| Delaware | 82-3720890 | |||||||

| (State or other jurisdiction of | (I.R.S. Employer | |||||||

| incorporation or organization) | Identification No.) | |||||||

| Klarabergsviadukten 70, Section C6 | ||||||||

| Box 13089, | SE- 103 02 | |||||||

| Stockholm, | ||||||||

| Sweden | ||||||||

| +46 | 8 527 762 00 | |||||||||||||||||||||||||

| (Registrant’s telephone number, including area code) | ||||||||||||||||||||||||||

| Securities registered pursuant to Section 12(b) of the Act: | ||||||||||||||||||||||||||

Title of each class: | Trading Symbol: | Name of each exchange on which registered: | ||||||

| Common Stock, par value $1.00 per share | VNE | New York Stock Exchange | ||||||

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes: ý ☒ No: ¨☐

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Exchange Act. Yes: ¨ ☐ No: ý☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15 (d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports) and (2) has been subject to such filing requirements for the past 90 days. Yes: ý ☒ No: ¨☐

Indicate by check mark whether the registrant has submitted electronically, every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (Section 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes: ý ☒ No: ¨☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act

| Large accelerated filer | Accelerated filer | |||||||||||||||||||

| Non-accelerated filer | Smaller reporting company | |||||||||||||||||||

| Emerging Growth Company | ||||||||||||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ¨☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes: ¨☐ No: ý☒

As of February 15,13, 2019, there were 87,178,772111,408,845 shares of common stock of Veoneer, Inc., par value $1.00 per share, outstanding.

Documents Incorporated by Reference

| Document | Where Incorporated | ||||

| Proxy Statement* | Part III (Items 10, 11, 12, 13 and 14) | ||||

*As stated under various Items of this Report, only certain specified portions of the registrant’s definitive Proxy Statement for the annual stockholders’ meeting to be held on May 8, 2019,6, 2020, to be dated on or around March 28, 201925, 2020 (the “2019“2020 Proxy Statement”) are incorporated by reference in this Report.

TABLE OF CONTENTS

| PART I | ||||||||

| Item 1. | ||||||||

| Item 1A. | ||||||||

| Item 1B. | ||||||||

| Item 2. | ||||||||

| Item 3. | ||||||||

| Item 4. | ||||||||

| PART II | ||||||||

| Item 5. | ||||||||

| Item 6. | ||||||||

| Item 7. | ||||||||

| Item 7A. | ||||||||

| Item 8. | ||||||||

| Item 9. | ||||||||

| Item 9A. | ||||||||

| Item 9B. | ||||||||

| PART III | ||||||||

| Item 10. | ||||||||

| Item 11. | ||||||||

| Item 12. | ||||||||

| Item 13. | ||||||||

| Item 14. | ||||||||

| PART IV | ||||||||

| Item 15. | ||||||||

| Item 16. | ||||||||

FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K contains forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. All statements contained in this Annual Report on Form 10-K other than statements of historical fact, including without limitation, statements regarding management’s examination of historical operating trends and data, estimates of future sales (including estimates related to order intake), operating margin, cash flow, taxes or other future operating performance or financial results, are forward-looking statements. In some cases, you can identify these statements by forward-looking words such as “estimates,” “expects,” “anticipates,” “projects,” “plans,” “intends,” “believes,” “may,” “likely,” “might,” “would,” “should,” “could,” or the negative of these terms and other comparable terminology, although not all forward-looking statements contain such words. We have based these forward-looking statements on our current expectations and assumptions and/or data available from third parties about future events and trends that we believe may affect our financial condition, results of operations, business strategy, short-term and long-term business operations and objectives and financial needs.

New risks and uncertainties arise from time to time, and it is not possible for our management to predict all risks, nor can we assess the impact of all factors on our business or the extent to which any factor, or combination of factors, may cause actual results to differ materially from those contained in any forward-looking statements we may make. Factors that could cause actual results to differ materially from these forward-looking statements include, without limitation, the following: the cyclical nature of automotive sales and production; changes in general industry and market conditions or regional growth or decline; our ability to achieve the intended benefits from our separation from our former parent; our ability to be awarded new business or loss of business from increased competition; higher than anticipated costs and use of resources related to developing new technologies; higher raw material, energy and commodity costs; component shortages; changes in customer and consumer preferences for end products; market acceptance of our new products; dependence on and relationships with customers and suppliers; unfavorable fluctuations in currencies or interest rates among the various jurisdictions in which we operate; costs or difficulties related to the integration of any new or acquired businesses and technologies; successful integration of acquisitions and operations of joint ventures; successful implementation of strategic partnerships and collaborations; product liability, warranty and recall claims and investigations and other litigation and customer reactions thereto; higher expenses for our pension and other post-retirement benefits, including higher funding needs for our pension plans; work stoppages or other labor issues; possible adverse results of future litigation, regulatory actions or investigations or infringement claims; our ability to protect our intellectual property rights; tax assessments by governmental authorities and changes in our tax rate; dependence on key personnel; legislative or regulatory changes impacting or limiting our business; political conditions; and other risks and uncertainties identified in Item 1A -“Risk Factors” and Item 7 - “Management’s Discussion and Analysis of Financial Condition and Results of Operations” in this Form 10-K.

For any forward-looking statements contained in this Annual Report on Form 10-K or any other document, we claim the protection of the safe harbor for forward-looking statements contained in the Private Securities Litigation Reform Act of 1995, and we assume no obligation to revise or publicly release the results of any revision to these forward-looking statements, except as required by law. Given these risks and uncertainties, readers are cautioned not to place undue reliance on such forward-looking statements.

3

Part I

Item 1. Business

General

Veoneer, Inc. (“Veoneer”, the “Company” or “we”) is a Delaware corporation with its principal executive officersoffice in Stockholm, Sweden. On June 29, 2018, weVeoneer became an independent company as a result of the separation of the Electronics segment from Autoliv, Inc. (“Autoliv”). Veoneer was incorporated under the laws of Delaware in 2017 for the purpose of holding this business. The separation was completed in the form of a pro rata distribution of 100% of the outstanding shares of Common Stock of Veoneer to the stockholders of Autoliv (the “Spin-Off”). The Company functions as a holding corporation and owns two principal subsidiaries, Veoneer AB and Veoneer US, Inc.

Shares of Veoneer common stock are traded on the New York Stock Exchange under the symbol “VNE”. Swedish Depository Receipts representing shares of Veoneer common stock (“SDRs”) trade on NASDAQ Stockholm under the symbol “VNE SDB”. Our fiscal year ends on December 31.

On June 14, 2019, the Company signed agreements with Nissin Kogyo Co. Ltd., its joint venture partner in Veoneer Nissin Brake Systems ("VNBS"), providing for certain structural changes to the joint venture and the funding of VNBS.

Pursuant to the agreements, Veoneer acquired Nissin Kogyo’s interests in the US operations of VNBS, referred to as Veoneer Brake Systems ("VBS"), and VNBS transferred or licensed the VNBS technologies necessary to operate the VBS business to VBS. VBS, including the transferred or licensed technologies, is a wholly-owned Veoneer business effective on the closing date, June 28, 2019.VNBS will also provide certain transition services to VBS.

On October 30, 2019, Veoneer signed agreements (the "Definitive Agreements") to sell its 51% ownership in Veoneer Nissin Brake Japan ("VNBJ") and Veoneer Nissin Brake China ("VNBZ") entities that comprise VNBS to its joint venture partner, Nissin-Kogyo Co., Ltd., and Honda Motor Co., Ltd. The transaction was completed on February 3,

2020 under the Definitive Agreements, and the VNBS joint venture was terminated. See Note 6 "Assets held for sale" for additional information.

Business

Veoneer is a global leader in the design, development, manufacture and sale of automotive safety electronics. Our ambition is to be a leading system supplier for advanced driver assistance systems ("ADAS"), Collaborative Driving, highly automated driving ("HAD") solutions, and autonomous drive ("AD") as well as a market leader in automotive safety electronics products.

Based on our purpose of "Creating Trust in Mobility", our safety systems are designed to make driving safer and easier, more comfortable and convenient, and to intervene before a collision. Our systems currently include restraint control electronics and crash sensors for deployment of airbags and seatbelt pretensioners, active safety sensors, controllers and software for both ADAS and AD solutions and brake control systems.

Veoneer’s head office is located in Stockholm, Sweden. As of December 31, 2018,2019, Veoneer had approximately 7,300 employees7,500 associates worldwide and a total headcountassociates of approximately 8,600,8,900, including temporary personnel.

Additional information required by this Item 1 regarding developments in the Company’s business during 20182019 is contained under Item 7 in this Annual Report.

Financial Information on Segments

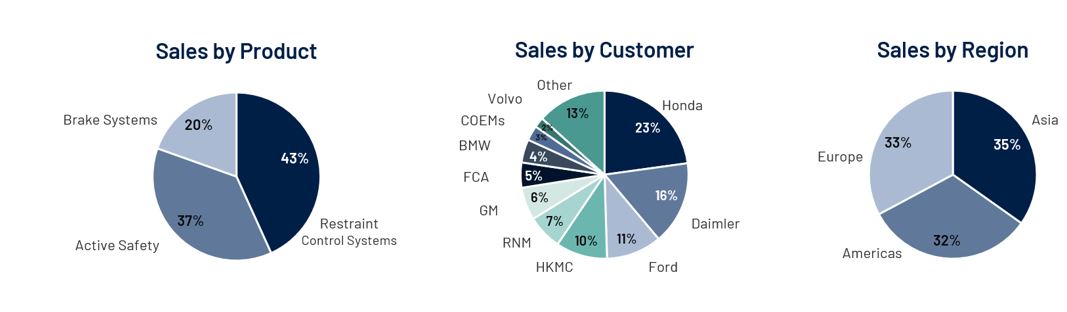

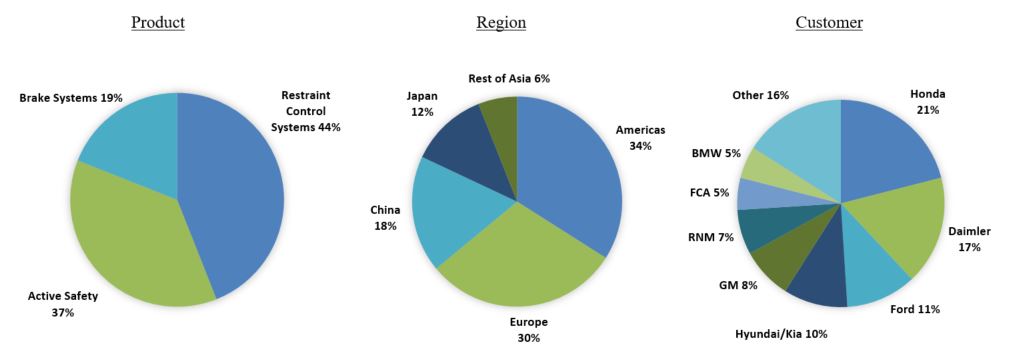

Veoneer reports its financial results in two segments: Electronics and Brake Systems.Systems. Our Electronics reporting segment consists of our active safetyActive Safety and restraint control systemsRestraint Control Systems product areas. Our Brake Systems reporting segment consists of our brake systemsBrake Systems product area, which are those products developed by Veoneer-Nissin Brake Systems (VNBS),VNBS, our joint venture with Nissin Kogyo the 49% owner in VNBS (a 51% owned subsidiary). and VBS.

On October 30, 2019 Veoneer announced the execution of definitive agreements to divest its 51% ownership in the remaining VNBS joint venture operations in Japan and China to Nissin Kogyo Co. Ltd. and Honda Motor Co. Ltd. On February 3, 2020,

4

Veoneer completed the divestiture of its VNBS joint venture interest. Veoneer is classifying this transaction, which was pending as of December 31, 2019, as "assets held for sale" in this Annual Report on Form 10-K, which resulted in no impairment charge.

Business Strategy

Products and Technology

Electronics Segment

We also provide restraint control systemsRestraint Control Systems such as ECUs and crash sensors for deployment of airbags and seatbelt pretensioners in the event of a collision.

Active Safety Products

Active safetySafety systems are designed to intervene before a collision to make accidents avoidable or reduce the severity of the crash, in addition to making driving easier as well as more comfortable and convenient.

We develop radar and vision technologies (including Veoneer’s internally developed vision algorithms for both mono-and-stereomono, stereo and thermal vision) that monitor the environment around the vehicle with features thatwhich can adjust engine output and steering or braking to avoid accidents. The goal of active safetyActive Safety technologies is to provide early warnings to alert drivers to take timely and appropriate action or trigger intelligent systems that affect the vehicle’s motion using braking and steering to avoid accidents, as well as to increase the comfort and convenience of driving. Active safetySafety systems can also improve the effectiveness of the restraint control systems which combine hazard information with traditional crash-sensing methods.

Active safetySafety functions include: Autonomous Emergency Braking (AEB), which brakes a vehicle autonomously; Adaptive Cruise Control (ACC), which keeps and adjusts the vehicle’s pre-set speed to keep a pre-set distance from vehicles ahead; Traffic Jam Assist and Highway Assist, which takes control of braking and acceleration in slow-moving traffic and highway speed, respectively; Forward Collision Warning; Blind Spot Detection; Rear Cross-Traffic Assist; Lane Departure Warning; Lane Centering Assist, Traffic Sign Detection; Light Source Recognition; Driver Monitoring for attention and drowsiness; Vehicle-to-Vehicle and Vehicle-to-Infrastructure communication; and Night Driving Assist.

Key systems usedincluded in the active safety functions and the Company’s capabilities,Company's Active Safety portfolio, either currently provided to the market or under activeproduct development, include:

Vision Systems: Vision systems are critical to driver assistance and safety functions. They support the driver in collision avoidance and mitigating the crash severity in the event of an accident. Using our internally developed software algorithms, the camera looks at the road ahead for other vehicles, road signs, lane markings and other key elementsroad attributes and provides information and warnings if the cara vehicle is approaching a potentially hazardous traffic situation. Vision systems are used in applications such as road-sign recognition, lane detection along with forward and pedestrian collision warnings. We offer forward looking mono- and stereo-vision systems:

•The mono-vision system is a forward-looking camera that is mounted behind the windshield in front of the rear-view mirror. Images are interpreted by algorithms that help identify objects and assist the driver with warnings or actuations such as lane keeping and automatic braking of the vehicle. Mono-vision systems provide a significant level of accident reductions targeting 5-star safety levels as well as driver comfort and convenience features like Adaptive Cruise Control.

5

•Stereo-vision system technology goes a step further and measures the entire driving environment in 3D.a 3D view. The system is capable of acting on any object without classification. Stereo-vision also provides free-space recognition, and road surface measurement down to millimeter level accuracy, which is important to original equipment manufacturers ("OEMs") to improve safety and comfort and provides depth perception for distance calculations due to the 3D capability.

Next generation vision systems and algorithms such as our fourth-generation mono-mono and stereo-cameras, which are currently under development and planned forwent into initial production in 2019, will support AD and European New Car Assessment Program (“NCAP”) 2020. Fifth generation vision systems, which are in the early planningdevelopment stages, and planned for production in 2022 will offer more than five times higher image resolution than the current generations of camera solutions, as well as offer multiple camera solutions. Selected customers where Veoneer has been awarded and sourced business for our vision systems include Geely, Mercedes-Benz, Volvo Cars, two major global OEMs, an Asian based OEM and one additional Asiana local Chinese OEM.

Radar Systems: Radar systems capture and analyze driving conditions and alert the driver to potentially dangerous events,situations, and can take control of the vehicle if the driver does not take timely, appropriate action. Radar systems are used in functions such as adaptive cruise controlACC and automatic emergency braking.AEB. Radar is important because it provides superior performance in poor weather conditions such as rain and fog and other situations with limited or poor visibility.visibility from the camera system. Fused with vision systems, higher levels of functional safety are possible, allowing a wider range of operating conditions. Our radar sensor portfolio includes: 25GHz ultra-wide band radar, 24 GHz narrow band radar, and 77GHz front and rear corner, and front center radars. Selected customers for our radar systems include Fiat Chrysler Automobiles (FCA), GAC, Geely, General MotorMotors (GM), Honda, Mercedes-Benz, Renault Nissan Mitsubishi, and Volvo Cars. Veoneer has been awarded and sourced business with 12 OEM customers.

ADAS Central Compute: ADAS ECUs: ADAS electronic control units ("ECU") are emerging products within the active safetyActive Safety market and are precursors to the autonomous vehicles of the future. Today, a limited number of OEMs are using separate ADAS ECUs, as most of the ADAS functionalities can be done in an integrated sensor-ECU.ECU. With future ADAS and AD systems increasing in complexity, the need for multi-sensor solutions and subsequently higher processing capabilities is expected to lead to more OEMs installing separate ADAS ECUs in their vehicles.

In the ADAS ECU, large quantities of data from the vehicle’s different sensors is validatedare analyzed and analyzed.validated. Advanced algorithms can then act in real time to warn the driver and control the vehicle throttle, braking and steering torque to follow a desired trajectory for fully automated driving.Automated Driving. We believe one of the biggest challenges self-driving cars will have to overcome is being able to react to the randomness of traffic flow, other drivers, and the fact that no two driving situations are ever the same.

vehicles are 50 to 100 times more intensiveextensive than the most advanced vehicle today. Meeting these demands will be thea major challenge in developing the next generation of ADAS ECUs, including data processing.

In 2016, we launched the world’s first ADAS ECU for mass production in Mercedes-Benz’s new E-class. We provide a similar solution to the updated Mercedes-Benz S-class.S-class, and have received new business awards with three additional customers launching over the next 18 months.

Night Vision Systems: Using passive infrared technology (thermal sensing), our night vision system identifies if pedestrians, animals or other certain other hazards are present in the danger zone of a vehicle, and alerts the driver, driver, particularly in nighttime, or other “dark”“challenging” conditions. Our night vision system is the key component in “dynamic light spot” pedestrian illumination system which allows more time for drivers to identify potential hazards at distances beyond normal head-lights. Our fourth-generation night vision system, expected inlaunching during 2020, will have improved field of view and detection distances, reduction in size, weight and cost, featuring enhanced algorithms for pedestrian, animal and vehicle detection as well as supporting night time automatic emergency brakingAEB solutions. Selected customers of the night vision system include Audi, BMW, GM, Mercedes-Benz, PSA, Porsche and Volkswagen.

Safety Domain ECUs: As activeActive and passive safetyPassive Safety features become more advanced, having dedicated ECUs for the various features increases the complexity, weight and cost of the vehicle architecture. The Safety Domain ECU replaces multiple dedicated ECUs across the vehicle by combining all activeActive and passive safetyPassive Safety ECUs into one powerful domain controller. This requires a highly powerful processor which is able to execute simultaneous computing. Techniques such as virtualization enable the safe and secure separation of computing tasks, as the other controllers are not affected if one virtual controller fails.

6

LiDAR: In 2017, we agreed to collaborate with Velodyne to expand and commercialize our LiDAR development. LiDAR is expected to be an important sensor technology for the future development of AD systems. Under the current non-exclusive agreement with Velodyne, Veoneer will act as the Tier-1 supplier to the OEMs for the Velodyne LiDAR sensors. WeVeoneer will provide project management services, product validation and verification, capabilities and system/interface packaging in supplyingand manufacturing to produce automotive-grade LiDAR systems to the OEMs. Our LiDAR product roadmap includes first providing it to test fleets of the OEMs and the robo-taxis market followed by developing a solid-state design for the consumer vehicle market. Building on this relationship, on January 7, 2019 the Company announced entry into a license and supply agreement with Velodyne whereby Velodyne will provide Veoneer US, Inc. with materials and rights to certain Velodyne intellectual property which would enable Veoneer US, IncInc. to sell, distribute, promote, manufacture and modify, including related research and development ("R&D") certain LiDAR products based on a Velodyne-authorized reference design.

Driver Monitoring: We have been developing solutions to address driver distraction and fatigue as they relate to traditional driving situations and driver attention for hands-free driving. In 2017, we entered into an agreement with Seeing Machines to accelerate this effort. This technology is expected to be necessary to achieve a 5-star NCAP rating in Europe in 2022 as well as Level 3 autonomy solutions worldwide.worldwide and is an option to meet the EU mandate for driver monitoring systems starting in 2022. Our non-exclusive agreement with Seeing Machines to utilize their reference design and market under a license, allowsprovides Veoneer the Company the abilitycapability to build hardware and feature level solutions on top of Seeing Machines’sMachines’ world leading head pose, gaze and recognition data outputs.

RoadScape: Our RoadScapeTM product line offers highly accurate satellite positioning along with world leading dead reckoning capabilities for increased precision in highway, urban and rural areas. Building on this, our RoadScapeTM platform provides a digital representation of the road ahead that can be further enhanced through probe data in the field and cloud connectivity. Finally, addingAdding RoadScapeTM communication technology allows for vehicle-to-vehicle, infrastructure and cloud connectivity for premonition and situational awareness in ADAS and AD.

Human Machine Interaction (“HMI”): Genuine Effective two-way communication between the vehicle and driver is critical to building driver trust and enhancing the driver experience. Veoneer’s Learning Intelligent Vehicle (“LIV”) is an artificial intelligence-equipped research vehicle that can understand and respond to context. LIV uses external and internal sensing combined with complex algorithmic artificial intelligence algorithms to create a unified contextual picture of what is going on with the occupants, vehicle, driving situation and then acts and serves as a “co-pilot” to communicate with drivers and passengers. Veoneer uses LIV to learn more aboutabout: task delegation, shared control, driver-vehicle collaboration; innovatecollaboration, innovative ways to increase driver understanding of an autonomous system;system, and to continually improve the system’s understanding of its human co-travelers.

Restraint Control Systems

The restraint control systemRestraint Control System is the brain triggering a vehicle’s passive safetyPassive Safety system in a crash situation. Restraint control systemsControl Systems consist of a restraint ECU and related remote crash sensors, including acceleration and pressure sensors. The ECU’sECUs algorithms decide when a seatbelt pretensioner should be triggered and an airbag system should be deployed.

The ECU is mounted centrally in the vehicle, well protected from the environment in the event of a crash, and is supported by crash sensors mounted in the door beam, the pillarpillars between the doors, the rocker panelpanels and/or in various locations at the front and rear of the vehicle. These “satellite” crash sensors provide acceleration data to enable early and appropriate deployment of the airbags and seatbelt pretensioners within milliseconds of a vehicle crash.

The ECU also contains certain sensors that are common with the brake system. We were the first to offer this type of solution, providing savings through the reduction in multiple sensors for measuring yaw rate, and consolidating this information on the vehicle data bus. Additionally, the restraint control systemRestraint Control System is capable of recording details of what happened before and during a crash event using an Event Data Recorder (“EDR”) with the restraint control ECU.

Selected customers include FCA, Ford, Geely, GM, Great Wall, Hyundai/Kia, Jaguar Land Rover, Mazda, PSA, Renault Nissan Mitsubishi, Suzuki and Volvo Cars.

Overview of Zenuity

In addition to our two segments, we are a 50% owner of Zenuity, our joint venture with Volvo Cars to develop decision making and vehicle control software for ADAS and AD.

7

All ADAS and AD features are based on a recommended reference architecture for customers that require a system level solution. In March 2018 Zenuity was selected by Geely as supplier for Geely’s first Level 3 project, which includes an ADAS electronic control unitsECU and software, radar systems, as well as mono-vision and stereo-vision camera systems.

As of December 31, 2018,2019, Zenuity had a team of over 600approximately 720 employees and consultants, ofclose to which 88%90% are software engineers who we believe have the necessary skills to develop these technologies. We expectthe decision making and vehicle control software for ADAS and AD. Zenuity is expected to supplydeliver software to its customers with Zenuity software during 2020.

Through the Company's owninternal product capabilities and extensive partnership network, Veoneer has one of the broadest ADAS and AD product portfolio offerings in the market, which includeincludes all major sensing technologies, decision making and vehicle control software, positioning and mapping technologies and cloud solutions.

Our product portfolio has been significantly expanded over the recent years (as illustrated below) from individual hardware sensing components to a full range of key functionsfeatures and capabilitiesfunctions, as outlined below.earlier. This enables usVeoneer to address our customer needs today, and likely in the future, bywith a complete system offering the entire spectrum of ADAS and AD solutions.solutions for consumer based vehicles and specific sub-system solutions for robo-taxi applications.

Brake Systems Segment

Our Brake Systems reporting segment consists of our brake systems product area, which are those products developed by our VNBS joint venture and VBS which provides brake control and actuation systems. VNBS providesand VBS provide products for both traditional and new next generation braking systems which we see as building blocks in the actuatoractuation area towards HAD.

VNBS suppliesand VBS supply brake systems, including the brake booster,boosters, hydraulic proportioning valves and electronic control modulemodules with sensors. The control module can modulate the brake pressure applied on each wheel individually to maintain optimum braking and offers features like Electronic Stability Control (“ESC”), Anti-locking Brakes (“ABS”) and Traction Control System.System ("TCS").

For traditional brakes, a vacuum produced by Internal Combustion Engines is necessary to amplify the force applied by the driver’s foot to convert it into hydraulic pressure to decelerate the vehicle. New drivetrains, such as Electric (“EV”) and Hybrid (“HEV”), do not provide the same source of energy for boosting the brake input from the driver. Therefore, VNBS hasVBS have developed new servo-assisted and integrated brake control systems that can work independent of the type of drivetrain used.

To improve the overall efficiency of vehicles, VNBS’these new braking systems also provide the opportunity to recover brake energy using electric motors as generators to charge batteries. This contrasts with conventional braking systems where the excess kinetic energy is converted to unwanted and wasted heat by friction in the brakes.

In January 2017, the Company announced that VNBSVBS is expanding its customer base beyond its primary customer Honda, winning lifetime contract order value of more than $1 billion for our new braking system with a Detroit based OEM on a major vehicle platform. Production for this awardednew business award is currently scheduled to begin in 2020. There is no minimum purchase value associated with this awarded business. The agreement will be governed by the OEM’s general terms and conditions and Veoneer and such OEM will enter into a commercial and program agreement that will set forth the specific commercial terms and functional requirements with respect to this order. The program life cycle is estimated to be six years. We received a secondsubsequent major orderorders from the same OEM atduring 2017 and 2018 to roll-out the end of 2017.same product on additional vehicle platforms and several models. The main opportunities we see in brake systems stem from its capabilities in regenerative braking technology which works well with combustion engine vehicles but is even more suitable for HEV and EV. We see significant opportunities to expand outside the current customer base, especially in combination with our strong customer relationships and our global footprint.

8

Acquisition, Partnership and Collaboration History

Our success and comprehensive product portfolio have partly been driven by acquisitions and partnerships, both being critical elements to succeed within the multifaceted autoautomotive safety electronics industry and to remain competitive against existing and new entrants looking to entermoving into various parts of the market. These partnerships and collaborations have a strategic importance in the near and long termlong-term to develop additional autonomous driving building blocks and bring potential productsnew technologies to market in future years.

Acquisitions, and Joint Ventures and Divestitures

October 2019: Veoneer signed definitive agreements to divest its remaining 51% ownership in the VNBS joint venture. The transaction closed February 3, 2020.

June 2019: Veoneer acquired Nissin Kogyo's 49% of their ownership stake in the US operations of the VNBS joint venture (VNBA).

February 2018: Zenuity announced the acquisition of Beyonav intellectual property and trademarks, a technology services company delivering innovative location-based solutions that go beyond traditional applications of navigation technology.

November 2017: WeVeoneer acquired Fotonic, a Swedish company with expertise in LiDAR and Time of Flight cameras, building on our collaboration with Velodyne that was established in June 2017. This acquisition addsadded to our portfolio the collaboration capabilities within LiDAR sensors, leveraging on our expertise in manufacturing and validation.

April 2017: WeVeoneer launched Zenuity, a strategic 50/50 joint venture with Volvo Cars. This joint venture is an industry first, where an OEM and Tier-1 supplier, both recognized as pioneers in automotive safety, formed a company to develop ADAS software towards AD. See details above.

April 2016: WeVeoneer formed VNBS, a 51/49 joint venture with Nissin Kogyo, a Japanese supplier of both traditional and new brake systems. The joint venture is fully consolidated by Veoneer. See details above.

Partnerships, Collaborations and Supplier Agreements

January 2019: The Company Veoneer announced entrythat it had entered into a license and supply agreement with Velodyne whereby Velodyne will provide Veoneer US, Inc. with materials and rights to certain Velodyne intellectual property which would enable Veoneer US, Inc. to sell, distribute, promote, manufacture and modify (including related R&D) certain LiDAR products based on a Velodyne-authorized reference design.

January 2018: Zenuity announced a non-exclusive collaboration with TomTom, to provide reference map architecture for the “Zenuity Connected Roadview” system for autonomous vehicles. TomTom’s High Definition (“HD”) Maps will power the localization, perception and path planning in the Zenuity AD software stack in combination with on-vehicle sensors such as cameras, radar and LiDAR to create continuously updated maps.

October 2017: WeVeoneer announced a non-exclusive collaboration with Massachusetts Institute of Technology AgeLab to develop deep learning algorithms that enable effective communication and transfer of control between driver and vehicle. This includes sensing driver gaze, emotion, cognitive load, drowsiness, hand position, posture and fusing this information with the perception of the driving environment to create safe and reliable vehicles that drivers can learn to trust.

September 2017: Zenuity announced a non-exclusive collaboration with Ericsson. The aim is to develop the Zenuity connected cloud, where Ericsson will contribute its “Internet of Things” accelerator platform aiming to integrate in-vehicle software and systems with connected safety data from other vehicles and infrastructure to potentially provide Over-the-Air real time updates across the vehicle fleet.

August 2017: WeVeoneer announced a non-exclusive collaboration with Seeing Machines, a pioneer in computer vision based human sensing technologies to develop next generation Driver Monitoring Systems for autonomous vehicles.

July 2017: WeVeoneer announced a non-exclusive collaboration with Velodyne to sell various LiDAR sensors as the Tier-1 supplier to the OEMs. See details above.

June 2017: WeVeoneer announced a non-exclusive early stage collaboration with NVIDIA, in combination with Zenuity, providing Veoneer and Zenuity with pre-commercial access to NVIDIA’s AI computing platform for autonomous driving. Actual production vehicles utilizing said platform are not planned for sale before 2021.

9

Market Overview and Competitive Landscape

Automotive Supplier Market Overview

The automotive production value chain is split among OEMs such as General Motors, Toyota and Volkswagen and automotive suppliers, such as ourselves, Aptiv, Bosch, Continental, Denso, Magna, Valeo and ZF. Veoneer acts mainly as a Tier-1 supplier to OEMs, meaning that we sell products directly to OEMs.

Our underlying market is primarily driven by two critical factors: Global Light Vehicle Production (“LVP”) and Content Per Vehicle (“CPV”), whereby CPV is the clear market driver for the growth of our total addressable market.Total Addressable Market ("TAM").

Light Vehicle Production: Over the last two decades, LVP has increased at an average annual growth rate of around 3% despite the cyclical nature of the automotive industry. The LVP is expected to growincrease from 85 million vehicles in 2020, to around 92 million in 2019, and 10697 million in 2025, fromwhere approximately 9186 million where produced in 2018,2019, according to IHS, The market is undergoing a shift from traditional internal combustion engine ("ICE") vehicles, to HEVs and EVs, as emission regulation becomesregulations become more stringent, and battery technology continues to evolve.evolve in cost and performance.

Content Per Vehicle: Unlike LVP, we can directly influence the CPV by introducing new technologies to the market. Looking ahead, we expect thatthe safety CPV growth will primarily be driven by active safetyActive Safety content (including software), with total active safetyActive Safety market growing from approximately $75$100 per vehicle in 20182019 to approximately $250$300 per vehicle in 2025, representing a compound annual growth rate ("CAGR") of roughly 19% from 2018 to 2025, as the demand for advanced active safety features grows.2025.

See Item 7 Management’s Discussion and Analysis ("MD&A") of Financial Condition and Results of Operations-Trends, Uncertainties and Opportunities” for additional information related to recent trends in LVP and CPV.

Active Safety Competitive Landscape

The active safetyActive Safety market isremains a highly fragmented and highly competitive. Competition is based primarily on technology, innovation, quality, delivery and price. Our future success will depend on our ability to develop advanced hardware and software technologiestechnology solutions and to maintain or improve on our already strong competitive position over our existing and any new competitors. Main competitors in active safetyActive Safety include Aptiv, Bosch, Continental, Denso, Magna, Mobis, Valeo, ZF, and Intel/Mobileye.Mobileye as a Tier 2 vision software provider.

On a broader scale, we have seen significant shifts in our competitive landscape over the last several years. Technology companies have increased their presence and influence in ADAS and AD either through acquisitions or forming “ecosystems” around certain technologies with OEMs and other suppliers. This has led to new industry entrants like Apple, Google,Waymo, Intel, Lyft, NVIDIA, Qualcomm and Uber, which also provide partnership or customer opportunities for Veoneer hardware and software solutions.

Through acquisitions, technology partnerships with customers and licensing agreements, along with our customers we have continuously added key building blocks and we estimate to have obtained a market share of 12%approximately 9% in active safetyActive Safety in 2018.2019. Zenuity has since inception formed several partnerships to establish a full-suitesoftware-suite ecosystem and competes with peer ecosystems such as the BMW/Intel/Mobileye collaboration.collaboration and GM Super Cruise program.

Restraint Control Systems Competitive Landscape

The market for restraint control systemsRestraint Control Systems, in comparison to the Active Safety market, remains relatively fragmentedconsolidated with both traditional electronics suppliers and some passive safetyPassive Safety suppliers. Over the past few years, we have seen our market share increase mainly due to cost efficient integration solutions and strong customer relationships built on quality and technology advancements. Currently we are thea leading supplier of restraint control systemsRestraint Control Systems with aan estimated market share of around 26%approximately 22% in 2018.2019. Our largest competitors include Bosch, Continental, Denso and ZF.

The total restraint control systems market amounted to approximately $4 billion in 2018 and is expected to remain at the same level until 2025. We believe that restraint control systems will play an integral role in a larger integration trend towards centralized Safety Domain Controllers in the future. In addition, our strong market position in restraint control systems will provide opportunities to become a leading supplier in the ADAS ECU and eventually the Safety Domain Controller market.

Brake Systems Competitive Landscape

Brake systems consists of brake control ECUs, including ABS and ESC as well as brake apply units. We estimate the total brake systems market to be approximately $12 billion in 2018,2019, with a projected CAGR of 3%5% through 2025. The main growth driver is higher installation rates of ESC systems in China and other emerging countries in Asia. Another major growth driver is more advanced and complex servo assisted systems and regenerative braking systems for HEVs and EVs. The ability to regenerate kinetic energy through braking is of growing importance as vehicle powertrainspower trains are becoming increasingly electrified. We estimate that VNBS and VBS combined had a market share of just aboveapproximately 4% in 2018.2019. Main competitors of VNBS include ADVICS, Bosch, Continental, Mando and ZF.

Research & Development and Intellectual Property

Our ability to maintain our position at the forefront of technologicaltechnology innovations and to serve customers on a local basis will be differentiating factors to our success. Therefore, we maintain one of the broadest global networks of technical engineering centers across all major automotive regions to develop and provide advanced products, processes and manufacturing support for our manufacturing sites and to provide our customers with local engineering capabilities and design development on a global basis.

We currently own or co-own approximately 738850 active patents and have approximately 710800 pending patent applications in the US and other jurisdictions. The active patents will expire between 20192020 and 2038.2039. We have registered the name Veoneer as a trademark in Sweden and are pursuing registration in other markets of interest. Depending on the jurisdiction, trademarks are generally valid as long as they are in use or their registrations are properly maintained, and they have not been found to have become generic.

We are actively pursuing opportunities to commercialize and license our technology to the automotive industries, and we selectively utilize other companies’ licenses through sublicensessub-licenses in order to support our business interests. These activities foster optimization of intellectual property rights.

We believe that our patents, trademarks and licenses, provide meaningful protection for our products and technical innovations and as a whole, to be material to our business. However, we do not consider our business or any of our business segments to be materially dependent upon any individual patent, trademark or license.

We seek to effectively manage fixed costs and efficiently rationalize capital spending by evaluating the market and profit potential of existing and new customer programs, including investments in innovation and technology. We maintain our engineering activities around our focused product portfolio and allocate our capital and resources to those products and distinctive technologies.

Our total research and development expenses, including engineering, net of customer reimbursements, were $562 million, $466 million $375 million and $300$375 million for the years ended December 31, 2019, 2018 and 2017, respectively. Veoneer's 50% share of Zenuity’s net expenses, as reported in loss from equity method investment, was $70 million, $63 million and 2016, respectively. Zenuity’s total expenses were $125$31 million for the yearyears ended December 31, 2018.2019, 2018 and 2017, respectively. These expensescosts were mainly related to research and development.

We believe that our engineering and technical expertise, together with our emphasis on continuing research and development, allows us to use the latest technologies, materials and processes to solve problems for our customers and to bring new innovative productsinnovations to market. We believe that a continued focus on engineering activities are criticalcrucial to maintaining our pipeline of technologically advanced products.technologies to become automotive grade products to meet our customer, regulatory and consumer demands.

Dependence on Customers

Veoneer serves most of the world’s major automotive OEMs and is not dependent on one single customer. Our customer base has consistently increased and become more diversified over the last five years, mainly driven by our active safetyActive Safety product offerings and VNBS.Brake Systems.

11

We typically supply products to our OEM customers through written contracts or purchase orders which are generally governed by general terms and conditions established by each OEM. These arrangements include terms regarding price, quality, technology and delivery. Although it may vary from customer to customer, our customer contracts generally require us to supply a customer’s annual requirements for a particular vehicle model and assembly facilities, rather than for manufacturing a specific quantity of products. Such contracts range from one year to the life of the model, which is generally four to seven years. Because we produce products for a broad cross section of vehicle models, we are not overly reliant on any one vehicle model or one particular product.

These contracts are often subject to renegotiation, sometimes as frequent as on an annual basis which may affect product pricing. In general, these arrangements with our customers provide that the customer can terminate them if we do not meet specified quality, delivery and cost requirements. Although these arrangements may be terminated at any time by our customers (but not typically by us), such terminations have historically been minimal and have not had a material impact on our results of operations. However, if terminations do occur in the future or if production under a contract winds down earlier than expected, then such event could have a material impact on our results of operations. The arrangements typically provide that we are subject to a warranty on the products supplied; in most cases, the duration of such warranty is coterminous with the warranty offered by the OEM to the end-user of the vehicle. We may also be obligated to share in all or a part of recall costs if the OEM recalls its vehicles for defects attributable to our products.

Veoneer Personnel

As of December 31, 2018,2019, we had a total of approximately 8,600 employees and consultants,8,900 total associates, with 4,6764,900 in engineering, 2,0832,000 in direct manufacturing and the remaining 2,000 in production and 1,346SG&A overhead functions. Included in production overhead,these figures are approximately 1,400 temporary associates, and the remainder employed in management, general and administrative functions. Withinwithin engineering, more than two thirds of the employeesassociates worked as software engineers.

In addition, Zenuity had approximately 600720 employees and consultants at the endas of 2018,December 31, 2019, of which approximately 88%close to 90% worked as software developers. In 2018,During 2019, approximately 1,100230 engineers were hired by Veoneer and more than 100approximately 70 were hired by Zenuity.

We consider our relationship with our personnel to be strong. We have not had any disputes which are significant or had a lasting impact on our relationship with our employees, customer perception of our employee practices or our business results.

Major unions to which some of our employees belong in Europe include: IG Metall in Germany; Unite in the United Kingdom; Confédération Générale des Travailleurs, Confédération Française Démocratique du Travail, and Force Ouvrière in France; and If Metall, Unionen, Sveriges Ingenjörer and Akademikerföreningen in Sweden.

In addition, our employees in other regions are represented by the following unions: Unifor and the International Association of Machinists and Aerospace Workers (“IAM”) in Canada and VNBS Roudou Kumiai in Japan.

In many European countries and in Canada, wages, salaries and general working conditions are negotiated with local unions and/or are subject to centrally negotiated collective bargaining agreements. The terms of our various agreements with unions typically range between one and three years. Some of our subsidiaries in Europe and Canada must negotiate with the applicable local unions with respect to important changes in operations, working and employment conditions. Twice a year, members of the Company’s management conduct a meeting with the European Works Council (“EWC”) to provide employee representatives with important information about the Company and a forum for the exchange of ideas and opinions.

In many Asia Pacific countries, the central or regional governments provide guidance each year for salary adjustments or statutory minimum wage for workers. Our employees may join associations in accordance with local legislation and rules, although the level of unionization varies significantly throughout our operations.

Inventory and Working Capital

We, as with other component manufactures in the automotive industry, ship our products to customer vehicle assembly facilities throughout the world on a “just-in-time” basis for our customers to maintain low inventory levels. Our suppliers (external suppliers as well as our own production sites) use a similar method in providing raw materials or sub-assemblies to us. In certain situations Veoneer utilizes consignment inventories with our supply base.

12

Sources and Availability of Raw Materials

We procure our raw materials and components from a variety of suppliers around the world. Generally, we seek to obtain materials in the region in which our products are manufactured to minimize transportation, currency risks and other costs. The most significant raw materials we use to manufacture our products are various electricalelectronic semi-conductor components and ferrous metals for brake systems. As of December 31, 2018,2019, we have not experienced any significant shortages of raw materials and normally do not carry inventories of such raw materials more than those reasonably required to meet our production and shipping schedules.

Commodity cost volatility is a challenge for us and our industry. We are continually seeking to manage these costs using a combination of strategies, including working with our suppliers to mitigate costs, seeking alternative product designs and material specifications, continuous improvement VEVAs (Value Engineering, Value Analysis), combining our purchase requirements with our customers and/or suppliers, changing suppliers, hedging certain commodities and other means. Our overall success in passing commodity cost increases on to our customers has been limited. We will continue our efforts to pass market-driven commodity cost increases to our customers in an effort to mitigate all or some of the adverse earnings impacts, including by seeking to renegotiate terms as contracts with our customers expire.

Seasonality

Our business is moderately seasonal. Our European customers generally reduce production during the months of July and August and for one week in December. Our North American customers historically reduce production during the month of July and halt operations for approximately one week in December. Our Chinese customers generally reduce production during the Chinese New Year period in February. Shut-down periods in the rest of the world generally vary by country. In addition, automotive production is traditionally reduced in the months of July, August and September due to the launch of parts production for new vehicle models. Accordingly, our results reflect this seasonality. In addition, engineering incomereimbursement tends to be skewed towards the fourth quarter.

Environmental Compliance

We are subject to various environmental regulations governing, among other things: (i) the generation, storage, handling, use, transportation, presence of, or exposure to hazardous materials; (ii) the emission and discharge of hazardous materials into the ground, air or water; (iii) the incorporation of certain chemical substances into our products, including electronic equipment; and (iv) the health and safety of our employees.

Most of the Company’s manufacturing processes consist of the assembly of components. As a result, the environmental impact from the Company’s plants is generally modest. While our businesses from time to time are subject to environmental investigations, there are no material environmental-related cases pending against the Company. Therefore, we do not incur (or expect to incur) any material costs or capital expenditures associated with maintaining facilities compliant with U.S. or non-U.S. environmental requirements. To reduce environmental risk, the Company has implemented an environmental management system in all plants globally and has adopted an environmental policy.

We are subject to various U.S. federal, state and local, and non-U.S., laws and regulations, including those related to environmental, health and safety, financial and other matters. We cannot predict the substance or impact of pending or future legislation or regulations, or the application thereof. The introduction of new laws or regulations or changes in existing laws or regulations that impact our business, or the interpretations thereof, could increase the costs of doing business for us or our customers or suppliers or restrict our actions and adversely affect our financial condition, operating results and cash flows.

We are also required to obtain permits from governmental authorities for certain of our operations.

Dependency on Government Contracts

We are not dependent on government contracts. Some R&D projects are partly financed by certain government agencies.

13

Joint Venture AgreementsVentures

Zenuity Joint Venture Agreement

Zenuity operates pursuant to the Joint Venture Agreement, dated April 18, 2017 (the “Zenuity JV Agreement”), between Volvo Cars and a subsidiary of Veoneer. The Zenuity JV Agreement describes the scope of the business activities of Zenuity, which is to develop automotive driver assistance and highly autonomous driving software solutions that can be supplied to Volvo Cars and other potential customers. In addition, Zenuity conducts research within the areas of human factors, vehicle environments and computer techniques to develop algorithms for driving assistance or automated driving. Zenuity owns and licenses certain intellectual property rights pursuant to commercialization agreements between the parties. Veoneer is the exclusive supplier and distribution channel for all Zenuity’s products sold to third parties; however, there is no exclusivity toward any customer or the owners. Volvo Cars can source such products directly from Zenuity. The parties also entered into a number of related agreements in connection with forming the joint venture, including an investment agreement, commercialization agreements and intellectual property license and assignment agreements pursuant to which Volvo Cars and Veoneer transferred certain intellectual property rights to Zenuity. A copy of the Zenuity JV Agreement has been filed with the U.S. Securities and Exchange Commission (the “SEC”).

Former VNBS Joint Venture Agreement

Brake Systems was formed by and operates pursuant to a number of agreements entered into between certain affiliates of each of Veoneer and Nissin Kogyo Ltd., Co. (“Nissin”), including a Share Purchase Agreement, dated September 9, 2015, and a Joint Venture Agreement, dated March 7, 2016 (the “VNBS JV Agreement”). The VNBS JV Agreement setsset forth the agreementsagreement between Veoneer and Nissin with respect to the ownership, capitalization, governance and operations of Brake Systems. It providesprovided that Veoneer ownswould own 51% of each of the entities that comprisecomprised Brake Systems and Nissin ownswould own the remaining 49% of each entity. A copy of the VNBS JV Agreement has beenwas filed with the SEC.

Pursuant to the agreements, Veoneer acquired Nissin’s interests in the US operations of VNBS, referred to as VBS, and VNBS transferred or licensed the VNBS technologies necessary to operate the VBS business to VBS. VBS, including the transferred or licensed technologies, became a formal negotiation processwholly-owned Veoneer business effective on the closing date, June 28, 2019.

Under the agreement, Nissin provided guarantees for certain VNBS commercial loans corresponding to 49% of the funding Veoneer had previously unilaterally provided to VNBS. During the nine months ended September 30, 2019, Veoneer received approximately $20 million as debt repayment from VNBS.

On October 30, 2019, Veoneer signed agreements (the "Definitive Agreements") to sell its 51% ownership in Veoneer Nissin Brake Japan ("VNBJ") and Veoneer Nissin Brake China ("VNBZ") entities that comprise VNBS to Nissin and Honda Motor Co., Ltd. The transaction was completed on February 3, 2020 under the Definitive Agreements, and the VNBS JV Agreement to find a resolution to the current funding situation.joint venture was terminated. See Note 6 "Assets held for sale" for additional information.

Spin-Off Related Agreements

As part of the Spin-Off, Autoliv underwent an internal reorganization, pursuant to which, among other things and subject to limited exceptions, all of the assets and liabilities (including whether accrued, contingent or otherwise, and subject to certain exceptions) associated with the electronics business of Autoliv were retained by or transferred to Veoneer or our subsidiaries and all other assets and liabilities (including whether accrued, contingent or otherwise, and subject to certain exceptions) of Autoliv were retained by or transferred to Autoliv or its subsidiaries (other than Veoneer).

Following the Spin-Off, the Company and Autoliv began operating independently and neither has any ownership interest in the other. To govern certain ongoing relationships between Veoneer and Autoliv after the Spin-Off and to provide mechanisms for an orderly transition, the Company and Autoliv entered into agreements pursuant to which certain services and rights are provided for following the Spin-Off, and the Company and Autoliv will indemnify each other against certain liabilities arising from our respective businesses.

Distribution Agreement

In connection with the internal reorganization, we entered into a Master Transfer Agreement with Autoliv which was amended and restated effective as of the Spin-Off (the “Distribution Agreement”). The Distribution Agreement governs

14

certain transfers of assets and assumptions of liabilities by each of Veoneer and Autoliv and the settlement or extinguishment of certain liabilities and other obligations among the companies and their subsidiaries. In particular, substantially all of the assets and liabilities associated with the separated Electronics business were retained by or transferred to Veoneer or its subsidiaries and all other assets and liabilities were retained by or transferred to Autoliv or its subsidiaries. The Distribution Agreement also provided the principal corporate transactions required to affect the Spin-Off, certain conditions to the Spin-Off and provisions governing the relationship between Veoneer and Autoliv with respect to and resulting from the completion of the Spin-Off. The Distribution Agreement also provides for indemnification obligations designed to make the Company financially responsible for substantially all liabilities that may exist relating to its business activities, whether incurred prior to or after the completion of the internal reorganization, as well as those obligations of Autoliv assumed by us pursuant to the Master Transfer Agreement; provided, however, certain warranty, recall and product liabilities for Electronics products manufactured prior to the completion of the internal reorganization were retained by Autoliv and Autoliv will indemnify us for any losses associated with such warranty, recall or product liabilities.

Employee Matters Agreement

The Employee Matters Agreement governs Autoliv’s and Veoneer’s compensation and employee benefit obligations with respect to the current and former employees and non-employee directors of each company. Under the agreement, Autoliv is responsible for liabilities associated with Autoliv allocated employees and liabilities associated with former employees and Veoneer is responsible for liabilities associated with Veoneer allocated employees, but Autoliv retains and continues to be responsible for certain post-retirement liabilities relating to plans sponsored by Autoliv. The Employee Matters Agreement provided for the conversion of the outstanding awards granted under the Autoliv equity compensation programs into adjusted awards relating to both shares of Autoliv and Veoneer common stock.

Tax Matters Agreement

The Tax Matters Agreement governs the respective rights, responsibilities and obligations of Autoliv and Veoneer with respect to tax liabilities and benefits, tax attributes, tax contests and other tax sharing regarding U.S. federal, state, local and foreign income taxes, other tax matters and related tax returns. The agreement also specifies the portion, if any, of this tax liability for which Veoneer will bear responsibility and provides for certain indemnification provisions with respect to amounts for which they are not responsible. In addition, under the agreement, each party is expected to be responsible for any taxes imposed on Autoliv that arise from the failure of the Spin-Off and certain related transactions to qualify as a tax-free transaction for U.S. federal income tax purposes.

Amended and Restated Transition Services Agreement

Under the Amended and Restated Transition Services Agreement (“TSA”), Autoliv and Veoneer agreed to provide to each other certain services for a limited time to help ensure an orderly transition following the Spin-Off. The services that Autoliv provides include certain finance, information technology, human resources and compensation, facilities, legal and compliance and other services. We pay Autoliv for any such services utilized at agreed amounts as set forth in the TSA. In addition, for a term set forth in the TSA, we and Autoliv may mutually agree on additional services to be provided by Autoliv to us that were provided to us by Autoliv prior to the distribution but were omitted from the TSA at pricing based on market rates that are reasonably agreed by the parties. The TSA terminates on April 1, 2020.

Available Information

We file or furnish with the SEC periodic reports and amendments thereto, which include annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, proxy statements and other information. Such reports, amendments, proxy statements and other information are made available free of charge on our corporate website at www.veoneer.com and are available as soon as reasonably practicable after they are electronically filed with the SEC. The SEC maintains an internet site that contains reports, proxy and information statements, and other information regarding issuers that file electronically with the SEC at http://www.sec.gov. Paper copies ocfof the above-mentioned documents can be obtained free of charge from the Company by contacting usour Investor Relations and Corporate Communications at: Veoneer, Inc., Box 13089, SE-103 02, Stockholm, Sweden or Veoneer, Inc., 2654526360 American Drive, Southfield, MI 48034.48034 or http://www.veoneer.com.

15

Item 1A. Risk Factors

Owning our common stock involves a high degree of risk. You should consider carefully the following risk factors and all other information contained in this Annual Report on Form 10-K. If any of the following risks, as well as additional risks and uncertainties not currently known to us or that we currently deem immaterial but are in fact material, occur, our business, liquidity, results of operations and financial condition could be materially and adversely affected. If this were to happen, the market price of our common stock could decline significantly, and you could lose all or a part of the value of your ownership in our common stock. Some statements in this information statement,Annual Report, including statements in the following risk factors, constitute forward-looking statements. Please refer to the section in this Annual Report entitled “Forward-Looking Statements.”

Risks Related to Our Industry

The cyclical nature of automotive sales and production can adversely affect our business. The market is currently experiencing a significant decline in light vehicle production (LVP) and LVP may decline for the next several years. A prolonged recession and/or a downturn in our industry or deteriorating performance of our business, could adversely affect our business and require impairments or restructuring actions.

Our business is related to LVP in the global market and by our customers, and automotive sales and LVP are critical drivers for our sales. Automotive sales and production are highly cyclical and can be affected by generalA prolonged downturn in or uncertainty relating to global or regional economic or industry conditions, or uncertainty, the level of consumer demand, recalls and other safety issues, labor relations issues, technological changes, fuel prices and availability, vehicle safety regulations and other regulatory requirements, governmental initiatives, trade agreements, political volatility, especially in energy producing countries and growth markets, changes in interest rate levels and credit availability and other factors. At various times some regions around the world may be more particularly impacted by these factors than other regions. Economic declines that result in aany significant reduction in automotive sales and productionand/or LVP by our customers, have in the past had, and may in the futurewhether due to general economic conditions or any other factors relevant to sales or LVP, will likely have a material adverse effect on our business, results of operations and financial condition. If global economic conditions deteriorate or economic uncertainty increases, our customers and potential customers may experience deterioration of their businesses, which may result in the delay or cancellation of plans to purchase our products.

Furthermore, our ability to generate cash from our operations is highly dependent on regional and global economic conditions, automotive sales and LVP. Additionally, we have a substantial number of important product and program launches in the next 18 months. These launches are important from both a sales and cash flow perspective. A continued lower LVP or lower sales volumes on these new vehicles being launched as well as lower sales on other vehicles may delay the return on our investment in R&D and a return on the resources expended to ensure timely and quality launches. Given the high level of R&D that is required in our products, including new product and program launches, a significantly negative cash flow could have a materially negative impact on our business. A prolonged downturn in global economic conditions or LVP would likely result in us experiencing a significantly negative cash flow.

Order intake and the dollar amount of the order intake are not necessarily indicative of future net sales revenues and are subject to a number of uncertainties. If order intake fails to translate into future net sales revenue it may adversely affect our business.

We monitor order intake to make certain predictions related to our capital needs and expenditures and in providing long-term targets, earnings guidance and estimates. Our order intake is the estimated future average annual sales attributable to documented new business awarded based on estimated average annual product volumes, average annual sales price for such products over their anticipated life, and exchange rates. Order intake is not recorded as revenue until the order is completed. The aggregate value of order intake is considered our “order book” and is part of it until the products are also affected by inventory levelsmanufactured and delivered to customers and we realize net sales revenue from such orders. Since the general lead time from an “order” to the start of production is three to four years and it may take several months for production of a certain vehicle model to fully ramp up, the assumptions we use to determine order intake may no longer be accurate at the time production begins or the order is completed. For example, active safety and restraint control systems order intake from 2013 to 2015 is reflected in sales from 2017 to 2019.

To determine our customers.estimated order intake, we make several assumptions related to vehicle production in a particular year of a particular model, annual product values, sales prices for such products and exchange rates. If any of the inputs to these assumptions fail to materialize as we expect, the net sales revenue actually realized may be adversely impacted. We cannot predict when our customers will decide to either increase or reduce inventory levels or whether new inventory levels will approximate historical inventory levels. This may exacerbate variability inOur customers generally do not guarantee order volumes. Additionally, the commercial success of the vehicle models which include our products will also impact whether our order intake and, as a result, our revenues and financial condition. Uncertainty regarding inventory levels may be exacerbated by consumer financing programs initiated or terminated by our customers or governments as such changes may affect the timing of their sales.

conditions or any other factors relevant to sales or LVP, will likely have a material adverse effect on whether net sales revenue is ultimately realized from our business, results of operations and financial condition.estimated order book.

16

Growth rates in safety content per vehicle, which may be impacted by changes in consumer trends and political decisions, could affect our results in the future.

Vehicles produced in different markets may have various safety content values. For now, our products are typically found in vehicles with higher safety content. Because growth in global LVP is highly concentrated in markets such as China and India, our operating results may suffer if the safety content per vehicle remains low in our growth markets. As safety content per vehicle is also an indicator of our sales development, should this trendstrend continue, the average safety systems per vehicle could decline.

Our estimate of total addressable market is subject to numerous uncertainties. If we have overestimated the size of our total addressable market, our future growth rate may be limited.

The Company’s estimates of total addressable market, or TAM, are based on a variety of inputs, including production estimates per product group (which are based in significant part on LVP data and estimates from IHS), and in particular in relation to content per vehicle, or CPV, estimates, the Company’s own market insights, estimates as to the pace and extent of standard-setting and regulatory change, internal market intelligence on prices and penetration/adoption rates of each expected product group and the Company’s history operating in the market (including, among other things, its order and bid experience).

We have not independently verified any third-party information, including LVP estimates by IHS, and cannot assure you of its accuracy or completeness. While we believe our market size estimates are reasonable, such information is inherently imprecise. For example, IHS’s January 2020 estimates of LVP over the time period from 2020 to 2023 are reduced by approximately 50 million vehicles compared to forecasts in June 2018 (around the time of the completion of our spin-off from Autoliv). Compared to forecasts in June 2018, the current global LVP forecast is 11% lower for 2019, 13% lower for 2020 and 12% lower for 2022. In Western Europe, the current forecast is 10% lower for 2019, 11% lower for 2020 and 5% lower for 2022. In North America, the current forecast is 7% lower for 2019, 6% lower for 2020 and 7% lower for 2022. In China, the current forecast is 18% lower for 2019, 22% lower for 2020 and 19% lower for 2022. If IHS or other third-party or internally generated data that is used in our estimates proves to be inaccurate or we make errors in our assumptions based on that data, our actual market may be more limited than our estimates. In addition, these inaccuracies or errors may cause us to misallocate capital and other critical business resources, which could harm our business. Even if our total addressable market meets our size estimates and experiences growth, we may not continue to grow our share of the market. Our growth is subject to many factors, including our success in implementing our business strategy, which is subject to many risks and uncertainties. Accordingly, the estimates of our total addressable market included in this Annual Report should not be taken as indicative of our ability to grow our business.

We operate in highly competitive markets.

The markets in which we operate are highly competitive. We compete with a number of companies that design, produce and sell similar products. Among other factors, our products compete on the basis of price, quality, manufacturing and distribution capability, design and performance, technological innovation, delivery and service. Some of our competitors are subsidiaries (or divisions, units or similar) of companies that are larger than we are and have greater financial and other resources than us. Some of our competitors as well as some of our customers have strategic relationships with outside partners, enabling them to pool resources. Additionally, some of our competitors may also have “preferred status” as a result of special relationships or ownership interests with certain customers. Our ability to compete successfully depends, in large part, on our ability to innovate and manufacture products that have commercial success with consumers, differentiatingdifferentiate our products from those of our competitors, deliveringdeliver quality products in the time frames required by our customers, create confidence in our financial stability, and achievingachieve best-cost production.

Furthermore, given that some of our competitors are larger than we are and have greater financial resources, our ability to create confidence in our customers and potential customers that we have the financial strength and resources to support their ambitious programs and can timely deliver quality products over the life of a vehicle program will also be a significant factor in our ability to be competitive. Because the supply chain in our industry is very complex and many of our competitors have greater financial resources, our customers and potential customers may consider us as a supply risk and become concerned that we will be unable to continue to provide products to them at a quality level that meets their needs. If we are unable to create confidence in our financial position, customers may choose other suppliers, which would have a material adverse effect on our business, results of operations and financial condition.

Our ability to maintain and improve existing products, while successfully developing and introducing distinctive new and enhanced products that anticipate changing customer and consumer preferences and capitalize upon emerging technologies will

17

be a significant factor in our ability to be competitive. If we are unsuccessful or are less successful than our competitors in predicting the course of market development, developing innovative products, processes, and/or use of materials or adapting to new technologies or evolving regulatory, industry or customer requirements, we will suffer from a competitive disadvantage. Further, the global automotive industry is experiencing a period of significant technological change, including a focus on environmentally sustainable products. As a result, the success of portions of our business requires us to develop, acquire and/or incorporate new technologies. There is a risk that our investments in research and development initiatives will not lead to successful new products and a corresponding increase in revenue. We may also encounter increased competition in the future from existing or new competitors. The inability to compete successfully could have a material adverse effect on our business, results of operations and financial condition.

We operate in a developing market that may be subject to greater uncertainty and fluctuations in levels of competition than a more mature market.

The field of active safety is a developing segment in the automotive industry and is expected to act as a basis for and enable the development and introduction of commercially viable autonomous vehicles. The number of competitors may increase as suppliers from outside the traditional automotive industry, such as Google, Argo, Uber, Lyft, Cruise, Samsung, Panasonic, Here, Tesla, Intel, NVIDIA and other technology companies, consider the significant business opportunities presented by autonomous driving. Some of our customers are also partnering together to develop autonomous driving solutions. The evolving nature of the competitive landscape creates greater uncertainty than the traditional automotive market.

Products and services provided by companies outside the automotive industry may also reduce demand for our products, which require substantial investment in research and development. For example, there has been an increase in consumer preferences for mobility on demand services, such as car- and ride-sharing, as opposed to automobile ownership, which may result in a long-term reduction in the number of vehicles per capita. Today, in most markets, active safety products are considered to be premium equipment rather than standard automotive safety items, which can create significant volatility in demand for certain of our products.