Indicate by check mark whether the registrant is an accelerated filera shell company (as defined inby Rule 12b-2 of the Exchange Act Rule 12b-2)Act).

Yesx No¨.

| Yeso | Nox |

The aggregate market value of the Common Stock of The Kroger Co. held by non-affiliates as of April 8, 2005: $11,616,627,274August 12, 2006: $16,271 million. There were 709,560,479 shares of Common Stock ($1 par value) outstanding as of March 30, 2007.

Documents Incorporated by Reference:

Proxy statement to be filed pursuant to Regulation 14A of the Exchange Act on or before May 31, 2005,June 4, 2007, incorporated by reference into Parts II andPart III of Form 10-K.

PART I

EXPLANATORY NOTE:ITEM 1.BUSINESS.

This Amendment No. 1 toThe Kroger Co. was founded in 1883 and incorporated in 1902. As of February 3, 2007, the Company was one of the largest retailers in the United States based on annual sales. The Company also manufactures and processes some of the food for sale in its supermarkets. The Company’s principal executive offices are located at 1014 Vine Street, Cincinnati, Ohio 45202, and its telephone number is (513) 762-4000. The Company maintains a web site (www.kroger.com) that includes additional information about the Company. The Company makes available through its web site, free of charge, its annual reports on Form 10-K, its quarterly reports on Form 10-Q and its current reports on Form 8-K, including amendments thereto. These forms are available as soon as reasonably practicable after the Company has filed or furnished them electronically with the SEC.

The Company’s revenues are earned and cash is filed solelygenerated as consumer products are sold to insertcustomers in its stores. The Company earns income predominantly by selling products at price levels that produce revenues in excess of its costs to make these products available to its customers. Such costs include procurement and distribution costs, facility occupancy and operational costs, and overhead expenses.

EMPLOYEES

The Company employs approximately 310,000 full and part-time employees. A majority of the Company’s employees are covered by collective bargaining agreements negotiated with local unions affiliated with one of several different international unions. There are approximately 320 such agreements, usually with terms of three to five years.

During fiscal 2007, the Company has major labor contracts expiring in southern California, Cincinnati, Detroit, Houston, Memphis, Toledo, Seattle and West Virginia. Negotiations in 2007 will be challenging as the Company must have competitive cost structures in each market while meeting our associates’ needs for good wages and affordable health care.

STORES

As of February 3, 2007, the Company operated, either directly or through its subsidiaries, 2,468 supermarkets and multi-department stores, 631 of which had fuel centers. Approximately 39% of these supermarkets were operated in Company-owned facilities, including some Company-owned buildings on leased land. The Company’s current strategy emphasizes self-development and ownership of store real estate. The Company’s stores operate under several banners that have strong local ties and brand equity. Supermarkets are generally operated under one of the following formats: combination food and drug stores (“combo stores”); multi-department stores; price impact warehouses; or marketplace stores.

The combo stores are the primary food store format. They are typically able to earn a conformed signaturereturn above the Company’s cost of capital by drawing customers from a 2 – 2½ mile radius. The Company believes this format is successful because the stores are large enough to offer the specialty departments that customers desire for one-stop shopping, including natural food and organic sections, pharmacies, general merchandise, pet centers and high-quality perishables such as fresh seafood and organic produce. Many combo stores include a fuel center.

Multi-department stores are significantly larger in size than combo stores. In addition to the Reportdepartments offered at a typical combo store, multi-department stores sell a wide selection of Independent Registered Public Accounting Firm appearinggeneral merchandise items such as apparel, home fashion and furnishings, electronics, automotive, toys and fine jewelry. Many multi-department stores include a fuel center.

Price impact warehouse stores offer a “no-frills, low cost” warehouse format and feature everyday low prices plus promotions for a wide selection of grocery and health and beauty care items. Quality meat, dairy, baked goods and fresh produce items provide a competitive advantage. The average size of a price impact warehouse store is similar to that of a combo store.

In addition to supermarkets, the Company operates, either directly or through subsidiaries, 779 convenience stores and 412 fine jewelry stores. Substantially all of our fine jewelry stores are operated in leased locations. Subsidiaries operated 687 of the convenience stores, while 92 were operated through franchise agreements. Approximately 44% of the convenience stores operated by subsidiaries were operated in Company-owned facilities. The convenience stores offer a limited assortment of staple food items and general merchandise and, in most cases, sell gasoline.

SEGMENTS

The Company operates retail food and drug stores, multi-department stores, jewelry stores, and convenience stores throughout the United States. The Company’s retail operations, which represent substantially all of the Company’s consolidated sales, earnings and total assets, are its only reportable segment. All of the Company’s operations are domestic. Revenues, profit and losses, and total assets are shown in the Company’s Consolidated Financial Statements set forth in Item 8 below.

MERCHANDISING AND MANUFACTURING

Corporate brand products play an important role in the Company’s merchandising strategy. Supermarket divisions typically stock approximately 11,000 private label items. The Company’s corporate brand products are produced and sold in three quality “tiers.” Private Selection is the premium quality brand designed to be a unique item in a category or to meet or beat the “gourmet” or “upscale” brands. The “banner brand” (Kroger, Ralphs, King Soopers, etc.), which conformed signature inadvertentlyrepresents the majority of the Company’s private label items, is designed to be equal to or better than the national brand and carries the “Try It, Like It, or Get the National Brand Free” guarantee. Kroger Value is the value brand, designed to deliver good quality at a very affordable price.

Approximately 55% of the corporate brand units sold are produced in the Company’s manufacturing plants; the remaining corporate brand items are produced to the Company’s strict specifications by outside manufacturers. The Company performs a “make or buy” analysis on corporate brand products and decisions are based upon a comparison of market-based transfer prices versus open market purchases. As of February 3, 2007, the Company operated 42 manufacturing plants. These plants consisted of 18 dairies, 11 deli or bakery plants, five grocery product plants, three beverage plants, three meat plants and two cheese plants.

EXECUTIVE OFFICERSOFTHE REGISTRANT

The disclosure regarding executive officers is set forth in Item 10 of Part III of this Form 10-K under the heading “Executive Officers of the Company,” and is incorporated herein by reference.

ITEM 1A.RISK FACTORS.

There are risks and uncertainties that can affect our business. The significant risk factors are discussed below. Please also see the “Outlook” section in Item 7 of this Form 10-K for forward-looking statements and factors that could cause us not to realize our goals or meet our expectations.

COMPETITIVE ENVIRONMENT

The operating environment for the food retailing industry continues to be characterized by intense price competition, aggressive supercenter expansion, increasing fragmentation of retail formats, entry of non-traditional competitors and market consolidation. Additionally, consumers are increasingly looking to restaurants to fulfill their food product needs. We have developed a strategic plan that we believe is a balanced approach that will enable Kroger to meet the wide-ranging needs and expectations of our customers. However, the nature and extent to which our competitors implement various pricing and promotional activities in response to increasing competition - including our execution of our strategic plan - and our response to these competitive actions, can adversely affect our profitability.

FOOD SAFETY

Customers count on Kroger to provide them with wholesome food products. Concerns regarding the safety of food products sold by Kroger could cause shoppers to avoid purchasing certain products from us, or to seek alternative sources of supply for all of their food needs, even if the basis for the concern is outside of our control. Any lost confidence on the part of our customers would be difficult and costly to reestablish. As such, any issue regarding the safety of any food items sold by Kroger, regardless of the cause, could have a substantial and adverse effect on our operations.

LABOR RELATIONS

A significant majority of our employees are covered by collective bargaining agreements with unions, and our relationship with those unions, including any work stoppages, could have an adverse impact on our financial results.

We are a party to approximately 320 collective bargaining agreements. We have major contracts expiring in 2007 in southern California, Cincinnati, Detroit, Houston, Memphis, Toledo, Seattle and West Virginia. In future negotiations with labor unions, we expect that rising health care, pension and employee benefit costs, among other issues, will continue to be important topics for negotiation. Upon the expiration of our collective bargaining agreements, work stoppages by the affected workers could occur if we are unable to negotiate acceptable contracts with labor unions. This could significantly disrupt our operations. Further, if we are unable to control health care, pension and wage costs, or gain operational flexibility under our collective bargaining agreements, we may experience increased operating costs and an adverse impact on future results of operations.

STRATEGY EXECUTION

Our strategy focuses on improving our customers’ shopping experience through enhanced service, product selection and value. Successful execution of this strategy requires a balance between sales growth and earnings growth. Maintaining this strategy requires the ability to identify and execute plans to generate cost savings and productivity improvements that can be invested in the merchandising and pricing initiatives necessary to support our customer-focused programs, as well as recognizing and implementing organizational changes as required. If we are unable to execute our plans, or if our plans fail to meet our customers’ expectations, our sales and earnings growth expectations could be adversely affected.

DATAAND TECHNOLOGY

Our business is increasingly dependent on information technology systems that are complex and vital to continuing operations. If we were to experience difficulties maintaining existing systems or implementing new systems, we could incur significant losses due to disruptions in our operations. Additionally, these systems contain valuable proprietary data that, if breached, would have an adverse effect on Kroger.

INDEBTEDNESS

As of year-end 2006, Kroger’s outstanding indebtedness, including capital leases and financing obligations, totaled approximately $7.1 billion. This indebtedness could reduce our ability to obtain additional financing for working capital, acquisitions or other purposes and could make us more vulnerable to economic downturns and competitive pressures. If debt markets do not permit us to refinance certain maturing debt, we may be required to dedicate a substantial portion of our cash flow from operations to payments on our indebtedness. Changes in our credit ratings, or in the interest rate environment, could have an adverse effect on our financing costs and structure.

LEGAL PROCEEDINGS

From time to time, we are a party to legal proceedings, including matters involving personnel and employment issues, personal injury, antitrust claims and other proceedings. Some of these proceedings, including product liability cases, could result in a substantial loss to Kroger in the event that other potentially responsible parties are unable (for financial reasons or otherwise) to satisfy a judgment entered against them. Others purport to be brought as class actions on behalf of similarly situated parties. We estimate our exposure to these legal proceedings and establish accruals for the estimated liabilities. Assessing and predicting the outcome of these matters involves substantial uncertainties. While we currently do not expect any outstanding legal proceedings to have a material effect on the financial condition of Kroger, unexpected outcomes in these legal proceedings, or changes in our evaluations or predictions about the proceedings, could have a material adverse effect on our financial results. Please also refer to the “Legal Proceedings” section in Item 3 below.

MULTI-EMPLOYER POST-RETIREMENT OBLIGATIONS

As discussed in more detail below in “Management’s Discussion and Analysis of Financial Condition and Results of Operation-Critical Accounting Policies-Post-Retirement Benefit Plans,” Kroger contributes to several multi-employer pension plans based on obligations arising under collective bargaining agreements with unions representing employees covered by those agreements. In addition to future contribution obligations that Kroger may have under those plans, there is a risk that the agencies that rate Kroger’s outstanding debt instruments could view the underfunded nature of these plans unfavorably when determining their ratings on the Company’s debt securities. Any downgrading of Kroger’s debt ratings likely would increase Kroger’s cost of borrowing.

INSURANCE

We use a combination of insurance and self-insurance to provide for potential liability for workers’ compensation, automobile and general liability, property, director and officers’ liability, and employee health care benefits. Any actuarial projection of losses is subject to a high degree of variability. Changes in legal trends and interpretations, variability in inflation rates, changes in the nature and method of claims settlement, benefit level changes due to changes in applicable laws, and changes in discount rates could all affect ultimate settlements of claims.

ITEM 1B.UNRESOLVED STAFF COMMENTS.

None.

ITEM 2.PROPERTIES.

As of February 3, 2007, the Company operated more than 3,500 owned or leased supermarkets, convenience stores, fine jewelry stores, distribution warehouses and food processing facilities through divisions, subsidiaries or affiliates. These facilities are located throughout the United States. A majority of the properties used to conduct the Company’s business are leased.

The Company generally owns store equipment, fixtures and leasehold improvements, as well as processing and manufacturing equipment. The total cost of the Company’s owned assets and capitalized leases at February 3, 2007, was omitted$20,982 million while the accumulated depreciation was $9,203 million.

Leased premises generally have base terms ranging from ten-to-twenty years with renewal options for additional periods. Some options provide the right to purchase the property after conclusion of the lease term. Store rentals are normally payable monthly at a stated amount or at a guaranteed minimum amount plus a percentage of sales over a stated dollar volume. Rentals for the distribution, processing and miscellaneous facilities generally are payable monthly at stated amounts. For additional information on lease obligations, see Note 8 to the Consolidated Financial Statements.

ITEM 3.LEGAL PROCEEDINGS.

On October 6, 2006, the Company petitioned the Tax Court (In Re: Ralphs Grocery Company and Subsidiaries, formerly known as Ralphs Supermarkets, Inc., Docket No. 20364-06) for a redetermination of deficiencies set by the Commissioner of Internal Revenue. The dispute at issue involves a 1992 transaction in which Ralphs Holding Company acquired the stock of Ralphs Grocery Company and made an election under Section 338(h)(10) of the Internal Revenue Code. The Commissioner has determined that the acquisition of the stock was not a purchase as defined by Section 338(h)(3) of the Internal Revenue Code and that the acquisition does not qualify as a purchase. The Company has strong arguments in favor of its position, but due to the inherent uncertainty involved in the litigation process, an adverse decision that could have a material adverse effect on the Company’s financial results is a possible outcome. As of February 3, 2007, an adverse decision would require a cash payment of approximately $363 million, including interest.

On February 2, 2004, the Attorney General for the State of California filed an action in Los Angeles federal court (California, ex rel Lockyer v. Safeway, Inc. dba Vons, a Safeway Company; Albertson’s, Inc. and Ralphs Grocery Company, a division of The Kroger Co., United States District Court Central District of California, Case No. CV04-0687) alleging that the Mutual Strike Assistance Agreement (the “Agreement”) between the Company, Albertson’s, Inc. and Safeway Inc. (collectively, the “Retailers”), which was designed to prevent the union from placing disproportionate pressure on one or more of the Retailers by picketing such Retailer(s) but not the other Retailer(s) during the labor dispute in southern California, violated Section 1 of the Sherman Act. The lawsuit seeks declarative and injunctive relief. On May 25, 2005, the Court denied a motion for a summary judgment filed by the defendants. Ralphs and the other defendants filed a notice of an interlocutory appeal to the United States Court of Appeals for the Ninth Circuit. On November 29, 2005, the appellate court dismissed the appeal. On December 7, 2006, the Court denied a motion for summary judgment filed by the State of California. The Company continues to believe it has strong defenses against this lawsuit and is vigorously defending it. Although this lawsuit is subject to uncertainties inherent to the litigation process, based on the information presently available to the Company, management does not expect that the ultimate resolution of this action will have a material adverse effect on the Company’s financial condition, results of operations or cash flows.

Ralphs Grocery Company is the defendant in a group of civil actions initially filed in 2003 and for which a coordination order was issued on January 20, 2004 inThe Great Escape Promotion Cases pending in the Superior Court of California, County of Los Angeles, Case No. JCCP No. 4343. The plaintiffs allege that Ralphs violated various laws protecting consumers in connection with a promotion pursuant to which Ralphs offered travel awards to customers. On February 22, 2006, the Court inThe Great Escape Promotion Cases issued an Order granting preliminary approval of the class action settlement. Notice of the class action settlement was sent to class members, and the Court issued an Order finally approving the class action settlement on August 25, 2006. The settlement involved the issuance of coupons and gift cards. While the ultimate cost of the settlement to Ralphs is largely dependent on the rate of coupon redemption, management does not expect that the ultimate resolution of this action will have a material adverse effect on the Company’s financial condition, results of operations or cash flows.

On August 12, 2000, Ralphs Grocery Company, along with several other potentially responsible parties, entered into a consent decree with the U. S. Environmental Protection Agency surrounding the purported release of volatile organic compounds in connection with industrial operations at a property located in Los Angeles, California. The consent decree followed the EPA’s earlier Administrative Order No. 97-18 in which the EPA sought remedial action pursuant to its authority under the Comprehensive Environmental Remediation, Compensation and Liability Act. Under the consent decree, Ralphs contributes a share of the costs associated with groundwater extraction and treatment, which share currently totals approximately $30,000-$40,000 per year. The treatment process is expected to continue until at least 2012.

Various claims and lawsuits arising in the normal course of business, including suits charging violations of certain antitrust, wage and hour, or civil rights laws, are pending against the Company. Some of these suits purport or have been determined to be class actions and/or seek substantial damages. Any damages that may be awarded in antitrust cases will be automatically trebled. Although it is not possible at this time to evaluate the merits of all of these claims and lawsuits, nor their likelihood of success, the Company is of the belief that any resulting liability will not have a material adverse effect on the Company’s financial position.

The Company continually evaluates its exposure to loss contingencies arising from pending or threatened litigation and believes it has made adequate provisions therefor. Nonetheless, assessing and predicting the outcomes of these matters involve substantial uncertainties. It remains possible that despite management’s current belief, material differences in actual outcomes or changes in management’s evaluation or predictions could arise that could have a material adverse impact on the Company’s financial condition or results of operation.

ITEM 4.SUBMISSION OF MATTERS TO A VOTE OF SECURITY HOLDERS.

None.

PART II

| ITEM 5. | MARKET FOR REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES. |

(a)

| COMMON STOCK PRICE RANGE | ||||||||||||

| 2006 | 2005 | |||||||||||

| Quarter | High | Low | High | Low | ||||||||

| 1st | $ | 20.98 | $ | 18.05 | $ | 18.22 | $ | 15.15 | ||||

| 2nd | $ | 23.23 | $ | 19.37 | $ | 20.00 | $ | 16.46 | ||||

| 3rd | $ | 24.15 | $ | 21.49 | $ | 20.88 | $ | 19.09 | ||||

| 4th | $ | 25.96 | $ | 21.12 | $ | 20.58 | $ | 18.42 | ||||

Main trading market: New York Stock Exchange (Symbol KR)

Number of shareholders of record at year-end 2006: 61,920

Number of shareholders of record at March 30, 2007: 53,435

The Company did not pay dividends on its Common Stock during fiscal year 2005. During fiscal 2006, the Company’s Board of Directors adopted a dividend policy and paid three quarterly dividends of $0.065 per share. On March 1, 2007, the Company paid its fourth quarterly dividend of $0.065 per share. On March 15, 2007, the Company announced that its Board of Directors had increased the quarterly dividend to $0.075 per share, payable on June 1, 2007, to shareholders of record at the close of business on May 15, 2007.

The information regarding equity compensation plans is set forth in Item 12 of this Form 10-K and is incorporated by reference into this Item 5.

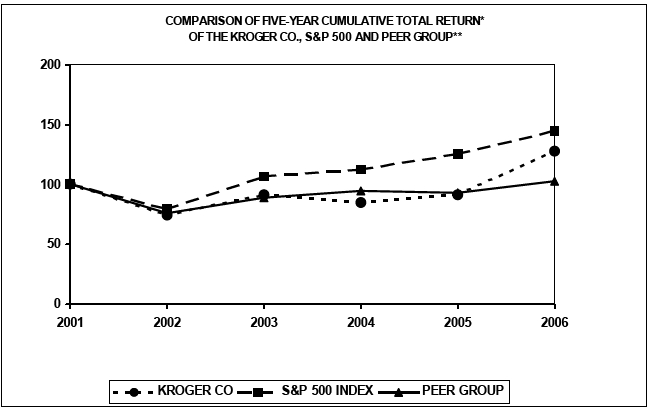

PERFORMANCE GRAPH

Set forth below is a line graph comparing the five-year cumulative total shareholder return on Kroger’s common stock, based on the market price of thecommon stock and assuming reinvestment of dividends, with the cumulative total return of companies in the Standard & Poor’s 500 Stock Index and the PeerGroup composed of food and drug companies.

Historically, our peer group has consisted of the major food store companies. In recent years there have been significant changes in the industry,including consolidation and increased competition from supercenters and drug chains. As a result, in 2003 we changed our peer group ( the “Peer Group”) toinclude companies operating supermarkets, supercenters and warehouse clubs in the United States as well as the major drug chains with which Kroger competes.

| Base | INDEXED RETURNS | |||||||||||

| Period | Years Ending | |||||||||||

| Company Name/Index | 2001 | 2002 | 2003 | 2004 | 2005 | 2006 | ||||||

| The Kroger Co. | 100 | 74.23 | 91.15 | 84.80 | 91.34 | 128.31 | ||||||

| S&P 500 Index | 100 | 79.50 | 106.98 | 112.69 | 125.80 | 144.66 | ||||||

| Peer Group | 100 | 76.05 | 88.72 | 94.99 | 93.12 | 102.54 | ||||||

Kroger’s fiscal year ends on the Saturday closest to January 31.

| * | Total assumes $100 invested on February 3, 2002, in The Kroger Co., S&P 500 Index and the Peer Group, with reinvestment of dividends. | |

| ** | The Peer Group consists of Albertson’s, Inc., Costco Wholesale Corp., CVS Corp, Delhaize Group SA (ADR), Great Atlantic & Pacific Tea Company, Inc., Koninklijke Ahold NV (ADR), Marsh Supermarkets Inc. (Class A), Safeway, Inc., Supervalu Inc., Target Corp., Wal-Mart Stores Inc., Walgreen Co., Whole Foods Market Inc. and Winn-Dixie Stores, Inc. Albertson’s, Inc., was substantially acquired by Supervalu in July 2006, and is included through 2005. Marsh Supermarkets was acquired by MarshSupermarkets Holding Corp. in September 2006, and is included through 2005. Winn-Dixie Stores emerged from bankruptcy in 2006 as a new issue and returnsfor the old and new issue were calculated then weighted to determine 2006 return. | |

Data supplied by Standard & Poor’s.

The foregoing Performance Graph will not be deemed incorporated by reference into any other filing, absent an express reference thereto.

(c)

| ISSUER PURCHASES OF EQUITY SECURITIES | ||||||||||

| Total Number of | Maximum Dollar | |||||||||

| Shares | Value of Shares | |||||||||

| Purchased as | that May Yet Be | |||||||||

| Part of Publicly | Purchased Under | |||||||||

| Total Number | Average | Announced | the Plans or | |||||||

| of Shares | Price Paid | Plans or | Programs(3) | |||||||

| Period(1) | Purchased | Per Share | Programs(2) | (in millions) | ||||||

| First period - four weeks | ||||||||||

| November 5, 2006 to December 2, 2006 | 1,176,497 | $ | 21.99 | 1,175,000 | $ | 297 | ||||

| Second period - four weeks | ||||||||||

| December 3, 2006 to December 30, 2006 | 1,203,899 | $ | 23.18 | 1,200,000 | $ | 271 | ||||

| Third period - five weeks | ||||||||||

| December 31, 2006 to February 3, 2007 | 2,205,944 | $ | 23.75 | 2,200,000 | $ | 233 | ||||

| Total | 4,586,340 | $ | 23.15 | 4,575,000 | $ | 233 | ||||

| (1) | The reported periods conform to the Company’s fiscal calendar composed of thirteen 28-day periods. The fourth quarter of 2006 contained two 28-day periods and one 35-day period. | |

| (2) | Shares were repurchased under (i) a $500 million stock repurchase program, authorized by the Board of Directors on May 4, 2006, and (ii) a program announced on December 6, 1999, to repurchase common stock to reduce dilution resulting from our employee stock option plans, which program is limited to proceeds received from exercises of stock options and the tax benefits associated therewith. The programs have no expiration date but may be terminated by the Board of Directors at any time. Total number of shares purchased includes shares that were surrendered to the Company by participants in the Company’s long-term incentive plans to pay for taxes on restricted stock awards. | |

| (3) | Amounts shown in this column reflect amounts remaining under the $500 million stock repurchase program referenced in Note 2 above. Amounts to be invested under the program utilizing option exercise proceeds are dependent upon option exercise activity. | |

ITEM 6.SELECTED FINANCIAL DATA.

| Fiscal Years Ended | ||||||||||||||||

| February 3, | January 28, | January 29, | January 31, | February 1, | ||||||||||||

| 2007 | 2006 | 2005 | 2004 | 2003 | ||||||||||||

| (53 weeks) | (52 weeks) | (52 weeks) | (52 weeks) | (52 weeks) | ||||||||||||

| (In millions, except per share amounts) | ||||||||||||||||

| Sales | $ | 66,111 | $ | 60,553 | $ | 56,434 | $ | 53,791 | $ | 51,760 | ||||||

| Earnings (loss) before cumulative effect of accounting | ||||||||||||||||

| change | 1,115 | 958 | (104 | ) | 285 | 1,218 | ||||||||||

| Cumulative effect of accounting change(1) | — | — | — | — | (16 | ) | ||||||||||

| Net earnings (loss) | 1,115 | 958 | (104 | ) | 285 | 1,202 | ||||||||||

| Diluted earnings (loss) per share: | ||||||||||||||||

| Earnings (loss) before cumulative effect of accounting | ||||||||||||||||

| change | 1.54 | 1.31 | (0.14 | ) | 0.38 | 1.54 | ||||||||||

| Cumulative effect of accounting change(1) | — | — | — | — | (0.02 | ) | ||||||||||

| Net earnings (loss) | 1.54 | 1.31 | (0.14 | ) | 0.38 | 1.52 | ||||||||||

| Total assets | 21,215 | 20,482 | 20,491 | 20,767 | 20,349 | |||||||||||

| Long-term liabilities, including obligations under capital | ||||||||||||||||

| leases and financing obligations | 8,711 | 9,377 | 10,537 | 10,515 | 10,569 | |||||||||||

| Shareowners’ equity | 4,923 | 4,390 | 3,619 | 4,068 | 3,937 | |||||||||||

| Cash dividends per common share(2) | 0.195 | — | — | — | — | |||||||||||

| (1) | Amounts are net of tax. | |

| (2) | During the fiscal year ended February 2, 2002, the Company was prohibited from paying cash dividends under the terms of its previous Credit Agreement. On May 22, 2002, the Company entered into a new Credit Agreement, at which time the restriction on payment of cash dividends was eliminated. | |

| ITEM 7. | MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATION. |

OUR BUSINESS

The Kroger Co. was founded in 1883 and incorporated in 1902. It is one of the nation’s largest retailers, operating 2,468 supermarket and multi-department stores under two dozen banners including Kroger, Ralphs, Fred Meyer, Food 4 Less, King Soopers, Smith’s, Fry’s, Fry’s Marketplace, Dillons, QFC and City Market. Of these stores, 631 had fuel centers. We also operate 779 convenience stores and 412 fine jewelry stores.

Kroger operates 42 manufacturing plants, primarily bakeries and dairies, which supply approximately 55% of the corporate brand units sold in the Company’s retail outlets.

Our revenues are earned and cash is generated as consumer products are sold to customers in our stores. We earn income predominately by selling products at price levels that produce revenues in excess of our costs to make these products available to our customers. Such costs include procurement and distribution costs, facility occupancy and operational costs, and overhead expenses. Our operations are reported as a single reportable segment: the retail sale of merchandise to individual customers.

OUR 2006 PERFORMANCE

The continued focus of our associates on delivering improved service, product selection and value to our customers generated a year of significantly improved identical supermarket sales growth, excluding fuel sales, in 2006. Our identical supermarket sales, excluding fuel sales, grew at 5.6% in 2006. These results followed strong 2005 identical supermarket sales, excluding fuel sales, of 3.5% in 2005 and 0.8% in 2004.

Increasing market share helped us achieve our results. Our internal analysis shows that we hold the #1 or #2 market share position in 38 of our 44 major markets. We define a major market as one in which we operate nine or more stores. Our share increased in 36 of these 44 major markets, declined in seven and remained unchanged in one. On a volume-weighted basis, our overall market share in these 44 major markets increased approximately 65 basis points during 2006.

We compete against a total of 1,262 supercenters, an increase of 133 over 2005. There are 34 major markets in which supercenters have achieved at least a #3 market share position. Our overall market share in these 34 major markets, on a volume-weighted basis, increased over 70 basis points during 2006. Our market share increased in 27 of these 34 major markets, declined in six and remained unchanged in one.

All of the market share estimates described above are based on our internal data and analysis. We believe they are reliable but can provide no other assurance of reliability. We believe this market share analysis illustrates that Kroger continued to achieve significant growth in 2006, even in the face of aggressive expansion in the supermarket industry by supercenters, intense price competition, increasing fragmentation of retail formats and market consolidation. Our retail price investments, combined with our service and selling initiatives, led to these market share gains in 2006. We believe there is still significant room for growth. In our 44 major markets, we estimate approximately 47% of the share in those markets continues to be held by competitors without our economies of scale.

We were able to balance our sales growth with earnings growth. Our net earnings increased 16.4% to $1.54 per diluted share in 2006, from $1.31 per diluted share in 2005. Earnings growth was primarily driven by strong identical supermarket sales growth, improving operating margins and fewer shares outstanding. In addition, fiscal 2006 included a 53rd week that benefited the year by an estimated $0.07 per diluted share, adjustments to certain deferred tax balances that benefited the year by $0.03 per diluted share, expense totaling $0.03 per diluted share for increases in legal reserves, and $0.06 per diluted share of expense for the adoption of stock option expensing.

FUTURE EXPECTATIONS

While we were pleased with our 2006 results, we must continue to adjust our business model to meet the changing needs and expectations of our customers. Our plan requires balance between sales growth, earnings growth and profitable capital investment.

We expect to achieve identical supermarket sales growth through merchandising and operating initiatives that improve the shopping experience for our customers and continue building customer loyalty. We expect identical supermarket sales growth, excluding fuel sales, of 3%-5% in 2007.

To the extent that these sales initiatives involve price reductions or additional costs, we expect they will be funded by operating cost reductions and productivity improvements. We expect sales improvements and cost reductions, combined with fewer shares outstanding, to drive earnings per share growth in 2007. We expect earnings per share in 2007 of $1.60-$1.65 per diluted share. This represents earnings per share growth of approximately 9%-12% in 2007, net of the effect of a 53rd week in fiscal 2006 of approximately $0.07 per diluted share.

In addition, on March 15, 2007, the Board of Directors declared an increase in Kroger’s quarterly dividend to $0.075 per share.

Further discussion on our industry, the current economic environment and our related strategic plans is included in the “Outlook” section.

RESULTSOF OPERATIONS

The following discussion summarizes our operating results for 2006 compared to 2005 and for 2005 compared to 2004.Comparability is affected by certain income and expense items that fluctuated significantly between and among the periods, including goodwill and asset impairment charges and a labor dispute in southern California in 2004.

Net Earnings (Loss)

Net earnings totaled $1,115 million for 2006, compared to net earnings totaling $958 million in 2005 and a net loss totaling $104 million in 2004. The increase in our net earnings for 2006, compared to 2005 and 2004, resulted from improvements in the southern California market and the leveraging of fixed costs with strong identical supermarket sales growth, as well as the effect of a 53rd week in 2006. In addition, 2004 was negatively affected by goodwill charges totaling $904 million, as well as a labor dispute in southern California.

Earnings per diluted share totaled $1.54 in 2006, compared to $1.31 per share in 2005 and a net loss of $0.14 per diluted share in 2004. Net earnings in 2006 benefited by $0.07 per share due to the 53rd week and $0.03 per share from the adjustment of certain deferred tax balances. Net earnings in 2006 also included expense of $0.03 per share recorded for legal reserves. Net earnings were reduced by $1.16 per share in 2004 due to the effects of goodwill impairment charges. Our earnings per share growth in 2006 and 2005 resulted from increased net earnings and the repurchase of Kroger stock. During fiscal 2006, we repurchased 29 million shares of Kroger stock for a total investment of $633 million. During fiscal 2005, we repurchased 15 million shares of our stock for a total investment of $252 million. During fiscal 2004, we repurchased 20 million shares of Kroger stock for a total investment of $319 million.

Sales

| Total Sales | ||||||||||||||

| (in millions) | ||||||||||||||

| Percentage | Percentage | |||||||||||||

| 2006 | Increase | 2005 | Increase | 2004 | ||||||||||

| Total food store sales without fuel | $ | 57,712 | 7.9 | % | $ | 53,472 | 4.6 | % | $ | 51,106 | ||||

| Total food store fuel sales | 4,455 | 26.3 | % | 3,526 | 53.0 | % | 2,305 | |||||||

| Total food store sales | $ | 62,167 | 9.1 | % | $ | 56,998 | 6.7 | % | $ | 53,411 | ||||

| Other sales(1) | 3,944 | 10.9 | % | 3,555 | 17.6 | % | 3,023 | |||||||

| Total Sales | $ | 66,111 | 9.2 | % | $ | 60,553 | 7.3 | % | $ | 56,434 | ||||

| (1) | Other sales primarily relate to sales at convenience stores, including fuel, jewelry stores and sales by our manufacturing plants to outside firms. |

The growth in our total sales was primarily the result of identical store sales increases, the addition of a 53rd week in 2006 and inflation in pharmacy and some perishable commodities. Increased transaction count and average transaction size were both responsible for our increases in identical supermarket sales, excluding retail fuel operations. After adjusting for the extra week in fiscal 2006, total sales increased 7.0% over fiscal 2005.

We define a supermarket as identical when it has been in operation without expansion or relocation for five full quarters. Differences between total supermarket sales and identical supermarket sales primarily relate to changes in supermarket square footage. We calculate annualized identical supermarket sales based on a summation of four quarters of identical supermarket sales. Our identical supermarket sales results are summarized in the table below, based on the 53-week period of 2006, compared to the same 53-week period of the previous year.

| Identical Supermarket Sales | |||||||

| (in millions) | |||||||

| 2006 | 2005 | ||||||

| Including supermarket fuel centers | $ | 59,592 | $ | 55,993 | |||

| Excluding supermarket fuel centers | $ | 55,399 | $ | 52,483 | |||

| Including supermarket fuel centers | 6.4 | % | 5.3 | % | |||

| Excluding supermarket fuel centers | 5.6 | % | 3.5 | % | |||

We define a supermarket as comparable when it has been in operation for five full quarters, including expansions and relocations. We calculate annualized comparable supermarket sales based on a summation of four quarters of comparable sales. Our annualized comparable supermarket sales results are summarized in the table below, based on the 53-week period of 2006, compared to the same 53-week period of the previous year.

| Comparable Supermarket Sales | |||||||

| (in millions) | |||||||

| 2006 | 2005 | ||||||

| Including supermarket fuel centers | $ | 61,045 | $ | 57,203 | |||

| Excluding supermarket fuel centers | $ | 56,702 | $ | 53,622 | |||

| Including supermarket fuel centers | 6.7 | % | 5.9 | % | |||

| Excluding supermarket fuel centers | 5.7 | % | 3.9 | % | |||

FIFO Gross Margin

We calculate First-In, First-Out (“FIFO”) Gross Margin as follows: Sales minus merchandise costs plus Last-In, First-Out (“LIFO”) charge (credit). Merchandise costs include advertising, warehousing and transportation, but exclude depreciation expense and rent expense. FIFO gross margin is an important measure used by our management to evaluate merchandising and operational effectiveness.

Our FIFO gross margin rates were 24.27%, 24.80% and 25.38% in 2006, 2005 and 2004, respectively. Retail fuel sales lowered our FIFO gross margin rate due to the very low FIFO gross margin on retail fuel sales as compared to non-fuel sales. Excluding the effect of retail fuel operations, our FIFO gross margin rates were 26.43%, 26.69% and 26.73% in 2006, 2005 and 2004, respectively. The decrease in our non-fuel FIFO gross margin rate reflects our continued reinvestment of operating cost savings into lower prices for our customers.

Operating, General and Administrative Expenses

Operating, general and administrative (“OG&A”) expenses consist primarily of employee-related costs such as wages, health care benefit costs and retirement plan costs. Among other items, rent expense, depreciation and amortization expense, and interest expense are not included in OG&A.

OG&A expenses, as a percent of sales, were 17.91%, 18.21% and 18.76% in 2006, 2005 and 2004, respectively. The growth in our retail fuel sales lowers our OG&A rate due to the very low OG&A rate on retail fuel sales as compared to non-fuel sales. Excluding the effect of retail fuel operations, our OG&A expenses, as a percent of sales, were 19.59%, 19.68% and 19.81% in 2006, 2005 and 2004, respectively. Excluding the effect of retail fuel operations, expenses recorded for legal reserves and stock option expense, our OG&A rate declined 28 basis points in 2006. This decrease was driven by identical store sales growth, by increasing store labor productivity, and by progress we have made in controlling our health care costs. These improvements were partially offset by increases in pension expense and credit card fees.

Rent Expense

Rent expense was $649 million in 2006, as compared to $661 million and $680 million in 2005 and 2004, respectively. Rent expense, as a percent of sales, was 0.98% in 2006, as compared to 1.09% in 2005 and 1.21% in 2004. The decrease in rent expense reflects our increasing sales leverage and our continued emphasis on ownership of real estate when available, as well as decreased charges for closed-store future rent liabilities in 2006 and 2005 compared to 2004.

Depreciation and Amortization Expense

Depreciation and amortization expense was $1,272 million, $1,265 million and $1,256 million for 2006, 2005 and 2004, respectively. The increases in depreciation and amortization expense were the result of capital expenditures totaling $1,777 million, $1,306 million and $1,634 million in 2006, 2005 and 2004, respectively. Depreciation and amortization expense, as a percent of sales, was 1.92%, 2.09% and 2.23% in 2006, 2005 and 2004, respectively. The decrease in our depreciation and amortization expense, as a percent of sales, is primarily the result of total sales increases.

Interest Expense

Net interest expense totaled $488 million, $510 million and $557 million for 2006, 2005 and 2004, respectively. The decrease in interest expense was the result of lower average borrowings. During 2006, we reduced total debt $173 million from $7.2 billion as of January 28, 2006, to $7.1 billion as of February 3, 2007. Interest expense in 2004 included $25 million related to the early retirement of debt.

Income Taxes

Our effective income tax rate was 36.2%, 37.2% and 136.4% for 2006, 2005 and 2004, respectively. The effective tax rates for 2006 and 2005 differ from the effective tax rate for 2004 due to the impairment of non-deductible goodwill in 2004. The effective income tax rates also differ from the expected federal statutory rate in all years presented due to the effect of state taxes as well as the adjustment of certain deferred tax balances in 2006.

During the reconciliation of our deferred tax balances, after the filing of annual federal and state tax returns, we identified adjustments to be made in the previous years’ deferred tax reconciliation. We corrected these deferred tax balances in our Consolidated Financial Statements for the year ended February 3, 2007, which resulted in a reduction of our 2006 provision for income tax expense of approximately $21 million and reduced the rate by 120 basis points. We do not believe these adjustments are material to our Consolidated Financial Statements for the year ended February 3, 2007, or to any prior years’ Consolidated Financial Statements. As a result, we have not restated any prior year amounts.

COMMON STOCK REPURCHASE PROGRAM

We maintain a stock repurchase program that complies with Securities Exchange Act Rule 10b5-1 to allow for the orderly repurchase of our common stock, from time to time. We made open market purchases totaling $374 million, $239 million and $291 million under this repurchase program during fiscal 2006, 2005 and 2004, respectively. In addition to this repurchase program, in December 1999 we began a program to repurchase common stock to reduce dilution resulting from our employee stock option plans. This program is solely funded by proceeds from stock option exercises, including the tax benefit from these exercises. We repurchased approximately $259 million, $13 million and $28 million under the stock option program during 2006, 2005 and 2004, respectively.

CAPITAL EXPENDITURES

Capital expenditures, including changes in construction-in-progress payable and excluding acquisitions, totaled $1,777 million in 2006 compared to $1,306 million in 2005 and $1,634 million in 2004. The decline in 2005 was the result of our emphasis on the tightening of capital and increasing our focus on remodels, merchandising and productivity projects. The table below shows our supermarket storing activity and our total food store square footage:

| Supermarket Storing Activity | ||||||||

| 2006 | 2005 | 2004 | ||||||

| Beginning of year | 2,507 | 2,532 | 2,532 | |||||

| Opened | 20 | 28 | 41 | |||||

| Opened (relocation) | 17 | 12 | 20 | |||||

| Acquired | 1 | 1 | 15 | |||||

| Acquired (relocation) | — | — | 3 | |||||

| Closed (operational) | (60 | ) | (54 | ) | (56 | ) | ||

| Closed (relocation) | (17 | ) | (12 | ) | (23 | ) | ||

| End of year | 2,468 | 2,507 | 2,532 | |||||

| Total food store square footage (in millions) | 142 | 142 | 141 | |||||

CRITICAL ACCOUNTING POLICIES

We have chosen accounting policies that we believe are appropriate to report accurately and fairly our operating results and financial position, and we apply those accounting policies in a consistent manner. Our significant accounting policies are summarized in Note 1 to the Consolidated Financial Statements.

The preparation of financial statements in conformity with generally accepted accounting principles (“GAAP”) requires us to make estimates and assumptions that affect the reported amounts of assets, liabilities, revenues, and expenses, and related disclosures of contingent assets and liabilities. We base our estimates on historical experience and other factors we believe to be reasonable under the circumstances, the results of which form the basis for making judgments about the carrying values of assets and liabilities that are not readily apparent from other sources. Actual results could differ from those estimates.

We believe that the following accounting policies are the most critical in the preparation of our financial statements because they involve the most difficult, subjective or complex judgments about the effect of matters that are inherently uncertain.

Self-Insurance Costs

We primarily are self-insured for costs related to workers’ compensation and general liability claims. The liabilities represent our best estimate, using generally accepted actuarial reserving methods, of the ultimate obligations for reported claims plus those incurred but not reported for all claims incurred through February 3, 2007. Case reserves are established for reported claims using case-basis evaluation of the underlying claim data and are updated as information becomes known.

For both workers’ compensation and general liability claims, we have purchased stop-loss coverage to limit our exposure to any significant exposure on a per claim basis. We are insured for covered costs in excess of these per claim limits. The liabilities for workers’ compensation claims are accounted for on a present value basis utilizing a risk-adjusted discount rate. A 25 basis point decrease in our discount rate would increase our liability by approximately $3 million. General liability claims are not discounted.

We are also similarly self-insured for property-related losses. We have purchased stop-loss coverage to limit our exposure to losses in excess of $25 million on a per claim basis, except in the case of an earthquake, for which stop-loss coverage is in excess of $50 million per claim, up to $200 million per claim in California and $300 million outside of California.

The assumptions underlying the ultimate costs of existing claim losses are subject to a high degree of unpredictability, which can affect the liability recorded for such claims. For example, variability in inflation rates of health care costs inherent in these claims can affect the amounts realized. Similarly, changes in legal trends and interpretations, as well as a change in the nature and method of how claims are settled can affect ultimate costs. Our estimates of liabilities incurred do not anticipate significant changes in historical trends for these variables, and any changes could have a considerable effect upon future claim costs and currently recorded liabilities.

Impairments of Long-Lived Assets

In accordance with Statement of Financial Accounting Standards (“SFAS”) No. 144, Accounting for the Impairment or Disposal of Long-Lived Assets, we monitor the carrying value of long-lived assets for potential impairment each quarter based on whether certain trigger events have occurred. These events include current period losses combined with a history of losses or a projection of continuing losses or a significant decrease in the market value of an asset. When a trigger event occurs, we perform an impairment calculation, comparing projected undiscounted cash flows, utilizing current cash flow information and expected growth rates related to specific stores, to the carrying value for those stores. If we identify impairment for long-lived assets to be held and used, we compare discounted future cash flows to the asset’s current carrying value. We record impairment when the carrying value exceeds the discounted cash flows. With respect to owned property and equipment held for disposal, we adjust the value of the property and equipment to reflect recoverable values based on our previous efforts to dispose of similar assets and current economic conditions. We recognize impairment for the excess of the carrying value over the estimated fair market value, reduced by estimated direct costs of disposal. We record costs to reduce the carrying value of long-lived assets in the Consolidated Statements of Operations as “Operating, general and administrative” expense.

The factors that most significantly affect the impairment calculation are our estimates of future cash flows. Our cash flow projections look several years into the future and include assumptions on variables such as inflation, the economy and market competition. Application of alternative assumptions and definitions, such as reviewing long-lived assets for impairment at a different organizational level, could produce significantly different results.

Goodwill

We review goodwill for impairment during the fourth quarter of each year, and also upon the occurrence of trigger events. The reviews are performed at the operating division level. Generally, fair value represents a multiple of earnings, or discounted projected future cash flows, and we compare fair value to the carrying value of a division for purposes of identifying potential impairment. We base projected future cash flows on management’s knowledge of the current operating environment and expectations for the future. If we identify potential for impairment, we measure the fair value of a division against the fair value of its underlying assets and liabilities, excluding goodwill, to estimate an implied fair value of the division’s goodwill. We recognize goodwill impairment for any excess of the carrying value of the division’s goodwill over the implied fair value. Results of the goodwill impairment reviews performed during 2006, 2005 and 2004 are summarized in Note 2 to the Consolidated Financial Statements.

The annual impairment review requires the extensive use of accounting judgment and financial estimates. Application of alternative assumptions and definitions, such as reviewing goodwill for impairment at a different organizational level, could produce significantly different results. Similar to our policy on impairment of long-lived assets, the cash flow projections embedded in our goodwill impairment reviews can be affected by several items such as inflation, the economy and market competition.

Intangible Assets

In addition to goodwill, we have recorded intangible assets totaling $26 million, $22 million and $28 million for leasehold equities, liquor licenses and pharmacy prescription file purchases, respectively, at February 3, 2007. Balances at January 28, 2006, were $35 million, $20 million and $30 million for lease equities, liquor licenses and pharmacy prescription files, respectively. We amortize leasehold equities over the remaining life of the lease. We do not amortize owned liquor licenses, however, we amortize liquor licenses that must be renewed over their useful lives. We amortize pharmacy prescription file purchases over seven years. We consider these assets annually during our testing for impairment.

Store Closing Costs

We provide for closed store liabilities relating to the present value of the estimated remaining noncancellable lease payments after the closing date, net of estimated subtenant income. We estimate the net lease liabilities using a discount rate to calculate the present value of the remaining net rent payments on closed stores. The closed store lease liabilities usually are paid over the lease terms associated with the closed stores, which generally have remaining terms ranging from one to 20 years. Adjustments to closed store liabilities primarily relate to changes in subtenant income and actual exit costs differing from original filing.estimates. Adjustments are made for changes in estimates in the period in which the change becomes known. We review store closing liabilities quarterly to ensure that any accrued amount that is not a sufficient estimate of future costs, or that no longer is needed for its originally intended purpose, is adjusted to income in the proper period.

We estimate subtenant income, future cash flows and asset recovery values based on our experience and knowledge of the market in which the closed store is located, our previous efforts to dispose of similar assets and current economic conditions. The ultimate cost of the disposition of the leases and the related assets is affected by current real estate markets, inflation rates and general economic conditions.

We reduce owned stores held for disposal to their estimated net realizable value. We account for costs to reduce the carrying values of property, equipment and leasehold improvements in accordance with our policy on impairment of long-lived assets. We classify inventory write-downs in connection with store closings, if any, in “Merchandise costs.” We expense costs to transfer inventory and equipment from closed stores as they are incurred.

Post-Retirement Benefit Plans

(a) Company-sponsored Pension Plans

Effective February 3, 2007, we adopted the recognition and disclosure provisions of SFAS No. 158,Employers’ Accounting for Defined Benefit Pension and Other Postretirement Plans-an amendment of FASB Statements No. 87, 99, 106 and 123(R), which required the recognition of the funded status of its retirement plans on the Consolidated Balance Sheet. We are now required to record, as a component of Accumulated Other Comprehensive Income (“AOCI”), actuarial gains or losses, prior service costs or credits and transition obligations that have not yet been recognized.

The determination of our obligation and expense for Company-sponsored pension plans and other post-retirement benefits is dependent upon our selection of assumptions used by actuaries in calculating those amounts. Those assumptions are described in Note 14 to the Consolidated Financial Statements and include, among others, the discount rate, the expected long-term rate of return on plan assets, average life expectancy and the rate of increases in compensation and health care costs. Actual results that differ from our assumptions are accumulated and amortized over future periods and, therefore, generally affect our recognized expense and recorded obligation in future periods. While we believe that our assumptions are appropriate, significant differences in our actual experience or significant changes in our assumptions, including the discount rate used and the expected return on plan assets, may materially affect our pension and other post-retirement obligations and our future expense. Note 14 to the Consolidated Financial Statements discusses the effect of a 1% change in the assumed health care cost trend rate on other post-retirement benefit costs and the related liability.

The objective of our discount rate assumption is to reflect the rate at which the pension benefits could be effectively settled. In making this determination, we take into account the timing and amount of benefits that would be available under the plans. Our methodology for selecting the discount rate as of year-end 2006 was to match the plan’s cash flows to that of a yield curve that provides the equivalent yields on zero-coupon corporate bonds for each maturity. Benefit cash flows due in a particular year can be “settled” theoretically by “investing” them in the zero-coupon bond that matures in the same year. The discount rate is the single rate that produces the same present value of cash flows. The selection of the 5.90% discount rate as of year-end 2006 represents the equivalent single rate under a broad-market AA yield curve constructed by our outside consultant, Mercer Human Resource Consulting. We utilized a discount rate of 5.70% for year-end 2005. The 20 basis point increase in the discount rate decreased the projected pension benefit obligation as of February 3, 2007, by approximately $68 million.

To determine the expected return on pension plan assets, we consider current and forecasted plan asset allocations as well as historical and forecasted returns on various asset categories. For 2006 and 2005, we assumed a pension plan investment return rate of 8.5%. Our pension plan’s average return was 9.7% for the 10 calendar years ended December 31, 2006, net of all investment management fees and expenses. Our actual return for the pension plan calendar year ending December 31, 2006, on that same basis, was 13.4%. We believe the pension return assumption is appropriate because we do not expect that future returns will achieve the same level of performance as the historical average annual return. We have been advised that during 2007 and 2008, the trustees plan to reduce from 50% to 42% the allocation of pension plan assets to domestic and international equities and increase from 18% to 27% the allocation to non-core assets, including inflation-linked bonds, commodities, hedge funds and real estate. Furthermore, in order to augment the return on domestic equities and investment grade debt securities during 2007 and 2008, the trustees plan to increase hedge funds within these sectors from 7% to 22%. Collectively, these changes should improve the diversification of pension plan assets. The trustees expect these changes will have little effect on the total return but will reduce the expected volatility of the return. See Note 14 to the Consolidated Financial Statements for more information on the asset allocations of pension plan assets.

Sensitivity to changes in the major assumptions used in the calculation of Kroger’s pension plan liabilities for the Qualified Plans is illustrated below (in millions).

| Projected Benefit | ||||||||||

| Percentage | Obligation | Expense | ||||||||

| Point Change | Decrease/(Increase) | Decrease/(Increase) | ||||||||

| Discount Rate | +/- 1.0 | % | $ | 350/($306 | ) | $ | 38/($36 | ) | ||

| Expected Return on Assets | +/- 1.0 | % | — | $ | 21/($21 | ) | ||||

In 2005, we updated the mortality table used to determine average life expectancy in the calculation of our pension obligation to the RP-2000 Projected to 2015 mortality table. The change in this assumption increased our projected benefit obligation by approximately $93 million at the time of the change, and is reflected in unrecognized actuarial (gain) loss as of the measurement date.

We contributed $150 million, $300 million and $35 million to our Company-sponsored pension plans in 2006, 2005 and 2004, respectively. Although we are not required to make cash contributions to our Company-sponsored pension plans during fiscal 2007, we contributed $50 million to the plans on February 5, 2007. We may elect to make additional voluntary contributions to our Company-sponsored pension plans in order to maintain our desired funding status. Additional contributions may be made if our cash flows from operations exceed our expectations. We expect any elective contributions made during 2007 will decrease our required contributions in future years. Among other things, investment performance of plan assets, the interest rates required to be used to calculate the pension obligations, and future changes in legislation, will determine the amounts of any additional contributions.

Effective January 1, 2007, the Cash Balance Plan was replaced with a 401(k) Retirement Savings Account Plan, which will provide both Company matching contributions and other Company contributions based upon length of service, to eligible employees. We expect to make matching contributions in 2007 of approximately 75 million.

(b) Multi-Employer Plans

We also contribute to various multi-employer pension plans based on obligations arising from most of our collective bargaining agreements. These plans provide retirement benefits to participants based on their service to contributing employers. The benefits are paid from assets held in trust for that purpose. Trustees are appointed in equal number by employers and unions. The trustees typically are responsible for determining the level of benefits to be provided to participants as well as for such matters as the investment of the assets and the administration of the plans.

We recognize expense in connection with these plans as contributions are funded, in accordance with GAAP. We made contributions to these plans, and recognized expense, of $204 million in 2006, $196 million in 2005, and $180 million in 2004. We estimate we would have contributed an additional $2 million in 2004 but our obligation to contribute was suspended during the southern California labor dispute.

Based on the most recent information available to us, we believe that the present value of actuarially accrued liabilities in most or all of these multi-employer plans substantially exceeds the value of the assets held in trust to pay benefits. We have attempted to estimate the amount by which these liabilities exceed the assets, (i.e., the amount of underfunding), as of December 31, 2006.Because Kroger is only one of a number of employers contributing to these plans, we also have attempted to estimate the ratio of Kroger’s contributions to the total of all contributions to these plans in a year as a way of assessing Kroger’s “share” of the underfunding. As of December 31, 2006, we estimate that Kroger’s share of the underfunding of multi-employer plans to which Kroger contributes was $600 million to $800 million, pre-tax, or $375 million to $500 million, after-tax. This represents a decrease in the amount of underfunding estimated as of December 31, 2005. This decrease is attributable to, among other things, the continuing benefit of plan design changes and the investment returns on assets held in trust for the plans during 2006. Our estimate is based on the best information available to us including actuarial evaluations and other data (that include the estimates of others), and such information may be outdated or otherwise unreliable. Our estimate is imprecise and not necessarily reliable.

We have made and disclosed this estimate not because this underfunding is a direct liability of Kroger. Rather, we believe the underfunding is likely to have important consequences. We expect our contributions to these multi-employer plans will continue to increase each year, and therefore the expense we recognize under GAAP will increase. In 2006, our contributions to these plans increased approximately 4% over the prior year and have grown at a compound annual rate of approximately 6% since 2003. We expect our contributions to increase by approximately 1.0% in 2007. The amount of increases in 2007 and beyond has been favorably affected by significant improvement in the values of assets held in trusts, by the labor agreements negotiated in southern California and elsewhere in recent years, and by related trustee actions. Although underfunding can result in the imposition of excise taxes on contributing employers, increased contributions can reduce underfunding so that excise taxes are not triggered. Our estimate of future contribution increases takes into account the avoidance of those taxes. Finally, underfunding means that, in the event we were to exit certain markets or otherwise cease making contributions to these funds, we could trigger a substantial withdrawal liability. Any adjustment for withdrawal liability will be recorded when it is probable that a liability exists and can be reasonably estimated, in accordance with SFAS No. 87, Employers’ Accounting for Pensions.

The amount of underfunding described above is an estimate and is disclosed for the purpose described. The amount could decline, and Kroger’s future expense would be favorably affected, if the values of net assets held in the trust significantly increase or if further changes occur through collective bargaining, trustee action or favorable legislation. On the other hand, Kroger’s share of the underfunding would increase and Kroger’s future expense could be adversely affected if net asset values decline, if employers currently contributing to these funds cease participation or if changes occur through collective bargaining, trustee action or adverse legislation.

Deferred Rent

We recognize rent holidays, including the time period during which we have access to the property for construction of buildings or improvements, as well as construction allowances and escalating rent provisions on a straight-line basis over the term of the lease. The deferred amount is included in Other Current Liabilities and Other Long-Term Liabilities on the Consolidated Balance Sheets.

Tax Contingencies

Various taxing authorities periodically audit our income tax returns. These audits include questions regarding our tax filing positions, including the timing and amount of deductions and the allocation of income to various tax jurisdictions. In evaluating the exposures connected with these various tax filing positions, including state and local taxes, we record allowances for probable exposures. A number of years may elapse before a particular matter, for which we have established an allowance, is audited and fully resolved. As of February 3, 2007, tax years 2002 through 2004 were undergoing examination by the Internal Revenue Service.

The establishment of our tax contingency allowances relies on the judgment of management to estimate the exposures associated with our various filing positions. Although management believes those estimates and judgments are reasonable, actual results could differ, resulting in gains or losses that may be material to our Consolidated Statements of Operations.

To the extent that we prevail in matters for which allowances have been established, or are required to pay amounts in excess of these allowances, our effective tax rate in any given financial statement period could be materially affected. An unfavorable tax settlement could require use of cash and result in an increase in our effective tax rate in the year of resolution. A favorable tax settlement would be recognized as a reduction in our effective tax rate in the year of resolution.

Share-Based Compensation Expense

Effective January 29, 2006, we adopted the fair value recognition provisions of SFAS No. 123(R),Share-Based Payment, using the modified prospective transition method and, therefore, have not restated results for prior periods. Under this method, we recognize compensation expense for all share-based payments granted on or after January 29, 2006, as well as all share-based payments granted prior to, but not yet vested as of, January 29, 2006, in accordance with SFAS No. 123(R). Under the fair value recognition provisions of SFAS No. 123(R), we recognize share-based compensation expense, net of an estimated forfeiture rate, over the requisite service period of the award.

Prior to the adoption of SFAS No. 123(R), we accounted for share-based payments under Accounting Principles Board (“APB”) Opinion No. 25,Accounting for Stock Issued to Employees and the disclosure provisions of SFAS No. 123, as amended. We recognized compensation expense for all share-based awards described above using the straight-line attribution method applied to the fair value of each option grant, over the requisite service period associated with each award. The requisite service period is typically consistent with the vesting period, except as noted below. Because awards typically vest evenly over the requisite service period, compensation cost recognized in 2006 is at least equal to the grant-date fair value of the vested portion of all outstanding options.

The weighted-average fair value of stock options granted during 2006, 2005 and 2004 was $6.90, $7.70 and $7.91, respectively. The fair value of each stock option grant was estimated on the date of grant using the Black-Scholes option-pricing model, based on the assumptions shown in the table below. The Black-Scholes model utilizes extensive accounting judgment and financial estimates, including the term employees are expected to retain their stock options before exercising them, the volatility of our stock price over that expected term, the dividend yield over the term and the number of awards expected to be forfeited before they vest. Using alternative assumptions in the calculation of fair value would produce fair values for stock option grants that could be different than those used to record share-based compensation expense in the Consolidated Statements of Operations.

The following table reflects the weighted-average assumptions used for grants awarded to option holders.

| 2006 | 2005 | 2004 | ||||||

| Weighted average expected volatility | 27.60 | % | 30.83 | % | 30.13 | % | ||

| Weighted average risk-free interest rate | 5.07 | % | 4.11 | % | 3.99 | % | ||

| Expected dividend yield | 1.50 | % | N/A | N/A | ||||

| Expected term | 7.5 years | 8.7 years | 8.7 years | |||||

The weighted-average risk-free interest rate was based on the yield of a treasury note as of the grant date, continuously compounded, which matures at a date that approximates the expected term of the options. Prior to 2006, we did not pay a dividend, so an expected dividend rate was not included in the determination of fair value for options granted during fiscal year 2005. Using a dividend yield of 1.50% to value options issued in 2005 would have decreased the fair value of each option by approximately $1.60. We determined expected volatility based upon historical stock volatilities. We also considered implied volatility. We determined expected term based upon a combination of historical exercise and cancellation experience, as well as estimates of expected future exercise and cancellation experience.

Under SFAS No. 123(R), we record expense for restricted stock awards in an amount equal to the fair market value of the underlying stock on the grant date of the award.

In 2006, we recognized total stock compensation expense of $72 million. This included $50 million for stock options and $22 million for restricted shares. A total of $18 million of the restricted stock expense was attributable to the wider distribution of restricted shares incorporated into the first quarter 2006 grant of share-based awards (as described in Note 10 to the Consolidated Financial Statements), and the remaining $4 million of restricted stock expense related to previously issued restricted stock awards. The incremental compensation expense attributable to the adoption of SFAS No. 123(R) in 2006 was $68 million, pre-tax, or $43 million and $0.06 per diluted share, after tax. In 2005, we recognized stock compensation cost of $7 million, pre-tax, related entirely to restricted stock grants.

These costs were recognized as operating, general and administrative costs in our Company’s Consolidated Statements of Operations. The cumulative effect of applying a forfeiture rate to unvested restricted shares at January 29, 2006 was not material. The pro forma earnings effect of stock options in prior years, in accordance with SFAS No. 123, is described below:

| (in millions, except per share amounts) | 2005 | 2004 | |||||

| Net earnings (loss), as reported | $ | 958 | $ | (104 | ) | ||

| Stock-based compensation expense included in net earnings, net of | |||||||

| income tax benefits | 5 | 8 | |||||

| Total stock-based compensation expense determined under fair value | |||||||

| method for all awards, net of income tax benefits(1) | (34 | ) | (48 | ) | |||

| Pro forma net earnings (loss) | $ | 929 | $ | (144 | ) | ||

| Earnings (loss) per basic common share, as reported | $ | 1.32 | $ | (0.14 | ) | ||

| Pro forma earnings (loss) per basic common share | $ | 1.28 | $ | (0.20 | ) | ||

| Earnings (loss) per diluted common share, as reported | $ | 1.31 | $ | (0.14 | ) | ||

| Pro forma earnings (loss) per diluted common share | $ | 1.27 | $ | (0.20 | ) | ||

| Refer to Note 10 of our Consolidated Financial Statements for a summary of the assumptions used for options issued in each year at an option price equal to the fair market value of the stock at the date of the grant. |

As of February 3, 2007, we had $92 million of total unrecognized compensation expense related to non-vested share-based compensation arrangements granted under equity award plans. We expected to recognize this cost over a weighted-average period of approximately one year. The total fair value of options that vested in 2006 was $44 million.

For share-based awards granted prior to the adoption of SFAS No. 123(R), the Company’s stock option grants generally contained retirement-eligibility provisions that caused the options to vest upon the earlier of the stated vesting date or retirement. We calculated compensation expense over the stated vesting periods, regardless of whether certain employees became retirement-eligible during the respective vesting periods. Upon the adoption of SFAS No. 123(R), we continued this method of recognizing compensation expense of awards granted prior to the adoption of SFAS No. 123(R). For awards granted on or after January 29, 2006,options vest based on the stated vesting date, even if an employee retires prior to the vesting date. However, the requisite service period ends on the employee’s retirement-eligible date. As a result, we recognize expense for stock option grants containing such retirement-eligibility provisions over the shorter of the vesting period or the period until employees become retirement-eligible (the requisite service period). As a result of retirement eligibility provisions in stock option awards granted on or after January 29, 2006, we recognized approximately $6 million of compensation expense in 2006 prior to the completion of stated vesting periods.

Shares issued as a result of stock option exercises may be newly issued shares or reissued treasury shares. We expect to reissue shares held in treasury upon exercise of these options.

Inventories

Inventories are stated at the lower of cost (principally on a LIFO basis) or market. In total, approximately 98% of inventories for 2006 and 2005, respectively, were valued using the LIFO method. Cost for the balance of the inventories was determined using the first-in, first-out (“FIFO”) method. Replacement cost was higher than the carrying amount by $450 million at February 3, 2007, and by $400 million at January 28, 2006. We follow the Link-Chain, Dollar-Value LIFO method for purposes of calculating our LIFO charge or credit.

The item-cost method of accounting to determine inventory cost before the LIFO adjustment is followed for substantially all store inventories at our supermarket divisions. This method involves counting each item in inventory, assigning costs to each of these items based on the actual purchase costs (net of vendor allowances and cash discounts) of each item and recording the actual cost of items sold. The item-cost method of accounting allows for more accurate reporting of periodic inventory balances and enables management to more precisely manage inventory and purchasing levels when compared to the methodology followed under the retail method of accounting.

We evaluate inventory shortages throughout the year based on actual physical counts in our facilities. We record allowances for inventory shortages based on the results of recent physical counts to provide for estimated shortages from the last physical count to the financial statement date.

Vendor Allowances