The following report of the compensation committeePerformance Graph section shall not be deemed to be “soliciting material” or “filed” or incorporated by reference in future filings with the SEC, or subject to be incorporated by reference into any other filing by Nikola Corporation under the Securities Actliabilities of 1933 orSection 18 of the Securities Exchange Act, of 1934, except to the extent that we specifically incorporate it by reference into a document filed under those Acts.the Securities Act or the Exchange Act.

The graph below indicates our cumulative 5-year total shareholder return on common stock with the cumulative total returns of the NASDAQ Composite index and the NASDAQ Clean Edge Green Energy index. The graph tracks the

performance of a $100 investment in our common stock and in each index (with the reinvestment of all dividends) from December 31, 2018 to December 31, 2023.

Issuer Purchases of Securities

None.

Item 6. [Reserved]

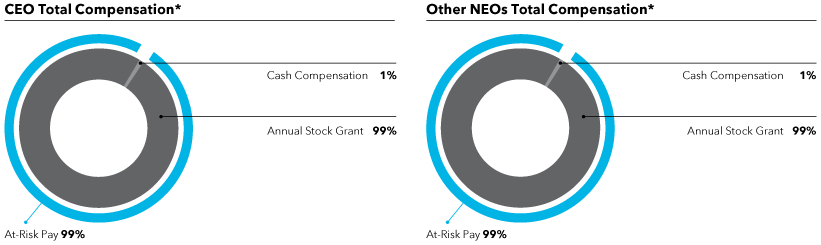

The compensation committee has reviewed and discussed the Compensation

Item 7. Management's Discussion and Analysis of Financial Condition and Results of Operations

You should read the following discussion and analysis of our financial condition and results of operations together with the consolidated financial statements and related notes that are included elsewhere in this Annual Report on Form 10-K. This discussion contains forward-looking statements based upon current expectations that involve risks and uncertainties. Our actual results may differ materially from those anticipated in these forward-looking statements as a result of various factors, including those set forth aboveunder "Forward-Looking Statements", “Risk Factors” and in other parts of this Annual Report on Form 10-K.

Overview

We are a technology innovator and integrator, working to decarbonize the trucking industry by developing innovative energy and transportation solutions. We are pioneering a business model that will enable fleets and end users to integrate next-generation truck technology, hydrogen refueling infrastructure, EV charging solutions, and related maintenance. By creating this ecosystem, we and our strategic business partners and suppliers hope to build a long-term competitive advantage for clean technology vehicles and next-generation fueling solutions.

Our expertise lies in design, innovation, and software and engineering. We assemble, integrate, and commission our vehicles in collaboration with our management. Based on its reviewbusiness partners and those discussions, the compensation committee recommendedsuppliers. Our approach is to leverage strategic partnerships to help lower cost, increase capital efficiency and increase speed to market.

We operate in two business units: Truck and Energy. The Truck business unit is commercializing FCEV and BEV Class 8 trucks that provide or are intended to provide environmentally friendly, cost-effective solutions to the boardshort, medium and long haul trucking sectors. The Energy business unit is developing hydrogen fueling infrastructure to support our FCEV trucks.

We commenced commercial production of directors that the CompensationTre BEV in the first quarter of 2022 and commenced commercial production of the Tre FCEV in the third quarter of 2023, both at our manufacturing facility in Coolidge, Arizona.

In January 2023, we announced our new global brand, HYLA, to encompass our energy products for procuring, distributing, and dispensing hydrogen to fuel our trucks. We expect to leverage multiple ownership structures where we either fully or partially own, or do not own, hydrogen production assets. In cases where we are able to source hydrogen supply, without ownership of hydrogen production assets, we expect to enter into long-term supply contracts where our costs and surety of supply are well-defined.

We intend to continue to develop our business, which includes the following ongoing activities:

•commercialize our heavy-duty trucks and other products;

•expand and maintain manufacturing facilities and equipment;

•invest in servicing our vehicles under warranty including repairs and service parts;

•develop, deploy, and maintain hydrogen fueling infrastructure;

•continue to invest in our technology;

•invest in marketing and advertising, sales, and distribution infrastructure for our products and services;

•maintain and improve our operational, financial and management information systems;

•hire and retain personnel;

•obtain, maintain, expand, and protect our intellectual property portfolio; and

•operate as a public company.

Comparability of Financial Information

On June 30, 2023, we completed the Assignment of Romeo, which was previously consolidated in our financial statements from the date of acquisition, October 14, 2022. The operating results of Romeo are reported in discontinued operations for the years ended December 31, 2023 and 2022. Our results for the periods presented, as discussed in this Management's Discussion and Analysis of Financial Condition and Results of Operations, include only results from continuing operations and exclude results related to our discontinued operation.

Key Factors Affecting Operating Results

We believe that our performance and future success depend on several factors that present significant opportunities for us but also pose risks and challenges, including those set forth in the section entitled "Risk Factors."

We require substantial additional capital to manufacture and validate our products and services and fund operations for the foreseeable future. Until we can generate sufficient revenue and positive gross margins, we expect to finance our operations through a combination of existing cash on hand, sales of stock, debt financings, strategic partnerships, and licensing arrangements. The amount and timing of our future funding requirements will depend on many factors, including the pace and results of our development and validation efforts, demand for our trucks and expense levels, among other things.

Truck Production and Shipments

We started serial production at our manufacturing facility in March 2022 and began sales of Tre BEV trucks in the second quarter of 2022. During the second half of 2023, production and shipment of the Tre BEV was suspended due to the voluntary recall of BEV trucks initiated during the third quarter of 2023. In response to the voluntary recall, we have placed a temporary hold on all new BEV truck shipments.

The recall was initiated in response to investigations prompted by a battery pack thermal event. To minimize vehicle downtime and maximize end user safety and satisfaction, the battery packs in trucks owned by dealers and their retail customers are being retrofit with battery packs from an alternative supplier. We accrued recall campaign costs of $65.8 million for the BEV trucks that are expected to be returned to dealers and their customers once the recall is complete, of which $3.0 million has been incurred through December 31, 2023. The battery replacement commenced in late 2023, with the first set of trucks expected to be returned to fleets starting late in the first quarter of 2024, pending supply chain or other issues.

As of December 31, 2023, all BEV truck inventory was classified as work in process inventory as we are retrofitting the BEV inventory with alternative battery packs.

The following is a summary of the number of Tre BEV trucks produced and shipped since we commenced commercial production:

| | | | | | | | | | | | | | | | | |

| Tre BEVs | Q1 2022 | Q2 2022 | Q3 2022 | Q4 2022 | YTD 2022 |

| Produced | N/A | 50 | 75 | 133 | 258 |

| Shipped | N/A | 48 | 63 | 20 | 131 |

| | | | | | | | | | | | | | | | | |

| Tre BEVs | Q1 2023 | Q2 2023 | Q3 2023 | Q4 2023 | YTD 2023 |

| Produced | 63 | 33 | N/A | N/A | 96 |

| Shipped | 31 | 45 | 3 | N/A | 79 |

During the second quarter of 2023, we transitioned the manufacturing line to a mixed model production line in preparation for the commencement of commercial production of the FCEV starting on July 31, 2023.

The following is a summary of the number of Tre FCEV trucks produced and shipped since we commenced commercial production:

| | | | | | | | | | | |

| FCEVs | Q3 2023 | Q4 2023 | YTD 2023 |

| Produced | — | 42 | 42 |

| Shipped | — | 35 | 35 |

As of December 31, 2023, we had no FCEV trucks in finished goods inventory. Among the seven trucks produced but not shipped, three are being used in an extended field test with a fleet partner, two are in continued validation and engineering and two are being used for service training/fleet demos.

The hydrogen fuel cell vehicle market and hydrogen infrastructure are early stage markets. As a result, we have and may continue to experience production shortages as a result of new technology supply chain challenges, including but not limited to supply chain shortages we experienced in 2023 with respect to hydrogen tanks and modular fuelers. Additionally, we may experience delays in deliveries of FCEV trucks due to lack of hydrogen infrastructure or supply for end users.

Basis of Presentation

Currently, we conduct business through one operating segment. See Note 2 in the accompanying audited consolidated financial statements for more information.

Components of Results of Operations

Revenues

Truck sales: During the years ended December 31, 2023 and 2022, our truck sales were derived from deliveries of our Tre FCEV and Tre BEV trucks to dealers.

Service and other: During the years ended December 31, 2023 and 2022, service and other revenues included sales from delivered MCTs and other charging products to dealers and fleet customers, hydrogen sales, and service parts and labor.

Cost of Revenues

Truck sales: Cost of revenues includes direct parts, material and labor costs, manufacturing overhead, including amortized tooling costs and depreciation of our manufacturing facility, freight and duty costs, reserves for estimated warranty expenses including recall campaigns, and inventory write-downs.

Service and other: Cost of revenues relate primarily to direct materials, labor, outsourced manufacturing services and fulfillment costs for the sale of MCTs and other charging products, hydrogen, and service parts and labor.

Research and Development Expense

Research and development expenses consist primarily of costs incurred for the discovery and development of our vehicles, which include:

•Personnel-related expenses, including salaries, benefits, and stock-based compensation expense, for personnel in our engineering and research functions;

•Fees paid to third parties such as consultants and contractors for outside development and validation activities;

•Expenses related to materials, supplies and third-party services, including prototype tooling and non-recurring engineering.

•Depreciation for prototyping equipment and R&D facilities; and

•Expenses related to operating the manufacturing facility until the start of commercial production. With the start of commercial production of the Tre BEV in 2022 and Tre FCEV in 2023, manufacturing costs, including labor and overhead, as well as inventory-related expenses related to our trucks, and related facility costs, are no longer recorded in research and development but are reflected in cost of revenues.

During the years ended December 31, 2023, 2022, and 2021, our research and development expenses were primarily incurred in connection with the development of the BEV and FCEV trucks.

As a part of an in-kind investment, Iveco agreed to provide us with $100.0 million in advisory services (based on pre-negotiated hourly rates), including project coordination, drawings, documentation support, engineering support, vehicle integration, and product validation support. During the year ended December 31, 2021, we utilized $46.3 million of advisory services which were recorded as research and development expense. As of December 31, 2021, the full amount of advisory services had been consumed.

Our research and development costs have decreased and are expected to remain relatively stable as we have commenced commercial production of the Tre BEV and Tre FCEV. We will continue to incur research and development expenses for personnel and outside development.

Selling, General, and Administrative Expense

Selling, general, and administrative expenses consist of personnel related expenses for our corporate, executive, finance, and other administrative functions, expenses for outside professional services, including legal, audit and accounting services, as well as expenses for facilities, depreciation, amortization, travel, marketing, and selling costs. Personnel related expenses consist of salaries, benefits, and stock-based compensation.

We expect our selling, general, and administrative expenses to decrease as we continue to stay focused on right-scaling the business and implement cost-cutting programs to enable cash preservation.

Loss on Supplier Deposits

Loss on supplier deposits consist of losses on deposits for tooling and long-term supply agreements.

Interest Expense, net

Interest expense consists of interest on our debt, financing obligation and finance lease liabilities. Interest income consists primarily of interest received or earned on our cash and cash equivalents balances.

Revaluation of Warrant Liability

The revaluation of warrant liability includes the net gains and losses from the remeasurement of the warrant liability. Warrants recorded as liabilities are recorded at their fair value and remeasured at each reporting period.

Gain on Divestiture of Affiliate

Gain on divestiture of affiliate consists of consideration for the divestiture of Nikola Iveco Europe GmbH and the related License Agreement, in excess of the basis of our investment as of the divestiture date.

Loss on Debt Extinguishment

Loss on debt extinguishment includes the loss on exchange of $100.0 million of June 2022 Toggle Convertible Notes for the issuance of $100.0 million April 2023 Toggle Convertible Notes. Additionally, loss on debt extinguishment includes losses incurred on conversions of the 8.25% Convertible Notes. Losses were calculated as the difference between the carrying value of notes extinguished and the fair value of the notes or consideration issued as of the exchange or upon conversion, as applicable.

Other Income (Expense), net

Other income (expense), net consists primarily of other miscellaneous non-operating items, such as government grants, subsidies, merchandising, revaluation gains and losses on derivative assets and liabilities and other instruments recognized at fair value, foreign currency gains and losses, and unrealized gains and losses on investments.

Income Tax Expense

Our income tax provision consists of an estimate for U.S. federal and state income taxes based on enacted rates, as adjusted for allowable credits, deductions, uncertain tax positions, changes in deferred tax assets and liabilities, and changes in the tax law. Due to cumulative losses, we maintain a valuation allowance against U.S. and state deferred tax assets. Cash paid for income taxes, net of refunds during the years ended December 31, 2023, 2022, and 2021 were not material.

Equity in Net Loss of Affiliates

Equity in net loss of affiliates consists of our net portion of gains and losses from equity method investments, primarily Nikola Iveco Europe GmbH through the date of divestiture on June 29, 2023.

Results of Operations

Comparison of Year Ended December 31, 2023 to Year Ended December 31, 2022

The following table sets forth our historical operating results for the periods indicated:

| | | | | | | | | | | | | | | | | | | | | | | |

| Years Ended December 31, | | | | |

| 2023 | | 2022 | | $ Change | | % Change |

| (in thousands, except share and per share data) |

| Revenues: | | | | | | | |

| Truck sales | $ | 30,061 | | | $ | 45,931 | | | $ | (15,870) | | | (35) | % |

| Service and other | 5,778 | | | 3,794 | | | 1,984 | | | 52 | % |

| Total revenues | 35,839 | | | 49,725 | | | (13,886) | | | (28) | % |

| Cost of revenues: | | | | | | | |

| Truck sales | 242,519 | | | 132,556 | | | 109,963 | | | 83 | % |

| Service and other | 7,387 | | | 3,138 | | | 4,249 | | | 135 | % |

| Total cost of revenues | 249,906 | | | 135,694 | | | 114,212 | | | 84 | % |

| Gross loss | (214,067) | | | (85,969) | | | (128,098) | | | 149 | % |

| Operating expenses: | | | | | | | |

| Research and development | 208,160 | | | 270,480 | | | (62,320) | | | (23) | % |

| Selling, general and administrative | 198,768 | | | 346,186 | | | (147,418) | | | (43) | % |

| Loss on supplier deposits | 28,834 | | | — | | | 28,834 | | | NM |

| Total operating expenses | 435,762 | | | 616,666 | | | (180,904) | | | (29) | % |

| Loss from operations | (649,829) | | | (702,635) | | | 52,806 | | | (8) | % |

| Other income (expense): | | | | | | | |

| Interest expense, net | (76,023) | | | (17,712) | | | (58,311) | | | 329 | % |

| Revaluation of warrant liability | 371 | | | 3,903 | | | (3,532) | | | (90) | % |

| Gain on divestiture of affiliate | 70,849 | | | — | | | 70,849 | | | NM |

| Loss on debt extinguishment | (31,025) | | | — | | | (31,025) | | | NM |

| Other expense, net | (162,534) | | | (1,023) | | | (161,511) | | | 15788 | % |

| Loss before income taxes and equity in net loss of affiliates | (848,191) | | | (717,467) | | | (130,724) | | | 18 | % |

| Income tax expense | 12 | | | 6 | | | 6 | | | 100 | % |

| Loss before equity in net loss of affiliates | (848,203) | | | (717,473) | | | (130,730) | | | 18 | % |

| Equity in net loss of affiliates | (16,418) | | | (20,665) | | | 4,247 | | | (21) | % |

| Net loss from continuing operations | $ | (864,621) | | | $ | (738,138) | | | $ | (126,483) | | | 17 | % |

| | | | | | | |

| Basic and diluted net loss per share: | | | | | | | |

| Net loss from continuing operations | $ | (1.08) | | | $ | (1.67) | | | $ | 0.59 | | | (35) | % |

| | | | | | | |

| Weighted-average shares outstanding, basic and diluted: | 800,030,551 | | | 441,800,499 | | | 358,230,052 | | | 81 | % |

Revenues

Truck Sales

Revenues related to truck sales decreased by $15.9 million, or 35%, from $45.9 million during the year ended December 31, 2022 to $30.1 million during the year ended December 31, 2023. The decrease is attributed to the hold on new BEV truck shipments in connection with the recall initiated during the third quarter of 2023. We shipped 131 Tre BEVs during the year ended December 31, 2022 compared to 79 during the year ended December 31, 2023. Additionally, during the year ended December 31, 2023, we recognized the impact of 13 Tre BEV repurchases or expected repurchases related to executed or expected cancellations of dealer agreements.

Decreases were partially offset by Tre FCEV truck shipments, commencing in the fourth quarter of 2023. During the year ended December 31, 2023, we transferred control of 35 Tre FCEV trucks to our dealer network.

Service and Other

Revenues related to service and other revenue increased by $2.0 million, or 52%, from $3.8 million during the year ended December 31, 2022 to $5.8 million during the year ended December 31, 2023. The increase was primarily driven by deliveries of MCTs and other charging products, hydrogen, and service parts and labor.

Cost of Revenues

Truck Sales

Cost of revenues related to truck sales increased by $110.0 million, or 83%, from $132.6 million during the year ended December 31, 2022 to $242.5 million during the year ended December 31, 2023. The increase is primarily attributed to the voluntary recall of BEV trucks in the second half of 2023. As a result of the recall, we accrued $65.8 million for estimated recall campaign costs, and wrote down $45.7 million for BEV battery pack and other BEV inventory components deemed excess and obsolete.

Outside of expenses directly related to the recall, cost of revenues increased related to the shipment of FCEV trucks starting in the fourth quarter of 2023, partially offset by a decrease in freight during the year ended December 31, 2023 of $18.4 million, and a decrease for BEV cost of revenues due to a decrease in the number of Tre BEVs shipped to our dealer network.

Service and other

Cost of revenues related to service and other revenue increased by $4.2 million, or 135%, from $3.1 million during the year ended December 31, 2022 to $7.4 million during the year ended December 31, 2023. The increase is driven by direct materials, outsourced services, inventory write-downs and fulfillment costs related to MCTs and other charging products, and cost of hydrogen, including transportation.

Research and Development

Research and development expenses decreased by $62.3 million, or 23%, from $270.5 million during the year ended December 31, 2022 to $208.2 million during the year ended December 31, 2023. This decrease was primarily due to decreased spending on purchased components, outside development, professional services, freight, and tooling related to Tre BEV and FCEV prototype builds of $54.9 million. Additional decreases were related to stock compensation for $13.2 million and travel for $2.1 million. These decreases were partially offset by an increase in personnel costs of $3.1 million related to higher labor costs and severance costs incurred related to reorganization in June 2023, higher depreciation and occupancy costs of $2.1 million related to equipment and software dedicated to research and development activities and hydrogen fuel costs of $1.9 million.

Selling, General, and Administrative

Selling, general, and administrative expenses decreased by $147.4 million, or 43%, from $346.2 million during the year ended December 31, 2022 to $198.8 million during the year ended December 31, 2023. The decrease primarily related to stock based compensation expense of $163.7 million, which decreased primarily due to the acceleration of stock compensation for the market based RSUs that were cancelled in the third quarter of 2022, along with a decrease of $10.0 million for a supply commitment revision fee recognized during the year ended December 31, 2022, a decrease of $3.5 million for professional services and a $1.2 million decrease for freight. Decreases were partially offset by increases in personnel costs of $12.9 million related to higher labor costs and severance costs incurred related to reorganization in June 2023, and additional depreciation expense of $10.3 million primarily related to the reassessment of useful lives for BEV demo trucks. Additional increases included costs related to occupancy, legal expenses and other general corporate expenses of $8.2 million.

Loss on Supplier Deposits

Loss on supplier deposits was $28.8 million for the year ended December 31, 2023, consisting of losses on deposits for tooling and long-term supply agreements.

Interest expense, net

Interest expense, net increased by $58.3 million, or 329%, from $17.7 million during the year ended December 31, 2022 to $76.0 million during the year ended December 31, 2023. The increase is primarily due to increases in interest expense on our Toggle Convertible Notes of $50.7 million, interest on our senior convertible notes of $13.4 million, interest on our financing obligations of $3.9 million, and interest on our finance leases of $0.7 million. These increases were partially offset by an increase in interest income earned on our cash and cash equivalent balances of $10.1 million.

Revaluation of Warrant Liability

The revaluation of warrant liability decreased $3.5 million, from $3.9 million during the year ended December 31, 2022 to $0.4 million during the year ended December 31, 2023, resulting from changes in fair value of our warrant liability.

Gain on Divestiture of Affiliate

Gain on divestiture of affiliate was $70.8 million for the year ended December 31, 2023, representing the consideration received for the divestiture of Nikola Iveco Europe GmbH and related License Agreement, in excess of the basis of our investment as of the divestiture date.

Loss on Debt Extinguishment

Loss on debt extinguishment includes a $20.4 million loss for the year ended December 31, 2023, representing the loss on exchange of $100.0 million of June 2022 Toggle Convertible Notes for the issuance of $100.0 million April 2023 Toggle Convertible Notes. Additionally, loss on debt extinguishment includes a $10.7 million loss for the year ended December 31, 2023 due to extinguishments of the 8.25% Convertible Notes for conversions.

Other Expense, net

Other expense, net increased by $161.5 million, from $1.0 million of expense during the year ended December 31, 2022 to $162.5 million of expense during the year ended December 31, 2023. The increase was driven primarily by an increase of net losses on revaluations of derivative assets and liabilities of $202.2 million compared to the prior year, along with losses on foreign currency valuation adjustments of $3.2 million and additional losses on sales of assets of $1.4 million. Increases were partially offset by a gain on revaluation of contingent stock consideration of $44.0 million and an increase in government grant income recognized of $1.8 million.

Income Tax Expense

Income tax expense for the years ended December 31, 2023 and 2022 was immaterial. We have cumulative net operating losses at the federal and state level and maintain a full valuation allowance against our net deferred taxes.

Equity in Net Loss of Affiliates

Equity in net loss of affiliates decreased by $4.2 million, from $20.7 million for the year ended December 31, 2022 to $16.4 million for the year endedDecember 31, 2023. The decrease was driven by a reduction of losses of $4.8 million for Nikola Iveco Europe GmbH, primarily attributed to the divestiture of this affiliate during the second quarter of 2023.

Comparison of Year Ended December 31, 2022 to Year Ended December 31, 2021

The following table sets forth our historical operating results for the periods indicated:

| | | | | | | | | | | | | | | | | | | | | | | |

| Years Ended December 31, | | | | |

| 2022 | | 2021 | | $ Change | | % Change |

| (in thousands, except share and per share data) |

| Revenues: | | | | | | | |

| Truck sales | $ | 45,931 | | | $ | — | | | $ | 45,931 | | | NM |

| Service and other | 3,794 | | | — | | | 3,794 | | | NM |

| Total revenues | 49,725 | | | — | | | 49,725 | | | NM |

| Cost of revenues: | | | | | | | |

| Truck sales | 132,556 | | | — | | | 132,556 | | | NM |

| Service and other | 3,138 | | | — | | | 3,138 | | | NM |

| Total cost of revenues | 135,694 | | | — | | | 135,694 | | | NM |

| Gross loss | (85,969) | | | — | | | (85,969) | | | NM |

| Operating expenses: | | | | | | | |

| Research and development | 270,480 | | | 292,951 | | | (22,471) | | | (8) | % |

| Selling, general and administrative | 346,186 | | | 400,575 | | | (54,389) | | | (14) | % |

| | | | | | | |

| Total operating expenses | 616,666 | | | 693,526 | | | (76,860) | | | (11) | % |

| Loss from operations | (702,635) | | | (693,526) | | | (9,109) | | | 1 | % |

| Other income (expense): | | | | | | | |

| Interest expense, net | (17,712) | | | (481) | | | (17,231) | | | 3582 | % |

| | | | | | | |

| | | | | | | |

| Revaluation of warrant liability | 3,903 | | | 3,051 | | | 852 | | | 28 | % |

| Other income (expense), net | (1,023) | | | 4,102 | | | (5,125) | | | (125) | % |

| Loss before income taxes and equity in net loss of affiliates | (717,467) | | | (686,854) | | | (30,613) | | | 4 | % |

| Income tax expense | 6 | | | 4 | | | 2 | | | 50 | % |

| Loss before equity in net loss of affiliates | (717,473) | | | (686,858) | | | (30,615) | | | 4 | % |

| Equity in net loss of affiliates | (20,665) | | | (3,580) | | | (17,085) | | | 477 | % |

| Net loss from continuing operations | $ | (738,138) | | | $ | (690,438) | | | $ | (47,700) | | | 7 | % |

| | | | | | | |

| | | | | | | |

| Net loss from continuing operations per share: | | | | | | | |

| Basic | $ | (1.67) | | | $ | (1.73) | | | $ | 0.06 | | | (3) | % |

| Diluted | $ | (1.67) | | | $ | (1.74) | | | $ | 0.07 | | | (4) | % |

| Weighted-average shares outstanding: | | | | | | | |

| Basic | 441,800,499 | | | 398,655,081 | | | 43,145,418 | | | 11 | % |

| Diluted | 441,800,499 | | | 398,784,392 | | | 43,016,107 | | | 11 | % |

Revenues

Revenues were $49.7 million for the year ended December 31, 2022, consisting of $45.9 million in truck revenue driven by sales of Tre BEV trucks and $3.8 million in service and other revenue driven by deliveries of MCT units, and other charging products.

Cost of Revenues

Cost of revenues related to truck sales were $132.6 million for the year ended December 31, 2022. Truck cost of revenues include direct materials, freight and duties for transportation of purchased parts, manufacturing labor and overhead including Coolidge plant facility costs and depreciation, inventory write-downs for net realizable value and obsolescence, and reserves for estimated warranty expenses. Given our inventory is stated at net realizable value, which is currently lower than the actual cost, any overhead including freight is expensed in the period incurred as opposed to being capitalized into inventory.

With the start of production late in the first quarter of 2022, we have experienced high fixed costs due to low volumes produced driving significantly negative margins.

Cost of revenues related to service and other revenue were $3.1 million for the year ended December 31, 2022, driven by direct materials, outsourced services, and fulfillment costs related to MCTs, other charging products, and battery product deliveries.

Research and Development

Research and development expenses decreased by $22.5 million, or 8%, from $293.0 million during the year ended December 31, 2021 to $270.5 million in the year ended December 31, 2022. The decrease was primarily due to a decrease of $54.3 million in outside development. The decrease was partially offset by an increase in personnel costs of $26.7 million driven by growth in our in-house engineering headcount, and an increase in freight for prototype components of $2.9 million.

Selling, General, and Administrative

Selling, general, and administrative expenses decreased by $54.4 million, or 14%, from $400.6 million during the year ended December 31, 2021 to $346.2 million during the year ended December 31, 2022. The decrease was primarily related to $125.0 million recognized in the third quarter of 2021 related to settlement of the SEC investigation, along with a decrease of $21.5 million for legal expenses related to Mr. Milton's indemnification agreement. These decreases were partially offset by an increase in stock-based compensation of $45.5 million, an increase in personnel costs of $22.9 million driven by an increase in headcount, an increase of $10.0 million for a supply commitment revision fee, and increase in professional services of $9.5 million primarily due to costs incurred for the acquisition of Romeo in October 2022.

Interest Expense, net

Interest expense, net increased by $17.2 million, or 3582%, from $0.5 million during the year ended December 31, 2021 to $17.7 million during the year ended December 31, 2022. The increase is primarily due to an increase in interest on our Toggle Convertible Notes of $15.1 million, interest on our financing obligations of $2.3 million, interest on our Collateralized Promissory Notes of $1.3 million, and interest on other debt of $0.5 million, partially offset by interest income earned on our cash and cash equivalents balances.

Revaluation of Warrant Liability

The revaluation of warrant liability increased $0.9 million, from $3.1 million during the year ended December 31, 2021 to $3.9 million during the year ended December 31, 2022, resulting from changes in the fair value of our warrant liability.

Other Income (Expense), net

Other income (expense), net decreased by $5.1 million, from $4.1 million of income during the year ended December 31, 2021 to $1.0 million of expense during the year ended December 31, 2022. The decrease was driven primarily by an incremental loss on revaluations of the derivative asset and liability of $3.8 million compared to the prior year, a decrease in government grant income recognized of $1.7 million, along with losses on foreign currency valuation adjustments, partially offset by an increase of $1.0 million related to a loss on sale of equipment recognized in the prior year.

Income Tax Expense (Benefit)

Income tax expense for the years ended December 31, 2022 and 2021 was immaterial. We have cumulative net operating losses at the federal and state level and maintain a full valuation allowance against our net deferred taxes.

Equity in Net Loss of Affiliates

Equity in net loss of affiliate increased by $17.1 million from $3.6 million for the year ended December 31, 2021 to $20.7 million for the year ended December 31, 2022. The increase was driven by additional losses of $16.5 million during the year ended December 31, 2022 related to Nikola Iveco Europe GmbH, attributed to research and development activities, and additional losses of $0.6 million related to Wabash Valley Resources, LLC ("WVR") for the year ended December 31, 2022.

Non-GAAP Financial Measures

In addition to our results determined in accordance with U.S. Generally Accepted Accounting Principles ("GAAP"), we believe the following non-GAAP measures are useful in evaluating operational performance. We use the following non-GAAP financial information to evaluate ongoing operations and for internal planning and forecasting purposes. We believe that non-GAAP financial information, when taken collectively, may be helpful to investors in assessing operating performance.

EBITDA and Adjusted EBITDA

“EBITDA” is defined as net loss from continuing operations before interest income or expense, income tax expense or benefit, and depreciation and amortization. “Adjusted EBITDA” is defined as EBITDA adjusted for stock-based compensation and other items determined by management. Adjusted EBITDA is intended as a supplemental measure of our performance that is neither required by, nor presented in accordance with, GAAP. We believe that the use of EBITDA and Adjusted EBITDA provides an additional tool for investors to use in evaluating ongoing operating results and trends and in comparing our financial measures with those of comparable companies, which may present similar non-GAAP financial measures to investors. However, you should be aware that when evaluating EBITDA and Adjusted EBITDA we may incur future expenses similar to those excluded when calculating these measures. In addition, our presentation of these measures should not be construed as an inference that our future results will be unaffected by unusual or non-recurring items. Our computation of Adjusted EBITDA may not be comparable to other similarly titled measures computed by other companies, because all companies may not calculate Adjusted EBITDA in the same fashion.

Because of these limitations, EBITDA and Adjusted EBITDA should not be considered in isolation or as a substitute for performance measures calculated in accordance with GAAP. We compensate for these limitations by relying primarily on our GAAP results and using EBITDA and Adjusted EBITDA on a supplemental basis. You should review the reconciliation of net loss from continuing operations to EBITDA and Adjusted EBITDA below and not rely on any single financial measure to evaluate our business.

The following table reconciles net loss from continuing operations to EBITDA and Adjusted EBITDA for the periods indicated:

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Three Months Ended December 31, | | Years Ended December 31, |

| 2023 | | 2022 | | 2023 | | 2022 | | 2021 |

| (in thousands) |

| Net loss from continuing operations | $ | (153,596) | | | $ | (175,966) | | | $ | (864,621) | | | $ | (738,138) | | | $ | (690,438) | |

| Interest expense, net | 4,761 | | | 6,958 | | | 76,023 | | | 17,712 | | | 481 | |

| Income tax expense | 11 | | | 3 | | | 12 | | | 6 | | | 4 | |

| Depreciation and amortization | 7,132 | | | 6,293 | | | 35,890 | | | 22,765 | | | 8,231 | |

| EBITDA | (141,692) | | | (162,712) | | | (752,696) | | | (697,655) | | | (681,722) | |

| Stock-based compensation | 6,475 | | | 41,231 | | | 75,391 | | | 252,445 | | | 205,711 | |

| Loss on supplier deposits | 10,401 | | | — | | | 28,834 | | | — | | | — | |

| Gain on divestiture of affiliate | — | | | — | | | (70,849) | | | — | | | — | |

| Loss on debt extinguishment | 10,663 | | | — | | | 31,025 | | | — | | | — | |

| Revaluation of financial instruments | 10,457 | | | (81) | | | 161,608 | | | (174) | | | (3,155) | |

| Romeo Acquisition transaction costs | — | | | 5,218 | | | — | | | 7,315 | | | — | |

Regulatory and legal matters(1) | 1,665 | | | (15,145) | | | 7,339 | | | 23,175 | | | 47,842 | |

| SEC settlement | — | | | — | | | — | | | — | | | 125,000 | |

| Adjusted EBITDA | $ | (102,031) | | | $ | (131,489) | | | $ | (519,348) | | | $ | (414,894) | | | $ | (306,324) | |

(1) Regulatory and legal matters include legal, advisory and other professional service fees incurred in connection with the short-seller article from September 2020, and investigations and litigation related thereto.

Non-GAAP Net Loss and Non-GAAP Net Loss Per Share, Basic and Diluted

Non-GAAP net loss and non-GAAP net loss per share, basic and diluted are presented as supplemental measures of our performance. Non-GAAP net loss is defined as net loss from continuing operations, basic and diluted adjusted for stock compensation expense and other items determined by management. Non-GAAP net loss per share, basic and diluted, is defined as non-GAAP net loss divided by weighted average shares outstanding, basic and diluted.

The following table reconciles net loss from continuing operations and net loss per share to non-GAAP net loss and non-GAAP net loss per share for the periods indicated:

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Three Months Ended December 31, | | Years Ended December 31, |

| 2023 | | 2022 | | 2023 | | 2022 | | 2021 |

| (in thousands, except share and per share data) |

| Net loss from continuing operations | $ | (153,596) | | | $ | (175,966) | | | $ | (864,621) | | | $ | (738,138) | | | $ | (690,438) | |

| Stock-based compensation | 6,475 | | | 41,231 | | | 75,391 | | | 252,445 | | | 205,711 | |

| Loss on supplier deposits | 10,401 | | | — | | | 28,834 | | | — | | | — | |

| Gain on divestiture of affiliate | — | | | — | | | (70,849) | | | — | | | — | |

| Loss on debt extinguishment | 10,663 | | | — | | | 31,025 | | | — | | | — | |

| Revaluation of financial instruments | 10,457 | | | (81) | | | 161,608 | | | (174) | | | (3,155) | |

| Romeo Acquisition transaction costs | — | | | 5,218 | | | — | | | 7,315 | | | — | |

Regulatory and legal matters(1) | 1,665 | | | (15,145) | | | 7,339 | | | 23,175 | | | 47,842 | |

| SEC settlement | — | | | — | | | — | | | — | | | 125,000 | |

| Non-GAAP net loss | $ | (113,935) | | | $ | (144,743) | | | $ | (631,273) | | | $ | (455,377) | | | $ | (315,040) | |

| | | | | | | | | |

| Non-GAAP net loss per share: | | | | | | | | | |

| Basic | $ | (0.11) | | | $ | (0.30) | | | $ | (0.79) | | | $ | (1.03) | | | $ | (0.79) | |

| Diluted | $ | (0.11) | | | $ | (0.30) | | | $ | (0.79) | | | $ | (1.03) | | | $ | (0.79) | |

| Weighted average shares outstanding: | | | | | | | | | |

| Basic | 1,078,090,959 | | | 487,551,035 | | | 800,030,551 | | | 441,800,499 | | | 398,655,081 | |

| Diluted | 1,078,090,959 | | | 487,551,035 | | | 800,030,551 | | | 441,800,499 | | | 398,784,392 | |

(1) Regulatory and legal matters include legal, advisory and other professional service fees incurred in connection with the short-seller article from September 2020, and investigations and litigation related thereto.

Adjusted Free Cash Flow

We define "Adjusted free cash flow", a non-GAAP financial measure, as net cash flow from operating activities less purchases of property, plant and equipment. Adjusted free cash flow is intended as a supplemental measure of our performance that is neither required by, nor presented in accordance with, GAAP.

Our use of Adjusted free cash flow has limitations as an analytical tool and should not be considered in isolation or as a substitute for an analysis of our results under GAAP. First, Adjusted free cash flow is not a substitute for net cash flow from operating activities. Second, other companies may calculate Adjusted free cash flow or similarly titled non-GAAP financial measures differently or may use other measures to evaluate their performance, all of which could reduce the usefulness of Adjusted free cash flow as a tool for comparison. Additionally, the utility of Adjusted free cash flow is further limited as it does not reflect our future contractual commitments and does not represent the total increase or decrease in our cash balance for a given period. Because of these and other limitations, Adjusted free cash flow should be considered along with net cash flow from operating activities and other comparable financial measures prepared and presented in accordance with GAAP.

The following table presents a reconciliation of net cash flow from operating activities, the most directly comparable financial measure calculated in accordance with GAAP, to Adjusted free cash flow for the periods indicated:

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | Three Months Ended December 31, | | Years Ended December 31, |

| | 2023 | | 2022 | | 2023 | | 2022 | | 2021 |

| | (in thousands) | | |

| Most comparable GAAP measure: | | | | | | | | | | |

| Net cash used for operating activities | | $ | (117,754) | | | $ | (150,104) | | | $ | (496,178) | | | $ | (581,563) | | | $ | (307,154) | |

| Net cash used for investing activities | | (11,107) | | | (55,702) | | | (66,749) | | | (225,645) | | | (207,481) | |

| Net cash provided by financing activities | | 230,726 | | | 115,925 | | | 742,983 | | | 598,876 | | | 187,598 | |

| | | | | | | | | | |

| Non-GAAP measure: | | | | | | | | | | |

| Net cash used for operating activities | | (117,754) | | | (150,104) | | | (496,178) | | | (581,563) | | | (307,154) | |

| Purchases of property, plant and equipment | | (12,107) | | | (49,821) | | | (120,516) | | | (168,257) | | | (179,269) | |

| Adjusted free cash flow | | $ | (129,861) | | | $ | (199,925) | | | $ | (616,694) | | | $ | (749,820) | | | $ | (486,423) | |

Liquidity and Capital Resources

In accordance with the ASC 205-40, Disclosure of Uncertainties about an Entity’s Ability to Continue as a Going Concern, (“ASC 205-40”), we have evaluated whether there are conditions and events, considered in the aggregate, that raise substantial doubt about our ability to continue as a going concern within one year after the date that the consolidated financial statements are issued.

As an early stage growth company, our ability to access capital is critical. Until we can generate sufficient revenue to cover our operating expenses, working capital and capital expenditures, we will need to raise additional capital. Additional stock financing may not be available on favorable terms and could be dilutive to current stockholders. Debt financing, if available, may involve restrictive covenants and dilutive financing instruments.

We intend to employ various strategies to obtain the required funding for future operations such as continuing to access capital through the Equity Distribution Agreement. However, the ability to access the Equity Distribution Agreement is dependent on the market price of our common stock, the registration of shares to be sold under the Equity Distribution Agreement and availability of sufficient authorized common stock, which cannot be assured, and as a result cannot be included as sources of liquidity for our ASC 205-40 analysis.

If capital is not available to us when, and in the amounts needed, we could be required to delay, scale back, or abandon some or all of our Annual Reportoperations and development programs, which would materially harm our business, financial condition and results of operations. The result of our ASC 205-40 analysis, due to uncertainties discussed above, is that there is substantial doubt about our ability to continue as a going concern through the next twelve months from the date of issuance of these consolidated financial statements.

Since inception, we financed our operations primarily from the sales of common stock, the business combination with VectoIQ Acquisition Corp., redemption of warrants, and the issuance of debt. As of December 31, 2023, our principal sources of liquidity were our cash and cash equivalents in the amount of $464.7 million.

During 2021, we entered into a common stock purchase agreement (the "First Tumim Purchase Agreement") with Tumim Stone Capital LLC ("Tumim") allowing us to issue shares of our common stock to Tumim for proceeds of up to $300.0 million. During the years ended December 31, 2023, 2022, 2021 and we sold 3,420,990, 17,248,244, and 14,213,498 shares of common stock, respectively, for proceeds of $8.4 million, $123.7 million, and $163.8 million, respectively, under the First Tumim Purchase Agreement. As of December 31, 2023 we sold in aggregate 34,882,732 shares of common stock to Tumim under the terms of the First Tumim Purchase Agreement for gross proceeds of $295.9 million, excluding the 155,703 commitment shares issued to Tumim as consideration for its irrevocable commitment to purchase shares of our common stock under the First Tumim Purchase Agreement. The First Tumim Purchase Agreement was terminated in the first quarter of 2023.

Additionally, during 2021, we entered into a second common stock purchase agreement with Tumim (the "Second Tumim Purchase Agreement" and, together with the First Tumim Purchase Agreement, the "Tumim Purchase Agreements") allowing us to issue shares of our common stock to Tumim for proceeds of up to an additional $300.0 million, provided that certain

conditions have been met. During the year ended December 31, 2023, we sold to Tumim 28,790,787 shares of common stock for proceeds of $59.2 million, excluding the 252,040 commitment shares issued to Tumim as a consideration for its irrevocable commitment to purchase shares of our common stock under the Second Tumim Purchase Agreement. The Second Tumim Purchase Agreement was terminated in the third quarter of 2023.

During the second quarter of 2022, we completed a private placement of $200.0 million aggregate principal amount of unsecured 8.00% / 11.00% convertible senior paid in kind ("PIK") toggle notes (the “June 2022 Toggle Convertible Notes"), which mature on FormMay 31, 2026. Net proceeds from the issuance were $183.2 million. The June 2022 Toggle Convertible Notes bear interest at 8.00% per annum, to the extent paid in cash ("Cash Interest"), and 11.00% per annum, to the extent paid in kind through the issuance of additional June 2022 Toggle Convertible Notes ("PIK Interest"). Interest is payable semi-annually in arrears on May 31 and November 30 of each year, beginning on November 30, 2022. We can elect to make any interest payment through Cash Interest, PIK Interest or any combination thereof.

10-KThe initial conversion rate is 114.3602 shares per $1,000 principal amount of the June 2022 Toggle Convertible Notes, subject to customary anti-dilution adjustments in certain circumstances, which represented an initial conversion price of approximately $8.74 per share. During the second quarter of 2023, we exchanged $100.0 million of June 2022 Toggle Convertible Notes for $100.0 million principal amount of unsecured 8.00% / 11.00% Series B convertible senior PIK toggle notes (the “April 2023 Toggle Convertible Notes"). The initial conversion rate for the April 2023 Toggle Convertible Notes is 686.8132 shares per $1,000 principal amount of the April 2023 Toggle Convertible Notes, subject to customary anti-dilution adjustments in certain circumstances, which represented an initial conversion price of approximately $1.46 per share. During the third quarter of 2023, the April 2023 Toggle Convertible Notes were converted in full for the issuance of 72,458,789 shares of our common stock.

Prior to February 28, 2026, the June 2022 Toggle Convertible Notes will be convertible at the option of the holders only upon the occurrence of specified events and during certain periods, and will be convertible on or after February 28, 2026, at any time until the close of business on the second scheduled trading day immediately preceding the maturity date of the June 2022 Toggle Convertible Notes.

During the third quarter of 2022, we entered into an Equity Distribution Agreement, which was subsequently amended and restated during the third quarter of 2023, with Citi pursuant to which we can issue and sell shares of our common stock with an aggregate maximum offering price of $600.0 million. During the years ended December 31, 2023 and 2022, we sold 68,351,243 and 45,324,227 shares, respectively, of common stock under the Equity Distribution Agreement. During the years ended December 31, 2023 and 2022, we received $117.5 million and $163.5 million, respectively, in net proceeds from the Equity Distribution Agreement after deduction of commissions and fees to the sales agent. As of December 31, 2023, we had approximately $311.7 million remaining available under the Equity Distribution Agreement.

During the fourth quarter of 2022, we entered into a securities purchase agreement with an investor pursuant to which we can issue and sell up to $125.0 million in initial principal amount of senior convertible notes (the "First Purchase Agreement Notes") in a registered direct offering. We consummated an initial closing for the sale of $50.0 million in aggregate principal amount of First Purchase Agreement Notes on December 30, 2022. During 2023, we consummated additional closings of $52.1 million in aggregate principal amount of First Purchase Agreement Notes. The First Purchase Agreement was terminated in the third quarter of 2023. As of December 31, 2023, all of the First Purchase Agreement Notes had been converted into common stock.

On April 4, 2023, we sold 29,910,715 shares of our common stock in an underwritten public offering (the "Public Offering") at an offering price of $1.12 per share, for net proceeds of $32.2 million after deducting underwriting discounts and commissions.

On March 29, 2023, we entered into a stock purchase agreement with an investor (the "Investor") pursuant to which the Investor agreed to purchase up to $100.0 million of shares of our common stock in a registered direct offering (the "Direct Offering"), with the actual amount of shares of common stock purchased in the Direct Offering reduced to the extent of the total number of shares sold in the Public Offering. The Direct Offering closed on April 11, 2023, and we sold 59,374,999 shares of common stock at the Public Offering price of $1.12 per share to the Investor for net proceeds of $63.2 million.

On August 3, 2023, we obtained stockholder approval to increase our authorized number of shares of common stock from 800,000,000 to 1,600,000,000. As of December 31, 2023, we had 140.4 million shares unreserved and unissued.

During the third quarter of 2023, we entered into a securities purchase agreement with an investor pursuant to which we can issue and sell up to $325.0 million in initial principal amount of senior convertible notes (the "Second Purchase Agreement Notes" and, together with the First Purchase Agreement Notes, the "Senior Convertible Notes") in a registered direct offering. We consummated an initial closing for the sale of $125.0 million in aggregate principal amount of Second Purchase Agreement

Notes on August 21, 2023. Additionally, during the third quarter of 2023, we consummated an additional closing of $40.0 million in aggregate principal amount of Second Purchase Agreement Notes. As of December 31, 2023, all of the Second Purchase Agreement Notes had been converted into common stock. The amount of additional notes that may be issued pursuant to the Second Purchase Agreement is limited by Nasdaq listing rules limiting the number of shares of common stock issuable upon conversion of the notes and is less than the remaining notional capacity under the agreement.

On December 12, 2023, we sold 133,333,334 shares of our common stock in an underwritten public offering (the "December 2023 Public Offering") at an offering price of $0.75 per share, for net proceeds of $95.6 million after deducting underwriting discounts and commissions.

On December 12, 2023, we sold $175.0 million aggregate principal amount of our 8.25% green convertible senior notes due 2026 (the "8.25% Convertible Notes") for net proceeds of $169.4 million after deducting underwriting discounts and commissions. As of December 31, 2023, holders of the 8.25% Convertible Notes converted aggregate principal amount of $153.4 million for issuance of 170,491,093 shares of our common stock.

As of December 31, 2023, our current assets were $572.4 million consisting primarily of cash and cash equivalents of $464.7 million and inventory of $62.6 million, and our current liabilities were $260.1 million, primarily comprised of accrued expenses and accounts payable, which includes $84.0 million related to the SEC settlement and $65.7 million for warranty reserves related primarily to the BEV recall.

Our short term liquidity will be utilized to execute our business strategy over the next twelve month period including (i) scaling the production, distribution and service of the FCEV and BEV trucks, (ii) performing the recall work related to our BEV recall (iii) maintaining the manufacturing facility, and (iv) establishing our initial energy infrastructure. However, actual results could vary materially and negatively as a result of a number of factors, including:

•our ability to manage the costs of manufacturing and servicing the FCEV and BEV trucks and our ability to drive the cost down with our suppliers;

•the amount and timing of cash generated from sales of our FCEV and BEV trucks and hydrogen infrastructure, and our ability to offer our products and services at competitive prices;

•the costs of maintaining our manufacturing facility, hydrogen refueling assets and equipment;

•our warranty claims experience should actual warranty claims differ significantly from estimates;

•our BEV truck recall campaign costs and timing;

•the scope, progress, results, costs, timing and outcomes of our ongoing validation and demos of our FCEV trucks;

•the costs and timing of development and deployment of our hydrogen distribution, dispensing and storage network;

•our ability to attract and retain strategic partners for development and maintenance of our hydrogen dispensing and storage network and the related costs and timing;

•the costs of maintaining, expanding and protecting our intellectual property portfolio, including potential litigation costs and liabilities;

•the costs of additional general and administrative personnel, including accounting and finance, legal and human resources, as well as costs related to litigation, investigations, or settlements;

•our ability to raise sufficient capital to finance our business, and our ability to increase our authorized common stock, which is subject to stockholder approval; and

•other risks discussed in the section entitled "Risk Factors."

For at least the next twelve months, we expect our principal demand for funds will be for our ongoing activities described above. In addition to those activities, our short term liquidity will be utilized to fund the current portion of non-cancellable commitments including leases, debt obligations and purchase commitments. Refer to Note 5, Leases, Note 8, Debt and Finance Lease Liabilities, and Purchase Commitments within Note 14, Commitments and Contingencies, for additional details.

Long-Term Liquidity Requirements

Until we can generate sufficient revenue and positive gross margins to cover operating expenses, working capital and capital expenditures, we expect to fund cash needs through a combination of equity and debt financing, and potentially through lease securitization, strategic collaborations, and licensing arrangements. If we raise funds by issuing equity or equity-linked securities, dilution to stockholders may result. Any equity or equity-linked securities issued may also provide for rights, preferences or privileges senior to those of holders of our common stock. If we raise funds by issuing debt securities, these debt securities would have rights, preferences and privileges senior to those of holders of our common stock. The terms of debt securities or other debt financing agreements could impose significant restrictions on our operations and may require us to pledge certain assets. The credit market and financial services industry have in the past, and may in the future, experience periods of upheaval that could impact the availability and cost of equity and debt financing.

As of December 31, 2023, our long-term liquidity requirements include debt repayments, lease arrangements, and long-term purchase commitments. Refer to Note 5, Leases, Note 8, Debt and Finance Lease Liabilities, and Purchase Commitments within Note 14, Commitments and Contingencies, for additional details.

Summary of Cash Flows

The following table provides a summary of cash flow data: | | | | | | | | | | | | | | | | | |

| Years Ended December 31, |

| 2023 | | 2022 | | 2021 |

| (in thousands) |

| Net cash used in operating activities | $ | (496,178) | | | $ | (581,563) | | | $ | (307,154) | |

| Net cash used in investing activities | (66,749) | | | (225,645) | | | (207,481) | |

| Net cash provided by financing activities | 742,983 | | | 598,876 | | | 187,598 | |

Cash Flows from Operating Activities

Our cash flows from operating activities are significantly affected by the growth of our business primarily related to manufacturing, research and development and selling, general, and administrative activities. Our operating cash flows are also affected by our working capital needs to support personnel-related expenditures and fluctuations in accounts payable and other current assets and liabilities.

Net cash used in operating activities was $496.2 million for the year ended December 31, 2023. The most significant component of our cash used during this period was a net loss from continuing operations of $864.6 million, which included $205.6 million non-cash net losses on revaluation of financial instruments, $79.2 million non-cash interest expense, non-cash expenses of $75.4 million related to stock-based compensation, gain on divestiture of affiliate of $70.8 million, $71.2 million in inventory write downs, other net non-cash charges of $72.5 million, and net cash outflows of $64.6 million from changes in operating assets and liabilities primarily driven by increases in prepaid expenses and other current assets and inventory, a decrease in accounts payable, accrued expenses and other current liabilities, partially offset by a decrease in accounts receivable, net.

Net cash used in operating activities was $581.6 million for the year ended December 31, 2022. The most significant component of our cash used during this period was a net loss from continuing operations of $738.1 million, which included non-cash expenses of $252.4 million related to stock-based compensation, $19.7 million related to inventory write-downs, $20.7 million equity in loss of affiliates, and $22.8 million related to depreciation and amortization, other non cash adjustments of $16.2 million and net cash outflows of $175.2 million from changes in operating assets and liabilities primarily driven by an increase in inventory and accounts receivable, partially offset by an increase in accounts payable and accrued expenses.

Net cash used in operating activities was $307.2 million for the year ended December 31, 2021. The most significant component of our cash used during this period was a net loss of $690.4 million, which included non-cash expenses of $205.7 million related to stock-based compensation, $46.3 million for in-kind services, $8.2 million related to depreciation and amortization, and $5.6 million for the issuance of commitment shares to Tumim, other non cash adjustments of $7.1 million and net cash inflows of $110.4 million from changes in operating assets and liabilities primarily driven by an increase in accounts payable and accrued expenses related to the liability for the SEC settlement, and increased spend on the development of our BEV and FCEV trucks, along with an increase in other long-term liabilities related to the SEC settlement, partially offset by an increase in inventory and prepaid expenses and other current assets.

Cash Flows from Investing Activities

Mary L. Petrovich, ChairCash flows from investing activities primarily relate to capital expenditures to support our growth. Net cash used in investing activities is expected to continue as we maintain our truck manufacturing facility in Coolidge, Arizona, and develop our hydrogen infrastructure network. As of December 31, 2023, we anticipate our capital expenditures for fiscal year 2024 to be approximately $65.0 million. Actual capital expenditures will also be dependent on availability of capital as well as third party lead times.

Net cash used in investing activities was $66.7 million for the year ended December 31, 2023, which was primarily due to $120.5 million in purchases of and deposits for capital equipment, costs of expansion of our facilities, and investments in our hydrogen infrastructure and $3.0 million in other investing outflows, partially offset by proceeds of $36.0 million related to the divestiture of Nikola Iveco Europe GmbH and dissolution of Nikola TA HRS 1, LLC ("TA"), and proceeds of $20.7 million related to the sale of assets to FFI.

Net cash used in investing activities was $225.6 million for the year ended December 31, 2022, which was primarily due to purchases and deposits for property and equipment, including construction for our manufacturing facility and purchases of capital equipment of $168.3 million, $27.8 million for issuance of senior secured debt to Romeo, $23.0 million in cash paid for investment in affiliates, and $6.6 million paid to settle the first price differential with WVR.

Net cash used in investing activities was $207.5 million for the year ended December 31, 2021, which was primarily due to purchases and deposits for property and capital equipment, including construction for our manufacturing facility and purchase of capital equipment of $179.3 million, $25.0 million in cash paid for investment in WVR, and $3.4 million paid to settle the first price differential with WVR.

Cash Flows from Financing Activities

Net cash provided by financing activities was $743.0 million for the year ended December 31, 2023, which was primarily due to proceeds from the issuance of convertible notes of $386.7 million, proceeds from public offerings of $128.2 million, proceeds from the issuance of common stock under the Equity Distribution Agreement of approximately $115.9 million, proceeds from the Tumim Purchase Agreements of approximately $67.6 million, proceeds from the registered direct offering of $63.2 million, and proceeds from the issuance of financing obligations of $56.1 million, partially offset by repayments of debt and notes payable of $45.5 million, payments for coupon make whole premiums of $35.2 million and other net finance inflows of $5.9 million.

Net cash provided by financing activities was $598.9 million for the year ended December 31, 2022, which was primarily due to proceeds from the issuance of convertible notes of approximately $233.2 million, proceeds from the issuance of common stock from the Equity Distribution Agreement of approximately $165.1 million, proceeds from First Tumim Purchase Agreement of approximately $123.7 million, net proceeds from issuance of promissory notes for $54.0 million, proceeds from financing obligations of $44.8 million, proceeds from the exercises of stock options of $6.9 million, and other financing activity of $1.7 million partially offset by a $30.5 million in payments of our debt, promissory notes and notes payable.

Net cash provided by financing activities was $187.6 million for the year ended December 31, 2021, which was primarily due to proceeds from the First Tumim Purchase Agreement of approximately $163.8 million, net proceeds from issuance of the promissory notes for $24.6 million, proceeds from the exercise of stock options of $4.8 million, partially offset by a $4.1 million payment of our term loan and other financing outflows of $1.5 million.

Off-Balance Sheet Arrangements

Since the date of incorporation, we have not engaged in any off-balance sheet arrangements, as defined in the rules and regulations of the SEC.

Critical Accounting Policies and Estimates

Our discussion and analysis of our financial condition and results of operations are based upon our financial statements, which have been prepared in accordance with GAAP. These principles require us to make certain estimates and assumptions. These estimates and assumptions affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities, as of the balance sheet date, as well as reported amounts of revenue and expenses during the reporting period. Our most significant estimates and judgments involve valuation of our stock-based compensation for the fair value of market-based restricted stock units, assignment of fair value and allocation of purchase price in connection with the Romeo Acquisition, the valuations of warrant liabilities, derivative liabilities, the Put Right and Price Differential, estimates related to our lease assumptions and revenue recognition, contingent liabilities, including litigation reserves, warranty reserves, including inputs and assumptions related to recall campaigns, and inventory valuation. Management bases its estimates on historical experience

and on various other assumptions believed to be reasonable, the results of which form the basis for making judgments about the carrying values of assets and liabilities. Actual results could differ from those estimates, and the results may be material.

Gerrit A. MarxWe believe that the accounting policies discussed below are critical to understanding our historical and future performance, as these policies relate to the more significant areas involving management's judgments and estimates.

While our significant accounting policies are described in the notes to our consolidated financial statements, we believe that the following accounting policies are most critical to understanding our financial condition and historical and future results of operations.

Stock-Based Compensation

The fair value of market based RSU awards is determined using a Monte Carlo simulation model that utilizes significant assumptions, including volatility, that determine the probability of satisfying the market condition stipulated in the award to calculate the fair value of the award. Significant judgment is required in determining the expected volatility of our common stock. Due to the limited history of trading of our common stock, we determine expected volatility based on a mix of historical volatility and a peer group of publicly traded companies.

Product Warranties and Recall Campaigns

Product warranty costs are recognized upon transfer of control of trucks to dealers, and are estimated based on factors including the length of the warranty (generally 2 to 5 years), product costs, and product failure rates. Warranty reserves are reviewed and adjusted quarterly to ensure that accruals are adequate to meet expected future warranty obligations. Estimating future warranty costs is highly subjective and requires significant management judgment. We believe that the accruals are adequate, however, based on the limited historical information available, it is possible that substantial additional charges may be required in future periods based on new information or changes in facts and circumstances. Our accrual includes estimates of the replacement costs for covered parts which is based on historical experience. This could be impacted by contractual changes with third-party suppliers or the need to identify new suppliers and the engineering and design costs that would accompany such a change.

Recall campaign costs are recognized when a product recall liability is probable and related amounts are reasonably estimable. Costs are estimated based on the number of trucks to be repaired and the required repairs including engineering and development, product costs, labor rates, and shipping. Estimating the cost to repair the trucks is highly subjective and requires significant management judgment. Based on information that is currently available, we believe that the accruals are adequate. It is possible that substantial additional charges may be required in future periods based on new information, changes in facts and circumstances, availability of materials from key suppliers, and actions that we may commit to or be required to undertake.

Recent Accounting Pronouncements

Note 2, Summary of Significant Accounting Policies, to our consolidated financial statements elsewhere in this Annual Report on Form 10-K, provides more information about recent accounting pronouncements, the timing of their adoption, and our assessment, to the extent we have made one, of their potential impact on our financial condition and results of operations.

Item 7A. Quantitative and Qualitative Disclosures About Market Risk

We are exposed to a variety of market and other risks, including the effects of changes in interest rates, inflation, and foreign currency exchange rates, as well as risks to the availability of funding sources, hazard events, and specific asset risks.

Interest Rate Risk

The market risk inherent in our financial instruments and our financial position represents the potential loss arising from adverse changes in interest rates. As of December 31, 2023 and 2022, we had cash and cash equivalents of $464.7 million and $225.9 million, respectively. As of December 31, 2023, we had a cash and cash equivalents balance of $29.8 million which consisted of interest-bearing money market accounts for which the fair market value would be affected by changes in the general level of U.S. interest rates. However, due to the short-term maturities and the low-risk profile of our investments, an immediate 10% change in interest rates would not have a material effect on the fair market value of our cash and cash equivalents. As of December 31, 2022, none of our cash and cash equivalents balance was invested in interest-bearing money market accounts.

Foreign Currency Risk

For the year ended December 31, 2023, 2022 and 2021, we recorded a $2.2 million loss, $1.0 million gain and $1.4 million gain, respectively, for foreign currency adjustments.

Item 8. Financial Statements and Supplementary Data

Index to Consolidated Financial Statements

Report of Independent Registered Public Accounting Firm

To the Stockholders and the Board of Directors of Nikola Corporation

Opinion on the Financial Statements

We have audited the accompanying consolidated balance sheets of Nikola Corporation (the Company) as of December 31, 2023 and 2022, the related consolidated statements of operations, comprehensive loss, stockholders' equity and cash flows for each of the three years in the period ended December 31, 2023, and the related notes (collectively referred to as the “consolidated financial statements”). In our opinion, the consolidated financial statements present fairly, in all material respects, the financial position of the Company at December 31, 2023 and 2022, and the results of its operations and its cash flows for each of the three years in the period ended December 31, 2023, in conformity with U.S. generally accepted accounting principles.

We also have audited, in accordance with the standards of the Public Company Accounting Oversight Board (United States) (PCAOB), the Company's internal control over financial reporting as of December 31, 2023, based on criteria established in Internal Control-Integrated Framework issued by the Committee of Sponsoring Organizations of the Treadway Commission (2013 framework) and our report dated February 28, 2024 expressed an adverse opinion thereon.

The Company's Ability to Continue as a Going Concern

The accompanying consolidated financial statements have been prepared assuming that the Company will continue as a going concern. As discussed in Note 1 to the financial statements, the Company has suffered recurring losses from operations and has stated that substantial doubt exists about the Company’s ability to continue as a going concern. Management's evaluation of the events and conditions and management’s plans regarding these matters are also described in Note 1. The consolidated financial statements do not include any adjustments that might result from the outcome of this uncertainty.

Basis for Opinion

These financial statements are the responsibility of the Company's management. Our responsibility is to express an opinion on the Company’s financial statements based on our audits. We are a public accounting firm registered with the PCAOB and are required to be independent with respect to the Company in accordance with the U.S. federal securities laws and the applicable rules and regulations of the Securities and Exchange Commission and the PCAOB.

We conducted our audits in accordance with the standards of the PCAOB. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement, whether due to error or fraud. Our audits included performing procedures to assess the risks of material misstatement of the financial statements, whether due to error or fraud, and performing procedures that respond to those risks. Such procedures included examining, on a test basis, evidence regarding the amounts and disclosures in the financial statements. Our audits also included evaluating the accounting principles used and significant estimates made by management, as well as evaluating the overall presentation of the financial statements. We believe that our audits provide a reasonable basis for our opinion.

Critical Audit Matter

The critical audit matter communicated below is a matter arising from the current period audit of the financial statements that was communicated or required to be communicated to the audit committee and that: (1) relates to accounts or disclosures that are material to the financial statements and (2) involved our especially challenging, subjective, or complex judgments. The communication of the critical audit matter does not alter in any way our opinion on the consolidated financial statements, taken as a whole, and we are not, by communicating the critical audit matter below, providing a separate opinion on the critical audit matter or on the account or disclosure to which it relates.

| | | | | | | | |

| | Product Warranties and Recall Campaigns |

| | |

| Description of the Matter | | The Company’s liabilities for product warranties and recall campaigns totaled $78.9 million at December 31, 2023. As discussed in Note 2 to the consolidated financial statements, the Company's liability for product warranties are estimated and recorded upon the transfer of control of trucks to dealers based on length of warranty, replacement product costs, and expected failure rates for certain components covered by the warranty. Recall campaign costs are accrued when a product recall liability is probable and related amounts are reasonably estimable. Recall campaign liabilities are primarily related to the number of trucks to be recalled and the replacement product costs. The Company periodically assesses the adequacy of its recorded product warranties and recall campaign liabilities and adjusts them as appropriate to reflect actual experience and change in estimates.

Auditing the Company’s product warranties and recall campaign liabilities is complex due to the significant estimation uncertainty and the application of significant management judgment regarding the product replacement costs and failure rates used in these calculations. |

| | |

| How We Addressed the Matter in Our Audit | | To evaluate product warranties and recall campaign liabilities, our audit procedures included, among others, testing the completeness and accuracy of the replacement costs used in the product warranties and recall campaign accrual calculations and evaluating the failure rates used in the product warranties accrual for reasonableness. We also evaluated the sufficiency of management’s disclosures related to the product warranties and recall campaigns.

|

/s/ Ernst & Young LLP

We have served as the Company's auditor since 2018.

Phoenix, Arizona

February 28, 2024

Report of Independent Registered Public Accounting Firm

To the Stockholders and the Board of Directors of Nikola Corporation

Opinion on Internal Control Over Financial Reporting