[X]ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

| ☒ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

[ ]

| ☐ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| For the transition period from ________________ to ________________ |

For the transition period from ________________to ________________

Commission file number:001-33706

Nevada | 98-0399476 | |

| (State or other jurisdiction of incorporation of organization) | (I.R.S. Employer Identification No.) |

500 North Shoreline, Ste. 800, Corpus Christi, Texas, U.S.A. | 78401 | |

| (U.S. corporate headquarters) | (Zip Code) |

1111 West Hastings Street, Suite 320, Vancouver, British Columbia, Canada V6E 2J31830 – 1188 West Georgia Street

Vancouver, British Columbia, CanadaV6E 4A2(Canadian corporate headquarters) (Zip Code) (Address of principal executive offices)(604) 682-9775(Registrant's telephone number, including area code)(361) 888-8235(Registrant’s telephone number, includingarea code)Securities registered pursuant to Section 12(b) of the Act:Title of each class: Trading Symbol(s) Name of each exchange on which registered: Common Stock Par Value $0.001 per shareUECNYSE MKT Equities ExchangeAmerican

Yes [ ]☒ No [X]

☐

Yes [ ]☐ No [X]

☒

Yes [X]☒ No [ ]

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of the registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. [ ]

☐

| ☐ Non-accelerated filer | ☐ Smaller reporting company | ||

| ☐ Emerging growth company | |||

Yes [ ]☐ No [X]

☒

$1,479,408,555.

__________

Explanatory Note:

September 28, 2023.

For the conveniencestaff (the “Staff”) of the reader, this Form 10-K/A sets forthSEC in connection with the Company’s annual report in its entirety, not just those portions that have been amended since the filing of the Original Report. Other than the amendments noted above, none of the disclosure contained in any other ItemStaff’s review of the Original Report, has been amended, updated or otherwise revised. Furthermore, noneincluding the Staff’s review of the Items, including the amendments as noted above, have been amended, updated or otherwise revised to reflect material subsequent events occurring after the filing date ofproperty disclosure requirements for registrants engaged in mining operations and reflected in the Original Report on October 15, 2012.

Pursuant to the requirements of the SEC, Report.

ii

FORWARD-LOOKING STATEMENTS

This annual report contains forward-looking statements

Country | State/Province | Project | Location (Latitude) | Location (Longitude) | Equity Interest | Operator | Stage | Mining Method | Mineralization Style |

| Allemand-Ross | 43.3101 | -105.7787 | 100% | UEC | Exploration Stage | ISR | Roll-Front | ||

| Antelope | 42.2263 | -107.9095 | 100% | UEC | Exploration Stage | ISR | Roll-Front | ||

| Barge | 43.2729 | -105.5905 | 100% | UEC | Exploration Stage | ISR | Roll-Front | ||

| Black Hills | 44.7764 | -104.8831 | 100% | UEC | Exploration Stage | ISR | Roll-Front | ||

| Brown Ranch | 43.7377 | -105.9684 | 100% | UEC | Exploration Stage | ISR | Roll-Front | ||

| Bull Springs | 42.1584 | -107.6305 | 100% | UEC | Exploration Stage | ISR | Roll-Front | ||

| Central Shirley Basin | 42.3378 | -106.4100 | 100% | UEC | Exploration Stage | ISR | Roll-Front | ||

| Charlie | 43.8274 | -106.0594 | 100% | UEC | Exploration Stage | ISR | Roll-Front | ||

| Christensen Ranch | 43.7982 | -106.0235 | 100% | UEC | Exploration Stage | ISR | Roll-Front | ||

| Clarkson Hills | 42.6593 | -106.7006 | 100% | UEC | Exploration Stage | ISR | Roll-Front | ||

| Crooks Creek | 42.2867 | -107.7660 | 100% | UEC | Exploration Stage | ISR | Roll-Front | ||

| Crook's Mountain | 42.3840 | -107.9060 | 100% | UEC | Exploration Stage | ISR | Roll-Front | ||

| Crossroads | 43.0040 | -105.6364 | 100% | UEC | Exploration Stage | ISR | Roll-Front | ||

| Cyclone Rim | 42.2943 | -108.3332 | 100% | UEC | Exploration Stage | ISR | Roll-Front | ||

| East Shirley Basin | 42.3192 | -106.1616 | 100% | UEC | Exploration Stage | ISR | Roll-Front | ||

| Gas Hills | 42.7094 | -107.6521 | 100% | UEC | Exploration Stage | ISR | Roll-Front | ||

| United States | Wyoming | Horse Creek | 42.5957 | -106.9867 | 100% | UEC | Exploration Stage | ISR | Roll-Front |

| Irigaray | 43.8683 | -106.1186 | 100% | UEC | Exploration Stage | ISR | Roll-Front | ||

| Jab/West Jab | 42.2209/42.2611 | -108.0439/ -108.1225 | 100% | UEC | Exploration Stage | ISR | Roll-Front | ||

| Ludeman | 42.9119 | -105.6277 | 100% | UEC | Exploration Stage | ISR | Roll-Front | ||

| Moore Ranch | 43.5652 | -105.8480 | 100% | UEC | Exploration Stage | ISR | Roll-Front | ||

| Mule Creek | 42.2118 | -105.8143 | 100% | UEC | Exploration Stage | ISR | Roll-Front | ||

| Niles Ranch | 43.8024 | -105.7961 | 100% | UEC | Exploration Stage | ISR | Roll-Front | ||

| Nine Mile Lake | 42.9807 | -106.3278 | 100% | UEC | Exploration Stage | ISR | Roll-Front | ||

| Pine Ridge | 43.4591 | -106.0725 | 100% | UEC | Exploration Stage | ISR | Roll-Front | ||

| Pine Tree U1 | 43.6173 | -105.7860 | 100% | UEC | Exploration Stage | ISR | Roll-Front | ||

| Pumpkin Creek | 43.8163 | -105.8955 | 100% | UEC | Exploration Stage | ISR | Roll-Front | ||

| Red Rim | 41.6502 | -107.5755 | 100% | UEC | Exploration Stage | ISR | Roll-Front | ||

| Reno Creek | 43.6796 | -105.7226 | 100% | UEC | Exploration Stage | ISR | Roll-Front | ||

| Ross Flats | 43.5224 | -105.8861 | 100% | UEC | Exploration Stage | ISR | Roll-Front | ||

| Sand Creek | 42.7007 | -105.2645 | 100% | UEC | Exploration Stage | ISR | Roll-Front | ||

| South Pine Ridge | 43.1204 | -105.9251 | 100% | UEC | Exploration Stage | ISR | Roll-Front | ||

| South Reno Creek | 43.6440 | -105.6199 | 100% | UEC | Exploration Stage | ISR | Roll-Front |

Country | State/Province | Project | Location (Latitude) | Location (Longitude) | Equity Interest | Operator | Stage | Mining Method | Mineralization Style |

Uranium Projects | |||||||||

| South Sweetwater | 41.9694 | -107.9820 | 100% | UEC | Exploration Stage | ISR | Roll-Front | ||

| Stewart Creek | 43.3124 | -105.7342 | 100% | UEC | Exploration Stage | ISR | Roll-Front | ||

| Taylor Ranch | 43.5578 | -106.0098 | 100% | UEC | Exploration Stage | ISR | Roll-Front | ||

| Twin Buttes | 42.2316 | -107.7205 | 100% | UEC | Exploration Stage | ISR | Roll-Front | ||

| West Beaver Rim | 42.5967 | -108.1568 | 100% | UEC | Exploration Stage | ISR | Roll-Front | ||

| West Crook's Creek | 42.2984 | -107.8603 | 100% | UEC | Exploration Stage | ISR | Roll-Front | ||

| West Sweetwater | 42.1318 | -108.0931 | 100% | UEC | Exploration Stage | ISR | Roll-Front | ||

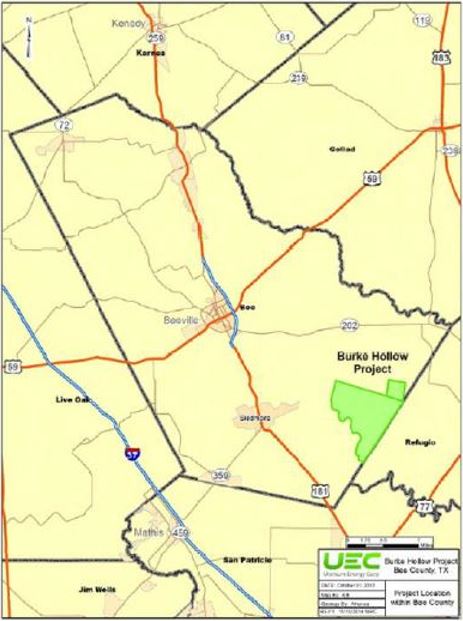

| Burke Hollow | 27.6756 | -97.5176 | 100% | UEC | Exploration Stage | ISR | Roll-Front | ||

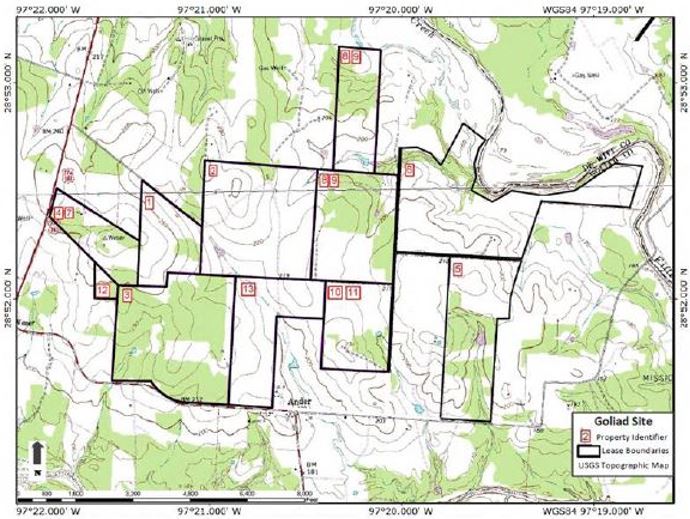

| Goliad | 28.8686 | -97.3433 | 100% | UEC | Exploration Stage | ISR | Roll-Front | ||

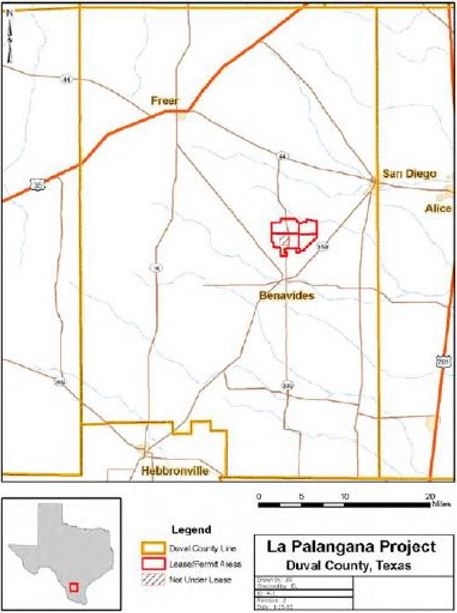

| Texas | La Palangana | 28.2638 | -98.3959 | 100% | UEC | Exploration Stage | ISR | Roll-Front | |

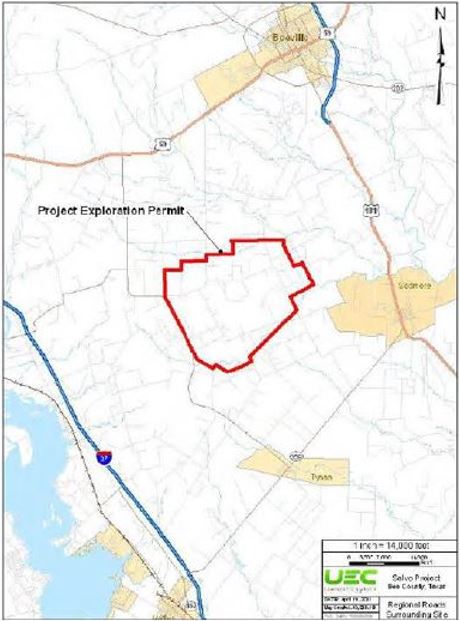

| Salvo | 28.2632 | -97.7889 | 100% | UEC | Exploration Stage | ISR | Roll-Front | ||

| Longhorn | 28.1700 | -98.1200 | 100% | UEC | Exploration Stage | ISR | Roll-Front | ||

| Anderson | 34.1829 | -113.1632 | 100% | UEC | Exploration Stage | Conventional | Tabular | ||

| Arizona | Los Cuatros | 33.548 | -112.322 | 100% | UEC | Exploration Stage | Conventional | Tabular | |

| Workman Creek | 33.50 | -110.57 | 100% | UEC | Exploration Stage | Conventional | Tabular | ||

| New Mexico | C de Baca | 34.18 | -107.15 | 100% | UEC | Exploration Stage | Conventional | Tabular | |

| Dalton Pass | 35.40 | -108.14 | 100% | UEC | Exploration Stage | Conventional | Tabular | ||

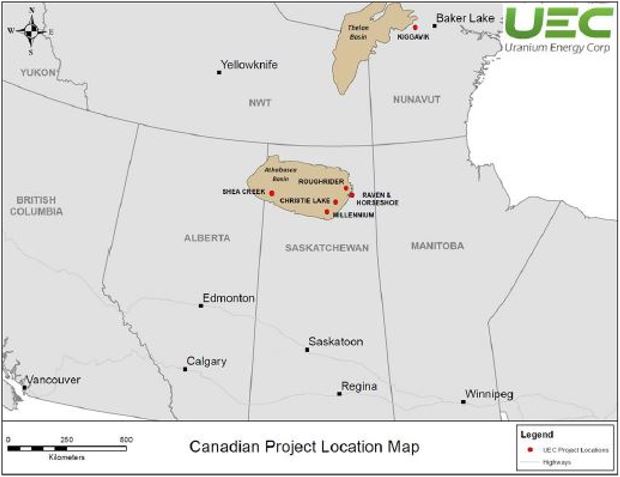

| Alexandra | 58.023 | -109.789 | 21.05% | Orano Canada Inc. | Exploration Stage | Conventional | Unconformity Related | ||

| Axis Lake | 59.304 | -106.136 | 100.00% | UEC | Exploration Stage | Conventional | Unconformity Related | ||

| Beatty River | 57.897 | -109.542 | 32.76% | Orano Canada Inc. | Exploration Stage | Conventional | Unconformity Related | ||

| Black Lake | 59.1167 | -105.905 | 51.43% | UEC | Exploration Stage | Conventional | Unconformity Related | ||

| Brander Lake | 58.2895 | -109.888 | 49.10% | Orano Canada Inc. | Exploration Stage | Conventional | Unconformity Related | ||

| Candle Lake | 57.9969 | -104.93 | 12.50% | Denison Mines Corp. | Exploration Stage | Conventional | Unconformity Related | ||

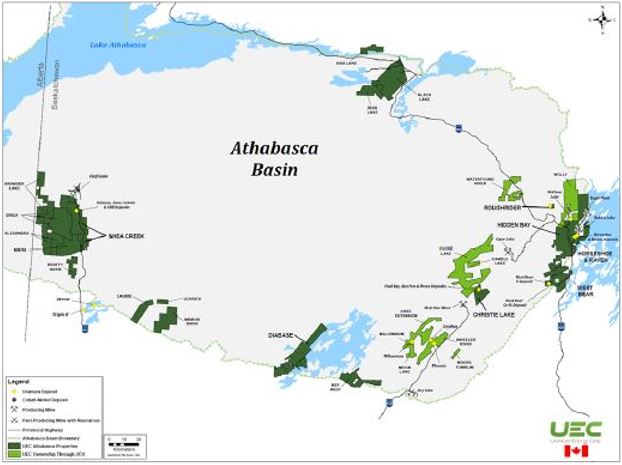

| Christie Lake | 57.8128 | -104.86 | 82.77% | UEC | Exploration Stage | Conventional | Unconformity Related | ||

| Close Lake | 57.9729 | -105.082 | 5.16% | Orano Canada Inc. | Exploration Stage | Conventional | Unconformity Related | ||

| Canada | Saskatchewan | Cree Extension | 57.5881 | -105.551 | 15.05% | Cameco Corporation | Exploration Stage | Conventional | Unconformity Related |

Diabase Peninsula | 57.4294 | -106.913 | 100.00% | UEC | Exploration Stage | Conventional | Unconformity Related | ||

| Erica | 58.1465 | -109.731 | 49.10% | Orano Canada Inc. | Exploration Stage | Conventional | Unconformity Related | ||

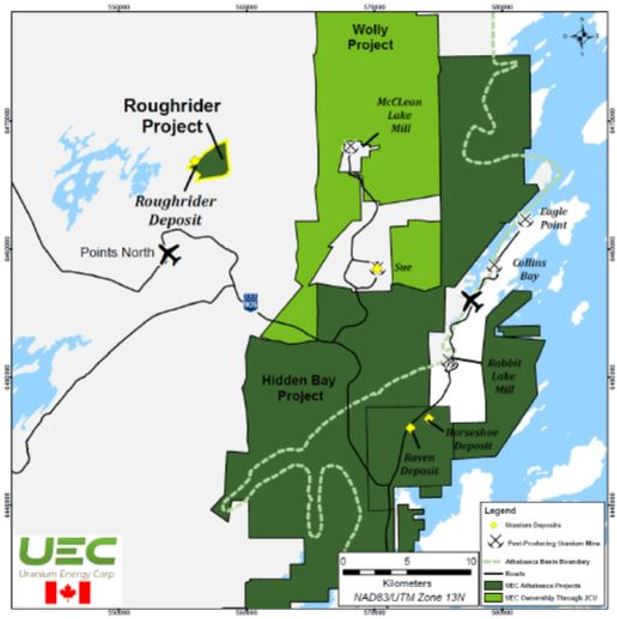

| Hidden Bay | 58.157 | -103.88 | 100.00% | UEC | Exploration Stage | Conventional | Unconformity Related | ||

| Horseshoe-Raven | 58.1331 | -103.76 | 100.00% | UEC | Exploration Stage | Conventional | Unconformity Related | ||

| Key West | 57.2731 | -106.217 | 100.00% | UEC | Exploration Stage | Conventional | Unconformity Related | ||

| Laurie | 57.6579 | -108.721 | 32.99% | Orano Canada Inc. | Exploration Stage | Conventional | Unconformity Related | ||

| Millennium | 57.5138 | -105.639 | 15.05% | Cameco Corporation | Exploration Stage | Conventional | Unconformity Related | ||

| Mirror River | 57.6078 | -108.423 | 32.34% | Orano Canada Inc. | Exploration Stage | Conventional | Unconformity Related | ||

| Moon Lake | 57.4669 | -105.634 | 10.07% | Orano Canada Inc. | Exploration Stage | Conventional | Unconformity Related | ||

| Moore Tomblin | 57.4512 | -105.135 | 6.80% | Orano Canada Inc. | Exploration Stage | Conventional | Unconformity Related | ||

| Nikita | 58.0107 | -109.574 | 12.72% | Orano Canada Inc. | Exploration Stage | Conventional | Unconformity Related | ||

Country | State/Province | Project | Location (Latitude) | Location (Longitude) | Equity Interest | Operator | Stage | Mining Method | Mineralization Style |

Uranium Projects | |||||||||

| Riou Lake | 59.0491 | -106.156 | 100.00% | UEC | Exploration Stage | Conventional | Unconformity Related | ||

| Roughrider | 58.3374 | -104.021 | 100.00% | UEC | Exploration Stage | Conventional | Unconformity Related | ||

| Shea Creek | 58.1804 | -109.49 | 49.10% | Orano Canada Inc. | Exploration Stage | Conventional | Unconformity Related | ||

| Uchrich | 57.7196 | -108.483 | 30.48% | Orano Canada Inc. | Exploration Stage | Conventional | Unconformity Related | ||

Waterfound River | 58.4588 | -104.548 | 12.90% | Orano Canada Inc. | Exploration Stage | Conventional | Unconformity Related | ||

| West Bear | 57.8744 | -103.975 | 100.00% | UEC | Exploration Stage | Conventional | Unconformity Related | ||

| Wheeler River | 57.5000 | -105.421 | 5.00% | Denison Mines Corp. | Development | Conventional | Unconformity Related | ||

| Wolly | 58.3927 | -103.799 | 6.38% | Orano Canada Inc. | Exploration Stage | Conventional | Unconformity Related | ||

| Nunavut | Kiggavik | 64.3752 | -97.7685 | 16.91% | Orano Canada Inc. | Exploration Stage | Conventional | Unconformity Related | |

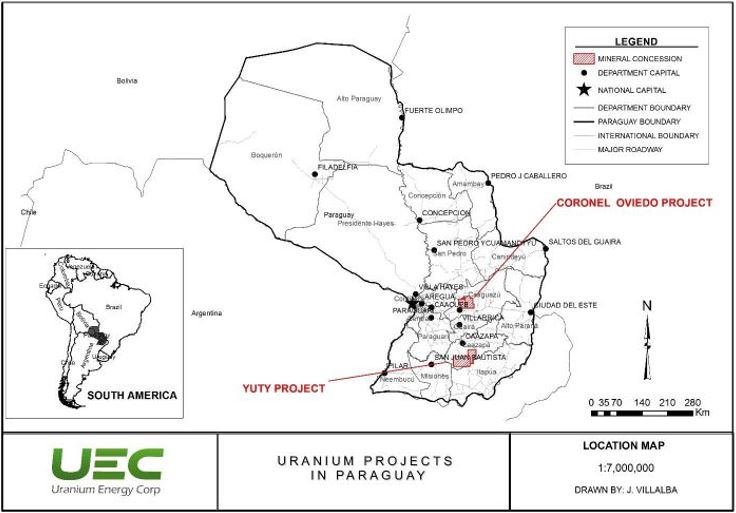

| Paraguay | Yuty | 25.2702 | 56.3125 | 100.00% | UEC | Exploration Stage | ISR | Roll-Front | |

| Oviedo | 25.2702 | 56.2828 | 100.00% | UEC | Exploration Stage | ISR | Roll-Front | ||

Titanium Projects | |||||||||

| Paraguay | Alto Parana | 24.8147 | 54.9083 | 100.00% | UEC | Exploration Stage | Conventional | Surficial | |

Acres | Hectares | State Leases | Fee Mineral Leases | Federal Lode Mining Claims | Provincial Mineral Dispositions | Provincial Mining Leases | |||||||||||||

Country | State/Province | Project | Total | Total | Number | Acres | Expiration Date | Number | Acres | Expiration Date | Number | Acres | Expiration Date | Number | Hectares | Expiration Date | Number | Hectares | Expiration Date |

Uranium Projects | |||||||||||||||||||

| Allemand-Ross | 13,331.72 | 5,395.16 | 3 | 958 | Annual | 7 | 3,333.72 | July 2025 - Feb 2029 (variable | 452 | 9,040 | Annual | ||||||||

| Antelope | 13,220 | 5,349.94 | 1 | 640 | Annual | 629 | 12,580 | Annual | |||||||||||

| Barge | 7,480 | 3,027.05 | 1 | 640 | Annual | 342 | 6,840 | Annual | |||||||||||

| Black Hills | 1,280 | 518.00 | 1 | 640 | Annual | 32 | 640 | Annual | |||||||||||

| Brown Ranch | 3,640 | 1,473.06 | 1 | 640 | Annual | 150 | 3,000 | Annual | |||||||||||

| Bull Springs | 5,702.8 | 2,307.84 | 2 | 1,922.8 | Annual | 189 | 3,780 | Annual | |||||||||||

| Central Shirley Basin | 2,380 | 963.15 | 2 | 760 | Annual | 81 | 1,620 | Annual | |||||||||||

| Charlie | 820 | 331.84 | 1 | 720 | Annual | 5 | 100 | Annual | |||||||||||

| United States | Wyoming | Christensen Ranch | 11,140 | 4,508.20 | 1 | 1,280 | Annual | 1 | 720 | Annual | 358 | 9,140 | Annual | ||||||

| Clarkson Hills | 400 | 161.87 | 20 | 400 | Annual | ||||||||||||||

| Crooks Creek | 6,979.25 | 2,824.40 | 6 | 2,599.25 | Annual | 219 | 4,380 | Annual | |||||||||||

| Crook's Mountain | 2,480 | 1,003.62 | 2 | 1,280 | Annual | 60 | 1,200 | Annual | |||||||||||

| Crossroads | 5,680 | 2,298.61 | 2 | 1,280 | Annual | 220 | 4,400 | Annual | |||||||||||

| Cyclone Rim | 4,280 | 1,732.06 | 0 | 0 | 214 | 4,280 | Annual | ||||||||||||

| East Shirley Basin | 4,599.90 | 1,861.51 | 4 | 2,099.9 | Annual | 125 | 2,500 | Annual | |||||||||||

| Gas Hills | 6,114.76 | 2,474.56 | 5 | 3,394.76 | Annual | 136 | 2,720 | Annual | |||||||||||

| Acres | Hectares | State Leases | Fee Mineral Leases | Federal Lode Mining Claims | Provincial Mineral Dispositions | Provincial Mining Leases | |||||||||||||

Country | State/Province | Project | Total | Total | Number | Acres | Expiration Date | Number | Acres | Expiration Date | Number | Acres | Expiration Date | Number | Hectares | Expiration Date | Number | Hectares | Expiration Date |

| Horse Creek | 540 | 218.53 | 27 | 540 | Annual | ||||||||||||||

| Irigaray | 2,320 | 938.87 | 2 | 480 | Annual | 92 | 1,840 | Annual | |||||||||||

| Jab/West Jab | 5,300 | 2,144.83 | 3 | 960 | Annual | 217 | 4,340 | Annual | |||||||||||

| Ludeman | 18,101.89 | 7,325.57 | 4 | 1,440 | Annual | 2 | 1,741.89 | Sept. 2026 and Jan. 2029 | 746 | 14,920 | Annual | ||||||||

| Moore Ranch | 4,180 | 1,691.59 | 3 | 1,280 | Annual | 4 | 1,180 | Aug. 2025 through Mar. 2027 (variable) | 86 | 1,720 | Annual | ||||||||

| Mule Creek | 260 | 105.22 | 13 | 260 | Annual | ||||||||||||||

| Niles Ranch | 3,560 | 1,440.68 | 6 | 2,560 | Annual | 50 | 1,000 | Annual | |||||||||||

| Nine Mile Lake | 2,620 | 1,060.28 | 3 | 1,280 | Annual | 67 | 1,340 | Annual | |||||||||||

| Pine Ridge | 3,780 | 1,529.71 | 2 | 720 | Annual | 153 | 3,060 | Annual | |||||||||||

| Pine Tree U1 | 1,540 | 623.22 | 1 | 80 | Annual | 73 | 1,460 | Annual | |||||||||||

| Pumpkin Creek | 1,000 | 404.69 | 50 | 1,000 | Annual | ||||||||||||||

| Red Rim | 680 | 275.19 | 34 | 680 | Annual | ||||||||||||||

| Reno Creek | 18,763 | 7,593.12 | 4 | 3,200 | Annual | 36 | 4,583 | Variable | 549 | 10,980 | Annual | ||||||||

| Ross Flats | 5,480 | 2,217.68 | 3 | 1,040 | Annual | 3 | 1,680 | Mar. 2027 | 138 | 2,760 | Annual | ||||||||

| Sand Creek | 3,000 | 1,214.06 | 3 | 1,920 | Annual | 54 | 1,080 | Annual | |||||||||||

| South Pine Ridge | 4,020 | 1,626.84 | 5 | 2,360 | Annual | 83 | 1,660 | Annual | |||||||||||

| South Reno Creek | 2,580 | 1,044.09 | 1 | 80 | Annual | 125 | 2,500 | Annual | |||||||||||

| South Sweetwater | 1,120 | 453.25 | 1 | 640 | Annual | 24 | 480 | Annual | |||||||||||

| Stewart Creek | 2,460 | 995.53 | 1 | 640 | Annual | 91 | 1,820 | Annual | |||||||||||

| Taylor Ranch | 3,940 | 1,594.46 | 7 | 2,880 | Annual | 53 | 1,060 | Annual | |||||||||||

| Twin Buttes | 7,740 | 3,132.27 | 3 | 1,600 | Annual | 307 | 6,140 | Annual | |||||||||||

| West Beaver Rim | 1,900 | 768.90 | 1 | 640 | Annual | 63 | 1,260 | Annual | |||||||||||

| West Crook's Creek | 1,520 | 615.12 | 1 | 640 | Annual | 44 | 880 | Annual | |||||||||||

| West Sweetwater | 1,080 | 437.06 | 54 | 1,080 | Annual | ||||||||||||||

| Burke Hollow | 17,511 | 7,086 | 1 | 17,511 | 2032 | ||||||||||||||

| Goliad | 636 | 257 | 7 | 636 | 2024 & 2025 | ||||||||||||||

| Texas | Palangana | 6,969 | 2,820 | 12 | 6,969 | 2025 thru 2032 | |||||||||||||

| Salvo | 800 | 324 | 2 | 800 | 2026 & 2027 | ||||||||||||||

| Longhorn | 594 | 240 | 40 | 594 | 2027 thru 2028 | ||||||||||||||

| Arizona | Anderson | 8,268 | 3,346 | 1 | 640 | 2024 | 386 | 7,628 | 2024 | ||||||||||

| Los Cuatros | 640 | 259 | 1 | 640 | 2024 | ||||||||||||||

| Acres | Hectares | State Leases | Fee Mineral Leases | Federal Lode Mining Claims | Provincial Mineral Dispositions | Provincial Mining Leases | |||||||||||||

Country | State/Province | Project | Total | Total | Number | Acres | Expiration Date | Number | Acres | Expiration Date | Number | Acres | Expiration Date | Number | Hectares | Expiration Date | Number | Hectares | Expiration Date |

| Workman Creek | 4,036 | 1,374 | 198 | 4,036 | 2024 | ||||||||||||||

New Mexico | C de Baca | 600 | 243 | 30 | 600 | 2024 | |||||||||||||

| Dalton Pass | 1,020 | 413 | 51 | 1,020 | 2024 | ||||||||||||||

| Alexandra | 36,485 | 14,765 | 6 | 14,765 | Oct. 4042 | ||||||||||||||

| Axis Lake | 13,045 | 5,279 | 3 | 5,279 | Aug. 2023 | ||||||||||||||

| Beatty River | 16,526 | 6,688 | 7 | 6,688 | Sept. 2027 | ||||||||||||||

| Canada | Saskatchewan | Black Lake | 78,335 | 31,701 | 13 | 31,701 | Nov. 2024 | ||||||||||||

| Brander Lake | 34,577 | 13,993 | 9 | 13,993 | Apr. 2035 | ||||||||||||||

| Candle Lake | 6,412 | 2,595 | 1 | 2,595 | Oct. 2038 | ||||||||||||||

| Christie Lake | 19,575 | 7,922 | 6 | 7,922 | Mar. 2044 | ||||||||||||||

| Christie West | 813 | 329 | 2 | 329 | Jun. 2023 | ||||||||||||||

| Close Lake | 95,578 | 38,679 | 21 | 38,679 | Oct. 2023 | ||||||||||||||

| Cree Extension | 30,115 | 12,187 | 11 | 12,187 | Aug. 2040 | ||||||||||||||

| Diabase Peninsula | 77,164 | 31,227 | 22 | 31,227 | |||||||||||||||

| Erica | 91,409 | 36,992 | 20 | 36,992 | Nov. 2036 | ||||||||||||||

| Hidden Bay | 126,933 | 51,368 | 45 | 51,368 | Aug. 2037 | ||||||||||||||

| Horseshoe-Raven | 11,085 | 4,486 | 1 | 4,486 | Feb. 2041 | ||||||||||||||

| Key West | 31,827 | 12,880 | 4 | 12,880 | Apr. 2024 | ||||||||||||||

| Laurie | 21,691 | 8,778 | 4 | 8,778 | May 2027 | ||||||||||||||

| Millennium | 1,458 | 590 | 1 | 590 | Feb. 2039 | ||||||||||||||

| Mirror River | 42,996 | 17,400 | 5 | 17,400 | Apr. 2024 | ||||||||||||||

| Moon Lake | 9,385 | 3,798 | 5 | 3,798 | Oct. 2039 | ||||||||||||||

| Moore Tomblin | 3,249 | 1,315 | 2 | 1,315 | May 2028 | ||||||||||||||

| Nikita | 37,390 | 15,131 | 6 | 15,131 | Jun. 2043 | ||||||||||||||

| Riou Lake | 27,634 | 11,183 | 14 | 11,183 | Nov. 2023 | ||||||||||||||

| Roughrider | 1,475 | 597 | 1 | 597 | Jan. 2028 | ||||||||||||||

| Shea Creek | 81,451 | 32,962 | 18 | 32,962 | Mar. 2035 | ||||||||||||||

| Uchrich | 5,592 | 2,263 | 1 | 2,263 | May 2027 | ||||||||||||||

| Waterfound River | 28,837 | 11,670 | 25 | 11,670 | Jul. 2031 | ||||||||||||||

| West Bear | 27,439 | 11,104 | 26 | 10,807 | Feb 2043 | 1 | 297 | June 2035 | |||||||||||

| Wheeler River | 28,961 | 11,720 | 19 | 11,720 | Oct. 2041 | ||||||||||||||

| Wolly | 58,564 | 23,700 | 17 | 23,700 | Nov. 2038 | ||||||||||||||

| Nunavut | Kiggavik | 45,638 | 18,469 | 37 | 18,469 | Oct. 2038 | |||||||||||||

| Paraguay | Yuty | 289,687 | 117,232 | ||||||||||||||||

| Oviedo | 223,754 | 90,550 | |||||||||||||||||

Titanium Projects | |||||||||||||||||||

| Paraguay | Alto Parana | 174,204 | 70,498 | ||||||||||||||||

Uranium Projects | ||||||||||

Texas | ||||||||||

Property | Fully Permitted to Mine | Partially Permitted to Mine | Not Permitted to Mine | RRC Exploration Permit | TCEQ Class 1 Well Permits | TCEQ Injection Control Permit | TCEQ Area Permit | TCEQ/EPA Aquifer Exemption | TCEQ Radioactive Materials License | Notes |

| Burke Hollow | X | Yes | 2 | Yes | Yes | Yes | Yes | Has all major permits, waiting on final production authorization | ||

| Goliad | X | Yes | 2 | Yes | Yes | Yes | Yes | Has all major permits and first production authorization | ||

| La Palangana | X | Yes | 2 | Yes | Yes | Yes | Yes | Has all major permits and four production authorizations | ||

| Salvo | X | No | 0 | No | No | No | No | |||

| Longhorn | X | No | 0 | No | No | No | No | |||

Wyoming | ||||||||||

Property | Fully Permitted to Mine | Partially Permitted to Mine | Not Permitted to Mine | Class III UIC Permit to Mine | WDEQ Class 1 Well Permits | Source and Byproduct Materials License | BLM Plan of Operations | WDEQ/EPA Aquifer Exemption | Notes | |

| Allemand-Ross | X | Drilling Notification DN339 | ||||||||

| Antelope | X | Yes | Drilling Notification DN353 | |||||||

| Barge | X | |||||||||

| Black Hills | X | |||||||||

| Brown Ranch | X | |||||||||

| Bull Springs | X | |||||||||

| Central Shirley Basin | X | |||||||||

| Charlie | X | Permitted as an open pit mine not ISR | ||||||||

| Christensen Ranch | X | Yes | Yes | Yes | Yes | |||||

| Clarkson Hill | X | |||||||||

| Crooks Creek | X | |||||||||

| Crook's Mountain | X | |||||||||

| Crossroads | X | |||||||||

| Cyclone Rim | X | |||||||||

| East Shirley Basin | X | |||||||||

| Gas Hills | X | |||||||||

| Horse Creek | X | |||||||||

| Irigaray Project | X | Yes | Yes | Yes | Yes | Irigaray mine expansion to north and south will require a permit revision. Drilling Notification DN342 | ||||

| Jab/West Jab | X | Drilling Notification DN353 | ||||||||

| Ludeman | X | Yes | Yes | Yes | ||||||

| Moore Ranch | X | Yes | Yes | Yes | Yes | |||||

| Mule Creek | X | |||||||||

| Niles Ranch | X | |||||||||

| Nine Mile Lake | X | Drilling Notification DN339 | ||||||||

| Pine Ridge | X | Drilling Notification DN342 | ||||||||

| Pine Tree U1 | X | Drilling Notification DN342 | ||||||||

| Pumpkin Creek | X | Drilling Notification DN342 | ||||||||

| Red Rim | X | |||||||||

| Reno Creek | X | Yes | Yes | Yes | Yes | North Reno Creek and SW Reno Creek Resource areas are permitted. | ||||

| Ross Flat | X | Drilling Notification DN342 | ||||||||

| Sand Creek | X | |||||||||

| South Pine Ridge | X | |||||||||

| South Reno Creek | X | |||||||||

| South Sweetwater | X | |||||||||

| Stewart Creek | X | |||||||||

| Taylor Ranch | X | Drilling Notification DN342 | ||||||||

| Twin Buttes | X | |||||||||

| West Beaver Rim | X | |||||||||

| West Crook's Creek | X | |||||||||

| West Sweetwater | X | |||||||||

Arizona | ||||||||||

Property | Fully Permitted to Mine | Partially Permitted to Mine | Not Permitted to Mine | Class III UIC Permit to Mine | WDEQ Class 1 Well Permits | Source and Byproduct Materials License | BLM Plan of Operations | WDEQ/EPA Aquifer Exemption | Notes | |

| Anderson | X | |||||||||

| Los Cuatros | X | |||||||||

| Workman Creek | X | |||||||||

New Mexico | ||||||||||

Property | Fully Permitted to Mine | Partially Permitted to Mine | Not Permitted to Mine | Class III UIC Permit to Mine | WDEQ Class 1 Well Permits | Source and Byproduct Materials License | BLM Plan of Operations | WDEQ/EPA Aquifer Exemption | Notes | |

| C de Baca | X | |||||||||

| Dalton Pass | X | |||||||||

Canada | ||||||||||

Property | Fully Permitted to Mine | Partially Permitted to Mine | Not Permitted to Mine | Notes | ||||||

| Alexandra | X | Exploration-Stage Project with no resources | ||||||||

| Axis Lake | X | Exploration-Stage Project with no resources | ||||||||

| Beatty River | X | Exploration-Stage Project with no resources | ||||||||

| Black Lake | X | Exploration-Stage Project with no resources | ||||||||

| Brander Lake | X | Exploration-Stage Project with no resources | ||||||||

| Candle Lake | X | Exploration-Stage Project with no resources | ||||||||

| Christie Lake | X | Exploration-Stage Project with resources | ||||||||

| Christie West | X | Exploration-Stage Project with no resources | ||||||||

| Close Lake | X | Exploration-Stage Project with no resources | ||||||||

| Cree Extension | X | Exploration-Stage Project with no resources | ||||||||

| Diabase Peninsula | X | Exploration-Stage Project with no resources | ||||||||

| Erica | X | Exploration-Stage Project with no resources | ||||||||

| Hidden Bay | X | Exploration-Stage Project with no resources | ||||||||

| Horseshoe-Raven | X | Exploration-Stage Project with resources | ||||||||

| Key West | X | Exploration-Stage Project with no resources | ||||||||

| Laurie | X | Exploration-Stage Project with no resources | ||||||||

| Millennium | X | Exploration-Stage Project with resources | ||||||||

| Mirror River | X | Exploration-Stage Project with no resources | ||||||||

| Moon Lake | X | Exploration-Stage Project with no resources | ||||||||

| Moore Tomblin | X | Exploration-Stage Project with no resources | ||||||||

| Nikita | X | Exploration-Stage Project with no resources | ||||||||

| Riou Lake | X | Exploration-Stage Project with no resources | ||||||||

| Roughrider | X | Exploration-Stage Project with resources | ||||||||

| Shea Creek | X | Exploration-Stage Project with resources | ||||||||

| Uchrich | X | Exploration-Stage Project with no resources | ||||||||

| Waterfound River | X | Exploration-Stage Project with no resources | ||||||||

| West Bear | X | Exploration-Stage Project with no resources |

| Wheeler River | X | Feasibility Field Test mining completed | ||||||||

| Wolly | X | Exploration-Stage Project with no resources | ||||||||

| Kiggavik | X | Development-Stage, not permitted to mine | ||||||||

Paraguay | ||||||||||

Property | Fully Permitted to Mine | Partially Permitted to Mine | Not Permitted to Mine | Notes | ||||||

| Yuty | X | Exploration-Stage Project with resources | ||||||||

| Oviedo | X | Exploration-Stage Project with no resources | ||||||||

Titanium Projects | ||||||||||

Paraguay | ||||||||||

Property | Fully Permitted to Mine | Partially Permitted to Mine | Not Permitted to Mine | Notes | ||||||

| Alto Parana | X | Exploration-Stage Project with no resources | ||||||||

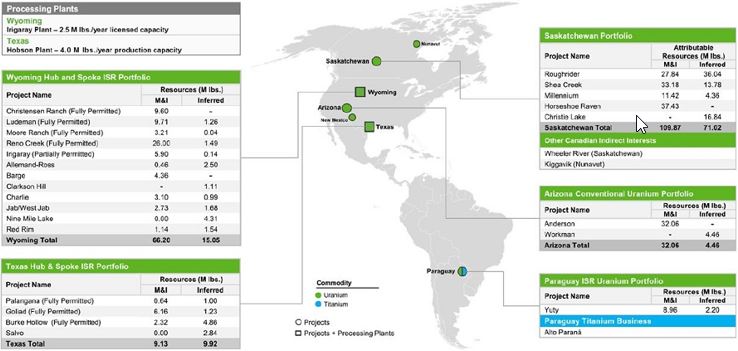

State/Province | Plant | Location (Latitude) | Location (Longitude) | Equity Interest | Operator | Status | Annual Permitted Production Capacity | Fully Permitted to Mine | Partially Permitted to Mine | Not Permitted to Mine | WDEQ Class 1 Well Permits | TCEQ Radioactive Materials License |

| Wyoming | Irigaray Central Processing Plant | 100% | UEC | Production Suspended | 2.5 Mlb/year | X | 2 | Yes | ||||

| Christensen Ranch Satellite Production Plant | 100% | UEC | Standby | 9,000 gpm | X | 4 | Yes | |||||

State/Province | Plant | Location (Latitude) | Location (Longitude) | Equity Interest | Operator | Status | Annual Permitted Production Capacity | Fully Permitted to Mine | Partially Permitted to Mine | Not Permitted to Mine | TCEQ Class 1 Well Permits | TCEQ Radioactive Materials License |

| Texas | Hobson Central Processing Plant | 28.945 | -97.989 | 100% | UEC | Production Suspended | 4.0 Mlb/year | X | 2 | Yes |

Uranium Oxide Mineral Resources | ||||||||||||||

Country | State/Province | Project | Measured | Indicated | Inferred | |||||||||

Tons ('000's) | Tonnes ('000's) | Grade (% U3O8) | Pounds U3O8 ('000's) | Tons ('000's) | Tonnes ('000's) | Grade (% U3O8) | Pounds U3O8 ('000's) | Tons ('000's) | Tonnes ('000's) | Grade (% U3O8) | Pounds U3O8 ('000's) | |||

| Allemand-Ross | 246 | 223 | 0.09% | 417 | 32 | 29 | 0.07% | 42 | 1,275 | 1,157 | 0.10% | 2,496 | ||

| Barge | 4,301 | 3,902 | 0.05% | 4,361 | ||||||||||

| Charlie | 1,255 | 1,139 | 0.12% | 3,100 | 411 | 373 | 0.12% | 988 | ||||||

| Christensen Ranch | 6,555 | 5,947 | 0.07% | 9,596 | ||||||||||

| Clarkson Hill | 957 | 868 | 0.06% | 1,113 | ||||||||||

| Irigaray | 3,881 | 3,521 | 0.08% | 5,899 | 104 | 94 | 0.07% | 141 | ||||||

| Wyoming | Jab/West Jab | 1,621 | 1,471 | 0.07% | 2,335 | 253 | 230 | 0.08% | 392 | 1,402 | 1,272 | 0.06% | 1,677 | |

| Ludeman | 2,674 | 2,426 | 0.09% | 5,017 | 2,660 | 2,413 | 0.09% | 4,697 | 866 | 786 | 0.07% | 1,258 | ||

| Moore Ranch | 2,675 | 2,427 | 0.06% | 3,210 | 46 | 42 | 0.05% | 44 | ||||||

| Nine Mile Lake | 3,405 | 3,089 | 0.04% | 4,308 | ||||||||||

| Red Rim | 337 | 306 | 0.17% | 1,142 | 473 | 429 | 0.16% | 1,539 | ||||||

| United States | Reno Creek | 14,990 | 13,599 | 0.04% | 12,920 | 16,980 | 15,404 | 0.04% | 13,070 | 1,920 | 1,742 | 0.04% | 1,490 | |

Wyoming Total | 22,206 | 20,145 | 0.05% | 23,899 | 36,254 | 32,889 | 0.06% | 42,299 | 10,859 | 9,851 | 0.07% | 15,054 | ||

| Burke Hollow | 70 | 64 | 0.08% | 115 | 1,337 | 1,213 | 0.09% | 2,209 | 2,494 | 2,263 | 0.10% | 4,859 | ||

| Goliad | 1,595 | 1,447 | 0.05% | 2,668 | 1,504 | 1,364 | 0.10% | 3,492 | 333 | 302 | 0.20% | 1,225 | ||

| Texas | Palangana | 232 | 210 | 0.13% | 643 | 302 | 274 | 0.18% | 1,001 | |||||

| Salvo | 1125 | 1,020 | 0.09% | 2,839 | ||||||||||

Texas Total | 1,665 | 1,510 | 0.08% | 2,783 | 3,073 | 2,788 | 0.10% | 6,344 | 5,469 | 4,961 | 0.09% | 9,924 | ||

| Anderson | 16,175 | 14,674 | 0.10% | 32,055 | ||||||||||

| Arizona | Workman Creek | 1,981 | 1,797 | 0.11% | 4,459 | |||||||||

Arizona Total | 16,175 | 14,674 | 0.10% | 32,055 | 1,981 | 1,797 | 0.11% | 4,459 | ||||||

United States Total | 23,871 | 21,655 | 0.06% | 26,682 | 55,502 | 50,351 | 0.07% | 80,698 | 18,309 | 16,610 | 0.08% | 29,437 | ||

| Christie Lake | 537 | 488 | 1.57% | 16,836 | ||||||||||

| Roughrider | 429 | 389 | 3.25% | 27,842 | 396 | 359 | 4.55% | 36,043 | ||||||

| Canada | Saskatchewan | Horseshoe-Raven | 11,412 | 10,353 | 0.16% | 37,426 | ||||||||

| Shea Creek | 1,113 | 1,009 | 1.49% | 33,175 | 679 | 616 | 1.02% | 13,775 | ||||||

| Millennium | 239 | 217 | 2.39% | 11,423 | 68 | 62 | 3.19% | 4,364 | ||||||

Canada Total | 13,192 | 11,968 | 0.42% | 109,867 | 1,681 | 1,525 | 2.11% | 71,019 | ||||||

| Paraguay | Yuty | 9,074 | 8,232 | 0.05% | 8,962 | 2,733 | 2,479 | 0.04% | 2,203 | |||||

Total Resources | 23,871 | 21,655 | 0.06% | 26,682 | 77,768 | 70,550 | 0.13% | 199,527 | 22,797 | 20,681 | 0.23% | 102,658 | ||

| 1. | The Mineral Resource estimates in this table meet S-K 1300 definitions. | |

| 2. | Mineral Resources are not Mineral Reserves and do not have demonstrated economic viability. | |

| 3. | The point of reference for mineral resources is in-situ at the Project. | |

| 4. | Mineral Resources are estimated using a long-term uranium price of $40 per pound for ISR projects and $65 per pound for conventional projects, except for the Canadian projects where a price of $56 per pound was used for the Roughrider Project, a price of $75 per pound was used for the Horseshoe-Raven Project, a price of $50 per pound was used for the Shea Creek Project, a price of $50 per pound was used for the Christie Lake Project and a price of $62 per pound was used for the Millennium Project. | |

| 5. | Mineral Resources in the table above are 100% attributable to the Company. Where JV projects have resources that are attributable to other companies, these resources are not listed in this table. | |

| 6. | Numbers may not add due to rounding. |

Uranium Oxide Resources | |||||||||||

FY 2022 | FY 2023 | YOY Change | |||||||||

Country | State/Province | Project | Measured Pounds U3O8 ('000's) | Indicated Pounds U3O8 ('000's) | Inferred Pounds U3O8 ('000's) | Measured Pounds U3O8 ('000's) | Indicated Pounds U3O8 ('000's) | Inferred Pounds U3O8 ('000's) | % Change in Measured Pounds | % Change in Indicated Pounds | % Change in Inferred Pounds |

| Allemand-Ross | 417 | 42 | 2,496 | 417 | 42 | 2,496 | 0% | 0% | 0% | ||

| Barge | 4,361 | 4,361 | 0% | ||||||||

| Charlie | 3,100 | 988 | 3,100 | 988 | 0% | 0% | |||||

| Christensen Ranch | 9,596 | 9,596 | 0% | ||||||||

| Clarkson Hill | 1,113 | 1,113 | 0% | ||||||||

| Irigaray | 5,899 | 141 | 5,899 | 141 | 0% | 0% | |||||

| Wyoming | Jab/West Jab | 2,335 | 392 | 1,677 | 2,335 | 392 | 1,677 | 0% | 0% | 0% | |

| Ludeman | 5,017 | 4,697 | 1,258 | 5,017 | 4,697 | 1,258 | 0% | 0% | 0% | ||

| Moore Ranch | 3,210 | 44 | 3,210 | 44 | 0% | 0% | |||||

| United States | Nine Mile Lake | 4,308 | 4,308 | 0% | |||||||

| Red Rim | 1,142 | 1,539 | 1,142 | 1,539 | 0% | 0% | |||||

| Reno Creek | 12,920 | 13,070 | 1,490 | 12,920 | 13,070 | 1,490 | 0% | 0% | 0% | ||

Wyoming Total | 23,899 | 42,299 | 15,054 | 23,899 | 42,299 | 15,054 | 0% | 0% | 0% | ||

| Burke Hollow | 115 | 2,209 | 4,859 | 115 | 2,209 | 4,859 | 0% | 0% | 0% | ||

| Texas | Goliad | 2,668 | 3,492 | 1,225 | 2,668 | 3,492 | 1,225 | 0% | 0% | 0% | |

| Palangana | 643 | 1,001 | 643 | 1,001 | 0% | 0% | |||||

| Salvo | 2,839 | 2,839 | 0% | ||||||||

Texas Total | 2,783 | 6,344 | 9,924 | 2,783 | 6,344 | 9,924 | 0% | 0% | 0% | ||

| Anderson | 32,055 | 32,055 | 0% | ||||||||

| Arizona | Workman Creek | 4,459 | 4,459 | 0% | |||||||

Arizona Total | 32,055 | 4,459 | 32,055 | 4,459 | 0% | 0% | |||||

United States Total | 26,682 | 80,698 | 29,437 | 26,682 | 80,698 | 29,437 | 0% | 0% | 0% | ||

| Christie Lake | 16,836 | 100% | |||||||||

| Roughrider | 27,842 | 36,043 | 100% | 100% | |||||||

| Canada | Saskatchewan | Horseshoe-Raven | 37,426 | 100% | |||||||

| Shea Creek | 33,175 | 13,775 | 100% | 100% | |||||||

| Millennium | 11,423 | 4,364 | 100% | 100% | |||||||

Canada Total | 109,867 | 71,019 | 100% | 100% | |||||||

| Paraguay | Yuty | 8,962 | 2,203 | 8,962 | 2,203 | 0% | 0% | ||||

Total Resources | 26,682 | 89,660 | 31,640 | 26,682 | 199,527 | 102,658 | 0% | 123% | 224% | ||

| 1. | The Mineral Resource estimates in this table meet S-K 1300 definitions. | |

| 2. | Mineral Resources are not Mineral Reserves and do not have demonstrated economic viability. | |

| 3. | The point of reference for mineral resources is in-situ at the Project. | |

| 4. | Mineral Resources are estimated using a long-term uranium price of $40 per pound for ISR projects and $65 per pound for conventional projects, except for the Canadian projects where a price of $56 per pound was used for the Roughrider Project, a price of $75 per pound was used for the Horseshoe-Raven Project, a price of $50 per pound was used for the Shea Creek Project, a price of $50 per pound was used for the Christie Lake Project and a price of $62 per pound was used for the Millennium Project.. | |

| 5. | Mineral Resources are 100% attributable to the Company. Where JV projects have resources that are attributable to other companies, these resources are not listed in this table. | |

| 6. | Numbers may not add due to rounding. |

our capital needs;

business plans; and

expectations.

While these forward-looking statements, and any assumptions upon which they are based, are made in good faith and reflect our current judgment regarding future events, our actual results will likely vary, sometimes materially, from any estimates, predictions, projections, assumptions or other future performance suggested herein. Some of the risks and assumptions include:

our need for additional financing;

our exploration activities may not result in commercially exploitable quantities of ore on our mineral properties;

the risks inherentprompt fission neutron (“PFN”) techniques. This technology has been employed in the exploration and development of sandstone uranium deposits in the U.S. since the 1950s. QA/QC of gamma-ray and PFN probes from each logging truck are required to maintain calibration by regular cross-checking the probes at a U.S. Department of Energy test pits located in George West, Texas, or Casper, Wyoming. The pit is set up for mineralslogging units to calibrate the probes with a known radioactive source. Each test run generates calibration files for the operator to review and make necessary tool adjustments. Calibration runs typically are made on a one- or two-month interval, and files with the test pit run results are maintained by the operator. The available data indicate that the logging provided by the Company and contract probe trucks at the various U.S. projects have maintained industry standard calibration procedures for their probes.

| ● | The Tullock member consists of sandstone, siltstone and sparse coal and carbonaceous shale; |

| ● | The Lebo member consists of abundant drab gray mudstone, minor siltstone and sandstone and sparse coal and carbonaceous shale beds; and |

| ● | The Tongue River member consists of interbedded sandstone, conglomerate, siltstone, mudstone, limestone, anomalously thick coal beds and carbonaceous shale beds. This member has been mined extensively for its coal beds, which can be hundreds of feet thick. |

our limited operating history;

ourconsists of sandstone, siltstone, shale, coal and local conglomerates. The Fort Union is overlain, often unconformably, by the Eocene Wind River Formation, which consists of sandstones, conglomerates, siltstones and shale. Overlying the Wind River Formation is the Oligocene White River Formation. The White River Formation also consists of sandstones, siltstone and shale, however, along with fluvial deposition of the sands and clays, substantial volumes of windblown volcanic ash (tuffs) were also deposited. This volcanic ash is regarded by many as the source of uranium for many Wyoming sandstone uranium deposits. Economic uranium deposits in the WRB typically occur as roll-front deposits in porous sandstones within the Wind River and Fort Union Formations.

commercial production.

our lack of insurance coverage;

the competitive environment in which we operate;

the level of government regulation, including environmental regulation;

changes in governmental regulationapproximately 14 miles then exit left onto Irigaray Road and administrative practices;

our dependence on key personnel;

conflicts of interest of our directors and officers;

our ability to fully implement our business plan;

our ability to effectively manage our growth; and

other regulatory, legislative and judicial developments.

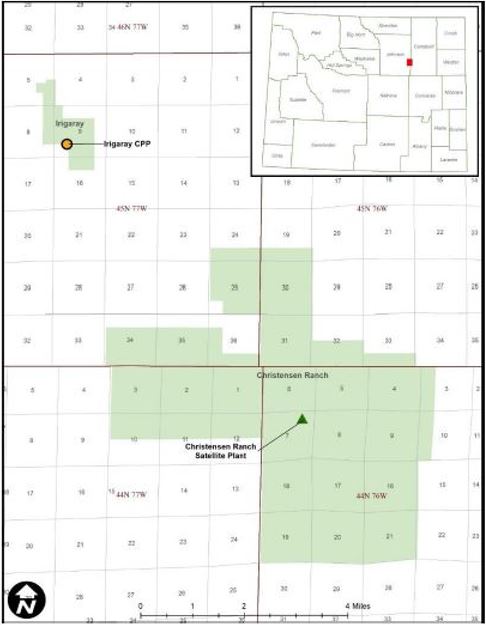

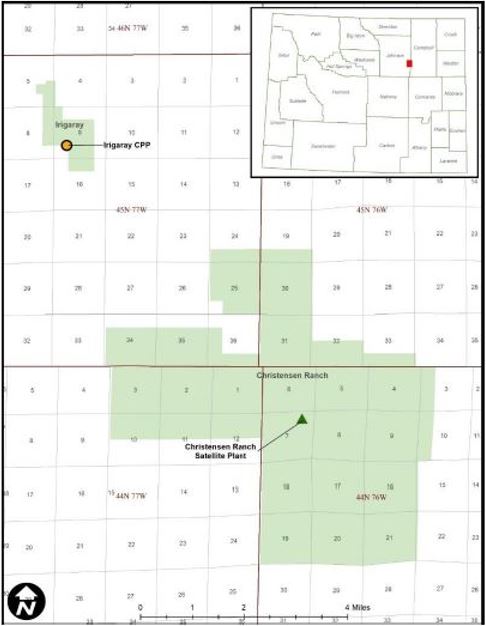

We advise the reader that these cautionary remarks expressly qualify in their entirety all forward-looking statements attributable to us or persons acting on our behalf. Important factors that you should also consider, include, but are not limitedfollow signs to the factors discussedIrigaray site. For access from Gillette, take State Highway 50 south approximately 25 miles exit right onto Black and Yellow Road, travel for approximately 20 miles and follow signs to Irigaray. The Irigaray Project Area is primarily located on private surface land, federal BLM land and a portion located on one section of state-managed land.

Year | Company | Operations/Activity | Amount (No. of Drill holes) | Results of Work |

1969 | Homestake Mining (“Homestake”) | Original controller of the Irigaray Project Area. | Approximately 1,340 | Right to mine secured. Preliminary delineation of mineralized areas. |

1975 | Westinghouse Electric Corporation (“Westinghouse”) | Acquired property from Homestake. The project was licensed for ISR production in 1978 and was operated by Wyoming Mineral Corporation, a subsidiary of Westinghouse. Operations ceased in 1982 due to market trends. | Approximately 470 | Delineation of mineralized areas. Began ISR production. |

1987 | Malapai Resources Company (“Malapai”) | Acquired property from Westinghouse. | None | Ownership transition. |

1990 | Total Minerals Corporation (“TOMIN”) and Électricité de France (“EDF”) | Acquired property from Malapai. TOMIN acted as project operator. | None | Ownership transition. |

1993 | COGEMA Resources, Inc. (“COGEMA”) (now Orano S.A.)/Areva | Replaced TOMIN as project operator in partnership with EDF. COGEMA acquired interests from TOMIN. | Approximately 20 | 0.74 million lb. of U3O8 produced from 1978 through 2000. |

2010 | Uranium One | Dried many millions of pounds from Christensen Ranch and through toll milling. | N/A | Decommissioned Irigaray wellfields. |

2021 | UEC | Irigaray Project Area acquired by UEC from Uranium One. | N/A | Ownership transition. |

2018. Permit to Mine No. 478 and Radioactive Materials License WYSUA-1341 are in good standing, with no violations of permit or license conditions. Mining permit requirements can be found in Wyoming Statutes §35-11-400 through 437, with specific laws for ISR mining in sections 426 – 436. Conditions of the Radioactive Materials License applicable to ISR mining are generally standard for all licensees. Requirements of Radioactive Materials Licenses are found in WDEQ, LQD/Uranium Recovery Program Chapter 4 Rules and Regulations for Licensing of Source and Byproduct Material. There are no materially significant encumbrances on the Irigaray Project. Standard encumbrances include reclamation bonding, mining and surface lease royalties.

Classification | Tons Ore (000’s) | Tonnes Ore (1000’s) | Average Grade (% eU3O8) | Pounds eU3O8 (000’s) |

| Measured | - | - | - | - |

| Indicated | 3,881 | 3,521 | 0.076 | 5,899.0 |

Total M&I | 3,881 | 3,521 | 0.076 | 5,899.0 |

| Inferred | 104 | 94 | 0.068 | 141.0 |

Total Resources | 3,985 | 3,615 | 0.076 | 6,040.0 |

| 1. | The sum of resource tons and lbs. may not add up to the reported total due to rounding. | |

| 2. | Measured, indicated and inferred mineral resources as defined in 17 CFR § 229.1300. | |

| 3. | GT Cutoff = 0.25 ft% eU3O8. | |

| 4. | All reported resources occur below the static water table. | |

| 5. | The point of reference for mineral resources is in-situ at the Project. | |

| 6. | Mineral resources that are not mineral reserves do not have demonstrated economic viability. | |

| 7. | A long-term uranium price of $40/lb U3O8 and an 80% metallurgical recovery factor were considered for the purposes of determining the reasonable prospect of economic extraction. |

iii

REFERENCES

As used in this annual report: (i)PRB.

iv

1

PART I

Corporate Organization

Uranium Energy Corp. was incorporated under the lawssoutheast of the Irigaray Central Processing Plant and is accessed by travelling west on Black and Yellow Road to Irigaray Road. The Christensen Ranch Project Area is primarily located on private surface land, with two portions located on federal BLM-managed land.

On December 31, 2007, we incorporated a wholly-owned subsidiary, UEC Resources Ltd., under the laws of the Province of British Columbia, Canada. Effective December 18, 2009, we acquired a 100% interestlate 1950s, small open pit mine operations were established in the South Texas Mining Venture, L.L.P. ("STMV"), a Texas limited liability partnership, from each of URN Resources Inc., a subsidiary of Uranium One Inc.,PRB. Early prospecting and Everest Exploration, Inc. (“STMV Acquisition”). On September 3, 2010, we incorporated a wholly-owned subsidiary, UEC Paraguay Corp., under the laws of the State of Nevada. Effective May 24, 2011, we acquired a 100% in interest in Piedra Rica Mining S.A., a private company incorporated in Paraguay. Effective September 9, 2011, we acquired a 100% interest in Concentric Energy Corp., a private company incorporated in the State of Nevada. Effective March 30, 2012, we acquired a 100% interest in Cue Resources Ltd., a publicly-traded company incorporated in the Province of British Columbia, Canada.

Our principal offices are located at 500 North Shoreline Boulevard, Suite 800N, Corpus Christi, Texas 78401exploration included geologic mapping and 1111 West Hastings Street, Suite 320, Vancouver, British Columbia, Canada V6E 2J3.

General Business

We are engaged in uranium mining and related activities, including exploration, pre-extraction, extraction and processing of uranium concentrates, on projects located in the United States and Paraguay. Our fully-licensed and 100%-owned Hobson Processing Facility (“Hobson” or the “Hobson Facility”) forms the basis for our regional operating strategy in the State of Texas, specifically the South Texas Uranium Belt, utilizing in-situ recovery mining. As a central processing site, Hobson processes uranium-loaded resins from our Palangana Mine and has the additional capacitygamma surveys, which led to process uranium-loaded resins from other satellite mining activities within the South Texas Uranium Belt as they enter uranium recovery. Since the commencement of uranium extraction in November 2010 to July 31, 2012, the Hobson Facility has processed 323,000 pounds of uranium concentrates.

At July 31, 2012, we had mineral rights located in the States of Arizona, Colorado, New Mexico, Texas and Wyoming and in Paraguay. We acquired these mineral rights for the purposes of uranium mining and related activities, including exploration, pre-extraction, extraction and processing of uranium concentrates. Many of the areas in which the Company has interests in have been the subject of historical exploration by other mining companies. Specific exploration targets may be identified internally by our geological team by utilizing this prior exploration work combined with our extensive exploration database.

Fiscal 2012

The following is a list of the material transactions for the fiscal year ended July 31, 2012:

Effective September 9, 2011, we acquired a 100% interest in the Anderson Project located in the State of Arizona through the acquisition of Concentric Energy Corp., a private company incorporated in the State of Nevada;

2

Effective November 30, 2011, we acquired a 100% interest in the Workman Creek Project located in the State of Arizona;

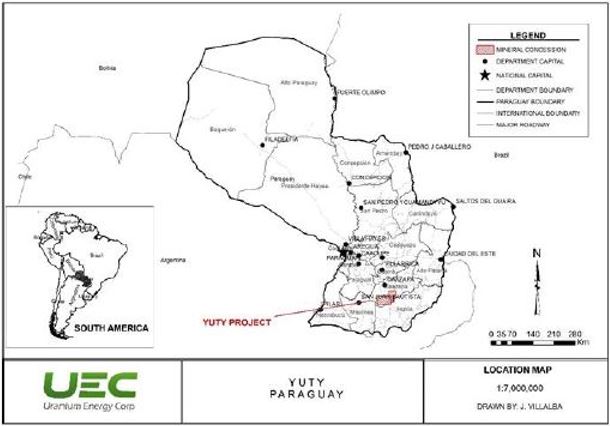

Effective March 30, 2012, we acquired a 100% interest in the Yuty Project located in the Republic of Paraguay through the acquisition of Cue Resources Ltd., a publicly-traded company incorporated in the Province of British Columbia, Canada;

Effective March 31, 2012, we acquired a 100% interest in a further two prospecting permits in the area of Coronel Oviedo, Paraguay, adjacent to the Company’s existing Coronel Oviedo Project;

On April 10, 2012, we closed a public offering of its common stock for gross proceeds of $22.5 million (net proceeds of $21.0 million) through the sale of 6,246,078 shares of the Company at a price of $3.60 per share;

Effective May 23, 2012, we acquired uranium rights through a mineral lease on the Slick Rock Project located in the State of Colorado;

During Fiscal 2012, we acquired uranium rights through a mineral lease on the Burke Hollow Project located in the State of Texas; and

During Fiscal 2012, we acquired uranium rights through a mineral lease on the Channen Project located in the State of Texas.

Background of the Uranium Industry

A relatively small number of companies operating in only a few countries are engaged in uranium production, with only five producers marketing 61% of the estimated world production in 2011. Roughly 73% of the world’s production in 2011 came from four countries: Kazakhstan, Canada, Australia and Niger. In 2009, Kazakhstan surpassed Canada as the largest global producer, a title Canada had held for 17 years.

Between 1960 and 1985, a significant amount of uranium exploration was conducted in the United States. In 2011, the United States was the largest consumerdiscoveries of uranium in the worldWasatch and Fort Union Formations. Extensive drill hole exploration has been utilized to locate deeper uranium mineralization since the 1960s to progress geologic models.

Year | Company | Operations/Activity | Amount (No. of Drill holes) | Results of Work |

1967 | Independent Operators | Assembled as a large land package by independent operators. | Approximately 4,860 | Right to mine secured. Preliminary delineation of mineralized areas. |

1979 | Arizona Public Services (“APS”), parent company of Malapai | APS became a 50% partner in 1979. | Approximately 2,220 | Delineation of mineralized areas. |

1981 | Malapai | Malapai assumed sole ownership of the Christensen Ranch Project Area by acquiring the interests of Wold Energy (“Wold”) and Western Nuclear Corporation (“WNC”). Malapai purchased the Irigaray Project Area from Westinghouse in 1987, and the Christensen Ranch Project Area was licensed for operations under the Irigaray U.S. NRC and Wyoming Department of Environmental Quality (“WDEQ”) license/permit in 1988. Uranium production by ISR was started by Malapai in 1989 and was placed on standby in 1990. | Approximately 1,460 | Delineation of mineralized areas. Began ISR production. |

1990 | TOMIN and EDF | EDF acquired the Irigaray and Christensen Ranch Project Areas from Malapai in 1990. TOMIN acted as project operator for EDF under a joint participation agreement. TOMIN restarted ISR operations in 1991. | Approximately 2,270 | Delineation of mineralized areas. Restarted ISR production. |

1993 | COGEMA and EDF | In 1993, COGEMA acquired the assets of TOMIN and changed the name of the operating entity to COGEMA Mining, Inc. EDF (now Malapai) was still owner of 29%, COGEMA, as operator, owned 71% through the joint participation agreement. | Approximately 3,690 | 3.70 million lbs of U3O8 produced from 1989 through 2000. |

2000 | COGEMA and Malapai | Groundwater restoration of Mine Units 2 through 6 was completed. The Christensen Ranch Project Area was placed on standby from 2006 through 2010, at which time COGEMA and Malapai sold the project to Uranium One and Uranium One USA, Inc. (collectively, “Uranium One”). | N/A | 188,000 lbs of U3O8 produced during restoration. |

2010 | Uranium One | Mine Units 7, 8 and 10 were installed and operated. A ramp up occurred in 2011, and a ramp down occurred in 2013 (all wellfield development ceased). Low production mode occurred in 2014 through 2018, and production ended in 2018, at which time the Christensen Ranch Project Area was placed on care and maintenance. | N/A | 2.6 million lbs of U3O8 produced. |

2021 | UEC | The Christensen Ranch Project Area acquired by UEC from Uranium One. | N/A | Ownership transition. |

Classification | Tons Ore (000’s) | Tonnes Ore (1000’s) | Average Grade (% eU3O8) | Pounds eU3O8 (000’s) |

| Measured | - | - | - | - |

| Indicated | 6,555 | 5,947 | 0.073 | 9,596 |

Total M&I | 6,555 | 5,947 | 0.073 | 9,596 |

| Inferred | - | - | - | - |

Total Resources | 6,555 | 5,947 | 0.073 | 9,596 |

| 1. | The sum of resource tons and lbs. may not add up to the reported total due to rounding. | |

| 2. | Measured, indicated, and inferred mineral resources as defined in 17 CFR § 229.1300. | |

| 3. | GT Cutoff = 0.25 ft% eU3O8. | |

| 4. | All reported resources occur below the static water table. | |

| 5. | The point of reference for mineral resources is in-situ at the Project. | |

| 6. | Mineral resources that are not mineral reserves do not have demonstrated economic viability. | |

| 7. | A long-term uranium price of $40/lb U3O8 and an 80% metallurgical recovery factor were considered for the purposes of determining the reasonable prospect of economic extraction. |

Year | Company | Operations/Activity | Amount (No. of Drill holes) | Results of Work |

1971 | Conoco Minerals (“Conoco”) and Kerr-McGee Corporation (“Kerr-McGee”) | Conoco and Kerr-McGee operated as a joint venture. Of the joint venture, Conoco controlled 50% of the Moore Ranch Project Area and served as the operator. | Approximately 2,700 rotary drill holes Approximately 130 core holes | Discovery and delineation of mineralized areas. Permitting and licensing of a proposed uranium processing facility known as Sand Rock Mill was completed through the WDEQ/LQD and the NRC. |

1983 | Wold and Kerr-McGee | Conoco sold its interests to Wold in 1983. Kerr-McGee retained the rights with Wold. Assessment drilling was conducted. | None | Retained mining claims. Mining claim assessment drilling. |

1989 | Rio Algom Mining Corp. (“Rio Algom”) | Rio Algom acquired the project in 1989. Rio Algom conducted mining claim assessment drilling to retain mining claims through 1992, which was the last year to allow mining claim assessment drilling. | None | Retained mining claims. Mining claim assessment drilling. |

1992 | Rio Algom | Claim maintenance paid directly to the BLM. No further drilling conducted. | None | Mining claims retained through payment. |

2002 | Power Resources, Inc. (“PRI”) (now Cameco Resources) | Rio Algom acquired by PRI. | None | Ownership transition. |

2004 | Energy Metals Corporation (“EMC”) | EMC acquired most of the mining claims and state leases. | N/A | Secured right to mine. |

2007 | Uranium One | Uranium One acquired EMC and all rights to the Moore Ranch Project Area. Uranium One completed verification and resource enhancement drilling, coring, baseline monitor wells, and pump test wells. The Moore Ranch Project Area is fully permitted by WDEQ/LQD in 2011 and the NRC in 2013. | Approximately 800 | Exploration efforts focused on developing and upgrading mineral resources. |

2021 | UEC | Moore Ranch Project Area acquired by UEC from Uranium One. | N/A | Ownership transition. |

Classification | Tons Ore (000’s) | Tonnes Ore (1000’s) | Average Grade (% eU3O8) | Pounds eU3O8 (000’s) |

| Measured | 2,675 | 2,427 | 0.06 | 3,210.0 |

| Indicated | - | - | - | - |

Total M&I | 2,675 | 2,427 | 0.06 | 3,210.0 |

| Inferred | 46 | 42 | 0.047 | 43.7 |

Total Resources | 2,721 | 2,469 | 0.06 | 3,253.7 |

| 1. | The sum of resource tons and lbs. may not add up to the reported total due to rounding. | |

| 2. | Measured, indicated, and inferred mineral resources as defined in 17 CFR § 229.1300. | |

| 3. | GT Cutoff = 0.3 ft% eU3O8. | |

| 4. | All reported resources occur below the static water table. | |

| 5. | The point of reference for mineral resources is in-situ at the Project. | |

| 6. | Mineral resources that are not mineral reserves do not have demonstrated economic viability. | |

| 7. | A long-term uranium price of $40/lb U3O8 and an 80% metallurgical recovery factor were considered for the purposes of determining the reasonable prospect of economic extraction. |

Year | Company | Operations/Activity | Amount (No. of Drill holes) | Results of Work |

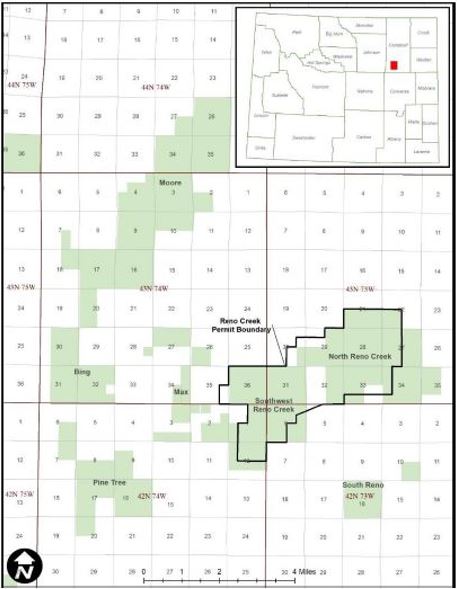

Reno Creek – North Reno Creek | ||||

Late 1960s | Rocky Mountain Energy Company (“RME”) | Drilled exploration holes at and around North Reno Creek resource area. | Approximately 5,800 | Delineated Approximately 10 miles of roll-front deposits. |

Mid 1970s | RME, Mono Power Company (“Mono”) and Halliburton Services | Partnership formed to develop North Reno Creek Resource Area using ISR methods. | N/A | Acquisition of the Reno Creek Project Area. |

1992 | Energy Fuels Nuclear Inc./International Uranium Corporation | Energy Fuels Nuclear Inc. acquired RME’s North Reno Creek Resource Area and later became International Uranium Corporation. | N/A | Acquisition of the Reno Creek Project Area. |

2001 | Rio Algom | Rio Algom acquired International Uranium Corporation’s property. | N/A | Acquisition of the Reno Creek Project Area. |

2001 | PRI | PRI acquired North Reno Creek Area and dropped claims in 2003. | N/A | Acquisition of the Reno Creek Project Area and mining claims dropped. |

2004 | Strathmore Minerals Corporation and American Uranium Corporation (“AUCA”) | Re-staked and filed new mining claims on approximately 16,000 acres. | N/A | Refiled mining claims and secured right to mine. |

2007 | AUCA | Advanced project through acquisition of most major permits and required authorizations. | N/A | Acquisition of the Reno Creek Project Area and secured permits and authorizations. |

2017 | UEC | Consolidated ownership of multiple resource areas and oversaw technical reporting and auditing of Project resources. | N/A | Consolidation of ownership. Auditing of project resources. |

Reno Creek – Southwest Reno Creek | ||||

Pre-2007 | AUCA and Tennessee Valley Authority JV | Controlled Southwest Reno Creek and drilled exploration holes. | Approximately 700 | Delineation of mineralized areas. |

2007 | AUCA | Advanced project through acquisition of most major permits and required authorizations. | N/A | Secured permits and required authorizations. |

2017 | UEC | Consolidated ownership of multiple Resource Areas and oversaw technical reporting and auditing of Project resources. | N/A | Consolidation of ownership. Auditing of the Reno Creek Project Area resources. |

Reno Creek – Moore, Pine Tree, and Bing | ||||

1960s | Utah International Mining Company | Exploration on Moore and Pine Tree Resource Areas. | N/A | Delineation of mineralized areas. |

Late 1970s | Pathfinder Mines, Inc. | Utah International Mining Company becomes Pathfinder Mines, Inc. and continues exploration on Moore and Pine Tree Resource Areas. | >1,560 | Delineation of mineralized areas. |

1980s | RME | Obtained ownership of Moore Area, continued exploration drilling until the 1990s. | >400 | Acquired the Reno Creek Project Area. Delineation of mineralized areas. |

1960s | Cleveland-Cliffs Iron Company | Exploration of Bing Area, drilled several hundred exploration holes and conducted limited hydrologic testing in the 1970s. | 177 | Delineation of mineralized areas through drilling and conducted hydrologic testing. |

2007 | AUCA | Consolidated the Resource Areas under one owner. | N/A | Consolidated ownership. |

2017 | UEC | Oversaw technical reporting and auditing of project resources. | N/A | Auditing of the Reno Creek Project Area resources. |

Classification | Tons Ore (000’s) | Tonnes Ore (1000’s) | Average Grade (% eU3O8) | Pounds eU3O8 (000’s) |

| Measured | 14,990 | 13,599 | 0.043 | 12,920.0 |

| Indicated | 16,980 | 15,404 | 0.039 | 13,070.0 |

Total M&I | 31,970 | 29,003 | 0.041 | 25,990.0 |

| Inferred | 1,920 | 1,742 | 0.039 | 1,490.0 |

Total Resources | 33,890 | 30,745 | 0.041 | 27,480.0 |

| 1. | The sum of resources tons and lbs. may not add up to the reported total due to rounding. | |

| 2. | Measured, indicated, and inferred mineral resources as defined in 17 CFR § 229.1300. | |

| 3. | GT Cutoff = 0.20 ft% eU3O8. | |

| 4. | All reported resources occur below the static water table. | |

| 5. | The point of reference for mineral resources is in-situ at the Project. | |

| 6. | Mineral resources that are not mineral reserves do not have demonstrated economic viability. | |

| 7. | A long-term uranium price of $40/lb U3O8 and an 80% metallurgical recovery factor were considered for the purposes of determining the reasonable prospect of economic extraction. |

Year | Company | Operations/Activity | Amount (No. of Drill holes) | Results of Work |

1960s-1970s | Cordero Mining | Numerous exploration companies including Teton Exploration (“Teton”), PRI, Uranium Resources, Inc. (“URI”) and Malapai (a subsidiary of APS) collectively explored in the Ludeman Project Area. | Approximately 5,420 | Explored for uranium roll-front mineralization and delineated deposits in the Ludeman Project Area. |

1980 | United Nuclear Corp. (“UNC”) and partner Teton | Constructed and operated the Leuenberger ISR pilot test facility for 12 months. Groundwater restoration was completed following production and a commercial permit to mine was granted. Due to a decline in the market, the permitted mine was not placed into commercial operation and the permit expired. | N/A | Produced 12,800 lbs of U3O8 from the pilot facility. |

1981 | URI | Constructed and operated the North Platte ISR project on a portion of the Ludeman Project Area. The pilot test facility produced for five months during 1982. | N/A | Produced 1,515 lbs of U3O8 from the pilot facility. |

1980s | Malapai | Permitted the Peterson Project for pilot operations but was never operated. | N/A | Facility was never operated. |

1985-Early 1990s | Central Electrical Generating Board of England (known as PRI) | Nedco and Union Pacific properties were consolidated into the Teton Leuenberger Project. PRI purchased the property and added to the acreage through the purchase of adjacent claim blocks owned by Kerr-McGee. | N/A | Ownership transition and growth in acreage through acquisitions. |

Late 1990s | PRI | Leuenberger properties were released due to declining market trends. Some claims reverted to previous owners. | N/A | Decrease in claims and generally the Ludeman Project Area. |

Early to Mid- 2000s | High Plains Uranium (“HPU”) and EMC | HPU held most claims and leases in the Ludeman Project Area. Energy Metals held the remaining claims in the Ludeman Project Area. | N/A | Claims and leases increased in the Ludeman Project Area. |

2007 | EMC | EMC acquired HPU. | N/A | Consolidation through acquisition. |

2007 | Uranium One | Uranium One acquired Energy Metals in late 2007 and continued exploration of the Ludeman Project Area from 2007 through 2012. The primary goals of drilling included exploration to establish continuity of regional ore trends, development drilling to determine the lateral extents of the ore body, stratigraphic investigation, confirmation of the location and nature of mineralization, and collection of cores for leach testing and analysis of uranium, mineralogy, trace metals, disequilibrium, permeability, porosity and density. Acquired the WDEQ/LQD mine permit and NRC license. | Approximately 2,180 | Continued exploration of the Ludeman Project Area. Additional holes included boreholes, core holes, and monitor wells. |

2021 | UEC | The Ludeman Project Area acquired by UEC from Uranium One. | N/A | Ownership transition. |

Classification | Tons Ore (000’s) | Tonnes Ore (1000’s) | Average Grade (% eU3O8) | Pounds eU3O8 (000’s) |

| Measured | 2,674 | 2,426 | 0.094 | 5,016.9 |

| Indicated | 2,660 | 2,413 | 0.088 | 4,696.9 |

Total M&I | 5,334 | 4,839 | 0.091 | 9,713.8 |

| Inferred | 866 | 786 | 0.073 | 1,258.0 |

Total Resources | 6,200 | 5,625 | 0.088 | 10,971.8 |

| 1. | The sum of measured and indicated tons and lbs. may not add up to the reported total due to rounding. | |

| 2. | Measured and indicated mineral resources as defined in 17 CFR § 229.1300. | |

| 3. | GT Cutoff = 0.25 ft% eU3O8. | |

| 4. | All reported resources occur below the static water table. | |

| 5. | The point of reference for mineral resources is in-situ at the Project. | |

| 6. | Mineral resources that are not mineral reserves do not have demonstrated economic viability. | |

| 7. | A long-term uranium price of $40/lb U3O8 and an 80% metallurgical recovery factor were considered for the purposes of determining the reasonable prospect of economic extraction. |

Year | Company | Operations/Activity | Amount (No. of Drill holes) | Results of Work |

1967 | Kerr-McGee, Homestake, Teton | Early uranium exploration was completed by the three companies in the Allemand-Ross Project Area. Exploration was typically for shallower mineralization (<1,000 ft). | Approximately 100 | Exploration of shallow mineralization (<1,000 ft). |

1971 | Conoco | Conoco staked lode mining claims in 1969. In 1970, Conoco entered an agreement with National Resources Corporation to earn in on the Allemand-Ranch land holdings. National Resources Corporation’s interests were acquired by Pioneer Nuclear in 1972 and the joint venture partnership was maintained until 1975. In 1979, Conoco continued to operate the drilling program. Conoco closed its mineral department in 1984. | Approximately 1,180 | A significant amount of the mineralization within the Allemand-Ross Project Area was delineated. |

1984 | Power Reactor and Nuclear Fuel Development Corporation (“PNC”) | PNC assumed control of the Allemand-Ross Project Area and continued exploration. | Approximately 50 | Additional exploration completed by PNC. |

Early 1990s | PNC | Mineral rights were allowed to lapse due to further declining uranium market conditions. | N/A | Lost mineral rights. |

Early 2000s-2005 | HPU and EMC | Claims and leases were acquired during the uranium market upswing. HPU held most claims and leases and EMC holding the remainder of the Allemand-Ross Project Area. | N/A | Mineral rights were acquired. |

2007 | EMC | EMC acquired HPU. The properties were consolidated. | N/A | Properties consolidated. |

2007 | Uranium One | Uranium One acquired EMC. Uranium One proceeded to conduct verification and resource enhancement drilling. Most drilling was completed between 2008 and 2010. | Approximately 300 | Additional exploration completed within the Allemand-Ross Project Area with average depths ranging from 1,118 ft to 1,546 ft. |

2021 | UEC | The Allemand-Ross Project Area acquired by UEC from Uranium One. | N/A | Ownership transition. |

Classification | Tons Ore (000’s) | Tonnes Ore (1000’s) | Average Grade (% eU3O8) | Pounds eU3O8 (000’s) |

| Measured | 246 | 223 | 0.085 | 417.0 |

| Indicated | 32 | 29 | 0.066 | 42.4 |

Total M&I | 278 | 252 | 0.083 | 459.4 |

| Inferred | 1,275 | 1,157 | 0.098 | 2,496.0 |

Total Resources | 1,553 | 1,409 | 0.095 | 2,955.4 |

| 1. | The sum of resource tons and lbs. may not add up to the reported total due to rounding. | |

| 2. | Measured and indicated mineral resources as defined in 17 CFR § 229.1300. | |

| 3. | GT Cutoff = 0.25 ft% eU3O8. | |

| 4. | All reported resources occur below the static water table. | |

| 5. | The point of reference for mineral resources is in-situ at the Project. | |

| 6. | Mineral resources that are not mineral reserves do not have demonstrated economic viability. | |

| 7. | A long-term uranium price of $40/lb U3O8 and an 80% metallurgical recovery factor were considered for the purposes of determining the reasonable prospect of economic extraction. |

Year | Company | Operations/Activity | Amount (No. of Drill holes) | Results of Work |

1969 | Mono and RME | Under a joint venture, Mono and RME conducted the initial exploration program through drilling. Upon successful exploration, the Bear Creek Uranium Company was formed under general partnership between Mono and RME. | Unspecified and included in the total estimate. | Successful exploration led to joint venture and mill construction. |

1975-1982 | Bear Creek Uranium Company | A mill was constructed in 1975. Open pit mining operations began in 1977 until 1982. Mining claims were dropped after 1982. | Approximately 6,880 | 4.7 million tons of material from open pit mining processed at the Bear Creek mill. |

2006 | EMC | EMC located the unpatented mining claims and acquired the state mineral leases. | N/A | Lapsed mineral leases acquired. |

2007 | Uranium One | Uranium One acquired EMC and all rights to the Barge Project Area. | None as of 2019. | No exploration had been completed. |

2021 | UEC | Barge Project Area acquired by UEC from Uranium One. | N/A | Ownership. |

Classification | Tons Ore (000’s) | Tonnes Ore (1000’s) | Average Grade (% eU3O8) | Pounds eU3O8 (000’s) |

| Measured | - | - | - | - |

| Indicated | 4,301 | 3,902 | 0.051 | 4,361.0 |

Total M&I | 4,301 | 3,902 | 0.051 | 4,361.0 |

| Inferred | - | - | - | - |

Total Resources | 4,301 | 3,902 | 0.051 | 4,361.0 |

| 1. | The sum of measured and indicated tons and lbs. may not add up to the reported total due to rounding. | |

| 2. | Measured and indicated mineral resources as defined in 17 CFR § 229.1300. | |

| 3. | GT Cutoff = 0.25 ft% eU3O8. | |

| 4. | All reported resources occur below the static water table. | |

| 5. | The point of reference for mineral resources is in-situ at the Project. | |

| 6. | Mineral resources that are not mineral reserves do not have demonstrated economic viability. | |

| 7. | A long-term uranium price of $40/lb U3O8 and an 80% metallurgical recovery factor were considered for the purposes of determining the reasonable prospect of economic extraction. |

Year | Company | Operations/Activity | Amount (No. of Drill holes) | Results of Work |

Jab | ||||

Unspecified | Silverbell Industries | Originator of the Jab/West Jab Project Area. | Not specified. | The Jab/West Jab Project Area initially developed. |

1972 | Union Carbide Corporation (“UCC”) | Delineated an area of shallow oxidized mineralization and completed feasibility studies for open pit mining. The plan was not executed, and a mining permit was prepared for the WDEQ/LQD. The permit was withdrawn due to the declining uranium market in 1982. | Approximately 1,830 | Delineation of shallow oxidized material. |

1985-2000 | Yellowstone Fuels | Property held until a decline in the uranium market in 2000. No data developed by Yellowstone Fuels were available for evaluation. | No data available. | The Jab/West Jab Project Area held but not substantially developed. |

West Jab | ||||

Unspecified | AMAX Petroleum Company | Originator of the Jab/West Jab Project Area. | Not specified. | The Jab/West Jab Project Area initially developed. |

1975-1983 | WNC | WNC drilled the Jab/West Jab Project Area until 1983 when uranium markets had dropped. WNC terminated claim. AMAX Petroleum Company regained control until the claims were dropped. | Approximately 1,020 | Exploration completed by WNC. |

Jab/West Jab | ||||

2006 | EMC | Identified the unpatented mining claims and acquired the state mineral leases. | N/A | Secured right to mine. |

2007 | Uranium One | Uranium One acquired EMC and all rights to the Jab/West Jab Project Area. | None as of 2019 | No exploration had been completed. Right to mine secured. |

2021 | UEC | The Jab/West Jab Project Area acquired by UEC from Uranium One. | N/A | Ownership transition. |

Classification | Tons Ore (000’s) | Tonnes Ore (1000’s) | Average Grade (% eU3O8) | Pounds eU3O8 (000’s) |

| Measured | 1,621 | 1,471 | 0.072 | 2,335.0 |

| Indicated | 253 | 230 | 0.077 | 392.0 |

Total M&I | 1,874 | 1,701 | 0.073 | 2,727.0 |

| Inferred | 1,402 | 1,272 | 0.06 | 1,677.0 |

Total Resources | 3,276 | 2,973 | 0.067 | 4,404.0 |

| 1. | The sum of resource tons and lbs. may not add up to the reported total due to rounding. | |

| 2. | Measured, indicated, and inferred mineral resources as defined in 17 CFR § 229.1300. | |

| 3. | GT Cutoff = 0.25 ft% eU3O8. | |

| 4. | Measured and indicated resources occur below the static water table. The inferred resources at Jab/West Jab occur above the water table and may not be amenable to ISR. | |

| 5. | The point of reference for mineral resources is in-situ at the Project. | |

| 6. | Mineral resources that are not mineral reserves do not have demonstrated economic viability. | |

| 7. | A long-term uranium price of $40/lb U3O8 and an 80% metallurgical recovery factor were considered for the purposes of determining the reasonable prospect of economic extraction. |

Year | Company | Operations/Activity | Amount (No. of Drill holes) | Results of Work |

1966 | Preston Oil Co. (“Preston Oil”) | Awarded the state lease for 720 acres. | None. | Right to mine secured. |

1966 | Inexco Oil Company (“Inexco”) | Inexco assigned lease from Preston Oil in 1966 and conducted exploration drilling program in 1969 and 1970. | 215 | Delineation of mineralized areas. |

1974 | Uranerz USA | Inexco formed a joint venture with Uranerz USA who became the operator. Over the next two years, Uranerz expanded the drilling program, including core drilling. | 715 | Delineation of mineralized areas. |

Not specified | Cotter Corporation (“Cotter”) | Cotter acquired the property and evaluated both conventional open pit and in situ mining methods. Cotter obtained a surface mining permit in 1979. A 200-foot-deep test pit was excavated in 1981 in a small mineralization area. The pit was subsequently reclaimed, but the state mining permit remains active. | Not specified | Falling uranium prices in the 1980’s halted further development. |

1994 | Cotter and PRI | PRI entered a joint venture agreement with Cotter and completed a feasibility study for development as an ISR mine (PRI, 1995). Completed additional drilling in 1994. | Not specified | The feasibility study was positive; however, the Charlie Project Area did not proceed, and the joint venture agreement expired. |

2014 | Cotter | In 2014 Cotter sought to convert the permit to ISR mining; however, that process has not been completed. | None | Unknown. |

2018 | Anfield Energy Inc. (“Anfield”) | Anfield acquired the Charlie Project Area from Cotter. | None | Oversaw technical reporting and auditing of Charlie Project Area resources. |

2021 | UEC | UEC acquired the Charlie Project Area from Anfield. | N/A | Ownership transition. |

Classification | Tons Ore (000’s) | Tonnes Ore (1000’s) | Average Grade (% eU3O8) | Pounds eU3O8 (000’s) |

| Measured | - | - | - | - |

| Indicated | 1,255 | 1,139 | 0.123 | 3,100.0 |

Total M&I | 1,255 | 1,139 | 0.123 | 3,100.0 |

| Inferred | 411 | 373 | 0.120 | 988.0 |

Total Resources | 1,666 | 1,512 | 0.123 | 4,088.0 |

| 1. | The sum of resource tons and lbs. may not add up to the reported total due to rounding. | |

| 2. | Measured, indicated, and inferred mineral resources as defined in 17 CFR § 229.1300. | |

| 3. | GT Cutoff = 0.20 ft% eU3O8. | |

| 4. | All reported resources occur below the static water table. | |

| 5. | The point of reference for mineral resources is in-situ at the Project. | |

| 6. | Mineral resources that are not mineral reserves do not have demonstrated economic viability. | |

| 7. | A long-term uranium price of $40/lb U3O8 and an 80% metallurgical recovery factor were considered for the purposes of determining the reasonable prospect of economic extraction. |

Year | Company | Operations/Activity | Amount (No. of Drill holes) | Results of Work |

Early 1950s | Independent operator | An internal report from 1969 states a Mr. Vickers reportedly discovered surficial mineralization and mined approximately 100 tons U3O8 at an average grade of 0.30%. Uranium was shipped to the AEC buying station at Edgemont, South Dakota. | None | Exploration and production of 100 tons U3O8. |

1972 | RME | RME acquired interest in the project in 1972 and conducted extensive drilling through 1978. Pilot scale ISR mining was conducted using four seven-spot patterns with a 50-foot radius. The first 3 patterns used sulfuric acid as the primary lixiviant and the fourth sodium carbonate-bicarbonate as the primary lixiviant. The U.S. Bureau of Mines assisted RME in conducting the pilot testing and documented the results in a publication titled “Case History of a Pilot-Scale Acidic In Situ Uranium Leaching Experiment” (Nigbor, N. T., et al, 1982). RME controlled the project until the late 1980s when the mineral interests were dropped due to declining uranium prices. | Approximately 1,100 | Exploration and pilot scale ISR mining. |

2005 and 2006 | EMC | EMC located unpatented mining lode claims and secured mineral leases and surface agreements within the area formerly held by RME. EMC conducted exploratory drilling and compiled previous data and maps for the project. | Approximately 45 | Secured right to mine. |

2008 | Uranium One | EMC was acquired by Uranium One. | None | Ownership transition. |

2016 | Anfield | Anfield purchased Nine Mile Lake Project from Uranium One. | None | Oversaw technical reporting and auditing of project resources. |

2022 | UEC | UEC acquired the Nine Mile Lake Project from Anfield. | N/A | Ownership transition. |

Classification | Tons Ore (000’s) | Tonnes Ore (1000’s) | Average Grade (% eU3O8) | Pounds eU3O8 (000’s) |

| Measured | - | - | - | - |

| Indicated | - | - | - | - |

Total M&I | - | - | - | - |

| Inferred | 3,405 | 3,089 | 0.036 | 4,308.0 |

Total Resources | 3,405 | 3,089 | 0.036 | 4,308.0 |

| 1. | The sum of resource tons and lbs. may not add up to the reported total due to rounding. | |

| 2. | Measured, indicated, and inferred mineral resources as defined in 17 CFR § 229.1300. | |

| 3. | GT Cutoff = 0.25 ft% eU3O8. | |

| 4. | All reported resources occur below the static water table. | |

| 5. | The point of reference for mineral resources is in-situ at the Project. | |

| 6. | Mineral resources that are not mineral reserves do not have demonstrated economic viability. | |

| 7. | A long-term uranium price of $40/lb U3O8 and an 80% metallurgical recovery factor were considered for the purposes of determining the reasonable prospect of economic extraction. |