UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-Q

☒ QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE

SECURITIES EXCHANGE ACT OF 1934

For the quarterly period ended June 30, 2022Quarterly Period Ended March 31, 2023

OR-OR-

☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF

THE SECURITIES EXCHANGE ACT OF 1934

DPL Inc.

(an Ohio corporation)

Commission File Number 1-9052

1065 Woodman Drive(Exact name of registrant as specified in its charter)

Dayton, Ohio 45432

| | | | | |

| Ohio |

937-259-7215

IRS Employer Identification No. 31-1163136

|

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) |

| 1065 Woodman Drive | |

| Dayton, Ohio | 45432 |

| (Address of principal executive offices) | (Zip Code) |

| Registrant's telephone number, including area code: | (937) 259-7215 |

Commission File Number 1-2385

THE DAYTON POWER AND LIGHT COMPANY

(Exact name of registrant as specified in its charter)

d/b/a AES Ohio

(an Ohio corporation)

| | | | | |

| Ohio |

Commission File Number 1-2385

1065 Woodman Drive

Dayton, Ohio 45432

937-259-7215

IRS Employer Identification No. 31-0258470

|

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) |

| 1065 Woodman Drive | |

| Dayton, Ohio | 45432 |

| (Address of principal executive offices) | (Zip Code) |

| Registrant's telephone number, including area code: | (937) 259-7215 |

| | | | | | | | |

| Securities registered pursuant to Section 12(b) of the Act: |

| Title of Each Class | Trading Symbol(s) | Name of Each Exchange on Which Registered |

| N/A | N/A | N/A |

| | |

Indicate by check mark whether each registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

| | | | | | | | | | | | | | |

| DPL Inc. | Yes | ☐ | No | ☑☒ |

| The Dayton Power and Light Company | Yes | ☐ | No | ☑☒ |

DPL Inc. and The Dayton Power and Light Company are voluntary filers. DPL Inc. and The Dayton Power and Light Company have filed all applicable reports under Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months.

Indicate by check mark whether each registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

| | | | | | | | | | | | | | |

| DPL Inc. | Yes | ☑☒ | No | ☐ |

| The Dayton Power and Light Company | Yes | ☑☒ | No | ☐ |

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer”, “smaller reporting company” and "emerging growth company" in Rule 12b-2 of the Exchange Act.

| | | | | | | | | | | | | | | | | |

| Large

accelerated

Filer | Accelerated

Filer | Non-accelerated Filer | Smaller

reporting

company | Emerging growth company |

| DPL Inc. | ☐ | ☐ | ☑☒ | ☐ | ☐ |

| Large

accelerated

Filer | Accelerated

Filer | Non-accelerated Filer | Smaller

reporting

company | Emerging growth company |

| The Dayton Power and Light Company | ☐ | ☐ | ☑☒ | ☐ | ☐ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act.

| | | | | |

| DPL Inc. | ☐ |

| The Dayton Power and Light Company | ☐ |

Indicate by check mark whether each registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

| | | | | | | | | | | | | | |

| DPL Inc. | Yes | ☐ | No | ☑☒ |

| The Dayton Power and Light Company | Yes | ☐ | No | ☑☒ |

All of the outstanding common stock of DPL Inc. is indirectly owned by The AES Corporation. All of the outstanding common stock of The Dayton Power and Light Company is owned by DPL Inc.

As of AugustMay 4, 2022,2023, each registrant had the following shares of common stock outstanding:

| | | | | | | | | | | | | | |

| Registrant | | Description | | Shares Outstanding |

| | | | |

| DPL Inc. | | Common Stock, no par value | | 1 |

| | | | |

| The Dayton Power and Light Company | | Common Stock, $0.01 par value | | 41,172,173 |

This combined Form 10-Q is separately filed by DPL Inc. and The Dayton Power and Light Company. Information contained herein relating to any individual registrant is filed by such registrant on its own behalf. Each registrant makes no representation as to information relating to a registrant other than itself.

DPL Inc. and AES Ohio

Quarter Ended June 30, 2022March 31, 2023

| | | | | | | | |

| Table of Contents | Page No. |

| Glossary of Terms | |

Forward-LookingForward–Looking Statements | |

| Part I Financial Information | |

| Item 1 | Financial Statements – DPL Inc. and AES Ohio (Unaudited) | |

| DPL Inc. | |

| Condensed Consolidated Statements of Operations | |

| Condensed Consolidated Statements of Comprehensive Income | |

| Condensed Consolidated Balance Sheets | |

| Condensed Consolidated Statements of Cash Flows | |

| Condensed Consolidated Statements of Shareholder's Deficit | |

| Notes to Unaudited Condensed Consolidated Financial Statements | |

| Note 1 – Overview and Summary of Significant Accounting PoliciesOVERVIEW AND SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES | |

| Note 2 – Regulatory Matters | |

| Note 3 – Fair Value | |

| Note 4 – Derivative Instruments and Hedging ActivitiesREGULATORY MATTERS | |

| Note 53 – DebtFAIR VALUE | |

| Note 64 – Income TaxesDERIVATIVE INSTRUMENTS AND HEDGING ACTIVITIES | |

| Note 75 – Benefit PlansDEBT | |

| Note 86 – Commitments and ContingenciesINCOME TAXES | |

| Note 7 – BENEFIT PLANS | |

| Note 8 – SHAREHOLDER'S DEFICIT | |

| Note 9 – Business SegmentsCOMMITMENTS AND CONTINGENCIES | |

| Note 10 – RevenueBUSINESS SEGMENTS | |

| Note 11 – Discontinued OperationsREVENUES | |

| Note 12 – Risks and UncertaintiesRISKS AND UNCERTAINTIES | |

| | |

| | |

| AES Ohio | |

| Condensed Statements of Operations | |

| Condensed Statements of Comprehensive Income | |

| Condensed Balance Sheets | |

| Condensed Statements of Cash Flows | |

| Condensed Statements of Shareholder's Equity | |

| Notes to Unaudited Condensed Financial Statements | |

| Note 1 – Overview and Summary of Significant Accounting PoliciesOVERVIEW AND SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES | |

| Note 2 – Regulatory MattersREGULATORY MATTERS | |

| Note 3 – FAIR VALUE | |

| Note 34 – Fair ValueDEBT | |

| Note 45 – DebtINCOME TAXES | |

| Note 56 – Income TaxesBENEFIT PLANS | |

| Note 6 – Benefit Plans | |

| Note 7 – Commitments and ContingenciesSHAREHOLDER'S EQUITY | |

| Note 8 – RevenueCOMMITMENTS AND CONTINGENCIES | |

| Note 9 – REVENUES | |

| Note 910 – Risks and UncertaintiesRISKS AND UNCERTAINTIES | |

| | |

| | |

| Item 2 | Management's Discussion and Analysis of Financial Condition and Results of Operations | |

| Executive Summary | |

| Results of Operations – DPL | |

| Results of Operations by Segment – DPL | |

| Results of Operations – AES Ohio | |

| Key Trends and Uncertainties | |

| Capital Resources and Liquidity | |

| Critical Accounting Policies and Estimates | |

| Item 3 | Quantitative and Qualitative Disclosures about Market Risk | |

| Item 4 | Controls and Procedures | |

| | |

DPL Inc. and AES Ohio

Quarter Ended March 31, 2023

| | | | | | | | |

| Table of Contents | Page No. |

| Part II Other Information | |

| Item 1 | Legal Proceedings | |

| Item 1A | Risk Factors | |

| Item 2 | Unregistered SalesSale of Equity Securities and Use of Proceeds | |

| Item 3 | Defaults Upon Senior Securities | |

| Item 4 | Mine Safety Disclosures | |

| Item 5 | Other Information | |

| Item 6 | Exhibits | |

| Signatures | |

GLOSSARY OF TERMS

The following select terms, abbreviations or acronyms are used in this Form 10-Q:

| | | | | |

| Term | Definition |

| 401(k) Plans | AES Ohio sponsors two defined contribution plans, The Dayton Power and Light Company Employee Savings Plan and The Dayton Power and Light Company Savings Plan for Collective Bargaining Employees |

| 2017 ESP | DP&L's ESP - approved October 20, 2017, effective November 1, 2017 |

| AES | The AES Corporation - a global power company and the ultimate parent company of DPL |

| AES Ohio | The Dayton Power and Light Company, which does business as AES Ohio |

| AES Ohio Credit Agreement | $175.0250.0 million AES Ohio Amended and Restated Credit Agreement, dated as of June 19, 2019 |

| AES Ohio Generation | AES Ohio Generation, LLC - a wholly-owned subsidiary of DPL, which previously operated EGUs and made wholesale sales |

| |

| AOCI | Accumulated Other Comprehensive Income |

| AOCL | Accumulated Other Comprehensive Loss |

| ASU | Accounting Standards Update |

| BIL | Bipartisan Infrastructure Law (Infrastructure Investment and Jobs Act) - the congressional act passed in November 2021 |

| CAA | U.S. Clean Air Act - the congressional act that directs the EPA’s regulation of stationary and mobile sources of air pollution to protect air quality and stratospheric ozone |

| CCR | Coal Combustion Residuals |

| Conesville | AES Ohio Generation's interest in Unit 4 at the Conesville EGU. This was sold on June 5, 2020. |

| COVID-19 | The disease caused by the novel coronavirus that resulted in a global pandemic beginning in 2020. |

| |

| DPL | DPL Inc. and its consolidated subsidiaries |

| DPL Credit Agreement | $90.040.0 million DPL Inc. Amended and Restated Credit Agreement, dated as of June 19, 2019 |

| DP&L | The Dayton Power and Light Company - the principal subsidiary of DPL and a public utility that delivers electricity to residential, commercial, industrial and governmental customers in a 6,000-square mile area of West Central Ohio. DP&L does business as AES Ohio. |

| EBITDA | Earnings before interest, taxes, depreciation and amortization |

| EGU | Electric Generating Unit |

| EPA | U.S. Environmental Protection Agency |

ERISA | The Employee Retirement Income Security Act of 1974 |

| ESP | The Electric Security Plan - a plan that a utility must file with the PUCO to establish SSO rates pursuant to Ohio law |

| ESP 1 | ESP originally approved by PUCO order dated June 24, 2009. After DP&L withdrew its 2017 ESP Application, the PUCO approved DP&L's request to revert to rates based on its ESP 1 rate plan effective December 19, 2019. DP&L is currently operating under this ESP 1 plan. |

| ESP 4 | DP&L's ESP filed September 26, 2022. DP&L expects approval in 2023. |

| FASB | Financial Accounting Standards Board |

| FASC | FASB Accounting Standards Codification |

| FERC | Federal Energy Regulatory Commission |

| Form 10-K | DPL’s and DP&L’s combined Annual Report on Form 10-K for the fiscal year ended December 31, 2021,2022, which was filed on February 28, 2022March 1, 2023 |

| First and Refunding Mortgage | DP&L’s First and Refunding Mortgage, dated October 1, 1935, as amended, with the Bank of New York Mellon as Trustee |

| GAAP | Generally Accepted Accounting Principles in the United States of America |

| |

| kWh | Kilowatt-hours - a measure of electrical energy equivalent to a power consumption of 1,000 watts for 1 hour |

| LIBOR | London Inter-Bank Offered Rate |

| Master Trust | DP&L established a Master Trust to hold assets that could be used for the benefit of employees participating in employee benefit plans |

| MATS | Mercury and Air Toxics Standards - the EPA’s rules for existing and new power plants under Section 112 of the CAA |

Merger | The merger of DPL and Dolphin Sub, Inc., a wholly-owned subsidiary of AES. On November 28, 2011, DPL became a wholly-owned subsidiary of AES. |

| Miami Valley Lighting | Miami Valley Lighting, LLC is a wholly-owned subsidiary of DPL established in 1985 to provide street and outdoor lighting services to customers in the Dayton region. Miami Valley Lighting serves businesses, communities and neighborhoods in West Central Ohio with over 70,000 lighting solutions for more than 190 businesses and 180 local governments. |

| MRO | Market Rate Option - a market-based plan that a utility may file with PUCO to establish SSO rates pursuant to Ohio law |

| MVIC | Miami Valley Insurance Company is a wholly-owned insurance subsidiary of DPL that provides insurance services to DPL and its subsidiaries |

MW | Megawatt, a unit of power equal to one million watts |

| NAAQS | National Ambient Air Quality Standards - the EPA’s health and environmental based standards for six specified pollutants, as found in the ambient air |

| NERC | North American Electric Reliability Corporation - a not-for-profit international regulatory authority whose mission is to assure the effective and efficient reduction of risks to the reliability and security of the electric grid |

NOx | |

| OAQDA | Nitrogen Oxide - an air pollutant regulated by the NAAQS under the CAAOhio Air Quality Development Authority |

| | | | | |

GLOSSARY OF TERMS (cont.) |

| |

| Term | Definition |

Ohio EPAOCC | The Office of the Ohio Environmental Protection AgencyConsumers’ Counsel (OCC) is the statewide legal representative for Ohio’s residential consumers in matters related to their investor-owned electric, natural gas, telephone, and water services. |

| |

| OVEC | Ohio Valley Electric Corporation - an electric generating company in which DP&L holds a 4.9% equity interest |

| Pension Plans | AES Ohio sponsors two defined benefit plans, The Dayton Power and Light Company Retirement Income Plan and The Dayton Power and Light Company Supplemental Executive Retirement Plan |

| PJM | PJM Interconnection, LLC, an RTO |

| PUCO | Public Utilities Commission of Ohio |

| RSC | The Rate Stabilization Charge is a non-bypassable rider intended to compensate DP&L for providing stabilized rates to customers. |

| RTO | Regional Transmission Organization - an entity that is independent from all generation and power marketing interests and has exclusive responsibility for grid operations, short-term reliability, and transmission service within a region |

| SEC | U.S. Securities and Exchange Commission |

SERP | Supplemental Executive Retirement Plan |

| Service Company | AES US Services, LLC - the shared services affiliate providing accounting, finance, and other support services to AES’ U.S. SBU businesses |

| SGF | Solar Generation Fund rider - a statewide program that collects monthly payments for all Ohio electric distribution utilities related to in-state solar and nuclear resources |

| SOFR | Secured Overnight Financing Rate |

| SSO | Standard Service Offer represents the regulated rates, authorized by the PUCO, charged to DP&L retail customers that take retail generation service from DP&L within DP&L’s service territory |

| T&D | Transmission and distribution |

| U.S. | United States of America |

| USD | U.S. dollar |

| USF | The Universal Service Fund is a statewide program which provides qualified low-income customers in Ohio with income-based bills and energy efficiency education programs |

U.S. SBU | U.S. and Utilities Strategic Business Unit, AES’ reporting unit covering the businesses in the United States, including DPL |

| Utility segment | DPL's Utility segment is made up of DP&L’s electric transmission and distribution businesses, which distribute electricity to residential, commercial, industrial and governmental customers |

FORWARD-LOOKINGFORWARD–LOOKING STATEMENTS

Certain statements contained in this report are “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. Matters discussed in this report that relate to events or developments that are expected to occur in the future, including management’s expectations, strategic objectives, business prospects, anticipated economic performance and financial condition and other similar matters constitute forward-looking statements. Forward-looking statements are based on management’s beliefs, assumptions and expectations of future economic performance, considering the information currently available to management. These statements are not statements of historical fact and are typically identified by terms and phrases such as “anticipate,” “believe,” “intend,” “estimate,” “expect,” “continue,” “should,” “could,” “may,” “plan,” “project,” “predict,” “will” and similar expressions. Such forward-looking statements are subject to risks and uncertainties and investors are cautioned that outcomes and results may vary materially from those projected due to various factors beyond our control, including but not limited to:

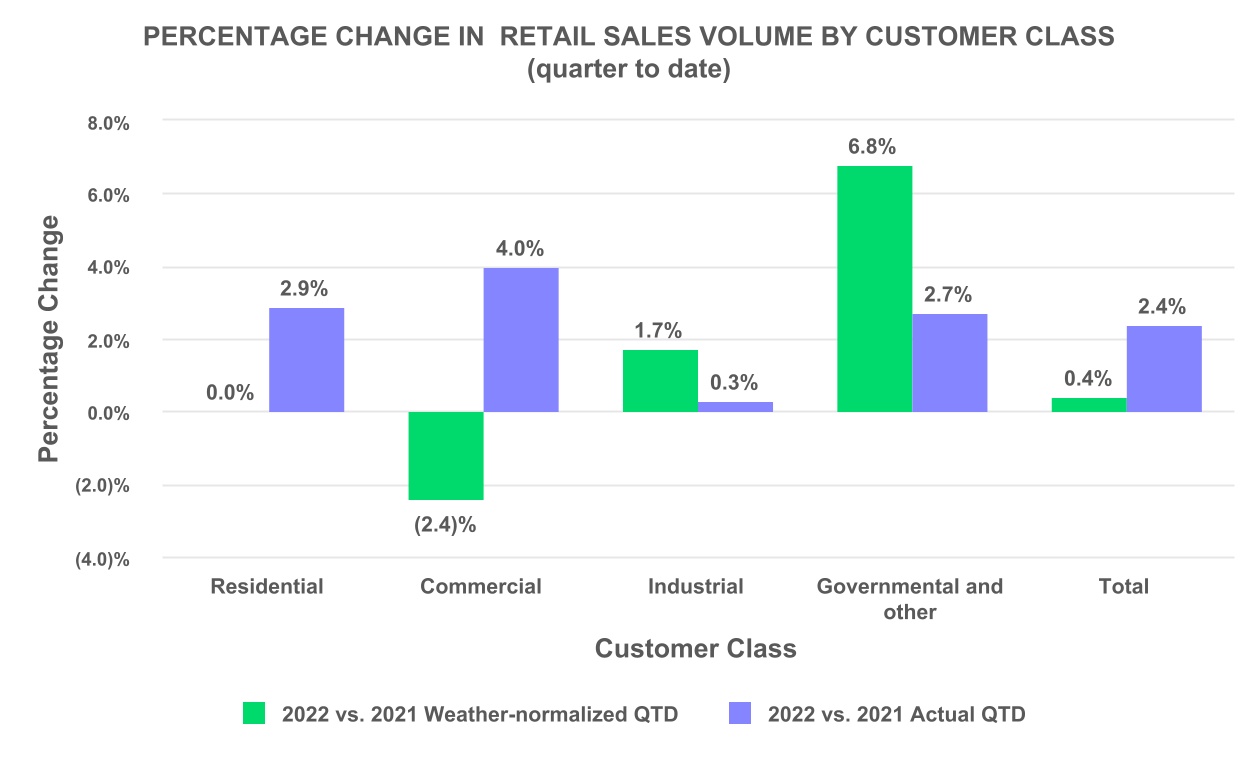

•impacts of weather on retail sales;

•growth in our service territory and changes in demand and demographic patterns;

•weather-related damage to our electrical system;

•performance of our suppliers;

•transmission and distribution system reliability and capacity;

•regulatory actions and outcomes, including, but not limited to, the review and approval of our rates and charges by the PUCO;

•federal and state legislation and regulations;

•changes in our credit ratings or the credit ratings of AES;

•fluctuations in the value of pension plan assets, fluctuations in pension plan expenses and our ability to fund defined benefit pension plans;

•changes in financial or regulatory accounting policies;

•environmental matters, including costs of compliance with, and liabilities related to, current and future environmental and climate change laws and requirements;

•interest rates and the use of interest rate hedges, inflation rates and other costs of capital;

•the availability of capital;

•the ability of subsidiaries to pay dividends or distributions to DPL;DPL;

•level of creditworthiness of counterparties to contracts and transactions;

•labor strikes or other workforce factors, including the ability to attract and retain key personnel;

•facility or equipment maintenance, repairs and capital expenditures;

•significant delays or unanticipated cost increases associated with construction or other projects;

•the availability and cost of funds to finance working capital and capital needs, particularly during periods when the time lag between incurring costs and recovery is long and the costs are material;

•local economic conditions;

•costs and effects of legal and administrative proceedings, audits, settlements, investigations and claims and the ultimate disposition of litigation; cyberattacks and information security breaches;

•industry restructuring, deregulation and competition;

•issues related to our participation in PJM, including the cost associated with membership, allocation of costs, costs associated with transmission expansion, the recovery of costs incurred and the risk of default of other PJM participants;

•changes in tax laws and the effects of our tax strategies;

•the use of derivative contracts;

•product development, technology changes and changes in prices of products and technologies;

•cyberattacks and information security breaches;

•the use of derivative contracts;

•catastrophic events such as fires, explosions, terrorist acts, acts of war, pandemic events, including the outbreak of COVID-19, or natural disasters such as floods, earthquakes, tornadoes, severe winds, ice or snowstorms, droughts, or other similar occurrences;occurrences, including as a result of climate change; and

•the risks and other factors discussed in this report and other DPL and DP&L filings with the SEC.

Forward-looking statements speak only as of the date of the document in which they are made. We disclaim any obligation or undertaking to provide any updates or revisions to any forward-looking statement to reflect any change in our expectations or any change in events, conditions or circumstances on which the forward-looking statement is based. If we do update one or more forward-looking statements, no inference should be made that we will make additional updates with respect to those or other forward-looking statements.

All of the above factors are difficult to predict, contain uncertainties that may materially affect actual results, and many are beyond our control. See Item 1A - Risk Factors to Part I in our Annual Report on Form 10-K and Item 1A - Risk Factors to Part II of this quarterly report and the “Management'sManagement's Discussion and Analysis of Financial Condition and Results of Operations”Operations section in our Form 10-K and in our Quarterly Report on Form 10-Q for the quarter ended March 31, 2022 and this Quarterly Report on Form 10-Q for a more detailed discussion of the foregoing and certain other factors that could cause actual results to differ materially from those reflected in such forward-looking statements and that should be considered in evaluating our outlook. These risks may also be specifically described in our Quarterly Reports on Form 10-Q in Part II, - Item 1A, Current Reports on Form 8-K and other documents that we may file from time to time with the SEC.

Our SEC filings are available to the public from the SEC’s website at www.sec.gov.

COMPANY WEBSITE

DP&L’s public internet site is www.aes-ohio.com. The information on this website is not incorporated by reference into this report.

| | |

| Part I – Financial Information |

This report includes the combined filing of DPL and DP&L. Throughout this report, the terms “we,” “us,” “our” and “ours” are used to refer to both DPL and DP&L,, respectively and altogether, unless the context indicates otherwise. Discussions or areas of this report that apply only to DPL or DP&L will be clearly noted in the applicable section.

| | |

| Item 1 – Financial Statements |

FINANCIAL STATEMENTS

DPL INC.

| | DPL Inc. | DPL Inc. | DPL Inc. |

| Condensed Consolidated Statements of Operations | Condensed Consolidated Statements of Operations | Condensed Consolidated Statements of Operations |

| (Unaudited) | (Unaudited) | (Unaudited) |

| | Three months ended | | Six months ended | | | Three months ended |

| | June 30, | | June 30, | | | March 31, |

| $ in millions | $ in millions | | 2022 | | 2021 | | 2022 | | 2021 | $ in millions | | | 2023 | | 2022 |

| Revenues | Revenues | | $ | 190.9 | | | $ | 148.1 | | | $ | 390.2 | | | $ | 323.3 | | Revenues | | | $ | 240.1 | | | $ | 199.3 | |

| | Operating costs and expenses | Operating costs and expenses | | Operating costs and expenses | | | |

| Net fuel cost | | — | | | 0.1 | | | — | | | 0.5 | | |

| | Net purchased power cost | Net purchased power cost | | 90.6 | | | 53.9 | | | 181.4 | | | 125.4 | | Net purchased power cost | | | 122.2 | | | 90.8 | |

| | Operation and maintenance | Operation and maintenance | | 43.1 | | | 38.0 | | | 83.9 | | | 72.8 | | Operation and maintenance | | | 54.0 | | | 40.8 | |

| Depreciation and amortization | Depreciation and amortization | | 20.1 | | | 18.9 | | | 39.6 | | | 38.0 | | Depreciation and amortization | | | 19.8 | | | 19.5 | |

| Taxes other than income taxes | Taxes other than income taxes | | 21.2 | | | 20.7 | | | 43.2 | | | 41.1 | | Taxes other than income taxes | | | 25.5 | | | 22.0 | |

| | Gain on disposal of business | Gain on disposal of business | | — | | | — | | | (0.6) | | | — | | Gain on disposal of business | | | — | | | (0.6) | |

| | Total operating costs and expenses | Total operating costs and expenses | | 175.0 | | | 131.6 | | | 347.5 | | | 277.8 | | Total operating costs and expenses | | | 221.5 | | | 172.5 | |

| | Operating income | Operating income | | 15.9 | | | 16.5 | | | 42.7 | | | 45.5 | | Operating income | | | 18.6 | | | 26.8 | |

| | Other expense, net: | Other expense, net: | | Other expense, net: | | | |

| Interest expense | Interest expense | | (16.5) | | | (15.6) | | | (32.0) | | | (31.2) | | Interest expense | | | (18.1) | | | (15.5) | |

| | Other income | | — | | | 0.6 | | | 0.4 | | | 1.1 | | |

| Other income, net | | Other income, net | | | 1.8 | | | 0.4 | |

| Total other expense, net | Total other expense, net | | (16.5) | | | (15.0) | | | (31.6) | | | (30.1) | | Total other expense, net | | | (16.3) | | | (15.1) | |

| | Income / (loss) from continuing operations before income tax | | (0.6) | | | 1.5 | | | 11.1 | | | 15.4 | | |

| Income before income tax | | Income before income tax | | | 2.3 | | | 11.7 | |

| | Income tax expense / (benefit) from continuing operations | | (0.8) | | | 0.9 | | | (4.5) | | | 0.6 | | |

| Income tax expense / (benefit) | | Income tax expense / (benefit) | | | 1.1 | | | (3.7) | |

| | Net income from continuing operations | | 0.2 | | | 0.6 | | | 15.6 | | | 14.8 | | |

| | Discontinued operations (Note 11): | | |

| Loss from discontinued operations before income tax | | — | | | (0.2) | | | — | | | (1.0) | | |

| | Income tax benefit from discontinued operations | | — | | | — | | | — | | | (0.2) | | |

| Net loss from discontinued operations | | — | | | (0.2) | | | — | | | (0.8) | | |

| | | Net income | Net income | | $ | 0.2 | | | $ | 0.4 | | | $ | 15.6 | | | $ | 14.0 | | Net income | | | $ | 1.2 | | | $ | 15.4 | |

See Notes to Condensed Consolidated Financial Statements.

| | | | | | | | | | | | | | | | | | | | | | | | | | |

| DPL Inc. |

| Condensed Consolidated Statements of Comprehensive Income |

| (Unaudited) |

| | Three months ended | | Six months ended |

| | June 30, | | June 30, |

| $ in millions | | 2022 | | 2021 | | 2022 | | 2021 |

| Net income | | $ | 0.2 | | | $ | 0.4 | | | $ | 15.6 | | | $ | 14.0 | |

| Derivative activity: | | | | | | | | |

| | | | | | | | |

| Reclassification to earnings, net of income tax effect of $0.0, $0.1, $0.1 and $0.1 for each respective period | | (0.3) | | | (0.2) | | | (0.4) | | | (0.4) | |

| Total derivative activity | | (0.3) | | | (0.2) | | | (0.4) | | | (0.4) | |

| Pension and postretirement activity: | | | | | | | | |

| Reclassification to earnings, net of income tax effect of $0.0, $(0.2), $(0.1) and $(0.3) for each respective period | | 0.3 | | | 0.5 | | | 0.5 | | | 1.0 | |

| Total change in unfunded pension and postretirement obligations | | 0.3 | | | 0.5 | | | 0.5 | | | 1.0 | |

| | | | | | | | |

| Other comprehensive income | | — | | | 0.3 | | | 0.1 | | | 0.6 | |

| | | | | | | | |

| Net comprehensive income | | $ | 0.2 | | | $ | 0.7 | | | $ | 15.7 | | | $ | 14.6 | |

| | | | | | | | | | | | | | | | | | |

| DPL Inc. |

| Condensed Consolidated Statements of Comprehensive Income |

| (Unaudited) |

| | | | Three months ended |

| | | | March 31, |

| $ in millions | | | | | | 2023 | | 2022 |

| Net income | | | | | | $ | 1.2 | | | $ | 15.4 | |

| Derivative activity: | | | | | | | | |

| | | | | | | | |

| Reclassification to earnings, net of income tax effect of $0.0 and $0.1 for each respective period | | | | | | (0.2) | | | (0.1) | |

| | | | | | | | |

| Unfunded pension and other postretirement activity: | | | | | | | | |

| Reclassification to earnings, net of income tax effect of $0.0 and $(0.1) for each respective period | | | | | | — | | | 0.2 | |

| | | | | | | | |

| | | | | | | | |

| Other comprehensive income / (loss) | | | | | | (0.2) | | | 0.1 | |

| | | | | | | | |

| Net Comprehensive income | | | | | | $ | 1.0 | | | $ | 15.5 | |

See Notes to Condensed Consolidated Financial Statements.

| | DPL Inc. | DPL Inc. | DPL Inc. |

| Condensed Consolidated Balance Sheets | Condensed Consolidated Balance Sheets | Condensed Consolidated Balance Sheets |

| (Unaudited) | (Unaudited) | (Unaudited) |

| $ in millions | $ in millions | | June 30, 2022 | | December 31, 2021 | $ in millions | | March 31, 2023 | | December 31, 2022 |

| ASSETS | ASSETS | | | | | ASSETS | | | | |

| Current assets: | Current assets: | | Current assets: | |

| Cash and cash equivalents | Cash and cash equivalents | | $ | 60.3 | | | $ | 26.6 | | Cash and cash equivalents | | $ | 21.0 | | | $ | 30.5 | |

| | Accounts receivable, net of allowance for credit losses of $0.3 and $0.3, respectively (Note 1) | | 85.1 | | | 71.5 | | |

| Accounts receivable, net of allowance for credit losses of $0.6 and $0.5, respectively (Note 1) | | Accounts receivable, net of allowance for credit losses of $0.6 and $0.5, respectively (Note 1) | | 96.7 | | | 91.9 | |

| Inventories | Inventories | | 17.9 | | | 14.4 | | Inventories | | 29.4 | | | 26.8 | |

| Taxes applicable to subsequent years | Taxes applicable to subsequent years | | 40.5 | | | 83.1 | | Taxes applicable to subsequent years | | 70.0 | | | 94.0 | |

| Regulatory assets, current | Regulatory assets, current | | 37.2 | | | 24.5 | | Regulatory assets, current | | 32.2 | | | 39.2 | |

| Taxes receivable | Taxes receivable | | 6.1 | | | 2.7 | | Taxes receivable | | 13.2 | | | 10.9 | |

| Prepayments and other current assets | Prepayments and other current assets | | 9.9 | | | 7.6 | | Prepayments and other current assets | | 7.7 | | | 3.9 | |

| | Total current assets | Total current assets | | 257.0 | | | 230.4 | | Total current assets | | 270.2 | | | 297.2 | |

| | Property, plant & equipment: | Property, plant & equipment: | | | | | Property, plant & equipment: | | | | |

| Property, plant & equipment | Property, plant & equipment | | 2,103.9 | | | 1,990.4 | | Property, plant & equipment | | 2,292.5 | | | 2,193.6 | |

| Less: Accumulated depreciation and amortization | Less: Accumulated depreciation and amortization | | (489.4) | | | (464.0) | | Less: Accumulated depreciation and amortization | | (512.6) | | | (505.7) | |

| | | | 1,614.5 | | | 1,526.4 | | | | 1,779.9 | | | 1,687.9 | |

| Construction work in process | Construction work in process | | 165.9 | | | 174.4 | | Construction work in process | | 163.1 | | | 197.1 | |

| Total net property, plant & equipment | Total net property, plant & equipment | | 1,780.4 | | | 1,700.8 | | Total net property, plant & equipment | | 1,943.0 | | | 1,885.0 | |

| | Other non-current assets: | Other non-current assets: | | | | | Other non-current assets: | | | | |

| Regulatory assets, non-current | Regulatory assets, non-current | | 166.8 | | | 176.8 | | Regulatory assets, non-current | | 133.9 | | | 129.8 | |

| Intangible assets, net of amortization | Intangible assets, net of amortization | | 43.1 | | | 33.7 | | Intangible assets, net of amortization | | 77.1 | | | 70.1 | |

| Other non-current assets | Other non-current assets | | 28.1 | | | 30.1 | | Other non-current assets | | 42.9 | | | 40.3 | |

| | Total other non-current assets | Total other non-current assets | | 238.0 | | | 240.6 | | Total other non-current assets | | 253.9 | | | 240.2 | |

| | Total assets | Total assets | | $ | 2,275.4 | | | $ | 2,171.8 | | Total assets | | $ | 2,467.1 | | | $ | 2,422.4 | |

| | LIABILITIES AND SHAREHOLDER'S DEFICIT | LIABILITIES AND SHAREHOLDER'S DEFICIT | | LIABILITIES AND SHAREHOLDER'S DEFICIT | |

| Current liabilities: | Current liabilities: | | Current liabilities: | |

| Short-term and current portion of long-term debt (Note 5) | Short-term and current portion of long-term debt (Note 5) | | $ | 50.2 | | | $ | 65.2 | | Short-term and current portion of long-term debt (Note 5) | | $ | 260.2 | | | $ | 155.2 | |

| Accounts payable | Accounts payable | | 98.1 | | | 111.0 | | Accounts payable | | 110.5 | | | 129.5 | |

| Accrued taxes | Accrued taxes | | 85.1 | | | 85.1 | | Accrued taxes | | 94.3 | | | 88.4 | |

| Accrued interest | Accrued interest | | 15.9 | | | 15.3 | | Accrued interest | | 20.7 | | | 16.1 | |

| Customer and supplier deposits | Customer and supplier deposits | | 29.6 | | | 15.0 | | Customer and supplier deposits | | 23.7 | | | 16.7 | |

| Regulatory liabilities, current | Regulatory liabilities, current | | 31.0 | | | 14.6 | | Regulatory liabilities, current | | 29.5 | | | 40.4 | |

| | Accrued and other current liabilities | Accrued and other current liabilities | | 15.3 | | | 17.1 | | Accrued and other current liabilities | | 23.2 | | | 20.9 | |

| | Total current liabilities | Total current liabilities | | 325.2 | | | 323.3 | | Total current liabilities | | 562.1 | | | 467.2 | |

| | Non-current liabilities: | Non-current liabilities: | | Non-current liabilities: | |

| Long-term debt (Note 5) | Long-term debt (Note 5) | | 1,534.8 | | | 1,395.3 | | Long-term debt (Note 5) | | 1,536.5 | | | 1,535.7 | |

| Deferred income taxes | Deferred income taxes | | 191.0 | | | 187.9 | | Deferred income taxes | | 204.1 | | | 199.0 | |

| Taxes payable | Taxes payable | | 40.9 | | | 83.6 | | Taxes payable | | 47.1 | | | 94.5 | |

| Regulatory liabilities, non-current | Regulatory liabilities, non-current | | 224.7 | | | 229.3 | | Regulatory liabilities, non-current | | 196.4 | | | 198.7 | |

| Accrued pension and other post-retirement benefits | | 53.7 | | | 62.3 | | |

| Accrued pension and other postretirement obligations | | Accrued pension and other postretirement obligations | | 34.7 | | | 41.8 | |

| | Other non-current liabilities | Other non-current liabilities | | 10.8 | | | 11.5 | | Other non-current liabilities | | 8.9 | | | 9.2 | |

| | Total non-current liabilities | Total non-current liabilities | | 2,055.9 | | | 1,969.9 | | Total non-current liabilities | | 2,027.7 | | | 2,078.9 | |

| | Commitments and contingencies (Note 8) | | 0 | | 0 | |

| Commitments and contingencies (Note 9) | | Commitments and contingencies (Note 9) | |

| | Common shareholder's deficit: | Common shareholder's deficit: | | Common shareholder's deficit: | |

| | Common stock: | Common stock: | | Common stock: | |

| 1,500 shares authorized; 1 share issued and outstanding | 1,500 shares authorized; 1 share issued and outstanding | | — | | | — | | 1,500 shares authorized; 1 share issued and outstanding | | — | | | — | |

| Other paid-in capital | Other paid-in capital | | 2,601.3 | | | 2,601.3 | | Other paid-in capital | | 2,601.3 | | | 2,601.3 | |

| Accumulated other comprehensive loss | Accumulated other comprehensive loss | | (4.7) | | | (4.8) | | Accumulated other comprehensive loss | | (2.6) | | | (2.4) | |

| Accumulated deficit | Accumulated deficit | | (2,702.3) | | | (2,717.9) | | Accumulated deficit | | (2,721.4) | | | (2,722.6) | |

| Total common shareholder's deficit | Total common shareholder's deficit | | (105.7) | | | (121.4) | | Total common shareholder's deficit | | (122.7) | | | (123.7) | |

| | Total liabilities and shareholder's deficit | Total liabilities and shareholder's deficit | | $ | 2,275.4 | | | $ | 2,171.8 | | Total liabilities and shareholder's deficit | | $ | 2,467.1 | | | $ | 2,422.4 | |

See Notes to Condensed Consolidated Financial Statements.

| | | | | | | | | | | | | | |

| DPL Inc. |

| Condensed Consolidated Statements of Cash Flows |

| (Unaudited) |

| | Six months ended June 30, |

| $ in millions | | 2022 | | 2021 |

| Cash flows from operating activities: | | | | |

| Net income | | $ | 15.6 | | | $ | 14.0 | |

| Adjustments to reconcile net income to net cash from operating activities: | | | | |

| Depreciation and amortization | | 39.6 | | | 38.0 | |

| | | | |

| | | | |

| Deferred income taxes | | (1.1) | | | 4.6 | |

| | | | |

| Gain on disposal of business | | (0.6) | | | — | |

| | | | |

| Changes in certain assets and liabilities: | | | | |

| Accounts receivable, net | | (13.6) | | | 4.4 | |

| Inventories | | (3.5) | | | (0.6) | |

| | | | |

| Taxes applicable to subsequent years | | 42.7 | | | 39.2 | |

| Deferred regulatory costs, net | | 9.1 | | | (9.8) | |

| Prepayments and other current assets | | (2.3) | | | (5.7) | |

| | | | |

| Accounts payable | | 3.1 | | | 4.1 | |

| Accrued taxes payable / receivable | | (46.0) | | | (57.5) | |

| Accrued interest | | 0.6 | | | (0.4) | |

| | | | |

| | | | |

| Accrued and other current liabilities | | 12.9 | | | (3.7) | |

| Accrued pension and other post-retirement benefits | | (8.5) | | | (11.4) | |

| Other | | 3.9 | | | 1.5 | |

| Net cash provided by operating activities | | 51.9 | | | 16.7 | |

| Cash flows from investing activities: | | | | |

| Capital expenditures | | (133.9) | | | (94.9) | |

| Cost of removal payments | | (8.1) | | | (9.2) | |

| | | | |

| | | | |

| | | | |

| | | | |

| | | | |

| | | | |

| Other investing activities, net | | (0.2) | | | (0.9) | |

| Net cash used in investing activities | | (142.2) | | | (105.0) | |

| Cash flows from financing activities: | | | | |

| Payments of deferred financing costs | | (1.0) | | | (0.4) | |

| Issuance of long-term debt | | 140.0 | | | — | |

| | | | |

| Borrowings from revolving credit facilities | | 130.0 | | | 80.0 | |

| Repayment of borrowings from revolving credit facilities | | (145.0) | | | — | |

| | | | |

| | | | |

| Net cash provided by financing activities | | 124.0 | | | 79.6 | |

| Cash, cash equivalents, and restricted cash: | | | | |

| Net change | | 33.7 | | | (8.7) | |

| Balance at beginning of period | | 26.7 | | | 25.5 | |

| Cash, cash equivalents, and restricted cash at end of period | | $ | 60.4 | | | $ | 16.8 | |

| Supplemental cash flow information: | | | | |

| Interest paid, net of amounts capitalized | | $ | 28.7 | | | $ | 29.6 | |

| | | | |

| Non-cash investing activities: | | | | |

| Accruals for capital expenditures | | $ | 26.6 | | | $ | 15.8 | |

| | | | |

| | | | |

| | | | | | | | | | | | | | |

| DPL Inc. |

| Condensed Consolidated Statements of Cash Flows |

| (Unaudited) |

| | Three months ended March 31, |

| $ in millions | | 2023 | | 2022 |

| Cash flows from operating activities: | | | | |

| Net income | | $ | 1.2 | | | $ | 15.4 | |

| Adjustments to reconcile net income to net cash from operating activities: | | | | |

| Depreciation and amortization | | 19.8 | | | 19.5 | |

| | | | |

| | | | |

| Deferred income taxes | | 3.7 | | | (0.4) | |

| | | | |

| Gain on disposal of business | | — | | | (0.6) | |

| | | | |

| Changes in certain assets and liabilities: | | | | |

| Accounts receivable, net | | (4.8) | | | (2.3) | |

| Inventories | | (2.5) | | | (3.0) | |

| | | | |

| Taxes applicable to subsequent years | | 24.0 | | | 22.3 | |

| Current and non-current regulatory assets and liabilities | | (11.4) | | | 10.4 | |

| | | | |

| | | | |

| Accounts payable | | (8.9) | | | (15.7) | |

| Accrued taxes payable / receivable | | (43.8) | | | (43.3) | |

| Accrued interest | | 4.6 | | | 3.0 | |

| | | | |

| | | | |

| | | | |

| Accrued pension and other post-retirement benefits | | (7.1) | | | (8.0) | |

| Other | | 3.1 | | | 2.5 | |

| Net cash used in operating activities | | (22.1) | | | (0.2) | |

| Cash flows from investing activities: | | | | |

| Capital expenditures | | (89.4) | | | (64.4) | |

| Cost of removal payments | | (3.2) | | | (5.0) | |

| | | | |

| | | | |

| | | | |

| | | | |

| | | | |

| | | | |

| Other investing activities, net | | 0.2 | | | 0.1 | |

| Net cash used in investing activities | | (92.4) | | | (69.3) | |

| Cash flows from financing activities: | | | | |

| | | | |

| | | | |

| | | | |

| Borrowings from revolving credit facilities | | 115.0 | | | 95.0 | |

| Repayment of borrowings from revolving credit facilities | | (10.0) | | | (20.0) | |

| | | | |

| | | | |

| Net cash provided by financing activities | | 105.0 | | | 75.0 | |

| Cash, cash equivalents, and restricted cash: | | | | |

| Net change | | (9.5) | | | 5.5 | |

| Balance at beginning of period | | 30.6 | | | 26.7 | |

| Cash, cash equivalents, and restricted cash at end of period | | $ | 21.1 | | | $ | 32.2 | |

| Supplemental cash flow information: | | | | |

| Interest paid, net of amounts capitalized | | $ | 12.9 | | | $ | 11.3 | |

| | | | |

| Non-cash investing activities: | | | | |

| Accruals for capital expenditures | | $ | 36.4 | | | $ | 23.7 | |

| | | | |

See Notes to Condensed Consolidated Financial Statements.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| DPL Inc. |

| Condensed Consolidated Statements of Shareholder's Deficit |

| (Unaudited) |

| | Common Stock (a) | | | | | | | | |

| $ in millions | | Outstanding Shares | | Amount | | Other

Paid-in

Capital | | Accumulated Other Comprehensive Loss | | Accumulated Deficit | | Total |

| Balance, January 1, 2022 | | 1 | | | $ | — | | | $ | 2,601.3 | | | $ | (4.8) | | | $ | (2,717.9) | | | $ | (121.4) | |

| Net comprehensive income | | | | | | | | 0.1 | | | 15.4 | | | 15.5 | |

| | | | | | | | | | | | |

| | | | | | | | | | | | |

| Balance, March 31, 2022 | | 1 | | | — | | | 2,601.3 | | | (4.7) | | | (2,702.5) | | | (105.9) | |

| Net comprehensive income | | | | | | | | — | | | 0.2 | | | 0.2 | |

| | | | | | | | | | | | |

| | | | | | | | | | | | |

| Balance, June 30, 2022 | | 1 | | | $ | — | | | $ | 2,601.3 | | | $ | (4.7) | | | $ | (2,702.3) | | | $ | (105.7) | |

| | | | | | | | | | | | |

| | | | | | | | | | | | |

| | | | | | | | | | | | |

| | | | | | | | | | | | |

| | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| DPL Inc. |

| Condensed Consolidated Statements of Shareholder's Deficit |

| (Unaudited) |

| | Common Stock (a) | | | | | | | | |

| $ in millions | | Outstanding Shares | | Amount | | Other

Paid-in

Capital | | Accumulated Other Comprehensive Loss | | Accumulated Deficit | | Total |

| Balance, January 1, 2023 | | 1 | | | $ | — | | | $ | 2,601.3 | | | $ | (2.4) | | | $ | (2,722.6) | | | $ | (123.7) | |

| Net income | | | | | | | | | | 1.2 | | | 1.2 | |

| Net comprehensive loss | | | | | | | | (0.2) | | | | | (0.2) | |

| | | | | | | | | | | | |

| | | | | | | | | | | | |

| Balance, March 31, 2023 | | 1 | | | $ | — | | | $ | 2,601.3 | | | $ | (2.6) | | | $ | (2,721.4) | | | $ | (122.7) | |

| | | | | | | | | | | | |

| | | | | | | | | | | | |

| | | | | | | | | | | | |

| | | | | | | | | | | | |

| | | | | | | | | | | | |

| | | | | | | | | | | | |

| | | | | | | | | | | | |

| | | | | | | | | | | | |

| | | | | | | | | | | | |

| | | | | | | | | | | | |

| | | | | | | | | | | | |

| | | Common Stock (a) | | | Common Stock (a) | |

| $ in millions | $ in millions | | Outstanding Shares | | Amount | | Other

Paid-in

Capital | | Accumulated Other Comprehensive Loss | | Accumulated Deficit | | Total | $ in millions | | Outstanding Shares | | Amount | | Other

Paid-in

Capital | | Accumulated Other Comprehensive Loss | | Accumulated Deficit | | Total |

| Balance, January 1, 2021 | | 1 | | | $ | — | | | $ | 2,468.8 | | | $ | (12.3) | | | $ | (2,740.0) | | | $ | (283.5) | | |

| Balance, January 1, 2022 | | Balance, January 1, 2022 | | 1 | | | $ | — | | | $ | 2,601.3 | | | $ | (4.8) | | | $ | (2,717.9) | | | $ | (121.4) | |

| Net income | | Net income | | 15.4 | | | 15.4 | |

| Net comprehensive income | Net comprehensive income | | 0.3 | | | 13.6 | | | 13.9 | | Net comprehensive income | | 0.1 | | | 0.1 | |

| | Balance, March 31, 2021 | | 1 | | | — | | | 2,468.8 | | | (12.0) | | | (2,726.4) | | | (269.6) | | |

| Net comprehensive income | | 0.3 | | | 0.4 | | | 0.7 | | |

| | Balance, June 30, 2021 | | 1 | | | $ | — | | | $ | 2,468.8 | | | $ | (11.7) | | | $ | (2,726.0) | | | $ | (268.9) | | |

| Balance, March 31, 2022 | | Balance, March 31, 2022 | | 1 | | | $ | — | | | $ | 2,601.3 | | | $ | (4.7) | | | $ | (2,702.5) | | | $ | (105.9) | |

| |

(a)1,500 shares authorized.

See Notes to Condensed Consolidated Financial Statements.

DPL Inc.

Notes to Unaudited Condensed Consolidated Financial Statements

For the three and six months ended June 30,March 31, 2023 and 2022 and 2021

1. Overview and Summary of Significant Accounting PoliciesOVERVIEW AND SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

DPL, an indirectly wholly-owned subsidiary of AES, is a diversified regional energy company organized in 1985 under the laws of Ohio. DPL has 1 reportable segment, owns all of the Utility segment. See Note 9 – Business Segments for more information relating to this reportable segment.outstanding common stock of DP&L, which does business as AES Ohio. Substantially all of DPL’s business consists of transmitting, distributing and selling of electric energy conducted through its principal subsidiary, AES Ohio. The terms “we,” “us,” “our” and “ours” are used to refer to DPL and its subsidiaries.

DPL is an indirectly wholly-owned subsidiary of AES. DP&L, a wholly-owned subsidiary of DPL that does business as AES Ohio, is a public utility incorporated in 1911 under the laws of Ohio. Beginning in 2001, Ohio law gave Ohio consumers the right to choose the electric generation supplier from whom they purchase retail generation service; however, retail transmission and distribution services are still regulated. AES Ohio has the exclusive right to provide such transmission and distribution services to approximately 535,000537,000 customers located in West Central Ohio. Additionally, Principal industries located in AES Ohio’s service territory include automotive, food processing, paper, plastic, manufacturing and defense. AES Ohio also provides retail SSO electric service to residential, commercial, industrial and governmental customers in a 6,000-square mile area of West Central Ohio. AES Ohio sources all of the generation for its SSO customers through a competitive bid process. Principal industries located in AES Ohio’s service territory include automotive, food processing, paper, plastic, manufacturing and defense. AES Ohio's sales reflect the general economic conditions, seasonal weather patterns of the area, the market price of electricity and customer energy efficiency initiatives. AES Ohio owns numerous transmission facilities. AES Ohio sells its proportional share of energy and capacity from its investment in OVEC into the wholesale market.

DPL’s other primary subsidiaries are MVIC and Miami Valley Lighting. MVIC is our captive insurance company that provides insurance services to AES Ohio and our other subsidiaries, and Miami Valley Lighting provides street and outdoor lighting services to customers in the Dayton region. In prior periods, AES Ohio Generation was also a primary subsidiary and sold all of its energy and capacity into the wholesale market. AES Ohio Generation retired its only remaining operating asset in May 2020 and sold it in June 2020. See Note 11 – Discontinued Operations for more information. DPL's subsidiaries are all wholly-owned. DPL also has a wholly-owned business trust, DPL Capital Trust II, formed for the purpose of issuing trust capital securities to investors.

AES Ohio’s electric transmission and distribution businesses are subject to rate regulation by federal and state regulators. Accordingly, AES Ohio applies the accounting standards for regulated operations to its electric transmission and distribution businesses and records regulatory assets when incurred costs are expected to be recovered in future customer rates and regulatory liabilities when current cost recoveries in customer rates relate to expected future costs or overcollections of riders.

Consolidation

DPL’s Condensed Consolidated Financial Statements include the accounts of DPL and its wholly-owned subsidiaries except for DPL Capital Trust II, which is not consolidated consistent with the provisions of GAAP.

Certain immaterial amounts from prior periods We have been reclassified to conform toevaluated subsequent events through the current period presentation.date this report is issued. All material intercompany accounts and transactions are eliminated in consolidation.

Interim Financial Presentation

The accompanying unaudited condensed consolidated financial statements and footnotes have been prepared in accordance with GAAP, as contained in the FASB ASC,FASC, for interim financial information and Article 10 of Regulation S-X issued by the SEC. Accordingly, they do not include all the information and footnotes required by GAAP for annual fiscal reporting periods. In the opinion of management, the interim financial information includes all adjustments of a normal recurring nature necessary for a fair presentation of the results of operations, financial position, comprehensive income, changes in common shareholder's deficit, and cash flows. The results of operations for the three and six months ended June 30, 2022March 31, 2023 are not necessarily indicative of expected results for the year ending December 31, 2022.2023. The accompanying condensed consolidated financial statements are unaudited and should be read in conjunction with the 20212022 audited consolidated financial statements and notes thereto, which are included in our Form 10-K.

Use of Management Estimates

The preparation of consolidated financial statements in conformity with GAAP requires us to make estimates and assumptions that affect the reported amounts of assets and liabilities, the disclosure of contingent assets and liabilities and the revenues and expenses of the periods reported. Actual results could differ from these estimates and assumptions.

Significant items subject to such estimates and assumptions include: recognition of revenue including unbilled revenues; the carrying value of

property, plant and equipment; the valuation of insurance and claims liabilities;unbilled revenues; the valuation of allowances for credit losses and deferred income taxes; regulatory assets and liabilities; liabilitiesreserves recorded for income tax exposures; litigation; contingencies; and assets and liabilities related to employee benefits.

Cash, Cash Equivalents and Restricted Cash

The following table summarizes cash, cash equivalents, and restricted cash amounts reported on the Condensed Consolidated Balance Sheets that reconcile to the total of such amounts as shown on the Condensed Consolidated Statements of Cash Flows:

| | $ in millions | $ in millions | | June 30, 2022 | | December 31, 2021 | $ in millions | | March 31, 2023 | | December 31, 2022 |

| Cash and cash equivalents | Cash and cash equivalents | | $ | 60.3 | | | $ | 26.6 | | Cash and cash equivalents | | $ | 21.0 | | | $ | 30.5 | |

| Restricted cash (included in Prepayments and other current assets) | | 0.1 | | | 0.1 | | |

Restricted cash (included in Prepayments and other current assets) | | Restricted cash (included in Prepayments and other current assets) | | 0.1 | | | 0.1 | |

| Cash, Cash Equivalents, and Restricted Cash, End of Period | Cash, Cash Equivalents, and Restricted Cash, End of Period | | $ | 60.4 | | | $ | 26.7 | | Cash, Cash Equivalents, and Restricted Cash, End of Period | | $ | 21.1 | | | $ | 30.6 | |

Accounts Receivable and Allowance for Credit Losses

The following table summarizes accounts receivable as of June 30, 2022March 31, 2023 and December 31, 2021:2022:

| | | June 30, | | December 31, | | | March 31, | | December 31, | |

| $ in millions | $ in millions | | 2022 | | 2021 | | $ in millions | | 2023 | | 2022 | |

| Accounts receivable, net: | Accounts receivable, net: | | | | | | Accounts receivable, net: | | | | | |

| Customer receivables | Customer receivables | | $ | 56.9 | | | $ | 42.3 | | | Customer receivables | | $ | 68.3 | | | $ | 61.3 | | |

| Unbilled revenue | Unbilled revenue | | 18.8 | | | 19.2 | | | Unbilled revenue | | 18.2 | | | 24.0 | | |

| Amounts due from affiliates | Amounts due from affiliates | | 4.5 | | | 3.1 | | | Amounts due from affiliates | | 3.8 | | | 3.2 | | |

| Due from PJM transmission enhancement settlement | | 1.7 | | | 1.7 | | | |

| Other | Other | | 3.5 | | | 5.5 | | | Other | | 7.0 | | | 3.9 | | |

| Allowance for credit losses | Allowance for credit losses | | (0.3) | | | (0.3) | | | Allowance for credit losses | | (0.6) | | | (0.5) | | |

| Total accounts receivable, net | Total accounts receivable, net | | $ | 85.1 | | | $ | 71.5 | | | Total accounts receivable, net | | $ | 96.7 | | | $ | 91.9 | | |

|

The following table is a roll forward of our allowance for credit losses related to the accounts receivable balances for the sixthree months ended June 30, 2022March 31, 2023 and 2021:2022:

| | $ in millions | $ in millions | | Beginning Allowance Balance | | Current Period Provision | | Write-offs Charged Against Allowances | | Recoveries Collected | | Ending Allowance Balance | $ in millions | | Beginning Allowance Balance | | Current Period Provision | | Write-offs Charged Against Allowances | | Recoveries Collected | | Ending Allowance Balance |

| 2023 | | 2023 | | $ | 0.5 | | | $ | 0.9 | | | $ | (1.1) | | | $ | 0.3 | | | $ | 0.6 | |

| 2022 | 2022 | | $ | 0.3 | | | $ | 0.7 | | | $ | (1.1) | | | $ | 0.4 | | | $ | 0.3 | | 2022 | | $ | 0.3 | | | $ | (0.1) | | | $ | (0.2) | | | $ | 0.2 | | | $ | 0.2 | |

| 2021 | | $ | 2.8 | | | $ | (0.2) | | | $ | (1.6) | | | $ | 0.7 | | | $ | 1.7 | | |

The allowance for credit losses primarily relates to utility customer receivables, including unbilled amounts. Expected credit loss estimates are developed by disaggregating customers into those with similar credit risk characteristics and using historical credit loss experience. In addition, we also consider how current and future economic conditions are expected to impact collectability, as applicable, including the economic impacts of the COVID-19 pandemic on our receivable balance as of June 30, 2022.collectability. Amounts are written off when reasonable collections efforts have been exhausted. During 2021, the current period provision and allowance for credit losses decreased due to lower past due customer receivable balances.

Inventories

Inventories consist of materials and supplies as of June 30, 2022March 31, 2023 and December 31, 2021.2022.

0Regulatory Accounting

As a regulated utility, AES Ohio applies the provisions of ASC 980 - Regulated Operations, which gives recognition to the ratemaking and accounting practices of the PUCO and the FERC. Regulatory assets generally represent incurred costs that have been deferred because such costs are probable of future recovery in customer rates. Regulatory assets can also represent performance incentives permitted by the regulator. Regulatory assets have been included as allowable costs for ratemaking purposes, as authorized by the PUCO or established regulatory practices. Regulatory liabilities generally represent obligations to make refunds or future rate reductions to customers for previous over collections or the deferral of revenues collected for costs that AES Ohio expects to incur in the future.

The deferral of costs (as regulatory assets) is appropriate only when the future recovery of such costs is probable. In assessing probability, we consider such factors as specific orders from the PUCO or the FERC, regulatory precedent and the current regulatory environment. To the extent recovery of costs is no longer deemed probable, related regulatory assets would be required to be expensed in current period earnings. Our regulatory assets and liabilities have been created pursuant to a specific order of the PUCO or the FERC or established regulatory

practices, such as other utilities under the jurisdiction of the PUCO or the FERC being granted recovery of similar costs. It is probable, but not certain, that these regulatory assets will be recoverable, subject to approval by the PUCO or the FERC. Regulatory assets and liabilities are classified as current or non-current based on the term in which recovery is expected. See Note 2 – REGULATORY MATTERS in Item 8.—Financial Statements and Supplementary Data of our Form 10-K for more information.

Accumulated other comprehensive loss

The amounts reclassified out of Accumulated other comprehensive lossAOCL by component during the three and six months ended June 30,March 31, 2023 and 2022 and 2021 are as follows:

| | Details about Accumulated Other Comprehensive Loss components | | Affected line item in the Condensed Consolidated Statements of Operations | | Three months ended | | Six months ended | |

| Details about AOCL components | | Details about AOCL components | | Affected line item in the Condensed Consolidated Statements of Operations | | | Three months ended |

| | | | | June 30, | | June 30, | | | | March 31, |

| $ in millions | $ in millions | | | | 2022 | | 2021 | | 2022 | | 2021 | $ in millions | | | | | 2023 | | 2022 |

| Net gains on cash flow hedges (Note 4): | Net gains on cash flow hedges (Note 4): | | | | | | | | | Net gains on cash flow hedges (Note 4): | | | | | |

| | Interest expense | | $ | (0.3) | | | $ | (0.3) | | | $ | (0.5) | | | $ | (0.5) | | | Interest expense | | | $ | (0.2) | | | $ | (0.2) | |

| | Income tax effect | | — | | | 0.1 | | | 0.1 | | | 0.1 | | | Income tax effect | | | — | | | 0.1 | |

| | Net of income taxes | | (0.3) | | | (0.2) | | | (0.4) | | | (0.4) | | | Net of income taxes | | | (0.2) | | | (0.1) | |

| | | Amortization of defined benefit pension items (Note 7): | | |

| Amortization of unfunded pension and other postretirement obligations (Note 7): | | Amortization of unfunded pension and other postretirement obligations (Note 7): | | | |

| | Other expense | | 0.3 | | | 0.7 | | | 0.6 | | | 1.3 | | | Other expense | | | — | | | 0.3 | |

| | Income tax effect | | — | | | (0.2) | | | (0.1) | | | (0.3) | | | Income tax effect | | | — | | | (0.1) | |

| | Net of income taxes | | 0.3 | | | 0.5 | | | 0.5 | | | 1.0 | | | Net of income taxes | | | — | | | 0.2 | |

| | Total reclassifications for the period, net of income taxes | Total reclassifications for the period, net of income taxes | | $ | — | | | $ | 0.3 | | | $ | 0.1 | | | $ | 0.6 | | Total reclassifications for the period, net of income taxes | | | $ | (0.2) | | | $ | 0.1 | |

|

The changes in the components of Accumulated other comprehensive lossAOCL during the sixthree months ended June 30, 2022March 31, 2023 are as follows:

| | $ in millions | $ in millions | | Change in cash flow hedges | | Change in unfunded pension and postretirement benefit obligations | | Total | $ in millions | | Change in cash flow hedges | | Change in unfunded pension and other postretirement obligations | | Total |

| Balance as of January 1, 2022 | | $ | 12.8 | | | $ | (17.6) | | | $ | (4.8) | | |

| Balance as of January 1, 2023 | | Balance as of January 1, 2023 | | $ | 12.0 | | | $ | (14.4) | | | $ | (2.4) | |

| | | Amounts reclassified from AOCL to earnings | Amounts reclassified from AOCL to earnings | | (0.4) | | | 0.5 | | | 0.1 | | Amounts reclassified from AOCL to earnings | | (0.2) | | | — | | | (0.2) | |

| | | Balance as of June 30, 2022 | | $ | 12.4 | | | $ | (17.1) | | | $ | (4.7) | | |

| Balance as of March 31, 2023 | | Balance as of March 31, 2023 | | $ | 11.8 | | | $ | (14.4) | | | $ | (2.6) | |

Accounting for Taxes Collected from Customers and Remitted to Governmental Authorities

AES Ohio collects certain excise taxes levied by state or local governments from its customers. These taxes are accounted for on a net basis and not included in revenue. The amounts of such taxes collected for the three and six months ended June 30,March 31, 2023 and 2022 and 2021 were as follows:

| | | Three months ended | | Six months ended | | | Three months ended |

| | June 30, | | June 30, | | | March 31, |

| $ in millions | $ in millions | | 2022 | | 2021 | | 2022 | | 2021 | $ in millions | | | 2023 | | 2022 |

| Excise taxes collected | Excise taxes collected | | $ | 11.5 | | | $ | 11.3 | | | $ | 24.6 | | | $ | 24.2 | | Excise taxes collected | | | $ | 12.0 | | | $ | 13.1 | |

New Accounting Pronouncements Adopted in 20222023

The following table provides a brief description of recentWe have assessed and determined that the new accounting pronouncements that had an impact on our consolidated financial statements.

| | | | | | | | | | | |

ASU Number and Name | Description | Date of Adoption | Effect on the financial statements upon adoption |

2020-04 and 2021-01, Reference Rate Form (Topic 848): Facilitation of the Effects of Reference Rate Reform on Financial Reporting | The amendments in these updates provide optional expedients and exceptions for applying GAAP to contracts, hedging relationships and other transactions that reference to LIBOR or another reference rate expected to be discontinued by reference rate reform, and clarify that certain optional expedients and exceptions in Topic 848 for contract modifications and hedge accounting apply to derivatives that are affected by the discounting transition. These amendments are effective for a limited period of time (March 12, 2020 - December 31, 2022). | Effective for all entities as of March 12, 2020 through December 31, 2022 | We are implementing the reference rate reform and doadopted did not expect these amendments to have a material impact on our consolidated financial statements. See Implementation for further details. |

New Accounting Pronouncements Issued But Not Yet Effective

We have assessed and determined that the new accounting pronouncements issued but not yet effective are not expected to have a material impact on our consolidated financial statements.

2. Regulatory MattersREGULATORY MATTERS

Distribution Rate CaseAES Ohio ESPs and Comprehensive Settlement

On November 30, 2020, AES Ohio ESP filed a new distribution– Ohio law requires utilities to file either an ESP or MRO plan to establish SSO rates. From November 1, 2017 through December 18, 2019, AES Ohio operated pursuant to an approved ESP, which was initially approved on October 20, 2017 (ESP 3). On December 18, 2019, the PUCO approved AES Ohio's Notice of Withdrawal and reversion to its prior rate case withplan (ESP 1). Among other items, the PUCO. This rate case proposes a revenue increase of $120.8 million per year and incorporatesPUCO Order approving the DIR investments that were planned and approved in the last rate case but not yet included in distribution rates, other distribution investments since September 2015 and investments necessitated by the tornados that occurred on Memorial Day in 2019. The rate case also includes a proposal for increased tree-trimming expenses and certain customer demand-side management programs and recovery of prior-approved regulatory assets for tree trimming, uncollectible expenses and rate case expense. A hearing on this case was held in January 2022, and the case is pending a commission order. Certain parties that have intervened in the distribution rate case have argued that ESP 1 incorporatesrate plan includes reinstating the non-bypassable RSC Rider, which provides annual revenues of approximately $79.0 million. The OCC has appealed to the Ohio Supreme Court the PUCO's decision approving the reversion to ESP 1 as well as argued for a distribution rate freeze. Oral arguments regardingrefund of the potential rate freeze were held in May 2022.RSC revenues dating back to August 2021. A decision is pending. We are unable to predict the outcome of the distribution rate case,this appeal, but if the PUCO were to impose athis results in terms that are more adverse than AES Ohio's current ESP rate freeze that precludes AES Ohio’s ability to implement a distribution rate increase during ESP 1,plan, it could have a material adverse effect on our results of operations, financial condition and cash flows.

3. Fair ValueComprehensive Settlement - On October 23, 2020, AES Ohio entered into a Stipulation and Recommendation with the staff of the PUCO, various customers and organizations representing customers of AES Ohio and certain other parties with respect to, among other matters, AES Ohio's applications pending at the PUCO for (i) approval of AES Ohio's plan to modernize its distribution grid (the Smart Grid Plan), (ii) findings that DP&L passed the SEET for 2018 and 2019, and (iii) findings that AES Ohio's current ESP 1 satisfies the SEET and the more favorable in the aggregate (MFA) regulatory test. On June 16, 2021, the PUCO issued their opinion and order accepting the stipulation as filed. The OCC appealed the final PUCO order to the Ohio Supreme Court on December 6, 2021. Oral arguments regarding this appeal are expected but not yet scheduled.

ESP 4– AES Ohio is currently operating pursuant to ESP 1. On September 26, 2022, AES Ohio filed its latest ESP (ESP 4) with the PUCO. ESP 4 is a comprehensive plan to enhance and upgrade its network and improve service reliability, provide greater safeguards for price stability and continue investments in local economic development. As part of this plan, AES Ohio intends to increase investments in the distribution infrastructure and deploy a proactive vegetation management program. The plan also includes proposals for new customer programs, including renewable options, electric vehicle programs and energy efficiency programs for residential and low-income customers. ESP 4 also seeks to recover outstanding regulatory assets not currently in rates. AES Ohio did not propose that the RSC would continue as part of ESP 4.

On April 10, 2023, AES Ohio entered into a Stipulation and Recommendation with the PUCO Staff and seventeen parties (the “Settlement”) with respect to AES Ohio’s ESP 4 application, pending at the PUCO. The Settlement is subject to, and conditioned upon, approval by the PUCO. The Settlement would provide for a three-year ESP without a rate stability charge, and, in addition to other items, provides for the following:

•A Distribution Investment Rider for the term of the ESP allowing for the timely recovery of distribution investments by AES Ohio based on a 9.999% return on equity, subject to revenue caps;

•The recovery of approximately $66.0 million related to past expenditures by AES Ohio plus future carrying costs and the recovery of incremental vegetation management expenses up to certain annual limits during the term of ESP 4; and

•Funding of programs for assistance to low-income customers and for economic development.

Upon approval of this Settlement, the distribution rates that were approved by the PUCO in December 2022, and are described in the paragraph below, will become effective. An evidentiary hearing began May 2, 2023, and AES Ohio expects an order by the PUCO in the third quarter of 2023.

Distribution Rate Case

On November 30, 2020, AES Ohio filed a new distribution rate case application with the PUCO to increase AES Ohio’s base rates for electric distribution service to address, in part, increased costs of materials and labor and substantial investments to improve distribution structures. On December 14, 2022, the PUCO issued an order on the application. Among other matters, the order:

•Establishes a revenue increase of $75.6 million for AES Ohio’s base rates for electric distribution service and

•Provides for a return on equity of 9.999% and a cost of long-term debt of 4.4% on a distribution rate base of $783.5 million and based on a capital structure of 53.87% equity and 46.13% long-term debt.

As noted above, these rates will go into effect when the PUCO approves AES Ohio's Settlement regarding ESP 4.

3. FAIR VALUE

The fair value of currentour financial assets and liabilities and other deposits approximateapproximates their reported carrying amounts. The estimated fair values of our assets and liabilities have been determined using available market information. Because these amounts are estimates and based on hypothetical transactions to sell assets or transfer liabilities, the use of different market assumptions and/or estimation methodologies may have a material effect on the estimated fair value amounts. For further information on our valuation techniques and policies, see Note 4—Fair Value4– FAIR VALUE in Item 8.—Financial Statements and Supplementary Data of our Form 10-K.

Financial Assets

AES Ohio established a Master Trust to hold assets that could be used for the benefit of employees participating in employee benefit plans and theseplans. These assets are not used for general operating purposes. These assets are primarily comprised of open-ended mutual funds, which are valued using the net asset value per unit. These investmentsassets are recorded at fair value within Other non-current assets on the Condensed Consolidated Balance Sheets and are classified as equity investments. We recorded net unrealized gains / (losses) related to equity investments still held as of $(0.9)March 31, 2023 and 2022 of $0.3 million and $0.3$(0.5) million during the three months ended June 30,March 31, 2023 and 2022, and 2021, respectively, and $(1.6) million and $0.5 million during the six months ended June 30, 2022 and 2021, respectively. These amounts are included in "Other income"Other income, net in our Condensed Consolidated Statements of Operations.

Recurring Fair Value Measurements

The following table presents the fair value, carrying value and cost of our non-derivative instruments as of June 30, 2022 and December 31, 2021.

| | | | | | | | | | | | | | | | | | | | | | | | | | |

| | June 30, 2022 | | December 31, 2021 |

| $ in millions | | Cost | | Fair Value | | Cost | | Fair Value |

| Assets | | | | | | | | |

| Money market funds | | $ | 0.4 | | | $ | 0.4 | | | $ | 0.4 | | | $ | 0.4 | |

| Equity securities | | 1.8 | | | 3.8 | | | 1.9 | | | 5.1 | |

| Debt securities | | 3.7 | | | 3.3 | | | 3.8 | | | 3.9 | |

| | | | | | | | |

| | | | | | | | |

| | | | | | | | |

| Total | | $ | 5.9 | | | $ | 7.5 | | | $ | 6.1 | | | $ | 9.4 | |

These financial instruments are not subject to master netting agreements or collateral requirements and, as such, are presented in the Condensed Consolidated Balance Sheets at their gross fair value.

We did not have any transfers of the fair values of our financial instruments between Level 1, Level 2 or Level 3 of the fair value hierarchy during the sixthree months ended June 30, 2022March 31, 2023 or 2021.2022.

Recurring Fair Value Measurements

The fair value of assets and liabilities as of June 30, 2022March 31, 2023 and December 31, 20212022 measured on a recurring basis and the respective category within the fair value hierarchy for DPL is as follows:

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | Fair value as of March 31, 2023 | | Fair value as of December 31, 2022 |

| $ in millions | $ in millions | | Fair value as of June 30, 2022 | | Fair value as of December 31, 2021 | $ in millions | | Level 1 | | Level 2 | | Level 3 | | Total | | Level 1 | | Level 2 | | Level 3 | | Total |

| | Level 1 | | Level 2 | | Level 3 | | Total | | Level 1 | | Level 2 | | Level 3 | | Total | |

| Assets | Assets | | | | | | | | | | | | | | | | | Assets | | | | | | | | | | | | | | | | |

| Master Trust assets | Master Trust assets | | Master Trust assets | |

| Money market funds | Money market funds | | $ | 0.4 | | | $ | — | | | $ | — | | | $ | 0.4 | | | $ | 0.4 | | | $ | — | | | $ | — | | | $ | 0.4 | | Money market funds | | $ | 0.3 | | | $ | — | | | $ | — | | | $ | 0.3 | | | $ | 0.5 | | | $ | — | | | $ | — | | | $ | 0.5 | |

| Equity securities | | — | | | 3.8 | | | — | | | 3.8 | | | — | | | 5.1 | | | — | | | 5.1 | | |

| Debt securities | | — | | | 3.3 | | | — | | | 3.3 | | | — | | | 3.9 | | | — | | | 3.9 | | |

| Mutual funds | | Mutual funds | | 7.1 | | | — | | | — | | | 7.1 | | | 7.0 | | | — | | | — | | | 7.0 | |

| | | Total assets | Total assets | | $ | 0.4 | | | $ | 7.1 | | | $ | — | | | $ | 7.5 | | | $ | 0.4 | | | $ | 9.0 | | | $ | — | | | $ | 9.4 | | Total assets | | $ | 7.4 | | | $ | — | | | $ | — | | | $ | 7.4 | | | $ | 7.5 | | | $ | — | | | $ | — | | | $ | 7.5 | |

Financial Instruments not Measured at Fair Value in the Condensed Consolidated Balance Sheets

The fair value of long-term debt is based on current public market prices for disclosure purposes only. These fair value inputs are considered Level 2 in the fair value hierarchy. As the Wright-Patterson Air Force Base note is not publicly traded, the fair value inputs are considered Level 3 in the fair value hierarchy as there are no observable inputs. Unrealized gains or losses are not recognized in the financial statements as long-term debt is presented at carrying value, net of unamortized premium or discount and unamortized deferred financing costs in the financial statements. The long-term debt amounts include the current portion payable in the next twelve months and have maturities that range from 2025 to 2061.

The following table presents the carrying amount, fair value, and fair value hierarchy of our financial liabilities that are not measured at fair value in the Condensed Consolidated Balance Sheets as of the periods indicated, but for which fair value is disclosed:

| | | | Carrying Amount | | Fair value as of June 30, 2022 | | Carrying Amount | | Fair value as of December 31, 2021 | | Carrying Amount | | Fair value as of March 31, 2023 | | Carrying Amount | | Fair value as of December 31, 2022 |

| $ in millions | $ in millions | | Level 1 | | Level 2 | | Level 3 | | Total | | Level 1 | | Level 2 | | Level 3 | | Total | $ in millions | | Level 1 | | Level 2 | | Level 3 | | Total | | Level 1 | | Level 2 | | Level 3 | | Total |

| Liabilities | Liabilities | | | | | | | | | | | | | | | | | | | | | Liabilities | | | | | | | | | | | | | | | | | | | | |

| Long-term debt | Long-term debt | | $ | 1,535.0 | | | $ | — | | | $ | 1,399.6 | | | $ | 17.1 | | | $ | 1,416.7 | | | $ | 1,395.5 | | | $ | — | | | $ | 1,502.5 | | | $ | 17.2 | | | $ | 1,519.7 | | Long-term debt | | $ | 1,536.7 | | | $ | — | | | $ | 1,392.0 | | | $ | 17.0 | | | $ | 1,409.0 | | | $ | 1,535.9 | | | $ | — | | | $ | 1,376.4 | | | $ | 17.0 | | | $ | 1,393.4 | |

4. Derivative Instruments and Hedging ActivitiesDERIVATIVE INSTRUMENTS AND HEDGING ACTIVITIES

For further information on our derivative and hedge accounting policies, see Note 1 – OVERVIEW AND SUMMARY OF SIGNIFICANT ACCOUNTING POLICIESOverview and Summary of Significant Accounting Policies – Financial Derivatives and Note 5 - Derivative Instruments and Hedging Activities– DERIVATIVE INSTRUMENTS AND HEDGING ACTIVITIES of Item 8 – Financial Statements and Supplementary Data in our Form 10-K.

Cash Flow Hedges

WeDPL previously entered intoused derivative financial instruments primarily to manage the interest rate derivative contracts to manage interest rate exposure related to anticipated borrowings of fixed-raterisk associated with our long-term debt. These interest rate derivative contracts were settled in 2013, and we continue to amortize amounts out of AOCL into interest expense.

The following tables provide information concerning gains or losses recognized in AOCL for the cash flow hedges for the three and six months ended June 30, 2022March 31, 2023 and 2021:2022:

| | | Three months ended | | Six months ended | | | Three months ended |

| | June 30, 2022 | | June 30, 2021 | | June 30, 2022 | | June 30, 2021 | | | March 31, 2023 | | March 31, 2022 |

| | Interest | | Interest | | Interest | | Interest | | | Interest | | Interest |

| $ in millions (net of tax) | $ in millions (net of tax) | | Rate Hedge | | Rate Hedge | | Rate Hedge | | Rate Hedge | $ in millions (net of tax) | | | Rate Hedge | | Rate Hedge |

| Beginning accumulated derivative gains in AOCL | Beginning accumulated derivative gains in AOCL | | $ | 12.7 | | | $ | 13.4 | | | $ | 12.8 | | | $ | 13.6 | | Beginning accumulated derivative gains in AOCL | | | $ | 12.0 | | | $ | 12.8 | |

| | Net gains reclassified to earnings | Net gains reclassified to earnings | | | | | | | Net gains reclassified to earnings | | | |

| Interest expense | Interest expense | | (0.3) | | | (0.2) | | | (0.4) | | | (0.4) | | Interest expense | | | (0.2) | | | (0.1) | |

| | Ending accumulated derivative gains in AOCL | Ending accumulated derivative gains in AOCL | | $ | 12.4 | | | $ | 13.2 | | | $ | 12.4 | | | $ | 13.2 | | Ending accumulated derivative gains in AOCL | | | $ | 11.8 | | | $ | 12.7 | |