UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, DC 20549

FORM 10-Q

|

| | | | |

x

☒ | Quarterly Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 |

For the quarterly period ended September 30, 20172020

or

|

| | | | |

o

☐ | Transition Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 |

Commission File Number: 1-9819

DYNEX CAPITAL, INC.

(Exact name of registrant as specified in its charter) |

| | | | | | | | | | | | | | | | | | | |

| Virginia | | 52-1549373 |

| (State or other jurisdiction of | (I.R.S. Employer |

| incorporation or organization) | | (IRS Employer Identification No.) |

| |

4991 Lake Brook Drive, Suite 100 Glen Allen, Virginia | 23060-9245 | | |

| Glen Allen, | Virginia | | 23060-9245 |

| (Address of principal executive offices) | | (Zip Code) |

| | | (804) | 217-5800 | |

(804) 217-5800

(Registrant’s telephone number, including area code) |

| | | | | | | | | | | | | | |

| Securities registered pursuant to Section 12(b) of the Act: | | |

| Title of each class | | Trading Symbol(s) | | Name of each exchange on which registered |

| Common Stock, par value $0.01 per share | | DX | | New York Stock Exchange |

| 7.625% Series B Cumulative Redeemable Preferred Stock, par value $0.01 per share | | DXPRB | | New York Stock Exchange |

| 6.900% Series C Fixed-to-Floating Rate Cumulative Redeemable Preferred Stock, par value $0.01 per share | | DXPRC | | New York Stock Exchange |

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Yes x☒ No o☐

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

Yes x☒ No o☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and "emerging growth company" in Rule 12b-2 of the Exchange Act.

|

| | | | | | | | | | |

| Large accelerated filer | o☐ | Accelerated filer | x☒ |

| Non-accelerated filer | o (Do not check if a smaller reporting company)

☐ | Smaller reporting company | o☐ |

| | Emerging growth company | o☐ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. o☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

Yes o☐ No x☒

On October 31, 2017,30, 2020, the registrant had 53,219,28623,144,606 shares outstanding of common stock, $0.01 par value, which is the registrant’s only class of common stock.

DYNEX CAPITAL, INC.

FORM 10-Q

INDEX

| | | | | | | | | | | |

| | | Page |

| PART I. FINANCIAL INFORMATION | |

| | | |

| Item 1. | Financial Statements | Page |

| | |

| | | |

| | | |

| | | |

| | Consolidated Balance Sheets as of September 30, 20172020 (unaudited) and December 31, 20162019 | |

| | | |

| | Consolidated Statements of Comprehensive Income (Loss) for the three and nine months ended September 30, 20172020 (unaudited) and September 30, 20162019 (unaudited) | |

| | | |

| | Consolidated StatementStatements of Shareholders' Equity for the nine months ended September 30, 20172020 and September 30, 2019 (unaudited) | |

| | | |

| | Consolidated Statements of Cash Flows for the nine months ended September 30, 20172020 (unaudited) and September 30, 20162019 (unaudited) | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | |

| | | |

| Item 1. | Legal Proceedings | | | |

| Item 1A. | | |

| Risk Factors | | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| Item 5. | | |

| Other Information | | | |

| Item 6. | | |

| Exhibits | | | |

| | | |

| |

PART I. FINANCIAL INFORMATION

ITEM 1. FINANCIAL STATEMENTS

DYNEX CAPITAL, INC.

CONSOLIDATED BALANCE SHEETS

(amounts in thousands except share data) |

| | | | | | | |

| | September 30, 2017 | | December 31, 2016 |

| ASSETS | (unaudited) | |

|

| Mortgage-backed securities (including pledged of $2,714,312 and $3,150,610, respectively) | $ | 2,921,444 |

| | $ | 3,212,084 |

|

| Mortgage loans held for investment, net | 16,523 |

| | 19,036 |

|

| Cash and cash equivalents | 117,702 |

| | 74,120 |

|

| Restricted cash | 43,987 |

| | 24,769 |

|

| Derivative assets | 368 |

| | 28,534 |

|

| Receivable for securities sold | 13,435 |

| | — |

|

| Principal receivable on investments | 3,359 |

| | 11,978 |

|

| Accrued interest receivable | 19,267 |

| | 20,396 |

|

| Other assets, net | 7,193 |

| | 6,814 |

|

| Total assets | $ | 3,143,278 |

| | $ | 3,397,731 |

|

| | | | |

| LIABILITIES AND SHAREHOLDERS’ EQUITY |

|

| | |

|

| Liabilities: | |

| | |

|

| Repurchase agreements | $ | 2,519,230 |

| | $ | 2,898,952 |

|

| Payable for unsettled securities | 77,357 |

| | — |

|

| Non-recourse collateralized financing | 5,706 |

| | 6,440 |

|

| Derivative liabilities | 133 |

| | 6,922 |

|

| Accrued interest payable | 2,720 |

| | 3,156 |

|

| Accrued dividends payable | 11,620 |

| | 12,268 |

|

| Other liabilities | 2,413 |

| | 2,809 |

|

| Total liabilities | 2,619,179 |

| | 2,930,547 |

|

| |

|

| | |

| Shareholders’ equity: | |

| | |

|

| Preferred stock, par value $.01 per share; 50,000,000 shares authorized; 5,665,101 and 4,571,937 shares issued and outstanding, respectively ($141,628 and $114,298 aggregate liquidation preference, respectively) | $ | 135,828 |

| | $ | 110,005 |

|

Common stock, par value $.01 per share, 200,000,000 shares authorized; 51,262,350 and 49,153,463 shares issued and outstanding, respectively | 513 |

| | 492 |

|

| Additional paid-in capital | 742,845 |

| | 727,369 |

|

| Accumulated other comprehensive income (loss) | 5,886 |

| | (32,609 | ) |

| Accumulated deficit | (360,973 | ) | | (338,073 | ) |

| Total shareholders' equity | 524,099 |

| | 467,184 |

|

| Total liabilities and shareholders’ equity | $ | 3,143,278 |

| | $ | 3,397,731 |

|

See notes to the unaudited consolidated financial statements.

DYNEX CAPITAL, INC.

CONSOLIDATED STATEMENTS OF COMPREHENSIVE INCOME

(UNAUDITED)

(amounts in thousands except per share data)

|

| | | | | | | | | | | | | | | |

| | Three Months Ended | | Nine Months Ended |

| | September 30, | | September 30, |

| | 2017 | | 2016 | | 2017 | | 2016 |

| Interest income | $ | 23,103 |

| | $ | 21,135 |

| | $ | 70,378 |

| | 69,040 |

|

| Interest expense | 9,889 |

| | 6,068 |

| | 26,122 |

| | 18,478 |

|

| Net interest income | 13,214 |

| | 15,067 |

| | 44,256 |

| | 50,562 |

|

| | | | | | | | |

| Gain (loss) on derivative instruments, net | 5,993 |

| | 2,409 |

| | (9,634 | ) | | (62,153 | ) |

| Loss on sale of investments, net | (5,211 | ) | | — |

| | (10,628 | ) | | (4,238 | ) |

| Fair value adjustments, net | 23 |

| | 34 |

| | 63 |

| | 86 |

|

| Other (loss) income, net | (109 | ) | | 545 |

| | (150 | ) | | 898 |

|

| General and administrative expenses: | | | | |

|

| | |

| Compensation and benefits | (2,070 | ) | | (1,736 | ) | | (6,356 | ) | | (5,829 | ) |

| Other general and administrative | (1,529 | ) | | (1,619 | ) | | (5,620 | ) | | (5,288 | ) |

| Net income (loss) | 10,311 |

| | 14,700 |

| | 11,931 |

| | (25,962 | ) |

| Preferred stock dividends | (2,808 | ) | | (2,294 | ) | | (7,885 | ) | | (6,882 | ) |

| Net income (loss) to common shareholders | $ | 7,503 |

| | $ | 12,406 |

| | $ | 4,046 |

| | $ | (32,844 | ) |

| | | | | | | | |

| Other comprehensive income: | | | | |

|

| | |

| Unrealized gain on available-for-sale investments, net | $ | 981 |

| | $ | 769 |

| | $ | 28,087 |

| | $ | 61,260 |

|

| Reclassification adjustment for loss on sale of investments, net | 5,211 |

| | — |

| | 10,628 |

| | 4,238 |

|

| Reclassification adjustment for de-designated cash flow hedges | (48 | ) | | (99 | ) | | (220 | ) | | (152 | ) |

| Total other comprehensive income | 6,144 |

| | 670 |

| | 38,495 |

| | 65,346 |

|

| Comprehensive income to common shareholders | $ | 13,647 |

| | $ | 13,076 |

| | $ | 42,541 |

| | $ | 32,502 |

|

| | | | | | | | |

| Net income (loss) per common share-basic and diluted | $ | 0.15 |

| | $ | 0.25 |

| | $ | 0.08 |

| | $ | (0.67 | ) |

| Weighted average common shares-basic and diluted | 49,832 |

| | 49,147 |

| | 49,411 |

| | 49,102 |

|

| | | | | | | | | | | |

| | September 30, 2020 | | December 31, 2019 |

| ASSETS | (unaudited) | | |

| Cash and cash equivalents | $ | 158,897 | | | $ | 62,582 | |

| Restricted cash | 26,006 | | | 71,648 | |

| Mortgage-backed securities (including pledged of $2,766,132 and $5,024,625, respectively), at fair value | 2,995,660 | | | 5,188,163 | |

| Mortgage loans held for investment (includes $6,921 and $8,857 at fair value, respectively); see Note 1 | 6,921 | | | 9,405 | |

| Receivable for securities sold | 1,145 | | | 0 | |

| Derivative assets | 4,266 | | | 4,290 | |

| Accrued interest receivable | 15,340 | | | 26,209 | |

| Other assets, net | 6,804 | | | 8,307 | |

| Total assets | $ | 3,215,039 | | | $ | 5,370,604 | |

| | | |

| LIABILITIES AND SHAREHOLDERS’ EQUITY | | | |

| Liabilities: | | | |

| Repurchase agreements | $ | 2,594,683 | | | $ | 4,752,348 | |

| Payable for unsettled securities | 190 | | | 6,180 | |

| Non-recourse collateralized financing | 645 | | | 2,733 | |

| Derivative liabilities | 5,164 | | | 974 | |

| Accrued interest payable | 1,059 | | | 15,585 | |

| Accrued dividends payable | 5,755 | | | 6,280 | |

| Other liabilities | 3,990 | | | 3,516 | |

| Total liabilities | $ | 2,611,486 | | | $ | 4,787,616 | |

| | | |

| Shareholders’ equity: | | | |

| Preferred stock, par value $0.01 per share; 50,000,000 shares authorized; 7,248,330 and 6,788,330 shares issued and outstanding, respectively ($181,208 and $169,708 aggregate liquidation preference, respectively) | $ | 174,709 | | | $ | 162,807 | |

Common stock, par value $0.01 per share, 90,000,000 shares authorized; 23,145,238 and 22,945,993 shares issued and outstanding, respectively | 231 | | | 229 | |

| Additional paid-in capital | 859,089 | | | 858,347 | |

| Accumulated other comprehensive income | 88,729 | | | 173,806 | |

| Accumulated deficit | (519,205) | | | (612,201) | |

| Total shareholders’ equity | 603,553 | | | 582,988 | |

| Total liabilities and shareholders’ equity | $ | 3,215,039 | | | $ | 5,370,604 | |

See notes to the unaudited consolidated financial statements.

DYNEX CAPITAL, INC.

CONSOLIDATED STATEMENTSTATEMENTS OF SHAREHOLDERS’ EQUITYCOMPREHENSIVE INCOME (LOSS)

(UNAUDITED)(unaudited)

($amounts in thousands)thousands except per share data)

| | | | | | | | | | | | | | | | | | | | | | | |

| Three Months Ended | | Nine Months Ended |

| September 30, | | September 30, |

| | 2020 | | 2019 | | 2020 | | 2019 |

| Interest income | $ | 20,088 | | | $ | 44,502 | | | $ | 79,764 | | | $ | 128,207 | |

| Interest expense | 3,375 | | | 31,256 | | | 30,327 | | | 88,345 | |

| Net interest income | 16,713 | | | 13,246 | | | 49,437 | | | 39,862 | |

| | | | | | | |

| Gain (loss) on derivative instruments, net | 7,974 | | | (50,709) | | | (196,156) | | | (229,941) | |

| Gain (loss) on sale of investments, net | 20,846 | | | 4,605 | | | 298,728 | | | (5,755) | |

| Fair value adjustments, net | 194 | | | (13) | | | 154 | | | (42) | |

| Other operating (expense) income, net | (207) | | | 25 | | | (852) | | | 50 | |

| General and administrative expenses: | | | | | | | |

| Compensation and benefits | (2,402) | | | (1,786) | | | (7,301) | | | (5,430) | |

| Other general and administrative | (2,393) | | | (1,972) | | | (6,926) | | | (6,547) | |

| Net income (loss) | 40,725 | | | (36,604) | | | 137,084 | | | (207,803) | |

| Preferred stock dividends | (3,252) | | | (3,341) | | | (10,346) | | | (9,606) | |

| Preferred stock redemption charge | 0 | | | 0 | | | (3,914) | | | 0 | |

| Net income (loss) to common shareholders | $ | 37,473 | | | $ | (39,945) | | | $ | 122,824 | | | $ | (217,409) | |

| | | | | | | |

| Other comprehensive income: | | | | | | | |

| Unrealized gain on available-for-sale investments, net | $ | 27,844 | | | $ | 59,800 | | | $ | 213,651 | | | $ | 247,199 | |

| Reclassification adjustment for (gain) loss on sale of investments, net | (20,846) | | | (4,605) | | | (298,728) | | | 5,755 | |

| Reclassification adjustment for de-designated cash flow hedges | 0 | | | 0 | | | 0 | | | (165) | |

| Total other comprehensive income (loss) | 6,998 | | | 55,195 | | | (85,077) | | | 252,789 | |

| Comprehensive income to common shareholders | $ | 44,471 | | | $ | 15,250 | | | $ | 37,747 | | | $ | 35,380 | |

| | | | | | | |

| Net income (loss) per common share-basic and diluted | $ | 1.62 | | | $ | (1.65) | | | $ | 5.33 | | | $ | (9.12) | |

| Weighted average common shares-basic and diluted | 23,141 | | | 24,174 | | | 23,054 | | | 23,847 | |

|

| | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | Preferred Stock | | Common Stock | | Additional Paid-in Capital | | Accumulated Other Comprehensive (Loss) Income | | Accumulated Deficit | | Total Shareholders' Equity |

| | Shares | Amount | Shares | Amount |

| Balance as of December 31, 2016 | 4,571,937 |

| $ | 110,005 |

| | 49,153,463 |

| $ | 492 |

| | $ | 727,369 |

| | $ | (32,609 | ) | | $ | (338,073 | ) | | $ | 467,184 |

|

| Stock issuance | 1,093,164 |

| 25,884 |

| | 2,048,288 |

| 21 |

| | 14,474 |

| | — |

| | — |

| | 40,379 |

|

| Restricted stock granted, net of amortization | — |

| — |

| | 138,166 |

| 1 |

| | 1,565 |

| | — |

| | — |

| | 1,566 |

|

| Adjustments for tax withholding on share-based compensation | — |

| — |

| | (77,567 | ) | (1 | ) | | (520 | ) | | — |

| | — |

| | (521 | ) |

| Stock issuance costs | — |

| (61 | ) | | — |

| — |

| | (43 | ) | | — |

| | — |

| | (104 | ) |

| Net income | — |

| — |

| | — |

| — |

| | — |

| | — |

| | 11,931 |

| | 11,931 |

|

| Dividends on preferred stock | — |

| — |

| | — |

| — |

| | — |

| | — |

| | (7,885 | ) | | (7,885 | ) |

| Dividends on common stock | — |

| — |

| | — |

| — |

| | — |

| | — |

| | (26,946 | ) | | (26,946 | ) |

| Other comprehensive income | — |

| — |

| | — |

| — |

| | — |

| | 38,495 |

| | — |

| | 38,495 |

|

| Balance as of September 30, 2017 | 5,665,101 |

| $ | 135,828 |

| | 51,262,350 |

| $ | 513 |

| | $ | 742,845 |

| | $ | 5,886 |

| | $ | (360,973 | ) | | $ | 524,099 |

|

DYNEX CAPITAL, INC.

CONSOLIDATED STATEMENTS OF SHAREHOLDERS’ EQUITY

(unaudited)

($ in thousands)

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Preferred Stock | | Common Stock | | Additional

Paid-in

Capital | | Accumulated

Other

Comprehensive

Income (Loss) | | Accumulated

Deficit | | Total Shareholders’ Equity |

| Shares | Amount | Shares | Amount |

Balance as of

December 31, 2019 | 6,788,330 | | $ | 162,807 | | | 22,945,993 | | $ | 229 | | | $ | 858,347 | | | $ | 173,806 | | | $ | (612,201) | | | $ | 582,988 | |

| Cumulative effect of change in accounting principle | — | | — | | | — | | — | | | — | | | — | | | (548) | | | (548) | |

| Stock issuance | 4,460,000 | | 107,988 | | | — | | — | | | — | | | — | | | — | | | 107,988 | |

| Redemption of preferred stock | (4,000,000) | | (96,086) | | | — | | — | | | — | | | — | | | (3,914) | | | (100,000) | |

| Restricted stock granted, net of amortization | — | | — | | | 67,511 | | 1 | | | 306 | | | — | | | — | | | 307 | |

| Stock repurchase | — | | — | | | (18,782) | | 0 | | | (206) | | | — | | | — | | | (206) | |

| Adjustments for tax withholding on share-based compensation | — | | — | | | (12,744) | | 0 | | | (235) | | | — | | | — | | | (235) | |

| Stock issuance costs | — | | — | | | — | | — | | | (9) | | | — | | | — | | | (9) | |

| Net loss | — | | — | | | — | | — | | | — | | | — | | | (98,479) | | | (98,479) | |

| Dividends on preferred stock | — | | — | | | — | | — | | | — | | | — | | | (3,841) | | | (3,841) | |

| Dividends on common stock | — | | — | | | — | | — | | | — | | | — | | | (10,330) | | | (10,330) | |

| Other comprehensive income | — | | — | | | — | | — | | | — | | | 72,972 | | | — | | | 72,972 | |

Balance as of

March 31, 2020 | 7,248,330 | | $ | 174,709 | | | 22,981,978 | | $ | 230 | | | $ | 858,203 | | | $ | 246,778 | | | $ | (729,313) | | | $ | 550,607 | |

| Restricted stock granted, net of amortization | — | | — | | | 172,782 | | 1 | | | 422 | | | — | | | — | | | 423 | |

| Stock repurchase | — | | — | | | (14,143) | | — | | | (166) | | | — | | | — | | | (166) | |

| Stock issuance costs | — | | — | | | — | | — | | | (8) | | | — | | | — | | | (8) | |

| Net income | — | | — | | | — | | — | | | — | | | — | | | 194,838 | | | 194,838 | |

| Dividends on preferred stock | — | | — | | | — | | — | | | — | | | — | | | (3,253) | | | (3,253) | |

| Dividends on common stock | — | | — | | | — | | — | | | — | | | — | | | (9,925) | | | (9,925) | |

| Other comprehensive loss | — | | — | | | — | | — | | | — | | | (165,047) | | | — | | | (165,047) | |

Balance as of

June 30, 2020 | 7,248,330 | | $ | 174,709 | | | 23,140,617 | | $ | 231 | | | $ | 858,451 | | | $ | 81,731 | | | $ | (547,653) | | | $ | 567,469 | |

| Stock issuance | — | | — | | | 5,219 | | 0 | | | 85 | | | — | | | — | | | 85 | |

| Restricted stock granted, net of amortization | — | | — | | | — | | — | | | 568 | | | — | | | — | | | 568 | |

| Adjustments for tax withholding on share-based compensation | — | | — | | | (598) | | — | | | (10) | | | — | | | — | | | (10) | |

| Stock issuance costs | — | | — | | | — | | — | | | (5) | | | — | | | — | | | (5) | |

| Net income | — | | — | | | — | | — | | | — | | | — | | | 40,725 | | | 40,725 | |

| Dividends on preferred stock | — | | — | | | — | | — | | | — | | | — | | | (3,252) | | | (3,252) | |

| Dividends on common stock | — | | — | | | — | | — | | | — | | | — | | | (9,025) | | | (9,025) | |

| Other comprehensive income | — | | — | | | — | | — | | | — | | | 6,998 | | | — | | | 6,998 | |

Balance as of

September 30, 2020 | 7,248,330 | | $ | 174,709 | | | 23,145,238 | | $ | 231 | | | $ | 859,089 | | | $ | 88,729 | | | $ | (519,205) | | | $ | 603,553 | |

| | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Preferred Stock | | Common Stock | | Additional

Paid-in

Capital | | Accumulated

Other

Comprehensive

Income (Loss) | | Accumulated

Deficit | | Total Shareholders’ Equity |

| Shares | Amount | Shares | Amount |

| Balance as of December 31, 2018 | 5,954,594 | | $ | 142,883 | | | 20,939,073 | | $ | 209 | | | $ | 818,861 | | | $ | (35,779) | | | $ | (399,021) | | | $ | 527,153 | |

| Stock issuance | 213,468 | | 5,015 | | | 3,109,047 | | 31 | | | 53,841 | | | — | | | — | | | 58,887 | |

| Restricted stock granted, net of amortization | — | | — | | | 50,821 | | 1 | | | 297 | | | — | | | — | | | 298 | |

| Adjustments for tax withholding on share-based compensation | — | | — | | | (16,231) | | 0 | | | (296) | | | — | | | — | | | (296) | |

| Stock issuance costs | — | | — | | | — | | — | | | (212) | | | — | | | — | | | (212) | |

| Net loss | — | | — | | | — | | — | | | — | | | �� | | | (52,214) | | | (52,214) | |

| Dividends on preferred stock | — | | — | | | — | | — | | | — | | | — | | | (3,059) | | | (3,059) | |

| Dividends on common stock | — | | — | | | — | | — | | | — | | | — | | | (12,350) | | | (12,350) | |

| Other comprehensive income | — | | — | | | — | | — | | | — | | | 86,467 | | | — | | | 86,467 | |

Balance as of

March 31, 2019 | 6,168,062 | | $ | 147,898 | | | 24,082,710 | | $ | 241 | | | $ | 872,491 | | | $ | 50,688 | | | $ | (466,644) | | | $ | 604,674 | |

| Stock issuance | 346,068 | | 8,173 | | | 547,071 | | 5 | | | 9,874 | | | — | | | — | | | 18,052 | |

| Restricted stock granted, net of amortization | — | | — | | | 17,183 | | 0 | | | 296 | | | — | | | — | | | 296 | |

| Stock issuance costs | — | | — | | | — | | — | | | (28) | | | — | | | — | | | (28) | |

| Net loss | — | | — | | | — | | — | | | — | | | — | | | (118,985) | | | (118,985) | |

| Dividends on preferred stock | — | | — | | | — | | — | | | — | | | — | | | (3,206) | | | (3,206) | |

| Dividends on common stock | — | | — | | | — | | — | | | — | | | — | | | (13,292) | | | (13,292) | |

| Other comprehensive income | — | | — | | | — | | — | | | — | | | 111,127 | | | — | | | 111,127 | |

Balance as of

June 30, 2019 | 6,514,130 | | 156,071 | | | 24,646,964 | | 246 | | | 882,633 | | | 161,815 | | | (602,127) | | | 598,638 | |

| Stock issuance | 274,200 | | 6,736 | | | 8,300 | | 0 | | | 137 | | | — | | | — | | | 6,873 | |

| Restricted stock granted, net of amortization | — | | — | | | 0 | | 0 | | | 306 | | | — | | | — | | | 306 | |

| Stock repurchase | — | | — | | | (1,709,271) | | (17) | | | (25,017) | | | — | | | — | | | (25,034) | |

| Stock issuance costs | — | | — | | | — | | — | | | (9) | | | — | | | — | | | (9) | |

| Net loss | — | | — | | | — | | — | | | — | | | — | | | (36,604) | | | (36,604) | |

| Dividends on preferred stock | — | | — | | | — | | — | | | — | | | — | | | (3,341) | | | (3,341) | |

| Dividends on common stock | — | | — | | | — | | — | | | — | | | — | | | (11,577) | | | (11,577) | |

| Other comprehensive income | — | | — | | | — | | — | | | — | | | 55,195 | | | — | | | 55,195 | |

Balance as of

September 30, 2019 | 6,788,330 | | $ | 162,807 | | | 22,945,993 | | $ | 229 | | | $ | 858,050 | | | $ | 217,010 | | | $ | (653,649) | | | $ | 584,447 | |

See notes to the unaudited consolidated financial statements.

DYNEX CAPITAL, INC.

CONSOLIDATED STATEMENTS OF CASH FLOWS

(UNAUDITED)(unaudited)

| | | | Nine Months Ended | | Nine Months Ended |

| | September 30, | | September 30, |

| | 2017 | | 2016 | | 2020 | | 2019 |

| Operating activities: | | | | Operating activities: | | | |

| Net income (loss) | $ | 11,931 |

| | $ | (25,962 | ) | Net income (loss) | $ | 137,084 | | | $ | (207,803) | |

| Adjustments to reconcile net income (loss) to cash provided by operating activities: | |

| | |

| Adjustments to reconcile net income (loss) to cash provided by operating activities: | | |

| Decrease in accrued interest receivable | 1,129 |

| | 3,263 |

| |

| (Decrease) increase in accrued interest payable | (436 | ) | | 420 |

| |

| Decrease (increase) in accrued interest receivable | | Decrease (increase) in accrued interest receivable | 10,869 | | | (3,075) | |

| Decrease in accrued interest payable | | Decrease in accrued interest payable | (14,526) | | | (3,122) | |

| Loss on derivative instruments, net | 9,634 |

| | 62,153 |

| Loss on derivative instruments, net | 196,156 | | | 229,941 | |

| Loss on sale of investments, net | 10,628 |

| | 4,238 |

| |

| (Gain) loss on sale of investments, net | | (Gain) loss on sale of investments, net | (298,728) | | | 5,755 | |

| Fair value adjustments, net | (63 | ) | | (86 | ) | Fair value adjustments, net | (154) | | | 42 | |

| Amortization of investment premiums, net | 122,621 |

| | 112,418 |

| Amortization of investment premiums, net | 96,018 | | | 98,327 | |

| Other amortization and depreciation, net | 983 |

| | 1,186 |

| Other amortization and depreciation, net | 1,428 | | | 1,186 | |

| Stock-based compensation expense | 1,567 |

| | 2,066 |

| Stock-based compensation expense | 1,299 | | | 899 | |

| Increase in other assets and liabilities, net | (1,905 | ) | | (2,060 | ) | |

| Change in other assets and liabilities, net | | Change in other assets and liabilities, net | 530 | | | (6) | |

| Net cash and cash equivalents provided by operating activities | 156,089 |

| | 157,636 |

| Net cash and cash equivalents provided by operating activities | 129,976 | | | 122,144 | |

| Investing activities: | |

| | |

| Investing activities: | | | |

| Purchase of investments | (772,590 | ) | | (96,816 | ) | Purchase of investments | (2,436,953) | | | (2,833,348) | |

| Principal payments received on investments | 248,298 |

| | 337,719 |

| Principal payments received on investments | 344,055 | | | 347,565 | |

| Proceeds from sales of investments | 792,984 |

| | 94,033 |

| Proceeds from sales of investments | 4,401,909 | | | 1,033,066 | |

| Principal payments received on mortgage loans held for investment, net | 2,641 |

| | 3,709 |

| |

| Distributions received from limited partnership | — |

| | 10,835 |

| |

| Net receipts (payments) on derivatives, including terminations | 11,743 |

| | (24,483 | ) | |

| Principal payments received on mortgage loans held for investment | | Principal payments received on mortgage loans held for investment | 2,170 | | | 1,677 | |

| Net payments on derivatives, including terminations | | Net payments on derivatives, including terminations | (197,932) | | | (229,001) | |

| Other investing activities | (214 | ) | | (105 | ) | Other investing activities | 0 | | | (183) | |

| Net cash and cash equivalents provided by investing activities | 282,862 |

| | 324,892 |

| |

| Net cash and cash equivalents provided by (used in) investing activities | | Net cash and cash equivalents provided by (used in) investing activities | 2,113,249 | | | (1,680,224) | |

| Financing activities: | |

| | |

| Financing activities: | | | |

| Borrowings under repurchase agreements | 60,229,426 |

| | 19,293,243 |

| Borrowings under repurchase agreements | 28,304,165 | | | 93,107,875 | |

| Repayments of repurchase agreement borrowings and FHLB advances | (60,609,148 | ) | | (19,661,384 | ) | |

| Repayments of repurchase agreement borrowings | | Repayments of repurchase agreement borrowings | (30,461,830) | | | (91,502,990) | |

| Principal payments on non-recourse collateralized financing | (747 | ) | | (1,443 | ) | Principal payments on non-recourse collateralized financing | (2,107) | | | (517) | |

| Proceeds from issuance of preferred stock | 25,884 |

| | — |

| Proceeds from issuance of preferred stock | 107,988 | | | 19,924 | |

| Proceeds from issuance of common stock | 14,495 |

| | 102 |

| Proceeds from issuance of common stock | 0 | | | 63,889 | |

| Cash paid for redemption of preferred stock | | Cash paid for redemption of preferred stock | (100,000) | | | 0 | |

| Cash paid for stock issuance costs | (61 | ) | | — |

| Cash paid for stock issuance costs | 0 | | | (185) | |

| Cash paid for repurchases of common stock | — |

| | (310 | ) | |

| Cash paid for common stock repurchases | | Cash paid for common stock repurchases | (372) | | | (25,034) | |

| Payments related to tax withholding for stock-based compensation | (521 | ) | | (485 | ) | Payments related to tax withholding for stock-based compensation | (245) | | | (296) | |

| Dividends paid | (35,479 | ) | | (39,285 | ) | Dividends paid | (40,151) | | | (54,355) | |

| Net cash and cash equivalents used in financing activities | (376,151 | ) | | (409,562 | ) | |

| Net cash and cash equivalents (used in) provided by financing activities | | Net cash and cash equivalents (used in) provided by financing activities | (2,192,552) | | | 1,608,311 | |

| | | | | | | | |

| Net increase in cash, cash equivalents, and restricted cash | 62,800 |

| | 72,966 |

| Net increase in cash, cash equivalents, and restricted cash | 50,673 | | | 50,231 | |

| Cash, cash equivalents, and restricted cash at beginning of period | 98,889 |

| | 85,125 |

| Cash, cash equivalents, and restricted cash at beginning of period | 134,230 | | | 88,704 | |

| Cash, cash equivalents, and restricted cash at end of period | $ | 161,689 |

| | $ | 158,091 |

| Cash, cash equivalents, and restricted cash at end of period | $ | 184,903 | | | $ | 138,935 | |

| Supplemental Disclosure of Cash Activity: | |

| | |

| Supplemental Disclosure of Cash Activity: | | | |

| Cash paid for interest | $ | 26,766 |

| | $ | 18,185 |

| Cash paid for interest | $ | 44,216 | | | $ | 91,624 | |

See notes to the unaudited consolidated financial statements.

NOTES TO THE UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS

DYNEX CAPITAL, INC.

(amounts in thousands except share data)

NOTE 1 – ORGANIZATION AND SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

Organization

Dynex Capital, Inc., ("Company" (“Company”) was incorporated in the Commonwealth of Virginia on December 18, 1987 and commenced operations in February 1988. The Company is an internally managed mortgage real estate investment trust, or mortgage REIT, which primarily earns income from investing on a leveraged basis in debt securities, the majority of which are specified pools of Agency and non-Agency mortgage-backed securities (“MBS”) consisting of commercial MBS (“CMBS”), residential MBS (“RMBS”), commercial MBS (“CMBS”) and CMBS interest-only ("IO"(“IO”) securities thatand non-Agency MBS, which consist mainly of CMBS IO. Agency MBS have a guaranty of principal payment by a U.S. government-sponsored entity (“GSE”) such as Fannie Mae and Freddie Mac which are in conservatorship and are currently supported by a senior preferred stock purchase agreement from U.S. Treasury. Non-Agency MBS are issued or guaranteed by the U.S. Government or U.S. Government sponsored agencies ("Agency MBS")non-governmental enterprises and MBS issued by others ("non-Agency MBS"). Wedo not have a guaranty of principal payment. The Company also investinvests in other types of mortgage-related securities, such as to-be-announced securities (“TBA”TBAs” or “TBA securities”).

Impact of COVID-19

As a result of the economic, health and market turmoil brought about by the coronavirus (“COVID-19”) forward contracts forpandemic, fixed income and equity markets experienced severe disruption which began in mid-March of 2020. The disruption resulted in a substantial rally in interest rates and a decline in fair value of MBS, which led to significant demands on liquidity from margin calls from derivative and repurchase agreement counterparties. During this time, the purchase or saleCompany met all margin calls and was not forced to sell any assets. Since early in the second quarter of generic (also referred2020, fixed income markets, equity markets and Agency MBS prices have stabilized with the Federal Reserve announcing multiple programs to as "non-specified"support economic activity and to support the smooth functioning of markets. In addition, the U.S. Congress passed the Coronavirus Aid, Relief, and Economic Security (“CARES”) poolsAct to provide economic relief, which included certain assistance to homeowners and renters. Though these supportive actions have helped cushion the economic damage from the disruption of Agency MBS.the pandemic to date, the Company is not able to predict the impact these policies may have on its investments over the longer term, particularly if a resurgence in cases of COVID-19 causes further damage to the economy.

Basis of Presentation

The accompanying unaudited consolidated financial statements of Dynex Capital, Inc.the Company and its subsidiaries (together, “Dynex” or, as appropriate, the “Company”) have been prepared in accordance with accounting principles generally accepted in the United States of America (“GAAP”) for interim financial information and with the instructions to the Quarterly Report on Form 10-Q and Article 10, Rule 10-01 of Regulation S-X promulgated by the Securities and Exchange Commission (the “SEC”). Accordingly, they do not include all of the information and notes required by GAAP for complete financial statements. In the opinion of management, all significant adjustments, consisting of normal recurring accruals, considered necessary for a fair presentation of the consolidated financial statements have been included.included; however, uncertainty over the continuing impact that COVID-19 will have on the global economy and on the Company’s business makes any estimates and assumptions as of September 30, 2020 inherently less certain than they would be absent the current and potential impacts of COVID-19. Operating results for the three and nine months ended September 30, 20172020 are not necessarily indicative of the results that may be expected for any other interim periods or for the entire year ending December 31, 2017.2020. The unaudited consolidated financial statements included herein should be read in conjunction with the audited financial statements and notes thereto included in the Company’s Annual Report on Form 10-K for the year ended December 31, 20162019 (the “2019 Form 10-K”) filed with the SEC.

Consolidation and Variable Interest Entities

The consolidated financial statements include the accounts of the Company and the accounts of its majority owned subsidiaries and variable interest entities ("VIE"(“VIE”) for which it is the primary beneficiary. As a primary beneficiary, the Company has both the power to direct the activities that most significantly impact the economic performance of the VIE and a right to receive benefits or absorb losses of the entity that could be potentially significant to the VIE. The Company is required to reconsider its evaluation of whether to consolidate a VIE each reporting period, based upon changes in the facts and circumstances pertaining to the VIE. The Company consolidates certain trusts through which it has securitized mortgage loans as a result of not meeting the sale criteria under GAAP at the time the financial assets were transferred to the trust. All intercompany accounts and transactions have been eliminated in consolidation.

The Company consolidates a VIE if the Company is determined to be the VIE’s primary beneficiary, which is defined as the party that has both: (i) the power to control the activities that most significantly impact the VIE’s financial

NOTES TO THE UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS

DYNEX CAPITAL, INC.

(amounts in thousands except share data)

performance and (ii) the right to receive benefits or absorb losses that could potentially be significant to the VIE. The Company reconsiders its evaluation of whether to consolidate a VIE on an ongoing basis, based on changes in the facts and circumstances pertaining to the VIE.

The Company consolidates a securitization trust, which has residential mortgage loans included in “mortgage loans held for investment” on its consolidated balance sheet, of which a portion is pledged as collateral for one remaining bond recorded as “non-recourse collateralized financing” on its consolidated balance sheet. The Company owns the subordinate class in the trust and has been deemed the primary beneficiary.

Though the Company invests in Agency and non-Agency MBS which are generally considered to be interests in VIEs, the Company does not consolidate these entities because it does not meet the criteria necessary to be deemed a primary beneficiary.

Use of Estimates

The preparation of financial statements in conformity with GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and the disclosure of contingent assets and liabilities at the date of the financial statements as well as the reported amounts of revenue and expenses during the reported period. Actual results could differ from those estimates. The most significant estimates used by management include, but are not limited to, amortization of premiums and discounts and fair value measurements of its investments, and other-than-temporary impairments.investments. These items are discussed further below within this note to the consolidated financial statements.

Income Taxes

The Company has elected to be taxed as a real estate investment trust ("REIT"(“REIT”) under the Internal Revenue Code of 1986 and the corresponding provisions of state law. To qualify as a REIT, the Company must meet certain tests including investing in primarily real estate-related assets and the required distribution of at least 90% of its annual REIT taxable income to stockholdersshareholders after consideration of its net operating loss ("NOL"(“NOL”) carryforward and not including taxable income retained in its taxable subsidiaries. As a REIT, the Company generally will not be subject to federal income tax on the amount of its income or capital gains that is distributed as dividends to shareholders.

The Company assesses its tax positions for all open tax years and determines whether the Company has any material unrecognized liabilities in accordance with Accounting Standards Codification ("ASC") Topic 740. The Companyand records these liabilities, if any, to the extent they are deemed more likely than not to have been incurred.

Net Income (Loss) Per Common Share

The Company calculates basic net income (loss) per common share by dividing net income (loss) to common shareholders for the period by weighted-average shares of common stock outstanding for that period. The Company did not have any potentially dilutive securities outstanding during the three orand nine months ended September 30, 20172020 or September 30, 2016.2019.

Holders of unvested shares of the Company'sCompany’s issued and outstanding restricted common stock are eligible to receive non-forfeitable dividends. As such, these unvested shares are considered participating securities as per ASC Topic 260-10 and therefore are included in the computation of basic net income (loss) per common share using the two-class method. Upon vesting, restrictions on transfer expire on each share of restricted stock, and each such share of restricted stock represents one unrestricted share of common stock.

Because the Company's 8.50% Series A Cumulative Redeemable Preferred Stock (the “Series A Preferred Stock”) andCompany’s 7.625% Series B Cumulative Redeemable Preferred Stock (the “Series B Preferred Stock”) and its 6.900% Series C Fixed-to-Floating Rate Cumulative Redeemable Preferred Stock (the “Series C Preferred Stock”) (collectively, the “Preferred Stock”) are redeemable at the Company'sCompany’s option for cash only and may convert into shares of common stock only upon a change of control of the Company (and subject to other circumstances) as described in Article IIIB and Article IIIC of the Company’s Articles of Amendment to the Restated Articles of Incorporation (the “Restated

NOTES TO THE UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS

DYNEX CAPITAL, INC.

(amounts in thousands except share data)

Articles of Incorporation, as amended”), the effect of those shares and their related dividends is excluded from the calculation of diluted net income (loss) per common share.

Cash and Cash Equivalents

Cash and cash equivalents include cash on hand and highly liquid investments with original maturities of three months or less.less as well as unrestricted demand deposits at highly rated financial institutions. The Company’s cash balances fluctuate throughout the year and may exceed Federal Deposit Insurance Company insured limits from time to time. Although the Company bears risk to amounts in excess of those insured by the FDIC, it does not anticipate any losses as a result.

Restricted Cash

Restricted cash consists of cash the Company has pledged to cover initial and variation margin with its financing and certain derivative counterparties.

The Company early adopted Accounting Standards Update ("ASU") No. 2016-18, Statement of Cash Flows (Topic 230) - Restricted Cash, which requires amounts generally described as restricted cash or restricted cash equivalents to be included with cash and cash equivalents when reconciling the beginning of period and end of period total amounts shown on the statement of cash flows. Because this ASU is to be applied retrospectively to each period presented, "net cash and cash equivalents used in financing activities" on the Company's consolidated statement of cash flows for the nine months ended September 30, 2016 now omits "increase in restricted cash" previously reported in the Quarterly Report on Form 10-Q for that period, and that increase is now included within "net increase in cash, cash equivalents, and restricted cash" for that period in order to conform to the current period's presentation.

The following table provides a reconciliation of cash, cash equivalents, and restricted cash reported on the Company's consolidated balance sheet as of September 30, 20172020 that sum to the total of the same such amounts shown on the Company'sCompany’s consolidated statement of cash flows for the nine months ended September 30, 2017:2020:

| | | | | | | | |

| | September 30, 2020 |

| Cash and cash equivalents | | $ | 158,897 | |

| Restricted cash | | 26,006 | |

| Total cash, cash equivalents, and restricted cash shown on consolidated statement of cash flows | | $ | 184,903 | |

|

| | | | |

| | | September 30, 2017 |

| Cash and cash equivalents | | $ | 117,702 |

|

| Restricted cash | | 43,987 |

|

| Total cash, cash equivalents, and restricted cash shown on consolidated statement of cash flows | | $ | 161,689 |

|

Mortgage-Backed Securities

The Company's investments in Agency and non-Agency RMBS, CMBS, and CMBS IO securitiesCompany’s MBS are designated as available-for-sale ("AFS"(“AFS”) and are recorded at fair value on the Company'sCompany’s consolidated balance sheet. Changes in unrealized gain (loss) on the Company'sCompany’s MBS are reported in other comprehensive income ("OCI"(“OCI”) until itthe investment is sold matures, or is determined to be other than temporarily impaired.matures. Although the Company generally intends to hold its AFS securities until maturity, it may sell any of these securities as part of the overall management of its business. Upon the sale of an AFS security, any unrealized gain or loss is reclassified out of accumulated other comprehensive income ("AOCI"(“AOCI”) into net income as a realized "gain“gain (loss) on sale of investments, net"net” using the specific identification method.

The fair value of the Company’s MBS pledged as collateral against repurchase agreements and derivative instruments are included in MBSis disclosed parenthetically on the Company’s consolidated balance sheets with the fair value of the MBS pledged as collateral disclosed parenthetically.sheets.

Interest Income, Premium Amortization, and Discount Accretion.Interest income on MBS is accrued based on the outstanding principal balance (or notional balance in the case of interest-only, or "IO",“IO” securities) and their contractual terms. Premiums andor discounts onassociated with the Company'spurchase of Agency MBS as well as any non-Agency MBS rated 'AA'‘AA’ and higher at the time of purchase are amortized or accreted into interest income over the expectedprojected life of such securities using the effective yield method, and adjustments to premium amortization and discount accretion are made for actual cash payments. The Company may also adjust premium amortization and discount accretion for changes in projected future cash payments. The Company'sCompany’s projections of future cash payments are based on input and analysis received from external sources and internal models and include assumptions about the amount and timing of loan prepayment rates, fluctuations in interest rates, credit losses, and other factors. On at least a quarterly basis, the Company reviews and makes any necessary adjustments to its cash flow projections and updates the yield recognized on these assets.

The Company does not estimate future prepayments on its fixed-rate Agency RMBS.

The Company holds certaincurrently hold any non-Agency MBS that hadwere purchased at a discount with credit ratings of less than 'AA' at the time of purchase‘AA’ or were not rated by any of the nationally recognized credit rating agencies. A portionagencies at the time of these non-Agency MBS were purchased at discounts to their par value, which management does not believe to be substantial. The discount is accreted into income over the security's expected life based on management's estimate of the security's projected cash flows. Future changes in the timing of projected cash flows or differences arising between projected cash flows and actual cash flows received may result in a prospective change in the effective yield on those securities.purchase.

Determination of MBS Fair Value.The Company estimates the fair value of the majority of its MBS based upon prices obtained from third-party pricing services and broker quotes. The remainder of the Company'sCompany’s MBS are valued by discounting the estimated future cash flows derived from cash flow models that utilize information such as the security'ssecurity’s coupon rate, estimated prepayment speeds, expected weighted average life, collateral composition, estimated future interest

NOTES TO THE UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS

DYNEX CAPITAL, INC.

(amounts in thousands except share data)

rates, expected losses, and credit enhancements as well as certain other relevant information. ReferPlease refer to Note 5 for further discussion of MBS fair value measurements.

Other-than-Temporary Impairment. AnAllowance for Credit Losses.The Company recently adopted Accounting Standards Codification Topic 326, Financial Instruments - Credit Losses. On at least a quarterly basis, the Company evaluates any MBS is considered impaired when itswith a fair value is less than its amortized cost. The Company evaluates all of its impaired MBScost for other-than-temporary impairments ("OTTI") on at least a quarterly basis. An impairment is considered other-than-temporary if: (1) the Company intends to sell the MBS; (2) it is more likely than not that the Company will be required to sell the MBS before its fair value recovers; or (3) the Company does not expect to recover the full amortized cost basis of the MBS.credit losses. If either of the first two conditions is met, the entire amount of the impairment is recognized in earnings. If the impairment is solely due to the inability to fully recover the amortized cost basis, the security is further analyzed to quantify any credit loss, which is the difference between the present value of cash flows expected to be collected on the MBS andis less than its amortized cost. Thecost, the difference is recorded as an allowance for credit loss if any, is thenthrough net income up to and not exceeding the amount that the amortized cost exceeds current fair value. Subsequent changes in credit loss estimates are recognized in earnings whilein the balance of impairment related to other factors is recognizedperiod in other comprehensive income.

Followingwhich they occur. Because the recognition of an OTTI through earnings, a new cost basis is established for the security. Any subsequent recoveries in fair value may be accreted back into the amortized cost basismajority of the MBSCompany’s investments are higher credit quality and most are guaranteed by a GSE, the Company is not likely to have an allowance for credit losses recorded on a prospective basis through interest income. Please see Note 2 for additional information related to the Company's evaluation for OTTI.its consolidated balance sheet.

Repurchase Agreements

The Company'sCompany’s repurchase agreements, which are used to finance its purchases of MBS, are accounted for as secured borrowings under which the Company pledges its securities as collateral to secure a loan, which is equal in value to a specified percentage of the estimated fair value of the pledged collateral. The Company retains beneficial ownership of the pledged collateral. At the maturity of a repurchase agreement, the Company is required to repay the loan and concurrently receives back its pledged collateral from the lender or, with the consent of the lender, the Company may renew the agreement at the then prevailing financing rate. A repurchase agreement lender may require the Company to pledge additional collateral in the event of a decline in the fair value of the collateral pledged. Repurchase agreement financing is recourse to the Company and the assets pledged. Most of the Company’s repurchase agreements are based on the September 1996 version of the Bond Market Association Master Repurchase Agreement, which generally provides that the lender, as buyer, is responsible for obtaining collateral valuations from a generally recognized source agreed to by both the Company and the lender, or, in an instance when such source is not available, the value determination is made by the lender.

Derivative Instruments

The Company'sCompany’s derivative instruments generally include interest rate swaps, futures, options, and forward contracts for the purchase or sale of generic Agency RMBS on a non-specified pool basis, commonly referred to as "TBA securities" or "TBA contracts".to-be-announced (“TBA”) securities. Derivative instruments are accounted forreported at thetheir fair value of their unit of account. Derivative instrumentson the Company’s consolidated balance sheet as derivative assets if in a gain position are reportedor as derivative assets and derivative instrumentsliabilities if in a loss position, are reported as derivative liabilities onat the Company's consolidated balance sheet.end of the period reported. All periodic interest benefits/costs and changes in fair value of derivative instruments, including gains and losses realized upon termination, maturity, or settlement are recorded in "gain“gain (loss) on derivative instruments, net"net” on the Company'sCompany’s consolidated statement of comprehensive income.income (loss). Cash receipts and payments related to derivative instruments are classified in the investing activities section of ourthe consolidated statements of cash flows in accordance with the underlying nature or purpose of the derivative transactions.

OurGenerally, the Company enters into pay-fixed interest rate swaps, which involve the receipt of variable-rate amounts from a counterparty in exchange for the Company making fixed-rate payments over the life of the interest rate swap agreements are privately negotiated inwithout exchange of the over-the-counter ("OTC") market and the majority of theseunderlying notional amount. The Company’s interest rate swap agreements are centrally cleared through the Chicago Mercantile Exchange ("CME"(“CME”) with the rest being subject to bilateral agreements between the Company and the swap counterparty.. The Company'sCompany’s CME cleared swaps require that the Company post initial margin as determined by the CME,collateral, and in addition, variation margin is exchanged, typically in cash, for changes in the fair value of the CME cleared swaps. Beginning in January 2017, as a result of a change in the CME's rulebook, theThe exchange of variation margin for CME cleared swaps is legally considered to be the settlement of the derivative itself as opposed to a pledge of collateral. Accordingly, beginning in 2017, the Company accounts for the daily exchange of variation margin associated with its CME cleared interest rate swaps as a direct increase or decrease to the carrying value of the related derivative asset or liability. The carrying valueSince December 31, 2019, the Company has significantly reduced its volume of CME cleared interest rate swaps due to management’s expectations of historically low financing costs for the near term and the increase in margin requirements from counterparties since the onset of the pandemic.

The Company enters into long and short positions in U.S. Treasury futures contracts, which are valued based on exchange pricing with daily margin settlements. The Company realizes gains or losses on these contracts upon expiration at an amount equal to the Company's consolidated balance sheets isdifference between the unsettledcurrent fair value of those instruments.the underlying asset and the contractual price of

NOTES TO THE UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS

DYNEX CAPITAL, INC.

(amounts in thousands except share data)

the futures contract. Unlike interest rate swaps, the Company does not treat the daily margin exchanges for its U.S. Treasury futures as legal settlement of the instrument.

The Company currently holds put options on U.S. Treasury futures which provide the Company the right, but not an obligation, to buy U.S. Treasury futures at a predetermined notional amount and stated term in the future. Put options on U.S. Treasury futures are valued based on exchange pricing without daily exchanges of margin amounts. The Company records the premium paid for the option contract as a derivative asset on its consolidated balance sheet and adjusts the balance for changes in fair value through “gain (loss) on derivative instruments” until the option is exercised or the contract expires. The Company may also purchase options for interest rate swaps (“interest rate swaptions”) and defer the premium payment until the effective date. The premium payable and underlying swaption are accounted for as a single unit of account.

A TBA security is a forward contract (“TBA contract”) for the purchase (“long position”) or sale (“short position”) of a genericnon-specified Agency MBS at a predetermined price with certain principal and interest terms and certain types of collateral, but the particular Agency securities to be delivered are not identified until shortly before the TBA settlement date. The Company executes TBA dollar roll transactions which effectively delay the settlement of a forward purchase of a TBA Agency RMBS by entering into an offsettingaccounts for long and short position (referred to as a "pair off"), net settling the paired-off positions in cash, and simultaneously entering a similar TBA contract for a later settlement date. TBA securities purchased for a forward settlement month are generally priced at a discount relative to TBA securities sold for settlement in the current month. This discount, often referred to as “drop income” is the economic equivalent of net interest income on the underlying Agency securities over the roll period (interest income less implied financing cost).

The Company accounts for TBA securitiesTBAs as derivative instruments because the Company cannot assert that it is probable at inception and throughout the term of an individual TBA contracttransaction that its settlement will result in physical delivery of the underlying Agency RMBS or that the individual TBA contracttransaction will not settle in the shortest time period possible.

Please refer to Note 4 for additional information regarding the Company'sCompany’s derivative instruments as well as Note 5 for information on how the fair value of these instruments are calculated.

Share-Based Compensation

Pursuant to the Company’s 20092020 Stock and Incentive Plan (the “2020 Plan”), the Company may grant share-based compensation to eligible employees, non-employee directors or consultants or advisersadvisors to the Company, including restricted stock awards, stock options, stock appreciation rights, dividend equivalent rights, performance shares, andunits, restricted stock units.units, and performance cash awards. The Company'sCompany’s restricted stock currently issued and outstanding under this plan may be settled only in shares of its common stock, and therefore are treated as equity awards with their fair value measured at the grant date and recognized as compensation cost over the requisite service period with a corresponding credit to shareholders'shareholders’ equity. The requisite service period is the period during which an employeea participant is required to provide service in exchange for an award, which is equivalent to the vesting period specified in the terms of the time-based restricted stock award. None of the Company'sCompany’s restricted stock awards have performance basedperformance-based conditions. The Company does not currently have any share-based compensation issued or outstanding other than restricted stock issued to its employees, officers, and directors.

Contingencies

In the normal course of business, there may be various lawsuits, claims, and other contingencies pending against the Company. On a quarterly basis, the Company evaluates whether to establish provisions for estimated losses from those matters. The Company recognizes a liability for a contingent loss when: (a) the underlying causal event has occurred prior to the balance sheet date; (b) it is probable that a loss has been incurred; and (c) there is a reasonable basis for estimating that loss. A liability is not recognized for a contingent loss when it is only possible or remotely possible that a loss has been incurred, however, possible contingent losses shall be disclosed. If the contingent loss (or an additional loss in excess of any accrual) is at least a reasonable possibility and material, then the Company discloses a reasonable estimate of the possible loss or range of loss, if such reasonable estimate can be made. If the Company cannot make a reasonable estimate of the possible material loss, or range of loss, then that fact is disclosed.

RecentAs previously disclosed in the 2019 Form 10-K, the receiver (the “Receiver”) for one of the plaintiffs awarded damages in a judgment (the "DCI Judgment") against Dynex Commercial, Inc. ("DCI"), a subsidiary of a former affiliate of the Company, filed a separate claim in May 2018 against the Company seeking payment of the damages awarded in connection with the DCI Judgment, alleging that the Company breached a litigation cost sharing agreement, as amended (the "Agreement"), that was initially entered into by the Company and DCI in December 2000. On November 21, 2019, the U.S. District Court, Northern District of Texas ("Northern District Court") granted in part and denied in part summary judgment on the Receiver’s claim and the Company’s claim for offset and recoupment. The Northern District Court found that the

NOTES TO THE UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS

DYNEX CAPITAL, INC.

(amounts in thousands except share data)

Company breached the Agreement and therefore must pay damages to the Receiver. The Northern District Court simultaneously granted the Company’s motion for summary judgment finding that DCI also breached the Agreement and that the Company can recover amounts due to it from DCI under the Agreement. The Receiver subsequently filed a claim for damages with the Northern District Court of approximately $12,600, while the Company filed claims for damages ranging from $13,300 to $30,600, including interest. The Receiver filed objections (the "Objections") with the Northern District Court to, among other things, the Company recovering amounts incurred prior to entry into the Agreement and amounts incurred under the Agreement after January 31, 2006, including interest, which is the date that DCI’s corporate existence ceased under Virginia law. The Company has disputed the Receiver’s Objections, arguing, among other things, that the Receiver's Objections are not supportable under Virginia law and has further refined its damages claim to range from $13,300 based on simple interest to $17,800 based on a combination of simple and compound interest, which the Company believes is supportable under Virginia law. There have been no material developments in this matter during the three months ended September 30, 2020. After consultation with litigation counsel, the Company believes, based upon information currently available and its evaluation of Virginia law, that the likelihood of loss is not probable, and given the range of potential claims for damages by the Company to offset the Receiver's claims, the amount of possible loss cannot be reasonably estimated, and therefore, no contingent liability has been recorded.

Recently Issued and Adopted Accounting Pronouncements

The Company evaluates Accounting Standards Updates (“ASU”) issued by the Financial Accounting Standards Board ("FASB"(“FASB”) on at least a quarterly basis to evaluate applicability and significance of any impact on its financial condition and results of operations. There were no accounting pronouncements issued ASU No. 2017-08, Receivables-Nonrefundable Fees and Other Costs, which shortensduring the amortization period for certain callable debt securities held at a premium, requiring the premium to be amortized to the earliest call date. The amendments in this ASUnine months ended September 30, 2020 that are effective for fiscal years, and interim periods within those fiscal years, beginning after December 15, 2018 and early adoption is permitted. The amendments in this Update should be applied using the modified-retrospective transition approach and will require disclosures for the change in accounting principle. The Company does not expect this ASUexpected to have a material impact on the Company'sCompany’s financial condition or results of operations.

As of January 1, 2020, the Company elected the fair value option for its mortgage loans held for investment pursuant to the provisions of ASU No. 2019-05, Financial Instruments—Credit Losses (Topic 326) Targeted Transition Relief, which was issued in May of 2019. Management chose to elect the fair value option for its mortgage loans because the majority of the Company’s investments are represented on its consolidated balance sheet at fair value. The election of the fair value option resulted in a cumulative adjustment of $(548) to retained earnings on its consolidated balance sheet as of January 1, 2020. The election of the fair value option for its mortgage loans did not have a material impact on its consolidated financial statements.

In March 2020, FASB issued ASU No. 2017-12, Derivatives and Hedging2020-04, Reference Rate Reform (Topic 815)848): Targeted Improvements to Accounting for Hedging Activities, which contains significant amendments to hedge accounting with the main objective of better aligning an entity’s risk management activities and financial reporting for hedging relationships through changes to both the designation and measurement guidance for qualifying hedging relationships and the presentation of hedge results. To meet that objective, the amendments expand and refine hedge accounting for both non-financial and financial risk components and align the recognition and presentationFacilitation of the effectsEffects of the hedging instrumentReference Rate Reform on Financial Reporting, which provides optional expedients and the hedged item in the financial statements. This ASU also includes certain targeted improvementsexceptions to ease the application of current guidanceGAAP requirements for modifications on debt instruments, leases, derivatives, and other contracts, related to the assessmentexpected market transition from LIBOR, and certain other floating rate benchmark indices to alternative reference rates. ASU 2020-04 generally considers contract modifications related to reference rate reform to be an event that does not require contract remeasurement at the modification date nor a reassessment of hedge effectivenessa previous accounting determination. The guidance in ASU 2020-04 is optional and may be elected over time, through December 31, 2022, as well as changes to current disclosure requirements. The amendments in this ASU are effective for public business entities for fiscal years beginning after December 15, 2018, and interim periods within those fiscal years, and early adoption is permitted. All transition requirements and elections will be applied to hedging relationships existing on the date of adoption. The effect of adoption will be reflected as of the beginning of the fiscal year of adoption, and the amended presentation and disclosure guidance is required only prospectively.reference rate reform activities occur. The Company does not currently apply hedge accounting, but is evaluating the impactbelieve this ASU wouldwill have a material impact on its consolidated financial statements if the Company elects to adopt hedge accountingstatements.

NOTES TO THE UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS

DYNEX CAPITAL, INC.

(amounts in the future.thousands except share data)

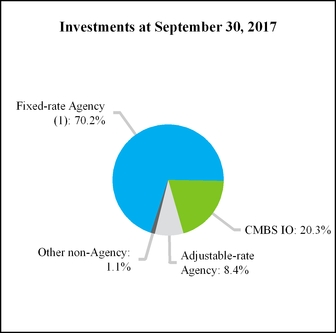

NOTE 2 – MORTGAGE-BACKED SECURITIES

The majority of the Company'sCompany’s MBS are pledged as collateral for the Company's secured borrowings.Company’s repurchase agreements. The following tables present the Company’s MBS by investment type (including securities pending settlement) as of the dates indicated:

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | September 30, 2020 |

| | Par | | Net Premium (Discount) | | Amortized Cost | | Gross Unrealized Gain | | Gross Unrealized Loss | | Fair Value |

| Agency RMBS | $ | 2,159,813 | | | $ | 65,064 | | | $ | 2,224,877 | | | $ | 56,928 | | | $ | 0 | | | $ | 2,281,805 | |

| Agency CMBS | 271,764 | | | 3,445 | | | 275,209 | | | 23,495 | | | 0 | | | 298,704 | |

CMBS IO (1) | 0 | | | 405,736 | | | 405,736 | | | 9,497 | | | (1,480) | | | 413,753 | |

| Non-Agency other | 1,630 | | | (517) | | | 1,113 | | | 333 | | | (48) | | | 1,398 | |

| Total MBS: | $ | 2,433,207 | | | $ | 473,728 | | | $ | 2,906,935 | | | $ | 90,253 | | | $ | (1,528) | | | $ | 2,995,660 | |

|

| | | | | | | | | | | | | | | | | | | | | | | | | | |

| | September 30, 2017 |

| | Par | | Net Premium (Discount) | | Amortized Cost | | Gross Unrealized Gain | | Gross Unrealized Loss | | Fair Value | | WAC (1) |

| CMBS: | | | | | | | | | | | | | |

| Agency | $ | 1,302,237 |

| | $ | 12,688 |

| | 1,314,925 |

| | $ | 6,187 |

| | $ | (13,623 | ) | | 1,307,489 |

| | 2.99 | % |

| Non-Agency | 40,780 |

| | (4,452 | ) | | 36,328 |

| | 2,877 |

| | — |

| | 39,205 |

| | 5.48 | % |

| | 1,343,017 |

| | 8,236 |

| | 1,351,253 |

| | 9,064 |

| | (13,623 | ) | | 1,346,694 |

| | |

CMBS IO (2): | | | | | | | | | | | | | |

| Agency | — |

| | 394,380 |

| | 394,380 |

| | 7,592 |

| | (164 | ) | | 401,808 |

| | 0.63 | % |

| Non-Agency | — |

| | 322,735 |

| | 322,735 |

| | 6,254 |

| | (330 | ) | | 328,659 |

| | 0.61 | % |

| | — |

| | 717,115 |

| | 717,115 |

| | 13,846 |

| | (494 | ) | | 730,467 |

| | |

| RMBS: | | | | | | | | | | | | | |

| Agency fixed-rate | 522,099 |

| | 19,163 |

| | 541,262 |

| | — |

| | (1,903 | ) | | 539,359 |

| | 3.52 | % |

| Agency adjustable-rate | 294,254 |

| | 11,011 |

| | 305,265 |

| | 1,263 |

| | (2,746 | ) | | 303,782 |

| | 3.05 | % |

| Non-Agency | 1,113 |

| | — |

| | 1,113 |

| | 49 |

| | (20 | ) | | 1,142 |

| | 6.75 | % |

| | 817,466 |

| | 30,174 |

| | 847,640 |

| | 1,312 |

| | (4,669 | ) | | 844,283 |

| | |

| | | | | | | | | | | | | |

|

|

| Total AFS securities: | $ | 2,160,483 |

| | $ | 755,525 |

| | $ | 2,916,008 |

| | $ | 24,222 |

| | $ | (18,786 | ) | | $ | 2,921,444 |

| | |

| |

(1) | The weighted average coupon ("WAC") is the gross interest rate of the security weighted by the outstanding principal balance (or by notional balance in the case of an IO security). |

| |

(2) | The notional balance for Agency CMBS IO and non-Agency CMBS IO was $14,253,392 and $11,061,377, respectively, as of September 30, 2017. |

(1) The notional balance for Agency CMBS IO and non-Agency CMBS IO was $12,344,492 and $9,485,281 respectively, as of September 30, 2020. |

| | | | | | | | | | | | | | | | | | | | | | | | | | |

| | December 31, 2016 |

| | Par | | Net Premium (Discount) | | Amortized Cost | | Gross Unrealized Gain | | Gross Unrealized Loss | | Fair Value | | WAC (1) |

| CMBS: | | | | | | | | | | | | | |

| Agency | $ | 1,152,586 |

| | $ | 13,868 |

| | $ | 1,166,454 |

| | $ | 6,209 |

| | $ | (28,108 | ) | | $ | 1,144,555 |

| | 3.12 | % |

| Non-Agency | 79,467 |

| | (6,718 | ) | | 72,749 |

| | 5,467 |

| | — |

| | 78,216 |

| | 4.72 | % |

| | 1,232,053 |

| | 7,150 |

| | 1,239,203 |

| | 11,676 |

| | (28,108 | ) | | 1,222,771 |

| | |

CMBS IO (2): | | | | | | | | | | | | | |

| Agency | — |

| | 411,737 |

| | 411,737 |

| | 3,523 |

| | (3,362 | ) | | 411,898 |

| | 0.67 | % |

| Non-Agency | — |

| | 346,155 |

| | 346,155 |

| | 1,548 |

| | (5,055 | ) | | 342,648 |

| | 0.61 | % |

| | — |

| | 757,892 |

| | 757,892 |

| | 5,071 |

| | (8,417 | ) | | 754,546 |

| | |

| RMBS: | | | | | | | | | | | | | |

| Agency adjustable-rate | $ | 1,157,258 |

| | $ | 57,066 |

| | $ | 1,214,324 |

| | $ | 2,832 |

| | $ | (15,951 | ) | | $ | 1,201,205 |

| | 3.05 | % |

| Non-Agency | 33,572 |

| | (24 | ) | | 33,548 |

| | 64 |

| | (50 | ) | | 33,562 |

| | 3.58 | % |

| | 1,190,830 |

| | 57,042 |

| | 1,247,872 |

| | 2,896 |

| | (16,001 | ) | | 1,234,767 |

| | |

|

|

| | | |

|

| |

|

| | | |

|

| | |

| Total AFS securities: | $ | 2,422,883 |

| | $ | 822,084 |

| | $ | 3,244,967 |

| | $ | 19,643 |

| | $ | (52,526 | ) | | $ | 3,212,084 |

| |

|

|

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | December 31, 2019 |

| | Par | | Net Premium (Discount) | | Amortized Cost | | Gross Unrealized Gain | | Gross Unrealized Loss | | Fair Value |

| Agency RMBS | $ | 2,563,684 | | | $ | 55,770 | | | $ | 2,619,454 | | | $ | 69,082 | | | $ | (462) | | | $ | 2,688,074 | |

| Agency CMBS | 1,890,186 | | | 15,414 | | | 1,905,600 | | | 93,763 | | | (6) | | | 1,999,357 | |

CMBS IO (1) | 0 | | | 488,145 | | | 488,145 | | | 11,760 | | | (863) | | | 499,042 | |

| Non-Agency other | 1,938 | | | (780) | | | 1,158 | | | 552 | | | (20) | | | 1,690 | |

| Total MBS: | $ | 4,455,808 | | | $ | 558,549 | | | $ | 5,014,357 | | | $ | 175,157 | | | $ | (1,351) | | | $ | 5,188,163 | |

(1) The notional balance for the Agency CMBS IO and non-Agency CMBS IO was $13,404,824 and $9,799,629, respectively, as of December 31, 2019.

| |

(1) | The WAC is the gross interest rate of the pool of mortgages underlying the security weighted by the outstanding principal balance (or by notional balance in the case of an IO security). |

| |

(2) | The notional balance for the Agency CMBS IO and non-Agency CMBS IO was $13,106,912 and $10,884,964, respectively, as of December 31, 2016. |

Actual maturities of MBS are affected by the contractual lives of the underlying mortgage collateral, periodic payments of principal, prepayments of principal, and the payment priority structure of the security; therefore, actual maturities are generally shorter than the securities' stated contractual maturities.

The following table presents information regarding the sales included in "loss"gain (loss) on sale of investments, net" on the Company'sCompany’s consolidated statements of comprehensive income (loss) for the periods indicated:

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Three Months Ended | | Nine Months Ended |

| September 30, | | September 30, |

| 2020 | | 2019 | | 2020 | | 2019 |

| Proceeds Received | | Realized Gain (Loss) | | Proceeds Received | | Realized Gain (Loss) | | Proceeds Received | | Realized Gain (Loss) | | Proceeds Received | | Realized Gain (Loss) |

Agency RMBS (1) | $ | 0 | | | $ | 1 | | | $ | 591,206 | | | $ | 4,458 | | | $ | 2,187,956 | | | $ | 75,824 | | | $ | 796,699 | | | $ | 506 | |

| Agency CMBS | 403,095 | | | 20,845 | | | 0 | | | 0 | | | 2,215,098 | | | 222,904 | | | 213,199 | | | (6,493) | |

| Agency CMBS IO | — | | | — | | | 9,308 | | | 147 | | | — | | | — | | | 23,168 | | | 232 | |

| $ | 403,095 | | | $ | 20,846 | | | $ | 600,514 | | | $ | 4,605 | | | $ | 4,403,054 | | | $ | 298,728 | | | $ | 1,033,066 | | | $ | (5,755) | |

(1) Additional realized gain for Agency RMBS relates to change in effective rate due to paydown that occurred between trade date of sale in second quarter of 2020 and settlement date in third quarter.

NOTES TO THE UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS

DYNEX CAPITAL, INC.

(amounts in thousands except share data)

|

| | | | | | | | | | | | | | | |

| | Three Months Ended |

| | September 30, |

| | 2017 | | 2016 |

| | Proceeds Received | | Realized Gain (Loss) | | Proceeds Received | | Realized Gain (Loss) |

| Agency RMBS | $ | 393,502 |

| | $ | (5,160 | ) | | $ | — |

| | $ | — |

|

| Agency CMBS | 13,433 |

| | (51 | ) | | — |

| | — |

|

| | $ | 406,935 |

| | $ | (5,211 | ) | | $ | — |

| | $ | — |

|

| | | | | | | | |

| | Nine Months Ended |

| | September 30, |

| | 2017 | | 2016 |

| | Proceeds Received | | Realized Gain (Loss) | | Proceeds Received | | Realized Gain (Loss) |

| Agency RMBS | $ | 716,560 |

| | $ | (12,392 | ) | | $ | 54,178 |

| | $ | (3,010 | ) |

| Agency CMBS | 206,993 |

| | 523 |

| | — |

| | — |

|

| Non-Agency CMBS | 35,705 |

| | 1,199 |

| | 33,640 |

| | (1,228 | ) |

| Non-Agency RMBS | 16,407 |

| | 42 |

| | — |

| | — |

|

| | $ | 975,665 |

| | $ | (10,628 | ) | | $ | 87,818 |

| | $ | (4,238 | ) |

The following table presents certain information for those MBSthe AFS securities in an unrealized loss position as of the dates indicated:

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | September 30, 2020 | | December 31, 2019 |

| Fair Value | | Gross Unrealized Losses | | # of Securities | | Fair Value | | Gross Unrealized Losses | | # of Securities |

| Continuous unrealized loss position for less than 12 months: | | | | | | | | | | | |

| Agency MBS | $ | 36,664 | | | $ | (503) | | | 16 | | $ | 215,792 | | | $ | (1,139) | | | 27 |

| Non-Agency MBS | 46,835 | | | (897) | | | 30 | | 13,607 | | | (146) | | | 7 |

| | | | | | | | | | | |

| Continuous unrealized loss position for 12 months or longer: | | | | | | | | | | | |

| Agency MBS | $ | 689 | | | $ | (107) | | | 3 | | $ | 75,745 | | | $ | (35) | | | 2 |

| Non-Agency MBS | 100 | | | (21) | | | 4 | | 1,099 | | | (31) | | | 5 |

|

| | | | | | | | | | | | | | | | | | | |

| | September 30, 2017 | | December 31, 2016 |

| | Fair Value | | Gross Unrealized Losses | | # of Securities | | Fair Value | | Gross Unrealized Losses | | # of Securities |

| Continuous unrealized loss position for less than 12 months: | | | | | | | | | | | |

| Agency MBS | $ | 1,377,438 |

| | $ | (13,201 | ) | | 76 | | $ | 1,738,094 |

| | $ | (38,469 | ) | | 133 |

| Non-Agency MBS | 38,979 |

| | (151 | ) | | 6 | | 205,484 |

| | (2,773 | ) | | 48 |

| | | | | | | | | | | | |

| Continuous unrealized loss position for 12 months or longer: | | | | | | | | | | | |

| Agency MBS | $ | 206,045 |

| | $ | (5,236 | ) | | 17 | | $ | 427,405 |