0000828944us-gaap:AccumulatedNetUnrealizedInvestmentGainLossMember2023-01-012023-12-31

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K | | | | | |

| (Mark One) |

| ☒ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| For the fiscal year ended December 31, 20212023 |

| OR |

| ☐ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to |

| Commission file number 001-35638 |

| WSFS FINANCIAL CORPORATION |

| (Exact Name of Registrant as Specified in its Charter) |

| | | | | | | | |

| Delaware | | 22-2866913 |

| (State or other Jurisdiction of Incorporation or Organization) | | (I.R.S. Employer Identification No.) |

| 500 Delaware Avenue, Wilmington, Delaware | | 19801 |

| (Address of Principal Executive Offices) | | (Zip Code) |

Registrant’s Telephone Number, Including Area Code: (302) 792-6000 |

| | | | | | | | | | | | | | |

| Securities registered pursuant to Section 12(b) of the Act: |

| Title of Each Class | | Trading Symbol(s) | | Name of Each Exchange on Which Registered |

| Common Stock, $0.01 par value | | WSFS | | Nasdaq Global Select Market |

| Securities registered pursuant to Section 12(g) of the Act: None |

Indicate by check if the registrant is a well-known seasoned issuer as defined in Rule 405 of the Securities Act. Yes x No ☐

Indicate by check if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Exchange Act. Yes ☐ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes x No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company or an emerging growth company. See definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| | | | | | | | | | | | | | | | | | | | |

| Large accelerated filer | | x | | Accelerated filer | | ☐ |

| Non-accelerated filer | | ☐ | | Smaller reporting company | | ☐ |

| Emerging growth company | | ☐ | | | | |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management's assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15. U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☒

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to § 240.10D-1(b). ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ☐ No x

The aggregate market value of the voting and non-voting common equity held by nonaffiliates of the registrant, based on the closing price of the registrant’s common stock as quoted on Nasdaq as of June 30, 2021,2023, was $2,185,763,654.$2,282,293,260. For purposes of this calculation only, affiliates are deemed to be directors, executive officers and beneficial owners of greater than 10% of the registrant's outstanding common stock.

As of February 24, 2022,26, 2024, there were issued and outstanding 65,378,95560,280,040 shares of the registrant’s common stock, par value $0.01 per share.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the Registrant’s Proxy Statement for the 20222024 Annual Meeting of Stockholders are incorporated by reference in Part III hereof.

WSFS FINANCIAL CORPORATION

TABLE OF CONTENTS

| | | | | | | | |

| | |

| | | Page |

| | |

| Item 1. | | |

| Item 1A. | | |

| Item 1B. | | |

| Item 1C. | | |

| Item 2. | | |

| Item 3. | | |

| Item 4. | | |

| | |

| | |

| Item 5. | | |

| Item 6. | | |

| Item 7. | | |

| Item 7A. | | |

| Item 8. | | |

| Item 9. | | |

| Item 9A. | | |

| Item 9B. | | |

| Item 9C. | | |

| | |

| | |

| Item 10. | | |

| Item 11. | | |

| Item 12. | | |

| Item 13. | | |

| Item 14. | | |

| | |

| | |

| Item 15. | | |

| Item 16. | | |

| | |

FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K, and exhibits hereto, contains estimates, predictions, opinions, projections and other “forward-looking statements” as that phrase is defined in the Private Securities Litigation Reform Act of 1995. Such statements include, without limitation, references to the Company’s predictions or expectations of future business or financial performance as well as its goals and objectives for future operations, financial and business trends, business prospects and management’s outlook or expectations for earnings, revenues, expenses, capital levels, liquidity levels, asset quality or other future financial or business performance, strategies or expectations. The words “believe,” “expect,” “anticipate,” “plan,” “estimate,” “target,” “project” and similar expressions, among others, generally identify forward-looking statements. Such forward-looking statements are based on various assumptions (some of which may be beyond the Company’s control) and are subject to risks and uncertainties (which change over time) and other factors which could cause actual results to differ materially from those currently anticipated. Such risks and uncertainties include, but are not limited to:

•difficult market conditions and unfavorable economic trends in the United States generally and in financial markets, particularly in the markets in which the Company operates and in which its loans are concentrated, including an increase indifficult and unfavorable conditions and trends related to housing markets, costs of living, unemployment levels, inflation,interest rates, supply chain issues, inflation, and slowdowns in economic growth,growth;

•the impacts related to or resulting from bank failures and other economic industry volatility, including as a result of the novel coronaviruspotential increased regulatory requirements and its variants (COVID-19) pandemic;costs and potential impacts to macroeconomic conditions;

•possible additional loan losses and impairment of the collectability of loans;

•additional credit, fraud and litigation risks associated with our PPP lending activities;

•the economic and financial impact of federal, state and local emergency orders, vaccine mandates and other actions taken in response to the COVID-19 pandemic;

•the continuation of these conditions related to the COVID-19 pandemic, including whether due to a resurgence or additional waves of COVID-19 infections or variants thereof, particularly as the geographic areas in which we operate, how quickly and to what extent normal economic and operating conditions can resume and continue, and the potential waning of vaccine effectiveness or effects of low vaccination rates;

•the Company’s level of nonperforming assets and the costs associated with resolving problem loans including litigation and other costs and complying with government-imposed foreclosure moratoriums;

•changes in market interest rates, which may increase funding costs and reduce earning asset yields and thus reduce margin;

•the impact of changes in interest rates and the credit quality and strength of underlying collateral and the effect of such changes on the market value of the Company’s investment securities portfolio;portfolio, which could impact market confidence in our operations;

•the credit risk associated with the substantial amount of commercial mortgage,real estate, commercial and industrial, and construction and land development and commercial and industrial loans in the Company’sCompany's loan portfolio;

•the extensive federal and state regulation, supervision and examination governing almost every aspect of the Company’s operations, and potential expenses associated with complying with such regulations;

•the Company’s ability to comply with applicable capital and liquidity requirements, including its ability to generate liquidity internally or raise capital on favorable terms;

•possible changes in trade, monetary and fiscal policies and stimulus programs, laws and regulations and other activities of governments, agencies, and similar organizations, and the uncertainty of the short- and long-term impacts of such changes;

•any impairments of the Company’sCompany's goodwill or other intangible assets;

•conditions in the financial markets, that may limit the Company’s access to additional funding to meet its liquidity needs;

•the discontinued publication of London Inter-Bank Offered Rate (LIBOR) and the transition to an alternative reference interest rate, such as the Secured Overnight Financing Rate (SOFR), including methodologies for calculating the rate that are different from the LIBOR methodology and changed language for existing and new floating or adjustable rate contracts;

•the success of the Company's growth plans including its plans to grow the commercial small business leasing portfolio and residential, small business and Small Business Administration (SBA) portfolios, and wealth management business following its recent acquisition of Bryn Mawracross our WSFS Bank, Corporation (BMBC);Cash Connect

•the Company’s ability to successfully integrate and fully realize the cost savings and other benefits of its acquisitions, manage risks related to business disruption following those acquisitions, and post-acquisition Customer acceptance of the Company’s products and services and related Customer disintermediation, including its recent acquisition of BMBC;disintermediation;

•negative perceptions or publicity with respect to the Company generally and, in particular, the Company’s trust and wealth management business;

•failure of the financial andand/or operational controls of the Company’s Cash Connect® division;and/or Wealth Management segments;

•adverse judgments or other resolution of pending and future legal proceedings, and cost incurred in defending such proceedings;

•the Company’sCompany's reliance on third parties for certain important functions, including the operation of its core systems, and any failures by such third parties;

•system failures or cybersecurity incidents or other breaches of the Company’s network security, particularly given widespread remote working arrangements;

•the Company’s ability to recruit and retain key Associates;

•

the effects of problems encountered by other financial institutions that adversely affect the Company or the banking industry generally;

•the effects of weather, including climate change, and natural disasters such as floods, droughts, wind, tornadoes and hurricanes as well as effects from geopolitical instability, armed conflicts, public health crises and man-made disasters including terrorist attacks;

•the effects of regional or national civil unrest (including any resulting branch or ATM closures or damage);

•possible changes in the speed of loan prepayments by the Company’s Customers and loan origination or sales volumes;

•possible changes in market valuations and/or the speed of prepayments of mortgage-backed securities (MBS) due to changes in the interest rate environment and the related acceleration of premium amortization on prepayments in the event that prepayments accelerate;

•regulatory limits on the Company’s ability to receive dividends from its subsidiaries and pay dividends to its stockholders;

•any reputation, credit, interest rate, market, operational, litigation, legal, liquidity, regulatory and compliance risk resulting from developments related to any of the risks discussed above;

•any compounding effects or unexpected interactions of the risks discussed above; and

•other risks and uncertainties, including those discussed herein under the heading “Risk Factors” and in other documents filed by the Company with the Securities and Exchange Commission (SEC) from time to time.

The Company cautions readers not to place undue reliance on any such forward-looking statements, which speak only as of the date they are made. The Company disclaims any duty to revise or update any forward-looking statement, whether written or oral, that may be made from time to time by or on behalf of the Company for any reason, except as specifically required by law.

As used in this Annual Report on Form 10-K, the terms “WSFS”, “the Company”, “registrant”, “we”, “us”, and “our” mean WSFS Financial Corporation and its subsidiaries, on a consolidated basis, unless the context indicates otherwise.

The following are registered trademarks of the Company: Bryn Mawr Trust®, Cash Connect®, Christiana Trust Company of Delaware®,NewLane Finance®, Powdermill® Financial Solutions, West Capital Management®, WSFS Institutional Services®, WSFS Mortgage®and WSFS Wealth® Investments. Any other trademarks appearing in this Annual Report on Form 10-K are the property of their respective holders.

PART I

ITEM 1. BUSINESS

OUR BUSINESS

WSFS Financial Corporation (the Company or WSFS) is a savings and loan holding company headquartered in Wilmington, Delaware. Substantially all of our assets are held by the Company's subsidiary, Wilmington Savings Fund Society, FSB (WSFS Bank or the Bank), one of the ten oldest bank and trust companies in the United States (U.S.) continuously operating under the same name. With $15.8$20.6 billion in assets and $34.6$84.3 billion in assets under management (AUM) and assets under administration (AUA) at December 31, 2021,2023, WSFS Bank is the oldest and largest locally-managed bank and trust company headquartered in the DelawareGreater Philadelphia and Greater PhiladelphiaDelaware region. As a federal savings bank that was formerly chartered as a state mutual savings bank, WSFS Bank enjoys a broader scope of permissible activities than most other financial institutions.

A fixture in the community, WSFS Bank has been in operation for more than 189191 years. In addition to its focus on stellar customer experiences, WSFS Bank has continued to fuel growth and remain a leader in our community. We are a relationship-focused and locally-managed community banking institution.and wealth franchise, complemented by nationwide businesses. Our mission is simple: “We Stand for Service.” Our strategy of “Engaged Associates, living our culture, making a better life for allenriching the Communities we serve” focuses on exceeding customerCustomer expectations, delivering stellar experiences and building customer advocacy through highly-trained, relationship-oriented, friendly, knowledgeable and empowered Associates. As of December 31, 2021,2023, we serviced our Customers primarily from our 112114 offices located in Pennsylvania (52)(57), Delaware (42)(40), New Jersey (16)(14), VirginiaFlorida (1), Nevada (1) and NevadaVirginia (1), our ATM network, our website at www.wsfsbank.com and our mobile apps.

Subsidiaries

As of December 31, 2021,2023, the Company had six consolidated subsidiaries: WSFS Bank, The Bryn Mawr Trust Company of Delaware (BMT-DE), Bryn Mawr Capital Management, LLC (BMCM), WSFS Wealth Management, LLC (Powdermill®), WSFS CapitalSPE Services, LLC, and 601 Perkasie, LLC.

•BMT-DE, a Delaware state chartered non-depository trust company, supplements our existing Wealth Management LLC (West Capital),segment by offering Delaware advantage trust services including directed trusts, asset protection trusts and dynasty trusts via centers of influence such as estate planning attorneys. BMT-DE has approximately $53.0 billion in AUM and AUA at December 31, 2023.

•BMCM is a registered investment adviser and provides fee-only asset management services. On January 1, 2023, WSFS subsidiaries Cypress Capital Management, LLC (Cypress), Christiana Trust Companyand West Capital Management, LLC merged and rebranded as BMCM. In the third quarter of 2023, BMCM expanded its business in Southern Delaware® (Christiana Trust DE), and WSFS SPE Services, LLC.established a new presence in Boca Raton, Florida with the acquisition of a registered investment advisory firm's business based in Rehoboth Beach, Delaware. BMCM had approximately $3.3 billion in AUM and AUA at December 31, 2023.

•Powdermill® provides multi-family office services to affluent clientele in the local community and throughout the U.S.

•West Capital, a registered investment adviser, provides fee-only wealth management services tailored to the needs of high net worth individuals operating under a multi-family office philosophy. West Capital had approximately $947.5 million in AUM at December 31, 2021, compared to approximately $806.5 million at December 31, 2020.

•Cypress provides asset management services. As a registered investment adviser and fee-only wealth management firm, Cypress had approximately $1.3 billion in AUM at December 31, 2021 compared to approximately $1.2 billion at December 31, 2020.

•Christiana Trust DE supplements our existing Wealth Management segment by offering Delaware advantage trust services including directed trusts, asset protection trusts and dynasty trusts.

•WSFS SPE Services, LLC provides commercial domicile services which include providing employees, directors, subleases of office facilities and registered agent services in Delaware and Nevada.

•601 Perkasie, LLC was formed to hold certain tax credit investments.

As of December 31, 2021,2023, WSFS Bank had two wholly ownedwholly-owned subsidiaries: Beneficial Equipment Finance Corporation (BEFC), and 1832 Holdings, Inc. WSFS Bank had one majority-owned subsidiary, NewLane Finance Company (NewLane Finance®).

•BEFC, a small equipment and fixed assets leasing company, was acquired during the Beneficial Bancorp, Inc. (Beneficial) acquisition and is in the business of leasing small equipment and fixed assets.acquisition. Subsequent to the Beneficial acquisition, theBEFC ceased origination of new leases and its leasing operations of BEFC were combined with NewLane Finance®, described below.

•1832 Holdings, Inc. was formed to hold certain debt and equity investment securities.

•NewLane Finance® originates small business leases and provides commercial financing to businesses nationwide, targeting various equipment categories including technology, software, office, medical, veterinary and other areas. In addition, NewLane Finance® offers new product offerings for insurance through a newly-formedits subsidiary, Prime Protect.

As of December 31, 2021,2023, WSFS had onethree unconsolidated subsidiary,subsidiaries, WSFS Capital Trust III (the Trust), whichRoyal Bancshares Capital Trust I, and Royal Bancshares Capital Trust II.

•The Trust was formed in 2005 to issue $67.0 million aggregate principal amount of Pooled Floating Rate Capital Securities. These securities are currently callable and have a maturity date of June 1, 2035. The proceeds from this issue were used to fund the redemption of $51.5 million Floating Rate WSFS Capital Trust I Preferred Securities (formerly, WSFS Capital Trust I). WSFS Capital Trust I invested all of the proceeds from the sale of the Pooled Floating Rate Capital Securities in our Junior Subordinated Debentures. Although WSFS owns $2.0 million of the common securities of the Trust, the Trust is not consolidated into the Company’s Consolidated Financial Statements as the Company is not deemed to be the primary beneficiary of the entity.

•Royal Bancshares Capital Trust I (Trust I) and Royal Bancshares Capital Trust II (Trust II) (collectively, the RBC Trusts), which were acquired from Bryn Mawr Bank Corporation. The RBC Trusts were utilized for the sole purpose of issuing and selling capital securities representing preferred beneficial interests. Although WSFS owns an aggregate of $0.8 million of the common securities of Trust I and Trust II, the RBC Trusts are not consolidated into the Company’s Consolidated Financial Statements as the Company is not deemed to be the primary beneficiary of these entities.

Segment Information

For financial reporting purposes, our business has three segments: WSFS Bank, Cash Connect® and Wealth Management. The WSFS Bank segment provides loans and leases, deposits and other financial products to commercial and retailconsumer customers. Cash Connect® provides ATM vault cash, smart safe and other cash logistics services in the U.S, through strategic partnershipsservicing non-bank ATMs and smart safes nationwide and supporting ATMs for WSFS Bank Customers with severalone of the largest branded ATM networks manufacturers and service providers in the cash logistics industry.our region. The Wealth Management segment provides a broad array of planning and advisor services, investment management, personal and institutional trust services, and credit and deposit products to individuals, corporate, and institutional clients.

WSFS Bank

As of December 31, 2021,2023, WSFS Bank's banking business had a total loan and lease portfolio of $7.9 billion, which was funded primarily through commercial relationships and retail and customer-generated deposits.$12.8 billion. We have built a $6.2$9.9 billion commercial loan and lease portfolio by recruiting seasoned commercial lenders in our markets, offering the high level of service and flexibility typically associated with a community bank and through acquisitions. We fund this businessour lending businesses primarily with deposits generated through commercial relationships and retailconsumer deposits, as well as through our digital banking platforms.

WSFS Bank also offers a broad variety of consumer loan products, retail securities and insurance brokerage services through our retail branches, and mortgage and title services in collaboration withthrough WSFS Mortgage®. Our WSFS Mortgage® business is a mortgage banking company and abstract and title company specializing in a variety of residential mortgage and refinancing solutions.

Cash Connect®

Our Cash Connect® business is a premier provider of ATM vault cash, smart safe (safes that automatically accept, validate, record and hold cash in a secure environment) and other cash logistics services through strategic partnerships with several of the largest networks, manufacturers and service providers in the U.S.ATM industry. Cash Connect® services non-bank and WSFS-branded ATMs and smart safes nationwide. As of December 31, 2021,2023, Cash Connect® manages approximately $1.7$1.9 billion in total cash and services approximately 27,40033,000 non-bank ATMs and approximately 6,3008,700 smart safes nationwide. Cash Connect® provides related services such as online reporting and ATM cash management, predictive cash ordering and reconcilement services, armored carrier management, loss protection ATM processing equipment sales and deposit safe cash logistics. As of December 31, 2021,2023, Cash Connect® also supports over 600590 owned andor branded ATMs for WSFS Bank, which has one of the largest branded ATM networks in our market.

Wealth Management

Our Wealth Management business provides a broad array of planning and advisory services, investment management, trust services, and credit and deposit products to individual, corporate, and institutional clients through multiple integrated businesses.clients. Combined, these businesses had $34.6$84.3 billion of AUM and AUA at December 31, 2021. WSFS Wealth2023.

Bryn Mawr Trust® Investments provides financialis our predominant Private Wealth Management brand, providing advisory, investment management and trustee services to institutions, affluent and high-net-worth individuals. Private Wealth Management, which includes Private Banking, serves high-net-worth clients and institutions by providing trustee and advisory services, along with insurancefinancial planning, customized investment strategies, brokerage products such as annuities and brokerage products. Cypress,customized banking services including credit and deposit products tailored to its clientele. Private Wealth Management includes businesses that operate under the bank’s charter, through a broker/dealer and as a registered investment adviser, is aadvisor (RIA). It generates revenue through fee-only wealth management firm managing a “balanced” investment style portfolio focused on preservation of capitalarrangements, net interest income and generating current income. West Capital, a registered investment adviser, is aother fee-only wealth management firm operating under a multi-family office philosophy to provide customized solutions to institutionsservices such as estate administration, trust tax planning and high-net-worth individuals. The trust division of WSFS, comprised of WSFS Institutional Services® and Christiana Trust DE, provides trustee, agency, bankruptcy administration, custodial and commercial domicile services to institutional and corporate clients and special purpose vehicles. Christiana Trust DE also provides personal trust and fiduciary services to families and individuals across the U.S. Powdermill®custody. Powdermill® is a multi-family office specializing in providing independent solutions to high-net-worth individuals, families and corporate executives through a coordinated, centralized approach.

The Bryn Mawr Trust Company of Delaware provides personal trust and fiduciary services to families and individuals across the U.S. and internationally. WSFS Wealth Client Management serves high-net-worthInstitutional Services® provides trustee, agency, bankruptcy administration, custodial and commercial domicile services to institutional, corporate clients by delivering credit and deposit products and partnering with other Wealth Management businesses to provide comprehensive solutions to clients.special purpose vehicles.

For segment financial information for the years ended December 31, 2021, 20202023, 2022 and 2019,2021, see Note 21 to the Consolidated Financial Statements in this report.

Recent Business Developments

•Acquisition and Integration Efforts: On January 1, 2022, we completed our acquisition of Bryn Mawr Bank Corporation (BMBC), a Pennsylvania corporation and the parent holding company of The Bryn Mawr Trust Company, a Pennsylvania chartered bank and wholly owned subsidiary of BMBC. Our bank technology, branding, and branch conversion is scheduled to occur later in the first quarter of 2022, with our Trust and Wealth integration expected to follow in late 2022 or early 2023. Throughout this document, we refer to these acquired entities collectively as “Bryn Mawr Trust.”

•Upstart Strategic Partnership: During 2021 we launched our strategic partnership with Upstart Holdings, Inc. (Upstart), a leading white label lending-as-a-service platform provider specializing in risk-based priced unsecured consumer loans. With this relationship WSFS is now able to deliver an AI enabled underwriting program customized to our specifications. The Upstart partnership enables WSFS to digitize our unsecured personal loan product, acquire new in-footprint customers, and provides cross-sell opportunities within our footprint.

•Future Forward: Throughout the COVID-19 pandemic, our Retail branch office locations remained open servicing our Customers while following the recommended Federal, State and local guidance, including appropriate personal protective equipment and social distancing. During 2021, we began a phased transition to the office at our corporate locations with approximately 30% of Associates in these locations working from the office at least 3 days per week. As we move into 2022, we look to further expand our Future Forward initiative and transition more Associates into office locations while taking the appropriate precautions. Our Future Forward strategy is also focused on our current and future office capacity and including assessment of our current space utilized by us and potential for optimization in this area. This strategy will continue to evolve as we progress into 2022.

WSFS DIFFERENTIATION STRATEGY

While most banks offer similar products and services, weWe believe that WSFS, through its provenour unique competitive position in our market as the only community bank with a full suite of product offerings to compete with larger institutions, diversified and resilient fee income, and high-touch customer service, model, sets itself apart from other banks in our market and the industry in general. In addition, community banks such as WSFS have been able to distinguish themselves from large national or international banks by providing our Customers with the service levels, responsiveness and local decision making they prefer.

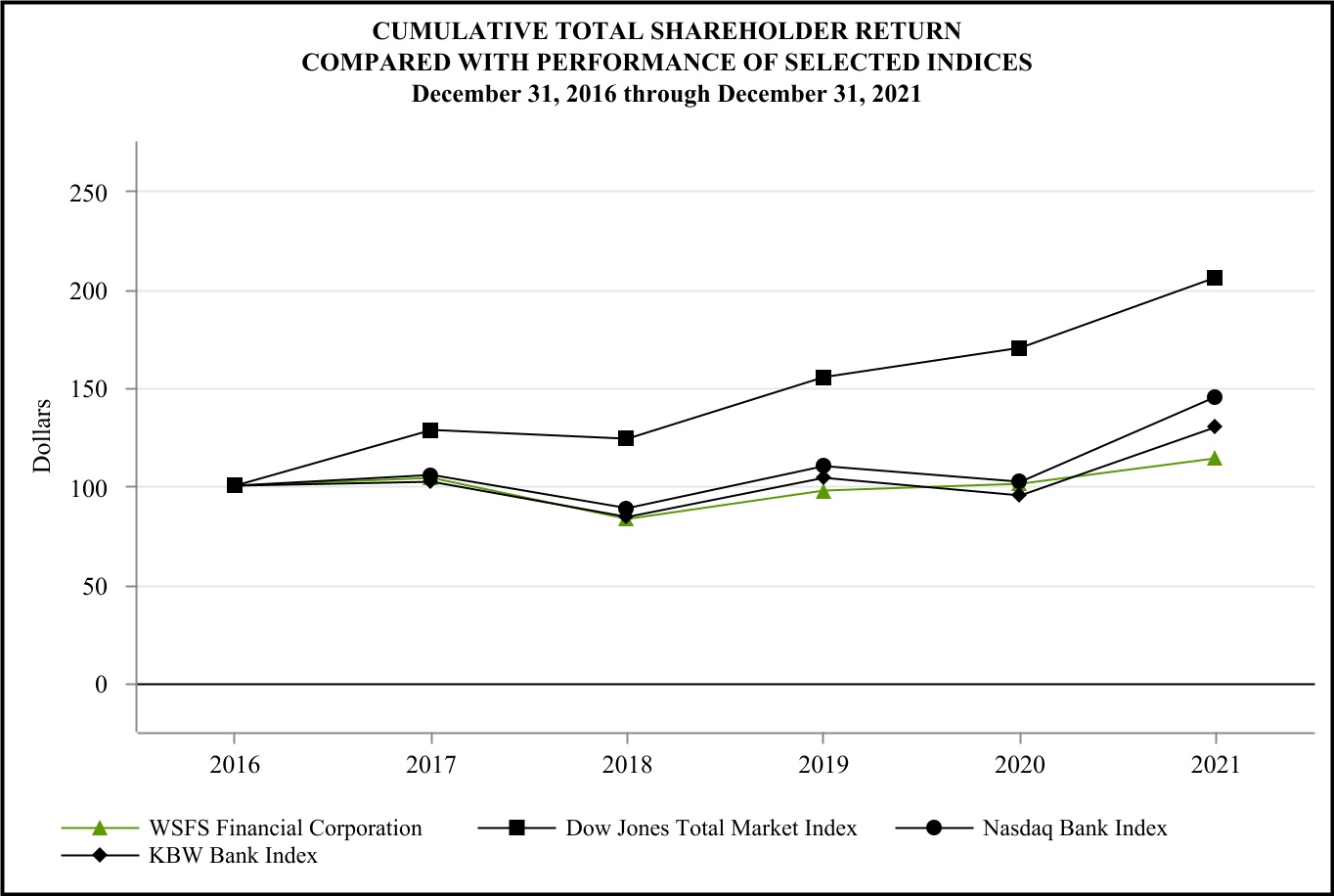

Our focus on this differentiation strategy supports our core franchise with a mix of organic and acquisition-related growth and builds value for our stockholders. Since December 31, 2017,2018, our commercial loans and leases, which exclude loans held-for-sale, have grown 146% from $4.0 billion to $6.2$9.9 billion at December 31, 2021, a 9% compound annual growth rate (CAGR).2023. Over the same period, customer deposits have grown 202% from $5.0$5.4 billion to $13.2 billion, a 21% CAGR. For further details, refer to the Comparative Stock Performance Graph in Item 5. Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities.$16.4 billion.

The following factors summarize what we believe is our differentiation strategy:

Our Mission

We Stand for Service® is our mission and our daily call to action. Since 1832, WSFS has been a service-oriented, locally managedlocally-managed community banking institution serving Greater Philadelphia and Delaware Valleyregion families and businesses. We strive to meet our Customers’ evolving banking needs and to exceed their expectations each and every day.

Values

Our values address integrity, service, accountability, transparency, honesty, growth and desire to improve. They are the corefoundation of our culture. They define us and serve as our moral compass. Our values are rooted in integrity; we do the right thing, unconditionally. We live our values every day; they nourish our culture they make us whoand practiced over time, become “the WSFS way.” Our values are the fuel that ignites our virtuous cycle: when we aredo well, our Community does well and when our Community does well, we live them every day.

At WSFS, we:do well.

•Do the right thingService: Serving others is fundamental to our mission and grounds our purpose. We serve by listening, caring, collaborating, volunteering and “getting things done” for those who rely on us to be there for them.

•Serve othersTruth: The truth is non-negotiable. The truth brings clarity to a challenging situation or sensitive matter; it guides us with confidence and conviction. Being open and honest earns trust and underpins our conversations, decisions and communications.

•Are welcoming, openRespect: We value and candid

•Growrespect each other and improveall we serve. The many unique attributes of our team makes us stronger. Respecting others’ beliefs, experiences, perspectives and feelings sparks dialogue, facilitates learning and growth, drives change, inspires innovation and builds valued relationships.

Human SigmaEngagement and Culture

Our business model is designed using the science of Human Sigma, which is built on a foundation of engagement. The Human SigmaOur model identified by Gallup, Inc. (Gallup), begins with Associates (employees) who take ownership for their responsibilities and impact; as such, they are more likely to consistently perform at a higher level. We significantly invest in our culture ofand engagement which underpinsas they underpin all that we do at WSFS, including attracting, inspiring and retaining our Associates, delivering stellar Customer experiences and strengthening the well-being of our communities. Our culture is based on the fundamental principal of “a really good life.”communities as evidenced by our Vision: "We envision a day when everyone will thrive." Our strategy, “Engaged Associates, living our culture, making a better life for allenriching the Communities we serve” builds upon that principal.

Our strategy in action starts aour virtuous cycle whereby, as we do better, our community does better and as our community does better, we do better.cycle. It’s a simple premise that plays out in a big way every day. Research studies validate the direct link between engagement and a company’s financial performance. Our strategy, which drives our virtuous cycle, ensuresis built upon that research and reinforces our culture that is evidenced in our Company results.

Human Resources

At December 31, 2021,2023, we had 1,8392,229 full-time equivalent Associates. Our Associates are not represented by a collective bargaining unit and we believe our relationship with our Associates is strong.

During 2021,2023, WSFS captured the voice of our Associates and our Customers through multiple channels including our ongoing partnership with Gallup Inc. (Gallup), which was used to measure our Associate and Customer engagement.

Surveys conducted for us by Gallup indicate that, in 2021:

•Our Associate engagement survey results placed WSFS in the 93rd88th percentile of Gallup's global overall company-level database. Our Associate engagement ratio was 16.5:12.4:1, which means there were 16.512.4 engaged Associates for every actively disengaged Associate. This compares to a U.S. working population ratio of 2.1:1.

•Our culture of inclusion index of 4.484.38 placed WSFS in the 74th percentiletop quartile of Gallup's global overall workgroup-level database. We believe these results reflect that Associates are encouraged to be themselves, are a valued part of their teams, experience strength-based developments, have inclusive conversations and trust in the Company's mission, values and leadership.

•62.7% of Customers surveyed ranked WSFS a “five” out of five, strongly agreeing with the statement “WSFS is the perfect bank for people like me,” which placed WSFS in the 71st percentile of Gallup's global overall customer database. Our Customer engagement ratio was 6.1:1, which means there were 6.1 engaged Customers for every actively disengaged Customer.

•Customer loyalty grewremained consistent during the year, as measured by our Net Promoter Scores (NPS). Our branch networkWSFS achieved an overall NPS of 79.368.1 in 2021 compared to 72.3 in 2020. The fourth quarter of 2021 resulted2023, which placed WSFS in the highest quarter performance since program inception.top quartile of Medallia's global database of financial services companies for relationship surveys.

By fostering a culture of engaged and empowered Associates, we believe we have become the employer and bank of choice in our market. In 2021,2023, we were honored to receive the following accolades:

•Ranked #10 in the United States on the Forbes America’s Best Banks Listing;

•Received The Gallup Exceptional Workplace Award for the fifthseventh time;

•Named a Top Workplace in Delawareto Forbes' list of America's Best Banks for the 15thfourth year in a row;

•Named a Top Workplace2023 honoree of The Civic 50 Greater Philadelphia by the Philadelphia Foundation, in Philadelphiapartnership with Points of Light and southeastern PAother local partners, for the seventhsecond year in a row;

•Selected as Reader's Pick for Named to the 'Soaring 76', recognizing us as one"Best of the 76 fastest growing companiesBiz" for Customer Service in the Greater Philadelphia region for the fifth yearSouth Jersey Magazine;

•Recognized in a row by the Philadelphia Business Journal;Newsweek's List of America's Best Regional Banks and Credit Unions 2024; and

•Named "Bestone of Biz Editor's Pick" for customer serviceAmerica's Best Midsize Employers in 2023 by Forbes.

During 2023, our Associates continued to embody our strategy through the South Jersey Business Magazine; andfollowing community enrichment activities:

•Volunteered more than 18,000 hours during 2023 through Team WSFS, our corporate volunteer program;

•Recognized by The ForumIn June, we held our first-ever "We Stand for Service Day", during which approximately 1,200 of Executive Women as a "Championour Associates provided nearly 5,000 hours of Board Diversity."

Diversity, Equityservice to more than 80 nonprofit and Inclusion

Diversity, Equitycommunity organizations across the Greater Philadelphia, Southern New Jersey and Inclusion (DE&I) is rooted in the values of WSFS, which is led by our Director of DE&I, Michelle Burroughs, who was hired in October 2021. Our DE&I efforts focus on educating, supporting, managing and implementing diversity and inclusion strategies and programs, and creating and delivering initiatives designed to sustain a culture of inclusion.

During 2021, the Company completed the following DE&I accomplishments:

•Created DE&I Strategic Pillars and socialized with Executive Leadership Team;Delaware region.

•CompletedWe contributed $4.9 million to the DE&I Steering Committee Charter and structure;WSFS CARES Foundation, the charitable giving arm of WSFS Bank, to enhance community support activities, which included a one-time $2.0 million special contribution in the fourth quarter.

•Established 2022 Focus Areas for DE&I Steering CommitteeThe WSFS CARES Foundation provided grants and Strategic Pillars;

•Completed "Listening Tours" with approximately 50 Associatesdonations totaling more than $2.7 million to capture qualitative data regarding DE&I;more than 390 community organizations located across Delaware, New Jersey and

•Established report routine with Voice Pennsylvania, bolstering our key pillars of Customer team that will review Customer discrimination data.support including community investments, affordable housing, revitalization and business economic empowerment, education and leadership development, and strengthening those in need.

Diversity, Equity and Inclusion

Beyond having diverse talent and Customers, WSFS works to create a truly inclusive environment with opportunities to find commonalities, build relationships and provide support to our diverse Communities from different backgrounds and cultures. We are committed to enhancing workforce diversity, creating developmental opportunities and continually improving hiring practices to retain our status as an employer of choice.

During 2023, the Company completed the following Diversity, Equity, and Inclusion (DEI) accomplishments:

•The number of Associates engaged as members of one or more Resource groups more than doubled compared to 2022.

•Launched the inaugural cohort of a formalized, 9-month mentoring program for Associates in Resource Groups.

•Implemented monthly challenges to increase leadership opportunities to engage in DEI trainings, conversations, and activities.

•Developed an interactive DEI scorecard to assist with monitoring trends and reporting data for each Executive Leadership Team member.

•Facilitated Implicit Bias and Ally Training to Associates.

•Successfully launched an external DEI page on the company website.

•Integrated the ability to display pronouns into email signatures.

•Established DEI engagement goals for Executive Leadership Team.

•Implemented a recognition program which allows Associates the opportunity to recognize colleagues for demonstrating behaviors that promote inclusion and belonging.

Community Banking Model

Our size and community banking model play a key role in our success. Our approach to business combines a service-oriented culture with a full complement of products and services, all aimed at meeting the needs of our retail,consumer, business and wealth Customers. We believe the essence of being a community bank means that we are:

•Small enough to offer Customers responsive, personalized service and direct access to decision makers, yet

•Large enough to provide the products, services and balance sheet lending capacity needed by our target market Customers.

As the financial services industry has consolidated, many independent banks have been acquired by national companies that have centralized their decision-making authority and focused their product offerings on a regional or even national customer base. As a result, many of these banks have lost the deep knowledge of the local markets expected by our Customer base. We believe this trend has underserved small and medium size business owners who have become accustomed to dealing directly with their bank’s senior executives, discouraged retailconsumer customers who often experience deteriorating levels of service in branches and other service outlets, and resulted in less empowered bank employees who are less engaged to provide good and timely service to their customers.

We have created the largest, premier, locally-headquarteredlocally headquartered community bank in the DelawareGreater Philadelphia and Greater PhiladelphiaDelaware region, offering the benefits of local market knowledge and decision-making, a full-service product suite, the balance sheet to compete with larger regional and national banks, and most importantly, a culture of engaged Associates that bring to life WSFS’ mission of We Stand For Service in our daily delivery of stellar Customer experiences.

WSFS Bank offers:

•One primary point of contact: Each of our relationship managers is responsible for understanding his or hertheir Customers’ needs and bringing together the right resources in WSFS Bank to meet those needs.

•A customized approach to serving our Customers: We believe that this gives us an advantage over our competitors who are too large or centralized to offer customized products or services.

•Products and services that our Customers value: This includes a broad array of banking, cashtreasury management, capital markets and trust and wealth management products, as well as a legal lending limit high enough to meet the credit needs of our Customers, especially as they grow.

•Rapid response and a company that is easy to do business with: Our Customers tell us this is an important differentiator from larger in-market competitors.

Our Diversified Business

Diversified Revenue Streams

With over 25 discrete lines of business, our diversified revenue model is a key differentiator for the Company. We focus on relationship-based lending which provides the potential for higher profit margins, more resilient deposits and strong consumer relationships. In addition, our diversified fee revenue businesses, which include banking fees, Wealth, Trust, Cash Connect®, and capital markets, account for 32.8% of our noninterest income and further differentiate us from our peers and provide additional growth opportunities for the Company.

Balance Sheet Management

We put a great deal of focus on actively managing our balance sheet. This manifests itself in:

•Prudent capital levels - Maintaining prudent capital levels is key to our operating philosophy. At December 31, 2021 all regulatory capital levels for the Bank were in excess of "well-capitalized" levels. For the capital position of the Bank and the Company, refer to Note 13 of the Consolidated Financial Statements. At December 31, 2021, the Company's common equity to assets ratio was 12.29% and its tangible common equity to tangible assets ratio, which is a non-GAAP financial measure, was 9.14%. For a reconciliation of tangible common equity and tangible assets to net income and total assets, the most comparable measures in accordance with U.S. generally accepted accounting principles (GAAP), refer to “Reconciliation of non-GAAP financial measures included in Item 1” located at the end of this section.

•Disciplined lending - We maintain discipline in our lending with a particular focus on portfolio diversification and granularity. Diversification includes limits on loans to one borrower as well as industry and product concentrations. We supplement this portfolio diversification with a disciplined underwriting process and the benefit of knowing our customers. We have also taken a proactive approach to identifying credit-related trends in our local economy and have responded to areas of concern.

•Focus on credit quality - We seek to control credit risk in our investment portfolio and use this portion of our balance sheet primarily to help us manage liquidity and interest rate risk, while providing marginal income and tax relief. Our philosophy and pre-purchase due diligence have allowed us to control credit risk in our investment portfolio.

•Asset/liability management strategies - Our investment portfolio is consistent with the approved risk appetite of our Board of Directors. We work to optimize duration, yield and liquidity and to minimize credit risk within policy guidelines. The concentration in agency MBS (98%(96% of investment portfolio) and bank qualified municipal bonds (2%(4% of investment portfolio) provides liquidity, yield and credit to meet the intended risk profile.

Disciplined Capital Management

We understand that our capital (or stockholders’ equity) belongs to our stockholders. They have entrusted this capital to us with the expectation that it will earn an appropriate return relative to the risks we take. Mindful of this balance, we prudently, but aggressively, manage our capital.

Maintaining prudent capital levels is key to our operating philosophy. At December 31, 2023 all regulatory capital levels for the Bank were in excess of "well-capitalized" levels. For the capital position of the Bank and the Company, refer to Note 13 of the Consolidated Financial Statements. At December 31, 2023, the Company's common equity to assets ratio was 12.03% and its tangible common equity to tangible assets ratio, which is a non-GAAP financial measure, was 7.52%. For a reconciliation of tangible common equity and tangible assets to net income and total assets, the most comparable measures in accordance with U.S. generally accepted accounting principles (GAAP), refer to “Reconciliation of non-GAAP financial measures included in Item 1” located at the end of this section.

We continue to execute our current Board-approved share repurchase plan,plans, as well as any future Board-approved share repurchase plans, including opportunistically repurchasing shares, based on current valuation levels, above our stated practice of returning a minimum of 25%35% of annual net income to stockholders through dividends and share repurchases. All share repurchases were temporarily suspended upon the announcement of the signing of the Merger Agreement with BMBC on March 10, 2021. We resumed repurchases during the first quarter of 2022 following the close of our combination with Bryn Mawr Trust on January 1, 2022.

Performance Expectations and Alignment with Stockholder Priorities

We are focused on high-performing, long-term financial goals. We define “high-performing” as the top quintile of a relevant peer group in return on assets (ROA).key financial metrics. Management incentives are, in large part, based on driving performance of ROA as well as return on average tangible common equity (ROTCE), which is a non-GAAP financial measure, and EPS growth.EPS. More details on management incentive plans will be included in the proxy statement for our 20222024 Annual Meeting of Stockholders.

For the year ended December 31, 2021,2023, WSFS reported ROA of 1.82%1.33%. Core ROA, which excludes non-core items and is a non-GAAP financial measure, was 1.80%1.38% for the year ended December 31, 2021.2023.

Core ROA for 20212023 excludes (i) securities gains, (ii) realized and realized/unrealized gains and losses on equity investments, net,(ii) valuation adjustments related to our derivative liability established from the sale of 360,000 Visa Class B shares in 2Q 2020, (iii) loss on debt extinguishment,FDIC special assessment, (iv) corporate development and restructuring expense, (v) recovery of legal settlement,certain contributions to the WSFS CARES Foundation, and (vi) contributionincome tax adjustments related to WSFS CARES Foundation.bank-owned life insurance (BOLI) policy surrender.

For a reconciliation of Core ROA to ROA, the most comparable GAAP measure, refer to “Reconciliation of non-GAAP financial measures included in Item 1” located at the end of this section.

Growth Plans

We have achieved success over the long-term in lending and deposit gathering, growing the Wealth Management segment’s client base and product offerings and growing Cash Connect®’s customer base and services. Our success has been the result of a focused strategy that provides service, responsiveness and careful execution in a consolidating marketplace.

We plan to continue to grow by:

•DevelopingRecruiting and developing talented, service-focused Associates: We have successfully recruited Associates with strong ties to, and the passion to serve, their communities to enhance our service in existing markets and to provide a strong start in new communities. We also focus on developing talent and leadership from our current Associate base to better equipprepare those Associates for their jobsroles and prepare them for leadership roles at WSFS.to ensure we have bench strength across our various lines of business. Our strategy continues to be diligent on attracting, retaining and rewarding the best talent, which we believe has positioned us well in the current climate of the Great Resignation that has seen many employees of U.S. companies reconsider their priorities and voluntarily resign.climate.

•Embracing the Human Sigma concept: We are committed to building Associate Engagementengagement and Customer Advocacyloyalty and advocacy as a way to differentiate ourselves and grow our franchise.

•Building fee income through investment in and growth of our Wealth Management and Cash Connect® segments.

◦Wealth Management experienced near-record growth during 2021 in AUA/AUM and corresponding AUM-based revenues largely due to market performance.ended 2023 31% above 2022 balances. WSFS Institutional Services® ended 20212023 as the securitization industry's fourth most active trustee for U.S. Asset and Mortgage Backed Securities by number of deals completed according to Asset-Backed Alert’s ABS Database.

◦Cash Connect® saw sustained demand forincreased fee revenue due to the rising interest rate environment, increasing market share in the ATM vault cash space, and related services duringcontinued growth in the on-going COVID-19 pandemic, andsmart safe space. The division, in partnership with our retail strategy, continued to serve the DelawareGreater Philadelphia and the Greater PhiladelphiaDelaware region through the WSFS ATM network. The number of owned andor branded ATMs was 609590 as of December 31, 2021.2023.

•Continuing strong growth in commercial and retailconsumer lending by:

◦Offering local decision-making by seasoned banking professionals with significant local market experience.

◦Executing our community banking model that combines stellar experiences with the banking products and services our business customers demand.

◦Continuing to grow our NewLane Finance® leasing business.

◦Adding seasoned lending professionals that have helped us win customers in our Delaware, southeastern Pennsylvania and southern New Jersey markets, which contributes to our expanding commercial small business leasing portfolio and residential, small business and SBA portfolios in the footprint we operate.markets.

◦Leveraging our strategic partnership withpartnerships, including Spring EQ, LLC, Upstart, a leading white label lending-as-a-service platform provider specializing in risk-based priced unsecured consumer loans, which we launched in 2021.LendKey Technologies, Inc, and Cred Technologies (cred.ai).

•Continuing to grow deposits by:

◦OfferingProviding a stellar experience to our Customers and offering products through an expanded and updatedour branch network, increasing our market presence in Philadelphia,Delaware, southeastern Pennsylvania and southern New Jersey.

◦Providing a stellar experience to our Customers.

◦Further expanding our commercialCommercial and Small Business Customer relationships with deposit and cash management products.

◦Expanding services within WSFS Institutional Services® and increasing cross-sell opportunities within Private Wealth Management.

◦Finding creative ways to build deposit market share such as targeted marketing programs.

•Continuing investment inEnhancing our Delivery Transformation initiative (described in greater detail in “Innovation” below)capabilities to increase adoption and usageserve the needs of digital channels aligned with our strategyCustomers through our Capital Markets division by:

◦Improving branch NPS scoresMaking strategic investments to build our Interest Rate Derivatives, Foreign Exchange, and expanding NPS surveys to our contact center.Trade Finance lines of business.

◦Deploying MedalliaEmploying products and services that enable customers to better manage their own market risk exposures, providing additional sources of non-interest fee income for real-time customer feedback from our branches and contact center.

◦Expanding DocuSign capabilities to improve turnaround time and document retention across the Company.

◦Executing multichannel target marketing campaigns with our Customers.Making continued investments in a team of highly experienced markets personnel and improved technology solutions.

◦Implementing Salesforce to support our customer relationship managementDelivering the capabilities of a globally capable financial institution with focus on change management, adoption and governance.a locally headquartered team that is fully embedded in the WSFS culture.

•Seeking targeted, strategic opportunities in our non-banking businesses while we focus on optimizing our recent franchise investments.

•Continuing investment in our franchise to increase adoption and usage of digital channels aligned with our strategy by

◦Enabling business outcomes through optimizing and leveraging the full capabilities of current and future investments in our franchise to increase Associate efficiencies and improve the overall Customer experience.

◦Building out Salesforce to support our customer relationship management with focus on change management, adoption and governance

◦Increased control, transparency, automation & efficiencies through platform integrations, enhancements and bot implementations

◦Advancing how we use data, the deployment of artificial intelligence, and predictive modeling to create operational efficiencies and redesign business models

◦Continue to build upon people, processes and controls within a focus on information security and fraud prevention

Disciplined Cost Management

We maintain a disciplined cost management strategy while continuing to make prudent investments in our businesses through the lens of our Strategic Plan. This wasis evident in management's execution of the cost synergies and branch optimization plan following the acquisition of Beneficial. Further, we have experienced and continue to anticipate increased costs as a result of our previously announced Delivery Transformation initiative andcontinued investment in marketing technology,the franchise, fully supported by business cases indicating strong return on investment, and driving our future growth.

Innovation

Our organization is committed to product and service innovation as a means to drive growth and to stay ahead of changing customer demands and emerging competition. We are focused on developing and maintaining a strong “culture of innovation” that solicits, captures, prioritizes and executes innovation initiatives, including feedback from our customers, as well as leveraging technology from product creation to process improvements. Cash Connect®, a premier provider of ATM vault cash, smart safe and other cash logistics services in the U.S., serves as an innovation engine by driving enhancements such as mobile phone cash withdrawals from WSFS ATMs, and has developed best-in-class cash logistics and reconciliation software. WSFS Institutional Services®, which offers owner and indenture trustee services for asset-backed securities, custody, escrow, verification agent services as well as numerous other services, has partnered with several technology firms and fintechs to enhance and expand our client offerings. These innovations have created internal efficiencies and valued services for our local banking customers, institutional clients and merchants across the nation. We intend to continue to leverage technology and innovation to grow our business and to successfully execute on our strategy.

In 2019, we embarked on a multi-year Delivery Transformation initiative focusedWe maintain an organizational philosophy of continuous, prudent investment in technology to continue to meet our customer needs. We focus on melding our physical and digital delivery, consistent with our brand, by enabling our Associates with the latest technology and actionable data to better serve our Customers. Industry and customer behavior trends continue to shift as observed in reduced branch traffic and increased mobile adoption.digital channel adoption. As such, we have concluded that we need to stay nimble as we transform our delivery channels to meet these new expectations. Our transformationcontinued investment includes optimizing our physical branch network and making strategic investments in meaningful technology solutions, supported by specialized talent. Those investments are expected to provide our Customers with leading edge products and elevate our Associates, as they strive to serve in a competitive and compelling way. We are designing and integrating solutions to provide personalized experiences to our Customers, while retaining the essence of what makes WSFS great. Through our Delivery Transformationinvestments in the franchise and our ongoing commitment to Stellar Service, we intend to continue to lead the community and regional banking industry with regards to service delivery and Customer experience.

Our organization is committed to product and service innovation as a means to drive growth and to stay ahead of changing customer demands and emerging competition. We are focused on developing and maintaining a strong “culture of innovation” that solicits, captures, prioritizes and executes innovation initiatives, including feedback from our customers, as well as leveraging technology from product creation to process improvements.We have embraced a partnership model to help diversify our consumer business and learn from innovators in the industry. We position ourselves with strategic partners when it is the best experience for our Customers and aligned to our strategic plan. Through these partnerships, we look forward to offering and supporting even more innovative products to the financial services marketplace, continuing our organizational learning in this fast-developing space, and participating in value creation for our stockholders. These current partnerships include:

•LendKey Technologies, Inc.: A digital lending platform that specializes in student loans and student loan refinancing.

•Spring EQ, LLC: A digital mortgage solution specializing in home equity, refinancing, cash out, and home purchase loans.

•Cred Technologies (cred.ai): A Philadelphia-based fintech company that provides a high-tech, mobile-first everyday card spending experience. Through our partnership with cred.ai, we issue credit cards and provide deposit accounts.

•Upstart: A leading white label lending-as-a-service platform provider specializing in risk-based priced unsecured consumer loans. Our partnership with Upstart allowed us to expand our personal loan offerings to a wider, more inclusive Customer base while diversifying our business and creating more digital-friendly Customer experiences.

Previously, we partnered with•LendKey Technologies, Inc.: A digital lending platform that specializes in student loans and made an investment in Social Finance, Inc. (SoFi), an online personal financestudent loan refinancing.

•Cred Technologies (cred.ai): A Philadelphia-based fintech company that provides a full suite of products. During 2021,high-tech, mobile-first everyday card spending experience. Through our partnership with cred.ai, we liquidated our investment in SoFi for a net gain of $4.4 million.issue credit cards and provide deposit accounts.

Enterprise Risk Management

We manage our risks through our Enterprise Risk Management (ERM) program administered by the Chief Risk Officer (CRO) and ERM department. Our stand-alone ERM department is separate from our lines of business. Formal Risk Appetite Statementsrisk appetite statements have been developed for each risk category throughout the institution; these statements are reviewed and approved by the Board annually. From a regulatory perspective, our ERM program is evaluated as part of the regular Safety and Soundness examination by the Office of the Comptroller of the Currency (OCC).

Key Risk Indicators (KRIs) or Riskrisk metrics are continually monitored in relation to risk appetite though a Risk Assessment Summary dashboard. Each KRI has an assigned quantitative tolerance level which considers our overall risk appetite, regulatory requirements, the bank’s peer group statistics, best practices, and general industry guidelines. As part of our ERM program, approximately 90100 KRIs are monitored company-wide. In the event that risk levels exceed our defined risk appetite, management action is required.

The CRO and the ERM department conduct meetings with managementfacilitates a risk liaison program, consisting of individuals in the first line of defense that monitor and report risks from their respective business lineslines. ERM engages and support areashas credible challenge discussions with Risk Liaisons and business line leaders to discuss and gather information for ERM reporting. ERM reporting is also provided to the Board of Directors quarterly. In addition, our Management Risk Committee (MRC), which meets each quarter, provides management governance and oversight of the Company's risk management program on an enterprise-wide basis, and includes members of the Company's executive and senior management teams.

Market Demographics

Our primary market is Delaware and the Greater Philadelphia and Delaware region, including southeastern Pennsylvania and southern New Jersey. This market benefits from an urban concentration as well as from a unique political, legal, tax and business environment. The following table shows key demographics for our markets compared to the national average.

| | | | | | | | | | | | | | | | | | | | | | | | | | |

| (Most recent available statistics) | | Delaware | | Southeastern Pennsylvania(1) | | Southern New Jersey(2) | | National

Average |

Unemployment (For November 2021) (3) (4) (5) | | 5.1% | | 4.1% | | 5.0% | | 4.2% |

Median Household Income (2015-2019) (6) | | $68,287 | | $80,261 | | $78,934 | | $62,843 |

Population Growth (2010-2020) (7) | | 10.3% | | 5.2% | | 2.4% | | 7.4% |

| | | | | | | | | | | | | | | | | | | | | | | | | | |

| (Most recent available statistics) | | Delaware | | Southeastern Pennsylvania(1) | | Southern New Jersey(2) | | National

Average |

Unemployment (For November 2023) (3) (4) (5) | | 4.2% | | 2.8% | | 4.2% | | 3.7% |

Median Household Income (2018-2022) (6) | | $79,325 | | $95,554 | | $92,310 | | $75,149 |

Population Growth (2020-2022) (7) | | 3.0% | | (0.5)% | | 0.6% | | 0.5% |

(1)Comprised of Bucks, Chester, Delaware, Montgomery, and Philadelphia Counties

(2)Comprised of Burlington and Camden Counties

(3)Bureau of Labor Statistics - Delaware and National unemployment rates are as of November 2021,2023, seasonally adjusted

(4)Bureau of Labor Statistics - Southeastern Pennsylvania unemployment rate is a simple average of the November 20212023 not seasonally adjusted unemployment rates for Bucks, Chester, Delaware, Montgomery, and Philadelphia Counties

(5)Bureau of Labor Statistics - Southern New Jersey unemployment rate is a simple average of the November 20212023 not seasonally adjusted unemployment rates for Burlington and Camden Counties

(6)U.S. Census Bureau - Quick Facts 20152018 - 20192022

(7)U.S. Census Bureau - Quick Facts 20102020 - 20202022

DISTRIBUTION OF ASSETS, LIABILITIES AND STOCKHOLDERS’ EQUITY

Condensed average balance sheets for each of the last two years and analyses of net interest income and changes in net interest income due to changes in volume and rate are presented in “Results of Operations” included in the section entitled “Management’s Discussion and Analysis of Financial Condition and Results of Operations.”

CREDIT EXTENSION ACTIVITIES

Over the past several years we have focused on growing the more profitable, relationship-oriented segments of our loan portfolio.portfolio as well as growing our consumer portfolio primarily through our consumer partnerships. Our current portfolio lending activity is concentrated on small- to mid-sized businesses in the mid-Atlantic region of the U.S., primarily in Delaware, southeastern Pennsylvania, southern New Jersey, Maryland and northern Virginia. Based on current market conditions, we expect our focus on growing commercial and industrial loans and other relationship-based commercial loans to continue during the remainder of 20222024 and beyond.

The following table shows the composition of our loan and lease portfolio at year-end for the last two years:

| | | |

| | | | | At December 31, | | At December 31, |

| (Dollars in thousands) | (Dollars in thousands) | | 2021 | | 2020 | |

| | | | Amount | | Percent | | Amount | | Percent | |

| | |

| | |

| Types of Loans | Types of Loans | | | | | | | | | |

Commercial and industrial(1) | | $ | 1,918,043 | | | 24.6 | % | | $ | 2,700,418 | | | 30.7 | % | |

| Types of Loans | |

| Types of Loans | |

| Commercial and industrial | |

| Commercial and industrial | |

| Commercial and industrial | |

| Owner-occupied commercial | |

| Owner-occupied commercial | |

| Owner-occupied commercial | Owner-occupied commercial | | 1,341,707 | | | 17.2 | | | 1,332,727 | | | 15.2 | | |

| Commercial mortgages | Commercial mortgages | | 1,881,510 | | | 24.2 | | | 2,086,062 | | | 23.7 | | |

| Commercial mortgages | |

| Commercial mortgages | |

| Construction | Construction | | 687,213 | | | 8.8 | | | 716,275 | | | 8.1 | | |

| Construction | |

| Construction | |

| Commercial small business leases | |

| Commercial small business leases | |

| Commercial small business leases | Commercial small business leases | | 352,276 | | | 4.5 | | | 248,885 | | | 2.8 | | |

| Residential(2) | | 546,667 | | | 7.0 | | | 774,455 | | | 8.8 | | |

Consumer(3) | | 1,158,573 | | | 14.9 | | | 1,165,917 | | | 13.3 | | |

Residential(1) | |

| Residential(1) | |

| Residential(1) | |

Consumer(2) | |

Consumer(2) | |

Consumer(2) | |

| | Gross loans and leases | |

| | Gross loans and leases | |

| | Gross loans and leases | Gross loans and leases | | 7,885,989 | | | 101.2 | | | 9,024,739 | | | 102.6 | | |

| Less: | Less: | | |

| Less: | |

| Less: | |

| | Allowance for credit losses | Allowance for credit losses | | 94,507 | | | 1.2 | | | 228,804 | | | 2.6 | | |

Net loans and leases(4) | | $ | 7,791,482 | | | 100.0 | % | | $ | 8,795,935 | | | 100.0 | % | |

| | Allowance for credit losses | |

| | Allowance for credit losses | |

Net loans and leases(3) | |

Net loans and leases(3) | |

Net loans and leases(3) | |

(1)Includes $31.5 million and $751.2 million of PPP loans at December 31, 2021 and 2020, respectively.

(2)Includes reverse mortgages, at fair value of $3.9$2.8 million and $10.1$2.4 million at December 31, 20212023 and 2020,2022, respectively.

(3)(2)Includes home equity lines of credit, installment loans unsecured lines of credit and education loans.

(4)(3)Excludes $113.329.3 million and $197.5$43.0 million of commercial and industrial loans and residential loans held for sale at December 31, 20212023 and 2020,2022, respectively.

The following table shows the remaining contractual maturity and rate sensitivity of the loan portfolio by loan category as of December 31, 2021.2023. Loans may be pre-paid, so the actual maturity may differ from the contractual maturity. Prepayments tend to be highly dependent upon the interest rate environment. Loans having no stated maturity or repayment schedule are reported in the "Less than One Year" category.

| | (Dollars in thousands) | (Dollars in thousands) | | Less than One Year | | One to Five Years | | Five to Fifteen Years | | Over Fifteen Years | | Total | (Dollars in thousands) | | Less than One Year | | One to Five Years | | Five to Fifteen Years | | Over Fifteen Years | | Total |

Commercial and industrial(1) | | | | | | | | | | |

| Commercial and industrial | |

| Interest rate: | Interest rate: | |

| Interest rate: | |

| Interest rate: | |

| Fixed | |

| Fixed | |

| Fixed | Fixed | | $ | 2,694 | | | $ | 353,443 | | | $ | 184,525 | | | $ | 48,104 | | | $ | 588,766 | |

| Adjustable | Adjustable | | 204,697 | | | 803,975 | | | 295,743 | | | 24,862 | | | 1,329,277 | |

| Total | Total | | $ | 207,391 | | | $ | 1,157,418 | | | $ | 480,268 | | | $ | 72,966 | | | $ | 1,918,043 | |

| Owner-occupied commercial | Owner-occupied commercial | |

| Interest rate: | Interest rate: | |

| Interest rate: | |

| Interest rate: | |

| Fixed | |

| Fixed | |

| Fixed | Fixed | | $ | 3,247 | | | $ | 319,842 | | | $ | 291,038 | | | $ | 206,156 | | | $ | 820,283 | |

| Adjustable | Adjustable | | 14,059 | | | 160,111 | | | 287,282 | | | 59,972 | | | 521,424 | |

| Total | Total | | $ | 17,306 | | | $ | 479,953 | | | $ | 578,320 | | | $ | 266,128 | | | $ | 1,341,707 | |

| Commercial mortgages | Commercial mortgages | |

| Interest rate: | Interest rate: | |

| Interest rate: | |

| Interest rate: | |

| Fixed | |

| Fixed | |

| Fixed | Fixed | | $ | 9,988 | | | $ | 506,952 | | | $ | 233,631 | | | $ | 157,139 | | | $ | 907,710 | |

| Adjustable | Adjustable | | 16,543 | | | 402,286 | | | 492,934 | | | 62,037 | | | 973,800 | |

| Total | Total | | $ | 26,531 | | | $ | 909,238 | | | $ | 726,565 | | | $ | 219,176 | | | $ | 1,881,510 | |

| Construction | Construction | |

| Interest rate: | Interest rate: | |

| Interest rate: | |

| Interest rate: | |

| Fixed | |

| Fixed | |

| Fixed | Fixed | | $ | 788 | | | $ | 19,089 | | | $ | 19,198 | | | $ | 4,817 | | | $ | 43,892 | |

| Adjustable | Adjustable | | 41,108 | | | 479,838 | | | 118,586 | | | 3,789 | | | 643,321 | |

| Total | Total | | $ | 41,896 | | | $ | 498,927 | | | $ | 137,784 | | | $ | 8,606 | | | $ | 687,213 | |

| Commercial small business leases | Commercial small business leases | |

| Interest rate: | Interest rate: | |

| Interest rate: | |

| Interest rate: | |

| Fixed | |

| Fixed | |

| Fixed | Fixed | | $ | — | | | $ | 274,525 | | | $ | 77,751 | | | $ | — | | | $ | 352,276 | |

| Adjustable | Adjustable | | — | | | — | | | — | | | — | | | — | |

| Total | Total | | $ | — | | | $ | 274,525 | | | $ | 77,751 | | | $ | — | | | $ | 352,276 | |

Residential(2) | |

Residential(1) | |

| Interest rate: | |

| Interest rate: | |

| Interest rate: | Interest rate: | |

| Fixed | Fixed | | $ | 684 | | | $ | 25,498 | | | $ | 99,525 | | | $ | 312,979 | | | $ | 438,686 | |

Adjustable(3) | | — | | | 588 | | | 15,681 | | | 87,778 | | | 104,047 | |

| Fixed | |

| Fixed | |

Adjustable(2) | |

| Total | Total | | $ | 684 | | | $ | 26,086 | | | $ | 115,206 | | | $ | 400,757 | | | $ | 542,733 | |

| Consumer | Consumer | |

| Interest rate: | Interest rate: | |

| Interest rate: | |

| Interest rate: | |

| Fixed | |

| Fixed | |

| Fixed | Fixed | | $ | 30 | | | $ | 104,613 | | | $ | 312,498 | | | $ | 303,808 | | | $ | 720,949 | |

| Adjustable | Adjustable | | 14,973 | | | 18,912 | | | 57,369 | | | 346,370 | | | 437,624 | |

| Total | Total | | $ | 15,003 | | | $ | 123,525 | | | $ | 369,867 | | | $ | 650,178 | | | $ | 1,158,573 | |

| Total loans and leases | Total loans and leases | | $ | 308,811 | | | $ | 3,469,672 | | | $ | 2,485,761 | | | $ | 1,617,811 | | | $ | 7,882,055 | |

|

(1) Includes $31.5 million of PPP loans.

(2) Excludes reverse mortgages at fair value of $3.9$2.8 million.

(3)(2) Includes hybrid adjustable-rate mortgages.

Commercial Lending

Pursuant to section 5(c) of the Home Owners’ Loan Act (HOLA), federal savings banks are generally permitted to invest up to 400% of their total regulatory capital in nonresidential real estate loans and up to 20% of their assets in commercial loans, but no more than 10% may be in loans that do not qualify as small business loans. As a federal savings bank that was formerly chartered as a Delaware savings bank, the Bank has certain additional lending authority.

Commercial, owner-occupied commercial, commercial mortgage and construction loans have higher levels of risk than residential lending. These loans typically involve larger loan balances concentrated with single borrowers or groups of related borrowers. In addition, the payment experience on loans secured by income-producing properties is typically dependent on the successful operation of the related real estate project and may be more subject to adverse conditions in the commercial real estate market or in the general economy than residential loans. The majority of our commercial and commercial mortgage loans are concentrated in Delaware and Pennsylvania.

We offer commercial mortgage loans on multi-family properties and on other commercial real estate. Generally, loan-to-value ratios for these loans do not exceed 80% of appraised value at origination.

Our commercial mortgage portfolio was $1.9$3.8 billion at December 31, 2021.2023. Generally, this portfolio is diversified by property type, with no type representing more than 27%30% of the portfolio. The three largest type istypes are retail-related (non-mall, neighborhood shopping centers and other retail), residential multi-family, and office with outstanding balances of $496.0 million$1.1 billion, $1.0 billion and $0.7 billion at December 31, 2021.2023, respectively. The average size of a loan in the commercial mortgage portfolio is $0.7$1.1 million and only nine46 loans are greater than $12.0 million, with one loaneight loans greater than $24.0 million.

We offer commercial construction loans to developers. In some cases these loans are made as “construction/permanent” loans, which provides for disbursement of loan funds during construction with the option of conversion to mini-permanent loans (one - five years) upon completion of construction. These construction loans are short-term, usually not exceeding three years, with interest rates generally indexed to our WSFS prime rate, the “Wall Street” prime rate or LIBOR,the Secured Overnight Financing Rate (SOFR), and are adjusted periodically as these indices change. The loan appraisal process includes the same evaluation criteria as required for permanent mortgage loans, but also takes into consideration: completed plans, specifications, comparables and cost estimates. Prior to approval of each loan, these criteria are used as a basis to determine the appraised value of the subject property when completed. Our policy requires that all appraisals be reviewed independently from our commercial business development staff. At origination, the loan-to-value ratios for construction loans generally do not exceed 75%. The initial interest rate on the permanent portion of the financing is determined by the prevailing market rate at the time of conversion to the permanent loan. At December 31, 2021, $1.12023, $1.8 billion was committed for construction loans, of which $687.2 million$1.0 billion was outstanding. Also at December 31, 2021,2023, the residential construction and land development (CLD) portfolio represented $316.7$607.4 million, or 4%5%, of total loans and the commercial CLD portfolio represented $279.9$204.1 million, or 4%2%, of total loans. At December 31, 2021,2023, the construction portfolio included $38.3$101.6 million of “land hold” loans, which are land loans not currently being developed.