Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes: ý ☒No: ¨☐

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Exchange Act. Yes: ¨ ☐No: ý☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15 (d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports) and (2) has been subject to such filing requirements for the past 90 days. Yes: ý ☒No: ¨☐

Indicate by check mark whether the registrant has submitted electronically, every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (Section 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes: ý ☒No: ¨☐

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ¨☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☒

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes: ¨☐ No: ý☒

Prior to the separation of the registrant from Autoliv, Inc., on June 29, 2018, the registrant was a wholly-owned subsidiary of Autoliv, Inc. Consequently, there was no

The aggregate market value of the registrant'sregistrant’s voting and non-voting common stockequity held by non-affiliates of the registrant as ofon June 29, 2018, the30, 2021 (the last business day of the most recently completed second fiscal quarter.quarter) was approximately $2.58 billion.

As of February 15, 2019,March 30, 2022, there were 87,178,772112,140,210 shares of common stock of Veoneer, Inc., par value $1.00 per share, outstanding.

Documents Incorporated

DOCUMENTS INCORPORATED BY REFERENCE

None.

EXPLANATORY NOTE

Veoneer, Inc., referred to in this report as “Veoneer,” “the Company,” “we,” “us,” and “our,” is filing this Amendment No. 1 on Form 10-K/A (this “Amendment”) to its Annual Report on Form 10-K for the year ended December 31, 2021, originally filed with the Securities and Exchange Commission (the “SEC”) on February 17, 2022 (the “Original Report”), for the sole purpose of including the information required by ReferencePart III, Items 10 through 14, of Form 10-K. This information was previously omitted from the Original Report in reliance on General Instruction G(3) to Form 10-K, which permits the information in Part III to be incorporated in the Form 10-K by reference from our definitive proxy statement if such statement is filed no later than 120 days after our fiscal year end. We are filing this Amendment to provide information required in Part III of Form 10-K for the fiscal year ended December 31, 2021, because the Company does not intend to file a definitive proxy statement containing such information within 120 days of December 31, 2021.

|

| |

Document | Where Incorporated |

Proxy Statement* | Part III (Items 10, 11, 12, 13 and 14) |

*As statedIn accordance with Rule 12b-15 under variousthe Securities Exchange Act of 1934, as amended (the “Exchange Act”), Part III, Items 10 through 14 of the Original Report are hereby amended and restated in their entirety, and Part IV, Item 15 of the Original Report is hereby amended and restated only with respect to the addition of the new certifications by our principal executive officer and principal financial officer filed herewith. Except as described above or as otherwise expressly provided by the terms of this Report, only certain specified portionsAmendment, no other changes have been made to the Original Report. This Amendment does not reflect events occurring after the filing of the registrant’sOriginal Report, does not modify or update in any way the disclosures contained in the Original Report, and does not modify or update those disclosures that may be affected by subsequent events. Accordingly, this Amendment should be read in conjunction with the Original Report and with our filings with the SEC subsequent to the Original Report.

On October 4, 2021, Veoneer entered into a definitive Proxy Statementagreement with SSW HoldCo LP (“SSW”), a Delaware limited partnership, SSW Merger Sub Corp, a Delaware corporation and a direct, wholly owned subsidiary of SSW (“Merger Sub”), and QUALCOMM Incorporated (“Qualcomm”) providing for the annual stockholders’ meetingmerger of Merger Sub with and into the Company, with the Company continuing as a wholly owned subsidiary of SSW (the “Merger”).

Shortly after the closing of the Merger, it is contemplated that SSW will sell Veoneer's dedicated software unit, referred to as the Arriver business, to Qualcomm and retain Veoneer’s Tier-1 supplier businesses.

Pursuant to the Merger Agreement, at the effective time of the Merger (the “Effective Time”):

| • | each share of common stock, par value $1.00 per share, of the Company (the “Common Stock”) issued and outstanding immediately prior to the Effective Time (other than any shares cancelled pursuant to the Merger Agreement) will be converted into the right to receive $37.00 per share of Common Stock in cash, without interest and subject to any tax withholding required by applicable law (the “Merger Consideration”); |

| • | each Company stock option (whether or not vested) that is outstanding immediately prior to the Effective Time will automatically vest (if unvested) and be cancelled and converted into the right to receive an amount in cash, without interest and subject to any tax withholding required by applicable law, equal to the product of (i) the excess, if any, of (A) the Merger Consideration over (B) the per-share exercise price for such Company stock option and (ii) the total number of shares of Common Stock underlying such Company stock option, provided, that if the exercise price per share of Common Stock of such Company stock option is equal to or greater than the Merger Consideration, such Company stock option shall be cancelled without any cash payment or other consideration being made in respect thereof; |

| • | each Company time-based restricted stock unit that is outstanding immediately prior to the Effective Time will automatically vest (if unvested) and be cancelled and converted into the right to receive an amount in cash, without interest and subject to any tax withholding required by applicable law, equal to the product of (i) the total number of shares of Common Stock underlying such Company time-based restricted stock unit (including any shares of Common Stock in respect of dividend equivalent units credited thereon) and (ii) the Merger Consideration; and |

| • | each Company performance-based restricted stock unit that is outstanding immediately prior to the Effective Time will automatically vest (if unvested) and be cancelled and converted into the right to receive an amount in cash, without interest and subject to any tax withholding required by applicable law, equal to the product of (i) the number of shares of Company Common Stock underlying such Company PSU (including any shares of Common Stock in respect of dividend equivalent units credited thereon) determined based on the attainment of the applicable performance metrics at (x) the actual level of performance for any performance periods that have concluded prior to the date of the Merger Agreement, and (y) the greater of the target level of performance or actual level of performance measured through the date on which the Closing of the Merger occurs (as determined by the Board), for any performance periods that would otherwise conclude following the date of the Merger Agreement, in each case, and (ii) the Merger Consideration. |

In connection with the Merger, the Company’s securities will be held on May 8, 2019, to be dated on or around March 28, 2019 (the “2019 Proxy Statement”) are incorporated by reference in this Report.de-listed from the New York Stock Exchange and de-registered under the Exchange Act as soon as practicable following the Effective Time.

TABLE OF CONTENTS

VEONEER, INC.

FORM 10-K/A

For the Year Ended December 31, 2021

PART III

|

| | |

| | |

| PART I | |

Item 1. | | |

Item 1A. | | |

Item 1B. | | |

Item 2. | | |

Item 3. | | |

Item 4. | | |

| PART II | |

Item 5. | | |

Item 6. | | |

Item 7. | | |

Item 7A. | | |

Item 8. | | |

Item 9. | | |

Item 9A. | | |

Item 9B. | | |

| PART III | |

| Item 10. | | 4 |

| Item 11. | | 11 |

| Item 12. | | 34 |

| Item 13. | | 35 |

| Item 14. | | 36 |

| | | |

| PART IV | | |

| Item 15. | | 37 |

| Signatures | |

Part III

Item 16.10. | | Directors, Executive Officers and Corporate Governance |

FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K contains forward-looking statements withinThe Company’s bylaws (the “Bylaws”) provide that the meaningsize of the Private Securities Litigation Reform Act of 1995. All statements contained in this Annual Report on Form 10-K other than statements of historical fact, including without limitation, statements regarding management’s examination of historical operating trends and data, estimates of future sales (including estimates related to order intake), operating margin, cash flow, taxes or other future operating performance or financial results, are forward-looking statements. In some cases, you can identify these statements by forward-looking words such as “estimates,” “expects,” “anticipates,” “projects,” “plans,” “intends,” “believes,” “may,” “likely,” “might,” “would,” “should,” “could,” or the negative of these terms and other comparable terminology, although not all forward-looking statements contain such words. We have based these forward-looking statements on our current expectations and assumptions and/or data available from third parties about future events and trends that we believe may affect our financial condition, results of operations, business strategy, short-term and long-term business operations and objectives and financial needs.

New risks and uncertainties ariseBoard shall be fixed from time to time exclusively by the Board. The Board has currently fixed the size of the Board at seven. The Board currently consists of seven members divided into three classes.

The directors designated in the first class have terms expiring in 2022 (Class I); the directors designated in the second class have terms expiring in 2023 (Class II); and itthe directors designated in the third class have terms expiring in 2024 (Class III). Each director will be elected at such meetings to serve a term of three years, with each director’s term to expire at the annual meeting held three years after the director’s election.

Below are biographical summaries current as of the date of this Form 10-K/A for each of our directors.

Class I Directors

Mark Durcan

Director Since: June 29, 2018

Current Other Public Directorships: Advanced Micro Devices, Inc., AmerisourceBergen Corporation, and ASML Holding NV

Age: 60 | | Mr. Durcan served as Chief Executive Officer of Micron Technology, Inc., a memory and storage solutions company, from February 2012 until May 2017. Mr. Durcan joined Micron Technology in 1984 and held a variety of senior leadership positions at the company, including President and Chief Operating Officer from June 2007 to February 2012, Chief Operating Officer from February 2006 to 2007 and Chief Technical Officer from 1998 to February 2006. Mr. Durcan has been a member of the board of directors of Advanced Micro Devices, Inc. since October 2017, a director of St. Luke’s Health System of Idaho since February 2017, a director of AmerisourceBergen Corporation since September 2015, and a member of the Supervisory Board of ASML Holding NV, a manufacturer of chip-making equipment, since April 2020. Mr. Durcan also served on the board of the Semiconductor Industry Association from 2011 to 2017. Mr. Durcan holds a Bachelor of Science and Master of Chemical Engineering degree from Rice University and is currently a member of its Board of Trustees.

Qualifications: Mr. Durcan is a seasoned business executive who brings demonstrated skill in the areas of strategic planning, semiconductor technology, finance and corporate governance to the Board.

|

Jonas Synnergren

Director Since: June 29, 2018

Current Other Public Directorships: Nordea

Age: 44 | | Mr. Synnergren has been a partner at Cevian Capital AB, investment advisor to the international investment firm, Cevian Capital since 2009 and was promoted to Senior Partner in 2020. Mr. Synnergren joined Cevian in 2007 and has been head of Cevian’s Swedish office since 2012. In 2006 Mr. Synnergren was Interim CEO and Head of Investor Relations and Business Development of Svalan Konsortier AB, a Swedish Real Estate fund based in Stockholm. From 2000 to 2006, Mr. Synnergren worked for the Boston Consulting Group, ultimately as a Project Leader, where he led projects related to strategy, organization and operational efficiency, including IT-related assignments. During his time with the Boston Consulting Group, Mr. Synnergren’s main focus was financial services. Mr. Synnergren served on the board of directors of Tieto Corporation, a Finnish IT software and services company, from 2012 through early 2019. Mr. Synnergren has served on the board of directors of Nordea, a Nordic bank headquartered in Finland, since May 28, 2020. Mr. Synnergren has also served on the Nomination Committee of Ericsson, a Swedish telecom equipment company, since 2019. Mr. Synnergren served on the Nomination Board of Metso, a Finnish industry machinery company, from 2014 to 2016. Mr. Synnergren has a Master of Science in Economics and Business from the Stockholm School of Economics, including studying at HEC Paris.

Qualifications: The Board benefits from Mr. Synnergren’s deep knowledge of capital markets, mergers and acquisitions and investment expertise. |

Mr. Synnergren was initially appointed as a director of the Company pursuant to the terms of a Cooperation Agreement between the Company and Cevian Capital II GP Limited (“Cevian”), and its affiliates (the “Cooperation Agreement”), as described below under “Relationships and Related Party Transactions – Stockholder Agreements- Cooperation Agreement with Cevian Capital II GP Limited”. As of the date of this Report, Cevian owns at least 8% of the outstanding common stock of the Company. Pursuant to the terms of the Cooperation Agreement, Mr. Synnergren has agreed to offer his resignation from the Board if Cevian no longer owns at least 8% of the then-outstanding shares of common stock of Veoneer.

Class II Directors

Kazuhiko Sakamoto

Director Since: June 29, 2018

Age: 76 | | Mr. Sakamoto has served as an outside auditor of Zenitaka Corporation, a mid-sized construction company listed on the Tokyo Stock Exchange, since 2016. Mr. Sakamoto previously served in a number of senior executive roles at Marubeni Corporation, one of Japan’s leading general trading houses, and Marubeni Construction Material Lease Co. Ltd., a company affiliated with Marubeni Corporation, over the course of 40 years. Mr. Sakamoto served as a director of Autoliv, Inc. from 2007 until the Spin-off (as defined below). He has a degree from Keio University, and attended the Harvard University Research Institute for International Affairs. Qualifications: Mr. Sakamoto brings to the Board a unique set of skills and insights gained through his extensive business experience in both Asia and North America.

|

Wolfgang Ziebart

Director Since: June 29, 2018

Current Other Public Directorships: Nordex SE

Age: 72 | | Dr. Ziebart had a distinguished career with BMW beginning in 1977, which took him to the Board of Management, where he was responsible for R&D and Purchasing. From 2000 to 2004, he was Member of the Board of Management of automotive supplier Continental, where he was in charge of the electronics and the brake business. Between 2004 and 2008, he was President and CEO of Infineon Technologies AG, a global semiconductor and system solutions provider listed on the Frankfurt Stock Exchange. Dr. Ziebart was also previously employed by Jaguar Land Rover, where he served in a consulting role related to product development. Dr. Ziebart serves on the Supervisory Board of Webasto SE, an automotive supplier, mainly for body systems, and is the Chairman of the Supervisory Board of Nordex SE, a wind turbine manufacturer. Dr. Ziebart served as a director of Autoliv, Inc. from 2008 to 2013, and from December 2015 until the Spin-off. Dr. Ziebart holds a doctorate degree in mechanical engineering from the Technical University of Munich in Germany. Qualifications: Dr. Ziebart brings to the Board his extensive knowledge of the automotive industry, gained through his years of experience, including, in particular, with engineering and development.

|

Class III Directors

Robert W. Alspaugh

Director Since: June 29, 2018

Current Other Public Directorships: Triton International Ltd.

Age: 75 | | Mr. Alspaugh had a 36-year career with KPMG, serving in a number of roles, including as the senior partner for a diverse array of companies across a broad range of industries. He has worked with global companies in Europe and Japan in addition to those headquartered in the U.S. Mr. Alspaugh also serves on the board of directors of Triton International Ltd., which is a public company, and DSGI Technologies, Inc., a private company. Mr. Alspaugh served on the board of Autoliv, Inc. from 2006 until the Spin-off. Mr. Alspaugh has a BBA degree, summa cum laude, in Accounting from Baylor University. Qualifications: Mr. Alspaugh brings his technical skills and knowledge gained through his extensive global business experience to the Board. |

Jan Carlson

Director Since: April 1, 2018

Current Other Public Directorships: Autoliv, Inc. and Telefonaktiebolaget LM Ericsson

Age: 61 | | Mr. Carlson has been the Chairman of the Board of Veoneer since the Spin-off, and President and Chief Executive Officer of Veoneer since April 1, 2018. Before the Spin-off, Mr. Carlson served as the President and Chief Executive Officer of Autoliv since April 1, 2007. Mr. Carlson joined Autoliv in 1999 as President of Autoliv Electronics, and later served as Vice President, Engineering and a member of Autoliv’s Executive Committee. Mr. Carlson was appointed Chairman of the board of directors of Autoliv in May 2014 and continues to serve in that role. Mr. Carlson has served on the board of directors of Telefonaktiebolaget LM Ericsson since February 2017. Mr. Carlson has been nominated for election to the board of directors of AB Volvo, a commercial transport solutions company, at its Annual General Meeting scheduled to be held on April 6, 2022. Mr. Carlson has a Master of Science degree in Physics and Electrical Engineering from the University of Linköping in Sweden and was appointed Technology Honorary Doctorate by the University in May 2018. Qualifications: Mr. Carlson brings his extensive knowledge of Veoneer’s operations, business and industry to the Board and Mr. Carlson’s role as Chief Executive Officer of Veoneer provides the Board with insight into the day-to-day operations of the Company. |

James M. Ringler

Director Since: April 1, 2018

Current Other Public Directorships: Autoliv, Inc., TechnipFMC plc, JBT Corporation, and Teradata Corporation

Age: 76 | | Mr. Ringler served as Vice Chairman of Illinois Tool Works Inc. between 1999 and 2004. Prior to joining Illinois Tool Works, Mr. Ringler served in a number of executive positions at Premark International, Inc., including as Chairman, President, and Chief Executive Officer until the company merged with Illinois Tool Works in 1999. Mr. Ringler served as a director of Autoliv, Inc. from 2002 until 2021, and also serves on the board of directors of TechnipFMC plc and JBT Corporation. Mr. Ringler also previously served on the board of directors of Teradata Corporation until 2021. Mr. Ringler holds a Bachelor of Science degree in Business Administration and an MBA degree in Finance from the State University of New York. Qualifications: Mr. Ringler brings to the Board his business and management experience in multiple executive positions at Premark International, Inc. and Illinois Tool Works and his deep knowledge of manufacturing, technology and corporate governance gained through his extensive service on the boards of directors of public companies in a wide variety of industries. |

Executive Officers of the Company

Set forth below is information regarding our current executive officers of the Company as defined in Rule 3b-7 under the Securities Exchange Act of 1934, as amended, who are not also directors:

Ray Pekar

Executive Officer Since: March 1, 2021

Title: CFO and Executive Vice President, Finance Age: 59

| | Mr. Pekar has served as the Chief Financial Officer and Executive Vice President, Finance of the Company since March 2021. Mr. Pekar joined the Company in April 2018 as Vice President, Investor Relations, in connection with the spin-off of the Company by Autoliv, Inc. Prior to that, Mr. Pekar served in various roles of increasing responsibility at Autoliv, Inc. beginning in 1996, including Vice President, IR and M&A from January 2005 until April 2018 and VP Finance and Tech Center General Manager for North America from June 1998 until January 2005. Mr. Pekar holds a Bachelor of Commerce Degree from the University of Windsor with a concentration in finance and accounting. He is also a CPA, CMA receiving his accreditation in Ontario, Canada.

|

Matthias Bieler

Executive Officer Since: February 1, 2020

Title: Executive Vice President, Business Unit

Europe

Age: 55

| | Mr. Bieler has served as Executive Vice President, Business Area Vision & DMS since April 1, 2021. Prior to that he served as Executive Vice President, Business Unit Europe of the Company (beginning in February 2020) and as Vice President and Managing Director for VW, PAS and JLR (beginning in November 2019). Prior to joining the Company, Mr. Bieler was self-employed for several years after holding multiple senior management positions within program management, business development and sales in Europe and China for TRW Automotive, and then, following its acquisition of TRW Automotive, as a Senior Vice President for ZF Friedrichshafen from 2015-2017. Mr. Bieler holds an engineering degree in electrical engineering from University of Paderborn and an Executive MBA from Henley Management College. |

Robert Bisciotti

Executive Officer Since: August 1, 2020

Title: Executive Vice President, Business Unit North America

Age: 59 | | Mr. Bisciotti has served as Executive Vice President, Business Unit North America since August 1, 2020. Mr. Bisciotti previously served as the Company’s Vice President and Managing Director-Ford Business Unit since July 2018. Prior to joining the Company, Mr. Bisciotti was the VP-Autoliv Electronics Europe and America, VP-ANBS Operations & Sales, VP-Autoliv NA Sales at Autoliv, Inc. Mr. Bisciotti holds a Bachelor’s degree in Electrical Engineering and an MBA from Villanova University.

|

Steven Jenkins

Executive Officer Since: May 1, 2021

Title: Chief Technology Officer

Age: 43 | | Mr. Jenkins has served as Chief Technology Officer since April 2021. Prior to that, he served as Director of Technical Competence since December 2018 and as Department Manager of Software Engineering from June 2016 until December 2018. Prior to joining the Company, Mr. Jenkins served as Department Manager – Software Engineering for Autoliv, Inc. from October 2017 until April 2018 and as a Manager – Systems Design for Autoliv, Inc. from June 2016 until September 2017. Prior to his career at Autoliv, Mr. Jenkins served as a Software Engineering Manager at Arris, Inc. from May 2013 until May 2016. Mr. Jenkins holds a Bachelor’s degree in Computer Science from University of Bradford. |

Thomas Jönsson

Executive Officer Since: April 1, 2018

Title: Executive Vice President, Communications and Investor Relations

Age: 56 | | Mr. Jönsson has served as Executive Vice President, Communications and Investor Relations of the Company since April 1, 2018. Prior to joining the Company, Mr. Jönsson served as Vice President, Corporate Communications of Autoliv since May 2013. Prior to joining Autoliv in January 2013, Mr. Jönsson served from June 2010 to December 2012 as Vice President of Brand and External Communications for TeliaSonera, a leading Nordic and Baltic telecommunications company. Before joining TeliaSonera, Mr. Jönsson had an international career working for Nokia and Intel Corporation. Mr. Jönsson studied Business Administration at the University of Stockholm.

|

| | |

Mikael Landberg

Executive Officer Since: March 1, 2020

Title: Executive Vice President, Human Resources

Age: 53 | | Mr. Landberg has served as Executive Vice President, Human Resources of the Company since March 1, 2020. Immediately prior to joining the Company, he served as the Chief Human Resources Officer of Sweco AB since January 2018. Prior to that, Mr. Landberg worked for DeLaval for almost ten years, where he served in progressively senior positions and was appointed Senior Vice President of Human Resources in 2012. Mr. Landberg holds a Bachelor´s degree in Human Resources, Industrial Relations and Labour Relations from Uppsala University, and an Executive MBA from the Stockholm School of Economics. |

| | |

Christer Lundström

Executive Officer Since: May 6, 2020

Title: Executive Vice President, Quality

Age: 57 | | Mr. Lundström has served as Executive Vice President, Operations & Quality of the Company since May 1, 2021. From May 6, 2021 until May 1, 2021. Mr. Lundström served as Executive Vice President, Quality (beginning May 6, 2021), and Senior Vice President, Quality (beginning March 19, 2020) of the Company. Prior to coming to work for the Company, Mr. Lundström was employed by Volvo Car Corporation, based in Gothenburg, Sweden, from May 1989 until March 18, 2020. From 2011 until 2016, Mr. Lundström had the position Vice President, Manufacturing Quality and from 2016 until the end of his employment on March 18, 2020, Vice President, Marketing, Sales, and Service Quality. Mr. Lundström has a Master of Science degree in Computer Science and Computer Engineering. |

| | |

Christoph Schmickler

Executive Officer Since: May 10, 2021 Title: Executive Vice President, ADAS ECU & Integration Product Area

Age: 54

| | Mr. Schmickler has served as the Company’s Executive Vice President, ADAS ECU & Integration beginning in May 10, 2021, and as Senior Vice President and Managing Director, Business Unit, Europe of the Company beginning in 2020. Prior to joining the Company, Mr. Schmickler served as Vice President, Sales and Business Development at Zenuity GmbH (2017-2020), and Director, Business Development, Europe Active Safety (2012-2016) for Autoliv Electronics. |

| | |

Lars Sjöbring

Executive Officer Since: April 1, 2018

Title: Executive Vice President, Legal Affairs, General Counsel and Secretary

Age: 54 | | Mr. Sjöbring has served as Executive Vice President, Legal Affairs, General Counsel and Secretary of the Company since April 1, 2018. Prior to that, Mr. Sjöbring served as Group Vice President, Legal Affairs, General Counsel and Secretary of Autoliv since November 2015. Mr. Sjöbring served as Senior Vice President and General Counsel of Transocean Ltd., a leading international provider of offshore contract drilling services, from March 2014 through November 2015. Prior to his time with Transocean, Mr. Sjöbring served as Autoliv’s Vice President, Legal Affairs, General Counsel and Secretary from September 2007 until February 2014. Over the course of his career, Mr. Sjöbring has also held various positions at Telia AB, Skadden Arps, Slate, Meagher and Flom LLP and Nokia Corporation. Mr. Sjöbring holds Master of Law degrees from the University of Lund in Sweden and Amsterdam School of International Relations (ASIR) in the Netherlands and a Master of Corporate Law degree from Fordham University School of Law in New York.

|

| | |

Chris Van Dan Elzen

Executive Officer Since: May 1, 2021

Title: Executive Vice President, Radar

Age: 50 | | Mr. Van Dan Elzen has served as Executive Vice President, Radar at Veoneer since May 2021. Mr. Van Dan Elzen previously held the positions of Vice President and Managing Director from July 2019 until May 2021, and Vice President, Product Planning from April 2018 until July 2019 at the Company. Prior to joining Veoneer, Mr. Van Dan Elzen held the positions of Vice President Product Planning from December 2016 until April 2018 and Senior Director Business Development from October 2016 until December 2016 at Autoliv, Inc. Mr. Van Dan Elzen has a Master of Science in Engineering from Oakland University, Rochester, Michigan, and three Bachelor of Science degrees in engineering from Oakland University, Rochester, Michigan, as well as Master of Business Administration from University of Michigan, Ann Arbor, Michigan. |

Corporate Governance Guidelines and Code of Conduct and Ethics

The Board has adopted Corporate Governance Guidelines to guide the Board in the exercise of its responsibilities and a Code of Conduct and Ethics for Directors to assist the individual directors in fulfilling their duties as members of the Board. The Company also has Standards of Business Conduct and Ethics that apply to all employees of the Company and a Code of Conduct and Ethics for Senior Officers (the Code of Conduct and Ethics for Directors, Code of Conduct and Ethics for Senior Officers, and Standards of Business Conduct and Ethics are collectively referred to herein as the “Codes”).

The Company has also adopted a written policy regarding related person transactions (the “Related Person Transactions Policy”). The Company’s Corporate Governance Guidelines, the Codes and the Related Person Transactions Policy, and any amendments or waivers related thereto, are posted on the Company’s website at www.Veoneer.com – Who we are – Governance, and can also be obtained from the Company in print by request using the contact information below.

Board Committees

Committees of the Board

There are three standing committees of the Board: the Audit Committee, the Compensation Committee and the Nominating and Corporate Governance Committee. The Board has determined that all members of the Audit, the Compensation, and the Nominating and Corporate Governance Committees qualify as independent directors under the applicable rules of the NYSE, the Sarbanes-Oxley Act of 2002, as amended, and the rules and regulations promulgated by the SEC. While no formal policy exists regarding the attendance of the CEO and the Chairman at committee meetings, the practice of the Board is to invite the CEO and the Chairman to attend each committee meeting and excuse them when matters relating to them are discussed. The Lead Independent Director is also invited to attend all committee meetings. The following table shows the composition of the committees of the Board:

| Audit Committee | Compensation Committee | Nominating and Corporate Governance Committee |

| Robert W. Alspaugh (Chair) | James M. Ringler (Chair) | Wolfgang Ziebart (Chair) |

| Jonas Synnergren | Mark Durcan | James M. Ringler |

| Wolfgang Ziebart | Kazuhiko Sakamoto | Jonas Synnergren |

The Audit Committee

The Audit Committee appoints, subject to stockholder ratification, the Company’s independent auditors and is responsible for the compensation, retention and oversight of the work of the independent auditors and for any special assignments given to such auditors. The Audit Committee reviews the independence of the independent auditors and considers whether there should be a regular rotation of the independent auditors. In addition, the Audit Committee evaluates the lead audit partner’s qualifications and performance. The Audit Committee also evaluates the selection of the lead audit partner, including his or her qualifications and performance. The Audit Committee also (i) reviews the annual audit and its scope, including the results of the independent auditors’ audit and management’s responses thereto; (ii) reviews the performance of the independent auditors, including the lead partner; (iii) approves any non-audit services provided to the Company by its independent auditors; (iv) reviews possible violations of the Company’s business ethics and conflicts of interest policies; (v) reviews any major accounting changes made or contemplated; (vi) reviews the effectiveness and efficiency of the Company’s internal audit staff; and (vii) monitors legal, regulatory and financial risk, including those related to ethics practices and information technology (including cybersecurity), as well as discusses risk oversight and management as part of its obligations under the NYSE’s listing standards. In addition, the Audit Committee confirms that no restrictions have been imposed by Company personnel on the scope of the independent auditors’ examinations. The Audit Committee is also responsible for our managementthe review and approval of related person transactions. Members of this committee are Mr. Alspaugh (Chairman), Mr. Synnergren and Dr. Ziebart. The Audit Committee met eight times in 2021.

The Compensation Committee

The Compensation Committee advises the Board with respect to predict all risks, nor can we assess the impact of all factors on our business or the extent to which any factor, or combination of factors, may cause actual results to differ materially from those contained in any forward-looking statements we may make. Factors that could cause actual results to differ materially from these forward-looking statements include, without limitation, the following: the cyclical nature of automotive sales and production; changes in general industry and market conditions or regional growth or decline; our ability to achieve the intended benefits from our separation from our former parent; our abilitycompensation to be awarded new business or loss of business from increased competition; higher than anticipated costs and use of resources related to developing new technologies; higher raw material, energy and commodity costs; component shortages; changes in customer and consumer preferences for end products; market acceptance of our new products; dependence on and relationships with customers and suppliers; unfavorable fluctuations in currencies or interest rates among the various jurisdictions in which we operate; costs or difficulties relatedpaid to the integrationdirectors and executive officers of any new or acquired businessesthe Company and technologies; successful integrationis responsible for approving the terms of acquisitionscontracts to be entered into with the senior executives of the Company. The committee also administers the Company’s cash and operations of joint ventures; successful implementation of strategic partnershipsstock incentive plans and collaborations; product liability, warrantyreviews and recall claims and investigations and other litigation and customer reactions thereto; higher expenses for our pension and other post-retirement benefits, including higher funding needs for our pension plans; work stoppages or other labor issues; possible adverse results of future litigation, regulatory actions or investigations or infringement claims; our ability to protect our intellectual property rights; tax assessments by governmental authorities and changes in our tax rate; dependence on key personnel; legislative or regulatory changes impacting or limiting our business; political conditions; and other risks and uncertainties identified in Item 1A -“Risk Factors” and Item 7 - “Management’sdiscusses with management the Company’s Compensation Discussion and Analysis of Financial Condition and Results of Operations”(“CD&A”) included in this Form 10-K.Proxy Statement. The committee also oversees the Company’s human capital management, including executive succession planning, leadership development, diversity and inclusion, and pay equality. Members of this committee are Mr. Ringler (Chairman), Mr. Durcan and Mr. Sakamoto. The Compensation Committee met seven times in 2021.

For any forward-looking statements contained in this Annual Report on Form 10-K or any other document, we claim the protection

The Nominating and Corporate Governance Committee

The Nominating and Corporate Governance Committee identifies and recommends individuals qualified to serve as members of the safe harborBoard and assists the Board by reviewing the composition of the Board and its committees, monitoring a process to assess Board effectiveness, and developing and implementing the Company’s Corporate Governance Guidelines. The committee also oversees the Company’s sustainability, corporate social responsibility and corporate citizenship policies and practices and reviews the Company’s disclosure containing significant information relating to matters within the committee’s mandate. The Nominating and Corporate Governance Committee will consider stockholder nominees for forward-looking statements contained inelection to the Private Securities Litigation Reform ActBoard if timely advance written notice of 1995, and we assume no obligation to revise or publicly releasesuch nominees is received by the resultsSecretary of any revision to these forward-looking statements, except as required by law. Given these risks and uncertainties, readers are cautioned not to place undue reliance on such forward-looking statements.

Part I

Item 1. Business

General

Veoneer, Inc. (“Veoneer”, the “Company” or “we”) is a Delaware corporation withCompany at its principal executive officersoffices in Stockholm, Sweden. accordance with the Bylaws, a copy of which may be obtained by written request to the Company’s Secretary or on the Company’s website at www.Veoneer.com – Who we are – Governance. Members of this committee are Dr. Ziebart (Chairman) and Messrs. Ringler and Synnergren. The Nominating and Corporate Governance Committee met five times in 2021.

Corporate Governance

The Spin-off

On June 29, 2018 we(the “Spin-off Effective Date”), Veoneer, Inc. became an independent, publicly traded company as a result of the separation of the Electronics segment from Autoliv, Inc. (“Autoliv”). Veoneer was incorporated under the laws of Delaware in 2017 for the purpose of holding this business. The separation was completed in the form of a pro rata distribution on the Spin-off Effective Date (the “Spin-off”) of 100% of the outstanding shares of Common Stock of Veoneer to the stockholders of Autoliv (the “Spin-Off”). The Company functions as a holding corporation and owns two principal subsidiaries, Veoneer AB and Veoneer US, Inc.

Shares of Veoneer common stock are traded on the New York Stock Exchange under the symbol “VNE”. Swedish Depository Receipts representing shares of Veoneer common stock (“SDRs”) trade on NASDAQ Stockholm under the symbol “VNE SDB”. Our fiscal year ends on December 31.

Business

Veoneer is a global leader in the design, development, manufacture and sale of automotive safety electronics. Our ambition is to be a leading system supplier for advanced driver assistance systems ("ADAS"), Collaborative Driving, highly automated driving ("HAD") solutions, and autonomous drive ("AD") as well as a market leader in automotive safety electronics products.

Based on our purpose of "Creating Trust in Mobility", our safety systems are designed to make driving safer and easier, more comfortable and convenient, and to intervene before a collision. Our systems currently include restraint control electronics and crash sensors for deployment of airbags and seatbelt pretensioners, active safety sensors, controllers and software for both ADAS and AD solutions and brake control systems.

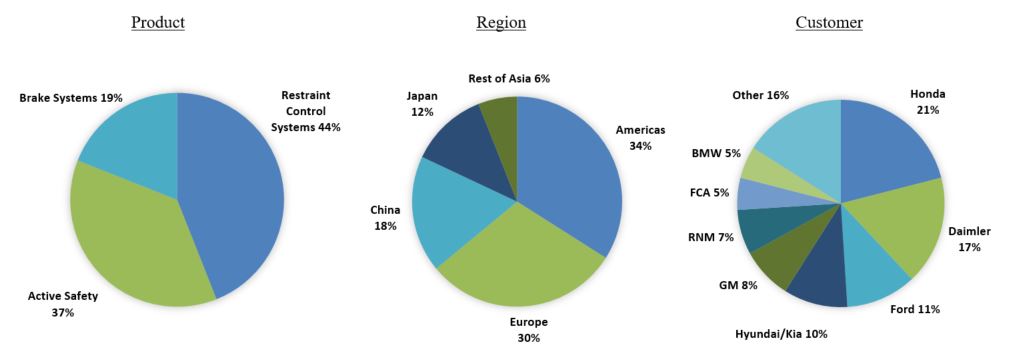

Including joint venture operations, Veoneer has 10 manufacturing sites and operates in 13 countries and its customers include the world’s largest car manufacturers. Veoneer’s sales in 2018 were $2.2 billion, approximately 37% of which consisted of active safety products, approximately 44% of which consisted of restraint control systems and approximately 19% of which consisted of brake systems products. Our business is conducted primarily in Europe, the Americas and Asia.

Veoneer’s head office is located in Stockholm, Sweden. As of December 31, 2018, Veoneer had approximately 7,300 employees worldwide and a total headcount of approximately 8,600, including temporary personnel.

Additional information required by this Item 1 regarding developments in the Company’s business during 2018 is contained under Item 7 in this Annual Report.

Financial Information on Segments

Veoneer reports its financial results in two segments: Electronics and Brake Systems. Our Electronics reporting segment consists of our active safety and restraint control systems product areas. Our Brake Systems reporting segment consists of our brake systems product area, which are those products developed by Veoneer-Nissin Brake Systems (VNBS), our joint venture with Nissin Kogyo the 49% owner in VNBS (a 51% owned subsidiary).

Business Strategy

We believe the Company is well-positioned for growth from increasing long-term global vehicle production volumes, increased demand for safety and collaborative and autonomous driving products, and new business wins with existing and new customers. We are focused on accelerating the commercialization of active safety and collaborative and autonomous driving by providing the software, sensors and computers required to do so.

Products and Technology

Electronics Segment

We provide advanced active safety sensors, used for ADAS, HAD and AD solutions, such as vision and radar systems, ADAS Electronic Control Units (“ECUs”), night vision and positioning systems. Through Zenuity, our 50% owned joint venture with Volvo Car Corporation ("Volvo Cars"), we develop an advanced software stack for sensor fusion and decision control for ADAS, HAD and AD solutions. In addition, we offer driver monitoring systems, LiDAR sensors and other technologies critical for AD solutions by leveraging our partnership network and internally developed intellectual property.

We also provide restraint control systems such as ECUs and crash sensors for deployment of airbags and seatbelt pretensioners in the event of a collision.

Active Safety Products

Active safety systems are designed to intervene before a collision to make accidents avoidable or reduce the severity of the crash in addition to making driving easier as well as more comfortable and convenient.

We develop radar and vision technologies (including Veoneer’s internally developed vision algorithms for both mono-and-stereo vision) that monitor the environment around the vehicle with features that adjust engine output and steering or braking to avoid accidents. The goal of active safety technologies is to provide early warnings to alert drivers to take timely and appropriate action or trigger intelligent systems that affect the vehicle’s motion using braking and steering to avoid accidents, as well as to increase the comfort and convenience of driving. Active safety systems can also improve the effectiveness of the restraint control systems which combine hazard information with traditional crash-sensing methods.

Active safety functions include: Autonomous Emergency Braking, which brakes a vehicle autonomously; Adaptive Cruise Control, which keeps and adjusts the vehicle’s pre-set speed to keep a pre-set distance from vehicles ahead; Traffic Jam Assist and Highway Assist, which takes control of braking and acceleration in slow-moving traffic and highway speed, respectively; Forward Collision Warning; Blind Spot Detection; Rear Cross-Traffic Assist; Lane Departure Warning; Lane Centering Assist, Traffic Sign Detection; Light Source Recognition; Driver Monitoring for attention and drowsiness; Vehicle-to-Vehicle and Vehicle-to-Infrastructure communication; and Night Driving Assist.

Key systems used in the active safety functions and the Company’s capabilities, currently provided to the market or under active development, include:

Vision Systems: Vision systems are critical to driver assistance and safety functions. They support the driver in collision avoidance and mitigating severity in the event of an accident. Using our software algorithms, the camera looks at the road ahead for other vehicles, road signs, lane markings and other key elements and provides information and warnings if the car is approaching a potentially hazardous traffic situation. Vision systems are used in applications such as road-sign recognition, lane detection along with forward and pedestrian collision warnings. We offer forward looking mono- and stereo-vision systems:

•The mono-vision system is a forward-looking camera that is mounted behind the windshield in front of the rear-view mirror. Images are interpreted by algorithms that help identify objects and assist the driver with warnings or actuations such as lane keeping and automatic braking of the vehicle. Mono-vision systems provide a significant level of accident reductions targeting 5-star safety levels as well as driver comfort and convenience features like Adaptive Cruise Control.

•Stereo-vision system technology goes a step further and measures the entire driving environment in 3D. The system is capable of acting on any object without classification. Stereo-vision also provides free-space recognition, road surface measurement down to millimeter level accuracy, which is important to original equipment manufacturers ("OEMs") to improve safety and comfort and provides depth perception for distance calculations due to the 3D capability.

Next generation vision systems and algorithms such as our fourth-generation mono- and stereo-cameras, which are currently under development and planned for production in 2019 will support AD and European New Car Assessment Program (“NCAP”) 2020. Fifth generation vision systems, which are in the early planning stages, and planned for production in 2022 will offer more than five times higher image resolution than the current generations as well as offer multiple camera solutions. Selected customers for our vision systems include Geely, Mercedes-Benz, Volvo Cars and one additional Asian OEM.

Radar Systems: Radar systems capture and analyze driving conditions and alert the driver to potentially dangerous events, and can take control of the vehicle if the driver does not take timely appropriate action. Radar systems are used in functions such as adaptive cruise control and automatic emergency braking. Radar is important because it provides superior performance in poor weather conditions such as rain and fog and other situations with poor visibility. Fused with vision systems, higher levels of functional safety are possible allowing a wider range of operating conditions. Our radar sensor portfolio includes: 25GHz ultra-wide band radar, 24 GHz narrow band radar, and 77GHz front and rear corner, and front center radars. Selected customers for our radar systems include Fiat Chrysler Automobiles (FCA), Geely, General Motor (GM), Honda, Mercedes-Benz, Renault Nissan Mitsubishi, and Volvo Cars.

ADAS ECUs: ADAS electronic control units ("ECU") are emerging products within the active safety market and are precursors to the autonomous vehicles of the future. Today, a limited number of OEMs are using separate ADAS ECUs, as most of the ADAS functionalities can be done in an integrated sensor-ECU. With future ADAS and AD systems increasing in complexity, the need for multi-sensor solutions and subsequently higher processing capabilities is expected to lead to more OEMs installing separate ADAS ECUs in their vehicles.

In the ADAS ECU, large quantities of data from the vehicle’s different sensors is validated and analyzed. Advanced algorithms can then act in real time to warn the driver and control the vehicle throttle, braking and steering torque to follow a desired trajectory for fully automated driving. We believe one of the biggest challenges self-driving cars will have to overcome is being able to react to the randomness of traffic flow, other drivers, and the fact that no two driving situations are ever the same.

By using deep learning (artificial intelligence) and sensor fusion, algorithms in the ADAS ECU can likely be improved in such a way that the vehicle will be able to make better decisions than a human driver could. This processing must be done with multiple levels of redundancy to ensure the highest level of safety. The computing demands of driverless

vehicles are 50 to 100 times more intensive than the most advanced vehicle today. Meeting these demands will be the major challenge in developing the next generation of ADAS ECUs including data processing.

In 2016, we launched the world’s first ADAS ECU for mass production in Mercedes-Benz’s new E-class. We provide a similar solution to the updated Mercedes-Benz S-class.

Night Vision Systems: Using passive infrared technology, our night vision system identifies if pedestrians, animals or certain other hazards are present in the danger zone of a vehicle, and alerts the driver, driver, particularly in nighttime, or other “dark” conditions. Our night vision system is the key component in “dynamic light spot” pedestrian illumination system which allows more time for drivers to identify potential hazards at distances beyond normal head-lights. Our fourth-generation night vision system, expected in 2020, will have improved field of view and detection distances, reduction in size, weight and cost featuring enhanced algorithms for pedestrian, animal and vehicle detection as well as supporting night time automatic emergency braking solutions. Selected customers of the night vision system include Audi, BMW, GM, Mercedes-Benz, PSA, Porsche and Volkswagen.

Safety Domain ECUs: As active and passive safety features become more advanced, having dedicated ECUs for the various features increases the complexity and cost of the vehicle architecture. The Safety Domain ECU replaces multiple dedicated ECUs across the vehicle by combining all active and passive safety ECUs into one powerful domain controller. This requires a highly powerful processor which is able to execute simultaneous computing. Techniques such as virtualization enable the safe and secure separation of computing tasks, as the other controllers are not affected if one virtual controller fails.

LiDAR: In 2017, we agreed to collaborate with Velodyne to expand and commercialize our LiDAR development. LiDAR is expected to be an important sensor technology for the future development of AD systems. Under the current agreement with Velodyne, Veoneer will act as the Tier-1 supplier to the OEMs for the Velodyne LiDAR sensors. We will provide project management services, product validation and verification capabilities and system/interface packaging in supplying automotive-grade LiDAR systems to the OEMs. Our LiDAR product roadmap includes first providing it to test fleets of the OEMs and the robo-taxis market followed by developing a solid-state design for the consumer vehicle market. Building on this relationship, on January 7, 2019 the Company announced entry into a license and supply agreement with Velodyne whereby Velodyne will provide Veoneer US, Inc. with materials and rights to certain Velodyne intellectual property which would enable Veoneer US, Inc to sell, distribute, promote, manufacture and modify, including related research and development ("R&D") certain LiDAR products based on a Velodyne-authorized reference design.

Driver Monitoring: We have been developing solutions to address driver distraction and fatigue as they relate to traditional driving situations and driver attention for hands-free driving. In 2017 we entered into an agreement with Seeing Machines to accelerate this effort. This technology is expected to be necessary to achieve a 5-star NCAP rating in Europe in 2022 as well as Level 3 autonomy solutions worldwide. Our non-exclusive agreement with Seeing Machines to utilize their reference design and market under a license, allows the Company the ability to build hardware and feature level solutions on top of Seeing Machines’s world leading head pose, gaze and recognition data outputs.

RoadScape: Our RoadScapeTM product line offers highly accurate satellite positioning along with world leading dead reckoning capabilities for increased precision in urban areas. Building on this, RoadScapeTM provides a digital representation of the road ahead that can be further enhanced through probe data in the field and cloud connectivity. Finally, adding RoadScapeTM communication technology allows for vehicle-to-vehicle, infrastructure and cloud connectivity for premonition and situational awareness in ADAS and AD.

Human Machine Interaction (“HMI”): Genuine two-way communication between vehicle and driver is critical to building driver trust and enhancing the driver experience. Veoneer’s Learning Intelligent Vehicle (“LIV”) is an artificial intelligence-equipped research vehicle that can understand and respond to context. LIV uses external and internal sensing combined with complex algorithmic artificial intelligence to create a unified contextual picture of what is going on with the occupants, vehicle, driving situation and then acts and serves as a “co-pilot” to communicate with drivers and passengers. Veoneer uses LIV to learn more about task delegation, shared control, driver-vehicle collaboration; innovate ways to increase driver understanding of an autonomous system; and to continually improve the system’s understanding of its human co-travelers.

Restraint Control Systems

The restraint control system is the brain triggering a vehicle’s passive safety system in a crash situation. Restraint control systems consist of a restraint ECU and related remote crash sensors, including acceleration and pressure sensors. The ECU’s algorithms decide when a seatbelt pretensioner should be triggered and an airbag system should be deployed.

The ECU is mounted centrally in the vehicle, well protected in the event of a crash, and is supported by crash sensors mounted in the door beam, the pillar between the doors, the rocker panel and/or in various locations at the front and rear of the vehicle. These “satellite” crash sensors provide acceleration data to enable early and appropriate deployment of the airbags and seatbelt pretensioners within milliseconds of a vehicle crash.

The ECU also contains certain sensors that are common with the brake system. We were the first to offer this type of solution, providing savings through the reduction in multiple sensors for measuring yaw rate, and consolidating this information on the vehicle data bus. Additionally, the restraint control system is capable of recording details of what happened before and during a crash event using an Event Data Recorder (“EDR”) with the restraint control ECU.

Selected customers include FCA, Ford, Geely, GM, Great Wall, Hyundai/Kia, Jaguar Land Rover, Mazda, PSA, Renault Nissan Mitsubishi, Suzuki and Volvo Cars.

Overview of Zenuity

In addition to our two segments, we are a 50% owner of Zenuity, our joint venture with Volvo Cars to develop decision making software for ADAS and AD.

All ADAS and AD features are based on a recommended reference architecture for customers that require a system level solution. In March 2018 Zenuity was selected by Geely as supplier for Geely’s Level 3 project, which includes ADAS electronic control units and software, radar systems, as well as mono-vision and stereo-vision camera systems.

As of December 31, 2018, Zenuity had a team of over 600 employees and consultants, of which 88% are software engineers who we believe have the necessary skills to develop these technologies. We expect to supply customers with Zenuity software during 2020.

Through the Company's own product capabilities and extensive partnership network, Veoneer has one of the broadest ADAS and AD product portfolio offerings, which include all major sensing technologies, decision making software, positioning and mapping technologies and cloud solutions.

Our product portfolio has been significantly expanded over the recent years (as illustrated below) from individual hardware sensing components to a full range of key functions and capabilities as outlined below. This enables us to address our customer needs today, and likely in the future, by offering the entire spectrum of ADAS and AD solutions.

Brake Systems Segment

Our Brake Systems reporting segment consists of our brake systems product area, which are those products developed by VNBS which provides brake control and actuation systems. VNBS provides products for both traditional and new braking systems which we see as building blocks in the actuator area towards HAD.

VNBS supplies brake systems, including the brake booster, hydraulic proportioning valves and electronic control module with sensors. The control module can modulate the brake pressure applied on each wheel individually to maintain optimum braking and offers features like Electronic Stability Control (“ESC”), Anti-locking Brakes (“ABS”) and Traction Control System.

For traditional brakes, a vacuum produced by Internal Combustion Engines is necessary to amplify the force applied by the driver’s foot to convert it into hydraulic pressure to decelerate the vehicle. New drivetrains, such as Electric (“EV”) and Hybrid (“HEV”), do not provide the same source of energy for boosting the brake input from the driver. Therefore, VNBS has developed new servo-assisted and integrated brake control systems that can work independent of the type of drivetrain used.

To improve the overall efficiency of vehicles, VNBS’ new braking systems also provide the opportunity to recover brake energy using electric motors as generators to charge batteries. This contrasts with conventional braking systems where the excess kinetic energy is converted to unwanted and wasted heat by friction in the brakes.

VNBS currently produces brake systems capable of coping with regenerative braking and has developed an upgraded Electronic Brake Boost system for market introduction expected towards the end of 2019. This system integrates the hydraulic brake modulator with the electronic brake control unit and the brake fluid reservoir into a single unit (so called “one box” design). Scalability and cost competitiveness of this technology qualifies VNBS to participate in the growth of brake-by-wire systems needed for regenerative braking while delivering superior braking performance to support the growing need for external brake requests such as Automated Emergency Braking and other functionalities.

In January 2017 the Company announced that VNBS is expanding its customer base beyond its primary customer Honda, winning lifetime contract order value of more than $1 billion for our new braking system with a Detroit based OEM on a major vehicle platform. Production for this awarded business is currently scheduled to begin in 2020. There is no minimum purchase value associated with this awarded business. The agreement will be governed by the OEM’s general terms and conditions and Veoneer and such OEM will enter into a commercial and program agreement that will set forth the specific commercial terms and functional requirements with respect to this order. The program life cycle is estimated to be six years. We received a second major order from the same OEM at the end of 2017. The main opportunities we see in brake systems stem from its capabilities in regenerative braking technology which works well with combustion engine vehicles but is even more suitable for HEV and EV. We see significant opportunities to expand outside the current customer base, especially in combination with our strong customer relationships and global footprint.

Acquisition, Partnership and Collaboration History

Our success and comprehensive product portfolio have partly been driven by acquisitions and partnerships, both critical elements to succeed within the multifaceted auto safety electronics industry and to remain competitive against existing and new entrants looking to enter the market. These partnerships and collaborations have a strategic importance in the near and long term to develop additional autonomous driving building blocks and bring potential products to market in future years.

Acquisitions and Joint Ventures

February 2018: Zenuity announced the acquisition of Beyonav intellectual property and trademarks, a technology services company delivering innovative location-based solutions that go beyond traditional applications of navigation technology.

November 2017: We acquired Fotonic, a Swedish company with expertise in LiDAR and Time of Flight cameras, building on our collaboration with Velodyne that was established in June 2017. This acquisition adds to our portfolio the collaboration capabilities within LiDAR sensors, leveraging on our expertise in manufacturing and validation.

April 2017: We launched Zenuity, a strategic 50/50 joint venture with Volvo Cars. This joint venture is an industry first, where an OEM and Tier-1 supplier, both recognized as pioneers in automotive safety, formed a company to develop ADAS software towards AD. See details above.

April 2016: We formed VNBS, a 51/49 joint venture with Nissin Kogyo, a Japanese supplier of both traditional and new brake systems. The joint venture is fully consolidated by Veoneer. See details above.

Partnerships, Collaborations and Supplier Agreements

January 2019: The Company announced entry into a license and supply agreement with Velodyne whereby Velodyne will provide Veoneer US, Inc. with materials and rights to certain Velodyne intellectual property which would enable Veoneer US, Inc. to sell, distribute, promote, manufacture and modify (including related R&D) certain LiDAR products based on a Velodyne-authorized reference design.

January 2018: Zenuity announced a non-exclusive collaboration with TomTom, to provide reference map architecture for the “Zenuity Connected Roadview” system for autonomous vehicles. TomTom’s High Definition (“HD”) Maps will power the localization, perception and path planning in the Zenuity AD software stack in combination with on-vehicle sensors such as cameras, radar and LiDAR to create continuously updated maps.

October 2017: We announced a non-exclusive collaboration with Massachusetts Institute of Technology AgeLab to develop deep learning algorithms that enable effective communication and transfer of control between driver and vehicle. This includes sensing driver gaze, emotion, cognitive load, drowsiness, hand position, posture and fusing this information with the perception of the driving environment to create safe and reliable vehicles that drivers can learn to trust.

September 2017: Zenuity announced a non-exclusive collaboration with Ericsson. The aim is to develop the Zenuity connected cloud, where Ericsson will contribute its “Internet of Things” accelerator platform aiming to integrate in-vehicle software and systems with connected safety data from other vehicles and infrastructure to potentially provide Over-the-Air real time updates across the vehicle fleet.

August 2017: We announced a non-exclusive collaboration with Seeing Machines, a pioneer in computer vision based human sensing technologies to develop next generation Driver Monitoring Systems for autonomous vehicles.

July 2017: We announced a non-exclusive collaboration with Velodyne to sell various LiDAR sensors as the Tier-1 supplier to the OEMs. See details above.

June 2017: We announced a non-exclusive early stage collaboration with NVIDIA, in combination with Zenuity, providing Veoneer and Zenuity with pre-commercial access to NVIDIA’s AI computing platform for autonomous driving. Actual production vehicles utilizing said platform are not planned for sale before 2021.

Market Overview and Competitive Landscape

Automotive Supplier Market Overview

The automotive production value chain is split among OEMs such as General Motors, Toyota and Volkswagen and automotive suppliers, such as ourselves, Aptiv, Bosch, Continental, Denso, Magna, Valeo and ZF. Veoneer acts mainly as a Tier-1 supplier to OEMs, meaning that we sell products directly to OEMs.

Our underlying market is primarily driven by two critical factors: Global Light Vehicle Production (“LVP”) and Content Per Vehicle (“CPV”), whereby CPV is the clear market driver for the growth of our total addressable market.

Light Vehicle Production: Over the last two decades, LVP has increased at an average annual growth rate of around 3% despite the cyclical nature of the automotive industry. LVP is expected to grow to around 92 million in 2019, and 106 million in 2025, from approximately 91 million in 2018, according to IHS, The market is undergoing a shift from traditional internal combustion engine vehicles, to HEVs and EVs, as emission regulation becomes more stringent, and battery technology continues to evolve.

Content Per Vehicle: Unlike LVP, we can directly influence the CPV by introducing new technologies to the market. Looking ahead, we expect that safety CPV growth will primarily be driven by active safety content (including software), with total active safety market growing from approximately $75 per vehicle in 2018 to approximately $250 per vehicle in 2025, representing a compound annual growth rate ("CAGR") of roughly 19% from 2018 to 2025, as the demand for advanced active safety features grows.

See Item 7 Management’s Discussion and Analysis ("MD&A") of Financial Condition and Results of Operations-Trends, Uncertainties and Opportunities” for additional information related to recent trends in LVP and CPV.

Active Safety Competitive Landscape

The active safety market is highly fragmented and highly competitive. Competition is based primarily on technology, innovation, quality, delivery and price. Our future success will depend on our ability to develop advanced hardware and software technologies and to maintain or improve on our already strong competitive position over our existing and any new competitors. Main competitors in active safety include Aptiv, Bosch, Continental, Denso, Magna, Valeo, ZF, and Intel/Mobileye.

On a broader scale, we have seen significant shifts in our competitive landscape over the last several years. Technology companies have increased their presence and influence in ADAS and AD either through acquisitions or forming “ecosystems” around certain technologies with OEMs and other suppliers. This has led to new industry entrants like Apple, Google, Intel, NVIDIA, Qualcomm and Uber, which also provide partnership or customer opportunities for Veoneer hardware and software solutions.

Through acquisitions, technology partnerships with customers and licensing agreements we have continuously added key building blocks and we estimate to have obtained a market share of 12% in active safety in 2018. Zenuity has since inception formed several partnerships to establish a full-suite ecosystem and competes with peer ecosystems such as the BMW/Intel/Mobileye collaboration.

Restraint Control Systems Competitive Landscape

The market for restraint control systems remains relatively fragmented with both traditional electronics suppliers and some passive safety suppliers. Over the past few years, we have seen our market share increase mainly due to cost efficient integration solutions and strong customer relationships built on quality and technology advancements. Currently we are the leading supplier of restraint control systems with a market share of around 26% in 2018. Our largest competitors include Bosch, Continental, Denso and ZF.

The total restraint control systems market amounted to approximately $4 billion in 2018 and is expected to remain at the same level until 2025. We believe that restraint control systems will play an integral role in a larger integration trend towards centralized Safety Domain Controllers in the future. In addition, our strong market position in restraint control systems will provide opportunities to become a leading supplier in the ADAS ECU and eventually the Safety Domain Controller market.

Brake Systems Competitive Landscape

Brake systems consists of brake control ECUs, including ABS and ESC as well as brake apply units. We estimate the total brake systems market to be approximately $12 billion in 2018, with a projected CAGR of 3% through 2025. The main growth driver is higher installation rates of ESC systems in China and other emerging countries in Asia. Another major growth driver is more advanced and complex servo assisted systems and regenerative braking systems for HEVs and EVs. The ability to regenerate kinetic energy through braking is of growing importance as vehicle powertrains are becoming increasingly electrified. We estimate that VNBS had a market share of just above 4% in 2018. Main competitors of VNBS include ADVICS, Bosch, Continental, Mando and ZF.

Research & Development and Intellectual Property

Our ability to maintain our position at the forefront of technological innovations and to serve customers on a local basis will be differentiating factors to our success. Therefore, we maintain one of the broadest global networks of technical engineering centers across all major automotive regions to develop and provide advanced products, processes and manufacturing support for our manufacturing sites and to provide our customers with local engineering capabilities and design development on a global basis.

We currently own or co-own approximately 738 active patents and have approximately 710 pending patent applications in the US and other jurisdictions. The active patents will expire between 2019 and 2038. We have registered the name Veoneer as a trademark in Sweden and are pursuing registration in other markets of interest. Depending on the jurisdiction, trademarks are generally valid as long as they are in use or their registrations are properly maintained, and they have not been found to have become generic.

We are actively pursuing opportunities to commercialize and license our technology to the automotive industries, and we selectively utilize other companies’ licenses through sublicenses in order to support our business interests. These activities foster optimization of intellectual property rights.

We believe that our patents, trademarks and licenses, provide meaningful protection for our products and technical innovations and as a whole, to be material to our business. However, we do not consider our business or any of our business segments to be materially dependent upon any individual patent, trademark or license.

We seek to effectively manage fixed costs and efficiently rationalize capital spending by evaluating the market and profit potential of existing and new customer programs, including investments in innovation and technology. We maintain our engineering activities around our focused product portfolio and allocate our capital and resources to those products and distinctive technologies.

Our total research and development expenses, including engineering, net of customer reimbursements, were $466 million, $375 million and $300 million for the years ended December 31, 2018, 2017 and 2016, respectively. Zenuity’s total expenses were $125 million for the year ended December 31, 2018. These expenses were mainly related to research and development.

We believe that our engineering and technical expertise, together with our emphasis on continuing research and development, allows us to use the latest technologies, materials and processes to solve problems for our customers and to bring new innovative products to market. We believe that continued engineering activities are critical to maintaining our pipeline of technologically advanced products.

Dependence on Customers

Veoneer serves most of the world’s major automotive OEMs and is not dependent on one single customer. Our customer base has consistently increased and diversified over the last five years, mainly driven by our active safety product offerings and VNBS.

In 2018 we served a total of 16 customers and our largest customers were Honda (21% of sales), Daimler (17% of sales), Ford (11% of sales), Hyundai/Kia (10% of sales), General Motors (8% of sales), Renault Nissan Mitsubishi (7% of sales) FCA (5% of sales) and BMW (5% of sales). Some of the concentration is driven by the concentration in the automotive industry, with the five largest OEMs in 2018 accounting for 49% of global LVP and the ten largest for 74%, according to IHS.

We typically supply products to our OEM customers through written contracts or purchase orders which are generally governed by general terms and conditions established by each OEM. These arrangements include terms regarding price, quality, technology and delivery. Although it may vary from customer to customer, our customer contracts generally require us to supply a customer’s annual requirements for a particular vehicle model and assembly facilities, rather than for manufacturing a specific quantity of products. Such contracts range from one year to the life of the model, which is generally four to seven years. Because we produce products for a broad cross section of vehicle models, we are not overly reliant on any one vehicle model or one particular product.

These contracts are often subject to renegotiation, sometimes as frequent as on an annual basis which may affect product pricing. In general, these arrangements with our customers provide that the customer can terminate them if we do not meet specified quality, delivery and cost requirements. Although these arrangements may be terminated at any time by our customers (but not typically by us), such terminations have historically been minimal and have not had a material impact on our results of operations. However, if terminations do occur in the future or if production under a contract winds down earlier than expected, then such event could have a material impact on our results of operations. The arrangements typically provide that we are subject to a warranty on the products supplied; in most cases, the duration of such warranty is coterminous with the warranty offered by the OEM to the end-user of the vehicle. We may also be obligated to share in all or a part of recall costs if the OEM recalls its vehicles for defects attributable to our products.

Veoneer Personnel

As of December 31, 2018, we had a total of approximately 8,600 employees and consultants, with 4,676 in engineering, 2,083 in production and 1,346 in production overhead, and the remainder employed in management, general and administrative functions. Within engineering, more than two thirds of the employees worked as software engineers.

In addition, Zenuity had approximately 600 employees and consultants at the end of 2018, of which approximately 88% worked as software developers. In 2018, approximately 1,100 engineers were hired by Veoneer and more than 100 were hired by Zenuity.

We consider our relationship with our personnel to be strong. We have not had any disputes which are significant or had a lasting impact on our relationship with our employees, customer perception of our employee practices or our business results.

Major unions to which some of our employees belong in Europe include: IG Metall in Germany; Unite in the United Kingdom; Confédération Générale des Travailleurs, Confédération Française Démocratique du Travail, and Force Ouvrière in France; and If Metall, Unionen, Sveriges Ingenjörer and Akademikerföreningen in Sweden.

In addition, our employees in other regions are represented by the following unions: Unifor and the International Association of Machinists and Aerospace Workers (“IAM”) in Canada and VNBS Roudou Kumiai in Japan.

In many European countries and in Canada, wages, salaries and general working conditions are negotiated with local unions and/or are subject to centrally negotiated collective bargaining agreements. The terms of our various agreements with unions typically range between one and three years. Some of our subsidiaries in Europe and Canada must negotiate with the applicable local unions with respect to important changes in operations, working and employment conditions. Twice a year, members of the Company’s management conduct a meeting with the European Works Council (“EWC”) to provide employee representatives with important information about the Company and a forum for the exchange of ideas and opinions.

In many Asia Pacific countries, the central or regional governments provide guidance each year for salary adjustments or statutory minimum wage for workers. Our employees may join associations in accordance with local legislation and rules, although the level of unionization varies significantly throughout our operations.

Inventory and Working Capital

We, as with other component manufactures in the automotive industry, ship our products to customer vehicle assembly facilities throughout the world on a “just-in-time” basis for our customers to maintain low inventory levels. Our suppliers (external suppliers as well as our own production sites) use a similar method in providing raw materials to us.

Sources and Availability of Raw Materials