UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

| | | | | |

| ☒ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 20192023

OR

| | | | | |

| ☐ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 FOR THE TRANSITION PERIOD FROM TO |

Commission File Number 001-38846

Lyft, Inc.

(Exact name of Registrantregistrant as specified in its Charter)charter)

| | | | | |

| Delaware | 20-8809830 |

(State or other jurisdiction of

incorporation or organization) | (I.R.S. Employer

Identification No.) |

| | | | | |

185 Berry Street, Suite 5000400 San Francisco, California | 94107 |

| (Address of principal executive offices) | (Zip Code) |

Registrant’s telephone number, including area code: (844) 250-2773

Securities registered pursuant to Section 12(b) of the Act:

| | | | | | | | | | | | | | |

| Title of each class | | Trading

Symbol(s) | | Name of each exchange on which registered |

| Class A common stock, par value of $0.00001 per share | | LYFT | | Nasdaq Global Select Market |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the Registrantregistrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐☒ No ☒☐

Indicate by check mark if the Registrantregistrant is not required to file reports pursuant to Section 13 or 15(d) of the Act. Yes ☐ No ☒

Indicate by check mark whether the Registrant:registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrantregistrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the Registrantregistrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the Registrantregistrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| | | | | | | | | | | |

| Large accelerated filer | ☐☒ | Accelerated filer | ☐ |

| Non-accelerated filer | ☒☐ | Smaller reporting company | ☐ |

| Emerging growth company | ☐ | | |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the Registrantregistrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☒

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

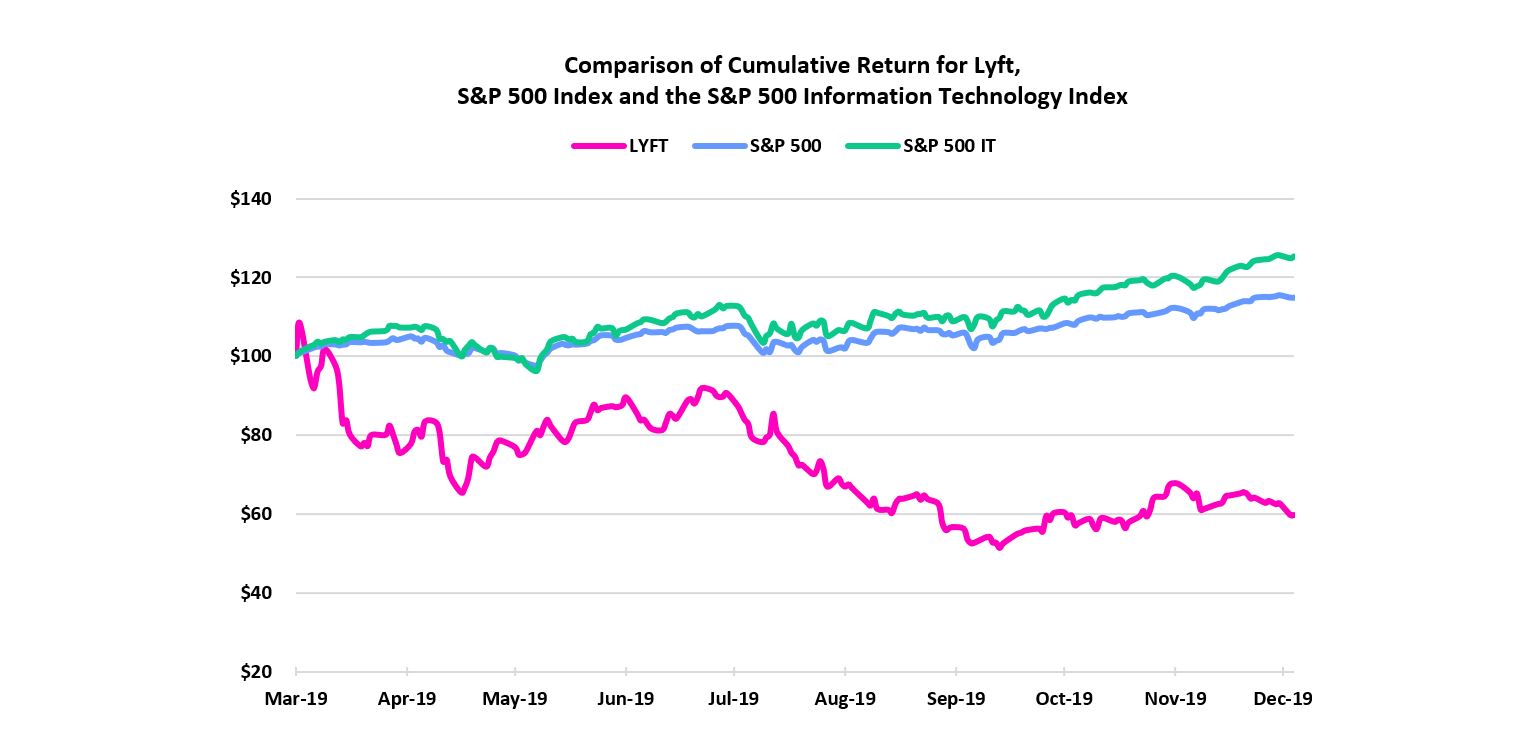

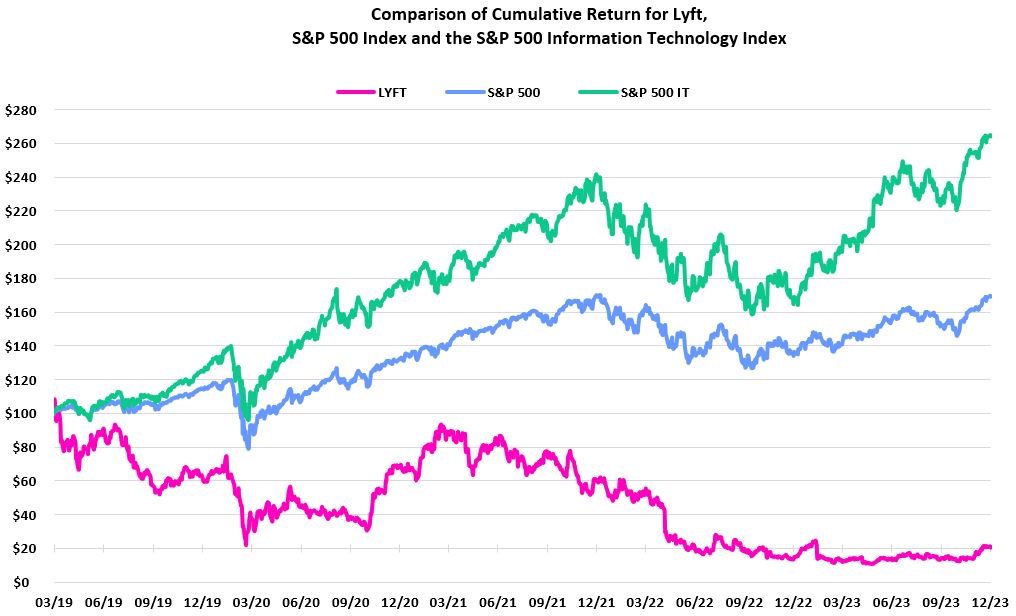

The aggregate market value of the Registrant’sregistrant’s common stock held by non-affiliates of the Registrantregistrant on June 28, 2019,30, 2023, the last business day of its most recently completed second fiscal quarter, was $14.1$3.6 billion based on the closing sales price of the Registrant’sregistrant’s Class A common stock on that date.

On February 21, 2020,12, 2024, the Registrantregistrant had 297,836,880391,240,004 shares of Class A common stock and 8,802,6298,566,629 shares of Class B common stock outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant’s Proxy Statement for the 20202024 Annual Meeting of Stockholders are incorporated herein by reference in Part III of this Annual Report on Form 10-K to the extent stated herein. Such proxy statement will be filed with the Securities and Exchange Commission within 120 days of the registrant’s fiscal year ended December 31, 2019.

Table of Contents

| | | | | | | | |

| | Page |

| PART I | | |

| Item 1. | | |

| Item 1A. | | |

| Item 1B. | | |

| Item 1C. | | |

| Item 2. | | |

| Item 3. | | |

| Item 4. | | |

| | |

| PART II | | |

| Item 5. | | |

| Item 6. | | |

| Item 7. | | |

| Item 7A. | | |

| Item 8. | | |

| Item 9. | | |

| Item 9A. | | |

| Item 9B. | | |

| Item 9C. | | |

| | |

| PART III | | |

| Item 10. | | |

| Item 11. | | |

| Item 12. | | |

| Item 13. | | |

| Item 14. | | |

| | |

| PART IV | | |

| Item 15. | | |

| Item 16. | | |

NOTE ABOUT FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K contains forward-looking statements within the meaning of the federal securities laws, which statements involve substantial risks and uncertainties. Forward-looking statements generally relate to future events or our future financial or operating performance. In some cases, you can identify forward-looking statements because they contain words such as “may,” “will,” “should,” “expect,” “plan,” “anticipate,” “could,” “intend,” “target,” “project,” “contemplate,” “believe,” “estimate,” “predict,” “potential” or “continue” or the negative of these words or other similar terms or expressions that concern our expectations, strategy, plans or intentions. Forward-looking statements contained in this Annual Report on Form 10-K include statements about:

•our future financial performance, including our expectations regarding our revenue, cost of revenue, operating expenses, capital expenditures, our ability to determine insurance, legal and other reserves and our ability to achieve and maintain future profitability;

•the sufficiency of our cash, cash equivalents and short-term investments to meet our liquidity needs;

•the demand for our platform or for Transportation-as-a-Service networks in general;

•our ability to attract and retain drivers and riders;

•our ability to develop new offerings and bring them to market in a timely manner and update and make enhancements to our platform;

•our ability to compete with existing and new competitors in existing and new markets and offerings;

•our prices and pricing methodologies and our expectations for the impact of pricing on our competitive position and our financial results;

•our future operating performance, including but not limited to our expectations regarding future Gross Bookings, Rides and Active Riders;

•our expectations regarding outstanding and potential litigation, including with respect to the classification of drivers on our platform;

•our expectations regarding the effects of existing and developing laws and regulations, including with respect to the classification of drivers on our platform, taxation, privacy and data protection;

•our ability to manage and insure risks associated with our Transportation-as-a-Service network, including auto-related and operations-relatedoperations related risks, and our expectations regarding insurance costs and estimated insurance reserves;

•our expectations regarding new and evolving markets and our efforts to address these markets, including our autonomous vehiclesvehicle programs, Light Vehicles, Flexdrive, and bikes and scooters as well as Express Drive, Driver Centers and Lyft Rentals;Drive;

•our ability to develop and protect our brand;

•our ability to maintain the security and availability of our platform;

•our expectations and management of future growth;growth and business operations, including our prior plans of termination;

•our expectations concerning relationships with third parties;

•our ability to maintain, protect and enhance our intellectual property;

•our expectations concerning macroeconomic conditions, including the impact of inflation, uncertainty in the global banking and financial services markets and the COVID-19 pandemic;

•our disclosure controls and procedures, including changes thereto;

•our ability to service our existing debt; and

•our ability to successfully acquire and integrate companies and assets; and

•the increased expenses associated with being a public company.assets.

We caution you that the foregoing list may not contain all of the forward-looking statements made in this Annual Report on Form 10-K.

You should not rely upon forward-looking statements as predictions of future events. We have based the forward-looking statements contained in this Annual Report on Form 10-K primarily on our current expectations and projections about future events and trends that we believe may affect our business, financial condition, results of operations and prospects. The outcome of the events described in these forward-looking statements is subject to risks, uncertainties and other factors, including those described in the section titled “Risk Factors” and elsewhere in this Annual Report on Form 10-K. Moreover, we operate in a very competitive and rapidly changing environment. New risks and uncertainties emerge from time to time and it is not possible for us to predict all risks and uncertainties that could have an impact on the forward-looking statements contained in this Annual Report on Form 10-K. We cannot assure you that the results, events and circumstances reflected in the forward-looking statements will be achieved or occur, and actual results, events or circumstances could differ materially from those described in the forward-looking statements.

The forward-looking statements made in this Annual Report on Form 10-K relate only to events as of the date on which the statements are made. We undertake no obligation to update any forward-looking statements made in this Annual Report on Form 10-K to reflect events or circumstances after the date of this Annual Report on Form 10-K or to reflect new information or the occurrence of unanticipated events, except as required by law. We may not actually achieve the plans, intentions or expectations disclosed in our forward-looking statements and you should not place undue reliance on our forward-looking statements. Our forward-looking statements do not reflect the potential impact of any future acquisitions, mergers, dispositions, joint ventures or investments we may make.

In addition, statements that “we believe” and similar statements reflect our beliefs and opinions on the relevant subject. These statements are based upon information available to us as of the date of this Annual Report on Form 10-K, and while we believe such information forms a reasonable basis for such statements, such information may be limited or incomplete, and our statements should not be read to indicate that we have conducted an exhaustive inquiry into, or review of, all potentially available relevant information. These statements are inherently uncertain and investors are cautioned not to unduly rely upon these statements.

PART I

Item 1. Business.

Our Mission

Improve people’s lives with the world’s best transportation.

Overview

Lyft, Inc. (the “Company” or “Lyft”) started a movement to revolutionize transportation. In 2012, we launched our peer-to-peer marketplace for on-demand ridesharing and have continued to pioneer innovations aligned with our mission.innovations. Today, Lyft is one of the largest and fastest-growingmultimodal transportation networks in the United States and Canada.

We believe that cities should be built for people, not cars. Mass car ownership in the twentieth century brought unprecedented freedom to individuals and spurred significant economic growth. However, in the process, city infrastructure became overwhelmingly devoted to cars. Roads and parking lots have replaced too much green space. Mass car ownership strains our cities and reduces the very freedom that cars once provided. Car ownership has also economically burdened consumers and can equate to a substantial portion of a household’s transportation spend despite the average car being parked and unused a majority of the time.

Consumers are seeking better waysan important purpose, which is to get around. They have grown accustomed to the convenience and immediacy of the on-demand economy and expect their experiences to be more simple and enjoyable. Existing transportation options have failed to meet this shift in consumer demand, creating the opportunity for a better solution.

We believe thatriders out into the world is at the beginning ofso they can live their lives together, and to provide drivers a shift away from car ownershipway to Transportation-as-a-Service (“TaaS”). Lyft is at the forefront of this massive societal change. work that gives them control over their time and money.

Our ridesharing marketplace connects drivers with riders via the Lyft mobile application (the “Lyft App”) in cities across the United States and in select cities in Canada. We believe that our ridesharing marketplace allows our riders to use their car less and offers a viable alternative to car ownership while providing drivers on our platform the freedom and independence to choose when, where, how long and on what platforms they work. As this evolution continues, we believe there is a massive opportunity for us to improve the lives of our riders by connecting them to more affordable and convenient transportation options.

We are laser-focused on revolutionizing transportation and continue to lead the market in innovation. We have established a scaled network of users that is brought together by our robust technology platform (the “Lyft Platform”) that powers millions of rides and connections every day. We leverage our technology platform, the scale and density of our user network and insights from our increasinga significant number of rides to continuously improve our ridesharing marketplace efficiency and develop new offerings. For example, we pioneered Shared Rides, providing lower-cost ridesWe’ve also taken steps to riders traveling similar routes while improvingensure our network is well positioned to benefit from technological innovation in mobility.

Our offerings on the efficiency of our network. In 2018, we were the first to launch a publicly-available commercial autonomous offering in the United States.

Today, our offeringsLyft App include an expanded set of transportation modes in select cities, such as access to a network of shared bikes and scooters (“Light Vehicles”) for shorter rides and first-mile and last-mile legs of multimodal trips, information about nearby public transit routes,trips.

Substantially all of our revenue is generated from our ridesharing marketplace that connects drivers and riders. We collect service fees and commissions from drivers for their use of our ridesharing marketplace. As drivers accept more rider leads, Gross Bookings1 and Rides1 increase, driving more revenue. We also generate revenue from riders renting Light Vehicles, drivers renting vehicles through Express Drive and by making our ridesharing marketplace available to organizations through our Lyft Business offerings, such as our Concierge and Lyft RentalsPass programs. In 2021, we began generating revenues from licensing and data access agreements. In 2022, we began generating revenues from the sale of bikes and bike station software and hardware sales substantially through our acquisition of PBSC Urban Solutions Inc (“PBSC”).

Riders and drivers want and value choice, and we believe there remains an opportunity for growth in our marketplace. In September 2023, we launched Women+ Connect, a new feature that offers women and nonbinary drivers the option to offer riders an extensive view of transportation options when planning any trip.turn on a preference within the Lyft App to prioritize matches with nearby women and nonbinary riders. We believe our transportation network offersare focused on delivering a viable alternative to car ownership. We anticipate the demand for our offeringsgreat rideshare experience and will continue to grow as moreinnovate for drivers and more people discover the convenience, experienceriders, creating an increasingly differentiated service over time. We are committed to building a durable, healthy and affordability of using Lyft.profitable business for riders, drivers and shareholders.

To advance our mission,Additionally, we aim to build the defining brand ofadvocate through our generation and to promote a company culture based on our unique values and commitment to social and environmental responsibility. Through our Lyft Up initiatives, we’re working to make sure people have access to affordable, reliable transportation to get where they need to go - no matter their income or zip code. We believecan’t talk about work that serves customer needs and social goals without mentioning our brand represents freedom at your fingertips: freedom fromresponsibility to our shared environment - the stressesair we breathe and the resilience of car ownershipcommunities we serve. We’re working to make the Lyft Platform more sustainable by helping drivers transition to electric vehicles (“EVs”), riders take more sustainable transportation modes, and freedom to dobusinesses reduce their carbon footprint. We’ve achieved significant growth in EV rides on our platform by investing in EV driver incentives, expanding the Express Drive EV rental program, helping drivers access discounted fast charging and see more. In addition, we have three core values: 1) Be yourself, 2) Uplift others and 3) Make it happen. These values have given rise to a unique company culture that fosters an amazing community of drivers, riders and employees, and have helped establish Lyft as a widely-trusted and recognized brand. advocating for smart EV policy.

We believe many users are loyal to Lyft because of our values, brand and commitment to social and environmental responsibility.

Our values, brand innovation and focused execution have driven significant growth in revenue and the number of usersfocus on customer experience are key differentiators for our platform. As ridesharing becomes more mainstream, webusiness. We continue to believe that users are increasingly choosing services, including a ridesharing platformtransportation network, based on brand affinity and value alignment.For the quarter ended December 31, 2019,alignment and we had 22.9 million Active Riders.

Lyft’s Market Opportunity

Transportation is a massive market. Transportation costs are a substantial expenditureaim to make it easy for both drivers and riders to choose Lyft every household, often more than healthcare and entertainment expenditures. We believe we are still in the very early phases of capturing this massive opportunity as rideshare represents a small percentage of vehicle miles travelled. We also believe that we have a significant incremental opportunity to address transportation spend by businesses and organizations. Our market opportunity today includes transportation spend in the United States and Canada. In the transportation ecosystem, we are one of only two companies that have established a TaaS network at scale across the United States.

Changes in society and the transportation industry are catalyzing a complete transformation of the massive transportation market:

•Consumers increasingly value accessibility and experiences over ownership

•Rise of on-demand services, specifically within the younger demographic

•Greater affinity towards mission-driven brands

•Increased demand for flexible work opportunities

•Emergence of new modes of transportation, such as our network of shared bikes and scooters

•Development of autonomous vehicles

The Lyft Solutiontime.

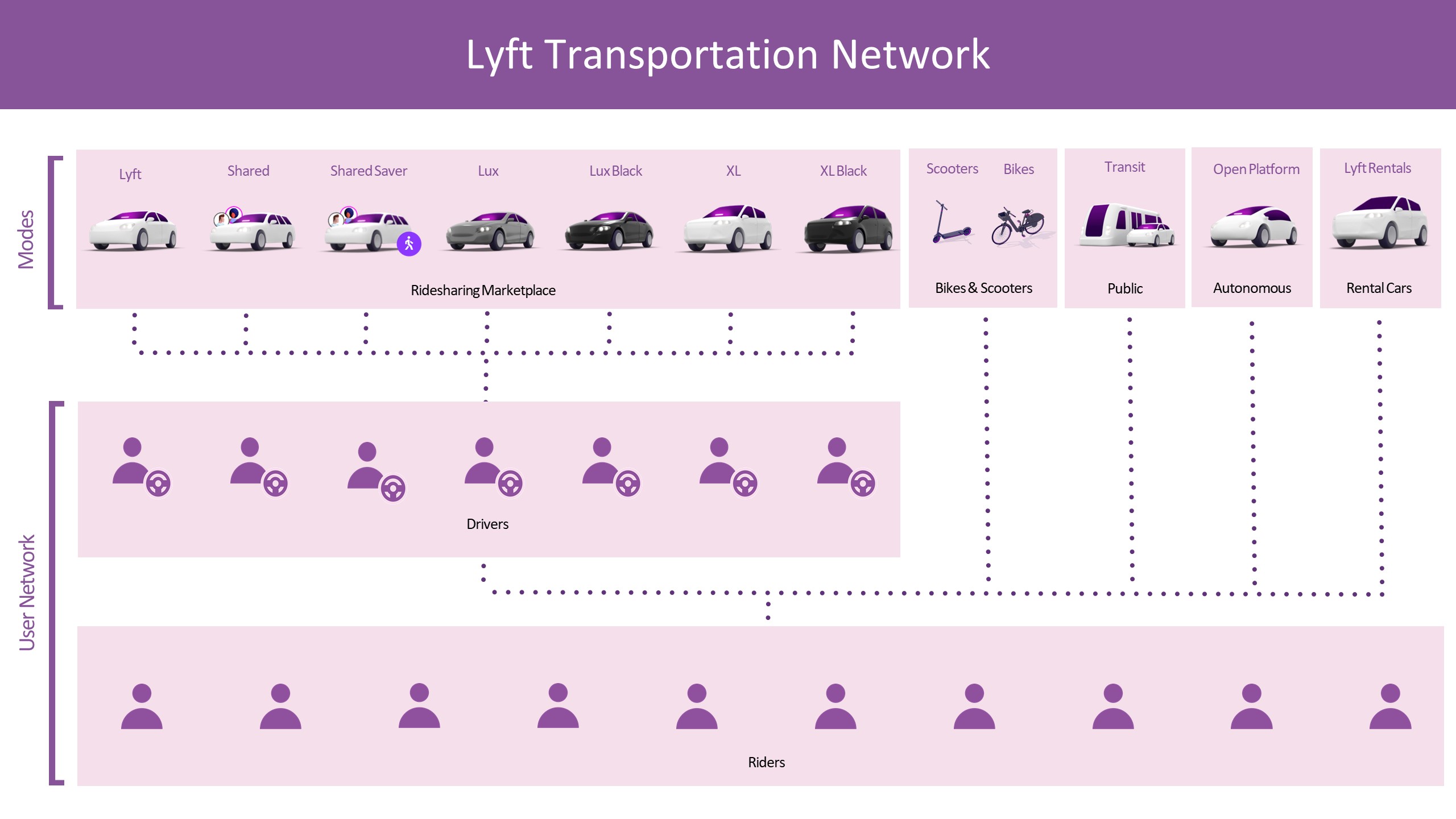

Our Transportation Network

Our transportation network offers riders seamless, personalized and on-demand access to a variety of mobility options.

Our transportation network is primarily comprised of:

•Ridesharing Marketplace.Our core offering since 2012 connects drivers with riders who need to get somewhere.riders. The scale of our network enables us to predict demand and proactively incentivize drivers to be available for rides in the right place at the right time. This allows us to optimize earning opportunities for drivers and offer convenient rides for riders, creating sustainable value to both sides of our marketplace. Our ridesharing marketplace connects drivers with riders in cities across the United States and in select cities in Canada. In addition to our standard rideshare offering, riders can select a variety of other rideshare offerings which include, but are not limited to, Wait & Save, Priority Pickup, XL, Extra Comfort and Black.

1 Beginning in the third quarter of 2023, we began presenting Gross Bookings and Rides as our key business metrics, which we believe best align with how management assesses our performance and measures achievement against our strategic priorities and opportunities. For the definition of Gross Bookings and Rides, refer to the “Definitions of Key Metrics” section within Item 7 of Part II of this Annual Report on Form 10-K.

•BikesExpress Drive. Our car rental program for drivers, including those who want to drive using our platform but do not have access to a vehicle that meets our requirements. Through our Express Drive program, drivers can enter into rental agreements with our independently managed subsidiary, Flexdrive, and Scooters. our rental car partners for vehicles that may be used to provide ridesharing services on the Lyft Platform.

•Light Vehicles.We have a network of shared bikes and scooters in a number of cities to address the needs of ridersusers who are looking for options that are more active usually lower-priced, and often more cost-effective and efficient for short trips during heavy traffic.shorter trips. These transportation modes can also help supplement the first-mile and last-mile of a multimodal trip with public transit.

We utilize data-driven insights to improve our network of shared bikes and scooters. For our offering, we use data science and real-time analytics to understand and predict rider behavior and bike and scooter movement. This informs the on-the-ground teams that support our operations. Our platform technology helps us optimize bike and scooter distribution and rebalancing, which helps reduce operational costs, maximize availability and improve the rider experience.

Lyft bikes are standard and electric pedal-assist bicycles. Riders use the Lyft App, a dedicated program-specific partner app, key fobs, station kiosks, or local transit cards, where applicable, to access the network. Through our acquisition of Motivate in 2018, we believe we operate the largest bike sharing platform in the United States and are well-positioned to lead sustainable mobility in the markets we serve. This platform brings expertise in managing bike share systems in partnership with cities and local governments across the country, currently operating in nine major cities across the United States. Lyft has exclusive city partnerships in a majority of locations where we operate a bike share program including New York City, the San Francisco Bay Area, Chicago and Boston.

Riders can access Lyft scooters via our Lyft App in nine major cities in the United States. When in a service area, riders can see available scooters nearby. They can reserve a scooter ahead of time or use the Lyft App to scan the QR code on a nearby scooter to begin a ride.

•Public Transit. Available in select cities, our Transit offering integrates third-party public transit data into the Lyft App to offer riders a robust view of transportation options around them and allows them to see transit routes to their destinations. Providing real-time public transit information is another step toward providing effective, equitable and sustainable transportation to our communities, and creating a more seamless and connected transportation network. We do not monetize our Transit offering, but it is designed to increase engagement with our platform. We are providing Transit products in eight major cities.

•Autonomous Vehicles. We have a number of strategic partnerships that offer access to autonomous vehicles including Waymo and Aptiv. Our Open Platform partnership with Aptiv has enabled the commercial deployment of a fleet of autonomous vehicles on our platform in Las Vegas. We have facilitated over 100,000 rides in Aptiv autonomous vehicles with a safety driver since January 2018.

•Lyft Rentals. In 2019, we began to test car rentals for riders. This offering is in addition to Express Drive which is our flexible car rentals program for drivers who want to drive using our platform but do not have access to a vehicle that meets our requirements. Lyft Rentals is being offered to riders in two metropolitan areas and offers an attractive option for users who have long-distance trips, like a weekend away.

We have established one of the largest transportation networks in the United States and Canada with 22.9 million Active Riders for the quarter ended December 31, 2019. While network scale is important, we recognize that transportation happens locally. We currently operate in over 300 markets across the United States and Canada, each with its own unique user network. Our dynamic platform adjusts to the specific attributes of each market on a real-time basis.

Drivers

The drivers on our platform are active members of their communities. They are parents, students, business owners, retirees and everything in between. We work hard to serve the community of drivers on our platform, empowering them to bedrive on their own bosses andflexible terms while providing them the opportunity to focus their time on what matters most. Key benefits to driversDrivers on our platform also have key benefits, which include:

•Flexibility. We offer drivers the flexibility to generate income on their own schedule, so they can best prioritize what is important in their lives.

•Technology.Our predictive technology around ride volume and demand enables us to share key information with drivers about when and where to drive in order to maximize their earnings on a real-time basis.

•Transparent and Consistent Pay: We've released multiple products over the years such as upfront pay where drivers can see ride information and what they’ll earn before accepting a ride. We also launched the Weekly Pay Statement for a clearer, more comprehensive view of driver's pay details.

•Insurance.We procure insurance that helps protect transportation network company (“TNC”) drivers against financial losses related to automobile accidents while on the platform. We also provide drivers support in emergency situations and accidents.

•Community Standards. To help us uphold high community standards, we give both drivers and riders the opportunity to rate each other after a ride. If a rider is rated three stars or below,ride booked through the Lyft reviews the situation and contacts the driver if necessary to follow up on the ride experience.App.

•All transactions are processed through our platform, soSupport. We offer drivers do not need to worry about carrying cash.

•Our Driver Hubs and certain field locations in major cities serve as gathering places and offer in-person support and a personal connection to Lyft employees. In addition, drivers have access to 24/7 support and earnings tools as well as education resources and other support to meet their personal goals.

Riders

We care deeply about the riders on our platform and work to build long-term relationships with them by:

•developing simple, elegant and intuitive solutions;

•focusing intensely on the user experience, including soliciting feedback and following up if necessary on the ride experience;

•engendering a sense of mutual respect and fair treatment; and

•promoting trust and safety within our network.

We believe this approach fuels our word-of-mouth referrals and reinforces our community’s desire to use Lyft over alternatives. Our network continues to grow with Active Riders increasing 23% in the fourth quarter of 2019 compared to the same period in 2018.

Our riders are as diverse and dynamic as the communities we serve. They represent all adult age groups and backgrounds and use Lyft to commute to and from work, explore their cities, spend more time at local businesses and stay out longer knowing they can get a reliable ride home. For our ridesharing marketplace,Unless otherwise stated, riders are passengers who request rides from drivers. For bikes, scootersdrivers in our ridesharing marketplace and consumer car rentals, riders are the renters of a shared bike, scooter or automobile.

automobile available on the Lyft App. We work hard to provide our riders with a quality experience every time they open the Lyft App, in order to earn the right to have Lyft be their transportation network of choice. KeyRiders on our platform also have key benefits, to our riderswhich include:

•Selection and Convenience. We designed the Lyft App with a focus on simplicity, efficiency and convenience. Riders enter their destination and are then presented with a range of transportation options to select from based on their needs and preferences. Our proprietary technology efficiently matches riders with drivers through advanced dispatching algorithms providing faster arrival times, localized pricing and maximum availability. We continuously aim to reduce friction in the booking process with features like “one tap ride” so riders can enter their destinations quickly. Additional transportation modes, such as bikes and scooters,Light Vehicles, offer riders more options for shorter trips. We also continue to launch new features, such as Women+ Connect. The more rides that are taken on our platform, the better we are able to offer our riders personalized experiences most suitable to the trip being planned.their trip.

•Availability.Availability and Reliability. We strive to ensure that riders can get a ride when they want one. We leverage our proprietary dispatch platform and data to help drivers and riders connect efficiently and reduce wait times. Our machine learning algorithms continuously trainAs of November 2023, scheduled rides to the airport are backed by our optimization models and dynamically incentivize driverson-time pickup promise in certain major markets. If a ride is more than ten minutes late for a scheduled pick-up, we will offer up to be on our platform when and where riders are seeking transportation. We are also expanding our recently introduced network of shared bikes and scooters. The high availability of our platform and the breadth of our offerings have made us the preferred transportation network$100 in Lyft credits to make up for millions of riders.it.

•Affordability. Our platform empowers riders to choose from a broad set of transportation options to easily optimize for cost, comfort and time. For our ridesharing marketplace,Wait & Save, a substantial and growing portion of rides, offers riders are presented with upfront estimated prices priora way to taking the trip sosave money when they can anticipate the total cost. We also introduced lower-cost options for riders to get aroundaren’t in select cities, including Shared and Shared Saver Rides, a network of shared bikes and scooters and Transit with affordability in mind.hurry.

•Trust and Safety. Since day one, we have worked continuously to improveenhance the safety of our platform and the ridesharing industry by developing innovative products, policies and processes. Before givingWe have a ride on the Lyft platform, all driver-applicants are screened for disqualifying criminal offenses and driving incidents. All approved Lyft drivers are also required to complete mandatory Community Safety Education. We conduct continuous criminal monitoring which provides Lyft with daily monitoring and immediate notification of any disqualifying criminal convictions and driving infractions. Any driver who does not meet applicable regulations and our internaldedicated safety criteria on both the annual and continuous screenings is barred from our platform. During the ride, we have designed numerous safety features into the Lyft experience.

◦Share Route, which allows riders to share their location with family and friends;

◦Emergency access to 911 within the app;

◦Smart Trip Check-In (which we expect to roll out in the near future): in some cases, if we notice your ride has stopped too soon or for an unusual amount of time Lyft will ask drivers and riders if they need support and, if necessary, give the option to request emergency assistance;

◦Partnershipresponse team, a partnership with ADT, where pilot usersInc. (“ADT”) to aid in emergencies, and work with leading national organizations to inform our safety policies. We are ablealways working to signal to ADT that they are in need of assistance;make Lyft as safe as we can.

◦In-app photos of the driver and vehicle, with license plate numbers and vehicle information;Business

◦Real-time ride tracking;We work with organizations across a wide range of industries to deliver transportation solutions. Our comprehensive set of solutions allows clients to design, manage and pay for ground transportation programs that contribute to productivity and satisfaction while reducing cost and streamlining operations.

◦Digital receipts; and

◦Two-way rating system with mandatory secondary feedback. If a driver is rated four stars or below, Lyft obtains detailed feedback, reviews the situation, and follows up if necessary on the ride experience.

◦We have also announced a new, enhanced identity verification process, which combines driver's license verification and photographic identity verification to prevent identity fraud on our platform.

Our Technology Infrastructure and Operations

We organize our product teams with a full-stack development model, integrating product management, engineering, analytics, data science and design. We focus on affordability, reliability, efficiency, optimization and cohesion when developing our software. Our offerings are mobile-first and platform agnostic. We seek to continuously improve our platformthe Lyft Platform and the Lyft App. Our offerings are built on a scalable technology platform that enables us to manage peaks in demand.

We have a commercial agreement with AWSAmazon Web Services (“AWS”) for cloud services provided by AWS to help deliver and host our platform. As a result of our partnership, we believe we are more resilient to surges in demand on our platform or product changes we may introduce. Our commercial agreement with AWS will remain in effect until terminated by AWS or us. AWS may only terminateRefer to Note 9 “Commitments and Contingencies” to the agreementconsolidated financial statements for convenience after March 31, 2022, and only after complying with certain advance notice requirements. AWS may also terminate the agreement for cause upon a breach of the agreement or for failure to pay amounts due, in each case, subject to AWS providing prior written notice and a 30-day cure period. We committed to spend an aggregate of at least $300 million between January 2019 and December 2021 on AWS services. If we fail to meet the minimum purchase commitment during any year, we may be required to pay the difference. We pay AWS monthly, and we may pay more than the minimum purchase commitment to AWS based on usage.information regarding this agreement.

We designed our platform with multiple layers of redundancy to guard against data loss and deliver high availability. Incremental backups are performed hourly or more frequentlyBoth incremental and full backups are performed daily. In addition, as a default,and redundant copies of content are stored independently in at least two separate geographic regions and replicated reliably within each region.regions. We are also investing in iterating and continuously improving our data privacy and security foundation, and continually review and implement the most relevant policies.

Our Intellectual Property

We believe that our intellectual property rights are valuable and important to our business. We rely on trademarks, patents, copyrights, trade secrets, license agreements, intellectual property assignment agreements, confidentiality procedures, non-disclosure agreements and employee non-disclosure and invention assignment agreements to establish and protect our proprietary rights. Though we rely in part upon these legal and contractual protections, we believe that factors such as the skills and ingenuity of our employees and the functionality and frequent enhancements to our solutions are larger contributors to our success in the marketplace.

We have invested in a patent program to identify and protect a substantial portion of our strategic intellectual property in ridesharing, autonomous vehicle technology, telecommunications, networking and other technologies relevant to our business. As of December 31, 2019, we held 248 issued U.S. patents and had 348 U.S. patent applications pending. We also held 36 issued patents in foreign jurisdictions and had 161 applications pending in foreign jurisdictions. We continually review our development efforts to assess the existence and patentability of new intellectual property.

We have an ongoing trademark and service mark registration program pursuant to which we register our brand names and product names, taglines and logos in the United States and other countries to the extent we determine appropriate and cost-effective. We also have common law rights in some trademarks. In addition, we have registered domain names for websites that we use in our business, such as www.lyft.com and other variations.

We intend to pursue additional intellectual property protection to the extent we believe it would be beneficial and cost-effective. Despite our efforts to protect our intellectual property rights, they may not be respected in the future or may be invalidated, circumvented or challenged. For additional information, see the sections titled “Risk Factors—Risks Related to Our Business and Industry—Claims by others that we infringed their proprietary technology or other intellectual property rights could harm our business” and “Risk Factors—Risks Related to Our Business and Industry—Failure to protect or enforce our intellectual property rights could harm our business, financial condition and results of operations.”

Our Growth Strategy

Transportation is a massive market. We are in the very early phase of capturing this large opportunity. Our key growth strategies include our plans to:

•Increase Our Use Cases. We continuously work to extend our offerings to make Lyft the transportation network of choice across an expanding range of use cases. We offer products to simplify travel decision-making and expand the potential uses for our platform, such as subscription plans including Lyft Pink, commuter services, first-mile and last-mile services and university safe rides programs. We also provide centralized tools and enterprise transportation solutions tailored to businesses, such as our Concierge offering, which enables organizations to manage the transportation needs of their customers, employees and constituents.

•Grow Our Rider Base. We see opportunities to continue to grow our rider base. We intend to drive organic adoption in our rider base by continuing to make investments in our brand and growth marketing to increase consumer awareness. We also may offer discounts for first time riders to try Lyft and incentives for existing drivers and riders to refer new riders, and we plan to continue to add density to our ridesharing marketplace by attracting and retaining drivers to our platform to further improve the rider experience. Additionally, we are expanding our platform coverage beyond the geographies and markets we currently serve. We also believe we will benefit from demographic trends, such as the growing percentage of the population who are born as digital natives accustomed to on-demand and shared offerings.

•Expand Our Transportation Offerings. We continue to make Lyft an everyday experience for riders through our transportation network designed to address a wide range of mobility needs. For example, in 2018 we launched a network of shared bikes and scooters and will continue to supplement and scale modes in order to offer riders more transportation options. We also launched Shared Saver in 2019, which offers our riders the option to walk a short distance for our most affordable ride offering to date. More recently we added Lyft Rentals in two cities to add an attractive daily option for users planning to travel longer distances. By expanding our transportation offerings, we can offer riders options that best fit their criteria directly from the Lyft App, which increases rider engagement.

•Grow Our Share of Rider Transportation Spend. As we continue to increase rider loyalty to our brand and expand our use cases and the breadth of our multimodal offerings, we believe we will also increase our share of rider transportation spend. For example, a rider may start using our ridesharing offering for a night out and then choose Lyft again for travel to the airport. Once they have experienced the reliability and convenience of Lyft, they may incorporate Shared Rides into their daily commute, rent one of our shared bikes or scooters for shorter rides or when connecting to public transit, and rent one of our Lyft Rentals vehicles for long-distance trips, like a weekend away. We are also investing to increase our share of more valuable rides to grow our share of rider transportation spend. In addition, usage of our platform typically increases over time.

•Increase Value to the Driver Community. We strive to provide the best and most fulfilling economic opportunities for the community of drivers on our platform. We continuously seek to launch and improve programs and initiatives that enhance the driver experience on our platform. Our Express Drive program, which connects drivers with rental cars, continued to grow in 2019. We continue to invest in this program and expect that our acquisition of Flexdrive, one of our longstanding Express Drive partners, will improve our offering for drivers. We are also investing in Driver Centers and related partnerships that can offer affordable and convenient vehicle maintenance to the driver community. In addition to helping drivers access and maintain vehicles, we are committed to delivering innovative solutions that offer drivers fast and affordable access to their earnings. For example, we were the first ridesharing company to offer instant payouts to drivers through the Lyft App when we launched Express pay in 2015. In 2019, we further improved access to driver earnings by launching Lyft Direct, our no-fee bank account and debit card for drivers that allows drivers to receive payment instantly after every ride. We believe that our efforts to improve the driver experience allows us to increase driver satisfaction and loyalty to Lyft.

•Invest in Technology to Strengthen Our Network and Increase Efficiency. Our investments in proprietary technologies and predictive analytics leverage insights derived from the rich set of data generated by our platform. These investments allow us to deliver an affordable, convenient and high-quality experience for our riders and increase the earnings of drivers. Our investments in mapping, routing, payments, in-app navigation and matching technologies are key to integrating technology and leveraging data science into our platform in order to increase the efficiency of our platform and improve safety. In addition, we are investing in autonomous technology, which we believe will be a critical part of the future of transportation.

•Pursue M&A and Strategic Partnerships. In November 2018, we acquired Motivate, the largest bike sharing platform in the United States at the time and, from time to time, we have made other acquisitions of businesses and technologies. We will continue to selectively pursue acquisitions that contribute to the growth of our current business, help us expand into adjacent markets or add new capabilities to our platform. We believe drivers and riders on our platform will also benefit from a broader partner ecosystem that expands our marketing and loyalty programs and employee ride solutions. We have built strong relationships with transportation suppliers, state and local governments and technology solutions providers. We intend to continue to pursue acquisitions and partnerships that contribute to our growth.

Our Brand and Marketing

We aim to build the defining brand of our generation. We believe that our brand represents freedom at your fingertips: freedom from the stresses of driving and car ownership and freedom to do and see more. Our unique values and culture are reflected in our brand. We drive awareness of our brand through our marketing efforts, which highlight our offerings, the simplicity of our user experience and our commitment to community, and we also benefit from the evangelism by our users.

Values and Culture

Building community and having a positive local impact is fundamental to who we are. We approach working with our partners, cities and municipalities in a collaborative manner and seek to establish mutually beneficial relationships based on trust, respect and a common objective of improving people’s lives by improving transportation.

Millions of people lack access to basic needs because they can’t get a ride. Through our LyftUp initiative, we’re working to make sure everyone has access to affordable, reliable transportation to get where they need to go — no matter their age, income, or zip code.

This vision has been core to our business from the start. We believe more than 40% of Lyft rides start or end in low-income areas. In a number of cities, our riders can now find public transit, shared rides, bikes, and scooters all in the same app. Every day, Lyft helps unlock access for millions of people — providing a crucial entry point for upward mobility.

We built LyftUp to account for those still left behind. LyftUp aims to bridge some of the most serious outstanding transportation gaps. Through LyftUp, we partner with leading nonprofit organizations to provide free and discounted car, bike, and scooter rides to individuals and families in need.

Our five primary programs are:

•Grocery Access - rides to/from the grocery store for families living in areas without sufficient grocery store access;

•Jobs Access - rides to/from job interviews, job trainings, and the first few weeks of a new job;

•Voting Access - free and discounted rides to the polls;

•Disaster Response - rides to access vital services leading up to and in the wake of disasters and other local emergencies; and

•Bikeshare Access - discounted bikeshare memberships for eligible applicants who qualify for federal/state/local assistance programs, and free passes to thousands of young people ages 16 to 20 years old.

All of this work directly ties back to Lyft's mission of improving people's lives with the world's best transportation, and we're proud to work with amazing community partners to bring these programs to life.

Lastly, Lyft was founded on the belief that technology will enable us to dramatically reduce carbon emissions from the transportation system. In 2019, we launched electric vehicles through our Express Drive rental program, and we now offer several lower-carbon modes in the Lyft App: shared rides, bikes, scooters, and transit.

Brand Marketing

Our marketing efforts are designed to educate people about Lyft in creative and memorable ways, generating brand awareness among potential drivers and riders.

•Lyft-Produced Content. Lyft will produce content and post on various platforms, such as Undercover Lyft where celebrities are disguised as drivers.

•Popular Culture. Ad placement in pop culture such as television series and movies.

•Marketing Partnerships. We have marketing partnerships with leading brands, such as J.P. Morgan (Chase), Delta Air Lines, Hilton, and Walt Disney Parks & Resorts.

•Local Events. Our goal in sponsoring local events is to boost brand awareness at locally relevant times and use cases.

•Outdoor Advertising. To build unaided awareness, we have outdoor billboard campaigns in key markets.

•Specialty Modes. In select markets, riders may experience specialty or promotional ride modes for local events and organizations.

•Lyft Amp. Lyft Amps are bright, oval-shaped devices that sit on certain drivers’ dashboards which enhance the user experience, boost our brand awareness, and help promote safety. Amps assist rider identification of their driver’s vehicles and also display a personalized greeting and ETA during non-Shared Rides to inform riders of the estimated time to their destination.

Performance Marketing

We use a variety of channels to drive adoption of our platform and maintain driver and rider loyalty. We use specific channels and initiatives that enable us to measure the impact of our marketing spend. We currently attract new drivers and riders through a variety of marketing channels, including referrals, affiliate programs, partnerships, display advertising, radio, video, social media, email, search engine optimization and keyword search campaigns. After signup, we continue to engage riders through a variety of initiatives, such as promotions, emails and in-app notifications.

Our Proprietary Data-Driven Technology Platform

Our robust technology platform powers the millions of rides and connections that we facilitate every day and provides insights that drive our platform in real-time. We leverage historical data to continuously improve experiences for drivers and riders on our platform. Our platform analyzes large datasets covering the ride lifecycle, from when drivers go online and riders request rides, to when they match, which route to take and any feedback given after the rides. Utilizing machine learning capabilities to predict future behavior based on many years of historical data and use cases, we employ various levers to balance supply and demand in the marketplace, creating increased driver earnings while maintaining strong service levels for riders. We also leverage our data science and algorithms to inform our product development,development.

Our Intellectual Property

We believe that our intellectual property rights are valuable and important to our business. We rely on trademarks, patents, copyrights, trade secrets, license agreements, intellectual property assignment agreements, confidentiality procedures, non-disclosure agreements and employee non-disclosure and invention assignment agreements to establish and protect our proprietary rights. Though we rely in part upon these legal and contractual protections, we believe that factors such as the introductionskills and ingenuity of Lyft Pink.

Ridesharing Marketplace Efficiency

Duringour employees and the matching process, we leveragefunctionality and frequent enhancements to our proprietary dispatch platformsolutions and dataofferings are larger contributors to help drivers and riders connect efficiently. Factors such as distance, destination, route, traffic and travel time contribute to determining both driver to rider matching as well as rider-to-rider matching for Shared and Shared Saver Rides. Prior to a match, we give drivers a simple, reliable signal about where to drive and often an incentive to increase earnings. We also focus on providing predictable, competitive and sustainable prices that optimize value for our riders as well as help increase conversion. Our machine learning algorithms continuously train our optimization models and dynamically balance current and future supply and demand withinsuccess in the marketplace.

Optimizing Marketplace Supply

Once drivers sign upWe have invested in a patent program to identify and begin driving,protect a substantial portion of our predictive analytics and dynamic pricing algorithms help us to align driver incentives to encourage drivers to be available, at the right times,strategic intellectual property in areas of high demand. This helps provide drivers with potentially higher earning opportunities by allowing them to maximize their earnings per hour, which can elevate driver satisfaction, increase supply in peak hours and improve the overall efficiency of the marketplace.

Managing and Anticipating Rider Demand

Our pricing algorithms use real-time ride cost estimates, demand elasticity and data about traffic, weatherridesharing, autonomous vehicle-related technology, micro-mobility, telecommunications, networking and other travel conditionstechnologies relevant to optimize ride pricesour business. We hold numerous issued and balance supplypending patents in the U.S. and demand inforeign jurisdictions and continually review our ridesharing marketplace. This allows usdevelopment efforts to offer consistently competitive ride prices, reduce rider wait timesassess the existence and maximize rider utilizationpatentability of our platform,new intellectual property.

We have an ongoing trademark and service mark registration program pursuant to which we believe leadsseek to long-term driverregister our brand names and rider loyalty.

Improving Shared Ride Efficiency

We believe Sharedproduct names, taglines and Shared Saver Rides will provide a significant foundation for sustainable mobility. We aim to provide the most reliable and sustainable shared ride offering to improve efficiency and density of the marketplace and reduce congestion on city roads. We also aim to maximize the number of potential rides while minimizing costs by increasing the utilization rate of driver hours. To that end, we continually improve our core marketplace technology through enhancements in dispatching, mapping, routing and in-app navigation to improve matching among other areas. By increasing the percentage of rides that match and the quality of the matches, we can increase the efficiency of Shared and Shared Saver Rides.

The Lyft Driver Experience

We help drivers on our platform generate earnings while maintaining a flexible schedule. For these drivers, it all begins with the Lyft Driver app. After extensive background and safety checks, drivers can gain access to our platform and begin driving.

•The Lyft Driver App. Drivers only have to tap ‘Go Online’ in the Lyft Driver app to begin receiving ride requests. Once matched, drivers will get a notification to accept the ride and receive the rider’s pickup spot. On-screen instructions and directions make it easy to pick up riders, navigate to destinations and drop off riders. Drivers and riders may then rate each other at the end of the ride.

•Driver Dashboard. In the Lyft Driver app, we offer drivers a dashboard that shows the total earnings they can expect to see transferred to their bank accounts. In this dashboard, we offer detailed views of earnings activity, ride count and time spent, to help drivers understand and maximize their earnings. We provide an in-app Driver Console with additional tools and analytics to help drivers measure ride demand, pinpoint the best times to drive each day, set earnings goals and help them monitor their earnings progress. Drivers also gain real-time visibility into currently available incentives.

•Lyft Direct. We offer drivers a no-fee, secure, online bank account and debit card. Drivers with a Lyft Direct Debit get earnings paid immediately after a ride is completed without any transfer or rush fees. In addition, drivers who use the card receive cash back on everyday purchases like gas.

•In-app Tipping. Lyft was the first ridesharing platform to offer In-app Tipping, making it easy for riders to tip right from the app. 100% of tips from riders go to drivers. We built tipping into the Lyft App to encourage great hospitality, and to make it easy for riders to show their appreciation. Since 2016, drivers have earned over $1.1 billion in tips through the Lyft App.

•Driver Destination Mode. Destination Mode matches drivers with rides getting them closer to their intended destination by a specific time. We allow drivers to set a targeted arrival time so they can maximize earnings until the time they chose to go offline, or we allow them to specify a destination so they only receive priority matched rides going in the same direction.

•Express Drive. Express Drive is our flexible car rentals program for drivers. It is designed for those who want to drive using our platform but do not have access to a vehicle that meets our requirements. Express Drive offers a preferred weekly rate on cars rented from Hertz and Flexdrive Services, LLC (“Flexdrive”, formerly known as the Select Express Drive Partner), a company we recently acquired. Refer to Note 16 “Subsequent Events” to our consolidated financial statements for information regarding this acquisition. Express Drive has grown steadily since it began in 2016, with tens of thousands of cars now available in over 30 cities nationwide.

•Driver Hubs. Our Driver Hubs and service desks are currently in 35 cities across North America. These facilities are used for driver onboarding, answering driver questions and providing free inspections in select markets. They feature refreshments, access to clean bathrooms and help desks for easy access to the Lyft support team. The Driver Hubs are also used for driver events and educational sessions.

•Driver Centers. Lyft Driver Centers offer standard maintenance as well as services and repairs including free diagnostic inspection. We operated five driver centers as of December 31, 2019.

The Lyft Rider Experience

We provide a variety of offerings to solve the transportation needs of our riders. This starts with the Lyft App, which is a core part of the Lyft rider experience. To provide riders with the best experience, we are also continually adding new features, rider modes and payment models to address the needs of specific groups of riders, such as businesses and government entities.

Lyft App

The Lyft App provides a variety of ride modes to fit riders’ transportation needs. The Lyft App is designed to be fast, simple and purposeful. When a user opens the Lyft App all ride options available in that location are shown in a unified experience including scooters, bikes, public transit, car rentals, Shared and Shared Saver Rides, regular rides, big rides, and even more.

Subscription Plans and Ride Passes

Offering subscription plans and passes allows us to provide more earning opportunities for drivers and is an important step toward providing transportation options to address the range of riders’ budgets and make car ownership optional. Lyft Pink is our latest membership subscription program that offers an elevated Lyft experience with preferred pricing to enable riders to unlock all that their city has to offer. Lyft Pink members receive 15% savings on unlimited car rides, relaxed cancellations, priority airport pick-ups and more. The amount of revenue recognized from subscription plans and Ride Passes, and related breakage amounts, were not material for the years ended December 31, 2019, 2018 and 2017.

Lyft Business

Lyft is evolving how businesses large and small take care of their people’s transportation needs across sectors including corporate, healthcare, auto, education and government. Our comprehensive set of solutions allows customers to design, manage and pay for ground transportation programs that contribute to productivity and satisfaction while reducing cost, improving transparency and streamlining operations.

Corporate Business Travel

We partner with leading travel and expense management companies like SAP Concur, Certify and Expensify to deliver seamless experiences that are changing how our customers do business by making travel easier for everyone involved. Tools and features such as automated expensing and centralized payment improve policy adherence for travelers and offer greater visibility for travel managers. Benefits such as real-time reporting on rides and costs as well as detailed ride data and classification make it easier to attribute, reconcile and reimburse expense spend.

Concierge

Originally developed for large healthcare partners to help improve access to quality care, our Concierge offering is now used by organizations of all types to access our network and request or schedule rides for other people. The majority of our ride modes are available through Concierge with features including real-time ride tracking, 24-hour customer support and the option to request a ride for someone as soon as they are ready or schedule a ride up to a week in advance. Organizations can also choose to build a seamless transportation experience in their own applications using the Lyft Concierge API.

Concierge leads the industry in:

•Simplify Transportation for Businesses. Concierge allows organizations to arrange rides for their customers, guests and patients from one central dashboard, even if they don’t have the Lyft App or a smartphone. Customers can reduce cost, save time and streamline transportation with our courtesy ride tool.

•Improve Healthcare. Many Americans miss or delay medical care annually because they cannot get a ride to the doctor. Healthcare transportation brokers like Logisticare Circulation use our Concierge offering to provide patients with a reliable way to get to important healthcare appointments on time.

Enterprise Programs

We offer various enterprise programs, including monthly ride credits for daily commutes, supplementing public transit by providing rides for the first and last leg of commute trips, late-night rides home and shuttle replacement rides. Companies like Slack provide monthly Lyft credits as a benefit to employees to ensure convenient and cost-effective late-night transportation from the office.

Events

We offer transportation solutions that can be customized for events such as recruiting events, conferences, celebrations, meetings and company retreats. Organizations or individuals can create in-app experiences and custom codes for attendees to ride to and from events.

Our Commitment to Trust & Safety

A strong guiding principle since day one has been to build a community that drivers and riders trust. Trust is the foundation of our relationship with drivers and riders on our platform, and we take significant measures every day that are focused on their safety. This dedication led our customer support to be recently named number one in Newsweek’s 2019 America’s Best Customer Service rankings for the Taxi and Peer-to-Peer Ridesharing category.

To ensure we are delivering exceptional service levels and upholding high quality standards, we have established our Customer Experience and Trust, or CET, team as a key part of our organization. With over 550 employees as of December 31, 2019, CET is in charge of fielding customer support inquiries and is available through multiple channels, including via self-service and assisted support directly within our apps. Our CET team focuses on driving results based on experience-based metrics including First Contact Resolution, which is the number of support tickets resolved during first contact with a driver or rider, and Net Promoter Score. CET aims to eliminate bad customer experiences, quickly resolve problems when they occur and maintain trust with drivers and riders. We also use third parties to help Lyft deliver best-in-class support.

The ways we promote safety include:

•Critical Response Line. Our Trust & Safety team of specialists within CET that handle sensitive issues regarding behavior or safety incidents on our platform. Available 24/7, they work with many teams on highly visible cases to provide a high quality of care.

•Driving Record and Background Checks. Every driver is screened before they are permitted to drive on our platform, starting with professional third-party background and driving record checks. To promote a consistently high-quality experience, we ensure vehicles meet our criteria for vehicle age before drivers are accepted to drive these vehicles on our platform. We conduct continuous monitoring which provides Lyft with daily monitoring and expeditious notification of any disqualifying criminal convictions and driving infractions. Any driver who does not meet applicable regulations and our internal safety criteria on both the annual and continuous screenings is barred from our platform.

•Two-Way Ratings. Our two-way ratings system helps promote the safety and comfort of the Lyft community by offering a channel for drivers and riders to provide anonymous feedback on their Lyft experiences. At the end of each ride, drivers and riders are prompted to rate each other on a scale of 1-5 stars. Our ratings system allows drivers and riders to provide anonymous feedback. We take rider ratings and driver feedback very seriously. If a driver is rated four stars or below, Lyft requests feedback, reviews the situation, and follows up if necessary. If a rider is rated three stars or below, Lyft reviews the situation and contacts the driver if necessary to follow up on the ride experience.

•Zero-Tolerance Policy. Lyft maintains a zero-tolerance drug and alcohol policy for drivers on our platform. We also do not allow riders to have open alcohol containers in-ride and can deactivate riders from the platform for violating this policy.

•Community Safety Education. All approved Lyft drivers are required to complete mandatory Community Safety Education.

•Newly Designed Safety Features. In 2019, we launched more than 15 new safety features, including increased anti-fraud measures and requiring feedback for any rides less than four stars. During the ride, we have designed numerous safety features into the Lyft experience and will continue to innovate to ensure the safety of our riders and drivers. Some recently designed safety features include:

◦Share Route, which allows riders to share their location with family and friends;

◦Emergency access to 911 within the app;

◦Smart Trip Check-In (which we expect to roll out in the near future): in some cases, if we notice your ride has stopped too soon or for an unusual amount of time, Lyft will ask drivers and riders if they need support and, if necessary, give the option to request emergency assistance;

◦Partnership with ADT, where pilot users are able to signal to ADT that they are in need of assistance;

◦In-app photos of the driver and vehicle, with license plate numbers and vehicle information;

◦Real-time ride tracking, digital receipts; and

◦Two-way rating system with mandatory secondary feedback.

•Lyft Insurance Protection. We were the first ridesharing platform to introduce insurance protection that provides drivers with additional liability coverages. We provide primary liability coverage for TNC drivers from the moment they are matched with a rider until that rider is dropped off. Our auto liability insurance will apply as primary to a driver’s standard personal automobile insurance policy when matched with a rider.

•Bikes and Scooters. Safety is a key tenet that guides our work with bikes and scooters. We are providing the necessary education and support for all riders and are working with partners to provide the capital and technology solutions to expand protected bike lanes and reduce speeding. We are working with organizations, like Together For Safer Roads, that collaborate with local bike and pedestrian advocates to help protect our community members. We are also giving away free helmets in select markets for our riders.

Government Regulation

We are subject to a wide variety of laws and regulationslogos in the United States and other jurisdictions. These laws, regulationscountries to the extent we determine appropriate and standards governing issuescost-effective. We also have common law rights in some trademarks. In addition, we have registered domain names for websites that we use in our business, such as TNCs, ridesharing, worker classification, laborwww.lyft.com and employment, anti-discrimination, payments, gift cards, whistleblowing and worker confidentiality obligations, product liability, defects, maintenance and repairs, personal injury, text messaging, subscription services,other variations.

We intend to pursue additional intellectual property consumer protection taxation, privacy, data security, competition, unionizingto the extent we believe it would be beneficial and collective action, arbitration agreements and class action waiver provisions, terms of service, mobile application accessibility, autonomous vehicles, bike and scooter sharing, insurance, vehicle rentals, money transmittal, non-emergency medical transportation, environmental health and safety and background checks, are often complex and subjectcost-effective. Despite our efforts to varying interpretations, in many cases due to their lack of specificity. As a result, their application in practiceprotect our intellectual property rights, they may change or develop over time through judicial decisions or as new guidance or interpretations are provided by regulatory and governing bodies, such as federal, state and local administrative agencies.

The ridesharing industry and our business model are relatively nascent and rapidly evolving. When we introduced a peer-to-peer ridesharing marketplace in 2012, the laws and regulations in place at the time did not directly address our offerings. Laws and regulations that were in existence at that time, and some that have since been adopted, were often applied to our industry and our business in a manner that limited our relationships with drivers or otherwise inhibited the growth of our ridesharing marketplace. We have been proactively working with federal, state and local governments and regulatory bodies to ensure that our ridesharing marketplace and other offerings are available broadlybe respected in the United States and Canada. In part due to our efforts, a large majority of U.S. states have adopted laws related to TNCs to address the unique issues of the ridesharing industry. New laws and regulations and changes to existing laws and regulations continue to be adopted, implemented and interpreted in response to our industry and related technologies. As we expand our business into new markets or introduce new offerings into existing markets, regulatory bodies or courts may claim that we or users on our platform are subject to additional requirements, or that we are prohibited from conducting our business in certain jurisdictions, or that users on our platform are prohibited from using our platform, either generally or with respect to certain offerings. Certain jurisdictions and governmental entities, including airports, require us to obtain permits, pay fees or comply with certain reporting and other compliance requirements to provide our ridesharing, bike and scooter sharing, Lyft Rentals and autonomous vehicle offerings. These jurisdictions and governmental entities may reject our applications for permits, revoke existing or deny renewals of permits to operate, delay our ability to operate, increase their fees, charge new types of fees, or impose fines and penalties, including as a result of errors in, or failures to comply with, reporting or other requirements related to our product offerings.

Recent financial, political and other events may increase the level of regulatory scrutiny on larger companies, technology companies in general and companies engaged in dealings with independent contractors. Regulatory bodies may enact new laws or promulgate new regulations that are adverse to our business, or, due to changes in our operations and structure or partner relationships as a result of changes in the market or otherwise, they may view matters or interpret laws and regulations differently than they have in the past or in a manner adverse to our business. For example, a new law in California, known as Assembly Bill 5, codifies and extends an employment classification test in Dynamex Operations West, Inc. v. Superior Court, which established a new standard for determining employee or independent contractor status. The passage of this bill has led to and could continue to lead to additional challenges to the independent contractor classification of drivers using the Lyft Platform. Such regulatory scrutiny or action may create different or conflicting obligations from one jurisdiction to another. Additionally, from time to time we invest resources in an attempt to influence or challenge legislation and other regulatory matters pertinent to our operations, particularly those related to the ridesharing industry.

We have been subject to intense regulatory pressure from state and municipal regulatory authorities across the United States and Canada, and a number of them have imposed limitations on or attempted to ban ridesharing and bike and scooter sharing. For example, in December 2018, the New York City Taxi & Limousine Commission adopted rules governing minimum driver earnings calculations and utilization rates applicable to our ridesharing platform, as well as certain other ridesharing platforms. In January 2019, we filed an Article 78 Petition through two of our subsidiaries challenging these rules before the Supreme Court of the State of New York, which was denied in May 2019. In December 2019, we appealed this decision and litigation is ongoing. Other jurisdictions in which we currently operatefuture or may want to operate could follow suit. We could also face similar regulatory restrictions from foreign regulators as we expand operations internationally, particularly in areas where we face competition from local incumbents.

Additionally, because we receive, use, transmit, disclose and store personally identifiablebe invalidated, circumvented or challenged. For additional information, and other data relating to drivers and riders on our platform, we are subject to numerous local, municipal, state, federal and international laws and regulations that address privacy, data protection andsee the collection, storing, sharing, use, transfer, disclosure and protection of certain types of data. Such regulations include the Controlling the Assault of Non-Solicited Pornography and Marketing Act, Canada’s Anti-Spam Law, the Telephone Consumer Protection Act of 1991, or TCPA, the U.S. Federal Health Insurance Portability and Accountability Act of 1996, or HIPAA, Section 5(a) of the Federal Trade Commission Act, and, effective as of January 1, 2020, the CCPA.

See the sections titled “Risk Factors,” including the subsections titled “Risk Factors—Risks Related to Our BusinessRegulatory and Industry—Challenges to contractor classification of driversLegal Factors—Claims by others that usewe infringed their proprietary technology or other intellectual property rights could harm our platform may have adverse business, financial, tax, legalbusiness” and other consequences to our business,” “Risk Factors—Risks Related to Our BusinessRegulatory and Industry—Our business is subjectLegal Factors—Failure to a wide range of laws and regulations, many of which are evolving, and failure to comply with such laws and regulationsprotect or enforce our intellectual property rights could harm our business,” “Risk Factors—Risks Related to Our Business and Industry—We rely on third-party payment processors to process payments made by riders and payments made to drivers on our platform, and if we cannot manage our relationships with such third parties and other payment-related risks, our business, financial condition and results of operations could be adversely affected,operations.” “Risk Factors—Risks Related

Our Growth Strategy

Transportation represents a massive market opportunity, one that we are in the very early stages of addressing. Our key growth strategies include our plans to:

•Increase Rider Use Cases. We are continuously working to Our Businessmake Lyft the transportation network of choice across an expanding range of use cases. We offer products to simplify travel decision-making, for example with our Lyft Pink subscription plan, Lyft Pass commuter programs, first-mile and Industry—Changeslast-mile services and university ride smart programs. We

also provide centralized tools and enterprise transportation solutions, such as our Concierge offering, that enable organizations to manage the transportation needs of customers, employees and other constituents.