UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

x QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the quarterly period ended SeptemberJune 30, 20172019

Commission File No. 001-11241

CATERPILLAR FINANCIAL SERVICES CORPORATION

(Exact name of Registrant as specified in its charter)

|

| | |

| Delaware | 37-1105865 |

| (State of incorporation) | (IRS Employer I.D. No.) |

| | |

2120 West End Ave. , Nashville, Tennessee | 37203-0001 |

| (Address of principal executive offices) | (Zip Code) |

Registrant's telephone number, including area code:(615) 341-1000

|

| | | | |

| Securities registered pursuant to Section 12(b) of the Act: |

| Title of each class | Trading Symbol(s) | | Name of each exchange on which registered |

| Medium-Term Notes, Series H, 3.300% Notes Due 2024 | CAT/24 | | New York Stock Exchange

|

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes [ü ] No [ ]

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes [ü ] No [ ]

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of "large accelerated filer," "accelerated filer," "smaller reporting company," and "emerging growth company" in Rule 12b-2 of the Exchange Act.

|

| | | | |

| Large accelerated filer | [ ] | | Accelerated filer | [ ] |

| Non-accelerated filer | [ü ] | (Do not check if a smaller reporting company) | |

| | | Smaller reporting company | [ ] |

| | | | Emerging growth company | [ ] |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. [ ]

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

Yes [ ] No [ü ]

As of NovemberAugust 1, 2017,2019, one share of common stock of the registrant was outstanding, which is owned by Caterpillar Inc.

The registrant is a wholly owned subsidiary of Caterpillar Inc. and meets the conditions set forth in General Instruction (H)(1)(a) and (b) of Form 10-Q, and is therefore filing this form with the reduced disclosure format.

PART I. FINANCIAL INFORMATION

ITEM 1. CONSOLIDATED FINANCIAL STATEMENTS (Unaudited)

In addition to the accompanying unaudited consolidated financial statements for Caterpillar Financial Services Corporation (together with its subsidiaries, "Cat Financial," "the Company," "we," "us" or "our"), we suggest that you read our 20162018 Annual Report on Form 10-K filed with the Securities and Exchange Commission (SEC) on February 15, 2017.14, 2019. The Company files electronically with the SEC required reports on Form 8-K, Form 10-Q, Form 10-K and10-K; registration statements on Form S-3S-3; and other forms or reports as required. The public may read and copy any materials the Company has filed with the SEC at the SEC’s Public Reference Room at 100 F Street, N.E., Washington, D.C. 20549. The public may obtain information on the operation of the Public Reference Room by calling the SEC at 1-800-SEC-0330. The SEC maintains a website (www.sec.gov) that contains reports, proxy and information statements, and other information regarding issuers that file electronically with the SEC. Copies of our annual report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and any amendments to these reports filed or furnished with the SEC are available free of charge through Caterpillar Inc.'sCaterpillar’s website (www.caterpillar.com/secfilings) as soon as reasonably practicable after filing with the SEC. Copies may also be obtained free of charge by writing to: Legal Dept., Caterpillar Financial Services Corporation, 2120 West End Ave., Nashville, Tennessee 37203-0001. In addition, the public may obtain more detailed information about our parent company, Caterpillar, Inc. (together with its subsidiaries, "Caterpillar" or "Cat") by visiting its website (www.caterpillar.com). None of the information contained at any time on our website Caterpillar’s website or the SEC’sCaterpillar’s website is incorporated by reference into this document.

Caterpillar Financial Services Corporation

CONSOLIDATED STATEMENTS OF PROFIT

(Unaudited)

(Dollars in Millions)

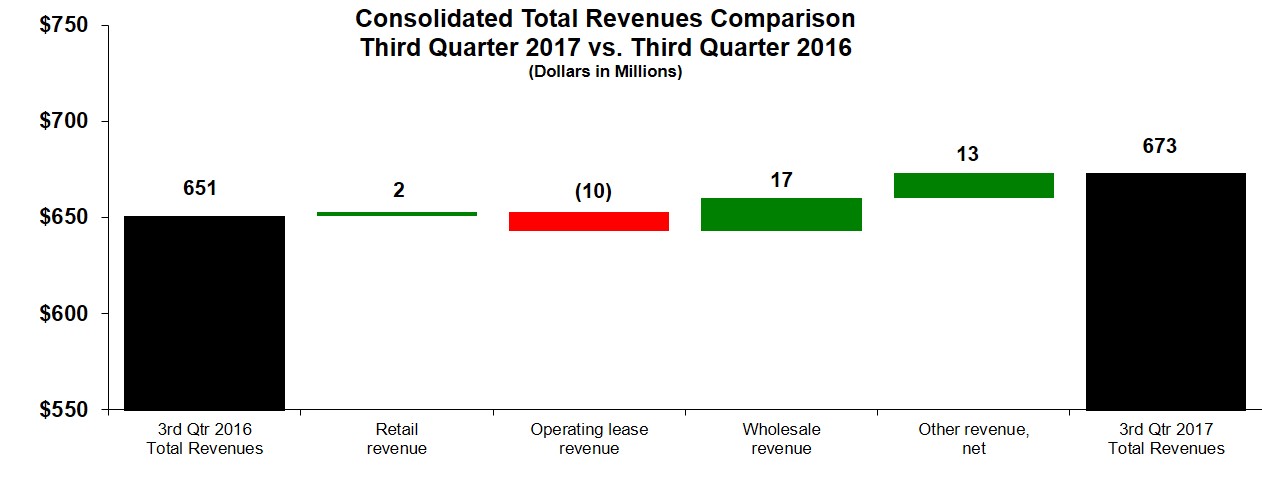

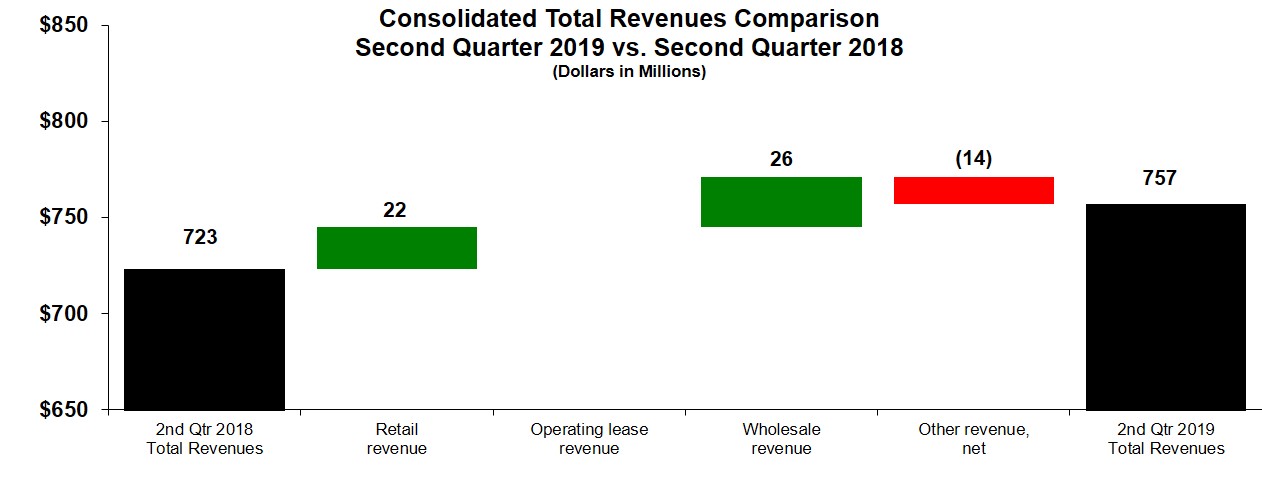

| | | | Three Months Ended

September 30, | | Nine Months Ended

September 30, | Three Months Ended

June 30, | | Six Months Ended

June 30, |

| | 2017 |

| 2016 | | 2017 | | 2016 | 2019 |

| 2018 | | 2019 | | 2018 |

| | | | | | | | | | | | | | | |

| Revenues: | | | | | | | | | | | | | | |

| Retail finance | $ | 309 |

| | $ | 307 |

| | $ | 924 |

| | $ | 914 |

| $ | 350 |

| | $ | 328 |

| | $ | 685 |

| | $ | 645 |

|

| Operating lease | 247 |

| | 257 |

| | 737 |

| | 756 |

| 257 |

| | 257 |

| | 515 |

| | 501 |

|

| Wholesale finance | 79 |

| | 62 |

| | 222 |

| | 202 |

| 131 |

| | 105 |

| | 250 |

| | 196 |

|

| Other, net | 38 |

| | 25 |

| | 128 |

| | 81 |

| 19 |

| | 33 |

| | 43 |

| | 71 |

|

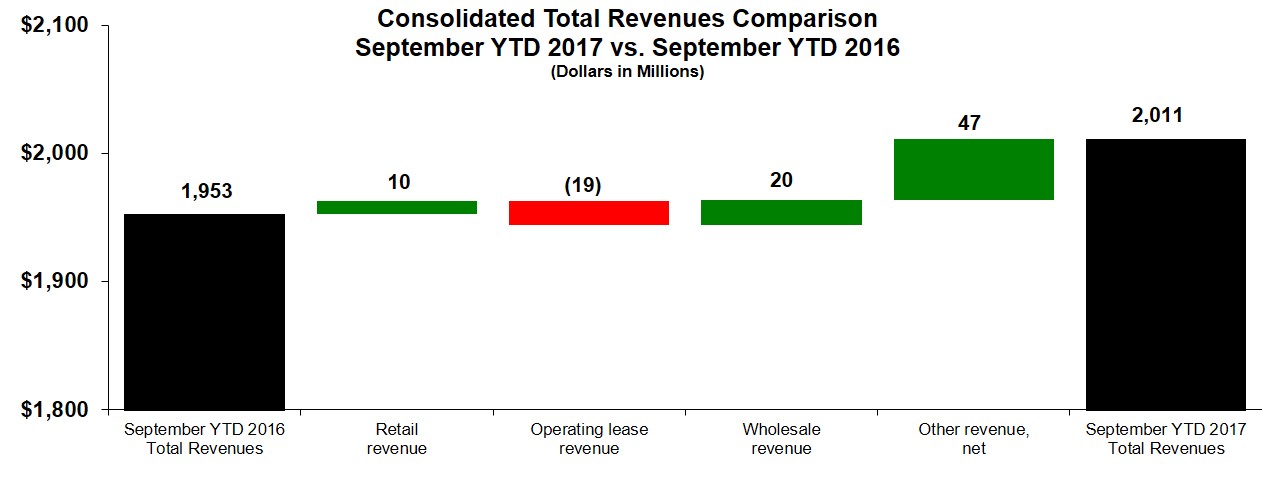

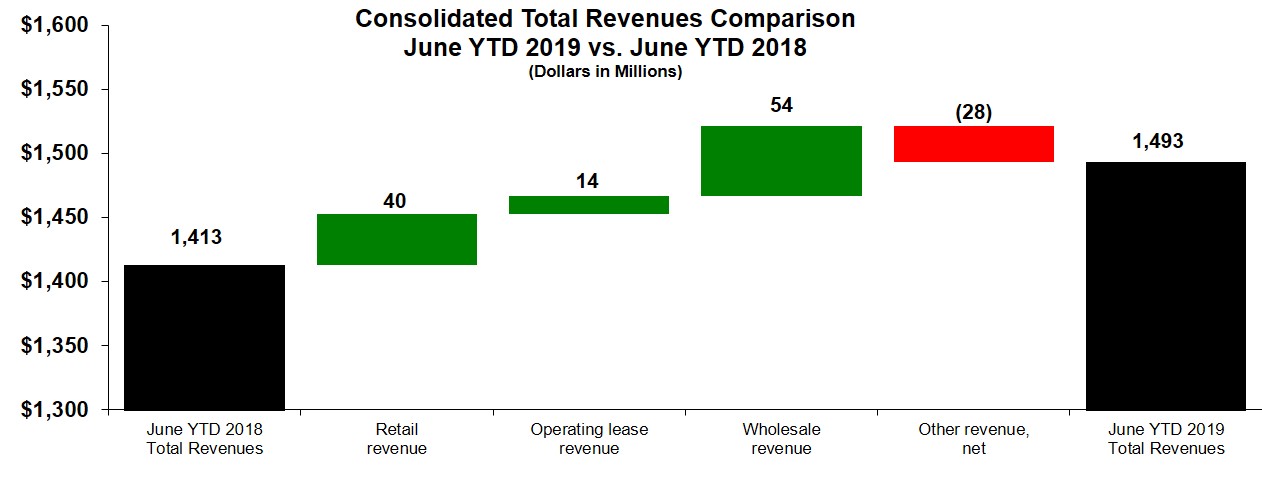

| Total revenues | 673 |

| | 651 |

| | 2,011 |

| | 1,953 |

| 757 |

| | 723 |

| | 1,493 |

| | 1,413 |

|

| | | | | | | | | | | | | | | |

| Expenses: | |

| | |

| | |

| | |

| |

| | |

| | |

| | |

|

| Interest | 169 |

| | 151 |

| | 499 |

| | 458 |

| 200 |

| | 190 |

| | 401 |

| | 364 |

|

| Depreciation on equipment leased to others | 201 |

| | 213 |

| | 608 |

| | 627 |

| 204 |

| | 209 |

| | 406 |

| | 408 |

|

| General, operating and administrative | 113 |

| | 97 |

| | 319 |

| | 292 |

| 126 |

| | 107 |

| | 250 |

| | 217 |

|

| Provision for credit losses | 48 |

| | 29 |

| | 82 |

| | 96 |

| 71 |

| | 104 |

| | 124 |

| | 171 |

|

| Other | 12 |

| | 12 |

| | 36 |

| | 31 |

| 9 |

| | 8 |

| | 19 |

| | 17 |

|

| Total expenses | 543 |

| | 502 |

| | 1,544 |

| | 1,504 |

| 610 |

| | 618 |

| | 1,200 |

| | 1,177 |

|

| | | | | | | | | | | | | | | |

| Other income (expense) | (4 | ) | | (3 | ) | | (10 | ) | | (10 | ) | (6 | ) | | (5 | ) | | (10 | ) | | (12 | ) |

| | | | | | | | | | | | | | | |

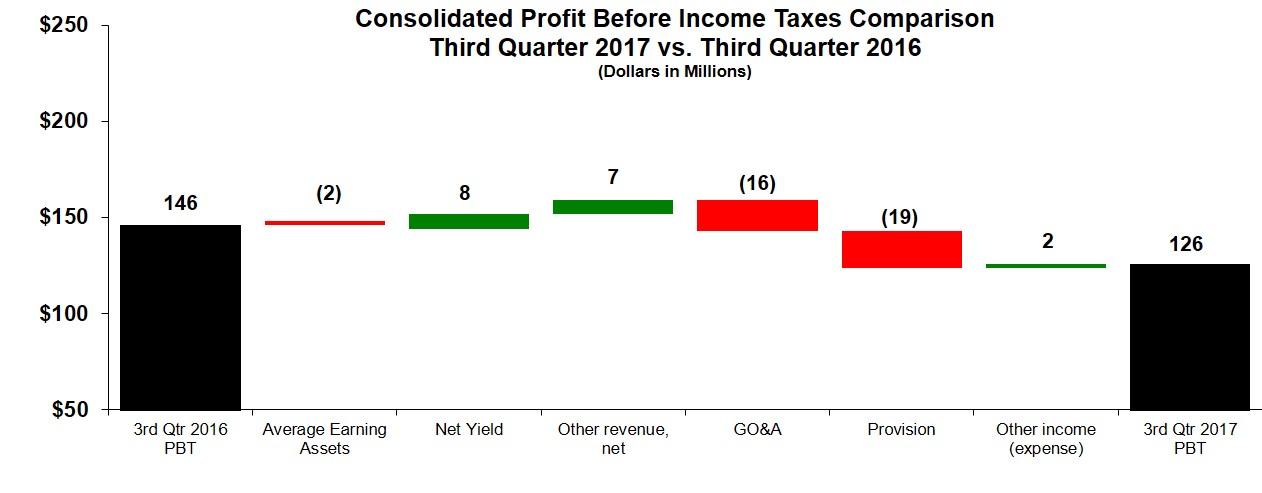

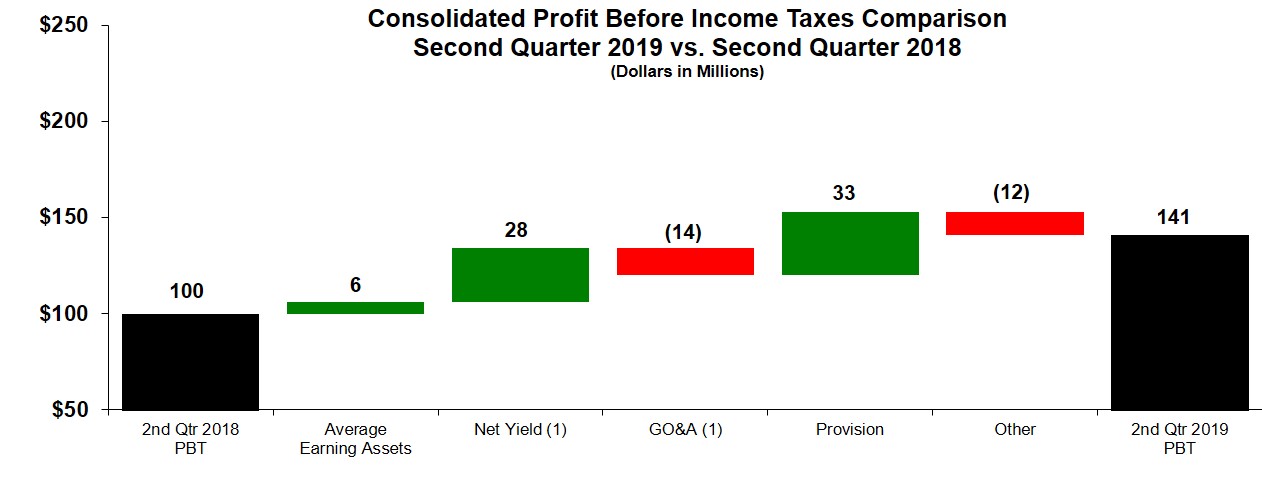

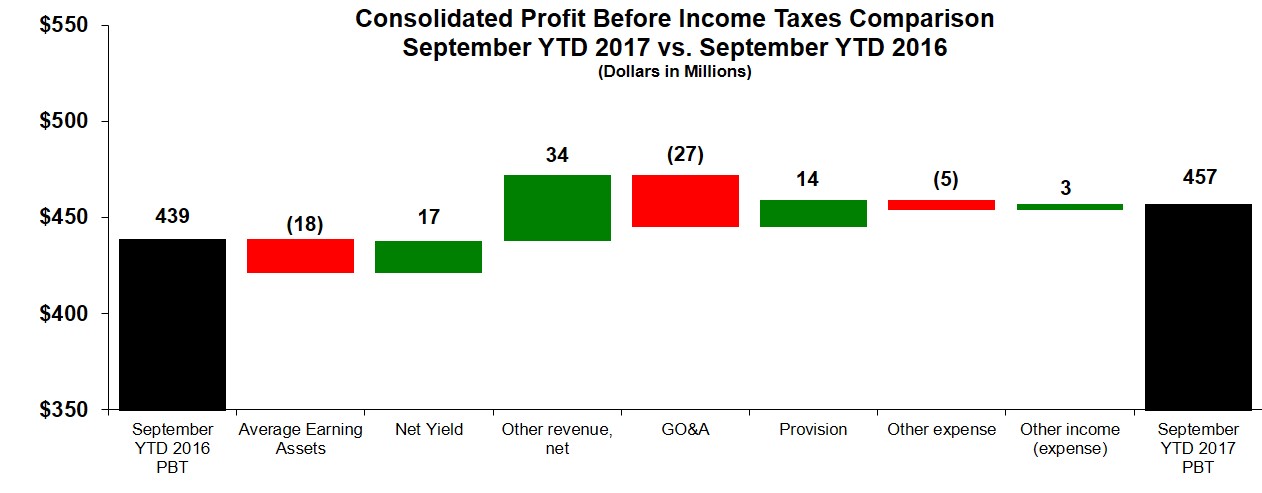

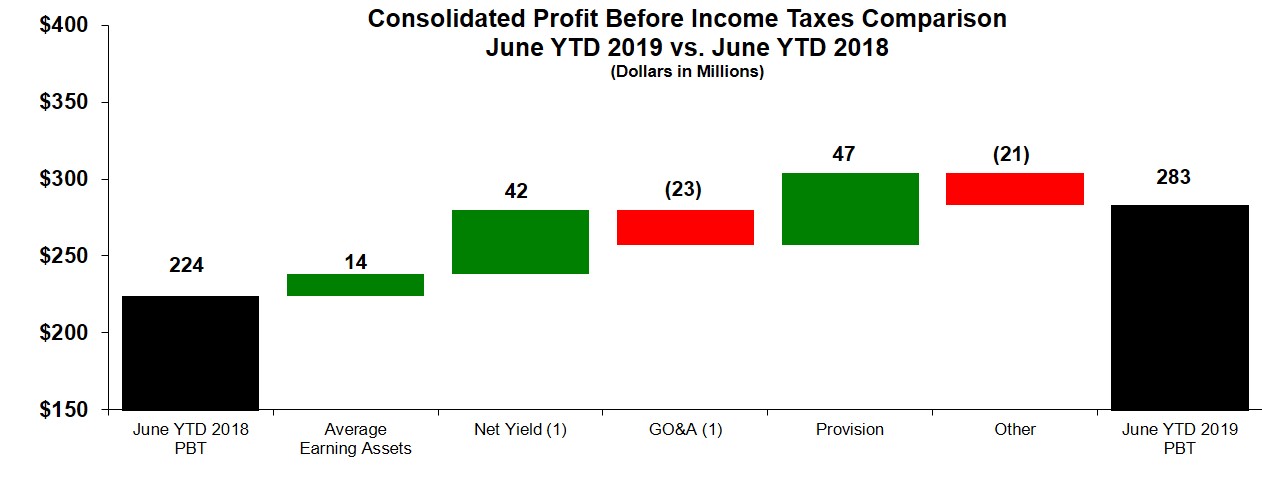

| Profit before income taxes | 126 |

| | 146 |

| | 457 |

| | 439 |

| 141 |

| | 100 |

| | 283 |

| | 224 |

|

| | | | | | | | | | | | | | | |

| Provision for income taxes | 38 |

| | 48 |

| | 137 |

| | 136 |

| 57 |

| | 24 |

| | 95 |

| | 53 |

|

| | | | | | | | | | | | | | | |

| Profit of consolidated companies | 88 |

| | 98 |

| | 320 |

| | 303 |

| 84 |

| | 76 |

| | 188 |

| | 171 |

|

| | | | | | | | | | | | | | | |

| Less: Profit attributable to noncontrolling interests | 2 |

| | 1 |

| | 5 |

| | 4 |

| 5 |

| | 5 |

| | 11 |

| | 9 |

|

| | | | | | | | | | | | | | | |

Profit 1 | $ | 86 |

| | $ | 97 |

| | $ | 315 |

| | $ | 299 |

| |

Profit(1) | | $ | 79 |

| | $ | 71 |

| | $ | 177 |

| | $ | 162 |

|

| | | | | | | | | | | | | | | |

1(1) Profit attributable to Caterpillar Financial Services Corporation.

See Notes to Consolidated Financial Statements (unaudited).

Caterpillar Financial Services Corporation

CONSOLIDATED STATEMENTS OF COMPREHENSIVE INCOME

(Unaudited)

(Dollars in Millions)

| | | | Three Months Ended

September 30, | | Nine Months Ended

September 30, | Three Months Ended

June 30, | | Six Months Ended

June 30, |

| | 2017 |

| 2016 | | 2017 | | 2016 | 2019 |

| 2018 | | 2019 | | 2018 |

| | | | | | | | | | | | | | | |

| Profit of consolidated companies | $ | 88 |

| | $ | 98 |

| | $ | 320 |

| | $ | 303 |

| $ | 84 |

| | $ | 76 |

| | $ | 188 |

| | $ | 171 |

|

| | | | | | | | | | | | | | | |

| Other comprehensive income (loss), net of tax: | | | | | | | | | | | | | | |

Foreign currency translation, net of tax (expense)/benefit of:

2017 $30 three months, $94 nine months;

2016 $4 three months, $21 nine months | 154 |

| | (5 | ) | | 395 |

| | 100 |

| |

Foreign currency translation, net of tax (expense)/benefit of:

2019 $7 three months, $3 six months; 2018 $(31) three months, $(15) six months | | 18 |

| | (262 | ) | | 33 |

| | (191 | ) |

| Derivative financial instruments: | | | | | | | | | | | | | | |

Gains (losses) deferred, net of tax (expense)/benefit of: 2017 $8 three months, $22 nine months; 2016 $5 three months, $8 nine months | (14 | ) | | (10 | ) | | (41 | ) | | (15 | ) | |

(Gains) losses reclassified to earnings, net of tax expense/(benefit) of:

2017 $(7) three months, $(23) nine months;

2016 $(3) three months, $(6) nine months | 11 |

| | 7 |

| | 41 |

| | 13 |

| |

| Available-for-sale securities: | | | | | | | | |

Gains (losses) deferred, net of tax (expense)/benefit of:

2017 $0 three months, $0 nine months;

2016 $(1) three months, $(1) nine months | (1 | ) | | 1 |

| | — |

| | (1 | ) | |

(Gains) losses reclassified to earnings, net of tax expense/(benefit) of:

2017 $0 three months, $0 nine months;

2016 $0 three months, $0 nine months | — |

| | — |

| | — |

| | — |

| |

Gains (losses) deferred, net of tax (expense)/benefit of:

2019 $5 three months, $6 six months; 2018 $(29) three months, $(22) six months | | (19 | ) | | 99 |

| | (22 | ) | | 73 |

|

(Gains) losses reclassified to earnings, net of tax expense/(benefit) of:

2019 $- three months, $3 six months; 2018 $28 three months, $23 six months | | (3 | ) | | (96 | ) | | (14 | ) | | (76 | ) |

| Total Other comprehensive income (loss), net of tax | 150 |

| | (7 | ) | | 395 |

| | 97 |

| (4 | ) | | (259 | ) | | (3 | ) | | (194 | ) |

| |

|

| | | | | | |

|

| | | | | | |

| Comprehensive income (loss) | 238 |

| | 91 |

| | 715 |

| | 400 |

| 80 |

| | (183 | ) | | 185 |

| | (23 | ) |

| | | | | | | | | | | | | | | |

Less: Comprehensive income (loss) attributable to the noncontrolling interests | 5 |

| | 1 |

| | 11 |

| | 2 |

| 3 |

| | (3 | ) | | 11 |

| | 7 |

|

| | | | | | | | | | | | | | | |

Comprehensive income (loss) attributable to Caterpillar Financial Services Corporation | $ | 233 |

| | $ | 90 |

| | $ | 704 |

| | $ | 398 |

| $ | 77 |

| | $ | (180 | ) | | $ | 174 |

| | $ | (30 | ) |

| | | | | | | | | | | | | | | |

See Notes to Consolidated Financial Statements (unaudited).

Caterpillar Financial Services Corporation

CONSOLIDATED STATEMENTS OF FINANCIAL POSITION

(Unaudited)

(Dollars in Millions, except share data)

| | | | September 30,

2017 | | December 31,

2016 | June 30,

2019 | | December 31,

2018 |

| Assets: | | | | | | |

| Cash and cash equivalents | $ | 710 |

| | $ | 1,795 |

| $ | 760 |

| | $ | 766 |

|

| Finance receivables, net | 26,597 |

| | 26,212 |

| 28,297 |

| | 27,923 |

|

| Notes receivable from Caterpillar | 1,577 |

| | 530 |

| 640 |

| | 662 |

|

| Equipment on operating leases, | |

| | |

| |

| less accumulated depreciation | 3,580 |

| | 3,708 |

| |

| Deferred and refundable income taxes | 156 |

| | 119 |

| |

| Equipment on operating leases, net | | 3,575 |

| | 3,562 |

|

| Other assets | 1,063 |

| | 1,251 |

| 1,293 |

| | 1,268 |

|

| Total assets | $ | 33,683 |

| | $ | 33,615 |

| $ | 34,565 |

| | $ | 34,181 |

|

| | | | | | | |

| Liabilities and shareholder’s equity: | |

| | |

| |

| | |

|

| Payable to dealers and others | $ | 142 |

| | $ | 140 |

| $ | 411 |

| | $ | 117 |

|

| Payable to Caterpillar - other | 60 |

| | 49 |

| |

| Payable to Caterpillar - borrowings and other | | 1,389 |

| | 1,601 |

|

| Accrued expenses | 241 |

| | 172 |

| 289 |

| | 259 |

|

| Income taxes payable | 95 |

| | 32 |

| |

| Payable to Caterpillar - borrowings | 1,493 |

| | 1,637 |

| |

| Short-term borrowings | 5,459 |

| | 7,094 |

| 5,266 |

| | 5,723 |

|

| Current maturities of long-term debt | 5,614 |

| | 6,155 |

| 6,235 |

| | 5,820 |

|

| Long-term debt | 16,015 |

| | 14,382 |

| 17,107 |

| | 16,995 |

|

| Deferred income taxes and other liabilities | 864 |

| | 969 |

| |

| Other liabilities | | 834 |

| | 817 |

|

| Total liabilities | 29,983 |

| | 30,630 |

| 31,531 |

| | 31,332 |

|

| | | | | | | |

| Commitments and contingent liabilities (Notes 7 and 9) |

|

| |

|

| |

| Commitments and contingent liabilities (Notes 8 and 10) | |

|

| |

|

|

| | | | | | | |

| Common stock - $1 par value | | | |

| | | |

|

| Authorized: 2,000 shares; Issued and | |

| | |

| |

| | |

|

| outstanding: one share (at paid-in amount) | 745 |

| | 745 |

| 745 |

| | 745 |

|

| Additional paid-in capital | 2 |

| | 2 |

| 2 |

| | 2 |

|

| Retained earnings | 3,423 |

| | 3,108 |

| 2,954 |

| | 2,874 |

|

| Accumulated other comprehensive income/(loss) | (606 | ) | | (995 | ) | (831 | ) | | (925 | ) |

| Noncontrolling interests | 136 |

| | 125 |

| 164 |

| | 153 |

|

| Total shareholder’s equity | 3,700 |

| | 2,985 |

| 3,034 |

| | 2,849 |

|

| | | | | | | |

| Total liabilities and shareholder’s equity | $ | 33,683 |

| | $ | 33,615 |

| $ | 34,565 |

| | $ | 34,181 |

|

| | | | | | | |

See Notes to Consolidated Financial Statements (unaudited).

Caterpillar Financial Services Corporation

CONSOLIDATED STATEMENTS OF CHANGES IN SHAREHOLDER'S EQUITY

(Unaudited)

(Dollars in Millions)

|

| | | | | | | | | | | | | | | | | | | | | | | |

Nine Months Ended

September 30, 2016 | Common stock | | Additional paid-in capital | | Retained earnings | | Accumulated other comprehensive income/(loss) | | Noncontrolling interests | | Total |

| Balance at December 31, 2015 | $ | 745 |

| | $ | 2 |

| | $ | 2,999 |

| | $ | (897 | ) | | $ | 126 |

| | $ | 2,975 |

|

| Profit of consolidated companies | |

| | |

| | 299 |

| | |

| | 4 |

| | 303 |

|

| Foreign currency translation, net of tax | |

| | |

| | |

| | 102 |

| | (2 | ) | | 100 |

|

| Derivative financial instruments, net of tax | |

| | |

| | |

| | (2 | ) | | |

| | (2 | ) |

| Available-for-sale securities, net of tax | | | | | | | (1 | ) | | | | (1 | ) |

| Balance at September 30, 2016 | $ | 745 |

| | $ | 2 |

| | $ | 3,298 |

| | $ | (798 | ) | | $ | 128 |

| | $ | 3,375 |

|

| | | | | | | | | | | | |

Nine Months Ended

September 30, 2017 | |

| | |

| | |

| | |

| | |

| | |

|

| Balance at December 31, 2016 | $ | 745 |

| | $ | 2 |

| | $ | 3,108 |

| | $ | (995 | ) | | $ | 125 |

| | $ | 2,985 |

|

| Profit of consolidated companies | |

| | |

| | 315 |

| | |

| | 5 |

| | 320 |

|

| Foreign currency translation, net of tax | |

| | |

| | |

| | 389 |

| | 6 |

| | 395 |

|

| Derivative financial instruments, net of tax | |

| | |

| | |

| | — |

| | |

| | — |

|

| Available-for-sale securities, net of tax | | | | | | | — |

| | | | — |

|

| Balance at September 30, 2017 | $ | 745 |

| | $ | 2 |

| | $ | 3,423 |

| | $ | (606 | ) | | $ | 136 |

| | $ | 3,700 |

|

| | | | | | | | | | | | |

|

| | | | | | | | | | | | | | | | | | | | | | | |

| Three Months Ended June 30, 2018 | Common stock | | Additional paid-in capital | | Retained earnings | | Accumulated other comprehensive income/(loss) | | Noncontrolling interests | | Total |

| Balance at March 31, 2018 | $ | 745 |

| | $ | 2 |

| | $ | 3,060 |

| | $ | (533 | ) | | $ | 150 |

| | $ | 3,424 |

|

| Profit of consolidated companies | | | | | 71 |

| | | | 5 |

| | 76 |

|

| Foreign currency translation, net of tax | | | | | | | (254 | ) | | (8 | ) | | (262 | ) |

| Derivative financial instruments, net of tax | | | | | | | 3 |

| | | | 3 |

|

| Balance at June 30, 2018 | $ | 745 |

| | $ | 2 |

| | $ | 3,131 |

| | $ | (784 | ) | | $ | 147 |

| | $ | 3,241 |

|

| | | | | | | | | | | | |

| Three Months Ended June 30, 2019 | | | | | | | | | | | |

| Balance at March 31, 2019 | $ | 745 |

| | $ | 2 |

| | $ | 2,875 |

| | $ | (829 | ) | | $ | 161 |

| | $ | 2,954 |

|

| Profit of consolidated companies | | | | | 79 |

| | | | 5 |

| | 84 |

|

| Foreign currency translation, net of tax | | | | | | | 20 |

| | (2 | ) | | 18 |

|

| Derivative financial instruments, net of tax | | | | | | | (22 | ) | | | | (22 | ) |

| Balance at June 30, 2019 | $ | 745 |

| | $ | 2 |

| | $ | 2,954 |

| | $ | (831 | ) | | $ | 164 |

| | $ | 3,034 |

|

| | | | | | | | | | | | |

| Six Months Ended June 30, 2018 | | | | | | | | | | | |

| Balance at December 31, 2017 | $ | 745 |

| | $ | 2 |

| | $ | 2,969 |

| | $ | (592 | ) | | $ | 140 |

| | $ | 3,264 |

|

| Profit of consolidated companies | |

| | |

| | 162 |

| | |

| | 9 |

| | 171 |

|

| Foreign currency translation, net of tax | |

| | |

| | |

| | (189 | ) | | (2 | ) | | (191 | ) |

| Derivative financial instruments, net of tax | |

| | |

| | |

| | (3 | ) | | |

| | (3 | ) |

| Balance at June 30, 2018 | $ | 745 |

| | $ | 2 |

| | $ | 3,131 |

| | $ | (784 | ) | | $ | 147 |

| | $ | 3,241 |

|

| | | | | | | | | | | | |

| Six Months Ended June 30, 2019 | |

| | |

| | |

| | |

| | |

| | |

|

| Balance at December 31, 2018 | $ | 745 |

| | $ | 2 |

| | $ | 2,874 |

| | $ | (925 | ) | | $ | 153 |

| | $ | 2,849 |

|

| Profit of consolidated companies | |

| | |

| | 177 |

| | |

| | 11 |

| | 188 |

|

| Foreign currency translation, net of tax | |

| | |

| | |

| | 33 |

| | — |

| | 33 |

|

| Derivative financial instruments, net of tax | |

| | |

| | |

| | (36 | ) | | |

| | (36 | ) |

Adjustment to adopt new accounting guidance(1) | | | | | (97 | ) | | 97 |

| | | | — |

|

| Balance at June 30, 2019 | $ | 745 |

| | $ | 2 |

| | $ | 2,954 |

| | $ | (831 | ) | | $ | 164 |

| | $ | 3,034 |

|

| | | | | | | | | | | | |

(1) See Note 2 regarding new accounting guidance related to reclassification of certain tax effects from accumulated other comprehensive income/(loss).

See Notes to Consolidated Financial Statements (unaudited).

Caterpillar Financial Services Corporation

CONSOLIDATED STATEMENTS OF CASH FLOWS

(Unaudited)

(Dollars in Millions)

| | | | Nine Months Ended

September 30, | Six Months Ended

June 30, |

| | 2017 | | 2016 | 2019 | | 2018 |

| Cash flows from operating activities: | | | | | | |

| Profit of consolidated companies | $ | 320 |

| | $ | 303 |

| $ | 188 |

| | $ | 171 |

|

| Adjustments for non-cash items: | |

| | |

| |

| | |

|

| Depreciation and amortization | 616 |

| | 635 |

| 413 |

| | 414 |

|

| Amortization of receivables purchase discount | (180 | ) | | (158 | ) | (231 | ) | | (177 | ) |

| Provision for credit losses | 82 |

| | 96 |

| 124 |

| | 171 |

|

| Other, net | 12 |

| | 81 |

| 74 |

| | 67 |

|

| Changes in assets and liabilities: | |

| | |

| |

| | |

|

| Receivables from others | 69 |

| | 10 |

| |

| Other receivables/payables with Caterpillar | 1 |

| | (2 | ) | |

| Other assets | | 56 |

| | (1 | ) |

| Payable to dealers and others | (31 | ) | | 30 |

| 294 |

| | (42 | ) |

| Accrued interest payable | 3 |

| | (17 | ) | |

| Accrued expenses and other liabilities, net | (4 | ) | | 22 |

| |

| Income taxes payable | 38 |

| | 100 |

| |

| Settlements of designated derivatives | (7 | ) | | 36 |

| |

| Debt exchange premium | — |

| | (33 | ) | |

| Accrued expenses | | (38 | ) | | (13 | ) |

| Other payables with Caterpillar | | (4 | ) | | (29 | ) |

| Other liabilities | | 31 |

| | (52 | ) |

| Net cash provided by operating activities | 919 |

| | 1,103 |

| 907 |

| | 509 |

|

| | | | | | | |

| Cash flows from investing activities: | |

| | |

| |

| | |

|

| Capital expenditures for equipment on operating leases and other capital expenditures | (1,018 | ) | | (1,265 | ) | |

| Expenditures for equipment on operating leases | | (694 | ) | | (799 | ) |

| Capital expenditures - excluding equipment on operating leases | | (11 | ) | | (95 | ) |

| Proceeds from disposals of equipment | 753 |

| | 497 |

| 354 |

| | 454 |

|

| Additions to finance receivables | (9,765 | ) | | (8,888 | ) | (7,027 | ) | | (6,823 | ) |

| Collections of finance receivables | 10,192 |

| | 9,307 |

| 6,543 |

| | 6,142 |

|

| Net changes in Caterpillar purchased receivables | (161 | ) | | 580 |

| 15 |

| | (608 | ) |

| Proceeds from sales of receivables | 98 |

| | 55 |

| 119 |

| | 124 |

|

| Net change in variable lending to Caterpillar | (1,051 | ) | | (1,001 | ) | 69 |

| | (39 | ) |

| Additions to other notes receivable with Caterpillar | (53 | ) | | (91 | ) | (80 | ) | | (90 | ) |

| Collections on other notes receivable with Caterpillar | 56 |

| | 46 |

| 33 |

| | 42 |

|

| Proceeds from sale of securities | 4 |

| | — |

| |

| Restricted cash and cash equivalents activity, net | (2 | ) | | 7 |

| |

| Settlements of undesignated derivatives | 23 |

| | (23 | ) | (31 | ) | | (4 | ) |

| Net cash provided by (used for) investing activities | (924 | ) | | (776 | ) | (710 | ) | | (1,696 | ) |

| | | | | | | |

| Cash flows from financing activities: | |

| | |

| |

| | |

|

| Net change in variable lending from Caterpillar | (105 | ) | | 466 |

| (118 | ) | | (109 | ) |

| Proceeds from borrowings with Caterpillar | — |

| | 253 |

| |

| Payments on borrowings with Caterpillar | (49 | ) | | (3 | ) | (93 | ) | | — |

|

| Proceeds from debt issued (original maturities greater than three months) | 6,972 |

| | 4,424 |

| 5,340 |

| | 4,307 |

|

| Payments on debt issued (original maturities greater than three months) | (5,714 | ) | | (5,077 | ) | (4,897 | ) | | (4,433 | ) |

| Short-term borrowings, net (original maturities three months or less) | (2,207 | ) | | (365 | ) | (436 | ) | | 1,453 |

|

| Net cash provided by (used for) financing activities | (1,103 | ) | | (302 | ) | (204 | ) | | 1,218 |

|

| | | | | | | |

| Effect of exchange rate changes on cash and cash equivalents | 23 |

| | 10 |

| |

| Effect of exchange rate changes on cash, cash equivalents and restricted cash | | (2 | ) | | (9 | ) |

| | | | | | | |

| Increase/(decrease) in cash and cash equivalents | (1,085 | ) | | 35 |

| |

| Cash and cash equivalents at beginning of year | 1,795 |

| | 1,016 |

| |

| Cash and cash equivalents at end of period | $ | 710 |

| | $ | 1,051 |

| |

| Increase/(decrease) in cash, cash equivalents and restricted cash | | (9 | ) | | 22 |

|

Cash, cash equivalents and restricted cash at beginning of year(1) | | 773 |

| | 732 |

|

Cash, cash equivalents and restricted cash at end of period(1) | | $ | 764 |

| | $ | 754 |

|

| | | | | | | |

| Non-cash activity: In September 2016, $381 million of medium-term notes with varying interest rates and maturity dates were exchanged for $366 million of 1.93% medium-term notes due in 2021 and $15 million of cash. In addition, a debt exchange premium of $33 million was paid and is included in the operating section of the Consolidated Statements of Cash Flows. | |

(1) As of June 30, 2019 and December 31, 2018, restricted cash, which is included in Other assets in the Consolidated Statements of Financial Position, was $4 million and $7 million, respectively. Restricted cash primarily includes cash related to syndication activities.

See Notes to Consolidated Financial Statements (unaudited).

Notes to Consolidated Financial Statements

(Unaudited)

In the opinion of management, the accompanying unaudited consolidated financial statements include all adjustments, consisting only of normal recurring adjustments, necessary for a fair statement of (a) the consolidated profit for the three and ninesix months ended SeptemberJune 30, 20172019 and 2016,2018, (b) the consolidated comprehensive income for the three and ninesix months ended SeptemberJune 30, 20172019 and 2016,2018, (c) the consolidated financial position as of SeptemberJune 30, 20172019 and December 31, 2016,2018, (d) the consolidated changes in shareholder's equity for the ninethree and six months ended SeptemberJune 30, 20172019 and 20162018 and (e) the consolidated cash flows for the ninesix months ended SeptemberJune 30, 20172019 and 2016.2018. The preparation of financial statements, in conformity with generally accepted accounting principles in the United States of America (U.S. GAAP) and pursuant to the rules and regulations of the Securities and Exchange Commission (SEC), requires management to make estimates and assumptions that affect reported amounts. Significant estimates include residual values for leased assets, allowance for credit losses and income taxes. Actual results may differ from these estimates.

Interim results are not necessarily indicative of results for a full year. The information included in this Form 10-Q should be read in conjunction with the audited consolidated financial statements and notes thereto included in our annual report on Form 10-K for the year ended December 31, 2016 (20162018 (2018 Form 10-K) filed with the SEC on February 15, 2017.14, 2019. The December 31, 20162018 financial position data included herein was derived from the audited consolidated financial statements included in the 20162018 Form 10-K but does not include all disclosures required by U.S. GAAP. Certain amounts for prior periods have been reclassified to conform to thewith current period financial statement presentation.

We consolidate all variable-interestvariable interest entities (VIEs) where we are the primary beneficiary. For VIEs, we assess whether we are the primary beneficiary as prescribed by the accounting guidance on the consolidation of VIEs. The primary beneficiary of a VIE is the party that has both the power to direct the activities that most significantly impact the entity’s economic performance and the obligation to absorb losses or the right to receive benefits that could potentially be significant to the entity. Please refer to Note 78 for more information.

We have customers and dealers that are VIEs of which we are not the primary beneficiary. Although we have provided financial support to these entities and therefore have a variable interest, we do not have the power to direct the activities that most significantly impact their economic performance. Our maximum exposure to loss from our involvement with these VIEs is limited to the credit risk inherently present in the financial support that we have provided. These risks are evaluated and reflected in our financial statements as part of our overall portfolio of finance receivables and related allowance for credit losses.

| |

| 2. | New Accounting Pronouncements |

| |

| A. | Adoption of New Accounting Standards |

Revenue recognitionLease accounting (Accounting Standards Update (ASU) 2016-02) – In May 2014,February 2016, the Financial Accounting Standards Board (FASB) issued new revenue recognition guidance to provide a single, comprehensive revenue recognition model for all contracts with customers. Under the new guidance, an entity will recognize revenue to depict the transfer of promised goods or services to customers at an amount that the entity expects to be entitled to in exchange for those goods or services. A five step model has been introduced for an entity to apply when recognizing revenue. The new guidance also includes enhanced disclosure requirements and is effective January 1, 2018. Entities have the option to apply the new guidance under a retrospective approach to each prior reporting period presented, or a modified retrospective approach with the cumulative effect of initially applying the new guidance recognized at the date of initial application within the Consolidated Statement of Changes in Shareholder's Equity. We will adopt the new guidance effective January 1, 2018 under the modified retrospective approach. We have completed our evaluation of the impact of the new standard and do not expect the adoption to have a material impact on our financial statements.

Recognition and measurement of financial assets and financial liabilities – In January 2016, the FASB issued accounting guidance that affects the accounting for equity investments, financial liabilities accounted for under the fair value option and the presentation and disclosure requirements for financial instruments. Under the new guidance, all equity investments in unconsolidated entities (other than those accounted for using the equity method of accounting) will generally be measured at fair value through earnings. There will no longer be an available-for-sale classification for equity securities with readily determinable fair values. For financial liabilities when the fair value option has been elected, changes in fair value due to instrument-specific credit risk will be recognized separately in other comprehensive income. In addition, the FASB clarified guidance related to the valuation allowance assessment when recognizing deferred tax assets resulting from unrealized losses on available-for-sale debt securities. The new guidance is effective January 1, 2018, with the cumulative effect adjustment from initially applying the new guidance recognized in the Consolidated Statement of Financial Position as of the beginning of the year of adoption. We do not expect the adoption to have a material impact on our financial statements.

Lease accounting – In February 2016, the FASB issued accounting guidance that revises the accounting for leases. Under the new guidance, lessees are required to recognize a right-of-use asset and a lease liability for substantially all leases. The new guidance will continue to classify leases as either financing or operating, with classification affecting the pattern of expense recognition. The accounting applied by a lessor under the new guidance will be substantially equivalent to current lease accounting guidance. The new guidance iswas effective January 1, 2019 with early adoption permitted. The new standard is required to beand was applied withusing a modified retrospective approach through a cumulative effect adjustment to eachretained earnings as of January 1, 2019. The prior reporting period presentedcomparative information has not been recasted and continues to be reported under the accounting guidance in effect for those periods.

The new guidance provides for certaina number of optional practical expedients.expedients in transition. We are inelected the process"package of evaluating the effect ofpractical expedients," which allows us not to reassess under the new guidance our prior conclusions about lease identification, lease classification and initial direct costs. We did not elect the use-of-hindsight practical expedient. In addition, the new guidance provides practical expedients for an entity’s ongoing lessee accounting. We have elected not to separate lease and non-lease components for the majority of our asset classes. We have elected the short-term lease recognition exemption for all leases that qualify which means we will not recognize right-of-use assets or lease liabilities for these leases with a term of twelve months or less.

The most significant effects of adoption relate to the recognition of right-of-use assets and lease liabilities on our balance sheet for operating leases and providing new disclosures about our leasing activities. The adoption did not have a material impact on our results of operations.

In March 2019, the FASB issued Leases - Codification improvements (ASU 2019-01) which amended the new leasing guidance. Under these amendments, lessors that are not manufacturers or dealers will use their cost, less any discounts that may apply, as the fair value of the underlying asset, and lessors within the scope of Financial Services-Depository and Lending guidance will present all principal payments received under leases within investment activities on the statement of cash flows. We adopted the new guidance effective January 1, 2019, and the adoption did not have a material impact to our financial statements.

See Note 4 for additional information.

Reclassification of certain tax effects from accumulated other comprehensive income (ASU 2018-02) – In February 2018, the FASB issued accounting guidance to allow a reclassification from accumulated other comprehensive income (AOCI) to retained earnings for stranded tax effects resulting from U.S. tax reform legislation. We adopted the guidance effective January 1, 2019 and the resulting reclassification was included in the period of adoption. The reclassification resulted in decreased retained earnings and increased AOCI of $97 million.

The following ASUs were effective January 1, 2019 and did not have a material impact on our financial statements.statements:

|

| |

| ASU | Description |

| 2017-12 | Derivatives and hedging - Targeted improvements |

| |

| B. | Accounting Standards Issued But Not Yet Adopted |

Measurement of creditCredit losses on financial instruments(ASU 2016-13) – In June 2016, the FASB issued accounting guidance to introduce a new model for recognizing credit losses on financial instruments based on an estimate of current expected credit losses. The new guidance will apply to loans, accounts receivable, trade receivables, other financial assets measured at amortized cost, loan commitments and other off-balance sheet credit exposures. The new guidance will also apply to debt securities and other financial assets measured at fair value through other comprehensive income. The new guidance is effective January 1, 2020, with early adoption permitted beginning January 1, 2019. We are in the process of evaluatingAn implementation team continues to evaluate data requirements and methodologies and has started designing new processes and controls. The team is also modeling results to assess the effect of the new guidance on our financial statements. We plan to adopt the new guidance effective January 1, 2020.

Classification for certain cash receiptsWe consider the applicability and cash payments – In August 2016, the FASB issued accounting guidance relatedimpact of all ASUs. ASUs not listed above were assessed and either determined to the presentation and classification of certain transactions in the statement of cash flows where diversity in practice exists. The guidance is effective January 1, 2018 with early adoption permitted. We dobe not expect the adoptionapplicable or not expected to have a material impact on our financial statements.

Classification of restricted cash – In November 2016, the FASB issued accounting guidance related to the presentation and classification of changes in restricted cash on the statement of cash flows where diversity in practice exists. The new standard is required to be applied with a retrospective approach. The guidance is effective January 1, 2018 with early adoption permitted. We do not expect the adoption to have a material impact on our financial statements.

Derivatives and hedging – In August 2017, the FASB issued accounting guidance to better align hedge accounting with a company’s risk management activities, simplify the application of hedge accounting and improve the disclosures of hedging arrangements. The new guidance is required to be applied on a modified retrospective basis. The guidance is effective January 1, 2019, with early adoption permitted. We are in the process of evaluating the effect of the new guidance on our financial statements.

A summary of finance receivables included in the Consolidated Statements of Financial Position was as follows:

|

| | | | | | | | |

| (Millions of dollars) | | September 30,

2017 | | December 31,

2016 |

Finance leases and installment sale contracts – Retail (1) | | $ | 14,172 |

| | $ | 13,565 |

|

| Retail notes receivable | | 9,711 |

| | 10,195 |

|

| Wholesale notes receivable | | 3,753 |

| | 3,457 |

|

| Finance leases and installment sale contracts – Wholesale | | 118 |

| | 103 |

|

| | | 27,754 |

| | 27,320 |

|

| Less: Unearned income | | (814 | ) | | (765 | ) |

| Recorded investment in finance receivables | | 26,940 |

| | 26,555 |

|

| Less: Allowance for credit losses | | (343 | ) | | (343 | ) |

| Total finance receivables, net | | $ | 26,597 |

|

| $ | 26,212 |

|

| | | | | |

|

| | | | | | | | |

| (Millions of dollars) | | June 30,

2019 | | December 31,

2018 |

Retail loans, net(1) | | $ | 15,482 |

| | $ | 15,509 |

|

Retail leases, net(2) | | 7,683 |

| | 7,499 |

|

| Caterpillar purchased receivables, net | | 4,837 |

| | 4,691 |

|

Wholesale loans, net(1) | | 729 |

| | 626 |

|

| Wholesale leases, net | | 89 |

| | 109 |

|

| Recorded investment in finance receivables | | 28,820 |

| | 28,434 |

|

| Less: Allowance for credit losses | | (523 | ) | | (511 | ) |

Total finance receivables, net(3) | | $ | 28,297 |

|

| $ | 27,923 |

|

| | | | | |

(1)Includes $0failed sale leasebacks.

(2) Includes $9 million of finance leases with Caterpillar as of June 30, 2019 and $4December 31, 2018.

(3)Includes $65 million and $0 million of finance receivables classified as held for sale as of SeptemberJune 30, 20172019 and December 31, 2016,2018, respectively.

Allowance for Credit Losses

The allowance for credit losses is an estimate of the losses inherent in our finance receivable portfolio and includes consideration of accounts that have been individually identified as impaired, as well as pools of finance receivables where it is probable that certain receivables in the pool are impaired but the individual accounts cannot yet be identified. In identifying and measuring impairment, management takes into consideration past loss experience, known and inherent risks in the portfolio, adverse situations that may affect the borrower’s ability to repay, estimated value of underlying collateral and current economic conditions.

Accounts are identified for individual review based on past-due status and information available about the customer, such as financial statements, news reports and published credit ratings, as well as general information regarding industry trends and the economic environment in which our customers operate. The allowance for credit losses attributable to finance receivables that are individually evaluated and determined to be impaired is based either on the present value of expected future cash flows discounted at the receivables' effective interest rate, the fair value of the collateral for collateral-dependent receivables or the observable market price of the receivable. In determining collateral value, we estimate the current fair market value of the collateral less selling costs. We also consider credit enhancements such as additional collateral and contractual third-party guarantees. The allowance for credit losses attributable to the remaining accounts not yet individually identified as impaired is estimated based on loss forecast models utilizing probabilities of default, our estimate of the loss emergence period and the estimated loss given default. In addition, qualitative factors not able to be fully captured in our loss forecast models including industry trends, macroeconomic factors and model imprecision are considered in the evaluation of the adequacy of the allowance for credit losses. These qualitative factors are subjective and require a degree of management judgment.

Our allowance for credit losses is segregated into three portfolio segments:

Customer - Finance receivables with retailend-user customers.

Dealer - Finance receivables with Caterpillar dealers.

Caterpillar Purchased Receivables - Trade receivables purchased from Caterpillar entities.

A portfolio segment is the level at which the Company develops a systematic methodology for determining its allowance for credit losses.

We further evaluate our portfolio segments by the class of finance receivables, which is defined as a level of information (below a portfolio segment) in which the finance receivables have the same initial measurement attribute and a similar method for assessing and monitoring credit risk. Typically, our finance receivables within a geographic area have similar credit risk profiles and methods for assessing and monitoring credit risk. Our classes, which align with management reporting for credit losses, are as follows:

North America - Includes financeFinance receivables originated in the United States and Canada.

EuropeEAME - Includes financeFinance receivables originated in Europe, Africa, the Middle East and the Commonwealth of Independent States.

Asia/Pacific - Includes financeFinance receivables originated in Australia, New Zealand, China, Japan, Southeast Asia and Southeast Asia.India.

Mining - Includes financeFinance receivables related to large mining customers worldwide and project financing in various countries.

Latin America - Includes financeFinance receivables originated in Mexico and Central and South American countries.

Caterpillar Power Finance - Includes financeFinance receivables originated worldwide related to marine vessels with Caterpillar engines worldwide and Caterpillar electrical power generation, gas compression and co-generation systems and non-Caterpillar equipment that is powered by these systems worldwide.systems.

Our allowance for credit losses as of SeptemberJune 30, 20172019 was $343$523 million or 1.271.81 percent of our recorded investment in finance receivables compared with $343$511 million or 1.291.80 percent as of December 31, 2016.2018. An analysis of the allowance for credit losses was as follows:

| | | (Millions of dollars) | | | | | | | | | | | | | | |

| | September 30, 2017 | June 30, 2019 |

| Allowance for Credit Losses: | Customer | | Dealer | | Caterpillar Purchased Receivables | | Total | Customer | | Dealer | | Caterpillar Purchased Receivables | | Total |

| Balance at beginning of year | $ | 331 |

| | $ | 10 |

| | $ | 2 |

| | $ | 343 |

| $ | 486 |

| | $ | 21 |

| | $ | 4 |

| | $ | 511 |

|

| Receivables written off | (119 | ) | | — |

| | — |

| | (119 | ) | (125 | ) | | — |

| | — |

| | (125 | ) |

| Recoveries on receivables previously written off | 31 |

| | — |

| | — |

| | 31 |

| 21 |

| | — |

| | — |

| | 21 |

|

| Provision for credit losses | 80 |

| | — |

| | — |

| | 80 |

| 99 |

| | 24 |

| | 1 |

| | 124 |

|

| Adjustment due to sale of receivables | (1 | ) | | — |

| | — |

| | (1 | ) | (9 | ) | | — |

| | — |

| | (9 | ) |

| Foreign currency translation adjustment | 9 |

| | — |

| | — |

| | 9 |

| 1 |

| | — |

| | — |

| | 1 |

|

| Balance at end of period | $ | 331 |

| | $ | 10 |

| | $ | 2 |

| | $ | 343 |

| $ | 473 |

| | $ | 45 |

| | $ | 5 |

| | $ | 523 |

|

| | | | | | | | | | | | | | | |

| Individually evaluated for impairment | $ | 100 |

| | $ | — |

| | $ | — |

| | $ | 100 |

| $ | 266 |

| | $ | 39 |

| | $ | — |

| | $ | 305 |

|

| Collectively evaluated for impairment | 231 |

| | 10 |

| | 2 |

| | 243 |

| 207 |

| | 6 |

| | 5 |

| | 218 |

|

| Ending Balance | $ | 331 |

| | $ | 10 |

| | $ | 2 |

| | $ | 343 |

| $ | 473 |

| | $ | 45 |

| | $ | 5 |

| | $ | 523 |

|

| | | | | | | | | | | | | | | |

| Recorded Investment in Finance Receivables: | |

| | |

| | |

| | |

| |

| | |

| | |

| | |

|

| Individually evaluated for impairment | $ | 869 |

| | $ | — |

| | $ | — |

| | $ | 869 |

| $ | 789 |

| | $ | 78 |

| | $ | — |

| | $ | 867 |

|

| Collectively evaluated for impairment | 18,704 |

| | 4,544 |

| | 2,823 |

| | 26,071 |

| 18,758 |

| | 4,358 |

| | 4,837 |

| | 27,953 |

|

| Ending Balance | $ | 19,573 |

| | $ | 4,544 |

| | $ | 2,823 |

| | $ | 26,940 |

| $ | 19,547 |

| | $ | 4,436 |

| | $ | 4,837 |

| | $ | 28,820 |

|

| | | | | | | | | | | | | | | |

| | | (Millions of dollars) | | | | | | | | | | | | | | |

| | December 31, 2016 | December 31, 2018 |

| Allowance for Credit Losses: | Customer | | Dealer | | Caterpillar Purchased Receivables | | Total | Customer | | Dealer | | Caterpillar Purchased Receivables | | Total |

| Balance at beginning of year | $ | 327 |

| | $ | 9 |

| | $ | 2 |

| | $ | 338 |

| $ | 353 |

| | $ | 9 |

| | $ | 3 |

| | $ | 365 |

|

| Receivables written off | (158 | ) | | — |

| | — |

| | (158 | ) | (235 | ) | | — |

| | — |

| | (235 | ) |

| Recoveries on receivables previously written off | 35 |

| | — |

| | — |

| | 35 |

| 46 |

| | — |

| | — |

| | 46 |

|

| Provision for credit losses | 132 |

| | 1 |

| | — |

| | 133 |

| 337 |

| | 12 |

| | 1 |

| | 350 |

|

| Adjustment due to sale of receivables | (8 | ) | | — |

| | — |

| | (8 | ) | (7 | ) | | — |

| | — |

| | (7 | ) |

| Foreign currency translation adjustment | 3 |

| | — |

| | — |

| | 3 |

| (8 | ) | | — |

| | — |

| | (8 | ) |

| Balance at end of year | $ | 331 |

| | $ | 10 |

| | $ | 2 |

| | $ | 343 |

| $ | 486 |

| | $ | 21 |

| | $ | 4 |

| | $ | 511 |

|

| | | | | | | | | | | | | | | |

| Individually evaluated for impairment | $ | 85 |

| | $ | — |

| | $ | — |

| | $ | 85 |

| $ | 288 |

| | $ | 14 |

| | $ | — |

| | $ | 302 |

|

| Collectively evaluated for impairment | 246 |

| | 10 |

| | 2 |

| | 258 |

| 198 |

| | 7 |

| | 4 |

| | 209 |

|

| Ending Balance | $ | 331 |

| | $ | 10 |

| | $ | 2 |

| | $ | 343 |

| $ | 486 |

| | $ | 21 |

| | $ | 4 |

| | $ | 511 |

|

| | | | | | | | | | | | | | | |

| Recorded Investment in Finance Receivables: | |

| | |

| | |

| | |

| |

| | |

| | |

| | |

|

| Individually evaluated for impairment | $ | 786 |

| | $ | — |

| | $ | — |

| | $ | 786 |

| $ | 859 |

| | $ | 78 |

| | $ | — |

| | $ | 937 |

|

| Collectively evaluated for impairment | 18,859 |

| | 4,479 |

| | 2,431 |

| | 25,769 |

| 18,724 |

| | 4,082 |

| | 4,691 |

| | 27,497 |

|

| Ending Balance | $ | 19,645 |

| | $ | 4,479 |

| | $ | 2,431 |

| | $ | 26,555 |

| $ | 19,583 |

| | $ | 4,160 |

| | $ | 4,691 |

| | $ | 28,434 |

|

| | | | | | | | | | | | | | | |

Credit quality of finance receivables

At origination, we evaluate credit risk based on a variety of credit quality factors including prior payment experience, customer financial information, credit-rating agency ratings, loan-to-value ratios and other internal metrics. On an ongoing basis, we monitor credit quality based on past-due status and collection experience as there is a meaningful correlation between the past-due status of customers and the risk of loss.

In determining past-due status, we consider the entire recorded investment in finance receivablereceivables past due when any installment is over 30 days past due. The tables below summarize our recorded investment in finance receivables by aging category.

| | | (Millions of dollars) | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | September 30, 2017 | June 30, 2019 |

| | 31-60 Days Past Due | | 61-90 Days Past Due | | 91+ Days Past Due | | Total Past Due | | Current | | Recorded Investment in Finance Receivables | | 91+ Still Accruing | 31-60 Days Past Due | | 61-90 Days Past Due | | 91+ Days Past Due | | Total Past Due | | Current | | Recorded Investment in Finance Receivables | | 91+ Still Accruing |

| Customer | |

| | |

| | |

| | | | | | | | | |

| | |

| | |

| | | | | | | | |

| North America | $ | 64 |

| | $ | 17 |

| | $ | 49 |

| | $ | 130 |

| | $ | 7,916 |

| | $ | 8,046 |

| | $ | 8 |

| $ | 90 |

| | $ | 17 |

| | $ | 44 |

| | $ | 151 |

| | $ | 7,899 |

| | $ | 8,050 |

| | $ | 12 |

|

| Europe | 27 |

| | 9 |

| | 56 |

| | 92 |

| | 2,642 |

| | 2,734 |

| | 4 |

| |

| EAME | | 29 |

| | 13 |

| | 167 |

| | 209 |

| | 2,885 |

| | 3,094 |

| | 7 |

|

| Asia/Pacific | 27 |

| | 13 |

| | 17 |

| | 57 |

| | 2,299 |

| | 2,356 |

| | 9 |

| 38 |

| | 15 |

| | 25 |

| | 78 |

| | 3,033 |

| | 3,111 |

| | 12 |

|

| Mining | 8 |

| | 4 |

| | 52 |

| | 64 |

| | 1,682 |

| | 1,746 |

| | 1 |

| 3 |

| | 13 |

| | 19 |

| | 35 |

| | 1,814 |

| | 1,849 |

| | — |

|

| Latin America | 53 |

| | 28 |

| | 180 |

| | 261 |

| | 1,672 |

| | 1,933 |

| | — |

| 44 |

| | 17 |

| | 85 |

| | 146 |

| | 1,398 |

| | 1,544 |

| | — |

|

| Caterpillar Power Finance | 11 |

| | 34 |

| | 124 |

| | 169 |

| | 2,589 |

| | 2,758 |

| | 11 |

| 7 |

| | 13 |

| | 296 |

| | 316 |

| | 1,583 |

| | 1,899 |

| | — |

|

| Dealer | |

| | |

| | |

| | | | | | | | | |

| | |

| | |

| | | | | | | | |

| North America | — |

| | — |

| | — |

| | — |

| | 2,816 |

| | 2,816 |

| | — |

| — |

| | — |

| | — |

| | — |

| | 2,524 |

| | 2,524 |

| | — |

|

| Europe | — |

| | — |

| | — |

| | — |

| | 350 |

| | 350 |

| | — |

| |

| EAME | | — |

| | — |

| | — |

| | — |

| | 603 |

| | 603 |

| | — |

|

| Asia/Pacific | — |

| | — |

| | — |

| | — |

| | 580 |

| | 580 |

| | — |

| — |

| | — |

| | — |

| | — |

| | 515 |

| | 515 |

| | — |

|

| Mining | — |

| | — |

| | — |

| | — |

| | 5 |

| | 5 |

| | — |

| — |

| | — |

| | — |

| | — |

| | 4 |

| | 4 |

| | — |

|

| Latin America | 5 |

| | — |

| | 3 |

| | 8 |

| | 783 |

| | 791 |

| | — |

| 1 |

| | 1 |

| | 79 |

| | 81 |

| | 706 |

| | 787 |

| | 1 |

|

| Caterpillar Power Finance | — |

| | — |

| | — |

| | — |

| | 2 |

| | 2 |

| | — |

| — |

| | — |

| | — |

| | — |

| | 3 |

| | 3 |

| | — |

|

Caterpillar Purchased Receivables | |

| | |

| | |

| | | | | | | | | |

| | |

| | |

| | | | | | | | |

| North America | 13 |

| | 5 |

| | 3 |

| | 21 |

| | 1,666 |

| | 1,687 |

| | 3 |

| 14 |

| | 9 |

| | 17 |

| | 40 |

| | 3,220 |

| | 3,260 |

| | |

| Europe | 2 |

| | — |

| | — |

| | 2 |

| | 333 |

| | 335 |

| | — |

| |

| EAME | | 1 |

| | — |

| | 2 |

| | 3 |

| | 510 |

| | 513 |

| | |

| Asia/Pacific | 1 |

| | — |

| | — |

| | 1 |

| | 396 |

| | 397 |

| | — |

| — |

| | 2 |

| | 3 |

| | 5 |

| | 587 |

| | 592 |

| | |

| Mining | — |

| | — |

| | — |

| | — |

| | — |

| | — |

| | — |

| — |

| | — |

| | — |

| | — |

| | — |

| | — |

| | |

| Latin America | — |

| | — |

| | — |

| | — |

| | 400 |

| | 400 |

| | — |

| — |

| | — |

| | — |

| | — |

| | 465 |

| | 465 |

| | |

| Caterpillar Power Finance | — |

| | — |

| | — |

| | — |

| | 4 |

| | 4 |

| | — |

| — |

| | — |

| | — |

| | — |

| | 7 |

| | 7 |

| | |

| Total | $ | 211 |

| | $ | 110 |

| | $ | 484 |

| | $ | 805 |

| | $ | 26,135 |

| | $ | 26,940 |

| | $ | 36 |

| $ | 227 |

| | $ | 100 |

| | $ | 737 |

| | $ | 1,064 |

| | $ | 27,756 |

| | $ | 28,820 |

| | $ | 32 |

|

| | | | | | | | | | | | | | | | | | | | | | | | | | | |

(1) Caterpillar Purchased Receivables are non-interest bearing trade receivables purchased at a discount.

| | | (Millions of dollars) | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | December 31, 2016 | December 31, 2018 |

| | 31-60 Days Past Due | | 61-90 Days Past Due | | 91+ Days Past Due | | Total Past Due | | Current | | Recorded Investment in Finance Receivables | | 91+ Still Accruing | 31-60 Days Past Due | | 61-90 Days Past Due | | 91+ Days Past Due | | Total Past Due | | Current | | Recorded Investment in Finance Receivables | | 91+ Still Accruing |

| Customer | |

| | |

| | |

| | | | | | | | | |

| | |

| | |

| | | | | | | | |

| North America | $ | 50 |

| | $ | 16 |

| | $ | 59 |

| | $ | 125 |

| | $ | 8,051 |

| | $ | 8,176 |

| | $ | 5 |

| $ | 65 |

| | $ | 18 |

| | $ | 84 |

| | $ | 167 |

| | $ | 7,883 |

| | $ | 8,050 |

| | $ | 14 |

|

| Europe | 16 |

| | 12 |

| | 39 |

| | 67 |

| | 2,388 |

| | 2,455 |

| | 6 |

| |

| EAME | | 19 |

| | 9 |

| | 153 |

| | 181 |

| | 2,850 |

| | 3,031 |

| | 5 |

|

| Asia/Pacific | 18 |

| | 7 |

| | 15 |

| | 40 |

| | 1,944 |

| | 1,984 |

| | 4 |

| 25 |

| | 9 |

| | 8 |

| | 42 |

| | 2,923 |

| | 2,965 |

| | 5 |

|

| Mining | 3 |

| | 2 |

| | 63 |

| | 68 |

| | 1,756 |

| | 1,824 |

| | 2 |

| 28 |

| | 1 |

| | 9 |

| | 38 |

| | 1,642 |

| | 1,680 |

| | — |

|

| Latin America | 40 |

| | 33 |

| | 214 |

| | 287 |

| | 1,808 |

| | 2,095 |

| | — |

| 38 |

| | 29 |

| | 71 |

| | 138 |

| | 1,421 |

| | 1,559 |

| | — |

|

| Caterpillar Power Finance | 11 |

| | 9 |

| | 73 |

| | 93 |

| | 3,018 |

| | 3,111 |

| | 1 |

| 10 |

| | 1 |

| | 384 |

| | 395 |

| | 1,903 |

| | 2,298 |

| | — |

|

| Dealer | |

| | |

| | |

| | | | | | | | | |

| | |

| | |

| | | | | | | | |

| North America | — |

| | — |

| | — |

| | — |

| | 2,705 |

| | 2,705 |

| | — |

| — |

| | — |

| | — |

| | — |

| | 2,210 |

| | 2,210 |

| | — |

|

| Europe | — |

| | — |

| | — |

| | — |

| | 336 |

| | 336 |

| | — |

| |

| EAME | | — |

| | — |

| | — |

| | — |

| | 619 |

| | 619 |

| | — |

|

| Asia/Pacific | — |

| | — |

| | — |

| | — |

| | 582 |

| | 582 |

| | — |

| — |

| | — |

| | — |

| | — |

| | 514 |

| | 514 |

| | — |

|

| Mining | — |

| | — |

| | — |

| | — |

| | 6 |

| | 6 |

| | — |

| — |

| | — |

| | — |

| | — |

| | 4 |

| | 4 |

| | — |

|

| Latin America | — |

| | — |

| | — |

| | — |

| | 848 |

| | 848 |

| | — |

| — |

| | — |

| | 78 |

| | 78 |

| | 731 |

| | 809 |

| | — |

|

| Caterpillar Power Finance | — |

| | — |

| | — |

| | — |

| | 2 |

| | 2 |

| | — |

| — |

| | — |

| | — |

| | — |

| | 4 |

| | 4 |

| | — |

|

Caterpillar Purchased Receivables | |

| | |

| | |

| | | | | | | | | |

| | |

| | |

| | | | | | | | |

| North America | 11 |

| | 3 |

| | 1 |

| | 15 |

| | 1,303 |

| | 1,318 |

| | 1 |

| 22 |

| | 12 |

| | 18 |

| | 52 |

| | 2,982 |

| | 3,034 |

| | |

| Europe | — |

| | — |

| | 1 |

| | 1 |

| | 268 |

| | 269 |

| | — |

| |

| EAME | | 1 |

| | — |

| | 1 |

| | 2 |

| | 546 |

| | 548 |

| | |

| Asia/Pacific | — |

| | — |

| | — |

| | — |

| | 475 |

| | 475 |

| | — |

| 5 |

| | 1 |

| | 1 |

| | 7 |

| | 756 |

| | 763 |

| | |

| Mining | — |

| | — |

| | — |

| | — |

| | — |

| | — |

| | — |

| — |

| | — |

| | — |

| | — |

| | — |

| | — |

| | |

| Latin America | — |

| | — |

| | — |

| | — |

| | 366 |

| | 366 |

| | — |

| — |

| | — |

| | — |

| | — |

| | 338 |

| | 338 |

| | |

| Caterpillar Power Finance | — |

| | — |

| | — |

| | — |

| | 3 |

| | 3 |

| | — |

| — |

| | — |

| | — |

| | — |

| | 8 |

| | 8 |

| | |

| Total | $ | 149 |

| | $ | 82 |

| | $ | 465 |

| | $ | 696 |

| | $ | 25,859 |

| | $ | 26,555 |

| | $ | 19 |

| $ | 213 |

| | $ | 80 |

| | $ | 807 |

| | $ | 1,100 |

| | $ | 27,334 |

| | $ | 28,434 |

| | $ | 24 |

|

| | | | | | | | | | | | | | | | | | | | | | | | | | | |

(1) Caterpillar Purchased Receivables are non-interest bearing trade receivables purchased at a discount.

Impaired finance receivables

For all classes, a finance receivable is considered impaired, based on current information and events, if it is probable that we will be unable to collect all amounts due according to the contractual terms. Impaired finance receivables include finance receivables that have been restructured and are considered to be Troubled Debt Restructures.troubled debt restructures.

There were $78 million in impaired finance receivables with a related allowance of $39 million and $14 million as of June 30, 2019 and December 31, 2018, respectively, for the Dealer portfolio segment, all of which was in Latin America. There were no impaired finance receivables as of SeptemberJune 30, 20172019 and December 31, 2016,2018, for the Dealer and Caterpillar Purchased Receivables portfolio segments.segment. Our recorded investment in impaired finance receivables and the related unpaid principal balances and allowance for the Customer portfolio segment were as follows:

| | | (Millions of dollars) | | | | | | | | | | | | | | | | | | | | | | |

| | As of September 30, 2017 | | As of December 31, 2016 | As of June 30, 2019 | | As of December 31, 2018 |

Impaired Finance Receivables With No Allowance Recorded | Recorded Investment | | Unpaid Principal Balance | | Related Allowance | | Recorded Investment | | Unpaid Principal Balance | | Related Allowance | Recorded Investment | | Unpaid Principal Balance | | Related Allowance | | Recorded Investment | | Unpaid Principal Balance | | Related Allowance |

| North America | $ | 16 |

| | $ | 21 |

| | $ | — |

| | $ | 10 |

| | $ | 10 |

| | $ | — |

| $ | 11 |

| | $ | 11 |

| | $ | — |

| | $ | 10 |

| | $ | 10 |

| | $ | — |

|

| Europe | 47 |

| | 47 |

| | — |

| | 49 |

| | 48 |

| | — |

| |

| EAME | | 1 |

| | 1 |

| | — |

| | 1 |

| | 1 |

| | — |

|

| Asia/Pacific | 32 |

| | 31 |

| | — |

| | 3 |

| | 2 |

| | — |

| — |

| | — |

| | — |

| | 1 |

| | 1 |

| | — |

|

| Mining | 127 |

| | 125 |

| | — |

| | 129 |

| | 129 |

| | — |

| 26 |

| | 26 |

| | — |

| | 33 |

| | 33 |

| | — |

|

| Latin America | 60 |

| | 60 |

| | — |

| | 68 |

| | 68 |

| | — |

| 21 |

| | 21 |

| | — |

| | 29 |

| | 29 |

| | — |

|

| Caterpillar Power Finance | 187 |

| | 200 |

| | — |

| | 271 |

| | 271 |

| | — |

| 52 |

| | 52 |

| | — |

| | 69 |

| | 83 |

| | — |

|

| Total | $ | 469 |

| | $ | 484 |

| | $ | — |

| | $ | 530 |

| | $ | 528 |

| | $ | — |

| $ | 111 |

| | $ | 111 |

| | $ | — |

| | $ | 143 |

| | $ | 157 |

| | $ | — |

|

Impaired Finance Receivables With An Allowance Recorded | |

| | |

| | |

| | |

| | |

| | |

| |

| | |

| | |

| | |

| | |

| | |

|

| North America | $ | 36 |

| | $ | 35 |

| | $ | 13 |

| | $ | 61 |

| | $ | 60 |

| | $ | 22 |

| $ | 28 |

| | $ | 28 |

| | $ | 10 |

| | $ | 40 |

| | $ | 41 |

| | $ | 14 |

|

| Europe | 8 |

| | 8 |

| | 5 |

| | 7 |

| | 7 |

| | 3 |

| |

| EAME | | 101 |

| | 101 |

| | 56 |

| | 92 |

| | 92 |

| | 57 |

|

| Asia/Pacific | 25 |

| | 25 |

| | 3 |

| | 50 |

| | 50 |

| | 8 |

| 10 |

| | 10 |

| | 3 |

| | 4 |

| | 4 |

| | 2 |

|

| Mining | — |

| | — |

| | — |

| | — |

| | — |

| | — |

| 63 |

| | 62 |

| | 20 |

| | 56 |

| | 55 |

| | 26 |

|

| Latin America | 92 |

| | 104 |

| | 35 |

| | 93 |

| | 104 |

| | 34 |

| 70 |

| | 69 |

| | 26 |

| | 75 |

| | 75 |

| | 25 |

|

| Caterpillar Power Finance | 239 |

| | 241 |

| | 44 |

| | 45 |

| | 44 |

| | 18 |

| 406 |

| | 420 |

| | 151 |

| | 449 |

| | 455 |

| | 164 |

|

| Total | $ | 400 |

| | $ | 413 |

| | $ | 100 |

| | $ | 256 |

| | $ | 265 |

| | $ | 85 |

| $ | 678 |

| | $ | 690 |

| | $ | 266 |

| | $ | 716 |

| | $ | 722 |

| | $ | 288 |

|

| Total Impaired Finance Receivables | |

| | |

| | |

| | |

| | |

| | |

| |

| | |

| | |

| | |

| | |

| | |

|

| North America | $ | 52 |

| | $ | 56 |

| | $ | 13 |

| | $ | 71 |

| | $ | 70 |

| | $ | 22 |

| $ | 39 |

| | $ | 39 |

| | $ | 10 |

| | $ | 50 |

| | $ | 51 |

| | $ | 14 |

|

| Europe | 55 |

| | 55 |

| | 5 |

| | 56 |

| | 55 |

| | 3 |

| |

| EAME | | 102 |

| | 102 |

| | 56 |

| | 93 |

| | 93 |

| | 57 |

|

| Asia/Pacific | 57 |

| | 56 |

| | 3 |

| | 53 |

| | 52 |

| | 8 |

| 10 |

| | 10 |

| | 3 |

| | 5 |

| | 5 |

| | 2 |

|

| Mining | 127 |

| | 125 |

| | — |

| | 129 |

| | 129 |

| | — |

| 89 |

| | 88 |

| | 20 |

| | 89 |

| | 88 |

| | 26 |

|

| Latin America | 152 |

| | 164 |

| | 35 |

| | 161 |

| | 172 |

| | 34 |

| 91 |

| | 90 |

| | 26 |

| | 104 |

| | 104 |

| | 25 |

|

| Caterpillar Power Finance | 426 |

| | 441 |

| | 44 |

| | 316 |

| | 315 |

| | 18 |

| 458 |

| | 472 |

| | 151 |

| | 518 |

| | 538 |

| | 164 |

|

| Total | $ | 869 |

| | $ | 897 |

| | $ | 100 |

| | $ | 786 |

| | $ | 793 |

| | $ | 85 |

| $ | 789 |

| | $ | 801 |

| | $ | 266 |

| | $ | 859 |

| | $ | 879 |

| | $ | 288 |

|

| | | | | | | | | | | | | | | | | | | | | | | |

| | | (Millions of dollars) | | | | | | | | | | | | | | |

| | Three Months Ended

September 30, 2017 | | Three Months Ended

September 30, 2016 | Three Months Ended

June 30, 2019 | | Three Months Ended

June 30, 2018 |

Impaired Finance Receivables With No Allowance Recorded | Average Recorded Investment | | Interest Income Recognized | | Average Recorded Investment | | Interest Income Recognized | Average Recorded Investment | | Interest Income Recognized | | Average Recorded Investment | | Interest Income Recognized |

| North America | $ | 14 |

| | $ | 1 |

| | $ | 24 |

| | $ | — |

| $ | 10 |

| | $ | — |

| | $ | 18 |

| | $ | 1 |

|

| Europe | 47 |

| | — |

| | 49 |

| | 1 |

| |

| EAME | | 1 |

| | — |

| | 7 |

| | — |

|

| Asia/Pacific | 30 |

| | 1 |

| | 1 |

| | — |

| — |

| | — |

| | 29 |

| | — |

|

| Mining | 128 |

| | 1 |

| | 90 |

| | 2 |

| 29 |

| | 1 |

| | 45 |

| | 1 |

|

| Latin America | 68 |

| | 1 |

| | 58 |

| | — |

| 20 |

| | 1 |

| | 43 |

| | — |

|

| Caterpillar Power Finance | 171 |

| | 1 |

| | 282 |

| | 3 |

| 41 |

| | — |

| | 189 |

| | 1 |

|

| Total | $ | 458 |

| | $ | 5 |

| | $ | 504 |

| | $ | 6 |

| $ | 101 |

| | $ | 2 |

| | $ | 331 |

| | $ | 3 |

|

Impaired Finance Receivables With An Allowance Recorded | |

| | |

| | |

| | |

| |

| | |

| | |

| | |

|

| North America | $ | 44 |

| | $ | — |

| | $ | 42 |

| | $ | — |

| $ | 35 |

| | $ | — |

| | $ | 56 |

| | $ | — |

|

| Europe | 6 |

| | — |

| | 10 |

| | — |

| |

| EAME | | 94 |

| | — |

| | 48 |

| | 1 |

|

| Asia/Pacific | 28 |

| | 1 |

| | 35 |

| | — |

| 9 |

| | — |

| | 5 |

| | — |

|

| Mining | — |

| | — |

| | 19 |

| | — |

| 39 |

| | — |

| | 64 |

| | 1 |

|

| Latin America | 102 |

| | 1 |

| | 67 |

| | 1 |

| 74 |

| | 2 |

| | 65 |

| | 1 |

|

| Caterpillar Power Finance | 251 |

| | 3 |

| | 43 |

| | — |

| 443 |

| | 4 |

| | 356 |

| | 3 |

|

| Total | $ | 431 |

| | $ | 5 |

| | $ | 216 |

| | $ | 1 |

| $ | 694 |

| | $ | 6 |

| | $ | 594 |

| | $ | 6 |

|

| Total Impaired Finance Receivables | |

| | |

| | |

| | |

| |

| | |

| | |

| | |

|

| North America | $ | 58 |

| | $ | 1 |

| | $ | 66 |

| | $ | — |

| $ | 45 |

| | $ | — |

| | $ | 74 |

| | $ | 1 |

|

| Europe | 53 |

| | — |

| | 59 |

| | 1 |

| |

| EAME | | 95 |

| | — |

| | 55 |

| | 1 |

|

| Asia/Pacific | 58 |

| | 2 |

| | 36 |

| | — |

| 9 |

| | — |

| | 34 |

| | — |

|

| Mining | 128 |

| | 1 |

| | 109 |

| | 2 |

| 68 |

| | 1 |

| | 109 |

| | 2 |

|

| Latin America | 170 |

| | 2 |

| | 125 |

| | 1 |

| 94 |

| | 3 |

| | 108 |

| | 1 |

|

| Caterpillar Power Finance | 422 |

| | 4 |

| | 325 |

| | 3 |

| 484 |

| | 4 |

| | 545 |

| | 4 |

|

| Total | $ | 889 |

| | $ | 10 |

| | $ | 720 |

| | $ | 7 |

| $ | 795 |

| | $ | 8 |

| | $ | 925 |

| | $ | 9 |

|

| | | | | | | | | | | | | | | |

| | | (Millions of dollars) | | | | | | | | | | | | | | |

| | Nine Months Ended

September 30, 2017 | | Nine Months Ended

September 30, 2016 | Six Months Ended

June 30, 2019 | | Six Months Ended

June 30, 2018 |

Impaired Finance Receivables With No Allowance Recorded | Average Recorded Investment | | Interest Income Recognized | | Average Recorded Investment | | Interest Income Recognized | Average Recorded Investment | | Interest Income Recognized | | Average Recorded Investment | | Interest Income Recognized |

| North America | $ | 12 |

| | $ | 1 |

| | $ | 19 |

| | $ | 1 |

| $ | 10 |

| | $ | — |

| | $ | 18 |

| | $ | 1 |

|

| Europe | 48 |

| | 1 |

| | 45 |

| | 1 |

| |

| EAME | | 1 |

| | — |

| | 23 |

| | — |

|

| Asia/Pacific | 22 |

| | 2 |

| | 2 |

| | — |

| — |

| | — |

| | 31 |

| | 1 |

|

| Mining | 128 |

| | 5 |

| | 84 |

| | 3 |

| 30 |

| | 1 |

| | 78 |

| | 2 |

|

| Latin America | 69 |

| | 2 |

| | 39 |

| | — |

| 23 |

| | 1 |

| | 44 |

| | 1 |

|

| Caterpillar Power Finance | 233 |

| | 7 |

| | 269 |

| | 8 |

| 51 |

| | 1 |

| | 178 |

| | 3 |

|

| Total | $ | 512 |

| | $ | 18 |

| | $ | 458 |

| | $ | 13 |

| $ | 115 |

| | $ | 3 |

| | $ | 372 |

| | $ | 8 |

|

Impaired Finance Receivables With An Allowance Recorded | |

| | |

| | |

| | |

| |

| | |

| | |

| | |

|

| North America | $ | 52 |

| | $ | 1 |

| | $ | 28 |

| | $ | — |

| $ | 37 |

| | $ | 1 |

| | $ | 53 |

| | $ | 1 |

|

| Europe | 6 |

| | — |

| | 11 |

| | — |

| |

| EAME | | 94 |

| | 1 |

| | 32 |

| | 1 |

|

| Asia/Pacific | 35 |

| | 2 |

| | 34 |

| | 2 |

| 8 |

| | — |

| | 6 |

| | — |

|

| Mining | — |

| | — |

| | 15 |

| | — |

| 42 |

| | 1 |

| | 36 |

| | 1 |

|

| Latin America | 101 |

| | 3 |

| | 59 |

| | 2 |

| 75 |

| | 3 |

| | 76 |

| | 2 |

|

| Caterpillar Power Finance | 141 |

| | 4 |

| | 50 |

| | 1 |

| 446 |

| | 7 |

| | 355 |

| | 4 |

|

| Total | $ | 335 |

| | $ | 10 |

| | $ | 197 |

| | $ | 5 |

| $ | 702 |

| | $ | 13 |

| | $ | 558 |

| | $ | 9 |

|

| Total Impaired Finance Receivables | |

| | |

| | |

| | |

| |

| | |

| | |

| | |

|

| North America | $ | 64 |

| | $ | 2 |

| | $ | 47 |

| | $ | 1 |

| $ | 47 |

| | $ | 1 |

| | $ | 71 |

| | $ | 2 |

|

| Europe | 54 |

| | 1 |

| | 56 |

| | 1 |

| |

| EAME | | 95 |

| | 1 |

| | 55 |

| | 1 |

|

| Asia/Pacific | 57 |

| | 4 |

| | 36 |

| | 2 |

| 8 |

| | — |

| | 37 |

| | 1 |

|

| Mining | 128 |

| | 5 |

| | 99 |

| | 3 |

| 72 |

| | 2 |

| | 114 |

| | 3 |

|

| Latin America | 170 |

| | 5 |

| | 98 |

| | 2 |

| 98 |

| | 4 |

| | 120 |

| | 3 |

|

| Caterpillar Power Finance | 374 |

| | 11 |

| | 319 |

| | 9 |

| 497 |

| | 8 |

| | 533 |

| | 7 |

|

| Total | $ | 847 |

| | $ | 28 |

| | $ | 655 |

| | $ | 18 |

| $ | 817 |

| | $ | 16 |

| | $ | 930 |

| | $ | 17 |

|

| | | | | | | | | | | | | | | |