UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

☑ Annual Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934

For the fiscal year ended December 31, 20202023

or

☐ Transition Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934

Commission file number 001-37697

CENTENNIAL RESOURCE DEVELOPMENT, INC.PERMIAN RESOURCES CORPORATION

(Exact name of registrant as specified in its charter)

| | | | | | | | |

| Delaware | | 47-5381253 |

| (State of Incorporation) | | (I.R.S. Employer Identification No.) |

1001 Seventeenth Street,300 N. Marienfeld St., Suite 18001000

Denver, Colorado 80202Midland, Texas 79701

(Registrant’s telephone number, including area code): (720) 499-1400(432) 695-4222

Securities registered pursuant to Section 12(b) of the Act:

| | | | | | | | | | | | | | |

| Title of each class | | Trading Symbol(s) | | Name of each exchange on which registered |

| Class A Common Stock, par value $0.0001 per share | | CDEVPR | | The NASDAQNew York Stock Market LLCExchange |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☒ No ☐

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to the filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the Registrant has submitted electronically and posted on its corporate website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. (See definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act).

| | | | | | | | | | | | | | | | | | | | | | | | | | |

| Large accelerated filer | | Accelerated filer | | Non-accelerated filer

| | Smaller reporting company | | Emerging growth company |

☐ | | ☒ | | ☐ | | ☐ | | ☒☐ | | ☐ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C.7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☒

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

The aggregate market value of the voting and non-voting common stock held by non-affiliates of the registrant as of June 30, 2020,2023, the last business day of the registrant’s most recently completed second fiscal quarter, was approximately $162,307,533$2,940,481,909 based on the closing price of the shares of common stock on that date. While shares of Class C Common Stock are not listed for public trading, they are exchangeable for shares of Class A Common Stock at any time on a share-for-share basis, and the calculation of aggregate market value assumes all outstanding shares of Class C Common Stock were exchanged for Class A Common Stock as of June 30, 2023.

As of February 19, 2021,23, 2024, there were 278,916,306540,951,732 shares of Class A Common Stock, par value $0.0001 per share outstanding and 230,910,435 shares of Class C Common Stock , par value $0.0001 per share, outstanding.

Documents Incorporated by Reference:

Portions of the registrant’s definitive proxy statement for its 20212024 Annual Meeting of Stockholders, which will be filed with the United States Securities and Exchange Commission within 120 days of December 31, 2020,2023, are incorporated by reference into Part III of this Form 10-K for the year ended December 31, 2020.

TABLE OF CONTENTS

GLOSSARY OF OILUNITS OF MEASUREMENTS AND NATURAL GASINDUSTRY TERMS

The following are abbreviations and definitions of certain terms used in this Annual Report on Form 10-K, which are commonly used in the oil and natural gas industry:

Bbl. One stock tank barrel of 42 U.S. gallons liquid volume used herein in reference to crude oil, condensate or NGLs.

Bbl/d. One Bbl per day.

Boe. One barrel of oil equivalent, calculated by converting natural gas to oil equivalent barrels at a ratio of six Mcf of natural gas to one Bbl of oil. This is an energy content correlation and does not reflect a value or price relationship between the commodities.

Boe/d. One Boe per day.

Btu. One British thermal unit, which is the quantity of heat required to raise the temperature of a one-pound mass of water by one-degree Fahrenheit.

Completion. The process of preparing an oil and gas wellbore for production through the installation of permanent production equipment, as well as perforation and fracture stimulation to initiate production.

Development well. A well drilled within the proved area of an oil or natural gas reservoir to the depth of a stratigraphic horizon known to be productive.

Differential. An adjustment to the price of oil or natural gas from an established spot market price to reflect differences in the quality, gathering, processing and transportation fees and location of oil or natural gas.

Exploratory well. A well drilled to find a new field or to find a new reservoir in a field previously found to be productive of oil or natural gas in another reservoir.

Extension well. A well drilled to extend the limits of a known reservoir.

Field. An area consisting of a single reservoir or multiple reservoirs all grouped on, or related to, the same individual geological structural feature or stratigraphic condition. The field name refers to the surface area, although it may refer to both the surface and the underground productive formations.

Formation. A layer of rock which has distinct characteristics that differs from nearby rock.

Henry Hub price. A natural gas benchmark price quoted at settlement date average.

Horizontal drilling. A drilling technique used in certain formations where a well is drilled vertically to a certain depth and then drilled at a right angle within a specified interval.

ICE Brent. Brent crude oil traded on the Intercontinental Exchange, Inc. (ICE).

LIBOR. London Interbank Offered Rate.

MBbl. One thousand barrels of crude oil, condensate or NGLs.

MBoe. One thousand Boe.

Mcf. One thousand cubic feet of natural gas.

Mcf/d. One Mcf per day.

MMBtu. One million British thermal units.

MMcf. One million cubic feet of natural gas.

NGL. Natural gas liquids. These are naturally occurring substances found in natural gas, including ethane, butane, isobutane, propane and natural gasoline, that can be collectively removed from produced natural gas, separated in these substances and sold.

NYMEX. The New York Mercantile Exchange.

NYSE. The New York Stock Exchange.

Operator. The individual or company responsible for the development and/or production of an oil or natural gas well or lease.

Proved developed reserves. Reserves that can be expected to be recovered through existing wells with existing equipment and operating methods or in which the cost of the required equipment is relatively minor compared with the cost of a new well.

Proved reserves. The estimated quantities of oil, NGLs and natural gas that geological and engineering data demonstrate with reasonable certainty to be commercially recoverable in future years from known reservoirs under existing economic and operating conditions.

Proved undeveloped reserves or PUD. Proved reserves that are expected to be recovered from new wells on undrilled acreage, or from existing wells where a relatively major expenditure is required for completion.

Realized price. The cash market price less differentials.

Reserves. Estimated remaining quantities of oil and natural gas and related substances anticipated to be economically producible, as of a given date, by application of development projects to known accumulations. In addition, there must exist, or there must be a reasonable expectation that there will exist, the legal right to produce or a revenue interest in the production, installed means of delivering oil and natural gas or related substances to market and all permits and financing required to implement the project.

Reservoir. A porous and permeable underground formation containing a natural accumulation of producible oil and/or natural gas that is confined by impermeable rock or water barriers and is individual and separate from other reservoirs.

Royalty interest. An interest in an oil or gas property entitling the owner to shares of the production free of costs of exploration, development and production operations.

SOFR. Secured Overnight Funding Rate.

Spot market price. The cash market price without reduction for expected quality, location, transportation and demand adjustments.

Unproved reserves. Reserves attributable to unproved properties with no proved reserves.

Wellbore. The hole drilled by a drill bit that is equipped for oil and natural gas production once the well has been completed. Also called well or borehole.

Working interest. The interest in an oil and gas property (typically a leasehold interest) that gives the owner the right to drill, produce and conduct operations on the property and to a share of production, subject to all royalties and other burdens and to all costs of exploration, development and operations and all risks in connection therewith.

Workover. Operations on a producing well to restore or increase production.

WTI. West Texas Intermediate is a grade of crude oil used as a benchmark in oil pricing.

GLOSSARY OF CERTAIN OTHER TERMS

The following are definitions of certain other terms that are used in this Annual Report:

Business Combination. The acquisition of approximately 89% of the outstanding membership interests in CRP from the Centennial Contributors, which closed on October 11, 2016, and the other transactions contemplated by the Contribution Agreement.

Centennial Contributors. The legacy owners of CRP, who sold approximately 89% of the outstanding membership interests in CRP to the Company in connection with the Business Combination. On April 2, 2020, the Centennial Contributors converted all of their remaining CRP Common Units (and corresponding shares of Class C Common Stock) for Class A Common Stock, which eliminated their entire ownership interest in CRP.

The Company, We, Our or Us. (i) Centennial Resource Development, Inc. and its consolidated subsidiaries including CRP, following the closing of the Business Combination and (ii) Silver Run Acquisition Corporation prior to the closing of the Business Combination.

Class A Common Stock. Our Class A Common Stock, par value $0.0001 per share, also referred to as our Common Stock.

Class C Common Stock. Our Class C Common Stock, par value $0.0001 per share, which was issued to the Centennial Contributors in connection with the Business Combination, all of which have been converted for Class A Common Stock and are no longer outstanding.

Contribution Agreement. The Contribution Agreement, dated as of July 6, 2016, among the Centennial Contributors, CRP and NewCo, as amended by Amendment No. 1 thereto, dated as of July 29, 2016, and the Joinder Agreement, dated as of October 7, 2016, by the Company.

CRP. Centennial Resource Production, LLC, a Delaware limited liability company.

CRP Common Units. The units representing common membership interests in CRP.

GMT Acquisition. The acquisition of certain undeveloped acreage and producing oil and natural gas properties of GMT Exploration Company LLC, which closed on June 8, 2017.

IPO. Our initial public offering of units, which closed on February 29, 2016.

NewCo. New Centennial, LLC, a Delaware limited liability company controlled by affiliates of Riverstone.

Private Placement Warrants. Our 8,000,000 outstanding warrants for the purchase of shares of Class A Common Stock, which were purchased by our Sponsor in a private placement simultaneously with the closing of our IPO.

Riverstone. Riverstone Investment Group LLC and its affiliates, including Silver Run Sponsor, LLC, a Delaware limited liability company, collectively.

Silverback. Silverback Exploration, LLC and Silverback Operating, LLC, collectively.

Silverback Acquisition. The acquisition of leasehold interests and related upstream assets in Reeves County, Texas from Silverback, which closed on December 28, 2016.

Voting common stock. Our Class A Common Stock and Class C Common Stock.

CAUTIONARY STATEMENT CONCERNING FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K (the “Annual Report”), includes “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933, as amended (the “Securities Act”), and Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”). All statements, other than statements of historical fact included in this Annual Report, regarding our strategy, future operations, financial position, estimated revenues and losses, projected costs, prospects, plans and objectives of management are forward-looking statements. When used in this Annual Report, the words “could,” “may,” “believe,” “anticipate,” “intend,” “estimate,” “expect,” “project,” “goal,” “plan,” “target” and similar expressions are intended to identify forward-looking statements, although not all forward-looking statements contain such identifying words. These forward-looking statements are based on management’s current expectations and assumptions about future events and are based on currently available information as to the outcome and timing of future events. When considering forward-looking statements, you should keep in mind the risk factors and other cautionary statements described in Item 1A. Risk Factors in this Annual Report.

Forward-looking statements may include statements about:

•volatility of oil, natural gas and NGL prices or a prolonged period of low oil, natural gas or NGL prices and the effects of actions by, or disputes among or between, members of the Organization of Petroleum Exporting Countries (“OPEC”), such as Saudi Arabia, and other oil and natural gas producing countries, such as Russia, with respect to production levels or other matters related to the price of oil;

•political and economic conditions in or affecting other producing regions or countries, including the effects of excess supply of oilMiddle East, Russia, Eastern Europe, Africa and natural gas resulting from the reduced demand caused by the Coronavirus Disease 2019 (“COVID-19”) pandemic and the actions by certain oil and natural gas producing countries;South America;

•our business strategy and future drilling plans;

•our reserves and our ability to replace the reserves we produce through drilling and property acquisitions;

•our drilling prospects, inventories, projects and programs;

•our financial strategy, return of capital program, leverage, liquidity and capital required for our development program;

•our realized oil, natural gas and NGL prices;

•the timing and amount of our future production of oil, natural gas and NGLs;

•our ability to identify, complete and effectively integrate acquisitions of properties or businesses;

•our ability to realize the anticipated benefits and synergies from the Earthstone Merger and effectively integrate the acquired assets (as defined below);

•our hedging strategy and results;

•our competition and government regulations;

•our ability to obtain permits and governmental approvals;

•our pending legal or environmental matters;

•the marketing and transportation of our oil, natural gas and NGLs;

•our leasehold or business acquisitions;

•cost of developing or operating our properties;

•our anticipated rate of return;

•general economic conditions;

•weather conditions in the areas where we operate;

•credit markets;

•our ability to make dividends, distributions and share repurchases;

•uncertainty regarding our future operating results; and

•our plans, objectives, expectations and intentions contained in this Annual Report that are not historical.

We caution you that these forward-looking statements are subject to all of the risks and uncertainties, most of which are difficult to predict and many of which are beyond our control, incident to the development, production, gathering and sale of oil and natural gas. These risks include, but are not limited to, commodity price volatility, inflation, lack of availability of drilling and production equipment and services, risks relating to the merger of the Company with Earthstone Energy, Inc (the “Earthstone

Merger”), environmental risks, drilling and other operating risks, regulatory changes, the uncertainty inherent in estimating reserves and in projecting future rates of production, cash flow and access to capital, the timing of development expenditures and the other risks described in Item 1A. Risk Factors in this Annual Report.

Reserve engineering is a process of estimating underground accumulations of oil and natural gas that cannot be measured in an exact way. The accuracy of any reserve estimate depends on the quality of available data, the interpretation of such data and price and cost assumptions made by reserve engineers. In addition, the results of drilling, testing and production activities may

justify revisions of estimates that were made previously. If significant, such revisions would change the schedule of any further production and development drilling. Accordingly, reserve estimates may differ significantly from the quantities of oil and natural gas that are ultimately recovered.

Should one or more of the risks or uncertainties described in this Annual Report occur, or should underlying assumptions prove incorrect, our actual results and plans could differ materially from those expressed in any forward-looking statements.

All forward-looking statements, expressed or implied, included in this Annual Report are expressly qualified in their entirety by this cautionary statement. This cautionary statement should also be considered in connection with any subsequent written or oral forward-looking statements that we or persons acting on our behalf may issue.

Except as otherwise required by applicable law, we disclaim any duty to update any forward-looking statements, all of which are expressly qualified by the statements in this section, to reflect events or circumstances after the date of this Annual Report.

Risk Factors Summary

The following is a summary of the principal risks that could materially adversely affect our business, financial condition and results of operations. Refer to Risk Factors under Part I, Item 1A of this Annual Report for a more detailed description of each risk factor.

Risks Related to Commodity Prices

•Commodity prices are volatile, and a sustained period of low commodity prices for oil, natural gas and NGLs could adversely affect our business, financial condition and results of operations.

•If commodity prices decrease to a level such that our future undiscounted cash flows from our properties are less than their carrying value, we may be required to take write-downs of the carrying values of our properties.

Risks Related to Our Reserves, Leases and Drilling Locations

•Reserve estimates depend on many assumptions that may turn out to be inaccurate. Any material inaccuracies in reserve estimates or underlying assumptions will materially affect the quantities and present value of our reserves.

•Unless we replace our reserves with new reserves and develop those reserves, our reserves and production will decline, which would adversely affect our future cash flows and results of operations.

•Our use of seismic data is subject to interpretation and may not accurately identify the presence of oil and natural gas, which could adversely affect the results of our drilling operations.

•The development of our estimated PUDs may take longer and may require higher levels of capital expenditures than we currently anticipate. Therefore, our estimated PUDs may not be ultimately developed or produced.

•Certain of our undeveloped leasehold acreage is subject to leases that will expire over the next several years unless production is established on units containing the acreage, the primary term is extended through continuous drilling provisions or the leases are renewed.

•Our identified drilling locations are scheduled out over many years, making them susceptible to uncertainties that could materially alter the occurrence or timing of their drilling.

•Properties that we decide to drill may not yield oil or natural gas in commercially viable quantities.

Risks Related to Our Operations

•Our development and acquisition projects require substantial capital expenditures. We may be unable to obtain required capital or financing on satisfactory terms, which could lead to a decline in our ability to access or grow production and reserves.

•Drilling for and producing oil and natural gas are high risk activities with many uncertainties that could adversely affect our business, financial condition or results of operations. Additionally, we may not be insured for, or our insurance may be inadequate to protect us against, these risks.

•Many of our properties are in areas that may have been partially depleted or drained by offset wells and certain of our wells may be adversely affected by actions other operators may take when drilling, completing, or operating wells that they own.

•Part of our strategy involves using some of the latest available horizontal drilling and completion techniques, which involve risks and uncertainties in their application.

•Our operations are substantially dependent on the availability of water. Restrictions on our ability to obtain water may have an adverse effect on our financial condition, results of operations and cash flows.

•Our ability to produce crude oil, natural gas and NGLs economically and in commercial quantities could be impaired if we are unable to acquire adequate supplies of water for our drilling operations or are unable to recycle or dispose of the produced water we produce in an economical and environmentally safe manner.

•Our producing properties are concentrated in the Permian Basin, making us vulnerable to risks associated with operating in a single geographic area.

•The marketability of our production is dependent upon transportation and other facilities, most of which we do not control. If these facilities are unavailable, or if we are unable to access these facilities on commercially reasonable terms, our operations could be interrupted and our revenues reduced.

•We have entered into multi-year agreements with some of our suppliers, service providers and the purchasers of our oil and natural gas, which contain minimum volume commitments. Any failure by us to satisfy the minimum volume commitments could lead to contractual penalties that could adversely affect our results of operations and financial position.

•The unavailability or high cost of additional drilling rigs, equipment, supplies, personnel and oilfield services could adversely affect our ability to execute our development plans within our budget and on a timely basis.

•We could experience periods of higher costs if commodity prices rise. These increases could reduce our profitability, cash flow and ability to complete development activities as planned.

•We depend upon a small number of significant purchasers for the sale of most of our oil, natural gas and NGL production.

•We may incur losses as a result of title defects in the properties in which we invest.

•Multi-well pad drilling may result in volatility in our operating results.

•We may be unable to make attractive acquisitions or successfully integrate acquired businesses, and any inability to do so may disrupt our business and hinder our ability to grow.

•A security interruption or failure with respect to our information technology systems could harm our ability to effectively operate our business.

Risks Related to Our Derivative Transactions, Debt and Access to Capital

•Our derivative activities could result in financial losses or could reduce our earnings.

•Our leverage and debt service obligations may adversely affect our financial condition, results of operations, business prospects and our ability to make payments on our outstanding debt.

•We may not be able to generate sufficient cash to service all of OpCo’s indebtedness and may be forced to take other actions to satisfy OpCo’s obligations under applicable debt instruments, which may not be successful.

•Restrictions in OpCo’s existing and future debt agreements could limit our growth and ability to engage in certain activities.

•If OpCo is unable to comply with the restrictions and covenants in the agreements governing its indebtedness, there could be a default under the terms of these agreements, which could result in an acceleration of payment of funds that OpCo has borrowed.

•Any significant reduction in the borrowing base under OpCo’s revolving credit facility as a result of the periodic borrowing base redeterminations or otherwise may negatively impact our ability to fund our operations.

•If we experience liquidity concerns, we could face a downgrade in our debt ratings which could restrict our access to, and negatively impact the terms of, current or future financings or trade credit.

•Increases in interest rates could adversely affect our business.

Risks Related to Legislative and Regulatory Initiatives

•Climate change laws and regulations restricting emissions of GHGs could increase our costs and reduce demand for the oil and natural gas we produce, while potential physical effects of climate change could disrupt our production and cause us to incur significant costs in preparing for or responding to those effects.

•Federal, state and local legislative and regulatory initiatives relating to hydraulic fracturing as well as governmental reviews of such activities could result in increased costs and additional operating restrictions or delays in the completion of oil and natural gas wells and adversely affect our production.

•Conservation measures, technological advances and negative shift in market perception toward the oil and natural gas industry could reduce demand for oil and natural gas.

•Our operations may be exposed to significant delays, costs and liabilities as a result of environmental and occupational health and safety requirements applicable to our business activities.

•Restrictions on drilling activities intended to protect certain species of wildlife may adversely affect our ability to conduct drilling activities in areas where we operate.

•A negative shift in investor sentiment towards the oil and natural gas industry and increased attention to environmental, social and governance (“ESG”) and conservation matters may adversely impact our business.

•Any restrictions on oil and natural gas development on federal lands has the potential to adversely impact our operations.

•Tax laws and regulations may change over time, and any such changes could adversely affect our business and financial condition.

•Changes in laws or regulations, or a failure to comply with any laws and regulations, may adversely affect our business, investments and results of operations.

Risks Related to Our Common Stock and Capital Structure

•A negative shift in investor sentiment towards the oil and gas industry could adversely affect our ability to raise equity and debt capital.

•Our principal stockholders hold substantial voting power of our outstanding voting common stock.

•There may be future sales or other dilution of our equity, which may adversely affect the market price of our common stock.

•The declaration of dividends and any repurchases of our common stock are each within the discretion of our board of directors based upon a review of relevant considerations, and there is no guarantee that we will pay any dividends on or repurchase shares of our common stock in the future or at levels anticipated by our stockholders.

•Provisions contained in our Charter and Bylaws, as well as provisions of Delaware law, could impair a takeover attempt, which may adversely affect the market price of our common stock.

•The Charter designates the Court of Chancery of the State of Delaware as the sole and exclusive forum for substantially all actions and proceedings that may be initiated by stockholders, which could limit shareholders’ ability to obtain a favorable judicial forum for disputes with us or our directors, officers, employees or agents.

Risks Related to the Earthstone Merger

•We may be unable to integrate the business of the Company and Earthstone successfully or realize the anticipated benefits of the Earthstone Merger.

•The financial forecasts disclosed in connection with the announcement of the Earthstone Merger are based on various assumptions that may not be realized.

•The synergies attributable to the Earthstone Merger may vary from expectations.

PART I

ITEMS 1 AND 2. BUSINESS AND PROPERTIES

Overview

Centennial Resource Development, Inc.Permian Resources Corporation is an independent oil and natural gas company focused on driving sustainable returns through the responsible acquisition, optimization and development of unconventionalhigh-return crude oil and associated liquids-rich natural gas reserves in the Permian Basin.reserves. Throughout this Annual Report, unless the context otherwise indicates, all references to the “Company,” “Centennial,“Permian Resources,” “we,” “us,” or “our” refer to Centennial Resource Development, Inc.Permian Resources Corporation and its consolidated subsidiary, Centennial Resource Production,Permian Resources Operating, LLC (“CRP”OpCo”).

Our principal business objective is to increasedeliver leading shareholder valuereturns by building a premier development company focused on horizontal drilling in the Delaware Basin. We intendleveraging our high-quality asset base and technical expertise to growsustainably and responsibly develop our production and oil and natural gas reserves by developingresources to meet the world’s need for affordable, abundant energy. We intend to drive disciplined production growth through optimized development of our acreageassets with an increased focus on optimizing drilling and completion results, drilling extended laterals and managing costs, with anthe overall objective of improving our rates of return, on all wells drilledgenerating sustainable free cash flow, maintaining a strong and thereby fundingflexible balance sheet and maximizing returns to our drilling and development capex entirely from cash flows from operations.shareholders. We also intendlook for opportunities to increase scale and grow production and reservesoptimize our portfolio of high-return, long-life inventory through selectiveaccretive acquisitions that meet our strategic and financial objectives.

Organizational StructureBusiness Combinations

On October 11, 2016,November 1, 2023, we completed the acquisitionmerger (the “Earthstone Merger”) with Earthstone Energy, Inc. (“Earthstone”). Earthstone was an independent oil and gas company engaged in the operation and development of oil and natural gas properties. The Earthstone Merger added approximately 89%223,000 net leasehold acres and significant core inventory locations to our position in the Permian Basin in both Texas and New Mexico and was completed to drive long-term accretion across our key financial and operating metrics, enhance shareholder returns and improve capital efficiency. As a part of the outstanding membership interests in CRP was consummated (the “Business Combination”). CRP is currently a wholly-owned subsidiaryEarthstone Merger consideration, approximately 161.2 million shares of Centennial Resource Development due to various equity transactions.

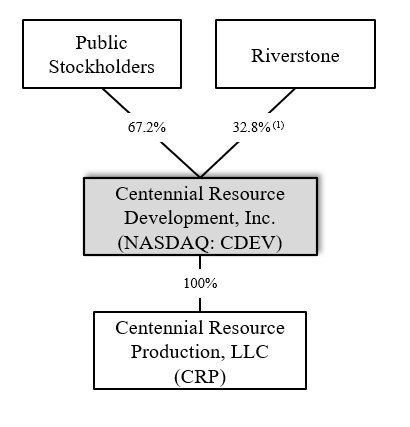

The following diagram illustrates the current ownership structure of the company as of December 31, 2020, including the voting interests of our equity holders:

(1) The above diagram excludes 8,000,000 outstanding Private Placement Warrants, each of which is exercisable for one share of Class A Common Stock at a priceand 49.5 million shares of $11.50 per shareour Class C Common Stock (with underlying units of OpCo) were issued to Earthstone’s equity holders. Certain operational and will expirefinancial information set forth in this Annual Report on October 11, 2021 (five years afterForm 10-K does not include the activity of Earthstone for periods prior to the completion of the Business Combination) or earlier upon redemption or liquidation. As of December 31, 2020, Riverstone Investment GroupEarthstone Merger on November 1, 2023.

On September 1, 2022, we completed the merger (the “Colgate Merger”) with Colgate Energy Partners III, LLC (“Riverstone”Colgate”) owns 6,826,502 Private Placement Warrants. Colgate was an independent oil and Mark G. Papa,gas exploration and development company with properties located in the Delaware Basin. The Colgate Merger was completed to provide increases to our former Chief Executive Officeroperational and Chairman, owns 1,173,498.financial scale, drive accretion across our key financial and operating metrics, and enhance the combined company’s shareholder returns. As a part of the Merger consideration, 269.3 million shares of our Class C Common Stock and underlying units of OpCo were issued to Colgate’s equity holders. Certain operational and financial information set forth in this Annual Report on Form 10-K does not include the activity of Colgate for periods prior to the completion of the Colgate Merger on September 1, 2022.

Refer to Note 2—Business Combinations under Part II, Item 8

Description of Our Properties

Our assets are concentrated in the Delaware Basin, a sub-basincore of the Permian Basin and our properties consist of large, contiguous acreage blocks in West Texas and New Mexico. As a result, we are able to efficiently develop our drilling inventory and focus on maximizing returns to our stakeholders. We have established commercial production on our acreage using horizontal drilling from ten distinct zones: the Avalon Shale, 1st Bone Spring Sand, 2nd Bone Spring Sand, 2nd Bone Spring Shale, 3rd Bone Spring Sand, 3rd Bone Spring Shale, Upper Wolfcamp A, Lower Wolfcamp A, Wolfcamp B and Wolfcamp C. Our development drilling plan is comprised exclusively of horizontal drilling with an ongoing focus on optimizing completions, improving drilling results and managing costs.

As of December 31, 2020,2023, we have leased or acquired approximately 81,657407,000 net leasehold acres 97% of which we operate. In addition, we own 1,472and approximately 68,000 net mineral acres in the Delaware Basin.royalty acres. Approximately 71%70% of our total acreage is located in Texas primarily Reeves County, in the southern portion of the Delaware Basin and the remaining 29%30% is located in Lea County, New Mexico, in the northern portion of the Delaware Basin. Over 88% of our net acreage is held by production as of December 31, 2020. The relatively high proportion of our operated acreage that is held by production gives us significant operational control and capital spending flexibility. This allows us to execute our development program with significant control over the timing and allocation of capital expenditures and application of the optimal drilling and completion techniques to efficiently develop our resource base as evidenced by our operational flexibility executed in 2020.

During the first quarter of 2020, we operated a five-rig drilling program completing 22 gross operated wells and planned to operate a similar drilling and completion program for the remainder of the year. However, in response to significant market deterioration and declines in the oil and natural gas commodity prices, both stemming from the COVID-19 pandemic and tensions between members of OPEC and other important oil producing countries like Russia, we suspended our drilling program at the end of the first quarter of 2020. We continued with no rigs in operation until the end of the third quarter of 2020 when markets and commodity prices began to recover. During August of 2020, we also completed five gross operated wells that had been drilled but left uncompleted earlier in the year. We operated one drilling rig through the fourth quarter of 2020 and ended the year with two drilling rigs in operation. These operational decisions allowed us to preserve liquidity, conserve our reserve base and develop our properties during periods of higher economic opportunity. Refer to Item 7, Management Discussion and Analysis of Financial Condition and Result of Operations under Part II, Item 7 of this Annual Report for further discussion on the 2020 market conditions and our operational activity.Mexico.

Proved Oil and Gas Reserves

Reserve estimates are inherently imprecise, and estimates for new discoveries and undeveloped locations are more imprecise than reserve estimates for producing oil and gas properties. Accordingly, these estimates are expected to change as new information becomes available. The pre-tax PV 10% amounts shown in the following table are not intended to represent the current market value of our estimated proved reserves. The actual quantities and present value of our estimated proved reserves may be more or less than we have estimated, due to a number of factors. The following table should be read along with Item 1A. Risk Factors in this Annual Report.

The following table summarizes estimated proved reserves, pre-tax PV 10%, and standardized measure of discounted future cash flows for the periods indicated:

| | | | | | | | | | | | | | | | | |

| December 31, 2020 | | December 31, 2019 | | December 31, 2018 |

| Proved developed reserves: | | | | | |

| Oil (MBbls) | 70,716 | | | 74,842 | | | 63,317 | |

| Natural gas (MMcf) | 279,556 | | | 237,791 | | | 180,542 | |

| NGL (MBbls) | 31,672 | | | 32,743 | | | 23,093 | |

Total proved developed reserves (MBoe)(1) | 148,981 | | | 147,216 | | | 116,500 | |

| Proved undeveloped reserves: | | | | | |

| Oil (MBbls) | 79,776 | | | 75,317 | | | 79,449 | |

| Natural gas (MMcf) | 248,231 | | | 264,639 | | | 222,310 | |

| NGL (MBbls) | 28,773 | | | 34,499 | | | 28,825 | |

Total proved undeveloped reserves (MBoe)(1) | 149,921 | | | 153,923 | | | 145,326 | |

| Total proved reserves: | | | | | |

| Oil (MBbls) | 150,492 | | | 150,159 | | | 142,766 | |

| Natural gas (MMcf) | 527,787 | | | 502,430 | | | 402,852 | |

| NGL (MBbls) | 60,445 | | | 67,242 | | | 51,918 | |

Total proved reserves (MBoe)(1) | 298,902 | | | 301,139 | | | 261,826 | |

| | | | | |

| Proved developed reserves % | 50 | % | | 49 | % | | 44 | % |

| Proved undeveloped reserves % | 50 | % | | 51 | % | | 56 | % |

| | | | | |

| Reserve values (in millions): | | | | | |

| Standard measure of discounted future net cash flows | $ | 1,184.7 | | | $ | 2,062.4 | | | $ | 2,479.9 | |

| Discounted future income tax expense | 4.4 | | | 135.5 | | | 499.6 | |

Total proved pre-tax PV 10%(2) | $ | 1,189.1 | | | $ | 2,197.9 | | | $ | 2,979.5 | |

| | | | | | | | | | | | | | | | | |

| December 31, 2023 | | December 31, 2022 | | December 31, 2021 |

| Proved developed reserves: | | | | | |

| Oil (MBbls) | 271,328 | | | 156,941 | | | 77,973 | |

| Natural gas (MMcf) | 1,441,914 | | | 652,270 | | | 326,223 | |

| NGL (MBbls) | 192,368 | | | 74,940 | | | 30,318 | |

Total proved developed reserves (MBoe)(1) | 704,015 | | | 340,593 | | | 162,662 | |

| Proved undeveloped reserves: | | | | | |

| Oil (MBbls) | 122,008 | | | 130,091 | | | 75,480 | |

| Natural gas (MMcf) | 324,176 | | | 381,301 | | | 250,782 | |

| NGL (MBbls) | 45,046 | | | 47,911 | | | 25,265 | |

Total proved undeveloped reserves (MBoe)(1) | 221,083 | | | 241,553 | | | 142,542 | |

| Total proved reserves: | | | | | |

| Oil (MBbls) | 393,336 | | | 287,032 | | | 153,453 | |

| Natural gas (MMcf) | 1,766,090 | | | 1,033,571 | | | 577,005 | |

| NGL (MBbls) | 237,414 | | | 122,851 | | | 55,583 | |

Total proved reserves (MBoe)(1) | 925,098 | | | 582,146 | | | 305,204 | |

| | | | | |

| Proved developed reserves % | 76 | % | | 59 | % | | 53 | % |

| Proved undeveloped reserves % | 24 | % | | 41 | % | | 47 | % |

| | | | | |

| Reserve values (in millions): | | | | | |

| Standard measure of discounted future net cash flows | $ | 9,526.2 | | | $ | 9,425.6 | | | $ | 3,396.3 | |

| Discounted future income tax expense | 1,581.5 | | | 2,289.1 | | | 481.2 | |

Total proved pre-tax PV 10%(2) | $ | 11,107.7 | | | $ | 11,714.7 | | | $ | 3,877.5 | |

(1) Calculated by converting natural gas to oil equivalent barrels at a ratio of six Mcf of natural gas to one Boe.

(2) Total proved pre-tax PV 10% (“Pre-tax PV 10%”) is a supplemental non-GAAP financial measure as defined by the SEC U.S. Securities and Exchange Commission (“SEC”) and is derived from the standardized measure of discounted future net cash flows (the ‘‘Standardized Measure’’), which is the most directly comparable U.S. generally accepted accounting principles (“GAAP”) financial measure. Pre-tax PV 10% is computed on the same basis as the Standardized Measure but without deducting future income taxes. We believe Pre-tax PV 10% is a useful measure for investors when evaluating the relative monetary significance of our oil and natural gas properties. We further believe investors may utilize our Pre-tax PV 10% as a basis for comparison of the relative size and value of our proved reserves to other companies because many factors that are unique to each individual company impact the amount of future income taxes to be paid. Our management uses this measure when assessing the potential return on investment related to our oil and gas properties and acquisitions. However, Pre-tax PV 10% is not a substitute for the Standardized Measure. Our Pre-tax PV 10% and Standardized Measure do not purport to present the fair value of our proved oil, NGL and natural gas reserves.

Proved Undeveloped Reserves. Our proved undeveloped (“PUD”) reserves decreased by 4.020.5 MMBoe on a net basis from December 31, 20192022 to December 31, 2020,2023, and the following table provides a reconciliation of the changes to our PUD reserves that occurred during the year:

| | | | | |

| (MBoe) | 20202023 |

| Proved undeveloped reserves at January 1, 2023 | 241,553 | | 153,923 |

TransferredTransfers to proved developed reserves | (18,622)(91,234) | |

| Revisions to previous estimates | (37,471)(34,872) | |

| Extensions and discoveries | 52,09147,947 | |

| |

| |

| Purchase of reserves in place | 57,689 | |

| Proved undeveloped reserves at December 31, 2023 | 221,083 | | 149,921 |

During 2020, we spent $158.3 millionThe decrease in capital expendituresproved undeveloped reserves was primarily attributable to convert 18.6converting 91.2 MMBoe of PUD reserves to proved developed reserves. Furthermore, we added 52.1 MMBoe of PUD reserves during the year through extensions and discoveries,2023, for which mainly related to new locations added based on our 2020 drilling results. The majority of these new PUD locations were on our New Mexico acreage within the 2nd and 3rd Bone Spring formations, and we also added locationsspent $870.6 million in the Wolfcamp C and 3rd Bone Spring on our Texas acreage position. Totalcapital expenditures. Additionally, total revisions to previous estimates reduced PUD reserves by a net amount of 37.534.9 MMBoe. Negative revisions during 2020 totaled 114.02023 mainly related to (i) 22.3 MMBoe and consisted of (i) 83.9 MMBoe of downward pricing adjustments, (ii) 25.4 MMBoe of negative revisions associated with PUD locations that were eithermainly reclassified to unproved reserves or removed due to changes inmade to our active development program,plan (ii) 7.6 MMBoe of downward revisions related to lowered estimates associated with timing and performance, and (iii) 4.05.0 MMBoe of reduced PUD reserves removedfrom lower average commodity prices for PUD locations no longer expected to be developed within five years of their initial recording.the year ended 2023. These downward revisionsdecreases in proved undeveloped reserves were partially offset by 76.5adding 57.7 MMBoe of upward revisions primarily relatedPUD reserves, the significant majority of which were from properties acquired in the Earthstone Merger on November 1, 2023 (Refer to reductions to our operating costs and per-well capital expenditures realizedNote 2—Business Combinations under Part II, Item 8 of this Annual Report for further details on the Earthstone Merger). Additionally, we added 47.9 MMBoe of PUD reserves during the year through extensions and applieddiscoveries as a result of our 2023 drilling results, which mainly related to our reserve estimates.new locations added in the various Bone Spring and Wolfcamp formations on the Company’s acreage position in the Delaware Basin. All of our PUD locations are scheduled to be drilled within five years of their initial booking. Our PUD to proved developed reserves conversion rate was 13%38% in 2020, which is lower than historical conversion rates due to our reduced 2020 drilling activity as previously discussed.2023.

For additional information and for a discussion of material changes on our total proved reserves, see Supplemental Information About Oil & Natural Gas Producing Activities, Item 8. Financial Statements and Supplementary Data of this Annual Report.

Preparation of Reserve Estimates

Our proved reserves are estimated by an independent engineering firm, Netherland, Sewell & Associates, Inc. (“NSAI”). Reserve estimates are prepared in accordance with the definitions and regulations of the SEC and the Financial Accounting Standards Board (the “FASB”) using a deterministic method, which includes decline curve analysis, production performance analysis, offset analogies, and in some cases a combination of these methodologies.

Controls over Reserve Estimation

We maintain adequate and effective internal controls over the reserve estimation process and the underlying data which the reserve estimates are based upon. Our reserves estimation process is coordinated by our internal reserves department, which consists of qualified petroleum engineers and is overseen by our Vice President of Strategic Planning and Corporate Reserves.Reserves Manager. Reserve information, including models and other technical data, are stored on a secured database on our network. Certain non-technical inputs used in the reserves estimation process such as ownership interest percentages, oil and natural gas production, commodity prices, price differentials, operating and development costs and plug and abandonment estimates are obtained by other departments and are subject to our internal control process.departments. Annually, our internal reserves department prepares a preliminary reserve database and meets with NSAI to discuss the assumptions and methods to be used in the year-end proved reserve estimation process and to review field performance and our future development plans. Following this review, the reserve database and supporting data is furnished to NSAI for their independent estimates and final report.

Qualifications of Responsible Technical Persons

Our Vice President of Strategic Planning and Corporate Reserves Jeff Thompson,Manager, Joseph Jones, is responsible for overseeing the preparation of the reserves estimates. Mr. ThompsonJones has held this position at CentennialPermian Resources since July 2017September 2022 after formerly serving in a similar role for Colgate prior to the Colgate Merger and has over 1510 years of relevant experience in reservoir engineering and reserve estimation. He holds a Bachelor of Science degree in petroleum engineering from the University of Oklahoma and is a Registered Professional Engineer in Oklahoma and member of the Society of Petroleum Engineers.Texas A&M University.

NSAI was founded in 1961 and performs consulting petroleum engineering services under Texas Board of Professional Engineers Registration No. F-2699. Within NSAI, the technical persons primarily responsible for preparing the estimates set forth in the NSAI reservereserves report incorporated herein are Mr. Neil H. LittleMs. Lily W. Cheung and Mr. Edward C. Roy III. Mr. Little,Zachary R. Long. Ms. Cheung, a Licensed Professional Engineer in the State of Texas (No. 117966)107207), has been practicing consulting petroleum engineering at NSAI since 20112007 and has over 4 years of prior industry experience. She graduated from Massachusetts Institute of Technology in 2003 with a Bachelor of Science Degree in Mechanical Engineering and from University of Texas at Austin in 2007 with a Master of Business

over 9 years of prior industry experience. He graduated from Rice University with a Bachelor of Science Degree in Chemical Engineering and from University of Houston with a Master of Business Administration Degree. Mr. Roy,Long, a Licensed Professional Geoscientist in the State of Texas, Geology (No. 2364)11792), has been practicing consulting petroleum geoscience at NSAI since 20082007 and has over 112 years of prior industry experience. He graduated from Texas Christian University of Louisiana at Lafayette in 2003 with a Bachelor of Science Degree in Petroleum Geology and from Texas A&M University in 2005 with a Master’sMaster of Science Degree in Geology.Geophysics. Both technical principals meet or exceed the education, training, and experience requirements set forth in the Standards Pertaining to the Estimating and Auditing of Oil and Gas Reserves Information promulgated by the Society of Petroleum Engineers; both are proficient in judiciously applying industry standard practices to engineering and geoscience evaluations as well as applying SEC and other industry reservereserves definitions and guidelines.

Production

The following table sets forth information regarding net production of oil, natural gas and NGLs, and certain price and cost information for each of the periods indicated:

| | | | | | | | | | | | | | | | | |

| Year Ended December 31, |

| 2020 | | 2019 | | 2018 |

| Net production: | | | | | |

| Oil (MBbls) | 13,207 | | | 15,582 | | | 12,679 | |

| Natural gas (MMcf) | 41,302 | | | 41,703 | | | 31,707 | |

| NGL (MBbls) | 4,490 | | | 5,234 | | | 4,332 | |

Total (MBoe)(1) | 24,581 | | | 27,766 | | | 22,295 | |

| Average sales price (excluding effect of hedges): | | | | | |

| Oil (per Bbl) | $ | 36.02 | | | $ | 52.02 | | | $ | 55.98 | |

| Natural gas (per Mcf) | 1.13 | | | 1.07 | | | 1.97 | |

| NGL (per Bbl) | 12.91 | | | 17.03 | | | 27.45 | |

Total per BOE(1) | $ | 23.61 | | | $ | 34.01 | | | $ | 39.97 | |

| Operating costs per Boe: | | | | | |

| Lease operating expenses | $ | 4.45 | | | $ | 5.26 | | | $ | 3.74 | |

| Severance and ad valorem taxes | 1.60 | | | 2.28 | | | 2.54 | |

| Gathering, processing and transportation expenses | 2.90 | | | 2.62 | | | 2.58 | |

| | | | | | | | | | | | | | | | | |

| Year Ended December 31, |

| 2023 | | 2022 | | 2021 |

| Net production: | | | | | |

| Oil (MBbls) | 35,560 | | | 18,235 | | | 11,701 | |

| Natural gas (MMcf) | 119,182 | | | 59,692 | | | 40,741 | |

| NGL (MBbls) | 15,569 | | | 6,750 | | | 3,752 | |

Total (MBoe)(1) | 70,992 | | | 34,934 | | | 22,243 | |

| Average sales price (excluding effect of hedges): | | | | | |

| Oil (per Bbl) | $ | 75.84 | | | $ | 88.95 | | | $ | 63.50 | |

Natural gas price excluding the effects of GP&T (per Mcf)(2) | 1.60 | | | 4.86 | | | 3.67 | |

NGL price excluding the effects of GP&T (per Bbl)(3) | 22.83 | | | 35.97 | | | 36.61 | |

Total per Boe(1) | $ | 45.68 | | | $ | 61.69 | | | $ | 46.30 | |

| Operating costs per Boe: | | | | | |

| Lease operating expenses | $ | 5.26 | | | $ | 4.92 | | | $ | 4.78 | |

| Severance and ad valorem taxes | 3.39 | | | 4.46 | | | 3.02 | |

| Gathering, processing and transportation expenses | 1.26 | | | 2.80 | | | 3.86 | |

(1) Calculated by converting natural gas to oil equivalent barrels at a ratio of six Mcf of natural gas to one Boe.

(2) Natural gas average sales price excludes $0.41 per Mcf of gathering, processing and transportation costs (“GP&T”) for the year ended December 31, 2023, $0.22 for the year ended December 31, 2022 and none for the year ended December 31, 2021.

(3) NGL average sales price excludes $4.71 per Bbl of GP&T charges for the year ended December 31, 2023, $1.56 per Bbl for the year ended December 31, 2022 and none for the year ended December 31, 2021.

Productive Wells

As of December 31, 2020,2023, we owned an approximate 75%83% average working interest in 5342,577 gross (400(2,143 net) operated productive wells and an approximate 11% average working interest in 1,094 gross (120 net) non-operated productive wells. Our wells are primarily oil wells (517 gross/387(3,150 gross, 2,018 net productive oil wells) that produce associated liquids-rich natural gas. Productive wells consist of producing wells, wells capable of production and wells awaiting connection to production facilities. Gross wells are the total number of producing wells in which we have an interest, operated and non-operated, and net wells are the sum of our fractional working interests owned in gross wells.

Acreage

The following table sets forth information as of December 31, 20202023 relating to our gross and net developed and undeveloped leasehold acreage. Developed acreage consists of acres spaced or assigned to productive wells and does not include undrilled acreage held by production under the terms of the lease. Undeveloped acreage is defined as acres on which wells have not been drilled or completed to a point that would permit the production of commercial quantities of oil or natural gas, regardless of whether such acreage contains proved reserves.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Developed Acreage(3) | | Undeveloped Acreage(3) | | Total Acreage(3) |

Gross(1) | | Net(2) | | Gross(1) | | Net(2) | | Gross(1) | | Net(2) |

| 60,267 | | | 45,579 | | | 45,983 | | | 36,078 | | | 106,250 | | | 81,657 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Developed Acreage | | Undeveloped Acreage | | Total Acreage |

Gross(1) | | Net(2) | | Gross(1) | | Net(2) | | Gross(1) | | Net(2) |

| 433,957 | | | 345,390 | | | 109,534 | | | 61,663 | | | 543,491 | | | 407,053 | |

(1) A gross acre is an acre in which a working interest is owned. The number of gross acres is the total number of acres in which a working interest is owned.

(2) A net acre is deemed to exist when the sum of the fractional ownership working interests in gross acres equals one. The number of net acres is the sum of the fractional working interests owned in gross acres expressed as whole numbers and fractions thereof.

(3) Does not include our 1,472 net mineral acres.

The following table sets forth the gross and net undeveloped acreage, as of December 31, 2020,2023, that will expire over the next five years unless production is established within the spacing units covering the acreage, the lease is renewed or extended under continuous drilling provisions prior to the primary term expiration dates, or pursuant to other terms of the lease agreements.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| 2021 | | 2022 | | 2023 | | 2024 | | 2025 |

| Gross | | Net | | Gross | | Net | | Gross | | Net | | Gross | | Net | | Gross | | Net |

| 7,776 | | | 5,017 | | | 4,183 | | | 2,171 | | | 1,335 | | | 211 | | | 1,320 | | | 1,081 | | | 320 | | | 320 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| 2024 | | 2025 | | 2026 | | 2027 | | 2028 |

| Gross | | Net | | Gross | | Net | | Gross | | Net | | Gross | | Net | | Gross | | Net |

| 1,620 | | | 766 | | | 1,519 | | | 930 | | | 3,402 | | | 1,700 | | | 1,120 | | | 533 | | | 213 | | | 200 | |

Drilling Results

The following table sets forth the results of our drilling activity, as defined by wells placed on production, for the periods indicated. Productive wells are exploratory, development or extension wells that produce, or are capable of producing, commercial quantities of hydrocarbons, regardless of whether they produce a reasonable rate of return. Dry wells are exploratory, development or extension wells that prove to be incapable of producing hydrocarbons in sufficient quantities to justify incurring the costs associated with completion as an oil or gas well.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Year Ended December 31, |

| 2020 | | 2019 | | 2018 |

| Gross | | Net | | Gross | | Net | | Gross | | Net |

| Development Wells: | | | | | | | | | | | |

Productive(1) | 31 | | | 29.5 | | | 84 | | | 73.6 | | | 80 | | | 72.4 | |

Dry(2) | 1 | | | 1.0 | | | 2 | | | 2.0 | | | — | | | — | |

| 32 | | | 30.5 | | | 86 | | | 75.6 | | | 80 | | | 72.4 | |

| Exploratory Wells: | | | | | | | | | | | |

Productive(1) | — | | | — | | | — | | | — | | | — | | | — | |

| Dry | 1 | | | 1.0 | | | — | | | — | | | — | | | — | |

| 1 | | | 1.0 | | | — | | | — | | | — | | | — | |

| Total | 33 | | | 31.5 | | | 86 | | | 75.6 | | | 80 | | | 72.4 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Year Ended December 31, |

| 2023 | | 2022 | | 2021 |

| Gross | | Net | | Gross | | Net | | Gross | | Net |

| Development Wells: | | | | | | | | | | | |

| Productive | 183 | | | 150.2 | | | 95 | | | 84.9 | | | 42 | | | 38.0 | |

Dry(1) | 2 | | | 1.8 | | | 3 | | | 2.8 | | | — | | | — | |

| 185 | | | 152.0 | | | 98 | | | 87.7 | | | 42 | | | 38.0 | |

| Exploratory Wells: | | | | | | | | | | | |

| Productive | — | | | — | | | — | | | — | | | — | | | — | |

| Dry | — | | | — | | | — | | | — | | | — | | | — | |

| — | | | — | | | — | | | — | | | — | | | — | |

| Total | 185 | | | 152.0 | | | 98 | | | 87.7 | | | 42 | | | 38.0 | |

(1) Although a well may be classified as productive upon completion, future changes in oil and natural gas prices, operating costs and production may result in the well becoming uneconomical, particularly exploratory wells where there is no production history.

(2) The developmental dry hole category includes wells that were unsuccessful due to mechanical issues that occurred during drilling.

As of December 31, 2020,2023, we had 923 gross (8.4(19.5 net) operated wells in the process of drilling completingand 45 gross (36.3 net) operated wells in the process of completion or waiting on completion.

Delivery Commitments

The table below summarizes our firm sales agreements for crude oil, and natural gas, both of which provideprovides for gross firm sales over the contractual terms:

| | | | | | | | | | | | | | | | | | | | | | | | | | |

| | Oil Volume Commitments(1)(2) | | Gas Volume Commitments(1)(3) |

| Period | | Total (Bbl) | | Daily (Bbls/d) | | Total (MMBtu) | | Daily (MMBtu/d) |

| 2021 | | 14,000,000 | | | 38,300 | | | 30,150,000 | | | 82,600 | |

| 2022 | | 18,250,000 | | | 50,000 | | | 12,450,000 | | | 41,000 | |

| 2023 | | 20,075,000 | | | 55,000 | | | — | | | — | |

| 2024 | | 10,980,000 | | | 30,100 | | | — | | | — | |

| 2025 | | 4,530,000 | | | 30,000 | | | — | | | — | |

| Total | | 67,835,000 | | | | | 42,600,000 | | | |

| | | | | | | | | | | | | | |

| | Oil Volume Commitments(1) |

| Period | | Total (Bbl) | | Daily (Bbls/d) |

| 2024 | | 10,610,000 | | | 29,000 | |

| 2025 | | 4,380,000 | | | 29,000 | |

| | | | |

| | | | |

| Total | | 14,990,000 | | | |

(1) Above volumes represent the total gross volumes we are required to deliver per thesepursuant to agreements with carriers, which gross volumes are not comparable to our net production presented in Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operation in this Annual Report, as amounts therein are reflected net of all royalties, overriding royalties and production due to others.

(2) WeThese total oil volumes committed are only requiredsubject to physically deliver 30,000 Bbls/d of the total committed gross volumes of crude oil during the years 2021 through May 2025, andfinancial ship-or-pay penalties if thesesuch physical delivery commitments are not met, a financial obligation would arise. Failure to deliver the remainder of the committed gross volumes of crude oil under these agreements could result, and during 2020 did result, in a reduction of our future firm takeaway capacity at the purchasers’ discretion in accordance with the terms of the agreements.

(3) We are not required to physically deliver these gross volumes over the terms of the agreements, but if the volumetric commitments are not met and the purchaser incurs financial damages, we are required to pay for any differences between the contracted prices and current market prices for replacement volumes bought by the purchaser.

met. We believe our current production and reserves are sufficient to fulfill these physical delivery commitments, and production under the agreements is not tied to any specific property. Therefore, if our production is not sufficient to satisfy the firm delivery commitments above, we believe we can purchase sufficient volumes in the market at index-related prices to satisfy our commitments. See also Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations — Contractual Obligations, in this Annual Report for discussion of our firm transportation commitments related to natural gas deliveries.

Title to Properties

We believe that we have satisfactory title to substantially all of our producing properties in accordance with generally accepted industry standards. Individual properties may be subject to burdens such as royalty, overriding royalty, working and other outstanding interests customary in the industry. In most cases, we investigate title and obtain title opinions from counsel only when we acquire producing properties or before commencement of drilling operations.

Marketing and Customers

We market the majority of the production from properties we operate on account of both ourselves and that of the other working interest owners in these properties. We generally sell our oil, natural gas and NGL production to purchasers at prevailing market prices, which in certain cases are adjusted for contractual differentials, and the majority of our revenue contracts have terms greater than twelve months.

We normally sell production to a relatively small number of customers, as is customary in our business. The table below summarizes the purchasers that accounted for 10% or more of our total net revenues for the periods presented:

| | | | | | | | | | | | | | | | | |

| Year Ended December 31, |

| 2020 | | 2019 | | 2018 |

| BP America | 47 | % | | 37 | % | | 18 | % |

| Shell Trading (US) Company | 20 | % | | 11 | % | | 19 | % |

| Eagleclaw Midstream Ventures, LLC | 8 | % | | 8 | % | | 12 | % |

| ExxonMobil Oil Corporation | 4 | % | | 26 | % | | — | % |

| | | | | | | | | | | | | | | | | |

| Year Ended December 31, |

| 2023 | | 2022 | | 2021 |

| BP America | 20 | % | | 34 | % | | 50 | % |

| Shell Trading (US) Company | 20 | % | | 21 | % | | 22 | % |

| Enterprise Crude Oil, LLC | 30 | % | | 18 | % | | — | % |

| Kinetik Holdings Inc. | 5 | % | | 8 | % | | 11 | % |

During these periods, no other purchaser accounted for 10% or more of our net revenues. The loss of any of our major purchasers could materially and adversely affect our revenues in the near-term. However, since crude oil and natural gas are fungible products with well-established markets and numerous purchasers and are based on current demand for oil and natural

gas, we believe that the loss of any major purchaser would not have a material adverse effect on our financial condition or results of operations.

Competition

The oil and natural gas industry is a highly competitive environment. We compete with both major integrated and other independent oil and natural gas companies in all aspects of our business including exploring, developing and operating our properties as well as transporting and marketing our production. Competitive conditions may be affected by future legislation and regulations as the United States develops new energy and climate-related policies. In addition, some of our competitors may have a competitive advantage when responding to factors that affect the supply and demand for oil and natural gas production, such as price fluctuations (including basis differentials), domestic and foreign political conditions, weather conditions, the proximity and capacity of natural gas pipelines and other transportation facilities and overall economic conditions. We also face indirect competition from alternative energy sources. Our ability to acquire additional prospects and to find and develop reserves in the

future will depend on our ability to evaluate and select suitable properties and to consummate transactions in a highly competitive environment.

Transportation

During the initial development of our fields, we consider all gathering and delivery infrastructure options in the areas of our production. The majority of our oil production is sold at the leasewellhead as it enters third-party gathering pipelines. The purchaser then transports the oil by pipeline or truck to a tank farm, another pipeline or a refinery. Our natural gas is either transported by gathering lines from the wellhead to a central delivery point and is then gathered by third-party lines to a gas processing facility or gathered by a third-party directly from the wellhead.

Regulation of the Oil and Natural Gas Industry

Our operations are subject to extensive federal, state and local laws and regulations. All of the jurisdictions in which we own or operate producing properties have statutory provisions regulating the development and production of oil and natural gas, including, but not limited to, provisions related to permits for the drilling of wells, bonding requirements to drill or operate wells, the location of wells, the method of drilling and casing wells, the surface use and restoration of properties upon which wells are drilled, sourcing and disposal of water used in the drilling and completion process, and the abandonment of wells. Our operations are also subject to various conservation laws and regulations including, but not limited to, the regulation of the size of drilling and spacing units or proration units, the number of wells which may be drilled in an area, and the unitization or pooling of crude oil or natural gas wells, as well as regulations that generally prohibit the venting or flaring of natural gas and impose certain requirements regarding the ratability or fair apportionment of production from fields and individual wells.

Failure to comply with applicable laws and regulations can result in substantial penalties. The regulatory burden on the industry increases the cost of doing business and affects profitability. Although we believe we are in substantial compliance with all applicable laws and regulations, such laws and regulations are frequently amended or reinterpreted. Therefore, we are unable to predict the future costs or impact of compliance. Additional proposals and proceedings affecting the oil and natural gas industry are regularly considered by Congress, the states, regulatory authorities, including the Federal Energy Regulatory Commission (“FERC”), and the courts. We cannot predict when or whether any such proposals may become effective.

We believe we are in substantial compliance with currently applicable laws and regulations and that continued substantial compliance with existing requirements will not have a material adverse effect on our financial position, cash flows or results of operations. However, current regulatory requirements may change, currently unforeseen environmental, health or safety incidents may occur or past non-compliance with environmental, health and safety laws or regulations may be discovered. In addition, governmental, scientific, and public concern over the threat of climate change arising from increasing global greenhouse gas (“GHG”) emissions has resulted in higher political and regulatory risks in the United States, including climate change related pledges made by certain administrations. President Biden has issued several executive orders focused on addressing climate change since taking office, which may impact the costs to produce, or demand for, oil and natural gas. Additionally, in November 2021, the Biden administration released “The Long-Term Strategy of the United States: Pathways to Net-Zero Greenhouse Gas Emissions by 2050,” which establishes a roadmap to net zero emissions in the United States by 2050 through, among other things, improving energy efficiency; decarbonizing energy sources via electricity, hydrogen, and sustainable biofuels; and reducing non-carbon dioxide GHG emissions, such as methane and nitrous oxide. The Biden administration has also proposed certain changes to the leasing and permitting programs for oil and natural gas development on federal lands, including imposing bans on new oil and gas leasing, cancelling issued oil and gas leases, and removing public lands from future oil and gas leasing.

Regulation of Production of Oil and Natural Gas

The production of oil, natural gas and NGLs is subject to regulation under a wide range of local, state and federal statutes, rules, orders and regulations. Federal, state and local statutes and regulations require permits for drilling operations, drilling bonds and reports concerning operations. We own interests in properties located in New Mexico and Texas, which regulate drilling and operating activities by, among other things, requiring permits for the drilling of wells, maintaining bonding requirements in order to drill or operate wells, and regulating the location of wells, the method of drilling and casing wells, the surface use and restoration of properties upon which wells are drilled and the plugging and abandonment of wells. The laws of New Mexico and Texas also govern a number of conservation matters, including provisions for the unitization or pooling of oil and natural gas properties, the establishment of maximum allowable rates of production from oil and natural gas wells, the regulation of well spacing or density, and plugging and abandonment of wells. The effect of these regulations is to limit the amount of oil, natural gas and NGLs that we can produce from our wells and to limit the number of wells or the locations where we can drill, although we can apply for exceptions to such regulations or to have reductions in well spacing or density. Moreover, New Mexico and Texas impose a production or severance tax with respect to the production and sale of oil, natural gas and NGLs within their jurisdiction.

Our competitors in the oil and natural gas industry are subject to the same regulatory requirements and restrictions that affect our operations, and as a result we do not expect compliance with such regulatory requirements to affect our operations in any way

that is of material difference from our competitors who are similarly situated. However, the failure to comply with these rules and regulations can result in substantial penalties.

Regulation of Sales and Transportation of Oil

Sales of oil, condensate and NGLs from our producing wells are not currently regulated and are made at negotiated prices. Nevertheless, Congress could enact price controls in the future.

Sales of oil are affected by the availability, terms and conditions and cost of transportation services. The transportation of oil in common carrier pipelines is also subject to rate and access regulation. FERC regulates the transportation in interstate commerce of crude oil, petroleum products, NGLs and other forms of liquid fuel under the Interstate Commerce Act.

Intrastate oil pipeline transportation rates are subject to regulation by state regulatory commissions. The basis for intrastate oil pipeline regulation, and the degree of regulatory oversight and scrutiny given to intrastate oil pipeline rates, varies from state to state. We rely on third-party pipeline systems to transport the majority of crude oil produced by ours wells. Insofar as effective interstate and intrastate rates and regulations regarding access are equally applicable to all comparable shippers, we believe that the regulation of oil transportation will not affect our operations in any way that is of material difference from those of our competitors who are similarly situated.

Changes in FERC or state policies and regulations or laws may adversely affect the availability and reliability of firm and/or interruptible transportation service on interstate and intrastate pipelines, and we cannot predict what future action FERC or state regulatory bodies will take. We do not believe, however, that any regulatory changes will affect us in a way that materially differs from the way they will affect other oil producers and marketers with which we compete.

Regulation of Transportation and Sales of Natural Gas

Historically, the transportation and sale of natural gas in interstate commerce have been regulated by agencies of the U.S. federal government, primarily FERC. In the past, the federal government regulated the prices at which natural gas could be sold. While sales by producers of natural gas can currently be made at uncontrolled market prices, Congress could reenact price controls in the future. Deregulation of wellhead natural gas sales began with the enactment of the Natural Gas Policy Act of 1978 (the “NGPA”) and culminated in adoption of the Natural Gas Wellhead Decontrol Act, which removed controls affecting wellhead sales of natural gas effective January 1, 1993. The transportation and sale for resale of natural gas in interstate commerce is regulated primarily under the Natural Gas Act of 1938 (the “NGA”), and by regulations and orders promulgated under the NGA by FERC. In certain limited circumstances, intrastate transportation and wholesale sales of natural gas may also be affected directly or indirectly by laws enacted by Congress and by FERC regulations.