UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

☒QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the quarterly period ended June 30, 2019March 31, 2020

or

☐TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from to

Commission file number 001-16383

CHENIERE ENERGY, INC.

(Exact name of registrant as specified in its charter)

|

| | | |

| Delaware | 95-4352386 |

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) |

| | | |

700 Milam Street | , | Suite 1900 | |

Houston | , | Texas | 77002 |

(Address of principal executive offices) | (Zip |

700 Milam Street, Suite 1900

Houston, Texas77002

(Address of principal executive offices) (Zip Code)

(713) 375-5000

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

|

| | |

| Title of each class | Trading Symbol | Name of each exchange on which registered |

| Common Stock, $ 0.003 par value | LNG | NYSE American |

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

|

| | | | | |

| | Large accelerated filer | ☒ | | Accelerated filer | ☐ |

| | Non-accelerated filer | ☐ | | Smaller reporting company | ☐ |

| | | | | Emerging growth company | ☐ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

As of August 2, 2019,April 24, 2020, the issuer had 256,779,983252,107,558 shares of Common Stock outstanding.

CHENIERE ENERGY, INC.

TABLE OF CONTENTS

DEFINITIONS

As used in this quarterly report, the terms listed below have the following meanings:

Common Industry and Other Terms

|

| | |

| Bcf | | billion cubic feet |

| Bcf/d | | billion cubic feet per day |

| Bcf/yr | | billion cubic feet per year |

| Bcfe | | billion cubic feet equivalent |

| DOE | | U.S. Department of Energy |

| EPC | | engineering, procurement and construction |

| FERC | | Federal Energy Regulatory Commission |

| FTA countries | | countries with which the United States has a free trade agreement providing for national treatment for trade in natural gas |

| GAAP | | generally accepted accounting principles in the United States |

| Henry Hub | | the final settlement price (in USD per MMBtu) for the New York Mercantile Exchange’s Henry Hub natural gas futures contract for the month in which a relevant cargo’s delivery window is scheduled to begin |

| LIBOR | | London Interbank Offered Rate |

| LNG | | liquefied natural gas, a product of natural gas that, through a refrigeration process, has been cooled to a liquid state, which occupies a volume that is approximately 1/600th of its gaseous state |

| MMBtu | | million British thermal units, an energy unit |

| mtpa | | million tonnes per annum |

| non-FTA countries | | countries with which the United States does not have a free trade agreement providing for national treatment for trade in natural gas and with which trade is permitted |

| SEC | | U.S. Securities and Exchange Commission |

| SPA | | LNG sale and purchase agreement |

| TBtu | | trillion British thermal units, an energy unit |

| Train | | an industrial facility comprised of a series of refrigerant compressor loops used to cool natural gas into LNG |

| TUA | | terminal use agreement |

Abbreviated Legal Entity Structure

The following diagram depicts our abbreviated legal entity structure as of June 30, 2019,March 31, 2020, including our ownership of certain subsidiaries, and the references to these entities used in this quarterly report:

Unless the context requires otherwise, references to “Cheniere,” the “Company,” “we,” “us” and “our” refer to Cheniere Energy, Inc. and its consolidated subsidiaries, including our publicly traded subsidiary, Cheniere Partners.

Unless the context requires otherwise, references to the “CCH Group” refer to CCH HoldCo II, CCH HoldCo I, CCH, CCL and CCP, collectively.

| |

| PART I. | FINANCIAL INFORMATION |

| |

| ITEM 1. | CONSOLIDATED FINANCIAL STATEMENTS |

CHENIERE ENERGY, INC. AND SUBSIDIARIES

CONSOLIDATED BALANCE SHEETS (1)

(in millions, except share data)

| | | | June 30, | | December 31, | March 31, | | December 31, |

| | 2019 | | 2018 | 2020 | | 2019 |

| ASSETS | (unaudited) | | | (unaudited) | | |

| Current assets | | | | | | |

| Cash and cash equivalents | $ | 2,279 |

| | $ | 981 |

| $ | 2,399 |

| | $ | 2,474 |

|

| Restricted cash | 1,161 |

| | 2,175 |

| 430 |

| | 520 |

|

| Accounts and other receivables | 433 |

| | 585 |

| 468 |

| | 491 |

|

| Inventory | 290 |

| | 316 |

| 239 |

| | 312 |

|

| Derivative assets | 127 |

| | 63 |

| 322 |

| | 323 |

|

| Other current assets | 135 |

| | 114 |

| 79 |

| | 92 |

|

| Total current assets | 4,425 |

| | 4,234 |

| 3,937 |

| | 4,212 |

|

| | | | | | | |

| Property, plant and equipment, net | 29,073 |

| | 27,245 |

| 29,802 |

| | 29,673 |

|

| Operating lease assets, net | 502 |

| | — |

| 350 |

| | 439 |

|

| Debt issuance costs, net | 55 |

| | 72 |

| |

| Non-current derivative assets | 103 |

| | 54 |

| 705 |

| | 174 |

|

| Goodwill | 77 |

| | 77 |

| 77 |

| | 77 |

|

| Deferred tax assets | | 400 |

| | 529 |

|

| Other non-current assets, net | 337 |

| | 305 |

| 476 |

| | 388 |

|

| Total assets | $ | 34,572 |

| | $ | 31,987 |

| $ | 35,747 |

| | $ | 35,492 |

|

| | | | | | | |

| LIABILITIES AND STOCKHOLDERS’ EQUITY | |

| | |

| | | |

| Current liabilities | |

| | |

| |

| | |

|

| Accounts payable | $ | 120 |

| | $ | 58 |

| $ | 29 |

| | $ | 66 |

|

| Accrued liabilities | 1,572 |

| | 1,169 |

| 922 |

| | 1,281 |

|

| Current debt | — |

| | 239 |

| 2,137 |

| | — |

|

| Deferred revenue | 136 |

| | 139 |

| 94 |

| | 161 |

|

| Current operating lease liabilities | 292 |

| | — |

| 178 |

| | 236 |

|

| Derivative liabilities | 84 |

| | 128 |

| 244 |

| | 117 |

|

| Other current liabilities | 3 |

| | 9 |

| 53 |

| | 13 |

|

| Total current liabilities | 2,207 |

| | 1,742 |

| 3,657 |

| | 1,874 |

|

| | | | | | | |

| Long-term debt, net | 29,944 |

| | 28,179 |

| 28,940 |

| | 30,774 |

|

| Non-current operating lease liabilities | 202 |

| | — |

| 164 |

| | 189 |

|

| Non-current finance lease liabilities | 58 |

| | 57 |

| 58 |

| | 58 |

|

| Non-current derivative liabilities | 94 |

| | 22 |

| 186 |

| | 151 |

|

| Other non-current liabilities | 44 |

| | 58 |

| 23 |

| | 11 |

|

| | | | | | | |

| Commitments and contingencies (see Note 16) |

|

| |

|

| |

| Commitments and contingencies (see Note 17) | |

|

| |

|

|

| | | | | | | |

| Stockholders’ equity | |

| | |

| |

| | |

|

| Preferred stock, $0.0001 par value, 5.0 million shares authorized, none issued | — |

| | — |

| — |

| | — |

|

| Common stock, $0.003 par value | | | |

| |

| Authorized: 480.0 million shares at June 30, 2019 and December 31, 2018 | | | | |

| Issued: 270.5 million shares at June 30, 2019 and 269.8 million shares at December 31, 2018 |

|

| |

|

| |

| Outstanding: 257.5 million shares at June 30, 2019 and 257.0 million shares at December 31, 2018 | 1 |

| | 1 |

| |

| Treasury stock: 13.0 million shares and 12.8 million shares at June 30, 2019 and December 31, 2018, respectively, at cost | (423 | ) | | (406 | ) | |

| Common stock, $0.003 par value, 480.0 million shares authorized | | | | |

| Issued: 272.8 million shares at March 31, 2020 and 270.7 million shares at December 31, 2019 | |

|

| |

|

|

| Outstanding: 252.1 million shares at March 31, 2020 and 253.6 million shares at December 31, 2019 | | 1 |

| | 1 |

|

| Treasury stock: 20.7 million shares and 17.1 million shares at March 31, 2020 and December 31, 2019, respectively, at cost | | (868 | ) | | (674 | ) |

| Additional paid-in-capital | 4,097 |

| | 4,035 |

| 4,196 |

| | 4,167 |

|

| Accumulated deficit | (4,129 | ) | | (4,156 | ) | (3,133 | ) | | (3,508 | ) |

| Total stockholders’ deficit | (454 | ) | | (526 | ) | |

| Total stockholders’ equity (deficit) | | 196 |

| | (14 | ) |

| Non-controlling interest | 2,477 |

| | 2,455 |

| 2,523 |

| | 2,449 |

|

| Total equity | 2,023 |

| | 1,929 |

| 2,719 |

| | 2,435 |

|

| Total liabilities and equity | $ | 34,572 |

| | $ | 31,987 |

| |

| Total liabilities and stockholders’ equity | | $ | 35,747 |

| | $ | 35,492 |

|

| |

| (1) | Amounts presented include balances held by our consolidated variable interest entity (“VIE”), Cheniere Partners, as further discussed in Note 8— Non-controlling Interest and Variable Interest Entity. As of March 31, 2020, total assets and liabilities of Cheniere Partners, which are included in our Consolidated Balance Sheets, were $19.0 billion and $18.4 billion, respectively, including $1.7 billion of cash and cash equivalents and $0.1 billion of restricted cash. |

The accompanying notes are an integral part of these consolidated financial statements.

3

CHENIERE ENERGY, INC. AND SUBSIDIARIES

CONSOLIDATED STATEMENTS OF OPERATIONS

(in millions, except per share data)

(unaudited)

| | | | Three Months Ended June 30, | | Six Months Ended June 30, | Three Months Ended March 31, |

| | 2019 | | 2018 | | 2019 | | 2018 | 2020 | | 2019 |

| Revenues | | | | | | | | | | |

| LNG revenues | $ | 2,173 |

| | $ | 1,442 |

| | $ | 4,316 |

| | $ | 3,608 |

| $ | 2,568 |

| | $ | 2,143 |

|

| Regasification revenues | 67 |

| | 65 |

| | 133 |

| | 130 |

| 67 |

| | 66 |

|

| Other revenues | 52 |

| | 36 |

| | 104 |

| | 47 |

| 74 |

| | 52 |

|

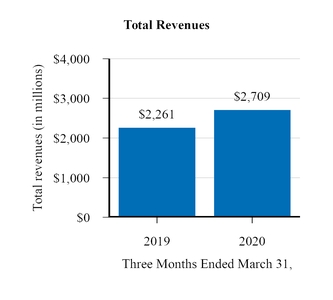

| Total revenues | 2,292 |

| | 1,543 |

| | 4,553 |

| | 3,785 |

| 2,709 |

| | 2,261 |

|

| | | | | | | | | | | |

| Operating costs and expenses | | | | | | | | | | |

| Cost of sales (excluding depreciation and amortization expense shown separately below) | 1,277 |

| | 873 |

| | 2,491 |

| | 2,051 |

| |

| Cost of sales (excluding items shown separately below) | | 724 |

| | 1,214 |

|

| Operating and maintenance expense | 295 |

| | 147 |

| | 516 |

| | 287 |

| 316 |

| | 221 |

|

| Development expense | 3 |

| | 3 |

| | 4 |

| | 4 |

| 4 |

| | 1 |

|

| Selling, general and administrative expense | 77 |

| | 73 |

| | 150 |

| | 140 |

| 81 |

| | 73 |

|

| Depreciation and amortization expense | 204 |

| | 111 |

| | 348 |

| | 220 |

| 233 |

| | 144 |

|

| Impairment expense and loss on disposal of assets | 4 |

| | — |

| | 6 |

| | — |

| 5 |

| | 2 |

|

| Total operating costs and expenses | 1,860 |

| | 1,207 |

| | 3,515 |

| | 2,702 |

| 1,363 |

| | 1,655 |

|

| | | | | | | | | | | |

| Income from operations | 432 |

| | 336 |

| | 1,038 |

| | 1,083 |

| 1,346 |

| | 606 |

|

| | | | | | | | | | | |

| Other income (expense) | | | | | | | | | | |

| Interest expense, net of capitalized interest | (372 | ) | | (216 | ) | | (619 | ) | | (432 | ) | (412 | ) | | (247 | ) |

| Loss on modification or extinguishment of debt | — |

| | (15 | ) | | — |

| | (15 | ) | (1 | ) | | — |

|

| Derivative gain (loss), net | (74 | ) | | 32 |

| | (109 | ) | | 109 |

| |

| Other income | 16 |

| | 10 |

| | 32 |

| | 17 |

| |

| Interest rate derivative loss, net | | (208 | ) | | (35 | ) |

| Other income, net | | 9 |

| | 16 |

|

| Total other expense | (430 | ) | | (189 | ) | | (696 | ) | | (321 | ) | (612 | ) | | (266 | ) |

| | | | | | | | | | | |

| Income before income taxes and non-controlling interest | 2 |

|

| 147 |

|

| 342 |

|

| 762 |

| 734 |

|

| 340 |

|

| Income tax benefit (provision) | — |

|

| 3 |

|

| (3 | ) |

| (12 | ) | |

| Income tax provision | | (131 | ) |

| (3 | ) |

| Net income | 2 |

|

| 150 |

|

| 339 |

|

| 750 |

| 603 |

|

| 337 |

|

| Less: net income attributable to non-controlling interest | 116 |

|

| 168 |

|

| 312 |

|

| 411 |

| 228 |

|

| 196 |

|

| Net income (loss) attributable to common stockholders | $ | (114 | ) |

| $ | (18 | ) |

| $ | 27 |

|

| $ | 339 |

| |

| Net income attributable to common stockholders | | $ | 375 |

|

| $ | 141 |

|

| | Net income (loss) per share attributable to common stockholders—basic (1) | $ | (0.44 | ) |

| $ | (0.07 | ) |

| $ | 0.11 |

|

| $ | 1.42 |

| |

| Net income (loss) per share attributable to common stockholders—diluted (1) | $ | (0.44 | ) | | $ | (0.07 | ) | | $ | 0.11 |

| | $ | 1.40 |

| |

| Net income per share attributable to common stockholders—basic (1) | | $ | 1.48 |

|

| $ | 0.55 |

|

| Net income per share attributable to common stockholders—diluted (1) | | $ | 1.43 |

| | $ | 0.54 |

|

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Weighted average number of common shares outstanding—basic | 257.4 |

| | 242.8 |

| | 257.3 |

| | 239.2 |

| 253.0 |

| | 257.1 |

|

| Weighted average number of common shares outstanding—diluted | 257.4 |

| | 242.8 |

| | 258.6 |

| | 241.7 |

| 299.6 |

| | 258.5 |

|

(1) | |

| (1) | Earnings per share in the table may not recalculate exactly due to rounding because it is calculated based on whole numbers, not the rounded numbers presented. |

The accompanying notes are an integral part of these consolidated financial statements.

4

CHENIERE ENERGY, INC. AND SUBSIDIARIES

CONSOLIDATED STATEMENTS OF STOCKHOLDERS’ EQUITY

(in millions)

(unaudited)

|

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Three and Six Months Ended June 30, 2019 | | | | | | | | | | | | | | | |

| | Total Stockholders’ Equity | | | |

| | Common Stock | | Treasury Stock | | Additional Paid-in Capital | | Accumulated Deficit | | Non-controlling Interest | | Total Equity |

| | Shares | | Par Value Amount | | Shares | | Amount | | | | |

| Balance at December 31, 2018 | 257.0 |

|

| $ | 1 |

|

| 12.8 |

|

| $ | (406 | ) |

| $ | 4,035 |

|

| $ | (4,156 | ) |

| $ | 2,455 |

|

| $ | 1,929 |

|

| Vesting of restricted stock units | 0.6 |

| | — |

| | — |

| | — |

| | — |

| | — |

| | — |

| | — |

|

| Share-based compensation | — |

| | — |

| | — |

| | — |

| | 28 |

| | — |

| | — |

| | 28 |

|

| Shares withheld from employees related to share-based compensation, at cost | (0.2 | ) | | — |

| | 0.2 |

| | (12 | ) | | — |

| | — |

| | — |

| | (12 | ) |

| Net income attributable to non-controlling interest | — |

| | — |

| | — |

| | — |

| | — |

| | — |

| | 196 |

| | 196 |

|

| Distributions and dividends to non-controlling interest | — |

| | — |

| | — |

| | — |

| | — |

| | — |

| | (144 | ) | | (144 | ) |

| Net income | — |

| | — |

| | — |

| | — |

| | — |

| | 141 |

| | — |

| | 141 |

|

| Balance at March 31, 2019 | 257.4 |

| | 1 |

| | 13.0 |

| | (418 | ) | | 4,063 |

| | (4,015 | ) | | 2,507 |

| | 2,138 |

|

| Vesting of restricted stock units | 0.1 |

| | — |

| | — |

| | — |

| | — |

| | — |

| | — |

| | — |

|

| Share-based compensation | — |

| | — |

| | — |

| | — |

| | 33 |

| | — |

| | — |

| | 33 |

|

| Shares withheld from employees related to share-based compensation, at cost | — |

| | — |

| | — |

| | (2 | ) | | — |

| | — |

| | — |

| | (2 | ) |

| Shares repurchased, at cost | — |

| | — |

| | — |

| | (3 | ) | | — |

| | — |

| | — |

| | (3 | ) |

| Net income attributable to non-controlling interest | — |

| | — |

| | — |

| | — |

| | — |

| | — |

| | 116 |

| | 116 |

|

| Equity portion of convertible notes, net | — |

| | — |

| | — |

| | — |

| | 1 |

| | — |

| | — |

| | 1 |

|

| Distributions and dividends to non-controlling interest | — |

| | — |

| | — |

| | — |

| | — |

| | — |

| | (146 | ) | | (146 | ) |

| Net loss | — |

| | — |

| | — |

| | — |

| | — |

| | (114 | ) | | — |

| | (114 | ) |

| Balance at June 30, 2019 | 257.5 |

| | $ | 1 |

| | 13.0 |

| | $ | (423 | ) | | $ | 4,097 |

| | $ | (4,129 | ) | | $ | 2,477 |

| | $ | 2,023 |

|

|

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Three Months Ended March 31, 2020 | | | | | | | | | | | | | | | |

| | Total Stockholders’ Equity | | | |

| | Common Stock | | Treasury Stock | | Additional Paid-in Capital | | Accumulated Deficit | | Non-controlling Interest | | Total Equity |

| | Shares | | Par Value Amount | | Shares | | Amount | | | | |

| Balance at December 31, 2019 | 253.6 |

|

| $ | 1 |

|

| 17.1 |

|

| $ | (674 | ) |

| $ | 4,167 |

|

| $ | (3,508 | ) |

| $ | 2,449 |

|

| $ | 2,435 |

|

| Vesting of restricted stock units and performance stock units | 2.1 |

| | — |

| | — |

| | — |

| | — |

| | — |

| | — |

| | — |

|

| Share-based compensation | — |

| | — |

| | — |

| | — |

| | 29 |

| | — |

| | — |

| | 29 |

|

| Issued shares withheld from employees related to share-based compensation, at cost | (0.7 | ) | | — |

| | 0.7 |

| | (39 | ) | | — |

| | — |

| | — |

| | (39 | ) |

| Shares repurchased, at cost | (2.9 | ) | | — |

| | 2.9 |

| | (155 | ) | | — |

| | — |

| | — |

| | (155 | ) |

| Net income attributable to non-controlling interest | — |

| | — |

| | — |

| | — |

| | — |

| | — |

| | 228 |

| | 228 |

|

| Distributions and dividends to non-controlling interest | — |

| | — |

| | — |

| | — |

| | — |

| | — |

| | (154 | ) | | (154 | ) |

| Net income | — |

| | — |

| | — |

| | — |

| | — |

| | 375 |

| | — |

| | 375 |

|

| Balance at March 31, 2020 | 252.1 |

| | $ | 1 |

| | 20.7 |

| | $ | (868 | ) | | $ | 4,196 |

| | $ | (3,133 | ) | | $ | 2,523 |

| | $ | 2,719 |

|

|

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Three Months Ended March 31, 2019 | | | | | | | | | | | | | | | |

| | Total Stockholders’ Equity | | | |

| | Common Stock | | Treasury Stock | | Additional Paid-in Capital | | Accumulated Deficit | | Non-controlling Interest | | Total

Equity |

| | Shares | | Par Value Amount | | Shares | | Amount | | | | |

| Balance at December 31, 2018 | 257.0 |

| | $ | 1 |

| | 12.8 |

| | $ | (406 | ) | | $ | 4,035 |

| | $ | (4,156 | ) | | $ | 2,455 |

| | $ | 1,929 |

|

| Vesting of restricted stock units | 0.6 |

| | — |

| | — |

| | — |

| | — |

| | — |

| | — |

| | — |

|

| Share-based compensation | — |

| | — |

| | — |

| | — |

| | 28 |

| | — |

| | — |

| | 28 |

|

| Issued shares withheld from employees related to share-based compensation, at cost | (0.2 | ) | | — |

| | 0.2 |

| | (12 | ) | | — |

| | — |

| | — |

| | (12 | ) |

| Net income attributable to non-controlling interest | — |

| | — |

| | — |

| | — |

| | — |

| | — |

| | 196 |

| | 196 |

|

| Distributions and dividends to non-controlling interest | — |

| | — |

| | — |

| | — |

| | — |

| | — |

| | (144 | ) | | (144 | ) |

| Net income | — |

| | — |

| | — |

| | — |

| | — |

| | 141 |

| | — |

| | 141 |

|

| Balance at March 31, 2019 | 257.4 |

| | $ | 1 |

| | 13.0 |

| | $ | (418 | ) | | $ | 4,063 |

| | $ | (4,015 | ) | | $ | 2,507 |

| | $ | 2,138 |

|

The accompanying notes are an integral part of these consolidated financial statements.

5

CHENIERE ENERGY, INC. AND SUBSIDIARIES

CONSOLIDATED STATEMENTS OF STOCKHOLDERS’ EQUITY—CONTINUED

(in millions)

(unaudited)

|

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Three and Six Months Ended June 30, 2018 | | | | | | | | | | | | | | | |

| | Total Stockholders’ Equity | | | |

| | Common Stock | | Treasury Stock | | Additional Paid-in Capital | | Accumulated Deficit | | Non-controlling Interest | | Total

Equity |

| | Shares | | Par Value Amount | | Shares | | Amount | | | | |

| Balance at December 31, 2017 | 237.6 |

| | $ | 1 |

| | 12.5 |

| | $ | (386 | ) | | $ | 3,248 |

| | $ | (4,627 | ) | | $ | 3,004 |

| | $ | 1,240 |

|

| Vesting of restricted stock units | 0.3 |

| | — |

| | — |

| | — |

| | — |

| | — |

| | — |

| | — |

|

| Share-based compensation | — |

| | — |

| | — |

| | — |

| | 16 |

| | — |

| | — |

| | 16 |

|

| Shares withheld from employees related to share-based compensation, at cost | — |

| | — |

| | 0.1 |

| | (6 | ) | | — |

| | — |

| | — |

| | (6 | ) |

| Net income attributable to non-controlling interest | — |

| | — |

| | — |

| | — |

| | — |

| | — |

| | 243 |

| | 243 |

|

| Distributions and dividends to non-controlling interest | — |

| | — |

| | — |

| | — |

| | — |

| | — |

| | (143 | ) | | (143 | ) |

| Net income | — |

| | — |

| | — |

| | — |

| | — |

| | 357 |

| | — |

| | 357 |

|

| Balance at March 31, 2018 | 237.9 |

| | 1 |

| | 12.6 |

| | (392 | ) | | 3,264 |

| | (4,270 | ) | | 3,104 |

| | 1,707 |

|

| Issuance of stock to acquire additional interest in Cheniere Holdings | 10.3 |

| | — |

| | — |

| | — |

| | 376 |

| | — |

| | (376 | ) | | — |

|

| Share-based compensation | — |

| | — |

| | — |

| | — |

| | 23 |

| | — |

| | — |

| | 23 |

|

| Shares withheld from employees related to share-based compensation, at cost | (0.1 | ) | | — |

| | — |

| | (2 | ) | | — |

| | — |

| | — |

| | (2 | ) |

| Net income attributable to non-controlling interest | — |

| | — |

| | — |

| | — |

| | — |

| | — |

| | 168 |

| | 168 |

|

| Equity portion of convertible notes, net | — |

| | — |

| | — |

| | — |

| | 1 |

| | — |

| | — |

| | 1 |

|

| Distributions and dividends to non-controlling interest | — |

| | — |

| | — |

| | — |

| | — |

| | — |

| | (145 | ) | | (145 | ) |

| Net loss | — |

| | — |

| | — |

| | — |

| | — |

| | (18 | ) | | — |

| | (18 | ) |

| Balance at June 30, 2018 | 248.1 |

| | $ | 1 |

| | 12.6 |

| | $ | (394 | ) | | $ | 3,664 |

| | $ | (4,288 | ) | | $ | 2,751 |

| | $ | 1,734 |

|

The accompanying notes are an integral part of these consolidated financial statements.

6

CHENIERE ENERGY, INC. AND SUBSIDIARIES

CONSOLIDATED STATEMENTS OF CASH FLOWS

(in millions)

(unaudited)

| | | | Six Months Ended June 30, | Three Months Ended March 31, |

| | 2019 | | 2018 | 2020 | | 2019 |

| Cash flows from operating activities | | | | | | |

| Net income | $ | 339 |

| | $ | 750 |

| $ | 603 |

| | $ | 337 |

|

| Adjustments to reconcile net income to net cash provided by operating activities: | | | | | | |

| Depreciation and amortization expense | 348 |

| | 220 |

| 233 |

| | 144 |

|

| Share-based compensation expense | 61 |

| | 58 |

| 29 |

| | 28 |

|

| Non-cash interest expense | 93 |

| | 30 |

| 17 |

| | 33 |

|

| Amortization of debt issuance costs, deferred commitment fees, premium and discount | 44 |

| | 35 |

| |

| Amortization of operating lease assets | 158 |

| | — |

| |

| Amortization of debt issuance costs, premium and discount | | 32 |

| | 18 |

|

| Non-cash operating lease costs | | 96 |

| | 79 |

|

| Loss on modification or extinguishment of debt | — |

| | 15 |

| 1 |

| | — |

|

| Total losses (gains) on derivatives, net | (147 | ) | | 4 |

| |

| Net cash provided by (used for) settlement of derivative instruments | 62 |

| | (8 | ) | |

| Total gains on derivatives, net | | (459 | ) | | (122 | ) |

| Net cash provided by settlement of derivative instruments | | 91 |

| | 16 |

|

| Impairment expense and loss on disposal of assets | 6 |

| | — |

| 5 |

| | 2 |

|

| Other | 2 |

| | (5 | ) | |

| Impairment or loss on equity method investments | | 1 |

| | — |

|

| Deferred taxes | | 129 |

| | — |

|

| Changes in operating assets and liabilities: | | | | | | |

| Accounts and other receivables | 59 |

| | 80 |

| 23 |

| | 99 |

|

| Inventory | 33 |

| | 10 |

| 74 |

| | 44 |

|

| Other current assets | (46 | ) | | (61 | ) | 13 |

| | (15 | ) |

| Accounts payable and accrued liabilities | (80 | ) | | (132 | ) | (176 | ) | | (146 | ) |

| Deferred revenue | (2 | ) | | (13 | ) | (67 | ) | | (31 | ) |

| Operating lease liabilities | (163 | ) | | — |

| (90 | ) | | (85 | ) |

| Finance lease liabilities | | — |

| | 1 |

|

| Other, net | (7 | ) | | (1 | ) | 19 |

| | 10 |

|

| Net cash provided by operating activities | 760 |

| | 982 |

| 574 |

| | 412 |

|

| | | | | | | |

| Cash flows from investing activities | | | | | | |

| Property, plant and equipment, net | (1,508 | ) | | (1,508 | ) | (556 | ) | | (625 | ) |

| Investment in equity method investment | (34 | ) | | — |

| (90 | ) | | (24 | ) |

| Other | — |

| | 16 |

| (8 | ) | | (2 | ) |

| Net cash used in investing activities | (1,542 | ) | | (1,492 | ) | (654 | ) | | (651 | ) |

| | | | | | | |

| Cash flows from financing activities | | | | | | |

| Proceeds from issuances of debt | 2,021 |

| | 1,799 |

| 596 |

| | 692 |

|

| Repayments of debt | (630 | ) | | (281 | ) | (300 | ) | | (441 | ) |

| Debt issuance and deferred financing costs | (20 | ) | | (46 | ) | |

| Debt extinguishment costs | — |

| | (8 | ) | |

| Debt issuance and other financing costs | | (33 | ) | | — |

|

| Distributions and dividends to non-controlling interest | (290 | ) | | (288 | ) | (154 | ) | | (144 | ) |

| Payments related to tax withholdings for share-based compensation | (14 | ) | | (8 | ) | (39 | ) | | (12 | ) |

| Repurchase of common stock | (3 | ) | | — |

| (155 | ) | | — |

|

| Other | 2 |

| | — |

| — |

| | (1 | ) |

| Net cash provided by financing activities | 1,066 |

| | 1,168 |

| |

| Net cash provided by (used in) financing activities | | (85 | ) | | 94 |

|

| | | | | | | |

| Net increase in cash, cash equivalents and restricted cash | 284 |

| | 658 |

| |

| Net decrease in cash, cash equivalents and restricted cash | | (165 | ) | | (145 | ) |

| Cash, cash equivalents and restricted cash—beginning of period | 3,156 |

| | 2,613 |

| 2,994 |

| | 3,156 |

|

| Cash, cash equivalents and restricted cash—end of period | $ | 3,440 |

| | $ | 3,271 |

| $ | 2,829 |

| | $ | 3,011 |

|

Balances per Consolidated Balance Sheet:

| | | | | March 31, |

| | June 30, 2019 | 2020 |

| Cash and cash equivalents | $ | 2,279 |

| $ | 2,399 |

|

| Restricted cash | 1,161 |

| 430 |

|

| Total cash, cash equivalents and restricted cash | $ | 3,440 |

| $ | 2,829 |

|

The accompanying notes are an integral part of these consolidated financial statements.

76

CHENIERE ENERGY, INC. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

(unaudited)

NOTE 1—NATURE OF OPERATIONS AND BASIS OF PRESENTATION

We ownare operating and operate twoconstructing 2 natural gas liquefaction and export facilities at Sabine Pass and Corpus Christi. The Sabine Pass LNG terminal is located in Cameron Parish, Louisiana, on the Sabine-Neches Waterway less than four miles from the Gulf Coast. Cheniere Partners, through its subsidiary SPL, is in various stages of constructing andcurrently operating six5 natural gas liquefaction facilitiesTrains and is constructing 1 additional Train for a total production capacity of approximately 30 mtpa of LNG (the “SPL Project”) at the Sabine Pass LNG terminal adjacent to the existing regasification facilities through a wholly owned subsidiary, SPL. Trains 1 through 5 are operational and Train 6 is under construction.terminal. The Sabine Pass LNG terminal has operational regasification facilities owned by Cheniere Partners’ wholly owned subsidiary, SPLNG, that include pre-existing infrastructure of 5 LNG storage tanks, 2 marine berths and vaporizers. Cheniere Partners also owns a 94-mile pipeline that interconnects the Sabine Pass LNG terminal with a number of large interstate pipelines owned by Cheniere Partners’ wholly owned(the “Creole Trail Pipeline”) through its subsidiary, CTPL. As of March 31, 2020, we owned 100% of the general partner interest and 48.6% of the limited partner interest in Cheniere Partners.

The Corpus Christi LNG terminal is located near Corpus Christi, Texas and is operated and constructed by our wholly owned subsidiary, CCL. We are currently operating 2 Trains and are constructing 1 additional Train for a total production capacity of approximately 15 mtpa of LNG. We also operate a 23-mile natural gas supply pipeline that interconnects the Corpus Christi LNG terminal with several interstate and intrastate natural gas pipelines (the “Corpus Christi Pipeline” and together with the liquefaction facilities,Trains, the “CCL Project”) through our wholly owned subsidiary, CCP. The CCL Project, is being developed in stages with the first phase being three Trains (“Phase 1”). The first stage includes Trains 1 and 2, twoonce fully constructed, will contain 3 LNG storage tanks one completeand 2 marine berth and a second partial berth and all of the CCL Project’s necessary infrastructure facilities (“Stage 1”). The second stage includes Train 3, one LNG storage tank and the completion of the second partial berth (“Stage 2”). Train 1 is operational, Train 2 is undergoing commissioning and Train 3 is under construction.berths.

Additionally, separate from the CCH Group, we are developing an expansion of the Corpus Christi LNG terminal adjacent to the CCL Project (“Corpus Christi Stage 3”) and filed an application with FERC in June 2018through our subsidiary CCL Stage III, for sevenup to 7 midscale Trains with an expected aggregate nominaltotal production capacity of approximately 9.510 mtpa of LNG. We received approval from FERC in November 2019 to site, construct and one LNG storage tank.operate the expansion project.

We remain focused on expansionoperational excellence and customer satisfaction. Increasing demand of LNG has allowed us to expand our existing sites by leveraging existing infrastructure.liquefaction infrastructure in a financially disciplined manner. We continue to considerhold significant land positions at both the Sabine Pass LNG terminal and the Corpus Christi LNG terminal which provide opportunity for further liquefaction capacity expansion. The development of these sites or other projects, including infrastructure projects in support of natural gas supply and LNG demand, which,will require, among other things, will require acceptable commercial and financing arrangements before we make a final investment decision (“FID”).

Basis of Presentation

The accompanying unaudited Consolidated Financial Statements of Cheniere have been prepared in accordance with GAAP for interim financial information and with Rule 10-01 of Regulation S-X. Accordingly, they do not include all of the information and footnotes required by GAAP for complete financial statements and should be read in conjunction with the Consolidated Financial Statements and accompanying notes included in our annual report on Form 10-K for the year ended December 31, 20182019.. In our opinion, all adjustments, consisting only of normal recurring adjustments necessary for a fair presentation, have been included.

Results of operations for the three and six months ended June 30, 2019March 31, 2020 are not necessarily indicative of the results of operations that will be realized for the year ending December 31, 2019.2020.

Recent Accounting Standards

We adopted ASU 2016-02,In March 2020, the Financial Accounting Standards Board (“FASB”) issued Accounting Standards Update (“ASU”) 2020-04, LeasesReference Rate Reform (Topic 842)848): Facilitation of the Effects of Reference Rate Reform on Financial Reporting,. This guidance primarily provides temporary optional expedients which simplify the accounting for contract modifications to existing debt agreements expected to arise from the market transition from LIBOR to alternative reference rates. The optional expedients were available to be used upon issuance of this guidance but we have not yet applied the guidance because we have not yet modified any of our existing contracts for reference rate reform. Once we apply an optional expedient to a modified contract and adopt this standard, the guidance will be applied to all subsequent amendments thereto (“ASC 842”) on January 1, 2019 usingapplicable contract modifications until December 31, 2022, at which time the optional transition approach to apply the standard at the beginning of the first quarter of 2019 withexpedients are no retrospective adjustments to prior periods. The adoption of the standard resulted in the recognition of right-of-use assets and lease liabilities for operating leases of approximately $550 million on our Consolidated Balance Sheets, with no material impact on our Consolidated Statements of Operations or Consolidated Statements of Cash Flows. We have elected the practical expedients to (1) carryforward prior conclusions related to lease identification and classification for existing leases, (2) combine lease and non-lease components of an arrangement for all classes of leased assets, (3) omit short-term leases with a term of 12 months or less from recognition on the balance sheet and (4) carryforward our existing accounting for land easements not previously accounted for as leases. See Note 11—Leases for additional information on our leases following the adoption of this standard.longer available.

CHENIERE ENERGY, INC. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—CONTINUED

(unaudited)

NOTE 2—RESTRICTED CASH

Restricted cash consists of funds that are contractually andor legally restricted as to usage or withdrawal and have been presented separately from cash and cash equivalents on our Consolidated Balance Sheets. As of June 30, 2019March 31, 2020 and December 31, 2018,2019, restricted cash consisted of the following (in millions):

| | | | | June 30, | | December 31, | | March 31, | | December 31, |

| | | 2019 | | 2018 | | 2020 | | 2019 |

| Current restricted cash | | | | | | | | |

| SPL Project | | $ | 596 |

| | $ | 756 |

| | $ | 109 |

| | $ | 181 |

|

| Cheniere Partners and cash held by guarantor subsidiaries | | — |

| | 785 |

| |

| CCL Project | | 279 |

| | 289 |

| | 94 |

| | 80 |

|

| Cash held by our subsidiaries restricted to Cheniere | | 286 |

| | 345 |

| | 227 |

| | 259 |

|

| Total current restricted cash | | $ | 1,161 |

| | $ | 2,175 |

| | $ | 430 |

| | $ | 520 |

|

Pursuant to the accounts agreements entered into with the collateral trustees for the benefit of SPL’s debt holders and CCH’s debt holders, SPL and CCH are required to deposit all cash received into reserve accounts controlled by the collateral trustees. The usage or withdrawal of such cash is restricted to the payment of liabilities related to the SPL Project and the CCL Project (collectively, the “Liquefaction Projects”) and other restricted payments.

In May 2019, Cheniere Partners entered into the $1.5 billion credit facilities (the “2019 CQP Credit Facilities”), which replaced the previous $2.8 billion credit facilities (the “2016 CQP Credit Facilities”). The cash held by Cheniere Partners and its guarantor subsidiaries was restricted in use under the terms of the 2016 CQP Credit Facilities and the related depositary agreement governing the extension of credit to Cheniere Partners, but is no longer restricted under the 2019 CQP Credit Facilities.

NOTE 3—ACCOUNTS AND OTHER RECEIVABLES

As of June 30, 2019March 31, 2020 and December 31, 2018,2019, accounts and other receivables consisted of the following (in millions):

| | | | | June 30, | | December 31, | | March 31, | | December 31, |

| | | 2019 | | 2018 | | 2020 | | 2019 |

| Trade receivables | | | | | | | | |

| SPL and CCL | | $ | 257 |

| | $ | 330 |

| | $ | 304 |

| | $ | 328 |

|

| Cheniere Marketing | | 145 |

| | 205 |

| | 88 |

| | 113 |

|

| Other accounts receivable | | 31 |

| | 50 |

| | 76 |

| | 50 |

|

| Total accounts and other receivables | | $ | 433 |

| | $ | 585 |

| | $ | 468 |

| | $ | 491 |

|

NOTE 4—INVENTORY

As of June 30, 2019March 31, 2020 and December 31, 2018,2019, inventory consisted of the following (in millions):

| | | | | June 30, | | December 31, | | March 31, | | December 31, |

| | | 2019 | | 2018 | | 2020 | | 2019 |

| Natural gas | | $ | 19 |

| | $ | 30 |

| | $ | 13 |

| | $ | 16 |

|

| LNG | | 38 |

| | 24 |

| | 35 |

| | 67 |

|

| LNG in-transit | | 104 |

| | 173 |

| | 48 |

| | 93 |

|

| Materials and other | | 129 |

| | 89 |

| | 143 |

| | 136 |

|

| Total inventory | | $ | 290 |

| | $ | 316 |

| | $ | 239 |

| | $ | 312 |

|

CHENIERE ENERGY, INC. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—CONTINUED

(unaudited)

NOTE 5—PROPERTY, PLANT AND EQUIPMENT

As of June 30, 2019March 31, 2020 and December 31, 2018,2019, property, plant and equipment, net consisted of the following (in millions):

| | | | | June 30, | | December 31, | | March 31, | | December 31, |

| | | 2019 | | 2018 | | 2020 | | 2019 |

| LNG terminal costs | | | | | | | | |

| LNG terminal and interconnecting pipeline facilities | | $ | 23,650 |

| | $ | 13,386 |

| | $ | 27,330 |

| | $ | 27,305 |

|

| LNG site and related costs | | 319 |

| | 86 |

| | 322 |

| | 322 |

|

| LNG terminal construction-in-process | | 6,529 |

| | 14,864 |

| | 4,233 |

| | 3,903 |

|

| Accumulated depreciation | | (1,625 | ) | | (1,299 | ) | | (2,272 | ) | | (2,049 | ) |

| Total LNG terminal costs, net | | 28,873 |

| | 27,037 |

| | 29,613 |

| | 29,481 |

|

| Fixed assets and other | | |

| | |

| | |

| | |

|

| Computer and office equipment | | 22 |

| | 17 |

| | 23 |

| | 23 |

|

| Furniture and fixtures | | 22 |

| | 22 |

| | 22 |

| | 22 |

|

| Computer software | | 104 |

| | 100 |

| | 112 |

| | 110 |

|

| Leasehold improvements | | 42 |

| | 41 |

| | 43 |

| | 42 |

|

| Land | | 59 |

| | 59 |

| | 59 |

| | 59 |

|

| Other | | 20 |

| | 21 |

| | 24 |

| | 21 |

|

| Accumulated depreciation | | (127 | ) | | (111 | ) | | (149 | ) | | (141 | ) |

| Total fixed assets and other, net | | 142 |

| | 149 |

| | 134 |

| | 136 |

|

| Assets under finance lease | | | | | | | | |

| Tug vessels | | 60 |

| | 60 |

| | 60 |

| | 60 |

|

| Accumulated depreciation | | (2 | ) | | (1 | ) | | (5 | ) | | (4 | ) |

| Total assets under finance lease, net | | 58 |

| | 59 |

| | 55 |

| | 56 |

|

| Property, plant and equipment, net | | $ | 29,073 |

| | $ | 27,245 |

| | $ | 29,802 |

| | $ | 29,673 |

|

Depreciation expense was $203$232 million and $111$143 million during the three months ended June 30,March 31, 2020 and 2019, and 2018, respectively, and $346 million and $219 million during the six months ended June 30, 2019 and 2018, respectively.

We realizerealized offsets to LNG terminal costs for salesof $202 million during the three months ended March 31, 2019 that were related to the sale of commissioning cargoes thatbecause these amounts were earned or loaded prior to the start of commercial operations of the respective TrainTrains of the Liquefaction Projects, during the testing phase for its construction. We realized offsets to LNG terminal costs of $202 million during the six months ended June 30, 2019 for sales of commissioning cargoes from the Liquefaction Projects. We did not0t realize any offsets to LNG terminal costs during the three months ended June 30, 2019 and the three and six months ended June 30, 2018.March 31, 2020.

NOTE 6—DERIVATIVE INSTRUMENTS

We have entered into the following derivative instruments that are reported at fair value:

interest rate swaps (“CCH Interest Rate Derivatives”) to hedge the exposure to volatility in a portion of the floating-rate interest payments underon CCH’s amended and restated credit facilities (“CCH Interest Rate Derivatives”facility (the “CCH Credit Facility”) and to hedge against changes in interest rates that could impact anticipated future issuance of debt by CCH, which is anticipated by the end of 2020 (“CCH Interest Rate Forward Start Derivatives” and, collectively with the CCH Interest Rate Derivatives, the “Interest Rate Derivatives”);

commodity derivatives consisting of natural gas supply contracts for the commissioning and operation of the SPL Project, CCL ProjectLiquefaction Projects and potential future development of Corpus Christi Stage 3 (“Physical Liquefaction Supply Derivatives”) and associated economic hedges (collectively, the “Liquefaction Supply Derivatives”);

financial derivatives to hedge the exposure to the commodity markets in which we have contractual arrangements to purchase or sell physical LNG (“LNG Trading Derivatives”); and

foreign currency exchange (“FX”) contracts to hedge exposure to currency risk associated with both LNG Trading Derivatives and operations in countries outside of the United States (“FX Derivatives”).

We recognize our derivative instruments as either assets or liabilities and measure those instruments at fair value. None of our derivative instruments are designated as cash flow or fair value hedging instruments, and changes in fair value are recorded within our Consolidated Statements of Operations to the extent not utilized for the commissioning process.

CHENIERE ENERGY, INC. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—CONTINUED

(unaudited)

The following table shows the fair value of our derivative instruments that are required to be measured at fair value on a recurring basis as of June 30, 2019March 31, 2020 and December 31, 2018,2019, which are classified as derivative assets, non-current derivative assets, derivative liabilities or non-current derivative liabilities in our Consolidated Balance Sheets (in millions):

| | | | Fair Value Measurements as of | Fair Value Measurements as of |

| | June 30, 2019 | | December 31, 2018 | March 31, 2020 | | December 31, 2019 |

| | Quoted Prices in Active Markets

(Level 1) | | Significant Other Observable Inputs

(Level 2) | | Significant Unobservable Inputs

(Level 3) | | Total | | Quoted Prices in Active Markets

(Level 1) | | Significant Other Observable Inputs

(Level 2) | | Significant Unobservable Inputs

(Level 3) | | Total | Quoted Prices in Active Markets

(Level 1) | | Significant Other Observable Inputs

(Level 2) | | Significant Unobservable Inputs

(Level 3) | | Total | | Quoted Prices in Active Markets

(Level 1) | | Significant Other Observable Inputs

(Level 2) | | Significant Unobservable Inputs

(Level 3) | | Total |

| CCH Interest Rate Derivatives asset (liability) | $ | — |

| | $ | (88 | ) | | $ | — |

| | $ | (88 | ) | | $ | — |

| | $ | 18 |

| | $ | — |

| | $ | 18 |

| |

| CCH Interest Rate Derivatives liability | | $ | — |

| | $ | (197 | ) | | $ | — |

| | $ | (197 | ) | | $ | — |

| | $ | (81 | ) | | $ | — |

| | $ | (81 | ) |

| CCH Interest Rate Forward Start Derivatives liability | — |

| | (7 | ) | | — |

| | (7 | ) | | — |

| | — |

| | — |

| | — |

| — |

| | (92 | ) | | — |

| | (92 | ) | | — |

| | (8 | ) | | — |

| | (8 | ) |

| Liquefaction Supply Derivatives asset (liability) | — |

| | 1 |

| | 89 |

| | 90 |

| | 6 |

| | (19 | ) | | (29 | ) | | (42 | ) | |

| Liquefaction Supply Derivatives asset | | 1 |

| | 3 |

| | 674 |

| | 678 |

| | 5 |

| | 6 |

| | 138 |

| | 149 |

|

| LNG Trading Derivatives asset (liability) | (4 | ) | | 51 |

| | — |

| | 47 |

| | 1 |

| | (25 | ) | | — |

| | (24 | ) | (3 | ) | | 188 |

| | — |

| | 185 |

| | — |

| | 165 |

| | — |

| | 165 |

|

| FX Derivatives asset | — |

| | 10 |

| | — |

| | 10 |

| | — |

| | 15 |

| | — |

| | 15 |

| — |

| | 23 |

| | — |

| | 23 |

| | — |

| | 4 |

| | — |

| | 4 |

|

We value our CCH Interest Rate Derivatives and CCH Interest Rate Forward Start Derivatives using an income-based approach utilizing observable inputs to the valuation model including interest rate curves, risk adjusted discount rates, credit spreads and other relevant data. We value our LNG Trading Derivatives and our Liquefaction Supply Derivatives using a market or option-based approach incorporating present value techniques, as needed, using observable commodity price curves, when available, and other relevant data. We value our FX Derivatives with a market approach using observable FX rates and other relevant data.

The fair value of our Physical Liquefaction Supply Derivatives is predominantly driven by observable and unobservable market commodity prices and, as applicable to our natural gas supply contracts, our assessment of the associated conditions precedent,events deriving fair value, including evaluating whether the respective market is available as pipeline infrastructure is developed. The fair value of our Physical Liquefaction Supply Derivatives incorporates risk premiums related to the satisfaction of conditions precedent, such as completion and placement into service of relevant pipeline infrastructure to accommodate marketable physical gas flow. As of June 30, 2019March 31, 2020 and December 31, 2018,2019, some of our Physical Liquefaction Supply Derivatives existed within markets for which the pipeline infrastructure was under development to accommodate marketable physical gas flow.

We include a portion of our Physical Liquefaction Supply Derivatives as Level 3 within the valuation hierarchy as the fair value is developed through the use of internal models which incorporate significant unobservable inputs. In instances where observable data is unavailable, consideration is given to the assumptions that market participants would use in valuing the asset or liability. This includes assumptions about market risks, such as future prices of energy units for unobservable periods, liquidity, volatility and contract duration. In determining and recording fair value, we do not use third party sources that derive price based on proprietary models or market surveys.

The Level 3 fair value measurements of natural gas positions within our Physical Liquefaction Supply Derivatives could be materially impacted by a significant change in certain natural gas and international LNG prices. The following table includes quantitative information for the unobservable inputs for our Level 3 Physical Liquefaction Supply Derivatives as of June 30, 2019:March 31, 2020:

|

| | | | | | | | |

| | | Net Fair Value Asset (Liability) (in millions) | | Valuation Approach | | Significant Unobservable Input | | Range of Significant Unobservable Inputs Range/ Weighted Average (1) |

| Physical Liquefaction Supply Derivatives | | $89674 | | Market approach incorporating present value techniques | | Henry Hub Basis Spreadbasis spread | | $(0.700)(0.619) - $0.056$0.054 / (0.027) |

| | | | | Option pricing model | | International LNG pricing spread, relative to Henry Hub (1)(2) | | 128%48% - 176%154% / 117% |

(1) Unobservable inputs were weighted by the relative fair value of the instruments.

(2) Spread contemplates U.S. dollar-denominated pricing.

CHENIERE ENERGY, INC. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—CONTINUED

(unaudited)

Increases or decreases in basis or pricing spreads, in isolation, would decrease or increase, respectively, the fair value of our Physical Liquefaction Supply Derivatives.

The following table shows the changes in the fair value of our Level 3 Physical Liquefaction Supply Derivatives during the three and six months ended June 30,March 31, 2020 and 2019 and 2018 (in millions):

| | | | | Three Months Ended June 30, | | Six Months Ended June 30, | | Three Months Ended March 31, |

| | | 2019 | | 2018 | | 2019 | | 2018 | | 2020 | | 2019 |

| Balance, beginning of period | | $ | 31 |

| | $ | 10 |

| | $ | (29 | ) | | $ | 43 |

| | $ | 138 |

| | $ | (29 | ) |

| Realized and mark-to-market gains (losses): | | | | | | | | | |

| Realized and mark-to-market gains: | | | | | |

| Included in cost of sales | | 7 |

| | (1 | ) | | 23 |

| | (12 | ) | | 534 |

| | 12 |

|

| Purchases and settlements: | | | | | | | | | | | | |

| Purchases | | 50 |

| | 6 |

| | 50 |

| | 6 |

| | 1 |

| | 1 |

|

| Settlements | | 1 |

| | (4 | ) | | 45 |

| | (25 | ) | | — |

| | 47 |

|

| Transfers out of Level 3 (1) | | — |

| | 1 |

| | — |

| | — |

| | 1 |

| | — |

|

| Balance, end of period | | $ | 89 |

| | $ | 12 |

| | $ | 89 |

| | $ | 12 |

| | $ | 674 |

| | $ | 31 |

|

| Change in unrealized gains (losses) relating to instruments still held at end of period | | $ | 7 |

| | $ | (1 | ) | | $ | 23 |

| | $ | (12 | ) | |

| Change in unrealized gains relating to instruments still held at end of period | | | $ | 534 |

| | $ | 12 |

|

(1) Transferred to Level 2 as a result of observable market for the underlying natural gas purchase agreements.

Derivative assets and liabilities arising from our derivative contracts with the same counterparty are reported on a net basis, as all counterparty derivative contracts provide for the unconditional right of set-off in the event of default. The use of derivative instruments exposes us to counterparty credit risk, or the risk that a counterparty will be unable to meet its commitments in instances when our derivative instruments are in an asset position. Additionally, counterparties are at risk that we will be unable to meet our commitments in instances where our derivative instruments are in a liability position. We incorporate both our own nonperformance risk and the respective counterparty’s nonperformance risk in fair value measurements. In adjusting the fair value of our derivative contracts for the effect of nonperformance risk, we have considered the impact of netting and any applicable credit enhancements, such as collateral postings, set-off rights and guarantees.

Interest Rate Derivatives

During the six months ended June 30, 2019, there were no changes to the terms of the CCH Interest Rate Derivatives entered into by CCH to protect against volatility of future cash flows and hedge a portion of the variable interest payments on its credit facility (the “CCH Credit Facility”).

In June 2019, we entered into the CCH Interest Rate Forward Start Derivatives to hedge against changes in interest rates that could impact anticipated future issuance of debt by CCH, which is anticipated by the end of 2020.

Cheniere Partners previously had interest rate swaps (“CQP Interest Rate Derivatives” and, collectively with the CCH Interest Rate Derivatives and the CCH Interest Rate Forward Start Derivatives, the “Interest Rate Derivatives”) to hedge a portion of the variable interest payments on its credit facilities, which were terminated in October 2018.

As of June 30, 2019,March 31, 2020, we had the following Interest Rate Derivatives outstanding:

|

| | | | | | | | | | | | |

| | | Initial Notional AmountAmounts | | Maximum Notional Amount | | | | | | |

| | March 31, 2020 | | December 31, 2019 | | Effective Date | | Maturity Date | | Weighted Average Fixed Interest Rate Paid | | Variable Interest Rate Received |

| CCH Interest Rate Derivatives | | $29 million4.7 billion | | $4.74.5 billion | | May 20, 2015 | | May 31, 2022 | | 2.30% | | One-month LIBOR |

| CCH Interest Rate Forward Start Derivatives | | $1.0 billion750 million | | $1.0 billion750 million | | JuneSeptember 30, 2020

| | September 30,December 31, 2030

| | 2.11%2.06% | | Three-month LIBOR |

CHENIERE ENERGY, INC. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—CONTINUED

(unaudited)

The following table shows the fair value and location of the Interest Rate Derivatives on our Consolidated Balance Sheets (in millions):

| | | | June 30, 2019 | | December 31, 2018 | March 31, 2020 | | December 31, 2019 |

| | CCH Interest Rate Derivatives | | CCH Interest Rate Forward Start Derivatives | | Total | | CCH Interest Rate Derivatives | | CCH Interest Rate Forward Start Derivatives | | Total | CCH Interest Rate Derivatives | | CCH Interest Rate Forward Start Derivatives | | Total | | CCH Interest Rate Derivatives | | CCH Interest Rate Forward Start Derivatives | | Total |

| Consolidated Balance Sheet Location | | | | | | | | | | | | | | | | | | | | | | |

| Derivative assets | $ | — |

| | $ | — |

| | $ | — |

| | $ | 10 |

| | $ | — |

| | $ | 10 |

| |

| Non-current derivative assets | — |

| | — |

| | — |

| | 8 |

| | — |

| | 8 |

| |

| Total derivative assets | — |

|

| — |

|

| — |

|

| 18 |

|

| — |

|

| 18 |

| |

| | | | | |

|

| | | | | |

|

| |

| Derivative liabilities | (21 | ) | | — |

| | (21 | ) | | — |

| | — |

| | — |

| $ | (92 | ) | | $ | (92 | ) | | $ | (184 | ) | | $ | (32 | ) | | $ | (8 | ) | | $ | (40 | ) |

| Non-current derivative liabilities | (67 | ) | | (7 | ) | | (74 | ) | | — |

| | — |

| | — |

| (105 | ) | | — |

| | (105 | ) | | (49 | ) | | — |

| | (49 | ) |

| Total derivative liabilities | (88 | ) |

| (7 | ) |

| (95 | ) |

| — |

|

| — |

|

| — |

| $ | (197 | ) |

| $ | (92 | ) |

| $ | (289 | ) |

| $ | (81 | ) |

| $ | (8 | ) |

| $ | (89 | ) |

| | | | | |

|

| | | | | |

|

| |

| Derivative asset (liability), net | $ | (88 | ) |

| $ | (7 | ) |

| $ | (95 | ) |

| $ | 18 |

|

| $ | — |

|

| $ | 18 |

| |

CHENIERE ENERGY, INC. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—CONTINUED

(unaudited)

The following table shows the changes in the fair value and settlements of our Interest Rate Derivatives recorded in interest rate derivative gain (loss),loss, net on our Consolidated Statements of Operations during the three and six months ended June 30,March 31, 2020 and 2019 and 2018 (in millions):

|

| | | | | | | | | | | | | | | | |

| | | Three Months Ended June 30, | | Six Months Ended June 30, |

| | | 2019 | | 2018 | | 2019 | | 2018 |

| CCH Interest Rate Derivatives gain (loss) | | $ | (67 | ) | | $ | 29 |

| | $ | (102 | ) | | $ | 98 |

|

| CCH Interest Rate Forward Start Derivatives loss | | (7 | ) | | — |

| | (7 | ) | | — |

|

| CQP Interest Rate Derivatives gain | | — |

| | 3 |

| | — |

| | 11 |

|

|

| | | | | | | | |

| | | Three Months Ended March 31, |

| | | 2020 | | 2019 |

| CCH Interest Rate Derivatives loss | | $ | (123 | ) | | $ | (35 | ) |

| CCH Interest Rate Forward Start Derivatives loss | | (85 | ) | | — |

|

Commodity Derivatives

SPL, CCL and CCL Stage III have entered into physical natural gas supply contracts and associated economic hedges to purchase natural gas for the commissioning and operation of the SPL Project, the CCL ProjectLiquefaction Projects and potential future development of Corpus Christi Stage 3, respectively, which are primarily indexed to the natural gas market and international LNG indices. The remaining terms of the index-based physical natural gas supply contracts range up to approximately 15 years, some of which commence upon the satisfaction of certain conditions precedent.events or states of affairs.

We have entered into, and may from time to time enter into, financial LNG Trading Derivatives in the form of swaps, forwards, options or futures to economically hedge exposure to the commodity markets in which we have contractual arrangements to purchase or sell physical LNG. We have entered into LNG Trading Derivatives to secure a fixed price position to minimize future cash flow variability associated with LNG purchase and sale transactions.

CHENIERE ENERGY, INC. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—CONTINUED

(unaudited)

The following table shows the fair value and location of our Liquefaction Supply Derivatives and LNG Trading Derivatives (collectively, “Commodity Derivatives”) on our Consolidated Balance Sheets (in millions, except notional amount):

| | | | June 30, 2019 | | December 31, 2018 | March 31, 2020 | | December 31, 2019 |

| | Liquefaction Supply Derivatives (1) | | LNG Trading Derivatives (2) | | Total | | Liquefaction Supply Derivatives (1) | | LNG Trading Derivatives (2) | | Total | Liquefaction Supply Derivatives (1) | | LNG Trading Derivatives (2) | | Total | | Liquefaction Supply Derivatives (1) | | LNG Trading Derivatives (2) | | Total |

| Consolidated Balance Sheet Location | | | | | | | | | | | | | | | | | | | | | | |

| Derivative assets | $ | 24 |

| | $ | 92 |

| | $ | 116 |

| | $ | 13 |

| | $ | 24 |

| | $ | 37 |

| $ | 113 |

| | $ | 190 |

| | $ | 303 |

| | $ | 93 |

| | $ | 225 |

| | $ | 318 |

|

| Non-current derivative assets | 94 |

| | 9 |

| | 103 |

| | 46 |

| | — |

| | 46 |

| 665 |

| | 35 |

| | 700 |

| | 174 |

| | — |

| | 174 |

|

| Total derivative assets | 118 |

| | 101 |

| | 219 |

| | 59 |

| | 24 |

| | 83 |

| 778 |

| | 225 |

| | 1,003 |

| | 267 |

| | 225 |

| | 492 |

|

| | | | | | | | | | | | | | | | | | | | | | | |

| Derivative liabilities | (13 | ) | | (50 | ) | | (63 | ) | | (79 | ) | | (48 | ) | | (127 | ) | (19 | ) | | (40 | ) | | (59 | ) | | (16 | ) | | (60 | ) | | (76 | ) |

| Non-current derivative liabilities | (15 | ) | | (4 | ) | | (19 | ) | | (22 | ) | | — |

| | (22 | ) | (81 | ) | | — |

| | (81 | ) | | (102 | ) | | — |

| | (102 | ) |

| Total derivative liabilities | (28 | ) | | (54 | ) | | (82 | ) | | (101 | ) | | (48 | ) | | (149 | ) | (100 | ) | | (40 | ) | | (140 | ) | | (118 | ) | | (60 | ) | | (178 | ) |

| | | | | | | | | | | | | | | | | | | | | | | |

| Derivative asset (liability), net | $ | 90 |

| | $ | 47 |

| | $ | 137 |

| | $ | (42 | ) | | $ | (24 | ) | | $ | (66 | ) | |

| Derivative asset, net | | $ | 678 |

| | $ | 185 |

| | $ | 863 |

| | $ | 149 |

| | $ | 165 |

| | $ | 314 |

|

| | | | | | | | | | | | | | | | | | | | | | | |

| Notional amount, net (in TBtu) (3) | 6,781 |

| | 50 |

| | | | 5,832 |

| | 12 |

| | | 10,988 |

| | 22 |

| | | | 9,177 |

| | 4 |

| | |

| |

| (1) | Does not include collateral callsposted with counterparties by us of $6$11 million and $5$7 million for such contracts, which are included in other current assets in our Consolidated Balance Sheets as of June 30, 2019March 31, 2020 and December 31, 2018,2019, respectively. Includes derivative assets of $2 million and $2 million and non-current assets of $1$4 million and $3 million as of June 30, 2019March 31, 2020 and December 31, 2018,2019, respectively, and non-current assets of $2 million as of both March 31, 2020 and December 31, 2019 for a natural gas supply contractcontracts that SPL and CCL hashave with a related party.parties. |

| |

| (2) | Does not include collateral posted with counterparties by us of $15$11 million and $9$5 million deposited for such contracts, which are included in other current assets in our Consolidated Balance Sheets as of June 30, 2019March 31, 2020 and December 31, 2018,2019, respectively. |

| |

| (3) | SPL had secured up to approximately 3,437Includes 198 TBtu and 3,464120 TBtu as of June 30, 2019March 31, 2020 and December 31, 2018, respectively. CCL had secured up to approximately 2,787 TBtu and 2,801 TBtu of natural gas feedstock through2019, respectively, for natural gas supply contracts as of June 30, 2019that SPL and December 31, 2018, respectively, of which 57 TBtu and 55 TBtu, respectively, were for a natural gas supply contract CCL hashave with a related party. Corpus Christi Stage 3 had secured up to approximately 754 TBtu of natural gas feedstock through natural gas supply contracts as of June 30, 2019.parties. |

CHENIERE ENERGY, INC. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—CONTINUED

(unaudited)

The following table shows the changes in the fair value, settlements and location of our Commodity Derivatives recorded on our Consolidated Statements of Operations during the three and six months ended June 30,March 31, 2020 and 2019 and 2018 (in millions):

| | | | Consolidated Statements of Operations Location (1) | | Three Months Ended June 30, | | Six Months Ended June 30, | Consolidated Statements of Operations Location (1) | | Three Months Ended March 31, |

| | | 2019 | | 2018 | | 2019 | | 2018 | | 2020 | | 2019 |

| LNG Trading Derivatives gain (loss) | LNG revenues | | $ | 94 |

| | $ | (76 | ) | | $ | 158 |

| | $ | (70 | ) | |

| LNG Trading Derivatives gain | | LNG revenues | | $ | 140 |

| | $ | 64 |

|

| LNG Trading Derivatives loss | Cost of sales | | (51 | ) | | — |

| | (51 | ) | | — |

| Cost of sales | | (34 | ) | | — |

|

| Liquefaction Supply Derivatives gain (loss) (2) | LNG revenues | | (1 | ) | | — |

| | 1 |

| | — |

| LNG revenues | | (1 | ) | | 2 |

|

| Liquefaction Supply Derivatives gain (loss) (2)(3) | Cost of sales | | 57 |

| | (3 | ) | | 139 |

| | (53 | ) | |

| Liquefaction Supply Derivatives gain (2)(3) | | Cost of sales | | 537 |

| | 82 |

|

| |

| (1) | Fair value fluctuations associated with commodity derivative activities are classified and presented consistently with the item economically hedged and the nature and intent of the derivative instrument. |

| |

| (2) | Does not include the realized value associated with derivative instruments that settle through physical delivery. |

| |

| (3) | Includes $24CCL recorded $23 million and $36$10 million that CCL recorded in cost of sales under a natural gas supply contract with a related party during the three and six months ended June 30,March 31, 2020 and 2019, respectively, including $1 million of Liquefaction Supply Derivatives gain and $2 million of Liquefaction Supply Derivatives loss, respectively. Of this amount, $4As of March 31, 2020 and December 31, 2019, $7 million wasand $3 million, respectively, were included in accrued liabilities as of June 30, 2019. CCL did not have any transactions during the three and six months ended June 30, 2018 underrelated to this contract. |

CHENIERE ENERGY, INC. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—CONTINUED

(unaudited)

FX Derivatives

Cheniere Marketing has entered into FX Derivatives to protect against the volatility in future cash flows attributable to changes in international currency exchange rates. The FX Derivatives economically hedge the foreign currency exposure arising from cash flows expended for both physical and financial LNG transactions.

The following table shows the fair value and location of our FX Derivatives on our Consolidated Balance Sheets (in millions):

| | | | | Fair Value Measurements as of | | Fair Value Measurements as of |

| | Consolidated Balance Sheet Location | | June 30, 2019 | | December 31, 2018 | Consolidated Balance Sheet Location | | March 31, 2020 | | December 31, 2019 |

| FX Derivatives | Derivative assets | | $ | 11 |

| | $ | 16 |

| Derivative assets | | $ | 19 |

| | $ | 5 |

|

| FX Derivatives | Derivative liabilities | | — |

| | (1 | ) | Non-current derivative assets | | 5 |

| | — |

|

| FX Derivatives | Non-current derivative liabilities | | (1 | ) | | — |

| Derivative liabilities | | (1 | ) | | (1 | ) |

The total notional amount of our FX Derivatives was $942$496 million and $379$827 million as of June 30, 2019March 31, 2020 and December 31, 2018,2019, respectively.

The following table shows the changes in the fair value, settlements and location of our FX Derivatives recorded on our Consolidated Statements of Operations during the three and six months ended June 30,March 31, 2020 and 2019 and 2018 (in millions):

|

| | | | | | | | | | | | | | | | | |

| | | | Three Months Ended June 30, | | Six Months Ended June 30, |

| | Consolidated Statements of Operations Location | | 2019 | | 2018 | | 2019 | | 2018 |

| FX Derivatives gain | LNG revenues | | $ | — |

| | $ | 12 |

| | $ | 9 |

| | $ | 10 |

|

|

| | | | | | | | | |

| | | | Three Months Ended March 31, |

| | Consolidated Statements of Operations Location | | 2020 | | 2019 |

| FX Derivatives gain | LNG revenues | | $ | 25 |

| | $ | 9 |

|

CHENIERE ENERGY, INC. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—CONTINUED

(unaudited)

Consolidated Balance Sheet Presentation

Our derivative instruments are presented on a net basis on our Consolidated Balance Sheets as described above. The following table shows the fair value of our derivatives outstanding on a gross and net basis (in millions):

| | | | | Gross Amounts Recognized | | Gross Amounts Offset in the Consolidated Balance Sheets | | Net Amounts Presented in the Consolidated Balance Sheets | | Gross Amounts Recognized | | Gross Amounts Offset in the Consolidated Balance Sheets | | Net Amounts Presented in the Consolidated Balance Sheets |

| Offsetting Derivative Assets (Liabilities) | | |

| As of June 30, 2019 | | | | | | | |

| As of March 31, 2020 | | | | | | | |

| CCH Interest Rate Derivatives | | $ | (88 | ) | | $ | — |

| | $ | (88 | ) | | $ | (197 | ) | | $ | — |

| | $ | (197 | ) |

| CCH Interest Rate Forward Start Derivatives | | (7 | ) | | — |

| | (7 | ) | | (92 | ) | | — |

| | (92 | ) |

| Liquefaction Supply Derivatives | | 121 |

| | (3 | ) | | 118 |

| | 796 |

| | (18 | ) | | 778 |

|

| Liquefaction Supply Derivatives | | (35 | ) | | 7 |

| | (28 | ) | | (104 | ) | | 4 |

| | (100 | ) |

| LNG Trading Derivatives | | 109 |

| | (8 | ) | | 101 |

| | 225 |

| | — |

| | 225 |

|

| LNG Trading Derivatives | | (62 | ) | | 8 |

| | (54 | ) | | (47 | ) | | 7 |

| | (40 | ) |

| FX Derivatives | | 21 |

| | (10 | ) | | 11 |

| | 27 |

| | (3 | ) | | 24 |

|

| FX Derivatives | | (11 | ) | | 10 |

| | (1 | ) | | (1 | ) | | — |

| | (1 | ) |

| As of December 31, 2018 | | | | | |

|

| |

| As of December 31, 2019 | | | | | | |

|

|

| CCH Interest Rate Derivatives | | $ | 19 |

| | $ | (1 | ) | | $ | 18 |

| | $ | (81 | ) | | $ | — |

| | $ | (81 | ) |

| CCH Interest Rate Forward Start Derivatives | | | (8 | ) | | — |

| | (8 | ) |

| Liquefaction Supply Derivatives | | 95 |

| | (36 | ) | | 59 |

| | 281 |

| | (14 | ) | | 267 |

|

| Liquefaction Supply Derivatives | | (121 | ) | | 20 |

| | (101 | ) | | (126 | ) | | 8 |

| | (118 | ) |

| LNG Trading Derivatives | | 112 |

| | (88 | ) | | 24 |

| | 229 |

| | (4 | ) | | 225 |

|

| LNG Trading Derivatives | | (92 | ) | | 44 |

| | (48 | ) | | (60 | ) | | — |

| | (60 | ) |

| FX Derivatives | | 30 |

| | (14 | ) | | 16 |

| | 9 |

| | (4 | ) | | 5 |

|

| FX Derivatives | | (2 | ) | | 1 |

| | (1 | ) | | (6 | ) | | 5 |

| | (1 | ) |

CHENIERE ENERGY, INC. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—CONTINUED

(unaudited)

NOTE 7—OTHER NON-CURRENT ASSETS

As of June 30, 2019March 31, 2020 and December 31, 2018,2019, other non-current assets, net consisted of the following (in millions):

| | | | | June 30, | | December 31, | | March 31, | | December 31, |

| | | 2019 | | 2018 | | 2020 | | 2019 |

| Advances made to municipalities for water system enhancements | | $ | 89 |

| | $ | 90 |

| | $ | 86 |

| | $ | 87 |

|

| Advances and other asset conveyances to third parties to support LNG terminals | | 55 |

| | 54 |

| | 60 |

| | 55 |

|

| Advances made under EPC and non-EPC contracts | | | 7 |

| | 29 |

|

| Equity method investments | | | 197 |

| | 108 |

|

| Debt issuance costs and debt discount, net | | | 48 |

| | 45 |

|

| Tax-related payments and receivables | | 21 |

| | 21 |

| | 20 |

| | 20 |

|

| Equity method investments | | 124 |

| | 94 |

| |

| Advances made under EPC and non-EPC contracts | | 11 |

| | 14 |

| |

| Other | | 37 |

| | 32 |

| | 58 |

| | 44 |

|

| Total other non-current assets, net | | $ | 337 |

| | $ | 305 |

| | $ | 476 |

| | $ | 388 |

|

Equity Method Investments

Our equity method investments consist of interests in privately-held companies. In 2017, we acquired an equity interest in Midship Holdings, LLC (“Midship Holdings”), which manages the business and affairs of Midship Pipeline Company, LLC (“Midship Pipeline”). Midship Pipeline is currently constructing an approximately 200-mile natural gas pipeline project (the “Midship Project”) that connects production in the Anadarko Basin to Gulf Coast markets. Construction of the Midship Project commenced in the first quarter of 2019.

Subsequent to Midship Project obtaining its financing in the form of credit facilities, in conjunction with existing equity, Midship Holdings is able to finance its current activities without additional subordinated financial support. As a result of the total equity investment at risk being sufficient to finance its activities, Midship Holdings is no longer a variable interest entity. We continue to report Midship Holdings, which we account for as an equity method

investment dueinvestment. See Note 8—Other Non-Current Assets of our Notes to Consolidated Financial Statements in our ability to exercise significant influence overannual report on Form 10-K for the operating and financial policies of Midship Holdings through our non-controlling voting rights on its board of managers. year ended December 31, 2019 for further information.

Our investment in Midship Holdings, net of impairment losses, was $117$195 million and $85$105 million at June 30, 2019March 31, 2020 and December 31, 2018,2019, respectively.