UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

___________________________________________________

FORM 10-Q

|

| | | | |

| ☒ | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF

THE SECURITIES EXCHANGE ACT OF 1934

|

For the quarterly period ended March 31, 20202021

|

| | | | |

| ☐ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

|

| | | | |

| Commission File Number: | 1-9047 |

Independent Bank Corp.

(Exact name of registrant as specified in its charter)

___________________________________________________

|

| |

Massachusetts | 04-2870273 |

(State or other jurisdiction of

incorporation or organization)

| (I.R.S. Employer

Identification No.)

|

|

| | | | |

| MA | 04-2870273 |

(State or other jurisdiction of

incorporation or organization) | (I.R.S. Employer

Identification No.) |

| | | | | | | | | | | | | | |

| Office Address: | 2036 Washington Street, | Hanover, | MassachusettsMA | 02339 |

| Mailing Address: | 288 Union Street, | Rockland, | MassachusettsMA | 02370 |

| (Address of principal executive offices, including zip code) |

(781) 878-6100

(Registrant’s telephone number, including area code)

|

| | | | | | | |

| Securities registered pursuant to Section 12(b) of the Act: |

| Title of each Class | Trading Symbol | Name of each exchange on which registered |

| Common Stock, $0.01 par value per share | INDB | NASDAQThe Nasdaq Global Select Market |

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No o

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes x No o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and "emerging growth company" in Rule 12b-2 of the Exchange Act.

| | | | | | | | | | | |

| Large Accelerated Filer | x | Accelerated Filer | ☐ |

| | | |

Large Accelerated Filer | x | Accelerated Filer | ☐ |

| | | |

| Non-accelerated Filer | ☐ | Smaller Reporting Company | ☐ |

| | | |

| | Emerging Growth Company | ☐ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. o

|

| | | | | | | | | | | | | |

| Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act.) | Yes | ☐ | No | ☒ |

As of May 6, 2020,4, 2021, there were 32,934,65633,030,954 shares of the issuer’s common stock outstanding, par value $0.01 per share.

| Table of Contents |

| |

| PAGE |

| |

| |

| |

| |

| |

| |

| |

| |

Condensed Notes to Consolidated Financial Statements - March 31, 20192021 | |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

|

| | | | |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| Exhibit 31.1 – Certification 302 | |

| Exhibit 31.2 – Certification 302 | |

| Exhibit 32.1 – Certification 906 | |

| Exhibit 32.2 – Certification 906 | |

PART 1. FINANCIAL INFORMATION

Item 1. Financial Statements

INDEPENDENT BANK CORP.

CONSOLIDATED BALANCE SHEETS

(Unaudited—Dollars in thousands)

| | | | | | | | | | | |

| March 31

2021 | | December 31

2020 |

| Assets |

| Cash and due from banks | $ | 126,651 | | | $ | 169,460 | |

| Interest-earning deposits with banks | 1,642,688 | | | 1,127,176 | |

| Securities | | | |

| Trading | 3,269 | | | 2,838 | |

| Equity | 22,419 | | | 22,107 | |

| Available for sale (amortized cost $593,167 and $395,453) | 600,213 | | | 412,860 | |

| Held to maturity (fair value $820,430 and $752,177) | 805,529 | | | 724,512 | |

| Total securities | 1,431,430 | | | 1,162,317 | |

| Loans held for sale (at fair value) | 41,632 | | | 58,104 | |

| Loans | | | |

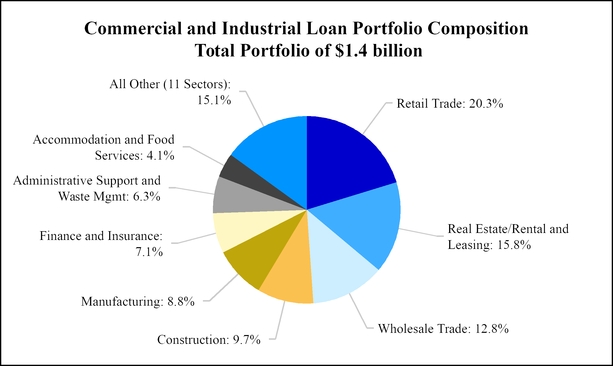

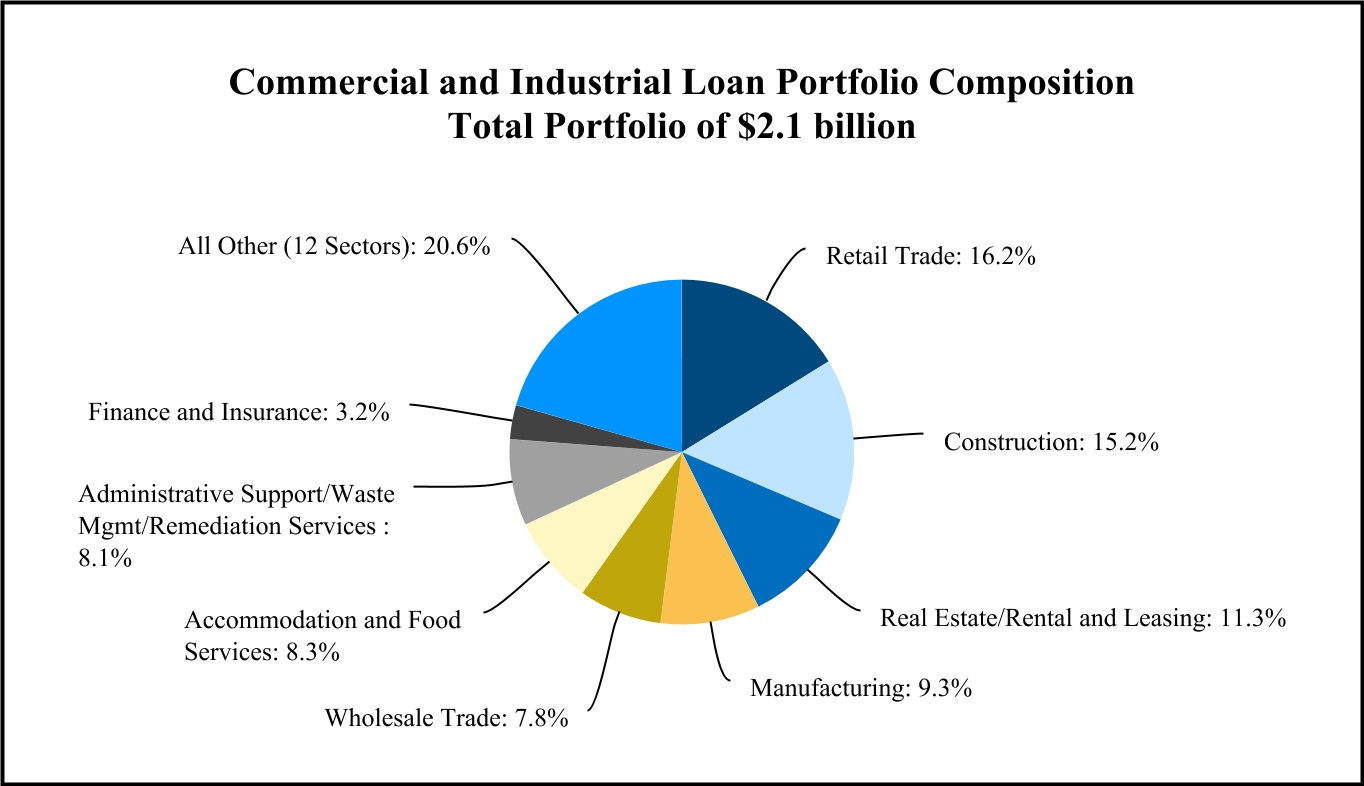

| Commercial and industrial | 2,086,671 | | | 2,103,152 | |

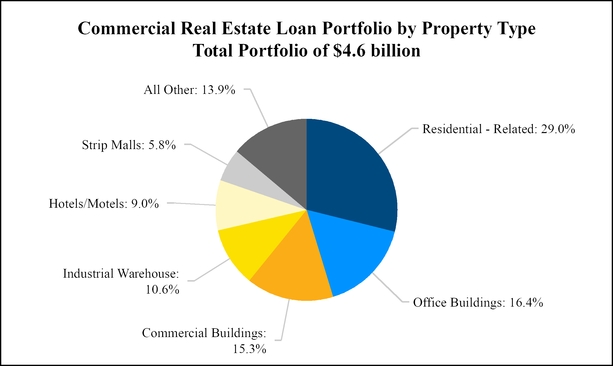

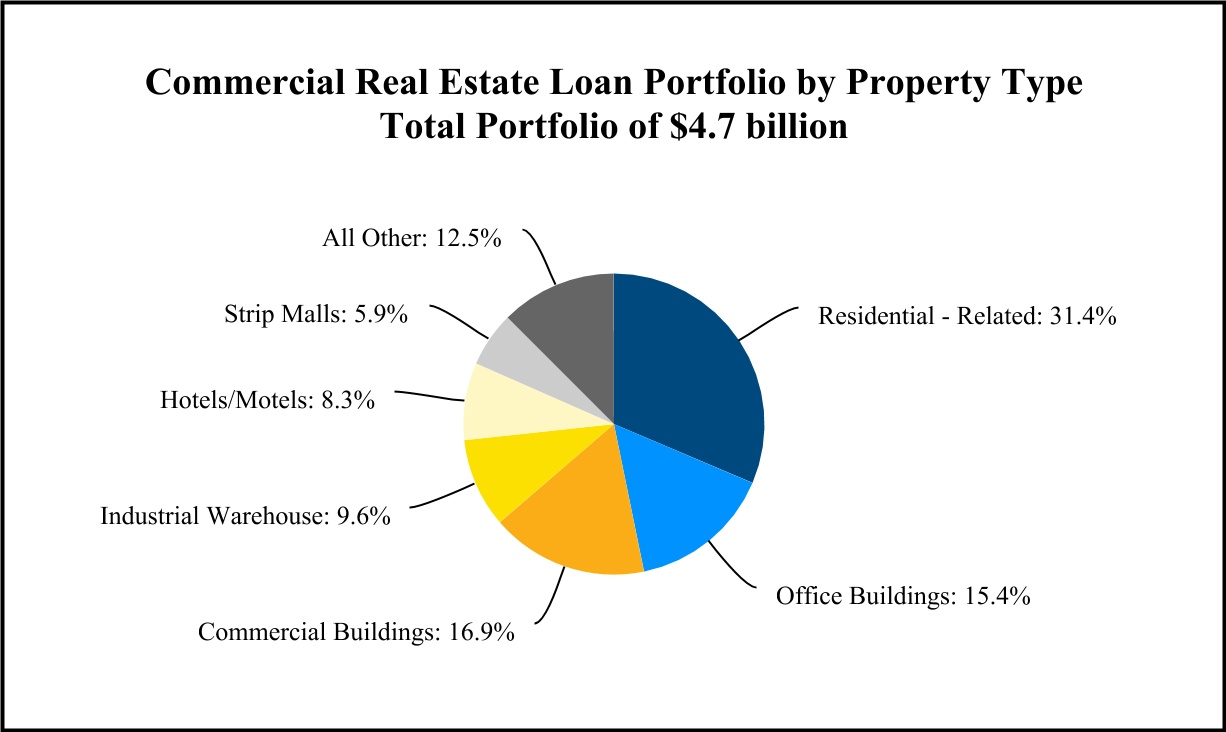

| Commercial real estate | 4,177,617 | | | 4,173,927 | |

| Commercial construction | 516,362 | | | 553,929 | |

| Small business | 174,211 | | | 175,023 | |

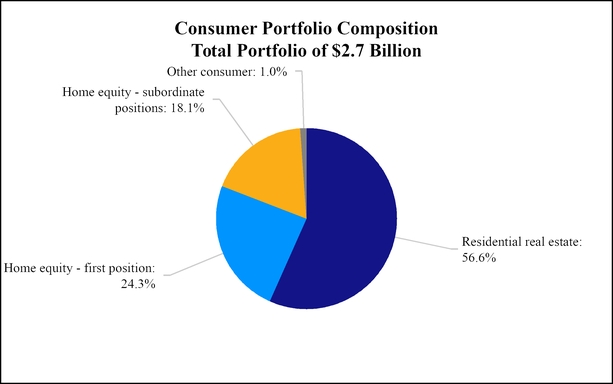

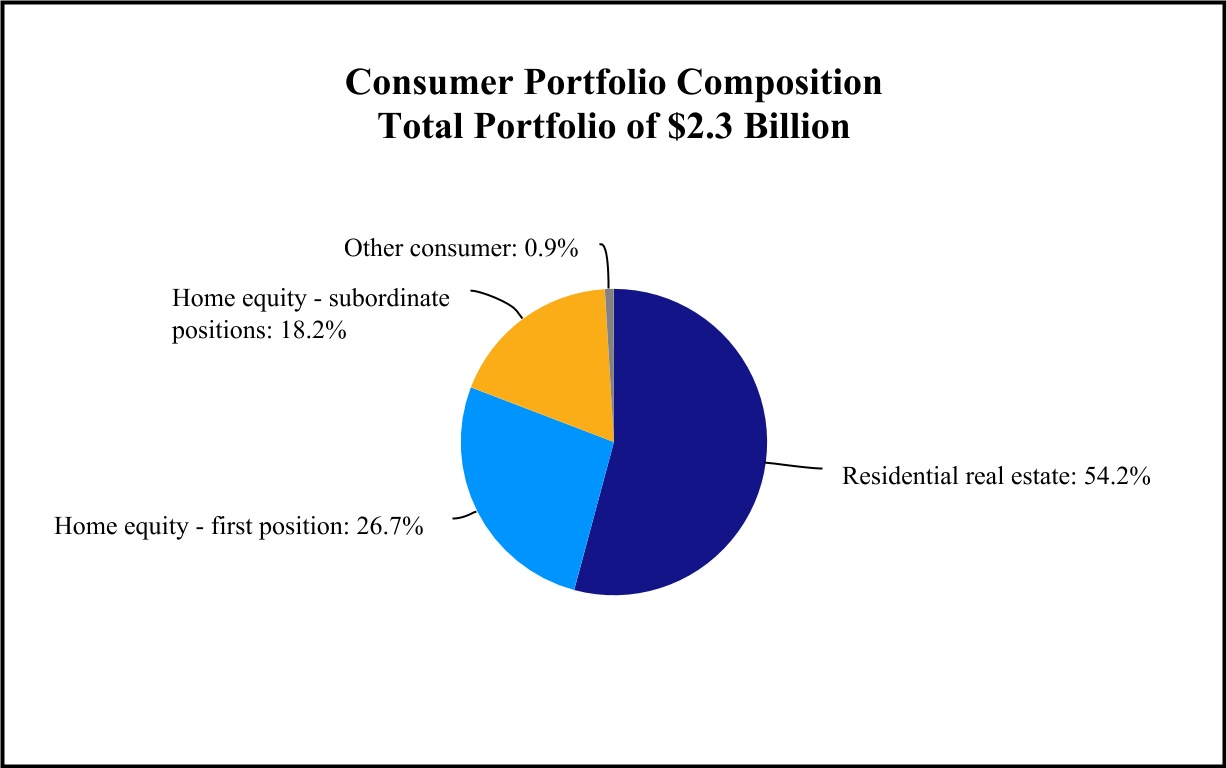

| Residential real estate | 1,241,789 | | | 1,296,183 | |

| Home equity - first position | 610,907 | | | 633,142 | |

| Home equity - subordinate positions | 417,588 | | | 435,648 | |

| Other consumer | 21,546 | | | 21,862 | |

| Total loans | 9,246,691 | | | 9,392,866 | |

| Less: allowance for credit losses | (107,549) | | | (113,392) | |

| Net loans | 9,139,142 | | | 9,279,474 | |

| Federal Home Loan Bank stock | 10,250 | | | 10,250 | |

| Bank premises and equipment, net | 115,945 | | | 116,393 | |

| Goodwill | 506,206 | | | 506,206 | |

| Other intangible assets | 21,689 | | | 23,107 | |

| Cash surrender value of life insurance policies | 241,365 | | | 200,525 | |

| | | |

| Other assets | 496,916 | | | 551,289 | |

| Total assets | $ | 13,773,914 | | | $ | 13,204,301 | |

| Liabilities and Stockholders' Equity |

| Deposits | | | |

| Noninterest-bearing demand deposits | $ | 4,136,259 | | | $ | 3,762,306 | |

| Savings and interest checking accounts | 4,242,235 | | | 4,047,332 | |

| Money market | 2,346,985 | | | 2,232,903 | |

| Time certificates of deposit of $100,000 and over | 465,182 | | | 525,424 | |

| Other time certificates of deposits | 402,863 | | | 425,205 | |

| Total deposits | 11,593,524 | | | 10,993,170 | |

| Borrowings | | | |

| Federal Home Loan Bank borrowings | 35,717 | | | 35,740 | |

| | | |

| | | |

| | | |

| Long-term borrowings (less unamortized debt issuance costs of $26 and $40) | 28,099 | | | 32,773 | |

|

| | | | | | | |

| | March 31

2020 | | December 31

2019 |

| Assets |

| Cash and due from banks | $ | 125,638 |

| | $ | 114,686 |

|

| Interest-earning deposits with banks | 345,739 |

| | 36,288 |

|

| Securities | | | |

| Trading | 2,247 |

| | 2,179 |

|

| Equity | 19,439 |

| | 21,261 |

|

| Available for sale (amortized cost $419,452 and $420,703) | 437,296 |

| | 426,424 |

|

| Held to maturity (fair value $809,355 and $753,263) | 777,798 |

| | 740,806 |

|

| Total securities | 1,236,780 |

| | 1,190,670 |

|

| Loans held for sale (at fair value) | 43,756 |

| | 33,307 |

|

| Loans | | | |

| Commercial and industrial | 1,448,224 |

| | 1,395,036 |

|

| Commercial real estate | 4,061,347 |

| | 4,002,359 |

|

| Commercial construction | 527,138 |

| | 547,293 |

|

| Small business | 177,820 |

| | 174,497 |

|

| Residential real estate | 1,528,416 |

| | 1,590,569 |

|

| Home equity - first position | 656,994 |

| | 649,255 |

|

| Home equity - subordinate positions | 489,276 |

| | 484,543 |

|

| Other consumer | 27,215 |

| | 30,087 |

|

| Total loans | 8,916,430 |

| | 8,873,639 |

|

| Less: allowance for credit losses | (92,376 | ) | | (67,740 | ) |

| Net loans | 8,824,054 |

| | 8,805,899 |

|

| Federal Home Loan Bank stock | 23,274 |

| | 14,424 |

|

| Bank premises and equipment, net | 121,873 |

| | 123,674 |

|

| Goodwill | 506,206 |

| | 506,206 |

|

| Other intangible assets | 27,466 |

| | 29,286 |

|

| Cash surrender value of life insurance policies | 197,772 |

| | 197,372 |

|

| Other assets | 527,682 |

| | 343,353 |

|

| Total assets | $ | 11,980,240 |

| | $ | 11,395,165 |

|

| Liabilities and Stockholders' Equity |

| Deposits | | | |

| Noninterest-bearing demand deposits | $ | 2,820,312 |

| | $ | 2,662,591 |

|

| Savings and interest checking accounts | 3,428,546 |

| | 3,232,909 |

|

| Money market | 1,897,632 |

| | 1,856,552 |

|

| Time certificates of deposit of $100,000 and over | 629,528 |

| | 663,645 |

|

| Other time certificates of deposits | 640,180 |

| | 731,670 |

|

| Total deposits | 9,416,198 |

| | 9,147,367 |

|

| Borrowings | | | |

| Federal Home Loan Bank borrowings | 358,591 |

| | 115,748 |

|

| | | Long-term borrowings (less unamortized debt issuance costs of $80 and $94) | 74,920 |

| | 74,906 |

| |

| Junior subordinated debentures (less unamortized debt issuance costs of $39 and $40) | 62,849 |

| | 62,848 |

| |

| Subordinated debentures (less unamortized debt issuance costs of $375 and $399) | 49,625 |

| | 49,601 |

| |

| Junior subordinated debentures (less unamortized debt issuance costs of $37 and $37) | | Junior subordinated debentures (less unamortized debt issuance costs of $37 and $37) | 62,851 | | | 62,851 | |

| Subordinated debentures (less unamortized debt issuance costs of $280 and $304) | | Subordinated debentures (less unamortized debt issuance costs of $280 and $304) | 49,720 | | | 49,696 | |

| Total borrowings | 545,985 |

| | 303,103 |

| Total borrowings | 176,387 | | | 181,060 | |

| Other liabilities | 338,401 |

| | 236,552 |

| Other liabilities | 288,632 | | | 327,386 | |

| Total liabilities | 10,300,584 |

| | 9,687,022 |

| Total liabilities | 12,058,543 | | | 11,501,616 | |

| Commitments and contingencies | — |

| | — |

| Commitments and contingencies | 0 | | | 0 | |

| Stockholders' equity | | | | Stockholders' equity | |

| Preferred stock, $.01 par value, authorized: 1,000,000 shares, outstanding: none | — |

| | — |

| |

Common stock, $.01 par value, authorized: 75,000,000 shares,

issued and outstanding: 33,260,005 shares at March 31, 2020 and 34,377,388 shares at December 31, 2019 (includes 147,892 and 147,184 shares of unvested participating restricted stock awards, respectively) | 331 |

| | 342 |

| |

| Value of shares held in rabbi trust at cost: 133,857 shares at March 31, 2020 and 143,820 shares at December 31, 2019 | (4,604 | ) | | (4,735 | ) | |

| Preferred stock, $0.01 par value, authorized: 1,000,000 shares, outstanding: NaN | | Preferred stock, $0.01 par value, authorized: 1,000,000 shares, outstanding: NaN | 0 | | | 0 | |

Common stock, $0.01 par value, authorized: 75,000,000 shares, issued and outstanding: 33,024,882 shares at March 31, 2021 and 32,965,692 shares at December 31, 2020 (includes 144,790 and 135,205 shares of unvested participating restricted stock awards, respectively) | | Common stock, $0.01 par value, authorized: 75,000,000 shares, issued and outstanding: 33,024,882 shares at March 31, 2021 and 32,965,692 shares at December 31, 2020 (includes 144,790 and 135,205 shares of unvested participating restricted stock awards, respectively) | 329 | | | 328 | |

| Value of shares held in rabbi trust at cost: 83,629 shares at March 31, 2021 and 84,126 shares at December 31, 2020 | | Value of shares held in rabbi trust at cost: 83,629 shares at March 31, 2021 and 84,126 shares at December 31, 2020 | (3,080) | | | (3,066) | |

| Deferred compensation and other retirement benefit obligations | 4,604 |

| | 4,735 |

| Deferred compensation and other retirement benefit obligations | 3,080 | | | 3,066 | |

| Additional paid in capital | 962,513 |

| | 1,035,450 |

| Additional paid in capital | 946,002 | | | 945,638 | |

| Retained earnings | 667,084 |

| | 654,182 |

| Retained earnings | 741,883 | | | 716,024 | |

| Accumulated other comprehensive income, net of tax | 49,728 |

| | 18,169 |

| Accumulated other comprehensive income, net of tax | 27,157 | | | 40,695 | |

| Total stockholders’ equity | 1,679,656 |

| | 1,708,143 |

| Total stockholders’ equity | 1,715,371 | | | 1,702,685 | |

| Total liabilities and stockholders' equity | $ | 11,980,240 |

| | $ | 11,395,165 |

| Total liabilities and stockholders' equity | $ | 13,773,914 | | | $ | 13,204,301 | |

The accompanying condensed notes are an integral part of these unaudited consolidated financial statements.

INDEPENDENT BANK CORP.

CONSOLIDATED STATEMENTS OF INCOME

(Unaudited—Dollars in thousands, except per share data)

| | | | Three Months Ended | | | Three Months Ended |

| | March 31 | | | March 31 |

| | 2020 | | 2019 | | | 2021 | | 2020 |

| Interest income | | | | Interest income | | | | |

| Interest and fees on loans | $ | 99,022 |

| | $ | 83,608 |

| Interest and fees on loans | | $ | 92,383 | | | $ | 99,022 | |

| Taxable interest and dividends on securities | 7,957 |

| | 7,465 |

| Taxable interest and dividends on securities | | 6,627 | | | 7,957 | |

| Nontaxable interest and dividends on securities | 9 |

| | 13 |

| Nontaxable interest and dividends on securities | | 5 | | | 9 | |

| Interest on loans held for sale | 232 |

| | 31 |

| Interest on loans held for sale | | 296 | | | 232 | |

| Interest on federal funds sold and short-term investments | 160 |

| | 426 |

| Interest on federal funds sold and short-term investments | | 326 | | | 160 | |

| Total interest and dividend income | 107,380 |

| | 91,543 |

| Total interest and dividend income | | 99,637 | | | 107,380 | |

| Interest expense | | | | Interest expense | | | | |

| Interest on deposits | 10,892 |

| | 7,028 |

| Interest on deposits | | 2,711 | | | 10,892 | |

| Interest on borrowings | 2,184 |

| | 1,990 |

| Interest on borrowings | | 1,342 | | | 2,184 | |

| Total interest expense | 13,076 |

| | 9,018 |

| Total interest expense | | 4,053 | | | 13,076 | |

| Net interest income | 94,304 |

| | 82,525 |

| Net interest income | | 95,584 | | | 94,304 | |

| Provision for credit losses | 25,000 |

| | 1,000 |

| Provision for credit losses | | (2,500) | | | 25,000 | |

| Net interest income after provision for credit losses | 69,304 |

| | 81,525 |

| Net interest income after provision for credit losses | | 98,084 | | | 69,304 | |

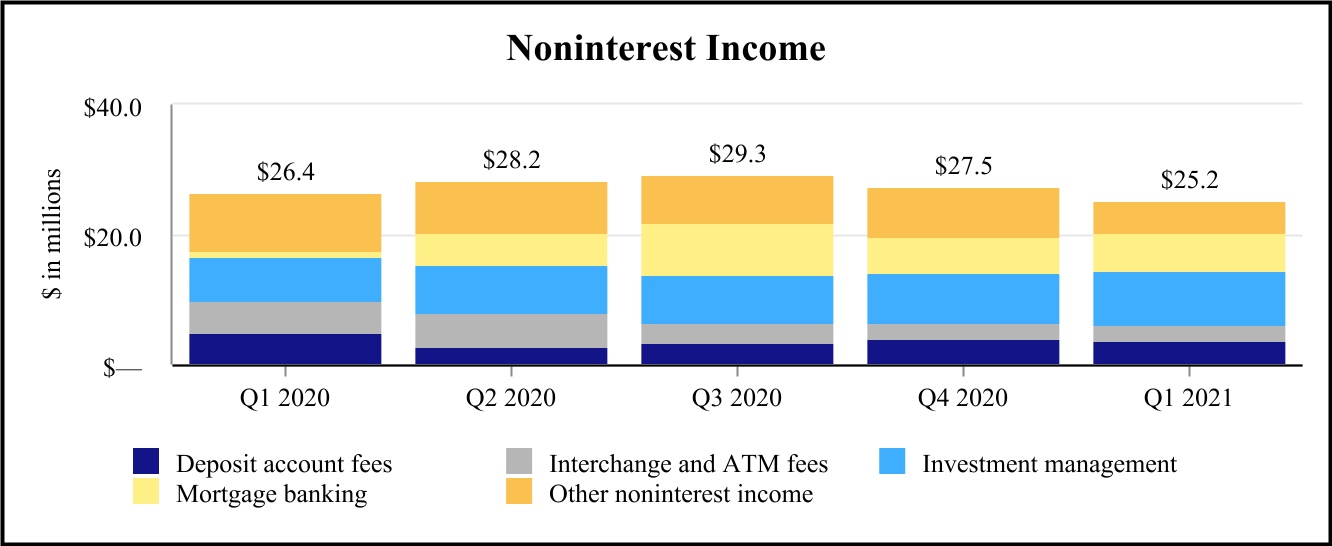

| Noninterest income | | | | Noninterest income | | | | |

| Deposit account fees | 4,970 |

| | 4,406 |

| Deposit account fees | | 3,584 | | | 4,970 | |

| Interchange and ATM fees | 4,896 |

| | 4,516 |

| Interchange and ATM fees | | 2,720 | | | 4,896 | |

| Investment management | 6,829 |

| | 6,748 |

| Investment management | | 8,304 | | | 6,829 | |

| Mortgage banking income | 861 |

| | 806 |

| Mortgage banking income | | 5,740 | | | 861 | |

| Increase in cash surrender value of life insurance policies | | Increase in cash surrender value of life insurance policies | | 1,323 | | | 1,276 | |

| Gain on life insurance benefits | 357 |

| | — |

| Gain on life insurance benefits | | 258 | | | 357 | |

| Increase in cash surrender value of life insurance policies | 1,276 |

| | 972 |

| |

| Loan level derivative income | 3,597 |

| | 641 |

| Loan level derivative income | | 173 | | | 3,597 | |

| | Other noninterest income | 3,649 |

| | 3,444 |

| Other noninterest income | | 3,144 | | | 3,649 | |

| Total noninterest income | 26,435 |

| | 21,533 |

| Total noninterest income | | 25,246 | | | 26,435 | |

| Noninterest expenses | | | | Noninterest expenses | | | | |

| Salaries and employee benefits | 37,349 |

| | 33,117 |

| Salaries and employee benefits | | 39,889 | | | 37,349 | |

| Occupancy and equipment expenses | 9,317 |

| | 7,130 |

| Occupancy and equipment expenses | | 9,273 | | | 9,317 | |

| Data processing and facilities management | 1,658 |

| | 1,326 |

| Data processing and facilities management | | 1,665 | | | 1,658 | |

| FDIC assessment | — |

| | 616 |

| FDIC assessment | | 1,050 | | | — | |

| Advertising expense | 1,105 |

| | 1,213 |

| |

| | Consulting expense | 1,336 |

| | 764 |

| Consulting expense | | 2,391 | | | 1,336 | |

| Core deposit amortization | 1,531 |

| | 857 |

| Core deposit amortization | | 1,392 | | | 1,531 | |

| Merger and acquisition expense | — |

| | 1,032 |

| |

| | Software maintenance | 1,685 |

| | 1,165 |

| Software maintenance | | 1,970 | | | 1,685 | |

| Unrealized loss on equity securities | 1,799 |

| | — |

| Unrealized loss on equity securities | | 0 | | | 1,799 | |

| Other noninterest expenses | 11,060 |

| | 9,091 |

| Other noninterest expenses | | 12,052 | | | 12,165 | |

| Total noninterest expenses | 66,840 |

| | 56,311 |

| Total noninterest expenses | | 69,682 | | | 66,840 | |

| Income before income taxes | 28,899 |

| | 46,747 |

| Income before income taxes | | 53,648 | | | 28,899 | |

| Provision for income taxes | 2,148 |

| | 11,522 |

| Provision for income taxes | | 11,937 | | | 2,148 | |

| Net income | $ | 26,751 |

| | $ | 35,225 |

| Net income | | $ | 41,711 | | | $ | 26,751 | |

| Basic earnings per share | $ | 0.78 |

| | $ | 1.25 |

| Basic earnings per share | | $ | 1.26 | | | $ | 0.78 | |

| Diluted earnings per share | $ | 0.78 |

| | $ | 1.25 |

| Diluted earnings per share | | $ | 1.26 | | | $ | 0.78 | |

| Weighted average common shares (basic) | 34,184,431 |

| | 28,106,184 |

| Weighted average common shares (basic) | | 32,995,332 | | | 34,184,431 | |

| Common share equivalents | 36,827 |

| | 54,466 |

| Common share equivalents | | 30,098 | | | 36,827 | |

| Weighted average common shares (diluted) | 34,221,258 |

| | 28,160,650 |

| Weighted average common shares (diluted) | | 33,025,430 | | | 34,221,258 | |

| Cash dividends declared per common share | $ | 0.46 |

| | $ | 0.44 |

| Cash dividends declared per common share | | $ | 0.48 | | | $ | 0.46 | |

The accompanying condensed notes are an integral part of these unaudited consolidated financial statements.

INDEPENDENT BANK CORP.

CONSOLIDATED STATEMENTS OF COMPREHENSIVE INCOME

(Unaudited—Dollars in thousands)

| | | | Three Months Ended | | | Three Months Ended |

| | March 31 | | | March 31 |

| | 2020 | | 2019 | | | 2021 | | 2020 |

| Net income | $ | 26,751 |

| | $ | 35,225 |

| Net income | | $ | 41,711 | | | $ | 26,751 | |

| Other comprehensive income, net of tax | | | | Other comprehensive income, net of tax | | |

| Net change in fair value of securities available for sale | 9,347 |

| | 4,729 |

| Net change in fair value of securities available for sale | | (7,774) | | | 9,347 | |

| Net change in fair value of cash flow hedges | 22,984 |

| | 3,285 |

| Net change in fair value of cash flow hedges | | (6,583) | | | 22,984 | |

| Net change in other comprehensive income for defined benefit postretirement plans | (772 | ) | | 40 |

| Net change in other comprehensive income for defined benefit postretirement plans | | 819 | | | (772) | |

| Total other comprehensive income | 31,559 |

| | 8,054 |

| |

| Total other comprehensive income (loss) | | Total other comprehensive income (loss) | | (13,538) | | | 31,559 | |

| Total comprehensive income | $ | 58,310 |

| | $ | 43,279 |

| Total comprehensive income | | $ | 28,173 | | | $ | 58,310 | |

The accompanying condensed notes are an integral part of these unaudited consolidated financial statements.

INDEPENDENT BANK CORP.

CONSOLIDATED STATEMENTS OF STOCKHOLDERS’ EQUITY

Three Months Ended March 31, 20202021 and 20192020

(Unaudited—Dollars in thousands, except per share data)

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Common Stock Outstanding | | Common Stock | | Value of Shares Held in Rabbi Trust at Cost | | Deferred Compensation Obligation | | Additional Paid in Capital | | Retained Earnings | | Accumulated Other

Comprehensive Income (Loss) | | Total |

| Balance December 31, 2020 | 32,965,692 | | $ | 328 | | | $ | (3,066) | | | $ | 3,066 | | | $ | 945,638 | | | $ | 716,024 | | | $ | 40,695 | | | $ | 1,702,685 | |

| | | | | | | | | | | | | | | |

| Net income | — | | | — | | | — | | | — | | | — | | | 41,711 | | | — | | | 41,711 | |

| Other comprehensive loss | — | | | — | | | — | | | — | | | — | | | — | | | (13,538) | | | (13,538) | |

| Common dividend declared ($0.48 per share) | — | | | — | | | — | | | — | | | — | | | (15,852) | | | — | | | (15,852) | |

| | | | | | | | | | | | | | | |

| Proceeds from exercise of stock options, net of cash paid | 4,744 | | | — | | | — | | | — | | | (57) | | | — | | | — | | | (57) | |

| Stock based compensation | — | | | — | | | — | | | — | | | 1,150 | | | — | | | — | | | 1,150 | |

| Restricted stock awards issued, net of awards surrendered | 48,106 | | | 1 | | | — | | | — | | | (1,221) | | | — | | | — | | | (1,220) | |

| Shares issued under direct stock purchase plan | 6,340 | | | — | | | — | | | — | | | 492 | | | — | | | — | | | 492 | |

| | | | | | | | | | | | | | | |

| Deferred compensation and other retirement benefit obligations | — | | | — | | | (14) | | | 14 | | | — | | | — | | | — | | | 0 | |

| Balance March 31, 2021 | 33,024,882 | | | $ | 329 | | | $ | (3,080) | | | $ | 3,080 | | | $ | 946,002 | | | $ | 741,883 | | | $ | 27,157 | | | $ | 1,715,371 | |

| | | | | | | | | | | | | | | |

| Balance December 31, 2019 | 34,377,388 | | | $ | 342 | | | $ | (4,735) | | | $ | 4,735 | | | $ | 1,035,450 | | | $ | 654,182 | | | $ | 18,169 | | | $ | 1,708,143 | |

| Cumulative effect accounting adjustment (1) | — | | | — | | | — | | | — | | | — | | | 1,553 | | | — | | | 1,553 | |

| | | | | | | | | | | | | | | |

| Net income | — | | | — | | | — | | | — | | | — | | | 26,751 | | | — | | | 26,751 | |

| Other comprehensive income | — | | | — | | | — | | | — | | | — | | | — | | | 31,559 | | | 31,559 | |

| Common dividend declared ($0.46 per share) | — | | | — | | | — | | | — | | | — | | | (15,402) | | | — | | | (15,402) | |

| | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | |

| Stock based compensation | — | | | — | | | — | | | — | | | 850 | | | — | | | — | | | 850 | |

| Restricted stock awards issued, net of awards surrendered | 42,531 | | | 1 | | | — | | | — | | | (1,133) | | | — | | | — | | | (1,132) | |

| Shares issued under direct stock purchase plan | 7,009 | | | 0 | | | — | | | — | | | 560 | | | — | | | — | | | 560 | |

| Shares repurchased under share repurchase program | (1,166,923) | | | (12) | | | — | | | — | | | (73,214) | | | — | | | — | | | (73,226) | |

| Deferred compensation and other retirement benefit obligations | — | | | — | | | 131 | | | (131) | | | — | | | — | | | — | | | 0 | |

| Balance March 31, 2020 | 33,260,005 | | | $ | 331 | | | $ | (4,604) | | | $ | 4,604 | | | $ | 962,513 | | | $ | 667,084 | | | $ | 49,728 | | | $ | 1,679,656 | |

|

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | Common Stock Outstanding | | Common Stock | | Value of Shares Held in Rabbi Trust at Cost | | Deferred Compensation Obligation | | Additional Paid in Capital | | Retained Earnings | | Accumulated Other

Comprehensive Income/(Loss) | | Total |

| Balance December 31, 2019 | 34,377,388 |

| | $ | 342 |

| | $ | (4,735 | ) | | $ | 4,735 |

| | $ | 1,035,450 |

| | $ | 654,182 |

| | $ | 18,169 |

| | $ | 1,708,143 |

|

| Cumulative effect accounting adjustment (1) | — |

| | — |

| | — |

| | — |

| | — |

| | 1,553 |

| | — |

| | 1,553 |

|

| Net income | — |

| | — |

| | — |

| | — |

| | — |

| | 26,751 |

| | — |

| | 26,751 |

|

| Other comprehensive income | — |

| | — |

| | — |

| | — |

| | — |

| | — |

| | 31,559 |

| | 31,559 |

|

| Common dividend declared ($0.46 per share) | — |

| | — |

| | — |

| | — |

| | — |

| | (15,402 | ) | | — |

| | (15,402 | ) |

| Stock based compensation | — |

| | — |

| | — |

| | — |

| | 850 |

| | — |

| | — |

| | 850 |

|

| Restricted stock awards issued, net of awards surrendered | 42,531 |

| | 1 |

| | — |

| | — |

| | (1,133 | ) | | — |

| | — |

| | (1,132 | ) |

| Shares issued under direct stock purchase plan | 7,009 |

| | — |

| | — |

| | — |

| | 560 |

| | — |

| | — |

| | 560 |

|

| Shares repurchased under share repurchase program | (1,166,923 | ) | | (12 | ) | | — |

| | — |

| | (73,214 | ) | | — |

| | — |

| | (73,226 | ) |

| Deferred compensation and other retirement benefit obligations | — |

| | — |

| | 131 |

| | (131 | ) | | — |

| | — |

| | — |

| | — |

|

| Balance March 31, 2020 | 33,260,005 |

| | $ | 331 |

|

| $ | (4,604 | ) |

| $ | 4,604 |

|

| $ | 962,513 |

|

| $ | 667,084 |

|

| $ | 49,728 |

|

| $ | 1,679,656 |

|

| | | | | | | | | | | | | | | | |

| Balance December 31, 2018 | 28,080,408 |

| | $ | 279 |

| | $ | (4,718 | ) | | $ | 4,718 |

| | $ | 527,648 |

| | $ | 546,736 |

| | $ | (1,173 | ) | | $ | 1,073,490 |

|

| Net income | — |

| | — |

| | — |

| | — |

| | — |

| | 35,225 |

| | — |

| | 35,225 |

|

| Other comprehensive loss | — |

| | — |

| | — |

| | — |

| | — |

| | — |

| | 8,054 |

| | 8,054 |

|

| Common dividend declared ($0.44 per share) | — |

| | — |

| | — |

| | — |

| | — |

| | (12,379 | ) | | — |

| | (12,379 | ) |

| Proceeds from exercise of stock options, net of cash paid | 6,000 |

| | — |

| | — |

| | — |

| | 165 |

| | — |

| | — |

| | 165 |

|

| Stock based compensation | — |

| | — |

| | — |

| | — |

| | 915 |

| | — |

| | — |

| | 915 |

|

| Restricted stock awards issued, net of awards surrendered | 44,407 |

| | 1 |

| | — |

| | — |

| | (1,420 | ) | | — |

| | — |

| | (1,419 | ) |

| Shares issued under direct stock purchase plan | 6,689 |

| | — |

| | — |

| | — |

| | 487 |

| | — |

| | — |

| | 487 |

|

| Deferred compensation and other retirement benefit obligations | — |

| | — |

| | 119 |

| | (119 | ) | | — |

| | — |

| | — |

| | — |

|

| Balance March 31, 2019 | 28,137,504 |

| | $ | 280 |

| | $ | (4,599 | ) | | $ | 4,599 |

| | $ | 527,795 |

| | $ | 569,582 |

| | $ | 6,881 |

| | $ | 1,104,538 |

|

| |

(1) | Represents adjustment needed to reflect the cumulative impact on retained earnings pursuant to the Company's adoption of Accounting Standards Update 2016-13. The adjustment presented includes $1.1 million ($817,000, net of tax) attributable to the change in accounting methodology for estimating the allowance for credit losses and $1.0 million ($736,000, net of tax) related to the reserve for unfunded commitments resulting from the Company's adoption of the standard. Amount shown in the table above is presented net of tax. |

The accompanying condensed notes are an integral part of these unaudited consolidated financial statements.

INDEPENDENT BANK CORP.

CONSOLIDATED STATEMENTS OF CASH FLOWS

(Unaudited—Dollars in thousands)

|

| | | | | | | |

| | Three Months Ended |

| | March 31 |

| | 2020 | | 2019 |

| Cash flow from operating activities | | | |

| Net income | $ | 26,751 |

| | $ | 35,225 |

|

| Adjustments to reconcile net income to net cash provided by (used in) operating activities | | | |

| Depreciation and amortization | 6,992 |

| | 4,101 |

|

| Change in unamortized net loan costs and premiums | (735 | ) | | (453 | ) |

| Provision for loan losses | 25,000 |

| | 1,000 |

|

| Deferred income tax expense | 3,108 |

| | 539 |

|

| Net (gain) loss on equity securities | 1,801 |

| | (907 | ) |

| Net loss on bank premises and equipment | 420 |

| | 25 |

|

| Realized gain on sale leaseback transaction | (145 | ) | | (145 | ) |

| Stock based compensation | 850 |

| | 915 |

|

| Increase in cash surrender value of life insurance policies | (1,276 | ) | | (972 | ) |

| Gain on life insurance benefits | (357 | ) | | — |

|

| Operating lease payments | (2,926 | ) | | (2,165 | ) |

| Change in fair value on loans held for sale | 914 |

| | (1 | ) |

| Net change in: | | | |

| Trading assets | (68 | ) | | (333 | ) |

| Loans held for sale | (11,363 | ) | | 846 |

|

| Other assets | (151,830 | ) | | 1,721 |

|

| Other liabilities | 92,461 |

| | (5,228 | ) |

| Total adjustments | (37,154 | ) | | (1,057 | ) |

| Net cash provided by (used in) operating activities | (10,403 | ) | | 34,168 |

|

| Cash flows provided by (used in) investing activities | | | |

| Purchases of equity securities | (108 | ) | | (105 | ) |

| Proceeds from maturities and principal repayments of securities available for sale | 31,280 |

| | 11,318 |

|

| Purchases of securities available for sale | (30,095 | ) | | — |

|

| Proceeds from maturities and principal repayments of securities held to maturity | 48,183 |

| | 19,003 |

|

| Purchases of securities held to maturity | (84,824 | ) | | (30,502 | ) |

| Net redemption (purchases) of Federal Home Loan Bank stock | (8,850 | ) | | 8,016 |

|

| Investments in low income housing projects | (5,934 | ) | | (292 | ) |

| Purchases of life insurance policies | (93 | ) | | (93 | ) |

| Proceeds from life insurance policies | 1,326 |

| | — |

|

| Net increase in loans | (41,283 | ) | | (70,378 | ) |

| Purchases of bank premises and equipment | (1,749 | ) | | (3,713 | ) |

| Proceeds from the sale of bank premises and equipment | 9 |

| | 13 |

|

| Net cash used in investing activities | (92,138 | ) | | (66,733 | ) |

| Cash flows provided by (used in) financing activities | | | |

| Net increase (decrease) in time deposits | (125,396 | ) | | 12,464 |

|

| Net increase in other deposits | 394,438 |

| | 24,034 |

|

| Net advances (repayments) of short-term Federal Home Loan Bank borrowings | 257,826 |

| | (122,046 | ) |

| | | | | | | | | | | |

| | Three Months Ended |

| March 31 |

| 2021 | | 2020 |

| Cash flow from operating activities | | | |

| Net income | $ | 41,711 | | | $ | 26,751 | |

| Adjustments to reconcile net income to net cash provided by (used in) operating activities | | | |

| Depreciation and amortization | 8,228 | | | 6,992 | |

| Change in unamortized net loan costs and premiums | (10,318) | | | (735) | |

| | | |

| Provision for credit losses | (2,500) | | | 25,000 | |

| Deferred income tax expense | 567 | | | 3,108 | |

| Net (gain) loss on equity securities | (316) | | | 1,801 | |

| | | |

| | | |

| Net loss on bank premises and equipment | 4 | | | 420 | |

| | | |

| | | |

| | | |

| | | |

| Realized gain on sale leaseback transaction | (145) | | | (145) | |

| Stock based compensation | 1,150 | | | 850 | |

| | | |

| Increase in cash surrender value of life insurance policies | (1,323) | | | (1,276) | |

| Gain on life insurance benefits | (258) | | | (357) | |

| Operating lease payments | (3,077) | | | (2,926) | |

| Change in fair value on loans held for sale | 1,764 | | | (255) | |

| Net change in: | | | |

| Trading assets | (431) | | | (68) | |

| | | |

| Loans held for sale | 14,708 | | | (10,194) | |

| Other assets | 70,901 | | | (151,830) | |

| Other liabilities | (53,201) | | | 92,461 | |

| Total adjustments | 25,753 | | | (37,154) | |

| Net cash provided by (used in) operating activities | 67,464 | | | (10,403) | |

| Cash flows used in investing activities | | | |

| | | |

| | | |

| Purchases of equity securities | (124) | | | (108) | |

| | | |

| Proceeds from maturities and principal repayments of securities available for sale | 26,092 | | | 31,280 | |

| Purchases of securities available for sale | (223,986) | | | (30,095) | |

| Proceeds from maturities and principal repayments of securities held to maturity | 68,497 | | | 48,183 | |

| Purchases of securities held to maturity | (149,453) | | | (84,824) | |

| Net purchases of Federal Home Loan Bank stock | 0 | | | (8,850) | |

| Investments in low income housing projects | (6,632) | | | (5,934) | |

| Purchases of life insurance policies | (40,093) | | | (93) | |

| Proceeds from life insurance policies | 576 | | | 1,326 | |

| Net (increase) decrease in loans | 153,150 | | | (41,283) | |

| | | |

| Purchases of bank premises and equipment | (2,524) | | | (1,749) | |

| Proceeds from the sale of bank premises and equipment | 4 | | | 9 | |

| | | |

| | | |

| | | |

| Net cash used in investing activities | (174,493) | | | (92,138) | |

| Cash flows provided by financing activities | | | |

| Net decrease in time deposits | (82,569) | | | (125,396) | |

| Net increase in other deposits | 682,938 | | | 394,438 | |

| | | |

| Net advances of short-term Federal Home Loan Bank borrowings | 0 | | | 257,826 | |

| | | |

| Repayments of long-term Federal Home Loan Bank borrowings | 0 | | | (15,000) | |

| | | |

| | | |

| | | |

| | | |

| | | |

|

| | | | | | | |

| Repayments of long-term Federal Home Loan Bank borrowings | (15,000 | ) | | — |

|

| Proceeds from line of credit, net of issuance costs | — |

| | 49,993 |

|

| Proceeds from long-term debt, net of issuance costs | — |

| | 74,914 |

|

| Repayments of junior subordinated debentures, net of issuance costs | — |

| | (3,093 | ) |

| Proceeds from subordinated debentures, net of issuance costs | — |

| | 49,556 |

|

| Net proceeds from exercise of stock options | — |

| | 165 |

|

| Restricted stock awards issued, net of awards surrendered | (1,132 | ) | | (1,419 | ) |

| Proceeds from shares issued under direct stock purchase plan | 560 |

| | 487 |

|

| Payments for shares repurchased under share repurchase program | (73,226 | ) | | — |

|

| Common dividends paid | (15,126 | ) | | (10,671 | ) |

| Net cash provided by financing activities | 422,944 |

| | 74,384 |

|

| Net increase in cash and cash equivalents | 320,403 |

| | 41,819 |

|

| Cash and cash equivalents at beginning of year | 150,974 |

| | 250,455 |

|

| Cash and cash equivalents at end of period | $ | 471,377 |

| | $ | 292,274 |

|

| Supplemental schedule of noncash activities | | | |

| Net increase in capital commitments relating to low income housing project investments | $ | 14,394 |

| | $ | — |

|

| Initial recognition of operating leases upon adoption of Accounting Standards Update 2016-02 (1) | $ | — |

| | $ | 32,777 |

|

| Recognition of operating lease at commencement | $ | 2,223 |

| | $ | 2,926 |

|

10

| |

(1) | Represents adjustment needed to reflect the opening balance of the Company's Right of Use ("ROU") assets and lease liabilities pursuant to the adoption of Accounting Standards Update 2016-02 effective January 1, 2019. Upon adoption, the Company recognized on its balance sheet ROU assets of approximately $32.8 million, with a corresponding operating lease liability of approximately $34.1 million, with an adjustment to remove the Company's existing deferred rent liability of approximately $1.3 million. |

| | | | | | | | | | | |

| Repayments of long-term debt, net of issuance costs | (4,688) | | | 0 | |

| | | |

| | | |

| Net proceeds from exercise of stock options | (57) | | | 0 | |

| Restricted stock awards issued, net of awards surrendered | (1,220) | | | (1,132) | |

| Proceeds from shares issued under direct stock purchase plan | 492 | | | 560 | |

| Payments for shares repurchased under share repurchase program | 0 | | | (73,226) | |

| Common dividends paid | (15,164) | | | (15,126) | |

| Net cash provided by financing activities | 579,732 | | | 422,944 | |

| Net increase in cash and cash equivalents | 472,703 | | | 320,403 | |

| Cash and cash equivalents at beginning of year | 1,296,636 | | | 150,974 | |

| Cash and cash equivalents at end of period | $ | 1,769,339 | | | $ | 471,377 | |

| Supplemental schedule of noncash activities | | | |

| | | |

| | | |

| Net increase in capital commitments relating to low income housing project investments | $ | 24,014 | | | $ | 14,394 | |

| | | |

| Right-of-use assets obtained in exchange for new lease obligations | $ | 0 | | | $ | 2,223 | |

| | | |

| | | |

| | | |

| | | |

The accompanying condensed notes are an integral part of these unaudited consolidated financial statements.

CONDENSED NOTES TO UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS

NOTE 1 - BASIS OF PRESENTATION

Independent Bank Corp. (the “Company”) is a state chartered, federally registered bank holding company, incorporated in 1985. The Company is the sole stockholder of Rockland Trust Company (“Rockland Trust” or the “Bank”), a Massachusetts trust company chartered in 1907.

All material intercompany balances and transactions have been eliminated in consolidation. Certain previously reported amounts have been reclassified to conform to the current year’s presentation.

The accompanying unaudited consolidated financial statements have been prepared in accordance with accounting principles generally accepted in the United States of America ("GAAP") for interim financial information and with the instructions to Form 10-Q and Article 10 of Regulation S-X. Accordingly, they do not include all of the information and notes required by GAAP for complete financial statements. In the opinion of management, all adjustments considered necessary for a fair presentation of the financial statements, primarily consisting of normal recurring adjustments, have been included. Results for the quarterthree months ended March 31, 20202021 are not necessarily indicative of the results that may be expected for the year ending December 31, 20202021 or any other interim period.

For further information, refer to the consolidated financial statements and notes thereto included in the Company’s Annual Report on Form 10-K for the year ended December 31, 2019,2020, filed with the Securities and Exchange Commission.Commission (the "2020 Form 10-K").

NOTE 2 - RECENT ACCOUNTING STANDARDS UPDATES

Financial Accounting Standards Board ("FASB") Accounting Standards Codification ("ASC") Topic 326 "Financial Instruments - Credit Losses" Update No. 2016-13.The standard was issued in June 2016 and has been amended three times by the FASB (collectively, the "updates"). The purpose of the updates is to provide financial statement users with more decision-useful information about the expected credit losses on financial instruments and other commitments to extend credit held by a reporting entity at each reporting date. To achieve this objective, these updates replace the incurred loss impairment methodology in current GAAP with a methodology, referred to as the current expected credit losses ("CECL") methodology, that reflects expected credit losses and requires consideration of a broader range of reasonable and supportable information to inform credit loss estimates. The updates affect loans, debt securities, trade receivables, net investments in leases, off-balance sheet credit exposures, reinsurance receivables, and any other financial assets not excluded from the scope that have the contractual right to receive cash. The Company adopted the CECL standard effective January 1, 2020.

The Company adopted the standard using the modified retrospective method for all financial assets measured at amortized cost, net investment in leases and off-balance sheet credit exposures. Results for reporting periods beginning after January 1, 2020 are presented under the CECL standard, while prior period results are presented under standards previously applicable under GAAP. The cumulative effect of the Company's adoption resulted in an immaterial increase to retained earnings as of the January 1, 2020 adoption date. This transition adjustment was a result of the change in allowance methodology, including the impact to the reserve on unfunded commitments resulting from the application of new guidance under CECL, as well as the day one gross-up of purchased credit deteriorated ("PCD") assets. The standard was adopted using the prospective transition approach for PCD assets that were previously classified as purchased credit impaired ("PCI") assets. As prescribed by the standard, management did not reassess whether PCI assets met the criteria of PCD assets at the date of adoption. On January 1, 2020, the amortized cost basis of the PCD assets were adjusted to reflect estimated credit losses, with the remaining non-credit related discount, calculated based on the adjusted amortized cost, and will be accreted into interest income on a straight line basis over the remaining contractual term of the asset. See Note 3 Securities and Note 4 Loans, Allowance for Credit Losses and Credit Quality for further details surrounding the Company's adoption of CECL, related accounting policy updates and full disclosures required under the standard.

FASB ASC Topic 848 "Reference Rate Reform" Update No. 2020-04. Update No. 2020-04 was issued in March 2020 to provide optional expedients and exceptions for applying generally accepted accounting principles (GAAP)GAAP to certain contracts, hedging relationships, and other transactions affected by reference rate reform if certain criteria are met. The amendments in this update apply only to contracts, hedging relationships, and other transactions that reference the London Interbank Offered Rate ("LIBOR") or another reference rate expected to be discontinued because of reference rate reform. The expedients and exceptions provided by the amendments dowill not apply to contract modifications made and hedging relationship entered into or evaluated after December 31, 2022, except for hedging relationships existing as of December 31, 2022 thatfor which an entity has elected certain optional expedients for and that are retained through the end of the hedging relationship. The amendments in this update are effective for all entities as of March 12, 2020 through December 31, 2022 and do not apply to contract modifications made after December 31, 2022. FASB ASC Topic 848 "Reference Rate Reform" Update No. 2021-01 was subsequently issued in January 2021 and expanded application of the optional expedients to derivative transactions affected by the discounting transition. The Company has not yet adopted the amendments in this updatethese updates and is

currently in the process of reviewing its contracts and existing processes in order to assess the risks and potential impact of the transition away from LIBOR.

NOTE 3 - SECURITIES

Investment securities are classified at the time of purchase as available for sale, held to maturity, trading, or equity. Classification is constantly re-evaluated for consistency with corporate goals and objectives. Trading and equity securities are recorded at fair value with subsequent changes in fair value recorded in earnings. Debt securities that management has the positive intent and ability to hold to maturity are classified as held to maturity and recorded at amortized cost. Securities not classified as held to maturity or trading are classified as available for sale and recorded at fair value, with changes in fair value excluded from earnings and reported in other comprehensive income, net of related tax. Purchase premiums and discounts are recognized in interest income, using the interest method, to arrive at periodic interest income at a constant effective yield, thereby reflecting the securities market yield. Gains and losses on the sale of securities are recorded on the trade date and are determined using the specific identification method.

Accrued interest receivable balances are excluded from the amortized cost of held to maturity securities and the fair value of available for sale securities and are included within Other Assets on the consolidated balance sheet. Management has elected not to measure an allowance for credit losses on these balances as the Company employs a timely write-off policy. It is the Company's policy that a security is placed on nonaccrual status at the time any principal or interest payments become 90 days delinquent, and interest earned but not collected for a security placed on non-accrual is reversed against interest income.

Allowance for Credit Losses - Available for Sale Securities

The Company's available for sale securities are carried at fair value. For available for sale securities in an unrealized loss position, management will first evaluate whether there is intent to sell, or if it is more likely than not that the Company will be required to sell a security prior to anticipated recovery of its amortized cost basis. If either of these criteria are met, the Company will record a write-down of the security's amortized cost basis to fair value through income. For those available for sale securities which do not meet the intent or requirement to sell criteria, management will evaluate whether the decline in fair value is a result of credit related matters or other factors. In performing this assessment, Management considers the creditworthiness of the issuer including whether the security is guaranteed by the U.S. Federal Government or other government agency, the extent to which fair value is less than amortized cost, and changes in credit rating during the period, among other factors. If this assessment indicates the existence of credit losses, the security will be written down to fair value, as determined by a discounted cash flow analysis. To the extent the estimated cash flows do not support the amortized cost, the deficiency is considered to be due to credit loss and is recognized in earnings.

Changes in the allowance for credit losses are recorded as a provision for (or reversal of) credit loss expense. Losses are charged against the allowance when the uncollectibility of a security is confirmed, or when either of the aforementioned criteria surrounding intent or requirement to sell have been met.

Allowance for Credit Losses - Held to Maturity Securities

The Company measures expected credit losses on held to maturity securities on a collective basis by major security type. Management classifies the held-to maturity portfolio into the following major security types: U.S. Government Agency, U.S. Treasury, Agency Mortgage-Backed Securities, Agency Collateralized Mortgage Obligations, Small Business Administration Pooled Securities, and Single Issuer Trust Preferred Securities. Securities in the Company's held to maturity portfolio are primarily guaranteed by either the U.S. Federal Government or other government sponsored agencies with a long history of no credit losses. As a result, Management has determined these securities to have a zero loss expectation and therefore does not estimate an allowance for credit losses on these securities.

Trading Securities

The Company had trading securities of $2.2$3.3 million and $2.8 million as of March 31, 20202021 and December 31, 2019.2020, respectively. These securities are held in a rabbi trust and will be used for future payments associated with the Company’s nonqualifiednon-qualified 401(k) Restoration Plan and NonqualifiedNon-qualified Deferred Compensation Plan.

Equity Securities

The Company had equity securities of $19.4$22.4 million and $21.3$22.1 million as of March 31, 20202021 and December 31, 2019,2020, respectively. These securities consist primarily of mutual funds held in a rabbi trust and will be used for future payments associated with the Company’s supplemental executive retirement plans.

The following table represents a summary of the gains and losses recognized within non-interest income and non-interest expense within the consolidated statements of income that relate to equity securities for the periods indicated:

|

| | | | | | | |

| | Three Months Ended |

| | March 31 |

| | 2020 | | 2019 |

| Net gains (losses) recognized during the period on equity securities | $ | (1,801 | ) | | $ | 907 |

|

| Less: net gains recognized during the period on equity securities sold during the period | 6 |

| | 3 |

|

| Unrealized gains (losses) recognized during the reporting period on equity securities still held at the reporting date | $ | (1,807 | ) | | $ | 904 |

|

| | | | | | | | | | | | | | | |

| Three Months Ended | | |

| March 31 | | |

| 2021 | | 2020 | | | | |

| Dollars in thousands |

| Net gains (losses) recognized during the period on equity securities | $ | 316 | | | $ | (1,801) | | | | | |

| Less: net gains recognized during the period on equity securities sold during the period | 29 | | | 6 | | | | | |

| Unrealized gains (losses) recognized during the reporting period on equity securities still held at the reporting date | $ | 287 | | | $ | (1,807) | | | | | |

Available for Sale Securities

The following table summarizes the amortized cost, allowance for credit losses, and fair value of available for sale securities and the corresponding amounts of gross unrealized gains and losses recognized in accumulated other comprehensive income(loss)income (loss) as of the dates indicated:

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | March 31, 2021 | | December 31, 2020 |

| | Amortized

Cost | | Gross

Unrealized

Gains | | Gross Unrealized

Losses | | Allowance for credit losses | | Fair

Value | | Amortized

Cost | | Gross

Unrealized

Gains | | Gross Unrealized

Losses | | Allowance for credit losses | | Fair

Value |

| | (Dollars in thousands) |

| | | | | | | | | | | | | | | | | | | |

| U.S. government agency securities | $ | 169,091 | | | $ | 1,209 | | | $ | (2,244) | | | $ | 0 | | | $ | 168,056 | | | $ | 22,476 | | | $ | 1,640 | | | $ | 0 | | | $ | 0 | | | $ | 24,116 | |

| Agency mortgage-backed securities | 286,512 | | | 7,561 | | | (3,898) | | | 0 | | | 290,175 | | | 224,293 | | | 9,337 | | | (1) | | | 0 | | | 233,629 | |

| Agency collateralized mortgage obligations | 78,952 | | | 2,688 | | | (11) | | | 0 | | | 81,629 | | | 88,687 | | | 3,083 | | | (87) | | | 0 | | | 91,683 | |

| | | | | | | | | | | | | | | | | | | |

| State, county, and municipal securities | 540 | | | 15 | | | 0 | | | 0 | | | 555 | | | 790 | | | 17 | | | 0 | | | 0 | | | 807 | |

| Single issuer trust preferred securities issued by banks | 489 | | | 0 | | | (1) | | | 0 | | | 488 | | | 489 | | | 0 | | | (1) | | | 0 | | | 488 | |

| Pooled trust preferred securities issued by banks and insurers | 1,412 | | | 0 | | | (348) | | | 0 | | | 1,064 | | | 1,429 | | | 0 | | | (373) | | | 0 | | | 1,056 | |

| Small business administration pooled securities | 56,171 | | | 2,075 | | | 0 | | | 0 | | | 58,246 | | | 57,289 | | | 3,792 | | | 0 | | | 0 | | | 61,081 | |

| Total available for sale securities | $ | 593,167 | | | $ | 13,548 | | | $ | (6,502) | | | $ | 0 | | | $ | 600,213 | | | $ | 395,453 | | | $ | 17,869 | | | $ | (462) | | | $ | 0 | | | $ | 412,860 | |

| | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | |

|

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | March 31, 2020 | | December 31, 2019 |

| | Amortized

Cost | | Gross

Unrealized

Gains | | Gross Unrealized

Losses | | Allowance for credit losses | | Fair

Value | | Amortized

Cost | | Gross

Unrealized

Gains | | Gross Unrealized

Losses | | Fair

Value |

| | (Dollars in thousands) |

| U.S. government agency securities | $ | 22,474 |

| | $ | 1,818 |

| | $ | — |

| | $ | — |

| | $ | 24,292 |

| | $ | 32,473 |

| | $ | 642 |

| | $ | — |

| | $ | 33,115 |

|

| Agency mortgage-backed securities | 247,675 |

| | 11,110 |

| | (1 | ) | | — |

| | 258,784 |

| | 243,548 |

| | 3,456 |

| | (4 | ) | | 247,000 |

|

| Agency collateralized mortgage obligations | 83,183 |

| | 4,027 |

| | — |

| | — |

| | 87,210 |

| | 87,305 |

| | 1,225 |

| | (19 | ) | | 88,511 |

|

| State, county, and municipal securities | 1,126 |

| | 18 |

| | — |

| | — |

| | 1,144 |

| | 1,377 |

| | 19 |

| | — |

| | 1,396 |

|

| Single issuer trust preferred securities issued by banks | 489 |

| | — |

| | (53 | ) | | — |

| | 436 |

| | 488 |

| | 5 |

| | — |

| | 493 |

|

| Pooled trust preferred securities issued by banks and insurers | 1,443 |

| | — |

| | (434 | ) | | — |

| | 1,009 |

| | 1,488 |

| | — |

| | (374 | ) | | 1,114 |

|

| Small business administration pooled securities | 63,062 |

| | 1,359 |

| | — |

| | — |

| | 64,421 |

| | 54,024 |

| | 771 |

| | — |

| | 54,795 |

|

| Total available for sale securities | $ | 419,452 |

| | $ | 18,332 |

| | $ | (488 | ) | | $ | — |

| | $ | 437,296 |

| | $ | 420,703 |

| | $ | 6,118 |

| | $ | (397 | ) | | $ | 426,424 |

|

As noted in the table above, theThe Company did not record an allowancea provision for estimated credit losses on any available for sale securities during the three months ended March 31, 2021 and 2020. Excluded from the table above is accrued interest on available for sale securities of $1.6$2.0 million and $1.2 million as of March 31, 2021 and December 31, 2020, respectively, which is included within Other Assetsother assets on the consolidated balance sheet.sheets. Additionally, the Company did not record any write-offs of accrued interest income on available for sale securities during the three months ended March 31, 2021 and 2020. NoFurthermore, 0 securities held by the Company were delinquent on contractual payments as of March 31, 2020, nor were any securities placed on non-accrual status during the three months then ended.as of March 31, 2021 and December 31, 2020.

When securities are sold, the adjusted cost of the specific security sold is used to compute the gain or loss on the sale. The Company had no sales of securities available for sale during the three months ended March 31, 20202021 and 2019,2020, and therefore no gains or losses were realized during the periods presented.

The following table showstables show the gross unrealized losses and fair value of the Company’s available for sale securities which are in an unrealized loss position, and for which the Company has not recorded an allowancea provision for credit losses as of March 31, 2020.losses. These available for sale securities are aggregated by major security type and length of time that individual securities have been in a continuous unrealized loss position:

|

| | | | | | | | | | | | | | | | | | | | | | | | | | |

| | March 31, 2020 |

| | | | Less than 12 months | | 12 months or longer | | Total |

| | # of holdings | | Fair Value | | Unrealized Losses | | Fair Value | | Unrealized Losses | | Fair Value | | Unrealized Losses |

| | (Dollars in thousands) |

| Agency mortgage-backed securities | 1 |

| | 86 |

| | (1 | ) | | — |

| | — |

| | 86 |

| | (1 | ) |

| Single issuer trust preferred securities issued by banks and insurers | 1 |

| | 436 |

| | (53 | ) | | — |

| | — |

| | 436 |

| | (53 | ) |

| Pooled trust preferred securities issued by banks and insurers | 1 |

| | — |

| | — |

| | 1,009 |

| | (434 | ) | | 1,009 |

| | (434 | ) |

| Total temporarily impaired available for sale securities | 3 |

| | $ | 522 |

| | $ | (54 | ) | | $ | 1,009 |

| | $ | (434 | ) | | $ | 1,531 |

| | $ | (488 | ) |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | March 31, 2021 |

| | | | Less than 12 months | | 12 months or longer | | Total |

| | # of

holdings | | Fair

Value | | Unrealized

Losses | | Fair

Value | | Unrealized

Losses | | Fair

Value | | Unrealized

Losses |

| | (Dollars in thousands) |

| U.S. government agency securities | 4 | | | $ | 113,171 | | | $ | (2,244) | | | $ | 0 | | | $ | 0 | | | $ | 113,171 | | | $ | (2,244) | |

| Agency mortgage-backed securities | 8 | | | 98,873 | | | (3,898) | | | 0 | | | 0 | | | 98,873 | | | (3,898) | |

| Agency collateralized mortgage obligations | 1 | | | 9,519 | | | (11) | | | 0 | | | 0 | | | 9,519 | | | (11) | |

| | | | | | | | | | | | | |

| Single issuer trust preferred securities issued by banks and insurers | 1 | | | 0 | | | 0 | | | 488 | | | (1) | | | 488 | | | (1) | |

| Pooled trust preferred securities issued by banks and insurers | 1 | | | 0 | | | 0 | | | 1,064 | | | (348) | | | 1,064 | | | (348) | |

| | | | | | | | | | | | | |

| Total impaired available for sale securities | 15 | | | $ | 221,563 | | | $ | (6,153) | | | $ | 1,552 | | | $ | (349) | | | $ | 223,115 | | | $ | (6,502) | |

| | | | | | | | | | | | | |

| December 31, 2020 |

| | | Less than 12 months | | 12 months or longer | | Total |

| # of

holdings | | Fair

Value | | Unrealized

Losses | | Fair

Value | | Unrealized

Losses | | Fair

Value | | Unrealized

Losses |

| (Dollars in thousands) |

| | | | | | | | | | | | | |

| Agency mortgage-backed securities | 3 | | | 437 | | | (1) | | | 0 | | | 0 | | | 437 | | | (1) | |

| Agency collateralized mortgage obligations | 2 | | | 23,323 | | | (87) | | | 0 | | | 0 | | | 23,323 | | | (87) | |

| | | | | | | | | | | | | |

| Single issuer trust preferred securities issued by banks and insurers | 1 | | | 488 | | | (1) | | | 0 | | | 0 | | | 488 | | | (1) | |

| Pooled trust preferred securities issued by banks and insurers | 1 | | | 0 | | | 0 | | | 1,056 | | | (373) | | | 1,056 | | | (373) | |

| | | | | | | | | | | | | |

| Total impaired available for sale securities | 7 | | | $ | 24,248 | | | $ | (89) | | | $ | 1,056 | | | $ | (373) | | | $ | 25,304 | | | $ | (462) | |

The Company does not intend to sell these investments and has determined, based upon available evidence, that it is more likely than not that the Company will not be required to sell each security before the recovery of its amortized cost basis. In addition, management does not believe that any of the securities are impaired due to reasons of credit quality. As a result, the Company did not recognize an allowancea provision for credit losses on these investments duringfor the three months ended March 31, 2021 and 2020. The Company made this determination by reviewing various qualitative and quantitative factors regarding each investment category, such as current market conditions, extent and nature of changes in fair value, issuer rating changes and trends, volatility of earnings, and current analysts’ evaluations.

As a result of the Company’s review of these qualitative and quantitative factors, the causes of the impairments listed in the table above by category arewere as follows at March 31, 2020:

| |

• | Agency Mortgage-Backed Securities: These portfolios have contractual terms that generally do not permit the issuer to settle the securities at a price less than the current par value of the investment. The decline in market value of these securities is attributable to changes in interest rates and not credit quality. Additionally, these securities are implicitly guaranteed by the U.S. Government or one of its agencies.

|

| |

• | Single Issuer Trust Preferred Securities: This portfolio consists of one security, which is investment grade. The unrealized loss on this security is attributable to the illiquid nature of the trust preferred market in the current economic environment. Management evaluates various financial metrics for the issuers, including regulatory capital ratios of the issuers.

|

| |

• | Pooled Trust Preferred Securities: This portfolio consists of one below investment grade security which is performing. The unrealized loss on this security is attributable to the illiquid nature of the trust preferred market in the current economic and regulatory environment. Management evaluates collateral credit and instrument structure, including current and expected deferral and default rates and timing. In addition, discount rates are determined by evaluating comparable spreads observed currently in the market for similar instruments.

|

•Pooled Trust Preferred Securities: This portfolio consists of one below investment grade security which is performing. The unrealized loss on this security is attributable to the illiquid nature of the trust preferred market in the current economic and regulatory environment. Management evaluates collateral credit and instrument

structure, including current and expected deferral and default rates and timing. In addition, discount rates are determined by evaluating comparable spreads observed currently in the market for similar instruments.

Held to Maturity Securities

The following table summarizes the amortized cost, fair value and allowance for credit losses of held to maturity securities and the corresponding amounts of gross unrealized gains and losses recognized in accumulated other comprehensive income(loss)income (loss) as of the dates indicated:

|

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | March 31, 2020 | | December 31, 2019 |

| | Amortized

Cost | | Gross

Unrealized

Gains | | Gross Unrealized

Losses | | Allowance for credit losses | | Fair

Value | | Amortized

Cost | | Gross

Unrealized

Gains | | Gross Unrealized

Losses | | Fair

Value |

| | (Dollars in thousands) |

| U.S. government agency securities | $ | — |

| | $ | — |

| | $ | — |

| | $ | — |

| | $ | — |

| | $ | 12,874 |

| | $ | 123 |

| | $ | — |

| | $ | 12,997 |

|

| U.S. Treasury securities | 4,029 |

| | 110 |

| | — |

| | — |

| | 4,139 |

| | 4,032 |

| | 21 |

| | — |

| | 4,053 |

|

| Agency mortgage-backed securities | 463,632 |

| | 18,864 |

| | (133 | ) | | — |

| | 482,363 |

| | 397,414 |

| | 8,445 |

| | (57 | ) | | 405,802 |

|

| Agency collateralized mortgage obligations | 277,921 |

| | 11,981 |

| | — |

| | — |

| | 289,902 |

| | 293,662 |

| | 4,501 |

| | (849 | ) | | 297,314 |

|

| Single issuer trust preferred securities issued by banks | 1,500 |

| | — |

| | (10 | ) | | — |

| | 1,490 |

| | 1,500 |

| | — |

| | (10 | ) | | 1,490 |

|

| Small business administration pooled securities | 30,716 |

| | 745 |

| | — |

| | — |

| | 31,461 |

| | 31,324 |

| | 338 |

| | (55 | ) | | 31,607 |

|

| Total held to maturity securities | $ | 777,798 |

| | $ | 31,700 |

| | $ | (143 | ) | | $ | — |

| | $ | 809,355 |

| | $ | 740,806 |

| | $ | 13,428 |

| | $ | (971 | ) | | $ | 753,263 |

|

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | March 31, 2021 | | December 31, 2020 |

| | Amortized

Cost | | Gross

Unrealized

Gains | | Gross Unrealized

Losses | | Allowance for credit losses | | Fair

Value | | Amortized

Cost | | Gross

Unrealized

Gains | | Gross Unrealized

Losses | | Allowance for credit losses | | Fair

Value |

| | (Dollars in thousands) |

| | | | | | | | | | | | | | | | | | | |

| U.S. Treasury securities | $ | 4,014 | | | $ | 43 | | | $ | 0 | | | $ | 0 | | | $ | 4,057 | | | $ | 4,017 | | | $ | 60 | | | $ | 0 | | | $ | 0 | | | $ | 4,077 | |

| Agency mortgage-backed securities | 417,811 | | | 13,069 | | | (4,252) | | | 0 | | | 426,628 | | | 356,085 | | | 18,036 | | | 0 | | | 0 | | | 374,121 | |

| Agency collateralized mortgage obligations | 355,686 | | | 7,474 | | | (2,158) | | | 0 | | | 361,002 | | | 335,993 | | | 8,466 | | | (340) | | | 0 | | | 344,119 | |

| | | | | | | | | | | | | | | | | | | |

| Single issuer trust preferred securities issued by banks | 1,500 | | | 8 | | | 0 | | | 0 | | | 1,508 | | | 1,500 | | | 0 | | | (2) | | | 0 | | | 1,498 | |

| Small business administration pooled securities | 26,518 | | | 717 | | | 0 | | | 0 | | | 27,235 | | | 26,917 | | | 1,445 | | | 0 | | | 0 | | | 28,362 | |

| | | | | | | | | | | | | | | | | | | |

| Total held to maturity securities | $ | 805,529 | | | $ | 21,311 | | | $ | (6,410) | | | $ | 0 | | | $ | 820,430 | | | $ | 724,512 | | | $ | 28,007 | | | $ | (342) | | | $ | 0 | | | $ | 752,177 | |

As noted in the table above, theThe Company did not record an allowancea provision for estimated credit losses on any held to maturity securities during the three months ended March 31, 2021 and 2020. Excluded from the table above is accrued interest on held to maturity securities of $2.0$1.6 million and $1.5 million as of March 31, 2021 and December 31, 2020, respectively, which is included within Other Assetsother assets on the consolidated balance sheet.sheets. Additionally, the Company did not record any write-offs of accrued interest income on held to maturity securities during the three months ended March 31, 2021 and 2020. NoFurthermore, 0 securities held by the Company were delinquent on contractual payments as of March 31, 2020, nor were any securities placed on non-accrual status during the three months then ended.as of March 31, 2021 and December 31, 2020.

When securities are sold, the adjusted cost of the specific security sold is used to compute the gain or loss on the sale. The Company had no sales of held to maturity securities during the three months ended March 31, 20202021 and 2019,2020, and therefore no gains or losses were realized during the periods presented.

The Company monitors the credit quality of held to maturity securities through the use of credit ratings. Credit ratings are monitored by the Company on at least a quarterly basis. As of March 31, 2020,2021, all held to maturity securities held by the Company were rated investment grade or higher.

The actual maturities of certain available for sale or held to maturity securities may differ from the contractual maturities because borrowers may have the right to call or prepay obligations with or without call or prepayment penalties. A schedule of the contractual maturities of available for sale and held to maturity securities as of March 31, 20202021 is presented below:

| | | | Due in one year or less | | Due after one year to five years | | Due after five to ten years | | Due after ten years | | Total | | Due in one year or less | | Due after one year to five years | | Due after five to ten years | | Due after ten years | | Total |

| | Amortized Cost | | Fair Value | | Amortized Cost | | Fair Value | | Amortized Cost | | Fair Value | | Amortized Cost | | Fair Value | | Amortized Cost | | Fair Value | | Amortized

Cost | | Fair

Value | | Amortized

Cost | | Fair

Value | | Amortized

Cost | | Fair

Value | | Amortized

Cost | | Fair

Value | | Amortized

Cost | | Fair

Value |

| | (Dollars in thousands) | | (Dollars in thousands) |

| Available for sale securities | | | | | | | | | | | | | | | | | | | | Available for sale securities | |

| U.S. government agency securities | $ | — |

| | $ | — |

| | $ | 10,002 |

| | $ | 10,351 |

| | $ | 12,472 |

| | $ | 13,941 |

| | $ | — |

| | $ | — |

| | $ | 22,474 |

| | $ | 24,292 |

| U.S. government agency securities | $ | 10,001 | | | $ | 10,180 | | | $ | 0 | | | $ | 0 | | | $ | 159,090 | | | $ | 157,876 | | | $ | 0 | | | $ | 0 | | | $ | 169,091 | | | $ | 168,056 | |

| Agency mortgage-backed securities | — |

| | — |

| | 72,092 |

| | 75,268 |

| | 41,885 |

| | 44,607 |

| | 133,698 |

| | 138,909 |

| | 247,675 |

| | 258,784 |

| Agency mortgage-backed securities | 0 | | | 0 | | | 80,169 | | | 82,809 | | | 98,747 | | | 96,914 | | | 107,596 | | | 110,452 | | | 286,512 | | | 290,175 | |

| Agency collateralized mortgage obligations | — |

| | — |

| | — |

| | — |

| | — |

| | — |

| | 83,183 |

| | 87,210 |

| | 83,183 |

| | 87,210 |

| Agency collateralized mortgage obligations | 0 | | | 0 | | | 0 | | | 0 | | | 0 | | | 0 | | | 78,952 | | | 81,629 | | | 78,952 | | | 81,629 | |

| | State, county, and municipal securities | 250 |

| | 250 |

| | 687 |

| | 691 |

| | 189 |

| | 203 |

| | — |

| | — |

| | 1,126 |

| | 1,144 |

| State, county, and municipal securities | 350 | | | 351 | | | 0 | | | 0 | | | 190 | | | 204 | | | 0 | | | 0 | | | 540 | | | 555 | |

| Single issuer trust preferred securities issued by banks | — |

| | — |

| | — |

| | — |

| | — |

| | — |

| | 489 |

| | 436 |

| | 489 |

| | 436 |

| Single issuer trust preferred securities issued by banks | 0 | | | 0 | | | 0 | | | 0 | | | 0 | | | 0 | | | 489 | | | 488 | | | 489 | | | 488 | |

| Pooled trust preferred securities issued by banks and insurers | — |

| | — |

| | — |

| | — |

| | — |

| | — |

| | 1,443 |

| | 1,009 |

| | 1,443 |

| | 1,009 |

| Pooled trust preferred securities issued by banks and insurers | 0 | | | 0 | | | 0 | | | 0 | | | 0 | | | 0 | | | 1,412 | | | 1,064 | | | 1,412 | | | 1,064 | |

| Small business administration pooled securities | — |

| | — |

| | — |

| | — |

| | — |

| | — |

| | 63,062 |

| | 64,421 |

| | 63,062 |

| | 64,421 |

| Small business administration pooled securities | 0 | | | 0 | | | 0 | | | 0 | | | 0 | | | 0 | | | 56,171 | | | 58,246 | | | 56,171 | | | 58,246 | |

| Total available for sale securities | $ | 250 |

| | $ | 250 |

| | $ | 82,781 |

| | $ | 86,310 |

| | $ | 54,546 |

| | $ | 58,751 |

| | $ | 281,875 |

| | $ | 291,985 |

| | $ | 419,452 |

| | $ | 437,296 |

| Total available for sale securities | $ | 10,351 | | | $ | 10,531 | | | $ | 80,169 | | | $ | 82,809 | | | $ | 258,027 | | | $ | 254,994 | | | $ | 244,620 | | | $ | 251,879 | | | $ | 593,167 | | | $ | 600,213 | |

| Held to maturity securities | | | | | | | | | | | | | | | | | | | | Held to maturity securities | | | | | | | | | | | | | | | | | | | |

| | U.S. Treasury securities | $ | — |

| | $ | — |

| | $ | 4,029 |

| | $ | 4,139 |

| | $ | — |

| | $ | — |

| | $ | — |

| | $ | — |

| | $ | 4,029 |

| | $ | 4,139 |

| U.S. Treasury securities | $ | 4,014 | | | $ | 4,057 | | | $ | 0 | | | $ | 0 | | | $ | 0 | | | $ | 0 | | | $ | 0 | | | $ | 0 | | | $ | 4,014 | | | $ | 4,057 | |

| Agency mortgage-backed securities | 8,619 |

| | 8,715 |

| | 1,902 |

| | 1,951 |

| | 48,123 |

| | 50,345 |

| | 404,988 |

| | 421,352 |

| | 463,632 |

| | 482,363 |

| Agency mortgage-backed securities | 0 | | | 0 | | | 4,614 | | | 4,869 | | | 128,958 | | | 127,901 | | | 284,239 | | | 293,858 | | | 417,811 | | | 426,628 | |

| Agency collateralized mortgage obligations | — |

| | — |

| | — |

| | — |

| | — |

| | — |

| | 277,921 |

| | 289,902 |

| | 277,921 |

| | 289,902 |

| Agency collateralized mortgage obligations | 0 | | | 0 | | | 0 | | | 0 | | | 0 | | | 0 | | | 355,686 | | | 361,002 | | | 355,686 | | | 361,002 | |

| | Single issuer trust preferred securities issued by banks | — |

| | — |

| | — |

| | — |

| | 1,500 |

| | 1,490 |

| | — |

| | — |

| | 1,500 |

| | 1,490 |

| Single issuer trust preferred securities issued by banks | 0 | | | 0 | | | 0 | | | 0 | | | 1,500 | | | 1,508 | | | 0 | | | 0 | | | 1,500 | | | 1,508 | |

| Small business administration pooled securities | — |

| | — |

| | — |

| | — |

| | — |

| | — |

| | 30,716 |

| | 31,461 |

| | 30,716 |

| | 31,461 |

| Small business administration pooled securities | 0 | | | 0 | | | 0 | | | 0 | | | 0 | | | 0 | | | 26,518 | | | 27,235 | | | 26,518 | | | 27,235 | |

| | Total held to maturity securities | $ | 8,619 |

| | $ | 8,715 |

| | $ | 5,931 |

| | $ | 6,090 |

| | $ | 49,623 |

| | $ | 51,835 |

| | $ | 713,625 |

| | $ | 742,715 |

| | $ | 777,798 |

| | $ | 809,355 |

| Total held to maturity securities | $ | 4,014 | | | $ | 4,057 | | | $ | 4,614 | | | $ | 4,869 | | | $ | 130,458 | | | $ | 129,409 | | | $ | 666,443 | | | $ | 682,095 | | | $ | 805,529 | | | $ | 820,430 | |

| Total | $ | 8,869 |

| | $ | 8,965 |

| | $ | 88,712 |

| | $ | 92,400 |

| | $ | 104,169 |

| | $ | 110,586 |

| | $ | 995,500 |

| | $ | 1,034,700 |

| | $ | 1,197,250 |

| | $ | 1,246,651 |

| Total | $ | 14,365 | | | $ | 14,588 | | | $ | 84,783 | | | $ | 87,678 | | | $ | 388,485 | | | $ | 384,403 | | | $ | 911,063 | | | $ | 933,974 | | | $ | 1,398,696 | | | $ | 1,420,643 | |

Included in the table above are $4.1$3.3 million of callable securities at March 31, 2020.2021.

The carrying value of securities pledged to secure public funds, trust deposits, and for other purposes, as required or permitted by law, was $459.5$420.2 million and $375.5$419.6 million at March 31, 20202021 and December 31, 2019,2020, respectively.

At March 31, 20202021 and December 31, 2019,2020, the Company had 0 investments in obligations of individual states, counties, or municipalities which exceeded 10% of consolidated stockholders’ equity.