UNITED STATES SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

________________________________________________________

FORM 10-Q

________________________________________________________ |

| | |

ý☒ | | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the quarterly period ended September 30, 20182019

OR

|

| | |

¨☐ | | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Commission file number 1-3932

WHIRLPOOL CORPORATION

(Exact name of registrant as specified in its charter)

|

| | | |

| Delaware | | 38-1490038 |

| (State of Incorporation) | | (I.R.S. Employer Identification No.) |

| | | | |

2000 North M-63 | | |

| Benton Harbor, | Michigan | | 49022-2692 |

| (Address of principal executive offices) | | (Zip Code) |

Registrant's telephone number, including area code (269) (269) 923-5000

Securities registered pursuant to Section 12(b) of the Act:

|

| | | | | | |

| Title of each class | | Trading symbol(s) | | Name of each exchange on which registered |

| Common stock, par value $1.00 per share | | WHR | | Chicago Stock Exchange | and | New York Stock Exchange |

| 0.625% Senior Notes due 2020 | | WHR 20 | | New York Stock Exchange |

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yesý☒ No ¨☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yesý☒ No ¨

☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of "large accelerated filer," "accelerated filer," "smaller reporting company," and "emerging growth company" in Rule 12b-2 of the Exchange Act.

|

| | | |

Large accelerated filerý | ☒ | Accelerated filer¨ | ☐ |

Non-accelerated filer¨ (Do not check if a smaller reporting company) | ☐ | Smaller reporting company¨ | ☐ |

| | | Emerging growth company¨ | ☐ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ¨☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨☐ No ý

☒

Number of shares outstanding of each of the issuer's classes of common stock, as of the latest practicable date:

|

| | |

| Class of common stock | | Shares outstanding at October 19, 201818, 2019 |

| Common stock, par value $1 per share | | 63,808,27563,199,776 |

WHIRLPOOL CORPORATION

QUARTERLY REPORT ON FORM 10-Q

Three and Nine Months Ended September 30, 20182019

TABLE OF CONTENTS

|

| | |

| | | PAGE |

| |

| Item 1. | | |

| | | |

| | | |

| | | |

| | | |

| Item 2. | | |

| Item 3. | | |

Item 4. | | |

| | |

| |

Item 1. | | |

Item 1A. | | |

Item 2. | | |

Item 3. | | |

| Item 4. | | |

Item 5. | | |

Item 6. | | |

| | | |

| |

| Item 1. | | |

| Item 1A. | | |

| Item 2. | | |

| Item 3. | | |

| Item 4. | | |

| Item 5. | | |

| Item 6. | | |

| | |

| |

FORWARD-LOOKING STATEMENTS

The Private Securities Litigation Reform Act of 1995 provides a safe harbor for forward-looking statements made by us or on our behalf. Certain statements contained in this quarterly report, including those within the forward-looking perspective section within this report's Management's Discussion and Analysis, and other written and oral statements made from time to time by us or on our behalf do not relate strictly to historical or current facts and may contain forward-looking statements that reflect our current views with respect to future events and financial performance. As such, they are considered "forward-looking statements" which provide current expectations or forecasts of future events. Such statements can be identified by the use of terminology such as "may," "could," "will," "should," "possible," "plan," "predict," "forecast," "potential," "anticipate," "estimate," "expect," "project," "intend," "believe," "may impact," "on track," and similar words or expressions. Our forward-looking statements generally relate to our growth strategies, financial results, product development, and sales efforts. These forward-looking statements should be considered with the understanding that such statements involve a variety of risks and uncertainties, known and unknown, and may be affected by inaccurate assumptions. Consequently, no forward-looking statement can be guaranteed and actual results may vary materially.

This document contains forward-looking statements about Whirlpool Corporation and its consolidated subsidiaries ("Whirlpool") that speak only as of this date. Whirlpool disclaims any obligation to update these statements. Forward-looking statements in this document may include, but are not limited to, statements regarding expected earnings per share, cash flow, productivity and raw material prices. Many risks, contingencies and uncertainties could cause actual results to differ materially from Whirlpool's forward-looking statements. Among these factors are: (1) intense competition in the home appliance industry reflecting the impact of both new and established global competitors, including Asian and European manufacturers, and the impact of the changing retail environment; (2) Whirlpool's ability to maintain or increase sales to significant trade customers and the ability of these trade customers to maintain or increase market share; (3) Whirlpool's ability to maintain its reputation and brand image; (4) the ability of Whirlpool to achieve its business plans, productivity improvements, and cost control objectives, and to leverage its global operating platform, and accelerate the rate of innovation; (5) Whirlpool's ability to obtain and protect intellectual property rights; (6) acquisition and investment-related risks, including risks associated with our past acquisitions, and risks associated with our increased presence in emerging markets; (7) risks related to our international operations, including changes in foreign regulations, regulatory compliance and disruptions arising from political, legal and economic instability; (8) information technology system failures, data security breaches, network disruptions, and cybersecurity attacks; (9) product liability and product recall costs; (10) the ability of suppliers of critical parts, components and manufacturing equipment to deliver sufficient quantities to Whirlpool in a timely and cost-effective manner; (11) our ability to attract, develop and retain executives and other qualified employees; (12) the impact of labor relations; (13) fluctuations in the cost of key materials (including steel, resins, copper and aluminum) and components and the ability of Whirlpool to offset cost increases; (14) Whirlpool's ability to manage foreign currency fluctuations; (15) impacts from goodwill impairment and related charges; (16) triggering events or circumstances impacting the carrying value of our long-lived assets; (17) inventory and other asset risk; (18) the uncertain global economy and changes in economic conditions which affect demand for our products; (19) health care cost trends, regulatory changes and variations between results and estimates that could increase future funding obligations for pension and postretirement benefit plans; (20) litigation, tax, and legal compliance risk and costs, especially if materially different from the amount we expect to incur or have accrued for, and any disruptions caused by the same; (21) the effects and costs of governmental investigations or related actions by third parties; and (22) changes in the legal and regulatory environment including environmental, health and safety regulations, and taxes and tariffs.

We undertake no obligation to update any forward-looking statement, and investors are advised to review disclosures in our filings with the SEC. It is not possible to foresee or identify all factors that could cause actual results to differ from expected or historic results. Therefore, investors should not consider the foregoing factors to be an exhaustive statement of all risks, uncertainties, or factors that could potentially cause actual results to differ from forward-looking statements.

Additional information concerning these and other factors can be found in "Risk Factors" in Part II, Item 1A of this report.

Unless otherwise indicated, the terms "Whirlpool," "the Company," "we," "us," and "our" refer to Whirlpool Corporation and its consolidated subsidiaries.

Website Disclosure

We routinely post important information for investors on our website, whirlpoolcorp.com, in the "Investors" section. We also intend to useupdate the Hot Topics Q&A portion of this webpage as a means of disclosing material, non-public information and for complying with our disclosure obligations under Regulation FD. Accordingly, investors should monitor the Investors section of our website, in addition to following our press releases, SEC filings, public conference calls, presentations and webcasts. The information contained on, or that may be accessed through, our webpage is not incorporated by reference into, and is not a part of, this document.

|

|

| PART I. FINANCIAL INFORMATION |

|

| |

| ITEM 1. | FINANCIAL STATEMENTS |

TABLE OF CONTENTS

|

| |

| | PAGE |

| FINANCIAL STATEMENTS AND SUPPLEMENTARY DATA | |

| |

| |

| |

| | | | | PAGE | | PAGE |

NOTES TO THE CONSOLIDATED CONDENSED FINANCIAL STATEMENTS (UNAUDITED) | | 1. | Basis of Presentation | | | |

| 2. | Revenue Recognition | | | |

| 3. | Cash, Cash Equivalents and Restricted Cash | | | |

| 4. | Inventories | | | |

| 5. | Property, Plant and Equipment | | | |

| 6. | Financing Arrangements | | | |

| 7. | Commitments and Contingencies | | | |

| 8. | Pension and Other Postretirement Benefit Plans | | | |

| 9. | Hedges and Derivative Financial Instruments | | | |

| 10. | Fair Value Measurements | | | |

| 11. | Stockholders' Equity | | | |

| 12. | Restructuring Charges | | | |

| 13. | Income Taxes | | | |

| 14. | Segment Information | | | |

| 15. | Assets and Liabilities Held for Sale | | | |

| 16. | Goodwill and Other Intangibles | | | |

| 17. | | | |

WHIRLPOOL CORPORATION

CONSOLIDATED CONDENSED STATEMENTS OF COMPREHENSIVE INCOME (LOSS) (UNAUDITED)

FOR THE PERIODS ENDED SEPTEMBER 30

(Millions of dollars, except per share data)

|

|

|

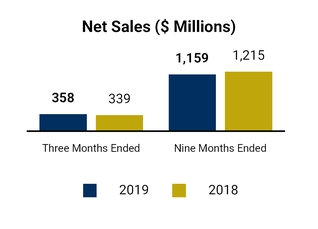

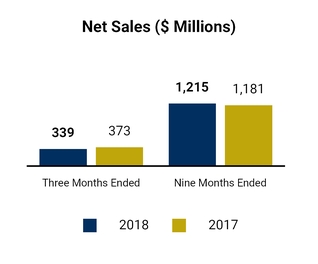

| | | Three Months Ended | | Nine Months Ended | Three Months Ended | | Nine Months Ended |

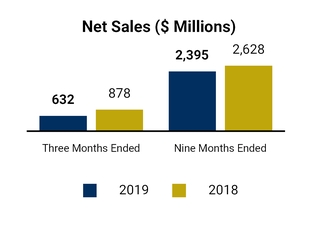

| | 2018 | | 2017 | | 2018 | | 2017 | 2019 | | 2018 | | 2019 | | 2018 |

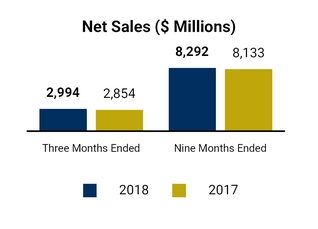

| Net sales | $ | 5,326 |

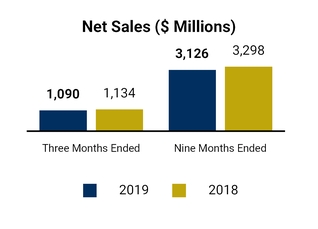

| | $ | 5,418 |

| | $ | 15,377 |

| | $ | 15,551 |

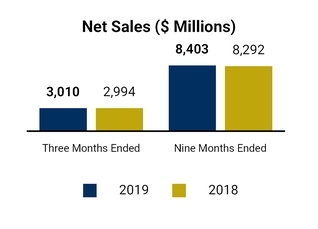

| $ | 5,091 |

| | $ | 5,326 |

| | $ | 15,037 |

| | $ | 15,377 |

|

| Expenses | | | | | | | | | | | | | | |

| Cost of products sold | 4,431 |

| | 4,503 |

| | 12,790 |

| | 12,934 |

| 4,350 |

| | 4,431 |

| | 12,552 |

| | 12,790 |

|

| Gross margin | 895 |

| | 915 |

| | 2,587 |

| | 2,617 |

| 741 |

| | 895 |

| | 2,485 |

| | 2,587 |

|

| Selling, general and administrative | 550 |

| | 521 |

| | 1,596 |

| | 1,546 |

| 491 |

| | 550 |

| | 1,580 |

| | 1,596 |

|

| Intangible amortization | 18 |

| | 18 |

| | 58 |

| | 52 |

| 17 |

| | 18 |

| | 53 |

| | 58 |

|

| Restructuring costs | 28 |

| | 45 |

| | 216 |

| | 150 |

| 56 |

| | 28 |

| | 142 |

| | 216 |

|

| Impairment of goodwill and other intangibles | — |

| | — |

| | 747 |

| | — |

| — |

| | — |

| | — |

| | 747 |

|

| (Gain) loss on sale and disposal of businesses | | (516 | ) | | — |

| | (437 | ) | | — |

|

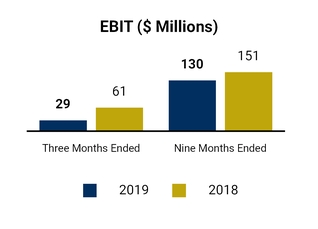

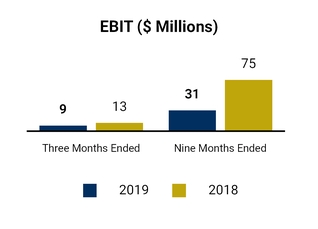

| Operating profit (loss) | 299 |

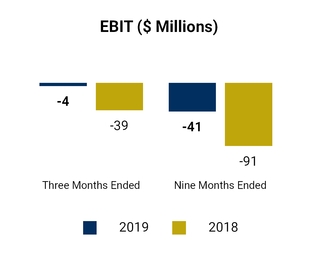

| | 331 |

| | (30 | ) | | 869 |

| 693 |

| | 299 |

| | 1,147 |

| | (30 | ) |

| Other (income) expense | | | | |

| |

| | | | |

| |

|

| Interest and sundry (income) expense | 24 |

| | 21 |

| | 106 |

| | 69 |

| (29 | ) | | 24 |

| | (222 | ) | | 106 |

|

| Interest expense | 52 |

| | 42 |

| | 141 |

| | 122 |

| 45 |

| | 52 |

| | 148 |

| | 141 |

|

| Earnings (loss) before income taxes | 223 |

| | 268 |

| | (277 | ) | | 678 |

| 677 |

| | 223 |

| | 1,221 |

| | (277 | ) |

| Income tax (benefit) expense | 7 |

| | (4 | ) | | 52 |

| | 69 |

| |

| Income tax expense | | 313 |

| | 7 |

| | 311 |

| | 52 |

|

| Net earnings (loss) | 216 |

| | 272 |

| | (329 | ) | | 609 |

| 364 |

| | 216 |

| | 910 |

| | (329 | ) |

| Less: Net earnings (loss) available to noncontrolling interests | 6 |

| | (4 | ) | | 24 |

| | (9 | ) | |

| Less: Net earnings available to noncontrolling interests | | 6 |

| | 6 |

| | 14 |

| | 24 |

|

| Net earnings (loss) available to Whirlpool | $ | 210 |

| | $ | 276 |

| | $ | (353 | ) | | $ | 618 |

| $ | 358 |

| | $ | 210 |

| | $ | 896 |

| | $ | (353 | ) |

| Per share of common stock | | | | | | | | | | | | | | |

| Basic net earnings (loss) available to Whirlpool | $ | 3.25 |

| | $ | 3.78 |

| | $ | (5.18 | ) | | $ | 8.36 |

| $ | 5.62 |

| | $ | 3.25 |

| | $ | 14.04 |

| | $ | (5.18 | ) |

| Diluted net earnings (loss) available to Whirlpool | $ | 3.22 |

| | $ | 3.72 |

| | $ | (5.18 | ) | | $ | 8.23 |

| $ | 5.57 |

| | $ | 3.22 |

| | $ | 13.93 |

| | $ | (5.18 | ) |

| Dividends declared | $ | 1.15 |

| | $ | 1.10 |

| | $ | 3.40 |

| | $ | 3.20 |

| $ | 1.20 |

| | $ | 1.15 |

| | $ | 3.55 |

| | $ | 3.40 |

|

| Weighted-average shares outstanding (in millions) | | | | | | | | | | | | | | |

| Basic | 64.5 |

| | 72.9 |

| | 68.2 |

| | 73.9 |

| 63.6 |

| | 64.5 |

| | 63.8 |

| | 68.2 |

|

| Diluted | 65.3 |

| | 74.0 |

| | 68.2 |

| | 75.1 |

| 64.2 |

| | 65.3 |

| | 64.3 |

| | 68.2 |

|

| | | | | | | | | | | | | | | |

| Comprehensive income (loss) | $ | 130 |

| | $ | 286 |

| | $ | (573 | ) | | $ | 694 |

| $ | 419 |

| | $ | 130 |

| | $ | 1,002 |

| | $ | (573 | ) |

The accompanying notes are an integral part of these Consolidated Condensed Financial Statements.

WHIRLPOOL CORPORATION

CONSOLIDATED CONDENSED BALANCE SHEETS

(Millions of dollars, except share data)

| | | | (Unaudited) | | | (Unaudited) | | |

| September 30, 2018 |

| December 31, 2017 | September 30, 2019 |

| December 31, 2018 |

| Assets |

|

|

|

|

|

|

| Current assets |

|

|

|

|

|

|

| Cash and cash equivalents | $ | 1,032 |

|

| $ | 1,196 |

| $ | 993 |

|

| $ | 1,498 |

|

| Accounts receivable, net of allowance of $151 and $157, respectively | 2,881 |

|

| 2,665 |

| |

| Accounts receivable, net of allowance of $127 and $136, respectively | | 2,588 |

|

| 2,210 |

|

| Inventories | 2,873 |

|

| 2,988 |

| 2,883 |

|

| 2,533 |

|

| Prepaid and other current assets | 862 |

|

| 1,081 |

| 911 |

|

| 839 |

|

| Assets held for sale | 813 |

| | — |

| — |

| | 818 |

|

| Total current assets | 8,461 |

|

| 7,930 |

| 7,375 |

|

| 7,898 |

|

| Property, net of accumulated depreciation of $6,216 and $6,825, respectively | 3,396 |

|

| 4,033 |

| |

| Property, net of accumulated depreciation of $6,331 and $6,190, respectively | | 3,203 |

|

| 3,414 |

|

| Right of use assets | | 746 |

| | — |

|

| Goodwill | 2,478 |

|

| 3,118 |

| 2,420 |

|

| 2,451 |

|

| Other intangibles, net of accumulated amortization of $512 and $476, respectively | 2,325 |

|

| 2,591 |

| |

| Other intangibles, net of accumulated amortization of $572 and $527, respectively | | 2,217 |

|

| 2,296 |

|

| Deferred income taxes | 2,103 |

|

| 2,013 |

| 2,031 |

|

| 1,989 |

|

| Other noncurrent assets | 330 |

|

| 353 |

| 414 |

|

| 299 |

|

| Total assets | $ | 19,093 |

|

| $ | 20,038 |

| $ | 18,406 |

|

| $ | 18,347 |

|

| Liabilities and stockholders' equity |

|

|

|

|

|

|

| Current liabilities |

|

|

|

|

|

|

| Accounts payable | $ | 4,200 |

|

| $ | 4,797 |

| $ | 4,229 |

|

| $ | 4,487 |

|

| Accrued expenses | 751 |

|

| 674 |

| 626 |

|

| 690 |

|

| Accrued advertising and promotions | 728 |

|

| 853 |

| 755 |

|

| 827 |

|

| Employee compensation | 363 |

|

| 414 |

| 430 |

|

| 393 |

|

| Notes payable | 2,153 |

|

| 450 |

| 941 |

|

| 1,034 |

|

| Current maturities of long-term debt | 260 |

|

| 376 |

| 546 |

|

| 947 |

|

| Other current liabilities | 740 |

|

| 941 |

| 973 |

|

| 811 |

|

| Liabilities held for sale | 479 |

| | — |

| — |

| | 489 |

|

| Total current liabilities | 9,674 |

|

| 8,505 |

| 8,500 |

|

| 9,678 |

|

| Noncurrent liabilities |

|

|

|

|

|

|

| Long-term debt | 4,768 |

|

| 4,392 |

| 4,105 |

|

| 4,046 |

|

| Pension benefits | 542 |

|

| 1,029 |

| 530 |

|

| 637 |

|

| Postretirement benefits | 316 |

|

| 352 |

| 310 |

|

| 318 |

|

| Lease liabilities | | 617 |

| | — |

|

| Other noncurrent liabilities | 485 |

|

| 632 |

| 395 |

|

| 463 |

|

| Total noncurrent liabilities | 6,111 |

|

| 6,405 |

| 5,957 |

|

| 5,464 |

|

| Stockholders' equity |

|

|

|

|

|

|

| Common stock, $1 par value, 250 million shares authorized, 112 million shares issued, and 64 million and 71 million shares outstanding, respectively | 112 |

|

| 112 |

| |

| Common stock, $1 par value, 250 million shares authorized, 112 million shares issued, and 63 million and 64 million shares outstanding, respectively | | 112 |

|

| 112 |

|

| Additional paid-in capital | 2,777 |

|

| 2,739 |

| 2,786 |

|

| 2,768 |

|

| Retained earnings | 6,837 |

|

| 7,352 |

| 7,659 |

|

| 6,933 |

|

| Accumulated other comprehensive loss | (2,590 | ) |

| (2,331 | ) | (2,603 | ) |

| (2,695 | ) |

| Treasury stock, 48 million and 41 million shares, respectively | (4,776 | ) |

| (3,674 | ) | |

| Treasury stock, 49 million and 48 million shares, respectively | | (4,926 | ) |

| (4,827 | ) |

| Total Whirlpool stockholders' equity | 2,360 |

|

| 4,198 |

| 3,028 |

|

| 2,291 |

|

| Noncontrolling interests | 948 |

|

| 930 |

| 921 |

|

| 914 |

|

| Total stockholders' equity | 3,308 |

|

| 5,128 |

| 3,949 |

|

| 3,205 |

|

| Total liabilities and stockholders' equity | $ | 19,093 |

|

| $ | 20,038 |

| $ | 18,406 |

|

| $ | 18,347 |

|

The accompanying notes are an integral part of these Consolidated Condensed Financial Statements.

WHIRLPOOL CORPORATION

CONSOLIDATED CONDENSED STATEMENTS OF CASH FLOWS (UNAUDITED)

FOR THE PERIODS ENDED SEPTEMBER 30

(Millions of dollars)

| |

| Nine Months Ended | Nine Months Ended |

| 2018 |

| 2017 | 2019 |

| 2018 |

| Operating activities |

|

|

|

|

|

|

| Net earnings (loss) | $ | (329 | ) |

| $ | 609 |

| $ | 910 |

|

| $ | (329 | ) |

| Adjustments to reconcile net earnings to cash provided by (used in) operating activities: |

|

|

|

|

|

|

| Depreciation and amortization | 491 |

|

| 487 |

| 443 |

|

| 491 |

|

| Impairment of goodwill and other intangibles | 747 |

| | — |

| — |

| | 747 |

|

| (Gain) loss on sale and disposal of businesses | | (437 | ) | | — |

|

| Changes in assets and liabilities: |

|

|

|

|

|

|

| Accounts receivable | (585 | ) |

| (259 | ) | (517 | ) |

| (585 | ) |

| Inventories | (271 | ) |

| (589 | ) | (525 | ) |

| (271 | ) |

| Accounts payable | (122 | ) |

| 107 |

| (110 | ) |

| (122 | ) |

| Accrued advertising and promotions | (95 | ) |

| 18 |

| (62 | ) |

| (95 | ) |

| Accrued expenses and current liabilities | 196 |

|

| (154 | ) | 29 |

|

| 196 |

|

| Taxes deferred and payable, net | (105 | ) |

| (144 | ) | (59 | ) |

| (105 | ) |

| Accrued pension and postretirement benefits | (433 | ) |

| (85 | ) | (72 | ) |

| (433 | ) |

| Employee compensation | 35 |

|

| 49 |

| 77 |

|

| 35 |

|

| Other | (144 | ) |

| (72 | ) | (243 | ) |

| (144 | ) |

| Cash used in operating activities | (615 | ) |

| (33 | ) | (566 | ) |

| (615 | ) |

| Investing activities |

|

|

|

|

|

|

| Capital expenditures | (330 | ) |

| (371 | ) | (306 | ) |

| (330 | ) |

| Proceeds from sale of assets and business | 27 |

|

| 5 |

| 1,034 |

|

| 27 |

|

| Proceeds from held-to-maturity securities | 60 |

| | — |

| — |

| | 60 |

|

| Investment in related businesses | (25 | ) |

| (35 | ) | — |

|

| (25 | ) |

| Other | (4 | ) |

| 1 |

| (5 | ) |

| (4 | ) |

| Cash used in investing activities | (272 | ) |

| (400 | ) | |

| Cash provided by (used in) investing activities | | 723 |

|

| (272 | ) |

| Financing activities |

|

|

|

|

|

|

| Proceeds from borrowings of long-term debt | 703 |

|

| — |

| |

| Net proceeds from borrowings of long-term debt | | 699 |

|

| 703 |

|

| Repayments of long-term debt | (381 | ) |

| (261 | ) | (946 | ) |

| (381 | ) |

| Net proceeds from short-term borrowings | 1,761 |

|

| 1,365 |

| |

| Net proceeds (repayments) from short-term borrowings | | (63 | ) |

| 1,761 |

|

| Dividends paid | (232 | ) |

| (235 | ) | (229 | ) |

| (232 | ) |

| Repurchase of common stock | (1,102 | ) |

| (550 | ) | (100 | ) |

| (1,102 | ) |

| Common stock issued | 7 |

|

| 33 |

| 5 |

|

| 7 |

|

| Other | (6 | ) |

| (17 | ) | (7 | ) |

| (6 | ) |

| Cash provided by financing activities | 750 |

|

| 335 |

| |

| Cash provided by (used in) financing activities | | (641 | ) |

| 750 |

|

| Effect of exchange rate changes on cash, cash equivalents and restricted cash | (74 | ) |

| 55 |

| (55 | ) |

| (74 | ) |

| Decrease in cash, cash equivalents and restricted cash | (211 | ) |

| (43 | ) | (539 | ) |

| (211 | ) |

| Cash, cash equivalents and restricted cash at beginning of period | 1,293 |

|

| 1,240 |

| 1,538 |

|

| 1,293 |

|

| Cash, cash equivalents and restricted cash at end of period | $ | 1,082 |

|

| $ | 1,197 |

| $ | 999 |

|

| $ | 1,082 |

|

The accompanying notes are an integral part of these Consolidated Condensed Financial Statements.

NOTES TO THE CONSOLIDATED CONDENSED FINANCIAL STATEMENTS (UNAUDITED)

(1) BASIS OF PRESENTATION

General Information

The accompanying unaudited Consolidated Condensed Financial Statements have been prepared in accordance with accounting principles generally accepted in the United States of America ("GAAP") for interim financial information, and with the instructions to Form 10-Q and Article 10 of Regulation S-X. Accordingly, they do not include all information or footnotes required by GAAP for complete financial statements. As a result, this Form 10-Q should be read in conjunction with the Consolidated Financial Statements and accompanying Notes in our Form 10-K for the year ended December 31, 2017.2018.

Management believes that the accompanying Consolidated Condensed Financial Statements reflect all adjustments, including normal recurring items, considered necessary for a fair presentation of the interim periods.

We are required to make estimates and assumptions that affect the amounts reported in the Consolidated Condensed Financial Statements and accompanying Notes. Actual results could differ materially from those estimates.

Certain prior year amounts in the Consolidated Condensed Financial Statements have been reclassified to conform with current year presentation. Assets and liabilities related to the sale of Embraco which met the held for sale criteria as of September 30, 2018 have been presented separately in the Consolidated Condensed Balance Sheet. See Note 15 to the Consolidated Condensed Financial Statements.

We have eliminated all material intercompany transactions in our Consolidated Condensed Financial Statements. We do not consolidate the financial statements of any company in which we have an ownership interest of 50% or less, unless that company is deemed to be a variable interest entity ("VIE") of which we are the primary beneficiary. VIEs are consolidated when the company is the primary beneficiary of these entities and has the ability to directly impact the activities of these entities.

Related Party TransactionOut-of-Period Adjustments

During the third quarter of 2019, we recorded a net adjustment of $34 million related to prior years resulting from the one time transition tax deemed repatriation on earnings of certain foreign subsidiaries that were previously tax deferred and related impacts. This adjustment resulted in a decrease of net earnings available to Whirlpool of India Limited (Whirlpool India),$34 million and a majority-owned subsidiarydecrease of Whirlpool Corporation, acquired a 49% equity interest$0.53 in Elica PB Indiadiluted earnings per share for $22 million. As part of the agreement, Whirlpool India received an optionthree and nine months ended 2019. The Company determined the impact was not material to acquire the remaining equity interest in the future for fair value,prior years' financial statements and the non-Whirlpool India shareholders of Elica PB India received an optionis not expected to sell their remaining equity interest to Whirlpool India in the future for fair value, which could be material to the financial statements depending onConsolidated Statement of Comprehensive Income (Loss) for the performanceyear ending December 31, 2019.

In addition, during the third quarter of 2019 we recorded an adjustment of $22 million related to the venture. We accountfirst quarter of 2019 resulting from other foreign subsidiary income items and corresponding tax credit impacts. This adjustment resulted in a decrease of $22 million in net earnings available to Whirlpool and a decrease of $0.34 in diluted earnings per share for our minority interest under the equity methodthree months ended September 30, 2019. The Consolidated Condensed Statement of accounting.Comprehensive Income (Loss) for the nine months ended September 30, 2019 is not impacted by this adjustment.

Adoption of New Accounting Standards

On January 1, 2018,2019, we adopted Accounting Standards Update ("ASU"(“ASU”) No. 2014-09, "Revenue from Contracts with Customers2017-12, "Derivatives and Hedging (Topic 606)815): Targeted Improvements to Accounting for Hedging Activities." using the modified retrospective method. Under the modified retrospective method, we recognized the cumulative effectThe adoption of initially applying the new revenuethis standard as an increase to the opening balance of retained earnings. This adjustment did not have a material impact on our financial statements.Consolidated Condensed Financial Statements, however we have expanded our use of hedge accounting to hedge contractually specified components in commodity contracts designated as cash flow hedges. For additional information on the required disclosures related to the impact of adopting this standard, see Note 210 to the Consolidated Condensed Financial Statements.

In October 2016,

On January 1, 2019, we adopted ASU No. 2016-02, "Leases (Topic 842)" and as part of that process the Financial Accounting Standards Board ("FASB") issued ASU 2016-16, "Income Taxes (Topic 740): Intra-Entity Transfers of Assets Other Than Inventory," which requires an entity to recognizeCompany made the income tax consequences of an intra-entity transfer of an asset other than inventory when the transfer occurs. The amendments were effective for fiscal years, and interim periods within those fiscal years, beginning after December 15, 2017, and should be applied on a modified retrospective basis through a cumulative-effect adjustment directly to retained earnings at the beginning of the period of adoption. Early adoption is permitted in the first interim period of an annual reporting period for which financial statements have not been issued. following elections:

The Company adopteddid not elect the accounting standard on January 1, 2018hindsight practical expedient, for all leases.

The Company elected the package of practical expedients and, recognizedas a $56 million increaseresult, did not reassess prior conclusions related to the opening balance of retained earnings.contracts containing leases, lease classification and initial direct costs for all leases.

In January 2017,March 2018, the FASB issued ASU 2017-04, "Intangibles - Goodwillapproved an optional transition method that allows companies to use the effective date as the date of initial application on transition. The Company elected this transition method, and Other (Topic 350): Simplifying the Test for Goodwill Impairment". The guidance in ASU 2017-04 eliminates the requirement to determine the fair value of individual assets and liabilities ofas a reporting unit to measure goodwill impairment. Under the amendments in the new standard, goodwill impairment testing will be performed by comparing the fair value of the reporting unit with its carrying amount

and recognizing an impairment chargeresult, did not adjust its comparative period financial information or make the newly required lease disclosures for periods before the amount by which the carrying amount exceeds the reporting unit's fair value. The new standard is effective for annual and interim goodwill impairment tests in fiscal years beginning after December 15, 2019, and should be applied on a prospective basis. Early adoption is permitted for annual or interim goodwill impairment testing performed after January 1, 2017. date.

The Company elected to early adoptmake the accounting policy election for short-term leases resulting in lease payments being recorded as an expense on a straight-line basis over the lease term.

The Company elected to not separate lease and non-lease components for all leases.

The Company did not elect the land easement practical expedient.

Upon adoption, we recognized the cumulative effect of initially applying this new standard resulting in the second quarteraddition of 2018. approximately $858 million of right of use assets, of which $46 million were classified as held for sale, as well as the corresponding short-term and long-term lease liabilities. Additionally, the Company has sold and leased back a group of properties in our Latin American region and, upon adoption, the Company recorded a cumulative adjustment to retained earnings of approximately $82 million related to deferred gains associated with these transactions.

For additional information on the required disclosures related to the impact of goodwill impairment and related charges,adopting this standard, see Note 3 to the Consolidated Condensed Financial Statements.

For additional information on held for sale assets, see Note 16 to the Consolidated Condensed Financial Statements.

We adopted the following standards,standard, none of which have a material impact on our Consolidated Condensed Financial Statements:

|

| | |

| Standard | | Effective Date |

2016-012019-07 | Financial Instruments - Overall (Subtopic 825-10): RecognitionCodification Updates to SEC Sections: Amendments to SEC Paragraphs Pursuant to SEC Final Releases No. 33-10532, Disclosure Update and Measurement of Financial AssetsSimplification, and Financial LiabilitiesNos. 33-10231 and 33-10441, Investment Company Reporting Modernization, and Miscellaneous Updates | JanuaryJuly 1, 2018 |

2016-04 | Liabilities-Extinguishments of Liabilities (Subtopic 405-20): Recognition of Breakage for Certain Prepaid Stored-Value Products | January 1, 2018 |

2016-15 | Statement of Cash Flows (Topic 230): Classification of Certain Cash Receipts and Cash Payments | January 1, 2018 |

2016-18 | Statement of Cash Flows (Topic 230): Restricted Cash | January 1, 2018 |

2017-01 | Business Combinations (Topic 805): Clarifying the Definition of a Business | January 1, 2018 |

2017-09 | Compensation-Stock Compensation (Topic 718): Scope of Modification Accounting | January 1, 20182019 |

All other newly issued and effective accounting standards during 20182019 were not relevant or material to the Company.

Accounting Pronouncements Issued But Not Yet Effective

In FebruaryNovember 2018, the FASB issued ASU 2018-02, "Income Statement - Reporting Comprehensive Income2018-18, "Collaborative Arrangements (Topic 220)808): Reclassification of Certain Tax Effects from Accumulated Other Comprehensive Income".Clarifying the Interaction between Topic 808 and Topic 606." The new standard givesclarifies that certain transactions between participants in a collaborative arrangement should be accounted for under Topic 606 when the counterparty is a customer for a good or service that is a distinct unit of account. The amendments also preclude entities the option to reclassify to retained earnings tax effects related to items in accumulated other comprehensive income asfrom presenting consideration from transactions with a result of the tax reform.collaborator that is not a customer together with revenue recognized from contracts with customers. The new standard is effective for fiscal years beginning after December 15, 2018,2019, and interim periods within those fiscal years. Early adoption is permitted in any interim period after issuance.for entities that have adopted ASC 606. The standard should be applied retrospectively to the period when ASC 606 was initially adopted. The Company is currently evaluating the impact of adopting this guidance.

In August 2017, the FASB issued ASU 2017-12, "Derivatives and Hedging (Topic 815): Targeted Improvements to Accounting for Hedging Activities". The new standard is effective for fiscal years beginning after December 15, 2018, and interim periods within those fiscal years. Early adoption is permitted in any interim period after issuance. All transition requirements and elections should be applied to hedging relationships existing (that is, hedging relationships in which the hedging instrument has not expired, been sold, terminated, or exercised or the entity has not removed the designation of the hedging relationship) on the date of adoption. The effect of adoption should be reflected as of the beginning of the fiscal year in which the entity adopts. The Company is currently evaluating the impact of adopting this guidance.

In February 2016, the FASB issued ASU No. 2016-02, "Leases (Topic 842)". The guidance in ASU 2016-02 supersedes the lease recognition requirements in ASC Topic 840, Leases (FAS 13). The new standard establishes a right-of-use (ROU) model that requires a lessee to record a ROU asset and a lease liability on the balance sheet for leases with terms longer than 12 months. Leases will be classified as either finance or operating, with classification affecting the pattern of expense recognition in the income statement. The new standard is effective for fiscal years beginning after December 15, 2018, including interim periods within those fiscal years, with early adoption permitted. The Company is currently planning to elect the package of practical expedients to not reassess prior conclusions related to contracts containing leases, lease classification and initial direct costs and is evaluating other practical expedients available under the guidance. In March 2018, the FASB approved a new, optional transition method that will give companies the option to use the effective date as the date of initial application on transition. The Company plans to elect this transition method, and as a result, the Company will not adjust its comparative period financial information or make the new required lease disclosures for periods before the effective date.

In connection with the adoption of the new lease accounting standard, we established a cross functional project management implementation team. As part of that process, we have completed scoping reviews and we continue to make progress in updating business process, systems, accounting policies and internal controls and continue to execute our implementation strategy.

The implementation strategy to obtain and summarize our leases includes utilizing surveys to centrally gather more information about the Company's existing leases, lease processes, and contracts that may contain leases, including service agreements. To ensure completeness of the population of lease contracts, the results of the survey are being cross-referenced against other available lease information such as year-end disclosures and lease expense. As of September 30, 2018, the Company has obtained the relevant lease contract data points and is updating our lease accounting system.

The Company anticipates the adoption of this new standard will result in a material increase in ROU assets and liabilities on our consolidated balance sheet. The impact on the Company's consolidated statement of income is being evaluated. As the impact of this standard is non–cash in nature, we do not anticipate its adoption having an impact on the Company's Consolidated Condensed Statement of Cash Flows.

The FASB has issued the following relevant standards, which are not expected to have a material impact on our Consolidated Condensed Financial Statements:

|

| | |

| Standard | | Effective Date |

| 2016-13 | Financial Instruments - Credit Losses (Topic 326): Measurement of Credit Losses on Financial Instruments | January 1, 2020 |

| 2018-13 | Fair Value Measurement (Topic 820): Disclosure Framework - Changes to the Disclosure Requirements for Fair Value Measurement | January 1, 2020 |

| 2018-14 | Compensation - Retirement Benefits - Defined Benefit Plans - General (Subtopic 715-20): Disclosure Framework - Changes to the Disclosure Requirements for Defined Benefit Plans | January 1, 2021 |

| 2018-15 | Intangibles - Goodwill and Other - Internal-Use Software (Subtopic 350-40): Customer's Accounting for Implementation Costs Incurred In a Cloud Computing Arrangement That Is a Service Contract | January 1, 2020 |

| 2018-17 | Consolidation (Topic 810): Targeted Improvements to Related Party Guidance for Variable Interest Entities | January 1, 2020 |

All other issued and not yet effective accounting standards are not relevant or material to the Company.

(2) REVENUE RECOGNITION

Revenue from Contracts with Customers

On January 1, 2018, we adopted Topic 606 using the modified retrospective method, as a result, we recognized the cumulative effect of initially applying the new revenue standard as an adjustment to the opening balance of retained earnings. This adjustment did not have a material impact on our Consolidated Condensed Financial Statements. Results for reporting periods beginning after January 1, 2018 are presented under Topic 606, while prior period amounts are not adjusted and continue to be reported in accordance with our historic accounting under Revenue Recognition ("Topic 605"). The adoption of Topic 606 did not have a material impact on our Consolidated Condensed Statements of Comprehensive Income (Loss) and Consolidated Condensed Balance Sheets.

The adoption of Topic 606 represents a change in accounting principle that will provide financial statement readers with enhanced revenue recognition disclosures. In accordance with Topic 606, revenue is recognized when obligations under the terms of a contract with our customer are satisfied; generally this occurs with the transfer of control of our products or services. Revenue is measured as the amount of consideration we expect to receive in exchange for transferring products or providing services. Certain customers may receive cash and/or non-cash incentives, which are accounted for as variable consideration. To achieve this core principle, the Company applies the following five steps:

1. Identify the contract with a customer

A contract with a customer exists when (i) the Company enters into an agreement with a customer that defines each party's rights regarding the products or services to be transferred and identifies the payment terms related to these products or services, (ii) both parties to the contract are committed to perform their respective obligations, (iii) the contract has commercial substance, and (iv) the Company determines that collection of substantially all consideration for products or services that are transferred is probable based on the customer's intent and ability to pay the promised consideration. The Company applies judgment in determining the customer's ability and intention to pay, which is based on a variety of factors including the customer's payment history or, in the case of a new customer, published credit and financial information pertaining to the customer.

2. Identify the performance obligations in the contract

Performance obligations promised in a contract are identified based on the products or services that will be transferred to the customer that are both capable of being distinct, whereby the customer can benefit from the product or service either on its own or together with other resources that are readily available from third parties or from the Company, and are distinct in the context of the contract, whereby the transfer of the products or services is separately identifiable from other promises in the contract. To the extent a contract includes multiple promised products or services, the Company must apply judgment to determine whether promised products or services are capable of being distinct and distinct in the context of the contract. If these criteria are not met, the promised products or services are accounted for as a combined performance obligation. The Company has elected to account for shipping and handling activities as a fulfillment cost as permitted by the standard.

3. Determine the transaction price

The transaction price is determined based on the consideration to which the Company will be entitled in exchange for transferring products or services to the customer. To the extent the transaction price is variable, revenue is recognized at an amount equal to the consideration to which the Company expects to be entitled. This estimate includes customer sales incentives which are accounted for as a reduction to revenue and estimated primarily using the expected value method. Determining the transaction price requires significant judgment, which is discussed by revenue category in further detail below.

In practice, we do not offer extended payment terms beyond one year to customers. As such, we do not adjust our consideration for financing arrangements.

4. Allocate the transaction price to performance obligations in the contract

If the contract contains a single performance obligation, the entire transaction price is allocated to the single performance obligation. Contracts that contain multiple performance obligations require an allocation of the transaction price to each performance obligation based on a relative standalone selling price basis unless a portion of the variable consideration related to the contract is allocated entirely to a performance obligation. The Company determines standalone selling price based on the price at which the performance obligation is sold separately.

5. Recognize revenue when or as the Company satisfies a performance obligation

The Company generally satisfies performance obligations at a point in time. Revenue is recognized based on the transaction price at the time the related performance obligation is satisfied by transferring a promised product or service to a customer. The impact to revenue related to prior period performance obligations in the three and nine months ended September 30, 2018 is immaterial.

Disaggregation of Revenue

The following table presents our disaggregated revenues by revenue source. We sell products within all product categories in each operating segment. Revenues related to compressors are fully reflected in our Latin America segment. For additional information on the disaggregated revenues by geographicalgeographic regions, see Note 1415 to the Consolidated Condensed Financial Statements.

|

| | | | | | | | |

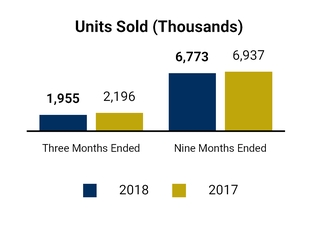

| | | Three Months Ended September 30, | | Nine Months Ended September 30, |

| Millions of dollars | | 2018 | | 2018 |

| Major product categories: | | | | |

| Laundry | | $ | 1,580 |

| | $ | 4,605 |

|

| Refrigeration | | 1,577 |

| | 4,474 |

|

| Cooking | | 1,204 |

| | 3,342 |

|

| Dishwashing | | 421 |

| | 1,229 |

|

| Total major product category net sales | | $ | 4,782 |

| | $ | 13,650 |

|

| Compressors | | 266 |

| | 847 |

|

| Spare parts and warranties | | 246 |

| | 768 |

|

| Other | | 32 |

| | 112 |

|

| Total net sales | | $ | 5,326 |

| | $ | 15,377 |

|

Major Product Category Sales

Whirlpool Corporation manufactures and markets a full line of home appliances andRevenues related products and services. Our major product categories include the following: refrigeration, laundry, cooking, and dishwashing. The refrigeration product category includes refrigerators, freezers, ice makers and refrigerator water filters. The laundry product category includes laundry appliances and related laundry accessories. The cooking category includes cooking appliances and other small domestic appliances. The dishwashing product category includes dishwasher appliances and related accessories. In addition, we also produce hermetic compressors for refrigeration systems which is not considered a major product category.

For product sales and compressors, we transfer control and recognize a sale when we ship the product from our manufacturing facility to our customer or when the customer receives the product based upon agreed shipping terms. Each unit sold is considered an independent, unbundled performance obligation. We do not have any additional performance obligations other than product sales that are material in the context of the contract. The amount of consideration we receive and revenue we recognize varies due to sales incentives and returns we offer to our customers. When we give our customers the right to return eligible products, we reduce revenue for our estimate of the expected returns which is primarily based on an analysis of historical experience.

Spare Parts & Warranties

Spare parts are primarily sold to parts distributors and retailers, with a small number of sales to end consumers. For spare part sales, we transfer control and recognize a sale when we ship the product to our customer or when the customer receives product based upon agreed shipping terms. Each unit sold is considered an independent, unbundled performance obligation. We do not have any additional performance obligations other than spare part sales that are material in the context of the contract. The amount of consideration we receive and revenue we recognize varies due to sales incentives and returns we offer to our customers. When we give our customers the right to return eligible products, we reduce revenue for our estimate of the expected returns which is primarily based on an analysis of historical experience.

Warranties are classified as either assurance type or service type warranties. A warranty is considered an assurance type warranty if it provides the consumer with assurance that the product will function as intended. A warranty that goes above and beyond ensuring basic functionality is considered a service type warranty. The Company offers certain limited warranties that are assurance type warranties and extended service arrangements that are service type warranties. Assurance type warranties are not accounted for as separate performance obligations under the revenue model. If a service type warranty is sold with a product or separately, revenue is recognized over the life of the warranty. The Company evaluates warranty offerings in comparison to industry standards and market expectations to determine appropriate warranty classification. Industry standards and market expectations are determined by jurisdictional laws, competitor offerings and customer expectations. Market expectations and industry standards can vary based on product type and geography. The Company primarily offers assurance type warranties.

Whirlpool sells certain extended service arrangements separately from the sale of products. Whirlpool acts as a sales agent under some of these arrangements whereby the Company receives a fee that is recognized as revenue upon

the sale of the extended service arrangement. The Company is also the principal for certain extended service arrangements. Revenue related to these arrangements is recognized ratably over the contract term.

Other Revenue

Other revenue sources include subscription arrangements and licenses as described below.

The Company has a water subscriptionformer compressor business were fully reflected in our Latin America segment which providesthrough June 30, 2019. We completed the customer with a water filtration system that is deliveredsale of our compressor business on July 1, 2019. For additional information on the sale of Embraco, see Note 16 to the consumer's home. Our water subscription contracts represent a performance obligation that is satisfied over time andConsolidated Condensed Financial Statements.

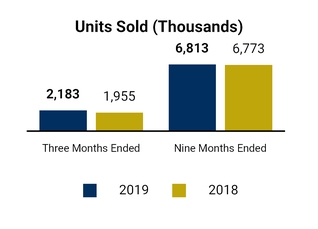

|

| | | | | | | | | | | | | | | | |

| | | Three Months Ended September 30, | | Nine Months Ended September 30, |

| Millions of dollars | | 2019 | | 2018 | | 2019 | | 2018 |

| Major product categories: | | | | | | | | |

| Laundry | | $ | 1,576 |

| | $ | 1,580 |

| | $ | 4,531 |

| | $ | 4,605 |

|

| Refrigeration | | 1,673 |

| | 1,577 |

| | 4,694 |

| | 4,474 |

|

| Cooking | | 1,183 |

| | 1,204 |

| | 3,289 |

| | 3,342 |

|

| Dishwashing | | 414 |

| | 421 |

| | 1,169 |

| | 1,229 |

|

| Total major product category net sales | | $ | 4,846 |

| | $ | 4,782 |

| | $ | 13,683 |

| | $ | 13,650 |

|

| Compressors | | — |

| | 266 |

| | 557 |

| | 847 |

|

| Spare parts and warranties | | 227 |

| | 246 |

| | 749 |

| | 768 |

|

| Other | | 18 |

| | 32 |

| | 48 |

| | 112 |

|

| Total net sales | | $ | 5,091 |

| | $ | 5,326 |

| | $ | 15,037 |

| | $ | 15,377 |

|

The impact to revenue is recognized as the performance obligation is completed. The installation and maintenance of the water filtration system are not distinct services in the context of the contract (i.e., the customer views all activities associated with the arrangement as one singular value proposition). The contract term is generally less than one year for these arrangements and revenue is recognized based on the monthly invoiced amount which directly corresponds to the value of our performance completed to date.

We license our brands in arrangements that do not include other performance obligations. Whirlpool licensing provides a right of access to the Company's intellectual property throughout the license period. Whirlpool recognizes licensing revenue over the life of the license contract as the underlying sale or usage occurs. As a result, we recognize revenue for these contracts at the amount which directly corresponds to the value provided to the customer.

Costs to Obtain or Fulfill a Contract

We do not capitalize costs to obtain a contract because a nominal number of contracts have terms that extend beyond one year. The Company does not have a significant amount of capitalized costs related to fulfillment.

Sales Tax and Other Non Income Taxes

The Company is subject to certain non-income taxes in certain jurisdictions including butprior period performance obligations was not limited to sales tax, value added tax, excise tax and other taxes we collect concurrent with revenue-producing activities that are excluded from the transaction price, and therefore, excluded from revenue.

Bad Debt Expense

Formaterial for the three and nine months ended September 30, 2018, we recorded $29 million of bad2019.

Bad Debt Expense

Bad debt expense related to trade customer insolvencywas not material for the three and nine months ended September 30, 2019.

(3) LEASES

Leases

We lease certain manufacturing facilities, warehouses/distribution centers, office space, land, vehicles, and equipment. At lease inception, we determine the lease term by assuming the exercise of a U.S. retailer and a Brazilian retailer, in the amountthose renewal options that are reasonably assured. Leases with an initial term of $17 million and $12 million, respectively. There was an immaterial amount of bad debt expense12 months or less are not recorded in the prior periods.Consolidated Condensed Balance Sheets and we recognize lease expense for these leases on a straight-line basis over the lease term. The Company had operating lease costs of approximately $150 million for the nine months endedSeptember 30, 2019.

Financial Statement ImpactAs of Adopting Topic 606September 30, 2019, we have approximately $82 million of non-cancelable operating lease commitments, primarily for warehouses, that have not yet commenced. These operating leases are expected to commence between fiscal year 2019 and fiscal year 2020 with lease terms of up to 15 years.

On January 1, 2018,At September 30, 2019, we adopted Topic 606 usinghave 0 leases classified as financing leases and we have approximately $885 million of non-cancelable operating lease commitments, excluding variable consideration. The undiscounted annual future minimum lease payments are summarized by year in the modified retrospective method. In previoustable below:

|

| | | |

| Maturity of Lease Liabilities | Operating Leases (in millions) |

| 2019 | $ | 45 |

|

| 2020 | 166 |

|

| 2021 | 139 |

|

| 2022 | 119 |

|

| 2023 | 107 |

|

| After 2023 | 309 |

|

| Total lease payments | $ | 885 |

|

| Less: interest | 123 |

|

| Present value of lease liabilities | $ | 762 |

|

The long-term portion of the lease liabilities included in the amounts above is $617 million. The remainder of our lease liabilities are included in other current liabilities in the Consolidated Condensed Balance Sheets.

At September 30, 2019, the weighted average remaining lease term and weighted average discount rate for operating leases was 7 years and 5%, respectively.

During the nine months ended September 30, 2019 the cash paid for amounts included in the measurement of the liabilities and the operating cash flows was $147 million. The right of use assets obtained in exchange for new liabilities was $39 million in the nine months ended.

As the Company's lease agreements normally do not provide an implicit interest rate, we apply the Company's incremental borrowing rate based on the information available at commencement date in determining the present value of future lease payments. Relevant information used in determining the Company's incremental borrowing rate includes the duration of the lease, location of the lease, and the Company's credit risk relative to risk-free market rates.

Many of our Brazilian operations earned tax credits underleases include renewal options that can extend the Brazilian government's export incentive program (BEFIEX). These credits reduced Brazilian federal excise taxes on domestic sales. Prior to the adoptionlease term. The execution of Topic 606, the excise taxes inthose renewal options is at our Brazilian operations weresole discretion and reflected in revenue. In accordance with Topic 606, we madethe lease term when they are reasonably certain to be exercised.

Certain leases also include options to purchase the underlying asset at fair market value. If leased assets have leasehold improvements, typically the depreciable life of those leasehold improvements are limited by the expected lease term. Additionally, certain lease agreements include lease payment adjustments for inflation.

Our lease agreements do not contain any material residual value guarantees or material restrictive covenants.

We rent or sublease certain real estate to third parties. Our sublease portfolio primarily consists of operating leases within our warehouses, resulting in a policy election to exclude non-income taxes from the transaction price. As a result, these credits in 2018 are reflected in other income. Based on our evaluation, we determined no significant changes are required to our business processes, systems and controls to effectively report revenue recognition under the new standard. Adoption of the new standard does not materially change the timing ornominal amount of revenue recognizedsublease income in our Consolidated Condensed Financial Statements.2019.

(3)(4) CASH, CASH EQUIVALENTS AND RESTRICTED CASH

The following table provides a reconciliation of cash, cash equivalents and restricted cash as reported within our Consolidated Condensed Statements of Cash Flows:

| | | | September 30 | September 30, |

| Millions of dollars | 2018 | | 2017 | 2019 | | 2018 |

| Cash and cash equivalents as presented in our Consolidated Condensed Balance Sheets | 1,032 |

| | 1,087 |

| $ | 993 |

| | $ | 1,032 |

|

Restricted cash included in prepaid and other current assets (1) | 45 |

| | 47 |

| 6 |

| | 45 |

|

Restricted cash included in other noncurrent assets (1) | 5 |

| | 63 |

| — |

| | 5 |

|

| Cash, cash equivalents and restricted cash as presented in our Consolidated Condensed Statements of Cash Flows | $ | 1,082 |

| | $ | 1,197 |

| $ | 999 |

| | $ | 1,082 |

|

(1)Change in restricted cash resulted inreflects realization of foreign currency translation adjustments of $3$1 million and ($5 million),$3 million, respectively, for the nine months ended September 30, 20182019 and 20172018 compared to the prior year.fiscal year end.

|

| | | | | | | |

| | December 31, |

| Millions of dollars | 2017 | | 2016 |

| Cash and cash equivalents as presented in our Consolidated Balance Sheets | 1,196 |

| | 1,085 |

|

| Restricted cash included in prepaid and other current assets | 48 |

| | 45 |

|

| Restricted cash included in other noncurrent assets | 49 |

| | 110 |

|

| Cash, cash equivalents and restricted cash as presented in our Consolidated Statements of Cash Flows | $ | 1,293 |

| | $ | 1,240 |

|

|

| | | | | | | |

| | December 31, |

| Millions of dollars | 2018 | | 2017 |

| Cash and cash equivalents as presented in our Consolidated Balance Sheets | $ | 1,498 |

| | $ | 1,196 |

|

| Restricted cash included in prepaid and other current assets | 40 |

| | 48 |

|

| Restricted cash included in other noncurrent assets | — |

| | 49 |

|

| Cash, cash equivalents and restricted cash as presented in our Consolidated Statements of Cash Flows | $ | 1,538 |

| | $ | 1,293 |

|

Restricted cash can only be used to fund capital expenditures and technical resources to enhance Whirlpool China's research and development and working capital, as required by the terms of the Whirlpool China (formerly Hefei Sanyo) acquisition completed in October 2014.

(4)(5) INVENTORIES

The following table summarizes our inventory for the periods presented:at September 30, 2019 and December 31, 2018:

|

| | | | | | | | |

| Millions of dollars |

| September 30, 2019 |

| December 31, 2018 |

| Finished products |

| $ | 2,414 |

|

| $ | 2,076 |

|

| Raw materials and work in process |

| 627 |

|

| 617 |

|

|

| 3,041 |

|

| 2,693 |

|

| Less: excess of FIFO cost over LIFO cost |

| (158 | ) |

| (160 | ) |

| Total inventories |

| $ | 2,883 |

|

| $ | 2,533 |

|

|

| | | | | | | | |

| Millions of dollars |

| September 30, 2018 |

| December 31, 2017 |

| Finished products |

| $ | 2,385 |

|

| $ | 2,374 |

|

| Raw materials and work in process |

| 624 |

|

| 725 |

|

|

| 3,009 |

|

| 3,099 |

|

| Less: excess of FIFO cost over LIFO cost |

| (136 | ) |

| (111 | ) |

| Total inventories |

| $ | 2,873 |

|

| $ | 2,988 |

|

LIFO inventories represented 42%44% and 38%41% of total inventories at September 30, 20182019 and December 31, 2017,2018, respectively.

(5)(6) PROPERTY, PLANT & EQUIPMENT

The following table summarizes our property, plant and equipment as ofat September 30, 20182019 and December 31, 2017:2018:

|

| | | | | | | | |

| Millions of dollars |

| September 30, 2019 |

| December 31, 2018 |

| Land |

| $ | 98 |

|

| $ | 102 |

|

| Buildings |

| 1,585 |

|

| 1,593 |

|

| Machinery and equipment |

| 7,851 |

|

| 7,909 |

|

| Accumulated depreciation |

| (6,331 | ) |

| (6,190 | ) |

| Property, plant and equipment, net |

| $ | 3,203 |

|

| $ | 3,414 |

|

|

| | | | | | | | |

| Millions of dollars |

| September 30, 2018 |

| December 31, 2017 |

| Land |

| $ | 122 |

|

| $ | 123 |

|

| Buildings |

| 1,671 |

|

| 1,789 |

|

| Machinery and equipment |

| 7,819 |

|

| 8,946 |

|

| Accumulated depreciation |

| (6,216 | ) |

| (6,825 | ) |

| Property, plant and equipment, net |

| $ | 3,396 |

|

| $ | 4,033 |

|

During the nine months ended September 30, 2018,2019, we disposed of buildings, machinery and equipment no longer in use with a net book value of $25$57 million, and certain land use rights were transferredprimarily related to the China government resulting in a $27 million gain recorded in cost of products sold.Naples asset impairment charges.

For additional information, see Note 13 to the Consolidated Condensed Financial Statements.

(6)(7) FINANCING ARRANGEMENTS

Debt Offering

On November 9, 2017, Whirlpool Finance Luxembourg S.à. r.l., an indirect, wholly-owned finance subsidiary ofFebruary 26, 2019, Whirlpool Corporation completed a debtbond offering consisting of €600$700 million (approximately $699 million as of the date of issuance)in principal amount of 1.100% notes4.75% Senior Notes due in 2027. The Company has fully and unconditionally guaranteed these notes.2029. The notes contain covenants that limit Whirlpool Corporation's ability to incur certain liens or enter into certain sale and lease-back transactions. In addition, if we experience a specific kind of change of control, we are required to make an offer to purchase all of the notes at a purchase price of 101% of the principal amount thereof, plus accrued and unpaid interest. The notes are registered under the Securities Act of 1933, as amended, pursuant to our Registration Statement on Form S-3 (File No.333-203704-1)No.333-224381) previously filed with the Securities and Exchange Commission on October 25, 2016. Commission.

Debt Repayment

On August 9, 2019, we repaid $1.0 billion pursuant to our April 23, 2018 Term Loan Agreement with Citibank, N.A., as Administrative Agent, and certain other financial institutions, representing full repayment of amounts borrowed under the term loan. As previously disclosed, we agreed to repay this term loan amount with the net cash proceeds received from the sale of our Embraco business unit to Nidec Corporation, which closed on July 1, 2019.

On February 27, 2019, we repaid €600 million (approximately $673 million) pursuant to our June 5, 2018 Term Loan Agreement with Wells Fargo Bank, National Association, as Administrative Agent, and certain other financial institutions (the "Whirlpool EMEA Finance Term Loan"), representing full repayment of amounts borrowed under the Whirlpool EMEA Finance Term Loan. On March 1, 2019, $250 million of 2.40% senior notes matured and were repaid. On April 26, 2018, $363 million of 4.50% senior notes matured and were repaid. On November 1, 2017, $300 million of 1.65% senior notes matured and were repaid. On March 1, 2017, $250 million of 1.35% senior notes matured and were repaid.

Term Loan Agreements

On June 5, 2018, the Company and its indirect wholly-owned subsidiary, Whirlpool EMEA Finance S.à. r.l., entered into a Term Loan Agreement (the "Whirlpool EMEA Finance Term Loan") with Wells Fargo Bank, National Association, as Administrative Agent, and certain other financial institutions. Wells Fargo Securities, LLC acted as Sole Lead Arranger and Sole Bookrunner for the Whirlpool EMEA Finance Term Loan. The Whirlpool EMEA Finance Term Loan Agreement provides for an aggregate lender commitment of €600 million (approximately $703 million as of June 5, 2018) and is recorded in long-term debt of our Consolidated Condensed Balance Sheets. The Whirlpool EMEA Finance Term Loan has a maturity date of December 1, 2019, and contains an unconditional Company guarantee for repayment of amounts borrowed by Whirlpool EMEA Finance S.à. r.l. under the term loan facility. The Company and Whirlpool EMEA Finance S.à. r.l. also agree to repay outstanding loan amounts with the proceeds received from any future capital markets transaction involving Whirlpool EMEA Finance S.à. r.l. as issuer or the Company as issuer or guarantor.

The interest and fee rates payable with respect to the term loan facility based on the Company's current debt rating are as follows: (1) the spread over EURIBOR is 1.00%; (2) the spread over prime is 0.125%; and (3) the ticking fee is 0.125%, as of the date hereof. The Whirlpool EMEA Finance Term Loan Agreement, as amended August 30, 2018, contains customary covenants and warranties including, among other things, a Company debt to capitalization ratio of less than or equal to 0.65 to 1.00 as of the last day of each fiscal quarter, and a Company rolling twelve month interest coverage ratio required to be greater than or equal to 3.0 to 1.0 for each fiscal quarter. In addition, the covenants limit the Company's ability to (or to permit any subsidiaries to), subject to various exceptions and limitations: (i) merge with other companies; (ii) create liens on its property; (iii) incur debt or off-balance sheet obligations at the subsidiary level; (iv) enter into transactions with affiliates, except on an arms-length basis or with or between subsidiaries; (v) enter into agreements restricting the payment of subsidiary dividends or restricting the making of loans or repayment of debt by subsidiaries to the Company or other subsidiaries; and (vi) enter into agreements restricting the creation of

liens on its assets. The covenants also provide that Whirlpool EMEA Finance S.à. r.l must at all times remain a wholly-owned subsidiary of the Company.

On April 23, 2018 the Company entered into, and on May 14, 2018 and August 30, 2018 the Company amended, a Term Loan Agreement (the "Term Loan Agreement") by and among the Company, Citibank, N.A., as Administrative Agent, JPMorgan Chase Bank, N.A. as Syndication Agent, and certain other financial institutions. Citibank, N.A., JPMorgan Chase Bank, N.A., BNP Paribas Securities Corp., Mizuho Bank, Ltd., and Wells Fargo Securities, LLC acted as Joint Lead Arrangers and Joint Bookrunners for the Term Loan Agreement. The Term Loan Agreement provides for an aggregate lender commitment of $1.0 billion and is recorded in notes payable of our Consolidated Condensed Balance Sheets. The Term Loan Agreement has a maturity date of April 22, 2019, which date may be extended by the Company, in its discretion, prior to the maturity date for an additional six months. The Company also has agreed to repay the outstanding term loan amounts with the net cash proceeds received from the closing of the Embraco sale transaction. The proceeds of the Term Loan Agreement were used to fund accelerated share repurchases through a modified Dutch auction tender offer.

The interest and fee rates payable with respect to the term loan facility based on the Company's current debt rating are as follows: (1) the spread over LIBOR is 1.125%; (2) the spread over prime is 0.125%; and (3) the ticking fee is 0.125%, as of the date hereof. The Term Loan Agreement, as amended, contains customary covenants and warranties including, among other things, a debt to capitalization ratio of less than or equal to 0.65 to 1.00 as of the last day of each fiscal quarter, and a rolling twelve month interest coverage ratio required to be greater than or equal to 3.0 to 1.0 for each fiscal quarter. In addition, the covenants limit the Company's ability to (or to permit any subsidiaries to), subject to various exceptions and limitations: (i) merge with other companies; (ii) create liens on its property; (iii) incur debt or off-balance sheet obligations at the subsidiary level; (iv) enter into transactions with affiliates, except on an arms-length basis or with or between subsidiaries; (v) enter into agreements restricting the payment of subsidiary dividends or restricting the making of loans or repayment of debt by subsidiaries to the Company or other subsidiaries; and (vi) enter into agreements restricting the creation of liens on its assets.

Credit Facilities

On September 27, 2017,August 6, 2019, Whirlpool Corporation exercised its commitment increase and term extension rights under the Thirdentered into a Fourth Amended and Restated Long-Term Credit Agreement (the "Amended Long-Term Facility") by and among the Company, certain other borrowers, the lenders referred to therein, JPMorgan Chase Bank, N.A. as Administrative Agent, and Citibank, N.A., as Syndication Agent. In connection with this exercise, the Company entered into a Consent to Commitment Increase agreement with the Administrative Agent, which increasesThe Amended Long-Term Facility provides aggregate borrowing capacity underof $3.5 billion, an increase of $500 million from the Company's prior amended and restated credit agreement. The Amended Long-Term Facility from $2.5 billion to $3.0 billion, and the Administrative Agent received extension request consents fromhas a majority of lenders, which extends the terminationmaturity date of theAugust 6, 2024, unless earlier terminated, and amends and restates in its entirety our previously existing Third Amended and Restated Long-Term Facility by one year, toCredit Agreement, dated May 17, 2022.2016, as amended.

The interest and fee rates payable with respect to the Amended Long-Term Facility based on our current debt rating are as follows: (1) the spread over LIBOREURIBOR is 1.125%; (2) the spread over prime is 0.125%; and (3) the unused commitmentticking fee is 0.125%0.100%. The Amended Long-Term Facility as amended August 30, 2018, contains customary covenants and warranties including, among other things, a debt to capitalization ratio of less than or equal to 0.65 to 1.00 as of the last day of each fiscal quarter, and a rolling twelve month interest coverage ratio required to be greater than or equal to 3.0 to 1.0 for each fiscal quarter. In addition, the covenants limit our ability to (or to permit any subsidiaries to), subject to various exceptions and limitations: (i) merge with other companies; (ii) create liens on our property; (iii) incur debt or off-balance sheet obligations at the subsidiary level; (iv) enter into transactions with affiliates, except on an arms-length basis or with or between subsidiaries; (v) enter into agreements restricting the payment of subsidiary dividends or restricting the making of loans or repayment of debt by subsidiaries to the Company or other subsidiaries; and (vi) enter into agreements restricting the creation of liens on our assets.level.

In addition to the committed $3.0$3.5 billion Amended Long-Term Facility, we have a committed European facility and committed credit facilities in Brazil. The European facility provides borrowings up to €250 million (approximately $290 million at September 30, 2018 and $300 million at December 31, 2017), maturing on September 26, 2019. The committed credit facilities in Brazil provide borrowings up to 1.0 billion Brazilian reais (approximately $250$240 million at September 30, 20182019 and $302$258 million at December 31, 2017)2018), maturing through 2019.2022. On August 5, 2019 we terminated a €250 million European revolving credit facility that we entered into in July 2015. The termination of this facility did not have a material impact on our Consolidated Condensed Financial Statements.

We had no0 borrowings outstanding under the committed credit facilities at September 30, 20182019 or December 31, 20172018.

Notes Payable

Notes payable, which consist of short-term borrowings payable to banks or commercial paper, are generally used to fund working capital requirements. The proceeds of the term loan, included in short-term borrowings, were used to fund accelerated share repurchases through a modified Dutch auction tender offer in the second quarter of 2018. Additionally notes payable were used to fund the $350 million of discretionary pension contributions in September 2018. The fair value of our notes payable approximates the carrying amount due to the short maturity of these obligations. As previously disclosed, during the third quarter of 2019 we repaid the $1 billion term loan.

The following table summarizes the carrying value of notes payable at September 30, 20182019 and December 31, 2017.2018:

|

| | | | | | | | |

| Millions of dollars | | September 30, 2019 | | December 31, 2018 |

| Commercial paper | | $ | 711 |

| | $ | — |

|

| Short-term borrowings due to banks | | 230 |

| | 1,034 |

|

| Total notes payable | | $ | 941 |

| | $ | 1,034 |

|

Transfers and Servicing of Financial Assets

In an effort to manage economic and geographic trade customer risk, from time to time, the Company will transfer, primarily without recourse, accounts receivable balances of certain customers to financial institutions resulting in a nominal impact recorded in interest and sundry (income) expense. These transactions are accounted for as sales of the receivables resulting in the receivables being de-recognized from the Consolidated Condensed Balance Sheets.

|

| | | | | | | | |

| Millions of dollars | | September 30, 2018 | | December 31, 2017 |

| Commercial paper | | $ | 907 |