UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-Q

xQUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the Quarterly Period Ended March 31,September 30, 2019

OR

¨ oTRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the Transition Period from to

COMMISSION FILE NUMBER: 000-16509

|

|

| CITIZENS, INC. |

| (Exact name of registrant as specified in its charter) |

|

| |

| Colorado | 84-0755371 |

| (State or other jurisdiction of | (I.R.S. Employer |

| incorporation or organization) | (I.R.S. Employer Identification No.) |

| | |

2900 Esperanza Crossing,14231 Tandem Blvd, 2nd Floor | |

| Austin, Texas | 7875878728 |

| (Address of principal executive offices) | (Zip Code) |

| | |

| 2900 Esperanza Crossing, 2nd Floor |

| (512) 837-7100 | N/AAustin, Texas 78758 |

| (Registrant's telephone number, including area code:) | (Former name, former address and former fiscal year, if changed since last report:) |

|

| | |

| Securities registered pursuant to Section 12(b) of the Act |

|

| Class A Common Stock | CIA | NYSE |

| (Title of Each Class) | (Trading Symbol(s)) | (Name of Each Exchange on Which Registered) |

|

| | | | | |

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. xYes o No |

| |

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). xYes o No |

| |

| Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See the definitions of "large accelerated filer," "accelerated filer," "smaller reporting company" and "emerging growth company" in Rule 12b-2 of the Exchange Act: |

| | Large accelerated filer ¨o | Accelerated filer x | Non-accelerated filer ¨o | Smaller reporting company ¨o | Emerging growth company ¨o |

| | | | | | |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period forcomplying with anyneworrevisedfinancialaccountingstandardsprovidedpursuanttoSection13(a)oftheExchangeAct. ¨o |

| |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). ¨o Yes x No |

|

| | |

Securities registered pursuant to Section 12(b) of the Act |

|

Class A Common Stock | CIA | New York Stock Exchange |

(Title of Each Class) | (Trading Symbol(s)) | (Name of Each Exchange on Which Registered) |

As of April 29,November 1, 2019,, the Registrant had 52,364,993 shares of Class A common stock, no par value, outstanding and 1,001,714 shares of Class B common stock, no par value, outstanding.

THIS PAGE INTENTIONALLY LEFT BLANK

TABLE OF CONTENTS

|

| | | |

| | | | Page Number |

| Part I. FINANCIAL INFORMATION | Financial Information |

| | | |

| | Item 1. | | |

| | | | |

| | | | |

| | | | |

| | | | |

| | | | |

| | | | |

| | | | |

| | | | |

| | | |

| | | |

| | | | |

| | | | |

| | | | |

| | Item 2. | | |

| | | | |

| | Item 3. | | |

| | | | |

| | Item 4. | | |

| | | | |

| Part II. | Other Information OTHER INFORMATION | |

| | | | |

| | Item 1. | | |

| | | | |

| | Item 1A. | | |

| | | | |

| | Item 2. | | |

| | | | |

| | Item 3. | | |

| | | | |

| | Item 4. | | |

| | | | |

| | Item 5. | | |

| | | | |

| | Item 6. | | |

September 30, 2019 Form | 10-Q 1

PART I. FINANCIAL INFORMATION

Item 11.. FINANCIAL STATEMENTS

CITIZENS, INC. AND CONSOLIDATED SUBSIDIARIES Consolidated Statements of Financial Position (In thousands) |

| | | | | | |

| | | | |

| | | | |

| | March 31, 2019 | | December 31, 2018 |

| Assets | (Unaudited) | | |

| Investments: | | | |

| Fixed maturities available-for-sale, at fair value (cost: $1,259,353 and $1,223,747 in 2019 and 2018, respectively) | $ | 1,295,514 |

| | 1,231,039 |

|

| Equity securities, at fair value | 15,672 |

| | 15,068 |

|

| Mortgage loans on real estate | 185 |

| | 186 |

|

| Policy loans | 81,474 |

| | 80,825 |

|

| Real estate held for investment (less $1,309 and $1,284 accumulated depreciation in 2019 and 2018, respectively) | 5,693 |

| | 5,718 |

|

| Real estate held for sale (less $4,411 accumulated depreciation in 2018) | — |

| | 1,483 |

|

| Other long-term investments | 22 |

| | 22 |

|

| Short-term investments | 7,914 |

| | 7,865 |

|

| Total investments | 1,406,474 |

| | 1,342,206 |

|

| Cash and cash equivalents | 34,093 |

| | 45,492 |

|

| Accrued investment income | 18,155 |

| | 18,467 |

|

| Reinsurance recoverable | 3,587 |

| | 3,664 |

|

| Deferred policy acquisition costs | 154,076 |

| | 155,747 |

|

| Cost of customer relationships acquired | 14,697 |

| | 15,225 |

|

| Goodwill | 12,624 |

| | 12,624 |

|

| Other intangible assets | 955 |

| | 956 |

|

| Property and equipment, net | 7,046 |

| | 5,943 |

|

| Due premiums, net (less $1,663 and $1,990 allowance for doubtful accounts in 2019 and 2018, respectively) | 11,083 |

| | 13,325 |

|

| Prepaid expenses | 823 |

| | 284 |

|

| Other assets | 1,943 |

| | 1,628 |

|

| Total assets | $ | 1,665,556 |

| | 1,615,561 |

|

(Continued)CITIZENS, INC. AND CONSOLIDATED SUBSIDIARIES Consolidated Statements of Financial Position |

| | | | | | |

| | | | |

| | | | |

| (In thousands) | September 30, 2019 | | December 31, 2018 |

| Assets | (Unaudited) | | |

| Investments: | | | |

| Fixed maturities available-for-sale, at fair value (cost: $1,278,293 and $1,223,747 in 2019 and 2018, respectively) | $ | 1,369,648 |

| | 1,231,039 |

|

| Equity securities, at fair value | 15,845 |

| | 15,068 |

|

| Mortgage loans on real estate | 180 |

| | 186 |

|

| Policy loans | 81,964 |

| | 80,825 |

|

| Real estate held for investment (less $1,284 accumulated depreciation in 2018) | — |

| | 5,718 |

|

| Real estate held-for-sale (less $1,325 and $4,411 accumulated depreciation in 2019 and 2018, respectively) | 2,571 |

| | 1,483 |

|

| Other long-term investments | 22 |

| | 22 |

|

| Short-term investments | 2,453 |

| | 7,865 |

|

| Total investments | 1,472,683 |

| | 1,342,206 |

|

| Cash and cash equivalents | 47,147 |

| | 45,492 |

|

| Accrued investment income | 17,648 |

| | 18,467 |

|

| Reinsurance recoverable | 3,596 |

| | 3,664 |

|

| Deferred policy acquisition costs | 150,289 |

| | 155,747 |

|

| Cost of customer relationships acquired | 13,741 |

| | 15,225 |

|

| Goodwill | 12,624 |

| | 12,624 |

|

| Other intangible assets | 953 |

| | 956 |

|

| Property and equipment, net | 6,639 |

| | 5,943 |

|

| Due premiums, net (less $1,640 and $1,990 allowance for doubtful accounts in 2019 and 2018, respectively) | 10,737 |

| | 13,325 |

|

| Prepaid expenses | 983 |

| | 284 |

|

| Other assets | 1,319 |

| | 1,628 |

|

| Total assets | $ | 1,738,359 |

| | 1,615,561 |

|

See accompanying notesNotes to consolidated financial statements.Consolidated Financial Statements.

September 30, 2019 Form | 10-Q 2

CITIZENS, INC. AND CONSOLIDATED SUBSIDIARIES Consolidated Statements of Financial Position (In thousands, except share amounts) | |

CITIZENS, INC. AND CONSOLIDATED SUBSIDIARIES Consolidated Statements of Financial Position, Continued

| | CITIZENS, INC. AND CONSOLIDATED SUBSIDIARIES Consolidated Statements of Financial Position, Continued

|

| | | | | | | | |

| | | | | |

| | March 31, 2019 | | December 31, 2018 | |

| (In thousands, except share amounts) | | September 30, 2019 | | December 31, 2018 |

| Liabilities and Stockholders' Equity | (Unaudited) | | | (Unaudited) | | |

| Liabilities: | | | | | | |

| Policy liabilities: | | | | | | |

| Future policy benefit reserves: | | | | | | |

| Life insurance | $ | 1,191,545 |

| | 1,179,946 |

| $ | 1,206,042 |

| | 1,179,946 |

|

| Annuities | 76,500 |

| | 76,377 |

| 76,427 |

| | 76,377 |

|

| Accident and health | 938 |

| | 944 |

| 997 |

| | 944 |

|

| Dividend accumulations | 26,984 |

| | 26,250 |

| 28,400 |

| | 26,250 |

|

| Premiums paid in advance | 43,448 |

| | 48,553 |

| 42,591 |

| | 48,553 |

|

| Policy claims payable | 8,174 |

| | 7,614 |

| 8,095 |

| | 7,614 |

|

| Other policyholders' funds | 15,767 |

| | 10,760 |

| 16,400 |

| | 10,760 |

|

| Total policy liabilities | 1,363,356 |

| | 1,350,444 |

| 1,378,952 |

| | 1,350,444 |

|

| Commissions payable | 1,922 |

| | 1,901 |

| 2,096 |

| | 1,901 |

|

| Current federal income tax payable | 46,952 |

| | 41,281 |

| 47,861 |

| | 41,281 |

|

| Deferred federal income tax liability | 7,873 |

| | 5,709 |

| |

| Deferred federal income tax payable | | 12,081 |

| | 5,709 |

|

| Payable for securities in process of settlement | 4,884 |

| | — |

| 6,030 |

| | — |

|

| Other liabilities | 28,675 |

| | 28,493 |

| 29,997 |

| | 28,493 |

|

| Total liabilities | 1,453,662 |

| | 1,427,828 |

| 1,477,017 |

| | 1,427,828 |

|

Commitments and contingencies (Note 7) |

|

| |

|

|

|

| |

|

|

| Stockholders' equity: | |

| | |

| |

| | |

|

| Class A, no par value, 100,000,000 shares authorized, 52,364,993 and 52,215,852 shares issued and outstanding in 2019 and 2018, respectively, including shares in treasury of 3,135,738 in 2019 and 2018 | 260,876 |

| | 259,793 |

| 261,346 |

| | 259,793 |

|

| Class B, no par value, 2,000,000 shares authorized, 1,001,714 shares issued and outstanding in 2019 and 2018 | 3,184 |

| | 3,184 |

| 3,184 |

| | 3,184 |

|

| Accumulated deficit | (73,401 | ) | | (69,599 | ) | (75,920 | ) | | (69,599 | ) |

| Accumulated other comprehensive income: | |

| | |

| |

| | |

|

| Unrealized gains on securities, net of tax | 32,246 |

| | 5,366 |

| |

| Net unrealized gains on securities, net of tax | | 83,743 |

| | 5,366 |

|

| Treasury stock, at cost | (11,011 | ) | | (11,011 | ) | (11,011 | ) | | (11,011 | ) |

| Total stockholders' equity | 211,894 |

| | 187,733 |

| 261,342 |

| | 187,733 |

|

| Total liabilities and stockholders' equity | $ | 1,665,556 |

| | 1,615,561 |

| $ | 1,738,359 |

| | 1,615,561 |

|

See accompanying notesNotes to consolidated financial statements.

Consolidated Financial Statements.

September 30, 2019 Form | 10-Q 3

CITIZENS, INC. AND CONSOLIDATED SUBSIDIARIES Consolidated Statements of Comprehensive Income Three Months Ended March 31, (In thousands, except per share amounts) (Unaudited)

| |

CITIZENS, INC. AND CONSOLIDATED SUBSIDIARIES Consolidated Statements of Comprehensive Income (Unaudited)

| | CITIZENS, INC. AND CONSOLIDATED SUBSIDIARIES Consolidated Statements of Comprehensive Income (Unaudited)

|

| | | 2019 | | 2018 | |

Three Months Ended September 30,

(In thousands, except per share amounts) | | 2019 | | 2018

(As Restated*) |

| Revenues: | | | | | | | | |

| Premiums: | | | | | | | | | | |

| Life insurance | | | $ | 40,980 |

| | | | 42,529 |

| $ | 44,502 |

| | 45,898 |

|

| Accident and health insurance | | | 323 |

| | | | 291 |

| 350 |

| | 323 |

|

| Property insurance | | | 1,161 |

| | | | 1,209 |

| 1,157 |

| | 1,208 |

|

| Net investment income | | | 13,796 |

| | | | 13,771 |

| 15,039 |

| | 13,587 |

|

| Realized investment gains (losses), net | | | 5,961 |

| | | | (575 | ) | 72 |

| | (498 | ) |

| Other income | | | 185 |

| | | | 208 |

| 347 |

| | 643 |

|

| Total revenues | | | 62,406 |

| | | | 57,433 |

| 61,467 |

| | 61,161 |

|

| Benefits and expenses: | | | |

| | | | |

| |

| Benefits and Expenses: | | |

| | |

|

| Insurance benefits paid or provided: | | | |

| | | | |

| |

| | |

|

| Claims and surrenders | | | 23,033 |

| | | | 21,151 |

| 28,751 |

| | 25,076 |

|

| Increase in future policy benefit reserves | | | 12,299 |

| | | | 14,608 |

| 6,409 |

| | 1,653 |

|

| Policyholders' dividends | | | 1,182 |

| | | | 1,307 |

| 1,560 |

| | 1,595 |

|

| Total insurance benefits paid or provided | | | 36,514 |

| | | | 37,066 |

| 36,720 |

| | 28,324 |

|

| Commissions | | | 7,884 |

| | | | 8,959 |

| 8,879 |

| | 8,656 |

|

| Other general expenses | | | 14,132 |

| | | | 6,507 |

| 11,530 |

| | 12,402 |

|

| Capitalization of deferred policy acquisition costs | | | (4,828 | ) | | | | (5,963 | ) | (5,984 | ) | | (5,561 | ) |

| Amortization of deferred policy acquisition costs | | | 6,277 |

| | | | 7,606 |

| 7,835 |

| | 11,412 |

|

| Amortization of cost of customer relationships acquired | | | 419 |

| | | | 679 |

| 355 |

| | 366 |

|

| Total benefits and expenses | | | 60,398 |

| | | | 54,854 |

| 59,335 |

| | 55,599 |

|

| Income before federal income tax | | | 2,008 |

| | | | 2,579 |

| 2,132 |

| | 5,562 |

|

| Federal income tax expense | | | 5,810 |

| | | | 2,542 |

| 86 |

| | 12,671 |

|

| Net income (loss) | | | (3,802 | ) | | | | 37 |

| 2,046 |

| | (7,109 | ) |

| Per Share Amounts: | | | |

| | |

| | |

| |

| | |

|

| Basic and diluted earnings (losses) per share of Class A common stock | $ | (0.08 | ) | | |

| | — |

| | |

| 0.04 |

| | (0.14 | ) |

| Basic and diluted earnings (losses) per share of Class B common stock | (0.04 | ) | | |

| | — |

| | |

| 0.02 |

| | (0.07 | ) |

| Other comprehensive income (loss): | |

| | |

| | | | |

| |

| Other Comprehensive Income (Loss): | | |

| | |

|

| Unrealized gains (losses) on available-for-sale debt securities: | |

| | |

| | |

| | |

| |

| | |

|

| Unrealized holding gains (losses) arising during period | |

| | 28,801 |

| | |

| | (18,098 | ) | 24,201 |

| | (2,236 | ) |

| Reclassification adjustment for losses included in net income | |

| | 104 |

| |

|

| | 259 |

| |

| Reclassification adjustment for losses (gains) included in net income | | (53 | ) | | 656 |

|

| Unrealized gains (losses) on available-for-sale debt securities, net | |

| | 28,905 |

| | |

| | (17,839 | ) | 24,148 |

| | (1,580 | ) |

| Income tax expense (benefit) on unrealized gains (losses) on available-for-sale debt securities | |

| | 2,025 |

| | |

| | (3,735 | ) | |

| Income tax expense on unrealized gains (losses) on available-for-sale debt securities | | 1,627 |

| | 454 |

|

| Other comprehensive income (loss) | |

| | 26,880 |

| | |

| | (14,104 | ) | 22,521 |

| | (2,034 | ) |

| Total comprehensive income (loss) | |

| | $ | 23,078 |

| | |

| | (14,067 | ) | $ | 24,567 |

| | (9,143 | ) |

* See Note 1 in the Notes to Consolidated Financial Statements

See accompanying notesNotes to consolidated financial statements.Consolidated Financial Statements.

September 30, 2019 Form | 10-Q 4

|

| | | | | | | | | | | | | | | | | | |

| CITIZENS, INC. AND CONSOLIDATED SUBSIDIARIES |

| Consolidated Statements of Stockholders' Equity |

| Three Months Ended March 31, 2019 and 2018 |

| (In thousands) |

| (Unaudited) |

| | | | | | | | | | | | |

| | Common Stock | | Accumulated deficit | | Accumulated other comprehensive income (loss) | | Treasury stock | | Total Stockholders' equity |

| | Class A | | Class B | | | | |

| Balance at December 31, 2017 | $ | 259,383 |

| | 3,184 |

| | (54,375 | ) | | 26,332 |

| | (11,011 | ) | | 223,513 |

|

| Accounting standards adopted January 1, 2018 | — |

| | — |

| | (4,162 | ) | | 4,162 |

| | — |

| | — |

|

| Balance at January 1, 2018 | 259,383 |

| | 3,184 |

| | (58,537 | ) | | 30,494 |

| | (11,011 | ) | | 223,513 |

|

| | | | | | | | | | | | |

| Comprehensive loss: | |

| | |

| | |

| | |

| | |

| | |

|

| Net income | — |

| | — |

| | 37 |

| | — |

| | — |

| | 37 |

|

| Unrealized investment losses, net | — |

| | — |

| | — |

| | (14,104 | ) | | — |

| | (14,104 | ) |

| Total comprehensive loss | — |

| | — |

| | 37 |

| | (14,104 | ) | | — |

| | (14,067 | ) |

| Balance at March 31, 2018 | $ | 259,383 |

| | 3,184 |

| | (58,500 | ) | | 16,390 |

| | (11,011 | ) | | 209,446 |

|

| | | | | | | | | | | | |

| Balance at December 31, 2018 | $ | 259,793 |

| | 3,184 |

| | (69,599 | ) | | 5,366 |

| | (11,011 | ) | | 187,733 |

|

| Comprehensive income: | |

| | |

| | |

| | |

| | |

| | |

|

| Net loss | — |

| | — |

| | (3,802 | ) | | — |

| | — |

| | (3,802 | ) |

| Unrealized investment gains, net | — |

| | — |

| | — |

| | 26,880 |

| | — |

| | 26,880 |

|

| Total comprehensive income | — |

| | — |

| | (3,802 | ) | | 26,880 |

| | — |

| | 23,078 |

|

| Stock-based compensation | 1,083 |

| | — |

| | — |

| | — |

| | — |

| | 1,083 |

|

| Balance at March 31, 2019 | $ | 260,876 |

| | 3,184 |

| | (73,401 | ) | | 32,246 |

| | (11,011 | ) | | 211,894 |

|

CITIZENS, INC. AND CONSOLIDATED SUBSIDIARIES Consolidated Statements of Comprehensive Income (Unaudited)

|

| | | | | | |

Nine Months Ended September 30,

(In thousands, except per share amounts) | 2019 | | 2018

(As Restated*) |

| Revenues: | | | |

| Premiums: | | | |

| Life insurance | $ | 127,795 |

| | 133,058 |

|

| Accident and health insurance | 1,018 |

| | 915 |

|

| Property insurance | 3,464 |

| | 3,615 |

|

| Net investment income | 44,150 |

| | 41,169 |

|

| Realized investment gains (losses), net | 3,164 |

| | (1,251 | ) |

| Other income | 1,148 |

| | 930 |

|

| Total revenues | 180,739 |

| | 178,436 |

|

| Benefits and Expenses: | |

| | |

|

| Insurance benefits paid or provided: | |

| | |

|

| Claims and surrenders | 78,808 |

| | 66,844 |

|

| Increase in future policy benefit reserves | 28,180 |

| | 32,816 |

|

| Policyholders' dividends | 4,165 |

| | 4,516 |

|

| Total insurance benefits paid or provided | 111,153 |

| | 104,176 |

|

| Commissions | 25,147 |

| | 26,284 |

|

| Other general expenses | 37,611 |

| | 33,375 |

|

| Capitalization of deferred policy acquisition costs | (16,224 | ) | | (17,164 | ) |

| Amortization of deferred policy acquisition costs | 21,043 |

| | 26,218 |

|

| Amortization of cost of customer relationships acquired | 1,192 |

| | 1,517 |

|

| Total benefits and expenses | 179,922 |

| | 174,406 |

|

| Income before federal income tax | 817 |

| | 4,030 |

|

| Federal income tax expense | 7,138 |

| | 13,660 |

|

| Net loss | (6,321 | ) | | (9,630 | ) |

| Per Share Amounts: | |

| | |

|

| Basic and diluted losses per share of Class A common stock | (0.13 | ) | | (0.19 | ) |

| Basic and diluted losses per share of Class B common stock | (0.06 | ) | | (0.10 | ) |

| Other Comprehensive Income (Loss): | |

| | |

|

| Unrealized gains (losses) on available-for-sale debt securities: | |

| | |

|

| Unrealized holding gains (losses) arising during period | 84,222 |

| | (32,663 | ) |

| Reclassification adjustment for losses (gains) included in net income | (30 | ) | | 1,002 |

|

| Unrealized gains (losses) on available-for-sale debt securities, net | 84,192 |

| | (31,661 | ) |

| Income tax expense (benefit) on unrealized gains (losses) on available-for-sale debt securities | 5,815 |

| | (5,852 | ) |

| Other comprehensive income (loss) | 78,377 |

| | (25,809 | ) |

| Total comprehensive income (loss) | $ | 72,056 |

| | (35,439 | ) |

* See Note 1 in the Notes to Consolidated Financial Statements

See accompanying notesNotes to consolidated financial statements.

Consolidated Financial Statements.

September 30, 2019 Form | 10-Q 5

CITIZENS, INC. AND CONSOLIDATED SUBSIDIARIES Consolidated Statements of Cash Flows Three Months Ended March 31, (In thousands) (Unaudited) |

| | | | | | |

| | 2019 | | 2018 |

| Cash flows from operating activities: | | | |

| Net income (loss) | $ | (3,802 | ) | | 37 |

|

| Adjustments to reconcile net income (loss) to net cash provided by operating activities: | |

| | |

|

| Realized (gains) losses on sale of investments and other assets | (5,961 | ) | | 575 |

|

| Net deferred policy acquisition costs | 1,449 |

| | 1,643 |

|

| Amortization of cost of customer relationships acquired | 419 |

| | 679 |

|

| Depreciation | 396 |

| | 437 |

|

| Amortization of premiums and discounts on investments | 4,043 |

| | 4,155 |

|

| Stock-based compensation | 1,460 |

| | — |

|

| Deferred federal income tax benefit | 140 |

| | (1,793 | ) |

| Change in: | |

| | |

|

| Accrued investment income | 312 |

| | 310 |

|

| Reinsurance recoverable | 77 |

| | (65 | ) |

| Due premiums | 2,242 |

| | 1,870 |

|

| Future policy benefit reserves | 12,217 |

| | 14,757 |

|

| Other policyholders' liabilities | 1,195 |

| | 2,352 |

|

| Federal income tax payable | 5,671 |

| | 4,335 |

|

| Commissions payable and other liabilities | 204 |

| | (6,872 | ) |

| Other, net | (2,139 | ) | | (429 | ) |

| Net cash provided by operating activities | 17,923 |

| | 21,991 |

|

| Cash flows from investing activities: | |

| | |

|

| Purchase of fixed maturities, available-for-sale | (74,209 | ) | | (43,914 | ) |

| Sale of fixed maturities, available-for-sale | 7,659 |

| | — |

|

| Maturities and calls of fixed maturities, available-for-sale | 31,631 |

| | 16,501 |

|

| Maturities and calls of fixed maturities, held-to-maturity | — |

| | 2,295 |

|

| Principal payments on mortgage loans | 2 |

| | 2 |

|

| Increase in policy loans, net | (650 | ) | | (1,901 | ) |

| Sale of other long-term investments and real estate | 6,996 |

| | 1 |

|

| Sale of property and equipment | 18 |

| | — |

|

| Purchase of property and equipment | (257 | ) | | (61 | ) |

| Net cash used in investing activities | (28,810 | ) | | (27,077 | ) |

| | | | |

| See accompanying notes to consolidated financial statements. |

|

| | | | | | | | | | | | | | | | | | |

| CITIZENS, INC. AND CONSOLIDATED SUBSIDIARIES |

| Consolidated Statements of Stockholders' Equity |

| (Unaudited) |

| | | | | | | | | | | | |

| | Common Stock | | Accumulated

deficit | | Accumulated other comprehensive income | | Treasury

stock | | Total

Stock-holders'

equity |

| (In thousands) | Class A | | Class B | | | | |

| | | | | | | | | | | |

| Balance at December 31, 2018 | $ | 259,793 |

| | 3,184 |

| | (69,599 | ) | | 5,366 |

| | (11,011 | ) | | 187,733 |

|

| Comprehensive income: | | | | | | | | | | | |

| Net loss | — |

| | — |

| | (3,802 | ) | | — |

| | — |

| | (3,802 | ) |

| Unrealized investment gains, net | — |

| | — |

| | — |

| | 26,880 |

| | — |

| | 26,880 |

|

| Total comprehensive income | — |

| | — |

| | (3,802 | ) | | 26,880 |

| | — |

| | 23,078 |

|

| Stock-based compensation | 1,083 |

| | — |

| | — |

| | — |

| | — |

| | 1,083 |

|

| Balance at March 31, 2019 | 260,876 |

| | 3,184 |

| | (73,401 | ) | | 32,246 |

| | (11,011 | ) | | 211,894 |

|

| Comprehensive income: | |

| | |

| | |

| | |

| | |

| | |

|

| Net loss | — |

| | — |

| | (4,565 | ) | | — |

| | — |

| | (4,565 | ) |

| Unrealized investment gains, net | — |

| | — |

| | — |

| | 28,976 |

| | — |

| | 28,976 |

|

| Total comprehensive income | — |

| | — |

| | (4,565 | ) | | 28,976 |

| | — |

| | 24,411 |

|

| Stock-based compensation | 127 |

| | — |

| | — |

| | — |

| | — |

| | 127 |

|

| Balance at June 30, 2019 | 261,003 |

| | 3,184 |

| | (77,966 | ) | | 61,222 |

| | (11,011 | ) | | 236,432 |

|

| Comprehensive income: | |

| | |

| | |

| | |

| | |

| | |

|

| Net income | — |

| | — |

| | 2,046 |

| | — |

| | — |

| | 2,046 |

|

| Unrealized investment gains, net | — |

| | — |

| | — |

| | 22,521 |

| | — |

| | 22,521 |

|

| Total comprehensive income | — |

| | — |

| | 2,046 |

| | 22,521 |

| | — |

| | 24,567 |

|

| Stock-based compensation | 343 |

| | — |

| | — |

| | — |

| | — |

| | 343 |

|

| Balance at September 30, 2019 | $ | 261,346 |

| | 3,184 |

| | (75,920 | ) | | 83,743 |

| | (11,011 | ) | | 261,342 |

|

See accompanying Notes to Consolidated Financial Statements.

September 30, 2019 Form | 10-Q 6

CITIZENS, INC. AND CONSOLIDATED SUBSIDIARIES Consolidated Statements of Cash Flows, Continued Three Months Ended March 31, (In thousands) (Unaudited) |

| | | | | | |

| | 2019 | | 2018 |

| Cash flows from financing activities: | | | |

| Annuity deposits | $ | 1,541 |

| | 1,775 |

|

| Annuity withdrawals | (1,676 | ) | | (1,506 | ) |

| Other | (377 | ) | | — |

|

| Net cash provided by (used in) financing activities | (512 | ) | | 269 |

|

| Net decrease in cash and cash equivalents | (11,399 | ) | | (4,817 | ) |

| Cash and cash equivalents at beginning of year | 45,492 |

| | 46,064 |

|

| Cash and cash equivalents at end of period | $ | 34,093 |

| | 41,247 |

|

|

| | | | | | | | | | | | | | | | | | |

| CITIZENS, INC. AND CONSOLIDATED SUBSIDIARIES |

| Consolidated Statements of Stockholders' Equity, Continued |

| (Unaudited) |

| | | | | | | | | | | | |

| | Common Stock | | Accumulated

deficit | | Accumulated other comprehensive income (loss) | | Treasury

stock | | Total

Stock-holders'

equity |

| (In thousands) | Class A | | Class B | | | | |

| | | | | | | | | | | |

| Balance at December 31, 2017 | $ | 259,383 |

| | 3,184 |

| | (54,375 | ) | | 26,332 |

| | (11,011 | ) | | 223,513 |

|

| Accounting standards adopted January 1, 2018 | — |

| | — |

| | (4,162 | ) | | 4,162 |

| | — |

| | — |

|

| Balance at January 1, 2018 | 259,383 |

| | 3,184 |

| | (58,537 | ) | | 30,494 |

| | (11,011 | ) | | 223,513 |

|

| Comprehensive loss: | | | | | | | | | | | |

| Net income | — |

| | — |

| | 37 |

| | — |

| | — |

| | 37 |

|

| Unrealized investment losses, net | — |

| | — |

| | — |

| | (14,104 | ) | | — |

| | (14,104 | ) |

| Total comprehensive loss | — |

| | — |

| | 37 |

| | (14,104 | ) | | — |

| | (14,067 | ) |

| Balance at March 31, 2018 | 259,383 |

| | 3,184 |

| | (58,500 | ) |

| 16,390 |

| | (11,011 | ) | | 209,446 |

|

| Comprehensive loss: | |

| | |

| | |

| | |

| | |

| | |

|

| Net loss | — |

| | — |

| | (2,558 | ) | | — |

| | — |

| | (2,558 | ) |

| Unrealized investment losses, net | — |

| | — |

| | — |

| | (9,671 | ) | | — |

| | (9,671 | ) |

| Total comprehensive loss | — |

| | — |

| | (2,558 | ) | | (9,671 | ) | | — |

| | (12,229 | ) |

| Stock-based compensation | 213 |

| | — |

| | — |

| | — |

| | — |

| | 213 |

|

| Balance at June 30, 2018 | 259,596 |

| | 3,184 |

| | (61,058 | ) | | 6,719 |

| | (11,011 | ) | | 197,430 |

|

| Comprehensive loss: | |

| | |

| | |

| | |

| | |

| | |

|

| Net loss (as restated*) | — |

| | — |

| | (7,109 | ) | | — |

| | — |

| | (7,109 | ) |

| Unrealized investment losses, net | — |

| | — |

| | — |

| | (2,854 | ) | | — |

| | (2,854 | ) |

| Unrealized gain from held-to-maturity securities transferred to available-for-sale | — |

| | — |

| | — |

| | 820 |

| | — |

| | 820 |

|

| Total comprehensive loss (as restated*) | — |

| | — |

| | (7,109 | ) | | (2,034 | ) | | — |

| | (9,143 | ) |

| Stock-based compensation | 97 |

| | — |

| | — |

| | — |

| | — |

| | 97 |

|

| Balance at September 30, 2018 (as restated*) | $ | 259,693 |

| | 3,184 |

| | (68,167 | ) | | 4,685 |

| | (11,011 | ) | | 188,384 |

|

* See Note 1 in the Notes to Consolidated Financial Statements

See accompanying Notes to Consolidated Financial Statements.

September 30, 2019 Form | 10-Q 7

CITIZENS, INC. AND CONSOLIDATED SUBSIDIARIES Consolidated Statements of Cash Flows (Unaudited)

|

| | | | | | |

Nine Months Ended September 30,

(In thousands) | 2019 | | 2018

(As Restated*) |

| Cash flows from operating activities: | | | |

| Net income (loss) | $ | (6,321 | ) | | (9,630 | ) |

| Adjustments to reconcile net income (loss) to net cash provided by operating activities: | |

| | |

|

| Realized (gains) losses on sale of investments and other assets | (3,164 | ) | | 1,251 |

|

| Net deferred policy acquisition costs | 4,819 |

| | 9,054 |

|

| Amortization of cost of customer relationships acquired | 1,192 |

| | 1,517 |

|

| Depreciation | 1,269 |

| | 921 |

|

| Amortization of premiums and discounts on investments | 10,422 |

| | 12,781 |

|

| Stock-based compensation | 1,930 |

| | 310 |

|

| Deferred federal income tax benefit | 560 |

| | 59,329 |

|

| Change in: | |

| | |

|

| Accrued investment income | 819 |

| | 673 |

|

| Reinsurance recoverable | 68 |

| | 89 |

|

| Due premiums | 2,588 |

| | 427 |

|

| Future policy benefit reserves | 27,994 |

| | 33,425 |

|

| Other policyholders' liabilities | 2,309 |

| | 1,413 |

|

| Federal income tax payable | 6,580 |

| | (45,678 | ) |

| Commissions payable and other liabilities | 1,699 |

| | 558 |

|

| Other, net | (1,851 | ) | | (1,205 | ) |

| Net cash provided by operating activities | 50,913 |

| | 65,235 |

|

| Cash flows from investing activities: | |

| | |

|

| Purchase of fixed maturities, available-for-sale | (210,445 | ) | | (109,642 | ) |

| Sale of fixed maturities, available-for-sale | 39,708 |

| | 1,084 |

|

| Maturities and calls of fixed maturities, available-for-sale | 111,757 |

| | 51,190 |

|

| Maturities and calls of fixed maturities, held-to-maturity | — |

| | 20,699 |

|

| Purchase of equity securities | — |

| | (9 | ) |

| Principal payments on mortgage loans | 6 |

| | 7 |

|

| Increase in policy loans, net | (1,141 | ) | | (5,277 | ) |

| Sale of other long-term investments and real estate | 6,981 |

| | 14 |

|

| Sale of property and equipment | 15 |

| | — |

|

| Purchase of property and equipment | (509 | ) | | (437 | ) |

| Maturity of short-term investments | 7,940 |

| | — |

|

| Purchase of short-term investments | (2,456 | ) | | — |

|

| Net cash used in investing activities | (48,144 | ) | | (42,371 | ) |

| * See Note 1 in the Notes to Consolidated Financial Statements | | | |

See accompanying Notes to Consolidated Financial Statements. | |

September 30, 2019 Form | 10-Q 8

CITIZENS, INC. AND CONSOLIDATED SUBSIDIARIES Consolidated Statements of Cash Flows, Continued (Unaudited)

|

| | | | | | |

Nine Months Ended September 30,

(In thousands) | 2019 | | 2018

(As Restated*) |

| Cash flows from financing activities: | |

| | |

|

| Annuity deposits | $ | 4,948 |

| | 5,222 |

|

| Annuity withdrawals | (5,685 | ) | | (5,397 | ) |

| Other | (377 | ) | | — |

|

| Net cash used in financing activities | (1,114 | ) | | (175 | ) |

| Net increase in cash and cash equivalents | 1,655 |

| | 22,689 |

|

| Cash and cash equivalents at beginning of year | 45,492 |

| | 46,064 |

|

| Cash and cash equivalents at end of period | $ | 47,147 |

| | 68,753 |

|

| * See Note 1 in the Notes to Consolidated Financial Statements | | | |

Supplemental Disclosures of Noncash Investing and Financing Activities:

SUPPLEMENTAL DISCLOSURES OF NONCASH INVESTING AND FINANCING ACTIVITIES:

During the threenine months ended March 31,September 30, 2019 and 2018, various fixed maturity issuers exchanged securities with book values of $8.8$12.2 million and $2.5 million, respectively, for securities of equal value. There were none during the three months ended March 31, 2018.

The Company had net unsettled security trades of $4.9$6.0 million at March 31,September 30, 2019 and none at March 31,September 30, 2018.

See accompanying notesNotes to consolidated financial statements.Consolidated Financial Statements.

7

September 30, 2019 Form | 10-Q 9

CITIZENS, INC. AND CONSOLIDATED SUBSIDIARIES

Notes to Consolidated Financial Statements |

| | |

CITIZENS, INC. | NOTES TO CONSOLIDATED FINANCIAL STATEMENTS |

| | (Unaudited) |

| | |

March 31, 2019

(Unaudited)

(1) Financial StatementsFINANCIAL STATEMENTS

Basis of Presentation and ConsolidationBASIS OF PRESENTATION AND CONSOLIDATION

The consolidated financial statements include the accounts and operations of Citizens, Inc. ("Citizens"), a Colorado corporation, and its wholly-owned subsidiaries, CICA Life Insurance Company of America ("CICA"), CICA Life Ltd. ("CICA Ltd."), Citizens National Life Insurance Company ("CNLIC"), CICA Life Ltd. ("CICA Ltd."), Security Plan Life Insurance Company ("SPLIC"), Security Plan Fire Insurance Company ("SPFIC"), Magnolia Guaranty Life Insurance Company ("MGLIC") and Computing Technology, Inc. ("CTI"). All significant inter-company accounts and interactions have been eliminated. Citizens and its wholly-owned subsidiaries are collectively referred to as the "Company," "we,""Company", "we", "us" or "our.""our".

The consolidated statements of financial position as of March 31,September 30, 2019,, the consolidated statements of comprehensive income and stockholders' equity for the three and nine months ended March 31,September 30, 2019 and March 31,September 30, 2018 and the consolidated statements of stockholders' equity and cash flows for the threenine months ended March 31,September 30, 2019 and March 31,September 30, 2018 have been prepared by the Company without audit. In the opinion of management, all normal and recurring adjustments to present fairly the financial position, results of operations, and changes in cash flows at March 31,September 30, 2019 and for comparative periods have been made. The consolidated financial statements have been prepared in accordance with United States Generally Accepted Accounting Principles ("U.S. GAAP") for interim financial information and with the instructions to Form 10-Q adopted by the Securities and Exchange Commission ("SEC"). Accordingly, the consolidated financial statements do not include all the information and footnotes required for complete financial statements and should be read in conjunction with the Company’s consolidated financial statements and notes thereto included in our Annual Report on Form 10-K for the year ended December 31, 2018.2018. Operating results for the interim periods disclosed herein are not necessarily indicative of the results that may be expected for a full year or any future period.

We provide primarily life insurance and a small amount of health insurance policies through our insurance subsidiaries - CICA, CNLIC, CICA Ltd., SPLIC MGLIC and CNLIC.MGLIC. CICA and CNLIC issued ordinary whole-life policies, credit life and disability, and accident and health related policies, throughout the Midwest and southern U.S. until they ceased most domestic sales beginning January 1, 2017. CICA Ltd. primarily issues endowment and ordinary whole-life policies to non-U.S. residents. SPLIC offers final expense and home service life insurance in Louisiana, Arkansas and Mississippi, andMississippi. SPFIC, a wholly-owned subsidiary of SPLIC, writes a limited amount of property insurance in Louisiana. MGLIC provides industrial life policies through independent funeral homes in Mississippi.

CTI provides data processing systems and services to the Company.

Use

September 30, 2019 Form | 10-Q 10

|

| | |

CITIZENS, INC. | NOTES TO CONSOLIDATED FINANCIAL STATEMENTS |

| | (Unaudited) |

| | |

We converted to a new actuarial valuation software solution impacting both the Home Service Insurance and Life Insurance segments, providing enhanced modeling capabilities for the ordinary whole life policies of SPLIC as of July 1, 2019 and the ordinary whole life and endowment policies of CICA and CICA Ltd. as of July 1, 2018. The total impact of these system conversions reflected in the accompanying consolidated financial statements as of and for the three and nine months ended September 30, 2019 and 2018 are summarized in the table below.

|

| | | | | | | |

| (In thousands) | | September 30, 2019 | | September 30, 2018 |

| Increase (Decrease) | | | | |

| Consolidated Statements of Financial Position | | | | |

| Deferred policy acquisition costs | | $ | (1,396 | ) | | (4,339 | ) |

| Future policy benefit reserves: | | | | |

| Life insurance | | (2,299 | ) | | (10,197 | ) |

| | | | | |

| Consolidated Statement of Comprehensive Income | | | | |

| Decrease in future policy benefit reserves | | (2,299 | ) | | (10,197 | ) |

| Amortization of deferred policy acquisition costs | | 1,396 |

| | 4,339 |

|

| Income before federal income tax | | 903 |

| | 5,858 |

|

| Federal income tax expense | | 190 |

| | 1,230 |

|

| Net income | | $ | 713 |

| | 4,628 |

|

USE OF ESTIMATES

The preparation of consolidated financial statements in conformity with U.S. GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and the disclosure of contingent assets and liabilities at the date of the consolidated financial statements and the reported amounts of revenues and expenses during the reporting period. Actual results could differ from those estimates.

Significant estimates include those used in the evaluation of other-than-temporary impairments on debt and equity securities, actuarially determined assets and liabilities and assumptions, tests of goodwill impairment, valuation allowance on deferred tax assets, valuation of uncertain tax positions and contingencies relating to litigation and regulatory matters. Certain of these estimates are particularly sensitive to market conditions, and deterioration and/or volatility in the worldwide debt or equity markets could have a material impact on the consolidated financial statements.

RESTATEMENT

As disclosed in Note 14. Quarterly Financial Information (Unaudited) in the notes to our consolidated financial statements included in our Annual Report on Form 10-K for the year ended December 31, 2018, the Company has restated its unaudited consolidated financial information as of and for the three and nine month periods ended September 30, 2018 to correct an immaterial error related to the accounting for the income tax effects of the novation of international insurance policies to our Bermuda-based subsidiary on July 1, 2018.

8

September 30, 2019 Form | 10-Q 11

CITIZENS, INC. AND CONSOLIDATED SUBSIDIARIES

Notes to Consolidated Financial Statements, Continued |

| | |

CITIZENS, INC. | NOTES TO CONSOLIDATED FINANCIAL STATEMENTS |

| | (Unaudited) |

| | |

March 31, 2019

(Unaudited)

Significant Accounting PoliciesFederal income tax expense and net income (loss) have been restated herein to properly reflect the reduction in federal income tax expense as compared to originally reported amounts. Basic & diluted earnings (losses) per share of Class A common stock and Class B common stock were also restated. The table below reflects the line items adjusted as a result of the restatement as of September 30, 2018 and for the three and nine months ended September 30, 2018.

|

| | | | | | | | | | |

| (In thousands, except per share amounts) | | As Previously Reported | | Adjustments | | As Restated |

| For the Three Months Ended September 30, 2018 | | | | | | |

| Consolidated Statement of Comprehensive Income | | | | | | |

| Federal income expense (benefit) | | $ | 20,316 |

| | (7,645 | ) | | 12,671 |

|

| Net income (loss) | | (14,754 | ) | | 7,645 |

| | (7,109 | ) |

| Basic and diluted earnings (losses) per share of Class A common stock | | (0.30 | ) | | 0.16 |

| | (0.14 | ) |

| Basic and diluted earnings (losses) per share of Class B common stock | | (0.14 | ) | | 0.07 |

| | (0.07 | ) |

| Total comprehensive income (loss) | | (16,788 | ) | | 7,645 |

| | (9,143 | ) |

|

| | | | | | | | | | |

| For the Nine Months Ended September 30, 2018 | | | | | | |

| Consolidated Statement of Comprehensive Income | | | | | | |

| Federal income expense (benefit) | | $ | 21,305 |

| | (7,645 | ) | | 13,660 |

|

| Net income (loss) | | (17,275 | ) | | 7,645 |

| | (9,630 | ) |

| Basic and diluted earnings (losses) per share of Class A common stock | | (0.35 | ) | | 0.16 |

| | (0.19 | ) |

| Basic and diluted earnings (losses) per share of Class B common stock | | (0.17 | ) | | 0.07 |

| | (0.10 | ) |

| Total comprehensive income (loss) | | (43,084 | ) | | 7,645 |

| | (35,439 | ) |

|

| | | | | | | | | | |

| As of September 30, 2018 | | | | | | |

| Consolidated Statements of Stockholders' Equity | | | | | | |

| Balance at June 30, 2018 | | $ | 197,430 |

| | — |

| | 197,430 |

|

| Net income (loss) | | (14,754 | ) | | 7,645 |

| | (7,109 | ) |

| Total comprehensive income (loss) | | (16,788 | ) | | 7,645 |

| | (9,143 | ) |

| Accumulated deficit | | (75,812 | ) | | 7,645 |

| | (68,167 | ) |

| Balance at September 30, 2018 | | 180,739 |

| | 7,645 |

| | 188,384 |

|

|

| | | | | | | | | | |

| For the Nine Months Ended September 30, 2018 | | | | | | |

| Consolidated Statements of Cash Flows | | | | | | |

| Net income (loss) | | $ | (17,275 | ) | | 7,645 |

| | (9,630 | ) |

| Deferred federal income tax (expense) benefit | | 67,040 |

| | (7,711 | ) | | 59,329 |

|

| Federal income tax payable | | (45,744 | ) | | 66 |

| | (45,678 | ) |

| Net cash provided by operating activities | | 65,235 |

| | — |

| | 65,235 |

|

SIGNIFICANT ACCOUNTING POLICIES

For a description of our significant accounting policies, see Note 1. Summary of Significant Accounting Policies in the notes to our consolidated financial statements included in our Annual Report on Form 10-K for the year ended December 31, 2018, which should be read in conjunction with these accompanying consolidated financial statements.

September 30, 2019 Form | 10-Q 12

|

| | |

CITIZENS, INC. | NOTES TO CONSOLIDATED FINANCIAL STATEMENTS |

| | (Unaudited) |

| | |

(2) Accounting PronouncementsACCOUNTING PRONOUNCEMENTS

Accounting Standards Recently AdoptedACCOUNTING STANDARDS RECENTLY ADOPTED

In February 2016, the Financial Accounting Standards Board ("FASB") issued Accounting Standards Update ("ASU") 2016-02, Leases (Topic 842). The ASU requires organizations that lease assets, referred to as "lessees," to recognize on the consolidated statement of financial position the rights and obligations created by those leases. The ASU also requires disclosures to help investors and other financial statement users better understand the amount, timing, and uncertainty of cash flows arising from leases. These disclosures include qualitative and quantitative requirements, providing additional information about the amounts recorded in the consolidated financial statements. The ASU on leases became effective for public companies for fiscal years, and interim periods within those fiscal years, beginning after December 15, 2018.

The Company has several lease agreements, such as district office locations related to our Home Service Insurance segment. The Company adopted this standard effective January 1, 2019 and recognizes these lease agreements on the consolidated statements of financial position as a right-of-use asset and a corresponding lease liability. See Note 9. Leases for further discussions.discussion.

In March 2017, the FASB issued ASU No. 2017-08, Receivables-Nonrefundable Fees and Other Costs (Subtopic 310-20). The amendments in this ASU shorten the amortization period for certain callable debt securities held at a premium. Specifically, the amendments require the premium to be amortized to the earliest call date. The amendments do not require an accounting change for securities held at a discount; the discount continues to be amortized to maturity. The Company has a large portfolio of callable debt securities purchased at a premium. As such, the Company had already been amortizing the premium to the earliest call date (yield to worst)., thus adoption of this guidance as of January 1, 2019 did not have a material impact on our consolidated financial statements. For public business entities, the amendments in this ASU are effective for fiscal years, and interim periods within those fiscal years, beginning after December 15, 2018.

In June 2018, the FASB issued ASU No. 2018-07, Compensation - StockCompensation-Stock Compensation (Topic 718), Improvements to Nonemployee Share-Based Payment Accounting. This ASU is intended to simplify aspects of share-based compensation issued to non-employees by making the guidance consistent with the accounting for employee share-based compensation. This ASU is effective for annual periods beginning after December 15, 2018 and interim periods within those annual periods, with early adoption permitted. We adopted the provisions of this ASU in the first quarteras of January 1, 2019. This guidance did not have a material impact on our consolidated financial statements.

Accounting Standards Not Yet AdoptedACCOUNTING STANDARDS NOT YET ADOPTED

In June 2016, the FASB issued ASU No. 2016-13, Financial Instruments-Credit Losses (Topic 326), with the main objective to provide financial statement users with more decision-useful information about the expected credit losses on financial instruments and other commitments to extend credit held by a reporting entity at each reporting date. The ASU requires a financial asset (or a group of financial assets) measured at amortized cost basis to be presented at the net amount expected to be collected. The allowance for credit losses is a valuation account that is deducted from the amortized cost basis of the financial asset(s) to present the net carrying value at the amount expected to be collected on the financial asset. The income statement reflects the measurement of credit losses for newly recognized financial assets, as well as the expected increases or decreases of expected credit losses that have taken place during the period. Credit losses on available-for-sale debt securities should be measured in a manner similar to current U.S. GAAP; however, the credit losses are recorded through an allowance for credit losses rather than as a write-down. This approach is an improvement to current U.S. GAAP because an entity will be able to record reversals of credit losses (in situations in which the estimate of credit losses declines) in current period net income, which in turn should align the income statement recognition of credit losses with the reporting period in which changes occur. Current U.S. GAAP prohibits reflecting

CITIZENS, INC. AND CONSOLIDATED SUBSIDIARIES

Notes to Consolidated Financial Statements, Continued

March 31, 2019

(Unaudited)

those improvements in current-period earnings. For public business entities, the amendments in this ASU will be effective for fiscal years beginning after December 15, 2019, including interim periods within those fiscal years.

September 30, 2019 Form | 10-Q 13

|

| | |

CITIZENS, INC. | NOTES TO CONSOLIDATED FINANCIAL STATEMENTS |

| | (Unaudited) |

| | |

The Company is evaluatinghas evaluated the impact this guidance will have on our consolidated financial statements. This guidance could have a materialstatements and expects the impact on the Company's consolidated financial statements.to be immaterial.

In August 2018, the FASB issued ASU No. 2018-12, Financial Services-Insurance (Topic 944): Targeted Improvements to the Accounting for Long-Duration Contracts. This ASU amends four key areas of the accounting and impacts disclosures for long-duration insurance and investment contracts:

Requires updated assumptions for liability measurement. Assumptions used to measure the liability for traditional insurance contracts, which are typically determined at contract inception, will now be reviewed at least annually, and, if there is a change, updated, with the effect recorded in net income;

Standardizes the liability discount rate. The liability discount rate will be a market-observable discount rate (upper-medium grade fixed-income instrument yield), with the effect of rate changes recorded in other comprehensive income;

Provides greater consistency in measurement of market risk benefits. The two previous measurement models have been reduced to one measurement model (fair value), resulting in greater uniformity across similar market-based benefits and better alignment with the fair value measurement of derivatives used to hedge capital market risk;

Simplifies amortization of deferred acquisition costs. Previous earnings-based amortization methods have been replaced with a more level amortization basis; and

Requires enhanced disclosures. The new disclosures include rollforwards and information about significant assumptions and the effects of changes in those assumptions.

For calendar-year public companies, the changes will be effective on January 1, 2021.2022. The Company is evaluating the impact this guidance will have on our consolidated financial statements. This new guidance is expected to have a material impact on our consolidated financial statements.

In August 2018, the FASB issued ASU No. 2018-13, Disclosure Framework - ChangesFramework-Changes to the Disclosure Requirements for Fair Value Measurement. This ASU eliminates, adds and modifies certain disclosure requirements for fair value measurements. Among the changes, entities will no longer be required to disclose the amount of and reasons for transfers between Level 1 and Level 2 of the fair value hierarchy, but will be required to disclose the range and weighted average used to develop significant unobservable inputs for Level 3 fair value measurements. This ASU will be effective for interim and annual reporting periods beginning after December 15, 2019; however, early adoption is permitted. Entities are also allowed to elect early adoption of the eliminated or modified disclosure requirements and delay adoption of the new disclosure requirements until their effective date. As this ASU only revises disclosure requirements, it is not expected to have a material impact on the Company’s consolidated financial statements.

In September 2018, the FASB issued ASU No. 2018-15, Customer’s Accounting for Implementation Costs Incurred in a Cloud Computing Arrangement That Is a Service Contract. This ASU requires an entity in a cloud computing arrangement (i.e., hosting arrangement) that is a service contract to follow the internal-use software guidance in ASC 350-40 to determine which implementation costs to capitalize as assets or expense as incurred. Capitalized implementation costs should be presented in the same line item on the balance sheet as amounts prepaid for the hosted service, if any (generally as an "other asset"). The capitalized costs will be amortized over the term of the hosting arrangement, with the amortization expense being presented in the same income statement line item as the fees paid for the hosted service. This ASU will be effective for interim and annual reporting periods beginning after December 15, 2019; early adoption is permitted. We are evaluating the impact of this guidance on our limited cloud computing arrangements and our consolidated financial statements.

No other new accounting pronouncement issued or effective during the fiscal year had, or is expected to have, a material impact on our consolidated financial statements.

CITIZENS, INC. AND CONSOLIDATED SUBSIDIARIES

Notes to Consolidated Financial Statements, Continued

March 31, 2019

(Unaudited)

(3) Segment InformationSEGMENT INFORMATION

The Company has two reportable segments: Life Insurance and Home Service Insurance. The Life Insurance and

September 30, 2019 Form | 10-Q 14

|

| | |

CITIZENS, INC. | NOTES TO CONSOLIDATED FINANCIAL STATEMENTS |

| | (Unaudited) |

| | |

Home Service Insurance portions of the Company constitute separate businesses. CICA, CICA Ltd. and CNLIC constitute the Life Insurance segment, and SPLIC, SPFIC and MGLIC constitute the Home Service Insurance segment. In addition to the Life Insurance and Home Service Insurance business, the Company also operates other non-insurance ("Other Non-Insurance Enterprises") portions of the Company, which primarily include the Company's IT and Corporate-support functions, and are included in the tables presented below to properly reconcile the segment information with the consolidated financial statements of the Company.

The accounting policies of the reportable segments and Other Non-Insurance Enterprises are presented in accordance with U.S. GAAP and are the same as those used in the preparation of the consolidated financial statements. The Company evaluates profit and loss performance based on U.S. GAAP income before federal income taxes for its two reportable segments.

The Company's Other Non-Insurance Enterprises are the only reportable difference between segments and consolidated operations.

|

| | | | | | | | | | | | |

| | Three Months Ended |

| | March 31, 2019 |

| | Life Insurance | | Home Service Insurance | | Other Non-Insurance Enterprises | | Consolidated |

| | (In thousands) |

| Revenues: | | | | | | | |

| Premiums | $ | 30,914 |

| | 11,550 |

| | — |

| | 42,464 |

|

| Net investment income | 10,169 |

| | 3,086 |

| | 541 |

| | 13,796 |

|

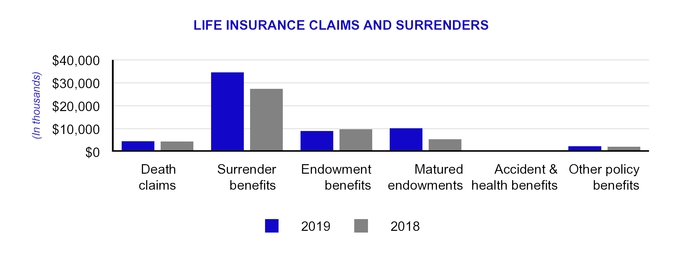

| Realized investment gains, net | 5,457 |

| | 484 |

| | 20 |

| | 5,961 |

|

| Other income | 183 |

| | 1 |

| | 1 |

| | 185 |

|

| Total revenue | 46,723 |

| | 15,121 |

| | 562 |

| | 62,406 |

|

| Benefits and expenses: | | | |

| | |

| | |

|

| Insurance benefits paid or provided: | |

| | |

| | |

| | |

|

| Claims and surrenders | 17,162 |

| | 5,871 |

| | — |

| | 23,033 |

|

| Increase in future policy benefit reserves | 11,313 |

| | 986 |

| | — |

| | 12,299 |

|

| Policyholders' dividends | 1,172 |

| | 10 |

| | — |

| | 1,182 |

|

| Total insurance benefits paid or provided | 29,647 |

| | 6,867 |

| | — |

| | 36,514 |

|

| Commissions | 4,373 |

| | 3,511 |

| | — |

| | 7,884 |

|

| Other general expenses | 6,205 |

| | 5,070 |

| | 2,857 |

| | 14,132 |

|

| Capitalization of deferred policy acquisition costs | (3,702 | ) | | (1,126 | ) | | — |

| | (4,828 | ) |

| Amortization of deferred policy acquisition costs | 5,441 |

| | 836 |

| | — |

| | 6,277 |

|

| Amortization of cost of customer relationships acquired | 122 |

| | 297 |

| | — |

| | 419 |

|

| Total benefits and expenses | 42,086 |

| | 15,455 |

| | 2,857 |

| | 60,398 |

|

| Income (loss) before federal income tax expense | $ | 4,637 |

| | (334 | ) | | (2,295 | ) | | 2,008 |

|

|

| | | | | | | | | | | | |

| | Life Insurance | | Home Service Insurance | | Other Non-Insurance Enterprises | | Consolidated |

| Three Months Ended September 30, 2019 | | | |

| (In thousands) | | | |

| | | | | | | | |

| Revenues: | | | | | | | |

| Premiums | $ | 34,385 |

| | 11,624 |

| | — |

| | 46,009 |

|

| Net investment income | 11,340 |

| | 3,309 |

| | 390 |

| | 15,039 |

|

| Realized investment gains, net | 61 |

| | 3 |

| | 8 |

| | 72 |

|

| Other income (loss) | 349 |

| | (2 | ) | | — |

| | 347 |

|

| Total revenue | 46,135 |

| | 14,934 |

| | 398 |

| | 61,467 |

|

| Benefits and expenses: | | | |

| | |

| | |

|

| Insurance benefits paid or provided: | |

| | |

| | |

| | |

|

| Claims and surrenders | 22,533 |

| | 6,218 |

| | — |

| | 28,751 |

|

| Increase in future policy benefit reserves | 7,667 |

| | (1,258 | ) | | — |

| | 6,409 |

|

| Policyholders' dividends | 1,551 |

| | 9 |

| | — |

| | 1,560 |

|

| Total insurance benefits paid or provided | 31,751 |

| | 4,969 |

| | — |

| | 36,720 |

|

| Commissions | 5,386 |

| | 3,493 |

| | — |

| | 8,879 |

|

| Other general expenses | 5,358 |

| | 4,669 |

| | 1,503 |

| | 11,530 |

|

| Capitalization of deferred policy acquisition costs | (4,743 | ) | | (1,241 | ) | | — |

| | (5,984 | ) |

| Amortization of deferred policy acquisition costs | 5,960 |

| | 1,875 |

| | — |

| | 7,835 |

|

| Amortization of cost of customer relationships acquired | 113 |

| | 242 |

| | — |

| | 355 |

|

| Total benefits and expenses | 43,825 |

| | 14,007 |

| | 1,503 |

| | 59,335 |

|

| Income (loss) before income tax expense | $ | 2,310 |

| | 927 |

| | (1,105 | ) | | 2,132 |

|

11

September 30, 2019 Form | 10-Q 15

CITIZENS, INC. AND CONSOLIDATED SUBSIDIARIES

Notes to Consolidated Financial Statements, Continued |

| | |

CITIZENS, INC. | NOTES TO CONSOLIDATED FINANCIAL STATEMENTS |

| | (Unaudited) |

| | |

March 31, 2019

(Unaudited)

|

| | | | | | | | | | | | |

| | Three Months Ended |

| | March 31, 2018 |

| | Life Insurance | | Home Service Insurance | | Other Non-Insurance Enterprises | | Consolidated |

| | (In thousands) |

| Revenues: | | | | | | | |

| Premiums | $ | 32,360 |

| | 11,669 |

| | — |

| | 44,029 |

|

| Net investment income | 10,130 |

| | 3,302 |

| | 339 |

| | 13,771 |

|

| Realized investment losses, net | (185 | ) | | (352 | ) | | (38 | ) | | (575 | ) |

| Other income (loss) | 209 |

| | (1 | ) | | — |

| | 208 |

|

| Total revenue | 42,514 |

| | 14,618 |

| | 301 |

| | 57,433 |

|

| Benefits and expenses: | |

| | |

| | |

| | |

|

| Insurance benefits paid or provided: | |

| | |

| | |

| | |

|

| Claims and surrenders | 15,291 |

| | 5,860 |

| | — |

| | 21,151 |

|

| Increase in future policy benefit reserves | 13,582 |

| | 1,026 |

| | — |

| | 14,608 |

|

| Policyholders' dividends | 1,297 |

| | 10 |

| | — |

| | 1,307 |

|

| Total insurance benefits paid or provided | 30,170 |

| | 6,896 |

| | — |

| | 37,066 |

|

| Commissions | 5,228 |

| | 3,731 |

| | — |

| | 8,959 |

|

Other general expenses(1) | (884 | ) | | 5,544 |

| | 1,847 |

| | 6,507 |

|

| Capitalization of deferred policy acquisition costs | (4,640 | ) | | (1,323 | ) | | — |

| | (5,963 | ) |

| Amortization of deferred policy acquisition costs | 6,540 |

| | 1,066 |

| | — |

| | 7,606 |

|

| Amortization of cost of customer relationships acquired | 152 |

| | 527 |

| | — |

| | 679 |

|

| Total benefits and expenses | 36,566 |

| | 16,441 |

| | 1,847 |

| | 54,854 |

|

| Income (loss) before federal income tax expense | $ | 5,948 |

| | (1,823 | ) | | (1,546 | ) | | 2,579 |

|

(1)During the three months ended March 31, 2018, the Company reduced its estimate of the liability accrued for policies that are not in compliance with Section 7702 of the Internal Revenue Code from $12.3 million to $5.1 million, as we continue to refine our estimates. The decrease is primarily related to the Life Insurance segment, which when offset by the impact of increased compliance costs, resulted in a negative amount reported for other general expenses for the Life Insurance segment for the three months ended March 31, 2018. For further information, refer to disclosures under the "Qualification of Life Products" heading within Note 7 in the Company's notes to consolidated financial statements. |

| | | | | | | | | | | | |

| | Life Insurance | | Home Service Insurance | | Other Non-Insurance Enterprises | | Consolidated |

| Nine Months Ended September 30, 2019 | | | |

| (In thousands) | | | |

| | | | | | | | |

| Revenues: | | | | | | | |

| Premiums | $ | 97,439 |

| | 34,838 |

| | — |

| | 132,277 |

|

| Net investment income | 33,121 |

| | 9,720 |

| | 1,309 |

| | 44,150 |

|

| Realized investment gains (losses), net | 5,586 |

| | 639 |

| | (3,061 | ) | | 3,164 |

|

| Other income | 1,146 |

| | — |

| | 2 |

| | 1,148 |

|

| Total revenue | 137,292 |

| | 45,197 |

| | (1,750 | ) | | 180,739 |

|

| Benefits and expenses: | | | |

| | |

| | |

|

| Insurance benefits paid or provided: | |

| | |

| | |

| | |

|

| Claims and surrenders | 61,011 |

| | 17,797 |

| | — |

| | 78,808 |

|

| Increase in future policy benefit reserves | 27,499 |

| | 681 |

| | — |

| | 28,180 |

|

| Policyholders' dividends | 4,136 |

| | 29 |

| | — |

| | 4,165 |

|

| Total insurance benefits paid or provided | 92,646 |

| | 18,507 |

| | — |

| | 111,153 |

|

| Commissions | 14,435 |

| | 10,712 |

| | — |

| | 25,147 |

|

| Other general expenses | 18,021 |

| | 15,071 |

| | 4,519 |

| | 37,611 |

|

| Capitalization of deferred policy acquisition costs | (12,465 | ) | | (3,759 | ) | | — |

| | (16,224 | ) |

| Amortization of deferred policy acquisition costs | 17,454 |

| | 3,589 |

| | — |

| | 21,043 |

|

| Amortization of cost of customer relationships acquired | 373 |

| | 819 |

| | — |

| | 1,192 |

|

| Total benefits and expenses | 130,464 |

| | 44,939 |

| | 4,519 |

| | 179,922 |

|

| Income (loss) before federal income tax expense | $ | 6,828 |

| | 258 |

| | (6,269 | ) | | 817 |

|

12

September 30, 2019 Form | 10-Q 16

|

| | |

CITIZENS, INC. | NOTES TO CONSOLIDATED FINANCIAL STATEMENTS |

| | (Unaudited) |

| | |

|

| | | | | | | | | | | | |

| | Life Insurance | | Home Service Insurance | | Other Non-Insurance Enterprises | | Consolidated |

| Three Months Ended September 30, 2018 | | | |

| (In thousands) | | | |

| | | | | | | | |

| Revenues: | | | | | | | |

| Premiums | $ | 35,784 |

| | 11,645 |

| | — |

| | 47,429 |

|

| Net investment income | 10,062 |

| | 3,276 |

| | 249 |

| | 13,587 |

|

| Realized investment gains (losses), net | (475 | ) | | (32 | ) | | 9 |

| | (498 | ) |

| Other income | 643 |

| | — |

| | — |

| | 643 |

|

| Total revenue | 46,014 |

| | 14,889 |

| | 258 |

| | 61,161 |

|

| Benefits and expenses: | |

| | |

| | |

| | |

|

| Insurance benefits paid or provided: | |

| | |

| | |

| | |

|

| Claims and surrenders | 19,212 |

| | 5,864 |

| | — |

| | 25,076 |

|

| Increase in future policy benefit reserves | 544 |

| | 1,109 |

| | — |

| | 1,653 |

|

| Policyholders' dividends | 1,581 |

| | 14 |

| | — |

| | 1,595 |

|

| Total insurance benefits paid or provided | 21,337 |

| | 6,987 |

| | — |

| | 28,324 |

|

| Commissions | 4,712 |

| | 3,944 |

| | — |

| | 8,656 |

|

| Other general expenses | 6,583 |

| | 4,502 |

| | 1,317 |

| | 12,402 |

|

| Capitalization of deferred policy acquisition costs | (3,873 | ) | | (1,688 | ) | | — |

| | (5,561 | ) |

| Amortization of deferred policy acquisition costs | 10,132 |

| | 1,280 |

| | — |

| | 11,412 |

|

| Amortization of cost of customer relationships acquired | 150 |

| | 216 |

| | — |

| | 366 |

|

| Total benefits and expenses | 39,041 |

| | 15,241 |

| | 1,317 |

| | 55,599 |

|

| Income (loss) before income tax expense | $ | 6,973 |

| | (352 | ) | | (1,059 | ) | | 5,562 |

|

September 30, 2019 Form | 10-Q 17

|

| | |

CITIZENS, INC. | NOTES TO CONSOLIDATED FINANCIAL STATEMENTS |

| | (Unaudited) |

| | |

|

| | | | | | | | | | | | |

| | Life Insurance | | Home Service Insurance | | Other Non-Insurance Enterprises | | Consolidated |

| Nine Months Ended September 30, 2018 | | | |

| (In thousands) | | | |

| | | | | | | | |

| Revenues: | | | | | | | |

| Premiums | $ | 102,537 |

| | 35,051 |

| | — |

| | 137,588 |

|

| Net investment income | 30,331 |

| | 9,894 |

| | 944 |

| | 41,169 |

|

| Realized investment losses, net | (684 | ) | | (535 | ) | | (32 | ) | | (1,251 | ) |

| Other income (loss) | 931 |

| | (1 | ) | | — |

| | 930 |

|

| Total revenue | 133,115 |

| | 44,409 |

| | 912 |

| | 178,436 |

|

| Benefits and expenses: | |

| | |

| | |

| | |

|

| Insurance benefits paid or provided: | |

| | |

| | |

| | |

|

| Claims and surrenders | 49,522 |

| | 17,322 |

| | — |

| | 66,844 |

|

| Increase in future policy benefit reserves | 29,509 |

| | 3,307 |

| | — |

| | 32,816 |

|

| Policyholders' dividends | 4,483 |

| | 33 |

| | — |

| | 4,516 |

|

| Total insurance benefits paid or provided | 83,514 |

| | 20,662 |

| | — |

| | 104,176 |

|

| Commissions | 14,717 |

| | 11,567 |

| | — |

| | 26,284 |

|

| Other general expenses | 12,607 |

| | 15,438 |

| | 5,330 |

| | 33,375 |

|

| Capitalization of deferred policy acquisition costs | (12,663 | ) | | (4,501 | ) | | — |

| | (17,164 | ) |

| Amortization of deferred policy acquisition costs | 22,912 |

| | 3,306 |

| | — |

| | 26,218 |

|

| Amortization of cost of customer relationships acquired | 434 |

| | 1,083 |

| | — |

| | 1,517 |

|

| Total benefits and expenses | 121,521 |

| | 47,555 |

| | 5,330 |

| | 174,406 |

|

| Income (loss) before federal income tax expense | $ | 11,594 |

| | (3,146 | ) | | (4,418 | ) | | 4,030 |

|

September 30, 2019 Form | 10-Q 18

CITIZENS, INC. AND CONSOLIDATED SUBSIDIARIES

Notes to Consolidated Financial Statements, Continued |

| | |

CITIZENS, INC. | NOTES TO CONSOLIDATED FINANCIAL STATEMENTS |

| | (Unaudited) |

| | |

March 31, 2019

(Unaudited)

(4) Earnings Per ShareEARNINGS PER SHARE

The following tables set forth the computation of basic and diluted earnings per share.

|

| | | | | | |

| Three Months Ended September 30, | 2019 | | 2018

(As Restated*) |

| (In thousands, except per share amounts) | |

| | | | |

| Basic and diluted earnings per share: | | | |

| Numerator: | | | |

| Net income (loss) | $ | 2,046 |

| | (7,109 | ) |

| Net income (loss) allocated to Class A common stock | $ | 2,026 |

| | (7,036 | ) |

| Net income (loss) allocated to Class B common stock | 20 |

| | (73 | ) |

| Net income (loss) | $ | 2,046 |

| | (7,109 | ) |

| | | | |

| Denominator: | | | |

| Weighted average shares of Class A outstanding - basic | 49,229 |

| | 49,080 |

|

| Weighted average shares of Class A outstanding - diluted | 49,327 |

| | 49,127 |

|

| Weighted average shares of Class B outstanding - basic and diluted | 1,002 |

| | 1,002 |

|

| Basic and diluted earnings (loss) per share of Class A common stock | $ | 0.04 |

| | (0.14 | ) |

| Basic and diluted earnings (loss) per share of Class B common stock | 0.02 |

| | (0.07 | ) |

* See Note 1 in the Notes to Consolidated Financial Statements

|

| | | | | | |

| Nine Months Ended September 30, | 2019 | | 2018

(As Restated*) |

| (In thousands, except per share amounts) | |

| | | | |

| Basic and diluted earnings per share: | | | |

| Numerator: | | | |

| Net loss | $ | (6,321 | ) | | (9,630 | ) |

| Net loss allocated to Class A common stock | $ | (6,257 | ) | | (9,533 | ) |

| Net loss allocated to Class B common stock | (64 | ) | | (97 | ) |

| Net loss | $ | (6,321 | ) | | (9,630 | ) |

| | | | |

| Denominator: | | | |

| Weighted average shares of Class A outstanding - basic | 49,229 |

| | 49,080 |

|

| Weighted average shares of Class A outstanding - diluted | 49,327 |

| | 49,127 |

|

| Weighted average shares of Class B outstanding - basic and diluted | 1,002 |

| | 1,002 |

|

| Basic and diluted loss per share of Class A common stock | $ | (0.13 | ) | | (0.19 | ) |

| Basic and diluted loss per share of Class B common stock | (0.06 | ) | | (0.10 | ) |

* See Note 1 in the Notes to Consolidated Financial Statements

September 30, 2019 Form | 10-Q 19

|

| | |

CITIZENS, INC. | NOTES TO CONSOLIDATED FINANCIAL STATEMENTS |

| | (Unaudited) |

| | | | |

|

| | | | | | |

| | Three Months Ended |

| March 31, 2019 | | March 31, 2018 |

| | (In thousands, except per share amounts) |

| Basic and diluted earnings per share: | | | |

| Numerator: | | | |

| Net income (loss) | $ | (3,802 | ) | | 37 |

|

| Net income (loss) allocated to Class A common stock | $ | (3,764 | ) | | 37 |

|

| Net income (loss) allocated to Class B common stock | (38 | ) | | — |

|

| Net income (loss) | $ | (3,802 | ) | | 37 |

|

| Denominator: | | | |

| Weighted average shares of Class A outstanding - basic | 49,229 |

| | 49,080 |

|

| Weighted average shares of Class A outstanding - diluted | 49,267 |

| | 49,080 |

|

| Weighted average shares of Class B outstanding - basic and diluted | 1,002 |

| | 1,002 |

|

| Basic and diluted earnings (loss) per share of Class A common stock | $ | (0.08 | ) | | — |

|

| Basic and diluted earnings (loss) per share of Class B common stock | (0.04 | ) | | — |

|

(5) InvestmentsINVESTMENTS

The Company invests primarily in fixed maturity securities, which totaled 90.0%90.1% of total cash, cash equivalents and investments at March 31,September 30, 2019. The Company's cash, cash equivalents and investments are listed below.

|

| | | | | | | | | | | | |

| | March 31, 2019 | | December 31, 2018 |

| | Carrying Value | | % of Total Carrying Value | | Carrying Value | | % of Total Carrying Value |

| | (In thousands) | | | | (In thousands) | | |

| Fixed maturity securities | $ | 1,295,514 |

| | 90.0 |

| | $ | 1,231,039 |

| | 88.7 |

| Equity securities | 15,672 |

| | 1.1 |

| | 15,068 |

| | 1.1 |

| Mortgage loans | 185 |

| | — |

| | 186 |

| | — |

| Policy loans | 81,474 |

| | 5.7 |

| | 80,825 |

| | 5.8 |

| Real estate and other long-term investments | 5,715 |