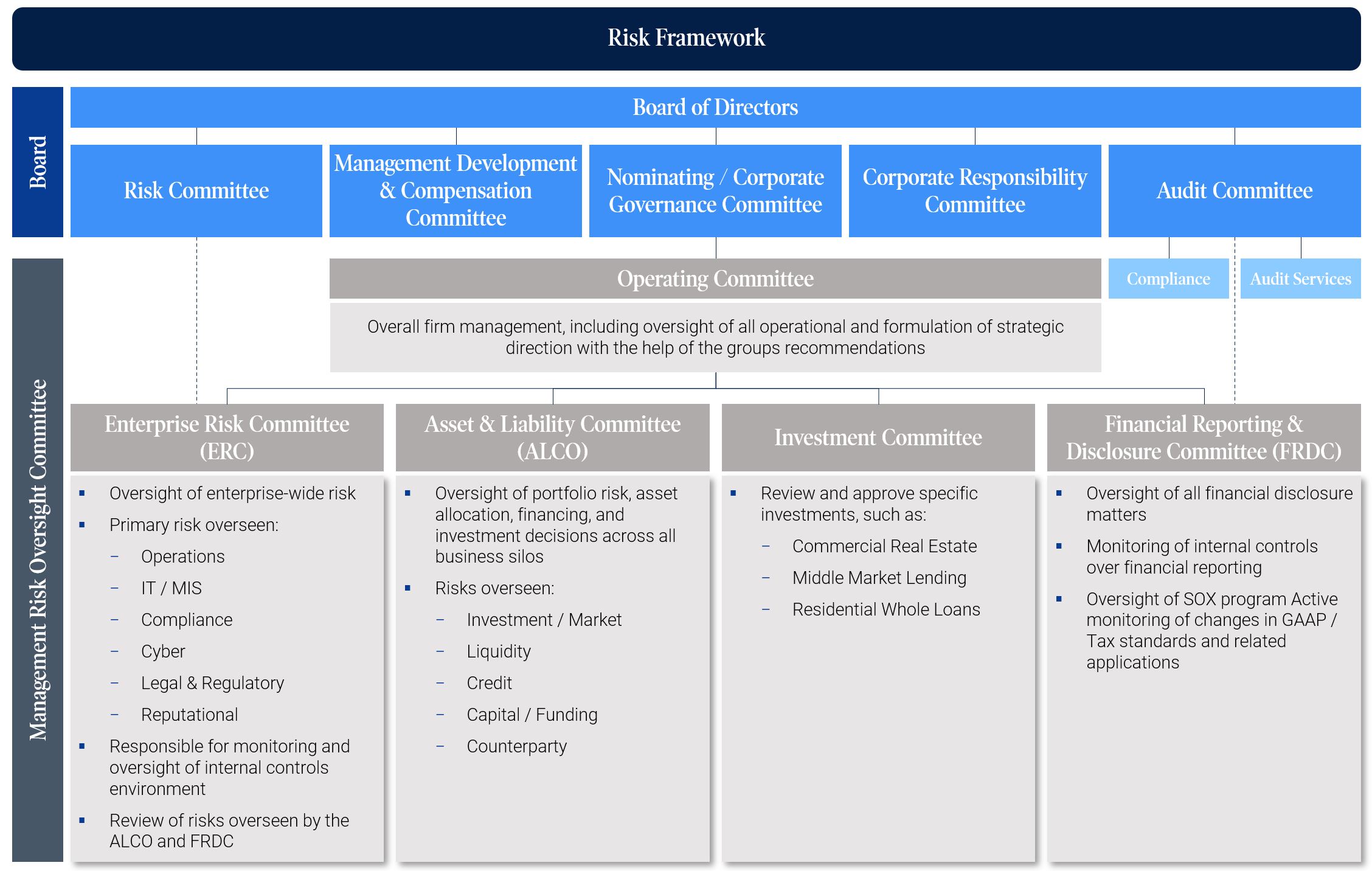

Risk Management

Risk is a natural element of our business. Effective risk management is of critical importance to our business strategy. The objective of our risk management framework is to identify, measure, monitor and control the key risks to which we are subject. Our approach to risk management is comprehensive and has been designed to foster a holistic view of risk. For a full discussion of our risk management process and policies please refer to the section titled “Risk Management” of Part II, Item 7. “Management’s Discussion and Analysis of Financial Condition and Results of Operations.”

Closing of the Internalization and Termination of the Management Agreement

On February 12, 2020, we entered into an internalization agreement (the “Internalization Agreement”) with our Former Manager and certain affiliates of our Former Manager. Pursuant to the Internalization Agreement, we agreed to acquire all of the outstanding equity interests of our Former Manager and our Former Manager’s direct and indirect parent companies from their respective owners (the “Internalization”) for nominal cash consideration ($1.00). In connection with the closing of the Internalization, on June 30, 2020, we acquired all of the assets and liabilities of our Former Manager (the net effect of which was immaterial in amount), and we transitioned from an externally-managed REIT to an internally-managed REIT. At the closing, all employees of our Former Manager became our employees. The parties also terminated the Amended and Restated Management Agreement by and between us and our Former Manager (the “Management Agreement”) and therefore we no longer pay a management fee to, or reimburse expenses of, our Former Manager. Pursuant to the Internalization Agreement, our Former Manager waived any termination fee. For additional information about the Internalization, see the Note titled “Related Party Transactions” in the Notes to the Consolidated Financial Statements included in Item 15. “Exhibits, Financial Statement Schedules.”

Information about our Executive Officers

The following table sets forth certain information as of January 31, 2021February 15, 2024 concerning our executive officers:

| | | | | | | | |

| Name | Age | Title |

| | |

| David L. Finkelstein | 4851 | Chief Executive Officer and Chief Investment Officer |

| Serena Wolfe | 4144 | Chief Financial Officer |

| Steven F. Campbell | 4851 | President and Chief Operating Officer |

Timothy P. Coffey | 47 | Chief Credit Officer |

Ilker Ertas | 50 | Head of Securitized Products |

| Anthony C. Green | 4649 | Chief Corporate Officer, Chief Legal Officer and Secretary |

David L. Finkelstein has served as the Chief Executive Officer of Annaly since March 2020 and Chief Investment Officer of Annaly since November 2016.2022. Mr. Finkelstein previously served as President of Annaly from March 2020 until December 2022 and Annaly’s Chief Investment Officer from November 2016 until December 2021. Prior to that, Mr. Finkelstein served as Annaly’s Chief Investment Officer, Agency and RMBS beginning in February 2015 and as Annaly’s Head of Agency Trading beginning in August 2013. Prior to joining Annaly in 2013, Mr. Finkelstein served for four years as an Officer in the Markets Group of the Federal Reserve Bank of New York where he was the primary strategist and policy advisor for the MBS purchase

ANNALY CAPITAL MANAGEMENT, INC. AND SUBSIDIARIES

ITEM 1. BUSINESS

program. Mr. Finkelstein has over 2025 years of experience in fixed income investments. Prior to the Federal Reserve Bank of New York, Mr. Finkelstein held Agency MBS trading positions at Salomon Smith Barney, Citigroup Inc. and Barclays PLC. Mr. Finkelstein is a member of the Treasury Market Practices Group sponsored by the Federal Reserve Bank of New York, as well as a member of the Financial Sector Advisory Council of the Federal Reserve Bank of Dallas. Mr. Finkelstein received his B.A. in Business Administration from the University of Washington and his M.B.A. from the University of Chicago, Booth School of Business. Mr. Finkelstein also holds the Chartered Financial Analyst® designation.

Serena Wolfe has served as Chief Financial Officer of Annaly since December 2019. Prior to joining Annaly in 2019, Ms. Wolfe served as a Partner at Ernst & Young (“EY”) since 2011 and as its Central Region Real Estate Hospitality & Construction (“RHC”) leader from 2017 to November 2019, managing the go-to-market efforts and client relationships across

ANNALY CAPITAL MANAGEMENT, INC. AND SUBSIDIARIES

ITEM 1. BUSINESS

the sector. Ms. Wolfe was previously also EY’s Global RHC Assurance Leader. Ms. Wolfe practiced with EY for over 20 years, including six years with EY Australia and 16 years with the U.S. practice. Ms. Wolfe currently serves on the boards of Lennar Corporation and Doma Holdings, Inc. Ms. Wolfe graduated from the University of Queensland with a Bachelor of Commerce in Accounting. She is a Certified Public Accountant in the states of New York California, Illinois and Pennsylvania.California.

Steven F. Campbell has served as President of Annaly since December 2022 and Chief Operating Officer of Annaly since June 2020. Prior to this position,these positions, Mr. Campbell served in a number of other senior roles at Annaly, including as Head of Business Operations from September 2019 to June 2020, Head of Credit Operations and Enterprise Risk from February 2018 to September 2019, Chief Operating Officer of Annaly Commercial Real Estate Group from December 2016 to February 2018 and Head of Credit Strategy from April 2015 to February 2018. Mr. Campbell has over 2025 years of experience in financial services. Prior to joining Annaly in 2015, Mr. Campbell held various roles over six years at Fortress Investment Group LLC, including serving as a Managing Director in the Credit Funds business. Prior to that, Mr. Campbell held positions at General Electric Capital Corporation and D.B. Zwirn & Co,Co., L.P. with a focus on credit and debt restructuring. Mr. Campbell currently serves on the Advisory Board for the Fitzgerald Institute of Real Estate at the University of Notre Dame. Mr. Campbell received a B.B.A. from the University of Notre Dame and a M.B.A. from the University of Chicago, Booth School of Business.

Timothy P. Coffey has served as Chief Credit Officer of Annaly since January 2016. Mr. Coffey served as Annaly’s Head of Middle Market Lending from 2010 until January 2016. Mr. Coffey has over 20 years of experience in leveraged finance and has held a variety of origination, execution, structuring and distribution positions. Prior to joining Annaly in 2010, Mr. Coffey served as Managing Director and Head of Debt Capital Markets in the Leverage Finance Group at Bank of Ireland. Prior to that, Mr. Coffey held positions at Scotia Capital, the holding company of Saul Steinberg’s Reliance Group Holdings and SC Johnson International. Mr. Coffey received his B.A. in Finance from Marquette University.

Ilker Ertas has served as Head of Securitized Products at Annaly since February 2019. Prior to this position, Mr. Ertas served in a number of other senior roles at Annaly, including as Head of RMBS Portfolios from February 2018 to February 2019, Head of Trading from February 2017 to February 2018, Head of Asset Trading from October 2016 to February 2017 and Managing Director, Agency & Residential Credit from June 2015 to October 2016. Mr. Ertas has 20 years of experience in U.S. fixed income markets. Prior to joining Annaly in 2015, Mr. Ertas was at Citigroup Inc., where he was most recently a Managing Director and Head of Mortgage Derivatives Trading. Mr. Ertas has also held mortgage trading positions at Barclays PLC and Lehman Brothers Holdings Inc. Mr. Ertas received a B.S. in Industrial Engineering from Bogazici University in Istanbul, Turkey and a M.B.A. from the Yale School of Management.

Anthony C. Green has served as Chief Corporate Officer of Annaly since January 2019 and as Chief Legal Officer and Secretary of Annaly since March 2017. Mr. Green previously served as Annaly’s Deputy General Counsel from 2009 until February 2017. Prior to joining Annaly, Mr. Green was a partner in the Corporate, Securities, Mergers & Acquisitions Group at the law firm K&L Gates LLP. Mr. Green has over 20 years of experience in corporate and securities law. Mr. Green holds a B.A. in Economics and Political Science from the University of Pennsylvania and a J.D. and LL.M. in International and Comparative Law from Cornell Law School.

Human Capital

In connection with the closing of the Internalization on June 30, 2020, we transitioned from an externally-managed REIT to an internally-managed REIT. Our human capital groupHuman Capital team oversees our human capitalcompany’s workforce management to ensure that it isits objectives are strategically integrated with ourthe firm’s goals and business plans. We proactively review human capital management best practices to continually enhance our employee experience. In addition, the Management Development and Compensation (“MDC”) Committee of the Board provides independent oversight of the our policies and strategies related to human capital management. Further, the Chair of the MDC Committee liaises on certain human capital topics with the Chair of the Corporate Responsibility Committee of the Board as appropriate.

As of December 31, 2020,2023, we had 180187 employees.

Our People and Culture

We recognize that ourOur employees are our most important asset,the driving force behind Annaly’s success, and we are committed to promoting their well-being, engagement, and development and fullto help them reach their highest potential. We areOur culture is focused on fostering ana diverse, inclusive and rewarding work environment for all our employees, with ongoing opportunities for career development, and wellness support that seeks to facilitate the achievement of their professional goals.and empowerment.

Our culture is built on sixfive core values: ownership, humility, accountability, communication, collaboration and diversity, equity and inclusion and humility.inclusion. These values are embedded in our professional and personal conduct and are crucial to how we operate our business. All employees are responsible for upholding these values, which form the bedrock of our culture and are vital to the continued success of our company. Guided by these values, we are committed to attracting, developing and retaining the best talent, with diverse experiences, perspectives and backgrounds.

We utilize employee surveys, including an annual engagement survey, to create an open and honest feedback forum,channels that foster our ability to actively engage and involve our employees in the design and evolution of our culture and our human capital strategies to enhance our overall productivity and mitigate risk. Our leaders review and incorporate survey feedback to increase employee engagement and drive positive changes throughout the firm.our company. We remain committed to maintaining an environment of consistent feedback as we strive for high employment satisfaction levels.

ANNALY CAPITAL MANAGEMENT, INC. AND SUBSIDIARIES

ITEM 1. BUSINESS

COVID-19

In response to COVID-19, our employees have largely worked remotely since March 2020. We supported our employees’ remote working through stipends to upgrade home office equipment. Since September 2020, there are a limited number of employees who voluntarily work in the office on occasion. We implemented a regular Coronavirus testing protocol to optimize our ability to provide a safe work environment. In addition to addressing physical health and safety concerns, we recognize that the pandemic has affected people’s daily emotional lives and mental health. As a result, we have increased our mental health offerings and hosted a multitude of virtual seminars to help keep our employees connected with one another and to equip them with tools to help alleviate some of the increased stress and burdens.

Diversity, Equity & Inclusion

The diversity of our employees brings a critical range of thought and experience throughoutenables our company cultivatingto cultivate innovation, fresh perspectives and vital new ideas.agility. Diversity, equity and inclusion are essential tenets of our corporate culture. Our human capital management group,Human Capital team, in coordination with our recently named Head of Inclusion andan Inclusion Support Committee of Executive Sponsors, is responsible for overseeing and continuing to improveadvance our diversity, equity and inclusion initiatives.

We are committed to achievingpromoting diversity, including gender and racial/ethnic diversity, across all levels of our company. With 50%62% of total employeesour Operating Committee and 58% of our overall population in 20202023 identifying as either female and/or racially/ethnically diverse, we are driven by the belief that having a diverse group of employees supports our continued long-term growth. In 2017, we launchedsuccess. Hosting over 30 community building events in 2023, our seven employee network groups, which include the Women’s Interactive Network which provides(“WIN”), the Asian American and Pacific Islander Employee Network, the Black Employee Network, the Latin American Employee Network, the Disabilities Within a Family Network, the Veteran’s Employee Network and the Annaly Pride Network, continue to evolve and advance. These employee networks help strengthen our inclusive culture by fostering a sense of belonging and engagement through targeted development and networking opportunities, knowledge exchanges, mentorship, coaching and volunteer efforts. Our

Additionally, we recognize and understand that education, candid conversations and continued training are key to embedding and advancing diversity, equity and inclusion within our organization and culture. To further promote and foster such a foundation, our efforts also include offering firm-wide initiatives like antraining on topics such as unconscious bias, training program offered in 2020allyship and inclusive leadership. To that end, we have hosted various forums for employees to establish foundational knowledge, language and understanding to support the strategic diversity and inclusion efforts of the firm, organizing forums toopenly discuss employees’their views and have provided opportunities for employee connection and networking, as well as actively seekingsought out feedback fromthrough periodic employee surveys.

Employee Development,Compensation, Benefits and Wellness

We seek to invest in and promote talent to cultivate a high-performance culture and build on the capabilities and full potential of our employees. We invest in a wide range of benefits and wellness initiatives for our employees to support healthy lifestyles and choices.

Our employee compensation program includes base salary, annual incentive bonuses and stock-based awards. Employee compensation packages are designed to align employee and stockholder interests and to provide incentives to attract, retain and motivate talented employees.

In addition, we invest in a wide range of benefits and wellness initiatives that support healthy lifestyles and choices for our employees. We offer employees benefits including health and insurance coverage, health savings and flexible spending accounts, telemedicine benefits, 401(K)401(k) plans, paid time off and family care resources. We also sponsor a wide range of initiatives that promote employee wellness and mental well-being, including access to talk therapy, health coaching, stress management support and a dedicated Wellness Week that includes a number of health and wellness related activities and seminars. Over the last few years, we have enhanced our parental and family care benefits to provide extended leave and fertility assistance.

At Annaly, we understand that it is our responsibility to provide an environment where our employees feel safe, motivated, empowered, and prepared, regardless of whatever challenges may arise. In addition to addressing physical health and safety concerns, we recognize that people’s daily emotional lives and mental health play a key role in their overall wellness. As such, we continue to evaluate ways to promote and expand our mental health offerings. Additionally, we recognize that part of meeting employee needs includes institutionalizing broader and longer-term flexibility where appropriate. Flexibility comes in many forms at Annaly, including vacation and sick time, hybrid work options and location strategy. We remain committed to evaluating the evolving definition of flexibility and promoting programs and practices that foster inclusivity and well-being both personally and professionally.

Learning and Development

We seek to advance and promote our employees’ capabilities and full potential by investing in a number of targeted learning and development opportunities. By aligning with our overall business strategy, we design our learning and development objectives to meet our employees’ needs and interests. Additionally, we have both a tuition reimbursement and learning reimbursement plan to cover all or part ofthat provide financial support toward the cost of education that furthersfurthering employee education in a fieldan area directly related to their specific job.

WeTo promote a sense of purpose, accountability and broader exposure, we offer a number of learning and development programs tailored to our employee needs and interestsnetworking opportunities that include senior leader-led small group sessions as well as our overall strategicone-on-one employee knowledge share sessions across the firm. More broadly, we continue to offer firmwide learning sessions that focus on core business objectives. For example,strategies and initiatives to foster holistic and inclusive learning. Further, we offer targeted professional development training for employees at various stages in their career. In 2020, we began offering firm-widefacilitate individual style and culture sessions where we facilitate discussionswith new employees to gain insights onpromote professional awareness and understanding of our company’s culture enhancement priorities.initiatives.

Corporate and Employee Philanthropy and Volunteerism

Our corporate giving has been focused on high-impact programs that seek to advance social issues we are committed to, including combating homelessness and advancing the professional development of women and underrepresented groups. In 2020, we also provided support to COVID-19 relief effortsgroups in our New York City community.finance. Annaly and our employees endeavor to meaningfully contribute to the communities where we live, work and invest by

ANNALY CAPITAL MANAGEMENT, INC. AND SUBSIDIARIES

ITEM 1. BUSINESS

partnering with well-established non-profit organizations and through Annaly’s corporate giving, employee volunteerism and our employee charity match program.

Regulatory Requirements

The financial services industry is subject to extensive regulation and supervision, and changes to regulations and supervisory practices are continuously being considered by regulators and policy makers worldwide. We continue to assess our business, risk management and compliance practices to conform to developments in the regulatory environment.

We have elected, organized and operated in a manner that qualifies us to be taxed as a REIT under the Internal Revenue Code of 1986, as amended and regulations promulgated thereunder (the “Code”). So long as we qualify for taxation as a REIT, we generally will not be subject to U.S. federal income tax on our taxable income that is distributed to our stockholders. Furthermore, substantially all of our assets, other than our taxable REIT subsidiaries (“TRSs”), consistsconsist of qualified REIT real estate assets (of the type described in Section 856(c)(5) of the Code).

We regularly monitor our investments and the income from these investments and, to the extent we enter into hedging transactions, we monitor income from our hedging transactions as well, so as to ensure at all times that we maintain our qualification as a REIT, and our exemption from registration under the Investment Company Act.Act and our exemption from registration as a commodity pool operator ("CPO") with the U.S. Commodity Futures Trading Commission ("CFTC").

Arcola is a member of FINRA, an SEC registered broker-dealer and is subject to regulations of the securities business that include but are not limited to trade practices, use and safekeeping of funds and securities, capital structure, recordkeeping and conduct of directors, officers and employees. As a self-clearing, registered broker dealer,broker-dealer, Arcola is required to maintain minimum net capital by the SEC and FINRA. Arcola consistently operates with capital in excess of its regulatory capital requirements as defined by SEC Rule 15c3-1.

ANNALY CAPITAL MANAGEMENT, INC. AND SUBSIDIARIES

ITEM 1. BUSINESS

We have a subsidiary that is registered with the SEC as an investment adviser under the Investment Advisers Act. As a result, we are subject to the anti-fraud provisions of the Investment Advisers Act and to fiduciary duties derived from these provisions that apply to our relationships with that subsidiary’s clients. These provisions and duties impose restrictions and obligations on us with respect to our dealings with our subsidiary’s clients, including, for example, restrictions on agency, cross and principal transactions. Our registered investment adviser subsidiary is subject to periodic SEC examinations and other requirements under the Investment Advisers Act and related regulations primarily intended to benefit advisory clients. These additional requirements relate to, among other things, maintaining an effective and comprehensive compliance program, recordkeeping and reporting requirements and disclosure requirements.

We also have a subsidiary that operates as a licensed mortgage aggregator and master servicer, which subjects it to individual state licensing laws and to supervision and examination by federal authorities, including the Consumer Financial Protection Bureau ("CFPB"), the U.S. Department of Housing and Urban Development (“HUD”), the SEC as well as various state licensing, supervisory and administrative agencies. We and our subsidiaries must also comply with a large number of federal, state and local consumer protection laws including, among others, the Gramm-Leach-Bliley Act, the Fair Debt Collection Practices Act, Real Estate Settlement Procedures Act, the Truth in Lending Act, and the Fair Credit Reporting Act, as well as state foreclosure laws and federal and local bankruptcy rules. These laws and regulations, which are frequently amended and adjusted, have, in recent years, led to an increase in both the scope of the requirements and the intensity of the supervision to which we are subject.

The financial services industryCFTC has jurisdiction over the regulation of swaps. The CFTC has asserted that this causes the operators of mortgage REITs that use swaps as part of their business model to fall within the statutory definition of CPO, and absent relief from the Market Participants Division of the CFTC, such operators generally much register as CPOs or qualify for an exemption from registration. On December 7, 2012, as a result of numerous requests for no-action relief from the CPO registration requirement for operators of mortgage REITs, the Division of Swap Dealer and Intermediary Oversight (the predecessor to the Market Participants Division) of the CFTC issued no-action relief entitled “No-Action Relief from the Commodity Pool Operator Registration Requirement for Commodity Pool Operators of Certain Pooled Investment Vehicles Organized as Mortgage Real Estate Investment Trusts” that permits a CPO to receive relief from the requirement to register by filing a claim to perfect the use of the relief. A claim submitted by a CPO will be effective upon filing, so long as the claim is subjectmaterially complete. The conditions that must be met relate to extensive regulationinitial margin and supervisionpremiums requirements, net income derived annually from commodity interest positions that are not qualifying hedging transactions, marketing of interests in the U.S. The Dodd-Frank Wall Street Reformmortgage REIT to the public and Consumer Protection Actidentification of 2010 (“Dodd-Frank Act”) and the rules thereunder significantly alteredentity as a mortgage real estate investment trust in its federal tax filings with the financial regulatory regime within which financial institutions operate. Other reformsIRS. We have been adopted or are being considered by other regulators and policy makers worldwide. We will continue to assess our business, risk management and compliance practices to conform to developmentssubmitted a claim for the relief set forth in the regulatory environment.no-action relief entitled “No-Action Relief from the Commodity Pool Operator Registration Requirement for Commodity Pool Operators of Certain Pooled Investment Vehicles Organized as Mortgage Real Estate Investment Trusts” and believe we meet the criteria for such relief set forth therein.

ANNALY CAPITAL MANAGEMENT, INC. AND SUBSIDIARIES

ITEM 1. BUSINESS

Competition

We operate in a highly competitive market for investment opportunities and competitionopportunities. Competition may limit our ability to acquire desirable investments in our target assets and could also affect the pricing of these investments. In acquiring our target assets, we will compete with financial institutions, institutional investors, other lenders, government entities and certain other REITs. For a full discussion of the risks associated with competition see the “Risks Related to Our Investing, Portfolio Management and Financing Activities” section in Item 1A. “Risk Factors.”

Corporate Governance

We strive to conduct our business in accordance with the highest ethical standards and in compliance with applicable governmental laws, rules and regulations. Our notable governance practices and policies include:

•We closed our management internalization transaction on June 30, 2020 and transitioned from an externally-managed REIT to an internally-managed REIT.

•Our Board is composed of a majority of independent directors, and our Audit, Management Development and Compensation, and Nominating/Corporate Governance Committees are composed exclusively of independent directors.

•We have separated the roles of Chair of the Board and Chief Executive Officer, and appointed an independent Chair of the Board.

•In December 2018, we amended our bylaws to declassify our Board over a three-year period with allAll directors standing forare elected on an annual election by our company’s annual meeting of stockholders in 2021.basis.

•We have adopted an enhanced director refreshment policy, which provides that an independent director may not stand for re-election at the next annual meeting of stockholders taking place at the end of his or her term following the earlier of his or her: (i) 15th anniversary of service on our Board or (ii) 73rd birthday.

•We have adopted a Code of Business Conduct and Ethics, which sets forth the basic principles and guidelines for resolving various legal and ethical questions that may arise in the workplace and in the conduct of our business. This code is applicable to our directors, officers and employees.

•We have adopted Corporate Governance Guidelines which, in conjunction with the charters of our Board committees, provide the framework for the governance of our company.

•We have procedures by which any of our employees, officers or directors may raise concerns

confidentially about our company’s conduct, accounting, internal controls or auditing matters with the Chair of the Board, the independent directors, or the Chair of the Audit Committee or through our whistleblower phone hotline or e-mail inbox.

•We have adopted an Insider Trading Policy that prohibits our directors, officers and employees, as well as those of our subsidiaries from buying or selling our securities on the basis of material nonpublic information and prohibits communicating material nonpublic information about our company to others. Our Insider Trading Policy prohibits our directors, officers and employees, from (1) holding our stock in a margin account as eligible collateral, or otherwise pledging our stock as collateral for a loan, or (2) engaging in any hedging transactions with respect to our equity securities held by them.

•Our executive officers are subject to a robusttwo clawback policy, which includes triggers forpolicies, one that covers financial restatements and a second for misconduct.

•Our executive officers are subject to stock ownership guidelines and holding restrictions.

ANNALY CAPITAL MANAGEMENT, INC. AND SUBSIDIARIES

ITEM 1. BUSINESSStockholders holding 25% of our common stock have the right to call a special meeting.

Distributions

In accordance with the requirements for maintaining REIT status, we intend to distribute to stockholders aggregate dividends equaling at least 90% of our REIT taxable income (determined without regard to the deduction of dividends paid and by excluding any net capital gain) for each taxable year and will endeavor to distribute at least 100% of our REIT taxable income so as not to be subject to tax. Distributions of economic profits from our enterprise could be classified as return of capital due to differences between book and tax accounting rules. We may make additional returns of capital when the potential risk-adjusted returns from new investments fail to exceed our cost of capital. Subject to the limitations of applicable securities and state corporation laws, we can return capital by making purchases of our own capital stock or through payment of dividends.

ANNALY CAPITAL MANAGEMENT, INC. AND SUBSIDIARIES

ITEM 1. BUSINESS

Available Information

Our website is www.annaly.com. We make available on this website under “Investors - SEC Filings,” free of charge, our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and any amendments to those reports as soon as reasonably practicable after we electronically file or furnish such materials to the SEC pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 (the “Securities Exchange Act”). Our website and the information contained therein are not incorporated into this annual report on Form 10-K.

Also posted on our website, and available in print upon request of any stockholder to our Investor Relations Department, are charters for our Audit Committee, Management Development and Compensation Committee, Nominating/Corporate Governance Committee, Risk Committee and Corporate Responsibility Committee, our Corporate Governance Guidelines and our Code of Business Conduct and Ethics. Within the time period required by the SEC, we will post on our website any amendment to the Code of Business Conduct and Ethics and any waiver applicable to any executive officer, director or senior financial officer.

Our Investor Relations Department can be contacted at:

Annaly Capital Management, Inc.

1211 Avenue of the Americas

New York, New York 10036

Attn: Investor Relations

Telephone: 888-8ANNALY

E-mail: investor@annaly.com

The SEC also maintains a website that contains reports, proxy and information statements and other information we file with the SEC at www.sec.gov.

ANNALY CAPITAL MANAGEMENT, INC. AND SUBSIDIARIES

Item 1A. Risk Factors

An investment in our stock involves a number of risks. Before making an investment decision, you should carefully consider all of the risks described in this annual report on Form 10-K. If any of the risks discussed in this annual report on Form 10-K actually occur, our business, financial condition and results of operations could be materially adversely affected. If this were to occur, the trading price of our stock could decline significantly and you may lose all or part of your investment. Readers should not consider any descriptions of these factors to be a complete set of all potential risks that could affect us.

INDEX TO ITEM 1A. RISK FACTORS

ANNALY CAPITAL MANAGEMENT, INC. AND SUBSIDIARIES

Item 1A. Risk Factors

Summary of Risk Factors

Risks Related to COVID-19

•COVID-19 has affected, and will likely continue to affect, the U.S. economy, the mortgage REIT industry and our business.

•We cannot predict the effect that government policies, laws and plans in response to the COVID-19 pandemic will have on us.

Risks Related to Our Investing, Portfolio ManagementLiquidity and Financing Activities

•We may change our policies without stockholder approval.Funding

•Our strategy involves the use of leverage, which increases the risk that we may incur substantial losses.

•Our use of leverage may causeresult in margin calls and defaults and force us to sell assets under adverse market conditions.

•We may exceed our target leverage ratios, or weratios.

•We may not be able to achieve our optimal leverage.

•Failure to procure or renew funding on favorable terms, or at all, would adversely affect our results and financial condition.

•Failure to effectively manage our liquidity would adversely affect our results and financial condition.

•Risk management policiesVolatile market conditions for our assets can result in contraction in liquidity for those assets and procedures may not adequately identify all risks to our businesses.the related financing.

•An increase or decrease in prepayment rates may adversely affect our profitability.

•We are subject to reinvestment risk.

•Volatile market conditions for mortgages and mortgage-related assets can result in a significant contraction in liquidity.

•Competition may limit our ability to acquire desirable investments in our target assets and also affect the pricing of these assets.

•Increases in interest payments on our borrowings relative to the interest earnedwe earn on our interest earning assets may adversely affect our profitability.

•Differences in timing of interest rate adjustments on our interest earning assets and our borrowings may adversely affect profitability.

•Changes in the method pursuant to which LIBOR is determined and potential discontinuation of LIBOR may affect our results.

•An increase in interest rates may adversely affect the market value of our interest earning assets and, therefore, also our book value.

•We may experience declines in market value of our assets resulting in us recording impairments, which may effect on our results.

•The soundness of other financial institutions could adversely affect us.

•Our hedging strategies may be costly or ineffective and our use of derivatives may expose us to counterparty and liquidity risks.profitability.

•It may be uneconomical to "roll"“roll” our TBA dollar roll transactions or we may be unable to meet margin calls on our TBA contracts.

•Any incorrect, misleading or incomplete information used in connection with analytical models would subjectOur use of derivatives may expose us to potentialcounterparty and liquidity risks.

•Securitizations expose us to additional risks.

•Our use of non-recourse securitizations may expose us to risks which could result in losses to us.

•Counterparties may require us to enter into covenants that restrict our investment strategy.

•We may be unable to profitably execute or participate in future securitization transactions.

Risks of Ownership of Our Common Stock

•Our charter does not permit ownership of over 9.8% in number of shares or value of our common stock or any class of our preferred stock.

•Provisions contained in Maryland law may have anti-takeover effects, potentially preventing investors from receiving a “control premium” for their shares.

•We have not established a minimum dividend payment level and cannot assure stockholders of our ability to pay dividends in the future.

•Our reported GAAP financial results may not be an accurate indicator of future taxable income and dividend distributions.

Compliance, Regulatory & Legal Risks

•Accounting rules related to certain of our transactions are highly complex and involve significant judgment and assumptions.

•We are dependent on information systems and third parties; system failures or cybersecurity incidents could disrupt our business.

•Securitizations, including non-recourse securitizations, Our application of GAAP may expose usproduce financial results that fluctuate from one period to additional risks.

•Counterparties may require us to enter into restrictive covenants relating to our operations that may inhibit our ability to grow.

•We may enter into new lines of business, acquire other companies or engage in other strategic initiatives.

•We are subject to risks and liabilities in connection with sponsoring, investing in and managing new funds and other accounts.

•Investments in MSRs may expose us to additional risks.

•We depend on third-party service providers, including mortgage loan servicers, for a variety of services related to our business.

•Purchases and sales of Agency MBS by Federal Reserve may adversely affect the price and return associated with Agency MBS.another.

•New laws may be passed affecting the relationship between Fannie Mae, and Freddie Mac and the federal government.

Risks Related To Our Credit Assets

•We invest in securities in the credit risk transfer sector that are subject to mortgage credit risk.

•Prolonged economic slowdown or declining real estate values could impair the assets we may own and adversely affect our results.

•Geographic concentration exposes investors to greater risk of default and loss.

•Inadequate property insurance coverage could have an adverse impact on our operating results.

•We may incur losses when a borrower defaults on a loan and the underlying collateral value is less than the amount due.

•Our assets may become non-performing or sub-performing assets, which are subject to increased risks relative to performing loans.

•We may be required to repurchase commercial or residential mortgage loans or indemnify investors.

•Our due diligence of potential assets may not reveal all liabilities and other weaknesses.

•When we foreclose on an asset, we may come to own and operate the property securing the loan.

•Financial covenants could adversely affect our ability to conduct our business.

•Proposals to acquire mortgage loans by eminent domain may adversely affect the value of our assets.

•Our investments in corporate loans and debt securities for middle market companies carry risks.

Risks Related To Commercial Real Estate Debt, Preferred Equity Investments, Net Lease Real Estate Assets and Other Equity

•The real estate assets we acquire are subject to risks particular to real property, which may adversely affect our returns

•Commercial loan assets we originate and/or acquire depend on the ability of property owner to generate net income from operating.

•Commercial and non-Agency mortgage-backed securities we acquire may be subject to losses.

•Borrowers may be unable to repay the Remaining Principal Balance on the Maturity Date.

•The B-Notes that we originate and acquire may be subject to risks related to their privately negotiated structure and terms.

•The mezzanine loan assets and other subordinate debt positions that we originate and acquire involve greater risks of loss.

•We are subject to additional risks associated with loan participations and co-lending arrangements.

•Construction loans involve an increased risk of loss.

ANNALY CAPITAL MANAGEMENT, INC. AND SUBSIDIARIES

Item 1A. Risk Factors

•We may experience losses if the creditworthiness of our tenants deteriorates and they are unable to meet their lease obligations.

•Lease expirations, lease defaults and lease terminations may adversely affect our revenue.

•Our real estate investments are illiquid.

•We may not control the special servicing of the mortgage loans included in the commercial MBS in which we invest.

•Joint venture investments could be adversely affected by our lack of sole decision-making authority.

Risks Related To Our Residential Credit Business

•Our investments in non-Agency MBS or other investment assets of lower credit quality involve credit risk.

•Our investments in non-Agency MBS are collateralized by non-prime loans and may also include subprime mortgage loans.

•Our investments may include subordinated tranches of non-Agency MBS, which are subordinate in payment to senior securities.

•We are subject to counterparty risk and may be unable to seek indemnity or demand repurchase of residential whole loans.

•Our investments in residential whole loans subject us to servicing-related risks, including those associated with foreclosure.

•Challenges to the MERS® System could materially and adversely affect our business, results of operations and financial condition.

•We may be subject to liability for potential violations of truth-in-lending or other similar consumer protection laws and regulations.

•We may not be able to obtain or maintain the governmental licenses requiredcompliance with laws and regulations applicable to operate our Residential Credit and MSR businesses, including through the manner in which we oversee the compliance obligations of our third party service providers.

•Changes in laws or regulations governing our operations or our failure to comply with those laws or regulations may adversely affect our business.

•Our abilityThe increased focus on ESG and climate change issues by investors, governmental bodies and other stakeholders, as well as existing and proposed laws and regulations related to profitably execute or participate in future securitizations transactions, including, in particular, securitizations of residential mortgage loans, is dependent on numerous factors and if we are not able to achieve our desired level of profitability or if we are unable to execute or participate in future securitizations, or incur losses in connection therewith, it could have a material adverse impact onthese topics, may adversely affect our business and financial results.results and damage our reputation.

Risks Related to Our Business Structure

•We may be exposedare subject to complex and evolving laws, regulations, rules, standards and contractual obligations regarding data privacy and security, which could increase the cost of doing business, compliance risks to which we have not historically been exposed as a result of the Internalization.and potential liability.

•The departure of anyWe are subject to risks and liabilities in connection with sponsoring, investing in and managing new funds and other investment accounts, including potential regulatory risks.

•Loss of our key personnel could materially andInvestment Company Act exemption from registration would adversely affect us.

Risks Related to Our Taxation as a REIT