(Mark One)

| x | |||||

| QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the quarterly period ended September 30, 2017March 31, 2024

OR

| ¨ | |||||

| TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the transition period from to

Commission file number 1-10258

Tredegar Corporation

(Exact Name of Registrant as Specified in Its Charter)

| Virginia | 54-1497771 | |||||||

(State or Other Jurisdiction of Incorporation or Organization) | (I.R.S. Employer Identification No.) | |||||

1100 Boulders Parkway | |||||||||||

| Richmond, | Virginia | 23225 | |||||||||

| (Address of Principal Executive Offices) | (Zip Code) | ||||||||||

Registrant’s Telephone Number, Including Area Code: (804) 330-1000

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||||||

| Common stock, no par value | ||||||||

| TG | New York Stock Exchange | |||||||

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ¨ | Accelerated filer | x | Smaller reporting company | |||||||||||||||||||

| Non-accelerated filer | ¨ | Emerging growth company | |||||||||||||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act.¨

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨☐ No x

The number of shares of Common Stock, no par value, outstanding as of October 26, 2017: 33,026,931

May 3, 2024: 34,484,893

Tredegar Corporation

Table of Contents

| Page | |||||||||||

PART I - FINANCIAL INFORMATION

Tredegar Corporation

Condensed Consolidated Balance Sheets

(In Thousands, Except Share Data)

(Unaudited)

| September 30, | December 31, | ||||||

| 2017 | 2016 | ||||||

| Assets | |||||||

| Current assets: | |||||||

| Cash and cash equivalents | $ | 31,850 | $ | 29,511 | |||

| Accounts and other receivables, net of allowance for doubtful accounts and sales returns of $3,124 in 2017 and $3,102 in 2016 | 126,964 | 97,388 | |||||

| Income taxes recoverable | 8,260 | 7,518 | |||||

| Inventories | 82,426 | 66,069 | |||||

| Prepaid expenses and other | 8,354 | 7,738 | |||||

| Total current assets | 257,854 | 208,224 | |||||

| Property, plant and equipment, at cost | 881,139 | 797,630 | |||||

| Less accumulated depreciation | (571,062 | ) | (536,905 | ) | |||

| Net property, plant and equipment | 310,077 | 260,725 | |||||

| Goodwill and other intangibles, net | 188,334 | 151,423 | |||||

| Other assets and deferred charges | 55,683 | 30,790 | |||||

| Total assets | $ | 811,948 | $ | 651,162 | |||

| Liabilities and Shareholders’ Equity | |||||||

| Current liabilities: | |||||||

| Accounts payable | $ | 95,684 | $ | 81,342 | |||

| Accrued expenses | 41,776 | 38,647 | |||||

| Total current liabilities | 137,460 | 119,989 | |||||

| Long-term debt | 177,000 | 95,000 | |||||

| Deferred income taxes | 25,767 | 21,110 | |||||

| Other noncurrent liabilities | 97,807 | 104,280 | |||||

| Total liabilities | 438,034 | 340,379 | |||||

| Commitments and contingencies (Notes 1 and 12) | |||||||

| Shareholders’ equity: | |||||||

| Common stock, no par value (issued and outstanding - 33,026,931 at September 30, 2017 and 32,933,807 at December 31, 2016) | 34,027 | 32,007 | |||||

| Common stock held in trust for savings restoration plan (70,884 shares at September 30, 2017 and 69,622 shares at December 31, 2016) | (1,520 | ) | (1,497 | ) | |||

| Accumulated other comprehensive income (loss): | |||||||

| Foreign currency translation adjustment | (84,153 | ) | (93,970 | ) | |||

| Gain on derivative financial instruments | 1,151 | 863 | |||||

| Pension and other post-retirement benefit adjustments | (84,373 | ) | (90,127 | ) | |||

| Retained earnings | 508,782 | 463,507 | |||||

| Total shareholders’ equity | 373,914 | 310,783 | |||||

| Total liabilities and shareholders’ equity | $ | 811,948 | $ | 651,162 | |||

| March 31, | December 31, | ||||||||||

| 2024 | 2023 | ||||||||||

| Assets | |||||||||||

| Current assets: | |||||||||||

| Cash and cash equivalents | $ | 3,493 | $ | 9,660 | |||||||

| Restricted cash | 1,299 | 3,795 | |||||||||

| Accounts and other receivables, net | 73,032 | 67,938 | |||||||||

| Income taxes recoverable | 793 | 1,182 | |||||||||

| Inventories | 86,822 | 82,037 | |||||||||

| Prepaid expenses and other | 9,438 | 12,065 | |||||||||

| Total current assets | 174,877 | 176,677 | |||||||||

| Property, plant and equipment, at cost | 540,856 | 541,046 | |||||||||

| Less: accumulated depreciation | (362,884) | (357,591) | |||||||||

| Net property, plant and equipment | 177,972 | 183,455 | |||||||||

| Right-of-use leased assets | 16,761 | 11,848 | |||||||||

| Identifiable intangible assets, net | 9,364 | 9,851 | |||||||||

| Goodwill | 35,717 | 35,717 | |||||||||

| Deferred income taxes | 24,320 | 25,034 | |||||||||

| Other assets | 3,520 | 3,879 | |||||||||

| Total assets | $ | 442,531 | $ | 446,461 | |||||||

| Liabilities and Shareholders’ Equity | |||||||||||

| Current liabilities: | |||||||||||

| Accounts payable | $ | 84,925 | $ | 95,023 | |||||||

| Accrued expenses | 23,083 | 24,442 | |||||||||

| Lease liability, short-term | 2,871 | 2,107 | |||||||||

| ABL revolving facility (matures June 30, 2026) | 128,330 | 126,322 | |||||||||

| Income taxes payable | 225 | 1,210 | |||||||||

| Total current liabilities | 239,434 | 249,104 | |||||||||

| Lease liability, long-term | 15,318 | 10,942 | |||||||||

| Long-term debt | 20,000 | 20,000 | |||||||||

| Pension and other postretirement benefit obligations, net | 6,582 | 6,643 | |||||||||

| Other non-current liabilities | 4,382 | 4,119 | |||||||||

| Total liabilities | 285,716 | 290,808 | |||||||||

| Shareholders’ equity: | |||||||||||

| Common stock, no par value (authorized shares 150,000,000, issued and outstanding 34,533,870 shares at March 31, 2024 and 34,408,638 shares at December 31, 2023) | 61,959 | 61,606 | |||||||||

| Common stock held in trust for savings restoration plan (118,543 shares at March 31, 2024 and 118,543 shares at December 31, 2023) | (2,233) | (2,233) | |||||||||

| Accumulated other comprehensive income (loss): | |||||||||||

| Foreign currency translation adjustment | (84,985) | (83,037) | |||||||||

| Gain (loss) on derivative financial instruments | 297 | 801 | |||||||||

| Pension and other postretirement benefit adjustments | 512 | 539 | |||||||||

| Retained earnings | 181,265 | 177,977 | |||||||||

| Total shareholders’ equity | 156,815 | 155,653 | |||||||||

| Total liabilities and shareholders’ equity | $ | 442,531 | $ | 446,461 | |||||||

See accompanying notes to the condensed consolidated financial statements.

2

Tredegar Corporation

Condensed Consolidated Statements of Income (Loss)

(In Thousands, Except Per Share Data)

(Unaudited)

| Three Months Ended September 30, | Nine Months Ended September 30, | ||||||||||||||

| 2017 | 2016 | 2017 | 2016 | ||||||||||||

| Revenues and other items: | |||||||||||||||

| Sales | $ | 247,121 | $ | 207,702 | $ | 715,494 | $ | 623,569 | |||||||

| Other income (expense), net | 34 | 388 | 38,055 | 1,481 | |||||||||||

| 247,155 | 208,090 | 753,549 | 625,050 | ||||||||||||

| Costs and expenses: | |||||||||||||||

| Cost of goods sold | 196,393 | 166,622 | 575,614 | 499,504 | |||||||||||

| Freight | 8,621 | 7,153 | 24,840 | 21,221 | |||||||||||

| Selling, general and administrative | 21,214 | 17,383 | 63,438 | 57,027 | |||||||||||

| Research and development | 4,455 | 4,519 | 14,028 | 14,458 | |||||||||||

| Amortization of intangibles | 1,658 | 1,019 | 4,550 | 2,965 | |||||||||||

| Interest expense | 1,757 | 886 | 4,579 | 2,918 | |||||||||||

| Asset impairments and costs associated with exit and disposal activities, net of adjustments | 361 | 1,129 | 653 | 2,355 | |||||||||||

| Total | 234,459 | 198,711 | 687,702 | 600,448 | |||||||||||

| Income before income taxes | 12,696 | 9,379 | 65,847 | 24,602 | |||||||||||

| Income taxes (benefit) | 4,422 | (2,669 | ) | 9,667 | 1,864 | ||||||||||

| Net income | $ | 8,274 | $ | 12,048 | $ | 56,180 | $ | 22,738 | |||||||

Earnings per share: | |||||||||||||||

| Basic | $ | 0.25 | $ | 0.37 | $ | 1.71 | $ | 0.69 | |||||||

| Diluted | $ | 0.25 | $ | 0.37 | $ | 1.70 | $ | 0.69 | |||||||

| Shares used to compute earnings per share: | |||||||||||||||

| Basic | 32,954 | 32,818 | 32,945 | 32,730 | |||||||||||

| Diluted | 32,954 | 32,828 | 32,952 | 32,733 | |||||||||||

| Dividends per share | $ | 0.11 | $ | 0.11 | $ | 0.33 | $ | 0.33 | |||||||

| Three Months Ended March 31, | |||||||||||||||||||||||

| 2024 | 2023 | ||||||||||||||||||||||

| Revenues and other items: | |||||||||||||||||||||||

| Sales | $ | 175,736 | $ | 191,122 | |||||||||||||||||||

| Other income (expense), net | 8 | 280 | |||||||||||||||||||||

| 175,744 | 191,402 | ||||||||||||||||||||||

| Costs and expenses: | |||||||||||||||||||||||

| Cost of goods sold | 142,043 | 159,525 | |||||||||||||||||||||

| Freight | 6,666 | 6,043 | |||||||||||||||||||||

| Selling, general and administrative | 18,258 | 19,006 | |||||||||||||||||||||

| Research and development | 352 | 1,205 | |||||||||||||||||||||

| Amortization of identifiable intangibles | 464 | 503 | |||||||||||||||||||||

| Pension and postretirement benefits | 54 | 3,418 | |||||||||||||||||||||

| Interest expense | 3,455 | 2,311 | |||||||||||||||||||||

| Asset impairments and costs associated with exit and disposal activities, net of adjustments | 507 | 69 | |||||||||||||||||||||

| Total | 171,799 | 192,080 | |||||||||||||||||||||

| Income (loss) before income taxes | 3,945 | (678) | |||||||||||||||||||||

| Income tax expense (benefit) | 657 | 331 | |||||||||||||||||||||

| Net income (loss) | $ | 3,288 | $ | (1,009) | |||||||||||||||||||

| Earnings (loss) per share: | |||||||||||||||||||||||

| Basic | $ | 0.10 | $ | (0.03) | |||||||||||||||||||

| Diluted | $ | 0.10 | $ | (0.03) | |||||||||||||||||||

| Shares used to compute earnings (loss) per share: | |||||||||||||||||||||||

| Basic | 34,323 | 33,895 | |||||||||||||||||||||

| Diluted | 34,323 | 33,895 | |||||||||||||||||||||

See accompanying notes to the condensed consolidated financial statements.

3

Tredegar Corporation

Condensed Consolidated Statements of Comprehensive Income (Loss)

(In Thousands)

(Unaudited)

| Three Months Ended March 31, | |||||||||||

| 2024 | 2023 | ||||||||||

| Net income (loss) | $ | 3,288 | $ | (1,009) | |||||||

| Other comprehensive income (loss): | |||||||||||

| Unrealized foreign currency translation adjustment (net of tax expense of $221 in 2024 and net of tax expense of $436 in 2023) | (1,948) | 1,120 | |||||||||

| Derivative financial instruments adjustment (net of tax benefit of $140 in 2024 and net of tax expense of $836 in 2023) | (504) | 1,269 | |||||||||

| Amortization of prior service costs and net gains or losses (net of tax benefit of $8 in 2024 and net of tax expense of $637 in 2023) | (27) | 2,287 | |||||||||

| Other comprehensive income (loss) | (2,479) | 4,676 | |||||||||

| Comprehensive income (loss) | $ | 809 | $ | 3,667 | |||||||

| Three Months Ended September 30, | |||||||

| 2017 | 2016 | ||||||

| Net income | $ | 8,274 | $ | 12,048 | |||

| Other comprehensive income (loss): | |||||||

| Foreign currency translation adjustment (net of tax of $251 in 2017 and tax benefit of $77 in 2016) | 7,143 | (719 | ) | ||||

| Derivative financial instruments adjustment (net of tax of $186 in 2017 and tax benefit of $31 in 2016) | 326 | (54 | ) | ||||

| Amortization of prior service costs and net gains or losses (net of tax of $1,057 in 2017 and tax of $1,120 in 2016) | 1,854 | 1,966 | |||||

| Other comprehensive income (loss) | 9,323 | 1,193 | |||||

| Comprehensive income (loss) | $ | 17,597 | $ | 13,241 | |||

| Nine Months Ended September 30, | |||||||

| 2017 | 2016 | ||||||

| Net income | $ | 56,180 | $ | 22,738 | |||

| Other comprehensive income (loss): | |||||||

| Foreign currency translation adjustment (net of tax of $481 in 2017 and tax benefit of $307 in 2016) | 9,817 | 22,929 | |||||

| Derivative financial instruments adjustment (net of tax of $162 in 2017 and tax of $567 in 2016) | 288 | 963 | |||||

| Amortization of prior service costs and net gains or losses (net of tax of $3,279 in 2017 and tax of $3,186 in 2016) | 5,754 | 6,573 | |||||

| Other comprehensive income (loss) | 15,859 | 30,465 | |||||

| Comprehensive income (loss) | $ | 72,039 | $ | 53,203 | |||

See accompanying notes to the condensed consolidated financial statements.

4

Tredegar Corporation

Condensed Consolidated Statements of Cash Flows

(In Thousands)

(Unaudited)

| Nine Months Ended September 30, | |||||||

| 2017 | 2016 | ||||||

| Cash flows from operating activities: | |||||||

| Net income | $ | 56,180 | $ | 22,738 | |||

| Adjustments for noncash items: | |||||||

| Depreciation | 25,072 | 21,004 | |||||

| Amortization of intangibles | 4,550 | 2,965 | |||||

| Deferred income taxes | (104 | ) | (5,122 | ) | |||

| Accrued pension and post-retirement benefits | 7,645 | 8,168 | |||||

| (Gain)/loss on investment accounted for under the fair value method | (24,800 | ) | 200 | ||||

| (Gain)/loss on asset impairments and divestitures | 50 | 412 | |||||

| Net (gain)/loss on disposal of assets | 412 | — | |||||

| Gain from insurance recoveries | — | (1,634 | ) | ||||

| Changes in assets and liabilities, net of effects of acquisitions and divestitures: | |||||||

| Accounts and other receivables | (16,925 | ) | (4,919 | ) | |||

| Inventories | (4,220 | ) | (5,188 | ) | |||

| Income taxes recoverable/payable | (603 | ) | (4,095 | ) | |||

| Prepaid expenses and other | 129 | (514 | ) | ||||

| Accounts payable and accrued expenses | 8,674 | 4,857 | |||||

| Pension and postretirement benefit plan contributions | (4,642 | ) | (7,143 | ) | |||

| Other, net | 2,093 | 2,818 | |||||

| Net cash provided by operating activities | 53,511 | 34,547 | |||||

| Cash flows from investing activities: | |||||||

| Capital expenditures | (37,245 | ) | (30,912 | ) | |||

| Acquisition | (87,110 | ) | — | ||||

| Proceeds from the sale of assets and other | 121 | 1,399 | |||||

| Net cash used in investing activities | (124,234 | ) | (29,513 | ) | |||

| Cash flows from financing activities: | |||||||

| Borrowings | 173,250 | 61,000 | |||||

| Debt principal payments | (91,250 | ) | (73,250 | ) | |||

| Dividends paid | (10,901 | ) | (10,834 | ) | |||

| Debt financing costs | — | (2,509 | ) | ||||

| Proceeds from exercise of stock options and other | 695 | 1,948 | |||||

| Net cash provided by (used in) financing activities | 71,794 | (23,645 | ) | ||||

| Effect of exchange rate changes on cash | 1,268 | 2,811 | |||||

| Increase (decrease) in cash and cash equivalents | 2,339 | (15,800 | ) | ||||

| Cash and cash equivalents at beginning of period | 29,511 | 44,156 | |||||

| Cash and cash equivalents at end of period | $ | 31,850 | $ | 28,356 | |||

| Three Months Ended March 31, | |||||||||||

| 2024 | 2023 | ||||||||||

| Cash flows from operating activities: | |||||||||||

| Net income (loss) | $ | 3,288 | $ | (1,009) | |||||||

| Adjustments for noncash items: | |||||||||||

| Depreciation | 6,252 | 6,340 | |||||||||

| Amortization of identifiable intangibles | 464 | 503 | |||||||||

| Reduction of right-of-use lease asset | 610 | 551 | |||||||||

| Deferred income taxes | 623 | 411 | |||||||||

| Accrued pension and post-retirement benefits | 54 | 3,418 | |||||||||

| Stock-based compensation expense | 686 | 186 | |||||||||

| Gain on investment in kaléo | — | (262) | |||||||||

| Changes in assets and liabilities: | |||||||||||

| Accounts and other receivables | (5,337) | (4,320) | |||||||||

| Inventories | (5,481) | 14,840 | |||||||||

| Income taxes recoverable/payable | (580) | (1,156) | |||||||||

| Prepaid expenses and other | 1,890 | 1,816 | |||||||||

| Accounts payable and accrued expenses | (10,306) | (28,977) | |||||||||

| Lease liability | (689) | (558) | |||||||||

| Pension and postretirement benefit plan contributions | (158) | (154) | |||||||||

| Other, net | 965 | (737) | |||||||||

| Net cash provided by (used in) operating activities | (7,719) | (9,108) | |||||||||

| Cash flows from investing activities: | |||||||||||

| Capital expenditures | (2,461) | (9,025) | |||||||||

| Proceeds from the sale of kaléo | — | 262 | |||||||||

| Proceeds from the sale of assets | 83 | — | |||||||||

| Net cash provided by (used in) investing activities | (2,378) | (8,763) | |||||||||

| Cash flows from financing activities: | |||||||||||

| Borrowings | 179,248 | 37,250 | |||||||||

| Debt principal payments | (177,240) | (19,250) | |||||||||

| Dividends paid | — | (4,419) | |||||||||

| Net cash provided by (used in) financing activities | 2,008 | 13,581 | |||||||||

| Effect of exchange rate changes on cash | (574) | 83 | |||||||||

| Increase (decrease) in cash, cash equivalents and restricted cash | (8,663) | (4,207) | |||||||||

| Cash, cash equivalents and restricted cash at beginning of period | 13,455 | 19,232 | |||||||||

| Cash, cash equivalents and restricted cash at end of period | $ | 4,792 | $ | 15,025 | |||||||

See accompanying notes to the condensed consolidated financial statements.

5

Tredegar Corporation

Condensed Consolidated StatementStatements of Shareholders’ Equity

(In Thousands, Except Share and Per Share Data)

(Unaudited)

The following summarizes the changes in shareholders’ equity for the three month period ended March 31, 2024:

Accumulated Other Comprehensive Income (Loss) | |||||||||||||||||||||||||||

Common Stock | Retained Earnings | Trust for Savings Restoration Plan | Foreign Currency Translation | Gain (Loss) on Derivative Financial Instruments | Pension & Other Post-retirement Benefit Adjust. | Total Shareholders’ Equity | |||||||||||||||||||||

| Balance at January 1, 2017 | $ | 32,007 | $ | 463,507 | $ | (1,497 | ) | $ | (93,970 | ) | $ | 863 | $ | (90,127 | ) | $ | 310,783 | ||||||||||

| Net income | — | 56,180 | — | — | — | — | 56,180 | ||||||||||||||||||||

| Other comprehensive income (loss): | |||||||||||||||||||||||||||

| Foreign currency translation adjustment (net of tax of $481) | — | — | — | 9,817 | — | — | 9,817 | ||||||||||||||||||||

| Derivative financial instruments adjustment (net of tax of $162) | — | — | — | — | 288 | — | 288 | ||||||||||||||||||||

| Amortization of prior service costs and net gains or losses (net of tax of $3,279) | — | — | — | — | — | 5,754 | 5,754 | ||||||||||||||||||||

| Cash dividends declared ($0.33 per share) | — | (10,901 | ) | — | — | — | — | (10,901 | ) | ||||||||||||||||||

| Stock-based compensation expense | 1,298 | — | — | — | — | — | 1,298 | ||||||||||||||||||||

| Issued upon exercise of stock options & other | 695 | — | — | — | — | — | 695 | ||||||||||||||||||||

| Cumulative effect adjustment for adoption of stock-based comp accounting guidance | 27 | (27 | ) | — | — | — | — | — | |||||||||||||||||||

| Tredegar common stock purchased by trust for savings restoration plan | — | 23 | (23 | ) | — | — | — | — | |||||||||||||||||||

| Balance at September 30, 2017 | $ | 34,027 | $ | 508,782 | $ | (1,520 | ) | $ | (84,153 | ) | $ | 1,151 | $ | (84,373 | ) | $ | 373,914 | ||||||||||

| Common Stock | Retained Earnings | Trust for Savings Restoration Plan | Accumulated Other Comprehensive Income (Loss) | Total Shareholders’ Equity | |||||||||||||||||||||||||

| Balance January 1, 2024 | $ | 61,606 | $ | 177,977 | $ | (2,233) | $ | (81,697) | $ | 155,653 | |||||||||||||||||||

| Net income (loss) | — | 3,288 | — | — | 3,288 | ||||||||||||||||||||||||

| Foreign currency translation adjustment | — | — | — | (1,948) | (1,948) | ||||||||||||||||||||||||

| Derivative financial instruments adjustment | — | — | — | (504) | (504) | ||||||||||||||||||||||||

| Amortization of prior service costs and net gains or losses | — | — | — | (27) | (27) | ||||||||||||||||||||||||

| Stock-based compensation expense | 579 | — | — | — | 579 | ||||||||||||||||||||||||

| Repurchase of employee common stock for tax withholdings | (226) | — | — | — | (226) | ||||||||||||||||||||||||

| Balance March 31, 2024 | $ | 61,959 | $ | 181,265 | $ | (2,233) | $ | (84,176) | $ | 156,815 | |||||||||||||||||||

The following summarizes the changes in shareholders’ equity for the three month period ended March 31, 2023:

| Common Stock | Retained Earnings | Trust for Savings Restoration Plan | Accumulated Other Comprehensive Income (Loss) | Total Shareholders’ Equity | |||||||||||||||||||||||||

| Balance at January 1, 2023 | $ | 58,824 | $ | 292,721 | $ | (2,188) | $ | (147,595) | $ | 201,762 | |||||||||||||||||||

| Net income (loss) | — | (1,009) | — | — | (1,009) | ||||||||||||||||||||||||

| Foreign currency translation adjustment | — | — | — | 1,120 | 1,120 | ||||||||||||||||||||||||

| Derivative financial instruments adjustment | — | — | — | 1,269 | 1,269 | ||||||||||||||||||||||||

| Amortization of prior service costs and net gains or losses | — | — | — | 2,287 | 2,287 | ||||||||||||||||||||||||

| Cash dividends declared ($0.13 per share) | — | (4,419) | — | — | (4,419) | ||||||||||||||||||||||||

| Stock-based compensation expense | 853 | — | — | — | 853 | ||||||||||||||||||||||||

| Repurchase of employee common stock for tax withholdings | (254) | (254) | |||||||||||||||||||||||||||

| Tredegar common stock purchased by trust for savings restoration plan | — | 15 | (15) | — | — | ||||||||||||||||||||||||

| Balance at March 31, 2023 | $ | 59,423 | $ | 287,308 | $ | (2,203) | $ | (142,919) | $ | 201,609 | |||||||||||||||||||

See accompanying notes to the condensed consolidated financial statements.

6

TREDEGAR CORPORATION

NOTES TO THE CONDENSED CONSOLIDATED INTERIM FINANCIAL STATEMENTS

(Unaudited)

1. BASIS OF PRESENTATION In the opinion of management, the accompanying condensed consolidated financial statements of Tredegar Corporation and its subsidiaries (“Tredegar,” “the Company,” “we,” “us” or “our”) contain all adjustments necessary to state fairly, in all material respects, Tredegar’s condensed consolidated financial position as of March 31, 2024, the condensed consolidated results of operations for the three months ended March 31, 2024 and 2023, the condensed consolidated cash flows for the three months ended March 31, 2024 and 2023, and the condensed consolidated changes in shareholders’ equity for the three months ended March 31, 2024 and 2023, in accordance with U.S. generally accepted accounting principles (“GAAP”). All such adjustments, unless otherwise detailed in the notes to the condensed consolidated |

The Company operates on a calendar fiscal year except for the Aluminum Extrusions segment, which operates on a 52/53-week fiscal year basis. As such, the fiscal thirdfirst quarter for 20172024 and 20162023 for this segment references 13-week periods ended September 24, 2017March 31, 2024 and September 25, 2016,March 26, 2023, respectively. The Company does not believe the impact of reporting the results of this segment as stated above is material to the consolidated financial results.

The Company may fund or receive cash from the Aluminum Extrusions segment based on Aluminum Extrusion’s cash flows from operations during the intervening period from Aluminum Extrusion’s fiscal quarter end and the Company’s fiscal quarter end.

The condensed consolidated financial position datastatements as of December 31, 20162023 that is included herein was derived from the audited consolidated financial statements provided in the Company’s Annual Report on Form 10-K for the year ended December 31, 20162023 (“20162023 Form 10-K”) but does not include all disclosures required by United States generally accepted accounting principles (“GAAP”).GAAP. These financial statements should be read in conjunction with the audited consolidated financial statements and related notes included in the Company’s 20162023 Form 10-K.

The results of operations for the three and nine months ended September 30, 2017,March 31, 2024, are not necessarily indicative of the results to be expected for the full year. Certain prior year balances

Sale of Flexible Packaging Films

On September 1, 2023, the Company announced that it had entered into a definitive agreement to sell its Flexible Packaging Films business (also referred to as "Terphane") to Oben Group (the “Contingent Terphane Sale”). Completion of the sale is contingent upon the satisfaction of customary closing conditions, including the receipt of certain competition filing approvals by authorities in Brazil and Colombia. On October 27, 2023, the Company filed the requisite competition forms with the Administrative Council for Economic Defense (“CADE”) in Brazil. The regulatory review process is ongoing and in line with the Company’s expectations. CADE’s maximum deadline for completing its review is no later than November 18, 2024. The merger review regarding the transaction was cleared by the Colombian authority in early February 2024.

Closure of PE Films Technical Center

In August 2023, the Company adopted a plan to close the PE Films technical center in Richmond, VA and reduce its efforts to develop and sell films supporting the semiconductor market. Future research & development activities for PE Films will be performed at the production facility in Pottsville, PA. PE Films continues to have been reclassifiednew business opportunities primarily relating to conformsurface protection films that protect components of flat panel and flexible displays. All activities ceased at the PE Films technical center in Richmond, VA as of the end of the first quarter of 2024. The Company recognized expense incurred through March 31, 2024 associated with current year presentation (see Note 13the exit activities of $0.2 million for additional detail)building closure costs. In addition, the Company recognized a non-cash loss on the lease abandonment ($0.3 million).

7

Supply Chain Financing

Accounting standards not yet adopted

In October 2023, the Financial Accounting Standards Board ("FASB") issued Accounting Standards Update ("ASU") 2023-06 to amend various paragraphs in the westernAccounting Standards Codification ("ASC") to primarily reflect the issuance of U.S., designs Securities and manufactures a wide rangeExchange Commission ("SEC") Staff Bulletin No. 33-10532. ASU 2023-06 will impact various disclosure areas, including the statement of extruded aluminum products, including branded flooring trimscash flows, accounting changes and TSLOTSTM, as well as OEM (original equipment manufacturer) components for truck grills, solar panels, fitness equipmenterror corrections, earnings per share, debt, equity, derivatives, and other applications. As a resulttransfers of financial assets. The amendments in this transaction, Futura is now a wholly-owned subsidiary of the William L. Bonnell Company, Inc. (which is a wholly-owned subsidiary of Tredegar) and operates as a division of Bonnell Aluminum, and its results of operations are included in Tredegar’s consolidated financial statements fromASU 2023-06 will be effective on the date of acquisition.

| (in Thousands) | |||

| Accounts receivable | $ | 6,680 | |

| Inventories | 10,342 | ||

| Prepaid expenses and other current assets | 240 | ||

| Property, plant & equipment | 32,662 | ||

| Identifiable intangible assets: | |||

| Customer relationships | 24,000 | ||

| Trade names | 6,700 | ||

| Trade payables & accrued expenses | (8,135 | ) | |

| Total identifiable net assets | 72,489 | ||

| Adjusted Net Purchase Price | 82,860 | ||

| Goodwill | $ | 10,371 | |

In November 2023, the FASB issued ASU 2023-07 to improve reportable segment disclosure and requirements, primarily through the enhanced disclosures about significant segment expenses. ASU 2023-07 expands public entities’ segment disclosures by requiring disclosure of significant segment expenses that are regularly provided to the chief operating decision maker ("CODM") and included within each reported measure of segment profit or loss, an amount and description of its strong name recognitioncomposition for other segment items, and competitive advantageinterim disclosures of a reportable segment’s profit or loss and assets. This ASU is effective for fiscal years beginning after December 15, 2023 and interim period beginning after December 15, 2024, with early adoption permitted. The amendments in this ASU are to be applied retrospectively to all prior periods presented in the financial statements. The Company is currently evaluating the impact of this standard on our consolidated financial statements and related disclosures.

In December 2023, the FASB issued ASU 2023-09 to improve the income tax disclosures related to the rate reconciliation and income taxes paid information and to improve the effectiveness of income tax disclosures. The amendments in this ASU will require the Company to disclose specified additional information in its target markets.

2. ACCOUNTS AND OTHER RECEIVABLES

As of March 31, 2024 and December 31, 2023, accounts and other receivables, net include the following:

| (In thousands) | March 31, 2024 | December 31, 2023 | |||||||||

| Customer receivables | $ | 73,333 | $ | 67,183 | |||||||

| Other receivables | 1,754 | 3,056 | |||||||||

| Total accounts and other receivables | 75,087 | 70,239 | |||||||||

| Less: Allowance for bad debts | (2,055) | (2,301) | |||||||||

| Total accounts and other receivables, net | $ | 73,032 | $ | 67,938 | |||||||

3. INVENTORIES

The components of inventories are as iffollows:

| (In thousands) | March 31, 2024 | December 31, 2023 | |||||||||

| Finished goods | $ | 28,939 | $ | 29,821 | |||||||

| Work-in-process | 9,835 | 7,830 | |||||||||

| Raw materials | 25,182 | 21,939 | |||||||||

| Stores, supplies and other | 22,866 | 22,447 | |||||||||

| Total | $ | 86,822 | $ | 82,037 | |||||||

8

4. PENSION AND OTHER POSTRETIREMENT BENEFITS

Tredegar sponsored a noncontributory defined benefit (pension) plan covering certain current and former U.S. employees. As of January 31, 2018, the acquisitionplan no longer accrued benefits associated with crediting employees for service, thereby freezing all future benefits under the plan. On February 10, 2022, Tredegar announced the initiation of Futura had been consummated ata process to terminate and settle its frozen defined benefit pension plan through lump sum distributions and the beginningpurchase of 2016,annuity contracts. On November 3, 2023, the pension plan termination and is not necessarily indicative of the Company’s financial performance if the acquisition had actually been consummated as of that date, or of future performance. The supplemental unaudited pro forma measures for the three and nine months ended September 30, 2017 and 2016 are presented below:

| Tredegar Pro Forma Results with Futura Acquisition | Three Months Ended | Nine Months Ended | |||||||||||||

| September 30, | September 30, | ||||||||||||||

| (In Thousands, Except Per Share Data) | 2017 | 2016 | 2017 | 2016 | |||||||||||

| Sales | $ | 247,121 | $ | 228,176 | $ | 722,505 | $ | 681,686 | |||||||

| Net income | $ | 8,274 | $ | 13,225 | $ | 55,835 | $ | 25,559 | |||||||

| Earnings per share: | |||||||||||||||

| Basic | $ | 0.25 | $ | 0.40 | $ | 1.69 | $ | 0.78 | |||||||

| Diluted | $ | 0.25 | $ | 0.40 | $ | 1.69 | $ | 0.78 | |||||||

Tredegar also has a non-qualified supplemental pension plan covering certain employees. Effective December 31, 2005, further participation in this plan was terminated and benefit accruals for existing participants were frozen. Pension expense recognized for this plan was immaterial in the three months ended March 31, 2024 and 2023. This information has been included in the pension benefit table below.

The components of net periodic benefit cost for the Company applied at an annual rate of 3.0% to the $87.0 million Initial Cash Funding, minus (v) the pro forma pre-acquisition period income taxes applied at a rate of 39.1% to the pro forma pre-acquisition earnings before income taxes computed from items (ii) through (iv).

| Pension Benefits | Other Post-Retirement Benefits | ||||||||||||||||||||||

| Three Months Ended March 31, | Three Months Ended March 31, | ||||||||||||||||||||||

| (In thousands) | 2024 | 2023 | 2024 | 2023 | |||||||||||||||||||

| Service cost | $ | — | $ | — | $ | 3 | $ | 3 | |||||||||||||||

| Interest cost | 19 | 3,027 | 67 | 71 | |||||||||||||||||||

| Expected return on plan assets | — | (2,607) | — | — | |||||||||||||||||||

| Amortization of prior service costs, (gains) losses and net transition asset | 5 | 2,983 | (40) | (59) | |||||||||||||||||||

| Net periodic benefit cost | $ | 24 | $ | 3,403 | $ | 30 | $ | 15 | |||||||||||||||

Pension and other postretirement liabilities were $7.2 million and $7.3 million at March 31, 2024 and December 31, 2023, respectively ($0.6 million and $0.7 million included in “Accrued expenses” at March 31, 2024 and December 31, 2023, respectively, with the remainder included in “Pension and other postretirement benefit obligations, net” in the condensed consolidated balance sheets).

| (In Thousands) | Severance (a) | Asset Impairments | Other (b) | Total | |||||||||||

| Balance at January 1, 2017 | $ | 1,854 | $ | — | $ | 554 | $ | 2,408 | |||||||

| Changes in 2017: | |||||||||||||||

| Charges | 300 | 50 | 303 | 653 | |||||||||||

| Cash spent | (1,068 | ) | — | (307 | ) | (1,375 | ) | ||||||||

| Charges against assets | — | (50 | ) | — | (50 | ) | |||||||||

| Balance at September 30, 2017 | $ | 1,086 | $ | — | $ | 550 | $ | 1,636 | |||||||

(a) Severance primarily includes severance payments associated with the consolidation of North American PE Films manufacturing facilities. (b) Other primarily includes other shutdown-related costs associated with the shutdown and sale of the Company’s aluminum extrusions manufacturing facility in Kentland, Indiana. | |||||||||||||||

5. EARNINGS PER SHARE

Basic earnings per share is computed by dividing net income (loss) by the restructuring were $1.4 million inweighted average number of shares of common stock outstanding. Diluted earnings per share is computed by dividing net income (loss) by the first nine months of 2017, which includes capital expenditures of $0.1 million. Total cash expenditures for the project since inception were $15.5 million, which includes $11.2 million for capital expenditures. Additional cash payments for remaining accrued costs of approximately $1 million are expected to be paid within the next 12 months.

| September 30, | December 31, | |||||||

| (In Thousands) | 2017 | 2016 | ||||||

| Finished goods | $ | 21,442 | $ | 16,215 | ||||

| Work-in-process | 10,695 | 8,590 | ||||||

| Raw materials | 32,061 | 23,733 | ||||||

| Stores, supplies and other | 18,228 | 17,531 | ||||||

| Total | $ | 82,426 | $ | 66,069 | ||||

| Three Months Ended | Nine Months Ended | ||||||||||

| September 30, | September 30, | ||||||||||

| (In Thousands) | 2017 | 2016 | 2017 | 2016 | |||||||

| Weighted average shares outstanding used to compute basic earnings per share | 32,954 | 32,818 | 32,945 | 32,730 | |||||||

| Incremental dilutive shares attributable to stock options and restricted stock | — | 10 | 7 | 3 | |||||||

| Shares used to compute diluted earnings per share | 32,954 | 32,828 | 32,952 | 32,733 | |||||||

| Three Months Ended March 31, | |||||||||||||||||||||||

| (In thousands) | 2024 | 2023 | |||||||||||||||||||||

| Weighted average shares outstanding used to compute basic earnings per share | 34,323 | 33,895 | |||||||||||||||||||||

| Incremental dilutive shares attributable to stock options and restricted stock | — | — | |||||||||||||||||||||

| Shares used to compute diluted earnings per share | 34,323 | 33,895 | |||||||||||||||||||||

Incremental shares attributable to stock options and restricted stock are computed under the treasury stock method using the average market price during the related period. ForAverage out-of-the-money options to purchase shares that were excluded from the calculation of incremental shares attributable to stock options and restricted stock were 2,870,670 for the three and nine months ended September 30, 2017,March 31, 2024. If the Company had reported net income for the three months ended March 31, 2023, the average out-of-the-money options to purchase shares that were excluded from the calculation of incremental shares attributable to stock options and restricted stock were 479,651 and 386,729, respectively. For the three and nine months ended September 30, 2016, average out-of-the-money options to purchase shares that were excluded from the calculation of incremental shares attributable to stock options and restricted stock were 493,119 and 643,010, respectively.would have been 2,645,365.

9

| (In Thousands) | Foreign currency translation adjustment | Gain (loss) on derivative financial instruments | Pension and other post-retirement benefit adjustments | Total | |||||||||||

| Beginning balance, January 1, 2017 | $ | (93,970 | ) | $ | 863 | $ | (90,127 | ) | $ | (183,234 | ) | ||||

| Other comprehensive income (loss) before reclassifications | 9,817 | 817 | — | 10,634 | |||||||||||

| Amounts reclassified from accumulated other comprehensive income (loss) | — | (529 | ) | 5,754 | 5,225 | ||||||||||

| Net other comprehensive income (loss) - current period | 9,817 | 288 | 5,754 | 15,859 | |||||||||||

| Ending balance, September 30, 2017 | $ | (84,153 | ) | $ | 1,151 | $ | (84,373 | ) | $ | (167,375 | ) | ||||

6. ACCUMULATED OTHER COMPREHENSIVE INCOME (LOSS)

The following table summarizes the after-tax changes in accumulated other comprehensive income (loss) by component for the ninethree months ended September 30, 2016:March 31, 2024.

| (In thousands) | Foreign Currency Translation | Gain (Loss) on Derivative Financial Instruments | Pension & Other Postretirement Benefit Adjust | Total Accumulated Other Comprehensive Income (Loss) | |||||||||||||||||||

| Balance at January 1, 2024 | $ | (83,037) | $ | 801 | $ | 539 | $ | (81,697) | |||||||||||||||

| Other comprehensive income (loss) | (1,727) | 282 | — | (1,445) | |||||||||||||||||||

| Income tax (expense) benefit | (221) | (112) | — | (333) | |||||||||||||||||||

| Other comprehensive income (loss), net of tax | (1,948) | 170 | — | (1,778) | |||||||||||||||||||

| Reclassification adjustment to net income (loss) | — | (927) | (35) | (962) | |||||||||||||||||||

| Income tax (expense) benefit | — | 253 | 8 | 261 | |||||||||||||||||||

| Reclassification adjustment to net income (loss), net of tax | — | (674) | (27) | (701) | |||||||||||||||||||

| Other comprehensive income (loss), net of tax | (1,948) | (504) | (27) | (2,479) | |||||||||||||||||||

| Balance at March 31, 2024 | $ | (84,985) | $ | 297 | $ | 512 | $ | (84,176) | |||||||||||||||

| (In Thousands) | Foreign currency translation adjustment | Gain (loss) on derivative financial instruments | Pension and other post-retirement benefit adjustments | Total | |||||||||||

| Beginning balance, January 1, 2016 | $ | (112,807 | ) | $ | (373 | ) | $ | (95,539 | ) | $ | (208,719 | ) | |||

| Other comprehensive income (loss) before reclassifications | 22,929 | (60 | ) | — | 22,869 | ||||||||||

| Amounts reclassified from accumulated other comprehensive income (loss) | — | 1,023 | 6,573 | 7,596 | |||||||||||

| Net other comprehensive income (loss) - current period | 22,929 | 963 | 6,573 | 30,465 | |||||||||||

| Ending balance, September 30, 2016 | $ | (89,878 | ) | $ | 590 | $ | (88,966 | ) | $ | (178,254 | ) | ||||

| (In thousands) | Foreign Currency Translation | Gain (Loss) on Derivative Financial Instruments | Pension & Other Postretirement Benefit Adjust | Total Accumulated Other Comprehensive Income (Loss) | |||||||||||||||||||

| Balance at January 1, 2023 | $ | (86,079) | $ | (2,480) | $ | (59,036) | $ | (147,595) | |||||||||||||||

| Other comprehensive income (loss) | 1,557 | 3,078 | — | 4,635 | |||||||||||||||||||

| Income tax (expense) benefit | (437) | (1,087) | — | (1,524) | |||||||||||||||||||

| Other comprehensive income (loss), net of tax | 1,120 | 1,991 | — | 3,111 | |||||||||||||||||||

| Reclassification adjustment to net income (loss) | — | (973) | 2,924 | 1,951 | |||||||||||||||||||

| Income tax (expense) benefit | — | 251 | (637) | (386) | |||||||||||||||||||

| Reclassification adjustment to net income (loss), net of tax | — | (722) | 2,287 | 1,565 | |||||||||||||||||||

| Other comprehensive income (loss), net of tax | 1,120 | 1,269 | 2,287 | 4,676 | |||||||||||||||||||

| Balance at March 31, 2023 | $ | (84,959) | $ | (1,211) | $ | (56,749) | $ | (142,919) | |||||||||||||||

| (In Thousands) | Amount reclassified from other comprehensive income (loss) | Location of gain (loss) reclassified from accumulated other comprehensive income (loss) to net income (loss) | |||

| Gain (loss) on derivative financial instruments: | |||||

| Aluminum future contracts, before taxes | $ | 231 | Cost of sales | ||

| Foreign currency forward contracts, before taxes | 15 | Cost of sales | |||

| Total, before taxes | 246 | ||||

| Income tax expense (benefit) | 90 | Income taxes | |||

| Total, net of tax | $ | 156 | |||

| Amortization of pension and other post-retirement benefits: | |||||

| Actuarial gain (loss) and prior service costs, before taxes | $ | (2,911 | ) | (a) | |

| Income tax expense (benefit) | (1,057 | ) | Income taxes | ||

| Total, net of tax | $ | (1,854 | ) | ||

| (In Thousands) | Amount reclassified from other comprehensive income (loss) | Location of gain (loss) reclassified from accumulated other comprehensive income (loss) to net income (loss) | |||

| Gain (loss) on derivative financial instruments: | |||||

| Aluminum future contracts, before taxes | $ | 785 | Cost of sales | ||

| Foreign currency forward contracts, before taxes | 46 | Cost of sales | |||

| Total, before taxes | 831 | ||||

| Income tax expense (benefit) | 302 | Income taxes | |||

| Total, net of tax | $ | 529 | |||

| Amortization of pension and other post-retirement benefits: | |||||

| Actuarial gain (loss) and prior service costs, before taxes | $ | (9,033 | ) | (a) | |

| Income tax expense (benefit) | (3,279 | ) | Income taxes | ||

| Total, net of tax | $ | (5,754 | ) | ||

| (In Thousands) | Amount reclassified from other comprehensive income (loss) | Location of gain (loss) reclassified from accumulated other comprehensive income (loss) to net income (loss) | |||

| Gain (loss) on derivative financial instruments: | |||||

| Aluminum future contracts, before taxes | $ | (160 | ) | Cost of sales | |

| Foreign currency forward contracts, before taxes | 15 | Cost of sales | |||

| Total, before taxes | (145 | ) | |||

| Income tax expense (benefit) | (53 | ) | Income taxes | ||

| Total, net of tax | $ | (92 | ) | ||

| Amortization of pension and other post-retirement benefits: | |||||

| Actuarial gain (loss) and prior service costs, before taxes | $ | (3,086 | ) | (a) | |

| Income tax expense (benefit) | (1,120 | ) | Income taxes | ||

| Total, net of tax | $ | (1,966 | ) | ||

| (In Thousands) | Amount reclassified from other comprehensive income (loss) | Location of gain (loss) reclassified from accumulated other comprehensive income (loss) to net income (loss) | |||

| Gain (loss) on derivative financial instruments: | |||||

| Aluminum future contracts, before taxes | $ | (1,669 | ) | Cost of sales | |

| Foreign currency forward contracts, before taxes | 46 | Cost of sales | |||

| Total, before taxes | (1,623 | ) | |||

| Income tax expense (benefit) | (600 | ) | Income taxes | ||

| Total, net of tax | $ | (1,023 | ) | ||

| Amortization of pension and other post-retirement benefits: | |||||

| Actuarial gain (loss) and prior service costs, before taxes | $ | (9,759 | ) | (a) | |

| Income tax expense (benefit) | (3,186 | ) | Income taxes | ||

| Total, net of tax | $ | (6,573 | ) | ||

7. DERIVATIVES

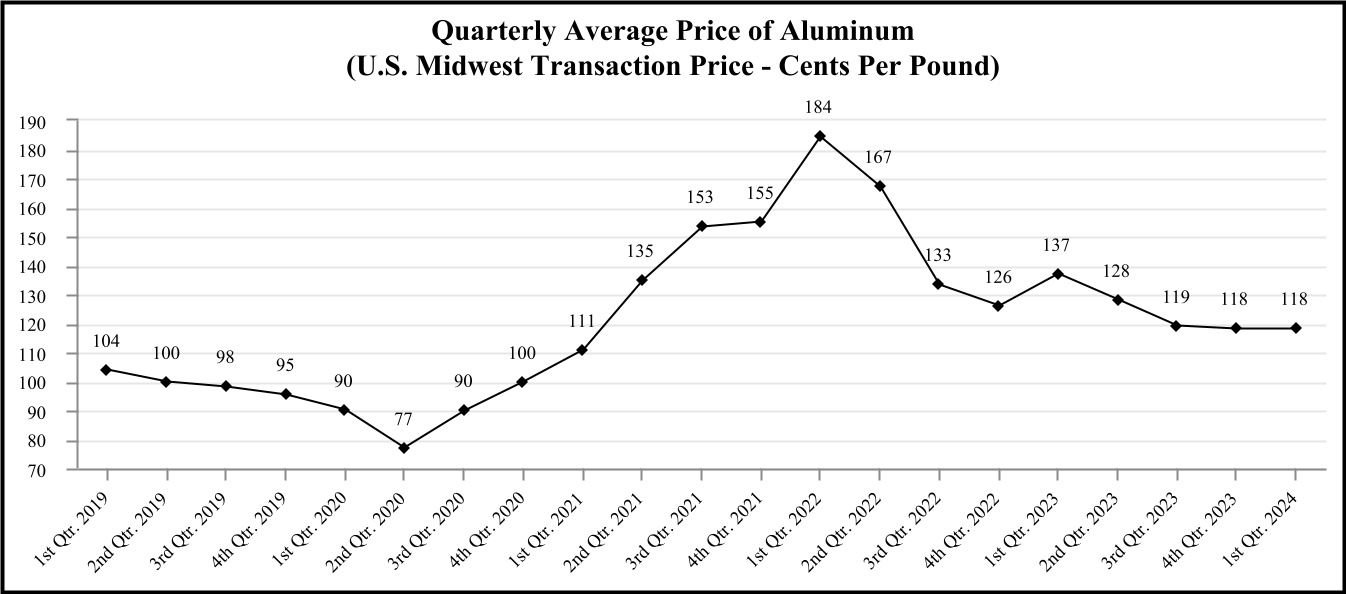

Tredegar uses derivative financial instruments for the purpose of hedging margin exposure from fixed-price forward sales contracts in Aluminum Extrusions and deferred charges”exposure from currency volatility that exists as part of ongoing business operations in the consolidated balance sheets) was $45.0 million at September 30, 2017Flexible Packaging Films. These derivative financial instruments are designated as and $20.2 million at December 31, 2016. An unrealized loss of $1.3 million wasqualify as cash flow hedges and are recognized in the third quarter of 2016. Unrealized gains of $24.8 million and an unrealized loss of $0.2 million were recognized incondensed consolidated balance sheet at fair value. If individual derivative instruments with the first nine months of 2017 and 2016, respectively. There was no change in the estimated fair value from June 30, 2017 to September 30, 2017, as appreciation in value from the discount rate for one quarter was offset bysame counterparty can be settled on a change in the present value of projected cash flows versus prior projections. Unrealized gains (losses) associated with this investment are included in “Other income (expense), net” in the consolidated statements of income and separately stated in the net sales and operating profit by segment table in Note 10.

| Unaudited (In Thousands) | September 30, 2017 | December 31, 2016 | September 30, 2017 | December 31, 2016 | ||||||||||||

| Assets: | Liabilities & Equity: | |||||||||||||||

| Cash & short-term investments | $ | 104,753 | $ | 102,329 | ||||||||||||

| Restricted cash | 31 | 31 | Current liabilities | $ | 85,086 | $ | 50,134 | |||||||||

| Other current assets | 39,059 | 15,391 | Long term debt, net | 138,305 | 143,380 | |||||||||||

| Property & equipment | 10,399 | 13,011 | Other noncurrent liabilities | 807 | 822 | |||||||||||

| Other long-term assets | 494 | 472 | Equity | (69,462 | ) | (63,102 | ) | |||||||||

| Total assets | $ | 154,736 | $ | 131,234 | Total liabilities & equity | $ | 154,736 | $ | 131,234 | |||||||

| Three Months Ended September 30, | Nine Months Ended September 30, | ||||||||||||||

| Unaudited (In Thousands) | 2017 | 2016 | 2017 | 2016 | |||||||||||

| Revenues | $ | 58,822 | $ | 17,377 | $ | 148,761 | $ | 29,347 | |||||||

Cost of goods sold, R&D and SG&A expenses before depreciation & amortization | (52,072 | ) | (19,046 | ) | (137,411 | ) | (50,442 | ) | |||||||

| Depreciation & amortization | (1,245 | ) | (1,278 | ) | (3,723 | ) | (3,477 | ) | |||||||

| Operating income (loss) | 5,505 | (2,947 | ) | 7,627 | (24,572 | ) | |||||||||

| Gain on contract termination | — | — | — | 18,075 | |||||||||||

| Net interest expense and other net | (4,767 | ) | (4,848 | ) | (14,408 | ) | (14,535 | ) | |||||||

| Income tax benefit (expense) | (244 | ) | — | (734 | ) | (8 | ) | ||||||||

| Net income (loss) | $ | 494 | $ | (7,795 | ) | $ | (7,515 | ) | $ | (21,040 | ) | ||||

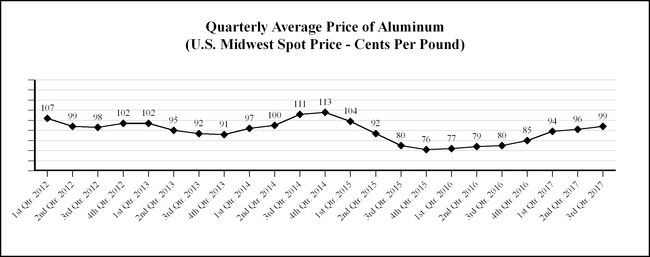

In the normal course of business, Aluminum Extrusions enters into fixed-price forward sales contracts with certaina small subset of its customers for the future sale of fixed quantities of aluminum extrusions at scheduled intervals. In order to hedge margin exposure created from the fixing of future sales prices relative to volatile raw material (aluminum) costs, Aluminum Extrusions enters into a combination of forward purchase commitments and futures contracts to acquire or hedge aluminum, based on the

10

scheduled purchases for the firm sales commitments. The fixed-price firm sales commitments and related hedging instruments generally have durations of not moregenerally no longer than 12 months, and themonths. The notional amount of aluminum futures contracts that hedged future purchases of aluminum to meet fixed-price forward sales contract obligations was $7.1$6.8 million (7.4(5.1 million pounds of aluminum) at September 30, 2017March 31, 2024 and $8.0$7.7 million (9.6(5.6 million pounds of aluminum) at December 31, 2016.2023.

The table below summarizes the location and gross amounts of aluminum futures contract fair values (Level 2) in the condensed consolidated balance sheets as of September 30, 2017March 31, 2024 and December 31, 2016:

| September 30, 2017 | December 31, 2016 | ||||||||||

| (In Thousands) | Balance Sheet Account | Fair Value | Balance Sheet Account | Fair Value | |||||||

| Derivatives Designated as Hedging Instruments | |||||||||||

| Asset derivatives: Aluminum futures contracts | Prepaid expenses and other | $ | 792 | Prepaid expenses and other | $ | 308 | |||||

| Liability derivatives: Aluminum futures contracts | Prepaid expenses and other | $ | (25 | ) | Prepaid expenses and other | $ | (37 | ) | |||

| Net asset (liability) | $ | 767 | $ | 271 | |||||||

| March 31, 2024 | December 31, 2023 | ||||||||||||||||||||||

| (In thousands) | Balance Sheet Account | Fair Value | Balance Sheet Account | Fair Value | |||||||||||||||||||

| Derivatives Designated as Hedging Instruments | |||||||||||||||||||||||

Asset derivatives: Aluminum futures contracts | Other assets | 28 | Other assets | — | |||||||||||||||||||

Liability derivatives: Aluminum futures contracts | Accrued expenses | (318) | Accrued expenses | (483) | |||||||||||||||||||

| Aluminum futures contracts | Other non-current liabilities | — | Other non-current liabilities | (9) | |||||||||||||||||||

| Net asset (liability) | $ | (290) | $ | (492) | |||||||||||||||||||

In the event that a counterparty to an aluminum fixed-price forward sales contract chooses not to take delivery of its aluminum extrusions, the customer is contractually obligated to compensate Aluminum Extrusions for any losses on the related aluminum futures and/or forward contracts through the date of cancellation.

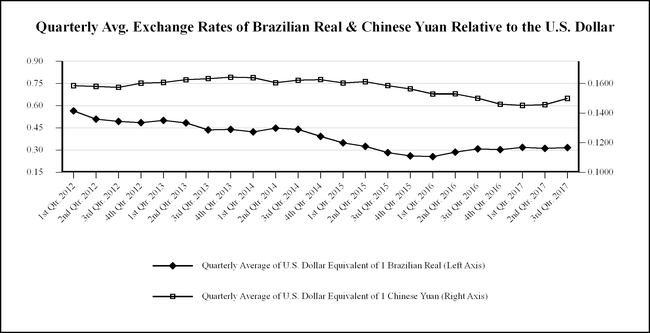

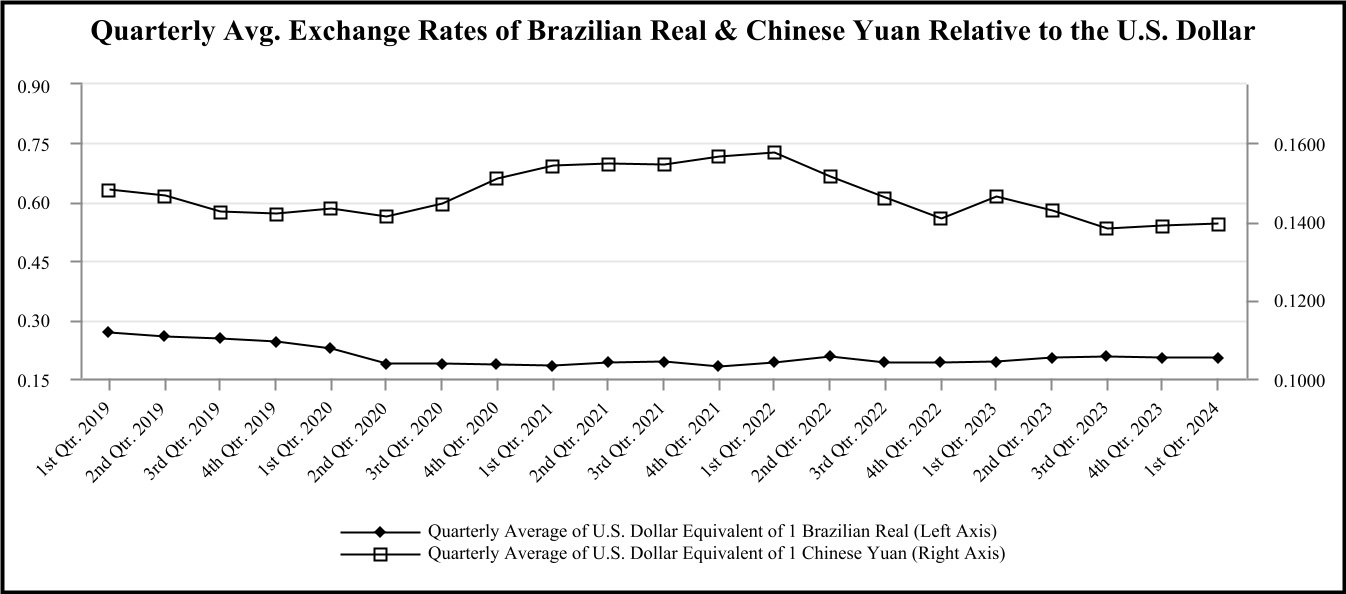

The Company's earnings are exposed to foreign currency exchange risk primarily through the translation of the financial statements of subsidiaries that have a functional currency other than the U.S. Dollar. On September 29, 2017,The Company estimates that the net mismatch translation exposure for the Flexible Packaging FilmsFilm's business unit in Brazil (“Terphane Ltda.”) entered into 15 monthlyof its sales and raw materials quoted or priced in U.S. Dollars and its variable conversion, fixed conversion and sales, general and administrative costs (before depreciation and amortization) quoted or priced in Brazilian Real ("R$") will result in an annual net cost of R$139 million for the full year of 2024.

Terphane Ltda. had the following outstanding foreign exchange average forward rate contracts to purchase Brazilian Real (“R$”) and sell U.S. Dollars covering the period from October 2017 through December 2018. as of March 31, 2024:

| USD Notional Amount (000s) | Average Forward Rate Contracted on USD/BRL | R$ Equivalent Amount (000s) | Applicable Month | Estimated % of Terphane Ltda. R$ Operating Cost Exposure Hedged | ||||||||||

| $1,827 | 5.3373 | R$9,751 | Apr-24 | 84% | ||||||||||

| $1,798 | 5.3588 | R$9,635 | May-24 | 83% | ||||||||||

| $1,812 | 5.3708 | R$9,732 | Jun-24 | 84% | ||||||||||

| $1,804 | 5.3848 | R$9,714 | Jul-24 | 84% | ||||||||||

| $1,806 | 5.4014 | R$9,755 | Aug-24 | 84% | ||||||||||

| $1,857 | 5.4107 | R$10,048 | Sep-24 | 87% | ||||||||||

| $1,851 | 5.4225 | R$10,037 | Oct-24 | 87% | ||||||||||

| $1,837 | 5.4403 | R$9,994 | Nov-24 | 86% | ||||||||||

| $1,801 | 5.4580 | R$9,830 | Dec-24 | 85% | ||||||||||

| $16,393 | 5.3984 | R$88,496 | 84% | |||||||||||

These foreign currency exchange contracts have been designated and qualify as cash flow hedges of Terphane Ltda.'s’s forecasted sales to customers quoted or priced in U.S. Dollars over that period. By changing the currency risk associated with these U.S. Dollar sales, the derivatives have the effect of offsetting operating costs quoted or priced in Brazilian Real and decreasing the net exposure to Brazilian Real in the condensed consolidated statements of income.

11

The aggregate notional amounttable below summarizes the location and gross amounts of open foreign exchange contracts at September 30, 2017 was $18.75 million (R$60.7 million). Thecurrency forward rates contracted andcontract fair values (Level 2) in the related market ratescondensed consolidated balance sheets as of September 30, 2017 were the same,March 31, 2024 and accordingly the fair value of all 15 open forward contracts were zero at that date.December 31, 2023:

| March 31, 2024 | December 31, 2023 | |||||||||||||||||||||||||

| (In thousands) | Balance Sheet Account | Fair Value | Balance Sheet Account | Fair Value | ||||||||||||||||||||||

| Derivatives Designated as Hedging Instruments | ||||||||||||||||||||||||||

Asset derivatives: Foreign currency forward contracts | Prepaid expenses and other | $ | 1,154 | Prepaid expenses and other | $ | 2,050 | ||||||||||||||||||||

| Foreign currency forward contracts | Other assets | — | Other assets | 146 | ||||||||||||||||||||||

Liability derivatives: Foreign currency forward contracts | Accrued expenses | (6) | Other non-current liabilities | — | ||||||||||||||||||||||

| Foreign currency forward contracts | Other non-current liabilities | (2) | Other non-current liabilities | — | ||||||||||||||||||||||

| Net asset (liability) | $ | 1,146 | $ | 2,196 | ||||||||||||||||||||||

These derivative contracts involve elements of market risk that are not reflected on the condensed consolidated balance sheet, including the risk of dealing with counterparties and their ability to meet the terms of the contracts. The counterparties to any forward purchase commitments are major aluminum brokers and suppliers, and the counterparties to any aluminum futures contracts are major financial institutions. Fixed-price forward sales contracts are only made available

to the best and most credit-worthy customers. The counterparties to the Company’s foreign currency cash flow hedge contracts are major financial institutions.

The pre-tax effect on net income (loss) and other comprehensive income (loss) of derivative instruments classified as cash flow hedges and described in the previous paragraphs for the three and nine month periods ended September 30, 2017March 31, 2024 and 20162023 is summarized in the table below:

| (In Thousands) | Cash Flow Derivative Hedges | ||||||||||||||

| Aluminum Futures Contracts | Foreign Currency Forwards | ||||||||||||||

| Three Months Ended September 30, | |||||||||||||||

| 2017 | 2016 | 2017 | 2016 | ||||||||||||

| Amount of pretax gain (loss) recognized in other comprehensive income (loss) | $ | 757 | $ | (230 | ) | $ | — | $ | — | ||||||

| Location of gain (loss) reclassified from accumulated other comprehensive income (loss) into net income (loss) (effective portion) | Cost of sales | Cost of sales | Cost of sales | Cost of sales | |||||||||||

| Amount of pretax gain (loss) reclassified from accumulated other comprehensive income (loss) to net income (loss) (effective portion) | $ | 231 | $ | (160 | ) | $ | 15 | $ | 15 | ||||||

| Aluminum Futures Contracts | Foreign Currency Forwards | ||||||||||||||

| Nine Months Ended September 30, | |||||||||||||||

| 2017 | 2016 | 2017 | 2016 | ||||||||||||

| Amount of pre-tax gain (loss) recognized in other comprehensive income (loss) | $ | 1,281 | $ | (93 | ) | $ | — | $ | — | ||||||

| Location of gain (loss) reclassified from accumulated other comprehensive income (loss) into net income (loss) (effective portion) | Cost of sales | Cost of sales | Cost of sales | Cost of sales | |||||||||||

| Amount of pre-tax gain (loss) reclassified from accumulated other comprehensive income (loss) to net income (loss) (effective portion) | $ | 785 | $ | (1,669 | ) | $ | 46 | $ | 46 | ||||||

| Cash Flow Derivative Hedges | ||||||||||||||||||||||||||||||||

| Three Months Ended March 31, | ||||||||||||||||||||||||||||||||

| Aluminum Futures Contracts | Foreign Currency Forwards | |||||||||||||||||||||||||||||||

| (In thousands) | 2024 | 2023 | 2024 | 2023 | ||||||||||||||||||||||||||||

| Amount of pre-tax gain (loss) recognized in other comprehensive income (loss) | $ | 721 | $ | 1,402 | $ | — | $ | (439) | $ | — | $ | 1,676 | ||||||||||||||||||||

| Location of gain (loss) reclassified from accumulated other comprehensive income (loss) into net income (effective portion) | Cost of goods sold | Cost of goods sold | Cost of goods sold | Selling, general & admin | Cost of goods sold | Selling, general & admin | ||||||||||||||||||||||||||

| Amount of pre-tax gain (loss) reclassified from accumulated other comprehensive income (loss) to net income (effective portion) | $ | 519 | $ | 672 | $ | 15 | $ | 393 | $ | 15 | $ | 286 | ||||||||||||||||||||

As of September 30, 2017,March 31, 2024, the Company expects $0.5$0.4 million of unrealized after-tax gains on aluminum and foreign currency derivative instruments reported in accumulated other comprehensive income (loss) to be reclassified to earnings within the next 12 months. For the three and nine month periods ended September 30, 2017March 31, 2024 and 2016,2023, net gains or losses realized, from previously unrealized net gains or losses on hedges that had been discontinued, were not material.

8. INCOME TAXES

Tredegar recorded tax expense (benefit) of $0.7 million on pre-tax income (loss) of $3.9 million in the first three months of 2024. The effective tax rate in the first three months of 2024 was 16.7% and (48.8)% in the first three months of 2023. The change in effective tax rate was primarily due to pre-tax income in the first quarter of 2024 versus a pre-tax loss in the first three months of 2023.

The components of net periodic benefit costeffective tax rate for the pensionfirst three months of 2024 varies from the 21% statutory rate primarily due to foreign rate differences and other post-retirement benefit programs reflected in consolidated results are shown below:

| Pension Benefits | Other Post-Retirement Benefits | ||||||||||||||

| Three Months Ended September 30, | Three Months Ended September 30, | ||||||||||||||

| (In Thousands) | 2017 | 2016 | 2017 | 2016 | |||||||||||

| Service cost | $ | 29 | $ | 54 | $ | 7 | $ | 8 | |||||||

| Interest cost | 3,103 | 3,263 | 73 | 67 | |||||||||||

| Expected return on plan assets | (3,743 | ) | (4,070 | ) | — | — | |||||||||

| Amortization of prior service costs, gains or losses and net transition asset | 2,996 | 3,135 | (84 | ) | (49 | ) | |||||||||

| Net periodic benefit cost | $ | 2,385 | $ | 2,382 | $ | (4 | ) | $ | 26 | ||||||

| Pension Benefits | Other Post-Retirement Benefits | ||||||||||||||

| Nine Months Ended September 30, | Nine Months Ended September 30, | ||||||||||||||

| 2017 | 2016 | 2017 | 2016 | ||||||||||||

| Service cost | $ | 145 | $ | 178 | $ | 25 | $ | 29 | |||||||

| Interest cost | 9,431 | 9,993 | 226 | 236 | |||||||||||

| Expected return on plan assets | (11,216 | ) | (12,027 | ) | — | — | |||||||||

| Amortization of prior service costs, (gains) losses and net transition asset | 9,241 | 9,903 | (207 | ) | (144 | ) | |||||||||

| Net periodic benefit cost | $ | 7,601 | $ | 8,047 | $ | 44 | $ | 121 | |||||||

| Three Months Ended September 30, | Nine Months Ended September 30, | ||||||||||||||

| (In Thousands) | 2017 | 2016 | 2017 | 2016 | |||||||||||

| Net Sales | |||||||||||||||

| PE Films | $ | 89,723 | $ | 82,179 | $ | 265,773 | $ | 251,473 | |||||||

| Flexible Packaging Films | 26,628 | 27,303 | 79,925 | 80,888 | |||||||||||

| Aluminum Extrusions | 122,149 | 91,067 | 344,956 | 269,987 | |||||||||||

| Total net sales | 238,500 | 200,549 | 690,654 | 602,348 | |||||||||||

| Add back freight | 8,621 | 7,153 | 24,840 | 21,221 | |||||||||||

| Sales as shown in the Consolidated Statements of Income | $ | 247,121 | $ | 207,702 | $ | 715,494 | $ | 623,569 | |||||||

| Operating Profit (Loss) | |||||||||||||||

| PE Films: | |||||||||||||||

| Ongoing operations | $ | 11,251 | $ | 9,011 | $ | 30,965 | $ | 23,564 | |||||||

| Plant shutdowns, asset impairments, restructurings and other | (919 | ) | (1,187 | ) | (3,890 | ) | (3,678 | ) | |||||||

| Flexible Packaging Films: | |||||||||||||||

| Ongoing operations | (1,074 | ) | 93 | (3,392 | ) | 1,184 | |||||||||

| Plant shutdowns, asset impairments, restructurings and other | — | — | 11,856 | — | |||||||||||

| Aluminum Extrusions: | |||||||||||||||

| Ongoing operations | 12,601 | 9,427 | 34,201 | 27,786 | |||||||||||

| Plant shutdowns, asset impairments, restructurings and other | (377 | ) | 1,405 | (3,147 | ) | 840 | |||||||||

| Total | 21,482 | 18,749 | 66,593 | 49,696 | |||||||||||

| Interest income | 42 | 70 | 171 | 158 | |||||||||||

| Interest expense | 1,757 | 886 | 4,579 | 2,918 | |||||||||||

| Gain (loss) on investment accounted for under fair value method | — | (1,300 | ) | 24,800 | (200 | ) | |||||||||

| Stock option-based compensation costs | 111 | 31 | 153 | 24 | |||||||||||

| Corporate expenses, net | 6,960 | 7,223 | 20,985 | 22,110 | |||||||||||

| Income before income taxes | 12,696 | 9,379 | 65,847 | 24,602 | |||||||||||

| Income taxes | 4,422 | (2,669 | ) | 9,667 | 1,864 | ||||||||||

| Net income | $ | 8,274 | $ | 12,048 | $ | 56,180 | $ | 22,738 | |||||||

| (In Thousands) | September 30, 2017 | December 31, 2016 | |||||

| PE Films | $ | 295,181 | $ | 278,558 | |||

| Flexible Packaging Films | 153,488 | 156,836 | |||||

| Aluminum Extrusions | 268,994 | 147,639 | |||||

| Subtotal | 717,663 | 583,033 | |||||

| General corporate | 62,435 | 38,618 | |||||

| Cash and cash equivalents | 31,850 | 29,511 | |||||

| Total | $ | 811,948 | $ | 651,162 | |||

Percent of Income Before Income Taxes | |||||

| Nine Months Ended September 30, | 2017 | 2016 | |||

| Income tax expense at federal statutory rate | 35.0 | 35.0 | |||

| Foreign rate differences | 1.5 | 1.1 | |||

| State taxes, net of federal income tax benefit | 1.3 | 0.7 | |||

| Changes in estimates related to prior year tax provision | 0.5 | (1.6 | ) | ||

| Non-deductible expenses | 0.5 | 1.6 | |||

| Valuation allowance for foreign operating loss carry-forwards | 0.4 | 0.3 | |||

| Unremitted earnings from foreign operations | 0.2 | (1.1 | ) | ||

| Valuation allowance for capital loss carry-forwards | — | (0.4 | ) | ||

| Income tax contingency accruals and tax settlements | (0.4 | ) | 1.3 | ||

| Remitted earnings from foreign operations | (0.6 | ) | (23.8 | ) | |

| Research and development tax credit | (0.7 | ) | (1.8 | ) | |

| Domestic production activities deduction | (0.9 | ) | (3.8 | ) | |

| Foreign investment write-up | (3.5 | ) | 0.1 | ||

| Settlement of Terphane acquisition escrow | (6.4 | ) | — | ||

| Worthless stock deduction | (12.2 | ) | — | ||

| Effective income tax rate | 14.7 | 7.6 | |||

12

The Brazilian federal statutory income tax rate is a composite of 34.0% (25.0% of income tax and 9.0% of social contribution on income). Terphane Ltda.’s manufacturing facility in Brazil is the beneficiary of certain income tax incentives that allow for a reduction in the statutory Brazilian federal income tax rate to 15.25% levied on the operating profit on certain of its products. The incentives have been granted for a 10-year period, which has afrom the commencement date of January 1, 2015. No benefit was recognized2015 and expiring at the end of 2024.

9. BUSINESS SEGMENTS

The Company’s business segments are Aluminum Extrusions, PE Films, and Flexible Packaging Films. Information by business segment is reported below. There are no accounting transactions between segments and no allocations to segments.

The Company’s reportable segments are based on its method of internal reporting, which is generally segregated by differences in products. Accounting standards for presentation of segments require an approach based on the way the Company organizes the segments for making operating decisions and how the CODM assesses performance. Earnings before interest, taxes, depreciation and amortization ("EBITDA") from these tax incentivesongoing operations is the key profitability measure used by the CODM (Tredegar’s President and Chief Executive Officer) for purposes of assessing financial performance. The Company uses sales less freight (“net sales”) as its measure of revenues from external customers at the segment level. This measure is separately included in the first nine months of 2017 or 2016.

The following table presents net sales and EBITDA from ongoing operations by segment for the utilization of assumed capital losses onthree months ended March 31, 2024 and 2023:

13

| Three Months Ended March 31, | |||||||||||||||||||||||

| (In thousands) | 2024 | 2023 | |||||||||||||||||||||

| Net Sales | |||||||||||||||||||||||

| Aluminum Extrusions | $ | 114,222 | $ | 133,370 | |||||||||||||||||||

| PE Films | 24,735 | 20,182 | |||||||||||||||||||||

| Flexible Packaging Films | 30,113 | 31,527 | |||||||||||||||||||||

| Total net sales | 169,070 | 185,079 | |||||||||||||||||||||

| Add back freight | 6,666 | 6,043 | |||||||||||||||||||||

| Sales as shown in the condensed consolidated statements of income (loss) | $ | 175,736 | $ | 191,122 | |||||||||||||||||||

| EBITDA from Ongoing Operations | |||||||||||||||||||||||

| Aluminum Extrusions: | |||||||||||||||||||||||

| Ongoing operations: | |||||||||||||||||||||||

| EBITDA | $ | 12,540 | $ | 14,638 | |||||||||||||||||||

| Depreciation & amortization | (4,542) | (4,411) | |||||||||||||||||||||

| EBIT | 7,998 | 10,227 | |||||||||||||||||||||

| Plant shutdowns, asset impairments, restructurings and other | (1,167) | (493) | |||||||||||||||||||||

| PE Films: | |||||||||||||||||||||||

| Ongoing operations: | |||||||||||||||||||||||

| EBITDA | 6,904 | 1,849 | |||||||||||||||||||||

| Depreciation & amortization | (1,329) | (1,643) | |||||||||||||||||||||

| EBIT | 5,575 | 206 | |||||||||||||||||||||

| Plant shutdowns, asset impairments, restructurings and other | (504) | 2 | |||||||||||||||||||||

| Flexible Packaging Films: | |||||||||||||||||||||||

| Ongoing operations: | |||||||||||||||||||||||

| EBITDA | 1,963 | 1,350 | |||||||||||||||||||||

| Depreciation & amortization | (751) | (700) | |||||||||||||||||||||

| EBIT | 1,212 | 650 | |||||||||||||||||||||

| Plant shutdowns, asset impairments, restructurings and other | — | (78) | |||||||||||||||||||||

| Total | 13,114 | 10,514 | |||||||||||||||||||||

| Interest income | 22 | 44 | |||||||||||||||||||||

| Interest expense | 3,455 | 2,311 | |||||||||||||||||||||

| Gain on investment in kaleo, Inc. | — | 262 | |||||||||||||||||||||

| Stock option-based compensation costs | — | 231 | |||||||||||||||||||||

| Corporate expenses, net | 5,736 | 8,956 | |||||||||||||||||||||

| Income (loss) before income taxes | 3,945 | (678) | |||||||||||||||||||||

| Income tax expense (benefit) | 657 | 331 | |||||||||||||||||||||

| Net income (loss) | $ | 3,288 | $ | (1,009) | |||||||||||||||||||

The following table presents identifiable assets by segment at March 31, 2024 and December 31, 2023:

| (In thousands) | March 31, 2024 | December 31, 2023 | |||||||||

| Aluminum Extrusions | $ | 264,300 | $ | 255,756 | |||||||

| PE Films | 57,925 | 56,536 | |||||||||

| Flexible Packaging Films | 81,290 | 84,062 | |||||||||

| Subtotal | 403,515 | 396,354 | |||||||||

| General corporate | 34,224 | 36,652 | |||||||||

| Cash, cash equivalents and restricted cash | 4,792 | 13,455 | |||||||||

| Total | $ | 442,531 | $ | 446,461 | |||||||

14

The following tables disaggregate the Company’s revenue by geographic area and product group for the three months ended March 31, 2024 and 2023:

| Net Sales by Geographic Area (a) | |||||||||||||||||||||||

| Three Months Ended March 31, | |||||||||||||||||||||||

| (In thousands) | 2024 | 2023 | |||||||||||||||||||||

| United States | $ | 132,627 | $ | 150,611 | |||||||||||||||||||

| Exports from the United States to: | |||||||||||||||||||||||

| Asia | 8,825 | 5,732 | |||||||||||||||||||||

| Latin America | 1,331 | 1,859 | |||||||||||||||||||||

| Canada | 4,539 | 4,284 | |||||||||||||||||||||

| Europe | 255 | 860 | |||||||||||||||||||||

| Operations outside the United States: | |||||||||||||||||||||||

| Brazil | 21,331 | 21,628 | |||||||||||||||||||||

| Asia | 162 | 105 | |||||||||||||||||||||

| Total | $ | 169,070 | $ | 185,079 | |||||||||||||||||||

| (a) Export sales relate mostly to PE Films. Operations in Brazil relate to Flexible Packaging Films. | |||||||||||||||||||||||

The Company’s facilities in Pottsville, PA (“PV”) and Guangzhou, China (“GZ”) have a tolling arrangement whereby certain investmentssurface protection films are manufactured in GZ for a fee with raw materials supplied from PV that were recognized in prior years. Income taxes in 2016 included the partial reversal of a valuation allowance of $0.1 million relatedare then shipped by GZ directly to the expected limitations on the utilization of assumed capital losses on certain investments. The Company had a valuation allowance for excess capital losses from investments and other related items of $11.2 million at September 30, 2017. Tredegar continues to evaluate opportunities to utilize these loss carryforwards prior to their expiration at various datescustomers principally in the future. As events and circumstances warrant, allowances will be reversed when it is more likely than not that future taxable income will exceed deductible amounts, thereby resultingAsian market, but paid by customers directly to PV. Amounts associated with this intercompany tolling arrangement are reported in the realization of deferred tax assets.

| Net Sales by Product Group | |||||||||||||||||||||||

| Three Months Ended March 31, | |||||||||||||||||||||||

| (In thousands) | 2024 | 2023 | |||||||||||||||||||||

| Aluminum Extrusions: | |||||||||||||||||||||||

| Nonresidential building & construction | $ | 66,347 | $ | 78,629 | |||||||||||||||||||

| Consumer durables | 7,984 | 10,347 | |||||||||||||||||||||

| Automotive | 10,606 | 12,122 | |||||||||||||||||||||

| Residential building & construction | 7,902 | 11,603 | |||||||||||||||||||||

| Electrical | 5,836 | 8,129 | |||||||||||||||||||||

| Machinery & equipment | 12,195 | 10,724 | |||||||||||||||||||||

| Distribution | 3,352 | 1,816 | |||||||||||||||||||||

| Subtotal | 114,222 | 133,370 | |||||||||||||||||||||

| PE Films: | |||||||||||||||||||||||

| Surface protection films | 17,011 | 12,855 | |||||||||||||||||||||

| Overwrap packaging | 7,724 | 7,327 | |||||||||||||||||||||

| Subtotal | 24,735 | 20,182 | |||||||||||||||||||||

| Flexible Packaging Films | 30,113 | 31,527 | |||||||||||||||||||||

| Total | $ | 169,070 | $ | 185,079 | |||||||||||||||||||

10. DEBT

ABL Facility

On December 27, 2023, the Company entered into Amendment No. 3 (the “ABL Facility”) to the Second Amended and Restated Credit Agreement, which provides the Company with a $180 million senior secured asset-based revolving credit facility that will expire on June 30, 2026. On April 16, 2024, the Company entered into Amendment No. 4 (the "Amendment") that, among other items: (i) moves the ABL Adjustment Date (defined below) from March 31, 2025 to September 30, 2025 and (ii) requires weekly reporting of the borrowing base financial covenant. The ABL Facility is secured by substantially all assets of the Company and its domestic subsidiaries, including equity in certain material first-tier foreign subsidiaries. Availability for

15

borrowings under the ABL Facility is governed by a borrowing base, determined by the application of specified advance rates against eligible assets, including a portion of trade accounts receivable, inventory, cash and cash equivalents, owned real properties, and owned machinery and equipment. Upon the earlier of September 30, 2025 or the date the Company receives the proceeds from the sale of Terphane (the “ABL Adjustment Date”), the $180 million ABL Facility will be reduced to $125 million. As of March 31, 2024, availability under the ABL Facility was $22.2 million, after reducing the borrowing base by the aggregate outstanding borrowings of $128.3 million, standby letters of credit of $13.1 million, and the adoptionMinimum Liquidity (as defined in the ABL Facility) financial covenant.

Outstanding borrowings accrue interest at the rates elected by the Company depending on the type of this guidance didloan and denomination of such borrowing. With respect to revolving loans denominated in U.S. Dollars, the Company may elect interest rates at:

•Alternate Base Rate (“ABR”) plus 2.50% before the ABL Adjustment Date and the applicable ABR Spread (as defined in the ABL Facility) after the ABL Adjustment Date are determined in accordance with an excess availability-based pricing grid. ABR is defined, in part, as the greater of (a) the Prime Rate in effect on such day, (b) the Federal Reserve Bank of New York Rate in effect on such day plus ½ of 1% and (c) the Adjusted Term SOFR Rate (defined below) for a one-month period plus 1%; or

•The Adjusted Term Secured Overnight Financing Rate ("SOFR") Rate plus 3.50% before the ABL Adjustment Date and the applicable Term Benchmark Spread (as defined in the ABL Facility) are determined in accordance with an excess availability-based pricing grid after the ABL Adjustment Date. Adjusted Term SOFR Rate is defined as the Term SOFR Rate plus 0.10%, subject to an initial Floor (as defined in the ABL Facility) of 0%.

Interest rate indices for select non-U.S. dollar borrowings, including borrowings denominated in Euro, Pounds Sterling, Swiss Francs and Japanese Yen, remain consistent with the Second Amended and Restated Credit Agreement.

Based upon the quarterly average of daily availability under the ABL Facility, the interest rate pricing grid applicable after the ABL Adjustment Date will be as follows:

| Pricing under the ABL Facility (Basis Points) | |||||||||||

| Quarter Average of Daily Availability | Term Benchmark Spread | ABR Spread | Commitment Fee* | ||||||||

| > 66% of $125 million aggregate commitment | 225.0 | 125.0 | 40.0 | ||||||||

| ≤ 66% but > 33% of $125 million aggregate commitment | 250.0 | 150.0 | 40.0 | ||||||||

| ≤ 33% of $125 million aggregate commitment | 275.0 | 175.0 | 40.0 | ||||||||

*The Commitment Fee before the ABL Adjustment Date and after the ABL Adjustment Date remain the same as reflected in this table. | |||||||||||