0001818874srt:MaximumMembersofi:OtherFinancingNotesMemberus-gaap:LondonInterbankOfferedRateLIBORMemberus-gaap:NotesPayableOtherPayablesMember2021-12-31

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

| | | | | |

x☒ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 20212023

or

| | | | | |

| ☐ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission file number 001-39606

SoFi Technologies, Inc.

(Exact name of registrant as specified in its charter)

| | | | | | | | |

| Delaware | | 98-1547291 |

| (State or other jurisdiction of incorporation or organization) | | (I.R.S. Employer Identification No.) |

234 1st Street San Francisco, California | | 94105 |

| (Address of Principal Executive Offices) | | (Zip Code) |

Registrant’s telephone number, including area code: (855) 456-7634

Securities registered pursuant to Section 12(b) of the Act:

| | | | | | | | | | | | | | |

| Title of each class | | Trading Symbol(s) | | Name of each exchange on which registered |

| Common stock, $0.0001 par value per share | | SOFI | | The Nasdaq Global Select Market |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐ No x☒

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No x☒

Indicate by check mark whether the registrant:registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports);, and (2) has been subject to such filing requirements for the past 90 days. Yes x☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes x No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| | | | | | | | | | | | | | |

| Large accelerated filer | x☒ | | Accelerated filer | ☐

|

| Non-accelerated filer | ☐ | | Smaller reporting company | ☐ |

| | | Emerging growth company | ☐ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 74262(b)) by the registered public accounting firm that prepared or issued its audit report. ☒

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.1D-1(b). ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ☐ No x☒

The aggregate market value of the voting and non-voting common equity of the Registrant held by non-affiliates as of June 30, 2021: $10.02023: $7.4 billion

The number of shares of the registrant’s common stock, par value $0.0001 per share, outstanding as of February 15, 20222024 was 828,591,590976,736,877 shares.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the Proxy Statement for the 20222024 Annual Meeting of Stockholders are incorporated by reference in Part III. The Proxy Statement will be filed with the Securities and Exchange Commission within 120 days of the Registrant’s fiscal year ended December 31, 2021.2023.

SOFI TECHNOLOGIES, INC.

TABLE OF CONTENTS

Glossary of Terms and Acronyms

| | | | | |

ACH: Automated clearing house | GAAP: U.S. Generally Accepted Accounting Principles |

AFS: Available-for-sale | GLBA: Gramm-Leach-Bliley Act |

ALCO: Asset Liability Committee | Golden Pacific: Golden Pacific Bancorp, Inc. |

AWS: Amazon Web Services | GSE: Government-Sponsored Enterprise |

AOCI: Accumulated other comprehensive income (loss) | HFI: Held for investment |

ASU: Accounting Standards Update | HFS: Held for sale |

ATDS: Automatic telephone dialing systems | HMDA: Home Mortgage Disclosure Act |

BHCA: Bank Holding Company Act of 1956, as amended | IRLC: Interest rate lock commitment |

BPS: Basis points | IRS: Internal Revenue Service |

BSA: Bank Secrecy Act | LIBOR: London Inter-Bank Offered Rate |

CALM: Capital and Asset Liability Management policy | MLA: Military Lending Act |

CARES Act: Coronavirus Aid, Relief, and Economic Security Act | MOHELA: Missouri Higher Education Loan Authority |

CCPA: California Consumer Privacy Act | MSB: Money services business |

CD: Community Development | MSRB: Municipal Securities Rulemaking Board |

CET1: Common Equity Tier 1 | NACHA: National Automated Clearinghouse Association |

CFP: Certified financial planners | Nasdaq: The Nasdaq Global Select Market |

CFPB: Consumer Financial Protection Bureau | OCC: Office of the Comptroller of the Currency |

CFTC: Commodity Futures Trading Commission | OFAC: Office of Foreign Assets Control |

CISO: Chief Information Security Officer | PCD: Purchased credit deteriorated |

CODM: Chief Operating Decision Maker | PFOF: Payment for order flow |

CPA: Colorado Privacy Act | PSU: Performance stock units |

CPPA: California Privacy Protection Act | QIA: Qatar Investment Authority |

CPRA: California Privacy Rights Act | RESPA: Real Estate Settlement Procedures Act |

CRA: Community Reinvestment Act | ROU: Right-of-use |

DACA: Deferred Access for Childhood Arrival | RSU: Restricted stock units |

DCF: Discounted cash flow | SCH: Social Capital Hedosophia Holdings Corp. V |

DE&I: Diversity, Equity and Inclusion | SCRA: Servicemembers’ Civil Relief Act |

DEP: Digital engagement practices | SEC: U.S. Securities and Exchange Commission |

Dodd-Frank Act: Dodd-Frank Wall Street Reform and Consumer | SPAC: Special purpose acquisition company |

| Protection Act of 2010 | Social Finance: Social Finance, Inc. |

DSU: Deferred stock units | SoFi Bank: SoFi Bank, National Association |

EC: European Commission | SoFi Capital Advisors: SoFi Capital Advisors, LLC |

ECOA: Equal Credit Opportunity Act | SoFi Securities: SoFi Securities LLC |

EFTA: Electronic Fund Transfer Act | SoFi Stadium: The LA Stadium and Entertainment District at Hollywood |

ESG: Environmental, social and corporate governance | Park in Inglewood, California |

ESIGN: Electronic Signatures in Global and National Commerce Act | SoFi Wealth: SoFi Wealth LLC |

ETF: Exchange-Traded Funds | SOFR: Secured Overnight Financing Rate |

FCA: Financial Conduct Authority | SPE: Special purpose entity |

FCRA: Fair Credit Reporting Act | SRO: Self-regulatory organizations |

FDCPA: Fair Debt Collection Practices Act | TBA: To-be-announced |

FDIA: Federal Deposit Insurance Act | TCJA: Tax Cuts and Jobs Act |

FDIC: Federal Deposit Insurance Corporation | TCPA: Federal Telephone Consumer Protection Act |

Federal Reserve: Board of Governors of the Federal Reserve System | Technisys: Technisys S.A., a Luxembourg société anonyme |

FHA: Fair Housing Act | TDR: Troubled debt restructuring |

FHFA: Federal Housing Finance Agency | TILA: Truth in Lending Act |

FHLB: Federal Home Loan Bank | UDAAP: Unfair, deceptive or abusive acts or practices |

FinCEN: Financial Crimes Enforcement Network | UETA: Uniform Electronic Transactions Act |

FINRA: Financial Industry Regulatory Authority | URG: Underrepresented Group |

FRB: Federal Reserve Bank of San Francisco | VA: United Stated Department of Veterans Affairs |

FTC: Federal Trade Commission | VIE: Variable interest entity |

FTP: Fund transfer pricing | Wyndham: Wyndham Capital Mortgage |

SoFi Technologies, Inc.

As used in this Annual Report on Form 10-K, unless the context requires otherwise, references to “SoFi”, the “Company”, “we”, “us”, and “our”, and similar references refer to SoFi Technologies, Inc. and its wholly-owned subsidiaries following the Business Combination (as defined herein) and to Social Finance, Inc. prior to the Business Combination.

Social Finance, Inc. (“Social Finance”) entered into a merger agreement (the “Agreement”) with Social Capital Hedosophia Holdings Corp. V (“SCH”) on January 7, 2021. The transactions contemplated by the terms of the Agreement were completed on May 28, 2021 (the “Closing”), in conjunction with which SCH changed its name to SoFi Technologies, Inc. (hereafter referred to, collectively with its subsidiaries, as “SoFi”, the “Company”, “we”, “us” or “our”, unless the context otherwise requires). The transactions contemplated in the Agreement are collectively referred to as the “Business Combination”. As a result of the Business Combination completed on May 28, 2021, share and per share amounts presented in this Annual Report on Form 10-K for periods prior to the Business Combination for Social Finance, Inc. have been retroactively converted by application of the exchange ratio of 1.7428. For more information regarding the Business Combination, see Item 8, Note 2 to the Notes to Consolidated Financial Statements included in this Annual Report on Form 10-K.

In March 2021,February 2022, we entered into an agreement to acquireacquired Golden Pacific Bancorp, Inc. (“Golden Pacific”), a bank holding company, and its wholly-owned subsidiary, Golden Pacific Bank, National Association, a national bank for a total cash purchase price of $22.3 million (the “Bank Merger”). The Bank Merger closed in February 2022,, after which we became a bank holding company and renamed Golden Pacific Bank as SoFi Bank, National Association (“SoFi Bank”).

In FebruaryMarch 2022, we entered into an agreement to acquireacquired Technisys S.A. (“Technisys”), a Luxembourg société anonyme and a cloud-native digital multi-product core banking platform for total purchase consideration, in the form of shares of SoFi common stock, of $1.1 billion (the “Technisys Merger”).

In April 2023, we acquired Wyndham, a fintech mortgage lender.

See Note 2. Business Combinations to the Notes to Consolidated Financial Statements within Part II, Item 8. for information on our business combinations.

Refer to Glossary of Terms and Acronyms for the definitions of certain terms, acronyms and abbreviations used in this document.

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K contains statements that are forward-looking and as such are not historical facts. This includes, without limitation, statements regarding the financial position, business strategy and the plans and objectives of management for our future operations; anticipated trends and prospects in the industries in which our business operates; and new products, services and related strategies.strategies; anticipated actions by governmental authorities; and macroeconomic conditions. These statements constitute projections, forecasts and forward-looking statements, and are not guarantees of performance. Such statements can be identified by the fact that they do not relate strictly to historical or current facts. When used in this Annual Report on Form 10-K, words such as “aim”, “allow”, “anticipate”, “believe”, “can”, “continue”, “could”, “estimate”, “expect”, “if”, “intend”, “likely”, “may”, “might”, “opportunity”, “plan”, “possible”, “potential”, “predict”, “project”, “should”, “strive”, “will”, “would” and similar expressions may identify forward-looking statements, but the absence of these words does not mean that a statement is not forward-looking.

Forward-looking statements are subject to risks, uncertainties and other factors described in Part I, Item 1A. “Risk Factors” and elsewhere in this Annual Report on Form 10-K mayand our other filings with the SEC and include, for example, statements about:

•the effect of and uncertainties related to the ongoing COVID-19 pandemic (including any government responses thereto) and any continued recovery from the impact of the COVID-19 pandemic;among other things:

•our ability to achieve and maintain profitability in the future;

•the impact on our business of the regulatory environment and complexities with compliance;

•our ability to respond to generalthe effect and impact of evolving laws, rules, regulations and government enforcement policies, including any federal or state loan forgiveness programs;

•the impact of adverse developments affecting the U.S. or global banking industry, including bank failures and liquidity concerns, which could cause economic conditions;and market volatility, and regulatory responses thereto;

•our ability to manage our growth effectively and our expectations regarding the development and expansion of our business;

•our ability to continue to originate and sell loans to third parties, and the impact of the performance of loans held on our balance sheet;

•our ability to access sources of capital on favorable terms, if at all, including debt financing, deposits and other sources of capital to finance operations and growth;

•the impact of and our ability to respond to general economic conditions and other macroeconomic and geopolitical factors, such as elevated and fluctuating interest rates, inflationary pressures, counterparty risk, changing customer

demand, capital markets volatility, instability in the financial services industry, a potential U.S. government shutdown, the possibility of a recession, and domestic or international conflicts or disputes;

•the success of our marketing efforts and our ability to expand our member base;

•our ability to grow market share in existing markets or any new markets we may enter;

•our ability to develop new products, features and functionality that are competitive and meet market needs;

•our ability to diversify our core student loan business into other lending products and broaden our suite of financial services offerings;

•our ability to realize the benefits of our strategy, including what we refer to as our Financial Services Productivity Loop, and achieve scale in our Financial Services segment;

•our ability to successfully operate as a bank holding company, and to own and operate SoFi Bank;

•our ability to make accurate credit and pricing decisions or effectively forecast our loss rates;

•our ability to establish and maintain an effective system of internal controls over financial reporting;

•our ability to maintain the listing of our securities on The Nasdaq Global Select Market (“Nasdaq”);the Nasdaq;

•our ability to realize the anticipated benefits of the Business Combination, the Bank Merger, the Technisys Merger, our acquisition of Wyndham, and the anticipated Technisys Merger;any other acquisitions we undertake, including our expectations with regards to such acquisitions;

•our ability to successfully expand our operations into foreign jurisdictions, including compliance with a variety of foreign laws; and

•the outcome of any legal or governmental proceedings that may be instituted against us.

These forward-lookingForward-looking statements are based on information available as of the date of this Annual Report on Form 10-K and reflect current expectations, forecasts and assumptions, and involve a number of judgments, risks and uncertainties. New risks and uncertainties emerge from time to time and it is not possible for us to predict all risks and uncertainties that could have an impact on the forward-looking statements contained in this Annual Report on Form 10-K. The results, events and circumstances reflected in the forward-looking statements may not be achieved or occur, and actual results, events or circumstances could differ materially from those described in the forward-looking statements. Accordingly, forward-looking statements should not be relied upon as representing our views as of any subsequent date, and we do not undertake any obligation to update forward-looking statements to reflect events or circumstances after the date they were made, whether as a result of new information, future events or otherwise, except as may be required under applicable securities laws.

As a result of a number of known and unknown risks and uncertainties, our actual results or performance may be materially different from those expressed or implied by these forward-looking statements. You should not place undue reliance on these forward-looking statements.

TRADEMARKS

This document contains references to trademarks, service marks and trade names owned by us or belonging to other entities. Solely for convenience, trademarks, service marks and trade names referred to in this document may appear without the ® or ™ symbols, but such references are not intended to indicate, in any way, that we or the applicable licensor will not assert, to the fullest extent under applicable law, our or its rights to these trademarks, service marks and trade names. SoFi Technologies does not intend its use or display of other companies’ trademarks, service marks or trade names to imply a relationship with, or endorsement or sponsorship of it by, any other companies. All trademarks, service marks and trade names included in this document are the property of their respective owners.

PART I

Item 1. Business

We are a member-centric, one-stop shop for financial services that, through our Lending and Financial Services products, allows members to borrow, save, spend, invest and protect their money. We refer to our customers as “members” and “clients”.

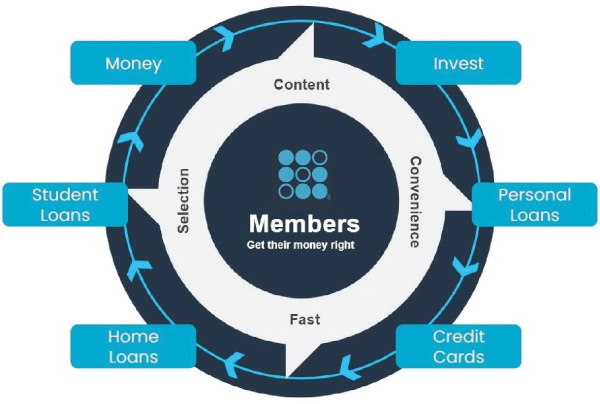

Our mission is to help our members achieve financial independence in order to realize their ambitions. To us, financial independence does not mean being wealthy, but rather represents the ability of our members to have the financial means to achieve their personal objectives at each stage of life, such as owning a home, having a family, or having a career of their choice — more simply stated, to have enough money to do what they want. We were founded in 2011 and have developed a suite of financial products that offers the speed, selection, content and convenience that only an integrated digital platform can provide. In order for us to achieve our mission, we have to help people get their money right, which means providing them with the ability to borrow better, save better, spend better, invest better and protect better. Everything we do today is geared toward helping our members “Get Your Money Right” and we strive to innovate and build ways for our members to achieve this goal.

In order to help achieve our mission, we offer personal loans, student loans, home loans and related servicing. We offer a variety of financial services products, such as SoFi Money, SoFi Credit Card, SoFi Invest and SoFi Relay, that provide more daily interactions with our members, as well as lending as a service which helps a broader range of borrowers to find lending solutions. We offer products and capabilities, such as SoFi At Work, that are designed to appeal to enterprises. We have created an innovative financial services platform designedalso made strategic acquisitions to offer best-in-class products to meet the broad objectives of our members and the lifecycle of their financial needs. We define a member as someone who has a lending relationship with us through origination and/or ongoing servicing, opened a financial services account, linked an external account tofurther expand our platform or signed upcapabilities for enterprises, which we believe will deepen our credit score monitoring service. Once someone becomesparticipation in the entire technology ecosystem powering digital financial services.

We have built a social area within our digital native application, which we refer to as the member they are always considered a member unless they violate our terms of service. Our members have continuous access to our certified financial planners (“CFPs”), our career advice services, our member events, our content, educational material, news, tools and calculators at no cost to the member. Additionally, our mobile app and website have ahome feed. The member home feed that is personalized and delivers content to a member about what they must do that day in their financial life, what they should consider doing that day in their financial life, and what they can do that day in their financial life. Through the member home feed, there are significant opportunities to build frequent engagement and, to date, the member home feed has been an important driver of new product adoption. The member home feed is an important part of our strategy and our ability to use data as a competitive advantage.

To complement these products and services, we believe in establishing partnerships with other enterprises to leverage our existing capabilities to reach a broader market and in building vertically-integrated technology platforms designed to manage and deliver our suite of products and technology solutions to our members and clients in a low-cost and differentiated manner.

Our three reportable segments and their primary product offerings as of December 31, 2023 were as follows:

_________________

(1)Lending as a service includes referred loans which are originated by a third-party partner to which we provide pre-qualified borrower referrals, certain loans which we originate and subsequently sell to a third-party partner, and certain loans associated with our Lantern Credit financial services marketplace platform.

Members

We believe we are inhave created an innovative financial services platform designed to offer best-in-class products to meet the early stagesbroad objectives of our members and the digital transformationlifecycle of their financial needs. Our platform offers our members (as defined under Part II, Item 7. “Key Business Metrics”) a suite of financial products and services, enabling them to borrow, save, spend, invest and protect their finances across one integrated platform, as well as personal financial management tools and benefits to complement our products. Our aim is to create a result, havebest-in-class, integrated financial services platform that will generate a substantial opportunityvirtuous cycle whereby positive member experiences will lead to continuenew product adoption by existing members and enhanced profitability for each additional product by lowering overall member acquisition costs and increasing the lifetime value of our members. We refer to growthis virtuous cycle as our member base and increase the number of products that our members use on the SoFi platform.“Financial Services Productivity Loop”, which is further discussed below.

Enterprises

In addition to benefiting our members, our products and capabilities are also designed to appeal to enterprises, such as financial services institutions that subscribe to our enterprise services called SoFi At Work, and have become interconnected with the SoFi platform. We have continued to expand our platform capabilities for enterprises through strategic acquisitions, including: (i) our acquisition of Galileo in 2020, which provides technology platform services to financial and non-financial institutions and which has allowed us to vertically integrate across more of our financial services, and our anticipated acquisition(ii) the Technisys Merger in the first quarter of Technisys in 2022, through which we will expandadded a cloud-native digital and core banking platform into our technology platform offerings and expanded our technology platform services to a broader international market.

While we primarily operate in the United States, we expanded into Hong Kong with our acquisition of 8 Limited (an investment business), we gained clients in Mexico and Colombia with our acquisition of Galileo, and we expect to further expand into Latin America with our anticipated acquisition of Technisys.

We believe that these These expansions will deepenhave deepened our participation in the entire technology ecosystem powering digital financial services, allowing us to not only reduce costs to operate our member-centric business, but also deliver increasing value to our enterprise customers. While our enterprises are not considered members, they are important contributors to the growth of the SoFi platform, and also have their own constituents who might benefit from our products in the future.

National Bank Charter

A key element of our long-term strategy to better serve our members has been to secure a national bank charter. In January 2022, we received regulatory approval to become a bank holding company and to acquire Golden Pacific, and its wholly-owned subsidiary, Golden Pacific Bank, National Association, a national bank (“Golden Pacific Bank”). We also received approval to change the composition of Golden Pacific Bank’s assets. We closed the Bank Merger in February 2022, after which we became a bank holding company and Golden Pacific Bank began operating as SoFi Bank. See “Management’s Discussion and Analysis of Financial Condition and Results of Operations—National Bank Charter” for additional information on our regulatory approval process and the Bank Merger.

We believe that operating as a bank holding company can enhance our overall profitability. While we have historically relied on third-party bank holding companies to provide banking services to our members (as discussed further in “Our Products” below), we believe that operating under a national bank charter will allow us to provide members and prospective members broader and more competitive options across their financial services needs, including deposit accounts and loan products, and lower our cost to fund loans (by utilizing our members deposits held at SoFi Bank to fund our loans), which we

believe will enable us to offer lower interest rates on loans to members as well as offer higher interest rates on deposit accounts. Following the Bank Merger, we have begun to transfer SoFi Money products to SoFi Bank and intend to continue to transfer our SoFi Money, lending, and SoFi Credit Card products to SoFi Bank over time.

Our Differentiation

In order to build best-in-class offerings, we focus on four differentiators: fast, selection, content and convenience.

(1)Fast — We aspire to be the fastest place for our members to responsibly do anything, whether it’s applying for a loan, getting a funded loan, opening an account, buying or selling a stock, uploading a mobile check, getting access to money, paying a friend, or accessing relevant financial content. Other than certain products acquired and offered through SoFi Bank, our products are all digital and we have a culture of iteration to help drive faster and faster services.

(2)Selection — Given the digital nature of our products, the permutations of features and services that can be made available to our members across their needs to borrow, save, spend, invest and protect are significant. We will continue to iterate, learn and innovate to broaden our selection in the same way we did by providing our members with the ability to buy single stocks without commissions, purchase fractional shares, invest in SoFi proprietary robo-advisory portfolios, and invest in SoFi-branded Exchange-Traded Funds.

(3)Content — Our financial education, insights, research content, actionable tools and advice are designed to provide meaningful value for our members. Our carefully-crafted and personalized content is offered through our member home feed and is designed to help our members get their money right. We strive to provide digestible financial education, meaningful answers, salient information, advice, credit scores, financial calculators, investment research and financial news that enhance member loyalty and increase the likelihood that members will use additional SoFi products in the future.

(4)Convenience — We hold ourselves accountable to providing the most convenient member experience possible in terms of ease of use, ubiquity, functionality, simplicity and responsive customer service. Our long-term goal is to provide the most convenient 24x7 service and dispel the historical construct of financial service availability based on 9-5 Monday through Friday.

Each product we offer is delivered in a member-centric way and is built and enhanced with these differentiators in mind. We believe that our member-centric one stop shop for financial services serves as a competitive differentiator for us relative to other financial services providers.

We offer our members a full suite of financial products and services all in one common mobile platform. To complement these products and services, we believe in building vertically-integrated technology platforms designed to manage and deliver the suite of solutions to our members in a low-cost and differentiated manner.

Our Strategy

The Financial Services Productivity Loop

We believe that developing a relationship with our members and gaining their trust is central to our success as a financial services platform. Moreover, we believe that some of the current frictions faced by other financial institutions are caused by a disjointed and non-seamless product experience, a lack of digital acquisition, subpar mobile web products instead of digital native apps and incomplete product offerings to meet a customer’s holistic financial needs. Through our mobile technology and continuous effort to improve our financial services products, we are seeking to build a financial services platform that members can access for all of their financial services needs.

Our strategy, which we refer to as the “Financial Services Productivity Loop”, is centered around building trust and a lifetime relationship with our members, which we believe will help build a sustainable competitive advantage. In order to deliver on our strategy, we must develop best-in-class unit economics and best-in-class products that build trust and reliability between our members and our platform. Our acquisition of SoFi Bank was also an important step in continuing to build best-in-class unit economics and best-in-class products, as we believe it will enable us to offer additional products and lower fees. When we do this on a member’s first product, and they later consider using an additional product, they are more likely to start with our platform and we have a higher chance that they will select one of our products to meet their other financial needs. This results in delivering more revenue per member with no second member acquisition costs, resulting in higher lifetime value per member. This also reinforces the benefits of our platform, which simplifies the entire financial ecosystem for our members, helping them get their money right. We are able to use the increased profits to further improve member benefits and product experience.

We believe we are in the early stages of realizing the benefits of the Financial Services Productivity Loop. During the year ended December 31, 2021, approximately 600,000 members became multi-product members. In addition to realizing the benefits of more of our members adopting multiple SoFi products, both in terms of additional revenue and lower member acquisition costs per product, the Financial Services Productivity Loop strategy delivers operating and technology efficiencies to deliver better unit economics on a per product basis. One of the success factors of our lending business is that it is vertically integrated across our technology stack, risk protocols and operations processes.

| | |

Financial Services Productivity Loop |

Our Products

We offer our members a suite of financial products and services all in one digital native application to help members get their money right. In 2011, we started our company with an innovative approach to the private student loan market and later expanded our lending product offerings to include personal loans and home loans. We have continued to expand our overall strategy to not only include products that enable our members to borrow better, but also to save better, spend better, invest better and protect better. In the first quarter of 2019, we launched SoFi Money, SoFi Invest and SoFi Relay. In that same quarter, we also redesigned our end-to-end approach to mortgage lending and relaunched home loans. In the third quarter of 2019, we introduced in-school loans and in the third quarter of 2020, we launched SoFi Credit Card, which was expanded to a broader market in the fourth quarter of 2020.

In addition, we have built a social area within our digital native application, which we refer to as the member home feed. In the member home feed, we show our members what is happening in their financial lives through personalized cards with relevant content, news and tools. Through the member home feed, there are significant opportunities to build frequent engagement and, to date, the member home feed has been an important and additional driver of new product adoption. The member home feed is an important part of our strategy and our ability to use data as a competitive advantage.

To complement these products and services, we believe in establishing partnerships to leverage our existing capabilities to reach a broader market and in building vertically-integrated technology platforms designed to manage and deliver our suite of solutions to our members in a low-cost and differentiated manner.

Our Reportable Segments

We conduct our business through three reportable segments: Lending, Technology Platform and Financial Services. Below is a discussion of our segments and their corresponding products.

Lending Segment

Our origins are in student loans. On the strength of our capabilities in student lending, we expanded into personal loans and home loans and related services. We believe that our market opportunity within each of these lending channels is significant. Our lending process primarily leverages an in-application, digital borrowing experience, which we believe serves as a competitive advantage as digital lending becomes increasingly ubiquitous. We expect to begin accepting new loan applications and originating new loans within SoFi Bank over time. As a bank holding company, we expect to be able to offer a wider range of loan sizes and interest rates through SoFi Bank.

Student Loans. We primarily operate in the student loan refinance space, with a focus on super-prime graduate school loans. We later expanded into “in-school” lending, which allows members to borrow funds while they attend school. We offer flexible loan sizes and repayment options, competitive rates, and the ability to lock in an interest rate for funding at a later time on our student loan products.

Personal Loans. We primarily originate personal loans for debt consolidation purposes and home improvement projects. We offer fixed and variable rate loans with no origination fees and flexible repayment terms, such as unemployment protection. There are other personal loan purposes or channels that we have not aggressively pursued, which we believe could represent opportunities for us in the future.

Home Loans. We have historically offered agency and non-agency loans for members purchasing a home or refinancing an existing mortgage. For our home loan products, we offer competitive rates, flexible down payment options for as little as 3% and educational tools and calculators.

A key element of our underwriting process is the ability to facilitate risk-based interest rates that are appropriate for each loan. Using SoFi’s proprietary risk models, we project quarterly loan performance, including expected losses and prepayments. The outcome of this process helps us determine a more data-driven, risk-adjusted interest rate that we can offer our members.

We have developed an extensive underwriting process across each lending product that is focused on willingness to pay (measured by credit attributes), ability to pay (measured through income verification), and capacity to pay (measured by debt service in relation to other loans). Our student loan and personal loan underwriting models consider credit reports, industry credit and bankruptcy prediction models, custom credit assessment models, and debt capacity analysis, as indicated by borrower free cash flow (defined as borrower monthly net income less revolving and installment payments less housing payments). We decreased our in-school loan minimum FICO requirement in conjunction with our launch of a revised underwriting strategy during 2021, which utilizes an advanced risk model that focuses on borrowers’ ability to pay and provides refined risk separation. Home loans originated by SoFi that are agency conforming loans are subject to credit, debt service, and collateral eligibility established by Fannie Mae. Existing members generally experience a higher approval rate than new members, subject to the existing member being in good standing on their existing products. Home loans originated by us that are non-agency loans are subject to our credit criteria, which typically includes a minimum tri-bureau credit score, established credit history requirements, income verification, as well as maximum qualified mortgage limits on debt-to-income service and caps on loan-to-value based on an accredited appraisal. We also leverage our data to provide existing members a streamlined application process through automation.

Our lending business is primarily a gain-on-sale model, whereby we seek to originate loans and recognize a gain from these loans when we sell them into either our whole loan or securitization channels. We sell our whole loans primarily to large financial institutions, such as bank holding companies, typically at a premium to par, and in excess of our costs to originate the loans. Our loan premiums fluctuate from time to time based on benchmark rates and credit spreads, and we are not guaranteed a gain on all or any of our loan sales. When securitizing loans, we first isolate the underlying loans in a trust and then sell the beneficial interests in the trust to a bankruptcy-remote entity. In securitization transactions that do not qualify for sale accounting, the related assets remain on our consolidated balance sheet and cash proceeds received are reported as liabilities, with related interest expense recognized over the life of the related borrowing. In securitization transactions that qualify for sale accounting, we typically have insignificant continuing involvement as an investor.

Prior to selling our loans, we hold our loans on our consolidated balance sheet at fair value and primarily rely upon warehouse financing and our own capital to enable us to expand our origination capabilities. By securing our national bank charter, we believe we can lower our cost of funding by utilizing our members’ deposits held at SoFi Bank to fund our loans. Net interest income, which we define as the difference between the earned interest income and interest expense to finance loans, is a key component of the profitability of our Lending segment.

In the case of both whole loan sales and securitizations, and with the exception of certain of our home loans, we also continue to retain servicing rights to our originated loans following transfer. We view servicing as an integral component of the Lending segment, as we believe our servicing function is an important asset because of the connection to the member it affords us throughout the life of the loan. We directly service all of the personal loans that we originate. We act as master servicer for, and rely on sub-servicers to directly service, all of our student loans and Federal National Mortgage Association (“FNMA”) conforming home loans. We believe this ongoing relationship with our members enhances the effectiveness of our Financial Services Productivity Loop by increasing member touchpoints and driving increases in the number of products per member.

Furthermore, our platform supports the full transaction lifecycle, including credit application, underwriting, approval, funding and servicing. Through data derived at loan origination and throughout the servicing process, SoFi has life-of-loan

performance data on each loan in its ecosystem that we originate and on which we retain servicing, which provides a meaningful data asset.

Technology Platform Segment

Our Technology Platform segment consists of Galileo, which we acquired in May 2020. Galileo is a provider of technology platform services to financial and non-financial institutions. Through Galileo, we provide services through a suite of program, event and authorization application programming interfaces for financial and non-financial institutions. Additionally, Galileo provides vertical integration benefits with SoFi Money and deposit accounts held at SoFi Bank.

We earn revenue on Galileo’s platform in the following two ways:

•Technology Platform Fees: We earn Technology Platform revenues for providing continuous delivery of an integrated technology platform as an outsourced service for financial and non-financial institutions. The platform fees we earn are based on access to the platform and are specific to the type of transaction. For example, we offer “event pricing”, which includes a specific charge for an account setup, an active account on file, use of Program, Event and Authorization Application Programming Interfaces (“APIs”), card activation, authorizations and processing, and card loads. In addition, we offer “partner pricing”, which is the back-end support we provide to Galileo’s clients, such as live agent customer service, chargeback and fraud analysis and credit bureau reporting, all within one integrated solution for our clients.

•Program Management Fees: Also referred to as “card program fees”, these transaction fees are generated from the creation and management of card programs issued by banks and requested by enterprise partners. In these arrangements, Galileo performs card management services and the revenue stems from the payment network and card program fees generated by the card program. This revenue is reduced by association and bank issuer costs, and a revenue share passed along to the enterprise partner that markets the card program. We categorize this class of revenue as payment network fees.

Galileo typically enters into multi-year service contracts with its clients. The contracts provide for a variety of integrated platform services, which vary by client and are generally either non-cancellable or cancellable with a substantive payment. Pricing structures under these contracts are typically volume-based, or a combination of activity- and volume-based, and payment terms are predominantly monthly in arrears. Most of Galileo’s contracts contain minimum monthly payments with agreed upon monthly service levels and may contain penalties if service levels are not met.

The Technology Platform segment historically included our minority ownership of Apex Clearing Holdings, LLC (“Apex”), a technology-enabled provider of investment custody and clearing brokerage services, in which we invested in December 2018 and which investment was called by the seller in January 2021. Apex continues to provide investment custody and clearing services for SoFi Invest, including for our brokerage activities, under a multi-year revenue sharing arrangement.

Financial Services Segment

Our digital suite of financial services products, by nature, provides more daily interactions with our members and is, therefore, differentiated from our lending products, which inherently have less consistent touchpoints with our members. We offer a suite of financial services solutions, including cash management and investment services across our SoFi Money, SoFi Invest, SoFi Credit Card and SoFi Relay products. SoFi Money is a digitally-native, mobile cash management experience for our members. Following the Bank Merger, we have begun to transfer SoFi Money products to deposit accounts held at SoFi Bank. SoFi Invest is a mobile-first investment platform offering members access to trading and advisory solutions, such as active investing, robo-advisory and digital assets accounts. SoFi Credit Card has no annual fee and is designed to help our members save, invest and pay down debt through a variable rewards program, with higher rewards offerings when redeeming into other SoFi products, such as SoFi Money or deposit accounts held at SoFi Bank, SoFi Invest or SoFi personal or student loans. To complement these products, we offer financial tracking through SoFi Relay, and partner with other enterprises through loan referrals and our SoFi At Work service. We also developed a financial services marketplace platform branded Lantern Credit to help applicants that do not qualify for SoFi products with alternative products from other providers, as well as providing a product comparison experience.

SoFi Money. SoFi Money is a digital, mobile cash management account offered by SoFi Securities LLC (“SoFi Securities”), a FINRA registered broker dealer. The SoFi Money account is a brokerage account powered by the SoFi application and SoFi Money Debit Card.

Prior to becoming a bank holding company, we exclusively relied on member bank holding companies (each a “Member Bank”) to provide cash management services to our members through our bank sweep program at our broker-dealer

subsidiary, wherein our members place funds on deposit with us that are then swept out and placed on deposit with Member Banks. We continue to rely on Member Banks to provide such cash management services for our members’ SoFi Money accounts, which we expect to transition to deposits held at SoFi Bank over time, as further discussed below. We generate interest income from deposits sitting in our various Member Banks, which rates are determined with each bank and are variable in nature, and which is reduced by the interest fees paid to members. We create and manage the digital, mobile cash management experience for our members. We also earn payment network fees on member expenditures via SoFi-branded debit cards issued by one of our Member Banks. Payment network fees are reduced by direct fees payable to card associations and the Member Bank.

The Bancorp Bank (“Bancorp”) is the issuer of all SoFi Money debit cards and sponsors access to debit networks for payment transactions, funding transactions and associated settlement of funds under a sponsorship agreement with SoFi Securities. Additionally, Bancorp provides sponsorship and support for ACH, check, and wire transactions along with associated funds settlement. The SoFi Money product also utilizes a sweep administrator, UMB Bank, National Association (“UMB”), to sweep funds to and from the SoFi Money program banks, as necessary, under a program broker agreement between SoFi Securities and UMB and program account and program bank agreements with a variety of sweep program banks. SoFi Securities’ agreement with Bancorp provides for receipt by Bancorp of program revenue and transaction fees, and is subject to a minimum monthly card activity fee. The agreement with Bancorp is terminable by SoFi Securities with 120 days prior notice. The program broker agreement between SoFi Securities and UMB provides for one-year terms that automatically renew and is terminable by either party with at least 90 days’ written notice prior to the end of the current term. The program account agreements and program bank agreements between SoFi Securities, UMB and the sweep banks provide for the rate of interest payable on the balances in a member’s SoFi Money account and include certain maximum transfer requirements on transfers. These arrangements are generally terminable upon termination of SoFi Securities’ sweep arrangement with UMB.

As a bank holding company, in 2022 we have begun to allow existing members to convert their SoFi Money cash management accounts into deposit accounts held at SoFi Bank, which allows us to offer both checking and savings features and higher interest rates on the accounts, and through which SoFi Bank is expected to use the deposit accounts as an alternative and more cost-effective source of funding for loans. Additionally, through SoFi Bank we expect to, among other things, issue debit cards and provide ACH, check, and wire transaction services over time.

We believe SoFi Money and deposit accounts held at SoFi Bank are attractive to our members and prospective members because our digital banking platform allows members to spend, save and earn interest and rewards in flexible ways, all within our mobile application. Finally, our “vaults” feature provides a nimble account balance resource that can facilitate budgeting and saving, and provides members with enhanced tracking visibility toward their financial goals.

SoFi Invest. SoFi Invest is a digital brokerage service that provides a streamlined mobile investing experience through which we offer multiple ways to invest and give members access to active investing, robo-advisory and digital assets services. Our active investing service enables members to buy and sell stocks and exchange-traded funds, or ETFs. Our robo-advisory service offers managed portfolios of stocks, bonds and ETFs. Our digital assets service allows members to buy and sell select digital assets. Furthermore, our innovative “stock bits” feature allows members to purchase fractional shares in various companies.

Our interactive investing experience fosters virality by allowing members to engage with other investors’ activity on the platform. Finally, consistent with our aim for our members to “Get Your Money Right” and as part of our commitment to helping our members, we provide access to CFPs at no cost to the member. Additionally, we provide introductory brokerage services to our members and have invested heavily to create an appealing mobile investing experience. While we do not charge trading fees, other than for digital assets trading and for accounts on our 8 Limited platform, our platform benefits from increasing assets under management, as we generate interest income on cash balances that we hold. We also earn brokerage revenue through share lending and pay for order flow arrangements.

With respect to our digital assets trading activities, we do not hold or store members’ digital assets, but instead rely on a third-party custodian, and we hold an immaterial amount of digital assets in order to facilitate paying new member bonuses when members initiate their first digital assets trade. We do this for member convenience to facilitate a seamless payment of digital assets. In connection with our approval as a bank holding company, the Board of Governors of the Federal Reserve (the “Federal Reserve”) determined that the activities of SoFi Digital Assets, LLC in providing members with the ability to buy or sell various digital currencies through SoFi Digital Assets, LLC's omnibus account with a third-party custodian is not a permissible activity under the Bank Holding Company Act and Regulation Y. However, under Section 4 of the Bank Holding Company Act, the Federal Reserve has permitted us to continue our current digital assets related offering for a two-year conformance period from the date we became a bank holding company, with the possibility for three one-year extensions, provided that we do not expand our impermissible activities, except as authorized by the Bank Holding Company Act and

Regulation Y, or increase our established risk limits for total customer digital assets maintained in wallets that are accessible online, referred to as “hot wallets”, or held on balance sheet.

Through our “stock bits” offering, members with SoFi Invest active brokerage accounts may buy or sell fractional shares in a variety of equity securities. Members can place orders in dollars or shares. During the course of a trading day, all member orders are consolidated into a single order for each equity security, which may be a sell or buy order. These fractional orders are rounded up to the next whole share and executed as a market order prior to market close on a standard trading day. Following market close, we allocate the trades to each individual member.

Within our SoFi Invest product, we also believe there are opportunities to generate incremental future revenue through margin lending and options. Through our acquisition of 8 Limited in 2020, we expanded SoFi Invest into the Hong Kong market. We view SoFi Invest as an attractive first product for members who may later become deposit account holders or borrow with SoFi.

Other. We launched the SoFi Credit Card in the second half of 2020. We expect to transition the SoFi Credit Card assets to SoFi Bank, which is not expected to impact the member experience. Additionally, we developed SoFi Relay within the SoFi mobile application, a personal finance management product which allows members to track all of their financial accounts in one place and utilize credit score monitoring services. Further, we leverage our technology and information infrastructure to offer services to other enterprises, such as loan referrals, referral fulfillment and SoFi At Work, which is a platform we offer to enterprises that are looking for a seamless way to provide financial benefits to their employees, such as student loan payments made on their employees’ behalf, for which we earn a fee. We have also developed a financial services marketplace platform branded as Lantern Credit to help applicants that do not qualify for SoFi products find alternative products, as well as providing a product comparison experience. Our other services also include SoFi Protect, which partners with providers who offer products to help our members protect their assets, including insurance providers across auto, life, homeowners, property and casual, and renters products and estate planning. Finally, beginning in 2021, we earned revenues for providing equity capital markets services, either by serving in underwriting syndicates or for providing dealer services in partnership with underwriting syndicates in connection with helping companies successfully complete the business combination or initial public offering (“IPO”) process, as well as advisory services, inclusive of obtaining required shareholder votes.

We believe that the content and features we provide within our mobile application can spur more financial education, which leads to more ways for our members to engage in getting their money right and will ultimately demonstrate the effectiveness of our Financial Services Productivity Loop. SoFi Relay also provides us with unified intelligence about our members and offers us meaningful insights about what SoFi products may help our members best achieve their financial goals.

We earn revenues in connection with our Financial Services segment through various partnerships and our SoFi Money and SoFi Invest products in the following ways:

•Brokerage fees: We earn brokerage fees from our share lending and payment for order flow arrangements related to our SoFi Invest product (for which Apex serves as principal, and we are an agent), exchange conversion services and digital assets activity. In our share lending arrangements and payment for order flow arrangements with Apex, we do not oversee the execution of the transactions by our members, but benefit through a negotiated multi-year revenue sharing arrangement, since our members' brokerage activity drives the share lending and payment for order flow volume. Apex connects with market makers (order flow) and institutions (share lending) to facilitate the service and is responsible for execution. Apex carries inventory risk with the share lending and fractional share programs and ultimately is responsible for successful order routing to market makers that trigger the payment for order flow revenue, and therefore is in control of this offering. Apex sets the gross price and negotiates with market makers and institutions as part of our order flow and share lending arrangements. We have no discretion or visibility into this pricing and, instead, negotiate a net fee for our order flow and share lending arrangements, which is settled with Apex rather than with market makers or other institutions. In our digital assets arrangements, our fee is calculated as a negotiated percentage of the transaction volume. In our exchange conversion arrangements, we earn fees for exchanging one currency for another. Historically, these fees have not been a significant portion of our total net revenue. Our arrangements with Apex are governed by an agreement which contains certain minimum monthly requirements and which is terminable by either party upon notice. Although we no longer have an equity method investment in Apex as of December 31, 2021, Apex continues to provide the services under this agreement.

Beginning in the fourth quarter of 2021, we introduced a flat monthly platform fee that is charged to members associated with our 8 Limited business in Hong Kong. The fee is assessed at each month end on all members with at least one open 8 Limited brokerage account (with the exception of accounts for which the applicable fee exceeds the account’s net asset value at month end) regardless of the volume or frequency of trading activity during the month. The fee is deducted directly from the member’s primary brokerage account.

•Referral fees: Through strategic partnerships, we earn a specified referral fee in connection with referral activity we facilitate through our platform. Referral fees are paid to us by third-party partners that offer services to end users who do not use one of our product offerings, but who were referred to the partners through our platform. As such, the third-party enterprise partners are our customers in these referral arrangements. Beginning in the third quarter of 2021, referral fees also include referral fulfillment fees earned for providing pre-qualified borrower referrals to a third-party partner who separately contracts with a loan originator. The referral fulfillment fee is determined as either of two fixed amounts based on the aggregate origination principal balance of the loan. As such, the third-party partner is our customer in this referral fulfillment arrangement.

•Payment network fees: We earn payment network fees, which primarily constitute interchange fees from our SoFi Money and SoFi Credit Card products, which are reduced by fees payable to card associations and the issuing bank holding company. These fees are remitted by merchants and are calculated by multiplying a set fee percentage (as stipulated by the debit card payment network) by the transaction volume processed through such network. We arrange for performance by a card association and the bank issuer to enable certain aspects of the SoFi branded transaction card process. We enter into contracts with both parties that establish the shared economics of SoFi branded transaction cards. As we continue to transition our SoFi Money cash management accounts to deposit accounts held at SoFi Bank, we expect to decrease certain fees payable to third parties over time.

•Enterprise service fees: These fees are earned in connection with services we provide to enterprise partners through our At Work product, such as when we facilitate transactions for the benefit of their employees, such as 529 plan contributions or student loan payments. In the second quarter of 2021, enterprise services also included fees for providing advisory services to an enterprise partner to facilitate reaching a quorum on their shareholder vote. Our fee for these advisory services was a success-based fee for achieving contractually-specified targets.

•Equity capital markets fees: Equity capital markets fees consist of underwriting fees and dealer fees. Beginning in the second quarter of 2021, we earned underwriting fees related to our membership in underwriting syndicates for IPOs. Beginning in the fourth quarter of 2021, we also earned dealer fees for providing dealer services in partnership with underwriting syndicates for IPOs. We are engaged to place IPO shares that are allocated to us by the underwriters with third-party investors for which we have received a confirmed order. We recognize both types of equity capital markets fees on the applicable trade date.

•Net interest income: Our SoFi Invest and SoFi Money products also generate net interest income based on the cash balances held in these accounts. Historically, this income has not been a significant portion of our total net revenue. As a bank holding company, we expect to reduce our interest expense as we are able to increasingly use deposit accounts as an alternative and more cost-effective and less interest-rate sensitive source of funding for loans. Additionally, through operating under a national bank charter, we expect to be able to offer a wider range of loan sizes and interest rates through SoFi Bank, which we expect to positively impact our interest income.

Competition

We compete at multiple levels, including: (i) competition among other personal loan, student loan, credit card and residential mortgage lenders; (ii) competition for money deposits among other banks, some challenger banks and a variety of technology and retail companies; (iii) competition for investment accounts among other introductory brokerage firms and a variety of technology and other companies; (iv) competition for subscribers to financial services content; and (v) competition among other technology platforms for the enterprise services we provide, such as platform-as-a-service through Galileo.

Competition to fund prime loans. The prime lending market is highly fragmented and competitive. We face competition from a diverse landscape of consumer lenders, including other banks, credit unions and specialty finance lenders, as well as alternative technology-enabled lenders.

Competition to acquire money accounts. Although we now operate a bank, many other banks are larger, have been in business longer and often have greater brand awareness than us. Some large technology and retail companies have large consumer bases and strong balance sheets, which could enhance their competitive ability.

Competition to acquire investment brokerage accounts. The leading incumbent brokerage firms are larger, have been in business longer and generally have greater brand awareness than us. We also face competition from neo-brokerage platforms that provide some of the same features as us, such as a mobile brokerage experience and fractional share investing. In addition, technology and other companies have begun to offer some basic investing features and the ability to buy and sell digital assets.

Competition to attract financial services content viewership. There are many sources of financial news in the marketplace, many of which are more established and have a larger subscriber base.

Competition for debit and credit card sponsors, particularly some challenger banks who need a platform-as-a-service solution, such as the one provided by Galileo. Generally, these arrangements are multi-year contracts, which require us to spend the necessary resources on implementation and interconnecting new customers onto our platform. We face competition from larger institutions that could make investments into an integrated platform-as-a-service solution, and also undercut our pricing, preventing our current customers from renewing, while also impeding our attempts to acquire new members.

Marketing

Our sales and marketing efforts are designed to drive brand awareness, improve member acquisition efficiency and accelerate our Financial Services Productivity Loop. We attract and retain members through multiple marketing channels, including social media, traditional media such as the press, online affiliations, search engine optimization, search engine marketing, offline partnerships, preapproved direct mailings and television advertising. We continue to optimize our marketing strategy through a focus on our full suite of financial products and iterate on opportunities to accelerate the Financial Services Productivity Loop.

Government Supervision and Regulation

We are subject to extensive and complex rules and regulations, licensing and examination by various federal, state and local government authorities designed to, among other things, protect depositors, borrowers and customers. The following is a summary of certain aspects of the various statutes and regulations applicable to us and our subsidiaries. This summary is not a comprehensive analysis of all applicable laws, and is qualified by reference to the full text of statutes and regulations referenced below.

As a bank holding company, we are subject to regulation, supervision and examination by the Federal Reserve under the Bank Holding Company Act of 1956, as amended (“BHCA”), and SoFi Bank is subject to regulation, supervision and examination by the Office of the Comptroller of the Currency (the “OCC”).

SoFi Bank

In February 2022, we closed the Bank Merger, pursuant to which we became a bank holding company and began operating as SoFi Bank. Golden Pacific’s community bank business continues to operate as a division of SoFi Bank.

As a bank holding company, we offer checking and savings accounts and credit cards through SoFi Bank. We are originating all new loan applications within SoFi Bank, and we intend to continue to explore other products for SoFi Bank over time. The key current and expected financial benefits to us of operating a national bank include: (i) lowering our cost to fund loans, as we can utilize deposits held at SoFi Bank to fund loans, which have a lower borrowing cost of funds than our warehouse and securitization financing model, (ii) increasing our flexibility to hold loans on our balance sheet for longer periods, thereby enabling us to earn interest on these loans for a longer period, (iii) supporting origination volume growth by providing an alternative financing option, while also maintaining our warehouse capacity, and (iv) through deposits, providing us with meaningful member data that can allow us to better serve our members’ financial needs. See Part I, Item 1A. “Risk Factors” for a discussion of certain potential risks related to being a bank holding company.

International Operations

While we primarily operate in the United States, we also operate internationally in Latin America and Canada, largely through our Technology Platform segment, as well as in Hong Kong through SoFi Holdings (Hong Kong) Limited (an investment business).

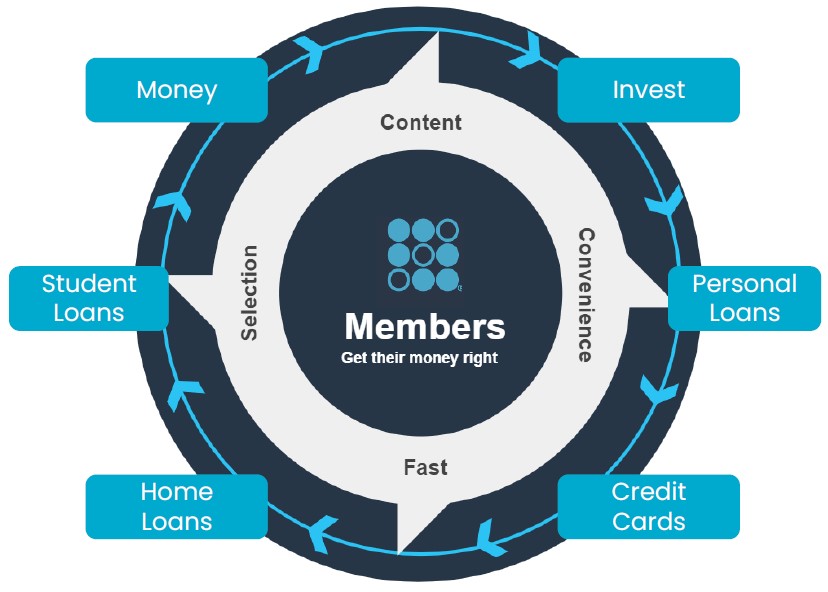

In order to build best-in-class offerings, we focus on four differentiators: fast, selection, content and convenience.

(1)Fast — We aspire to be the fastest place for our members to responsibly do anything, whether it’s applying for a loan, getting a funded loan, opening an account, buying or selling a stock, uploading a mobile check, getting access to money, paying a friend, or accessing relevant financial content. Other than certain products acquired and offered through SoFi Bank, our products are all digital and we have a culture of iteration to help drive faster and faster services.

(2)Selection — Given the digital nature of our products, the permutations of features and services that can be made available to our members across their needs to borrow, save, spend, invest and protect are significant. We will continue to iterate, learn and innovate to broaden our selection in the same way we did this year by providing our members with

competitive interest rates on checking and savings accounts, options trading, “Pay in 4” (a buy now, pay later product), and SoFi Plus membership benefits.

(3)Content — Our financial education, insights, research content, actionable tools and advice are designed to provide meaningful value for our members. Our carefully-crafted and personalized content is offered through our member home feed and is designed to help our members get their money right. We strive to provide digestible financial education, meaningful answers, salient information, advice, credit scores, financial calculators, investment research and financial news that enhance member loyalty and increase the likelihood that members will use additional SoFi products in the future.

(4)Convenience — We hold ourselves accountable and aim to provide the most convenient member experience possible in terms of ease of use, ubiquity, functionality, simplicity and responsive customer service. Our long-term goal is to provide the most convenient 24x7 service and dispel the historical construct of financial service availability based on 9-5 Monday through Friday.

Each product we offer is delivered in a member-centric way and is built and enhanced with these differentiators in mind. We believe that our member-centric, one-stop shop for financial services serves as a competitive differentiator for us relative to other financial services providers.

We offer our members a full suite of financial products and services all in one common mobile platform. To complement these products and services, we believe in building vertically-integrated technology platforms designed to manage and deliver the suite of solutions to our members in a low-cost and differentiated manner.

The Financial Services Productivity Loop We believe that developing a relationship with our members and gaining their trust is central to our success as a financial services platform. Moreover, we believe that some of the current frictions faced by other financial institutions are caused by a disjointed and non-seamless product experience, a lack of digital customer acquisition, subpar mobile web products instead of digital native apps and incomplete product offerings to meet a customer’s holistic financial needs. Through our mobile technology and continuous effort to improve our financial services products, we are seeking to build a financial services platform that can support all of our members’ financial services needs throughout their lifetime.

Our strategy, which is rooted in what we refer to as our “Financial Services Productivity Loop”, is centered around building trust and a lifetime relationship with our members, which we believe will help build a sustainable competitive advantage.

| | |

| Financial Services Productivity Loop |

In order to deliver on our strategy, we must develop best-in-class unit economics and best-in-class products that build trust and reliability between our members and our platform. Our acquisition of SoFi Bank was also an important step in continuing to build best-in-class unit economics and best-in-class products, as it has enabled us to achieve lower cost of funding through deposits, and improved unit economics and engagement on SoFi Money. When we do this on a member’s first product, and they later consider using an additional product, we believe they are more likely to start with our platform and we have a

higher chance that they will select one of our products to meet their other financial needs. This results in delivering more revenue per member with no second member acquisition costs, resulting in higher lifetime value per member. This also reinforces the benefits of our platform, which simplifies the entire financial ecosystem for our members, helping them get their money right. We are able to use the increased profits to further improve member benefits and product experience.

In addition to realizing the benefits of more of our members adopting multiple SoFi products, the Financial Services Productivity Loop strategy delivers operating and technology efficiencies to deliver better unit economics on a per product basis. One of the success factors of our lending business is that it is vertically integrated across our technology stack, risk protocols and operations processes.

We conduct our business through three reportable segments: Lending, Technology Platform and Financial Services. Below is a discussion of our segments and their primary products and non-product offerings.

Lending Segment

We offer personal loans, student loans, home loans and related servicing. We believe that our market opportunity within each of these lending channels is significant. Our lending process primarily leverages an in-application, digital borrowing experience, which we believe serves as a competitive advantage as digital lending becomes increasingly ubiquitous. Furthermore, our platform supports the full transaction lifecycle, including credit application, underwriting, approval, funding and servicing. Through data derived at loan origination and throughout the servicing process, SoFi has life-of-loan performance data on each loan in our ecosystem that we originate and on which we retain servicing, which provides a meaningful data asset. Net interest income, which we define as the difference between the earned interest income and interest expense to finance loans, is a key component of the profitability of our Lending segment.

Personal Loans. We originate personal loans to help our members with a variety of financial needs, such as debt consolidation, home improvement projects, family planning, travel and weddings, to name a few. We offer fixed rate loans with flexible repayment terms, including unemployment protection. We generally offer loan sizes of $5,000 to $100,000, subject to legal and/or licensing requirements, with terms generally ranging from 2 to 7 years. We regularly update the annual percentage rates offered on our personal loans.

Student Loans. We operate in the student loan refinance space, with a focus on prime and super-prime school loans, as well as the “in-school” lending space, which allows members to borrow funds while they attend school. We offer flexible loan sizes, repayment options and competitive rates. Within student loan refinancing, we generally offer loan sizes of $5,000 or higher, subject to legal and/or licensing requirements, with terms generally ranging from 5 to 20 years. Within in-school loans, we generally offer loan sizes of $1,000 or higher, subject to legal and/or licensing requirements, with terms generally ranging from 5 to 15 years. We regularly update the annual percentage rates offered on our fixed and variable-rate student loans.

Home Loans. We offer agency, non-agency and, beginning in the second quarter of 2023, certain government loans (e.g., VA and Federal Housing Administration loans) for members purchasing a home or refinancing an existing mortgage. For our home loan products, we offer competitive rates, flexible down payment options for as little as 3% (or 0% for VA loans), a close on time guarantee, and educational tools and calculators. For one-unit properties, we generally offer loan sizes of $75,000 to $766,550 for in conforming normal cost areas (with exceptions for smaller loan sizes considered on a case-by-case basis), up to $1,149,825 in conforming high cost areas (GSE-eligible loans above the normal conforming limit, which is determined by county). For multi-unit properties, we offer loan sizes up to $2,211,600. In addition, we offer loan sizes up to $3,000,000 for jumbo loans (loans in the jumbo loan program), up to $1,500,000 for VA loans, and up to $472,030 for Federal Housing Administration loans in most areas. Our fixed rate home loans generally have terms of 10, 15, 20, 25 or 30 years. We offer adjustable rate mortgage products for conforming and jumbo loans, with a fixed rate for 5, 7 or 10 years followed by rate adjustments every six months for the remainder of the 30-year term, and for VA and Federal Housing Administration loans, with a fixed rate for 5 years followed by rate adjustments every year for the remainder of the 30-year term. We regularly update the annual percentage rates offered on our home loans.

Lending Model

We originate loans through our lending business, and have the option of pursuing a gain-on-sale origination model, whereby we seek to recognize a gain from these loans and sell them into either our whole loan or securitization channels, or holding loans on our balance sheet when advantageous. This enables us to maximize our return and balance our risk by earning

interest on these loans for a longer period and to be selective in our sales arrangements. We expect to benefit from the continued mix towards deposit funding through operating SoFi Bank.