UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K/A

Amendment No. 110-K

(Mark One)

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 20072008

OR

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Commission file number: 000-27163

Kana Software, Inc.

(Exact Name of Registrant as Specified in its Charter)

| Delaware | 77-0435679 | |

(State or Other Jurisdiction of Incorporation or Organization) | (I.R.S. Employer Identification No.) | |

181 Constitution Drive Menlo Park, California | 94025 | |

| (Address of Principal Executive Offices) | (Zip Code) | |

(650) 614-8300

(Registrant’s Telephone Number, Including Area Code)

Securities registered pursuant to Section 12(b) of the Act:

None

Securities registered pursuant to Section 12(g) of the Act:

Common Stock, $0.001 par value per share

(Title of Class)class)

Indicate by check mark if the Registrant is a well-known seasoned issuer as defined in Rule 405 of the Securities Act. Yes ¨ No x

Indicate by check mark if the Registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No x

Indicate by check mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrantregistrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 229.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ¨ No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405)229.405 of this chapter) is not contained herein, and will not be contained, to the best of the Registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K/A10-K or any amendment to this Form 10-K/A.10-K. ¨

Indicate by check mark whether the Registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer”, “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer ¨ | Accelerated filer | |||

| Non-accelerated filer | Smaller reporting company ¨ | |||

Indicate by check mark whether the Registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x

As of June 29, 2007,30, 2008, the last business day of the Registrant’s most recently completed second fiscal quarter, the aggregate market value of the voting stock held by non-affiliates of the Registrant was approximately $93,546,679$43,734,118 based upon the closing sales price of the Registrant’s common stockCommon Stock as reported on the Over the Counter Bulletin Board of $3.10.$1.27.

As of March 31, 2008,At April 30, 2009 the Registrant had outstanding approximately 41,212,57841,214,666 shares of common stock,Common Stock, $0.001 par value per share.

EXPLANATORY NOTEDOCUMENTS INCORPORATED BY REFERENCE

This Amendment No. 1 on Form 10-K/A supplements ourPortions of the Registrant’s Proxy Statement for the 2008 Annual Meeting of Stockholders are incorporated herein by reference in Part III of this Annual Report on Form 10-K forto the year ended December 31, 2007 that we filed on March 17, 2008 with the Securities and Exchange Commission. We are filing this Amendment No. 1 to provide the information required by Items 10, 11, 12, 13 and 14 of Part III and to update the information contained in Item 15 of Part IV. Except as described above, no other amendments are being made to our Annual Report on Form 10-K filed on March 17, 2008.extent stated herein.

Form 10-K/A10-K

For the Fiscal Year Ended December 31, 20072008

TABLE OF CONTENTS

| Page | ||||

Item 1 | 1 | |||

Item 1A | 7 | |||

Item 1B | 22 | |||

Item 2 | 22 | |||

Item 3 | 22 | |||

Item 4 | 23 | |||

| ||||

Item 5 | Market for the Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities | 24 | ||

Item 6 | 25 | |||

Item 7 | Management’s Discussion and Analysis of Financial Condition and Results of Operations | 28 | ||

Item 7A | 47 | |||

Item 8 | 48 | |||

Item 9 | Changes in and Disagreements with Accountants on Accounting and Financial Disclosure | 80 | ||

Item 9A(T) | 80 | |||

Item 9B | 82 | |||

Item 10 | ||||

| 83 | ||||

Item | ||||

| 83 | ||||

Item | Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters | |||

| 83 | ||||

Item | Certain Relationships and Related Transactions, and Director Independence | |||

Item 14 | 83 | |||

| ||||

Item | ||||

In addition to historical information, this report contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934. The forward-looking statements are not historical facts but rather are based on current expectations, estimates and projections about our business and industry, and our beliefs and assumptions. Words such as “anticipate,” “believe,” “estimate,” “expect,” “intend,” “plan,” “will” and variations of these words and similar expressions identify forward-looking statements. These statements are not guarantees of future performance and are subject to risks, uncertainties and other factors, many of which are beyond our control, are difficult to predict and could cause actual results to differ materially from those expressed or forecasted in the forward-looking statements. These risks and uncertainties include, but are not limited to, those described in Item 1A “Risk Factors” and elsewhere in this report. Forward-looking statements that were believed to be true at the time made may ultimately prove to be incorrect or false. We undertake no obligation to revise or publicly release the results of any revision to these forward-looking statements. Given these risks and uncertainties, readers are cautioned not to place undue reliance on such forward-looking statements.

| ITEM 1. | BUSINESS. |

Overview

KANA Software, Inc. (the “Company” or “KANA”) offers an innovative approach to customer service with cost-effective solutions that enhance the quality of multi-channel customer service interactions. Built on open standards for a high degree of adaptability and integration, KANA solutions intelligently automate the processes needed to successfully serve our clients’ customers, so that our clients can deliver higher value service at lower cost, increasing customer retention and loyalty. We provide an integrated solution which enables organizations to deliver consistent, managed service across all channels, including e-mail, chat, call centers and Web self-service, ensuring a consistent service experience across communication channels. We are headquartered in Menlo Park, California with offices throughout the United States, as well as Europe and Japan.

We were incorporated in July 1996 in California and reincorporated in Delaware in September 1999. References in this Annual Report on Form 10-K to “we,” “our” and “us” collectively refer to KANA, our predecessor and our subsidiaries and their predecessors. Our principal executive offices are located at 181 Constitution Drive, Menlo Park, California 94025 and our telephone number is (650) 614-8300. Our Internet website is located at http://www.kana.com.

Our Strategy

Deliver world-class products & solutions to Global 2000 enterprises, and enable these organizations to improve customer loyalty and retention, increase corporate revenue and reduce the cost of service. We believe that a significant percentage of an enterprise’s cost of providing service to its customers resides in efficiently and effectively managing and resolving individual customer questions and problems, or cases. These cases must be received, routed, tracked and resolved by customer service agents. While many enterprises possess technology capable of routing and tracking cases, the actual resolution of customer issues is largely unautomated, and therefore is particularly costly. Our knowledge-powered customer service solutions focus on automating the service experience across multiple channels. The majority of our license revenues are for applications that are used by our customers’ agents (Assisted Service), or directly by their customers (Web Self-Service), empowering them with knowledge and information to resolve their issues.

Partner with the world’s leading systems integrators. Our strategy is to focus our efforts on the sale of software and support and to enter into strategic relationships with leading systems integrators in order to provide our customers with a wide range of implementation, systems integration, and consulting services. Our professional services organization was augmented in 2007 by our acquisition of eVergance Partners LLC

(“eVergance”), a consulting and services firm that provides our systems integrator partners with additional resources and subject matter expertise on our applications. Our customers can benefit from these systems integrators’ deep knowledge of our products, as well as their industry expertise and proven integration success. In addition, these systems integrators employ larger sales forces than we do, and we generally coordinate our sales efforts with them.

Deliver industry-specific applications. Some industries, such as banking, telecommunications, and healthcare, have exceptionally high volumes of customer interactions, and providing consistent and accurate feedback to customers of companies in these industries has become increasingly difficult as the products and offerings of such companies have become increasingly complicated. We continue to expand our portfolio of applications through our professional services and systems integrator relationships.

Products

We provide a suite of customer service software solutions. Around the world, our multi-channel customer service solutions are helping Global 2000 companies provide more intelligent, effective interactions with customers, helping them build loyal and lasting customer relationships while reducing costs in the contact center.

Our suite of multi-channel solutions is built on open standards for a high degree of adaptability and flexibility. Our solutions provide a critical link between call centers and transactional back end systems, allowing organizations to have effective, efficient interactions with customers across points of contact (including Web, telephone and e-mail) and throughout the enterprise. We employ robust reporting tools across our entire product family to allow companies to continually analyze and improve their customer and partner relationships. These features enable Global 2000 companies and other enterprises to reduce the cost of information access for their employees, customers and partners while creating profitable customer relationships.

Our customers can deploy our multi-channel solutions as a complete suite or as separate applications. Our solutions include the following products:

KANA IQ—Bringing together a self-service application for customers and an assisted-service solution for contact center agents, KANA IQ is a sophisticated knowledge management application that guides customers and agents through the process of finding answers, enabling them to quickly and accurately locate the information they need.

KANA Response—KANA Response is a robust e-mail management system which intelligently automates the process of managing high-volume email and Web forms in the contact center.

KANA Response Live—KANA Response Live delivers comprehensive live chat and Web page co-browsing so that Web self-service customers can engage in online “conversations” with agents.

KANA Contact Center—KANA Contact Center is a multi-channel customer service application for contact centers that provides an intelligent agent desktop with one-stop access to relevant customers and service data, multi-channel history, request management, and extranet workflow.

Our applications are designed to easily integrate with other enterprise software and legacy systems. They can be installed on systems running Solaris, AIX, Linux or Windows operating systems, and provide customers with capabilities for personalization, customer profile management, inquiry management, universal business rules, knowledge management, and workflow. They can be linked with customers’ legacy systems allowing customers to design their systems to preserve previous investments. Our service-oriented architecture uses data modeling to make data located in external systems available in our application without requiring the data to be moved or replicated. Our applications are built on a single Web-architected platform, which offers a service-oriented framework that provides our customers with full access to our applications using a standard Web browser and without requiring them to install additional software on their individual computers.

Alliances

We enter into strategic relationships with leading systems integrators that have developed significant expertise with our applications and are able to provide customers with a wide range of consulting, implementation and systems integration services. In addition, many of these systems integrators act as resellers for our products, and we rely on them for assistance in driving our sales efforts. We believe that support for our products by these systems integrators is increasingly important in influencing new customers’ decisions to license our products. In addition to our consulting services and systems integration subsidiary, eVergance, we work with several third-party systems integrators and consulting firms, including IBM Global Business Services (“IBM”). These systems integrators have been integral to our success in selling our products to large-organizations such as ATT, Bank of America, Cummins, DVLA, JetBlue, Metlife, O2, and TD Waterhouse.

Services and Support

Customer Support. Our customer support group uses our own applications to provide multi-channel global support for our customers and partners.

Professional Services. Our worldwide consulting and education services group provides business and technical expertise to support our customers and alliance partners. Our consulting services group works closely with our customers to address the people and process areas common to every enterprise deployment along with systems integrators during implementations to lend technical experience and functional product expertise and to assist the systems integrators in providing our customers with high-quality, successful, enterprise-wide implementations. Education services provide a full set of training programs and materials for our customers and partners, including a comprehensive set of courses for end users, business consultants and developers, which are available through instructor-led, Web-based, and on-site classes.

Sales

Our sales strategy is to focus on Global 2000 companies through our direct sales force. We have commercial sales teams that cover named accounts within geographical territories, as well as a vertical account manager for the federal government. We maintain direct sales personnel across North America and in Europe and Japan. Our Inside Sales Organization focuses on a departmental strategy within the Global 2000 and the high end of the mid-market. We also have a Renewals team that works with our existing customers to renew their maintenance and support agreements.

Customers

Our customers range from Global 2000 companies to growing companies who want to differentiate their businesses through the delivery of superior customer service. The following is a list of customers that we believe are representative of our overall customer base:

Financial Services | Communications | |

| Bank of America | AT&T | |

| Bank Leumi | Brighthouse Networks | |

| Barclays | BSkyB | |

| Capital One | Com Hem | |

| ING Postbank | COX Communications | |

| JP Morgan Chase | Hutchison 3G | |

| Principal Financial Group | O2 | |

| TD Ameritrade | Sprint | |

| TD Waterhouse UK | Telekom Austria | |

| Wells Fargo | Telenor | |

Time Warner Cable | ||

T-Mobile |

Health Care | Government | |

| Abbott Laboratories | City of Amsterdam/Gemeente Amsterdam | |

| Aetna | Defense Information Systems Agency | |

| Allergan | Her Majesty Revenues & Customs (HMRC) | |

| Cigna HealthCare | United States Postal Services | |

| Highmark Inc. | ||

| Kaiser Permanente | ||

| MetLife | ||

| United HealthGroup | ||

| WellPoint | ||

High Technology | Travel/Hospitality | |

| Dell Computer Corp. | American Airlines | |

| DST Systems | Avis Budget Group | |

| Garmin | Best Western International | |

| IBM | Carlson Companies | |

| Palm | Disney | |

| Siemens | Icelandair | |

| Sony | JetBlue Airways | |

| Xerox | Northwest Airlines | |

| Yahoo! | Priceline.com | |

| Starwood Hotels & Resorts | ||

America West Airlines | ||

Retail | ||

| American Girl | ||

| Avon.com | ||

| Barnes & Noble | ||

| Best Buy | ||

| Carphone Warehouse | ||

| eBay, Inc. | ||

| Estee Lauder | ||

| Home Depot | ||

| JC Penney | ||

| Sears | ||

| Staples.com | ||

| Target | ||

| The Gap | ||

| Tiffany & Company | ||

No customer accounted for 10% or more of our total revenues in 2008. A portion of our license and services revenues in any given quarter has been, and we expect will continue to be, generated from a limited number of customers. We consider ourselves to be in a single industry segment—specifically, the licensing and support of our software applications. Revenue classification is based upon customer location. See Note 12 of the Notes to the Consolidated Financial Statements in Item 8 of this Annual Report on Form 10-K for geographic information on revenues for the years ended December 31, 2008, 2007, and 2006 and long-lived assets for the years ended December 31, 2008 and 2007.

Research and Development

We believe that strong product development capabilities are essential to our strategy of enhancing our core technology, developing additional applications incorporating that technology and maintaining the competitiveness of our product and service offerings. We have invested significant time and resources in creating a structured process for undertaking all product development.

Our success significantly depends on our ability to enhance our existing customer service solutions and to develop new services, functionality and technology that address the increasingly sophisticated and varied needs of our existing and prospective customers. The challenges of developing new products and enhancements require us to commit a substantial amount of resources. We might not be able to develop or introduce new products on a timely or cost-effective basis, or at all, which could lead existing and potential customers to choose a competitor’s products.

Our research and development expenses were $13.8 million, $12.7 million and $10.8 million in 2008, 2007 and 2006, respectively.

Competition

The market for our products and services is intensely competitive, evolving and subject to rapid technological change. We currently face competition for our products from software designed by our customers’ in-house development teams and by third parties. We expect these competing software applications to continue to be a major source of competition for the foreseeable future. Our primary competitors for customer relationship management (“CRM”) software platforms are larger, more established companies such as Oracle. We also face competition from companies such as Chordiant Software, Salesforce.com, Consona, eGain, RightNow, InQuira and Pegasystems with respect to several specific applications we offer. We may face increased competition upon introduction of new products or upgrades from competitors.

We believe that the principal competitive factors affecting our industry include having a significant base of customers recommending our products, the breadth and depth of a given solution, product cost, product quality and performance, customer service, product scalability and reliability, product features, ability to implement solutions and perception of financial position. We believe that our products currently compete favorably with respect to many of these factors, and, in particular, that our Web-based architecture provides us with a competitive advantage because it allows for greater product scalability and rapid implementation. However, we may not be able to maintain our competitive position against current and potential competitors, especially those with greater financial, marketing, service, support, technical and other resources, and who may, for example, be able to add features or functionality to their competing products more quickly or decide to sell their competing products to their existing customer bases for other products.

Seasonality

Our business is influenced by seasonal trends, largely due to customer buying patterns. These trends may include higher license revenues in the fourth quarter as many customers complete annual budgetary cycles and lower license revenues in the first quarter and summer months when many of our prospects and customers experience lower sales. Our professional services are negatively impacted in the fourth quarter due to the holiday season, in which fewer billable hours are available for our consultants. In addition, our international operations experience a slowdown in the summer months.

Intellectual Property

We rely upon a combination of patent, copyright, trade secret and trademark laws, and contractual restrictions, such as confidentiality agreements and licenses, to establish and protect our proprietary rights. We currently have five issued U.S. patents, three of which expire in 2018 and two of which expire in 2020, and a number of U.S. patent applications pending. We have also filed international patent applications corresponding to some of our U.S. applications. In addition, we have several trademarks that are registered or pending registration in the U.S. and abroad. Although we rely on patent, copyright, trade secret and trademark laws to protect our technology, we believe that factors such as the technological and creative skills of our personnel, new product development, frequent product enhancements and reliable product maintenance are more essential to establishing and maintaining a technology leadership position.

Despite our efforts to protect our proprietary rights, unauthorized parties may attempt to copy or otherwise obtain and use our products or technology or to develop products with the same functionality as our products. Policing unauthorized use of our products is difficult. Also, the laws of other countries in which we market our products may offer little or no effective protection of our proprietary technology. Furthermore, our competitors could independently develop technologies equivalent to ours, and our intellectual property rights may not be broad enough for us to prevent such competitors from selling products incorporating those technologies. Reverse engineering, unauthorized copying or other misappropriation of our proprietary technology could enable third parties to benefit from our technology without paying us for it, which would significantly harm our business.

Substantial litigation regarding intellectual property rights exists in our industry. We expect that software in our industry may be increasingly subject to third-party infringement claims as the number of competitors grows and the functionality of products in different industry segments overlaps. Some of our competitors in the market for customer communications software may have filed or may intend to file patent applications covering aspects of their technology that they may claim our technology infringes. Such competitors could make a claim of infringement against us with respect to our products and technology. Third parties may currently have, or may eventually be issued, patents upon which our current or future products or technology infringe. Any of these third parties might make a claim of infringement against us. See Item 1A “Risk Factors”—“We may become involved in litigation over proprietary rights, which could be costly and time consuming.”

Backlog

As of December 31, 2008 and 2007, we had $16.4 million and $20.1 million, respectively, in backlog, which relates to firm orders, with $86,000 and $419,000, respectively, not expected to be recognized within one year due to the timing of obligations in the underlying agreements. The majority of these firm orders relate to annual support contracts, and were invoiced and recorded as deferred revenue as of December 31, 2008 and 2007.

Employees

As of December 31, 2008, we had 229 full-time employees, compared to 225 full-time employees as of December 31, 2007. Of the 229 employees as of December 31, 2008, 69 were in our services and support group, 60 were in sales and marketing, 65 were in research and development and 35 were in finance, legal, information technology (“IT”) and administration.

| ITEM 1A. | RISK FACTORS. |

We operate in a dynamic and rapidly changing business environment that involves substantial risks and uncertainty, including but not limited to the specific risks identified below. The risks described below are not the only ones facing our company. Additional risks not presently known to us, or that we currently deem immaterial, may become important factors that impair our business operations. Any of these risks could cause, or contribute to causing, our actual results to differ materially from expectations. Prospective and existing investors are strongly urged to carefully consider the various cautionary statements and risks set forth in this report and our other public filings.

Risks Related to Our Business and Industry

Current uncertainty in global economic conditions makes it particularly difficult to predict demand and other related matters and makes it more likely that our actual results could differ materially from expectations.

Our operations and performance depend on worldwide economic conditions, which have recently deteriorated significantly in the United States and other countries, and may remain depressed for the foreseeable future. These conditions make it difficult for our customers and potential customers to accurately forecast and plan future business activities, and could cause our customers and potential customers to slow or reduce spending on our products and services. Furthermore, during challenging economic times, our customers may face issues gaining timely access to sufficient credit, which could impact their willingness to make purchases or their ability to make timely payments to us. If that were to occur, we may experience decreased sales, be required to increase our allowance for doubtful accounts and our days sales outstanding could be negatively impacted. We cannot predict the timing, strength or duration of any economic slowdown or subsequent economic recovery, worldwide, in the United States, or in our industry. These and other economic factors could have a material adverse effect on demand for our products and services, on our ability to predict future operating results, and on our financial condition and operating results.

In periods of worsening economic conditions, our exposure to credit risk and payment delinquencies on our accounts receivable significantly increases.

A substantial majority of our outstanding accounts receivables are not covered by collateral. In addition, our standard terms and conditions permit payment within a specified number of days following the receipt of our product. While we have procedures to monitor and limit exposure to credit risk on our receivables, there can be no assurance such procedures will effectively limit our credit risk and avoid losses. As economic conditions deteriorate, certain of our customers have faced and may face liquidity concerns and have delayed and may delay or may be unable to satisfy their payment obligations, which would have a material adverse effect on our financial condition and operating results.

We have a history of losses and may not be able to generate sufficient revenues to achieve and maintain profitability.

Since we began operations in 1997, our revenues have not been sufficient to support our operations, and we have incurred substantial operating losses every year. As of December 31, 2008, our accumulated deficit was approximately $4.3 billion, which includes approximately $2.7 billion related to goodwill impairment charges. Our stockholders’ equity at December 31, 2008 was $2.6 million. We continue to commit a substantial investment of resources to sales, product marketing and developing new products and enhancements, and we will need to increase our revenues to achieve profitability and positive cash flows. Our expectations as to when we can achieve positive cash flows, and as to our future cash balances, are subject to a number of assumptions, including assumptions regarding improvements in general economic conditions and customer purchasing and payment patterns, many of which are beyond our control. Our history of losses has previously caused some of our potential customers to question our viability, which has in turn hampered our ability to sell some of our products. Additionally, our revenues have been affected by the current downturn in economic conditions, both

generally and in our market. As a result of these conditions, we have experienced and expect to continue to experience difficulties in attracting new customers, which means that, even if sales of our products and services grow, we may continue to experience losses, which may cause the price of our stock to decline.

Our ability to continue as a going concern is at risk.

Our independent public accounting firm has issued an opinion on our consolidated financial statements that states that the consolidated financial statements were prepared assuming we will continue as a going concern and further states that our recurring losses from operations, negative working capital, negative cash flow from operations and accumulated deficit raise substantial doubt about our ability to continue as a going concern. The global economic downturn created a substantially more difficult business environment in 2008, affecting our liquidity and operating performance. If our revenues do not improve and we are unable to reduce operating expenses sufficiently and we do not obtain additional financing, we may become unable to pay our operating expenses on a timely basis due to a lack of sufficient liquidity. We can give no assurances as to whether we will be able to implement cost reduction initiatives, increase revenues, or obtain debt or equity financing, in order to provide sufficient liquidity for us to continue as a going concern.

The relatively large size of many of our expected license transactions could contribute to our failure to meet expected sales in any given quarter and could materially harm our operating results.

Our revenues and results of operations may fluctuate as a result of a variety of factors. Our revenues are especially subject to fluctuation because they depend on the completion of relatively large orders for our products and related services. The average size of our license transactions is generally large relative to our total revenues in any quarter, particularly as we have focused on larger enterprise customers, on licensing our more comprehensive integrated products, and have involved systems integrators in our sales process. If sales expected from a specific customer in a particular quarter are not realized in that quarter, we are unlikely to be able to generate revenue from alternate sources in time to compensate for the shortfall. Fluctuations in our results of operations may be due to a number of additional factors, including, but not limited to, our ability to retain and increase our customer base, changes in our pricing policies or those of our competitors, the timing and success of new product introductions by us or our competitors, the sales cycle for our products, our fixed expenses, the purchasing and budgeting cycles of our clients, and the decline in general economic, industry and market conditions.

This dependence on large orders makes our revenues and operating results more likely to vary from quarter to quarter, and more difficult to predict, because the loss of any particular large order is significant. In recent periods, we have experienced increases in the length of a typical sales cycle. This trend may add to the uncertainty of our future operating results and reduce our ability to anticipate our future revenues. Moreover, to the extent that significant sales occur earlier than anticipated, revenues for subsequent quarters may be lower than expected. As a result, our operating results could suffer if any large orders are delayed or canceled in any future period. In part as a result of this aspect of our business, our quarterly revenues and operating results may fluctuate in future periods and we may fail to meet the expectations of investors and public market analysts, which could cause the price of our common stock to decline.

We may not be able to forecast our revenues accurately because our products have a long and variable sales cycle and we rely on systems integrators for sales.

The long sales cycle for our products may cause license revenues and operating results to vary significantly from period to period. To date, the sales cycle for most of our product sales has taken anywhere from 6 to 9 months. Our sales cycle typically requires pre-purchase evaluation by a significant number of individuals within our customers’ organizations. Along with third parties that often jointly market our software with us, we invest significant amount of time and resources educating and providing information to prospective customers regarding the use and benefits of our products. Many of our customers evaluate our software slowly and

deliberately, depending on the specific technical capabilities of the customer, the size of the deployment, the complexity of the customer’s network environment, and the quantity of hardware and the degree of hardware configuration necessary to deploy our products.

Furthermore, we rely to a significant extent on systems integrators to identify, influence and manage large transactions with customers, and we expect this trend to continue as our industry consolidates. Selling our products in conjunction with our systems integrators who incorporate our products into their offerings can involve a particularly long and unpredictable sales cycle, as it typically takes more time for the prospective customer to evaluate proposals from multiple vendors. In addition, when systems integrators propose the use of our products to their customers, it is typically part of a larger project, which can require additional levels of customer approvals. We have little or no control over the sales cycle of an integrator-led transaction or our customers’ budgetary constraints and internal decision-making and acceptance processes.

As a result of increasingly long sales cycles, we have faced increased difficulty in predicting our operating results for any given period, and have experienced significant unanticipated fluctuations in our revenues from period to period. Any failure to achieve anticipated revenues for a period could cause our stock price to decline.

If we fail to generate sufficient revenues to support our business and require additional financing, failure to obtain such financing would affect our ability to maintain our operations and to grow our business, and the terms of any financing we obtain may impair the rights of our existing stockholders.

If we fail to generate sufficient revenues to support our business, we may need to seek additional financing to fund our operations or growth. If we raise additional funds through the issuance of equity or convertible debt securities, the percentage ownership of our stockholders would be reduced and the securities we issue might have rights, preferences and privileges senior to those of our current stockholders. Moreover, because of current volatility in the global capital markets and among financial institutions, including a tightening in the capital and credit markets, if we were to seek funding from the capital or credit markets, we may not be able to secure funding on terms acceptable to us or at all.

If adequate funds were not available on acceptable terms, our ability to achieve or sustain positive cash flows, maintain current operations, fund any potential expansion, take advantage of unanticipated opportunities, develop or enhance products or services, or otherwise respond to competitive pressures would be significantly limited. Furthermore, any failure to raise sufficient capital in a timely fashion could prevent us from growing or pursuing our strategies or cause us to limit our operations and cause potential customers to question our financial viability. We had cash and cash equivalents of $7.0 million at December 31, 2008, and as of such date, had contractual commitments of $10.2 million in 2009. It is possible that our cash position could decrease over the next few quarters and some customers could become increasingly concerned about our cash situation and our ongoing ability to update and maintain our products. This could significantly harm our sales efforts.

Our cash and cash equivalents could be adversely affected if the financial institutions in which we hold our cash and cash equivalents fail.

Our cash and cash equivalents are highly liquid investments with original maturities of three months or less at the time of purchase. We maintain the cash and cash equivalents with reputable major financial institutions. Deposits with these banks exceed the Federal Deposit Insurance Corporation (“FDIC”) insurance limits or similar limits in foreign jurisdictions. While we monitor daily the cash balances in the operating accounts and adjust the balances as appropriate, these balances could be impacted if one or more of the financial institutions with which we deposit fails or is subject to other adverse conditions in the financial or credit markets. To date we have experienced no loss or lack of access to our invested cash or cash equivalents; however, we can provide no assurance that access to our invested cash and cash equivalents will not be impacted by adverse conditions in the financial and credit markets.

Our business relies heavily on customer service solutions, and these solutions may not gain market acceptance.

We have made customer service solutions our main focus and, have allocated a significant portion of our research and development and marketing resources to the development and promotion of such products. If these products are not accepted by potential customers, our business would be materially adversely affected. For our current business model to succeed, we believe that we will need to convince new and existing customers of the merits of purchasing our customer service solutions over traditional CRM solutions and competitors’ customer service solutions. Many of these customers have previously invested substantial resources in adopting and implementing their existing CRM products, whether such products are ours or are those of our competitors. We may be unable to convince customers and potential customers of the benefits of purchasing substantial new software packages that provide our specific customer service capabilities. If our strategy of offering customer service solutions fails, we may not be able to sell sufficient quantities of our product offerings to generate significant license revenues, and our business could be harmed.

Our expenses are generally fixed and we will not be able to reduce these expenses quickly if we fail to meet our revenue expectations.

Most of our expenses, such as employee compensation, are relatively fixed in the short term. Other expenses like leases are fixed and are more long term. Moreover, our forecast is based, in part, upon our expectations regarding future revenue levels. As a result, in any particular quarter our total revenues can be below expectation and we could not proportionately reduce operating expenses for that quarter. Accordingly, such a revenue shortfall would have a disproportionate negative effect on our expected operating results for that quarter.

If we fail to grow our customer base or generate repeat business, our operating results could be harmed.

Our business model generally depends on the sale of our products to new customers as well as on expanded use of our products within our customers’ organizations. If we fail to grow our customer base or generate repeat and expanded business from our current and future customers, our business and operating results will be seriously harmed. In some cases, our customers initially make a limited purchase of our products and services for pilot programs. These customers may not purchase additional licenses to expand their use of our products. If these customers do not successfully develop and deploy initial applications based on our products, they may choose not to purchase deployment licenses or additional development licenses. In addition, as we introduce new versions of our products, new product lines or new product features, our current customers might not require the additional functionality we offer and might not ultimately license these products. Furthermore, because the total amount of maintenance and support fees we receive in any period depends in large part on the size and number of licenses that we have previously sold, any downturn in our software license revenues would negatively affect our future services revenue. Also, if customers elect not to renew their support agreements, our services revenue could decline significantly. If customers are unable to pay for their current products or are unwilling to purchase additional products, our revenues would decline. Additionally, a substantial percentage of our sales come from repeat customers. If a significant existing customer or a group of existing customers decide not to repeat business with us, our revenues would decline and our business would be harmed.

We face substantial competition and may not be able to compete effectively.

The market for our products and services is intensely competitive, evolving, and subject to rapid technological change. From time to time, our competitors reduce the prices of their products and services (substantially in certain cases) to obtain new customers. Competitive pressures could make it difficult for us to acquire and retain customers and could require us to reduce the price of our products. Any such changes would likely reduce margins and could adversely affect operating results.

Our customers’ requirements and the technology available to satisfy those requirements are continually changing. Therefore, we must be able to respond to these changes in order to remain competitive. Changes in our

products may also make it more difficult for our sales force to sell effectively. In addition, changes in customers’ demand for the specific products, product features and services of other companies may result in our products becoming uncompetitive. We expect the intensity of competition to increase in the future. Furthermore, we could lose market share if our competitors introduce new competitive products, add new functionality, acquire competitive products, reduce prices or form strategic alliances with other companies. We may not be able to compete successfully against current and future competitors, and competitive pressures may seriously harm our business.

Our competitors vary in size and in the scope and breadth of products and services offered. We currently face competition with our products from systems designed in-house and by our competitors. We expect that these systems will continue to be a major source of competition for the foreseeable future. Our primary competitors for electronic CRM platforms are larger, more established companies such as Oracle. We also face competition from Chordiant Software, Salesforce.com, Consona, eGain, RightNow, Inquira and Pegasystems with respect to specific applications we offer. We may face increased competition upon introduction of new products or upgrades from competitors, or if we expand our product line through acquisition of complementary businesses or otherwise. As we have combined and enhanced our product lines to offer a more comprehensive software solution, we are increasingly competing with large, established providers of customer management and communication solutions as well as other competitors. Our combined product line may not be sufficient to successfully compete with the product offerings available from these companies, which could slow our growth and harm our business.

Many of our competitors have longer operating histories, significantly greater financial, technical, marketing and other resources, significantly greater name recognition and a larger installed base of customers than we have. As a result, our competitors may be able to respond more quickly than we can to new or changing opportunities, technologies, standards or client requirements or devote greater resources to the promotion and sale of their products and services than we can. In addition, many of our competitors have well-established relationships with our current and potential customers and have extensive knowledge of our industry. We may lose potential customers to competitors for various reasons, including the ability or willingness of competitors to offer lower prices and other incentives that we cannot match. It is possible that new competitors or alliances among competitors may emerge and rapidly acquire significant market share. We also expect that competition will increase as a result of recent industry consolidations, as well as anticipated future consolidations.

We rely on marketing, technology and distribution relationships for the sale, installation and support of our products that may generally be terminated at any time, and if our current and future relationships are not successful, our growth might be limited.

We rely on marketing and technology relationships with a variety of companies, including systems integrators and consulting firms that, among other things, generate leads for the sale of our products and provide our customers with implementation and ongoing support. If we cannot maintain successful marketing and technology relationships or if we fail to enter into such additional relationships, we could have difficulty expanding the sales of our products and our growth might be limited.

A portion of our revenues depends on leads generated by systems integrators and their recommendations of our products. If systems integrators do not successfully market our products, our operating results will be materially harmed. In addition, many of our direct sales are to customers that will be relying on systems integrators to implement our products, and if systems integrators are not familiar with our technology or able to successfully implement our products, our operating results will be materially harmed. We expect to continue increasing our leverage of systems integrators as indirect sales channels and, if this strategy is successful, our dependence on the efforts of these third parties for revenue growth and customer service will remain high. Our reliance on third parties for these functions has reduced our control over such activities and reduced our ability to perform such functions internally. If we come to rely primarily on a single systems integrator that subsequently terminates its relationship with us, becomes insolvent or is acquired by another company with which we have no

relationship, or decides not to provide implementation services related to our products, we may not be able to internally generate sufficient revenues or increase the revenues generated by our other systems integrator relationships to offset the resulting lost revenues. Furthermore, systems integrators typically suggest our solution in combination with other products and services, some of which may compete with our solution. Systems integrators are not required to promote any fixed quantities of our products, are not bound to promote our products exclusively and may act as indirect sales channels for our competitors. If systems integrators choose not to promote our products or if they develop, market or recommend software applications that compete with our products, our business will be harmed.

In addition to relying on systems integrators to recommend our products, we also rely on systems integrators and other third-party resellers to install and support our products. If the companies providing these services fail to implement our products successfully for our customers, the customer may be unable to complete implementation on the schedule that it had anticipated and we may have increased customer dissatisfaction or difficulty making future sales as a result. We might not be able to maintain our relationships with systems integrators and other indirect sales channel partners and enter into additional relationships that will provide timely and cost-effective customer support and service. If we cannot maintain successful relationships with our indirect sales channel partners, we might have difficulty expanding the sales of our products and our growth could be limited. In addition, if such third parties do not provide the support our customers need, we may be required to hire subcontractors to provide these professional services. Increased use of subcontractors would harm our margins because it costs us more to hire subcontractors to perform these services than it would to provide the services ourselves.

Because certain customers account for a substantial portion of our revenues, the loss of a significant customer could cause a substantial decline in our revenues.

No customer accounted for 10% or more of our revenues in 2006, 2007 or 2008. However, if we lose a number of major customers, or if contracts are delayed or cancelled or we do not contract with new major customers, our revenues and net loss would be adversely affected. In addition, customers that have accounted for significant revenues in the past may not generate revenues in any future period, and our failure to obtain new significant customers or additional orders from existing customers could materially affect our operating results.

We may not receive significant revenues from our current research and development efforts for several years, if at all.

Developing and localizing software is expensive and the investment in product development often involves a long payback cycle. We have and expect to continue making significant investments in software research and development and related product opportunities. Enhancing our products and pursuing new product developments require high levels of expenditures for research and development that could adversely affect our operating results if not offset by revenue increases. We believe that we must continue to dedicate a significant amount of resources to our research and development efforts to maintain our competitive position. However, we do not expect to receive significant revenues from these investments for several years, if at all.

If our cost reduction and restructuring efforts are ineffective, our revenues and profitability may be hurt.

During the year ended December 31, 2008 we implemented various cost reduction and restructuring activities to reduce operating costs. The expense related to our reduction in work force was approximately $737,000 and expense related to ceasing use of two of our offices was approximately $64,000. We also wrote off approximately $263,000 of capitalized costs related to an internal use software project that was abandoned. Additionally, during the year ended December 31, 2008 we recorded a restructuring recovery of $482,000 as a result of the extension of a sublease on one of the properties in our restructuring accrual. In September 2007, we agreed with the landlord of one of the facilities included in our restructuring accrual to surrender the remaining term of the lease in exchange for a lump sum cash payment. As a result of this agreement, we recorded additional

restructuring expense of approximately $319,000. We also undertook various cost reduction and restructuring activities in July 2007. The expense related to our reduction in work force was approximately $240,000 and expense related to ceasing use of one of our offices was approximately $8,000. These cost reduction and restructuring activities may not produce the full efficiencies and benefits we expect or the efficiencies and benefits might be delayed. There can be no assurance that these efforts, as well as any potential future cost reduction and restructuring activities, will not adversely affect our business, operations or customer perceptions, or result in additional future charges.

We may be unable to hire and retain the skilled personnel necessary to develop and grow our business.

We rely on the continued service of our senior management and other key employees and the hiring of new qualified employees. In the software industry, there is substantial and continuous competition for highly skilled business, product development, technical and other personnel. Given the concern over our long-term financial strength, we may not be successful in recruiting and integrating new personnel and retaining and motivating existing personnel, which could lead to increased turnover and reduce our ability to meet the needs of our current and future customers. Because our stock price declined drastically in recent years, and has not experienced any sustained recovery from the decline, stock-based compensation, including options to purchase our common stock, may have diminished the effectiveness as employee hiring and retention devices. If we are unable to retain qualified personnel, we could face disruptions to operations, loss of key information, expertise or know-how and unanticipated additional recruitment and training costs. If employee turnover increases, our ability to provide customer service and execute our strategy would be negatively affected.

For example, our ability to increase revenues in the future depends considerably upon our success in training and retaining effective direct sales personnel and the success of our direct sales force. We might not be successful in these efforts. Our products and services require sophisticated sales efforts. We have experienced significant turnover in our sales force including domestic senior sales management, and may experience further turnover in future periods. It generally takes a new salesperson nine or more months to become productive, and they may not be able to generate new sales. Our business will be harmed if we fail to retain qualified sales personnel, or if newly hired salespeople fail to develop the necessary sales skills or develop these skills more slowly than anticipated. Additionally, we continue to need to recruit experienced developers as a result of our back-shoring initiative.

If we fail to respond to changing customer preferences in our market, demand for our products and our ability to enhance our revenues will suffer.

If we do not continue to improve our products and develop new products that keep pace with competitive product introductions and technological developments, satisfy diverse and rapidly evolving customer requirements, and achieve market acceptance, we might be unable to attract new customers. Our industry is characterized by rapid and substantial developments in the technologies and products that enjoy widespread acceptance among prospective and existing customers. The development of proprietary technology and necessary service enhancements entails significant technical and business risks and requires substantial expenditures and lead-time. We might not be successful in marketing and supporting our products or developing and marketing other product enhancements and new products that respond to technological advances and market changes, on a timely or cost-effective basis. In addition, even if these products are developed and released, they might not achieve market acceptance. We have experienced delays in releasing new products and product enhancements in the past and could experience similar delays in the future. These delays or problems in the installation or implementation of our new releases could cause us to lose customers.

Our failure to manage multiple technologies and technological change could reduce demand for our products.

Rapidly changing technology and operating systems, changes in customer requirements, and evolving industry standards might impede market acceptance of our products. Our products are designed based upon

currently prevailing technology to work on a variety of hardware and software platforms used by our customers. However, our software may not operate correctly on evolving versions of hardware and software platforms, programming languages, database environments and other systems that our customers use. If new technologies emerge that are incompatible with our products, or if competing products emerge that are based on new technologies or new industry standards and that perform better or cost less than our products, our key products could become obsolete and our existing and potential customers could seek alternatives to our products. We must constantly modify and improve our products to keep pace with changes made to these platforms and to database systems and other back-office applications and Internet-related applications. Furthermore, software adapters are necessary to integrate our products with other systems and data sources used by our customers. We must develop and update these adapters to reflect changes to these systems and data sources in order to maintain the functionality provided by our products. As a result, uncertainties related to the timing and nature of new product announcements, introductions or modifications by vendors of operating systems, databases, CRM software, Web servers and other enterprise and Internet-based applications could delay our product development, increase our product development expense or cause customers to delay evaluation, purchase and deployment of our analytics products. If we fail to modify or improve our products in response to evolving industry standards, our products could rapidly become obsolete.

Our success depends upon our ability to develop new products and enhance our existing products on a timely basis.

The challenges of developing new products and enhancements require us to commit a substantial investment of resources to development, and we might not be able to develop or introduce new products on a timely or cost-effective basis, or at all, which could be exploited by our competitors and lead potential customers to choose alternative products. To be competitive, we must develop and introduce on a timely basis new products and product enhancements for companies with significant e-business customer interactions needs. Our ability to deliver competitive products may be negatively affected by the diversion of resources to development of our suite of products, and responding to changes in competitive products and in the demands of our customers. If we experience product delays in the future, we may face:

customer dissatisfaction;

cancellation of orders and license agreements;

negative publicity;

loss of revenues; and

slower market acceptance.

Furthermore, delays in bringing new products or enhancements to market can result, for example, from loss of institutional knowledge through reductions in force, or the existence of defects in new products or their enhancements.

Failure to license necessary third-party software incorporated in our products could cause delays or reductions in our sales.

We license third-party software that we incorporate into our products. These licenses may not continue to be available on commercially reasonable terms or at all. Some of this technology would be difficult to replace. The loss of any of these licenses could result in delays or reductions of our applications until we identify, license and integrate, or develop equivalent software. If we are required to enter into license agreements with third parties for replacement technology, we could face higher royalty payments and our products may lose certain attributes or features. In the future, we might need to license other software to enhance our products and meet evolving customer needs. If we are unable to do this, we could experience reduced demand for our products.

Defects in third-party products associated with our products could impair our products’ functionality and injure our reputation.

The effective implementation of our products depends upon the successful operation of third-party products in conjunction with our products. Any undetected defects in these third-party products could prevent the implementation or impair the functionality of our products, delay new product introductions or injure our reputation.

Given that our stock price is near its historical low, we may be subject to takeover overtures that will divert the attention of our management and Board, and require us to incur expenses for outside advisors.

Given that our stock price is near its historical low, we may be subject to takeover overtures. Evaluating and addressing these overtures would require the time and attention of our management and Board, divert them from their focus on our business, and require us to incur additional expenses on outside legal, financial and other advisors, all of which could materially and adversely affect our business, financial condition and results of operations.

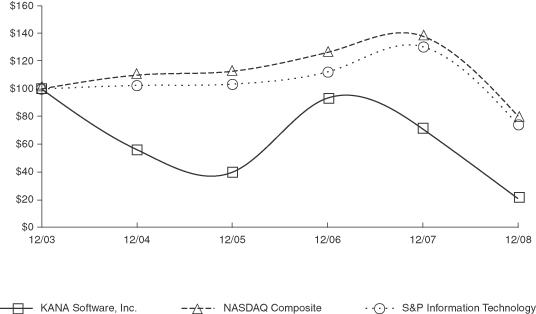

Our common stock is currently quoted on the OTCBB.

Our common stock was delisted from The NASDAQ Stock Market effective at the opening of business on October 17, 2005. From October 17, 2005 to December 4, 2006, our common stock was quoted on the “Pink Sheets” and as of December 5, 2006, our common stock has been quoted on Over the Counter Bulletin Board (“OTCBB”). The OTCBB is generally considered less efficient than The NASDAQ Stock Market. Quotation of our common stock on the OTCBB may reduce the liquidity of our securities, limit the number of investors who trade in our securities, result in a lower stock price and larger spread in the bid and ask prices for shares of our common stock and could have an adverse effect on us. Additionally, we may become subject to the SEC rules that affect “penny stocks,” which are stocks below $5.00 per share that are not quoted on The NASDAQ Stock Market. These SEC rules would make it more difficult for brokers to find buyers for our securities and could lower the net sales prices that our stockholders are able to obtain. If our price of common stock remains low, we may not be able to raise equity capital.

Our listing on the OTCBB and the declines in our stock price may greatly impair our ability to raise additional necessary capital through equity or debt financing, and significantly increase the dilution to our current stockholders caused by any issuance of equity in financing or other transactions. The price at which we would issue shares in such transactions is generally based on the market price of our common stock and a decline in the stock price could result in our need to issue a greater number of shares to raise a given amount of funding.

In addition, because our common stock is not listed on a principal national exchange, we are subject to Rule 15g-9 under the Exchange Act, which imposes additional sales practice requirements on broker-dealers that sell low-priced securities to persons other than established customers and institutional accredited investors. For transactions covered by this rule, a broker-dealer must make a special suitability determination for the purchaser and have received the purchaser’s written consent to the transaction prior to sale. Consequently, the rule may affect the ability of broker-dealers to sell our common stock and affect the ability of holders to sell their shares of our common stock in the secondary market. Moreover, investors may be less interested in purchasing low-priced securities because the brokerage commissions, as a percentage of the total transaction value, tend to be higher for such securities, and some investment funds will not invest in low-priced securities (other than those which focus on small-capitalization companies or low-priced securities).

Our stock price has been highly volatile and has experienced a significant decline, and may continue to be volatile and decline.

The trading price of our common stock has fluctuated widely in the past and we expect that it will continue to do so in the future, as a result of a number of factors, many of which are outside our control, such as:

price and volume fluctuations in the overall stock market;

the impact of announcements related to the effects of the global economic downturn and programs intended to address it;

variations in our actual and anticipated operating results;

changes in our earnings estimates by analysts;

the volatility inherent in stock prices within the emerging sector within which we conduct business; and

the volume of trading in our common stock, including sales of substantial amounts of common stock issued upon the exercise of outstanding options and warrants.

In addition, stock markets in general have, and particularly The NASDAQ Stock Market and the OTCBB have, experienced extreme price and volume fluctuations that have affected the market prices of many technology and computer software companies, particularly Internet-related companies. Such fluctuations have often been unrelated or disproportionate to the operating performance of these companies. These broad market fluctuations could adversely affect the market price of our common stock. In the past, following periods of volatility in the market price of a particular company’s securities, securities class action litigation has often been brought against that company. Securities class action litigation could result in substantial costs and a diversion of our management’s attention and resources.

Since becoming a publicly traded security listed on The NASDAQ Stock Market in September 1999, our common stock has reached a sales price high of $1,698.10 per share and a sales price low of $0.46 per share. Our common stock is currently quoted on the OTCBB and the last reported sales price of our shares on May 14, 2009 was $0.72 per share.

Our pending patents may never be issued and, even if issued, may provide little protection.

Our success and ability to compete depend upon the protection of our software and other proprietary technology rights. We currently have five issued U.S. patents, three of which expire in 2018 and two of which expire in 2020, and multiple U.S. patent applications pending relating to our software. None of our technology is patented outside of the United States. It is possible that:

our pending patent applications may not result in the issuance of patents;

any issued patents may not be broad enough to protect our proprietary rights;

any issued patents could be successfully challenged by one or more third parties, which could result in our loss of the right to prevent others from exploiting the inventions claimed in those patents;

current and future competitors may independently develop similar technology, duplicate our products or design around any of our patents; and

effective patent protection may not be available in every country in which we do business.

We rely upon trademarks, copyrights and trade secrets to protect our proprietary rights, which may not be sufficient to protect our intellectual property.

In addition to patents, we rely on a combination of laws, such as copyright, trademark and trade secret laws, and contractual restrictions, such as confidentiality agreements and licenses, to establish and protect our proprietary rights. However, despite the precautions that we have taken:

laws and contractual restrictions may not be sufficient to prevent misappropriation of our technology or deter others from developing similar technologies;

current federal laws that prohibit software copying provide only limited protection from software “pirates,” and effective trademark, copyright and trade secret protection may be unavailable or limited in foreign countries;

other companies may claim common law trademark rights based upon state or foreign laws that precede the federal registration of our marks; and

policing unauthorized use of our products and trademarks is difficult, expensive and time-consuming, and we may be unable to determine the extent of this unauthorized use.

Also, the laws of some other countries in which we market our products may offer little or no effective protection of our proprietary technology. Consequently, we may be unable to prevent our proprietary technology from being exploited abroad, which could diminish international sales or require costly efforts to protect our technology. Reverse engineering, unauthorized copying or other misappropriation of our proprietary technology could enable third parties to benefit from our technology without paying us for it, which would significantly harm our business.

We may become involved in litigation over proprietary rights, which could be costly and time consuming.

The software industry is characterized by the existence of a large number of patents, trademarks and copyrights and by frequent litigation based on allegations of infringement or other violations of intellectual property rights, and our technologies may not be able to withstand any third-party claims or rights against their use. Some of our competitors in the market for customer communications software may have filed or may intend to file patent applications covering aspects of their technology that they may claim our technology infringes. Such competitors could make a claim of infringement against us with respect to our products and technology. Additionally, third parties may currently have, or may eventually be issued, patents upon which our current or future products or technology infringe and any of these third parties might make a claim of infringement against us. For example, during 2006 and 2007, we were involved in litigation brought by Polaris IP, LLC against us and certain of our customers that claimed that certain of our products violate patents held by them.

As we grow, the possibility of intellectual property rights claims against us increases. We may not be able to withstand any third-party claims and regardless of the merits of the claim, any intellectual property claims could be inherently uncertain, time-consuming and expensive to litigate or settle. Many of our software license agreements require us to indemnify our customers from any claim or finding of intellectual property infringement. We periodically receive notices from customers regarding patent license inquiries they have received which may or may not implicate our indemnity obligations. Any litigation, brought by others, or us could result in the expenditure of significant financial resources and the diversion of management’s time and efforts. In addition, litigation in which we are accused of infringement might cause product shipment delays, require us to develop alternative technology or require us to enter into royalty or license agreements, which might not be available on acceptable terms, or at all. If an infringement claim is made against us, we may not be able to develop non-infringing technology or license the infringing or similar technology on a timely and cost-effective basis. As a result, our business could be significantly harmed.

We may face liability claims that could result in unexpected costs and damages to our reputation.

Our licenses with customers generally contain provisions designed to limit our exposure to potential product liability claims, such as disclaimers of warranties and limitations on liability for special, consequential and incidental damages. In addition, our license agreements generally limit the amounts recoverable for damages to the amounts paid by the licensee to us for the product or service giving rise to the damages. However, some domestic and international jurisdictions may not enforce these contractual limitations on liability. We may be subject to claims based on errors in our software or mistakes in performing our services including claims relating to damages to our customers’ internal systems. A product liability claim could divert the attention of our management and key personnel, could be expensive to defend and could result in adverse settlements and judgments.

We may face higher costs and lost sales if our software contains errors.

We face the possibility of higher costs as a result of the complexity of our products and the potential for undetected errors. Due to the critical nature of many of our products and services, errors could be particularly problematic. In the past, we have discovered software errors in some of our products after their introduction. We only have a few “beta” customers that test new features and functionality of our software before we make these features and functionalities generally available to our customers. If we are not able to detect and correct errors in our products or releases before commencing commercial shipments, we could face:

loss of or delay in revenues expected from new products and an immediate and significant loss of market share;

loss of existing customers that upgrade to new products and of new customers;

failure to achieve market acceptance;

diversion of development resources;

injury to our reputation;

increased service and warranty costs;

legal actions by customers; and

increased insurance costs.

Any of the foregoing potential results of errors in our software could adversely affect our business, financial condition and results of operations.

Our security could be breached, which could damage our reputation and deter customers from using our services.

We must protect our computer systems and network from physical break-ins, security breaches, and other disruptive problems caused by the Internet or other users. Computer break-ins could jeopardize the security of information stored in and transmitted through our computer systems and network, which could adversely affect our ability to retain or attract customers, damage our reputation, and subject us to litigation. We have been in the past, and could be in the future, subject to denial of service, vandalism, and other attacks on our systems by Internet hackers. Although we intend to continue to implement security technology and establish operational procedures to prevent break-ins, damage and failures, these security measures may fail. Our insurance coverage in certain circumstances may be insufficient to cover losses that may result from such events.

We have significant international sales and are subject to risks associated with operating in international markets.

A substantial proportion of our revenues are generated from sales outside North America, exposing us to additional financial and operational risks. Sales outside North America represented 25%, 25% and 32% of our total revenues for 2008, 2007 and 2006, respectively. We have established offices in the United States, Europe and Japan. Sales outside North America could increase as a percentage of total revenues as we attempt to expand our international operations. In addition to the additional costs and uncertainties of being subject to international laws and regulations, international operations require significant management attention and financial resources, as well as additional support personnel. To the extent our international operations grow, we will also need to, among other things, expand our international sales channel management and support organizations and develop relationships with international service providers and additional distributors and systems integrators. International operations are subject to many inherent risks, including:

political, social and economic instability, including conflicts in the Middle East and elsewhere abroad, terrorist attacks and security concerns in general;

adverse changes in tariffs, duties, price controls and other protectionist laws and business practices that favor local competitors;

fluctuations in currency exchange rates;

longer collection periods and difficulties in collecting receivables from foreign entities;

exposure to different legal standards and burdens of complying with a variety of foreign laws, including employment, tax, privacy and data protection laws and regulations;

reduced protection for our intellectual property in some countries;

increases in tax rates;

greater seasonal fluctuations in business activity;

expenses associated with localizing products for foreign countries, including translation into foreign languages;

difficulty and cost of staffing and managing international operations; and

import and export license requirements and restrictions of the United States and each other country in which we operate.