On March 12, 2020, the U.S. Securities and Exchange Commission voted to adopt amendmentsdiscretionary bonuses were awarded to the

"accelerated filer" and "large accelerated filer" definitions in Rule 12b-2 under the Securities Exchange Act of 1934. The amendments increased the transition thresholds for large accelerated filers to exit the large accelerated filer status from $500 million to $560 million. The measurement is performed annually each June 30th using that day's Class A common stock closing price applied to the number of Class A commons shares considered to be publicly traded float, which is defined as the number of shares available to the public for trading in the secondary market without restriction. This excludes, among others, shares held by officers and directors. As of June 30, 2020, the Company's public float was less than $560 million and changed the Company's filing status from large accelerated filer to accelerated filer. At June 30, 2021, there was no change in the Company's filing status as an accelerated filer.Named Executive Officers.

Equity Security Holders

The number of stockholders of record on March 7, 2022 was as follows:

| | | | | |

Class A Common Stock | 2,047 | |

Class B Common Stock | 2 | |

Dividends

Class B common stockholders receive dividends at one-half the per share amount declared on Class A common stock. During 2021, NWLGI paid cash dividends on its Class A and Class B common stock in the amounts of $1.2 million and $36,000, respectively. During 2020, the Company also paid cash dividends on its Class A and Class B common stock in the amounts of $1.2 million and $36,000, respectively. Payment of dividends is within the discretion of the Company’s Board of Directors.

Payment of dividends by National Western Life Insurance Company ("National Western") to NWLGI, as the sole owner of National Western, are also within the discretion of National Western's Board of Directors, but are subject to prescribed limitations set by the Colorado Division of Insurance without prior approval. The Company’s general policy is to reinvest earnings internally to finance the development of new business, provide for potential acquisitions, and to lend support to its financial strength ratings assigned by independent rating agencies. In the years ended December 31, 2021 and 2020, National Western did not declare or pay dividends to NWLGI.

Securities Authorized For Issuance Under Equity Compensation Plans

The Company currently has one equity compensation plan, thatwhich was originally approved by security holdersNWLIC’s stockholders in 2008. ThisThat equity plan was assumed by NWLGI from National WesternNWLIC in 2015 pursuant to the terms of the holding company reorganization. TheThereafter, the plan was amended, restated and approved by stockholders of NWLGI in June 2016, extending its term for ten years from the date of stockholder approval. There are no outstanding options atIn December 2022, this plan was amended and restated by the Board of Directors to make certain technical and administrative changes. This amended and restated incentive plan, as amended, is referred to in this annual report as the “Amended Incentive Plan.” As of December 31, 2021 under the plan which would otherwise entitle option holders to shares. At December 31, 2021,2023, there were a total of 291,000 shares of Class A common stock remain availableStock that were authorized for future issuance underupon the plan.

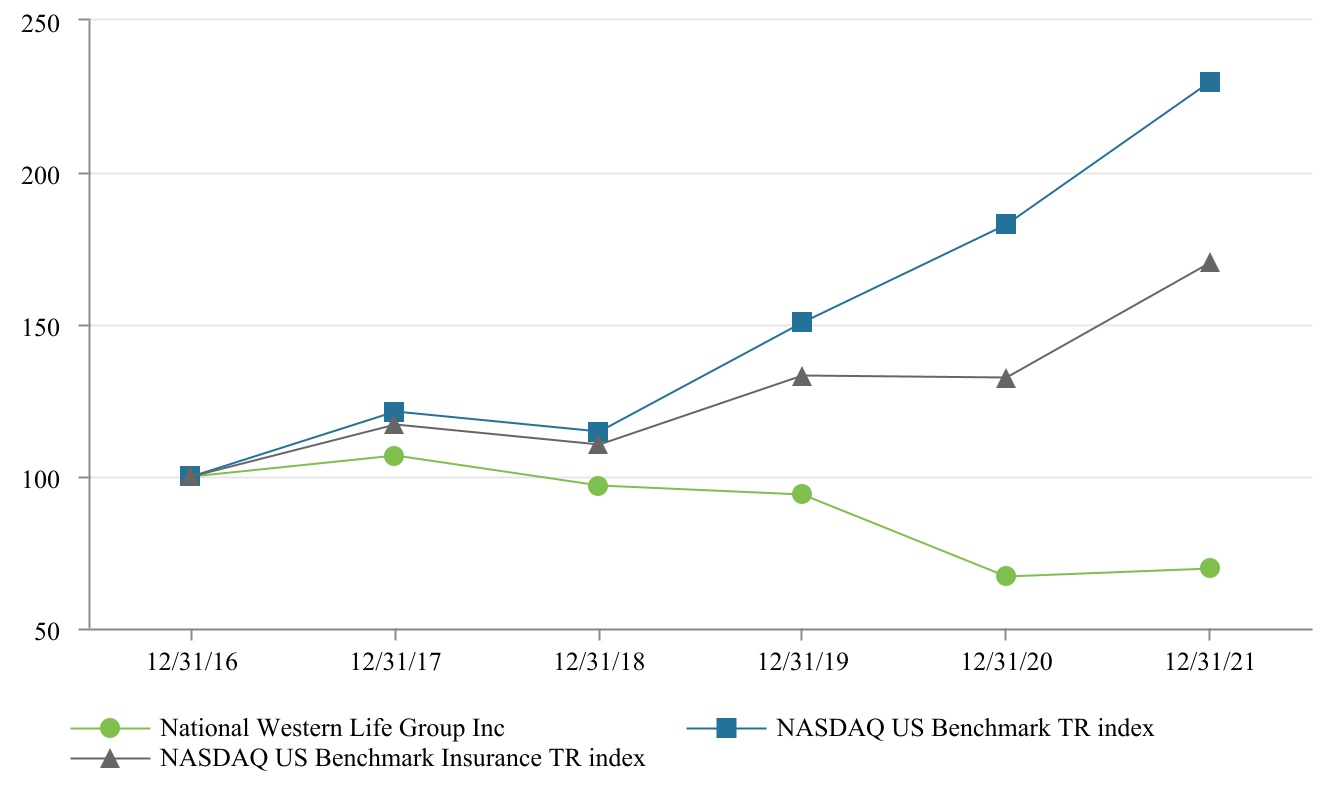

Performance Graph

The following graph compares the annual percentage change in the Company's cumulative total return on its common stock over the past five years with the total returnsettlement or exercise, as applicable, of companies comprising the NASDAQ - U.S. Benchmark TR index and the NASDAQ - US Benchmark Insurance TR index. The graph assumes that the value of the Company's Class A common stock and each index was $100 at December 31, 2016, and that all dividends were reinvested. The NASDAQ US Benchmark TR index replaces the NASDAQ Stock Market (US Companies) Index and the NASDAQ US Benchmark Insurance TR index replaces the NASDAQ Insurance Index in this analysis and going forward, as the CRSP Index data is no longer accessible.

Issuer Purchases of Equity Securities

Effective August 22, 2008, National Western adopted and implemented a limited stock buy-back program associated with the 2008 Incentive Plan which provides Option Holders the additional alternative of selling shares acquired through the exercise of options directly back to the Company. This plan and program was assumed by NWLGI from National Western in 2015awards granted pursuant to the terms of the holding company reorganization. The program provides Option Holders with the ability to elect to sell acquired shares back to the Company at any time within ninety (90) days after the exercise of options at the prevailing market price as of the date of notice of election. As of December 31, 2021, there are no options outstanding under the plan.

The following table sets forth the Company’s issuance and repurchase activity of its Class A common shares from Option Holders for the quarter ended December 31, 2021.

| | | | | | | | | | | | | | | | | | | | | | | | | | |

Period | | Total Number of Shares Purchased | | Average Price Paid Per Share | | Total Number of Shares Purchased as Part of Publicly Announced Plans or Programs | | Approximate Dollar Value of Shares that May yet Be Purchased Under the Plans or Programs |

| | | | | | | | |

October 1, 2021 through October 31, 2021 | | — | | | $ | — | | | N/A | | N/A |

November 1, 2021 through November 30, 2021 | | — | | | $ | — | | | N/A | | N/A |

December 1, 2021 through December 31, 2021 | | — | | | $ | — | | | N/A | | N/A |

| | | | | | | | |

Total | | — | | | $ | — | | | N/A | | N/A |

Purchased shares are reported in the Company's Consolidated Financial Statements as authorized and unissued.

ITEM 7. MANAGEMENT’S DISCUSSION AND ANALYSIS

OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

Forward-Looking Statements

The Private Securities Litigation Reform Act of 1995 provides a “safe harbor” for forward-looking statements. Certain information contained herein or in other written or oral statements made by or on behalf of National Western Life Group, Inc. and its subsidiaries (the "Company") are or may be viewed as forward-looking. Although the Company has taken appropriate carehistorically granted stock options, in developing any such information, forward-looking information involves risks and uncertainties that could significantly impact actual results. These risks and uncertainties include, but are not limited to, matters described in the Company's filings such as exposure to market risks, anticipated cash flows or operating performance, future capital needs, and statutory or regulatory related issues. However, as a matter of policy, the Company does not make any specific projections as to future earnings, nor does it endorse any projections regarding future performance that may be made by others. Whether or not actual results differ materially from forward-looking statements may depend on numerous foreseeable and unforeseeable events or developments. Also, the Company undertakes no obligation to publicly update or revise any forward-looking statements, whether as a result of new information, future developments, or otherwise.

Management’s discussion and analysis of the financial condition and results of operations (“MD&A”) of National Western Life Group, Inc. ("NWLGI") for the three years ended December 31, 2021 follows. Where appropriate, discussion specific to the insurance operations of National Western Life Insurance Company is denoted by "National Western" or "NWLIC". This discussion should be read in conjunction with the Company’s Consolidated Financial Statements and related notes beginning on page 97 of this report.

Effective January 31, 2019, the Company completed its previously announced acquisition of Ozark National Life Insurance Company ("Ozark National") and N.I.S. Financial Services, Inc. ("NIS") following the receipt of regulatory approvals. NWLGI and National Western paid cash in an aggregate amount of approximately $205.4 million in exchange for all of the outstanding stock of Ozark National (wholly owned by National Western) and NIS (wholly owned by NWLGI). The eleven month results of Ozark National and NIS are included in the Company's Consolidated Financial Statements as of and for the year ended December 31, 2019 and reference to each is made in this MD&A where appropriate.

Overview

National Western has historically provided life insurance products on a global basis for the savings and protection needs of policyholders and issued annuity contracts for the asset accumulation and retirement needs of contract holders, both domestic and international residents. As disclosed in the Company's 2018 filings, the Company discontinued accepting applications for its international life insurance products from all foreign residents in other countries in the second quarter of 2018.

The Company, National Western and Ozark National, accepts funds from policyholders or contract holders and establishes a liability representing future obligations to pay the policy or contract holders and their beneficiaries. To ensure the Company will be able to pay these future commitments, the funds received as premium payments and deposits are invested in high quality investments, primarily fixed income securities.

Due to the business of accepting funds to pay future obligations in later years and the underlying economics, the relevant factors affecting the Company’s overall business and profitability include the following:

| | | | | |

● | the level of sales and premium revenues collected |

● | the volume of life insurance and annuity business in force |

● | persistency of policies and contracts |

● | the ability to price products to earn acceptable margins over benefit costs and expenses |

● | return on investments sufficient to produce acceptable spread margins over interest crediting rates |

● | investment credit quality which minimizes the risk of default or impairment |

● | levels of policy benefits and costs to acquire business |

● | the ability to manage the level of operating expenses |

● | effect of interest rate changes on revenues and investments including asset and liability matching |

● | maintaining adequate levels of capital and surplus |

● | corporate tax rates and the treatment of financial statement items under tax rules and accounting |

● | actual levels of surrenders, withdrawals, claims and interest spreads |

● | changes in assumptions for amortization of deferred policy acquisition expenses and deferred sales inducements |

● | changes in the fair value of derivative index options and embedded derivatives pertaining to fixed-index life and annuity products |

● | pricing and availability of adequate counterparties for reinsurance and index option contracts |

● | litigation subject to unfavorable judicial development, including the time and expense of litigation |

The Company monitors these factors continually as key business indicators. The discussion that follows in this Item 6 includes these indicators and presents information useful to an overall understanding of the Company’s business performance in 2021, incorporating required disclosures in accordance with the rules and regulations of the Securities Exchange Commission ("SEC").

Impact of Recent Business Environment

The Company's business is generally aided by an economic environment experiencing growth, whether moderate or vibrant, characterized by improving employment data and increases in personal income. Important metrics indicating sustained economic growth over the longer term principally revolve around employment and confidence, both consumer and business sentiment.

The COVID-19 pandemic not only affected how businesses conducted operations but also introduced a great deal of uncertainty to the life insurance industry. The morbidity exposure of COVID-19 translated into a higher death claim incidence throughout the industry and was a frequently discussed item in company earnings releases. In 2021, the Company (National Western and Ozark National) incurred approximately $32 million in net death claims for which COVID-19 was identified as the cause of death, an increase from $8 million in the preceding year. However, composite reports tracking the incidence of COVID-19 death activity appear to suggest that a peak occurred in the third quarter of 2021 with noticeable declines observed thereafter.

Another consequence of the pandemic has been the impact on investment yields and asset valuations. Interest rates have hovered at levels making traditional industry investments in fixed income debt securities insufficient to price products competitively or to meet minimum interest rate guarantees without reducing internal rates of return below required targets. Seizing on this situation, large investment entities have entered the industry through acquisitions or reinsurance transactions in order to tap insurance company portfolios of low yielding assets with the goal of using specific investment expertise to roll these assets into higher yielding, and higher risk, assets. While the COVID-19 environment has not caused widespread declines in the value of invested assets through downgrades in credit market securities, insurers have still faced fair value decreases resulting in unrealized losses, impairment-related losses or sizable additions being made to the allowance for current credit losses in financial statements.

In recent years, in an attempt to acquire additional investment yield in the low rate environment, life insurers substantially increased allocations to BBB- rated bonds. In a recession, many of these investment grade corporate credits are at risk for downgrades, as well as the potential to default. Risk-based capital (RBC) formulas assess higher required capital charges as investment quality declines. A meaningful shift of BBB- rated debt securities to non-investment grade categories could have significant implications in terms of required capital levels which would depress RBC ratios of impacted insurers. Life insurance companies also have a large exposure to real estate in its investment portfolios through commercial mortgage, direct real estate investment, alternative investment funds, and mortgage-backed securities. These investments are highly dependent upon occupancy and payment of rent and lease obligations.

With regard to the credit market, industry analysts and observers generally agree that a sudden jump in interest rate levels would be harmful to life insurers with interest-sensitive products as it could provide an impetus for abnormal levels of product surrenders and withdrawals at the same time fixed debt securities held by insurers declined in market value. The current rise of inflation rates has prompted Federal Reserve officials to begin signalling their intent to commence with a series of interest rate increases in order to head off the crippling effects of rising prices. Ultimately, a mix of monetary policy adjustments, fiscal policy, and economic fundamentals will determine the degree of interest rate increases and the speed of such shifts. It is uncertain what impacts, if any, such movements would have on the Company’s business, results of operations, cash flows or financial condition.

In an environment such as this, the need for a strong capital position that can cushion against unexpected bumps is critical for stability and ongoing business activity. The Company's operating strategy continues to be focused on maintaining capital levels substantially above regulatory and rating agency requirements. In addition, its business model is predicated upon steady growth in invested assets while managing the block of business within profitability objectives. A key premise of the Company's financial management is maintaining a high quality investment portfolio, well matched in terms of duration with policyholder obligations, that continues to outperform the industry with respect to adverse impairment experience. This discipline enables the Company to sustain resources more than adequate to fund future growth and absorb abnormal periods of cash outflows.

Critical Accounting Policies

Accounting policies discussed below are those considered critical to an understanding of the Company’s financial statements.

Impairment of Investment Securities. The Company’s accounting policy requires that a decline in the value of a security below its amortized cost basis be evaluated to determine if the decline is a result of credit loss. The primary factors considered in evaluating whether a decline in value for fixed income and equity securities without readily determinable fair values is a result of credit loss are: (a) the length of time and the extent to which the fair value has been less than cost, (b) the reasons for the decline in value (credit event, interest rate related, credit spread widening), (c) the overall financial condition as well as the near-term prospects of the issuer, (d) whether the debtor is current on contractually obligated principal and interest payments, and (e) that the Company does not intend or be required to sell the investment prior to recovery. In addition, certain securitized financial assets with contractual cash flows are evaluated periodically by the Company to update the estimated cash flows over the life of the security. If the Company determines that the fair value of the securitized financial asset is less than its carrying amount and there has been a decrease in the present value of the estimated cash flows since the previous purchase or prior impairment, then a credit loss charge is recognized. The Company would recognize impairment of securities due to changing interest rates or market dislocations only if the Company intended to sell the securities prior to recovery. When a security is deemed to be impaired, a charge is recorded equal to the difference between the fair value and amortized cost basis of the security. In compliance with GAAP guidance after adoption of ASU 2016-13, Financial Instruments-Credit Losses the estimated credit loss is recorded as an allowance with changes in the allowance recorded to Net investment income in the Consolidated Statements of Earnings.

Deferred Policy Acquisition Costs (“DPAC”). The Company is required to defer certain policy acquisition costs and amortize them over future periods. These costs include commissions and certain other expenses that vary with and are directly associated with acquiring new business. The deferred costs are recorded as an asset commonly referred to as deferred policy acquisition costs. The DPAC asset balance is subsequently charged to income over the lives of the underlying contracts in relation to the anticipated emergence of revenue or profits. Actual revenue or profits can vary from Company estimates resulting in increases or decreases in the rate of amortization. The Company performs regular evaluations of its universal life and annuity contracts to determine if actual experience or other evidence suggests that earlier estimates should be revised. Assumptions considered significant include surrender and lapse rates, mortality, expense levels, investment performance, and estimated interest spread. Should actual experience dictate that the Company change its assumptions regarding the emergence of future revenues or profits (commonly referred to as “unlocking”), the Company would record a charge or addition to bring its DPAC balance to the level it would have been if using the new assumptions from the inception date of each policy.

DPAC is also subject to periodic recoverability and loss recognition testing. These tests ensure that the present value of future contract-related cash flows will support the capitalized DPAC balance to be amortized in the future. The present value of these cash flows, less the benefit reserve, is compared with the unamortized DPAC balance and if the DPAC balance is greater, the deficiency is charged to expense as a component of amortization and the asset balance is reduced to the recoverable amount. For more information about accounting for DPAC see Note (1), Summary of Significant Accounting Policies, in the accompanying Notes to Consolidated Financial Statements in this report.

Deferred Sales Inducements ("DSI"). Costs related to sales inducements offered on sales to new customers, principally on investment type contracts and primarily in the form of additional credits to the customer’s account value or enhancements to interest credited for a specified period, which are beyond amounts currently being credited to existing contracts, are deferred and recorded as other assets. All other sales inducements are expensed as incurred and included in interest credited to contract holders’ funds. Deferred sales inducements are amortized to income using the same methodology and assumptions as DPAC, and are included in interest credited to contract holders’ funds. Deferred sales inducements are also periodically reviewed for recoverability. For more information about accounting for deferred sales inducementssee Note (1), Summary of Significant Accounting Policies, in the accompanying Notes to Consolidated Financial Statements in this report.

Value of Business Acquired ("VOBA"). VOBA is a purchase accounting convention for life insurance companies in business combinations based upon an actuarial determination of the difference between the fair value of policyholder liabilities acquired and the same policyholder liabilities measured in accordance with the acquiring company's accounting policies. The difference, referred to as VOBA, is an intangible asset subject to periodic amortization. Similar to DPAC and DSI, VOBA is subject to periodic analysis assessing recoverability.

Future Policy Benefits. Because of the long-term nature of insurance contracts, the Company is liable for policy benefit payments many years into the future. The liability for future policy benefits represents estimates of the present value of the Company’s expected benefit payments, net of the related present value of future net premium collections. For traditional life insurance contracts, this is determined by standard actuarial procedures, using assumptions as to mortality (life expectancy), morbidity (health expectancy), persistency, and interest rates, which are based on the Company’s experience with similar products. The assumptions used are those considered to be appropriate at the time the policies are issued. An additional provision is made on most products to allow for possible adverse deviation from the assumptions assumed. For universal life and annuity products, the Company’s liability is the amount of the contract’s account balance. Account balances are also subject to minimum liability calculations as a result of minimum guaranteed interest rates in the policies. While management and Company actuaries have used their best judgment in determining the assumptions and in calculating the liability for future policy benefits, there is no assurance that the estimate of the liabilities reflected in the financial statements represents the Company’s ultimate obligation. In addition, significantly different assumptions could result in materially different reported amounts. A discussion of the assumptions used to calculate the liability for future policy benefits is reported in Note (1), Summary of Significant Accounting Policies, in the accompanying Notes to Consolidated Financial Statements in this report.

Revenue Recognition. Premium income for the Company’s traditional life insurance contracts is generally recognized as the premium becomes due from policyholders. For annuity and universal life contracts, the amounts collected from policyholders are considered deposits and are not included in revenue. For these contracts, fee income consists of policy charges for policy administration, cost of insurance charges and surrender charges assessed against policyholders’ account balances which are recognized in the period the services are provided.

Investment activities of the Company are integral to its insurance operations. Since life insurance benefits may not be paid until many years into the future, the accumulation of cash flows from premium receipts are invested with income reported as revenue when earned. Anticipated yields on investments are reflected in premium rates, contract liabilities, and other product contract features. These anticipated yields are implied in the interest required on the Company’s net insurance liabilities (future policy benefits less deferred acquisition costs) and contractual interest obligations in its insurance and annuity products. The Company benefits to the extent actual net investment income exceeds the required interest on net insurance liabilities and manages the rates it credits on its products to maintain the targeted excess or “spread” of investment earnings over interest credited. The Company will continue to be required to provide for future contractual obligations in the event of a decline in investment yield. For more information concerning revenue recognition, investment accounting, and interest sensitivity, please refer to Note (1), Summary of Significant Accounting Policies, and Note (3), Investments, in the accompanying Notes to Consolidated Financial Statements in this report, and the discussions under Investments in Item 6 of this report.

Pension Plans and Other Postretirement Benefits. The Company sponsors a qualified defined benefit pension plan, which was frozen effective December 31, 2007, covering substantially all employees at that time, and three non-qualified defined benefit plans covering certain senior officers. In addition, the Company has postretirement health care benefits for certain senior officers. The freeze of the qualified benefit pension plan ceased future benefit accruals to all participants and closed the Plan to any new participants. In addition, all participants became immediately 100% vested in their accrued benefits as of that date. In accordance with prescribed accounting standards, the Company annually reviews plan assumptions.

The Company annually reviews its pension benefit plans' assumptions which include the discount rate, the expected long-term rate of return on plan assets, and the compensation increase rate. The assumed discount rate is set based on the rates of return on high quality long-term fixed income investments currently available and expected to be available during the period to maturity of the pension benefits. The assumed long-term rate of return on plan assets is generally set at the rate expected to be earned based on the long-term investment policy of the plans, the various classes of the invested funds, input of the plan’s investment advisors and consulting actuary, and the plan’s historic rate of return. The compensation rate increase assumption is generally set at a rate consistent with current and expected long-term compensation and salary policy, including inflation. These assumptions involve uncertainties and judgment, and therefore actual performance may not be reflective of the assumptions.

Other postretirement benefit assumptions include future events affecting retirement age, mortality, dependency status, per capita claims costs by age, health care trend rates, and discount rates. Per capita claims cost by age is the current cost of providing postretirement health care benefits for one year at each age from the youngest age to the oldest age at which plan participants are expected to receive benefits under the plan. Health care trend rates involve assumptions about the annual rate(s) of change in the cost of health care benefits currently provided by the plan, due to factors other than changes in the composition of the plan population by age and dependency status. These rates implicitly consider estimates of health care inflation, changes in utilization, technological advances, and changes in health status of the participants.

Share-Based Payments. Liability awards under a share-based payment arrangement have been measured based on the awards’ fair value at the reporting date. The Black-Scholes valuation method is used to estimate the fair value of the options. This fair value calculation of the options includes assumptions relative to the following:

| | | | | |

● | exercise price |

● | expected term based on contractual term and perceived future behavior relative to exercise |

● | current price |

● | expected volatility |

● | risk-free interest rates |

● | expected dividends |

These assumptions are continually reviewed by the Company and adjustments may be made based upon current facts and circumstances.

Other significant accounting policies, although not involving the same level of measurement uncertainties as those discussed above, but nonetheless important to an understanding of the financial statements, are described in Note (1), Summary of Significant Accounting Policies, in the accompanying Notes to Consolidated Financial Statements in this report.

RESULTS OF OPERATIONS

The Company’s Consolidated Financial Statements are prepared in accordance with U.S. generally accepted accounting principles (“GAAP”). In addition, the Company regularly evaluates operating performance using non-GAAP financial measures which exclude or segregate derivative and realized investment gains and losses from operating revenues. Similar measures are commonly used in the insurance industry in order to assess profitability and results from ongoing operations. The Company believes that the presentation of these non-GAAP financial measures enhances the understanding of the Company’s results of operations by highlighting the results from ongoing operations and the underlying profitability factors of the Company’s business. The Company excludes or segregates derivative and realized investment gains and losses because such items are often the result of events which may or may not be at the Company’s discretion and the fluctuating effects of these items could distort trends in the underlying profitability of the Company’s business. Therefore, in the following sections discussing consolidated operations and segment operations, appropriate reconciliations have been included to report information management considers useful in enhancing an understanding of the Company’s operations to reportable GAAP balances reflected in the Consolidated Financial Statements.

Consolidated Operations

Revenues. The following details Company revenues:

| | | | | | | | | | | | | | | | | |

| | Years Ended December 31, |

| | 2021 | | 2020 | | 2019 |

| | (In thousands) |

| | | | | |

| Universal life and annuity contract charges | $ | 134,254 | | | 145,405 | | | 149,721 | |

| Traditional life premiums | 90,043 | | | 92,542 | | | 90,248 | |

| Net investment income (excluding index option derivatives) | 441,812 | | | 402,448 | | | 432,285 | |

| Other revenues | 22,314 | | | 18,522 | | | 17,486 | |

| | | | | |

| | | | | |

| Derivative gain, index options | 120,718 | | | 14,754 | | | 123,207 | |

| Net realized investment gains | 14,950 | | | 21,071 | | | 6,241 | |

| | | | | |

| Total revenues | $ | 824,091 | | | 694,742 | | | 819,188 | |

Universal life and annuity contract revenues - Revenues for universal life and annuity products consist of policy charges for the cost of insurance, administration charges, and surrender charges assessed against policyholder account balances, less reinsurance premiums. As depicted in the following table, revenues for universal life and annuity contract charges decreased in 2021 compared to 2020 due to lower surrender charge revenue from terminated policies and lower cost of insurance charges associated with decreased levels of universal life insurance in force.

| | | | | | | | | | | | | | | | | |

| | Years Ended December 31, |

| Contract Charges: | 2021 | | 2020 | | 2019 |

| | (In thousands) |

| | | | | |

| Cost of insurance and administrative charges | $ | 122,961 | | | 124,821 | | | 126,049 | |

| Surrender charges | 25,363 | | | 26,623 | | | 33,079 | |

| Other charges | 4,347 | | | 11,430 | | | 8,171 | |

| Gross contract revenues | 152,671 | | | 162,874 | | | 167,299 | |

| | | | | |

| Reinsurance premiums | (18,417) | | | (17,469) | | | (17,578) | |

| | | | | |

| Net contract charges | $ | 134,254 | | | 145,405 | | | 149,721 | |

Cost of insurance charges were $95.9 million in 2021 compared to $98.9 million in 2020 and $102.0 million in 2019. Cost of insurance charges typically trend with the size of the universal life insurance block in force and the amount of new business issued during the period. The volume of universal life insurance in force during 2021 decreased to $12.7 billion from $13.5 billion at year-end 2020 and $14.4 billion at year-end 2019. Administrative charges were $27.1 million, $25.9 million, and $24.1 million for the years ended December 31, 2021, 2020 and 2019, respectively, and correlate with new universal life insurance business sales by the number of policies placed, the amount of premiums received and the volume of insurance issued.

Surrender charges assessed against policyholder account balances upon withdrawal were $25.4 million in 2021 compared to $26.6 million in 2020 and $33.1 million in 2019. The Company earns surrender charge income that is assessed upon policy terminations, however, the Company’s overall profitability is enhanced when policies remain in force and additional contract revenues are realized and the Company continues to make an interest rate spread equivalent to the difference it earns on its investment and the amounts that it credits to policyholders. While policy lapse rates in 2021 for the domestic life insurance and international life insurance segments were somewhat lower than those experienced in 2020, the annuities segment continued to exhibit a higher lapse rate due to liquidity demands prompted by the pandemic crisis. Surrender charge income recognized is also dependent upon the duration of policies at the time of surrender (i.e. later duration policy surrenders have lower surrender charges assessed and earlier policy surrenders have a higher surrender charge assessed). The declining trend in assessed surrender charges is indicative of policy surrenders later in the surrender charge period.

Other charges include the net amortization into income of the premium load on single premium life insurance products which is deferred at the inception of the policy. The net income reported for this activity is dependent upon the level of amortization of accumulated deferrals compared to current premium loads being deferred. In addition, as part of the Company's annual unlocking analysis, a prospective unlocking of the unearned revenue reserve was done for each year shown. The effect of the unlocking in the year ended December 31, 2021 was a decrease in other charges revenue of $(0.6) million while the effect of the unlockings increased other charges revenue by $5.9 million and $0.5 million in the years ended December 31, 2020 and 2019, respectively.

Traditional life premiums - Traditional life premiums include the activity of Ozark National subsequent to their acquisition on January 31, 2019. Ozark National's principal product is a non-participating whole life insurance policy with premiums remitted primarily on a monthly basis. The product is sold in tandem with a mutual fund investment product offered through its broker-dealer affiliate, NIS. Traditional life insurance premiums for products such as whole life and term life are recognized as revenues over the premium-paying period. A sizable portion of National Western's traditional life business resided in the International Life insurance segment which ceased accepting new applications in 2018. However, National Western’s overall life insurance sales focus has historically been primarily centered around universal life products. The addition of Ozark National's business of repetitive paying permanent life insurance adds an important complement to National Western's life insurance sales. Included in the amounts for the years ended December 31, 2021, 2020, and 2019 is $73.5 million, $74.8 million, and $69.0 million, respectively, of life insurance renewal premium from Ozark National. Universal life products, especially National Western’s equity indexed universal life products, which offer the opportunity for consumers to acquire life insurance protection and receive credited interest linked in part to an outside market index, have been the more popular product offerings in the Company’s markets.

Net investment income (with and without derivatives) - A detail of net investment income is provided below.

| | | | | | | | | | | | | | | | | |

| | Years Ended December 31, |

| | 2021 | | 2020 | | 2019 |

| | (In thousands) |

| | | | | |

| Gross investment income: | | | | | |

| Debt and equities | $ | 309,082 | | | 373,479 | | | 403,372 | |

| Mortgage loans | 20,155 | | | 13,162 | | | 12,595 | |

| Policy loans | 2,667 | | | 3,361 | | | 3,539 | |

| Short-term investments | 293 | | | 2,160 | | | 2,974 | |

| Other invested assets | 16,321 | | | 12,698 | | | 13,057 | |

| | | | | |

| Total investment income | 348,518 | | | 404,860 | | | 435,537 | |

| Less: investment expenses | 2,762 | | | 2,412 | | | 3,252 | |

| | | | | |

| Net investment income (excluding derivatives and trading securities) | 345,756 | | | 402,448 | | | 432,285 | |

| Index option derivative gain | 120,718 | | | 14,754 | | | 123,207 | |

| Embedded derivative on reinsurance | 84,725 | | | — | | | — | |

| Trading securities market adjustments | 11,331 | | | — | | | — | |

| | | | | |

| Net investment income | $ | 562,530 | | | 417,202 | | | 555,492 | |

The Company’s strategy is to invest a substantial portion of its cash flows in fixed debt securities within its guidelines for credit quality, duration, and diversification. National Western's debt and equities investment income continues to experience higher yielding debt securities maturing or being called by borrowers and being replaced with lower yielding securities in the current interest rate environment. In addition, the excess of annuity outflows over inflows has caused the debt security portfolio to contract. As part of the acquisition of Ozark National and NIS in the first quarter of 2019, a sizable part of National Western's investable cash resources were applied toward the purchase of the two companies and then subsequently to pay back line of credit borrowings of $75 million used to fund a part of the acquisition price.

The Company's investable funds are derived from incremental cash flow from new business and investment income from its portfolio above its operational requirements to pay policy benefits, commissions, and expenses. The debt securities portfolio increased from $10.5 billion at December 31, 2019 to $10.8 billion at December 31, 2020, largely the result of recording certain holdings at fair value instead of amortized cost as had been done previously. At December 31, 2021, the debt securities portfolio declined to $10.1 billion. Investment yields on new bond purchases in 2021 and 2020 were less than the portfolio's weighted average yield after exceeding the portfolio yield in the prior two years. The portfolio weighted average yield was approximately 3.62% at December 31, 2021, while the yield on debt security purchases to fund insurance operations was 3.02%, 3.33%, and 4.06% in 2021, 2020, and 2019, respectively. Ozark National's weighted average portfolio yield at December 31, 2021 was 3.62%. Bond portfolio yields have continued to be impacted by higher yielding debt securities maturing or being called by borrowers with the proceeds being reinvested into lower yielding securities.

Fair value changes of equity securities are included in the Consolidated Statements of Earnings as a component of net investment income. For the years ended December 31, 2021, 2020, and 2019 an unrealized gain (loss) of $6.0 million, $(1.0) million, and $3.5 million, respectively, has been included in net investment income reflecting the change in fair value of equity securities during the periods. The carrying value of the Company’s portfolio of equity securities was $28.2 million at December 31, 2021.

Prior to 2020, the Company’s new mortgage loan activity had been challenged by the low level of interest rates and highly competitive underwriting of commercial properties. The COVID-19 pandemic crisis further impeded the underwriting of new loan applications early in 2020 until clarity regarding the impacts of closing down the economy upon commercial real estate became discernible. Eventually the volume of new mortgage loan originations during the latter half of 2020 resumed a pace closer to that of the pre-pandemic environment. Additional resources were added with the goal of increasing mortgage loan investments to a more appreciable percentage of total invested assets. The Company originated new mortgage loans in the amount of $183.6 million, $80.2 million, and $121.4 in 2021, 2020, and 2019, respectively. Mortgage loan investment income also benefits from incremental contributions from loan prepayment fees and profit participation receipts.

Policy loan and other invested asset balances outstanding have remained relatively stable over the past few years. During the latter part of 2020, National Western, in order to obtain incremental investment yield, expanded its invested asset vehicles to include alternative investments. These assets are typically syndicated, targeted capital pools with specific investment objectives managed by investment firms having specific expertise in designated asset opportunities. At December 31, 2021 and 2020, the Company held balances of $67.7 million and $28.9 million, respectively, in this investment category.

Effective January 1, 2021, the Company's net investment income is reduced for amounts ceded to the reinsurer under the funds withheld reinsurance agreement associated with funds withheld assets. For the year ended December 31, 2021, the Company ceded net investment income of $55.1 million, substantially comprised of investment income from debt securities.

The Company adopted new accounting guidance pertaining to current expected credit losses on financial instruments ("CECL") in 2020. The adoption as of January 1, 2020 was reported as a change in accounting with initial balances recorded and $3.0 million, net of taxes, charged to retained earnings. Remeasurement of the CECL allowance during 2020 resulted in a decrease in the allowance of $2.0 million for the year ended December 31, 2020 which is netted in gross investment income. During the year ended December 31, 2021, remeasurement of the CECL allowance resulted in an increase to the allowance of $0.5 million.

In order to evaluate underlying profitability and results from ongoing operations, net investment income performance is analyzed excluding derivative gain (loss), which is a common practice in the insurance industry. Although this is considered a non-GAAP financial measure, Company management believes this financial measure provides useful supplemental information by removing the swings associated with fair value changes on derivative instruments. Net investment income and average invested assets shown below includes cash and cash equivalents. Net investment income performance is summarized as follows:

| | | | | | | | | | | | | | | | | | | | |

| | | Years Ended December 31, |

| | | 2021 | | 2020 | | 2019 |

| | | (In thousands except percentages) |

| | | | | | |

| Excluding derivatives and trading securities: | | | | | | |

| Net investment income | | $ | 345,756 | | | 402,448 | | | 432,285 | |

| Average invested assets, at amortized cost | | 9,420,544 | | | 10,994,033 | | | 10,881,052 | |

| Annual yield on average invested assets | | 3.67 | % | | 3.66 | % | | 3.97 | % |

| | | | | | |

| Including derivatives and trading securities: | | | | | | |

| Net investment income | | $ | 562,530 | | | 417,202 | | | 555,492 | |

| Average invested assets, at amortized cost | | 11,163,776 | | | 11,139,238 | | | 10,967,188 | |

| Annual yield on average invested assets | | 5.04 | % | | 3.75 | % | | 5.07 | % |

The decline in average invested asset yield, excluding derivatives and trading securities, from 2019 to 2020 is due to the Company continuing to obtain lower yields on newly invested cash inflows as higher yielding assets mature or are called. The average invested asset yield in 2021 remained level with 2020 reflecting diversification during 2021 into other invested assets, namely commercial mortgage loans and alternative investments, which have incrementally higher yields.

The pattern in average invested asset yield, including derivatives and trading securities, incorporates increases and decreases in the fair value of index options purchased by National Western to support its fixed-index products as well as net investment income from the embedded derivative funds withheld liability. Fair values of the purchased call options recorded net gains in 2021, 2020, and 2019 corresponding to the movement in the S&P 500 Index® during these periods (the primary index the fixed-index products employ). Refer to the derivatives discussion following this section for a more detailed explanation.

Other revenues - Other revenues pertain to NIS, the broker-dealer affiliate of Ozark National; the operations of Braker P III ("BP III"), a subsidiary which owns and manages a commercial office building which includes the home office operations of National Western; and a maintenance expense allowance earned by National Western for administering the funds withheld block of annuity policies ceded to a third party reinsurer. The operations of the Company’s previously owned two nursing home operations in Reno, Nevada and San Marcos, Texas are included in the results for the year ended December 31, 2019 up to their respective dates of sales.

NIS revenues were $12.5 million, $9.9 million, and $8.2 million for the years ended December 31, 2021, 2020, and 2019, respectively. NIS revenues in 2019 were for the period subsequent to its acquisition effective January 31, 2019.

Revenues associated with BP III were $5.1 million, $4.7 million, and $3.9 million in December 31, 2021, 2020, and 2019, respectively, reflecting additional tenant leases subsequently executed. The facility is currently fully leased.

Under terms of the funds withheld reinsurance contract, National Western earns a monthly expense allowance equal to the average policy count of the funds withheld reinsurance block of business multiplied by a stated amount per policy. In the year ended December 31, 2021, the Company reported $5.4 million as maintenance expense allowance revenue.

The Company closed on the sale of its Reno nursing home operations effective February 1, 2019 and on the sale of its San Marcos nursing home operations effective May 1, 2019. Revenues associated with these operations were $(0.2) million, $(0.6) million, and $4.3 million in 2021, 2020, and 2019, respectively. In addition, net gains from the sale of personal property and equipment at the Reno facility of $1.4 million are included in 2019 revenues.

The Company's acquisition of Ozark National (by National Western) included a contingent payment provision that was dependent upon the subsequent persistency of Ozark National's in force block of business that was acquired. The Company had been progressively accruing for this potential obligation in its financial statements. During 2020, the Company executed an agreement with the seller under which both parties agreed that the Company had fulfilled its payment obligation under the Stock Purchase Agreement executed October 3, 2018. Consequently, the Company reversed the contingent payment amounts previously accrued and recognized as Other revenues $4.1 million in the year ended December 31, 2020.

Other revenues also include semi-annual distributions from the life interest in the Libbie Shearn Moody Trust. Revenues recognized from these distributions were $5.7 million, $5.3 million, and $6.7 million for the years ended December 31, 2021, 2020, and 2019, respectively.

Index option derivative gain (loss) - Index options are derivative financial instruments used to hedge the equity return component of National Western’s fixed-index products. Derivative gain or loss includes the amounts realized from the sale or expiration of the options. Since the index options do not meet the requirements for hedge accounting under GAAP, they are marked to fair value on each reporting date and the resulting unrealized gain or loss is reflected as a component of net investment income. As the options hedging the notional amount of policyholder contract obligations are purchased as close as possible to like amounts, the amount of the options returns tend to correlate closely with indexed interest credited.

Gains and losses from index options are substantially due to changes in equity market conditions. Index options are intended to act as hedges to match the returns on the product’s underlying reference index and the rise or decline in the index relative to the index level at the time of the option purchase which causes option values to likewise rise or decline. As income from index options fluctuates with the underlying index, the contract interest expense to policyholder accounts for the Company’s fixed-index products also fluctuates in a similar manner and direction. The Company recorded derivative gain (loss) and contract interest amounts as shown below.

| | | | | | | | | | | | | | | | | |

| | Years Ended December 31, |

| | 2021 | | 2020 | | 2019 |

| | (In thousands) |

| | | | | |

| Index option derivatives: | | | | | |

| Unrealized gain (loss) | $ | (16,564) | | | (9,740) | | | 152,993 | |

| Realized gain (loss) | 137,282 | | | 24,494 | | | (29,786) | |

| | | | | |

| Total gain included in net investment income | $ | 120,718 | | | 14,754 | | | 123,207 | |

| | | | | |

| Total contract interest | $ | 213,184 | | | 206,250 | | | 295,330 | |

The economic impact of option performance in the Company's financial statements is not generally determined solely by the option gain or loss included in net investment income as there is a corresponding amount recorded in the contract interest expense line. The Company's profitability with respect to these options is largely dependent upon the purchase cost of the option remaining within the financial budget for acquiring options embedded in the product pricing. Option prices vary with interest rates, volatility, and dividend yields among other things. As option prices vary, the Company manages for the variability by making offsetting adjustments to product caps, participation rates, and management fees. For the periods shown, the Company's option costs have generally been within the product pricing budgets.

The financial statement investment spread, the difference between investment income and interest credited to contract holders, is subject to variations from option performance during any given period. For example, many of the Company's equity-index annuity products provide for the collection of asset management fees. These asset management fees are assessed when returns on expiring options are positive, and they are collected prior to passing any additional returns above the assessed management fees to the policy contractholders. During periods of positive returns, the collected asset management fees serve to increase the financial statement spread by increasing option realized gains reported as investment income in an amount greater than interest credited to policy contractholders which is reported as contract interest expense. Asset management fees collected in 2021, 2020, and 2019 were $5.8 million, $30.7 million, and $15.9 million, respectively. While the level of asset management fees collected is dependent upon equity market performance, the reduced amount in 2021 is primarily the result of the Company's change in option hedging to an "out-of-the-money" basis during the second quarter of 2020. Consequently, no asset management fees were collected during the third and fourth quarters of 2021 as the out-of-the-money hedges constituted all hedges maturing during these time periods. Though asset management fees are no longer being collected, the costs to purchase the out-of-the-money options similarly decreases.

Net realized investment gains (losses) - Realized gains (losses) on investments generally include proceeds from bond calls, sales and impairment write-downs, as well as gains and losses on the sale of real estate property. Net gains reported in 2021 consisted of gross gains of $16.4 million which were mostly from bond calls of debt securities in the available-for-sales category, offset by gross losses of $(1.4) million. Gross losses include $1.4 million pertaining to property held by Ozark National which was sold during 2021. Gross gains in 2020 and 2019 include proceeds from bond calls of securities classified in the held-to-maturity category at that time.

Included the year ended December 31, 2019 gross gains is $5.7 million from the sale of land and building associated with the nursing home in Reno, Nevada and a $3.2 million gain on the sale of the Company's former Austin, Texas home office facility. Included in 2019 gross losses is a $2.0 million loss on the sale of the building pertaining to the San Marcos, Texas nursing home and an other-than-temporary impairment on a single debt security credit in the amount of $7.8 million.

Prior to January 1, 2020 and the adoption of the new accounting guidance on current expected credit losses, the Company recorded impairment write-downs when a decline in value was considered to be other-than-temporary and full recovery of the investment was not expected. Impairments due to credit factors were recorded in the Company’s Consolidated Statements of Earnings while non-credit (liquidity) impairment losses were included in the Consolidated Statements of Comprehensive Income (Loss). Under current expected credit loss accounting guidance, credit loss allowances for available-for-sale debt securities are recorded following the same process previously applied for impairment accounting and are recorded through net investment income in the Consolidated Statement of Earnings. Impairment or valuation write-downs recorded prior to January 1, 2020 under previous accounting guidance totaled $7.8 million in the year ended December 31, 2019.

Benefits and Expenses. The following details benefits and expenses.

| | | | | | | | | | | | | | | | | |

| | Years Ended December 31, |

| | 2021 | | 2020 | | 2019 |

| | (In thousands) |

| | | | | |

| Life and other policy benefits | $ | 187,577 | | | 131,337 | | | 137,342 | |

| Amortization of deferred transaction costs | 69,461 | | | 140,503 | | | 116,802 | |

| Universal life and annuity contract interest | 213,184 | | | 206,250 | | | 295,330 | |

| Other operating expenses | 126,612 | | | 104,584 | | | 104,558 | |

| | | | | |

| Totals | $ | 596,834 | | | 582,674 | | | 654,032 | |

Life and other policy benefits - Life and other policy benefits include death claims of $96.3 million, $72.5 million and $65.8 million for 2021, 2020 and 2019, respectively. Included in the amounts for the years ended December 31, 2021, 2020, and 2019, are $39.6 million, $37.0 million and $29.3 million in death claims pertaining to Ozark National. Death claim amounts are subject to variation from period to period. Death claims reported in 2021 and 2020 include net benefit amounts (after reinsurance) pertaining to death from COVID-19 of $23.5 million and $5.1 million for National Western and $8.2 million and $2.8 million for Ozark National. In 2021, the number of National Western life insurance claims incurred was level with that of 2020 while the average dollar amount per net claim increased 42% to $61,900 from $43,600. National Western’s mortality experience has generally been consistent with or better than its product pricing assumptions. The average net claim for Ozark National during 2021 increased to $15,400 from the 2020 period amount of $14,800. The average face amount of insurance in force for Ozark National was $33,600 at December 31, 2021. Mortality exposure is managed through reinsurance treaties under which the Company's retained maximum net amount at risk on any one life is capped at $500,000. Ozark National's retained maximum net amount at risk is capped at $200,000 under its reinsurance treaties with limited exceptions related to the conversion of child protection and guaranteed insurability riders.

Life and other policy benefits also includes policy liabilities held associated with the Company's traditional life products, including riders such as the guaranteed minimum withdrawal benefit rider ("WBR"), a popular rider to National Western's equity-indexed annuity products. The increases in these liabilities for National Western were $46.5 million, $10.7 million, and $24.4 million in 2021, 2020, and 2019, respectively. In each of these years, National Western unlocked its policy benefit reserves associated with the WBR which resulted in an increase/(decrease) to the policy benefit liability of $27.4 million, $(11.9) million, and $0.7 million in 2021, 2020, and 2019, respectively. The 2020 adjustment included an unlocking amount pertaining to mortality experience on payout annuities with life contingencies of $(3.3) million.

Life and other policy benefits in the years ended December 31, 2021, 2020, and 2019 includes changes in traditional life reserves and miscellaneous benefit payments associated with Ozark National's operations of $29.5 million, $30.7 million, and $30.5 million, respectively, reflecting normal business conditions.

Amortization of deferred transaction costs - Life insurance companies are required to defer certain expenses that vary with, and are directly related to, the cost of acquiring new business. The majority of these acquisition expenses consist of commissions paid to agents, underwriting costs, and certain marketing expenses. Recognition of these deferred policy acquisition costs (“DPAC”) as an expense in the Consolidated Financial Statements occurs over future periods in relation to the expected emergence of profits priced into the products sold. This emergence of profits is based upon assumptions regarding premium payment patterns, mortality, persistency, investment performance, and expense patterns. Companies are required to review universal life and annuity contract assumptions periodically to ascertain whether actual experience has deviated significantly from that assumed. If it is determined that a significant deviation has occurred, the emergence of profits pattern is to be "unlocked" and reset based upon the actual experience. DPAC balances are also adjusted each period to reflect current policy lapse or termination rates, expense levels and credited rates on policies as compared to anticipated experience (“true-up”) with the adjustment reflected in current period amortization expense. In accordance with GAAP guidance, the Company must also write off deferred acquisition costs and unearned revenue liabilities upon internal replacement of certain contracts as well as annuitizations of deferred annuities.

The following table identifies the effects of unlocking adjustments on DPAC balances recorded through amortization expense separate from recurring amortization expense components for 2021, 2020, and 2019.

| | | | | | | | | | | | | | | | | |

| | Years Ended December 31, |

| Amortization of DPAC | 2021 | | 2020 | | 2019 |

| | (In thousands) |

| | | | | |

| Unlocking adjustments | $ | (36,510) | | | 22,358 | | | (8,643) | |

| Other amortization components | 84,349 | | | 107,917 | | | 117,748 | |

| | | | | |

| Totals | $ | 47,839 | | | 130,275 | | | 109,105 | |

The amortization amounts for the years ended December 31, 2021, 2020, and 2019 were comprised of DPAC amortization by National Western of $47.2 million, $129.7 million, and $108.4 million and by Ozark National of $0.6 million, $0.6 million, and $0.7 million. Ozark National's deferred policy acquisition cost balance was initiated February 1, 2019 following its acquisition by National Western.

In 2021, the Company unlocked its DPAC balances for: (1) mortality rates, lapse rates, portfolio yield rates and spreads, and increased cost of insurance ("COI") charges on International universal life products inforce which collectively increased DPAC balances (and decreased amortization expense) on its Life segment by $33.3 million; and (2) surrender rates, annuitization rates, portfolio yield rates and spreads, mortality experience on payout annuities, and utilization of the Company's withdrawal benefit rider which collectively increased DPAC balances (and decreased amortization expense) on its Annuity segment by $3.2 million.

In 2020, the Company unlocked its DPAC balances for: (1) mortality rates, lapse rates, portfolio yield rates and spreads, which collectively decreased DPAC balances (and increased amortization expense) on its Life segment by $7.4 million; and (2) surrender rates, annuitization rates, portfolio yield rates and spreads, mortality experience on payout annuities, and utilization of the Company's withdrawal benefit rider which collectively decreased DPAC balances (and increased amortization expense) on its Annuity segment by $15.0 million.

In 2019, the Company unlocked its DPAC balances for: (1) mortality rates, lapse rates, portfolio yield rates and spreads, and maintenance expense on its International life business which collectively increased DPAC balances (and reduced amortization expense) on its Life segment by $11.2 million; and (2) surrender rates, annuitization rates, portfolio yield rates and spreads, and utilization of the Company's withdrawal benefit rider which collectively decreased DPAC balances (and increased amortization expense) on its Annuity segment by $2.6 million.

As the DPAC balance is an asset on the Company's Consolidated Balance Sheets, GAAP provides for an earned interest return on the unamortized balance each period. The earned interest serves to increase the DPAC balance and reduce other amortization component expense. The rate at which the DPAC balance earns interest is the average credited interest rate on universal life and annuity policies in force, including credited interest on equity-indexed policies. The amount of earned interest on DPAC balances was $32.7 million, $17.2 million, and $12.0 million in 2021, 2020, and 2019, respectively, each decreasing other amortization component expense. The increasing interest amounts reflect larger realized returns on equity-index products, particularly life insurance products.

As part of the purchase accounting required with the acquisition of Ozark National effective January 31, 2019, the Company recorded an intangible asset of $145.8 million referred to as the value of business acquired ("VOBA"). VOBA represents the difference between the acquired assets and liabilities of Ozark National measured in accordance with the Company's accounting policies and the fair value of these same assets and liabilities. During the year ended December 31, 2020, the cash value of certain acquired reserves was increased which resulted in a commensurate $35.1 million increase in both the traditional life reserve liability and the related VOBA balance reported on the Consolidated Balance Sheets. The VOBA balance sheet amount is amortized following a methodology similar to that used for amortizing deferred policy acquisition costs. In the years ended December 31, 2021, 2020, and 2019 the Company's VOBA amortization was $8.5 million, and $10.2 million, and $7.7 million, respectively.

Universal life and annuity contract interest - The Company closely monitors its credited interest rates on interest sensitive policies (National Western products), taking into consideration such factors as profitability goals, policyholder benefits, product marketability, and economic market conditions. As long-term interest rates change, the Company's credited interest rates are often adjusted accordingly, taking into consideration the factors described above. The difference between yields earned on investments over policy credited rates is often referred to as the "interest spread."

Contract interest reported in the financial statements also encompasses the performance of the index options associated with the Company's fixed-index products. As previously noted, the market value changes of these derivative features resulted in net realized and unrealized gains/(losses) in 2021, 2020, and 2019 of $120.7 million, $14.8 million, and $123.2 million, respectively. In 2021, this figure was comprised of unrealized losses totaling $(16.6) million offset by realized gains of $137.3 million. In 2020, this figure was comprised of unrealized losses totaling $(9.7) million offset by realized gains of $24.5 million. In 2019, the amount consisted of unrealized gains of $153.0 million offset by realized losses of $(29.8) million. These returns similarly increased/(decreased) the computed average credited rates for the periods shown above. Policyholders of equity-indexed products cannot receive an interest credit below 0% according to the policy contract terms.

| | | | | | | | | | | | | | | | | |

| Contract Interest Expense | December 31, |

| 2021 | | 2020 | | 2019 |

| |

| | | | | |

| Gross reserve changes | $ | 24,250 | | | 18,748 | | | 26,893 | |

| Ceded reserve changes under funds withheld | (26,429) | | | — | | | — | |

| Unlocking adjustments, net | (14,547) | | | 17,180 | | | 10,274 | |

| Asset management fees collected | (5,835) | | | (30,675) | | | (15,856) | |

| Projected asset management fees | 6,477 | | | 34,426 | | | (33,600) | |

| Other embedded derivative components | 5,814 | | | (5,188) | | | 6,389 | |

| | | | | |

| Totals | $ | (10,270) | | | 34,491 | | | (5,900) | |

Contract interest expense includes reserve changes for immediate annuities, two tier annuities, excess death benefit reserves, excess annuitizations, and amortization of deferred sales inducement balances. These gross reserve items are offset by policy charges assessed for policies having the withdrawal benefit rider (WBR). As changes in these items collectively impact contract interest expense, financial statement interest spread is also affected. Netted against reserve changes in the years ended December 31, 2021, 2020, and 2019 are WBR assessed policy charges of $28.2 million, $24.8 million, and $23.8 million, respectively.

Beginning in 2021, reserve changes associated with funds withheld annuity policies are ceded to the reinsurer and no longer reflected in the financial statements of the Company. Accordingly, contract interest expense is adjusted to remove these expense items which are shown in the above table for the year ended December 31, 2021. In addition to these amounts, the Company also cedes the fixed interest credited on the funds withheld annuity policies. For the year ended December 31, 2021, the fixed interest credited ceded was $29.8 million.

Generally, the impact of the market value change of index options on asset values aligns closely with the movement of the embedded derivative liability held for the Company's fixed-index products such that the net effect upon pretax earnings is negligible (i.e. net realized and unrealized gains/(losses) included in net investment income approximate the change in contract interest associated with the corresponding embedded derivative liability change). However, other aspects of the embedded derivatives can cause deviations to occur between the change in index option asset values included in net investment income and the change in the embedded derivative liability included in contract interest. As noted in the discussion of net investment income, the collection of asset management fees in a period can cause investment income to increase marginally higher than contract interest expense since these collected fees are deducted from indexed interest credited to policyholders. As shown in the table above, the collection of asset management fees are deductions from contract interest expense.

Accounting rules require the embedded derivative liability to include a projection of asset management fees estimated to be collected in the succeeding fiscal year due to the Company's historical practice of purchasing options priced to incorporate an expected probability of collecting asset management fees (referred to as "at the money hedging"). This projection for the embedded derivative liability is based upon the most recent performance of the reference equity index. Increases in projected asset management fees to be collected reduce contract interest expense while decreases in projected asset management fees to be collected increase contract interest expense. During the years ended December 31, 2021, 2020, and 2019, contract interest was increased/(decreased) by $6.5 million, $34.4 million, and $(33.6) million, respectively, for the projected change in asset management fees to be collected. During 2020, the Company changed its embedded derivative hedging process to incorporate "out-of-the-money" hedging which reduces option costs and eliminates the requirement for estimating probability projections of collected asset management fees. The remaining inventory of at the money option hedges purchase with a one year term completed its roll over to out-of-the-money hedges during the second quarter of 2021. Consequently, the embedded derivative liability component for projected asset management fees to be collected was phased out as of the end of the 2021 second quarter. Refer to Note (3) Derivative Investments in the accompanying Notes to Consolidated Financial Statements in this report for further information.

Other embedded derivative components include changes pertaining to other modeling differences, changes in future interest adjustments, and the change in the host contract component of the embedded derivative products. In the first quarter of 2020, the Company incurred an additional charge to contract interest of $12.1 million pertaining to an assumption regarding the embedded derivative option budget which was made several years ago when the Company's investment portfolio yield was higher. The combination of the embedded derivative option budget being out of date relative to the Company's current investment portfolio yield and the historically low interest rate levels introduced an embedded derivative floor which prevented the Company's contract interest expense from declining in tandem with the option value decreases recorded in net investment income. The Company subsequently unlocked for this out of date embedded derivative option budget assumption to reflect the Company's current investment portfolio yield. The effect of the unlocking was to remove the embedded derivative floor and reverse the contract interest charge recorded in the first quarter of 2020 so that there was no effect for this occurrence for the year ended December 31, 2020.

Another contract interest expense component is the amortization of deferred sales inducements (included in Gross reserve changes above). Similar to deferred policy acquisition costs, the Company defers sales inducements in the form of first year credited interest bonuses on annuity products that are directly related to the production of new business. These bonus interest charges are deferred and amortized using the same methodology and assumptions used to amortize other capitalized acquisition costs and the amortization is included in contract interest. In addition, deferred sales inducement balances ("DSI") are also reviewed periodically to ascertain whether actual experience has deviated significantly from that assumed (unlock) and are adjusted to reflect current policy lapse or termination rates, expense levels and credited rates on policies compared to anticipated experience (true-up). These adjustments, plus or minus, are included in contract interest expense. As part of the DPAC balance unlockings for the Annuity segment previously discussed for 2021, 2020, and 2019, the Company also unlocked its DSI balance. The effect of these prospective unlockings was to increase/(decrease) the DSI balance by $1.0 million, $(4.4) million, and $(0.6) million, respectively. These amounts are included in the previous table in the Unlocking adjustments line.

Other operating expenses - Other operating expenses consist of general administrative expenses, licenses and fees, commissions not subject to deferral, real estate expenses, brokerage expenses, compensation costs, and reinsurance ceded commission expense. These are summarized in the table that follows.

| | | | | | | | | | | | | | | | | |

| Years Ended December 31, |

| 2021 | | 2020 | | 2019 |

| (In thousands) |

| | | | | |

| General administrative expenses | $ | 51,317 | | | 42,688 | | | 42,353 | |

| | | | | |

| Compensation expenses | 40,178 | | | 30,372 | | | 31,956 | |

| Commission expenses | 10,810 | | | 11,159 | | | 10,502 | |

| Real estate expenses | 5,947 | | | 5,598 | | | 5,236 | |

| Brokerage expenses (NIS) | 6,123 | | | 5,085 | | | 4,372 | |

| Reinsurance ceded commission expense | 12 | | | — | | | — | |

| Taxes, licenses and fees | 12,225 | | | 9,682 | | | 10,139 | |

| | | | | |

| Totals | $ | 126,612 | | | 104,584 | | | 104,558 | |

General administrative expenses include software amortization of previously capitalized information technology (IT) expenditures including National Western's proprietary policy administration systems. Software costs, including amortization expense, for 2021, 2020, and 2019 were $13.8 million, $12.6 million, and $12.7 million, respectively. Other IT expenditures include consulting costs for system implementations, assistance with analysis involving a security incident experienced by National Western, and contractor resources to fill IT staffing shortages. These amounts in the years ended December 31, 2021 and 2020 were $17.5 million and $10.4 million, respectively. General administrative expenses also include payments and provisions made relating to potential or contingent legal liabilities and legal fees. Expenses in this category were $6.0 million, $2.8 million, and $3.8 million in 2021, 2020, and 2019, respectively. The 2021 amount includes $4.4 million accrued for potential settlement of a class action lawsuit pertaining to the IT security incident experienced by National Western. General administrative expenses for the year ended December 31, 2019 include a $3.3 million broker fee paid in connection with the acquisition of Ozark National and NIS which closed early in 2019. GAAP precludes this fee from being part of the purchase price for acquiring these businesses. General administrative expenses in the years ended December 31, 2021, 2020, and 2019 include Ozark National expenses in the amount of $4.3 million, $4.4 million, and $4.2 million, respectively.

General administrative expenses include nursing home expenses that reflect the operations of the Company's two facilities which were sold during 2019. The Reno, Nevada nursing home was sold effective February 1, 2019, while the San Marcos, Texas nursing home sale closed effective May 1, 2019. Expenses shown for 2019 reflect operations up to the date of sale for each facility. The Company must maintain the legal entities for a specified time period subsequent to each sale and incur various record safekeeping and other administrative expenses in the interim.

Compensation expenses include share-based compensation costs related to outstanding vested and nonvested stock appreciation rights ("SARs"), restricted stock units ("RSUs"), and performance share units ("PSUs"). The related share-based compensation costs move in tandem not only with the number of awards outstanding but also with the movement in the market price of the Company's Class A common stock as a result of marking the SARs, RSUs and PSUs, to fair value under the liability method of accounting. Consequently, the related expense amount varies positive or negative in any given period. In the amounts shown above, share-based compensation expense totaled $5.8 million in 2021, $(2.2) million in 2020, and $2.4 million in 2019. The negative expense level in 2020 reflects a change in the Company's Class A common share price to $206.44 at December 31, 2020 from $290.88 at December 31, 2019. In addition to the changes in price of the Company's Class A common shares, there were 64,157, 40,990, and 20,380 SARs granted to officers in 2021, 2020, and 2019, respectively. Refer to Note (12) Stockholders' Equity in the accompanying Notes to Consolidated Financial Statements of this report for a discussion of performance share awards.

Commission expenses in 2021, 2020, and 2019 include Ozark National non-deferrable commissions of $3.0 million, $3.1 million, and $3.2 million, respectively.

Real estate expenses pertain to the commercial building operated by Braker P III. The building was acquired at year-end 2016 and National Western relocated to this facility during the fourth quarter of 2017. The trending increase in the level of operating expenses reflects the addition of new tenants and associated operating expenses. At December 31, 2021, the facility was fully occupied.