UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

|

| |

| ☒ | Quarterly Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 |

For Quarterly Period Endedthe quarterly period ended July 31, 2019April 30, 2020

|

| |

| ☐ | Transition Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 |

For the transition period from to

Commission File Number 1-8597

The Cooper Companies, Inc.

(Exact name of registrant as specified in its charter)

|

| |

| Delaware | 94-2657368 |

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) |

6140 Stoneridge Mall6101 Bollinger Canyon Road, Suite 590500,

San Ramon, Pleasanton, CACalifornia 9458894583

(Address of principal executive offices) (Zip Code)

Registrant’s telephone number, including area code (925) 460-3600

Securities registered pursuant to Section 12(b) of the Act:

|

| | | | |

| Title of each class | | Trading Symbol | | Name of each exchange on which registered |

| Common Stock, $.10 par value | | COO | | The New York Stock Exchange |

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or emerging growth company. See definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and "emerging growth company" in Rule 12b-2 of the Exchange Act.

|

| | | | |

| Large accelerated filer | ☒ | | Accelerated filer | ☐ |

| Non-accelerated filer | ☐ | | Smaller reporting company | ☐ |

| Emerging growth company | ☐ | | | |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act.): Yes ☐ No ☒

Indicate the number of shares outstanding of each of issuer’s classes of common stock, as of the latest practicable date.

On August 23, 2019, 49,573,612May 29, 2020, 53,333,091 shares of Common Stock, $.10 par value, were outstanding.

INDEX

|

| | |

| | | Page No. |

| PART I. | | |

| | | |

| Item 1. | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| | |

| | | |

| | | |

| | | |

| | | |

| | | |

| Item 2. | | |

| | | |

| Item 3. | | |

| | | |

| Item 4. | | |

| | | |

| PART II. | | |

| | | |

| Item 1. | | |

| | | |

| Item 1A. | | |

| | | |

| Item 2. | | |

| | | |

| Item 3. | | |

| | | |

| Item 4. | | |

| | | |

| Item 5. | | |

| | | |

| Item 6. | | |

| | |

| |

PART I. FINANCIAL INFORMATION

Item 1. Unaudited Financial Statements

THE COOPER COMPANIES, INC. AND SUBSIDIARIES

Consolidated Statements of Income and Comprehensive Income (Loss)

Periods Ended July 31,

April 30,

(In millions, except for earnings per share)

(Unaudited)

| | | | Three Months | | Nine Months | Three Months | | Six Months |

| 2019 | | 2018 | | 2019 | | 2018 | 2020 | | 2019 | | 2020 | | 2019 |

| Net sales (Note 2) | $ | 679.4 |

| | $ | 660.0 |

| | $ | 1,961.8 |

| | $ | 1,881.3 |

| |

| Net sales | | $ | 524.9 |

| | $ | 654.3 |

| | $ | 1,171.1 |

| | $ | 1,282.4 |

|

| Cost of sales | 228.7 |

| | 233.2 |

| | 660.0 |

| | 679.1 |

| 201.4 |

| | 221.7 |

| | 421.1 |

| | 431.3 |

|

| Gross profit | 450.7 |

| | 426.8 |

| | 1,301.8 |

| | 1,202.2 |

| 323.5 |

| | 432.6 |

| | 750.0 |

| | 851.1 |

|

| Selling, general and administrative expense | 249.8 |

| | 251.0 |

| | 746.6 |

| | 724.7 |

| 237.2 |

| | 246.8 |

| | 495.5 |

| | 496.8 |

|

| Research and development expense | 21.5 |

| | 22.5 |

| | 63.4 |

| | 62.2 |

| 23.8 |

| | 21.0 |

| | 46.0 |

| | 42.0 |

|

| Amortization of intangibles | 37.2 |

| | 37.7 |

| | 110.7 |

| | 110.5 |

| 33.9 |

| | 36.9 |

| | 68.8 |

| | 73.5 |

|

| Impairment of intangibles | — |

| | — |

| | — |

| | 24.4 |

| |

| Gain on sale of an intangible (Note 5) | — |

| | — |

| | (19.0 | ) | | — |

| |

| Gain on sale of an intangible | | — |

| | (19.0 | ) | | — |

| | (19.0 | ) |

| Operating income | 142.2 |

| | 115.6 |

| | 400.1 |

| | 280.4 |

| 28.6 |

| | 146.9 |

| | 139.7 |

| | 257.8 |

|

| Interest expense | 16.7 |

|

| 22.8 |

|

| 53.3 |

|

| 59.9 |

| 12.8 |

|

| 18.5 |

|

| 24.4 |

|

| 36.6 |

|

| Other (income) expense, net | (1.5 | ) |

| 2.4 |

|

| (2.1 | ) |

| 1.3 |

| |

| Other expense (Income), net | | 6.8 |

|

| 0.3 |

|

| 8.9 |

|

| (0.7 | ) |

| Income before income taxes | 127.0 |

| | 90.4 |

| | 348.9 |

| | 219.2 |

| 9.0 |

| | 128.1 |

| | 106.4 |

| | 221.9 |

|

| Provision (benefit) for income taxes (Note 7) | 6.9 |

| | (10.4 | ) | | 3.2 |

| | 180.0 |

| |

| (Benefit) Provision for income taxes (Note 7) | | (2.5 | ) | | 5.7 |

| | 4.4 |

| | (3.6 | ) |

| Net income | $ | 120.1 |

| | $ | 100.8 |

| | $ | 345.7 |

| | $ | 39.2 |

| $ | 11.5 |

| | $ | 122.4 |

| | $ | 102.0 |

| | $ | 225.5 |

|

| Earnings per share - basic (Note 8) | $ | 2.43 |

| | $ | 2.05 |

| | $ | 7.00 |

| | $ | 0.80 |

| |

| Earnings per share - diluted (Note 8) | $ | 2.40 |

| | $ | 2.03 |

| | $ | 6.91 |

| | $ | 0.79 |

| |

| Earnings per share (Note 8): | | | | | | | | |

| Basic | | $ | 0.23 |

| | $ | 2.48 |

| | $ | 2.07 |

| | $ | 4.57 |

|

| Diluted | | $ | 0.23 |

| | $ | 2.45 |

| | $ | 2.05 |

| | $ | 4.52 |

|

| Number of shares used to compute earnings per share: |

| |

| |

| |

|

| |

| |

| |

|

| Basic | 49.5 |

| | 49.1 |

| | 49.4 |

| | 49.0 |

| 49.2 |

| | 49.4 |

| | 49.2 |

| | 49.3 |

|

| Diluted | 50.1 |

| | 49.7 |

| | 50.0 |

| | 49.6 |

| 49.6 |

| | 50.0 |

| | 49.7 |

| | 49.9 |

|

| Other comprehensive income, net of tax: | | | | | | | | |

| Cash flow hedge | | $ | (13.5 | ) | | — |

| | $ | (13.5 | ) | | — |

|

| Foreign currency translation adjustment | | (68.9 | ) | | (18.6 | ) | | (52.2 | ) | | 14.1 |

|

| Comprehensive (loss) income | | $ | (70.9 | ) | | $ | 103.8 |

| | $ | 36.3 |

| | $ | 239.6 |

|

See

The accompanying notes.notes are an integral part of these Consolidated Condensed Financial Statements.

THE COOPER COMPANIES, INC. AND SUBSIDIARIES

Consolidated Statements of Comprehensive Income

Periods Ended July 31,

(In millions)

(Unaudited)

|

| | | | | | | | | | | | | | | |

| | Three Months | | Nine Months |

| | 2019 | | 2018 | | 2019 | | 2018 |

| Net income | $ | 120.1 |

| | $ | 100.8 |

| | $ | 345.7 |

| | $ | 39.2 |

|

| Other comprehensive loss: | | | | | | | |

| Foreign currency translation adjustment, net of tax | (65.2 | ) | | (69.6 | ) | | (51.1 | ) | | (10.3 | ) |

| Comprehensive income | $ | 54.9 |

| | $ | 31.2 |

| | $ | 294.6 |

| | $ | 28.9 |

|

See accompanying notes.

THE COOPER COMPANIES, INC. AND SUBSIDIARIES

Consolidated Condensed Balance Sheets

(In millions)

(Unaudited)millions, unaudited)

| | | | July 31, 2019 | | October 31, 2018 | April 30, 2020 | | October 31, 2019 |

| ASSETS | | | | | | |

| Current assets: | | | | | | |

| Cash and cash equivalents | $ | 112.7 |

| | $ | 77.7 |

| $ | 79.8 |

| | $ | 89.0 |

|

| Trade accounts receivable, net of allowance for doubtful accounts of $17.1 at July 31, 2019 and $19.0 at October 31, 2018 | 404.7 |

| | 374.7 |

| |

| Trade accounts receivable, net of allowance for doubtful accounts of $13.4 at April 30, 2020 and $16.4 at October 31, 2019 | | 368.8 |

| | 435.3 |

|

| Inventories (Note 4) | 502.1 |

| | 468.8 |

| 568.2 |

| | 506.9 |

|

| Prepaid expense and other current assets | 131.3 |

| | 169.7 |

| 149.4 |

| | 132.2 |

|

| Total current assets | 1,150.8 |

| | 1,090.9 |

| 1,166.2 |

| | 1,163.4 |

|

| Property, plant and equipment, at cost | 2,086.9 |

| | 1,930.3 |

| 2,309.5 |

| | 2,193.9 |

|

| Less: accumulated depreciation and amortization | 1,021.5 |

| | 954.3 |

| 1,113.4 |

| | 1,061.8 |

|

| | 1,065.4 |

| | 976.0 |

| 1,196.1 |

| | 1,132.1 |

|

| Operating lease right-of-use assets (Note 2) | | 255.5 |

| | — |

|

| Goodwill (Note 5) | 2,391.4 |

| | 2,392.1 |

| 2,400.0 |

| | 2,428.9 |

|

| Other intangibles, net (Note 5) | 1,438.6 |

| | 1,521.3 |

| 1,337.7 |

| | 1,405.3 |

|

| Deferred tax assets | 63.1 |

| | 58.4 |

| 77.0 |

| | 78.0 |

|

| Other assets | 63.5 |

| | 74.1 |

| 77.5 |

| | 66.8 |

|

| | $ | 6,172.8 |

| | $ | 6,112.8 |

| |

| Total assets | | $ | 6,510.0 |

| | $ | 6,274.5 |

|

| LIABILITIES AND STOCKHOLDERS’ EQUITY | | | | | | |

| Current liabilities: | | | | | | |

| Short-term debt (Note 6) | $ | 390.0 |

| | $ | 37.1 |

| $ | 554.5 |

| | $ | 563.7 |

|

| Accounts payable | 141.5 |

| | 146.4 |

| 128.7 |

| | 150.1 |

|

| Employee compensation and benefits | 89.5 |

| | 94.0 |

| 86.3 |

| | 104.7 |

|

| Operating lease liabilities | | 31.5 |

| | — |

|

| Other current liabilities | 268.4 |

| | 259.0 |

| 224.3 |

| | 292.1 |

|

| Total current liabilities | 889.4 |

| | 536.5 |

| 1,025.3 |

| | 1,110.6 |

|

| Long-term debt (Note 6) | 1,422.6 |

| | 1,985.7 |

| 1,344.8 |

| | 1,262.6 |

|

| Deferred tax liabilities | 31.5 |

| | 31.0 |

| 26.8 |

| | 28.0 |

|

| Long-term tax payable | 124.8 |

| | 141.5 |

| 158.9 |

| | 124.8 |

|

| Operating lease liabilities | | 232.7 |

| | — |

|

| Accrued pension liability and other | 89.0 |

| | 110.3 |

| 94.0 |

| | 119.9 |

|

| Total liabilities | 2,557.3 |

| | 2,805.0 |

| $ | 2,882.5 |

| | $ | 2,645.9 |

|

| Contingencies (see Note 13) |

| |

| |

| Contingencies (Note 13) | |

| |

|

| Stockholders’ equity: |

| | | | | |

| Preferred stock, 10 cents par value, shares authorized: 1.0; zero shares issued or outstanding | — |

| | — |

| — |

| | — |

|

| Common stock, 10 cents par value, shares authorized: 120.0; issued 53.2 at July 31, 2019 and 52.8 at October 31, 2018 | 5.3 |

| | 5.3 |

| |

| Common stock, 10 cents par value, shares authorized: 120.0; issued 53.3 at April 30, 2020 and 53.2 at October 31, 2019 | | 5.3 |

| | 5.3 |

|

| Additional paid-in capital | 1,607.6 |

| | 1,572.1 |

| 1,626.5 |

| | 1,615.0 |

|

| Accumulated other comprehensive loss | (481.8 | ) | | (430.7 | ) | (512.8 | ) | | (447.1 | ) |

| Retained earnings | 2,905.4 |

| | 2,576.0 |

| 3,126.9 |

| | 3,026.4 |

|

| Treasury stock at cost: 3.6 shares at July 31, 2019 and 3.6 shares at October 31, 2018 | (421.2 | ) | | (415.1 | ) | |

| Treasury stock at cost: 4.2 shares at April 30, 2020 and 4.1 shares at October 31, 2019 | | (618.6 | ) | | (571.2 | ) |

| Total Cooper stockholders’ equity | | 3,627.3 |

| | 3,628.4 |

|

| Noncontrolling interests | 0.2 |

| | 0.2 |

| 0.2 |

| | 0.2 |

|

| Stockholders’ equity (Note 10) | 3,615.5 |

| | 3,307.8 |

| 3,627.5 |

| | 3,628.6 |

|

| | $ | 6,172.8 |

| | $ | 6,112.8 |

| |

| Total liabilities and stockholders’ equity | | $ | 6,510.0 |

| | $ | 6,274.5 |

|

See

The accompanying notes.notes are an integral part of these Consolidated Condensed Financial Statements.

THE COOPER COMPANIES, INC. AND SUBSIDIARIES

Consolidated Condensed Statements of Stockholders' Equity

| | | Consolidated Condensed Statements of Stockholders' Equity | |

| | Common Shares | | Treasury Stock | | Additional Paid-In Capital | | Accumulated

Other

Comprehensive

Income (Loss) | | Retained Earnings | | Treasury Stock | | Noncontrolling Interests | | Total

Stockholders'

Equity | Common Shares | | Treasury Stock | | Additional Paid-In Capital | | Accumulated

Other

Comprehensive

Income (Loss) | | Retained Earnings | | Treasury Stock | | Noncontrolling Interests | | Total

Stockholders'

Equity |

| (In millions) | Shares | | Amount | | Shares | | Amount | | | | | Shares | | Amount | | Shares | | Amount | | | | |

| Balance at November 1, 2017 | 48.8 |

| | $ | 4.9 |

| | 3.6 |

| | $ | 0.3 |

| | $ | 1,526.7 |

| | $ | (375.3 | ) | | $ | 2,434.2 |

| | $ | (415.1 | ) | | $ | 0.1 |

| | $ | 3,175.8 |

| |

| Net loss | — |

| | — |

| | — |

| | — |

| | — |

| | — |

| | (122.5 | ) | | — |

| | — |

| | (122.5 | ) | |

| Balance at November 1, 2018 | | 49.2 |

| | $ | 5.0 |

| | 3.6 |

| | $ | 0.3 |

| | $ | 1,572.1 |

| | $ | (430.7 | ) | | $ | 2,576.0 |

| | $ | (415.1 | ) | | $ | 0.2 |

| | $ | 3,307.8 |

|

| Net income | | — |

| | — |

| | — |

| | — |

| | — |

| | — |

| | 103.2 |

| | — |

| | — |

| | 103.2 |

|

| Other comprehensive income, net of tax | — |

| | — |

| | — |

| | — |

| | — |

| | 102.3 |

| | — |

| | — |

| | — |

| | 102.3 |

| — |

| | — |

| | — |

| | — |

| | — |

| | 32.7 |

| | — |

| | — |

| | — |

| | 32.7 |

|

| Issuance of common stock for stock plans, net | 0.2 |

| | 0.1 |

| | — |

| | — |

| | (10.6 | ) | | — |

| | — |

| | — |

| | — |

| | (10.5 | ) | 0.1 |

| | — |

| | — |

| | — |

| | (9.0 | ) | | — |

| | — |

| | — |

| | — |

| | (9.0 | ) |

| Dividends on common stock | — |

| | — |

| | — |

| | — |

| | — |

| | — |

| | (1.4 | ) | | — |

| | — |

| | (1.4 | ) | |

| Treasury stock repurchase | | — |

| | — |

| | — |

| | — |

| | — |

| | — |

| | — |

| | (6.1 | ) | | — |

| | (6.1 | ) |

| Dividends on common stock ($0.03 per share) | | — |

| | — |

| | — |

| | — |

| | — |

| | — |

| | (1.5 | ) | | — |

| | — |

| | (1.5 | ) |

| Share-based compensation expense | — |

| | — |

| | — |

| | — |

| | 12.7 |

| | — |

| | — |

| | — |

| | — |

| | 12.7 |

| — |

| | — |

| | — |

| | — |

| | 11.7 |

| | — |

| | — |

| | — |

| | — |

| | 11.7 |

|

| Balance at January 31, 2018 | 49.0 |

| | $ | 5.0 |

| | 3.6 |

| | $ | 0.3 |

| | $ | 1,528.8 |

| | $ | (273.0 | ) | | $ | 2,310.3 |

| | $ | (415.1 | ) | | $ | 0.1 |

| | $ | 3,156.4 |

| |

| ASU 2016-16 adoption | | — |

| | — |

| | — |

| | — |

| | — |

| | — |

| | (13.3 | ) | | — |

| | — |

| | (13.3 | ) |

| Balance at January 31, 2019 | | 49.3 |

| | $ | 5.0 |

| | 3.6 |

| | $ | 0.3 |

| | $ | 1,574.8 |

| | $ | (398.0 | ) | | $ | 2,664.4 |

| | $ | (421.2 | ) | | $ | 0.2 |

| | $ | 3,425.5 |

|

| Net income | — |

| | — |

| | — |

| | — |

| | — |

| | — |

| | 60.9 |

| | — |

| | — |

| | 60.9 |

| — |

| | — |

| | — |

| | — |

| | — |

| | — |

| | 122.4 |

| | — |

| | — |

| | 122.4 |

|

| Other comprehensive loss, net of tax | — |

| | — |

| | — |

| | — |

| | — |

| | (43.0 | ) | | — |

| | — |

| | — |

| | (43.0 | ) | — |

| | — |

| | — |

| | — |

| | — |

| | (18.6 | ) | | — |

| | — |

| | — |

| | (18.6 | ) |

| Issuance of common stock for stock plans, net | 0.1 |

| | — |

| | — |

| | — |

| | 0.1 |

| | — |

| | — |

| | — |

| | — |

| | 0.1 |

| 0.2 |

| | — |

| | — |

| | — |

| | 4.5 |

| | — |

| | — |

| | — |

| | — |

| | 4.5 |

|

| Share-based compensation expense | — |

| | — |

| | — |

| | — |

| | 13.6 |

| | — |

| | — |

| | — |

| | — |

| | 13.6 |

| — |

| | — |

| | — |

| | — |

| | 8.4 |

| | — |

| | — |

| | — |

| | — |

| | 8.4 |

|

| Balance at April 30, 2018 | 49.1 |

| | $ | 5.0 |

| | 3.6 |

| | $ | 0.3 |

| | $ | 1,542.5 |

| | $ | (316.0 | ) | | $ | 2,371.2 |

| | $ | (415.1 | ) | | $ | 0.1 |

| | $ | 3,188.0 |

| |

| Balance at April 30, 2019 | | 49.5 |

| | $ | 5.0 |

| | 3.6 |

| | $ | 0.3 |

| | $ | 1,587.7 |

| | $ | (416.6 | ) | | $ | 2,786.8 |

| | $ | (421.2 | ) | | $ | 0.2 |

| | $ | 3,542.2 |

|

| | | | | | | | | | | | | | | | | | | | | |

| Balance at November 1, 2019 | | 49.1 |

| | $ | 4.9 |

| | 4.1 |

| | $ | 0.4 |

| | $ | 1,615.0 |

| | $ | (447.1 | ) | | $ | 3,026.4 |

| | $ | (571.2 | ) | | $ | 0.2 |

| | $ | 3,628.6 |

|

| Net income | — |

| | — |

| | — |

| | — |

| | — |

| | — |

| | 100.8 |

| | — |

| | — |

| | 100.8 |

| — |

| | — |

| | — |

| | — |

| | — |

| | — |

| | 90.5 |

| | — |

| | — |

| | 90.5 |

|

| Other comprehensive loss, net of tax | — |

| | — |

| | — |

| | — |

| | — |

| | (69.6 | ) | | — |

| | — |

| | — |

| | (69.6 | ) | |

| Other comprehensive income, net of tax | | — |

| | — |

| | — |

| | — |

| | — |

| | 16.7 |

| | — |

| | — |

| | — |

| | 16.7 |

|

| Issuance of common stock for stock plans, net | — |

| | — |

| | — |

| | — |

| | 0.8 |

| | — |

| | — |

| | — |

| | — |

| | 0.8 |

| 0.1 |

| | — |

| | — |

| | — |

| | (13.2 | ) | | — |

| | — |

| | — |

| | — |

| | (13.1 | ) |

Dividends on common stock

| — |

| | — |

| | — |

| | — |

| | — |

| | — |

| | (1.5 | ) | | — |

| | — |

| | (1.5 | ) | |

| Dividends on common stock ($0.03 per share) | | — |

| | — |

| | — |

| | — |

| | — |

| | — |

| | (1.5 | ) | | — |

| | — |

| | (1.5 | ) |

| Share-based compensation expense | — |

| | — |

| | — |

| | — |

| | 8.1 |

| | — |

| | — |

| | — |

| | — |

| | 8.1 |

| — |

| | — |

| | — |

| | — |

| | 9.7 |

| | — |

| | — |

| | — |

| | — |

| | 9.7 |

|

| Balance at July 31, 2018 | 49.1 |

| | $ | 5.0 |

| | 3.6 |

| | $ | 0.3 |

| | $ | 1,551.4 |

| | $ | (385.6 | ) | | $ | 2,470.5 |

| | $ | (415.1 | ) | | $ | 0.1 |

| | $ | 3,226.6 |

| |

| Balance at January 31, 2020 | | 49.2 |

| | $ | 4.9 |

| | 4.1 |

| | $ | 0.4 |

| | $ | 1,611.6 |

| | $ | (430.4 | ) | | $ | 3,115.4 |

| | $ | (571.2 | ) | | $ | 0.2 |

| | $ | 3,730.9 |

|

| Net income | | — |

| | — |

| | — |

| | — |

| | — |

| | — |

| | 11.5 |

| | — |

| | — |

| | 11.5 |

|

| Other comprehensive income, net of tax | | — |

| | — |

| | — |

| | — |

| | — |

| | (82.4 | ) | | — |

| | — |

| | — |

| | (82.4 | ) |

| Issuance of common stock for stock plans, net | | 0.1 |

| | — |

| | — |

| | — |

| | 5.0 |

| | — |

| | — |

| | — |

| | — |

| | 5.0 |

|

| Treasury stock repurchase | | (0.2 | ) | | — |

| | 0.2 |

| | — |

| | — |

| | — |

| | — |

| | (47.8 | ) | | — |

| | (47.8 | ) |

| Issuance of common stock for employee stock purchase plan | | — |

| | — |

| | — |

| | — |

| | 0.6 |

| | — |

| | — |

| | 0.4 |

| | — |

| | 1.0 |

|

| Share-based compensation expense | | — |

| | — |

| | — |

| | — |

| | 9.3 |

| | — |

| | — |

| | — |

| | — |

| | 9.3 |

|

| Balance at April 30, 2020 | | 49.1 |

| | $ | 4.9 |

| | 4.3 |

| | $ | 0.4 |

| | $ | 1,626.5 |

| | $ | (512.8 | ) | | $ | 3,126.9 |

| | $ | (618.6 | ) | | $ | 0.2 |

| | $ | 3,627.5 |

|

THE COOPER COMPANIES, INC. AND SUBSIDIARIES

The accompanying notes are an integral part of these Consolidated Condensed Financial Statements.

|

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Consolidated Condensed Statements of Stockholders' Equity |

| | Common Shares | | Treasury Stock | | Additional Paid-In Capital | | Accumulated

Other

Comprehensive

Income (Loss) | | Retained Earnings | | Treasury Stock | | Noncontrolling Interests | | Total

Stockholders'

Equity |

| (In millions) | Shares | | Amount | | Shares | | Amount | | | | | | |

| Balance at November 1, 2018 | 49.2 |

| | $ | 5.0 |

| | 3.6 |

| | $ | 0.3 |

| | $ | 1,572.1 |

| | $ | (430.7 | ) | | $ | 2,576.0 |

| | $ | (415.1 | ) | | $ | 0.2 |

| | $ | 3,307.8 |

|

| Net income | — |

| | — |

| | — |

| | — |

| | — |

| | — |

| | 103.2 |

| | — |

| | — |

| | 103.2 |

|

| Other comprehensive income, net of tax | — |

| | — |

| | — |

| | — |

| | — |

| | 32.7 |

| | — |

| | — |

| | — |

| | 32.7 |

|

| Issuance of common stock for stock plans, net | 0.1 |

| | — |

| | — |

| | — |

| | (9.0 | ) | | — |

| | — |

| | — |

| | — |

| | (9.0 | ) |

| Treasury stock repurchase | — |

| | — |

| | — |

| | — |

| | — |

| | — |

| | — |

| | (6.1 | ) | | — |

| | (6.1 | ) |

| Dividends on common stock | — |

| | — |

| | — |

| | — |

| | — |

| | — |

| | (1.5 | ) | | — |

| | — |

| | (1.5 | ) |

| Share-based compensation expense | — |

| | — |

| | — |

| | — |

| | 11.7 |

| | — |

| | — |

| | — |

| | — |

| | 11.7 |

|

| ASU 2016-16 adoption (1) | — |

| | — |

| | — |

| | — |

| | — |

| | — |

| | (13.3 | ) | | — |

| | — |

| | (13.3 | ) |

| Balance at January 31, 2019 | 49.3 |

| | $ | 5.0 |

| | 3.6 |

| | $ | 0.3 |

| | $ | 1,574.8 |

| | $ | (398.0 | ) | | $ | 2,664.4 |

| | $ | (421.2 | ) | | $ | 0.2 |

| | $ | 3,425.5 |

|

| Net income | — |

| | — |

| | — |

| | — |

| | — |

| | — |

| | 122.4 |

| | — |

| | — |

| | 122.4 |

|

| Other comprehensive loss, net of tax | — |

| | — |

| | — |

| | — |

| | — |

| | (18.6 | ) | | — |

| | — |

| | — |

| | (18.6 | ) |

| Issuance of common stock for stock plans, net | 0.2 |

| | — |

| | — |

| | — |

| | 4.5 |

| | — |

| | — |

| | — |

| | — |

| | 4.5 |

|

| Share-based compensation expense | — |

| | — |

| | — |

| | — |

| | 8.4 |

| | — |

| | — |

| | — |

| | — |

| | 8.4 |

|

| Balance at April 30, 2019 | 49.5 |

| | $ | 5.0 |

| | 3.6 |

| | $ | 0.3 |

| | $ | 1,587.7 |

| | $ | (416.6 | ) | | $ | 2,786.8 |

| | $ | (421.2 | ) | | $ | 0.2 |

| | $ | 3,542.2 |

|

| Net income | — |

| | — |

| | — |

| | — |

| | — |

| | — |

| | 120.1 |

| | — |

| | — |

| | 120.1 |

|

| Other comprehensive loss, net of tax | — |

| | — |

| | — |

| | — |

| | — |

| | (65.2 | ) | | — |

| | — |

| | — |

| | (65.2 | ) |

| Issuance of common stock for stock plans, net | 0.1 |

| | — |

| | — |

| | — |

| | 12.2 |

| | — |

| | — |

| | — |

| | — |

| | 12.2 |

|

| Dividends on common stock | — |

| | — |

| | — |

| | — |

| | — |

| | — |

| | (1.5 | ) | | — |

| | — |

| | (1.5 | ) |

| Share-based compensation expense | — |

| | — |

| | — |

| | — |

| | 7.7 |

| | — |

| | — |

| | — |

| | — |

| | 7.7 |

|

| Balance at July 31, 2019 | 49.6 |

| | $ | 5.0 |

| | 3.6 |

| | $ | 0.3 |

| | $ | 1,607.6 |

| | $ | (481.8 | ) | | $ | 2,905.4 |

| | $ | (421.2 | ) | | $ | 0.2 |

| | $ | 3,615.5 |

|

See accompanying notes to consolidated financial statements.

(1) We adopted ASU 2016-16, Income Taxes (Topic 740): Intra-Entity Transfers of Assets Other Than Inventory in the first quarter of fiscal 2019. Refer to “Note 1. General" for further information.

THE COOPER COMPANIES, INC. AND SUBSIDIARIES

Consolidated Condensed Statements of Cash Flows

NineSix Months Ended July 31,April 30,

(In millions)

(Unaudited)millions, unaudited)

| | | | 2019 | | 2018 | 2020 | | 2019 |

| Cash flows from operating activities: | | | | | | |

| Net income | $ | 345.7 |

| | $ | 39.2 |

| $ | 102.0 |

| | $ | 225.5 |

|

| Depreciation and amortization | 210.2 |

| | 204.6 |

| 139.4 |

| | 139.5 |

|

| Gain on sale of an intangible (Note 5) | (19.0 | ) | | — |

| |

| Impairment of intangibles | — |

| | 24.4 |

| |

| Increase in operating capital | (22.1 | ) | | (141.1 | ) | |

| Gain on sale of an intangible | | — |

| | (19.0 | ) |

| Decrease in operating capital | | (119.8 | ) | | (19.7 | ) |

| Other non-cash items | (1.5 | ) | | 305.2 |

| 33.9 |

| | (9.7 | ) |

| Net cash provided by operating activities | 513.3 |

| | 432.3 |

| 155.5 |

| | 316.6 |

|

| Cash flows from investing activities: | | | | | | |

| Purchases of property, plant and equipment | (207.3 | ) | | (150.2 | ) | (158.3 | ) | | (131.9 | ) |

| Acquisitions of businesses and assets, net of cash acquired, and other | (59.1 | ) | | (1,320.8 | ) | (11.2 | ) | | (50.8 | ) |

| Net cash used in investing activities | (266.4 | ) | | (1,471.0 | ) | (169.5 | ) | | (182.7 | ) |

| Cash flows from financing activities: | | | | | | |

| Proceeds from long-term debt | 576.8 |

| | 2,073.1 |

| 1,862.0 |

| | 424.8 |

|

| Repayments of long-term debt | (1,140.8 | ) | | (971.1 | ) | (1,781.3 | ) | | (938.8 | ) |

| Net proceeds from short-term debt | 351.8 |

| | 21.0 |

| |

| Net proceeds (payments) related to share-based compensation awards | 7.7 |

| | (9.8 | ) | |

| Net (repayments) proceeds from short-term debt | | (10.0 | ) | | 417.4 |

|

| Net payments related to share-based compensation awards | | (8.4 | ) | | (4.3 | ) |

| Dividends on common stock | (1.5 | ) | | (1.5 | ) | (1.5 | ) | | (1.5 | ) |

| Repurchase of common stock | (6.1 | ) | | — |

| (47.8 | ) | | (6.1 | ) |

| Debt acquisition costs | (0.2 | ) | | (3.9 | ) | |

| Payment of contingent consideration | — |

| | (0.1 | ) | |

| Net cash (used in) provided by financing activities | (212.3 | ) | | 1,107.7 |

| |

| Issuance of common stock for employee stock purchase plan | | 0.9 |

| | — |

|

| Debt issuance costs | | (5.5 | ) | | (0.2 | ) |

| Net cash provided by (used in) financing activities | | 8.4 |

| | (108.7 | ) |

| Effect of exchange rate changes on cash, cash equivalents and restricted cash | (1.6 | ) | | (2.2 | ) | (3.1 | ) | | (0.5 | ) |

| Net increase in cash, cash equivalents and restricted cash | 33.0 |

| | 66.8 |

| |

| Net (decrease) increase in cash, cash equivalents and restricted cash | | (8.7 | ) | | 24.7 |

|

| Cash, cash equivalents and restricted cash at beginning of period | 80.2 |

| | 88.8 |

| 89.5 |

| | 80.2 |

|

| Cash, cash equivalents and restricted cash at end of period | $ | 113.2 |

| | $ | 155.6 |

| $ | 80.8 |

| | $ | 104.9 |

|

| Reconciliation of cash flow information: | | | | | | |

| Cash and cash equivalents | $ | 112.7 |

| | $ | 155.6 |

| $ | 79.8 |

| | $ | 104.6 |

|

| Restricted cash included in other current assets | 0.5 |

| | — |

| 1.0 |

| | 0.3 |

|

| Total cash, cash equivalents, and restricted cash | $ | 113.2 |

| | $ | 155.6 |

| |

| Total cash, cash equivalents and restricted cash | | $ | 80.8 |

| | $ | 104.9 |

|

The accompanying notes are an integral part of these Consolidated Condensed Financial Statements.

6

See accompanying notes.

THE COOPER COMPANIES, INC. AND SUBSIDIARIES

Notes to Consolidated Condensed Financial Statements

(Unaudited)

Note 1. General

The accompanying unauditedConsolidated Condensed Financial Statements of the Cooper Companies, Inc. and its subsidiaries (the Company) have been prepared in accordance with U.S. GAAP for interim consolidated condensedfinancial information and with the requirements of Regulation S-X, Rule 10-01 for financial statements required to be filed as a part of this Quarterly Report on Form 10-Q. Unless the context requires otherwise, terms "the Company", "we", "us", and "our" are used to refer collectively to the Cooper Companies, Inc. and its subsidiaries.

The accompanying Consolidated Condensed Financial Statements and related notes should be read in conjunction with the audited Consolidated Financial Statements of the Cooper Companies, Inc. and its subsidiaries (the Company) and related notes as contained in the Company’s Annual Report on Form 10-K for the fiscal year ended October 31, 2018.2019. The unaudited interim financial statementsConsolidated Condensed Financial Statements include all adjustments (consisting only of normal recurring adjustments) and accruals necessary in the judgment of management for a fair statement of the results for the periods presented. Readers should not assume that the results reported here either indicate or guarantee future performance. The terms "the Company", "we", "us", and "our" are used to refer collectively to the Cooper Companies, Inc. and its subsidiaries.

Accounting Pronouncements Recently AdoptedPolicies

In JulyThere have been no material changes to our significant accounting policies described in our Annual Report on Form 10-K for the fiscal year ended October 31, 2019, except as it relates to the FASB issued ASU 2019-07, Codification Updates to SEC Sections. The ASU clarifies or improves the disclosure and presentation requirementsadoption of a variety of codification topics by aligning them with the SEC’s regulations, thereby eliminating redundancies and making the codification easier to apply. The Company adopted this guidance during third quarter of fiscal 2019, and it did not have a material impact on the Company’s reported consolidated financial results.

In March 2017, the Financial Accounting Standards Board (FASB) issued Accounting Standards Update (ASU) 2017-07,2016-02, Compensation - Retirement BenefitsLeases (Topic 715): Improving the Presentation of Net Periodic Pension Cost and Net Periodic Postretirement Benefit Cost. The ASU requires an entity to disaggregate the service cost component from the other components of net benefit cost. The service cost component is now presented in the same income statement line as other compensation costs arising from services rendered by the pertinent employees during the period and the other components of net benefit costs are presented separately as other income/expense below operating income. The Company adopted this guidance on November 1, 2018, and it did not have a material impact on the Company’s reported consolidated financial results.

In October 2016, the FASB issued ASU 2016-16, Income Taxes (Topic 740): Intra-Entity Transfers of Assets Other Than Inventory842), which requires entitiesis described below.

Leases

We consider an arrangement a lease if the arrangement transfers the right to recognizecontrol the income tax consequences on an intra-entity transferuse of an identified asset other than inventory whenin exchange for consideration. We have operating leases, but do not have material financing leases. Lease right-of-use assets represent the transfer occurs. The ASU changesright to use an underlying asset for the timinglease term, and lease liabilities represent the obligation to make payments arising from the lease agreement. These assets and liabilities are recognized at the commencement of the recognitionlease based upon the present value of the income tax consequencesfuture minimum lease payments over the lease term.

The lease term reflects the noncancelable period of non-inventory transfers which under previous guidance deferred the income tax consequences untillease together with periods covered by an option to extend or terminate the asset was sold to an outside party or otherwise recognized. The guidance for the amendments of ASU 2016-16 requires companies to apply a modified retrospective approach with a cumulative catch-up adjustment to opening retained earningslease when management is reasonably certain that it will exercise such option. Changes in the periodlease term assumption could impact the right-of-use assets and lease liabilities recognized on the balance sheet. As our leases typically do not contain a readily determinable implicit rate, we determine the present value of adoption. The Company adopted ASU 2016-16 in the first quarter of fiscal 2019lease liability using our incremental borrowing rate at the lease commencement date based on the lease term on a modified retrospectivecollateralized basis.

Estimates

The Company recordedWorld Health Organization has categorized the cumulative effectCoronavirus disease 2019 ("COVID-19") as a pandemic. The COVID-19 pandemic has caused a severe global health crisis, along with economic and societal disruptions and uncertainties, which have negatively impacted business and healthcare activity globally. As a result of healthcare systems responding to the demands of managing the pandemic, governments around the world imposing measures designed to reduce the transmission of the change as a decreaseCOVID-19 virus, and individuals responding to retained earningsthe concerns of approximately $13.3 million. contracting the COVID-19 virus, many of our optical retailers, hospital, medical office and fertility clinic customers have closed their facilities, restricted access, or delayed or cancelled patient visits, exams and elective medical procedures. This has had, and we believe will continue to have, an adverse effect on our sales, operating results and cash flows, although the extent of which is uncertain.

The cumulative effect adjustment representspreparation of Consolidated Condensed Financial Statements in conformity with GAAP requires management to make estimates and assumptions that affect the recognition of unrecognized income tax effects from intra-entity transfersreported amounts of assets other than inventory that occurred prior toand liabilities and disclosure of contingent assets and liabilities at the date of adoption.

In May 2014, the FASB issued ASU 2014-09, Revenuefinancial statements, as well as the reported amounts of revenue and expenses during the reporting period. Actual results could differ from Contracts with Customers (Topic 606).those estimates particularly as it relates to estimates reliant on forecasts and other assumptions reasonably available to the Company and the uncertain future impacts of the COVID-19 pandemic and related economic disruptions. The ASU requires revenue recognition to depict the transfer of goods or services to customers at an amount that reflects the considerationextent to which the entity expectsCOVID-19 pandemic and related economic disruptions impact our business and financial results will depend on future developments including, but not limited to, be entitled in exchange for those goodsthe continued spread, duration and severity of the COVID-19 pandemic; the occurrence, spread, duration and severity of any subsequent wave or services. The amendments inwaves of outbreaks after the ASU can be applied either retrospectivelyinitial outbreak has subsided; the actions taken by the U.S. and foreign governments to each prior reporting period presentedcontain the COVID-19 pandemic, address its impact or alternatively,respond to the modified retrospective transition method whereby the company recognizes the cumulative effect of initially applying the guidance as an opening balance sheet adjustment to equity in the period of initial application. This alternative approach must be supplemented by additional disclosures.reduction

We adopted ASU 2014-09 on November 1, 2018, using the modified retrospective transition method. We did not recognize any cumulative effect of initially applying the new revenue standard as an adjustment to our opening balance of retained earnings due to its immaterial impact. The comparative information has not been restated and continues to be reported under the accounting standards in effect for those periods. There was no material impact of ASU 2014-09 to our financial statements during the three and nine months ended July 31, 2019. We do not expect the adoption of the new revenue standard to have a material impact to our net income on an ongoing basis.7

THE COOPER COMPANIES, INC. AND SUBSIDIARIES

Notes to Consolidated Condensed Financial Statements

(Unaudited)

allowance for doubtful accounts and credit losses

the carrying value of the goodwill and other long-lived assets.

There was not a material impact to the above estimates in the Company’s Consolidated Condensed Financial Statements for the three and six months ended April 30, 2020. The Company appliesCompany’s future assessment of the provisionsmagnitude and duration of Accounting Standards Codification (ASC) 606-10 or ASU 2014-09, Revenue from Contracts with Customers,COVID-19, as well as other factors, could result in material changes to the estimates and all related appropriate guidance. The Company recognizes revenue under the core principle to depict the transfer of controlmaterial impacts to the Company’s customersConsolidated Condensed Financial Statements in an amount reflecting the consideration to which the Company expects to be entitled. In order to achieve that core principle, the Company applies the following five step approach: (1) identify the contract with a customer, (2) identify the performance obligations in the contract, (3) determine the transaction price, (4) allocate the transaction price to the performance obligations in the contract, and (5) recognize revenue when a performance obligation is satisfied. For a complete discussion of accounting for net product revenue, see Note 2. Revenue Recognition.future reporting periods.

Accounting Pronouncements Issued Not YetRecently Adopted

In November 2018, the FASB issued ASU 2018-18, ICollaborative Arrangements (Topic 808), Clarifying the Interaction between Topic 808 and Topic 606. This guidance amended Topic 808 and Topic 606 to clarify that transactions in a collaborative arrangement should be accounted for under Topic 606 when the counterparty is a customer for a distinct good or service (i.e., unit of account). The amendments preclude an entity from presenting consideration from a transaction in a collaborative arrangement as revenue from contracts with customers if the counterparty is not a customer for that transaction. We are currently evaluating the impact of ASU 2018-18 which is effective for the Company in our fiscal year and interim periods beginning on November 1, 2020.

In August 2018, the FASB issued ASU 2018-15, Intangibles-Goodwill and Other - Internal Use Software (Subtopic 350-40): Customer's Accounting for Implementation Costs Incurred in a Cloud Computing Arrangement That is a Service Contract. This guidance requires companies to apply the internal-use software guidance in ASC 350-40 to implementation costs incurred in a hosting arrangement that is a service contract to determine whether to capitalize certain implementation costs or expense them as incurred. We are currently evaluating the impact of ASU 2018-15 which is effective for the Company in our fiscal year and interim periods beginning on November 1, 2020.

Inn February 2016, the FASBFinancial Accounting Standards Board (FASB) issued ASU 2016-02, Leases (Topic 842). ASU 2016-02 requires that a lessee recognize the assets and liabilities that arise from operating leases. A lessee should recognize in the statement of financial position a liability to make lease payments (the lease liability) and a right-of-use (ROU) asset representing its right to use the underlying asset for the lease term. For leases with a term of 12 months or less, a lessee is permitted to make an accounting policy election by class of underlying asset not to recognize lease assets and lease liabilities. In transition, lessees and lessors are required to recognize and measure leases at the beginning of the earliest period presented using a modified retrospective approach. In July 2018, the FASB issued ASU 2018-10, Codification Improvements to Topic 842, Leases and ASU 2018-11, Leases Topic 842 Target improvements,, which provides an additional (and optional) transition method whereby the new lease standard is applied at the adoption date and recognized as an adjustment to retained earnings. In March 2019, the FASB issued ASU 2019-01, Leases (Topic 842) Codification Improvements, which further clarifies the determination of fair value of the underlying asset by lessors that are not manufacturers or dealers and modifies transition disclosure requirements for changes in accounting principles and other technical updates.

We adopted this standard using the optional transition method and recorded an adjustment to the Consolidated Condensed Balance Sheet on November 1, 2019. We have implemented changes to certain business processes, systems and internal controls to support adoption of the new standard and the related disclosure requirements, including the implementation of a third-party leasing software solution. We elected the package of transition expedients, which allows us to keep our existing lease classifications and not reassess whether any existing contracts as of the date of adoption are leases or contain leases and not reassess initial direct costs. In addition, we elected the practical expedients to combine lease and non-lease components for our leases, and for leases with an initial term of 12 months or less to recognize the associated lease payments in the Consolidated Statements of Income and Comprehensive Income on a straight-line basis over the lease term.

As of April 30, 2020, the aggregate balances of lease right-of-use assets and lease liabilities were $255.5 million and $264.2 million, respectively. The standard did not affect our Consolidated Statements of Income and Comprehensive Income or Consolidated Condensed Statements of Cash Flows. We will continue to disclose comparative reporting periods prior to November 1, 2019 under the previous accounting guidance, ASC 840 Leases.

THE COOPER COMPANIES, INC. AND SUBSIDIARIES

Notes to Consolidated Condensed Financial Statements

(Unaudited)

Accounting Pronouncements Issued Not Yet Adopted

In June 2016, the FASB issued ASU No. 2016-13, “Financial Instruments-Credit Losses (Topic 326): Measurement of Credit Losses on Financial Instruments” and subsequent amendments to the initial guidance: ASU 2018-19 “Codification Improvements to Topic 326, Financial Instruments-Credit Losses”, ASU 2019-04 “Codification Improvements to Topic 326, Financial Instruments-Credit Losses, Topic 815, Derivatives and Hedging, and Topic 825, Financial Instruments”, ASU 2019-05 “Financial Instruments-Credit Losses”, ASU 2019-11 “Codification Improvements to Topic 326, Financial Instruments - Credit Losses” (collectively, “Topic 326”), ASU 2020-02 Financial Instruments—Credit Losses (Topic 326) and Leases (Topic 842) and ASU 2020-03 CodificationImprovementstoFinancialInstruments. Topic 326 requires measurement and recognition of expected credit losses for financial assets held. Topic 326 is effective for fiscal years and interim periods within those fiscal years beginning after December 15, 2019, which means it will be effective for our fiscal year beginning November 01, 2020. Early adoption is permitted. We are currently evaluating the impact of Topic 326 on our Consolidated Condensed Financial Statements.

In November 2018, the FASB issued ASU 2018-18, Collaborative Arrangements (Topic 808), Clarifying the Interaction between Topic 808 and Topic 606. This guidance amended Topic 808 and Topic 606 to clarify that transactions in a collaborative arrangement should be accounted for under Topic 606 when the counterparty is a customer for a distinct good or service (i.e., unit of account). The amendments preclude an entity from presenting consideration from a transaction in a collaborative arrangement as revenue from contracts with customers if the counterparty is not a customer for that transaction. This guidance is effective for fiscal years, and interim periods within those fiscal years, beginning after December 15, 2019, which means it will be effective for our fiscal year beginning November 1, 2020. Early adoption is permitted. The adoption of this guidance will not have a material impact on our Consolidated Condensed Financial Statements.

In December 2019, the FASB issued ASU 2019-12, Income Taxes (Topic 740): Simplifying the Accounting for Income Taxes. This guidance removes certain exceptions to the general principles in Topic 740 and enhances and simplifies various aspects of the income tax accounting guidance, including requirements such as tax basis step-up in goodwill obtained in a transaction that is not a business combination, ownership changes in investments, and interim-period accounting for enacted changes in tax law. This standard is effective for fiscal years and interim periods within those fiscal years beginning after December 15, 2020. Early adoption is permitted. We are currently evaluating the impact of ASU 2019-12 on our Consolidated Condensed Financial Statements, which is effective for the Company in our fiscal year and interim periods beginning on November 1, 2019.2021.

In January 2020, the FASB issued ASU 2020-01 Investments-Equity Securities (Topic 321), Investments-Equity Method and Joint Ventures (Topic 323), and Derivatives and Hedging (Topic 815) - Clarifying the Interactions between Topic 321, Topic 323, and Topic 815. This guidance addresses accounting for the transition into and out of the equity method and provides clarification of the interaction of rules for equity securities, the equity method of accounting, and forward contracts and purchase options on certain types of securities. This standard is effective for fiscal years and interim periods within those fiscal years beginning after December 15, 2020. Early adoption is permitted. We anticipate this standardare currently evaluating the impact of ASU 2020-01 on our Consolidated Condensed Financial Statements, which is effective for the Company in our fiscal year and interim periods beginning on November 1, 2021.

In March 2020, the FASB issued ASU 2020-04, ReferenceRateReform (Topic848): Facilitation of the Effects of Reference Rate Reform on Financial Reporting. This guidance provides optional expedients and exceptions for applying generally accepted accounting principles (GAAP) to contracts, hedging relationships, and other transactions affected by reference rate reform if certain criteria are met. The amendments apply only to contracts, hedging relationships, and other transactions that reference LIBOR or another reference rate expected to be discontinued because of reference rate reform. This guidance is effective for all entities as of March 12, 2020 through December 31, 2022. We are currently evaluating the impact of ASU 2020-04 on our Consolidated Condensed Financial Statements.

No other recently issued accounting pronouncements had or are expected to have a material impact on our Consolidated Balance Sheets and related disclosures due to the recognition of ROU assets and lease liabilities for operating leases. However, we do not expect the adoption to have a material impact on our Consolidated Statements of Income. We are continuing to assess and evaluate the potential impacts of the standard as well as the election of transition method and certain practical expedients available within ASU 2019-01. We are in the process of documenting and analyzing our lease contracts, assessing business processes and controls, implementing a system solution and completing our analysis of information necessary to determine the impact to the consolidated financial statements.Condensed Financial Statements.

Note 2. Revenue Recognition

Product Revenue, Net

The Company sells its products principally to a limited number of distributors, group purchasing organizations, eye care or health care professionals including independent practices, corporate retailers, hospitals and clinics or authorized resellers (collectively, its Customers). These Customers subsequently resell the Company’s products to eye care or health care

THE COOPER COMPANIES, INC. AND SUBSIDIARIES

Notes to Consolidated Condensed Financial Statements

(Unaudited)

providers and patients. In addition to product supply and distribution agreements with Customers, the Company enters into arrangements with health care providers and payors that provide for government-mandated and/or privately-negotiated rebates, chargebacks and discounts with respect to the purchase of the Company’s products. The Company considers customer purchase orders, which in some cases are governed by master sales agreements, to be contracts with a customer. In situations where sales are to a distributor, the Company has concluded that its contracts are with the distributor. As part of its consideration of the contract, the Company evaluates certain factors including the customer’s ability to pay (or credit risk). For each contract, the Company considers the promise to transfer products, each of which is distinct, to be the identified performance obligations.

Revenues from product sales are recognized when the Customer obtains control of the Company’s product, which occurs at a point in time, typically upon shipment or delivery to the Customer. When the Company performs shipping and handling activities after the transfer of control to the Customer (e.g., when control transfers prior to delivery), they are considered as fulfillment activities, and accordingly, the costs are accrued for when the related revenue is recognized. Taxes collected from Customers relating to product sales and remitted to governmental authorities are excluded from revenues. The Company does not have any revenue recognized on payment expected to be received more than one year after the transfer of control of the products. The Company expenses incremental costs of obtaining a contract as and when incurred if the expected amortization period of the asset that the Company would have recognized is one year or less. See Note14. Business Segment Information, for disaggregation of revenue.

Reserves for Variable Consideration

Revenues from product sales are recorded at the net sales price (transaction price), which includes estimates of variable consideration for which reserves are established and which result from discounts, returns, chargebacks, rebates and other allowances that are offered within contracts between the Company and its Customers, health care providers, payors and other indirect customers relating to the Company’s sales of its products. These reserves are based on the amounts earned or to be claimed on the related sales and are classified primarily in current liabilities. Variable consideration is estimated based on the most likely amount or expected value approach, depending on which method the Company expects to better predict the amount of consideration to which it will be entitled. Once the Company elects one of the methods to estimate variable consideration for a particular type of performance obligation, the Company applies that method consistently.

Where appropriate, these estimates take into consideration a range of possible outcomes which are probability-weighted for relevant factors such as the Company’s historical experience, current contractual and statutory requirements, specific known market events and trends, industry data and forecasted customer buying and payment patterns. Overall, these reserves reflect the Company’s best estimates of the amount of consideration to which it is entitled based on the terms of the contract. Actual amounts of consideration ultimately received may differ from the Company’s estimates. If actual results in the future vary from the Company’s estimates, the Company adjusts these estimates, which would affect net product revenue and earnings in the period such variances become known.

Trade Discounts and AllowancesNote 2. Leases

The Company generally provides Customersprimarily has operating leases for office, manufacturing and warehouse space, vehicles, and office equipment. Our leases expire on various dates between 2020 and 2045, some of which could include options to extend the lease.

Lease right-of-use assets and liabilities are recognized at the commencement date based on the present value of lease payments over the lease term. As these leases do not provide an implicit rate, we use our incremental borrowing rate based on the information available at the lease's commencement date in determining the present value of lease payments. We consider information including, but not limited to, the lease term, our credit rating and interest rates of similar debt instruments with discounts, whichcomparable credit ratings and security interests. The lease right-of-use assets are increased by any lease prepayments made and reduced by any lease incentives such as tenant improvement allowances. Options to extend the lease term are included in the lease term when it is reasonably certain that we will exercise the extension option.

The Company’s operating leases typically include incentive feesnon-lease components such as common-area maintenance costs. We have elected to include non-lease components with lease payments for the purpose of calculating lease right-of-use assets and liabilities, to the extent that they are fixed. Non-lease components that are stated innot fixed are expensed as incurred as variable lease payments.

Leases with a term of one year or less are not recognized on our Consolidated Condensed Balance Sheet, while the Company’s contracts and are recorded as a reduction of revenue in the period the related product revenue is recognized. In addition, the Company receives sales order management, data and distribution services from certain Customers. To the extent the services received are distinct from the Company’s sale of products to the Customer and have readily determinable fair value, theseassociated lease payments are classified in selling, general and administrative expensesrecorded in the Consolidated Statements of Income ofand Comprehensive Income on a straight-line basis over the Company.

Product Returnslease term.

Consistent with industry practice, the Company generally offers Customers a limited rightCommitments under finance lease arrangements of return for a product that has been purchased from the Company. The Company estimates the amount$1.9 million as of its product sales that may be returned by its CustomersApril 30, 2020 are not significant and records this estimate as a reduction of revenueare not included in the perioddisclosure tables below.

The following table presents information about leases on the related product revenue is recognized. There is inherent judgmentConsolidated Condensed Balance Sheet:

|

| | | |

| (In millions) | April 30, 2020 |

| Operating Leases | |

| Operating lease right-of-use assets | $ | 255.5 |

|

| | |

| Operating lease liabilities, current | 31.5 |

|

| Operating lease liabilities, non-current | 232.7 |

|

| Total operating lease liabilities | $ | 264.2 |

|

| | |

Weighted average remaining lease term (in years)

| 11.6 |

|

| Weighted average discount rate | 3 | % |

The following table presents information about lease expense in estimating future refundsour Consolidated Statements of Income and Comprehensive Income:

|

| | | | | | | |

| Periods Ended April 30, | Three Months | | Six Months |

| (In millions) | 2020 | | 2020 |

| Operating lease expense | $ | 9.7 |

| | $ | 19.6 |

|

| Short-term lease expense | 1.5 |

| | 2.6 |

|

| Variable lease expense | 0.4 |

| | 0.8 |

|

THE COOPER COMPANIES, INC. AND SUBSIDIARIES

Notes to Consolidated Condensed Financial Statements

(Unaudited)

The following table presents supplemental cash flow information about the Company’s leases:

|

| | | | | | | |

| Periods Ended April 30, | Three Months | | Six Months |

| (In millions) | 2020 | | 2020 |

| Cash paid for amounts included in the measurement of lease liabilities: | | | |

| Operating cash flows from operating leases | $ | 9.7 |

| | $ | 19.6 |

|

Maturity of Lease Liabilities

The minimum rental payments required under operating leases that have initial or remaining noncancelable lease terms in excess of one year as they are susceptible to factors outside of our influence. However, we have significant experienceApril 30, 2020 are:

|

| | | |

| (In millions) | |

| Remainder of 2020 | $ | 19.1 |

|

| 2021 | 36.5 |

|

| 2022 | 32.6 |

|

| 2023 | 29.2 |

|

| 2024 | 27.1 |

|

| 2025 and thereafter | 173.9 |

|

| Total lease payments | 318.4 |

|

| Less: interest | 54.2 |

|

| Present value of lease liabilities | $ | 264.2 |

|

As previously disclosed in estimating the amount of refunds, based primarilyCompany’s Annual Report on historical data. Our refund liabilityForm 10-K for product returns was $9.9 million at Julythe fiscal year ended October 31, 2019, which is included in Accrued Liabilities on our Condensed Consolidated Balance Sheets and represents the expected value ofunder previous lease accounting standard ASC 840, Leases, the aggregate refunds that will be due to our customers.future noncancelable minimum rental payments on its operating leases, as of October 31, 2019, were as follows:

|

| | | |

| (In millions) | |

| 2020 | $ | 38.5 |

|

| 2021 | 34.9 |

|

| 2022 | 31.2 |

|

| 2023 | 28.0 |

|

| 2024 | 26.5 |

|

| 2025 and thereafter | 173.6 |

|

| Total future minimum lease payments | $ | 332.7 |

|

THE COOPER COMPANIES, INC. AND SUBSIDIARIES

Notes to Consolidated Condensed Financial Statements

(Unaudited)

Rebates and Chargebacks

Rebates are estimated based on contractual terms, historical experience, customer mix, trend analysis and projected market conditions in the various markets served.

Chargebacks for fees and discounts to providers represent the estimated obligations resulting from contractual commitments to sell products to qualified healthcare providers at prices lower than the list wholesale prices charged to the Company’s direct customers. For certain office and surgical products in CooperSurgical, customers charge the Company for the difference between what they pay for the product and the ultimate selling price to the qualified healthcare providers. These reserves are established in the same period that the related revenue is recognized, resulting in a reduction of product revenue. Chargeback amounts are generally determined at the time of resale to the qualified healthcare provider by Customers. CooperSurgical rebates are predominately related to the Medicaid rebate provision that is estimated based upon contractual terms, historical experience, and trend analysis.

Contract balances

The timing of billing and revenue recognition primarily occurs simultaneously. The Company does not have material contract assets or liabilities.

Note 3. Acquisitions

The following is a summary of the allocation of the total purchase consideration for business and asset acquisitions that the Company completed during fiscal 20192020 and 2018:2019: | | | (In millions) | July 31, 2019 | | October 31, 2018 | April 30, 2020 | | October 31, 2019 |

| Customer relationships | | $ | 6.5 |

| | $ | 7.5 |

|

| Technology | $ | 12.3 |

| | $ | — |

| — |

| | 12.3 |

|

| Customer relationships | 7.5 |

| | 23.5 |

| |

| Trademarks | 10.2 |

| | 100.0 |

| — |

| | 10.2 |

|

| Composite intangible asset | — |

| | 1,061.9 |

| |

| Other | 0.1 |

| | 4.2 |

| — |

| | 0.1 |

|

| Total identifiable intangible assets | $ | 30.1 |

| | $ | 1,189.6 |

| $ | 6.5 |

| | $ | 30.1 |

|

| Goodwill | 35.8 |

| | 70.6 |

| 1.9 |

| | 29.8 |

|

| Net tangible assets | 1.3 |

| | 59.6 |

| 0.8 |

| | 7.3 |

|

| Total purchase price | $ | 67.2 |

| | $ | 1,319.8 |

| $ | 9.2 |

| | $ | 67.2 |

|

All the acquisitions were funded by cash generated from operations or facility borrowings.

For business acquisitions, we recorded the tangible and intangible assets acquired and liabilities assumed at their fair values as of the applicable date of acquisition. For assetsasset acquisitions, we recorded the tangible and intangible assets acquired and liabilities assumed at their estimated and relative fair values as of the applicable date of acquisition.

We believe these acquisitions strengthen CooperSurgical's and CooperVision's businesses through the addition of new distributors or complementary products and services.

The pro forma results of operations have not been presented because the effect of the business combinations described below were not material to our consolidated results of operations.

Fiscal Year 20192020

On December 31, 2018,13, 2019, CooperSurgical completed the acquisition of Incisive Surgical Inc., a privately-held U.S.distributor of in vitro fertilization (IVF) medical device company that develops mechanical surgical solutions for skin closure.devices and systems. The purchase price allocation is preliminary and we are in the process of finalizing information primarily related to taxes and the corresponding impact on goodwill.

Fiscal Year 2019

On December 28, 2018, CooperVision completed the acquisition of Blanchard Contact Lenses. Blanchard is a privately-held scleral lens company, which expands CooperVision's specialty and scleral lens portfolio. The purchase price allocation is preliminary and we are in the process of finalizing information primarily related to property plant and equipment, taxes and the corresponding impact on goodwill.

THE COOPER COMPANIES, INC. AND SUBSIDIARIES

Notes to Consolidated Condensed Financial Statements

(Unaudited)

The pro forma results of operations of these acquisitions have not been presented because the effects of the business combinations described above, individually and in the aggregate, were not material to our reported consolidated financial results.

Fiscal Year 2018

PARAGARD

On November 1, 2017, CooperSurgical acquired the assets of the PARAGARD Intrauterine Device (IUD) business (PARAGARD) from Teva Pharmaceuticals Industries Limited for $1.1 billion. This asset acquisition broadened and strengthened CooperSurgical's product portfolio. PARAGARD® is the only hormone-free, long lasting, reversible contraceptive approved by the United States Food and Drug Administration (FDA) available in the United States.

The following table summarizes the relative fair values of net assets acquired and liabilities assumed using the cost accumulation and allocation model:

|

| | | |

| (In millions) | Relative Fair Value |

Composite intangible asset (1) | $ | 1,061.9 |

|

Assembled workforce intangible asset (2) | 1.2 |

|

| Property, plant and equipment | 2.0 |

|

Inventory (3) | 47.3 |

|

| Other assets | 9.4 |

|

| Total assets acquired | $ | 1,121.8 |

|

| Less: liabilities assumed | 16.4 |

|

| Total Purchase Price | $ | 1,105.4 |

|

The Company proportionally allocated the acquisition costs to the net assets acquired. The acquisition-related costs included advisory, legal, valuation and other professional fees.

(1) Composite Intangible asset consists of technology, trade name, New Drug Application (NDA) approval and physician relationships, which have been valued as a single composite intangible asset as they are inextricably linked. The composite asset was identified as the primary asset acquired, was valued using the Multi-Period Excess Earnings Method and will be amortized over 15 years.

(2) An assembled workforce was recognized as a separate acquired intangible asset, given the purchase of assets and will be amortized over 5 years.

(3) Inventory relative fair value includes step up of $45.4 million.

Other Acquisitions

On April 3,December 31, 2018, CooperSurgical completed the acquisition of The LifeGlobal Group (LifeGlobal). LifeGlobal wasIncisive Surgical Inc., a privately heldprivately-held U.S. medical device company that specializes primarily in in-vitro fertilization (IVF) media. LifeGlobal’s product categories include media products as well as IVF laboratory air filtration products and dishware. We have completed the purchase price allocationdevelops mechanical surgical solutions for this acquisition.

On January 4, 2018, CooperVision acquired Blueyes Ltd, a long-standing distribution partner, with a leading position in the distribution of contact lenses to the Optical and Pharmacy sector in Israel. We have completed the purchase price allocation for this acquisition.

On December 1, 2017, CooperVision acquired Paragon Vision Sciences, a leading provider of orthokeratology (ortho-k) specialty contact lenses and oxygen permeable rigid contact lens materials. Ortho-k contact lenses are overnight lenses which enable corneal topography correction for myopia (nearsightedness) patients. We have completed the purchase price allocation for this acquisition.

THE COOPER COMPANIES, INC. AND SUBSIDIARIES

Notes to Consolidated Condensed Financial Statements

(Unaudited)

Note 4. Inventories

| | | (In millions) | July 31, 2019 | | October 31, 2018 | April 30, 2020 | | October 31, 2019 |

| Raw materials | $ | 127.1 |

| | $ | 112.5 |

| $ | 141.1 |

| | $ | 131.4 |

|

| Work-in-process | 13.4 |

| | 12.6 |

| 13.0 | | 13.3 |

| Finished goods | 361.6 |

| | 343.7 |

| 414.1 | | 362.2 |

| | $ | 502.1 |

| | $ | 468.8 |

| |

| Total inventories | | $ | 568.2 |

| | $ | 506.9 |

|

Inventories are stated at the lower of cost and net realizable value. Cost is computed using standard cost that approximates actual cost, on a first-in, first-out basis.

THE COOPER COMPANIES, INC. AND SUBSIDIARIES

Notes to Consolidated Condensed Financial Statements

(Unaudited)

Note 5. Intangible Assets

Goodwill

|

| | | | | | | | | | | |

| (In millions) | CooperVision | | CooperSurgical | | Total |

| Balance at October 31, 2017 | $ | 1,735.7 |

| | $ | 619.1 |

| | $ | 2,354.8 |

|

| Net additions during the year ended October 31, 2018 | 36.8 |

| | 34.4 |

| | 71.2 |

|

| Translation | (29.6 | ) | | (4.3 | ) | | (33.9 | ) |

| Balance at October 31, 2018 | 1,742.9 |

| | 649.2 |

| | 2,392.1 |

|

| Net additions during the nine months ended July 31, 2019 | 13.8 |

| | 22.0 |

| | 35.8 |

|

| Translation | (33.0 | ) | | (3.5 | ) | | (36.5 | ) |

| Balance at July 31, 2019 | $ | 1,723.7 |

| | $ | 667.7 |

| | $ | 2,391.4 |

|

|

| | | | | | | | | | | |

| (In millions) | CooperVision | | CooperSurgical | | Total |

| Balance at October 31, 2019 | 1,765.4 |

| | 663.5 |

| | 2,428.9 |

|

| Current period additions | — |

| | 1.9 |

| | 1.9 |

|

| Foreign currency translation adjustment | (27.2 | ) | | (3.6 | ) | | (30.8 | ) |

| Balance at April 30, 2020 | $ | 1,738.2 |

| | $ | 661.8 |

| | $ | 2,400.0 |

|

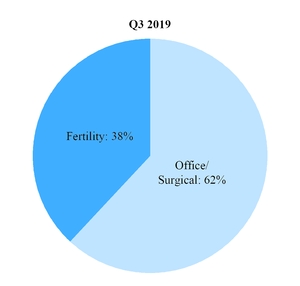

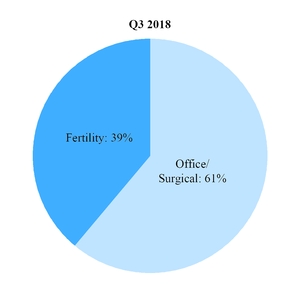

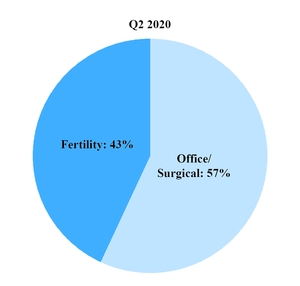

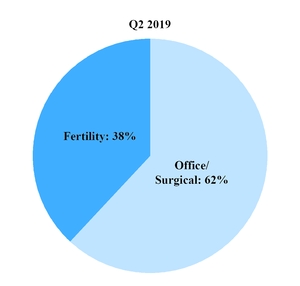

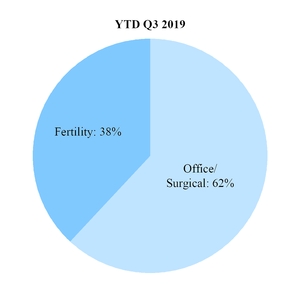

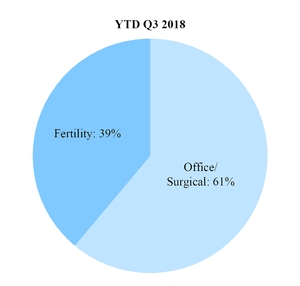

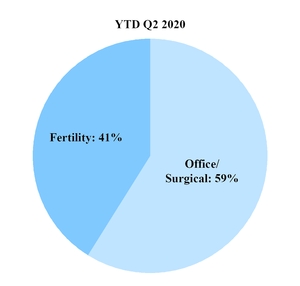

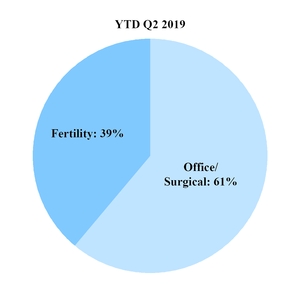

Effective April 30, 2019, there was a change in the reporting units as a result of realignment in the internal reporting structure of the business around markets and customers at CooperSurgical. As such, Cooper Surgical has evolved into 2 reporting units, namely, Office/Surgical and Fertility, which reflects management oversight of operations. The change in reporting units did not result in a change in operating segments. We allocated CooperSurgical's goodwill based on relative fair values utilizing the discounted cash flow method and guideline public company method as our allocation base, and the allocated fair values exceeded the carrying values for each of the 3 reporting units as of April 30, 2019.

We evaluateCompany evaluates goodwill for impairment annually during the fiscal third quarter and when an event occurs or circumstances change such that it is reasonably possible that impairment may exist. We accountThe Company accounts for goodwill, evaluates and evaluate ourtests goodwill balances and test them for impairment in accordance with related accounting standards. WeThe Company performed ouran annual impairment assessment in our third quarter of fiscal 2019, and 2018, and ourits analysis indicated that we hadthere was 0 impairment of goodwill in our reporting units.

Other Intangible Assets

|

| | | | | | | | | | | | | | | | | |

| | April 30, 2020 | | October 31, 2019 | | |

| (In millions) | Gross Carrying Amount | | Accumulated Amortization | | Gross Carrying Amount | | Accumulated Amortization | | Weighted Average Amortization Period (in years) |

| Intangible assets with definite lives: | | | | | | | | | |

| Trademarks | $ | 147.7 |

| | $ | 32.3 |

| | $ | 148.5 |

| | $ | 27.3 |

| | 14 |

| Composite intangible asset | 1,061.9 |

| | 177.0 |

| | 1,061.9 |

| | 141.6 |

| | 15 |

| Technology | 399.3 |

| | 236.2 |

| | 399.9 |

| | 221.2 |

| | 11 |

| Customer relationships | 357.7 |

| | 203.5 |

| | 357.6 |

| | 194.0 |

| | 13 |

| License and distribution rights and other | 27.9 |

| | 16.7 |

| | 27.9 |

| | 15.3 |

| | 11 |

| | 1,994.5 |

| | $ | 665.7 |

| | 1,995.8 |

| | $ | 599.4 |

| | 14 |

| Less: accumulated amortization and translation | 665.7 |

| | | | 599.4 |

| | | | |

| Intangible assets with definite lives, net | 1,328.8 |

| | | | 1,396.4 |

| | | | |

| | | | | | | | | | |

Intangible assets with indefinite lives, net (1) | 8.9 |

| | | | 8.9 |

| | | | |

| | | | | | | | | | |

| Total other intangibles, net | $ | 1,337.7 |

| | | | $ | 1,405.3 |

| | | | |

(1) Intangible assets with indefinite lives include technology and trademarks.

Balances include foreign currency translation adjustments.

We performed a qualitative assessment to test each reporting unit's goodwill for impairment. Qualitative factors considered in this assessment include industry and market considerations, overall financial performance and other relevant events and factors affecting each reporting unit. Based on our qualitative assessment, if we determine that the fair value of a reporting unit is more likely than not to be less than its carrying amount, the fair value of a reporting unit will be compared with its carrying amount and an impairment charge will be recognized for the amount that the carrying value exceeds the fair value of the reporting unit. A reporting unit is the level of reporting at which goodwill is tested for impairment. Our reporting units are CooperVision, Office/Surgical and Fertility reflecting the current way we manage our business. Goodwill impairment analysis and measurement is a process that requires significant judgment. If our common stock price trades below book value per share, there are changes in market conditions or a future downturn in our business, or a future goodwill impairment test indicates an impairment of our goodwill, we may have to recognize a non-cash impairment of goodwill that could be material and could adversely affect our results of operations in the period recognized and also adversely affect our total assets and stockholders' equity.

THE COOPER COMPANIES, INC. AND SUBSIDIARIES

Notes to Consolidated Condensed Financial Statements

(Unaudited)

Other Intangible Assets

|

| | | | | | | | | | | | | | | | | |

| | July 31, 2019 | | October 31, 2018 | | |

| (In millions) | Gross Carrying Amount | | Accumulated Amortization | | Gross Carrying Amount | | Accumulated Amortization | | Weighted Average Amortization Period (In years) |

| Intangible assets with definite lives: | | | | | | | | | |

| Trademarks | $ | 148.3 |

| | $ | 24.6 |

| | $ | 138.1 |

| | $ | 16.9 |

| | 14 |

| Composite intangible asset | 1,061.9 |

| | 123.9 |

| | 1,061.9 |

| | 70.8 |

| | 15 |

| Technology | 398.8 |

| | 213.0 |

| | 387.2 |

| | 190.7 |

| | 11 |

| Customer relationships | 356.1 |

| | 187.0 |

| | 350.0 |

| | 168.6 |

| | 13 |

License and distribution rights and other (1) | 27.8 |

| | 14.7 |

| | 74.9 |

| | 52.7 |

| | 11 |

| | 1,992.9 |

| | $ | 563.2 |

| | 2,012.1 |

| | $ | 499.7 |

| | 14 |

| Less: accumulated amortization and translation | 563.2 |

| | | | 499.7 |

| | | | |

| Intangible assets with definite lives, net | 1,429.7 |

| | | | 1,512.4 |

| | | | |

| | | | | | | | | | |

Intangible assets with indefinite lives, net (2) | 8.9 |

| | | | 8.9 |

| | | | |