UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-K

| | | | | | | | | | | |

| ☒ | | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| | For the Fiscal Year ended | December 31, 20222023 |

| ☐ | | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the Transition period from to . |

Commission File Number: 333-203369

Clearway Energy LLC

(Exact name of registrant as specified in its charter) | | | | | | | | | | | |

| Delaware | | 32-0407370 |

| (State or other jurisdiction of incorporation or organization) | | (I.R.S. Employer Identification No.) |

| 300 Carnegie Center, Suite 300 | Princeton | New Jersey | 08540 |

| (Address of principal executive offices) | (Zip Code) |

(609) 608-1525

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

None

Securities registered pursuant to Section 12(g) of the Act:

None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes o No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Exchange Act. Yes x No o

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No o

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes x No o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| | | | | | | | | | | |

| Large accelerated filer | ☐ | Accelerated filer | ☐ |

| Non-accelerated filer | ☒ | Smaller reporting company | ☐ |

| | Emerging growth company | ☐ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. o

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ☐ No x

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☐

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Clearway Energy LLC’s outstanding equity interests are held by Clearway Energy, Inc. and Clearway Energy Group LLC and there are no equity interests held by non-affiliates.

Indicate the number of shares outstanding of each of the registrant’s classes of common stock as of the latest practicable date. There is no public market for the registrant’s outstanding units.

| | | | | |

| Class | Outstanding at January 31, 20232024 |

| Class A Units | 34,613,853 |

| Class B Units | 42,738,750 |

| Class C Units | 82,283,46082,391,441 |

| Class D Units | 42,336,750 |

Documents Incorporated by Reference:

None.

TABLE OF CONTENTS

Index | | | | | |

| GLOSSARY OF TERMS | |

| PART I | |

| Item 1 — Business | |

| Item 1A — Risk Factors | |

| Item 1B — Unresolved Staff Comments | |

| Item 1C — Cybersecurity | |

| Item 2 — Properties | |

| Item 3 — Legal Proceedings | |

| Item 4 — Mine Safety Disclosures | |

| PART II | |

| Item 5 — Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities | |

| Item 6 — Reserved | |

| Item 7 — Management’s Discussion and Analysis of Financial Condition and Results of Operations | |

| Item 7A — Quantitative and Qualitative Disclosures About Market Risk | |

| Item 8 — Financial Statements and Supplementary Data | |

| Item 9 — Changes in and Disagreements with Accountants on Accounting and Financial Disclosure | |

| Item 9A — Controls and Procedures | |

| Item 9B — Other Information | |

| PART III | |

| Item 10 — Information about Directors, Executive Officers and Corporate Governance | |

| Item 11 — Executive Compensation | |

| Item 12 — Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters | |

| Item 13 — Certain Relationships and Related Transactions, and Director Independence | |

| Item 14 — Principal Accounting Fees and Services | |

| PART IV | |

| Item 15 — Exhibits, Financial Statement Schedules | |

| EXHIBIT INDEX | |

| Item 16 — Form 10-K Summary | |

GLOSSARY OF TERMS

When the following terms and abbreviations appear in the text of this report, they have the meanings indicated below:

| | | | | |

| |

2025 Senior Notes | $600 million aggregate principal amount of 5.75% unsecured senior notes due 2025, issued by Clearway Energy Operating LLC, which were repaid in March 2021 |

2026 Senior Notes | $350 million aggregate principal amount of 5.00% unsecured senior notes due 2026, issued by Clearway Energy Operating LLC, which were repaid in October 2021 |

| 2028 Senior Notes | $850 million aggregate principal amount of 4.75% unsecured senior notes due 2028, issued by Clearway Energy Operating LLC |

| 2031 Senior Notes | $925 million aggregate principal amount of 3.75% unsecured senior notes due 2031, issued by Clearway Energy Operating LLC |

| 2032 Senior Notes | $350 million aggregate principal amount of 3.75% unsecured senior notes due 2032, issued by Clearway Energy Operating LLC |

| Adjusted EBITDA | A non-GAAP measure, represents earnings before interest (including loss on debt extinguishment), tax, depreciation and amortization adjusted for mark-to-market gains or losses, asset write offs and impairments; and factors which the Company does not consider indicative of future operating performance |

| ARO | Asset Retirement Obligation |

| |

| ASC | The FASB Accounting Standards Codification, which the FASB established as the source of authoritative GAAP |

| ASU | Accounting Standards Updates – updates to the ASC |

| ATM Program | At-The-Market Equity Offering Program |

| BESS | Battery energy storage system |

| BlackRock | BlackRock, Inc. |

| Black Start | The capability of a generating asset to restore the grid in the event of a blackout without relying on the external electric power transmission network |

| Bridge Loan Agreement | Senior secured bridge credit agreement entered into by Clearway Energy Operating LLC that provides a term loan facility in an aggregate principal amount of $335 million that was repaid on May 3, 2022 |

| CAFD | A non-GAAP measure, Cash Available for Distribution is defined as of December 31, 20222023 as Adjusted EBITDA plus cash distributions/return of investment from unconsolidated affiliates, cash receipts from notes receivable, cash contributions from noncontrolling interests, adjustments to reflect sales-type lease cash payments and payments for lease expenses, less cash distributions to noncontrolling interests, maintenance capital expenditures, pro-rata Adjusted EBITDA from unconsolidated affiliates, cash interest paid, income taxes paid, principal amortization of indebtedness, changes in prepaid and accrued capacity payments, and adjusted for development expenses |

| Capistrano Wind Portfolio | Five wind projects representing 413 MW of capacity, which includes Broken Bow and Crofton Bluffs located in Nebraska, Cedro Hill located in Texas and Mountain Wind Power I1 and II2 located in Wyoming |

CARES Act | The Coronavirus Aid, Relief, and Economic Security Act |

| CEG | Clearway Energy Group LLC (formerly Zephyr Renewables LLC) |

| CEG Master Services Agreement | Amended and Restated Master Services Agreements, entered intodated as of August 31, 2018 and amended on February 2, 2023, betweenamong the Company, Clearway Energy, LLC andInc., Clearway Energy Operating LLC and CEG |

CEG ROFO Agreement | Right of First Offer Agreement, entered into as of August 31, 2018, by and between Clearway Energy Group LLC and Clearway Energy, Inc., and solely for purposes of Section 2.4, GIP III Zephyr Acquisition Partners, L.P., as amended by the First Amendment dated February 14, 2019, the Second Amendment dated August 1, 2019, the Third Amendment dated December 6, 2019, the Fourth Amendment dated November 2, 2020 and the Fifth Amendment dated August 2, 2021 |

| Clearway, Inc. | Clearway Energy, Inc., the holder of the Company’s Class A and Class C units |

| Clearway Energy Group LLC | The holder of all shares of Clearway, Inc.’s Class B and Class D common sharesstock and the Company’s Class B and Class D units and, from time to time, possibly shares of Clearway, Inc.’s Class A and/or Class C common stock |

| Clearway Energy Operating LLC | The holder of the project assets that are owned by the Company |

| Clearway Renew | Clearway Renew LLC, a subsidiary of CEG, and its wholly-owned subsidiaries |

| COD | Commercial Operation Date |

| Code | Internal Revenue Code of 1986, as amended |

| Company | Clearway Energy LLC, together with its consolidated subsidiaries |

| CVSR | California Valley Solar Ranch |

| | | | | |

| CVSR Holdco | CVSR Holdco LLC, the indirect owner of CVSR |

DGPV Holdco 1 | DGPV Holdco 1 LLC |

DGPV Holdco 2 | DGPV Holdco 2 LLC |

DGPV Holdco 3 | DGPV Holdco 3 LLC |

Distributed Solar

| Solar power projects, typically less than 20 MW in size (on an alternating current, or AC, basis), that primarily sell power produced to customers for usage on site, or are interconnected to sell power into the local distribution grid |

| Drop Down Assets | Assets under common control acquired by the Company from CEG |

| | | | | |

| EPA | United States Environmental Protection Agency |

ERCOT

| Electric Reliability Council of Texas, the ISO and the regional reliability coordinator of the various electricity systems within Texas |

| EWG | Exempt Wholesale Generator |

| Exchange Act | The Securities Exchange Act of 1934, as amended |

| FASB | Financial Accounting Standards Board |

| FERC | Federal Energy Regulatory Commission |

| FPA | Federal Power Act |

| FWS | U.S. Fish & Wildlife Service |

| GAAP | Accounting principles generally accepted in the U.S. |

| GenConn | GenConn Energy LLC |

| GHG | Greenhouse gas |

| GIM | Global Infrastructure Management, LLC, the manager of GIP |

| GIP | Global Infrastructure Partners |

GIP Transaction | On August 31, 2018, NRG transferred its full ownership interest in the Company to Clearway Energy Group LLC and subsequently sold 100% of its interests in Clearway Energy Group LLC, which includes NRG's renewable energy development and operations platform, to an affiliate of GIP. GIP, NRG and the Company also entered into a consent and indemnity agreement in connection with the purchase and sale agreement, which was signed on February 6, 2018 |

| HLBV | Hypothetical Liquidation at Book Value |

| IRA | Inflation Reduction Act of 2022 |

| IRS | Internal Revenue Service |

| ISO | Independent System Operator, also referred to as an RTO |

| ITC | Investment Tax Credit |

| KKR | KKR Thor Bidco, LLC, an affiliate of Kohlberg Kravis Roberts & Co. L.P. |

| kWh | Kilowatt Hour |

| LIBOR | London Inter-Bank Offered Rate |

| |

| MBTA | Migratory Bird Treaty Act |

| Mesquite Star | Mesquite Star Special, LLC |

| MMBtu | Million British Thermal Units |

| Mt. Storm | NedPower Mount Storm LLC |

| MW | Megawatt |

| MWh | Saleable megawatt hours, net of internal/parasitic load megawatt-hours |

| MWt | Megawatts Thermal Equivalent |

| NEPA | National Environmental Policy Act |

| NERC | North American Electric Reliability Corporation |

| Net Exposure | Counterparty credit exposure to Clearway Energy LLC, net of collateral |

| |

| NOLs | Net Operating Losses |

NOx | Nitrogen Oxides |

| NPNS | Normal Purchases and Normal Sales |

| | | | | |

NPPD | Nebraska Public Power District |

| NRG | NRG Energy, Inc. |

| OCI/OCL | Other comprehensive income/loss |

| O&M | Operations and Maintenance |

| PG&E | Pacific Gas and Electric Company |

| |

| PJM | PJM Interconnection, LLC |

| PPA | Power Purchase Agreement |

| PTC | Production Tax Credit |

| PUCT | Public Utility Commission of Texas |

| PUHCA | Public Utility Holding Company Act of 2005 |

| PURPA | Public Utility Regulatory Policies Act of 1978 |

| QF | Qualifying Facility under PURPA |

| RA | Resource adequacy |

| | | | | |

| RENOM | Clearway Renewable Operation & Maintenance LLC, a wholly-owned subsidiary of CEG |

ROFORosie Central BESS | Right of First OfferRosie BESS Devco LLC |

| |

| RPS | Renewable Portfolio Standards |

RPV Holdco | RPV Holdco 1 LLC |

| RTO | Regional Transmission Organization |

| SCE | Southern California Edison |

| SEC | U.S. Securities and Exchange Commission |

| Senior Notes | Collectively, the 2028 Senior Notes, the 2031 Senior Notes and the 2032 Senior Notes |

SO2 | Sulfur Dioxide |

| SOFR | Secured Overnight Financing Rate |

| SPP | Solar Power Partners |

| SREC | Solar Renewable Energy Credit |

| Tax Act | Tax Cuts and Jobs Act of 2017

| Thermal Business | The Company’s thermal business, which consistsconsisted of thermal infrastructure assets that provideprovided steam, hot water and/or chilled water, and in some instances electricity, to commercial businesses, universities, hospitals and governmental units |

| Thermal Disposition | On May 1, 2022, the Company completed theThe Company’s sale of 100% of its interests in the Thermal Business to KKR, which was completed on May 1, 2022 |

| TotalEnergies | TotalEnergies SE |

| U.S. | United States of America |

U.S. DOE | U.S. Department of Energy |

| Utah Solar Portfolio | Seven utility-scale solar farms located in Utah, representing 530 MW of capacity |

Utility Scale Solar

| Solar power projects, typically 20 MW or greater in size (on an alternating current, or AC, basis), that are interconnected into the transmission or distribution grid to sell power at a wholesale level |

| VIE | Variable Interest Entity |

| |

PART I

Item 1 — Business

General

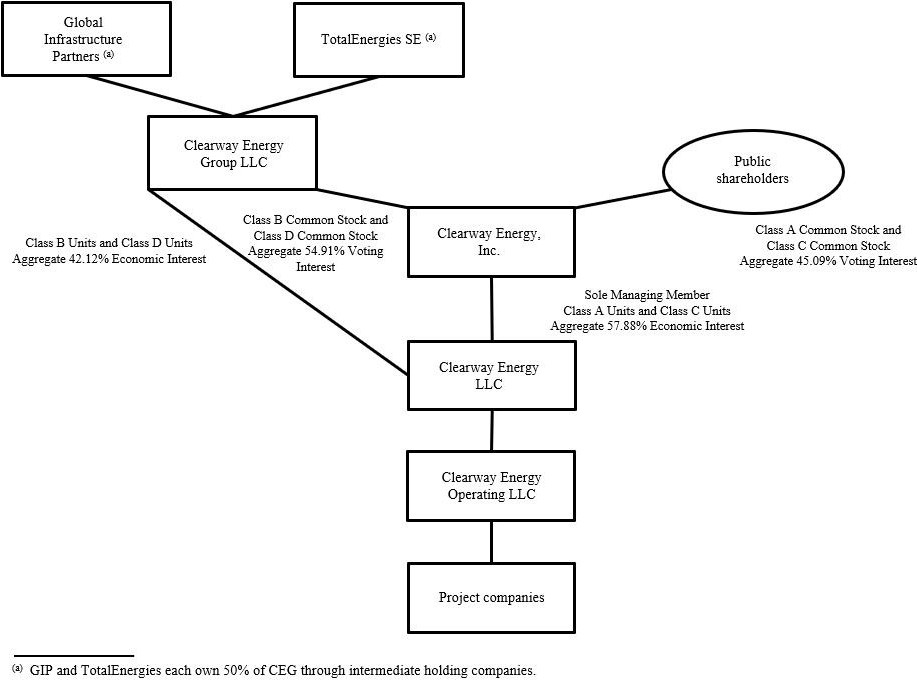

Clearway Energy LLC, together with its consolidated subsidiaries, or the Company, is an energy infrastructure investor with a focus on investments in clean energy and owner of modern, sustainable and long-term contracted assets across North America. The Company was formed as a Delaware limited liability company on March 5, 2013. The Company is sponsored by GIP and TotalEnergies through the portfolio company, Clearway Energy Group LLC, or CEG, which becameis equally owned by GIP and TotalEnergies as of September 12, 2022, when TotalEnergies acquired, through its investment in an intermediate holding company, 50% of GIP’s interest in CEG.TotalEnergies. GIP is an independent infrastructure fund manager that makes equity and debt investments in infrastructure assets and businesses. TotalEnergies is a global multi-energy company. CEG is a leading developer of renewable energy infrastructure in the U.S. On January 12, 2024, BlackRock entered into a definitive agreement to acquire 100% of the business and assets of GIM, which is the investment manager of the GIP funds that own an interest in CEG. BlackRock has indicated that the transaction is expected to close in the third quarter of 2024, subject to regulatory approvals and other customary closing conditions. BlackRock is a publicly-traded global investment management firm.

The Company is one of the largest renewable energy owners in the U.S. with over 5,500approximately 6,000 net MW of installed wind, solar and solar generationenergy storage projects. The Company’s over 8,000approximately 8,500 net MW of assets also includes approximately 2,500 net MW of environmentally-sound, highly efficient natural gas-fired generation facilities. Through this environmentally-sound, diversified and primarily contracted portfolio, the Company endeavors to increase distributions to its unit holders. The majority of the Company’s revenues are derived from long-term contractual arrangements for the output or capacity from these assets. The weighted average remaining contract duration of these offtake agreements was approximately 1110 years as of December 31, 20222023 based on CAFD.

On May 1, 2022, the Company completed the sale of 100% of its interests in the Thermal Business to KKR. For further details of the Thermal Disposition, refer to Item 15 — Note 3, Acquisitions and Dispositions.

A complete listing of the Company’s interests in facilities, operations and/or projects owned or leased as of December 31, 20222023 can be found in Item 2 — Properties.

History

The Company was formed as a Delaware limited liability company by NRG on March 5, 2013. On August 31, 2018, NRG transferred its full ownership interest in Clearway Energy, Inc, or Clearway, Inc., and its subsidiaries to CEG, the holder of NRG’s renewable energy development and operations platform, and subsequently sold 100% of its interest in CEG to GIP. On September 12, 2022, GIP sold 50% of its interest in CEG through an intermediate holding company to TotalEnergies.

The Company is a holding company for the companies that directly and indirectly own and operate Clearway Energy, Inc.’s, or Clearway, Inc., business. As of December 31, 2022, CEG which is equally owned by GIP and TotalEnergies, controls Clearway, Inc., and Clearway, Inc. in turn, as the sole managing member of the Company, controls the Company and its subsidiaries. Clearway, Inc. consolidates the results of the Company through its controlling interest, with CEG’s interest shown as contributed capital in the Company’s consolidated financial statements. The holders of Clearway, Inc.’s outstanding shares of Class A and Class C common stock are entitled to dividends as declared. CEG receives its distributions from the Company through its ownership of the Company’s Class B and Class D units. From time to time, CEG may also hold shares of Clearway Inc’s Class A and/or Class C common stock.

As of December 31, 2022,2023, CEG owned 42,738,750 of the Company’s Class B units and 42,336,750 of the Company’s Class D units, while Clearway, Inc. owned 34,613,853 of the Company’s Class A units and 82,283,46082,391,441 of the Company’s Class C units. Clearway, Inc., through its holdings of Class A units and Class C units, owned a 57.88%57.90% economic interest in the Company as of December 31, 2022.2023. Additionally, GIP,CEG, through CEG’sits holdings of Class B units and Class D units, owned a 42.12%42.10% economic interest in the Company as of December 31, 2022.2023.

The diagram below represents a summarized structure of the Company as of December 31, 2022:2023:

Business Strategy

The Company’s primary business strategy is to focus on the acquisition and ownership of assets with predictable, long-term cash flows in order that it may be able to increase the distributions to Clearway, Inc. over time without compromising the ongoing stability of the business.

The Company’s plan for executing its business strategy includes the following key components:

Focus on contracted renewable energy and conventional generation. The Company owns and operates utility scale and distributed renewable energy and natural gas-fired generation assets, as well as energy storage assets, with proven technologies, generally low operating risks and stable cash flows. The Company believes by focusing on this core asset class and leveraging its industry knowledge, it will maximize its strategic opportunities, be a leader in operational efficiency and maximize its overall financial performance.

Growing the business through acquisitions of contracted operating assets. The Company believes that its base of operations provides a platform for strategic growth through cash accretive and tax advantaged acquisitions complementary to its existing portfolio. In addition to acquiring generation facilities from third parties where the Company believes its knowledge of the market and operating expertise provides it with a competitive advantage, the Company may consummate future acquisitions from CEG. The Company believes that CEG’s project development expertise provides the Company access to a development platform with an extensive pipeline of potential renewable energy and energy storage projects that are aligned to support the Company’s growth. The Company and CEG work collaboratively in considering new assets to be acquired by the Company. The assets listed below all of which are included in co-investment partnerships, represent the Company’s currently committed investments in projects with CEG:

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Asset | | Technology | | Gross Capacity (MW) | | State | | Estimated COD | | Status |

Daggett Solar 3Cedar Creek | | Solar/StorageWind | | 300160 | | CAID | | 1H23 | | Committed1H24 |

Daggett Solar 2Cedro Hill Repowering | | Solar/StorageWind | | 182160 | | CATX | | 2H23 | | Committed2H24 |

| | | | | | | | |

AricaTexas Solar Nova 2 (a)

| | Solar | | Solar/Storage | | 263 | | CA | | 2H23 | | Committed |

Victory Pass | | Solar/Storage | | 200 | | CATX | | 2H23 | | Committed1H24 |

(a) Included in a co-investment partnership.

Primary focus on North America. The Company intends to focus its investments in North America. The Company believes that industry fundamentals in North America present it with significant opportunity to grow its portfolio without creating significant exposure to currency and sovereign risk. By focusing its efforts on North America, the Company believes it will best leverage its regional knowledge of power markets, industry relationships and skill sets to maximize the performance of the Company.

Maintain sound financial practices to grow the distributions. The Company intends to maintain a commitment to disciplined financial analysis and a balanced capital structure to enable it to increase its distributions over time and serve the long-term interests of its unit holders. The Company’s financial practices include a risk and credit policy focused on transacting with creditworthy counterparties; a financing policy, which focuses on seeking an optimal capital structure through various capital formation alternatives to minimize interest rate and refinancing risks, ensure stable distributions and maximize value. The Company intends to evaluate various alternatives for financing future acquisitions and refinancing of existing project-level debt, in each case, to reduce the cost of debt, extend maturities and maximize CAFD.

Competition

Power generation is a capital-intensive business with numerous and diverse industry participants. The Company competes on the basis of the location of its plants and on the basis of contract price and terms of individual projects. Within the power industry, there is a wide variation in terms of the capabilities, resources, nature and identity of the companies with whom the Company competes depending on the market. Competitors for energy supply are utilities, independent power producers and other providers of distributed generation. The Company also competes to acquire new projects with renewable developers who retain renewable power plant ownership, independent power producers, financial investors and other growth-oriented companies. Competitive conditions may be substantially affected by capital market conditions and by various forms of energy legislation and regulation considered by federal, state and local legislatures and administrative agencies, including tax policy. Such laws and regulations may substantially increase the costs of acquiring, constructing and operating projects, and it could be difficult for the Company to adapt to and operate under such laws and regulations.

Competitive Strengths

Stable, high quality cash flows. The Company’s facilities have a stable, predictable cash flow profile consisting of predominantly long-life electric generation assets that primarily sell electricity under long-term fixed priced contracts or pursuant to regulated rates with investment-grade and certain other creditworthy counterparties. The majority of the Company’s facilities have minimal fuel risk. Forrisk, as the Renewables facilities have no fuel costs, however, the Company’s merchant conventional assets currently contracted under tolling agreements, fuel is provided by the toll counterparty or the cost thereof is a pass-through cost under the Contract for Differences. When the tolling agreements expire, the conventional assets will need to procure their own fuel. The Renewable facilities have no fuel costs. The offtake agreements for the Company’s conventional and renewable generation facilities have a weighted-average remaining duration, based on CAFD, of approximately 1110 years as of December 31, 2022,2023, providing long-term cash flow stability. The Company’s generation offtake agreements with counterparties for whom credit ratings are available have a weighted-average Moody’s rating of Ba1 based on rated capacity under contract. All of the Company’s assets are in the U.S. and accordingly have no currency or repatriation risks.

Environmentally well-positioned portfolio of assets. The Company’s portfolio of electric generation assets consists of over 5,500approximately 6,000 net MW of renewable generation capacityinstalled wind, solar and energy storage projects that are predominantly non-emitting sources of power generation. Additionally, the Company’s California conventional assets consist of efficient gas generation facilities that support electric system reliability. The Company does not anticipate having to expend any significant capital expenditures in the foreseeable future to comply with current environmental regulations applicable to its generation assets. Taken as a whole, the Company believes its strategy will be a net beneficiary of current and potential environmental legislation and regulatory requirements that may serve as a catalyst for capacity retirements and improve market opportunities for environmentally well-positioned assets like the Company’s assets once its current offtake agreements expire.

High quality, long-lived assets with low operating and capital requirements. The Company benefits from a portfolio of relatively youngernewer assets. The Company’s assets are largely comprised of proven and reliable technologies, provided by leading original wind, solar and windenergy storage equipment manufacturers, such asincluding First Solar, General Electric, Siemens Energy AG, SunPower, Corporation, or SunPower, First Solar Inc., or First Solar, Vestas Mitsubishi, Trina Solar, JA Solar and Siemens Gamesa.Wärtsilä. Given the modern nature of the portfolio, which includes a substantial number of relatively low operating and maintenance cost wind, solar and wind generation assets,energy storage projects, the Company expects to achieve high fleet availability and expend modest maintenance-related capital expenditures.

Significant scale and diversity. The Company is one of the largest renewable energy owners in the U.S. with over 5,500approximately 6,000 net MW of installed wind, solar and solar generationenergy storage projects. The Company’s over 8,000approximately 8,500 net MW of assets also includes approximately 2,500 net MW of environmentally-sound, highly efficient natural gas-fired generation facilities. The Company’s contracted renewable and conventional generation assets benefit from significant diversification in terms of technology, fuel type, counterparty and geography. The Company believes its scale and access to best practices across the fleet improves its business development opportunities through enhanced industry relationships, reputation and understanding of regional power market dynamics. Furthermore, the Company’s diversification reduces its operating risk profile and reliance on any single market.

Relationship with GIP, TotalEnergies and CEG. The Company believes that its relationship with GIP, TotalEnergies and CEG provides significant benefits. Global Infrastructure Management, LLC, or GIM, the manager of GIP, is an independent infrastructure fund manager that makes equity and debt investments in infrastructure assets and businesses in both the Organization for Economic Co-operation and Development (OECD) and select emerging market countries. GIM has a strong track record of investment and value creation in the renewable energy sector. GIM also has extensive experience with publicly traded yield vehicles and development platforms, ranging from Europe’s first application of a yield company/development company model to the largest renewable platform in Asia-Pacific. TotalEnergies is a global multi-energy company that produces and markets energies in more than 130 countries. Additionally, the Company believes that CEG provides the Company access to a highly capable renewable development and operations platform that is aligned to support the Company’s growth.

Segment Review

The following tables summarize the Company’s operating revenues, net income (loss) and assets by segment, for the years ended December 31, 2022, 2021 and 2020, as discussed in Item 15 — Note 13,12, Segment Reporting.

| | | | | | | | | | | | | | | | | | | | | | | | |

| Year ended December 31, 2023 | |

| (In millions) | Conventional Generation | | Renewables | | Corporate | | Total | |

| Operating revenues | $ | 420 | | | $ | 894 | | | $ | — | | | $ | 1,314 | | |

| | | | | | | | |

| Net income (loss) | 109 | | | (12) | | | (110) | | | (13) | | |

| Total assets | 2,058 | | | 12,205 | | | 425 | | | 14,688 | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Year ended December 31, 2022 |

| (In millions) | Conventional Generation | | Renewables | | Thermal | | Corporate | | Total |

| Operating revenues | $ | 417 | | | $ | 696 | | | $ | 77 | | | $ | — | | | $ | 1,190 | |

| | | | | | | | | |

Net income (loss) (a) | 161 | | | (58) | | | 17 | | | 1,162 | | | 1,282 | |

| Total assets | 2,251 | | | 9,515 | | | — | | | 546 | | | 12,312 | |

(a) Corporate net income includes the $1.29 millionbillion gain on the sale of the Thermal Business to KKR, which was completed on May 1, 2022.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Year ended December 31, 2021 |

| (In millions) | Conventional Generation | | Renewables | | Thermal | | Corporate | | Total |

| Operating revenues | $ | 441 | | | $ | 641 | | | $ | 204 | | | $ | — | | | $ | 1,286 | |

| | | | | | | | | |

| Net income (loss) | 172 | | | (65) | | | 22 | | | (192) | | | (63) | |

| Total assets | 2,442 | | | 9,603 | | | 631 | | | 42 | | | 12,718 | |

| | Year ended December 31, 2020 |

| Year ended December 31, 2021 | | | Year ended December 31, 2021 |

| (In millions) | (In millions) | Conventional Generation | | Renewables | | Thermal | | Corporate | | Total | (In millions) | Conventional Generation | | Renewables | | Thermal | | Corporate | | Total |

| Operating revenues | Operating revenues | $ | 437 | | | $ | 569 | | | $ | 193 | | | $ | — | | | $ | 1,199 | |

| | Net income (loss) | Net income (loss) | 140 | | | (108) | | | 3 | | | (87) | | | (52) | |

| Net income (loss) | |

| Net income (loss) | |

Policy Incentives

U.S. federal, state and local governments have established various policy incentives to support the development, financing, ownership and operation of renewable energy projects. These incentives include PTCs, ITCs, accelerated tax depreciation, cash grants, tax abatements and RPS programs which have the effect of decreasing the costs and risks associated with developing and operating such projects or creating demand for renewable energy assets. In particular,

•Owners of wind facilities are eligible to claim the PTC, or an ITC in lieu of the PTC, provided that certain requirements are met. Similarly, owners of solar facilities are eligible to claim the ITC or, for facilities placed in service after August 16, 2022, the PTC, or an ITC in lieu of the PTC, provided certain requirements are met. Additionally, owners of energy storage facilities are eligible to claim the ITC for facilities placed in service after December 31, 2022, provided certain requirements are met. The PTC is an annual credit that is based on the amount of electricity sold by the facility during the first ten years after the facility is first placed in service. The ITC is a one-time credit that is based on a percentage of the cost of the facility and is claimed for the tax year in which the facility is first placed in service. Depending on the type of taxpayer, the PTC or ITC may be sold to an unrelated third party for cash, or in certain cases, direct payment from the government may be received. In order to qualify for the full amount of these credits in the case of facilities whose construction beginsbegan on or after January 29,30, 2023, certain prevailing wage and apprenticeship requirements generally must be satisfied, the details of which have been released only in part with additional details expected in future guidance.satisfied. For facilities that begin construction after December 31, 2024, the PTC and ITC will no longer apply and such facilities may instead be eligible for the clean electricity production credit or clean electricity investment credit, respectively. In order to qualify for these new credits, the facility’s greenhouse gas emissions cannot be greater than zero.

•Pursuant to the U.S. federal Modified Accelerated Cost Recovery System, or MACRS, wind and solar projects are generally depreciable for tax purposes over a five-year period (before taking into account certain conventions) even though the useful life of such projects is generally much longer than five years. The Tax ActFederal income tax law also provides for immediate and 100% expensing and deductibility for eligible property acquired and placed in service after September 27, 2017, and before January 1, 2023, with phase downs permitting 80%, 60%, 40% and 20% expensing and deductibility for property acquired and placed in service during 2023, 2024, 2025 and 2026, respectively.

•RPS programs, currently in place in certain states and territories, require electricity providers in the state or territory to meet a certain percentage of their retail sales with energy from renewable sources. Additionally, other states in the U.S. have set renewable energy goals to reduce GHG emissions from historic levels. The Company believes that these standards and goals will create incremental demand for renewable energy in the future.

The elimination of, loss of, or reduction in, the incentives discussed above could decrease the attractiveness of renewable energy projects to developers, including, but not limited to, CEG, which could reduce the Company'sCompany’s acquisition or development opportunities. Such an elimination, loss or reduction could also reduce the Company’s willingness to pursue or develop certain renewable energy projects due to higher operating costs or decreased revenues under its PPAs.

Regulatory Matters

As owners of power plants and participants in wholesale energy markets, certain of the Company’s subsidiaries are subject to regulation by various federal and state government agencies. These agencies include FERC and the PUCT, as well as other public utility commissions in certain states where the Company’s assets are located. Each of the Company’s U.S. generating facilities qualifies as an EWG or QF. In addition, the Company is subject to the market rules, procedures and protocols of the various ISO and RTO markets in which it participates. Likewise, certain of the Company’s subsidiaries must also comply with the mandatory reliability requirements imposed by NERC and the regional reliability entities in the regions where the Company has generating facilities subject to NERC’s reliability authority.The Company’s operations within the ERCOT footprint are not subject to rate regulation by FERC, as they are deemed to operate solely within the ERCOT market and not in interstate commerce. These operations are subject to regulation by PUCT. Similarly, the Company’s operations within Hawaii are not subject to rate regulation by FERC, as they are deemed to operate solely within the State of Hawaii and not in interstate commerce.

FERC

FERC, among other things, regulates the transmission and the wholesale sale of electricity in interstate commerce under the authority of the FPA. The transmission and sale of electric energy occurring wholly within ERCOT and Hawaii is not subject to FERC’s jurisdiction. Under existing regulations, FERC has the authority to determine whether an entity owning a generation facility is an EWG, as defined in the PUHCA. FERC also has the authority to determine whether a generation facility meets the applicable criteria of a QF under the PURPA. Each of the Company’s U.S. generating facilities qualifies as either an EWG or QF.

The FPA gives FERC exclusive rate-making jurisdiction over the wholesale sale of electricity and transmission of electricity in interstate commerce of public utilities (as defined by the FPA). Under the FPA, FERC, with certain exceptions, regulates owners and operators of facilities used for the wholesale sale of electricity or transmission in interstate commerce as public utilities, and is charged with ensuring that market rules are just and reasonable.

Public utilities are required to obtain FERC’s acceptance, pursuant to Section 205 of the FPA, of their rate schedules for the wholesale sale of electricity. Several of the Company’s QF generating facilities and all of the Company’s non-QF generating facilities located in the U.S. outside of ERCOT and Hawaii make sales of electricity pursuant to market-based rates, as opposed to traditional cost-of-service regulated rates. FERC conducts a review of the market-based rates of Company public utilities and potential market power every three years according to a regional schedule established by FERC.

In accordance with the Energy Policy Act of 2005, FERC has approved the NERC as the national Energy Reliability Organization, or ERO. As the ERO, NERC is responsible for the development and enforcement of mandatory reliability standards for the wholesale electric power system, with such authority delegated in part to regional reliability entities charged with enforcement of mandatory reliability standards for the region which they are responsible for overseeing.

The PURPA was passed in 1978 in large part to promote increased energy efficiency and development of independent power producers. The PURPA created QFs to further both goals, and FERC is primarily charged with administering the PURPA as it applies to QFs. QFs are exempt from certain regulations under the FPA.

The PUHCA provides FERC with certain authority over and access to books and records of public utility holding companies not otherwise exempt by virtue of their ownership of EWGs and QFs. The Company is exempt from many of the accounting, record retention, and reporting requirements of the PUHCA.

Environmental Matters

The Company is subject to a wide range of environmental laws during the development, construction, ownership and operation of facilities. These existing and future laws generally require that governmental permits and approvals be obtained before construction and maintained during operation of facilities. The Company is obligated to comply with all environmental laws and regulations applicable within each jurisdiction and required to implement environmental programs and procedures to monitor and control risks associated with the construction, operation and decommissioning of regulated or permitted energy assets. Federal and state environmental laws have historically become more stringent over time, although this trend could change in the future.

A number of regulations that may affect the Company are under review for potential revision or rescission in 2023.2024. The Company will evaluate the impact of the legislation and regulations as they are revised but cannot fully predict the impact of each until anticipated revisions and legal challenges are resolved. To the extent that proposed legislation and new or revised regulations restrict or otherwise impact the Company’s operations, the proposed legislation and regulations could have a negative impact on the Company’s financial performance.

Proposed Federal MBTA Incidental Take Legislation and Regulations— On October 4, 2021, U.S. Fish and Wildlife Service, (FWS)or FWS, issued the final MBTA rule, effective December 3, 2021, restoring the MBTA to prohibit the incidental take of migratory birds. In 2021, FWS issued an advance notice of proposed rulemaking (ANPR) advising that it intends to gather information necessary to develop proposed regulations to authorize the incidental take of migratory birds under prescribed conditions and prepare a draft environmental review pursuant to the National Environmental Policy Act.Act, or NEPA. Throughout 2022, FWS sought comments on the content of the proposed rule. The Company worked with renewable industry groupsIn November 2023, FWS withdrew the draft MBTA permit program rule from the Office of Information and Regulatory Affairs to provideaddress technical comments on the proposed rule development.received from agencies. FWS is currently considering how to drafthas indicated that the rule and expectsis likely to issuebe published in the noticesecond half of proposed rulemaking early in 2023.2024.

Proposed Federal Eagle Incidental Take Permit Proposed Rule — On September 30, 2022, FWS published in the Federal Register a draft rule revising the eagle incidental take permit program. Comments on the revised rule were due by the end of November 2022, but a 30-day extension was issued withcontinued to be accepted during 2023. The final comments due by December 30, 2022. The Company worked with renewable industry groups to provide comments on the proposed rule in advance of the cut-off date. FWS is currently reviewing comments and it is not clear how the comments will be incorporated into the final rule or how FWS will structure the revisions to the eagle incidental take permit program.rule was published in the Federal Register on February 12, 2024 and will become effective on April 13, 2024. The final rule is anticipated to provide an expedited eagle take permitting and lower cost path for many wind facilities.

Local California Air District Rules — Air districts, including the Bay Area Air Quality Management District and the San Diego Air Pollution Control District, have recently proposed and/or updated new source review permitting requirements, including to incorporate public notice requirements as well as updates to its respective rules to amend, as applicable, Best Available Control Technology criteria for stationary emissions sources including gas turbines, Toxic Air Contaminant Health Risk reporting and general reporting requirements.programs addressing toxic air contaminants. Rulemaking in the Los Angeles Air Basin, as regulated by South Coast Air Quality Management District, or SCAQMD, continues to update command-and-control regulations that limit NOx emissions for stationary sources in preparation for sunsetting SCAQMD’s Regional Clean Air Market, or RECLAIM, NOx cap and trade program in the next few years. The Company’s conventional generation plants meet the district’s existing and proposed amendments to command-and-control regulations. Proposed updates to local California Air District Rules are not expected to affect the operations nor compliance of the Company’s conventional generation plants.

Amendments to NEPA — On June 3, 2023, President Biden signed the Fiscal Responsibility Act of 2023, or FRA, into law, which includes amendments to the NEPA, aimed at streamlining the environmental review process. Following the FRA, on July 31, 2023, the White House Council on Environmental Quality, or CEQ, published a proposed rule, the Bipartisan Permitting Reform Implementation Rule, which seeks to revise, update and modernize the existing regulations under the NEPA and includes provisions regarding robust public involvement, environmental justice, and climate change, or the Phase 2 Proposed Rule. The public comment period on the Phase 2 Proposed Rule closed on September 29, 2023 and the final rule has not yet been published.

Customers

The Company sells its electricity and environmental attributes, including RECs, primarily to local utilities under contractual arrangements. During the year ended December 31, 2022,2023, the Company derived approximately 33%24% of its consolidated revenue from Southern California Edison, or SCE, and approximately 25%17% of its consolidated revenue from PG&E.

Human Capital

As of December 31, 2022,2023, the Company had 5861 employees. The Company also depends upon personnel of CEG for the provision of asset management, administration and O&M services.

The Company focuses on attracting, developing and retaining a team of highly talented and motivated employees. The Company regularly conducts assessments of its compensation and benefit practices and pay levels to help ensure that staff members are compensated equitably and competitively. The Company devotes extensive resources to staff development and training, including tuition assistance for career-enhancing academic and professional programs. Employee performance is measured in part based on goals that are aligned with the Company’s annual objectives. The Company recognizes that its success is based on the talents and dedication of those it employs, and the Company is highly invested in their success.

The Company is committed to maintaining a workplace that acknowledges, encourages, and values diversity and inclusion and provides its employees with unconscious bias training. The Company believes that individual differences, experiences, and strengths enrich the culture and fabric of its organization. Having employees with backgrounds and orientations that reflect a variety of viewpoints and experiences also helps the Company to better understand the needs of its customers and the communities in which it operates.

By leveraging the multitude of backgrounds and perspectives of its team and developing ongoing relationships with diverse vendors, the Company achieves a collective strength that enhances the workplace and makes the Company a better business partner to its customers and others with a stake in the Company’s success.

The Company also has an Equity, Partnership & Inclusion Council, or EPIC. As part of its commitment, the Company provides education on topics related to diversity, inclusion and equity. The Company identified three areas of focus: Our People,People; Our Product &Brand, Customers and Community; and Our Purchasing. With the involvement of its employees, EPIC is advancing efforts in each of these areas to identify and implement opportunities for the Company to address equity, partnership and inclusion issues in its business activities.

Our People focuses on education and training; diversity, equity and inclusion policies and recruitment strategies; community and industry partnerships; and maintaining high employee engagement and retention.

Our ProductBrand, Customers & CustomersCommunity focuses on pursuing opportunities that provide more equitable access to renewable energyenergy; broadening participation for low-to-moderate income customers;small to medium enterprises; supporting the diversity, equity and inclusion goals of the Company’s offtakers; building robust community engagement relationships; and meaningfully representing that work in the external market.

Our Purchasing focuses on establishing a non-discriminatory practices standard for the Company’s suppliers, diverse vendor sourcing and benchmarking.

In addition to the personnel of CEG, the Company relies on other third-party service providers in the daily operations of its conventional facilities and certain renewable facilities.

Environmental, Social and Governance (ESG)

The Company is committed to engaging with its stakeholders on environmental, social and governance, or ESG, matters in a proactive, holistic and integrated manner. The Company strives to provide recent, credible and comparable data to ESG agencies while engaging institutional investors and investor advocacy organizations around ESG issues. The Company’s Corporate Governance, Conflictsissues and Nominating Committeeto comply with ESG disclosure requirements. Clearway, Inc.’s Board of Directors reviews developing trends and emerging ESG matters as well as the Company’s strategies, activities, policies and communications regarding ESG matters, and makes recommendations to the Company’s Board of Directors regardingreviews and considers potential actions by the Company.Company could take regarding ESG matters.

Aligned with the Company’s strategy of owning and acquiring environmentally-sound power generation and energy storage assets, the Company has issued $2.1 billion of corporate green bonds under a green bond framework that applies the net proceeds to finance or refinance, in part or in full, new and existing projects and assets meeting certain criteria focused on the supply of energy from renewable resources, including solar energy and wind energy. The Company’s projects and alignment of its Green Bond Principles (2018) are reviewed by Sustainalytics, an outside consultant with recognized expertise in ESG research and analysis.

As discussed in greater detail above, the Company, through EPIC, has focused its diversity, equity and inclusion efforts in three areas: Our People,People; Our Product &Brand, Customers and Community; and Our Purchasing – through its launch of EPIC.Purchasing. With the involvement of the Company’s employees, EPIC is advancing efforts in each of these areas to identify and implement opportunities for the Company to address equity, partnership and inclusion issues in its business activities.

Available Information

The Company’s annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, and amendments to those reports filed or furnished pursuant to section 13(a) or 15(d) of the Exchange Act are available free of charge through the SEC’s website, www.sec.gov, and through the “Investor Relations” section of Clearway, Inc.’s website, www.clearwayenergy.com, as soon as reasonably practicable after they are electronically filed with, or furnished to, the SEC. The Company also routinely posts press releases, presentations, webcasts, and other information regarding the Company on Clearway, Inc.’s website. The information posted on Clearway, Inc.’s website is not a part of this report.

Item 1A — Risk Factors

Summary of Risk Factors

The Company’s business is subject to numerous risks and uncertainties, discussed in more detail in the following section. These risks include, among others, the following key risks:

Risks Related to the Company’s Business

•The Company’s ability to grow and make acquisitions through cash on hand is limited.

•The Company may not be able to effectively identify or consummate any future acquisitions on favorable terms, or at all, and future acquisitions may not be accretive as a result of incorrect assumptions in the Company’s evaluation of such acquisitions, unforeseen consequences or other external events beyond the Company’s control.

•Counterparties to the Company’s offtake agreements may not fulfill their obligations and, as the contracts expire, the Company may not be able to replace them with agreements on similar terms in light of increasing competition in the markets in which the Company operates.

•The Company’s ability to effectively consummate future acquisitions will also depend on the Company’s ability to arrange the required or desired financing for acquisitions.

•The Company’s indebtedness could adversely affect its ability to raise additional capital to fund the Company’s operations or pay distributions.

•The operation of electric generation facilities depends on suitable meteorological conditions and involves significant risks and hazards customary to the power industry that could have a material adverse effect on the Company’s business, financial condition, results of operations and cash flows. These facilities may operate without long-term power sales agreements.

•Maintenance, expansion and refurbishment of electric generation facilities involve significant risks that could result in unplanned power outages or reduced output.

•Supplier and/or customer concentration at certain of the Company’s facilities may expose the Company to significant financial credit or performance risks.

•The Company currently owns, and in the future may acquire, certain assets in which the Company has limited control over management decisions and its interests in such assets may be subject to transfer or other related restrictions.

•The Company’s assets areCompany is exposed to risks inherent in the use of interest rate swaps and theenergy-related financial instruments. The Company may be exposed to additional risks in the future if it utilizes other derivative instruments.

•The Company does not own all of the land on which its power generation and energy storage assets are located, which could result in disruption to its operations. The Company’s use and enjoyment of real property rights for its projects may be adversely affected by the rights of lienholders and leaseholders that are superior to those of the grantors of those real property rights to the Company.

•The Company’s businesses are subject to physical, market and economic risks relating to potential effects of climate change and public and governmental initiatives to address climate change.

•Risks that are beyond the Company’s control, including but not limited to acts of terrorism or related acts of war, natural disaster,disasters, severe weather, changes in weather patterns, flooding, pandemics (such as the COVID-19 pandemic), inflation, supply chain disruptions, hostile cyber intrusions or other catastrophic events, could have a material adverse effect on the business, financial condition, results of operations and cash flows.

•The operation of the Company’s businesses is subject to cyber-based security and integrity risk.

•The Company relies on electric distribution and transmission facilities that it does not own or control and that are subject to transmission constraints within a number of the Company’s regions.If these facilities fail to provide the Company with adequate transmission capacity, it may be restricted in its ability to deliver electric power to its customers and may either incur additional costs or forego revenues.

•The Company’s costs, results of operations, financial condition and cash flows could be adversely impacted by the disruption of the fuel supplies necessary to generate power at its conventional generation facilities.

•The Company depends on key personnel and its ability to attract and retain additional skilled management and other personnel, the loss of any of which could have a material adverse effect on the Company’s financial condition and results of operations.

•The Company may potentially be adversely affected by emerging technologies that may over time impact capacity markets and the energy industry overall.

Risks Related to the Company’s Relationship with GIP, TotalEnergies and CEG

•GIP and TotalEnergies, through their equal ownership of CEG, the Company’s controlling shareholder of Clearway, Inc., exercise substantial influence over the Company. The Company is highly dependent on GIP, TotalEnergies and CEG.

•CEG controls the Company and has the ability to designate a majority of the members of Clearway, Inc.’s Board.

•The Company may not be able to consummate future acquisitions from CEG.

•The Company may be unable to terminate the CEG Master Services Agreement, in certain circumstances.

•If CEG terminates the CEG Master Services Agreement or defaults in the performance of its obligations under the agreement, the Company may be unable to contract with a substitute service provider on similar terms, or at all.

Risks Related to Regulation

•The Company’s business is subject to restrictions resulting from environmental, health and safety laws and regulations.

•The electric generation business is subject to substantial governmental regulation, including environmental laws, and may be adversely affected by changes in laws or regulations, as well as liability under, or any future inability to comply with, existing or future regulations or other legal requirements.

•The Company’s business is subject to complex and evolving U.S. laws and regulations regarding privacy and data protection.

•Government regulations providing incentives for renewable power generation could change at any time and such changes may negatively impact the Company’s growth strategy.

Risks Related to the Company’s Business

Pursuant to the Company’s cash distribution policy, the Company intends to distribute a significant amount of the CAFD through regular quarterly distributions, and the Company’s ability to grow and make acquisitions through cash on hand is limited.

The Company expects to distribute a significant amount of the CAFD each quarter and to rely primarily upon external financing sources, including the issuance of debt and equity securities and, if applicable, borrowings under the Company’s revolving credit facility to fund acquisitions and growth capital expenditures. The Company may be precluded from pursuing otherwise attractive acquisitions if the projected short-term cash flow from the acquisition or investment is not adequate to service the capital raised to fund the acquisition or investment, after giving effect to the Company’s available cash reserves. The incurrence of bank borrowings or other debt by Clearway Energy Operating LLC or by the Company’s project-level subsidiaries to finance the Company’s growth strategy will result in increased interest expense and the imposition of additional or more restrictive covenants, which, in turn, may impact the cash distributions the Company makes to Clearway, Inc. and CEG.

The Company may not be able to effectively identify or consummate any future acquisitions on favorable terms, or at all, and future acquisitions may not be accretive as a result of incorrect assumptions in the Company’s evaluation of such acquisitions, unforeseen consequences or other external events beyond the Company’s control.

The Company’s business strategy includes growth through the acquisitions of additional generation assets (including through corporate acquisitions). This strategy depends on the Company’s ability to successfully identify and evaluate acquisition opportunities and consummate acquisitions on favorable terms. However, the number of acquisition opportunities is limited. In addition, the Company will compete with other companies for these limited acquisition opportunities, which may increase the Company’s cost of making acquisitions or cause the Company to refrain from making acquisitions at all. Some of the Company’s competitors for acquisitions are much larger than the Company with substantially greater resources. These companies may be able to pay more for acquisitions and may be able to identify, evaluate, bid for and purchase a greater number of assets than the Company’s financial or human resources permit. If the Company is unable to identify and consummate future acquisitions, it will impede the Company’s ability to execute its growth strategy and limit the Company’s ability to increase the amount of distributions paid to holders of Clearway, Inc.’s common stock.

The Company’s ability to acquire future renewable facilities may depend on the viability of renewable assets generally. These assets currently are largely contingent on public policy mechanisms including ITCs, cash grants, loan guarantees, accelerated depreciation, RPS and carbon trading plans. These mechanisms have been implemented at the state and federal levels to support the development of renewable generation, demand-side and smart grid and other clean infrastructure technologies. The availability and continuation of public policy support mechanisms will drive a significant part of the economics and viability of the Company’s growth strategy and expansion into clean energy investments.

The acquisition of companies and assets are subject to substantial risks, including the failure to identify material problems during due diligence (for which the Company may not be indemnified post-closing) and the risk of overpaying for assets (or not making acquisitions on an accretive basis). The integration and consolidation of acquisitions requires substantial human, financial and other resources and, ultimately, the Company’s acquisitions may divert management’s attention from the Company’s existing business concerns, disrupt the Company’s ongoing business or not be successfully integrated. There can be no assurances that any future acquisitions will perform as expected or that the returns from such acquisitions will support the financing utilized to acquire them or maintain them. A failure to achieve the financial returns the Company expects when it acquires generation assets could have a material adverse effect on the Company’s ability to grow its business and make cash distributions to its unit holders. Any failure of the Company’s acquired generation assets to be accretive or difficulty in integrating such acquisition into the Company’s business could have a material adverse effect on the Company’s ability to grow its business and make cash distributions to its unit holders. As a result, the consummation of acquisitions could have a material adverse effect on the Company’s business, financial condition, results of operations, cash flows and ability to pay distributions to its unit holders.

Counterparties to the Company’s offtake agreements may not fulfill their obligations and, as the contracts expire, the Company may not be able to replace them with agreements on similar terms in light of increasing competition in the markets in which the Company operates.

A significant portion of the electric power the Company generates is sold under long-term offtake agreements with public utilities or industrial or commercial end-users, with a weighted average remaining duration, based on CAFD, of approximately 11 years. As of December 31, 2022, the largest customers of the Company’s power generation assets, including assets in which the Company has less than a 100% membership interest, were SCE and PG&E, which represented 33% and 25%, respectively, of total consolidated revenues generated by the Company during the year ended December 31, 2022.

If, for any reason, any of the purchasers of power under these agreements are unable or unwilling to fulfill their related contractual obligations or if they refuse to accept delivery of power delivered thereunder or if they otherwise terminate such agreements prior to the expiration thereof, the Company’s assets, liabilities, business, financial condition, results of operations and cash flows could be materially and adversely affected. Furthermore, to the extent any of the Company’s power purchasers are, or are controlled by, governmental entities, the Company’s facilities may be subject to legislative or other political action that may impair their contractual performance.

The power generation industry is characterized by intense competition and the Company’s electric generation assets encounter competition from utilities, industrial companies and independent power producers, in particular with respect to uncontracted output. In recent years, there has been increasing competition among generators for offtake agreements and this has contributed to a reduction in electricity prices in certain markets characterized by excess supply above designated reserve margins. In light of these market conditions, the Company may not be able to replace an expiring or terminated agreement with an agreement on equivalent terms and conditions, including at prices that permit operation of the related facility on a profitable basis. In addition, the Company believes many of its competitors have well-established relationships with the Company’s current and potential suppliers, lenders and customers, and have extensive knowledge of its target markets. As a result, these competitors may be able to respond more quickly than the Company to evolving industry standards and changing customer requirements. The adoption of more advanced technology could reduce its competitors’ power production costs resulting in their having a lower cost structure than is achievable with the technologies currently employed by the Company and adversely affect its ability to compete for offtake agreement renewals. If the Company is unable to replace an expiring or terminated offtake agreement, the affected facility may temporarily or permanently cease operations. External events, such as a severe economic downturn or force majeure events, could also impair the ability of some counterparties to the Company’s offtake agreements and other customer agreements to pay for energy and/or other products and services received.

The Company’s inability to enter into new or replacement offtake agreements or to compete successfully against current and future competitors in the markets in which the Company operates could have a material adverse effect on the Company’s business, financial condition, results of operations and cash flows.

The Company’s ability to effectively consummate future acquisitions will also depend on the Company’s ability to arrange the required or desired financing for acquisitions.

The Company may not have sufficient availability under the Company’s credit facilities or have access to project-level financing on commercially reasonable terms when acquisition opportunities arise. An inability to obtain the required or desired financing could significantly limit the Company’s ability to consummate future acquisitions and effectuate the Company’s growth strategy. If financing is available, utilization of the Company’s credit facilities or project-level financing for all or a portion of the purchase price of an acquisition could significantly increase the Company’s interest expense, impose additional or more restrictive covenants and reduce CAFD. The Company’s ability to consummate future acquisitions may also depend on the Company’s ability to obtain any required regulatory approvals for such acquisitions.

The Company’s indebtedness could adversely affect its ability to raise additional capital to fund the Company’s operations or pay distributions. It could also expose the Company to the risk of increased interest rates and limit the Company’s ability to react to changes in the economy or the Company’s industry as well as impact the Company’s results of operations, financial condition and cash flows.

As of December 31, 2022, the Company had approximately $6,872 million of total consolidated indebtedness, $4,745 million of which was incurred by the Company’s non-guarantor subsidiaries. In addition, the Company’s share of its unconsolidated affiliates’ total indebtedness and letters of credit outstanding as of December 31, 2022, totaled approximately $325 million and $37 million, respectively (calculated as the Company’s unconsolidated affiliates’ total indebtedness as of such date multiplied by the Company’s percentage membership interest in such assets).

The Company’s substantial debt could have important negative consequences on the Company’s financial condition, including:

•increasing the Company’s vulnerability to general economic and industry conditions;

•requiring a substantial portion of the Company’s cash flow from operations to be dedicated to the payment of principal and interest on the Company’s indebtedness, therefore reducing the Company’s ability to pay distributions to Clearway, Inc. and CEG or to use the Company’s cash flow to fund its operations, capital expenditures and future business opportunities;

•limiting the Company’s ability to enter into long-term power sales or fuel purchases which require credit support;

•limiting the Company’s ability to fund operations or future acquisitions;

•restricting the Company’s ability to make certain distributions to Clearway, Inc. and CEG and the ability of the Company’s subsidiaries to make certain distributions to it, in light of restricted payment and other financial covenants in the Company’s credit facilities and other financing agreements;

•exposing the Company to the risk of increased interest rates because certain of the Company’s borrowings, which may include borrowings under the Company’s revolving credit facility, are at variable rates of interest;

•limiting the Company’s ability to obtain additional financing for working capital including collateral postings, capital expenditures, debt service requirements, acquisitions and general corporate or other purposes; and

•limiting the Company’s ability to adjust to changing market conditions and placing it at a competitive disadvantage compared to the Company’s competitors who have less debt.

The Company’s revolving credit facility contains financial and other restrictive covenants that limit the Company’s ability to return capital to unit holders or otherwise engage in activities that may be in the Company’s long-term best interests. The Company’s inability to satisfy certain financial covenants could prevent the Company from paying cash distributions, and the Company’s failure to comply with those and other covenants could result in an event of default which, if not cured or waived, may entitle the related lenders to demand repayment or enforce their security interests, which could have a material adverse effect on the Company’s business, financial condition, results of operations and cash flows. In addition, failure to comply with such covenants may entitle the related lenders to demand repayment and accelerate all such indebtedness.

The agreements governing the Company’s project-level financing contain financial and other restrictive covenants that limit the Company’s project subsidiaries’ ability to make distributions to the Company or otherwise engage in activities that may be in the Company’s long-term best interests. The project-level financing agreements generally prohibit distributions from the project entities to the Company unless certain specific conditions are met, including the satisfaction of certain financial ratios. The Company’s inability to satisfy certain financial covenants may prevent cash distributions by the particular project(s) to it and, the Company’s failure to comply with those and other covenants could result in an event of default which, if not cured or waived may entitle the related lenders to demand repayment or enforce their security interests, which could have a material adverse effect on the Company’s business, results of operations and financial condition. In addition, failure to comply with such covenants may entitle the related lenders to demand repayment and accelerate all such indebtedness. If the Company is unable to make distributions from the Company’s project-level subsidiaries, it would likely have a material adverse effect on the Company’s ability to pay distributions to Clearway, Inc. and CEG.

Letter of credit facilities to support project-level contractual obligations generally have a limited term that may require future renewal, at which time the Company or relevant project-level subsidiary will need to satisfy applicable financial ratios and covenants. If the Company is unable to renew the Company’s letters of credit as expected or replace them with letters of credit under different facilities on favorable terms or at all, the Company may experience a material adverse effect on its business, financial condition, results of operations and cash flows. Furthermore, such inability may constitute a default under certain project-level financing arrangements, restrict the ability of the project-level subsidiary to make distributions to it and/or reduce the amount of cash available at such subsidiary to make distributions to the Company.

In addition, the Company’s ability to arrange financing, either at the corporate level or at a non-recourse project-level subsidiary, and the costs of such capital, are dependent on numerous factors, including:

•general economic and capital market conditions;

•credit availability from banks and other financial institutions;

•investor confidence in the Company, its partners, Clearway, Inc. (as the Company’s sole managing member), or GIP and TotalEnergies, through CEG, as Clearway, Inc.’s principal stockholder (on a combined voting basis) and the regional wholesale power markets;

•the Company’s financial performance and the financial performance of the Company subsidiaries;

•the Company’s level of indebtedness and compliance with covenants in debt agreements;

•maintenance of acceptable project credit ratings or credit quality;

•cash flow; and

•provisions of tax and securities laws that may impact raising capital.

The Company may not be successful in obtaining additional capital for these or other reasons. Furthermore, the Company may be unable to refinance or replace project-level financing arrangements or other credit facilities on favorable terms or at all upon the expiration or termination thereof. The Company’s failure, or the failure of any of the Company’s projects, to obtain additional capital or enter into new or replacement financing arrangements when due may constitute a default under such existing indebtedness and may have a material adverse effect on the Company’s business, financial condition, results of operations and cash flows.

Certain of the Company’s long-term bilateral contracts result from state-mandated procurements and could be declared invalid by a court of competent jurisdiction.

A portion of the Company’s revenues are derived from long-term bilateral contracts with utilities that are regulated by their respective states and have been entered into pursuant to certain state programs. Certain long-term contracts that other companies have with state-regulated utilities have been challenged in federal court and have been declared unconstitutional on the grounds that the rate for energy and capacity established by the contracts impermissibly conflicts with the rate for energy and capacity established by FERC pursuant to the FPA. If certain of the Company’s state-mandated agreements with utilities are ever held to be invalid or unenforceable due to the financial conditions or other conditions of such utility, the Company may be unable to replace such contracts, which could have a material adverse effect on the Company’s business, financial condition, results of operations and cash flows.

The generation of electric energy from solar and wind energy sources depends heavily on suitable meteorological conditions.