UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K/A10-K

☒(Mark One)

x ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) 4 OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended ended: December 31 2020, 2023

or

☐o TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from _________________ to ____________________

Commission File Number No. 000-49709

CARDIFF LEXINGTON CORP.

(Exact name of registrant as specified in its charter)

| (Exact name of registrant as specified in its charter) |

| Nevada | 84-1044583 | |

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |

| 3753 Howard Hughes Parkway, Suite 200, Las Vegas, NV | 89169 | |

| (Address of principal executive offices) | (Zip Code) |

401 East Las Olas Blvd., Suite 1400, Ft. Lauderdale, FL 33301

(Address of principal executive offices)

(844) 628-2100

(Registrant's telephone no., including area code)

| (844) 628-2100 |

| (Registrant’s telephone number, including area code) |

Securities registered pursuant to Section 12(b) of the Act: None

Securities registered pursuant to Section 12(g) of the Act:

Par Value Common Stock, $0.001 Common Stock

(Title of each class)par value

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐¨No☒.x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Exchange Act. Yes ☐¨No☒.x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Yes☒x No ☐¨

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

Yes☒x No ☐

¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer”,filer,” “smaller reporting company”,company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act. (Check one)

| Large accelerated filer | Accelerated filer | ||

| Non-accelerated filer | Smaller reporting company | ||

| Emerging growth company | ¨ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐¨

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its annualaudit report. ☐¨

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ¨

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ¨

Indicate by check mark whether registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

Yes ☐¨ No ☒x

State the aggregate market valueAs of the voting and non-voting common equity held by non-affiliates computed by reference to the price at which the common equity was last sold, or the average bid and asked price of such common equity, as of theSeptember 30, 2023 (the last business day of the registrant’s most recently completed second fiscal quarter. $1,990,001.00quarter), the aggregate market value of the registrant’s common stock held by non-affiliates (based upon the closing price of such shares as reported on OTC Pink Market) was approximately $868,776. Shares held by each executive officer and director and by each person who owns 10% or more of the outstanding common stock have been excluded from the calculation in that such persons may be deemed to be affiliates of the registrant. This determination of affiliate status is not necessarily a conclusive determination for other purposes.

CommonAs of March 22, 2024, there were a total of shares outstanding at March 30, 2021 is 109,944,821 with a par value of $0.001.common stock of the registrant issued and outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

None.

EXPLANATORY NOTECardiff Lexington Corporation

Cardiff Lexington Corp. ("Cardiff” or the “Company”), is filing this Amendment No. 2 (the “2020 Form 10-K/A”) to its Annual Report on Form 10-K for the year ended

Year Ended December 31, 2020 (the “2020 Form 10-K”) originally filed with the U.S. Securities and Exchange Commission (“SEC”) on March 31, 2021, and as amended on April 2, 2021. This 2020 Form 10-K/A is being filed to restate its financial statements as of and for the years ended December 31, 2020 and 2019, and accompanying notes to the financial statements included in the Amendment, including a description of the impact of restatement on previously reported quarterly amounts for the three-month, six-month, and nine-month periods ended March 31, June 30, and September 30, respectively.2023

The restatement primarily relates to the accounting for (1) the valuation of embedded derivative liabilities in certain matured convertible notes and (2) the accounting treatment for changes in certain rights and privileges with respect to certain classes of preferred stock on January 10, 2020.TABLE OF CONTENTS

Although this Form amends and restates the original Form in its entirety, except for the information described above, this Form does not reflect events occurring after the filing of the original Form 10-K and unless otherwise stated herein, the information contained in this Form is current only as of the date of the original filing. Except as noted herein, no other changes have been made to the original Form. Accordingly, this form should be read in conjunction with the Company's filings made with the U.S. Securities and Exchange Commission subsequent to the filing of the original Forms. The sections of the original Forms affected by the restatement should no longer be relied upon.

In connection with the restatement, the Company’s management reassessed the effectiveness of its disclosure controls and procedures as of December 31, 2020. As a result of that reassessment, the Company’s management determined that its disclosure controls and procedures as of December 31, 2020 were not effective solely as a result of its accounting for the embedded derivative liabilities and the amendment of certain classes of preferred stock. For more information, see Item 9A included in this Amendment.

The Company has not amended its previously filed Quarterly Reports on Form 10-Q or any Current Report on Form 8-K (whether filed or furnished) that are for or relate to the periods affected by the restatement. The financial information that has been previously filed or otherwise reported for these periods is superseded by the information in this Amendment.

See Note 2 to the Notes to Financial Statements included in Part II, Item 8 of this Amendment for additional information on the restatement and the related financial statement effects.

The following items are amended in this Amendment: (i) Part II, Item 8. Financial Statements and Supplementary Data; (ii) Part II, Item 9A. Controls and Procedures; and (iii) Part IV, Item 15. Exhibits, Financial Statement Schedules. Additionally, in accordance with Rule 12b-15 under the Securities Exchange Act of 1934, as amended, the Company is including with this Amendment currently dated certifications from our principal executive officer and principal financial officer. These certifications are filed or furnished, as applicable, as Exhibits.

FORM 10-K/A

CARDIFF LEXINGTON CORP

PART IINDEX

| Item 1. | 1 | |

| Item 1A. | Risk Factors. | 15 |

| Item 1B. | 32 | |

| Item 1C. | Cybersecurity. | 32 |

| Item | 33 | |

| Item 3. | Legal Proceedings. | 33 |

| Item 4. | Mine Safety |

| Item 15. | Exhibit and Financial Statement | |

| Item 16. | ||

| ||

| i |

INTRODUCTORY NOTES

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTSUse of Terms

Except as otherwise indicated by the context and for the purposes of this report only, references in this report to “we,” “us,” “our” and “our company” are to Cardiff Lexington Corporation, a Nevada corporation, and its consolidated subsidiaries.

Special Note Regarding Forward-Looking Statements

This Annual Report on Form 10-K/A (this “Report”)report contains “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933, as amended, (the “Securities Act”),or the Securities Act, and Section 21E of the Securities Exchange Act of 1934, as amended, (the “Exchange Act”). Forward- looking statements discuss mattersor the Exchange Act, that are notbased on our management’s beliefs and assumptions and on information currently available to us. All statements other than statements of historical facts. Because they discussfacts are forward-looking statements. These statements relate to future events or conditions, forward-looking statements may include words such as “anticipate,” “believe,” “estimate,” “intend,” “could,” “should,” “would,” “may,” “seek,” “plan,” “might,” “will,” “expect,” “predict,” “project,” “forecast,” “potential,” “continue” negatives thereof or similar expressions. Forward-looking statements speak only as of the date they are made, are based on various underlying assumptionsto our future financial performance and current expectations about the future and are not guarantees. Such statements involve known and unknown risks, uncertainties and other factors that may cause our actual results, levellevels of activity, performance or achievementachievements to be materially different from theany future results, levels of operationsactivity, performance or plansachievements expressed or implied by such forward-looking statements.

We cannot predict all the risks and uncertainties. Accordingly, such information should not be regarded as representations that the results or conditions described in such statements or that our objectives and plans will be achieved, and we do not assume any responsibility for the accuracy or completeness of any of these forward-looking statements. TheseForward-looking statements include, but are not limited to, statements about:

| · | our ability to successfully identify and acquire additional businesses; | |

| · | our ability to effectively integrate and operate the businesses that we acquire; | |

| · | our expectations around the performance of our current businesses; | |

| · | our ability to maintain our business model and improve our capital efficiency; | |

| · | our ability to effectively manage the growth of our business; | |

| · | our ability to maintain profitability; | |

| · | the competitive environment in which our businesses operate; | |

| · | trends in the industries in which our businesses operate; | |

| · | the regulatory environment in which our businesses operate under; | |

| · | changes in general economic or business conditions or economic or demographic trends in the United States, including changes in interest rates and inflation; | |

| · | our ability to service and comply with the terms of indebtedness; | |

| · | our ability to retain or replace qualified employees of our businesses; | |

| · | labor disputes, strikes or other employee disputes or grievances; | |

| · | casualties, condemnation or catastrophic failures with respect to any of our business’ facilities; | |

| · | costs and effects of legal and administrative proceedings, settlements, investigations and claims; and | |

| · | extraordinary or force majeure events affecting the business or operations of our businesses. |

In some cases, you can identify forward-looking statements by terms such as “may,” “could,” “will,” “should,” “would,” “expect,” “plan,” “intend,” “anticipate,” “believe,” “estimate,” “predict,” “potential,” “project” or “continue” or the negative of these terms or other comparable terminology. These statements are found at various places throughout this Report and include information concerning possible or assumed future results of our operations, including statements about potential acquisition or merger targets; business strategies; future cash flows; financing plans; plans and objectives of management; any other statements regarding future acquisitions, future cash needs, future operations, business plans and future financial results, and any other statements that areonly predictions. You should not historical facts.

Theseplace undue reliance on forward-looking statements represent our intentions, plans, expectations, assumptions,because they involve known and beliefs about future events and are subject tounknown risks, uncertainties and other factors. Many of those factors, which are, outside ofin some cases, beyond our control and which could materially affect results. Factors that may cause actual results to differ materially from thecurrent expectations include, among other things, those listed under Item 1A “Risk Factors” and elsewhere in this report. If one or more of these risks or uncertainties occur, or if our underlying assumptions prove to be incorrect, actual events or results expressedmay vary significantly from those implied or impliedprojected by thosethe forward-looking statements. Considering these risks, uncertaintiesNo forward-looking statement is a guarantee of future performance.

| ii |

In addition, statements that “we believe” and assumptions,similar statements reflect our beliefs and opinions on the events described in the forward- lookingrelevant subject. These statements might not occur or might occurare based upon information available to a different extent or at a different time than we have described. You are cautioned not to place undue reliance on these forward-looking statements, which speak onlyus as of the date of this Report. All subsequent writtenreport, and oralwhile we believe such information forms a reasonable basis for such statements, such information may be limited or incomplete, and our statements should not be read to indicate that we have conducted an exhaustive inquiry into, or review of, all potentially available relevant information. These statements are inherently uncertain and investors are cautioned not to unduly rely upon these statements.

The forward-looking statements concerning other matters addressedmade in this Report and attributablereport relate only to usevents or any person actinginformation as of the date on our behalfwhich the statements are made in this report. Except as expressly qualified in their entiretyrequired by the cautionary statements contained or referredfederal securities laws, there is no undertaking to in this Report.

Except to the extent required by law, we undertake no obligation topublicly update or revise any forward-looking statements, whether as a result of new information, future events, a change in events, conditions,changed circumstances or assumptions underlying such statements, or otherwise.any other reason.

Reverse Stock Split

On January 9, 2024, we effected a 1-for-75,000 reverse split of our outstanding common stock. All share and per share data set forth in this report has been retroactively adjusted to reflect this reverse stock split.

| ITEM 1. |

Overview

HistoryWe are an acquisition holding company focused on locating undervalued and Operationundercapitalized companies, primarily in the healthcare industry, and providing them capitalization and leadership to maximize the value and potential of their private enterprises while also providing diversification and risk mitigation for our stockholders. Specifically, we have and will continue to look at a diverse variety of acquisitions in the Businesshealthcare sector in terms of growth stages and capital structures and we intend to focus our portfolio of subsidiaries approximately as follows: 80% will be targeted to established profitable niche small to mid-sized healthcare companies and 20% will be targeted to second stage startups in healthcare and related financial services (emerging businesses with a strong organic growth plan that is materially cash generative).

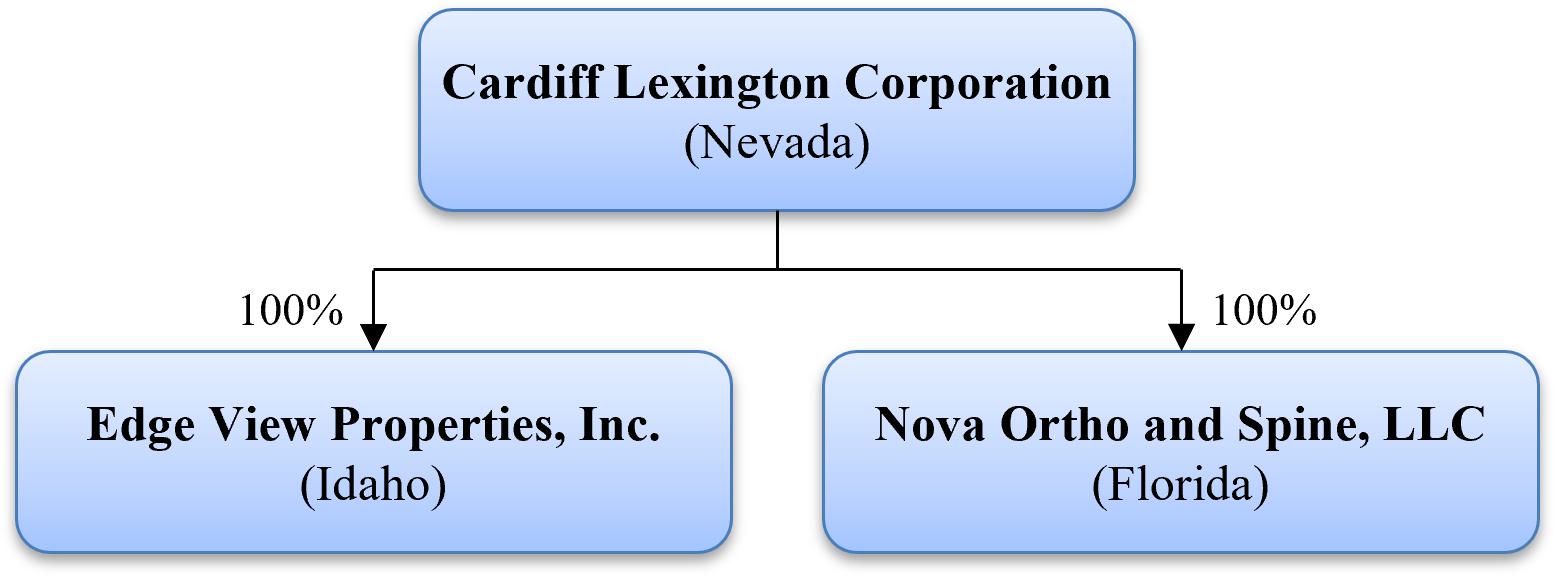

Legacy Card Company,On May 31, 2021, we acquired Nova Ortho and Spine, LLC, (“Legacy”) was formedor Nova, which operates a group of regional primary specialty and ancillary care facilities throughout Florida that provide traumatic injury victims with primary care evaluations, interventional pain management, and specialty consultation services. We focus on plaintiff related care are and a highly efficient provider of emergency medical condition, or EMC, assessments. We provide a full range of diagnostic and surgical services for injuries and disorders of the skeletal system and associated bones, joints, tendons, muscles, ligaments, and nerves. From sports injuries, to sprains, strains, and fractures, our doctors are dedicated to helping patients return to active lifestyles.

We also own a real estate company, Edge View Properties, Inc., or Edge View, which we acquired on July 16, 2014. Edge View owns five (5) acres zoned medium density residential (MDR) with 12 lots already platted, six (6) acres zoned high-density residential (HDR) that can be platted in various configurations to meet current housing needs, and twelve (12) acres zoned in Lemhi County as Agriculture that is available for further annexation into the City of Salmon for development, as well as a California limited liability companycommon area for landowners to view wildlife, provide access to the Salmon River and fishing in a two (2) acre pond. Management has invested years working to develop a new and exciting housing development in Salmon, Idaho and plans to enter into a joint venture agreement with a developer for this planned concept development.

Our Corporate History and Structure

We were incorporated on August 29, 2001. On April 18, 2005, Legacy converted to a Nevada corporation.September 3, 1986 in Colorado as Cardiff International Inc. On November 10, 2005, Legacywe merged with Legacy Card Company and became Cardiff Lexington Corp (formerly Cardiff International, Inc.) (“Cardiff Lexington”, the “Company”), a publicly traded Colorado corporation.Corporation. On August 27, 2014, Cardiff Lexingtonwe redomiciled toand became a corporation under the laws of Florida. On April 13, 2021, we redomiciled and became a corporation under the laws of Nevada.

In the first quarterAll of 2013, Cardiff Lexingtonour operations are conducted through our operating subsidiaries, Nova and Edge View. Nova was restructured into a holding company that began targeting the acquisition of undervalued, niche companies with high growth potential, income-producing commercial real estate properties, or high return investments, with the goal of generating the net income required to support a consistent dividend to our shareholders. The reason for this strategy was to protect our shareholders by acquiring profitable small- to minimum-sized businesses with little to no debt, and provide financing and management support to enhance their ability to provide acceptable returns to investors. New classes of preferred stock have been and may continue to be created to streamline voting rights, avoid debt, and acquire new businesses. By December 31, 2020, we had acquired ten businesses. Four of the acquired businesses were merged into two, one was discontinued, and two were sold during 2020. Accordingly, we currently operate the following four businesses, each as a separate subsidiary:

Cardiff Lexington divested its holdingsorganized in the food services sector: Repicci's Italian IceState of Florida on December 3, 2018 and Gelato and Romeo's New York Style Pizza. The companies’ restaurant franchise operations have been hard hit by the economic pressure of the COVID-19 pandemic and the subsequent directives and responses to this crisis taken by the federal, state, and local government. In light of current circumstances arising from the COVID-19 pandemic, management is continuing to evaluate alternatives to mitigate the negative effects of the pandemic on the Company and its shareholders. Cardiff Lexington Board of Directors has narrowed its forward focus to acquisitionsEdge View was incorporated in the financial services, healthcare and real estate sectors.State of Idaho on February 9, 2005.

Cardiff Lexington is a diversified holding company that operates much like a cooperative, leveraging proven management in private companies that become subsidiaries underThe following chart depicts our umbrella. Our current emphasis is on the financial services, healthcare, and real estate sectors. Our platform provides an “Equity Exit or Equity Capitalization” strategy for acquisitions as well as a diversified investment platform for investors that is intended to mitigate risk. Our “Buy and Build” strategy seeks niche companies which complement existing subsidiaries. Our acquisition strategy is driven by structure, transaction value, alignment, resources and return on investment. Our acquisition strategy is not limited by geographic location, and is focused on proven management teams, attractive markets, and historical operating margins. We target acquisitions of mature, high growth, niche companies. Cardiff Lexington’s strategy identifies and empowers select, income-producing, middle market private businesses and commercial real estate properties.organizational structure:

| 1 |

The target company’s management team typically maintains controlDuring the year ended December 31, 2023, we sold our financial services (tax resolution) business, Platinum Tax Defenders, or Platinum Tax, that we acquired on July 31, 2018, which was a full-service tax resolution firm located in Los Angeles, California. Through this subsidiary, we provided fee-based tax resolution services to individuals and companies that have federal and state tax liabilities by assisting clients to settle outstanding tax debts.

We also previously owned all of the day-to-day operations. Acquisitions become standalone autonomous subsidiaries that gainequity interests of We Three, LLC, d/b/a Affordable Housing Initiative, or AHI, an affordable home acquirer located in Maryville, Tennessee. On October 31, 2022, we entered into a buyback agreement to sell AHI back to the advantagesoriginal owners in exchange for the return of a publicly traded company without losing their independent management control. Management enjoys175,045 shares of series F preferred stock by the advantageoriginal owners and our issuance of improved valuation, liquidity, synergies, and support, along with diversification and asset appreciation through collective subsidiary performance. Diversification and pooled resources leverage value and mitigate risk.67,500 shares of series B preferred stock to the original owners.

Cardiff Lexington provides these companies both 1) the enhanced ability to raise money for operations or expansion, and 2) an equity exit and liquidity strategy for the owner, heirs, and/or Investors.Our Business Strategy

For investors, Cardiff Lexington provides a diversified lower riskWe employ an acquisition and value creation strategy, with the goal of locating undervalued and undercapitalized healthcare companies and providing them capitalization and leadership in order to protect and safely enhance their investment by continually adding assets and holdings.

Cardiff Lexington employs a merge, acquire, and hold strategy to maximize the value and potential of their private, often family run, enterprises while also providing diversification and risk mitigation for all shareholders.

Cardiff Lexingtonour stockholders. Our primary focus is ledon the healthcare sector, with holdings and real estate, where we utilize our management team’s relationship networks, industry experiences and deal sourcing capabilities to target companies we believe have an experienced management team and compelling assets which we believe are well positioned for growth. Our culture emphasizes core values, teamwork, accountability, and performance. Specifically, we have and will continue to look at a diverse variety of acquisitions in the healthcare sector in terms of growth stages and capital structures and we intend to focus our portfolio of subsidiaries approximately as follows: 80% will be targeted to established profitable niche small to mid-sized healthcare companies and 20% will be targeted to second stage startups in healthcare and related financial services (emerging businesses with a strong organic growth plan that is materially cash generative). Our acquisition strategy is driven by strongstructure, transaction value, alignment, resources and talented rosterreturn on investment. As we identify potential targets, it is also our strategy and goal to identify and recruit the right operating executive partners that have the requisite tools and experience to manage and grow our existing and newly acquired subsidiaries. Based on our management’s long history and experience in building relationships with a vast number of executives and advisors providing expert acquisition, market guidance and added value fortheir teams, we are confident that we have placed or left successful executives in charge of our current subsidiaries and investors.will be able to identify appropriate executives to add long term value to any future acquisitions.

Impact of COVID-19 Pandemic

The outbreak of a novel coronavirus throughoutAfter our acquisitions, the world, includingentities become wholly owned subsidiaries and the United States, during early calendar year 2020 has caused widespread business and economic disruption through mandated and voluntary business closings and restrictions on the movement and activities of people (“COVID-19 Pandemic”). We are subject to risks and uncertainties as a result of the COVID-19 Pandemic. See “Management’s Discussion and Analysis of Financial Condition and Results of Operations” for discussion on results of operationstarget company’s management team either maintains responsibility for the year ended December 31, 2020. The extent of the impact of the COVID-19 Pandemic on the Company's business is highly uncertain and difficultday-to-day operations or we locate suitable executives to predict, as the response to the COVID-19 Pandemic is rapidly evolving in many countries, including the United States and other markets where the Company operates. It is expected that many of the Company's customers and suppliers will continue to be impacted by these closings and restrictions which could materially and adversely affect demand for our products, our ability to obtain or deliver inventory or services, and our ability to collect accounts receivables as customers face higher liquidity and solvency risk. Furthermore, capital markets and economies worldwide have also been negatively impacted by the COVID-19 Pandemic, and it is possible that economic distress will continue in many marketsovertake responsibility for the foreseeable future. Such economic disruption could have a material adverse effect on our business. Policymakers around the world have responded with fiscal and monetary policy actions to support the economy. The magnitude and overall effectiveness of these actions remains uncertain.

The Company’s restaurant franchise operations have been severely and adversely affected by the economic pressure of the COVID-19 pandemic and the subsequent directives and responses to the crisis taken by the federal, state, and local governments. In light of circumstances arising from the COVID-19 Pandemic, management divested of all food service operations and is continuing to evaluate the Company’s current operations and acquisition opportunities to mitigate the impact of the pandemic and maximize shareholder value.

The decrease in revenue in 2020 is primarily attributable to the COVID-19 Pandemic. Both the affordable housing and financial services segments of the economy have been adversely affected by the COVID-19 Pandemic, due mainly to the significant increase in unemployment, which directly affected our subsidiaries prospects and customer base. We believe the segment of the population which was adversely affected by unemployment overlaps significantly with the customer base of our affordable housing and financial services businesses and, consequently, these customers were no longer able to afford our services.

Human Capital

Collectively, Cardiff Lexington and its subsidiaries employ approximately 37 employees and anticipates hiring additional personnel with new acquisitions.entities. We believe that we have good relationscan then provide these entities with our employeessome of the benefits of being a publicly traded company, including but not limited to, providing them with increased access to funding that we can obtain on their behalf in the capital markets for operations or expansion and our employeesmanagement team’s experience operating businesses. Our combined acquisition and value creation strategy drives our goal to deliver our public stockholders an opportunity to own a long term, stable, durable compounding equity investment that can produce strong returns.

Our Market Opportunity

Utilizing our management teams and principals’ expansive network of relationships, we believe there are not represented by any collective bargaining groupa substantial number of small to mid-sized healthcare companies, second stage startups – emerging businesses with a strong organic growth plan that is materially cash generative and income producing real estate holdings that we can seek to acquire that can potentially generate attractive returns for our stockholders. We further believe the economic and market dislocation resulting from the COVID-19 pandemic enhanced our opportunity to obtain potentially profitable businesses, which are facing lingering working capital challenges post pandemic, but have rebounded and returned to or agreement. Wenear previous levels of profitability. In this environment, we believe the expertise and relationships of our abilitymanagement team represent a compelling value proposition for potential business targets looking for additional working capital infusion, a pathway to attractexit some equity, and retain employees is a keyleadership to a successful acquisition strategy.assist them to grow and expand.

| 2 |

CompetitionOur Acquisition Process

In evaluating a potential target business, we conduct a comprehensive due diligence review to determine a company’s quality and its intrinsic value. That due diligence review may include, among other things, financial statement analysis, detailed document reviews, multiple meetings with management, consultations with relevant industry experts, competitors, customers, and suppliers, as well as a review of additional information that we will seek to obtain as part of our analysis of a target company. Upon the consummation of an acquisition agreement with a target company, it becomes a wholly owned subsidiary of our company.

We areanticipate structuring our acquisitions in such a small capitalization holdingway so that the post-business combination subsidiary company that seeks to enable businesses to take advantagewill own or acquire 100% of the potential accessequity interests or assets of the target business or businesses. We may, however, structure future acquisitions such that the post-business combination company owns or acquires less than 100% of such interests or assets of the target business in order to meet certain objectives of the target management team or stockholders or for other reasons, but we will only complete such acquisition if the post-business subsidiary company owns or acquires 50% or more of the outstanding voting securities of the target or otherwise acquires a controlling interest in the target sufficient for it not to be required to register as an investment company under the Investment Company Act of 1940, as amended, or the Investment Company Act.

If our board of directors is not able to independently determine the fair market value of the target business or businesses, we will obtain an opinion from an independent investment banking firm or an independent valuation or appraisal firm with respect to the satisfaction of such criteria. While we consider it unlikely that our board of directors will not be able to make an independent determination of the fair market value of a target business or businesses, it may be unable to do so if the board of directors is less familiar or experienced with the target company’s business, there is a significant amount of uncertainty as to the value of the company’s assets or prospects, including if such company is at an early stage of development, operations or growth, or if the anticipated transaction involves a complex financial analysis or other specialized skills and the board of directors determines that outside expertise would be helpful or necessary in conducting such analysis.

We finance acquisitions primarily through additional equity and debt financings. We believe that having the ability to finance most, if not all, acquisitions with the general capital markets providedresources raised by affiliation with a publicly traded company. Cardiff Lexington began targetingour company, rather than financing relating to the acquisition of undervalued, niche companiesindividual businesses, provides us with high growth potential, income-producing commercial real estate properties,an advantage in acquiring attractive businesses by minimizing delay and high return investments, all designedclosing conditions that are often related to generate sufficient earningsacquisition-specific financings. Because the timing and size of acquisitions cannot be readily predicted, we may need to pay a consistent dividendbe able to obtain funding on short notice to benefit fully from attractive acquisition opportunities. The sale of additional shares of any class of equity will be subject to market conditions and investor demand for such shares at prices that may not be in the best interest of our stockholders. The sale of additional equity securities could also result in dilution to our shareholders.stockholders. The incurrence of indebtedness would result in increased debt service obligations and could require us to agree to operating and financial covenants that would restrict our operations. Financing may not be available in amounts or on terms acceptable to us, if at all. See also Item 1A “Risk Factors—Risks Related to Our Business and Structure—We may not be able to successfully fund acquisitions due to the unavailability of equity or debt financing on acceptable terms, which could impede the implementation of our acquisition strategy.”

The time required to select and evaluate a target business and to structure and complete acquisitions, and the costs associated with this process, are not currently ascertainable with any degree of certainty. Any costs incurred with respect to the identification and evaluation of a prospective target business with which any acquisition is intendednot ultimately completed will result in our incurring losses and will reduce the funds we can use to mitigate riskcomplete another acquisition.

Members of our management team, including our officers and directors, will directly or indirectly own a majority of our securities following this offering and, accordingly, may have a conflict of interest in determining whether a particular target company is an appropriate business with which to shareholders by building a diversified portfolio of profitable small- to minimum-sized businesses with little to no debt, seeking support with both financing and management that had the ability to offer a return to investors. We will continue to establish new classes of preferred stock to streamline voting rights, negate debt, and acquire new businesses in the financial services and healthcare, and real estate sectors.effectuate our initial business combination.

We facehave not selected any specific business combination target for our next acquisition, and we have not entered into any letters of intent, nor has anyone on our behalf, initiated any substantive acquisition discussions, directly or indirectly, with any specific business combination target.

| 3 |

To the extent we effect any future acquisition with a company or business that may be financially unstable or in its early stages of development or growth, we may be affected by numerous risks inherent in such company or business. Although our management will endeavor to evaluate the risks inherent in a particular target business, we cannot assure you that we will properly ascertain or assess all significant competitionrisk factors.

There are several risks associated with our acquisition strategy, including the following risks, which are described more fully in the markets in which our subsidiaries operate. Platinum TaxItem 1A “Risk Factors—Risks Related to Our Business and Key Tax have significant competition in most of the markets in which they operate from other local tax resolution entitiesStructure”:

| · | our acquisition strategy exposes us to substantial risk; | |

| · | we may experience difficulty as we evaluate, acquire and integrate businesses that we may acquire, which could result in drains on our resources, including the attention of our management, and disruptions of our on-going business; | |

| · | we may not be able to effectively integrate the businesses that we acquire; | |

| · | we face competition for businesses that fit our acquisition strategy and, therefore, we may have to acquire targets at sub-optimal prices or, alternatively, forego certain acquisition opportunities; | |

| · | we may not be able to successfully fund acquisitions due to the unavailability of debt or equity financing on acceptable terms, which could impede the implementation of our acquisition strategy; and | |

| · | we may change our management and acquisition strategies without the consent of our stockholders, which may result in a determination by us to pursue riskier business activities. |

Competition

In identifying, evaluating, and from larger national companies. AHI has significantselecting potential target business for acquisition, we may encounter intense competition from other entities having a business objective similar to ours, including blank check companies, private companies in the areaequity groups and a few real estate investment trusts, which compete in the manufactured housing communities Edgeview competes in the highly competitive housing industry. Someleveraged buyout funds, and operating businesses seeking strategic acquisitions. Many of our subsidiaries’these entities are well established and have extensive experience identifying and effecting acquisitions directly or through affiliates. Moreover, many of these competitors may have advantages over us in terms ofpossess greater operational, financial, management ortechnical, human, and other resources than us. Our ability to acquire larger target businesses will be limited by our available financial resources. This inherent limitation gives others an advantage in particular markets orpursuing the acquisition of a target business. Any of these factors may place us at a competitive disadvantage in general. Our market position depends on our financing, development and operation capabilities, reputation, experience and track record. There can be no assurance that our current or potential competitors will not offer products or services comparable or superior to those that our subsidiaries offer. Increased competition may result in price reductions, reduced profit margins and loss of market share.successfully negotiating an acquisition.

Proprietary InformationCompetitive Strengths

We own the following trademarks: Cardiff USA; Mission Tuition, Legacy Card Company and Small Cap Rescue.believe that we have several competitive advantages that differentiate us from other holding companies. Our competitive strengths include:

| · | Management Operating and Investing Experience. Our directors and executive officers have significant executive, investment and operational experience in the management and growing of small and middle market companies. We believe that this breadth of experience provides us with a competitive advantage in evaluating businesses and acquisition opportunities. | |

| · | Extensive Network of Small to Middle Market Companies. As a result of their experience with acquisitions and in providing services to small to middle market companies around the United States, our management team members have developed a broad array of contacts at private and closely held companies. We believe that these contacts will be important in generating potential acquisition opportunities for us. |

Government

| 4 |

| · | Public Company Benefits. We believe our structure will make us an attractive business transaction partner to prospective acquisition targets. As an existing public company, we will be able to raise capital to deploy to our acquired businesses for their business operations. Additionally, we will be able to offer to the employees of our subsidiaries equity in our company as an additional means of creating management incentives that are better aligned with stockholder’s interests. | |

| · | Maintaining of day-to-day control of operations. As part of our acquisition criteria for a target company, we search for companies with what we believe are strong management teams, which allows us to have the management team maintain control of the day-to-day operations of the companies. We believe this model is attractive to target companies with management desiring to obtain the benefits of being a public company while maintaining control over the operations of their company. |

Intellectual Property

We do not have any intellectual property at our holding company.

Employees

As of December 31, 2023, our company had three full-time employees (excluding our operating subsidiaries described below). None of our employees are represented by labor unions, and we believe that we have an excellent relationship with our employees.

Regulation

We do not expect tothat our holding company will be subject to material governmental regulation. However, it is our policy to fully comply with all governmental regulation and regulatory authorities.

ResearchHealthcare Business

Our healthcare business is operated by Nova, which we acquired on May 31, 2021. This business accounted for all of our revenues for the years ended December 31, 2023 and Development2022.

Overview

We operate a group of regional primary specialty and ancillary care facilities throughout Florida that provide traumatic injury victims with primary care evaluations, interventional pain management, and specialty consultation services. We focus on plaintiff related care are investing inand a highly efficient provider of EMC assessments. We provide a full range of diagnostic and surgical services for injuries and disorders of the development of a new website that will effectively present the Company’s acquisition strategyskeletal system and its benefitsassociated bones, joints, tendons, muscles, ligaments, and nerves. From sports injuries, to prospective acquisition targetssprains, strains, and the communities we serve, as well as keep investors informed offractures, our progress in executing our strategy.doctors are dedicated to helping patients return to active lifestyles.

Environmental ComplianceThe Healthcare Market

We believeThe healthcare sector is defined as end users whose primary business is the delivery of medical, patient care or treatment, medical diagnostic services, or medical care provided in connection with disaster relief, including, but not limited to (i) professional medical and healthcare service companies, businesses, institutions and enterprises, (ii) medical diagnostics facilities and laboratories having patient interaction, (iii) government and private organizations providing medical care in connection with disaster relief and (iv) firms selling products or services into such end users. Examples of such end users are: hospitals, including their pharmacies; integrated medical service provider networks and their member facilities; surgery centers, including their pharmacies; blood banks; bone and tissue centers; physician and medical clinic offices including their pharmacies; psychiatric health facilities, including their pharmacies; clinics in retail outlets that we are not subject to any material costs for compliance with any environmental laws.

How to Obtain our SEC Filings

We file annual, quarterly, and special reports, information statements, and other information with the Securities and Exchange Commission (the “SEC”). Reports, information statements and other information filed with the SEC can be inspected and copied at the public referenceperform or provide medical services or care; long-term medical care facilities, including their pharmacies; medical care components of the SEC at 100 F Street N.E., Washington, DC 20549. Such material may also be accessed electronically by means of the SEC's website at www.sec.gov.

Our investor relations department can be contacted at our principal executive office located at, 401 East Las Olas Blvd. Unit 1400, Fort Lauderdale, FL 33301. Our telephone number is (844-628-2100).Red Cross or other disaster relief organizations; and dental care facilities.

We provide a full range of diagnostic and surgical services for injuries and disorders of the skeletal system and associated bones, joints, tendons, muscles, ligaments, and nerves. Orthopedic and pain procedure services include hip and knee replacement, shoulder reconstruction, fracture care and hand surgery, as well as spinal surgery.

Our service model is designed to promote referral relationships, facilitate patient access, and coordinate administration among medical providers, personal injury attorneys, and chiropractors. This “referral relationship” approach to case management results in increased revenue as attorneys consider the value of our patient management process when brokering settlements. As EMC and early stage continued care providers, we believe that we have superior access to patient information to determine the validity of each case and manage cases appropriately.

Revenue is primarily provided by bodily injury policies, general liability policies, and personal injury protection policies, which partially insulates our business from the declining reimbursement programs paid from or correlated to Medicare/Medicaid and traditional health insurance companies.

Healthcare Facilities

We currently operate ten facilities, most of which were opened in the last twenty-four months. As of December 31, 2023, management estimates that the ten facilities are operating at 35% capacity. We believe that the most important factors relating to the overall utilization of a facility include adequate working capital, the quality and market position of the facility and the number, quality and specialties of physicians providing patient care within the facility. Other factors that affect utilization include general and local economic conditions, market penetration, the degree of outpatient use, the availability of reimbursement programs such as Medicare and Medicaid, and demographic changes such as the growth in local populations. Utilization across the industry is also being affected by improvements in clinical practice, medical technology and pharmacology. Current industry trends in utilization and occupancy have been significantly affected by changes in reimbursement policies of third party payers. We are also unable to predict the extent to which these industry trends will continue or accelerate.

Customers, Sales and Marketing

As of December 31, 2023, we provide services to approximately 150-180 patients per month at ten facilities. Patients are primarily referred through a growing network of personal injury attorneys, insurance carriers, physical therapy providers, and chiropractic care providers.

Competition

The health care industry is highly competitive. In recent years, competition among healthcare providers for patients has intensified in the United States due to, among other things, regulatory and technological changes, increasing use of managed care payment systems, cost containment pressures and a shift toward outpatient treatment. In all of the geographical areas in which we operate, there are other facilities that provide services comparable to those offered by our facilities. In addition, some of our competitors include hospitals that are owned by tax-supported governmental agencies or by nonprofit corporations and may be supported by endowments and charitable contributions and exempt from property, sale and income taxes. Such exemptions and support are not available to us.

Certain of our competitors may have greater financial resources, be better equipped and offer a broader range of services than us. The increase in outpatient treatment and diagnostic facilities, outpatient surgical centers and freestanding ambulatory surgical also increases competition for us.

| 6 |

The number and quality of the physicians on a facility’s staff are important factors in determining a facility’s success and competitive advantage. Typically, physicians are responsible for making admissions decisions and for directing the course of patient treatment. We believe that physicians refer patients to a facility primarily on the basis of the patient’s needs, the quality of other physicians on the medical staff, the location of the facility and the breadth and scope of services offered at the facility. We strive to retain and attract qualified doctors by maintaining high ethical and professional standards and providing adequate support personnel, technologically advanced equipment and facilities that meet the needs of those physicians.

In addition, we depend on the efforts, abilities, and experience of our medical support personnel, including our nurses, pharmacists and lab technicians and other health care professionals. We compete with other health care providers in recruiting and retaining qualified management, nurses and other medical personnel. Our healthcare facilities are experiencing the effects of a nationwide staffing shortage, which has caused and may continue to cause an increase in salaries, wages and benefits expense in excess of the inflation rate. In addition, there are requirements to maintain specified nurse-staffing levels. To the extent we cannot meet those levels, we may be required to limit the healthcare services provided, which would have a corresponding adverse effect on our net operating revenues.

Although most of our revenue is provided by bodily injury policies, general liability policies, and personal injury protection policies, our ability to negotiate favorable service contracts with purchasers of group health care services also affects our competitive position and significantly affects the revenues and operating results of our facilities. Managed care plans attempt to direct and control the use of services and to demand that we accept lower rates of payment. In addition, employers and traditional health insurers are increasingly interested in containing costs through negotiations with facilities for managed care programs and discounts from established charges. In return, facilities secure commitments for a larger number of potential patients. Generally, facilities compete for service contracts with group health care service purchasers on the basis of price, market reputation, geographic location, quality and range of services, quality of the medical staff and convenience. The importance of obtaining contracts with managed care organizations varies from market to market depending on the market strength of such organizations.

A key element of our growth strategy is expansion through opening additional locations and the acquisition of additional facilities in select markets. The competition to acquire healthcare facilities is significant. We compete for acquisitions with other for-profit healthcare companies, private equity and venture capital firms, as well as not-for-profit entities. Some of our competitors have greater resources than we do. We intend to selectively seek opportunities to expand our base of operations by adhering to our disciplined program of rational growth but may not be successful in accomplishing acquisitions on favorable terms.

Competitive Strengths

We believe that we have several competitive advantages, including the following:

| · | Broad array of services focusing on plaintiff related care. We provide a full range of diagnostic and surgical services for injuries and disorders of the skeletal system and associated bones, joints, tendons, muscles, ligaments, and nerves with a focus on plaintiff related care. From sports injuries, to sprains, strains, and fractures, orthopedic and pain procedure services include hip and knee replacement, shoulder reconstruction, fracture care and hand surgery, as well as spinal surgery. Our service model is designed to promote referral relationships, facilitate patient access, and coordinate administration among medical providers, personal injury attorneys, and chiropractors. As a result, our revenue is primarily provided by bodily injury policies, general liability policies, and personal injury protection policies, which partially insulates our business from the declining reimbursement programs paid from or correlated to Medicare/ Medicaid and traditional health insurance companies. | |

| · | Opportunities for accelerated growth. We have a track record of delivering strong growth through a combination of organic growth, new contract additions and selective acquisitions. Organic growth has historically been supported by consistent underlying market volume trends, stable pricing and a diversified payor mix. We believe that our networks of high-quality providers position us to take advantage of these trends. We have successfully executed on new contract growth by providing a set of differentiated services and delivering integrated, efficient, high-quality care, which has helped us expand our relationships with our existing customers and compete effectively in the bidding process for new contracts. Additionally, we believe we will have opportunities to expand our services through acquisitions, as discussed in more detail below. |

| 7 |

| · | Focus on clinical excellence. We are focused on achieving the best clinical outcomes for our patients through the application of rigorous recruiting and credentialing standards, the promotion of a physician-led leadership culture and the monitoring of our clinical quality measures. Through extensive clinical and leadership development programs, we train our healthcare professionals to continually enhance their skills and deliver innovative and patient-focused experiences and outcomes. We provide internally developed continuing medical education accredited courses to our healthcare professionals, including instructor-led and on-line education sessions. We have developed and implemented quality measurement systems that track multiple key indicators, which assist our professionals in systematically monitoring, examining and analyzing outcomes and processes. These quality measurement systems are supplemented by our active peer review infrastructure designed to ensure the development and implementation of actionable items that will improve patient outcomes. Our ability to deliver high levels of customer service and patient care is a direct result of this focus, which helps us to differentiate our services, and to attract and retain providers. | |

| · | Ability to attract and retain high-quality providers. Through our processes, we are able to identify and target high-quality providers to match the needs of our customers. We believe that our operating infrastructure enables us to provide attractive opportunities for our providers to enhance their skills through extensive clinical and leadership development programs. We believe that our differentiated recruiting, training and development programs strengthen our customer and provider relationships, enhance our contract and clinician retention rates and allow us to efficiently recruit providers to support our new contract pipeline. |

Growth Strategies

The key elements of our strategy to grow our business include:

| · | Capitalize on organic growth opportunities. As noted above, management estimates that our ten facilities are operating at 35% capacity as of December 31, 2023. Accordingly, we believe that we have an opportunity for organic growth at our existing facilities. We also believe our physician-led, patient-focused culture and approach to clinical solutions will allow us to continue to successfully recruit and retain clinical professionals. | |

| · | Supplement organic growth with strategic acquisitions. The market in which we compete is highly fragmented, presenting significant opportunities for additional acquisitions. We will continue to follow a disciplined strategy in exploring future acquisitions by analyzing the strategic rationale, financial impact and organic growth profile of each potential opportunity. Our current focus for future acquisitions is MRI imaging, followed by medical billing and outpatient surgery centers. We have been in discussions with several privately owned MRI facilities. Key targets are strategically located within our market territory. We believe that the addition of these profitable businesses would be immediately enhanced by significant additional new business that we would direct to them. | |

| · | Enhance operational efficiencies and productivity. We believe there are significant opportunities to continue to build upon our success in improving our productivity and profitability. We continue to focus on initiatives to improve productivity, including more efficient scheduling, continued use of mid-level providers, enhancing our leadership training programs, improving and realigning compensation programs. We believe that our processes related to managed care contracting, billing, coding, collection and compliance have driven a strong track record of efficient revenue cycle management. We have made significant investments in infrastructure, including management information systems that we believe will continue to enable us to improve clinical results and key client metrics while reducing the cost of providing patient care. We have dedicated teams with business and clinical expertise that are responsible for implementing best practices. Furthermore, we will continue to utilize risk mitigation programs for loss prevention and early intervention. We believe that our significant investments in scalable technology systems will facilitate additional cost reductions and efficiencies. |

Intellectual Property

Our healthcare business does not own any intellectual property.

| 8 |

Employees and Medical Staff

As of December 31, 2023, we had 10 employees. Our facilities are staffed by licensed physicians who have been admitted to the medical staff of individual facilities. Members of the medical staff of our facilities also serve on the medical staffs of facilities not owned by us and may terminate their affiliation with our facilities at any time. Each of our facilities is managed on a day-to-day basis by a managing director. In addition, a Board of Governors, including members of the facility’s medical staff, governs the medical, professional and ethical practices at each facility. We believe that our relations with our employees are satisfactory.

None of our employees are represented by labor unions, and we believe that we have an excellent relationship with our employees.

Regulation

The healthcare industry is subject to numerous laws, regulations and rules including, among others, those related to government healthcare participation requirements, various licensure and accreditations, reimbursement for patient services, health information privacy and security rules, and Medicare and Medicaid fraud and abuse provisions (including, but not limited to, federal statutes and regulations prohibiting kickbacks and other illegal inducements to potential referral sources, false claims submitted to federal or state health care programs and self-referrals by physicians). Providers that are found to have violated any of these laws and regulations may be excluded from participating in government healthcare programs, subjected to significant fines or penalties and/or required to repay amounts received from the government for previously billed patient services. Although we believe our policies, procedures and practices comply with governmental regulations, no assurance can be given that we will not be subjected to additional governmental inquiries or actions, or that we would not be faced with sanctions, fines or penalties if so subjected. Even if we were to ultimately prevail, a significant governmental inquiry or action under one of the above laws, regulations or rules could have a material adverse impact on us.

Licensing, Certification and Accreditation: All of our facilities are subject to compliance with various federal, state and local statutes and regulations and receive periodic inspection by state licensing agencies to review standards of medical care, equipment and cleanliness. Our facilities s must also comply with the conditions of participation and licensing requirements of federal, state and local health agencies, as well as the requirements of municipal building codes, health codes and local fire departments. Various other licenses and permits are also required in order to dispense narcotics, operate pharmacies, handle radioactive materials and operate certain equipment. All of our eligible hospitals have been accredited by The Joint Commission. All of our facilities are certified as providers of Medicare and Medicaid services by the appropriate governmental authorities. If any of our facilities were to lose its Joint Commission accreditation or otherwise lose its certification under the Medicare and Medicaid programs, the facility may be unable to receive reimbursement from the Medicare and Medicaid programs and other payers. We believe our facilities are in substantial compliance with current applicable federal, state, local and independent review body regulations and standards. The requirements for licensure, certification and accreditation are subject to change and, in order to remain qualified, it may become necessary for us to make changes in our facilities, equipment, personnel and services in the future, which could have a material adverse impact on operations.

Certificates of Need: Many states, including Florida, have enacted certificates of need, or CON, laws as a condition prior to capital expenditures, construction, expansion, modernization or initiation of major new services. Failure to obtain necessary state approval can result in our inability to complete an acquisition, expansion or replacement, the imposition of civil or, in some cases, criminal sanctions, the inability to receive Medicare or Medicaid reimbursement or the revocation of a facility’s license, which could harm our business. In addition, significant CON reforms have been proposed in a number of states that would increase the capital spending thresholds and provide exemptions of various services from review requirements. In the past, we have not experienced any material adverse effects from those requirements, but we cannot predict the impact of these changes upon our operations.

| 9 |

Conversion Legislation: Many states have enacted or are considering enacting laws affecting the conversion or sale of not-for-profit healthcare facilities to for-profit entities. These laws generally require prior approval from the attorney general, advance notification and community involvement. In addition, attorneys general in states without specific conversion legislation may exercise discretionary authority over these transactions. Although the level of government involvement varies from state to state, the trend is to provide for increased governmental review and, in some cases, approval of a transaction in which a not-for-profit entity sells a health care facility to a for-profit entity. The adoption of new or expanded conversion legislation and the increased review of not-for-profit conversions may limit our ability to grow through acquisitions of not-for-profit facilities.

Utilization Review: Federal regulations require that admissions and utilization of facilities by Medicare and Medicaid patients must be reviewed in order to ensure efficient utilization of facilities and services. The law and regulations require Peer Review Organizations, or PROs, to review the appropriateness of Medicare and Medicaid patient admissions and discharges, the quality of care provided, the validity of diagnosis related group classifications and the appropriateness of cases of extraordinary length of stay. PROs may deny payment for services provided, assess fines and also have the authority to recommend to the Department of Health and Human Services, or HHS, that a provider that is in substantial non-compliance with the standards of the PRO be excluded from participating in the Medicare program. We have contracted with PROs to perform the required reviews.

Audits: Most healthcare facilities are subject to federal audits to validate the accuracy of Medicare and Medicaid program submitted claims. If these audits identify overpayments, we could be required to pay a substantial rebate of prior years’ payments subject to various administrative appeal rights. The federal government contracts with third-party “recovery audit contractors” and “Medicaid integrity contractors,” on a contingent fee basis, to audit the propriety of payments to Medicare and Medicaid providers. Similarly, Medicare zone program integrity contractors target claims for potential fraud and abuse. Additionally, Medicare administrative contractors must ensure they pay the right amount for covered and correctly coded services rendered to eligible beneficiaries by legitimate providers. The Centers for Medicare and Medicaid Services announced its intent to consolidate many of these Medicare and Medicaid program integrity functions into new unified program integrity contractors, though it remains unclear what effect, if any, this consolidation may have. We have undergone claims audits related to our receipt of federal healthcare payments during the last three years, the results of which have not required material adjustments to our consolidated results of operations. However, potential liability from future federal or state audits could ultimately exceed established reserves, and any excess could potentially be substantial. Further, Medicare and Medicaid regulations also provide for withholding Medicare and Medicaid overpayments in certain circumstances, which could adversely affect our cash flow.

The Stark Law: The Social Security Act includes a provision commonly known as the “Stark Law.” This law prohibits physicians from referring Medicare and Medicaid patients to entities with which they or any of their immediate family members have a financial relationship unless an exception is met. These types of referrals are known as “self-referrals.” Sanctions for violating the Stark Law include civil penalties up to $26,125 for each violation, and up to $174,172 for sham arrangements. There are a number of exceptions to the self-referral prohibition, including an exception for a physician’s ownership interest in an entire facility as opposed to an ownership interest in a facility department unit, service or subpart. However, federal laws and regulations now limit the ability of facilities relying on this exception to expand aggregate physician ownership interest or to expand certain facilities. This regulation also places a number of compliance requirements on physician-owned facilities related to reporting of ownership interest. There are also exceptions for many of the customary financial arrangements between physicians and providers, including employment contracts, leases and recruitment agreements that adhere to certain enumerated requirements. The Centers for Medicare and Medicaid Services, or CMS, issued a final rule in 2020 that created a new Stark exception for value-based models. Although the final regulations provide exceptions to the Stark Law, there may remain regulatory risks for participating hospitals, as well as financial and operational risks. We monitor all aspects of our business and have developed a comprehensive ethics and compliance program that is designed to meet or exceed applicable federal guidelines and industry standards. Nonetheless, because the law in this area is complex and constantly evolving, there can be no assurance that federal regulatory authorities will not determine that any of our arrangements with physicians violate the Stark Law.

| 10 |

Anti-kickback Statute: A provision of the Social Security Act known as the “anti-kickback statute” prohibits healthcare providers and others from directly or indirectly soliciting, receiving, offering or paying money or other remuneration to other individuals and entities in return for using, referring, ordering, recommending or arranging for such referrals or orders of services or other items covered by a federal or state health care program. However, changes to the anti-kickback statute have reduced the intent required for violation; one is no longer required to have actual knowledge or specific intent to commit a violation of the anti-kickback statute in order to be found in violation of such law. The anti-kickback statute contains certain exceptions, and the Office of the Inspector General of the Department of Health and Human Services, or the OIG, has issued regulations that provide for “safe harbors,” from the federal anti-kickback statute for various activities. These activities, which must meet certain requirements, include (but are not limited to) the following: investment interests, space rental, equipment rental, practitioner recruitment, personnel services and management contracts, sale of practice, referral services, warranties, discounts, employees, group purchasing organizations, waiver of beneficiary coinsurance and deductible amounts, managed care arrangements, obstetrical malpractice insurance subsidies, investments in group practices, freestanding surgery centers, donation of technology for electronic health records and referral agreements for specialty services. In 2020, the OIG issued a final rule that established an anti-kickback statute safe harbor for value based models. Although the final regulations provide safe harbors, there may remain regulatory risks for participating facilities, as well as financial and operational risks. The fact that conduct or a business arrangement does not fall within a safe harbor or exception does not automatically render the conduct or business arrangement illegal under the anti-kickback statute. However, such conduct and business arrangements may lead to increased scrutiny by government enforcement authorities. Although we believe that our arrangements with physicians and other referral sources have been structured to comply with current law and available interpretations, there can be no assurance that all arrangements comply with an available safe harbor or that regulatory authorities enforcing these laws will determine these financial arrangements do not violate the anti-kickback statute or other applicable laws. Violations of the anti-kickback statute may be punished by a criminal fine of up to $100,000 for each violation or imprisonment, however, under 18 U.S.C. Section 3571, this fine may be increased to $250,000 for individuals and $500,000 for organizations. Civil money penalties may include fines of up to $105,563 per violation and damages of up to three times the total amount of the remuneration and/or exclusion from participation in Medicare and Medicaid.

Similar State Laws: Many states, including Florida, have adopted laws that prohibit payments to physicians in exchange for referrals similar to the anti-kickback statute and the Stark Law, some of which apply regardless of the source of payment for care. These statutes typically provide criminal and civil penalties as well as loss of licensure. In many instances, the state statutes provide that any arrangement falling in a federal safe harbor will be immune from scrutiny under the state statutes. However, in most cases, little precedent exists for the interpretation or enforcement of these state laws. These laws and regulations are extremely complex and, in many cases, we do not have the benefit of regulatory or judicial interpretation. It is possible that different interpretations or enforcement of these laws and regulations could subject our current or past practices to allegations of impropriety or illegality or could require us to make changes in our facilities, equipment, personnel, services, capital expenditure programs and operating expenses. A determination that we have violated one or more of these laws, or the public announcement that we are being investigated for possible violations of one or more of these laws, could have a material adverse effect on our business, financial condition or results of operations and our business reputation could suffer significantly. In addition, we cannot predict whether other legislation or regulations at the federal or state level will be adopted, what form such legislation or regulations may take or what their impact on us may be. If we are deemed to have failed to comply with the anti-kickback statute, the Stark Law or other applicable laws and regulations, we could be subjected to liabilities, including criminal penalties, civil penalties (including the loss of our licenses to operate one or more facilities), and exclusion of one or more facilities from participation in the Medicare, Medicaid and other federal and state health care programs. The imposition of such penalties could have a material adverse effect on our business, financial condition or results of operations.

Federal False Claims Act and Similar State Regulations: A current trend affecting the health care industry is the increased use of the federal False Claims Act, and, in particular, actions being brought by individuals on the government’s behalf under the False Claims Act’s qui tam, or whistleblower, provisions. Whistleblower provisions allow private individuals to bring actions on behalf of the government by alleging that the defendant has defrauded the Federal government. When a defendant is determined by a court of law to have violated the False Claims Act, the defendant may be liable for up to three times the actual damages sustained by the government, plus mandatory civil penalties of between $12,537 to $25,076 for each separate false claim. There are many potential bases for liability under the False Claims Act. Liability often arises when an entity knowingly submits a false claim for reimbursement to the federal government. The Fraud Enforcement and Recovery Act of 2009, or FERA, amended and expanded the number of actions for which liability may attach under the False Claims Act, eliminating requirements that false claims be presented to federal officials or directly involve federal funds. FERA also clarifies that a false claim violation occurs upon the knowing retention, as well as the receipt, of overpayments. In addition, recent changes to the anti-kickback statute have made violations of that law punishable under the civil False Claims Act. Further, a number of states have adopted their own false claims provisions as well as their own whistleblower provisions whereby a private party may file a civil lawsuit on behalf of the state in state court. The False Claims Act requires that federal healthcare program overpayments be returned within 60 days from the date the overpayment was identified, or by the date any corresponding cost report was due, whichever is later. Failure to return an overpayment within this period may result in additional civil False Claims Act liability.

| 11 |

Other Fraud and Abuse Provisions: The Social Security Act also imposes criminal and civil penalties for submitting false claims to Medicare and Medicaid. False claims include, but are not limited to, billing for services not rendered, billing for services without prescribed documentation, misrepresenting actual services rendered in order to obtain higher reimbursement and cost report fraud. Like the anti-kickback statute, these provisions are very broad. Further, the Health Insurance Portability and Accountability Act of 1996, or HIPAA, broadened the scope of the fraud and abuse laws by adding several criminal provisions for health care fraud offenses that apply to all health benefit programs, whether or not payments under such programs are paid pursuant to federal programs. HIPAA also introduced enforcement mechanisms to prevent fraud and abuse in Medicare. There are civil penalties for prohibited conduct, including, but not limited to billing for medically unnecessary products or services.