We may become subject to claims of infringement or misappropriation of the intellectual property rights of others, which could prohibit us from developing our products, require us to obtain licenses from third parties or to develop non-infringing alternatives and subject us to substantial monetary damages.

Third parties could, in the future, assert infringement or misappropriation claims against us with respect to products we develop. Whether a product infringes a patent or misappropriates other intellectual property involves complex legal and factual issues, the determination of which is often uncertain. Therefore, we cannot be certain that we have not infringed the intellectual property rights of others. There may be third-party patents or patent applications with claims to materials, formulations, methods of manufacture or methods for use related to the use or manufacture of our products, and our potential competitors may assert that some aspect of our product infringes their patents. Because patent applications may take years to issue, there also may be applications now pending of which we are unaware that may later result in issued patents upon which our products could infringe. There also may be existing patents or pending patent applications of which we are unaware upon which our products may inadvertently infringe.

Any infringement or misappropriation claim could cause us to incur significant costs, place significant strain on our financial resources, divert management’s attention from our business and harm our reputation. If the relevant patents in such claim were upheld as valid and enforceable and we were found to infringe them, we could be prohibited from manufacturing or selling any product that is found to infringe unless we could obtain licenses to use the technology covered by the patent or are able to design around the patent. We may be unable to obtain such a license on terms acceptable to us, if at all, and we may not be able to redesign our products to avoid infringement, which could materially impact our revenue. A court could also order us to pay compensatory damages for such infringement, plus prejudgment interest and could, in addition, treble the compensatory damages and award attorney fees. These damages could be substantial and could harm our reputation, business, financial condition and operating results. A court also could enter orders that temporarily, preliminarily or permanently enjoin us and our customers from making, using, or selling products, and could enter an order mandating that we undertake certain remedial activities. Depending on the nature of the relief ordered by the court, we could become liable for additional damages to third parties.

The prosecution and enforcement of patents licensed to us by third parties are not within our control. Without these technologies, our products may not be successful and our business would be harmed if the patents were infringed on or misappropriated without action by such third parties.

We may be subject to damages resulting from claims that we, our employees, or our independent contractors have wrongfully used or disclosed alleged trade secrets of others.

Some of our employees were previously employed at other dietary supplement, nutraceutical, food and beverage, functional food, analytical laboratories, pharmaceutical and cosmetic companies. We may also hire additional employees who are currently employed at other such companies, including our competitors. Additionally, consultants or other independent agents with which we may contract may be or have been in a contractual arrangement with one or more of our competitors. We may be subject to claims that these employees or independent contractors have used or disclosed such other party’s trade secrets or other proprietary information. Litigation may be necessary to defend against these claims. Even if we are successful in defending against these claims, litigation could result in substantial costs and be a distraction to our management. If we fail to defend such claims, in addition to paying monetary damages, we may lose valuable intellectual property rights or personnel. A loss of key personnel or their work product could hamper or prevent our ability to market existing or new products, which could severely harm our business.

Litigation may harm our business.

Substantial, complex or extended litigation could cause us to incur significant costs and distract our management. For example, lawsuits by employees, stockholders, collaborators, distributors, customers, competitors or others could be very costly and substantially disrupt our business. Disputes from time to time with such companies, organizations or individuals are not uncommon, and we cannot assure you that we will always be able to resolve such disputes or on terms favorable to us. As further described in Part I, Item 3 of this Annual Report on Form 10-K, we are currently involved in substantial and complex litigation with Elysium. Unexpected results could cause us to have financial exposure in these matters in excess of recorded reserves and insurance coverage, requiring us to provide additional reserves to address these liabilities, therefore impacting profits.

Our sales and results of operations for our core standards and contract services segment depend on our customers’ research and development efforts and their ability to obtain funding for these efforts.

Our core standards and contract services segment customers include researchers at pharmaceutical and biotechnology companies, chemical and related companies, academic institutions, government laboratories and private foundations. Fluctuations in the research and development budgets of these researchers and their organizations could have a significant effect on the demand for our products. Our customers determine their research and development budgets based on several factors, including the need to develop new products, the availability of governmental and other funding, competition and the general availability of resources. As we continue to expand our international operations, we expect research and development spending levels in markets outside of the United States will become increasingly important to us.

Research and development budgets fluctuate due to changes in available resources, spending priorities, general economic conditions, institutional and governmental budgetary limitations and mergers of pharmaceutical and biotechnology companies. Our business could be harmed by any significant decrease in life science and high technology research and development expenditures by our customers. In particular, a small portion of our sales has been to researchers whose funding is dependent on grants from government agencies such as the United States National Institute of Health, the National Science Foundation, the National Cancer Institute and similar agencies or organizations. Government funding of research and development is subject to the political process, which is often unpredictable. Other departments, such as Homeland Security or Defense, or general efforts to reduce the United States federal budget deficit could be viewed by the government as a higher priority. Any shift away from funding of life science and high technology research and development or delays surrounding the approval of governmental budget proposals may cause our customers to delay or forego purchases of our products and services, which could seriously damage our business.

Some of our customers receive funds from approved grants at a particular time of year, many times set by government budget cycles. In the past, such grants have been frozen for extended periods or have otherwise become unavailable to various institutions without notice. The timing of the receipt of grant funds may affect the timing of purchase decisions by our customers and, as a result, cause fluctuations in our sales and operating results.

Demand for our products and services are subject to the commercial success of our customers’ products, which may vary for reasons outside our control.

Even if we are successful in securing utilization of our products in a customer’s manufacturing process, sales of many of our products and services remain dependent on the timing and volume of the customer’s production, over which we have no control. The demand for our products depends on regulatory approvals and frequently depends on the commercial success of the customer’s supported product. Regulatory processes are complex, lengthy, expensive, and can often take years to complete.

We may bear financial risk if we under-price our contracts or overrun cost estimates.

In cases where our contracts are structured as fixed price or fee-for-service with a cap, we bear the financial risk if we initially under-price our contracts or otherwise overrun our cost estimates. Such underpricing or significant cost overruns could have a material adverse effect on our business, results of operations, financial condition and cash flows.

We rely on single or a limited number of third-party suppliers for the raw materials required to produce our products.

Our dependence on a limited number of third-party suppliers or on a single supplier, and the challenges we may face in obtaining adequate supplies of raw materials, involve several risks, including limited control over pricing, availability, quality and delivery schedules. We cannot be certain that our current suppliers will continue to provide us with the quantities of these raw materials that we require or satisfy our anticipated specifications and quality requirements. Any supply interruption in limited or sole sourced raw materials could materially harm our ability to manufacture our products until a new source of supply, if any, could be identified and qualified. Although we believe there are other suppliers of these raw materials, we may be unable to find a sufficient alternative supply channel in a reasonable time or on commercially reasonable terms. Any performance failure on the part of our suppliers could delay the development and commercialization of our products, or interrupt production of then existing products that are already marketed, which would have a material adverse effect on our business.

We maynot be successful in acquiring complementary businesses or products on favorable terms.

As part of our business strategy, we intend to consider acquisitions of similar or complementary businesses or products. No assurance can be given that we will be successful in identifying attractive acquisition candidates or completing acquisitions on favorable terms. In addition, any future acquisitions will be accompanied by the risks commonly associated with acquisitions. These risks include potential exposure to unknown liabilities of acquired companies or to acquisition costs and expenses, the difficulty and expense of integrating the operations and personnel of the acquired companies, the potential disruption to the business of the combined company and potential diversion of our management's time and attention, the impairment of relationships with and the possible loss of key employees and clients as a result of the changes in management, the incurrence of amortization expenses and write-downs and dilution to the shareholders of the combined company if the acquisition is made for stock of the combined company. In addition, successful completion of an acquisition may depend on consents from third parties, including regulatory authorities and private parties, which consents are beyond our control. There can be no assurance that products, technologies or businesses of acquired companies will be effectively assimilated into the business or product offerings of the combined company or will have a positive effect on the combined company's revenues or earnings. Further, the combined company may incur significant expense to complete acquisitions and to support the acquired products and businesses. Any such acquisitions may be funded with cash, debt or equity, which could have the effect of diluting or otherwise adversely affecting the holdings or the rights of our existing stockholders.

If we experience a significant disruption in our information technology systems or if we fail to implement new systems and software successfully, our business could be adversely affected.

We depend on information systems throughout our company to control our manufacturing processes, process orders, manage inventory, process and bill shipments and collect cash from our customers, respond to customer inquiries, contribute to our overall internal control processes, maintain records of our property, plant and equipment, and record and pay amounts due vendors and other creditors. If we were to experience a prolonged disruption in our information systems that involve interactions with customers and suppliers, it could result in the loss of sales and customers and/or increased costs, which could adversely affect our overall business operation.

Our cash flows and capital resources may be insufficient to make required payments on future indebtedness.

On November 4, 2016, we entered into entered into a business financing agreement (the “Financing Agreement”) with Western Alliance Bank (“Western Alliance”), to establish a formula based revolving credit line pursuant to which the Company may borrow an aggregate principal amount of up to $5,000,000, subject to the terms and conditions of the Financing Agreement. The interest rate will be calculated at a floating rate per month equal to (a) the greater of (i) 3.50% per year or (ii) the Prime Rate published in the Money Rates section of the Western Edition of The Wall Street Journal, or such other rate of interest publicly announced by Lender as its Prime Rate, plus (b) 2.50 percentage points. Any borrowings, interest or other fees or obligations that the Company owes Western Alliance pursuant to the Financing Agreement (the “Obligations”) will be become due and payable on November 4, 2018.

As of December 30, 2017, and March 14, 2018, we did not have any indebtedness under the Financing Agreement. However, we may incur indebtedness in the future and such indebtedness could have important consequences to you. For example, it could:

●

make it difficult for us to satisfy our other debt obligations;

●

make us more vulnerable to general adverse economic and industry conditions;

●

limit our ability to obtain additional financing for working capital, capital expenditures, acquisitions and other general corporate requirements;

●

expose us to interest rate fluctuations because the interest rate on the debt under the Financing Agreement is variable;

●

require us to dedicate a portion of our cash flow from operations to payments on our debt, thereby reducing the availability of our cash flow for operations and other purposes;

●

limit our flexibility in planning for, or reacting to, changes in our business and the industry in which we operate; and

●

place us at a competitive disadvantage compared to competitors that may have proportionately less debt and greater financial resources.

In addition, our ability to make payments or refinance our obligations depends on our successful financial and operating performance, cash flows and capital resources, which in turn depend upon prevailing economic conditions and certain financial, business and other factors, many of which are beyond our control. These factors include, among others:

●

economic and demand factors affecting our industry;

●

increased operating costs;

●

competitive conditions; and

●

other operating difficulties.

If our cash flows and capital resources are insufficient to fund our debt service obligations, we may be forced to reduce or delay capital expenditures, sell material assets or operations, obtain additional capital or restructure our debt. In the event that we are required to dispose of material assets or operations to meet our debt service and other obligations, the value realized on such assets or operations will depend on market conditions and the availability of buyers. Accordingly, any such sale may not, among other things, be for a sufficient dollar amount. Our obligations pursuant to the Financing Agreement are secured by a security interest in all of our assets, exclusive of intellectual property. The foregoing encumbrances may limit our ability to dispose of material assets or operations. We also may not be able to restructure our indebtedness on favorable economic terms, if at all.

We may incur additional indebtedness in the future. Our incurrence of additional indebtedness would intensify the risks described above.

The Financing Agreement contains various covenants limiting the discretion of our management in operating our business.

The Financing Agreement contains various restrictive covenants that limit our management's discretion in operating our business. These instruments limit our ability to, among other things:

●

make investments, including capital expenditures;

●

sell or acquire assets outside the ordinary course of business; and

●

make fundamental business changes.

If we fail to comply with the restrictions in the Financing Agreement, a default may allow the creditors under the relevant instruments to accelerate the related debt and to exercise their remedies under these agreements, which will typically include the right to declare the principal amount of that debt, together with accrued and unpaid interest and other related amounts, immediately due and payable, to exercise any remedies the creditors may have to foreclose on assets that are subject to liens securing that debt and to terminate any commitments they had made to supply further funds.

If we are unable to maintain sales, marketing and distribution capabilities or maintain arrangements with third parties to sell, market and distribute our products, our business may be harmed.

To achieve commercial success for our products, we must sell our product lines and/or technologies at favorable prices. In addition to being expensive, maintaining such a sales force is time-consuming. Qualified direct sales personnel with experience in the natural products industry are in high demand, and there can be no assurance that we will be able to hire or retain an effective direct sales team. Similarly, qualified independent sales representatives both within and outside the United States are in high demand, and we may not be able to build an effective network for the distribution of our product through such representatives. There can be no assurance that we will be able to enter into contracts with representatives on terms acceptable to us. Furthermore, there can be no assurance that we will be able to build an alternate distribution framework should we attempt to do so.

We may also need to contract with third parties in order to market our products. To the extent that we enter into arrangements with third parties to perform marketing and distribution services, our product revenue could be lower and our costs higher than if we directly marketed our products. Furthermore, to the extent that we enter into co-promotion or other marketing and sales arrangements with other companies, any revenue received will depend on the skills and efforts of others, and we do not know whether these efforts will be successful. If we are unable to establish and maintain adequate sales, marketing and distribution capabilities, independently or with others, we will not be able to generate product revenue, and may not become profitable.

Risks Related to Regulatory Approval of Our Products and Other Government Regulations

Changes in government regulation or in practices relating to the pharmaceutical, dietary supplement, food and cosmetic industry could decrease the need for the services we provide.

Governmental agencies throughout the world, including in the United States, strictly regulate the pharmaceutical, dietary supplement, food and cosmetic industries. Changes in regulation, such as a relaxation in regulatory requirements or the introduction of simplified drug approval procedures, or an increase in regulatory requirements that we may have difficulty satisfying or that make our services less competitive, could eliminate or substantially reduce the demand for our services. Also, if the government makes efforts to contain drug costs and pharmaceutical and biotechnology company profits from new drugs, or if health insurers were to change their practices with respect to reimbursements for pharmaceutical products, our customers may spend less, or reduce their spending on research and development.

Compliance with stringent and changing global privacy and data security laws and regulations could result in additional costs and liabilities to us or inhibit our ability to collect and, if applicable, process data globally, and the failure or perceived failure to comply with such laws and regulations could have a material adverse effect on our business, financial condition or results of operations.

We collect, receive, store, process, use, generate, transfer, disclose, make accessible, protect and share personal information and other sensitive information, including but not limited to proprietary and confidential business information, trade secrets, intellectual property, information collected about patients in connection with clinical trials and sensitive third-party information necessary to operate our business, for legal and marketing purposes. Accordingly, we are, or may become, subject to numerous federal, state, local, and foreign data privacy and security laws, regulations, guidance and industry standards as well as external and internal privacy and security policies, contracts and other obligations that apply to the processing of personal data by us and on our behalf. The legal framework for the collection, use, safeguarding, sharing, transfer and other processing of information worldwide is rapidly evolving and may remain unsettled for the foreseeable future.

Outside the United States, an increasing number of laws, regulations, and industry standards apply to data privacy and security. For example, the European Union’s General Data Protection Regulation (GDPR) and the United Kingdom’s GDPR (UK GDPR) imposes strict obligations on the processing of personal data, including, without limitation, personal health data. The GDPR and UK GDPR set out extensive compliance requirements, including providing detailed disclosures about how personal data is collected and processed, demonstrating that an appropriate legal basis is in place or otherwise exists to justify data processing activities; granting new rights for data subjects in regard to their personal data, as well as enhancing pre-existing rights (e.g., data subject access requests); requiring the appointment of a data protection officer in certain circumstances; mandating the appointment of representatives in the United Kingdom and/or the EEA in certain circumstances; introducing new data transfer frameworks such as the EU-U.S. Data Privacy Framework and the U.K. – U.S. Data Bridge, introducing the obligation to notify data protection regulators or supervisory authorities (and in certain cases, affected individuals) of significant data breaches; imposing limitations on retention of personal data; maintaining a record of data processing; and complying with the principle of accountability and the obligation to demonstrate compliance through policies, procedures, training and audit.

Legal developments in Europe have created complexity and uncertainty regarding transfers of personal data from the European Economic Area, or EEA, to the United States. We continue to execute contracts involving the transfer of personal data outside of the European Economic Area with the Standard Contractual Clauses in the ordinary course. As supervisory authorities issue further guidance on personal data export mechanisms, including updates to the Standard Contractual Clauses, and/or start taking enforcement action, we could suffer additional costs, complaints and/or regulatory investigations or fines, and/or if we or third

parties we work with are otherwise unable to transfer personal data between and among countries and regions in which we conduct business.

Following the United Kingdom’s withdrawal from the EEA and the EU, we also have to comply with the UK-specific requirements related to data protection, including with respect to transfer of personal data outside of the UK, which increases our regulatory compliance burden. The UK updated its transfer mechanism and we continue to execute contracts involving the transfer of personal data outside of the United Kingdom with the new UK-specific transfer tools in the ordinary course.

If we cannot implement a valid compliance mechanism for cross-border data transfers, we may face increased exposure to regulatory actions, substantial fines, and injunctions against processing or transferring personal data from Europe or elsewhere. The inability to import personal data to the United States could significantly and negatively impact our business operations, including by limiting our ability to collaborate with parties that are subject to European and other data privacy and security laws; or requiring us to increase our personal data processing capabilities and infrastructure in Europe and/or elsewhere at significant expense.

Additionally, in the United States, federal, state, and local governments have enacted numerous data privacy and security laws, including data breach notification laws, personal data privacy laws, and consumer protection laws. Each of these state laws adds potential compliance and risk for us with respect to data necessary to operate our business.

A United States federal privacy bill advanced to the U.S. House of Representatives on July 20, 2022, which has been amended as of December 30, 2022, and recommended for passage as law, would establish new requirements for how companies handle personal data, including information that identifies or is reasonably linked to an individual, such as our consumers. If this bill becomes law, we may be required to implement certain security practices to protect and secure personal data against unauthorized access, and we may be subject to further requirements for complying with this requirement if the FTC issues related regulations. Additionally, if we become subject to new data privacy laws, at the state level, the risk of enforcement action against us could increase because we may become subject to additional obligations, and the number of individuals or entities that can initiate actions against us may increase (including individuals, via a private right of action, and state actors).Other data privacy and security laws have been proposed at the federal, state, and local levels in recent years, which could further complicate compliance efforts.

Our obligations related to data privacy and security are quickly changing in an increasingly stringent fashion, creating some uncertainty as to the effective future legal framework. Additionally, these obligations may be subject to differing applications and interpretations, which may be inconsistent or in conflict among jurisdictions. Preparing for and complying with these obligations requires us to devote significant resources (including, without limitation, financial and time-related resources). These obligations may necessitate changes to our information technologies, systems, and practices and to those of any third parties that process personal data on our behalf. In addition, these obligations may require us to change our business model. Collectively, these laws may increase our compliance costs and potential liability. Although we endeavor to comply with our published policies, other documentation, and all applicable privacy and security laws, we may at times fail to do so or may be perceived to have failed to do so. Moreover, despite our efforts, our personnel or third parties upon whom we rely may fail to comply with such obligations, which could negatively impact our business operations and compliance posture. For example, any failure by a third-party processor to comply with applicable law, regulations, or contractual obligations could result in adverse effects, including inability to operate our business and proceedings against us by governmental entities or others. If we fail, or are perceived to have failed, to address or comply with obligations related to data privacy and security, we could face government enforcement actions that could include investigations, fines, penalties, audits and inspections; additional reporting requirements and/or oversight; temporary or permanent bans on all or some processing of personal data; orders to destroy or not use personal data; and imprisonment of company officials. Further, individuals or other relevant stakeholders could sue us for our actual or perceived failure to comply with our data privacy and security obligations, including, without limitation, in class action litigation. Any of these events could have a material adverse effect on our reputation, business, or financial condition, and could lead to a loss of actual or prospective customers, collaborators or partners; result in an inability to process personal data or to operate in certain jurisdictions; limit our ability to develop or commercialize our products; or require us to revise or restructure our operations. Moreover, such suits, even if we are not found liable, could be expensive and time-consuming to defend and could result in adverse publicity that could harm our business or have other material adverse effects. Additionally, we expect that there will continue to be new proposed laws and regulations concerning data privacy and security, and we cannot yet determine the impact such future laws, regulations and standards may have on our business.

We are subject to regulation by various federal, state and foreign agencies that require us to comply with a wide variety of regulations, including those regarding the manufacture of products, advertising and product label claims, the distribution of our products and environmental matters. Failure to comply with these regulations could subject us to fines, penalties and additional costs.

Some of our operations are subject to regulation by various United States federal agencies and similar state and international agencies, including the Department of Commerce, the FDA, the FTC, the Department of Transportation and the Department of Agriculture. These regulations govern a wide variety of product activities, from design and development to labeling, manufacturing, handling, sales and distribution of products. If we fail to comply with any of these regulations, we may be subject to fines or penalties, have to recall products and/or cease their manufacture and distribution, which would increase our costs and reduce our sales.

We are also subject to various federal, state, local and international laws and regulations that govern the handling, transportation, manufacture, use and sale of substances that are or could be classified as toxic or hazardous substances. Some risk of environmental damage is inherent in our operations and the products we manufacture, sell, or distribute. In addition, we may incur substantial costs in order to comply with current or future environmental, health and safety laws and regulations. Current or future environmental laws and regulations may impair our research, development or production efforts. In addition, failure to comply with these laws and regulations may result in substantial fines, penalties or other sanctions. Any failure by us to comply with the applicable government regulations could also result in product recalls or impositions of fines and restrictions on our ability to carry on with or expand in a portion or possibly all of our operations. If we fail to comply with any or all of these regulations, we may be subject to fines or penalties, have to recall products and/or cease their manufacture and distribution, which would increase our costs and reduce our sales.

Government regulations of our customer’s business are extensive and are constantly changing. Changes in these regulations can significantly affect customer demand for our products and services.

The process by which our customers’ industries are regulated is controlled by government agencies and depending on the market segment can be very expensive, time consuming, and uncertain. Changes in regulations or the enforcement practices of current regulations could have a negative impact on our customers and, in turn, our business. At this time, it is unknown how the FDA will interpret and to what extent it will enforce GMPs,Good Manufacturing Practices, and other regulations that will likely affect many of our customers. These uncertainties may have a material impact on our results of operations, as lack of enforcement or an interpretation of the regulations that lessens the burden of compliance for the dietary supplement marketplace may cause a reduced demand for our products and services.

Changes in government regulation or in practices relatingrelated to the pharmaceutical, dietary supplement, food and cosmetic industry could decrease the need for the services we provide.

Governmental agencies throughout the world, including in the United States, strictly regulate the pharmaceutical, dietary supplement, food and cosmetic industries. Our business involves helping pharmaceutical and biotechnology companies navigate the regulatory drug approval process. Changes in regulation, such as a relaxation in regulatory requirements or the introduction of simplified drug approval procedures, or an increase in regulatory requirements that we have difficulty satisfying or that make our services less competitive, could eliminate or substantially reduce the demand for our services. Also, if the government makes efforts to contain drug costs and pharmaceutical and biotechnology company profits from new drugs, our customers may spend less, or reduce their spending on research and development. If health insurers were to change their practices with respect to reimbursements for pharmaceutical products, our customers may spend less, or reduce their spending on research and development.

If we should in the future become required to obtain regulatory approvalapprovals to market and sell our goods we will not be ablecould adversely affect our ability to generate any revenues until such approval is received.

revenues.

The pharmaceutical industry isindustries within which we operate are subject to stringent regulationand constantly evolving regulations by a wide range of authorities. While weauthorities worldwide. We believe that, given our present business, weproducts are not currently required to obtain regulatory approval to market our goods because, among other things, we do not (i) producefollowing all applicable regulations in those jurisdictions within which they are sold or market any clinical devices or other products, or (ii) sell any medical products or services to the customer, wemarketed. We cannot predict whether regulatory clearancehow regulations will be requiredevolve or what new requirements may arise in the future and, if so, whether or how such clearance will at such time be obtained forchanges may affect any products that we are developing or may attempt to develop. Should such regulatory approval in the future be required,Depending on how regulations evolve, our goods may be suspended or may not be able to be marketed and sold in the United States or in other markets until we have completed theachieved appropriate regulatory clearance processcompliance as and if implemented by the FDA.FDA or other regulatory body. In certain markets and product categories, regulatory approval is a prerequisite for marketing and selling our products. These markets and categories may require adherence to specific regulatory standards, and any failure to obtain or maintain necessary approvals or changes in requirements in these regions could adversely impact our ability to sell our goods there. Satisfaction of regulatory requirements typically takesmay take many years, is dependent upon the type, complexity and novelty of the product or service and would require the expenditure of substantial resources.

If regulatory clearance of a good that we propose to propose to market and sell is granted, this clearance may be limited to those particular countries, states and conditions for which the good is demonstrated to be safe and effective, which wouldcould limit our ability to generate revenue. We cannot ensure that any good that we develop will meet all of the applicable regulatory requirements needed to receive marketing clearance. Failure to obtain regulatory approval will prevent commercialization of our goods where such clearance is necessary. There can be no assurance that we will obtain regulatory approval of our proposed goods that may require it.

Risks Related to the Securities Markets and Ownership of our Equity Securities

The market price of our common stock may be volatile and adversely affected by several factors.

The market price of our common stock could fluctuate significantly in response to various factors and events, including, but not limited to:

•our ability to develop and commercialize our products;

●

•our ability to integrate operations, technology, products and services;

●

•our ability to execute our business plan;

●

•our operating results are below expectations;

●

•our issuance of additional securities, including debt or equity or a combination thereof,;

●

•announcements of technological innovations or new products by us or our competitors;

●

•acceptance of and demand for our products by consumers;

●

•media coverage or social media attention regarding our industry or us;

•litigation, arbitration, or other adverse non-judicial proceedings;

●

•disputes with or our inability to collect from significant customers;

●

•loss of any strategic relationship;

●

•industry developments, including, without limitation, changes in healthcare policies or practices;

●

•economic and other external factors;

●

•reductions in purchases from our large customers;

•sales of our common stock by us, our insiders or other stockholders;

● •short positions, hedging, or other transactions in our securities;

•period-to-period fluctuations in our financial results; and

●

•whether an active trading market in our common stock develops and is maintained.

In addition, the securities markets have from time to time experienced significant price and volume fluctuations that are unrelated to the operating performance of particular companies. These market fluctuations may also materially and adversely affect the market price of our common stock.

We have not paid cash dividends in the past and do not expect to pay cash dividends in the foreseeable future. Any return on investment may be limited to the value of our common stock.

We have never paid cash dividends on our capital stock and do not anticipate paying cash dividends on our capital stock in the foreseeable future. The payment of dividends on our capital stock will depend on our earnings, financial condition and other business and economic factors affecting us at such time as the board of directors may consider relevant. If we do not pay dividends, our common stock may be less valuable because a return on your investment will only occur if the common stock price appreciates.

We have a significant number of outstanding options and unvested restricted stock units. Future sales of these shares could adversely affect the market price of our common stock.

As of December 31, 2023, we had outstanding options for an aggregate of approximately 11.6 million shares of common stock at a weighted average exercise price of $3.68 per share and approximately 0.6 million of unvested restricted stock units. The holders may sell many of these shares in the public markets from time to time, without limitations on the timing, amount or method of sale. As and when our stock price rises, if at all, more outstanding options will be in-the-money and the holders may exercise their options and sell a large number of shares. This could cause the market price of our common stock to decline.

We have a limited operating history in China and we face risks with respect to conducting business in connection with our joint venture in China due to certain legal, political, economic and social uncertainties relating to China.

During fiscal year 2022, we entered into an agreement to form a joint venture to expand the Company’s market strategy to include opportunities in Mainland China and its territories, excluding Hong Kong, Macau and Taiwan. Operating activity under the joint venture was not material during the year ended December 31, 2023. Our participation in the joint venture in China is subject to general, as well as industry-specific, economic, political and legal developments and risks in China. The Chinese government exercises significant control over the Chinese economy, including but not limited to, controlling capital investments, allocating resources, setting monetary policy, controlling and monitoring foreign exchange rates, implementing and overseeing tax regulations, providing preferential treatment to certain industry segments or companies and issuing necessary licenses to conduct business. In addition, we could face additional risks resulting from changes in China’s data privacy and cybersecurity requirements. Accordingly, any adverse change in the Chinese economy, the Chinese legal system or Chinese governmental, economic or other policies could have a material adverse effect on our joint venture in China and our prospects generally.

We face additional risks in China due to China’s historically limited recognition and enforcement of contractual and intellectual property rights. We may experience difficulty enforcing our intellectual property rights in China. Unauthorized use of our technologies and intellectual property rights by partners or competitors may dilute or undermine the strength of our brands. If we cannot adequately monitor the use of our technologies and products, or enforce our intellectual property rights in China or contractual restrictions relating to use of our intellectual property by Chinese companies, our revenue could be adversely affected.

Our joint venture will be subject to laws and regulations applicable to foreign investment in China. There are uncertainties regarding the interpretation and enforcement of laws, rules and policies in China. Because many laws and regulations are relatively new, the interpretations of many laws, regulations and rules are not always uniform. Moreover, the interpretation of statutes and regulations may be subject to government policies reflecting domestic political agendas. Enforcement of existing laws or contracts based on existing law may be uncertain and sporadic. As a result of the foregoing, it may be difficult for us to obtain swift or equitable enforcement of laws ostensibly designed to protect companies like ours, which could have a material adverse effect on our business and results of operations. There is no guarantee that we will be able to successfully launch our joint venture.

Our ability to use our net operating loss (NOL) carryforwards and certain other tax attributes may be limited.

Our federal net operating losses (NOLs) generated in taxable years beginning on or prior to December 31, 2017 could expire unused. Under current law, federal NOLs incurred in taxable years beginning after December 31, 2017, may be carried forward indefinitely, but the deductibility of such federal NOLs in tax years beginning after December 31, 2017, is limited to 80% of taxable income. It is uncertain if and to what extent various states will conform to federal tax laws. In addition, under Sections 382 and 383 of the Internal Revenue Code of 1986, as amended, and corresponding provisions of state law, if a corporation undergoes an “ownership change,” which is generally defined as a greater than 50% change (by value) in its equity ownership over a three-year period, the corporation’s ability to use its pre-change NOL carryforwards and other pre-change tax attributes (such as research tax credits) to offset its post-change income or taxes may be limited. We may experience ownership changes in the future as a result of subsequent shifts in our stock ownership, some of which may be outside of our control. As a result, if we earn net taxable income, our ability to use our pre-ownership change NOL carryforwards to offset U.S. federal taxable income may be subject to limitations, which could potentially result in increased future tax liability to us. In addition, at the state level, there may be periods during which the use of NOLs is suspended or otherwise limited, which could accelerate or permanently increase state taxes owed.

Our bylaws, as amended (Bylaws) provide that the Court of Chancery of the State of Delaware is the exclusive forum for certain disputes between us and our stockholders, which could limit our stockholders’ ability to obtain a favorable judicial forum for disputes with us or our directors, officers or employees.

Our Bylaws provide that the Court of Chancery of the State of Delaware will be the sole and exclusive forum for the following types of actions or proceedings under Delaware statutory or common law: (i) any derivative action or proceeding brought on our behalf, (ii) any action asserting a claim of breach of a fiduciary duty owed by any of our directors or officers to our company or our stockholders, (iii) any action asserting a claim against our company arising pursuant to any provision of the Delaware General Corporation Law or our amended and restated certificate of incorporation or Bylaws, or (iv) any action asserting a claim against our company governed by the internal affairs doctrine.

This choice of forum provision may limit a stockholder’s ability to bring certain claims in a judicial forum that it finds favorable for disputes with us or any of our directors, officers, other employees or stockholders, which may discourage lawsuits with respect to such claims, although our stockholders will not be deemed to have waived our compliance with federal securities laws and the rules and regulations thereunder. While the Delaware courts have determined that such choice of forum provisions are facially valid and several state trial courts have enforced such provisions, there is no guarantee that courts of appeal will affirm the enforceability of such provisions and a stockholder may nevertheless seek to bring a claim in a venue other than that designated in the exclusive forum provision. If a court were to find this choice of forum provision to be inapplicable or unenforceable in an action, we may incur additional costs associated with resolving such action in other jurisdictions, which could adversely affect our business and financial condition.

General Risks

We may become involved in securities class action litigation that could divert management’s attention and harm our business.

The stock market has experienced extreme price and volume fluctuations. These fluctuations have often been unrelated or disproportionate to the operating performance of the companies involved. If these fluctuations occur in the future, the market price of our shares could fall regardless of our operating performance. In the past, following periods of volatility in the market price of a particular company’s securities, securities class action litigation has often been brought against that company. If the market price or volume of our shares suffers extreme fluctuations, then we may become involved in this type of litigation, which would be expensive and divert management’s attention and resources from managing our business.

As a public company, we may also from time to time make forward-looking statements about future operating results and provide some financial guidance to the public markets. Projections may not be made in a timely manner, or we might fail to reach expected performance levels and could materially affect the price of our shares. Any failure to meet published forward-looking statements that adversely affect the stock price could result in losses to investors, stockholder lawsuits or other litigation, sanctions or restrictions issued by the Securities and Exchange Commission.

Our failure to establish and maintain effective internal control over financial reporting could result in material misstatements in our financial statements, our failure to meet our reporting obligations and cause investors to lose confidence in our reported financial information, which in turn could cause the trading price of our common stock to decline.

Maintaining effective internal control over financial reporting is necessary for us to produce reliable and timely financial statements and disclosures. If we identify material weaknesses in our internal controls and/or fail to establish and maintain effective controls and procedures and internal control over financial reporting it could result in material misstatements in our financial statements and/or a failure to meet our reporting and financial obligations, each of which could have a material adverse effect on our financial condition and the trading price of our common stock. The SEC has proposed a new rule regarding climate change that, if adopted, requires significant new disclosure obligations of us and requires us to update and develop our controls to accommodate these new obligations.

Environmental, social and governance matters may impact our business and reputation.

Companies across many industries are facing increased scrutiny, including by consumers, investors, employees and other stakeholders, as well as by governmental and non-governmental organizations surrounding environmental, social and governance (ESG) practices. This increased scrutiny and changing expectations with respect to the Company’s ESG practices as well as new rules and regulations may result in additional costs or risks. The SEC has proposed new rules regarding climate change that, if adopted, require significant new disclosure obligations of us and require us to update and develop our controls to accommodate these new obligations. Standards and research regarding ESG practices could change as a result of these rules. In addition, the State of California recently passed the Climate Corporate Data Accountability Act and the Climate-Related Financial Risk Act that will impose broad climate-related disclosure obligations on certain companies doing business in California, starting in 2026. New or revised laws and regulations or new interpretations of existing laws and regulations, such as those related to climate change, could affect the operation of our properties or result in significant additional expense and restrictions on our business operations. If we are unable to satisfy such new criteria, investors may conclude that our policies with respect to corporate responsibility are inadequate. We risk damage to our brand and reputation in the event that our corporate responsibility procedures or standards do not meet the standards set by various constituencies, which could lead to the loss of existing or potential customers and reduced sales. There can be no assurance that investors or other constituents will not publicly advocate for us to not make corporate governance changes or engage in corporate actions and responding to challenges could be costly and time consuming.

Developing and achieving ESG initiatives may result in increased costs in our supply chain, fulfillment, and/or corporate business operations, and could deviate from our initial estimates and have a material adverse effect on our business and financial condition. Furthermore, if our competitors’ corporate responsibility performance is perceived to be greater than ours, potential or current investors may elect to invest with our competitors instead. Investor advocacy groups, certain institutional investors, investment funds and other influential investors are increasingly focused on ESG practices and in recent years have placed increasing importance on the non-financial impacts of their investments. Topics taken into account in such assessments include, among others, the company’s efforts and impacts on climate change and human rights, ethics and compliance with law and the role of the Company’s board of directors in supervising various sustainability issues. In light of investors’ and other stakeholders’ increased focus on ESG matters, there can be no certainty that we will manage such issues successfully, or that we will successfully meet our investors’ or society’s ESG expectations. While our mission is to promote healthy aging, if our ESG practices do not meet investor or other industry stakeholder expectations, which continue to evolve, we may incur additional costs and our brand’s ability to attract and retain qualified employees and business may be harmed.

Changes in tax laws or regulations that are applied adversely to us or our customers may have a material adverse effect on our business, cash flow, financial condition or results of operations.

New income, sales, use or other tax laws, statutes, rules, regulations or ordinances could be enacted at any time, which could adversely affect our business operations and financial performance. Further, existing tax laws, statutes, rules, regulations or ordinances could be interpreted, changed, modified or applied adversely to us. For example, the Biden administration and Congress have proposed various U.S. federal tax law changes, which if enacted could have a material impact on our business, cash flows, financial condition or results of operations. In addition, it is uncertain if and to what extent various states will conform to federal tax laws. Future tax reform legislation could have a material impact on the value of our deferred tax assets, could result in significant one-time charges, and could increase our future U.S. tax expense.

Our shares of common stock may be thinly traded, so you may be unable to sell at or near ask prices or at all.

We cannot predict the extent to which an active public market for our common stock will develop or be sustained. This situation may be attributable to a number of factors, including the fact that we are a small company that is relatively unknown to stock analysts, stock brokers, institutional investors and others in the investment community who generate or influence sales volume, and that even if we came to the attention of such persons, they tend to be risk averse and would be reluctant to follow an unproven company such as ours or purchase or recommend the purchase of our shares until such time as we have become more seasoned and viable. As a consequence, there may be periods of several days or weeks when trading activity in our shares is minimal or non-existent, as compared to a seasoned issuer which has a large and steady volume of trading activity that will generally support continuous sales without an adverse effect on share price. We cannot assure you that a broader or more active public trading market for our common stock will develop or be sustained, or that current trading levels will be sustained or not diminish.

We have not paid cash dividends in the past and do not expect to pay cash dividends in the foreseeable future. Any return on investment may be limited to the value of our common stock.

We have never paid cash dividends on our capital stock and do not anticipate paying cash dividends on our capital stock in the foreseeable future. The payment of dividends on our capital stock will depend on our earnings, financial condition and other business and economic factors affecting us at such time as the board of directors may consider relevant. If we do not pay dividends, our common stock may be less valuable because a return on your investment will only occur if the common stock price appreciates.

The recently passed comprehensive tax reform bill could adversely affect our business and financial condition.

On December 22, 2017, President Trump signed into law new legislation that significantly revises the Internal Revenue Code of 1986, as amended. The newly enacted federal income tax law, among other things, contains significant changes to corporate taxation, including reduction of the corporate tax rate from a top marginal rate of 35% to a flat rate of 21%, limitation of the tax deduction for interest expense to 30% of adjusted earnings (except for certain small businesses), limitation of the deduction for net operating losses to 80% of current year taxable income and elimination of net operating loss carrybacks, one time taxation of offshore earnings at reduced rates regardless of whether they are repatriated, elimination of U.S. tax on foreign earnings (subject to certain important exceptions), immediate deductions for certain new investments instead of deductions for depreciation expense over time, and modifying or repealing many business deductions and credits (including reducing the business tax credit for certain clinical testing expenses incurred in the testing of certain drugs for rare diseases or conditions). Notwithstanding the reduction in the corporate income tax rate, the overall impact of the new federal tax law is uncertain and our business and financial condition could be adversely affected. In addition, it is unknown if and to what extent various states will conform to the newly enacted federal tax law. The impact of this tax reform on holders of our common stock is likewise uncertain and could be adverse. We urge our stockholders to consult with their legal and tax advisors with respect to this legislation and the potential tax consequences of investing in or holding our common stock.

Stockholders may experience significant dilution if future equity offerings are used to fund operations or acquire complementary businesses.

If future operations or acquisitions are financed through the issuance of additional equity securities, stockholders could experience significant dilution. Securities issued in connection with future financing activities or potential acquisitions may have rights and preferences senior to the rights and preferences of our common stock. In addition, the issuance of shares of our common stock upon the exercise of outstanding options or warrants may result in dilution to our stockholders.

Item 1B. Unresolved Staff Comments

None.

Item 1C. Cybersecurity

Cybersecurity Risk Management and Strategy

We are a global bioscience company dedicated to healthy aging. In the ordinary course of our business, we may become involvedcollect, process, store and transmit proprietary, confidential and sensitive information, including personal information (including health information), intellectual property, trade secrets, and proprietary business information owned or controlled by ourselves or other parties. We use our data centers and our networks, and those of third parties, to store and access our proprietary business and other sensitive information. We rely upon third parties service providers and technologies to operate critical business systems to process confidential and personal information in securities class action litigationa variety of contexts, including, without limitation, third-party providers of cloud-based infrastructure, employee email, and other functions. We have established cybersecurity risk management policies and procedures aimed at safeguarding the confidentiality, integrity, and availability of our critical systems and information, including those involving third-party service providers. Further, we are actively working to enhance our policies and procedures into a more comprehensive cybersecurity risk management program, our current measures are designed to address cybersecurity risks effectively. Our cybersecurity risk management policies and procedures include the ChromaDex Incident Management Plan.

We design and assess our policies and procedures based on the National Institute of Standards and Technology Cybersecurity Framework (NIST CSF framework). This does not imply that could divert management’s attentionwe follow or meet any particular technical standards, specifications, or requirements, only that we use the NIST CSF framework as a guide to help us identify, assess, and harmmanage cybersecurity risks relevant to our business. For example, we periodically perform independent third-party security audits and assess potential risks.

The stock market in general,Our cybersecurity risk management policies and procedures are integrated into our overall enterprise risk management program, and shares common methodologies, reporting channels and governance processes that apply across the stocksenterprise risk management program to other legal, compliance, strategic, operational, and financial risk areas.

Our cybersecurity risk management policies and volume fluctuations. These fluctuations have often been unrelatedprocedures include:

–risk assessments designed to help identify material cybersecurity risks to our critical systems, information, products, services, and our broader enterprise IT environment;

–a security team, led by our Vice President of IT (VP of IT), principally responsible for managing our (1) cybersecurity risk assessment processes, (2) security controls, and (3) responses to cybersecurity incidents;

–the use of external service providers, where appropriate, to assess, test or disproportionate to the operating performance of the companies involved. If these fluctuations occur in the future, the market priceotherwise assist with aspects of our shares could fall regardlesssecurity controls and designed to anticipate cyber-attacks and prevent breaches;

–cybersecurity awareness training of our operating performance. In the past, following periods of volatility in the market price of employees, incident response personnel, and senior management;

–a particular company’s securities, securities class action litigation has often been brought againstcybersecurity incident response plan that company. If the market price or volume of our shares suffers extreme fluctuations, then we may become involved in this type of litigation, which would be expensiveincludes procedures for responding to cybersecurity incidents; and divert management’s attention

–a third-party risk management process for service providers, suppliers, and resources from managing our business.vendors.

As a public company, we may also from time to time make forward-looking statements about future operating results and provide some financial guidance to the public markets. Projections may not be made in a timely manner or we might fail to reach expected performance levels and could materially affect the price of our shares. Any failure to meet published forward-looking statements that adversely affect the stock price could result in losses to investors, stockholder lawsuits or other litigation, sanctions or restrictions issued by the SEC.

We have not identified risks from known cybersecurity threats, including as a significant numberresult of outstanding optionsany prior cybersecurity incidents, that have materially affected or are reasonably likely to materially affect us, including our operations, business strategy, results of operations, or financial condition.

Cybersecurity Governance

Our Board considers cybersecurity risk as part of its risk oversight function. In connection with the Audit Committee’s oversight of the Company’s risk management, the Audit Committee reviews with management, at least annually, the Company’s cybersecurity risk exposure and warrants,the steps management has taken to monitor or mitigate such exposure, including reviewing risk assessments from management with respect to our information technology systems and future salesprocedures, and overseeing our cybersecurity risk management processes. In addition, management will update the Audit Committee and the full Board, as necessary, regarding cybersecurity incidents, that we may experience.

Our management team, including our VP of these shares could adversely affectIT, is responsible for assessing and managing our material risks from cybersecurity threats. The team has primary responsibility for our overall cybersecurity risk management policies and procedures and supervises both our internal cybersecurity personnel and our retained external cybersecurity consultants. Our management team’s cybersecurity risk management is led by our VP of IT, who has experience across technology-enabled growth, information security, infrastructure, operations and compliance.

Our management team supervises efforts to prevent, detect, mitigate, and remediate cybersecurity risks and incidents through various means, which may include briefings from internal security personnel; threat intelligence and other information obtained from governmental, public or private sources, including external consultants engaged by us; and alerts and reports produced by security tools deployed in the market price of our common stock.IT environment.

Item 2. Properties

As of December 30, 2017, we had outstanding options exercisable for an aggregate of 6,534,167 shares of common stock at a weighted average exercise price of $3.59 per share and outstanding warrants exercisable for an aggregate of 470,444 shares of common stock at a weighted average exercise price of $4.15 per share. The holders may sell many of these shares in the public markets from time to time, without limitations on the timing, amount or method of sale. As and when our stock price rises, if at all, more outstanding options and warrants will be in-the-money and the holders may exercise their options and warrants and sell a large number of shares. This could cause the market price of our common stock to decline.

Item 1B. | Unresolved Staff Comments |

None.

As of December 30, 2017,31, 2023, we lease approximately 15,000 square feet of office space in Irvine, California with 2 years remaining on the lease,(i) approximately 10,000 square feet of space for research and development laboratory in Longmont, Colorado with 7 years remaining on the lease, approximately 4,500 square feet of office space in Los Angeles, California with 4three years remaining on the lease, (ii) approximately 20,000 square feet of space for a research and development laboratory in Longmont, Colorado with two years remaining on the lease, and (iii) approximately 2,3008,000 square feet of office space in Rockville, MarylandTustin, California with 3five years remaining on the lease. We do not own any real estate. The below table illustrates the use of each property by our business segments.

| | | | | | | | |

| Business Segment | | Property Used |

IngredientsConsumer Products | | All properties |

Consumer ProductsIngredients | | All properties |

CoreAnalytical Reference Standards and Contract Services | | Irvine, CA, Longmont, CO and Rockville, MDAll properties |

We also rent an apartment with approximately 1,000 square feet in Foothill Ranch, California, and an apartment with less than 1,100 square feet in Longmont, Colorado. We use the apartments to accommodate our traveling employees to each of our California and Colorado locations. We do not own any real estate. For the year ended December 30, 2017,31, 2023, our total annual rentalrent expense was approximately $729,000.$1,214,000.

Item 3. Legal Proceedings

On December 29, 2016, ChromaDex, Inc. filed a complaint (the “Complaint”)The information set forth under the heading “Legal Proceedings” in the United States District Court for the Central District of California, naming Elysium Health, Inc. (together with Elysium Health, LLC, “Elysium”) as defendant. Among other allegations, ChromaDex, Inc. allegedNote 16, Commitments and Contingencies, in the Complaint that (i) Elysium breached the Supply Agreement, dated June 26, 2014, by and between ChromaDex, Inc. and Elysium (the “pTeroPure® Supply Agreement”), by failing to make payments to ChromaDex, Inc. for purchases of pTeroPure® pursuantNotes to the pTeroPure® Supply Agreement, (ii) Elysium breached the Supply Agreement, dated February 3, 2014,Consolidated Financial Statements in Item 8 of Part II of this Form 10-K, is incorporated herein by and between ChromaDex, Inc. and Elysium, as amended (the “NIAGEN® Supply Agreement”), by failing to make payments to ChromaDex, Inc. for purchasesreference. For additional discussion of NIAGEN® pursuant to the NIAGEN® Supply Agreement, (iii) Elysium breached the Trademark License and Royalty Agreement, dated February 3, 2014, by and between ChromaDex, Inc. and Elysium (the “License Agreement”), by failing to make payments to ChromaDex, Inc. for royalties due pursuant to the License Agreement and (iv) certain officers of Elysium made false promises and representations to induce ChromaDex, Inc. into providing large supplies of pTeroPure® and NIAGEN® to Elysium pursuant to the pTeroPure® Supply Agreement and NIAGEN® Supply Agreement. ChromaDex, Inc. is seeking punitive damages, money damages and interest.

-32-

risks associated with legal proceedings, see Item 1A, Risk Factors.On January 25, 2017, Elysium filed an answer and counterclaims (the “Counterclaim”) in response to the Complaint. Among other allegations, Elysium alleges in the Counterclaim that (i) ChromaDex, Inc. breached the NIAGEN® Supply Agreement by not issuing certain refunds or credits to Elysium and for violating certain confidential information provisions, (ii) ChromaDex, Inc. breached the implied covenant of good faith and fair dealing pursuant to the NIAGEN® Supply Agreement, (iii) ChromaDex, Inc. breached certain confidential provisions of the pTeroPure® Supply Agreement, (iv) ChromaDex, Inc. fraudulently induced Elysium into entering into the License Agreement (the “Fraud Claim”), (v) ChromaDex, Inc.’s conduct constitutes misuse of its patent rights (the “Patent Claim”) and (vi) ChromaDex, Inc. has engaged in unlawful or unfair competition under California state law (the “Unfair Competition Claim”). Elysium is seeking damages for ChromaDex, Inc.’s alleged breaches of the NIAGEN® Supply Agreement and pTeroPure® Supply Agreement, and compensatory damages, punitive damages and/or rescission of the License Agreement and restitution of any royalty payments conveyed by Elysium pursuant to the License Agreement, and a declaratory judgment that ChromaDex, Inc. has engaged in patent misuse.

On February 15, 2017, ChromaDex, Inc. filed an amended complaint. In the amended complaint, ChromaDex, Inc. re-alleges the claims in the Complaint, and also alleges that Elysium willfully and maliciously misappropriated ChromaDex, Inc.’s trade secrets. On February 15, 2017, ChromaDex, Inc. also filed a motion to dismiss the Fraud Claim, the Patent Claim and the Unfair Competition Claim. On March 1, 2017, Elysium filed a motion to dismiss ChromaDex, Inc.'s fraud and trade secret misappropriation causes of action. On March 6, 2017, Elysium filed a first amended counterclaim. On March 20, 2017, ChromaDex, Inc. moved to dismiss Elysium's amended fraud, declaratory judgment of patent misuse and the Unfair Competition Claim. On May 10, 2017, the court ruled on the motions to dismiss, denying ChromaDex, Inc.’s motion as to Elysium’s fraud and declaratory judgment claims and granting ChromaDex, Inc.’s motion with prejudice as to Elysium’s Unfair Competition Claim. With respect to Elysium’s motion, the court granted the motion with prejudice as to ChromaDex, Inc.’s fraud claim and granted with leave to amend the motion as to ChromaDex, Inc.’s trade secret misappropriation claims. On May 24, 2017, ChromaDex, Inc. answered the first amended counterclaim and asserted several affirmative defenses. Also on May 24, 2017, ChromaDex, Inc. filed a second amended complaint, amending the trade secret misappropriation claims and addressing Elysium’s declaratory judgment of patent misuse counterclaim. On June 7, 2017, ChromaDex, Inc. filed a third amended complaint dismissing the trade secret misappropriation claims and asserting two breach of contract claims for Elysium’s failure to pay for the product delivered. On June 16, 2017, Elysium answered the third amended complaint. On August 14, 2017, ChromaDex, Inc. moved for judgment on the pleadings as to Elysium’s declaratory judgment of patent misuse counterclaim. On September 26, 2017, the court denied ChromaDex’s motion without prejudice and directed Elysium to file an amended counterclaim if it intended to maintain its declaratory judgment counterclaim. On October 11, 2017, Elysium filed a second amended counterclaim, re-alleging the claims in the first amended counterclaim and adding a claim for unjust enrichment and restitution of the royalties Elysium paid to ChromaDex, Inc. pursuant to the License Agreement. On October 25, 2017, ChromaDex, Inc. filed a motion to dismiss the declaratory judgment of patent misuse and unjust enrichment claims and/or strike allegations in the unjust enrichment claim contained in the second amended counterclaim. On November 28, 2017, the court denied the motion. ChromaDex, Inc. answered the second amended counterclaim on December 12, 2017. The parties are currently in discovery.

On July 17, 2017, Elysium filed petitions with the U.S. Patent and Trademark Office for inter partes review of U.S. Patent No. 8,197,807 (the “’807 Patent”) and 8,383,086 (the “’086 Patent”), patents to which ChromaDex, Inc. is the exclusive licensee. The U.S. Patent Trial and Appeal Board (“PTAB”) denied institution of an inter partes review for the ’807 Patent on January 18, 2018. For the ’086 patent, on January 29, 2018 the PTAB granted institution of an inter partes review as to claims 1, 3, 4, and 5 and denied institution as to claim 2.

On September 27, 2017, Elysium Health Inc. ("Elysium Health") filed a complaint in the United States District Court for the Southern District of New York, against ChromaDex, Inc. (the “SDNY Complaint”). Elysium Health alleges in the SDNY Complaint that ChromaDex, Inc. made false and misleading statements in a citizen petition to the Food and Drug Administration it filed on or about August 18, 2017. Among other allegations, Elysium Health avers that the citizen petition made Elysium Health’s product appear dangerous, while casting ChromaDex, Inc.’s own product as safe. The SDNY Complaint asserts four claims for relief: (i) false advertising under the Lanham Act, 15 U.S.C. § 1125(a); (ii) trade libel; (iii) deceptive business practices under New York General Business Law § 349; and (iv) tortious interference with prospective economic relations. ChromaDex, Inc. denies the claims in the SDNY Complaint and intends to defend against them vigorously. On October 26, 2017, ChromaDex, Inc. moved to dismiss the SDNY Complaint on the grounds that, inter alia, its statements in the citizen petition are immune from liability under the Noerr-Pennington Doctrine, the litigation privilege, and New York’s Anti-SLAPP statute, and that the SDNY Complaint failed to state a claim. Elysium Health opposed the motion on November 2, 2017. ChromaDex, Inc. filed its reply on November 9, 2017. The motion is currently pending.

On October 26, 2017, ChromaDex, Inc. filed a complaint in the United States District Court for the Southern District of New York against Elysium Health (the “ChromaDex SDNY Complaint”). ChromaDex alleges that Elysium Health made material false and misleading statements to consumers in the promotion, marketing, and sale of its health supplement product, Basis, and asserts five claims for relief: (i) false advertising under the Lanham Act, 15 U.S.C. §1125(a); (ii) unfair competition under 15 U.S.C. § 1125(a); (iii) deceptive practices under New York General Business Law § 349; (iv) deceptive practices under New York General Business Law § 350; and (v) tortious interference with prospective economic advantage. On November 16, 2017, Elysium Health moved to dismiss for failure to state a claim. ChromaDex, Inc. opposed the motion on November 30, 2017 and Elysium Health filed a reply on December 7, 2017. On November 3, 2017, the Court consolidated the SDNY Complaint and the ChromaDex SDNY Complaint actions under the caption In re Elysium Health-ChromaDex Litigation, 17-cv-7394, and stayed discovery in the consolidated action pending a Court-ordered mediation. The mediation was unsuccessful and the motion is currently pending.

The Company is unable to predict the outcome of these matters and, at this time, cannot reasonably estimate the possible loss or range of loss with respect to the legal proceedings discussed herein. As of December 31, 2017, ChromaDex, Inc. did not accrue a potential loss for the Counterclaim or the SDNY Complaint because ChromaDex, Inc. believes that the allegations are without merit and thus it is not probable that a liability has been incurred.

From time to time we are involved in legal proceedings arising in the ordinary course of our business. We believe that there is no other litigation pending that is likely to have, individually or in the aggregate, a material adverse effect on our financial condition or results of operations.

Item 4. | Item 4. Mine Safety Disclosures |

Not applicable.

Item 5. | Item 5. Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities |

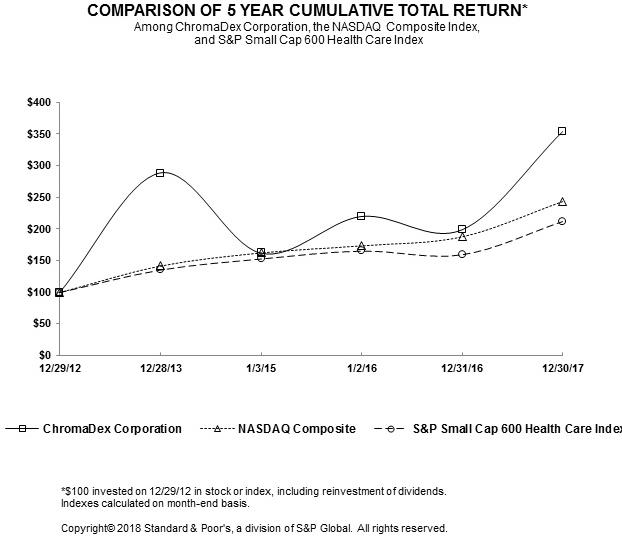

Since April 25, 2016, our common stock has been traded on The NASDAQNasdaq Capital Market (“NASDAQ”)(NASDAQ) under the symbol “CDXC.” From November 10, 2014 to April 22, 2016, our common stock had been traded on the top tier of the OTC Markets Group, Inc. (the “OTCQX”) under the symbol “CDXC.”

On April 13, 2016, the Company effected a 1-for-3 reverse stock split. All information presented herein has been retrospectively adjusted to reflect the reverse stock split as if it took place as of the earliest period presented. An additional 1,632 shares were issued to round up fractional shares as a result of the reverse stock split.