UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D. C. 20549

______________________________________________

FORM 10-Q

______________________________________________

(Mark one)

|

| |

| ý | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the quarterly period ended March 31, 20192020

or

|

| |

| o | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Commission File Number: 1-8182

PIONEER ENERGY SERVICES CORP.

(Exact name of registrant as specified in its charter)

____________________________________________

|

| | |

TEXASDELAWARE | | 74-2088619 |

(State or other jurisdiction of incorporation or organization) | | (I.R.S. Employer Identification Number) |

| | | |

1250 N.E. Loop 410, Suite 1000 San Antonio, Texas | | 78209 |

| (Address of principal executive offices) | | (Zip Code) |

Registrant’s telephone number, including area code: (855) 884-0575

|

|

| | |

| Securities registered pursuant to Section 12(b) of the Act |

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered |

Common Stock | PES | New York Stock Exchange |

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No o

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes x No o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

|

| | | |

| Large accelerated filer | o | Accelerated filer | x |

| | | o |

| Non-accelerated filer | ox | Smaller reporting company | ox |

| | | |

| Emerging Growth Company | o |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ¨

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x

Indicate by check mark whether the registrant has filed all documents and reports required to be filed by Sections 12, 13, or 15(d) of the Securities Exchange Act of 1934 subsequent to the distribution of securities under a plan confirmed by a court. Yes x No ¨

As of AprilJune 15, 2019,2020, there were 78,466,2601,048,185 shares of common stock, par value $0.10$0.001 per share, of the registrant outstanding.

EXPLANATORY NOTE

As previously disclosed in the Current Report on Form 8-K filed by Pioneer Energy Services Corp. (the “Company”) on March 2, 2020, the Company commenced a voluntary restructuring under Chapter 11 of the U.S. Bankruptcy Code on March 1, 2020. The Company has had to devote a significant amount of time, resources and administrative support to simultaneously support managing the Company and managing its restructuring, while also monitoring how these ongoing processes may affect the disclosures to be included in this Form 10-Q and other reports; all of which were made more difficult due to the coronavirus (“COVID-19”) pandemic and disruptions associated with the COVID-19 pandemic. The Company was unable to file this Form 10-Q by the original deadline due to the outbreak of, and local, state and federal governmental responses to, the COVID-19 pandemic. Office closures limited access to the Company’s facilities by the Company’s financial reporting and accounting staff, as well as other advisors involved in the preparation of this Form 10-Q, led to communications and similar delays among such persons, and impacted our ability to fulfill required preparation and review processes and procedures with respect to this Form 10-Q, thus additional time was required to complete this Form 10-Q. As previously disclosed in the Current Report on Form 8-K filed by the Company on May 15, 2020, the Company announced that it was delaying the filing of its Quarterly Report on Form 10-Q for the quarter ended March 31, 2020 for the foregoing reasons in reliance on an order (Release No. 34-88465) issued by the Securities and Exchange Commission that provides conditional relief to public companies that are unable to timely comply with a filing deadline due to circumstances related to the COVID-19 pandemic.

As previously disclosed in the Current Report on Form 8-K filed by the Company on June 2, 2020, the Company announced that it had emerged from Chapter 11 (the “Emergence 8-K”). As more fully described in the Emergence 8-K, pursuant to the Chapter 11 plan of reorganization approved by the Bankruptcy Court, on May 29, 2020, among other things:

the Company converted from a Texas corporation to a Delaware corporation;

all the outstanding common stock was canceled, and holders thereof received an aggregate of 5.75% of the proforma common equity (subject to dilution from the convertible notes and new management incentive plan), at a conversion rate of 0.0006849838 new shares for each old share;

the $300 million principal amount of the Company’s Senior Notes due 2022 was canceled in exchange for 94.25% of the proforma common equity (subject to dilution from the convertible notes and new management incentive plan);

the amounts outstanding under the Company’s debtor-in-possession credit facility were repaid and the existing term loan was repaid with proceeds from the issuance of the senior secured notes and convertible notes referenced below;

the Company entered into a $75 millionsenior secured asset-based revolving credit agreement;

the Company issued $78,125,000 of its floating rate senior secured notes due 2025; and

the Company issued $129,771,000 aggregate principal amount of its 5% convertible senior unsecured pay-in-kind notes due 2025, which are convertible into 75 shares of Common Stock per $1,000 principal amount of the convertible notes, subject to customary anti-dilution adjustments, which notes have the right to vote together with the common stock on an “as-converted” basis on all matters to be voted on by the Company’s stockholders.

TABLE OF CONTENTS

PART I. FINANCIAL INFORMATION

| |

| ITEM 1. | FINANCIAL STATEMENTS |

PIONEER ENERGY SERVICES CORP. AND SUBSIDIARIES (DEBTOR IN POSSESSION)

CONDENSED CONSOLIDATED BALANCE SHEETS

| | | | March 31,

2019 | | December 31,

2018 | March 31,

2020 | | December 31,

2019 |

| | (unaudited) | | (audited) | (unaudited) | | (audited) |

| | (in thousands, except share data) | (in thousands, except share data) |

| ASSETS | | |

| Current assets: | | | | | | |

| Cash and cash equivalents | $ | 26,855 |

| | $ | 53,566 |

| $ | 15,457 |

| | $ | 24,619 |

|

| Restricted cash | 998 |

| | 998 |

| 998 |

| | 998 |

|

| Receivables: | | | | | | |

| Trade, net of allowance for doubtful accounts | 90,816 |

| | 76,924 |

| 64,836 |

| | 79,135 |

|

| Unbilled receivables | 27,535 |

| | 24,822 |

| 12,015 |

| | 12,590 |

|

| Insurance recoveries | 23,427 |

| | 23,656 |

| 22,379 |

| | 22,873 |

|

| Other receivables | 6,307 |

| | 5,479 |

| 3,693 |

| | 8,928 |

|

| Inventory | 20,229 |

| | 18,898 |

| 21,619 |

| | 22,453 |

|

| Assets held for sale | 4,794 |

| | 3,582 |

| 1,825 |

| | 3,447 |

|

| Prepaid expenses and other current assets | 7,307 |

| | 7,109 |

| 8,129 |

| | 7,869 |

|

| Total current assets | 208,268 |

| | 215,034 |

| 150,951 |

| | 182,912 |

|

| Property and equipment, at cost | 1,125,170 |

| | 1,118,215 |

| 1,083,512 |

| | 1,119,546 |

|

| Less accumulated depreciation | 607,403 |

| | 593,357 |

| 643,558 |

| | 648,376 |

|

| Net property and equipment | 517,767 |

| | 524,858 |

| 439,954 |

| | 471,170 |

|

| Deferred income taxes | | 9,264 |

| | 11,540 |

|

| Operating lease assets | 9,423 |

| | — |

| 7,972 |

| | 7,264 |

|

| Other noncurrent assets | 1,633 |

| | 1,658 |

| 7,593 |

| | 1,068 |

|

| Total assets | $ | 737,091 |

| | $ | 741,550 |

| $ | 615,734 |

| | $ | 673,954 |

|

| | | | | | | |

| LIABILITIES AND SHAREHOLDERS’ EQUITY | | | | |

| LIABILITIES AND STOCKHOLDERS’ EQUITY | | | | |

| Current liabilities: | | | | | | |

| Accounts payable | $ | 38,163 |

| | $ | 34,134 |

| $ | 28,774 |

| | $ | 32,551 |

|

| Deferred revenues | 1,659 |

| | 1,722 |

| 997 |

| | 1,339 |

|

| Commitment premium | | 9,584 |

| | — |

|

| Debtor in possession financing | | 4,000 |

| | — |

|

| Accrued expenses: | | | | | | |

| Payroll and related employee costs | 24,699 |

| | 24,598 |

| |

| Employee compensation and related costs | | 10,300 |

| | 13,781 |

|

| Insurance claims and settlements | 22,819 |

| | 23,593 |

| 22,239 |

| | 22,873 |

|

| Insurance premiums and deductibles | 5,543 |

| | 5,482 |

| 5,831 |

| | 5,940 |

|

| Interest | 1,460 |

| | 6,148 |

| 107 |

| | 5,452 |

|

| Other | 10,233 |

| | 9,091 |

| 11,196 |

| | 9,645 |

|

| Total current liabilities | 104,576 |

| | 104,768 |

| 93,028 |

| | 91,581 |

|

| Long-term debt, less unamortized discount and debt issuance costs | 465,315 |

| | 464,552 |

| 170,921 |

| | 467,699 |

|

| Noncurrent operating lease liabilities | 6,929 |

| | — |

| 6,434 |

| | 5,700 |

|

| Deferred income taxes | 4,844 |

| | 3,688 |

| 3,256 |

| | 4,417 |

|

| Other noncurrent liabilities | 4,460 |

| | 3,484 |

| 383 |

| | 481 |

|

| Total liabilities | 586,124 |

| | 576,492 |

| |

| Commitments and contingencies (Note 11) |

| |

| |

| Shareholders’ equity: | | | | |

| Total liabilities not subject to compromise | | 274,022 |

| | 569,878 |

|

| Commitments and contingencies (Note 12) | | | | |

| Liabilities subject to compromise | | 306,419 |

| | — |

|

| Stockholders’ equity: | | | | |

| Preferred stock, 10,000,000 shares authorized; none issued and outstanding | — |

| | — |

| — |

| | — |

|

| Common stock $.10 par value; 200,000,000 shares authorized; 78,456,260 and 78,214,550 shares outstanding at March 31, 2019 and December 31, 2018, respectively | 7,933 |

| | 7,900 |

| |

| Common stock $.10 par value; 200,000,000 shares authorized; 79,579,571 and 79,202,216 shares outstanding at March 31, 2020 and December 31, 2019, respectively | | 8,062 |

| | 8,008 |

|

| Additional paid-in capital | 551,382 |

| | 550,548 |

| 553,484 |

| | 553,210 |

|

| Treasury stock, at cost; 874,391 and 789,532 shares at March 31, 2019 and December 31, 2018, respectively | (5,085 | ) | | (4,965 | ) | |

| Treasury stock, at cost; 1,041,565 and 877,047 shares at March 31, 2020 and December 31, 2019, respectively | | (5,097 | ) | | (5,090 | ) |

| Accumulated deficit | (403,263 | ) | | (388,425 | ) | (521,156 | ) | | (452,052 | ) |

| Total shareholders’ equity | 150,967 |

| | 165,058 |

| |

| Total liabilities and shareholders’ equity | $ | 737,091 |

| | $ | 741,550 |

| |

| Total stockholders’ equity | | 35,293 |

| | 104,076 |

|

| Total liabilities and stockholders’ equity | | $ | 615,734 |

| | $ | 673,954 |

|

See accompanying notes to condensed consolidated financial statements.

PIONEER ENERGY SERVICES CORP. AND SUBSIDIARIES (DEBTOR IN POSSESSION)

CONDENSED CONSOLIDATED STATEMENTS OF OPERATIONS

(unaudited)

| | | | Three months ended March 31, | Three months ended March 31, |

| | 2019 | | 2018 | 2020 | | 2019 |

| | (in thousands, except per share data) | (in thousands, except per share data) |

| | | | | | | |

| Revenues | $ | 146,568 |

| | $ | 144,478 |

| $ | 114,322 |

| | $ | 146,568 |

|

| | | | | | | |

| Costs and expenses: | | | | | | |

| Operating costs | 108,585 |

| | 102,766 |

| 92,022 |

| | 108,585 |

|

| Depreciation | 22,653 |

| | 23,747 |

| 21,984 |

| | 22,653 |

|

| General and administrative | 19,758 |

| | 19,194 |

| 14,655 |

| | 19,758 |

|

| Bad debt expense (recovery), net | 62 |

| | (52 | ) | |

| Pre-petition restructuring charges | | 17,074 |

| | — |

|

| Impairment | 1,046 |

| | — |

| 17,853 |

| | 1,046 |

|

| Bad debt expense, net | | 727 |

| | 62 |

|

| Gain on dispositions of property and equipment, net | (1,075 | ) | | (335 | ) | (717 | ) | | (1,075 | ) |

| Total costs and expenses | 151,029 |

| | 145,320 |

| 163,598 |

| | 151,029 |

|

| Loss from operations | (4,461 | ) | | (842 | ) | (49,276 | ) | | (4,461 | ) |

| | | | | | | |

| Other income (expense): | | | | | | |

| Interest expense, net of interest capitalized | (9,885 | ) | | (9,513 | ) | (8,651 | ) | | (9,885 | ) |

| Other income, net | 684 |

| | 504 |

| |

| Reorganization items | | (6,663 | ) | | — |

|

| Other income (expense), net | | (5,545 | ) | | 684 |

|

| Total other expense, net | (9,201 | ) | | (9,009 | ) | (20,859 | ) | | (9,201 | ) |

| | | | | | | |

| Loss before income taxes | (13,662 | ) | | (9,851 | ) | (70,135 | ) | | (13,662 | ) |

| Income tax expense | (1,453 | ) | | (1,288 | ) | |

| Income tax (expense) benefit | | 1,031 |

| | (1,453 | ) |

| Net loss | $ | (15,115 | ) | | $ | (11,139 | ) | $ | (69,104 | ) | | $ | (15,115 | ) |

| | | | | | | |

| Loss per common share - Basic | $ | (0.19 | ) | | $ | (0.14 | ) | $ | (0.88 | ) | | $ | (0.19 | ) |

| | | | | | | |

| Loss per common share - Diluted | $ | (0.19 | ) | | $ | (0.14 | ) | $ | (0.88 | ) | | $ | (0.19 | ) |

| | | | | | | |

| Weighted average number of shares outstanding—Basic | 78,311 |

| | 77,606 |

| 78,753 |

| | 78,311 |

|

| | | | | | | |

| Weighted average number of shares outstanding—Diluted | 78,311 |

| | 77,606 |

| 78,753 |

| | 78,311 |

|

See accompanying notes to condensed consolidated financial statements.

PIONEER ENERGY SERVICES CORP. AND SUBSIDIARIES (DEBTOR IN POSSESSION)

CONDENSED CONSOLIDATED STATEMENTS OF SHAREHOLDERS’STOCKHOLDERS’ EQUITY

(unaudited)

| | | | As of and for the three months ended March 31, 2019 | As of and for the three months ended March 31, 2020 |

| | Shares | | Amount | | Additional Paid In Capital | | Accumulated Deficit | | Total Shareholders’ Equity | Shares | | Amount | | Additional Paid In Capital | | Accumulated Deficit | | Total Stockholders’ Equity |

| Common | | Treasury | Common | | Treasury | Common | | Treasury | Common | | Treasury |

| | (in thousands) | (in thousands) |

| Balance as of December 31, 2018 | 79,005 |

| | (790 | ) | | $ | 7,900 |

| | $ | (4,965 | ) | | $ | 550,548 |

| | $ | (388,425 | ) | | $ | 165,058 |

| |

| Balance as of December 31, 2019 | | 80,079 |

| | (877 | ) | | $ | 8,008 |

| | $ | (5,090 | ) | | $ | 553,210 |

| | $ | (452,052 | ) | | $ | 104,076 |

|

| Net loss | — |

| | — |

| | — |

| | — |

| | — |

| | (15,115 | ) | | (15,115 | ) | — |

| | — |

| | — |

| | — |

| | — |

| | (69,104 | ) | | (69,104 | ) |

| Purchase of treasury stock | — |

| | (84 | ) | | — |

| | (120 | ) | | — |

| | — |

| | (120 | ) | — |

| | (165 | ) | | — |

| | (7 | ) | | — |

| | — |

| | (7 | ) |

| Cumulative-effect adjustment due to adoption of ASC Topic 842 | — |

| | — |

| | — |

| | — |

| | — |

| | 277 |

| | 277 |

| |

| Issuance of restricted stock | 326 |

| | — |

| | 33 |

| | — |

| | (33 | ) | | — |

| | — |

| 542 |

| | — |

| | 54 |

| | — |

| | (54 | ) | | — |

| | — |

|

| Stock-based compensation expense | — |

| | — |

| | — |

| | — |

| | 867 |

| | — |

| | 867 |

| — |

| | — |

| | — |

| | — |

| | 328 |

| | — |

| | 328 |

|

| Balance as of March 31, 2019 | 79,331 |

| | (874 | ) | | $ | 7,933 |

| | $ | (5,085 | ) | | $ | 551,382 |

| | $ | (403,263 | ) | | $ | 150,967 |

| |

| Balance as of March 31, 2020 | | 80,621 |

| | (1,042 | ) | | $ | 8,062 |

| | $ | (5,097 | ) | | $ | 553,484 |

| | $ | (521,156 | ) | | $ | 35,293 |

|

| | | | As of and for the three months ended March 31, 2018 | As of and for the three months ended March 31, 2019 |

| | Shares | | Amount | | Additional Paid In Capital | | Accumulated Deficit | | Total Shareholders’ Equity | Shares | | Amount | | Additional Paid In Capital | | Accumulated Deficit | | Total Stockholders’ Equity |

| Common | | Treasury | Common | | Treasury | Common | | Treasury | Common | | Treasury |

| | (in thousands) | (in thousands) |

| Balance as of December 31, 2017 | 78,350 |

| | (631 | ) | | $ | 7,835 |

| | $ | (4,416 | ) | | $ | 546,158 |

| | $ | (339,481 | ) | | $ | 210,096 |

| |

| Balance as of December 31, 2018 | | 79,004 |

| | (790 | ) | | $ | 7,900 |

| | $ | (4,965 | ) | | $ | 550,548 |

| | $ | (388,425 | ) | | $ | 165,058 |

|

| Net loss | — |

| | — |

| | — |

| | — |

| | — |

| | (11,139 | ) | | (11,139 | ) | — |

| | — |

| | — |

| | — |

| | — |

| | (15,115 | ) | | (15,115 | ) |

| Purchase of treasury stock | — |

| | (28 | ) | | — |

| | (96 | ) | | — |

| | — |

| | (96 | ) | — |

| | (84 | ) | | — |

| | (120 | ) | | — |

| | — |

| | (120 | ) |

| Cumulative-effect adjustment due to adoption of ASC Topic 606 | — |

| | — |

| | — |

| | — |

| | — |

| | 67 |

| | 67 |

| |

| Cumulative-effect adjustment due to adoption of ASC Topic 842 | | — |

| | — |

| | — |

| | — |

| | — |

| | 277 |

| | 277 |

|

| Issuance of restricted stock | 105 |

| | — |

| | 10 |

| | — |

| | (10 | ) | | — |

| | — |

| 326 |

| | — |

| | 33 |

| | — |

| | (33 | ) | | — |

| | — |

|

| Stock-based compensation expense | — |

| | — |

| | — |

| | — |

| | 1,259 |

| | — |

| | 1,259 |

| — |

| | — |

| | — |

| | — |

| | 867 |

| | — |

| | 867 |

|

| Balance as of March 31, 2018 | 78,455 |

| | (659 | ) | | $ | 7,845 |

| | $ | (4,512 | ) | | $ | 547,407 |

| | $ | (350,553 | ) | | $ | 200,187 |

| |

| Balance as of March 31, 2019 | | 79,330 |

| | (874 | ) | | $ | 7,933 |

| | $ | (5,085 | ) | | $ | 551,382 |

| | $ | (403,263 | ) | | $ | 150,967 |

|

See accompanying notes to consolidated financial statements.

PIONEER ENERGY SERVICES CORP. AND SUBSIDIARIES (DEBTOR IN POSSESSION)

CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS

(unaudited)

| | | | Three months ended March 31, | Three months ended March 31, |

| | 2019 | | 2018 | 2020 | | 2019 |

| | (in thousands) | (in thousands) |

| Cash flows from operating activities: | | | | | | |

| Net loss | $ | (15,115 | ) | | $ | (11,139 | ) | $ | (69,104 | ) | | $ | (15,115 | ) |

| Adjustments to reconcile net loss to net cash provided by (used in) operating activities: | | | | |

| Adjustments to reconcile net loss to net cash used in operating activities: | | | | |

| Depreciation | 22,653 |

| | 23,747 |

| 21,984 |

| | 22,653 |

|

| Allowance for doubtful accounts, net of recoveries | 62 |

| | (52 | ) | 727 |

| | 62 |

|

| Gain on dispositions of property and equipment, net | (1,075 | ) | | (335 | ) | (717 | ) | | (1,075 | ) |

| Reorganization items | | 988 |

| | — |

|

| Stock-based compensation expense | 867 |

| | 1,259 |

| 328 |

| | 867 |

|

| Phantom stock compensation expense | 848 |

| | 430 |

| (3 | ) | | 848 |

|

| Amortization of debt issuance costs and discount | 763 |

| | 707 |

| 1,219 |

| | 763 |

|

| Impairment | 1,046 |

| | — |

| 17,853 |

| | 1,046 |

|

| Deferred income taxes | 1,156 |

| | 911 |

| 1,115 |

| | 1,156 |

|

| Change in other noncurrent assets | 699 |

| | (463 | ) | 690 |

| | 699 |

|

| Change in other noncurrent liabilities | (20 | ) | | 1,414 |

| (562 | ) | | (20 | ) |

| Changes in current assets and liabilities: | | | | | | |

| Receivables | (17,488 | ) | | (3,296 | ) | 14,234 |

| | (17,488 | ) |

| Inventory | (1,293 | ) | | (2,042 | ) | 834 |

| | (1,293 | ) |

| Prepaid expenses and other current assets | (178 | ) | | 882 |

| (1,253 | ) | | (178 | ) |

| Accounts payable | 2,339 |

| | 51 |

| (4,114 | ) | | 2,339 |

|

| Deferred revenues | (64 | ) | | (108 | ) | (342 | ) | | (64 | ) |

| Commitment premium | | 9,584 |

| | — |

|

| Accrued expenses | (5,990 | ) | | (6,908 | ) | 1,148 |

| | (5,990 | ) |

| Net cash provided by (used in) operating activities | (10,790 | ) | | 5,058 |

| |

| Net cash used in operating activities | | (5,391 | ) | | (10,790 | ) |

| | | | | | | |

| Cash flows from investing activities: | | | | | | |

| Purchases of property and equipment | (16,844 | ) | | (11,657 | ) | (7,503 | ) | | (16,844 | ) |

| Proceeds from sale of property and equipment | 1,043 |

| | 1,283 |

| 727 |

| | 1,043 |

|

| Proceeds from insurance recoveries | — |

| | 523 |

| |

| Net cash used in investing activities | (15,801 | ) | | (9,851 | ) | (6,776 | ) | | (15,801 | ) |

| | | | | | | |

| Cash flows from financing activities: | | | | | | |

| Debt issuance costs | — |

| | (33 | ) | |

| Proceeds from DIP Facility | | 4,000 |

| | — |

|

| DIP Facility issuance costs | | (988 | ) | | — |

|

| Purchase of treasury stock | (120 | ) | | (96 | ) | (7 | ) | | (120 | ) |

| Net cash used in financing activities | (120 | ) | | (129 | ) | |

| Net cash provided by (used in) financing activities | | 3,005 |

| | (120 | ) |

| | | | | | | |

| Net decrease in cash, cash equivalents and restricted cash | (26,711 | ) | | (4,922 | ) | (9,162 | ) | | (26,711 | ) |

| Beginning cash, cash equivalents and restricted cash | 54,564 |

| | 75,648 |

| 25,617 |

| | 54,564 |

|

| Ending cash, cash equivalents and restricted cash | $ | 27,853 |

| | $ | 70,726 |

| $ | 16,455 |

| | $ | 27,853 |

|

| | | | | | | |

| Supplementary disclosure: | | | | | | |

| Interest paid | $ | 13,887 |

| | $ | 13,515 |

| $ | 4,306 |

| | $ | 13,887 |

|

| Income tax paid | $ | 1,013 |

| | $ | 658 |

| $ | 623 |

| | $ | 1,013 |

|

| Reorganization items paid | | $ | 2,322 |

| | — |

|

| Noncash investing and financing activity: | | | | | | |

| Change in capital expenditure accruals | $ | 1,531 |

| | $ | 2,931 |

| $ | 358 |

| | $ | 1,531 |

|

See accompanying notes to condensed consolidated financial statements.

PIONEER ENERGY SERVICES CORP. AND SUBSIDIARIES (DEBTOR IN POSSESSION)

NOTES TO UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

1. Organization and Summary of Significant Accounting Policies

Business

Pioneer Energy Services Corp. provides land-based drilling services and production services to a diverse group of oil and gas exploration and production companies in the United States and internationally in Colombia.

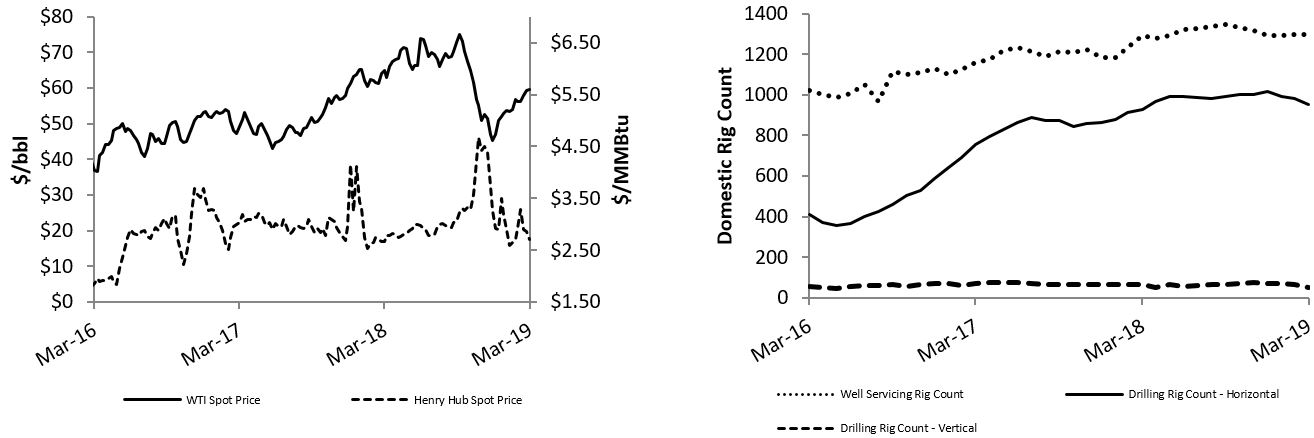

Our drilling services business segments provide contract land drilling services through three domestic divisions which are located in the Marcellus/Utica, Permian Basin and Eagle Ford, and Bakken regions, and internationally in Colombia. We provide a comprehensive service offering which includes the drilling rig, crews, supplies, and most of the ancillary equipment needed to operate our drilling rigs. Our drilling rigs are equipped with 1,500 horsepower or greater drawworks, arefleet is 100% pad-capable and offeroffers the latest advancements in pad drilling. The following table summarizes our current rig fleet count and composition for each drilling services business segment:

|

| | | | | | | |

| | Multi-well, Pad-capable |

| | AC rigs | | SCR rigs | | Total |

| Domestic drilling | 17 |

| | — |

| | 17 |

| International drilling | — |

| | 8 |

| | 8 |

| | | | | | 25 |

Our production services business segments provide a range of well, wireline and coiled tubing services to a diverse group of explorationproducers primarily in Texas and production companies, with our operations concentrated in the major domestic onshore oil and gas producing regions in the Gulf Coast, Mid-Continent and Rocky Mountain states.regions, as well as in North Dakota, Louisiana and Mississippi. As of March 31, 2019,2020, the fleet countcounts for each of our production services business segments arewere as follows:

| | | | 550 HP | | 600 HP | | Total | 550 HP | | 600 HP | | Total |

| Well servicing rigs, by horsepower (HP) rating | 113 | | 12 | | 125 |

| 111 | | 12 | | 123 |

| | | | |

| | | Total | | Total |

| Wireline services units | Wireline services units | | 93 |

| Wireline services units | | 93 |

| Coiled tubing services units | Coiled tubing services units | | 9 |

| Coiled tubing services units | | 9 |

Basis of Presentation

The accompanying unaudited condensed consolidated financial statements include the accounts of Pioneer Energy Services Corp. and our wholly ownedwholly-owned subsidiaries. All intercompany balances and transactions have been eliminated in consolidation. The accompanying unaudited condensed consolidated financial statements have been prepared in accordance with accounting principles generally accepted in the United States of America for interim financial information and with the instructions to Form 10-Q and Rule 10-01 of Regulation S-X. Accordingly, they do not include all of the information and footnotes required by generally accepted accounting principles for complete financial statements. In the opinion of our management, all adjustments (consisting of normal, recurring accruals) necessary for a fair presentation have been included. We suggest that you read these unaudited condensed consolidated financial statements together with the consolidated financial statements and the related notes included in our annual report on Form 10-K for the year ended December 31, 2018.2019.

Chapter 11 Cases — On March 1, 2020 (the “Petition Date”), Pioneer and certain of our domestic subsidiaries (collectively, the “Debtors”) filed voluntary petitions (the “Bankruptcy Petitions”) for reorganization under title 11 of the United States Code (the “Bankruptcy Code”) in the United States Bankruptcy Court for the Southern District of Texas (the “Bankruptcy Court”). On May 11, 2020, the Bankruptcy Court confirmed the plan of reorganization that was filed with the Bankruptcy Court on March 2, 2020, and on May 29, 2020 (the “Effective Date”), the conditions to effectiveness of the plan were satisfied and we emerged from Chapter 11. See Note 2, Chapter 11 Cases and Subsequent Events,for more information.

Use of Estimates — In preparing the accompanying unaudited condensed consolidated financial statements, we make various estimates and assumptions that affect the amounts of assets and liabilities we report as of the dates of the balance sheets and income and expenses we report for the periods shown in the income statements and statements of cash flows. Our actual results could differ significantly from those estimates. Material estimates that are particularly susceptible to significant changes in the near term relate to our estimates of certain variable revenues and amortization periods of certain deferred

revenues and costs associated with drilling daywork contacts, our estimates of projected cash flows and fair values for impairment evaluations, our estimate of the valuation allowance for deferred tax assets, and our estimate of the liability relating to the self-insurance portion of our health and workers’ compensation insurance and our estimate of compensation related accruals.insurance.

Subsequent Events — In preparing the accompanying unaudited condensed consolidated financial statements, we have reviewed events that have occurred after March 31, 2019,2020, through the filing of this Form 10-Q, for inclusion as necessary. See Note 2, Chapter 11 Cases and Subsequent Events,for more information.

Reclassifications—Certain amounts in the unaudited condensed consolidated financial statements for the prior year periods have been reclassified to conform to the current year’s presentation.

Change in Accounting Principle and Recently Issued Accounting Standards

Changes to accounting principles generally accepted in the United States of America (“U.S. GAAP”) are established by the Financial Accounting Standards Board (FASB) in the form of Accounting Standards Updates (ASUs) to the FASB Accounting Standards Codification (ASC). We consider the applicability and impact of all ASUs. Any ASUs not listed below were assessed and we have determined to be either not applicablethat there are currently no new or are expected torecently adopted ASUs which we believe will have an immateriala material impact on our consolidated financial position and results of operations.

Leases. In February 2016, the FASB issued ASU No. 2016-02, Leases, which among other things, requires lessees to recognize substantially all leases on the balance sheet, with expense recognition that is similar to the former lease standard, and aligns the principles of lessor accounting with the principles of the FASB’s new revenue guidance in ASC Topic 606. In July 2018, the FASB issued ASU No. 2018-11, Leases: Targeted Improvements, which provides an option to apply the guidance prospectively, and provides a practical expedient allowing lessors to combine the lease and non-lease components of revenues where the revenue recognition pattern is the same and where the lease component, when accounted for separately, would be considered an operating lease. The practical expedient also allows a lessor to account for the combined lease and non-lease components under ASC Topic 606, Revenue from Contracts with Customers, when the non-lease component is the predominant element of the combined component.

As a lessor, we elected to apply the practical expedient which allows us to continue to recognize our revenues (both lease and service components) under ASC Topic 606, and continue to present them as one revenue stream in our unaudited condensed consolidated statements of operations. As a lessee, this standard primarily impacts our accounting for long-term real estate and office equipment leases, for which we recognized an operating lease asset and a corresponding operating lease liability on our unaudited condensed consolidated balance sheet of $9.8 million at the adoption date of January 1, 2019. For leases that commenced prior to adoption of ASC Topic 842, we elected to apply the package of practical expedients which allows us to carry forward the historical lease classification. The adoption of ASC Topic 842 also resulted in a cumulative effect adjustment of $0.3 million after applicable income taxes, related to the write off of previously unamortized deferred lease liabilities at the date of adoption. For more information about the accounting under ASC Topic 842, and disclosures under the new standard, see Note 3, Leases.

Additional Detail of Account Balances

Cash Equivalents and Restricted Cash Equivalents — CashWe had no cash equivalents at March 31, 2019 and2020. Cash equivalents at December 31, 20182019 were $17.7$8.9 million, and $40.6 million, respectively, consisting of investments in highly-liquid money-market mutual funds. Our restricted cash balance reflects the portion of net proceeds from the issuance of our senior secured term loan which are currently held in a restricted account until the completion of certain administrative tasks related to providing access rights to certain of our real property.

Other Receivables — Our other receivables primarily consist of recoverable taxes related to our international operations, as well as vendor rebates and net income tax receivables.

Prepaid Expenses and Other Current Assets — Prepaid expenses and other current assets include items such as insurance, rent deposits, software subscriptions, and other fees.fees, including professional fee deposits associated with the Chapter 11 Cases. We routinely expense these items in the normal course of business over the periods that we benefit from these expenses. Prepaid expenses and other current assets also include deferred mobilization costs for short-term drilling contracts.contracts and demobilization revenues recognized on drilling contracts expiring in the near term.

Other Noncurrent Assets — Other noncurrent assets consist of prepaid taxes in Colombia which are creditable against future income taxes, deferred mobilization costs on long-term drilling contracts, cash deposits related to the deductibles on our workers’ compensation insurance policies, the noncurrent portion of prepaid insurance premiums, and deferred compensation plan investments.

Other Accrued Expenses — Our other accrued expenses include accruals for items such as sales taxes, property taxes, withholding tax liabilityliabilities related to our international operations, and professional and other fees.fees, including those associated with the Chapter 11 Cases. We routinely expense these items in the normal course of business over the periods these expenses benefit. Our other accrued expenses also includes the current portion of the lease liability associated with our long-term operating leases.

Other Noncurrent Liabilities — Our other noncurrent liabilities consist of the noncurrent portion of deferred mobilization revenues and liabilities associated with our long-term compensation plans.

2. Chapter 11 Cases and Subsequent Events

Reorganization and Chapter 11 Proceedings

In an effort to achieve liquidity that would be sufficient to meet all of our commitments, we took a number of actions, including minimizing capital expenditures and reducing recurring expenses. However, we believed that even after taking these actions, we would not have sufficient liquidity to satisfy all of our future financial obligations, comply with our debt covenants, and execute our business plan. As a result, we filed a petition for reorganization under Chapter 11 of the Bankruptcy Code on March 1, 2020.

On March 1, 2020 (the “Petition Date”), Pioneer Energy Services Corp. (“Pioneer”) and its affiliates Pioneer Coiled Tubing Services, LLC, Pioneer Drilling Services, Ltd., Pioneer Fishing & Rental Services, LLC, Pioneer Global Holdings, Inc., Pioneer Production Services, Inc., Pioneer Services Holdings, LLC, Pioneer Well Services, LLC, Pioneer Wireline Services Holdings, Inc., Pioneer Wireline Services, LLC (collectively with Pioneer, the “Pioneer RSA Parties”) filed voluntary petitions (the “Bankruptcy Petitions”) for reorganization under title 11 of the United States Code (the “Bankruptcy Code”)

in the United States Bankruptcy Court for the Southern District of Texas (the “Bankruptcy Court”). The Chapter 11 proceedings were being jointly administered under the caption In re Pioneer Energy Services Corp. et al (the “Chapter 11 Cases”).

In connection with the Bankruptcy Petitions, the Pioneer RSA Parties entered into a restructuring support agreement (the “RSA”) with holders of approximately 99% in aggregate principal amount of our outstanding Term Loan (the “Consenting Term Lenders”) and holders of approximately 75% in aggregate principal amount of our Senior Notes (the “Consenting Noteholders” and together with the Consenting Term Lenders, the “Consenting Creditors”). Pursuant to the RSA, the Consenting Creditors and the Pioneer RSA Parties made certain customary commitments to each other, including the Consenting Noteholders committing to vote for, and the Consenting Creditors committing to support, the restructuring transactions (the “Restructuring”) to be effectuated through a plan of reorganization that incorporates the economic terms included in the RSA (the “Plan”). The Pioneer RSA Parties filed the Plan with the Bankruptcy Court on March 2, 2020.

After commencement of the Chapter 11 Cases, we continued to operate our businesses as “debtors-in-possession” under the jurisdiction of the Bankruptcy Court and in accordance with the applicable provisions of the Bankruptcy Code and orders of the Bankruptcy Court.

On May 11, 2020, the Bankruptcy Court entered an order, Docket No. 331 (the “Confirmation Order”) confirming the Plan. On May 29, 2020 (the “Effective Date”) the conditions to effectiveness of the Plan were satisfied and we emerged from Chapter 11.

The commencement of the Chapter 11 Cases constituted an event of default that accelerated our obligations under our Senior Notes, the Prepetition ABL Facility, and Term Loan. Under the Bankruptcy Code, holders of our Senior Notes and the lenders under our Term Loan and the Prepetition ABL Facility were stayed from taking any action against us as a result of this event of default. On the Effective Date, all applicable agreements governing the obligations under the Term Loan, Senior Notes and Prepetition ABL Facility were terminated. The Term Loan and Prepetition ABL Facility were paid in full and all outstanding obligations under the Senior Notes were canceled in exchange for 94.25% of the proforma common equity (subject to the dilution from the Convertible Notes and new management incentive plan).

On the Effective Date, we entered into a $75 million senior secured asset-based revolving credit agreement (the “ABL Credit Facility”), and issued $129.8 million of aggregate principal amount of 5% convertible senior unsecured pay-in-kind notes due 2025 (the “Convertible Notes”) and $78.1 million of aggregate principal amount of floating rate senior secured notes due 2025 (the “Senior Secured Notes”).

Also on the Effective Date, by operation of the Plan, all agreements, instruments, and other documents evidencing, relating to or connected with any equity interests of the Company, including the existing common stock, issued and outstanding immediately prior to the Effective Date, and any rights of any holder in respect thereof, were deemed canceled, discharged and of no force or effect. Pursuant to the Plan, we issued a total of 1,049,804 shares of our new common stock, with approximately 94.25% of such new common stock being issued to holders of the Senior Notes outstanding immediately prior to the Effective Date. Holders of the existing common stock received an aggregate of 5.75% of the proforma common equity (subject to the dilution from the Convertible Notes and new management incentive plan), at a conversion rate of 0.0006849838 new shares for each existing share.

As part of the transactions undertaken pursuant to the Plan, we converted from a Texas corporation to a Delaware corporation, filed the Certificate of Incorporation of the Company with the office of the Secretary of State of the State of Delaware and adopted Amended and Restated Bylaws of the Company.

Backstop Commitment Agreement

Prior to filing the Plan, we entered into a separate backstop commitment agreement with the Consenting Noteholders and certain members of our senior management (the “Backstop Commitment Agreement”), pursuant to which the Consenting Noteholders and certain members of our senior management committed to backstop approximately $118 million and $1.8 million, respectively, of new convertible bonds to be issued in a rights offering. As consideration for this commitment, we committed to make an aggregate payment of $9.4 million and $0.1 million to the Consenting Noteholders and certain members of our senior management, respectively, in the form of additional new convertible bonds, or in cash if the Backstop Commitment Agreement was terminated under certain circumstances as forth therein. As a result, we incurred a liability and expense at the time we entered into the Backstop Commitment Agreement for the aggregate amount of $9.6 million (the “Commitment Premium”) which was recognized in our condensed consolidated financial statements as of and for the

three months ended March 31, 2020. The Commitment Premium was settled in conjunction with our emergence from Chapter 11 and the issuance of the Convertible Notes.

Debtor-in-Possession Financing

On February 28, 2020, we received commitments pursuant to the Commitment Letter from PNC Bank, N.A. for a $75 million asset-based revolving loan debtor-in-possession financing facility (the “DIP Facility”) and a $75 million asset-based revolving exit financing facility. On March 3, 2020, with the approval of the Bankruptcy Court, we entered into the DIP Facility and used the proceeds thereunder to refinance all outstanding letters of credit under the Prepetition ABL Facility in connection with the termination of the Prepetition ABL Facility and to pay fees and expenses in connection with the Chapter 11 proceedings and transaction and professional fees related thereto.

The DIP Facility provided financing with a 5-month maturity, bearing interest at a rate of LIBOR plus 200 basis points per annum, and contained customary covenants and events of default.

As of March 31, 2020, we had $4.0 million outstanding under our DIP Facility. The DIP Facility was terminated upon our emergence from the Chapter 11 Cases on May 29, 2020.

Post-Emergence Debt Instruments

ABL Credit Facility — On the Effective Date, pursuant to the terms of the Plan, we entered into a senior secured asset-based revolving credit agreement in an aggregate amount of $75 million (the “ABL Credit Facility”) among us and our domestic subsidiaries as borrowers (the “Borrowers”), the lenders party thereto and PNC Bank, National Association as administrative agent. Among other things, proceeds of loans under the ABL Credit Facility may be used to pay fees and expenses associated with the ABL Credit Facility and finance ongoing working capital and general corporate needs.

The maturity date of loans made under the ABL Credit Facility is the earliest of 90 days prior to maturity of the Senior Secured Notes or the Convertible Notes (both of which are described further below) and May 29, 2025. Borrowings under the ABL Credit Facility will bear interest at a rate of (i) the LIBOR rate, with a LIBOR rate floor of 0%, plus an applicable margin in the range of 175 to 225 basis points per annum, or (ii) the base rate plus an applicable margin in the range of 75 to 125 basis points per annum, in both cases based on the average excess availability, as defined in the ABL Credit Facility.

The ABL Credit Facility s guaranteed by the Borrowers and is secured by a first lien on the Borrowers’ accounts receivable and inventory, and the cash proceeds thereof, and a second lien on substantially all of the other assets and properties of the Borrowers.

The ABL Credit Facility limits our annual capital expenditures to 125% of the budget set forth in the projections for any fiscal year and provides that if our availability falls below $11.25 million (15% of the maximum revolver amount), we will be required to comply with a fixed charge coverage ratio of 1.0 to 1.0, all of which is defined in the ABL Credit Facility. As of May 31, 2020, we had no borrowings and approximately $7.1 million in outstanding letters of credit under the ABL Credit Facility and subject to the availability requirements in the ABL Credit Facility, based on eligible accounts receivable and inventory balances at May 31, 2020, availability under the ABL Credit Facility was $20.3 million, which our access to would be limited by our requirement to maintain 15% available or comply with a fixed charge coverage ratio, as described above.

Convertible Notes Indenture and Convertible Notes due 2025 — We entered into an indenture, dated as of the Effective Date, among the Company and Wilmington Trust, N.A., as trustee (the “Convertible Notes Indenture”), and issued $129.8 million aggregate principal amount of convertible senior unsecured pay-in-kind notes due 2025 thereunder (the “Convertible Notes”).

The Convertible Notes are general unsecured obligations which will mature on November 15, 2025, unless earlier accelerated, redeemed, converted or repurchased, and bear interest at a fixed rate of 5% per annum, which will be payable semi-annually in-kind in the form of an increase to the principal amount. The Convertible Notes are convertible at the option of the holders at any time into shares of our common stock and will convert mandatorily into our common stock at maturity; provided, however, that if the value of our common stock otherwise deliverable in connection with a mandatory conversion of a Convertible Note on the maturity date would be less than the principal amount of such Convertible Note plus accrued and unpaid interest, then the Convertible Note will instead convert into an amount of cash equal to the principal amount thereof

plus accrued and unpaid interest. The initial conversion rate is 75 shares of common stock per $1,000 principal amount of the Convertible Notes. The conversion rate is subject to customary anti-dilution adjustments.

If we undergo a “fundamental change” as defined in the Convertible Notes Indenture, subject to certain conditions, holders may require us to repurchase all or any portion of their Convertible Notes for cash at an amount equal to 100% of the principal amount of the Convertible Notes to be repurchased plus any accrued and unpaid interest. In the case of certain fundamental change events that constitute merger events (as defined in the Convertible Notes Indenture), we have a superseding right to cause the mandatory conversion of all or part of the Convertible Notes into a number of shares of common stock, per $1,000 principal amount of Convertible Notes, equal to the then-current conversion rate or the cash value of such number of shares of common stock (but not less than the principal amount).

Holders of Convertible Notes are entitled to vote on all matters on which holders of our common stock generally are entitled to vote (or, if any, to take action by written consent of the holders of our common stock), voting together as a single class together with the shares of our common stock and not as a separate class, on an as-converted basis, at any annual or special meeting of holders of our common stock and each holder is entitled to such number of votes as such holder would receive on an as-converted basis on the record date for such vote.

The Convertible Notes Indenture contains customary events of default and covenants that limit our ability and the ability of certain of our subsidiaries to incur, assume or guarantee additional indebtedness and create liens and enter into mergers or consolidations.

Senior Secured Notes Indenture and Senior Secured Notes due 2025 — We entered into an indenture, dated as of the Effective Date, among the Company, the subsidiary guarantors party thereto and Wilmington Trust, N.A., as trustee (the “Senior Secured Notes Indenture”), and issued $78.1 million aggregate principal amount of floating rate senior secured notes due 2025 (the “Senior Secured Notes”) thereunder. The Senior Secured Notes are guaranteed on a senior secured basis by our existing subsidiaries that also guarantee our obligations under the ABL Credit Facility (the “Guarantors”) on a full and unconditional basis and are secured by a second lien on the accounts receivable and inventory and a first lien on substantially all of the other assets and properties (including the cash proceeds thereof) of the Company and the Guarantors.

The Senior Secured Notes will mature on May 15, 2025 and interest will accrue at the rate of LIBOR plus 9.5% per annum, with a LIBOR rate floor of 1.5%, payable quarterly in arrears on February 15, May 15, August 15 and November 15 of each year, commencing on August 15, 2020. With respect to any interest payment due on or prior to May 29, 2021, 50% of the interest will be payable in cash and 50% of the interest will be paid in-kind in the form of an increase to the principal amount; however, a majority in interest of the holders of the Senior Secured Notes may elect to have 100% of the interest due on or prior to May 29, 2021 payable in-kind. For all interest periods commencing on or after May 15, 2024, the interest rate for the Senior Secured Notes will be a rate equal to LIBOR plus 10.5%, with a LIBOR rate floor of 1.5%.

We may redeem all or part of the Senior Secured Notes on or after June 1, 2021 at redemption prices (expressed as percentages of the principal amount) equal to (i) 104% for the twelve-month period beginning on June 1, 2021; (ii) 102% for the twelve-month period beginning on June 1, 2022; (iii) 101% for the twelve-month period beginning on June 1, 2023 and (iii) 100% for the twelve-month period beginning June 1, 2024 and at any time thereafter, plus accrued and unpaid interest at the redemption date. Notwithstanding the foregoing, if a change of control (as defined in the Senior Secured Notes Indenture) occurs prior to June 1, 2022, we may elect to purchase all remaining outstanding Senior Secured Notes not tendered to us as described below at a redemption price equal to 103% of the principal amount thereof, plus accrued and unpaid interest, if any, thereon to the applicable redemption date. If a change of control (as defined in the Senior Secured Notes Indenture) occurs, holders of the Senior Secured Notes will have the right to require us to repurchase all or any part of their Senior Secured Notes at a purchase price equal to 101% of the aggregate principal amount of the Senior Secured Notes repurchased, plus accrued and unpaid interest, if any, to the repurchase date.

The Senior Secured Notes Indenture contains a minimum asset coverage ratio of 1.5 to 1.0 as of any June 30 or December 31. The Senior Secured Notes Indenture provides for certain customary events of default and contains covenants that limit, among other things, our ability and the ability of certain of our subsidiaries, to incur, assume or guarantee additional indebtedness; pay dividends or distributions on capital stock or redeem or repurchase capital stock; make investments; repay junior debt; sell stock of its subsidiaries; transfer or sell assets; enter into sale and lease back transactions; create liens; enter into transactions with affiliates; and enter into mergers or consolidations.

Chapter 11 Accounting

The accompanying unaudited condensed consolidated financial statements contemplate our continuation as a going concern and have been prepared in accordance with FASB ASC Topic 852, Reorganizations.

Pre-petition restructuring charges — All expenses and losses incurred prior to the Petition Date which were related to the Chapter 11 proceedings are presented as pre-petition restructuring charges in our condensed consolidated statements of operations, including $9.6 million of expense incurred for the Commitment Premium pursuant to the Backstop Commitment Agreement.

Reorganization items — Any expenses, gains, and losses incurred subsequent to and as a direct result of the Chapter 11 proceedings are presented as reorganization items in our condensed consolidated statements of operations. Reorganization items consisted of the following for the three months ended March 31, 2020 (amounts in thousands):

|

| | | |

| Legal and professional fees | $ | 6,150 |

|

| DIP facility costs | 513 |

|

| | $ | 6,663 |

|

Liabilities subject to compromise — Pre-petition unsecured and under-secured obligations that may be impacted by the Chapter 11 Cases have been classified as liabilities subject to compromise on our condensed consolidated balance sheet. As of March 31, 2020, liabilities subject to compromise consisted of the following (amounts in thousands):

|

| | | |

| Senior Notes | $ | 300,000 |

|

| Unamortized debt issuance costs on Senior Notes | (2,003 | ) |

| Accrued interest on Senior Notes | 8,422 |

|

| | $ | 306,419 |

|

Contractual interest expense on our Senior Notes totaled $4.6 million for the three months ended March 31, 2020, which is in excess of the $3.1 million included in interest expense on our condensed consolidated statement of operations because we discontinued accruing interest on the Petition Date in accordance with the terms of the Plan and ASC Topic 852. See Note 6, Debt and DIP Financing for more information.

Fresh Start Accounting — We expect to adopt the fresh start accounting rules upon emergence from Chapter 11, in which case our assets and liabilities will be recorded at fair value as of the fresh start reporting date, which may differ materially from the recorded values of assets and liabilities on our consolidated balance sheets.

Debtor Financial Statements

Following are the consolidated financial statements of the entities included in the Chapter 11 Cases:

PIONEER ENERGY SERVICES CORP. DEBTOR ENTITIES (DEBTOR IN POSSESSION)

CONDENSED COMBINED BALANCE SHEET

(unaudited)

|

| | | |

| | March 31, 2020 |

| | (in thousands) |

| ASSETS | |

| Current assets: | |

| Cash and cash equivalents | $ | 7,938 |

|

| Restricted cash | 998 |

|

| Receivables, net of allowance | 84,674 |

|

| Intercompany receivables, net | 32,599 |

|

| Inventory | 9,530 |

|

| Assets held for sale | 1,825 |

|

| Prepaid expenses and other current assets | 7,127 |

|

| Total current assets | 144,691 |

|

| Net property and equipment | 412,711 |

|

| Investment in subsidiaries | 549,536 |

|

| Deferred income taxes | 38,948 |

|

| Operating lease assets | 7,441 |

|

| Other noncurrent assets | 1,754 |

|

| Total assets | $ | 1,155,081 |

|

| | |

| LIABILITIES AND STOCKHOLDERS’ EQUITY | |

| Current liabilities: | |

| Accounts payable | $ | 23,166 |

|

| Deferred revenues | 428 |

|

| Commitment premium | 9,584 |

|

| Debtor in possession financing | 4,000 |

|

| Accrued expenses | 48,480 |

|

| Total current liabilities | 85,658 |

|

| Long-term debt, less unamortized discount and debt issuance costs | 170,921 |

|

| Noncurrent operating lease liabilities | 6,058 |

|

| Deferred income taxes | 42,204 |

|

| Other noncurrent liabilities | 383 |

|

| Total liabilities not subject to compromise | 305,224 |

|

| Liabilities subject to compromise | 306,419 |

|

| Stockholders’ equity | 543,438 |

|

| Total liabilities and stockholders’ equity | $ | 1,155,081 |

|

PIONEER ENERGY SERVICES CORP. DEBTOR ENTITIES (DEBTOR IN POSSESSION)

CONDENSED COMBINED STATEMENT OF OPERATIONS

(unaudited)

|

| | | |

| | Three months ended March 31, 2020 |

| | (in thousands) |

| | |

| Revenues | $ | 99,867 |

|

| | |

| Costs and expenses: | |

| Operating costs | 79,885 |

|

| Depreciation | 20,683 |

|

| General and administrative | 14,155 |

|

| Pre-petition restructuring charges | 17,074 |

|

| Impairment | 17,853 |

|

| Bad debt expense, net | 727 |

|

| Gain on dispositions of property and equipment, net | (717 | ) |

| Intercompany leasing | (1,215 | ) |

| Total costs and expenses | 148,445 |

|

| Loss from operations | (48,578 | ) |

| | |

| Other income (expense): | |

| Equity in losses of subsidiaries | (31,726 | ) |

| Interest expense, net of interest capitalized | (8,668 | ) |

| Reorganization items | (6,663 | ) |

| Other income (expense), net | 197 |

|

| Total other expense, net | (46,860 | ) |

| | |

| Loss before income taxes | (95,438 | ) |

| Income tax (expense) benefit | 1,116 |

|

| Net loss | $ | (94,322 | ) |

PIONEER ENERGY SERVICES CORP. DEBTOR ENTITIES (DEBTOR IN POSSESSION)

CONDENSED COMBINED STATEMENT OF CASH FLOWS

(unaudited)

|

| | | |

| | Three months ended March 31, 2020 |

| | (in thousands) |

| | |

| Cash flows from operating activities | $ | (4,277 | ) |

| | |

| Cash flows from investing activities: | |

| Purchases of property and equipment | (6,180 | ) |

| Proceeds from sale of property and equipment | 876 |

|

| | (5,304 | ) |

| | |

| Cash flows from financing activities: | |

| Proceeds from DIP Facility | 4,000 |

|

| DIP Facility issuance costs | (988 | ) |

| Purchase of treasury stock | (7 | ) |

| Intercompany contributions | 53 |

|

| | 3,058 |

|

| | |

| Net decrease in cash, cash equivalents and restricted cash | (6,523 | ) |

| Beginning cash, cash equivalents and restricted cash | 15,459 |

|

| Ending cash, cash equivalents and restricted cash | $ | 8,936 |

|

Other Subsequent Events

In April 2020, we closed our coiled tubing operations and idled all our coiled tubing equipment, which were subsequently placed as held for sale.

3. Revenue from Contracts with Customers

Our production services business segments earn revenues for well servicing, wireline services and coiled tubing services pursuant to master services agreements based on purchase orders or other contractual arrangements with the client. Production services jobs are generally short-term (ranging in duration from several hours to less than 30 days) and are charged at current market rates for the labor, equipment and materials necessary to complete the job. Production services jobs are varied in nature but typically represent a single performance obligation, either for a particular job, a series of distinct jobs, or a period of time during which we stand ready to provide services as our client needs them. Revenue is recognized for these services over time, as the services are performed.

Our drilling services business segments earn revenues by drilling oil and gas wells for our clients under daywork contracts. Daywork contracts are comprehensive agreements under which we provide a comprehensive service offering, including the drilling rig, crew, supplies, and most of the ancillary equipment necessary to operate the rig. Contract modifications that extend the term of a dayrate contract are generally accounted for prospectively as a separate dayrate contract. We account for our services provided under daywork contracts as a single performance obligation comprised of a series of distinct time increments which are satisfied over time. Accordingly, dayrate revenues are recognized in the period during which the services are performed.

With most drilling contracts, we also receive payments contractually designated for the mobilization and demobilization of drilling rigs and other equipment to and from the client’s drill site. Revenues associated with the mobilization and demobilization of our drilling rigs to and from the client’s drill site do not relate to a distinct good or service and are recognized ratably over the related contract term.

The amount of demobilization revenue that we ultimately collect is dependent upon the specific contractual terms, most of which include provisions for reduced (or no) payment for demobilization when, among other things, the contract is renewed or extended with the same client, or when the rig is subsequently contracted with another client prior to the termination of the current contract. Since revenues associated with demobilization activity are typically variable, at each period end, they are estimated at the most likely amount, and constrained when the likelihood of a significant reversal is probable. Any change in the expected amount of demobilization revenue is accounted for with the net cumulative impact of the change in estimate recognized in the period during which the revenue estimate is revised.

The upfront costs that we incur to mobilize the drilling rig to our client’s initial drilling site are capitalized and recognized ratably over the term of the related contract, including any contracted renewal or extension periods, which is our estimate of the period during which we expect to benefit from the cost of mobilizing the rig. Costs associated with the final demobilization at the end of the contract term are expensed when incurred, when the demobilization activity is performed.

We also act as a principal for certain reimbursable services and auxiliary equipment provided by us to our clients, for which we incur costs and earn revenues, many of which are variable, or dependent upon the activity that is actually performed each day under the related contract. Accordingly, reimbursements that we receive for out-of-pocket expenses are recorded as revenues and the out-of-pocket expenses for which they relate are recorded as operating costs during the period to which they relate within the series of distinct time increments.

All of our revenues are recognized net of sales taxes, when applicable.

Contract Asset and Liability Balances and Contract Cost Assets

Contract asset and contract liability balances relate to demobilization and mobilization revenues, respectively. Demobilization revenue that we expect to receive is recognized ratably over the related contract term, but invoiced upon completion of the demobilization activity. Mobilization revenue, which is typically collected upon the completion of the initial mobilization activity, is deferred and recognized ratably over the related contract term. Contract asset and liability

balances are netted at the contract level, with the net current and noncurrent portions separately classified in our condensed consolidated balance sheets, and the resulting contract liabilities are referred to herein as “deferred revenues.” When demobilization revenues are recognized prior to the activity being performed, they are not yet billable, and the resulting contract assets are included in our other current assets in our unaudited condensed consolidated financial statements.

Contract cost assets represent the costs associated with the initial mobilization required in order to fulfill the contract, which are deferred and recognized ratably over the period during which we expect to benefit from the mobilization, or the period during which we expect to satisfy the performance obligations of the related contract. Contract cost assets are presented as either current or noncurrent, according to the duration of the original contract to which it relates, and referred to herein as “deferred costs.”

Our current and noncurrent deferred revenues, contract assets and deferred costs as of March 31, 20192020 and December 31, 20182019 were as follows (amounts in thousands):

| | | | March 31, 2019 | | December 31, 2018 | March 31, 2020 | | December 31, 2019 |

| Current deferred revenues | $ | 1,659 |

| | $ | 1,722 |

| $ | 997 |

| | $ | 1,339 |

|

| Current deferred costs | 1,621 |

| | 1,543 |

| 591 |

| | 1,071 |

|

| Current contract assets | | 795 |

| | — |

|

| | | | | | | |

| Noncurrent deferred revenues | $ | 428 |

| | $ | 437 |

| $ | — |

| | $ | 57 |

|

| Noncurrent deferred costs | 676 |

| | 679 |

| 142 |

| | 267 |

|

The changes in deferred revenue and costcontract balances during the three months ended March 31, 20192020 are primarily related to increased deferred mobilization revenue and cost balances for the deployment of one international rig and two domestic rigs under new term contracts in 2019, mostly offset by the amortization of deferred revenues and costs during the period.period, partially offset by increases related to two rigs deployed under new contracts in 2020, and an increase in demobilization revenues recognized on contracts that are expected to expire or be terminated in the near term. Amortization of deferred revenues and costs during the three months ended March 31, 20192020 and 20182019 were as follows (amounts in thousands):

| | | | Three months ended March 31, | Three months ended March 31, |

| | 2019 | | 2018 | 2020 | | 2019 |

| Amortization of deferred revenues | $ | 954 |

| | $ | 499 |

| $ | 1,613 |

| | $ | 954 |

|

| Amortization of deferred costs | 986 |

| | 463 |

| 1,263 |

| | 986 |

|

In February 2019, onelate March 2020, rather than terminating their contracts with us, several of our domestic clients elected to early terminate their contract with ustemporarily stack the rigs and makeplace them on an upfront early termination payment based onextended standby for a per dayreduced revenue rate forand the remaining termoption to reactivate the rig through the remainder of the contract resultingterm.

4. Property and Equipment

Capital Expenditures — Our capital expenditure additions were $7.9 million and $18.4 million, including the impact of accruals for capital additions, during the three months ended March 31, 2020 and 2019, respectively. Capital additions during the three months ended March 31, 2020 primarily related to routine expenditures to maintain our fleets, while capital additions during the corresponding period also included the completion of construction on our 17th AC drilling rig which we deployed in $0.4March 2019, and various vehicle and ancillary equipment purchases and upgrades.

Gain/Loss on Disposition of Property — We recognized net gains of $0.7 million and $1.1 million during the three months ended March 31, 2020 and 2019, respectively, on the disposition or sale of revenues associatedvarious property and equipment, including drill pipe and collars and certain older and/or underutilized equipment.

Assets Held for Sale — We have various equipment designated as held for sale with the 34 days that were remaining under the contract term. We subsequently placed this rig with another client. Asvalues of $1.8 million and $3.4 million in aggregate as of March 31, 2020 and December 31, 2019, respectively, primarily consisting of real estate property for two wireline locations closed during 2019 that were sold in 2020, and the remaining equipment from two SCR drilling rigs which were dismantled for spare parts.

During the three months ended March 31, 2020 and 2019, we recognized impairment charges of $1.5 million and $1.0 million, respectively, to reduce the carrying values of assets which were classified as held for sale, to their estimated fair values, based on expected sales prices which are classified as Level 3 inputs as defined by ASC Topic 820, Fair Value Measurements and Disclosures.

Impairments — In accordance with ASC Topic 360, Property, Plant and Equipment, we monitor all but oneindicators of potential impairments. We evaluate for potential impairment of long-lived assets when indicators of impairment are present, which may include, among other things, significant adverse changes in industry trends (including revenue rates, utilization rates, oil and natural gas market prices, and industry rig counts). In performing an impairment evaluation, we estimate the future undiscounted net cash flows from the use and eventual disposition of the assets grouped at the lowest level that independent cash flows can be identified. We perform an impairment evaluation and estimate future undiscounted cash flows for each of our 25 rigsasset groups separately, which are earning under daywork contracts, 14our domestic drilling services, international drilling services, well servicing, wireline services and coiled tubing services segments. If the sum of the estimated future undiscounted net cash flows is less than the carrying amount of the asset group, then we determine the fair value of the asset group, and the amount of an impairment charge would be measured as the difference between the carrying amount and the fair value of the assets.

Due to the significant decline in industry conditions, commodity prices, and projected utilization of equipment, as well as the COVID-19 pandemic’s impact on our industry, our projected cash flows declined during the first quarter of 2020, and we performed recoverability testing on all our reporting units. As a result of this analysis, we incurred impairment charges of $16.4 million to reduce the carrying values of our coiled tubing assets to their estimated fair values. For all our other reporting units, excluding coiled tubing, we determined that the sum of the estimated future undiscounted net cash flows were in excess of the carrying amounts and that no impairment existed for these reporting units at March 31, 2020.

The assumptions we use in the evaluation for impairment are inherently uncertain and require management judgment. Although we believe the assumptions and estimates used in our impairment analysis are reasonable, different assumptions and estimates could materially impact the analysis and resulting conclusions. The most significant inputs used in our impairment analysis include the projected utilization and pricing of our services, as well as the estimated proceeds upon any future sale or disposal of the assets, all of which are domestic term contracts. Our international drilling contractsclassified as Level 3 inputs as defined by ASC Topic 820, Fair Value Measurements and Disclosures. If commodity prices decrease or remain at current levels for an extended period of time, or if the demand for any of our services decreases below what we are cancelable bycurrently projecting, our clients without penalty, althoughestimated cash flows may decrease and our estimates of the contracts require 15fair value of certain assets may decrease as well. If any of the foregoing were to 30 days notice and payment for demobilization services. The spot contracts for our domestic drilling rigs are also terminable by our client with 30 days notice, but typically do not include a required payment for demobilization services.occur, we could incur impairment charges on the related assets.

3.5. Leases

As a drilling and production services provider, we provide the drilling rigs and production services equipment which are necessary to fulfill our performance obligations and which are considered leases under ASU No. 2016-02, Leases, ((together with its amendments, herein referred to as “ASC Topic 842”). However, ASU No. 2018-11, Leases: Targeted Improvements, allows lessors to (i) combine the lease and non-lease components of revenues when the revenue recognition pattern is the same and when the lease component, when accounted for separately, would be considered an operating lease, and (ii) account for the combined lease and non-lease components under ASC Topic 606, Revenue from Contracts with Customers, when the non-lease component is the predominant element of the combined component. We elected to apply this expedient and therefore continue to recognize our revenues (both lease and service components) under ASC Topic 606, and continue to present them as one revenue stream in our unaudited condensed consolidated statements of operations.

As a lessee, we lease our corporate office headquarters in San Antonio, Texas, and we conduct our business operations through 2819 other regional offices located throughout the United States and internationally in Colombia. These operating locations typically include regional offices, storage and maintenance yards and employee housing sufficient to support our operations in the area. We lease most of these properties under non-cancelable term and month-to-month operating leases, many of which contain renewal options that can extend the lease term from onethree months to five years and some of which contain escalation clauses. We also lease various items of supplemental equipment, typically under cancelable short-term and very short term (less than 30 days) leases. Due to the nature of our business, any option to renew these short-term leases, and the options to extend certain of our long-term real estate leases, are generally not considered reasonably certain to be exercised. Therefore,

the periods covered by such optional periods are not included in the determination of the term of the lease, and the lease payments during these periods are similarly excluded from the calculation of operating lease asset and lease liability balances.

In accordance with ASC Topic 842, we recognize an operating lease asset and a corresponding operating lease liability for all our long-term leases, which include real estate and office equipment leases, for which we elected to combine, or not separate, the lease and non-lease components, and therefore, all fixed charges associated with non-lease components are included in the lease payments and the calculation of the operating lease asset and associated lease liability. The operating lease asset and operating lease liability are discounted at the rate which represents our secured incremental borrowing rate, as most of our leases do not provide an implicit rate, and which we estimate based on the rate in effect under our asset-based lending facility.

We recognize rent expense on a straight-line basis, except for certain variable expenses which are recognized when the variability is resolved, typically during the period in which they are paid. Variable lease payments typically include charges for property taxes and insurance, and some leases contain variable payments related to non-lease components, including common area maintenance and usage of office equipment (for example, copiers), which totaled approximately $0.3 million during the three months ended March 31, 2019. The following table summarizes our lease expense recognized, for the three months ending March 31, 2019, excluding variable lease costs (amounts in thousands):

| | | | Three months ended March 31, |

| | | | 2020 | | 2019 |

| Long-term operating lease expense | $ | 842 |

| $ | 662 |

| | $ | 842 |

|

| Short-term operating lease expense | $ | 3,403 |

| 3,526 |

| | 3,403 |

|

The following table summarizes the amount and timing of our obligations associated with our long-term operating leases (amounts in thousands):

| | | | March 31, 2019 | | December 31, 2018 | March 31, 2020 | | December 31, 2019 |

| Within 1 year | $ | 2,878 |

| | $ | 3,318 |

| $ | 2,413 |

| | $ | 2,496 |

|

| In the second year | 2,045 |

| | 2,032 |

| 1,966 |

| | 1,933 |

|

| In the third year | 1,761 |

| | 1,721 |

| 1,592 |

| | 1,447 |

|

| In the fourth year | 1,355 |

| | 1,407 |

| 1,259 |

| | 1,117 |

|

| In the fifth year | 1,007 |

| | 1,110 |

| 1,176 |

| | 912 |

|

| Thereafter | 1,496 |

| | 1,738 |

| 1,079 |

| | 811 |

|

| Total undiscounted lease obligations | $ | 10,542 |

| | $ | 11,326 |

| $ | 9,485 |

| | $ | 8,716 |

|

| Impact of discounting | (1,098 | ) | | | (967 | ) | | (818 | ) |

| Discounted value of operating lease obligations | $ | 9,444 |

| | | $ | 8,518 |

| | 7,898 |

|

| | | | | | | |

| Current operating lease liabilities | $ | 2,515 |

| | | $ | 2,084 |

| | 2,198 |

|

| Noncurrent operating lease liabilities | 6,929 |

| | | 6,434 |

| | 5,700 |

|

| | $ | 9,444 |

| | | $ | 8,518 |

| | 7,898 |

|

The following table summarizes the weighted-average remaining lease term and discount rate associated with our long-term operating leases:

|

| | |

| March 31, 2019 |

Weighted-average remaining lease term (in years) | 4.9 |

|

Weighted-average discount rate | 4.5 | % |

4. Property and Equipment