UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C.

FORM 10-Q

QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF

THE SECURITIES EXCHANGE ACT OF 1934

| For the quarterly period ended | Commission file number 1–6770 |

MUELLER INDUSTRIES, INC.

(Exact name of registrant as specified in its charter)

Delaware | 25-0790410 |

| (State or other jurisdiction | (I.R.S. Employer |

| of incorporation or organization) | Identification No.) |

| 8285 Tournament Drive, Suite 150 | |

Memphis, Tennessee | 38125 |

| (Address of principal executive offices) | (Zip Code) |

(901) 753-3200

(Registrant's telephone number, including area code)

Indicate by check mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Yesx No☐

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yesx NoNo☐☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of "large accelerated filer", "accelerated filer", and "smaller reporting company" in Rule 12b-2 of the Exchange Act.

Large accelerated filer ☒ | Accelerated filer ☐ |

Non-accelerated filer ☐ | Smaller reporting company ☐ |

Indicate by check mark whether the Registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

YesYes ☐o No☒

The number of shares of the Registrant's common stock outstanding as of October 19, 2015,April 25, 2016, was 57,158,180.57,126,707.

MUELLER INDUSTRIES, INC.

FORM 10-Q

For the Quarterly Period Ended September 26, 2015April 2, 2016

__________________________

As used in this report, the terms "Company," "Mueller," and "Registrant" mean Mueller Industries, Inc. and its consolidated subsidiaries taken as a whole, unless the context indicates otherwise.

__________________________

Page Number | ||

2

MUELLER INDUSTRIES, INC.

(Unaudited)

| For the Quarter Ended | For the Nine Months Ended | For the Quarter Ended | ||||||||||||||||||||||||||

| (In thousands, except per share data) | September 26, 2015 | September 27, 2014 | September 26, 2015 | September 27, 2014 | April 2, 2016 | March 28, 2015 | ||||||||||||||||||||||

| Net sales | $ | 535,184 | $ | 602,820 | $ | 1,628,019 | $ | 1,826,885 | $ | 532,809 | $ | 537,242 | ||||||||||||||||

| Cost of goods sold | 467,167 | 521,278 | 1,398,366 | 1,574,830 | 446,642 | 460,834 | ||||||||||||||||||||||

| Depreciation and amortization | 8,749 | 8,952 | 24,790 | 25,651 | 8,920 | 7,853 | ||||||||||||||||||||||

| Selling, general, and administrative expense | 32,241 | 34,004 | 98,492 | 100,512 | 35,780 | 32,831 | ||||||||||||||||||||||

| Gain on sale of assets | — | — | (15,376 | ) | (1,417 | ) | ||||||||||||||||||||||

| Severance | — | 860 | 3,442 | 3,072 | ||||||||||||||||||||||||

| Operating income | 27,027 | 37,726 | 118,305 | 124,237 | 41,467 | 35,724 | ||||||||||||||||||||||

| Interest expense | (1,682 | ) | (1,430 | ) | (5,977 | ) | (3,913 | ) | (1,848 | ) | (2,076 | ) | ||||||||||||||||

| Other income, net | 164 | 225 | 534 | 440 | 245 | 105 | ||||||||||||||||||||||

| �� | ||||||||||||||||||||||||||||

| Income before income taxes | 25,509 | 36,521 | 112,862 | 120,764 | 39,864 | 33,753 | ||||||||||||||||||||||

| Income tax expense | (5,223 | ) | (12,199 | ) | (36,374 | ) | (36,279 | ) | (14,121 | ) | (11,413 | ) | ||||||||||||||||

| Loss from unconsolidated subsidiary, net of tax | (2,191 | ) | — | (2,191 | ) | — | ||||||||||||||||||||||

| Income from unconsolidated affiliates | 2,922 | — | ||||||||||||||||||||||||||

| Consolidated net income | 18,095 | 24,322 | 74,297 | 84,485 | 28,665 | 22,340 | ||||||||||||||||||||||

| Net income attributable to noncontrolling interest | (295 | ) | (499 | ) | (868 | ) | (911 | ) | (35 | ) | (362 | ) | ||||||||||||||||

| Net income attributable to Mueller Industries, Inc. | $ | 17,800 | $ | 23,823 | $ | 73,429 | $ | 83,574 | $ | 28,630 | $ | 21,978 | ||||||||||||||||

| Weighted average shares for basic earnings per share | 56,375 | 56,107 | 56,272 | 55,999 | 56,467 | 56,193 | ||||||||||||||||||||||

| Effect of dilutive stock-based awards | 598 | 637 | 690 | 746 | 495 | 731 | ||||||||||||||||||||||

| Adjusted weighted average shares for diluted earnings per share | 56,973 | 56,744 | 56,962 | 56,745 | 56,962 | 56,924 | ||||||||||||||||||||||

| Basic earnings per share | $ | 0.32 | $ | 0.42 | $ | 1.30 | $ | 1.49 | $ | 0.51 | $ | 0.39 | ||||||||||||||||

| Diluted earnings per share | $ | 0.31 | $ | 0.42 | $ | 1.29 | $ | 1.47 | $ | 0.50 | $ | 0.39 | ||||||||||||||||

| Dividends per share | $ | 0.075 | $ | 0.075 | $ | 0.225 | $ | 0.225 | $ | 0.075 | $ | 0.075 | ||||||||||||||||

| See accompanying notes to condensed consolidated financial statements. | See accompanying notes to condensed consolidated financial statements. | See accompanying notes to condensed consolidated financial statements. | ||||||||||||||||||||||||||

3

MUELLER INDUSTRIES, INC.

(Unaudited)

| For the Quarter Ended | For the Nine Months Ended | |||||||||||||||||||

| (In thousands) | September 26, 2015 | September 27, 2014 | September 26, 2015 | September 27, 2014 | ||||||||||||||||

| Consolidated net income | $ | 18,095 | $ | 24,322 | $ | 74,297 | $ | 84,485 | ||||||||||||

| Other comprehensive (loss) income, net of tax: | ||||||||||||||||||||

| Foreign currency translation | (12,153 | ) | (6,661 | ) | (13,501 | ) | (3,698 | ) | ||||||||||||

| Net change with respect to derivative instruments and hedging activities | (915 | ) | (1 | ) | (174 | ) | (2 | ) | (2,016 | ) | (3 | ) | (1,650 | ) | (4) | |||||

| Net actuarial loss on pension and postretirement obligations | 1,231 | (5 | ) | 646 | (6 | ) | 2,000 | (7 | ) | 490 | (8) | |||||||||

| Other, net | (53 | ) | (1 | ) | (46 | ) | 7 | |||||||||||||

| Total other comprehensive loss | (11,890 | ) | (6,190 | ) | (13,563 | ) | (4,851 | ) | ||||||||||||

| Consolidated comprehensive income | 6,205 | 18,132 | 60,734 | 79,634 | ||||||||||||||||

| Comprehensive loss (income) attributable to noncontrolling interest | 709 | (889 | ) | 534 | (548 | ) | ||||||||||||||

| Comprehensive income attributable to Mueller Industries, Inc. | $ | 6,914 | $ | 17,243 | $ | 61,268 | $ | 79,086 | ||||||||||||

| See accompanying notes to condensed consolidated financial statements. | ||||||||||||||||||||

| For the Quarter Ended | ||||||||

| (In thousands) | April 2, 2016 | March 28, 2015 | ||||||

| Consolidated net income | $ | 28,665 | $ | 22,340 | ||||

| Other comprehensive income (loss), net of tax: | ||||||||

| Foreign currency translation | (1,111 | ) | (8,404 | ) | ||||

| Net change with respect to derivative instruments and hedging activities, net of tax of $(221) in 2016 and $274 in 2015 | 594 | (198 | ) | |||||

| Net actuarial loss on pension and postretirement obligations, net of tax of $(398) in 2016 and $(501) in 2015 | 1,172 | 1,416 | ||||||

| Other, net | 14 | (27 | ) | |||||

| Total other comprehensive income (loss) | 669 | (7,213 | ) | |||||

| Comprehensive income | 29,334 | 15,127 | ||||||

| Comprehensive loss attributable to noncontrolling interest | 739 | 345 | ||||||

| Comprehensive income attributable to Mueller Industries, Inc. | $ | 30,073 | $ | 15,472 | ||||

| See accompanying notes to condensed consolidated financial statements. | ||||||||

MUELLER INDUSTRIES, INC.

(Unaudited)

| (In thousands, except share data) | September 26, 2015 | December 27, 2014 | April 2, 2016 | December 26, 2015 | ||||||||||||||

| Assets | ||||||||||||||||||

| Current assets: | ||||||||||||||||||

| Cash and cash equivalents | $ | 220,745 | $ | 352,134 | $ | 270,149 | $ | 274,844 | ||||||||||

| Accounts receivable, less allowance for doubtful accounts of $623 in 2015 and $666 in 2014 | 299,417 | 275,065 | ||||||||||||||||

| Accounts receivable, less allowance for doubtful accounts of $496 in 2016 and $623 in 2015 | 275,881 | 251,571 | ||||||||||||||||

| Inventories | 250,799 | 256,585 | 240,608 | 239,378 | ||||||||||||||

| Other current assets | 54,538 | 57,429 | 34,123 | 34,608 | ||||||||||||||

| Total current assets | 825,499 | 941,213 | 820,761 | 800,401 | ||||||||||||||

| Property, plant, and equipment, net | 270,655 | 245,910 | 278,481 | 280,224 | ||||||||||||||

| Goodwill | 163,063 | 102,909 | ||||||||||||||||

| Investment in unconsolidated subsidiary | 63,709 | — | ||||||||||||||||

| Goodwill, net | 121,112 | 120,252 | ||||||||||||||||

| Intangible assets, net | 40,617 | 40,636 | ||||||||||||||||

| Investment in unconsolidated affiliates | 68,822 | 65,900 | ||||||||||||||||

| Other assets | 50,600 | 38,064 | 31,227 | 31,388 | ||||||||||||||

| Total assets | $ | 1,373,526 | $ | 1,328,096 | $ | 1,361,020 | $ | 1,338,801 | ||||||||||

| Liabilities | ||||||||||||||||||

| Current liabilities: | ||||||||||||||||||

| Current portion of debt | $ | 13,756 | $ | 36,194 | $ | 4,583 | $ | 11,760 | ||||||||||

| Accounts payable | 113,597 | 100,735 | 98,324 | 88,051 | ||||||||||||||

| Accrued wages and other employee costs | 34,042 | 41,595 | 27,974 | 35,636 | ||||||||||||||

| Other current liabilities | 68,146 | 59,545 | 71,727 | 73,982 | ||||||||||||||

| Total current liabilities | 229,541 | 238,069 | 202,608 | 209,429 | ||||||||||||||

| Long-term debt, less current portion | 204,500 | 205,250 | 206,000 | 204,250 | ||||||||||||||

| Pension liabilities | 17,323 | 20,070 | 16,319 | 17,449 | ||||||||||||||

| Postretirement benefits other than pensions | 26,701 | 21,486 | 17,396 | 17,427 | ||||||||||||||

| Environmental reserves | 21,566 | 21,842 | 20,932 | 20,943 | ||||||||||||||

| Deferred income taxes | 22,142 | 24,556 | 8,310 | 7,161 | ||||||||||||||

| Other noncurrent liabilities | 3,570 | 1,389 | 2,973 | 2,440 | ||||||||||||||

| Total liabilities | 525,343 | 532,662 | 474,538 | 479,099 | ||||||||||||||

| Equity | ||||||||||||||||||

| Mueller Industries, Inc. stockholders' equity: | ||||||||||||||||||

| Preferred stock - $1.00 par value; shares authorized 5,000,000; none outstanding | — | — | — | — | ||||||||||||||

| Common stock - $.01 par value; shares authorized 100,000,000; issued 80,183,004; outstanding 57,158,013 in 2015 and 56,901,445 in 2014 | 802 | 802 | ||||||||||||||||

| Common stock - $.01 par value; shares authorized 100,000,000; issued 80,183,004; outstanding 57,126,707 in 2016 and 57,158,608 in 2015 | 802 | 802 | ||||||||||||||||

| Additional paid-in capital | 269,529 | 268,575 | 273,576 | 271,158 | ||||||||||||||

| Retained earnings | 1,053,395 | 992,798 | 1,087,927 | 1,063,543 | ||||||||||||||

| Accumulated other comprehensive loss | (55,084 | ) | (42,923 | ) | (53,547 | ) | (54,990 | ) | ||||||||||

| Treasury common stock, at cost | (453,209 | ) | (457,102 | ) | (453,954 | ) | (453,228 | ) | ||||||||||

| Total Mueller Industries, Inc. stockholders' equity | 815,433 | 762,150 | 854,804 | 827,285 | ||||||||||||||

| Noncontrolling interest | 32,750 | 33,284 | 31,678 | 32,417 | ||||||||||||||

| Total equity | 848,183 | 795,434 | 886,482 | 859,702 | ||||||||||||||

| Commitments and contingencies | — | — | — | — | ||||||||||||||

| Total liabilities and equity | $ | 1,373,526 | $ | 1,328,096 | $ | 1,361,020 | $ | 1,338,801 | ||||||||||

| See accompanying notes to condensed consolidated financial statements. | See accompanying notes to condensed consolidated financial statements. | See accompanying notes to condensed consolidated financial statements. | ||||||||||||||||

5

MUELLER INDUSTRIES, INC.

(Unaudited)

| For the Nine Months Ended | For the Quarter Ended | |||||||||||||||||

| (In thousands) | September 26, 2015 | September 27, 2014 | April 2, 2016 | March 28, 2015 | ||||||||||||||

| Cash flows from operating activities | ||||||||||||||||||

| Consolidated net income | $ | 74,297 | $ | 84,485 | $ | 28,665 | $ | 22,340 | ||||||||||

| Reconciliation of consolidated net income to net cash provided by operating activities: | ||||||||||||||||||

| Depreciation and amortization | 25,132 | 25,888 | 9,011 | 8,015 | ||||||||||||||

| Stock-based compensation expense | 4,611 | 4,957 | 1,236 | 1,349 | ||||||||||||||

| Equity in losses of unconsolidated subsidiary | 2,191 | — | ||||||||||||||||

| Gain on disposal of assets | (14,875 | ) | (1,146 | ) | ||||||||||||||

| Impairment charges | 570 | — | ||||||||||||||||

| Equity in earnings of unconsolidated affiliates | (2,922 | ) | — | |||||||||||||||

| (Gain) loss on disposal of properties | (23 | ) | 1 | |||||||||||||||

| Deferred income taxes | (8,262 | ) | (6,908 | ) | 1,895 | (570 | ) | |||||||||||

| Income tax benefit from exercise of stock options | (953 | ) | (829 | ) | (96 | ) | (69 | ) | ||||||||||

| Changes in assets and liabilities, net of businesses acquired: | ||||||||||||||||||

| Changes in assets and liabilities: | ||||||||||||||||||

| Receivables | 5,249 | (62,854 | ) | (25,089 | ) | (36,692 | ) | |||||||||||

| Inventories | 29,901 | (14,868 | ) | (1,631 | ) | 7,534 | ||||||||||||

| Other assets | 4,302 | (15,272 | ) | (370 | ) | 9,257 | ||||||||||||

| Current liabilities | (27,580 | ) | (8,675 | ) | 655 | (7,389 | ) | |||||||||||

| Other liabilities | 740 | (797 | ) | (704 | ) | (131 | ) | |||||||||||

| Other, net | 145 | 223 | (291 | ) | 245 | |||||||||||||

| Net cash provided by operating activities | 95,468 | 4,204 | 10,336 | 3,890 | ||||||||||||||

| Cash flows from investing activities | ||||||||||||||||||

| Capital expenditures | (22,502 | ) | (28,406 | ) | (5,892 | ) | (7,392 | ) | ||||||||||

| Acquisition of businesses, net of cash acquired | (107,405 | ) | (30,137 | ) | ||||||||||||||

| Net withdrawals from restricted cash balances | 1,822 | 2,507 | ||||||||||||||||

| Investment in unconsolidated subsidiary | (65,900 | ) | — | |||||||||||||||

| Proceeds from sales of assets | 5,521 | 4,920 | ||||||||||||||||

| Net withdrawals from (deposits into) restricted cash | 84 | (12,593 | ) | |||||||||||||||

| Proceeds from the sale of assets | 1 | 492 | ||||||||||||||||

| Net cash used in investing activities | (188,464 | ) | (51,116 | ) | (5,807 | ) | (19,493 | ) | ||||||||||

| Cash flows from financing activities | ||||||||||||||||||

| Repayments of long-term debt | (250 | ) | (250 | ) | ||||||||||||||

| Dividends paid to stockholders of Mueller Industries, Inc. | (12,669 | ) | (12,606 | ) | (4,236 | ) | (4,216 | ) | ||||||||||

| Issuance of long-term debt | — | 12,008 | ||||||||||||||||

| Repayment of debt by joint venture, net | (21,597 | ) | (3,170 | ) | (7,024 | ) | (3,817 | ) | ||||||||||

| Net cash used to settle stock-based awards | (718 | ) | (887 | ) | ||||||||||||||

| Repurchase of common stock | — | (58 | ) | |||||||||||||||

| Repayments of long-term debt | (750 | ) | (800 | ) | ||||||||||||||

| Issuance of debt | 2,000 | — | ||||||||||||||||

| Net cash received to settle stock-based awards | 361 | 93 | ||||||||||||||||

| Income tax benefit from exercise of stock options | 953 | 829 | 96 | 69 | ||||||||||||||

| Net cash used in financing activities | (34,781 | ) | (4,684 | ) | (9,053 | ) | (8,121 | ) | ||||||||||

| Effect of exchange rate changes on cash | (3,612 | ) | (346 | ) | (171 | ) | (1,516 | ) | ||||||||||

| Decrease in cash and cash equivalents | (131,389 | ) | (51,942 | ) | (4,695 | ) | (25,240 | ) | ||||||||||

| Cash and cash equivalents at the beginning of the period | 352,134 | 311,800 | �� | 274,844 | 352,134 | |||||||||||||

| Cash and cash equivalents at the end of the period | $ | 220,745 | $ | 259,858 | $ | 270,149 | $ | 326,894 | ||||||||||

| See accompanying notes to condensed consolidated financial statements. | See accompanying notes to condensed consolidated financial statements. | See accompanying notes to condensed consolidated financial statements. | ||||||||||||||||

6

MUELLER INDUSTRIES, INC.

(Unaudited)

General

Certain information and footnote disclosures normally included in annual financial statements prepared in accordance with accounting principles generally accepted in the United States have been condensed or omitted. Results of operations for the interim periods presented are not necessarily indicative of results which may be expected for any other interim period or for the year as a whole. This Quarterly Report on Form 10-Q should be read in conjunction with the Company's Annual Report on Form 10-K, including the annual financial statements incorporated therein.

The accompanying unaudited interim financial statements include all normal recurring adjustments which are, in the opinion of management, necessary for a fair presentation of the results for the interim periods presented.included herein. The fiscal quarter ended April 2, 2016 contained 14 weeks, while the fiscal quarter ended March 28, 2015 contained 13 weeks.

Note 1 – Earnings per Common Share

Basic per share amounts have been computed based on the average number of common shares outstanding. Diluted per share amounts reflect the increase in average common shares outstanding that would result from the assumed exercise of outstanding stock options and vesting of restricted stock awards, computed using the treasury stock method. Approximately 383579 thousand stock basedand 180 thousand stock-based awards were excluded from the computation of diluted earnings per share for the quarterquarters ended September 26,April 2, 2016 and March 28, 2015, respectively, because they were antidilutive.

Note 2 – Commitments and Contingencies–Segment Information

| (In thousands) | September 26, 2015 | December 27, 2014 | ||||||||

| Raw materials and supplies | $ | 55,522 | $ | 53,586 | ||||||

| Work-in-process | 38,689 | 39,707 | ||||||||

| Finished goods | 162,780 | 168,481 | ||||||||

| Valuation reserves | (6,192 | ) | (5,189 | ) | ||||||

| Inventories | $ | 250,799 | $ | 256,585 | ||||||

Piping Systems

Piping Systems is composed of Standard Products (SPD),the following operating segments: Domestic Piping Systems Group, Canadian Operations, European Operations, Trading Group, and Mexican Operations.Mueller-Xingrong, the Company's Chinese joint venture. The OEM segment is composed of Industrial Products (IPD), Engineered Products (EPD), and Jiangsu Mueller–Xingrong Copper Industries Limited (Mueller-Xingrong). These segments are classified primarily by the markets for their products. Performance of segments is generally evaluated by their operating income.

Industrial Metals is composed of the following operating segments: Brass Rod & Copper Bar Products, Impacts & Micro Gauge, and Brass Value-Added Products. These businesses manufacture brass rod, impact extrusions, and forgings, as well as a wide variety of end products including plumbing brass, automotive components, valves, fittings, and fittings. EPD manufacturesgas assemblies. These products are manufactured in the U.S. and fabricatessold primarily to OEMs in the U.S, many of which are in the industrial, construction, heating, ventilation, and air-conditioning, plumbing, and refrigeration markets.

7

Climate

Climate is composed of the following operating segments: Refrigeration Products, Fabricated Tube Products, Westermeyer, and Turbotec. These domestic businesses manufacture and fabricate valves and assemblies primarily for the heating, ventilation, air-conditioning, and refrigeration air-conditioning, gas appliance, and barbecue grill markets and specialty copper, copper-alloy, and aluminum tube. Mueller-Xingrong manufactures engineered copper tube primarily for air-conditioning applications. These products are sold primarily to OEM customers.in the U.S.

Summarized segment information is as follows:

| For the Quarter Ended September 26, 2015 | For the Quarter Ended April 2, 2016 | ||||||||||||||||||||||||||||||||||||

| (In thousands) | Plumbing & Refrigeration Segment | OEM Segment | Corporate and Eliminations | Total | Piping Systems | Industrial Metals | Climate | Corporate and Eliminations | Total | ||||||||||||||||||||||||||||

| Net sales | $ | 325,022 | $ | 212,596 | $ | (2,434 | ) | $ | 535,184 | $ | 368,890 | $ | 134,521 | $ | 30,706 | $ | (1,308 | ) | $ | 532,809 | |||||||||||||||||

| Cost of goods sold | 280,891 | 188,665 | (2,389 | ) | 467,167 | 313,792 | 109,229 | 23,705 | (84 | ) | 446,642 | ||||||||||||||||||||||||||

| Depreciation and amortization | 4,468 | 3,839 | 442 | 8,749 | 5,649 | 2,135 | 599 | 537 | 8,920 | ||||||||||||||||||||||||||||

| Selling, general, and administrative expense | 20,104 | 6,814 | 5,323 | 32,241 | 18,290 | 3,245 | 2,523 | 11,722 | 35,780 | ||||||||||||||||||||||||||||

| Operating income | $ | 19,559 | $ | 13,278 | $ | (5,810 | ) | 27,027 | 31,159 | 19,912 | 3,879 | (13,483 | ) | 41,467 | |||||||||||||||||||||||

| Interest expense | (1,682 | ) | (1,848 | ) | |||||||||||||||||||||||||||||||||

| Other income, net | 164 | 245 | |||||||||||||||||||||||||||||||||||

| Income before income taxes | $ | 25,509 | |||||||||||||||||||||||||||||||||||

| Income before taxes | $ | 39,864 | |||||||||||||||||||||||||||||||||||

| For the Quarter Ended March 28, 2015 | ||||||||||||||||||||

| (In thousands) | Piping Systems | Industrial Metals | Climate | Corporate and Eliminations | Total | |||||||||||||||

| Net sales | $ | 361,482 | $ | 151,036 | $ | 25,811 | $ | (1,087 | ) | $ | 537,242 | |||||||||

| �� | ||||||||||||||||||||

| Cost of goods sold | 312,690 | 127,724 | 21,267 | (847 | ) | 460,834 | ||||||||||||||

| Depreciation and amortization | 5,187 | 1,655 | 425 | 586 | 7,853 | |||||||||||||||

| Selling, general, and administrative expense | 17,346 | 2,698 | 1,854 | 10,933 | 32,831 | |||||||||||||||

| Operating income | 26,259 | 18,959 | 2,265 | (11,759 | ) | 35,724 | ||||||||||||||

| Interest expense | (2,076 | ) | ||||||||||||||||||

| Other income, net | 105 | |||||||||||||||||||

| Income before taxes | $ | 33,753 | ||||||||||||||||||

| For the Quarter Ended September 27, 2014 | |||||||||||||||||

| (In thousands) | Plumbing & Refrigeration Segment | OEM Segment | Corporate and Eliminations | Total | |||||||||||||

| Net sales | $ | 357,843 | $ | 247,883 | $ | (2,906 | ) | $ | 602,820 | ||||||||

| Cost of goods sold | 308,927 | 215,225 | (2,874 | ) | 521,278 | ||||||||||||

| Depreciation and amortization | 5,287 | 3,148 | 517 | 8,952 | |||||||||||||

| Selling, general, and administrative expense | 22,613 | 5,533 | 5,858 | 34,004 | |||||||||||||

| Severance | 860 | — | — | 860 | |||||||||||||

| Operating income | $ | 20,156 | $ | 23,977 | $ | (6,407 | ) | 37,726 | |||||||||

| Interest expense | (1,430 | ) | |||||||||||||||

| Other income, net | 225 | ||||||||||||||||

| Income before income taxes | $ | 36,521 | |||||||||||||||

| For the Nine Months Ended September 26, 2015 | |||||||||||||||||

| (In thousands) | Plumbing & Refrigeration Segment | OEM Segment | Corporate and Eliminations | Total | |||||||||||||

| Net sales | $ | 957,375 | $ | 678,293 | $ | (7,649 | ) | $ | 1,628,019 | ||||||||

| Cost of goods sold | 819,591 | 586,305 | (7,530 | ) | 1,398,366 | ||||||||||||

| Depreciation and amortization | 13,568 | 9,827 | 1,395 | 24,790 | |||||||||||||

| Selling, general, and administrative expense | 61,117 | 19,534 | 17,841 | 98,492 | |||||||||||||

| Gain on sale of assets | (15,376 | ) | — | — | (15,376 | ) | |||||||||||

| Severance | 3,442 | — | — | 3,442 | |||||||||||||

| Operating income | $ | 75,033 | $ | 62,627 | $ | (19,355 | ) | 118,305 | |||||||||

| Interest expense | (5,977 | ) | |||||||||||||||

| Other income, net | 534 | ||||||||||||||||

| Income before income taxes | $ | 112,862 | |||||||||||||||

| (In thousands) | April 2, 2016 | December 26, 2015 | ||||||

| Segment assets: | ||||||||

| Piping Systems | $ | 815,400 | $ | 811,343 | ||||

| Industrial Metals | 193,662 | 174,897 | ||||||

| Climate | 41,172 | 39,876 | ||||||

| General Corporate | 310,786 | 312,685 | ||||||

| $ | 1,361,020 | $ | 1,338,801 | |||||

Note 3 – Inventories

| For the Nine Months Ended September 27, 2014 | |||||||||||||||||

| (In thousands) | Plumbing & Refrigeration Segment | OEM Segment | Corporate and Eliminations | Total | |||||||||||||

| Net sales | $ | 1,093,060 | $ | 743,322 | $ | (9,497 | ) | $ | 1,826,885 | ||||||||

| Cost of goods sold | 934,208 | 650,020 | (9,398 | ) | 1,574,830 | ||||||||||||

| Depreciation and amortization | 14,803 | 9,123 | 1,725 | 25,651 | |||||||||||||

| Selling, general, and administrative expense | 66,023 | 15,700 | 18,789 | 100,512 | |||||||||||||

| Gain on sale of assets | (1,417 | ) | — | — | (1,417 | ) | |||||||||||

| Severance | 3,072 | — | — | 3,072 | |||||||||||||

| Operating income | $ | 76,371 | $ | 68,479 | $ | (20,613 | ) | 124,237 | |||||||||

| Interest expense | (3,913 | ) | |||||||||||||||

| Other income, net | 440 | ||||||||||||||||

| Income before income taxes | $ | 120,764 | |||||||||||||||

| (In thousands) | April 2, 2016 | December 26, 2015 | ||||||

| Raw materials and supplies | $ | 53,983 | $ | 58,987 | ||||

| Work-in-process | 37,656 | 25,161 | ||||||

| Finished goods | 154,592 | 161,410 | ||||||

| Valuation reserves | (5,623 | ) | (6,180 | ) | ||||

| Inventories | $ | 240,608 | $ | 239,378 | ||||

Note 4 – Derivative Instruments and Hedging Activities

The Company's earnings and cash flows are subject to fluctuations due to changes in commodity prices, foreign currency exchange rates, and interest rates. The Company uses derivative instruments such as commodity futures contracts, foreign currency forward contracts, and interest rate swaps to manage these exposures.

All derivatives are recognized in the Condensed Consolidated Balance Sheets at their fair value. On the date the derivative contract is entered into, it is either a) designated as (i) a hedge of a forecasted transaction or the variability of cash flow to be paid (cash flow hedge), or (ii) a hedge of the fair value of a recognized asset or liability (fair value hedge) or b) not designated in a hedge accounting relationship, even though the derivative contract was executed to mitigate an economic exposure, as the Company does not enter into derivative contracts for trading purposes (economic hedge). Changes in the fair value of a derivative instrument that is qualified, designated and highly effective as a cash flow hedge are recorded in accumulated other comprehensive income (AOCI), to the extent effective, until they are reclassified to earnings in the same period or periods during which the hedged transaction affects earnings. Changes in the fair value of a derivative instrument that is qualified, designated and highly effective as a fair value hedge, along with the gain or loss on the hedged recognized asset or liability that is attributable to the hedged risk, are recorded in current earnings. Changes in the fair value of undesignated derivative instruments and the ineffective portion of designated derivative instruments are reported in current earnings.

The Company documents all relationships between hedging instruments and hedged items, as well as the risk-management objective and strategy for undertaking various hedge transactions. This process includes linking all derivatives that are designated as fair value hedges to specific assets and liabilities in the Condensed Consolidated Balance Sheets and linking cash flow hedges to specific forecasted transactions or variability of cash flow.

The Company also assesses, both at the hedge's inception and on an ongoing basis, whether the designated derivatives that are used in hedging transactions are highly effective in offsetting changes in cash flow or fair values of hedged items. When a derivative is determined not to be highly effective as a hedge or the underlying hedged transaction is no longer probable of occurring, hedge accounting is discontinued prospectively, in accordance with the derecognition criteria for hedge accounting.

Commodity Futures Contracts

Copper and brass represent the largest component of the Company's variable costs of production. The cost of these materials is subject to global market fluctuations caused by factors beyond the Company's control. The Company occasionally enters into forward fixed-price arrangements with certain customers; the risk of these arrangements is generally managed with commodity futures contracts. These futures contracts have been designated as cash flow hedges.

At April 2, 2016, the Company held open futures contracts to purchase approximately $23.7 million of copper over the next nine months related to fixed price sales orders. The fair value of those futures contracts was a $21 thousand net gain position, which was determined by obtaining quoted market prices (level 1 within the fair value hierarchy). In the next twelve months, the Company will reclassify into earnings realized gains or losses relating to cash flow hedges. At April 2, 2016, this amount was approximately $105 thousand of deferred net losses, net of tax.

The Company may also enter into futures contracts to protect the value of inventory against market fluctuations. At April 2, 2016, the Company held open futures contracts to sell approximately $21.0 million of copper over the next four months related to copper inventory. The fair value of those futures contracts was a $307 thousand loss position, which was determined by obtaining quoted market prices (level 1 within the fair value hierarchy).

9

Foreign Currency Forward Contracts

The Company has entered into certain contracts to purchase heavy machinery and equipment denominated in euros.

In anticipation of entering into these contracts, the Company entered into forward contracts to purchase euros to protect itself against adverse foreign exchange rate fluctuations.

At April 2, 2016, the Company held open forward contracts to purchase approximately 2.7 million euros over the next eight months. The fair value of these contracts, which was determined by obtaining quoted market prices (level 1 within the fair value hierarchy), was an $88 thousand gain position. At April 2, 2016, there was $184 thousand of deferred net gains, net of tax, included in AOCI that are expected to be reclassified into depreciation expense over the useful life of the heavy machinery and equipment.

Interest Rate Swap

On February 20, 2013, the Company entered into a two-year forward-starting interest rate swap agreement with an effective date of January 12, 2015, and an underlying notional amount of $200.0 million, pursuant to which the Company receives variable interest payments based on one-month LIBOR and pays fixed interest at a rate of 1.4 percent. Based on the Company's current variable premium pricing on its Term Loan Facility, the all-in fixed rate as of the effective date is 2.7 percent. The interest rate swap will mature on December 11, 2017, and is structured to offset the interest rate risk associated with the Company's floating-rate, LIBOR-based Term Loan Facility Agreement. The swap was designated and accounted for as a cash flow hedge from inception.

The fair value of the interest rate swap is estimated based on the present value of the difference between expected cash flows calculated at the contracted interest rate and the expected cash flows at the current market interest rate using observable benchmarks for LIBOR forward rates at the end of the period (level 2 within the fair value hierarchy). Interest payable and receivable under the swap agreement is accrued and recorded as an adjustment to interest expense. The fair value of the interest rate swap was a $2.3 million loss position at April 2, 2016, and there was $1.5 million of deferred net losses, net of tax, included in AOCI that are expected to be reclassified into interest expense over the term of the hedged item.

10

The Company presents its derivative assets and liabilities in our Condensed Consolidated Balance Sheets on a net basis by counterparty. The following table summarizes the location and fair value of the derivative instruments and disaggregates our net derivative assets and liabilities into gross components on a contract-by-contract basis:

| Asset Derivatives | Liability Derivatives | |||||||||||||||||

| Fair Value | Fair Value | |||||||||||||||||

| (In thousands) | Balance Sheet Location | April 2, 2016 | December 26, 2015 | Balance Sheet Location | April 2, 2016 | December 26, 2015 | ||||||||||||

| Hedging instrument: | ||||||||||||||||||

| Commodity contracts - gains | Other current assets | $ | 654 | $ | 60 | Other current liabilities | $ | 122 | $ | 238 | ||||||||

| Commodity contracts - losses | Other current assets | (82 | ) | — | Other current liabilities | (979 | ) | (1,864 | ) | |||||||||

| Foreign currency contracts - gains | Other current assets | 88 | — | Other current liabilities | — | 34 | ||||||||||||

| Foreign currency contracts - losses | Other current assets | — | — | Other current liabilities | — | (75 | ) | |||||||||||

| Interest rate swap | Other assets | — | — | Other liabilities | (2,319 | ) | (1,692 | ) | ||||||||||

Total derivatives (1) | $ | 660 | $ | 60 | $ | (3,176 | ) | $ | (3,359 | ) | ||||||||

(1) Does not include the impact of cash collateral provided to counterparties. | ||||||||||||||||||

The following tables summarize the effects of derivative instruments in our Condensed Consolidated Statements of Income:

| Three Months Ended | |||||||||

| (In thousands) | Location | April 2, 2016 | March 28, 2015 | ||||||

| Fair value hedges: | |||||||||

| (Loss) gain on commodity contracts (qualifying) | Cost of goods sold | $ | (50 | ) | $ | 213 | |||

| Gain (loss) on hedged item - Inventory | Cost of goods sold | 62 | (247 | ) | |||||

| Undesignated derivatives: | |||||||||

| Gain on commodity contracts (nonqualifying) | Cost of goods sold | $ | 494 | $ | 234 | ||||

The following tables summarize amounts recognized in and reclassified from AOCI during the period:

| Three Months Ended April 2, 2016 | |||||||||

| (In thousands) | Gain (Loss) Recognized in AOCI (Effective Portion), Net of Tax | Classification Gains (Losses) | Loss (Gain) Reclassified from AOCI (Effective Portion), Net of Tax | ||||||

| Cash flow hedges: | |||||||||

| Commodity contracts | $ | 873 | Cost of goods sold | $ | 68 | ||||

| Foreign currency contracts | 66 | Depreciation expense | — | ||||||

| Interest rate swap | (470 | ) | Interest expense | 69 | |||||

| Other | (12 | ) | Other | — | |||||

| Total | $ | 457 | Total | $ | 137 | ||||

11

| Three Months Ended March 28, 2015 | |||||||||

| (In thousands) | Gain (Loss) Recognized in AOCI (Effective Portion), Net of Tax | Classification Gains (Losses) | Loss (Gain) Reclassified from AOCI (Effective Portion), Net of Tax | ||||||

| Cash flow hedges: | |||||||||

| Commodity contracts | $ | 274 | Cost of goods sold | $ | 571 | ||||

| Foreign currency contracts | (55 | ) | Depreciation expense | — | |||||

| Interest rate swap | (1,032 | ) | Interest expense | 68 | |||||

| Other | (24 | ) | Other | — | |||||

| Total | $ | (837 | ) | Total | $ | 639 | |||

The Company enters into futures and forward contracts that closely match the terms of the underlying transactions. As a result, the ineffective portion of the open hedge contracts through April 2, 2016 was not material to the Condensed Consolidated Statements of Income.

The Company primarily enters into International Swaps and Derivatives Association master netting agreements with major financial institutions that permit the net settlement of amounts owed under their respective derivative contracts. Under these master netting agreements, net settlement generally permits the Company or the counterparty to determine the net amount payable for contracts due on the same date and in the same currency for similar types of derivative transactions. The master netting agreements generally also provide for net settlement of all outstanding contracts with a counterparty in the case of an event of default or a termination event. The Company does not offset fair value amounts for derivative instruments and fair value amounts recognized for the right to reclaim cash collateral. At April 2, 2016 and December 26, 2015, the Company had recorded restricted cash in other current assets of $2.7 million and $2.6 million, respectively, as collateral related to open derivative contracts under the master netting arrangements.

Note 5 –Benefit– Investment in Unconsolidated Affiliates

The Company owns a 50 percent interest in Tecumseh Products Holdings LLC (Joint Venture), an unconsolidated affiliate that acquired Tecumseh Products Company (Tecumseh) during 2015. The Company also owns 50 percent interest in a second unconsolidated affiliate that provided financing to Tecumseh in conjunction with the acquisition. These investments are accounted for using the equity method of accounting as the Company can exercise significant influence but does not own a majority equity interest or otherwise control the repective entities. Under the equity method of accounting, these investments are stated at initial cost and are adjusted for subsequent additional investments and the Company's proportionate share of earnings or losses and distributions.

The Company records its proportionate share of the investee's net income or loss one quarter in arrears as income (loss) from unconsolidated affiliates in the Condensed Consolidated Statements of Income.

The following tables present summarized financial information derived from the Company's equity method investees' combined consolidated financial statements, which are prepared in accordance with U.S. GAAP.

| (In thousands) | December 31, 2015 | September 30, 2015 | ||||||

| Current assets | $ | 225,500 | $ | 251,389 | ||||

| Noncurrent assets | 118,600 | 112,156 | ||||||

| Current liabilities | 138,781 | 178,784 | ||||||

| Noncurrent liabilities | 71,700 | 63,643 | ||||||

12

| For the Quarter Ended | ||||||||

| (In thousands) | December 31, 2015 | September 30, 2015 | ||||||

| Net sales | $ | 151,600 | $ | — | ||||

| Gross profit | 18,000 | — | ||||||

| Net income | 5,843 | — | ||||||

Included in the equity method investees' net income for the quarter ended December 31, 2015 is a gain of $17.1 million that resulted from the allocation of the purchase price, which was finalized during the quarter. That gain was offset by restructuring and impairment charges of $5.3 million and operating losses of $6.0 million.

Note 6 – Benefits Plans

The Company sponsors several qualified and nonqualified pension plans and other postretirement benefit plans for certain of its employees. The components of net periodic benefit cost (income) are as follows:

| For the Quarter Ended | For the Nine Months Ended | For the Quarter Ended | ||||||||||||||||||||||||||

| (In thousands) | September 26, 2015 | September 27, 2014 | September 26, 2015 | September 27, 2014 | April 2, 2016 | March 28, 2015 | ||||||||||||||||||||||

| Pension benefits: | ||||||||||||||||||||||||||||

| Service cost | $ | 250 | $ | 199 | $ | 750 | $ | 596 | $ | 195 | $ | 272 | ||||||||||||||||

| Interest cost | 2,041 | 2,064 | 6,122 | 6,191 | 1,975 | 2,054 | ||||||||||||||||||||||

| Expected return on plan assets | (2,654 | ) | (3,202 | ) | (7,963 | ) | (9,604 | ) | (2,466 | ) | (2,654 | ) | ||||||||||||||||

| Amortization of prior service cost | — | 1 | — | 1 | ||||||||||||||||||||||||

| Amortization of net loss | 774 | 714 | ||||||||||||||||||||||||||

| Net periodic benefit cost | $ | 478 | $ | 386 | ||||||||||||||||||||||||

| Other benefits: | ||||||||||||||||||||||||||||

| Service cost | $ | 62 | $ | 96 | ||||||||||||||||||||||||

| Interest cost | 156 | 196 | ||||||||||||||||||||||||||

| Amortization of prior service (credit) cost | (224 | ) | 2 | |||||||||||||||||||||||||

| Amortization of net loss | 685 | 188 | 2,055 | 565 | 2 | 3 | ||||||||||||||||||||||

| Net periodic benefit (income) cost | $ | 322 | $ | (750 | ) | $ | 964 | $ | (2,251 | ) | $ | (4 | ) | $ | 297 | |||||||||||||

| Other benefits: | ||||||||||||||||||||||||||||

| Service cost | $ | 90 | $ | 88 | $ | 270 | $ | 264 | ||||||||||||||||||||

| Interest cost | 193 | 181 | 579 | 544 | ||||||||||||||||||||||||

| Amortization of prior service cost (credit) | 2 | — | 5 | (1 | ) | |||||||||||||||||||||||

| Amortization of net gain | (7 | ) | (55 | ) | (20 | ) | (164 | ) | ||||||||||||||||||||

| Net periodic benefit cost | $ | 278 | $ | 214 | $ | 834 | $ | 643 | ||||||||||||||||||||

Note 7 – Derivative InstrumentsCommitments and Hedging ActivitiesContingencies

The Company is involved in certain litigation as a result of claims that arose in the ordinary course of business, which management believes will not have a material adverse effect on the Company's earningsfinancial position, results of operations, or cash flows. It may also realize the benefit of certain legal claims and cash flowslitigation in the future; these gain contingencies are subject to fluctuations due to changes in commodity prices, foreign currency exchange rates, and interest rates. The Company uses derivative instruments such as commodity futures contracts, foreign currency forward contracts, and interest rate swaps to manage these exposures.

Guarantees

Guarantees, in the dateform of letters of credit, are issued by the derivative contract is entered into, it is designated as (i) a hedgeCompany generally to assure the payment of a forecasted transaction or the variability of cash flow to be paid (cash flow hedge), or (ii) a hedgeinsurance deductibles and certain retiree health benefits. The terms of the fair valueguarantees are generally one year but are renewable annually as required. These letters are primarily backed by the Company's revolving credit facility. The maximum payments that the Company could be required to make under its guarantees at April 2, 2016 were $6.6 million.

Note 8 – Income Taxes

The Company's effective tax rate for the first quarter of a recognized asset or liability (fair value hedge). Changes in the fair value of a derivative that is qualified, designated and highly effective as a cash flow hedge are recorded in accumulated other comprehensive income (AOCI), to the extent effective, until they are reclassified to earnings in2016 was 35 percent compared with 34 percent for the same period or periods during whichlast year. The items impacting the hedged transaction affects earnings. Changes ineffective tax rate for the fair valuefirst quarter of a derivative that is qualified, designated and highly effective as a fair value hedge, along with the gain or loss on the hedged recognized asset or liability that is2016 were primarily attributable to reductions for the hedged risk, are recorded in current earnings. Changes in the fair valueU.S. production activities deduction of undesignated derivative instruments$0.9 million and the ineffective portioneffect of designated derivative instruments are reportedforeign tax rates lower than statutory tax rates of $1.1 million. These items were partially offset by the provision for state income taxes, net of the federal benefit, of $0.8 million and the recording of the basis difference in current earnings.

$1.0 million.

| Asset Derivatives | Liability Derivatives | |||||||||||||||||

| Fair Value | Fair Value | |||||||||||||||||

| (In thousands) | Balance Sheet Location | Sept. 26, 2015 | Dec. 27, 2014 | Balance Sheet Location | Sept. 26, 2015 | Dec. 27, 2014 | ||||||||||||

| Hedging instrument: | ||||||||||||||||||

| Commodity contracts - gains | Other current assets | $ | 511 | $ | 99 | Other current liabilities | $ | 61 | $ | 15 | ||||||||

| Commodity contracts - losses | Other current assets | — | (4 | ) | Other current liabilities | (1,912 | ) | (832 | ) | |||||||||

| Foreign currency contracts | Other current assets | — | — | Other current liabilities | (23 | ) | (81 | ) | ||||||||||

| Interest rate swap | Other assets | — | — | Other liabilities | (2,817 | ) | (927 | ) | ||||||||||

Total derivatives (1) | $ | 511 | $ | 95 | $ | (4,691 | ) | $ | (1,825 | ) | ||||||||

(1) Does not include the impact of cash collateral received from or provided to counterparties. | ||||||||||||||||||

| Three Months Ended | Nine Months Ended | ||||||||||||||||

| (In thousands) | Location | Sept. 26, 2015 | Sept. 27, 2014 | Sept. 26, 2015 | Sept. 27, 2014 | ||||||||||||

| Fair value hedges: | |||||||||||||||||

| Gain on commodity contracts (qualifying) | Cost of goods sold | $ | 1,831 | $ | 1,100 | $ | 3,300 | $ | 7,371 | ||||||||

| Loss on hedged item - Inventory | Cost of goods sold | (1,943 | ) | (922 | ) | (3,593 | ) | (6,702 | ) | ||||||||

| Three Months Ended | Nine Months Ended | ||||||||||||||||

| (In thousands) | Location | Sept. 26, 2015 | Sept. 27, 2014 | Sept. 26, 2015 | Sept. 27, 2014 | ||||||||||||

| Undesignated derivatives: | |||||||||||||||||

| Gain on commodity contracts (nonqualifying) | Cost of goods sold | $ | 1,143 | $ | — | $ | 2,422 | $ | 1,466 | ||||||||

| Three Months Ended September 26, 2015 | ||||||||||

| (In thousands) | (Loss) Gain Recognized in AOCI (Effective Portion), Net of Tax | Classification Gains (Losses) | (Gain) Loss Reclassified from AOCI (Effective Portion), Net of Tax | |||||||

| Cash flow hedges: | ||||||||||

| Commodity contracts | $ | (2,046 | ) | Cost of goods sold | $ | 1,708 | ||||

| Foreign currency contracts | (7 | ) | Depreciation expense | — | ||||||

| Interest rate swap | (632 | ) | Interest expense | 58 | ||||||

| Three Months Ended September 27, 2014 | ||||||||||

| (In thousands) | (Loss) Gain Recognized in AOCI (Effective Portion), Net of Tax | Classification Gains (Losses) | (Gain) Loss Reclassified from AOCI (Effective Portion), Net of Tax | |||||||

| Cash flow hedges: | ||||||||||

| Commodity contracts | $ | (202 | ) | Cost of goods sold | $ | (174 | ) | |||

| Foreign currency contracts | (181 | ) | Depreciation expense | (46 | ) | |||||

| Interest rate swap | 430 | Interest expense | — | |||||||

| Nine Months Ended September 26, 2015 | ||||||||||

| (In thousands) | (Loss) Gain Recognized in AOCI (Effective Portion), Net of Tax | Classification Gains (Losses) | Loss (Gain) Reclassified from AOCI (Effective Portion), Net of Tax | |||||||

| Cash flow hedges: | ||||||||||

| Commodity contracts | $ | (2,931 | ) | Cost of goods sold | $ | 2,198 | ||||

| Foreign currency contracts | (59 | ) | Depreciation expense | — | ||||||

| Interest rate swap | (1,397 | ) | Interest expense | 189 | ||||||

| Other | (16 | ) | Other | |||||||

| Nine Months Ended September 27, 2014 | ||||||||||

| (In thousands) | (Loss) Gain Recognized in AOCI (Effective Portion), Net of Tax | Classification Gains (Losses) | Loss (Gain) Reclassified from AOCI (Effective Portion), Net of Tax | |||||||

| Cash flow hedges: | ||||||||||

| Commodity contracts | $ | (634 | ) | Cost of goods sold | $ | 285 | ||||

| Foreign currency contracts | (184 | ) | Depreciation expense | (283 | ) | |||||

| Interest rate swap | (837 | ) | Interest expense | — | ||||||

| Other | 3 | Other | ||||||||

The difference between the effective tax rate and the amount computed using the U.S. federal statutory tax rate for the first quarter of 2015 was primarily attributable to reductions for the U.S. production activities deduction of $1.0 million and the effect of foreign tax rates lower than statutory tax rates of $0.5 million. These items were partially offset by the provision for state income taxes, net of the federal benefit, of $0.8 million.

The Company files a consolidated U.S. federal income tax return and numerous consolidated and separate-company income tax returns in many state, local, and foreign jurisdictions. The statute of limitations is open for the Company's federal tax return and most state income tax returns for 2012 and all subsequent years and is open for certain state and foreign returns for earlier tax years due to ongoing audits and differing statute periods. The Internal Revenue Service is currently auditing the Company's 2013 federal tax return. While the Company believes that it is adequately reserved for possible future audit adjustments, the final resolution of these examinations cannot be determined with certainty and could result in final settlements that differ from current estimates.

Note 89 – Accumulated Other Comprehensive Income

AOCI includes certain foreign currency translation adjustments from those subsidiaries not using the U.S. dollar as their functional currency, net deferred gains and losses on certain derivative instruments accounted for as cash flow hedges, adjustments to pension and OPEB liabilities, and unrealized gains and losses on marketable securities classified as available-for-sale.

The following table provides changes in AOCI by component, net of taxes and noncontrolling interest (amounts in parentheses indicate debits to AOCI):

| For the Nine Months Ended September 26, 2015 | ||||||||||||||||||||

| (In thousands) | Cumulative Translation Adjustment | Unrealized (Losses)/Gains on Derivatives | Minimum Pension/OPEB Liability Adjustment | Unrealized Gains on Equity Investments | Total | |||||||||||||||

| Balance at December 27, 2014 | $ | (7,076 | ) | $ | (953 | ) | $ | (35,164 | ) | $ | 270 | $ | (42,923 | ) | ||||||

| Other comprehensive (loss) income before reclassifications | (12,099 | ) | (4,403 | ) | 510 | (46 | ) | (16,038 | ) | |||||||||||

| Amounts reclassified from AOCI | — | 2,387 | 1,490 | — | 3,877 | |||||||||||||||

| Net current-period other comprehensive income | (12,099 | ) | (2,016 | ) | 2,000 | (46 | ) | (12,161 | ) | |||||||||||

| Balance at September 26, 2015 | $ | (19,175 | ) | $ | (2,969 | ) | $ | (33,164 | ) | $ | 224 | $ | (55,084 | ) | ||||||

| For the Quarter Ended April 2, 2016 | ||||||||||||||||||||

| (In thousands) | Cumulative Translation Adjustment | Unrealized (Losses)/Gains on Derivatives | Minimum Pension/OPEB Liability Adjustment | Unrealized Gains on Equity Investments | Total | |||||||||||||||

| Balance at December 26, 2015 | $ | (24,773 | ) | $ | (2,009 | ) | $ | (28,429 | ) | $ | 221 | $ | (54,990 | ) | ||||||

| Other comprehensive income (loss) before reclassifications | (337 | ) | 457 | 760 | 14 | 894 | ||||||||||||||

| Amounts reclassified from accumulated OCI | — | 137 | 412 | — | 549 | |||||||||||||||

| Net current-period other comprehensive income | (337 | ) | 594 | 1,172 | 14 | 1,443 | ||||||||||||||

| Balance at April 2, 2016 | $ | (25,110 | ) | $ | (1,415 | ) | $ | (27,257 | ) | $ | 235 | $ | (53,547 | ) | ||||||

| For the Quarter Ended March 28, 2015 | ||||||||||||||||||||

| (In thousands) | Cumulative Translation Adjustment | Unrealized (Losses)/Gains on Derivatives | Minimum Pension/OPEB Liability Adjustment | Unrealized Gains on Equity Investments | Total | |||||||||||||||

| Balance at December 27, 2014 | $ | (7,076 | ) | $ | (953 | ) | $ | (35,164 | ) | $ | 270 | $ | (42,923 | ) | ||||||

| Other comprehensive income (loss) before reclassifications | (7,697 | ) | (837 | ) | 895 | (27 | ) | (7,666 | ) | |||||||||||

| Amounts reclassified from accumulated OCI | — | 639 | 521 | — | 1,160 | |||||||||||||||

| Net current-period other comprehensive income | (7,697 | ) | (198 | ) | 1,416 | (27 | ) | (6,506 | ) | |||||||||||

| Balance at March 28, 2015 | $ | (14,773 | ) | $ | (1,151 | ) | $ | (33,748 | ) | $ | 243 | $ | (49,429 | ) | ||||||

| For the Nine Months Ended September 27, 2014 | ||||||||||||||||||||

| (In thousands) | Cumulative Translation Adjustment | Unrealized (Losses)/Gains on Derivatives | Minimum Pension/OPEB Liability Adjustment | Unrealized Gains on Equity Investments | Total | |||||||||||||||

| Balance at December 28, 2013 | $ | (462 | ) | $ | 1,546 | $ | (12,158 | ) | $ | 255 | $ | (10,819 | ) | |||||||

| Other comprehensive (loss) income before reclassifications | (3,337 | ) | (1,652 | ) | 143 | 7 | (4,839 | ) | ||||||||||||

| Amounts reclassified from AOCI | — | 2 | 347 | — | 349 | |||||||||||||||

| Net current-period other comprehensive income | (3,337 | ) | (1,650 | ) | 490 | 7 | (4,490 | ) | ||||||||||||

| Balance at September 27, 2014 | $ | (3,799 | ) | $ | (104 | ) | $ | (11,668 | ) | $ | 262 | $ | (15,309 | ) | ||||||

Reclassification adjustments out of AOCI were as follows:

| Amount reclassified from AOCI | Amount reclassified from AOCI | |||||||||||||||||

| For the Three Months Ended | For the Quarter Ended | |||||||||||||||||

| (In thousands) | Sept. 26, 2015 | Sept. 27, 2014 | Affected line item | April 2, 2016 | March 28, 2015 | Affected line item | ||||||||||||

| Unrealized losses/(gains) on derivatives: | ||||||||||||||||||

| Commodity contracts | $ | 2,339 | $ | (214 | ) | Cost of goods sold | $ | 237 | $ | 762 | Cost of goods sold | |||||||

| Foreign currency contracts | — | (71 | ) | Depreciation expense | ||||||||||||||

| Interest rate swap | 91 | — | Interest expense | 108 | 106 | Interest expense | ||||||||||||

| (664 | ) | 65 | Income tax (expense) benefit | (208 | ) | (229 | ) | Income tax expense | ||||||||||

| 1,766 | (220 | ) | Net of tax | 137 | 639 | Net of tax | ||||||||||||

| — | — | Noncontrolling interest | — | — | Noncontrolling interest | |||||||||||||

| $ | 1,766 | $ | (220 | ) | Net of tax and noncontrolling interest | $ | 137 | $ | 639 | Net of tax and noncontrolling interest | ||||||||

| Amortization of net loss and prior service cost on employee benefit plans | $ | 680 | $ | 134 | Selling, general, and administrative expense | $ | 552 | $ | 719 | Selling, general, and administrative expense | ||||||||

| (188 | ) | (19 | ) | Income tax expense | (140 | ) | (198 | ) | Income tax expense | |||||||||

| 492 | 115 | Net of tax | 412 | 521 | Net of tax | |||||||||||||

| — | — | Noncontrolling interest | — | — | Noncontrolling interest | |||||||||||||

| $ | 492 | $ | 115 | Net of tax and noncontrolling interest | $ | 412 | $ | 521 | Net of tax and noncontrolling interest | |||||||||

| Amount reclassified from AOCI | |||||||||

| For the Nine Months Ended | |||||||||

| (In thousands) | Sept. 26, 2015 | Sept. 27, 2014 | Affected line item | ||||||

| Unrealized losses/(gains) on derivatives: | |||||||||

| Commodity contracts | $ | 2,990 | $ | 351 | Cost of goods sold | ||||

| Foreign currency contracts | — | (446 | ) | Depreciation expense | |||||

| Interest rate swap | 295 | — | Interest expense | ||||||

| (898 | ) | 97 | Income tax (expense) benefit | ||||||

| 2,387 | 2 | Net of tax | |||||||

| — | — | Noncontrolling interest | |||||||

| $ | 2,387 | $ | 2 | Net of tax and noncontrolling interest | |||||

| Amortization of net loss and prior service cost on employee benefit plans | $ | 2,040 | $ | 401 | Selling, general, and administrative expense | ||||

| (550 | ) | (54 | ) | Income tax expense | |||||

| 1,490 | 347 | Net of tax | |||||||

| — | — | Noncontrolling interest | |||||||

| $ | 1,490 | $ | 347 | Net of tax and noncontrolling interest | |||||

Note 1110 – Recently Issued Accounting Standards

In May 2014,March 2016, the Financial Accounting Standards Board (FASB) issued ASU (Accounting Standards Update) No. 2015-09, Compensation – Stock Compensation (Topic 718): Improvement to Employee Share-Based Payment Accounting Standards Update (ASU)(ASU 2016-09). The ASU requires all income tax effects of awards to be recognized in the income statement when the awards vest or are settled. It will also allow a company to make a policy election to account for forfeitures as they occur. The guidance is effective for public business entities in interim and fiscal periods beginning after December 15, 2016. Early adoption is permitted, but all of the guidance must be adopted in the same period. The Company is in the process of evaluating the impact of ASU 2016-09 on its Condensed Consolidated Financial Statements.

15

In February 2016, the FASB issued ASU No. 2016-02, Leases (Topic 842) (ASU 2016-02). ASU 2016-02 requires an entity to recognize a right-of-use asset and lease liability for all leases with terms of more than 12 months. Recognition, measurement and presentation of expenses will depend on classification as a financing or operating lease. The amendments also require certain quantitative and qualitative disclosures about leasing arrangements. The ASU will be effective for interim and fiscal periods beginning after December 15, 2018. Early adoption is permitted. The updated guidance requires a modified retrospective adoption. The Company is still evaluating the effects that the provision of ASU 2016-02 will have on its Condensed Consolidated Financial Statements.

In April 2015, the FASB issued ASU No. 2015-03, Interest – Imputation of Interest (Topic 835-30): Simplifying the Presentation of Debt Issue Costs (ASU 2015-03). The ASU simplifies the presentation of debt issuance costs by requiring debt issuance costs related to a recognized debt liability to be presented on the balance sheet as a direct deduction from the debt liability rather than as a separate asset. In circumstances in which there is not an associated debt liability amount recorded in the financial statements when the debt issuance costs are incurred, they will be reported on the balance sheet as an asset until the debt liability is recorded. The guidance is effective for public business entities in interim and fiscal periods beginning after December 15, 2015. Retrospective application is required. The Company adopted ASU 2015-03 effective December 27, 2015. The adoption of the ASU did not have a material impact on the Company's Condensed Consolidated Financial Statements.

In May 2014, the FASB issued ASU No. 2014-09, Revenue from Contracts with Customers (Topic 606) (ASU 2014-09). The ASU will supersede virtually all existing revenue recognition guidance under U.S. GAAP and will be effective for annual reporting periods beginning after December 15, 2017. The fundamental principles of the new guidance are that companies should recognize revenue in a manner that reflects the timing of the transfer of services to customers and the amount of revenue recognized reflects the consideration that a company expects to receive for the goods and services provided. The new guidance establishes a five-step approach for the recognition of revenue. The Company is in the process of evaluating the impact of ASU 2014-09 on its Condensed Consolidated Financial Statements.

In April 2015,February 2016, the FASB issued ASU No. 2015-04, Compensation – Retirement Benefits (Topic 715): Practical ExpedientCompany entered into an agreement providing for the Measurement Datepurchase of an Employers' Defined Benefit Obligationa 60 percent equity interest in Jungwoo Metal Ind. Co., LTD (Jungwoo) for KRW 25 billion or approximately $22.0 million. Jungwoo is a manufacturer of copper-based pipe joining products headquartered in Seoul, South Korea and Plan Assets (ASU 2015-04).serves markets worldwide. The ASU allows employers with fiscal year-ends that do not coincide with a calendar month-endtransaction was subject to make an accounting policy election to measure defined benefit plan assetscertain closing conditions, including Korean regulatory approval, and obligations as of the end of the month closest to their fiscal year-ends. The new guidance is effective for public business entities in interim and fiscal periods beginning after December 15, 2015. Prospective application is required, and early adoption is permitted. The Company will continue to measure its defined benefit plan assets and obligation at fiscal year-end and will not elect to change the measurement date to a calendar month-end.was completed on April 26, 2016.

| Item 2. | Management's Discussion and Analysis of Financial Condition and Results of Operations |

General Overview

We are a leading manufacturer of copper, brass, aluminum, and plastic products. The range of these products is broad: copper tube and fittings; line sets; brass and copper alloy rod, bar, and shapes; aluminum and brass forgings; aluminum and copper impact extrusions; plastic fittings and valves; refrigeration valves and fittings; fabricated tubular products; and steel nipples. We also resell imported brass and plastic plumbing valves, malleable iron fittings, faucets and plumbing specialty products. OurMueller's operations are located throughout the United States and in Canada, Mexico, Great Britain, and China.

| · | Piping Systems: The |

| · |

| · | Climate: The |

New housing starts and commercial construction are important determinants of the Company's sales to the HVAC,heating, ventilation, and air-conditioning, refrigeration, and plumbing markets because the principal end use of a significant portion of our products is in the construction of single and multi-family housing and commercial buildings. Repairs and remodeling projects are also important drivers of underlying demand for these products.

Residential construction activity has shown improvement in recent years, but remains at levels below long-term historical averages. Continued improvement is expected, but may be tempered by continuing low labor participation rates, the pace of household formations, higher interest rates, and tighter lending standards. Per the U.S. Census Bureau, the September 2015March 2016 seasonally adjusted annual rate of new housing starts was 1.21.1 million compared with the September 2014March 2015 rate of 1.0 million. While mortgageMortgage rates have risen in 2015 and 2014, they remain at historically low levels, as the average 30-year fixed mortgage rate was 3.833.74 percent for the first ninethree months of 20152016 and 4.173.85 percent for the twelve months ended December 2014.2015.

The private non-residential construction sector, which includes offices, industrial, health care and retail projects, began showing improvement in 2016 and 2015 and 2014 fromafter declines in previous years. Per the U.S. Census Bureau, the actual (not seasonally adjusted) value of private nonresidentialnon-residential construction put in place was $389.0 billion in 2015 compared to $347.7 billion in 2014 compared to $312.3 billion in 2013.2014. The seasonally adjusted annual value of private nonresidential value ofnon-residential construction put in place was $404.7$398.3 billion in August 2015February 2016 compared to the December 20142015 rate of $352.7$392.8 billion and the August 2014February 2015 rate of $346.3$360.2 billion. We expect that most of these conditions will continue to improve.

Profitability of certain of ourthe Company's product lines depends upon the "spreads" between the costscost of raw materialsmaterial and the selling prices of ourits products. The open market prices for copper cathode and scrap, for example, influence the selling price of copper tube, a principal product manufactured by the Company. We attempt to minimize the effects on profitability from fluctuations in material costs by passing through these costs to our customers. Our earnings and cash flow are dependent upon these spreads that fluctuate based upon market conditions.

Earnings and profitability are also impacted by unit volumes that are subject to market trends, such as substitute products, imports, technologies, and market share. In core product lines, we intensively manage our pricing structure while attempting to maximize itsour profitability. From time-to-time, this practice results in lost sales opportunities and lower volume. For plumbing systems, plastics are the primary substitute product; these products represent an increasing share of consumption. U.S. consumption of copper tube is still predominantly supplied by U.S. manufacturers. For certain air-conditioning and refrigeration applications, aluminum-basedaluminum based systems are the primary substitution threat. We cannot predict the acceptance or the rate of switching that may occur. In recent years, brass rod consumption in the U.S. has declined due to the outsourcing of many manufactured products from offshore regions.

Results of Operations

Consolidated Results

The following table compares summary operating results for the thirdfirst quarter of 20152016 and 2014:2015:

| Three Months Ended | Percent Change | Nine Months Ended | Percent Change | Three Months Ended | Percent Change | |||||||||||||||||||||||||||||||||

| (In thousands) | Sept. 26, 2015 | Sept. 27, 2014 | 2015 vs. 2014 | Sept. 26, 2015 | Sept. 27, 2014 | 2015 vs. 2014 | April 2, 2016 | March 28, 2015 | 2016 vs. 2015 | |||||||||||||||||||||||||||||

| Net sales | $ | 535,184 | $ | 602,820 | (11.2 | ) | % | $ | 1,628,019 | $ | 1,826,885 | (10.9 | )% | $ | 532,809 | $ | 537,242 | (0.8 | )% | |||||||||||||||||||

| Operating income | 27,027 | 37,726 | (28.4 | ) | 118,305 | 124,237 | (4.8 | ) | 41,467 | 35,724 | 16.1 | |||||||||||||||||||||||||||

| Net income | 17,800 | 23,823 | (25.3 | ) | 73,429 | 83,574 | (12.1 | ) | 28,630 | 21,978 | 30.3 | |||||||||||||||||||||||||||

The following are components of changes in net sales compared to the prior year:

| Quarter-to-Date | Year-to-Date | ||||||||

| 2015 vs. 2014 | 2015 vs. 2014 | ||||||||

| Net selling price in core product lines | (10.5 | ) | % | (8.3 | ) | % | |||

| Unit sales volume in core product lines | (7.0 | ) | (3.2 | ) | |||||

| Acquisitions & new products | 9.9 | 3.8 | |||||||

| Dispositions | (2.9 | ) | (2.8 | ) | |||||

| Other | (0.7 | ) | (0.4 | ) | |||||

| (11.2 | ) | % | (10.9 | ) | % | ||||

| 2016 vs. 2015 | |||||

| Net selling price in core product lines | (14.0 | ) | % | ||

| Unit sales volume in core product lines | (1.1 | ) | |||

| Acquisitions | 14.0 | ||||

| Other | 0.3 | ||||

| (0.8 | ) | % | |||

The decreaseincrease in net sales during the third quarter of 2015 was primarily due to (i) lower net selling prices of $63.3 million in our core product lines, primarily copper tube and brass rod, (ii) lower unit sales volume of $42.2 million, primarily in our OEM segment, and (iii) the absence of sales of $15.7 million recorded by Primaflow, a business we sold during November 2014. These decreases were offset by $40.4$57.3 million of sales recorded by Great Lakes Copper Ltd. (Great Lakes), acquired in July 2015, $11.2$12.3 million of sales recorded by Sherwood Valve Products, LLC (Sherwood), acquired in June 2015, and $5.6 million of sales recorded by Turbotec Products, Inc. (Turbotec), acquired in March 2015.

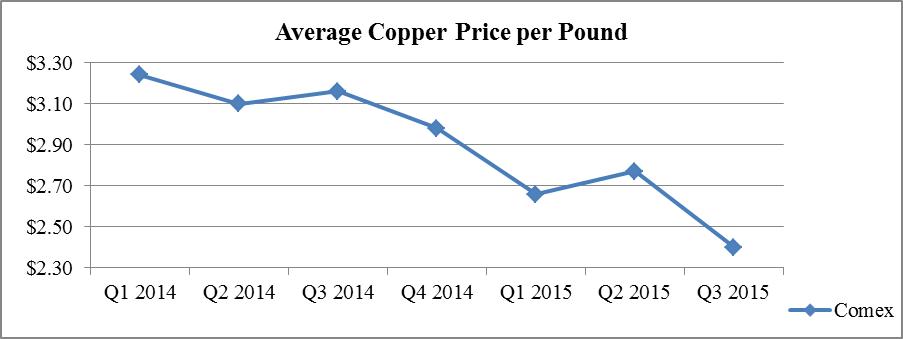

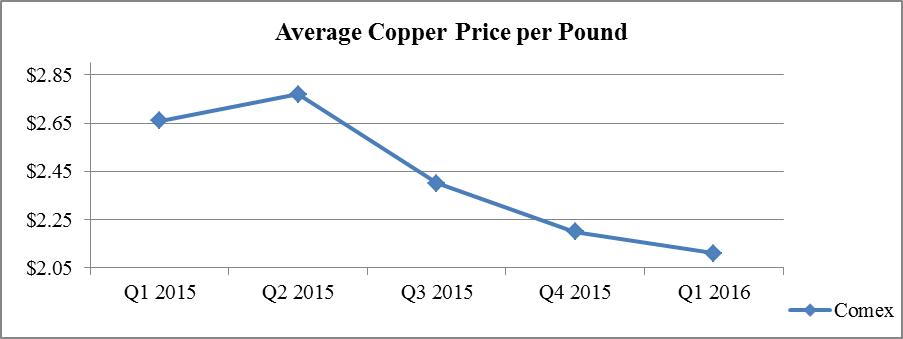

Net selling prices generally fluctuate with changes in raw material costs. Changes in raw material costs are generally passed through to customers by adjustments to selling prices. The following graph shows the Comex average copper price per pound by quarter for the current and prior fiscal years:

| Three Months Ended | Nine Months Ended | |||||||||||||||||||

| (In thousands) | Sept. 26, 2015 | Sept. 27, 2014 | Sept. 26, 2015 | Sept. 27, 2014 | ||||||||||||||||

| Cost of goods sold | $ | 467,167 | $ | 521,278 | $ | 1,398,366 | $ | 1,574,830 | ||||||||||||

Depreciation and amortization | 8,749 | 8,952 | 24,790 | 25,651 | ||||||||||||||||

| Selling, general and administrative expense | 32,241 | 34,004 | 98,492 | 100,512 | ||||||||||||||||

| Gain on sale of assets | — | — | (15,376 | ) | (1,417 | ) | ||||||||||||||

| Severance | — | 860 | 3,442 | 3,072 | ||||||||||||||||

| $ | 508,157 | $ | 565,094 | $ | 1,509,714 | $ | 1,702,648 | |||||||||||||

| Three Months Ended | Nine Months Ended | |||||||||||||||||||

| Sept. 26, 2015 | Sept. 27, 2014 | Sept. 26, 2015 | Sept. 27, 2014 | |||||||||||||||||

| Cost of goods sold | 87.3 | % | 86.5 | % | 85.9 | % | 86.2 | % | ||||||||||||

Depreciation and amortization | 1.6 | 1.5 | 1.5 | 1.4 | ||||||||||||||||

| Selling, general and administrative expense | 6.0 | 5.6 | 6.0 | 5.5 | ||||||||||||||||

| Gain on sale of assets | — | — | (0.9 | ) | (0.1 | ) | ||||||||||||||

| Severance | — | 0.1 | 0.2 | 0.2 | ||||||||||||||||

| 94.9 | % | 93.7 | % | 92.7 | % | 93.2 | % | |||||||||||||

| Three Months Ended | Percent Change | Nine Months Ended | Percent Change | |||||||||||||||||||||||

| (In thousands) | Sept. 26, 2015 | Sept. 27, 2014 | 2015 vs. 2014 | Sept. 26, 2015 | Sept. 27, 2014 | 2015 vs. 2014 | ||||||||||||||||||||

| Net sales | $ | 325,022 | $ | 357,843 | (9.2 | ) | % | $ | 957,375 | $ | 1,093,060 | (12.4 | )% | |||||||||||||

| Operating income | 19,559 | 20,156 | (3.0 | ) | 75,033 | 76,371 | (1.8 | ) | ||||||||||||||||||

| Quarter-to-Date | Year-to-Date | ||||||||

| 2015 vs. 2014 | 2015 vs. 2014 | ||||||||

| Net selling price in core product lines | (11.9 | )% | (9.2 | )% | |||||

| Unit sales volume in core product lines | (3.5 | ) | (2.0 | ) | |||||

| Acquisitions & new products | 9.9 | 3.7 | |||||||

| Dispositions | (2.9 | ) | (4.7 | ) | |||||

| Other | (0.8 | ) | (0.2 | ) | |||||

| (9.2 | )% | (12.4 | )% | ||||||

The following tables compare cost of goods sold and operating expenses as dollar amounts and as a percent of net sales for the thirdfirst quarter of 20152016 and 2014:

| Three Months Ended | Nine Months Ended | |||||||||||||||||||

| (In thousands) | Sept. 26, 2015 | Sept. 27, 2014 | Sept. 26, 2015 | Sept. 27, 2014 | ||||||||||||||||

| Cost of goods sold | $ | 280,891 | $ | 308,927 | $ | 819,591 | $ | 934,208 | ||||||||||||

Depreciation and amortization | 4,468 | 5,287 | 13,568 | 14,803 | ||||||||||||||||

| Selling, general and administrative expense | 20,104 | 22,613 | 61,117 | 66,023 | ||||||||||||||||

| Gain on sale of assets | — | — | (15,376 | ) | (1,417 | ) | ||||||||||||||

| Severance | — | 860 | 3,442 | 3,072 | ||||||||||||||||

| $ | 305,463 | $ | 337,687 | $ | 882,342 | $ | 1,016,689 | |||||||||||||

| Three Months Ended | Nine Months Ended | |||||||||||||||||||

| Sept. 26, 2015 | Sept. 27, 2014 | Sept. 26, 2015 | Sept. 27, 2014 | |||||||||||||||||

| Cost of goods sold | 86.4 | % | 86.3 | % | 85.6 | % | 85.5 | % | ||||||||||||

Depreciation and amortization | 1.4 | 1.5 | 1.4 | 1.4 | ||||||||||||||||

| Selling, general and administrative expense | 6.2 | 6.3 | 6.4 | 6.0 | ||||||||||||||||

| Gain on sale of assets | — | — | (1.6 | ) | (0.1 | ) | ||||||||||||||

| Severance | — | 0.3 | 0.4 | 0.2 | ||||||||||||||||

| 94.0 | % | 94.4 | % | 92.2 | % | 93.0 | % | |||||||||||||

| Three Months Ended | ||||||||

| (In thousands) | April 2, 2016 | March 28, 2015 | ||||||

| Cost of goods sold | $ | 446,642 | $ | 460,834 | ||||

| Depreciation and amortization | 8,920 | 7,853 | ||||||

| Selling, general, and administrative expense | 35,780 | 32,831 | ||||||

| Operating expenses | $ | 491,342 | $ | 501,518 | ||||

| Three Months Ended | ||||||||

| April 2, 2016 | March 28, 2015 | |||||||

| Cost of goods sold | 83.8 | % | 85.8 | % | ||||

| Depreciation and amortization | 1.7 | 1.5 | ||||||

| Selling, general, and administrative expense | 6.7 | 6.1 | ||||||

| Operating expenses | 92.2 | % | 93.4 | % | ||||

The decrease in cost of goods sold during the third quarter of 2015 was primarily due to the decrease in the average cost of copper, andour principal raw material, partially offset by the decreaseincrease in sales volume.volume related to the businesses acquired. Depreciation and amortization forincreased in the thirdfirst quarter of 2015 was consistent with the expense recorded2016 primarily as a result of depreciation and amortization of long-lived assets for the third quarter of 2014.businesses acquired. Selling, general, and administrative expenses increased for the first quarter of 2016 primarily as a result of incremental expenses associated with businesses acquired during 2015.

Interest expense decreased slightly in the first quarter of 2016 primarily as a result of decreased borrowing costs at Mueller-Xingrong. Other income, net, for the first quarter of 2016 was consistent with the first quarter of 2015.

Our effective tax rate for the first quarter of 2016 was 35 percent compared with 34 percent for the same period last year. The difference between the effective tax rate and the amount computed using the U.S. federal statutory tax rate for the first quarter of 2016 was primarily attributable to reductions for the U.S. production activities deduction of $0.9 million and the effect of foreign tax rates lower than statutory tax rates of $1.1 million. These items were partially offset by the provision for state income taxes, net of the federal benefit, of $0.8 million and the recording of the basis difference in unconsolidated affiliates of $1.0 million.

The difference between the effective tax rate and the amount computed using the U.S. federal statutory tax rate for the first quarter of 2015 was primarily attributable to reductions for the U.S. production activities deduction of $1.0 million and the effect of foreign tax rates lower than statutory tax rates of $0.5 million. These items were partially offset by the provision for state income taxes, net of the federal benefit, of $0.8 million.

We own a 50 percent interest in Tecumseh Products Holdings LLC, an unconsolidated affiliate that acquired Tecumseh Products Company (Tecumseh) during the third quarter of 2015, primarily due2015. We also own a 50 percent interest in a second unconsolidated affiliate that provided financing to (i) a decreaseTecumseh in conjunction with the acquisition. We account for these investments using the equity method of $2.8 million in selling, general, and administrative expenses related toaccounting. For the sale of Primaflow and (ii) lower employment costs, including incentive compensation, of $1.3 million. These decreases were offset by (i) selling, general, and administrative expenses of $1.1 million associated with Great Lakes and (ii) increased professional fees of $0.8 million related to consultation for the upgrade of our ERP system. The thirdfirst quarter of 2014 included $0.92016, we recognized $2.9 million of severance charges related toincome on these investments. Included in income from unconsolidated affiliates is a gain that resulted from the rationalizationallocation of Yorkshire.

The following table compares summary operating results for the thirdfirst quarter of 20152016 and 20142015 for the businesses comprising our OEMPiping Systems segment:

| Three Months Ended | Percent Change | Nine Months Ended | Percent Change | Three Months Ended | Percent Change | |||||||||||||||||||||||||||||||||

| (In thousands) | Sept. 26, 2015 | Sept. 27, 2014 | 2015 vs. 2014 | Sept. 26, 2015 | Sept. 27, 2014 | 2015 vs. 2014 | April 2, 2016 | March 28, 2015 | 2016 vs. 2015 | |||||||||||||||||||||||||||||

| Net sales | $ | 212,596 | $ | 247,883 | (14.2 | ) | % | $ | 678,293 | $ | 743,322 | (8.7 | )% | $ | 368,890 | $ | 361,482 | 2.0 | % | |||||||||||||||||||

| Operating income | 13,278 | 23,977 | (44.6 | ) | 62,627 | 68,479 | (8.5 | ) | 31,159 | 26,259 | 18.7 | |||||||||||||||||||||||||||

The following are components of changes in net sales compared to the prior year:

| Quarter-to-Date | Year-to-Date | ||||||||

| 2015 vs. 2014 | 2015 vs. 2014 | ||||||||

| Net selling price in core product lines | (8.5 | )% | (6.9 | )% | |||||

| Unit sales volume in core product lines | (12.0 | ) | (4.9 | ) | |||||

| Acquisitions & new products | 7.8 | 4.0 | |||||||

| Other | (1.5 | ) | (0.9 | ) | |||||

| (14.2 | )% | (8.7 | )% | ||||||

| 2016 vs. 2015 | |||||

| Net selling price in core product lines | (14.7 | ) | % | ||

| Unit sales volume in core product lines | 0.9 | ||||

| Acquisitions | 15.9 | ||||

| Other | (0.1 | ) | |||

| 2.0 | % | ||||

The decreaseincrease in net sales during the third quarter of 2015 was primarily due to (i) lower$57.3 million of sales recorded by Great Lakes and (ii) higher unit sales volume in the segment's domestic core product lines, primarily copper tube. These increases were offset by (i) lower net selling prices of $27.2$53.0 million in the segment's core product lines primarily brass rod and commercial tube, and (ii) lower net selling prices of $21.1 milliona decrease in sales by the segment's core product lines. These decreases were offset by $11.2 million of sales recorded by Sherwood and $5.6 million of sales recorded by Turbotec.

The following tables compare cost of goods sold and operating expenses as dollar amounts and as a percent of net sales for the thirdfirst quarter of 20152016 and 2014:2015: