QuickLinks-- Click here to rapidly navigate through this document

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D. C.D.C. 20549 FORM 10-K/A

AMENDMENT NO. 1Form 10-K

ý |

| |

| (Mark One) | | |

|

þ | | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| | For the fiscal year ended December 31, 20032006 |

OR

|

o |

| TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Commission file number: 1-14569 |

Commission file number 1-14569

PLAINS ALL AMERICAN PIPELINE, L.P.

(Exact name of registrant as specified in its charter) | | |

Delaware

(State or other jurisdiction of

incorporation or organization)76-0582150

(I.R.S. Employer Identification No.)

Delaware | | 76-0582150 |

(State or other jurisdiction of | | (I.R.S. Employer |

incorporation or organization) | | Identification No.) |

333 Clay Street, Suite 1600,

Houston, Texas 77002

(Address of principal executive offices)

(Zip (Zip Code) (713) 646-4100

(Registrant'sRegistrant’s telephone number, including area code) Securities registered pursuant to Section 12(b) of the Act:

| | | |

|---|

Title of each class

| | Each Class | | Name of each exchangeEach Exchange on which registered

Which Registered |

|---|

|

| Common Units | | New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act:

None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes þ No o

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No þ

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports)

, and (2) has been subject to such filing requirements for the past 90 days. Yes

ýþ No

o Indicate by check mark whether the registrant is an accelerated filer (as defined in Rule 12b-2 of the Act). Yes ý No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 ofRegulation S-K is not contained herein, and will not be contained, to the best of registrant'sregistrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of thisForm 10-K or any amendment to thisForm 10-K. þ

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer. See definition of “accelerated filer and large accelerated filer” inRule 12b-2 of the Exchange Act. (Check one):

Large Accelerated Filer þ Accelerated Filer o Non-Accelerated Filer o Indicate by check mark if the registrant is a shell company (as defined inRule 12b-2 of the Exchange Act). Yes o No þ

The aggregate value of the Common Units held by non-affiliates of the registrant (treating all executive officers and directors of the registrant and holders of 10% or more of the Common Units outstanding, for this purpose, as if they may be affiliates of the registrant) was approximately

$1.1$2.7 billion on June 30,

2003,2006, based on

$31.48$43.67 per unit, the closing price of the Common Units as reported on the New York Stock Exchange on such date.

At February

17, 2004,20, 2007, there were outstanding

57,162,638109,405,178 Common

Units and 1,307,190 Class B Common Units.

DOCUMENTS INCORPORATED BY REFERENCE: NoneREFERENCE

NONE

PLAINS ALL AMERICAN PIPELINE, L.P. AND SUBSIDIARIES

FORM 10-K/A—200310-K — 2006 ANNUAL REPORT

Introductory Note Plains All American Pipeline, L.P. is filing this Amendment No. 1 on Form 10-K/A ("Amendment No. 1") to reflect certain revisions to disclosures previously included in its Annual Report on Form 10-K for the fiscal year ended December 31, 2003, which was originally filed on March 1, 2004 (the "Original Filing"). The revisions to the Original Filing relate to a recently completed reviewTable of the Original Filing by the Securities and Exchange Commission's Division of Corporation Finance.

The following Items of the Original Filing are amended by this Amendment No. 1:

Contents Please note that the information contained in this Form 10-K/A, including the financial statements and notes thereto, do not reflect events occurring after the date of the Original Filing, except as reflected in "Note 16—Subsequent Events (Unaudited)" in the "Notes to the Consolidated Financial Statements." For a description of these events, please read Plains All American Pipeline, L.P.'s reports filed under the Exchange Act of 1934, as amended, since March 1, 2004.

PLAINS ALL AMERICAN PIPELINE, L.P. AND SUBSIDIARIES

FORM 10-K/A—2003 ANNUAL REPORT

Table of Contents

FORWARD-LOOKING STATEMENTS

All statements

included in this report, other than statements of historical fact,

included in this report are forward-looking statements, including but not limited to statements identified by the words

"anticipate," "believe," "estimate," "expect," "plan," "intend"“anticipate,” “believe,” “estimate,” “expect,” “plan,” “intend” and

"forecast,"“forecast,” and similar expressions and statements regarding our business strategy, plans and objectives of our management for future operations.

The absence of these words, however, does not mean that the statements are not forward-looking. These statements reflect our current views with respect to future events, based on what we believe are reasonable assumptions. Certain factors could cause actual results to differ materially from results anticipated in the forward-looking statements. These factors include, but are not limited to:

•abrupt or severe production declines or production interruptions in outer continental shelf production located offshore California and transported on our pipeline system;

•declines in volumes shipped on the Basin Pipeline and our other pipelines by third party shippers;

•the availability of adequate third-party production volumes for transportation and marketing in the areas in which we operate;

•demand for various grades of crude oil and resulting changes in pricing conditions or transmission throughput requirements;

•fluctuations in refinery capacity in areas supplied by our transmission lines;

•the effects of competition;

•the success of our risk management activities;

•the impact of crude oil price fluctuations;

•the availability of, and ability to consummate, acquisition or combination opportunities;

•successful integration and future performance of acquired assets;

•continued creditworthiness of, and performance by, counterparties;

•successful third-party drilling efforts in areas in which we operate pipelines or gather crude oil;

•our levels of indebtedness and our ability to receive credit on satisfactory terms;

•shortages or cost increases of power supplies, materials or labor;

•weather interference with business operations or project construction;

•the impact of current and future laws and governmental regulations;

•the currency exchange rate of the Canadian dollar;

•environmental liabilities that are not covered by an indemnity, insurance or existing reserves;

•fluctuations in the debt and equity markets including the price of our units at the time of vesting under our Long-Term Incentive Plan; and

•general economic, market or business conditions.

| | |

| • | our failure to successfully integrate the business operations of Pacific Energy Partners L.P. (“Pacific”) or our failure to successfully integrate any future acquisitions; |

|

| • | the failure to realize the anticipated cost savings, synergies and other benefits of the merger with Pacific; |

|

| • | the success of our risk management activities; |

|

| • | environmental liabilities or events that are not covered by an indemnity, insurance or existing reserves; |

|

| • | maintenance of our credit rating and ability to receive open credit from our suppliers and trade counterparties; |

|

| • | abrupt or severe declines or interruptions in outer continental shelf production located offshore California and transported on our pipeline systems; |

|

| • | failure to implement or capitalize on planned internal growth projects; |

|

| • | the availability of adequate third party production volumes for transportation and marketing in the areas in which we operate, and other factors that could cause declines in volumes shipped on our pipelines by us and third party shippers; |

|

| • | fluctuations in refinery capacity in areas supplied by our mainlines, and other factors affecting demand for various grades of crude oil, refined products and natural gas and resulting changes in pricing conditions or transmission throughput requirements; |

|

| • | the availability of, and our ability to consummate, acquisition or combination opportunities; |

|

| • | our access to capital to fund additional acquisitions and our ability to obtain debt or equity financing on satisfactory terms; |

|

| • | future performance of acquired assets or businesses and the risks associated with operating in lines of business that are distinct and separate from our historical operations; |

|

| • | unanticipated changes in crude oil market structure and volatility (or lack thereof); |

|

| • | the impact of current and future laws, rulings and governmental regulations; |

|

| • | the effects of competition; |

|

| • | continued creditworthiness of, and performance by, our counterparties; |

|

| • | interruptions in service and fluctuations in tariffs or volumes onthird-party pipelines; |

|

| • | increased costs or lack of availability of insurance; |

|

| • | fluctuations in the debt and equity markets, including the price of our units at the time of vesting under our Long-Term Incentive Plans; |

|

| • | the currency exchange rate of the Canadian dollar; |

|

| • | shortages or cost increases of power supplies, materials or labor; |

|

| • | weather interference with business operations or project construction; |

|

| • | risks related to the development and operation of natural gas storage facilities; |

|

| • | general economic, market or business conditions; and |

|

| • | other factors and uncertainties inherent in the transportation, storage, terminalling and marketing of crude oil, refined products and liquefied petroleum gas and other natural gas related petroleum products. |

Other factors described herein,elsewhere in this document, or factors that are unknown or unpredictable, could also have a material adverse effect on future results. Please read "Risk Factors“Risks Related to Our Business"Business” discussed in Item 7. "Management's Discussion and Analysis of Financial Condition and Results of Operations."1A. “Risk Factors.” Except as required by applicable securities laws, we do not intend to update these forward-looking statements and information.

Items 1 and 2. Business and Properties Plains All American Pipeline, L.P. is a publicly traded Delaware limited partnership (the "Partnership"), formed in 1998September 1998. Our operations are conducted directly and indirectly through our primary operating subsidiaries. As used in thisForm 10-K, the terms “Partnership,” “Plains,” “we,” “us,” “our,” “ours” and similar terms refer to Plains All American Pipeline, L.P. and its subsidiaries, unless the context indicates otherwise.

We are engaged in

interstatethe transportation, storage, terminalling and

intrastatemarketing of crude oil,

transportation,refined products and

crude oil gathering, marketing, terminalling and storage, as well as the marketing and storage of liquefied petroleum gas and other

natural gas-related petroleum products. We refer to liquefied petroleum gas and other natural gas related petroleum products

primarilycollectively as “LPG.” Through our 50% equity ownership in

Texas, California, Oklahoma, Louisiana and the Canadian Provinces of Alberta and Saskatchewan. Our operations can be categorized into two primary business activities:•Crude Oil Pipeline Transportation Operations. We ownPAA/Vulcan Gas Storage, LLC (“PAA/Vulcan”), we develop and operate approximately 7,000 milesnatural gas storage facilities.

Prior to the fourth quarter of gathering2006, we managed our operations through two segments. Due to our growth, especially in the facilities portion of our business (most notably in conjunction with the Pacific acquisition), we have revised the manner in which we internally evaluate our segment performance and mainlinedecide how to allocate resources to our segments. As a result, we now manage our operations through three operating segments: (i) Transportation, (ii) Facilities, and (iii) Marketing.

Transportation — Our transportation segment operations generally consist of fee-based activities associated with transporting volumes of crude oil and refined products on pipelines locatedand gathering systems. We generate revenue through a combination of tariffs,third-party leases of pipeline capacity, transportation fees, barrel exchanges and buy/sell arrangements.

As of December 31, 2006, we employed a variety of owned or leased long-term physical assets throughout the United States and Canada.Canada in this segment, including approximately:

| | |

| • | 20,000 miles of active pipelines and gathering systems; |

|

| • | 30 million barrels of tank capacity used primarily to facilitate pipeline throughput; and |

|

| • | 57 transport and storage barges and 30 transport tugs through our 50% interest in Settoon Towing, LLC (“Settoon Towing”). |

We also include in this segment our equity earnings from our investments in the Butte Pipe Line Company (“Butte”) and Frontier Pipeline Company (“Frontier”) pipeline systems, in which we own minority interests, and Settoon Towing, in which we own a 50% interest.

Facilities — Our activities from pipelinefacilities segment operations generally consist of transportingfee-based activities associated with providing storage, terminalling and throughput services for crude oil, forrefined products and LPG, as well as LPG fractionation and isomerization services. We generate revenue through a fee, third partycombination ofmonth-to-month and multi-year leases and processing arrangements.

As of pipeline capacity, barrel exchangesDecember 31, 2006, we owned and buy/sell arrangements.

•Gathering, Marketing, Terminallingemployed a variety of long-term physical assets throughout the United States and Storage Operations. We own and operateCanada in this segment, including: | | |

| • | approximately 30 million barrels of active, above-ground terminalling and storage facilities; |

|

| • | approximately 1.3 million barrels of active, underground terminalling and storage facilities; and |

|

| • | a fractionation plant in Canada with a processing capacity of 4,400 barrels per day, and a fractionation and isomerization facility in California with an aggregate processing capacity of 22,000 barrels per day. |

At year-end 2006, we were in the process of constructing approximately 24.012.5 million barrels of additional above-ground crude oil terminalling and storage facilities, including tankage associated with our pipeline systems. These facilities include a crude oil terminalling and storage facility at Cushing, Oklahoma. Cushing,the majority of which we referexpect to place in this report asservice during 2007.

Our facilities segment also includes our equity earnings from our investment in PAA/Vulcan. At December 31, 2006, PAA/Vulcan owned and operated approximately 25.7 billion cubic feet of underground storage capacity and

1

is constructing an additional 24 billion cubic feet of underground storage capacity, which is expected to be placed in service in stages over the Cushing Interchange, is onenext three years.

Marketing — Our marketing segment operations generally consist of the largestfollowing merchant activities:

| | |

| • | the purchase of U.S. and Canadian crude oil at the wellhead and the bulk purchase of crude oil at pipeline and terminal facilities, as well as the purchase of foreign cargoes at their load port and various other locations in transit; |

|

| • | the storage of inventory during contango market conditions; |

|

| • | the purchase of refined products and LPG from producers, refiners and other marketers; |

|

| • | the resale or exchange of crude oil, refined products and LPG at various points along the distribution chain to refiners or other resellers to maximize profits; and |

|

| • | arranging for the transportation of crude oil, refined products and LPG on trucks, barges, railcars, pipelines and ocean-going vessels to our terminals and third-party terminals. |

Our marketing activities are designed to produce a stable baseline of results in a variety of market hubsconditions, while at the same time providing upside exposure to opportunities inherent in the United Statesvolatile market conditions. These activities utilize storage facilities at major interchange and the designated delivery point for NYMEX crude oil futures contracts. We utilize our storage tanks to counter-cyclically balance our gatheringterminalling locations and marketing operations and to execute various hedging strategies to stabilize profits and reduce the negative impact of market volatility and provide counter-cyclical balance.

Except for pre-defined inventory positions, our policy is generally to purchase only product for which we have a market, to structure our sales contracts so that price fluctuations do not materially affect the segment profit we receive, and not to acquire and hold physical inventory, futures contracts or other derivative products for the purpose of speculating on commodity price changes.

In addition to substantial working inventories and working capital associated with its merchant activities, the marketing segment also employs significant volumes of crude oil and LPG as linefill or minimum inventory requirements under service arrangements with transportation carriers and terminalling providers. The marketing segment also employs trucks, trailers, barges, railcars and leased storage.

As of December 31, 2006, the marketing segment owned crude oil and LPG classified as long-term assets and a variety of owned or leased long-term physical assets throughout the United States and Canada, including approximately:

| | |

| • | 7.9 million barrels of crude oil and LPG linefill in pipelines owned by the Partnership; |

|

| • | 1.5 million barrels of crude oil and LPG linefill in pipelines owned by third parties; |

|

| • | 500 trucks and 600 trailers; and |

|

| • | 1,300 railcars. |

In connection with its operations, the marketing segment secures transportation and facilities services from the Partnership’s other two segments as well as third-party service providers undermonth-to-month and multi-year arrangements. Inter-segment transportation service rates are based on posted tariffs for pipeline transportation services. Facilities segment services are also obtained at rates consistent with rates charged to third parties for similar services; however, certain terminalling and storage rates are discounted to our marketing segment to reflect the fact that these services may be canceled on short notice to enable the facilities segment to provide services to third parties.

Counter-Cyclical Balance

Access to storage tankage by our marketing segment provides a counter-cyclical balance that has a stabilizing effect on our operations and cash flow associated with this segment. The strategic use of our terminalling and storage assets in conjunction with our marketing operations generally provides us with the flexibility to maintain a base level of margin irrespective of crude oil market volatility.conditions and, in certain circumstances, to realize incremental

2

margin during volatile market conditions. See

"—“— Crude Oil Volatility; Counter-Cyclical Balance; Risk

Management." Our terminalling and storage operations also generate revenue at the Cushing Interchange and our other locations through a combination of storage and throughput charges to third parties. Our gathering and marketing operations include:•the purchase of crude oil at the wellhead and the bulk purchase of crude oil at pipeline and terminal facilities;

•the transportation of crude oil on trucks, barges and pipelines;

•the subsequent resale or exchange of crude oil at various points along the crude oil distribution chain; and

•the purchase of liquified petroleum gas and other petroleum products (collectively "LPG") from producers, refiners and other marketers, and the sale of LPG to wholesalers, retailers and industrial end users.

Management.”

Our principal business strategy is to

capitalize onprovide competitive and efficient midstream transportation, terminalling, storage and marketing services to our producer, refiner and other customers, and to address the regional

crude oil supply and demand imbalances

for crude oil, refined products and LPG that exist in the United States and Canada by combining the strategic location and distinctive capabilities of our transportation,

terminalling and

terminallingstorage assets with our extensive marketing and distribution

expertiseexpertise. We believe successful execution of this strategy will enable us to generate sustainable earnings and cash flow.

We intend to executegrow our business strategy by:

| | |

| • | optimizing our existing assets and realizing cost efficiencies through operational improvements; |

|

| • | developing and implementing internal growth projects that (i) address evolving crude oil, refined product and LPG needs in the midstream transportation and infrastructure sector and (ii) are well positioned to benefit from long-term industry trends and opportunities; |

|

| • | utilizing our assets along the Gulf, West and East Coasts along with our Cushing Terminal and leased assets to increase our presence in the waterborne importation of foreign crude oil; |

|

| • | establishing a presence in the refined product supply and marketing sector; |

|

| • | selectively pursuing strategic and accretive acquisitions of crude oil, refined product and LPG transportation, terminalling, storage and marketing assets that complement our existing asset base and distribution capabilities; and |

|

| • | using our terminalling and storage assets in conjunction with our marketing activities to address physical market imbalances, mitigate inherent risks and increase margin. |

PAA/Vulcan’s natural gas storage assets are also well-positioned to benefit from long-term industry trends and

optimizing throughput on our existing pipelineopportunities. Our natural gas storage growth strategies are to develop and

gathering assets and realizing cost efficiencies through operational improvements;•utilizing and expanding our Cushing Terminal and our other assets to service the needs of refinersimplement internal growth projects and to profit from merchant activities that take advantage of crude oil pricing and quality differentials;

•- selectively

pursuingpursue strategic and accretive acquisitions of crude oil transportation assets, including pipelines, gathering systems, terminallingnatural gas storage projects and storage facilitiesfacilities. We also intend to prudently and economically leverage our asset base, knowledge base and skill sets to participate in other assetsenergy-related businesses that have characteristics and opportunities similar to, or that otherwise complement, our existing asset base and distribution capabilities; and

•optimizing and expanding our Canadian operations and our presence in the Gulf Coast and Gulf of Mexico to take advantage of anticipated increases in the volume and qualities of crude oil produced in these areas.

To a lesser degree, we also engage in a similar business strategy with respect to the wholesale marketing and storage of LPG, which we began as a result of an acquisition in mid 2001. Since that time, the portion of our Gathering, Marketing, Terminalling and Storage Operations segment profit associated with those activities has increased from $4.2 million in 2001 to $10.0 million in 2002 and $11.6 million in 2003. The segment profit for 2001 reflects results from July 1 through December 31.

activities.

Targeted Credit Profile

We believe that a major factor in our continued success

will beis our ability to maintain a competitive cost of capital and access to the capital markets.

Since our initial public offering in 1998, we have consistently communicated to the financial community our intentionWe intend to maintain a

strong credit profile that we believe is consistent with an investment grade credit rating. We have targeted a general credit profile with the following attributes:

| | |

| • | an average long-termdebt-to-total capitalization ratio of approximately 50%; |

|

| • | an average long-termdebt-to-EBITDA multiple of approximately 3.5x or less (EBITDA is earnings before interest, taxes, depreciation and amortization); and |

|

| • | an averageEBITDA-to-interest coverage multiple of approximately 3.3x or better. |

The first two of these three metrics include long-term debt-to-total capitalization ratiodebt as a critical measure. In certain market conditions, we also incur short-term debt in connection with marketing activities that involve the simultaneous purchase and forward sale of approximately 60% or less;

•an averagecrude oil. The crude oil purchased in these transactions is hedged, is required to be stored on amonth-to-month basis and is sold to high-credit quality counterparties. We do not consider the working capital borrowings associated with this activity to be part of our long-term debt-to-EBITDA ratiocapital structure. These borrowings are self-liquidating as they are repaid with sales proceeds following delivery of approximately 3.5x or less (EBITDA is earnings before interest, taxes, depreciationthe crude oil. We also anticipate performing similar activities for refined products as we expand our presence in the refined products supply and amortization); andmarketing sector.

•an average EBITDA-to-interest coverage ratio of approximately 3.3x or better.3 As of December 31, 2003, we were within our targeted credit profile.

In order for us to maintain our targeted credit profile and achieve growth through

internal growth projects and acquisitions, we intend to fund

acquisitions using approximately equal proportionsat least 50% of

the capital requirements associated with these activities with equity and

debt. In certain cases, acquisitions will initially be financed using debt since it is difficult to predict the actual timingcash flow in excess of

accessing the market to raise equity. Accordingly, fromdistributions. From time to time, we may be

temporarily outside the parameters of our targeted credit

profile.profile as, in certain cases, these capital expenditures and acquisitions may be financed initially using debt or there may be delays in realizing anticipated synergies from acquisitions or contributions to adjusted EBITDA from capital expansion projects. In this instance, “adjusted EBITDA” means earnings before interest, tax, depreciation, amortization, Long-Term Incentive Plan charges and gains and losses attributable to Statement of Financial Accounting Standards No. 133 “Accounting for Derivative Instruments and Hedging Activities,” as amended (“SFAS 133”). At December 2003, Moody's Investors Service raised31, 2006, we were above our targeted parameter for the long-termdebt-to-EBITDA ratio (due primarily to the closing of the Pacific acquisition in November 2006) and within the parameters of the other credit metrics. Based on our December 31, 2006 long-term debt balance and the midpoint of our adjusted EBITDA guidance for 2007 furnished in aForm 8-K dated February 22, 2007, our long-termdebt-to-adjusted-EBITDA multiple would be 3.8.

Credit Rating

As of February 2007, our senior unsecured

rating to Ba1, affirmed our senior implied credit rating of Ba1 and placed us on review for a possible ratings

upgrade. In November 2003,with Standard &

Poor's raisedPoor’s and Moody’s Investment Services were BBB- negative outlook and Baa3 stable outlook, respectively, both of which are considered “investment grade.” We have targeted the attainment of even stronger investment grade ratings of mid to high-BBB and Baa categories for Standard & Poor’s and Moody’s Investment Services, respectively. We cannot give assurance that our

senior unsecured ratingcurrent ratings will remain in effect for any given period of time, that we will be able to

BBB- (the same rating as our senior implied rating) from BB+. You should noteattain the higher ratings we have targeted or that one or both of these ratings will not be lowered or withdrawn entirely by the ratings agency. Note that a credit rating is not a recommendation to buy, sell or hold securities, and may be

subject to revisionrevised or

withdrawalwithdrawn at any time.

We believe that the following competitive strengths position us successfully to successfully execute our principal business strategy:

| | |

| • | Many of our transportation segment and facilities segment assets are strategically located and operationally flexible and have additional capacity or expansion capability. The majority of our primary transportation segment assets are in crude oil service, are located in well-established oil producing regions and transportation corridors, and are connected, directly or indirectly, with our facilities segment assets located at major trading locations and premium markets that serve as gateways to major North American refinery and distribution markets where we have strong business relationships. |

|

| • | We possess specialized crude oil market knowledge. We believe our business relationships with participants in various phases of the crude oil distribution chain, from crude oil producers to refiners, as well as our own industry expertise, provide us with an extensive understanding of the North American physical crude oil markets. |

|

| • | Our business activities are counter-cyclically balanced. We believe the balance of activities provided by our marketing segment provides us with a counter-cyclical balance that generally affords us the flexibility (i) to maintain a base level of margin irrespective of crude oil market conditions and (ii), in certain circumstances, to realize incremental margin during volatile market conditions. |

|

| • | We have the evaluation, integration and engineering skill sets and the financial flexibility to continue to pursue acquisition and expansion opportunities. Over the past nine years, we have completed and integrated approximately 45 acquisitions with an aggregate purchase price of approximately $5.1 billion ($2.6 billion excluding the Pacific acquisition, for which we are still in the process of integrating). We have also implemented internal expansion capital projects totaling over $700 million. In addition, we believe we have significant resources to finance future strategic expansion and acquisition opportunities. As of December 31, 2006, we had approximately $1.3 billion available under our committed credit facilities, subject to continued covenant compliance. We believe we have one of the strongest capital structures relative to other master limited partnerships with capitalizations greater than $1.0 billion. In addition, the investors in our general partner are diverse and financially strong and have demonstrated their support by providing |

4

•Our pipeline assets are strategically located and have additional capacity. Our primary crude oil pipeline transportation and gathering assets are located in well-established oil producing regions and are connected, directly or indirectly, with our terminalling and storage assets that service major North American refinery and distribution markets where we have strong business relationships. These assets are strategically positioned to maximize the value of our crude oil by transporting it to major trading locations and premium markets. Certain of our pipeline networks currently possess additional capacity that can accommodate increased demand without significant additional capital investment.

| | |

| | capital to help finance previous acquisitions and expansion activities. We believe they are supportive long-term sponsors of the partnership. |

•Our Cushing Terminal is strategically located, operationally flexible and readily expandable. Our Cushing Terminal interconnects with the Cushing Interchange's major inbound and outbound pipelines, providing access to both foreign and domestic crude oil. Our Cushing Terminal is the most modern large-scale terminalling and storage facility at the Cushing Interchange, incorporating (i) operational enhancements designed to safely and efficiently terminal, store, blend and segregate large volumes and multiple varieties of crude oil and (ii) extensive environmental safeguards. Since completing the initial construction of the Cushing Terminal in 1994, we have completed three expansion phases of approximately 1.1 million barrels each, thus expanding the facility to its current capacity of 5.3 million barrels. In January 2004, we announced the commencement of our Phase IV expansion project, which will increase capacity by an incremental 1.1 million barrels, or approximately 20% of current capacity. | | |

| • | We have an experienced management team whose interests are aligned with those of our unitholders. Our executive management team has an average of more than 20 years industry experience, with an average of more than 15 years with us or our predecessors and affiliates. Certain members of our senior management team own an approximate 5% interest in our general partner and collectively own approximately 850,000 common units, including fully vested options. In addition, through grants of phantom units, the senior management team also owns significant contingent equity incentives that generally vest upon achievement of performance objectives, continued service or both. These interests give management a vested interest in our continued success. |

We believe that the facility can be further expandedmany of these competitive strengths have similar application to meet additional demand should market conditions warrant. In addition, we own approximately 18.7 million barrels of above-ground crude oil terminalling and storage assets elsewhereour efforts to expand our presence in the United Statesrefined products, LPG and Canada that complement our Cushing Terminal and enable us to serve the needs of our customers.

•We possess specialized crude oil market knowledge. We believe our business relationships with participants in all phases of the crude oil distribution chain, from crude oil producers to refiners, as well as our own industry expertise, provide us with an extensive understanding of the North American physical crude oil markets.

•The combination of our business activities provide a counter-cyclical balance. We believe the manner in which we integrate the activities of our gathering and marketing operations with our terminalling andnatural gas storage operations provides a counter-cyclical balance to our business, irrespective of the structure of the crude oil market. In combination with our pipeline transportation operations, we believe these activities have a stabilizing effect on our cash flow from operations.

•- sectors.

We have the financial flexibility to continue to pursue expansion and acquisition opportunities. We believe we have significant resources to finance strategic expansion and acquisition opportunities, including our ability to issue additional partnership units, borrow under our credit facilities and issue additional notes in the long-term debt capital markets. We have committed senior unsecured facilities totaling $750 million. Under our committed facilities, each bank has committed to lend to us its pro rata share of the total facility amount. These credit facilities are available for working capital purposes and to fund capital expenditures, including acquisitions. At December 31, 2003, we had approximately $596.8 million of unused capacity under these credit facilities. We also have a $200 million uncommitted facility to finance the purchase of hedged crude oil inventory. Under our uncommitted facility, the banks have made no binding commitment to lend; rather, the banks can exercise discretion with respect to each borrowing request. Once they have agreed to lend, however, the amounts associated with any particular borrowing becomes "committed" in that the banks have no discretion to demand prepayment. The uncommitted facility is secured by the purchased inventory and related receivables. At December 31, 2003, we have approximately $100 million outstanding under our hedged crude oil inventory facility resulting in unused uncommitted capacity of approximately $100 million under this facility. Our usage is subject to covenant compliance. See Item 7. "Management's Discussion and Analysis of Financial Condition and Results of Operations—Liquidity and Capital Resources."

•We have an experienced management team whose interests are aligned with those of our stakeholders. Our executive management team has an average of more than 20 years industry experience, with an average of over 15 years with us or our predecessors and affiliates. Members of our senior management team own a 4% interest in our general partner, approximately 400,000 common units and, through phantom unit grants and options, own contingent equity incentives that vest

Organizational History

We were formed

as a master limited partnership in September 1998 to acquire and operate the midstream crude oil

businessbusinesses and assets of

Plains Resources Inc. and its wholly-owned subsidiaries ("Plains Resources") as a

separate, publicly traded master limited partnership.predecessor entity. We completed our initial public offering in November 1998.

As a result of subsequent equity offerings and the purchase inSince June 2001,

by senior management and a group of financial investors of majority control of our general partner and a portion of the limited partner units held by Plains Resources, Plains Resources' overall effective ownership in us was reduced to approximately 22% as of February 17, 2004. See Item 12. "Security Ownership of Certain Beneficial Owners and Management and Related Unitholders' Matters." As a result of the 2001 transaction, our 2% general partner interest ishas been held by Plains AAP, L.P., a Delaware limited partnership. Plains All American GP LLC, a Delaware limited liability company, is Plains AAP, L.P.'s’s general partner. Unless the context otherwise requires, we use the term "general partner"“general partner” to refer to both Plains AAP, L.P. and Plains All American GP LLC. Plains AAP, L.P. and Plains All American GP LLC are essentially held by 7 owners with the largest interest, 44%, held by Plains Resources. We use the phrase "former general partner" to refer to the subsidiaryseven owners. See Item 12. “Security Ownership of Plains Resources that formerly held the general partner interest.

Certain Beneficial Owners and Management and Related Unitholder Matters — Beneficial Ownership of General Partner Interest.”

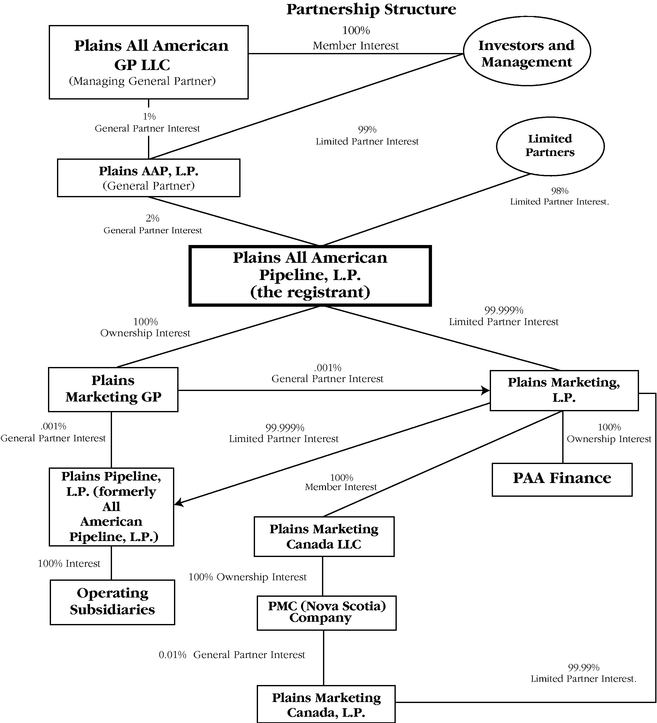

Partnership Structure and Management Our operations are conducted through, and our operating assets are owned by, our subsidiaries.

We own our interests in our subsidiaries through two operating partnerships,Our general partner, Plains

Marketing,AAP, L.P.

and Plains Pipeline, L.P. Our Canadian operations are conducted through Plains Marketing Canada, L.P. We currently have fewer than 20 subsidiaries, although we may form new subsidiaries from time to time in connection with acquisitions., is managed by its general partner, Plains All American GP LLC, manageswhich has ultimate responsibility for conducting our operationsbusiness and activitiesmanaging our operations. See Item 10. “Directors and employsExecutive Officers of our officersGeneral Partner and personnel, who devote 100% of their efforts to the management of the Partnership.Corporate Governance.” Our general partner does not receive a management fee or other compensation in connection with its management of our business, but it is reimbursed for substantially all direct and indirect expenses incurred on our behalf. Canadian personnel are employed by Plains Marketing Canada L.P.'s general partner, PMC (Nova Scotia) Company.

Our general partner owns all of the incentive distribution rights. These rights provide that our general partner receives an increasing percentage of cash distributions (in addition to its 2% general partner interest) as distributions reach and exceed certain threshold levels. See Item 5. "Market for the Registrant's Common Units and Related Unitholder Matters—Cash Distribution Policy."

The chart belowon the next page depicts the current organizationstructure and ownership of the Plains All American Pipeline, L.P. and certain subsidiaries.

5

Partnership the operating partnershipsStructure

| |

| (1) | Based on Form 4 filings for executive officers and directors, 13D filings for Paul G. Allen and Richard Kayne and other information believed to be reliable for the remaining investors, this group, or affiliates of such investors, owns approximately 26 million limited partner units, representing approximately 23.5% of the limited partner interest. |

Acquisitions

The acquisition of assets and

the subsidiaries.

Acquisitionsbusinesses that are strategic and Dispositions

Ancomplementary to our existing operations constitutes an integral component of our business strategy and growth objective is to acquireobjective. Such assets and operationsbusinesses include crude oil related assets, refined products assets and LPG assets, as well as other energy transportation related assets that are strategichave characteristics and complementaryopportunities similar to these business lines and enable us to leverage our existing operations.asset base, knowledge base and skill sets. We have established a target to complete, on average, $200 million to $300 million in acquisitions per year, subject to availability of attractive assets on acceptable terms. SinceBetween 1998 and December 31, 2006, we have completed numerousapproximately 45 acquisitions for an aggregatea cumulative purchase price of approximately $1.3$5.1 billion. In addition, from time to time

6

The following table summarizes acquisitions greater than $50 million that we have

sold assets that are no longer considered essential to our operations. During 2003,completed over the past five years:

| | | | | | | | | |

| | | | | | | Approximate

| |

Acquisition | | Date | | Description | | Purchase Price | |

| | | | | | | (In millions) | |

| |

| Pacific Energy Partners LP | | November 2006 | | Merger of Pacific Energy Partners with and into the Partnership | | $ | 2,456 | |

| Products Pipeline System | | September 2006 | | Three refined products pipeline systems | | $ | 66 | |

| Crude Oil Systems | | July 2006 | | 64.35% interest in theClovelly-to-Meraux Pipeline system; 100% interest in the BayMarchand-to-Ostrica-to-Alliance system and various interests in the High Island Pipeline System (2) | | $ | 130 | |

| Andrews Petroleum and Lone Star Trucking | | April 2006 | | Isomerization, fractionation, marketing and transportation services | | $ | 220 | |

| South Louisiana Gathering and Transportation Assets (SemCrude) | | April 2006 | | Crude oil gathering and transportation assets, including inventory, and related contracts in South Louisiana | | $ | 129 | |

| Investment in Natural Gas Storage Facilities | | September 2005 | | Joint venture with Vulcan Gas Storage LLC to develop and operate natural gas storage facilities. | | $ | 125 | (1) |

| Link Energy LLC | | April 2004 | | The North American crude oil and pipeline operations of Link Energy, LLC (‘‘Link”) | | $ | 332 | |

| Capline and Capwood Pipeline Systems | | March 2004 | | An approximate 22% undivided joint interest in the Capline Pipeline System and an approximate 76% undivided joint interest in the Capwood Pipeline System | | $ | 159 | |

| Shell West Texas Assets | | August 2002 | | Basin Pipeline System, Permian Basin Pipeline System and the Rancho Pipeline System | | $ | 324 | |

| | |

| (1) | | Represents 50% of the purchase price for the acquisition made by our joint venture. The joint venture completed an acquisition for approximately $250 million during 2005. |

|

| (2) | | Our interest in the High Island Pipeline System was relinquished in November 2006. |

Pacific Energy Acquisition

On November 15, 2006 we completed

ten acquisitions for aggregate considerationour acquisition of

approximately $159.5 million. In addition, in December 2003, we signed a definitive agreement with Shell Pipeline CompanyPacific pursuant to

acquire entities owning pipelinean Agreement and

terminal assets for $158 million. Following is a brief descriptionPlan of

this pendingMerger dated June 11, 2006. The merger-related transactions included: (i) the acquisition

acquisitions completed in 2003 that exceeded $15 millionfrom LB Pacific, LP and

major acquisitions and dispositions that have occurred since our initial public offering in November 1998. On December 16, 2003, we entered into a definitive agreement to acquire all of Shell Pipeline Company LP's ("SPLC"its affiliates (“LB Pacific”) interests in two entities. The principal assets of the entities are: (i) an approximate 22% undivided jointgeneral partner interest in the Capline Pipe Line System, and (ii) an approximate 76% undivided joint interest in the Capwood Pipeline System. The Capline Pipeline System is a 667-mile, 40-inch mainline crude oil pipeline originating in St. James, Louisiana, and terminating in Patoka, Illinois. The Capline system is operated by Shell Pipeline Company, LP and is oneincentive distribution rights of the primary transportation routes for crude oil shipped into the Midwestern U.S., accessing over 2.7 million barrels of refining capacity in PADD II, including refineries owned by ConocoPhillips, ExxonMobil, BP, MarathonAshland, CITGO and Premcor. Capline has direct connections to a significant amount of sweet and light sour crude production in the Gulf of Mexico. In addition, with its two active docks capable of handling 600,000-barrel tankersPacific as well as access to LOOP, the Louisiana Offshore Oil Port, the Capline System is a key transporter of sweetapproximately 5.2 million Pacific common units and light sour foreign crude to PADD II. Withapproximately 5.2 million Pacific subordinated units for a total system operating capacity of 1.14$700 million barrels per day, approximately 248,000 barrels per day are subject to the interest being acquired. During 2003, throughput on the interest in the Capline System we are acquiring averaged approximately 125,000 barrels per day.

The Capwood Pipeline System is a 57-mile, 20-inch mainline crude oil pipeline originating in Patoka, Illinois, and terminating in Wood River, Illinois. The Capwood system has an operating capacity of 277,000 barrels per day of crude oil. Of that capacity, approximately 211,000 barrels per day are subject to the interest we are acquiring. The Capwood System has the ability to deliver crude at Wood River to several other PADD II refineries and pipelines, including those owned by Koch and ConocoPhillips. Movements on the Capwood system are driven by the volumes shipped on Capline as well as Canadian crude that can be delivered to Patoka via the Mustang Pipeline. After closing, we anticipate that we will assume the operatorship of the Capwood system from SPLC. During 2003, throughput on the interest being acquired averaged approximately 107,000 barrels per day.

This acquisition is expected to close during the first quarter of 2004. While we believe it is reasonable to expect the acquisition to close in the first quarter of 2004, we can provide no assurance as to when or whether the acquisition will close.

In November 2003, we completed(ii) the acquisition of the South Saskatchewan Pipeline System from South Saskatchewan Pipe Line Company.balance of Pacific’s equity through aunit-for-unit exchange in which each Pacific unitholder (other than LB Pacific) received 0.77 newly issued Partnership common units for each

7

Pacific common unit. The

South Saskatchewan Pipeline System originates approximately 75 miles southwesttotal value of

Swift Current, Saskatchewan, and traverses north and east until it reaches its terminus at Regina, Saskatchewan. The system consists of a 158-mile, 16-inch mainline and

203 miles of gathering lines ranging in diameter from three to twelve inches. In 2002, the system transported approximately 52,000 barrels of crude oil per day. During the period of 2003 that we owned the system, it transported approximately 52,000 barrels of crude oil per day. At Regina, the system can deliver crude oil to the Enbridge Pipeline System, as well as to local markets, and through the Enbridge connection crude can be delivered into our Wascana Pipeline System. Total purchase price for these assetstransaction was approximately $48 million,$2.5 billion, including the assumption of debt and estimated transaction costs.

In October 2003, we completed the acquisition Upon completion of the ArkLaTex Pipeline System from Link Energy (formerly EOTT Energy).merger-related transactions, the general partner and limited partner ownership interests in Pacific were extinguished and Pacific was merged with and into the Partnership. The ArkLaTex Pipeline System consists of 240assets acquired in the Pacific acquisition included approximately 4,500 miles of active crude oil pipeline and gathering systems and mainline550 miles of refined products pipelines, and connects to our Red River Pipeline System near Sabine, Texas. Also included in the transaction were 470,000over 13 million barrels of active crude oil and 9 million barrels of refined products storage capacity, the assignmenta fleet of certainapproximately 75 owned or leased trucks and approximately 1.9 million barrels of Link Energy's crude oil supply contracts and crude oilrefined products linefill and working inventory comprising approximately 108,000 barrels.inventory. The total purchase price for thesePacific assets of approximately $21.3 million included approximately $14.0 million of cash paid to Link Energy forcomplement our existing asset base in California, the pipeline system, approximately $2.9 million of cash paid to Link Energy to purchase crude oil linefillRocky Mountains and working inventory, approximately $3.6 million for estimated near-term capital costs and transaction costs and approximately $0.8 million associatedCanada, with the satisfaction of outstanding claims for accounts receivable and inventory balances.

In June 2003, the Partnership acquired the Iraan to Midland Pipeline System from a unit of Marathon Ashland Petroleum LLC ("MAP") for aggregate consideration of approximately $17.6 million. The Iraan to Midland Pipeline System is a 16-inch, 95-mile mainline crude oil pipeline that originates in Iraan, Texas and terminates in Midland, Texas. At Midland, the system has the ability to deliver crude oil to our Basin Pipeline System and to the Mesa Pipeline System. In 2002, the Iraan to Midland Pipeline System transported approximately 21,000 barrels per day of crude oil.minimal asset overlap but attractive potential vertical integration opportunities. The results of operations and assets of the Iraan to Midland Pipeline Systemand liabilities from this acquisition (the “Pacific acquisition”) have been included in our consolidated financial statements and our pipeline operations since June 30, 2003.November 15, 2006. The aggregate purchase price allocation related to the Pacific acquisition is preliminary and subject to change. See Note 3 to our Consolidated Financial Statements.

Other 2006 Acquisitions

During 2006, we completed six additional acquisitions for aggregate consideration of approximately $565 million. These acquisitions included

$13.6 million(i) 100% of the equity interests of Andrews Petroleum and Lone Star Trucking, which provide isomerization, fractionation, marketing and transportation services to producers and customers of natural gas liquids (collectively, the “Andrews acquisition”), (ii) crude oil gathering and transportation assets and related contracts in

cash, approximately $3.6 million associated with the satisfaction of outstanding claims for accounts receivable and inventory balances, and approximately $0.4 million of estimated transaction costs. In June 2003, we completed(“SemCrude”), (iii) interests in various crude oil pipeline systems in Canada and the acquisition ofU.S. including a package of terminalling and gathering assets from El Paso Corporation for approximately $13.4 million, including transaction costs. These assets are located100% interest in southern Louisiana and includethe Bay Marchand-to-Ostrica-to-Alliance (“BOA”) Pipeline, various interests in five pipelinesthe High Island Pipeline System (“HIPS”), and gathering systems and two terminal facilities. These assets complement our existing activities in south Louisiana and we believe will help leverage our exposure to the growing volume of crude oil and condensate production from the Gulf of Mexico. The results of operations and assets from this acquisition have been included in our consolidated financial statements and in our pipeline operations segment since June 1, 2003. The assets acquired in this acquisition include a 331/3%64.35% interest in Atchafalayathe Clovelly-to-Meraux (“CAM”) Pipeline L.L.C. In December 2003, we acquired the remaining 662/3% interests in 2 separate transactions totaling $4.4 million.

In March 2003, we completed the acquisition of a West Texas crude oil gathering system, from Navajo Refining Company, L.P. for approximately $24.3 million, including transaction costs. The assets are located in the Permian Basin in West Texas and consist of approximately 315 miles of active crude

oil gathering lines. The results of operations and assets from this acquisition have been included in our consolidated financial statements and in our pipeline operations segment since March 1, 2003.

In February 2003, we completed the acquisition of a 347-mile crude oil pipeline from BP Pipelines (North America) Inc. for approximately $19.4 million, including transaction costs. The system originates at Sabine in East Texas and terminates near Cushing, Oklahoma. Subsequent to the acquisition, we connected the pipeline system to our Cushing Terminal. The system also includes approximately 645,000 barrels of crude oil storage capacity. The results of operations and assets from this acquisition have been included in our consolidated financial statements and in our pipeline operations segment since February 1, 2003. This pipeline complements our existing assets in East Texas.

On August 1, 2002, we acquired interests in approximately 2,000 miles of gathering and mainline crude oil pipelines and approximately 8.9 million barrels (net to our interest) of above-ground crude oil terminalling and storage assets in West Texas from Shell Pipeline Company LP and Equilon Enterprises LLC (the "Shell acquisition"). The primary assets included in the transaction are interests in the Basin Pipeline System ("Basin System"), the Permian Basin Gathering System ("Permian Basin System") and the Rancho Pipeline System ("Rancho System"). The total purchase price of $324.4 million consisted of (i) $304.0 million in cash, which was borrowed under our revolving credit facility, (ii) approximately $9.1 million related to the settlement of pre-existing accounts receivable and inventory balances and (iii) approximately $11.3 million of estimated transaction and closing costs.

The acquired assets are primarily fee-based mainline crude oil pipeline transportation assets that gather crude oil in the Permian Basin and transport that crude oil to major market locations in the Mid-Continent and Gulf Coast regions. The acquired assets complement our existing asset infrastructure in West Texas and represent a transportation link to Cushing, Oklahoma, where we provide storage and terminalling services. In addition, we believe that the Basin system is poised to benefit from potential shut-downs of refineries and other pipelines due to the shifting market dynamics in the West Texas area. As was contemplated at the time of the acquisition, the Rancho system was taken out of service in March 2003, pursuant to the terms of its operating agreement. See "—Shutdown and Partial Sale of Rancho Pipeline System."

In early 2000, we articulated to the financial community our intent to establish a strong Canadian operation that complements our operations in the United States. In 2001, after evaluating the marketplace and analyzing potential opportunities, we consummated the two transactions detailed below in 2001. The combination of these assets, an established fee-based pipeline transportation business and a rapidly-growing, entrepreneurial gathering and marketing business, allowed us to optimize both businesses and establish what we believe to be a solid foundation for future growth in Canada.

CANPET Energy Group, Inc. In July 2001, we purchased substantially all of the assets of CANPET Energy Group Inc., a Calgary-based Canadian crude oil and LPG marketing company, for approximately $24.6 million plus $25.0 million for additional inventory owned by CANPET. In December 2003 we recorded an additional $24.3 million related to a portion of the purchase price that had previously been deferred subject to various performance standards of the business acquired. See Note 7 "Partners' Capital and Distributions" in the "Notes to the Consolidated Financial Statements." The principal assets acquired included a crude oil handling facility, a 130,000-barrel tank facility, LPG facilities, existing business relationships and operating inventory.

Murphy Oil Company Ltd. Midstream Operations In May 2001, we completed the acquisition of substantially all of the Canadian crude oil pipeline, gathering, storage and terminalling assets of Murphy Oil Company Ltd. for approximately $161.0 million in cash, including financing and transaction costs. The purchase price included $6.5 million for excess inventory in the systems. The principal assets acquired include (i) approximately 560 miles of crude oil and condensate mainlines (including dual lines on which condensate is shipped for blending purposes and blended crude is shipped in the opposite direction) and associated gathering and lateral lines, (ii) approximately 1.1 million barrels of crude oil storage and terminalling capacity located primarily in Kerrobert, Saskatchewan, (iii) approximately 254,000 barrels of pipeline linefill and tank inventories, and (iv) 121 trailers used primarily for crude oil transportation.

West Texas Gathering System

In July 1999, we completed the acquisition of the West Texas Gathering Systemthree refined products pipeline systems from Chevron Pipe Line Company for approximately $36.0 million, including transaction costs. The assets acquired include approximately 420 miles of crude oil mainlines, approximately 295 miles of associated gathering and lateral lines, and approximately 2.9 million barrels of tankage located along the system.

Scurlock Permian In May 1999, we completed the acquisition of Scurlock Permian LLC ("Scurlock") and certain other pipeline assets from Marathon Ashland Petroleum LLC. Including working capital adjustments and closing and financing costs, the cash purchase price was approximately $141.7 million. Financing for the acquisition was provided through $117.0 million of borrowings under our revolving credit facility and the sale of 1.3 million Class B Common Units to our former general partner for total cash consideration of $25.0 million.

Scurlock, previously a wholly owned subsidiary of Marathon Ashland Petroleum, was engaged in crude oil transportation, gathering and marketing. The assets acquired included approximately 2,300 miles of active pipelines, numerous storage terminals and a fleet of trucks. The largest asset consists of an approximately 920-mile pipeline and gathering system located in the Spraberry Trend in West Texas that extends into Andrews, Glasscock, Martin, Midland, Regan and Upton Counties, Texas. The assets we acquired also included approximately one million barrels of crude oil linefill.

Consistent with our business strategy, we are continuously engaged in discussions with potential sellers regarding the possible purchase by us of

midstreamassets and operations that are strategic and complementary to our existing operations. Such assets and operations include crude oil

related assets, refined products assets, LPG assets and, through our interest in PAA/Vulcan, natural gas storage assets.

In addition, we have in the past and intend in the future to evaluate and pursue other energy related assets that have characteristics and opportunities similar to these business lines and enable us to leverage our asset base, knowledge base and skill sets. Such acquisition efforts

may involve participation by us in processes that have been made public

and involve a number of potential buyers,

and are commonly referred to as

"auction"“auction” processes, as well as situations

wherein which we believe we are the only party or one of a

very limited number of potential buyers in negotiations with the potential seller. These acquisition efforts often involve assets which, if acquired,

wouldcould have a material effect on our financial condition and results of operations.

We

Crude Oil Market Overview

Our assets and our business strategy are

currently involved in advanced discussions with a potential seller regarding the purchasedesigned to service our producer and refiner customers by

us ofaddressing regional crude oil

pipeline, terminalling, storagesupply and

gathering and marketing assets for an aggregate purchase price, including assumed liabilities and obligations, ranging from $300 million to $400 million. Such transaction is subject to confirmatory due diligence, negotiation of a mutually acceptable definitive purchase and sale agreement, regulatory approval and approval of both our board of directors anddemand imbalances that

of the seller. In connection with our acquisition activities, we routinely incur third party costs, which are capitalized and deferred pending final outcome of the transaction. Deferred costs associated with successful transactions are capitalized as part of the transaction, while deferred costs associated with

unsuccessful transactions are expensed at the time of such final determination. We had a total of approximately $0.4 million in deferred costs at December 31, 2003. We estimate that our deferred acquisition costs will increaseexist in the first quarter of 2004 byUnited States and Canada. According to the Energy Information Administration (“EIA”), during the twelve months ended October 2006, the United States consumed approximately $0.7 million. We can give no assurance that our current or future acquisition efforts will be successful or that any such acquisition will be completed on terms considered favorable to us.

We acquired the Rancho Pipeline System in conjunction with the Shell acquisition. The Rancho Pipeline System Agreement dated November 1, 1951, pursuant to which the system was constructed and operated, terminated in March 2003. Upon termination, the agreement required the owners to take the pipeline system, in which we owned an approximate 50% interest, out of service. Accordingly, we notified our shippers and did not accept nominations for movements after February 28, 2003. This shutdown was contemplated at the time of the acquisition and was accounted for under purchase accounting in accordance with SFAS No. 141 "Business Combinations." The pipeline was shut down on March 1, 2003 and a purge of the crude oil linefill was completed in April 2003. In June 2003, we completed transactions whereby we transferred all of our ownership interest in approximately 240 miles of the total 458 miles of the pipeline in exchange for $4.0 million and approximately 500,000 barrels of crude oil tankage in West Texas. The remaining portion will either be sold or salvaged. No gain or loss has been recorded on the shutdown of the Rancho System or these transactions.

In March 2000, we sold the segment of the All American Pipeline that extends from Emidio, California to McCamey, Texas to a unit of El Paso Corporation for $129.0 million. Except for minor third party volumes, one of our subsidiaries, Plains Marketing, L.P., was the sole shipper on this segment of the pipeline since its predecessor acquired the line from the Goodyear Tire & Rubber Company in July 1998. We realized net proceeds of approximately $124.0 million after the associated transaction costs and estimated costs to remove equipment. We used the proceeds from the sale to reduce outstanding debt. We recognized a gain of approximately $20.1 million in connection with the sale.

We had suspended shipments of crude oil on this segment of the pipeline in November 1999. At that time, we owned approximately 5.215.2 million barrels of crude oil inper day, while only producing 5.1 million barrels per day. Accordingly, the segmentUnited States relies on foreign imports for nearly 66% of the pipeline. We soldcrude oil used by U.S. domestic refineries. This imbalance represents a continuing trend. Foreign imports of crude oil into the U.S. have tripled over the last 21 years, increasing from 3.2 million barrels per day in 1985 to 10.2 million barrels per day for the 12 months ended October 2006, as U.S. refinery demand has increased and domestic crude oil production has declined due to natural depletion.

The Department of Energy segregates the United States into five Petroleum Administration Defense Districts (“PADDs”) which are used by the energy industry for reporting statistics regarding crude oil supply and demand. The table below sets forth supply, demand and shortfall information for each PADD for the twelve months ended October 2006 and is derived from information published by the EIA (see EIA website at www.eia.doe.gov).

8

| | | | | | | | | | | | | |

| | | Regional

| | | Refinery

| | | Supply

| |

Petroleum Administration Defense District | | Supply | | | Demand | | | Shortfall | |

| | | (Millions of barrels per day) | |

| |

| PADD I (East Coast) | | | 0.0 | | | | 1.5 | | | | (1.5 | ) |

| PADD II (Midwest) | | | 0.5 | | | | 3.3 | | | | (2.8 | ) |

| PADD III (South) | | | 2.8 | | | | 7.2 | | | | (4.4 | ) |

| PADD IV (Rockies) | | | 0.3 | | | | 0.5 | | | | (0.2 | ) |

| PADD V (West Coast) | | | 1.5 | | | | 2.7 | | | | (1.2 | ) |

| | | | | | | | | | | | | |

Total U.S. | | | 5.1 | | | | 15.2 | | | | (10.1 | ) |

Although PADD III has the largest supply shortfall, PADD II is believed to be the most critical region with respect to supply and transportation logistics because it is the largest, most highly populated area of the U.S. that does not have direct access to oceanborne cargoes.

Over the last 21 years, crude oil production in PADD II has declined from approximately 1.0 million barrels per day to approximately 450,000 barrels per day. Over this same time period, refinery demand has increased from approximately 2.7 million barrels per day in 1985 to 3.3 million barrels per day for the twelve months ended October 2006. As a result, the volume of crude oil transported into PADD II has increased 71%, from 1.7 million barrels per day to 2.9 million barrels per day. This aggregate shortfall is principally supplied by direct imports from Canada to the north and from the Gulf Coast area and the Cushing Interchange to the south.

The logistical transportation, terminalling and storage challenges associated with regional volumetric supply and demand imbalances are further complicated by the fact that crude oil from November 1999different sources is not fungible. The crude slate available to February 2000U.S. refineries consists of a substantial number of different grades and varieties of crude oil. Each crude grade has distinguishing physical properties, such as specific gravity (generally referred to as light or heavy), sulfur content (generally referred to as sweet or sour) and metals content as well as varying economic attributes. In many cases, these factors result in the need for net proceedssuch grades to be batched or segregated in the transportation and storage processes, blended to precise specifications or adjusted in value. In addition, from time to time, natural disasters and geopolitical factors, such as hurricanes, earthquakes, tsunamis, inclement weather, labor strikes, refinery disruptions, embargoes and armed conflicts, may impact supply, demand and transportation and storage logistics.

Refined Products Market Overview

Once crude oil is transported to a refinery, it is broken down into different petroleum products. These “refined products” fall into three major categories: fuels such as motor gasoline and distillate fuel oil (diesel fuel); finished non-fuel products such as solvents and lubricating oils; and feedstocks for the petrochemical industry such as naphtha and various refinery gases. Demand is greatest for products in the fuels category, particularly motor gasoline.

The characteristics of the gasoline produced depend upon the setup of the refinery at which it is produced and the type of crude oil that is used. Gasoline characteristics are also impacted by other ingredients that may be blended into it, such as ethanol. The performance of the gasoline must meet industry standards and environmental regulations that vary based on location.

After crude oil is refined into gasoline and other petroleum products, the products must be distributed to consumers. The majority of products are shipped by pipeline to storage terminals near consuming areas, and then loaded into trucks for delivery to gasoline stations or other end users. Some of the products which are used as feedstocks are typically transported by pipeline to chemical plants.

Demand for refined products is increasing and is affected by price levels, economic growth trends and, to a lesser extent, weather conditions. According to the EIA, consumption of refined products in the United States has risen steadily from approximately $100.015.7 million barrels per day in 1985 to approximately 20.7 million barrels per day for the twelve months ended October 2006, an increase of 31%. By 2030, the EIA estimates that the U.S. will consume approximately 27.6 million barrels per day of refined products, an increase of 33% over the last twelve

9

months’ levels. We believe that the additional demand will be met by growth in the capacity of existing refineries through large expansion projects and “capacity creep” as well as increased imports of refined products, both of which werewe believe will generate incremental demand for midstream infrastructure, such as pipelines and terminals.

We believe that demand for refined products pipeline and terminalling infrastructure will also increase as a result of:

| | |

| • | multiple specifications of existing products (also referred to as boutique gasoline blends); |

|

| • | specification changes to existing products, such as ultra low sulfur diesel; |

|

| • | new products, such as bio-fuels; |

|

| • | the aging of existing infrastructure; and |

|

| • | the potential reduction in storage capacity due to regulations governing the inspection, repair, alteration and construction of storage tanks. |

We intend to grow our asset base in the refined products business through expansion projects and future acquisitions. Consistent with our plan to apply our proven business model to these assets, we also intend to optimize the value of our refined products assets and better serve the needs of our customers by building a complementary refined products supply and marketing business.

LPG Products Market Overview

LPGs are a group ofhydrogen-based gases that are derived from crude oil refining and natural gas processing. They include ethane, propane, normal butane, isobutane and other related products. For transportation purposes, these gases are liquefied through pressurization. LPG is also imported into the U.S. from Canada and other parts of the world.

LPGs are principally used as feedstock for petrochemical production processes. Individual LPG products have specific uses. For example, propane is used for working capital purposes.home heating, water heating, cooking, crop drying and tobacco curing. As a motor fuel, propane is burned in internal combustion engines that power over-the-road vehicles, forklifts and stationary engines. Ethane is used primarily as a petrochemical feedstock. Normal butane is used as a petrochemical feedstock, as a blend stock for motor gasoline, and to derive isobutane through isomerization. Isobutane is principally used in refinery alkylation to enhance the octane content of motor gasoline or in the production of isooctane or other octane additives. Certain LPGs are also used as diluent in the transportation of heavy oil, particularly in Canada.

According to the EIA, consumption of LPGs in the United States has risen steadily from approximately 1.6 million barrels per day in 1985 to approximately 2.1 million barrels per day for the twelve months ended October 2006, an increase of 33%. By 2030, the EIA estimates that the U.S. will consume approximately 2.4 million barrels per day of LPGs, an increase of 13% over the last twelve months’ levels. We recognizedbelieve that the additional demand will result in an aggregate gainincreased demand for LPG infrastructure, including pipelines, storage facilities, processing facilities and import terminals.

We intend to grow our asset base in the LPG business through expansion projects and future acquisitions. We believe that our asset base, which is principally located in the upper tier of the U.S., Oklahoma and California, provides flexibility in meeting the needs of our customers and opportunities to capitalize on regional supply/demand imbalances in LPG markets.

Natural Gas Storage Market Overview

After treatment for impurities such as carbon dioxide and hydrogen sulfide and processing to separate heavier hydrocarbons from the gas stream, natural gas from one source generally is fungible with natural gas from any other source. Because of its fungibility and physical volatility and the fact that it is transported in a gaseous state, natural gas presents different logistical transportation challenges than crude oil and refined products; however, we believe the U.S. natural gas supply and demand situation will ultimately face storage challenges very similar to those that exist in the North American crude oil sector. We believe these factors will result in an increased need and an

10

attractive valuation for natural gas storage facilities in order to balance market demands. From 1990 to 2005, domestic natural gas production grew approximately $44.6 million,2% while domestic natural gas consumption rose approximately 15%, resulting in an approximate 175% increase in the domestic supply shortfall over that time period. In addition, significant excess domestic production capacity contractually withheld from the market bytake-or-pay contracts between natural gas producers and purchasers in the late 1980s and early 1990s has since been eliminated. This trend of an increasing domestic supply shortfall is expected to continue. By 2030, the EIA estimates that the U.S. will require approximately 5.5 trillion cubic feet of annual net natural gas imports (or approximately 15 billion cubic feet per day) to meet its demand, nearly 1.4 times the 2005 annual shortfall.

The vast majority of the projected supply shortfall is expected to be met with imports of liquefied natural gas (LNG). According to the Federal Energy Regulatory Commission (“FERC”) as of January 2007, plans for 34 new LNG terminals in the United States and Bahamas have been proposed, 17 of which approximately $28.1 million was recognizedare to be situated along the Gulf Coast. Of the 17 proposed Gulf Coast facilities, three are under construction, nine have been approved by the appropriate regulatory agencies, and five have been proposed to the appropriate regulatory agencies. These facilities will be used to re-gasify the LNG prior to shipment in 2000pipelines to natural gas markets.

Normal depletion of regional natural gas supplies will require additional storage capacity to pre-position natural gas supplies for seasonal usage. In addition, we believe that the growth of LNG as a supply source will also increase the demand for natural gas storage as a result of inconsistent surges and shortfalls in

connectionsupply based on LNG tanker deliveries, similar in many respects to the issues associated with